Modeling the Dynamics of Correlations among Implied Volatilities

|

|

|

- Benjamin Black

- 5 years ago

- Views:

Transcription

1 Draf of May 2, 2014 forhcoming in The Review of Finance Modeling he Dynamics of Correlaions among Implied Volailiies Rober Engle* and Sephen Figlewski** Implied volailiy (IV) reflecs boh expeced empirical volailiy and also risk premia. Sochasic variaion in eiher creaes unhedged risk in a dela hedged opions posiion. We develop EGARCH / DCC models for he dynamics of volailiies and correlaions among daily IVs from opions on 28 large cap socks. The daa srong suppor a general correlaion srucure and also a 1-facor model wih he VIX index as he common facor. Using IVs from socks ha are eiher highly correlaed wih he arge sock's IV or in he same indusry ogeher wih he VIX can significanly improve hedging of individual IV changes. JEL Classificaions: G13, G12, C32 Keywords: sochasic volailiy, hedging correlaion, implied volailiy, GARCH * Professor of Finance NYU Sern School of Business ** Professor of Finance NYU Sern School of Business We hank Amru Nashikkar and Yinghua Liu for heir assisance in he esimaions and David Hai of OpionMerics for providing addiional daa. Valuable commens and suggesions from Gurdip Bakshi, Liuren Wu, Rober Hodrick, and paricipans a he 2012 Sern Volailiy Insiue Conference and he 2012 OpionMerics conference, as well as wo referees and he edior are graefully acknowledged. We graefully acknowledge funding suppor from he NASDAQ OMX Educaional Foundaion. 1

2 Modeling he Dynamics of Correlaions among Implied Volailiies ABSTRACT Implied volailiy (IV) reflecs boh expeced empirical volailiy and also risk premia. Sochasic variaion in eiher creaes unhedged risk in a dela hedged opions posiion. We develop EGARCH / DCC models for he dynamics of volailiies and correlaions among daily IVs from opions on 28 large cap socks. The daa srong suppor a general correlaion srucure and also a 1-facor model wih he VIX index as he common facor. Using IVs from socks ha are eiher highly correlaed wih he arge sock's IV or in he same indusry ogeher wih he VIX can significanly improve hedging of individual IV changes. JEL Classificaions: G13, G12, C32 Keywords: sochasic volailiy, hedging correlaion, implied volailiy, GARCH 2

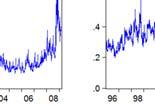

3 1. INTRODUCTION Implied volailiy, he volailiy value ha goes ino he marke's opion pricing formula, is a "risk neural" value, ha impounds boh he marke's objecive esimae of he fuure realized volailiy, and also he marke's olerance for volailiy risk. In he Black-Scholes (BS) model, insananeous volailiy is a known consan or, a wors, a nonsochasic funcion of ime. Empirically, sochasic variaion in volailiy produces risk in a real world dela hedged posiion in wo ways. The underlying sock's realized volailiy can be larger or smaller han expeced, leading o hedging errors whose size is deermined by he opion's gamma. Shocks o he marke's volailiy risk premium also change opion prices. Even if an opion wrier has hedged dela, gamma, and hea, an increase in implied volailiy causes an increase in an opion's price, and an immediae mark o marke loss on he posiion. The price sensiiviy o a change in implied volailiy (IV) is measured by vega, he parial derivaive of he (marke's) opion pricing formula wih respec o he volailiy parameer. Neiher empirical volailiy nor risk premia are direcly observable and boh can change unpredicably over ime. However, o he exen ha hese flucuaions are independen across socks, vega risk can be reduced hrough porfolio diversificaion. The focus in his paper is on modeling he dynamics of implied volailiies across socks in order o enhance our undersanding of vega risk and o develop ools for evaluaing and managing i. In he model exposiion, "volailiy" should be undersood as implied raher han realized or empirical volailiy. Figure 1 plos daily ime series of implied volailiies for 28 large socks over he period from Jan. 4, 1996 hrough Feb. 22, The socks are idenified by heir icker symbols and he corresponding company names are shown in Table I. Individual sock 1 These are composie implied volailiies from a he money calls and pus wih a weighed average ime o mauriy of 30 days. The consrucion mehod is described more fully below, in Secion 4. 3

4 IVs vary widely over ime, bu he flucuaions do no appear o be independen. Disinc paerns are visible, wih mos socks showing high values of implied volailiy from , low IVs in , and very high volailiies a he end of he sample in This paern suggess ha IVs are parially driven by one or more common facors. The las graph in he lower righ corner of Figure 1 is for he VIX index. The VIX was inroduced by he Chicago Board Opions Exchange in 1993 as a kind of marke implied volailiy index. The compuaion formula for he VIX was revised in 2003; he curren VIX reflecs an average implied volailiy for 30-day opions on he Sandard and Poor's 500 index. 2 Is ime paern closely resembles hose of he individual socks. We explore below using he VIX index as a proxy for he common facor in explaining he dynamics of IVs and he correlaions among hem. A a single poin in ime, opions on a given sock generally exhibi a range of implied volailiies for conracs wih a single expiraion, ha praciioners summarize in he volailiy "smile" or "skew." More generally, he "volailiy surface" refers o he full se of conracs wih all mauriies aken ogeher. 3 Aemps o model he dynamics of he volailiy surface find evidence of muliple underlying facors relaed o is level, slope and curvaure, as in he erm srucure of ineres raes. 4 However, we will no aemp o incorporae muliple facors ino a model of IV dynamics here. We develop a saisical model which allows changes in implied volailiies, volailiies of implied volailiies and correlaions of IVs among a se of underlying socks, where a sock's IV is measured by a composie of he implied volailiies of near o mauriy a-he-money calls and pus. The model correlaions can be used o assess he risk of a book of opions wrien on a collecion of underlying asses. Such a ool can be useful in developing hedging sraegies for a markemaker's porfolio of dela-gamma hedged posiions, as well as for risks associaed wih more exoic dispersion rades or volailiy producs such as variance swaps, VIX fuures or he newly offered VolConracs TM from VOLX, raded on he CME. 2 See CBOE (2003) for a full descripion of he VIX index and is mehod of calculaion. 3 See Gaheral (2006). 4 See Con and da Fonseca (2002) or Daglish e al. (2007). 4

5 The nex secion is an overview of he lieraure. Secion 3 develops he GARCHfamily models for he dynamics of IVs and heir correlaions. Secion 4 describes he daa se, covering 28 socks in he period , and Secion 5 presens he esimaion resuls for he models. Secion 6 explores he use of he 1-facor model in designing vega risk hedges for individual socks by combining posiions in he VIX index wih IV posiions in a small number of relaed socks. Secion 7 concludes. 2. REVIEW OF THE LITERATURE The original Black-Scholes (1973) consan volailiy framework allows an opion o be valued based on a coninuously rebalanced dela hedge agains he underlying sock. Bu in he real world large sock price changes expose hedgers o gamma risk ha increases wih he underlying sock's volailiy. Moreover, volailiy iself varies sochasically over ime, which inroduces addiional volailiy-relaed risk ha is no presen, or hedgeable, wihin he BS model. Hull and Whie (1987) and Heson (1993) inroduced opion models for reurns processes wih sochasic volailiy. Andersen, Benzoni and Lund (2002) and Eraker e al (2003) added sochasic jumps o he reurns process and o volailiy, and Pan (2002) incorporaed hem ino an opion model. Parameer esimaion is challenging in hese models, however, because volailiy is an unobservable sochasic laen facor. As an alernaive model of ime-varying volailiy, he GARCH framework has a major advanage ha here is only a single source of risk. 5 The shocks o reurns are also he shocks o reurns variance, so here are no laen facors. Boh he reurns equaion and he variance equaion are fied direcly from observed reurns. The common finding of srong negaive correlaion beween sock reurns and reurns variances is capured in a GARCH specificaion by an asymmery erm ha increases fuure volailiy more following a negaive reurn han a posiive reurn of he same size, as in he Glosen- Jagannahan-Runkle (1993) version of GARCH, or Nelson's (1991) EGARCH model. In sandard heory, sock risk can be reduced hrough diversificaion, bu no eliminaed because individual socks covary srongly wih a common marke facor. By 5 See Engle (1982), Bollerslev (1986), or Barone-Adesi e al. (2008). 5

6 conras, in Black-Scholes an opion can be perfecly hedged by aking a dynamic offseing posiion in is underlying sock. Correlaion beween he underlying sock's reurn and reurns on oher socks, or he marke as a whole, only become imporan for opions based on muliple underlying socks. 6,7 Bu once volailiy is allowed o be sochasically ime-varying, dela hedging leaves unhedged volailiy risk. Combining dela hedges ino a porfolio can miigae his risk, bu i canno be eliminaed if implied volailiy shocks are correlaed across socks. In ha case, i may even be appropriae o incorporae an opion's sensiiviy o "nondiversifiable" vega risk ino a heoreical pricing framework for opions, similar o he Capial Asse Pricing Model for socks, alhough we do no aemp o do ha here. GARCH-family models ha can apply o a porfolio of socks mus allow he individual pairwise correlaions o be ime-varying along wih he volailiies. The problem is ha wih n socks, here are (n 2 n)/2 disinc correlaions. To keep he number of fied parameers from geing ou of hand, various consrained models have been developed, wih he mos popular being he class of models wih dynamic condiional correlaion (DCC). See, for example, Engle (2002) or Engle (2009). The discussion and aricles cied so far have focused on modeling he underlying sock's "rue" or "empirical" or "real world" reurns process. Under BS assumpions, risk preferences don' affec he opion value direcly; he only difference beween he empirical disribuion and he risk neuralized disribuion is a difference in heir means. The volailiy inpu o he model should be he marke's bes esimae of he square roo of he sock's inegraed reurn variance from he presen o opion expiraion, which in Black-Scholes is he same under he risk neural measure. In ha case, he implied volailiy (IV) obained from an opion's marke price by invering he BS model is he marke's objecive forecas of fuure volailiy. Bu i was clear from he beginning ha his does no work in he real world. The ubiquious volailiy smile shows ha opion pricing under he risk neural measure and under he real world empirical measure are no he same. 6 See Sulz (1982) or Borovkova e al. (2007), for example. 7 By conras, derivaives based on credi porfolios depend very heavily on he correlaion in defaul risk among he componen securiies. 6

7 Risk exposures ha canno be perfecly hedged can be expeced o be priced in he marke. Sochasic volailiy is one such risk facor, and as Bakshi and Kapadia (2003), Carr and Wu (2008), and ohers have shown, implied volailiy is on average well above he underlying sock's realized volailiy over he opion's lifeime. The marke price of volailiy risk is posiive. 8 Opion prices impound he dynamics of reurns under he real world measure and also ime variaion in he marke's olerance for opion-relaed risk. Thus, a rise in expeced real world volailiy will increase IV and opion value. Bu an opion's price can also move wihou any change in he sock price or he rue expeced volailiy if risk aiudes change. In a dela hedge, any unexpeced change in IV produces an opion price shock. As Green and Figlewski (1999) amply documened, reurns on dela-hedged opion posiions in he real world are exposed o subsanial flucuaions in heir supposedly riskless reurns due o vega risk. If dela hedging is no riskless, opions marke makers and sock porfolio managers are now in a similar siuaion. Opion posiions can be dela hedged agains sock price changes, bu vega risk has o be managed. Dynamic models of he volailiy surface have been developed o predic expeced changes in IVs, see Gaheral (2006) or Derman e al. (1995) for insance, and unhedgeable vega risk mus be diversified. The same issue as wih sock porfolios arises wih opions: Is vega risk "idiosyncraic" so ha is effec is largely eliminaed in a broadly diversified porfolio of dela hedges, or is here a common "marke" IV facor ha will always remain? 9 And even wihou a common facor, as long as IV shocks are no perfecly independen across opions, knowledge of 8 The marke price of volailiy risk is ofen said o be negaive, no posiive. In mos cases, his is simply a differen way of describing he same phenomenon. Risk neural volailiy is higher han empirical volailiy, which causes he prices of opions o be higher han if here were no volailiy risk premium. Invesors pay a posiive premium o buy opions, because heir posiive exposure o volailiy is a hedge of volailiy risk. The reurns on hose high-priced opions will hen be lower on average, so he effec of he volailiy risk premium on opion reurns is negaive. 9 Driessen e al. (2009) find ha only marke-wide volailiy risk is priced, while i is no priced a he individual sock level. 7

8 heir covariance srucure allows more efficien diversificaion hrough consrucion of minimum vega risk porfolios of dela hedges. In 1993, he Chicago Board Opions Exchange inroduced he VIX index o measure he implied volailiy from opions on he overall sock marke. Given is apparen connecion o marke risk aiudes, he VIX is ofen known as he marke's "fear gauge." 10 The VIX has been found o be a viable measure of he common componen of IV flucuaions for individual opions and porfolios of opions. Recenly inroduced fuures conracs and opions ied o he VIX allow direc hedging of he vega exposure o his common facor. While some research has been done on modeling he connecion beween he VIX and IVs from opions on individual socks o suppor "dispersion" rading, ours is he firs paper o apply mulivariae GARCH mehodology o explore he dynamics of changes in IVs and he correlaions among hem THE MODEL Risk managers, opions raders and sraegiss mus undersand he risk exposure of an opions porfolio ha includes conracs wrien on a number of underlying asses wih various srikes and mauriies. By invoking a heoreical pricing model, such as Black Scholes, i is easy o evaluae he Greek leer risks of a porfolio of opions wih a single underlying asse. Traders aim o reduce risk by holding hedged porfolios ha are approximaely unaffeced by small movemens in he underlying asse prices and, ideally, in heir volailiies. Dela hedging an opion posiion agains he underlying sock is relaively easy; vega hedging is no. Wih muliple underlyings, only he porfolio delas are ypically evaluaed. 10 See Whaley (2000). 11 See, for example, Jacquier and Slaoui (2007). The CBOE (2009) recenly inroduced a new Implied Correlaion Index based on he dispersion beween he VIX and he average implied volailiy among opions on he socks ha make up he index. 8

9 Consider a collecion of opions whose prices a ime are given by a vecor p. The price vecor for he underlying asses, arranged in he same fashion, is given by s and he (Black Scholes) implied volailiies are sacked ino a vecor v. The dela marix for his se of opions is defined by p Δ = (1) s ' Mos elemens of his marix are zero, in heory, since he price of an opion on one asse should be unaffeced by a change in anoher asse's price as long as he underlying is unchanged. There may be addiional parameers in dela, and each of hese mus be evaluaed a he ime he hedge or risk measure is compued. A porfolio wih a % vecor W denoing W i unis of each opion i would be valued a π = W ' p. To make his porfolio dela neural, offseing posiions would be aken in he underlying asses o give a value for he hedged porfolio of '( ) π = W p Δ s (2) In heory his porfolio has no risk exposure from small movemens in any of he componens of s. When implied volailiy changes, he opion prices will also change. The vega marix for he vecor of opions is defined as: p Λ = (3) v ' If here is only one opion for each underlying, Λ would be expeced o be a diagonal marix. Wih muliple opions per sock, i would become block diagonal. Since he derivaive of s wih respec o v is zero, he vega for he dela neural porfolio in (2) is 9

10 π = W ' Λ v ' (4) Only if W ' Λ = 0, will his porfolio be independen of he dynamics of he implied volailiies. In heory his can be achieved in a hedge ha offses he volailiy exposure wih respec o each of he underlyings, bu his is rarely possible in pracice. If he changes in individual implied volailiies are highly correlaed hen a shor volailiy posiion in one asse can be hedged by a long volailiy posiion in anoher and he vega risk in he overall porfolio can be minimized. This leads o a need for a dynamic covariance marix of he implied volailiies of he underlyings. The focus of he paper is on developing expressions for ha IV covariance marix. The volailiy in he reurns equaion of a ypical GARCH model is a forecas of he volailiy of reurns over he nex day. For long horizon forecass, he expeced average volailiy of volailiy for reurns becomes very small as he new informaion has a relaively small effec on he long run average forecass. We model he behavior of he volailiy of IV over he nex day. Bu implied volailiy is a forecas of he average reurn volailiy over he remaining life of an opion, which will generally be many days or even years. Even so, we do no necessarily expec volailiy of volailiy for IVs o become very small a longer horizons, because IVs impound risk preferences in addiion o volailiy expecaions. Changes in marke risk premia may have a large effec on long mauriy conracs. A model for he dynamics of implied volailiies will provide a mehod for calculaing he condiional covariance marix for a se of dela-hedged equiy opion posiions. As par of his model, he covariance marix will be dynamic, wih differen correlaions in he shor and long run. Furhermore, allowing mean reversion in volailiies will produce some predicabiliy in he IVs, alhough probably no in he opion reurns hemselves. The heoreical models we develop below build up his covariance marix elemen by elemen by specifying he dynamics of each single opion's implied volailiy, and he correlaion beween he IVs for a pair of opions wrien on differen socks. For underlying asse i, he one monh a he money implied volailiy on day is denoed v i,. We consider he saisical model for he change in IV 10

11 v i, log( ) = i, + i, i,, i, ~ IID(0,1) vi, 1 ψ σ ε ε (5) where his noaion indicaes ha he errors are independen over ime wih mean zero and variance one. The funcions ( i,, i, ) ψ σ are he condiional mean and sandard deviaion of he change in log IV and are measurable wih respec o informaion a -1. Noe ha we are now changing from he coninuous-ime seing of heoreical opion pricing models o he discree-ime framework of volailiy modeling under GARCH. We model volailiy as a predicable mean revering process. A simple specificaion for he expeced change in log volailiy is an AR(1): E vi, log = θ 1, i θ 2, i log( vi, 1) (6) vi, where he subscrips indicae ha he hea parameers can vary over names bu no over ime. 3.1 VOLATILITY OF VOLATILITY The condiional variance of he log of he implied volailiy, σ,, is a measure of he volailiy of (implied) volailiy. Is dynamics can be parameerized naurally in he same way as is done for he reurn volailiies of regular asses. One difference is ha, unlike securiy reurns, he change in implied volailiy can have a non-rivial mean erm ha mus be aken ou before he volailiy of volailiy is measured. In his sudy we use he EGARCH volailiy process, as i easily accommodaes he non-sandard asymmery in volailiy ha is found in virually all volailiy of volailiy models. log ( σ 2 ) ( 2 i, φ1, i φ2, i εi, 1 φ3, iεi, 1 φ4, ilog σi, 1) = (7) Sandard TARCH specificaions which differ from (7) by having he variance on he lef hand side raher han is log, ofen maximize he likelihood funcion wih a negaive value 11

12 of he parameer φ 3,i ha measures he asymmeric par of volailiy. In such a model, here is a possibiliy of a negaive volailiy, especially during he esimaion procedure. Tha is no a problem wih EGARCH. I is very common wih financial asses o find ha negaive reurns have a bigger impac on fuure volailiy han posiive reurns. However for opions, declines in IV are found o have a smaller impac on fuure volailiy of volailiy han increases do. This is consisen wih he familiar posiive skew in reurns on volailiy conracs, which is opposie o he skew observed in mos asse classes. 12 Consequenly, we expec φ 3,i > 0. Wih his volailiy process i is simple o model joinly he mean and he volailiy of each individual log implied volailiy. The final specificaion decision is wha disribuion o assume for he, residuals. The normal is a sandard choice, bu i is found ha financial daa are more consisen wih faer-ailed disribuions. In he empirical resuls presened below, we have assumed a Suden- disribuion, wih he degrees of freedom, which deermines ail faness, as a parameer o be fied for our socks. Typical degrees of freedom values urn ou o be around 4, which implies quie fa ails. 3.2 CORRELATIONS The condiional correlaions beween wo implied log volailiies are given by ( ψ ) ( ) ( ( )) ( log ( / ) ψ ) log ( / ) log ( / ) log / E 1 v, v, 1, v, v, 1, ρ, = i i i j j j ij (8) Var v v Var v v 1 i, i, 1 1 j, j, 1 Direc subsiuion from (5) implies ha ρ ( ε ε ) = E (9) ij, 1 i, j, 12 Also, as poined ou in Engle (2011) and Engle and Misry (2007), his is likely o be a propery of any hedging porfolio since increases in he level of volailiy are likely o signal ha invesors need a larger hedge and hence need o purchase addiional volailiy exposure, hereby driving up is price. 12

13 Ineresingly, he condiional correlaions beween log IVs are simply he correlaions beween he disurbances. These correlaions will be esimaed wih dynamic srucure so ha hey can evolve over ime. The Dynamic Condiional Correlaion or DCC model of Engle (2002, 2009) is ideally suied o his problem. In ha model, he dependen variables are firs adjused for means and volailiies and hen he correlaions are compued for he sandardized reurns, which are inerpreed as he epsilons. The DCC model esimaes a full se of correlaions a one ime wih a very resriced parameerizaion. Leing ε be an n x 1 vecor of sandardized log volailiy residuals, he objecive is o esimae he correlaion marix which is defined as ( ) R = E εε (10) 1 ' The model for hese correlaions is given by he following hree equaions: T 1 R = εε ' T (11) = 1 ( 1 1' ) ( 1 ) Q = R+ α ε ε R + β Q R (12) ( ) ( ) 1/2 1/2 R = diag Q Q diag Q (13) Equaion (11) calculaes he uncondiional correlaions of he ε 's. Equaion (12) creaes a marix Q ha evolves based on jus wo unknown parameers α and β which govern he decay of correlaion informaion. The Q marix is approximaely a correlaion marix bu i does no have ones on he diagonal every ime period. Equaion (13) convers he Q marix ino a proper correlaion marix R and is he only place where a non-lineariy is inroduced. This non-lineariy is a naural consequence of esimaing correlaions which are bounded as a funcion of daa which are no. The wo unknown parameers of he DCC model can be esimaed wih maximum likelihood. However, subsanial research shows ha here are biases for large sysems 13

14 ha le alpha approach zero. Several alernaive esimaion sraegies have been proposed and in his analysis one of he simples bu very effecive sraegies called he MacGyver mehod is applied, see Engle (2009, 2009a). This mehod esimaes n(n-1)/2 bivariae models, as in Equaion (14). R 1 T i, j εi, ε j, T = 1 = (14) ( ) ( ) Q = R + α ε ε R + β Q R (15) ij, i, j i, j i, 1 j, 1 i, j i, j ij, 1 i, j ( ) 1/2 ( ) 1/2 R = Q Q Q (16) ij, ii, ij, jj, wihou imposing he resricion ha alpha and bea mus be he same for all i and j. Then he medians of hese wo series are compued and used in (15)-(16) in place of α i,j and β i,j o compue all he correlaions. In his way ouliers are ignored and usable esimaes are obained even if some of he bivariae pairs fail o converge or lie ouside he naural (0,1) inerval. This mehod is compared wih composie likelihood by Engle e al. (2008). 3.3 A ONE-FACTOR MODEL Empirically i is clear ha he correlaions beween implied volailiy innovaions are much smaller han he (uncondiional) correlaions beween IV levels. For some periods, all IVs are above he long run average and a oher imes none are. This suggess a facor model or some exogenous driving variables. The models for he ψ i, for each asse would depend upon variables from he oher asses, so ha shor run correlaions can become bigger due o he feedback. To incorporae his effec, we inroduce a common erm ino he mean IV change for each asse. In he same way ha he S&P 500 index serves as a proxy for he "marke porfolio," a naural choice for a measure of aggregae marke implied volailiy is he VIX. This index is closely relaed o he implied volailiies of 30-day opions on he S&P500 index and i impounds a forecas of fuure volailiy. Suppose he changes in log VIX saisfy he same model discussed above. 14

15 VIX log( ) VIX 1 = ψ + σ ε VIX, VIX, VIX, = θ + θ log( VIX ) + σ ε (17) 1, VIX 2, VIX 1 VIX, VIX, 2 2 log( σ ) φ + φ ε + φ ε φ log( σ ) (18) VIX, = 1, VIX 2, VIX VIX, 1 3, VIX VIX, 1 + 4, VIX VIX, 1 The research on sochasic volailiy provides srong evidence ha reurns variances are mean-revering. In (17), he long erm mean will be absorbed in he consan erm θ 1,VIX,, and θ 2,VIX should be negaive. Consider now he following model for he dynamics of a single sock's v i, where mean reversion for he individual sock's log variance and he VIX and are incorporaed in he θ 3,i and θ 4,i erms: v log v i, i, 1 = VIX θ 1, i + θ 2, i log + θ 3, i log( vi, 1) + θ 4, i log( VIX 1) + VIX 1 σ i, ε i, (19) In his specificaion, he variance equaion is sill given by Equaion (7), bu ε i, now refers only o he volailiy of he change in v i ha is independen of he change in VIX. This 1-facor model permis economy-wide informaion as refleced in he VIX o influence volailiies in all names simulaneously. The conemporaneous relaion beween VIX and each name provides an explanaion for he correlaion in IVs. Thus he second coefficien θ 2,i is he volailiy equivalen of he bea ha is rouinely calculaed in analyses of equiy reurns. In addiion, boh v i and VIX are mean-revering, a possibly differen raes. In his specificaion, he consan erm absorbs he long run means while he erms muliplied by θ 3,i and θ 4,i capure he effecs of reversion from he dae -1 levels oward hose long erm means. Given he way v i,-1 and VIX -1 ener Equaion (19), we expec θ 3,i < 0 and θ 4,i > 0. To he exen ha an individual sock's IV and he VIX are coinegraed, mean reversion here would essenially be reversion oward heir long erm relaionship. In ha case, one migh expec hese coefficiens also o be of similar magniude. We find boh of hese properies in he coefficien esimaes repored in Table III below. 15

16 4. DATA We will proceed o esimae he 0-facor model described above in Equaions (5)- (7), and he 1-facor model of (17)-(19) using daily reurns for a sample of large socks. The ime period covered is January 4, 1996 hrough February 27, To creae a sample of large acively raded socks, he firms originally seleced for he sudy were he 30 members of he Dow Jones Indusrial Average. Two socks were eliminaed due o mergers and oher changes in index composiion, leaving 28 firms, wih a oal of 378 pairwise correlaions among hem. The lis of firms and heir icker symbols is shown in Table I. The implied volailiies used in he sudy are drawn from he OpionMerics daabase, available hrough he Wharon Research Daa Services (WRDS) sysem. The GARCH models for individual sock volailiies are fied o sandardized IVs for a he money opions wih mauriies of 30 calendar days. The mehodology is essenially he same as for he original compuaion of he CBOE's VIX index, using weighed averages of IVs from raded opions. Specifically, o ge he sandardized call IV, OpionMerics averages he IVs from he wo calls wih he leas ou of he money and he leas in he money srikes, for he longes available mauriy less han 30 days. These IVs are weighed so ha he weighed average of he srikes equals he curren sock price. A similar averaging is done for calls wih he same srikes and he shores mauriy greaer han or equal o 30 days. The wo blended IVs are hen averaged using weighs such ha he weighed average mauriy is 30 days. This gives a composie implied volailiy for call opions. The equivalen calculaion is hen done wih four pu opions whose srikes bracke he curren forward price for he sock and whose mauriies bracke 30 days, o ge a pu IV. We hen ake a simple average of hese OpionMerics sandardized call and pu IVs o ge a single overall IV per sock per day which becomes he v i, series in he model. In he 1-facor model, he dynamics of individual sock IVs are assumed o be correlaed wih he acual (new) VIX index repored by he CBOE as a proxy for he 16

17 aggregae volailiy of he whole sock marke. 13 Daa on he VIX index was downloaded from he Chicago Board Opions Exchange websie. 5. EMPIRICAL ESTIMATION OF THE CORRELATION MODELS Each elemen of he correlaion marix R defined in (14)-(16) corresponds o a pair of opions, whose IVs are assumed o vary sochasically over ime. The individual sock volailiies are assumed o follow eiher (5)-(6), in he 0-facor model, or (19), in he 1-facor model. The esimaed parameers for he wo models are presened in Tables II and III. In Table II, he firs wo lines show he averages across all socks of he individual coefficiens and heir -saisics. The nex wo lines fi he 0-facor model for he VIX index, followed by resuls for he 28 individual socks. All coefficiens are highly saisically significan on average. The mean value of he auoregressive coefficien θ 2 is significanly negaive bu very small, indicaing only a mild degree of mean reversion in implied volailiies a a daily inerval, for boh he average sock in he sample and for he VIX index. Among he individual socks, 26 ou of 28 of he θ 2i esimaes are significanly negaive, and only 2 are posiive: for AXP (American Express) and for BAC (Bank of America). We suspec ha his resul for he wo large banks may be an arifac resuling from he insabiliy in he banking secor in lae 2008 and The resuls for he volailiy of volailiy equaion show he expeced posiive signs on φ 2, φ 3, and φ 4. Log variance oday is srongly relaed o yeserday's log variance and he size of yeserday's IV shock. The posiive and highly significan esimae for he φ 3 coefficien, averaging 0.070, indicaes asymmery in he IV process, such ha a posiive shock increases fuure IV by more han a negaive shock of he same size. 13 The procedure for compuing he VIX index was changed from he original mehod in In his sudy we use he new VIX ha is exraced by a nonparameric procedure from ou of he money calls and pus over a wide range of srike prices. 17

18 Ineresingly, he asymmery coefficien for he VIX is almos wice as large as he average across single socks. Among he individual equaions, every one shows posiive esimaes for he coefficien on he absolue value of yeserday's shock φ 2, none wih a - saisic below 10. Similarly, he coefficien on lagged volailiy of volailiy, φ 4, is highly significan, wih he lowes -saisic being In all bu wo cases φ 3 is posiive and i is significan in all bu one of hese. Table III presens he esimaion resuls for he 1-facor model, wih he (new) VIX index as he proxy for he common facor. As in Table II, every model coefficien was highly significan on average. The average value for θ 2, he sensiiviy o he common facor, was wih an average -saisic of more han 31. This coefficien was highly significan for every individual sock, ranging in value beween and wih a -saisic above 20 in every case. This provides srong evidence ha here is a common facor driving individual sock implied volailiies ha can be well proxied by he VIX index. The esimaes for θ 3 were also highly significan and all were negaive, indicaing mean reversion of he individual IVs oward is long run value, bu he small values for he coefficien, he larges in absolue value being , indicae ha he speed of convergence is fairly slow. The θ 4 coefficiens on he VIX mean correcion erm were of comparable size o hose for θ 3 bu all were posiive. A noable difference beween he variance equaions for he 0-facor and he 1-facor specificaions is ha boh he φ 3 and φ 4 coefficiens are smaller in Table III han in Table II. Idiosyncraic IV variance is less persisen han oal variance for individual names and less asymmerical. In he EGARCH specificaion, sabiliy of he sysem is ensured if φ 4 is below 1.0. In boh Table II and Table III, esimaes of φ 4 are less han 1.0 wih a high degree of saisical significance in every case. We noe also ha he -disribued shocks were found o have quie fa ails, wih he degrees of freedom parameer averaging under 4 for boh specificaions. The Macgyver procedure compues values for α ij and β ij in (15) across all pairs (i,j), akes he median α and β, and applies hem o consruc esimaes for he dynamics of he pairwise correlaions beween ε i and ε j. The resuling ime series of he mean correlaion across pairs for he 0-facor model and he 1-facor model are ploed in 18

19 Figure 2. The variabiliy in average correlaion over ime is sriking. Because he 1- facor model removes he common facor associaed wih he VIX index, he average correlaion for he residuals is boh lower and less variable over ime han correlaions in he 0-facor model ha reas he VIX facor as being par of he ε i and ε j residuals. 6. HEDGING DYNAMIC VEGA RISK This secion illusraes how our analysis can be applied o hedging vega, a derivaive securiy's exposure o he risk of an adverse change in is implied volailiy. Exising VIX fuures provide linear payoffs proporional o he change in he VIX index, which we have aken as a proxy for he common implied volailiy facor. For convenience, in our examples we will assume ha here exis comparable linear payoff conracs on individual sock IVs, such ha he change in value for conrac i is proporional o he change in v i. 14 This is mean o be jus an illusraion of how our analysis could be used o se up a vega hedge using a single "marke" IV conrac and a small number of conracs on individual sock IVs. We do no ry o opimize is performance ou of sample, for example, or moderae he effec of exreme parameer esimaes for some days. Le P denoe a single asse, a porfolio of securiies, or any oher posiion whose reurns R P are correlaed wih hose of a se H of hedging securiies, R Hi. 15 A sandard resul from he hedging lieraure is ha he vecor of risk minimizing quaniies for he hedging securiies, W * H, is given by 14 If, insead, he hedging securiies are individual sock opions or dela-hedges, he following equaions mus be modified o include he opion vegas, in order o conver he changes in he IV's ino dollar values. 15 In his secion, we are absracing from hedging possible exposure o oher sources of risk, noably from changes in he prices of he underlying asses. In hedging an acual porfolio of equiy opions, dela will ypically be neuralized and oher Greek leer risks may be hedged also. The hedging sraegy described here should be used o hedge he exposure o IV changes ha are independen of hose oher risk facors. 19

20 W = Var( R ) Cov( R, R ) (20) * 1 H H P H where Var(R H ) is he variance-covariance marix of he hedging securiies' reurns and Cov(R P,R H ) is he vecor of covariances beween he arge porfolio and he hedge securiy reurns. 6.1 HEDGING COMMON FACTOR AND IDIOSYNCRATIC VEGA RISK FOR A SINGLE NAME In applying our 1-facor correlaion model o he vega hedging problem, we will approximae he change in log IV by he percenage IV change: log( ) = (21) The firs equaliy holds in coninuous-ime; he second holds approximaely over a shor discree ime inerval Δ. Since our observaion inervals are mosly 1 day and never more han 5 calendar days, he approximaion is very close. Equaion (19) shows he model dynamics for an individual sock's implied volailiy v i in erms of he curren and previous period values of he VIX. Using (21), he sochasic par of Δv i is, [, ] =,,,, +,, (22) In our single-sock hedging examples, he dimension of he arge porfolio of linear payoffs o be hedged is 1, bu for greaer generaliy, we show he hedging soluion for a porfolio P ha may conain N P differen IV exposures. Le H denoe he porfolio of N H hedging asses, and W, v, θ 2, σ, and ε all denoe vecors of he corresponding individual parameer values from a se of securiies indicaed by subscrip P or H. For noaional convenience we will suppress he dependence of he risk parameers on, excep where i is needed. 20

21 The symbol will denoe he Hadamard produc, meaning elemen by elemen muliplicaion of wo vecors. For example, σ ε diag(σ) ε produces a vecor wih individual elemens σ i ε i. Thus, Σ PH, he N P x N H covariance marix for he idiosyncraic porions of he IV changes beween he securiies in P and hose in H is Σ E[( v oσ oε )( v oσ o ε )' ] (23) PH P P P H H H The variance-covariance marices for he arge and hedge porfolios, Σ P and Σ H, are defined analogously. The change in porfolio P is given by W P ' Δv P and he change in he hedging porfolio H is W H ' Δv H. Boh he arge porfolio and he hedging porfolio are exposed o common facor risk. This hedging problem differs from he general case because here is a conrac on he VIX ha has only common facor exposure and no idiosyncraic vega risk. This allows he minimum variance hedge o use derivaives on single socks o hedge he exposure o idiosyncraic IV changes, and he VIX conrac o eliminae he combined common facor risk from he arge and he hedging porfolios ogeher. From (22), he ime-varying sensiiviy of securiy i o he dae realizaion of he common facor is given by v i, θ 2,i ε VIX,. For any values of W P and W H, oal sensiiviy o ε VIX, of he overall hedged posiion is hen, +, which can be compleely offse by shoring he following amoun of he VIX conrac = (, +, )/ (24) Using(23) in Equaion (20) o solve for he quaniies of he hedging asses o sell agains porfolio P o minimize he idiosyncraic porion of he risk,, gives 21

22 = Σ Σ (25) The minimum vega risk hedge will have no common facor risk and idiosyncraic vega risk wih oal variance = Σ + Σ + 2 Σ (26) Table IV repors on he firs of wo experimens o illusrae he performance of hedges consruced using (24) and (25) wih he single-facor model parameer esimaes for our sample of socks. Firs, in every period we consider hedging each individual sock i's IV over he nex period by consrucing a hedge from he VIX conrac and implied volailiy conracs on he sock wih he highes esimaed period idiosyncraic IV correlaion wih sock i. The able shows he average hedge performance across socks and over ime in erms of he sandard deviaion in volailiy poins of he unhedged posiion, a hedge using only he VIX conrac, and an exended hedge wih boh he VIX and single sock IV conracs. On average, he one-day sandard deviaion of he change in IV across our 28 socks was , (2.27 percenage poins in annualized volailiy). Opimally hedging his vega risk using jus he VIX conrac would have reduced he average sandard deviaion of he hedged posiions o Adding a posiion in he mos correlaed single sock conrac would have reduced he hedge sandard deviaion a lile furher, o The saisical significance of his improvemen in hedge performance was gauged in wo ways. Differences in he squared hedging errors from he differen sraegies were compued for each single sock, and -saisics on he mean differences among hem were calculaed. The hird column of he able repor he averages of hose -saisics across socks. The average -saisic on he difference beween he unhedged posiion and he exended hedge averaged more han 3.0. No all socks showed significan improvemen. For 20 of 28 socks, he exended hedge significanly reduced he sandard deviaion of he change in is IV, bu in 5 cases i increased and he oher 3 showed an improvemen ha was no saisically significan. 22

23 The fourh column repors on he difference in squared hedging errors beween he exended hedges and hedges using only he VIX index o offse risk exposure o he common IV facor. The VIX by iself was quie effecive, achieving almos as good performance as he exended hedges and wih considerably lower variabiliy across names, such ha he -saisic on he improvemen over he unhedged posiion was The performance of he exended hedge relaive o he VIX only hedge was posiive bu no significan on average. Even so, he exended hedges were significanly beer han VIX only hedges for 10 of he socks, while in no case did he VIX only hedge significanly ouperform he exended hedge. In order o judge saisical significance for he whole sample ogeher, we creaed a pooled sample, esimaed he average difference in mean squared error, and compued - saisics using robus sandard errors correced for heeroskedasiciy across names and for conemporaneous correlaion in he errors. 16 These resuls, shown in columns 5 and 6, confirm wha he averages across names showed: boh he exended hedge and VIX only sraegies significanly reduced risk, bu exending he hedge by adding volailiy conracs on he single name whose correlaion was prediced o be he greaes on each dae gave raher limied improvemen. One reason for his is ha simply picking he sock wih he highes esimaed correlaion on each dae will end o selec ouliers and socks wih posiive esimaion errors. One way o reduce his problem in pracice could be o focus on correlaions over longer ime windows, for example selecing no he single sock wih he highes esimaed correlaion on dae, bu raher he one ha was, say, in he op 5 mos frequenly over he pas monh. A more naural way o use he dynamic IV correlaion model in hedging is o selec hedging socks ha are expeced on a priori grounds o be closely correlaed wih he arge porfolio, for example, socks from he same indusry. Our sample is limied o only 28 socks, bu hree of hem are drug companies, hree are banks, and here are hree oher ses of wo socks each from he same SIC 4-digi indusry. Table V explores hedging each of he welve socks for which his can be done using he VIX and one or wo oher socks from he same indusry. 16 The procedure is implemened in EViews, using Whie's robus procedure for cross-secion esimaion. 23

24 The improvemen in hedging performance is subsanial, especially for he hedges wih 2 socks in he same indusry. Of he welve, nine showed significan improvemen and only one of he hedges failed. For seven of hem, he exended hedge did significanly beer han hedging wih he VIX alone, and in no case did he VIX only hedge bea he exended hedge significanly. 7. CONCLUDING COMMENTS Alhough he original Black-Scholes model did no envision changes in he volailiy parameer, sochasic changes in implied volailiies are an imporan source of risk for real world opions markemakers. Correlaion in IV changes prevens his vega risk from being eliminaed by diversificaion in a porfolio of dela hedged opions posiions. Empirical volailiies and correlaions have been found o be sysemaically imevarying in ways ha can be capured wih GARCH-family models. This paper has explored wheher correlaions in implied volailiy changes also show dynamics ha can be capured wih mulivariae GARCH models. We developed wo such models using EGARCH, which is beer suied o modeling volailiies ha mus remain nonnegaive, and Dynamic Condiional Correlaion (DCC) for modeling correlaion dynamics. One specificaion has ime-varying correlaions driven by shocks ha are possibly correlaed across socks bu wihou a single common facor, and in he second model, IV changes are also correlaed hrough exposure o a single marke volailiy process ha we proxied by he VIX index. Our esimaes srongly suppored boh models in US equiy daa. There was a sligh bu significan degree of mean reversion in he "reurn" equaion (θ 2 = on average in he 0-facor model). In he 1-facor model, among 28 large socks, every one showed a srong correlaion beween is IV change and he change in he VIX, wih an average of for θ 2 in ha model. In he volailiy of volailiy equaions, boh specificaions showed a srong posiive asymmery. In he 0-facor model, for 25 ou of 28 socks, a posiive shock o implied volailiy increases fuure IV volailiy significanly 24

25 more han a negaive shock of he same size. For 19 socks, he coefficien on lagged variance exceeded 0.9 for he 0-facor model. The idiosyncraic IV changes in he 1- facor model showed less asymmery and less persisence. The use of he Suden - disribuion raher han he normal o model he shocks helped o reduce he impac of ouliers. The esimaed degrees of freedom averaged under 4.0 across socks, meaning he disribuion had very fa ails. We described in general how o use our model o consruc a dynamic hedge for he vega risk of an opion posiion, or porfolio, wih a hedging porfolio of IV exposures. Using he fied model coefficiens o hedge a single opion's vega risk wih he VIX and volailiy conracs on one oher name suggesed ha significan risk reducion could be achieved by offseing exposure o a common implied volailiy risk facor and also hedging he idiosyncraic residuals from he IV dynamics equaions. Turning our essenially saisical resuls ino an operaional hedging sraegy should involve a careful effor o limi he effecs of sampling noise and o incorporae non-saisical informaion such as he arge firm's indusry ino he hedge design. 25

26 References Andersen, T., Benzoni, L., and Lund, J. (2002). An empirical invesigaion of coninuous-ime equiy reurn models, Journal of Finance 57, Andersen, T., Bollerslev, T., Diebold, F., and Labys, P. (2003). Modeling and forecasing realized volailiy. Economerica 71, Bakshi, G., Cao, C. and Chen, Z. (1997). Empirical performance of alernaive opion pricing models, Journal of Finance 52, Bakshi, G. and Kapadia, N. (2003). Volailiy risk premiums embedded in individual equiy opions: some new insighs, Journal of Derivaives 11, Barone-Adesi, G., Engle, R. F., and Mancini, L. (2008). A GARCH opion pricing model wih filered hisorical simulaion, Review of Financial Sudies 21, Black, F. and Scholes M. (1973). The pricing of opions and corporae liabiliies, Journal of Poliical Economy 81, Bollerslev, T. (1986). Generalized auoregressive condiional heeroskedasiciy, Journal of Economerics 31, Borovkova, S., Permana F. and van der Weide, H. (2007). A closed form approach o valuaion and hedging of baske and spread opion, Journal of Derivaives 14,

27 Carr, P. and Wu L. (2009). Variance risk premiums, Review of Financial Sudies 22, Chicago Board Opions Exchange (2003). VIX CBOE Volailiy Index, hp:// Chicago Board Opions Exchange (2009). CBOE S&P 500 Implied Correlaion Index, hp:// Chrisoffersen, P., Jacobs, K., and Chang, B. Y. (2013). Forecasing wih opion implied informaion, in G. Ellio and A. Timmermann (eds.), Handbook of Economic Forecasing, Vol. 2, Elsevier, Amserdam, Neherlands. Con, R., and da Fonseca, J. (2002). Dynamics of implied volailiy surfaces, Quaniaive Finance 2, Daglish, T., Hull, J., and Suo, W. (2007). Volailiy surfaces: heory, rules of humb, and empirical evidence. Quaniaive Finance 7, Demeerfi, K, Derman, E., Kamal, M., and Zou, J. (1999). A guide o volailiy and variance swaps, Journal of Derivaives 6,

28 Derman, E., Kani, I., and Zou, J. (1995). The Local Volailiy Surface: Unlocking he Informaion in Index Opion Prices, Goldman Sachs Research Noes. Driessen, J., Maenhou, P., and Vilkov, G. (2009). The price of correlaion risk: evidence from equiy opions, Journal of Finance 64, Engle, R. (1982). Auoregressive Condiional Heeroscedasiciy wih esimaes of he variance of Unied Kingdom inflaion, Economerica 50, Engle, R. (2002). Dynamic condiional correlaion: a simple class of mulivariae generalized auoregressive condiional heeroskedasiciy models, Journal of Business and Economic Saisics 20, Engle, R. (2009). Anicipaing Correlaions, Princeon Universiy Press, Princeon New Jersey. Engle, R. (2009a). High dimension dynamic correlaions, in: J. L. Casle and N. Shephard (eds.), The Mehodology and Pracice of Economerics: A Fesschrif in Honour of David F. Hendry, Oxford Universiy Press, Oxford, U.K. Engle, R. (2011). Long-erm skewness and sysemic risk, Journal of Financial Economerics, 9,

29 Engle, R. and Misry, A. (2014). Priced risk and asymmeric volailiy in he crosssecion of skewness, Journal of Economerics, forhcoming. Engle, R., and Rangel, J.G. (2008). The Spline-GARCH model for low-frequency volailiy and is global macroeconomic causes, Review of Financial Sudies 21, Engle, R., Shephard, N., and Sheppard, K. (2008). Fiing and esing vas dimensional ime-varying covariance models, unpublished working paper, Universiy of Oxford. Eraker, B., Johannes, M., and Polson, N. (2003). The impac of jumps in volailiy and reurns, Journal of Finance 58, Gaheral, J. (2006). The Volailiy Surface: A Praciioner's Guide, Wiley Finance, Hoboken, New Jersey. Giamouridis, D. and Skiadopoulos, G. (2012). The informaional conen of financial opions for quaniaive asse managemen, in: B. Scherer and K. Winson (eds.), The Oxford Handbook of Quaniaive Asse Managemen, Oxford Universiy Press, Oxford, U.K. Glosen, L., Jagannahan, R., and Runkle, D. (1993). On he relaion beween he expeced value and he volailiy of he nominal excess reurn on socks. Journal of Finance 48,

30 Green, T.C. and Figlewski, S. (1999). Marke risk and model risk for a financial insiuion wriing opions, Journal of Finance 54, Harrison, J. M. and Kreps, D. (1979). Maringales and arbirage in muliperiod securiies markes," Journal of Economic Theory 20, Heson, S. (1993). A closed-form soluion for opions wih sochasic volailiy wih applicaions o bond and currency opions, Review of Financial Sudies 6, Hull, J., and Whie, A. (1987) The pricing of opions on asses wih sochasic volailiies. Journal of Finance 42, Jackwerh, J.C. (2004). Opion-Implied Risk-Neural Disribuions and Risk Aversion, Research Foundaion of AIMR, Charloesville, Virginia. Jacquier, A. and Slaoui, S. (2010). Variance dispersion and correlaion swaps, unpublished working paper, available a hp://papers.ssrn.com/sol3/papers.cfm?absrac_id= OpionMerics, (2008). Ivy DB File and Daa Reference Manual, Version Nelson, D. (1991). Condiional heeroskedasiciy in asse reurns: A new approach, Economerica 59,

31 Pan, J. (2002). The jump-risk premia implici in opions: Evidence from an inegraed ime-series sudy, Journal of Financial Economics 63, Poon, S. and Granger, C.W.J. (2003). "Forecasing volailiy in financial markes: a review, Journal of Economic Lieraure 41, Whaley, R. (2000). The invesor fear gauge, Journal of Porfolio Managemen 26,

32 Table I: Socks in he Daa Sample Ticker Symbol AA AXP BA BAC C CAT CVX DD DIS GE GM HD HPQ IBM INTC JNJ JPM KO MCD MMM MRK MSFT PFE T UTX VZ WMT XOM Company Name Alcoa American Express Boeing Bank of America Ciigroup Caerpillar Chevron Du Pon Disney General Elecric General Moors Home Depo Hewle Packard Inernaional Business Machines Inel Johnson & Johnson JP Morgan Chase Coca Cola McDonalds 3M CO Merck Microsof Pfizer AT&T Unied Technologies Verizon Walmar Exxon Mobil 32

33 Table II: EGARCH Esimaes for Sock Implied Volailiies wih No Common Facor Noes: The able repors he esimaed coefficiens and -saisics (in parenheses) from he 0-facor model: = + log( ) + ( ) = φ + φ + φ + φ ( ) Ticker -dis θ 1i θ 2i φ 1i φ 2i φ 3i φ 4i d.f. Sample averages (-3.42) (-4.20) (-14.05) (18.08) (8.23) (285.59) VIX Index (4.25) (-3.88) (-9.32) (6.13) (12.01) (167.75) AA (-3.87) (-4.19) (-15.53) (18.91) (4.74) (430.21) AXP (3.63) (2.53) (-14.23) (15.13) (19.78) (643.38) BA (-3.54) (-4.01) (-14.25) (16.05) (7.47) (59.48) BAC (3.06) (1.83) (-15.54) (13.81) (16.73) (994.88) C (-1.51) (-2.46) (-12.30) (16.07) (8.66) (334.32) CAT (-4.36) (-4.69) (-15.80) (19.57) (5.91) (87.07) CVX (-4.17) (-4.42) (-11.99) (16.34) (3.04) (258.91) DD (-2.07) (-2.60) (-7.78) (10.01) (7.12) (539.03) DIS (-5.20) (-6.27) (-14.19) (19.59) (10.46) (73.57) GE (-2.35) (-3.21) (-12.96) (15.37) (9.91) (240.69) GM (-3.58) (-4.31) (-16.62) (19.09) (9.58) (331.63) HD (-4.68) (-5.55) (-10.15) (10.57) (10.99) (184.76) HPQ (-4.12) (-6.00) (-23.58) (33.60) (10.13) (49.82) 33

34 Table II: coninued Ticker θ 1i θ 2i φ 1i φ 2i φ 3i φ 4i -dis d.f. IBM (-6.07) (-7.43) (-16.68) (16.68) (14.84) (49.45) INTC (-6.21) (-7.64) (-15.56) (16.04) (11.37) (102.77) JNJ (-3.09) (-3.64) (-15.06) (20.58) (2.03) (138.03) JPM (-2.55) (-3.31) (-21.09) (27.67) (8.30) (605.28) KO (-2.92) (-3.55) (-13.06) (15.61) (5.52) (68.60) MCD (-5.44) (-5.73) (-15.20) (21.64) (-0.57) (98.10) MMM (-1.42) (-2.31) (-9.89) (12.65) (19.07) (399.26) MRK (-8.42) (-8.54) (-8.25) (10.55) (-3.28) (1,046.1) MSFT (-3.15) (-4.62) (-17.55) (24.37) (12.05) (50.03) PFE (-5.58) (-6.02) (-11.69) (17.97) (0.07) (299.09) T (-3.72) (-4.67) (-13.11) (30.82) (6.33) (283.91) UTX (-4.24) (-4.98) (-13.81) (14.66) (10.89) (111.49) VZ (-2.40) (-3.06) (-19.79) (27.81) (7.02) (159.04) WMT (-1.80) (-2.37) (-8.60) (12.18) (8.26) (177.54) XOM (-6.08) (-6.43) (-9.17) (12.99) (4.01) (180.16) 34

35 Table III: EGARCH Esimaes for Sock Implied Volailiies wih One Common Facor Noes: The able repors he esimaed coefficiens and -saisics (in parenheses) from he 1-facor model: = + log + log( ) + log( ) + ( ) = φ + φ + φ + φ ( ) Ticker θ 1i θ 2i θ 3i θ 4i φ 1i φ 2i φ 3i φ 4i Sample averages 35 -dis d.f (-5.86) (31.58) (-6.25) (5.37) (-6.14) (8.24) (1.90) (74.56) AA (-6.34) (21.34) (-6.63) (5.53) (-4.32) (5.72) (.75) (311.96) AXP (-5.61) (37.87) (-5.59) (5.51) (-6.15) (8.20) (3.14) (97.46) BA (-8.13) (31.84) (-8.58) (7.64) (-6.11) (8.21) (.80) (7.61) BAC (-5.39) (30.59) (-5.12) (5.30) (-6.52) (8.33) (2.67) (163.66) C (-5.34) (37.15) (-5.56) (5.15) (-5.46) (7.55) (3.33) (199.53) CAT (-5.20) (28.16) (-5.92) (4.54) (-5.80) (8.27) (.79) (19.22) CVX (-4.88) (26.14) (-5.64) (3.66) (-5.41) (7.95) (-.06) (127.20) DD (-7.35) (33.80) (-7.61) (7.04) (-5.84) (7.37) (.85) (5.57) DIS (-6.90) (27.65) (-7.02) (6.61) (-7.24) (9.44) (3.41) (19.36) GE (-6.89) (47.90) (-7.12) (6.62) (-7.43) (10.10) (.57) (36.88) GM (-3.57) (26.43) (-4.02) (2.84) (-6.16) (7.74) (2.27) (153.59) HD (-7.42) (37.06) (-7.54) (7.21) (-5.42) (7.87) (2.19) (9.53) HPQ (-3.15) (28.78) (-3.87) (2.88) (-7.13) (9.52) (2.78) (15.02)

36 Table III: coninued Ticker θ 1i θ 2i θ 3i θ 4i φ 1i φ 2i φ 3i φ 4i -dis d.f. IBM (-2.77) (38.60) (-3.62) (2.42) (-5.75) (7.34) (4.38) (8.23) INTC (-6.43) (36.76) (-7.49) (5.85) (-5.62) (8.12) (3.32) (20.91) JNJ (-5.77) (25.75) (-6.33) (4.90) (-7.63) (9.72) (1.02) (25.20) JPM (-7.14) (35.93) (-7.12) (7.03) (-6.41) (8.26) (4.80) (226.24) KO (-5.31) (33.00) (-5.71) (4.87) (-6.69) (8.79) (1.87) (13.72) MCD (-7.71) (23.60) (-7.85) (6.88) (-6.51) (9.24) (.00) (27.84) MMM (-5.88) (33.48) (-6.40) (5.36) (-6.49) (8.37) (1.32) (15.95) MRK (-6.49) (29.99) (-6.61) (5.86) (-4.01) (5.22) (2.55) (305.57) MSFT (-5.11) (37.51) (-6.11) (4.75) (-7.49) (10.32) (4.36) (11.16) PFE (-5.63) (29.31) (-6.22) (4.77) (-4.61) (6.39) (.44) (93.35) T (-5.82) (22.26) (-6.00) (5.46) (-7.70) (10.92) (-.22) (33.27) UTX (-6.69) (29.14) (-7.22) (6.15) (-6.46) (8.19) (2.41) (20.26) VZ (-5.57) (23.27) (-5.69) (5.26) (-7.28) (9.32) (1.37) (24.03) WMT (-5.32) (34.64) (-5.41) (5.03) (-5.51) (7.58) (1.20) (20.01) XOM (-6.22) (36.39) (-6.91) (5.12) (-4.69) (6.72) (.89) (75.38) 36

37 Table IV: Hedging Vega Risk for an Individual Sock wih he Mos Highly Correlaed 1, 2, or 3 Socks The Table presens resuls of vega hedging each individual sock's implied volailiy changes using linear payoff derivaive conracs ied o he VIX index and o he IVs of one oher single sock. Hedge performance is he sandard deviaion of he change in he value of a porfolio consising of a linear volailiy conrac on a single name by iself, on he sock's IV hedged wih only VIX conracs, and on an "exended" hedge using VIX conracs plus volailiy conracs on he oher sock in he sample wih he mos highly correlaed idiosyncraic IV risk exposures on each dae. Columns 3 and 4 show, respecively, he average -saisic across names on he difference in mean squared error beween he unhedged posiion and a hedged posiion, and beween he exended hedge and he hedge wih only he VIX. Columns 5 and 6 repor -saisics on he difference in mean squared error for he pooled sample, using robus sandard errors ha are correced for heeroskedasiciy across names and conemporaneous correlaion in he errors. # hedging socks Hedge performance Hedge vs Unhedged -saisics on he Difference in Mean Squared Hedging Error Average across Individual Names Full sample wih Robus Sandard Errors Exended hedge vs VIX only Hedge vs Unhedged Exended hedge vs VIX only No hedge VIX only VIX

38 Table V: Hedging Vega Risk for an Individual Sock wih Socks from he Same Indusry The Table presens resuls of vega hedging an individual sock's implied volailiy changes using linear payoff derivaive conracs ied he VIX index and o he IVs of one or wo oher socks from he same 4-digi SIC indusry classificaion. Hedge performance in columns 5-7 is, respecively, he sandard deviaion of he change in he value of a porfolio consising of a linear volailiy conrac on a single sock by iself, on he sock hedged wih only VIX conracs, and on an "exended" hedge using VIX conracs and volailiy conracs on he hedging socks. Columns 8 and 9 repor, respecively, he -saisics on he difference in mean squared error beween he unhedged posiion and a hedged posiion, and beween he exended hedge and he hedge wih only he VIX. Targe sock SIC Code Hedging socks Hedge performance -saisics on he difference in squared errors Unhedged 38 VIX only hedge Exended hedge Exended hedge vs Unhedged Exended hedge vs VIX only MRK 2834 JNJ PFE PFE 2834 JNJ MRK JNJ 2834 MRK PFE BAC 6021 C JPM C 6021 BAC JPM JPM 6021 BAC C CVX 2911 XOM XOM 2911 CVX HPQ 3570 IBM IBM 3570 HPQ T 4813 VZ VZ 4813 T

39 Figure 1: Implied Volailiies of 28 Socks and he VIX Index,

The Mathematics Of Stock Option Valuation - Part Four Deriving The Black-Scholes Model Via Partial Differential Equations

The Mahemaics Of Sock Opion Valuaion - Par Four Deriving The Black-Scholes Model Via Parial Differenial Equaions Gary Schurman, MBE, CFA Ocober 1 In Par One we explained why valuing a call opion as a sand-alone

The Mahemaics Of Sock Opion Valuaion - Par Four Deriving The Black-Scholes Model Via Parial Differenial Equaions Gary Schurman, MBE, CFA Ocober 1 In Par One we explained why valuing a call opion as a sand-alone

INSTITUTE OF ACTUARIES OF INDIA

INSIUE OF ACUARIES OF INDIA EAMINAIONS 23 rd May 2011 Subjec S6 Finance and Invesmen B ime allowed: hree hours (9.45* 13.00 Hrs) oal Marks: 100 INSRUCIONS O HE CANDIDAES 1. Please read he insrucions on

INSIUE OF ACUARIES OF INDIA EAMINAIONS 23 rd May 2011 Subjec S6 Finance and Invesmen B ime allowed: hree hours (9.45* 13.00 Hrs) oal Marks: 100 INSRUCIONS O HE CANDIDAES 1. Please read he insrucions on

On the Impact of Inflation and Exchange Rate on Conditional Stock Market Volatility: A Re-Assessment

MPRA Munich Personal RePEc Archive On he Impac of Inflaion and Exchange Rae on Condiional Sock Marke Volailiy: A Re-Assessmen OlaOluwa S Yaya and Olanrewaju I Shiu Deparmen of Saisics, Universiy of Ibadan,

MPRA Munich Personal RePEc Archive On he Impac of Inflaion and Exchange Rae on Condiional Sock Marke Volailiy: A Re-Assessmen OlaOluwa S Yaya and Olanrewaju I Shiu Deparmen of Saisics, Universiy of Ibadan,

INSTITUTE OF ACTUARIES OF INDIA

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 05 h November 007 Subjec CT8 Financial Economics Time allowed: Three Hours (14.30 17.30 Hrs) Toal Marks: 100 INSTRUCTIONS TO THE CANDIDATES 1) Do no wrie your

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 05 h November 007 Subjec CT8 Financial Economics Time allowed: Three Hours (14.30 17.30 Hrs) Toal Marks: 100 INSTRUCTIONS TO THE CANDIDATES 1) Do no wrie your

1 Purpose of the paper

Moneary Economics 2 F.C. Bagliano - Sepember 2017 Noes on: F.X. Diebold and C. Li, Forecasing he erm srucure of governmen bond yields, Journal of Economerics, 2006 1 Purpose of he paper The paper presens

Moneary Economics 2 F.C. Bagliano - Sepember 2017 Noes on: F.X. Diebold and C. Li, Forecasing he erm srucure of governmen bond yields, Journal of Economerics, 2006 1 Purpose of he paper The paper presens

Asymmetry and Leverage in Stochastic Volatility Models: An Exposition

Asymmery and Leverage in Sochasic Volailiy Models: An xposiion Asai, M. a and M. McAleer b a Faculy of conomics, Soka Universiy, Japan b School of conomics and Commerce, Universiy of Wesern Ausralia Keywords:

Asymmery and Leverage in Sochasic Volailiy Models: An xposiion Asai, M. a and M. McAleer b a Faculy of conomics, Soka Universiy, Japan b School of conomics and Commerce, Universiy of Wesern Ausralia Keywords:

Financial Econometrics Jeffrey R. Russell Midterm Winter 2011

Name Financial Economerics Jeffrey R. Russell Miderm Winer 2011 You have 2 hours o complee he exam. Use can use a calculaor. Try o fi all your work in he space provided. If you find you need more space

Name Financial Economerics Jeffrey R. Russell Miderm Winer 2011 You have 2 hours o complee he exam. Use can use a calculaor. Try o fi all your work in he space provided. If you find you need more space

Comparison of back-testing results for various VaR estimation methods. Aleš Kresta, ICSP 2013, Bergamo 8 th July, 2013

Comparison of back-esing resuls for various VaR esimaion mehods, ICSP 3, Bergamo 8 h July, 3 THE MOTIVATION AND GOAL In order o esimae he risk of financial invesmens, i is crucial for all he models o esimae

Comparison of back-esing resuls for various VaR esimaion mehods, ICSP 3, Bergamo 8 h July, 3 THE MOTIVATION AND GOAL In order o esimae he risk of financial invesmens, i is crucial for all he models o esimae

Ch. 10 Measuring FX Exposure. Is Exchange Rate Risk Relevant? MNCs Take on FX Risk

Ch. 10 Measuring FX Exposure Topics Exchange Rae Risk: Relevan? Types of Exposure Transacion Exposure Economic Exposure Translaion Exposure Is Exchange Rae Risk Relevan?? Purchasing Power Pariy: Exchange

Ch. 10 Measuring FX Exposure Topics Exchange Rae Risk: Relevan? Types of Exposure Transacion Exposure Economic Exposure Translaion Exposure Is Exchange Rae Risk Relevan?? Purchasing Power Pariy: Exchange

Models of Default Risk

Models of Defaul Risk Models of Defaul Risk 1/29 Inroducion We consider wo general approaches o modelling defaul risk, a risk characerizing almos all xed-income securiies. The srucural approach was developed

Models of Defaul Risk Models of Defaul Risk 1/29 Inroducion We consider wo general approaches o modelling defaul risk, a risk characerizing almos all xed-income securiies. The srucural approach was developed

A Note on Missing Data Effects on the Hausman (1978) Simultaneity Test:

Simultaneity Test:") A Noe on Missing Daa Effecs on he Hausman (978) Simulaneiy Tes: Some Mone Carlo Resuls. Dikaios Tserkezos and Konsaninos P. Tsagarakis Deparmen of Economics, Universiy of Cree, Universiy Campus, 7400,

A Noe on Missing Daa Effecs on he Hausman (978) Simulaneiy Tes: Some Mone Carlo Resuls. Dikaios Tserkezos and Konsaninos P. Tsagarakis Deparmen of Economics, Universiy of Cree, Universiy Campus, 7400,

Volatility and Hedging Errors

Volailiy and Hedging Errors Jim Gaheral Sepember, 5 1999 Background Derivaive porfolio bookrunners ofen complain ha hedging a marke-implied volailiies is sub-opimal relaive o hedging a heir bes guess of

Volailiy and Hedging Errors Jim Gaheral Sepember, 5 1999 Background Derivaive porfolio bookrunners ofen complain ha hedging a marke-implied volailiies is sub-opimal relaive o hedging a heir bes guess of

DYNAMIC ECONOMETRIC MODELS Vol. 7 Nicolaus Copernicus University Toruń Krzysztof Jajuga Wrocław University of Economics

DYNAMIC ECONOMETRIC MODELS Vol. 7 Nicolaus Copernicus Universiy Toruń 2006 Krzyszof Jajuga Wrocław Universiy of Economics Ineres Rae Modeling and Tools of Financial Economerics 1. Financial Economerics

DYNAMIC ECONOMETRIC MODELS Vol. 7 Nicolaus Copernicus Universiy Toruń 2006 Krzyszof Jajuga Wrocław Universiy of Economics Ineres Rae Modeling and Tools of Financial Economerics 1. Financial Economerics

Optimal Early Exercise of Vulnerable American Options

Opimal Early Exercise of Vulnerable American Opions March 15, 2008 This paper is preliminary and incomplee. Opimal Early Exercise of Vulnerable American Opions Absrac We analyze he effec of credi risk

Opimal Early Exercise of Vulnerable American Opions March 15, 2008 This paper is preliminary and incomplee. Opimal Early Exercise of Vulnerable American Opions Absrac We analyze he effec of credi risk

FORECASTING WITH A LINEX LOSS: A MONTE CARLO STUDY

Proceedings of he 9h WSEAS Inernaional Conference on Applied Mahemaics, Isanbul, Turkey, May 7-9, 006 (pp63-67) FORECASTING WITH A LINEX LOSS: A MONTE CARLO STUDY Yasemin Ulu Deparmen of Economics American

Proceedings of he 9h WSEAS Inernaional Conference on Applied Mahemaics, Isanbul, Turkey, May 7-9, 006 (pp63-67) FORECASTING WITH A LINEX LOSS: A MONTE CARLO STUDY Yasemin Ulu Deparmen of Economics American

Macroeconomics II A dynamic approach to short run economic fluctuations. The DAD/DAS model.

Macroeconomics II A dynamic approach o shor run economic flucuaions. The DAD/DAS model. Par 2. The demand side of he model he dynamic aggregae demand (DAD) Inflaion and dynamics in he shor run So far,

Macroeconomics II A dynamic approach o shor run economic flucuaions. The DAD/DAS model. Par 2. The demand side of he model he dynamic aggregae demand (DAD) Inflaion and dynamics in he shor run So far,

Estimating Earnings Trend Using Unobserved Components Framework

Esimaing Earnings Trend Using Unobserved Componens Framework Arabinda Basisha and Alexander Kurov College of Business and Economics, Wes Virginia Universiy December 008 Absrac Regressions using valuaion

Esimaing Earnings Trend Using Unobserved Componens Framework Arabinda Basisha and Alexander Kurov College of Business and Economics, Wes Virginia Universiy December 008 Absrac Regressions using valuaion

The Correlation Risk Premium: Term Structure and Hedging

: erm Srucure and Hedging Gonçalo Faria (1),* and Rober Kosowski (2),* (1) CEF.UP, Universiy of Poro; (2) Imperial College Business School, CEPR, Oxford-Man Insiue of Quaniaive Finance. Nespar Inernaional

: erm Srucure and Hedging Gonçalo Faria (1),* and Rober Kosowski (2),* (1) CEF.UP, Universiy of Poro; (2) Imperial College Business School, CEPR, Oxford-Man Insiue of Quaniaive Finance. Nespar Inernaional

R e. Y R, X R, u e, and. Use the attached excel spreadsheets to

HW # Saisical Financial Modeling ( P Theodossiou) 1 The following are annual reurns for US finance socks (F) and he S&P500 socks index (M) Year Reurn Finance Socks Reurn S&P500 Year Reurn Finance Socks

HW # Saisical Financial Modeling ( P Theodossiou) 1 The following are annual reurns for US finance socks (F) and he S&P500 socks index (M) Year Reurn Finance Socks Reurn S&P500 Year Reurn Finance Socks

FINAL EXAM EC26102: MONEY, BANKING AND FINANCIAL MARKETS MAY 11, 2004

FINAL EXAM EC26102: MONEY, BANKING AND FINANCIAL MARKETS MAY 11, 2004 This exam has 50 quesions on 14 pages. Before you begin, please check o make sure ha your copy has all 50 quesions and all 14 pages.

FINAL EXAM EC26102: MONEY, BANKING AND FINANCIAL MARKETS MAY 11, 2004 This exam has 50 quesions on 14 pages. Before you begin, please check o make sure ha your copy has all 50 quesions and all 14 pages.

UCLA Department of Economics Fall PhD. Qualifying Exam in Macroeconomic Theory

UCLA Deparmen of Economics Fall 2016 PhD. Qualifying Exam in Macroeconomic Theory Insrucions: This exam consiss of hree pars, and you are o complee each par. Answer each par in a separae bluebook. All

UCLA Deparmen of Economics Fall 2016 PhD. Qualifying Exam in Macroeconomic Theory Insrucions: This exam consiss of hree pars, and you are o complee each par. Answer each par in a separae bluebook. All

An Incentive-Based, Multi-Period Decision Model for Hierarchical Systems

Wernz C. and Deshmukh A. An Incenive-Based Muli-Period Decision Model for Hierarchical Sysems Proceedings of he 3 rd Inernaional Conference on Global Inerdependence and Decision Sciences (ICGIDS) pp. 84-88

Wernz C. and Deshmukh A. An Incenive-Based Muli-Period Decision Model for Hierarchical Sysems Proceedings of he 3 rd Inernaional Conference on Global Inerdependence and Decision Sciences (ICGIDS) pp. 84-88

This specification describes the models that are used to forecast

PCE and CPI Inflaion Differenials: Convering Inflaion Forecass Model Specificaion By Craig S. Hakkio This specificaion describes he models ha are used o forecas he inflaion differenial. The 14 forecass

PCE and CPI Inflaion Differenials: Convering Inflaion Forecass Model Specificaion By Craig S. Hakkio This specificaion describes he models ha are used o forecas he inflaion differenial. The 14 forecass

Available online at ScienceDirect

Available online a www.sciencedirec.com ScienceDirec Procedia Economics and Finance 8 ( 04 658 663 s Inernaional Conference 'Economic Scienific Research - Theoreical, Empirical and Pracical Approaches',

Available online a www.sciencedirec.com ScienceDirec Procedia Economics and Finance 8 ( 04 658 663 s Inernaional Conference 'Economic Scienific Research - Theoreical, Empirical and Pracical Approaches',

Pricing Vulnerable American Options. April 16, Peter Klein. and. Jun (James) Yang. Simon Fraser University. Burnaby, B.C. V5A 1S6.

Yang. Simon Fraser University. Burnaby, B.C. V5A 1S6.") Pricing ulnerable American Opions April 16, 2007 Peer Klein and Jun (James) Yang imon Fraser Universiy Burnaby, B.C. 5A 16 pklein@sfu.ca (604) 268-7922 Pricing ulnerable American Opions Absrac We exend

Pricing ulnerable American Opions April 16, 2007 Peer Klein and Jun (James) Yang imon Fraser Universiy Burnaby, B.C. 5A 16 pklein@sfu.ca (604) 268-7922 Pricing ulnerable American Opions Absrac We exend

Hedging Performance of Indonesia Exchange Rate

Hedging Performance of Indonesia Exchange Rae By: Eneng Nur Hasanah Fakulas Ekonomi dan Bisnis-Manajemen, Universias Islam Bandung (Unisba) E-mail: enengnurhasanah@gmail.com ABSTRACT The flucuaion of exchange

Hedging Performance of Indonesia Exchange Rae By: Eneng Nur Hasanah Fakulas Ekonomi dan Bisnis-Manajemen, Universias Islam Bandung (Unisba) E-mail: enengnurhasanah@gmail.com ABSTRACT The flucuaion of exchange

An Analytical Implementation of the Hull and White Model

Dwigh Gran * and Gauam Vora ** Revised: February 8, & November, Do no quoe. Commens welcome. * Douglas M. Brown Professor of Finance, Anderson School of Managemen, Universiy of New Mexico, Albuquerque,

Dwigh Gran * and Gauam Vora ** Revised: February 8, & November, Do no quoe. Commens welcome. * Douglas M. Brown Professor of Finance, Anderson School of Managemen, Universiy of New Mexico, Albuquerque,

High and low frequency correlations in global equity markets

BIS CCA-007-2010 May 2010 High and low frequency correlaions in global equiy markes A presenaion prepared for he BIS CCA Conference on Sysemic risk, bank behaviour and regulaion over he business cycle

BIS CCA-007-2010 May 2010 High and low frequency correlaions in global equiy markes A presenaion prepared for he BIS CCA Conference on Sysemic risk, bank behaviour and regulaion over he business cycle

Portfolio investments accounted for the largest outflow of SEK 77.5 billion in the financial account, which gave a net outflow of SEK billion.

BALANCE OF PAYMENTS DATE: 27-11-27 PUBLISHER: Saisics Sweden Balance of Paymens and Financial Markes (BFM) Maria Falk +46 8 6 94 72, maria.falk@scb.se Camilla Bergeling +46 8 6 942 6, camilla.bergeling@scb.se

BALANCE OF PAYMENTS DATE: 27-11-27 PUBLISHER: Saisics Sweden Balance of Paymens and Financial Markes (BFM) Maria Falk +46 8 6 94 72, maria.falk@scb.se Camilla Bergeling +46 8 6 942 6, camilla.bergeling@scb.se

On the Relationship between Time-Varying Price dynamics of the Underlying. Stocks: Deregulation Effect on the Issuance of Third-Party Put Warrant

On he Relaionship beween Time-Varying Price dynamics of he Underlying Socks: Deregulaion Effec on he Issuance of Third-Pary Pu Warran Yi-Chen Wang * Deparmen of Financial Operaions, Naional Kaohsiung Firs

On he Relaionship beween Time-Varying Price dynamics of he Underlying Socks: Deregulaion Effec on he Issuance of Third-Pary Pu Warran Yi-Chen Wang * Deparmen of Financial Operaions, Naional Kaohsiung Firs

4452 Mathematical Modeling Lecture 17: Modeling of Data: Linear Regression

Mah Modeling Lecure 17: Modeling of Daa: Linear Regression Page 1 5 Mahemaical Modeling Lecure 17: Modeling of Daa: Linear Regression Inroducion In modeling of daa, we are given a se of daa poins, and

Mah Modeling Lecure 17: Modeling of Daa: Linear Regression Page 1 5 Mahemaical Modeling Lecure 17: Modeling of Daa: Linear Regression Inroducion In modeling of daa, we are given a se of daa poins, and

a. If Y is 1,000, M is 100, and the growth rate of nominal money is 1 percent, what must i and P be?

Problem Se 4 ECN 101 Inermediae Macroeconomics SOLUTIONS Numerical Quesions 1. Assume ha he demand for real money balance (M/P) is M/P = 0.6-100i, where is naional income and i is he nominal ineres rae.

Problem Se 4 ECN 101 Inermediae Macroeconomics SOLUTIONS Numerical Quesions 1. Assume ha he demand for real money balance (M/P) is M/P = 0.6-100i, where is naional income and i is he nominal ineres rae.

Advanced Forecasting Techniques and Models: Time-Series Forecasts

Advanced Forecasing Techniques and Models: Time-Series Forecass Shor Examples Series using Risk Simulaor For more informaion please visi: www.realopionsvaluaion.com or conac us a: admin@realopionsvaluaion.com

Advanced Forecasing Techniques and Models: Time-Series Forecass Shor Examples Series using Risk Simulaor For more informaion please visi: www.realopionsvaluaion.com or conac us a: admin@realopionsvaluaion.com

Pricing FX Target Redemption Forward under. Regime Switching Model

In. J. Conemp. Mah. Sciences, Vol. 8, 2013, no. 20, 987-991 HIKARI Ld, www.m-hikari.com hp://dx.doi.org/10.12988/ijcms.2013.311123 Pricing FX Targe Redempion Forward under Regime Swiching Model Ho-Seok

In. J. Conemp. Mah. Sciences, Vol. 8, 2013, no. 20, 987-991 HIKARI Ld, www.m-hikari.com hp://dx.doi.org/10.12988/ijcms.2013.311123 Pricing FX Targe Redempion Forward under Regime Swiching Model Ho-Seok

Proceedings of the 48th European Study Group Mathematics with Industry 1

Proceedings of he 48h European Sudy Group Mahemaics wih Indusry 1 ADR Opion Trading Jasper Anderluh and Hans van der Weide TU Delf, EWI (DIAM), Mekelweg 4, 2628 CD Delf jhmanderluh@ewiudelfnl, JAMvanderWeide@ewiudelfnl

Proceedings of he 48h European Sudy Group Mahemaics wih Indusry 1 ADR Opion Trading Jasper Anderluh and Hans van der Weide TU Delf, EWI (DIAM), Mekelweg 4, 2628 CD Delf jhmanderluh@ewiudelfnl, JAMvanderWeide@ewiudelfnl

A Method for Estimating the Change in Terminal Value Required to Increase IRR

A Mehod for Esimaing he Change in Terminal Value Required o Increase IRR Ausin M. Long, III, MPA, CPA, JD * Alignmen Capial Group 11940 Jollyville Road Suie 330-N Ausin, TX 78759 512-506-8299 (Phone) 512-996-0970

A Mehod for Esimaing he Change in Terminal Value Required o Increase IRR Ausin M. Long, III, MPA, CPA, JD * Alignmen Capial Group 11940 Jollyville Road Suie 330-N Ausin, TX 78759 512-506-8299 (Phone) 512-996-0970

Financial Markets And Empirical Regularities An Introduction to Financial Econometrics

Financial Markes And Empirical Regulariies An Inroducion o Financial Economerics SAMSI Workshop 11/18/05 Mike Aguilar UNC a Chapel Hill www.unc.edu/~maguilar 1 Ouline I. Hisorical Perspecive on Asse Prices

Financial Markes And Empirical Regulariies An Inroducion o Financial Economerics SAMSI Workshop 11/18/05 Mike Aguilar UNC a Chapel Hill www.unc.edu/~maguilar 1 Ouline I. Hisorical Perspecive on Asse Prices

Empirical analysis on China money multiplier

Aug. 2009, Volume 8, No.8 (Serial No.74) Chinese Business Review, ISSN 1537-1506, USA Empirical analysis on China money muliplier SHANG Hua-juan (Financial School, Shanghai Universiy of Finance and Economics,

Aug. 2009, Volume 8, No.8 (Serial No.74) Chinese Business Review, ISSN 1537-1506, USA Empirical analysis on China money muliplier SHANG Hua-juan (Financial School, Shanghai Universiy of Finance and Economics,

VaR and Low Interest Rates

VaR and Low Ineres Raes Presened a he Sevenh Monreal Indusrial Problem Solving Workshop By Louis Doray (U de M) Frédéric Edoukou (U de M) Rim Labdi (HEC Monréal) Zichun Ye (UBC) 20 May 2016 P r e s e n

VaR and Low Ineres Raes Presened a he Sevenh Monreal Indusrial Problem Solving Workshop By Louis Doray (U de M) Frédéric Edoukou (U de M) Rim Labdi (HEC Monréal) Zichun Ye (UBC) 20 May 2016 P r e s e n

(1 + Nominal Yield) = (1 + Real Yield) (1 + Expected Inflation Rate) (1 + Inflation Risk Premium)

= (1 + Real Yield) (1 + Expected Inflation Rate) (1 + Inflation Risk Premium)") 5. Inflaion-linked bonds Inflaion is an economic erm ha describes he general rise in prices of goods and services. As prices rise, a uni of money can buy less goods and services. Hence, inflaion is an

5. Inflaion-linked bonds Inflaion is an economic erm ha describes he general rise in prices of goods and services. As prices rise, a uni of money can buy less goods and services. Hence, inflaion is an

Stock Market Behaviour Around Profit Warning Announcements

Sock Marke Behaviour Around Profi Warning Announcemens Henryk Gurgul Conen 1. Moivaion 2. Review of exising evidence 3. Main conjecures 4. Daa and preliminary resuls 5. GARCH relaed mehodology 6. Empirical

Sock Marke Behaviour Around Profi Warning Announcemens Henryk Gurgul Conen 1. Moivaion 2. Review of exising evidence 3. Main conjecures 4. Daa and preliminary resuls 5. GARCH relaed mehodology 6. Empirical

The Binomial Model and Risk Neutrality: Some Important Details

The Binomial Model and Risk Neuraliy: Some Imporan Deails Sanjay K. Nawalkha* Donald R. Chambers** Absrac This paper reexamines he relaionship beween invesors preferences and he binomial opion pricing

The Binomial Model and Risk Neuraliy: Some Imporan Deails Sanjay K. Nawalkha* Donald R. Chambers** Absrac This paper reexamines he relaionship beween invesors preferences and he binomial opion pricing

Reconciling Gross Output TFP Growth with Value Added TFP Growth

Reconciling Gross Oupu TP Growh wih Value Added TP Growh Erwin Diewer Universiy of Briish Columbia and Universiy of New Souh Wales ABSTRACT This aricle obains relaively simple exac expressions ha relae

Reconciling Gross Oupu TP Growh wih Value Added TP Growh Erwin Diewer Universiy of Briish Columbia and Universiy of New Souh Wales ABSTRACT This aricle obains relaively simple exac expressions ha relae

Subdivided Research on the Inflation-hedging Ability of Residential Property: A Case of Hong Kong

Subdivided Research on he -hedging Abiliy of Residenial Propery: A Case of Hong Kong Guohua Huang 1, Haili Tu 2, Boyu Liu 3,* 1 Economics and Managemen School of Wuhan Universiy,Economics and Managemen