Chapter 2. Time Value of Money (TVOM) Principles of Engineering Economic Analysis, 5th edition

|

|

|

- Linda James

- 5 years ago

- Views:

Transcription

1 Chapter 2 Time Value of Money (TVOM)

2 Cash Flow Diagrams $5,000 $5,000 $5,000 ( + ) ( - ) Time $2,000 $3,000 $4,000

3 Example 2.1: Cash Flow Profiles for Two Investment Alternatives (EOY) CF(A) CF(B) CF(B-A) End of Year 0 -$100,000 -$100,000 $0 1 $10,000 $50,000 $40,000 2 $20,000 $40,000 $20,000 3 $30,000 $30,000 $0 4 $40,000 $20,000 -$20,000 5 $50,000 $10,000 -$40,000 Sum $50,000 $50,000 $0 Although the two investment alternatives have the same bottom line, there are obvious differences. Which would you prefer, A or B? Why?

4 Example 2.1: (cont.) ( + ) $10,000 $20,000 $30,000 $40,000 $50,000 Inv. A ( - ) End of Year $100,000 Inv. B ( + ) $50,000 $40,000 $30,000 $20, End of Year $10,000 ( - ) $100,000

5 Example 2.1: (cont.) Principle #7 Consider only differences in cash flows among investment alternatives $40,000 ( + ) ( - ) $20,000 $ End of Year $20,000 Inv. B Inv. A $40,000

6 Example 2.2 Which would you choose? Alternative C (+) (-) 0 $3,000 $3,000 $3, $6,000 $3,000 $3,000 $3,000 Alternative D (+) (-) $6,000

(-) 0 1 2 3 4 $2000 Alternative E-F 3 4 $1000")

7 Example 2.3 Which would you choose? $2,000 $2,000 $2,000 $3,000 Alternative E (+) (-) $2000 Alternative E-F 3 4 $1000 Alternative F $4000 $2,000 $3,000 $2,000 $1,000 (+) 0 (-) $4,000

8 Simple interest calculation: F n P( 1 in) Compound Interest Calculation: F n F (1 n 1 i ) Where P = present value of single sum of money F n = accumulated value of P over n periods i = interest rate per period n = number of periods

9 Example 2.7: Simple Interest Calculation Robert borrows $4,000 from Susan and agrees to pay $1,000 plus accrued interest at the end of the first year and $3,000 plus accrued interest at the end of the fourth year. What should be the size of the payments if 8% simple interest is used? 1 st payment = $1, ($4,000) = $1,320 2 nd payment = $3, ($3,000)(3) = $3,720 Remaining period after 1 st payment

10 Example 2.7: (Cont.) Simple Interest Cash Flow Diagram $720 $320 $3,000 $1, $4,000 Principal payment Interest payment

11 RULES Discounting Cash Flow 1. Money has time value! 2. Cash flows cannot be added unless they occur at the same point(s) in time 3. Multiply a cash flow by (1+i) to move it forward one time unit 4. Divide a cash flow by (1+i) to move it backward one time unit

12 Compound Interest Cash Flow Diagram We ll soon learn that the compounding effect is $ $320 $3,000 $1, $4,000 Principal payment Interest payment

13 Example 2.8: (Lender s Perspective) Value of $10,000 Investment 10% per year Start of Year Value of Investment Interest Earned End of Year Value of Investment 1 $10, $1, $11, $11, $1, $12, $12, $1, $13, $13, $1, $14, $14, $1, $16, This means this amount at end of year 5 is equivalent to 10,000 at time zero (present)

14 Example 2.8: (Borrower s Perspective) Value of $10,000 Investment 10% per year Year Unpaid Balance at the Beginning of the Year Annual Interest Payment Unpaid Balance at the End of the Year 1 $10, $1, $0.00 $11, $11, $1, $0.00 $12, $12, $1, $0.00 $13, $13, $1, $0.00 $14, $14, $1, $16, $0.00

15 Compounding of Money Beginning of Period Amount Owed at Beginning (PW) Interest Earned End of Period Amount Owed at End (FW) 1 P Pi 1 P(1+i) 2 P(1+i) P(1+i)i 2 P(1+i) 2 3 P(1+i) 2 P(1+i) 2 i 3 P(1+i) 3 4 P(1+i) 3 P(1+i) 3 i 4 P(1+i) 4 5 P(1+i) 4 P(1+i) 4 i 5 P(1+i) n-1 P(1+i) n-2 P(1+i) n-2 i n-1 P(1+i) n-1 n P(1+i) n-1 P(1+i) n-1 i n P(1+i) n

16 Discounted Cash Flow Formulas F = P (1 + i) n (2.8) F = P (F P i%, n) Vertical line means given P = F (1 + i) -n (2.9) = F/(1 + i) n P = F (P F i%, n)

17 Excel DCF Worksheet Functions F = P (1 + i) n (2.1) F = P (F P i%, n) F =FV(i%,n,,-P) P = F (1 + i) -n (2.3) P = F (P F i%, n) P =PV(i%,n,,-F)

18 F = P(1 + i) n F = P(F P i%,n) F =FV(i%,n,,-P) single sum, future worth factor P = F(1 + i) -n P = F(P F i%,n) P =PV(i%,n,,-F) single sum, present worth factor

19 F = P(1+i) n F = P(F P i%, n) F =FV(i%,n,,-P) P = F(1+i) -n P = F(P F i%, n) P =PV(i%,n,,-F) F n-1 n P P occurs n periods before F (F occurs n periods after P)

20 Relationships among P, F, and A P occurs at the same time as A 0, i.e., at t = 0 F occurs at the same time as A n, i.e., at t = n

21 Discounted Cash Flow (DCF) Methods DCF values are tabulated in the Appendixes Financial calculators can be used Financial spreadsheet software is available, e.g., Excel financial functions include PV, NPV, PMT, FV IRR, MIRR, RATE NPER

22 Example 2.9 Dia St. John borrows $1,000 at 12% compounded annually. The loan is to be repaid after 5 years. How much must she repay in 5 years?

23 Dia St. John borrows $1,000 at 12% compounded annually. The loan is to be repaid after 5 years. How much must she repay in 5 years? F = P(F P i%, n) F = $1,000(F P 12%,5) F = $1,000(1.12) 5 F = $1,000( ) F = $1, Example 2.9

24 Dia St. John borrows $1,000 at 12% compounded annually. The loan is to be repaid after 5 years. How much must she repay in 5 years? F = P(F P i, n) F = $1,000(F P 12%,5) F = $1,000(1.12) 5 F = $1,000( ) F = $1, F =FV(12%,5,,-1000) F = $1, Example 2.9

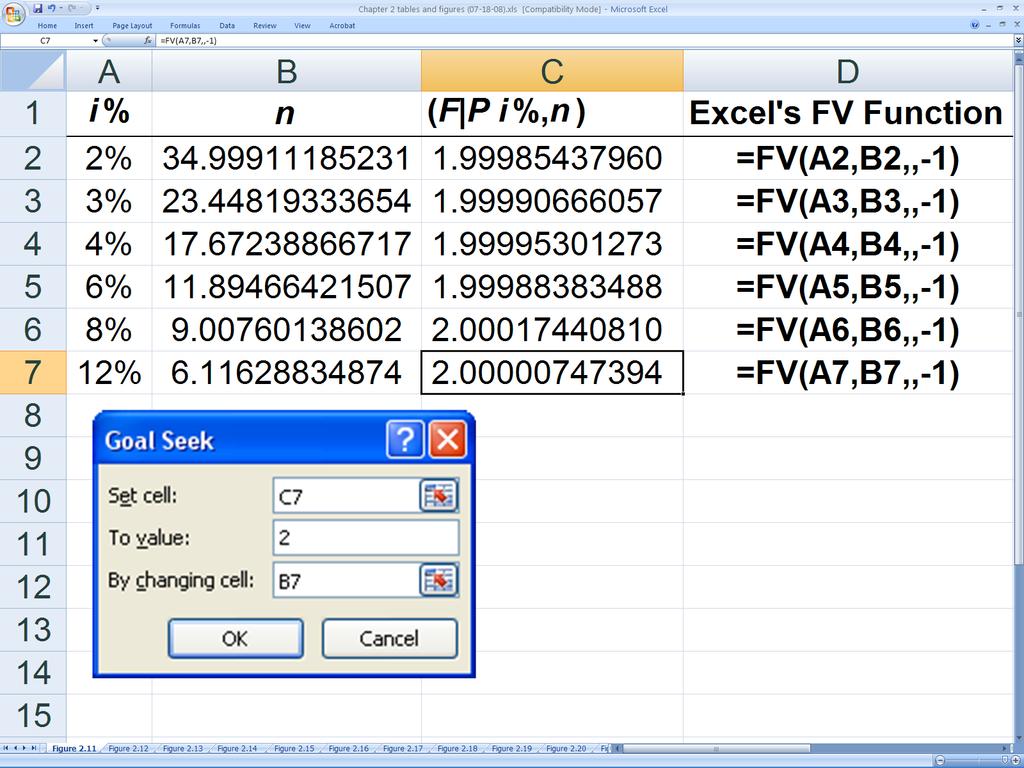

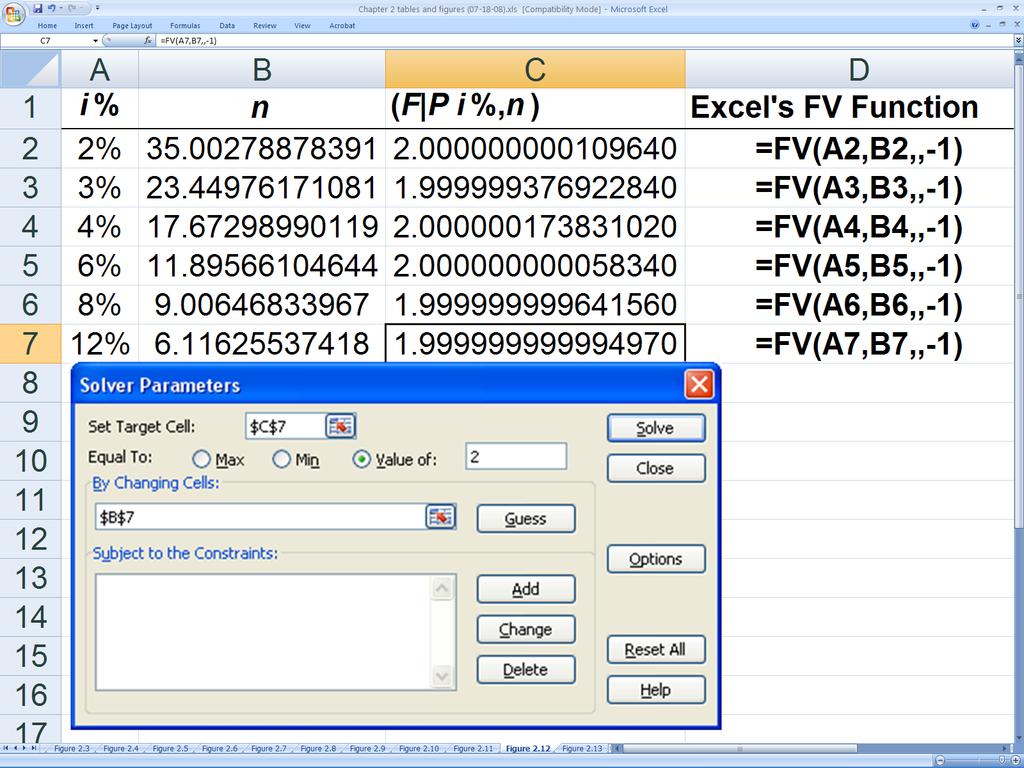

25 Example 2.10 How long does it take for money to double in value, if you earn (a) 2%, (b) 3%, (c) 4%, (d) 6%, (e) 8%, or (f) 12% annual compound interest?

26 Example 2.10 How long does it take for money to double in value, if you earn (a) 2%, (b) 3%, (c) 4%, (d) 6%, (e) 8%, or (f) 12% annual compound interest? I can think of six ways to solve this problem: 1) Solve using the Rule of 72 2) Use the interest tables; look for F P factor equal to 2.0 3) Solve numerically; n = log(2)/log(1+i) 4) Solve using Excel NPER function: =NPER(i%,,-1,2) 5) Solve using Excel GOAL SEEK tool 6) Solve using Excel SOLVER tool

27 Example 2.10 How long does it take for money to double in value, if you earn (a) 2%, (b) 3%, (c) 4%, (d) 6%, (e) 8%, or (f) 12% annual compound interest? RULE OF 72 Divide 72 by interest rate to determine how long it takes for money to double in value. (Quick, but not always accurate.)

28 How long does it take for money to double in value, if you earn (a) 2%, (b) 3%, (c) 4%, (d) 6%, (e) 8%, or (f) 12% annual compound interest? (a) 72/2 = 36 yrs (b) 72/3 = 24 yrs (c) 72/4 = 18 yrs (d) 72/6 = 12 yrs (e) 72/8 = 9 yrs (f) 72/12 = 6 yrs Example 2.10 Rule of 72 solution

29 How long does it take for money to double in value, if you earn (a) 2%, (b) 3%, (c) 4%, (d) 6%, (e) 8%, or (f) 12% annual compound interest? (a) yrs (b) yrs (c) yrs (d) yrs (e) yrs (f) yrs Example 2.10 Using interest tables & interpolating

30 How long does it take for money to double in value, if you earn (a) 2%, (b) 3%, (c) 4%, (d) 6%, (e) 8%, or (f) 12% annual compound interest? (a) log 2/log 1.02 = yrs (b) log 2/log 1.03 = yrs (c) log 2/log 1.04 = yrs (d) log 2/log 1.06 = yrs (e) log 2/log 1.08 = yrs (f) log 2/log 1.12 = yrs Example 2.10 Mathematical solution

31 How long does it take for money to double in value, if you earn (a) 2%, (b) 3%, (c) 4%, (d) 6%, (e) 8%, or (f) 12% annual compound interest? Using the Excel NPER function (a) n =NPER(2%,,-1,2) = yrs (b) n =NPER(3%,,-1,2) = yrs (c) n =NPER(4%,,-1,2) = yrs (d) n =NPER(6%,,-1,2) = yrs (e) n =NPER(8%,,-1,2) = yrs (f) n =NPER(12%,,-1,2) = yrs Example 2.10 Identical solution to that obtained mathematically

32 How long does it take for money to double in value, if you earn (a) 2%, (b) 3%, (c) 4%, (d) 6%, (e) 8%, or (f) 12% annual compound interest? (a) n = yrs (b) n = yrs (c) n = yrs (d) n = yrs (e) n =9.008 yrs (f) n =6.116 yrs Example 2.10 Using the Excel GOAL SEEK tool Solution obtained differs from that obtained mathematically; red digits differ

33

34 How long does it take for money to double in value, if you earn (a) 2%, (b) 3%, (c) 4%, (d) 6%, (e) 8%, or (f) 12% annual compound interest? (a) n = yrs (b) n = yrs (c) n = yrs (d) n = yrs (e) n =9.006 yrs (f) n =6.116 yrs Example 2.10 Using the Excel SOLVER tool Solution differs from mathematical solution, but at the 6 th to 10 th decimal place

35

36 F P Example How long does it take for money to triple in value, if you earn (a) 4%, (b) 6%, (c) 8%, (d) 10%, (e) 12%, (f) 15%, (g) 18% interest?

37 F P Example How long does it take for money to triple in value, if you earn (a) 4%, (b) 6%, (c) 8%, (d) 10%, (e) 12%, (f) 15%, (g) 18% interest? 1 st option log equation 2 nd option by using interest tables 3 rd option using different excel equation solving tools

38 How long does it take for money to triple in value, if you earn (a) 4%, (b) 6%, (c) 8%, (d) 10%, (e) 12%, (f) 15%, (g) 18% interest? (a) n =NPER(4%,,-1,3) = (b) n =NPER(6%,,-1,3) = (c) n =NPER(8%,,-1,3) = (d) n =NPER(10%,,-1,3) = (e) n =NPER(12%,,-1,3) = (f) n =NPER(15%,,-1,3) = (g) n =NPER(18%,,-1,3) = F P Example

39 Example 2.11 How much must you deposit, today, in order to accumulate $10,000 in 4 years, if you earn 5% compounded annually on your investment? P =PV(5%,4,, ) P = $

40 How much must you deposit, today, in order to accumulate $10,000 in 4 years, if you earn 5% compounded annually on your investment? P = F(P F i, n) P = $10,000(P F 5%,4) P = $10,000( )= 8, OR P = $10,000(1.05) -4 P = $8, P =PV(5%,4,,-10000) P = $ Example 2.11

41 How much must you deposit, today, in order to accumulate $10,000 in 4 years, if you earn 5% compounded annually on your investment? P = F(P F i, n) P = $10,000(P F 5%,4) P = $10,000(1.05) -4 P = $10,000( ) P = $8, P =PV(5%,4,,-10000) P = $8, Example 2.11

42 Computing the Present Worth of Multiple Cash flows P P n A t (1 i) t 0 n t 0 A t ( P t F i%, t) (2.12) (2.13)

43 Example 2.12 Determine the present worth equivalent of the CFD shown below, using an interest rate of 10% compounded annually. ( + ) $50,000 $40,000 $30,000 $40,000 $50, End of Year i = 10%/year ( - ) $100,000

44 Example 2.12 ( + ) $50,000 $40,000 $30,000 $40,000 $50, End of Year i = 10%/year ( - ) $100,000 End of Year Cash Flow Present Future (P F 10%,n) PV(10%,n,,-CF) (F P 10%,5-n) (n) (CF) Worth Worth FV(10%,5-n,,-CF) 0 -$100, $100, $100, $161, $161, $50, $45, $45, $73, $73, $40, $33, $33, $53, $53, $30, $22, $22, $36, $36, $40, $27, $27, $44, $44, $50, $31, $31, $50, $50, SUM $59, $59, $95, $95, P =NPV(10%,50000,40000,30000,40000,50000) = $59,418.45

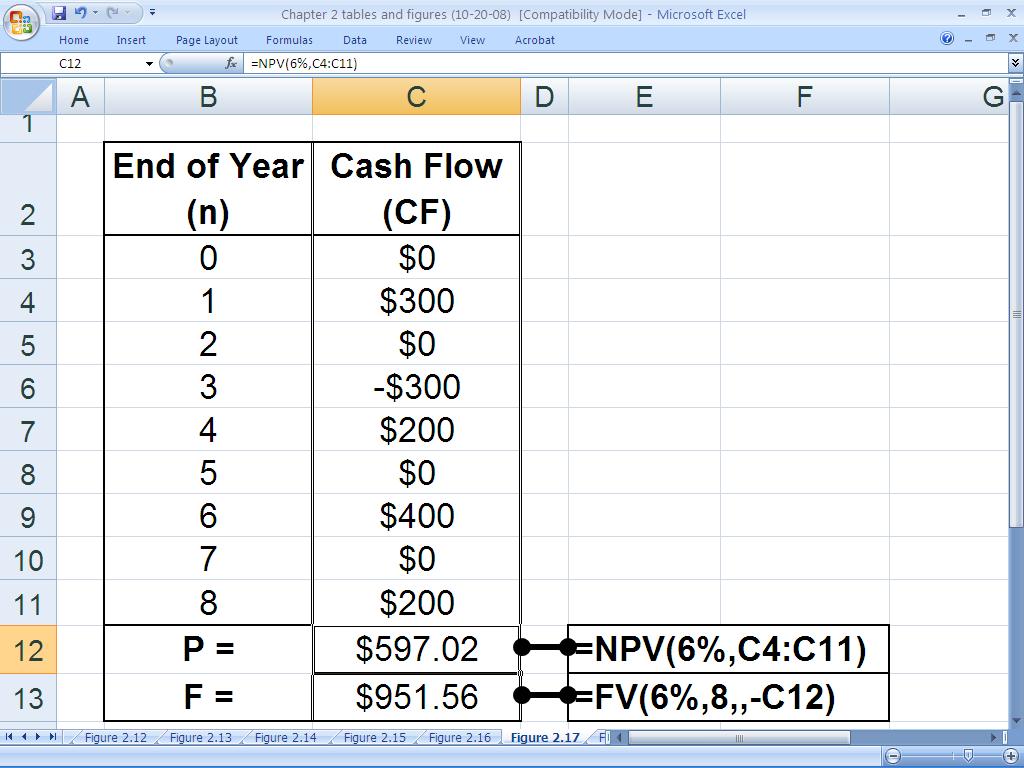

45 Determine the present worth equivalent of the following series of cash flows. Use an interest rate of 6% per interest period. P = $300(P F 6%,1)- $300(P F 6%,3)+$200(P F 6%,4)+$400(P F 6%,6) +$200(P F 6%,8) = $ P =NPV(6%,300,0,-300,200,0,400,0,200) P =$ Example 2.13 & 2.16 End of Period Cash Flow 0 $0 1 $300 2 $0 3 -$300 4 $200 5 $0 6 $400 7 $0 8 $200

46 Computing the Future worth of Multiple cash Flows ) %, ( ) (1 1 1 t n i P F A F i A F n t t t n n t t (2.15) (2.16)

47 Example 2.15 Determine the future worth equivalent of the CFD shown below, using an interest rate of 10% compounded annually. ( + ) $50,000 $40,000 $30,000 $40,000 $50, End of Year i = 10%/year ( - ) $100,000

48 Example 2.15 ( + ) $50,000 $40,000 $30,000 $40,000 $50, End of Year i = 10%/year ( - ) $100,000 End of Year Cash Flow Present Future (P F 10%,n) PV(10%,n,,-CF) (F P 10%,5-n) (n) (CF) Worth Worth FV(10%,5-n,,-CF) 0 -$100, $100, $100, $161, $161, $50, $45, $45, $73, $73, $40, $33, $33, $53, $53, $30, $22, $22, $36, $36, $40, $27, $27, $44, $44, $50, $31, $31, $50, $50, SUM $59, $59, $95, $95, F =10000*FV(10%,5,,-NPV(10%,5,4,3,4,5)+10) = $95,694.00

-$300(F P 6%,5) +$200(F P 6%,4)+$400(F P 6%,2)+$200 F = $951.59 F =FV(6%,8,,-NPV(6%,300,0,-300,200,0,400,0,200)) F =$951.")

49 Example 2.14 & 2.16 Determine the future worth equivalent of the following series of cash flows. Use an interest rate of 6% per interest period. End of Period Cash Flow F = $300(F P 6%,7)-$300(F P 6%,5) +$200(F P 6%,4)+$400(F P 6%,2)+$200 F = $ F =FV(6%,8,,-NPV(6%,300,0,-300,200,0,400,0,200)) F =$ $0 1 $300 2 $0 3 -$300 4 $200 5 $0 6 $400 7 $0 8 $200 (The 3 difference in the answers is due to round-off error in the tables in Appendix A.)

50

51 Some Common Cash Flow Series Uniform Series A t = A t = 1,,n Gradient Series A t = 0 t = 1 = A t-1 +G t = 2,,n = (t-1)g t = 1,,n Geometric Series A t = A t = 1 = A t-1 (1+j)t = 2,,n = A 1 (1+j) t-1 t = 1,,n

52 Relationships among P, F, and A P occurs at the same time as A 0, i.e., at t = 0 (one period before the first A in a uniform series) F occurs at the same time as A n, i.e., at t = n (the same time as the last A in a uniform series) Be careful in using the formulas we develop

53 DCF Uniform Series Formulas A A A A A A P occurs 1 period before first A P = A[(1+i) n -1]/[i(1+i) n ] P P = A(P A i%,n) P = [ =PV(i%,n,-A) ] A = Pi(1+i) n /[(1+i) n -1] A = P(A P i%,n) A = [ =PMT(i%,n,-P) ]

54 DCF Uniform Series Formulas A A A A A A P occurs 1 period before first A P = A[(1+i) n -1]/[i(1+i) n ] P P = A(P A i%,n) P =PV(i%,n,-A) A = Pi(1+i) n /[(1+i) n -1] A = P(A P i%,n) A =PMT(i%,n,-P)

55 DCF Uniform Series Formulas A A A A A A F = A[(1+i) n -1]/i F occurs at the same time as last A F = A(F A i%,n) F F = [ =FV(i%,n,-A) ] A = Fi/[(1+i) n -1] A = F(A F i%,n) A = [ =PMT(i%,n,,-F) ]

56 DCF Uniform Series Formulas A A A A A A F = A[(1+i) n -1]/i F occurs at the same time as last A F = A(F A i%,n) F F =FV(i%,n,-A) A = Fi/[(1+i) n -1] A = F(A F i%,n) A =PMT(i%,n,,-F)

57 Uniform Series of Cash Flows Discounted Cash Flow Formulas n (1 i) 1 n i(1 i) P = A(P A i%,n) = A (2.22) n i(1 i) n (1 i) 1 A = P(A P i%,n) = P (2.25) P occurs one period before the first A F = A(F A i%,n) = A (1 i) n 1 (2.28) i i A = F(A F i%,n) = F n (2.30) (1 i) 1 F occurs at the same time as the last A

58 Troy Long deposits a single sum of money in a savings account that pays 5% compounded annually. How much must he deposit in order to withdraw $2,000/yr for 5 years, with the first withdrawal occurring 1 year after the deposit? P = $2000(P A 5%,5) P = $2000( ) = $ P =PV(5%,5,-2000) P = $ Example 2.17

59 Troy Long deposits a single sum of money in a savings account that pays 5% compounded annually. How much must he deposit in order to withdraw $2,000/yr for 5 years, with the first withdrawal occurring 1 year after the deposit? P = $2,000(P A 5%,5) P = $2,000( ) = $8, P =PV(5%,5,-2000) P = $ Example 2.17

60 Troy Long deposits a single sum of money in a savings account that pays 5% compounded annually. How much must he deposit in order to withdraw $2,000/yr for 5 years, with the first withdrawal occurring 1 year after the deposit? P = $2,000(P A 5%,5) P = $2,000( ) = $8, P =PV(5%,5,-2000) P = $8, Example 2.17

61 Troy Long deposits a single sum of money in a savings account that pays 5% compounded annually. How much must he deposit in order to withdraw $2,000/yr for 5 years, with the first withdrawal occurring 3 years after the deposit? P = $2000(P A 5%,5)(P F 5%,2) P = $2000( )( ) = $ P =PV(5%,2,,-PV(5%,5,-2000)) P = $ Example 2.18

62 Troy Long deposits a single sum of money in a savings account that pays 5% compounded annually. How much must he deposit in order to withdraw $2,000/yr for 5 years, with the first withdrawal occurring 3 years after the deposit? P = $2,000(P A 5%,5)(P F 5%,2) P = $2,000( )( ) = $7, P =PV(5%,2,,-PV(5%,5,-2000)) P = $ Example 2.18

63 Troy Long deposits a single sum of money in a savings account that pays 5% compounded annually. How much must he deposit in order to withdraw $2,000/yr for 5 years, with the first withdrawal occurring 3 years after the deposit? P = $2,000(P A 5%,5)(P F 5%,2) P = $2,000( )( ) = $7, P =PV(5%,2,,-PV(5%,5,-2000)) P = $7, Example 2.18

64 Rachel Townsley invests $10,000 in a fund that pays 8% compounded annually. If she makes 10 equal annual withdrawals from the fund, how much can she withdraw if the first withdrawal occurs 1 year after her investment? A = $10,000(A P 8%,10) A = $10,000( ) = $ A =PMT(8%,10,-10000) A = $ Example 2.19

65 Rachel Townsley invests $10,000 in a fund that pays 8% compounded annually. If she makes 10 equal annual withdrawals from the fund, how much can she withdraw if the first withdrawal occurs 1 year after her investment? A = $10,000(A P 8%,10) A = $10,000( ) = $1, A =PMT(8%,10,-10000) A = $ Example 2.19

66 Rachel Townsley invests $10,000 in a fund that pays 8% compounded annually. If she makes 10 equal annual withdrawals from the fund, how much can she withdraw if the first withdrawal occurs 1 year after her investment? A = $10,000(A P 8%,10) A = $10,000( ) = $1, A =PMT(8%,10,-10000) A = $1, Example 2.19

67 Example 2.22 (note the skipping) Suppose Rachel delays the first withdrawal for 2 years. How much can be withdrawn each of the 10 years? A = $10,000(F P 8%,2)(A P 8%,10) A = $10,000( )( ) A = $ A =PMT(8%,10-FV(8%,2,,-10000)) A = $

68 Suppose Rachel delays the first withdrawal for 2 years. How much can be withdrawn each of the 10 years? A = $10,000(F P 8%,2)(A P 8%,10) A = $10,000( )( ) A = $1, A =PMT(8%,10-FV(8%,2,,-10000)) A = $ Example 2.22

69 Suppose Rachel delays the first withdrawal for 2 years. How much can be withdrawn each of the 10 years? A = $10,000(F P 8%,2)(A P 8%,10) A = $10,000( )( ) A = $1, A =PMT(8%,10,-FV(8%,2,,-10000)) A = $1, Example 2.22

70 Example 2.20 A firm borrows $2,000,000 at 12% annual interest and pays it back with 10 equal annual payments. What is the payment?

71 A firm borrows $2,000,000 at 12% annual interest and pays it back with 10 equal annual payments. What is the payment? A = $2,000,000(A P 12%,10) A = $2,000,000( ) A = $353,960 Example 2.20

72 A firm borrows $2,000,000 at 12% annual interest and pays it back with 10 equal annual payments. What is the payment? A = $2,000,000(A P 12%,10) A = $2,000,000( ) A = $353,960 A =PMT(12%,10, ) A = $353, Example 2.20

73 Example 2.21 Suppose the firm pays back the loan over 15 years in order to obtain a 10% interest rate. What would be the size of the annual payment?

74 Suppose the firm pays back the loan over 15 years in order to obtain a 10% interest rate. What would be the size of the annual payment? A = $2,000,000(A P 10%,15) A = $2,000,000( ) A = $262,940 Example 2.21

75 Suppose the firm pays back the loan over 15 years in order to obtain a 10% interest rate. What would be the size of the annual payment? A = $2,000,000(A P 10%,15) A = $2,000,000( ) A = $262,940 A =PMT(10%,15, ) Example 2.21 A = $262, Extending the loan period 5 years reduced the payment by $91,020.78

76 Luis Jimenez deposits $1,000/yr in a savings account that pays 6% compounded annually. How much will be in the account immediately after his 30 th deposit? F = $1000(F A 6%,30) F = $1000( ) = $79, F =FV(6%,30,-1000) A = $78, Example 2.23

77 Luis Jimenez deposits $1,000/yr in a savings account that pays 6% compounded annually. How much will be in the account immediately after his 30 th deposit? F = $1,000(F A 6%,30) F = $1,000( ) = $79, F =FV(6%,30,-1000) A = $78, Example 2.23

78 Luis Jimenez deposits $1,000/yr in a savings account that pays 6% compounded annually. How much will be in the account immediately after his 30 th deposit? F = $1,000(F A 6%,30) F = $1,000( ) = $79, F =FV(6%,30,-1000) A = $79, Example 2.23

79 Example 2.24 Andrew Brewer invests $5,000/yr and earns 6% compounded annually. How much will he have in his investment portfolio after 15 yrs? 20 yrs? 25 yrs? 30 yrs? (What if he earns 3%/yr?) F = $5000(F A 6%,15) = $5000( ) = $116, F = $5000(F A 6%,20) = $5000( ) = $183, F = $5000(F A 6%,25) = $5000( ) = $274, F = $5000(F A 6%,30) = $5000( ) = $395, F = $5000(F A 3%,15) = $5000( ) = $92, F = $5000(F A 3%,20) = $5000( ) = $134, F = $5000(F A 3%,25) = $5000( ) = $182, F = $5000(F A 3%,30) = $5000( ) = $237,877.10

80 Example 2.24 Andrew Brewer invests $5,000/yr and earns 6% compounded annually. How much will he have in his investment portfolio after 15 yrs? 20 yrs? 25 yrs? 30 yrs? (What if he earns 3%/yr?) F = $5,000(F A 6%,15) = $5,000( ) = $116, F = $5,000(F A 6%,20) = $5,000( ) = $183, F = $5,000(F A 6%,25) = $5,000( ) = $274, F = $5,000(F A 6%,30) = $5,000( ) = $395, F = $5000(F A 3%,15) = $5000( ) = $92, F = $5000(F A 3%,20) = $5000( ) = $134, F = $5000(F A 3%,25) = $5000( ) = $182, F = $5000(F A 3%,30) = $5000( ) = $237,877.10

81 Example 2.24 Andrew Brewer invests $5,000/yr and earns 6% compounded annually. How much will he have in his investment portfolio after 15 yrs? 20 yrs? 25 yrs? 30 yrs? (What if he earns 3%/yr?) F = $5,000(F A 6%,15) = $5,000( ) = $116, F = $5,000(F A 6%,20) = $5,000( ) = $183, F = $5,000(F A 6%,25) = $5,000( ) = $274, F = $5,000(F A 6%,30) = $5,000( ) = $395, F = $5,000(F A 3%,15) = $5,000( ) = $92, F = $5,000(F A 3%,20) = $5,000( ) = $134, F = $5,000(F A 3%,25) = $5,000( ) = $182, F = $5,000(F A 3%,30) = $5,000( ) = $237,877.10

82 Example 2.24 Andrew Brewer invests $5,000/yr and earns 6% compounded annually. How much will he have in his investment portfolio after 15 yrs? 20 yrs? 25 yrs? 30 yrs? (What if he earns 3%/yr?) F = $5,000(F A 6%,15) = $5,000( ) = $116, F = $5,000(F A 6%,20) = $5,000( ) = $183, F = $5,000(F A 6%,25) = $5,000( ) = $274, F = $5,000(F A 6%,30) = $5,000( ) = $395, F = $5,000(F A 3%,15) = $5,000( ) = $92, F = $5,000(F A 3%,20) = $5,000( ) = $134, F = $5,000(F A 3%,25) = $5,000( ) = $182, F = $5,000(F A 3%,30) = $5,000( ) = $237, Twice the time at half the rate is best! (1 + i) n

83 Andrew Brewer invests $5,000/yr and earns 6% compounded annually. How much will he have in his investment portfolio after 15 yrs? 20 yrs? 25 yrs? 30 yrs? (What if he earns 3%/yr?) F =FV(6%,15,-5000) = $116, F =FV(6%,20,-5000) = $183, F =FV(6%,25,-5000) = $274, F =FV(6%,30,-5000) = $395, F =FV(3%,15,-5000) = $92, F =FV(3%,20,-5000) = $134, F =FV(3%,25,-5000) = $182, F =FV(3%,30,-5000) = $237, Example 2.24

84 Andrew Brewer invests $5,000/yr and earns 6% compounded annually. How much will he have in his investment portfolio after 15 yrs? 20 yrs? 25 yrs? 30 yrs? (What if he earns 3%/yr?) F =FV(6%,15,-5000) = $116, F =FV(6%,20,-5000) = $183, F =FV(6%,25,-5000) = $274, F =FV(6%,30,-5000) = $395, F =FV(3%,15,-5000) = $92, F =FV(3%,20,-5000) = $134, F =FV(3%,25,-5000) = $182, Example 2.24 F =FV(3%,30,-5000) = $237, Twice the time at half the rate is best! (1 + i) n

85 If Coby Durham earns 7% on his investments, how much must he invest annually in order to accumulate $1,500,000 in 25 years? A = $1,500,000(A F 7%,25) A = $1,500,000( ) A = $23,715 A =PMT(7%,25,, ) A = $23, Example 2.25

86 If Coby Durham earns 7% on his investments, how much must he invest annually in order to accumulate $1,500,000 in 25 years? A = $1,500,000(A F 7%,25) A = $1,500,000( ) A = $23,715 A =PMT(7%,25,, ) A = $23, Example 2.25

87 If Coby Durham earns 7% on his investments, how much must he invest annually in order to accumulate $1,500,000 in 25 years? A = $1,500,000(A F 7%,25) A = $1,500,000( ) A = $23,715 A =PMT(7%,25,, ) A = $23, Example 2.25

88 Example 2.26 If Crystal Wilson earns 10% on her investments, how much must she invest annually in order to accumulate $1,000,000 in 40 years? A = $1,000,000(A F 10%,40) A = $1,000,000( ) A = $ A =PMT(10%,40,, ) A = $

89 Example 2.26 If Crystal Wilson earns 10% on her investments, how much must she invest annually in order to accumulate $1,000,000 in 40 years? A = $1,000,000(A F 10%,40) A = $1,000,000( ) A = $2, A =PMT(10%,40,, ) A = $

90 Example 2.26 If Crystal Wilson earns 10% on her investments, how much must she invest annually in order to accumulate $1,000,000 in 40 years? A = $1,000,000(A F 10%,40) A = $1,000,000( ) A = $2, A =PMT(10%,40,, ) A = $2,259.41

91 Example 2.27 $500,000 is spent for a SMP machine in order to reduce annual expenses by $92,500/yr. At the end of a 10-year planning horizon, the SMP machine is worth $50,000. Based on a 10% TVOM, a) what single sum at t = 0 is equivalent to the SMP investment? b) what single sum at t = 10 is equivalent to the SMP investment? c) what uniform annual series over the 10-year period is equivalent to the SMP investment?

92 Example 2.27 (Solution) P = -$500,000 + $92,500(P A 10%,10) + $50,000(P F 10%,10) P = -$500,000 + $92,500( ) + $50,000( ) P = $87, P =PV(10%,10,-92500,-50000) P = $87,649.62(Chapter 5) F = -$500,000(F P 10%,10) + $92,500(F A 10%,10) + $50,000 F = -$500,000( ) + $92,500( ) + $50,000 F = $227, F =FV(10%,10,-92500,500000) F = $227, (Chapter 6)

93 Example 2.27 (Solution) A = -$500,000(A P 10%,10) + $92,500 + $50,000(A F 10%,10) A = -$500,000( ) + $92,500 + $50,000( ) A = $14, A =PMT(10%,10,500000,-50000) A = $14,264.57(Chapter 7)

94 P = A A = P F = A A = F [(1 + i) n 1] i(1 + i) n [ i(1 + i) n ] (1 + i) n 1 [ ] (1 + i) n 1 i [ i ] (1 + i) n 1 uniform series, present worth factor = A(P A i%,n) =PV(i%,n,-A) uniform series, capital recovery factor = P(A P i%,n) =PMT(i%,n,-P) uniform series, future worth factor = A(F A i%,n) =FV(i%,n,-A) uniform series, sinking fund factor = F(A F i%,n) =PMT(i%,n,,-F)

Chapter 2. Time Value of Money (TVOM) Principles of Engineering Economic Analysis, 5th edition

Principles of Engineering Economic Analysis, 5th edition") Chapter 2 Time Value of Money (TVOM) Cash Flow Diagrams (EOY) Example 2.1 Cash Flow Profiles for Two Investment Alternatives End of Year (EOY) CF(A) CF(B) CF(B-A) 0 -$100,000 -$100,000 $0 1 $10,000 $50,000

Chapter 2 Time Value of Money (TVOM) Cash Flow Diagrams (EOY) Example 2.1 Cash Flow Profiles for Two Investment Alternatives End of Year (EOY) CF(A) CF(B) CF(B-A) 0 -$100,000 -$100,000 $0 1 $10,000 $50,000

Multiple Compounding Periods in a Year. Principles of Engineering Economic Analysis, 5th edition

Multiple Compounding Periods in a Year Example 2.36 Rebecca Carlson purchased a car for $25,000 by borrowing the money at 8% per year compounded monthly. She paid off the loan with 60 equal monthly payments,

Multiple Compounding Periods in a Year Example 2.36 Rebecca Carlson purchased a car for $25,000 by borrowing the money at 8% per year compounded monthly. She paid off the loan with 60 equal monthly payments,

IE463 Chapter 2. Objective. Time Value of Money (Money- Time Relationships)

") IE463 Chapter 2 Time Value of Money (Money- Time Relationships) Objective Given a cash flow (or series of cash flows) occurring at some point in time, the objective is to find its equivalent value at another

IE463 Chapter 2 Time Value of Money (Money- Time Relationships) Objective Given a cash flow (or series of cash flows) occurring at some point in time, the objective is to find its equivalent value at another

Engineering Economy Chapter 4 More Interest Formulas

Engineering Economy Chapter 4 More Interest Formulas 1. Uniform Series Factors Used to Move Money Find F, Given A (i.e., F/A) Find A, Given F (i.e., A/F) Find P, Given A (i.e., P/A) Find A, Given P (i.e.,

Engineering Economy Chapter 4 More Interest Formulas 1. Uniform Series Factors Used to Move Money Find F, Given A (i.e., F/A) Find A, Given F (i.e., A/F) Find P, Given A (i.e., P/A) Find A, Given P (i.e.,

Engineering Economics

Economic Analysis Methods Engineering Economics Day 3: Rate of Return Analysis Three commonly used economic analysis methods are 1. Present Worth Analysis 2. Annual Worth Analysis 3. www.engr.sjsu.edu/bjfurman/courses/me195/presentations/engeconpatel3nov4.ppt

Economic Analysis Methods Engineering Economics Day 3: Rate of Return Analysis Three commonly used economic analysis methods are 1. Present Worth Analysis 2. Annual Worth Analysis 3. www.engr.sjsu.edu/bjfurman/courses/me195/presentations/engeconpatel3nov4.ppt

CHAPTER 7: ENGINEERING ECONOMICS

CHAPTER 7: ENGINEERING ECONOMICS The aim is to think about and understand the power of money on decision making BREAKEVEN ANALYSIS Breakeven point method deals with the effect of alternative rates of operation

CHAPTER 7: ENGINEERING ECONOMICS The aim is to think about and understand the power of money on decision making BREAKEVEN ANALYSIS Breakeven point method deals with the effect of alternative rates of operation

Time Value of Money and Economic Equivalence

Time Value of Money and Economic Equivalence Lecture No.4 Chapter 3 Third Canadian Edition Copyright 2012 Chapter Opening Story Take a Lump Sum or Annual Installments q q q Millionaire Life is a lottery

Time Value of Money and Economic Equivalence Lecture No.4 Chapter 3 Third Canadian Edition Copyright 2012 Chapter Opening Story Take a Lump Sum or Annual Installments q q q Millionaire Life is a lottery

Solutions to end-of-chapter problems Basics of Engineering Economy, 2 nd edition Leland Blank and Anthony Tarquin

Solutions to end-of-chapter problems Basics of Engineering Economy, 2 nd edition Leland Blank and Anthony Tarquin Chapter 2 Factors: How Time and Interest Affect Money 2.1 (a) (F/P,10%,20) = 6.7275 (b)

Solutions to end-of-chapter problems Basics of Engineering Economy, 2 nd edition Leland Blank and Anthony Tarquin Chapter 2 Factors: How Time and Interest Affect Money 2.1 (a) (F/P,10%,20) = 6.7275 (b)

Engineering Economics ECIV 5245

Engineering Economics ECIV 5245 Chapter 3 Interest and Equivalence Cash Flow Diagrams (CFD) Used to model the positive and negative cash flows. At each time at which cash flow will occur, a vertical arrow

Engineering Economics ECIV 5245 Chapter 3 Interest and Equivalence Cash Flow Diagrams (CFD) Used to model the positive and negative cash flows. At each time at which cash flow will occur, a vertical arrow

Chapter 3 Mathematics of Finance

Chapter 3 Mathematics of Finance Section R Review Important Terms, Symbols, Concepts 3.1 Simple Interest Interest is the fee paid for the use of a sum of money P, called the principal. Simple interest

Chapter 3 Mathematics of Finance Section R Review Important Terms, Symbols, Concepts 3.1 Simple Interest Interest is the fee paid for the use of a sum of money P, called the principal. Simple interest

FINANCE FOR EVERYONE SPREADSHEETS

FINANCE FOR EVERYONE SPREADSHEETS Some Important Stuff Make sure there are at least two decimals allowed in each cell. Otherwise rounding off may create problems in a multi-step problem Always enter the

FINANCE FOR EVERYONE SPREADSHEETS Some Important Stuff Make sure there are at least two decimals allowed in each cell. Otherwise rounding off may create problems in a multi-step problem Always enter the

Chapter 8. Rate of Return Analysis. Principles of Engineering Economic Analysis, 5th edition

Chapter 8 Rate of Return Analysis Systematic Economic Analysis Technique 1. Identify the investment alternatives 2. Define the planning horizon 3. Specify the discount rate 4. Estimate the cash flows 5.

Chapter 8 Rate of Return Analysis Systematic Economic Analysis Technique 1. Identify the investment alternatives 2. Define the planning horizon 3. Specify the discount rate 4. Estimate the cash flows 5.

TIME VALUE OF MONEY. Lecture Notes Week 4. Dr Wan Ahmad Wan Omar

TIME VALUE OF MONEY Lecture Notes Week 4 Dr Wan Ahmad Wan Omar Lecture Notes Week 4 4. The Time Value of Money The notion on time value of money is based on the idea that money available at the present

TIME VALUE OF MONEY Lecture Notes Week 4 Dr Wan Ahmad Wan Omar Lecture Notes Week 4 4. The Time Value of Money The notion on time value of money is based on the idea that money available at the present

3. Time value of money. We will review some tools for discounting cash flows.

1 3. Time value of money We will review some tools for discounting cash flows. Simple interest 2 With simple interest, the amount earned each period is always the same: i = rp o where i = interest earned

1 3. Time value of money We will review some tools for discounting cash flows. Simple interest 2 With simple interest, the amount earned each period is always the same: i = rp o where i = interest earned

3. Time value of money

1 Simple interest 2 3. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

1 Simple interest 2 3. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

1) Cash Flow Pattern Diagram for Future Value and Present Value of Irregular Cash Flows

Cash Flow Pattern Diagram for Future Value and Present Value of Irregular Cash Flows") Topics Excel & Business Math Video/Class Project #45 Cash Flow Analysis for Annuities: Savings Plans, Asset Valuation, Retirement Plans and Mortgage Loan. FV, PV and PMT. 1) Cash Flow Pattern Diagram for

Topics Excel & Business Math Video/Class Project #45 Cash Flow Analysis for Annuities: Savings Plans, Asset Valuation, Retirement Plans and Mortgage Loan. FV, PV and PMT. 1) Cash Flow Pattern Diagram for

Cha h pt p er 2 Fac a t c o t rs r : s : H o H w w T i T me e a n a d I nte t r e e r s e t s A f f e f c e t c t M oney

Chapter 2 Factors: How Time and Interest Affect Money 2-1 LEARNING OBJECTIVES 1. F/P and P/F factors 2. P/A and A/P factors 3. Interpolate for factor values 4. P/G and A/G factors 5. Geometric gradient

Chapter 2 Factors: How Time and Interest Affect Money 2-1 LEARNING OBJECTIVES 1. F/P and P/F factors 2. P/A and A/P factors 3. Interpolate for factor values 4. P/G and A/G factors 5. Geometric gradient

FE Review Economics and Cash Flow

4/4/16 Compound Interest Variables FE Review Economics and Cash Flow Andrew Pederson P = present single sum of money (single cash flow). F = future single sum of money (single cash flow). A = uniform series

4/4/16 Compound Interest Variables FE Review Economics and Cash Flow Andrew Pederson P = present single sum of money (single cash flow). F = future single sum of money (single cash flow). A = uniform series

FINANCIAL DECISION RULES FOR PROJECT EVALUATION SPREADSHEETS

FINANCIAL DECISION RULES FOR PROJECT EVALUATION SPREADSHEETS This note is some basic information that should help you get started and do most calculations if you have access to spreadsheets. You could

FINANCIAL DECISION RULES FOR PROJECT EVALUATION SPREADSHEETS This note is some basic information that should help you get started and do most calculations if you have access to spreadsheets. You could

7 - Engineering Economic Analysis

Construction Project Management (CE 110401346) 7 - Engineering Economic Analysis Dr. Khaled Hyari Department of Civil Engineering Hashemite University Introduction Is any individual project worthwhile?

Construction Project Management (CE 110401346) 7 - Engineering Economic Analysis Dr. Khaled Hyari Department of Civil Engineering Hashemite University Introduction Is any individual project worthwhile?

What is Value? Engineering Economics: Session 2. Page 1

Engineering Economics: Session 2 Engineering Economic Analysis: Slide 26 What is Value? Engineering Economic Analysis: Slide 27 Page 1 Review: Cash Flow Equivalence Type otation Formula Excel Single Uniform

Engineering Economics: Session 2 Engineering Economic Analysis: Slide 26 What is Value? Engineering Economic Analysis: Slide 27 Page 1 Review: Cash Flow Equivalence Type otation Formula Excel Single Uniform

Chapter 4. Discounted Cash Flow Valuation

Chapter 4 Discounted Cash Flow Valuation Appreciate the significance of compound vs. simple interest Describe and compute the future value and/or present value of a single cash flow or series of cash flows

Chapter 4 Discounted Cash Flow Valuation Appreciate the significance of compound vs. simple interest Describe and compute the future value and/or present value of a single cash flow or series of cash flows

Interest: The money earned from an investment you have or the cost of borrowing money from a lender.

8.1 Simple Interest Interest: The money earned from an investment you have or the cost of borrowing money from a lender. Simple Interest: "I" Interest earned or paid that is calculated based only on the

8.1 Simple Interest Interest: The money earned from an investment you have or the cost of borrowing money from a lender. Simple Interest: "I" Interest earned or paid that is calculated based only on the

Chapter 5. Learning Objectives. Principals Applied in this Chapter. Time Value of Money. Principle 1: Money Has a Time Value.

Chapter 5 Time Value of Money Learning Objectives 1. Construct cash flow timelines to organize your analysis of problems involving the time value of money. 2. Understand compounding and calculate the future

Chapter 5 Time Value of Money Learning Objectives 1. Construct cash flow timelines to organize your analysis of problems involving the time value of money. 2. Understand compounding and calculate the future

Chapter 5. Time Value of Money

Chapter 5 Time Value of Money Using Timelines to Visualize Cashflows A timeline identifies the timing and amount of a stream of payments both cash received and cash spent - along with the interest rate

Chapter 5 Time Value of Money Using Timelines to Visualize Cashflows A timeline identifies the timing and amount of a stream of payments both cash received and cash spent - along with the interest rate

CE 231 ENGINEERING ECONOMY PROBLEM SET 1

CE 231 ENGINEERING ECONOMY PROBLEM SET 1 PROBLEM 1 The following two cash-flow operations are said to be present equivalent at 10 % interest rate compounded annually. Find X that satisfies the equivalence.

CE 231 ENGINEERING ECONOMY PROBLEM SET 1 PROBLEM 1 The following two cash-flow operations are said to be present equivalent at 10 % interest rate compounded annually. Find X that satisfies the equivalence.

Chapter 6. Learning Objectives. Principals Applies in this Chapter. Time Value of Money

Chapter 6 Time Value of Money 1 Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate the present and future values of each. 2. Calculate the present value of

Chapter 6 Time Value of Money 1 Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate the present and future values of each. 2. Calculate the present value of

LESSON 2 INTEREST FORMULAS AND THEIR APPLICATIONS. Overview of Interest Formulas and Their Applications. Symbols Used in Engineering Economy

Lesson Two: Interest Formulas and Their Applications from Understanding Engineering Economy: A Practical Approach LESSON 2 INTEREST FORMULAS AND THEIR APPLICATIONS Overview of Interest Formulas and Their

Lesson Two: Interest Formulas and Their Applications from Understanding Engineering Economy: A Practical Approach LESSON 2 INTEREST FORMULAS AND THEIR APPLICATIONS Overview of Interest Formulas and Their

TIME VALUE OF MONEY (TVM) IEG2H2-w2 1

IEG2H2-w2 1") TIME VALUE OF MONEY (TVM) IEG2H2-w2 1 After studying TVM, you should be able to: 1. Understand what is meant by "the time value of money." 2. Understand the relationship between present and future value.

TIME VALUE OF MONEY (TVM) IEG2H2-w2 1 After studying TVM, you should be able to: 1. Understand what is meant by "the time value of money." 2. Understand the relationship between present and future value.

Chapter 4 The Time Value of Money

Chapter 4 The Time Value of Money Copyright 2011 Pearson Prentice Hall. All rights reserved. Chapter Outline 4.1 The Timeline 4.2 The Three Rules of Time Travel 4.3 Valuing a Stream of Cash Flows 4.4 Calculating

Chapter 4 The Time Value of Money Copyright 2011 Pearson Prentice Hall. All rights reserved. Chapter Outline 4.1 The Timeline 4.2 The Three Rules of Time Travel 4.3 Valuing a Stream of Cash Flows 4.4 Calculating

MULTIPLE-CHOICE QUESTIONS Circle the correct answer on this test paper and record it on the computer answer sheet.

M I M E 3 1 0 E N G I N E E R I N G E C O N O M Y Class Test #2 Thursday, 23 March, 2006 90 minutes PRINT your family name / initial and record your student ID number in the spaces provided below. FAMILY

M I M E 3 1 0 E N G I N E E R I N G E C O N O M Y Class Test #2 Thursday, 23 March, 2006 90 minutes PRINT your family name / initial and record your student ID number in the spaces provided below. FAMILY

Simple Interest: Interest earned on the original investment amount only. I = Prt

c Kathryn Bollinger, June 28, 2011 1 Chapter 5 - Finance 5.1 - Compound Interest Simple Interest: Interest earned on the original investment amount only If P dollars (called the principal or present value)

c Kathryn Bollinger, June 28, 2011 1 Chapter 5 - Finance 5.1 - Compound Interest Simple Interest: Interest earned on the original investment amount only If P dollars (called the principal or present value)

Understanding Interest Rates

Money & Banking Notes Chapter 4 Understanding Interest Rates Measuring Interest Rates Present Value (PV): A dollar paid to you one year from now is less valuable than a dollar paid to you today. Why? -

Money & Banking Notes Chapter 4 Understanding Interest Rates Measuring Interest Rates Present Value (PV): A dollar paid to you one year from now is less valuable than a dollar paid to you today. Why? -

Financial Functions HNDA 1 st Year Computer Applications. By Nadeeshani Aththanagoda. Bsc,Msc ATI-Section Anuradhapura

Financial Functions HNDA 1 st Year Computer Applications By Nadeeshani Aththanagoda. Bsc,Msc ATI-Section Anuradhapura Financial Functions This section will cover the built-in Excel Financial Functions.

Financial Functions HNDA 1 st Year Computer Applications By Nadeeshani Aththanagoda. Bsc,Msc ATI-Section Anuradhapura Financial Functions This section will cover the built-in Excel Financial Functions.

IE2140 Engineering Economy Tutorial 3 (Lab 1) Using Excel Financial Functions for Project Evaluation

Using Excel Financial Functions for Project Evaluation") IE2140 Engineering Economy Tutorial 3 (Lab 1) Using Excel Financial Functions for Project Evaluation 1. Objectives and Overview Solutions Guide by Hong Lanqing, Wang Xin and Mei Wenjie The objective of

IE2140 Engineering Economy Tutorial 3 (Lab 1) Using Excel Financial Functions for Project Evaluation 1. Objectives and Overview Solutions Guide by Hong Lanqing, Wang Xin and Mei Wenjie The objective of

Section 5.1 Simple and Compound Interest

Section 5.1 Simple and Compound Interest Question 1 What is simple interest? Question 2 What is compound interest? Question 3 - What is an effective interest rate? Question 4 - What is continuous compound

Section 5.1 Simple and Compound Interest Question 1 What is simple interest? Question 2 What is compound interest? Question 3 - What is an effective interest rate? Question 4 - What is continuous compound

CAPITAL BUDGETING Shenandoah Furniture, Inc.

CAPITAL BUDGETING Shenandoah Furniture, Inc. Shenandoah Furniture is considering replacing one of the machines in its manufacturing facility. The cost of the new machine will be $76,120. Transportation

CAPITAL BUDGETING Shenandoah Furniture, Inc. Shenandoah Furniture is considering replacing one of the machines in its manufacturing facility. The cost of the new machine will be $76,120. Transportation

Simple Interest. Simple Interest is the money earned (or owed) only on the borrowed. Balance that Interest is Calculated On

only on the borrowed. Balance that Interest is Calculated On") MCR3U Unit 8: Financial Applications Lesson 1 Date: Learning goal: I understand simple interest and can calculate any value in the simple interest formula. Simple Interest is the money earned (or owed)

MCR3U Unit 8: Financial Applications Lesson 1 Date: Learning goal: I understand simple interest and can calculate any value in the simple interest formula. Simple Interest is the money earned (or owed)

Year 10 Mathematics Semester 2 Financial Maths Chapter 15

Year 10 Mathematics Semester 2 Financial Maths Chapter 15 Why learn this? Everyone requires food, housing, clothing and transport, and a fulfilling social life. Money allows us to purchase the things we

Year 10 Mathematics Semester 2 Financial Maths Chapter 15 Why learn this? Everyone requires food, housing, clothing and transport, and a fulfilling social life. Money allows us to purchase the things we

Running head: THE TIME VALUE OF MONEY 1. The Time Value of Money. Ma. Cesarlita G. Josol. MBA - Acquisition. Strayer University

Running head: THE TIME VALUE OF MONEY 1 The Time Value of Money Ma. Cesarlita G. Josol MBA - Acquisition Strayer University FIN 534 THE TIME VALUE OF MONEY 2 Abstract The paper presents computations about

Running head: THE TIME VALUE OF MONEY 1 The Time Value of Money Ma. Cesarlita G. Josol MBA - Acquisition Strayer University FIN 534 THE TIME VALUE OF MONEY 2 Abstract The paper presents computations about

REVIEW MATERIALS FOR REAL ESTATE FUNDAMENTALS

REVIEW MATERIALS FOR REAL ESTATE FUNDAMENTALS 1997, Roy T. Black J. Andrew Hansz, Ph.D., CFA REAE 3325, Fall 2005 University of Texas, Arlington Department of Finance and Real Estate CONTENTS ITEM ANNUAL

REVIEW MATERIALS FOR REAL ESTATE FUNDAMENTALS 1997, Roy T. Black J. Andrew Hansz, Ph.D., CFA REAE 3325, Fall 2005 University of Texas, Arlington Department of Finance and Real Estate CONTENTS ITEM ANNUAL

Chapter 15 Inflation

Chapter 15 Inflation 15-1 The first sewage treatment plant for Athens, Georgia cost about $2 million in 1964. The utilized capacity of the plant was 5 million gallons/day (mgd). Using the commonly accepted

Chapter 15 Inflation 15-1 The first sewage treatment plant for Athens, Georgia cost about $2 million in 1964. The utilized capacity of the plant was 5 million gallons/day (mgd). Using the commonly accepted

ME 353 ENGINEERING ECONOMICS Sample Second Midterm Exam

ME 353 ENGINEERING ECONOMICS Sample Second Midterm Exam Scoring gives priority to the correct formulation. Numerical answers without the correct formulas for justification receive no credit. Decisions

ME 353 ENGINEERING ECONOMICS Sample Second Midterm Exam Scoring gives priority to the correct formulation. Numerical answers without the correct formulas for justification receive no credit. Decisions

An Introduction to Capital Budgeting Methods

An Introduction to Capital Budgeting Methods Econ 466 Spring, 2010 Chapters 9 and 10 Consider the following choice You have an opportunity to invest $20,000 in one of the following capital assets. You

An Introduction to Capital Budgeting Methods Econ 466 Spring, 2010 Chapters 9 and 10 Consider the following choice You have an opportunity to invest $20,000 in one of the following capital assets. You

IE463 Chapter 3. Objective: INVESTMENT APPRAISAL (Applications of Money-Time Relationships)

") IE463 Chapter 3 IVESTMET APPRAISAL (Applications of Money-Time Relationships) Objective: To evaluate the economic profitability and liquidity of a single proposed investment project. CHAPTER 4 2 1 Equivalent

IE463 Chapter 3 IVESTMET APPRAISAL (Applications of Money-Time Relationships) Objective: To evaluate the economic profitability and liquidity of a single proposed investment project. CHAPTER 4 2 1 Equivalent

Example. Chapter F Finance Section F.1 Simple Interest and Discount

Math 166 (c)2011 Epstein Chapter F Page 1 Chapter F Finance Section F.1 Simple Interest and Discount Math 166 (c)2011 Epstein Chapter F Page 2 How much should be place in an account that pays simple interest

Math 166 (c)2011 Epstein Chapter F Page 1 Chapter F Finance Section F.1 Simple Interest and Discount Math 166 (c)2011 Epstein Chapter F Page 2 How much should be place in an account that pays simple interest

3.1 Simple Interest. Definition: I = Prt I = interest earned P = principal ( amount invested) r = interest rate (as a decimal) t = time

r = interest rate (as a decimal) t = time") 3.1 Simple Interest Definition: I = Prt I = interest earned P = principal ( amount invested) r = interest rate (as a decimal) t = time An example: Find the interest on a boat loan of $5,000 at 16% for

3.1 Simple Interest Definition: I = Prt I = interest earned P = principal ( amount invested) r = interest rate (as a decimal) t = time An example: Find the interest on a boat loan of $5,000 at 16% for

Copyright 2015 by the McGraw-Hill Education (Asia). All rights reserved.

. All rights reserved.") Copyright 2015 by the McGraw-Hill Education (Asia). All rights reserved. Key Concepts and Skills Be able to compute: The future value of an investment made today The present value of cash to be received

Copyright 2015 by the McGraw-Hill Education (Asia). All rights reserved. Key Concepts and Skills Be able to compute: The future value of an investment made today The present value of cash to be received

7.7 Technology: Amortization Tables and Spreadsheets

7.7 Technology: Amortization Tables and Spreadsheets Generally, people must borrow money when they purchase a car, house, or condominium, so they arrange a loan or mortgage. Loans and mortgages are agreements

7.7 Technology: Amortization Tables and Spreadsheets Generally, people must borrow money when they purchase a car, house, or condominium, so they arrange a loan or mortgage. Loans and mortgages are agreements

IE 343 Midterm Exam 1

IE 343 Midterm Exam 1 Feb 17, 2012 Version A Closed book, closed notes. Write your printed name in the spaces provided above on every page. Show all of your work in the spaces provided. Interest rate tables

IE 343 Midterm Exam 1 Feb 17, 2012 Version A Closed book, closed notes. Write your printed name in the spaces provided above on every page. Show all of your work in the spaces provided. Interest rate tables

CHAPTER 2. Financial Mathematics

CHAPTER 2 Financial Mathematics LEARNING OBJECTIVES By the end of this chapter, you should be able to explain the concept of simple interest; use the simple interest formula to calculate interest, interest

CHAPTER 2 Financial Mathematics LEARNING OBJECTIVES By the end of this chapter, you should be able to explain the concept of simple interest; use the simple interest formula to calculate interest, interest

CHAPTER 4. The Time Value of Money. Chapter Synopsis

CHAPTER 4 The Time Value of Money Chapter Synopsis Many financial problems require the valuation of cash flows occurring at different times. However, money received in the future is worth less than money

CHAPTER 4 The Time Value of Money Chapter Synopsis Many financial problems require the valuation of cash flows occurring at different times. However, money received in the future is worth less than money

Capital Leases I: Present and Future Value

Spreadsheet Models for Managers 9/1 Session 9 Capital Leases I: Present and Future Value Worksheet Functions Non-Uniform Payments Last revised: July 6, 2011 Review of last time: Financial Models 9/2 Three

Spreadsheet Models for Managers 9/1 Session 9 Capital Leases I: Present and Future Value Worksheet Functions Non-Uniform Payments Last revised: July 6, 2011 Review of last time: Financial Models 9/2 Three

6.1 Simple and Compound Interest

6.1 Simple and Compound Interest If P dollars (called the principal or present value) earns interest at a simple interest rate of r per year (as a decimal) for t years, then Interest: I = P rt Accumulated

6.1 Simple and Compound Interest If P dollars (called the principal or present value) earns interest at a simple interest rate of r per year (as a decimal) for t years, then Interest: I = P rt Accumulated

Copyright 2016 by the UBC Real Estate Division

DISCLAIMER: This publication is intended for EDUCATIONAL purposes only. The information contained herein is subject to change with no notice, and while a great deal of care has been taken to provide accurate

DISCLAIMER: This publication is intended for EDUCATIONAL purposes only. The information contained herein is subject to change with no notice, and while a great deal of care has been taken to provide accurate

??? Basic Concepts. ISyE 3025 Engineering Economy. Overview. Course Focus 2. Have we got a deal for you! 5. Pay Now or Pay Later 4. The Jackpot!

ISyE 3025 Engineering Economy Copyright 1999. Georgia Tech Research Corporation. All rights reserved. Basic Concepts Jack R. Lohmann School of Industrial and Systems Engineering Georgia Institute of Technology

ISyE 3025 Engineering Economy Copyright 1999. Georgia Tech Research Corporation. All rights reserved. Basic Concepts Jack R. Lohmann School of Industrial and Systems Engineering Georgia Institute of Technology

Solutions to Questions - Chapter 3 Mortgage Loan Foundations: The Time Value of Money

Solutions to Questions - Chapter 3 Mortgage Loan Foundations: The Time Value of Money Question 3-1 What is the essential concept in understanding compound interest? The concept of earning interest on interest

Solutions to Questions - Chapter 3 Mortgage Loan Foundations: The Time Value of Money Question 3-1 What is the essential concept in understanding compound interest? The concept of earning interest on interest

Financial institutions pay interest when you deposit your money into one of their accounts.

KEY CONCEPTS Financial institutions pay interest when you deposit your money into one of their accounts. Often, financial institutions charge fees or service charges for providing you with certain services

KEY CONCEPTS Financial institutions pay interest when you deposit your money into one of their accounts. Often, financial institutions charge fees or service charges for providing you with certain services

Our Own Problems and Solutions to Accompany Topic 11

Our Own Problems and Solutions to Accompany Topic. A home buyer wants to borrow $240,000, and to repay the loan with monthly payments over 30 years. A. Compute the unchanging monthly payments for a standard

Our Own Problems and Solutions to Accompany Topic. A home buyer wants to borrow $240,000, and to repay the loan with monthly payments over 30 years. A. Compute the unchanging monthly payments for a standard

Fin 5413: Chapter 04 - Fixed Interest Rate Mortgage Loans Page 1 Solutions to Problems - Chapter 4 Fixed Interest Rate Mortgage Loans

Fin 5413: Chapter 04 - Fixed Interest Rate Mortgage Loans Page 1 Solutions to Problems - Chapter 4 Fixed Interest Rate Mortgage Loans Problem 4-1 A borrower makes a fully amortizing CPM mortgage loan.

Fin 5413: Chapter 04 - Fixed Interest Rate Mortgage Loans Page 1 Solutions to Problems - Chapter 4 Fixed Interest Rate Mortgage Loans Problem 4-1 A borrower makes a fully amortizing CPM mortgage loan.

5.3 Amortization and Sinking Funds

5.3 Amortization and Sinking Funds Sinking Funds A sinking fund is an account that is set up for a specific purpose at some future date. Typical examples of this are retirement plans, saving money for

5.3 Amortization and Sinking Funds Sinking Funds A sinking fund is an account that is set up for a specific purpose at some future date. Typical examples of this are retirement plans, saving money for

SOLUTIONS TO SELECTED PROBLEMS. Student: You should work the problem completely before referring to the solution. CHAPTER 1

SOLUTIONS TO SELECTED PROBLEMS Student: You should work the problem completely before referring to the solution. CHAPTER 1 Solutions included for problems 1, 4, 7, 10, 13, 16, 19, 22, 25, 28, 31, 34, 37,

SOLUTIONS TO SELECTED PROBLEMS Student: You should work the problem completely before referring to the solution. CHAPTER 1 Solutions included for problems 1, 4, 7, 10, 13, 16, 19, 22, 25, 28, 31, 34, 37,

Lesson FA xx Capital Budgeting Part 2C

- - - - - - Cover Page - - - - - - Lesson FA-20-170-xx Capital Budgeting Part 2C These notes and worksheets accompany the corresponding video lesson available online at: Permission is granted for educators

- - - - - - Cover Page - - - - - - Lesson FA-20-170-xx Capital Budgeting Part 2C These notes and worksheets accompany the corresponding video lesson available online at: Permission is granted for educators

Lecture 3. Chapter 4: Allocating Resources Over Time

Lecture 3 Chapter 4: Allocating Resources Over Time 1 Introduction: Time Value of Money (TVM) $20 today is worth more than the expectation of $20 tomorrow because: a bank would pay interest on the $20

Lecture 3 Chapter 4: Allocating Resources Over Time 1 Introduction: Time Value of Money (TVM) $20 today is worth more than the expectation of $20 tomorrow because: a bank would pay interest on the $20

IE 343 Midterm Exam. March 7 th Closed book, closed notes.

IE 343 Midterm Exam March 7 th 2013 Closed book, closed notes. Write your name in the spaces provided above. Write your name on each page as well, so that in the event the pages are separated, we can still

IE 343 Midterm Exam March 7 th 2013 Closed book, closed notes. Write your name in the spaces provided above. Write your name on each page as well, so that in the event the pages are separated, we can still

Advanced Cost Accounting Acct 647 Prof Albrecht s Notes Capital Budgeting

Advanced Cost Accounting Acct 647 Prof Albrecht s Notes Capital Budgeting Drawing a timeline can help in identifying all the amounts for computations. I ll present two models. The first is without taxes.

Advanced Cost Accounting Acct 647 Prof Albrecht s Notes Capital Budgeting Drawing a timeline can help in identifying all the amounts for computations. I ll present two models. The first is without taxes.

CHAPTER 4 SIMPLE AND COMPOUND INTEREST INCLUDING ANNUITY APPLICATIONS. Copyright -The Institute of Chartered Accountants of India

CHAPTER 4 SIMPLE AND COMPOUND INTEREST INCLUDING ANNUITY APPLICATIONS SIMPLE AND COMPOUND INTEREST INCLUDING ANNUITY- APPLICATIONS LEARNING OBJECTIVES After studying this chapter students will be able

CHAPTER 4 SIMPLE AND COMPOUND INTEREST INCLUDING ANNUITY APPLICATIONS SIMPLE AND COMPOUND INTEREST INCLUDING ANNUITY- APPLICATIONS LEARNING OBJECTIVES After studying this chapter students will be able

January 29. Annuities

January 29 Annuities An annuity is a repeating payment, typically of a fixed amount, over a period of time. An annuity is like a loan in reverse; rather than paying a loan company, a bank or investment

January 29 Annuities An annuity is a repeating payment, typically of a fixed amount, over a period of time. An annuity is like a loan in reverse; rather than paying a loan company, a bank or investment

Chapter 5. Interest Rates ( ) 6. % per month then you will have ( 1.005) = of 2 years, using our rule ( ) = 1.

6. % per month then you will have ( 1.005) = of 2 years, using our rule ( ) = 1.") Chapter 5 Interest Rates 5-. 6 a. Since 6 months is 24 4 So the equivalent 6 month rate is 4.66% = of 2 years, using our rule ( ) 4 b. Since one year is half of 2 years ( ).2 2 =.0954 So the equivalent

Chapter 5 Interest Rates 5-. 6 a. Since 6 months is 24 4 So the equivalent 6 month rate is 4.66% = of 2 years, using our rule ( ) 4 b. Since one year is half of 2 years ( ).2 2 =.0954 So the equivalent

Outline of Review Topics

Outline of Review Topics Cash flow and equivalence Depreciation Special topics Comparison of alternatives Ethics Method of review Brief review of topic Problems 1 Cash Flow and Equivalence Cash flow Diagrams

Outline of Review Topics Cash flow and equivalence Depreciation Special topics Comparison of alternatives Ethics Method of review Brief review of topic Problems 1 Cash Flow and Equivalence Cash flow Diagrams

Sample Investment Device CD (Certificate of Deposit) Savings Account Bonds Loans for: Car House Start a business

Savings Account Bonds Loans for: Car House Start a business") Simple and Compound Interest (Young: 6.1) In this Lecture: 1. Financial Terminology 2. Simple Interest 3. Compound Interest 4. Important Formulas of Finance 5. From Simple to Compound Interest 6. Examples

Simple and Compound Interest (Young: 6.1) In this Lecture: 1. Financial Terminology 2. Simple Interest 3. Compound Interest 4. Important Formulas of Finance 5. From Simple to Compound Interest 6. Examples

Engineering Economy. Lecture 8 Evaluating a Single Project IRR continued Payback Period. NE 364 Engineering Economy

Engineering Economy Lecture 8 Evaluating a Single Project IRR continued Payback Period Internal Rate of Return (IRR) The internal rate of return (IRR) method is the most widely used rate of return method

Engineering Economy Lecture 8 Evaluating a Single Project IRR continued Payback Period Internal Rate of Return (IRR) The internal rate of return (IRR) method is the most widely used rate of return method

Chapter 5 - Level 3 - Course FM Solutions

ONLY CERTAIN PROBLEMS HAVE SOLUTIONS. THE REMAINING WILL BE ADDED OVER TIME. 1. Kathy can take out a loan of 50,000 with Bank A or Bank B. With Bank A, she must repay the loan with 60 monthly payments

ONLY CERTAIN PROBLEMS HAVE SOLUTIONS. THE REMAINING WILL BE ADDED OVER TIME. 1. Kathy can take out a loan of 50,000 with Bank A or Bank B. With Bank A, she must repay the loan with 60 monthly payments

Texas Instruments 83 Plus and 84 Plus Calculator

Texas Instruments 83 Plus and 84 Plus Calculator For the topics we cover, keystrokes for the TI-83 PLUS and 84 PLUS are identical. Keystrokes are shown for a few topics in which keystrokes are unique.

Texas Instruments 83 Plus and 84 Plus Calculator For the topics we cover, keystrokes for the TI-83 PLUS and 84 PLUS are identical. Keystrokes are shown for a few topics in which keystrokes are unique.

Section 4B: The Power of Compounding

Section 4B: The Power of Compounding Definitions The principal is the amount of your initial investment. This is the amount on which interest is paid. Simple interest is interest paid only on the original

Section 4B: The Power of Compounding Definitions The principal is the amount of your initial investment. This is the amount on which interest is paid. Simple interest is interest paid only on the original

ExcelBasics.pdf. Here is the URL for a very good website about Excel basics including the material covered in this primer.

Excel Primer for Finance Students John Byrd, November 2015. This primer assumes you can enter data and copy functions and equations between cells in Excel. If you aren t familiar with these basic skills

Excel Primer for Finance Students John Byrd, November 2015. This primer assumes you can enter data and copy functions and equations between cells in Excel. If you aren t familiar with these basic skills

These terms are the same whether you are the borrower or the lender, but I describe the words by thinking about borrowing the money.

Simple and compound interest NAME: These terms are the same whether you are the borrower or the lender, but I describe the words by thinking about borrowing the money. Principal: initial amount you borrow;

Simple and compound interest NAME: These terms are the same whether you are the borrower or the lender, but I describe the words by thinking about borrowing the money. Principal: initial amount you borrow;

Real Estate. Refinancing

Introduction This Solutions Handbook has been designed to supplement the HP-12C Owner's Handbook by providing a variety of applications in the financial area. Programs and/or step-by-step keystroke procedures

Introduction This Solutions Handbook has been designed to supplement the HP-12C Owner's Handbook by providing a variety of applications in the financial area. Programs and/or step-by-step keystroke procedures

Mathematics of Finance

CHAPTER 55 Mathematics of Finance PAMELA P. DRAKE, PhD, CFA J. Gray Ferguson Professor of Finance and Department Head of Finance and Business Law, James Madison University FRANK J. FABOZZI, PhD, CFA, CPA

CHAPTER 55 Mathematics of Finance PAMELA P. DRAKE, PhD, CFA J. Gray Ferguson Professor of Finance and Department Head of Finance and Business Law, James Madison University FRANK J. FABOZZI, PhD, CFA, CPA

Chapter 9, Mathematics of Finance from Applied Finite Mathematics by Rupinder Sekhon was developed by OpenStax College, licensed by Rice University,

Chapter 9, Mathematics of Finance from Applied Finite Mathematics by Rupinder Sekhon was developed by OpenStax College, licensed by Rice University, and is available on the Connexions website. It is used

Chapter 9, Mathematics of Finance from Applied Finite Mathematics by Rupinder Sekhon was developed by OpenStax College, licensed by Rice University, and is available on the Connexions website. It is used

Manual for SOA Exam FM/CAS Exam 2.

Manual for SOA Exam FM/CAS Exam 2. Chapter 2. Cashflows. c 2009. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam FM/CAS Exam 2, Financial Mathematics. Fall 2009 Edition,

Manual for SOA Exam FM/CAS Exam 2. Chapter 2. Cashflows. c 2009. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam FM/CAS Exam 2, Financial Mathematics. Fall 2009 Edition,

2. I =interest (in dollars and cents, accumulated over some period)

") A. Recap of the Variables 1. P = principal (as designated at some point in time) a. we shall use PV for present value. Your text and others use P for PV (We shall do it sometimes too!) 2. I =interest (in

A. Recap of the Variables 1. P = principal (as designated at some point in time) a. we shall use PV for present value. Your text and others use P for PV (We shall do it sometimes too!) 2. I =interest (in

Finance Notes AMORTIZED LOANS

Amortized Loans Page 1 of 10 AMORTIZED LOANS Objectives: After completing this section, you should be able to do the following: Calculate the monthly payment for a simple interest amortized loan. Calculate

Amortized Loans Page 1 of 10 AMORTIZED LOANS Objectives: After completing this section, you should be able to do the following: Calculate the monthly payment for a simple interest amortized loan. Calculate

Chapter 15B and 15C - Annuities formula

Chapter 15B and 15C - Annuities formula Finding the amount owing at any time during the term of the loan. A = PR n Q Rn 1 or TVM function on the Graphics Calculator Finding the repayment amount, Q Q =

Chapter 15B and 15C - Annuities formula Finding the amount owing at any time during the term of the loan. A = PR n Q Rn 1 or TVM function on the Graphics Calculator Finding the repayment amount, Q Q =

Computational Mathematics/Information Technology

Computational Mathematics/Information Technology 2009 10 Financial Functions in Excel This lecture starts to develop the background for the financial functions in Excel that deal with, for example, loan

Computational Mathematics/Information Technology 2009 10 Financial Functions in Excel This lecture starts to develop the background for the financial functions in Excel that deal with, for example, loan

Fin 5413: Chapter 06 - Mortgages: Additional Concepts, Analysis, and Applications Page 1

Fin 5413: Chapter 06 - Mortgages: Additional Concepts, Analysis, and Applications Page 1 INTRODUCTION Solutions to Problems - Chapter 6 Mortgages: Additional Concepts, Analysis, and Applications The following

Fin 5413: Chapter 06 - Mortgages: Additional Concepts, Analysis, and Applications Page 1 INTRODUCTION Solutions to Problems - Chapter 6 Mortgages: Additional Concepts, Analysis, and Applications The following

IE463 Chapter 4. Objective: COMPARING INVESTMENT AND COST ALTERNATIVES

IE463 Chapter 4 COMPARING INVESTMENT AND COST ALTERNATIVES Objective: To learn how to properly apply the profitability measures described in Chapter 3 to select the best alternative out of a set of mutually

IE463 Chapter 4 COMPARING INVESTMENT AND COST ALTERNATIVES Objective: To learn how to properly apply the profitability measures described in Chapter 3 to select the best alternative out of a set of mutually

8Syllabus topic F3 Depreciation and loans

Depreciation and loans 8Syllabus topic F3 Depreciation and loans This topic will develop your understanding of reducing balance loans and that an asset may depreciate over time rather than appreciate.

Depreciation and loans 8Syllabus topic F3 Depreciation and loans This topic will develop your understanding of reducing balance loans and that an asset may depreciate over time rather than appreciate.

Appendix A Financial Calculations

Derivatives Demystified: A Step-by-Step Guide to Forwards, Futures, Swaps and Options, Second Edition By Andrew M. Chisholm 010 John Wiley & Sons, Ltd. Appendix A Financial Calculations TIME VALUE OF MONEY

Derivatives Demystified: A Step-by-Step Guide to Forwards, Futures, Swaps and Options, Second Edition By Andrew M. Chisholm 010 John Wiley & Sons, Ltd. Appendix A Financial Calculations TIME VALUE OF MONEY

Compound Interest: Present Value

8.3 Compound Interest: Present Value GOL Determine the present value of an amount being charged or earning compound interest. YOU WILL NEED graphing calculator spreadsheet software LERN BOUT the Math nton

8.3 Compound Interest: Present Value GOL Determine the present value of an amount being charged or earning compound interest. YOU WILL NEED graphing calculator spreadsheet software LERN BOUT the Math nton

3.1 Mathematic of Finance: Simple Interest

3.1 Mathematic of Finance: Simple Interest Introduction Part I This chapter deals with Simple Interest, and teaches students how to calculate simple interest on investments and loans. The Simple Interest

3.1 Mathematic of Finance: Simple Interest Introduction Part I This chapter deals with Simple Interest, and teaches students how to calculate simple interest on investments and loans. The Simple Interest

A Brief Guide to Engineering Management Financial Calculations in ENGM 401 Section B1 Winter 2009

A Brief Guide to Engineering Management Financial Calculations in ENGM 401 Section B1 Winter 2009 MG Lipsett 2008 last updated December 8, 2008 Introduction This document provides concise explanations

A Brief Guide to Engineering Management Financial Calculations in ENGM 401 Section B1 Winter 2009 MG Lipsett 2008 last updated December 8, 2008 Introduction This document provides concise explanations

2/22/2017. Engineering Economics Knowledge. Engineering Economics FE REVIEW COURSE SPRING /22/2017

FE REVIEW COURSE SPRING 2017 Engineering Economics Paige Harris 2/22/2017 Engineering Economics Knowledge 4 6 problems Discounted cash flow Equivalence, PW, equivalent annual worth, FW, rate of return

FE REVIEW COURSE SPRING 2017 Engineering Economics Paige Harris 2/22/2017 Engineering Economics Knowledge 4 6 problems Discounted cash flow Equivalence, PW, equivalent annual worth, FW, rate of return

Copyright Disclaimer under Section 107 of the Copyright Act 1976, allowance is made for "fair use" for purposes such as criticism, comment, news

Copyright Disclaimer under Section 107 of the Copyright Act 1976, allowance is made for "fair use" for purposes such as criticism, comment, news reporting, teaching, scholarship, and research. Fair use

Copyright Disclaimer under Section 107 of the Copyright Act 1976, allowance is made for "fair use" for purposes such as criticism, comment, news reporting, teaching, scholarship, and research. Fair use

Chapter 7 Rate of Return Analysis

Chapter 7 Rate of Return Analysis 1 Recall the $5,000 debt example in chapter 3. Each of the four plans were used to repay the amount of $5000. At the end of 5 years, the principal and interest payments

Chapter 7 Rate of Return Analysis 1 Recall the $5,000 debt example in chapter 3. Each of the four plans were used to repay the amount of $5000. At the end of 5 years, the principal and interest payments

ECONOMIC ANALYSIS AND LIFE CYCLE COSTING SECTION I

ECONOMIC ANALYSIS AND LIFE CYCLE COSTING SECTION I ECONOMIC ANALYSIS AND LIFE CYCLE COSTING Engineering Economy and Economics 1. Several questions on basic economics. 2. Several problems on simple engineering

ECONOMIC ANALYSIS AND LIFE CYCLE COSTING SECTION I ECONOMIC ANALYSIS AND LIFE CYCLE COSTING Engineering Economy and Economics 1. Several questions on basic economics. 2. Several problems on simple engineering

The three formulas we use most commonly involving compounding interest n times a year are

Section 6.6 and 6.7 with finance review questions are included in this document for your convenience for studying for quizzes and exams for Finance Calculations for Math 11. Section 6.6 focuses on identifying

Section 6.6 and 6.7 with finance review questions are included in this document for your convenience for studying for quizzes and exams for Finance Calculations for Math 11. Section 6.6 focuses on identifying

Chapter 9. Capital Budgeting Decision Models

Chapter 9 Capital Budgeting Decision Models Learning Objectives 1. Explain capital budgeting and differentiate between short-term and long-term budgeting decisions. 2. Explain the payback model and its

Chapter 9 Capital Budgeting Decision Models Learning Objectives 1. Explain capital budgeting and differentiate between short-term and long-term budgeting decisions. 2. Explain the payback model and its

4: Single Cash Flows and Equivalence

4.1 Single Cash Flows and Equivalence Basic Concepts 28 4: Single Cash Flows and Equivalence This chapter explains basic concepts of project economics by examining single cash flows. This means that each

4.1 Single Cash Flows and Equivalence Basic Concepts 28 4: Single Cash Flows and Equivalence This chapter explains basic concepts of project economics by examining single cash flows. This means that each

Activity 1.1 Compound Interest and Accumulated Value

Activity 1.1 Compound Interest and Accumulated Value Remember that time is money. Ben Franklin, 1748 Reprinted by permission: Tribune Media Services Broom Hilda has discovered too late the power of compound

Activity 1.1 Compound Interest and Accumulated Value Remember that time is money. Ben Franklin, 1748 Reprinted by permission: Tribune Media Services Broom Hilda has discovered too late the power of compound