Agenda. Learning Objectives. Corporate Risk Management. Chapter 20. Learning Objectives Principles Used in This Chapter

|

|

|

- Rosaline Parker

- 6 years ago

- Views:

Transcription

1 Chapter 20 Corporate Risk Management Agenda Learning Objectives Principles Used in This Chapter 1. Five-Step Corporate Risk Management Process 2. Managing Risk with Insurance Contracts 3. Managing Risk by Hedging with Forward Contracts 4. Managing Risk with Exchange-Traded Financial Derivatives 5. Valuing Options and Swaps Learning Objectives 1. Define risk management in the context of the five-step risk management process. 2. Understand how insurance contracts can be used to manage risk. 3 Use forward contracts to hedge commodity price risk 3. Use forward contracts to hedge commodity price risk. 4. Understand the advantages and disadvantages of using exchange traded futures and option contracts to hedge price risk. 5. Understand how to value option and how swaps work. 1

2 Principles Used in This Chapter Principle 2: There is a Risk-Return Tradeoff. Business is inherently risky but a lot of risk that a firm is exposed to are at least partially controllable through the use of financial contracts. Corporations are devoting increasing amounts of time and resources to the active management of their risk exposure Five Step Corporate Risk Management Process Five Step Corporate Risk Management Process 1. Identify and understand the firm s major risks. 2. Decide which type of risks to keep and which to transfer. 3. Decide how much risk to assume. 4. Incorporate risk into all the firm s decisions and processes. 5. Monitor and manage the risk that the firm assumes. 2

3 Step1: Identify and Understand the Firm s Major Risks Identifying risks relates to understanding the factors that drive the firm s cash flow volatility. For example: Demand risk - fluctuations in demand Commodity risk fluctuations in prices of raw materials Country risk unfavorable government policies Operational risk cost overruns in firm s operations Exchange rate risk changes in exchange rates Step1: Identify and Understand the Firm s Major Risks All the listed sources of risk (except operational risk) are external to the firm. Risk management generally focuses on managing external factors that cause volatility in firm s cash flows. Step 2: Decide Which Type of Risk to Keep and Which to Transfer This is perhaps the most critical step. For example, oil and gas exploration and production firms have historically i chosen to assume the risk of fluctuations ti in the price of oil and gas. However, some firms have chosen to actively manage the risk. 3

4 Step 3: Decide How Much Risk to Assume Figure 20-1 illustrates the cash flow distributions for three risk management strategies. The specific strategy chosen will depend upon the firm s attitude to risk and the cost/benefit analysis of risk management strategies. Step 4: Incorporate Risk into All the Firm s Decisions and Processes In this step, the firm must implement a system for controlling the firm s risk exposure. For example, for those risks that will be transferred, the firm must determine an appropriate means of transferring risk such as developing a hedging strategy or buying an insurance policy. 4

5 Step 5: Monitor and Manage the Risk the Firm Assumes An effective monitoring system ensures that the firm s dayto-day decisions are consistent with its chosen risk profile. This may involve centralizing the firm s risk exposure with a chief risk officer who assumes responsibility for monitoring and regularly reporting to the CEO and to the firm s board Managing grisk with Insurance Contracts Managing Risk with Insurance Contracts Insurance is a method of transferring risk from the firm to an outside party, in exchange for a premium. There are many types of insurance contracts that provide protection against various events. 5

6 20.3 Managing Risk by Hedging with Forward Contracts Managing Risk by Hedging with Forward Contracts Hedging refers to a strategy designed to offset the exposure to price risk. Example 20.1 If you are planning to purchase 1 million Euros in 6 months, you may be concerned that if Euro strengthens it will cost you more in U.S. dollars. Such risk can be mitigated with forward contracts. 6

7 Managing Risk by Hedging with Forward Contracts Forward contract is a contract wherein a price is agreedupon today for asset to be sold or purchased in the future. Since the price is locked-in today, risk from future price fluctuation is reduced. These contracts are privately negotiated with an intermediary such as an investment bank. Managing Risk by Hedging with Forward Contracts Thus in example 20.1, you could negotiate a rate today for Euros (say 1 Euro = $1.35) using a forward contract. In 6-months, regardless of whether Euro has appreciated or depreciated, your obligation will be to buy 1 million Euros at $1.35 each or $1.35 million. Managing Risk by Hedging with Forward Contracts The following table shows potential future scenarios and the cash flows. It is seen that Forward contract helps to reduce risk if Euro appreciates. However, if Euro depreciates, Forward contract obligates the firm to pay a higher amount. Future Cost with a Cost without a Effect of Exchange Rate of Euro Forward Contract Forward contract Forward Contract $1.20 $1.35 million $1.20 million Unfavorable $1.30 $1.35 million $1.30 million Unfavorable $1.40 $1.35 million $1.40 million Favorable $1.50 $1.35 million $1.50 million Favorable 7

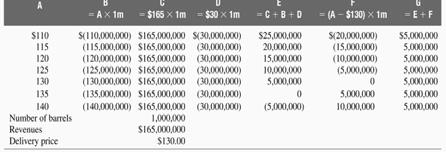

8 Checkpoint 20.1 Hedging Crude Oil Price Risk Using Forward Contracts Progressive Refining Inc. operates a specialty refining company that refines crude oil and sells the refined by-products to the cosmetic and plastic industries. The firm is currently planning for its refining needs for one year hence. The firm s analysts estimate that Progressive will need to purchase 1 million barrels of crude oil at the end of the current year to provide the feedstock for its refining needs for the coming year. The 1 million barrels of crude will be converted into byproducts at an average cost of $30 per barrel. Progressive will then sell the by-products for $165 per barrel. The current spot price of oil is $125 per barrel, and Progressive has been offered a forward contract by its investment banker to purchase the needed oil for a delivery price in one year of $130 per barrel. a. Ignoring taxes, if oil prices in one year are as low as $110 or as high as $140, what will be Progressive s profits (assuming the firm does not enter into the forward contract)? b. If the firm were to enter into the forward contract to purchase oil for $130 per barrel, demonstrate how this would effectively lock in the firm s cost of fuel today, thus hedging the risk that fluctuating crude oil prices pose for the firm s profits for the next year. Checkpoint 20.1 Checkpoint

9 Checkpoint 20.1 Checkpoint 20.1 Checkpoint

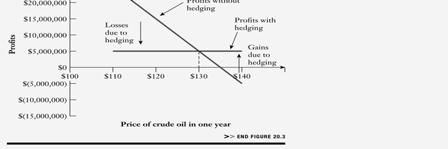

10 Checkpoint 20.1: Check Yourself Consider the profits that Progressive might earn if it chooses to hedge only 80% of its anticipated 1 million barrels of crude oil under the conditions above. Step 1: Picture the Problem The figure shows that the future price of crude oil could have a dramatic impact on the total cost of 1 million barrels of crude oil. If the price is not managed it will significantly affect the If the price is not managed, it will significantly affect the future profits of the firm. 10

11 Step 2: Decide on a Solution Strategy The firm can hedge its risk by purchasing a forward contract. This will lock-in the future price of oil at the forward rate of $130 per barrel. Step 3: Solve The table on the next slide contains the calculation of firm profits for the case where the price of crude oil is not hedged (column E), the payoff to the forward contract (column F) and firm profits where the price of crude is 80% hedged d (column G). Step 3: Solve 80% Hedged Price of Oil/bbl Total Cost of Oil Total Revenues Total Refining Costs Unhedged Annual Profits Profit/Loss on Forward Contract 80% Hedged Annual Profits A B=Ax1m C D=$30x1m E=C+B+D =(A- $130)x1mx%Hedge G=E+F $110 $(110,000,000) $165,000,000 $(30,000,000) $25,000,000 $(16,000,000) $9,000, (115,000,000) $165,000,000 (30,000,000) $20,000,000 $(12,000,000) 8,000, (120,000,000) $165,000,000 (30,000,000) $15,000,000 $(8,000,000) 7,000, (125,000,000) $165,000,000 (30,000,000) $10,000,000 $(4,000,000) 6,000, (130,000,000) $165,000,000 (30,000,000) $5,000,000 $ 5,000, (135,000,000) $165,000,000 (30,000,000) $0 $4,000,000 4,000, (140,000,000) $165,000,000 (30,000,000) $(5,000,000) $8,000,000 3,000,000 11

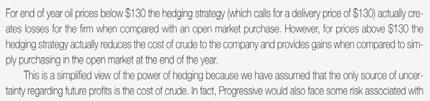

12 Step 4: Analyze The total cost of crude oil increases as the price of crude oil increases. The unhedged annual profits range from a loss of $5 million to a gain of $25 million. With 80% hedging, losses are avoided and the firm ends with profits ranging from $3 million to $5million. The forward contract obviously benefits the firm when the price of oil is higher than $130. Hedging Currency Risk Using Forward Contracts Currency risk can be hedged using forward contracts. For example, Disney expects to receive 500 million from its Tokyo operations in 3 months. Disney can lock-in the exchange rate to avoid any losses if the Yen weakens in 3 months. Hedging Currency Risk Using Forward Contracts Disney will follow a 2-step procedure to hedge its currency risk: 1. (Today): Enter into a forward contract which requires Disney to sell 500 million at the forward rate of say $0.0095/. 2. (In three months): Disney will convert its 500 million at the contracted forward rate, yielding $4,750,000 ( 500 m $0.0095=$4,750,000). With a forward contract, Disney will receive $4,750,000 regardless of the exchange rate in the market. 12

13 Limitations of Forward Contract 1. Credit or default risk: Both parties are exposed to the risk that the other party may default on their obligation. 2. Sharing of strategic information: The parties know what specific risk is being hedged. 3. It is hard to determine the market values of negotiated contracts as these contracts are not traded. Limitations of Forward Contract These limitations of forward contracts can be addressed by using exchange-traded contracts such as exchange traded futures, options, and swap contracts Managing Risk with Exchange-Traded Derivatives 13

14 Managing Risk with Exchange-Traded Derivatives A derivative contract is a security whose value is derived from the value of the underlying asset or security. In the examples considered on forward contract, the underlying assets were oil and currency. Exchange traded derivatives cannot be customized (like forward contracts) and are available only for specific assets and for limited set of maturities. Futures Contract A futures contract is a contract to buy or sell a stated commodity (such as wheat) or a financial claim (such as U.S. Treasuries) at a specified price at some future specified time. These contracts, like forward contracts, can be used to lock-in future prices. Futures Contract There are two categories of futures contracts: Commodity futures are traded on agricultural products, metals, wood products, and fibers. Financial futures include, for example, Treasuries, Eurodollars, foreign currencies, and stock indices. Financial futures dominate the futures market. 14

15 Managing Default Risk in Futures Market Default is prevented in futures contract in two ways: 1.Margin Futures exchanges require participants to post collateral called margin. 2.Marking to Market Daily gains or losses from a firm s futures contract are transferred to or from its margin account. Hedging with Futures Contract Similar to forward contracts, firms can use futures contract to hedge their price risk. If the firm is planning to buy, it can enter into a long hedge by purchasing the appropriate futures contract. If the firm is planning to sell, it can sell (or short) a futures contract. This is known as a short hedge. 15

16 Hedging with Futures Contract There are practical limitations with futures contract: It may not be possible to find a futures contract on the exact asset. The hedging firm may not know the exact date when the hedged asset will be bought or sold. The maturity of the futures contract may not match the anticipated risk exposure period of the underlying asset. Hedging with Futures Contract Basis risk is the failure of the hedge for any of the above reasons. Basis risk occurs whenever the price of the asset that underlies the futures contract is not perfectly correlated with the price risk the firm is trying to hedge. Hedging with Futures Contract If a specific asset is not available, the best alternative is to use an asset whose price changes are highly correlated with the asset. For example, hedging corn with soybean future if the prices of the two commodities are highly correlated. If a contract with exact duration is not available, the analysts must select a contract that most nearly matches the maturity of the firm s risk exposure. 16

17 Option Contracts Options are rights (not an obligation) to buy or sell a given number of shares or an asset at a specific price over a given period. The option owner s right to buy is known as a call option while the right to sell is known as a put option. Option Contracts Exercise price: The price at which the asset can be bought or sold. Option premium: The price paid for the option. Option expiration date: The date on which the option contract expires. American option: These options can be exercised anytime up to the expiration date of the contract. European option: These options can be exercised only on the expiration date. Option Contracts For example, if you buy a call option on 100 shares of XYZ stock at a premium of $4.50 and exercise price of $40 maturing in 90 days. You can buy the XYZ stock at $40 even though the You can buy the XYZ stock at $40, even though the market price of the stock maybe above $40. If the stock price is below $40, you will choose not to use your option contract and will lose the premium paid. 17

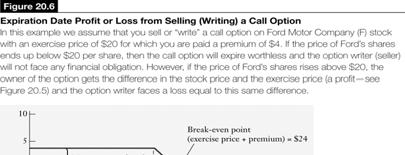

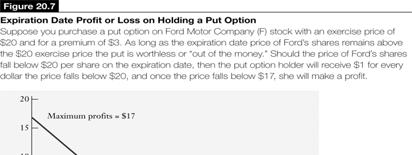

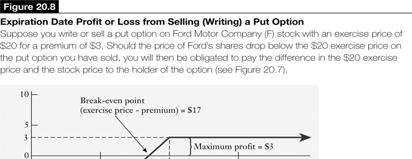

18 Option Contracts For example, if you buy a put option on 100 shares of ABC stock at a premium of $10.50 and exercise price of $70 maturing in 90 days. You can sell the ABC stock at $70, even though the market price of the stock maybe below $70. If the market price of stock is above $70, you will choose not to use your option contract and will lose the premium paid. A Graphical Look at Option Pricing Relationships Figures 20-5 to Figures 20-8 graphically illustrate the expiration date profit or loss from the following option positions: Buying a call option (figure 20-5) Selling or writing a call option (figure 20-6) Buying a put option (figure 20-7) Selling or writing a put option (figure 20-8) The graphs are based on the following assumptions: Exercise price for call and put options = $20 Call premium = $4 Put premium = $3 18

19 19

20 A Graphical Look at Option Pricing Relationships Buy Call Write Call Buy Put Write Put Maximum Profit Unlimited Premium Exercise Price - Premium Premium Maximum Loss Premium Unlimited Premium Exercise Price - Premium Future Market Expectation Bullish Bearish Bearish Bullish Break-even Point Exercise Price + Premium Exercise Price + Premium Exercise Price Premium Exercise Price - Premium 20.5 Valuing Options and Swaps Valuing Options and Swaps The value of option can be regarded as the present value of the expected payout when the option expires. The most popular option pricing model is the Black- Scholes Option Pricing Model (BS-OPM). 20

21 Black-Scholes Option Pricing Model There are six variables that impact the price of an option: 1. The price of the underlying stock 2. The option s exercise or strike price 3. The length of time left until expiration 4. The expected stock price volatility 5. The risk free rate of interest 6. The underlying stock s dividend yield Black-Scholes Option Pricing Model What IF Value of Call option Value of Put Option Price of underlying stock increases Increases Decreases Exercise price is higher Decreases Increases Time to expiration is longer Increases Increases Stock price volatility is higher over the life of the option Increases Increases Risk-free rate of interest is higher Increases Decreases The stock pays dividend Decreases Increases Black-Scholes Option Pricing Model Black-Scholes option pricing model for call options is stated as follows: 21

variance in the returns of the stock is.")

22 Checkpoint 20.3 Valuing a Call Option Using the Black-Scholes Model Consider the following call option: the current price of the stock on which the call option is written is $32.00; the exercise or strike price of the call option is $30.00; the maturity of the option is.25 years; the (annualized) variance in the returns of the stock is.16; and the risk-free rate of interest is 4% per annum. Use the Black-Scholes option pricing model to estimate the value of the call option. Checkpoint 20.3 Checkpoint

23 Checkpoint 20.3: Check Yourself Estimate the value of the above call option when the exercise price is $25. Step 1: Picture the Problem Given: Current price of stock = $32 Exercise price = $25 Maturity = 90 days or 0.25 years Variance in stock returns =.16 Risk-free rate =12% per annum Step 1: Picture the Problem Stock Price Call Premium Exercise Price Exercised or Not Profit or Loss A B C D E =Max(O, A-C)-B $20 ($5) $25 No ($5) Profit when stock is $25 or $32 $25 ($5) $25 No ($5) $30 ($5) $25 Yes $0 $32 ($5) $25 Yes $2 $35 ($5) $25 Yes $5 $40 ($5) $25 Yes $10 Break-even point 23

24 Step 1: Picture the Problem $12 Profits from Buying Calls $10 $8 Profits, Exercise Pric ce =$25 $6 $4 $2 $0 $0 $5 $10 $15 $20 $25 $30 $35 $40 $45 ($2) ($4) ($6) Stock Price Step 2: Decide on a Solution Strategy Equation 20-1 can be used to determine the value of call option using Black-Scholes option pricing model. Step 3: Solve Line d-1 (steps) Computation 1 In(S/E) R=.5(Variance) xt line 2* Numerator line 1+line txvariance.16* Sqrt(T*Variance) sqrt(line5) d-1 line 4/line

25 Step 3: Solve Line d-2 (steps) Computation o 8 txvariance.16* sqrt(t*variance) sqrt (line 8) d-2 line (7-9) N(d1) Normsdist (line7) N(d2) Normsdist (line10) Step 3: Solve Line Call value (steps) Computation o 13 S*N(d-1) $32*line R*t -0.12* exp^(-r*t) exp (line 14) E*e^RT*N(d-2) $25*line 15*line Call Value Line 13-Line Step 4: Analyze The value of this option is $7.95 using BS-OPM. The current stock price of $32 represents a $7 profit over the exercise price of $25. The additional $0.95 can be seen as the time value of the call option Premium available in the market for the possibility that stock price may rise even higher over the next 90 days. 25

26 Swap Contract A swap contract involves the swapping or trading of one set of payments for another. A currency swap involves exchange of debt obligations in different currencies. An interest rate swap involves trading of fixed interest payments for variable or floating rate interest rate payments between two currencies. A swap contract can be thought of as a series of forward contracts. Swap Contract Figure illustrates 5-year fixed for floating interest rate swap and a notational principal of $250 million. Notational principal is the amount used to calculate payments for the contract but this amount does not change hands. The floating rate = 6-month LIBOR The fixed rate = 9.75% Interest is paid semi-annually. 26

Chapter 20. Corporate Risk Management. Copyright 2011 Pearson Prentice Hall. All rights reserved.

Chapter 20 Corporate Risk Management 1 Chapter 14 Contents 1. Five-Step Corporate Risk Management Process 2. Managing Risk with Insurance Contracts 3. Managing Risk by Hedging with Forward Contracts 4.

Chapter 20 Corporate Risk Management 1 Chapter 14 Contents 1. Five-Step Corporate Risk Management Process 2. Managing Risk with Insurance Contracts 3. Managing Risk by Hedging with Forward Contracts 4.

Forwards, Futures, Options and Swaps

Forwards, Futures, Options and Swaps A derivative asset is any asset whose payoff, price or value depends on the payoff, price or value of another asset. The underlying or primitive asset may be almost

Forwards, Futures, Options and Swaps A derivative asset is any asset whose payoff, price or value depends on the payoff, price or value of another asset. The underlying or primitive asset may be almost

Copyright 2009 Pearson Education Canada

CHAPTER NINE Qualitative Questions 1. What is the difference between a call option and a put option? For an option buyer, a call option is the right to buy, while a put option is the right to sell. For

CHAPTER NINE Qualitative Questions 1. What is the difference between a call option and a put option? For an option buyer, a call option is the right to buy, while a put option is the right to sell. For

CIS March 2012 Diet. Examination Paper 2.3: Derivatives Valuation Analysis Portfolio Management Commodity Trading and Futures.

CIS March 2012 Diet Examination Paper 2.3: Derivatives Valuation Analysis Portfolio Management Commodity Trading and Futures Level 2 Derivative Valuation and Analysis (1 12) 1. A CIS student was making

CIS March 2012 Diet Examination Paper 2.3: Derivatives Valuation Analysis Portfolio Management Commodity Trading and Futures Level 2 Derivative Valuation and Analysis (1 12) 1. A CIS student was making

SOCIETY OF ACTUARIES FINANCIAL MATHEMATICS. EXAM FM SAMPLE QUESTIONS Financial Economics

SOCIETY OF ACTUARIES EXAM FM FINANCIAL MATHEMATICS EXAM FM SAMPLE QUESTIONS Financial Economics June 2014 changes Questions 1-30 are from the prior version of this document. They have been edited to conform

SOCIETY OF ACTUARIES EXAM FM FINANCIAL MATHEMATICS EXAM FM SAMPLE QUESTIONS Financial Economics June 2014 changes Questions 1-30 are from the prior version of this document. They have been edited to conform

Derivatives Questions Question 1 Explain carefully the difference between hedging, speculation, and arbitrage.

Derivatives Questions Question 1 Explain carefully the difference between hedging, speculation, and arbitrage. Question 2 What is the difference between entering into a long forward contract when the forward

Derivatives Questions Question 1 Explain carefully the difference between hedging, speculation, and arbitrage. Question 2 What is the difference between entering into a long forward contract when the forward

Q&A, 10/08/03. To buy and sell options do we need to contact the broker or can it be dome from programs like Bloomberg?

Q&A, 10/08/03 Dear Students, Thanks for asking these great questions! The answer to my question (what is a put) I you all got right: put is an option contract giving you the right to sell. Here are the

Q&A, 10/08/03 Dear Students, Thanks for asking these great questions! The answer to my question (what is a put) I you all got right: put is an option contract giving you the right to sell. Here are the

Answers to Selected Problems

Answers to Selected Problems Problem 1.11. he farmer can short 3 contracts that have 3 months to maturity. If the price of cattle falls, the gain on the futures contract will offset the loss on the sale

Answers to Selected Problems Problem 1.11. he farmer can short 3 contracts that have 3 months to maturity. If the price of cattle falls, the gain on the futures contract will offset the loss on the sale

PRACTICE QUESTIONS DERIVATIVES MARKET (DEALERS) MODULE

MODULE") PRACTICE QUESTIONS DERIVATIVES MARKET (DEALERS) MODULE 1. Swaps can be regarded as portfolios of. [ 1 Mark ] (a) Future Contracts (b) Option Contracts (c) Call Options (d) Forward Contracts 2. A stock

PRACTICE QUESTIONS DERIVATIVES MARKET (DEALERS) MODULE 1. Swaps can be regarded as portfolios of. [ 1 Mark ] (a) Future Contracts (b) Option Contracts (c) Call Options (d) Forward Contracts 2. A stock

Options Markets: Introduction

17-2 Options Options Markets: Introduction Derivatives are securities that get their value from the price of other securities. Derivatives are contingent claims because their payoffs depend on the value

17-2 Options Options Markets: Introduction Derivatives are securities that get their value from the price of other securities. Derivatives are contingent claims because their payoffs depend on the value

Financial Markets and Products

Financial Markets and Products 1. Which of the following types of traders never take position in the derivative instruments? a) Speculators b) Hedgers c) Arbitrageurs d) None of the above 2. Which of the

Financial Markets and Products 1. Which of the following types of traders never take position in the derivative instruments? a) Speculators b) Hedgers c) Arbitrageurs d) None of the above 2. Which of the

Answers to Selected Problems

Answers to Selected Problems Problem 1.11. he farmer can short 3 contracts that have 3 months to maturity. If the price of cattle falls, the gain on the futures contract will offset the loss on the sale

Answers to Selected Problems Problem 1.11. he farmer can short 3 contracts that have 3 months to maturity. If the price of cattle falls, the gain on the futures contract will offset the loss on the sale

Problems and Solutions Manual

Problems and Solutions Manual to accompany Derivatives: Principles & Practice Rangarajan K. Sundaram Sanjiv R. Das April 2, 2010 Sundaram & Das: Derivatives - Problems and Solutions..................................1

Problems and Solutions Manual to accompany Derivatives: Principles & Practice Rangarajan K. Sundaram Sanjiv R. Das April 2, 2010 Sundaram & Das: Derivatives - Problems and Solutions..................................1

Appendix A Financial Calculations

Derivatives Demystified: A Step-by-Step Guide to Forwards, Futures, Swaps and Options, Second Edition By Andrew M. Chisholm 010 John Wiley & Sons, Ltd. Appendix A Financial Calculations TIME VALUE OF MONEY

Derivatives Demystified: A Step-by-Step Guide to Forwards, Futures, Swaps and Options, Second Edition By Andrew M. Chisholm 010 John Wiley & Sons, Ltd. Appendix A Financial Calculations TIME VALUE OF MONEY

Risk Management Using Derivatives Securities

Risk Management Using Derivatives Securities 1 Definition of Derivatives A derivative is a financial instrument whose value is derived from the price of a more basic asset called the underlying asset.

Risk Management Using Derivatives Securities 1 Definition of Derivatives A derivative is a financial instrument whose value is derived from the price of a more basic asset called the underlying asset.

Financial Markets & Risk

Financial Markets & Risk Dr Cesario MATEUS Senior Lecturer in Finance and Banking Room QA259 Department of Accounting and Finance c.mateus@greenwich.ac.uk www.cesariomateus.com Session 3 Derivatives Binomial

Financial Markets & Risk Dr Cesario MATEUS Senior Lecturer in Finance and Banking Room QA259 Department of Accounting and Finance c.mateus@greenwich.ac.uk www.cesariomateus.com Session 3 Derivatives Binomial

BBK3273 International Finance

BBK3273 International Finance Prepared by Dr Khairul Anuar L6: Transaction Exposure www.notes638.wordpress.com Contents 1. Transaction Exposure 2. Policies for Hedging Transaction Exposure 3. Hedging Exposure

BBK3273 International Finance Prepared by Dr Khairul Anuar L6: Transaction Exposure www.notes638.wordpress.com Contents 1. Transaction Exposure 2. Policies for Hedging Transaction Exposure 3. Hedging Exposure

2. Futures and Forward Markets 2.1. Institutions

2. Futures and Forward Markets 2.1. Institutions 1. (Hull 2.3) Suppose that you enter into a short futures contract to sell July silver for $5.20 per ounce on the New York Commodity Exchange. The size

2. Futures and Forward Markets 2.1. Institutions 1. (Hull 2.3) Suppose that you enter into a short futures contract to sell July silver for $5.20 per ounce on the New York Commodity Exchange. The size

Strike Bid Ask Strike Bid Ask # # # # Expected Price($)

") 1 Exercises on Stock Options The price of XYZ stock is $201.09, and the bid/ask prices of call and put options on this stock which expire in two months are shown below (all in dollars). Call Options Put

1 Exercises on Stock Options The price of XYZ stock is $201.09, and the bid/ask prices of call and put options on this stock which expire in two months are shown below (all in dollars). Call Options Put

Functional Training & Basel II Reporting and Methodology Review: Derivatives

Functional Training & Basel II Reporting and Methodology Review: Copyright 2010 ebis. All rights reserved. Page i Table of Contents 1 EXPOSURE DEFINITIONS...2 1.1 DERIVATIVES...2 1.1.1 Introduction...2

Functional Training & Basel II Reporting and Methodology Review: Copyright 2010 ebis. All rights reserved. Page i Table of Contents 1 EXPOSURE DEFINITIONS...2 1.1 DERIVATIVES...2 1.1.1 Introduction...2

11 06 Class 12 Forwards and Futures

11 06 Class 12 Forwards and Futures From banks to futures markets Financial i l markets as insurance markets Instruments and exchanges; The counterparty risk problem 1 From last time Banks face bank runs

11 06 Class 12 Forwards and Futures From banks to futures markets Financial i l markets as insurance markets Instruments and exchanges; The counterparty risk problem 1 From last time Banks face bank runs

Chapter 11 Currency Risk Management

Chapter 11 Currency Risk Management Note: In these problems, the notation / is used to mean per. For example, 158/$ means 158 per $. 1. To lock in the rate at which yen can be converted into U.S. dollars,

Chapter 11 Currency Risk Management Note: In these problems, the notation / is used to mean per. For example, 158/$ means 158 per $. 1. To lock in the rate at which yen can be converted into U.S. dollars,

JEM034 Corporate Finance Winter Semester 2017/2018

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #7 Olga Bychkova Topics Covered Today Risk Management (chapter 26 in BMA) Hedging with Forwards and Futures Futures and Spot Contracts Swaps Hedging

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #7 Olga Bychkova Topics Covered Today Risk Management (chapter 26 in BMA) Hedging with Forwards and Futures Futures and Spot Contracts Swaps Hedging

Chapter 8. Swaps. Copyright 2009 Pearson Prentice Hall. All rights reserved.

Chapter 8 Swaps Introduction to Swaps A swap is a contract calling for an exchange of payments, on one or more dates, determined by the difference in two prices A swap provides a means to hedge a stream

Chapter 8 Swaps Introduction to Swaps A swap is a contract calling for an exchange of payments, on one or more dates, determined by the difference in two prices A swap provides a means to hedge a stream

BBK3273 International Finance

BBK3273 International Finance Prepared by Dr Khairul Anuar L6: Transaction Exposure www.notes638.wordpress.com Contents 1. Transaction Exposure 2. Policies for Hedging Transaction Exposure 3. Hedging Exposure

BBK3273 International Finance Prepared by Dr Khairul Anuar L6: Transaction Exposure www.notes638.wordpress.com Contents 1. Transaction Exposure 2. Policies for Hedging Transaction Exposure 3. Hedging Exposure

Introduction, Forwards and Futures

Introduction, Forwards and Futures Liuren Wu Options Markets Liuren Wu ( ) Introduction, Forwards & Futures Options Markets 1 / 31 Derivatives Derivative securities are financial instruments whose returns

Introduction, Forwards and Futures Liuren Wu Options Markets Liuren Wu ( ) Introduction, Forwards & Futures Options Markets 1 / 31 Derivatives Derivative securities are financial instruments whose returns

Finance 100 Problem Set 6 Futures (Alternative Solutions)

") Finance 100 Problem Set 6 Futures (Alternative Solutions) Note: Where appropriate, the final answer for each problem is given in bold italics for those not interested in the discussion of the solution.

Finance 100 Problem Set 6 Futures (Alternative Solutions) Note: Where appropriate, the final answer for each problem is given in bold italics for those not interested in the discussion of the solution.

The following table summarizes the unhedged and hedged profit calculations:

Chapter 4 Introduction to Risk Management Question 4.1 The following table summarizes the unhedged and hedged calculations: Copper price in one year Total cost short forward Net income on hedged $0.70

Chapter 4 Introduction to Risk Management Question 4.1 The following table summarizes the unhedged and hedged calculations: Copper price in one year Total cost short forward Net income on hedged $0.70

AGRICULTURAL RISK MANAGEMENT. Global Grain Geneva November 12, 2013

AGRICULTURAL RISK MANAGEMENT Global Grain Geneva November 12, 2013 Managing Price Risk is Easier to Swallow Than THE ALTERNATIVE Is Your Business Protected Is Your Business Protected Is Your Business Protected

AGRICULTURAL RISK MANAGEMENT Global Grain Geneva November 12, 2013 Managing Price Risk is Easier to Swallow Than THE ALTERNATIVE Is Your Business Protected Is Your Business Protected Is Your Business Protected

1. Risk Management: Forwards and Futures 3 2. Risk Management: Options Risk Management: Swaps Key Formulas 65

1. Risk Management: Forwards and Futures 3 2. Risk Management: Options 21 3. Risk Management: Swaps 51 4. Key Formulas 65 2014 Allen Resources, Inc. All rights reserved. Warning: Copyright violations will

1. Risk Management: Forwards and Futures 3 2. Risk Management: Options 21 3. Risk Management: Swaps 51 4. Key Formulas 65 2014 Allen Resources, Inc. All rights reserved. Warning: Copyright violations will

Currency Option Combinations

APPENDIX5B Currency Option Combinations 160 In addition to the basic call and put options just discussed, a variety of currency option combinations are available to the currency speculator and hedger.

APPENDIX5B Currency Option Combinations 160 In addition to the basic call and put options just discussed, a variety of currency option combinations are available to the currency speculator and hedger.

UNIVERSITÀ DEGLI STUDI DI TORINO SCHOOL OF MANAGEMENT AND ECONOMICS SIMULATION MODELS FOR ECONOMICS. Final Report. Stop-Loss Strategy

UNIVERSITÀ DEGLI STUDI DI TORINO SCHOOL OF MANAGEMENT AND ECONOMICS SIMULATION MODELS FOR ECONOMICS Final Report Stop-Loss Strategy Prof. Pietro Terna Edited by Luca Di Salvo, Giorgio Melon, Luca Pischedda

UNIVERSITÀ DEGLI STUDI DI TORINO SCHOOL OF MANAGEMENT AND ECONOMICS SIMULATION MODELS FOR ECONOMICS Final Report Stop-Loss Strategy Prof. Pietro Terna Edited by Luca Di Salvo, Giorgio Melon, Luca Pischedda

AFM 371 Winter 2008 Chapter 26 - Derivatives and Hedging Risk Part 2 - Interest Rate Risk Management ( )

") AFM 371 Winter 2008 Chapter 26 - Derivatives and Hedging Risk Part 2 - Interest Rate Risk Management (26.4-26.7) 1 / 30 Outline Term Structure Forward Contracts on Bonds Interest Rate Futures Contracts

AFM 371 Winter 2008 Chapter 26 - Derivatives and Hedging Risk Part 2 - Interest Rate Risk Management (26.4-26.7) 1 / 30 Outline Term Structure Forward Contracts on Bonds Interest Rate Futures Contracts

STRATEGIES WITH OPTIONS

MÄLARDALEN UNIVERSITY PROJECT DEPARTMENT OF MATHEMATICS AND PHYSICS ANALYTICAL FINANCE I, MT1410 TEACHER: JAN RÖMAN 2003-10-21 STRATEGIES WITH OPTIONS GROUP 3: MAGNUS SÖDERHOLTZ MAZYAR ROSTAMI SABAHUDIN

MÄLARDALEN UNIVERSITY PROJECT DEPARTMENT OF MATHEMATICS AND PHYSICS ANALYTICAL FINANCE I, MT1410 TEACHER: JAN RÖMAN 2003-10-21 STRATEGIES WITH OPTIONS GROUP 3: MAGNUS SÖDERHOLTZ MAZYAR ROSTAMI SABAHUDIN

FNCE4830 Investment Banking Seminar

FNCE4830 Investment Banking Seminar Introduction on Derivatives What is a Derivative? A derivative is an instrument whose value depends on, or is derived from, the value of another asset. Examples: Futures

FNCE4830 Investment Banking Seminar Introduction on Derivatives What is a Derivative? A derivative is an instrument whose value depends on, or is derived from, the value of another asset. Examples: Futures

Finance 527: Lecture 30, Options V2

Finance 527: Lecture 30, Options V2 [John Nofsinger]: This is the second video for options and so remember from last time a long position is-in the case of the call option-is the right to buy the underlying

Finance 527: Lecture 30, Options V2 [John Nofsinger]: This is the second video for options and so remember from last time a long position is-in the case of the call option-is the right to buy the underlying

Swaptions. Product nature

Product nature Swaptions The buyer of a swaption has the right to enter into an interest rate swap by some specified date. The swaption also specifies the maturity date of the swap. The buyer can be the

Product nature Swaptions The buyer of a swaption has the right to enter into an interest rate swap by some specified date. The swaption also specifies the maturity date of the swap. The buyer can be the

CHAPTER 17 OPTIONS AND CORPORATE FINANCE

CHAPTER 17 OPTIONS AND CORPORATE FINANCE Answers to Concept Questions 1. A call option confers the right, without the obligation, to buy an asset at a given price on or before a given date. A put option

CHAPTER 17 OPTIONS AND CORPORATE FINANCE Answers to Concept Questions 1. A call option confers the right, without the obligation, to buy an asset at a given price on or before a given date. A put option

Accounting for Derivatives

Accounting for Derivatives Publication Date: August 2015 1 Accounting for Derivatives Copyright 2015 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any form or by any

Accounting for Derivatives Publication Date: August 2015 1 Accounting for Derivatives Copyright 2015 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any form or by any

FNCE 302, Investments H Guy Williams, 2008

Sources http://finance.bi.no/~bernt/gcc_prog/recipes/recipes/node7.html It's all Greek to me, Chris McMahon Futures; Jun 2007; 36, 7 http://www.quantnotes.com Put Call Parity THIS IS THE CALL-PUT PARITY

Sources http://finance.bi.no/~bernt/gcc_prog/recipes/recipes/node7.html It's all Greek to me, Chris McMahon Futures; Jun 2007; 36, 7 http://www.quantnotes.com Put Call Parity THIS IS THE CALL-PUT PARITY

Finance 402: Problem Set 7 Solutions

Finance 402: Problem Set 7 Solutions Note: Where appropriate, the final answer for each problem is given in bold italics for those not interested in the discussion of the solution. 1. Consider the forward

Finance 402: Problem Set 7 Solutions Note: Where appropriate, the final answer for each problem is given in bold italics for those not interested in the discussion of the solution. 1. Consider the forward

Portfolio Management Philip Morris has issued bonds that pay coupons annually with the following characteristics:

Portfolio Management 010-011 1. a. Critically discuss the mean-variance approach of portfolio theory b. According to Markowitz portfolio theory, can we find a single risky optimal portfolio which is suitable

Portfolio Management 010-011 1. a. Critically discuss the mean-variance approach of portfolio theory b. According to Markowitz portfolio theory, can we find a single risky optimal portfolio which is suitable

Introduction to Forwards and Futures

Introduction to Forwards and Futures Liuren Wu Options Pricing Liuren Wu ( c ) Introduction, Forwards & Futures Options Pricing 1 / 27 Outline 1 Derivatives 2 Forwards 3 Futures 4 Forward pricing 5 Interest

Introduction to Forwards and Futures Liuren Wu Options Pricing Liuren Wu ( c ) Introduction, Forwards & Futures Options Pricing 1 / 27 Outline 1 Derivatives 2 Forwards 3 Futures 4 Forward pricing 5 Interest

Chapter 5. Risk Handling Techniques: Diversification and Hedging. Risk Bearing Institutions. Additional Benefits. Chapter 5 Page 1

Chapter 5 Risk Handling Techniques: Diversification and Hedging Risk Bearing Institutions Bearing risk collectively Diversification Examples: Pension Plans Mutual Funds Insurance Companies Additional Benefits

Chapter 5 Risk Handling Techniques: Diversification and Hedging Risk Bearing Institutions Bearing risk collectively Diversification Examples: Pension Plans Mutual Funds Insurance Companies Additional Benefits

CHAPTER 16: MANAGING BOND PORTFOLIOS

CHAPTER 16: MANAGING BOND PORTFOLIOS 1. The percentage change in the bond s price is: Duration 7.194 y = 0.005 = 0.0327 = 3.27% or a 3.27% decline. 1+ y 1.10 2. a. YTM = 6% (1) (2) (3) (4) (5) PV of CF

CHAPTER 16: MANAGING BOND PORTFOLIOS 1. The percentage change in the bond s price is: Duration 7.194 y = 0.005 = 0.0327 = 3.27% or a 3.27% decline. 1+ y 1.10 2. a. YTM = 6% (1) (2) (3) (4) (5) PV of CF

Mathematics of Finance II: Derivative securities

Mathematics of Finance II: Derivative securities MHAMED EDDAHBI King Saud University College of Sciences Mathematics Department Riyadh Saudi Arabia e mail: meddahbi@ksu.edu.sa Second term 2015 2016 Chapter

Mathematics of Finance II: Derivative securities MHAMED EDDAHBI King Saud University College of Sciences Mathematics Department Riyadh Saudi Arabia e mail: meddahbi@ksu.edu.sa Second term 2015 2016 Chapter

Interest Rates & Credit Derivatives

Interest Rates & Credit Derivatives Ashish Ghiya Derivium Tradition (India) 25/06/14 1 Agenda Introduction to Interest Rate & Credit Derivatives Practical Uses of Derivatives Derivatives Going Wrong Practical

Interest Rates & Credit Derivatives Ashish Ghiya Derivium Tradition (India) 25/06/14 1 Agenda Introduction to Interest Rate & Credit Derivatives Practical Uses of Derivatives Derivatives Going Wrong Practical

Call Options - Outline

Call Options - Outline 1 B.1.1 Call Options - Part 1 Quick Review of a Long Forward Call Option Details To Exercise or Not To Exercise Purchased Call Payoff Exercises B.1.1 Call Options - Part 1 1 / 9

Call Options - Outline 1 B.1.1 Call Options - Part 1 Quick Review of a Long Forward Call Option Details To Exercise or Not To Exercise Purchased Call Payoff Exercises B.1.1 Call Options - Part 1 1 / 9

FNCE4830 Investment Banking Seminar

FNCE4830 Investment Banking Seminar Introduction on Derivatives What is a Derivative? A derivative is an instrument whose value depends on, or is derived from, the value of another asset. Examples: Futures

FNCE4830 Investment Banking Seminar Introduction on Derivatives What is a Derivative? A derivative is an instrument whose value depends on, or is derived from, the value of another asset. Examples: Futures

Chapter 14. Exotic Options: I. Question Question Question Question The geometric averages for stocks will always be lower.

Chapter 14 Exotic Options: I Question 14.1 The geometric averages for stocks will always be lower. Question 14.2 The arithmetic average is 5 (three 5s, one 4, and one 6) and the geometric average is (5

Chapter 14 Exotic Options: I Question 14.1 The geometric averages for stocks will always be lower. Question 14.2 The arithmetic average is 5 (three 5s, one 4, and one 6) and the geometric average is (5

SOCIETY OF ACTUARIES EXAM IFM INVESTMENT AND FINANCIAL MARKETS EXAM IFM SAMPLE QUESTIONS AND SOLUTIONS DERIVATIVES

SOCIETY OF ACTUARIES EXAM IFM INVESTMENT AND FINANCIAL MARKETS EXAM IFM SAMPLE QUESTIONS AND SOLUTIONS DERIVATIVES These questions and solutions are based on the readings from McDonald and are identical

SOCIETY OF ACTUARIES EXAM IFM INVESTMENT AND FINANCIAL MARKETS EXAM IFM SAMPLE QUESTIONS AND SOLUTIONS DERIVATIVES These questions and solutions are based on the readings from McDonald and are identical

Pricing Options with Mathematical Models

Pricing Options with Mathematical Models 1. OVERVIEW Some of the content of these slides is based on material from the book Introduction to the Economics and Mathematics of Financial Markets by Jaksa Cvitanic

Pricing Options with Mathematical Models 1. OVERVIEW Some of the content of these slides is based on material from the book Introduction to the Economics and Mathematics of Financial Markets by Jaksa Cvitanic

CHAPTER 10 INTEREST RATE & CURRENCY SWAPS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS

CHAPTER 10 INTEREST RATE & CURRENCY SWAPS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Describe the difference between a swap broker and a swap dealer. Answer:

CHAPTER 10 INTEREST RATE & CURRENCY SWAPS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Describe the difference between a swap broker and a swap dealer. Answer:

Financial Markets and Products

Financial Markets and Products 1. Eric sold a call option on a stock trading at $40 and having a strike of $35 for $7. What is the profit of the Eric from the transaction if at expiry the stock is trading

Financial Markets and Products 1. Eric sold a call option on a stock trading at $40 and having a strike of $35 for $7. What is the profit of the Eric from the transaction if at expiry the stock is trading

University of Siegen

University of Siegen Faculty of Economic Disciplines, Department of economics Univ. Prof. Dr. Jan Franke-Viebach Seminar Risk and Finance Summer Semester 2008 Topic 4: Hedging with currency futures Name

University of Siegen Faculty of Economic Disciplines, Department of economics Univ. Prof. Dr. Jan Franke-Viebach Seminar Risk and Finance Summer Semester 2008 Topic 4: Hedging with currency futures Name

Volatility Monitor. 3 rd Quarter 2012 OCTOBER 11, John W. Labuszewski

Volatility Monitor 3 rd Quarter 2012 OCTOBER 11, 2012 John W. Labuszewski Managing Director Research & Product Development 312-466-7469 jlab@cmegroup.com Volatility is one of several key inputs into mathematical

Volatility Monitor 3 rd Quarter 2012 OCTOBER 11, 2012 John W. Labuszewski Managing Director Research & Product Development 312-466-7469 jlab@cmegroup.com Volatility is one of several key inputs into mathematical

TABLE OF CONTENTS Chapter 1: Introduction 4 The use of financial derivatives and the importance of options between a buyer and a seller 5 The scope

TABLE OF CONTENTS Chapter 1: Introduction 4 The use of financial derivatives and the importance of options between a buyer and a seller 5 The scope of the work 6 Chapter 2: Derivatives 7 2.1 Introduction

TABLE OF CONTENTS Chapter 1: Introduction 4 The use of financial derivatives and the importance of options between a buyer and a seller 5 The scope of the work 6 Chapter 2: Derivatives 7 2.1 Introduction

Managing Financial Risk with Forwards, Futures, Options, and Swaps. Second Edition

Managing Financial Risk with Forwards, Futures, Options, and Swaps Second Edition Managing Financial Risk with Forwards, Futures, Options, and Swaps Second Edition Fred R. Kaen Contents About This Course

Managing Financial Risk with Forwards, Futures, Options, and Swaps Second Edition Managing Financial Risk with Forwards, Futures, Options, and Swaps Second Edition Fred R. Kaen Contents About This Course

READING 8: RISK MANAGEMENT APPLICATIONS OF FORWARDS AND FUTURES STRATEGIES

READING 8: RISK MANAGEMENT APPLICATIONS OF FORWARDS AND FUTURES STRATEGIES Modifying a portfolio duration using futures: Number of future contract to be bought or (sold) (target duration bond portfolio

READING 8: RISK MANAGEMENT APPLICATIONS OF FORWARDS AND FUTURES STRATEGIES Modifying a portfolio duration using futures: Number of future contract to be bought or (sold) (target duration bond portfolio

Commodity Options : Gold, Crude, Copper, Silver

Commodity Options : Gold, Crude, Copper, Silver WHY OPTIONS? An option contract offers the best of both worlds. It will offer the buyer of the contract protection if the price of the underlying moves against

Commodity Options : Gold, Crude, Copper, Silver WHY OPTIONS? An option contract offers the best of both worlds. It will offer the buyer of the contract protection if the price of the underlying moves against

A CLEAR UNDERSTANDING OF THE INDUSTRY

A CLEAR UNDERSTANDING OF THE INDUSTRY IS CFA INSTITUTE INVESTMENT FOUNDATIONS RIGHT FOR YOU? Investment Foundations is a certificate program designed to give you a clear understanding of the investment

A CLEAR UNDERSTANDING OF THE INDUSTRY IS CFA INSTITUTE INVESTMENT FOUNDATIONS RIGHT FOR YOU? Investment Foundations is a certificate program designed to give you a clear understanding of the investment

Financial Derivatives Section 1

Financial Derivatives Section 1 Forwards & Futures Michail Anthropelos anthropel@unipi.gr http://web.xrh.unipi.gr/faculty/anthropelos/ University of Piraeus Spring 2018 M. Anthropelos (Un. of Piraeus)

Financial Derivatives Section 1 Forwards & Futures Michail Anthropelos anthropel@unipi.gr http://web.xrh.unipi.gr/faculty/anthropelos/ University of Piraeus Spring 2018 M. Anthropelos (Un. of Piraeus)

Futures and Forward Markets

Futures and Forward Markets (Text reference: Chapters 19, 21.4) background hedging and speculation optimal hedge ratio forward and futures prices futures prices and expected spot prices stock index futures

Futures and Forward Markets (Text reference: Chapters 19, 21.4) background hedging and speculation optimal hedge ratio forward and futures prices futures prices and expected spot prices stock index futures

Investing over the life-cycle building wealth. Introduction:

Investing over the life-cycle building wealth Introduction: Many investors are currently confused as to how best to approach the construction of an appropriate portfolio of investments, in order to build

Investing over the life-cycle building wealth Introduction: Many investors are currently confused as to how best to approach the construction of an appropriate portfolio of investments, in order to build

Lecture 11. SWAPs markets. I. Background of Interest Rate SWAP markets. Types of Interest Rate SWAPs

Lecture 11 SWAPs markets Agenda: I. Background of Interest Rate SWAP markets II. Types of Interest Rate SWAPs II.1 Plain vanilla swaps II.2 Forward swaps II.3 Callable swaps (Swaptions) II.4 Putable swaps

Lecture 11 SWAPs markets Agenda: I. Background of Interest Rate SWAP markets II. Types of Interest Rate SWAPs II.1 Plain vanilla swaps II.2 Forward swaps II.3 Callable swaps (Swaptions) II.4 Putable swaps

Basic Option Strategies

Page 1 of 9 Basic Option Strategies This chapter considers trading strategies for profiting from our ability to conduct a fundamental and technical analysis of a stock by extending our MCD example. In

Page 1 of 9 Basic Option Strategies This chapter considers trading strategies for profiting from our ability to conduct a fundamental and technical analysis of a stock by extending our MCD example. In

HEDGING WITH FUTURES AND BASIS

Futures & Options 1 Introduction The more producer know about the markets, the better equipped producer will be, based on current market conditions and your specific objectives, to decide whether to use

Futures & Options 1 Introduction The more producer know about the markets, the better equipped producer will be, based on current market conditions and your specific objectives, to decide whether to use

Final Exam. 5. (21 points) Short Questions. Parts (i)-(v) are multiple choice: in each case, only one answer is correct.

Short Questions. Parts (i)-(v) are multiple choice: in each case, only one answer is correct.") Final Exam Spring 016 Econ 180-367 Closed Book. Formula Sheet Provided. Calculators OK. Time Allowed: 3 hours Please write your answers on the page below each question 1. (10 points) What is the duration

Final Exam Spring 016 Econ 180-367 Closed Book. Formula Sheet Provided. Calculators OK. Time Allowed: 3 hours Please write your answers on the page below each question 1. (10 points) What is the duration

Chapter 1 Introduction. Options, Futures, and Other Derivatives, 8th Edition, Copyright John C. Hull

Chapter 1 Introduction 1 What is a Derivative? A derivative is an instrument whose value depends on, or is derived from, the value of another asset. Examples: futures, forwards, swaps, options, exotics

Chapter 1 Introduction 1 What is a Derivative? A derivative is an instrument whose value depends on, or is derived from, the value of another asset. Examples: futures, forwards, swaps, options, exotics

Deutsche Bank Foreign Exchange Management at Deutsche Bank

Deutsche Bank www.deutschebank.nl Foreign Exchange Management at Deutsche Bank Foreign Exchange Management at Deutsche Bank 1. Why is this prospectus important? In this prospectus we will provide general

Deutsche Bank www.deutschebank.nl Foreign Exchange Management at Deutsche Bank Foreign Exchange Management at Deutsche Bank 1. Why is this prospectus important? In this prospectus we will provide general

Derivatives and Hedging. Mike Loritz and Tim Woods

MHM Executive Education Series: Derivatives and Hedging Presented by: Mike Loritz and Tim Woods August 16, 2012 Agenda Basics - Overview of the definition of a derivative Identification and accounting

MHM Executive Education Series: Derivatives and Hedging Presented by: Mike Loritz and Tim Woods August 16, 2012 Agenda Basics - Overview of the definition of a derivative Identification and accounting

In the previous session we learned about the various categories of Risk in agriculture. Of course the whole point of talking about risk in this

In the previous session we learned about the various categories of Risk in agriculture. Of course the whole point of talking about risk in this educational series is so that we can talk about managing

In the previous session we learned about the various categories of Risk in agriculture. Of course the whole point of talking about risk in this educational series is so that we can talk about managing

Agenda. Learning Objectives. Chapter 19. International Business Finance. Learning Objectives Principles Used in This Chapter

Chapter 19 International Business Finance Agenda Learning Objectives Principles Used in This Chapter 1. Foreign Exchange Markets and Currency Exchange Rates 2. Interest Rate and Purchasing-Power Parity

Chapter 19 International Business Finance Agenda Learning Objectives Principles Used in This Chapter 1. Foreign Exchange Markets and Currency Exchange Rates 2. Interest Rate and Purchasing-Power Parity

covered warrants uncovered an explanation and the applications of covered warrants

covered warrants uncovered an explanation and the applications of covered warrants Disclaimer Whilst all reasonable care has been taken to ensure the accuracy of the information comprising this brochure,

covered warrants uncovered an explanation and the applications of covered warrants Disclaimer Whilst all reasonable care has been taken to ensure the accuracy of the information comprising this brochure,

Economic Risk and Decision Analysis for Oil and Gas Industry CE School of Engineering and Technology Asian Institute of Technology

Economic Risk and Decision Analysis for Oil and Gas Industry CE81.98 School of Engineering and Technology Asian Institute of Technology January Semester Presented by Dr. Thitisak Boonpramote Department

Economic Risk and Decision Analysis for Oil and Gas Industry CE81.98 School of Engineering and Technology Asian Institute of Technology January Semester Presented by Dr. Thitisak Boonpramote Department

Solutions of Exercises on Black Scholes model and pricing financial derivatives MQF: ACTU. 468 S you can also use d 2 = d 1 σ T

1 KING SAUD UNIVERSITY Academic year 2016/2017 College of Sciences, Mathematics Department Module: QMF Actu. 468 Bachelor AFM, Riyadh Mhamed Eddahbi Solutions of Exercises on Black Scholes model and pricing

1 KING SAUD UNIVERSITY Academic year 2016/2017 College of Sciences, Mathematics Department Module: QMF Actu. 468 Bachelor AFM, Riyadh Mhamed Eddahbi Solutions of Exercises on Black Scholes model and pricing

Mathematics of Finance II: Derivative securities

Mathematics of Finance II: Derivative securities M HAMED EDDAHBI King Saud University College of Sciences Mathematics Department Riyadh Saudi Arabia Second term 2015 2016 M hamed Eddahbi (KSU-COS) Mathematics

Mathematics of Finance II: Derivative securities M HAMED EDDAHBI King Saud University College of Sciences Mathematics Department Riyadh Saudi Arabia Second term 2015 2016 M hamed Eddahbi (KSU-COS) Mathematics

BARINGS GLOBAL CREDIT INCOME OPPORTUNITIES FUND Summary Prospectus November 1, 2018

BARINGS GLOBAL CREDIT INCOME OPPORTUNITIES FUND Summary Prospectus November 1, 2018 Class/Ticker Symbol Class A BXIAX Class C BXICX Class I BXITX Class Y BXIYX Before you invest, you may want to review

BARINGS GLOBAL CREDIT INCOME OPPORTUNITIES FUND Summary Prospectus November 1, 2018 Class/Ticker Symbol Class A BXIAX Class C BXICX Class I BXITX Class Y BXIYX Before you invest, you may want to review

Derivative Instruments And Hedging Activities

Activities Activities Activities [Abstract] Activities 3 Months Ended Mar. 31, 2012 NOTE 12. DERIVATIVE FINANCIAL INSTRUMENTS AND HEDGING ACTIVITIES People's United Financial uses derivative financial

Activities Activities Activities [Abstract] Activities 3 Months Ended Mar. 31, 2012 NOTE 12. DERIVATIVE FINANCIAL INSTRUMENTS AND HEDGING ACTIVITIES People's United Financial uses derivative financial

Exercise Session #7 Suggested Solutions

JEM034 Corporate Finance Winter Semester 207/208 Instructor: Olga Bychkova Date: 2//207 Exercise Session #7 Suggested Solutions Problem. 22.9 Describe each of the following situations in the language of

JEM034 Corporate Finance Winter Semester 207/208 Instructor: Olga Bychkova Date: 2//207 Exercise Session #7 Suggested Solutions Problem. 22.9 Describe each of the following situations in the language of

FNCE4040 Derivatives Chapter 1

FNCE4040 Derivatives Chapter 1 Introduction The Landscape Forwards and Option Contracts What is a Derivative? A derivative is an instrument whose value depends on, or is derived from, the value of another

FNCE4040 Derivatives Chapter 1 Introduction The Landscape Forwards and Option Contracts What is a Derivative? A derivative is an instrument whose value depends on, or is derived from, the value of another

Derivatives and Hedging for Accountants. Course #6270/QAS6270 Exam Packet

Derivatives and Hedging for Accountants Course #6270/QAS6270 Exam Packet DERIVATIVES AND HEDGING FOR ACCOUNTANTS (COURSE #6270/QAS6270) COURSE DESCRIPTION A derivative is a financial product that derives

Derivatives and Hedging for Accountants Course #6270/QAS6270 Exam Packet DERIVATIVES AND HEDGING FOR ACCOUNTANTS (COURSE #6270/QAS6270) COURSE DESCRIPTION A derivative is a financial product that derives

Managing Feed and Milk Price Risk: Futures Markets and Insurance Alternatives

Managing Feed and Milk Price Risk: Futures Markets and Insurance Alternatives Dillon M. Feuz Department of Applied Economics Utah State University 3530 Old Main Hill Logan, UT 84322-3530 435-797-2296 dillon.feuz@usu.edu

Managing Feed and Milk Price Risk: Futures Markets and Insurance Alternatives Dillon M. Feuz Department of Applied Economics Utah State University 3530 Old Main Hill Logan, UT 84322-3530 435-797-2296 dillon.feuz@usu.edu

UNIVERSITY OF AGDER EXAM. Faculty of Economicsand Social Sciences. Exam code: Exam name: Date: Time: Number of pages: Number of problems: Enclosure:

UNIVERSITY OF AGDER Faculty of Economicsand Social Sciences Exam code: Exam name: Date: Time: Number of pages: Number of problems: Enclosure: Exam aids: Comments: EXAM BE-411, ORDINARY EXAM Derivatives

UNIVERSITY OF AGDER Faculty of Economicsand Social Sciences Exam code: Exam name: Date: Time: Number of pages: Number of problems: Enclosure: Exam aids: Comments: EXAM BE-411, ORDINARY EXAM Derivatives

Chapter 8 Outline. Transaction exposure Should the Firm Hedge? Contractual hedge Risk Management in practice

Chapter 8 Outline Transaction exposure Should the Firm Hedge? Contractual hedge Risk Management in practice 1 / 51 Transaction exposure Transaction exposure measures gains or losses that arise from the

Chapter 8 Outline Transaction exposure Should the Firm Hedge? Contractual hedge Risk Management in practice 1 / 51 Transaction exposure Transaction exposure measures gains or losses that arise from the

Options Strategies. BIGSKY INVESTMENTS.

Options Strategies https://www.optionseducation.org/en.html BIGSKY INVESTMENTS www.bigskyinvestments.com 1 Getting Started Before you buy or sell options, you need a strategy. Understanding how options

Options Strategies https://www.optionseducation.org/en.html BIGSKY INVESTMENTS www.bigskyinvestments.com 1 Getting Started Before you buy or sell options, you need a strategy. Understanding how options

EXAMINATION II: Fixed Income Analysis and Valuation. Derivatives Analysis and Valuation. Portfolio Management. Questions.

EXAMINATION II: Fixed Income Analysis and Valuation Derivatives Analysis and Valuation Portfolio Management Questions Final Examination March 2010 Question 1: Fixed Income Analysis and Valuation (56 points)

EXAMINATION II: Fixed Income Analysis and Valuation Derivatives Analysis and Valuation Portfolio Management Questions Final Examination March 2010 Question 1: Fixed Income Analysis and Valuation (56 points)

Derivatives Analysis & Valuation (Futures)

") 6.1 Derivatives Analysis & Valuation (Futures) LOS 1 : Introduction Study Session 6 Define Forward Contract, Future Contract. Forward Contract, In Forward Contract one party agrees to buy, and the counterparty

6.1 Derivatives Analysis & Valuation (Futures) LOS 1 : Introduction Study Session 6 Define Forward Contract, Future Contract. Forward Contract, In Forward Contract one party agrees to buy, and the counterparty

18. Forwards and Futures

18. Forwards and Futures This is the first of a series of three lectures intended to bring the money view into contact with the finance view of the world. We are going to talk first about interest rate

18. Forwards and Futures This is the first of a series of three lectures intended to bring the money view into contact with the finance view of the world. We are going to talk first about interest rate

Eurocurrency Contracts. Eurocurrency Futures

Eurocurrency Contracts Futures Contracts, FRAs, & Options Eurocurrency Futures Eurocurrency time deposit Euro-zzz: The currency of denomination of the zzz instrument is not the official currency of the

Eurocurrency Contracts Futures Contracts, FRAs, & Options Eurocurrency Futures Eurocurrency time deposit Euro-zzz: The currency of denomination of the zzz instrument is not the official currency of the

FOREX RISK MANAGEMENT STRATEGIES FOR INDIAN IT COMPANIES

FOREX RISK MANAGEMENT STRATEGIES FOR INDIAN IT COMPANIES Mihir Dash Alliance Business School mihir@alliancebschool.ac.in +91-994518465 ABSTRACT Foreign exchange risk is the effect that unanticipated exchange

FOREX RISK MANAGEMENT STRATEGIES FOR INDIAN IT COMPANIES Mihir Dash Alliance Business School mihir@alliancebschool.ac.in +91-994518465 ABSTRACT Foreign exchange risk is the effect that unanticipated exchange

Chapter 22 examined how discounted cash flow models could be adapted to value

ch30_p826_840.qxp 12/8/11 2:05 PM Page 826 CHAPTER 30 Valuing Equity in Distressed Firms Chapter 22 examined how discounted cash flow models could be adapted to value firms with negative earnings. Most

ch30_p826_840.qxp 12/8/11 2:05 PM Page 826 CHAPTER 30 Valuing Equity in Distressed Firms Chapter 22 examined how discounted cash flow models could be adapted to value firms with negative earnings. Most

MiFID II: Information on Financial instruments

MiFID II: Information on Financial instruments A. Introduction This information is provided to you being categorized as a Professional client to inform you on financial instruments offered by Rabobank

MiFID II: Information on Financial instruments A. Introduction This information is provided to you being categorized as a Professional client to inform you on financial instruments offered by Rabobank

Portfolio Management

Portfolio Management 010-011 1. Consider the following prices (calculated under the assumption of absence of arbitrage) corresponding to three sets of options on the Dow Jones index. Each point of the

Portfolio Management 010-011 1. Consider the following prices (calculated under the assumption of absence of arbitrage) corresponding to three sets of options on the Dow Jones index. Each point of the

Financial Derivatives. Futures, Options, and Swaps

Financial Derivatives Futures, Options, and Swaps Defining Derivatives A derivative is a financial instrument whose value depends on is derived from the value of some other financial instrument, called

Financial Derivatives Futures, Options, and Swaps Defining Derivatives A derivative is a financial instrument whose value depends on is derived from the value of some other financial instrument, called

INV2601 DISCUSSION CLASS SEMESTER 2 INVESTMENTS: AN INTRODUCTION INV2601 DEPARTMENT OF FINANCE, RISK MANAGEMENT AND BANKING

INV2601 DISCUSSION CLASS SEMESTER 2 INVESTMENTS: AN INTRODUCTION INV2601 DEPARTMENT OF FINANCE, RISK MANAGEMENT AND BANKING Examination Duration of exam 2 hours. 40 multiple choice questions. Total marks

INV2601 DISCUSSION CLASS SEMESTER 2 INVESTMENTS: AN INTRODUCTION INV2601 DEPARTMENT OF FINANCE, RISK MANAGEMENT AND BANKING Examination Duration of exam 2 hours. 40 multiple choice questions. Total marks

Econ 340: Money, Banking and Financial Markets Midterm Exam, Spring 2009

Econ 340: Money, Banking and Financial Markets Midterm Exam, Spring 2009 1. On September 18, 2007 the U.S. Federal Reserve Board began cutting its fed funds rate (short term interest rate) target. This

Econ 340: Money, Banking and Financial Markets Midterm Exam, Spring 2009 1. On September 18, 2007 the U.S. Federal Reserve Board began cutting its fed funds rate (short term interest rate) target. This

Dynamic Risk Management. Education Session IASB Meeting, September 2017 Agenda Paper 4. Ross Turner Industry Fellow September 2017

1 Dynamic Risk Management Education Session IASB Meeting, September 2017 Agenda Paper 4 Ross Turner Industry Fellow September 2017 Copyright IFRS Foundation. All rights reserved Disclaimer IASB Meeting,

1 Dynamic Risk Management Education Session IASB Meeting, September 2017 Agenda Paper 4 Ross Turner Industry Fellow September 2017 Copyright IFRS Foundation. All rights reserved Disclaimer IASB Meeting,

MTP_Final_Syllabus 2016_Dec2017_Set 2 Paper 14 Strategic Financial Management

Paper 14 Strategic Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 14 Strategic Financial Management Full

Paper 14 Strategic Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 14 Strategic Financial Management Full

Financial Economics 4378 FALL 2013 FINAL EXAM There are 10 questions Total Points 100. Question 1 (10 points)

") Financial Economics 4378 FALL 2013 FINAL EXAM There are 10 questions Total Points 100 Name: Question 1 (10 points) A trader currently holds 300 shares of IBM stock. The trader also has $15,000 in cash.

Financial Economics 4378 FALL 2013 FINAL EXAM There are 10 questions Total Points 100 Name: Question 1 (10 points) A trader currently holds 300 shares of IBM stock. The trader also has $15,000 in cash.