Assessing payment mechanisms for Myanmar

|

|

|

- Cathleen Short

- 5 years ago

- Views:

Transcription

1

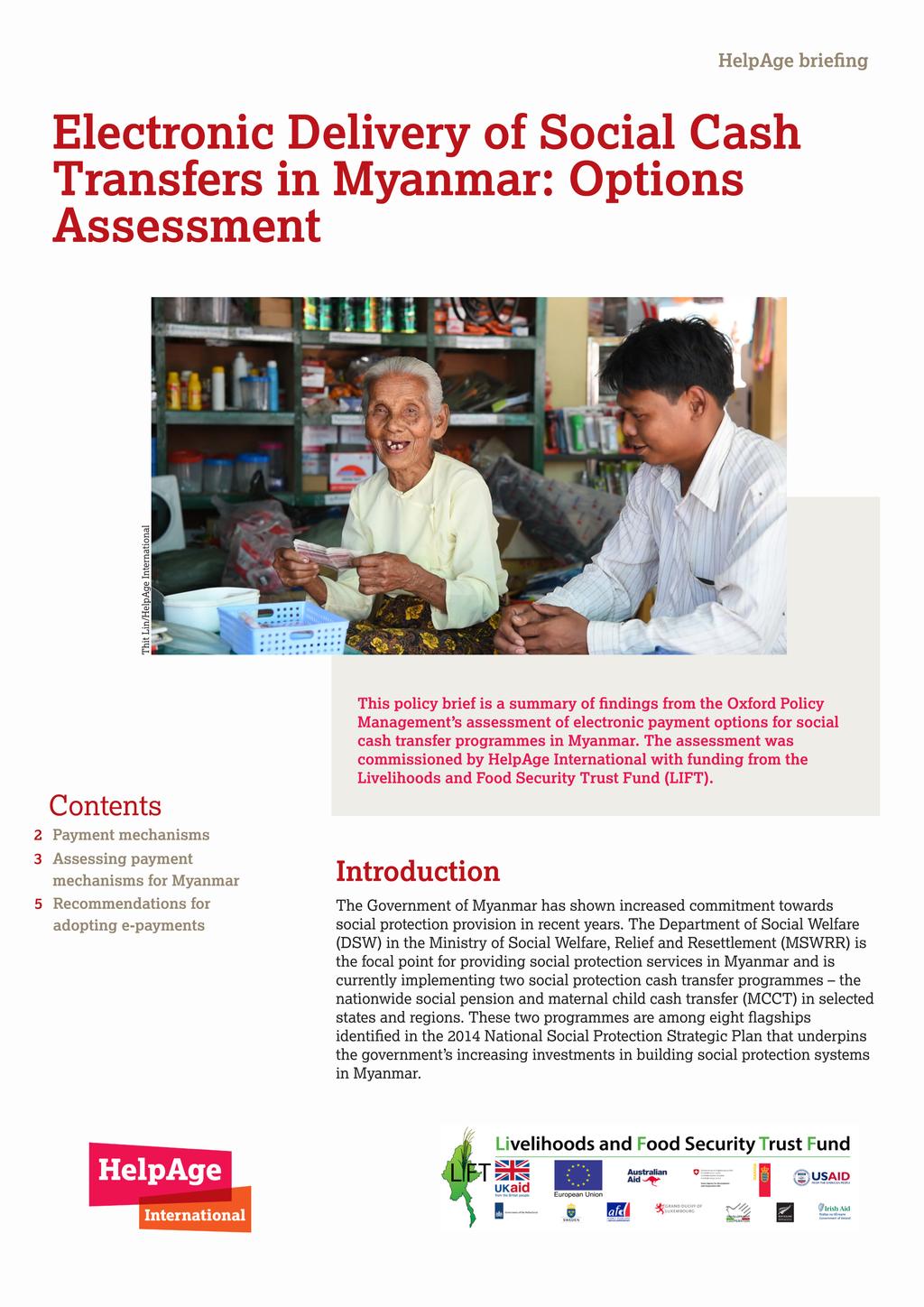

2 Whilst cash transfers are becoming increasingly important in the country, their delivery mechanism typically remains manual physical cash delivered by hand. Many other developing countries now use electronic payment systems to deliver social payments. In recent years, an exponential growth in the coverage and take up of mobile phones in Myanmar, coupled with changes in regulation and increased market competition, have now allowed the possibility of using e-payments for social transfers. Here we assess the feasibility of using e-payments (especially mobile money) to deliver social protection transfers (focussing on the National Social Pension programme). Payment mechanisms The way social protection transfers are paid can affect the impact of the programme and the costs and risks faced by both implementers and recipients. The goal of a payment system is to successfully distribute the correct benefit amount to the right people at the right time and with the right frequency, while minimising costs to both the programme and the recipients. There are several ways to make payments in cash transfer programmes. Different combinations of payment instruments (cash, cards, mobile money, vouchers etc.) can utilise different payment devices (POS, ATMs, mobile phones etc.) to deliver payments at different payment points (mobile vehicles, post offices, agent shops, bank branches etc.). The combination of a specific payment instrument, payment device and payment point can be termed a payment modality or payment mechanism. All payment mechanisms for social protection programmes involve transfer of funds and authorisation at the central level from the Ministry of Finance (or a donor account) to a Programme Administrator (usually a line department in a relevant ministry). The Programme Administrator then provides payment instructions based on programme records or a Management Information System (MIS) to deliver payments to recipients. However, the operationalisation of e-payments often requires contracting an external Payment Service Provider (PSP) to deliver payments and relies on an automated MIS. PSPs are essentially financial services providers and can include banks, microfinance institutions or mobile money operators. It is important to recognise that no payment mechanism is perfect and the adoption of a mechanism to deliver cash payments in social protection programmes is driven by a number of inherent characteristics such as functionality, coverage, interoperability, open versus closed loop systems, cost, and registration and authentication. Thit Lin/HelpAge International 2. Electronic Delivery of Social Cash Transfers in Myanmar: Options Assessment

3 Assessing payment mechanisms for Myanmar This assessment was conducted with specific focus on the National Social Pension Programme that the Department of Social Welfare is currently implementing nationwide in Myanmar, which currently targets everyone aged 90 and older. For implementing the Social Pension programme from beneficiary/recipient identification and registration to delivery of payments to the recipients DSW relies mainly on the General Administration Department (GAD) under the Ministry of Home Affairs. Township GAD offices and ward/ village administrators therefore play a central role in programme delivery. The current processes in beneficiary registration, MIS and payments (payroll generation, payment disbursement and reconciliation) all rely on manual systems and checks. In order to utilise e-payment mechanisms such as mobile money, these systems would need to be strengthened by improving staff capacity, digitising information channels and databases and changing communication flows. Depending on the payment mechanism adopted, and the roles and responsibilities assigned to DSW versus GAD, the flow of funds can be digitised at any administrative level. Thit Lin/HelpAge International Globally, there is a consensus that e-payments are a promising way to deliver cash to beneficiaries with flexibility, speed, reduced costs, reduced leakages in the system, and transparency. 3. Electronic Delivery of Social Cash Transfers in Myanmar: Options Assessment

4 Below, we draw on the adapted Inter-Agency Social Protection 1 criteria framework to assess the feasibility of using mobile money to deliver social pension payments in Myanmar. Enabling environment Accessibility Robustness Integration There are two major Central Bank instructions concerning PSPs: The Mobile Banking Directive (2013) and Mobile Financial Services Regulation (2016). Both allow for various types of transactions (P2B, P2P, G2P etc. 2 ) and require providers to offer wallet-level interoperability. Existing review of evidence and stakeholder interviews indicate that the regulatory environment in Myanmar is conducive to the development and use of e-payments including mobile money. There is no indication of changes to current regulation, although active enforcement of certain aspects such as interoperability is currently weak. The National Social Pension targets the very elderly who are more likely to be immobile and suffer from age-related disability. They may find manual cash payments, handed to recipients in households, more accessible than mobile money. At the same time, disability and mobility are less important considerations if payments are already accessed by proxies and trust between the recipients and proxies is high. In general, the adoption of mobile money for social transfers can be quicker and easier as the general usage of mobile money increases and there is greater adoption of e-payments across the society. Overall, if the National Social Pension expands to include everyone aged 85 years and above, the increase in scale of payments is likely to affect the accessibility of manual cash payments in terms of higher costs to village/ward administrators and poorer accuracy of payroll data. In this instance, mobile money payments could be more accessible provided adequate service coverage at the village level and greater interoperability across Payment Service Providers. The current manual payment mechanism is functional but inadequate in terms of checks and balances on the quality of service delivery and security of payments. Although there are no reported instances of fraud or corruption at the Union (national) level, the current system of grievance redressal, M&E and administrative data management (MIS) does not allow for detection of fraud. Without access to village level data, it is not possible to estimate the existence or prevalence of malpractice in the manual payments process. Nevertheless, there are several ways in which the existing manual system of cash payments can result in leakages and fraud. The use of mobile money to deliver the Social Pension could provide greater security in terms of checks and balances on the payments made to recipients. A regulated mobile money operator will be required to maintain high standards of data security for customers by the Central Bank, but these systems should be audited as well by the DSW. However, the use of mobile money does not alleviate all security concerns. Payment mechanisms for the National Social Pension in particular should focus on immediate need for cash out i.e. withdrawal of the full balance by the recipient. Nevertheless, in theory the use of savings enabled mechanisms can improve financial inclusion of Social Pension recipients. This is more likely in instances where payments are received by proxies. The use of manual cash payments does not enable or encourage savings or use of other financial services. The use of mobile money through e-wallets can enable savings, with higher amounts expected if PSPs are commercial banks and lower amounts if PSPs are mobile money operators. Typically, when social grant recipients are provided with a transaction account, they withdraw the full amount of the transfer in a single transaction. However, the National Social Pension is not a poverty-targeted social protection programme, so the income profile of recipients will vary, making it difficult to anticipate how payments will be used. It is likely that using a savings enabled account in itself may not translate into widespread gains in financial inclusion 1 ISPA, Social Protection Payment Delivery Mechanisms - What Matters Guidance Note (Inter Agency Social Protection Assessments, 2016), 2 P2B: Person-to-business; P2P: Person-to-person; G2P: Government-to-person 4. Electronic Delivery of Social Cash Transfers in Myanmar: Options Assessment

5 Recommendations for adopting e-payments Transitioning from manual cash payments to e-payments presents several challenges for social protection programmes. However, there is consensus that e-payments are a promising way to deliver cash to beneficiaries with flexibility, speed, reduced costs, reduced leakages in the system, and transparency. The transition process normally starts with pilots of e-payments in certain areas, and decisions to scale up are based on the performance of the pilot. During the transition, programmes might retain some payments in cash (especially in remote areas with poor network access), while testing the performance of one or more payment mechanisms in selected areas. A review of global evidence suggests that there are clear gains to be made from switching from manual payment mechanisms to e-payments. However, the case for Myanmar must be assessed based on the country context, the capacity of DSW to implement e-payments, market conditions and other factors. Below, we list some considerations if e-payments are used for government-implemented social protection cash transfers. We focus specifically on the National Social Pension Programme implemented by DSW. 1. Transition to e-payments should be a medium to long term goal. In the short term, DSW should prioritise capacity building, expansion of cash transfer programmes and strengthening internal systems. Last mile delivery challenges will remain in the short term as village level presence of pay agents is not universal. The implementation of cash transfers will continue to require GAD s support at both the township and village/ward level in the short to medium term. It is also crucial to get an accurate understanding of some key social pension programme characteristics before changes are made to the current payment system. More research is also needed to better understand the community level context in which e-payments for cash transfers will operate. DSW can capitalise on market trends towards increasing take-up of e-payments, as well as policy efforts to increase financial inclusion. Thit Lin/HelpAge International 5. Electronic Delivery of Social Cash Transfers in Myanmar: Options Assessment

6 2. E-payments cannot work without strengthening other implementation processes and improving DSW capacity. The use of electronic payments requires strengthening of related processes such as identity verification, MIS, grievance redressal channels and effective monitoring and evaluation at the programme level. Moreover, these systems need to be upgraded with a view to use e-payments in the future. A social protection programme with a paper-based record system cannot move from manual to e-payments. In the same vein, switching to e-payments per se will not eliminate all risks of fraud or error, so a functional grievance redressal mechanism and M&E system need to be in place. Strengthening existing systems and testing new ones require increased capacity, especially to engage with third parties contracted to deliver payments. This includes sufficient capacity within DSW to set out clear terms of reference and requests for proposals, negotiate with Payment Service Providers and liaise with regulatory authorities and other concerned line departments. It also requires capacity to monitor the enforcement of contracts and continuously engage with PSPs throughout the life of the programme. 3. It is likely that a mixed model works best for the social protection programmes, with a mix of manual and e-payments, and potentially multiple service providers. Given the diversity of programme recipients, geography and DSW capacity across Myanmar, it is unlikely that e-payment mechanisms such as mobile money will act as a universal solution. In Myanmar, it is likely that e-payments will be feasible and easier to roll out in urban areas, with manual payments continuing for remote rural areas. In addition to various payment mechanisms, DSW may require different Payment Service Providers if coverage of one PSP is not universal and/or regulatory authorities do not allow monopolisation of the market, or to allow recipients to choose the best service for them. This is likely to add complexity in the implementation of other processes, requiring greater capacity to manage different payment mechanisms and negotiate with different PSPs. However, the need to use multiple PSPs may diminish as interoperability improves. There is increased convergence towards different types of PSPs in Myanmar offering mobile money products with varying degrees of functionality. The starting point for assessing the suitability of these options would be coverage and distribution of cash-out points. 4. Maintain stakeholder commitment, across the board, throughout the transition to e-payments. It is important to consider the priorities of the different stakeholders involved (ministry line departments, programme donors, Payment Service Providers and beneficiaries). There should also be a business case for everyone along the entire chain of stakeholders such as PSPs, pay agents, and village officials. There is increasing competition between PSPs in Myanmar to provide mobile money products. However, currently there are no PSPs with the coverage and scale suitable to deliver nationwide payments, and in all likelihood national coverage will only come through interoperability or aggregators. DSW therefore needs to negotiate carefully with PSPs, as well as regulatory authorities, to ensure that any public-private collaboration is attractive to all parties and results in a more cost-effective solution for the government. DSW would need to involve the Central Bank and Ministry of Planning and Finance at an early stage to discuss the business case for switching to e-payments and the use of one or more private sector PSPs. 6. Electronic Delivery of Social Cash Transfers in Myanmar: Options Assessment

7 5. Prioritise social protection objectives over financial inclusion objectives in the short term. Formal financial inclusion is not a primary objective of the cash transfer programmes in the Myanmar National Social Protection Strategic Plan, so e-payment mechanisms should be savings enabled, rather than savings encouraged. If reliable payments are not prioritised first, the resulting risks could include lack of trust and/or understanding of the new payment system by beneficiaries, which might discourage them to use the system for anything beyond collecting their social cash transfers and, in turn, undermine financial inclusion goals. 6. Adopt an approach which provides choice and drives competition in the long term. In the long term, improved financial inclusion itself can drive the adoption of e-payments in social protection programmes. In an ideal scenario, all recipients of social protection programmes should have access to an account a bank account, e-wallet or other transaction account that should be able to receive payments from the government. Adopting this approach means that social protection recipients are provided with the choice and flexibility of using the Payment Service Providers and products of their choice. It is then up to the government to deliver e-payments to their accounts, negotiating with different PSPs on transaction charges and implementation modalities so that end-line recipients receive the full benefit amount. This approach can also use market competition in a way that allows PSPs to register customers, competitively, and encourage innovation amongst service providers so they can offer better coverage and functionality of their e-products. However, adopting this approach would still necessitate effective enforcement of regulation, strengthening of internal systems at DSW and continuous monitoring and evaluation to ensure the welfare of social protection recipients. 7. Determining cost efficiency of manual versus e-payments is challenging in the short term. Assessing the cost efficiency of various implementation modalities is important for DSW given resource constraints and the need to set policy and budget priorities in the long term. However, at the current stage, assessing the cost efficiency of manual versus e-payments is difficult for a number of reasons. The costs of operationalising e-payments depend on the type of e-payment mechanism that is chosen and the division of roles across DSW, GAD and Payment Service Providers. The user fees and implementation costs currently charged by private sector PSPs will likely change in the future. Furthermore, these costs are negotiated on an individual basis and require ex-ante negotiation. Understanding costs of manual payments is difficult as these are delivered through GAD and budgeting in DSW is not activity based. In comparison to other payment mechanisms, a basic mobile money mechanism generally provides the option of relatively low set-up costs. If DSW decides to use the option of e-wallets, there will be costs associated with helping recipients to register their SIM cards. However, if over-the-counter payments are used, recipients will not need to be registered. Regardless of the type of mobile money product used, there are significant costs associated with training DSW and GAD staff, village/ward officials and recipients. 7. Electronic Delivery of Social Cash Transfers in Myanmar: Options Assessment

8 This policy brief draws on a report titled Options Assessment for Electronic Cash Transfer Delivery, Myanmar, by Farhat, M., Lynn, T.A., For the full report in English please visit HelpAge International is a global network of organisations promoting the right of all older people to lead dignified, healthy and secure lives. HelpAge International Myanmar Country Office No.25/E, Sein Villa, Thiri Mingalar Avenue Street, Ward No.7, Yankin township, Yangon, Myanmar Tel (+95-1) HelpAge International East Asia/Pacific Regional Office 6 Soi 17 Nimmanhemin Road Suthep, Muang, Chiang Mai Thailand Tel: Fax: Registered charity number: Copyright HelpAge International 2018 This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License, Any parts of this publication may be reproduced for non-profit and educational purposes. Please clearly credit HelpAge International and send us a copy or link. Acknowledgements: We thank the European Union and governments of Australia, Denmark, France, Ireland, Italy, Luxembourg, the Netherlands, New Zealand, Sweden, Switzerland, the United Kingdom, the United States of America for their kind contributions to improving the livelihoods and food security of rural people in Myanmar. We would also like to thank the Mitsubishi Corporation, as a private sector donor. Disclaimer: This document is supported with financial assistance from Australia, Denmark, the European Union, France, Ireland, Italy, Luxembourg, the Netherlands, New Zealand, Sweden, Switzerland, the United Kingdom, the United States of America, and the Mitsubishi Corporation. The views expressed herein are not to be taken to reflect the official opinion of any of the LIFT donors. Funded by: 8. Electronic Delivery of Social Cash Transfers in Myanmar: Options Assessment

SMART MONEY MANAGEMENT

How much money did you earn last month? When was the last time you borrowed money? Have you opened a savings account? Why do you have to pay interest on a loan? With many tips and useful tools SMART MONEY

How much money did you earn last month? When was the last time you borrowed money? Have you opened a savings account? Why do you have to pay interest on a loan? With many tips and useful tools SMART MONEY

How to use the tool for successful delivery of SP payments?

The ISPA Tool Webinar Series Presents: THE ISPA TOOL: How to use the tool for successful delivery of SP payments? November 9 th, 2016 follow the conversation #ISPA_payments 1 PRESENTERS follow the conversation

The ISPA Tool Webinar Series Presents: THE ISPA TOOL: How to use the tool for successful delivery of SP payments? November 9 th, 2016 follow the conversation #ISPA_payments 1 PRESENTERS follow the conversation

BRITISH EXPORTERS ASSOCIATION

BRITISH EXPORTERS ASSOCIATION Broadway House, Tothill Street, London SW1H 9NQ Tel.: 020 7222 5419 FAX: 020 7799 2468 email: hughbailey@bexa.co.uk www.bexa.co.uk 9 th October 2015 Overview of BExA Concessional

BRITISH EXPORTERS ASSOCIATION Broadway House, Tothill Street, London SW1H 9NQ Tel.: 020 7222 5419 FAX: 020 7799 2468 email: hughbailey@bexa.co.uk www.bexa.co.uk 9 th October 2015 Overview of BExA Concessional

Al-Amal Microfinance Bank

Impact Brief Series, Issue 1 Al-Amal Microfinance Bank Yemen The Taqeem ( evaluation in Arabic) Initiative is a technical cooperation programme of the International Labour Organization and regional partners

Impact Brief Series, Issue 1 Al-Amal Microfinance Bank Yemen The Taqeem ( evaluation in Arabic) Initiative is a technical cooperation programme of the International Labour Organization and regional partners

DRAFT FEASIBILITY STUDY REPORT: TECHNICAL OPTIONS TO IMPLEMENT A UNIVERSAL SOCIAL PENSION IN MYANMAR

DRAFT FEASIBILITY STUDY REPORT: TECHNICAL OPTIONS TO IMPLEMENT A UNIVERSAL SOCIAL PENSION IN MYANMAR COMPLETED BY: SHARLENE RAMKISSOON, CONSULTANT DEVELOPMENT PATHWAYS COMPLETED FOR: MINISTRY OF SOCIAL

DRAFT FEASIBILITY STUDY REPORT: TECHNICAL OPTIONS TO IMPLEMENT A UNIVERSAL SOCIAL PENSION IN MYANMAR COMPLETED BY: SHARLENE RAMKISSOON, CONSULTANT DEVELOPMENT PATHWAYS COMPLETED FOR: MINISTRY OF SOCIAL

Version September Creating smart SEPA Solutions. A convenient and secure way to make payments. SEPA Direct Debit for Consumers

Creating smart SEPA Solutions Version 1.0 - September 2010 A convenient and secure way to make payments SEPA Direct Debit for Consumers 1 All you need to know about SEPA EPC Brochures* Making SEPA a Reality

Creating smart SEPA Solutions Version 1.0 - September 2010 A convenient and secure way to make payments SEPA Direct Debit for Consumers 1 All you need to know about SEPA EPC Brochures* Making SEPA a Reality

Food Security Policy Project Research Highlights Myanmar

Food Security Policy Project Research Highlights Myanmar December 2017 #9 AGRICULTURAL CREDIT ACCESS AND UTILIZATION IN MYANMAR S DRY ZONE Khun Moe Htun and Myat Su Tin INTRODUCTION This research highlight

Food Security Policy Project Research Highlights Myanmar December 2017 #9 AGRICULTURAL CREDIT ACCESS AND UTILIZATION IN MYANMAR S DRY ZONE Khun Moe Htun and Myat Su Tin INTRODUCTION This research highlight

TERMS OF REFERENCE Social protection technical support, Myanmar

TERMS OF REFERENCE Social protection technical support, Myanmar HelpAge is seeking a consultant to carry out two separate but interrelated assignments related to social protection cash transfers in Myanmar.

TERMS OF REFERENCE Social protection technical support, Myanmar HelpAge is seeking a consultant to carry out two separate but interrelated assignments related to social protection cash transfers in Myanmar.

Presented by Samuel O Ochieng MGCSD KENYA CT- OVC MIS AND POSSIBLE USES TO IMPROVE THE COORDINATION OF SOCIAL PROTECTION PROGRAMMES

Presented by Samuel O Ochieng MGCSD KENYA Policy dialogue expert workshop and south to south learning event Brasília, Brazil 3-5 December 2012 CT- OVC MIS AND POSSIBLE USES TO IMPROVE THE COORDINATION

Presented by Samuel O Ochieng MGCSD KENYA Policy dialogue expert workshop and south to south learning event Brasília, Brazil 3-5 December 2012 CT- OVC MIS AND POSSIBLE USES TO IMPROVE THE COORDINATION

Cheque imaging explained

Cheque imaging explained 22nd March 2017 The Cheque and Credit Clearing Company (C&CCC) is currently managing a programme to introduce a new, easier and quicker way of clearing cheques across the UK. Called

Cheque imaging explained 22nd March 2017 The Cheque and Credit Clearing Company (C&CCC) is currently managing a programme to introduce a new, easier and quicker way of clearing cheques across the UK. Called

Consultancy Announcement

Consultancy Announcement Title of Consultant : Monitoring and Evaluation Consultant Timeframe : 5 months (November 2018 March 2019) BACKGROUND My Justice: Strengthening Women s Access to Justice in Mon

Consultancy Announcement Title of Consultant : Monitoring and Evaluation Consultant Timeframe : 5 months (November 2018 March 2019) BACKGROUND My Justice: Strengthening Women s Access to Justice in Mon

EAP DRM KnowledgeNotes Disaster Risk Management in East Asia and the Pacific

Public Disclosure Authorized EAP DRM KnowledgeNotes Disaster Risk Management in East Asia and the Pacific Working Paper Series No. 15 Public Disclosure Authorized The World Bank/Mara Warwick Public Disclosure

Public Disclosure Authorized EAP DRM KnowledgeNotes Disaster Risk Management in East Asia and the Pacific Working Paper Series No. 15 Public Disclosure Authorized The World Bank/Mara Warwick Public Disclosure

Access to Cash Review Post Office Response

Access to Cash Review Post Office Response About the Post Office Post Office is the UK's largest retail network. With over 11,500 branches, we are within 3 miles of 99.7% of the population. Our branches

Access to Cash Review Post Office Response About the Post Office Post Office is the UK's largest retail network. With over 11,500 branches, we are within 3 miles of 99.7% of the population. Our branches

LIFT Call for Proposals. Digitisation of nutrition/1,000 day messaging

LIFT Call for Proposals Digitisation of nutrition/1,000 day messaging Ref no: Release date: 10 January 2018 Deadline: Title: Duration: 1 st February 2018, 9am (Myanmar time) Digitisation of nutrition/1,000

LIFT Call for Proposals Digitisation of nutrition/1,000 day messaging Ref no: Release date: 10 January 2018 Deadline: Title: Duration: 1 st February 2018, 9am (Myanmar time) Digitisation of nutrition/1,000

Payment Systems Briefing

Payment Systems Briefing Harish Natarajan Social Safety Nets Core Course 2010 Washington DC. December 9, 2010 Payment Systems Development Group The World Bank Payment Systems Development Group Help develop

Payment Systems Briefing Harish Natarajan Social Safety Nets Core Course 2010 Washington DC. December 9, 2010 Payment Systems Development Group The World Bank Payment Systems Development Group Help develop

PAKISTAN. QUICKSIGHTS REPORT FOURTH ANNUAL FII TRACKER SURVEY Fieldwork completed in October December 2016

QUICKSIGHTS REPORT FOURTH ANNUAL FII TRACKER SURVEY Fieldwork completed in October 206 December 206 Key definitions Access Access to a bank account or mobile money account means an individual can use bank/mobile

QUICKSIGHTS REPORT FOURTH ANNUAL FII TRACKER SURVEY Fieldwork completed in October 206 December 206 Key definitions Access Access to a bank account or mobile money account means an individual can use bank/mobile

Reaping the benefits of ID systems for delivering Social Protection. Robert Palacios, Lead Pensions, World Bank Pension Core Course April 30, 2015

Reaping the benefits of ID systems for delivering Social Protection Robert Palacios, Lead Pensions, World Bank Pension Core Course April 30, 2015 Harnessing the ID system for SP Program specific Ensure

Reaping the benefits of ID systems for delivering Social Protection Robert Palacios, Lead Pensions, World Bank Pension Core Course April 30, 2015 Harnessing the ID system for SP Program specific Ensure

Cabinet Committee on State Sector Reform and Expenditure Control STAGE 2 OF TRANSFORMING NEW ZEALAND S REVENUE SYSTEM

Cabinet Committee on State Sector Reform and Expenditure Control In Confidence Office of the Minister of Revenue STAGE 2 OF TRANSFORMING NEW ZEALAND S REVENUE SYSTEM Proposal 1. This paper provides an

Cabinet Committee on State Sector Reform and Expenditure Control In Confidence Office of the Minister of Revenue STAGE 2 OF TRANSFORMING NEW ZEALAND S REVENUE SYSTEM Proposal 1. This paper provides an

Seminar on Strengthening Social Protection Systems in Namibia

Seminar on Strengthening Social Protection Systems in Namibia PRESENTATION OVERVIEW 1. Social Support Model in Malawi 2. Objectives of the Policy/Programme 3. Interventions 4. Challenges 5. Reforms to

Seminar on Strengthening Social Protection Systems in Namibia PRESENTATION OVERVIEW 1. Social Support Model in Malawi 2. Objectives of the Policy/Programme 3. Interventions 4. Challenges 5. Reforms to

Bank of Mauritius. National Payment Switch

Bank of Mauritius National Payment Switch January 2016 1 Introduction The Bank of Mauritius (Bank) is empowered under the Bank of Mauritius Act to safeguard the safety, soundness and efficiency of payment,

Bank of Mauritius National Payment Switch January 2016 1 Introduction The Bank of Mauritius (Bank) is empowered under the Bank of Mauritius Act to safeguard the safety, soundness and efficiency of payment,

Increasing efficiency and effectiveness of Cash Transfer Schemes for improving school attendance

MINISTRY OF PLANNING AND INVESTMENT Increasing efficiency and effectiveness of Cash Transfer Schemes for improving school attendance Lessons from a Public Expenditure Tracking Survey of the implementation

MINISTRY OF PLANNING AND INVESTMENT Increasing efficiency and effectiveness of Cash Transfer Schemes for improving school attendance Lessons from a Public Expenditure Tracking Survey of the implementation

BlackRock is pleased to have the opportunity to respond to the Call for Evidence AIFMD passport and third country AIFMs.

8 th January 2015 European Securities and Markets Authority 103 Rue de Grenelle 75007 Paris France Submitted via electronic submission RE: Call for evidence AIFMD passport and third country AIFMs Dear

8 th January 2015 European Securities and Markets Authority 103 Rue de Grenelle 75007 Paris France Submitted via electronic submission RE: Call for evidence AIFMD passport and third country AIFMs Dear

Brainstorming Meeting on Impact Financing in the Fisheries Sector in Structurally Weak and Vulnerable Economies. Concept Note

Brainstorming Meeting on Impact Financing in the Fisheries Sector in Structurally Weak and Vulnerable Economies Concept Note 1 Brainstorming Meeting on Impact Financing in the Fisheries Sector in Structurally

Brainstorming Meeting on Impact Financing in the Fisheries Sector in Structurally Weak and Vulnerable Economies Concept Note 1 Brainstorming Meeting on Impact Financing in the Fisheries Sector in Structurally

Instant Payments. 9th Conference on Payments and Securities Settlement Systems, Ohrid, 5-8 June 2016 Richard Derksen

9th Conference on Payments and Securities Settlement Systems, Ohrid, 5-8 June 2016 Richard Derksen Contents 1. Definition and background 2. Instant Payments in the Netherlands 3. Status in Europe 4. Specific

9th Conference on Payments and Securities Settlement Systems, Ohrid, 5-8 June 2016 Richard Derksen Contents 1. Definition and background 2. Instant Payments in the Netherlands 3. Status in Europe 4. Specific

Hang Seng Credit Card Benefits Directory

Hang Seng Credit Card Benefits Directory Content 1. Important Points to Remember Page 1 2. Customer Privileges - Hang Seng Credit Card Membership Rewards Programme Page 2 - Online Shopping Security Page

Hang Seng Credit Card Benefits Directory Content 1. Important Points to Remember Page 1 2. Customer Privileges - Hang Seng Credit Card Membership Rewards Programme Page 2 - Online Shopping Security Page

Q&A of ODA and ODA Loans. This chapter provides essential information on Japan s official development assistance (ODA) and ODA loans.

and ODA loans.") 5 Q&A of ODA and ODA Loans This chapter provides essential information on Japan s official development assistance (ODA) and ODA loans. 1. Japan s ODA Q.What is ODA? A. ODA is the assistance to developing

5 Q&A of ODA and ODA Loans This chapter provides essential information on Japan s official development assistance (ODA) and ODA loans. 1. Japan s ODA Q.What is ODA? A. ODA is the assistance to developing

Financial Inclusion Glossary

Financial Inclusion Glossary In order to achieve full financial inclusion we must agree on what it means. Defining financial inclusion requires building out a shared language and describing how various

Financial Inclusion Glossary In order to achieve full financial inclusion we must agree on what it means. Defining financial inclusion requires building out a shared language and describing how various

TREATY SERIES 2003 Nº 2. Convention on Combating Bribery of Foreign Public Officials in International Business Transactions

TREATY SERIES 2003 Nº 2 Convention on Combating Bribery of Foreign Public Officials in International Business Transactions Done at Paris on 17 December 1997 Signed on behalf of Ireland on 17 December 1997

TREATY SERIES 2003 Nº 2 Convention on Combating Bribery of Foreign Public Officials in International Business Transactions Done at Paris on 17 December 1997 Signed on behalf of Ireland on 17 December 1997

TERMS OF REFERENCE Overview assessment of DSW institutional structure. 1. Background

TERMS OF REFERENCE Overview assessment of DSW institutional structure 1. Background HelpAge International has supported Myanmar since 2004 and has been an implementing partner of the Livelihoods and Food

TERMS OF REFERENCE Overview assessment of DSW institutional structure 1. Background HelpAge International has supported Myanmar since 2004 and has been an implementing partner of the Livelihoods and Food

Recommendation of the Council on Good Practices for Public Environmental Expenditure Management

Recommendation of the Council on for Public Environmental Expenditure Management ENVIRONMENT 8 June 2006 - C(2006)84 THE COUNCIL, Having regard to Article 5 b) of the Convention on the Organisation for

Recommendation of the Council on for Public Environmental Expenditure Management ENVIRONMENT 8 June 2006 - C(2006)84 THE COUNCIL, Having regard to Article 5 b) of the Convention on the Organisation for

Sudan. Sudan is a lower-middle income country with a gross national income (GNI) of USD 1 220

of USD 1 220") 00 Sudan INTRODUCTION Sudan is a lower-middle income country with a gross national income (GNI) of USD 1 220 per capita (2009) which has grown at an average rate of 7% per annum since 2005 (WDI, 2011).

00 Sudan INTRODUCTION Sudan is a lower-middle income country with a gross national income (GNI) of USD 1 220 per capita (2009) which has grown at an average rate of 7% per annum since 2005 (WDI, 2011).

Distributional Implications of the Welfare State

Agenda, Volume 10, Number 2, 2003, pages 99-112 Distributional Implications of the Welfare State James Cox This paper is concerned with the effect of the welfare state in redistributing income away from

Agenda, Volume 10, Number 2, 2003, pages 99-112 Distributional Implications of the Welfare State James Cox This paper is concerned with the effect of the welfare state in redistributing income away from

Overview of the Social Transfers Policy Framework. NAP 2 Pillars Key features of the HSCT Who are the stakeholders? How will it be implemented?

Overview of the Social Transfers Policy Framework. NAP 2 Pillars Key features of the HSCT Who are the stakeholders? How will it be implemented? Where will it be implemented? When will it be implemented?

Overview of the Social Transfers Policy Framework. NAP 2 Pillars Key features of the HSCT Who are the stakeholders? How will it be implemented? Where will it be implemented? When will it be implemented?

Chair, Cabinet Government Administration and Expenditure Review Committee

In Confidence Office of the Minister of Revenue Chair, Cabinet Government Administration and Expenditure Review Committee February 2018 Update Delivering the next step in the Transformation of New Zealand

In Confidence Office of the Minister of Revenue Chair, Cabinet Government Administration and Expenditure Review Committee February 2018 Update Delivering the next step in the Transformation of New Zealand

IMPLEMENTING THE PARIS DECLARATION AT THE COUNTRY LEVEL

CHAPTER 6 IMPLEMENTING THE PARIS DECLARATION AT THE COUNTRY LEVEL 6.1 INTRODUCTION The six countries that the evaluation team visited vary significantly. Table 1 captures the most important indicators

CHAPTER 6 IMPLEMENTING THE PARIS DECLARATION AT THE COUNTRY LEVEL 6.1 INTRODUCTION The six countries that the evaluation team visited vary significantly. Table 1 captures the most important indicators

Women s Economic Empowerment Update

Gender Equality and Financial Services for the Poor Women s Economic Empowerment Update 2018 Bill & Melinda Gates Foundation AREAS I WILL COVER TODAY The Gates Foundation s new Gender Equality Strategy:

Gender Equality and Financial Services for the Poor Women s Economic Empowerment Update 2018 Bill & Melinda Gates Foundation AREAS I WILL COVER TODAY The Gates Foundation s new Gender Equality Strategy:

World Bank Conditionality Review Nordic-Baltic Position Paper

World Bank Conditionality Review Nordic-Baltic Position Paper Key Points The Nordic and Baltic Countries (NBC:s) welcome the World Bank review of conditionality, and as input into the review process suggest

World Bank Conditionality Review Nordic-Baltic Position Paper Key Points The Nordic and Baltic Countries (NBC:s) welcome the World Bank review of conditionality, and as input into the review process suggest

Universal Social Protection

Universal Social Protection Universal pensions in South Africa Older Persons Grant South Africa is ranked as an upper-middle income country but characterized by high poverty incidence and inequality among

Universal Social Protection Universal pensions in South Africa Older Persons Grant South Africa is ranked as an upper-middle income country but characterized by high poverty incidence and inequality among

Advocacy with older people: Some practical suggestions. Advocacy by older people, with older people and for older people

Advocacy with older people: Advocacy by older people, with older people and for older people Advocacy with older people: HelpAge International is a global network of not-for-profit organisations with a

Advocacy with older people: Advocacy by older people, with older people and for older people Advocacy with older people: HelpAge International is a global network of not-for-profit organisations with a

THE FUTURE OF CASH AND PAYMENTS

THE FUTURE OF CASH AND PAYMENTS Retail Banking Research January 2010 CONFIDENTIALITY AND COPYRIGHT This report is published by Retail Banking Research Ltd (RBR). The information and data within this report

THE FUTURE OF CASH AND PAYMENTS Retail Banking Research January 2010 CONFIDENTIALITY AND COPYRIGHT This report is published by Retail Banking Research Ltd (RBR). The information and data within this report

TANZANIA. QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted September-October December 2015

QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted September-October 2015 December 2015 GLOSSARY Access Access to a bank, NBFI or mobile money account; those with access have used the services either via

QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted September-October 2015 December 2015 GLOSSARY Access Access to a bank, NBFI or mobile money account; those with access have used the services either via

IATI Country Pilot Synthesis Report May June 2010

IATI Country Pilot Synthesis Report May June 2010 Executive Summary Overall goal of pilots The country pilots have successfully proved the IATI concept that it is possible get data from multiple donor

IATI Country Pilot Synthesis Report May June 2010 Executive Summary Overall goal of pilots The country pilots have successfully proved the IATI concept that it is possible get data from multiple donor

CAMBODIA. Cambodia is a low-income country with a gross national income (GNI) of USD 610 per

of USD 610 per") 00 CAMBODIA INTRODUCTION Cambodia is a low-income country with a gross national income (GNI) of USD 610 per capita in 2009 (WDI, 2011). It has a population of approximately 15 million and more than a quarter

00 CAMBODIA INTRODUCTION Cambodia is a low-income country with a gross national income (GNI) of USD 610 per capita in 2009 (WDI, 2011). It has a population of approximately 15 million and more than a quarter

METRICS FOR IMPLEMENTING COUNTRY OWNERSHIP

METRICS FOR IMPLEMENTING COUNTRY OWNERSHIP The 2014 policy paper of the Modernizing Foreign Assistance Network (MFAN), The Way Forward, outlines two powerful and mutually reinforcing pillars of aid reform

METRICS FOR IMPLEMENTING COUNTRY OWNERSHIP The 2014 policy paper of the Modernizing Foreign Assistance Network (MFAN), The Way Forward, outlines two powerful and mutually reinforcing pillars of aid reform

Rwanda. Rwanda is a low-income country with a gross national income (GNI) of USD 490

of USD 490") 00 Rwanda INTRODUCTION Rwanda is a low-income country with a gross national income (GNI) of USD 490 per capita in 2009 (WDI, 2011). It has a population of approximately 10 million with 77% of the population

00 Rwanda INTRODUCTION Rwanda is a low-income country with a gross national income (GNI) of USD 490 per capita in 2009 (WDI, 2011). It has a population of approximately 10 million with 77% of the population

OECD THEMATIC FOLLOW-UP REVIEW OF POLICIES TO IMPROVE LABOUR MARKET PROSPECTS FOR OLDER WORKERS. ITALY (situation early 2012)

") OECD THEMATIC FOLLOW-UP REVIEW OF POLICIES TO IMPROVE LABOUR MARKET PROSPECTS FOR OLDER WORKERS ITALY (situation early 2012) In 2011, the employment rate for the population aged 50-64 in Italy was 5.9

OECD THEMATIC FOLLOW-UP REVIEW OF POLICIES TO IMPROVE LABOUR MARKET PROSPECTS FOR OLDER WORKERS ITALY (situation early 2012) In 2011, the employment rate for the population aged 50-64 in Italy was 5.9

EUA MEMBER CONSULTATION A CONTRIBUTION TO THE ERASMUS+ MID-TERM REVIEW

EUA MEMBER CONSULTATION A CONTRIBUTION TO THE ERASMUS+ MID-TERM REVIEW Participation in sub-questionnaires on specific actions KA1: Student Mobility KA1: Staff Mobility KA2: Strategic Partnerships

EUA MEMBER CONSULTATION A CONTRIBUTION TO THE ERASMUS+ MID-TERM REVIEW Participation in sub-questionnaires on specific actions KA1: Student Mobility KA1: Staff Mobility KA2: Strategic Partnerships

OECD Recommendation on Consumer Dispute Resolution and Redress

OECD Recommendation on Consumer Dispute Resolution and Redress ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT The OECD is a unique forum where the governments of 30 democracies work together to

OECD Recommendation on Consumer Dispute Resolution and Redress ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT The OECD is a unique forum where the governments of 30 democracies work together to

Chapter 2. Non-core funding of multilaterals

2. NON-CORE FUNDING OF MULTILATERALS 45 Chapter 2 Non-core funding of multilaterals This chapter concludes that non-core funding can contribute to a wide range of complementary activities, although they

2. NON-CORE FUNDING OF MULTILATERALS 45 Chapter 2 Non-core funding of multilaterals This chapter concludes that non-core funding can contribute to a wide range of complementary activities, although they

Livelihoods and Food Security Trust Fund (LIFT) Delta 3 Call for Proposals (CfP)

Delta 3 Call for Proposals (CfP)") Ref no: Livelihoods and Food Security Trust Fund (LIFT) Delta 3 Call for Proposals (CfP) CfP/LIFT/2015/2/Delta3 Release date: 12 March 2015 Deadline: Title: Duration: 27 April 2015, noon (1200h) Delta

Ref no: Livelihoods and Food Security Trust Fund (LIFT) Delta 3 Call for Proposals (CfP) CfP/LIFT/2015/2/Delta3 Release date: 12 March 2015 Deadline: Title: Duration: 27 April 2015, noon (1200h) Delta

FIDUCIARY ARRANGEMENTS FOR SECTORWIDE APPROACHES (SWAPS)

") FIDUCIARY ARRANGEMENTS FOR SECTORWIDE APPROACHES (SWAPS) OPERATIONS POLICY AND COUNTRY SERVICES APRIL 2, 2002 FIDUCIARY ARRANGEMENTS FOR SECTORWIDE APPROACHES (SWAPS) CONTENTS Page I. Introduction..1 II.

FIDUCIARY ARRANGEMENTS FOR SECTORWIDE APPROACHES (SWAPS) OPERATIONS POLICY AND COUNTRY SERVICES APRIL 2, 2002 FIDUCIARY ARRANGEMENTS FOR SECTORWIDE APPROACHES (SWAPS) CONTENTS Page I. Introduction..1 II.

Basic banking services

Presentation to the European Parliament by London Economics 25 January 2012 1 Presentation outline Basic facts and benefits 2 and benefits Background Access to basic banking is essential in modern society,

Presentation to the European Parliament by London Economics 25 January 2012 1 Presentation outline Basic facts and benefits 2 and benefits Background Access to basic banking is essential in modern society,

Cash transfers in emergencies: A practical field guide

Cash transfers in emergencies: A practical field guide 1 2 Contents Section 1: Cash transfer overview 1 What is the role of cash transfers in emergencies The importance of responding to and involving older

Cash transfers in emergencies: A practical field guide 1 2 Contents Section 1: Cash transfer overview 1 What is the role of cash transfers in emergencies The importance of responding to and involving older

Ways to increase employment

Ways to increase employment Iceland Luxembourg Spain Canada Italy Norway Denmark Germany Portugal Ireland Japan Belgium Switzerland Austria Slovenia United States New Zealand Finland France Netherlands

Ways to increase employment Iceland Luxembourg Spain Canada Italy Norway Denmark Germany Portugal Ireland Japan Belgium Switzerland Austria Slovenia United States New Zealand Finland France Netherlands

PNPM SUPPORT FACILITY (PSF) Project Proposal

Project Proposal") PNPM SUPPORT FACILITY (PSF) Project Proposal Project Title: Objective: Executing Agency: Estimated Duration: Estimated Budget: Geographic Coverage: Implementation Arrangements: PNPM Mandiri Revolving Loan

PNPM SUPPORT FACILITY (PSF) Project Proposal Project Title: Objective: Executing Agency: Estimated Duration: Estimated Budget: Geographic Coverage: Implementation Arrangements: PNPM Mandiri Revolving Loan

Universal Social Protection

Universal Social Protection The Universal Pension Scheme in Zanzibar Zanzibar Universal Pension Scheme (ZUPS) Zanzibar made history in April 2016 when it implemented the Zanzibar Universal Pension Scheme

Universal Social Protection The Universal Pension Scheme in Zanzibar Zanzibar Universal Pension Scheme (ZUPS) Zanzibar made history in April 2016 when it implemented the Zanzibar Universal Pension Scheme

SGX INTRODUCES A NEW REGULATORY FRAMEWORK FOR SECONDARY LISTINGS

NOVEMBER 2014 1 SGX INTRODUCES A NEW REGULATORY FRAMEWORK FOR SECONDARY LISTINGS The Singapore Exchange ( SGX ) announced that it commenced a new regulatory framework for secondary listings and secondary-listed

NOVEMBER 2014 1 SGX INTRODUCES A NEW REGULATORY FRAMEWORK FOR SECONDARY LISTINGS The Singapore Exchange ( SGX ) announced that it commenced a new regulatory framework for secondary listings and secondary-listed

Targets and Indicators for Active Ageing

Targets and Indicators for Active Ageing Daw Rupar Mya Director Department of Social Welfare Ministry of Social Welfare, Relief and Resettlement The Republic of the Union of Myanmar 51.486 millions ppl

Targets and Indicators for Active Ageing Daw Rupar Mya Director Department of Social Welfare Ministry of Social Welfare, Relief and Resettlement The Republic of the Union of Myanmar 51.486 millions ppl

Delivering services through Citizen Terminals and Mobile Municipal Offices in rural areas. AFE-INNONVET workshop, 8-9 October 2015

Delivering services through Citizen Terminals and Mobile Municipal Offices in rural areas AFE-INNONVET workshop, 8-9 October 2015 Agenda 1. Demographic change in the Free State of Saxony 2. Multi-channel

Delivering services through Citizen Terminals and Mobile Municipal Offices in rural areas AFE-INNONVET workshop, 8-9 October 2015 Agenda 1. Demographic change in the Free State of Saxony 2. Multi-channel

HIGHLIGHTS 2016 OECD PERFORMANCE BUDGETING SURVEY: Integrating performance and results in budgeting

HIGHLIGHTS 2016 OECD PERFORMANCE BUDGETING SURVEY: Integrating performance and results in budgeting This booklet presents highlights from the 2016 OECD performance budgeting survey. The data is preliminary

HIGHLIGHTS 2016 OECD PERFORMANCE BUDGETING SURVEY: Integrating performance and results in budgeting This booklet presents highlights from the 2016 OECD performance budgeting survey. The data is preliminary

Improving the home buying and selling process: UK Finance response to the DCLG call for evidence

Improving the home buying and selling process: UK Finance response to the DCLG call for evidence 15 December 2017 Introduction UK Finance represents around 300 firms in the UK providing credit, banking,

Improving the home buying and selling process: UK Finance response to the DCLG call for evidence 15 December 2017 Introduction UK Finance represents around 300 firms in the UK providing credit, banking,

Paper 3 Measuring Performance in Public Financial Management

Paper 3 Measuring Performance in Public Financial Management Key Issues 1. Effective financial management of public resources is essential to achieve the objectives of development programmes. It also promotes

Paper 3 Measuring Performance in Public Financial Management Key Issues 1. Effective financial management of public resources is essential to achieve the objectives of development programmes. It also promotes

SOCIAL AND ECONOMIC EMPOWERMENT OF OLDER PERSONS IN MYANMAR THROUGH OLDER PEOPLE SELF-HELP GROUPS. Tapan Barman, HelpAge Myanmar

SOCIAL AND ECONOMIC EMPOWERMENT OF OLDER PERSONS IN MYANMAR THROUGH OLDER PEOPLE SELF-HELP GROUPS Tapan Barman, HelpAge Myanmar HelpAge International s Partners in Myanmar National Young Men Christian

SOCIAL AND ECONOMIC EMPOWERMENT OF OLDER PERSONS IN MYANMAR THROUGH OLDER PEOPLE SELF-HELP GROUPS Tapan Barman, HelpAge Myanmar HelpAge International s Partners in Myanmar National Young Men Christian

THE REPUBLIC OF UGANDA

THE REPUBLIC OF UGANDA REPORT OF THE AUDITOR GENERAL ON THE FINANCIAL STATEMENTS OF THE ENERGY FOR RURAL TRANSFORMATION PROJECT II (ERT II) PRIVATE SECTOR FOUNDATION (PSFU) COMPONENT (IDA CREDIT AGREEMENT

THE REPUBLIC OF UGANDA REPORT OF THE AUDITOR GENERAL ON THE FINANCIAL STATEMENTS OF THE ENERGY FOR RURAL TRANSFORMATION PROJECT II (ERT II) PRIVATE SECTOR FOUNDATION (PSFU) COMPONENT (IDA CREDIT AGREEMENT

BANGLADESH. QUICKSIGHTS REPORT FOURTH ANNUAL FII TRACKER SURVEY Fieldwork completed in September December 2016

QUICKSIGHTS REPORT FOURTH ANNUAL FII TRACKER SURVEY Fieldwork completed in September 016 December 016 Key definitions Access Access to a bank account or mobile money account means an individual can use

QUICKSIGHTS REPORT FOURTH ANNUAL FII TRACKER SURVEY Fieldwork completed in September 016 December 016 Key definitions Access Access to a bank account or mobile money account means an individual can use

INDIA. QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted June through October, January 2016*

QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted June through October, 2015 January 2016* *Revised April 2016 KEY DEFINITIONS Access Access to a bank, NBFI or mobile money account; those with access have

QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted June through October, 2015 January 2016* *Revised April 2016 KEY DEFINITIONS Access Access to a bank, NBFI or mobile money account; those with access have

OECD THEMATIC FOLLOW-UP REVIEW OF POLICIES TO IMPROVE LABOUR MARKET PROSPECTS FOR OLDER WORKERS. NORWAY (situation mid-2012)

") OECD THEMATIC FOLLOW-UP REVIEW OF POLICIES TO IMPROVE LABOUR MARKET PROSPECTS FOR OLDER WORKERS NORWAY (situation mid-2012) In 2011, the employment rate for the population aged 50-64 in Norway was 1.2

OECD THEMATIC FOLLOW-UP REVIEW OF POLICIES TO IMPROVE LABOUR MARKET PROSPECTS FOR OLDER WORKERS NORWAY (situation mid-2012) In 2011, the employment rate for the population aged 50-64 in Norway was 1.2

CE TEXTE N'EST DISPONIBLE QU'EN VERSION ANGLAISE

CE TEXTE N'EST DISPONIBLE QU' VERSION ANGLAISE ANNEX 1 1. IDTIFICATION Title/Number Support Services to the National Authorising Officer CRIS NO: FED/2009/021-496 Total cost Total: 315,800 (EC Contribution:

CE TEXTE N'EST DISPONIBLE QU' VERSION ANGLAISE ANNEX 1 1. IDTIFICATION Title/Number Support Services to the National Authorising Officer CRIS NO: FED/2009/021-496 Total cost Total: 315,800 (EC Contribution:

What You Should Know CPEL Payment Services Directive 2

What You Should Know CPEL Payment Services Directive 2 GENERAL BACKGROUND - PAYMENT SERVICES DIRECTIVE (PSD) AND PAYMENT SERVICES DIRECTVE 2 (PSD2) 1. What is the PSD and what changes did it introduce

What You Should Know CPEL Payment Services Directive 2 GENERAL BACKGROUND - PAYMENT SERVICES DIRECTIVE (PSD) AND PAYMENT SERVICES DIRECTVE 2 (PSD2) 1. What is the PSD and what changes did it introduce

AUSTRAC Guidance Note. Risk management and AML/CTF programs

AUSTRAC Guidance Note Risk management and AML/CTF programs AUSTRAC Guidance Note Risk management and AML/CTF programs Anti-Money Laundering and Counter-Terrorism Financing Act 2006 Contents Page 1. Introduction

AUSTRAC Guidance Note Risk management and AML/CTF programs AUSTRAC Guidance Note Risk management and AML/CTF programs Anti-Money Laundering and Counter-Terrorism Financing Act 2006 Contents Page 1. Introduction

Implications of the New Cooperative Act on the Financial Sector in Nepal

Implications of the New Cooperative Act on the Financial Sector in Nepal Definition A cooperative (also known as co-operative, co-op, or coop) is "an autonomous association of persons united voluntarily

Implications of the New Cooperative Act on the Financial Sector in Nepal Definition A cooperative (also known as co-operative, co-op, or coop) is "an autonomous association of persons united voluntarily

BANGLADESH. QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted August-September November 2015

QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted August-September 2015 November 2015 Notable statistics Bangladesh is experiencing a shift in the primary means of financial access. o o o In 2013 and 2014,

QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted August-September 2015 November 2015 Notable statistics Bangladesh is experiencing a shift in the primary means of financial access. o o o In 2013 and 2014,

Targeting aid to reach the poorest people: LDC aid trends and targets

Targeting aid to reach the poorest people: LDC aid trends and targets Briefing 2015 April Development Initiatives exists to end extreme poverty by 2030 www.devinit.org Focusing aid on the poorest people

Targeting aid to reach the poorest people: LDC aid trends and targets Briefing 2015 April Development Initiatives exists to end extreme poverty by 2030 www.devinit.org Focusing aid on the poorest people

Taxation of non-controlled offshore investment in equity

Taxation of non-controlled offshore investment in equity An officials issues paper on suggested legislative amendments December 2003 Prepared by the Policy Advice Division of the Inland Revenue Department

Taxation of non-controlled offshore investment in equity An officials issues paper on suggested legislative amendments December 2003 Prepared by the Policy Advice Division of the Inland Revenue Department

Japanese Pension System and Its Outlook.

Japanese Pension System and Its Outlook www.japanmacroadvisors.com info@japanmacroadvisors.com Executive Summary The Japanese public pension scheme covers all people but so far a household of a retired

Japanese Pension System and Its Outlook www.japanmacroadvisors.com info@japanmacroadvisors.com Executive Summary The Japanese public pension scheme covers all people but so far a household of a retired

SUMMARY OF RESULTS PUBLIC CONSULTATION ON FINANCIAL AND INSURANCE

EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Indirect Taxation and Tax administration VAT and other turnover taxes SUMMARY OF RESULTS PUBLIC CONSULTATION ON FINANCIAL AND INSURANCE

EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Indirect Taxation and Tax administration VAT and other turnover taxes SUMMARY OF RESULTS PUBLIC CONSULTATION ON FINANCIAL AND INSURANCE

Recommendation of the Council on Tax Avoidance and Evasion

Recommendation of the Council on Tax Avoidance and Evasion OECD Legal Instruments This document is published under the responsibility of the Secretary-General of the OECD. It reproduces an OECD Legal Instrument

Recommendation of the Council on Tax Avoidance and Evasion OECD Legal Instruments This document is published under the responsibility of the Secretary-General of the OECD. It reproduces an OECD Legal Instrument

INTERIM MANAGEMENT STATEMENT QUARTER ENDED 30 SEPTEMBER 2011

INTERIM MANAGEMENT STATEMENT QUARTER ENDED 30 SEPTEMBER 2011 6 October 2011 Financial summary Growth in net fees for the quarter ended 30 September 2011 (Q1) (versus the same period last year) actual growth

INTERIM MANAGEMENT STATEMENT QUARTER ENDED 30 SEPTEMBER 2011 6 October 2011 Financial summary Growth in net fees for the quarter ended 30 September 2011 (Q1) (versus the same period last year) actual growth

Swiss Data Privacy statement

Applicant Privacy Notice Before we begin This notice (Privacy Notice) applies to personal information relating to your application for employment with HSBC Group held by HSBC Private Bank (Suisse) SA or

Applicant Privacy Notice Before we begin This notice (Privacy Notice) applies to personal information relating to your application for employment with HSBC Group held by HSBC Private Bank (Suisse) SA or

Recommendation of the Council on Establishing and Implementing Pollutant Release and Transfer Registers (PRTRs)

") Recommendation of the Council on Establishing and Implementing Pollutant Release and Transfer Registers (PRTRs) OECD Legal Instruments This document is published under the responsibility of the Secretary-General

Recommendation of the Council on Establishing and Implementing Pollutant Release and Transfer Registers (PRTRs) OECD Legal Instruments This document is published under the responsibility of the Secretary-General

Launch of the SEPA Instant Credit Transfer scheme PRESS KIT - NOVEMBER 2017

Launch of the SEPA Instant Credit Transfer scheme PRESS KIT - NOVEMBER 2017 INTRODUCTION November 2017 sees the launch of a pioneering initiative in the world of payments. The SEPA Instant Credit Transfer

Launch of the SEPA Instant Credit Transfer scheme PRESS KIT - NOVEMBER 2017 INTRODUCTION November 2017 sees the launch of a pioneering initiative in the world of payments. The SEPA Instant Credit Transfer

PRODUCT HIGHLIGHTS SHEET

Prepared on: 31 July 2018 This Product Highlights Sheet is an important document. It highlights the key terms and risks of this investment product and complements the Prospectus 1. It is important to read

Prepared on: 31 July 2018 This Product Highlights Sheet is an important document. It highlights the key terms and risks of this investment product and complements the Prospectus 1. It is important to read

Research Brief. Sultan Hafeez Rahman, Md. Shanawez Hossain, Mohammed Misbah Uddin

Research Brief Public Finance and Revenue Mobilization in Union Parishads Abstract Sultan Hafeez Rahman, Md. Shanawez Hossain, Mohammed Misbah Uddin July 2016 Despite the long history of local government

Research Brief Public Finance and Revenue Mobilization in Union Parishads Abstract Sultan Hafeez Rahman, Md. Shanawez Hossain, Mohammed Misbah Uddin July 2016 Despite the long history of local government

4 An external evaluator measures success rates as pre-defined by SFI and the outcome payer. SFI: Innovating Social Change with Impact Capital

SFI: Innovating Social Change with Impact Capital The value of the Social Impact Bond (SIB), also known as the Pay -for-success model, is its unique ability to find mutual benefit for investors with different

SFI: Innovating Social Change with Impact Capital The value of the Social Impact Bond (SIB), also known as the Pay -for-success model, is its unique ability to find mutual benefit for investors with different

Performance Budgeting (PB) in OECD Countries

in OECD Countries") Performance Budgeting (PB) in OECD Countries Teresa Curristine, Budgeting and Public Expenditures Division, Public Governance Directorate, OECD 6 th Annual Meeting of Latin American Senior Budget Officials

Performance Budgeting (PB) in OECD Countries Teresa Curristine, Budgeting and Public Expenditures Division, Public Governance Directorate, OECD 6 th Annual Meeting of Latin American Senior Budget Officials

Public consultation on long-term and sustainable investment

Case Id: 5a0bdff8-2c24-45af-b83c-2d5eea3336e3 Date: 25/03/2016 15:15:12 Public consultation on long-term and sustainable investment Fields marked with are mandatory. Introduction Fostering growth and investment

Case Id: 5a0bdff8-2c24-45af-b83c-2d5eea3336e3 Date: 25/03/2016 15:15:12 Public consultation on long-term and sustainable investment Fields marked with are mandatory. Introduction Fostering growth and investment

Evaluation of the European Union s Co-operation with Kenya Country level evaluation

"FICHE CONTRADICTOIRE" Evaluation of the European Union s Co-operation with Kenya Country level evaluation Recommendations Responses of Services: Follow-up (one year later) GENERAL RECOMMENDATIONS 1 Give

"FICHE CONTRADICTOIRE" Evaluation of the European Union s Co-operation with Kenya Country level evaluation Recommendations Responses of Services: Follow-up (one year later) GENERAL RECOMMENDATIONS 1 Give

Payment Acceptance Services

Payment Acceptance Services Provided by Elavon 1 Merchant Acquiring Services About Us Santander Corporate & Commercial has an international footprint with a presence in 10 core countries and many more

Payment Acceptance Services Provided by Elavon 1 Merchant Acquiring Services About Us Santander Corporate & Commercial has an international footprint with a presence in 10 core countries and many more

SELECTED MAJOR SOCIAL SECURITY PENSION REFORMS IN EUROPE, Source: ISSA Databases

SELECTED MAJOR SOCIAL SECURITY PENSION REFORMS IN EUROPE, 1995-2014 Source: ISSA Databases COUNTRY AREA YR SUMMARY OBJECTIVE POSSIBLE EVALUATION CRITERIA* United Kingdom Pensions 2014 Replacing public

SELECTED MAJOR SOCIAL SECURITY PENSION REFORMS IN EUROPE, 1995-2014 Source: ISSA Databases COUNTRY AREA YR SUMMARY OBJECTIVE POSSIBLE EVALUATION CRITERIA* United Kingdom Pensions 2014 Replacing public

Link Scheme Holdings Ltd CPMI - IOSCO Disclosure for the LINK Payment System 31 st December 2018

Link Scheme Holdings Ltd CPMI - IOSCO Disclosure for the LINK Payment System 31 st December 2018 Responding Institution: Jurisdiction: Authorities Regulating: Link Scheme Holdings Ltd UK (English Law)

Link Scheme Holdings Ltd CPMI - IOSCO Disclosure for the LINK Payment System 31 st December 2018 Responding Institution: Jurisdiction: Authorities Regulating: Link Scheme Holdings Ltd UK (English Law)

PRIVACY NOTICE LAST UPDATED: SEPT. 2018

PRIVACY NOTICE LAST UPDATED: SEPT. 2018 HOW THE BANK USES YOUR PERSONAL DATA This privacy notice provides an overview of how Hellenic Bank Public Company Ltd (the Bank ) processes your personal data. Personal

PRIVACY NOTICE LAST UPDATED: SEPT. 2018 HOW THE BANK USES YOUR PERSONAL DATA This privacy notice provides an overview of how Hellenic Bank Public Company Ltd (the Bank ) processes your personal data. Personal

Promoting Fairness and Sustainability of Pension Systems in East and Southeast Asia

Promoting Fairness and Sustainability of Pension Systems in East and Southeast Asia Dr. Donghyun PARK, Asian Development Bank (dpark@adb.org) UNESCAP Regional Consultation on Strengthening Income Support

Promoting Fairness and Sustainability of Pension Systems in East and Southeast Asia Dr. Donghyun PARK, Asian Development Bank (dpark@adb.org) UNESCAP Regional Consultation on Strengthening Income Support

London School of Hygiene and Tropical Medicine. Affording Our Future Conference Wellington, December, 2012

How and why has health system spending grown and how does the system need to adapt to remain sustainable in the face of long term health conditions? Nicholas Mays London School of Hygiene and Tropical

How and why has health system spending grown and how does the system need to adapt to remain sustainable in the face of long term health conditions? Nicholas Mays London School of Hygiene and Tropical

BUSINESS MENU PLAN LIFE OR CRITICAL ILLNESS COVER

BUSINESS MENU PLAN LIFE OR CRITICAL ILLNESS COVER Plan details - January 2018 Protection - Business Menu Plan WE GIVE THIS BOOKLET OF TERMS AND CONDITIONS TO EVERYONE WHO BUYS LIFE OR CRITICAL ILLNESS

BUSINESS MENU PLAN LIFE OR CRITICAL ILLNESS COVER Plan details - January 2018 Protection - Business Menu Plan WE GIVE THIS BOOKLET OF TERMS AND CONDITIONS TO EVERYONE WHO BUYS LIFE OR CRITICAL ILLNESS

GLOBAL FINTECH HACKCELERATOR

GLOBAL FINTECH HACKCELERATOR Industry Problem Statements Version 2018.05.21 Organised by In partnership with In collaboration with Global FinTech Hackcelerator Powered by 80 Problem statements The global

GLOBAL FINTECH HACKCELERATOR Industry Problem Statements Version 2018.05.21 Organised by In partnership with In collaboration with Global FinTech Hackcelerator Powered by 80 Problem statements The global

Money Matters: Designing Effective CDD Disbursement Mechanisms

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized SOCIAL DEVELOPMENT HOW TO SERIES vol. 4 February 2008 Money Matters: Designing Effective

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized SOCIAL DEVELOPMENT HOW TO SERIES vol. 4 February 2008 Money Matters: Designing Effective

Forest Carbon Partnership Facility (FCPF) Readiness Fund

Readiness Fund") Forest Carbon Partnership Facility (FCPF) Readiness Fund FY15 Budget Status and FY16 Proposed Budget for the FCPF Readiness Fund May 2015 This note is designed to (A) present the status of the FY15 budget

Forest Carbon Partnership Facility (FCPF) Readiness Fund FY15 Budget Status and FY16 Proposed Budget for the FCPF Readiness Fund May 2015 This note is designed to (A) present the status of the FY15 budget

Sub-national Public Finance Management in Myanmar

Sub-national Public Finance Management in Myanmar Budget Brief Series: Tanintharyi No.2 June 218 Introduction 1. Public finance management will play an essential role in Tanintharyi s development, as well

Sub-national Public Finance Management in Myanmar Budget Brief Series: Tanintharyi No.2 June 218 Introduction 1. Public finance management will play an essential role in Tanintharyi s development, as well

Responding to the Earthquake in Nepal. Avani Dixit, Disaster Risk Management Specialist Jyoti Pandey, Social Protection Analyst

Responding to the Earthquake in Nepal Avani Dixit, Disaster Risk Management Specialist Jyoti Pandey, Social Protection Analyst Earthquake and the response needs Housing reconstruction project: Grant &

Responding to the Earthquake in Nepal Avani Dixit, Disaster Risk Management Specialist Jyoti Pandey, Social Protection Analyst Earthquake and the response needs Housing reconstruction project: Grant &

Pensions at a Glance 2009: Retirement-Income Systems in OECD Countries

Pensions at a Glance 2009: Retirement-Income Systems in OECD Countries Summary in English The crisis and pension policy The headline figures are frightening. Due to the financial crisis, private pension

Pensions at a Glance 2009: Retirement-Income Systems in OECD Countries Summary in English The crisis and pension policy The headline figures are frightening. Due to the financial crisis, private pension