Social Security Basics

|

|

|

- Alexander Rich

- 5 years ago

- Views:

Transcription

1 Savvy Social Security Planning for Boomers Orientation Series Social Security Basics By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC 1

2 Key things to know How benefits are calculated 2

3 Key things to know How benefits are calculated Effect of early or delayed claiming 3

4 Key things to know How benefits are calculated Effect of early or delayed claiming Rules for spouses & divorced spouses 4

5 Key things to know How benefits are calculated Effect of early or delayed claiming Rules for spouses & divorced spouses Rules for widows and widowers 5

6 Key things to know How benefits are calculated Effect of early or delayed claiming Rules for spouses & divorced spouses Rules for widows and widowers How working affects benefits 6

7 Key things to know How benefits are calculated Effect of early or delayed claiming Rules for spouses & divorced spouses Rules for widows and widowers How working affects benefits How COLAs affect benefits 7

8 Key things to know How benefits are calculated Effect of early or delayed claiming Rules for spouses & divorced spouses Rules for widows and widowers How working affects benefits How COLAs affect benefits Taxation of benefits 8

9 Key things to know Windfall Elimination Provision & Government Pension Offset 9

10 Key things to know Windfall Elimination Provision & Government Pension Offset Medicare 10

11 Key things to know Windfall Elimination Provision & Government Pension Offset Medicare Solvency issues and reform proposals 11

12 How benefits are calculated Pages of the Financial Advisor s Guide to Savvy Social Security Planning for Boomers 12

13 How benefits are calculated Steps in calculating primary insurance amount or PIA (SSA does this; you don t) 1. Tally each year's earnings on which Social Security taxes were paid 13

14 How benefits are calculated Steps in calculating primary insurance amount or PIA (SSA does this; you don t) 1. Tally each year's earnings on which Social Security taxes were paid 2. Apply index factor to each year's earnings (varies with age) 14

15 How benefits are calculated Steps in calculating primary insurance amount or PIA (SSA does this; you don t) 1. Tally each year's earnings on which Social Security taxes were paid 2. Apply index factor to each year's earnings (varies with age) 3. Take 35 highest years' earnings and find the total 15

16 How benefits are calculated Steps in calculating primary insurance amount or PIA (SSA does this; you don t) 1. Tally each year's earnings on which Social Security taxes were paid 2. Apply index factor to each year's earnings (varies with age) 3. Take 35 highest years' earnings and find the total 4. Divide total by 420 (the number of months in 35 years) 16

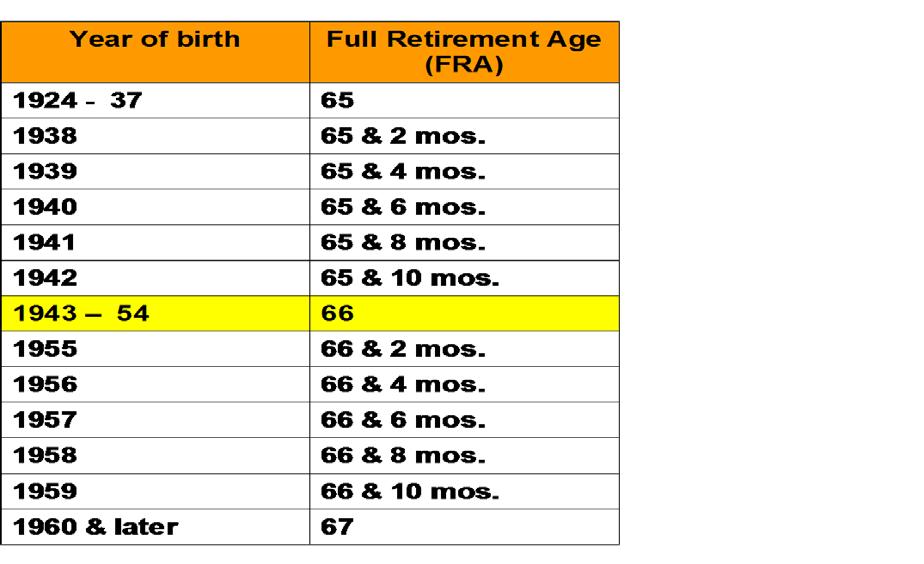

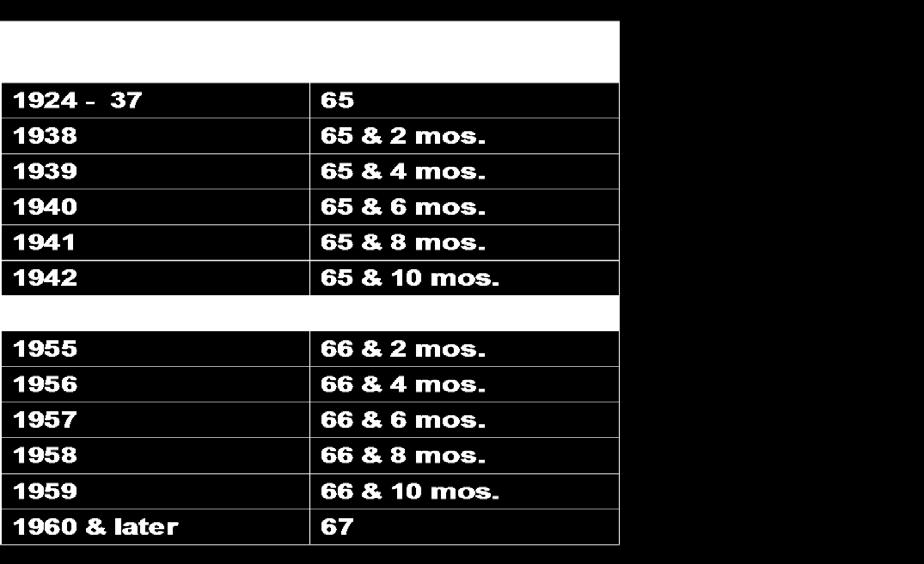

17 How benefits are calculated Steps in calculating primary insurance amount or PIA (SSA does this; you don t) 1. Tally each year's earnings on which Social Security taxes were paid 2. Apply index factor to each year's earnings (varies with age) 3. Take 35 highest years' earnings and find the total 4. Divide total by 420 (the number of months in 35 years) 5. Result is AIME, or average indexed monthly earnings 17

18 How benefits are calculated Steps in calculating primary insurance amount or PIA (SSA does this; you don t) 1. Tally each year's earnings on which Social Security taxes were paid 2. Apply index factor to each year's earnings (varies with age) 3. Take 35 highest years' earnings and find the total 4. Divide total by 420 (the number of months in 35 years) 5. Result is AIME, or average indexed monthly earnings 6. Apply formula to AIME: multiply "bend points" by 90%, 32%, and 15% 18

19 How benefits are calculated Steps in calculating primary insurance amount or PIA (SSA does this; you don t) 1. Tally each year's earnings on which Social Security taxes were paid 2. Apply index factor to each year's earnings (varies with age) 3. Take 35 highest years' earnings and find the total 4. Divide total by 420 (the number of months in 35 years) 5. Result is AIME, or average indexed monthly earnings 6. Apply formula to AIME: multiply "bend points" by 90%, 32%, and 15% 7. Total = PIA 19

20 Benefits based on highest 35 years of earnings up to taxable maximum Maximum Taxable Social Security Earnings Year Max earnings Year Max earnings Year Max earnings 1968 $7, $37, $76, $7, $39, $80, $7, $42, $84, $7, $43, $87, $9, $45, $87, $10, $48, $90, $13, $51, $94, $14, $53, $97, $15, $55, $102, $16, $57, $106, $17, $60, $106, $22, $61, $106, $25, $72, $110, $29, $65, $113, $32, $68, $117, $35, $72, $118,500 Social Security Administration 20

21 Average Indexed Monthly Earnings (AIME) for baby boomer born in 1954 Maximum earnings since 1976 $3,961,077 in total indexed earnings 420 months = $9,431 AIME 21

22 Primary Insurance Amount (PIA) Baby Boomer born in 1954 Maximum Social Security earnings every year since age 22 AIME = $9,431 PIA formula: $856 x.90 = $ $4,301 x.32 = $1, ($5,157 - $856 = $4,301) $4,274 x.15 = $ ($9,431 - $5,157 = $4,274) Total = $2, PIA = $2, Amount worker will receive at full retirement age 22

23 Effect of early or delayed claiming Pages of the Financial Advisor s Guide to Savvy Social Security Planning for Boomers 23

24 Full retirement age 24

25 Effect of early or delayed claiming Benefit for baby boomer born Age % of PIA Benefit if PIA is $2,700* , , ⅔ 2, ⅓ 2, , , , , ,564 *Not counting cost-of-living adjustments 25

26 Effect of early or delayed claiming Benefit for baby boomer born Age % of PIA Benefit if PIA is $2,700 Benefit with 2.7% COLAs ,025 2, ,160 2, ⅔ 2,340 2, ⅓ 2,520 2, ,700 3, ,916 3, ,132 3, ,348 4, ,564 4,411 26

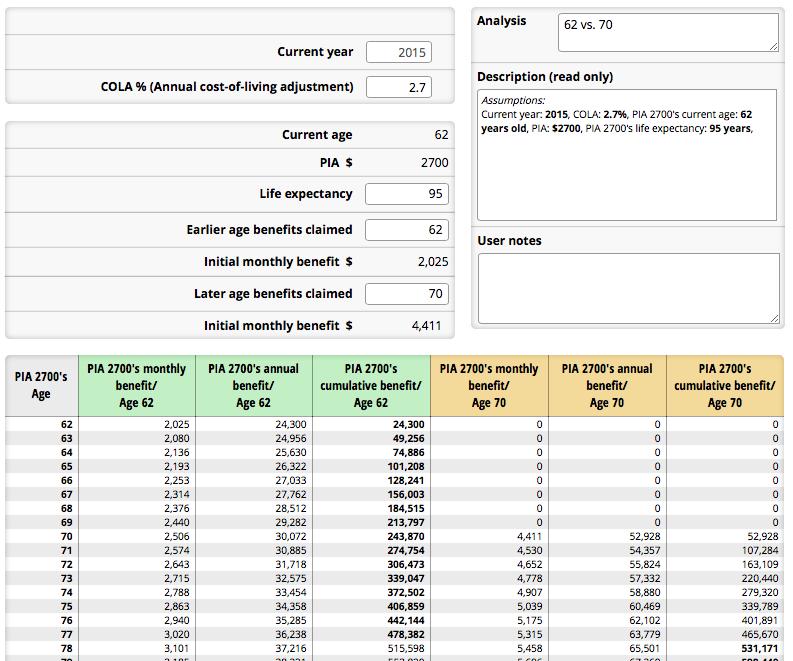

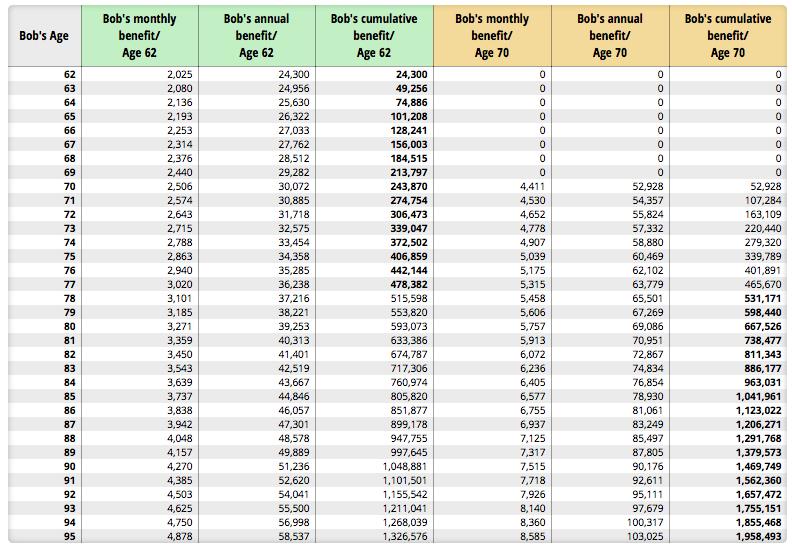

27 Two ways to analyze claiming decision Breakeven age Relative income 27

28 How to analyze claiming decision Breakeven age Considers cumulative benefits under two claiming scenarios 28

29 How to analyze claiming decision Breakeven age Considers cumulative benefits under two claiming scenarios Calculates catch-up age at which cumulative benefits from later-claiming scenario overtake cumulative benefits from early-claiming scenario 29

30 How to analyze claiming decision Breakeven age Considers cumulative benefits under two claiming scenarios Calculates catch-up age at which cumulative benefits from later-claiming scenario overtake cumulative benefits from early-claiming scenario Views Social Security as an asset 30

31 31

32 How to analyze claiming decision Relative income Considers relative income under two claiming scenarios 32

33 How to analyze claiming decision Relative income Considers relative income under two claiming scenarios Compares income at an advanced age (say, 85) under early vs. late claiming scenarios 33

34 Income How to analyze claiming decision Considers relative income under two claiming scenarios Compares income at an advanced age (say, 85) under early vs. late claiming scenarios Views Social Security as longevity insurance 34

35 35

36 Rules for spouses Pages 51-52, 81-93, of the Financial Advisor s Guide to Savvy Social Security Planning for Boomers 36

37 Rules for spouses Traditional: Nonworking wife receives 50% of husband s PIA if she applies at FRA (or 35% at 62) 37

38 Rules for spouses Traditional: Nonworking wife receives 50% of husband s PIA if she applies at FRA (or 35% at 62) If wife has own earnings, and if she applies before FRA, she ll receive her own reduced benefit first. If spousal benefit is higher, an amount will be added so combined benefit equals spousal benefit. If spousal benefit is not higher, she will not be paid a spousal benefit. 38

39 Rules for spouses Traditional: Nonworking wife receives 50% of husband s PIA if she applies at FRA (or 35% at 62) If wife has own earnings, and if she applies before FRA, she ll receive her own reduced benefit first. If spousal benefit is higher, an amount will be added so combined benefit equals spousal benefit. If spousal benefit is not higher, she will not be paid a spousal benefit. If application is made after FRA, a spouse can choose to receive own or spousal benefit (i.e., can restrict application to spousal benefit and let own benefit build delayed credits. Budget Act update: must be born before 1954 to file restricted application) 39

40 Rules for spouses Traditional: Nonworking wife receives 50% of husband s PIA if she applies at FRA (or 35% at 62) If wife has own earnings, and if she applies before FRA, she ll receive her own reduced benefit first. If spousal benefit is higher, an amount will be added so combined benefit equals spousal benefit. If spousal benefit is not higher, she will not be paid a spousal benefit. If application is made after FRA, a spouse can choose to receive own or spousal benefit (i.e., can restrict application to spousal benefit and let own benefit build delayed credits. Budget Act update: must be born before 1954 to file restricted application.) Husband must file for benefits in order for wife to receive spousal benefit (and vice versa) 40

41 Rules for spouses Traditional: Nonworking wife receives 50% of husband s PIA if she applies at FRA (or 35% at 62) If wife has own earnings, and if she applies before FRA, she ll receive her own reduced benefit first. If spousal benefit is higher, an amount will be added so combined benefit equals spousal benefit. If spousal benefit is not higher, she will not be paid a spousal benefit. If application is made after FRA, a spouse can choose to receive own or spousal benefit (i.e., can restrict application to spousal benefit and let own benefit build delayed credits. Budget Act update: must be born before 1954 to file restricted application.) Husband must file for benefits in order for wife to receive spousal benefit (and vice versa) No delayed credits for spousal benefits 41

42 Rules for spouses Key takeaway: Coordination of spousal benefits is extremely complex. Better to work with actual cases than try to apply rules of thumb. (Estimate benefit amounts and use Spousal Planning Calculator) 42

43 Strategies from the Center for Retirement Research at Boston College File and suspend Claim now claim more later 43

44 Strategies from the Center for Retirement Research at Boston College File and suspend High-earning husband files for own benefit at 66 to make wife eligible for her spousal benefit 44

45 Strategies from the Center for Retirement Research at Boston College File and suspend High-earning husband files for own benefit at 66 to make wife eligible for her spousal benefit Husband suspends own benefit to earn DRCs to age 70 45

46 Strategies from the Center for Retirement Research at Boston College File and suspend High-earning husband files for own benefit at 66 to make wife eligible for her spousal benefit Husband suspends own benefit to earn DRCs to age 70 Budget Act update: No spousal or dependent benefits payable on a benefit suspended after April 30,

47 Example of file and suspend Jack and Jill are both

48 Example of file and suspend Jack and Jill are both 66. Jack s PIA = $2,000. He plans to delay his benefit to age

49 Example of file and suspend Jack and Jill are both 66. Jack s PIA = $2,000. He plans to delay his benefit to age 70. JilI s PIA = $800. She wants to start benefits now. 49

50 Example of file and suspend Jack and Jill are both 66. Jack s PIA = $2,000. He plans to delay his benefit to age 70. JilI s PIA = $800. She wants to start benefits now. If Jill files for Social Security, she will receive her own benefit of $800 per month. She is not eligible for a spousal benefit because Jack hasn t filed. 50

51 Example of file and suspend Jack and Jill are both 66. Jack s PIA = $2,000. He plans to delay his benefit to age 70. JilI s PIA = $800. She wants to start benefits now. If Jill files for Social Security, she will receive her own benefit of $800 per month. She is not eligible for a spousal benefit because Jack hasn t filed. So Jack files and suspends (before April 30, 2016). Jill files for her spousal benefit and receives $1,000 per month. 51

52 Example of file and suspend Jack and Jill are both 66. Jack s PIA = $2,000. He plans to delay his benefit to age 70. JilI s PIA = $800. She wants to start benefits now. If Jill files for Social Security, she will receive her own benefit of $800 per month. She is not eligible for a spousal benefit because Jack hasn t filed. So Jack files and suspends (before April 30, 2016). Jill files for her spousal benefit and receives $1,000 per month. When Jack turns 70 he resumes his benefit and receives 4 years worth of 8% annual delayed credits, or $2,640 per month 52

53 Strategies from the Center for Retirement Research at Boston College Claim now, claim more later or restricted application High-earning husband files a restricted application for his spousal benefit at 66 (wife must have filed for her own benefit) 53

54 Strategies from the Center for Retirement Research at Boston College Claim now, claim more later High-earning husband files a restricted application for his spousal benefit at 66 (wife must have filed for her own benefit) Husband switches to his own benefit at 70 54

55 Strategies from the Center for Retirement Research at Boston College Claim now, claim more later High-earning husband files a restricted application for his spousal benefit at 66 (wife must have filed for her own benefit) Husband switches to his own benefit at 70 Budget Act Update: Restricted application available only to spouses born before

56 Example of claim now, claim more later Dan and Dora are both 66 56

57 Example of claim now, claim more later Dan and Dora are both 66 Dan s PIA is $2,000. He wants to delay benefits to age

58 Example of claim now, claim more later Dan and Dora are both 66 Dan s PIA is $2,000. He wants to delay benefits to age 70 Dora s PIA is $1,800. She wants to start benefits now. 58

59 Example of claim now, claim more later Dan and Dora are both 66 Dan s PIA is $2,000. He wants to delay benefits to age 70 Dora s PIA is $1,800. She wants to start benefits now Dora files for her benefit and receives $1,800 per month. 59

60 Example of claim now, claim more later Dan and Dora are both 66 Dan s PIA is $2,000. He wants to delay benefits to age 70 Dora s PIA is $1,800. She wants to start benefits now Dora files for her benefit and receives $1,800 per month Dan files for his spousal benefit and receives $900 per month. 60

61 Example of claim now, claim more later Dan and Dora are both 66 Dan s PIA is $2,000. He wants to delay benefits to age 70 Dora s PIA is $1,800. She wants to start benefits now Dora files for her benefit and receives $1,800 per month Dan files for his spousal benefit and receives $900 per month When Dan turns 70 he switches to his maximum benefit of $2,640 per month. 61

62 Rules for divorced spouses Page 53, 97-98, of the Financial Advisor s Guide to Savvy Social Security Planning for Boomers 62

63 Rules for divorced spouses Same rules as for spousal benefits if applicant: Is at least 62 63

64 Rules for divorced spouses Same rules as for spousal benefits if applicant: Is at least 62 Was married to worker at least 10 years 64

65 Rules for divorced spouses Same rules as for spousal benefits if applicant: Is at least 62 Was married to worker at least 10 years Is currently unmarried 65

66 Rules for divorced spouses Same rules as for spousal benefits if applicant: Is at least 62 Was married to worker at least 10 years Is currently unmarried Former spouse must be at least 62 (does not need to have filed for benefits if divorce occurred more than two years ago) 66

67 Rules for divorced spouses Same rules as for spousal benefits if applicant: Is at least 62 Was married to worker at least 10 years Is currently unmarried Former spouse must be at least 62 (does not need to have filed for benefits if divorce occurred more than two years ago) Worker s own benefit (and benefits for current spouse) not affected 67

68 Rules for divorced spouses Same rules as for spousal benefits if applicant: Is at least 62 Was married to worker at least 10 years Is currently unmarried Former spouse must be at least 62 (does not need to have filed for benefits if divorce occurred more than two years ago) Worker s own benefit (and benefits for current spouse) not affected Strategy for divorced clients: Receive divorced-spouse benefit from while delaying own benefit (Budget Act update: must have been born before 1954) 68

69 Rules for divorced spouses Key takeaway: Ask about former marriages. Integrate divorced-spouse benefits into the planning 69

70 Rules for widows and widowers Pages 92-93, of the Financial Advisor s Guide to Savvy Social Security Planning for Boomers 70

71 Rules for widows and widowers Survivor benefit = 100% of deceased spouse's benefit including delayed credits (even if benefit is unclaimed due to delaying to 70) 71

72 Rules for widows and widowers Survivor benefit = 100% of deceased spouse's benefit including delayed credits (even if benefit is unclaimed due to delaying to 70) Can apply for survivor benefit at age 60 but benefit will be reduced; widows should be encouraged to file at 66 to maximize income in old age (can receive own benefit from 62 to 66 if qualify) 72

73 Rules for widows and widowers Survivor benefit = 100% of deceased spouse's benefit including delayed credits (even if benefit is unclaimed due to delaying to 70) Can apply for survivor benefit at age 60 but benefit will be reduced; widows should be encouraged to file at 66 to maximize income in old age (can receive own benefit from 62 to 66 if qualify) Remarriage before age 60 negates survivor benefit unless that marriage ends 73

74 Rules for widows and widowers Survivor benefit = 100% of deceased spouse's benefit including delayed credits (even if benefit is unclaimed due to delaying to 70) Can apply for survivor benefit at age 60 but benefit will be reduced; widows should be encouraged to file at 66 to maximize income in old age (can receive own benefit from 62 to 66 if qualify) Remarriage before age 60 negates survivor benefit unless that marriage ends Strategy for high-earning widow(ers): Take survivor benefit at 60 and switch to maximum earned benefit at 70 (earnings test applies before FRA) 74

75 Rules for widows and widowers Key takeaways: High-earning spouse should delay to age 70 in order to maximize survivor benefit. Coordinate survivor and earned benefits for widow(er)s entitled to both. 75

76 How working affects benefits Pages 53-54, of the Financial Advisor s Guide to Savvy Social Security Planning for Boomers 76

77 How working affects benefits Earnings test if under FRA: $1 in benefits withheld for every $2 earned over $15,720 in

78 How working affects benefits Earnings test if under FRA: $1 in benefits withheld for every $2 earned over $15,720 in 2016 Earnings test in year attain FRA, in months before birth month: $1 in benefits withheld for every $3 earned over $41,880 in

79 How working affects benefits Earnings test if under FRA: $1 in benefits withheld for every $2 earned over $15,720 in 2016 Earnings test in year attain FRA, in months before birth month: $1 in benefits withheld for every $3 earned over $41,880 in 2016 Earnings test applies to all benefits -- retirement, spousal, survivor -- while under FRA 79

80 How working affects benefits Earnings test if under FRA: $1 in benefits withheld for every $2 earned over $15,720 in 2016 Earnings test in year attain FRA, in months before birth month: $1 in benefits withheld for every $3 earned over $41,880 in 2016 Earnings test applies to all benefits -- retirement, spousal, survivor -- while under FRA At FRA benefit will be adjusted to remove actuarial reduction for months in which benefit was withheld 80

81 How working affects benefits Earnings test if under FRA: $1 in benefits withheld for every $2 earned over $15,720 in 2016 Earnings test in year attain FRA, in months before birth month: $1 in benefits withheld for every $3 earned over $41,880 in 2016 Earnings test applies to all benefits -- retirement, spousal, survivor -- while under FRA At FRA benefit will be adjusted to remove actuarial reduction for months in which benefit was withheld After FRA no reduction in benefits for working 81

82 How working affects benefits Earnings test if under FRA: $1 in benefits withheld for every $2 earned over $15,720 in 2016 Earnings test in year attain FRA, in months before birth month: $1 in benefits withheld for every $3 earned over $41,880 in 2016 Earnings test applies to all benefits -- retirement, spousal, survivor -- while under FRA At FRA benefit will be adjusted to remove actuarial reduction for months in which benefit was withheld After FRA no reduction in benefits for working Don't confuse reduction of benefits with taxation of benefits 82

83 How working affects benefits Key takeaway: Consider client s earnings when deciding when to apply 83

84 How COLAs affect benefits Pages 54-55, of the Financial Advisor s Guide to Savvy Social Security Planning for Boomers 84

85 How COLAs affect benefits Cost-of-living adjustment announced in October; affects benefits received in January 85

86 How COLAs affect benefits Cost-of-living adjustment announced in October; affects benefits received in January COLAs based on CPI-W from 4 th quarter of one year through 3 rd quarter of next 86

87 How COLAs affect benefits Cost-of-living adjustment announced in October; affects benefits received in January COLAs based on CPI-W from 4 th quarter of one year through 3 rd quarter of next COLA for 2016: 0% 87

88 How COLAs affect benefits Cost-of-living adjustment announced in October; affects benefits received in January COLAs based on CPI-W from 4 th quarter of one year through 3 rd quarter of next COLA for 2016: 0% For long-term planning, trustees estimate annual COLAs of 2.7% 88

89 How COLAs affect benefits Key takeaway: COLAs magnify impact of early or delayed benefits. (See Calculators) 89

90 Taxation of benefits Pages of the Financial Advisor s Guide to Savvy Social Security Planning for Boomers 90

91 Taxation of Social Security benefits Filing status Provisional income* Amount of SS subject to tax Married filing jointly Under $32,000 $32,000 - $44,000 Over $44,000 0 Up to 50% Up to 85% Single, head of household, qualifying widow(er), married filing separately & living apart from spouse Under $25,000 $25,000 - $34,000 Over $34,000 0 Up to 50% Up to 85% Married filing separately and living with spouse Over 0 Up to 85% *Provisional income = AGI + one-half of SS benefit + tax-exempt interest 91

92 Taxation of benefits Key takeaway: Consider taxation of benefits when deciding when to apply. May be better to delay Social Security and draw from IRAs and other resources first. Engage tax advisor for complete tax analysis. 92

93 Windfall Elimination Provision Pages of the Financial Advisor s Guide to Savvy Social Security Planning for Boomers 93

94 Windfall Elimination Provision If client worked in non-social Security covered job, Social Security benefit may be reduced 94

95 Windfall Elimination Provision If client worked in non-social Security covered job, Social Security benefit may be reduced First bend point reduced to 40%-90% depending on how long worked in Social Security-covered job (no reduction if 30 years of substantial earnings; see table on page 56) 95

96 Windfall Elimination Provision If client worked in non-social Security covered job, Social Security benefit may be reduced First bend point reduced to 40%-90% depending on how long worked in Social Security-covered job (no reduction if 30 years of substantial earnings; see table on page 56) Maximum WEP reduction for person turning 62 in 2016: $428 96

97 Windfall Elimination Provision If client worked in non-social Security covered job, Social Security benefit may be reduced First bend point reduced to 40%-90% depending on how long worked in Social Security-covered job (no reduction if 30 years of substantial earnings; see table on page 56) Maximum WEP reduction for person turning 62 in 2016: $428 Key takeaway: Always ask clients about work history and prepare for WEP reduction if main career was in non Social Security-covered job (most common: civil service, teachers & health care workers who opted out of Social Security) 97

98 Government Pension Offset Pages 57 and 93 of the Financial Advisor s Guide to Savvy Social Security Planning for Boomers 98

99 Government Pension Offset Similar to WEP but affects spousal and survivor benefits if wife (or husband) receives a pension from non Social Security-covered job 99

100 Government Pension Offset Similar to WEP but affects spousal and survivor benefits if wife (or husband) receives a pension from non Social Security-covered job Spousal/survivor benefit reduced by two-thirds of the amount of the pension 100

101 Government Pension Offset Similar to WEP but affects spousal and survivor benefits if wife (or husband) receives a pension from non Social Security-covered job Spousal/survivor benefit reduced by two-thirds of the amount of the pension Example: wife (or husband) receives $3,000/month pension from teaching job. Any spousal or survivor benefits she/he may be entitled to will be reduced by $2,000 (two-thirds of $3,000) 101

102 Government Pension Offset Similar to WEP but affects spousal and survivor benefits if wife (or husband) receives a pension from non Social Security-covered job Spousal/survivor benefit reduced by two-thirds of the amount of the pension Example: wife (or husband) receives $3,000/month pension from teaching job. Any spousal or survivor benefits she/he may be entitled to will be reduced by $2,000 (two-thirds of $3,000) Key takeaway: Always ask about work history and pensions from non Social Security-covered jobs. Prepare clients for GPO reduction when estimating benefits. 102

103 Medicare Pages of the Financial Advisor s Guide to Savvy Social Security Planning for Boomers 103

104 Medicare starts at age 65 Medicare 104

105 Medicare Medicare starts at age 65 If already receiving Social Security, Medicare is automatic 105

106 Medicare Medicare starts at age 65 If already receiving Social Security, Medicare is automatic If delaying benefits, should apply for Medicare 3 months prior to 65 th birthday; if fail to apply by 4 th month after 65 th birthday, penalty will be added to Part B premium 106

107 Medicare Medicare starts at age 65 If already receiving Social Security, Medicare is automatic If delaying benefits, should apply for Medicare 3 months prior to 65 th birthday; if fail to apply by 4 th month after 65 th birthday, penalty will be added to Part B premium If still working and covered by employer plan (or spouse's group plan) that covers 20 or more employees, can delay applying for Medicare with no penalty 107

108 Medicare Medicare starts at age 65 If already receiving Social Security, Medicare is automatic If delaying benefits, should apply for Medicare 3 months prior to 65 th birthday; if fail to apply by 4 th month after 65 th birthday, penalty will be added to Part B premium If still working and covered by employer plan (or spouse's group plan), can delay applying for Medicare with no penalty Medicare involves deductibles and copayments and does not cover everything; supplemental insurance may be necessary 108

109 Medicare Medicare starts at age 65 If already receiving Social Security, Medicare is automatic If delaying benefits, should apply for Medicare 3 months prior to 65 th birthday; if fail to apply by 4 th month after 65 th birthday, penalty will be added to Part B premium If still working and covered by employer plan (or spouse's group plan), can delay applying for Medicare Medicare involves deductibles and copayments and does not cover everything; supplemental insurance may be necessary Medicare does not cover long-term care 109

110 Medicare Key takeaway: Every boomer needs a crash course in Medicare in order to avoid penalties, take advantage of benefits, and purchase additional coverage as needed. 110

111 Solvency issues and reform proposals Pages of the Financial Advisor s Guide to Savvy Social Security Planning for Boomers 111

112 Solvency issues and reform proposals According to the 2015 trustees report released in July 2015: The OASDI trust fund currently holds $2.7 trillion in special-issue Treasury securities 112

113 Solvency issues and reform proposals According to the 2015 trustees report released in July 2015: The OASDI trust fund currently holds $2.7 trillion in special-issue Treasury securities In 2014, total income was $884 billion, total expenses were $859 billion for an increase to the trust fund of $25 billion 113

114 Solvency issues and reform proposals According to the 2015 trustees report released in July 2015: The OASDI trust fund currently holds $2.7 trillion in special-issue Treasury securities In 2014, total income was $884 billion, total expenses were $859 billion for an increase to the trust fund of $25 billion Income is expected to exceed costs until

115 Solvency issues and reform proposals According to the 2015 trustees report released in July 2015: The OASDI trust fund currently holds $2.7 trillion in special-issue Treasury securities In 2014, total income was $884 billion, total expenses were $859 billion for an increase to the trust fund of $25 billion Income is expected to exceed costs until 2022 Starting in 2022, trust fund Treasury securities will begin to be liquidated 115

116 Solvency issues and reform proposals According to the 2015 trustees report released in July 2015: The OASDI trust fund currently holds $2.7 trillion in special-issue Treasury securities In 2014, total income was $884 billion, total expenses were $859 billion for an increase to the trust fund of $25 billion Income is expected to exceed costs until 2022 Starting in 2022, trust fund Treasury securities will begin to be liquidated By 2034 trust fund will be exhausted; income will be enough to pay 79% of promised benefits 116

117 Solvency issues and reform proposals According to the 2015 trustees report released in July 2015: The OASDI trust fund currently holds $2.7 trillion in special-issue Treasury securities In 2014, total income was $884 billion, total expenses were $859 billion for an increase to the trust fund of $25 billion Income is expected to exceed costs until 2022 Starting in 2022, trust fund Treasury securities will begin to be liquidated By 2034 trust fund will be exhausted; income will be enough to pay 79% of promised benefits Numbers are revised each year as actual experience and assumptions change 117

118 Solvency issues and reform proposals According to the 2015 trustees report released in July 2015: The OASDI trust fund currently holds $2.7 trillion in special-issue Treasury securities In 2014, total income was $884 billion, total expenses were $859 billion for an increase to the trust fund of $25 billion Income is expected to exceed costs until 2022 Starting in 2022, trust fund Treasury securities will begin to be liquidated By 2034 trust fund will be exhausted; income will be enough to pay 79% of promised benefits Numbers are revised each year as actual experience and assumptions change Social Security reform may include raising payroll taxes on high-income workers, raising the retirement age, revising the formula for future benefits, changing the COLA formula, or some combination of these 118

119 Where to go for more information 119

120 Where to go for more information See list of articles and papers in Appendix B 120

121 Where to go for more information See list of articles and papers in Appendix B Watch your for biweekly newsletter 121

122 Where to go for more information See list of articles and papers in Appendix B Watch your for biweekly newsletter Read all previous newsletters posted on (Note: newsletters prior to Nov. 2, 2015 were written under the old rules) 122

123 Where to go for more information See list of articles and papers in Appendix B Watch your for weekly newsletter Read all previous newsletters posted on (Note: newsletters prior to Nov. 2, 2015 were written under the old rules) Post questions on 123

124 Where to go for more information See list of articles and papers in Appendix B Watch your for weekly newsletter Read all previous newsletters posted on (Note: newsletters prior to Nov. 2, 2015 were written under the old rules) Post questions on Go to use search tool 124

125 Where to go for more information See list of articles and papers in Appendix B Watch your for weekly newsletter Read all previous newsletters posted on (Note: newsletters prior to Nov. 2, 2015 were written under the old rules) Post questions on Go to use search tool Call the SSA hotline at

126 Good luck! 126

Savvy Social Security Planning for Boomers. By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC

Savvy Social Security Planning for Boomers By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC 1 Two ways Social Security planning can help your business Reach out to new clients

Savvy Social Security Planning for Boomers By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC 1 Two ways Social Security planning can help your business Reach out to new clients

5 Keys to Profitable Social Security Planning

5 Keys to Profitable Social Security Planning What Advisors Need to Know to Optimize Clients Retirement Benefits By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC 1 2 Common

5 Keys to Profitable Social Security Planning What Advisors Need to Know to Optimize Clients Retirement Benefits By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC 1 2 Common

Savvy Social Security Planning: What baby boomers need to know to maximize retirement income

Savvy Social Security Planning: What baby boomers need to know to maximize retirement income NOT FDIC-INSURED l MAY LOSE VALUE l NO BANK GUARANTEE Copyright 2016 Horsesmouth, LLC. All Rights Reserved.

Savvy Social Security Planning: What baby boomers need to know to maximize retirement income NOT FDIC-INSURED l MAY LOSE VALUE l NO BANK GUARANTEE Copyright 2016 Horsesmouth, LLC. All Rights Reserved.

Savvy Social Security Planning: What baby boomers need to know to maximize retirement income. Copyright 2015 Horsesmouth, LLC. All Rights Reserved.

Savvy Social Security Planning: What baby boomers need to know to maximize retirement income Copyright 2015 Horsesmouth, LLC. All Rights Reserved. 1 Baby Boomers Want to Know: Will Social Security be there

Savvy Social Security Planning: What baby boomers need to know to maximize retirement income Copyright 2015 Horsesmouth, LLC. All Rights Reserved. 1 Baby Boomers Want to Know: Will Social Security be there

Savvy Social Security Planning: What Baby Boomers Need to Know to Maximize Retirement Income

Savvy Social Security Planning: What Baby Boomers Need to Know to Maximize Retirement Income Presented by Wakefield Hare, CFP Copyright 2013 Horsesmouth, LLC. All Rights Reserved. 1 2 Baby boomers want

Savvy Social Security Planning: What Baby Boomers Need to Know to Maximize Retirement Income Presented by Wakefield Hare, CFP Copyright 2013 Horsesmouth, LLC. All Rights Reserved. 1 2 Baby boomers want

Savvy Social Security Planning: What Baby Boomers Need to Know to Maximize Retirement Income

Savvy Social Security Planning: What Baby Boomers Need to Know to Maximize Retirement Income Copyright 2017 Horsesmouth, LLC. All Rights Reserved. 1 Baby boomers want to know: Will Social Security be there

Savvy Social Security Planning: What Baby Boomers Need to Know to Maximize Retirement Income Copyright 2017 Horsesmouth, LLC. All Rights Reserved. 1 Baby boomers want to know: Will Social Security be there

Savvy Social Security Planning:

Savvy Social Security Planning: What Baby Boomers Need to Know to Maximize Retirement Income Copyright 2017 Horsesmouth, LLC. All Rights Reserved. 1 Baby boomers want to know: Will Social Security be there

Savvy Social Security Planning: What Baby Boomers Need to Know to Maximize Retirement Income Copyright 2017 Horsesmouth, LLC. All Rights Reserved. 1 Baby boomers want to know: Will Social Security be there

Top 10 Social Security Questions Asked by Baby Boomers... And How To Answer Them

Top 10 Social Security Questions Asked by Baby Boomers... And How To Answer Them By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC 1 Elaine Floyd, CFP Director of Retirement

Top 10 Social Security Questions Asked by Baby Boomers... And How To Answer Them By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC 1 Elaine Floyd, CFP Director of Retirement

Savvy Social Security Planning:

Savvy Social Security Planning: What Baby Boomers Need to Know to Maximize Retirement Income Copyright 2015 Horsesmouth, LLC. All Rights Reserved. 1 Baby boomers want to know: Will Social Security be there

Savvy Social Security Planning: What Baby Boomers Need to Know to Maximize Retirement Income Copyright 2015 Horsesmouth, LLC. All Rights Reserved. 1 Baby boomers want to know: Will Social Security be there

SAVVY SOCIAL SECURITY

RETIREMENT PLAN SERVICES SAVVY SOCIAL SECURITY What Baby Boomers Need to Know to Potentially Maximize Retirement Income John K. Kriel, CRPC, CRPS Senior Retirement Consultant Lincoln Financial Group Products

RETIREMENT PLAN SERVICES SAVVY SOCIAL SECURITY What Baby Boomers Need to Know to Potentially Maximize Retirement Income John K. Kriel, CRPC, CRPS Senior Retirement Consultant Lincoln Financial Group Products

Top 10 Social Security Questions Asked by Baby Boomers... And How To Answer Them

Top 10 Social Security Questions Asked by Baby Boomers... And How To Answer Them By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC 1 Question #1 I applied for early benefits

Top 10 Social Security Questions Asked by Baby Boomers... And How To Answer Them By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC 1 Question #1 I applied for early benefits

By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC

New Spousal Claiming Rules Every Advisor Must Know for 2016 and Beyond! and Top 10 Social Security Questions Asked by Baby Boomers... And How To Answer Them By Elaine Floyd, CFP Director of Retirement

New Spousal Claiming Rules Every Advisor Must Know for 2016 and Beyond! and Top 10 Social Security Questions Asked by Baby Boomers... And How To Answer Them By Elaine Floyd, CFP Director of Retirement

Everything You Want to Know About Social Security

2015 CliftonLarsonAllen Wealth Advisors, LLC Everything You Want to Know About Social Security CliftonLarsonAllen Wealth Advisors, LLC James P. Clemensen, CFP CLAconnect.com/privateclient Table Of Contents

2015 CliftonLarsonAllen Wealth Advisors, LLC Everything You Want to Know About Social Security CliftonLarsonAllen Wealth Advisors, LLC James P. Clemensen, CFP CLAconnect.com/privateclient Table Of Contents

Social Security Planning Presented by: Diane M. Pearson, CFP, PPC, CDFA

Social Security Planning Presented by: Diane M. Pearson, CFP, PPC, CDFA 1 Copyright 2018 Horsesmouth, LLC. All Rights Reserved. WHAT YOU NEED TO KNOW TO MAXIMIZE RETIREMENT INCOME This webinar is provided

Social Security Planning Presented by: Diane M. Pearson, CFP, PPC, CDFA 1 Copyright 2018 Horsesmouth, LLC. All Rights Reserved. WHAT YOU NEED TO KNOW TO MAXIMIZE RETIREMENT INCOME This webinar is provided

By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC

New Spousal Claiming Rules Every Advisor Must Know for 2016 and Beyond! and Top 10 Social Security Questions Asked by Baby Boomers... And How To Answer Them By Elaine Floyd, CFP Director of Retirement

New Spousal Claiming Rules Every Advisor Must Know for 2016 and Beyond! and Top 10 Social Security Questions Asked by Baby Boomers... And How To Answer Them By Elaine Floyd, CFP Director of Retirement

Savvy Social Security Planning for Boomers

May 22-25, 2016 Los Angeles Convention Center Los Angeles, California Savvy Social Security Planning for Boomers Presented by Lee Claymore, CFP FM11 5/23/2016 11:00 AM - 12:30 PM The handouts and presentations

May 22-25, 2016 Los Angeles Convention Center Los Angeles, California Savvy Social Security Planning for Boomers Presented by Lee Claymore, CFP FM11 5/23/2016 11:00 AM - 12:30 PM The handouts and presentations

By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC

New Spousal Claiming Rules Every Advisor Must Know for 2016 and Beyond! and Top 10 Social Security Questions Asked by Baby Boomers... And How To Answer Them By Elaine Floyd, CFP Director of Retirement

New Spousal Claiming Rules Every Advisor Must Know for 2016 and Beyond! and Top 10 Social Security Questions Asked by Baby Boomers... And How To Answer Them By Elaine Floyd, CFP Director of Retirement

Doug Lindsey, CFP MGM, LLC Albuquerque, NM

Doug Lindsey, CFP MGM, LLC Albuquerque, NM 505-346-3434 doug@mgm-llc.com www.mgm-llc.com Copyright 2013 Horsesmouth, LLC. All Rights Reserved. 1 Savvy Social Security Planning: What Financial Professionals

Doug Lindsey, CFP MGM, LLC Albuquerque, NM 505-346-3434 doug@mgm-llc.com www.mgm-llc.com Copyright 2013 Horsesmouth, LLC. All Rights Reserved. 1 Savvy Social Security Planning: What Financial Professionals

Savvy Social Security Planning:

Savvy Social Security Planning: What CPAs, Attorneys, and Other Professionals Need to Know About Social Security Claiming Strategies Presented by: Diane M. Pearson, CFP, PPC, CDFA Wealth Advisor and Shareholder

Savvy Social Security Planning: What CPAs, Attorneys, and Other Professionals Need to Know About Social Security Claiming Strategies Presented by: Diane M. Pearson, CFP, PPC, CDFA Wealth Advisor and Shareholder

abacus planning group

abacus planning group smart financial decisions Social Security Claiming Strategies Kirkland Watson Financial Summit Tuesday, November 15, 2011 X. Alexandra Chastain, CFP, Susan Amick McCants, CFP and

abacus planning group smart financial decisions Social Security Claiming Strategies Kirkland Watson Financial Summit Tuesday, November 15, 2011 X. Alexandra Chastain, CFP, Susan Amick McCants, CFP and

NOT FDIC INSURED MAY LOSE VALUE NO BANK GUARANTEE

2019 Social Security quick reference NOT FDIC INSURED MAY LOSE VALUE NO BANK GUARANTEE Full Retirement Age (FRA) Year of Birth 1943 1954 66 Full Retirement Age (FRA) 1955 66 and 2 months 1956 66 and 4

2019 Social Security quick reference NOT FDIC INSURED MAY LOSE VALUE NO BANK GUARANTEE Full Retirement Age (FRA) Year of Birth 1943 1954 66 Full Retirement Age (FRA) 1955 66 and 2 months 1956 66 and 4

UNDERSTANDING SOCIAL SECURITY RETIREMENT BENEFITS

UNDERSTANDING SOCIAL SECURITY RETIREMENT CONTENTS Individual Collection Decision... 3 Qualifying For Benefits... 3 Collecting Benefits...3-5 } At Full Retirement Age } Earlier } Earlier While Working }

UNDERSTANDING SOCIAL SECURITY RETIREMENT CONTENTS Individual Collection Decision... 3 Qualifying For Benefits... 3 Collecting Benefits...3-5 } At Full Retirement Age } Earlier } Earlier While Working }

Your guide to filing for Social Security

RETIREMENT INSTITUTE SM Social Security Your guide to filing for Social Security It s a choice of a lifetime. Make it count. 2 Social Security It s more than a monthly check As you approach retirement,

RETIREMENT INSTITUTE SM Social Security Your guide to filing for Social Security It s a choice of a lifetime. Make it count. 2 Social Security It s more than a monthly check As you approach retirement,

Retirement Rules of Thumb! Presented By: Meredith M. Ehn Advisor Participant Services Francis Investment Counsel

Retirement Rules of Thumb! Presented By: Meredith M. Ehn Advisor Participant Services Francis Investment Counsel Journey of the American Worker working/saving freedom date retirement Journey of the American

Retirement Rules of Thumb! Presented By: Meredith M. Ehn Advisor Participant Services Francis Investment Counsel Journey of the American Worker working/saving freedom date retirement Journey of the American

Benefits Presented by: Kelli Send Principal Senior Vice President Participant Services Francis Investment Counsel LLC

Maximizing Social Maximizing Security Benefits Social Security Benefits Presented by: Kelli Send Principal Senior Vice President Participant Services Francis Investment Counsel LLC What we will cover today

Maximizing Social Maximizing Security Benefits Social Security Benefits Presented by: Kelli Send Principal Senior Vice President Participant Services Francis Investment Counsel LLC What we will cover today

Diane Owens, Speaker & Consultant Step Up Your Social Security

Diane Owens, Speaker & Consultant Step Up Your Social Security Benefit rate depends on your age when you start your benefits: Early Retirement reduced based on # of months before your Full Retirement Age

Diane Owens, Speaker & Consultant Step Up Your Social Security Benefit rate depends on your age when you start your benefits: Early Retirement reduced based on # of months before your Full Retirement Age

Social Security. The choice of a lifetime. Your choice on when to file could increase your annual benefit by as much as 76% 1

Social Security Guide NATIONWIDE RETIREMENT INSTITUTE Social Security The choice of a lifetime Your choice on when to file could increase your annual benefit by as much as 76% 1 1 Nationwide as of November

Social Security Guide NATIONWIDE RETIREMENT INSTITUTE Social Security The choice of a lifetime Your choice on when to file could increase your annual benefit by as much as 76% 1 1 Nationwide as of November

Your Customized Social Security Spousal Planning Analysis

Your Customized Social Security Spousal Planning Analysis Prepared For Joe and Anne Sample June 06, 2016 Prepared By Baird Advisor Robert W. Baird & Co. 777 East Wisconsin Ave Milwaukee, WI 53202 Page

Your Customized Social Security Spousal Planning Analysis Prepared For Joe and Anne Sample June 06, 2016 Prepared By Baird Advisor Robert W. Baird & Co. 777 East Wisconsin Ave Milwaukee, WI 53202 Page

Social Security and Medicare Changes for 2019: What Clients Need to Know

Social Security and Medicare Changes for 2019: What Clients Need to Know By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC 1 The Opportunities for Education and Advice 2 Education

Social Security and Medicare Changes for 2019: What Clients Need to Know By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC 1 The Opportunities for Education and Advice 2 Education

SOCIAL SECURITY YOU R OV E RV I EW OF ADR

YOU R 2 0 1 8 OV E RV I EW OF This booklet is being provided as a supplement to the Social Security and insurance sales presentation titled Strategies to Potentially Increase Your Social Security Benefits.

YOU R 2 0 1 8 OV E RV I EW OF This booklet is being provided as a supplement to the Social Security and insurance sales presentation titled Strategies to Potentially Increase Your Social Security Benefits.

How to Use the Savvy Social Security Calculators

How to Use the Savvy Social Security Calculators The Savvy Social Security Calculators utilize Excel spreadsheets to help you run various scenarios when doing Social Security planning for clients. They

How to Use the Savvy Social Security Calculators The Savvy Social Security Calculators utilize Excel spreadsheets to help you run various scenarios when doing Social Security planning for clients. They

A Guide to Social Security: Know your options, maximize your benefits

A Guide to Social Security: Know your options, maximize your benefits Content provided by Nuveen. Nuveen, LLC, formerly known as TIAA Global Asset Management, delivers the expertise of TIAA Investments

A Guide to Social Security: Know your options, maximize your benefits Content provided by Nuveen. Nuveen, LLC, formerly known as TIAA Global Asset Management, delivers the expertise of TIAA Investments

Maximizing Your Social Security Retirement Benefits

Maximizing Your Social Security Benefits Inside the Black Box Avram L. Sacks, Esq.* avram@asackslaw.com 773 206 0276 Chicago Center for Torah and Chesed Skokie, IL July 31, 2016 *Member: National Academy

Maximizing Your Social Security Benefits Inside the Black Box Avram L. Sacks, Esq.* avram@asackslaw.com 773 206 0276 Chicago Center for Torah and Chesed Skokie, IL July 31, 2016 *Member: National Academy

MAXIMIZING YOUR SOCIAL SECURITY RETIREMENT BENEFITS

MAXIMIZING YOUR SOCIAL SECURITY RETIREMENT BENEFITS Take the first step toward understanding when and how to apply. KEY TAKEAWAYS Deciding when and how to start drawing Social Security retirement benefits

MAXIMIZING YOUR SOCIAL SECURITY RETIREMENT BENEFITS Take the first step toward understanding when and how to apply. KEY TAKEAWAYS Deciding when and how to start drawing Social Security retirement benefits

Your Customized Social Security Analysis. Joe and Mary Sample 9/1/2013. Baird Advisor Robert W. Baird & Co (800)

") Your Customized Social Security Analysis Joe and Mary Sample 9/1/ Baird Advisor Robert W. Baird & Co (800) 800-1234 This report shows the Social Security income stream you can expect to receive under differing

Your Customized Social Security Analysis Joe and Mary Sample 9/1/ Baird Advisor Robert W. Baird & Co (800) 800-1234 This report shows the Social Security income stream you can expect to receive under differing

Social Security The Choice of a Lifetime. Timothy O Mara, Vice President, Nationwide Retirement Institute

Social Security The Choice of a Lifetime Timothy O Mara, Vice President, Nationwide Retirement Institute FOR BROKER/DEALER USE ONLY NOT FOR USE WITH THE GENERAL PUBLIC Important things to keep in mind

Social Security The Choice of a Lifetime Timothy O Mara, Vice President, Nationwide Retirement Institute FOR BROKER/DEALER USE ONLY NOT FOR USE WITH THE GENERAL PUBLIC Important things to keep in mind

Securing Your Retirement. Transforming Social Security Into a Winning Retirement Strategy

Securing Your Retirement Transforming Social Security Into a Winning Retirement Strategy Living Longer Life Expectancy Upon Retirement at Age 65 Male Age 65 50% chance of living to 87 25% chance of living

Securing Your Retirement Transforming Social Security Into a Winning Retirement Strategy Living Longer Life Expectancy Upon Retirement at Age 65 Male Age 65 50% chance of living to 87 25% chance of living

Social Security and Your Retirement

Social Security and Your Retirement January 2013 ACI-1111-3702 American Century Investment Services, Inc. Distributor 2013 American Century Investments Proprietary Holdings, Inc. All rights reserved. Social

Social Security and Your Retirement January 2013 ACI-1111-3702 American Century Investment Services, Inc. Distributor 2013 American Century Investments Proprietary Holdings, Inc. All rights reserved. Social

2018 Social Security Reference Guide

2018 Social Security Reference Guide TABLE OF CONTENTS Important Ages... 1 Full Retirement Age (FRA)... 1 Milestone Ages... 1 Retirement Benefits... 2 Requirements to Qualify for Social Security Retirement

2018 Social Security Reference Guide TABLE OF CONTENTS Important Ages... 1 Full Retirement Age (FRA)... 1 Milestone Ages... 1 Retirement Benefits... 2 Requirements to Qualify for Social Security Retirement

39 Broadway, 23rd floor, New York, NY 10006, phone: (888) ext.1,

ext.1,") 39 Broadway, 23rd floor, New York, NY 10006, phone: (888) 336-6884 ext.1, www.horsesmouth.com Hi all Savvy Social Security Planners! It's been a while since I've issued an update, but a lot of good information

39 Broadway, 23rd floor, New York, NY 10006, phone: (888) 336-6884 ext.1, www.horsesmouth.com Hi all Savvy Social Security Planners! It's been a while since I've issued an update, but a lot of good information

A Guide to Understanding Social Security Retirement Benefits

Private Wealth Management Products & Services A Guide to Understanding Social Security Retirement Benefits Social Security Eligibility Requirements Workers who pay Social Security taxes on their wages

Private Wealth Management Products & Services A Guide to Understanding Social Security Retirement Benefits Social Security Eligibility Requirements Workers who pay Social Security taxes on their wages

A Guide to Understanding Social Security Retirement Benefits

Private Wealth Management Products & Services A Guide to Understanding Social Security Retirement Benefits Social Security Eligibility Requirements Workers who pay Social Security taxes on their wages

Private Wealth Management Products & Services A Guide to Understanding Social Security Retirement Benefits Social Security Eligibility Requirements Workers who pay Social Security taxes on their wages

Your Customized Social Security Spousal Planning Analysis

Your Customized Social Security Spousal Planning Analysis Prepared For John and Mary Boomer September 29, 2015 Prepared By Steven Van Metre Steven Van Metre Financial 5901 Sundale Ave Ste B Bakersfield

Your Customized Social Security Spousal Planning Analysis Prepared For John and Mary Boomer September 29, 2015 Prepared By Steven Van Metre Steven Van Metre Financial 5901 Sundale Ave Ste B Bakersfield

The Curse of the WEP-GPO: Why Some Clients Face Reduced Benefits or Worse. What Advisors Need to Know About These Rare But Painful Rules.

The Curse of the WEP-GPO: Why Some Clients Face Reduced Benefits or Worse. What Advisors Need to Know About These Rare But Painful Rules. The Curse of the WEP-GPO: Why Some Clients Face Reduced Benefits,

The Curse of the WEP-GPO: Why Some Clients Face Reduced Benefits or Worse. What Advisors Need to Know About These Rare But Painful Rules. The Curse of the WEP-GPO: Why Some Clients Face Reduced Benefits,

SOCIAL SECURITY YOUR 2016 OVERVIEW OF

This booklet is being provided as a supplement to the Social Security and insurance sales presentation titled Strategies to Potentially Increase Your Social Security Benefi ts. It is intended as an overview

This booklet is being provided as a supplement to the Social Security and insurance sales presentation titled Strategies to Potentially Increase Your Social Security Benefi ts. It is intended as an overview

Social Security Eligibility. Amount of the Social Security Benefit. Primary Insurance Amount (PIA) Windfall Benefits Elimination Provision (WEP)

Windfall Benefits Elimination Provision (WEP)") Social Security Retirement Benefits Social Security Eligibility Amount of the Social Security Benefit Primary Insurance Amount (PIA) Windfall Benefits Elimination Provision (WEP) Social Security Benefit

Social Security Retirement Benefits Social Security Eligibility Amount of the Social Security Benefit Primary Insurance Amount (PIA) Windfall Benefits Elimination Provision (WEP) Social Security Benefit

Social Security and Retirement Planning: A Hit or Myth Proposition

Social Security and Retirement Planning: A Hit or Myth Proposition New Hampshire Government Finance Officers Association Presentation May 3, 2018 Kurt Czarnowski Czarnowski Consulting: Expert Answers to

Social Security and Retirement Planning: A Hit or Myth Proposition New Hampshire Government Finance Officers Association Presentation May 3, 2018 Kurt Czarnowski Czarnowski Consulting: Expert Answers to

Social Security 76% 1. The choice of a lifetime. Your choice on when to file could increase your annual benefit by as much as

Social Security Guide NATIONWIDE RETIREMENT INSTITUTE SM Social Security The choice of a lifetime Your choice on when to file could increase your annual benefit by as much as 76% 1 1 Nationwide as of May

Social Security Guide NATIONWIDE RETIREMENT INSTITUTE SM Social Security The choice of a lifetime Your choice on when to file could increase your annual benefit by as much as 76% 1 1 Nationwide as of May

Maximizing your Social Security retirement benefits

Maximizing your Social Security retirement benefits Your first step toward understanding when and how to apply Within your retirement income plan, Social Security retirement benefits should be considered

Maximizing your Social Security retirement benefits Your first step toward understanding when and how to apply Within your retirement income plan, Social Security retirement benefits should be considered

Social Security 76% 1. The choice of a lifetime. Your choice on when to file could increase your annual benefit by as much as

Social Security Guide NATIONWIDE RETIREMENT INSTITUTE Social Security The choice of a lifetime Your choice on when to file could increase your annual benefit by as much as 76% 1 1 Nationwide as of May

Social Security Guide NATIONWIDE RETIREMENT INSTITUTE Social Security The choice of a lifetime Your choice on when to file could increase your annual benefit by as much as 76% 1 1 Nationwide as of May

Social Security 76% 1. The choice of a lifetime. Your choice on when to file could increase your annual benefit by as much as

Social Security Guide NATIONWIDE RETIREMENT INSTITUTE Social Security The choice of a lifetime Your choice on when to file could increase your annual benefit by as much as 76% 1 1 Nationwide as of May

Social Security Guide NATIONWIDE RETIREMENT INSTITUTE Social Security The choice of a lifetime Your choice on when to file could increase your annual benefit by as much as 76% 1 1 Nationwide as of May

How to Maximize Social Security Benefits Now

MERS of Michigan 2018 Retirement Conference October 5, 2018 How to Maximize Social Security Benefits Now Mary Beth Franklin, CFP Contributing Editor Investment News MBF01 For most retirees, Social Security

MERS of Michigan 2018 Retirement Conference October 5, 2018 How to Maximize Social Security Benefits Now Mary Beth Franklin, CFP Contributing Editor Investment News MBF01 For most retirees, Social Security

Social Security & Medicare: Everything You Didn t Know to Ask

Social Security & Medicare: Everything You Didn t Know to Ask This material is not intended to replace the advice of a qualified attorney, tax advisor, investment professional, or insurance agent. Before

Social Security & Medicare: Everything You Didn t Know to Ask This material is not intended to replace the advice of a qualified attorney, tax advisor, investment professional, or insurance agent. Before

Helping to Secure Your Clients Retirement Transforming Social Security Into a Winning Retirement Strategy

Helping to Secure Your Clients Retirement Transforming Social Security Into a Winning Retirement Strategy FOR FINANCIAL PROFESSIONAL USE ONLY. Not to be shown or distributed to clients. Living Longer Life

Helping to Secure Your Clients Retirement Transforming Social Security Into a Winning Retirement Strategy FOR FINANCIAL PROFESSIONAL USE ONLY. Not to be shown or distributed to clients. Living Longer Life

How to Maximize Social Security Benefits

NAIFA Nebraska Statewide CE Credit Day March 14, 2018 How to Maximize Social Security Benefits Mary Beth Franklin, CFP Contributing Editor Investment News MBF01 MBF02 Remember the old analogy for the three

NAIFA Nebraska Statewide CE Credit Day March 14, 2018 How to Maximize Social Security Benefits Mary Beth Franklin, CFP Contributing Editor Investment News MBF01 MBF02 Remember the old analogy for the three

For Jack and Jill Sample. Presented by: Michael Merlob, FSA Phone:

For and Sample Presented by: Michael Merlob, FSA Phone: 954-295-254 Email: michael.merlob@foster-foster.com Important Notes This report of your Social Security benefits is based on the information you

For and Sample Presented by: Michael Merlob, FSA Phone: 954-295-254 Email: michael.merlob@foster-foster.com Important Notes This report of your Social Security benefits is based on the information you

Social Security fundamentals

Page 1 of 12 Guidelines for making well-informed decisions Table of contents 2 Key concept #1: Social Security will be around into the foreseeable future 3 Key concept #2: How benefits are calculated 4

Page 1 of 12 Guidelines for making well-informed decisions Table of contents 2 Key concept #1: Social Security will be around into the foreseeable future 3 Key concept #2: How benefits are calculated 4

SOCIAL SECURITY CLAIMING STRATEGIES MAXIMIZING YOUR LIFETIME ANNUITY

SOCIAL SECURITY CLAIMING STRATEGIES MAXIMIZING YOUR LIFETIME ANNUITY Who am I? Deborah L. Petrone, CPA, Mtax, CGMA, NSSA Senior Tax Manager Apple Growth Partners dpetrone@applegrowth,com 2275 State Route

SOCIAL SECURITY CLAIMING STRATEGIES MAXIMIZING YOUR LIFETIME ANNUITY Who am I? Deborah L. Petrone, CPA, Mtax, CGMA, NSSA Senior Tax Manager Apple Growth Partners dpetrone@applegrowth,com 2275 State Route

7/6/2016. Social Security Update: Agenda. Social Security Question Preview

Social Security Update: New Rules Require New Strategies Jonathan Dumas, CFP Advisor Dean, Jacobson Financial Services Insurance Sales Presentation Prudential Annuities, its distributors and representatives

Social Security Update: New Rules Require New Strategies Jonathan Dumas, CFP Advisor Dean, Jacobson Financial Services Insurance Sales Presentation Prudential Annuities, its distributors and representatives

Recent Developments. Social Security & Medicare Updates for Financial Advisors. Agenda

Social Security & Medicare Updates for Financial Advisors Sue Denny Cincinnati Public Affairs Specialist susan.denny@ssa.gov 1 866 593 1519 ext. 10856 513 684 2688 (fax) Agenda Recent Developments my Social

Social Security & Medicare Updates for Financial Advisors Sue Denny Cincinnati Public Affairs Specialist susan.denny@ssa.gov 1 866 593 1519 ext. 10856 513 684 2688 (fax) Agenda Recent Developments my Social

Social Security. Know your options to help maximize your benefits FOR INVESTORS. Not FDIC Insured May Lose Value No Bank Guarantee

Social Security Know your options to help maximize your benefits FOR INVESTORS Not FDIC Insured May Lose Value No Bank Guarantee What you need to know before you collect Today s agenda: Social Security

Social Security Know your options to help maximize your benefits FOR INVESTORS Not FDIC Insured May Lose Value No Bank Guarantee What you need to know before you collect Today s agenda: Social Security

MAXIMIZING YOUR SOCIAL SECURITY RETIREMENT BENEFITS

MAXIMIZING YOUR SOCIAL SECURITY RETIREMENT BENEFITS The information contained herein has been obtained from sources considered reliable, but we do not guarantee that the foregoing is accurate or complete.

MAXIMIZING YOUR SOCIAL SECURITY RETIREMENT BENEFITS The information contained herein has been obtained from sources considered reliable, but we do not guarantee that the foregoing is accurate or complete.

Understanding Social Security and Medicare

Understanding Social Security and Medicare How these programs fit into your retirement strategies Allianz Life Insurance Company of New York Allianz Life Insurance Company of North America ENT-1520-N Social

Understanding Social Security and Medicare How these programs fit into your retirement strategies Allianz Life Insurance Company of New York Allianz Life Insurance Company of North America ENT-1520-N Social

How to Use the Savvy Social Security Calculators

appendix a How to Use the Savvy Social Security Calculators The Savvy Social Security Calculators on the enclosed CD utilize Excel spreadsheets to help you run various scenarios when doing Social Security

appendix a How to Use the Savvy Social Security Calculators The Savvy Social Security Calculators on the enclosed CD utilize Excel spreadsheets to help you run various scenarios when doing Social Security

What You Need to Know About Social Security

What You Need to Know About Social Security Social Security is an important piece of many American s retirement income and it was only designed to replace a portion of your income and survivor needs. Your

What You Need to Know About Social Security Social Security is an important piece of many American s retirement income and it was only designed to replace a portion of your income and survivor needs. Your

Social Security Planning Strategies

Private Wealth Management Products & Services Social Security Planning Strategies Basic Social Security Planning Strategies One of the biggest decisions a retiree and their family will face is when to

Private Wealth Management Products & Services Social Security Planning Strategies Basic Social Security Planning Strategies One of the biggest decisions a retiree and their family will face is when to

Congressional Research Service Report for Congress Social Security Primer, April 30, 2012

Congressional Research Service Report for Congress Social Security Primer, April 30, 2012 Click to open document in a browser 2012ARD 094-204 112th Congress Social Security Primer Dawn Nuschler Specialist

Congressional Research Service Report for Congress Social Security Primer, April 30, 2012 Click to open document in a browser 2012ARD 094-204 112th Congress Social Security Primer Dawn Nuschler Specialist

Today s agenda. Social Security The choice of a lifetime. Social Security basics. Making your Social Security decision

Today s agenda Social Security The choice of a lifetime Social Security basics Making your Social Security decision 3 Social Security The choice of a lifetime 4 WHY SOCIAL SECURITY IS THE CHOICE OF A LIFETIME

Today s agenda Social Security The choice of a lifetime Social Security basics Making your Social Security decision 3 Social Security The choice of a lifetime 4 WHY SOCIAL SECURITY IS THE CHOICE OF A LIFETIME

Health Care and Long-Term Care Study, a consumer study of U.S. adults ages 50 and up, Nationwide/Harris Poll Survey (November 2016).

.") 1 Health Care and Long-Term Care Study, a consumer study of U.S. adults ages 50 and up, Nationwide/Harris Poll Survey (November 2016). 1 Important things to keep in mind Not a deposit Not FDIC or NCUSIF

1 Health Care and Long-Term Care Study, a consumer study of U.S. adults ages 50 and up, Nationwide/Harris Poll Survey (November 2016). 1 Important things to keep in mind Not a deposit Not FDIC or NCUSIF

The Social Side of Retirement SM

The Social Side of Retirement SM Exploring Social Security Retirement Benefits TABLE OF CONTENTS 2 Social Security and you 3 Filing for benefits 6 Benefits for spouses 8 How spousal benefits work 13 Working

The Social Side of Retirement SM Exploring Social Security Retirement Benefits TABLE OF CONTENTS 2 Social Security and you 3 Filing for benefits 6 Benefits for spouses 8 How spousal benefits work 13 Working

Social Security. What s in it for you. Presented by Cindi Hill, Aug. 5, CUNA Mutual Retirement Solutions People driven. Outcome focused.

Social Security. What s in it for you. Presented by Cindi Hill, Aug. 5, 2015. Agenda. 1. The value of Social Security 2. Rules of the road 3. Ways to maximize benefits 4. Summary Page 2 What lies ahead?

Social Security. What s in it for you. Presented by Cindi Hill, Aug. 5, 2015. Agenda. 1. The value of Social Security 2. Rules of the road 3. Ways to maximize benefits 4. Summary Page 2 What lies ahead?

SOCIAL SECURITY INFORMATION Annual Delegates Meeting

SOCIAL SECURITY INFORMATION 2017 Annual Delegates Meeting IN THE BEGINNING The Social Security Act was signed into law on August 14, 1935. Taxes were collected for the first time in January 1937 and the

SOCIAL SECURITY INFORMATION 2017 Annual Delegates Meeting IN THE BEGINNING The Social Security Act was signed into law on August 14, 1935. Taxes were collected for the first time in January 1937 and the

Social Security Planning Strategies

Private Wealth Management Products & Services Social Security Planning Strategies Social Security Planning Considerations One of the biggest decisions a retiree and their family will face is when to start

Private Wealth Management Products & Services Social Security Planning Strategies Social Security Planning Considerations One of the biggest decisions a retiree and their family will face is when to start

Social Security income benefit strategies under the new law

Social Security income benefit strategies under the new law Allianz Life Insurance Company of North America Allianz Life Insurance Company of New York ENT-1511-N Page 1 of 12 What s your Social Security

Social Security income benefit strategies under the new law Allianz Life Insurance Company of North America Allianz Life Insurance Company of New York ENT-1511-N Page 1 of 12 What s your Social Security

Social Security. What s in it for you.

Social Security. What s in it for you. Presented by Michael Mason, March 9, 2016. Agenda. 1. The role of Social Security 2. Understanding your benefit 3. How to maximize your benefit Page 2 What lies ahead?

Social Security. What s in it for you. Presented by Michael Mason, March 9, 2016. Agenda. 1. The role of Social Security 2. Understanding your benefit 3. How to maximize your benefit Page 2 What lies ahead?

Social Security.

Social Security www.socialsecurity.gov History of Social Security Programs 1935 Retirement Insurance 1939 Survivors Insurance 1956 Disability Insurance 1965 Medicare Program 1972 Supplemental Security

Social Security www.socialsecurity.gov History of Social Security Programs 1935 Retirement Insurance 1939 Survivors Insurance 1956 Disability Insurance 1965 Medicare Program 1972 Supplemental Security

Understanding Social Security

Understanding Social Security Guide for Advisors A Look at the Big Picture For Financial Professional Use Only. Not for Use With Consumers. Is Your Clients Picture of Retirement Incomplete? Building retirement

Understanding Social Security Guide for Advisors A Look at the Big Picture For Financial Professional Use Only. Not for Use With Consumers. Is Your Clients Picture of Retirement Incomplete? Building retirement

Social Security Calculator. Prepared For Tom and Jane

Social Security Calculator Prepared For Tom and Jane May 02, 2016 IMPORTANT DISCLOSURE INFORMATION IMPORTANT: The projections and other information generated by the MoneyGuidePro Social Security Calculator

Social Security Calculator Prepared For Tom and Jane May 02, 2016 IMPORTANT DISCLOSURE INFORMATION IMPORTANT: The projections and other information generated by the MoneyGuidePro Social Security Calculator

Social Security - Retire Ready

H.Haller Financial Howard Haller, CFP 28 West Bridge Street Saugerties, NY 12477 845-246-1618 fritz@hhallerfinancial.com www.hhallerfinancial.com Social Security - Retire Ready 2/26/2014 Page 1 of 16,

H.Haller Financial Howard Haller, CFP 28 West Bridge Street Saugerties, NY 12477 845-246-1618 fritz@hhallerfinancial.com www.hhallerfinancial.com Social Security - Retire Ready 2/26/2014 Page 1 of 16,

Social Security: With You Through Life s Journey. Produced at U.S. taxpayer expense

Social Security: With You Through Life s Journey Produced at U.S. taxpayer expense Over 60 Million Receiving Benefits 9 million Disabled Workers, 2 million Dependents 4 million Widows/ Widowers 41 million

Social Security: With You Through Life s Journey Produced at U.S. taxpayer expense Over 60 Million Receiving Benefits 9 million Disabled Workers, 2 million Dependents 4 million Widows/ Widowers 41 million

Nebraska Wealth Management Conference Omaha October 18, Social Security: Long-term Prognosis/Retirement Planning

Nebraska Wealth Management Conference Omaha October 18, 2016 Social Security: Long-term Prognosis/Retirement Planning Mary Beth Franklin, CFP Contributing Editor Investment News MBF01 Social Security:

Nebraska Wealth Management Conference Omaha October 18, 2016 Social Security: Long-term Prognosis/Retirement Planning Mary Beth Franklin, CFP Contributing Editor Investment News MBF01 Social Security:

Optimizing Social Security Benefits. Thursday, February 18, 2016 Susan Amick McCants, CFP Edward W. Kramer, CFP

Optimizing Social Security Benefits Thursday, February 18, 2016 Susan Amick McCants, CFP Edward W. Kramer, CFP Goals Social Security overview Claiming decision tree Strategies to maximize payment options

Optimizing Social Security Benefits Thursday, February 18, 2016 Susan Amick McCants, CFP Edward W. Kramer, CFP Goals Social Security overview Claiming decision tree Strategies to maximize payment options

The Broken Three-Legged Stool

FPA of Michigan 2017 Annual Fall Symposium October 18, 2017 The Broken Three-Legged Stool Mary Beth Franklin, CFP Contributing Editor Investment News Mary Beth Franklin, CFP 1 Remember the old analogy

FPA of Michigan 2017 Annual Fall Symposium October 18, 2017 The Broken Three-Legged Stool Mary Beth Franklin, CFP Contributing Editor Investment News Mary Beth Franklin, CFP 1 Remember the old analogy

Challenge. If you have any questions on the book or on planning your retirement please contact the author Marc Bautis.

Retirement Fitness Challenge The Retirement Fitness Challenge, while simple in concept, is an evolving program that presents different layers of complexity based on each retiree s unique needs. The following

Retirement Fitness Challenge The Retirement Fitness Challenge, while simple in concept, is an evolving program that presents different layers of complexity based on each retiree s unique needs. The following

What to Know, What to Ask By Joan Entmacher, Benjamin Veghte, and Kristen Arnold

Claiming Social Security Benefits NATIONAL ACADEMY OF SOCIAL INSURANCE What to Know, What to Ask By Joan Entmacher, Benamin Veghte, and Kristen Arnold Thinking about retirement? Deciding when to take Social

Claiming Social Security Benefits NATIONAL ACADEMY OF SOCIAL INSURANCE What to Know, What to Ask By Joan Entmacher, Benamin Veghte, and Kristen Arnold Thinking about retirement? Deciding when to take Social

Social Security.

Social Security www.socialsecurity.gov Save for a Secure Future Social Security is the foundation for a secure retirement, but you also will need other savings and investments. If you want to learn more

Social Security www.socialsecurity.gov Save for a Secure Future Social Security is the foundation for a secure retirement, but you also will need other savings and investments. If you want to learn more

2018 UPDATED EDITION: Social Security Cheat Sheet

2018 UPDATED EDITION: Social Security Cheat Sheet Visit Us Online: www.retirementyou.com At Retirement You, we believe in Motivation Through Education. Because knowledge is power, but only if you use

2018 UPDATED EDITION: Social Security Cheat Sheet Visit Us Online: www.retirementyou.com At Retirement You, we believe in Motivation Through Education. Because knowledge is power, but only if you use

Claiming Social Security

Claiming Social Security A NARFE Federal Benefits Institute Webinar Presented by Tammy Flanagan 1 When do you plan to claim Social Security retirement benefits: I am already receiving my Social Security

Claiming Social Security A NARFE Federal Benefits Institute Webinar Presented by Tammy Flanagan 1 When do you plan to claim Social Security retirement benefits: I am already receiving my Social Security

A TALE OF TWO COUPLES

Maximizing Social For You and Your Clients Inside the Black Box Avram L. Sacks, Esq.* avram@asackslaw.com 773 206 0276 4th Annual Elder Law Boot Camp: Beyond Basics Illinois State Bar Association Elder

Maximizing Social For You and Your Clients Inside the Black Box Avram L. Sacks, Esq.* avram@asackslaw.com 773 206 0276 4th Annual Elder Law Boot Camp: Beyond Basics Illinois State Bar Association Elder

Diane Owens, Speaker & Consultant, Step Up Your Social Security

Diane Owens, Speaker & Consultant, Step Up Your Social Security How Age Affects Benefits Benefits Based on Lifetime Earnings If You Work & Get Benefits Spouse s and Widow s Options Don t Forget Medicare

Diane Owens, Speaker & Consultant, Step Up Your Social Security How Age Affects Benefits Benefits Based on Lifetime Earnings If You Work & Get Benefits Spouse s and Widow s Options Don t Forget Medicare

Seminar Goals 11/16/2016. Introductions

Introductions Prince William County Public Schools Deborah Sparks, Director of Benefits & Retirement Services Kristin Brittigan, Benefits Specialist Retirement Services Virginia Retirement System (VRS)

Introductions Prince William County Public Schools Deborah Sparks, Director of Benefits & Retirement Services Kristin Brittigan, Benefits Specialist Retirement Services Virginia Retirement System (VRS)

SOCIAL SECURITY SIMPLIFIED

Webcast Premiere SOCIAL SECURITY SIMPLIFIED Dan Tambellini, CFP Judith Ward, CFP Roger Young, CFP December 13, 2017 7 p.m. (ET) With You Today Dan Tambellini, CFP Relationship Manager Roger Young, CFP

Webcast Premiere SOCIAL SECURITY SIMPLIFIED Dan Tambellini, CFP Judith Ward, CFP Roger Young, CFP December 13, 2017 7 p.m. (ET) With You Today Dan Tambellini, CFP Relationship Manager Roger Young, CFP

1-47 TABLE PERCENTAGE OF WORKERS ELECTING SOCIAL SECURITY RETIREMENT BENEFITS AT VARIOUS AGES, SELECTED YEARS

1-47 TABLE 1-13 -- NUMBER OF SOCIAL SECURITY RETIRED WORKER NEW BENEFIT AWARDS AND PERCENT RECEIVING REDUCED BENEFITS BECAUSE OF ENTITLEMENT BEFORE FRA, SELECTED YEARS 1956-2002 [Number in millions] Year

1-47 TABLE 1-13 -- NUMBER OF SOCIAL SECURITY RETIRED WORKER NEW BENEFIT AWARDS AND PERCENT RECEIVING REDUCED BENEFITS BECAUSE OF ENTITLEMENT BEFORE FRA, SELECTED YEARS 1956-2002 [Number in millions] Year

Social Security Using Social Security The Red Headed Step Child, in Retirement Planning.

Social Security Using Social Security The Red Headed Step Child, in Retirement Planning. History of Social Security Started in 1935 under President Roosevelt In Response to the Great Depression Benefits