Global Macroeconomic Outlook March LOWDER BROOK DRIVE SUITE 1100 WESTWOOD MA FAX

|

|

|

- Jodie Stevens

- 5 years ago

- Views:

Transcription

1 March 208 M E K E T A I N V E S T M E N T G R O U P 00 LOWDER BROOK DRIVE SUITE 00 WESTWOOD MA FAX

2 Global Economic Outlook The IMF continues to forecast a slight pick-up in growth over the next two years followed by a decline as output gaps close in advanced economies and the tailwinds of fiscal policy in the U.S. eventually wane. Risks are balanced over the short-term, but medium-term risks weigh to the downside, including antitrade sentiment, geopolitical tensions, and tightening financial conditions. The IMF s forecast for 208 and 209 global growth remained the same at 3.9%, a level slightly above the 3.8% level of 207. In the IMF s April update, growth projections for advanced economies increased for 208 (2.5% versus 2.2%) and remained the same for 209 (2.2%) as global growth momentum continues, financial conditions remain supportive, and U.S. tax reforms take effect. The IMF projects further increases in U.S. (2.9% versus 2.7%) and European (2.4% versus 2.2%) growth in 208 and U.S. growth in 209 (2.7% versus 2.5%). Projections for emerging economy growth remained unchanged for 208 (4.9%) and increased slightly for 209 (5.% versus 5.0%) with wide variations across countries. Growth in China is expected to moderate, with 208 and 209 growth rate projections unchanged at 6.6% and 6.4%, respectively. The IMF projects improved growth in India, Brazil, and Mexico. Slow growth is expected for Russia in 208 (.7%) and 209 (.5%). Overall, inflation is expected to decline slightly over the next two years, remaining below the long-term averages. IMF 208 Forecast Real GDP (%) Inflation (%) IMF Actual IMF IMF 209 Forecast 0 Year Average 208 Forecast 209 Forecast Actual 0 Year Average World U.S European Union Japan China Emerging Markets (ex. China) Source: IMF. World Economic Outlook. October 207 edition with April 208 update. Actual 0 Year Average represents data from 2007 to 207.

3 Global Economic Outlook (continued) Global Macroeconomic Outlook Tax cuts could provide a modest boost to growth, but it will likely be short lived. We could be moving into a period of coordinated monetary tightening across central banks. The balance of fiscal and monetary policy globally remains a key issue. Under new chair Jerome Powell, the Federal Reserve increased interest rates for the sixth time at their March meeting. Markets expect the Fed to increase rates two or three more times in 208 and to continue to reduce its balance sheet. Tax cuts and the changing complexion of the Fed could lead to further tightening. Of all the major central banks, the Bank of Japan (BOJ) is showing no signs of pulling back from its unprecedented monetary stimulus, as inflation remains stubbornly low. At their March meeting the BOJ made no changes to their stimulative efforts, keeping bank deposit rates negative (-0.%), and continuing to target a 0% yield on the 0-year government bond. At their meeting in March, the European Central Bank held rates steady and plans to continue asset purchases through September. They removed language in their statement that indicated they were ready to increase the level of bond purchases, signaling that its quantitative easing could be ending in the short-term. The strengthening euro is also a key consideration that could create a headwind to the bank s inflation target of close to 2%. China s central bank, the People s Bank of China (PBOC), continues to quietly tighten monetary policy. In March after the Federal Reserve s rate increase, the PBOC increased rates again, although by a smaller amount. Several issues are of primary concern: ) the potential for simultaneous monetary tightening globally; 2) uncertainty related to the U.S. economy and policies; 3) declining growth in China, along with uncertain fiscal and monetary policies; and 4) political uncertainty in Europe and risks related to the U.K. s exit from the European Union.

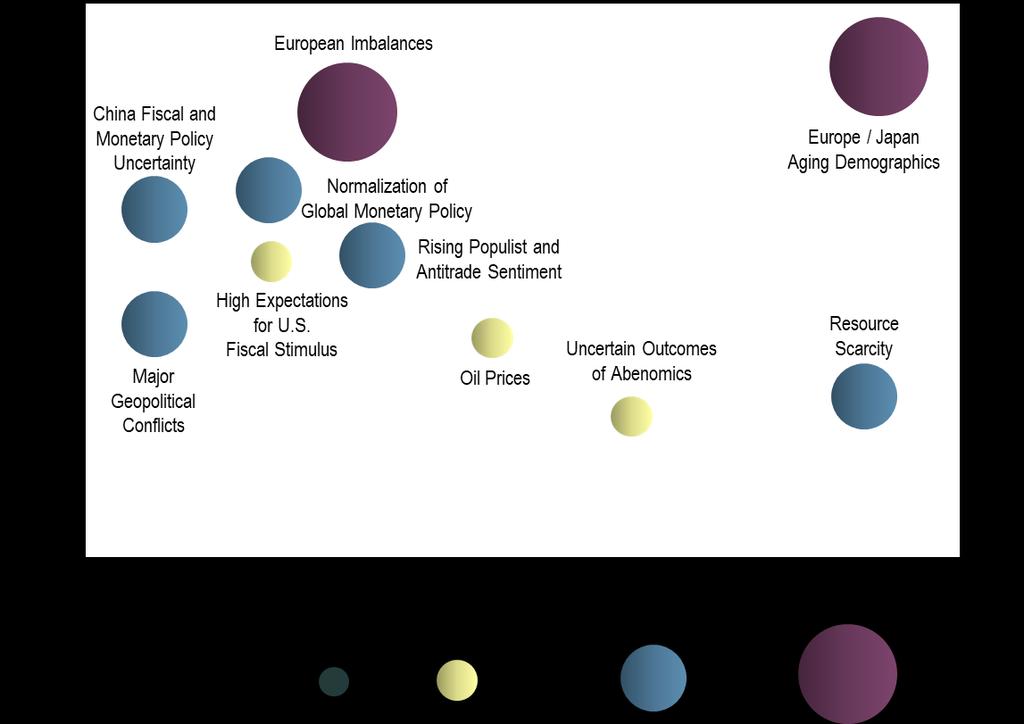

4 Macroeconomic Risk Matrix

5 Macroeconomic Risk Overviews China Fiscal and Monetary Policy Uncertainty Europe/Japan Aging Demographics High Expectations for U.S. Fiscal Stimulus European Imbalances Major Geopolitical Conflicts The process of transitioning from a growth model based on fixed asset investment by the government to a model of consumption-based growth will be difficult. Given the significant turnover in positions related to elections at the communist party s congress, policy uncertainty exists going forward including the management of debt levels and the regulation of state-owned enterprises. The management of capital outflows is another key issue in China. They have made some efforts to tighten regulations to stem outflows, but higher rates and growth in the U.S., and elsewhere, could add to outflow pressures. Were China to abandon its support for the yuan, the resulting major devaluation of the currency could prove particularly disruptive to global markets and trade. The hot property market and the growing mountain of debt in the corporate sector remain other key risks. In Japan and Europe, birth rates have declined for decades, resulting in populations becoming older and smaller relative to the rest of the world. These demographic trends will have negative long-term impacts on GDP growth and fiscal budgets, amplifying debt problems. Post U.S. presidential election, hopes have been high for new policies lowering taxes, increasing infrastructure spending, and reducing regulations. The recent reduction in taxes could lead to an increase in economic activity, but questions remain about how much has already been priced into markets and the late cycle timing of the cuts. The potential for disappointment remains as the stimulus could further fan inflation and the rate of the Fed s monetary tightening. The crisis is rooted in structural issues in the Eurozone related to the combination of a single currency combined with 7 fiscal authorities. Within the European Union, tensions exist, as highlighted in the U.K. referendum, related to policies on immigration, laws, and budgetary contributions. The referendum late last year in Catalonia Spain and elections in Germany highlight the political uncertainties. Additional countries leaving either group, particularly the Eurozone, could set a dangerous precedent, especially if they ultimately experience growth. Tensions with North Korea appear to have softened, while the ongoing conflict in Syria has flared-up. After heightened rhetoric from the U.S. and North Korea, progress has been made, with a meeting between North and South Korea, a visit by U.S. CIA director, Michael Pompeo, and plans for a meeting between President Trump and Kim Jong Un. In Syria, after a suspected chemical attack the U.S. and its allies launched strategic missile attacks increasing the tensions with Syria and its ally, Russia. Other outstanding issues include tensions between the U.S./Saudi Arabia and Iran along with ongoing conflicts in Yemen and Afghanistan.

6 Macroeconomic Risk Overviews (continued) Normalization of Global Monetary Policy Oil Prices Resource Scarcity Rising Populist and Antitrade Sentiment Uncertain Outcomes of Abenomics After the Global Financial Crisis, major central banks injected massive amounts of liquidity into the market by purchasing bonds from banks (i.e., quantitative easing). They also reduced short-term interest rates to record lows. The U.S. central bank has ended its bond-buying program, started to increase interest rates, and began reducing its balance sheet. Although other central banks, like Japan (BOJ) and Europe (ECB), continue to stimulate their economies, discussions have started about reducing stimulus. If major central banks start to tighten their policies at the same time it could lead to higher rates, less liquidity, and overall lower economic activity. Oil prices rallied significantly from their bottom, but they remain off their peaks. An extended period of relatively lower oil prices would hurt countries that depend on higher prices. Although OPEC has extended their production cuts into 208 to help prices, increased production from the U.S. shale industry acts as a counter force. The risk of increased geopolitical tensions also exists with depressed oil prices. The growing world population, urbanization, and a growing middle class, particularly in emerging economies, could all lead to a scarcity of resources, including food, water, land, energy, and minerals. As demand continues to grow and supply declines, certain commodity prices may skyrocket, hurting the living standards of many and increasing the risk of geopolitical conflicts. Recent tariffs imposed by the U.S. and China, along with the last U.S. presidential election and the U.K. vote to leave the European Union ( Brexit ) and other votes in Europe, highlight the growing populist/antitrade sentiment. Stagnant wages, growing inequality, and the perception of jobs being lost abroad are key contributors. Reducing trade and imposing tariffs will likely lead to inflation, reduced efficiencies, and heightened tensions between countries. Japan is engaged in a historic stimulus program, referred to as Abenomics to fight its decades of deflation. The plan includes monetary, fiscal, and structural components. Recently Japan has experienced economic improvements, but the risk remains of overshooting with its policies, which could prove disruptive to markets and growth.

7 Positive Macroeconomic Trends Matrix

8 Positive Macroeconomic Trends Overviews Global Fiscal Stimulus Growth of Emerging Markets Middle Class Improvements in Education/Healthcare Oil Prices Stabilization of Japanese and European Economies U.S. Employment Given the slow growth globally, and the likely tightening of monetary stimulus, there could be a shift to fiscal stimulus. Recent U.S. tax cuts should help growth domestically and abroad, particularly for key trading partners like Mexico and Canada. With interest rates still low, borrowing for infrastructure investments is affordable. Increased fiscal stimulus could help growth while reducing the reliance on monetary policy. In emerging economies, the middle class is projected to grow significantly over the next twenty years. This growing middle class should increase consumption globally, which in turn will drive GDP growth and create jobs. Literacy rates and average life spans have increased globally, particularly in emerging economies. Higher literacy rates will drive future growth, helping people learn new skills and improve existing skills. Longer lives increase incentives for long-term investments in education and training, resulting in a more productive work force and ultimately more growth. Although oil prices recently increased, they remain below their prior peak. Lower oil prices will likely have a positive impact on global growth, particularly for energy importers like China, Japan, and India. Consumers should benefit from lower oil prices, in the form of lower prices for gasoline and heating oil. Despite some recent talks of tightening monetary policy, the Japanese and European central banks continue their respective asset purchase programs and maintain interest rates at historic lows. Unemployment has come down in both areas and Japan has moved from deflation to inflation. Continued improvements in economic conditions in Europe and Japan could also be beneficial for global trade. U.S. investors could particularly benefit from these conditions if the dollar remains weak. The U.S. unemployment rate has steadily declined since its post Global Financial Crisis peak. Hourly earnings growth has not reached levels that it has in prior recoveries, but has increased from its lows. Improvements in the U.S. labor market, along with the recent tax cuts, should stimulate consumption and growth for both U.S. and foreign goods. A lower unemployment rate and higher consumption will also lead to higher tax revenue that should partly offset the deficit pressures from the recent tax reforms.

9 Global Nominal Gross Domestic Product (GDP) Growth 0% 8% Represents Projected Global Growth 6% 4% 2% 0% -2% Higher global growth is expected in 208, driven by robust trade, the fiscal stimulus in the U.S., and continued growth in Europe. Going forward, the potential for trade wars, higher inflation, and policy tightening remain headwinds to the global economy. Source: Oxford Economics. Updated March 208. GDP data after 207 are estimates.

10 U.S. and China Tariffs The U.S. and China, the world s two largest economies, are locked in a back-and-forth of trade tariff threats totaling over $00 billion in goods. The tension started as the U.S. administration looked to make good on its promise to bring jobs back to the U.S., particularly in the manufacturing sector. Thus far, the U.S. has announced tariffs on solar panels (30%), steel (25%), and aluminum (0%) imports, as well as proposed $50 billion in tariffs on other Chinese goods with China responding with similar tariffs across U.S. goods. Tariffs typically result in higher prices (inflation) and ultimately weigh on growth. This could particularly affect emerging economies. In addition, tariffs targeted to protect domestic producers will also hurt companies that use the items as an input (e.g., steel) weighing on margins and potentially leading to higher prices.

11 Billions of USD % of GDP Global Macroeconomic Outlook Global Monetary Policy FED ECB BOJ BOE SNB PBOC % of GDP $24,000 $22,000 $20,000 $8,000 $6,000 $4,000 $2,000 $0,000 $8,000 $6,000 $4,000 $2,000 50% 45% 40% 35% 30% 25% 20% 5% 0% 5% $0 0% Since the Global Financial Crisis, major central banks have dramatically increased their balance sheets to levels close to 45% of their aggregate GDP. The U.S. already started reducing its balance sheet and it is likely that the ECB will end its asset purchases by the end of 208. Less demand from central banks for bonds could weigh on overall economic activity and risk assets as interest rates rise, demand for credit falls, and liquidity declines. Bloomberg. Data is as of March 3, 208.

12 Major Currency Values versus the U.S. Dollar 30 Trade Weighted U.S. Dollar Index The U.S. dollar continued its slide in the first quarter falling.5% versus a basket of its peers. Fears of a trade war, inflationary pressures, and anticipation of a higher deficit from the recent tax cuts have depressed the dollar despite higher rates in the U.S. and fiscal stimulus. The weakening dollar lessened the burden for countries with dollar-denominated debt and boosted international equity returns for U.S. investors. Source: Federal Reserve Bank of St. Louis. Data is as of March 3, 208.

13 VIX Global Macroeconomic Outlook Volatility 45 VIX Index Average Average Supportive monetary policy, positive economic growth globally, and strategies that bet against volatility all contributed to the low levels of volatility in 207. In February, volatility spiked driven by an unwinding of short volatility trades and investors coming to terms with the fact that inflation and rates could be rising. Although volatility spiked recently, the increase brought the VIX to only slightly above its long-term average at quarter-end. Bloomberg. Data is as of March 3, 208.

14 Fed Balance Sheet ($Billions) Global Macroeconomic Outlook U.S. Monetary Policy, 2 Federal Funds Rate (Upper Bound) Federal Reserve Long Run Projection Market Expectations Federal Reserve Year-End Estimates (Mid point) 5,000 7% 4,500 6% 4,000 5% 3,500 $.5T 4% 3% 2.88% 3.38% 2.88% 3,000 2, % 2.44% 2.52% 2%.75% 2.08% % 0% -% Long Run 2,000,500, In March, the U.S. Federal Reserve continued its pace of steadily increasing interest rates announcing its sixth increase, to a range of.50% to.75%. This represented the first rate hike under the new head of the Fed, Jerome Powell. Expectations are for several more rate hikes this year with the trend persisting of market expectations being lower than the central bank s estimates. The Fed recently began the process of reducing their over $4 trillion balance sheet, with a target of reducing it by $.5 trillion by Less demand for bonds by the Fed could lead to further interest rate increases. Source for Monetary Policy: Bloomberg. Data is as of March 3, Source for Balance Sheet: Oxford Economics Data is as of March 3, 208.

15 U.S. Real Gross Domestic Product (GDP) Growth 0% 8% 6% 4% 2% 0% -2% -4% -6% -8% Personal consumption expenditures Net exports of goods and services Gross Domestic Product Gross private domestic investment Government consumption expenditures and gross investment -0% Mar-2008 Mar-2009 Mar-200 Mar-20 Mar-202 Mar-203 Mar-204 Mar-205 Mar-206 Mar-207 Mar-208 The initial estimate of first quarter U.S. GDP growth came in at 2.3%, below the prior reading of 2.9%, but above the 2.0% expected by economists. For the trailing year, GDP grew at a 2.9% rate. Consumer spending slowed in the first quarter contributing to the decline from the prior quarter, but this could change going forward as the impact of the recent tax reductions are felt. Source: U.S. Bureau of Economic Analysis. Data is as of the first quarter of 208 and represents the first estimate.

16 U.S. Employment & Wages 2% Unemployment Rate YoY % Change in Hourly Earnings 0% 8% 6% 4% 2% 0% In the first quarter, the unemployment rate was unchanged at 4.%, a level well below the 0.0% peak. Although the unemployment rate has substantially declined, labor force participation remains low and broader measures of unemployment that include discouraged and underemployed workers are high. Wage growth has plateaued at a level well below prior cycles, partly due to declining productivity, low labor force participation, and globalization. Source: Bureau of Labor Statistics. Data is as of March 3, 208.

17 Real GDP (YoY %) Core CPI (YoY %) ISM PMI Core CPI (YoY %) Global Macroeconomic Outlook U.S. Inflation Real GDP vs. Core CPI (Lagged 8 Months) Real GDP Core CPI ISM PMI vs. Core CPI (Lagged 2 Months) ISM PMI Core CPI Inflation is considered a lagging indicator representing the economic conditions of the past. This leads to economic conditions today being a means of forecasting future inflations levels. Real GDP and manufacturing indicators, like the ISM Purchasing Managers Index, have historically been reasonable indicators of future inflation and are both pointing to increasing inflationary pressures. Source: Bloomberg. Data is as of March 3, 208.

18 Government Bond Yield Curves United States Japan 3.5% Mar-8 Dec-7.0% Mar-8 Dec-7 3.0% 0.8% 2.5% 0.6% 2.0% 0.4%.5% 0.2%.0% 0.0% 0.5% -0.2% 0.0% 3.5% 3.0% 2.5% 2.0%.5%.0% 0.5% 0.0% -0.5% -.0% 3M 6M Y 2Y 3Y 5Y 7Y 0Y 30Y Mar-8 Italy Dec-7 3M 6M Y 2Y 3Y 5Y 7Y 0Y 30Y Germany The entire yield curve in the U.S. increased in the first quarter and continued to flatten due to fears that a pick-up in inflation could lead to the Federal Reserve increasing the pace of its rate hikes. In Europe and Japan, large portions of the yield curves remain negative. Rates largely declined in Italy with the exception of short-term rates. In Japan, rates were similar to the end of 207 with slight changes in short- and long-term rates, while results in Germany were mixed. -0.4%.5%.0% 0.5% 0.0% -0.5% -.0% 3M 6M Y 2Y 3Y 5Y 7Y 0Y 30Y Mar-8 Dec-7 3M 6M Y 2Y 3Y 5Y 7Y 0Y 30Y Source: Bloomberg. Data is as of March 3, 208.

19 Unemployment Inflation Unemployment Inflation Global Macroeconomic Outlook Japan and Europe Economic Conditions 4.0% EU Unemployment EU Inflation 5.0% 5.5% Japan Unemployment Japan Inflation 4.0% 2.0% 4.0% 5.0% 3.0% 0.0% 3.0% 4.5% 2.0% 8.0% 2.0% 4.0%.0% 6.0%.0% 3.5% 0.0% 4.0% 0.0% 3.0% -.0% 2.0% -.0% 2.5% -2.0% 0.0% % 2.0% % In Europe, employment growth remained strong, and inflation picked up, as lending and investment increased. Rising demand abroad and sustained monetary policy support have helped the Japanese economy with unemployment falling and inflation picking up. Improving economic conditions could continue to attract capital, but also lead to reduced monetary support. Source: Bloomberg. Inflation Data is as of March 3, 208 and unemployment data is as of February 28, 208.

20 Emerging Market GDP 5% Brazil Russia India China 2% 9% 6% 3% 0% -3% -6% -9% Growth in emerging economies continues strong but uneven, with debt levels remaining a key risk. China s stimulus, along with stable growth in developed economies, has helped export-focused countries. China s economy is forecasted to slow as they reposition the economy and deal with lingering debt issues. India remains a bright spot, with higher growth forecasted. The IMF projects growth from Russia and Brazil. Going forward, higher rates in the U.S., antitrade policies, and heightened geopolitical tensions could reverse the flow of the recent hot money into emerging markets and hurt returns. Source: IMF. World Economic Outlook. October edition with April 208 update. Estimates start after 206.

21 China Import Growth (USD, YoY %) China M Growth (%) % of GDP Global Macroeconomic Outlook China Stimulus 2 China Import Growth (USD, YoY) China M Growth Central Government Local Government Nonfinancial Corporations Financial Corporations Households After a difficult 205, China launched a stimulus program similar to that during the Global Financial Crisis, in an effort to stabilize the economy. They have since pulled back from this stimulus. Demand from China for imports has been a key driver in emerging market growth. A decrease in demand from China or an overall reduction in global trade driven by tariffs could hurt emerging economies. In the coming years, China will need to manage the process of transitioning to an economy based on consumption and not investment, while reducing debt levels and dealing with financial risks. Source for China Import Growth and M Growth: Bloomberg. Data is as of March 3, Source for China Debt: Oxford Economics/Haver Analytics.

22 Summary Global Macroeconomic Outlook Four primary concerns face the global economy: ) the potential for simultaneous monetary tightening globally; 2) uncertainty related to U.S. policies; 3) declining growth in China, along with uncertain fiscal and monetary policies; and 4) political uncertainty in Europe and risks related to the U.K. s exit from the European Union. Since the Global Financial Crisis, central banks worldwide have attempted to support markets and the economy through low interest rates and bond-purchasing programs (i.e., quantitative easing). Balance sheets have close to doubled since the GFC and equal around 45% of aggregate GDP. The U.S. has been increasing rates and reducing its balance sheet, with other central banks likely to follow shortly. Simultaneous tightening across central banks could lead to higher interest rates, less liquidity, and slower economic activity. The U.S. has experienced largely stable growth since the end of the financial crisis, but at levels below prior recoveries. Inflation and wage growth remain low despite the declining unemployment rate. Inflationary pressures could be building given where we are in the economic cycle, the recent tax legislation, and heightened rhetoric about tariffs. An acceleration in prices could lead the Fed to increase its pace of tightening. Political gridlock and uncertainty related to the new administration s policies remain other key issues. Over the coming years, China will likely continue to manage a repositioning and slowing of its economy, which could have a meaningful impact on countries that depend on its trade. Uncertainties related to the policies of the recently elected officials at the Communist Party s congress, growing debt, particularly in the corporate sector, and recent tariffs between China and the U.S. remain key issues. Another devaluation of the yuan could disrupt capital markets, weigh on domestic demand, and hurt countries with competing exports. The referendum in Catalonia Spain and the elections in Germany showed that political uncertainties remain in Europe. The on-going negotiations of the U.K. to leave the EU is another key issue. Uncertainty related to the negotiations should affect foreign investment and consumption. Moves by other countries to leave the EU, or the Eurozone, would be disruptive to markets and growth.

Global Macroeconomic Outlook March 2017

March 2017 M E K E T A I N V E S T M E N T G R O U P 100 LOWDER BROOK DRIVE SUITE 1100 WESTWOOD MA 02090 781 471 3500 FAX 781 471 3411 Global Economic Outlook 1 For the first time in six years, the IMF

March 2017 M E K E T A I N V E S T M E N T G R O U P 100 LOWDER BROOK DRIVE SUITE 1100 WESTWOOD MA 02090 781 471 3500 FAX 781 471 3411 Global Economic Outlook 1 For the first time in six years, the IMF

Global Macroeconomic Outlook September LOWDER BROOK DRIVE SUITE 1100 WESTWOOD MA FAX

September 208 M E K E T A I N V E S T M E N T G R O U P 00 LOWDER BROOK DRIVE SUITE 00 WESTWOOD MA 02090 78 47 3500 FAX 78 47 34 Global Economic Outlook Risk continues to increase for the global economy

September 208 M E K E T A I N V E S T M E N T G R O U P 00 LOWDER BROOK DRIVE SUITE 00 WESTWOOD MA 02090 78 47 3500 FAX 78 47 34 Global Economic Outlook Risk continues to increase for the global economy

Global Macroeconomic Outlook March 2016

Prepared by Meketa Investment Group Global Economic Outlook Projections for global growth continue to be lowered, as the economic recovery in many countries remains weak. The IMF reduced their 206 global

Prepared by Meketa Investment Group Global Economic Outlook Projections for global growth continue to be lowered, as the economic recovery in many countries remains weak. The IMF reduced their 206 global

Global Macroeconomic Outlook December LOWDER BROOK DRIVE SUITE 1100 WESTWOOD MA FAX

December 208 M E K E T A I N V E S T M E N T G R O U P 00 LOWDER BROOK DRIVE SUITE 00 WESTWOOD MA 02090 78 47 3500 FAX 78 47 34 Global Economic Outlook The IMF continues to reduce their projections for

December 208 M E K E T A I N V E S T M E N T G R O U P 00 LOWDER BROOK DRIVE SUITE 00 WESTWOOD MA 02090 78 47 3500 FAX 78 47 34 Global Economic Outlook The IMF continues to reduce their projections for

B-GUIDE: Economic Outlook

Aug-12 Apr-13 Dec-13 Aug-14 Apr-15 Dec-15 Aug-16 Apr-17 Jul-15 Nov-15 Mar-16 Jul-16 Nov-16 Mar-17 Jul-17 Quarterly Economic Outlook: Quarter 4 2017 4 January 2018 B-GUIDE: Economic Outlook The economy

Aug-12 Apr-13 Dec-13 Aug-14 Apr-15 Dec-15 Aug-16 Apr-17 Jul-15 Nov-15 Mar-16 Jul-16 Nov-16 Mar-17 Jul-17 Quarterly Economic Outlook: Quarter 4 2017 4 January 2018 B-GUIDE: Economic Outlook The economy

Explore the themes and thinking behind our decisions.

ASSET ALLOCATION COMMITTEE VIEWPOINTS First Quarter 2017 These views are informed by a subjective assessment of the relative attractiveness of asset classes and subclasses over a 6- to 18-month horizon.

ASSET ALLOCATION COMMITTEE VIEWPOINTS First Quarter 2017 These views are informed by a subjective assessment of the relative attractiveness of asset classes and subclasses over a 6- to 18-month horizon.

Global Macroeconomic Monthly Review

Global Macroeconomic Monthly Review October 16 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Please see disclaimer on the last page of this report 1 Key Issues Global

Global Macroeconomic Monthly Review October 16 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Please see disclaimer on the last page of this report 1 Key Issues Global

PMI and economic outlook

PMI and economic outlook Chris Williamson Chief Business Economist, IHS Markit 1 st November 2017 2 PMI coverage Current coverage Expansion pipeline 40+ Countries covered 27,000+ Companies surveyed every

PMI and economic outlook Chris Williamson Chief Business Economist, IHS Markit 1 st November 2017 2 PMI coverage Current coverage Expansion pipeline 40+ Countries covered 27,000+ Companies surveyed every

Interest Rate Forecast

Interest Rate Forecast Economics January Highlights Global growth firms Waiting for Trumponomics Bank of Canada on hold Recent growth momentum in the global economy continued in December and looks to extend

Interest Rate Forecast Economics January Highlights Global growth firms Waiting for Trumponomics Bank of Canada on hold Recent growth momentum in the global economy continued in December and looks to extend

Explore the themes and thinking behind our decisions.

ASSET ALLOCATION COMMITTEE VIEWPOINTS Fourth Quarter 2016 These views are informed by a subjective assessment of the relative attractiveness of asset classes and subclasses over a 6- to 18-month horizon.

ASSET ALLOCATION COMMITTEE VIEWPOINTS Fourth Quarter 2016 These views are informed by a subjective assessment of the relative attractiveness of asset classes and subclasses over a 6- to 18-month horizon.

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

Global Macroeconomic Monthly Review

Global Macroeconomic Monthly Review August 14 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department 1 Please see disclaimer on the last page of this report Key Issues Global

Global Macroeconomic Monthly Review August 14 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department 1 Please see disclaimer on the last page of this report Key Issues Global

2018 ECONOMIC OUTLOOK

LPL RESEARCH WEEKLY ECONOMIC COMMENTARY December 4 207 208 ECONOMIC OUTLOOK EXPECT BETTER GROWTH WORLDWIDE John Lynch Chief Investment Strategist, LPL Financial Barry Gilbert, PhD, CFA Asset Allocation

LPL RESEARCH WEEKLY ECONOMIC COMMENTARY December 4 207 208 ECONOMIC OUTLOOK EXPECT BETTER GROWTH WORLDWIDE John Lynch Chief Investment Strategist, LPL Financial Barry Gilbert, PhD, CFA Asset Allocation

Economic & Capital Market Outlook Third Quarter, 2018

Economic & Capital Market Outlook Third Quarter, 2018 Economic Outlook The domestic economy is functioning as well as any period since 2007, however we expect economic growth to slow next year. Measured

Economic & Capital Market Outlook Third Quarter, 2018 Economic Outlook The domestic economy is functioning as well as any period since 2007, however we expect economic growth to slow next year. Measured

Global economy in charts

Global economy in charts Ian Stewart, Debapratim De, Tom Simmons & Peter Ireson Economics & Markets Research, Deloitte, London Summary 1. Global activity easing 2. Slowdown most apparent in euro area 3.

Global economy in charts Ian Stewart, Debapratim De, Tom Simmons & Peter Ireson Economics & Markets Research, Deloitte, London Summary 1. Global activity easing 2. Slowdown most apparent in euro area 3.

Global Economic Outlook

Global Economic Outlook Will the growth continue and at what pace? Latin American Conference São Paulo August 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary Information

Global Economic Outlook Will the growth continue and at what pace? Latin American Conference São Paulo August 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary Information

Global Economic Outlook Brittle Strength

Global Economic Outlook Brittle Strength RISI North American Conference October 2017 Lasse Sinikallas Director Macroeconomics Agenda 1. Global Snapshot Steady 2. North America Performing 3. China In Transition

Global Economic Outlook Brittle Strength RISI North American Conference October 2017 Lasse Sinikallas Director Macroeconomics Agenda 1. Global Snapshot Steady 2. North America Performing 3. China In Transition

Global Economic Outlook

Global Economic Outlook Will growth continue and at what pace? North American Conference San Francisco October 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary Information

Global Economic Outlook Will growth continue and at what pace? North American Conference San Francisco October 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary Information

Global Economic Outlook

Global Economic Outlook Will growth continue and at what pace? International Containerboard Conference Chicago November 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary

Global Economic Outlook Will growth continue and at what pace? International Containerboard Conference Chicago November 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary

Leumi. Global Economics Monthly Review. Arie Tal, Research Economist. May 8, The Finance Division, Economics Department. leumiusa.

Global Economics Monthly Review May 8, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report Key

Global Economics Monthly Review May 8, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report Key

Summary. Economic Update 1 / 7 May Global Global GDP growth is forecast to accelerate to 2.9% in 2017 and maintain at 3.0% in 2018.

Economic Update Economic Update 1 / 7 Summary 2 Global Global GDP growth is forecast to accelerate to 2.9% in 2017 and maintain at 3.0% in 2018. 3 Eurozone The eurozone s recovery appears to strengthen

Economic Update Economic Update 1 / 7 Summary 2 Global Global GDP growth is forecast to accelerate to 2.9% in 2017 and maintain at 3.0% in 2018. 3 Eurozone The eurozone s recovery appears to strengthen

Q WestEnd Advisors. Macroeconomic Highlights. (888)

") Q1 2017 WestEnd Advisors Macroeconomic Highlights www.westendadvisors.com info@westendadvisors.com (888) 500-9025 1 U.S. Economic Picture Prior to the November Election 3-Month Moving Average 1.0 0.5 0.0-0.5-1.0-1.5-2.0

Q1 2017 WestEnd Advisors Macroeconomic Highlights www.westendadvisors.com info@westendadvisors.com (888) 500-9025 1 U.S. Economic Picture Prior to the November Election 3-Month Moving Average 1.0 0.5 0.0-0.5-1.0-1.5-2.0

October 2016 Market Update

Market Update (10/2016) Allianz Investment Management LLC October 2016 Market Update Key Points The lack of further easing measures from both the Bank of Japan and the European Central Bank are causing

Market Update (10/2016) Allianz Investment Management LLC October 2016 Market Update Key Points The lack of further easing measures from both the Bank of Japan and the European Central Bank are causing

April 13, Economics Research - Globanomics - Q4/16. Globanomics. World s Dashboard of Economic Indicators Q4 2016

April 13, 2017 Economics Research - Globanomics - Q4/16 Globanomics World s Dashboard of Economic Indicators Q4 2016 Globanomics: Global Economic Indicators Q4 16 1 Quarter at a Glance The IMF revised

April 13, 2017 Economics Research - Globanomics - Q4/16 Globanomics World s Dashboard of Economic Indicators Q4 2016 Globanomics: Global Economic Indicators Q4 16 1 Quarter at a Glance The IMF revised

Global MT outlook: Will the crisis in emerging markets derail the recovery?

Global MT outlook: Will the crisis in emerging markets derail the recovery? John Walker Chairman and Chief Economist jwalker@oxfordeconomics.com March 2014 Oxford Economics Oxford Economics is one of the

Global MT outlook: Will the crisis in emerging markets derail the recovery? John Walker Chairman and Chief Economist jwalker@oxfordeconomics.com March 2014 Oxford Economics Oxford Economics is one of the

Growth and Inflation Prospects and Monetary Policy

Growth and Inflation Prospects and Monetary Policy 1. Growth and Inflation Prospects and Monetary Policy The Thai economy expanded by slightly less than the previous projection due to weaker-than-anticipated

Growth and Inflation Prospects and Monetary Policy 1. Growth and Inflation Prospects and Monetary Policy The Thai economy expanded by slightly less than the previous projection due to weaker-than-anticipated

Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy March 2017 Global Stock Markets Rally likely to Continue, Driven by Strong Earnings & Strengthening GDP Growth.

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy March 2017 Global Stock Markets Rally likely to Continue, Driven by Strong Earnings & Strengthening GDP Growth.

Global Economic Outlook - July 2017

Global Economic Outlook - July 2017 June 28, 2017 by Carl Tannenbaum, Asha Bangalore, Ankit Mital, Brian Liebovich of Northern Trust Global economic activity has generally been good during the first six

Global Economic Outlook - July 2017 June 28, 2017 by Carl Tannenbaum, Asha Bangalore, Ankit Mital, Brian Liebovich of Northern Trust Global economic activity has generally been good during the first six

Global growth fragile: The global economy is projected to grow at 3.5% in 2019 and 3.6% in 2020, 0.2% and 0.1% below October 2018 projections.

Monday January 21st 19 1:05pm International Prepared by: Ravi Kurjah, Senior Economic Analyst (Research & Analytics) ravi.kurjah@firstcitizenstt.com World Economic Outlook: A Weakening Global Expansion

Monday January 21st 19 1:05pm International Prepared by: Ravi Kurjah, Senior Economic Analyst (Research & Analytics) ravi.kurjah@firstcitizenstt.com World Economic Outlook: A Weakening Global Expansion

Fourth Quarter Market Outlook. Kim Huebner, CFA Don Powell, CFA Joseph Styrna, CFA

Fourth Quarter 2017 Market Outlook Kim Huebner, CFA Don Powell, CFA Joseph Styrna, CFA Economic Outlook Growth Increasing, Spending Modest, Low Unemployment 2017 2016 2015 2014 2013 2012 2011 GDP* Q3:

Fourth Quarter 2017 Market Outlook Kim Huebner, CFA Don Powell, CFA Joseph Styrna, CFA Economic Outlook Growth Increasing, Spending Modest, Low Unemployment 2017 2016 2015 2014 2013 2012 2011 GDP* Q3:

World Economy: Prospects and Risks Masahiro Kawai Graduate School of Public Policy Univ. of Tokyo

World Economy: Prospects and Risks Masahiro Kawai Graduate School of Public Policy Univ. of Tokyo Seoul 13 June 2017 Prospects of the World Economy The world economy is growing in 2017 The US Fed continues

World Economy: Prospects and Risks Masahiro Kawai Graduate School of Public Policy Univ. of Tokyo Seoul 13 June 2017 Prospects of the World Economy The world economy is growing in 2017 The US Fed continues

Economic Outlook In the Shoes of an FOMC Member

Economic Outlook In the Shoes of an FOMC Member This material must be read in conjunction with the disclosure statement. 9 April 2018 PRESENTED BY: MARKUS SCHOMER Chief Economist PineBridge Investments

Economic Outlook In the Shoes of an FOMC Member This material must be read in conjunction with the disclosure statement. 9 April 2018 PRESENTED BY: MARKUS SCHOMER Chief Economist PineBridge Investments

Economic and Financial Markets Monthly Review & Outlook Detailed Report January 2018

Economic and Financial Markets Monthly Review & Outlook Detailed Report January 1 NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Overview of the Economy Business and economic confidence continue to

Economic and Financial Markets Monthly Review & Outlook Detailed Report January 1 NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Overview of the Economy Business and economic confidence continue to

Summary. Economic Update 1 / 7 December 2017

Economic Update Economic Update 1 / 7 Summary 2 Global Strengthening of the pickup in global growth, with GDP expected to increase 2.9% in 2017 and 3.1% in 2018. 3 Eurozone The eurozone recovery is upholding

Economic Update Economic Update 1 / 7 Summary 2 Global Strengthening of the pickup in global growth, with GDP expected to increase 2.9% in 2017 and 3.1% in 2018. 3 Eurozone The eurozone recovery is upholding

Quarterly Economic Outlook: Quarter on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War

Foregin Direct Investment (Billion USD) China U.S. Asia World Quarterly Economic Outlook: Quarter 3 2018 on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War Thai Economy: Thai

Foregin Direct Investment (Billion USD) China U.S. Asia World Quarterly Economic Outlook: Quarter 3 2018 on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War Thai Economy: Thai

Leumi. Global Economics Monthly Review. Gil M. Bufman, Chief Economist Arie Tal, Research Economist. March 13, 2018

Global Economics Monthly Review March 13, 2018 Gil M. Bufman, Chief Economist Arie Tal, Research Economist The Finance Division, Economics Department Please note that we will not publish the monthly review

Global Economics Monthly Review March 13, 2018 Gil M. Bufman, Chief Economist Arie Tal, Research Economist The Finance Division, Economics Department Please note that we will not publish the monthly review

Summary of Opinions at the Monetary Policy Meeting 1,2 on March 14 and 15, 2019

Not to be released until 8:50 a.m. Japan Standard Time on Tuesday, March 26, 2019. March 26, 2019 Bank of Japan Summary of Opinions at the Monetary Policy Meeting 1,2 on March 14 and 15, 2019 I. Opinions

Not to be released until 8:50 a.m. Japan Standard Time on Tuesday, March 26, 2019. March 26, 2019 Bank of Japan Summary of Opinions at the Monetary Policy Meeting 1,2 on March 14 and 15, 2019 I. Opinions

The Prospects Service

The Prospects Service LEADING ECONOMIC ANALYSIS, FORECASTS AND DATA Global Prospects, January 2017 Toplines The world economy remains in a stage of heightened uncertainty, with ongoing Brexit negotiations,

The Prospects Service LEADING ECONOMIC ANALYSIS, FORECASTS AND DATA Global Prospects, January 2017 Toplines The world economy remains in a stage of heightened uncertainty, with ongoing Brexit negotiations,

Mexico Economic Outlook 3Q18. August 2018

Mexico Economic Outlook 3Q18 August 2018 Key messages Global growth continues, but risks are intensifying. The economy grew 2.1% in the first half of the year. Downward bias in our growth forecast for

Mexico Economic Outlook 3Q18 August 2018 Key messages Global growth continues, but risks are intensifying. The economy grew 2.1% in the first half of the year. Downward bias in our growth forecast for

March PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy March 2016 Stocks likely to Recover Further with Improving Growth & Recession Fears Easing, Fresh Stimulus from

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy March 2016 Stocks likely to Recover Further with Improving Growth & Recession Fears Easing, Fresh Stimulus from

September PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy September 2015 Stock Market Volatility likely to Remain Elevated in Near-term on China Concerns & Fed Uncertainty.

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy September 2015 Stock Market Volatility likely to Remain Elevated in Near-term on China Concerns & Fed Uncertainty.

ECONOMIC OUTLOOK FINALLY, SYNCHRONIZED GLOBAL GROWTH

ECONOMIC OUTLOOK FINALLY, SYNCHRONIZED GLOBAL GROWTH Augustine Faucher Chief Economist November 13, 2017 Senior Economic Advisor Chief Economist BETTER GROWTH THIS YEAR, AND AN UPGRADE TO 2018 World output,

ECONOMIC OUTLOOK FINALLY, SYNCHRONIZED GLOBAL GROWTH Augustine Faucher Chief Economist November 13, 2017 Senior Economic Advisor Chief Economist BETTER GROWTH THIS YEAR, AND AN UPGRADE TO 2018 World output,

U.S. Economic Outlook with Focus on Maine: Shining Amidst Global Gloom

U.S. Economic Outlook with Focus on Maine: Shining Amidst Global Gloom Michael Dolega Senior Economist, TD Economics 15 Annual MEREDA Forecast Conference Portland, Maine January, 15 Key Themes Global economic

U.S. Economic Outlook with Focus on Maine: Shining Amidst Global Gloom Michael Dolega Senior Economist, TD Economics 15 Annual MEREDA Forecast Conference Portland, Maine January, 15 Key Themes Global economic

Latin America Outlook. 1st QUARTER 2018

Latin America Outlook 1st QUARTER Main messages 1. Strong global growth continues. Forecasts revised up in in most areas. Growth stabilizing in. 2. Growth recovers in Latin America, reaching close to potential

Latin America Outlook 1st QUARTER Main messages 1. Strong global growth continues. Forecasts revised up in in most areas. Growth stabilizing in. 2. Growth recovers in Latin America, reaching close to potential

Fourth Quarter Market Outlook. Jason Bulinski, CFA Donald A. Powell, CFA Joseph Styrna, CFA

Fourth Quarter 2018 Market Outlook Jason Bulinski, CFA Donald A. Powell, CFA Joseph Styrna, CFA Economic Outlook Growth: Strong 2018, But Expecting Slowdown in 2019 Growth & Jobs 2018 2017 2016 2015 2014

Fourth Quarter 2018 Market Outlook Jason Bulinski, CFA Donald A. Powell, CFA Joseph Styrna, CFA Economic Outlook Growth: Strong 2018, But Expecting Slowdown in 2019 Growth & Jobs 2018 2017 2016 2015 2014

Economic and Portfolio Outlook 4th Quarter 2014 (Released October 2014)

") Economic and Portfolio Outlook 4th Quarter 2014 (Released October 2014) Our economic outlook for the fourth quarter of 2014 for the U.S. is continued slow growth. We stated in our 3 rd quarter Economic

Economic and Portfolio Outlook 4th Quarter 2014 (Released October 2014) Our economic outlook for the fourth quarter of 2014 for the U.S. is continued slow growth. We stated in our 3 rd quarter Economic

OVERVIEW. The EU recovery is firming. Table 1: Overview - the winter 2014 forecast Real GDP. Unemployment rate. Inflation. Winter 2014 Winter 2014

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

ORSO 職業退休計劃. Fidelity Advantage Portfolio Fund

ORSO 職業退休計劃 Fidelity Advantage Portfolio Fund Semi-Annual Report and Accounts For the period ended 30 June 2018 SEMI-ANNUAL REPORT AND ACCOUNTS - FOR THE PERIOD ENDED 30TH JUNE 2018 Contents Pages Management

ORSO 職業退休計劃 Fidelity Advantage Portfolio Fund Semi-Annual Report and Accounts For the period ended 30 June 2018 SEMI-ANNUAL REPORT AND ACCOUNTS - FOR THE PERIOD ENDED 30TH JUNE 2018 Contents Pages Management

Global economic issues and the impact on Shipping

1st Annual Marine Money Cyprus Forum Global economic issues and the impact on Shipping Andreas Assiotis, PhD 26 April 2017 Table of contents 1 2 3 4 5 Economic Fundamentals and Global Drivers 3 Global

1st Annual Marine Money Cyprus Forum Global economic issues and the impact on Shipping Andreas Assiotis, PhD 26 April 2017 Table of contents 1 2 3 4 5 Economic Fundamentals and Global Drivers 3 Global

The Global Economy Heightened Risks

The Global Economy Heightened Risks RISI North American Conference 5 October, 2016 David Katsnelson Director, Macroeconomics Agenda 1. Global Snapshot 2. USA Steady Growth 3. Europe Growing Slowly 4. China

The Global Economy Heightened Risks RISI North American Conference 5 October, 2016 David Katsnelson Director, Macroeconomics Agenda 1. Global Snapshot 2. USA Steady Growth 3. Europe Growing Slowly 4. China

March 22, 2017 Boston, MA

March 22, 2017 Boston, MA Make or Break: Five Pivotal Drivers in 2017 Holly H. MacDonald Chief Investment Strategist Past performance is no guarantee of future results. This material is provided for your

March 22, 2017 Boston, MA Make or Break: Five Pivotal Drivers in 2017 Holly H. MacDonald Chief Investment Strategist Past performance is no guarantee of future results. This material is provided for your

Global Investment Outlook for 2H 2016

Global Investment Outlook for 2H 2016 Major central banks apart the Fed may stay in easing mode due to heightened economic and political risks. China s economy in 2H 2016 may continue to stabilize but

Global Investment Outlook for 2H 2016 Major central banks apart the Fed may stay in easing mode due to heightened economic and political risks. China s economy in 2H 2016 may continue to stabilize but

FY2016, FY2017 Economic Outlook The global economy will gradually pick up. Will Trump change the world?

Mizuho Economic Outlook & Analysis December 2016 FY2016, FY2017 Economic Outlook The global economy will gradually pick up. Will Trump change the world? The Japanese economy will lift off from the landing

Mizuho Economic Outlook & Analysis December 2016 FY2016, FY2017 Economic Outlook The global economy will gradually pick up. Will Trump change the world? The Japanese economy will lift off from the landing

Economic Activity, Prices, and Monetary Policy in Japan

November 8, 2017 Bank of Japan Economic Activity, Prices, and Monetary Policy in Japan Speech at a Meeting with Business Leaders in Miyazaki Yukitoshi Funo Member of the Policy Board (English translation

November 8, 2017 Bank of Japan Economic Activity, Prices, and Monetary Policy in Japan Speech at a Meeting with Business Leaders in Miyazaki Yukitoshi Funo Member of the Policy Board (English translation

Financial Market Outlook: Further Stock Gain on Faster GDP Rebound and Earnings Recovery. Year-end Target Raised

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: FurtherStock Gains Likely, Year-end Target Raised. Bond Under Pressure

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: FurtherStock Gains Likely, Year-end Target Raised. Bond Under Pressure

GLOBAL OUTLOOK ECONOMIC WATCH. July 2017

GLOBAL OUTLOOK ECONOMIC WATCH July 2017 Positive global outlook, with projections revised across areas The global outlook remains positive. Our BBVA-GAIN model estimates global GDP growth at 1% QoQ in,

GLOBAL OUTLOOK ECONOMIC WATCH July 2017 Positive global outlook, with projections revised across areas The global outlook remains positive. Our BBVA-GAIN model estimates global GDP growth at 1% QoQ in,

Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy John Praveen, PhD Chief Investment Strategist FOR MORE INFORMATION CONTACT: Mayura Hooper Phone: 973-367-7930 Email:

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy John Praveen, PhD Chief Investment Strategist FOR MORE INFORMATION CONTACT: Mayura Hooper Phone: 973-367-7930 Email:

SEPTEMBER Overview

Overview SEPTEMBER 214 Global growth. Global growth has been weaker than expected so far this year, as economic activity disappointed in a number of major countries in the first six months (Figure 1).

Overview SEPTEMBER 214 Global growth. Global growth has been weaker than expected so far this year, as economic activity disappointed in a number of major countries in the first six months (Figure 1).

Outlook and Market Review Third Quarter 2018

Outlook and Market Review Third Quarter The U. S. economy grew at a 3.5% rate in the third quarter of following a 4.2% growth rate in the prior quarter, according to the revision by the Bureau of Economic

Outlook and Market Review Third Quarter The U. S. economy grew at a 3.5% rate in the third quarter of following a 4.2% growth rate in the prior quarter, according to the revision by the Bureau of Economic

Explore the themes and thinking behind our decisions.

ASSET ALLOCATION COMMITTEE VIEWPOINTS Fourth Quarter 2017 These views are informed by a subjective assessment of the relative attractiveness of asset classes and subclasses over a 6- to 18-month horizon.

ASSET ALLOCATION COMMITTEE VIEWPOINTS Fourth Quarter 2017 These views are informed by a subjective assessment of the relative attractiveness of asset classes and subclasses over a 6- to 18-month horizon.

ECONOMIC RECOVERY AT CRUISE SPEED

EBF Economic Outlook Nr 43 May 2018 2018 SPRING OUTLOOK ON THE EURO AREA ECONOMIES IN 2018-2019 ECONOMIC RECOVERY AT CRUISE SPEED EDITORIAL TEAM: Francisco Saravia (author), Helge Pedersen - Chair of the

EBF Economic Outlook Nr 43 May 2018 2018 SPRING OUTLOOK ON THE EURO AREA ECONOMIES IN 2018-2019 ECONOMIC RECOVERY AT CRUISE SPEED EDITORIAL TEAM: Francisco Saravia (author), Helge Pedersen - Chair of the

Insolvency forecasts. Economic Research August 2017

Insolvency forecasts Economic Research August 2017 Summary We present our new insolvency forecasting model which offers a broader scope of macroeconomic developments to better predict insolvency developments.

Insolvency forecasts Economic Research August 2017 Summary We present our new insolvency forecasting model which offers a broader scope of macroeconomic developments to better predict insolvency developments.

Eurozone Economic Watch. July 2018

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

Prudential International Investments Advisers, LLC. Global Investment Strategy March 2010

Prudential International Investments Advisers, LLC. Global Investment Strategy March 2010 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Prudential International Investments Advisers, LLC. Global Investment Strategy March 2010 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Explore the themes and thinking behind our decisions.

ASSET ALLOCATION COMMITTEE VIEWPOINTS Third Quarter 2017 These views are informed by a subjective assessment of the relative attractiveness of asset classes and subclasses over a 6- to 18-month horizon.

ASSET ALLOCATION COMMITTEE VIEWPOINTS Third Quarter 2017 These views are informed by a subjective assessment of the relative attractiveness of asset classes and subclasses over a 6- to 18-month horizon.

Fed monetary policy amid a global backdrop of negative interest rates

Fed monetary policy amid a global backdrop of negative interest rates Kathy Bostjancic Head of US Macro Investor Services kathybostjancic@oxfordeconomics.com April 2016 Oxford Economics forecast highlights

Fed monetary policy amid a global backdrop of negative interest rates Kathy Bostjancic Head of US Macro Investor Services kathybostjancic@oxfordeconomics.com April 2016 Oxford Economics forecast highlights

Leumi. Global Economics Monthly Review. Arie Tal, Research Economist. July 12, Capital Markets Division, Economics Department. leumiusa.

Global Economics Monthly Review July 12, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report

Global Economics Monthly Review July 12, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report

Prudential International Investments Advisers, LLC. Global Investment Strategy October 2009

Prudential International Investments Advisers, LLC. Global Investment Strategy October 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Prudential International Investments Advisers, LLC. Global Investment Strategy October 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Investment Perspective

JANUARY 2015 Investment Perspective Major U.S. stock indexes increased in 2014 supported by improvement in our economy, earnings and valuations. The S&P 500 gained +13.7% while the Dow Industrials was

JANUARY 2015 Investment Perspective Major U.S. stock indexes increased in 2014 supported by improvement in our economy, earnings and valuations. The S&P 500 gained +13.7% while the Dow Industrials was

Hamid Rashid, Ph.D. Chief Global Economic Monitoring Unit Development Policy Analysis Division UNDESA, New York

Hamid Rashid, Ph.D. Chief Global Economic Monitoring Unit Development Policy Analysis Division UNDESA, New York 1 Global macroeconomic trends Major headwinds Risks and uncertainties Policy questions and

Hamid Rashid, Ph.D. Chief Global Economic Monitoring Unit Development Policy Analysis Division UNDESA, New York 1 Global macroeconomic trends Major headwinds Risks and uncertainties Policy questions and

The Global Economy Heightened Risks

The Global Economy Heightened Risks RISI Latin American Conference 16 August, 2016 David Katsnelson Director, Macroeconomics Agenda 1. Global Snapshot A Two-Track World 2. Latin America Some Improvement

The Global Economy Heightened Risks RISI Latin American Conference 16 August, 2016 David Katsnelson Director, Macroeconomics Agenda 1. Global Snapshot A Two-Track World 2. Latin America Some Improvement

World Economy Geopolitics Investment Strategy. The Impact of EU s Sovereign Risks on Turkish Economy. Presentation given by

World Economy Geopolitics Investment Strategy OUTLOOK FOR WORLD S MAJOR FINANCIAL MARKETS The Impact of EU s Sovereign Risks on Turkish Economy Presentation given by Dr. Michael Ivanovitch, President MSI

World Economy Geopolitics Investment Strategy OUTLOOK FOR WORLD S MAJOR FINANCIAL MARKETS The Impact of EU s Sovereign Risks on Turkish Economy Presentation given by Dr. Michael Ivanovitch, President MSI

Global Risk Outlook May 2016

Global Risk Outlook May 2016 Scott Livermore Managing Director and COO slivermore@oxfordeconomics.com About Oxford Economics Oxford Economics is a world leader in global forecasting and quantitative analysis.

Global Risk Outlook May 2016 Scott Livermore Managing Director and COO slivermore@oxfordeconomics.com About Oxford Economics Oxford Economics is a world leader in global forecasting and quantitative analysis.

Monthly Bulletin of Economic Trends: Review of the Australian Economy

MELBOURNE INSTITUTE Applied Economic & Social Research Monthly Bulletin of Economic Trends: Review of the Australian Economy March 2018 Released on 22 March 2018 Outlook for Australia 1 Economic Activity

MELBOURNE INSTITUTE Applied Economic & Social Research Monthly Bulletin of Economic Trends: Review of the Australian Economy March 2018 Released on 22 March 2018 Outlook for Australia 1 Economic Activity

Market Watch. July Review Global economic outlook. Australia

Market Watch Latest monthly commentary from the Investment Markets Research team at BT. Global economic outlook Australia Available data for the June quarter is consistent with a moderation in GDP growth

Market Watch Latest monthly commentary from the Investment Markets Research team at BT. Global economic outlook Australia Available data for the June quarter is consistent with a moderation in GDP growth

Yukitoshi Funo: Economic activity and prices in Japan, and monetary policy

Yukitoshi Funo: Economic activity and prices in Japan, and monetary policy Speech by Mr Yukitoshi Funo, Member of the Policy Board of the Bank of Japan, at a meeting with business leaders, Hyogo, 23 March

Yukitoshi Funo: Economic activity and prices in Japan, and monetary policy Speech by Mr Yukitoshi Funo, Member of the Policy Board of the Bank of Japan, at a meeting with business leaders, Hyogo, 23 March

South African Reserve Bank STATEMENT OF THE MONETARY POLICY COMMITTEE. Issued by Lesetja Kganyago, Governor of the South African Reserve Bank

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 30 March 2017 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the previous

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 30 March 2017 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the previous

Global Economics Monthly Review

Global Economics Monthly Review January 8 th, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Please see important disclaimer on the last page of this report 1 Key Issues Global

Global Economics Monthly Review January 8 th, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Please see important disclaimer on the last page of this report 1 Key Issues Global

Summary of Opinions at the Monetary Policy Meeting 1,2 on September 20 and 21, 2017

Not to be released until 8:50 a.m. Japan Standard Time on Friday, September 29, 2017. September 29, 2017 Bank of Japan Summary of Opinions at the Monetary Policy Meeting 1,2 on September 20 and 21, 2017

Not to be released until 8:50 a.m. Japan Standard Time on Friday, September 29, 2017. September 29, 2017 Bank of Japan Summary of Opinions at the Monetary Policy Meeting 1,2 on September 20 and 21, 2017

Rebalancing Economic Themes and Emerging Risks for the Balance of 2016

Rebalancing Economic Themes and Emerging Risks for the Balance of 2016 Page 1 Themes Oil s Not Well A world of cheap petroleum Eastern Anxiety China attempts a difficult transition Growing Prospects Central

Rebalancing Economic Themes and Emerging Risks for the Balance of 2016 Page 1 Themes Oil s Not Well A world of cheap petroleum Eastern Anxiety China attempts a difficult transition Growing Prospects Central

Global Economy & the Machine Tool Outlook. Jan 2010 Rhys Herbert

Global Economy & the Machine Tool Outlook Jan 21 Rhys Herbert rherbert@oxfordeconomics.com Which scenario do you favour? Short-term outlook (a) W -shaped cycle Growth initially boosted by inventory rebuild

Global Economy & the Machine Tool Outlook Jan 21 Rhys Herbert rherbert@oxfordeconomics.com Which scenario do you favour? Short-term outlook (a) W -shaped cycle Growth initially boosted by inventory rebuild

Weekly Economic Commentary

LPL FINANCIAL RESEARCH Weekly Economic Commentary May 28, 2013 Gauging Global Growth in 2013: An Update John Canally, CFA Economist LPL Financial Highlights Our long-held forecast for real GDP growth for

LPL FINANCIAL RESEARCH Weekly Economic Commentary May 28, 2013 Gauging Global Growth in 2013: An Update John Canally, CFA Economist LPL Financial Highlights Our long-held forecast for real GDP growth for

The Thai economy is viewed to moderate from last assessment from the intensified impact of the euro area s crisis on merchandise exports, which, in

1 I. Economic and inflation outlook II. Monetary policy stances going forward 2 I. Economic and inflation outlook II. Monetary policy stances going forward 3 The Thai economy is viewed to moderate from

1 I. Economic and inflation outlook II. Monetary policy stances going forward 2 I. Economic and inflation outlook II. Monetary policy stances going forward 3 The Thai economy is viewed to moderate from

NOVEMBER 2018 Summary global growth is above average but slowing

EMBARGOED UNTIL: 11.AM THURSDAY 1 NOVEMBER 1 THE FORWARD VIEW GLOBAL NOVEMBER 1 Summary global growth is above average but slowing While global growth remains above average, available GDP data for Q point

EMBARGOED UNTIL: 11.AM THURSDAY 1 NOVEMBER 1 THE FORWARD VIEW GLOBAL NOVEMBER 1 Summary global growth is above average but slowing While global growth remains above average, available GDP data for Q point

GAUGING GLOBAL GROWTH

LPL RESEARCH WEEKLY ECONOMIC COMMENTARY April 13 15 GAUGING GLOBAL GROWTH AN UPDATE FOR 15 & 16 John Canally Chief Economic Strategist, LPL Financial KEY TAKEAWAYS The market continues to expect that global

LPL RESEARCH WEEKLY ECONOMIC COMMENTARY April 13 15 GAUGING GLOBAL GROWTH AN UPDATE FOR 15 & 16 John Canally Chief Economic Strategist, LPL Financial KEY TAKEAWAYS The market continues to expect that global

Solutions Conference Year End Global Economy & World Political Outlook Leon C. LaBrecque, JD, CPA, CFP, CFA RAIN IN EUROPE?

Solutions Conference Year End 2014 Global Economy & World Political Outlook Leon C. LaBrecque, JD, CPA, CFP, CFA RAIN IN EUROPE? Global Equity Markets: Returns EAFE Return to Reach 2007 peak* EME Return

Solutions Conference Year End 2014 Global Economy & World Political Outlook Leon C. LaBrecque, JD, CPA, CFP, CFA RAIN IN EUROPE? Global Equity Markets: Returns EAFE Return to Reach 2007 peak* EME Return

Economic and Financial Markets Monthly Review & Outlook Detailed Report October 2017

Economic and Financial Markets Monthly Review & Outlook Detailed Report October 17 NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Overview of the Economy Business and economic confidence indicators

Economic and Financial Markets Monthly Review & Outlook Detailed Report October 17 NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Overview of the Economy Business and economic confidence indicators

Economic Indicators. Roland Berger Institute

Economic Indicators Roland Berger Institute November 2018 Overview Key points Economic Indicators A publication, compiled by the Roland Berger Institute, that provides you with the most important macroeconomic

Economic Indicators Roland Berger Institute November 2018 Overview Key points Economic Indicators A publication, compiled by the Roland Berger Institute, that provides you with the most important macroeconomic

Minutes of the Monetary Policy Council decision-making meeting held on 6 July 2016

Minutes of the Monetary Policy Council decision-making meeting held on 6 July 2016 At the meeting, members of the Monetary Policy Council discussed monetary policy against the background of macroeconomic

Minutes of the Monetary Policy Council decision-making meeting held on 6 July 2016 At the meeting, members of the Monetary Policy Council discussed monetary policy against the background of macroeconomic

Quarterly market summary

Quarterly market summary 3rd Quarter 2017 Economic overview Economic data released during the quarter seemed to signal a continuation of synchronised global recovery in almost all regions. This is being

Quarterly market summary 3rd Quarter 2017 Economic overview Economic data released during the quarter seemed to signal a continuation of synchronised global recovery in almost all regions. This is being

Monthly Economic Insight

Monthly Economic Insight Prepared by : TMB Analytics Date: 22 February 2018 Executive Summary Synchronized global economic growth continued to brighten global economic outlook and global trade outlook.

Monthly Economic Insight Prepared by : TMB Analytics Date: 22 February 2018 Executive Summary Synchronized global economic growth continued to brighten global economic outlook and global trade outlook.

WORLD ECONOMIC OUTLOOK January 2018 Research Department, International Monetary Fund

WORLD ECONOMIC OUTLOOK January 2018 Research Department, International Monetary Fund Global activity has gained further momentum Global growth picked up further in 2017H2; outlook is for higher annual

WORLD ECONOMIC OUTLOOK January 2018 Research Department, International Monetary Fund Global activity has gained further momentum Global growth picked up further in 2017H2; outlook is for higher annual

The Turkish Economy. Dynamics of Growth

The Economy in Turkey in 2018 2018 1 The Turkish Economy The Turkish economy grew at a rate of 3.2% in 2016, largely due to the attempted coup and terror attacks. The outlook was negative in the beginning

The Economy in Turkey in 2018 2018 1 The Turkish Economy The Turkish economy grew at a rate of 3.2% in 2016, largely due to the attempted coup and terror attacks. The outlook was negative in the beginning

Our goal is to provide a clear perspective on the global financial markets, as well as a logical framework to discuss them, thereby enabling

Our goal is to provide a clear perspective on the global financial markets, as well as a logical framework to discuss them, thereby enabling investors to recognize both the opportunities and risks that

Our goal is to provide a clear perspective on the global financial markets, as well as a logical framework to discuss them, thereby enabling investors to recognize both the opportunities and risks that

Legal & General Mixed Investment 0-35% Fund Annual Manager s Short Report for the year ended 31 July Distribution Number 27

Mixed Investment 0-35% Fund Annual Manager s Short Report for the year ended 31 July 2018 Distribution Number 27 Investment Objective and Policy This Fund aims to deliver long term capital growth which

Mixed Investment 0-35% Fund Annual Manager s Short Report for the year ended 31 July 2018 Distribution Number 27 Investment Objective and Policy This Fund aims to deliver long term capital growth which

INDEX. Forex market outlook Donald Trump s rise and impact on the US dollar. Fed s policy and their hawkish stance

FOREX MARKET OUTLOOK 2018 1 INDEX Forex market outlook 2018 Donald Trump s rise and impact on the US dollar Fed s policy and their hawkish stance EUR/USD s recovery and Euro zone s political challenges

FOREX MARKET OUTLOOK 2018 1 INDEX Forex market outlook 2018 Donald Trump s rise and impact on the US dollar Fed s policy and their hawkish stance EUR/USD s recovery and Euro zone s political challenges

2014 Annual Review & Outlook

2014 Annual Review & Outlook As we enter 2014, the current economic expansion is 4.5 years in duration, roughly the average life of U.S. economic expansions. There is every reason to believe it will continue,

2014 Annual Review & Outlook As we enter 2014, the current economic expansion is 4.5 years in duration, roughly the average life of U.S. economic expansions. There is every reason to believe it will continue,

Global Investment Outlook

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook 2015 Year Ahead - Global Investment Outlook Stocks likely to Post Solid Gains in 2015 Fuelled by Fresh QE Stimulus in Eurozone

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook 2015 Year Ahead - Global Investment Outlook Stocks likely to Post Solid Gains in 2015 Fuelled by Fresh QE Stimulus in Eurozone

June 2013 Equities Rally Drive Global Re-rating

June 2013 Equities Rally Drive Global Re-rating Since the lows of 2011, global equities have rallied 30% while Earnings per Share remained flat. This has been the biggest mid-cycle re-rating of global

June 2013 Equities Rally Drive Global Re-rating Since the lows of 2011, global equities have rallied 30% while Earnings per Share remained flat. This has been the biggest mid-cycle re-rating of global

Global Sovereign Conference Singapore 6 September

Global Sovereign Conference Singapore September 1 --- --- Politics, Populism and the Global Economy Brian Coulton Chief Economist --- --- Key Messages World economy muddling along but global macro risks

Global Sovereign Conference Singapore September 1 --- --- Politics, Populism and the Global Economy Brian Coulton Chief Economist --- --- Key Messages World economy muddling along but global macro risks