The End of the Tobacco Transition Payment Program. Blake Brown, Professor and Extension Economist, NCSU November 14, 2013

|

|

|

- Loraine Barnett

- 6 years ago

- Views:

Transcription

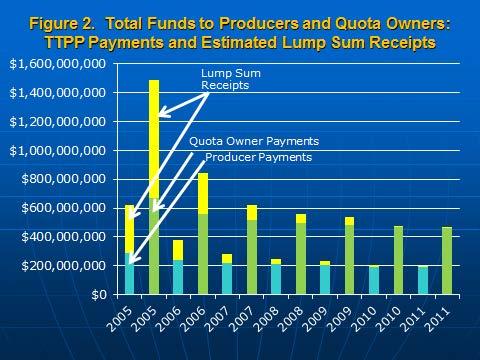

1 The End of the Tobacco Transition Payment Program Blake Brown, Professor and Extension Economist, NCSU November 14, 2013 With the last Tobacco Transition Payment Program (TTPP), commonly referred to as the tobacco buyout, payment scheduled for January 2014 many in agriculture are speculating what the impact might be on rural economies and, in particular, tobacco production. With about $9.6 billion in payments to tobacco quota owners and growers over 10 years, , the TTPP has large impacts on rural economies in tobacco growing states. As of 2012 $1.74 billion had been paid out by USDA directly to tobacco growers and $4.11 billion directly to former quota owners. In addition many quota owners and growers opted to sell their stream of payments to financial institutions offering a lump-sum in return (i.e. securitizing the payment stream). $1.79 billion had been paid to the financial institutions that purchased streams of TTPP payments. The TTPP ended the federal tobacco price support and quota program in 2004, deregulating U.S. tobacco production and providing compensation to quota owners and tobacco farmers over a 10 year period Total U.S. tobacco production had been restricted under the federal program by poundage quotas and acreage allotments set annually by USDA and allocated based on historical production dating back to For each pound of quota owned quota owners received $7 in 10 equal annual installments. Producers received $7 for each pound of quota owned plus $3 for each pound of quota grown during the last three years of the tobacco program, also in 10 equal annual installments. Most producers were also quota owners. (During the tobacco program many producers rented quota from non-growers, producing tobacco with both quota owned and quota rented.) Quota owners and producers were permitted to sell the stream of payments to a third party. The $9.6 billion cost of the TTPP is paid by USDA who recoups all the cost through annual assessments on tobacco product manufacturers. The TTPP payments have been a significant source of revenues flowing into state economies. Tables 1 and 2 give the 2005 TTPP payments by state for quota owners and producers. The first payments made in January of 2005 reflect the magnitude in terms of both value and number of people impacted since in January, 2005 financial institutions had not yet purchased any of the payments. Over 384 thousand payments were made to quota owners in Another 182,649 payments were sent to producers, but in most cases producers were also receiving a quota owner payment. Just prior to the buyout there were over 38,000 individual flue-cured tobacco quotas and over 240,000 individual burley tobacco quotas. (Many of these quotas were owned by more than one person which may be why the total number of payments in 2005 were so large.) Around 2/3 of the flue-cured quotas were owned by nonproducers. In burley the portion owned by non-producers may have been even higher. In 2005 North Carolina, the largest tobacco producing state, tobacco producer and quota owner payments totaled $392.4 million. For comparison the next largest payout was the Master Settlement Agreement (MSA) in which tobacco manufacturers paid the state of North Carolina $148.7 million in In the second largest tobacco state, Kentucky, producer and quota owner payments were $221.8 million in MSA payments to Kentucky in 2005 were $112.3 million. Figure 1 shows the TTPP payments and

2 their breakdown between quota owners, producers and financial institutions purchasing (securitizing) payment streams. By 2012 about 1/3 of quota owner and producer payments had been securitized, referred to as taking a lump sum for your payments. To do this, financial institutions paid the quota owner or producer a lump sum in return for the remaining annual TTPP payments. The financial institutions paid a lump sum that was discounted considering current and future interest rates at the time. Most discount rates were very competitive since the stream of TTPP payments were considered very safe in terms of certainty of payment. In the early years of the payments, a lump sum equivalent to 83% of the sum of the remaining payments was not uncommon. This equates to roughly a 4% discount rate, which in 2005, was close to the rate on 10 year Treasury bills. The largest portion of lump sums were completed in the fall of 2005, after the first TTPP payment had been received in early 2005 and before the second TTPP payment was received in January For example if a quota owner was scheduled to receive a TTPP payment of $1,000 per year and this quota owner sold his remaining stream of payments in fall 2005 ($9,000 in TTPP payments over 9 years, ) then the quota owner would have received a lump sum of $7,470 in late 2005 in addition to the $1,000 TTPP payment received the previous January. Receipts of lump sum payments from financial institutions in late 2005 by quota owners and producers in all tobacco states are estimated to have been about $1.16 billion. TTPP payments in January 2005 to producers and quota owners were $287 million and $667 million, respectively. So over $2.1 billion in lump sum and TTPP payments flowed into tobacco states in 2005 via producers and quota owners (Figure 2). Another large portion of payments were securitized in 2006 for the payments. The portion securitized in subsequent years was much smaller (Figures 1 and 2). Where did the payments come from? Quota owner and producer payments are a transfer from tobacco product manufacturers with much the same effect as a tax. Manufacturers may have absorbed some of the assessment from profits or reductions in costs. Most likely much of the assessment was passed to tobacco product consumers in the form of higher product prices. The 2005 TTPP payments equated to about $0.05 per pack of cigarettes sold in Financial institutions from around the US provided lump sums to TTPP recipients much in the same form as loans in return for recipients remaining stream of payments. What did quota owners and producers do with their lump sums and TTPP payments? Many quota owners that were not active producers were already retirees, often former tobacco farmers, who relied on the rent from quota for retirement income. Hopefully the prevalent use of the payments for this group was that the TTPP stream or a lump sum was put in savings and then drawn on as a continuing source for retirement income. Some quota owners were heirs of former tobacco farmers who still owned the family farm but did not grow tobacco. Some non-producers had purchased land with tobacco quota. For many in these latter groups the quota rent may not have been a critical component of their income, but the buyout offered an opportunity to get a guaranteed sum over 10 years or a lump

3 sum. How this group used the money for consumption, investment, or savings probably varies widely depending on how dependent they were on the quota rent during the tobacco program. Among tobacco producers many were near retirement age. Most in this group used the TTPP payment stream or lump sum to retire immediately. The exodus of tobacco farmers after the buyout was large. The number of tobacco farmers declined from about 57 thousand in the 2002 Census of Agriculture to 16,234 in the 2007 census. Part of this decline can be attributed to the way tobacco producers were defined during the tobacco program. Non-producing quota owners were counted as tobacco farmers during the program years if they shared in the risk of growing the tobacco by sharing in the cost and revenue of growing the tobacco with a grower who used the non-producing quota owner s quota. The decline is also due in part to farmers who exited tobacco production to non-farm jobs. Some farmers were part-time farmers growing tobacco, particularly burley, who dropped tobacco from their farms. But a large share of exiting farmers is attributable to farmers retiring with the end of the program. Producers that expected to remain active farmers used their TTPP payments or lump sums in a variety of ways. Many used the payments to reduce debt. Some used the funds to diversify or expand their operations in farm enterprises other than tobacco. Some used their funds to expand their tobacco operations. Were all these investments good ones? Undoubtedly mistakes were made. Alternative enterprises were sometimes not as lucrative as they appeared. Demand for U.S. tobacco declined more dramatically than most, including this economist, could imagine due to large increases in state and federal excise taxes and comprehensive smoking bans. Consequently consolidation in tobacco farming was greater than expected and the amount contracted for by buyers smaller than expected. There were tobacco farmers that tried to expand and produce in the unregulated era after the program who were either not competitive in terms of cost of production or who decided that the profits margins were not sufficient to keep them in tobacco production. Nine years after the buyout most of these producers have exited tobacco production. How will the end of the TTPP payments affect tobacco production? Concerns have been raised that some farmers have been using the TTPP to subsidize tobacco production and that as soon as the payments end there will be a large exodus of tobacco producers. There are probably some farmers who have done this and will exit production after But since the TTPP was not tied to any requirement to produce tobacco the only reason tobacco farmers had for continuing production was if they thought it would be profitable. The decoupling of TTPP payments from tobacco production increased the probability that decisions to continue tobacco farming were based on expected profitability, not contingent on receipt of TTPP payments. While there is little hard data to go on and this conclusion is based on anecdotal evidence and general behavior by businesses, the end of the TTPP is likely to have little effect on tobacco production. Other factors such as the emergence of e-cigarettes, increasing regulation of tobacco products, increases in excise taxes, competition from other tobacco producing countries, exchange rates, and whether or not robust demand from Asia for tobacco continues will be much more important in determining future U.S. tobacco production levels. There are many factors, some of them quite ominous, that will have potentially large impacts on U.S. tobacco production, but the end of the TTPP is not likely one of them.

4 Will the end of the TTPP be felt in rural communities in tobacco producing states? The answer is certainly yes. The TTPP brought unprecedented funds to a large number of citizens in rural tobacco producing communities. But even this situation should not be a crisis scenario. All involved in the tobacco buyout have known with certainty that the payments would end after 10 years. Again in every situation where funds are received there are some who spend irresponsibly and others who make honest mistakes in investment and consumption decisions. However most have likely consumed, invested, or saved the payments with the end in mind. All will bemoan the end of the payments, but the end should not be a surprise. One final fly in the ointment has arisen as this article is written. The Office of Management and Budget decided that the final TTPP payment should be subject to sequestration and be reduced by up to 7.2%. This decision was completely unexpected by all involved since the TTPP payments are backed and completely funded from a trust fund of assessments on the tobacco industry (i.e. at no cost, not even administrative, to the government). All involved including the financial institutions buying payment streams viewed the TTPP payments with the certainty of Treasury Bills. While the end of the TTPP payments should not be disruptive because the end was expected, an unexpected reduction in the last TTPP payment is disruptive. A reduction of 7.2% would be over $68 million dollars not flowing to quota owners, producers and financial institutions. Congressional offices involved in bringing resolution to this unexpected problem seemed confident that the reduction will be restored stay tuned.

5 Table TTPP to Quota Owners by State State Number of of 2005 Implied Over 10 years Average 2005 Payment Total Average Implied Over 10 Years AL 71 $ 347,306 $ 3,473,064 $ 4,892 $ 48,916 FL 502 $ 8,378,140 $ 83,781,404 $ 16,690 $ 166,895 GA 5,876 $ 42,854,888 $ 428,548,883 $ 7,293 $ 72,932 IN 7,859 $ 5,981,167 $ 59,811,668 $ 761 $ 7,611 KA 26 $ 24,144 $ 241,437 $ 929 $ 9,286 KY 141,264 $ 173,276,502 $1,732,765,020 $ 1,227 $ 12,266 MN 28 $ 26,755 $ 267,554 $ 956 $ 9,556 MO 1,455 $ 2,225,371 $ 22,253,714 $ 1,529 $ 15,295 NC 94,678 $ 274,253,512 $2,742,535,117 $ 2,897 $ 28,967 OH 8,558 $ 7,473,636 $ 74,736,361 $ 873 $ 8,733 OK 1 $ 713 $ 7,133 $ 713 $ 7,133 SC 17,874 $ 50,381,675 $ 503,816,754 $ 2,819 $ 28,187 TN 74,355 $ 50,472,183 $ 504,721,826 $ 679 $ 6,788 VA 25,677 $ 45,340,891 $ 453,408,907 $ 1,766 $ 17,658 WV 2,944 $ 1,385,493 $ 13,854,925 $ 471 $ 4,706 WI 3,162 $ 4,691,981 $ 46,919,810 $ 1,484 $ 14,839 US 384,330 $ 667,114,358 $6,671,143,577 $ 1,736 $ 17,358 Source: USDA-Farm Service Agency Table TTPP to Producers by State State Number of of 2005 Implied for 10 Average 2005 Payment per Recipient Average Total per Recipient of 10 AL 24 $ 148,956 $ 1,489,561 $ 6,207 $ 62,065 FL 334 $ 3,598,760 $ 35,987,601 $ 10,775 $ 107,747 GA 3,688 $ 18,291,371 $ 182,913,706 $ 4,960 $ 49,597 IN 2,683 $ 2,594,548 $ 25,945,480 $ 967 $ 9,670 KA 19 $ 10,548 $ 105,481 $ 555 $ 5,552 KY 80,498 $ 74,002,167 $ 740,021,668 $ 919 $ 9,193 MO 901 $ 952,103 $ 9,521,033 $ 1,057 $ 10,567 NC 45,347 $ 118,136,768 $1,181,367,679 $ 2,605 $ 26,052 OH 4,365 $ 3,068,833 $ 30,688,331 $ 703 $ 7,031 OK 4 $ 257 $ 2,573 $ 64 $ 643 SC 7,368 $ 21,653,935 $ 216,539,352 $ 2,939 $ 29,389 TN 22,656 $ 22,737,052 $ 227,370,516 $ 1,004 $ 10,036 VA 12,496 $ 19,819,039 $ 198,190,386 $ 1,586 $ 15,860 WV 990 $ 708,562 $ 7,085,617 $ 716 $ 7,157 WI 1,276 $ 1,282,308 $ 12,823,081 $ 1,005 $ 10,049 US 182,649 $ 287,005,206 $2,870,052,064 $ 1,571 $ 15,713 Source: USDA-Farm Service Agency

6

CRS Report for Congress

Order Code RL31790 CRS Report for Congress Received through the CRS Web Tobacco Quota Buyout Proposals in the 108 th Congress Updated April 6, 2004 Jasper Womach Agriculture Policy Specialist Resources,

Order Code RL31790 CRS Report for Congress Received through the CRS Web Tobacco Quota Buyout Proposals in the 108 th Congress Updated April 6, 2004 Jasper Womach Agriculture Policy Specialist Resources,

CRS Report for Congress Received through the CRS Web

CRS Report for Congress Received through the CRS Web Order Code RS21642 October 14, 2003 Comparing Quota Buyout Payments for Peanuts and Tobacco Summary Jasper Womach Specialist in Agricultural Policy

CRS Report for Congress Received through the CRS Web Order Code RS21642 October 14, 2003 Comparing Quota Buyout Payments for Peanuts and Tobacco Summary Jasper Womach Specialist in Agricultural Policy

WikiLeaks Document Release

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RL31790 Tobacco Quota Buyout Proposals in the 108th Congress Jasper Womach, Resources, Science, and Industry Division November

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RL31790 Tobacco Quota Buyout Proposals in the 108th Congress Jasper Womach, Resources, Science, and Industry Division November

12/7/2007 GOALS TODAY. Introduction. Provide a basic overview of crop insurance for tobacco in North Carolina

Crop Insurance for Tobacco: Issues and Updates Rod M. Rejesus Assistant Professor and Extension Specialist Dept. of Ag. and Resource Economics NC State University Raleigh, NC 27695 Tobacco Day 2007 Johnston

Crop Insurance for Tobacco: Issues and Updates Rod M. Rejesus Assistant Professor and Extension Specialist Dept. of Ag. and Resource Economics NC State University Raleigh, NC 27695 Tobacco Day 2007 Johnston

Buying and Selling Burley Quota: What Factors Should Farmers Consider?

AEC-76 Buying and Selling Burley Quota: What Factors Should Farmers Consider? William M. Snell and Orlando D. Chambers 1 Introduction The Farm Poundage Quota Revisions Act (FPQRA) of 1990 gives all burley

AEC-76 Buying and Selling Burley Quota: What Factors Should Farmers Consider? William M. Snell and Orlando D. Chambers 1 Introduction The Farm Poundage Quota Revisions Act (FPQRA) of 1990 gives all burley

Comparative Revenues and Revenue Forecasts Prepared By: Bureau of Legislative Research Fiscal Services Division State of Arkansas

Comparative Revenues and Revenue Forecasts 2010-2014 Prepared By: Bureau of Legislative Research Fiscal Services Division State of Arkansas Comparative Revenues and Revenue Forecasts This data shows tax

Comparative Revenues and Revenue Forecasts 2010-2014 Prepared By: Bureau of Legislative Research Fiscal Services Division State of Arkansas Comparative Revenues and Revenue Forecasts This data shows tax

Wanted: Energetic Ag Department to Make New Loans & Grow Profits. Refresh Webinar December 13, Bank Panel Introductions

Wanted: Energetic Ag Department to Make New Loans & Grow Profits Refresh Webinar December 13, 2017 Bank Panel Introductions Introducing Our Panelists WA OR CA NV ID UT AZ MT WY CO NM Patrick Hogrefe EVP,

Wanted: Energetic Ag Department to Make New Loans & Grow Profits Refresh Webinar December 13, 2017 Bank Panel Introductions Introducing Our Panelists WA OR CA NV ID UT AZ MT WY CO NM Patrick Hogrefe EVP,

Brady Brewer, Allen Featherstone, Christine Wilson, and Brian Briggeman Department of Agricultural Economics Kansas State University

Agricultural Lender Survey Brady Brewer, Allen Featherstone, Christine Wilson, and Brian Briggeman Department of Agricultural Economics Kansas State University Results: Fall Survey, 2015 Survey Summary

Agricultural Lender Survey Brady Brewer, Allen Featherstone, Christine Wilson, and Brian Briggeman Department of Agricultural Economics Kansas State University Results: Fall Survey, 2015 Survey Summary

NEVADA TAX REVENUE COMPARED TO THE UNITED STATES

Page 1 EXECUTIVE SUMMARY Applied Analysis was retained by the Las Vegas Convention and Visitors Authority (the LVCVA ) to review and analyze the economic impacts associated with its various operations

Page 1 EXECUTIVE SUMMARY Applied Analysis was retained by the Las Vegas Convention and Visitors Authority (the LVCVA ) to review and analyze the economic impacts associated with its various operations

Proposed Tobacco Quota Buyout Legislation: Effects on Tennessee Tobacco Farms 1,2

Agricultural Policy Analysis Center The University of Tennessee 310 Morgan Hall Knoxville, TN 37996-4519 Phone (865) 974-7407 FAX (865) 974-7298 www.agpolicy.org Proposed Tobacco Quota Buyout Legislation:

Agricultural Policy Analysis Center The University of Tennessee 310 Morgan Hall Knoxville, TN 37996-4519 Phone (865) 974-7407 FAX (865) 974-7298 www.agpolicy.org Proposed Tobacco Quota Buyout Legislation:

Property Tax Relief in New England

Property Tax Relief in New England January 23, 2015 Adam H. Langley Senior Research Analyst Lincoln Institute of Land Policy www.lincolninst.edu Property Tax as a % of Personal Income OK AL IN UT SD MS

Property Tax Relief in New England January 23, 2015 Adam H. Langley Senior Research Analyst Lincoln Institute of Land Policy www.lincolninst.edu Property Tax as a % of Personal Income OK AL IN UT SD MS

Commodity Taxes: Experiences with Tobacco and Alcohol Taxation

Commodity Taxes: Experiences with Tobacco and Alcohol Taxation Frank J. Chaloupka, University of Illinois at Chicago NAS Tax Policy Webinar on Commodity Taxes April 30, 2018 Overview Impact of Tobacco

Commodity Taxes: Experiences with Tobacco and Alcohol Taxation Frank J. Chaloupka, University of Illinois at Chicago NAS Tax Policy Webinar on Commodity Taxes April 30, 2018 Overview Impact of Tobacco

Commodity Taxes: Experiences with Tobacco and Alcohol Taxation

Commodity Taxes: Experiences with Tobacco and Alcohol Taxation Frank J. Chaloupka, University of Illinois at Chicago NAS Tax Policy Webinar on Commodity Taxes April 30, 2018 Overview Impact of Tobacco

Commodity Taxes: Experiences with Tobacco and Alcohol Taxation Frank J. Chaloupka, University of Illinois at Chicago NAS Tax Policy Webinar on Commodity Taxes April 30, 2018 Overview Impact of Tobacco

An Overview of New Hampshire s Tax System

An Overview of New Hampshire s Tax System Presentation to the House Ways & Means Committee January 9, 2013 Jeff McLynch Executive Director New Hampshire Fiscal Policy Institute 603.856.8337 jmclynch@nhfpi.org

An Overview of New Hampshire s Tax System Presentation to the House Ways & Means Committee January 9, 2013 Jeff McLynch Executive Director New Hampshire Fiscal Policy Institute 603.856.8337 jmclynch@nhfpi.org

PRODUCER ANNUITY SUITABILITY TRAINING REQUIREMENTS BY STATE As of September 11, 2017

PRODUCER ANNUITY SUITABILITY TRAINING REQUIREMENTS BY STATE As of September 11, 2017 This document provides a summary of the annuity training requirements that agents are required to complete for each

PRODUCER ANNUITY SUITABILITY TRAINING REQUIREMENTS BY STATE As of September 11, 2017 This document provides a summary of the annuity training requirements that agents are required to complete for each

Yolanda K. Kodrzycki New England Public Policy Center Federal Reserve Bank of Boston

The Growing Instability of Revenues over the Business Cycle: Putting the New England States in Perspective Yolanda K. Kodrzycki New England Public Policy Center Federal Reserve Bank of Boston Lincoln Institute

The Growing Instability of Revenues over the Business Cycle: Putting the New England States in Perspective Yolanda K. Kodrzycki New England Public Policy Center Federal Reserve Bank of Boston Lincoln Institute

State and Local Sales Tax Revenue Losses from E-Commerce: Estimates as of July 2004

State and Local Sales Tax Revenue Losses from E-Commerce: Estimates as of July 2004 by Dr. Donald Bruce, Research Assistant Professor dbruce@utk.edu and Dr. William F. Fox, Professor and Director billfox@utk.edu

State and Local Sales Tax Revenue Losses from E-Commerce: Estimates as of July 2004 by Dr. Donald Bruce, Research Assistant Professor dbruce@utk.edu and Dr. William F. Fox, Professor and Director billfox@utk.edu

Old Dominion University 2013 National Economic Outlook

Old Dominion University 2013 National Economic Outlook January 30, 2013 Professor Vinod Agarwal Professor Mohammad Najand Professor Gary A. Wagner www.odu.edu/forecasting 1 Presentation Outline 2012 Scorecard

Old Dominion University 2013 National Economic Outlook January 30, 2013 Professor Vinod Agarwal Professor Mohammad Najand Professor Gary A. Wagner www.odu.edu/forecasting 1 Presentation Outline 2012 Scorecard

The Entry, Performance, and Viability of De Novo Banks

The Entry, Performance, and Viability of De Novo Banks Yan Lee and Chiwon Yom* FEDERAL DEPOSIT INSURANCE CORPORATION *The views expressed here are solely of the authors and do not necessarily reflect the

The Entry, Performance, and Viability of De Novo Banks Yan Lee and Chiwon Yom* FEDERAL DEPOSIT INSURANCE CORPORATION *The views expressed here are solely of the authors and do not necessarily reflect the

Federal Reserve Bank of Dallas. November 7, 2005 SUBJECT

Federal Reserve Bank of Dallas 2200 N. PEARL ST. DALLAS, TX 75201-2272 November 7, 2005 Notice 05-70 TO: The Chief Executive Officer of each financial institution and foreign banking organization in the

Federal Reserve Bank of Dallas 2200 N. PEARL ST. DALLAS, TX 75201-2272 November 7, 2005 Notice 05-70 TO: The Chief Executive Officer of each financial institution and foreign banking organization in the

Medicare Index Report: Annual Enrollment Period for 2019 Coverage

Medicare Index Report: Annual Enrollment Period for 2019 Coverage This report examines costs and shopping trends in the Medicare insurance market during Medicare s Annual Enrollment Period (AEP) for 2019

Medicare Index Report: Annual Enrollment Period for 2019 Coverage This report examines costs and shopping trends in the Medicare insurance market during Medicare s Annual Enrollment Period (AEP) for 2019

Summary of Ratepayer-Funded Electric Efficiency Impacts, Budgets, and Expenditures

Summary of Ratepayer-Funded Electric Efficiency Impacts, Budgets, and Expenditures IEE Brief January 2012 Summary of Ratepayer-Funded Electric Efficiency Impacts, Budgets and Expenditures (2010-2011)

Summary of Ratepayer-Funded Electric Efficiency Impacts, Budgets, and Expenditures IEE Brief January 2012 Summary of Ratepayer-Funded Electric Efficiency Impacts, Budgets and Expenditures (2010-2011)

The Science Behind Tobacco Taxation

The Science Behind Tobacco Taxation Frank J. Chaloupka University of Illinois at Chicago National Conference on Tobacco or Health Fundamentals of Tobacco Tax Increases: Science, Methods, and Messaging

The Science Behind Tobacco Taxation Frank J. Chaloupka University of Illinois at Chicago National Conference on Tobacco or Health Fundamentals of Tobacco Tax Increases: Science, Methods, and Messaging

Each team will complete and turn in only one YELLOW copy of these six pages. Other copies can be used to make notes and calculations

Each team will complete and turn in only one YELLOW copy of these six pages. Other copies can be used to make notes and calculations 2004 National FFA Farm Business Management Career Development Event

Each team will complete and turn in only one YELLOW copy of these six pages. Other copies can be used to make notes and calculations 2004 National FFA Farm Business Management Career Development Event

Brady Brewer, Allen Featherstone, Christine Wilson, and Brian Briggeman Department of Agricultural Economics Kansas State University

Agricultural Lender Survey Brady Brewer, Allen Featherstone, Christine Wilson, and Brian Briggeman Department of Agricultural Economics Kansas State University Results: March Survey, 215 Survey Summary

Agricultural Lender Survey Brady Brewer, Allen Featherstone, Christine Wilson, and Brian Briggeman Department of Agricultural Economics Kansas State University Results: March Survey, 215 Survey Summary

Oregon: Where Taxes Are Low, Fees Are High and Revenue Is Slightly Below Average

Issue Brief March 6, 2012 Oregon: Where Taxes Are Low, Fees Are High and Revenue Is Slightly Below Average The money we pay in fees and taxes helps create jobs, build a strong economy, and preserve Oregon

Issue Brief March 6, 2012 Oregon: Where Taxes Are Low, Fees Are High and Revenue Is Slightly Below Average The money we pay in fees and taxes helps create jobs, build a strong economy, and preserve Oregon

AGRICULTURAL LENDER SURVEY. Spring 2018 Report

Spring 218 Report TABLE OF CONTENTS Contents Author Information 1 Executive Summary 2 Survey Overview and Demographic Information 3 Interest Rates 5 Spread Over Cost of Funds 6 Farm Loan Volume 7 Non-Performing

Spring 218 Report TABLE OF CONTENTS Contents Author Information 1 Executive Summary 2 Survey Overview and Demographic Information 3 Interest Rates 5 Spread Over Cost of Funds 6 Farm Loan Volume 7 Non-Performing

State Treatment of Social Security Treatment of Pension Income Other Income Tax Breaks Property Tax Breaks

State-By-State Tax Breaks for Seniors, 2016 State Treatment of Social Security Treatment of Pension Income Other Income Tax Breaks Property Tax Breaks AL Payments from defined benefit private plans are

State-By-State Tax Breaks for Seniors, 2016 State Treatment of Social Security Treatment of Pension Income Other Income Tax Breaks Property Tax Breaks AL Payments from defined benefit private plans are

Unemployment Insurance Benefit Adequacy: How many? How much? How Long?

Unemployment Insurance Benefit Adequacy: How many? How much? How Long? Joel Sacks, Deputy Commissioner Washington State Employment Security Department March 1, 2012 1 Outline How many get unemployment

Unemployment Insurance Benefit Adequacy: How many? How much? How Long? Joel Sacks, Deputy Commissioner Washington State Employment Security Department March 1, 2012 1 Outline How many get unemployment

Tax Breaks for Elderly Taxpayers in the States in 2016

AL Payments from defined benefit private plans are exempt; most public systems are exempt; military and US Civil service are exempt Special Homestead ion for 65+ +25.2% +2.4% AK No PIT Homestead ion for

AL Payments from defined benefit private plans are exempt; most public systems are exempt; military and US Civil service are exempt Special Homestead ion for 65+ +25.2% +2.4% AK No PIT Homestead ion for

Eye on the South Carolina Housing Market presented at 2008 HBA of South Carolina State Convention August 1, 2008

Eye on the South Carolina Housing Market presented at 28 HBA of South Carolina State Convention August 1, 28 Robert Denk Assistant Staff Vice President, Forecasting & Analysis 2, US Single Family Housing

Eye on the South Carolina Housing Market presented at 28 HBA of South Carolina State Convention August 1, 28 Robert Denk Assistant Staff Vice President, Forecasting & Analysis 2, US Single Family Housing

A Briefing on Georgia s Budget FY14-FY15. Dr. Carolyn Bourdeaux Andrew Young School of Policy Studies at Georgia State University

A Briefing on Georgia s Budget FY14-FY15 Dr. Carolyn Bourdeaux Andrew Young School of Policy Studies at Georgia State University 20,000 18,000 Georgia's State Tax Revenues 1984-2014 In FY14, Georgia is

A Briefing on Georgia s Budget FY14-FY15 Dr. Carolyn Bourdeaux Andrew Young School of Policy Studies at Georgia State University 20,000 18,000 Georgia's State Tax Revenues 1984-2014 In FY14, Georgia is

Stand-Alone Prescription Drug Plans Dominated the Rural Market in 2011

Stand-Alone Prescription Drug Plans Dominated the Rural Market in 2011 Growth Driven by Medicare Advantage Prescription Drug Plan Enrollment Leah Kemper, MPH Abigail Barker, PhD Fred Ullrich, BA Lisa Pollack,

Stand-Alone Prescription Drug Plans Dominated the Rural Market in 2011 Growth Driven by Medicare Advantage Prescription Drug Plan Enrollment Leah Kemper, MPH Abigail Barker, PhD Fred Ullrich, BA Lisa Pollack,

2014 ANNUAL COOPERATIVE BUSINESS SURVEY

2014 ANNUAL COOPERATIVE BUSINESS SURVEY Final Report February 13, 2015 In collaboration with the National Society of Accountants for Cooperatives 1 Background and Acknowledgment The University of Wisconsin

2014 ANNUAL COOPERATIVE BUSINESS SURVEY Final Report February 13, 2015 In collaboration with the National Society of Accountants for Cooperatives 1 Background and Acknowledgment The University of Wisconsin

CAH Financial Indicators Report: Summary of Indicator Medians by State

Flex Monitoring Team Data Summary Report No. 26: CAH Financial Indicators Report: Summary of Indicator Medians by State March 2018 The Flex Monitoring Team is a consortium of the Rural Health Research

Flex Monitoring Team Data Summary Report No. 26: CAH Financial Indicators Report: Summary of Indicator Medians by State March 2018 The Flex Monitoring Team is a consortium of the Rural Health Research

The Economics of Homelessness

15 The Economics of Homelessness Despite frequent characterization as a psychosocial problem, the problem of homelessness is largely economic. People who become homeless have insufficient financial resources

15 The Economics of Homelessness Despite frequent characterization as a psychosocial problem, the problem of homelessness is largely economic. People who become homeless have insufficient financial resources

Cost and Coverage Implications of the ACA Medicaid Expansion: National and State by State Analysis

Cost and Coverage Implications of the ACA Medicaid Expansion: National and State by State Analysis Report Authors: John Holahan, Matthew Buettgens, Caitlin Carroll, and Stan Dorn Urban Institute November

Cost and Coverage Implications of the ACA Medicaid Expansion: National and State by State Analysis Report Authors: John Holahan, Matthew Buettgens, Caitlin Carroll, and Stan Dorn Urban Institute November

Obamacare in Pictures

Obamacare in Pictures VISUALIZING THE EFFECTS OF THE PATIENT PROTECTION AND AFFORDABLE CARE ACT Spring 2014 If you like your health care plan, can you really keep it? At least 4.7 million health care plans

Obamacare in Pictures VISUALIZING THE EFFECTS OF THE PATIENT PROTECTION AND AFFORDABLE CARE ACT Spring 2014 If you like your health care plan, can you really keep it? At least 4.7 million health care plans

SCHIP Reauthorization: The Road Ahead

SCHIP Reauthorization: The Road Ahead The State Children s Health Insurance Program: Past, Present and Future Jocelyn Guyer Georgetown University Health Policy Institute Center for Children and Families

SCHIP Reauthorization: The Road Ahead The State Children s Health Insurance Program: Past, Present and Future Jocelyn Guyer Georgetown University Health Policy Institute Center for Children and Families

FEDERAL LIFE INSURANCE COMPANY. Annuity Suitability Training

FEDERAL LIFE INSURANCE COMPANY Annuity Suitability Training For Agents Licensed in: AL, AR, AZ, GA, LA, NC, OK, PA and VA NAIC Suitability in Annuity Transactions (2006 version) Agents licensed in the

FEDERAL LIFE INSURANCE COMPANY Annuity Suitability Training For Agents Licensed in: AL, AR, AZ, GA, LA, NC, OK, PA and VA NAIC Suitability in Annuity Transactions (2006 version) Agents licensed in the

Rural Policy Brief Volume 10, Number 8 (PB ) April 2006 RUPRI Center for Rural Health Policy Analysis

April 2006 RUPRI Center for Rural Health Policy Analysis") Rural Policy Brief Volume 10, Number 8 (PB2006-8 ) April 2006 RUPRI Center for Rural Health Policy Analysis Medicare Part D: Early Findings on Enrollment and Choices for Rural Beneficiaries Authors: Timothy

Rural Policy Brief Volume 10, Number 8 (PB2006-8 ) April 2006 RUPRI Center for Rural Health Policy Analysis Medicare Part D: Early Findings on Enrollment and Choices for Rural Beneficiaries Authors: Timothy

Income Rider Issued by Athene Annuity and Life Company, West Des Moines, Iowa (05/16)

") Income Rider 65103 Issued by Athene Annuity and Life Company, West Des Moines, Iowa (05/16) Enjoy an income that lasts as long as your retirement does. 2 Athene Ascent Income Rider designed to provide

Income Rider 65103 Issued by Athene Annuity and Life Company, West Des Moines, Iowa (05/16) Enjoy an income that lasts as long as your retirement does. 2 Athene Ascent Income Rider designed to provide

Overpayments: How Do I Handle? Overpayments Happen! How Overpayments Happen API Fund for Payroll Education, Inc.

Overpayments: How Do I Handle? 2018 API Fund for Payroll Education, Inc. Overpayments Happen! How Overpayments Happen How Overpayments Happen How Overpayments Happen Keying errorrs How Overpayments Happen

Overpayments: How Do I Handle? 2018 API Fund for Payroll Education, Inc. Overpayments Happen! How Overpayments Happen How Overpayments Happen How Overpayments Happen Keying errorrs How Overpayments Happen

Who s Above the Social Security Payroll Tax Cap? BY NICOLE WOO, JANELLE JONES, AND JOHN SCHMITT*

Issue Brief September 2011 Center for Economic and Policy Research 1611 Connecticut Ave, NW Suite 400 Washington, DC 20009 tel: 202-293-5380 fax: 202-588-1356 www.cepr.net Who s Above the Social Security

Issue Brief September 2011 Center for Economic and Policy Research 1611 Connecticut Ave, NW Suite 400 Washington, DC 20009 tel: 202-293-5380 fax: 202-588-1356 www.cepr.net Who s Above the Social Security

Florida 1/1/2016 Workers Compensation Rate Filing

Florida 1/1/2016 Workers Compensation Rate Filing Kirt Dooley, FCAS, MAAA October 21, 2015 1 $ Billions 4.0 3.5 3.0 2.5 2.0 1.5 1.0 0.5 0.0 Florida s Workers Compensation Premium Volume 2.368 0.765 0.034

Florida 1/1/2016 Workers Compensation Rate Filing Kirt Dooley, FCAS, MAAA October 21, 2015 1 $ Billions 4.0 3.5 3.0 2.5 2.0 1.5 1.0 0.5 0.0 Florida s Workers Compensation Premium Volume 2.368 0.765 0.034

Aviva Announcing Changes to Products and Annuity Rates

September 9, 2011 Aviva Announcing Changes to Products and Annuity Rates This field update contains information on product and rate changes effective September 16, 2011. We want to thank you for all of

September 9, 2011 Aviva Announcing Changes to Products and Annuity Rates This field update contains information on product and rate changes effective September 16, 2011. We want to thank you for all of

Indian Roots, American Soil. A survey of Indian companies' state-by-state operations in the United States

Indian Roots, American Soil A survey of Indian companies' state-by-state operations in the United States Contents 3 Survey overview 9 Survey results Top 25 states with largest Indian investment 10 Texas

Indian Roots, American Soil A survey of Indian companies' state-by-state operations in the United States Contents 3 Survey overview 9 Survey results Top 25 states with largest Indian investment 10 Texas

CRS Report for Congress Received through the CRS Web

Order Code RS20343 Updated January 10, 2002 CRS Report for Congress Received through the CRS Web Federal Excise Taxes on Tobacco Products: Rates and Revenues Louis Alan Talley Specialist in Taxation Government

Order Code RS20343 Updated January 10, 2002 CRS Report for Congress Received through the CRS Web Federal Excise Taxes on Tobacco Products: Rates and Revenues Louis Alan Talley Specialist in Taxation Government

Multistate indirect tax trends and policies

Multistate indirect tax trends and policies Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate

Multistate indirect tax trends and policies Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate

State Postal Abbreviation Codes

State Postal Areviation Codes State Areviation State Areviation Alaama AL Montana MT Alaska AK Neraska NE Arizona AZ Nevada NV Arkansas AR New Hampshire NH California CA New Jersey NJ Colorado CO New Mexico

State Postal Areviation Codes State Areviation State Areviation Alaama AL Montana MT Alaska AK Neraska NE Arizona AZ Nevada NV Arkansas AR New Hampshire NH California CA New Jersey NJ Colorado CO New Mexico

ehealth, Inc Fall Cost Report for Individual and Family Policyholders

ehealth, Inc. 2010 Fall Cost Report for and Family Policyholders Table of Contents Page Methodology.................................................................. 2 ehealth, Inc. 2010 Fall Cost Report

ehealth, Inc. 2010 Fall Cost Report for and Family Policyholders Table of Contents Page Methodology.................................................................. 2 ehealth, Inc. 2010 Fall Cost Report

Percent of Employees Waiving Coverage 27.0% 30.6% 29.1% 23.4% 24.9%

Number of Health Plans Reported 18,186 3,561 681 2,803 3,088 Offer HRA or HSA 34.0% 42.7% 47.0% 39.7% 35.0% Annual Employer Contribution $1,353 $1,415 $1,037 $1,272 $1,403 Percent of Employees Waiving

Number of Health Plans Reported 18,186 3,561 681 2,803 3,088 Offer HRA or HSA 34.0% 42.7% 47.0% 39.7% 35.0% Annual Employer Contribution $1,353 $1,415 $1,037 $1,272 $1,403 Percent of Employees Waiving

DOWNLOAD OR READ : DEVELOPMENT OF THE INCOME SMOOTHING LITERATURE VOL 4 A FOCUS ON THE UNITED STATES PDF EBOOK EPUB MOBI

DOWNLOAD OR READ : DEVELOPMENT OF THE INCOME SMOOTHING LITERATURE 1893 1998 VOL 4 A FOCUS ON THE UNITED STATES PDF EBOOK EPUB MOBI Page 1 Page 2 development of the income smoothing literature 1893 1998

DOWNLOAD OR READ : DEVELOPMENT OF THE INCOME SMOOTHING LITERATURE 1893 1998 VOL 4 A FOCUS ON THE UNITED STATES PDF EBOOK EPUB MOBI Page 1 Page 2 development of the income smoothing literature 1893 1998

PORTFOLIO REVENUE EXPENSES PERFORMANCE WATCHLIST

July 2018 ASSET MANAGEMENT Low-Income Housing Tax Credit Portfolio Trends Analysis Enterprise s Low-Income Housing Tax Credit (LIHTC) Portfolio Trends Analysis provides important information to our management

July 2018 ASSET MANAGEMENT Low-Income Housing Tax Credit Portfolio Trends Analysis Enterprise s Low-Income Housing Tax Credit (LIHTC) Portfolio Trends Analysis provides important information to our management

Patient Protection and. Affordable Care Act: The Impact on Employers

Patient Protection and Affordable Care Act: The Impact on Employers April 2013 Agenda Introductions Individual Mandate Healthcare Exchange Overview Impact on Employers Essential Health Benefits Fees &

Patient Protection and Affordable Care Act: The Impact on Employers April 2013 Agenda Introductions Individual Mandate Healthcare Exchange Overview Impact on Employers Essential Health Benefits Fees &

HEALTH CHOICE SELECT AN AFFORDABLE APPROACH TO HEALTHCARE FOR

HEALTH CHOICE SELECT AN AFFORDABLE APPROACH TO HEALTHCARE FOR For agent training use only and not for general distribution Health Choice Select Approved States WA ME MT ND AK OR CA NV ID UT WY CO SD NE

HEALTH CHOICE SELECT AN AFFORDABLE APPROACH TO HEALTHCARE FOR For agent training use only and not for general distribution Health Choice Select Approved States WA ME MT ND AK OR CA NV ID UT WY CO SD NE

States and Medicaid Provider Taxes or Fees

March 2016 Fact Sheet States and Medicaid Provider Taxes or Fees Medicaid is jointly financed by states and the federal government. Provider taxes are an integral source of Medicaid financing governed

March 2016 Fact Sheet States and Medicaid Provider Taxes or Fees Medicaid is jointly financed by states and the federal government. Provider taxes are an integral source of Medicaid financing governed

CAH Financial Indicators Report: Summary of Indicator Medians by State

Flex Monitoring Team Data Summary Report No. 18: : Summary of Indicator Medians by State March 2016 The Flex Monitoring Team is a consortium of the Rural Health Research Centers located at the Universities

Flex Monitoring Team Data Summary Report No. 18: : Summary of Indicator Medians by State March 2016 The Flex Monitoring Team is a consortium of the Rural Health Research Centers located at the Universities

Rate Lock Hours: 7:30-4:00 PST Toll Free: (866) WHOLESALE RATESHEET Lock Desk: (866) FHA Loan Programs

WHOLESALE RATESHEET Lock Desk: (866) FHA Loan Programs") FHA Loan Programs FHA 30yr Fixed FHA 30yr Fixed High Balance FHA 15yr Fixed F30F H30F F15F 5.000 (6.000) (6.000) (6.000) (6.000) 4.625 (5.596) (5.471) (5.346) (5.221) 4.125 (4.870) (4.729) (4.566) (4.406)

FHA Loan Programs FHA 30yr Fixed FHA 30yr Fixed High Balance FHA 15yr Fixed F30F H30F F15F 5.000 (6.000) (6.000) (6.000) (6.000) 4.625 (5.596) (5.471) (5.346) (5.221) 4.125 (4.870) (4.729) (4.566) (4.406)

IBEW Local 716 Marital status. - - Married - spousal signature required*. First name MI Last name. City State ZIP code

21 Request for Systematic Disbursement IBEW Local Union No. 716 Retirement Plan Instructions Please print using blue or black ink. Please forward this form to your Fund office to complete the 'Your Plan

21 Request for Systematic Disbursement IBEW Local Union No. 716 Retirement Plan Instructions Please print using blue or black ink. Please forward this form to your Fund office to complete the 'Your Plan

FIRST TIME HOME BUYER S GUIDE TO FINANCING

FIRST TIME HOME BUYER S GUIDE TO FINANCING FIRST TIME HOME BUYER S GUIDE TO FINANCING CONTENTS Overview/Mortgage Solutions Financial Mission... 2 Get the Loan First: Pre-Approval... 3 What is FICO?...

FIRST TIME HOME BUYER S GUIDE TO FINANCING FIRST TIME HOME BUYER S GUIDE TO FINANCING CONTENTS Overview/Mortgage Solutions Financial Mission... 2 Get the Loan First: Pre-Approval... 3 What is FICO?...

Report to Congressional Defense Committees

Report to Congressional Defense Committees The Department of Defense Comprehensive Autism Care Demonstration December 2016 Quarterly Report to Congress In Response to: Senate Report 114-255, page 205,

Report to Congressional Defense Committees The Department of Defense Comprehensive Autism Care Demonstration December 2016 Quarterly Report to Congress In Response to: Senate Report 114-255, page 205,

Potential Impact of Proposed 2011 Standard Reinsurance Agreement

Potential Impact of Proposed 2011 Standard Reinsurance Agreement Analysis of Second Draft Released by Risk Management Agency on February 23, 2010 Aon Benfield 200 East Randolph Street Chicago, IL 60601

Potential Impact of Proposed 2011 Standard Reinsurance Agreement Analysis of Second Draft Released by Risk Management Agency on February 23, 2010 Aon Benfield 200 East Randolph Street Chicago, IL 60601

New York Life Retirement Plan Services Stable value toolkit for plan advisors.

stable value New York Life Retirement Plan Services Stable value toolkit for plan advisors. Used as both part of a diverse investment allocation and as a safe haven for the risk averse, it is estimated

stable value New York Life Retirement Plan Services Stable value toolkit for plan advisors. Used as both part of a diverse investment allocation and as a safe haven for the risk averse, it is estimated

Update: 50-State Survey of Retiree Health Care Liabilities Most recent data show changes to benefits, funding policies could help manage rising costs

A fact sheet from Dec 2018 Update: 50-State Survey of Retiree Health Care Liabilities Most recent data show changes to benefits, funding policies could help manage rising costs Getty Images Overview States

A fact sheet from Dec 2018 Update: 50-State Survey of Retiree Health Care Liabilities Most recent data show changes to benefits, funding policies could help manage rising costs Getty Images Overview States

National Employment Law Project UNEMPLOYMENT INSURANCE FINANCING: STATE TRUST FUNDS IN RECESSION AS OF SEPTEMBER 30, 2008

National Employment Law Project UNEMPLOYMENT INSURANCE FINANCING: STATE TRUST FUNDS IN RECESSION AS OF SEPTEMBER 30, 2008 Introduction In May 2008, NELP issued a briefing paper (Unemployment Insurance

National Employment Law Project UNEMPLOYMENT INSURANCE FINANCING: STATE TRUST FUNDS IN RECESSION AS OF SEPTEMBER 30, 2008 Introduction In May 2008, NELP issued a briefing paper (Unemployment Insurance

Medicaid Funding and Policies Is There a Medicaid Crisis? A Financial Diagnosis for State and Local Government

Medicaid Funding and Policies Is There a Medicaid Crisis? A Financial Diagnosis for State and Local Government Matt Powers Health Management Associates March 15, 2007 Main Points Medicaid Remains a Workhorse

Medicaid Funding and Policies Is There a Medicaid Crisis? A Financial Diagnosis for State and Local Government Matt Powers Health Management Associates March 15, 2007 Main Points Medicaid Remains a Workhorse

Age of Insured Discount

A discount may apply based on the age of the insured. The age of each insured shall be calculated as the policyholder s age as of the last day of the calendar year. The age of the named insured in the

A discount may apply based on the age of the insured. The age of each insured shall be calculated as the policyholder s age as of the last day of the calendar year. The age of the named insured in the

50% are at or over 48, 50% are at or under 48 years of age (median) Cancer/Tumor registrars taking the survey ranged in age from 22 to 69

Cancer/Tumor registrars taking the survey ranged in age from 22 to 69") Cancer/Tumor Registrar Summary Cancer/Tumor Registrar Total Responses: 238, with 210 full-time and 28 part-time registrars responding. We also polled 72 Cancer/Tumor Registry Managers. Cancer Registrar

Cancer/Tumor Registrar Summary Cancer/Tumor Registrar Total Responses: 238, with 210 full-time and 28 part-time registrars responding. We also polled 72 Cancer/Tumor Registry Managers. Cancer Registrar

Committee on Ways and Means Democrats

DRAFT Committee on Ways and Means Democrats Representative Sandy Levin - Ranking Member Report November 7, 2013 Millions of Unemployed Americans Will Lose Benefits Unless Congress Acts Over 3 Million Will

DRAFT Committee on Ways and Means Democrats Representative Sandy Levin - Ranking Member Report November 7, 2013 Millions of Unemployed Americans Will Lose Benefits Unless Congress Acts Over 3 Million Will

Nevada Labor Market Briefing: January Summary of Labor Market Economic Indicators

Nevada Labor Market Briefing: January 2019 Summary of Labor Market Economic Indicators Department of Employment, Training, & Rehabilitation Dr. Tiffany Tyler-Garner, Director Dennis Perea, Deputy Director

Nevada Labor Market Briefing: January 2019 Summary of Labor Market Economic Indicators Department of Employment, Training, & Rehabilitation Dr. Tiffany Tyler-Garner, Director Dennis Perea, Deputy Director

An Rx for Treasury Managers When Healthcare Reform Arrives

An Rx for Treasury Managers When Healthcare Reform Arrives October 29, 2013 Las Vegas, NV Dale Sorenson, CTP Vice President Associated Bank Rick Noble, CTP Staff Vice President WellPoint, Inc. Outlook

An Rx for Treasury Managers When Healthcare Reform Arrives October 29, 2013 Las Vegas, NV Dale Sorenson, CTP Vice President Associated Bank Rick Noble, CTP Staff Vice President WellPoint, Inc. Outlook

Online Appendix for: Consumption Reponses to In-Kind Transfers: Evidence from the Introduction of the Food Stamp Program

Online Appendix for: Consumption Reponses to In-Kind Transfers: Evidence from the Introduction of the Food Stamp Program Hilary W. Hoynes University of California, Davis and NBER hwhoynes@ucdavis.edu and

Online Appendix for: Consumption Reponses to In-Kind Transfers: Evidence from the Introduction of the Food Stamp Program Hilary W. Hoynes University of California, Davis and NBER hwhoynes@ucdavis.edu and

AGRICULTURAL LENDER SURVEY

AGRICULTURAL LENDER SURVEY SPRING 217 REPORT Semi-annual survey of agricultural lenders from across the nation. Brady Brewer, Assistant Professor, University of Georgia Allen Featherstone, Professor, Head

AGRICULTURAL LENDER SURVEY SPRING 217 REPORT Semi-annual survey of agricultural lenders from across the nation. Brady Brewer, Assistant Professor, University of Georgia Allen Featherstone, Professor, Head

2018 National Electric Rate Study

2018 National Electric Rate Study Ranking of Typical Residential, Commercial and Industrial Electric Bills LES Administrative Board June 15, 2018 Emily N. Koenig Director of Finance & Rates 1 Why is the

2018 National Electric Rate Study Ranking of Typical Residential, Commercial and Industrial Electric Bills LES Administrative Board June 15, 2018 Emily N. Koenig Director of Finance & Rates 1 Why is the

1/10/2008 GOALS TODAY. Introduction. Provide a basic overview of crop insurance alternatives for apple growers. apple insurance alternatives work

Crop Insurance Alternatives for Apple Growers Rod M. Rejesus Assistant Professor and Extension Specialist Dept. of Ag. and Resource Economics NC State University Raleigh, NC 27695 2008 SE Apple Growers

Crop Insurance Alternatives for Apple Growers Rod M. Rejesus Assistant Professor and Extension Specialist Dept. of Ag. and Resource Economics NC State University Raleigh, NC 27695 2008 SE Apple Growers

The Affordable Care Act and it s Impact on Employers

The Affordable Care Act and it s Impact on Employers Presented by Avalere Health, LLC Eric Hammelman, Vice President Mairin Brady, Senior Manager Agenda > The ACA Today: Implementation Update > Major Provisions

The Affordable Care Act and it s Impact on Employers Presented by Avalere Health, LLC Eric Hammelman, Vice President Mairin Brady, Senior Manager Agenda > The ACA Today: Implementation Update > Major Provisions

SCHIP: Let the Discussions Begin

Figure 0 SCHIP: Let the Discussions Begin Diane Rowland, Sc.D. Executive Vice President, Henry J. Kaiser Family Foundation and Executive Director, Kaiser Commission on for Alliance for Health Reform February

Figure 0 SCHIP: Let the Discussions Begin Diane Rowland, Sc.D. Executive Vice President, Henry J. Kaiser Family Foundation and Executive Director, Kaiser Commission on for Alliance for Health Reform February

While one in five Californians overall is uninsured, the rate among those who work is even higher: one in four.

: By the Numbers December 2013 Introduction California had the greatest number of uninsured residents of any state, 7 million, and the seventh largest percentage of uninsured residents under 65 in the

: By the Numbers December 2013 Introduction California had the greatest number of uninsured residents of any state, 7 million, and the seventh largest percentage of uninsured residents under 65 in the

The State of Children s Health

Figure 0 The State of Children s Health Robin Rudowitz Principal Policy Analyst Kaiser Commission on NCSL Annual Meeting Boston, MA August 8, 2007 Figure 1 SCHIP Builds on Medicaid for Children s Coverage

Figure 0 The State of Children s Health Robin Rudowitz Principal Policy Analyst Kaiser Commission on NCSL Annual Meeting Boston, MA August 8, 2007 Figure 1 SCHIP Builds on Medicaid for Children s Coverage

Mortgage. A Beginner s. Rates. Guide

Mortgage Rates A Beginner s Guide US Mortgage Corporation (NMLS ID#3901). Corporate Office is located at 201 Old Country Road, Suite 140, Melville, NY 11747; 631-580-2600 or (800) 562-6715 (LOANS15). Licensed

Mortgage Rates A Beginner s Guide US Mortgage Corporation (NMLS ID#3901). Corporate Office is located at 201 Old Country Road, Suite 140, Melville, NY 11747; 631-580-2600 or (800) 562-6715 (LOANS15). Licensed

Purdue Agricultural Economics Report

Purdue Agricultural Economics Report November 2011 Managing The Risk Capturing The Opportunity In Crop Farming Michael Boehlje and Brent Gloy*, Center for Commercial Agriculture Farming has always been

Purdue Agricultural Economics Report November 2011 Managing The Risk Capturing The Opportunity In Crop Farming Michael Boehlje and Brent Gloy*, Center for Commercial Agriculture Farming has always been

UTILIZATION OF CAPTIVES TODAY

UTILIZATION OF CAPTIVES TODAY November 20, 2015 Prepared by: Julie Patel Vice President Marsh Captive Solutions Utilization of Captives Today Objectives of Discussion 1. Captive Basics 2. The Process of

UTILIZATION OF CAPTIVES TODAY November 20, 2015 Prepared by: Julie Patel Vice President Marsh Captive Solutions Utilization of Captives Today Objectives of Discussion 1. Captive Basics 2. The Process of

Current Trends in the Medicaid RFP Procurement Landscape

Current Trends in the Medicaid RFP Procurement Landscape This is a Presentation Subtitle PRESENTED BY: Michael Lutz Avalere Health October 31, 2017 About Us Michael Lutz Vice President mlutz@avalere.com

Current Trends in the Medicaid RFP Procurement Landscape This is a Presentation Subtitle PRESENTED BY: Michael Lutz Avalere Health October 31, 2017 About Us Michael Lutz Vice President mlutz@avalere.com

New Tool Gauges Impact of Exchange Rates on States By Keith R. Phillips, Steve Brzezinski and Barbara Davalos

New Tool Gauges Impact of Exchange Rates on States By Keith R. Phillips, Steve Brzezinski and Barbara Davalos The RTWVD index will allow analysts to more precisely identify the exchange rates that most

New Tool Gauges Impact of Exchange Rates on States By Keith R. Phillips, Steve Brzezinski and Barbara Davalos The RTWVD index will allow analysts to more precisely identify the exchange rates that most

Domestic violence funding reduced from $1,253,000 to $1,000,000. $53,000 to fund elder law hotline eliminated.

Court Fees and Fines and State Appropriations by State* 2009-10 Amounts, Major Changes from 2009 Legislative Sessions Noted Revised 3/8/10 (**See note below related to court fees and fines) State Court

Court Fees and Fines and State Appropriations by State* 2009-10 Amounts, Major Changes from 2009 Legislative Sessions Noted Revised 3/8/10 (**See note below related to court fees and fines) State Court

Withdrawal Instructions - Eligible for Rollover

Withdrawal Instructions - Eligible for Rollover This form should be completed if: You have been terminated from your Employer for at least sixty (60) days and want to take a distribution of your vested

Withdrawal Instructions - Eligible for Rollover This form should be completed if: You have been terminated from your Employer for at least sixty (60) days and want to take a distribution of your vested

The State Tax Implications of Federal Tax Reform Legislation

The State Tax Implications of Federal Tax Reform Legislation Executive Committee Task Force on State and Local Taxation Phoenix, Arizona January 14, 2017 Joe Crosby, Multistate Associates Karl Frieden,

The State Tax Implications of Federal Tax Reform Legislation Executive Committee Task Force on State and Local Taxation Phoenix, Arizona January 14, 2017 Joe Crosby, Multistate Associates Karl Frieden,

Exhibit 1. The Impact of Health Reform: Percent of Women Ages Uninsured by State

Exhibit 1. The Impact of Health Reform: Percent of Women Ages 19 64 Uninsured by State 2008 09 2019 (estimated) OR CA 23% WA NV 23% AK ID AZ UT MT WY CO NM 28% ND SD NE KS TX 31% OK MN IA MO WI AR 25%

Exhibit 1. The Impact of Health Reform: Percent of Women Ages 19 64 Uninsured by State 2008 09 2019 (estimated) OR CA 23% WA NV 23% AK ID AZ UT MT WY CO NM 28% ND SD NE KS TX 31% OK MN IA MO WI AR 25%

WikiLeaks Document Release

WikiLeaks Document Release February 2, 29 Congressional Research Service Report 97-417 Tobacco-Related Programs and Activities of the U.S. Department of Agriculture: Operation and Cost Jasper Womach, Environment

WikiLeaks Document Release February 2, 29 Congressional Research Service Report 97-417 Tobacco-Related Programs and Activities of the U.S. Department of Agriculture: Operation and Cost Jasper Womach, Environment

Older consumers and student loan debt by state

August 2017 Older consumers and student loan debt by state New data on the burden of student loan debt on older consumers In January, the Bureau published a snapshot of older consumers and student loan

August 2017 Older consumers and student loan debt by state New data on the burden of student loan debt on older consumers In January, the Bureau published a snapshot of older consumers and student loan

Consumer-Driven Health Plans, HSAs & Tax-related Strategies to Control Health Costs

Richard Cauchi Program Director National Conference of State Legislatures Consumer-Driven Health Plans, HSAs & Tax-related Strategies to Control Health Costs Rev 9/4/06 NCSL FISCAL ANALYSTS SEMINAR September

Richard Cauchi Program Director National Conference of State Legislatures Consumer-Driven Health Plans, HSAs & Tax-related Strategies to Control Health Costs Rev 9/4/06 NCSL FISCAL ANALYSTS SEMINAR September

Tax Freedom Day 2019 is April 16th

Apr. 2019 Tax Freedom Day 2019 is April 16th Erica York Economist Madison Mauro Research Assistant Emma Wei Research Assistant Key Findings This year, Tax Freedom Day falls on April 16, or 105 days into

Apr. 2019 Tax Freedom Day 2019 is April 16th Erica York Economist Madison Mauro Research Assistant Emma Wei Research Assistant Key Findings This year, Tax Freedom Day falls on April 16, or 105 days into

Real Gross Domestic Product

Real Gross Domestic Product 6 5 4 3 2 1 0-1 -2-3 -4-5 -6-7 -8-9 Percent change from previous quarter at annual rate Q3 4.1% 6 5 4 3 2 1 0-1 -2-3 -4-5 -6-7 -8-9 -10 2005 2006 2007 2008 2009 2010 2011 2012

Real Gross Domestic Product 6 5 4 3 2 1 0-1 -2-3 -4-5 -6-7 -8-9 Percent change from previous quarter at annual rate Q3 4.1% 6 5 4 3 2 1 0-1 -2-3 -4-5 -6-7 -8-9 -10 2005 2006 2007 2008 2009 2010 2011 2012

National and Virginia Economic Outlook

National and Virginia Economic Outlook Association of Electric Cooperatives September 29, 215 Sonya Ravindranath Waddell Regional Economist Research Department The views and opinions expressed herein are

National and Virginia Economic Outlook Association of Electric Cooperatives September 29, 215 Sonya Ravindranath Waddell Regional Economist Research Department The views and opinions expressed herein are

Transition from NAFTA to USMCA October New Trade Deal Removes Uncertainty-

Transition from NAFTA to USMCA October 2018 -New Trade Deal Removes Uncertainty- SECRETARÍA DE ECONOMÍA MÉXICO MX-US Trade www.naftamexico.net More information: naftadsk@naftamexico.net 1 North America

Transition from NAFTA to USMCA October 2018 -New Trade Deal Removes Uncertainty- SECRETARÍA DE ECONOMÍA MÉXICO MX-US Trade www.naftamexico.net More information: naftadsk@naftamexico.net 1 North America

Application Trade Credit Insurance Multi Buyer

Chubb Global Markets Political Risk & Credit 1133 Avenue of the Americas New York, NY 10036 (212) 835-3138 (NY) (312) 612-8827 (Chicago) (213) 612-5512 (Los Angeles) Application Trade Credit Insurance

Chubb Global Markets Political Risk & Credit 1133 Avenue of the Americas New York, NY 10036 (212) 835-3138 (NY) (312) 612-8827 (Chicago) (213) 612-5512 (Los Angeles) Application Trade Credit Insurance

Taxing Food for Home Consumption

Taxing Food for Home Consumption Taxing the Poor: Road Map Regional differences in income poverty & poverty related outcomes Historical patterns of property tax Emergence of supermajority rules Growth

Taxing Food for Home Consumption Taxing the Poor: Road Map Regional differences in income poverty & poverty related outcomes Historical patterns of property tax Emergence of supermajority rules Growth

Analyzing State-Level Construction Fatality Rates,

Analyzing State-Level Construction Fatality Rates, 1992-2016 John Mendeloff Professor of Public Affairs University of Pittsburgh jmen@pitt.edu Wayne B. Gray Professor of Economics Clark University wgray@clarku.edu

Analyzing State-Level Construction Fatality Rates, 1992-2016 John Mendeloff Professor of Public Affairs University of Pittsburgh jmen@pitt.edu Wayne B. Gray Professor of Economics Clark University wgray@clarku.edu

Draft Document Not For Publication But For Discussion Purposes Only

Draft Document Not For Publication But For Discussion Purposes Only Nothing contained herein represents a final position or opinion of the State and Local Advisory Council. Readers should neither rely

Draft Document Not For Publication But For Discussion Purposes Only Nothing contained herein represents a final position or opinion of the State and Local Advisory Council. Readers should neither rely