Credit Derivatives CHAPTER 7

|

|

|

- Abraham Lewis

- 5 years ago

- Views:

Transcription

1 3 Credit Derivatives CHAPTER 7

2 Credit derivatives Collaterized debt obligation Credit default swap Credit spread options Credit linked notes Risks in credit derivatives

3 Credit Derivatives A credit derivative is a financial instrument whose value is determined by the default risk of the principal asset. Financial assets like forward, options and swaps form a part of Credit derivatives Borrowers can default and the lender will need protection against such default and in reality, a credit derivative is a way to insure such losses

4 Credit Derivatives Credit default swaps (CDS), total return swap, credit default swap options, collateralized debt obligations (CDO) and credit spread forwards are some examples of credit derivatives The credit quality of the borrower as well as the third party plays an important role in determining the credit derivative s value

5 Credit Derivatives Credit derivatives are fundamentally divided into two categories: funded credit derivatives and unfunded credit derivatives. There is a contract between both the parties stating the responsibility of each party with regard to its payment without resorting to any asset class

6 Credit Derivatives The level of risk differs in different cases depending on the third party and a fee is decided based on the appropriate risk level by both the parties. Financial assets like forward, options and swaps form a part of Credit derivatives The price for these instruments changes with change in the credit risk of agents such as investors and government

7

8 Credit derivatives Collaterized debt obligation Credit default swap Credit spread options Credit linked notes Risks in credit derivatives

9 Collaterized Debt obligation CDOs or Collateralized Debt Obligation are financial instruments that banks and other financial institutions use to repackage individual loans into a product sold to investors on the secondary market.

10 Collaterized Debt obligation A collateralized debt obligation (CDO) is an example of structured assetbacked security (ABS). Different assets which generate cash can be pooled together and then repackaged into various discrete tranches in order to sell it to the investors The junior tranches offer higher coupon rates because of the high risk involved.

11 Collaterized Debt obligation With the help of CDOs banks can give more loans because of greater liquidity. This happens because of more cash at their disposal

12 Collaterized Debt obligation One of the major advantages of CDO was its ability to provide liquidity to the economy and therefore they were a welcomed innovation in finance With the help of CDOs, banks and corporations had more money at their disposal which helped them to invest and give loan

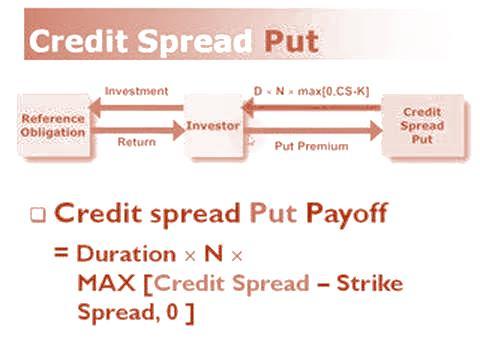

13 Collaterized Debt obligation CDOs are created with the help of a computer model An asset bubble was created because of the extra liquidity in the market Banks went on selling CDOs without thinking too much about the payments because they had sold these loans to investors and they were the one who would be affected if people default

14

15 Credit derivatives Collaterized debt obligation Credit default swap Credit spread options Credit linked notes Risks in credit derivatives

16 Credit Default Swaps A credit default swap is the most common form of credit derivative and may involve municipal bonds, emerging market bonds, mortgage-backed securities or corporate bonds

17 Credit Default Swaps Swap sellers use diversification to protect themselves They provide as sellers in different industries so that even if one of them defaults entirely they will be getting annual payments from the other industries to make up for the losses

18 Credit Default Swaps Until 2009 swaps were not regulated. It led to a situation where there was no one to see if the person selling the CDS even had enough money to pay the CDS buyer in case the bond had defaulted

19 Credit derivatives Collaterized debt obligation Credit default swap Credit spread options Credit linked notes Risks in credit derivatives

20 Credit Spread Options Yield difference between the U.S. Treasury bond and a debt security with the same maturity but with not so good quality is known as credit spread

21 Credit spread options. A strategy of buying low premium option and selling high premium option also comes under credit spread. Credit spreads are measured in basis points

22

23 Credit derivatives Collaterized debt obligation Credit default swap Credit spread options Credit linked notes Risks in credit derivatives

24 Credit linked notes A credit linked note (CLN) is a type of funded credit derivative. It is prepared as a security with an embedded credit default swap which helps the issuer in transferring credit risks to the investors

25 Credit linked notes The difference here is that the issuer is not under any obligation to repay the debt in case of a specified event.

26 Credit linked notes The motive of the deal is to pass the danger of specific default onto investors eager tolerate that danger in exchange for the higher earnings it makes obtainable. The CLNs themselves are typically backed by very highly rated collateral, such as U.S. Treasury securities.

27 Credit derivatives Collaterized debt obligation Credit default swap Credit spread options Credit linked notes Risks in credit derivatives

28 Risks in credit derivatives Credit derivatives are popular in the financial world where there is a lot of risk and where the yield is low Commercial banks, hedgers as well as insurance company show a lot of interest on credit derivates

29 Risks in credit derivatives While on one hand they provide high yield returns to a seller, on the other hand they help the buyer to manage portfolio risk Some insurance companies and commercial banks have the tendency to be too aggressive which leads to distortion of the prices

30 Risks in credit derivatives Many people entire the market because of the attractive high yield and they feel that they can absorb the risk but only a few of them are able to survive in the market and understand the risk of the credit derivates.

31 Risks in credit derivatives The increasing use of credit derivatives have increased the risk because many banks and insurance companies are taking on risks which they are not able to understand properly In contrast to other loans, the credit derivatives hold a vast number of debts from various organizations

32 Risks in credit derivatives In order to get more returns, some companies have focused the most on the most risky segment and thereby creating the probability of huge losses at the same time.

33 Risks in credit derivatives Investors need to be able to understand the likelihood of default by individual companies so that they know the total loss amount which they can incur. The situation is unsettling because insurance companies do not face the rigorous capital requirements.

34

35 Too many people spend money they haven't earned, to buy things they don't want, to impress people that they don't like. - Will Rogers

36 THANK YOU

MATH FOR CREDIT. Purdue University, Feb 6 th, SHIKHAR RANJAN Credit Products Group, Morgan Stanley

MATH FOR CREDIT Purdue University, Feb 6 th, 2004 SHIKHAR RANJAN Credit Products Group, Morgan Stanley Outline The space of credit products Key drivers of value Mathematical models Pricing Trading strategies

MATH FOR CREDIT Purdue University, Feb 6 th, 2004 SHIKHAR RANJAN Credit Products Group, Morgan Stanley Outline The space of credit products Key drivers of value Mathematical models Pricing Trading strategies

FINANCIAL INSTRUMENTS AND THEIR RISKS

FINANCIAL INSTRUMENTS AND THEIR RISKS This document presents an overview of the main financial instruments that Amundi uses in providing its investment services and the risks associated with these instruments.

FINANCIAL INSTRUMENTS AND THEIR RISKS This document presents an overview of the main financial instruments that Amundi uses in providing its investment services and the risks associated with these instruments.

Credit Derivatives. By A. V. Vedpuriswar

Credit Derivatives By A. V. Vedpuriswar September 17, 2017 Historical perspective on credit derivatives Traditionally, credit risk has differentiated commercial banks from investment banks. Commercial

Credit Derivatives By A. V. Vedpuriswar September 17, 2017 Historical perspective on credit derivatives Traditionally, credit risk has differentiated commercial banks from investment banks. Commercial

Example:(Schweser CFA Note: Automobile Loans Securitization)

") The Basic Structural Features of and Parties to a Securitization Transaction. ABS are most commonly backed by automobile loans, credit card receivables, home equity loans, manufactured housing loans, student

The Basic Structural Features of and Parties to a Securitization Transaction. ABS are most commonly backed by automobile loans, credit card receivables, home equity loans, manufactured housing loans, student

Maiden Lane LLC (A Special Purpose Vehicle Consolidated by the Federal Reserve Bank of New York)

") (A Special Purpose Vehicle Consolidated by the Federal Reserve Bank of New York) Consolidated Financial Statements for the Period March 14, 2008 to December 31, 2008, and Independent Auditors Report MAIDEN

(A Special Purpose Vehicle Consolidated by the Federal Reserve Bank of New York) Consolidated Financial Statements for the Period March 14, 2008 to December 31, 2008, and Independent Auditors Report MAIDEN

The Financial System. Sherif Khalifa. Sherif Khalifa () The Financial System 1 / 52

The Financial System 1 / 52") The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 52 Financial System Definition The financial system consists of those institutions in the economy that matches saving with

The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 52 Financial System Definition The financial system consists of those institutions in the economy that matches saving with

Credit Risk in Banking

Credit Risk in Banking CREDIT DERIVATIVES Hull J., Options, futures, and other derivatives, Ed. 7, chapter 23 Sebastiano Vitali, 2017/2018 Credit derivatives Credit derivatives are contracts where the

Credit Risk in Banking CREDIT DERIVATIVES Hull J., Options, futures, and other derivatives, Ed. 7, chapter 23 Sebastiano Vitali, 2017/2018 Credit derivatives Credit derivatives are contracts where the

1.2 Product nature of credit derivatives

1.2 Product nature of credit derivatives Payoff depends on the occurrence of a credit event: default: any non-compliance with the exact specification of a contract price or yield change of a bond credit

1.2 Product nature of credit derivatives Payoff depends on the occurrence of a credit event: default: any non-compliance with the exact specification of a contract price or yield change of a bond credit

A Review of Basel II on Securitisation of SME Loans Iwen Legro Amsterdam 2009

A Review of Basel II on Securitisation of SME Loans Iwen Legro Amsterdam 2009 - Public Version- A Review of Basel II on Securitisation of SME Loans Graduation study at Hypoport, Amsterdam Report of a

A Review of Basel II on Securitisation of SME Loans Iwen Legro Amsterdam 2009 - Public Version- A Review of Basel II on Securitisation of SME Loans Graduation study at Hypoport, Amsterdam Report of a

March 2017 For intermediaries and professional investors only. Not for further distribution.

Understanding Structured Credit March 2017 For intermediaries and professional investors only. Not for further distribution. Contents Investing in a rising interest rate environment 3 Understanding Structured

Understanding Structured Credit March 2017 For intermediaries and professional investors only. Not for further distribution. Contents Investing in a rising interest rate environment 3 Understanding Structured

COPYRIGHTED MATERIAL. 1 The Credit Derivatives Market 1.1 INTRODUCTION

1 The Credit Derivatives Market 1.1 INTRODUCTION Without a doubt, credit derivatives have revolutionised the trading and management of credit risk. They have made it easier for banks, who have historically

1 The Credit Derivatives Market 1.1 INTRODUCTION Without a doubt, credit derivatives have revolutionised the trading and management of credit risk. They have made it easier for banks, who have historically

The Financial System. Sherif Khalifa. Sherif Khalifa () The Financial System 1 / 55

The Financial System 1 / 55") The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 55 The financial system consists of those institutions in the economy that matches saving with investment. The financial system

The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 55 The financial system consists of those institutions in the economy that matches saving with investment. The financial system

Using derivatives to manage financial market risk and credit risk. Moorad Choudhry

Using derivatives to manage financial market risk and credit risk London School of Economics 15 October 2002 Moorad Choudhry www.yieldcurve.com Agenda o Risk o Hedging risk o Derivative instruments o Interest-rate

Using derivatives to manage financial market risk and credit risk London School of Economics 15 October 2002 Moorad Choudhry www.yieldcurve.com Agenda o Risk o Hedging risk o Derivative instruments o Interest-rate

Ch. 2 AN OVERVIEW OF THE FINANCIAL SYSTEM

Ch. 2 AN OVERVIEW OF THE FINANCIAL SYSTEM To "finance" something means to pay for it. Since money (or credit) is the means of payment, "financial" basically means "pertaining to money or credit." Financial

Ch. 2 AN OVERVIEW OF THE FINANCIAL SYSTEM To "finance" something means to pay for it. Since money (or credit) is the means of payment, "financial" basically means "pertaining to money or credit." Financial

Assets Eligible as Collateral under the Bank of Canada s Standing Liquidity Facility

Assets Eligible as Collateral under the Bank of Canada s Standing Liquidity Facility The Bank of Canada, through its Standing Liquidity Facility (SLF), provides access to liquidity to those institutions

Assets Eligible as Collateral under the Bank of Canada s Standing Liquidity Facility The Bank of Canada, through its Standing Liquidity Facility (SLF), provides access to liquidity to those institutions

Trading motivated by anticipated changes in the expected correlations of credit defaults and spread movements among specific credits and indices.

Arbitrage Asset-backed security (ABS) Asset/liability management (ALM) Assets under management (AUM) Back office Bankruptcy remoteness Brady bonds CDO capital structure Carry trade Collateralized debt

Arbitrage Asset-backed security (ABS) Asset/liability management (ALM) Assets under management (AUM) Back office Bankruptcy remoteness Brady bonds CDO capital structure Carry trade Collateralized debt

CREDIT DEFAULT SWAPS AND THEIR APPLICATION

CREDIT DEFAULT SWAPS AND THEIR APPLICATION Dr Ewelina Sokołowska, Dr Justyna Łapińska Nicolaus Copernicus University Torun, Faculty of Economic Sciences and Management, ul. Gagarina 11, 87-100 Toruń, e-mail:

CREDIT DEFAULT SWAPS AND THEIR APPLICATION Dr Ewelina Sokołowska, Dr Justyna Łapińska Nicolaus Copernicus University Torun, Faculty of Economic Sciences and Management, ul. Gagarina 11, 87-100 Toruń, e-mail:

Bond Buyer Conference Municipal Credit Default Swaps

Bond Buyer Conference Municipal Credit Default Swaps 20, 2008 This material has been prepared by Municipal Structured Products and is not a product of Lehman Brothers Research Department. It is for information

Bond Buyer Conference Municipal Credit Default Swaps 20, 2008 This material has been prepared by Municipal Structured Products and is not a product of Lehman Brothers Research Department. It is for information

Preview PP542. International Capital Markets. Gains from Trade. International Capital Markets. The Three Types of International Transaction Trade

Preview PP542 International Capital Markets Gains from trade Portfolio diversification Players in the international capital markets Attainable policies with international capital markets Offshore banking

Preview PP542 International Capital Markets Gains from trade Portfolio diversification Players in the international capital markets Attainable policies with international capital markets Offshore banking

Pierpont Securities LLC. pierpontsecurities.com 2012 Pierpont Securities, a member of FINRA and SIPC

Pierpont Securities LLC SECURITIZATION OVERVIEW SECURITIZATION Section I: Section II: Section III: Appendix: Definition Process Analysis Market Defined Terms P R O P R I E T A R Y A N D C O N F I D E N

Pierpont Securities LLC SECURITIZATION OVERVIEW SECURITIZATION Section I: Section II: Section III: Appendix: Definition Process Analysis Market Defined Terms P R O P R I E T A R Y A N D C O N F I D E N

Taiwan Ratings. An Introduction to CDOs and Standard & Poor's Global CDO Ratings. Analysis. 1. What is a CDO? 2. Are CDOs similar to mutual funds?

An Introduction to CDOs and Standard & Poor's Global CDO Ratings Analysts: Thomas Upton, New York Standard & Poor's Ratings Services has been rating collateralized debt obligation (CDO) transactions since

An Introduction to CDOs and Standard & Poor's Global CDO Ratings Analysts: Thomas Upton, New York Standard & Poor's Ratings Services has been rating collateralized debt obligation (CDO) transactions since

CHAPTER 6 SECURITIZATION

CHAPTER 6 SECURITIZATION Introduction Some companies or firms who are involved in sending the money or making credit sale must have a huge balance of receivables in their Balance Sheet. Though they have

CHAPTER 6 SECURITIZATION Introduction Some companies or firms who are involved in sending the money or making credit sale must have a huge balance of receivables in their Balance Sheet. Though they have

Role of Financial Markets and Institutions

International Financial Management By Jeff Madura Solution Manual 11th Edition International Financial Management By Jeff Madura Solution Manual 11th Edition Test Bank. Completed download Solutions Manual

International Financial Management By Jeff Madura Solution Manual 11th Edition International Financial Management By Jeff Madura Solution Manual 11th Edition Test Bank. Completed download Solutions Manual

An Introduction to Synthetic Collateralized Debt Obligations

An Introduction to Synthetic Collateralized Debt Obligations Department of Finance College of Business Administration Clarion University of Pennsylvania Clarion, PA 16214 mbrigida@clarion.edu September

An Introduction to Synthetic Collateralized Debt Obligations Department of Finance College of Business Administration Clarion University of Pennsylvania Clarion, PA 16214 mbrigida@clarion.edu September

Lecture 7 Foundations of Finance

Lecture 7: Fixed Income Markets. I. Reading. II. Money Market. III. Long Term Credit Markets. IV. Repurchase Agreements (Repos). 0 Lecture 7: Fixed Income Markets. I. Reading. A. BKM, Chapter 2, Sections

Lecture 7: Fixed Income Markets. I. Reading. II. Money Market. III. Long Term Credit Markets. IV. Repurchase Agreements (Repos). 0 Lecture 7: Fixed Income Markets. I. Reading. A. BKM, Chapter 2, Sections

GAUSSIAN COPULA What happens when models fail?

GAUSSIAN COPULA What happens when models fail? Erik Forslund forslune@student.chalmers.se Daniel Johansson johansson.gd@gmail.com November 23, 2012 Division of labour Both authors have contributed to all

GAUSSIAN COPULA What happens when models fail? Erik Forslund forslune@student.chalmers.se Daniel Johansson johansson.gd@gmail.com November 23, 2012 Division of labour Both authors have contributed to all

LESSONS. Corporate Securitization: Seven Lessons for a CFO

6 Corporate Securitization: Seven Lessons for a CFO 12 3RF Prof. Dr. Andre Thibeault Dr. Dennis Vink BBefore the subprime meltdown the asset-backed market had grown to become one of the largest capital

6 Corporate Securitization: Seven Lessons for a CFO 12 3RF Prof. Dr. Andre Thibeault Dr. Dennis Vink BBefore the subprime meltdown the asset-backed market had grown to become one of the largest capital

Bonds: An Introduction

Marblehead Financial Services Bill Bartin, CFP Located at Marblehead Bank 21 Atlantic Avenue Marblehead, MA 01945 781-476-0600 781-715-4629 wbartin@infinexgroup.com Bonds: An Introduction Page 1 of 6,

Marblehead Financial Services Bill Bartin, CFP Located at Marblehead Bank 21 Atlantic Avenue Marblehead, MA 01945 781-476-0600 781-715-4629 wbartin@infinexgroup.com Bonds: An Introduction Page 1 of 6,

The Financial Crisis. Dr. Myles Watts Department of Ag. Econ. & Econ. Montana State University and

The Financial Crisis Dr. Myles Watts Department of Ag. Econ. & Econ. Montana State University and November 2009 I. Situation Prior to 2006 II. III. IV. Discussion Outline Situation Changes Crisis Issues

The Financial Crisis Dr. Myles Watts Department of Ag. Econ. & Econ. Montana State University and November 2009 I. Situation Prior to 2006 II. III. IV. Discussion Outline Situation Changes Crisis Issues

How to Make Money. Building your Own Portfolio. Alexander Lin Joey Khoury. Professor Karl Shell ECON 4905

How to Make Money Building your Own Portfolio Alexander Lin Joey Khoury Professor Karl Shell ECON 4905 Agenda Types of Stock Fixed Income Securities Portfolio Maximization and Macroeconomic Considerations

How to Make Money Building your Own Portfolio Alexander Lin Joey Khoury Professor Karl Shell ECON 4905 Agenda Types of Stock Fixed Income Securities Portfolio Maximization and Macroeconomic Considerations

The Financial System. Sherif Khalifa. Sherif Khalifa () The Financial System 1 / 74

The Financial System 1 / 74") The Sherif Khalifa Sherif Khalifa () The 1 / 74 The financial system consists of those institutions that match saving with investment. The financial system channels funds from those who save to those with

The Sherif Khalifa Sherif Khalifa () The 1 / 74 The financial system consists of those institutions that match saving with investment. The financial system channels funds from those who save to those with

BTO s: The new CDO s?

Financial Risk (MVE220) BTO s: The new CDO s? Authors: Erik Johansson Rens IJsendijk Chalmers University of Technology, Gothenburg May 2017 1 Introduction The financial crisis of 2008 was the largest since

Financial Risk (MVE220) BTO s: The new CDO s? Authors: Erik Johansson Rens IJsendijk Chalmers University of Technology, Gothenburg May 2017 1 Introduction The financial crisis of 2008 was the largest since

EN Annex VI. Definitions of the CIC Table

Country ISO 3166-1-alpha-2 country code Identify the ISO 3166-1-alpha-2 country code where the asset is listed in. An asset is considered as being listed if it is negotiated on a regulated market or on

Country ISO 3166-1-alpha-2 country code Identify the ISO 3166-1-alpha-2 country code where the asset is listed in. An asset is considered as being listed if it is negotiated on a regulated market or on

Rating Methodology. Structured Finance. Global Credit-Linked Note and Repackaging Vehicle Rating Criteria. Updated May 2017

Rating Methodology Structured Finance Global Credit-Linked Note and Repackaging Vehicle Rating Criteria Related Research Updated May 2017 Each transaction will be accompanied with a transaction specific

Rating Methodology Structured Finance Global Credit-Linked Note and Repackaging Vehicle Rating Criteria Related Research Updated May 2017 Each transaction will be accompanied with a transaction specific

Derivatives: part I 1

Derivatives: part I 1 Derivatives Derivatives are financial products whose value depends on the value of underlying variables. The main use of derivatives is to reduce risk for one party. Thediverse range

Derivatives: part I 1 Derivatives Derivatives are financial products whose value depends on the value of underlying variables. The main use of derivatives is to reduce risk for one party. Thediverse range

Gaurav Pathak [ ] Pramod Bidrupane [ ] Rajesh Goli [ ] THE ROLE OF CREDIT DERIVATIVES IN PRECIPITATING THE CURRENT FINANCIAL CRISIS

![Gaurav Pathak [ ] Pramod Bidrupane [ ] Rajesh Goli [ ] THE ROLE OF CREDIT DERIVATIVES IN PRECIPITATING THE CURRENT FINANCIAL CRISIS](/thumbs/95/125043985.jpg "Gaurav Pathak [ ] Pramod Bidrupane [ ] Rajesh Goli [ ] THE ROLE OF CREDIT DERIVATIVES IN PRECIPITATING THE CURRENT FINANCIAL CRISIS") THE ROLE OF CREDIT DERIVATIVES IN PRECIPITATING THE CURRENT FINANCIAL CRISIS BFMS P C NARAYAN SUBMITTED BY Gaurav Pathak [2007021] Pramod Bidrupane [2007039] Rajesh Goli [2007044] IIM BANGALORE INTRODUCTION

THE ROLE OF CREDIT DERIVATIVES IN PRECIPITATING THE CURRENT FINANCIAL CRISIS BFMS P C NARAYAN SUBMITTED BY Gaurav Pathak [2007021] Pramod Bidrupane [2007039] Rajesh Goli [2007044] IIM BANGALORE INTRODUCTION

10th Symposium on Finance, Banking, and Insurance Universität Karlsruhe (TH), December 14 16, 2005

, December 14 16, 2005") 10th Symposium on Finance, Banking, and Insurance Universität Karlsruhe (TH), December 14 16, 2005 Plenary Lecture Heinz Hilgert Member of the Board, DZ BANK Transfer of Corporate Credit Risk within the

10th Symposium on Finance, Banking, and Insurance Universität Karlsruhe (TH), December 14 16, 2005 Plenary Lecture Heinz Hilgert Member of the Board, DZ BANK Transfer of Corporate Credit Risk within the

25 Oct 2010 QIAO Yang SHEN Si

Credit Derivatives: CDS, CDO and financial crisis 25 Oct 2010 QIAO Yang SHEN Si 1 Agenda Historical background: what is Credit Default Swaps (CDS) and Collateralized Default Obligation (CDO) Issue and

Credit Derivatives: CDS, CDO and financial crisis 25 Oct 2010 QIAO Yang SHEN Si 1 Agenda Historical background: what is Credit Default Swaps (CDS) and Collateralized Default Obligation (CDO) Issue and

Appendix Pricing and Valuation of Securities: Introduction to Common Types of Securities

Page 1 Appendix Pricing and Valuation of Securities: Introduction to Common Types of Securities This handout provides summary information for common security types held by entities in their investment

Page 1 Appendix Pricing and Valuation of Securities: Introduction to Common Types of Securities This handout provides summary information for common security types held by entities in their investment

AlphaCentric Income Opportunities Fund Class A: IOFAX Class C: IOFCX Class I: IOFIX SUMMARY PROSPECTUS AUGUST 1, 2017

AlphaCentric Income Opportunities Fund Class A: IOFAX Class C: IOFCX Class I: IOFIX SUMMARY PROSPECTUS AUGUST 1, 2017 Before you invest, you may want to review the Fund s complete prospectus, which contains

AlphaCentric Income Opportunities Fund Class A: IOFAX Class C: IOFCX Class I: IOFIX SUMMARY PROSPECTUS AUGUST 1, 2017 Before you invest, you may want to review the Fund s complete prospectus, which contains

1. Primary markets are markets in which users of funds raise cash by selling securities to funds' suppliers.

Test Bank Financial Markets and Institutions 6th Edition Saunders Complete download Financial Markets and Institutions 6th Edition TEST BANK by Saunders, Cornett: https://testbankarea.com/download/financial-markets-institutions-6th-editiontest-bank-saunders-cornett/

Test Bank Financial Markets and Institutions 6th Edition Saunders Complete download Financial Markets and Institutions 6th Edition TEST BANK by Saunders, Cornett: https://testbankarea.com/download/financial-markets-institutions-6th-editiontest-bank-saunders-cornett/

Financial Markets 1

318.06 Financial Markets 1 I. Market distinctions (rather than corporate bonds vs government bonds vs mortgages, which may be sold in different physical markets but are very similar) A. Capital market

318.06 Financial Markets 1 I. Market distinctions (rather than corporate bonds vs government bonds vs mortgages, which may be sold in different physical markets but are very similar) A. Capital market

Chapter 11: Financial Markets Section 2

Chapter 11: Financial Markets Section 2 Objectives 1. Describe the characteristics of bonds as financial assets. 2. Identify different types of bonds. 3. Describe the characteristics of other types of

Chapter 11: Financial Markets Section 2 Objectives 1. Describe the characteristics of bonds as financial assets. 2. Identify different types of bonds. 3. Describe the characteristics of other types of

RETURN ENHANCEMENT WITH EUROPEAN ABS AND BANK LOANS IN SWISS INSTITUTIONAL PORTFOLIOS

H E A L T H W E A L T H C A R E E R RETURN ENHANCEMENT WITH EUROPEAN ABS AND BANK LOANS IN SWISS INSTITUTIONAL PORTFOLIOS JUNE 2017 INTRODUCTION In the aftermath of the global financial crisis, conventional

H E A L T H W E A L T H C A R E E R RETURN ENHANCEMENT WITH EUROPEAN ABS AND BANK LOANS IN SWISS INSTITUTIONAL PORTFOLIOS JUNE 2017 INTRODUCTION In the aftermath of the global financial crisis, conventional

INS Mutual Funds and Individual Securities Exam Study Guide

INS Mutual Funds and Individual Securities Exam Study Guide This document contains the questions that will be on the exam. When you have studied the course materials, reviewed the questions in this document,

INS Mutual Funds and Individual Securities Exam Study Guide This document contains the questions that will be on the exam. When you have studied the course materials, reviewed the questions in this document,

Mechanics and Benefits of Securitization

Mechanics and Benefits of Securitization Executive Summary Securitization is not a new concept. In its most basic form, securitization dates back to the late 18th century. The first modern residential

Mechanics and Benefits of Securitization Executive Summary Securitization is not a new concept. In its most basic form, securitization dates back to the late 18th century. The first modern residential

P2.T6. Credit Risk Measurement & Management. Ashcroft & Schuermann, Understanding the Securitization of Subprime Mortgage Credit

P2.T6. Credit Risk Measurement & Management Ashcroft & Schuermann, Understanding the Securitization of Subprime Mortgage Credit Bionic Turtle FRM Study Notes Reading 48 By David Harper, CFA FRM CIPM www.bionicturtle.com

P2.T6. Credit Risk Measurement & Management Ashcroft & Schuermann, Understanding the Securitization of Subprime Mortgage Credit Bionic Turtle FRM Study Notes Reading 48 By David Harper, CFA FRM CIPM www.bionicturtle.com

I. Introduction to Bonds

University of California, Merced ECO 163-Economics of Investments Chapter 10 Lecture otes I. Introduction to Bonds Professor Jason Lee A. Definitions Definition: A bond obligates the issuer to make specified

University of California, Merced ECO 163-Economics of Investments Chapter 10 Lecture otes I. Introduction to Bonds Professor Jason Lee A. Definitions Definition: A bond obligates the issuer to make specified

Financial Markets and Institutions, 8e (Mishkin) Chapter 2 Overview of the Financial System. 2.1 Multiple Choice

Chapter 2 Overview of the Financial System. 2.1 Multiple Choice") Financial Markets and Institutions, 8e (Mishkin) Chapter 2 Overview of the Financial System 2.1 Multiple Choice 1) Every financial market performs the following function: A) It determines the level of

Financial Markets and Institutions, 8e (Mishkin) Chapter 2 Overview of the Financial System 2.1 Multiple Choice 1) Every financial market performs the following function: A) It determines the level of

The Investment Environment. Chapter 1

The Investment Environment Chapter 1 Real & Financial Assets Real assets = assets used to produce goods and services (productive capacity) physical assets (land, buildings, machinery etc.) human assets

The Investment Environment Chapter 1 Real & Financial Assets Real assets = assets used to produce goods and services (productive capacity) physical assets (land, buildings, machinery etc.) human assets

off their risks, and a market may rise to meet the trading demand.

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) Only small companies can go through financial markets to obtain financing. 2) The reinvestment of cash back into the

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) Only small companies can go through financial markets to obtain financing. 2) The reinvestment of cash back into the

RS Official Gazette, No 103/2016

RS Official Gazette, No 103/2016 Based on Article 21, paragraph 3, Article 23, paragraph 5 and Article 24, paragraphs 2 and 4 of the Law on Banks (RS Official Gazette, Nos 107/2005, 91/2010 and 14/2015)

RS Official Gazette, No 103/2016 Based on Article 21, paragraph 3, Article 23, paragraph 5 and Article 24, paragraphs 2 and 4 of the Law on Banks (RS Official Gazette, Nos 107/2005, 91/2010 and 14/2015)

Chapter 14. The Mortgage Markets. Chapter Preview

Chapter 14 The Mortgage Markets Chapter Preview The average price of a U.S. home is well over $208,000. For most of us, home ownership would be impossible without borrowing most of the cost of a home.

Chapter 14 The Mortgage Markets Chapter Preview The average price of a U.S. home is well over $208,000. For most of us, home ownership would be impossible without borrowing most of the cost of a home.

Securitisation: Benefits for Emerging Markets and Lessons from the Global Financial Crisis

Securitisation: Benefits for Emerging Markets and Lessons from the Global Financial Crisis SEC Securities Markets Workshop Washington DC May 1, 2009 1 Securitisation: Benefits for Emerging Markets Investors

Securitisation: Benefits for Emerging Markets and Lessons from the Global Financial Crisis SEC Securities Markets Workshop Washington DC May 1, 2009 1 Securitisation: Benefits for Emerging Markets Investors

A Multi-Agent Model of Financial Stability and Credit Risk Transfers of Banks

A Multi-Agent Model of Financial Stability and Credit Risk Transfers of Banks Presentation for Bank of Italy Workshop on ABM in Banking and Finance: Turin Feb 9-11 Sheri Markose,, Yang Dong, Bewaji Oluwasegun

A Multi-Agent Model of Financial Stability and Credit Risk Transfers of Banks Presentation for Bank of Italy Workshop on ABM in Banking and Finance: Turin Feb 9-11 Sheri Markose,, Yang Dong, Bewaji Oluwasegun

Structured Finance. Synthetic CDOs: A Growing Market for Credit Derivatives. Loan Products Special Report. Analysts

Loan Products Special Report Synthetic CDOs: A Growing Market for Credit Derivatives Analysts New York Roger Merritt 1 212 908-0636 roger.merritt@fitchratings.com Michael Gerity 1 212 908-0628 michael.gerity@fitchratings.com

Loan Products Special Report Synthetic CDOs: A Growing Market for Credit Derivatives Analysts New York Roger Merritt 1 212 908-0636 roger.merritt@fitchratings.com Michael Gerity 1 212 908-0628 michael.gerity@fitchratings.com

Credit derivatives are derivative contracts that seek to transfer

Introduction to Securitization by Frank J. Fabozzi and Vinod Kothari Copyright 2008 John Wiley & Sons, Inc. APPENDIX A Basics of Credit Derivatives Credit derivatives are derivative contracts that seek

Introduction to Securitization by Frank J. Fabozzi and Vinod Kothari Copyright 2008 John Wiley & Sons, Inc. APPENDIX A Basics of Credit Derivatives Credit derivatives are derivative contracts that seek

Mutual Fund Investing Exam Study Guide

Mutual Fund Investing Exam Study Guide This document contains all the questions that will included in the final exam, in the order that they will be asked. When you have studied the course materials, reviewed

Mutual Fund Investing Exam Study Guide This document contains all the questions that will included in the final exam, in the order that they will be asked. When you have studied the course materials, reviewed

MODERN PORTFOLIO THEORY AND INVESTMENT ANALYSIS 9 TH EDITION

Test Bank to accompany Modern Portfolio Theory and Investment Analysis, 9 th Edition MODERN PORTFOLIO THEORY AND INVESTMENT ANALYSIS 9 TH EDITION ELTON, GRUBER, BROWN, & GOETZMANN The following exam questions

Test Bank to accompany Modern Portfolio Theory and Investment Analysis, 9 th Edition MODERN PORTFOLIO THEORY AND INVESTMENT ANALYSIS 9 TH EDITION ELTON, GRUBER, BROWN, & GOETZMANN The following exam questions

CHAPTER 9 DEBT SECURITIES. by Lee M. Dunham, PhD, CFA, and Vijay Singal, PhD, CFA

CHAPTER 9 DEBT SECURITIES by Lee M. Dunham, PhD, CFA, and Vijay Singal, PhD, CFA LEARNING OUTCOMES After completing this chapter, you should be able to do the following: a Identify issuers of debt securities;

CHAPTER 9 DEBT SECURITIES by Lee M. Dunham, PhD, CFA, and Vijay Singal, PhD, CFA LEARNING OUTCOMES After completing this chapter, you should be able to do the following: a Identify issuers of debt securities;

Maiden Lane III LLC (A Special Purpose Vehicle Consolidated by the Federal Reserve Bank of New York)

") (A Special Purpose Vehicle Consolidated by the Federal Reserve Bank of New York) Financial Statements for the Year Ended December 31, 2009, and for the Period October 31, 2008 to December 31, 2008, and

(A Special Purpose Vehicle Consolidated by the Federal Reserve Bank of New York) Financial Statements for the Year Ended December 31, 2009, and for the Period October 31, 2008 to December 31, 2008, and

Retirement. on the Brain. Managing Risk: Step-by-step investing for tomorrow

Retirement on the Brain Managing Risk: Step-by-step investing for tomorrow Managing risk Understanding risk is crucial to overcoming the fear of investing. Managing risk explains the basic investing principles

Retirement on the Brain Managing Risk: Step-by-step investing for tomorrow Managing risk Understanding risk is crucial to overcoming the fear of investing. Managing risk explains the basic investing principles

APIR: PER0760AU ARSN: ISIN: AU60PER07600

JPMorgan Multi-Manager Alternatives Fund Supplementary Information APIR: PER0760AU ARSN: 612 459 864 ISIN: AU60PER07600 Benchmark: Bloomberg AusBond Bank Bill Index 1 PORTFOLIO ALLOCATION OF THE UNDERLYING

JPMorgan Multi-Manager Alternatives Fund Supplementary Information APIR: PER0760AU ARSN: 612 459 864 ISIN: AU60PER07600 Benchmark: Bloomberg AusBond Bank Bill Index 1 PORTFOLIO ALLOCATION OF THE UNDERLYING

Financial Markets and Institutions Final study guide Jon Faust Spring The final will be a 2 hour exam.

180.266 Financial Markets and Institutions Final study guide Jon Faust Spring 2014 The final will be a 2 hour exam. Bring a calculator: there will be some calculations. If you have an accommodation for

180.266 Financial Markets and Institutions Final study guide Jon Faust Spring 2014 The final will be a 2 hour exam. Bring a calculator: there will be some calculations. If you have an accommodation for

MORGAN STANLEY & CO. LLC (SEC I.D. No ) CONSOLIDATED STATEMENT OF FINANCIAL CONDITION AS OF DECEMBER 31, 2011 AND INDEPENDENT AUDITORS REPORT

CONSOLIDATED STATEMENT OF FINANCIAL CONDITION AS OF DECEMBER 31, 2011 AND INDEPENDENT AUDITORS REPORT") MORGAN STANLEY & CO. LLC (SEC I.D. No. 8-15869) CONSOLIDATED STATEMENT OF FINANCIAL CONDITION AS OF DECEMBER 31, 2011 AND INDEPENDENT AUDITORS REPORT ******** INDEPENDENT AUDITORS REPORT To the Board of

MORGAN STANLEY & CO. LLC (SEC I.D. No. 8-15869) CONSOLIDATED STATEMENT OF FINANCIAL CONDITION AS OF DECEMBER 31, 2011 AND INDEPENDENT AUDITORS REPORT ******** INDEPENDENT AUDITORS REPORT To the Board of

Securitization Structured finance solutions

Securitization Structured finance solutions March 2018 Brochure / report title goes here Section title goes here Contents 1. Preface 4 1.1 Introduction 4 1.2 The appeal of securitization 4 1.3 A new European

Securitization Structured finance solutions March 2018 Brochure / report title goes here Section title goes here Contents 1. Preface 4 1.1 Introduction 4 1.2 The appeal of securitization 4 1.3 A new European

Topics in Corporate Finance

Topics in Corporate Finance Securitisations Plan of the Introduction and overview of securitisations Securitisation in Practice (Richard Golding, Anthem Corporate Finance) Regulation and securitisation

Topics in Corporate Finance Securitisations Plan of the Introduction and overview of securitisations Securitisation in Practice (Richard Golding, Anthem Corporate Finance) Regulation and securitisation

Special Risks in Securities Trading

Special Risks in Securities Trading Information about the Stock Exchange Act growing together. Contents Pages Sections What this brochure is about 3 7 1 19 Transactions involving special risks 8 35 20

Special Risks in Securities Trading Information about the Stock Exchange Act growing together. Contents Pages Sections What this brochure is about 3 7 1 19 Transactions involving special risks 8 35 20

The State of New York Deferred Compensation Board Stable Income Fund INVESTMENT POLICIES AND GUIDELINES. Table of Contents

The State of New York Deferred Compensation Board Stable Income Fund INVESTMENT POLICIES AND GUIDELINES June 12, 2009 Table of Contents I. Investment Objectives II. Investment Strategy A. Permitted Investments

The State of New York Deferred Compensation Board Stable Income Fund INVESTMENT POLICIES AND GUIDELINES June 12, 2009 Table of Contents I. Investment Objectives II. Investment Strategy A. Permitted Investments

CRE FinanCE W. The Voice of Commercial Real Estate Finance. Autumn 2012 Volume 14 No.3. A publication of CRE Finance Council

A publication of CRE Finance Council CRE FinanCE W The Voice of Commercial Real Estate Finance Rld Autumn Issue 2012 is Sponsored by Autumn 2012 Volume 14 No.3 CMBS Opportunities: Any Floating-Rate Port

A publication of CRE Finance Council CRE FinanCE W The Voice of Commercial Real Estate Finance Rld Autumn Issue 2012 is Sponsored by Autumn 2012 Volume 14 No.3 CMBS Opportunities: Any Floating-Rate Port

CHAPTER 2: ASSET CLASSES AND FINANCIAL INSTRUMENTS

Chapter 2 - Asset Classes and Financial Instruments CHAPTER 2: ASSET CLASSES AND FINANCIAL INSTRUMENTS PROBLEM SETS 1. Preferred stock is like long-term debt in that it typically promises a fixed payment

Chapter 2 - Asset Classes and Financial Instruments CHAPTER 2: ASSET CLASSES AND FINANCIAL INSTRUMENTS PROBLEM SETS 1. Preferred stock is like long-term debt in that it typically promises a fixed payment

INDUSTRY MEMO ON ISSUES FOR SECURITISATION UNDER THE MARKET ABUSE DIRECTIVE

Commercial Mortgage Securities Association Europe / European Securitisation Forum INDUSTRY MEMO ON ISSUES FOR SECURITISATION UNDER THE MARKET ABUSE DIRECTIVE 1. Introduction: securitisation In this paper

Commercial Mortgage Securities Association Europe / European Securitisation Forum INDUSTRY MEMO ON ISSUES FOR SECURITISATION UNDER THE MARKET ABUSE DIRECTIVE 1. Introduction: securitisation In this paper

Special Risks in Securities Trading. 2 nd edition, 2008

ab Special Risks in Securities Trading 2 nd edition, 2008 Pages Margin numbers INTRODUCTION What this brochure is about 4 1 19 SECTION ONE Transactions involving special risks Options 8 20 85 Forwards

ab Special Risks in Securities Trading 2 nd edition, 2008 Pages Margin numbers INTRODUCTION What this brochure is about 4 1 19 SECTION ONE Transactions involving special risks Options 8 20 85 Forwards

Structured Finance, Risk Management, and the Recent Financial Crisis

Structured Finance, Risk Management, and the Recent Financial Crisis Georges Dionne Canada Research Chair in Risk Management, CIRPEE, and Department of Finance, HEC Montreal 20 October 2009 Abstract Structured

Structured Finance, Risk Management, and the Recent Financial Crisis Georges Dionne Canada Research Chair in Risk Management, CIRPEE, and Department of Finance, HEC Montreal 20 October 2009 Abstract Structured

Online Workshop (hard copy version) Member options regarding their Liquidating Trust

Member options regarding their Liquidating Trust") Online Workshop (hard copy version) Member options regarding their Liquidating Trust Introduction Welcome to a workshop developed to help you better understand the market for Restructured Notes that are

Online Workshop (hard copy version) Member options regarding their Liquidating Trust Introduction Welcome to a workshop developed to help you better understand the market for Restructured Notes that are

Overview of Financial Instruments and Financial Markets

CHAPTER 1 Overview of Financial Instruments and Financial Markets FRANK J. FABOZZI, PhD, CFA, CPA Professor in the Practice of Finance, Yale School of Management Issuers and Investors 3 Debt versus Equity

CHAPTER 1 Overview of Financial Instruments and Financial Markets FRANK J. FABOZZI, PhD, CFA, CPA Professor in the Practice of Finance, Yale School of Management Issuers and Investors 3 Debt versus Equity

MSRB Rule G-17: Interpretive Notice on Duties of Underwriters to Issuers

MSRB Rule G-17: Interpretive Notice on Duties of Underwriters to Issuers Webinar Part 2: Required Disclosure of Role, Obligations and Conflicts of Interest Required Underwriter Disclosures to Issuers Under

MSRB Rule G-17: Interpretive Notice on Duties of Underwriters to Issuers Webinar Part 2: Required Disclosure of Role, Obligations and Conflicts of Interest Required Underwriter Disclosures to Issuers Under

CDOs October 19, 2006

2006 Annual Meeting & Education Conference New York, NY CDOs Ozgur K. Bayazitoglu AIG Global Investment Group Keith M. Ashton TIAA-CREF Michael Lamont Deutsche Bank Securities Inc. Vicki E. Marmorstein

2006 Annual Meeting & Education Conference New York, NY CDOs Ozgur K. Bayazitoglu AIG Global Investment Group Keith M. Ashton TIAA-CREF Michael Lamont Deutsche Bank Securities Inc. Vicki E. Marmorstein

MONEY MARKET FUND GLOSSARY

MONEY MARKET FUND GLOSSARY 1-day SEC yield: The calculation is similar to the 7-day Yield, only covering a one day time frame. To calculate the 1-day yield, take the net interest income earned by the fund

MONEY MARKET FUND GLOSSARY 1-day SEC yield: The calculation is similar to the 7-day Yield, only covering a one day time frame. To calculate the 1-day yield, take the net interest income earned by the fund

Answers to Selected Problems

Answers to Selected Problems Problem 1.11. he farmer can short 3 contracts that have 3 months to maturity. If the price of cattle falls, the gain on the futures contract will offset the loss on the sale

Answers to Selected Problems Problem 1.11. he farmer can short 3 contracts that have 3 months to maturity. If the price of cattle falls, the gain on the futures contract will offset the loss on the sale

MORGAN STANLEY & CO. LLC CONSOLIDATED STATEMENT OF FINANCIAL CONDITION AS OF JUNE 30, 2017 (UNAUDITED) ********

********") MORGAN STANLEY & CO. LLC CONSOLIDATED STATEMENT OF FINANCIAL CONDITION AS OF JUNE 30, 2017 (UNAUDITED) ******** MORGAN STANLEY & CO. LLC CONSOLIDATED STATEMENT OF FINANCIAL CONDITION As of June 30, 2017

MORGAN STANLEY & CO. LLC CONSOLIDATED STATEMENT OF FINANCIAL CONDITION AS OF JUNE 30, 2017 (UNAUDITED) ******** MORGAN STANLEY & CO. LLC CONSOLIDATED STATEMENT OF FINANCIAL CONDITION As of June 30, 2017

Fixed-Income Securities Lecture 1: Overview

Philip H. Dybvig Washington University in Saint Louis Introduction Some of the players Some of the Securities Analytical tasks: overview Fixed-Income Securities Lecture 1: Overview Copyright c Philip H.

Philip H. Dybvig Washington University in Saint Louis Introduction Some of the players Some of the Securities Analytical tasks: overview Fixed-Income Securities Lecture 1: Overview Copyright c Philip H.

Introduction. Fixed-Income Securities Lecture 1: Overview. Generic issues for the players

Philip H. Dybvig Washington University in Saint Louis Introduction Some of the players Some of the Securities Analytical tasks: overview Fixed-Income Securities Lecture 1: Overview Introduction Fixed-income

Philip H. Dybvig Washington University in Saint Louis Introduction Some of the players Some of the Securities Analytical tasks: overview Fixed-Income Securities Lecture 1: Overview Introduction Fixed-income

Securitization. Spring Stephen Sapp

Securitization Spring 2014 Stephen Sapp What is Securitization? Grouping together a set of assets which generate cashflows, selling this portfolio to another entity to manage (i.e., collect the cashflows),

Securitization Spring 2014 Stephen Sapp What is Securitization? Grouping together a set of assets which generate cashflows, selling this portfolio to another entity to manage (i.e., collect the cashflows),

Financial Literacy: Investing

tocks: When you own stock in a company, the number of shares you own represent equity, also called ownership, in the company. he value of your investment is then based on the value of the company. Bonds:

tocks: When you own stock in a company, the number of shares you own represent equity, also called ownership, in the company. he value of your investment is then based on the value of the company. Bonds:

SECTION 1: LEGISLATIVE AND REGULATORY AUTHORITY INVESTMENTS

SECTION 1: LEGISLATIVE AND REGULATORY AUTHORITY INVESTMENTS The Municipal Act as well as a number of Ontario regulations govern municipal investments. The following provides the specific references that

SECTION 1: LEGISLATIVE AND REGULATORY AUTHORITY INVESTMENTS The Municipal Act as well as a number of Ontario regulations govern municipal investments. The following provides the specific references that

Chapter 02 Test Bank - Static

Chapter 02 Test Bank - Static Student: 1. Only small companies can go through financial markets to obtain financing. 2. The reinvestment of cash back into the firm's operations is an example of a flow

Chapter 02 Test Bank - Static Student: 1. Only small companies can go through financial markets to obtain financing. 2. The reinvestment of cash back into the firm's operations is an example of a flow

CHAPTER 14. Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS. Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved.

CHAPTER 14 Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS BODIE, KANE, MARCUS 14-2 Bond Characteristics

CHAPTER 14 Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS BODIE, KANE, MARCUS 14-2 Bond Characteristics

Derivatives Terms and Definitions Vademecum

Derivatives Terms and Definitions Vademecum 1st Edition 2011 www.morganlewis.de This Vademecum is as of January 2011 and provides initial guidance on certain derivatives terms and definitions. The terms

Derivatives Terms and Definitions Vademecum 1st Edition 2011 www.morganlewis.de This Vademecum is as of January 2011 and provides initial guidance on certain derivatives terms and definitions. The terms

Taxing Risk* Narayana Kocherlakota. President Federal Reserve Bank of Minneapolis. Economic Club of Minnesota. Minneapolis, Minnesota.

Taxing Risk* Narayana Kocherlakota President Federal Reserve Bank of Minneapolis Economic Club of Minnesota Minneapolis, Minnesota May 10, 2010 *This topic is discussed in greater depth in "Taxing Risk

Taxing Risk* Narayana Kocherlakota President Federal Reserve Bank of Minneapolis Economic Club of Minnesota Minneapolis, Minnesota May 10, 2010 *This topic is discussed in greater depth in "Taxing Risk

CRISIL s rating methodology for collateralised debt obligations (CDO) September 2018

September 2018") CRISIL s rating methodology for collateralised debt obligations (CDO) September 2018 Criteria contacts Somasekhar Vemuri Senior Director Rating Criteria and Product Development Email: somasekhar.vemuri@crisil.com

CRISIL s rating methodology for collateralised debt obligations (CDO) September 2018 Criteria contacts Somasekhar Vemuri Senior Director Rating Criteria and Product Development Email: somasekhar.vemuri@crisil.com

Glossary of Investment Terms

Glossary of Investment Terms Performance Measures Alpha: Alpha measures the difference between a portfolio s actual returns and its expected returns given its risk level as measured by its beta. A higher

Glossary of Investment Terms Performance Measures Alpha: Alpha measures the difference between a portfolio s actual returns and its expected returns given its risk level as measured by its beta. A higher

(A Special Purpose Vehicle Consolidated by the Federal Reserve Bank of New York)

") (A Special Purpose Vehicle Consolidated by the Federal Reserve Bank of New York) Consolidated Financial Statements as of and for the Years Ended December 31, 2013 and 2012, and Independent Auditors Report

(A Special Purpose Vehicle Consolidated by the Federal Reserve Bank of New York) Consolidated Financial Statements as of and for the Years Ended December 31, 2013 and 2012, and Independent Auditors Report

1. Only small companies can go through financial markets to obtain financing.

Fundamentals of Corporate Finance 8th Edition Brealey Test Bank Full Download: http://testbanklive.com/download/fundamentals-of-corporate-finance-8th-edition-brealey-test-bank/ Chapter 02 Financial Markets

Fundamentals of Corporate Finance 8th Edition Brealey Test Bank Full Download: http://testbanklive.com/download/fundamentals-of-corporate-finance-8th-edition-brealey-test-bank/ Chapter 02 Financial Markets

BOGAZICI UNIVERSITY - DEPARTMENT OF ECONOMICS FALL 2016 EC 344: MONEY, BANKING AND FINANCIAL INSTITUTIONS - PROBLEM SET 2 -

BOGAZICI UNIVERSITY - DEPARTMENT OF ECONOMICS FALL 2016 EC 344: MONEY, BANKING AND FINANCIAL INSTITUTIONS - PROBLEM SET 2 - DUE BY OCTOBER 10, 2016, 5 PM 1) Every financial market has the following characteristic.

BOGAZICI UNIVERSITY - DEPARTMENT OF ECONOMICS FALL 2016 EC 344: MONEY, BANKING AND FINANCIAL INSTITUTIONS - PROBLEM SET 2 - DUE BY OCTOBER 10, 2016, 5 PM 1) Every financial market has the following characteristic.

Real Estate Finance 101: The Basics Wednesday, October 17 th, :15 a.m. - 10:30 a.m. Presented by: Jay Rollins JCR Capital

Real Estate Finance 101: The Basics Wednesday, October 17 th, 2012 9:15 a.m. - 10:30 a.m. Presented by: Jay Rollins JCR Capital www.jcrcapital.com 1. Commercial real estate can be a huge wealth creator

Real Estate Finance 101: The Basics Wednesday, October 17 th, 2012 9:15 a.m. - 10:30 a.m. Presented by: Jay Rollins JCR Capital www.jcrcapital.com 1. Commercial real estate can be a huge wealth creator

CIS March 2012 Exam Diet

CIS March 2012 Exam Diet Examination Paper 2.2: Corporate Finance Equity Valuation and Analysis Fixed Income Valuation and Analysis Level 2 Corporate Finance (1 13) 1. Which of the following statements

CIS March 2012 Exam Diet Examination Paper 2.2: Corporate Finance Equity Valuation and Analysis Fixed Income Valuation and Analysis Level 2 Corporate Finance (1 13) 1. Which of the following statements

Lecture 5: The Repo Market

Lecture 5: The Repo Market Concepts and Buzzwords Repurchase Agreements (Repos) The Repo Market Uses of Repos in Practice Repo, reverse repo, repo rates, collateral, margin, haircut, matched book, special

Lecture 5: The Repo Market Concepts and Buzzwords Repurchase Agreements (Repos) The Repo Market Uses of Repos in Practice Repo, reverse repo, repo rates, collateral, margin, haircut, matched book, special

A CLEAR UNDERSTANDING OF THE INDUSTRY

A CLEAR UNDERSTANDING OF THE INDUSTRY IS CFA INSTITUTE INVESTMENT FOUNDATIONS RIGHT FOR YOU? Investment Foundations is a certificate program designed to give you a clear understanding of the investment

A CLEAR UNDERSTANDING OF THE INDUSTRY IS CFA INSTITUTE INVESTMENT FOUNDATIONS RIGHT FOR YOU? Investment Foundations is a certificate program designed to give you a clear understanding of the investment

BBM2153 Financial Markets and Institutions Prepared by Dr Khairul Anuar

BBM2153 Financial Markets and Institutions Prepared by Dr Khairul Anuar L6: The Bond Market www. notes638.wordpress.com 6-1 Chapter Preview In this chapter, we focus on longer-term securities: bonds. Bonds

BBM2153 Financial Markets and Institutions Prepared by Dr Khairul Anuar L6: The Bond Market www. notes638.wordpress.com 6-1 Chapter Preview In this chapter, we focus on longer-term securities: bonds. Bonds