|

|

|

- Pierce Lambert Preston

- 5 years ago

- Views:

Transcription

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27 CITY OF CRESCENT CITY FIREFIGHTERS' RETIREMENT TRUST FUND An actuarial valuation of the Fund has been completed and the results are presented in the enclosures. The Total Required Contribution to the Fund for the City's fiscal year ending September 30, 2017 along with an indication of the sources of contributions, is as follows: Valuation Date 10/1/ /1/2012 Applicable to Fiscal Year Ending 9/30/2017 9/30/2014 Total Required Contribution $10,275 $10,565 % of Total Annual Payroll Less Member Contributions $2,802 $2,375 % of Total Annual Payroll Equals Required City and State Contributions $7,473 $8,190 % of Total Annual Payroll Less Estimated State Contribution $8,811 $7,835 % of Total Annual Payroll Equals Balance From City $0 $355 % of Total Annual Payroll The required City and State contributions for fiscal 2017 will be $7,473, and for fiscal years 2018 and 2019 will be 14.0% of the pensionable payroll realized in that year. The actual City requirement will be this amount, less actual State Monies received in those years.

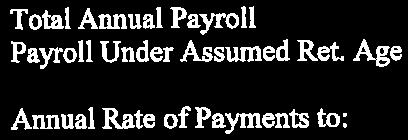

28 COMPARATIVE SUMMARY OF PRINCIPAL VALUATION RESULTS A. Participant Data 10/1/ /1/2012 Number Included Actives 12 9 Service Retirees 1 1 Beneficiaries 0 1 Terminated Vested 5 4 Disability Retirees 0 0 Total Total Annual Payroll $50,847 $43,178 Payroll Under Assumed Ret. Age 50,847 43,178 Annual Rate of Payments to: Service Retirees 11,370 11,370 Beneficiaries Terminated Vested 3,995 2,956 Disability Retirees 0 0 B. Assets Actuarial Value 490, ,272 Market Value 490, ,272 C. Liabilities Present Value of Benefits Active Members Retirement Benefits 120,743 91,342 Disability Benefits 2,761 1,803 Death Benefits 1, Vested Benefits 32,952 32,121 Refund of Contributions 1, Service Retirees 131, ,192 Beneficiaries 0 1,047 Terminated Vested 37,260 19,084 Disability Retirees 0 0 Total 327, ,325

29 10/1/ /1/2012 C. Liabilities - (Continued) Present Value of Future Salaries (Attained Age) 438, ,579 Present Value of Future Member Contributions 21,908 20,729 Normal Cost (Aggregate Method) 0 0 Present Value of Future Normal Costs (Entry Age) 50,658 47,302 Actuarial Accrued Liability 490, ,272 Unfunded Actuarial Accrued 0 0 Liability (UAAL) D. Actuarial Present Value of Accrued Benefits Vested Accrued Benefits Inactives 168, ,323 Actives 44,237 18,292 Member Contributions 15,742 10,162 Total 228, ,777 Non-vested Accrued Benefits 5,855 1,978 Total Present Value Accrued 234, ,755 Benefits Increase (Decrease) in Present Value of Accrued Benefits Attributable to: Plan Amendments 0 Assumption Changes 0 New Accrued Benefits 48,034 Benefits Paid (37,098) Interest 35,533 Other 0 Total: 46,469

30 Valuation Date 10/1/ /1/2012 Applicable to Fiscal Year Ending 9/30/2017 9/30/2014 E. Pension Cost Normal Cost ¹ $0 $0 % of Total Annual Payroll ¹ Required Expenses ¹ $10,275 $10,565 % of Total Annual Payroll ¹ Payment Required to Amortize Unfunded Actuarial Accrued Liability ¹ $0 $0 % of Total Annual Payroll ¹ Total Required Contribution $10,275 $10,565 % of Total Annual Payroll ¹ Expected Member Contributions $2,802 $2,375 % of Total Annual Payroll ¹ Expected City & State Contrib. $7,473 $8,190 % of Total Annual Payroll ¹ F. Past Contributions Plan Years Ending: 9/30/2015 9/30/2014 9/30/2013 Total Required Contribution $10,889 10,565 $981 City and State Requirement 8,522 8,190 0 Actual Contributions Made: Members 2,367 2,234 2,044 City State 8,811 10,015 12,884 Total 11,178 12,249 14,928 G. Net Actuarial Gain (Loss) N/A ¹ Contributions developed above have been adjusted with assumed interest and salary increase components.

31 H. Schedule Illustrating the Amortization of the Total Unfunded Actuarial Accrued Liability as of: Year Projected Unfunded Accrued Liability N/A - Aggregate Actuarial Cost Method I. (i) 3 Year Comparison of Actual and Assumed Salary Increases Actual Assumed Year Ended 9/30/ % Year Ended 9/30/ % 6.3% Year Ended 9/30/ % 6.3% (ii) 3 Year Comparison of Investment Return on Actuarial Value Actual Assumed Year Ended 9/30/ % 7.0% Year Ended 9/30/ % 7.0% Year Ended 9/30/ % 7.0% (iii) Average Annual Payroll Growth (a) Payroll as of: 10/1/2015 $50,847 10/1/ ,090 (b) Total Increase -14.0% (c) Number of Years (d) Average Annual Rate -1.5%

32 STATEMENT BY ENROLLED ACTUARY This actuarial valuation was prepared and completed by me or under my direct supervision, and I acknowledge responsibility for the results. To the best of my knowledge, the results are complete and accurate, and in my opinion, the techniques and assumptions used are reasonable and meet the requirements and intent of Part VII, Chapter 112, Florida Statutes. There is no benefit or expense to be provided by the plan and/or paid from the plan's assets for which liabilities or current costs have not been established or otherwise taken into account in the valuation. All known events or trends which may require a material increase in plan costs or required contribution rates have been taken into account in the valuation. Patrick T. Donlan, EA, ASA, MAAA Enrolled Actuary # Please let us know when the report is approved by the Board and unless otherwise directed we will provide copies of the report to the following offices to comply with Chapter 112 Florida Statutes: Mr. Keith Brinkman Bureau of Local Retirement Systems Post Office Box 9000 Tallahassee, FL Ms. Sarah Carr Municipal Police and Fire Pension Trust Funds Division of Retirement Post Office Box 3010 Tallahassee, FL

33 ACTUARIAL ASSUMPTIONS AND METHODS Mortality Rate Interest Rate Retirement Age RP 2000 Table - Sex Distinct. We feel this sufficiently accommodates expected mortality improvements for public safety employees. 7.0% per year compounded annually, gross of investment related expenses. This assumption was adopted following an experience study dated December 1, % per year eligible for Early Retirement. 10% per year eligible for Normal Retirement (with 100% at Age 52 with 25 Yrs of Service). Also, any member who has reached Normal Retirement Age on the valuation date is assumed to continue employment for one additional year. This assumption was adopted following an experience study dated December 1, Disability Rate Age % Becoming Disabled During the Year % This assumption was adopted following an experience study dated December 1, Termination Rate Service % Terminating During the Year 0-2 Years 15.0% 3+ Years 5.0% This assumption was adopted following an experience study dated December 1, Salary Increases Years of Service Salary Increase % 1 8.0% % % This assumption was adopted following an experience study dated December 1, Expenses Payroll Growth Assumption Funding Method $9,322 per year. Based on actual 2015 expenses. None. Aggregate Actuarial Cost Method.

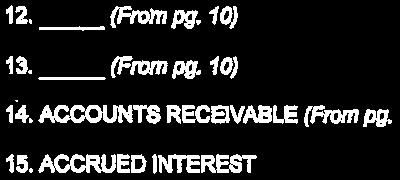

34 Crescent Ci~ CITY NAME Municipal Firefi ghters Pension Fund NAME OF PENSION FUND STATEMENT OF ASSETS AND LIABILITIES AS OF 9/30/15 Month/Day/Year ASSETS - MARKET VALUE 1 CASH, CHECKING AND SAVINGS (From pg.7) 2. CERTIFICATES OF DEPOSIT (From pg. 7) 3. SHORT TERM INVESTMENTS (From pg.8) 4. OTHER CASH AND EQUIVALENTS (From pg. 8) 5. u. s. BONDS AND BILLS (From pg. 8) 6. FEDERAL AGENCY GUARANTEED SECURITIES (From pg. 8) 7. CORPORATE BONDS (From pg. 8) 8. STOCKS (From pg. 9) 9. OTHER SECURITIES (From pg. 9) $185, $302, REAL ESTATE (From pg. 9) 11. INVESTMENTS HELD BY INSURANCE COMPANY (From pg. 9) 12. _ (From pg. 10) 13. (From pg. 10) 14. ACCOUNTS RECEIVABLE (From pg. 10) $2, ACCRUEDINTEREST 16. TOT AL ASSETS (sum oflines 1-15) ~-/ ----~~-$4_9_0_.4_76~. 2_2_ LIABILITIES 17. REFUNDS PAYABLE 18. PENSIONS PAYABLE 19. UNPAID EXPENSES 20. DROP PLAN PAYABLE 21. PREPAID CONTRIBUTIONS 22. ( 23. TOTAL LIABILITIES (sum of lines 17-22) 24. FUND BALANCE (subtract /me 23 from /me 16) <MUST agree with page 5, hne 25> $490, '-\. ' Revi d Novelllber 2015 ( 4 )

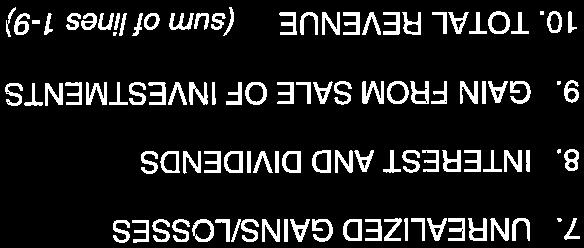

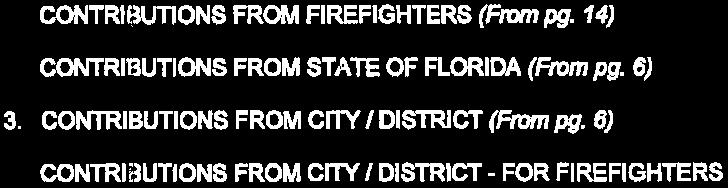

35 Crescent City CITY NAME Municipal Firefighters' Pension Fund NAME OF PENSION FUND STATEMENT OF REVENUES, EXPENDITURES & CHANGES IN FUND BALANCE FOR THE PERIOD ENDING 9/30/15 Month/Day/Year REVENUES 1. CONTRIBUTIONS FROM POLICE OFFICERS (From pg. 14) 2. CONTRIBUTIONS FROM STATE OF FLORIDA (From pg. 6) 3. CONTRIBUTIONS FROM CITY (From pg. 6) 4. CONTRIBUTIONS FROM CITY - FOR FIREFIGHTERS' 5. BUYBACKS/REPAYMENT OF CONTRIBUTIONS UNREALIZED GAINS/LOSSES 8. INTEREST AND DIVIDENDS 9. GAIN FROM SALE OF INVESTMENTS / / $2, \1~ $8, tr ($64,410.22) $56, TOTAL REVENUE (sum of lines 1-9) EXPENDITURES -~,,/'~~~~~$~3=,1~3~8._7=8 fl 11. RETIREMENT PENSION PAYMENTS (From pg. 12) $11, DISABILITY PENSION PAYMENTS (From pg. 12) 13. BENEFICIARY PENSION PAYMENTS (From pg. 12) 14. TOTAL PENSION PAYMENTS (sum oflines 11-13) $64.92 $11, rt/ 15. TERMINATION PAYMENTS (From pg. 13) 16. DROP PLAN PAYMENTS 17. INSURANCE PREMIUM PAYMENTS 18. EXPENSES (From pg. 6) $ $8, ~ LOSS FROM SALE OF INVESTMENTS 22. TOTAL EXPENDITURES (sum of lines 14-21) 23. NET INCREASE I (DECREASE) (subtract line 22 from line 10) 24. FUND BALANCE - BEGINNING OF YEAR: October 1, 2014 <MUST agree with prior year report page 5, line 25> 25. FUND BALANCE - END OF YEAR: September 30, 2015 (line 23 plus line 24) <MUST agree with page 4, line 24> / I I / / $20, ( ($17,617.74) $508, / $490,~76.22 \ Rev i sed November 2015 { 5 l

36

37

38

39

40 VALUATION PARTICIPANT RECONCILIATION 1. Active lives a. Number in prior valuation 10/1/12 9 b. Terminations i. Vested (partial or full) with deferred 1 benefits ii. Non-vested or full lump sum distribution 0 received c. Deaths i. Beneficiary receiving benefits 0 ii. No future benefits payable 0 d. Disabled 0 e. Retired 0 f. Voluntary withdrawal 0 g. Continuing participants 8 h. New entrants 4 i. Total active life participants in valuation Non-Active lives (including beneficiaries receiving benefits) Service Retirees, Vested Receiving Receiving Receiving Death Disability Vested Benefits Benefits Benefits Deferred Total a. Number prior valuation b. In c. Out d. Number current valuation

41 STATISTICAL DATA 10/1/ /1/2015 Number 9 12 Average Current Age Average Age at Employment Average Past Service Average Annual Salary $4,798 $4,237

42 AGE AND SERVICE DISTRIBUTION PAST SERVICE AGE Total Total

43 CHAPTER PLAN SUMMARY OF PLAN BENEFITS AS OF OCTOBER 1, 2015 CRESCENT CITY FIRE FIREFIGHTERS RETIREMENT PLAN BENEFIT EFFECTIVE DATE Age 55 October 1, 1986 Age 52 with 25 Years October 1, year Average Final Compensation October 1, 1986 New Disability October 1, 1986 Benefit Rate 2.0% MEMBER CONTRIBUTION RATE Firefighters 5% City for Firefighters 0% LATEST ACTUARIAL VALUATION October 1, 2012

44 CITY OF CRESCENT CITY POLICE OFFICERS' RETIREMENT TRUST FUND An actuarial valuation of the Fund has been completed and the results are presented in the enclosures. The Total Required Contribution to the Fund for the City's fiscal year ending September 30, 2017 along with an indication of the sources of contributions, is as follows: Valuation Date 10/1/ /1/2012 Applicable to Fiscal Year Ending 9/30/2017 9/30/2014 Total Required Contribution $23,630 $76,143 % of Total Annual Payroll Less Member Contributions 12,077 17,885 % of Total Annual Payroll Equals Required City and State Contribution 11,553 58,258 % of Total Annual Payroll Less Estimated State Contribution 15,655 16,143 % of Total Annual Payroll Equals Balance From City 0 42,115 % of Total Annual Payroll The required City and State contributions for fiscal 2017 will be $11,553, and for fiscal years 2018 and 2019 will be 5.1% of the pensionable payroll realized in that year. The actual City requirement will be this amount, less actual State Monies received in those years.

45 COMPARATIVE SUMMARY OF PRINCIPAL VALUATION RESULTS A. Participant Data 10/1/ /1/2012 Number Included Actives 4 7 Service Retirees 2 2 Beneficiaries 0 0 Terminated Vested 2 1 Disability Retirees 1 2 Total 9 12 Total Annual Payroll $216,684 $321,199 Payroll Under Assumed Ret. Age 216, ,199 Annual Rate of Payments to: Service Retirees 16,068 16,068 Beneficiaries 0 0 Terminated Vested 0 0 Disability Retirees 12,964 23,726 B. Assets Actuarial Value 820, ,553 Market Value 820, ,553 C. Liabilities Present Value of Benefits Active Members Retirement Benefits 505, ,805 Disability Benefits 8,972 14,802 Death Benefits 3,984 6,815 Vested Benefits 23,093 96,332 Refund of Contributions 10,918 20,419 Service Retirees 181, ,668 Beneficiaries 0 0 Terminated Vested 12,308 1,603 Disability Retirees 126, ,355 Total 873,169 1,147,799

46 10/1/ /1/2012 C. Liabilities - (Continued) Present Value of Future Salaries (Attained Age) 1,413,416 2,693,543 Present Value of Future Member Contributions 70, ,677 Normal Cost (Aggregate Method) 8,040 54,883 Present Value of Future Normal Costs (Entry Age) 173, ,067 Actuarial Accrued Liability 820, ,553 Unfunded Actuarial Accrued 0 0 Liability (UAAL) D. Actuarial Present Value of Accrued Benefits Vested Accrued Benefits Inactives 320, ,626 Actives 232, ,146 Member Contributions 66,897 76,022 Total 619, ,794 Non-vested Accrued Benefits 27,216 26,681 Total Present Value Accrued 647, ,475 Benefits Increase (Decrease) in Present Value of Accrued Benefits Attributable to: Plan Amendments 0 Assumption Changes 0 New Accrued Benefits (27,421) Benefits Paid (165,292) Interest 141,307 Other 0 Total: (51,406)

47 Valuation Date 10/1/ /1/2012 Applicable to Fiscal Year Ending 9/30/2017 9/30/2014 E. Pension Cost Normal Cost* $8,962 $61,121 % of Total Annual Payroll* Expenses* $14,668 $15,022 % of Total Annual Payroll* Payment Required to Amortize Unfunded Actuarial Accrued Liability* $0 $0 % of Total Annual Payroll* Total Required Contribution* $23,630 $76,143 % of Total Annual Payroll* Expected Member Contributions* $12,077 $17,885 % of Total Annual Payroll* Expected City & State Contrib.* $11,553 $58,258 % of Total Annual Payroll* F. Past Contributions Plan Years Ending: 9/30/2015 9/30/2014 9/30/2013 Total Required Contribution $49,048 $76,143 $57,477 City and State Requirement 37,901 58,258 42,963 Actual Contributions Made: Members 11,147 13,050 14,514 City 27,422 29,287 28,452 State 15,655 15,567 16,252 Total 54,224 57,904 59,218 G. Net Actuarial Gain (Loss) N/A * Contributions developed above have been adjusted for assumed interest and salary increase components

48 H. Schedule Illustrating the Amortization of the Total Unfunded Actuarial Accrued Liability as of: Year Projected Unfunded Accrued Liability N/A - Aggregate Actuarial Cost Method I. (i) 3 Year Comparison of Actual and Assumed Salary Increases Actual Assumed Year Ended 9/30/ % 7.1% Year Ended 9/30/ % 7.6% Year Ended 9/30/ % 7.6% (ii) 3 Year Comparison of Investment Return on Actuarial Value Actual Assumed Year Ended 9/30/ % 7.0% Year Ended 9/30/ % 7.0% Year Ended 9/30/ % 7.0% (iii) Average Annual Payroll Growth (a) Payroll as of: 10/1/2015 $216,684 10/1/ ,410 (b) Total Increase -17.7% (c) Number of Years (d) Average Annual Rate -1.9%

49 STATEMENT BY ENROLLED ACTUARY This actuarial valuation was prepared and completed by me or under my direct supervision, and I acknowledge responsibility for the results. To the best of my knowledge, the results are complete and accurate, and in my opinion, the techniques and assumptions used are reasonable and meet the requirements and intent of Part VII, Chapter 112, Florida Statutes. There is no benefit or expense to be provided by the plan and/or paid from the plan's assets for which liabilities or current costs have not been established or otherwise taken into account in the valuation. All known events or trends which may require a material increase in plan costs or required contribution rates have been taken into account in the valuation. Patrick T. Donlan, EA, ASA, MAAA Enrolled Actuary # Please let us know when the report is approved by the Board and unless otherwise directed we will provide copies of the report to the following offices to comply with Chapter 112 Florida Statutes: Mr. Keith Brinkman Bureau of Local Retirement Systems Post Office Box 9000 Tallahassee, FL Ms. Sarah Carr Municipal Police and Fire Pension Trust Funds Division of Retirement Post Office Box 3010 Tallahassee, FL

50 ACTUARIAL ASSUMPTIONS AND METHODS Mortality Rate Interest Rate Retirement Age RP 2000 Table - Sex Distinct. We feel this sufficiently accommodates expected mortality improvements for public safety employees. 7.00% per year compounded annually, gross of investment related expenses. This assumption was adopted following an experience study dated December 1, % per year eligible for Early Retirement. 10% per year eligible for Normal Retirement (with 100% at 3 years beyond Normal Retirement Date). Also, any member who has reached Normal Retirement Age on the valuation date is assumed to continue employment for one additional year. This assumption was adopted following an experience study dated December 1, Disability Rate Age % Becoming Disabled During the Year % This assumption was adopted following an experience study dated December 1, Termination Rate Service % Terminating During the Year 0-2 Years 20.0% 3-4 Years 15.0% 5+ Years 5.0% This assumption was adopted following an experience study dated December 1, Salary Increases Years of Service Salary Increase % 1 8.0% % % This assumption was adopted following an experience study dated December 1, Expenses Payroll Growth Assumption $13,159 per year. None.

51 Funding Method Aggregate Actuarial Cost Method.

52

53

54

55

56

57

58 VALUATION PARTICIPANT RECONCILIATION 1. Active lives a. Number in prior valuation 10/1/12 7 b. Terminations i. Vested (partial or full) with deferred 1 benefits ii. Non-vested or full lump sum distribution 4 received c. Deaths i. Beneficiary receiving benefits 0 ii. No future benefits payable 0 d. Disabled 0 e. Retired 0 f. Voluntary withdrawal 0 g. Continuing participants 2 h. New entrants 2 i. Total active life participants in valuation 4 2. Non-Active lives (including beneficiaries receiving benefits) Service Retirees, Vested Receiving Receiving Receiving Death Disability Vested Benefits Benefits Benefits Deferred Total a. Number prior valuation b. In c. Out d. Number current valuation

59 STATISTICAL DATA 10/1/ /1/2015 Number 7 4 Average Current Age Average Age at Employment Average Past Service Average Annual Salary $45,886 $54,171

60 AGE AND SERVICE DISTRIBUTION PAST SERVICE AGE Total Total

61 CHAPTER PLAN SUMMARY OF PLAN BENEFITS AS OF OCTOBER 1, 2012 CRESCENT CITY POLICE OFFICERS RETIREMENT PLAN BENEFIT EFFECTIVE DATE Age 55 October 1, 1986 Age 52 with 25 Years October 1, year Average Final Compensation October 1, 1986 New Disability October 1, 1986 Benefit Rate 2.0% MEMBER CONTRIBUTION RATE Police Officers 5% City for Police Officers 0% LATEST ACTUARIAL VALUATION October 1, 2012

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

100

101

102

103

104

105

106

107

108

109

110

111

112

113

114

115

116

117

118

119

120

121

122

123

124

125

126

127

128

129

130

131

132

133

134

135

136

137

138

139

140

141

142

143

144

145

146

147

148

149

150

151

152

153

154

155

156

157

158

159

160

161

162

163

164

165

166

167

168

169

170

171

172

173

174

175

176

177

178

179

180

181

182

183

184

185

186

187

188

189

190

191

192

193

194

195

196

197

198

199

200

201

202

203

204

205

206

207

208

209

210

211

212

213

214

215

216

217

218

219

220

221

222

223

224 March 17, 2016 Board of Trustees th Street Niceville, FL RE: GASB Statement No. 67 and No. 68 East Niceville Fire District Firefighters Pension Fund Dear Board: We are pleased to present to the Board a GASB Statement No. 67 and No. 68 measured as of September 30, 2015 for East Niceville Fire District Firefighters Pension Fund. The calculation of the liability associated with the benefits referenced in this report was performed for the purpose of satisfying the requirements of GASB No.67 and No.68 and is not applicable for purposes, such as determining the plans funding requirements. A calculation of the plan s liability for other purposes may produce significantly different results. The total pension liability, net pension liability, and certain sensitivity information shown in this report are based on an actuarial valuation performed as of October 1, The total pension liability was rolled-back from the valuation date to the plan s fiscal year ending September 30 th, 2015 to obtain the beginning amount using generally accepted actuarial principles. It is our opinion that the assumptions used for this purposes are internally consistent, reasonable, and comply with the requirements under GASB No.67 and No.68. Certain schedules should include a 10-year history of information. As provided for in GASB No. 67 and No.68, this historical information is only presented for the years in which the information was measured in conformity with the requirements of GASB No. 67 and No.68. To the best of our knowledge, these statements are complete and accurate and are in accordance with generally recognized actuarial practices and methods. If there are any questions, concerns, or comments about any of the items contained in this report, please contact me at Respectfully submitted, Foster & Foster, Inc. By: Patrick T. Donlan, ASA, MAAA Enrolled Actuary # PTD/lke Enclosures Parker Commons Blvd., Suite 104 Fort Myers, FL (239) Fax (239)

225 GASB 67 STATEMENT OF FIDUCIARY NET POSITION SEPTEMBER 30, 2015 ASSETS Cash and Cash Equivalents: Cash Total Cash and Equivalents Receivables: State Contributions Total Receivable Investments: Pooled/Common/Commingled Funds: Vanguard Wellington Total Investments Total Assets Total Liabilities NET POSITION RESTRICTED FOR PENSIONS MARKET VALUE 339, ,240 56,017 56, , , , ,381 East Niceville Fire District Firefighters' Pension Fund Foster & Foster 2

226 GASB 67 STATEMENT OF CHANGES IN FIDUCIARY NET POSITION FOR THE YEAR ENDED SEPTEMBER 30, 2015 Market Value Basis ADDITIONS Contributions: Member 18,575 Buy-Back 443 District 13,918 State 56,017 Total Contributions 88,953 Investment Income: Net Increase in Fair Value of Investments (7,619) Interest & Dividends 8,788 Less Investment Expense¹ 0 Net Investment Income 1,169 Total Additions 90,122 DEDUCTIONS Distributions to Members: Refunds of Member Contributions 2,901 Total Distributions 2,901 Administrative Expense 2,520 Total Deductions 5,421 Net Increase in Net Position 84,701 NET POSITION RESTRICTED FOR PENSIONS Beginning of the Year 591,680 End of the Year 676,381 ¹Investment related expenses include investment advisory, custodial and performance monitoring fees. East Niceville Fire District Firefighters' Pension Fund Foster & Foster 3

227 GASB 67 NOTES TO THE FINANCIAL STATEMENTS (For the Year Ended September 30, 2015) Plan Description Plan Administration The Plan is a single-employer defined benefit pension plan administered by the Plan's Board of Trustees comprised of: a. Two Commission appointees, b. Two Members of the Department elected by the membership, and c. Fifth Member elected by other four and appointed by Commission. Plan Membership as of October 1, 2015: Inactive Plan Members or Beneficiaries Currently Receiving Benefits - Inactive Plan Members Entitled to But Not Yet Receiving Benefits 1 Active Plan Members Benefits Provided The Plan provides retirement, termination, disability and death benefits. Normal Retirement: Date: The earlier of: 1) age 55 and the completion of 10 years of Credited Service, or 2) the attainment of age 52 and the completion of 25 years of credit service. Benefit: 3.00% of Average Final Compensation times Credited Service. Early Retirement: Date: Age 50 and 10 years of Credited Service. Accrued benefit, reduced 3.0% per year. Vesting: Schedule: 100% after 10 years of Credited Service. Benefit Amount: Member will receive the vested portion of his (her) accrued benefit payable at the otherwise Normal Retirement Date. Disability: Eligibility Service Incurred: Covered from Date of Employment. Eligibility Non-Service Incurred: 10 years of Credited Service. Benefit accrued to date of disability but not less than 42% of Average Final Compensation (Service Incurred) or 25% of Average Final Compensation (Not Service Incurred). Pre-Retirement Death Benefits: Vested: Monthly accrued benefit payable to designated beneficiary for 10 years at the otherwise Normal or Early Retirement Date. Non-Vested: Refund of accumulated contributions without interest. Contributions Firefighters - 5%. District for Firefighters - 0%. East Niceville Fire District Firefighters' Pension Fund Foster & Foster 4

228 GASB 67 Investments There is no investment policy available. The following asset classes were noted on the Annual Report as of September 30, 2015: Asset Class Target Allocation Cash 55% Pooled Funds 45% Total 100% Concentrations: The Plan did not hold investments in any one organization that represent 5 percent or more of the Pension Plan's Fiduciary Net Position. Rate of Return: For the year ended September 30, 2015, the annual money-weighted rate of return on Pension Plan investments, net of Pension Plan investment expense, was 0.09 percent. The money-weighted rate of return expresses investment performance, net of investment expense, adjusted for the changing amounts actually invested. East Niceville Fire District Firefighters' Pension Fund Foster & Foster 5

229 GASB 67 NET PENSION LIABILITY OF THE SPONSOR The components of the Net Pension Liability of the Sponsor on September 30, 2015 were as follows: Total Pension Liability $ 625,866 Plan Fiduciary Net Position $ (676,381) Sponsor's Net Pension Liability $ (50,515) Plan Fiduciary Net Position as a percentage of Total Pension Liability % Actuarial Assumptions: The Total Pension Liability was determined by an actuarial valuation as of October 1, 2015 using the following actuarial assumptions: Inflation 3.00% Salary Increases 5.50% % Discount Rate 7.00% Investment Rate of Return 7.00% Mortality Rate: RP-2000 Table - Sex Distinct. Disabled lives are set forward 5 years. We feel this assumption sufficiently accommodates future mortality improvements. The date of the most recent experience study for which significant assumptions are based upon is not available. The Long-Term Expected Rate of Return on Pension Plan investments was determined using a building-block method in which bestestimate ranges of expected future real rates of return (expected returns, net of Pension Plan investment expenses and inflation) are developed for each major asset class. These ranges are combined to produce the Long-Term Expected Rate of Return by weighting the expected future real rates of return by the target asset allocation percentage and by adding expected inflation. Best estimates of arithmetic real rates of return for each major asset class included in the Pension Plan's target asset allocation as of September 30, 2015 are summarized in the following table: Asset Class Cash Pooled Funds Long Term Expected Real Rate of Return N/A* N/A* * The Trust Fund has no performance evaluator. The asset class allocation is from the 2015 Annual Report. Discount Rate: The Discount Rate used to measure the Total Pension Liability was 7.00 percent. The projection of cash flows used to determine the Discount Rate assumed that Plan Member contributions will be made at the current contribution rate and that Sponsor contributions will be made at rates equal to the difference between actuarially determined contribution rates and the Member rate. Based on those assumptions, the Pension Plan's Fiduciary Net Position was projected to be available to make all projected future benefit payments of current plan members. Therefore, the Long-Term Expected Rate of Return on Pension Plan investments was applied to all periods of projected benefit payments to determine the Total Pension Liability. 1% Decrease Current Discount Rate 1% Increase 6.00% 7.00% 8.00% Sponsor's Net Pension Liability $ 53,835 $ (50,515) $ (136,786) East Niceville Fire District Firefighters' Pension Fund Foster & Foster 6

230 GASB 67 SCHEDULE OF CHANGES IN NET PENSION LIABILITY AND RELATED RATIOS Last 10 Fiscal Years 09/30/ /00/ /00/1900 Total Pension Liability Service Cost 69, Interest 41, Changes of benefit terms Differences between Expected and Actual Experience Changes of assumptions Contributions - Buy Back Benefit Payments, including Refunds of Employee Contributions (2,901) - - Net Change in Total Pension Liability 107, Total Pension Liability - Beginning 518, Total Pension Liability - Ending (a) $ 625,866 $ - $ - Plan Fiduciary Net Position Contributions - Employer 13, Contributions - State 56, Contributions - Employee 18, Contributions - Buy Back Net Investment Income 1, Benefit Payments, including Refunds of Employee Contributions (2,901) - - Administrative Expense (2,520) - - Net Change in Plan Fiduciary Net Position 84, Plan Fiduciary Net Position - Beginning 591, Plan Fiduciary Net Position - Ending (b) $ 676,381 $ - $ - Net Pension Liability - Ending (a) - (b) $ (50,515) $ - $ - Plan Fiduciary Net Position as a percentage of the Total Pension Liability % #DIV/0! #DIV/0! Covered Employee Payroll $ 408,671 $ - $ - Net Pension Liability as a percentage of Covered Employee Payroll % #DIV/0! #DIV/0! East Niceville Fire District Firefighters' Pension Fund Foster & Foster 7

231 GASB 67 SCHEDULE OF CONTRIBUTIONS Last 10 Fiscal Years 09/30/ /00/ /00/1900 Actuarially Determined Contribution 62, Contributions in relation to the Actuarially Determined Contributions 69, Contribution Deficiency (Excess) $ (7,894) $ - $ - Covered Employee Payroll $ 408,671 $ - $ - Contributions as a percentage of Covered Employee Payroll 17.11% #DIV/0! #DIV/0! Notes to Schedule Valuation Date: 10/01/2012 Actuarially determined contribution rates are calculated as of October 1, three years prior to the end of the fiscal year in which contributions are reported. Methods and assumptions used to determine contribution rates: Funding Method: Mortality Rate: Interest Rate: Inflation: Retirement Age: Disability Rates: Termination Rates: Salary Increases: Payroll Growth Assumption: Entry Age Normal Actuarial Cost Method. RP-2000 Table (sex distinct). 7.0% per year, compounded annually, net of investment related expenses. 3.0% per year. 10% (previously 5%) per year eligible for Early Retirement. 10% per year eligible for Normal Retirement (with 100% at Age 52 with 25 Y rs of Service). Also, any member who has reached Normal Retirement Age on the valuation date is assumed to continue employment for one additional year. % Becoming Disabled During Age the Year % % % % % Terminating Service During the Year 0-2 Years 15.0% 3+ Years 5.0% Previously age based assumption. Years of Service Salary Increase % 1 8.0% % % Previously 6% per year until the assumed retirement age. None. East Niceville Fire District Firefighters' Pension Fund Foster & Foster 8

232 GASB 67 SCHEDULE OF INVESTMENT RETURNS Last 10 Fiscal Years 09/30/ /00/ /00/1900 Annual Money-Weighted Rate of Return Net of Investment Expense 0.09% 0.00% 0.00% East Niceville Fire District Firefighters' Pension Fund Foster & Foster 9

233 GASB 68 NOTES TO THE FINANCIAL STATEMENTS (For the Year Ended September 30, 2015) General Information about the Pension Plan Plan Description Each person employed by the City Fire Department as full-time Firefighter becomes a member of the Plan as a condition of his employment. All Firefighters are therefore eligible for plan benefits as provided for in the plan document and by applicable law. The Plan is a single-employer defined benefit pension plan administered by the Plan's Board of Trustees comprised of: a. Two Commission appointees, b. Two Members of the Department elected by the membership, and c. Fifth Member elected by other four and appointed by Commission. Plan Membership as of October 1, 2015: Inactive Plan Members or Beneficiaries Currently Receiving Benefits - Inactive Plan Members Entitled to But Not Yet Receiving Benefits 1 Active Plan Members Benefits Provided The Plan provides retirement, termination, disability and death benefits. Normal Retirement: Date: The earlier of: 1) age 55 and the completion of 10 years of Credited Service, or 2) the attainment of age 52 and the completion of 25 years of credit service. Benefit: 3.00% of Average Final Compensation times Credited Service. Early Retirement: Date: Age 50 and 10 years of Credited Service. Accrued benefit, reduced 3.0% per year. Vesting: Schedule: 100% after 10 years of Credited Service. Benefit Amount: Member will receive the vested portion of his (her) accrued benefit payable at the otherwise Normal Retirement Date. Disability: Eligibility Service Incurred: Covered from Date of Employment. Eligibility Non-Service Incurred: 10 years of Credited Service. Benefit accrued to date of disability but not less than 42% of Average Final Compensation (Service Incurred) or 25% of Average Final Compensation (Not Service Incurred). Pre-Retirement Death Benefits: Vested: Monthly accrued benefit payable to designated beneficiary for 10 years at the otherwise Normal or Early Retirement Date. Non-Vested: Refund of accumulated contributions without interest. Contributions Firefighters - 5%. District for Firefighters - 0%. East Niceville Fire District Firefighters' Pension Fund Foster & Foster 10

234 GASB 68 Net Pension Liability The measurement date is September 30, The measurement period for the pension expense was October 1, 2014 to September 30, The reporting period is October 1, 2014 through September 30, The Sponsor's Net Pension Liability was measured as of September 30, The Total Pension Liability used to calculate the Net Pension Liability was determined as of that date. Actuarial Assumptions: The Total Pension Liability was determined by an actuarial valuation as of October 1, 2015 using the following actuarial assumptions: Inflation 3.00% Salary Increases 5.50% % Discount Rate 7.00% Investment Rate of Return 7.00% Mortality Rate: RP-2000 Table - Sex Distinct. Disabled lives are set forward 5 years. We feel this assumption sufficiently accommodates future mortality improvements. The date of the most recent experience study for which significant assumptions are based upon is not available. The Long-Term Expected Rate of Return on Pension Plan investments was determined using a building-block method in which bestestimate ranges of expected future real rates of return (expected returns, Net of Pension Plan investment expenses and inflation) are developed for each major asset class. These ranges are combined to produce the Long-Term Expected Rate of Return by weighting the expected future real rates of return by the target asset allocation percentage and by adding expected inflation. Best estimates of arithmetic real rates of return for each major asset class included in the Pension Plan's target asset allocation as of September 30, 2015 are summarized in the following table: Asset Class Target Allocation Long Term Expected Real Rate of Return Cash 55% N/A* Pooled Funds 45% N/A* Total 100% * The Trust Fund has no performance evaluator. The asset class allocation is from the 2015 Annual Report. Discount Rate: The Discount Rate used to measure the Total Pension Liability was 7.00 percent. The projection of cash flows used to determine the Discount Rate assumed that Plan Member contributions will be made at the current contribution rate and that Sponsor contributions will be made at rates equal to the difference between actuarially determined contribution rates and the Member rate. Based on those assumptions, the Pension Plan's Fiduciary Net Position was projected to be available to make all projected future benefit payments of current plan members. Therefore, the Long-Term Expected Rate of Return on Pension Plan investments was applied to all periods of projected benefit payments to determine the Total Pension Liability. East Niceville Fire District Firefighters' Pension Fund Foster & Foster 11

235 GASB 68 CHANGES IN NET PENSION LIABILITY Increase (Decrease) Total Pension Liability Plan Fiduciary Net Position Net Pension Liability (a) (b) (a)-(b) Balances at September 30, 2014 $ 518,009 $ 591,680 $ (73,671) Changes for a Year: Service Cost 69,276-69,276 Interest 41,039-41,039 Differences between Expected and Actual Experience Changes of assumptions Changes of benefit terms Contributions - Employer - 13,918 (13,918) Contributions - State - 56,017 (56,017) Contributions - Employee - 18,575 (18,575) Contributions - Buy Back Net Investment Income - 1,169 (1,169) Benefit Payments, including Refunds of Employee Contributions (2,901) (2,901) - Administrative Expense - (2,520) 2,520 Net Changes 107,857 84,701 23,156 Balances at September 30, 2015 $ 625,866 $ 676,381 $ (50,515) Sensitivity of the Net Pension Liability to changes in the Discount Rate. 1% Decrease Current Discount Rate 1% Increase 6.00% 7.00% 8.00% Sponsor's Net Pension Liability $ 53,835 $ (50,515) $ (136,786) Pension Plan Fiduciary Net Position. Detailed information about the pension Plan's Fiduciary Net Position is available in a separately issued Plan financial report. East Niceville Fire District Firefighters' Pension Fund Foster & Foster 12

236 GASB 68 PENSION EXPENSE AND DEFERRED OUTFLOWS OF RESOURCES AND DEFERRED INFLOWS OF RESOURCES RELATED TO PENSIONS For the year ended September 30, 2015, the Sponsor will recognize a Pension Expense of $58,554. On September 30, 2015, the Sponsor reported Deferred Outflows of Resources and Deferred Inflows of Resources related to pensions from the following sources: Deferred Outflows of Resources Deferred Inflows of Resources Differences between Expected and Actual Experience - - Changes of assumptions - - Net difference between Projected and Actual Earnings on Pension Plan investments 34,537 - Total $ 34,537 $ - Amounts reported as Deferred Outflows of Resources and Deferred Inflows of Resources related to pensions will be recognized in Pension Expense as follows: OUTFLOW INFLOW Year ended September 30: 2016 $ - $ - $ 8,635 $ 8, $ - $ - $ 8,634 $ 8, $ - $ - $ 8,634 $ 8, $ - $ - $ 8,634 $ 8, $ - $ - $ - $ - Thereafter $ - $ - $ - $ - East Niceville Fire District Firefighters' Pension Fund Foster & Foster 13

237 GASB 68 SCHEDULE OF CHANGES IN NET PENSION LIABILITY AND RELATED RATIOS Last 10 Fiscal Years 09/30/ /00/ /00/1900 Total Pension Liability Service Cost 69, Interest 41, Changes of benefit terms Differences between Expected and Actual Experience Changes of assumptions Contributions - Buy Back Benefit Payments, including Refunds of Employee Contributions (2,901) - - Net Change in Total Pension Liability 107, Total Pension Liability - Beginning 518, Total Pension Liability - Ending (a) $ 625,866 $ - $ - Plan Fiduciary Net Position Contributions - Employer 13, Contributions - State 56, Contributions - Employee 18, Contributions - Buy Back Net Investment Income 1, Benefit Payments, including Refunds of Employee Contributions (2,901) - - Administrative Expense (2,520) - - Net Change in Plan Fiduciary Net Position 84, Plan Fiduciary Net Position - Beginning 591, Plan Fiduciary Net Position - Ending (b) $ 676,381 $ - $ - Net Pension Liability - Ending (a) - (b) $ (50,515) $ - $ - Plan Fiduciary Net Position as a percentage of the Total Pension Liability % #DIV/0! #DIV/0! Covered Employee Payroll $ 408,671 $ - $ - Net Pension Liability as a percentage of Covered Employee Payroll % #DIV/0! #DIV/0! East Niceville Fire District Firefighters' Pension Fund Foster & Foster 14

238 GASB 68 SCHEDULE OF CONTRIBUTIONS Last 10 Fiscal Years 09/30/ /00/ /00/ /00/ /00/1900 Actuarially Determined Contribution 62, Contributions in relation to the Actuarially Determined Contributions 69, Contribution Deficiency (Excess) $ (7,894) $ - $ - $ - $ - Covered Employee Payroll $ 408,671 $ - $ - $ - $ - Contributions as a percentage of Covered Employee Payroll 17.11% #DIV/0! #DIV/0! #DIV/0! #DIV/0! Notes to Schedule Valuation Date: 10/01/2012 Actuarially determined contribution rates are calculated as of October 1, three years prior to the end of the fiscal year in which contributions are reported. Methods and assumptions used to determine contribution rates: Funding Method: Mortality Rate: Interest Rate: Inflation: Retirement Age: Disability Rates: Termination Rates: Salary Increases: Payroll Growth Assumption: Entry Age Normal Actuarial Cost Method. RP-2000 Table (sex distinct). 7.0% per year, compounded annually, net of investment related expenses. 3.0% per year. 10% (previously 5%) per year eligible for Early Retirement. 10% per year eligible for Normal Retirement (with 100% at Age 52 with 25 Y rs of Service). Also, any member who has reached Normal Retirement Age on the valuation date is assumed to continue employment for one additional year. % Becoming Disabled During Age the Year % % % % % Terminating Service During the Year 0-2 Years 15.00% 3+ Years 5.00% Previously age based assumption. Years of Service Salary Increase % % % % Previously 6% per year until the assumed retirement age. None. East Niceville Fire District Firefighters' Pension Fund Foster & Foster 15

239 GASB 68 COMPONENTS OF PENSION EXPENSE FISCAL YEAR SEPTEMBER 30, 2015 Net Pension Liability Deferred Inflows Deferred Outflows Pension Expense Beginning balance $ (73,671) $ - $ - $ - Total Pension Liability Factors: Service Cost 69, ,276 Interest 41, ,039 Changes in benefit terms Contributions - Buy Back Differences between Expected and Actual Experience with regard to economic or demographic assumptions Current year amortization of experience difference Change in assumptions about future economic or demographic factors or other inputs Current year amortization of change in assumptions Benefit Payments (2,901) - - (2,901) Net change 107, ,857 Plan Fiduciary Net Position: Contributions - Employer 13, Contributions - State 56, Contributions - Employee 18, (18,575) Contributions - Buy Back (443) Net Investment Income 44, (44,341) Difference between projected and actual earnings on Pension Plan investments (43,172) - 43,172 - Current year amortization - - (8,635) 8,635 Benefit Payments (2,901) - - 2,901 Administrative Expenses (2,520) - - 2,520 Net change 84,701-34,537 (49,303) Ending Balance $ (50,515) $ - $ 34,537 $ 58,554 East Niceville Fire District Firefighters' Pension Fund Foster & Foster 16

240 October 4, 2017 Board of Trustees City of Chattahoochee Municipal Firefighters Retirement Trust Fund P.O. Box 188 Chattahoochee, FL RE: GASB Statement No.67 and No.68 City of Chattahoochee Municipal Firefighters Retirement Trust Fund Dear Board: We are pleased to present to the Board GASB Statement No.67 and No.68 measured as of September 30, 2016 for the City of Chattahoochee Municipal Firefighters Retirement Trust Fund. The calculation of the liability associated with the benefits referenced in this report was performed for the purpose of satisfying the requirements of GASB No.67 and No.68 and is not applicable for other purposes, such as determining the plan s funding requirements. A calculation of the plan s liability for other purposes may produce significantly different results. The total pension liability, net pension liability, and certain sensitivity information shown in this report are based on an actuarial valuation performed as of October 1, It is our opinion that the assumptions used for this purposes are internally consistent, reasonable, and comply with the requirements under GASB No.67 and No.68. Certain schedules should include a 10-year history of information. As provided for in GASB No.67 and No.68, this historical information is only presented for the years in which the information was measured in conformity with the requirements of GASB No.67 and No.68. To the best of our knowledge, these statements are complete and accurate and are in accordance with generally recognized actuarial practices and methods. If there are any questions, concerns, or comments about any of the items contained in this report, please contact me at Respectfully submitted, Foster & Foster, Inc. By: Patrick T. Donlan, ASA, MAAA Enrolled Actuary # PTD/lke Enclosures Parker Commons Blvd., Suite 104 Fort Myers, FL (239) Fax (239)

241 GASB 67 STATEMENT OF FIDUCIARY NET POSITION SEPTEMBER 30, 2016 ASSETS Cash and Cash Equivalents: Certificates of Deposits Cash Total Cash and Equivalents Receivables: Additional City Contributions Accrued Interest Total Receivable Total Investments Total Assets Total Liabilities NET POSITION RESTRICTED FOR PENSIONS MARKET VALUE 350,000 68, ,452 2,821 4,561 7, , ,834 City of Chattahoochee Municipal Firefighters Retirement Trust Fund FOSTER & FOSTER 2

242 GASB 67 STATEMENT OF CHANGES IN FIDUCIARY NET POSITION FOR THE YEAR ENDED SEPTEMBER 30, 2016 Market Value Basis ADDITIONS Contributions: Member 2,815 City 30,680 Total Contributions 33,495 Investment Income: Net Increase in Fair Value of Investments 0 Interest & Dividends 2,436 Less Investment Expense¹ 0 Net Investment Income 2,436 Total Additions 35,931 DEDUCTIONS Distributions to Members: Benefit Payments 24,574 Refunds of Member Contributions 0 Total Distributions 24,574 Administrative Expense 0 Total Deductions 24,574 Net Increase in Net Position 11,357 NET POSITION RESTRICTED FOR PENSIONS Beginning of the Year 414,477 End of the Year 425,834 ¹Investment related expenses include investment advisory, custodial and performance monitoring fees. City of Chattahoochee Municipal Firefighters Retirement Trust Fund FOSTER & FOSTER 3

243 GASB 67 NOTES TO THE FINANCIAL STATEMENTS (For the Year Ended September 30, 2016) Plan Description Plan Administration The Plan is a single-employer defined benefit pension plan administered by the Plan's Board of Trustees comprised of: a. Two Commission appointees, b. Two Members of the Department elected by the Membership, and c. A fifth Member elected by other four and appointed by Commission. Plan Membership as of October 1, 2016: Inactive Plan Members or Beneficiaries Currently Receiving Benefits 5 Inactive Plan Members Entitled to But Not Yet Receiving Benefits 1 Active Plan Members Benefits Provided The Plan provides retirement, termination, disability and death benefits. Normal Retirement: Date: The earlier of: 1) age 55 and the completion of 10 years of Credited Service, or 2) the attainment of age 52 and the completion of 25 years of credit service. Benefit: 2.50% of Average Final Compensation times Credited Service. Early Retirement: Date: Age 50 and 10 years of Credited Service. Accrued benefit, reduced 3.0% per year. Vesting: Schedule: 100% after 10 years of Credited Service. Benefit Amount: Member will receive the vested portion of his (her) accrued benefit payable at the otherwise Normal Retirement Date. Disability: Eligibility Service Incurred: Covered from Date of Employment. Eligibility Non-Service Incurred: 10 years of Credited Service. Benefit accrued to date of disability but not less than 42% of Average Final Compensation (Service Incurred) or 25% of Average Final Compensation (Not Service Incurred). Pre-Retirement Death Benefits: Vested: Monthly accrued benefit payable to designated beneficiary for 10 years at the otherwise Normal or Early Retirement Date. Non-Vested: Refund of accumulated contributions without interest. Contributions Member Contributions 5.0% of Salary. City and State Contributions: Remaining amount necessary to pay current costs and amortize past service cost, if any, as provided in Part VII of Chapter 112, Florida Statutes. City of Chattahoochee Municipal Firefighters Retirement Trust Fund FOSTER & FOSTER 4

244 GASB 67 Investments Investment Policy: The following was the Board's adopted asset allocation policy as of September 30, 2016: Asset Class N/A Target Allocation N/A Concentrations: The Plan did not hold investments in any one organization that represent 5 percent or more of the Pension Plan's Fiduciary Net Position. Rate of Return: For the year ended September 30, 2016, the annual money-weighted rate of return on Pension Plan investments, net of Pension Plan investment expense, was 0.58 percent. The money-weighted rate of return expresses investment performance, net of investment expense, adjusted for the changing amounts actually invested. City of Chattahoochee Municipal Firefighters Retirement Trust Fund FOSTER & FOSTER 5

RE: GASB Statement No.67 and No.68 City of Holly Hill Police Officers Pension Board

February 2, 2018 Board of Trustees City of Holly Hill Police Officers' Pension Board 1065 Ridgewood Avenue Holly Hill, FL 32117 RE: GASB Statement No.67 and No.68 City of Holly Hill Police Officers Pension

February 2, 2018 Board of Trustees City of Holly Hill Police Officers' Pension Board 1065 Ridgewood Avenue Holly Hill, FL 32117 RE: GASB Statement No.67 and No.68 City of Holly Hill Police Officers Pension

CITY OF WEST MELBOURNE POLICE OFFICERS RETIREMENT PLAN ACTUARIAL VALUATION AS OF OCTOBER 1, 2015

CITY OF WEST MELBOURNE POLICE OFFICERS RETIREMENT PLAN ACTUARIAL VALUATION AS OF OCTOBER 1, 2015 CONTRIBUTIONS APPLICABLE TO THE PLAN/ FISCAL YEAR ENDING SEPTEMBER 30, 2017 February 1, 2016 Ms. Karan Rounsavall

CITY OF WEST MELBOURNE POLICE OFFICERS RETIREMENT PLAN ACTUARIAL VALUATION AS OF OCTOBER 1, 2015 CONTRIBUTIONS APPLICABLE TO THE PLAN/ FISCAL YEAR ENDING SEPTEMBER 30, 2017 February 1, 2016 Ms. Karan Rounsavall

CITY OF DADE CITY POLICE OFFICERS' PENSION FUND ACTUARIAL VALUATION AS OF OCTOBER 1, 2016

CITY OF DADE CITY POLICE OFFICERS' PENSION FUND ACTUARIAL VALUATION AS OF OCTOBER 1, 2016 CONTRIBUTIONS APPLICABLE TO THE PLAN/FISCAL YEAR ENDING SEPTEMBER 30, 2018 May 20, 2017 Board of Trustees City

CITY OF DADE CITY POLICE OFFICERS' PENSION FUND ACTUARIAL VALUATION AS OF OCTOBER 1, 2016 CONTRIBUTIONS APPLICABLE TO THE PLAN/FISCAL YEAR ENDING SEPTEMBER 30, 2018 May 20, 2017 Board of Trustees City

CITY OF DUNEDIN FIREFIGHTERS RETIREMENT SYSTEM ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2017

CITY OF DUNEDIN FIREFIGHTERS RETIREMENT SYSTEM ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2017 CONTRIBUTIONS APPLICABLE TO THE CITY'S PLAN/FISCAL YEAR ENDED SEPTEMBER 30, 2019 February 19, 2018 Board

CITY OF DUNEDIN FIREFIGHTERS RETIREMENT SYSTEM ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2017 CONTRIBUTIONS APPLICABLE TO THE CITY'S PLAN/FISCAL YEAR ENDED SEPTEMBER 30, 2019 February 19, 2018 Board

CITY OF PINELLAS PARK FIREFIGHTERS PENSION FUND ACTUARIAL VALUATION AS OF OCTOBER 1, 2016

CITY OF PINELLAS PARK FIREFIGHTERS PENSION FUND ACTUARIAL VALUATION AS OF OCTOBER 1, 2016 CONTRIBUTIONS APPLICABLE TO THE PLAN/ FISCAL YEAR ENDED SEPTEMBER 30, 2018 January 30, 2017 Board of Trustees City

CITY OF PINELLAS PARK FIREFIGHTERS PENSION FUND ACTUARIAL VALUATION AS OF OCTOBER 1, 2016 CONTRIBUTIONS APPLICABLE TO THE PLAN/ FISCAL YEAR ENDED SEPTEMBER 30, 2018 January 30, 2017 Board of Trustees City

CITY OF ORMOND BEACH FIREFIGHTERS PENSION TRUST FUND ACTUARIAL VALUATION AND REPORT AS OF OCTOBER 1, 2017

CITY OF ORMOND BEACH FIREFIGHTERS PENSION TRUST FUND ACTUARIAL VALUATION AND REPORT AS OF OCTOBER 1, 2017 CONTRIBUTIONS APPLICABLE TO THE PLAN/ FISCAL YEAR ENDED SEPTEMBER 30, 2019 December 15, 2017 Board

CITY OF ORMOND BEACH FIREFIGHTERS PENSION TRUST FUND ACTUARIAL VALUATION AND REPORT AS OF OCTOBER 1, 2017 CONTRIBUTIONS APPLICABLE TO THE PLAN/ FISCAL YEAR ENDED SEPTEMBER 30, 2019 December 15, 2017 Board

ENGLEWOOD AREA FIRE CONTROL DISTRICT FIREFIGHTERS' PENSION TRUST FUND ACTUARIAL VALUATION AS OF OCTOBER 1, 2016

ENGLEWOOD AREA FIRE CONTROL DISTRICT FIREFIGHTERS' PENSION TRUST FUND ACTUARIAL VALUATION AS OF OCTOBER 1, 2016 CONTRIBUTIONS APPLICABLE TO THE PLAN/FISCAL YEAR ENDING SEPTEMBER 30, 2018 December 8, 2016

ENGLEWOOD AREA FIRE CONTROL DISTRICT FIREFIGHTERS' PENSION TRUST FUND ACTUARIAL VALUATION AS OF OCTOBER 1, 2016 CONTRIBUTIONS APPLICABLE TO THE PLAN/FISCAL YEAR ENDING SEPTEMBER 30, 2018 December 8, 2016

RE: GASB Statement No. 67 and No. 68 City of Cape Coral Municipal General Employees Retirement Plan

February 21, 2017 Ms. Linda Runkle, Plan Administrator The Resource Centers, LLC P.O. Box 152665 Cape Coral, FL 33915-2665 RE: GASB Statement No. 67 and No. 68 City of Cape Coral Municipal General Employees

February 21, 2017 Ms. Linda Runkle, Plan Administrator The Resource Centers, LLC P.O. Box 152665 Cape Coral, FL 33915-2665 RE: GASB Statement No. 67 and No. 68 City of Cape Coral Municipal General Employees

CITY OF OVIEDO FIREFIGHTERS' PENSION TRUST FUND ACTUARIAL VALUATION AS OF OCTOBER 1, 2017

CITY OF OVIEDO FIREFIGHTERS' PENSION TRUST FUND ACTUARIAL VALUATION AS OF OCTOBER 1, 2017 CONTRIBUTIONS APPLICABLE TO THE PLAN FISCAL YEAR ENDING SEPTEMBER 30, 2019 November 22, 2017 Board of Trustees

CITY OF OVIEDO FIREFIGHTERS' PENSION TRUST FUND ACTUARIAL VALUATION AS OF OCTOBER 1, 2017 CONTRIBUTIONS APPLICABLE TO THE PLAN FISCAL YEAR ENDING SEPTEMBER 30, 2019 November 22, 2017 Board of Trustees

13420 Parker Commons Blvd., Suite 104 Fort Myers, FL (239) Fax (239)

Fax (239)") February 9, 2017 Mr. Scott Baur The Resource Centers, LLC P.O. Box 152665 Cape Coral, FL 33915-2665 RE: GASB Statement No. 67 and No. 68 City of Cape Coral Municipal Police Officers Retirement Plan Dear

February 9, 2017 Mr. Scott Baur The Resource Centers, LLC P.O. Box 152665 Cape Coral, FL 33915-2665 RE: GASB Statement No. 67 and No. 68 City of Cape Coral Municipal Police Officers Retirement Plan Dear

CITY OF CRESTVIEW POLICE OFFICERS' AND FIREFIGHTERS' RETIREMENT PLAN ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2016

CITY OF CRESTVIEW POLICE OFFICERS' AND FIREFIGHTERS' RETIREMENT PLAN ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2016 CONTRIBUTIONS APPLICABLE TO THE CITY'S PLAN/FISCAL YEAR ENDING SEPTEMBER 30, 2018 June

CITY OF CRESTVIEW POLICE OFFICERS' AND FIREFIGHTERS' RETIREMENT PLAN ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2016 CONTRIBUTIONS APPLICABLE TO THE CITY'S PLAN/FISCAL YEAR ENDING SEPTEMBER 30, 2018 June

CITY OF PENSACOLA FIREFIGHTERS RELIEF AND PENSION FUND ACTUARIAL VALUATION AND REPORT AS OF OCTOBER 1, 2014

CITY OF PENSACOLA FIREFIGHTERS RELIEF AND PENSION FUND ACTUARIAL VALUATION AND REPORT AS OF OCTOBER 1, 2014 CONTRIBUTIONS APPLICABLE TO THE PLAN/ FISCAL YEAR ENDED SEPTEMBER 30, 2016 2 January 20, 2015

CITY OF PENSACOLA FIREFIGHTERS RELIEF AND PENSION FUND ACTUARIAL VALUATION AND REPORT AS OF OCTOBER 1, 2014 CONTRIBUTIONS APPLICABLE TO THE PLAN/ FISCAL YEAR ENDED SEPTEMBER 30, 2016 2 January 20, 2015

CITY OF OCALA POLICE OFFICERS' RETIREMENT SYSTEM ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2015

CITY OF OCALA POLICE OFFICERS' RETIREMENT SYSTEM ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2015 CONTRIBUTIONS APPLICABLE TO THE PLAN/FISCAL YEAR ENDED SEPTEMBER 30, 2017 March 16, 2016 Board of Trustees

CITY OF OCALA POLICE OFFICERS' RETIREMENT SYSTEM ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2015 CONTRIBUTIONS APPLICABLE TO THE PLAN/FISCAL YEAR ENDED SEPTEMBER 30, 2017 March 16, 2016 Board of Trustees

TOWN OF MEDLEY POLICE OFFICERS' RETIREMENT SYSTEM. ACTUARIAL VALUATION AS OF OCTOBER 1, 2014 (Revised May 20, 2015)

") TOWN OF MEDLEY POLICE OFFICERS' RETIREMENT SYSTEM ACTUARIAL VALUATION AS OF OCTOBER 1, 2014 (Revised May 20, 2015) CONTRIBUTIONS APPLICABLE TO THE TOWN'S PLAN/FISCAL YEAR ENDED SEPTEMBER 30, 2016 2 May

TOWN OF MEDLEY POLICE OFFICERS' RETIREMENT SYSTEM ACTUARIAL VALUATION AS OF OCTOBER 1, 2014 (Revised May 20, 2015) CONTRIBUTIONS APPLICABLE TO THE TOWN'S PLAN/FISCAL YEAR ENDED SEPTEMBER 30, 2016 2 May

CITY OF MELBOURNE POLICE OFFICERS' RETIREMENT TRUST FUND OCTOBER 1, 2016 ACTUARIAL VALUATION REPORT

CITY OF MELBOURNE POLICE OFFICERS' RETIREMENT TRUST FUND OCTOBER 1, 2016 ACTUARIAL VALUATION REPORT CONTRIBUTIONS APPLICABLE TO THE PLAN/FISCAL YEAR ENDED SEPTEMBER 30, 2018 February 1, 2017 Board of Trustees

CITY OF MELBOURNE POLICE OFFICERS' RETIREMENT TRUST FUND OCTOBER 1, 2016 ACTUARIAL VALUATION REPORT CONTRIBUTIONS APPLICABLE TO THE PLAN/FISCAL YEAR ENDED SEPTEMBER 30, 2018 February 1, 2017 Board of Trustees

CITY OF NAPLES FIREFIGHTERS PENSION AND RETIREMENT SYSTEM ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2016

CITY OF NAPLES FIREFIGHTERS PENSION AND RETIREMENT SYSTEM ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2016 CONTRIBUTIONS APPLICABLE TO THE CITY'S PLAN/FISCAL YEAR ENDED SEPTEMBER 30, 2018 November 28,

CITY OF NAPLES FIREFIGHTERS PENSION AND RETIREMENT SYSTEM ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2016 CONTRIBUTIONS APPLICABLE TO THE CITY'S PLAN/FISCAL YEAR ENDED SEPTEMBER 30, 2018 November 28,

CITY OF HOLLYWOOD FIREFIGHTERS PENSION FUND ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2015

CITY OF HOLLYWOOD FIREFIGHTERS PENSION FUND ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2015 CONTRIBUTIONS APPLICABLE TO THE PLAN/ FISCAL YEAR ENDED SEPTEMBER 30, 2017 June 28, 2016 Board of Trustees c/o

CITY OF HOLLYWOOD FIREFIGHTERS PENSION FUND ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2015 CONTRIBUTIONS APPLICABLE TO THE PLAN/ FISCAL YEAR ENDED SEPTEMBER 30, 2017 June 28, 2016 Board of Trustees c/o

CITY OF TARPON SPRINGS FIREFIGHTERS' PENSION TRUST FUND ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2015

CITY OF TARPON SPRINGS FIREFIGHTERS' PENSION TRUST FUND ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2015 CONTRIBUTIONS APPLICABLE TO THE PLAN/ FISCAL YEAR ENDED SEPTEMBER 30, 2017 February 16, 2016 Ms.

CITY OF TARPON SPRINGS FIREFIGHTERS' PENSION TRUST FUND ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2015 CONTRIBUTIONS APPLICABLE TO THE PLAN/ FISCAL YEAR ENDED SEPTEMBER 30, 2017 February 16, 2016 Ms.

RE: Revised GASB Statement No.67 and No.68 Town of Longboat Key Police Officers Retirement System

February 21, 2018 Board of Trustees Town of Longboat Key 501 Bay Isles Road Longboat Key, FL 34228 RE: Revised GASB Statement No.67 and No.68 Town of Longboat Key Police Officers Retirement System Dear

February 21, 2018 Board of Trustees Town of Longboat Key 501 Bay Isles Road Longboat Key, FL 34228 RE: Revised GASB Statement No.67 and No.68 Town of Longboat Key Police Officers Retirement System Dear

CITY OF PALM COAST VOLUNTEER FIREFIGHTERS RETIREMENT TRUST FUND ACTUARIAL VALUATION AS OF OCTOBER 1, 2017

CITY OF PALM COAST VOLUNTEER FIREFIGHTERS RETIREMENT TRUST FUND ACTUARIAL VALUATION AS OF OCTOBER 1, 2017 CONTRIBUTIONS APPLICABLE TO THE PLAN/ FISCAL YEAR ENDED SEPTEMBER 30, 2019 January 22, 2018 Board

CITY OF PALM COAST VOLUNTEER FIREFIGHTERS RETIREMENT TRUST FUND ACTUARIAL VALUATION AS OF OCTOBER 1, 2017 CONTRIBUTIONS APPLICABLE TO THE PLAN/ FISCAL YEAR ENDED SEPTEMBER 30, 2019 January 22, 2018 Board

CITY OF KISSIMMEE MUNICIPAL POLICE OFFICERS RETIREMENT FUND ACTUARIAL VALUATION AS OF OCTOBER 1, 2017

CITY OF KISSIMMEE MUNICIPAL POLICE OFFICERS RETIREMENT FUND ACTUARIAL VALUATION AS OF OCTOBER 1, 2017 CONTRIBUTIONS APPLICABLE TO THE PLAN YEAR ENDED SEPTEMBER 30, 2018, AND THE CITY'S FISCAL YEAR ENDED

CITY OF KISSIMMEE MUNICIPAL POLICE OFFICERS RETIREMENT FUND ACTUARIAL VALUATION AS OF OCTOBER 1, 2017 CONTRIBUTIONS APPLICABLE TO THE PLAN YEAR ENDED SEPTEMBER 30, 2018, AND THE CITY'S FISCAL YEAR ENDED

CITY OF OCALA GENERAL EMPLOYEES RETIREMENT SYSTEM ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2015

CITY OF OCALA GENERAL EMPLOYEES RETIREMENT SYSTEM ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2015 CONTRIBUTIONS APPLICABLE TO THE PLAN/FISCAL YEAR ENDED SEPTEMBER 30, 2017 March 7, 2016 Board of Trustees

CITY OF OCALA GENERAL EMPLOYEES RETIREMENT SYSTEM ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2015 CONTRIBUTIONS APPLICABLE TO THE PLAN/FISCAL YEAR ENDED SEPTEMBER 30, 2017 March 7, 2016 Board of Trustees

CITY OF OCOEE MUNICIPAL POLICE OFFICERS' AND FIREFIGHTERS' RETIREMENT TRUST FUND ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2017

CITY OF OCOEE MUNICIPAL POLICE OFFICERS' AND FIREFIGHTERS' RETIREMENT TRUST FUND ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2017 CONTRIBUTIONS APPLICABLE TO THE CITY'S PLAN/FISCAL YEAR ENDING SEPTEMBER

CITY OF OCOEE MUNICIPAL POLICE OFFICERS' AND FIREFIGHTERS' RETIREMENT TRUST FUND ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2017 CONTRIBUTIONS APPLICABLE TO THE CITY'S PLAN/FISCAL YEAR ENDING SEPTEMBER

CITY OF OCALA POLICE OFFICERS' RETIREMENT SYSTEM ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2016

CITY OF OCALA POLICE OFFICERS' RETIREMENT SYSTEM ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2016 CONTRIBUTIONS APPLICABLE TO THE PLAN/FISCAL YEAR ENDED SEPTEMBER 30, 2018 February 10, 2017 Board of Trustees

CITY OF OCALA POLICE OFFICERS' RETIREMENT SYSTEM ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2016 CONTRIBUTIONS APPLICABLE TO THE PLAN/FISCAL YEAR ENDED SEPTEMBER 30, 2018 February 10, 2017 Board of Trustees

CITY OF MELBOURNE GENERAL EMPLOYEES' AND SPECIAL RISK CLASS EMPLOYEES' PENSION PLAN ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2017

CITY OF MELBOURNE GENERAL EMPLOYEES' AND SPECIAL RISK CLASS EMPLOYEES' PENSION PLAN ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2017 CONTRIBUTIONS APPLICABLE TO THE PLAN/FISCAL YEAR ENDED SEPTEMBER 30,

CITY OF MELBOURNE GENERAL EMPLOYEES' AND SPECIAL RISK CLASS EMPLOYEES' PENSION PLAN ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2017 CONTRIBUTIONS APPLICABLE TO THE PLAN/FISCAL YEAR ENDED SEPTEMBER 30,

CITY OF KISSIMMEE MUNICIPAL FIREFIGHTERS RETIREMENT PLAN ACTUARIAL VALUATION AS OF OCTOBER 1, 2017

CITY OF KISSIMMEE MUNICIPAL FIREFIGHTERS RETIREMENT PLAN ACTUARIAL VALUATION AS OF OCTOBER 1, 2017 CONTRIBUTIONS APPLICABLE TO THE PLAN YEAR ENDED SEPTEMBER 30, 2018, AND THE CITY'S FISCAL YEAR ENDED SEPTEMBER

CITY OF KISSIMMEE MUNICIPAL FIREFIGHTERS RETIREMENT PLAN ACTUARIAL VALUATION AS OF OCTOBER 1, 2017 CONTRIBUTIONS APPLICABLE TO THE PLAN YEAR ENDED SEPTEMBER 30, 2018, AND THE CITY'S FISCAL YEAR ENDED SEPTEMBER

CITY OF WINTER GARDEN PENSION PLAN FOR GENERAL EMPLOYEES ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2016

CITY OF WINTER GARDEN PENSION PLAN FOR GENERAL EMPLOYEES ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2016 CONTRIBUTIONS APPLICABLE TO THE CITY'S PLAN/FISCAL YEAR ENDING SEPTEMBER 30, 2018 March 6, 2017

CITY OF WINTER GARDEN PENSION PLAN FOR GENERAL EMPLOYEES ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2016 CONTRIBUTIONS APPLICABLE TO THE CITY'S PLAN/FISCAL YEAR ENDING SEPTEMBER 30, 2018 March 6, 2017

EAST NAPLES FIRE CONTROL AND RESCUE DISTRICT FIREFIGHTERS' PENSION PLAN ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2014

EAST NAPLES FIRE CONTROL AND RESCUE DISTRICT FIREFIGHTERS' PENSION PLAN ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2014 CONTRIBUTIONS APPLICABLE TO THE DISTRICT'S PLAN/FISCAL YEAR ENDED SEPTEMBER 30,

EAST NAPLES FIRE CONTROL AND RESCUE DISTRICT FIREFIGHTERS' PENSION PLAN ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2014 CONTRIBUTIONS APPLICABLE TO THE DISTRICT'S PLAN/FISCAL YEAR ENDED SEPTEMBER 30,

We are pleased to present to the Board the GASB Statement No. 67 measured as of December 31, 2013 for the Austin Police Retirement System.

November 26, 2014 Mr. Sam Jordan, CEO Austin Police Retirement System 2520 South IH 35, Suite 100 Austin, TX 78704 RE: GASB Statement No. 67 Austin Police Retirement System Dear Board: We are pleased to

November 26, 2014 Mr. Sam Jordan, CEO Austin Police Retirement System 2520 South IH 35, Suite 100 Austin, TX 78704 RE: GASB Statement No. 67 Austin Police Retirement System Dear Board: We are pleased to

CITY OF CAPE CORAL MUNICIPAL GENERAL EMPLOYEES' RETIREMENT PLAN ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2016

CITY OF CAPE CORAL MUNICIPAL GENERAL EMPLOYEES' RETIREMENT PLAN ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2016 CONTRIBUTIONS APPLICABLE TO THE PLAN/FISCAL YEAR ENDED SEPTEMBER 30, 2018 February 28, 2017

CITY OF CAPE CORAL MUNICIPAL GENERAL EMPLOYEES' RETIREMENT PLAN ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2016 CONTRIBUTIONS APPLICABLE TO THE PLAN/FISCAL YEAR ENDED SEPTEMBER 30, 2018 February 28, 2017

Please find enclosed the annual disclosures that satisfy the October 1, 2017 financial reporting requirements made under Section

May 23, 2018 VIA EMAIL Mr. Ryan Holt 7301 Gulf Blvd St. Pete Beach, FL 33706 Re: City of St. Pete Beach Firefighters' Retirement System Section 112.664, Florida Statutes Compliance Dear Ryan: Please find

May 23, 2018 VIA EMAIL Mr. Ryan Holt 7301 Gulf Blvd St. Pete Beach, FL 33706 Re: City of St. Pete Beach Firefighters' Retirement System Section 112.664, Florida Statutes Compliance Dear Ryan: Please find

Please find enclosed the annual disclosures that satisfy the October 1, 2017 financial reporting requirements made under Section

November 5, 2018 VIA EMAIL Ms. Karen Lauer City of New Port Richey Firefighters Retirement System 5919 Main Street New Port Richey, FL 34652 Re: City of New Port Richey Firefighters' Retirement System

November 5, 2018 VIA EMAIL Ms. Karen Lauer City of New Port Richey Firefighters Retirement System 5919 Main Street New Port Richey, FL 34652 Re: City of New Port Richey Firefighters' Retirement System

TOWN OF MEDLEY DEFINED BENEFIT PLAN ACTUARIAL VALUATION AS OF OCTOBER 1, 2017

TOWN OF MEDLEY DEFINED BENEFIT PLAN ACTUARIAL VALUATION AS OF OCTOBER 1, 2017 CONTRIBUTIONS APPLICABLE TO THE PLAN/FISCAL YEAR ENDED SEPTEMBER 30, 2018 May 10, 2018 Roy Danzinger Town of Medley 7777 NW

TOWN OF MEDLEY DEFINED BENEFIT PLAN ACTUARIAL VALUATION AS OF OCTOBER 1, 2017 CONTRIBUTIONS APPLICABLE TO THE PLAN/FISCAL YEAR ENDED SEPTEMBER 30, 2018 May 10, 2018 Roy Danzinger Town of Medley 7777 NW

Please find enclosed the annual disclosures that satisfy the October 1, 2015 financial reporting requirements made under Section

February 8, 2016 VIA EMAIL Ms. Lois Towey Assistant City Clerk City of Ormond Beach 22 South Beach St. Ormond Beach, Florida 32174 Re: City of Ormond Beach Police Officers' Pension Trust Fund Senate Bill

February 8, 2016 VIA EMAIL Ms. Lois Towey Assistant City Clerk City of Ormond Beach 22 South Beach St. Ormond Beach, Florida 32174 Re: City of Ormond Beach Police Officers' Pension Trust Fund Senate Bill

Please find enclosed the annual disclosures that satisfy the October 1, 2018 financial reporting requirements made under Section

January 7, 2019 VIA EMAIL Mr. Mike Lowell City of Temple Terrace Police Officers' Pension Board 11250 N. 56th Street Temple Terrace, FL 33687 Re: City of Temple Terrace Police Officers' Retirement System

January 7, 2019 VIA EMAIL Mr. Mike Lowell City of Temple Terrace Police Officers' Pension Board 11250 N. 56th Street Temple Terrace, FL 33687 Re: City of Temple Terrace Police Officers' Retirement System

Please find enclosed the annual disclosures that satisfy the October 1, 2017 financial reporting requirements made under Section

April 16, 2018 VIA EMAIL Mr. Bob Rogers 200-76th Avenue St. Pete Beach, FL 33706 Re: City of St. Pete Beach Police Officers' Retirement System Section 112.664, Florida Statutes Compliance Dear Bob: Please

April 16, 2018 VIA EMAIL Mr. Bob Rogers 200-76th Avenue St. Pete Beach, FL 33706 Re: City of St. Pete Beach Police Officers' Retirement System Section 112.664, Florida Statutes Compliance Dear Bob: Please

Please find enclosed the annual disclosures that satisfy the October 1, 2016 financial reporting requirements made under Section

August 30, 2017 VIA EMAIL Captain Stephen Aldrich City of Holly Hill Police Officers' Retirement Trust Fund City of Holly Hill 1065 Ridgewood Avenue Holly Hill, Florida 32117 Re: City of Holly Hill Police

August 30, 2017 VIA EMAIL Captain Stephen Aldrich City of Holly Hill Police Officers' Retirement Trust Fund City of Holly Hill 1065 Ridgewood Avenue Holly Hill, Florida 32117 Re: City of Holly Hill Police

CITY OF COCOA BEACH FIREFIGHTERS' RETIREMENT SYSTEM ACTUARIAL VALUATION REPORT PERFORMED AS OF OCTOBER 1, 2016

CITY OF COCOA BEACH FIREFIGHTERS' RETIREMENT SYSTEM ACTUARIAL VALUATION REPORT PERFORMED AS OF OCTOBER 1, 2016 WITH RESULTS APPLICABLE TO THE PLAN/FISCAL YEAR ENDED SEPTEMBER 30, 2018 November 14, 2016

CITY OF COCOA BEACH FIREFIGHTERS' RETIREMENT SYSTEM ACTUARIAL VALUATION REPORT PERFORMED AS OF OCTOBER 1, 2016 WITH RESULTS APPLICABLE TO THE PLAN/FISCAL YEAR ENDED SEPTEMBER 30, 2018 November 14, 2016

Please find enclosed the annual disclosures that satisfy the October 1, 2016 financial reporting requirements made under Section

April 17, 2017 VIA EMAIL Ms. Julie Enright, Plan Administrator City of Titusville Post Office Box 2806 Titusville, FL 32781-2806 Re: City of Titusville Police Officers' and Firefighters' Pension Plan Senate

April 17, 2017 VIA EMAIL Ms. Julie Enright, Plan Administrator City of Titusville Post Office Box 2806 Titusville, FL 32781-2806 Re: City of Titusville Police Officers' and Firefighters' Pension Plan Senate

Please find enclosed the annual disclosures that satisfy the October 1, 2014 financial reporting requirements made under Section

June 25, 2015 VIA EMAIL Ms. Ferrell Jenne, Plan Administrator Town of Indian River Shores Public Safety Officers and Firefighters Defined Benefit Plan Foster & Foster, Inc. 13420 Parker Commons Blvd.,

June 25, 2015 VIA EMAIL Ms. Ferrell Jenne, Plan Administrator Town of Indian River Shores Public Safety Officers and Firefighters Defined Benefit Plan Foster & Foster, Inc. 13420 Parker Commons Blvd.,

Please find enclosed the annual disclosures that satisfy the October 1, 2017 financial reporting requirements made under Section

March 9, 2018 VIA EMAIL Ms. Julie Enright Plan Administrator 555 S. Washington Avenue Titusville, FL 32796 Re: City of Oviedo Firefighters' Pension Trust Fund Section 112.664, Florida Statutes Compliance

March 9, 2018 VIA EMAIL Ms. Julie Enright Plan Administrator 555 S. Washington Avenue Titusville, FL 32796 Re: City of Oviedo Firefighters' Pension Trust Fund Section 112.664, Florida Statutes Compliance

Please find enclosed the annual disclosures that satisfy the October 1, 2014 financial reporting requirements made under Section

June 25, 2015 VIA EMAIL Scott Baur, Plan Administrator City of Cocoa Firefighters Retirement Plan The Resource Centers, LLC 4360 Northlake Blvd, Suite 206 Palm Beach Gardens, FL 33410 Re: Dear Scott: Senate

June 25, 2015 VIA EMAIL Scott Baur, Plan Administrator City of Cocoa Firefighters Retirement Plan The Resource Centers, LLC 4360 Northlake Blvd, Suite 206 Palm Beach Gardens, FL 33410 Re: Dear Scott: Senate

AUSTIN POLICE RETIREMENT SYSTEM ACTUARIAL VALUATION AS OF DECEMBER 31, 2016

AUSTIN POLICE RETIREMENT SYSTEM ACTUARIAL VALUATION AS OF DECEMBER 31, 2016 July 26, 2017 Ms. Pattie Featherston, Executive Director Austin Police Retirement System 20 South IH 35, Suite 100 Austin, TX

AUSTIN POLICE RETIREMENT SYSTEM ACTUARIAL VALUATION AS OF DECEMBER 31, 2016 July 26, 2017 Ms. Pattie Featherston, Executive Director Austin Police Retirement System 20 South IH 35, Suite 100 Austin, TX

Town of Longboat Key Consolidated Retirement System (Police Officers) Senate Bill 534 (Section , Florida Statutes) Compliance

Senate Bill 534 (Section , Florida Statutes) Compliance") July 27, 2016 VIA EMAIL Ms. Susan Smith Town of Longboat Key 501 Bay Isles Road Longboat Key, Florida 34228 Re: Town of Longboat Key Consolidated Retirement System (Police Officers) Senate Bill 534 (Section

July 27, 2016 VIA EMAIL Ms. Susan Smith Town of Longboat Key 501 Bay Isles Road Longboat Key, Florida 34228 Re: Town of Longboat Key Consolidated Retirement System (Police Officers) Senate Bill 534 (Section

Please find enclosed the annual disclosures that satisfy the October 1, 2017 financial reporting requirements made under Section

January 8, 2018 VIA EMAIL Ms. Lauren Boatwright Trust Manager Trustmark National Bank P.O. Box 469 Brewton, AL 36427 Re: City of Lynn Haven Police Officers' Retirement System Section 112.664, Florida Statutes

January 8, 2018 VIA EMAIL Ms. Lauren Boatwright Trust Manager Trustmark National Bank P.O. Box 469 Brewton, AL 36427 Re: City of Lynn Haven Police Officers' Retirement System Section 112.664, Florida Statutes

Please find enclosed the annual disclosures that satisfy the October 1, 2017 financial reporting requirements made under Section

January 8, 2018 VIA EMAIL Lt. Darrell Hernandez, Secretary City of Lynn Haven Firefighters' Pension Board 1412 Pennsylvania Avenue Lynn Haven, FL 32444-2398 Re: City of Lynn Haven Firefighters' Retirement

January 8, 2018 VIA EMAIL Lt. Darrell Hernandez, Secretary City of Lynn Haven Firefighters' Pension Board 1412 Pennsylvania Avenue Lynn Haven, FL 32444-2398 Re: City of Lynn Haven Firefighters' Retirement

Please find enclosed the annual disclosures that satisfy the October 1, 2017 financial reporting requirements made under Section

May 7, 2018 VIA EMAIL Captain Dave Foxall, Administrator Bradenton Firefighters Retirement System 1010 9th Avenue West Bradenton, FL 34205 Re: City of Bradenton Firefighters' Retirement System Section

May 7, 2018 VIA EMAIL Captain Dave Foxall, Administrator Bradenton Firefighters Retirement System 1010 9th Avenue West Bradenton, FL 34205 Re: City of Bradenton Firefighters' Retirement System Section

Please find enclosed the annual disclosures that satisfy the October 1, 2016 financial reporting requirements made under Section

May 8, 2017 VIA EMAIL Carol Godwin, Budget and Grants Analyst City of Fort Walton Beach General Retirement Fund 107 Miracle Strip Parkway, SW Fort Walton Beach, FL 32548 Re: City of Fort Walton Beach General

May 8, 2017 VIA EMAIL Carol Godwin, Budget and Grants Analyst City of Fort Walton Beach General Retirement Fund 107 Miracle Strip Parkway, SW Fort Walton Beach, FL 32548 Re: City of Fort Walton Beach General

Please find enclosed the annual disclosures that satisfy the October 1, 2017 financial reporting requirements made under Section

April 20, 2018 VIA EMAIL Sheila Hutcheson, Plan Administrator 3860 Grantline Road Mims, FL 32754 Re: City of Cocoa General Employees' Retirement Plan Section 112.664, Florida Statutes Compliance Dear Sheila:

April 20, 2018 VIA EMAIL Sheila Hutcheson, Plan Administrator 3860 Grantline Road Mims, FL 32754 Re: City of Cocoa General Employees' Retirement Plan Section 112.664, Florida Statutes Compliance Dear Sheila:

CITY OF HAINES CITY GENERAL EMPLOYEES' PENSION PLAN SECTION , FLORIDA STATUTES COMPLIANCE

CITY OF HAINES CITY GENERAL EMPLOYEES' PENSION PLAN SECTION 112.664, FLORIDA STATUTES COMPLIANCE With respect to the reporting standards for defined benefit retirement plans or systems contained in Section

CITY OF HAINES CITY GENERAL EMPLOYEES' PENSION PLAN SECTION 112.664, FLORIDA STATUTES COMPLIANCE With respect to the reporting standards for defined benefit retirement plans or systems contained in Section

DALLAS AREA RAPID TRANSIT (DART) EMPLOYEES DEFINED BENEFIT RETIREMENT PLAN ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2015

EMPLOYEES DEFINED BENEFIT RETIREMENT PLAN ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2015") DALLAS AREA RAPID TRANSIT (DART) EMPLOYEES DEFINED BENEFIT RETIREMENT PLAN ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2015 CONTRIBUTIONS APPLICABLE TO THE PLAN/FISCAL YEAR ENDING SEPTEMBER 30, 2016 March

DALLAS AREA RAPID TRANSIT (DART) EMPLOYEES DEFINED BENEFIT RETIREMENT PLAN ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2015 CONTRIBUTIONS APPLICABLE TO THE PLAN/FISCAL YEAR ENDING SEPTEMBER 30, 2016 March

CITY OF WINTER GARDEN PENSION PLAN FOR FIREFIGHTERS AND POLICE OFFICERS SECTION , FLORIDA STATUTES COMPLIANCE

CITY OF WINTER GARDEN PENSION PLAN FOR FIREFIGHTERS AND POLICE OFFICERS SECTION 112.664, FLORIDA STATUTES COMPLIANCE With respect to the reporting standards for defined benefit retirement plans or systems

CITY OF WINTER GARDEN PENSION PLAN FOR FIREFIGHTERS AND POLICE OFFICERS SECTION 112.664, FLORIDA STATUTES COMPLIANCE With respect to the reporting standards for defined benefit retirement plans or systems

DALLAS AREA RAPID TRANSIT (DART) EMPLOYEES DEFINED BENEFIT RETIREMENT PLAN ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2016

EMPLOYEES DEFINED BENEFIT RETIREMENT PLAN ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2016") DALLAS AREA RAPID TRANSIT (DART) EMPLOYEES DEFINED BENEFIT RETIREMENT PLAN ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2016 CONTRIBUTIONS APPLICABLE TO THE PLAN/FISCAL YEAR ENDING SEPTEMBER 30, 2017 February

DALLAS AREA RAPID TRANSIT (DART) EMPLOYEES DEFINED BENEFIT RETIREMENT PLAN ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2016 CONTRIBUTIONS APPLICABLE TO THE PLAN/FISCAL YEAR ENDING SEPTEMBER 30, 2017 February

CITY OF EVANSTON POLICE PENSION FUND ACTUARIAL VALUATION AS OF JANUARY 1, 2016

CITY OF EVANSTON POLICE PENSION FUND ACTUARIAL VALUATION AS OF JANUARY 1, 2016 CONTRIBUTIONS APPLICABLE TO THE PLAN/FISCAL YEAR ENDED DECEMBER 31, 2016 September 16, 2016 Board of Trustees City of Evanston

CITY OF EVANSTON POLICE PENSION FUND ACTUARIAL VALUATION AS OF JANUARY 1, 2016 CONTRIBUTIONS APPLICABLE TO THE PLAN/FISCAL YEAR ENDED DECEMBER 31, 2016 September 16, 2016 Board of Trustees City of Evanston

CITY OF CAPE CORAL MUNICIPAL FIREFIGHTERS' RETIREMENT PLAN SECTION , FLORIDA STATUTES COMPLIANCE

CITY OF CAPE CORAL MUNICIPAL FIREFIGHTERS' RETIREMENT PLAN SECTION 112.664, FLORIDA STATUTES COMPLIANCE With respect to the reporting standards for defined benefit retirement plans or systems contained

CITY OF CAPE CORAL MUNICIPAL FIREFIGHTERS' RETIREMENT PLAN SECTION 112.664, FLORIDA STATUTES COMPLIANCE With respect to the reporting standards for defined benefit retirement plans or systems contained

CITY OF ST. PETE BEACH FIREFIGHTERS RETIREMENT SYSTEM ACTUARIAL IMPACT STATEMENT #2 (MEMBERS USE EXCESS STATE MONIES RESERVE) March 14, 2017

March 14, 2017") CITY OF ST. PETE BEACH FIREFIGHTERS RETIREMENT SYSTEM ACTUARIAL IMPACT STATEMENT #2 (MEMBERS USE EXCESS STATE MONIES RESERVE) March 14, 2017 Attached hereto is a comparison of the impact on the Total Required