David Sung. President

|

|

|

- Bonnie Hutchinson

- 5 years ago

- Views:

Transcription

1 WELCOME

2 David Sung President

3 Agenda Introduction and Background Tax Reform: The Details Planning Options Case Study Q & A

4

5

6

7 These changes won t just affect the wealthy as the government has implied. they directly target small business owners who make daily sacrifices to keep their businesses alive, support their families and create jobs in their communities.

and to repay debt accrued during their studies.")

8 Physicians are up in arms because they do not have pensions or benefits and the tax changes will make it near impossible for them to save for retirement, to finance maternity or parental leave, to work part time while raising a family (or support a spouse doing so) and to repay debt accrued during their studies.

9 It is the farmers, mom and pop shops, and entrepreneurs, who invested everything into their businesses, that will be most affected by these changes.

10

11

12

13 Krista Ross CEO of the Fredericton Chamber of Commerce Characterizing the last 45 years of Canadian tax policy as loopholes is insulting to businesses that have worked within the rules in good faith to build their businesses, to save for retirement, and sometimes just to keep their doors open.

14

15

16 John Nicola Chairman & CEO

Change of tax rates")

17 Higher Taxes Actual and Possible Results % higher marginal tax over $200,000 Higher provincial rates in Ontario %>$220,000 Overall tax on first $200,000 lower Reduced TFSAs to $5500 No Income splitting of salaries Stock options fully taxed over $100,000 per year (may have different rules for CCPCs) Change of tax rates for professional corporations and ability to income split? 4% higher corporate tax on passive income

Change of")

18 Tax Reform 2017 Resurrected and improved Actual and Possible Results % higher marginal tax over $200,000 Higher provincial rates in Ontario %>$220,000 Overall tax on first $200,000 lower Reduced TFSAs to $5500 No Income splitting of salaries Stock options fully taxed over $100,000 per year (may have different rules for CCPCs) Change of tax rates for professional corporations and ability to income split? 4% higher corporate tax on passive income

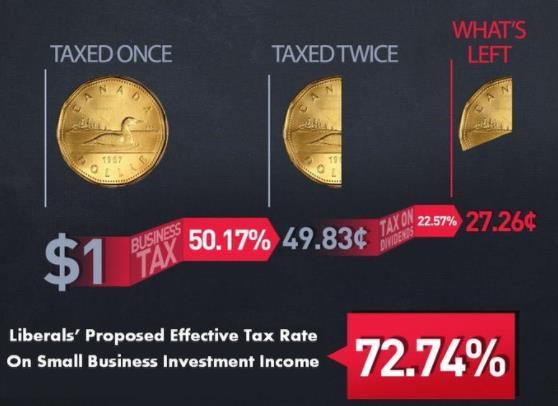

19 Tax Reform 2017 What s being plucked? Income Splitting of Dividends from private corporations Increase tax on passive corporate income that could reach 72% when paid out as dividends Pipeline planning that converts dividends to capital gains is prevented

20 And Now The Rest of The Story Paul Harvey

21 n 25% swing in 100 years Rising since the 70 s 10 developed countries either less upwardly mobile or less equal in income than us or both

Investable Net worth about")

22 Who are the 1% Who Are The 1%? 135,000 Households Average income $500,000+( based on $458,000 for 2013) Investable Net worth about $4Million Currently pay 20% of all personal income tax in Canada Equal to 11% of all businesses in Canada and 5% of self-employed Assuming 2/3rds of the 1% are professionals or business owners, then only 7% of all incorporated entities are owned by the 1% (93% are not)

23 Retiring MPs 3% per year of service Indexed for life Survivor benefits Cost for each $1000/year of annuity=$21000 (Couple age 65) Biggest pension $132,000/year =$2.8Million Income can be split for tax purposes with a spouse No tax on accumulation during working lifetime or until pension starts MP s fund less than 10% of the cost

Pension is split for tax purposes; therefore no OAS clawback First year retired income = $140,000/year ($70,000 each) Annual income tax (assume no other")

24 Indexed Pensions The Case of the retired Civil Servant Assumptions and Results Both age 65 Both worked but only one has a pension Pension is $100,000/year indexed with Survivor benefits Both get full CPP/ OAS (about $20,000/ year each indexed) Pension is split for tax purposes; therefore no OAS clawback First year retired income = $140,000/year ($70,000 each) Annual income tax (assume no other income) = $14,000 Average tax rate 20% Net spendable indexed income $112,000/year ($9300/month) Replacement Cost of all pensions combined = $3 Million (approx) Q: How much of these assets are part of their official net worth? A: Zero

25 What Else is in The Rest of the Story?

26 The Doctor and The Civil Servant Cheryl finishes residency at age 30 Starts GP practice with student debt of $175,000 Practice grosses $350,000 per year Overhead is 40% Starts taking salary to maximize RRSP s Is able to leave $50,000 per year in medco to save for retirement and future maternity leaves and payoff student debt. Bob graduates with B Comm. and joins civil service age 25 Entry level salary is $40,000/year Gets MBA at age 30 Moves up the ranks to ADM by age 50 Retires age 60 with salary of $200,000 per year Indexed pension at age 60 is $133,000/year

27 What Else Do We Need To Know? Bob s pension is fully guaranteed. No investment risk. To fund Bob s pension at 4% real rate of return is takes 50%+ of career income. If Bob s option is RRSP or DC pension his maximum contribution employer / employee is 18% of his salary or 36% of what his pension will be. The tax rate on this additional saving is 0% when earned and 0% when accumulating. Medcos tax rate is 13% when earned and 50% when accumulating. Cheryl funds 100% of savings for retirement and accepts risk on returns. Expected RRSP balance for Cheryl age 60 is $1.5M. Value of Medco savings $1.4M. Total $2.9M or 90% of the value of Bob s pension. Cheryl has to fund 100% of sick pay, holiday pay, maternity leave, health benefits. When Bob retires he lowers his tax by splitting pension income with his spouse. He can split income at 60. Jane has to wait until age 65

28 The Cost of Pensions

29 23 CEOs of Canadian Public Companies All of them have accrued pension benefits worth more than $10M Average for all 23 is $23M Total accrued benefits are $528M This does not include the present value of other benefits (such as health care) The total does not include the value of pensions or benefits for other senior management

30 Who is Getting the Benefit of Deferring Taxable Income? Private vs. Public Asset Accumulation in Tax-Deferred Plans Private companies are limited to statutory levels of RRSP s or IPP s Beyond that private companies use Retirement Compensation Arrangements (RCA s) to accumulate additional retirement assets (subject to a 50% withholding tax) Pension income received from public companies can be income split between employee and spouse. Private companies cannot accumulate this level of tax deferred pension or health benefits for either staff or shareholders. Public companies can use stock options to provide deferred compensation benefits taxed at 50% of regular income. Public companies pay tax at 26% on passive income or about half what private companies pay. Owner managers and professionals pay 100% of the cost of their retirement savings, heath benefits, CPP, and cannot receive UIC or Worker s compensation.

Sell to Jane $100,000 $470,000")

31 Selling the Family business $1,100,000 $730,000 Armco John Jane Sell to Armco Opco ($1.2M) Sell to Jane $100,000 $470,000 Government Aka Mordor

32 Selling the Family Farm Jim and Rita Luke $2M Farmco ($2M) Common shares $80,000 Annually 2017 $17, $33,500 Government Aka Mordor

33 Die With Their Boots On? +65% What price will sellers get if the tax cost selling to family is 400%+ More? -25%

34 Dead Money?

35 Morneau says tax changes will target dead money Small Business Who is hoarding the money? Public Companies $630 billion on balance sheets in % = 22% = 72% = Corporate Tax Personal Tax Total Tax = 26% = 23% = 49% How level is this playing field?

36 Taxable Income for a Balanced Portfolio 50% Return Breakdown Capital Gains 1.5% Deferred Gains 2.5% 0% 67% Dividends 1.0% 100% Interest, Rent, Foreign 2.0% Return of Capital 1.0% 0% Total return = 8% Taxable this year = 3.5%

Current Taxation Corporate Tax 49.7% $52,200 RDTOH 30.")

37 Tax Options for Passive Corporate Accounts $3-million value Total Return = $240,000 Taxable Return = $105,000 Total tax LRIP $54,900 (52.2%) Total tax GRIP $46,600 (44.4%) Current Taxation Corporate Tax 49.7% $52,200 RDTOH 30.7% $32,200 Net Corp Tax 19.0% $20,000 Dividend Paid to recover RDTOH $85,000 Personal tax (LRIP) -41.0% $34,900 Personal tax (GRIP)-31.0% $26,600

38 Tax Options for Passive Corporate Accounts $3-million value Total Return = $240,000 Taxable Return = $105,000 Blended Tax = 72% No CDA / RDTOH Dividend taxed at 41% personally

39 Longer Term Impact? What is longer term impact? Assume: 100% of taxable income left in corporation now 50% tax paid on earnings Dividends not used for compensation until retirement (then taxed as high as 41%) Impact on spendable returns after twenty years 70bps-100bps drop in net annual return if all income taxed corporately

40 Tax Options for Passive Corporate Accounts $3-million value Total Return = $240,000 Taxable Return = $105,000 Options to reduce or eliminate taxable income: Pay bonuses or salaries Make Charitable gifts Offset with interest expense Portfolio design Reasonableness will be a requirement

41 Individual Pension Plans

42 New IPP Age 60: Maximum Income & Past Service New IPP in Year Old Value of Pension ( ) Transfer From Employee s RRSP Employer Past Service Contribution 2017 Current Service Contribution 2017 Terminal Funding Total funding available Contributions $ 800,000 $ (490,000) $ 310,000 $ 40,000 $ 1,200,000 $ 1,550,000

43 IPP vs. RRSP: Terminal Funding at 65 Total funding $1,550,000 $1,200,000 $1,550,000 $26,000 $40,000 $310,000 RRSP IPP current IPP past service Terminal funding IPP total

44 IPP yes or no? Issues Limited to RRSP eligible assets Fully taxable in estate on second death (insured version is an option) Restricted liquidity When income received, it can be split with spouse. Future earnings to age 71 can be taxdeferred. Contributions tax deductible Offset high rate tax on passive income after retirement? Amortize funding over 10 years or more if required. Trigger pregnant gains in the year IPP funding occurs? Generally better than RRSPs after age 50

45 Is This True?

46 Life Insurance as an Asset Class Is Insurance and expense or asset? Can it be used to create an income during one s lifetime How does it compare to other fixed income asset classes? On risk? On return? How do you maximize benefits of insurance bought for needs?

47 Whole Life Par: The Basics $100,000 $90,000 $80,000 $70,000 $60,000 $50,000 $40,000 $30,000 $20,000 $10,000 $0 Tax Sheltered Tax-free earnings Pay for life insurance Costs and buy additional coverage Excess savings invested in par account

48 How Can Par Outperform Balanced Portfolios? Returns not mark to market Cash value guaranteed Balanced portfolio returns with bond like risk

49 Where Leverage Applies Fully taxable Low risk Borrow Funds BANK Put new capital into lower taxed asset classes

50 Things to Consider LOC better than term loan (flexibility, opportunistic, interest only on borrowed funds). No need to increase risk. Look for assets with high cash flow taxed at lower rates. Examples include rental income (return of capital) and writing calls and puts (capital gains), eligible dividends.

51 Mixing Passive and Active Income OPCO $1,000,000 Profit $3M portfolio $100,000 taxable income 100% Common Family Trust Salaries to maximize RRSPs Additional dividends for inactive spouse GRIP dividends to fund university Recover RDTOH

52 Future Models Investment and business loans in Holdco Distribute taxable income by bonus and IPP contribution Holdco $3M portfolio $75,000 of taxable income Beneficiary Family Trust Charitable Gifts Salaries at reasonable levels Fund balance of IPP OPCO $1,000,000 Profit No dividends Does loan to trust at prescribed rate work?

53 Pushback? Morneau dialed in to a conference call Thursday to reassure nervous MPs that the changes would not be applied retroactively, and business owners who use the system to plan for retirement wouldn't see any changes to their current nest egg. Rather, the changes would apply on investments moving forward.

54 Grandfathering? Will existing corporate passive assets continue to taxed under current rules? What about any earnings from those assets? Will CDA and RDTOH balances be kept? What about with respect to future RDTOH/CDA triggered by current assets? Will income splitting be allowed on current passive assets? What does reasonable mean? What financial organizations are able to track old and new assets within the same corporation for reporting purposes? (We would set up separate accounts.)

55

56

57 From Now On The Consequences Are Intentional Liberals have been told the following: Doctors and other professionals leaving Canada Private Corp vs. Public Corp tax rates on passive income Higher tax to transfer business and farms to family vs. strangers Recognition of spouse financial and labour involvement in CCPC Tax advantages they enjoy with DB pension plans Submissions have been made so far

58 What Questions Need To Be Asked? 1. Tax Freedom Day is June 8. Is that too soon or too late (U.S. April 24)? 2. The top 1% of tax filers pay 21% of all income tax. Is that too much or not enough? 3. If we are going to increase our tax burden should it be consumption taxes (GST), corporate taxes, or personal? 4. Can a consensus about approach become Tri-Partisan?

59 Tax Reform 2017 What might you want to do? 1. Maximize the use of Individual Pension Plans (IPPs) 2. Consider the use of a Retirement Compensation Arrangement (RCA) 3. Reduce taxable passive income inside a corporation by looking at how the returns are taxed 4. Combine existing or new insurance with leverage corporately 5. Hold off on triggering pregnant gains on corporate assets until after new rules are known 6. Lock in any loan arrangements to trusts or family at current prescribed rates 7. Review different approaches to sale of business once final rules are clear

60 Next Steps? Bespoke is an adjective for anything commissioned to a particular specification. "Custom-made." Solutions will differ for each family and also change over time. A custom approach is required.

61 THANK YOU

62 Question & Answer

CONTENTS VOLUME II VOLUME I. The detailed contents of both Volume I and II follow. The textbook is published in two Volumes:

CONTENTS The textbook is published in two Volumes: Volume I = Chapters 1 to 10 Volume II = Chapters 11 to 21 Chapter I Chapter II 1 Introduction To Federal Taxation In Canada 11 Taxable Income and Tax

CONTENTS The textbook is published in two Volumes: Volume I = Chapters 1 to 10 Volume II = Chapters 11 to 21 Chapter I Chapter II 1 Introduction To Federal Taxation In Canada 11 Taxable Income and Tax

How Finance s new proposals will affect tax planning for private companies. 1 August, 2017

How Finance s new proposals will affect tax planning for private companies 1 August, 2017 Today s presenters Gabriel Baron Tax Partner Private Client Services practice EY Ryan Ball Tax Partner Private

How Finance s new proposals will affect tax planning for private companies 1 August, 2017 Today s presenters Gabriel Baron Tax Partner Private Client Services practice EY Ryan Ball Tax Partner Private

CONTENTS VOLUME II VOLUME I. The detailed contents of both Volume I and II follow. The textbook is published in two Volumes:

CONTENTS The textbook is published in two Volumes: Volume I = Chapters 1 to 10 Volume II = Chapters 11 to 21 Chapter I Chapter II 1 Introduction To Federal Taxation In Canada 11 Taxable Income and Tax

CONTENTS The textbook is published in two Volumes: Volume I = Chapters 1 to 10 Volume II = Chapters 11 to 21 Chapter I Chapter II 1 Introduction To Federal Taxation In Canada 11 Taxable Income and Tax

Tax & estate planning update. Agenda. GOLOMBEK January Jamie Golombek - Managing Director, Tax & Estate Planning

Tax & estate planning update Jamie Golombek - Managing Director, Tax & Estate Planning Ottawa Estate Planning Council January 6, 2016 Agenda 1 1. Canadian tax update for individuals 2. Canadian tax update

Tax & estate planning update Jamie Golombek - Managing Director, Tax & Estate Planning Ottawa Estate Planning Council January 6, 2016 Agenda 1 1. Canadian tax update for individuals 2. Canadian tax update

Individual Pension Plans

Integrating IPPs in Fiscal and Retirement Planning June 16, 2010 IPPs Highlights Greater tax-sheltering than RRSPs Contributions and expenses are tax deductible May make up for investment losses Funds

Integrating IPPs in Fiscal and Retirement Planning June 16, 2010 IPPs Highlights Greater tax-sheltering than RRSPs Contributions and expenses are tax deductible May make up for investment losses Funds

Retiring Right: Understanding the Taxation of Retirement Income

January 2019 Retiring Right: Understanding the Taxation of Retirement Income Jamie Golombek & Tess Francis Tax & Estate Planning, CIBC Financial Planning and Advice The question isn't at what age I want

January 2019 Retiring Right: Understanding the Taxation of Retirement Income Jamie Golombek & Tess Francis Tax & Estate Planning, CIBC Financial Planning and Advice The question isn't at what age I want

REGISTERED RETIREMENT SAVINGS PLAN

REGISTERED RETIREMENT SAVINGS PLAN The 2014 RRSP contribution deadline is March 2, 2015 Registered Retirement Savings Plans (RRSPs) are an important financial and taxplanning vehicle to encourage retirement

REGISTERED RETIREMENT SAVINGS PLAN The 2014 RRSP contribution deadline is March 2, 2015 Registered Retirement Savings Plans (RRSPs) are an important financial and taxplanning vehicle to encourage retirement

CONTENTS CHAPTER 1. CHAPTER 1, continued CHAPTER 2. Introduction To Federal Taxation In Canada. Income Or Loss From An Office Or Employment.

xvii CONTENTS CHAPTER 1 Introduction To Federal Taxation In Canada The Canadian Tax System.......... 1 Alternative Tax Bases.......... 1 Taxable Entities In Canada........ 2 Federal Taxation And The Provinces....

xvii CONTENTS CHAPTER 1 Introduction To Federal Taxation In Canada The Canadian Tax System.......... 1 Alternative Tax Bases.......... 1 Taxable Entities In Canada........ 2 Federal Taxation And The Provinces....

CONTENTS VOLUME II VOLUME I. The detailed contents of both Volume I and II follow. The textbook is published in two Volumes:

CONTENTS The textbook is published in two Volumes: Volume I = Chapters 1 to 10 Volume II = Chapters 11 to 21 Chapter I Chapter II 1 To Federal Taxation In Canada 11 Taxable Income and Tax Payable For Individuals

CONTENTS The textbook is published in two Volumes: Volume I = Chapters 1 to 10 Volume II = Chapters 11 to 21 Chapter I Chapter II 1 To Federal Taxation In Canada 11 Taxable Income and Tax Payable For Individuals

Recent Tax Developments Impacting Insurance Planning

Recent Tax Developments Impacting Toronto, LL.B, CLU, TEP Overview Exempt Test Update New Charitable Gifting Legislation Trust Legislation LIA Grandfathering CRA Update Life insurance in spousal trusts

Recent Tax Developments Impacting Toronto, LL.B, CLU, TEP Overview Exempt Test Update New Charitable Gifting Legislation Trust Legislation LIA Grandfathering CRA Update Life insurance in spousal trusts

Ideally your contribution should be made as soon as possible in the year in order to shelter the investment income from tax.

Maximize RRSP Contributions. You should make your maximum RRSP contribution while you are working. You will get a tax deduction now at your current tax rate and you will be able to take the money out later

Maximize RRSP Contributions. You should make your maximum RRSP contribution while you are working. You will get a tax deduction now at your current tax rate and you will be able to take the money out later

CHAPTER 2 CHAPTER 1. Procedures And Administration. Introduction To Federal Taxation In Canada. xviii Table Of Contents (Volume 1)

") xviii Table Of Contents (Volume 1) CHAPTER 1 Introduction To Federal Taxation In Canada The Canadian Tax System.......... 1 Alternative Tax Bases.......... 1 Taxable Entities In Canada........ 2 Federal

xviii Table Of Contents (Volume 1) CHAPTER 1 Introduction To Federal Taxation In Canada The Canadian Tax System.......... 1 Alternative Tax Bases.......... 1 Taxable Entities In Canada........ 2 Federal

INCORPORATING YOUR FARM BUSINESS

INCORPORATING YOUR FARM BUSINESS If you carry on a farm business, and have significant income, transferring the farm business to a corporation may provide some benefits as there are tax planning opportunities

INCORPORATING YOUR FARM BUSINESS If you carry on a farm business, and have significant income, transferring the farm business to a corporation may provide some benefits as there are tax planning opportunities

Marital Status Single Married Common law Widowed

FINANCIAL PLANNING INFORMATION Date: IA Name: FPS Name: PERSONAL INFORMATION First name Last name Marital Status Single Married Common law Widowed Separated Divorced Date of birth Retirement age Date of

FINANCIAL PLANNING INFORMATION Date: IA Name: FPS Name: PERSONAL INFORMATION First name Last name Marital Status Single Married Common law Widowed Separated Divorced Date of birth Retirement age Date of

TAX PLANNING USING PRIVATE CORPORATIONS

TAX PLANNING USING PRIVATE CORPORATIONS A review of the July 18, 2017 proposals from the Department of Finance Jennifer Dunn, CPA, CA, TEP September 29, 2017 TAX PLANNING USING PRIVATE CORPORATIONS INCOME

TAX PLANNING USING PRIVATE CORPORATIONS A review of the July 18, 2017 proposals from the Department of Finance Jennifer Dunn, CPA, CA, TEP September 29, 2017 TAX PLANNING USING PRIVATE CORPORATIONS INCOME

10 Strategies to Pay Less Tax and Invest Wisely in Retirement

10 Strategies to Pay Less Tax and Invest Wisely in Retirement Agenda Overview, background 10 key strategies to minimize taxes and invest wisely in retirement 1. Spousal RRSPs 2. Tax-preferred investment

10 Strategies to Pay Less Tax and Invest Wisely in Retirement Agenda Overview, background 10 key strategies to minimize taxes and invest wisely in retirement 1. Spousal RRSPs 2. Tax-preferred investment

2018 Proposed Tax Changes. Holm Raiche Oberg Chartered Professional Accountants P.C. Ltd.

2018 Proposed Tax Changes Holm Raiche Oberg Chartered Professional Accountants P.C. Ltd. Introduction Who am I? I am not tiny! Came from truck drivers Dad told me to sit in a different chair NOT POLITICALLY

2018 Proposed Tax Changes Holm Raiche Oberg Chartered Professional Accountants P.C. Ltd. Introduction Who am I? I am not tiny! Came from truck drivers Dad told me to sit in a different chair NOT POLITICALLY

Owner-Manager Remuneration Update

Owner-Manager Remuneration Update Don Desaulniers and Kevin Stienstra Grant Thornton LLP Toronto Presentation Overview Summary of rate changes Ontario integration Salary vs Dividend planning Remuneration

Owner-Manager Remuneration Update Don Desaulniers and Kevin Stienstra Grant Thornton LLP Toronto Presentation Overview Summary of rate changes Ontario integration Salary vs Dividend planning Remuneration

2013 Personal Income Tax Update

2013 Personal Tax Presentation February 12, 2013 TITLE September 21, 2012 2013 Personal Income Tax Update Presented by: Kris Wirk Phone Number: 250 220 7311 Email: k.wirk@ddwca.com The enclosed presentation

2013 Personal Tax Presentation February 12, 2013 TITLE September 21, 2012 2013 Personal Income Tax Update Presented by: Kris Wirk Phone Number: 250 220 7311 Email: k.wirk@ddwca.com The enclosed presentation

CTF Policy Conference on Tax Planning Using Private Corporations (September 25, 2017): Questions from Participants

: Questions from Participants") 1 CTF Policy Conference on Tax Planning Using Private Corporations (September 25, 2017): Questions from Participants A. General 1. On what date will the new passive income rules become effective? When

1 CTF Policy Conference on Tax Planning Using Private Corporations (September 25, 2017): Questions from Participants A. General 1. On what date will the new passive income rules become effective? When

Navigator. Incorporating your farm. The. Is it right for you? Please contact us for more information about the topics discussed in this article.

The Navigator INVESTMENT, TAX AND LIFESTYLE PERSPECTIVES FROM RBC WEALTH MANAGEMENT SERVICES Incorporating your farm Is it right for you? On July 18, 2017 the federal government released a consultation

The Navigator INVESTMENT, TAX AND LIFESTYLE PERSPECTIVES FROM RBC WEALTH MANAGEMENT SERVICES Incorporating your farm Is it right for you? On July 18, 2017 the federal government released a consultation

Looking back to 2013 and FORWARD TO 2014

YEAR-END TAX PLANNER 2013/2014 IN THIS ISSUE Federal Highlights 1 Provincial Highlights 1 Sales Tax Highlights 1 International Highlights 2 Entrepreneurs 2 Personal Tax Matters 4 United States Matters

YEAR-END TAX PLANNER 2013/2014 IN THIS ISSUE Federal Highlights 1 Provincial Highlights 1 Sales Tax Highlights 1 International Highlights 2 Entrepreneurs 2 Personal Tax Matters 4 United States Matters

Current Income Tax Issues for Agriculture

Current Income Tax Issues for Agriculture Presented by Vern H. Peters, CPA, CA Tax Partner (2016/01/26) Current Income Tax Issues > Incorporation > Succession > Exit 1 Incorporation Incorporation > In

Current Income Tax Issues for Agriculture Presented by Vern H. Peters, CPA, CA Tax Partner (2016/01/26) Current Income Tax Issues > Incorporation > Succession > Exit 1 Incorporation Incorporation > In

Tax & Estate Planning for HNW Clients

Tax & Estate Planning for HNW Clients October 11, 2012 Wood Gundy National Business Conference Jamie Golombek Managing Director CIBC Private Wealth Management High Net Worth Integrated Advisory Offer Bringing

Tax & Estate Planning for HNW Clients October 11, 2012 Wood Gundy National Business Conference Jamie Golombek Managing Director CIBC Private Wealth Management High Net Worth Integrated Advisory Offer Bringing

SAMPLE PLAN FOR ILLUSTRATIVE PURPOSES ONLY

RBC Wealth Management Prepared exclusively for Bob and Mary Smith Halifax, Nova Scotia January 2017 Prepared by: The Wealth Management Services Team and John Bell RBC Wealth Management Table of Contents

RBC Wealth Management Prepared exclusively for Bob and Mary Smith Halifax, Nova Scotia January 2017 Prepared by: The Wealth Management Services Team and John Bell RBC Wealth Management Table of Contents

AGENDA: Introduction Income Sprinkling Family Trusts Passive Investment Income Q&A

AGENDA: Introduction Income Sprinkling Family Trusts Passive Investment Income Q&A Introduction Allan Madan o CPA, CA Income Sprinkling Definition: o Tax strategy used to distribute income among family

AGENDA: Introduction Income Sprinkling Family Trusts Passive Investment Income Q&A Introduction Allan Madan o CPA, CA Income Sprinkling Definition: o Tax strategy used to distribute income among family

TAX TIPS. Audit Tax Advisory

Audit Tax Advisory TAX TIPS Crowe Soberman LLP Join our online community In this issue: Investment income 3 Facebook.com/CroweSoberman On Crowe Soberman s Facebook page, you can stay in the loop with the

Audit Tax Advisory TAX TIPS Crowe Soberman LLP Join our online community In this issue: Investment income 3 Facebook.com/CroweSoberman On Crowe Soberman s Facebook page, you can stay in the loop with the

Looking back to 2011 and FORWARD TO 2012

December 2011 YEAR-END TAX PLANNER 2011/2012 IN THIS ISSUE Federal Highlights 1 Provincial Highlights 1 Entrepreneurs 1 Personal Tax Matters 2 United States Matters 5 International Matters 5 Key Tax Dates

December 2011 YEAR-END TAX PLANNER 2011/2012 IN THIS ISSUE Federal Highlights 1 Provincial Highlights 1 Entrepreneurs 1 Personal Tax Matters 2 United States Matters 5 International Matters 5 Key Tax Dates

Year-End Tax Planner Our latest ideas and tips in reducing your 2018 tax burden

www.segalllp.com December 2018 Year-End Tax Planner Our latest ideas and tips in reducing your 2018 tax burden Welcome! Dear clients and friends, as we approach the end of another year, now would be a

www.segalllp.com December 2018 Year-End Tax Planner Our latest ideas and tips in reducing your 2018 tax burden Welcome! Dear clients and friends, as we approach the end of another year, now would be a

TAX LETTER. January 2016

TAX LETTER January 2016 DRAFT LEGISLATION FOR 2016 TAX CHANGES FINANCE PROPOSES CHANGES TO RULES GOVERNING SPOUSAL AND SIMILAR TRUSTS TAX-FREE TRANSFERS OF PROPERTY TO YOUR CORPORATION CAPITAL DIVIDENDS

TAX LETTER January 2016 DRAFT LEGISLATION FOR 2016 TAX CHANGES FINANCE PROPOSES CHANGES TO RULES GOVERNING SPOUSAL AND SIMILAR TRUSTS TAX-FREE TRANSFERS OF PROPERTY TO YOUR CORPORATION CAPITAL DIVIDENDS

Tax Toolkit TAX PLANNING

2017-2018 Tax Toolkit TAX PLANNING More opportunities for tax savings Contents More opportunities for tax savings 2 Jamie Golombek s tax tips 3 Not all fund distributions are created equal 4 Understanding

2017-2018 Tax Toolkit TAX PLANNING More opportunities for tax savings Contents More opportunities for tax savings 2 Jamie Golombek s tax tips 3 Not all fund distributions are created equal 4 Understanding

Personal Financial Plan

Personal Financial Plan Pete and Carrie Mitchell 918 Richmond Street Toronto, Ontario M5N 1V5 Disclaimer This document has been prepared to assist in the analysis of your current financial position, thereby

Personal Financial Plan Pete and Carrie Mitchell 918 Richmond Street Toronto, Ontario M5N 1V5 Disclaimer This document has been prepared to assist in the analysis of your current financial position, thereby

10/23/17 THE POTENTIAL IMPACT OF THE JULY 18, 2017 PROPOSED TAX CHANGES. Prepared for: 2017 CPA FORUM NORTH

THE POTENTIAL IMPACT OF THE JULY 18, 2017 PROPOSED TAX CHANGES Prepared for: 2017 CPA FORUM NORTH Jasper October 23, 2017 K. John Fuller, CPA, CA Jason Pisesky Page 2 Page 3 1 OVERVIEW OF PROPOSED AMENDMENTS

THE POTENTIAL IMPACT OF THE JULY 18, 2017 PROPOSED TAX CHANGES Prepared for: 2017 CPA FORUM NORTH Jasper October 23, 2017 K. John Fuller, CPA, CA Jason Pisesky Page 2 Page 3 1 OVERVIEW OF PROPOSED AMENDMENTS

INCORPORATING YOUR FARM BUSINESS

INCORPORATING YOUR FARM BUSINESS If you carry on a farm business, and have significant income, transferring the farm business to a corporation may provide some benefits as there are tax planning opportunities

INCORPORATING YOUR FARM BUSINESS If you carry on a farm business, and have significant income, transferring the farm business to a corporation may provide some benefits as there are tax planning opportunities

Owner-Manager Tax Planning 5 th Annual Tax Planning for the Wealthy Family

Owner-Manager Tax Planning 5 th Annual Tax Planning for the Wealthy Family James A. Hutchinson Miller Thomson LLP 416.597.4381 jhutchinson@millerthomson.com Wednesday, September 9, 2009 1 Overview 1. Personal

Owner-Manager Tax Planning 5 th Annual Tax Planning for the Wealthy Family James A. Hutchinson Miller Thomson LLP 416.597.4381 jhutchinson@millerthomson.com Wednesday, September 9, 2009 1 Overview 1. Personal

Pension Plan for Faculty, Librarians and Senior Administrative Officers of Mount Allison University

Pension Plan for Faculty, Librarians and Senior Administrative Officers of Mount Allison University DEC, 2014 CONTENTS INTRODUCTION... i YOUR RESPONSIBILITIES... ii 1. Am I eligible to join the Pension

Pension Plan for Faculty, Librarians and Senior Administrative Officers of Mount Allison University DEC, 2014 CONTENTS INTRODUCTION... i YOUR RESPONSIBILITIES... ii 1. Am I eligible to join the Pension

TAX & ESTATE PLANNING FOR BUSINESS OWNERS. Wilmot George, CFP, TEP, CHS Director, Tax and Estate Planning

TAX & ESTATE PLANNING FOR BUSINESS OWNERS Wilmot George, CFP, TEP, CHS Director, Tax and Estate Planning Canadian Small Business Some Stats 1 98% of all employer businesses are small businesses (2010)

TAX & ESTATE PLANNING FOR BUSINESS OWNERS Wilmot George, CFP, TEP, CHS Director, Tax and Estate Planning Canadian Small Business Some Stats 1 98% of all employer businesses are small businesses (2010)

Pensions Part 2 Defined Contribution Plans

June 3, 2010 Pensions Part 2 Defined Contribution Plans This article is the second part of a four-part series on employer retirement plans. Due to the complexity and variety of employer retirement plans,

June 3, 2010 Pensions Part 2 Defined Contribution Plans This article is the second part of a four-part series on employer retirement plans. Due to the complexity and variety of employer retirement plans,

2012 Year End Tax Tips

2012 Year End Tax Tips Jamie Golombek November 2012 It s the most wonderful time of the year! That s right, time to start your year-end tax planning so that any strategies that need to be implemented by

2012 Year End Tax Tips Jamie Golombek November 2012 It s the most wonderful time of the year! That s right, time to start your year-end tax planning so that any strategies that need to be implemented by

GREYHOUND WESTERN EMPLOYEES RETIREMENT INCOME PLAN YOUR PENSION PLAN SUMMARY

GREYHOUND WESTERN EMPLOYEES RETIREMENT INCOME PLAN YOUR PENSION PLAN SUMMARY November 2003 GREYHOUND WESTERN EMPLOYEES RETIREMENT INCOME PLAN PENSION PLAN SUMMARY YOUR RETIREMENT PLAN The Greyhound Western

GREYHOUND WESTERN EMPLOYEES RETIREMENT INCOME PLAN YOUR PENSION PLAN SUMMARY November 2003 GREYHOUND WESTERN EMPLOYEES RETIREMENT INCOME PLAN PENSION PLAN SUMMARY YOUR RETIREMENT PLAN The Greyhound Western

Tax Refresher for Advisors

Tax Refresher for Advisors Canadian income tax basics 1 Ian Tod, MBA, CFP, CLU Advanced Case Specialist, National Robert Hurdman, CFP Investment Specialist, Western Canada 2 Agenda 1 2 3 4 5 Progressive

Tax Refresher for Advisors Canadian income tax basics 1 Ian Tod, MBA, CFP, CLU Advanced Case Specialist, National Robert Hurdman, CFP Investment Specialist, Western Canada 2 Agenda 1 2 3 4 5 Progressive

A plain language review of the proposed tax legislation

A plain language review of the proposed tax legislation (and how it affects your clients) Wednesday October 11, 2017 7:30-9:30am Agenda 2 1 INTRO 5 TAX ON SPLIT INCOME 2 REVIEW OF POLICY CONCERNS 6 CAPITAL

A plain language review of the proposed tax legislation (and how it affects your clients) Wednesday October 11, 2017 7:30-9:30am Agenda 2 1 INTRO 5 TAX ON SPLIT INCOME 2 REVIEW OF POLICY CONCERNS 6 CAPITAL

2000 Academic Money Purchase Pension Plan

2000 Academic Money Purchase Pension Plan TABLE OF CONTENTS Introduction... 2 Eligibility... 2 Enrolling in the Plan... 2 Contributions... 2 Other Contributions... 3 Retirement Benefits... 4 Retirement

2000 Academic Money Purchase Pension Plan TABLE OF CONTENTS Introduction... 2 Eligibility... 2 Enrolling in the Plan... 2 Contributions... 2 Other Contributions... 3 Retirement Benefits... 4 Retirement

Tax Planning for Business Owners:

Tax Planning for Business Owners: 2017-18 If you make your daily bread in the business world as a self-employed person or corporate business owner, you have many opportunities to consider when it comes

Tax Planning for Business Owners: 2017-18 If you make your daily bread in the business world as a self-employed person or corporate business owner, you have many opportunities to consider when it comes

What is incorporation?

The Navigator INVESTMENT, TAX AND LIFESTYLE PERSPECTIVES FROM RBC WEALTH MANAGEMENT SERVICES Professional corporations Is incorporating your professional practice right for you? Bola Wealth Management

The Navigator INVESTMENT, TAX AND LIFESTYLE PERSPECTIVES FROM RBC WEALTH MANAGEMENT SERVICES Professional corporations Is incorporating your professional practice right for you? Bola Wealth Management

INCORPORATING YOUR BUSINESS

INCORPORATING YOUR BUSINESS If you carry on a business, there are many tax planning opportunities which become available to you by simply incorporating. By transferring your business to a corporation,

INCORPORATING YOUR BUSINESS If you carry on a business, there are many tax planning opportunities which become available to you by simply incorporating. By transferring your business to a corporation,

IPPs: Frequently Asked Questions

RBC Dominion Securities Inc. Individual Pension Plans (IPP) IPPs: Frequently Asked Questions General IPP Questions 1 2 3 4 5 6 7 8 9 10 What is an IPP? What is a defined benefit pension plan? Who calculates

RBC Dominion Securities Inc. Individual Pension Plans (IPP) IPPs: Frequently Asked Questions General IPP Questions 1 2 3 4 5 6 7 8 9 10 What is an IPP? What is a defined benefit pension plan? Who calculates

Proposed Tax Changes for Private Corporations

SEPTEMBER 2017 Drew Jackiw CPA, CA Partner Ryan Dorton, CPA, CA Partner www.jmhca.com Agenda 1. Background 2. Key Features of the Income Tax System 3. Tax Planning Strategies a) Income Sprinkling b) Passive

SEPTEMBER 2017 Drew Jackiw CPA, CA Partner Ryan Dorton, CPA, CA Partner www.jmhca.com Agenda 1. Background 2. Key Features of the Income Tax System 3. Tax Planning Strategies a) Income Sprinkling b) Passive

INDEX. Segregated funds, Structured pre-1990 contracts, settlements deferred annuities, accrual taxation rules,

INDEX 21-year deemed disposition rule, 328 329 Crummey trust and, 353 A Accounting for life insurance, 224 226 Accounting standards, 71 72 Accrual reporting annuities, 431 433 keyperson insurance strategy

INDEX 21-year deemed disposition rule, 328 329 Crummey trust and, 353 A Accounting for life insurance, 224 226 Accounting standards, 71 72 Accrual reporting annuities, 431 433 keyperson insurance strategy

YEAR-END INCOME TAX STRATEGIES FOR 2017 Tax and Estate Reports November 2017

YEAR-END INCOME TAX STRATEGIES FOR 2017 Tax and Estate Reports November 2017 As the holiday season approaches most of us are focused on spending time with family and friends. It s also the opportune time

YEAR-END INCOME TAX STRATEGIES FOR 2017 Tax and Estate Reports November 2017 As the holiday season approaches most of us are focused on spending time with family and friends. It s also the opportune time

TAX LETTER. April 2014

TAX LETTER April 2014 FEDERAL BUDGET TAX HIGHLIGHTS CHARITABLE DONATIONS MADE BY YOUR ESTATE ALLOWABLE BUSINESS INVESTMENT LOSSES TAX-FREE GIFTS FOR EMPLOYEES CAPITAL GAINS SPLITTING WITH YOUR MINOR CHILDREN

TAX LETTER April 2014 FEDERAL BUDGET TAX HIGHLIGHTS CHARITABLE DONATIONS MADE BY YOUR ESTATE ALLOWABLE BUSINESS INVESTMENT LOSSES TAX-FREE GIFTS FOR EMPLOYEES CAPITAL GAINS SPLITTING WITH YOUR MINOR CHILDREN

Update on the CCPC tax proposals December 2017

Update on the CCPC tax proposals December 2017 Debbie Pearl-Weinberg Executive Director, Tax and Estate Planning, CIBC Financial Planning and Advice Jamie Golombek Managing Director, Tax & Estate Planning,

Update on the CCPC tax proposals December 2017 Debbie Pearl-Weinberg Executive Director, Tax and Estate Planning, CIBC Financial Planning and Advice Jamie Golombek Managing Director, Tax & Estate Planning,

Welcome: Proposed Tax Changes for Private Corporations

Welcome: Proposed Tax Changes for Private Corporations WEBINAR: Proposed Tax Changes for Private Corporations September 18, 2017 2:30-4:30 PM EST Registration URL: https://attendee.gotowebinar.com/register/5371598472188728579

Welcome: Proposed Tax Changes for Private Corporations WEBINAR: Proposed Tax Changes for Private Corporations September 18, 2017 2:30-4:30 PM EST Registration URL: https://attendee.gotowebinar.com/register/5371598472188728579

Planning to retire on a low income: What you need to know. October 3, 2018 Don Mills Library John Stapleton

Planning to retire on a low income: What you need to know October 3, 2018 Don Mills Library John Stapleton Topics 1. What seniors get in Ontario 2. What does low income mean? 3. What does taxable income

Planning to retire on a low income: What you need to know October 3, 2018 Don Mills Library John Stapleton Topics 1. What seniors get in Ontario 2. What does low income mean? 3. What does taxable income

In assessing the benefits of incorporation the following four items represent the most significant tax benefits of incorporation:

Tax Implications of Using a Corporation This summary is intended to provide a general overview of the significant Canadian tax implications of using a corporation to carry on business. Given that the commercial

Tax Implications of Using a Corporation This summary is intended to provide a general overview of the significant Canadian tax implications of using a corporation to carry on business. Given that the commercial

REPORTER SPECIAL EDITION CORPORATE TAXATION UPDATE REVISIONS TO SMALL BUSINESS DEDUCTION

REPORTER SPECIAL EDITION NOV. 2016 ASSURANCE / TAX / BUSINESS ADVISORY SERVICES CORPORATE TAXATION UPDATE REVISIONS TO SMALL BUSINESS DEDUCTION In its budget of March 16, 2016, the Quebec government made

REPORTER SPECIAL EDITION NOV. 2016 ASSURANCE / TAX / BUSINESS ADVISORY SERVICES CORPORATE TAXATION UPDATE REVISIONS TO SMALL BUSINESS DEDUCTION In its budget of March 16, 2016, the Quebec government made

RRSP Contribution Limits Pension Adjustment (PA)... 9 RRSP Contribution Room... 9

... 9 RRSP Contribution Room... 9") Pension Plan for the Eligible Employees at the University of Saskatchewan (Research Pension Plan) Contents Introduction... 2 Eligibility... 2 Enrolling in the Plan... 2 Contributions... 2 Other Contributions...

Pension Plan for the Eligible Employees at the University of Saskatchewan (Research Pension Plan) Contents Introduction... 2 Eligibility... 2 Enrolling in the Plan... 2 Contributions... 2 Other Contributions...

Manitoba Multiple Trades

Manitoba Multiple Trades pension trust fund JUNE 2012 Important note The purpose of this outline is to explain briefly the main features of this pension plan. This outline does not create or confer any

Manitoba Multiple Trades pension trust fund JUNE 2012 Important note The purpose of this outline is to explain briefly the main features of this pension plan. This outline does not create or confer any

Navigator. Incorporate or not? The. Is incorporating your business right for you?

The Navigator INVESTMENT, TAX AND LIFESTYLE PERSPECTIVES FROM RBC WEALTH MANAGEMENT SERVICES Incorporate or not? Is incorporating your business right for you? Bola Wealth Management RBC Dominion Securities

The Navigator INVESTMENT, TAX AND LIFESTYLE PERSPECTIVES FROM RBC WEALTH MANAGEMENT SERVICES Incorporate or not? Is incorporating your business right for you? Bola Wealth Management RBC Dominion Securities

Aging and taxation: Retirement income and age-related tax issues

Tax & Estate Aging and taxation: Retirement income and age-related tax issues We all know the over-worn adage about the inevitability of death and taxes, but just because we recite it doesn t mean we have

Tax & Estate Aging and taxation: Retirement income and age-related tax issues We all know the over-worn adage about the inevitability of death and taxes, but just because we recite it doesn t mean we have

Death and Taxes It s Never Too Early To Plan. Franklin H. Famme, CPA, CA

Death and Taxes It s Never Too Early To Plan Franklin H. Famme, CPA, CA Benjamin Franklin Agenda Understanding Estates Taxes Upon Death Probate Income Tax Taxes After Death Understanding Estates Jointly-Held

Death and Taxes It s Never Too Early To Plan Franklin H. Famme, CPA, CA Benjamin Franklin Agenda Understanding Estates Taxes Upon Death Probate Income Tax Taxes After Death Understanding Estates Jointly-Held

TAX TIPS. Smart Decisions. Lasting Value. Audit Tax Advisory

TAX TIPS Smart Decisions. Lasting Value. Audit Tax Advisory Join our online community In this issue: Investment income 3 Facebook.com/CroweSoberman On Crowe Soberman s Facebook page, you can stay in the

TAX TIPS Smart Decisions. Lasting Value. Audit Tax Advisory Join our online community In this issue: Investment income 3 Facebook.com/CroweSoberman On Crowe Soberman s Facebook page, you can stay in the

RRSP OVERVIEW, STRATEGIES AND TIPS

E.E.S. FINANCIAL SERVICES LTD. 6090 Highway #7 East Markham, Ontario L3P 3B1 905-471-1337 1-866-590-0001 www.ees-financial.com 2017 2018 RRSP OVERVIEW, STRATEGIES AND TIPS Deadline for 2017 contributions

E.E.S. FINANCIAL SERVICES LTD. 6090 Highway #7 East Markham, Ontario L3P 3B1 905-471-1337 1-866-590-0001 www.ees-financial.com 2017 2018 RRSP OVERVIEW, STRATEGIES AND TIPS Deadline for 2017 contributions

a CANADIAN UNION OF PUBLIC EMPLOYEES EMPLOYEES PENSION PLAN (CEPP) MEMBER BOOKLET

MEMBER BOOKLET") Canadian Union of Public Employees Employees Pension Plan (CEPP) MEMBER BOOKLET a Also available on the CUPE Employees Pension Plan website www.cepp.ca Last update September 2013 This member booklet provides

Canadian Union of Public Employees Employees Pension Plan (CEPP) MEMBER BOOKLET a Also available on the CUPE Employees Pension Plan website www.cepp.ca Last update September 2013 This member booklet provides

Prepared for Mr. John Smith, Mrs Jane Smith March 13, 2013

Prepared for Mr. John Smith, Mrs Jane Smith March 13, 2013 Dan Dean, B.Sc., CFP, CLU DAN DEAN Financial 13135 156 Street NW Edmonton(Alberta) T5V 1V2 Telephone:780-487-7903 Fax:780-944-0683 deandanr@gmail.com

Prepared for Mr. John Smith, Mrs Jane Smith March 13, 2013 Dan Dean, B.Sc., CFP, CLU DAN DEAN Financial 13135 156 Street NW Edmonton(Alberta) T5V 1V2 Telephone:780-487-7903 Fax:780-944-0683 deandanr@gmail.com

University of New Brunswick

Pension Plan for Academic Employees T he UNB pension plan is designed to pay you a monthly income for life after you retire. The cost of providing this pension is shared equally by you and the University.

Pension Plan for Academic Employees T he UNB pension plan is designed to pay you a monthly income for life after you retire. The cost of providing this pension is shared equally by you and the University.

2013 Year End Tax Tips by Jamie Golombek

November 2013 2013 Year End Tax Tips by Jamie Golombek With December 31st fast approaching, here s our updated, annual look at some year-end tax tips you may wish to keep in mind as we enter the final

November 2013 2013 Year End Tax Tips by Jamie Golombek With December 31st fast approaching, here s our updated, annual look at some year-end tax tips you may wish to keep in mind as we enter the final

Budget 2018 What does it mean to you?

Budget 2018 What does it mean to you? March 2018 Tax alert On February 27, 2018, Finance Minister Bill Morneau presented the government s 2018-2019 federal budget. A full summary of the proposed tax measures

Budget 2018 What does it mean to you? March 2018 Tax alert On February 27, 2018, Finance Minister Bill Morneau presented the government s 2018-2019 federal budget. A full summary of the proposed tax measures

TAX NEWSLETTER. because that is the Part of the Income Tax Act that imposes this tax. November 2018

TAX NEWSLETTER November 2018 INTER-CORPORATE DIVIDENDS CHARITABLE DONATIONS ON DEATH TAXATION OF PUT AND CALL OPTIONS EMPLOYEE STOCK OPTIONS AROUND THE COURTS INTER-CORPORATE DIVIDENDS General Rule Normally,

TAX NEWSLETTER November 2018 INTER-CORPORATE DIVIDENDS CHARITABLE DONATIONS ON DEATH TAXATION OF PUT AND CALL OPTIONS EMPLOYEE STOCK OPTIONS AROUND THE COURTS INTER-CORPORATE DIVIDENDS General Rule Normally,

Retirement Checklist. Making the most of your retirement

Retirement Checklist Making the most of your retirement RBC Wealth Management RBC Wealth Management provides comprehensive services designed to address your multi-faceted financial concerns, simplify your

Retirement Checklist Making the most of your retirement RBC Wealth Management RBC Wealth Management provides comprehensive services designed to address your multi-faceted financial concerns, simplify your

Prepared for Mr. Eric Example, Mrs Celine Example July 30, 2013

Prepared for Mr. Eric Example, Mrs Celine Example July 30, 2013 Jean Le Conseiller Conseiller en sécurité financière Bons conseils et associés 1234, rue du Conseil Montréal(Québec) Telephone:514-555-5555

Prepared for Mr. Eric Example, Mrs Celine Example July 30, 2013 Jean Le Conseiller Conseiller en sécurité financière Bons conseils et associés 1234, rue du Conseil Montréal(Québec) Telephone:514-555-5555

2016 Edition Tax Tips for Investors

BMO Financial Group April 2016 2016 Edition Tax Tips for Investors Knowing how the tax rules affect your investments is essential to maximize your after-tax return. Keeping up to date on changes to the

BMO Financial Group April 2016 2016 Edition Tax Tips for Investors Knowing how the tax rules affect your investments is essential to maximize your after-tax return. Keeping up to date on changes to the

Understanding the TFSA

Understanding the TFSA Tax Free Savings Account capital ii corporation fisgardcapital2.com Table of Contents What Is A TFSA?... 1 Tax-Sheltered Savings... 1 Flexibility... 1 Who Could Benefit from a TFSA?...

Understanding the TFSA Tax Free Savings Account capital ii corporation fisgardcapital2.com Table of Contents What Is A TFSA?... 1 Tax-Sheltered Savings... 1 Flexibility... 1 Who Could Benefit from a TFSA?...

2012 Year End Tax Planning Considerations

2012 Year End Tax Planning Considerations Tax planning is a year-round activity and a vital component of the financial planning process. Since we are approaching the end of the calendar year, it is an

2012 Year End Tax Planning Considerations Tax planning is a year-round activity and a vital component of the financial planning process. Since we are approaching the end of the calendar year, it is an

Taking Action: CCPC tax proposals What you need to know (and do)

") September 2017 Taking Action: CCPC tax proposals What you need to know (and do) Debbie Pearl-Weinberg Executive Director, Tax and Estate Planning, CIBC Financial Planning and Advice Jamie Golombek Managing

September 2017 Taking Action: CCPC tax proposals What you need to know (and do) Debbie Pearl-Weinberg Executive Director, Tax and Estate Planning, CIBC Financial Planning and Advice Jamie Golombek Managing

Index. A Inventory valuation, 199. Landscaping, 209

Index A Inventory valuation, 199 Academic prize income, 134 Investigation of site, 210 Accounting net income vs. tax Landscaping, 209 net income, 41-2, 198-210 Lease cancellation cost, 209 Accounting depreciation

Index A Inventory valuation, 199 Academic prize income, 134 Investigation of site, 210 Accounting net income vs. tax Landscaping, 209 net income, 41-2, 198-210 Lease cancellation cost, 209 Accounting depreciation

DEFINED CONTRIBUTION RETIREMENT PLANS

DEFINED CONTRIBUTION RETIREMENT PLANS The and of Defined Contribution Pension Plans, Deferred Profit Sharing Plans and Group RRSP Plans DEFINED CONTRIBUTION PENSION PLAN 1. Employer has more control than

DEFINED CONTRIBUTION RETIREMENT PLANS The and of Defined Contribution Pension Plans, Deferred Profit Sharing Plans and Group RRSP Plans DEFINED CONTRIBUTION PENSION PLAN 1. Employer has more control than

Retirement Plan of the University of St. Michael s College

Retirement Plan of the University of St. Michael s College September 2013 Table of Contents INTRODUCTION.......................................... 4 BACKGROUND TO THE PLAN...................................

Retirement Plan of the University of St. Michael s College September 2013 Table of Contents INTRODUCTION.......................................... 4 BACKGROUND TO THE PLAN...................................

Retirement Checklist. Making the most of your retirement

Retirement Checklist Making the most of your retirement 2 Making the most of your retirement RBC Wealth Management RBC Wealth Management provides comprehensive services designed to address your multi-faceted

Retirement Checklist Making the most of your retirement 2 Making the most of your retirement RBC Wealth Management RBC Wealth Management provides comprehensive services designed to address your multi-faceted

2013 Year End Tax Tips

TAX TIPS 2013 Year End Tax Tips Jamie Golombek, CPA, CA, CFP, CLU, TEP Managing Director, Tax & Estate Planning, CIBC Wealth Advisory Services Jamie.Golombek@cibc.com With December 31 st fast approaching,

TAX TIPS 2013 Year End Tax Tips Jamie Golombek, CPA, CA, CFP, CLU, TEP Managing Director, Tax & Estate Planning, CIBC Wealth Advisory Services Jamie.Golombek@cibc.com With December 31 st fast approaching,

Update on Proposed Small Business Tax Changes. January 2018

Update on Proposed Small Business Tax Changes January 2018 PRESENTERS Jeff Saunders, CPA, CA, Partner Matt Mahoney, CPA, CA, Partner Rod Doyle, CPA, CA, Senior Manager 1 INTRODUCTION On July 18, 2017,

Update on Proposed Small Business Tax Changes January 2018 PRESENTERS Jeff Saunders, CPA, CA, Partner Matt Mahoney, CPA, CA, Partner Rod Doyle, CPA, CA, Senior Manager 1 INTRODUCTION On July 18, 2017,

TAX LETTER. August 2018

TAX LETTER August 2018 SUPERFICIAL LOSSES ROLLOVERS INTO CERTAIN PERSONAL TRUSTS SPLITTING PENSION INCOME WITH YOUR SPOUSE DEDUCTION OF LIFE INSURANCE PREMIUMS PRESCRIBED INTEREST RATES AROUND THE COURTS

TAX LETTER August 2018 SUPERFICIAL LOSSES ROLLOVERS INTO CERTAIN PERSONAL TRUSTS SPLITTING PENSION INCOME WITH YOUR SPOUSE DEDUCTION OF LIFE INSURANCE PREMIUMS PRESCRIBED INTEREST RATES AROUND THE COURTS

PPP PROPOSAL as at January 1st, 2018 for Dr. Age 60 of MPC

PPP PROPOSAL as at January 1st, 2018 for Dr. Age 60 of MPC Retirement at Age 65 Presented by INTEGRIS Pension Management Corp INTEGRIS Pension Management Corp E-mail: illustrations@integris-mgt.com Telephone:

PPP PROPOSAL as at January 1st, 2018 for Dr. Age 60 of MPC Retirement at Age 65 Presented by INTEGRIS Pension Management Corp INTEGRIS Pension Management Corp E-mail: illustrations@integris-mgt.com Telephone:

GLOSSARY A B C D E F G H I J L M N O P Q R S T U V W Z

1 Canadian Tax Principles Student Edition / Glossary lossary GLOSSARY A B C D E F G H I J L M N O P Q R S T U V W Z Canadian Tax Principles Student Edition / Glossary / A A A Accrual Basis - A method of

1 Canadian Tax Principles Student Edition / Glossary lossary GLOSSARY A B C D E F G H I J L M N O P Q R S T U V W Z Canadian Tax Principles Student Edition / Glossary / A A A Accrual Basis - A method of

CONTENTS VOLUME II VOLUME I. Detailed contents of Volume II, Chapters 11 to 21 follows. The textbook is published in two Volumes:

xi CONTENTS The textbook is published in two Volumes: Volume I = Chapters 1 to 10 Volume II = Chapters 11 to 21 Chapter VOLUME I Chapter VOLUME II 1 Introduction To Federal Taxation In Canada 11 Taxable

xi CONTENTS The textbook is published in two Volumes: Volume I = Chapters 1 to 10 Volume II = Chapters 11 to 21 Chapter VOLUME I Chapter VOLUME II 1 Introduction To Federal Taxation In Canada 11 Taxable

George will pay tax on the taxable portion of the gain at his marginal tax rate of 35%. His tax liability will be: $ x 35% = $133.

FILE 41: Taxation of Investments Taxation of Interest George Hammy invested in a Canada Savings Bond from which he received $765 in interest. George is in the 35% marginal tax bracket (federal and provincial

FILE 41: Taxation of Investments Taxation of Interest George Hammy invested in a Canada Savings Bond from which he received $765 in interest. George is in the 35% marginal tax bracket (federal and provincial

Creating Retirement Income With Registered Assets

Registered Retirement Savings Plans (RRSPs) represent the most effective way to save for retirement. Subject to contribution rules and limits, you are allowed to defer income taxes each year on the amount

Registered Retirement Savings Plans (RRSPs) represent the most effective way to save for retirement. Subject to contribution rules and limits, you are allowed to defer income taxes each year on the amount

2016 Federal Budget Federal Budget March 22, RBC Wealth Management Services

RBC Wealth Management Services 2016 Federal Budget 2016 Federal Budget March 22, 2016 A summary of the key tax measures that may have a direct impact on you Federal Minister of Finance, Bill Morneau, delivered

RBC Wealth Management Services 2016 Federal Budget 2016 Federal Budget March 22, 2016 A summary of the key tax measures that may have a direct impact on you Federal Minister of Finance, Bill Morneau, delivered

INDIVIDUAL PENSION PLAN (IPP)

") The information contained in this booklet is for education and information purposes only. Every effort has been made to ensure the accuracy of the information. Because all situations can not be included

The information contained in this booklet is for education and information purposes only. Every effort has been made to ensure the accuracy of the information. Because all situations can not be included

Taxation of Business Income and Methods of Withdrawing Cash from a Corporation

March 22, 2012 Taxation of Business Income and Methods of Withdrawing Cash from a Corporation Surplus Cash in a Corporation Part 3 As the owner-manager of your operating company, you may have surplus profits

March 22, 2012 Taxation of Business Income and Methods of Withdrawing Cash from a Corporation Surplus Cash in a Corporation Part 3 As the owner-manager of your operating company, you may have surplus profits

Reference Guide CHARITABLE GIVING

Reference Guide CHARITABLE GIVING In order to promote and encourage charitable giving, the Income Tax Act of Canada (the Act ) allows a tax credit to be claimed for eligible charitable gifts made by an

Reference Guide CHARITABLE GIVING In order to promote and encourage charitable giving, the Income Tax Act of Canada (the Act ) allows a tax credit to be claimed for eligible charitable gifts made by an

A Charitable Gift Annuity

A Charitable Gift Annuity Provide donors with an income stream and a means of supporting charities Through a combination of an annuity and a Donor Advised Fund, donors can be guaranteed a steady income

A Charitable Gift Annuity Provide donors with an income stream and a means of supporting charities Through a combination of an annuity and a Donor Advised Fund, donors can be guaranteed a steady income

INDEX. pro-rating, 11

INDEX A grandfathered policies, 11, 12, 13 21-year deemed disposition rule, keyperson insurance strategy and, 301 302 205, 207, 208 Crummey trust and, 325 pro-rating, 11 Accounting for life insurance,

INDEX A grandfathered policies, 11, 12, 13 21-year deemed disposition rule, keyperson insurance strategy and, 301 302 205, 207, 208 Crummey trust and, 325 pro-rating, 11 Accounting for life insurance,

THE ULTIMATE END-ALL-BE-ALL DEFINITIVE GUIDE TO. RRSP or TFSA WHICH WAY SHOULD YOU GO?

THE ULTIMATE END-ALL-BE-ALL DEFINITIVE GUIDE TO RRSP or TFSA WHICH WAY SHOULD YOU GO? The most common question I am asked is, Which is better RRSP or TFSA? And my answer is most often, It depends. Which

THE ULTIMATE END-ALL-BE-ALL DEFINITIVE GUIDE TO RRSP or TFSA WHICH WAY SHOULD YOU GO? The most common question I am asked is, Which is better RRSP or TFSA? And my answer is most often, It depends. Which

Update on the July 18 th Tax Proposals. Nathan Wright, LL.B., MTAX, TEP Founding Principal Ph: (416)

") Update on the July 18 th Tax Proposals Nathan Wright, LL.B., MTAX, TEP Founding Principal Ph: (416) 203-8338 E-mail: nwright@spectrumlawyers.ca July 18, 2017 Proposed Changes On July 18, 2017 Finance Minister

Update on the July 18 th Tax Proposals Nathan Wright, LL.B., MTAX, TEP Founding Principal Ph: (416) 203-8338 E-mail: nwright@spectrumlawyers.ca July 18, 2017 Proposed Changes On July 18, 2017 Finance Minister

2018 Year-End Tax Planning Tips

2018 Year-End Tax Planning Tips It s Never Too Early to Start Planning As the end of another year approaches, it s time to start thinking about ideas which may help lower your tax bill. When discussing

2018 Year-End Tax Planning Tips It s Never Too Early to Start Planning As the end of another year approaches, it s time to start thinking about ideas which may help lower your tax bill. When discussing

INCORPORATING YOUR PROFESSIONAL PRACTICE

INCORPORATING YOUR PROFESSIONAL PRACTICE REFERENCE GUIDE Most provinces and professional associations in Canada now permit professionals such as doctors, dentists, lawyers, and accountants to carry on

INCORPORATING YOUR PROFESSIONAL PRACTICE REFERENCE GUIDE Most provinces and professional associations in Canada now permit professionals such as doctors, dentists, lawyers, and accountants to carry on

EMPLOYEES PENSION PLAN

Effective 8 July 2019 Your Pension Plan was established on 1 January 1969 by Her Majesty in Right of Canada through the Minister of National Defence, pursuant to his authority and responsibility with respect

Effective 8 July 2019 Your Pension Plan was established on 1 January 1969 by Her Majesty in Right of Canada through the Minister of National Defence, pursuant to his authority and responsibility with respect

Canadian income tax system. For the purposes of this article, we assume you are a tax resident of Canada.

The Navigator RBC Wealth Management Services Tax planning basics This article provides an overview of the Canadian tax system, basic investments and how the two interact. By investing tax-efficiently,

The Navigator RBC Wealth Management Services Tax planning basics This article provides an overview of the Canadian tax system, basic investments and how the two interact. By investing tax-efficiently,

Insurance Solutions for Individual Needs

Insurance Solutions for Individual Needs This brochure looks at some of the different needs individuals can experience and it shows how insurance can help meet those needs. Leaving a Legacy at Death Life

Insurance Solutions for Individual Needs This brochure looks at some of the different needs individuals can experience and it shows how insurance can help meet those needs. Leaving a Legacy at Death Life