FCA Update March Presented by: Ian Fletcher FCA

|

|

|

- Loraine Terry

- 5 years ago

- Views:

Transcription

1 FCA Update March 2015 Presented by: Ian Fletcher FCA

2 Training disclaimer The current requirements with which an authorised person, and an approved person, must comply are set out in the Financial Services and Market Acts 2000, the regulations made under that Act and the rules in the FCA Handbook. Under that Act, FCA are given the power to give guidance and they do so extensively in the Handbook. FCA call this general guidance. FCA also give guidance to particular firms in their particular circumstances. They call this individual guidance. The information which we will give to you on this webinar is for training purposes only. It is not guidance in either of these two senses. I hope you will appreciate that I am not in a position to give you, or your firms, individual guidance. The purpose of this session is to give you a better understanding of FCA provisions and to enable you to apply them to your circumstances. The slides and notes for this webinar should be read in conjunction with the detailed legislation or regulations. No responsibility for loss occasioned by any person acting or refraining from action as a result of the material contained in this programme can be accepted by the authors or 2020 Innovation Training Limited.

3 Forthcoming FCA Webinars FCA Update 23 June 2015 Please contact the office on for booking and prices or see for further information

4 Objectives To provide an overview of regulation and legislation To review common problem areas To provide guidance on the audit and accounting work of an FCA authorised entity Revision of the year

5 Content New CPs and PSs CASS 7 June update

6 FCA Website Review Reminder of key areas Register CP and PS in YOUR FCA Dear CEO letters News sections

7 FCA Website Review

8 Consultation Paper Update

9 Recent CPs CP 14/25 - Changes to the Approved Persons Regime for Solvency II firms CP14/26 - Regulatory fees and levies: policy proposals for 2015/16 CP14/27 - Quarterly consultation No.7 CP14/28 - MIPRU Simplification CP14/29 Guaranteed Asset Protection insurance: a competition remedy CP14/29 - Technical annex CP14/30 Improving complaints handling CP14/31 Strengthening accountability in banking: forms, consequential and transitional aspects CP14/32 Bringing additional benchmarks into the regulatory and supervisory regime

10 Recent CPs CP15/1 - FCA Competition Concurrency Guidance and Handbook amendments CP15/2: Financial Services Compensation Scheme Management Expenses Levy Limit 2015/16 CP15/3: Buy-to-let mortgages: implementing the Mortgage Credit Directive Order 2015 CP15/4: Whistleblowing in deposit-takers, PRA-designated investment firms and insurers CP15/5: Approach to non-executive directors in banking and Solvency II firms & Application of the presumption of responsibility to Senior Managers in banking firms CP15/6: Consumer credit - proposed changes to FCA rules and guidance CP15/7: Proposed changes to FCA pension transfer rules CP15/8: Quarterly Consultation No.8 CP15/9: Strengthening accountability in banking: a new regulatory framework for individuals Feedback on FCA CP14/13 / PRA CP14/14 and consultation on additional guidance CP15/10: Strengthening accountability in banking: UK branches of foreign banks

11 CP 14/25 - Changes to the Approved Persons Regime for Solvency II firms Primarily this concerns the amount of capital that EU insurance companies must hold to reduce the risk of insolvency. This CP proposes changes to the Approved Persons Regime for Solvency II firms to address: The Financial Conduct Authority s (FCA) role in reviewing firms assessments of the fitness and propriety of certain important individuals within these firms; and Provisions in the Financial Services (Banking Reform) Act 2013 ( the Banking Reform Act ), which allow the regulators to apply Conduct Rules to certain individuals in FSMA-authorised firms.

12 Form A SUP Section

13 CP14/26 - Regulatory fees and levies: policy proposals for 2015/16 This forms part of the annual cycle of fees consultation. In October or November, FCA consult on any proposed changes to the underlying policy of the fee and levy regimes of the FCA, the Financial Ombudsman Service, the Financial Services Compensation Scheme (FSCS), the Money Advice Service and, from 2015/16, the Payment Systems Regulator (PSR). FCA expect to consult on the fee rates for the forthcoming year in the following March.

14 CP14/27 - Quarterly consultation No.7 This CP contains: Changes to SUP 16.6 compliance reports; Amendments to the Prospectus Rules, including the provisions about final terms Revoke the Building Societies Regulatory Guide Changes to the Training and Competence sourcebook list of appropriate qualifications

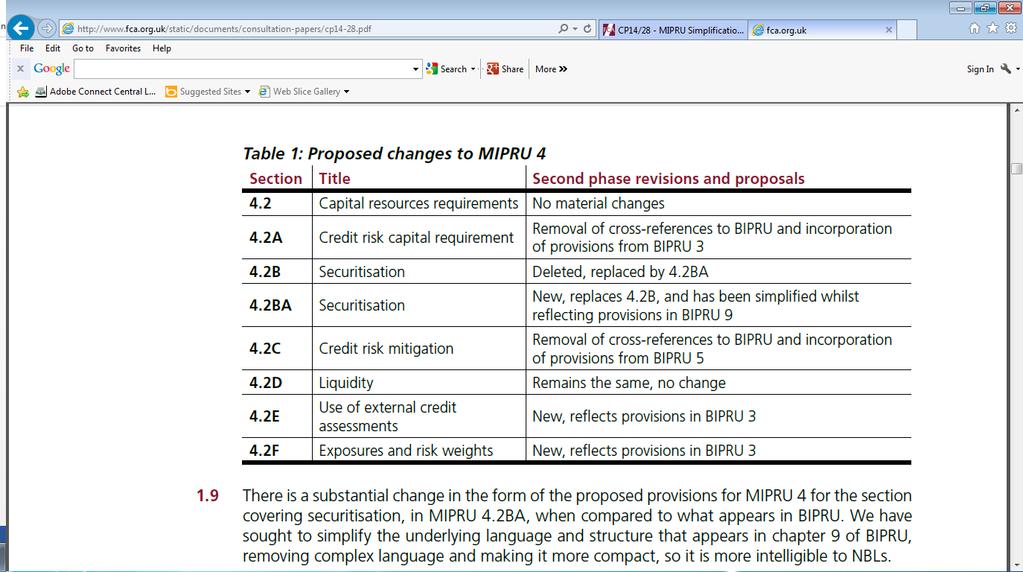

15 CP14/28 - MIPRU Simplification FCA are consulting on the changes they propose to the Handbook to make it simpler for certain mortgage firms to calculate their capital requirements. See table 1 : Proposed changes to MIPRU

16 TABLE 1

17 CP14/29 Guaranteed Asset Protection insurance: a competition remedy In July 2014, FCA published confirmed findings from the General Insurance Add-ons Market Study (the Market Study). The report examined how competition is affected by selling general insurance products as an add-on to a primary product. The main findings were: First, that the add-on mechanism has a clear impact on consumer behaviour. It often affects consumers decisionmaking and weakens engagement which in turn strengthens a structural point of sale advantage; and Second, there is a lack of transparency and comparability about the value provided by general insurance products leading to consumers getting poor value not just from some add-on products but also from standalone purchases.

18 CP14/29 Guaranteed Asset Protection insurance: a competition remedy In this paper FCA consult on rules to implement the deferred opt-in and requiring enhanced disclosure, subject to refinements they have made to take account of feedback received from stakeholders in response to the Market Study.

19 CP14/29 - Technical annex Technical Annex to Guaranteed Asset Protection insurance: a competition remedy CP14/29.

20 CP14/30 Improving complaints handling This paper proposes changes to FCA rules to improve complaints handling by, and access to the ombudsman service for customers of, firms in the compulsory jurisdiction. This paper also proposes changes to the voluntary jurisdiction and changes to the procedures of the ombudsman service.

21 CP14/31 Strengthening accountability in banking: forms, consequential and transitional aspects The proposals are intended to create a new framework to encourage individuals to take greater responsibility for their actions, and will make it easier for both firms and regulators to hold individuals to account: A new Senior Managers Regime (SMR) for individuals who are subject to regulatory approval, which will require firms to allocate a range of responsibilities to these individuals and to regularly vet their fitness and propriety. This will focus accountability on a narrower number of senior individuals in a firm than the current Approved Persons Regime (APR). A Certification Regime which will require relevant firms to assess the fitness and propriety of certain employees who could pose a risk of significant harm to the firm or any of its customers. A new set of Conduct Rules 5

22 Grandfathering SIF to SMR

23 CP14/32 Bringing additional benchmarks into the regulatory and supervisory regime Historically, benchmarks have not been regulated. Following misconduct related to the London Inter-Bank Offered Rate (LIBOR) benchmark, FCA were given powers to regulate benchmarks specified by the Government in April Currently, LIBOR is the only regulated benchmark. This consultation paper seeks views on how FCA generic approach to regulating benchmarks could be applied beyond LIBOR to other benchmark administrators (and benchmark submitters as appropriate). The CP considers regulating benchmarks in the following areas: Sterling Overnight Index Average (SONIA) (unsecured sterling); Repurchase Overnight Index Average (RONIA)(secured sterling); ISDAFIX (interest rate swaps); WM/Reuters (WMR) (forex) London 4pm Closing Spot Rate; London Gold Fixing (soon to be replaced by the LBMA Gold Price); LBMA Silver Price; and ICE Brent Index

24 CP15/1 - FCA Competition Concurrency Guidance and Handbook amendments The FCA obtains concurrent competition powers on 1 April This means they will have powers to enforce the prohibitions on anti-competitive behaviour in the Competition Act 1998 (CA98) and the Treaty on the Functioning of the European Union (TFEU) in relation to the provision of financial services. They will also have powers to carry out market studies, and make market investigation references to the Competition and Markets Authority (CMA) under the Enterprise Act 2002 (EA02), in relation to the provision of financial services. This CP seeks views on these powers.

25 CP15/2: Financial Services Compensation Scheme Management Expenses Levy Limit 2015/16 The MELL proposed for 2015/16 is 74.4m, consisting of: FSCS management expenses of 69.1m: this is the minimum amount that will be levied for 2015/16. A contingency reserve of 5.3m that allows the FSCS to levy additional funds, most likely at relatively short notice, without formal consultation by the FCA and PRA to meet contingencies that were not foreseen when the annual levy was raised.

26 CP15/3: Buy-to-let mortgages: implementing the Mortgage Credit Directive Order 2015 In chapter 2, FCA set out the following proposals: The registration processes that firms, with or without existing FCA permissions, will need to follow to register with FCA as CBTL firm; Aggregated data reporting from CBTL lenders to support the risk-based approach to supervision and inform FCA understanding of CBTL activity; Complaints handling rules to support the government s widening of the Financial Ombudsman Service s (the ombudsman service) compulsory jurisdiction to capture CBTL firms; and Modifications to other Handbook modules to incorporate CBTL, including changes to Supervision Manual (SUP), Enforcement Guidance (EG), Decision Procedures and Penalties Manual (DEPP), Perimeter Guidance (PERG), and the Glossary.

27 CP15/4: Whistleblowing in deposit-takers, PRAdesignated investment firms and insurers The FCA propose that relevant firms should: Put internal whistleblowing arrangements in place (if they are not already), and inform their UK-based employees about these arrangements (see chapter 2). Inform their UK-based employees that they can blow the whistle to the FCA or the PRA (see sections 2.6 and 2.7). Offer protections to all whistle-blowers, whatever their relationship with the firm and whatever the topic of their disclosure (see sections 2.15 to 2.18). Include a passage in new employment contracts and settlement agreements clarifying that nothing in that agreement prevents an employee, or ex-employee, from making a protected disclosure (see sections 2.22 to 2.26). Allocate the prescribed responsibility for whistleblowing under the Senior Managers Regime and Senior Insurance Managers Regime to an individual (referred to as the whistle-blowers champion ) with responsibility for: overseeing the effectiveness of internal whistleblowing arrangements, including arrangements for protecting whistle-blowers against detrimental treatment (see chapter 3) preparing an annual report to the board about their operation (see section 3.10 to 3.14), and reporting to the FCA where, in a case before an employment tribunal contested by the firm, the tribunal finds in favour of a whistle-blower (see section 3.16)

28 CP15/5: Approach to non-executive directors in banking and Solvency II firms & Application of the presumption of responsibility to Senior Managers in banking firms This paper sets out the FCA revised approach to independent non-executive directors ( NEDs ) in UK banks, building societies, credit unions and PRAdesignated investment firms1 (collectively relevant authorised persons 2) and Solvency II firms. Under the revised approach, the FCA will only make the following NEDs subject to approval and inclusion in the Senior Managers Regime (SMR) for relevant authorised persons: Chairman Chair of the Risk Committee Chair of the Audit Committee Chair of the Remuneration Committee Chair of the Nomination Committee Senior Independent Director

29 CP15/6: Consumer credit - proposed changes to FCA rules and guidance This consultation paper sets out proposals for amendments to the consumer credit regime, and invites views on them. Key proposals in this consultation paper are: Guarantor lending: to require firms to provide adequate pre-contract explanations to guarantors and to assess the guarantor s creditworthiness. Also, to impose other obligations on firms regarding guarantors, including treating guarantors fairly and with forbearance if they are in financial difficulty. High-cost short-term credit (HCSTC): to remove the exemption from the requirement to include a risk warning in financial promotions. Financial promotions: to amend the rules regarding relative prominence and the circumstances in which promotions must include a representative annual percentage rate of charge (APR), and to restate as a rule the current guidance on Principle 7 (that communications should be clear, fair and not misleading). Arrears, default and collection: to amend FCA rules to reflect policy intention and allow firms to introduce continuous payment authority (CPA) to collect repayments where a customer is in arrears or default and the lender is exercising forbearance.

30 CP15/7: Proposed changes to FCA pension transfer rules FCA propose to: amend the rules to incorporate the new specified activity of advising on conversions or transfers of safeguarded benefits to flexible benefits, and require that all advice on DB to DC pension transfers be provided or checked by a Pension Transfer Specialist.

31 CP15/8: Quarterly Consultation No.8 This has proposals to strengthen certain rules in CASS 6 and 7 (amongst others) The CASS 6 requirements FCA are proposing to amend affect: External custody reconciliations, and Registration and recording of legal title. The CASS 7 requirements FCA are proposing to amend affect: Use of the normal approach to client money segregation in relation to certain regulated clearing arrangements, and The delivery versus payment rules applicable to authorised fund managers and relating to regulated collective investment schemes.

32 CP15/9: Strengthening accountability in banking: a new regulatory framework for individuals Feedback on FCA CP14/13 / PRA CP14/14 and consultation on additional guidance HM Treasury has now announced that the new regime will need to come into force by 7 March FCA plan to publish final rules in the spring/summer. However, to give firms as much time as possible to prepare for the changes, they are providing in this paper a set of near-final rules on the new Senior Managers Regime (SMR), together with a steer on policy intentions for the whole regime, including the Certification Regime and the application of their Conduct Rules.

33 Background to CP 15/9 July The proposals were intended to encourage accountability for decision-making in relevant firms, focusing particularly on senior management, while aiming for good conduct at all levels. FCA proposals followed recommendations made by the Parliamentary Commission on Banking Standards (PCBS) and reflected the powers given to us in the Financial Services (Banking Reform) Act 2013 (the Act) These proposals were consulted on and it was felt banks needed more time to implement them. Hence 7 March Near final rules included in the CP to help prepare.

34 CP15/10: Strengthening accountability in banking: UK branches of foreign banks The new framework comprises the following two regimes, which aim to encourage individuals to take greater responsibility for their actions and make it easier for both firms and the regulators to hold individuals to account: A Senior Managers Regime (SMR) for individuals who are subject to regulatory approval (Senior Managers). The SMR seeks to promote a clear allocation of responsibilities to key decision-makers and strengthen their individual accountability through a robust initial and ongoing assessment of their fitness and propriety (by firms as well as by regulators) and strengthened powers of approval and enforcement for the regulators. A Certification Regime which will require relevant firms to assess and certify the fitness and propriety of employees deemed capable of causing significant harm to the firm or any of its customers at least annually.

35 POLICY STATEMENT UPDATE

36 Recent Policy Statements PS14/17 Retirement Reforms and the Guidance Guarantee, including feedback on CP14/11 PS14/18 Credit broking and fees PS15/1 Early implementation of the Transparency Directive s requirements for reports on payments to government PS15/2: Recovery and Resolution Directive, including feedback on CP14/15 and final rules PS15/3: Final rules for independent governance committees, including feedback on CP14/16 PS15/4: Retirement reforms and the guidance guarantee: retirement risk warnings PS15/5: Final rules for charges in workplace personal pension schemes and feedback on CP14/24 PS15/6: Bringing additional benchmarks into the regulatory and supervisory regime

37 PS14/17 Retirement Reforms and the Guidance Guarantee, including feedback on CP14/11

38 Retirement reforms and the Guidance Guarantee All consumers with Defined Contribution (DC) pensions should be entitled to free impartial guidance at retirement the Guidance Guarantee to help them make the most of their pension savings.

39 Retirement reforms and the Guidance Guarantee The 2014 Budget announced fundamental changes to the options consumers will have for accessing their DC pension savings at retirement. From the age of 55 consumers will be able to: take their pension savings as cash, and/or buy an annuity (or other income generating guaranteed products that may emerge), and/or use drawdown but without any limits applied

40 Retirement reforms and the Guidance Guarantee To support this increased flexibility the Government announced a Guidance Guarantee, which entitles everyone with a DC pension fund to access free (at the point of delivery), impartial guidance, including the option of a face-to-face conversation about their options when accessing their pension savings. It will not be mandatory for people to take this guidance to access their pension savings, but they will be signposted to the Guidance Service before they do.

41 Retirement reforms and the Guidance Guarantee The Pensions Advisory Service (TPAS) and the Money Advice Service (MAS) Only designated organisations which are independent and have no actual (or potential) conflict of interest will be allowed to provide the guidance. These are referred to as Delivery partners

42 6 April - Are they ready?

43 Retirement reforms and the Guidance Guarantee Formal role for the Financial Conduct Authority (FCA) in setting the standards for the delivery partners, maintaining the standards, monitoring compliance with those standards and collecting the levy, which will fund the provision of the guidance.

44 Retirement reforms and the Guidance Guarantee Chapter 2 of the consultation paper set out the proposed standards that will apply to the delivery partners Chapter 3 of the CP sought views on FCA provisional proposals for collecting the levy to fund the provision of the guidance.

45 Chapter 2 -Standards The standards cover the following areas: Ensuring the guidance is free at point of delivery Consistency and quality of the delivery of the guidance Professional standards Communications Systems and controls Complaint management The information the delivery partners will use in giving the guidance Content of the guidance session Helping the consumer to take the next step Providing a record of the guidance

46 Timetable First half 2015: Consultation on policy for making recommendations to designated guidance providers and the Treasury as part of our monitoring approach. Development of monitoring approach in liaison with the Treasury and designated guidance providers. Wider review of FCA rules in the pensions and retirement area. Second half 2015: Full review of designated guidance providers compliance with the standards.

47 And now for our on going saga about.

48 PS14/18 Credit broking and fees The FCA has significant concerns about the practices of some credit brokers particularly in the high-cost short-term credit (HCSTC) and other subprime credit markets which charge upfront fees to consumers.

49 PS14/18 Credit broking and fees Their primary concerns are as follows: consumers not realising they are dealing with a broker rather than a lender; a lack of informed consent to the taking of fees, for example where terms and conditions are hidden or misleading; consumers being misled as to the purpose of giving their payment details; firms passing on consumers details, including their payment details, without informed consent, to other firms who also take a fee; and consumers facing difficulty in identifying the firm that has taken a payment (and in obtaining a refund from the firm or a response to their complaint).

50 PS14/18 Credit broking and fees FCA state there is evidence that such practices are causing substantial harm to consumers, including vulnerable consumers and those in financial hardship (which may be aggravated by the taking of unexpected fees).

51 PS14/18 Credit broking and fees New rules 2 January They ban firms from charging fees, and from requesting payment details from customers for that purpose, unless: the firm has provided an explicit notice to the customer, in a durable medium (an information notice ), setting out: the firm s legal name a prominent statement that the firm is a credit broker (not a lender) or, if it is both a credit broker and a lender, a statement that it is acting as a credit broker and not as a lender a statement that a fee will, or (where relevant) may, be payable, the amount or likely amount of the fee and when and by what means the fee will be payable, and the customer has acknowledged receipt of the notice, and awareness of its contents, in a durable medium (the customer confirmation )

52 And now more from our friends in Brussels.

53 PS15/1 Early implementation of the Transparency Directive s requirements for reports on payments to government 28 August 2014 FCA published a consultation paper (CP) proposing, at the request of HM Treasury (the Treasury), to align the implementation of the requirement for reports on payments to governments (or country by country reporting) set out in Article 6 of the Transparency Directive (TD) (as revised by the Transparency Directive Amending Directive (TDAD)) with the implementation by the Department for Business, Innovation & Skills (BIS) of the country by country reporting requirements set out in Chapter 10 of the Accounting Directive (AD). FCA will implement this change to take effect for financial years beginning on or after 1 January Therefore they also publish the final rules that came into force on 22 December 2014 in relation to financial years beginning on or after 1 January 2015

54 PS of interest to: Issuers of securities admitted to trading on a regulated market where the UK acts as home Member State and our Disclosure Rules and Transparency Rules (DTRs) apply, and who are or who may be active in the extractive or logging of primary forest industries; listed companies who are required by LR9.2.6BR, LR R or LR18.4.3R to comply with DTR4 as if they were an issuer for the purposes of the DTRs and who are or who may be active in the extractive or logging of primary forest industries; issuers of securitised derivatives who, pursuant to LR BR, we consider should comply with DTR4 as if they were an issuer of debt securities as defined in the DTRs and who are or who may be active in the extractive or logging of primary forest industries; firms advising issuers; firms or persons investing or dealing in listed securities

55 PS15/2: Recovery and Resolution Directive, including feedback on CP14/15 and final rules On 1 August 2014 FCA published a Consultation Paper (CP) proposing changes to the Handbook that are required to transpose the Recovery and Resolution Directive (RRD) into the UK regulatory regime for FCA soloregulated investment firms (IFPRU 730k firms), as well as certain group entities, that fall within the scope of the RRD. Final rules come into force 1 January 2016

56 Recovery and Resolution Directive This sets out the proposed changes to FCA Handbook that are required to transpose the Recovery and Resolution Directive (RRD) into the UK regulatory regime for the investment firms and certain group entities that FCA regulate prudentially and that fall within the scope of the RRD.

57 Recovery and Resolution Directive The recovery and early intervention enhancements that the RRD is expected to bring to the prudential framework should make it less likely that banks and investment firms will fail, thereby improving stability in the financial sector in general.

58 Objective: The Directive aims to provide measures, tools and powers in respect of preparing for the recovery of firms in financial difficulty, early intervention in the event of problems, and the resolution of failed firms in a way that reduces the costs to the public and mitigates the impact on the financial system.

59 Recovery and Resolution Directive The proposals investment firms that are soloregulated by the FCA and that meet the definition in our Handbook of an IFPRU 730k firm. The current population covers approximately 230 firms. Recovery Notification of failure or likely to fail Resolution Intra-group financing Contractual obligations of bail-in

60 Content, frequency and submission of recovery plans

61 Recovery and Resolution Directive

62 AUTO ENROLMENT

63 PS15/3: Final rules for independent governance committees, including feedback on CP14/16 FCA are publishing rules to require the providers of workplace personal pension schemes to set up and maintain independent governance committees (IGCs). IGCs will have a duty to act in the interests of scheme members and will operate independently of the firm. They will assess and, where necessary, raise concerns about the value for money of workplace personal pension schemes. The rules will come into force on 6 April Firms will be expected to comply from that date. Firms that already have IGCs in place will need to ensure that they meet the rules from 6 April 2015

64 Proposed rules for independent governance committees By 2018, the time AE applies to all companies, it is estimated that between eight and nine million people will be newly saving, or saving more, in a workplace pension scheme. Many of these will be on low incomes and will not have made any active choice about how their pension savings are invested.

65 Proposed rules for independent governance committees The rules include new governance standards, a proposed charge cap on default funds, the banning of certain charging practices, and measures to improve the disclosure of costs and charges.

66 Proposed rules for independent governance committees IGCs will have a duty to act in the interests of scheme members and will operate independently of the firm. They will assess and, where necessary, raise concerns about the value for money of workplace personal pension schemes.

67 Proposed rules for independent governance committees The key duties of the IGC would be as follows: to act in the interests of relevant policyholders; to assess the value for money of the firm s workplace personal pension schemes; where the IGC finds problems with value for money, to raise concerns (as it sees fit) with the firm s board; to escalate concerns to the FCA, alert relevant scheme members and employers, and make its concerns public, and; to produce an annual report of its findings.

68 Proposed rules for independent governance committees FCA propose a comply or explain duty on firms, so that the firm must address the IGC s concerns or explain to the IGC why it does not intend to do so. FCA s objective is for firms to take actions that will ensure the value for money of workplace personal pension schemes on an ongoing basis.

69 Proposed rules for independent governance committees They allow firms with smaller and less complex workplace personal pension schemes to establish a governance advisory arrangement (GAA), as an alternative to an IGC. A GAA would involve the firm appointing another independent firm (a third party) to take on their IGC responsibilities. The third party may provide GAAs to multiple firms, with the potential for economies of scale and lower costs per firm.

70 Retirement risk warnings

71 Pensions reform The 2014 Budget announced proposals for fundamental changes to the options consumers will have for accessing their DC pension savings at retirement. These have been referred to as the pension freedoms. From April 2015, consumers aged 55 and over will be able to: take their pension savings as cash (in one lump sum or in smaller amounts over time) buy an annuity (or other income-generating guaranteed products) use a drawdown pension without any limits applied use any combination of these

72 PS15/4: Retirement reforms and the guidance guarantee: retirement risk warnings From April 2015, consumers will have greater choice about how they access their Defined Contribution (DC) pension savings. FCA are concerned that consumers may not be well equipped to make these important decisions, which for some may be irreversible. This concern applies particularly to consumers who are generally not engaged with retirement decision making, and who do not take regulated advice or the offer of guidance from Pension Wise (the Government s new pension guidance service). This could lead to poor outcomes for consumers. Therefore, as noted in their Dear CEO letter of 26 January, FCA are introducing new rules.

73 DEAR CEO ADDITIONAL PROTECTION

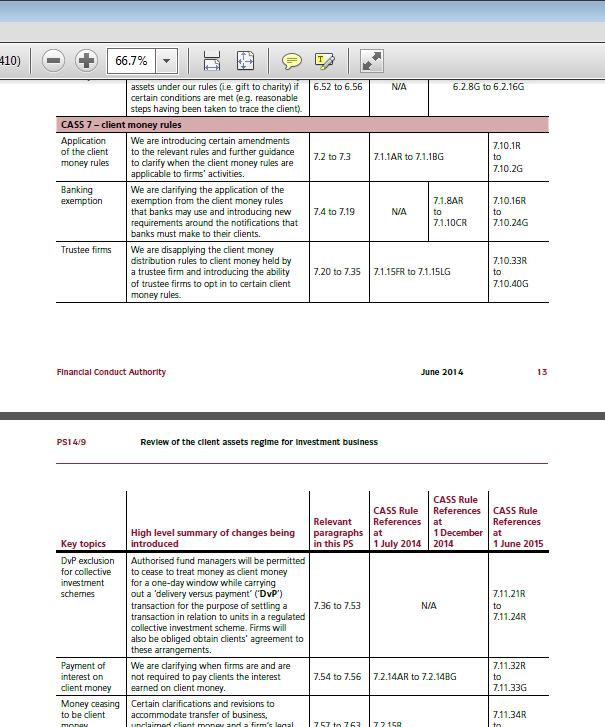

74 New Rules This Policy Statement will relevant to all those with an interest in pensions and retirement issues, including: Providers of pensions, including operators of Self Invested Personal Pensions (SIPPs) Providers of retirement income products Firms facilitating access to pension savings on an execution-only basis Trustees of DC pension schemes (and schemes with a DC element) Employer sponsors of DC schemes (and schemes with a DC element) Providers of other financial services and products that play a role in consumers retirement planning Those providing advice and information in this area already Distributors of financial products, in particular retirement income products

75 Rules The new rules will require firms to give appropriate retirement risk warnings to consumers accessing their pension savings. Firms must ask the consumer relevant questions, based on how the consumer wants to access their pension savings, to determine whether risk factors are present. If they are, risk warnings must be given. The risk warnings will relate to how the consumer has decided to access their pension savings and require the firms to ask the consumer questions to identify if a risk factor is present and therefore if a risk warning must be given. These new rules do not require firms to replicate the Pension Wise service. Instead, and in addition to Pension Wise, the rules ensure firms will flag specific risks to consumers, and give additional warnings.

76 The Process

77 PS15/5: Final rules for charges in workplace personal pension schemes and feedback on CP14/24

78 CP14/24 Charges in workplace personal pension schemes New governance standards A proposed charge cap on default funds The banning of certain charging practices Measures to improve the disclosure of costs and charges

79 CP14/24 Charges in workplace personal pension schemes A cap on the charges within default funds equivalent to 0.75% per annum of funds under management from April Preventing firms from paying or receiving consultancy charges from April Preventing firms from paying commission or other charges for advice which are not initiated by scheme members from April Preventing firms from using differential charges based on whether the member is currently contributing or not from April 2016.

80 PS15/6: Bringing additional benchmarks into the regulatory and supervisory regime The benchmarks being brought into scope are: Sterling Overnight Index Average (SONIA) Repurchase Overnight Index Average (RONIA) ISDAFIX (soon to be renamed the ICE Swap Rate) WM/Reuters (WMR) London 4pm Closing Spot Rate London Gold Fixing (soon to be replaced by the LBMA Gold Price) LBMA Silver Price ICE Brent Index (See CP 14/32 ABOVE)

81 PS14/9 - Review of the client assets regime for investment business This policy statement makes changes to the rules in Client Assets Sourcebook (CASS).

82 PS14/9 - Review of the client assets regime for investment business The changes affect around 1,500 FCAregulated firms that carry out investment business, from the largest investment banks to the smallest investment adviser, who collectively hold over 100 billion of client money and 10 trillion of custody assets.

83 Background to PS 14/9 CP 13/5 was as a result of FSA / FCA findings on handling of client assets 2010 Client Assets review Existing rules CP proposals PS confirmation / amendments / changes

84 Background -CP13/5 - Review of the client assets regime for investment business This paper consulted on material changes to the rules in relation to client money, custody assets and mandates Some of these proposals were more significant than others Individually each proposal was intended to address a particular risk identified in firms or clarify an existing requirement

85 CP13/5 - Review of the client assets regime for investment business This consultation paper proposed changes to the client assets rules that are applicable to firms that are subject to the client assets sourcebook (CASS) because they hold client money, custody assets, collateral and/or mandates (or rely on exemptions contained within CASS) in relation to investment business. This consultation will also interest Auditors in relation to the provision of client assets audit reports and auditors reports on different or alternative approaches/methods permitted by CASS.

86 CP13/5 - Review of the client assets regime for investment business The proposals in this Consultation Paper will not apply to general insurance intermediaries that only hold client money in accordance with CASS 5 (subject to the amendments proposed in CP 12/20).

87 CP13/5 - Review of the client assets regime for investment business Background: FCA (FSA) launched the Client Assets Unit in 2010, and in recent years they have driven improvements in the auditors reporting on client assets, as well as introducing the Client Money and Assets Return (CMAR) that firms submit monthly to them. This CP shows the concern the FCA has over firms holding Clients money and assets.

88 2010 Report FSA Poor management oversight and control Lack of trust status for segregated accounts Unclear arrangements for segregating and diversifying client money Incomplete or inaccurate records, accounts and reconciliations

89 Brief Reminder of Existing Rules CASS 7

90 Existing Rules CASS 7 MiFID rules apply to all DIF firms Principle based S & C Segregation and Identification Separate account Bank account rules Prompt and accurate payments into and out of account

91 Existing Rules CASS 7 Regular reconciliations Supervision and review of reconciliations Accounting records Auditors report Gabriel reporting

92 Changes in CASS 7 rules (Summarised from the CP) FCA discuss changes to the client money rules, which will affect all firms who hold client money. These changes are designed to clarify and enhance the regime to ensure the best protection of client money held in relation to investment business. PS RULE CHANGES 1 July, 1 December and 1 June 2015 (main rules)

93 1 July July 2014 certain rules and guidance came into force providing clarifications to existing requirements, introducing optional arrangements with which firms may choose to comply and limiting the placement of client money in new unbreakable term deposits. These include clarifications of application provisions and the introduction of the option to operate multiple client money pools

94 1 December December 2014 certain rules and guidance came into force relating to the provision of information to or obtaining the agreement of new clients and the documenting of agreements and arrangements with any new counterparties with whom firms deposit or otherwise place custody assets or client money, these include requirements to notify the client of certain matters if operating the banking exemption and mandating the use of template acknowledgment letters with new client bank accounts and client transaction accounts.

95 Templates

96 1 June 2015 June 2015 all of the remaining rules and guidance come into force and firms will need to ensure they fully comply with all of the new rules set out in Appendix 1 to the PS.

97 Summary in PS of Proposals

98 Outline Rule Changes

99 CP 13/5 - Details Client distribution regime IP regime Multiple pools clearing member firms EMIR indirect client clearing SAR review administration Compensation regimes FSCS CLIENT MONEY, CUSTODY, MANDATES NEW RULES

100 Client Money Rules CASS 7 Changes affect ALL firms holding client money Clarification of existing rules and added guidance to help firms identify and protect clients monies

101 CASS Proposals (cont.) Clarification of interest rules and when money ceases to be client money ( ) Transfer of business assignment clause instead of contacting each individual client, tightening up of wording of the clause (4.42)

102 Policy Statement - Rules Some minor amends and clarifications but proposals adopted Methodology for informing clients reference a transfer made clearer 25 retail and 100 other, de minimus limits

103 Proposals (cont.) Allocated but unclaimed money (4.48 et seq.) steps firms have to take to identify location etc. of client and for sums under 10 before giving the money to charity.

104 Segregation of Client Money CP proposes enhancements to rules (4.55) CASS 7.4 enhancement to ensure all client money held in appropriate manner with a suitable institution (4.58) Requirement to consider diversification and do enhanced due diligence on the banks with which they deposit client money (4.6) Client money account must be in the name of the firm

105 POLICY STATEMENT - RULES Proposals generally adopted In addition, periodic review of whether further segregation needed Introduction of an explicit requirement for firms to make a record of each periodic review of a bank and to keep that record from the date it conducts the periodic review until five years after the firm ceases to use that bank to hold client money

106 Unbreakable Client Money Deposits (4.63) Restriction on the use of term deposits and Notice accounts Enhances prompt withdrawals of client money rules

107 POLICY STATEMENT - RULES Amended the proposal to allow firms to place client money in term deposits for up to a maximum unbreakable term of 30 days

108 Immediate Segregation (4.67) All client money MUST be received directly into a client account No client money into firm s own account and then to client account

109 Physical Receipt and Allocation of Client Money (4.74) Practical problems with receipts e.g. HMRC refund covering large number of clients Mixture of cash, cheques, payment orders Risks for clients FCA PROPOSAL All client money to be banked no later than one business day following receipt PROPOSAL Cannot use client money until cleared PROPOSAL Unidentified receipts to be segregated until identified

110 POLICY STATEMENT - RULES The final rules make it clear that a firm should promptly, and in any event no later than one business day after the money becomes due and payable, pay the money to the client account or segregate that money in a client bank account.

111 Prudent over segregation of client money (4.82) Some firms do currently over-segregate money, e.g. to cover a specific situation or risk. FCA considers there is uncertainty and differing practices in industry PROPOSAL- clarification in the record keeping including oversight and calculation policies

112 POLICY STATEMENT - RULES The final rules include further detail on the contents of the policy document and the requirements to keep records of all prudent segregation payments made.

113 Alternative Approach (4.87) Money paid in and out of firm s own account rather than client accounts Relevant for multi currency and multi product companies FCA research in 2012 indicated some firms using approach inappropriately PROPOSAL Clarify when alternative approach relevant PROPOSAL Notify FCA no less than 3 months before adopting PROPOSAL Risk justification to be made on why alternative approach necessary, adequate systems and controls, buffer requirement, AUDITOR REPORT to FCA BEFORE adoption

114 POLICY STATEMENT - RULES Under the final rules, both those firms already using the alternative approach and any firms wishing to use it in the future will need to establish and document their reasons (as set out in the final rules) for using the alternative approach for a particular business line.

115 POLICY STATEMENT - RULES A firm will be required to review at least annually its reasons for continuing to operate the alternative approach for each business line Post review 6 months to change rather than 3

116 POLICY STATEMENT - RULES Both those firms currently using the alternative approach and those wishing to use it for a business line in the future will be required to obtain a report from their auditor before operating the alternative approach to client money segregation. For those firms already using the alternative approach the reasons for this stem from the fact that the amended rules impose new requirements on these firms. RAR report following FRC guidelines

117 POLICY STATEMENT - RULES FCA also amended rules to more closely reflect the drafting of the specific opinions they expect auditors to provide. This includes revisions to clarify that the auditor will be opining on whether a firms proposed use of the alternative approach, including its proposed calculation and maintenance of a cash buffer, is suitably designed to achieve compliance with FCA requirements.

118 Client Money held by third parties (4.97) Necessary by nature of some transactions, rules say firm keeps fiduciary responsibility to client unless TP has direct relationship with client PROPOSAL Clarification, money remains client money and therefore include these amounts in client money calculations

119 POLICY STATEMENT - RULES FCA are introducing these rules with only minor changes to reflect feedback. For example, final guidance makes it clear that firms may allow another person to hold client money for both contingent liability investments and non-margined transactions for a client.

120 Client money relating to custody assets held at custodians or sub custodians (4.101) Firms may deposit assets with third parties, dividends etc. may arise which is client money and should be held by the firm FCA variety of models used by firms and risk of confusion PROPOSAL Firm must recognise any money derived from CM assets as CM and held in a CM account in the name of the firm

121 Client Money Reconciliations and Recordkeeping (4.104) Firms must carry out internals daily, externals regularly (per MiFID) FCA some firms fail to do this, wide variety in methodology and MiFID interpretation of regularly PROPOSALS Internals daily, externals no less than monthly. Firms to justify timing of externals. Guidance on how reconciliations should be done (4.111) Technical proposals to improve clarity and address inconsistencies (a number of provisions to be made into rules) Non standard methodologies to be agreed in advance More detailed record keeping requirements - overarching requirement firm can determine how much money it holds for each client Notification concept of materiality introduced, breach and MUST notify FCA (4.117)

122 POLICY STATEMENT - RULES The new rules in the PS will place additional recordkeeping obligations on all firms subject to client money rules for investment firms. This includes a requirement for a firm to maintain its records in a way that allows it to promptly determine the total amount of client money it should be holding for each client. Under this rule, FCA expect that firms will need to ensure that they are able to determine the total amount of client money they should be holding for each client within two business days of having taken a decision to do so, or at the request of the FCA

123 POLICY STATEMENT - RULES FCA are introducing these rules largely as proposed in the CP, requiring all firms to undertake an internal client money reconciliation on a daily basis. This requirement forms an important part of the steps a firm should be taking to ensure the accuracy of its client money records and that it has adequate arrangements in place for the protection of client money.

124 POLICY STATEMENT - RULES Non standard approach - changes A firm need not specifically opine on whether its non-standard method provides or will provide an equivalent degree of protection, rather the firm should consider whether the method achieves the same specified outcome as if the firm had used one of the standard methods. Only material changes (rather than any changes) to a firm s non-standard method of internal client money reconciliation will oblige the firm to repeat the steps required under FCA rules to use that method (i.e. carry out a new assessment and obtain and provide a new auditor s report to them)

125 POLICY STATEMENT - RULES FCA are making rules that will require a firm to obtain a report from its auditor before engaging in a non-standard method of internal client money reconciliation. This report must be prepared on the basis of a reasonable assurance engagement.

126 POLICY STATEMENT - RULES FCA are introducing a new sub-chapter in the client money rules containing rules and guidance around the standard methods of internal client money reconciliations. However, based on feedback, they have made a number of amendments to the rules proposed in the CP to ensure clarity and remove any inconsistencies between the rules for client money reconciliations and other recordkeeping and segregation requirements.

127 Acknowledgement Letters (4.123) CASS 7.8 requires firms to exchange usual letters with banks on Trust status, set off etc. FCA notes variety of methodologies in applying rule PROPOSALS Standard template letters to be used Removal of 20 days grace period and applies to UK and foreign accounts opened Firms required to perform due diligence on authorisations etc. ALL EXISTING letters to be re done in template form (6 month transitional period) (4.134)

128 POLICY STATEMENT - RULES All firms holding client money under CASS 7 will be required to use the relevant templates and follow a set process for completing and exchanging acknowledgment letters FCA have finalised the drafting of the template acknowledgment letters based on feedback and following extensive engagement with the industry, including those banks, clearing houses and intermediate brokers with whom we understand a significant proportion of client money is placed both within the UK and overseas All firms will be prohibited from depositing client money in a client bank account or allowing a third party to hold client money on a client transaction account until the firm has completed and obtained a duly countersigned acknowledgment letter from the relevant bank or third party

129 Custody Rules CASS 6 (5.1) Designed to clarify and enhance the regime to ensure the best protection of custody assets held in relation to Investment Business. Brief summary of proposals follows, please refer to the CP / PS for detailed proposals.

130 Custody Rules CASS 6 (5.1) (Cont.) Physical share certificates clarification IN Delivery vs. payment execution definition changes and TOB Unclaimed custody assets reasonable steps firms must take Registration of assets identification clarifications Written custody agreements written agreements with TP mandatory Reconciliations internal and external rules strengthened, frequencies not less than 25 business days Physical not less than 6 monthly Policies and procedures for reconciliations to be documented, records kept and internal review ( 5.45)

131 POLICY STATEMENT - RULES Share certificates included in the custody rules Written agreements in! The revised rules generally restrict a firm from registering its own assets in the name of the client or any nominee in whose name a custody asset is also registered FCA are introducing our proposals for internal custody record checks as consulted, but with a number of important clarifications to the rules proposed in the CP (see 5.44 PS) FCA are largely introducing the rules they proposed in the CP for physical asset reconciliation without change (except for the proposed auditor s report) Based on feedback, FCA have decided not to proceed with the proposals to require specific auditor s assurance within the custody rules

132 POLICY STATEMENT - RULES FCA are introducing the proposals for external custody reconciliations as set out in the CP. However, based on feedback, they are requiring all firms to undertake external custody reconciliations as regularly as is necessary but at least on a monthly basis (as opposed to once every 25 business days). This is to bring this proposal into line with the frequency at which they expect firms to undertake external client money reconciliations. Annual review on the frequency of internal and external reconciliations to be done by firms.

133 Client Reporting and Information (CASS 9) (6.1) These obligations to report to clients are being strengthened Fair, clear and not misleading See 6.8 et seq. All clients (Money or assets) must HIGHLIGHT to their clients a summary of the key provisions within their client agreements which modify rights or protections from CASS rules STAND ALONE DOCUMENT (6.15)

FCA Update September Presented by: Ian Fletcher FCA

FCA Update September 2015 Presented by: Ian Fletcher FCA www.the2020group.com Training disclaimer The current requirements with which an authorised person, and an approved person, must comply are set out

FCA Update September 2015 Presented by: Ian Fletcher FCA www.the2020group.com Training disclaimer The current requirements with which an authorised person, and an approved person, must comply are set out

Client Money The new CASS regime under the FCA. 26 November 2013

Client Money The new CASS regime under the FCA 26 November 2013 Issues arising out of CP13/5 Ash Saluja 1 Scope and timing Revisions to rules on client assets for investment businesses i.e.: CASS 6 (custody

Client Money The new CASS regime under the FCA 26 November 2013 Issues arising out of CP13/5 Ash Saluja 1 Scope and timing Revisions to rules on client assets for investment businesses i.e.: CASS 6 (custody

Asset Management Market Study Interim Report: Annex 2 Recent regulatory developments

MS15/2.2: Annex 2 Market Study Interim Report: Annex 2 November 2016 Annex 2: Introduction 1. There has been a range of relevant in the asset management sector over the past year. This annex, while not

MS15/2.2: Annex 2 Market Study Interim Report: Annex 2 November 2016 Annex 2: Introduction 1. There has been a range of relevant in the asset management sector over the past year. This annex, while not

CLIENT MONEY AND ASSETS POLICY

CLIENT MONEY AND ASSETS POLICY CLIENT MONEY AND ASSETS POLICY Version: 2.1 31st July 2017 w w w.houseofborse.com HOUSE Of BÖRSE Limited is authorized and regulated by the Financial Conduct Authority. UK

CLIENT MONEY AND ASSETS POLICY CLIENT MONEY AND ASSETS POLICY Version: 2.1 31st July 2017 w w w.houseofborse.com HOUSE Of BÖRSE Limited is authorized and regulated by the Financial Conduct Authority. UK

PS 14/9: Review of the client assets for investment business BEST PRACTICE STATEMENTS CASS

PS 14/9: Review of the client assets for investment business BEST PRACTICE STATEMENTS CASS Table of Contents 1. Introduction... 1 2. Cass 6 Custody Asset Rules... 2 2.1 Registration of firm assets and

PS 14/9: Review of the client assets for investment business BEST PRACTICE STATEMENTS CASS Table of Contents 1. Introduction... 1 2. Cass 6 Custody Asset Rules... 2 2.1 Registration of firm assets and

Reader's Guide: An introduction to the Handbook

Reader's Guide: An introduction to the Handbook January 2019 Reader's Guide: An introduction to the Handbook Contents 1 What is the Handbook? 3 2 Where can I find the Handbook? 4 3 Structure of the Handbook

Reader's Guide: An introduction to the Handbook January 2019 Reader's Guide: An introduction to the Handbook Contents 1 What is the Handbook? 3 2 Where can I find the Handbook? 4 3 Structure of the Handbook

Background Material. Strengthening accountability in financial services

Background Material Strengthening accountability in financial services Contents Background materials for respondents Rationale for extending the accountability regime beyond banking Key elements of the

Background Material Strengthening accountability in financial services Contents Background materials for respondents Rationale for extending the accountability regime beyond banking Key elements of the

Gem Briefing Note 17/4

CP17/33 - Insurance Distribution Directive Implementation Consultation Paper 3 Introduction The IDD entered into force on 23 February 2016 and firms must follow its requirements from 23 February 2018.

CP17/33 - Insurance Distribution Directive Implementation Consultation Paper 3 Introduction The IDD entered into force on 23 February 2016 and firms must follow its requirements from 23 February 2018.

Supervisory Statement SS35/15 Strengthening individual accountability in insurance. July 2018 (Updating February 2018)

") Supervisory Statement SS35/15 Strengthening individual accountability in insurance July 2018 (Updating February 2018) Supervisory Statement SS35/15 Strengthening individual accountability in insurance

Supervisory Statement SS35/15 Strengthening individual accountability in insurance July 2018 (Updating February 2018) Supervisory Statement SS35/15 Strengthening individual accountability in insurance

Policy Statement PS16/16 Implementing audit committee requirements under the revised Statutory Audit Directive. May 2016

Policy Statement PS16/16 Implementing audit committee requirements under the revised Statutory Audit Directive May 2016 Prudential Regulation Authority 20 Moorgate London EC2R 6DA Prudential Regulation

Policy Statement PS16/16 Implementing audit committee requirements under the revised Statutory Audit Directive May 2016 Prudential Regulation Authority 20 Moorgate London EC2R 6DA Prudential Regulation

Strengthening accountability in banking. New publications intensify implementation requirements

Strengthening accountability in banking New publications intensify implementation requirements The UK regulatory authorities continue to develop their proposals for Strengthening accountability in banking:

Strengthening accountability in banking New publications intensify implementation requirements The UK regulatory authorities continue to develop their proposals for Strengthening accountability in banking:

Stand out for the right reasons Protecting Client Assets

www.pwc.co.uk/fsrr Stand out for the right reasons Protecting Client Assets July 2014 Shaking up the Client Assets regime The FCA significantly revised the UK Client Assets protection regime (CASS) when

www.pwc.co.uk/fsrr Stand out for the right reasons Protecting Client Assets July 2014 Shaking up the Client Assets regime The FCA significantly revised the UK Client Assets protection regime (CASS) when

A new regulatory focus: the PRA and FCA Senior Insurance Managers framework

1 Briefing note February 2015 A new regulatory focus: the PRA and FCA Senior Insurance Managers framework On 2 February 2015, the PRA and the FCA consultations, which together set out the framework for

1 Briefing note February 2015 A new regulatory focus: the PRA and FCA Senior Insurance Managers framework On 2 February 2015, the PRA and the FCA consultations, which together set out the framework for

FINAL NOTICE For the reasons given in this notice, the Authority hereby imposes on Sesame a financial penalty of 1,598,000.

FINAL NOTICE To: Sesame Limited Reference Number: 150427 Address: Independence House, Holly Bank Road Huddersfield HD3 3HN 29 October 2014 1. ACTION 1.1. For the reasons given in this notice, the Authority

FINAL NOTICE To: Sesame Limited Reference Number: 150427 Address: Independence House, Holly Bank Road Huddersfield HD3 3HN 29 October 2014 1. ACTION 1.1. For the reasons given in this notice, the Authority

CREDIT UNIONS SOURCEBOOK (AMENDMENT NO 8) INSTRUMENT 2016

INSTRUMENT 2016") CREDIT UNIONS SOURCEBOOK (AMENDMENT NO 8) INSTRUMENT 2016 Powers exercised A. The Financial Conduct Authority makes this instrument in the exercise of the powers and related provisions in or under the

CREDIT UNIONS SOURCEBOOK (AMENDMENT NO 8) INSTRUMENT 2016 Powers exercised A. The Financial Conduct Authority makes this instrument in the exercise of the powers and related provisions in or under the

Consultation Paper CP35/16 Whistleblowing in UK branches

Consultation Paper CP35/16 Whistleblowing in UK branches September 2016 Prudential Regulation Authority 20 Moorgate London EC2R 6DA Prudential Regulation Authority, registered office: 8 Lothbury, London

Consultation Paper CP35/16 Whistleblowing in UK branches September 2016 Prudential Regulation Authority 20 Moorgate London EC2R 6DA Prudential Regulation Authority, registered office: 8 Lothbury, London

Strengthening individual accountability in insurance: SIMR, conduct rules and approved persons

UPDATE: November 2015 Strengthening individual accountability in insurance: SIMR, conduct rules and approved persons Summary The PRA and FCA have published a number of policy statements and consultation

UPDATE: November 2015 Strengthening individual accountability in insurance: SIMR, conduct rules and approved persons Summary The PRA and FCA have published a number of policy statements and consultation

Payment Services and Electronic Money Our Approach

DRAFT FOR CONSULTATION Payment Services and Electronic Money Our Approach The FCA s role under the Payment Services Regulations 2017 and the Electronic Money Regulations 2011 DRAFT April 2017 1 DRAFT FOR

DRAFT FOR CONSULTATION Payment Services and Electronic Money Our Approach The FCA s role under the Payment Services Regulations 2017 and the Electronic Money Regulations 2011 DRAFT April 2017 1 DRAFT FOR

Senior Insurance Managers Regime. an initial assessment of SIMR's introduction

The Senior Insurance Managers Regime an initial assessment of SIMR's introduction 8 June 2016 Various teething problems remain post the Senior Insurance Managers Regime coming into effect on 7 March 2016.

The Senior Insurance Managers Regime an initial assessment of SIMR's introduction 8 June 2016 Various teething problems remain post the Senior Insurance Managers Regime coming into effect on 7 March 2016.

UNIT 1: THE INVESTMENT ENVIRONMENT V.13 TESTED FROM 1 DECEMBER 2015

INVESTMENT MANAGEMENT CERTIFICATE UNIT 1: THE INVESTMENT ENVIRONMENT V.13 TESTED FROM 1 DECEMBER 2015 UNIT AIMS By the end of this unit, learners should be able to demonstrate: An understanding of the

INVESTMENT MANAGEMENT CERTIFICATE UNIT 1: THE INVESTMENT ENVIRONMENT V.13 TESTED FROM 1 DECEMBER 2015 UNIT AIMS By the end of this unit, learners should be able to demonstrate: An understanding of the

Financial Services Authority

Financial Services Authority FINAL NOTICE To: Of: Rowan Dartington & Co Limited Colston Tower Colston Street Bristol BS1 4RD Date: 4 June 2010 TAKE NOTICE: the Financial Services Authority of 25 The North

Financial Services Authority FINAL NOTICE To: Of: Rowan Dartington & Co Limited Colston Tower Colston Street Bristol BS1 4RD Date: 4 June 2010 TAKE NOTICE: the Financial Services Authority of 25 The North

Countdown to MiFID II: Final rules for trading venues, participants and investment firms

Countdown to MiFID II: Final rules for trading venues, participants and investment firms On 31 March 2017, the Financial Conduct Authority (FCA) published its first policy statement (PS 17/5) on the implementation

Countdown to MiFID II: Final rules for trading venues, participants and investment firms On 31 March 2017, the Financial Conduct Authority (FCA) published its first policy statement (PS 17/5) on the implementation

The new FCA Handbook. Feedback on Regulatory Reform proposals relating to the FCA Handbook, including final Handbook rules.

Policy Statement PS13/5«««Financial Services Authority The new FCA Handbook Feedback on Regulatory Reform proposals relating to the FCA Handbook, including final Handbook rules March 2013 Contents Abbreviations

Policy Statement PS13/5«««Financial Services Authority The new FCA Handbook Feedback on Regulatory Reform proposals relating to the FCA Handbook, including final Handbook rules March 2013 Contents Abbreviations

MONTHLY REGULATORY UPDATE JANUARY 2017

MONTHLY REGULATORY UPDATE JANUARY 2017 6 February 2017 The following is a summary of the pronouncements issued since our last regulatory update for the financial services sector issued on 3 January 2017.

MONTHLY REGULATORY UPDATE JANUARY 2017 6 February 2017 The following is a summary of the pronouncements issued since our last regulatory update for the financial services sector issued on 3 January 2017.

For more information, please contact Branko Bjelobaba at Branko Ltd on (0800) or

or") A digestible aid to compliance The Branko Ltd FCA DIY Compliance Manual has developed into an industry standard since it was first produced in 2004 (and we continue to exclusively publish the BIBA version).

A digestible aid to compliance The Branko Ltd FCA DIY Compliance Manual has developed into an industry standard since it was first produced in 2004 (and we continue to exclusively publish the BIBA version).

FINAL NOTICE. To: City & Provincial To: Mr Zaffar Hassan Tanweer

FINAL NOTICE To: City & Provincial To: Mr Zaffar Hassan Tanweer FRN: 302147 IRN: ZHT01000 Address: 21 Halifax Road Denholme Bradford UNITED KINGDOM BD13 4EN Dated: 13 March 2014 1. ACTION 1.1. For the

FINAL NOTICE To: City & Provincial To: Mr Zaffar Hassan Tanweer FRN: 302147 IRN: ZHT01000 Address: 21 Halifax Road Denholme Bradford UNITED KINGDOM BD13 4EN Dated: 13 March 2014 1. ACTION 1.1. For the

ICE BENCHMARK ADMINISTRATION CONSULTATION AND FEEDBACK REQUEST: LIBOR CODE OF CONDUCT ICE Benchmark Administration Limited (IBA) is responsible for the end-to-end administration of four systemically important

ICE BENCHMARK ADMINISTRATION CONSULTATION AND FEEDBACK REQUEST: LIBOR CODE OF CONDUCT ICE Benchmark Administration Limited (IBA) is responsible for the end-to-end administration of four systemically important

The Senior Manager and Certification Regimes in Financial Services: Update and Practical Problems. Tom Ogg ELA National Conference, May 2016

The Senior Manager and Certification Regimes in Financial Services: Update and Practical Problems Tom Ogg ELA National Conference, May 2016 Road map Overview of SMCR Senior Managers Regime: Allocation

The Senior Manager and Certification Regimes in Financial Services: Update and Practical Problems Tom Ogg ELA National Conference, May 2016 Road map Overview of SMCR Senior Managers Regime: Allocation

FINAL NOTICE. Xcap Securities PLC FRN: London EC3V 3ND United Kingdom. Date: 31 May 2013 ACTION

FINAL NOTICE To: Xcap Securities PLC FRN: 504211 Address: 24 Cornhill London EC3V 3ND United Kingdom Date: 31 May 2013 ACTION 1. For the reasons given in this notice, the Financial Conduct Authority (

FINAL NOTICE To: Xcap Securities PLC FRN: 504211 Address: 24 Cornhill London EC3V 3ND United Kingdom Date: 31 May 2013 ACTION 1. For the reasons given in this notice, the Financial Conduct Authority (

The new FCA and PRA Senior Managers and Certification Regime and Code of Conduct. A guide to the current proposals. August

The new FCA and PRA Senior Managers and Certification Regime and Code of Conduct A guide to the current proposals August 2014 www.allenovery.com 2 The new FCA and PRA Senior Managers and Certification

The new FCA and PRA Senior Managers and Certification Regime and Code of Conduct A guide to the current proposals August 2014 www.allenovery.com 2 The new FCA and PRA Senior Managers and Certification

The FSA s role under the Electronic Money Regulations 2011

Financial Services Authority The FSA s role under the Electronic Money Regulations 2011 Our approach March 2011 Preface The second Electronic Money Directive (2EMD) will be implemented in the UK on 30

Financial Services Authority The FSA s role under the Electronic Money Regulations 2011 Our approach March 2011 Preface The second Electronic Money Directive (2EMD) will be implemented in the UK on 30

Strengthening accountability in banking

Strengthening accountability in banking BSA response to PRA CP 1/16 and FCA CP 16/1 4 February 2016 Introduction This brief response supports the proposals in, and comments on, PRA CP1/16 and FCA CP 16/1

Strengthening accountability in banking BSA response to PRA CP 1/16 and FCA CP 16/1 4 February 2016 Introduction This brief response supports the proposals in, and comments on, PRA CP1/16 and FCA CP 16/1

Details of FCA Consumer Credit Regime (13/29) 14 October 2013

14 October 2013") CPA Audit LLP, Talbot House, 8-9 Talbot Court, London EC3V 0BP Telephone: 020 7621 9010 Facsimile: 020 7621 9011 email: info@cpaaudit.co.uk web: www.cpaaudit.co.uk Details of FCA Consumer Credit Regime

CPA Audit LLP, Talbot House, 8-9 Talbot Court, London EC3V 0BP Telephone: 020 7621 9010 Facsimile: 020 7621 9011 email: info@cpaaudit.co.uk web: www.cpaaudit.co.uk Details of FCA Consumer Credit Regime

FINAL NOTICE. Mr Ian David Jones Arle Court, Hatherley Lane, Cheltenham, GL51 6PN

Financial Services Authority FINAL NOTICE To: Of: Individual Ref: Mr Ian David Jones Arle Court, Hatherley Lane, Cheltenham, GL51 6PN IDJ00004 Date: 21 September 2011 TAKE NOTICE: The Financial Services

Financial Services Authority FINAL NOTICE To: Of: Individual Ref: Mr Ian David Jones Arle Court, Hatherley Lane, Cheltenham, GL51 6PN IDJ00004 Date: 21 September 2011 TAKE NOTICE: The Financial Services

Financial Conduct Authority Pension Wise recommendation policy

Financial Conduct Authority Pension Wise recommendation policy July 2015 Policy Statement PS15/17 Pension Wise recommendation policy PS15/17 Contents Abbreviations used in this paper 3 1 Overview 5 2

Financial Conduct Authority Pension Wise recommendation policy July 2015 Policy Statement PS15/17 Pension Wise recommendation policy PS15/17 Contents Abbreviations used in this paper 3 1 Overview 5 2

Future regulatory treatment of CCA regulated first charge mortgages

Financial Conduct Authority Future regulatory treatment of CCA regulated first charge mortgages November 2015 Consultation Paper CP15/36* Future regulatory treatment of CCA regulated first charge mortgages

Financial Conduct Authority Future regulatory treatment of CCA regulated first charge mortgages November 2015 Consultation Paper CP15/36* Future regulatory treatment of CCA regulated first charge mortgages

Supervisory Statement SS28/15 Strengthening individual accountability in banking. September 2016 (Updating January 2016)

") Supervisory Statement SS28/15 Strengthening individual accountability in banking September 2016 (Updating January 2016) Prudential Regulation Authority 20 Moorgate London EC2R 6DA Prudential Regulation

Supervisory Statement SS28/15 Strengthening individual accountability in banking September 2016 (Updating January 2016) Prudential Regulation Authority 20 Moorgate London EC2R 6DA Prudential Regulation

Policy Statement PS28/17 PRA fees and levies: model transaction fees, fees and FSCS levies for insurers and fees for designated investment firms

Policy Statement PS28/17 PRA fees and levies: model transaction fees, fees and FSCS levies for insurers and fees for designated investment firms December 2017 Prudential Regulation Authority 20 Moorgate

Policy Statement PS28/17 PRA fees and levies: model transaction fees, fees and FSCS levies for insurers and fees for designated investment firms December 2017 Prudential Regulation Authority 20 Moorgate

Principals and their appointed representatives in the general insurance sector

Financial Conduct Authority Thematic Review TR16/6 Principals and their appointed representatives in the general insurance sector July 2016 Principals and their appointed representatives in the general

Financial Conduct Authority Thematic Review TR16/6 Principals and their appointed representatives in the general insurance sector July 2016 Principals and their appointed representatives in the general

Respond to the consultation proposals; and Highlight the need for a proportionate approach that avoids a onesize-fits-all

Elizabeth Richards Financial Conduct Authority 25 The North Colonnade Canary Wharf London E14 5HS 15 May 2015 Dear Elizabeth, AFM Response to Consultation Paper FCA CP15/4, PRA 6/15, Whistleblowing 1.

Elizabeth Richards Financial Conduct Authority 25 The North Colonnade Canary Wharf London E14 5HS 15 May 2015 Dear Elizabeth, AFM Response to Consultation Paper FCA CP15/4, PRA 6/15, Whistleblowing 1.

Principles applicable to auditors reports to regulators

Guidance for reporting in accordance with the Client Asset Requirements issued by the Irish Financial Services Regulatory Authority ( Financial Regulator ) in November 2007. This guidance is issued by

Guidance for reporting in accordance with the Client Asset Requirements issued by the Irish Financial Services Regulatory Authority ( Financial Regulator ) in November 2007. This guidance is issued by

Prudential Standard GOI 3 Risk Management and Internal Controls for Insurers

Prudential Standard GOI 3 Risk Management and Internal Controls for Insurers Objectives and Key Requirements of this Prudential Standard Effective risk management is fundamental to the prudent management

Prudential Standard GOI 3 Risk Management and Internal Controls for Insurers Objectives and Key Requirements of this Prudential Standard Effective risk management is fundamental to the prudent management

CROWDFUNDING AND THE PROMOTION OF NON-READILY REALISABLE SECURITIES INSTRUMENT 2014

CROWDFUNDING AND THE PROMOTION OF NON-READILY REALISABLE SECURITIES INSTRUMENT 2014 Powers exercised A. The Financial Conduct Authority makes this instrument in the exercise of the following powers and

CROWDFUNDING AND THE PROMOTION OF NON-READILY REALISABLE SECURITIES INSTRUMENT 2014 Powers exercised A. The Financial Conduct Authority makes this instrument in the exercise of the following powers and

Working Together. An Industry Guide to Lender and Intermediary Accountabilities and Responsibilities in Mortgage Sales and Servicing

Working Together An Industry Guide to Lender and Intermediary Accountabilities and Responsibilities in Mortgage Sales and Servicing Issued: September 2016 0 A joint AMI, CML and IMLA paper 1. Introduction

Working Together An Industry Guide to Lender and Intermediary Accountabilities and Responsibilities in Mortgage Sales and Servicing Issued: September 2016 0 A joint AMI, CML and IMLA paper 1. Introduction

Future regulatory treatment of CCA regulated first charge mortgages

Financial Conduct Authority Policy Statement PS16/7 Future regulatory treatment of CCA regulated first charge mortgages March 2016 Future regulatory treatment of CCA regulated first charge mortgages PS16/7

Financial Conduct Authority Policy Statement PS16/7 Future regulatory treatment of CCA regulated first charge mortgages March 2016 Future regulatory treatment of CCA regulated first charge mortgages PS16/7

Consultation Paper CP12/22. Financial Services Authority. Client assets regime: EMIR, multiple pools and the wider review

Consultation Paper CP12/22 Financial Services Authority Client assets regime: EMIR, multiple pools and the wider review September 2012 CP12/22 Contents Abbreviations used in this paper 3 1. Overview 5

Consultation Paper CP12/22 Financial Services Authority Client assets regime: EMIR, multiple pools and the wider review September 2012 CP12/22 Contents Abbreviations used in this paper 3 1. Overview 5

BENCHMARKS REGULATION (AMENDMENT) INSTRUMENT 2018

INSTRUMENT 2018") BENCHMARKS REGULATION (AMENDMENT) INSTRUMENT 2018 Powers exercised A. The Financial Conduct Authority makes this instrument in the exercise of the following powers and related provisions in: (1) the Financial

BENCHMARKS REGULATION (AMENDMENT) INSTRUMENT 2018 Powers exercised A. The Financial Conduct Authority makes this instrument in the exercise of the following powers and related provisions in: (1) the Financial

PRA RULEBOOK CRR FIRMS INSTRUMENT 2013

PRA RULEBOOK CRR FIRMS INSTRUMENT 2013 Powers exercised A. The Prudential Regulation Authority (the PRA ) makes this instrument in the exercise of the following powers and related provisions in the Financial

PRA RULEBOOK CRR FIRMS INSTRUMENT 2013 Powers exercised A. The Prudential Regulation Authority (the PRA ) makes this instrument in the exercise of the following powers and related provisions in the Financial

The Bank of England, Prudential Regulation Authority

Consultation Paper CP12/39 Financial Services Authority The Bank of England, Prudential Regulation Authority The PRA s approach to enforcement: consultation on proposed statutory statements of policy and

Consultation Paper CP12/39 Financial Services Authority The Bank of England, Prudential Regulation Authority The PRA s approach to enforcement: consultation on proposed statutory statements of policy and

Policy Statement PS3/17 The implementation of ring-fencing: reporting and residual matters responses to CP25/16 and Chapter 5 of CP36/16

Policy Statement PS3/17 The implementation of ring-fencing: reporting and residual matters responses to CP25/16 and Chapter 5 of CP36/16 February 2017 Prudential Regulation Authority 20 Moorgate London

Policy Statement PS3/17 The implementation of ring-fencing: reporting and residual matters responses to CP25/16 and Chapter 5 of CP36/16 February 2017 Prudential Regulation Authority 20 Moorgate London

Finance & investment briefing

Finance & investment briefing September 2017 Sackers finance & investment group takes a look at current issues of interest to pension scheme investors Finance & investment briefing September 2017 Abbreviations

Finance & investment briefing September 2017 Sackers finance & investment group takes a look at current issues of interest to pension scheme investors Finance & investment briefing September 2017 Abbreviations

LMA GUIDANCE: SENIOR INSURANCE MANAGERS REGIME (SIMR)

") LMA GUIDANCE: SENIOR INSURANCE MANAGERS REGIME (SIMR) JULY 2015 LMA GUIDANCE SENIOR INSURANCE MANAGERS REGIME (SIMR) 1. SUMMARY Starting November 2014, the PRA and FCA issued a joint series of three consultation

LMA GUIDANCE: SENIOR INSURANCE MANAGERS REGIME (SIMR) JULY 2015 LMA GUIDANCE SENIOR INSURANCE MANAGERS REGIME (SIMR) 1. SUMMARY Starting November 2014, the PRA and FCA issued a joint series of three consultation

GUIDELINES ON WHOLESALE FUNDS

GUIDELINES ON WHOLESALE FUNDS Issued by: Securities Commission Effective Date: 18 February 2009 CONTENTS 1.0 APPLICATION OF GUIDELINES 1 2.0 DEFINITIONS 1 3.0 ROLE AND DUTIES OF THE FUND MANAGER 6 4.0

GUIDELINES ON WHOLESALE FUNDS Issued by: Securities Commission Effective Date: 18 February 2009 CONTENTS 1.0 APPLICATION OF GUIDELINES 1 2.0 DEFINITIONS 1 3.0 ROLE AND DUTIES OF THE FUND MANAGER 6 4.0

BERMUDA MONETARY AUTHORITY THE INSURANCE CODE OF CONDUCT FEBRUARY 2010

Table of Contents 0. Introduction..2 1. Preliminary...3 2. Proportionality principle...3 3. Corporate governance...4 4. Risk management..9 5. Governance mechanism..17 6. Outsourcing...21 7. Market discipline

Table of Contents 0. Introduction..2 1. Preliminary...3 2. Proportionality principle...3 3. Corporate governance...4 4. Risk management..9 5. Governance mechanism..17 6. Outsourcing...21 7. Market discipline

Direct line: Local fax:

Direct line: 0207 066 3100 Local fax: 0207 066 3101 Email: martin.wheatley@fca.org.uk Financial Conduct Authority 25 The North Colonnade Canary Wharf London E14 5HS Andrew Tyrie MP Chairman of the Treasury

Direct line: 0207 066 3100 Local fax: 0207 066 3101 Email: martin.wheatley@fca.org.uk Financial Conduct Authority 25 The North Colonnade Canary Wharf London E14 5HS Andrew Tyrie MP Chairman of the Treasury

PRA RULEBOOK: CRR FIRMS: NON-CRR FIRMS: FITNESS AND PROPRIETY AMENDMENT INSTRUMENT 2016

PRA RULEBOOK: CRR FIRMS: NON-CRR FIRMS: FITNESS AND PROPRIETY AMENDMENT INSTRUMENT 2016 Powers exercised A. The Prudential Regulation Authority ( PRA ) makes this instrument in the exercise of the following

PRA RULEBOOK: CRR FIRMS: NON-CRR FIRMS: FITNESS AND PROPRIETY AMENDMENT INSTRUMENT 2016 Powers exercised A. The Prudential Regulation Authority ( PRA ) makes this instrument in the exercise of the following

Proposed Revision to the UK Stewardship Code Annex A - Revised UK Stewardship Code

Consultation Financial Reporting Council January 2019 Proposed Revision to the UK Stewardship Code Annex A - Revised UK Stewardship Code The FRC s mission is to promote transparency and integrity in business

Consultation Financial Reporting Council January 2019 Proposed Revision to the UK Stewardship Code Annex A - Revised UK Stewardship Code The FRC s mission is to promote transparency and integrity in business