$14,600,000 DUBLIN UNIFIED SCHOOL DISTRICT (Alameda County, California) 2016 Refunding General Obligation Bonds

|

|

|

- Rosamund Carson

- 5 years ago

- Views:

Transcription

1 NEW ISSUE - FULL BOOK-ENTRY RATINGS: Moody s: Aa1 Standard & Poor s: AA See RATINGS herein. In the opinion of Jones Hall, A Professional Law Corporation, San Francisco, California, Bond Counsel, subject, however to certain qualifications described in this Official Statement, under existing law, interest on the Bonds is excluded from gross income for federal income tax purposes, and such interest is not an item of tax preference for purposes of the federal alternative minimum tax imposed on individuals and corporations, although for the purpose of computing the alternative minimum tax imposed on certain corporations, interest on the Bonds is taken into account in determining certain income and earnings. In the further opinion of Bond Counsel, interest on the Bonds is exempt from California personal income taxes. See TAX MATTERS. $14,600,000 DUBLIN UNIFIED SCHOOL DISTRICT (Alameda County, California) 2016 Refunding General Obligation Bonds Dated: Date of Delivery Due: August 1, as shown on inside front cover Authority and Purpose. The Dublin Unified School District (Alameda County, California) 2016 Refunding General Obligation Bonds (the Bonds ) are being issued by the Dublin Unified School District (the District ) pursuant to a resolution of the Board of Trustees of the District adopted on October 11, 2016 (the Bond Resolution ) and a Paying Agent Agreement dated as of November 1, 2016 (the Paying Agent Agreement ) between the District and U.S. Bank National Association, as paying agent. The Bonds are being issued to advance refund, on a crossover basis, a portion of the District s outstanding General Obligation Bonds, Election of 2004, Series C (Capital Appreciation Bonds). See THE BONDS Authority For Issuance and THE FINANCING PLAN herein. Security. Following the Crossover Date (as defined herein), the Bonds are general obligations of the District, payable solely from ad valorem property taxes levied and collected by Alameda County (the County ). The County Board of Supervisors is empowered and is obligated to annually levy ad valorem taxes for the payment of interest on, and principal of, the Bonds upon all property subject to taxation by the District, without limitation of rate or amount (except certain personal property which is taxable at limited rates). Prior to the Crossover Date, interest on the Bonds is secured by and payable solely from proceeds of the Bonds deposited in escrow fund established with proceeds of the Bonds. The District has outstanding general obligation bonds that are secured by ad valorem taxes on the same basis as the Bonds. See SECURITY FOR THE BONDS. Book-Entry Only. The Bonds will be issued in book-entry form only, and will be initially issued and registered in the name of Cede & Co. as nominee of The Depository Trust Company ( DTC ). Purchasers will not receive physical certificates representing their interests in the Bonds. See THE BONDS and APPENDIX F - DTC AND THE BOOK- ENTRY ONLY SYSTEM. Payments. The Bonds are being issued as current interest bonds. Interest on the Bonds accrues from the date of delivery and is payable semiannually on February 1 and August 1 of each year, commencing February 1, 2017, to the person in whose name the Bond is registered. Payments of principal and interest on the Bonds will be paid by the Paying Agent to DTC for subsequent disbursement to DTC Participants who will remit such payments to the beneficial owners of the Bonds. The Bonds will be issued in denominations of $5,000 or any integral multiple thereof. See THE BONDS. Redemption. The Bonds are subject to optional redemption and mandatory sinking fund redemption prior to maturity as described herein. See THE BONDS Optional Redemption and Mandatory Sinking Fund Redemption. The following firm, serving as Municipal Advisor to the District, has structured this financing: MATURITY SCHEDULE (See inside cover) Cover Page. This cover page contains certain information for general reference only. It is not a summary of all the provisions of the Bonds. Prospective investors must read the entire Official Statement to obtain information essential to making an informed investment decision. The Bonds were sold pursuant to a competitive bidding process held on Wednesday, October 26, The Bonds will be offered when, as and if issued, subject to the approval as to legality by Jones Hall, A Professional Law Corporation, San Francisco, California, Bond Counsel to the District, and subject to certain other conditions. Jones Hall is also serving as Disclosure Counsel to the District. It is anticipated that the Bonds, in book-entry form, will be available for delivery through the facilities of DTC in New York, New York, on or about November 23, The date of this Official Statement is October 26, 2016.

2 MATURITY SCHEDULE Base CUSIP : 26362V Maturity Date (August 1) 2016 Refunding General Obligation Bonds Principal Amount Interest Rate Yield Price CUSIP 2031 $4,555, % 2.300% C KZ ,945, C LA4 $5,100, % Term Bonds Due August 1, 2030; Yield: 2.280%; Price: C; CUSIP : KY3 C: Priced to first optional call date of August 1, CUSIP Copyright 2015, CUSIP Global Services, and a registered trademark of American Bankers Association. CUSIP data herein is provided by CUSIP Global Services, which is managed on behalf of American Bankers Association by S&P Capital IQ. Neither the District nor the Purchaser takes any responsibility for the accuracy of the CUSIP data.

3 GENERAL INFORMATION ABOUT THIS OFFICIAL STATEMENT Use of Official Statement. This Official Statement is submitted in connection with the sale of the Bonds referred to herein and may not be reproduced or used, in whole or in part, for any other purpose. This Official Statement is not a contract between any bond owner and the District or the Purchaser. No Offering Except by This Official Statement. No dealer, broker, salesperson or other person has been authorized by the District or the Purchaser to give any information or to make any representations other than those contained in this Official Statement and, if given or made, such other information or representation must not be relied upon as having been authorized by the District or the Purchaser. No Unlawful Offers or Solicitations. This Official Statement does not constitute an offer to sell or the solicitation of an offer to buy nor may there be any sale of the Bonds by a person in any jurisdiction in which it is unlawful for such person to make such an offer, solicitation or sale. Information in Official Statement. The information set forth in this Official Statement has been furnished by the District and other sources which are believed to be reliable, but it is not guaranteed as to accuracy or completeness. Estimates and Forecasts. When used in this Official Statement and in any continuing disclosure by the District in any press release and in any oral statement made with the approval of an authorized officer of the District or any other entity described or referenced herein, the words or phrases will likely result, are expected to, will continue, is anticipated, estimate, project, forecast, expect, intend and similar expressions identify forward looking statements within the meaning of the Private Securities Litigation Reform Act of Such statements are subject to risks and uncertainties that could cause actual results to differ materially from those contemplated in such forward-looking statements. Any forecast is subject to such uncertainties. Inevitably, some assumptions used to develop the forecasts will not be realized and unanticipated events and circumstances may occur. Therefore, there are likely to be differences between forecasts and actual results, and those differences may be material. The information and expressions of opinion herein are subject to change without notice, and neither the delivery of this Official Statement nor any sale made hereunder shall, under any circumstances, give rise to any implication that there has been no change in the affairs of the District or any other entity described or referenced herein since the date hereof. Involvement of Purchaser. The following statement has been included in this Official Statement on behalf of the Purchaser of the Bonds: The Purchaser has reviewed the information in this Official Statement in accordance with, and as a part of, their responsibilities to investors under the Federal Securities Laws as applied to the facts and circumstances of this transaction, but the Purchaser does not guarantee the accuracy or completeness of such information. Stabilization of and Changes to Offering Prices. The Purchaser may overallot or take other steps that stabilize or maintain the market prices of the Bonds at levels above that which might otherwise prevail in the open market. If commenced, the Purchaser may discontinue such market stabilization at any time. The Purchaser may offer and sell the Bonds to certain securities dealers, dealer banks and banks acting as agent at prices lower than the public offering prices stated on the inside cover page of this Official Statement, and those public offering prices may be changed from time to time by the Purchaser. Document Summaries. All summaries of the Bond Resolution, the Paying Agent Agreement or other documents referred to in this Official Statement are made subject to the provisions of such documents and qualified in their entirety to reference to such documents, and do not purport to be complete statements of any or all of such provisions. No Securities Laws Registration. The Bonds have not been registered under the Securities Act of 1933, as amended, in reliance upon exceptions therein for the issuance and sale of municipal securities. The Bonds have not been registered or qualified under the securities laws of any state. Effective Date. This Official Statement speaks only as of its date, and the information and expressions of opinion contained in this Official Statement are subject to change without notice. Neither the delivery of this Official Statement nor any sale of the Bonds will, under any circumstances, give rise to any implication that there has been no change in the affairs of the District, the County, the other parties described in this Official Statement, or the condition of the property within the District since the date of this Official Statement. Website. The District maintains a website. However, the information presented on the website is not a part of this Official Statement and should not be relied upon in making an investment decision with respect to the Bonds.

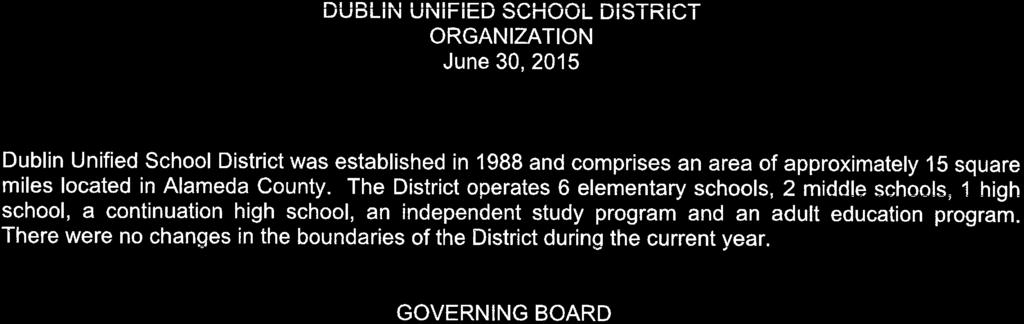

4 DUBLIN UNIFIED SCHOOL DISTRICT BOARD OF TRUSTEES OF THE DISTRICT Dan Cunningham, President Megan Rouse, Vice President Sameer Hakim, Trustee Amy Miller, Trustee Greg Tomlinson, Trustee DISTRICT ADMINISTRATION Dr. Leslie Boozer, Ed.D. and J.D., Superintendent Beverly Heironimus, CPA, Assistant Superintendent, Business Services PROFESSIONAL SERVICES MUNICIPAL ADVISOR KNN Public Finance, LLC Oakland, California BOND COUNSEL AND DISCLOSURE COUNSEL Jones Hall, A Professional Law Corporation San Francisco, California PAYING AGENT AND ESCROW AGENT U.S. Bank National Association San Francisco, California VERIFICATION AGENT Causey Demgen & Moore, P.C. Denver, Colorado

5 TABLE OF CONTENTS Page INTRODUCTION... 1 THE FINANCING PLAN... 4 The Refunded Bonds... 4 Deposits in Escrow Fund Crossover Refunding Structure... 4 SOURCES AND USES OF FUNDS... 5 THE BONDS... 6 Authority for Issuance... 6 Description of the Bonds... 6 Book-Entry Only System... 6 Optional Redemption... 7 Mandatory Sinking Fund Redemption... 7 Selection of Bonds for Redemption... 8 Notice of Redemption... 8 Partial Redemption of Bonds... 8 Right to Rescind Notice of Redemption... 8 Registration, Transfer and Exchange of Bonds... 8 Defeasance... 9 DEBT SERVICE SCHEDULES SECURITY FOR THE BONDS General Ad Valorem Taxes Debt Service Fund Not a County Obligation PROPERTY TAXATION Ad Valorem Property Taxation Assessed Valuations Appeals of Assessed Value Typical Tax Rates Tax Levies and Delinquencies Largest Secured Property Taxpayers in District Overlapping Debt Obligations TAX MATTERS CERTAIN LEGAL MATTERS Legality for Investment Absence of Litigation Compensation of Certain Professionals VERIFICATION OF MATHEMATICAL ACCURACY CONTINUING DISCLOSURE RATINGS COMPETITIVE SALE OF BONDS ADDITIONAL INFORMATION EXECUTION APPENDIX A - DUBLIN UNIFIED SCHOOL DISTRICT AUDITED FINANCIAL STATEMENTS FOR FISCAL YEAR A-1 APPENDIX B - GENERAL AND FINANCIAL INFORMATION FOR THE DUBLIN UNIFIED SCHOOL DISTRICT... B-1 APPENDIX C - GENERAL INFORMATION FOR THE CITY OF DUBLIN AND ALAMEDA COUNTYC-1 APPENDIX D - PROPOSED FORM OF OPINION OF BOND COUNSEL... D-1 APPENDIX E - FORM OF CONTINUING DISCLOSURE CERTIFICATE... E-1 APPENDIX F - DTC AND THE BOOK-ENTRY ONLY SYSTEM... F-1 APPENDIX G - ALAMEDA COUNTY INVESTMENT POLICY AND MONTHLY INVESTMENT REPORT... G-1

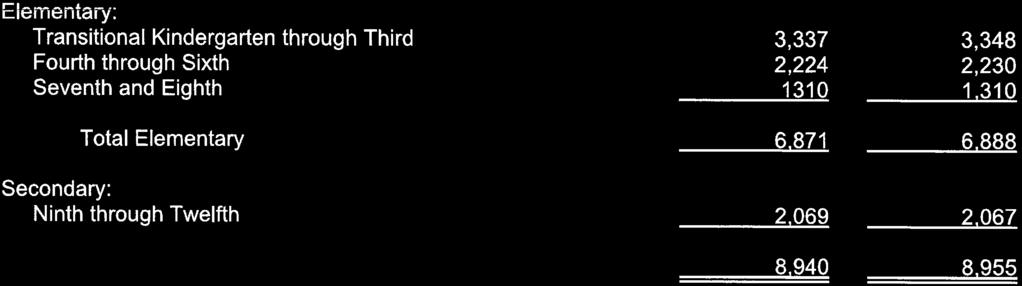

6 $14,600,000 DUBLIN UNIFIED SCHOOL DISTRICT (Alameda County, California) 2016 Refunding General Obligation Bonds The purpose of this Official Statement, which includes the cover page, inside cover page and attached appendices, is to set forth certain information concerning the sale and delivery of the 2016 Refunding General Obligation Bonds (the Bonds ) by the Dublin Unified School District (the District ). INTRODUCTION This Introduction is not a summary of this Official Statement. It is only a brief description of and guide to, and is qualified by, more complete and detailed information contained in the entire Official Statement and the documents summarized or described in this Official Statement. A full review should be made of the entire Official Statement. The offering of Bonds to potential investors is made only by means of the entire Official Statement. The District. The District is located in the City of Dublin (the City ) in the County of Alameda, California (the County ). The District was established in 1988 and comprises an area of approximately 15 square miles, which includes the City as well as a portion of Castro Valley. The District operates six elementary schools, two middle schools, one high school, a continuation high school, an independent study program and an adult education program. Enrollment in the District for the school year is budgeted for 10,635 students and average daily attendance is budgeted for 10,197 students. For more information regarding the District and its finances, see Appendix B attached hereto. See also Appendix C hereto for demographic and other statistical information regarding the County. Purpose of Issue. The Bonds are being issued by the District to refund on an advance crossover basis a portion of the District s outstanding General Obligation Bonds, Election of 2004, Series C (Capital Appreciation Bonds), originally issued in the aggregate principal amount of $14,998, (the 2004 Series C Bonds ), and to pay related costs of issuance. See THE FINANCING PLAN herein. Authority for Issuance. The Bonds are being issued pursuant to applicable provisions of the Government Code of the State of California, a resolution of the Board of Trustees of the District adopted October 11, 2016 (the Bond Resolution ), and a Paying Agent Agreement, dated as of November 1, 2016 (the Paying Agent Agreement ) between the District and U.S. Bank National Association, as paying agent (the Paying Agent ). See THE BONDS Authority for Issuance. -1-

7 Payment and Registration of the Bonds. The Bonds will be issued as current interest bonds. The Bonds will be dated their date of delivery (the Dated Date ) and will be issued as fully registered bonds, without coupons, in the denominations of $5,000 or any integral multiple thereof. The Bonds will mature on August 1 in the years indicated on the inside cover page hereof. See THE BONDS. The Bonds will be issued in book-entry form only, and will be initially issued and registered in the name of Cede & Co. as nominee for DTC. Purchaser will not receive physical certificates representing their interest in the Bonds. See THE BONDS and APPENDIX F - DTC AND THE BOOK-ENTRY ONLY SYSTEM. Redemption. The Bonds are subject to optional redemption and mandatory sinking fund redemption prior to maturity as described herein. See THE BONDS Optional Redemption and Mandatory Sinking Fund Redemption. Security and Sources of Payment for the Bonds. Following August 1, 2017 (the Crossover Date ), the Bonds are general obligation bonds of the District payable solely from ad valorem property taxes levied and collected by the County. The County is empowered and is obligated to annually levy ad valorem taxes for the payment of interest on, and principal of, the Bonds upon all property subject to taxation by the District, without limitation of rate or amount (except with respect to certain personal property which is taxable at limited rates). Prior to the Crossover Date, interest on the Bonds is secured by and payable solely from proceeds of the Bonds deposited into escrow funds established and funded with proceeds of the Bonds. See SECURITY FOR THE BONDS. Legal Matters. Issuance of the Bonds is subject to the approving opinion of Jones Hall, A Professional Law Corporation, San Francisco, California, as bond counsel ( Bond Counsel ), to be delivered in substantially the form attached hereto as Appendix D. Jones Hall, A Professional Law Corporation, San Francisco, California, will also serve as Disclosure Counsel to the District ( Disclosure Counsel ). Payment of the fees of Bond Counsel and Disclosure Counsel is contingent upon issuance of the Bonds. See APPENDIX D Form of Opinion of Bond Counsel. Tax-Exempt Status. In the opinion of Jones Hall, A Professional Law Corporation, bond counsel to the District ( Bond Counsel ), interest on the Bonds is excluded from gross income for federal income tax purposes and is not an item of tax preference for purposes of the federal individual and corporate alternative minimum taxes, although it is included in certain income and earnings in computing the alternative minimum tax imposed on certain corporations. In the further opinion of Bond Counsel, such interest is exempt from California personal income taxes. See TAX MATTERS and Appendix D hereto for the form of Bond Counsel s opinion to be delivered concurrently with the Bonds. Continuing Disclosure. The District will execute a Continuing Disclosure Certificate in connection with the issuance of the Bonds in the form attached hereto as Appendix E. See CONTINUING DISCLOSURE. Other Information. This Official Statement speaks only as of its date, and the information contained in this Official Statement is subject to change. Copies of documents referred to in this Official Statement and information concerning the Bonds are available from the District from the Superintendent s Office at Dublin Unified School District, 7471 Larkdale Avenue, Dublin, California 94568; telephone (925) The District may impose a charge for copying, mailing and handling. -2-

8 This Official Statement is not to be construed as a contract with the purchasers of the Bonds. Statements contained in this Official Statement which involve estimates, forecasts or matters of opinion, whether or not expressly so described herein, are intended solely as such and are not to be construed as representations of fact. The summaries and references to documents, statutes and constitutional provisions referred to herein do not purport to be comprehensive or definitive, and are qualified in their entireties by reference to each of such documents, statutes and constitutional provisions. The information set forth herein has been obtained from official sources which are believed to be reliable but it is not guaranteed as to accuracy or completeness, and is not to be construed as a representation by the District. The information and expressions of opinions herein are subject to change without notice and neither delivery of this Official Statement nor any sale made hereunder shall, under any circumstances, create any implication that there has been no change in the affairs of the District since the date hereof. This Official Statement is submitted in connection with the sale of the Bonds referred to herein and may not be reproduced or used, in whole or in part, for any other purpose. END OF INTRODUCTION -3-

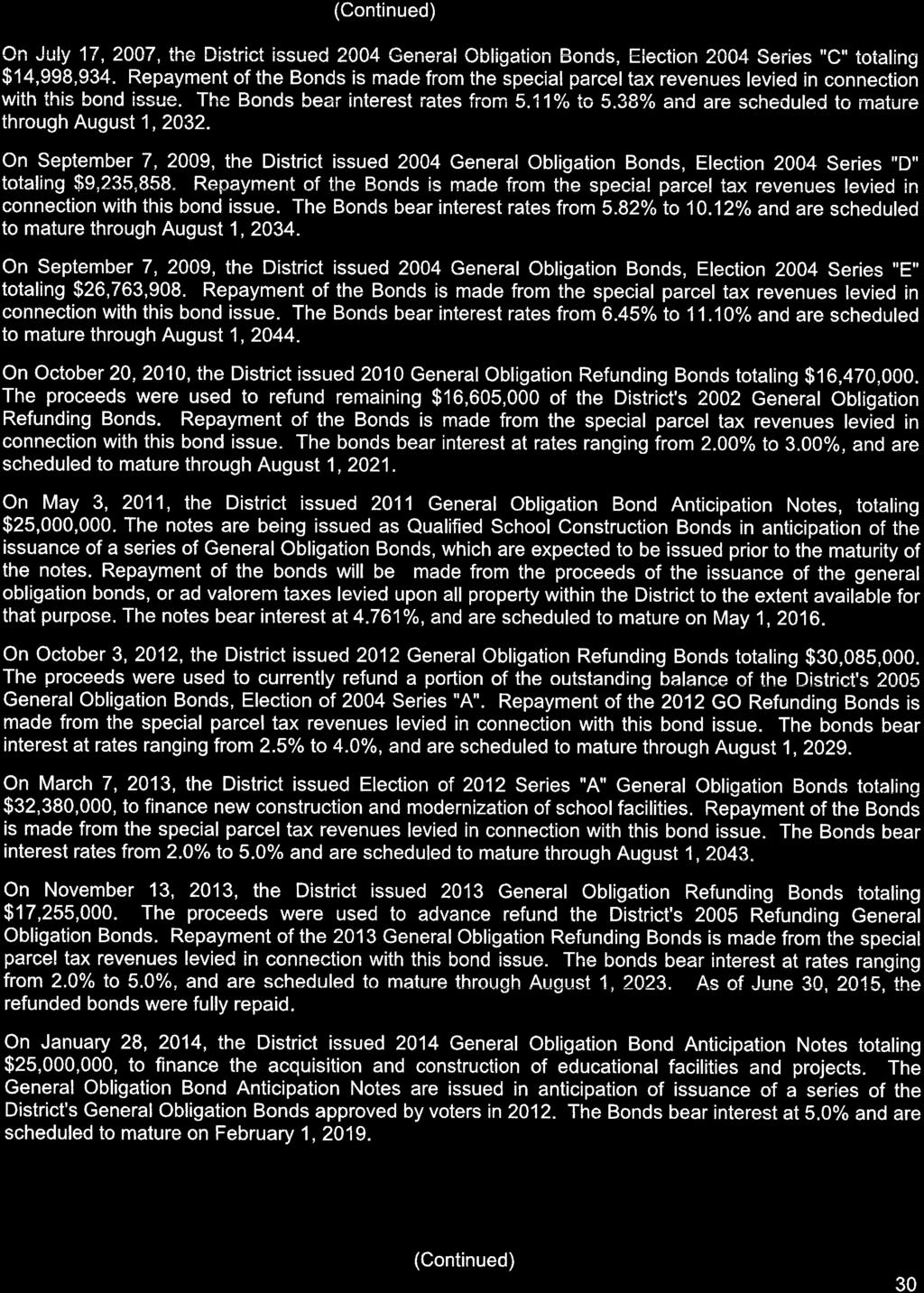

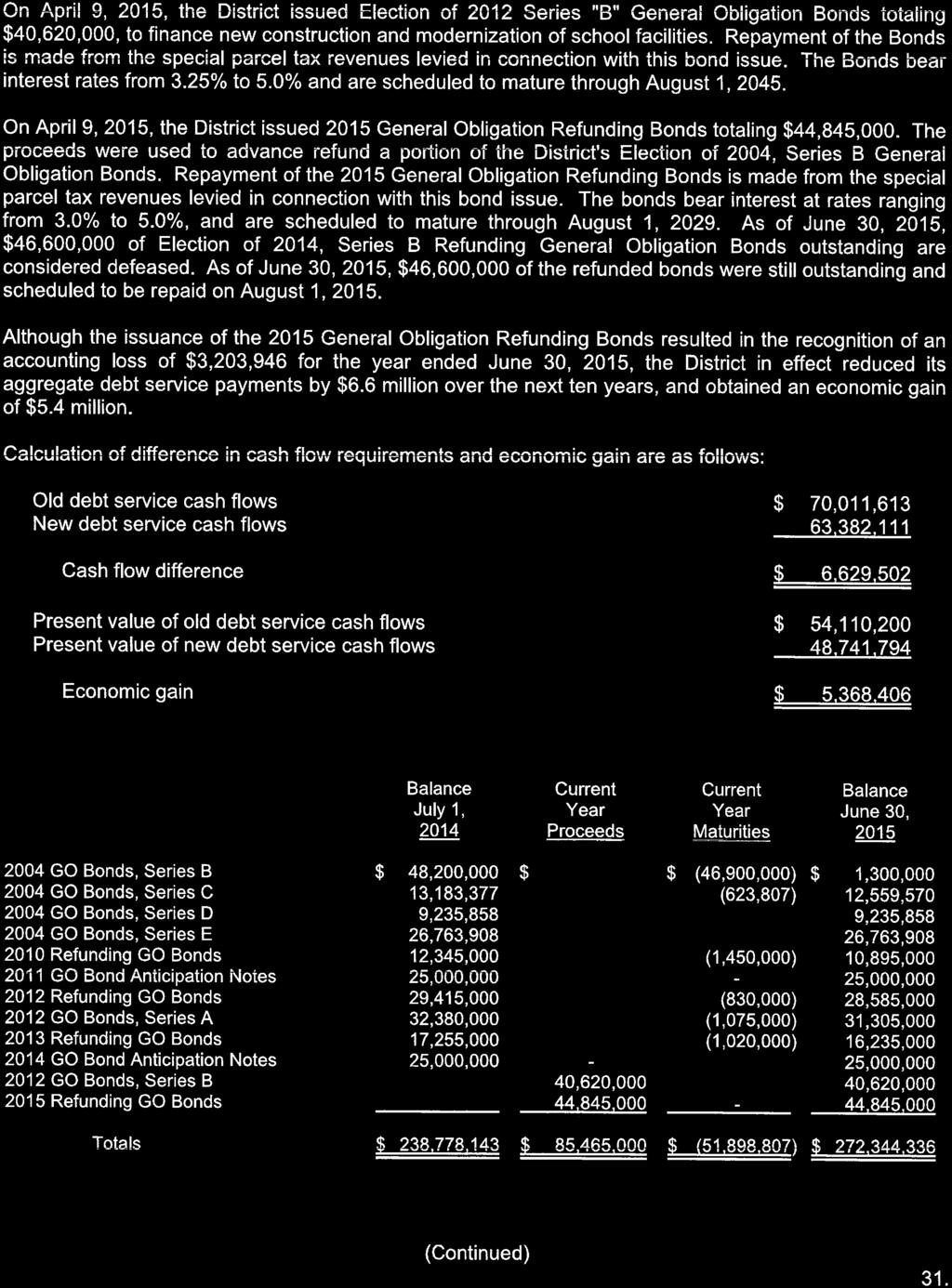

9 THE FINANCING PLAN The Refunded Bonds The Bonds are being issued by the District to advance refund, on a crossover basis, certain maturities of the 2004 Series C Bonds, as identified in the following table (the Refunded Bonds ). Maturities Payable from Escrow DUBLIN UNION HIGH SCHOOL DISTRICT Identification of Refunded 2004 Series C Bonds Original Denominational Amount Accreted Value Redemption Redemption CUSIP Upon Redemption Date Price 08/01/ V EB0 $737, $1,216, /01/ % 08/01/ V EC8 784, ,295, /01/ /01/ V ED6 3,002, ,963, /01/ /01/ V EE4 2,935, ,856, /01/ /01/ V EF1 2,866, ,747, /01/ $10,327, $17,079, CUSIP Copyright American Bankers Association. CUSIP data herein is provided by Standard & Poor s CUSIP Service Bureau, a division of McGraw Hill Companies, Inc. Neither the District nor the Purchaser are responsible for the accuracy of such data. Also referred to herein as the Crossover Date. Deposits in Escrow Fund; Crossover Refunding Structure The Bonds are being structured as crossover refunding bonds. The District will deliver the net proceeds of the Bonds to U.S. Bank National Association, San Francisco, California, as paying agent for the 2004 Series C Bonds (the Prior Paying Agent ), for deposit in an escrow fund (the "Escrow Fund") established under an Escrow Agreement (the Escrow Agreement ), between the District and U.S. Bank National Association (the Escrow Bank ). The Escrow Bank will invest such funds in United States governmental obligations and/or other obligations the timely payment of which is directly or indirectly guaranteed by the full faith and credit of the United States of America. Prior to and including the Crossover Date, amounts on deposit in the Escrow Fund will be applied to pay interest due on the Bonds. On the Crossover Date, the funds and investments in the Escrow Fund will be applied to pay interest due on the Bonds, and the redemption price of the Refunded Bonds. Sufficiency of the deposits in the Escrow Fund for the foregoing purposes will be verified by Causey Demgen & Moore P.C., certified public accountants, Denver, Colorado (the Verification Agent ). See VERIFICATION OF MATHEMATICAL ACCURACY herein. The amounts held by the Escrow Bank under the Escrow Agreement are pledged by the District solely to the payment of interest coming due and payable on the Bonds to and including the Crossover Date. The Refunded Bonds will remain outstanding until the Crossover Date, at which time they will be redeemed from amounts held for that purpose in the Escrow Fund. Prior to the Crossover Date, the Refunded Bonds will not be payable from amounts held in the Escrow Fund, but will continue to be payable from ad valorem property taxes levied for that purpose. -4-

10 SOURCES AND USES OF FUNDS The estimated sources and uses of funds with respect to the Bonds are as follows: Sources of Funds Principal Amount of Bonds $14,600, Net Original Issue Premium 3,048, Total Sources $17,648, Uses of Funds Deposit to Escrow Fund $17,488, Costs of Issuance (1) 160, Total Uses $17,648, (1) All estimated costs of issuance including, but not limited to, Purchaser s discount, printing costs, and fees of Bond Counsel, Disclosure Counsel, the Municipal Advisor, the Paying Agent, and the rating agencies. [Remainder of page intentionally left blank] -5-

11 THE BONDS Authority for Issuance The Bonds will be issued under the provisions of Articles 9 and 11 of Chapter 3 of Part 1 of Division 2 of Title 5 of the California Government Code, the Bond Resolution and the Paying Agent Agreement. The District has other outstanding general obligation bonds that are similarly secured by ad valorem property taxes. For a description of the District s outstanding general obligation bonds, see APPENDIX B - GENERAL AND FINANCIAL INFORMATION FOR THE DUBLIN UNIFIED SCHOOL DISTRICT- Long-Term Debt. Description of the Bonds Interest on the Bonds accrues from the dated date set forth on the inside cover hereof (the Dated Date ), and is payable semiannually on February 1 and August 1 of each year (each, as to the Bonds, a Bond Payment Date ) commencing February 1, Each Bond shall bear interest from the Bond Payment Date next preceding the date of registration and authentication thereof unless (i) it is registered and authenticated as of a Bond Payment Date, in which event it shall bear interest from such date, or (ii) it is registered and authenticated prior to a Bond Payment Date and after the close of business on the fifteenth (15th) day of the month preceding such Bond Payment Date, in which event it shall bear interest from such Bond Payment Date, or (iii) it is registered and authenticated prior to January 15, 2017, in which event it shall bear interest from the date of original delivery; provided, however, that if at the time of authentication of a Bond, interest is in default thereon, such Bond shall bear interest from the Bond Payment Date to which interest has previously been paid or made available for payment thereon. Interest on the Bonds, including the final interest payment upon maturity, is payable to the Owner thereof at such Owner s address as it appears on the bond register maintained by the Paying Agent at the close of business on the fifteenth (15th) day of the month preceding the Bond Payment Date (the Record Date ), or at such other address as the owner may have filed with the Paying Agent for that purpose. See also Book Entry Only System below. The Bonds shall be issued in denominations of $5,000 principal amount each or any integral multiple thereof. The Bonds mature on August 1 in the years and amounts set forth on the inside cover page hereof. While the Bonds are subject to the book-entry system, the principal, interest and any redemption premium with respect to a Bond will be paid by the Paying Agent to DTC, which in turn is obligated to remit such payment to its DTC Participants for subsequent disbursement to Beneficial Owners of the Bonds. See - Book-Entry Only System below and APPENDIX F DTC AND THE BOOK-ENTRY ONLY SYSTEM. Book-Entry Only System The Bonds will be issued in book-entry form only, and will be initially issued and registered in the name of Cede & Co. as nominee of The Depository Trust Company, New York, New York ( DTC ). Purchaser of the Bonds (the Beneficial Owners ) will not receive physical certificates representing their interest in the Bonds. Payments of principal of and -6-

12 interest on the Bonds will be paid by Bank of New York Mellon Trust Company, San Francisco, California, the designated paying agent for the Bonds (the Paying Agent ) to DTC for subsequent disbursement to DTC Participants which will remit such payments to the Beneficial Owners of the Bonds. As long as DTC s book-entry method is used for the Bonds, the Paying Agent will send any notice of prepayment or other notices to owners only to DTC. Any failure of DTC to advise any DTC Participant, or of any DTC Participant to notify any Beneficial Owner, of any such notice and its content or effect will not affect the validity or sufficiency of the proceedings relating to the prepayment of the Bonds called for prepayment or of any other action premised on such notice. See APPENDIX F - DTC AND THE BOOK-ENTRY ONLY SYSTEM. The Paying Agent, the District, and the Purchaser of the Bonds have no responsibility or liability for any aspects of the records relating to or payments made on account of beneficial ownership, or for maintaining, supervising or reviewing any records relating to beneficial ownership, of interests in the Bonds. Optional Redemption The Bonds are subject to redemption prior to maturity, as a whole or in part, in order of maturity as designated by the District, or if not designated, pro-rata among maturities and by lot within a maturity, at the option of the District, from any available source of funds, on August 1, 2026 and on any date thereafter, at a redemption price equal to the principal amount thereof together with accrued interest thereon to the date fixed for redemption, without premium. For the purpose of selection for optional redemption, Bonds will be deemed to consist of $5,000 portions. Mandatory Sinking Fund Redemption The Bonds maturing on August 1, 2030 (the Term Bonds ), are subject to mandatory sinking fund redemption on August 1 of each year in accordance with the schedule set forth below. The Term Bonds so called for mandatory sinking fund redemption shall be redeemed in the sinking fund payments amounts and on the dates set forth below, without premium. Term Bonds Maturing August 1, 2030 Redemption Date (August 1) Sinking Fund Redemption 2028 $375, , (maturity) 4,205,000 If any Term Bonds are redeemed pursuant to optional redemption, the total amount of all future sinking fund payments with respect to such Term Bonds shall be reduced by the aggregate principal amount of such Term Bonds so redeemed, to be allocated among such payments on a pro rata basis in integral multiples of $5,000 principal amount (or on such other basis as the District may determined) as set forth in written notice given by the District to the Paying Agent. -7-

13 Selection of Bonds for Redemption Whenever provision is made for the redemption of Bonds and less than all Outstanding Bonds are to be redeemed, the Paying Agent shall select Bonds for redemption by lot within a maturity. Redemption by lot shall be in such a manner as the Paying Agent may determine; provided, however, that the portion of any Bond to be redeemed in part will be in the principal amount of $5,000 or any integral multiple thereof. Notice of Redemption The Paying Agent is required to give notice of any redemption to be mailed, first class mail, postage prepaid, at least 30 days but not more than 60 days prior to the date fixed for redemption, to the respective Owners of any Bonds designated for redemption, at their addresses appearing on the Registration Books. Such mailing shall not be a condition precedent to such redemption and failure to mail or to receive any such notice shall not affect the validity of the proceedings for the redemption of such Bonds. Such notice shall (i) state the redemption date and the redemption price, (ii) if less than all of the then Outstanding Bonds are to be called for redemption, designate the serial numbers of the Bonds to be redeemed by giving the individual number of each Bond or by stating that all Bonds between two stated numbers, both inclusive, or by stating that all of the Bonds of one or more maturities have been called for redemption, (iii) require that such Bonds be then surrendered at the Principal Office of the Paying Agent for redemption at the said redemption price, and (iv) state that further interest on such Bonds will not accrue from and after the redemption date. Partial Redemption of Bonds Upon surrender of Bonds redeemed in part only, the District shall execute and the Paying Agent shall authenticate and deliver to the Owner, at the expense of the District, a new Bond or Bonds, of the same maturity, of authorized denominations in aggregate principal amount equal to the unredeemed portion of the Bond or Bonds. Right to Rescind Notice of Redemption The District has the right to rescind any notice of the optional redemption of Bonds by written notice to the Paying Agent on or prior to the dated fixed for redemption. Any notice of redemption shall be cancelled and annulled if for any reason funds will not be or are not available on the date fixed for redemption for the payment in full of the Bonds then called for redemption. The District and the Paying Agent have no liability to the Bond owners or any other party related to or arising from such rescission of redemption. The Paying Agent shall mail notice of such rescission of redemption in the same manner as the original notice of redemption was sent under the Paying Agent Agreement. Registration, Transfer and Exchange of Bonds If the book entry system is discontinued, the District shall cause the Paying Agent to maintain and keep at its principal corporate trust office all books and records necessary for the registration, exchange and transfer of the Bonds. -8-

14 If the book entry system is discontinued, the person in whose name a Bond is registered on the Bond Register shall be regarded as the absolute owner of that Bond. Payment of the principal of and interest on any Bond shall be made only to or upon the order of that person; neither the District, the County nor the Paying Agent shall be affected by any notice to the contrary, but the registration may be changed as provided in the Paying Agent Agreement. Any Bond may, in accordance with its terms, be transferred, upon the Registration Books, by the person in whose name it is registered, in person or by his duly authorized attorney, upon surrender of such Bond for cancellation at the Principal Office at the Paying Agent, accompanied by delivery of a written instrument of transfer in a form approved by the Paying Agent, duly executed. The District may charge a reasonable sum for each new Bond issued upon any transfer. Whenever any Bond or Bonds shall be surrendered for transfer, the District shall execute and the Paying Agent shall authenticate and deliver a new Bond or Bonds, for like aggregate principal amount. No transfers of Bonds shall be required to be made (a) fifteen (15) days prior to the date established by the Paying Agent for selection of Bonds for redemption or (b) with respect to a Bond which has been selected for redemption Bonds may be exchanged at the principal office of the Paying Agent in San Francisco, California, for a like aggregate principal amount of Bonds of authorized denominations and of the same maturity. The District may charge a reasonable sum for each new Bond issued upon any exchange (except in the case of any exchange of temporary Bonds for definitive Bonds). No exchanges of Bonds shall be required to be made (a) fifteen (15) days prior to the date established by the Paying Agent for selection of Bonds for redemption or (b) with respect to a Bond after such Bond has been selected for redemption. Defeasance The Bonds may be paid by the District, in whole or in part, in any one or more of the following ways: (a) (b) (c) by paying or causing to be paid the principal or redemption price of and interest on such Bonds, as and when the same become due and payable; by irrevocably depositing, in trust, at or before maturity, money or securities in the necessary amount (as provided in the Paying Agent Agreement) to pay or redeem such Bonds; or by delivering such Bonds to the Paying Agent for cancellation by it. Whenever in the Paying Agent Agreement it is provided or permitted that there be deposited with or held in trust by the Paying Agent money or securities in the necessary amount to pay or redeem any Bonds, the money or securities so to be deposited or held may be held by the Paying Agent in the funds and accounts established pursuant to the Paying Agent Agreement and will be: (i) lawful money of the United States of America in an amount equal to the Principal Amount of such Bonds and all unpaid interest thereon -9-

15 to maturity, except that, in the case of Bonds which are to be redeemed prior to maturity and in respect of which notice of such redemption is given as provided in the Paying Agent Agreement or provision satisfactory to the Paying Agent is made for the giving of such notice, the amount to be deposited or held will be the Principal Amount or redemption price of such Bonds and all unpaid interest thereon to the redemption date; or (ii) Federal Securities (not callable by the issuer thereof prior to maturity) the principal of and interest on which when due, in the opinion of a certified public accountant delivered to the County and the District, will provide money sufficient to pay the principal or redemption price of and all unpaid interest to maturity, or to the redemption date, as the case may be, on the Bonds to be paid or redeemed, as such principal or redemption price and interest become due, provided that, in the case of Bonds which are to be redeemed prior to the maturity thereof, notice of such redemption is given as provided in the Paying Agent Agreement or provision satisfactory to the Paying Agent is made for the giving of such notice. Notwithstanding any provisions of the Paying Agent Agreement, any moneys held by the Paying Agent in trust for the payment of the principal or redemption price of, or interest on, any Bonds and remaining unclaimed for one (1) year after the principal of all of the Bonds has become due and payable (whether at maturity or upon call for redemption or by acceleration as provided in the Paying Agent Agreement), if such moneys were so held at such date, or one (1) year after the date of deposit of such moneys if deposited after said date when all of the Bonds became due and payable, shall, upon request of the District, be repaid to the District free from the trusts created by the Paying Agent Agreement, and all liability of the Paying Agent with respect to such moneys shall thereupon cease; provided, however, that before the repayment of such moneys to the District as aforesaid, the Paying Agent may (at the cost of the District) first mail to the Owners of all Bonds which have not been paid at the addresses shown on the Registration Books a notice in such form as may be deemed appropriate by the Paying Agent, with respect to the Bonds so payable and not presented and with respect to the provisions relating to the repayment to the District of the moneys held for the payment thereof. Federal Securities means United States Treasury notes, bonds, bills or certificates of indebtedness, or obligations issued by any agency or department of the United States which are secured, directly or indirectly, by the full faith and credit of the United States. -10-

16 DEBT SERVICE SCHEDULES The Bonds. The following table shows the debt service schedule with respect to the Bonds, assuming no optional redemptions. DUBLIN UNIFIED SCHOOL DISTRICT Annual Bond Debt Service Schedule Bond Year Ending August 1 Bonds Principal Bonds Interest Bonds Total Debt Service* $ 475, $ 475, , , , , , , , , , , , , , , , , , , , , $ 375, , ,065, , , ,195, ,205, , ,859, ,555, , ,041, ,945, , ,192, Total $14,600, $10,133, $24,733, *Debt service payments through August 1, 2017, which is the Crossover Date, will be made from the Escrow Fund. Thereafter, debt service payments will be made from ad valorem tax collections. -11-

17 Combined Debt Service Schedule. The following table shows the combined debt service on all of the District s outstanding general obligation bonds and refunding bonds, including the Bonds described herein, assuming no optional redemptions. Such table does not include debt service on the District s Election of 2016, Series A General Obligation Bonds which have been authorized to be sold following the sale of the Bonds, and which are expected to be issued on the same date as the Bonds, the annual debt service on which is expected to range from approximately $1,650,000 to $10,000,000, from August 1, 2017 to August 1, For a description of the District s outstanding general obligation bonds, see APPENDIX B - GENERAL AND FINANCIAL INFORMATION FOR THE DUBLIN UNIFIED SCHOOL DISTRICT- Long-Term Debt. DUBLIN UNIFIED SCHOOL DISTRICT Combined General Obligation Bond Debt Service Schedule Bond Year Ending Aug Election Bonds (1) 2012 Election Bonds Other Outstanding Refunding Bonds (2) 2016 Refunding Bonds Aggregate Debt Service 2017 $8,105, $3,294, $3,620, $475, $15,496, ,283, ,798, ,801, , ,574, ,249, ,796, ,030, , ,766, ,691, ,854, ,258, , ,495, ,148, ,850, ,456, , ,145, ,628, ,845, ,761, , ,925, ,136, ,891, ,806, , ,523, ,667, ,960, , ,318, ,225, ,065, , ,981, ,813, ,221, , ,725, ,430, ,383, , ,504, ,967, ,552, ,065, ,585, ,390, ,729, ,195, ,315, ,928, ,916, ,859, ,704, ,388, ,112, ,041, ,542, ,884, ,318, ,192, ,394, ,827, ,532, ,360, ,693, ,756, ,449, ,604, ,998, ,602, ,558, ,245, ,804, ,564, ,508, ,072, ,615, ,786, ,401, ,721, ,073, ,794, ,883, ,377, ,261, ,102, ,697, ,799, ,935, ,032, ,967, ,935, ,379, ,315, ,935, ,749, ,684, ,138, ,138, Total $381,316, $132,866, $25,734, $24,733, $564,651, (1) Combined debt service for bonds issued pursuant to the District s 2004 authorization, including refunding bonds issued to refund such bonds, but not including the Bonds. See also Appendix B -Long-Term Debt. (2) Combined debt service on 2010 and 2013 Refunding Bonds, issued to refund bonds issued pursuant to the District s 1993 authorization. See also Appendix B -Long-Term Debt. -12-

18 SECURITY FOR THE BONDS General Following the Crossover Date, the Bonds will be general obligation bonds of the District payable by the District solely from ad valorem property taxes as more particularly described below. Prior to the Crossover Date, interest on the Bonds is not secured by ad valorem property taxes, but is secured by and payable by the District solely from proceeds of the Bonds deposited in the Escrow Fund. Any discussion herein describing the levy and collection of ad valorem property taxes for the Bonds applies only after the Crossover Date. See also THE FINANCING PLAN. Ad Valorem Taxes Bonds Payable from Ad Valorem Property Taxes. Following the Crossover Date, the Bonds will be general obligations of the District, payable solely from ad valorem property taxes levied and collected by the County. The County is empowered and is obligated to annually levy ad valorem taxes for the payment of the Bonds and the interest thereon upon all property within the District subject to taxation by the District, without limitation of rate or amount (except certain personal property which is taxable at limited rates). In no event is the District obligated to pay principal of and interest and redemption premium, if any, on the Bonds out of any funds or properties of the District other than ad valorem taxes levied upon all taxable property in the District following the Crossover Date; provided, however, nothing in the Bond Resolution prevents the District from making advances of its own moneys howsoever derived to any of the uses or purposes permitted by law. Other Bonds Payable from Ad Valorem Property Taxes. The District has previously issued other general obligation bonds, which are payable from ad valorem taxes on a parity basis. See DEBT SERVICE SCHEDULES - Combined General Obligation Bond Debt Service Schedule. In addition to the general obligation bonds issued by the District, there is other debt issued by entities with jurisdiction in the District, which is also payable from ad valorem taxes levied on property in the District. See PROPERTY TAXATION Direct and Overlapping Debt below. The Board of Trustees of the District has authorized the issuance of General Obligation Bonds, Election of 2016, Series A in the aggregate principal amount of not to exceed $60 million (the 2016 Series A Bonds ). The 2016 Series A Bonds are expected to be sold following the date of this Official Statement and to be delivered concurrently with the Bonds. The amount of annual debt service on the 2016 Series A Bonds is expected to range from approximately $1,650,000 to $10,000,000, from August 1, 2017 to August 1, Levy and Collection. The County will levy and collect such ad valorem taxes in such amounts and at such times as is necessary to ensure the timely payment of debt service. Such taxes, when collected, will be deposited into a debt service fund for the Bonds, which is maintained by the County and which is irrevocably pledged for the payment of principal of and interest on the Bonds when due. District property taxes are assessed and collected by the County in the same manner and at the same time, and in the same installments as other ad valorem taxes on real property, and will have the same priority, become delinquent at the same times and in the same proportionate amounts, and bear the same proportionate penalties and interest after -13-

19 delinquency, as do the other ad valorem taxes on real property. See PROPERTY TAXATION -Teeter Plan below. Statutory Lien on Ad Valorem Tax Revenues. Pursuant to Senate Bill 222 effective January 1, 2016, voter approved general obligation bonds which are secured by ad valorem tax collections, including the Bonds, are secured by a statutory lien on all revenues received pursuant to the levy and collection of the property tax imposed to service those bonds. Said lien attaches automatically and is valid and binding from the time the bonds are executed and delivered. The lien is enforceable against the school district or community college district, its successors, transferees, and creditors, and all others asserting rights therein, irrespective of whether those parties have notice of the lien and without the need for any further act. Annual Tax Rates. The amount of the annual ad valorem tax levied by the County to repay the Bonds will be determined by the relationship between the assessed valuation of taxable property in the District and the amount of debt service due on the Bonds. Fluctuations in the annual debt service on the Bonds and the assessed value of taxable property in the District may cause the annual tax rate to fluctuate. Economic and other factors beyond the District s control, such as economic recession, deflation of land values, a relocation out of the District or financial difficulty or bankruptcy by one or more major property taxpayers, or the complete or partial destruction of taxable property caused by, among other eventualities, earthquake, flood, fire, drought or other natural disaster, could cause a reduction in the assessed value within the District and necessitate a corresponding increase in the annual tax rate. Debt Service Fund As described herein, the County will establish a Debt Service Fund for the Bonds. The Debt Service Fund has been pledged for the payment of the principal of and interest and premium (if any) on the Bonds when and as the same become due. The collections deposited in the Debt Service Fund are secured by a statutory lien on all revenues received pursuant to the levy and collection of the property tax imposed to service the Bonds. Not a County Obligation Following the Crossover Date, the Bonds are payable solely from the proceeds of an ad valorem tax levied and collected by the County for the payment of principal and interest on the Bonds. Although the County is obligated to collect the ad valorem tax for the payment of the Bonds, the Bonds are not a debt of the County. -14-

20 PROPERTY TAXATION Ad Valorem Property Taxation Taxes are levied by the County for each fiscal year on taxable real and personal property which is situated in the District as of the preceding January 1. For assessment and collection purposes, property is classified either as secured or unsecured and is listed accordingly on separate parts of the assessment roll. The secured roll is that part of the assessment roll containing State-assessed public utilities property and real property having a tax lien which is sufficient, in the opinion of the County Assessor, to secure payment of the taxes. Other property is assessed on the unsecured roll. Property taxes on the secured roll are due in two installments, on November 1 and February 1 of each fiscal year. If unpaid, such taxes become delinquent on December 10 and April 10, respectively, and a 10 percent penalty attaches to any delinquent payment. Property on the secured roll with respect to which taxes are delinquent becomes tax defaulted on or about June 30 of the fiscal year. Such property may thereafter be redeemed by payment of a penalty of 1.5 percent per month to the time of redemption, plus costs and a redemption fee. If taxes are unpaid for a period of five years or more, the property is subject to sale by the Treasurer. Property taxes on the unsecured roll are due as of the January 1 lien date and become delinquent, if unpaid, on August 31. A 10 percent penalty attaches to delinquent unsecured taxes. If unsecured taxes are unpaid at 5:00 p.m. on October 31, an additional penalty of 1.5 percent attaches to them on the first day of each month until paid. The taxing authority has four ways of collecting delinquent unsecured personal property taxes: (1) bringing a civil action against the taxpayer; (2) filing a certificate in the office of the County Clerk specifying certain facts in order to obtain a lien on certain property of the taxpayer; (3) filing a certificate of delinquency for record in the County Clerk and County Recorder's office in order to obtain a lien on certain property of the taxpayer; and (4) seizing and selling personal property, improvements, or possessory interests belonging or assessed to the assessee. Assessed Valuations The assessed valuation of property in the District is established by the Contra Costa County Assessor, except for public utility property which is assessed by the State Board of Equalization. Assessed valuations are reported at 100 percent of the full value of the property, as defined in Article XIIIA of the California Constitution. Prior to , assessed valuations were reported at 25 percent of the full value of property. For a discussion of how properties currently are assessed, see CONSTITUTIONAL AND STATUTORY PROVISIONS AFFECTING DISTRICT REVENUES AND APPROPRIATIONS. Certain classes of property, such as churches, colleges, not-for-profit hospitals, and charitable institutions, are exempt from property taxation and do not appear on the tax rolls. No reimbursement is made by the State for such exemptions. -15-

21 Historical Assessed Valuation. Shown in the following table are recent assessed valuations for the District. DUBLIN UNIFIED SCHOOL DISTRICT Assessed Valuation Fiscal Year through Fiscal Year Fiscal Year Local Secured Utility Unsecured Total $8,387,779,912 $1,016,256 $218,156,134 $8,606,952, ,128,979,090 1,016, ,691,584 8,345,686, ,990,405,147 1,019, ,289,798 8,194,714, ,179,919,846 1,019, ,764,835 8,365,703, ,582,663,895 1,019, ,226,467 8,792,909, ,431,303,849 1,019, ,130,165 9,645,453, ,887,469, , ,047,093 11,116,721, ,373,907, , ,961,460 12,600,073, ,491,857, , ,546,917 13,746,609,425 Source: California Municipal Statistics, Inc. As indicated in the previous table, assessed valuations are subject to change in each year. Increases or decreases in assessed valuation may result from a variety of factors including but not limited to general economic conditions, supply and demand for real property in the area, government regulations such as zoning, and natural disasters such as earthquakes, fires, floods and droughts. With respect to droughts specifically, the State of California is currently facing water shortfalls, and on January 17, 2014, the Governor declared a state of drought emergency, calling on Californians to conserve water. As part of his declaration, the Governor directed State officials to assist agricultural producers and communities that may be economically impacted by dry conditions. Thereafter, the California State Water Resources Control Board (the Water Board ) issued a statewide notice of water shortages and potential future curtailment of water right diversions. On April 1, 2015, the Governor issued an executive order mandating certain conservation, which were implemented by an emergency regulation adopted by the Water Board on May 5, The temporary conservation measures have been extended and amended by subsequent executive orders of the Governor and related Water Board regulations, most recently with implementation of a stress test approach of water conservation, which requires local urban water agencies to ensure a three-year supply of water assuming three years of drought conditions. Those agencies with projected shortages are required to implement conservation measures through January The District cannot predict or make any representations regarding the effects that the current drought has had, or, if it should continue, may have on the value of taxable property within the District including the District, or to what extent the drought could cause disruptions to economic activity within the boundaries of the District including the District. Assessed Valuation by Jurisdiction. The following table shows the assessed valuation of local secured property within the District by jurisdiction for fiscal year

22 DUBLIN UNIFIED SCHOOL DISTRICT Assessed Valuation By Jurisdiction Fiscal Year Assessed Valuation % of Assessed Valuation % of Jurisdiction Jurisdiction: in School District School District of Jurisdiction in School District City of Dublin $13,742,624, % $13,742,624, % City of Pleasanton 750, $20,978,446, % Unincorporated Alameda County 3,235, $17,519,863, % Total District $13,746,609, % Alameda County $13,746,609, % $254,087,205, % Source: California Municipal Statistics, Inc. Assessed Valuation of Single Family Residential Parcels. The following table shows a breakdown of the assessed valuations of improved single-family residential parcels in the District, according to fiscal year assessed valuation. DUBLIN UNIFIED SCHOOL DISTRICT Summary of Per Parcel Assessed Valuation of Single Family Homes No. of Average Median Parcels Assessed Valuation Assessed Valuation Assessed Valuation Single Family Residential 10,786 $7,369,745,730 $683,270 $704, No. of % of Cumulative Total % of Cumulative Assessed Valuation Parcels (1) Total % of Total Valuation Total % of Total $0 - $99, % 5.173% $ 39,516, % 0.536% $100,000 - $199, ,490, $200,000 - $299, ,324, $300,000 - $399, ,480, $400,000 - $499, ,752, $500,000 - $599, ,477, $600,000 - $699,999 1, ,677, $700,000 - $799,999 1, ,061,065, $800,000 - $899,999 1, ,203,842, $900,000 - $999, ,851, $1,000,000 - $1,099, ,029, $1,100,000 - $1,199, ,822, $1,200,000 - $1,299, ,275, $1,300,000 - $1,399, ,429, $1,400,000 - $1,499, ,949, $1,500,000 - $1,599, ,160, $1,600,000 - $1,699, ,329, $1,700,000 - $1,799, ,487, $1,800,000 - $1,899, ,860, $1,900,000 - $1,999, ,900, $2,000,000 and greater ,021, Total 10, % $7,369,745, % (1) Improved single family residential parcels. Excludes condominiums and parcels with multiple family units. Source: California Municipal Statistics, Inc. -17-

23 Assessed Valuation by Land Use. The following The following table shows the assessed valuation in fiscal year for each land use category, as shown on County records. DUBLIN UNIFIED SCHOOL DISTRICT Assessed Valuation and Parcels by Land Use Fiscal Year % of No. of % of Non-Residential: Assessed Valuation (1) Total Parcels Total Agricultural/Rural $ 22,559, % % Commercial/Office 1,959,897, Vacant Commercial 232,710, Industrial 267,853, Vacant Industrial 1,430, Recreational 16,253, Government/Social/Institutional 27,755, Subtotal Non-Residential $2,528,460, % % Residential: Single Family Residence $ 7,369,745, % 10, % Condominium/Townhouse 1,741,230, , Residential Units 11,376, Residential Units/Apartments 803,966, Mobile Homes 1,361, Vacant Residential 1,035,716, , Subtotal Residential $10,963,397, % 18, % Total $13,491,857, % 18, % (1) Local Secured Assessed Valuation; excluding tax-exempt property. Source: California Municipal Statistics, Inc. Appeals of Assessed Value There are two types of appeals of assessed values that could adversely impact property tax revenues within the District. Appeals may be based on Proposition 8 of November 1978, which requires that for each January 1 lien date, the taxable value of real property must be the lesser of its base year value, annually adjusted by the inflation factor pursuant to Article XIIIA of the State Constitution, or its full cash value, taking into account reductions in value due to damage, destruction, depreciation, obsolescence, removal of property or other factors causing a decline in value. Under California law, property owners may apply for a reduction of their property tax assessment by filing a written application, in form prescribed by the State Board of Equalization, with the County board of equalization or assessment appeals board. In most cases, the appeal is filed because the applicant believes that present market conditions (such as residential home prices) cause the property to be worth less than its current assessed value. Proposition 8 reductions may also be unilaterally applied by the County Assessor. Any reduction in the assessment ultimately granted as a result of such appeal applies to the year for which application is made and during which the written application was filed. -18-

24 These reductions are subject to yearly reappraisals and are adjusted back to their original values when market conditions improve. Once the property has regained its prior value, adjusted for inflation, it once again is subject to the annual inflationary factor growth rate allowed under Article XIIIA. A second type of assessment appeal involves a challenge to the base year value of an assessed property. Appeals for reduction in the base year value of an assessment, if successful, reduce the assessment for the year in which the appeal is taken and prospectively thereafter. The base year is determined by the completion date of new construction or the date of change of ownership. Any base year appeal must be made within four years of the change of ownership or new construction date. The District cannot predict the changes in assessed values that might result from pending or future appeals by taxpayers. Any reduction in aggregate District assessed valuation due to appeals, as with any reduction in assessed valuation due to other causes, will cause the tax rate levied to repay the Bonds to increase accordingly, so that the fixed debt service on the Bonds (and other outstanding general obligation bonds, if any) may be paid. Typical Tax Rates The following table sets forth typical tax rates levied in Tax Rate Area (26-001) for fiscal years through DUBLIN UNIFIED SCHOOL DISTRICT Typical Total Tax Rates per $100 of Assessed Valuation (TRA ) Fiscal Years through Countywide Dublin Unified School District Chabot-Las Positas Com. Coll. District Flood Zone 7 State Water Project Bay Area Rapid Transit East Bay Regional Park District Total Tax Rate Source: California Municipal Statistics, Inc. -19-

25 Tax Levies and Delinquencies The following table shows tax charges, collections and delinquencies for secured property in the District with respect to the District s levy for debt service on outstanding general obligation bonds. Secured property taxes not relating to the one percent General Fund apportionment (which is provided for under the County s Teeter Plan described below) which are collected by the County are allocated to political subdivisions for which the County acts as tax-levying or tax-collecting agency, including the District, when the secured property taxes are actually collected, and the District is entitled to penalties and interest on such delinquent payments. Said levies, including for the Bonds, are not included in the below-described Teeter Plan. Fiscal Year DUBLIN UNIFIED SCHOOL DISTRICT Secured Tax Charges and Delinquencies Fiscal Years through Secured Tax Charge (1) Amount Delinquent June 30 % Delinquent June $6,323,956 $185, % ,792, , ,077, , ,544, , ,008, , ,878,754 89, ,446,805 77, ,712,603 73, ,615,700 69, ,624, , (1) Bond debt service levy collected by the County within the District. Source: California Municipal Statistics, Inc. For the District s share of the one percent general fund apportionment, the County has adopted the Alternative Method of Distribution of Tax Levies and Collections and of Tax Sale Proceeds (the "Teeter Plan") as provided for in the State Revenue and Taxation Code, which requires the County to pay 100% of such secured property taxes due to local agencies in the fiscal year such taxes are due. Pursuant to these provisions, each county operating under the Teeter Plan establishes a delinquency reserve and assumes responsibility for all secured delinquencies, assuming that certain conditions are met. Because of this method of tax collection, the K-12 districts located in the County are assured of their share of the one percent general fund apportionment, but are not entitled to share in any penalties due to delinquent payments with respect to the one percent general fund apportionment. The County does not include ad valorem taxes levied for general obligation bonds in the Teeter Plan. The Teeter Plan is subject to discontinuance at the County s option in the future or if demanded by the participating taxing agencies. -20-

26 Largest Secured Property Taxpayers in District The twenty taxpayers in the District with the greatest combined assessed valuation of taxable property on the fiscal year tax roll, and the assessed valuations thereof, are shown below. The more property (by assessed value) which is owned by a single taxpayer in the District, the greater amount of tax collections are exposed to weaknesses in the taxpayer s financial situation and ability or willingness to pay property taxes. Each taxpayer listed below is a unique name listed on the tax rolls. The District cannot determine from County assessment records whether individual persons, corporations or other organizations are liable for tax payments with respect to multiple properties held in various names that in aggregate may be larger than is suggested by the table below. DUBLIN UNIFIED SCHOOL DISTRICT Largest Secured Taxpayers Fiscal Year % of Property Owner Primary Land Use Assessed Valuation Total (1) 1. Avalon Dublin Station II LP Apartments $ 171,200, % 2. TRT NOIP Dublin LP Office Building 158,226, Toll Brothers Residential Development 129,986, Lennar Homes California Inc. Residential Development 122,185, Tassajara Road Apartments Investors Apartments 117,665, Dublin Station Owner LLC Apartments 111,322, Dublin Corporate Center Acquisition LLC Office Building 104,150, Essex Dublin Owner LP Apartments 103,468, Ross Dress for Less Inc. Office Building 101,458, Chang and Frederic and Jennifer Lin Apartments 92,677, Bere Island Properties I LLC Apartments 90,725, Tishman Speyer Archstone Smith Apartments 87,182, BIT Holdings Sixty-Three Inc. Shopping Center 77,748, ASVRF Dublin Place LP Shopping Center 74,420, Development Slutions WR LLC Undeveloped 70,069, Kaiser Foundation Hospitals Commercial Land 68,458, GS Dublin LLC Apartments 64,214, Regency Village Dublin LLC Shopping Center 56,803, SVF Waterford Dublin Corporation Shopping Center 55,069, PMI Springs LL Apartments 54,789, $1,911,823, % (1) Local Secured Assessed Valuation: $13,491,857,933 Source: California Municipal Statistics, Inc. -21-

27 Overlapping Debt Obligations Set forth below is a direct and overlapping debt report (the "Debt Report") prepared by California Municipal Statistics, Inc. and dated October 1, The Debt Report is included for general information purposes only. The District has not reviewed the Debt Report for completeness or accuracy and makes no representation in connection therewith. The Debt Report generally includes long-term obligations sold in the public credit markets by public agencies whose boundaries overlap the boundaries of the District in whole or in part. Such long-term obligations generally are not payable from revenues of the District (except as indicated) nor are they necessarily obligations secured by land within the District. In many cases, long-term obligations issued by a public agency are payable only from the general fund or other revenues of such public agency Assessed Valuation: $13,746,609,425 DUBLIN UNIFIED SCHOOL DISTRICT Statement of Direct and Overlapping Bonded Debt Dated as of October 1, 2016 DIRECT AND OVERLAPPING TAX AND ASSESSMENT DEBT: % Applicable Debt 10/1/16 Bay Area Rapid Transit District 2.128% $ 11,145,400 Chabot-Las Positas Community College District ,800,622 Dublin Unified School District ,242,619 (1) East Bay Regional Park District ,998,377 California Statewide Communities Development Authority 1915 Act Bonds ,771 TOTAL DIRECT AND OVERLAPPING TAX AND ASSESSMENT DEBT $362,129,789 OVERLAPPING GENERAL FUND DEBT: Alameda County General Fund Obligations 5.410% $48,316,548 Alameda County Pension Obligation Bonds ,548,710 Alameda-Contra Costa Transit District Certificates of Participation ,016 TOTAL OVERLAPPING GENERAL FUND DEBT $50,899,274 COMBINED TOTAL DEBT $413,029,063 (2) (1) Excludes Refunding Bonds to be sold and Election of 2016, Series A Bonds expected to be sold, but includes the District s bond anticipation notes issued in (2) Excludes tax and revenue anticipation notes, enterprise revenue, mortgage revenue and non-bonded capital lease obligations. Ratios to Assessed Valuation: Direct Debt ($279,242,619) % Total Direct and Overlapping Tax and Assessment Debt % Combined Total Debt % Source: California Municipal Statistics, Inc. -22-

28 TAX MATTERS Federal Tax Status. In the opinion of Jones Hall, A Professional Law Corporation, San Francisco, California, Bond Counsel, subject, however to certain qualifications set forth below, under existing law, the interest on the Bonds is excluded from gross income for federal income tax purposes, and such interest is not an item of tax preference for purposes of the federal alternative minimum tax imposed on individuals and corporations, although for the purpose of computing the alternative minimum tax imposed on certain corporations, such interest is taken into account in determining certain income and earnings. The opinions set forth in the preceding paragraph are subject to the condition that the District comply with all requirements of the Internal Revenue Code of 1986, as amended (the Tax Code ) that must be satisfied subsequent to the issuance of the Bonds in order that such interest be, or continue to be, excluded from gross income for federal income tax purposes. The District has covenanted to comply with each such requirement. Failure to comply with certain of such requirements may cause the inclusion of such interest in gross income for federal income tax purposes to be retroactive to the date of issuance of the Bonds. Tax Treatment of Original Issue Discount and Premium. If the initial offering price to the public (excluding bond houses and brokers) at which a Bond is sold is less than the amount payable at maturity thereof, then such difference constitutes "original issue discount" for purposes of federal income taxes and State of California personal income taxes. If the initial offering price to the public (excluding bond houses and brokers) at which a Bond is sold is greater than the amount payable at maturity thereof, then such difference constitutes "original issue premium" for purposes of federal income taxes and State of California personal income taxes. De minimis original issue discount and original issue premium is disregarded. Under the Tax Code, original issue discount is treated as interest excluded from federal gross income and exempt from State of California personal income taxes to the extent properly allocable to each owner thereof subject to the limitations described in the first paragraph of this section. The original issue discount accrues over the term to maturity of the Bond on the basis of a constant interest rate compounded on each interest or principal payment date (with straight-line interpolations between compounding dates). The amount of original issue discount accruing during each period is added to the adjusted basis of such Bonds to determine taxable gain upon disposition (including sale, redemption, or payment on maturity) of such Bond. The Tax Code contains certain provisions relating to the accrual of original issue discount in the case of purchasers of the Bonds who purchase the Bonds after the initial offering of a substantial amount of such maturity. Owners of such Bonds should consult their own tax advisors with respect to the tax consequences of ownership of Bonds with original issue discount, including the treatment of purchasers who do not purchase in the original offering, the allowance of a deduction for any loss on a sale or other disposition, and the treatment of accrued original issue discount on such Bonds under federal individual and corporate alternative minimum taxes. Under the Tax Code, original issue premium is amortized on an annual basis over the term of the Bond (said term being the shorter of the Bond's maturity date or its call date). The amount of original issue premium amortized each year reduces the adjusted basis of the owner of the Bond for purposes of determining taxable gain or loss upon disposition. The amount of original issue premium on a Bond is amortized each year over the term to maturity of the Bond on the basis of a constant interest rate compounded on each interest or principal payment date (with straight-line interpolations between compounding dates). Amortized bond premium is not -23-

29 deductible for federal income tax purposes. Owners of premium Bonds, including purchasers who do not purchase in the original offering, should consult their own tax advisors with respect to State of California personal income tax and federal income tax consequences of owning such Bonds. California Tax Status. In the further opinion of Bond Counsel, interest on the Bonds is exempt from California personal income taxes. Other Tax Considerations. Owners of the Bonds should also be aware that the ownership or disposition of, or the accrual or receipt of interest on, the Bonds may have federal or state tax consequences other than as described above. Bond Counsel expresses no opinion regarding any federal or state tax consequences arising with respect to the Bonds other than as expressly described above, including any opinion regarding federal tax consequences arising with respect to the ownership, sale or disposition of the Bonds, or the amount, accrual or receipt of interest on the Bonds. Form of Opinion. The proposed form of opinion of Bond Counsel relating to the Bonds is attached hereto as APPENDIX D. Legality for Investment CERTAIN LEGAL MATTERS Under provisions of the California Financial Code, the Bonds are legal investments for commercial banks in California to the extent that the Bonds, in the informed opinion of the bank, are prudent for the investment of funds of depositors, and under provisions of the California Government Code, the Bonds are eligible to secure deposits of public moneys in California. Absence of Litigation No litigation is pending or threatened concerning the validity of the Bonds, and a certificate to that effect will be furnished to Purchaser at the time of the original delivery of the Bonds. The District is not aware of any litigation pending or threatened that (i) questions the political existence of the District, (ii) contests the District's ability to receive ad valorem taxes or to collect other revenues or (iii) contests the District's ability to issue and retire the Bonds. The District is routinely subject to lawsuits and claims. In the opinion of the District, the aggregate amount of the uninsured liabilities of the District under these lawsuits and claims will not materially affect the financial position or operations of the District. Compensation of Certain Professionals Payment of the fees and expenses of Jones Hall, A Professional Law Corporation, as Bond Counsel and Disclosure Counsel to the District, and KNN Public Finance, LLC as Municipal Advisor to the District, is contingent upon issuance of the Bonds. -24-

30 VERIFICATION OF MATHEMATICAL ACCURACY The Verification Agent, upon delivery of the Bonds, will deliver a report of the mathematical accuracy of certain computations, contained in schedules provided to them on behalf of the District, relating to (a) the sufficiency of the anticipated amount of proceeds of the Bonds and other funds available to pay, when due, the principal, whether at maturity or upon prior redemption, interest and redemption premium requirements of the Refunded Bonds and (b) the yields on the amount of proceeds held and invested prior to redemption of the Refunded Bonds and on the Bonds considered by Bond Counsel in connection with the opinion rendered by Bond Counsel that the Bonds are not arbitrage bonds within the meaning of Section 148 of the Internal Revenue Code of 1986, as amended. The report of the Verification Agent will include the statement that the scope of their engagement is limited to verifying mathematical accuracy, of the computations contained in such schedules provided to them, and that they have no obligation to update their report because of events occurring, or data or information coming to their attention, subsequent to the date of their report. CONTINUING DISCLOSURE The District will execute a Continuing Disclosure Certificate in connection with the issuance of the Bonds in the form attached hereto as Appendix E. The District has covenanted therein, for the benefit of holders and beneficial owners of the Bonds to provide certain financial information and operating data relating to the District to the Municipal Securities Rulemaking Board (an Annual Report ) not later than nine months after the end of the District s fiscal year (which currently would be March 31), commencing March 31, 2017 with the report for the Fiscal Year, and to provide notices of the occurrence of certain enumerated events. The initial Annual Report will consist of this Official Statement. Such notices will be filed by the District with the Municipal Securities Rulemaking Board. The specific nature of the information to be contained in an Annual Report or the notices of enumerated events is set forth in APPENDIX E FORM OF CONTINUING DISCLOSURE CERTIFICATE. These covenants have been made in order to assist the Purchaser of the Bonds in complying with S.E.C. Rule 15c2-12(b)(5) (the Rule ). The District has prior undertakings pursuant to the Rule. In the previous five years, specific instances of non-compliance with prior undertakings are: (i) the District s annual report filing for its Election of 2004, Series A Bonds for fiscal year was filed approximately thirty days late, due to a filing deadline for annual reports which is eight months after the end of the fiscal year, not nine months, as is the case with the District s other undertakings, (ii) annual reports for fiscal years through did not include tax rate summary information for certain taxing entities, (iii) annual reports for fiscal years through did not include top taxpayer information, and (iv) event notices relating to insurer and underlying rating changes were not filed timely. Remedial filings have been made to address the foregoing items, as applicable, and the District has notified its dissemination agent to cause future compliance. Identification of the foregoing instances of non-compliance does not constitute a representation that such instances have been deemed material by the District, for purposes of the Rule. The District elected to participate in the Securities and Exchange Commission s (the Municipalities Continuing Disclosure Cooperation Initiative (the Initiative ) prior to the -25-

31 December 1, 2014 filing deadline. The purpose of the Initiative is to encourage issuers and underwriters of municipal securities to self-report possible violations involving materially inaccurate statements relating to prior compliance with their continuing disclosure undertakings. Neither the County nor any other entity other than the District shall have any obligation or incur any liability whatsoever with respect to the performance of the District s duties regarding continuing disclosure. RATINGS Moody s Investors Services ( Moody s ) and Standard & Poor s Ratings Services ( S&P ) have assigned ratings of Aa1 and AA, respectively, to the Bonds. The District has provided certain additional information and materials to Moody s (some of which does not appear in this Official Statement). Such rating reflects only the view of the rating agencies, and explanations of the significance of such rating may be obtained only from Moody s and S&P. There is no assurance that any credit ratings given to the Bonds will be maintained for any period of time or that the rating may not be lowered or withdrawn entirely by Moody s or S&P, in such agency s judgment, circumstances so warrant. Any such downward revision or withdrawal of a rating may have an adverse effect on the market price of the Bonds. COMPETITIVE SALE OF BONDS The Bonds were sold pursuant to a competitive bidding process held on October 26, 2016 pursuant to the terms set forth in an Official Notice of Sale with respect to the Bonds. The Bonds were awarded to Citigroup Global Markets Inc. (the Purchaser ), whose proposal represented the lowest true interest cost for the Bonds as determined in accordance with the Official Notice of Sale. The Purchaser has agreed to purchase the Bonds at a price of $17,615,008.80, which is equal to the initial principal amount of the Bonds of $14,600,000 plus an original issue premium of $3,048,895.40, less a Purchaser s discount of $33, The Purchaser intends to offer the Bonds to the public at the offering prices set forth on the inside cover page of this Official Statement. The Purchaser may offer and sell to certain dealers and others at a price lower than the offering prices stated on the inside cover page hereof. The offering price may be changed from time to time by the Purchaser. ADDITIONAL INFORMATION The discussions herein about the Bond Resolution, the Paying Agent Agreement and the Continuing Disclosure Certificate are brief outlines of certain provisions thereof. Such outlines do not purport to be complete and for full and complete statements of such provisions reference is made to such documents. Copies of these documents mentioned are available from the Purchaser and following delivery of the Bonds will be on file at the offices of the Paying Agent in San Francisco, California. -26-

32 References are also made herein to certain documents and reports relating to the District; such references are brief summaries and do not purport to be complete or definitive. Copies of such documents are available upon written request to the District. Any statements in this Official Statement involving matters of opinion, whether or not expressly so stated, are intended as such and not as representations of fact. This Official Statement is not to be construed as a contract or agreement between the District and the Purchaser or Owners of any of the Bonds. EXECUTION The execution and delivery of this Official Statement have been duly authorized by the District. DUBLIN UNIFIED SCHOOL DISTRICT By: /s/ Beverly Heironimus Assistant Superintendent, Business Services -27-

33 APPENDIX A DUBLIN UNIFIED SCHOOL DISTRICT AUDITED FINANCIAL STATEMENTS FOR FISCAL YEAR A-1

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89