The Importance of Accounting to the Crown Balance Sheet. The Treasury

|

|

|

- Magnus Rogers

- 6 years ago

- Views:

Transcription

1 The Importance of Accounting to the Crown Balance Sheet

2 Part 1: The International Story

3 Fra Luca Pacioli The father of accounting

4 Expense or Asset?

5

6 The first accounting principle? Unrealised profit should not be credited to income account of the corporation either directly or indirectly, through the medium of charging such unrealised profits amounts which would ordinarily fall to be charged against income account. Profit is deemed to be realised when a sale in the ordinary course of business is effected, unless circumstances are such that the collection of the sale price is not reasonably assured. An exception to the general rule may be made (for industries in which trade custom is to take inventories at net selling prices, which may exceed cost). Audits of Corporate Accounts, 1934 Special Committee on Co-Operation with Stock Exchanges

7 Where s the framework? Allocate revenues and costs to period Remove distortions True and fair, but prudent Avoid artificial fluctuations in net income Match Costs and Revenues Codify practice, seek general acceptance

8 A definition of income the maximum amount which can be spent during [a period] if there is to be an expectation of maintaining intact the capital value of prospective receipts (in money terms) 'the amount which a man can consume during a period and still remain as well off at the end of the period as he (thought he) was at the beginning John Hicks (1946)

9 The Conceptual Structure The Accounting Equation Assets Less Liabilities Equals Equity As a result of past events As a result of past events Definitional elements Present resources Present obligations That will provide future economic benefits That will involve economic sacrifice Movement in Equity in Period = Net Income in period

10 Johnsonville School Classroom 40,000 20,000 0 Historic cost

11 Johnsonville School Classroom 60,000 40,000 20,000 0 Historic cost Net present value

12 Johnsonville School Classroom 100,000 80,000 60,000 40,000 20,000 0 Historic cost Replacement cost Net present value

13 Johnsonville School Classroom 100,000 80,000 60,000 40,000 20,000 0 Historic cost Replacement cost Net present value Realisable value

14 Benefits of the Conceptual Framework Common frame of reference Discipline for consistency Less re-debate of issues Accountability Education Basis for gaps in GAAP

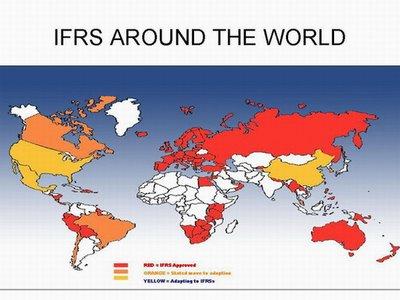

15 The rise of the Global Capital Market

16 2001 : A new Structure

17

18 Global Financial Crisis

19 International Public Sector Accounting Standards Board

20 IPSASB v IASB Sector Neutrality Characteristics of the public sector Service delivery objective broader information needs Involuntary Transfers and Non-Exchange Transactions Importance of the Approved Budget Nature and Purpose of Assets in the Public Sector Longevity of the Public Sector Regulatory Role of Public Sector Entities Importance of Statistical Bases of Accounting

21 The current challenge People are calling for: Decrease Volume/Complexity Increase Relevance to User Needs

22 IASB Conceptual Framework Developments

23 IPSASB : Hicks on Income No. 2 Hicks initial concept of income is fully determinable and objective only in the presence of complete and perfect markets (i.e., when every resource and claim on future cash flows has been commoditized into fully exchangeable assets and where everyone faces the same prices, including the discount rates A second definition of income: The amount that an entity can consume in a period and still expect to be able to consume the same amount in each ensuing period

24 Physical and financial assets a diminishing part of the story

25 Integrated Reporting on value creation

26 Illustrating the implications for the Crown Balance Sheet Reporting on the development of social policy obligations Political Announce - Approval of Execution of Services Promise Political Promise Policy Agreed Policy Budget Introduced a Budget Budget Approved Policy put in place a Contract Claim made Claim Goods approved Payment made Received ment of

27 The Importance of Accounting to the Crown Balance Sheet

28 Part 2: The New Zealand Story

29 1970's

30 The PM was an accountant!

31 In the 1970's Professional Standard Committee established to issue accounting standards NZ joined the International Accounting Standards Committee (IASC) Creation of International Federation of Accountants (IFAC) Accrual accounting evaluation begins in public sector Inflation (ie price level) accounting evaluation begins in private sector

32 1980s

33 In the 1980's NZ was one of only 9 countries around the world that actually "made" accounting standards from first principles Accounting standards did not have the force of law behind them, so there was no legal imperative to get things right Rogernomics followed by the 1987 crash drew attention to accountability Public Finance Act 1989 Sector neutral accounting seemed appropriate

34 1990's

35 In the early 1990's Finalisation of a "sector neutral" conceptual framework that gave equal weighting to "cash flows" and "service potential" Creation of Differential Reporting to recognise and solve the "cost/benefit" equation Financial Reporting Act 1993 providing a "one stop shop" for the accounting profession on accounting matters and creation of the ASRB Increasing influence of the International Accounting Standards Committee on NZ standard setting (particularly asset/liability recognition)

36 In the late 1990's The emergence of the G4+1 addressing conceptual framework matters so that International Accounting Standards (IAS) would be of better quality Heavy focus on defining "fair value" vs. "cost" On-going contribution to the IASC (Agriculture) First IPSASB standard issued (based on DNA found in the IASC standards

37 2000's

38 In the early 2000's Formation of the International Accounting Standards Board in London a full time, well funded Board with supporting resources The dotcom crash followed by the demise of World Com, Tyco, Enron and Arthur Andersen Ian Ball's appointed as CEO of IFAC (International Federation of Accountants) Continued active ASRB support of the IPSASB

39 Infrastructure investment and PPPs

40 During the mid 2000's Accounting Standards Review Board decided to "adapt" IFRS so that NZ could continue to have sector neutral financial standards Challenge for the public sector was getting enough airplay time at the FRSB to consider public sector issues given then 2005 start date for IFRS for listed companies around the world (eg Europe and Australia)

41 2009

42 Since 2009 Creation of the External Reporting Board (an independent Crown entity) with both an accounting and auditing mandate Private, but not public sector accounting alignment with Australia Auditor Regulation Act 2011 (does not cover the Office of the Auditor General

43 The future?

44 Biggest accounting issues Getting the cost/benefit equation correct Determination of fair value Impairment Social policy obligations (retirement) Likely divergence between IPSAS and IFRS Information overload ("excess baggage")

45 So to recap: Why is accounting so important to the Crown Balance sheet?

46 Final comments and questions

The Implementation of Accrual Accounting in the Public Sector New Zealand's Experience

The Implementation of Accrual Accounting in the Public Sector New Zealand's Experience Mark Hucklesby National Technical Director Grant Thornton New Zealand Session outline Putting accrual accounting for

The Implementation of Accrual Accounting in the Public Sector New Zealand's Experience Mark Hucklesby National Technical Director Grant Thornton New Zealand Session outline Putting accrual accounting for

01 Introduction to Financial Statements Acctg 102

Introduction to Financial s Describe the financial reporting environment and explain the accounting assumptions, principles, and qualitative characteristics underlying financial statements. Describe the

Introduction to Financial s Describe the financial reporting environment and explain the accounting assumptions, principles, and qualitative characteristics underlying financial statements. Describe the

UPDATE ON RECENT DEVELOPMENTS IN NEW ZEALAND

page 7.32 MEMORANDUM DATE: 8 NOVEMBER 2005 TO: MEMBERS OF THE IFAC INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARDS BOARD FROM: GREG SCHOLLUM, NEW ZEALAND REPRESENTATIVE SUBJECT: UPDATE ON RECENT DEVELOPMENTS

page 7.32 MEMORANDUM DATE: 8 NOVEMBER 2005 TO: MEMBERS OF THE IFAC INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARDS BOARD FROM: GREG SCHOLLUM, NEW ZEALAND REPRESENTATIVE SUBJECT: UPDATE ON RECENT DEVELOPMENTS

New Zealand Equivalent to International Accounting Standard 10 Events after the Reporting Period (NZ IAS 10)

") New Zealand Equivalent to International Accounting Standard 10 Events after the Reporting Period (NZ IAS 10) Issued November 2004 and incorporates amendments up to and including 30 June 2011 other than

New Zealand Equivalent to International Accounting Standard 10 Events after the Reporting Period (NZ IAS 10) Issued November 2004 and incorporates amendments up to and including 30 June 2011 other than

A snapshot of GAAP differences between IPSAS and IFRS. April 2013

A snapshot of GAAP differences between IPSAS and IFRS April 2013 Introduction for these governments. Many governments are exploring the adoption of accrual-based accounting frameworks in order to improve

A snapshot of GAAP differences between IPSAS and IFRS April 2013 Introduction for these governments. Many governments are exploring the adoption of accrual-based accounting frameworks in order to improve

New Accounting Standards and Interpretations for Tier 1 Public Sector and Not-for-Profit Public Benefit Entities

New Accounting Standards and Interpretations for Tier 1 Public Sector and Not-for-Profit Public Benefit Entities 31 March 2018 sued but not yet effective Introduction This document is applicable for Tier

New Accounting Standards and Interpretations for Tier 1 Public Sector and Not-for-Profit Public Benefit Entities 31 March 2018 sued but not yet effective Introduction This document is applicable for Tier

Proposals for the New Zealand Accounting Standards Framework

Proposals for the New Zealand Accounting Standards Framework Incorporating the Draft Tier Strategy and Presented to the Minister of Commerce in accordance with Section 34A of the Financial Reporting Act

Proposals for the New Zealand Accounting Standards Framework Incorporating the Draft Tier Strategy and Presented to the Minister of Commerce in accordance with Section 34A of the Financial Reporting Act

Agenda Item 13.2: IPSAS IFRS Alignment Dashboard

Agenda Item 13.2: IPSAS IFRS Alignment Dashboard João Fonseca, Principal IPSASB Meeting Toronto, Canada June 19 22, 2018 Page 1 Proprietary and Copyrighted Information Agenda Item 13.2 IPSAS IFRS Alignment

Agenda Item 13.2: IPSAS IFRS Alignment Dashboard João Fonseca, Principal IPSASB Meeting Toronto, Canada June 19 22, 2018 Page 1 Proprietary and Copyrighted Information Agenda Item 13.2 IPSAS IFRS Alignment

The Impact of IFRS Adoption on Public Sector Financial Statements

The Impact of IFRS Adoption on Public Sector Financial Statements Kathryn Trewavas November 2010 This is a draft report. Please do not quote without permission. Abstract Following a sector neutral approach

The Impact of IFRS Adoption on Public Sector Financial Statements Kathryn Trewavas November 2010 This is a draft report. Please do not quote without permission. Abstract Following a sector neutral approach

Topic 1: The International Accounting Environment and Financial Reporting

Topic 1: The International Accounting Environment and Financial Reporting USERS OF FINANCIAL STATEMENTS - Internal Users involves Management Accounting communicating to those within entity looking for

Topic 1: The International Accounting Environment and Financial Reporting USERS OF FINANCIAL STATEMENTS - Internal Users involves Management Accounting communicating to those within entity looking for

PUBLIC BENEFIT ENTITY STANDARDS. IMPACT ASSESSMENT FOR PUBLIC SECTOR PBEs

PUBLIC BENEFIT ENTITY STANDARDS IMPACT ASSESSMENT FOR PUBLIC SECTOR PBEs Prepared June 2012 Issued November 2013 This document contains assessments of the impact for public sector PBEs of transitioning

PUBLIC BENEFIT ENTITY STANDARDS IMPACT ASSESSMENT FOR PUBLIC SECTOR PBEs Prepared June 2012 Issued November 2013 This document contains assessments of the impact for public sector PBEs of transitioning

Events after the Reporting Period

IAS Standard 10 Events after the Reporting Period In April 2001 the International Accounting Standards Board (the Board) adopted IAS 10 Events After the Balance Sheet Date, which had originally been issued

IAS Standard 10 Events after the Reporting Period In April 2001 the International Accounting Standards Board (the Board) adopted IAS 10 Events After the Balance Sheet Date, which had originally been issued

New Accounting Standards and Interpretations for Tier 1 Public Sector and Notfor-Profit. Entities. 31 December 2016

New Accounting Standards and Interpretations for Tier 1 Public Sector and Notfor-Profit Public Benefit Entities 31 December Introduction This document is applicable for Tier 1 Public Benefit Entities (PBEs)

New Accounting Standards and Interpretations for Tier 1 Public Sector and Notfor-Profit Public Benefit Entities 31 December Introduction This document is applicable for Tier 1 Public Benefit Entities (PBEs)

Overview of Accounting Standards; IASs/IFRS and IPSAS Presentation by: CPA Daniel Kahi Monday, 10 September 2018

Overview of Accounting Standards; IASs/IFRS and IPSAS Presentation by: CPA Daniel Kahi Monday, 10 September 2018 Uphold public interest Presentation agenda Introduction ISAs / IFRSs IPSAS Concluding Remarks

Overview of Accounting Standards; IASs/IFRS and IPSAS Presentation by: CPA Daniel Kahi Monday, 10 September 2018 Uphold public interest Presentation agenda Introduction ISAs / IFRSs IPSAS Concluding Remarks

WARSAW 30 SEPTEMBER 2015 JOINT OUTREACH EVENT IASB EXPOSURE DRAFT ED/2015/3 CONCEPTUAL FRAMEWORK FOR FINANCIAL REPORTING

JOINT OUTREACH EVENT IASB EXPOSURE DRAFT ED/2015/3 CONCEPTUAL FRAMEWORK FOR FINANCIAL REPORTING WARSAW 30 SEPTEMBER 2015 This feedback statement has been prepared for the convenience of European constituents

JOINT OUTREACH EVENT IASB EXPOSURE DRAFT ED/2015/3 CONCEPTUAL FRAMEWORK FOR FINANCIAL REPORTING WARSAW 30 SEPTEMBER 2015 This feedback statement has been prepared for the convenience of European constituents

Agenda Item 1.7: IPSAS-IFRS Alignment Dashboard

Agenda Item 1.7: IPSAS-IFRS Alignment Dashboard João Fonseca, Principal IPSASB Meeting Washington D.C., USA March 12 15, 2019 Page 1 Proprietary and Copyrighted Information Agenda Item 1.7 Outline Change

Agenda Item 1.7: IPSAS-IFRS Alignment Dashboard João Fonseca, Principal IPSASB Meeting Washington D.C., USA March 12 15, 2019 Page 1 Proprietary and Copyrighted Information Agenda Item 1.7 Outline Change

New Zealand Equivalent to International Accounting Standard 34 Interim Financial Reporting (NZ IAS 34)

") New Zealand Equivalent to International Accounting Standard 34 Interim Financial Reporting (NZ IAS 34) Issued November 2004 and incorporates amendments up to and inclusing 31 October 2010 This Standard

New Zealand Equivalent to International Accounting Standard 34 Interim Financial Reporting (NZ IAS 34) Issued November 2004 and incorporates amendments up to and inclusing 31 October 2010 This Standard

TECHNICAL INFORMATION PAPER - VALUATIONS OF REAL PROPERTY, PLANT & EQUIPMENT FOR USE IN NEW ZEALAND FINANCIAL REPORTS

TECHNICAL INFORMATION PAPER - VALUATIONS OF REAL PROPERTY, PLANT & EQUIPMENT FOR USE IN NEW ZEALAND FINANCIAL REPORTS Reference Effective Review Owner NZVGNTIP# Valuations for Use in New Zealand Financial

TECHNICAL INFORMATION PAPER - VALUATIONS OF REAL PROPERTY, PLANT & EQUIPMENT FOR USE IN NEW ZEALAND FINANCIAL REPORTS Reference Effective Review Owner NZVGNTIP# Valuations for Use in New Zealand Financial

International Public Sector Accounting Standard 23 Revenue from Non-Exchange Transactions (Taxes and Transfers) IPSASB Basis for Conclusions

IPSASB Basis for Conclusions") International Public Sector Accounting Standard 23 Revenue from Non-Exchange Transactions (Taxes and Transfers) IPSASB Basis for Conclusions International Public Sector Accounting Standards, Exposure Drafts,

International Public Sector Accounting Standard 23 Revenue from Non-Exchange Transactions (Taxes and Transfers) IPSASB Basis for Conclusions International Public Sector Accounting Standards, Exposure Drafts,

Model financial statements

Model financial statements A guide to producing consolidated financial statements for entities which qualify for differential reporting Financial years ending on or after 31 December Introduction Welcome

Model financial statements A guide to producing consolidated financial statements for entities which qualify for differential reporting Financial years ending on or after 31 December Introduction Welcome

Intangible assets Issue paper presented at the EPSAS Working Group meeting Luxembourg, 7-8 May 2018

www.pwc.com Issue paper presented at the EPSAS Working Group meeting Luxembourg, Contents Introduction 3 Available accounting and reporting guidance 5 Country analysis 11 Matters for discussion 15 2 Introduction

www.pwc.com Issue paper presented at the EPSAS Working Group meeting Luxembourg, Contents Introduction 3 Available accounting and reporting guidance 5 Country analysis 11 Matters for discussion 15 2 Introduction

New Zealand Equivalent to International Accounting Standard 28 Investments in Associates and Joint Ventures (NZ IAS 28)

") New Zealand Equivalent to International Accounting Standard 28 Investments in Associates and Joint Ventures (NZ IAS 28) Issued June 2011 and incorporates amendments up to and including 30 November 2012

New Zealand Equivalent to International Accounting Standard 28 Investments in Associates and Joint Ventures (NZ IAS 28) Issued June 2011 and incorporates amendments up to and including 30 November 2012

International Federation of Accountants

International Federation of Accountants International Public Sector Accounting Standards Board John Stanford Deputy Director Ian Carruthers IPSASB Member & CIPFA Technical Director OECD Accrual Symposium

International Federation of Accountants International Public Sector Accounting Standards Board John Stanford Deputy Director Ian Carruthers IPSASB Member & CIPFA Technical Director OECD Accrual Symposium

Changing tack. A new financial reporting framework for public benefit entities. January 2017

Changing tack A new financial reporting framework for public benefit entities January 2017 Introduction Public benefit entities (PBEs) have experienced significant changes to their financial reporting

Changing tack A new financial reporting framework for public benefit entities January 2017 Introduction Public benefit entities (PBEs) have experienced significant changes to their financial reporting

Recognition of Deferred Tax Assets for Unrealised losses (Amendments to NZ IAS 12)

") Recognition of Deferred Tax Assets for Unrealised losses (Amendments to NZ IAS 12) This Standard was issued on 31 March 2016 by the New Zealand Accounting Standards Board of the External Reporting Board

Recognition of Deferred Tax Assets for Unrealised losses (Amendments to NZ IAS 12) This Standard was issued on 31 March 2016 by the New Zealand Accounting Standards Board of the External Reporting Board

NZ International Accounting Standard 27 (PBE) Consolidated and Separate Financial Statements (NZ IAS 27 (PBE))

Consolidated and Separate Financial Statements (NZ IAS 27 (PBE))") NZ International Accounting Standard 27 (PBE) Consolidated and Separate Financial Statements (NZ IAS 27 (PBE)) Issued November 2012 excluding consequential amendments resulting from early adoption of NZ

NZ International Accounting Standard 27 (PBE) Consolidated and Separate Financial Statements (NZ IAS 27 (PBE)) Issued November 2012 excluding consequential amendments resulting from early adoption of NZ

Financial Reporting Standard No. 44 (PBE) New Zealand Additional Disclosures (FRS-44 (PBE))

New Zealand Additional Disclosures (FRS-44 (PBE))") Financial Reporting Standard No. 44 (PBE) New Zealand Additional Disclosures (FRS-44 (PBE)) Issued November 2012 and incorporates amendments up to and including 31 August 2013 This Standard was issued

Financial Reporting Standard No. 44 (PBE) New Zealand Additional Disclosures (FRS-44 (PBE)) Issued November 2012 and incorporates amendments up to and including 31 August 2013 This Standard was issued

Corporate Reporting: Standard-setting and Work Programme

Corporate Reporting: Standard-setting and Work Programme Kevin Stevenson, Chairman and CEO, Australian Accounting Standards Board Executive in Residence & Fellow, Department of Accounting and Business

Corporate Reporting: Standard-setting and Work Programme Kevin Stevenson, Chairman and CEO, Australian Accounting Standards Board Executive in Residence & Fellow, Department of Accounting and Business

Reflections on financial reporting Surveying financial statements in annual reports 2011

Issue 7 June 2012 Reflections on financial reporting Surveying financial statements in annual reports 2011 Introduction Reflecting on 2011 financial statements, it was mostly steady as she goes with few

Issue 7 June 2012 Reflections on financial reporting Surveying financial statements in annual reports 2011 Introduction Reflecting on 2011 financial statements, it was mostly steady as she goes with few

PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 14 EVENTS AFTER THE REPORTING DATE (PBE IPSAS 14)

") PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 14 EVENTS AFTER THE REPORTING DATE (PBE IPSAS 14) This Standard was issued on 11 September 2014 by the New Zealand Accounting Standards

PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 14 EVENTS AFTER THE REPORTING DATE (PBE IPSAS 14) This Standard was issued on 11 September 2014 by the New Zealand Accounting Standards

New Zealand Equivalent to International Accounting Standard 28 Investments in Associates and Joint Ventures (NZ IAS 28)

") New Zealand Equivalent to International Accounting Standard 28 Investments in Associates and Joint Ventures (NZ IAS 28) Issued June 2011 and incorporates amendments to 31 December 2015 This Standard was

New Zealand Equivalent to International Accounting Standard 28 Investments in Associates and Joint Ventures (NZ IAS 28) Issued June 2011 and incorporates amendments to 31 December 2015 This Standard was

Financial Reporting Standard No. 44 New Zealand Additional Disclosures (FRS-44)

") Financial Reporting Standard No. 44 New Zealand Additional Disclosures (FRS-44) Issued April 2011 and incorporates amendments to 31 December 2015 This Standard was issued by the New Zealand Accounting

Financial Reporting Standard No. 44 New Zealand Additional Disclosures (FRS-44) Issued April 2011 and incorporates amendments to 31 December 2015 This Standard was issued by the New Zealand Accounting

Agenda Item 6: Leases

Agenda Item 6: Leases João Fonseca Manager, Standards Development and Technical Projects IPSASB Meeting New York, USA March 8-11, 2016 Page 1 Proprietary and Copyrighted Information Objective of Session

Agenda Item 6: Leases João Fonseca Manager, Standards Development and Technical Projects IPSASB Meeting New York, USA March 8-11, 2016 Page 1 Proprietary and Copyrighted Information Objective of Session

NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA) CPD CALENDAR FOR 2018

CPD CALENDAR FOR 2018") THEME AND TOPICS (1) IFRS, IPSAS AND ISA SEMINAR: GAAP vs IFRS Differences and Comparisons Latest Pronouncements issued by the IASB and IFRIC Review of first time adoption of IFRS Challenges and way Forward

THEME AND TOPICS (1) IFRS, IPSAS AND ISA SEMINAR: GAAP vs IFRS Differences and Comparisons Latest Pronouncements issued by the IASB and IFRIC Review of first time adoption of IFRS Challenges and way Forward

Accounting Alert. Quarterly update Public Benefit Entities What s new in financial reporting for December 2017? Accounting Alert.

Accounting Alert December 2017 Accounting Alert Quarterly update Public Benefit Entities What s new in financial reporting for December 2017? This quarterly update provides a high level overview of the

Accounting Alert December 2017 Accounting Alert Quarterly update Public Benefit Entities What s new in financial reporting for December 2017? This quarterly update provides a high level overview of the

PROJECT HISTORY. Contact: Stephenie Fox December 2014

PROJECT HISTORY Contact: Stephenie Fox (stepheniefox@ipsasb.org) December 2014 The IPSASB had agreed at its September 2014 meeting that the proposed IPSAS on First-time Adoption of Accrual Basis International

PROJECT HISTORY Contact: Stephenie Fox (stepheniefox@ipsasb.org) December 2014 The IPSASB had agreed at its September 2014 meeting that the proposed IPSAS on First-time Adoption of Accrual Basis International

New Zealand Equivalent to International Accounting Standard 7 Statement of Cash Flows (NZ IAS 7)

") New Zealand Equivalent to International Accounting Standard 7 Statement of Cash Flows (NZ IAS 7) Issued November 2004 and incorporates amendments up to and including 31 December 2012 This Standard was

New Zealand Equivalent to International Accounting Standard 7 Statement of Cash Flows (NZ IAS 7) Issued November 2004 and incorporates amendments up to and including 31 December 2012 This Standard was

Interim Financial Reporting and Impairment

IFRIC Interpretation 10 Interim Financial Reporting and Impairment This version includes amendments resulting from IFRSs issued up to 31 December 2010. IFRIC 10 Interim Financial Reporting and Impairment

IFRIC Interpretation 10 Interim Financial Reporting and Impairment This version includes amendments resulting from IFRSs issued up to 31 December 2010. IFRIC 10 Interim Financial Reporting and Impairment

EXPLANATORY GUIDE A1: GUIDE TO APPLICATION OF THE ACCOUNTING STANDARDS FRAMEWORK (EG A1)

") EXPLANATORY GUIDE A1: GUIDE TO APPLICATION OF THE ACCOUNTING STANDARDS FRAMEWORK (EG A1) Issued by the External Reporting Board April 2016 Relevant to reporting periods beginning on or after 1 January

EXPLANATORY GUIDE A1: GUIDE TO APPLICATION OF THE ACCOUNTING STANDARDS FRAMEWORK (EG A1) Issued by the External Reporting Board April 2016 Relevant to reporting periods beginning on or after 1 January

Progress report on IASB-FASB convergence work 21 April 2011

Progress report on IASB-FASB convergence work 21 April 2011 In a joint Statement issued in November 2009 we, the International Accounting Standards Board (IASB) and the US-based Financial Accounting Standards

Progress report on IASB-FASB convergence work 21 April 2011 In a joint Statement issued in November 2009 we, the International Accounting Standards Board (IASB) and the US-based Financial Accounting Standards

Agenda item 12: Revenue Education Session

Agenda item 12: Revenue Education Session Todd Beardsworth IPSASB Meeting March 10-13, 2015 Santiago, Chile Page 1 Objectives of this Education Session Consider the revenue model in IFRS 15, Revenue from

Agenda item 12: Revenue Education Session Todd Beardsworth IPSASB Meeting March 10-13, 2015 Santiago, Chile Page 1 Objectives of this Education Session Consider the revenue model in IFRS 15, Revenue from

New Zealand Equivalent to International Accounting Standard 28. Investments in Associates (NZ IAS 28)

") New Zealand Equivalent to International Accounting Standard 28 Investments in Associates (NZ IAS 28) Issued November 2004 and incorporates amendments up to and including 31 December 2009 other than consequential

New Zealand Equivalent to International Accounting Standard 28 Investments in Associates (NZ IAS 28) Issued November 2004 and incorporates amendments up to and including 31 December 2009 other than consequential

PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 8 INTERESTS IN JOINT VENTURES (PBE IPSAS 8)

") PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 8 INTERESTS IN JOINT VENTURES (PBE IPSAS 8) Issued September 2014 and incorporates amendments to 31 January 2017 other than consequential

PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 8 INTERESTS IN JOINT VENTURES (PBE IPSAS 8) Issued September 2014 and incorporates amendments to 31 January 2017 other than consequential

Financial reporting update

Financial reporting update Agenda What s new for 2017 o o Disclosure initiative Minor accounting standard changes PBEs For-Profits Major changes on the horizon Disclosure Initiative Objectives of financial

Financial reporting update Agenda What s new for 2017 o o Disclosure initiative Minor accounting standard changes PBEs For-Profits Major changes on the horizon Disclosure Initiative Objectives of financial

New Accounting Standards and Interpretations for Tier 1 Public Sector and Not-for-Profit Public Benefit Entities

New Accounting Standards and Interpretations for Tier 1 Public Sector and Not-for-Profit Public Benefit Entities 31 March 2017 New Accounting Standards and Interpretations for Tier 1 Public Benefit Entities

New Accounting Standards and Interpretations for Tier 1 Public Sector and Not-for-Profit Public Benefit Entities 31 March 2017 New Accounting Standards and Interpretations for Tier 1 Public Benefit Entities

New Zealand Equivalent to International Accounting Standard 34 Interim Financial Reporting (NZ IAS 34)

") New Zealand Equivalent to International Accounting Standard 34 Interim Financial Reporting (NZ IAS 34) Issued November 2004 and incorporates amendments up to and including 31 December 2012 This Standard

New Zealand Equivalent to International Accounting Standard 34 Interim Financial Reporting (NZ IAS 34) Issued November 2004 and incorporates amendments up to and including 31 December 2012 This Standard

Course Descriptions for the Department of Accounting

Course Descriptions for the Department of Accounting 53101 PRINCIPLES OF ACCOUNTING (1) {3} [3-3] Evolution of Accounting Science; Accounting as information system; accounting cycle; double entry; analysis

Course Descriptions for the Department of Accounting 53101 PRINCIPLES OF ACCOUNTING (1) {3} [3-3] Evolution of Accounting Science; Accounting as information system; accounting cycle; double entry; analysis

ICAEW REPRESENTATION 09/18

ICAEW REPRESENTATION 09/18 Accounting for Revenue and Non-Exchange Expenses ICAEW welcomes the opportunity to comment on the Accounting for Revenue and Non-Exchange Expenses consultation paper published

ICAEW REPRESENTATION 09/18 Accounting for Revenue and Non-Exchange Expenses ICAEW welcomes the opportunity to comment on the Accounting for Revenue and Non-Exchange Expenses consultation paper published

Statement of Comprehensive Income 1. Statement of Movements in Equity 1. Statement of Financial Position 2. Statement of Cash Flows 3

FORECAST FINANCIAL STATEMENTS FOR THE YEAR ENDED 30 JUNE 2013 INDEX Page Statement of Comprehensive Income 1 Statement of Movements in Equity 1 Statement of Financial Position 2 Statement of Cash Flows

FORECAST FINANCIAL STATEMENTS FOR THE YEAR ENDED 30 JUNE 2013 INDEX Page Statement of Comprehensive Income 1 Statement of Movements in Equity 1 Statement of Financial Position 2 Statement of Cash Flows

SUMMARY OF IASB WORK PLAN AS AT 14 NOVEMBER 2017

SUMMARY OF IASB WORK PLAN AS AT 14 NOVEMBER 2017 Page Standard-setting and Related Projects... 2 Conceptual Framework... 2 Disclosure Initiative Definition of Materiality... 3 Rate-regulated Activities...

SUMMARY OF IASB WORK PLAN AS AT 14 NOVEMBER 2017 Page Standard-setting and Related Projects... 2 Conceptual Framework... 2 Disclosure Initiative Definition of Materiality... 3 Rate-regulated Activities...

Adoption of International Financial Reporting Standards ( IFRS )

") 1 Adoption of International Financial Reporting Standards ( IFRS ) Simon Ball/Mike Brown 23 June 2005 2 Disclaimer This presentation provides illustrative statements for the year ended 31 March 2005 which

1 Adoption of International Financial Reporting Standards ( IFRS ) Simon Ball/Mike Brown 23 June 2005 2 Disclaimer This presentation provides illustrative statements for the year ended 31 March 2005 which

REVENUE. Meeting objectives Topic Agenda Item. Project management Decisions up to SEPTEMBER 2018 Meeting

Meeting: Meeting Location: International Public Sector Accounting Standards Board Kuala Lumpur, Malaysia Meeting Date: December 4 7, 2018 From: Amon Dhliwayo Agenda Item 10 For: Approval Discussion Information

Meeting: Meeting Location: International Public Sector Accounting Standards Board Kuala Lumpur, Malaysia Meeting Date: December 4 7, 2018 From: Amon Dhliwayo Agenda Item 10 For: Approval Discussion Information

Re: FEE comments on EFRAG Draft Endorsement Advice on IFRS 9 Financial Instruments.

Mr. Roger Marshall Acting President EFRAG 35 Square de Meeûs B-1000 Brussels Belgium commentletters@efrag.org 22 June 2015 Ref.: CRPG/PFK/PPA Dear Mr Marshall, Re: FEE comments on EFRAG Draft Endorsement

Mr. Roger Marshall Acting President EFRAG 35 Square de Meeûs B-1000 Brussels Belgium commentletters@efrag.org 22 June 2015 Ref.: CRPG/PFK/PPA Dear Mr Marshall, Re: FEE comments on EFRAG Draft Endorsement

International Financial Accounting and Policy. International Convergence of Financial Reporting. Harmonization

International Financial Accounting and Policy International Convergence of Financial Reporting Dinuka Perera ACA, ACMA (UK), CGMA, ACMA (SL), MBA (PIM - Sri J.) Harmonization What is harmonization? The

International Financial Accounting and Policy International Convergence of Financial Reporting Dinuka Perera ACA, ACMA (UK), CGMA, ACMA (SL), MBA (PIM - Sri J.) Harmonization What is harmonization? The

New Accounting Standards and Interpretations for Public Benefit Entities. 31 March 2014

New Accounting Standards and Interpretations for Public Benefit Entities 31 March 2014 Introduction This document is applicable for Public Benefit Entities (PBEs) applying New Zealand Equivalents to International

New Accounting Standards and Interpretations for Public Benefit Entities 31 March 2014 Introduction This document is applicable for Public Benefit Entities (PBEs) applying New Zealand Equivalents to International

Table 1 IPSAS and Equivalent IFRS Summary 1

Agenda Item 1.6 IPSAS IFRS Alignment Dashboard Table 1 IPSAS and Equivalent IFRS Summary 1 IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements IAS 1 17, Property,

Agenda Item 1.6 IPSAS IFRS Alignment Dashboard Table 1 IPSAS and Equivalent IFRS Summary 1 IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements IAS 1 17, Property,

REVENUE APPROACH TO IFRS 15

Meeting: Meeting Location: International Public Sector Accounting Standards Board Toronto, Canada Meeting Date: June 19 22, 2018 Agenda Item 8 For: Approval Discussion Information From: Amon Dhliwayo REVENUE

Meeting: Meeting Location: International Public Sector Accounting Standards Board Toronto, Canada Meeting Date: June 19 22, 2018 Agenda Item 8 For: Approval Discussion Information From: Amon Dhliwayo REVENUE

Public Sector Measurement

Public Sector Measurement Gwenda Jensen and John Stanford IPSASB Meeting March 6 9, 2018 New York, USA Page 1 Proprietary and Copyrighted Information Overview Introduction 1. ED, Objective, scope and definitions

Public Sector Measurement Gwenda Jensen and John Stanford IPSASB Meeting March 6 9, 2018 New York, USA Page 1 Proprietary and Copyrighted Information Overview Introduction 1. ED, Objective, scope and definitions

International Accounting: Introduction

International Accounting: Introduction Agenda 1. Introduction 2. Organisation of the IASB/IFRS Foundation 3. EC Regulation 4. Accounting principles and accounting standards 5. Components of financial statements

International Accounting: Introduction Agenda 1. Introduction 2. Organisation of the IASB/IFRS Foundation 3. EC Regulation 4. Accounting principles and accounting standards 5. Components of financial statements

IFRS Fair Value Measurement. Credibility. Professionalism. AccountAbility

IFRS 13 13 Fair Value Measurement Credibility. Professionalism. AccountAbility Agenda Objective Scope Definitions Measurement Disclosure Objective of IFRS 13 The IFRS applies to IFRSs that require or permit

IFRS 13 13 Fair Value Measurement Credibility. Professionalism. AccountAbility Agenda Objective Scope Definitions Measurement Disclosure Objective of IFRS 13 The IFRS applies to IFRSs that require or permit

Accounting Standards the International Setting

International Financial Reporting Standards Accounting Standards the International Setting Sir David Tweedie IASB Chairman The views expressed in this presentation are those of the presenter, not necessarily

International Financial Reporting Standards Accounting Standards the International Setting Sir David Tweedie IASB Chairman The views expressed in this presentation are those of the presenter, not necessarily

FINANCIAL INSTRUMENTS

FINANCIAL INSTRUMENTS Financial Instruments While the EBC notes many similarities between the accounting standards of financial instruments under IFRS and J-GAAP, there is one area where further alignment

FINANCIAL INSTRUMENTS Financial Instruments While the EBC notes many similarities between the accounting standards of financial instruments under IFRS and J-GAAP, there is one area where further alignment

The Conceptual Framework for Financial Reporting. The New name for Framework

The Conceptual Framework for Financial Reporting The New name for Framework 1 Earlier it was known as Framework for the Preparation and Presentation of Financial Statements 2 This presentation is based

The Conceptual Framework for Financial Reporting The New name for Framework 1 Earlier it was known as Framework for the Preparation and Presentation of Financial Statements 2 This presentation is based

Table 1 IPSAS and Equivalent IFRS Summary 2

IPSASB Meeting ( 2018) Agenda Item 1.6 IPSAS IFRS Alignment 1 Dashboard Table 1 IPSAS and Equivalent IFRS Summary 2 IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements

IPSASB Meeting ( 2018) Agenda Item 1.6 IPSAS IFRS Alignment 1 Dashboard Table 1 IPSAS and Equivalent IFRS Summary 2 IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements

LO.1 Describe the financial reporting environment and generally accepted accounting practice

NOTES Module 1 LO.1 Describe the financial reporting environment and generally accepted accounting practice What is accounting? The purpose of accounting is: 1. To identify, record, and communicate the

NOTES Module 1 LO.1 Describe the financial reporting environment and generally accepted accounting practice What is accounting? The purpose of accounting is: 1. To identify, record, and communicate the

response to consultation paper

IPSASB Consultation Paper Accounting for Revenue and Non-Exchange Expenses response to consultation paper 15 January 2018 CIPFA, the Chartered Institute of Public Finance and Accountancy, is the professional

IPSASB Consultation Paper Accounting for Revenue and Non-Exchange Expenses response to consultation paper 15 January 2018 CIPFA, the Chartered Institute of Public Finance and Accountancy, is the professional

IASB update: Progress and Plans

Agenda paper 2.1 International Financial Reporting Standards IASB update: Progress and Plans November 2014 The views expressed in this presentation are those of the presenter, not necessarily those of

Agenda paper 2.1 International Financial Reporting Standards IASB update: Progress and Plans November 2014 The views expressed in this presentation are those of the presenter, not necessarily those of

New Zealand Equivalent to International Accounting Standard 7 Statement of Cash Flows (NZ IAS 7)

") New Zealand Equivalent to International Accounting Standard 7 Statement of Cash Flows (NZ IAS 7) Issued November 2004 and incorporates amendments to 31 December 2016 other than consequential amendments

New Zealand Equivalent to International Accounting Standard 7 Statement of Cash Flows (NZ IAS 7) Issued November 2004 and incorporates amendments to 31 December 2016 other than consequential amendments

Request for Information: Comprehensive Review of IFRS for SMEs

30 November 2012 Level 7, 600 Bourke Street MELBOURNE VIC 3000 Postal Address PO Box 204 Collins Street West VIC 8007 Telephone: (03) 9617 7600 Facsimile: (03) 9617 7608 Mr Hans Hoogervorst Chairman International

30 November 2012 Level 7, 600 Bourke Street MELBOURNE VIC 3000 Postal Address PO Box 204 Collins Street West VIC 8007 Telephone: (03) 9617 7600 Facsimile: (03) 9617 7608 Mr Hans Hoogervorst Chairman International

Accounting Alert Quarterly update for Public Benefit Entities What s new in financial reporting for March 2016?

Quarterly update for Public Benefit Entities What s new in financial reporting for March 2016? This alert provides a high level overview of the new and revised financial reporting requirements that need

Quarterly update for Public Benefit Entities What s new in financial reporting for March 2016? This alert provides a high level overview of the new and revised financial reporting requirements that need

The Effects of Changes in Foreign Exchange Rates

International Public Sector Accounting Standards Board IPSAS 4 Issued January 2007 International Public Sector Accounting Standard The Effects of Changes in Foreign Exchange Rates International Public

International Public Sector Accounting Standards Board IPSAS 4 Issued January 2007 International Public Sector Accounting Standard The Effects of Changes in Foreign Exchange Rates International Public

MARCH 31, 2018 IPSASB EXPOSURE DRAFT 63: SOCIAL BENEFITS RESPONSE MANJ KALAR

MARCH 31, 2018 IPSASB EXPOSURE DRAFT 63: SOCIAL BENEFITS RESPONSE MANJ KALAR Manj has over 20 years experience working in public sector, focusing on implementation of accrual accounting across UK central

MARCH 31, 2018 IPSASB EXPOSURE DRAFT 63: SOCIAL BENEFITS RESPONSE MANJ KALAR Manj has over 20 years experience working in public sector, focusing on implementation of accrual accounting across UK central

1.1 This briefing provides an overview of IFRS 15 and issues around the adoption of the standard by charities.

\ PAPER 2 Briefing Committee Venue Charities SORP Committee CIPFA s Offices, Edinburgh Date 12 March 2018 Author Subject Secretariat to the Charities SORP Committee IFRS 15 Revenue from Contracts with

\ PAPER 2 Briefing Committee Venue Charities SORP Committee CIPFA s Offices, Edinburgh Date 12 March 2018 Author Subject Secretariat to the Charities SORP Committee IFRS 15 Revenue from Contracts with

What s new in financial reporting for March 2009? Quarterly Update

What s new in financial reporting for? Quarterly Update The analysis below provides a high level overview of new and revised financial reporting requirements that need to be considered for financial reporting

What s new in financial reporting for? Quarterly Update The analysis below provides a high level overview of new and revised financial reporting requirements that need to be considered for financial reporting

INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARDS - INTRODUCTION

INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARDS - INTRODUCTION IPSAS OBJECTIVES Comparability with other international organisations and national governments Enhanced governance and internal financial

INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARDS - INTRODUCTION IPSAS OBJECTIVES Comparability with other international organisations and national governments Enhanced governance and internal financial

Financial Statements. - Directors Responsibility Statement. - Consolidated Statement of Comprehensive Income

X.0 HEADER Financial Statements - Directors Responsibility Statement - Consolidated Statement of Comprehensive Income - Consolidated Statement of Financial Position - Consolidated Statement of Changes

X.0 HEADER Financial Statements - Directors Responsibility Statement - Consolidated Statement of Comprehensive Income - Consolidated Statement of Financial Position - Consolidated Statement of Changes

Module 1: The role and importance of financial reporting

MODULE 1: The role and importance of financial reporting Part A: The role and importance of financial reporting The role of financial reporting The importance of financial reporting Who must prepare general

MODULE 1: The role and importance of financial reporting Part A: The role and importance of financial reporting The role of financial reporting The importance of financial reporting Who must prepare general

Table 1 IPSAS and Equivalent IFRS Summary 2

Agenda Item 1.7 IPSAS IFRS Alignment 1 Dashboard Table 1 IPSAS and Equivalent IFRS Summary 2 IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements IAS 1 18, Segment

Agenda Item 1.7 IPSAS IFRS Alignment 1 Dashboard Table 1 IPSAS and Equivalent IFRS Summary 2 IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements IAS 1 18, Segment

OCI and relevance of performance measures: recent inquiry by IASB

International Financial Reporting Standards OCI and relevance of performance measures: recent inquiry by IASB Nov. 8, 2016, Maui Wei-Guo Zhang, IASB member The views expressed in this presentation are

International Financial Reporting Standards OCI and relevance of performance measures: recent inquiry by IASB Nov. 8, 2016, Maui Wei-Guo Zhang, IASB member The views expressed in this presentation are

ACCOUNTING STANDARDS BOARD DIRECTIVE 5 DETERMINING THE GRAP REPORTING FRAMEWORK

ACCOUNTING STANDARDS BOARD DIRECTIVE 5 DETERMINING THE GRAP REPORTING FRAMEWORK Issued by the Accounting Standards Board March 2009 Accounting Standards Board P O Box 74219 Lynnwood Ridge 0040 Fax: +27

ACCOUNTING STANDARDS BOARD DIRECTIVE 5 DETERMINING THE GRAP REPORTING FRAMEWORK Issued by the Accounting Standards Board March 2009 Accounting Standards Board P O Box 74219 Lynnwood Ridge 0040 Fax: +27

FINANCIAL STATEMENTS 2018

FINANCIAL STATEMENTS 2018 CONTENTS 2 Auditor s Report 7 Directors Responsibility Statement 8 Statement of Comprehensive Income 9 Statement of Financial Position 10 Statement of Changes in Equity 11 Statement

FINANCIAL STATEMENTS 2018 CONTENTS 2 Auditor s Report 7 Directors Responsibility Statement 8 Statement of Comprehensive Income 9 Statement of Financial Position 10 Statement of Changes in Equity 11 Statement

IFRS 9 Financial Instruments

November 2009 Project Summary and Feedback Statement IFRS 9 Financial Instruments Part 1: Classification and measurement Planned reform of financial instruments accounting 2009 2010 Q1 Q2 Q3 Q4 Q1 Q2 Q3

November 2009 Project Summary and Feedback Statement IFRS 9 Financial Instruments Part 1: Classification and measurement Planned reform of financial instruments accounting 2009 2010 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Accounting s Changing Landscape Keynote Address

Accounting s Changing Landscape Keynote Address Arn van Iersel, FCGA The Origins of Accounting The world s other oldest profession? Babylonian Accounting Records 4,500 B.C. Code of Hammurabi 2250 B.C.

Accounting s Changing Landscape Keynote Address Arn van Iersel, FCGA The Origins of Accounting The world s other oldest profession? Babylonian Accounting Records 4,500 B.C. Code of Hammurabi 2250 B.C.

On 15 September 2014, the President

Editor s Note W elcome to our third edition of ICPAK Technical e-newsletter. As you may be aware the mission of ICPAK is to oversee the development of the accountancy profession in Kenya through: supporting

Editor s Note W elcome to our third edition of ICPAK Technical e-newsletter. As you may be aware the mission of ICPAK is to oversee the development of the accountancy profession in Kenya through: supporting

IFRS Fair Value Measurement. Credibility. Professionalism. AccountAbility

IFRS 13 13 Fair Value Measurement Credibility. Professionalism. AccountAbility Agenda Objective Scope Definitions Measurement Disclosure Objective of IFRS 13 The IFRS applies to IFRSs that require or permit

IFRS 13 13 Fair Value Measurement Credibility. Professionalism. AccountAbility Agenda Objective Scope Definitions Measurement Disclosure Objective of IFRS 13 The IFRS applies to IFRSs that require or permit

Events after the Reporting Period

International Accounting Standard 10 Events after the Reporting Period This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 10 Events After the Balance Sheet Date was

International Accounting Standard 10 Events after the Reporting Period This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 10 Events After the Balance Sheet Date was

Business combinations

May 2004 The International Accounting Standards Board met in London on 18 and 19 May 2004, when it discussed: Business combinations (phase II) Consolidation Financial instruments Financial risk disclosures

May 2004 The International Accounting Standards Board met in London on 18 and 19 May 2004, when it discussed: Business combinations (phase II) Consolidation Financial instruments Financial risk disclosures

New Zealand Equivalent to International Financial Reporting Standard 4 Insurance Contracts (NZ IFRS 4)

") New Zealand Equivalent to International Financial Reporting Standard 4 Insurance Contracts (NZ IFRS 4) Issued November 2004 and incorporates amendments up to and including 30 June 2011 other than consequential

New Zealand Equivalent to International Financial Reporting Standard 4 Insurance Contracts (NZ IFRS 4) Issued November 2004 and incorporates amendments up to and including 30 June 2011 other than consequential

New Zealand Equivalent to International Accounting Standard 12 Income Taxes (NZ IAS 12)

") New Zealand Equivalent to International Accounting Standard 12 Income Taxes (NZ IAS 12) Issued November 2004 and incorporates amendments up to and including 31 December 2011 other than consequential amendments

New Zealand Equivalent to International Accounting Standard 12 Income Taxes (NZ IAS 12) Issued November 2004 and incorporates amendments up to and including 31 December 2011 other than consequential amendments

International Accounting Standard 10 Events after the Reporting Period

International Accounting Standard 10 Events after the Reporting Period Objective 1 The objective of this Standard is to prescribe: when an entity should adjust its financial statements for events after

International Accounting Standard 10 Events after the Reporting Period Objective 1 The objective of this Standard is to prescribe: when an entity should adjust its financial statements for events after

International Accounting Standards Board

International Accounting Standards Board International Accounting Standards Board The IASB agenda today and priorities for the future IASB is committed to develop, in the public interest, a single set

International Accounting Standards Board International Accounting Standards Board The IASB agenda today and priorities for the future IASB is committed to develop, in the public interest, a single set

IFRS AS A TOOL FOR CROSS- BORDER FINANCIAL REPORTING

IFRS AS A TOOL FOR CROSS- BORDER FINANCIAL REPORTING A paper presented by Ismai la M. Zakari FBR, FCA Managing Partner, (Chartered Accountants) Council Member, ICAN Learning Outcomes What is IFRS? What

IFRS AS A TOOL FOR CROSS- BORDER FINANCIAL REPORTING A paper presented by Ismai la M. Zakari FBR, FCA Managing Partner, (Chartered Accountants) Council Member, ICAN Learning Outcomes What is IFRS? What

Diploma in IFRS. Units with Learning Outcomes and Assessment Criteria

Diploma in IFRS Units with Learning Outcomes and Assessment Criteria Unit 1-IASB and regulatory framework Understand the need and role of the regulatory system Describe the impact of globalization Describe

Diploma in IFRS Units with Learning Outcomes and Assessment Criteria Unit 1-IASB and regulatory framework Understand the need and role of the regulatory system Describe the impact of globalization Describe

IFRS Update. International Financial Reporting Standards. OECD Accrual Accounting Symposium 7 March March 2013

4 March 2013 International Financial Reporting Standards IFRS Update OECD Accrual Accounting Symposium 7 March 2013 The views expressed in this presentation are those of the presenter, not necessarily

4 March 2013 International Financial Reporting Standards IFRS Update OECD Accrual Accounting Symposium 7 March 2013 The views expressed in this presentation are those of the presenter, not necessarily

IFRS 9 Implementation Workshop 31 st January 1 st February 2018

Historical Perspectives of IFRS 9 and the Implementation Guideline Presentation by: CPA Cliff Nyandoro IFRS 9 Implementation Workshop 31 st January 1 st February 2018 Uphold public interest PwC Why IFRS

Historical Perspectives of IFRS 9 and the Implementation Guideline Presentation by: CPA Cliff Nyandoro IFRS 9 Implementation Workshop 31 st January 1 st February 2018 Uphold public interest PwC Why IFRS

PROJECT BRIEF AND OUTLINE

INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARDS BOARD PROJECT BRIEF AND OUTLINE 1. Subject Financial Instruments: Presentation and Disclosure. 2. Project Rationale and Objectives a) Issue identification

INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARDS BOARD PROJECT BRIEF AND OUTLINE 1. Subject Financial Instruments: Presentation and Disclosure. 2. Project Rationale and Objectives a) Issue identification

Table 1 IPSAS and Equivalent IFRS Summary*

Agenda Item 13.3.2 IPSAS IFRS Alignment Dashboard Table 1 IPSAS and Equivalent IFRS Summary* IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements IAS 1 17, Property,

Agenda Item 13.3.2 IPSAS IFRS Alignment Dashboard Table 1 IPSAS and Equivalent IFRS Summary* IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements IAS 1 17, Property,

IAS 12 Income Taxes Recognising DTA s for unrealised losses on AFS debt securities

Mr Robert Garnett Chairman IFRS Interpretations Committee 30 Cannon Street London EC4M 6XH United Kingdom The European Insurance CFO Forum C/O Dieter Wemmer Zurich Financial Services Ltd Mythenquai 2 CH-8002

Mr Robert Garnett Chairman IFRS Interpretations Committee 30 Cannon Street London EC4M 6XH United Kingdom The European Insurance CFO Forum C/O Dieter Wemmer Zurich Financial Services Ltd Mythenquai 2 CH-8002

SUMMARY OF IASB WORK PLAN AS AT 23 AUGUST 2018

SUMMARY OF IASB WORK PLAN AS AT 23 AUGUST 2018 Page Standard-setting and Related Projects... 3 Management Commentary... 3 Rate-regulated Activities... 3 Research Projects... 4 Dynamic Risk Management...

SUMMARY OF IASB WORK PLAN AS AT 23 AUGUST 2018 Page Standard-setting and Related Projects... 3 Management Commentary... 3 Rate-regulated Activities... 3 Research Projects... 4 Dynamic Risk Management...

Tier 2 For-Profit Reporters

ILLUSTRATIVE FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2017 NEW ZEALAND EQUIVALENTS TO INTERNATIONAL FINANCIAL REPORTING STANDARDS REDUCED DISCLOSURE REGIME Tier 2 For-Profit Reporters RDR Layout (New

ILLUSTRATIVE FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2017 NEW ZEALAND EQUIVALENTS TO INTERNATIONAL FINANCIAL REPORTING STANDARDS REDUCED DISCLOSURE REGIME Tier 2 For-Profit Reporters RDR Layout (New