Update NASACT. GASB Update Due Process Documents

|

|

|

- Lee Ross

- 5 years ago

- Views:

Transcription

1 Update NASACT GASB Update Due Process Documents The views expressed in this presentation are those of the presenters. Official positions of the GASB are reached only after extensive due process and deliberations. Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

2 Opening Remarks MODERATOR R. Kinney Poynter Executive Director NASACT SPEAKER David Vaudt Chairman GASB SPEAKER David Bean Director of Research and Technical Activities GASB SPEAKER Michelle Czerkawski Senior Project Manager GASB SPEAKER Lisa Parker Senior Project Manager GASB SPEAKER Roberta Reese Senior Project Manager GASB SPEAKER Scott Reeser Supervising Project Manager GASB 2

3 Overview 3

4 Topics to be Covered Financial reporting model Implementation guide fiduciary activities Implementation guidance update Other projects 4

5 Financial Reporting Model 5

6 Preliminary Views: Financial Reporting Model Improvements Project objective and background Governmental funds - Concerns with current reporting - Short-term financial resources measurement focus Alternative views - Presentation Proprietary fund presentation Budgetary comparison reporting 6

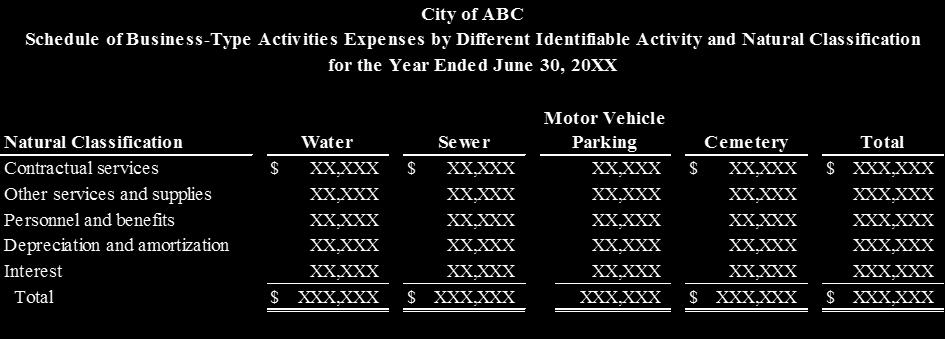

7 Preliminary Views: Financial Reporting Model Improvements Major component unit information Schedule of government-wide expenses by natural classification Feedback and next steps 7

8 Project Objective and Background Reexamination of the effectiveness of the financial reporting model Statements 34, 35, 37, 41, and 46, and Interpretation 6 Pre-agenda research showed model generally effective, targeted improvements possible Invitation to Comment, Financial Reporting Model Improvements Governmental Funds, issued December 2016 Preliminary Views, Financial Reporting Model Improvements, issued September

9 Concerns with Governmental Funds Financial Statements Lack of effectiveness of governmental fund information Lack of conceptual consistency Lack of guidance for complex transactions Lack of consistency in applying the current financial resources measurement focus and modified accrual basis of accounting 9

10 Recognition in Governmental Funds Short-term financial resources measurement focus Elements from short-term transactions recognized as the underlying transaction occurs Elements from long-term transactions recognized when payments are due Financial assets: cash, assets that are available to be converted to cash, and assets that are consumable in lieu of cash 10

11 Recognition in Governmental Funds Short-Term Transactions Normally are due to convert to or generate cash or require the use of cash within one year from the inception of the transaction Long-Term Transactions Normally are due to convert to or require the use of cash beyond one year from the inception of the transaction An entire class of transactions will either be short-term transactions or long-term transactions. Transactions within classes (for example, investments) are not treated differently. 11

12 Recognition in Governmental Funds Assets Assets include those from shortterm transactions that are receivable at period-end, as well as cash and other financial assets that are available to be converted to cash, or expected to be consumed within the subsequent reporting period Liabilities Liabilities arising from short-term transactions that are payable at year end Liabilities arising from long-term transactions are recognized when payments become due Assets arising from long-term transactions are recognized when payments are due 12

13 Recognition in Governmental Funds Outflows of Resources As spending occurs Spending from short-term transactions (such as use of goods and services and acquisition of capital assets) as the transactions occur Spending from long-term transactions as payments are due Inflows of Resources Inflows of resources from shortterm transactions (such as tax levies, grants, and changes in fair value of investments) as the transactions occur Inflows of resources arising from long-term transactions are recognized when payments become due 13

14 Messages Conveyed by Short-Term Financial Resources Measurement Focus Consistency in the reporting of balance sheet elements and financial resource flows elements Period-end balances from short-term transactions Spending of the period Inflows of resources from short-term transactions as they occur and long-term transactions when payment are due Fund balance that is available for spending Results useful in evaluating budgetary information 14

15 Recognition in Governmental Funds Deferred Outflows of Resources and Deferred Inflows of Resources Governed by concept of available for spending in a future period Outflows of resources that do not meet the definition of an asset and are inherently related to future spending Inflows of resources that do not meet the definition of a liability and can only be used for future spending Limited to circumstances identified by the GASB 15

16 Recognition Example Investments in Permanent Fund Beginning of year balance: $18,400,000 No maturities or purchase of investments; Change in fair value of $100,000; End of year balance: $18,500,000 Recognition Approach Balance Sheet Resource Flows Statement Current financial resources Investments of $18,500,000 Inflows of resources of $100,000 Short-term financial resources Investments of $18,500,000 Inflows of resources of $100,000 16

17 Recognition Example Other Taxes Receivable End of year balance: $13,342,623 Other taxes are associated with the current year; $3,342,623 of other taxes are due 3 months after year-end, $10,000,000 are due 6 months after year-end Recognition Approach Balance Sheet Resource Flows Statement Current financial resources Taxes receivable of $13,342,623 Inflows of resources of $3,342,623 and deferred inflow of resources of $10,000,000 Short-term financial resources Taxes receivable of $13,342,623 Inflows of resources of $13,342,623 17

18 Recognition Example Prepaid Items Beginning of year balance: $5,800 Spending on prepaid items during year: $60,000 End of year balance: $13,800 Recognition Approach Balance Sheet Resource Flows Statement Current financial resources Short-term financial resources Prepaid item and nonspendable fund balance of $13,800 Outflows of resources of $52,000 Prepaid item of $13,800 Outflows of resources of $52,000 18

19 Recognition Example Notes Receivable Related to Lending Beginning of year balance: $4,387,776 Collections during year: $645,000 End of year balance: $3,742,776 All scheduled to be collected beyond 3 months after period-end Recognition Approach Balance Sheet Resource Flows Statement Current financial resources Short-term financial resources Notes receivable and nonspendable fund balance of $3,742,776 No amounts recognized No amounts recognized Inflow of resources of $645,000 19

20 Recognition Example Accrued Interest on Long-Term Debt Beginning of year balance: $899,750 Accrued during in the current year: $2,394,534 Paid during the current year: $2,448,950 End of year balance: $845,334 Recognition Approach Balance Sheet Resource Flows Statement Current financial resources No amounts recognized Debt service expenditures of $2,448,950 Short-term financial resources Accrued interest payable of $845,334 Outflows of resources of $2,394,534 20

21 Recognition Example Tax Anticipation Notes Payable Beginning of year balance: $4,000,000 Repayments during in the current year: $4,000,000* Borrowings during the current year: $4,400,000* End of year balance: $4,400,000 Recognition Approach Balance Sheet Resource Flows Statement Current financial Tax anticipation note payable of No amounts recognized. resources $4,400,000 Short-term financial resources Tax anticipation note payable of $4,400,000 No amounts recognized. *Borrowings and repayments are disclosed. 21

22 Recognition Example Postemployment Benefits Pension plan is funded. Net pension liability is $826,333 at period-end. OPEB plan is pay-as-you-go. Net OPEB liability is $42,785,037 at period-end. Recognition Approach Pension OPEB Current financial resources Short-term financial resources No liability. No amount normally expected to be liquidated with available expendable resources. No liability. No amounts due. No liability. No amount normally expected to be liquidated with available expendable resources. No liability. No amounts due. 22

23 Recognition Example Bonds Payable Beginning of year balance: $33,414,493, all capital-related Principal paid during the current year: $8,331,457 End of year balance: $25,083,036 Recognition Approach Balance Sheet Resource Flows Statement Current financial No amounts recognized Expenditures of $8,331,457 resources Short-term financial resources No amounts recognized Outflows of resources of $8,331,457 23

24 Alternative Views Modify short-term financial resources - Recognize portion of long-term receivables due in the next reporting period (both as asset and inflows of resources) - Recognize portion of long-term liabilities due in the next reporting period (both as liability and outflows of resources) with exceptions: Pensions and other postemployment benefits Asset retirement obligations Replace concept of normally with contractual maturities (or amounts otherwise expected to be paid in cash or other fund financial resources) 24

25 Alternative Views (Continued) Examples - General obligation bond that will be called shortly after periodend using existing resources - Long-term debt payment due 1 month after period-end - Long-term debt payment due 11 months after period-end Government-wide statement of cash flows 25

26 Governmental Funds-Presentation Current and noncurrent format of resource flows statement Current includes all flows other than those that are noncurrent Noncurrent resource flows: those related to purchase and disposal of capital assets and issuance and repayment of long-term debt 26

27 Governmental Funds-Specific Terminology Titles Short-Term Financial Resources Balance Sheet Short-Term Financial Resource Flows Elements Short-term assets Short-term liabilities Deferred outflows of short-term financial resources Deferred inflows of short-term financial resources Short-term financial resources fund balances Inflows of short-term financial resources for current activities Outflows of short-term financial resources for current activities Net flows of short-term financial resources for noncurrent activity 27

28 Governmental Funds Specific Terminology This financial statement presents a short-term view of governmental fund activities and reports items of a longterm nature differently from how they are reported in the government-wide financial statements. 28

29 29

30 Proprietary Fund Financial Statement Presentation Continue separate presentation of operating and nonoperating revenues and expenses Operating revenues and expenses are those other than nonoperating Nonoperating revenues and expenses include: - Subsidies received and provided - Revenues and expenses related to financing - Resources from the disposal of capital assets and inventory - Investment income and expenses 30

31 Proprietary Fund Financial Statement Presentation Subtotal for operating income (loss) and noncapital subsidies Subsidies are: resources provided by another party or fund to keep rates lower than otherwise would be necessary to support the level of goods and services to be provided 31

32 32

33 Budgetary Comparison Information Presented in required supplementary information - Consistent with conceptual framework on methods of communication Required variance presentations - Final budget and actual amounts - Original and final budget 33

The existing alternative to present condensed major component unit financial statements in the notes to financial")

34 Major Component Unit Information If feasible, present in separate columns on the reporting entity s government-wide financial statements If not feasible, present in as combining financial statements after the fund financial statements (included in basic financial statements) The existing alternative to present condensed major component unit financial statements in the notes to financial statements would be eliminated 34

35 Government-Wide Expenses by Natural Classification Applicable to governments presenting a CAFR Presented as supplementary information Governmental activities by program or function (and natural classification) Business-type activities by different identifiable activity (and natural classification) No change to government-wide statement of activities 35

36 36

- March 14, 2019 in Flushing, NY (near LaGuardia airport) User forums - March 6, 2019 in Rosemont, IL - March 14, 2019 in Flushing, NY")

37 How to Provide Feedback Comment letter deadline February 15, 2019 Public hearings - March 5, 2019 in Rosemont, IL (near O Hare airport) - March 12, 2019 in Atlanta, GA (in conjunction with NASC) - March 14, 2019 in Flushing, NY (near LaGuardia airport) User forums - March 6, 2019 in Rosemont, IL - March 14, 2019 in Flushing, NY 37

- Debt service funds Target issuance of Exposure Draft: June 2020")

38 Next Steps Additional issues for Exposure Draft - Extraordinary and special items - Management s discussion and analysis (MD&A) - Debt service funds Target issuance of Exposure Draft: June

39 Concepts Recognition 39

40 Preliminary Views: Recognition of Elements of Financial Statements Hierarchy of recognition - Meet definition of asset or liability? - Meet definition of deferred outflow of resources or deferred inflow of resources? - Meet definition of outflow of resources or inflow or resources? 40

41 Preliminary Views: Recognition of Elements of Financial Statements Short-term financial resources measurement focus - Governmental funds - Recognizes elements arising from short-term transactions and other events as they occur - Recognizes elements arising from long-term transactions when payments are due Recognition concepts - Meet definition of element within context of short-term financial resources measurement focus - Sufficiently reflects qualitative characteristics, subject to limitations of financial reporting 41

42 Preliminary Views: Recognition of Elements of Financial Statements Economic resources measurement focus - Incorporates all outflows of resources, inflows of resources and all assets, liabilities, deferred outflows of resources, and deferred inflows of resources - Recognition concepts Meet the definition of an element Sufficiently reflect qualitative characteristics, subject to limitations of financial reporting 42

43 Implementation Guide Fiduciary Activities 43

44 Statement 84, Fiduciary Activities WHAT The Board issued Statement 84 to clarify when a government has a fiduciary responsibility and is required to present fiduciary fund financial statements WHY Guidance is needed by preparers and auditors for issues related to the implementation of Statement 84 WHEN Effective for fiscal years beginning after December 15, 2018 Earlier application is encouraged 44

45 Exposure Draft Proposed Implementation Guide, Fiduciary Activities WHAT GASB has cleared an Exposure Draft of a Proposed Implementation Guide, Fiduciary Activities, for public comment WHY Guidance is needed by preparers and auditors for issues related to the implementation of Statement 84 WHEN Comment deadline: February 28, 2019 Final Implementation Guide expected: June

46 Implementation Guidance A Focus on State Governments Identifying Fiduciary Activities - Fiduciary Component Units Control applicability - Pension and OPEB Arrangements That Are Not Component Units - Other Fiduciary Activities Assets are for the benefit of individuals Assets are for the benefit of organizations or other governments - Control of Assets - Own-source Revenues 46

47 Implementation Guidance A Focus on State Governments Reporting Fiduciary Activities in Fiduciary Funds - Investment Trust Funds - Private-Purpose Trust Funds - Custodial Funds Business-type activity exception Statement of Fiduciary Net Position - Liability to the Beneficiaries Statement of Changes in Fiduciary Net Position - Disaggregation Exception Reporting Fiduciary Component Units 47

48 Identifying Fiduciary Activities Q&As Fiduciary Component Units - Intended to clarify whether pension or OPEB plans (both defined benefit and defined contribution) that are administered through a trust or an equivalent arrangement are legally separate Potentially different answer for trust and equivalent arrangement (Q4.1-Q4.3) - Intended to clarify other Implications of Statement 14, as amended Financial accountability applicability (Q4.4-Q4.6) Implication of being legally obligated or otherwise assuming the obligation to make contributions to a pension or OPEB plan (Q4.7) 48

49 Identifying Fiduciary Activities Q&As Fiduciary Component Units - Control applicability Intended to clarify whether control of the assets is required when a government has determined the activity is a component unit (Q4.8) 49

50 Identifying Fiduciary Activities Q&As Pension and OPEB Arrangements That Are Not Component Units - Intended to clarify whether a government holding assets for a multiple employer pension or OPEB plan that is not administered through a trust that meets the specified criteria results in a fiduciary activity to be reported by any of the participating governments Government holding the assets versus the other government participants (Q4.9) 50

Contractor deposits/performance bonds (Q4.12-Q4.13) Retainage (Q4.14) Jail inmate accounts (Q4.15) Payroll clearing accounts (Q4.")

51 Identifying Fiduciary Activities Q&As Other Fiduciary Activities - Intended to clarify whether the following are considered to be fiduciary activities Seized assets (Q4.11) Contractor deposits/performance bonds (Q4.12-Q4.13) Retainage (Q4.14) Jail inmate accounts (Q4.15) Payroll clearing accounts (Q4.16) 51

52 Identifying Fiduciary Activities Q&As Assets Are For the Benefit of Individuals - Intended to clarify whether a government has administrative involvement or direct financial involvement with the assets Actual scenarios are analogized to the examples from Statement 24: o Monitors compliance with the requirements of the activity (established by the government or resource provider) o Determines eligible expenditures (established by the government or resource provider) o Has ability to exercise discretion over how the assets are allocated o Provides matching resources for the activities COMES DOWN TO WHO ESTABLISHES THE SPECIFIC GUIDELINES ON HOW THE RESOURCES CAN BE SPENT 52

53 Identifying Fiduciary Activities Q&As Assets Are For the Benefit of Individuals - Intended to clarify when a government has administrative involvement or direct financial involvement with the assets Inmate accounts- contraband purchases (Q4.25) University scholarships (Q4.26) 53

to a not-for-profit organization (Q4.")

54 Identifying Fiduciary Activities Q&As Assets Are For the Benefit of Organizations or Other Governments - Intended to clarify when assets are being held for the benefit of an individual or an other organization Funds received by a university from a foundation (Q4.28) Non-trust agreements to provide accounting and treasury services (including investing) to a not-for-profit organization (Q4.30-Q4.31) 54

55 Identifying Fiduciary Activities Q&As Control of Assets - Intended to clarify whether a government is controlling assets as described in paragraph 12 of Statement 84 College tuition savings plan (Q4.32) ABLE savings plan (Q4.34-Q4.35) Own-Source Revenues - Intended to clarify whether specific revenue sources would be considered own-source as described in paragraph 13 of Statement 84 Revenue-sharing agreements (Q4.36) University enrolled student activity fees (Q4.37) Prepaid college tuition plans (Q4.38) 55

56 Reporting Fiduciary Activities in Fiduciary Funds Q&As Investment Trust Funds - Intended to clarify how to report investment pools that are not administered through a trust that meets the criteria in paragraph 11c(1) of Statement 84 (Q4.41) Private-Purpose Trust Funds - Intended to clarify that a fiduciary activity administered through a trust that meets the criteria in Statement 84 that is not a pension (or other employee benefit) trust fund or an investment trust fund should be reported in a private-purpose trust fund (Q4.42) 56

of Statement 84 (Q4.")

57 Reporting Fiduciary Activities in Fiduciary Funds Q&As Custodial Funds - Intended to clarify how to report multiple external investment pools that are not administered through a trust that meets the criteria in paragraph 11c(1) of Statement 84 (Q4.44) Business-Type Activity Exception - Intended to clarify the exception provided in paragraph 19 of Statement 84 to business-type activities that are normally expected to hold assets, upon receipt, for three months or less (Q4.45) 57

58 Reporting Fiduciary Activities in Fiduciary Funds Q&As Statement of Fiduciary Net Position - Intended to clarify the liability to a beneficiary requirement when a government is compelled to disburse the resources (Q4.47) Statement of Changes in Fiduciary Net Position - Intended to clarify the disaggregation exception when resources are expected to be held for 3 months or less for one activity and for multiple activities (Q4.48-Q4.50) 58

Public university (Q4.")

59 Reporting Fiduciary Activities in Fiduciary Funds Q&As Reporting Fiduciary Component Units - Intended to clarify how to report a fiduciary component unit that has fiduciary component units of its own Public employee retirement system (Q4.51) Public university (Q4.53) 59

60 Effective Dates Effective date, except for questions 5.2 and Effective for financial reporting periods beginning after December 15, Effective date for questions 5.2 and Effective for financial reporting periods beginning after June 15, 2019 (same as Implementation Guide 2019-X). Earlier application is encouraged. 60

61 Transition Changes adopted to conform to the provisions in this Implementation Guide should be applied retroactively by restating financial statements, if practicable, for all prior periods presented. If restatement for prior periods is not practicable, the cumulative effect, if any, should be reported as a restatement of beginning fiduciary net position for the earliest period restated. 61

62 Implementation Guide Update 62

63 Implementation Guidance Update What: GASB has cleared an Exposure Draft of an implementation guidance update for public comment Why: Guidance is needed by preparers and auditors for issues related to previously issued standards When: Comment deadline: January 31 63

64 Issues Addressed in the Proposal Postemployment benefits - Selection of an index rate for purposes of the discount rate - Implicit rate subsidy as contributions subsequent to the measurement date Derivative instruments role of termination date in accounting for termination of an effective hedge Revenue recognition for expenditure-driven grants Insurance recoveries related to storm damage Intra-entity transfers of capital assets 64

65 Issues Addressed in the Proposal (cont.) Reporting amounts related to the long-term portion of notes receivable from transactions not yet recognized as revenue Tax abatement disclosures computation of the amount by which tax revenues were reduced Irrevocable split-interest agreements - Cash flows reporting for resources received - Remainder interest benefit to establish permanent endowment - General fund recognition of liability for remainder interest Technical corrections 65

66 Project Timeline Deliberations Began October 2018 Exposure Draft Cleared November 2018 Comment Deadline January 31, 2019 Final Guide Expected April

67 Other Projects 67

68 Other Projects Timetable Subscription-Based IT Arrangements Exposure Draft May 2019 Public-Private Partnerships Exposure Draft June 2019 Deferred Compensation Plans Exposure Draft June 2019 Omnibus Exposure Draft June 2019 Secured Overnight Financing Rate Exposure Draft August 2019 Implementation Guide Update Final April 2019 Implementation Guide Fiduciary Final June 2019 Implementation Guide Lease Exposure Draft February

69 Questions Website information:

70 70

71 Website Resources Free download of Statements, Implementation Guides, Concepts Statements and other pronouncements Free access to the basic view of Governmental Accounting Research System (GARS) Free copies of proposals Up-to-date information on current projects Articles and Fact Sheets about proposed and final pronouncements Form for submitting technical questions Educational materials, including podcasts 71

72 Questions and Answers MODERATOR R. Kinney Poynter Executive Director NASACT SPEAKER David Vaudt Chairman GASB SPEAKER David Bean Director of Research and Technical Activities GASB SPEAKER Michelle Czerkawski Senior Project Manager GASB SPEAKER Lisa Parker Senior Project Manager GASB SPEAKER Roberta Reese Senior Project Manager GASB SPEAKER Scott Reeser Supervising Project Manager GASB 72

Invitation to Comment, Financial Reporting Model Improvements Governmental Funds

Invitation to Comment, Financial Reporting Model Improvements Governmental Funds Opening Remarks MODERATOR R. Kinney Poynter Executive Director, NASACT SPEAKER David Vaudt Chairman GASB SPEAKER Roberta

Invitation to Comment, Financial Reporting Model Improvements Governmental Funds Opening Remarks MODERATOR R. Kinney Poynter Executive Director, NASACT SPEAKER David Vaudt Chairman GASB SPEAKER Roberta

Financial Reporting Model

Illinois GFOA Annual Conference, September 2018 Financial Reporting Model Frederick G. Lantz, C.P.A. Partner-in-Charge, Government Services, Sikich LLP Brian W. Caputo, Ph.D., C.P.A. Vice President for

Illinois GFOA Annual Conference, September 2018 Financial Reporting Model Frederick G. Lantz, C.P.A. Partner-in-Charge, Government Services, Sikich LLP Brian W. Caputo, Ph.D., C.P.A. Vice President for

GASB Update NASACT. July 18, 2018

NASACT GASB Update July 18, 2018 The views expressed in this presentation are those of the presenters. Official positions of the GASB are reached only after extensive due process and deliberations. 1 Opening

NASACT GASB Update July 18, 2018 The views expressed in this presentation are those of the presenters. Official positions of the GASB are reached only after extensive due process and deliberations. 1 Opening

Financial Reporting Model Improvements Governmental Funds

Financial Reporting Model Improvements Governmental Funds Feb. 8 2-3 p.m. ET 2 CPE FOS: ACCG Z Sample CPE OMB Tracking Circular Letter A-123 History 1981 OMB First Issued Circular No. A-123, Internal Control

Financial Reporting Model Improvements Governmental Funds Feb. 8 2-3 p.m. ET 2 CPE FOS: ACCG Z Sample CPE OMB Tracking Circular Letter A-123 History 1981 OMB First Issued Circular No. A-123, Internal Control

Déjà vu All Over Again! GASB Revisits the Financial Reporting Model

2018 CSFMO Annual Conference Déjà vu All Over Again! GASB Revisits the Financial Reporting Model February 22, 2018 David Sundstrom, Board Member, GASB Harriet Commons, Retired Finance Director/Treasurer,

2018 CSFMO Annual Conference Déjà vu All Over Again! GASB Revisits the Financial Reporting Model February 22, 2018 David Sundstrom, Board Member, GASB Harriet Commons, Retired Finance Director/Treasurer,

Financial Reporting Model Improvements Governmental Funds

December 7, 2016 Comments Due: March 31, 2017 Invitation to Comment of the Governmental Accounting Standards Board on major issues related to Financial Reporting Model Improvements Governmental Funds Project

December 7, 2016 Comments Due: March 31, 2017 Invitation to Comment of the Governmental Accounting Standards Board on major issues related to Financial Reporting Model Improvements Governmental Funds Project

GASB Update. Governmental Finance Officers Association of Alabama. February 4, Lisa R. Parker, CPA, CGMA, Senior Project Manager

Governmental Finance Officers Association of Alabama GASB Update February 4, 2019 Lisa R. Parker, CPA, CGMA, Senior Project Manager The views expressed in this presentation are those of Ms. Parker. Official

Governmental Finance Officers Association of Alabama GASB Update February 4, 2019 Lisa R. Parker, CPA, CGMA, Senior Project Manager The views expressed in this presentation are those of Ms. Parker. Official

The GASB s New Financial Reporting Model

The GASB s New Financial Reporting Model September 18, 2017 11:30 AM 12:30 PM Susannah Baney, Manager, Baker Tilly Virchow Krause LLP Christina Coyle, Finance Director, Village of Glen Ellyn Krisztina

The GASB s New Financial Reporting Model September 18, 2017 11:30 AM 12:30 PM Susannah Baney, Manager, Baker Tilly Virchow Krause LLP Christina Coyle, Finance Director, Village of Glen Ellyn Krisztina

Omnibus 201X. September 13, 2016 Comments Due: November 23, Proposed Statement of the Governmental Accounting Standards Board

September 13, 2016 Comments Due: November 23, 2016 Proposed Statement of the Governmental Accounting Standards Board Omnibus 201X This Exposure Draft of a proposed Statement of Governmental Accounting

September 13, 2016 Comments Due: November 23, 2016 Proposed Statement of the Governmental Accounting Standards Board Omnibus 201X This Exposure Draft of a proposed Statement of Governmental Accounting

Recent GASB Activity - Past

GASB Update 1 Recent GASB Activity - Past GASB 72 Fair value GASB 73 Certain pensions not administered through a trust GASB 76 GAAP hierarchy GASB 79 External investment pools 2 Recent GASB Activity -

GASB Update 1 Recent GASB Activity - Past GASB 72 Fair value GASB 73 Certain pensions not administered through a trust GASB 76 GAAP hierarchy GASB 79 External investment pools 2 Recent GASB Activity -

Latest Inventions from the Mind of GASB. March 15, Jerry E. Durham, CPA, CGFM, CFE

Latest Inventions from the Mind of GASB March 15, 2019 Jerry E. Durham, CPA, CGFM, CFE 1 Some GASB Concepts You Should Know Classification Measurement Focus Basis of Accounting Recognition Component Units

Latest Inventions from the Mind of GASB March 15, 2019 Jerry E. Durham, CPA, CGFM, CFE 1 Some GASB Concepts You Should Know Classification Measurement Focus Basis of Accounting Recognition Component Units

California Society of Municipal Finance Officers

California Society of Municipal Finance Officers GASB Update Waiting in the Wings The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB on accounting matters are

California Society of Municipal Finance Officers GASB Update Waiting in the Wings The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB on accounting matters are

GASB Update. Virginia GFOA Spring Conference. Current Technical Agenda. Paulina Haro

Virginia GFOA Spring Conference GASB Update Current Technical Agenda Paulina Haro The views expressed in this presentation are those of Ms Haro Official positions of the GASB are reached only after extensive

Virginia GFOA Spring Conference GASB Update Current Technical Agenda Paulina Haro The views expressed in this presentation are those of Ms Haro Official positions of the GASB are reached only after extensive

Implementation Guidance Update 2019

November 14, 2018 Comments Due: January 31, 2019 Proposed Implementation Guide of the Governmental Accounting Standards Board Implementation Guidance Update 2019 This Exposure Draft of a proposed Implementation

November 14, 2018 Comments Due: January 31, 2019 Proposed Implementation Guide of the Governmental Accounting Standards Board Implementation Guidance Update 2019 This Exposure Draft of a proposed Implementation

Governmental Accounting Standards Series

NO. 361 JANUARY 2017 Governmental Accounting Standards Series Statement No. 84 of the Governmental Accounting Standards Board Fiduciary Activities GOVERNMENTAL ACCOUNTING STANDARDS BOARD OF THE FINANCIAL

NO. 361 JANUARY 2017 Governmental Accounting Standards Series Statement No. 84 of the Governmental Accounting Standards Board Fiduciary Activities GOVERNMENTAL ACCOUNTING STANDARDS BOARD OF THE FINANCIAL

GASB Update. Virginia Government Finance Officers Association 2017 Spring Conference

Virginia Government Finance Officers Association 2017 Spring Conference GASB Update Scott Reeser, Supervising Project Manager Governmental Accounting Standards Board The views expressed in this presentation

Virginia Government Finance Officers Association 2017 Spring Conference GASB Update Scott Reeser, Supervising Project Manager Governmental Accounting Standards Board The views expressed in this presentation

A STAMPEDE OF NEW PRONOUNCEMENTS GASB UPDATE FOR GFOAT SPRING 2017 CONFERENCE

A STAMPEDE OF NEW PRONOUNCEMENTS GASB UPDATE FOR GFOAT SPRING 2017 CONFERENCE EFFECTIVE DATES JUNE 30, 2017 2017 STATEMENT 73 PENSIONS EMPLOYERS (OUTSIDE THE SCOPE OF STATEMENT 68) STATEMENT 74 OTHER POSTEMPLOYMENT

A STAMPEDE OF NEW PRONOUNCEMENTS GASB UPDATE FOR GFOAT SPRING 2017 CONFERENCE EFFECTIVE DATES JUNE 30, 2017 2017 STATEMENT 73 PENSIONS EMPLOYERS (OUTSIDE THE SCOPE OF STATEMENT 68) STATEMENT 74 OTHER POSTEMPLOYMENT

GASB Update. Rutgers Governmental Accounting and Auditing Update Conference. November 30, Michelle Czerkawski, Senior Project Manager, GASB

Rutgers Governmental Accounting and Auditing Update Conference GASB Update November 30, 2017 Michelle Czerkawski, Senior Project Manager, GASB The views expressed in this presentation are those of Ms.

Rutgers Governmental Accounting and Auditing Update Conference GASB Update November 30, 2017 Michelle Czerkawski, Senior Project Manager, GASB The views expressed in this presentation are those of Ms.

GASB Update. Alabama Government Finance Officers Association. February 22, Lisa R. Parker, CPA, CGMA

Alabama Government Finance Officers Association GASB Update February 22, 2018 Lisa R. Parker, CPA, CGMA The views expressed in this presentation are those of Ms. Parker. Official positions of the GASB

Alabama Government Finance Officers Association GASB Update February 22, 2018 Lisa R. Parker, CPA, CGMA The views expressed in this presentation are those of Ms. Parker. Official positions of the GASB

GASB Update. October 28, Jialan Su Project Manager Governmental Accounting Standards Board

GASB Update October 28, 2016 Jialan Su Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of Ms. Su. Official positions of the GASB on accounting

GASB Update October 28, 2016 Jialan Su Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of Ms. Su. Official positions of the GASB on accounting

Dean Michael Mead, GASB Senior Research Manager

GASB Update Ohio GFOA September 23, 2016 Dean Michael Mead, GASB Senior Research Manager The views expressed in this presentation are those of Mr. Mead. Official positions of the GASB on accounting matters

GASB Update Ohio GFOA September 23, 2016 Dean Michael Mead, GASB Senior Research Manager The views expressed in this presentation are those of Mr. Mead. Official positions of the GASB on accounting matters

David Alvarez, CPA, CVA, CGMA Partner Carr, Riggs & Ingram, LLC

GASB Update 2018 1 David Alvarez, CPA, CVA, CGMA Partner Carr, Riggs & Ingram, LLC dalvarez@cricpa.com Alan Jowers, CPA Partner Carr, Riggs & Ingram, LLC ajowers@cricpa.com 2 GASB Activity - Past GASB

GASB Update 2018 1 David Alvarez, CPA, CVA, CGMA Partner Carr, Riggs & Ingram, LLC dalvarez@cricpa.com Alan Jowers, CPA Partner Carr, Riggs & Ingram, LLC ajowers@cricpa.com 2 GASB Activity - Past GASB

GASB Update and Non-profit Reporting Model

GASB Update and Non-profit Reporting Model December 17, 2018 GASB Statement No. 88 Certain Disclosures Related to Debt, Including Direct Borrowings and Direct Placements Issued: March 2018 Effective Date:

GASB Update and Non-profit Reporting Model December 17, 2018 GASB Statement No. 88 Certain Disclosures Related to Debt, Including Direct Borrowings and Direct Placements Issued: March 2018 Effective Date:

GASB Update Lisa R. Parker Senior Project Manager Governmental Accounting Standards Board

GASB Update Lisa R. Parker Senior Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of Ms. Parker. Official positions of the GASB on accounting

GASB Update Lisa R. Parker Senior Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of Ms. Parker. Official positions of the GASB on accounting

Presented by: Frank Crawford, CPA Chris Pembrook, CPA, MBA, CGAP, CRFAC Crawford & Associates, P.C.

Presented by: Frank Crawford, CPA Chris Pembrook, CPA, MBA, CGAP, CRFAC Crawford & Associates, P.C. www.crawfordcpas.com chris@crawfordcpas.com frank@crawfordcpas.com @fcrawfordcpa (twitter) 1 To add some

Presented by: Frank Crawford, CPA Chris Pembrook, CPA, MBA, CGAP, CRFAC Crawford & Associates, P.C. www.crawfordcpas.com chris@crawfordcpas.com frank@crawfordcpas.com @fcrawfordcpa (twitter) 1 To add some

David Vaudt Michele Mark Levine Todd Buikema Stephen Gauthier James Falconer Zhikuan (Kuan) Hu Tony Boras Jim Phillips Melinda Gildart

Hu Tony Boras Jim Phillips Melinda Gildart") 1 2 Speakers David Vaudt, CPA Chairman, Governmental Accounting Standards Board (GASB) Stephen Gauthier, CPA Former Director, Technical Services Center, Government Finance Officers Association (GFOA) Tony

1 2 Speakers David Vaudt, CPA Chairman, Governmental Accounting Standards Board (GASB) Stephen Gauthier, CPA Former Director, Technical Services Center, Government Finance Officers Association (GFOA) Tony

Opening Remarks. SPEAKER David Bean Director of Research and Technical Activities GASB SPEAKER. SPEAKER David Vaudt Chairman GASB

GASB Update 2017 The views expressed in this presentation are those of the GASB Chairman and Staff. Official positions of the GASB on accounting matters are determined only after extensive due process

GASB Update 2017 The views expressed in this presentation are those of the GASB Chairman and Staff. Official positions of the GASB on accounting matters are determined only after extensive due process

Update. Governmental Accounting and Auditing Update

Update Governmental Accounting and Auditing Update The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB are reached only after extensive due process and deliberations.

Update Governmental Accounting and Auditing Update The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB are reached only after extensive due process and deliberations.

Financial Reporting for Postemployment Benefit Plans Other Than Pension Plans

May 28, 2014 Comments Due: August 29, 2014 Proposed Statement of the Governmental Accounting Standards Board Financial Reporting for Postemployment Benefit Plans Other Than Pension Plans This Exposure

May 28, 2014 Comments Due: August 29, 2014 Proposed Statement of the Governmental Accounting Standards Board Financial Reporting for Postemployment Benefit Plans Other Than Pension Plans This Exposure

Fiduciary Activities. December 17, 2018 Comments Due: February 28, Proposed Implementation Guide of the Governmental Accounting Standards Board

December 17, 2018 Comments Due: February 28, 2019 Proposed Implementation Guide of the Governmental Accounting Standards Board Fiduciary Activities This Exposure Draft of a proposed Implementation Guide

December 17, 2018 Comments Due: February 28, 2019 Proposed Implementation Guide of the Governmental Accounting Standards Board Fiduciary Activities This Exposure Draft of a proposed Implementation Guide

GASB Update. Georgia Fiscal Management Council October 4, 2016

GASB Update Georgia Fiscal Management Council October 4, 2016 Dean Michael Mead, Senior Research Manager The views expressed in this presentation are those of Mr. Mead. Official positions of the GASB on

GASB Update Georgia Fiscal Management Council October 4, 2016 Dean Michael Mead, Senior Research Manager The views expressed in this presentation are those of Mr. Mead. Official positions of the GASB on

Understanding Your Financial Statements

Understanding Your Financial Statements NHSAA & NHASBO BEST PRACTICES CONFERENCE 10.30.2017 & 10.31.2017 PLODZIK & SANDERSON, PA SCOTT EAGEN, CFE SENIOR MANAGER What s In Your Annual Financial Report *

Understanding Your Financial Statements NHSAA & NHASBO BEST PRACTICES CONFERENCE 10.30.2017 & 10.31.2017 PLODZIK & SANDERSON, PA SCOTT EAGEN, CFE SENIOR MANAGER What s In Your Annual Financial Report *

The opinions expressed in this presentation are those of Mrs. Parker. Official positions of the GASB are established only after extensive public due

GASB Update Lisa R. Parker, CPA Project Manager, Governmental Accounting Standards Board 22nd Governmental Accounting and Auditing Conference Alabama Society of CPA s December 2, 2010 Birmingham, Alabama

GASB Update Lisa R. Parker, CPA Project Manager, Governmental Accounting Standards Board 22nd Governmental Accounting and Auditing Conference Alabama Society of CPA s December 2, 2010 Birmingham, Alabama

GASB Update. Virginia GFOA Spring Conference. Current Pronouncements. Paulina Haro

Virginia GFOA Spring Conference GASB Update Current Pronouncements Paulina Haro The views expressed in this presentation are those of Ms Haro Official positions of the GASB are reached only after extensive

Virginia GFOA Spring Conference GASB Update Current Pronouncements Paulina Haro The views expressed in this presentation are those of Ms Haro Official positions of the GASB are reached only after extensive

Please note that all board decisions are tentative until a final pronouncement is issued.

MEMORANDUM TO: FROM: All NASACT Members and Other Interested Parties R. Kinney Poynter, Executive Director DATE: January 25, 2018 SUBJECT: January 23-24, 2018, GASB Meetings Gerry Boaz, CPA and CGFM, Technical

MEMORANDUM TO: FROM: All NASACT Members and Other Interested Parties R. Kinney Poynter, Executive Director DATE: January 25, 2018 SUBJECT: January 23-24, 2018, GASB Meetings Gerry Boaz, CPA and CGFM, Technical

GASB Update Florida School Finance Officers Association June 12, 2018

GASB Update Florida School Finance Officers Association June 12, 2018 2017 Becker Professional Education Corporation. All rights reserved. The copyright in this material is owned by Becker Professional

GASB Update Florida School Finance Officers Association June 12, 2018 2017 Becker Professional Education Corporation. All rights reserved. The copyright in this material is owned by Becker Professional

NASACT Emerging Leaders Conference

NASACT Emerging Leaders Conference GASB Update The view s expressed in this presentation are those of Mr. Bean. Official positions of the GASB are reached only after extensive due process and deliberations.

NASACT Emerging Leaders Conference GASB Update The view s expressed in this presentation are those of Mr. Bean. Official positions of the GASB are reached only after extensive due process and deliberations.

Understanding Your Financial Statements

Understanding Your Financial Statements NHASBO 5.04.2017 PLODZIK & SANDERSON, PA SCOTT EAGEN, CFE SENIOR MANAGER What s In Your Annual Financial Report Independent Auditor s Report Managements Discussion

Understanding Your Financial Statements NHASBO 5.04.2017 PLODZIK & SANDERSON, PA SCOTT EAGEN, CFE SENIOR MANAGER What s In Your Annual Financial Report Independent Auditor s Report Managements Discussion

GASB Update. New Hampshire Government Finance Officers Association. May 4, Lisa R. Parker, CPA, CGMA, Senior Project Manager

New Hampshire Government Finance Officers Association GASB Update May 4, 2018 Lisa R. Parker, CPA, CGMA, Senior Project Manager The views expressed in this presentation are those of Ms. Parker. Official

New Hampshire Government Finance Officers Association GASB Update May 4, 2018 Lisa R. Parker, CPA, CGMA, Senior Project Manager The views expressed in this presentation are those of Ms. Parker. Official

National Association of State Comptrollers

National Association of State Comptrollers GASB Update The views expressed in this presentation are those of Chair Vaudt, Vice-Chair Sylvis, and Mr. Bean. Official positions of the GASB on accounting matters

National Association of State Comptrollers GASB Update The views expressed in this presentation are those of Chair Vaudt, Vice-Chair Sylvis, and Mr. Bean. Official positions of the GASB on accounting matters

Council of State Governments Alan Conroy GASB Overview & Update

Council of State Governments Alan Conroy GASB Overview & Update The views expressed in this presentation are those of Mr. Conroy. Official positions of the GASB on accounting matters are determined only

Council of State Governments Alan Conroy GASB Overview & Update The views expressed in this presentation are those of Mr. Conroy. Official positions of the GASB on accounting matters are determined only

May 16, 2016 National Conference on Public Employee Retirement Systems

May 16, 2016 National Conference on Public Employee Retirement Systems GASB Update: What NCPERS Members Need to Know David A. Vaudt GASB Chair The views expressed in this presentation are those of Mr.

May 16, 2016 National Conference on Public Employee Retirement Systems GASB Update: What NCPERS Members Need to Know David A. Vaudt GASB Chair The views expressed in this presentation are those of Mr.

GAAP Update. Introduction / Summary 6/1/17. GASB Statement No. 73

GAAP Update Greg Allison, Teaching Professor UNC-CH SOG Lee Carter, Vice President Capital Management of the Carolinas GASB Statement No. 73 Accounting and Financial Reporting for Pensions and Financial

GAAP Update Greg Allison, Teaching Professor UNC-CH SOG Lee Carter, Vice President Capital Management of the Carolinas GASB Statement No. 73 Accounting and Financial Reporting for Pensions and Financial

UNAUDITED FINANCIAL REPORT FOR THE YEAR ENDED

UNAUDITED FINANCIAL REPORT FOR THE YEAR ENDED JUNE 30, 2017 JAMES MADISON UNIVERSITY UNAUDITED FINANCIAL REPORT 2016 2017 TABLE OF CONTENTS Pages MANAGEMENT S DISCUSSION AND ANALYSIS 1-11 FINANCIAL STATEMENTS:

UNAUDITED FINANCIAL REPORT FOR THE YEAR ENDED JUNE 30, 2017 JAMES MADISON UNIVERSITY UNAUDITED FINANCIAL REPORT 2016 2017 TABLE OF CONTENTS Pages MANAGEMENT S DISCUSSION AND ANALYSIS 1-11 FINANCIAL STATEMENTS:

June 28, 2017 Comments Due: September 25, Proposed Implementation Guide of the Governmental Accounting Standards Board

June 28, 2017 Comments Due: September 25, 2017 Proposed Implementation Guide of the Governmental Accounting Standards Board Implementation Guide No. 201X-Z, Accounting and Financial Reporting for Postemployment

June 28, 2017 Comments Due: September 25, 2017 Proposed Implementation Guide of the Governmental Accounting Standards Board Implementation Guide No. 201X-Z, Accounting and Financial Reporting for Postemployment

GAAP Update. Dean Michael Mead. Research Manager Governmental Accounting Standards Board. Maryland Association of CPAs April 30, 2010

GAAP Update Dean Michael Mead Research Manager Governmental Accounting Standards Board Maryland Association of CPAs April 30, 2010 The opinions expressed in this presentation are those of the presenter.

GAAP Update Dean Michael Mead Research Manager Governmental Accounting Standards Board Maryland Association of CPAs April 30, 2010 The opinions expressed in this presentation are those of the presenter.

Proposed Statement of the Governmental Accounting Standards Board

Issue Paper Attachment B June 0 Meeting NO. - JUNE XX, 0 Governmental Accounting Standards Series EXPOSURE DRAFT Proposed Statement of the Governmental Accounting Standards Board Financial Reporting for

Issue Paper Attachment B June 0 Meeting NO. - JUNE XX, 0 Governmental Accounting Standards Series EXPOSURE DRAFT Proposed Statement of the Governmental Accounting Standards Board Financial Reporting for

BLOOMINGTON-NORMAL AIRPORT AUTHORITY OF MCLEAN COUNTY, ILLINOIS FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT.

OF MCLEAN COUNTY, ILLINOIS FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT April 30, 2015 OF MCLEAN COUNTY, ILLINOIS TABLE OF CONTENTS Page(s) INDEPENDENT AUDITOR S REPORT... 1-3 MANAGEMENT S DISCUSSION

OF MCLEAN COUNTY, ILLINOIS FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT April 30, 2015 OF MCLEAN COUNTY, ILLINOIS TABLE OF CONTENTS Page(s) INDEPENDENT AUDITOR S REPORT... 1-3 MANAGEMENT S DISCUSSION

Overview: GASB Statement 68 on Pensions

Overview: GASB Statement 68 on Pensions Michelle Czerkawski, GASB Project Manager The views expressed in this presentation are those of Ms. Czerkawski. Official positions of the Governmental Accounting

Overview: GASB Statement 68 on Pensions Michelle Czerkawski, GASB Project Manager The views expressed in this presentation are those of Ms. Czerkawski. Official positions of the Governmental Accounting

October 10, Charles Tegen

GASB UPDATE Financial Reporting for Public Higher Education October 10, 2016 Charles Tegen ctegen@clemson.edu Agenda GASB and GASAC GASB Terms and Communication GASB Activities Newest Standards Exposure

GASB UPDATE Financial Reporting for Public Higher Education October 10, 2016 Charles Tegen ctegen@clemson.edu Agenda GASB and GASAC GASB Terms and Communication GASB Activities Newest Standards Exposure

Update. California Society of Municipal Finance Officers. GASB Update OPEB and so much more

Update California Society of Municipal Finance Officers GASB Update OPEB and so much more The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB are reached only

Update California Society of Municipal Finance Officers GASB Update OPEB and so much more The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB are reached only

11/7/2018. Emily Sobczak Greene Finney, LLP November, 2018

GAAP UPDATE 2018 Emily Sobczak Greene Finney, LLP November, 2018 GAAP Update Current Topics GASB 75 OPEB Reporting for Employers GASB 81 Irrevocable Split-Interest Agreements GASB 85 Omnibus 2017 GASB

GAAP UPDATE 2018 Emily Sobczak Greene Finney, LLP November, 2018 GAAP Update Current Topics GASB 75 OPEB Reporting for Employers GASB 81 Irrevocable Split-Interest Agreements GASB 85 Omnibus 2017 GASB

Proposed Statement of the Governmental Accounting Standards Board

NO. 34-P JUNE 27, 2011 Governmental Accounting Standards Series EXPOSURE DRAFT Proposed Statement of the Governmental Accounting Standards Board Financial Reporting for Pension Plans an amendment of GASB

NO. 34-P JUNE 27, 2011 Governmental Accounting Standards Series EXPOSURE DRAFT Proposed Statement of the Governmental Accounting Standards Board Financial Reporting for Pension Plans an amendment of GASB

May 28, 2014 Comments Due: August 29, Proposed Statement of the Governmental Accounting Standards Board

May 28, 2014 Comments Due: August 29, 2014 Proposed Statement of the Governmental Accounting Standards Board Accounting and Financial Reporting for Pensions and Financial Reporting for Pension Plans That

May 28, 2014 Comments Due: August 29, 2014 Proposed Statement of the Governmental Accounting Standards Board Accounting and Financial Reporting for Pensions and Financial Reporting for Pension Plans That

GASB Update. ACBO Conference. May 21, 2018

GASB Update ACBO Conference May 21, 2018 Jeff Jensen, CPA, Partner, Crowe Horwath LLP Matthew Nethaway, CPA, Partner, Crowe Horwath LLP Felipe Lopez, Vice President of Business Services, Cerritos College

GASB Update ACBO Conference May 21, 2018 Jeff Jensen, CPA, Partner, Crowe Horwath LLP Matthew Nethaway, CPA, Partner, Crowe Horwath LLP Felipe Lopez, Vice President of Business Services, Cerritos College

Accounting and Financial Reporting for Irrevocable Split-Interest Agreements

June 2, 2015 Comments Due: September 18, 2015 Proposed Statement of the Governmental Accounting Standards Board Accounting and Financial Reporting for Irrevocable Split-Interest Agreements This Exposure

June 2, 2015 Comments Due: September 18, 2015 Proposed Statement of the Governmental Accounting Standards Board Accounting and Financial Reporting for Irrevocable Split-Interest Agreements This Exposure

Montour School District

Montour School District Single Audit June 30, 2015 TABLE OF CONTENTS Independent Auditor's Report Management s Discussion and Analysis i Financial Statements: Government-Wide Financial Statements: Statement

Montour School District Single Audit June 30, 2015 TABLE OF CONTENTS Independent Auditor's Report Management s Discussion and Analysis i Financial Statements: Government-Wide Financial Statements: Statement

AGA Montgomery Chapter

AGA Montgomery Chapter GASB Update Past, Present, 1 and Future The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB on accounting matters are reached only after

AGA Montgomery Chapter GASB Update Past, Present, 1 and Future The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB on accounting matters are reached only after

FSFOA GASB Update. November 14, 2017

FSFOA GASB Update November 14, 2017 Course Topics Investments Fair Value OPEB Tax Abatements Pension Amendments Blending Criteria Irrevocable Split Interest Agreements Asset Retirement Obligations Fiduciary

FSFOA GASB Update November 14, 2017 Course Topics Investments Fair Value OPEB Tax Abatements Pension Amendments Blending Criteria Irrevocable Split Interest Agreements Asset Retirement Obligations Fiduciary

MILLCREEK TOWNSHIP SCHOOL DISTRICT

ERIE, PENNSYLVANIA FINANCIAL STATEMENTS YEAR ENDED YEAR ENDED CONTENTS Independent Auditor s Report 1-2 Page Management s Discussion and Analysis 3-14 Basic Financial Statements Government-wide Financial

ERIE, PENNSYLVANIA FINANCIAL STATEMENTS YEAR ENDED YEAR ENDED CONTENTS Independent Auditor s Report 1-2 Page Management s Discussion and Analysis 3-14 Basic Financial Statements Government-wide Financial

Town of Ogunquit, Maine

Audited Financial Statements and Other Financial Information Town of Ogunquit, Maine June 30, 2017 Proven Expertise and Integrity CONTENTS PAGE INDEPENDENT AUDITORS' REPORT 1-3 MANAGEMENT S DISCUSSION

Audited Financial Statements and Other Financial Information Town of Ogunquit, Maine June 30, 2017 Proven Expertise and Integrity CONTENTS PAGE INDEPENDENT AUDITORS' REPORT 1-3 MANAGEMENT S DISCUSSION

Governmental Accounting Standards Series

NO. 370 JUNE 2018 Governmental Accounting Standards Series Statement No. 89 of the Governmental Accounting Standards Board Accounting for Interest Cost Incurred before the End of a Construction Period

NO. 370 JUNE 2018 Governmental Accounting Standards Series Statement No. 89 of the Governmental Accounting Standards Board Accounting for Interest Cost Incurred before the End of a Construction Period

GASB Update Lisa R. Parker, CPA, CGMA Project Manager Governmental Accounting Standards Board

GASB Update Lisa R. Parker, CPA, CGMA Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of Ms. Parker. Official positions of the GASB on accounting

GASB Update Lisa R. Parker, CPA, CGMA Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of Ms. Parker. Official positions of the GASB on accounting

Certain Debt Extinguishment Issues

August 22, 2016 Comments Due: October 28, 2016 Proposed Statement of the Governmental Accounting Standards Board Certain Debt Extinguishment Issues This Exposure Draft of a proposed Statement of Governmental

August 22, 2016 Comments Due: October 28, 2016 Proposed Statement of the Governmental Accounting Standards Board Certain Debt Extinguishment Issues This Exposure Draft of a proposed Statement of Governmental

2018 GASB UPDATE P R E S E N T E D B Y : J I M C R E E D E N, M I K E B E H M E & J E S S I C A H A A G

2018 GASB UPDATE P R E S E N T E D B Y : J I M C R E E D E N, M I K E B E H M E & J E S S I C A H A A G GOALS FOR TODAY Recently issued pronouncements Projects in process How to stay informed 2 RECENTLY

2018 GASB UPDATE P R E S E N T E D B Y : J I M C R E E D E N, M I K E B E H M E & J E S S I C A H A A G GOALS FOR TODAY Recently issued pronouncements Projects in process How to stay informed 2 RECENTLY

Please note that all board decisions are tentative until a final pronouncement is issued.

MEMORANDUM TO: FROM: All NASACT Members and Other Interested Parties R. Kinney Poynter, Executive Director DATE: December 28, 2018 SUBJECT: October 2-4, 2018, GASB Meetings Gerry Boaz, CPA and CGFM, Technical

MEMORANDUM TO: FROM: All NASACT Members and Other Interested Parties R. Kinney Poynter, Executive Director DATE: December 28, 2018 SUBJECT: October 2-4, 2018, GASB Meetings Gerry Boaz, CPA and CGFM, Technical

Jersey Shore Area School District

Financial Statements and Supplementary Information Table of Contents Independent Auditors Report 1 Management s Discussion and Analysis (Unaudited) 4 Basic Financial Statements: Government-Wide Financial

Financial Statements and Supplementary Information Table of Contents Independent Auditors Report 1 Management s Discussion and Analysis (Unaudited) 4 Basic Financial Statements: Government-Wide Financial

ST. CHARLES COMMUNITY COLLEGE FINANCIAL STATEMENTS FOR THE YEARS ENDED JUNE 30, 2018 AND 2017

ST. CHARLES COMMUNITY COLLEGE FINANCIAL STATEMENTS FOR THE YEARS ENDED JUNE 30, 2018 AND 2017 ST. CHARLES COMMUNITY COLLEGE CONTENTS PAGE INDEPENDENT AUDITORS REPORT 1 MANAGEMENT S DISCUSSION AND ANALYSIS

ST. CHARLES COMMUNITY COLLEGE FINANCIAL STATEMENTS FOR THE YEARS ENDED JUNE 30, 2018 AND 2017 ST. CHARLES COMMUNITY COLLEGE CONTENTS PAGE INDEPENDENT AUDITORS REPORT 1 MANAGEMENT S DISCUSSION AND ANALYSIS

GASB Update Pamela Dolan, CPA Project Manager Governmental Accounting Standards Board

GASB Update Pamela Dolan, CPA Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of Ms. Dolan. Official positions of the GASB on accounting matters

GASB Update Pamela Dolan, CPA Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of Ms. Dolan. Official positions of the GASB on accounting matters

New Issues of Old Friends. GASB Update. The Year in Review Final Documents. Codification Original Pronouncements Comprehensive Implementation Guide

GASB Update The views expressed in this presentation are those of Dr. Smith. Official positions of the GASB are determined only after extensive due process and deliberation. The Year in Review Final Documents

GASB Update The views expressed in this presentation are those of Dr. Smith. Official positions of the GASB are determined only after extensive due process and deliberation. The Year in Review Final Documents

Kent County, Michigan. Annual Financial Report

Kent County, Michigan Annual Financial Report For the year ended June 30, 2018 Table of Contents For the year ended June 30, 2018 Financial Section Independent Auditor s Report... 1 Management s Discussion

Kent County, Michigan Annual Financial Report For the year ended June 30, 2018 Table of Contents For the year ended June 30, 2018 Financial Section Independent Auditor s Report... 1 Management s Discussion

MILLCREEK TOWNSHIP SCHOOL DISTRICT

ERIE, PENNSYLVANIA FINANCIAL STATEMENTS YEAR ENDED YEAR ENDED CONTENTS Independent Auditor s Report 1-2 Page Management s Discussion and Analysis 3-14 Basic Financial Statements Government-wide Financial

ERIE, PENNSYLVANIA FINANCIAL STATEMENTS YEAR ENDED YEAR ENDED CONTENTS Independent Auditor s Report 1-2 Page Management s Discussion and Analysis 3-14 Basic Financial Statements Government-wide Financial

Preliminary Views. Governmental Accounting Standards Series. Pension Accounting and Financial Reporting by Employers

NO. 34P JUNE 16, 2010 Governmental Accounting Standards Series Preliminary Views of the Governmental Accounting Standards Board on major issues related to Pension Accounting and Financial Reporting by

NO. 34P JUNE 16, 2010 Governmental Accounting Standards Series Preliminary Views of the Governmental Accounting Standards Board on major issues related to Pension Accounting and Financial Reporting by

9/27/16. North Carolina State Treasurer s Conference

North Carolina State Treasurer s Conference GASB Update The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB on accounting matters are reached only after extensive

North Carolina State Treasurer s Conference GASB Update The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB on accounting matters are reached only after extensive

Audited Financial Statements and Reports Required by Uniform Guidance As of and for the Year Ended June 30, 2018 Rogers State University

Audited Financial Statements and Reports Required by Uniform Guidance As of and for the Year Ended Rogers State University eidebailly.com Table of Contents As of and for the Year Ended Independent Auditor

Audited Financial Statements and Reports Required by Uniform Guidance As of and for the Year Ended Rogers State University eidebailly.com Table of Contents As of and for the Year Ended Independent Auditor

GASB Update October 22, 2015

GASB Update October 22, 2015 Smitty 1 Presentation Overview Pronouncements currently being implemented Proposals available for public comment Projects currently being deliberated by the Board GASB News

GASB Update October 22, 2015 Smitty 1 Presentation Overview Pronouncements currently being implemented Proposals available for public comment Projects currently being deliberated by the Board GASB News

GASB Update Pamela Dolan, CPA Project Manager Governmental Accounting Standards Board

GASB Update Pamela Dolan, CPA Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of Ms. Dolan. Official positions of the GASB on accounting matters

GASB Update Pamela Dolan, CPA Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of Ms. Dolan. Official positions of the GASB on accounting matters

Please note that all board decisions are tentative until a final pronouncement is issued.

MEMORANDUM TO: FROM: All NASACT Members and Other Interested Parties R. Kinney Poynter, Executive Director DATE: November 14, 2016 SUBJECT: September 13-15, 2016, GASB Meetings Gerry Boaz, CPA and CGFM,

MEMORANDUM TO: FROM: All NASACT Members and Other Interested Parties R. Kinney Poynter, Executive Director DATE: November 14, 2016 SUBJECT: September 13-15, 2016, GASB Meetings Gerry Boaz, CPA and CGFM,

Town of Harrison, Maine

Audited Financial Statements and Other Financial Information Town of Harrison, Maine June 30, 2018 Proven Expertise and Integrity CONTENTS PAGE INDEPENDENT AUDITORS' REPORT 1-3 MANAGEMENT S DISCUSSION

Audited Financial Statements and Other Financial Information Town of Harrison, Maine June 30, 2018 Proven Expertise and Integrity CONTENTS PAGE INDEPENDENT AUDITORS' REPORT 1-3 MANAGEMENT S DISCUSSION

22 nd Annual Governmental GAAP Update #GFOA. Speakers. Program Overview. Government Finance Officers Association

22 nd Annual Governmental GAAP Update #GFOA Government Finance Officers Association November 2, 2017 December 7, 2017 January 18, 2018 Speakers 2 Chris Morrill, Executive Director/CEO, GFOA Todd Buikema,

22 nd Annual Governmental GAAP Update #GFOA Government Finance Officers Association November 2, 2017 December 7, 2017 January 18, 2018 Speakers 2 Chris Morrill, Executive Director/CEO, GFOA Todd Buikema,

22 nd Annual Governmental GAAP Update #GFOA

22 nd Annual Governmental GAAP Update #GFOA Government Finance Officers Association November 2, 2017 December 7, 2017 January 18, 2018 2 Speakers Chris Morrill, Executive Director/CEO, GFOA Todd Buikema,

22 nd Annual Governmental GAAP Update #GFOA Government Finance Officers Association November 2, 2017 December 7, 2017 January 18, 2018 2 Speakers Chris Morrill, Executive Director/CEO, GFOA Todd Buikema,

22 nd Annual Governmental GAAP Update #GFOA

22 nd Annual Governmental GAAP Update #GFOA Government Finance Officers Association November 2, 2017 December 7, 2017 January 18, 2018 Speakers 2 Chris Morrill, Executive Director/CEO, GFOA Todd Buikema,

22 nd Annual Governmental GAAP Update #GFOA Government Finance Officers Association November 2, 2017 December 7, 2017 January 18, 2018 Speakers 2 Chris Morrill, Executive Director/CEO, GFOA Todd Buikema,

UNIVERSITY OF ALASKA

UNIVERSITY OF ALASKA (A Component Unit of the State of Alaska) Financial Statements (With Independent Auditors Report Thereon) University of Alaska (A Component Unit of the State of Alaska) Financial Statements

UNIVERSITY OF ALASKA (A Component Unit of the State of Alaska) Financial Statements (With Independent Auditors Report Thereon) University of Alaska (A Component Unit of the State of Alaska) Financial Statements

ACPEN. Effective Dates June-November, 2016 and GASB Update

ACPEN GASB Update The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB on accounting matters are reached only after extensive due process and deliberation. 1 Effective

ACPEN GASB Update The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB on accounting matters are reached only after extensive due process and deliberation. 1 Effective

GASB Update 2015 GFOAA Annual Conference Wesley A. Galloway, Project Manager Governmental Accounting Standards Board

GASB Update 2015 GFOAA Annual Conference Wesley A. Galloway, Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of [Mr./Ms. last name]. Official

GASB Update 2015 GFOAA Annual Conference Wesley A. Galloway, Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of [Mr./Ms. last name]. Official

Town of Wells, Maine

Audited Financial Statements and Other Financial Information Town of Wells, Maine June 30, 2018 Proven Expertise and Integrity CONTENTS PAGE INDEPENDENT AUDITORS' REPORT 1-3 MANAGEMENT S DISCUSSION AND

Audited Financial Statements and Other Financial Information Town of Wells, Maine June 30, 2018 Proven Expertise and Integrity CONTENTS PAGE INDEPENDENT AUDITORS' REPORT 1-3 MANAGEMENT S DISCUSSION AND

Town of Wells, Maine

Audited Financial Statements and Other Financial Information Town of Wells, Maine June 30, 2017 Proven Expertise and Integrity CONTENTS JUNE 30, 2017 PAGE INDEPENDENT AUDITORS' REPORT 1-3 MANAGEMENT S

Audited Financial Statements and Other Financial Information Town of Wells, Maine June 30, 2017 Proven Expertise and Integrity CONTENTS JUNE 30, 2017 PAGE INDEPENDENT AUDITORS' REPORT 1-3 MANAGEMENT S

1 NEW DEVELOPMENTS COPYRIGHTED MATERIAL INTRODUCTION

1 NEW DEVELOPMENTS Introduction 1 Recently Issued GASB Statements and Their Effective Dates 1 Most Recent GASB Statement: GASB Statement 58, Accounting and Financial Reporting for Chapter 9 Bankruptcies

1 NEW DEVELOPMENTS Introduction 1 Recently Issued GASB Statements and Their Effective Dates 1 Most Recent GASB Statement: GASB Statement 58, Accounting and Financial Reporting for Chapter 9 Bankruptcies

Please note that all board decisions are tentative until a final pronouncement is issued.

MEMORANDUM TO: FROM: All NASACT Members and Other Interested Parties R. Kinney Poynter, Executive Director DATE: July 18, 2017May 30, 2017 SUBJECT: May 23-25, 2017, GASB Meetings Gerry Boaz, CPA and CGFM,

MEMORANDUM TO: FROM: All NASACT Members and Other Interested Parties R. Kinney Poynter, Executive Director DATE: July 18, 2017May 30, 2017 SUBJECT: May 23-25, 2017, GASB Meetings Gerry Boaz, CPA and CGFM,

THE SCHOOL BOARD OF MIAMI-DADE COUNTY, FLORIDA STATEMENT OF NET POSITION JUNE 30, 2016 (amounts expressed in thousands)

") STATEMENT OF NET POSITION JUNE 30, 2016 (amounts expressed in thousands) Primary Government Total Governmental Activities ASSETS Current assets: Cash and cash equivalents $ 55,465 Investments 458,977 Cash

STATEMENT OF NET POSITION JUNE 30, 2016 (amounts expressed in thousands) Primary Government Total Governmental Activities ASSETS Current assets: Cash and cash equivalents $ 55,465 Investments 458,977 Cash

Governmental GAAP Edition. Warren Ruppel

Governmental GAAP 2016 Edition Warren Ruppel Chapter 1 New Developments... 1 Introduction... 1 Recently Issued GASB Statements and Their Effective Dates... 1 Exposure Drafts... 1 Exposure Draft Implementation

Governmental GAAP 2016 Edition Warren Ruppel Chapter 1 New Developments... 1 Introduction... 1 Recently Issued GASB Statements and Their Effective Dates... 1 Exposure Drafts... 1 Exposure Draft Implementation

The opinions expressed in this presentation are those of Mrs. Parker. Official positions of the GASB are established only after extensive public due

GASB Update Lisa R. Parker, CPA Project Manager, Governmental Accounting Standards Board Florida Institute of CPA s September 21, 2012 Ft. Lauderdale, Florida The opinions expressed in this presentation

GASB Update Lisa R. Parker, CPA Project Manager, Governmental Accounting Standards Board Florida Institute of CPA s September 21, 2012 Ft. Lauderdale, Florida The opinions expressed in this presentation

Financial Audit PALM BEACH STATE COLLEGE. For the Fiscal Year Ended June 30, Report No March 2016

March 2016 PALM BEACH STATE COLLEGE For the Fiscal Year Ended June 30, 2015 Financial Audit Sherrill F. Norman, CPA Auditor General Board of Trustees and President During the 2014-15 fiscal year, Dr. Dennis

March 2016 PALM BEACH STATE COLLEGE For the Fiscal Year Ended June 30, 2015 Financial Audit Sherrill F. Norman, CPA Auditor General Board of Trustees and President During the 2014-15 fiscal year, Dr. Dennis

NORTHWESTERN OKLAHOMA STATE UNIVERSITY

NORTHWESTERN OKLAHOMA STATE UNIVERSITY A DEPARTMENT OF THE REGIONAL UNIVERSITY SYSTEM OF OKLAHOMA ANNUAL FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT AS OF AND FOR THE YEAR ENDED JUNE 30, 2015

NORTHWESTERN OKLAHOMA STATE UNIVERSITY A DEPARTMENT OF THE REGIONAL UNIVERSITY SYSTEM OF OKLAHOMA ANNUAL FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT AS OF AND FOR THE YEAR ENDED JUNE 30, 2015

California Society of Municipal Financial Officers GASB A Look into the Future

California Society of Municipal Financial Officers GASB A Look into the Future The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB on accounting matters are determined

California Society of Municipal Financial Officers GASB A Look into the Future The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB on accounting matters are determined

WATER AND SEWERAGE SYSTEM OF DUPAGE COUNTY, ILLINOIS An Enterprise Fund of the DuPage County, Illinois

WATER AND SEWERAGE SYSTEM OF DUPAGE COUNTY, ILLINOIS An Enterprise Fund of the DuPage County, Illinois COMMUNICATION TO THOSE CHARGED WITH GOVERNANCE AND MANAGEMENT As of and for the Year Ended November

WATER AND SEWERAGE SYSTEM OF DUPAGE COUNTY, ILLINOIS An Enterprise Fund of the DuPage County, Illinois COMMUNICATION TO THOSE CHARGED WITH GOVERNANCE AND MANAGEMENT As of and for the Year Ended November

Financial Statements and Reports Required by Uniform Guidance June 30, 2018 and 2017 The University of Oklahoma - Norman Campus

Financial Statements and Reports Required by Uniform Guidance June 30, 2018 and 2017 The University of Oklahoma - Norman Campus eidebailly.com Table of Contents June 30, 2018 and 2017 Independent Auditor

Financial Statements and Reports Required by Uniform Guidance June 30, 2018 and 2017 The University of Oklahoma - Norman Campus eidebailly.com Table of Contents June 30, 2018 and 2017 Independent Auditor

Implementation Guide No. 201X-Y, Implementation Guidance Update 201X

November 16, 2016 Comments Due: January 31, 2017 Proposed Implementation Guide of the Governmental Accounting Standards Board Implementation Guide No. 201X-Y, Implementation Guidance Update 201X This Exposure

November 16, 2016 Comments Due: January 31, 2017 Proposed Implementation Guide of the Governmental Accounting Standards Board Implementation Guide No. 201X-Y, Implementation Guidance Update 201X This Exposure

COTATI-ROHNERT PARK UNIFIED SCHOOL DISTRICT COUNTY OF SONOMA ROHNERT PARK, CALIFORNIA

COTATI-ROHNERT PARK UNIFIED SCHOOL DISTRICT COUNTY OF SONOMA ROHNERT PARK, CALIFORNIA AUDIT REPORT JUNE 30, 2016 CHAVAN & ASSOCIATES, LLP CERTIFIED PUBLIC ACCOUNTANTS 1475 SARATOGA AVE., SUITE 180 SAN

COTATI-ROHNERT PARK UNIFIED SCHOOL DISTRICT COUNTY OF SONOMA ROHNERT PARK, CALIFORNIA AUDIT REPORT JUNE 30, 2016 CHAVAN & ASSOCIATES, LLP CERTIFIED PUBLIC ACCOUNTANTS 1475 SARATOGA AVE., SUITE 180 SAN

FINANCIAL STATEMENTS University of South Alabama Year ended September 30, 2002 with Report of Independent Auditors

FINANCIAL STATEMENTS University of South Alabama Year ended September 30, 2002 with Report of Independent Auditors Financial Statements Year ended September 30, 2002 Contents Management s Discussion and

FINANCIAL STATEMENTS University of South Alabama Year ended September 30, 2002 with Report of Independent Auditors Financial Statements Year ended September 30, 2002 Contents Management s Discussion and