Andreas Fagereng. Charles Gottlieb. Luigi Guiso

|

|

|

- Virgil Chapman

- 6 years ago

- Views:

Transcription

Charles Gottlieb (University of Cambridge) Luigi Guiso (EIEF) WU Symposium, Vienna, August")

1 Asset Market Participation and Portfolio Choice over the Life-Cycle Andreas Fagereng (Statistics Norway) Charles Gottlieb (University of Cambridge) Luigi Guiso (EIEF) WU Symposium, Vienna, August 2015

2 The two views Investor financial portfolio allocation over the life cycle (safe and risky investments): Practitioners view: invest heavily in stocks when young, rebalance as consumers gets older (Malkiel1996). Your age in bond Jack Bogle. Economists views - this may not always be true: Samuelson (1969), Mossin (1968), Merton (1969), but true when human capital accounted for (Merton 1971) Both views: all should participate in the risky assets markets

3 Merton (1971) implication: adding labor income Relevant wealth includes accumulated assets W(a) and human wealth H(a) (complete markets) Optimal share in stocks as a fraction of financial wealth is ( r) H ( a, T ) ( a) (1 ) 2 Wa ( ) And thus varies with age becasue Investors participate in stocks at all ages H ( a, T ) varies with age Wa ( ) Intuition: Human capital acts as a bond => when investors are flood with bond-like assets (at young ages) they invest a lot in stocks to attain the Merton share

4 Generalization of the Merton implication Does the basic Merton model implication generalize to the realistic case of uncertain and non-tradable labor income? With these features lifecycle consumption-portfolio problem has no closed form solution Over past decade a wave of computational models allow for many realistic features such as Uncertain labor income Incomplete markets (borrowing constraints) Non-standard preferences Bequests Correlated stock returns Basic Merton implication holds in these more general context

5 Empirical support for life cycle profile? If the risky share over the life cycle is driven by shrinking human capital (a fact of life) one would expect a strong evidence of rebalancing in the data. Haliassos et al (2001): the age profile of the risky share is relatively flat, though in some instances there does seem to be some moderate rebalancing. Empirical evidence: 1. based on cross sectional data (age vs cohort) 2. based surveys=> measurement problems. (lying about stocks and correlation of measurement error with age) 3. ignores that participation is a choice=> uncontrolled selection may contribute to failure to find evidence of rebalancing

6 This study: two tasks 1. Deal with the deficiencies of the empirical evidence Rely on data that should be free of most of the above concerns Model age profiles of participation and risky share accounting for time and cohort effects Account for the endogenous nature of participation Produces empirical age profiles for the portfolio share and participation with distinct patterns of adjustment Strong evidence of rebalancing along different margins 2. Propose a calibrated model that can: 1. come close to reproduce the age profile of the share and participation and the timing of adjustment along these two margins 2. is consistent with the level of the share for the stockholders

7 The administrative data Ideal data for our task: Long and complete household panel data from Norwegian Tax Registry, No attrition due to tracking Info on all households financial assets at the single instrument level Assets ownership and value reported to the tax authority by the bank, employers, or broker where the claim sits: More difficult to conceal information (no under or non-reporting) Absence of standard measurement error Households who exit are not replaced=> some attrition because Die (main reason 62%) Divorce (25%) Leave the country (13%) Focus on two assets model: stocks and bonds

8 Participation Share Participation shares in risky asset markets, selected cohorts Age

9 Risky Share Conditional risky Risky share share of financial by wealth, age selected and cohorts Suggestive of time effects, unclear cohort effects, declines with age Age

10 Conditional risky Financial share wealth, by selected age cohorts and cohort Suggestive of time effects, unclear cohort effects, declines with age

11 Modeling Two identification problems with the descriptive evidence in the figures 1. Separating age, time and cohort effects Impose two type of restrictions to identify the age profile 1. We follow Deaton-Paxson: add a trend and impose that deviations from trend sum to We impose causal mechanism on cohort effects: affected by stock market returns during impressionable years (Malmendier and Nagel, 2011, Giuliano and Spilimbergo, 2014) 2. Selection into participation: a two stage Heckman model Identification restriction: A measure of lifetime wealth (financial wealth + human capital) affects decision to participate but not the optimal share

12 Result: restricting cohort effects to youth experience share share share participation participation participation

13 Life cycle pattern of financial wealth

14 Key patterns: Dual adjustment Hump shape in participation => people enter and exit the stock market Participation peaks around retirement As people leave the labor market they also start leaving the stock market=> inconsistent with a once and forever participation cost Adjustment takes place along two margins with a specific timing Gradual rebalancing along the intensive margin well before retirement Exit from stocks after retirement Little wealth decumulation after retirement

15 Standard computational models Dynamics of the share consistent with those estimated by us but predicted level is too high Do not generate exit from the stock market and are silent about timing of exit over the life cycle Focus has been on limited (low) participation among the young Limited participation and exit among the elderly has been ignored (exception Allen Sue) We extend Cocco, Gomes and Maenhout (2005) to try account for these features by adding: 1. per-period participation cost 2. probability of tail risk 3. bequest motive

16 On tail risk Households in sample have had several experiences with large stock market crashes. Informed guess of tail event based on series of crashes, between 0.6% and 3.2%. Households are imperfectly diversified -> Even in years of not stock market crash some households may suffer substantial losses.

17 Baseline

18 Comparison with CGM (2005) Per period cost not enough to generate timely exit, also prob disasters needed

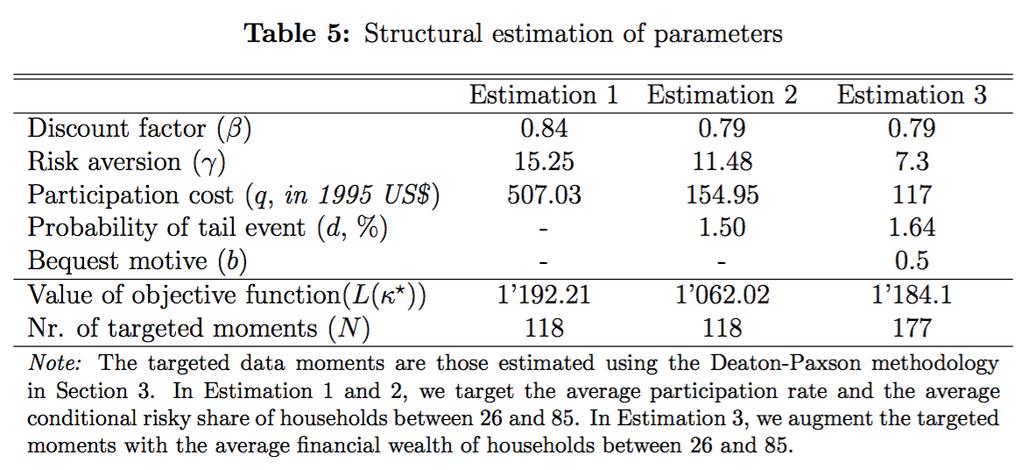

19 Estimates

20 Fit: estimate also disaster probability

21 Summing up We provide robust evidence that investors do indeed rebalance their portfolios over the life cycle Invariant to different ways to separate time, age and cohort effects Investors adjust along two margins with distinct timing Lowering the share in stocks when retirement comes into sight Exiting the stock market when they retire A model with a small per period participation cost a small age-invariant probability of disaster and relatively high risk aversion can come close to reproduce the dual pattern of adjustment and the level of the share over the life cycle

Optimal Life-Cycle Investing with Flexible Labor Supply: A Welfare Analysis of Default Investment Choices in Defined-Contribution Pension Plans

Optimal Life-Cycle Investing with Flexible Labor Supply: A Welfare Analysis of Default Investment Choices in Defined-Contribution Pension Plans Francisco J. Gomes, Laurence J. Kotlikoff and Luis M. Viceira

Optimal Life-Cycle Investing with Flexible Labor Supply: A Welfare Analysis of Default Investment Choices in Defined-Contribution Pension Plans Francisco J. Gomes, Laurence J. Kotlikoff and Luis M. Viceira

Optimal Life-Cycle Investing with Flexible Labor Supply: A Welfare Analysis of Life-Cycle Funds

American Economic Review: Papers & Proceedings 2008, 98:2, 297 303 http://www.aeaweb.org/articles.php?doi=10.1257/aer.98.2.297 Optimal Life-Cycle Investing with Flexible Labor Supply: A Welfare Analysis

American Economic Review: Papers & Proceedings 2008, 98:2, 297 303 http://www.aeaweb.org/articles.php?doi=10.1257/aer.98.2.297 Optimal Life-Cycle Investing with Flexible Labor Supply: A Welfare Analysis

Should Norway Change the 60% Equity portion of the GPFG fund?

Should Norway Change the 60% Equity portion of the GPFG fund? Pierre Collin-Dufresne EPFL & SFI, and CEPR April 2016 Outline Endowment Consumption Commitments Return Predictability and Trading Costs General

Should Norway Change the 60% Equity portion of the GPFG fund? Pierre Collin-Dufresne EPFL & SFI, and CEPR April 2016 Outline Endowment Consumption Commitments Return Predictability and Trading Costs General

Income Differences and Health Care Expenditures over the Life Cycle

Income Differences and Health Care Expenditures over the Life Cycle Serdar Ozkan Federal Reserve Board August 5, 2011 Motivation How do the low- and high-income households differ in the lifetime profile

Income Differences and Health Care Expenditures over the Life Cycle Serdar Ozkan Federal Reserve Board August 5, 2011 Motivation How do the low- and high-income households differ in the lifetime profile

The Effect of Uncertain Labor Income and Social Security on Life-cycle Portfolios

The Effect of Uncertain Labor Income and Social Security on Life-cycle Portfolios Raimond Maurer, Olivia S. Mitchell, and Ralph Rogalla September 2009 IRM WP2009-20 Insurance and Risk Management Working

The Effect of Uncertain Labor Income and Social Security on Life-cycle Portfolios Raimond Maurer, Olivia S. Mitchell, and Ralph Rogalla September 2009 IRM WP2009-20 Insurance and Risk Management Working

ON THE ASSET ALLOCATION OF A DEFAULT PENSION FUND

ON THE ASSET ALLOCATION OF A DEFAULT PENSION FUND Magnus Dahlquist 1 Ofer Setty 2 Roine Vestman 3 1 Stockholm School of Economics and CEPR 2 Tel Aviv University 3 Stockholm University and Swedish House

ON THE ASSET ALLOCATION OF A DEFAULT PENSION FUND Magnus Dahlquist 1 Ofer Setty 2 Roine Vestman 3 1 Stockholm School of Economics and CEPR 2 Tel Aviv University 3 Stockholm University and Swedish House

Precautionary Saving and Health Insurance: A Portfolio Choice Perspective

Front. Econ. China 2016, 11(2): 232 264 DOI 10.3868/s060-005-016-0015-0 RESEARCH ARTICLE Jiaping Qiu Precautionary Saving and Health Insurance: A Portfolio Choice Perspective Abstract This paper analyzes

Front. Econ. China 2016, 11(2): 232 264 DOI 10.3868/s060-005-016-0015-0 RESEARCH ARTICLE Jiaping Qiu Precautionary Saving and Health Insurance: A Portfolio Choice Perspective Abstract This paper analyzes

Determinants of Households Savings in Central, Eastern and Southeastern Europe

Determinants of Households Savings in Central, Eastern and Southeastern Europe Elisabeth Beckmann, Mariya Hake and Jarmila Urvova Oesterreichische Nationalbank (OeNB) Foreign Research Division XI. Emerging

Determinants of Households Savings in Central, Eastern and Southeastern Europe Elisabeth Beckmann, Mariya Hake and Jarmila Urvova Oesterreichische Nationalbank (OeNB) Foreign Research Division XI. Emerging

Wealth Returns Dynamics and Heterogeneity

Wealth Returns Dynamics and Heterogeneity Andreas Fagereng (Statistics Norway) Luigi Guiso (EIEF) Davide Malacrino (Stanford) Luigi Pistaferri (Stanford) Wealth distribution In many countries, and over

Wealth Returns Dynamics and Heterogeneity Andreas Fagereng (Statistics Norway) Luigi Guiso (EIEF) Davide Malacrino (Stanford) Luigi Pistaferri (Stanford) Wealth distribution In many countries, and over

NBER WORKING PAPER SERIES OPTIMAL LIFE-CYCLE INVESTING WITH FLEXIBLE LABOR SUPPLY: A WELFARE ANALYSIS OF LIFE-CYCLE FUNDS

NBER WORKING PAPER SERIES OPTIMAL LIFE-CYCLE INVESTING WITH FLEXIBLE LABOR SUPPLY: A WELFARE ANALYSIS OF LIFE-CYCLE FUNDS Francisco J. Gomes Laurence J. Kotlikoff Luis M. Viceira Working Paper 13966 http://www.nber.org/papers/w13966

NBER WORKING PAPER SERIES OPTIMAL LIFE-CYCLE INVESTING WITH FLEXIBLE LABOR SUPPLY: A WELFARE ANALYSIS OF LIFE-CYCLE FUNDS Francisco J. Gomes Laurence J. Kotlikoff Luis M. Viceira Working Paper 13966 http://www.nber.org/papers/w13966

LIFECYCLE INVESTING : DOES IT MAKE SENSE

Page 1 LIFECYCLE INVESTING : DOES IT MAKE SENSE TO REDUCE RISK AS RETIREMENT APPROACHES? John Livanas UNSW, School of Actuarial Sciences Lifecycle Investing, or the gradual reduction in the investment

Page 1 LIFECYCLE INVESTING : DOES IT MAKE SENSE TO REDUCE RISK AS RETIREMENT APPROACHES? John Livanas UNSW, School of Actuarial Sciences Lifecycle Investing, or the gradual reduction in the investment

Initial Conditions and Optimal Retirement Glide Paths

Initial Conditions and Optimal Retirement Glide Paths by David M., CFP, CFA David M., CFP, CFA, is head of retirement research at Morningstar Investment Management. He is the 2015 recipient of the Journal

Initial Conditions and Optimal Retirement Glide Paths by David M., CFP, CFA David M., CFP, CFA, is head of retirement research at Morningstar Investment Management. He is the 2015 recipient of the Journal

PhD Topics in Macroeconomics

PhD Topics in Macroeconomics Lecture 12: misallocation, part four Chris Edmond 2nd Semester 2014 1 This lecture Buera/Shin (2013) model of financial frictions, misallocation and the transitional dynamics

PhD Topics in Macroeconomics Lecture 12: misallocation, part four Chris Edmond 2nd Semester 2014 1 This lecture Buera/Shin (2013) model of financial frictions, misallocation and the transitional dynamics

Sang-Wook (Stanley) Cho

Cho") Beggar-thy-parents? A Lifecycle Model of Intergenerational Altruism Sang-Wook (Stanley) Cho University of New South Wales March 2009 Motivation & Question Since Becker (1974), several studies analyzing

Beggar-thy-parents? A Lifecycle Model of Intergenerational Altruism Sang-Wook (Stanley) Cho University of New South Wales March 2009 Motivation & Question Since Becker (1974), several studies analyzing

Saving During Retirement

Saving During Retirement Mariacristina De Nardi 1 1 UCL, Federal Reserve Bank of Chicago, IFS, CEPR, and NBER January 26, 2017 Assets held after retirement are large More than one-third of total wealth

Saving During Retirement Mariacristina De Nardi 1 1 UCL, Federal Reserve Bank of Chicago, IFS, CEPR, and NBER January 26, 2017 Assets held after retirement are large More than one-third of total wealth

Payout-Phase of Mandatory Pension Accounts

Goethe University Frankfurt, Germany Payout-Phase of Mandatory Pension Accounts Raimond Maurer (Budapest,24 th March 2009) (download see Rethinking Retirement Income Strategies How Can We Secure Better

Goethe University Frankfurt, Germany Payout-Phase of Mandatory Pension Accounts Raimond Maurer (Budapest,24 th March 2009) (download see Rethinking Retirement Income Strategies How Can We Secure Better

Forced Retirement Risk and Portfolio Choice

Forced Retirement Risk and Portfolio Choice Guodong Chen 1, Minjoon Lee 2, and Tong-yob Nam 3 1 New York University at Shanghai 2 Carleton University 3 Office of the Comptroller of the Currency, U.S. Department

Forced Retirement Risk and Portfolio Choice Guodong Chen 1, Minjoon Lee 2, and Tong-yob Nam 3 1 New York University at Shanghai 2 Carleton University 3 Office of the Comptroller of the Currency, U.S. Department

Consumption and Portfolio Decisions When Expected Returns A

Consumption and Portfolio Decisions When Expected Returns Are Time Varying September 10, 2007 Introduction In the recent literature of empirical asset pricing there has been considerable evidence of time-varying

Consumption and Portfolio Decisions When Expected Returns Are Time Varying September 10, 2007 Introduction In the recent literature of empirical asset pricing there has been considerable evidence of time-varying

ESSAYS IN ASSET PRICING AND REAL ESTATE

ESSAYS IN ASSET PRICING AND REAL ESTATE YU ZHANG Submitted in partial fulfillment of the requirements for the degree of Doctor of Philosophy under the Executive Committee of the Graduate School of Arts

ESSAYS IN ASSET PRICING AND REAL ESTATE YU ZHANG Submitted in partial fulfillment of the requirements for the degree of Doctor of Philosophy under the Executive Committee of the Graduate School of Arts

Heterogeneity in Returns to Wealth and the Measurement of Wealth Inequality 1

Heterogeneity in Returns to Wealth and the Measurement of Wealth Inequality 1 Andreas Fagereng (Statistics Norway) Luigi Guiso (EIEF) Davide Malacrino (Stanford University) Luigi Pistaferri (Stanford University

Heterogeneity in Returns to Wealth and the Measurement of Wealth Inequality 1 Andreas Fagereng (Statistics Norway) Luigi Guiso (EIEF) Davide Malacrino (Stanford University) Luigi Pistaferri (Stanford University

Depression Babies: Do Macroeconomic Experiences Affect Risk-Taking?

Depression Babies: Do Macroeconomic Experiences Affect Risk-Taking? October 19, 2009 Ulrike Malmendier, UC Berkeley (joint work with Stefan Nagel, Stanford) 1 The Tale of Depression Babies I don t know

Depression Babies: Do Macroeconomic Experiences Affect Risk-Taking? October 19, 2009 Ulrike Malmendier, UC Berkeley (joint work with Stefan Nagel, Stanford) 1 The Tale of Depression Babies I don t know

DISCUSSION OF CARDIA S PAPER. LI Xiaoxi LIU Xingyi WANG Yonglei

DISCUSSION OF CARDIA S PAPER LI Xiaoxi LIU Xingyi WANG Yonglei Agenda What is Ricardian Equivalence? What did Cardia do? Is the simulation credible? Are the reported results reasonable? What is Ricardian

DISCUSSION OF CARDIA S PAPER LI Xiaoxi LIU Xingyi WANG Yonglei Agenda What is Ricardian Equivalence? What did Cardia do? Is the simulation credible? Are the reported results reasonable? What is Ricardian

Life Cycle Uncertainty and Portfolio Choice Puzzles

Life Cycle Uncertainty and Portfolio Choice Puzzles Yongsung Chang University of Rochester Yonsei University Jay H. Hong University of Rochester Marios Karabarbounis Federal Reserve Bank of Richmond December

Life Cycle Uncertainty and Portfolio Choice Puzzles Yongsung Chang University of Rochester Yonsei University Jay H. Hong University of Rochester Marios Karabarbounis Federal Reserve Bank of Richmond December

Comments on: A. Armstrong, N. Draper, and E. Westerhout, The impact of demographic uncertainty on public finances in the Netherlands

Comments on: A. Armstrong, N. Draper, and E. Westerhout, The impact of demographic uncertainty on public finances in the Netherlands 1 1 University of Groningen; Institute for Advanced Studies (Vienna);

Comments on: A. Armstrong, N. Draper, and E. Westerhout, The impact of demographic uncertainty on public finances in the Netherlands 1 1 University of Groningen; Institute for Advanced Studies (Vienna);

Macroeconomic Experiences and Risk-Taking of Euro Area Households

Macroeconomic Experiences and Risk-Taking of Euro Area Households Miguel Ampudia (ECB) and Michael Ehrmann (Bank of Canada) Frankfurt, October 18th, 2013 The views expressed here are our own and not necessarily

Macroeconomic Experiences and Risk-Taking of Euro Area Households Miguel Ampudia (ECB) and Michael Ehrmann (Bank of Canada) Frankfurt, October 18th, 2013 The views expressed here are our own and not necessarily

Economics 230a, Fall 2014 Lecture Note 9: Dynamic Taxation II Optimal Capital Taxation

Economics 230a, Fall 2014 Lecture Note 9: Dynamic Taxation II Optimal Capital Taxation Capital Income Taxes, Labor Income Taxes and Consumption Taxes When thinking about the optimal taxation of saving

Economics 230a, Fall 2014 Lecture Note 9: Dynamic Taxation II Optimal Capital Taxation Capital Income Taxes, Labor Income Taxes and Consumption Taxes When thinking about the optimal taxation of saving

Discussion of Stock Market Investment: The Role of Human Capital by Athreya, Ionescu, Neelakantan Michael Haliassos, Goethe University Frankfurt,

Discussion of Stock Market Investment: The Role of Human Capital by Athreya, Ionescu, Neelakantan Michael Haliassos, Goethe University Frankfurt, CFS, CEPR, NETSPAR 1 Two puzzles: Stock Market Participation

Discussion of Stock Market Investment: The Role of Human Capital by Athreya, Ionescu, Neelakantan Michael Haliassos, Goethe University Frankfurt, CFS, CEPR, NETSPAR 1 Two puzzles: Stock Market Participation

The Welfare Cost of Asymmetric Information: Evidence from the U.K. Annuity Market

The Welfare Cost of Asymmetric Information: Evidence from the U.K. Annuity Market Liran Einav 1 Amy Finkelstein 2 Paul Schrimpf 3 1 Stanford and NBER 2 MIT and NBER 3 MIT Cowles 75th Anniversary Conference

The Welfare Cost of Asymmetric Information: Evidence from the U.K. Annuity Market Liran Einav 1 Amy Finkelstein 2 Paul Schrimpf 3 1 Stanford and NBER 2 MIT and NBER 3 MIT Cowles 75th Anniversary Conference

Household finance in Europe 1

IFC-National Bank of Belgium Workshop on "Data needs and Statistics compilation for macroprudential analysis" Brussels, Belgium, 18-19 May 2017 Household finance in Europe 1 Miguel Ampudia, European Central

IFC-National Bank of Belgium Workshop on "Data needs and Statistics compilation for macroprudential analysis" Brussels, Belgium, 18-19 May 2017 Household finance in Europe 1 Miguel Ampudia, European Central

Life-cycle Portfolio Allocation When Disasters are Possible

Life-cycle Portfolio Allocation When Disasters are Possible Daniela Kolusheva* November 2009 JOB MARKET PAPER Abstract In contrast to the predictions of life-cycle models with homothetic utility and risky

Life-cycle Portfolio Allocation When Disasters are Possible Daniela Kolusheva* November 2009 JOB MARKET PAPER Abstract In contrast to the predictions of life-cycle models with homothetic utility and risky

Retirement and Asset Allocation in Australian Households

Retirement and Asset Allocation in Australian Households Megan Gu School of Economics, The University of New South Wales September 2013 Abstract: This paper examines the effect of the retirement decision

Retirement and Asset Allocation in Australian Households Megan Gu School of Economics, The University of New South Wales September 2013 Abstract: This paper examines the effect of the retirement decision

Asset Location and Allocation with. Multiple Risky Assets

Asset Location and Allocation with Multiple Risky Assets Ashraf Al Zaman Krannert Graduate School of Management, Purdue University, IN zamanaa@mgmt.purdue.edu March 16, 24 Abstract In this paper, we report

Asset Location and Allocation with Multiple Risky Assets Ashraf Al Zaman Krannert Graduate School of Management, Purdue University, IN zamanaa@mgmt.purdue.edu March 16, 24 Abstract In this paper, we report

Investment Decisions in Retirement: The Role of Subjective Expectations

Investment Decisions in Retirement: The Role of Subjective Expectations Marco Angrisani a,, Michael D. Hurd b, and Erik Meijer a a University of Southern California and RAND Corporation b RAND Corporation,

Investment Decisions in Retirement: The Role of Subjective Expectations Marco Angrisani a,, Michael D. Hurd b, and Erik Meijer a a University of Southern California and RAND Corporation b RAND Corporation,

Federal Reserve Bank of Chicago

Federal Reserve Bank of Chicago Health and the Savings of Insured Versus Uninsured, Working-Age Households in the U.S. Maude Toussaint-Comeau and Jonathan Hartley WP 2009-23 Health and the Savings of Insured

Federal Reserve Bank of Chicago Health and the Savings of Insured Versus Uninsured, Working-Age Households in the U.S. Maude Toussaint-Comeau and Jonathan Hartley WP 2009-23 Health and the Savings of Insured

Retirement Saving, Annuity Markets, and Lifecycle Modeling. James Poterba 10 July 2008

Retirement Saving, Annuity Markets, and Lifecycle Modeling James Poterba 10 July 2008 Outline Shifting Composition of Retirement Saving: Rise of Defined Contribution Plans Mortality Risks in Retirement

Retirement Saving, Annuity Markets, and Lifecycle Modeling James Poterba 10 July 2008 Outline Shifting Composition of Retirement Saving: Rise of Defined Contribution Plans Mortality Risks in Retirement

When and How to Delegate? A Life Cycle Analysis of Financial Advice

When and How to Delegate? A Life Cycle Analysis of Financial Advice Hugh Hoikwang Kim, Raimond Maurer, and Olivia S. Mitchell Prepared for presentation at the Pension Research Council Symposium, May 5-6,

When and How to Delegate? A Life Cycle Analysis of Financial Advice Hugh Hoikwang Kim, Raimond Maurer, and Olivia S. Mitchell Prepared for presentation at the Pension Research Council Symposium, May 5-6,

MULTIVARIATE FRACTIONAL RESPONSE MODELS IN A PANEL SETTING WITH AN APPLICATION TO PORTFOLIO ALLOCATION. Michael Anthony Carlton A DISSERTATION

MULTIVARIATE FRACTIONAL RESPONSE MODELS IN A PANEL SETTING WITH AN APPLICATION TO PORTFOLIO ALLOCATION By Michael Anthony Carlton A DISSERTATION Submitted to Michigan State University in partial fulfillment

MULTIVARIATE FRACTIONAL RESPONSE MODELS IN A PANEL SETTING WITH AN APPLICATION TO PORTFOLIO ALLOCATION By Michael Anthony Carlton A DISSERTATION Submitted to Michigan State University in partial fulfillment

Optimal Decumulation of Assets in General Equilibrium. James Feigenbaum (Utah State)

") Optimal Decumulation of Assets in General Equilibrium James Feigenbaum (Utah State) Annuities An annuity is an investment that insures against mortality risk by paying an income stream until the investor

Optimal Decumulation of Assets in General Equilibrium James Feigenbaum (Utah State) Annuities An annuity is an investment that insures against mortality risk by paying an income stream until the investor

Household Finance in China

Household Finance in China Russell Cooper 1 and Guozhong Zhu 2 October 22, 2016 1 Department of Economics, the Pennsylvania State University and NBER, russellcoop@gmail.com 2 School of Business, University

Household Finance in China Russell Cooper 1 and Guozhong Zhu 2 October 22, 2016 1 Department of Economics, the Pennsylvania State University and NBER, russellcoop@gmail.com 2 School of Business, University

Household Portfolio Choice Before and After House Purchase

Household Portfolio Choice Before and After House Purchase Ran S. Lyng Jie Zhou This Version: January, 2017 Abstract We study the temporal patterns of household portfolio choice of liquid wealth over a

Household Portfolio Choice Before and After House Purchase Ran S. Lyng Jie Zhou This Version: January, 2017 Abstract We study the temporal patterns of household portfolio choice of liquid wealth over a

HOUSEHOLD DEBT AND CREDIT CONSTRAINTS: COMPARATIVE MICRO EVIDENCE FROM FOUR OECD COUNTRIES

HOUSEHOLD DEBT AND CREDIT CONSTRAINTS: COMPARATIVE MICRO EVIDENCE FROM FOUR OECD COUNTRIES Jonathan Crook (University of Edinburgh) and Stefan Hochguertel (VU University Amsterdam) Discussion by Ernesto

HOUSEHOLD DEBT AND CREDIT CONSTRAINTS: COMPARATIVE MICRO EVIDENCE FROM FOUR OECD COUNTRIES Jonathan Crook (University of Edinburgh) and Stefan Hochguertel (VU University Amsterdam) Discussion by Ernesto

The Distributions of Income and Consumption. Risk: Evidence from Norwegian Registry Data

The Distributions of Income and Consumption Risk: Evidence from Norwegian Registry Data Elin Halvorsen Hans A. Holter Serdar Ozkan Kjetil Storesletten February 15, 217 Preliminary Extended Abstract Version

The Distributions of Income and Consumption Risk: Evidence from Norwegian Registry Data Elin Halvorsen Hans A. Holter Serdar Ozkan Kjetil Storesletten February 15, 217 Preliminary Extended Abstract Version

Topic 2.3b - Life-Cycle Labour Supply. Professor H.J. Schuetze Economics 371

Topic 2.3b - Life-Cycle Labour Supply Professor H.J. Schuetze Economics 371 Life-cycle Labour Supply The simple static labour supply model discussed so far has a number of short-comings For example, The

Topic 2.3b - Life-Cycle Labour Supply Professor H.J. Schuetze Economics 371 Life-cycle Labour Supply The simple static labour supply model discussed so far has a number of short-comings For example, The

Ingmar Minderhoud, Roderick Molenaar and Eduard Ponds The Impact of Human Capital on Life- Cycle Portfolio Choice. Evidence for the Netherlands

Ingmar Minderhoud, Roderick Molenaar and Eduard Ponds The Impact of Human Capital on Life- Cycle Portfolio Choice Evidence for the Netherlands DP 10/2011-006 The Impact of Human Capital on Life-Cycle Portfolio

Ingmar Minderhoud, Roderick Molenaar and Eduard Ponds The Impact of Human Capital on Life- Cycle Portfolio Choice Evidence for the Netherlands DP 10/2011-006 The Impact of Human Capital on Life-Cycle Portfolio

Optimal Savings for Retirement: The Role of Individual Accounts

University of Konstanz Department of Economics Optimal Savings for Retirement: The Role of Individual Accounts Julia Le Blanc and Almuth Scholl Working Paper Series 2015-10 http://www.wiwi.uni-konstanz.de/econdoc/working-paper-series/

University of Konstanz Department of Economics Optimal Savings for Retirement: The Role of Individual Accounts Julia Le Blanc and Almuth Scholl Working Paper Series 2015-10 http://www.wiwi.uni-konstanz.de/econdoc/working-paper-series/

ASSET ALLOCATION IN ALTERNATIVE INVESTMENTS REISA April 15, Sameer Jain Chief Economist and Managing Director American Realty Capital

ASSET ALLOCATION IN ALTERNATIVE INVESTMENTS REISA April 15, 2013 Sameer Jain Chief Economist and Managing Director American Realty Capital Alternative Investments Investment Universe Non-Traditional Investments

ASSET ALLOCATION IN ALTERNATIVE INVESTMENTS REISA April 15, 2013 Sameer Jain Chief Economist and Managing Director American Realty Capital Alternative Investments Investment Universe Non-Traditional Investments

Forced Retirement Risk and Portfolio Choice. (Preliminary and Not for Circulation)

") Forced Retirement Risk and Portfolio Choice (Preliminary and Not for Circulation) Guodong Chen Minjoon Lee Tong Yob Nam January 29, 2017 Abstract Literature on the effect of labor income on portfolio choice

Forced Retirement Risk and Portfolio Choice (Preliminary and Not for Circulation) Guodong Chen Minjoon Lee Tong Yob Nam January 29, 2017 Abstract Literature on the effect of labor income on portfolio choice

Internet Appendix for Heterogeneity and Persistence in Returns to Wealth

Internet Appendix for Heterogeneity and Persistence in Returns to Wealth Andreas Fagereng ú Luigi Guiso Davide Malacrino Luigi Pistaferri November 2, 2016 In this Internet Appendix we provide supplementary

Internet Appendix for Heterogeneity and Persistence in Returns to Wealth Andreas Fagereng ú Luigi Guiso Davide Malacrino Luigi Pistaferri November 2, 2016 In this Internet Appendix we provide supplementary

Growth, demographic structure, and national saving in Taiwan. Angus Deaton and Christina Paxson

Growth, demographic structure, and national saving in Taiwan Angus Deaton and Christina Paxson Research Program in Development Studies Princeton University First Draft, May 1998 This version, June 1999

Growth, demographic structure, and national saving in Taiwan Angus Deaton and Christina Paxson Research Program in Development Studies Princeton University First Draft, May 1998 This version, June 1999

Wealth Analysis: Introduction to Household Portfolios

Wealth Analysis: Introduction to Household Portfolios Eva Sierminska CEPS/INSTEAD, Luxembourg and DIW Berlin VIIth Winter School on Inequality and Social Welfare Alba di Canazei, January 9-12, 2012 Outline

Wealth Analysis: Introduction to Household Portfolios Eva Sierminska CEPS/INSTEAD, Luxembourg and DIW Berlin VIIth Winter School on Inequality and Social Welfare Alba di Canazei, January 9-12, 2012 Outline

Topic 2.3b - Life-Cycle Labour Supply. Professor H.J. Schuetze Economics 371

Topic 2.3b - Life-Cycle Labour Supply Professor H.J. Schuetze Economics 371 Life-cycle Labour Supply The simple static labour supply model discussed so far has a number of short-comings For example, The

Topic 2.3b - Life-Cycle Labour Supply Professor H.J. Schuetze Economics 371 Life-cycle Labour Supply The simple static labour supply model discussed so far has a number of short-comings For example, The

Portfolio Choice with Illiquid Assets

Portfolio Choice with Illiquid Assets Andrew Ang Ann F Kaplan Professor of Business Columbia Business School and NBER Email: aa610@columbia.edu [co-authored with Dimitris Papanikolaou and Mark M Westerfield]

Portfolio Choice with Illiquid Assets Andrew Ang Ann F Kaplan Professor of Business Columbia Business School and NBER Email: aa610@columbia.edu [co-authored with Dimitris Papanikolaou and Mark M Westerfield]

Life Cycle Portfolio Choice with Liquid and Illiquid Financial Assets

ISSN 2279-9362 Life Cycle Portfolio Choice with Liquid and Illiquid Financial Assets Claudio Campanale Carolina Fugazza Francisco Gomes No. 269 October 2012 www.carloalberto.org/research/working-papers

ISSN 2279-9362 Life Cycle Portfolio Choice with Liquid and Illiquid Financial Assets Claudio Campanale Carolina Fugazza Francisco Gomes No. 269 October 2012 www.carloalberto.org/research/working-papers

Wealth Dynamics during Retirement: Evidence from Population-Level Wealth Data in Sweden

Wealth Dynamics during Retirement: Evidence from Population-Level Wealth Data in Sweden By Martin Ljunge, Lee Lockwood, and Day Manoli September 2014 ABSTRACT In this paper, we document the wealth dynamics

Wealth Dynamics during Retirement: Evidence from Population-Level Wealth Data in Sweden By Martin Ljunge, Lee Lockwood, and Day Manoli September 2014 ABSTRACT In this paper, we document the wealth dynamics

Problems. the net marginal product of capital, MP'

Problems 1. There are two effects of an increase in the depreciation rate. First, there is the direct effect, which implies that, given the marginal product of capital in period two, MP, the net marginal

Problems 1. There are two effects of an increase in the depreciation rate. First, there is the direct effect, which implies that, given the marginal product of capital in period two, MP, the net marginal

Life-Cycle Asset Allocation: A Model with Borrowing Constraints, Uninsurable Labor Income Risk and Stock-Market Participation Costs

Life-Cycle Asset Allocation: A Model with Borrowing Constraints, Uninsurable Labor Income Risk and Stock-Market Participation Costs Francisco Gomes London Business School and Alexander Michaelides University

Life-Cycle Asset Allocation: A Model with Borrowing Constraints, Uninsurable Labor Income Risk and Stock-Market Participation Costs Francisco Gomes London Business School and Alexander Michaelides University

An Introduction to Resampled Efficiency

by Richard O. Michaud New Frontier Advisors Newsletter 3 rd quarter, 2002 Abstract Resampled Efficiency provides the solution to using uncertain information in portfolio optimization. 2 The proper purpose

by Richard O. Michaud New Frontier Advisors Newsletter 3 rd quarter, 2002 Abstract Resampled Efficiency provides the solution to using uncertain information in portfolio optimization. 2 The proper purpose

Optimal Portfolio Choice for Long-Horizon Investors with Nontradable Labor Income

THE JOURNAL OF FINANCE VOL. LVI, NO. 2 APRIL 2001 Optimal Portfolio Choice for Long-Horizon Investors with Nontradable Labor Income LUIS M. VICEIRA* ABSTRACT This paper examines how risky labor income

THE JOURNAL OF FINANCE VOL. LVI, NO. 2 APRIL 2001 Optimal Portfolio Choice for Long-Horizon Investors with Nontradable Labor Income LUIS M. VICEIRA* ABSTRACT This paper examines how risky labor income

Saving and investing over the life cycle and the role of collective pension funds Bovenberg, Lans; Koijen, R.S.J.; Nijman, Theo; Teulings, C.N.

Tilburg University Saving and investing over the life cycle and the role of collective pension funds Bovenberg, Lans; Koijen, R.S.J.; Nijman, Theo; Teulings, C.N. Published in: De Economist Publication

Tilburg University Saving and investing over the life cycle and the role of collective pension funds Bovenberg, Lans; Koijen, R.S.J.; Nijman, Theo; Teulings, C.N. Published in: De Economist Publication

Motif Capital Horizon Models: A robust asset allocation framework

Motif Capital Horizon Models: A robust asset allocation framework Executive Summary By some estimates, over 93% of the variation in a portfolio s returns can be attributed to the allocation to broad asset

Motif Capital Horizon Models: A robust asset allocation framework Executive Summary By some estimates, over 93% of the variation in a portfolio s returns can be attributed to the allocation to broad asset

AGGREGATE IMPLICATIONS OF WEALTH REDISTRIBUTION: THE CASE OF INFLATION

AGGREGATE IMPLICATIONS OF WEALTH REDISTRIBUTION: THE CASE OF INFLATION Matthias Doepke University of California, Los Angeles Martin Schneider New York University and Federal Reserve Bank of Minneapolis

AGGREGATE IMPLICATIONS OF WEALTH REDISTRIBUTION: THE CASE OF INFLATION Matthias Doepke University of California, Los Angeles Martin Schneider New York University and Federal Reserve Bank of Minneapolis

Dynamic Asset Allocation for Hedging Downside Risk

Dynamic Asset Allocation for Hedging Downside Risk Gerd Infanger Stanford University Department of Management Science and Engineering and Infanger Investment Technology, LLC October 2009 Gerd Infanger,

Dynamic Asset Allocation for Hedging Downside Risk Gerd Infanger Stanford University Department of Management Science and Engineering and Infanger Investment Technology, LLC October 2009 Gerd Infanger,

Health Status and Portfolio Choice by Harvey S. Rosen, Princeton University Stephen Wu, Hamilton College. CEPS Working Paper No. 75.

Health Status and Portfolio Choice by Harvey S. Rosen, Princeton University Stephen Wu, Hamilton College CEPS Working Paper No. 75 October 2001 We are grateful to Princeton s Center for Economic Policy

Health Status and Portfolio Choice by Harvey S. Rosen, Princeton University Stephen Wu, Hamilton College CEPS Working Paper No. 75 October 2001 We are grateful to Princeton s Center for Economic Policy

Custom Financial Advice versus Simple Investment Portfolios: A Life Cycle Comparison

Custom Financial Advice versus Simple Investment Portfolios: A Life Cycle Comparison Hugh Hoikwang Kim, Raimond Maurer, and Olivia S. Mitchell PRC WP2016 Pension Research Council Working Paper Pension

Custom Financial Advice versus Simple Investment Portfolios: A Life Cycle Comparison Hugh Hoikwang Kim, Raimond Maurer, and Olivia S. Mitchell PRC WP2016 Pension Research Council Working Paper Pension

Household Finance in China

Household Finance in China Russell Cooper and Guozhong Zhu February 20, 2017 Abstract This paper studies household finance in China, focusing on the high saving rate, the low participation rate in the

Household Finance in China Russell Cooper and Guozhong Zhu February 20, 2017 Abstract This paper studies household finance in China, focusing on the high saving rate, the low participation rate in the

D S E Dipartimento Scienze Economiche

D S E Dipartimento Scienze Economiche Working Paper Department of Economics Ca Foscari University of Venice Renata Bottazzi Tullio Jappelli Mario Padula The Portfolio Effect of Pension Reforms ISSN: 1827/336X

D S E Dipartimento Scienze Economiche Working Paper Department of Economics Ca Foscari University of Venice Renata Bottazzi Tullio Jappelli Mario Padula The Portfolio Effect of Pension Reforms ISSN: 1827/336X

HOUSEHOLD RISKY ASSET CHOICE: AN EMPIRICAL STUDY USING BHPS

HOUSEHOLD RISKY ASSET CHOICE: AN EMPIRICAL STUDY USING BHPS by DEJING KONG A thesis submitted to the University of Birmingham for the degree of DOCTOR OF PHILOSOPHY Department of Economics Birmingham Business

HOUSEHOLD RISKY ASSET CHOICE: AN EMPIRICAL STUDY USING BHPS by DEJING KONG A thesis submitted to the University of Birmingham for the degree of DOCTOR OF PHILOSOPHY Department of Economics Birmingham Business

Borrowing Costs and the Demand for Equity over the Life Cycle

Borrowing Costs and the Demand for Equity over the Life Cycle No. 05 7 Steven J. Davis, Felix Kubler, and Paul Willen Abstract: We construct a life cycle model that delivers realistic behavior for both

Borrowing Costs and the Demand for Equity over the Life Cycle No. 05 7 Steven J. Davis, Felix Kubler, and Paul Willen Abstract: We construct a life cycle model that delivers realistic behavior for both

Reorienting Retirement Risk Management

Reorienting Retirement Risk Management EDITED BY Robert L. Clark and Olivia S. Mitchell 1 3 Great Clarendon Street, Oxford ox2 6dp Oxford University Press is a department of the University of Oxford. It

Reorienting Retirement Risk Management EDITED BY Robert L. Clark and Olivia S. Mitchell 1 3 Great Clarendon Street, Oxford ox2 6dp Oxford University Press is a department of the University of Oxford. It

MEASURING DYNAMIC INFLATION IN BRAZIL

MEASURING DYNAMIC INFLATION IN BRAZIL Angelo Polydoro Vagner Ardeo - Getulio Vargas Foundation 13 th OTTAWA GROUP MEETING DENMARK May 3th, 2013 MOTIVATION The static COLI framework considers a representative

MEASURING DYNAMIC INFLATION IN BRAZIL Angelo Polydoro Vagner Ardeo - Getulio Vargas Foundation 13 th OTTAWA GROUP MEETING DENMARK May 3th, 2013 MOTIVATION The static COLI framework considers a representative

Demography, Capital Flows and International Portfolio Choice over the Life-cycle

Demography, Capital Flows and International Portfolio Choice over the Life-cycle Margaret Davenport (University of Lausanne) Katja Mann (University of Bonn) EEA-ESEM Annual Congress 23 August 2017 Imbalances

Demography, Capital Flows and International Portfolio Choice over the Life-cycle Margaret Davenport (University of Lausanne) Katja Mann (University of Bonn) EEA-ESEM Annual Congress 23 August 2017 Imbalances

Long-Term Government Debt and Household Portfolio Composition

Long-Term Government Debt and Household Portfolio Composition Andreas Tischbirek University of Lausanne This version: December 218 Abstract Formal dynamic analyses of household portfolio choice in the

Long-Term Government Debt and Household Portfolio Composition Andreas Tischbirek University of Lausanne This version: December 218 Abstract Formal dynamic analyses of household portfolio choice in the

Investing over the life-cycle building wealth. Introduction:

Investing over the life-cycle building wealth Introduction: Many investors are currently confused as to how best to approach the construction of an appropriate portfolio of investments, in order to build

Investing over the life-cycle building wealth Introduction: Many investors are currently confused as to how best to approach the construction of an appropriate portfolio of investments, in order to build

LIFETIME FINANCIAL ADVICE: HUMAN CAPITAL, ASSET ALLOCATION, AND INSURANCE

CHAPTER 3 LIFETIME FINANCIAL ADVICE: HUMAN CAPITAL, ASSET ALLOCATION, AND INSURANCE Roger G. Ibbotson Moshe A. Milevsky Peng Chen, CFA Kevin X. Zhu In determining asset allocation, individuals must consider

CHAPTER 3 LIFETIME FINANCIAL ADVICE: HUMAN CAPITAL, ASSET ALLOCATION, AND INSURANCE Roger G. Ibbotson Moshe A. Milevsky Peng Chen, CFA Kevin X. Zhu In determining asset allocation, individuals must consider

HOW EARNINGS GROWTH THROUGHOUT THE LIFECYCLE IMPACTS RETIREMENT SAVINGS STRATEGIES

HOW EARNINGS GROWTH THROUGHOUT THE LIFECYCLE IMPACTS RETIREMENT SAVINGS STRATEGIES 5.1.2018 FPA Houston Dr. Derek T. Tharp Ph.D., CFP, CLU Researcher, Kitces.com Handouts/Materials: kitces.com/fpahs18

HOW EARNINGS GROWTH THROUGHOUT THE LIFECYCLE IMPACTS RETIREMENT SAVINGS STRATEGIES 5.1.2018 FPA Houston Dr. Derek T. Tharp Ph.D., CFP, CLU Researcher, Kitces.com Handouts/Materials: kitces.com/fpahs18

Economic Preparation for Retirement and the Risk of Out-of-pocket Long-term Care Expenses

Economic Preparation for Retirement and the Risk of Out-of-pocket Long-term Care Expenses Michael D Hurd With Susann Rohwedder and Peter Hudomiet We gratefully acknowledge research support from the Social

Economic Preparation for Retirement and the Risk of Out-of-pocket Long-term Care Expenses Michael D Hurd With Susann Rohwedder and Peter Hudomiet We gratefully acknowledge research support from the Social

Pension Reform in an OLG Model with Multiple Social Security Systems

ERC Working Papers in Economics 08/05 November 2008 Pension Reform in an OLG Model with Multiple Social Security Systems Çağaçan Değer Department of Economics Middle East Technical University Ankara 06531

ERC Working Papers in Economics 08/05 November 2008 Pension Reform in an OLG Model with Multiple Social Security Systems Çağaçan Değer Department of Economics Middle East Technical University Ankara 06531

Questions for Review. CHAPTER 16 Understanding Consumer Behavior

CHPTER 16 Understanding Consumer ehavior Questions for Review 1. First, Keynes conjectured that the marginal propensity to consume the amount consumed out of an additional dollar of income is between zero

CHPTER 16 Understanding Consumer ehavior Questions for Review 1. First, Keynes conjectured that the marginal propensity to consume the amount consumed out of an additional dollar of income is between zero

Long-term care risk, income streams and late in life savings

Long-term care risk, income streams and late in life savings Abstract We conduct and analyze a large experimental survey where participants made hypothetical allocations of their retirement savings to

Long-term care risk, income streams and late in life savings Abstract We conduct and analyze a large experimental survey where participants made hypothetical allocations of their retirement savings to

Asset Rich, but Income Poor: Australian Housing Wealth and Retirement in International Context

Asset Rich, but Income Poor: Australian Housing Wealth and Retirement in International Context Bruce Bradbury Social Policy Research Centre University of New South Wales Sydney, Australia b.bradbury@unsw.edu.au

Asset Rich, but Income Poor: Australian Housing Wealth and Retirement in International Context Bruce Bradbury Social Policy Research Centre University of New South Wales Sydney, Australia b.bradbury@unsw.edu.au

Housing prices, household debt and household consumption. Inquiry into housing policies, labour force participation and economic growth PEER REVIEWED

PEER REVIEWED EXECUTIVE SUMMARY Housing prices, household debt and household consumption Inquiry into housing policies, labour force participation and economic growth FOR THE AUTHORED BY Australian Housing

PEER REVIEWED EXECUTIVE SUMMARY Housing prices, household debt and household consumption Inquiry into housing policies, labour force participation and economic growth FOR THE AUTHORED BY Australian Housing

Discussion of. Size Premium Waves. by Bernard Kerskovic, Thilo Kind, and Howard Kung. Vadim Elenev. Johns Hopkins Carey

Discussion of Size Premium Waves by Bernard Kerskovic, Thilo Kind, and Howard Kung Vadim Elenev Johns Hopkins Carey Frontiers in Macrofinance Conference June 2018 Elenev Discussion: Herskovic, Kind, Kung

Discussion of Size Premium Waves by Bernard Kerskovic, Thilo Kind, and Howard Kung Vadim Elenev Johns Hopkins Carey Frontiers in Macrofinance Conference June 2018 Elenev Discussion: Herskovic, Kind, Kung

Pension Funds Performance Evaluation: a Utility Based Approach

Pension Funds Performance Evaluation: a Utility Based Approach Carolina Fugazza Fabio Bagliano Giovanna Nicodano CeRP-Collegio Carlo Alberto and University of of Turin CeRP 10 Anniversary Conference Motivation

Pension Funds Performance Evaluation: a Utility Based Approach Carolina Fugazza Fabio Bagliano Giovanna Nicodano CeRP-Collegio Carlo Alberto and University of of Turin CeRP 10 Anniversary Conference Motivation

Research. Evaluation of Retirement Strategies. 1. Retirement Strategies Key variables Key questions

Evaluation of Retirement Strategies 1. Retirement Strategies Key variables Key questions 2. Evaluation of Retirement Strategies Approaches proposed Pros, cons, and evidence 3. Concluding Thoughts Research

Evaluation of Retirement Strategies 1. Retirement Strategies Key variables Key questions 2. Evaluation of Retirement Strategies Approaches proposed Pros, cons, and evidence 3. Concluding Thoughts Research

Consumer protection and the design of the default option of a pan-european pension product

Consumer protection and the design of the default option of a pan-european pension product A. Berardi C. Tebaldi F. Trojani Foreword by John Y. Campbell This version: Milano, February 1st, 2018. The present

Consumer protection and the design of the default option of a pan-european pension product A. Berardi C. Tebaldi F. Trojani Foreword by John Y. Campbell This version: Milano, February 1st, 2018. The present

IEF. EIEF WORKING PAPER series. EIEF Working Paper 04/12 March Household Finance. An Emerging Field

EIEF WORKING PAPER series IEF Einaudi Institute for Economics and Finance EIEF Working Paper 04/12 March 2012 Household Finance. An Emerging Field by Luigi Guiso (EIEF) Paolo Sodini (Stockholm School of

EIEF WORKING PAPER series IEF Einaudi Institute for Economics and Finance EIEF Working Paper 04/12 March 2012 Household Finance. An Emerging Field by Luigi Guiso (EIEF) Paolo Sodini (Stockholm School of

Optimal Rules of Thumb for Consumption and. Portfolio Choice

Optimal Rules of Thumb for Consumption and Portfolio Choice David A. Love November 21, 2011 Abstract Conventional rules of thumb represent simple, but potentially inefficient, alternatives to dynamic programming

Optimal Rules of Thumb for Consumption and Portfolio Choice David A. Love November 21, 2011 Abstract Conventional rules of thumb represent simple, but potentially inefficient, alternatives to dynamic programming

On the Asset Allocation of a Default Pension Fund

THE JOURNAL OF FINANCE VOL. LXXIII, NO. 4 AUGUST 2018 On the Asset Allocation of a Default Pension Fund MAGNUS DAHLQUIST, OFER SETTY, and ROINE VESTMAN ABSTRACT We characterize the optimal default fund

THE JOURNAL OF FINANCE VOL. LXXIII, NO. 4 AUGUST 2018 On the Asset Allocation of a Default Pension Fund MAGNUS DAHLQUIST, OFER SETTY, and ROINE VESTMAN ABSTRACT We characterize the optimal default fund

The Long Term Evolution of Female Human Capital

The Long Term Evolution of Female Human Capital Audra Bowlus and Chris Robinson University of Western Ontario Presentation at Craig Riddell s Festschrift UBC, September 2016 Introduction and Motivation

The Long Term Evolution of Female Human Capital Audra Bowlus and Chris Robinson University of Western Ontario Presentation at Craig Riddell s Festschrift UBC, September 2016 Introduction and Motivation

How Persistent Low Expected Returns Alter Optimal Life Cycle Saving, Investment, and Retirement Behavior

How Persistent Low Expected Returns Alter Optimal Life Cycle Saving, Investment, and Retirement Behavior Vanya Horneff, Raimond Maurer, and Olivia S. Mitchell September 2017 PRC WP2017 Pension Research

How Persistent Low Expected Returns Alter Optimal Life Cycle Saving, Investment, and Retirement Behavior Vanya Horneff, Raimond Maurer, and Olivia S. Mitchell September 2017 PRC WP2017 Pension Research

Questions for Review. CHAPTER 17 Consumption

CHPTER 17 Consumption Questions for Review 1. First, Keynes conjectured that the marginal propensity to consume the amount consumed out of an additional dollar of income is between zero and one. This means

CHPTER 17 Consumption Questions for Review 1. First, Keynes conjectured that the marginal propensity to consume the amount consumed out of an additional dollar of income is between zero and one. This means

Appendix 4.A. A Formal Model of Consumption and Saving Pearson Addison-Wesley. All rights reserved

Appendix 4.A A Formal Model of Consumption and Saving How Much Can the Consumer Afford? The Budget Constraint Current income y; future income y f ; initial wealth a Choice variables: a f = wealth at beginning

Appendix 4.A A Formal Model of Consumption and Saving How Much Can the Consumer Afford? The Budget Constraint Current income y; future income y f ; initial wealth a Choice variables: a f = wealth at beginning

Discussion on Credit Cards and Consumption By Scott Fulford and Scott Schuh

Discussion on Credit Cards and Consumption By Scott Fulford and Scott Schuh Fumiko Hayashi Federal Reserve Bank of Kansas City Economics of Payments IX BIS November 16, 2018 The views are my own and do

Discussion on Credit Cards and Consumption By Scott Fulford and Scott Schuh Fumiko Hayashi Federal Reserve Bank of Kansas City Economics of Payments IX BIS November 16, 2018 The views are my own and do

Do Changes in Asset Prices Denote Changes in Wealth? When stock or bond prices drop sharply we are told that the nation's wealth has

Do Changes in Asset Prices Denote Changes in Wealth? Thomas Mayer When stock or bond prices drop sharply we are told that the nation's wealth has fallen. Some commentators go beyond such a vague statement

Do Changes in Asset Prices Denote Changes in Wealth? Thomas Mayer When stock or bond prices drop sharply we are told that the nation's wealth has fallen. Some commentators go beyond such a vague statement

1. Money in the utility function (continued)

") Monetary Economics: Macro Aspects, 19/2 2013 Henrik Jensen Department of Economics University of Copenhagen 1. Money in the utility function (continued) a. Welfare costs of in ation b. Potential non-superneutrality

Monetary Economics: Macro Aspects, 19/2 2013 Henrik Jensen Department of Economics University of Copenhagen 1. Money in the utility function (continued) a. Welfare costs of in ation b. Potential non-superneutrality

ECO 100Y INTRODUCTION TO ECONOMICS

Prof. Gustavo Indart Department of Economics University of Toronto ECO 100Y INTRODUCTION TO ECONOMICS Lecture 16. THE DEMAND FOR MONEY AND EQUILIBRIUM IN THE MONEY MARKET We will assume that there are

Prof. Gustavo Indart Department of Economics University of Toronto ECO 100Y INTRODUCTION TO ECONOMICS Lecture 16. THE DEMAND FOR MONEY AND EQUILIBRIUM IN THE MONEY MARKET We will assume that there are

Portfolio Choice and Asset Pricing with Investor Entry and Exit

Portfolio Choice and Asset Pricing with Investor Entry and Exit Yosef Bonaparte, George M. Korniotis, Alok Kumar May 6, 2018 Abstract We find that about 25% of stockholders enter/exit non-retirement investment

Portfolio Choice and Asset Pricing with Investor Entry and Exit Yosef Bonaparte, George M. Korniotis, Alok Kumar May 6, 2018 Abstract We find that about 25% of stockholders enter/exit non-retirement investment

ECONOMIC SURVEY OF NEW ZEALAND 2007: TWO BROAD APPROACHES FOR TAX REFORM

ECONOMIC SURVEY OF NEW ZEALAND 2007: TWO BROAD APPROACHES FOR TAX REFORM This is an excerpt of the OECD Economic Survey of New Zealand, 2007, from Chapter 4 www.oecd.org/eco/surveys/nz This section discusses

ECONOMIC SURVEY OF NEW ZEALAND 2007: TWO BROAD APPROACHES FOR TAX REFORM This is an excerpt of the OECD Economic Survey of New Zealand, 2007, from Chapter 4 www.oecd.org/eco/surveys/nz This section discusses

Pension Funds Performance Evaluation: a Utility Based Approach

Human Capital and Life-cycle Investing Pension Funds Performance Evaluation: a Utility Based Approach Giovanna Nicodano CeRP-Collegio Carlo Alberto and University of Turin Carolina Fugazza Fabio Bagliano

Human Capital and Life-cycle Investing Pension Funds Performance Evaluation: a Utility Based Approach Giovanna Nicodano CeRP-Collegio Carlo Alberto and University of Turin Carolina Fugazza Fabio Bagliano

Will Bequests Attenuate the Predicted Meltdown in Stock Prices When Baby Boomers Retire?

Will Bequests Attenuate the Predicted Meltdown in Stock Prices When Baby Boomers Retire? Andrew B. Abel The Wharton School of the University of Pennsylvania and National Bureau of Economic Research June

Will Bequests Attenuate the Predicted Meltdown in Stock Prices When Baby Boomers Retire? Andrew B. Abel The Wharton School of the University of Pennsylvania and National Bureau of Economic Research June