Making Access Possible (MAP) Zambia: Stakeholder presentation. Lusaka, 19 April 2017name

|

|

|

- Martha Green

- 5 years ago

- Views:

Transcription

")

1 Making Access Possible (MAP) Zambia: Stakeholder presentation Lusaka, 19 April 2017name

2 Agenda 1. Introduction to MAP 2. Contextual drivers 3. Understanding consumers and their needs 4. Provider and product overview 5. Priority focus areas

3 1. INTRODUCTION TO MAP

4

5 Why MAP? The value that MAP process provides

6 Where is MAP happening? MAP implementation and pipeline countries

7 MAP analysis process: MAP diagnostic components National Stakeholder Consultative Process Integrated MAP Diagnostic Demand Supply Regulation Context and behaviour Providers, products and services National objectives Needs Current usage Barriers and opportunities Financial sector infrastructure Sector strategy and objectives Distribution and connectivity Institutional structure Information and information providers Policy and regulatory laws and structure Strategy and Implementation Framework

8 MAP approach: Focused recommendations Public policy objectives Recommend public policy imperatives & enable private sector provision Understand client needs, behaviours and links to the real economy Farmers Micro- entrepreneu rs Commercial banks SFIs MFIs Community- based institutions Identify institutions best placed to meet those needs Identify products/delivery mechanisms to meet those needs Identify financial services with greatest potential to improve welfare Credit Savings Insurance Payments Mobile financial services, agents and electronic infrastructure

9 MAP analytic components: Demand, supply and regulation

10 MAP Process: An overview of the MAP process ESTABLISHMENT DIAGNOSTIC INCEPTION RESEARCH & ENGAGEMENT ROADMAP FORMULATION IMPLEMENTATION 8 12 MONTHS 2+ YEARS Stakeholder Engagement Stakeholder buy- in Establish relationships Gov t commitment Establish governance structures MAP Steer Com Stakeholder engagement Stakeholders involved in diagnostic visit Provide input at critical milestones in research Roadmap engagement Stakeholder workshop Feedback on diagnostic Roadmap development Facilitating implementation Coordinate with existing initiatives Support roadmap implementation Diagnostic Process Groundwork Kick- off workshop Diagnostic preparation Desktop research Appoint qualitative provider Info gathering, analysis and drafting In- country diagnostic visit Analysis and synthesis of findings Testing and refining diagnostic results Submit final diagnostic report Submit synthesis note Results placement Disseminate diagnostic and roadmap to feed into other local processes Drafting roadmap

11 MAP exists within existing policy processes: The National Financial Inclusion Strategy (NFIS) NFIS definition of Financial Inclusion: NFIS Vision: Access and informed usage of a broad range of quality and affordable savings, credit, payment, insurance, and investment products and services that meet the needs of individuals and businesses. Universal access and usage of a broad range of quality and affordable financial products and services. MAP provides an evidence base to support both the development and implementation of the NFIS Source: NFIS Draft, 2017

12 2. CONTEXTUAL DRIVERS

13 Context drives Financial Inclusion realities Government borrowing Crowding out retail credit Budget cuts Reliance on copper 77% of exports copper Citadel economy Low density in rural and poor areas constrain offerings Infrastructure developed in the urban centres Widespread informality and cash Cash is still king Informal savings widespread Established Social safety nets Free gov t primary healthcare Strong role of church and community

14 3. UNDERSTANDING CONSUMERS AND THEIR NEEDS

![Meet the consumer: Highly urbanized population, but strong farming community [My mother] lives](/docs-images/95/123028247/images/15-3.jpg "on a farm our late father left.")

15 Meet the consumer: Highly urbanized population, but strong farming community [My mother] lives on a farm our late father left. She rears chickens and grows vegetables which she sells and makes some money Yes, I have a phone 25% farmers I usually send her about K200 Mary K400 per month I have found value in keeping coins. I put them in a tin When I think of the interest, I think the bank might be good but then the interest is really low I have a savings account with Zanaco where I save some money for my children s school fees Source: FinScope (2015); Qualitative Interviews

16 Meet the consumer: Broad range of financial service needs Sends remittances via a bus Mary K400 per month Saves at home For security, store cash in an account Now uses Zoona to send money to her mother, which is a more efficient remittance method 25% farmers Chilimba member A potentially more effective savings vehicle for her children s education fund might be a savings group Source: FinScope (2015); Qualitative Interviews

17 Meet the consumer: Broad range of providers 100% 90% 80% Percentage of adults 70% 60% 50% 40% 30% 20% 10% 0% Sending over distance Life events Bill payments Growth Resilience Receiving income Local payments Liquidity Savings Credit Insurance Payments Source: FinScope, 2015

18 Meet the consumer: Breadth of uptake per product category Family & Friends Payments 34% 66% 0% 0% Insurance 97% 0% 0% Credit 5% 92% 23% 23% Savings 12% 9% 24% 55% 33% 33% 0% 20% 40% 60% 80% 100% Percentage of uptake Formal only Formal and informal Informal only Excluded Source: FinScope (2015)

19 Zambia compared to the region South Africa (2014) 75% 5% 5% 14% Uganda (2013) 20% 34% 31% 15% Kenya (2013) 32% 34% 7% 25% Swaziland (2014) 54% 11% 10% 26% Rwanda (2012) 23% 19% 30% 28% Tanzania (2012) 12% 40% 17% 31% Namibia (2014) 62% 3% 4% 31% Nigeria (2014) 36% 12% 12% 40% Zambia (2015) 25% 13% 21% 41% DRC (2014) 12% 24% 13% 52% Malawi (2014) 27% 7% 14% 52% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% Percentage of uptake Banked Other formal Informal Excluded Source: FinScope (2015)

20 Introducing the target markets Source: FinScope (2015)

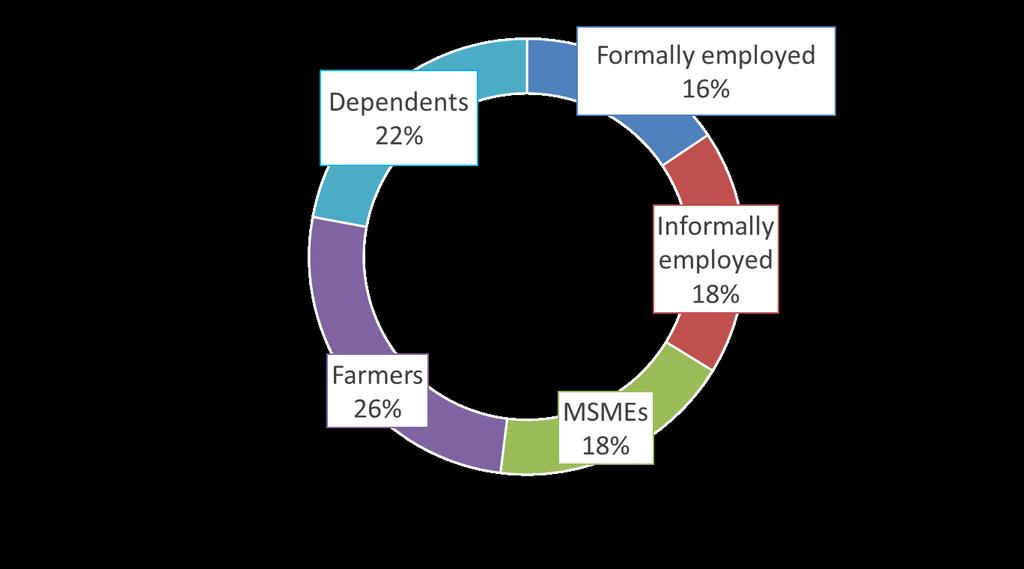

21 Introducing the target markets High income Formally employed 1.2m adults Median average age (34) Mostly male Low income Farmers 2m adults Oldest average age (40) Mostly male Informally employed 1.4m adults Median average age (34) Most male MSMEs 1.4m adults Median average age (36) Mostly female Dependents 1.7m adults Youngest average age (30) Most female Rural Urban Source: FinScope (2015)

22 Comparing overall uptake of financial products: Depth vs Breadth Size of bubble = number of adults in the target market Source: FinScope Consumer Surveys

23 Comparing overall uptake of financial products: Depth vs Breadth Size of bubble = number of adults in the target market Source: FinScope Consumer Surveys

24 Widespread use of and reliance on informal financial services across target markets 60% 50% % of adults in each group 40% 30% 20% 41% 11% 20% 10% 14% 10% 0% 13% Formally employed 24% 24% Informally employed 20% 19% MSMEs Farmers Dependents Informal Formal/Informal overlap Source: FinScope (2015)

25 Key Target Market Needs Key Need Formally Employed Informally Employed MSMEs Farmers Dependents Transfer of Value Liquidity Resilience Primary target market for insurance Meeting Goals Education Education Education + Productive assets Education + Productive assets Education

26 The role of consumer education Understanding of complex financial terms lacking But, wide range of financial tools used to meet different needs 250, 000 savings group members 790,000 members of Chilimbas 140,000 save with a church 850,000 save by buying farming or business inputs in advance 2.2.m save at home The other ways [than Zoona] are okay but because my mother is an elderly woman I don t think she can manage to keep up with the processes that are required for her to receive the money It [the Chilimba] encourages investing/saving which is my first priority Source: World Bank, 2016, FinScope, 2015

27 4. PROVIDER AND PRODUCT OVERVIEW

28 Uptake of non- cash payments products 2.7m use payments Total payments usage: 2015 Total payments usage: Male vs. female Formal Banked 0 500,000 1,000,000 1,500,000 Total payments usage: Target markets Total payments usage: Urban vs. Rural Other 24% 18% 58% Dependents 13% 17% 70% Farmers 10% 9% 80% MSMEs 16% 21% 62% Informally employed 7% 14% 80% Formally employed 60% 11% 29% Banked Formal Excluded Source: FinScope, 2015

29 Relative use of payments instruments: Cash is still king 8% 5% 4% % of adults report using Cash 9% Debit/ Credit card Mobile money Bank transfer 74% Post Office/ Western Union etc. Source: FinScope, 2015

30 Relative use of payments instruments: But Mobile is growing Average value of transactions (ZMW) ZMW 14,000 ZMW 12,000 ZMW 10,000 ZMW 8,000 ZMW 6,000 ZMW 4,000 ZMW 2,000 ZMW 0 Average value of transactions 12,656 4, Cheques EFT PoS Money transfers % of total volume of transactions 809 ATMs 34 Mobile 60% 50% 40% 30% 20% 10% 0% % of total volume of transactions Source: BOZ, 2017

31 Payments infrastructure: ATMs and PoS Devices lag behind other SADC countries ATMs per adults in SADC (PoS) 47m (ATM) 8m Volume of transactions (millions) Pos Devices per adults SADC Average = Source: IMF, 2016; FSDZ GIS data, 2016

32 Total cost using banking infrastructure: Rural vs. Urban divide K200 K180 K160 K (34% of income) Opportunity cost K4.48 Cost in ZMW K140 K120 K100 K80 K60 K40 K20 K0 >2.5x more expensive K65.90 (11% of income) Opportunity cost K2.11 Travel cost K20.00 *Basic account cost K43.79 Urban Travel cost K *Basic account cost K43.79 Rural Source: FinScope, 2015; Qualitative interviews, 2016, BOZ, 2016 *Based on basic consumer usage profile 2 ATM withdrawals & 1 deposit on a basic transactional account

33 Credit overview Total credit usage: use formal credit 2.3m use any credit Total credit usage: Male vs. female Family and Friends Informal Formal Banked 0 500,000 1,000,000 1,500,000 51% of total population is female 47% Total credit usage 53% Male Female Total credit usage: Target markets Other 11% 83% Dependents 19% 76% Farmers 24% 69% MSMEs 21% 71% Informally employed 23% 72% Formally employed 20% 62% Banked Formal Informal Family and Friends Excluded Total credit usage: Urban vs. Rural 45% of total population is Urban 45% Total credit usage 55% Rural Urban Source: FinScope, 2015

34 Credit market provision: Growing, but still behind global benchmarks Domestic credit as percentage of GDP Percentage of GDP 50% 45% 40% 35% 30% 25% 20% 15% 10% 5% 0% *Contracting retail Well below benchmarks % 34% 20% 15% Growing non- retail Lower middle income Mozambique Kenya Botswana Zambia Tanzania Source: World Bank Development indicators; FinScope 2015 * Only 1.3% of adults have retail bank lows; down 27% from 2009 to 2015

35 Credit market environment: Some positive steps but challenges remain Enabling environment Contract enforceability Judicial process quality Resolving solvency Credit information reporting Collateral registry Gaps in regulatory framework Impact assessments not informing implementation Regulation

36 Credit providers: Formal provision limited to corporates and formally employed *# of credit borrowers 300,000 Unregulated, formal source Informal Formal Number of borrowers 250, , , ,000 50,000 Total formal = Source: FinScope 2015, Stakeholder interviews * 1.7m adults (21%) borrow from family and friends

37 Credit products: Retail credit mostly payroll; limited SME and mortgage Mortgages SME Salary Extremely small mortgage market Recent high defaults Small SME loans market Expensive Mostly medium to large business Scheme/salary backed loans competitive Gov & formal employees Used as housing finance

38 Savings overview 1.7m use formal savings; 5.4m use any savings Source: FinScope, 2015

39 Zambia s savings culture Comparatively high national savings, despite decline in recent years Retail savings increased dramatically, but bank deposits declined since 2014 Source: World Bank Development indicators; FinScope 2015

40 Non- formal savings far more widely used than formal accounts 3,500,000 3,000,000 Number of adults 2,500,000 2,000,000 1,500,000 1,000, ,000 - Saving at home (in cash) Formal savings Informal savings Saving in kind (asset- based Source: FinScope, 2015

41 Bulk of deposit value with banks, but most popular saving mechanism is at home Formal Savings Products Dominated by Banks Largest collective book (K24.7b) Banks not expanding branches for deposits o Rising and smaller players are Bank products offer value only at higher amounts o Require larger deposits Informal Savings Products Dominated by Savings at Home Most clients (3.3m); Book = K3.3b) Savings groups realize positive returns at low values Low aggregated values intermediated informally o Efforts to mobilise informal savings may be misplaced o Higher aggregated funds retained in non- intermediated sector (family and friends)

42 Insurance overview use insurance Total insurance usage: 2015 Total insurance usage: Male vs. female Excluded Formal 0 5,000,000 10,000,000 Total insurance usage: Target markets Total insurance usage: Urban vs. Rural Other Dependents Farmers MSMEs Informally employed Formally employed Source: FinScope 2015 Formal 98% 99% 99% 98% 100% 86% Excluded

43 Insurance hardly used whilst many coping mechanisms are welfare reducing Source: FinScope, 2015

44 Zambia s insurance market dominated by compulsion and embedded products Stage 1: Establishment and corporate assets Stage 2: Early growth and compulsory Stage 3: Retail expansion Stage 4: Diversified retail 15% Life insurance penetration 0% % of adult population covered by insurance Ethiopia 0.04% Source: Chamberlain et al., 2017 Rwanda 0.08% Uganda 0.10% Tanzania 0.11% Zambia 0.35% GDP per capita Zimbabwe Kenya 2.20% 1.06% South Africa 10.9% Mauritius 4.10%

45 Mismatch between provider and consumer reported for insurance policies Provider reported*: > 1 million policies Consumer reported: < Source: FinScope 2015, Africa Microinsurance Landscape Survey, 2014 * The provider survey only covered products defined by the survey as microinsurance

46 5. PRIORITY FOCUS AREAS

47 PRIORITY 1: IMPROVE THE EASE WITH WHICH TO MAKE AND RECEIVE PAYMENTS

48 Biggest identified financial need is to transfer value % of adults that indicated using specified financial provider to meet each use case 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 0% Life events Resilience Sending over distance Growth Bill payments Liquidity Receiving income Local payments Formal Informal Family and friends Cash In Kind Source: FinScope, 2015

49 Digitising different types of payments have different time horizons and complexity Government payments Individual payments over distance Merchant spot payments Time and complexity to digitise

50 National payments: Digitise national payments where cash- out infrastructure exists, but not beyond Cash out points included: Bank branches, ATMs, MFIs, Post offices Bank agents and mobile money agents, Proportion of people that live within 15km of at least one cash- out point Region % of adults within 15km radius of cash- out point National 58% % of total population 100% Central 50% 10% Copperbelt 84% 15% Eastern 47% 12% Luapula 37% 7% Lusaka 95% 18% Muchinga 34% 6% Northern 37% 8% North- Western 28% 5% Source: Calculated from FSDZ GIS data Southern 50% 12%

51 Individual payments over distance: Bill payments over distance an underdeveloped opportunity for digital payments Market size Remittances 1.9m adults Bill payments 2m adults Local merchant payments 8.1m adults 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% % of adults that make each type of payment using each device Cash Bank transfer Mobile money Debit/ Credit card Post Office/ Western Union etc. Source: FinScope, 2015

52 Merchant spot payments: Develop and coordinate long- term strategy to digitise merchant payments Phase 1: Ensure consumers have access Infrastructure development Phase 2: Reduce barriers to digital payments Increase availability of cash to reduce barrier to digital Phase 3: Incentivise merchants to accept and consumers to use digital payments Digitise merchant suppliers Merchant acceptance business case Northern Central North- Southern Western Luapula Eastern Muchinga Copperbelt Lusaka Size of bubble indicates relative population Consumer use case

53 PRIORITY 2: SAVINGS PRODUCTS NOT MEETING NEEDS OF SAVERS OR PROVIDERS

54 Zambians save to meet many needs % of adults using savings to meet needs vs. credit and insurance Savings used more by vulnerable income groups, who: 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 0% Savings Credit Insurance 74% 54% 39% 40% Life events Growth Resilience Liquidity Use more non- formal mechanisms Use these more frequently Rate quick access, proximity, ease of use, and simplicity higher

55 Formal products not designed or priced to meet savings needs Saving to manage liquidity and resilience Nominal value of savings The cost of short term savings 100 Deposit Monthly fee One withdrawal & balance check Kwatcha 52 Value left The bank isn t working all the time, so if there is an emergency I can t get the money Informal trader 7 41 Proportion of nominal value of savings 100% 80% 60% 40% 20% 0% Saving to meet goals The cost of saving over time 40% 60% K50 pm Value left Cost 20% 80% K100 pm I have a bank account in Kabwe, two hours away. I know that if I have to travel two hours to make a withdrawal from my bank account, I will not squander the money Female farmer Low income clients prefer transactional based fees to fixed fees You opened a baby account for future planning and you don t have a child? Interviewer to single government employee Source: MAP Zambia qualitative interviews; BOZ, 2016

56 Opportunities Informal: Informal savings meeting broadest set of needs for majority of adults Explore further development of informal mechanisms, including replication, sustainability, aggregation and longer term mutualisation Explore formal recognition to encourage long term progression to larger structures Retailers, value chain providers and non- financial providers: Explore options to meet liquidity management (including living expenses), short and medium term resilience, and achieving goal needs Formal: Explore pricing models and product features that meet low income saver needs and behaviour Explore targeted, commitment devices. Products that are not easy to access except in an emergency, and are named after the purpose of saving. Product opportunities for targeted savings: Education, housing construction, Productive investment for MSMEs and farmers Increasing longer term deposits can alleviate mismatch on provider balance sheets, and support stronger credit market fundamentals over longer term

57 PRIORITY 3: ENSURING REGULATION AND POLICY THAT PRIORITISE FINANCIAL SERVICE MARKET DEVELOPMENT

58 Regulatory delays Key pieces of legislation are either significantly out of step with contemporary financial regulatory best practice or there are material gaps. Insurance Bill 2012 no Act Microfinance Services Bill (2014) no Act The Companies (Certificates Validation) (Amendment) Bill no Act Pensions and Insurance Authority (PIA) severely impact by delayed insurance Act. Financial services are not a core priority in policy overall Need to fast- track the drafting process and prioritize the passing of key bills Secondment of technical drafting team to assist Ministry of Justice Drafting Unit Technical assistance provided throughout the drafting process to facilitate the turnaround of amendments Increase the level of insight into financial matters in the legislature and broader executive spheres of government Appreciation of the sensitivity and impact of well drafted and timely financial legislation on development

59 Quick and unexpected changes in regulation Tendency to impose snap, broad ranging regulatory changes on banking and other financial institutions, without consultation nor appropriate transitionary periods Regulator can become a key source of risk to the financial services industry Unrealistic timing for financial institutions to restructure their balance sheets and long term positions. For example: Increased capital requirements for banks (+800%) Leasing companies (+5000%) MFIs (+2500%) Savings and credit facilities (+2500%) Some banks are in a dire situation as they could not meet the sudden high capital requirements or were not given sufficient time to adjust, and their impact in the financial services sphere has been substantially curtailed Increased statutory reserves Increase in statutory reserves curtailed the ability to lend and the appetite for deposits

60 Quick and unexpected changes in regulation Enduring legacy of market conduct snap changes; lessons learned Fallout of interest rate caps and reversal Snap implementation of interest rate caps against Regulatory Impact Assessment (RIA) advice materially eroded the capital of a significant number of financial institutions and their ability to expand market access Smaller institutions most severe impacted, particularly those with a niche focus and a higher potential to enable access to medium to lower income consumers Institutions have been severely weakened and it will take a considerable amount of consolidation and rebuilding of capital to effect broader access

RIA International best practice (in line with IAL principles) to be considered Consult")

61 Quick and unexpected changes in regulation Key need to follow and publish guidance of Regulatory Impact Assessments (RIA) RIA International best practice (in line with IAL principles) to be considered Consult banks and financial institutions and provide prudent space to adjust to regulatory changes Legislators need to be more broadly aware of the impact of timing and degree of change in regulation upon the financial sector

62 Other key regulatory issues Competition and consumer protection Consumers have inadequate access to redress The CPCC only handled a total of 923 consumer protection related cases between 1998 and 2010 Currently there are far too few incidents of consumer redress for the size of the financial services sector which can cause erosion of trust as most consumer complaints are unseen and not effectively dealt with No overarching regulation of credit Current framework is fragmented and doesn t cover all institutions This has created gaps, especially in terms of credit information sharing and credit market conduct such as: Definitions, degree, and manner of determining over- indebtedness, as well as measures against reckless lending (particularly in a very high interest market)

63 Opportunities to extend financial inclusion 1. Improve the ease with which to make and receive payments (including digital) 2. Savings products that better meet the needs of savers or providers 3. Regulation and policy that prioritise financial service market development

64 QUESTIONS

65 Please contact us at Thank You! Barry Cooper E- mail: Christiaan Loots E- mail: Jeremy Gray E- mail:

Making Access Possible (MAP) Zambia: Key Findings Presentation. Lusaka, 19 April 2017name

Zambia: Key Findings Presentation. Lusaka, 19 April 2017name") Making Access Possible (MAP) Zambia: Key Findings Presentation Lusaka, 19 April 2017name Presentation notes This presentation sets out some of the key findings from the MAP diagnostic analysis. The presentation

Making Access Possible (MAP) Zambia: Key Findings Presentation Lusaka, 19 April 2017name Presentation notes This presentation sets out some of the key findings from the MAP diagnostic analysis. The presentation

REPORT ON WOMEN S ACCESS TO FINANCIAL SERVICES IN ZAMBIA

REPORT ON WOMEN S ACCESS TO FINANCIAL SERVICES IN ZAMBIA WOMEN S ACCESS TO FINANCIAL SERVICES IN ZAMBIA TABLE OF CONTENTS EXECUTIVE SUMMARY 5 PART I BACKGROUND 9 1 Objectives and methodology 9 2 Overview

REPORT ON WOMEN S ACCESS TO FINANCIAL SERVICES IN ZAMBIA WOMEN S ACCESS TO FINANCIAL SERVICES IN ZAMBIA TABLE OF CONTENTS EXECUTIVE SUMMARY 5 PART I BACKGROUND 9 1 Objectives and methodology 9 2 Overview

FinScope Consumer Survey Malawi 2014

FinScope Consumer Survey Malawi 0 Introduction Malawi Government The Government of Malawi has increasingly recognised that access to financial services can play an important role in poverty alleviation

FinScope Consumer Survey Malawi 0 Introduction Malawi Government The Government of Malawi has increasingly recognised that access to financial services can play an important role in poverty alleviation

Financial Inclusion in SADC

Financial Inclusion in SADC Mbabane, Swaziland December 2017 Contents FinMark Trust FinScope as a tool of Financial Inclusion Current FinScope initiatives in SADC FinScope insights MSME Studies in SADC

Financial Inclusion in SADC Mbabane, Swaziland December 2017 Contents FinMark Trust FinScope as a tool of Financial Inclusion Current FinScope initiatives in SADC FinScope insights MSME Studies in SADC

MAP Zimbabwe Stakeholder Workshop: Key Findings

MAP Zimbabwe Stakeholder Workshop: Key Findings Presentation on the findings from the Making Access Possible (MAP) Diagnostic conducted in Zimbabwe Harare, Zimbabwe 14 December, 2015 Agenda MAP diagnostic

MAP Zimbabwe Stakeholder Workshop: Key Findings Presentation on the findings from the Making Access Possible (MAP) Diagnostic conducted in Zimbabwe Harare, Zimbabwe 14 December, 2015 Agenda MAP diagnostic

Although Financial Inclusion is higher amongst females in Cambodia, the income distribution shows a disparity favoring males

Although Financial Inclusion is higher amongst females in Cambodia, the income distribution shows a disparity favoring males 66 % 75 % 73 % 79 % 21 % 78 % headed vs. male headed households (Ownership)

Although Financial Inclusion is higher amongst females in Cambodia, the income distribution shows a disparity favoring males 66 % 75 % 73 % 79 % 21 % 78 % headed vs. male headed households (Ownership)

FinScope Consumer Survey Botswana 2014

FinScope Consumer Survey Botswana 2014 Introduction The government of Botswana in collaboration with the private sector are actively supporting growth and development of the financial sector. Financial

FinScope Consumer Survey Botswana 2014 Introduction The government of Botswana in collaboration with the private sector are actively supporting growth and development of the financial sector. Financial

Quick Facts. n n. Total population of Zambia million Total adult population 8.1 million. o o

FinScope Zambia 2015 Quick Facts n n Total population of Zambia 1 15.5 million Total adult population 8.1 million o o 54.8% of adults live in rural areas; 45.2% in urban areas 49.0% of adults are male;

FinScope Zambia 2015 Quick Facts n n Total population of Zambia 1 15.5 million Total adult population 8.1 million o o 54.8% of adults live in rural areas; 45.2% in urban areas 49.0% of adults are male;

MAP Myanmar Financial Inclusion Roadmap Workshop

MAP Myanmar Financial Inclusion Roadmap Workshop 2 nd National Conference on Financial Inclusion: Map Myanmar Financial Inclusion Roadmap Nay Pyi Taw, Myanmar, 21 May 2014 With: #mapfi What is MAP? Overarching

MAP Myanmar Financial Inclusion Roadmap Workshop 2 nd National Conference on Financial Inclusion: Map Myanmar Financial Inclusion Roadmap Nay Pyi Taw, Myanmar, 21 May 2014 With: #mapfi What is MAP? Overarching

Microinsurance Technical Advisory Group. MICROINSURANCE LANDSCAPE - ZAMBIA MICROINSURANCE FOCUS NOTE No. 9 JUNE Funded by

Microinsurance Technical Advisory Group FOCUS NOTE No. 9 JUNE 2018 Funded by ABOUT THIS FOCUS NOTE Since 2009, the Technical Advisory Group for Microinsurance (TAG) has been spearheading the development

Microinsurance Technical Advisory Group FOCUS NOTE No. 9 JUNE 2018 Funded by ABOUT THIS FOCUS NOTE Since 2009, the Technical Advisory Group for Microinsurance (TAG) has been spearheading the development

FinScope Consumer Survey Zimbabwe 2011

FinScope Consumer Survey Zimbabwe 2011 Republic of Zimbabwe Introduction The Government of Zimbabwe recognises the role played by the financial sector in facilitating economic growth. In order to develop

FinScope Consumer Survey Zimbabwe 2011 Republic of Zimbabwe Introduction The Government of Zimbabwe recognises the role played by the financial sector in facilitating economic growth. In order to develop

FINANCIAL INCLUSION IN AFRICA: THE ROLE OF INFORMALITY Leora Klapper and Dorothe Singer

FINANCIAL INCLUSION IN AFRICA: THE ROLE OF INFORMALITY Leora Klapper and Dorothe Singer OVERVIEW Global Findex: Goal to collect comparable cross-country data on financial inclusion by surveying individuals

FINANCIAL INCLUSION IN AFRICA: THE ROLE OF INFORMALITY Leora Klapper and Dorothe Singer OVERVIEW Global Findex: Goal to collect comparable cross-country data on financial inclusion by surveying individuals

Letshego Holdings Limited

Letshego Holdings Limited Building a leading African financial services group Agenda 1H 2015 Results Presentation strong performance, growth, and returns to shareholders Strategic update Diversification

Letshego Holdings Limited Building a leading African financial services group Agenda 1H 2015 Results Presentation strong performance, growth, and returns to shareholders Strategic update Diversification

Insurance innovation: needs, gaps and opportunities

Insurance innovation: needs, gaps and opportunities Innovation Forum and FSDU Insurance Challenge Fund Launch Kampala, 10 December 2018 Contents The changing insurance landscape globally The need for insurance:

Insurance innovation: needs, gaps and opportunities Innovation Forum and FSDU Insurance Challenge Fund Launch Kampala, 10 December 2018 Contents The changing insurance landscape globally The need for insurance:

Microinsurance Country Diagnostic & Stakeholder Dialogue in Nigeria Stakeholder meeting Abuja, Nigeria 24 October 2012

Microinsurance Country Diagnostic & Stakeholder Dialogue in Nigeria Stakeholder meeting Abuja, Nigeria 24 October 2012 Denise Dias, Denis Garand, Yemi Soladoye Consultants The Country Diagnostic Report

Microinsurance Country Diagnostic & Stakeholder Dialogue in Nigeria Stakeholder meeting Abuja, Nigeria 24 October 2012 Denise Dias, Denis Garand, Yemi Soladoye Consultants The Country Diagnostic Report

REPUBLIC OF ZAMBIA NATIONAL FINANCIAL SECTOR DEVELOPMENT POLICY

REPUBLIC OF ZAMBIA NATIONAL FINANCIAL SECTOR DEVELOPMENT POLICY 2017 2017 Ministry of Finance Economic Management Department Chimanga Road P.O. Box 50062 Lusaka, ZAMBIA Tel: +260-211-257-178 Website: www.mof.gov.zm

REPUBLIC OF ZAMBIA NATIONAL FINANCIAL SECTOR DEVELOPMENT POLICY 2017 2017 Ministry of Finance Economic Management Department Chimanga Road P.O. Box 50062 Lusaka, ZAMBIA Tel: +260-211-257-178 Website: www.mof.gov.zm

Outline. 1. The past 1.1. Overview 1.2. Legal Framework

Outline 1. The past 1.1. Overview 1.2. Legal Framework 2. The Present 2.1. Financial Inclusion Policies 2.2. Financial Education Initiatives 2.3. Financial Inclusion Indicators 3. The Future 3.1. Main

Outline 1. The past 1.1. Overview 1.2. Legal Framework 2. The Present 2.1. Financial Inclusion Policies 2.2. Financial Education Initiatives 2.3. Financial Inclusion Indicators 3. The Future 3.1. Main

FSDZ Multi Sector GIS Mapping Project Final Report 17th September 23 rd December 2015

FSDZ Multi Sector GIS Mapping Project Final Report 17th September 23 rd December 2015 Geo-Spatial Analysis: 3 Components 1). Access point data collection 3). Mapping Software 2). Add Poverty and other

FSDZ Multi Sector GIS Mapping Project Final Report 17th September 23 rd December 2015 Geo-Spatial Analysis: 3 Components 1). Access point data collection 3). Mapping Software 2). Add Poverty and other

Shapshot results from Tanzania, Kenya & Zambia

COMPARATIVE ANALYSIS OF SMALLHOLDER FARMERS IN KENYA, ZAMBIA AND TANZANIA Shapshot results from Tanzania, Kenya & Zambia Leesa Shrader AFA Program Director Washington DC, May 2018 Financial Inclusion and

COMPARATIVE ANALYSIS OF SMALLHOLDER FARMERS IN KENYA, ZAMBIA AND TANZANIA Shapshot results from Tanzania, Kenya & Zambia Leesa Shrader AFA Program Director Washington DC, May 2018 Financial Inclusion and

Measuring Financial Inclusion:

Measuring Financial Inclusion: The Global Findex Data Leora Klapper Finance and Private Sector Development Team Development Research Group World Bank GLOBAL FINDEX Financial Inclusion data In depth data

Measuring Financial Inclusion: The Global Findex Data Leora Klapper Finance and Private Sector Development Team Development Research Group World Bank GLOBAL FINDEX Financial Inclusion data In depth data

Tanzania Access to Insurance Diagnostic

Tanzania Access to Insurance Diagnostic Document 3: Insurance uptake 30/10/12 Final draft VERSION 3 30/10/12 Diagnostic series authored by Cenfri on behalf of FinMark Trust: Christine Hougaard Mia de Vos

Tanzania Access to Insurance Diagnostic Document 3: Insurance uptake 30/10/12 Final draft VERSION 3 30/10/12 Diagnostic series authored by Cenfri on behalf of FinMark Trust: Christine Hougaard Mia de Vos

FinScope Consumer Survey Botswana 2014

FinScope Consumer Survey Botswana 2014 LAUNCH PRESENTATION 14 July 2015 Making financial markets work for the poor Objectives of FinScope Botswana 2014 To describe the levels of financial inclusion (i.e.

FinScope Consumer Survey Botswana 2014 LAUNCH PRESENTATION 14 July 2015 Making financial markets work for the poor Objectives of FinScope Botswana 2014 To describe the levels of financial inclusion (i.e.

Community level impacts of financial inclusion in Kenya with particular focus on poverty eradication and employment creation

Community level impacts of financial inclusion in Kenya with particular focus on poverty eradication and employment creation By Matu Mugo Central Bank of Kenya UN Expert Group Meeting 8 th to 11 th May

Community level impacts of financial inclusion in Kenya with particular focus on poverty eradication and employment creation By Matu Mugo Central Bank of Kenya UN Expert Group Meeting 8 th to 11 th May

Rwanda Targeting 80 Per Cent Financial Inclusion in 2017

59 Rwanda Targeting 80 Per Cent Financial Inclusion in 2017 Rugazura Ephraim, Ph.D Scholar, Department of Rural Management, Annamalai University, Annamalainagar ABSTRACT Background: In order to achieve

59 Rwanda Targeting 80 Per Cent Financial Inclusion in 2017 Rugazura Ephraim, Ph.D Scholar, Department of Rural Management, Annamalai University, Annamalainagar ABSTRACT Background: In order to achieve

The Status of Agricultural and Rural Financial Services in Southern Africa Zambia Country Report

The Status of Agricultural and Rural Financial Services in Southern Africa Zambia Country Report Lemmy Manje, Melanie Newman Wilkinson Taj Pomodzi Hotel Friday, 13 th December 2013 Making financial markets

The Status of Agricultural and Rural Financial Services in Southern Africa Zambia Country Report Lemmy Manje, Melanie Newman Wilkinson Taj Pomodzi Hotel Friday, 13 th December 2013 Making financial markets

Leading global banking practices Emilio Pera, May 2013

Leading global banking practices Emilio Pera, May 203!@# Agenda Banking in Africa 2 Global Banking Outlook 3 Questions/discussion 2 Africa Attractiveness Getting down to business!@# How Infrastructure

Leading global banking practices Emilio Pera, May 203!@# Agenda Banking in Africa 2 Global Banking Outlook 3 Questions/discussion 2 Africa Attractiveness Getting down to business!@# How Infrastructure

FinScope SA 2013 Consumer Survey

FinScope SA Consumer Survey 1 Contents What did we do? Have people s lives changed? Where is the increase in credit? Are people saving? Is formal insurance replacing the informal? Increasing banking through

FinScope SA Consumer Survey 1 Contents What did we do? Have people s lives changed? Where is the increase in credit? Are people saving? Is formal insurance replacing the informal? Increasing banking through

Understanding the opportunity for MSME insurance: Evidence on MSME s risks and how they cope from 6 countries 4 November 2015

Understanding the opportunity for MSME insurance: Evidence on MSME s risks and how they cope from 6 countries 4 November 2015 Jeremy Gray International Microinsurance Conference 2015 Casablanca, Morocco

Understanding the opportunity for MSME insurance: Evidence on MSME s risks and how they cope from 6 countries 4 November 2015 Jeremy Gray International Microinsurance Conference 2015 Casablanca, Morocco

FinScope Consumer Survey Mauritius 2014

FinScope Consumer Survey Mauritius 2014 LAUNCH PRESENTATION October 2014 Making financial markets work for the poor CONTENTS Research Methodology Mauritius Context Income generating activities Incidence

FinScope Consumer Survey Mauritius 2014 LAUNCH PRESENTATION October 2014 Making financial markets work for the poor CONTENTS Research Methodology Mauritius Context Income generating activities Incidence

Financial Inclusion in ASEAN Presentation for the ASEAN Working Group on Financial Inclusion Kuala Lumpur, Malaysia, January 21, 2016

Financial Inclusion in ASEAN Presentation for the ASEAN Working Group on Financial Inclusion Kuala Lumpur, Malaysia, January 21, 2016 Jose De Luna Martinez World Bank Group Contents I. Financial inclusion

Financial Inclusion in ASEAN Presentation for the ASEAN Working Group on Financial Inclusion Kuala Lumpur, Malaysia, January 21, 2016 Jose De Luna Martinez World Bank Group Contents I. Financial inclusion

MAP Lao PDR Draft Financial Inclusion Roadmap, November 2016 Cedric Javary

MAP Lao PDR Draft Financial Inclusion Roadmap, 2016 2020 03 November 2016 Cedric Javary Agenda Promoters of the Financial Inclusion Roadmap The formulation process of the Roadmap Proposed vision and congruence

MAP Lao PDR Draft Financial Inclusion Roadmap, 2016 2020 03 November 2016 Cedric Javary Agenda Promoters of the Financial Inclusion Roadmap The formulation process of the Roadmap Proposed vision and congruence

Microinsurance: Strategies for accelerating uptake. Lemmy Manje OESAI Conference August 27, 2018

Microinsurance: Strategies for accelerating uptake Lemmy Manje OESAI Conference August 27, 2018 About FinProbity Solutions IDEAS TO ACTION Navigation Business Case for Insurance Inclusivity State of Insurance

Microinsurance: Strategies for accelerating uptake Lemmy Manje OESAI Conference August 27, 2018 About FinProbity Solutions IDEAS TO ACTION Navigation Business Case for Insurance Inclusivity State of Insurance

Setting the scene. Benjamin Davis Jenn Yablonski. Methodological issues in evaluating the impact of social cash transfers in sub Saharan Africa

Setting the scene Benjamin Davis Jenn Yablonski Methodological issues in evaluating the impact of social cash transfers in sub Saharan Africa Naivasha, Kenya January 19-21, 2011 Why are we holding this

Setting the scene Benjamin Davis Jenn Yablonski Methodological issues in evaluating the impact of social cash transfers in sub Saharan Africa Naivasha, Kenya January 19-21, 2011 Why are we holding this

Ask Afrika 2010 Making financial markets work for the poor

Ask Afrika 2010 Making financial markets work for the poor Give a man a fish Ask Afrika 2010 Making financial markets work for the poor 2 Ask Afrika 2010 Making financial markets work for the poor 3 Ask

Ask Afrika 2010 Making financial markets work for the poor Give a man a fish Ask Afrika 2010 Making financial markets work for the poor 2 Ask Afrika 2010 Making financial markets work for the poor 3 Ask

Financial Literacy in Africa A cross-country analysis using FinScope

Financial Literacy in Africa A cross-country analysis using FinScope Maya Makanjee FinMark Trust Promoting Financial Capability and Consumer Protection Accra, Ghana 8 September 2009 FinMark Trust Background

Financial Literacy in Africa A cross-country analysis using FinScope Maya Makanjee FinMark Trust Promoting Financial Capability and Consumer Protection Accra, Ghana 8 September 2009 FinMark Trust Background

Strategy for Measuring Financial Inclusion in Mexico

1 Strategy for Measuring Financial Inclusion in Mexico The 2009 Global AFI Policy Forum Nairobi, Kenya September 14, 2009 Raúl Hernández Coss Director General for Access to Finance Vicepresidency of Public

1 Strategy for Measuring Financial Inclusion in Mexico The 2009 Global AFI Policy Forum Nairobi, Kenya September 14, 2009 Raúl Hernández Coss Director General for Access to Finance Vicepresidency of Public

Importance of financial infrastructure to increase Access to Finance

Building a high performance SME business in the MENA Region Arab Monetary Fund & International Finance Corporation Dubai, 7-8 May 2013 Importance of financial infrastructure to increase Access to Finance

Building a high performance SME business in the MENA Region Arab Monetary Fund & International Finance Corporation Dubai, 7-8 May 2013 Importance of financial infrastructure to increase Access to Finance

THE LANDSCAPE OF FINANCIAL INCLUSION AND MICROFINANCE IN NIGERIA

THE LANDSCAPE OF FINANCIAL INCLUSION AND MICROFINANCE IN NIGERIA 1 Table of Content 1. About EFInA... 3 2. Background... 3 3. Demographic Profile of Nigerian Adults... 4 4. Landscape of Financial Access

THE LANDSCAPE OF FINANCIAL INCLUSION AND MICROFINANCE IN NIGERIA 1 Table of Content 1. About EFInA... 3 2. Background... 3 3. Demographic Profile of Nigerian Adults... 4 4. Landscape of Financial Access

Outline. Why a national financial inclusion strategy? Why digital? Where we want to go targets. Where we are now context.

National Financial Inclusion Strategy: Strategic Considerations Outline Why a national financial inclusion strategy? Why digital? Where we want to go targets Where we are now context Key thrusts Exploring

National Financial Inclusion Strategy: Strategic Considerations Outline Why a national financial inclusion strategy? Why digital? Where we want to go targets Where we are now context Key thrusts Exploring

FinScope. Consumer Survey Highlights. Demand for financial services. Togo 2016 MAKING ACCESS POSSIBLE

FinScope Consumer Survey Highlights Demand for financial services Togo 2016 MAKING ACCESS POSSIBLE Partnering for a common purpose Making Access Possible (MAP) is a diagnostic and programmatic framework

FinScope Consumer Survey Highlights Demand for financial services Togo 2016 MAKING ACCESS POSSIBLE Partnering for a common purpose Making Access Possible (MAP) is a diagnostic and programmatic framework

AGENT BANKING KNOWLEDGE EXCHANGE- CENTRAL BANK OF KENYA

AGENT BANKING KNOWLEDGE EXCHANGE- CENTRAL BANK OF KENYA 1 AGENDA The Policy Challenge. The Knowledge Exchange. Key Policy Insights. Resulting Outcomes. Lessons and Challenges. 2 THE POLICY CHALLENGE(1)

AGENT BANKING KNOWLEDGE EXCHANGE- CENTRAL BANK OF KENYA 1 AGENDA The Policy Challenge. The Knowledge Exchange. Key Policy Insights. Resulting Outcomes. Lessons and Challenges. 2 THE POLICY CHALLENGE(1)

TANZANIA. QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted September-October December 2015

QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted September-October 2015 December 2015 GLOSSARY Access Access to a bank, NBFI or mobile money account; those with access have used the services either via

QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted September-October 2015 December 2015 GLOSSARY Access Access to a bank, NBFI or mobile money account; those with access have used the services either via

BPS 2016 Annual Conference

BPS 2016 Annual Conference Private equity, retirement funds and job creation By: Alphonse Ndzinge 01 March 2016 1 Structure of Presentation Unemployment Stats The role of Private Equity for retirement

BPS 2016 Annual Conference Private equity, retirement funds and job creation By: Alphonse Ndzinge 01 March 2016 1 Structure of Presentation Unemployment Stats The role of Private Equity for retirement

Making Access Possible MWK. Malawi. Financial Inclusion Country Report MAKING ACCESS POSSIBLE

Making Access Possible MWK Malawi Financial Inclusion Country Report 2014 MAKING ACCESS POSSIBLE 1 PARTNERING FOR A COMMON PURPOSE Making Access Possible (MAP) is a multi-country initiative to support

Making Access Possible MWK Malawi Financial Inclusion Country Report 2014 MAKING ACCESS POSSIBLE 1 PARTNERING FOR A COMMON PURPOSE Making Access Possible (MAP) is a multi-country initiative to support

NIGERIA. QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted August-September December 2015

QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted August-September 2015 December 2015 KEY DEFINITIONS Access Access to a bank account or mobile money account means a respondent can use bank/mobile money

QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted August-September 2015 December 2015 KEY DEFINITIONS Access Access to a bank account or mobile money account means a respondent can use bank/mobile money

Presentation at the Conference <Finance for all: Promoting Financial Inclusion in Central Africa>, COBAC/BEAC/IMF, March 23, 2015

RWANDA s FINANCIAL INCLUSION SUCCESS STORY: UMURENGE SACCO PROGRAM IN RWANDA Presentation at the Conference , COBAC/BEAC/IMF, KAVUGIZO SHYAMBA Kevin OUTLINE 2 I.

RWANDA s FINANCIAL INCLUSION SUCCESS STORY: UMURENGE SACCO PROGRAM IN RWANDA Presentation at the Conference , COBAC/BEAC/IMF, KAVUGIZO SHYAMBA Kevin OUTLINE 2 I.

Terms of Reference for a Social Protection Risks and Needs Analysis in the Building and Construction Industry Value Chain

Terms of Reference for a Social Protection Risks and Needs Analysis in the Building and Construction Industry Value Chain 1. Background a. The UN Green Jobs Joint Program and its Social Protection Component

Terms of Reference for a Social Protection Risks and Needs Analysis in the Building and Construction Industry Value Chain 1. Background a. The UN Green Jobs Joint Program and its Social Protection Component

BVCMUN 2018 ORGANISATION FOR ECONOMIC COOPERATION AND DEVELOPMENT GLOBAL ACCESS TO FINANCIAL SERVICES FROM FAITH COMES STRENGTH

BVCMUN 2018 FROM FAITH COMES STRENGTH ORGANISATION FOR ECONOMIC COOPERATION AND DEVELOPMENT GLOBAL ACCESS TO FINANCIAL SERVICES 3rd-5th August, 2018 INDEX Topic Page Number Introduction 2 Micro-Macro relevance

BVCMUN 2018 FROM FAITH COMES STRENGTH ORGANISATION FOR ECONOMIC COOPERATION AND DEVELOPMENT GLOBAL ACCESS TO FINANCIAL SERVICES 3rd-5th August, 2018 INDEX Topic Page Number Introduction 2 Micro-Macro relevance

Report of the South Africa Financial Inclusion Workshop. 22 November 2017 The Wanderers Club Illovo

Report of the South Africa Financial Inclusion Workshop 22 November 2017 The Wanderers Club Illovo 1. OFFICIAL WELCOME 1.1 MR BRENDAN PEARCE, FINMARK TRUST The day s proceedings were officially opened

Report of the South Africa Financial Inclusion Workshop 22 November 2017 The Wanderers Club Illovo 1. OFFICIAL WELCOME 1.1 MR BRENDAN PEARCE, FINMARK TRUST The day s proceedings were officially opened

Trade in Services and Financial Inclusion. Hamid Mamdouh WTO April 2017

Trade in Services and Financial Inclusion Hamid Mamdouh WTO April 2017 Financial Exclusion: What Do We Know? Source: SOFI2016: Financial Inclusion infographic - Expanding Access to Financial Services How

Trade in Services and Financial Inclusion Hamid Mamdouh WTO April 2017 Financial Exclusion: What Do We Know? Source: SOFI2016: Financial Inclusion infographic - Expanding Access to Financial Services How

Understanding Rural Finance Issues and the Macro and Micro Operating Environment. Module 2 Rural Finance & Microfinance Actors and approaches

Understanding Rural Finance Issues and the Macro and Micro Operating Environment Module 2 Rural Finance & Microfinance Actors and approaches Rural and Agricultural Finance Module 2 Agenda Block 1 Introductions

Understanding Rural Finance Issues and the Macro and Micro Operating Environment Module 2 Rural Finance & Microfinance Actors and approaches Rural and Agricultural Finance Module 2 Agenda Block 1 Introductions

Making Access Possible (MAP) Malawi Stakeholder workshop

Malawi Stakeholder workshop") Making Access Possible (MAP) Malawi Stakeholder workshop Lilongwe, 23 April 2015 Presentation notes This presentation sets out some of the key findings from the MAP diagnostic analysis. The presentation

Making Access Possible (MAP) Malawi Stakeholder workshop Lilongwe, 23 April 2015 Presentation notes This presentation sets out some of the key findings from the MAP diagnostic analysis. The presentation

FinScope SZL. Micro, small and medium enterprises (MSME) survey

survey") FinScope SZL Micro, small and medium enterprises (MSME) survey Swaziland 2017 Partnering for a common purpose FinScope MSME Swaziland was designed to involve a range of stakeholders engaging in a comprehensive

FinScope SZL Micro, small and medium enterprises (MSME) survey Swaziland 2017 Partnering for a common purpose FinScope MSME Swaziland was designed to involve a range of stakeholders engaging in a comprehensive

Universal access to health and care services for NCDs by older men and women in Tanzania 1

Universal access to health and care services for NCDs by older men and women in Tanzania 1 1. Background Globally, developing countries are facing a double challenge number of new infections of communicable

Universal access to health and care services for NCDs by older men and women in Tanzania 1 1. Background Globally, developing countries are facing a double challenge number of new infections of communicable

QUARTERLY SURVEY OF BUSINESS OPINIONS AND EXPECTATIONS REPORT. First Quarter 2018, Vol 2.1

BANK Of ZAMBIA QUARTERLY SURVEY OF BUSINESS OPINIONS AND EXPECTATIONS REPORT First Quarter 8, Vol. Disclaimer: The opinions and expectations presented herein are of the respondents and not of the Bank

BANK Of ZAMBIA QUARTERLY SURVEY OF BUSINESS OPINIONS AND EXPECTATIONS REPORT First Quarter 8, Vol. Disclaimer: The opinions and expectations presented herein are of the respondents and not of the Bank

Contributing family workers and poverty. Shebo Nalishebo

Contributing family workers and poverty Shebo Nalishebo January 2013 Zambia Institute for Policy Analysis & Research 2013 Zambia Institute for Policy Analysis & Research (ZIPAR) CSO Annex Building Cnr

Contributing family workers and poverty Shebo Nalishebo January 2013 Zambia Institute for Policy Analysis & Research 2013 Zambia Institute for Policy Analysis & Research (ZIPAR) CSO Annex Building Cnr

Kyrgyz Republic: Borrowing by Individuals

Kyrgyz Republic: Borrowing by Individuals A Review of the Attitudes and Capacity for Indebtedness Summary Issues and Observations In partnership with: 1 INTRODUCTION A survey was undertaken in September

Kyrgyz Republic: Borrowing by Individuals A Review of the Attitudes and Capacity for Indebtedness Summary Issues and Observations In partnership with: 1 INTRODUCTION A survey was undertaken in September

SECTOR ASSESSMENT (SUMMARY): FINANCE 1

: FINANCE 1") Policy-Based Loan for Subprogram 3 of the Third Financial Sector Program (RRP CAM 42305) SECTOR ASSESSMENT (SUMMARY): FINANCE 1 1. Sector Performance, Problems, and Opportunities 1. Overall finance sector.

Policy-Based Loan for Subprogram 3 of the Third Financial Sector Program (RRP CAM 42305) SECTOR ASSESSMENT (SUMMARY): FINANCE 1 1. Sector Performance, Problems, and Opportunities 1. Overall finance sector.

Innovation Hubs and Accelerators. IAIS-A2ii Consultation Call, 22 March 2018

Innovation Hubs and Accelerators IAIS-A2ii Consultation Call, 22 March 2018 Technical expert Jeremy Gray Engagement Manager Cenfri Presenters IAIS representative Peter van den Broeke International Association

Innovation Hubs and Accelerators IAIS-A2ii Consultation Call, 22 March 2018 Technical expert Jeremy Gray Engagement Manager Cenfri Presenters IAIS representative Peter van den Broeke International Association

INDIA. QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted June through October, January 2016*

QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted June through October, 2015 January 2016* *Revised April 2016 KEY DEFINITIONS Access Access to a bank, NBFI or mobile money account; those with access have

QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted June through October, 2015 January 2016* *Revised April 2016 KEY DEFINITIONS Access Access to a bank, NBFI or mobile money account; those with access have

Africa s Fastest Fintech

Africa s Fastest Fintech Social Impact Evaluation September 2018 Who we are Since 2013 4G Capital has been developing and supporting MSMEs in East Africa by providing financial literacy and business training

Africa s Fastest Fintech Social Impact Evaluation September 2018 Who we are Since 2013 4G Capital has been developing and supporting MSMEs in East Africa by providing financial literacy and business training

Tariffs and Tariff Design Promoting Access to the Poor

Regulation for Practitioners Building Capacity through Participation Tariffs and Tariff Design Promoting Access to the Poor Gloria Magombo Energy Advisor gmagombo@satradehub.org July 27-31, Eskom Convention

Regulation for Practitioners Building Capacity through Participation Tariffs and Tariff Design Promoting Access to the Poor Gloria Magombo Energy Advisor gmagombo@satradehub.org July 27-31, Eskom Convention

International Monetary and Financial Committee

International Monetary and Financial Committee Thirty-Third Meeting April 16, 2016 IMFC Statement by Pravin Jamnadas Gordhan Minister of Finance, South Africa On behalf of Angola, Botswana, Burundi, Eritrea,

International Monetary and Financial Committee Thirty-Third Meeting April 16, 2016 IMFC Statement by Pravin Jamnadas Gordhan Minister of Finance, South Africa On behalf of Angola, Botswana, Burundi, Eritrea,

ធន គ រជ ត ន កម ព ជ NATIONAL BANK OF CAMBODIA

1 ធន គ រជ ត ន កម ព ជ NATIONAL BANK OF CAMBODIA Financial Inclusion in Cambodia: Issues and Challenges December 7-8, 2017 Presented by: Khou Vouthy (Ph.D.) Deputy Director General The views expressed in

1 ធន គ រជ ត ន កម ព ជ NATIONAL BANK OF CAMBODIA Financial Inclusion in Cambodia: Issues and Challenges December 7-8, 2017 Presented by: Khou Vouthy (Ph.D.) Deputy Director General The views expressed in

Developing a National Financial Literacy Strategy Tanzania

Developing a National Financial Literacy Strategy Tanzania Conference on "Promoting Financial Capability and Consumer Protection : Accra, 8-9 Sept 2009 By: Deogratias P. Macha Real Sector and Microfinance

Developing a National Financial Literacy Strategy Tanzania Conference on "Promoting Financial Capability and Consumer Protection : Accra, 8-9 Sept 2009 By: Deogratias P. Macha Real Sector and Microfinance

Inclusive Insurance Focus Note Series

Inclusive Insurance Focus Note Series Microinsurance Landscape 2015 Contents 03 About 04 Key Highlights 05 Introduction 08 Microinsurance Coverage 10 Distribution 11 Business Case 14 Client Value 15 Industry

Inclusive Insurance Focus Note Series Microinsurance Landscape 2015 Contents 03 About 04 Key Highlights 05 Introduction 08 Microinsurance Coverage 10 Distribution 11 Business Case 14 Client Value 15 Industry

MICROFINANCE IN LATIN AMERICA AND THE CARIBBEAN: PAST, PRESENT AND FUTURE

MICROFINANCE IN LATIN AMERICA AND THE CARIBBEAN: PAST, PRESENT AND FUTURE Nancy Lee General Manager MULTILATERAL INVESTMENT FUND Multilateral Investment Fund Member of the IDB Group Microfinance Trends

MICROFINANCE IN LATIN AMERICA AND THE CARIBBEAN: PAST, PRESENT AND FUTURE Nancy Lee General Manager MULTILATERAL INVESTMENT FUND Multilateral Investment Fund Member of the IDB Group Microfinance Trends

Microinsurance Development Strategy for Tanzania

Microinsurance Development Strategy for Tanzania Dr. Baghayo A. Saqware Member of Technical Working Team Chair of Education, Public Awareness Sub- Committee Need Improving risk management for majority

Microinsurance Development Strategy for Tanzania Dr. Baghayo A. Saqware Member of Technical Working Team Chair of Education, Public Awareness Sub- Committee Need Improving risk management for majority

Domestic Resource Mobilization in Africa

Domestic Resource Mobilization in Africa Yiagadeesen (Teddy) Samy Associate Professor Norman Paterson School of International Affairs and Institute of African Studies Carleton University March 12, 2015

Domestic Resource Mobilization in Africa Yiagadeesen (Teddy) Samy Associate Professor Norman Paterson School of International Affairs and Institute of African Studies Carleton University March 12, 2015

The Global Findex Database. Adults with an account at a formal financial institution (%) OTHER BRICS ECONOMIES REST OF DEVELOPING WORLD

OTHER BRICS ECONOMIES REST OF DEVELOPING WORLD") 08 NOTE NUMBER FINDEX NOTES Asli Demirguc-Kunt Leora Klapper Douglas Randall WWW.WORLDBANK.ORG/GLOBALFINDEX FEBRUARY 2013 The Global Findex Database Financial Inclusion in India In India 35 percent of

08 NOTE NUMBER FINDEX NOTES Asli Demirguc-Kunt Leora Klapper Douglas Randall WWW.WORLDBANK.ORG/GLOBALFINDEX FEBRUARY 2013 The Global Findex Database Financial Inclusion in India In India 35 percent of

The Mobile Money Revolution in Kenya Based on research by William Jack and Tavneet Suri

The Mobile Money Revolution in Kenya Based on research by William Jack and Tavneet Suri 1 An Efficient Financial System Decades of research: efficient financial systems are key to economic growth and poverty

The Mobile Money Revolution in Kenya Based on research by William Jack and Tavneet Suri 1 An Efficient Financial System Decades of research: efficient financial systems are key to economic growth and poverty

REPUBLIC OF ZAMBIA CENTRAL STATISTICAL OFFICE PRELIMINARY RESULTS OF THE 2012 LABOUR FORCE SURVEY

REPUBLIC OF ZAMBIA CENTRAL STATISTICAL OFFICE PRELIMINARY RESULTS OF THE 2012 LABOUR FORCE SURVEY This report presents preliminary results of the 2012 Labour Force Survey. The results presented herein

REPUBLIC OF ZAMBIA CENTRAL STATISTICAL OFFICE PRELIMINARY RESULTS OF THE 2012 LABOUR FORCE SURVEY This report presents preliminary results of the 2012 Labour Force Survey. The results presented herein

Rural Finance in China: Opportunities and Challenges

Rural Finance in China: Opportunities and Challenges Jinchang Lai Principal Operations Officer & Lead for Financial Infrastructure East Asia and Pacific Advisory Services CICA Annual Meeting, Hong Kong,

Rural Finance in China: Opportunities and Challenges Jinchang Lai Principal Operations Officer & Lead for Financial Infrastructure East Asia and Pacific Advisory Services CICA Annual Meeting, Hong Kong,

Financial Development, Financial Inclusion, and Growth in Africa

International Monetary Fund African Department Financial Development, Financial Inclusion, and Growth in Africa ECOWAS Regional Conference, Dakar, Senegal, Roger Nord Deputy Director African department

International Monetary Fund African Department Financial Development, Financial Inclusion, and Growth in Africa ECOWAS Regional Conference, Dakar, Senegal, Roger Nord Deputy Director African department

Scoping study: Overview of the housing 6inance sector in Zambia

Scoping study: Overview of the housing 6inance sector in Zambia Study commissioned by FINMARK TRUST May 2013, Lusaka Section I - Introduction Section II Context Section III Housing Finance Value Chain

Scoping study: Overview of the housing 6inance sector in Zambia Study commissioned by FINMARK TRUST May 2013, Lusaka Section I - Introduction Section II Context Section III Housing Finance Value Chain

SECURED TRANSACTIONS & COLLATERAL REGISTRY REFORMS RECENT DEVELOPMENTS IN AFRICA, MIDDLE EAST, EASTERN EUROPE, CENTRAL & SOUTH ASIA

SECURED TRANSACTIONS & COLLATERAL REGISTRY REFORMS RECENT DEVELOPMENTS IN AFRICA, MIDDLE EAST, EASTERN EUROPE, CENTRAL & SOUTH ASIA Murat Sultanov Secured Transactions Specialist February 09, 2017 Secured

SECURED TRANSACTIONS & COLLATERAL REGISTRY REFORMS RECENT DEVELOPMENTS IN AFRICA, MIDDLE EAST, EASTERN EUROPE, CENTRAL & SOUTH ASIA Murat Sultanov Secured Transactions Specialist February 09, 2017 Secured

The goals to Access / Financial Inclusion 2020 Briefing for World Bank Group President Dr. Jim Yong Kim Terence Gallagher Senior Specialist in Micro

The goals to Access / Financial Inclusion 2020 Briefing for World Bank Group President Dr. Jim Yong Kim Terence Gallagher Senior Specialist in Micro and Small Enterprise Finance Financial Institutions

The goals to Access / Financial Inclusion 2020 Briefing for World Bank Group President Dr. Jim Yong Kim Terence Gallagher Senior Specialist in Micro and Small Enterprise Finance Financial Institutions

Pyramids and frontiers of finance measuring access to finance. Forum for the Future. 24 October Mark Napier FinMark Trust

1 Pyramids and frontiers of finance measuring access to finance Forum for the Future Mark Napier FinMark Trust 24 October 2006 2 The concepts Access frontier Finance at the BoP Centrality of the consumer

1 Pyramids and frontiers of finance measuring access to finance Forum for the Future Mark Napier FinMark Trust 24 October 2006 2 The concepts Access frontier Finance at the BoP Centrality of the consumer

QUICKSIGHTS REPORT FOURTH ANNUAL FII TRACKER SURVEY

QUICKSIGHTS REPORT FOURTH ANNUAL FII TRACKER SURVEY Fieldwork conducted July - August 20 November 20 Key definitions Access to financial accounts Access to a bank account, mobile money account or an NBFI

QUICKSIGHTS REPORT FOURTH ANNUAL FII TRACKER SURVEY Fieldwork conducted July - August 20 November 20 Key definitions Access to financial accounts Access to a bank account, mobile money account or an NBFI

Terms of Reference. Challenges and opportunities for health finance in South Africa: a supply and regulation perspective

Terms of Reference Challenges and opportunities for health finance in South Africa: a supply and regulation perspective 28 October 2015 Page 2 1. Introduction Health risks are experienced by most households

Terms of Reference Challenges and opportunities for health finance in South Africa: a supply and regulation perspective 28 October 2015 Page 2 1. Introduction Health risks are experienced by most households

Innovation for Financial Inclusion: Indonesia s Perspective

2013/FMP/WKSP1/002 Session 1 Innovation for Financial Inclusion: Indonesia s Perspective Submitted by: Indonesia Workshop on Promoting Financial Access Through Innovative Delivery Channel to Enhance Financial

2013/FMP/WKSP1/002 Session 1 Innovation for Financial Inclusion: Indonesia s Perspective Submitted by: Indonesia Workshop on Promoting Financial Access Through Innovative Delivery Channel to Enhance Financial

double-clicking on the box) next to the appropriate response and specify if Other ].

![double-clicking on the box) next to the appropriate response and specify if Other ].](/thumbs/86/94292538.jpg "double-clicking on the box) next to the appropriate response and specify if Other ].") FinAccess Business Supply-side Questionnaire Name of the bank: Bank s activity: Commercial, Investment, Corporate, Retail, Other. [Put an X (by double-clicking on the box) next to the appropriate response

FinAccess Business Supply-side Questionnaire Name of the bank: Bank s activity: Commercial, Investment, Corporate, Retail, Other. [Put an X (by double-clicking on the box) next to the appropriate response

SECTOR ASSESSMENT (SUMMARY): FINANCE

: FINANCE") Inclusive Financial Sector Development Program, Subprogram 1 (RRP CAM 44263 013) SECTOR ASSESSMENT (SUMMARY): FINANCE 1. Sector Performance, Problems, and Opportunities a. Sector Context and Performance

Inclusive Financial Sector Development Program, Subprogram 1 (RRP CAM 44263 013) SECTOR ASSESSMENT (SUMMARY): FINANCE 1. Sector Performance, Problems, and Opportunities a. Sector Context and Performance

Expanding Financial Inclusion in Africa. SILC Meeting, Photo By Henry Tenenbaum, May 2016

Expanding Financial Inclusion in Africa SILC Meeting, Photo By Henry Tenenbaum, May 2016 SILC Financial Diaries: Case Study High-Income, High-Variation Household October 2016 Authors This case study was

Expanding Financial Inclusion in Africa SILC Meeting, Photo By Henry Tenenbaum, May 2016 SILC Financial Diaries: Case Study High-Income, High-Variation Household October 2016 Authors This case study was

Microinsurance Work for Small Farmers

Microinsurance Work for Small Farmers For Workshop on Climate Resilience on Agriculture July 10, 2012 Yoko Doi, Financial Specialist Financial and Private Sector Development Unit World Bank Jakarta Office

Microinsurance Work for Small Farmers For Workshop on Climate Resilience on Agriculture July 10, 2012 Yoko Doi, Financial Specialist Financial and Private Sector Development Unit World Bank Jakarta Office

FINANCIAL SERVICES LANDSCAPE IN NIGERIA (SUPPLY SIDE STUDY)

") FINANCIAL SERVICES LANDSCAPE IN NIGERIA (SUPPLY SIDE STUDY) Presentation to key stakeholders Robert Stone 10 August 2010 1 Outline 1. The objective and methodology of the survey 2. The Nigerian economy

FINANCIAL SERVICES LANDSCAPE IN NIGERIA (SUPPLY SIDE STUDY) Presentation to key stakeholders Robert Stone 10 August 2010 1 Outline 1. The objective and methodology of the survey 2. The Nigerian economy

Digital Financial Services: Indonesia Infrastructure Development for Financial Inclusion

2015/SMEWG40/026 Agenda Item: 13.2.1a Digital Financial Services: Indonesia Infrastructure Development for Financial Inclusion Purpose: Information Submitted by: Indonesia 40 th Small and Medium Enterprises

2015/SMEWG40/026 Agenda Item: 13.2.1a Digital Financial Services: Indonesia Infrastructure Development for Financial Inclusion Purpose: Information Submitted by: Indonesia 40 th Small and Medium Enterprises

SECURED TRANSACTIONS AND COLLATERAL REGISTRIES PEER TO PEER LEARNING EVENT

SECURED TRANSACTIONS AND COLLATERAL REGISTRIES PEER TO PEER LEARNING EVENT Presentation Title: Overview of Credit Reporting Worldwide Moyo Violet Ndonde Accra, Ghana - 3-5 July, 2012 -Session no. 2 Summary

SECURED TRANSACTIONS AND COLLATERAL REGISTRIES PEER TO PEER LEARNING EVENT Presentation Title: Overview of Credit Reporting Worldwide Moyo Violet Ndonde Accra, Ghana - 3-5 July, 2012 -Session no. 2 Summary

UGANDA WAVE 5 REPORT FIFTH ANNUAL FII TRACKER SURVEY. June Conducted July-August 2017

WAVE 5 REPORT FIFTH ANNUAL FII TRACKER SURVEY Conducted July-August 2017 June 2018 PUTTING THE USER FRONT AND CENTER The Financial Inclusion Insights (FII) program responds to the need identified by multiple

WAVE 5 REPORT FIFTH ANNUAL FII TRACKER SURVEY Conducted July-August 2017 June 2018 PUTTING THE USER FRONT AND CENTER The Financial Inclusion Insights (FII) program responds to the need identified by multiple

Credit: Challenges and Opportunities Presentation to OECD/US Treasury Conference on Financial Education Washington, May 2008

Credit: Challenges and Opportunities Presentation to OECD/US Treasury Conference on Financial Education Washington, May 2008 Presenter: Mary O Dea Consumer Director Financial Regulator (Ireland) Some future

Credit: Challenges and Opportunities Presentation to OECD/US Treasury Conference on Financial Education Washington, May 2008 Presenter: Mary O Dea Consumer Director Financial Regulator (Ireland) Some future

Click to edit Master title style

DIGITAL CREDIT IN TANZANIA: CUSTOMER EXPERIENCES & EMERGING RISKS Click to edit Master title style Photo: Hendri Lombard World Bank Photographer Name, CGAP Photo Contest Michelle Kaffenberger January 2018

DIGITAL CREDIT IN TANZANIA: CUSTOMER EXPERIENCES & EMERGING RISKS Click to edit Master title style Photo: Hendri Lombard World Bank Photographer Name, CGAP Photo Contest Michelle Kaffenberger January 2018

PRI REPORTING FRAMEWORK 2018 Direct Inclusive Finance

PRI REPORTING FRAMEWORK 2018 Direct Inclusive Finance November 2017 reporting@unpri.org +44 (0) 20 3714 3187 Understanding this document In addition to the detailed indicator text and selection options,

PRI REPORTING FRAMEWORK 2018 Direct Inclusive Finance November 2017 reporting@unpri.org +44 (0) 20 3714 3187 Understanding this document In addition to the detailed indicator text and selection options,

Getting Finance Indicators. Financial Analysis Unit Kumar / Lin / Safavian / Tzioumis April 25th, 2007

Getting Finance Indicators Financial Analysis Unit Kumar / Lin / Safavian / Tzioumis April 25th, 2007 1. Getting Finance Indicators Introduction A new set of indicators on household access to finance Challenge

Getting Finance Indicators Financial Analysis Unit Kumar / Lin / Safavian / Tzioumis April 25th, 2007 1. Getting Finance Indicators Introduction A new set of indicators on household access to finance Challenge

Training Programme Overview - Programme in Microinsurance Business Strategies for East African Markets

Training Programme Overview - Programme in Microinsurance Business Strategies for East African Markets VERSION 2.0 4/7/2010 Author: David Saunders Tel: +27 21 913 9510 Fax: +27 21 913 9644 E-mail: tessa@cenfi.org

Training Programme Overview - Programme in Microinsurance Business Strategies for East African Markets VERSION 2.0 4/7/2010 Author: David Saunders Tel: +27 21 913 9510 Fax: +27 21 913 9644 E-mail: tessa@cenfi.org

NIGERIA WAVE 4 REPORT FII TRACKER SURVEY. June Conducted August October 2016

NIGERIA WAVE 4 REPORT FII TRACKER SURVEY Conducted August October 2016 June 2017 PUTTING THE USER FRONT AND CENTER NIGERIA The Financial Inclusion Insights (FII) program responds to the need identified

NIGERIA WAVE 4 REPORT FII TRACKER SURVEY Conducted August October 2016 June 2017 PUTTING THE USER FRONT AND CENTER NIGERIA The Financial Inclusion Insights (FII) program responds to the need identified

FinScope. Consumer Survey Highlights. Madagascar 2016 MAKING ACCESS POSSIBLE

FinScope Consumer Survey Highlights Madagascar 2016 MAKING ACCESS POSSIBLE Partnering for a common purpose The FinScope survey is a research tool which was developed by FinMark Trust. It is a nationally

FinScope Consumer Survey Highlights Madagascar 2016 MAKING ACCESS POSSIBLE Partnering for a common purpose The FinScope survey is a research tool which was developed by FinMark Trust. It is a nationally

What is microinsurance and why does it matter?

Policy, regulation and supervision FOCUS NOTE 1 What is microinsurance and why does it matter? The rationale for microinsurance from a regulator s perspective March 2009 By Doubell Chamberlain, Christine

Policy, regulation and supervision FOCUS NOTE 1 What is microinsurance and why does it matter? The rationale for microinsurance from a regulator s perspective March 2009 By Doubell Chamberlain, Christine

SOUTH AFRICAN BANKING SECTOR OVERVIEW

1 SOUTH AFRICAN BANKING SECTOR OVERVIEW TABLE OF CONTENTS Sections Page 1 Background 1 2. Total Assets 1 3. Total liabilities 3 4. Credit extension 4 5. Branches and ATMs 5 6. Usage of payment systems

1 SOUTH AFRICAN BANKING SECTOR OVERVIEW TABLE OF CONTENTS Sections Page 1 Background 1 2. Total Assets 1 3. Total liabilities 3 4. Credit extension 4 5. Branches and ATMs 5 6. Usage of payment systems

SADC S Integrated Regional Payment Settlement System (SIRESS): The impact on cross-border trade

: The impact on cross-border trade") SADC S Integrated Regional Payment Settlement System (SIRESS): The impact on cross-border trade This policy note presents work in progress by the Southern African Business Forum (SABF) to initiate the

SADC S Integrated Regional Payment Settlement System (SIRESS): The impact on cross-border trade This policy note presents work in progress by the Southern African Business Forum (SABF) to initiate the

Expanding Financial Inclusion in Africa. SILC Meeting, Photo By Henry Tenenbaum, May 2016

Expanding Financial Inclusion in Africa SILC Meeting, Photo By Henry Tenenbaum, May 2016 SILC Financial Diaries: Case Study Low-Income, High-Variation Household October 2016 Authors This case study was

Expanding Financial Inclusion in Africa SILC Meeting, Photo By Henry Tenenbaum, May 2016 SILC Financial Diaries: Case Study Low-Income, High-Variation Household October 2016 Authors This case study was