One-Hour Crash Course on IRA Rollovers. Elaine Floyd, CFP Director, Retirement and Life Planning Horsesmouth

|

|

|

- Janel Baldwin

- 5 years ago

- Views:

Transcription

1 One-Hour Crash Course on IRA Rollovers Elaine Floyd, CFP Director, Retirement and Life Planning Horsesmouth

2 The Opportunity The value of rollover assets available this year will be nearly $347 billion, according Cogent, a market research firm. Advisors who are highly successful at obtaining business in this market capture an average rollover account size of $355,000, which is 2.4 times larger than those advisors who do not make this market a priority.

3 Capture More Retirement Rollovers 3 Marketing Ideas for Getting More Rollover Business from Clients, Prospects & COIs with Wendi Webb Director, Advisor/Client Solutions November 29, 2012

4 Campaign Overview Objective:To become known as the "Rollover Guy/Gal" through a series of workshops and other marketing activities focused on near-term rollover candidates Goals: Capture more rollover business Get in front of groups of qualified prospects Showcase retirement planning expertise Easy to repeat Make it easy for clients to bring you referrals Educate clients, prospects, and COIs Build reputation THE Rollover Guy

5 Today s Agenda Annuity vs. lump sum Triggering events What can and can t be rolled over Types of rollovers The 60-Day Rule Net unrealized appreciation Rolling to a Roth IRA The best ways to name beneficiaries How rollovers are treated in divorce How rollovers are reported Advisor/Client marketing solutions

6 Annuity vs. Lump Sum

7 Annuity or Lump Sum? Plan may offer lump sum or equivalent annuity Alternatives are actuarially equal based on certain assumptions: interest rates, average life expectancy Clients will ask: Should I take the annuity or the lump sum?

8 Reasons Why People Choose Annuity Helps you manage your budget because you get a predictable amount of money each month, just like a paycheck Gives you peace of mind because the payments will continue as long as you [and your spouse] live Ensures that your monthly income will not fall even if there is a large drop in the market Can help you remain independent because the money will never run out AARP Survey of Pension Plan and IRA Distribution Choices, April 2012 Worker s Retiree s 82% 81% 82% 81% 80% 79% 77% 78%

9 Reasons Why People Do Not Choose Annuity I want to keep the money around in case there is an emergency I don t think the lifelong monthly payments would be a good value for the money I may not live long enough to make the monthly payments worthwhile I think I could get a better return on my investment managing the money myself AARP Survey of Pension Plan and IRA Distribution Choices, April 2012 Worker s Retiree s 83% 75% 79% 74% 78% 62% 76% 66%

10 What Do They Ultimately Choose? Of workers and retirees with a defined contribution plan who were in a position to choose, 31% planned to elect a life annuity, and 24% of retirees had made a similar election. AARP Survey of Pension Plan and IRA Distribution Choices, April 2012

11 Advantages of Lump Sum Continued tax deferral if roll over More investment options More control over the assets (liquidity) More control over taxation (Roth conversion, timing of withdrawals)

12 Advantages of Lump Sum Lower expenses More flexible postdeath distribution options Hedge other annuity income such as Social Security No rush: can always buy annuity later

13 Questions to Ask How long are you likely to live? How good are your investing skills? What is the value of your lump sum? How large is your benefit? Will you change your mind? Deciding Between a Lump Sum and an Annuity Pension Rights Center, June 5, 2012

14 Triggering Events

15 Lump Sum Distribution Is Eligible for Favorable Tax Treatment If: Distributed from a qualified retirement plan (QRP) Due to employee s: Separation from service Attainment of age 59.5 (if plan allows) Death or disability

16 When in Doubt Ask if it is an Eligible Rollover Distribution Client should receive a written explanation from the plan stating that the distribution may be paid tax-free directly to IRA or other eligible plan (402f notice)

17 What Can and Can t Be Rolled Over

18 What CAN Be Rolled Over Cash Proceeds from sale of assets Property sale not taxable even if property gains value -- as long as entire proceeds from sale are rolled over If part of distribution is nontaxable and property is sold and only a portion is rolled over, client may designate which part of the rollover is nontaxable (get tax help) In-kind assets if custodian accepts

19 Loans What CAN T Be Rolled Over Hardship distributions Required minimum distributions (if client is over 70.5 and forced to take RMDs from plan usually not required if still employed unless 5% owner) Payments that are part of a series of substantially equal periodic payments (SEPPs) Different property: Can sell and roll over proceeds, but can t keep property and roll over same amount of cash

20 After-tax Contributions Can rollover to IRA but... IRA will forever comprise both taxable and after-tax money Must keep track of ratio of pretax to after-tax money custodian does not do this All IRAs are aggregated for this purpose Distributions must be prorated Roth conversions must be prorated Must file Form 8606 the year after the rollover and in any year there is a distribution

21 Over 70-1/2 Can roll over plan assets to IRA (even though can t contribute to IRA after 70-1/2) Rollover can t include any distributions required by plan RMDs on those assets start next year

22 What About? Self-employed individuals Separation from service doesn t apply Must be 59.5 or disabled In-service lump sum distributions Loans and hardship withdrawals don t count Plan may offer non-hardship withdrawals if over 59.5

23 Types of Rollovers

24 Types of Rollovers Qualified plan to IRA Qualified plan to qualified plan (if plan accepts) IRA to qualified plan (if plan accepts) IRA to IRA

25 3 Tax-Free Ways To Move a Lump Sum Distribution Rollover: Take receipt of funds, deposit to IRA or qualified plan within 60 days (20% withholding) Direct rollover or transfer: Check is made payable to new custodian; client touches the check but not the money (no withholding) Trustee-to-trustee transfer: Assets moved directly from one custodian to another; there is no distribution and no withholding

26 Rolling to a Qualified Plan Assets may come from an IRA or another qualified plan Qualified plan must agree to accept assets Must be an employee of the employer sponsoring the plan (e.g., can t be a contractor) If over 70.5, rolling to a qualified plan can avoid IRA RMDs However, if 5% owner must take RMDs as if funds were still in IRA New plan may require client to take RMDs Can t roll after-tax money to a qualified plan unless rolling from QRP to QRP by direct transfer

27 Rollover to Solo 401(k) QRP for sole proprietors (1 employee plus spouse) Allows loans (do not encourage this!) Does not avoid RMDs Main advantage of solo 401(k) is higher contribution limits; probably not worth it for rollovers

28 Rollover as Business Start-up Scheme for funding new business with QRP assets Client establishes a new corporation and associated qualified plan (the ROBS plan) Assets are rolled from QRP into new ROBS plan ROBS plan uses rollover assets to purchase stock in new business Assets end up in new business s checking account with no taxes due IRS does not like; although not illegal, will invite scrutiny

29 irs.gov/pub/irs irs-tege/rollover rollover_chart chart.pdf

30 The 60-Day Rule You generally must make the rollover contribution by the 60 th day after the day you receive the distribution from your IRA or qualified plan. IRS Publication 590

31 Rollovers Completed After the 60-Day Period Do not qualify for tax-free rollover treatment Must be treated as a taxable distribution in the year distributed (even if 60-day period expires in the next tax year) Premature distribution penalty may apply Excess contribution penalty may apply

32 How To Circumvent the 60-Day Rule Direct trustee-to-trustee transfer OR Direct rollover (check made payable to new custodian; does not have to be delivered within 60 days)

33 Waivers to 60-Day Rule Error by financial institution automatic waiver Case-by-case via private letter ruling ($$$)

34 Net Unrealized Appreciation

35 When Distribution Includes Employer Securities Net unrealized appreciation (NUA) is the excess of the stock s fair market value at the time of distribution over the plan s basis in the stock NUA is not taxable at time of distribution If stock is rolled over, NUA will ultimately be taxed as ordinary income when distributed from IRA If stock is not rolled over, NUA will be taxed as long-term capital gain whenever it is sold

36 To Get Capital Gains Tax Treatment of NUA: Do not roll over employer securities; place them in a taxable account instead Client will owe income tax on basis in year of distribution NUA and all future gains will be taxable at longterm capital gains rates

37 Example Bill retires and receives 10,000 shares of XYZ stock in a lump sum distribution The stock is worth $50/share at the time of the distribution, or $500,000 The plan s basis in the stock is $10, or $100,000 Bill places the stock in a taxable account and pays ordinary income tax on $100,000

38 What Happens When Bill Sells? If Bill sells the stock immediately for $500,000, he will report a $400,000 long-term capital gain ($500,000 - $100,000 basis = $400,000) If the stock appreciates to $600,000 and he sells within a year, he will report a $400,000 long-term capital gain and a $100,000 short-term capital gain

39 Consider Rolling Over Employer Client is under 59.5 Stock If: NUA is an insignificant amount Client plans to sell stock right away but leave proceeds invested for many years: need to analyze tradeoff between LTCG vs. tax deferral

40 NUA Mistakes Failing to hold out employer stock because of Negligence or Lack of understanding of the value of NUA tax treatment Temporarily rolling over employer stock Rollover election is irrevocable Once stock is placed in IRA, NUA will never qualify for LTCG tax treatment

41 Rolling to a Roth IRA

42 Qualified Plan Assets May Be Rolled Directly to a Roth IRA Full or partial rollover OK Assets are treated as a distribution and then as a rollover contribution to a Roth IRA

43 Taxation of Roth Rollovers Taxable amount rolled to Roth is taxable After-tax contributions may be rolled over tax free Cannot cherry pick the nontaxable portion and roll over only that amount However, unlike IRAs, QRP assets do not have to be aggregated when determining ratio of after-tax to pretax money Therefore, if there is more than one QRP account, you can choose the account with the most after-tax money to roll to a Roth

44 Example Full Rollover of One Account Linda has an IRA valued at $50,000 and two 401(k) accounts with a former employer valued at $100,000 and $150,000, respectively. The $100,000 account consists of $30,000 in after-tax contributions. If Linda converts the $100,000 account, the tax-free portion will be $30,000.

45 Example Partial Rollover of One Account Linda decides to convert just $30,000 of the $100,000 account. She may not cherry-pick the after-tax amount to convert. Rather, any amount she does convert would be tax-free in the same ratio as the total account: $30,000 to $100,000, or.3. If she converts $30,000, the tax-free portion would be $9,000 ($30,000 x.3).

46 Why Convert to a Roth? Expect higher taxes in the future Have a long investment time frame Can pay taxes on the conversion Want withdrawal flexibility (no RMDs provide tax diversification in retirement) Want to pass assets tax-free to heirs

47 Roth Caveat #1 Client has 2 QRP accounts, one with substantial after-tax contributions Don t roll both accounts into traditional IRA. This will dilute basis since all IRAs must be aggregated for the purpose of determining the taxable portion.

48 Example Steve has a contributory traditional IRA worth $100,000. He also has two qualified plan accounts. Account A is worth $150,000 and consists of $60,000 in after-tax contributions. Account B is worth $200,000 and is all pretax money. If Steve rolls Accounts A and B into an IRA, he will have IRAs totaling $450,000 with $60,000 basis. So of any partial conversions he might do, only 13% would be tax free ($60,000 $450,000). If he converts $150,000, only $19,500 would be tax free ($150,000 x.13). However, if he keeps Account A intact, he can convert the entire $150,000 account with his full $60,000 basis converted tax free.

49 Roth Caveat #2: If client will be converting IRA with basis, don t roll over plan assets to an IRA in the same year. This will cause unfavorable aggregation.

50 Example Christine has a $30,000 nondeductible IRA with $23,000 basis. She also has $300,000 in a qualified retirement plan that is rollover eligible. If she converts the $30,000 IRA without rolling over the $300,000, the tax-free portion of the Roth conversion will be $23,000. But if she rolls over the $300,000 to an IRA, the tax-free portion of the $30,000 conversion will be just $2,100. This was determined by first dividing the $23,000 basis by the $330,000 in total IRAs to get.07 as the tax-free multiplier. To determine the tax-free portion of any amount that Christine converts after rolling the $300,000 to an IRA, multiply the converted amount by.07 to get $2,100.

51 Roth Caveat #3 Don t allow non-spouse beneficiaries to roll over inherited plan assets to an IRA Inherited IRAs may not be converted to a Roth IRA Inherited plan assets may be rolled over to a Roth IRA

52 The Best Ways to Name Beneficiaries

53 Guidelines for Naming Beneficiaries Name a beneficiary Name a spouse as beneficiary Name a young person as beneficiary Split the IRA among beneficiaries Educate beneficiaries Don t spend the money Avoid the 5-year rule

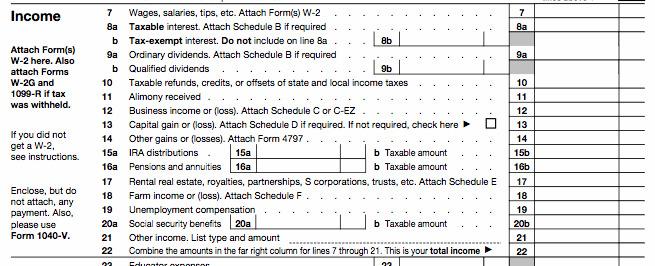

54 Beneficiary Mistakes Failing to coordinate the beneficiary designation with wills, trusts, and other dispositions Naming one s estate as beneficiary Writing all my children, equally Naming a minor without considering minor s guardian Failing to update beneficiary designation

55 How Rollovers Are Treated in Divorce

56 A Distribution Incident to Divorce May Be Rolled Over If: It would have been an eligible rollover distribution if it had been made to the employee, and It is made under a qualified domestic relations order (QDRO)

57 Qualified Domestic Relations Order (QDRO) Judgment issued under the domestic relations law of a state Gives to an alternate payee (e.g., former spouse) the right to receive all or part of the benefits that would be payable to a participant under the plan Requires certain specific information and cannot alter the amount or form of the benefits of the plan Income not subject to premature distribution penalty if taken prior to rollover

58 How Rollovers Are Reported

59

60

61 Reporting Rollovers Client will receive 1099-R with amount of distribution in Box 1 This amount must be entered on Line 16a of Form 1040 Subtract after-tax contributions Subtract amount rolled over Enter remaining amount, even if it s zero, on Line 16b. Write the word rollover next to line 16b

62 Questions about IRAs?

63 Marketing Your Rollover Services

64 Advisor/Client SolutionsA Marketing Campaigns Client Reprints Marketing Resources

65 Rollover Campaign(s) How to Capture More Rollover Business Webinar: Nov. 29, 2012

66 Rollover Marketing Options Rollover Workshop (Clients & Prospects) Rollover (Clients & Prospects) Rollover Memos (Clients, Prospects & COIs)

67 Rollover Promotion Materials Promotion Strategy Sheet Lunch n' Learn Checklist Marketing Postcard invitations Phone scripts Reminder s

68 Rollover Presentation Materials Workshop PPT: "How to Get Rollover Ready" Presentation Script Workshop Sign-In Sheet Workshop Evaluation Form Workshop Handouts Rollover Ready Checklist

69 Rollover Follow-Up Materials Follow-Up 3 messages Follow-up phone scripts 3 Client reprints Rollover Blunders Guide IRA Custodian Checklist 1st Year Retiree's Tax Checklist Retirement Ready Checklist

70 Other Marketing Options Marketing messages RO Blunders Guide Client checklists Drip Marketing 11 'One-Minute Memos' One series for clients & prospects Separate series for COIs

71 Have a Question? Send questions, comments, & feedback to: rollover@horsesmouth.com To learn more about the Advisor/Client Marketing Program, visit:

Frequently asked questions

Page 1 of 6 Frequently asked questions Distributions and rollovers from retirement accounts Choosing what to do with your retirement savings is an important decision. Tax implications are just one of several

Page 1 of 6 Frequently asked questions Distributions and rollovers from retirement accounts Choosing what to do with your retirement savings is an important decision. Tax implications are just one of several

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS (For Participant) A. TYPES OF PLAN DISTRIBUTIONS

A. TYPES OF PLAN DISTRIBUTIONS") SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS (For Participant) This notice explains how you can continue to defer federal income tax on your retirement plan savings in the Plan and contains important information

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS (For Participant) This notice explains how you can continue to defer federal income tax on your retirement plan savings in the Plan and contains important information

Taking Money Out of Retirement Plans

Taking Money Out of Retirement Plans Twila Slesnick, PhD, Enrolled Agent John C. Suttle, CPA, Attorney Chapter 1 Types of Retirement Plans... 1 Learning Objectives... 1 Introduction... 1 Qualified Plans...

Taking Money Out of Retirement Plans Twila Slesnick, PhD, Enrolled Agent John C. Suttle, CPA, Attorney Chapter 1 Types of Retirement Plans... 1 Learning Objectives... 1 Introduction... 1 Qualified Plans...

Taking Money Out of Retirement Plans

Taking Money Out of Retirement Plans 13 th Edition Twila Slesnick, PhD, Enrolled Agent John C. Suttle, CPA, Attorney Chapter 1 Types of Retirement Plans... 1 Learning Objectives... 1 Introduction... 1

Taking Money Out of Retirement Plans 13 th Edition Twila Slesnick, PhD, Enrolled Agent John C. Suttle, CPA, Attorney Chapter 1 Types of Retirement Plans... 1 Learning Objectives... 1 Introduction... 1

Savings Banks Employees Retirement Association

Savings Banks Employees Retirement Association IN-PLAN ROTH CONVERSION ELECTION FORM PLEASE NOTE: Your Plan must allow In-Plan Roth Rollovers Participant Name: (Please Print) Certificate No. Current Address

Savings Banks Employees Retirement Association IN-PLAN ROTH CONVERSION ELECTION FORM PLEASE NOTE: Your Plan must allow In-Plan Roth Rollovers Participant Name: (Please Print) Certificate No. Current Address

11 Biggest Rollover Blunders (and How to Avoid Them)

") 11 Biggest Rollover Blunders (and How to Avoid Them) Rolling over your funds for retirement presents a number of opportunities for error. Having a set of guidelines and preventive touch points is necessary

11 Biggest Rollover Blunders (and How to Avoid Them) Rolling over your funds for retirement presents a number of opportunities for error. Having a set of guidelines and preventive touch points is necessary

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS This notice explains how you can continue to defer federal income tax on your retirement plan savings in the Plan and contains important information you will

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS This notice explains how you can continue to defer federal income tax on your retirement plan savings in the Plan and contains important information you will

Distribution Request Form. Instructions

Distribution Request Form (Applicable to Plans that do not include Annuity Distribution Options.) A Distribution Request Form must be completed, signed and returned to the Plan Administrator to request

Distribution Request Form (Applicable to Plans that do not include Annuity Distribution Options.) A Distribution Request Form must be completed, signed and returned to the Plan Administrator to request

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS This notice explains how you can continue to defer federal income tax on your retirement plan savings in the Plan and contains important information you will

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS This notice explains how you can continue to defer federal income tax on your retirement plan savings in the Plan and contains important information you will

DISTRIBUTION FORM INSTRUCTION BOOKLET

403(b)(7) DISTRIBUTION FORM INSTRUCTION BOOKLET Not FDIC Insured May Lose Value Not Bank Guaranteed CONTENTS 2 Instructions 2 l s ri u i 3 Pe lty Exe p s ri u i 4 Ad i i s ri u i p i 4 re s ri u i 4 Roth

403(b)(7) DISTRIBUTION FORM INSTRUCTION BOOKLET Not FDIC Insured May Lose Value Not Bank Guaranteed CONTENTS 2 Instructions 2 l s ri u i 3 Pe lty Exe p s ri u i 4 Ad i i s ri u i p i 4 re s ri u i 4 Roth

MFS Retirement Strategies Stretch IRA and distribution options READY, SET, RETIRE. Taking income distributions during retirement

MFS Retirement Strategies Stretch IRA and distribution options READY, SET, RETIRE Taking income distributions during retirement ASSESS YOUR NEEDS INCOME WHEN YOU NEED IT Choosing the right income distribution

MFS Retirement Strategies Stretch IRA and distribution options READY, SET, RETIRE Taking income distributions during retirement ASSESS YOUR NEEDS INCOME WHEN YOU NEED IT Choosing the right income distribution

COLLIERS INTERNATIONAL USA, LLC And Affiliated Employers 401(K) Plan NOTICE OF DISTRIBUTION ELECTION

Plan NOTICE OF DISTRIBUTION ELECTION") COLLIERS INTERNATIONAL USA, LLC And Affiliated Employers 401(K) Plan NOTICE OF DISTRIBUTION ELECTION To: (Participant) Date: As a terminated participant in the Colliers International USA, LLC and Affiliated

COLLIERS INTERNATIONAL USA, LLC And Affiliated Employers 401(K) Plan NOTICE OF DISTRIBUTION ELECTION To: (Participant) Date: As a terminated participant in the Colliers International USA, LLC and Affiliated

INSTRUCTIONS TO REQUEST A BENEFIT PAYMENT

INSTRUCTIONS TO REQUEST A BENEFIT PAYMENT Participant 1. Read the enclosed notices, including the Notice to Terminated Participants and the Special Tax Notice Regarding Plan Payments. 2. Complete the enclosed

INSTRUCTIONS TO REQUEST A BENEFIT PAYMENT Participant 1. Read the enclosed notices, including the Notice to Terminated Participants and the Special Tax Notice Regarding Plan Payments. 2. Complete the enclosed

Rollover Distribution Notice

Rollover Distribution Notice GENERAL INFORMATION This notice contains important information you need before you decide how to receive your retirement plan benefits. This notice is provided to you by your

Rollover Distribution Notice GENERAL INFORMATION This notice contains important information you need before you decide how to receive your retirement plan benefits. This notice is provided to you by your

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS This Special Tax Notice Applies to Distributions from Section 401(a) Plans, Section 403(a) Annuity Plans, Section 403(b) Tax Sheltered Annuities and Section 457

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS This Special Tax Notice Applies to Distributions from Section 401(a) Plans, Section 403(a) Annuity Plans, Section 403(b) Tax Sheltered Annuities and Section 457

IN-SERVICE DISTRIBUTION

Plan Year 1999-2000 IN-SERVICE DISTRIBUTION FOR PERSONS 59 1/2 YEARS OF AGE OR OLDER Use this form to request a qualified distribution from your 401(k) account with our company plan if you are Still employed

Plan Year 1999-2000 IN-SERVICE DISTRIBUTION FOR PERSONS 59 1/2 YEARS OF AGE OR OLDER Use this form to request a qualified distribution from your 401(k) account with our company plan if you are Still employed

A GUIDE TO YOUR OPTIONS WHEN SEPARATING FROM SERVICE, INCLUDING THE SPECIAL TAX NOTICE

Distribution Options Guide A GUIDE TO YOUR OPTIONS WHEN SEPARATING FROM SERVICE, INCLUDING THE SPECIAL TAX NOTICE. www.modeferredcomp.org 800-392-0925 DISTRIBUTION OPTIONS WHEN SEPARATING FROM SERVICE

Distribution Options Guide A GUIDE TO YOUR OPTIONS WHEN SEPARATING FROM SERVICE, INCLUDING THE SPECIAL TAX NOTICE. www.modeferredcomp.org 800-392-0925 DISTRIBUTION OPTIONS WHEN SEPARATING FROM SERVICE

Distributions Options Guide

Distributions Options Guide A Guide to Your Options When Separating from Service Including the Special Tax Notice Retirement Savings, Simplified Your Distribution Options Upon separation of service and

Distributions Options Guide A Guide to Your Options When Separating from Service Including the Special Tax Notice Retirement Savings, Simplified Your Distribution Options Upon separation of service and

403(b) Plan DISTRIBUTION GUIDE

Plan DISTRIBUTION GUIDE") This Guide Includes: > 403(b) Distribution FAQs 403(b) Plan DISTRIBUTION GUIDE > Distribution Request Checklist > 403(b) Distribution Form > Special Tax Notice Learn about taking distributions from your

This Guide Includes: > 403(b) Distribution FAQs 403(b) Plan DISTRIBUTION GUIDE > Distribution Request Checklist > 403(b) Distribution Form > Special Tax Notice Learn about taking distributions from your

Legends Gaming, LLC Employees 401(k) Plan

Plan") Legends Gaming, LLC Employees 401(k) Plan ON-LINE DISTRIBUTION FORMS PACKAGE To: Plan Participant From: Retirement Direct The distribution you are entitled to receive from the above Plan is an eligible

Legends Gaming, LLC Employees 401(k) Plan ON-LINE DISTRIBUTION FORMS PACKAGE To: Plan Participant From: Retirement Direct The distribution you are entitled to receive from the above Plan is an eligible

QUALIFIED RETIREMENT PLAN AND 403(b)(7) CUSTODIAL ACCOUNT DISTRIBUTION REQUEST FORM

(7) CUSTODIAL ACCOUNT DISTRIBUTION REQUEST FORM") QUALIFIED RETIREMENT PLAN AND 403(b)(7) CUSTODIAL ACCOUNT DISTRIBUTION REQUEST FORM The Employee Retirement Income Security Act of 1974 (ERISA) requires that you receive the information contained in this

QUALIFIED RETIREMENT PLAN AND 403(b)(7) CUSTODIAL ACCOUNT DISTRIBUTION REQUEST FORM The Employee Retirement Income Security Act of 1974 (ERISA) requires that you receive the information contained in this

Rollovers from Employer-Sponsored Retirement Plans

Law Office Of Keith R. Miles, LLC Keith Miles Attorney-at-Law 2250 Oak Road PO Box 430 Snellville, GA 30078 678-666-0618 keithmiles@timetoestateplan.com www.timetoestateplan.com Rollovers from Employer-Sponsored

Law Office Of Keith R. Miles, LLC Keith Miles Attorney-at-Law 2250 Oak Road PO Box 430 Snellville, GA 30078 678-666-0618 keithmiles@timetoestateplan.com www.timetoestateplan.com Rollovers from Employer-Sponsored

SAMPLE COMPANY, INC. DEFINED BENEFIT PENSION PLAN NOTICE ON TERMINATION, RETIREMENT OR DISABILITY

SAMPLE COMPANY, INC. DEFINED BENEFIT PENSION PLAN NOTICE ON TERMINATION, RETIREMENT OR DISABILITY NAME OF PARTICIPANT: DATE: RE: Distribution of Plan Benefits Immediate Distribution You may elect to receive

SAMPLE COMPANY, INC. DEFINED BENEFIT PENSION PLAN NOTICE ON TERMINATION, RETIREMENT OR DISABILITY NAME OF PARTICIPANT: DATE: RE: Distribution of Plan Benefits Immediate Distribution You may elect to receive

Distribution Request Form. Instructions

Distribution Request Form (Applicable to Plans that do not include Annuity Distribution Options.) A Distribution Request Form must be completed, signed and returned to the Plan Administrator to request

Distribution Request Form (Applicable to Plans that do not include Annuity Distribution Options.) A Distribution Request Form must be completed, signed and returned to the Plan Administrator to request

APPLICATION FOR FULL REFUND

Municipal Employees Annuity and Benefit Fund of Chicago 221 North LaSalle Street, Suite 500, Chicago, Illinois 60601 Telephone: 312-236-4700 Fax: 312-236-2383 www.meabf.org APPLICATION FOR FULL REFUND

Municipal Employees Annuity and Benefit Fund of Chicago 221 North LaSalle Street, Suite 500, Chicago, Illinois 60601 Telephone: 312-236-4700 Fax: 312-236-2383 www.meabf.org APPLICATION FOR FULL REFUND

QP/401(k) DISTRIBUTION NOTICE

DISTRIBUTION NOTICE") QP/401(k) DISTRIBUTION NOTICE Important Information About Your Qualified Retirement Plan Distribution INTRODUCTION As a participant in your employer s qualified retirement plan, you have accumulated a

QP/401(k) DISTRIBUTION NOTICE Important Information About Your Qualified Retirement Plan Distribution INTRODUCTION As a participant in your employer s qualified retirement plan, you have accumulated a

TERMINATION FORM - 206

INSTRUCTIONS FOR COMPLETING TERMINATION FORM - 206 TERMINATION FORM - 206 Get your money fast! If your Plan Administrator has notified us of your termination, you may be able to easily process this 401(k)

INSTRUCTIONS FOR COMPLETING TERMINATION FORM - 206 TERMINATION FORM - 206 Get your money fast! If your Plan Administrator has notified us of your termination, you may be able to easily process this 401(k)

AFPlanServ 403(b) Plan Distribution Authorization Form

Plan Distribution Authorization Form") AFPlanServ 403(b) Plan Distribution Authorization Form Participant Instructions The AFPlanServ 403(b) Distribution Authorization Form must be submitted to AFPlanServ to approve a distribution or plan-to-plan

AFPlanServ 403(b) Plan Distribution Authorization Form Participant Instructions The AFPlanServ 403(b) Distribution Authorization Form must be submitted to AFPlanServ to approve a distribution or plan-to-plan

QRP Distribution Notice

QRP Distribution Notice Important Information About Your Qualified Retirement Plan Distribution INTRODUCTION As a participant in your employer s qualified retirement plan, you have accumulated a vested

QRP Distribution Notice Important Information About Your Qualified Retirement Plan Distribution INTRODUCTION As a participant in your employer s qualified retirement plan, you have accumulated a vested

Qualified Retirement Accounts Distribution Form

Qualified Retirement Accounts Distribution Form 800-525-1093 Use this form for a distribution from your qualified retirement account. Note: Do not use this form for distributions from an IRA or 403(b)(7).

Qualified Retirement Accounts Distribution Form 800-525-1093 Use this form for a distribution from your qualified retirement account. Note: Do not use this form for distributions from an IRA or 403(b)(7).

REQUEST FOR DISTRIBUTION OF BENEFITS

The Liberty National Life Insurance Company Defined Contribution Plan REQUEST FOR DISTRIBUTION OF BENEFITS INSTRUCTlONS: 1. Read the Retirement Annuity Explanation. 2. Read the Special Tax Notice Regarding

The Liberty National Life Insurance Company Defined Contribution Plan REQUEST FOR DISTRIBUTION OF BENEFITS INSTRUCTlONS: 1. Read the Retirement Annuity Explanation. 2. Read the Special Tax Notice Regarding

Rollover IRAs. Consider the advantages of consolidating your retirement savings PROOF 3

Rollover IRAs Consider the advantages of consolidating your retirement savings O O R P 3 F Consider the Advantages of Consolidating Your Retirement Savings If you have changed jobs, left the workforce

Rollover IRAs Consider the advantages of consolidating your retirement savings O O R P 3 F Consider the Advantages of Consolidating Your Retirement Savings If you have changed jobs, left the workforce

DISTRIBUTION ELECTION FORM

DISTRIBUTION ELECTION FORM (Please Print or Type) Participant Name (Last, First) Social Security No. Mailing Address City State Zip Daytime Phone Marital Status: [ ]Married [ ]Single Reason for distribution

DISTRIBUTION ELECTION FORM (Please Print or Type) Participant Name (Last, First) Social Security No. Mailing Address City State Zip Daytime Phone Marital Status: [ ]Married [ ]Single Reason for distribution

RETIREMENT PLAN LUMP SUM PAYMENT CALCULATION EXPLANATION

RETIREMENT PLAN LUMP SUM PAYMENT CALCULATION EXPLANATION The NKCH RETIREMENT PLAN is designed to provide participants with a monthly benefit at retirement, payable for their lifetime. The benefit is determined

RETIREMENT PLAN LUMP SUM PAYMENT CALCULATION EXPLANATION The NKCH RETIREMENT PLAN is designed to provide participants with a monthly benefit at retirement, payable for their lifetime. The benefit is determined

For Payments Not From a Designated Roth Account

Applies to Sections 401 and 403 SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS Retain For Your Records This notice is provided to you by Prudential Financial, Inc., on behalf of the plan administrator ( Plan

Applies to Sections 401 and 403 SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS Retain For Your Records This notice is provided to you by Prudential Financial, Inc., on behalf of the plan administrator ( Plan

CONSIDERING IRA ROLLOVERS. Making the right distribution decision now can make a big difference down the road.

CONSIDERING IRA ROLLOVERS Making the right distribution decision now can make a big difference down the road. CONSIDERING IRA ROLLOVERS ARE YOU CHANGING JOBS? CAREERS? RETIRING? If you are planning to

CONSIDERING IRA ROLLOVERS Making the right distribution decision now can make a big difference down the road. CONSIDERING IRA ROLLOVERS ARE YOU CHANGING JOBS? CAREERS? RETIRING? If you are planning to

Tax Information for Pension Distributions

Tax Information for Pension Distributions Information for: All Funds This fact sheet summarizes only the federal (not state or local) tax rules that might apply to your payment. The rules described below

Tax Information for Pension Distributions Information for: All Funds This fact sheet summarizes only the federal (not state or local) tax rules that might apply to your payment. The rules described below

TAX NOTICE (For Payments Not From a Designated Roth Account)

") 402(f) Notice Non-Roth YOUR ROLLOVER OPTIONS TAX NOTICE (For Payments Not From a Designated Roth Account) You are receiving this notice because all or a portion of a payment you are receiving from your

402(f) Notice Non-Roth YOUR ROLLOVER OPTIONS TAX NOTICE (For Payments Not From a Designated Roth Account) You are receiving this notice because all or a portion of a payment you are receiving from your

GENERAL INCOME TAX INFORMATION

GENERAL INCOME TAX INFORMATION TABLE OF CONTENTS Taxes on Loans from the Annuity Savings Fund 1 (Tier 1 and 2 Members Only) Taxes on the Withdrawal of the Annuity Savings Fund at Retirement 2 (Tier 1 and

GENERAL INCOME TAX INFORMATION TABLE OF CONTENTS Taxes on Loans from the Annuity Savings Fund 1 (Tier 1 and 2 Members Only) Taxes on the Withdrawal of the Annuity Savings Fund at Retirement 2 (Tier 1 and

For Payments From a Designated Roth Account

For Payments From a Designated Roth Account YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving from the [INSERT NAME OF PLAN] (the Plan ) is eligible

For Payments From a Designated Roth Account YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving from the [INSERT NAME OF PLAN] (the Plan ) is eligible

34 Make the Most of Your Employer Retirement Accounts

144 # 34 Make the Most of Your Employer Retirement Accounts By Barbara Camaglia, MBA, CFP, CFS, CPA Your eyes may glaze over at retirement-plan numbers 401(k), 403(b), 457 but you want to be sure you understand

144 # 34 Make the Most of Your Employer Retirement Accounts By Barbara Camaglia, MBA, CFP, CFS, CPA Your eyes may glaze over at retirement-plan numbers 401(k), 403(b), 457 but you want to be sure you understand

SPECIAL TAX NOTICE REGARDING PAYMENTS FROM THE PLAN

SPECIAL TAX NOTICE REGARDING PAYMENTS FROM THE PLAN This notice contains important information you will need should you decide to receive your retirement benefits under the Lockheed Martin Savings Plans.

SPECIAL TAX NOTICE REGARDING PAYMENTS FROM THE PLAN This notice contains important information you will need should you decide to receive your retirement benefits under the Lockheed Martin Savings Plans.

STD N402F ][03/14/16)( (f) NOTICE OF SPECIAL TAX RULES ON DISTRIBUTIONS

![STD N402F ][03/14/16)( (f) NOTICE OF SPECIAL TAX RULES ON DISTRIBUTIONS](/thumbs/85/92934653.jpg "STD N402F ][03/14/16)( (f) NOTICE OF SPECIAL TAX RULES ON DISTRIBUTIONS") 402(f) NOTICE OF SPECIAL TAX RULES ON DISTRIBUTIONS For Payments Not From a Designated Roth Account YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving

402(f) NOTICE OF SPECIAL TAX RULES ON DISTRIBUTIONS For Payments Not From a Designated Roth Account YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving

Qualified DISTRIBUTION NOTICE Retirement Plan Important Information About Your Qualified Retirement Plan Distribution

Qualified DISTRIBUTION NOTICE Retirement Plan Important Information About Your Qualified Retirement Plan Distribution INTRODUCTION As a participant in your employer s qualified retirement plan, you have

Qualified DISTRIBUTION NOTICE Retirement Plan Important Information About Your Qualified Retirement Plan Distribution INTRODUCTION As a participant in your employer s qualified retirement plan, you have

Retirement Matters: Distributions from Retirement Plans. Slide 1

Slide 1 If you re like many Americans, you ve been setting aside money for your retirement. Now that you re nearing retirement age, it may soon be time to start drawing money from your qualified retirement

Slide 1 If you re like many Americans, you ve been setting aside money for your retirement. Now that you re nearing retirement age, it may soon be time to start drawing money from your qualified retirement

If we receive request by 4:00pm ET on a business day, the transaction will be processed on that day unless you specify a future date below:

Jefferson National Life Insurance Company Regular Delivery: P.O. Box 36750, Louisville, KY 40233 Overnight: 9920 Corporate Campus Drive, Louisville, KY 40223 P: 866.667.0561 F: 866.667.0563 PARTIAL WITHDRAWAL

Jefferson National Life Insurance Company Regular Delivery: P.O. Box 36750, Louisville, KY 40233 Overnight: 9920 Corporate Campus Drive, Louisville, KY 40223 P: 866.667.0561 F: 866.667.0563 PARTIAL WITHDRAWAL

SPECIAL TAX NOTICE (For Payments From a Designated Roth Account) YOUR ROLLOVER OPTIONS

YOUR ROLLOVER OPTIONS") SPECIAL TAX NOTICE (For Payments From a Designated Roth Account) YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving from your retirement plan is

SPECIAL TAX NOTICE (For Payments From a Designated Roth Account) YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving from your retirement plan is

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS YOUR ROLLOVER OPTIONS

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving from your employer s retirement plan (the Plan ) is

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving from your employer s retirement plan (the Plan ) is

TAX NOTICE (For Payments Not From a Designated Roth Account)

") TAX NOTICE (For Payments Not From a Designated Roth Account) YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving from your employer s qualified retirement

TAX NOTICE (For Payments Not From a Designated Roth Account) YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving from your employer s qualified retirement

Special Tax Notice Regarding Payments YOUR ROLLOVER OPTIONS. Where may I roll over the payment?

Special Tax Notice Regarding Payments Products and financial services provided by American United Life Insurance Company a OneAmerica company One American Square, P.O. Box 368 Indianapolis, IN 46206-0368

Special Tax Notice Regarding Payments Products and financial services provided by American United Life Insurance Company a OneAmerica company One American Square, P.O. Box 368 Indianapolis, IN 46206-0368

chart RETIREMENT PLANS 8 RETIREMENT PLAN BENEFITS AVAILABLE RETIREMENT PLANS Retirement plans available to self-employed individuals include:

retirement plans Contributing to retirement plans can provide you with financial security as well as reducing and/or deferring your taxes. However, there are complex rules that govern the type of plans

retirement plans Contributing to retirement plans can provide you with financial security as well as reducing and/or deferring your taxes. However, there are complex rules that govern the type of plans

Notice Regarding Distributions to Terminated Participants: This notice explains what happens if the Distribution Election Form is not returned.

TO: FROM: RE: PLAN PARTICIPANT PREFERRED PENSION PLANNING CORPORATION 991 Route 22 West Bridgewater, NJ 08807 Phone: (908) 575-7575 Fax: (908) 575-8889 Email: distributions@preferredpension.com DISTRIBUTION

TO: FROM: RE: PLAN PARTICIPANT PREFERRED PENSION PLANNING CORPORATION 991 Route 22 West Bridgewater, NJ 08807 Phone: (908) 575-7575 Fax: (908) 575-8889 Email: distributions@preferredpension.com DISTRIBUTION

Special Tax Notice (This notice is required by the Internal Revenue Service.)

") Special Tax Notice (This notice is required by the Internal Revenue Service.) YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving from your employer

Special Tax Notice (This notice is required by the Internal Revenue Service.) YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving from your employer

Distribution Options. For Defined Contribution and 403(b) Plans Without Life Annuities

Plans Without Life Annuities") Distribution Options For Defined Contribution and 403(b) Plans Without Life Annuities Take the Time to Decide What will you do with your retirement savings? Life is full of changes. We retire. We change

Distribution Options For Defined Contribution and 403(b) Plans Without Life Annuities Take the Time to Decide What will you do with your retirement savings? Life is full of changes. We retire. We change

RETIREMENT ACCOUNT DISTRIBUTION FORM

RETIREMENT ACCOUNT DISTRIBUTION FORM 4010 Boy Scout Blvd., Suite 450 Tampa, Florida 33607 www.aspireonline.com RETIREMENT ACCOUNT DISTRIBUTION REQUEST CHECKLIST A Distribution Request Form must be completed,

RETIREMENT ACCOUNT DISTRIBUTION FORM 4010 Boy Scout Blvd., Suite 450 Tampa, Florida 33607 www.aspireonline.com RETIREMENT ACCOUNT DISTRIBUTION REQUEST CHECKLIST A Distribution Request Form must be completed,

Bellevue MEBT Plan. In-Service Withdrawal - Non-Hardship Forms

Bellevue MEBT Plan In-Service Withdrawal - Non-Hardship Forms Return these forms to: MEBT Service Center 5446 California Ave. SW Suite 200 Seattle, WA 98136 Fax: 206-938-5987 The following forms are included

Bellevue MEBT Plan In-Service Withdrawal - Non-Hardship Forms Return these forms to: MEBT Service Center 5446 California Ave. SW Suite 200 Seattle, WA 98136 Fax: 206-938-5987 The following forms are included

Introduction. Please read and follow all instructions carefully. Incomplete paperwork may cause delays or prevent your request from being processed.

Introduction Please read and follow all instructions carefully. Incomplete paperwork may cause delays or prevent your request from being processed. Critical information to consider: The Hardship Withdrawal

Introduction Please read and follow all instructions carefully. Incomplete paperwork may cause delays or prevent your request from being processed. Critical information to consider: The Hardship Withdrawal

Required Minimum Distributions

Required Minimum Distributions What You Need To Know When It Is Time To Start Distributions From Your Retirement Accounts What Are Required Minimum Distributions? Required minimum distributions (RMDs)

Required Minimum Distributions What You Need To Know When It Is Time To Start Distributions From Your Retirement Accounts What Are Required Minimum Distributions? Required minimum distributions (RMDs)

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy March 2018 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I Revocation 3

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy March 2018 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I Revocation 3

Three Tax-Diversification Strategies for Maximizing Wealth in Retirement

Three Tax-Diversification Strategies for Maximizing Wealth in Retirement Christine Fahlund, CFP, senior financial planner Tina Wilcox, QKA, relationship manager Copyright 2010 T. Rowe Price. All rights

Three Tax-Diversification Strategies for Maximizing Wealth in Retirement Christine Fahlund, CFP, senior financial planner Tina Wilcox, QKA, relationship manager Copyright 2010 T. Rowe Price. All rights

NATIONAL WESTERN LIFE INSURANCE COMPANY YOUR ROLLOVER OPTIONS

NATIONAL WESTERN LIFE INSURANCE COMPANY YOUR ROLLOVER OPTIONS This notice explains how you can continue to defer federal income tax on your retirement savings and contains important information you will

NATIONAL WESTERN LIFE INSURANCE COMPANY YOUR ROLLOVER OPTIONS This notice explains how you can continue to defer federal income tax on your retirement savings and contains important information you will

Instructions for Requesting an In-Service Withdrawal

Instructions for Requesting an In-Service Withdrawal Diocese of Metuchen 403(b) Plan Enclosed are the following items needed to request an In-Service Withdrawal from your retirement plan. Please review

Instructions for Requesting an In-Service Withdrawal Diocese of Metuchen 403(b) Plan Enclosed are the following items needed to request an In-Service Withdrawal from your retirement plan. Please review

Last Name First Name MI

Marsh & McLennan Companies 401(k) Savings & Investment Plan IN-PLAN ROTH CONVERSION REQUEST FORM Use this form as an active or terminated participant to request an In-Plan Roth conversion from your after

Marsh & McLennan Companies 401(k) Savings & Investment Plan IN-PLAN ROTH CONVERSION REQUEST FORM Use this form as an active or terminated participant to request an In-Plan Roth conversion from your after

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy Effective November 2016 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy Effective November 2016 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I

Capture More Retirement Rollovers

Capture More Retirement Rollovers Capture More Rollover Business from Clients, Prospects & COIs with Wendi Webb Director, Advisor/Client Solutions Aug 2, 2012 Advisor/Client Solutions Marketing Campaigns

Capture More Retirement Rollovers Capture More Rollover Business from Clients, Prospects & COIs with Wendi Webb Director, Advisor/Client Solutions Aug 2, 2012 Advisor/Client Solutions Marketing Campaigns

SPECIAL TAX NOTICE (For Payments Not From a Designated Roth Account) YOUR ROLLOVER OPTIONS

YOUR ROLLOVER OPTIONS") SPECIAL TAX NOTICE (For Payments Not From a Designated Roth Account) YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving from your retirement plan

SPECIAL TAX NOTICE (For Payments Not From a Designated Roth Account) YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving from your retirement plan

Special Tax Notice Regarding Distributions*

1901 Chestnut Avenue Glenview, Illinois 60025-1604 1-800-851-2201 wespath.org Special Tax Notice Regarding Distributions* Your Options You are receiving this notice because all or a portion of a Plan distribution

1901 Chestnut Avenue Glenview, Illinois 60025-1604 1-800-851-2201 wespath.org Special Tax Notice Regarding Distributions* Your Options You are receiving this notice because all or a portion of a Plan distribution

Distribution options summary

Distribution options summary For Governmental 457(b) Deferred Compensation Plans (for pre-tax deferral only) The Voya family of companies is committed to providing you with the information you need to

Distribution options summary For Governmental 457(b) Deferred Compensation Plans (for pre-tax deferral only) The Voya family of companies is committed to providing you with the information you need to

DISTRIBUTION PLANNING

DISTRIBUTION PLANNING In 5 Easy Steps 2.5 Million Baby Boomers Will Turn Age 70 in 2016 Get the Definitive Guide to RMD Planning at: www.irahelp.com/rmd-guide Calculating the Pro-Rata Rule in 5 Easy Steps

DISTRIBUTION PLANNING In 5 Easy Steps 2.5 Million Baby Boomers Will Turn Age 70 in 2016 Get the Definitive Guide to RMD Planning at: www.irahelp.com/rmd-guide Calculating the Pro-Rata Rule in 5 Easy Steps

YOUR ROLLOVER OPTIONS

YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you receive from the Plan is eligible to be rolled over to an IRA or an employer plan. This notice is intended

YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you receive from the Plan is eligible to be rolled over to an IRA or an employer plan. This notice is intended

IMPORTANT INFORMATION REGARDING DISTRIBUTIONS FROM YOUR 401(K) ACCOUNT

ACCOUNT") IMPORTANT INFORMATION REGARDING DISTRIBUTIONS FROM YOUR 401(K) ACCOUNT All distributions are issued in the form of a check, mailed to your address on file. Please make sure to have proper payee information

IMPORTANT INFORMATION REGARDING DISTRIBUTIONS FROM YOUR 401(K) ACCOUNT All distributions are issued in the form of a check, mailed to your address on file. Please make sure to have proper payee information

SPECIAL TAX NOTICE (For Payments Not From a Designated Roth Account) YOUR ROLLOVER

YOUR ROLLOVER") SPECIAL TAX NOTICE (For Payments Not From a Designated Roth Account) YOUR ROLLOVER You are receiving this notice because all or a portion of a payment you are receiving from your retirement plan is eligible

SPECIAL TAX NOTICE (For Payments Not From a Designated Roth Account) YOUR ROLLOVER You are receiving this notice because all or a portion of a payment you are receiving from your retirement plan is eligible

Your Rollover Options For Payments Not From a Designated Roth Account

This document combines two Rollover Options notices. The first notice describes the rollover and other tax rules that apply to payments from the Plan that are not from a designated Roth account. The second

This document combines two Rollover Options notices. The first notice describes the rollover and other tax rules that apply to payments from the Plan that are not from a designated Roth account. The second

Distribution Request Form Distribution of Traditional 401(k) to Roth IRA Request Form

to Roth IRA Request Form") Distribution Request Form Distribution of Traditional 401(k) to Roth IRA Request Form READ THE ATTACHED IRS SPECIAL TAX NOTICE: IF YOUR PLAN ALLOWS FOR AN ANNUITY OPTION, READ THE WRITTEN EXPLANATION OF

Distribution Request Form Distribution of Traditional 401(k) to Roth IRA Request Form READ THE ATTACHED IRS SPECIAL TAX NOTICE: IF YOUR PLAN ALLOWS FOR AN ANNUITY OPTION, READ THE WRITTEN EXPLANATION OF

YOUR ROLLOVER OPTIONS

For Payments From a Designated Roth Account YOUR ROLLOVER OPTIONS You are receiving this notice in the event that all or a portion of a payment you are receiving from the Plan is eligible to be rolled

For Payments From a Designated Roth Account YOUR ROLLOVER OPTIONS You are receiving this notice in the event that all or a portion of a payment you are receiving from the Plan is eligible to be rolled

DISTRIBUTION REQUEST TIMELINE

Distribution Request Form DISTRIBUTION REQUEST TIMELINE This form is to request a participant withdrawal from your retirement account with your employer. Whether you are rolling over the funds or taking

Distribution Request Form DISTRIBUTION REQUEST TIMELINE This form is to request a participant withdrawal from your retirement account with your employer. Whether you are rolling over the funds or taking

AUTOMATIC IRA ROLLOVER PAC

Plan Year 1999-2000 AUTOMATIC IRA ROLLOVER PAC FOR OUR COMPANY 401(K) PLAN Use this Automatic IRA Rollover Pac to... Indicate your distribution choice in the event that your employment with our company

Plan Year 1999-2000 AUTOMATIC IRA ROLLOVER PAC FOR OUR COMPANY 401(K) PLAN Use this Automatic IRA Rollover Pac to... Indicate your distribution choice in the event that your employment with our company

HILL BROTHERS CONSTRUCTION COMPANY, INC. STOCK OWNERSHIP PLAN

HILL BROTHERS CONSTRUCTION COMPANY, INC. STOCK OWNERSHIP PLAN As you may know, the Hill Brothers Construction Company, Inc. Stock Ownership Plan (the Plan ) is being terminated. As a result of the termination,

HILL BROTHERS CONSTRUCTION COMPANY, INC. STOCK OWNERSHIP PLAN As you may know, the Hill Brothers Construction Company, Inc. Stock Ownership Plan (the Plan ) is being terminated. As a result of the termination,

Savings Banks Employees Retirement Association

Savings Banks Employees Retirement Association 401(k) PLAN APPLICATION FOR WITHDRAWAL AT AGE 59 1/2 Participant Name: (Please Print) Certificate No. Current Address (required) (Street) (City, State Zip)

Savings Banks Employees Retirement Association 401(k) PLAN APPLICATION FOR WITHDRAWAL AT AGE 59 1/2 Participant Name: (Please Print) Certificate No. Current Address (required) (Street) (City, State Zip)

YOUR ROLLOVER OPTIONS

For Payments Not From a Designated Roth Account YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving from the [INSERT NAME OF PLAN] (the Plan ) is

For Payments Not From a Designated Roth Account YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving from the [INSERT NAME OF PLAN] (the Plan ) is

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS ROLLOVER OPTIONS

Page 1 of 5 You are receiving this notice because all or a portion of the payment that you are eligible to receive from the Chicago Regional Council of Carpenters Supplemental Retirement Fund is permitted

Page 1 of 5 You are receiving this notice because all or a portion of the payment that you are eligible to receive from the Chicago Regional Council of Carpenters Supplemental Retirement Fund is permitted

Death Claims These are given special handling by TCG. Please call us at call for assistance.

Death Claims These are given special handling by TCG. Please call us at call 1-800-943-9179 for assistance. Participant Information First Name MI Last Employer Street Address City State Zip (If the address

Death Claims These are given special handling by TCG. Please call us at call 1-800-943-9179 for assistance. Participant Information First Name MI Last Employer Street Address City State Zip (If the address

SPECIAL TAX NOTICE REGARDING PAYMENTS FROM QUALIFIED PLANS Excerpted from IRS Notice

SPECIAL TAX NOTICE REGARDING PAYMENTS FROM QUALIFIED PLANS Excerpted from IRS Notice 2002-3 This notice explains how you can continue to defer federal income tax on your retirement savings in your Employer

SPECIAL TAX NOTICE REGARDING PAYMENTS FROM QUALIFIED PLANS Excerpted from IRS Notice 2002-3 This notice explains how you can continue to defer federal income tax on your retirement savings in your Employer

Participant Distribution Notice

Participant Distribution Notice Plan Name: CITGO Petroleum Corporation Employees' Retirement and Savings Plan Plan Number: 87084 Date Generated: October 16, 2014 The CITGO Petroleum Corporation Employees'

Participant Distribution Notice Plan Name: CITGO Petroleum Corporation Employees' Retirement and Savings Plan Plan Number: 87084 Date Generated: October 16, 2014 The CITGO Petroleum Corporation Employees'

Special Tax Notice Regarding Plan Payments

Special Tax Notice Regarding Plan Payments Your Rollover Options for Payments Not From A Designated Roth Account You are receiving this notice because all or a portion of a payment you receive from your

Special Tax Notice Regarding Plan Payments Your Rollover Options for Payments Not From A Designated Roth Account You are receiving this notice because all or a portion of a payment you receive from your

DISTRIBUTION OPTIONS GENERAL INFORMATION ABOUT ROLLOVERS

PLUMBERS LOCAL UNION NO. 68 PLAN OF DEFINED CONTRIBUTION BENEFITS P.O. Box 8726 Houston, Texas 77249 713.869.2592 Fax: 713.862.4877 Toll Free: 800.833.2980 DISTRIBUTION OPTIONS You are receiving this notice

PLUMBERS LOCAL UNION NO. 68 PLAN OF DEFINED CONTRIBUTION BENEFITS P.O. Box 8726 Houston, Texas 77249 713.869.2592 Fax: 713.862.4877 Toll Free: 800.833.2980 DISTRIBUTION OPTIONS You are receiving this notice

Presented by Jeffrey Levine, CPA/PFS, CFP, CWS, MSA Program Leader, Savvy IRA Planning. Copyright 2018 Fully Vested Advice, Inc.

Presented by Jeffrey Levine, CPA/PFS, CFP, CWS, MSA Program Leader, Savvy IRA Planning 7 Deadly IRA Sins 1) Rollover Blunders 2) Non-spouse Beneficiary Mistakes 3) Spousal Beneficiary Mistakes 4) Failing

Presented by Jeffrey Levine, CPA/PFS, CFP, CWS, MSA Program Leader, Savvy IRA Planning 7 Deadly IRA Sins 1) Rollover Blunders 2) Non-spouse Beneficiary Mistakes 3) Spousal Beneficiary Mistakes 4) Failing

SPECIAL TAX NOTICE YOUR ROLLOVER OPTIONS

SPECIAL TAX NOTICE YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving from the Pfizer Consolidated Pension Plan (the Plan ) is eligible to be rolled

SPECIAL TAX NOTICE YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving from the Pfizer Consolidated Pension Plan (the Plan ) is eligible to be rolled

Lowe s 401(k) Plan SPECIAL TAX NOTICE AND YOUR ROLLOVER OPTIONS

Plan SPECIAL TAX NOTICE AND YOUR ROLLOVER OPTIONS") Lowe s 401(k) Plan SPECIAL TAX NOTICE AND YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving from the Lowe s 401(k) Plan (the Plan ) is eligible

Lowe s 401(k) Plan SPECIAL TAX NOTICE AND YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving from the Lowe s 401(k) Plan (the Plan ) is eligible

Net Unrealized Appreciation (NUA)

") Beacon Pointe Advisors 24 Corporate Plaza, Suite 150 Newport Beach, CA 92660 949-718-1600 info@bpadvisors.com www.bpadvisors.com Net Unrealized Appreciation (NUA) May 08, 2015 Page 1 of 6, see disclaimer

Beacon Pointe Advisors 24 Corporate Plaza, Suite 150 Newport Beach, CA 92660 949-718-1600 info@bpadvisors.com www.bpadvisors.com Net Unrealized Appreciation (NUA) May 08, 2015 Page 1 of 6, see disclaimer

Designating a Beneficiary for Your IRA

Retirement Planning Designating a Beneficiary for Your IRA You have likely named beneficiaries many times over the years for things like your life insurance policies, annuity contracts, IRAs, company pension

Retirement Planning Designating a Beneficiary for Your IRA You have likely named beneficiaries many times over the years for things like your life insurance policies, annuity contracts, IRAs, company pension

SPECIAL TAX NOTICE REGARDING RETIREMENT PLAN PAYMENTS

CUNA Mutual Retirement Solutions Phone: 800.999.8786 Fax: 608.236.8017 BenefitsForYou.com SPECIAL TAX NOTICE REGARDING RETIREMENT PLAN PAYMENTS Non-Roth Accounts YOUR ROLLOVER OPTIONS You are receiving

CUNA Mutual Retirement Solutions Phone: 800.999.8786 Fax: 608.236.8017 BenefitsForYou.com SPECIAL TAX NOTICE REGARDING RETIREMENT PLAN PAYMENTS Non-Roth Accounts YOUR ROLLOVER OPTIONS You are receiving

403(b) Distribution Guide. Learn about taking distributions from your 403(b) retirement savings. Accessing Your Retirement Savings Money

Distribution Guide. Learn about taking distributions from your 403(b) retirement savings. Accessing Your Retirement Savings Money") 403(b) Distribution Guide Accessing Your Retirement Savings Money Whether you are nearing retirement age, have separated from service or just encountered some unexpected expenses, FPS Trust can help you

403(b) Distribution Guide Accessing Your Retirement Savings Money Whether you are nearing retirement age, have separated from service or just encountered some unexpected expenses, FPS Trust can help you

Distribution Election Form

IMPORTANT INFORMATION Distribution Election Form Please complete the form in its entirety. Missing pages and/or incomplete forms will delay processing. After completion, please return form to Pension Inc.

IMPORTANT INFORMATION Distribution Election Form Please complete the form in its entirety. Missing pages and/or incomplete forms will delay processing. After completion, please return form to Pension Inc.

Special Tax Notice Regarding Plan Payment (the Plan )

") Special Tax Notice Regarding Plan Payment (the Plan ) SUMMARY This notice explains how you can continue to defer federal income tax on your retirement savings in Plan and contains important information

Special Tax Notice Regarding Plan Payment (the Plan ) SUMMARY This notice explains how you can continue to defer federal income tax on your retirement savings in Plan and contains important information

SPECIAL TAX NOTICE (For Payments Not From a Designated Roth Account)

") SPECIAL TAX NOTICE (For Payments Not From a Designated Roth Account) YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving from your retirement plan

SPECIAL TAX NOTICE (For Payments Not From a Designated Roth Account) YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving from your retirement plan

DISTRIBUTIONS FREQUENTLY ASKED QUESTIONS. Learn about taking distributions from your retirement savings account

DISTRIBUTIONS FREQUENTLY ASKED QUESTIONS Learn about taking distributions from your retirement savings account 4010 Boy Scout Blvd., Suite 450 Tampa, Florida 33607 www.aspireonline.com Frequently Asked

DISTRIBUTIONS FREQUENTLY ASKED QUESTIONS Learn about taking distributions from your retirement savings account 4010 Boy Scout Blvd., Suite 450 Tampa, Florida 33607 www.aspireonline.com Frequently Asked

YOUR ROLLOVER OPTIONS

For Payments Not From a Designated Roth Account YOUR ROLLOVER OPTIONS You are receiving this notice in the event that all or a portion of a payment you are receiving from the Plan is eligible to be rolled

For Payments Not From a Designated Roth Account YOUR ROLLOVER OPTIONS You are receiving this notice in the event that all or a portion of a payment you are receiving from the Plan is eligible to be rolled

Mailing Address: P.O. Box 9394 Des Moines, IA FAX (866)

") Mailing Address: P.O. Box 9394 Des Moines, IA 50306-9394 FAX (866) 704-3481 Principal Life Insurance Company Complete this form to withdraw part of your retirement funds while still employed. Participant

Mailing Address: P.O. Box 9394 Des Moines, IA 50306-9394 FAX (866) 704-3481 Principal Life Insurance Company Complete this form to withdraw part of your retirement funds while still employed. Participant