TIME AND EFFORT FEDERAL REQUIREMENT

|

|

|

- Linda Haynes

- 5 years ago

- Views:

Transcription

1 TIME AND EFFORT FEDERAL REQUIREMENT Alex Dominguez and Denise Dusek Education Service Center, Region 20 September 14, 2018 Revised 10/02/18 Revisions to Slides: 51, 55, 130, 137, 140; Added slides 4, 5, 76, 77, 84, 96, 154, 155, 168, 169, 178, 179

2 Learning Objectives Understand the basic requirements of time distribution reporting Determine the differences between single and multiple cost objectives and applicable time distribution documentation Review audit findings and best practices for compliance SEPTEMBER

3 Padlet only for use during the presentation. Data entry in Padlet will not be monitored after the session ends. Padlet Use Padlet to respond to group activity questions or to ask questions Click on the + or add button below the appropriate column and begin typing in the data entry box that appears SEPTEMBER

4 EDGAR and Uniform Guidance Throughout the presentation, we will use the terms EDGAR and Uniform Guidance interchangeably EDGAR is applicable to all federal education programs Uniform Guidance 2 CFR Part 200 is applicable to all federal programs Uniform Guidance 2 CFR Part 200 is included in EDGAR The rules concerning Time Distribution Reporting are found in the Uniform Guidance 2 CFR Part 200 EDGAR: Education Department General Administrative Regulations SEPTEMBER

5 EDGAR and Uniform Guidance Child Nutrition Programs administered by the United States Department of Agriculture (USDA) do not follow EDGAR, but are subject to the Uniform Guidance applicable to all federal programs Child Nutrition Services Update: Uniform Grant Guidance and Procurement, 1/8/2016 USDA Questions and Answers on the Transition to and Implementation of 2 CFR Part 200, 3/30/2015 SEPTEMBER

6 OVERVIEW SEPTEMBER

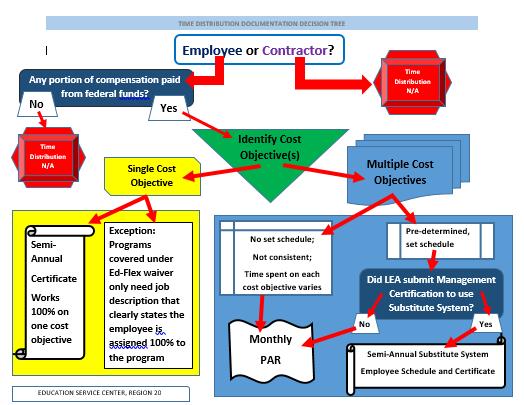

7 TIME DISTRIBUTION REPORTING Applicable to any employee* whose compensation for personal services is paid in whole or in part with Federal funds *N/A to contracted service providers SEPTEMBER

8 EDGAR requires time distribution documentation to ensure that charges to each Federal program reflect an accurate account of the employee s time and effort devoted to that program EDGAR: Education Department General Administrative Regulations SEPTEMBER

9 Time distribution reports demonstrate an employee s payroll costs paid with federal funds are allocable to the federal program EDGAR: Education Department General Administrative Regulations SEPTEMBER

10 Ensures the LEA does not over-charge the Federal grant award Ensures the Federal grant award is only charged in accordance to the benefit received EDGAR: Education Department General Administrative Regulations SEPTEMBER

11 Example of Importance of Time and Effort ABC ISD budgets a teacher s compensation to be paid 50% out of IDEA-B and 50% out of Title I, Part A However, the teacher actually spent 70% of their time teaching students with disabilities and 30% of their time performing Title I, Part A activities Without time distribution reporting, the IDEA-B grant would be undercharged by 20% and the Title I, Part A grant would be overcharged by 20% SEPTEMBER

12 FEDERAL REGULATIONS COMPENSATION SEPTEMBER

13 Cross-Cutting Federal Regulation Uniform Guidance Applicable to ALL Federal grants 2 CFR Compensation personal services Covers requirements for payroll expenditures with Federal funds 2 CFR (i) Standards for Documentation of Personnel Expenses (what we refer to as Time and Effort) Requirements of documentation supporting payroll expenditures Uniform Guidance 2 CFR Part 200 SEPTEMBER

14 2 CFR (a) Compensation for personal services includes all remuneration, paid currently or accrued, for services of employees rendered during the period of performance under the Federal award, including but not necessarily limited to wages and salaries. Compensation for personal services may also include fringe benefits which are addressed in Compensation fringe benefits. Uniform Guidance 2 CFR Part 200 SEPTEMBER

15 2 CFR (a)(1) Costs of compensation are allowable to the extent that they satisfy the specific requirements of this part, and that the total compensation for individual employees: (1) Is reasonable for the services rendered and conforms to the established written policy of the [LEA] consistently applied to both Federal and non-federal activities; Uniform Guidance 2 CFR Part 200 SEPTEMBER

(2) Costs of compensation are allowable to the extent that they satisfy the specific requirements of this part, and that the total compensation for individual employees: (2) Follows an")

16 2 CFR (a)(2) Costs of compensation are allowable to the extent that they satisfy the specific requirements of this part, and that the total compensation for individual employees: (2) Follows an appointment made in accordance with a[n] [LEA s] laws and/or rules or written policies and meets the requirements of Federal statute, where applicable; and Need Written Policy & Procedures Must meet allowable use of funds requirements for the relevant Federal grant Uniform Guidance 2 CFR Part 200 SEPTEMBER

17 2 CFR (a)(3) Costs of compensation are allowable to the extent that they satisfy the specific requirements of this part, and that the total compensation for individual employees: (3) Is determined and supported as provided in paragraph (i) of this section, Standards for Documentation of Personnel Expenses, when applicable. Uniform Guidance 2 CFR Part 200 SEPTEMBER

18 Documentation Standards 2 CFR (i)(1) Charges to Federal awards for salaries and wages must be based on records that accurately reflect the work performed. Uniform Guidance 2 CFR Part 200 SEPTEMBER

(1)(i) (i) These records must: Be supported by a system of internal control which provides reasonable assurance that the")

19 Documentation Standards 2 CFR (i)(1)(i) (i) These records must: Be supported by a system of internal control which provides reasonable assurance that the charges are accurate, allowable, and properly allocated; Uniform Guidance 2 CFR Part 200 SEPTEMBER

(1)(ii,iii) These records must: (ii) Be incorporated into the official records of the [LEA]; (iii) Reasonably reflect the total activity for which the")

20 Documentation Standards 2 CFR (i)(1)(ii,iii) These records must: (ii) Be incorporated into the official records of the [LEA]; (iii) Reasonably reflect the total activity for which the employee is compensated by the [LEA], not exceeding 100% of compensated activities; Uniform Guidance 2 CFR Part 200 SEPTEMBER

21 Documentation Standards 2 CFR (i)(1)(iv, v, vi) These records must: (iv) Encompass both federally assisted and all other activities compensated by the [LEA] on an integrated basis, but may include the use of subsidiary records as defined in the [LEA s] written policy; Written Policy & Procedures (v) Comply with the established accounting policies and practices of the [LEA]; and (vi) [Reserved] Uniform Guidance 2 CFR Part 200 SEPTEMBER

22 Documentation Standards 2 CFR (i)(1)(vii) These records must: (vii) Support the distribution of the employee s salary or wages among specific activities or cost objectives if the employee works on More than one Federal award; A Federal award and non-federal award; An indirect cost activity and a direct cost activity; Two or more indirect activities which are allocated using different allocation bases; or An unallowable activity and a direct or indirect cost activity Uniform Guidance 2 CFR Part 200 SEPTEMBER

23 Documentation Standards 2 CFR (i)(1)(viii) (viii) Budget estimates (i.e., estimates determined before the services are performed) alone do not qualify as support for charges to Federal awards, but may be used for interim accounting purposes, provided that: A. The system for establishing the estimates produces reasonable approximations of the activity actually performed; B. Significant changes in the corresponding work activity are identified and entered into the records in a timely manner ; and Uniform Guidance 2 CFR Part 200 SEPTEMBER

24 Documentation Standards 2 CFR (i)(1)(viii) (viii) Budget estimates (i.e., estimates determined before the services are performed) alone do not qualify as support for charges to Federal awards, but may be used for interim accounting purposes, provided that: C. The [LEA] s system of internal controls includes processes to review after-the-fact interim charges made to a Federal award based on budget estimates. All necessary adjustments must be made such that the final amount charged to the Federal award is accurate, allowable, and properly allocated. Uniform Guidance 2 CFR Part 200 SEPTEMBER

25 SUMMARY OF BASIC REQUIREMENTS OF DOCUMENTATION STANDARDS SEPTEMBER

26 Important Components LEA must have written policies and procedures Compensation charges to Federal awards are reasonable, accurate, allowable, and properly allocated LEA s records comply with EDGAR s documentation standards of 2 CFR (i) LEA reconciles budget to actual to ensure grant is not over-charged Uniform Guidance 2 CFR Part 200 SEPTEMBER

27 Essence of Time and Effort Compensation charges to Federal awards are properly allocated Compensation charges to the Federal program are aligned with the actual effort (activity) devoted to the program The Federal fund source is only being charged for activities related to the program Uniform Guidance 2 CFR Part 200 SEPTEMBER

28 COST OBJECTIVES SEPTEMBER

29 Cost Objectives Understanding cost objectives is important for ensuring compliance with the documentation standards of 2 CFR (i) Uniform Guidance 2 CFR Part 200 SEPTEMBER

30 Definition of Cost Objective 2 CFR Cost objective means a program, function, activity, award, organizational subdivision, contract, or work unit for which cost data are desired and for which provision is made to accumulate and measure the cost of processes, products, jobs, capital projects, etc. A cost objective may be a major function of the [LEA], a particular service or project, a Federal award, or an indirect cost activity, as described in Subpart E Cost Principles of this Part. Uniform Guidance 2 CFR Part 200 SEPTEMBER

31 Cost Objectives LEAs must carefully track and document the federal funds spent in carrying out each cost objective Time distribution records document the amount of time the employee spent on each cost objective Uniform Guidance 2 CFR Part 200 SEPTEMBER

32 Single Cost Objective A Single Cost Objective can be a single function, single grant, or single activity Example: A special education teacher works 100% of their time on special education activities USDE Guidance: Enclosure C Support for Salaries and Wages Of An Employee Working on a Single Cost Objective, September 7, 2012 SEPTEMBER

33 Concept 1 Single Cost Objective It is possible to work on a single cost objective even if an employee works on more than one Federal award IF the employee s activities could be fully funded from either grant USDE Guidance: Enclosure C Support for Salaries and Wages Of An Employee Working on a Single Cost Objective, September 7, 2012 SEPTEMBER

34 Single Cost Objective Example of Single Cost Objective employee working on more than one Federal award: A preschool special education teacher who is funded partially from IDEA-B Formula funds and partially from IDEA-B Preschool funds SEPTEMBER

35 Single Cost Objective Even though the preschool teacher is being split-funded from two separate Federal awards, it is considered a single cost objective because: Teaching preschool special education is an allowable activity under both IDEA-B Formula (ages 3-21) and IDEA-B Preschool (ages 3-5) Since the teacher s payroll costs could be paid 100% from either IDEA-B Formula or 100% from IDEA-B Preschool, it is considered a single cost objective SEPTEMBER

? Is that considered a single cost objective?")

36 Single Cost Objective What if the teacher worked part of the day teaching preschool students with disabilities (paid from IDEA-B Preschool funds) and part of the day teaching students with disabilities in middle school (paid from IDEA-B Formula funds)? Is that considered a single cost objective? SEPTEMBER

37 Single Cost Objective What if the teacher worked part of the day teaching preschool students with disabilities (paid from IDEA-B Preschool funds) and part of the day teaching students with disabilities in middle school (paid from IDEA-B Formula funds)? Is that considered a single cost objective? The teacher works with students with disabilities all day. No. Two different student population types IDEA-B Preschool funds cannot fully support the entire payroll costs (unallowable to use IDEA-B Preschool funds for ages 6-21) SEPTEMBER

38 Concept 2 Single Cost Objective It is possible to work on a single cost objective even if an employee is paid from a Federal award and a non-federal award IF the employee s activities could be fully funded from the Federal award alone USDE Guidance: Enclosure C Support for Salaries and Wages Of An Employee Working on a Single Cost Objective, September 7, 2012 SEPTEMBER

39 Single Cost Objective Example of Single Cost Objective employee paid from a Federal and a Non-Federal award: A supplemental math teacher serves low-achieving students and is paid partially from Title I, Part A funds and partially from State Compensatory Education (SCE) funds SEPTEMBER

40 Single Cost Objective Even though the math teacher is being split-funded from a Federal award (Title I, Part A) and state funds (SCE), it is considered a single cost objective because: Teaching math to low-achieving students is an allowable activity under both Title I, Part A and SCE Since the teacher s payroll costs could be paid 100% from Title I, Part A, it is considered a single cost objective SEPTEMBER

41 Single Cost Objective Another example of an employee being paid from a Federal award and Non-Federal award and being a Single Cost Objective: A special education teacher is paid partially from IDEA-B funds and partially from state or local funds, but works 100% of their time on special education activities SEPTEMBER

42 Single Cost Objective Key to determining whether an employee is working on a single cost objective: If the employee s payroll costs can be supported in full from each of the funding sources and the activities are allowable with each funding source SEPTEMBER

43 Group Activity: Single Cost Objective At your table, discuss different scenarios that would be considered Single Cost Objectives Enter your Single Cost Objective scenarios in Padlet in the second column T&E Single Cost Objectives Select the + or add button at the bottom of the column. Begin typing your scenario in the data entry box that appears Add as many scenarios as you would like, just click the + or add button again for each scenario you would like to enter SEPTEMBER

44 Multiple Cost Objectives An employee is considered to work on multiple cost objectives if the employee works on: More than one Federal award; (unless it meets the criteria of a single cost objective) A Federal award and a non-federal award; (unless it meets the criteria of a single cost objective) Concept 1 Concept 2 Uniform Guidance: 2 CFR (i)(1)(vii) SEPTEMBER

45 Multiple Cost Objectives An employee is considered to work on multiple cost objectives if the employee works on (continued): An indirect cost activity and a direct cost activity; Two or more indirect cost activities which are allocated using different allocation bases; Uniform Guidance: 2 CFR (i)(1)(vii) SEPTEMBER

46 Multiple Cost Objectives An employee is considered to work on multiple cost objectives if the employee works on (continued): An unallowable activity and a direct or indirect cost activity Uniform Guidance: 2 CFR (i)(1)(vii) SEPTEMBER

47 Concept 1 Multiple Cost Objectives Example of More Than One Federal Award: A teacher works part of the day teaching students with disabilities, paid with IDEA-B funds, and part of the day teaching ELL students, paid with Title III, Part A funds SEPTEMBER

classes SEPTEMBER")

48 Concept 2 Multiple Cost Objectives Example of Federal and non-federal Awards: A teacher works part of the day performing Title I, Part A activities and part of the day teaching GT (Gifted and Talented) classes SEPTEMBER

49 Cost Objectives Considerations Although the cost objective is connected to the employee s payroll fund source, the fund source alone does not determine the cost objective Significant factor in determining whether an employee works on Single or Multiple Cost Objectives: The number of cost objectives or activities or student population type, not the number of fund sources SEPTEMBER

50 Cost Objectives Considerations A work unit for which cost data are desired is a cost objective If your grant program requires a set-aside, statutory cap, or reservation requirement, these are considered cost objectives Concept 3 Uniform Guidance: 2 CFR Definition of Cost Objective SEPTEMBER

51 Cost Objectives Considerations Concept 3 Examples of Title I, Part A Cost Objectives: LEA-level Administration Parental Involvement (Set-Aside) PNP Equitable Services (Set-Aside) Title I, Part A Programmatic Costs SEPTEMBER

IDEA-B Programmatic Costs")

52 Concept 3 Cost Objectives Considerations Examples of IDEA-B Cost Objectives: Private School Proportionate Share Services CEIS (Coordinated Early Intervening Services) IDEA-B Programmatic Costs SEPTEMBER

53 Cost Objectives Considerations IDEA-B Proportionate Share funds as a cost objective: The LEA must differentiate between public school services and private school services A teacher paid with IDEA-B funds and serves both public and private school students with disabilities is working under multiple cost objectives Even though the teacher is serving students with disabilities 100% of the time TEA s Substitute System FAQ document; Q36 SEPTEMBER

54 Group Activity: Multiple Cost Objectives At your table, discuss different scenarios that would be considered Multiple Cost Objectives Enter your Multiple Cost Objective scenarios in Padlet in the third column T&E Multiple Cost Objectives Select the + or add button at the bottom of the column. Begin typing your scenario in the data entry box that appears Add as many scenarios as you would like, just click the + or add button again for each scenario you would like to enter SEPTEMBER

funds or SCE (refer to Q77 in TEA s SCE Q&A) funds should not")

55 Cost Objectives De Minimus Benefit Limited duties (5% or less), such as cafeteria or bus duty, won t deprive a benefit from the intended beneficiaries of the Federal program and therefore are not considered a separate cost objective The percentage is based on the employee s daily schedule Employees paid from Title III, Part A (ELL) funds or SCE (refer to Q77 in TEA s SCE Q&A) funds should not be assigned limited duties, such as cafeteria or bus duty SEPTEMBER

56 Additional Compensation Examples of additional compensation: Additional pay ( stipend ) for employee having an advanced or preferred degree Additional pay ( stipend ) for a certain position for recruitment and retention purposes Additional pay ( stipend ) for time spent attending a workshop for professional development outside the employee s normal working hours, such as a teacher on a 10-month contract obtaining professional development in the summer Extra duty pay for after-school activities, tutoring, summer school instruction, etc. SEPTEMBER

57 Additional Compensation Additional compensation may be paid with federal funds, if allowable under the grant Additional compensation paid from federal funds must comply with the Federal Cost Principles of 2 CFR , such as Consistent treatment: May use federal funds only in the same manner that is consistent with local salary schedules and local policy Must be reasonable and necessary Additional compensation paid with federal funds is subject to Time Distribution reporting (EDGAR Documentation of Personnel Expenses) Will be addressed in Documentation section of this presentation TEA s EDGAR FAQ document, Q 8.4 SEPTEMBER

58 COST OBJECTIVES TEST YOUR KNOWLEDGE SEPTEMBER

59 Activity Look at your hand-out of Test Your Knowledge scenarios and determine the answers Work alone or discuss with those at your table We will then answer each question as a group SEPTEMBER

60 Test Your Knowledge - Question A special education teacher works solely in the special education program 50% of the teacher s payroll costs are funded with Federal IDEA-B funds 50% of the teacher s payroll costs are funded with the State Special Education Allotment from the Foundation School Program (FSP) Is this teacher working on a Single Cost Objective or Multiple Cost Objectives? SEPTEMBER

61 Test Your Knowledge - Answer A special education teacher works solely in the special education program 50% of the teacher s payroll costs are funded with Federal IDEA-B funds 50% of the teacher s payroll costs are funded with the State Special Education Allotment from the Foundation School Program (FSP) SINGLE COST OBJECTIVE Although the employee is funded from multiple sources, the teacher s activities are solely devoted to the special education program The employee s compensation can be paid fully from either fund source SEPTEMBER

62 Test Your Knowledge - Question A teacher spends half the day working on special education activities and the other half of the day working on Title I, Part A activities Is this teacher working on a Single Cost Objective or Multiple Cost Objectives? SEPTEMBER

63 Test Your Knowledge - Answer A teacher spends half the day working on special education activities and the other half of the day working on Title I, Part A activities MULTIPLE COST OBJECTIVES These are multiple cost objectives because the teacher works with more than one student population type and with more than one Federal program The teacher s compensation cannot be paid fully from one of these fund sources SEPTEMBER

64 Test Your Knowledge - Question A Preschool Special Education teacher works solely in the special education program 80% of the teacher s payroll costs are funded with IDEA-B Formula funds 20% of the teacher s payroll costs are funded with IDEA-B Preschool funds Is this teacher working on a Single Cost Objective or Multiple Cost Objectives? SEPTEMBER

65 Test Your Knowledge - Answer A Preschool Special Education teacher works solely in the special education program 80% of the teacher s payroll costs are funded with IDEA-B Formula funds 20% of the teacher s payroll costs are funded with IDEA-B Preschool funds SINGLE COST OBJECTIVE Teaching preschool special education is an allowable activity under IDEA-B Formula funds and IDEA-B Preschool funds; therefore, the teacher is performing a single cost objective The employee s compensation can be paid fully from either fund source SEPTEMBER

66 Test Your Knowledge - Question A Special Education teacher works solely in the special education program, teaching preschool part of the day and middle school part of the day The teacher s payroll costs are funded partially with IDEA-B Preschool funds, and partially with State Special Education Allotment Is this teacher working on a Single Cost Objective or Multiple Cost Objectives? SEPTEMBER

67 Test Your Knowledge - Answer A Special Education teacher works solely in the special education program, teaching preschool part of the day and middle school part of the day The teacher s payroll costs are funded partially with IDEA-B Preschool funds and partially with State Special Education Allotment MULTIPLE COST OBJECTIVES IDEA-B Preschool grant is only allowable for ages 3-5 Although the State Special Education Allotment could fully fund the position, IDEA-B Preschool cannot fully support the position SEPTEMBER

68 Test Your Knowledge - Question A supplemental math teacher works solely with lowachieving students 70% of the teacher s payroll costs are funded with Title I, Part A funds 30% of the teacher s payroll costs are funded with State Compensatory Education (SCE) funds Is this teacher working on a Single Cost Objective or Multiple Cost Objectives? SEPTEMBER

69 Test Your Knowledge - Answer A supplemental math teacher works solely with low-achieving students 70% of the teacher s payroll costs are funded with Title I, Part A funds 30% of the teacher s payroll costs are funded with State Compensatory Education (SCE) funds SINGLE COST OBJECTIVE Teaching math to low-achieving students is a single cost objective because it can be fully supported under Title I, Part A or fully supported under SCE SEPTEMBER

70 Test Your Knowledge - Question A teacher spends ¾ of the day working on Title I, Part A activities and ¼ of the day working on Title I, Part C (Migrant) activities Is this teacher working on a Single Cost Objective or Multiple Cost Objectives? SEPTEMBER

71 Test Your Knowledge - Answer A teacher spends ¾ of the day working on Title I, Part A activities and ¼ of the day working on Title I, Part C (Migrant) activities MULTIPLE COST OBJECTIVES These are multiple cost objectives because the teacher works with more than one student population type and with more than one Federal program The teacher s compensation cannot be paid fully from one of these fund sources SEPTEMBER

72 Test Your Knowledge - Question A speech pathologist is paid 100% with IDEA-B Formula funds He spends a portion of his time providing services to the students with disabilities enrolled at his district He spends a portion of his time serving parentally-placed private school children with disabilities, as part of the proportionate share services Is this teacher working on a Single Cost Objective or Multiple Cost Objectives? SEPTEMBER

73 Test Your Knowledge - Answer A speech pathologist is paid 100% with IDEA-B Formula funds He spends a portion of his time providing services to the students with disabilities enrolled at his district and spends a portion of his time serving parentally-placed private school children with disabilities, as part of the proportionate share services MULTIPLE COST OBJECTIVES Although the speech pathologist is paid from one Federal fund source, cost data are required for the proportionate share services Therefore, proportionate share services is a separate cost objective from the regular program services SEPTEMBER

74 Test Your Knowledge - Question A special education teacher is assigned solely to the special education program, but is required to perform cafeteria duties for 20 minutes Is this teacher working on a Single Cost Objective or Multiple Cost Objectives? SEPTEMBER

75 Test Your Knowledge - Answer A special education teacher is assigned solely to the special education program, but is required to perform cafeteria duty for 20 minutes SINGLE COST OBJECTIVE Although the teacher is serving a variety of of student population types during the cafeteria duty, the small amount of time qualifies as de minimus benefit because it is limited duties The intended beneficiaries of the Federal program are not deprived SEPTEMBER

76 Test Your Knowledge - Question An employee is paid 100% from Title I, Part A funds. Half their time is spent on parental involvement activities and half their time is spent on LEA-level administration. Is this employee working on a Single Cost Objective or Multiple Cost Objectives? SEPTEMBER

77 Test Your Knowledge - Answer An employee is paid 100% from Title I, Part A funds. Half their time is spent on parental involvement activities and half their time is spent on LEA-level administration. MULTIPLE COST OBJECTIVES If a grant program requires set asides, statutory caps, or reservations, each of these are considered a cost objective Therefore, even though the employee is paid 100% from one federal award, the employee is working on multiple cost objectives since parental involvement and LEA-level administration are two separate cost objectives SEPTEMBER

78 DOCUMENTATION SEPTEMBER

79 Documentation New EDGAR is less prescriptive than old EDGAR Broad standards outlined in 2 CFR (i) LEA must have adequate internal controls to ensure charges to the Federal awards are reasonable, accurate, allowable, and allocable LEA must have written procedures Uniform Guidance 2 CFR Part 200 SEPTEMBER

80 Documentation New EDGAR is less prescriptive than old EDGAR, continued As long as the LEA s internal controls and documentation meet the EDGAR standards, the LEA has flexibility on how they comply with time distribution reporting Best Practice: Follow old EDGAR documentation standards: 2 CFR Part 225 (OMB Circular A-87) EDGAR: Education Department General Administrative Requirements SEPTEMBER

81 DOCUMENTATION: BEST PRACTICE FOR SINGLE COST OBJECTIVE: SEMI-ANNUAL CERTIFICATION SEPTEMBER

82 Best Practice for Single Cost Objective Employees complete Semi-Annual Certificates verifying they worked solely on the single Federal award or cost objective for the period of time covered by the certification Identify the Single Cost Objective on the form, not the source of funds Certificate is signed after-the-fact by either the employee or a supervisory official having firsthand knowledge of the work performed by the employee SEPTEMBER

83 Best Practice for Single Cost Objective Certificates completed and signed at least semi-annually (could be less than six months, but not more than six months), such as: Every six months (Aug-Jan; Feb-July) Based on semesters (Aug-Dec; Jan-May) If the employee works in the summer as well, add Jun-Jul as a third certification period Locally determined timeframe as long as it is after-the-fact and doesn t exceed a six-month period SEPTEMBER

84 Documentation for Single Cost Objective Neither USDE nor TEA mandates the use of a specific form for the periodic certification for Single Cost Objective employees However, the LEA must have a standard periodic certification form to be used by all their Single Cost Objective employees, which must include the elements listed on the next slide TEA s Federal Time and Effort Reporting Guidance Handbook for LEAs SEPTEMBER

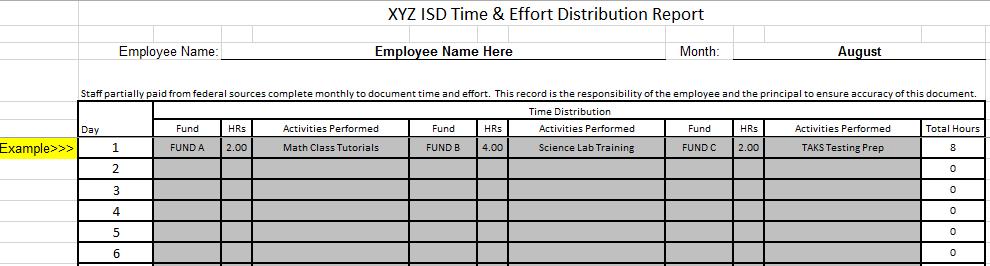

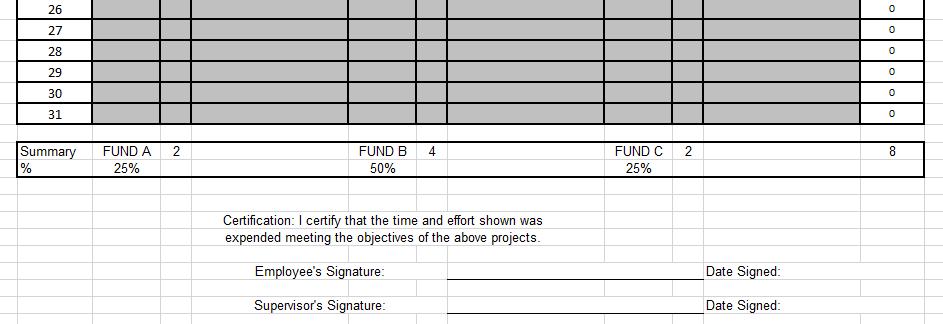

85 Documentation for Single Cost Objective Required Elements of Semi-Annual Certificate: Employer s Name Employee s Name and Position Name of Single Cost Objective under which the employee worked (this is not the fund source, it is the cost objective or activity) Reporting Period (at least semi-annual) Statement that the employee worked solely on that cost objective for the period covered by the certification Dated signature (after-the-fact) of the employee or of a supervisor with first-hand knowledge of the employee s activities TEA s Federal Time and Effort Reporting Guidance Handbook for LEAs SEPTEMBER

86 Sample Semi- Annual Certificate for Single Cost Objective

87 Audit Finding: Single Cost Objective Common Audit Finding: Certificate signed prior to end date Example: Certificate covers six month period: January through June The employee signed the form May 30 because that is the last day of school (not after-the fact) Solution: Change the certificate s period to cover January 1 - May 30 SEPTEMBER

88 ED-FLEX WAIVER AND TIME DISTRIBUTION REPORTING SEPTEMBER

89 Ed-Flex Waiver Texas annually seeks an Ed-Flex waiver from USDE, which allows TEA the authority to waive some federal education requirements One of the requirements Texas waives under its Ed-Flex authority is time and effort semi-annual certification for employees funded by certain grant programs Refer to TTAA Letter dated 07/13/2018 SEPTEMBER

90 Ed-Flex Waiver Employees who work on a Single Cost Objective and whose salaries are compensated by any Ed-Flex covered grant program are not required to submit: Semi-Annual Certification for Single Cost Objective Instead, the only required time distribution documentation is a job description that clearly states the employee is assigned 100% to the program or single cost objective Refer to TTAA Letter dated 07/13/2018 SEPTEMBER

91 Ed-Flex Waiver Covered Grant Programs under TEA s Ed-Flex Waiver: Title I, Part A (other than section 1111) Title I, Part C Title I, Part D Title II, Part A Title IV, Part A Carl D. Perkins Career and Technical Education Act of 2006 Refer to TTAA Letter dated 07/13/2018 SEPTEMBER

92 DOCUMENTATION: BEST PRACTICE FOR MULTIPLE COST OBJECTIVES: MONTHLY PAR SEPTEMBER

93 Best Practice for Multiple Cost Objectives Employees complete monthly PARs (Personnel Activity Reports) verifying the percentage of time they worked on each cost objective for the period of time covered by the PAR Identify each specific activity or cost objective and the actual amount of time or percentage worked on each PAR must account for the total activity (100%) for which the employee is compensated SEPTEMBER

94 Best Practice for Multiple Cost Objectives PAR is completed at least monthly and must coincide with one or more pay periods The PAR must be signed immediately after the last pay period of the time span being certified, as closely as possible PAR is signed after-the-fact Ensures the PAR represents actual hours worked rather than estimated hours SEPTEMBER

95 Best Practice for Multiple Cost Objectives PAR is signed by the employee Usually, only the employee knows how much time was spent on each activity each day, unless the employee has a set schedule Have local policy/procedure that if the employee is no longer with the LEA and did not sign the PAR, the supervisor with direct knowledge of the employee s schedule notates on the employee signature line that the employee is not available; the supervisor signs SEPTEMBER

96 Documentation for Multiple Cost Objectives Neither USDE nor TEA mandates the use of a specific form for the PARs for Multiple Cost Objectives employees However, the LEA must have a standard PAR form to be used by all their Multiple Cost Objective employees, which must include the employee s actual activity and the employee s signature TEA s Federal Time and Effort Reporting Guidance Handbook for LEAs SEPTEMBER

97 Sample PAR Courtesy of Ray Wilks, RTSBA Grand Prairie ISD

98

99 Monthly PAR Your LEA could choose to use TEA s Employee Schedule and Certificate form designed for the Substitute System* as your monthly PAR form Although the form is applicable to the Substitute System for certain employees and only covers a week, you could adapt it for use for your monthly PARs Recommended format because it covers all elements that would be reviewed in an audit or grant review *Substitute System is discussed later in this presentation TEA s Substitute System SEPTEMBER

100 Audit Finding: Multiple Cost Objectives Common Audit Finding: PAR total activity exceeds 100% Incorrect Example: Monthly PAR indicates: Title I, Part A Admin 100% Gifted & Talented Program 100% 200% Total activity must equal 100%, not 200% SEPTEMBER

101 Audit Finding: Multiple Cost Objectives Common Audit Finding: PAR total activity is less than 100% Incorrect Example: Monthly PAR of part-time employee indicates: Title I, Part A Admin 20% Gifted & Talented Program 30% 50% Total activity must equal 100% Regardless of whether the employee is full-time or part-time, the total activity must equal 100% SEPTEMBER

102 SUBSTITUTE SYSTEM IN LIEU OF MONTHLY PAR FOR ELIGIBLE EMPLOYEES SEPTEMBER

103 2 CFR (i)(5) For states, local governments and Indian tribes, substitute processes or systems for allocating salaries and wages to Federal awards may be used in place of or in addition to the records described in paragraph (1) [2 CFR (i)(1)] if approved by the cognizant agency for indirect cost. [TEA is the cognizant agency for ISDs and open-enrollment charter schools] Uniform Guidance 2 CFR Part 200 SEPTEMBER

104 Substitute System Approved by TEA May be used in lieu of monthly PAR for employees working on multiple cost objectives who have pre-determined, set schedules and work on only one activity at a time TEA s Substitute System SEPTEMBER

105 Substitute System Approved by TEA Optional Designed to ease the administrative burden of monthly PARs Allows for semi-annual reporting instead of monthly reporting for certain Multiple Cost Objective employees TEA s Substitute System SEPTEMBER

106 Substitute System LEA Eligibility The LEA must obtain approval from TEA to use the Substitute System Via submittal of TEA s Management Certificate LEA certifies their compliance with the TEA requirements for the Substitute System Management Certificate must be submitted to TEA annually TEA posts on their website a list of approved LEAs TEA s Substitute System SEPTEMBER

107 Sample Management Certification Form (top portion of form)

108 Sample Management Certification Form (lower portion of form)

109 Substitute System LEA Eligibility LEA must submit Management Certificate annually, but the submittal date determines when the system may be used during the school year To implement the Substitute System for the school year for the following semesters Submit the Management Certificate to TEA by. Fall 2018, Spring 2019, and Summer 2019 semesters September 15, 2018 Spring 2019 and Summer 2019 semesters only December 15, 2018 Summer 2019 semester only May 15, 2019 TEA s Substitute System SEPTEMBER

110 Substitute System LEA Eligibility Recommendation: Submit the Management Certificate for approval to use the Substitute System even if you currently do not have employees for whom the Substitute System would be applicable Submittal of the Management Certificate does not obligate the LEA to use the Substitute System Submittal of the Management Certificate ensures the LEA is eligible to use the Substitute System if it chooses to do so By submitting the Management Certificate, the LEA retains their eligibility to participate during the current year and will be eligible to use it immediately during the current year if staff become eligible TEA s Substitute System SEPTEMBER

111 Substitute System Employee Eligibility An employee must meet the following conditions to participate in the Substitute System: Employee works on Multiple Cost Objectives Employee works on a set schedule (pre-determined, consistent schedule) Employee does not work on the multiple activities or cost objectives at the exact same time on their schedule TEA s Substitute System SEPTEMBER

112 Substitute System Employee Eligibility Employees Ineligible to use the Substitute System: Employees working on a Single Cost Objective Use the Semi-Annual Certification for Single Cost Objective instead An employee whose schedule changes regularly, e.g., every month Use the monthly PAR instead An employee who works on the same programs on a regular basis but doesn t know from day to day how much time will be spent on each program (doesn t have a predetermined, set schedule) Use the monthly PAR instead TEA s Substitute System SEPTEMBER

113 Substitute System Employee Documentation Employees are required to complete an Employee Schedule and Certification Form at least semi-annually LEA uses TEA s form or develops their own form, provided it includes all required elements Employee Schedule and Certification Form are maintained locally; not submitted to TEA Employee Schedule and Certification Form completed after-the-fact, to ensure accuracy TEA s Substitute System SEPTEMBER

114 Substitute System Employee Documentation To meet the requirement that the Employee Certification coincides with one or more pay periods, the certification must be signed immediately after the last pay period of the time span being certified i.e., the last pay period of the school semester or six-month period Example: Staff are paid on the 25 th of each month; Auditors will look to see that semi-annual certifications were signed on or after the 26 th of the month that represents the mid-point of your school year TEA s Substitute System FAQ document, Q2 SEPTEMBER

115 Substitute System Employee Documentation The Employee Schedule and Certification form must: Include the specific activity/cost objective the employee worked on for each segment of the employee s schedule Account for the total hours the employee is compensated Be signed by the employee* and supervisor with first-hand knowledge of the employee s work If the employee is no longer with the LEA and did not sign the PAR, the supervisor with direct knowledge of the employee s schedule notates on the employee signature line that the employee is not available; the supervisor signs TEA s Substitute System FAQ document, Q24 SEPTEMBER

116 Substitute System Employee Documentation If the employee s pre-determined, set schedule changes by more than 10% occasionally (such as once every three or four months), the employee is still eligible to use the substitute system but must resubmit the Employee Schedule and Certification to reflect the new schedule TEA s Substitute System FAQ document, Q22 SEPTEMBER

117 Sample Employee Schedule for Substitute System SEPTEMBER

118 Sample Employee Certificate for Substitute System (Top portion of certificate)

119 Sample Employee Certificate for Substitute System (Lower portion of certificate)

120 Multiple Cost Objectives: Substitute System vs Monthly PAR Substitute System: Semi-Annual Certification PAR: Monthly Reporting LEA Eligibility: Only for LEAs with TEA approval to use the Substitute System LEA Eligibility: Applicable to any LEA Employee Eligibility: Only for Multiple Cost Employees with consistent schedule Employee Eligibility: Applicable to any Multiple Cost employee

121 SUMMARY OF DOCUMENTATION TYPES SEPTEMBER

122

123 Three Types of Time Distribution Reports Semi-Annual Certificate for Single Cost Objective employees Monthly Personnel Activity Reports (PARs) For employees with Multiple Cost objectives and inconsistent schedule OR all employees with Multiple Cost objectives (if not using the Substitute System for the Multiple Cost Objective employees with consistent schedule) The Substitute System, if LEA received approval by TEA For employees with Multiple Cost Objectives and consistent schedule Submitted at least semi-annually SEPTEMBER

for Multiple Cost Objectives *Recommendation: Add to written policies/procedures: If the employee is no longer with the LEA at the end of the")

124 Time Distribution Reports Must be Signed After-the-Fact by: Specify in written policies and procedures Semi-Annual Certification for Single Cost Objective Monthly PAR for Multiple Cost Objectives Semi-Annual Substitute System (in lieu of monthly PARs) for Multiple Cost Objectives *Recommendation: Add to written policies/procedures: If the employee is no longer with the LEA at the end of the designated certification period, the supervisor with direct knowledge of the employee s schedule notates on the employee signature line that the employee is not available, and then signs the certificate themselves Employee OR Supervisor with first-hand knowledge of employee s work Employee Only* Employee* AND Supervisor with first-hand knowledge of employee s work

125 DOCUMENTATION FOR ADDITIONAL COMPENSATION: SUBSTITUTES, STIPENDS, EXTRA-DUTY PAY ACTIVITIES SEPTEMBER

126 Documentation for Substitutes The LEA should have a local policy/procedure: All substitute pay is paid from state and/or local funds, not from federal or state grants, OR Substitute pay follows the same pay as the staff members for whom the substitute is working TEA s EDGAR FAQ document; Q8.3 SEPTEMBER

127 Documentation for Substitutes If substitute pay is paid from state/local funds, time distribution reporting is N/A If substitute pay follows the employee s federal funding distribution, the LEA should have some type of afterthe-fact documentation that identifies the employee for whom the substitute is working TEA s EDGAR FAQ document; Q8.3 SEPTEMBER

128 Documentation for Stipends Stipends paid from Federal Funds: For purposes of this presentation, stipends will be the terminology used to describe additional pay, such as Additional pay for employee having an advanced or preferred degree Additional pay for a certain position for recruitment and retention purposes Additional pay for time spent attending a workshop for professional development outside the employee s normal working hours, such as a teacher on a 10-month contract obtaining professional development in the summer SEPTEMBER

129 Documentation for Stipends Stipends may be paid with Federal funds only in the same manner that is consistent with local salary schedules and local policy, if allowable under the specific Federal grant Amount must be reasonable and necessary If stipends are paid with federal funds, time distribution documentation must be maintained TEA s EDGAR FAQ document; Q8.4 SEPTEMBER

![Best Practice: 3 Documents for Stipends 1) Document that informs employee they are receiving a stipend for [xx] purpose for $[xx] Supplemental Pay Agreement, if applicable 2) Payroll authorization](/docs-images/94/120808445/images/130-4.jpg "form 4.")

130 Best Practice: 3 Documents for Stipends 1) Document that informs employee they are receiving a stipend for [xx] purpose for $[xx] Supplemental Pay Agreement, if applicable 2) Payroll authorization form 4. Additional documentation as appropriate, such as proof of attendance if stipend is for professional development 3) Time Distribution Documentation, blanket certification or individual certification In most cases, an annual or semi-annual certification would be appropriate SEPTEMBER

131 SAMPLE SUPPLEMENTAL PAY AGREEMENT FORM (top portion of form)

132 SAMPLE SUPPLEMENTAL PAY AGREEMENT FORM (lower portion of form)

133 Recommended Time Distribution Documentation for Stipends Blanket certification signifying: Purpose and amount of the stipend Employee(s) receiving the stipend Fund source Time period for which the stipend is applicable Signed by supervisor, after-the-fact Completed at least semi-annually SEPTEMBER

134 SAMPLE of Blanket Certification for multiple employees receiving a stipend from federal funds 134

135 Documentation for Extra-Duty Pay Extra duty pay (tutoring, after school activities, summer instruction, etc) may be paid with Federal funds only in the same manner that is consistent with local salary schedules and local policy, if allowable under the specific Federal grant Amount must be reasonable and necessary If federal funds are used for extra duty pay, time distribution documentation must be maintained SEPTEMBER

136 Documentation for Extra-Duty Pay Considered a cost objective Treat the extra duty job separately from the regular, day job for purposes of time distribution reporting If the regular day job and the extra-duty job are both paid from federal funds, complete two, separate Time Distribution reports SEPTEMBER

137 Best Practice: 3 Documents for Extra Duty Pay 1) Extra-Duty Pay Agreement Form, providing employee with information of expected duties (must be allowable for the program), pay rate, time period for performance of activities, etc. 2) Time-sheets or other documentation submitted by the employee to document that activities were performed 3) Time Distribution documentation (based on various scenarios) SEPTEMBER

138 SAMPLE EXTRA-DUTY PAY AGREEMENT FORM (top portion of form)

139 SAMPLE EXTRA-DUTY PAY AGREEMENT FORM (lower portion of form)

140 Scenarios for Time Distribution Reports for Extra Duty Pay If both the additional compensation and the regular position are funded from Federal funds: Two types of time distribution reports are completed: The appropriate time distribution form applicable to the regular position Semi-Annual if Single Cost Objective; Monthly PAR or Substitute System if Multiple Cost Objectives Separate Time Distribution documentation completed for the additional compensation (typically semi-annual is appropriate since the extra duty activity is usually a single cost objective) SEPTEMBER

141 Scenarios for Time Distribution Reports for Extra Duty Pay If the additional compensation is funded from state or local funds, but the regular position is funded from Federal funds: The appropriate time distribution report is submitted only for the regular position Semi-Annual if Single Cost Objective; Monthly PAR or Substitute System for Multiple Cost Objectives Time distribution reporting is not required for the additional compensation paid from state or local funds SEPTEMBER

142 Scenarios for Time Distribution Reports for Extra Duty Pay If the additional compensation is funded from Federal funds, but the regular position is funded from state or local funds: Time Distribution documentation is completed only for the additional compensation (typically semi-annual is appropriate since the extra duty activity is usually a single cost objective) Time distribution reporting is not required for the regular position paid from state or local funds SEPTEMBER

143 ADDITIONAL COMPENSATION for Extra Duty Activities Job Duties Fund Source Type of Time Distribution Report: Two Separate Reports Regular Job Federal Semi-Annual if Single Cost Objective; Monthly PAR or Substitute System, as applicable, if Multiple Cost Objectives Extra-Duty Federal Separate Semi-Annual Certificate (typically)

144 ADDITIONAL COMPENSATION for Extra Duty Activities Job Duties Fund Source Type of Time Distribution Report: One Report only for Regular Job Regular Job Federal Semi-Annual if Single Cost Objective; Monthly PAR or Substitute System, as applicable, if Multiple Cost Objectives Extra-Duty State/Local N/A

145 ADDITIONAL COMPENSATION for Extra Duty Activities Job Duties Fund Source Regular Job State/Local N/A Type of Time Distribution Report: One Report only for Extra-Duty Extra-Duty Federal Semi-Annual Certificate (typically)

146 Important Considerations LEA must have adequate documentation to support the use of Federal funds for stipends or additional compensation LEA must document justification for use of Federal funds for the stipends or additional compensation SEPTEMBER

147 Important Considerations Payroll records must match payroll authorization forms, salary authorizations, personnel action forms, or other records that identify all sources of funding for which the employee is authorized to be paid SEPTEMBER

148 TIME DISTRIBUTION DOCUMENTATION TEST YOUR KNOWLEDGE SEPTEMBER

149 Activity Look at your hand-out of Test Your Knowledge scenarios used earlier for determining cost objectives and now determine the type of documentation needed for the various scenarios Work alone or discuss with those at your table We will then answer each question as a group SEPTEMBER

150 Test Your Knowledge - Question A special education teacher works solely in the special education program 50% of the teacher s payroll costs are funded with Federal IDEA-B funds 50% of the teacher s payroll costs are funded with the State Special Education Allotment from the Foundation School Program (FSP) What type of Time Distribution Report should the employee complete (best practice)? SEPTEMBER

151 Test Your Knowledge - Answer A special education teacher works solely in the special education program 50% of the teacher s payroll costs are funded with Federal IDEA-B funds 50% of the teacher s payroll costs are funded with the State Special Education Allotment from the Foundation School Program (FSP) SEMI-ANNUAL CERTIFICATE (SINGLE COST OBJECTIVE) Although the employee is funded from multiple sources, the teacher s activities are solely devoted to the special education program The employee s compensation can be paid fully from either fund source SEPTEMBER

152 Test Your Knowledge - Question A teacher spends half the day working on special education activities and the other half of the day working on Title I, Part A activities What type of Time Distribution Report should the employee complete (best practice)? SEPTEMBER

153 Test Your Knowledge - Answer A teacher spends half the day working on special education activities and the other half of the day working on Title I, Part A activities MONTHLY PAR OR SUBSTITUTE SYSTEM (MULTIPLE COST OBJECTIVES) These are multiple cost objectives because the teacher works with more than one student population type and with more than one Federal program The teacher s compensation cannot be paid fully from one of these fund sources SEPTEMBER

154 Test Your Knowledge - Question A teacher spends 100% of their time working on Title I, Part A activities What type of Time Distribution Report should the employee complete (best practice)? SEPTEMBER

155 Test Your Knowledge - Answer A teacher spends 100% of their time working on Title I, Part A activities NO TIME DISTRIBUTION REPORT IS REQUIRED Title I, Part A is covered under TEA s Ed-Flex waiver Therefore, the semi-annual certification for a Single Cost Objective position is waived However, the LEA must maintain an accurate, up-to-date job description that lists the current duties and responsibilities and states the employee is assigned 100% to the Title I, Part A program. The job description must be signed and dated by both the employee and the employee s supervisor SEPTEMBER

156 Test Your Knowledge - Question A Preschool Special Education teacher works solely in the special education program 80% of the teacher s payroll costs are funded with IDEA-B Formula funds 20% of the teacher s payroll costs are funded with IDEA-B Preschool funds What type of Time Distribution Report should the employee complete (best practice)? SEPTEMBER

157 Test Your Knowledge - Answer A Preschool Special Education teacher works solely in the special education program 80% of the teacher s payroll costs are funded with IDEA-B Formula funds 20% of the teacher s payroll costs are funded with IDEA-B Preschool funds SEMI-ANNUAL CERTIFICATE (SINGLE COST OBJECTIVE) Teaching preschool special education is an allowable activity under IDEA-B Formula funds and IDEA-B Preschool funds; therefore, the teacher is performing a single cost objective The employee s compensation can be paid fully from either fund source SEPTEMBER

158 Test Your Knowledge - Question A Special Education teacher works solely in the special education program, teaching preschool part of the day and middle school part of the day The teacher s payroll costs are funded partially with IDEA-B Preschool funds and partially with State Special Education Allotment What type of Time Distribution Report should the employee complete (best practice)? SEPTEMBER

159 Test Your Knowledge - Answer A Special Education teacher works solely in the special education program, teaching preschool part of the day and middle school part of the day The teacher s payroll costs are funded partially with IDEA-B Preschool funds and partially with State Special Education Allotment MONTHLY PAR OR SUBSTITUTE SYSTEM (MULTIPLE COST OBJECTIVES) IDEA-B Preschool grant is only allowable for ages 3-5 Although the State Special Education allotment could fully fund the position, IDEA-B Preschool cannot fully support the position SEPTEMBER

160 Test Your Knowledge - Question A supplemental math teacher works solely with lowachieving students 70% of the teacher s payroll costs are funded with Title I, Part A funds 30% of the teacher s payroll costs are funded with State Compensatory Education (SCE) funds What type of Time Distribution Report should the employee complete (best practice)? SEPTEMBER

161 Test Your Knowledge - Answer A supplemental math teacher works solely with low-achieving students 70% of the teacher s payroll costs are funded with Title I, Part A funds 30% of the teacher s payroll costs are funded with State Compensatory Education (SCE) funds SEMI-ANNUAL CERTIFICATE (SINGLE COST OBJECTIVE) Teaching math to low-achieving students is a single cost objective because it can be fully supported under Title I, Part A or fully supported under SCE SEPTEMBER

162 Test Your Knowledge - Question A teacher spends ¾ of the day working on Title I, Part A activities and ¼ of the day working on Title I, Part C (Migrant) activities What type of Time Distribution Report should the employee complete (best practice)? SEPTEMBER

These are multiple cost objectives because the teacher works with more than one student population type and with more than one Federal program The teacher s compensation")

163 Test Your Knowledge - Answer A teacher spends ¾ of the day working on Title I, Part A activities and ¼ of the day working on Title I, Part C (Migrant) activities MONTHLY PAR OR SUBSTITUTE SYSTEM (MULTIPLE COST OBJECTIVES) These are multiple cost objectives because the teacher works with more than one student population type and with more than one Federal program The teacher s compensation cannot be paid fully from one of these fund sources SEPTEMBER

164 Test Your Knowledge - Question A speech pathologist is paid 100% with IDEA-B Formula funds He spends a portion of his time providing services to the students with disabilities enrolled at his district He spends a portion of his time serving parentally-placed private school children with disabilities, as part of the proportionate share services What type of Time Distribution Report should the employee complete (best practice)? SEPTEMBER

165 Test Your Knowledge - Answer A speech pathologist is paid 100% with IDEA-B Formula funds He spends a portion of his time providing services to the students with disabilities enrolled at his district and spends a portion of his time serving parentally-placed private school children with disabilities, as part of the proportionate share services MONTHLY PAR OR SUBSTITUTE SYSTEM (MULTIPLE COST OBJECTIVES) Although the speech pathologist is paid from one Federal fund source, cost data is required for the proportionate share services Therefore, proportionate share services is a separate cost objective from the regular program services SEPTEMBER

166 Test Your Knowledge - Question A special education teacher is assigned solely to the special education program, but is required to perform cafeteria duties for 20 minutes What type of Time Distribution Report should the employee complete (best practice)? SEPTEMBER

167 Test Your Knowledge - Answer A special education teacher is assigned solely to the special education program, but is required to perform cafeteria duty for 20 minutes SEMI-ANNUAL CERTIFICATE (SINGLE COST OBJECTIVE) Although the teacher is serving a variety of of student population types during the cafeteria duty, the small amount of time qualifies as de minimus benefit because it is limited duties The intended beneficiaries of the Federal program are not deprived SEPTEMBER

168 Test Your Knowledge - Question An employee is paid 100% from Title I, Part A funds. Half their time is spent on parental involvement activities and half their time is spent on LEA-level administration. What type of Time Distribution Report should the employee complete (best practice)? SEPTEMBER

If a grant program requires set asides, statutory caps, or reservations, each of these are considered a cost objective Therefore, even")

169 Test Your Knowledge - Answer An employee is paid 100% from Title I, Part A funds. Half their time is spent on parental involvement activities and half their time is spent on LEA-level administration. MONTHLY PAR OR SUBSTITUTE SYSTEM (MULTIPLE COST OBJECTIVES) If a grant program requires set asides, statutory caps, or reservations, each of these are considered a cost objective Therefore, even though the employee is paid 100% from one federal award, the employee is working on multiple cost objectives since parental involvement and LEA-level administration are two separate cost objectives SEPTEMBER

170 Test Your Knowledge - Question A full-time aide is used by the LEA for special education activities part of the time and other federal programs part of the time. She does not have a set schedule for assisting the various programs, as it varies according to need. What type of Time Distribution Report should the employee complete (best practice)? SEPTEMBER

171 Test Your Knowledge - Answer A full-time aide is used by the LEA for special education activities part of the time and other federal programs part of the time. She does not have a set schedule for assisting the various programs, as it varies according to need. MONTHLY PAR (MULTIPLE COST OBJECTIVES) The employee is not eligible to use the Substitute System because she does not have a set schedule. SEPTEMBER

172 Test Your Knowledge - Question The LEA contracts with an Occupational Therapist (OT) to provide related services for the students with disabilities. Part of the time the OT provides services for the public school students, paid from IDEA-B funds, and part of the time the OT provides services for parentally placed private school children with disabilities, paid from IDEA-B proportionate share funds. What type of Time Distribution Report should the OT complete (best practice)? SEPTEMBER

173 Test Your Knowledge - Answer The LEA contracts with an Occupational Therapist (OT) to provide related services for the students with disabilities. Part of the time the OT provides services for the public school students, paid from IDEA-B funds, and part of the time the OT provides services for parentally placed private school children with disabilities, paid from IDEA-B proportionate share funds. NONE Time Distribution Reporting is not applicable to contractors; only applicable to employees paid in full or in part with Federal funds. SEPTEMBER

174 Test Your Knowledge - Question An LEA pays an elementary school teacher with local funds for her regular position, but pays her with Title I, Part A funds to provide after-school tutoring for low-achieving students What type of Time Distribution Report should the employee complete (best practice)? SEPTEMBER

175 Test Your Knowledge - Answer An LEA pays an elementary school teacher with local funds for her regular position, but pays her with Title I, Part A funds to provide after-school tutoring for low-achieving students SEMI-ANNUAL CERTIFICATE FOR THE EXTRA-DUTY PAY ONLY (Should also have Extra-Duty Pay Agreement Form & timesheets) The portion of her time spent on after-school tutoring is easily separated from her teaching position by her schedule. She only needs time distribution records for the time she works in the after-school program supported by Title I, Part A funds SEPTEMBER

176 Test Your Knowledge - Question An LEA pays a special education teacher with IDEA-B funds for her regular position, but pays her with Title I, Part A funds to provide after-school tutoring for low-achieving students What type of Time Distribution Report should the employee complete (best practice)? SEPTEMBER

177 Test Your Knowledge - Answer An LEA pays a special education teacher with IDEA-B funds for her regular position, but pays her with Title I, Part A funds to provide after-school tutoring for low-achieving students SEMI-ANNUAL CERTIFICATION FOR REGULAR JOB; and A SEPARATE SEMI-ANNUAL FORM FOR THE EXTRA-DUTY PAY (Should also have Extra-Duty Pay Agreement Form & timesheets) Treat the regular job separately from the extra-duty job She needs time distribution records for both jobs since both are paid from federal funds Each job needs a separate time distribution form SEPTEMBER

178 Test Your Knowledge - Question A special education teacher is paid from IDEA-B funds and works 100% of their time teaching students with disabilities Is a job description sufficient? SEPTEMBER

179 Test Your Knowledge - Answer A special education teacher is paid from IDEA-B funds and works 100% of their time teaching students with disabilities Is a job description sufficient? NO IDEA-B is not covered under the Ed-Flex waiver. Both a job description and semi-annual certification is required SEPTEMBER

180 JOB DESCRIPTIONS SEPTEMBER

181 Job Descriptions Maintaining signed job descriptions is considered to be an internal control activity that signifies the employee s understanding of his or her respective job duties. Signed and dated job descriptions that identify the funding source and duties related to the grant program are REQUIRED if using the Ed-Flex waiver in lieu of semi-annual time distribution certificates for SEPTEMBER

182 Job Descriptions Auditors and monitors often consider the lack of a signed job description to be an indicator of poor internal controls which, in combination with other poor controls, could lead to an audit or monitoring finding or comment. Subgrantees [LEAs] should [best practice] maintain signed job descriptions for all staff paid in full or in part with federal funds or staff paid with other funds whose salary is used to meet a federal matching or cost sharing requirement. TEA s EDGAR FAQ document; Q8.11 SEPTEMBER

183 Job Descriptions Include all the following components: Current duties and responsibilities List of all program or cost objectives under which the employee works Periodical updates when duties or responsibilities change Dated signature of both employee and employee s supervisor SEPTEMBER

184 Job Descriptions Job descriptions should be signed by the employee to ensure the employee understands their responsibilities and does not inadvertently perform duties unallowable for their fund source SEPTEMBER

185 Job Descriptions Job descriptions should be kept up-to-date If duties and responsibilities change during the year, revise accordingly in a timely manner Review and sign annually SEPTEMBER

186 Job Descriptions Single Cost Objective positions: Job descriptions should clearly state the position is supported by a Single Cost Objective If funding split among multiple sources, identify funding sources SEPTEMBER

187 Job Descriptions Multiple Cost Objectives position: Job descriptions should clearly state whether the position is supported by Multiple Cost Objectives and identify the cost objectives and funding sources SEPTEMBER

188 SAMPLE JOB DESCRIPTION (top portion)

189 SAMPLE JOB DESCRIPTION (middle portion)

190 SAMPLE JOB DESCRIPTION (lower portion)

191 RECONCILIATION FOR MULTIPLE COST OBJECTIVES SEPTEMBER

192 Reconciliation 2 CFR (i)(1)(viii) (viii) Budget estimates (i.e., estimates determined before the services are performed) alone do not qualify as support for charges to Federal awards, but may be used for interim accounting purposes, provided that: A. The system for establishing the estimates produces reasonable approximations of the activity actually performed; B. Significant changes in the corresponding work activity are identified and entered into the records in a timely manner ; and Uniform Guidance 2 CFR Part 200 SEPTEMBER

193 Reconciliation 2 CFR (i)(1)(viii) (viii) Budget estimates (i.e., estimates determined before the services are performed) alone do not qualify as support for charges to Federal awards, but may be used for interim accounting purposes, provided that: C. The [LEA] s system of internal controls includes processes to review after-the-fact interim charges made to a Federal award based on budget estimates. All necessary adjustments must be made such that the final amount charged to the Federal award is accurate, allowable, and properly allocated. Uniform Guidance 2 CFR Part 200 SEPTEMBER

194 Reconciliation The LEA must compare payroll costs based on initial budgets with the actual time and effort expended by the employee and certified on the PAR and make adjustments as needed SEPTEMBER

195 Reconciliation Any deviation between budgeted and actual costs must be adjusted by the end of the year to ensure all costs are allocable to the grant The final amount charged to the Federal grant must be accurate, allowable, and properly allocated SEPTEMBER

196 WRITTEN POLICIES & PROCEDURES SEPTEMBER

197 Written Policies and Procedures 2 CFR (a)(1) Costs of compensation are allowable to the extent that they satisfy the specific requirements of this part, and that the total compensation for individual employees: (1) Is reasonable for the services rendered and conforms to the established written policy of the [LEA] consistently applied to both Federal and non-federal activities; Uniform Guidance 2 CFR Part 200 SEPTEMBER

198 Written Policies and Procedures 2 CFR (i)(1)(ii,iii) These documentation of personnel records must: (ii) Be incorporated into the official records of the [LEA]; This means you should have your internal controls documented in your written policies and procedures Uniform Guidance 2 CFR Part 200 SEPTEMBER

199 Written Policies & Procedures LEA must demonstrate that it maintains and follows written policies and procedures for the Federal time distribution reporting requirement Written policies and procedures are important components of internal controls Adequate policies and procedures, properly implemented, are the key to compliance and successful audits! SEPTEMBER

200 Written Policies & Procedures Auditors or monitors check to ensure the following are documented: A specific administrative procedure that describes the circumstances under which employees are required to prepare time distribution reports SEPTEMBER

201 Written Policies & Procedures Auditors or monitors check to ensure the following are documented, continued: A specific administrative procedure that prescribes the frequency, form, and content of time distribution reports Procedures that include samples of the types of time distribution reports required SEPTEMBER

202 Written Policies & Procedures Auditors or monitors check to ensure the following are documented, continued: A specific administrative procedure that requires that employees working under Multiple Cost Objectives disclose on the time distribution report an after-the-fact distribution of 100 percent of the actual time spent on each activity/fund source SEPTEMBER

203 Written Policies & Procedures Auditors or monitors check to ensure the following are documented, continued: A specific administrative procedure that requires the allocation of payroll costs to Federal awards based upon the actual time reported by each employee paid from a Federal award SEPTEMBER

from TEA Desk Audit SEPTEMBER 2018")

204 Internal Controls Questionnaire regarding Administrative Procedures Manual (APM) from TEA Desk Audit SEPTEMBER

Federal Reporting -Time & Effort-

Federal Reporting -Time & Effort- Terry Harless, CPA Executive Director Internal Operations Who and Why? Any employee paid from federal funds. Serves as a receipt for federal funds spent. Why is T&E typically

Federal Reporting -Time & Effort- Terry Harless, CPA Executive Director Internal Operations Who and Why? Any employee paid from federal funds. Serves as a receipt for federal funds spent. Why is T&E typically

OMB CIRCULAR TUTORIAL BRUSTEIN & MANASEVIT, PLLC

EDGAR AND OMB CIRCULAR TUTORIAL BRETTE KAPLAN, ESQ. BKAPLAN@BRUMAN.COM BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM Ripped from the Headlines 2 Former Secretary of the Puerto Rico Department of Education

EDGAR AND OMB CIRCULAR TUTORIAL BRETTE KAPLAN, ESQ. BKAPLAN@BRUMAN.COM BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM Ripped from the Headlines 2 Former Secretary of the Puerto Rico Department of Education

SPECIAL EDUCATION IDEA Part B Fiscal Accountability Procedures Manual

SPECIAL EDUCATION IDEA Part B Fiscal Accountability Procedures Manual November, 2015 Revised 9-26-16 Arkansas State Department of Education IDEA Part B Fiscal Accountability I. IDEA Fiscal Accountability

SPECIAL EDUCATION IDEA Part B Fiscal Accountability Procedures Manual November, 2015 Revised 9-26-16 Arkansas State Department of Education IDEA Part B Fiscal Accountability I. IDEA Fiscal Accountability

Difficult Issues of Cost Allocation Carryover, Linkage. Leigh Manasevit Brustein & Manasevit, PLLC Fall Forum 2011

Difficult Issues of Cost Allocation Carryover, Linkage Leigh Manasevit Brustein & Manasevit, PLLC lmanasevit@bruman.com Fall Forum 2011 1 1. Direct Charge 2. Cost Allocation Plan (CAP) 3. Indirect Costs

Difficult Issues of Cost Allocation Carryover, Linkage Leigh Manasevit Brustein & Manasevit, PLLC lmanasevit@bruman.com Fall Forum 2011 1 1. Direct Charge 2. Cost Allocation Plan (CAP) 3. Indirect Costs

American Recovery and Reinvestment Act (ARRA) Funding Questions & Answers

Funding Questions & Answers") American Recovery and Reinvestment Act (ARRA) Funding Questions & Answers Index I. General Information II. Title I Part A Funds A. Carryover Limitation B. Supplement Not Supplant C. Maintenance of Effort

American Recovery and Reinvestment Act (ARRA) Funding Questions & Answers Index I. General Information II. Title I Part A Funds A. Carryover Limitation B. Supplement Not Supplant C. Maintenance of Effort

EDGAR AND OMB CIRCULAR TUTORIAL TIFFANY R. WINTERS, ESQ. BRUSTEIN & MANASEVIT, PLLC

EDGAR AND OMB CIRCULAR TUTORIAL TIFFANY R. WINTERS, ESQ. TWINTERS@BRUMAN.COM BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM Ripped from the Headlines 2 Former Secretary of the Puerto Rico Department of Education

EDGAR AND OMB CIRCULAR TUTORIAL TIFFANY R. WINTERS, ESQ. TWINTERS@BRUMAN.COM BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM Ripped from the Headlines 2 Former Secretary of the Puerto Rico Department of Education

Huron Intermediate School District. Finance Procedures

TABLE OF CONTENTS 3. Financial Regulations 3. Financial Control and Accounting Arrangements 3. Internal Financial Control and Data Security 5. Financial Management Systems 5. Budget Monitoring and Adjustments

TABLE OF CONTENTS 3. Financial Regulations 3. Financial Control and Accounting Arrangements 3. Internal Financial Control and Data Security 5. Financial Management Systems 5. Budget Monitoring and Adjustments

2 CFR 215 (A-110) or 2 CFR 230 (A-122) Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards.

or 2 CFR 230 (A-122) Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards.") Significant Changes for Selected Items of Cost Office of Management and Budget Guidance PART 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS Item of

Significant Changes for Selected Items of Cost Office of Management and Budget Guidance PART 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS Item of

Omni Circular Key Area #5 Indirect Costs and the Omni Circular: What to Expect. Total Cost of Federal Awards. Costing Options:

Omni Circular Key Area #5 Indirect Costs and the Omni Circular: What to Expect Leigh Manasevit, Esq. lmanasevit@bruman.com Spring Forum 2014 Total Cost of Federal Awards Indirect 10% Direct Indirect Direct

Omni Circular Key Area #5 Indirect Costs and the Omni Circular: What to Expect Leigh Manasevit, Esq. lmanasevit@bruman.com Spring Forum 2014 Total Cost of Federal Awards Indirect 10% Direct Indirect Direct

April 2017 ED Cross-Cutting Section ED DEPARTMENT OF EDUCATION CROSS-CUTTING SECTION INTRODUCTION. CFDA No. Program Name Listed as

April 2017 ED Cross-Cutting Section ED DEPARTMENT OF EDUCATION CROSS-CUTTING SECTION INTRODUCTION This section contains compliance requirements that apply to more than one Department of Education (ED)

April 2017 ED Cross-Cutting Section ED DEPARTMENT OF EDUCATION CROSS-CUTTING SECTION INTRODUCTION This section contains compliance requirements that apply to more than one Department of Education (ED)

IDEA-B LEA MAINTENANCE OF EFFORT (MOE) GUIDANCE HANDBOOK FOR FISCAL YEAR 2014 AND BEYOND

GUIDANCE HANDBOOK FOR FISCAL YEAR 2014 AND BEYOND") IDEA-B LEA MAINTENANCE OF EFFORT (MOE) GUIDANCE HANDBOOK FOR FISCAL YEAR 2014 AND BEYOND Texas Education Agency Version 1.0 (09/2013) Contents Introduction... 1 Relationship of Maintenance of Effort (MOE)

IDEA-B LEA MAINTENANCE OF EFFORT (MOE) GUIDANCE HANDBOOK FOR FISCAL YEAR 2014 AND BEYOND Texas Education Agency Version 1.0 (09/2013) Contents Introduction... 1 Relationship of Maintenance of Effort (MOE)

MISSISSIPPI DEPARTMENT OF EDUCATION

MISSISSIPPI DEPARTMENT OF EDUCATION Local Education Agency Federal Indirect Cost Proposal March 2016 Office of School Financial Services P. O. Box 771 Jackson, MS 39205 (601) 359-3294 Table of Contents

MISSISSIPPI DEPARTMENT OF EDUCATION Local Education Agency Federal Indirect Cost Proposal March 2016 Office of School Financial Services P. O. Box 771 Jackson, MS 39205 (601) 359-3294 Table of Contents

DEPARTMENT OF EDUCATION CROSS-CUTTING SECTION INTRODUCTION. CFDA No. Program Name Listed as

June 2016 Department of Education Cross-Cutting Section ED DEPARTMENT OF EDUCATION CROSS-CUTTING SECTION INTRODUCTION This section contains compliance requirements that apply to more than one Department

June 2016 Department of Education Cross-Cutting Section ED DEPARTMENT OF EDUCATION CROSS-CUTTING SECTION INTRODUCTION This section contains compliance requirements that apply to more than one Department

FY 15 IDEA Part B Allocations and Funding Issues

FY 15 IDEA Part B Allocations and Funding Issues 2014 Special Education Directors Conference Presented by: Tim Imler Presentation Outline FY 15 IDEA Regular and Preschool Grant Awards Allocation Variables

FY 15 IDEA Part B Allocations and Funding Issues 2014 Special Education Directors Conference Presented by: Tim Imler Presentation Outline FY 15 IDEA Regular and Preschool Grant Awards Allocation Variables

Division of Financial Compliance Update and Relevant information

Division of Financial Compliance Update and Relevant information Region 20 Education Service Center September 21, 2016 Topics Charter School Depository Contracts letter GASB 68 letter 313 Reporting Changes

Division of Financial Compliance Update and Relevant information Region 20 Education Service Center September 21, 2016 Topics Charter School Depository Contracts letter GASB 68 letter 313 Reporting Changes

Overview of the Title VI-B LEA Authenticated Application: Maintenance of Effort & Excess Cost. Revised 2/28/2013

Overview of the 2012-13 Title VI-B LEA Authenticated Application: Maintenance of Effort & Excess Cost Revised 2/28/2013 Contents Registering... 4 Sign-on... 5 Access Application... 6 Standalone District...

Overview of the 2012-13 Title VI-B LEA Authenticated Application: Maintenance of Effort & Excess Cost Revised 2/28/2013 Contents Registering... 4 Sign-on... 5 Access Application... 6 Standalone District...

Excess Costs. IDEA-B Requirement. Texas Education Agency (TEA)

") Excess Costs IDEA-B Requirement Texas Education Agency (TEA) Excess Costs -- Topics Code of Federal Regulations Definition Purpose Calculation Tool and Instructions Summary References Resources Part B

Excess Costs IDEA-B Requirement Texas Education Agency (TEA) Excess Costs -- Topics Code of Federal Regulations Definition Purpose Calculation Tool and Instructions Summary References Resources Part B

Fiscal Compliance for Special Education: Excess Cost