Demystifying Exotic Derivatives: What You Need to Know

|

|

|

- Jeffrey Green

- 6 years ago

- Views:

Transcription

1 Demystifying Exotic Derivatives: What You Need to Know Rutter Associates June 2, 2016 Abstract Exotic or complex derivatives are distinguished from their plain vanilla cousins only by the amount of reverse engineering required to value them and to analyze their risk/return trade-offs. Rutter Associates takes the mystery out of these instruments by plotting profit and loss profiles and simulating return distributions. Using Accumulators, Autocallables, KIKOs and TARNs as representatives of exotic derivatives commonly cited in the financial press, we present key information market participants need to assess in order to understand the derivative trades they are considering. 1

2 INTRODUCTION Derivative market participants engage in two broad activities: 1) hedging away unwanted risk exposures and 2) taking on new risk exposures or amplifying existing ones. The latter activity, often characterized as speculation, encompasses outright position taking, income generation (for example, covered call writing), and the creation of synthetic investment assets in replication strategies. For purposes of this note, we will define incremental risk mitigation as hedging and incremental risk acceptance as investing. Some participants are hedgers, some are investors and some engage in both hedging away unwanted risks and taking on risks in which they are comfortable investing. The first lesson Professor John Hull offers in his popular textbook Options, Futures and Other Derivatives to derivative endusers (primarily nonfinancial corporations but also including family offices and high net worth individuals) is, make sure you fully understand the trades you are doing 1. Derivative end-users have goals and face risks to the achievement of those goals: hedgers aim to use derivatives to reduce risk, and retain the risk of hedge ineffectiveness; investors use derivatives to accept risk in the pursuit of investment gain. Both hedgers and investors need the ability to price the derivatives they transact and to understand the risk/reward trade-offs they face throughout the life of their contracts. Many of the derivatives contracted by small to mid-sized nonfinancial corporate and high net worth retail end-users are of an exotic or complex nature that we discuss in our March News and Insights white paper, Calculating Derivative Complexity. There we define complexity as relating to the costs incurred in the modeling effort and data acquisition required to perform an adequate analysis of ex-ante derivative risk/return profiles and valuation and risk management throughout the derivative s life. We also cite four derivative structures that are commonly classified as exotic or complex in the literature: Accumulators, Autocallables, KIKOs and TARNs 2. Derivative end-users (both hedgers and investors) often choose to turn to independent and objective third parties (who are not compensated via sales commissions) in order to understand how well exotic and plain vanilla derivatives are suited to achieving their goals, to understand fully the market risks entailed in positions in the contracts, and to obtain independent price verification. In this note, we present Rutter Associates approach to evaluating the stand-alone market risks and the potential to achieve risky return goals of each of the four complex derivatives cited above. The first two examples are equity-linked derivatives, and the next two examples are foreign exchange-linked ( FX -linked) derivatives. Each presents counterparty credit risk that is beyond the scope of this note, and we do not consider the potential hedge applications of these derivatives (an end-user contemplating the use of any of these four in a hedge application would need to model the risk/return profile of the underlying account being hedged simultaneously with the derivative contract for a proper hedge evaluation). Thus, the end-user in each of the following examples is an investor and the return profiles are those of the particular derivative in isolation and not part of a hedged portfolio. This allows us to focus exclusively on the derivative contract being analyzed. 1 FORWARD ACCUMULATOR 1.1 How This Product Works A Forward Accumulator allows an end-user to accumulate a predefined number of shares of a single stock over a number of observation periods at a predefined price (the Forward Price or alternatively, the Strike Price ). The Forward Price is generally set 10% - 15% below the spot price at inception. Accumulators commonly span 1 to 2 years, divided into a number of periods containing roughly the same number of days, ranging from 10 days up to 30 days. During each period, the referenced stock s close price on each business day is observed to determine the number of shares to be accumulated. If the stock price is above the Forward Price, the end-user accumulates a predefined number of shares. However, if the stock price is below the Forward Price, the enduser accumulates the predefined number of shares multiplied by a leverage ratio. At the end of each 1 Hull, John. Options, Futures and Other Derivatives. 6th ed. Upper Saddle River, NJ: Prentice Hall, p Hughes, Jennifer. How South Korea is hurting European shares and the HK dollar, Financial Times, Markets Insights, February 4, 2016, 2

3 period, the accumulated shares will be delivered to the end-user in bulk. In exchange, the end-user will pay the dealer the Forward Price multiplied by the accumulated shares in that period. All Accumulators come with a knock-out feature, which means that if the referenced stock s price is above a predefined level (the Knock-Out Level ), the contract terminates immediately. A guarantee period is usually set for the first two observation periods. This means that if the Knock- Out Level is reached during the guarantee period, the contract will terminate after the guarantee period is over, guaranteeing some return to the enduser even if a knock-out event occurs in the days immediately following contract inception. 1.2 Example of an Accumulator This Accumulator example is a one-year transaction consisting of twenty-six 14-day periods. The referenced stock is the XYZ traded on Hong Kong Exchange. Stock price at inception is HKD , Forward Price is HKD and Knock-Out Level is HKD The daily number of shares to be accumulated is 1400, with a leverage ratio of 2 times (i.e., if the stock price is below the Forward Price, 2800 shares will be accumulated.) 1.3 Profit and Loss Profile Figure 1 shows the profit and loss profile for the enduser of this Accumulator on a daily basis 3, assuming no prior knock-out event. 1.4 Probabilities of Gain and Loss Figure 2 shows Rutter Associates simulation results, at inception and based on market-implied pricing (this includes interest rate term structure, implied volatilities, etc.), to determine the probabilities of the end-user s present value of profit and loss over the life of the trade. The results of this simulation demonstrate that the end-user might expect to earn a profit with 87.17% probability (earn 0 to HKD 1 million in 69.92% of the simulations; earn HKD 1 to 2 million in 12.88% of the simulations, and earn more than HKD 2 million up to HKD 6.3 million in 4.37% of the simulations) and to suffer a loss with 12.82% probability. These probabilities are consistent with the Forward Price being below the spot price at inception. It also illustrates both the probabilities of gains and losses for the end-user and the magnitude of these gains and losses. Averaging the results of each individual simulation provides an inception value for this trade. 1.5 Risk Associated with the Structure The parties to this transaction agreed to terms whereby the end-user is likely to come out ahead. In return, the end-user accepts the risk of a greater downside in the event of an adverse outcome. The two-to-one leverage inherent in this example is one of the features that enables the end-user to have a Forward Price below the current stock price at inception, and thus a greater probability of achieving a profit rather than a loss. The potential loss to the end-user from the Accumulator is only limited by the fact that the stock price cannot fall below zero. The higher potential loss is balanced by the higher probability of gain. Rutter Associates simulation analysis indicates that the end-user is positioned to lose more than HKD 13,846,013 5% of the time and HKD 27,005,386 1% of the time. In other words, in the risk-neutral world of market-implied pricing the 95 percentile Value at Risk ( VaR ) is HKD 13,846,013 and the 99 percentile VaR is HKD 27,005, Recommended Risk Monitoring and Management Rutter Associates suggests more detailed simulations as illustrated above and stress testing for more precise risk analysis in order to make informed decisions. 3 This payoff is based on the assumption that the number of shares is delivered on a daily basis, stocks are sold directly to reflect payoff, no liquidity issue is involved and bid-ask spread is zero. Bear in mind that in real contract terms, stocks are not delivered until the last day of each period. 3

4 Figure 1 Figure 2 4

5 2 AUTOCALLABLE 2.1 How This Product Works An Autocallable is an equity structured note: at inception, the end-user pays an upfront principal amount for that note. Subsequently, the end-user receives payments linked to the performance of reference stocks or stock indices observed on a series of pre-specified dates (the Observation Dates ) during the life of the note. The prices of the reference stocks (or stock indices) are recorded at inception (the Initial Levels ). On each Observation Date, the prices of the reference stocks or indices are observed. If the worst performing of the reference stocks or indices closes at or above its Initial Level at the first or subsequent Observation Dates, the note terminates immediately and the end-user receives 100% of its principal back plus accrued interest. The coupon of an Autocallable is usually significantly higher and therefore generally more attractive than the yield on an alternative fixed income investment with the same credit risk. If the note does not terminate before the final Observation Date and if the prices of all reference stocks are between their Initial Levels and the predefined lower prices (the Knock-In Levels ), the end-user of the note receives 100% of its principal back with NO coupon payment. It loses only the time value of its initial cash outlay. If on the final Observation Date, the price of the worst performing stock (or stock index) is below its Knock-In Level, the end-user receives only part of its principal back, i.e., it suffers the full percentage loss from the Initial Level of the worst performing stock or index. Possible Scenarios: 1. If on the first Observation Date, both the ABC index and the XYZ index are above their Initial Levels (HKD and EUR 9000 respectively), the note auto calls (i.e., terminates) and the end-user receives 100% of its principal plus 11% accrued interest (11% p.a. coupon for 1 year). 2. If the note does not auto call on the first Observation Date and on the second Observation Date both the ABC index and the XYZ index are above their Initial Levels (HKD and EUR 9000 respectively), the note auto calls and the end-user receives 100% of its principal plus 22% accrued interest (11% p.a. coupon for 2 years) 3. If the note has not previously auto called and on the final Observation Date both the ABC index and the XYZ index are above their Initial Levels (HKD and EUR 9000 respectively), the note terminates and the end-user receives 100% of its principal plus 33% accrued interest (11% p.a. coupon for 3 years). 4. If the note has not been auto called before the final Observation Date and both indices are between their Knock-In levels and Initial Levels, i.e., ABC index is between HKD 8400 to HKD and XYZ index is between EUR 5400 and EUR 9000 on the final Observation Date, the end-user receives 100% of its principal but no coupon. The end-user s loss is limited to the time value of its initial cash outlay (i.e., interest foregone) over three years. 2.2 Example of an Autocallable Let s examine an Autocallable with principal amount of USD 1,000,000 and a coupon of 11% per annum. The note is linked to the worst of performance of two referenced stock indices, ABC index and XYZ index. Their Initial Levels and Knock-In Levels are listed below in Table 1. There are 3 annual Observation Dates during the 3-year life of the note. The knock-in event is observed only on the final Observation Date, and the termination event (sometimes called the knock-out event) is observed on all three Observation Dates. 5. If on the final Observation Date, the worst performing index, say ABC index, is at HKD 8000, i.e., ABC index is at 57.14% ( 8000 ) of its Initial Level or has suffered a 42.86% loss from its Initial Level ( ), the end-user receives only 57.14% of its principal back. That is, the end-user suffers a 42.86% loss of its initial cash outlay plus the value of foregone interest. 2.3 Profit and Loss Profile Figure 3 shows the profit and loss profile for the end-user who purchases the Autocallable described 5

6 above, assuming no prior knock-out event. Although the Autocallable is not commonly labeled as an option transaction, the end-user is, in effect, selling a knock-in put option on the shares of the worst performing of the ABC index and XYZ index with the option strike prices at HKD and EUR 9000, respectively, and the Knock-In Level at HKD 8400 and EUR 5400, respectively. By selling this put option, the end-user earns an attractive coupon that is higher than coupons of alternative fixed income investments with the same credit risk. 2.4 Probabilities of Gain and Loss Figure 4 shows Rutter Associates simulation results, at inception and based on market-implied pricing, to determine the probabilities of the end-user s present value of profit and loss over the life of the trade. The results of this simulation demonstrate that the Autocallable end-user might expect to earn a profit with 38.84% probability (terminate at year 1 and earn 11% coupon, a discounted value of USD 104,305, in 25.66% of the cases; terminate at year 2 and earn 22% coupon, a discounted value of USD 197,187, in 8.71% of the cases; terminate at year 3 and earn 33% coupon, a discounted value of USD 278,666, in 4.47% of the cases) and to suffer a loss with 61.16% probability. In 34.38% of our simulations, the end-user receives initial principal cash outlay back and loses only the time value of money, i.e., a loss of USD 38,597; in 26.78% of our simulations the end-user loses more than USD 400,000 or a minimum of 40% of the end-user s initial cash outlay. Figure 4 illustrates both the probabilities of gains and losses for the end-user and the magnitude of these gains and losses. Averaging the results of each individual simulation provides an inception value for this trade. 2.5 Risk Associated with the Structure The end-user earns an attractive coupon that is higher than coupons of alternative fixed income investments with the same credit risk in return for accepting the risk of a greater downside in the event of an adverse outcome (i.e., in return for writing the knock-in put option discussed above). Because of the worst of performance payoff, the correlation between the two reference stock indices is an important factor in the analysis of the structure. All else equal, the lower the correlation, the worse for the end-user. This is because a lower correlation leads to a higher dispersion of returns on the reference indices, i.e., a higher possibility that the two indices move in different directions. And since the end-user will lose money in the event that any one of the index prices drops below its Knock-In Level, a lower correlation increases the probability of this event. Note also that in the Autocallable, the end-user transfers its FX risks to the dealer, thus the dealer will need to charge or price that accommodation into the trade via a factor known as a quanto adjustment. Rutter Associates simulation analysis indicates that the end-user is positioned to lose more than USD 625,479 5% of the time and USD 714,385 1% of the time. In other words, in the risk-neutral world of market-implied pricing the 95 percentile VaR is USD 625,479 and the 99 percentile VaR is USD 714, Recommended Risk Monitoring and Management Rutter Associates suggests more detailed simulations as illustrated above and stress testing for more precise risk analysis in order to make informed decisions. Reference Stocks Initial Levels Knock-In Levels ABC index HKD HKD 8400 (60% of Initial Level) XYZ index EUR 9000 EUR 5400 (60% of Initial Level) Table 1: Details of Autocallable 6

7 Figure 3 Figure 4 7

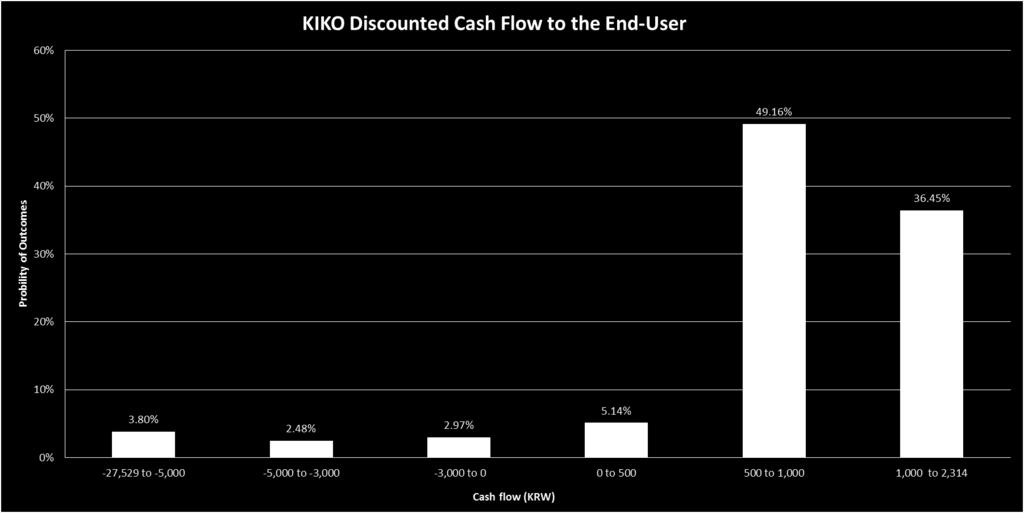

8 3 KIKO 3.1 How This Product Works KIKO is an acronym for knock-in & knock-out, and a FX KIKO refers to an exotic FX derivative trade in which the end-user buys a strip of put options and sells a strip of call options of notional amount typically twice that of the purchased puts. The strip of put options knocks out once a certain exchange rate (the Knock-Out Level ) is reached terminating the trade and limiting gains to the enduser; the call options knock out at the same Knock- Out Level and knock in at a certain FX level (the Knock-In Level ) beyond which losses to the enduser are not limited by any boundaries other than the near-absurd event of a zero currency value. Because the notional amount of the strip of calls is twice that of the puts (this is commonly referred to as leverage or gearing ) losses can accrue at twice the rate of gains. While gearing is typically two times, it can certainly be higher or lower. In practice, one of the most popular KIKO structures has the end-user purchasing a strip of in-themoney puts from a dealer and writing a strip of twice as many out-of-the money calls to the dealer with appropriately set gearing and Knock-In and Knock- Out Levels such that the initial outlay from the enduser of this structure is zero. 3.3 Profit and Loss Profile Figure 5 shows the profit and loss profile for the first put-call combination of the strip of 36. If on any monthly Settlement Date, the US dollar trades below 1000 KRW/USD and above 900 KRW/USD, assuming no prior knock-out event, the end-user will choose to sell dollars to the dealer for 1000 KRW/USD (in the illustration below, the end-user will profit from buying dollars for 950 KRW/USD and selling them to the dealer for 1000 KRW/USD). In this case, the end-user wins and the dealer loses. If on any monthly Settlement Date, the dollar trades below 900 KRW/USD, then the trade knocks out, i.e., the whole contract terminates. Assuming no prior knock-out event, if, on any monthly Settlement Date, the dollar trades above 1200 KRW/USD, all the call options knock in, meaning that the dealer may choose to buy dollars from the end-user for 1000 KRW/USD and subsequently sell the dollars for more than 1200 KRW/USD. And once all the call options knock in, the dealer will profit as long as the dollar trades above 1000 KRW/USD. In this case the dealer wins and the enduser loses. Note from the above that when the enduser loses, it does so at twice the rate at which it wins. This is the effect of gearing or leverage. 3.4 Probabilities of Gain and Loss 3.2 Example of a KIKO An end-user buys a series of puts on the US Dollar ( USD ) (or equivalently calls on the Korean Won ( KRW )) while selling a series of calls on the USD (equivalently puts on the KRW). The contract has 3-year maturity and monthly settlement (i.e., it embeds a strip of 36 calls and 36 puts). The notional amount of the purchased puts is set at USD 1 for illustrative purposes, and the notional amount on the calls is set at USD 2 to reflect the gearing. In both purchasing puts on USD and selling calls on USD, the end-user is betting against the dollar s appreciation. Figure 6 shows Rutter Associates simulation results for the entire strip of 36 puts and calls, at inception and based on market-implied pricing, to determine the probabilities of various levels of profit and loss. The results of this simulation demonstrate that the KIKO end-user might expect to earn a profit with 90.75% probability (5.14% probability of a profit up to KRW 500, 49.16% probability of a profit between KRW 500 and KRW 1,000 and 36.45% probability of a profit between KRW 1,000 and KRW 2,314) and to suffer a loss with 9.25% probability (3.80% probability of loss greater than KRW 5,000). Averaging the results of each individual simulation provides an inception value for this trade. 3.5 Risk Associated with the Structure The Knock-In/Knock-Out Levels, option strike price for both calls and puts (the Strike Price ), the When analyzed at trade inception, the end-user is spot FX rate at inception together with key KIKO likely to record a gain over the life of the KIKO. pricing inputs are summarized in Table 2. In return, the end-user accepts the risk of a greater 8

9 downside in the less likely event of an adverse outcome. We can see that the riskiness of the KIKO structure derives from the selling of embedded call options. The skewness of the return distribution arises from both the gearing on the written calls and the nature of the KIKO barriers that limit upside potential of the purchased puts but leave downside potential limited only by the near-absurd condition that the KRW becomes entirely worthless. Rutter Associates simulation analysis indicates that the end-user is positioned to lose more than KRW 3,959 5% of the time and KRW 8,924 1% of the time. In other words, in the risk-neutral world of market-implied pricing the 95 percentile VaR is KRW 3,959 and the 99 percentile VaR is KRW 8, Recommended Risk Monitoring and Management Rutter Associates suggests more detailed simulations as illustrated above and stress testing for more precise risk analysis in order to make informed decisions. Data Values FX are in KRW/USD unit Spot FX Rate at Inception 950 Strike Price 1000 Knock-Out Level 900 Knock-In Level 1200 Expiry 3 years Volatility 7% per year 3yr US Risk Free Rate 5.20% 3yr Korean Risk Free Rate 4.90% Payment Frequency Monthly Notional Amount of Call on USD KRW 2000 / USD 2 Notional Amount of Put on USD KRW 1000 / USD 1 Table 2: KIKO details 9

10 Figure 5 Figure 6 10

11 4 TARN (TARGET ACCRUAL REDEMP- TION NOTE) 4.1 How This Product Works Traditionally, the term TARN has meant a note that has a target accrual redemption amount, meaning that the return to the holder of the note is capped at a specified target amount. The term TARN has come to mean any transaction, whether in the form of a note or an unfunded derivative contract, in which the return to one of the parties is capped at a specified target amount. In a FX TARN, the end-user and the dealer exchange specified currencies, based on a predetermined exchange rate level (the Forward Price or alternatively, the Strike Price ) on a series of prespecified dates (the Settlement Dates ) during the life of the transaction. Unlike a regular FX forward contract, the FX TARN usually has different currency amounts to be exchanged when the FX rate is above or below the Forward Price. Although a TARN is not commonly labeled as an option transaction, the end-user is, in effect, buying a strip of call options and selling a strip of put options of notional typically twice that of the purchased calls. In addition to the target redemption termination provision, a TARN can also have a knock-out provision saying that if the level of the FX rate is over a predetermined price (the Knock-Out Level ) the TARN terminates. 4.2 Example of a TARN This TARN example is composed of 26 bi-weekly Settlement Dates over a one year tenor. The spot FX rate at inception is 102 JPY/AUD. On each Settlement Date 1. If the FX rate is equal to or greater than 97 JPY/AUD, the end-user receives AUD 2,000,000 and pays JPY 194,000,000, i.e., the end-user buys AUD 2,000,000 at the Forward Price of 97 JPY/AUD and the end-user has a profit of JPY 2,000,000 (FX rate-97) (the Profit Amount ). 2. If the FX rate is in between 97 JPY/AUD and 90 JPY/AUD, no payments occur. 3. If the FX rate is equal to or less than 90 JPY/AUD, the end-user receives AUD 4,000,000 and pays JPY 388,000,000, i.e., the end-user buys AUD 4,000,000 at the Forward Price of 97 JPY/AUD and the end-user has a loss of JPY 4,000,000 (97-FX rate). If the exchange rate moves to or above the Knock-Out Level of 105 JPY/AUD on any Settlement Date, the TARN transaction terminates immediately. If the aggregate Profit Amount to the end-user reaches or exceeds JPY 68,000,000 on any Settlement Date, the end-user only receives, on that date, a JPY amount such that the aggregate Profit Amount equals JPY 68,000,000, and the TARN transaction terminates immediately. The end-user received an upfront payment of JPY 41,000,000 at inception. The payoff schedule above is, in effect, that of the end-user buying a strip of call options on AUD with notional amount of AUD 2,000,000 and selling a strip of put options on AUD with notional amount twice that of the purchased calls. The call options have a Strike Price at 97 JPY/AUD and the Knock-Out Level at 105 JPY/AUD. The put options have the same Strike Price and Knock-Out Level with Knock- In Level at 90 JPY/AUD. 4.3 Profit and Loss Profile Figure 7 illustrates the profit and loss profile for the end-user on a Settlement Date, assuming there is no knock-out or the accrual target is not reached prior to this Settlement Date. 11

12 Figure 7 Figure 8 12

13 4.4 Probabilities of Gains and Losses Figure 8 shows Rutter Associates simulation results, at inception and based on market-implied pricing, to determine the probabilities of the end-user s present value of profit and loss over the life of the trade. The results of this simulation demonstrate that the end-user might expect to earn a profit of up to JPY mm with probability 80.68% and to suffer a loss of up to JPY 2,385.79mm with probability 19.32% (the expected loss, given that there is a loss, is JPY mm). These probabilities are consistent with the Forward Price being below the spot FX rate at inception. Figure 8 above illustrates both the probabilities of gains and losses for the end-user and the magnitude of these gains and losses. Averaging the results of each individual simulation provides an inception value for this trade. 4.5 Risk Associated with the Structure At inception of the trade, the dealer agrees to terms whereby the end-user is likely to come out ahead. In return, the end-user accepts the risk of a greater downside in the event of an adverse outcome. The two-to-one notional amount leverage inherent in this TARN example is one of the features that enables the end-user to achieve a Forward Price that is below the spot JPY/AUD exchange rate at inception and to set the Knock-In Level at a level that is well below the spot JPY/AUD exchange rate. As a result, the leverage is a factor in the probability of a gain for the end-user being greater than the probability of a loss. The potential loss to the end-user from the TARN transaction is only limited by the fact that the JPY/AUD exchange rate cannot fall below zero. The higher potential loss is balanced by the higher probability of gain. Rutter Associates simulation analysis indicates that the end-user is positioned to lose more than JPY 865,110,450 5% of the time and JPY 1,395,871,276 1% of the time. In other words, in the risk-neutral world of market-implied pricing the 95 percentile VaR is JPY 865,110,450 and the 99 percentile VaR is JPY 1,395,871, Recommended Risk Monitoring and Management Rutter Associates suggests more detailed simulations as illustrated above and stress testing for more precise risk analysis in order to make informed decisions. 5 Conclusion Professor Hull s advice, make sure you fully understand the trades you are doing 4, cannot be overemphasized. For complex or exotic derivatives, the end-user (whether hedging risk away or accepting risk in the pursuit of investment gains) must fully understand the trade and the rationale for entering into it. Further, he or she should be able to explain it to senior management and external stakeholders and not rely on the derivatives dealer for this. The end-user must also be able to value the derivative and to assess the incremental risks associated with the derivative. The end-user must not rely on the derivatives dealer for valuation and risk assessment. If the end-user does not have in-house capability in risk assessment and valuation, he or she should engage external resources. The four instruments examined in this note represent complicated trades for which risk/return analysis and valuation may present daunting challenges to some end-users. The Accumulator trade, perhaps the least complicated of the four, straddles the green and yellow zones of Rutter Associates Complexity Calculator when applied to the modeling expertise of our own quantitative analysts in Figure 9. For firms and individuals without such in-house capability, the Complexity Calculator will likely point solidly to the red (inputs to the calculator indicating that the end-user has no models and data for fair value determination and risk assessment, cannot quantify effect of leverage and cannot quantify downside potential) in Figure 10. For such red-zone situations, a derivative enduser would be wise to seek independent and objective expert assistance. 4 Hull, John. Options, Futures and Other Derivatives. 6th ed. Upper Saddle River, NJ: Prentice Hall, p

14 Figure 9 Figure 10 14

Product Disclosure Statement Structured Foreign Exchange Option Products 1 April 2019

Product Disclosure Statement Structured Foreign Exchange Option Products 1 April 2019 TABLE OF CONTENTS 1. INTRODUCTION... 1 1. INTRODUCTION... 3 2 ABOUT THIS PDS... 3 2.1 Purpose and Contents of this

Product Disclosure Statement Structured Foreign Exchange Option Products 1 April 2019 TABLE OF CONTENTS 1. INTRODUCTION... 1 1. INTRODUCTION... 3 2 ABOUT THIS PDS... 3 2.1 Purpose and Contents of this

Financial instruments and related risks

Financial instruments and related risks Foreign exchange products Money Market products Capital Market products Interest Rate products Equity products Version 1.0 August 2007 Index Introduction... 1 Definitions...

Financial instruments and related risks Foreign exchange products Money Market products Capital Market products Interest Rate products Equity products Version 1.0 August 2007 Index Introduction... 1 Definitions...

INVESTMENT SERVICES RULES FOR RETAIL COLLECTIVE INVESTMENT SCHEMES

INVESTMENT SERVICES RULES FOR RETAIL COLLECTIVE INVESTMENT SCHEMES PART B: STANDARD LICENCE CONDITIONS Appendix VI Supplementary Licence Conditions on Risk Management, Counterparty Risk Exposure and Issuer

INVESTMENT SERVICES RULES FOR RETAIL COLLECTIVE INVESTMENT SCHEMES PART B: STANDARD LICENCE CONDITIONS Appendix VI Supplementary Licence Conditions on Risk Management, Counterparty Risk Exposure and Issuer

Please refer to the Thai text for the official version

Unofficial Translation by the courtesy of The Foreign Banks' Association This translation is for the convenience of those unfamiliar with the Thai language. To Manager Please refer to the Thai text for

Unofficial Translation by the courtesy of The Foreign Banks' Association This translation is for the convenience of those unfamiliar with the Thai language. To Manager Please refer to the Thai text for

Deutsche Bank Global Markets Ex-Ante Cost Disclosure 2018

Deutsche Bank Global Markets Ex-Ante Cost Disclosure 2018 This document provides you with key information about Corporate Investment Bank Products. It is not marketing material. The purpose of this document

Deutsche Bank Global Markets Ex-Ante Cost Disclosure 2018 This document provides you with key information about Corporate Investment Bank Products. It is not marketing material. The purpose of this document

FNCE4830 Investment Banking Seminar

FNCE4830 Investment Banking Seminar Introduction on Derivatives What is a Derivative? A derivative is an instrument whose value depends on, or is derived from, the value of another asset. Examples: Futures

FNCE4830 Investment Banking Seminar Introduction on Derivatives What is a Derivative? A derivative is an instrument whose value depends on, or is derived from, the value of another asset. Examples: Futures

Foreign Currency Risk Management

Foreign Currency Risk Management Global Markets Introduction One of the key challenges for those engaged in international trade and overseas investment is managing foreign currency exposure. The document

Foreign Currency Risk Management Global Markets Introduction One of the key challenges for those engaged in international trade and overseas investment is managing foreign currency exposure. The document

An Introduction to Structured Financial Products (Continued)

") An Introduction to Structured Financial Products (Continued) Prof.ssa Manuela Pedio 20541 Advanced Quantitative Methods for Asset Pricing and Structuring Spring 2018 Outline and objectives The Nature of

An Introduction to Structured Financial Products (Continued) Prof.ssa Manuela Pedio 20541 Advanced Quantitative Methods for Asset Pricing and Structuring Spring 2018 Outline and objectives The Nature of

An Introduction to Structured Financial Products

An Introduction to Structured Financial Products Prof. Massimo Guidolin 20263 Advanced Tools for Risk Management and Pricing Spring 2015 Outline and objectives The Nature of Investment Certificates Market

An Introduction to Structured Financial Products Prof. Massimo Guidolin 20263 Advanced Tools for Risk Management and Pricing Spring 2015 Outline and objectives The Nature of Investment Certificates Market

Options Strategies. BIGSKY INVESTMENTS.

Options Strategies https://www.optionseducation.org/en.html BIGSKY INVESTMENTS www.bigskyinvestments.com 1 Getting Started Before you buy or sell options, you need a strategy. Understanding how options

Options Strategies https://www.optionseducation.org/en.html BIGSKY INVESTMENTS www.bigskyinvestments.com 1 Getting Started Before you buy or sell options, you need a strategy. Understanding how options

Basic Option Strategies

Page 1 of 9 Basic Option Strategies This chapter considers trading strategies for profiting from our ability to conduct a fundamental and technical analysis of a stock by extending our MCD example. In

Page 1 of 9 Basic Option Strategies This chapter considers trading strategies for profiting from our ability to conduct a fundamental and technical analysis of a stock by extending our MCD example. In

Hull, Options, Futures & Other Derivatives, 9th Edition

P1.T3. Financial Markets & Products Hull, Options, Futures & Other Derivatives, 9th Edition Bionic Turtle FRM Study Notes Reading 19 By David Harper, CFA FRM CIPM www.bionicturtle.com HULL, CHAPTER 1:

P1.T3. Financial Markets & Products Hull, Options, Futures & Other Derivatives, 9th Edition Bionic Turtle FRM Study Notes Reading 19 By David Harper, CFA FRM CIPM www.bionicturtle.com HULL, CHAPTER 1:

Sample Term Sheet. Warrant Definitions. Risk Measurement

INTRODUCTION TO WARRANTS This Presentation Should Help You: Understand Why Investors Buy s Learn the Basics about Pricing Feel Comfortable with Terminology Table of Contents Sample Term Sheet Scenario

INTRODUCTION TO WARRANTS This Presentation Should Help You: Understand Why Investors Buy s Learn the Basics about Pricing Feel Comfortable with Terminology Table of Contents Sample Term Sheet Scenario

FNCE4830 Investment Banking Seminar

FNCE4830 Investment Banking Seminar Introduction on Derivatives What is a Derivative? A derivative is an instrument whose value depends on, or is derived from, the value of another asset. Examples: Futures

FNCE4830 Investment Banking Seminar Introduction on Derivatives What is a Derivative? A derivative is an instrument whose value depends on, or is derived from, the value of another asset. Examples: Futures

CIS March 2012 Diet. Examination Paper 2.3: Derivatives Valuation Analysis Portfolio Management Commodity Trading and Futures.

CIS March 2012 Diet Examination Paper 2.3: Derivatives Valuation Analysis Portfolio Management Commodity Trading and Futures Level 2 Derivative Valuation and Analysis (1 12) 1. A CIS student was making

CIS March 2012 Diet Examination Paper 2.3: Derivatives Valuation Analysis Portfolio Management Commodity Trading and Futures Level 2 Derivative Valuation and Analysis (1 12) 1. A CIS student was making

1.2 Product nature of credit derivatives

1.2 Product nature of credit derivatives Payoff depends on the occurrence of a credit event: default: any non-compliance with the exact specification of a contract price or yield change of a bond credit

1.2 Product nature of credit derivatives Payoff depends on the occurrence of a credit event: default: any non-compliance with the exact specification of a contract price or yield change of a bond credit

An Introduction to Structured Financial Products

An Introduction to Structured Financial Products Prof. Massimo Guidolin 20263 Advanced Tools for Risk Management and Pricing Spring 2016 Outline and objectives The Nature of Investment Certificates Market

An Introduction to Structured Financial Products Prof. Massimo Guidolin 20263 Advanced Tools for Risk Management and Pricing Spring 2016 Outline and objectives The Nature of Investment Certificates Market

2. An equity-linked note that is designed to return at least the principal typically combines an option on an underlying equity asset with a.

1. Structured products: A. are only exposed to market risk B. are also referred to as hybrid products C. entitle holders to a share in the issuer s profits D. always provide higher returns compared to

1. Structured products: A. are only exposed to market risk B. are also referred to as hybrid products C. entitle holders to a share in the issuer s profits D. always provide higher returns compared to

Cross Currency Swaps. Savill Consulting 1

Cross Currency Swaps Savill Consulting 1 A forward FX rate is calculated using a no-arbitrage pricing model Assume a US-based investor has US$10.50 million to invest and a 12-mo time horizon. The current

Cross Currency Swaps Savill Consulting 1 A forward FX rate is calculated using a no-arbitrage pricing model Assume a US-based investor has US$10.50 million to invest and a 12-mo time horizon. The current

Best Practices for Foreign Exchange Risk Management in Volatile and Uncertain Times

erspective P Insights for America s Business Leaders Best Practices for Foreign Exchange Risk Management in Volatile and Uncertain Times Framing the Challenge The appeal of international trade among U.S.

erspective P Insights for America s Business Leaders Best Practices for Foreign Exchange Risk Management in Volatile and Uncertain Times Framing the Challenge The appeal of international trade among U.S.

November 22, GIPS Executive and Technical Committees CFA Institute 915 East High Street Charlottesville, VA 22902

November 22, 2017 GIPS Executive and Technical Committees CFA Institute 915 East High Street Charlottesville, VA 22902 RE: USIPC Comments on the Exposure Draft of GIPS Guidance Statement on Overlay Strategies

November 22, 2017 GIPS Executive and Technical Committees CFA Institute 915 East High Street Charlottesville, VA 22902 RE: USIPC Comments on the Exposure Draft of GIPS Guidance Statement on Overlay Strategies

Fx Derivatives- Simplified CA NAVEEN JAIN AUGUST 1, 2015

1 Fx Derivatives- Simplified CA NAVEEN JAIN AUGUST 1, 2015 Agenda 2 History of Fx Overview of Forex Markets Understanding Forex Concepts Hedging Instruments RBI Guidelines Current Forex Markets History

1 Fx Derivatives- Simplified CA NAVEEN JAIN AUGUST 1, 2015 Agenda 2 History of Fx Overview of Forex Markets Understanding Forex Concepts Hedging Instruments RBI Guidelines Current Forex Markets History

Derivatives Questions Question 1 Explain carefully the difference between hedging, speculation, and arbitrage.

Derivatives Questions Question 1 Explain carefully the difference between hedging, speculation, and arbitrage. Question 2 What is the difference between entering into a long forward contract when the forward

Derivatives Questions Question 1 Explain carefully the difference between hedging, speculation, and arbitrage. Question 2 What is the difference between entering into a long forward contract when the forward

GLOSSARY OF COMMON DERIVATIVES TERMS

Alpha The difference in performance of an investment relative to its benchmark. American Style Option An option that can be exercised at any time from inception as opposed to a European Style option which

Alpha The difference in performance of an investment relative to its benchmark. American Style Option An option that can be exercised at any time from inception as opposed to a European Style option which

Risk Management and Hedging Strategies. CFO BestPractice Conference September 13, 2011

Risk Management and Hedging Strategies CFO BestPractice Conference September 13, 2011 Introduction Why is Risk Management Important? (FX) Clients seek to maximise income and minimise costs. Reducing foreign

Risk Management and Hedging Strategies CFO BestPractice Conference September 13, 2011 Introduction Why is Risk Management Important? (FX) Clients seek to maximise income and minimise costs. Reducing foreign

EXAMINATION II: Fixed Income Valuation and Analysis. Derivatives Valuation and Analysis. Portfolio Management

EXAMINATION II: Fixed Income Valuation and Analysis Derivatives Valuation and Analysis Portfolio Management Questions Final Examination March 2016 Question 1: Fixed Income Valuation and Analysis / Fixed

EXAMINATION II: Fixed Income Valuation and Analysis Derivatives Valuation and Analysis Portfolio Management Questions Final Examination March 2016 Question 1: Fixed Income Valuation and Analysis / Fixed

Product Disclosure Statement

Product Disclosure Statement Vanilla Options and Structured Options Issued by EncoreFX (NZ) Limited 24th March 2017 This Product Disclosure Statement replaces the Product Disclosure Statement Vanilla Options

Product Disclosure Statement Vanilla Options and Structured Options Issued by EncoreFX (NZ) Limited 24th March 2017 This Product Disclosure Statement replaces the Product Disclosure Statement Vanilla Options

Financial Markets and Products

Financial Markets and Products 1. Which of the following types of traders never take position in the derivative instruments? a) Speculators b) Hedgers c) Arbitrageurs d) None of the above 2. Which of the

Financial Markets and Products 1. Which of the following types of traders never take position in the derivative instruments? a) Speculators b) Hedgers c) Arbitrageurs d) None of the above 2. Which of the

HSBC Bank Plc Global Markets MiFID II Ex-ante Costs and Charges Disclosures

HSBC Bank Plc Global Markets MiFID II Ex-ante Costs and Charges Disclosures PUBLIC Introduction Throughout this document references to we, our and us are references to HSBC Bank plc. References to you

HSBC Bank Plc Global Markets MiFID II Ex-ante Costs and Charges Disclosures PUBLIC Introduction Throughout this document references to we, our and us are references to HSBC Bank plc. References to you

YOUR GUIDE TO INVESTING IN LIQUID ALTERNATIVES

YOUR GUIDE TO INVESTING IN LIQUID ALTERNATIVES TABLE OF CONTENTS Alternative Investments 3 Defining alternative investments.............. 4 Alternative assets.................... 4 Alternative strategies..................

YOUR GUIDE TO INVESTING IN LIQUID ALTERNATIVES TABLE OF CONTENTS Alternative Investments 3 Defining alternative investments.............. 4 Alternative assets.................... 4 Alternative strategies..................

Corporate Financial Risk Management

Corporate Financial Risk Management Managing Interest Rate Expense Flows at Risk By: Darren Zuckerman, Solutions Consultant, Reval September 2011 CONTENT Executive Summary Inroduction Exposure Evaluation

Corporate Financial Risk Management Managing Interest Rate Expense Flows at Risk By: Darren Zuckerman, Solutions Consultant, Reval September 2011 CONTENT Executive Summary Inroduction Exposure Evaluation

Global Investment Opportunities and Product Disclosure

Global Investment Opportunities and Product Disclosure Our clients look to us, the Citi Private Bank, to help them diversify their investment portfolios across different currencies, asset classes and markets

Global Investment Opportunities and Product Disclosure Our clients look to us, the Citi Private Bank, to help them diversify their investment portfolios across different currencies, asset classes and markets

Leverage & Derivative Products

Leverage & Derivative Products Adam Cowperthwaite, Daiwa Capital Markets Hubbis Asian Wealth Management Forum 15 February 2011 When you combine ignorance and leverage, you get some pretty interesting results.

Leverage & Derivative Products Adam Cowperthwaite, Daiwa Capital Markets Hubbis Asian Wealth Management Forum 15 February 2011 When you combine ignorance and leverage, you get some pretty interesting results.

Glossary of Swap Terminology

Glossary of Swap Terminology Arbitrage: The opportunity to exploit price differentials on tv~otherwise identical sets of cash flows. In arbitrage-free financial markets, any two transactions with the same

Glossary of Swap Terminology Arbitrage: The opportunity to exploit price differentials on tv~otherwise identical sets of cash flows. In arbitrage-free financial markets, any two transactions with the same

Foreign exchange derivatives Commerzbank AG

Foreign exchange derivatives Commerzbank AG 2. The popularity of barrier options Isn't there anything cheaper than vanilla options? From an actuarial point of view a put or a call option is an insurance

Foreign exchange derivatives Commerzbank AG 2. The popularity of barrier options Isn't there anything cheaper than vanilla options? From an actuarial point of view a put or a call option is an insurance

Derivative Products Features and Risk Disclosures

Derivative Products Features and Risk Disclosures Table of Content 1 Warrants...2 2 Callable Bull/Bear Contracts (CBBC)...4 3 Exchange Traded Fund (ETF)...6 4 Listed equity linked instruments (ELI/ELN)...8

Derivative Products Features and Risk Disclosures Table of Content 1 Warrants...2 2 Callable Bull/Bear Contracts (CBBC)...4 3 Exchange Traded Fund (ETF)...6 4 Listed equity linked instruments (ELI/ELN)...8

Equity-Linked Deposit. DBS Bank (Hong Kong) Limited

Limited") Principal Brochure dated 2 April 2015 Equity-Linked Deposit DBS Bank (Hong Kong) Limited (incorporated in Hong Kong with limited liability and a licensed bank regulated by the Hong Kong Monetary Authority

Principal Brochure dated 2 April 2015 Equity-Linked Deposit DBS Bank (Hong Kong) Limited (incorporated in Hong Kong with limited liability and a licensed bank regulated by the Hong Kong Monetary Authority

Corporate Mentality on Foreign Exchange Hedging Karim Alidina Rotman MBA 2007

Corporate Mentality on Foreign Exchange Hedging Karim Alidina Rotman MBA 2007 karim.alidina07@rotman.utoronto.ca The views and recommendations in this presentation do not represent the views of RBC Capital

Corporate Mentality on Foreign Exchange Hedging Karim Alidina Rotman MBA 2007 karim.alidina07@rotman.utoronto.ca The views and recommendations in this presentation do not represent the views of RBC Capital

Information Statement & Disclosure for Material Risks

Information Statement & Disclosure for Material Risks Material Risks CFTC Rule 23.431(a)(1) requires Wells Fargo Bank, N.A. ( WFBNA, we, us or our ) to disclose to you the material risks of a swap before

Information Statement & Disclosure for Material Risks Material Risks CFTC Rule 23.431(a)(1) requires Wells Fargo Bank, N.A. ( WFBNA, we, us or our ) to disclose to you the material risks of a swap before

Over the Counter Options Oracle FLEXCUBE Universal Banking Europe Cluster Release [October] [2013]

![Over the Counter Options Oracle FLEXCUBE Universal Banking Europe Cluster Release [October] [2013]](/thumbs/74/71459347.jpg "Over the Counter Options Oracle FLEXCUBE Universal Banking Europe Cluster Release [October] [2013]") Over the Counter Options Oracle FLEXCUBE Universal Banking Europe Cluster Release 11.3.81.02.0 [October] [2013] 0 Table of Contents Over the Counter Options 1. ABOUT THIS MANUAL... 1-1 1.1 INTRODUCTION...

Over the Counter Options Oracle FLEXCUBE Universal Banking Europe Cluster Release 11.3.81.02.0 [October] [2013] 0 Table of Contents Over the Counter Options 1. ABOUT THIS MANUAL... 1-1 1.1 INTRODUCTION...

MEKETA INVESTMENT GROUP 100 Lowder Brook Drive, Suite 1100 Westwood, MA meketagroup.com

M E K E T A I N V E S T M E N T G R O U P BOSTON MA CHICAGO IL MIAMI FL PORTLAND OR SAN DIEGO CA LONDON UK DERIVATIVES: PRIMER Timur Kaya Yontar MEKETA INVESTMENT GROUP 100 Lowder Brook Drive, Suite 1100

M E K E T A I N V E S T M E N T G R O U P BOSTON MA CHICAGO IL MIAMI FL PORTLAND OR SAN DIEGO CA LONDON UK DERIVATIVES: PRIMER Timur Kaya Yontar MEKETA INVESTMENT GROUP 100 Lowder Brook Drive, Suite 1100

Double No Touch FX Option Strategies for Low Volatility Markets: A Case Study. Udi Sela September 2012

Double No Touch FX Option Strategies for Low Volatility Markets: A Case Study Udi Sela September 2012 About the Speaker Udi Sela has been active in foreign exchange derivatives markets over the last 18

Double No Touch FX Option Strategies for Low Volatility Markets: A Case Study Udi Sela September 2012 About the Speaker Udi Sela has been active in foreign exchange derivatives markets over the last 18

7. forward extra. 134 II/b. treasury deals for importers

7. forward extra MIFID complexity FX 3 product description A forward extra deal combines the security of a forward deal with the flexibility of an option. If you have a concrete idea about the maximum

7. forward extra MIFID complexity FX 3 product description A forward extra deal combines the security of a forward deal with the flexibility of an option. If you have a concrete idea about the maximum

Copyright 2015 by IntraDay Capital Management Ltd. (IDC)

") Copyright 2015 by IntraDay Capital Management Ltd. (IDC) All content included in this book, such as text, graphics, logos, images, data compilation etc. are the property of IDC. This book or any part thereof

Copyright 2015 by IntraDay Capital Management Ltd. (IDC) All content included in this book, such as text, graphics, logos, images, data compilation etc. are the property of IDC. This book or any part thereof

MAFS601A Exotic swaps. Forward rate agreements and interest rate swaps. Asset swaps. Total return swaps. Swaptions. Credit default swaps

MAFS601A Exotic swaps Forward rate agreements and interest rate swaps Asset swaps Total return swaps Swaptions Credit default swaps Differential swaps Constant maturity swaps 1 Forward rate agreement (FRA)

MAFS601A Exotic swaps Forward rate agreements and interest rate swaps Asset swaps Total return swaps Swaptions Credit default swaps Differential swaps Constant maturity swaps 1 Forward rate agreement (FRA)

Hedging Sales Revenue by Commodity Production

Hedging Sales Revenue by Commodity Production By: Andrew Volz, Solutions Consultant, Reval April 8, 2010 CONTENT Executive Summary Introduction Life Cycle of the Producer Evaluate the Ability to Hedge

Hedging Sales Revenue by Commodity Production By: Andrew Volz, Solutions Consultant, Reval April 8, 2010 CONTENT Executive Summary Introduction Life Cycle of the Producer Evaluate the Ability to Hedge

Executive Summary: A CVaR Scenario-based Framework For Minimizing Downside Risk In Multi-Asset Class Portfolios

Executive Summary: A CVaR Scenario-based Framework For Minimizing Downside Risk In Multi-Asset Class Portfolios Axioma, Inc. by Kartik Sivaramakrishnan, PhD, and Robert Stamicar, PhD August 2016 In this

Executive Summary: A CVaR Scenario-based Framework For Minimizing Downside Risk In Multi-Asset Class Portfolios Axioma, Inc. by Kartik Sivaramakrishnan, PhD, and Robert Stamicar, PhD August 2016 In this

China Post Global Funds

China Post Global Funds PRODUCT KEY FACTS Japan Small Cap Equity Fund ( Sub-Fund ) Issuer: China Post & Capital Global Asset Management Limited Quick facts This statement provides you with key information

China Post Global Funds PRODUCT KEY FACTS Japan Small Cap Equity Fund ( Sub-Fund ) Issuer: China Post & Capital Global Asset Management Limited Quick facts This statement provides you with key information

Financial Derivatives

Derivatives in ALM Financial Derivatives Swaps Hedge Contracts Forward Rate Agreements Futures Options Caps, Floors and Collars Swaps Agreement between two counterparties to exchange the cash flows. Cash

Derivatives in ALM Financial Derivatives Swaps Hedge Contracts Forward Rate Agreements Futures Options Caps, Floors and Collars Swaps Agreement between two counterparties to exchange the cash flows. Cash

WRITTEN NOTICE OPTION DELTA PERMISSION

WRITTEN NOTICE OPTION DELTA PERMISSION To: Investec Bank plc (FRN: 172330) ( the firm ) Reference Number: 2691623 Date: 9 September 2016 DECISIONS 1. In accordance with the discretions afforded to the

WRITTEN NOTICE OPTION DELTA PERMISSION To: Investec Bank plc (FRN: 172330) ( the firm ) Reference Number: 2691623 Date: 9 September 2016 DECISIONS 1. In accordance with the discretions afforded to the

Constructive Sales and Contingent Payment Options

Constructive Sales and Contingent Payment Options John F. Marshall, Ph.D. Marshall, Tucker & Associates, LLC www.mtaglobal.com Alan L. Tucker, Ph.D. Lubin School of Business Pace University www.pace.edu

Constructive Sales and Contingent Payment Options John F. Marshall, Ph.D. Marshall, Tucker & Associates, LLC www.mtaglobal.com Alan L. Tucker, Ph.D. Lubin School of Business Pace University www.pace.edu

Comparing the Performance of Annuities with Principal Guarantees: Accumulation Benefit on a VA Versus FIA

Comparing the Performance of Annuities with Principal Guarantees: Accumulation Benefit on a VA Versus FIA MARCH 2019 2019 CANNEX Financial Exchanges Limited. All rights reserved. Comparing the Performance

Comparing the Performance of Annuities with Principal Guarantees: Accumulation Benefit on a VA Versus FIA MARCH 2019 2019 CANNEX Financial Exchanges Limited. All rights reserved. Comparing the Performance

covered warrants uncovered an explanation and the applications of covered warrants

covered warrants uncovered an explanation and the applications of covered warrants Disclaimer Whilst all reasonable care has been taken to ensure the accuracy of the information comprising this brochure,

covered warrants uncovered an explanation and the applications of covered warrants Disclaimer Whilst all reasonable care has been taken to ensure the accuracy of the information comprising this brochure,

SUPPLEMENT 4 H2O BARRY SHORT FUND

SUPPLEMENT 4 H2O BARRY SHORT FUND Supplement dated 30 th November, 2016 to the Prospectus for H2O Global Strategies ICAV dated 22 nd December, 2015. This Supplement contains information relating specifically

SUPPLEMENT 4 H2O BARRY SHORT FUND Supplement dated 30 th November, 2016 to the Prospectus for H2O Global Strategies ICAV dated 22 nd December, 2015. This Supplement contains information relating specifically

FUNDAMENTALS OF FUTURES AND OPTIONS MARKETS

SEVENTH EDITION FUNDAMENTALS OF FUTURES AND OPTIONS MARKETS GLOBAL EDITION John C. Hull / Maple Financial Group Professor of Derivatives and Risk Management Joseph L. Rotman School of Management University

SEVENTH EDITION FUNDAMENTALS OF FUTURES AND OPTIONS MARKETS GLOBAL EDITION John C. Hull / Maple Financial Group Professor of Derivatives and Risk Management Joseph L. Rotman School of Management University

Borrowers Objectives

FIN 463 International Finance Cross-Currency and Interest Rate s Professor Robert Hauswald Kogod School of Business, AU Borrowers Objectives Lower your funding costs: optimal distribution of risks between

FIN 463 International Finance Cross-Currency and Interest Rate s Professor Robert Hauswald Kogod School of Business, AU Borrowers Objectives Lower your funding costs: optimal distribution of risks between

Types of Exposure. Forward Market Hedge. Transaction Exposure. Forward Market Hedge. Forward Market Hedge: an Example INTERNATIONAL FINANCE.

Types of Exposure INTERNATIONAL FINANCE Chapter 8 Transaction exposure sensitivity of realized domestic currency values of the firm s contractual cash flows denominated in foreign currencies to unexpected

Types of Exposure INTERNATIONAL FINANCE Chapter 8 Transaction exposure sensitivity of realized domestic currency values of the firm s contractual cash flows denominated in foreign currencies to unexpected

Fuel Hedging. Management. Strategien for Airlines, Shippers, VISHNU N. GAJJALA

Fuel Hedging andrisk Management Strategien for Airlines, Shippers, and Other Consumers S. MOHAMED DAFIR VISHNU N. GAJJALA WlLEY Contents Preface Acknovuledgments Almut the Aiithors xiii xix xxi CHAPTER

Fuel Hedging andrisk Management Strategien for Airlines, Shippers, and Other Consumers S. MOHAMED DAFIR VISHNU N. GAJJALA WlLEY Contents Preface Acknovuledgments Almut the Aiithors xiii xix xxi CHAPTER

KEY INFORMATION DOCUMENT- CFDs ON COMMODITIES

KEY INFORMATION DOCUMENT- CFDs ON COMMODITIES Purpose This document provides you with key information about this investment product. It is not marketing material. The information is required by law to

KEY INFORMATION DOCUMENT- CFDs ON COMMODITIES Purpose This document provides you with key information about this investment product. It is not marketing material. The information is required by law to

Chapter 14. Exotic Options: I. Question Question Question Question The geometric averages for stocks will always be lower.

Chapter 14 Exotic Options: I Question 14.1 The geometric averages for stocks will always be lower. Question 14.2 The arithmetic average is 5 (three 5s, one 4, and one 6) and the geometric average is (5

Chapter 14 Exotic Options: I Question 14.1 The geometric averages for stocks will always be lower. Question 14.2 The arithmetic average is 5 (three 5s, one 4, and one 6) and the geometric average is (5

Shorts and Derivatives in Portfolio Statistics

Shorts and Derivatives in Portfolio Statistics Morningstar Methodology Paper April 17, 2007 2007 Morningstar, Inc. All rights reserved. The information in this document is the property of Morningstar,

Shorts and Derivatives in Portfolio Statistics Morningstar Methodology Paper April 17, 2007 2007 Morningstar, Inc. All rights reserved. The information in this document is the property of Morningstar,

Special Risks in Securities Trading. 2 nd edition, 2008

ab Special Risks in Securities Trading 2 nd edition, 2008 Pages Margin numbers INTRODUCTION What this brochure is about 4 1 19 SECTION ONE Transactions involving special risks Options 8 20 85 Forwards

ab Special Risks in Securities Trading 2 nd edition, 2008 Pages Margin numbers INTRODUCTION What this brochure is about 4 1 19 SECTION ONE Transactions involving special risks Options 8 20 85 Forwards

Product Disclosure Statement

Product Disclosure Statement OzForex Limited trading as OFX (ABN: 65 092 375 703) ( OFX ) Revised as at: 15 MAY 2018 Version No: 1.6 Contents 1 PURPOSE 1.1 Information 1.2 No Financial Advice 1.3 Client

Product Disclosure Statement OzForex Limited trading as OFX (ABN: 65 092 375 703) ( OFX ) Revised as at: 15 MAY 2018 Version No: 1.6 Contents 1 PURPOSE 1.1 Information 1.2 No Financial Advice 1.3 Client

Financial Instruments Valuation and the Role of Quantitative Analysis in a Consulting Firm

Financial Instruments Valuation and the Role of Quantitative Analysis in a Consulting Firm Ľuboš Briatka Praha, May 29 th, 2012 Financial Instruments - definition A financial instrument is any contract

Financial Instruments Valuation and the Role of Quantitative Analysis in a Consulting Firm Ľuboš Briatka Praha, May 29 th, 2012 Financial Instruments - definition A financial instrument is any contract

Special Risks in Securities Trading

Special Risks in Securities Trading Information about the Stock Exchange Act growing together. Contents Pages Sections What this brochure is about 3 7 1 19 Transactions involving special risks 8 35 20

Special Risks in Securities Trading Information about the Stock Exchange Act growing together. Contents Pages Sections What this brochure is about 3 7 1 19 Transactions involving special risks 8 35 20

Derivatives Covering the Risk

2008 ANNUAL MEETING AND EDUCATION CONFERENCE American College of Investment Counsel New York, NY Derivatives Covering the Risk 2:45 p.m. - 4:00 p.m. October 23, 2008 MODERATOR: James M. Cain Sutherland

2008 ANNUAL MEETING AND EDUCATION CONFERENCE American College of Investment Counsel New York, NY Derivatives Covering the Risk 2:45 p.m. - 4:00 p.m. October 23, 2008 MODERATOR: James M. Cain Sutherland

You are about to purchase a product that is highly sophisticated and may be difficult to understand.

Key Information Document CFDs on FX Purpose This document is aimed at providing you with key information regarding this specific investment product and should not be taken as marketing material. It is

Key Information Document CFDs on FX Purpose This document is aimed at providing you with key information regarding this specific investment product and should not be taken as marketing material. It is

NINTH EDITION FUNDAMENTALS OF. John C. Hüll

NINTH EDITION FUNDAMENTALS OF FUTURES AND OPTIONS MARKETS John C. Hüll Maple Financial Group Professor of Derivatives and Risk Management Joseph L. Rotman School of Management University of Toronto PEARSON

NINTH EDITION FUNDAMENTALS OF FUTURES AND OPTIONS MARKETS John C. Hüll Maple Financial Group Professor of Derivatives and Risk Management Joseph L. Rotman School of Management University of Toronto PEARSON

Hull, Options, Futures & Other Derivatives Exotic Options

P1.T3. Financial Markets & Products Hull, Options, Futures & Other Derivatives Exotic Options Bionic Turtle FRM Video Tutorials By David Harper, CFA FRM 1 Exotic Options Define and contrast exotic derivatives

P1.T3. Financial Markets & Products Hull, Options, Futures & Other Derivatives Exotic Options Bionic Turtle FRM Video Tutorials By David Harper, CFA FRM 1 Exotic Options Define and contrast exotic derivatives

Investment Fundamentals Forum 21 January 2013

Investment Fundamentals Forum 21 January 2013 Understanding and Trading Equity & Related Products in Singapore Th ng Beng Hooi, CFA 1 Speaker Biography Th ng Beng Hooi, CFA is the Secretariat Director

Investment Fundamentals Forum 21 January 2013 Understanding and Trading Equity & Related Products in Singapore Th ng Beng Hooi, CFA 1 Speaker Biography Th ng Beng Hooi, CFA is the Secretariat Director

Issuer and Product Arranger

PRODUCT BOOKLET DATED 27 NOVEMBER 2017 Issuer and Product Arranger BANK OF CHINA (HONG KONG) LIMITED (incorporated in Hong Kong with limited liability, a licensed bank regulated by the Hong Kong Monetary

PRODUCT BOOKLET DATED 27 NOVEMBER 2017 Issuer and Product Arranger BANK OF CHINA (HONG KONG) LIMITED (incorporated in Hong Kong with limited liability, a licensed bank regulated by the Hong Kong Monetary

The Covered Call. - Own the stock - And Sell the Calls - Mildly Bullish

The Covered Call - Own the stock - And Sell the Calls - Mildly Bullish Introduction Selling Covered Call is one of the most well known option strategies. Before discussing the mechanics and applications

The Covered Call - Own the stock - And Sell the Calls - Mildly Bullish Introduction Selling Covered Call is one of the most well known option strategies. Before discussing the mechanics and applications

The role of the Model Validation function to manage and mitigate model risk

arxiv:1211.0225v1 [q-fin.rm] 21 Oct 2012 The role of the Model Validation function to manage and mitigate model risk Alberto Elices November 2, 2012 Abstract This paper describes the current taxonomy of

arxiv:1211.0225v1 [q-fin.rm] 21 Oct 2012 The role of the Model Validation function to manage and mitigate model risk Alberto Elices November 2, 2012 Abstract This paper describes the current taxonomy of

Lesson IX: Working within an International Context - Risks, Exposures and Hedging. Techniques

Lesson IX: Working within an Context - Risks, s and April 20, 2016 s Risk and Ad Hoc Table of Contents s Risk and Ad Hoc s Risk and Ad Hoc Risk vs Risk relates to the variability in the values of assets

Lesson IX: Working within an Context - Risks, s and April 20, 2016 s Risk and Ad Hoc Table of Contents s Risk and Ad Hoc s Risk and Ad Hoc Risk vs Risk relates to the variability in the values of assets

CHARACTERISTICS OF FINANCIAL INSTRUMENTS AND A DESCRIPTION OF

CHARACTERISTICS OF FINANCIAL INSTRUMENTS AND A DESCRIPTION OF RISK I. INTRODUCTION The purpose of this document is to provide customers with the essence of financial instruments offered on unregulated

CHARACTERISTICS OF FINANCIAL INSTRUMENTS AND A DESCRIPTION OF RISK I. INTRODUCTION The purpose of this document is to provide customers with the essence of financial instruments offered on unregulated

Financial Mathematics Principles

1 Financial Mathematics Principles 1.1 Financial Derivatives and Derivatives Markets A financial derivative is a special type of financial contract whose value and payouts depend on the performance of

1 Financial Mathematics Principles 1.1 Financial Derivatives and Derivatives Markets A financial derivative is a special type of financial contract whose value and payouts depend on the performance of

Structured Derivatives Valuation. Ľuboš Briatka. Praha, 7 June 2016

Structured Derivatives Valuation Ľuboš Briatka Praha, 7 June 2016 Global financial assets = 225 trillion USD Size of derivatives market = 710 trillion USD BIS Quarterly Review, September 2014 Size of derivatives

Structured Derivatives Valuation Ľuboš Briatka Praha, 7 June 2016 Global financial assets = 225 trillion USD Size of derivatives market = 710 trillion USD BIS Quarterly Review, September 2014 Size of derivatives

Lecture 4: Barrier Options

Lecture 4: Barrier Options Jim Gatheral, Merrill Lynch Case Studies in Financial Modelling Course Notes, Courant Institute of Mathematical Sciences, Fall Term, 2001 I am grateful to Peter Friz for carefully

Lecture 4: Barrier Options Jim Gatheral, Merrill Lynch Case Studies in Financial Modelling Course Notes, Courant Institute of Mathematical Sciences, Fall Term, 2001 I am grateful to Peter Friz for carefully

Interest Rate Swaps and Bank Regulation

Interest Rate Swaps and Bank Regulation Andrew H. Chen Southern Methodist University SINCE THEIR INTRODUCTION in the early 1980s, interest rate swaps have become one of the most powerful and popular risk-management

Interest Rate Swaps and Bank Regulation Andrew H. Chen Southern Methodist University SINCE THEIR INTRODUCTION in the early 1980s, interest rate swaps have become one of the most powerful and popular risk-management

Using Position in an Option & the Underlying

Week 8 : Strategies Introduction Assume that the underlying asset is a stock paying no income Assume that the options are EUROPEAN Ignore time value of money In figures o Dashed line relationship between

Week 8 : Strategies Introduction Assume that the underlying asset is a stock paying no income Assume that the options are EUROPEAN Ignore time value of money In figures o Dashed line relationship between

PRODUCT DISCLOSURE STATEMENT for. issued by OM Financial Limited

PRODUCT DISCLOSURE STATEMENT for Foreign Exchange Options issued by OM Financial Limited This document replaces the previous OM Financial Limited Product Disclosure Statement for Foreign Exchange Options

PRODUCT DISCLOSURE STATEMENT for Foreign Exchange Options issued by OM Financial Limited This document replaces the previous OM Financial Limited Product Disclosure Statement for Foreign Exchange Options

Exotic Derivatives & Structured Products. Zénó Farkas (MSCI)

") Exotic Derivatives & Structured Products Zénó Farkas (MSCI) Part 1: Exotic Derivatives Over the counter products Generally more profitable (and more risky) than vanilla derivatives Why do they exist? Possible

Exotic Derivatives & Structured Products Zénó Farkas (MSCI) Part 1: Exotic Derivatives Over the counter products Generally more profitable (and more risky) than vanilla derivatives Why do they exist? Possible

Overview of Financial Instruments and Financial Markets

CHAPTER 1 Overview of Financial Instruments and Financial Markets FRANK J. FABOZZI, PhD, CFA, CPA Professor in the Practice of Finance, Yale School of Management Issuers and Investors 3 Debt versus Equity

CHAPTER 1 Overview of Financial Instruments and Financial Markets FRANK J. FABOZZI, PhD, CFA, CPA Professor in the Practice of Finance, Yale School of Management Issuers and Investors 3 Debt versus Equity

MiFID II: Information on Financial instruments

MiFID II: Information on Financial instruments A. Introduction This information is provided to you being categorized as a Professional client to inform you on financial instruments offered by Rabobank

MiFID II: Information on Financial instruments A. Introduction This information is provided to you being categorized as a Professional client to inform you on financial instruments offered by Rabobank

7. forward extra. 80 II/a. treasury deals for exporters

7. forward extra MIFID complexity FX 3 product description A forward extra deal combines the security of a forward deal with the flexibility of an option. If you have a concrete idea of the maximum forint

7. forward extra MIFID complexity FX 3 product description A forward extra deal combines the security of a forward deal with the flexibility of an option. If you have a concrete idea of the maximum forint

Q Dividend Plus + Strategy with Option Overlay

Q1 2014 Dividend Plus + Strategy with Option Overlay MAI Firm Overview Independence and Innovation Who We Are Our heritage dates back to 1973 as an affiliate of IMG and we were later known as McCormack

Q1 2014 Dividend Plus + Strategy with Option Overlay MAI Firm Overview Independence and Innovation Who We Are Our heritage dates back to 1973 as an affiliate of IMG and we were later known as McCormack

1.3 Equity linked products Asian examples

1.3 Equity linked products Asian examples 2-Year USD Super Certificate Linked to Basket 2-Year JPY Early Redemption Equity-Redeemable Warrant Auto-Cancellable Equity Linked Swap 1 1 2-Year USD Super Certificate

1.3 Equity linked products Asian examples 2-Year USD Super Certificate Linked to Basket 2-Year JPY Early Redemption Equity-Redeemable Warrant Auto-Cancellable Equity Linked Swap 1 1 2-Year USD Super Certificate

MODULE 4 MODULE 4 INTRODUCTION PROGRAMME LEVERAGE AND MARGIN

INTRODUCTION PROGRAMME LEVERAGE AND MARGIN This module explains leverage and gearing and compares CFDs with non-geared investments. Additionally, there are a number of worked examples of how our margin

INTRODUCTION PROGRAMME LEVERAGE AND MARGIN This module explains leverage and gearing and compares CFDs with non-geared investments. Additionally, there are a number of worked examples of how our margin

Chapter 8 Outline. Transaction exposure Should the Firm Hedge? Contractual hedge Risk Management in practice

Chapter 8 Outline Transaction exposure Should the Firm Hedge? Contractual hedge Risk Management in practice 1 / 51 Transaction exposure Transaction exposure measures gains or losses that arise from the

Chapter 8 Outline Transaction exposure Should the Firm Hedge? Contractual hedge Risk Management in practice 1 / 51 Transaction exposure Transaction exposure measures gains or losses that arise from the

Learning takes you the extra mile. Rabobank Global Learning

Learning takes you the extra mile Rabobank Global Learning Release 38: 2016 FINANCIAL MARKETS COURSES Introduction to Financial Markets Financial Markets - An Introduction Money Markets - An Introduction

Learning takes you the extra mile Rabobank Global Learning Release 38: 2016 FINANCIAL MARKETS COURSES Introduction to Financial Markets Financial Markets - An Introduction Money Markets - An Introduction

Financial Instruments: basic definitions and derivatives

Risk and Accounting Financial Instruments: basic definitions and derivatives Marco Venuti 2018 Agenda Overview Definition of Financial Instrument Definition of Financial Asset Definition of Financial liability

Risk and Accounting Financial Instruments: basic definitions and derivatives Marco Venuti 2018 Agenda Overview Definition of Financial Instrument Definition of Financial Asset Definition of Financial liability

P1.T3. Financial Markets & Products. Hull, Options, Futures & Other Derivatives. Trading Strategies Involving Options

P1.T3. Financial Markets & Products Hull, Options, Futures & Other Derivatives Trading Strategies Involving Options Bionic Turtle FRM Video Tutorials By David Harper, CFA FRM 1 Trading Strategies Involving

P1.T3. Financial Markets & Products Hull, Options, Futures & Other Derivatives Trading Strategies Involving Options Bionic Turtle FRM Video Tutorials By David Harper, CFA FRM 1 Trading Strategies Involving

Over the Counter Options Version NT1368-ORACLE FCUBSV.UM [August] [2010] Oracle Part Number E

![Over the Counter Options Version NT1368-ORACLE FCUBSV.UM [August] [2010] Oracle Part Number E](/thumbs/76/73205954.jpg "Over the Counter Options Version NT1368-ORACLE FCUBSV.UM [August] [2010] Oracle Part Number E") Over the Counter Options Version-11.1 9NT1368-ORACLE FCUBSV.UM 11.1.0.0.0.0.0 [August] [2010] Oracle Part Number E51575-01 Document Control Author: Documentation Team Created on: October 01, 2008 Updated

Over the Counter Options Version-11.1 9NT1368-ORACLE FCUBSV.UM 11.1.0.0.0.0.0 [August] [2010] Oracle Part Number E51575-01 Document Control Author: Documentation Team Created on: October 01, 2008 Updated

2009 Structured Product Forum. FX Strategies

2009 Structured Product Forum FX Strategies 1 Structured Product Industry in 2009 Survive! Be informed Back to basics Work hard Stand out Develop new skills 2 and beyond Prosper! 3 2008-2009 RBS FX Credentials

2009 Structured Product Forum FX Strategies 1 Structured Product Industry in 2009 Survive! Be informed Back to basics Work hard Stand out Develop new skills 2 and beyond Prosper! 3 2008-2009 RBS FX Credentials

Important information about structured products

Important information about structured products Disclosure Highlights A structured product is an unsecured obligation of an issuer with a return, generally paid at maturity, that is linked to the performance

Important information about structured products Disclosure Highlights A structured product is an unsecured obligation of an issuer with a return, generally paid at maturity, that is linked to the performance

June 2014 / v.03. Special Risks in

June 2014 / v.03 Special Risks in Securities Trading Contents Introduction What this brochure is about Margin numbers 1-19 Section One: Transactions involving special risks Options Margin numbers 20-85

June 2014 / v.03 Special Risks in Securities Trading Contents Introduction What this brochure is about Margin numbers 1-19 Section One: Transactions involving special risks Options Margin numbers 20-85

GEARED INVESTING. An Introduction to Leveraged and Inverse Funds

GEARED INVESTING An Introduction to Leveraged and Inverse Funds Investors have long used leverage to increase their buying power and inverse strategies to profit during or protect a portfolio from declines.

GEARED INVESTING An Introduction to Leveraged and Inverse Funds Investors have long used leverage to increase their buying power and inverse strategies to profit during or protect a portfolio from declines.

Questions and answers (Q&A) on the PRIIPs KID

on the PRIIPs KID") JC 2017 49 20 November 2017 Questions and answers (Q&A) on the PRIIPs KID (Commission Delegated Regulation (EU) 2017/653) Table of Contents Acronyms and definitions used... 3 General topics [Last update

JC 2017 49 20 November 2017 Questions and answers (Q&A) on the PRIIPs KID (Commission Delegated Regulation (EU) 2017/653) Table of Contents Acronyms and definitions used... 3 General topics [Last update

3-MONTH AUD STRUCTURED DEPOSIT LINKED AUD/USD ( SD )

") 3-MONTH AUD STRUCTURED DEPOSIT LINKED AUD/USD ( SD ) SD is a deposit designed to enables Investors to potentially earn a higher coupon compared with ordinary time deposits. In exchange for this enhanced

3-MONTH AUD STRUCTURED DEPOSIT LINKED AUD/USD ( SD ) SD is a deposit designed to enables Investors to potentially earn a higher coupon compared with ordinary time deposits. In exchange for this enhanced

FIMMDA CODE OF CONDUCT FOR DERIVATIVES TRANSACTIONS

FIMMDA CODE OF CONDUCT FOR DERIVATIVES TRANSACTIONS (16 th AUGUST, 2007) FIXED INCOME MONEY MARKET & DERIVATIVES ASSOCIATION OF INDIA www.fimmda.org INTRODUCTION FIMMDA Code of Conduct for Derivatives

FIMMDA CODE OF CONDUCT FOR DERIVATIVES TRANSACTIONS (16 th AUGUST, 2007) FIXED INCOME MONEY MARKET & DERIVATIVES ASSOCIATION OF INDIA www.fimmda.org INTRODUCTION FIMMDA Code of Conduct for Derivatives