UNIVERSITY OF GEORGIA COOPERATIVE EXTENSION COST RECOVERY GUIDELINES FOR COUNTY EXTENSION PROGRAMS

|

|

|

- Claud Hubbard

- 5 years ago

- Views:

Transcription

1 UNIVERSITY OF GEORGIA COOPERATIVE EXTENSION COST RECOVERY GUIDELINES FOR COUNTY EXTENSION PROGRAMS Adopted July 24, 2013

2 INTRODUCTION These guidelines provide a framework through which county faculty/staff can expand their understanding of how cost recovery initiatives can support and enhance Extension programming during a time of limited federal, state, and county funding. These guidelines are not designed to answer all the questions associated with implementing a cost recovery program. We encourage and challenge you to utilize creative funding techniques including cost recovery programs to maintain and expand your educational efforts. TABLE OF CONTENTS Page Background and Philosophy 2 Guiding Principles 2 Cost Recovery Options and Types of Programs 4 Additional Overview of UGA Cooperative Extension 5 Cost Recovery Options and Programs Administration of Cost Recovery Guidelines 5 Sponsorship and Donations 6 Appendices A. Federal Cost Recovery Regulations 7 B. Extension Publications 8 C. Cost Recovery Worksheet (Example) 9 1 P age

3 BACKGROUND AND PHILOSOPHY As we look to the future, the goal of the University of Georgia Cooperative Extension is to maintain a strong presence at our land-grant institution and in the counties and cities throughout the state. In an environment of increasing pressures on traditional sources of funding at the federal, state and local levels, maintaining our capacity will require that we enhance our ability to generate funds from other sources. One of the ways to accomplish this is to seek funding for programs through sponsorships, advertising or by charging a fee to participants. This shift recognizes the valuable continuing need for a federal, state and county funding partnership for Cooperative Extension. However, ways to develop partial self-support for many of our programs must be explored and implemented to the fullest extent possible. Recovering costs associated with Extension programs and services is not a new idea. Extension has been charging fees to cover some of the costs of existing programs for a long time. Sometimes the costs of programs and services targeted for specific audiences have been fully recovered through grants, contracts, agreements, and MOUs. It is the intent of these Cost Recovery Guidelines to outline procedures and strategies for recovering some costs for local programs to aid in strengthening our programs for Georgia residents. GUIDING PRINCIPLES Extension supports the recovery of costs associated with programs and services for the public good and also for programs associated with developing and implementing high-quality customized programming and services that result from specific requests from exclusive audiences. Cost recovery associated with educational program delivery in Extension is guided by the following considerations: Cost recovery associated with Extension programming must be consistent with the UGA Cooperative Extension mission and program direction. Cost recovery practices are not intended to limit audience participation, impact, or involvement. UGA Cooperative Extension programs are open to all regardless of individual ability to pay or program source of funding; part of a complete budget plan should include provisions to reduce or waive fees when limited resource participants need financial assistance. There is no hard and fast rule for defining limited resource participants. It will be at the discretion of the faculty/staff member to determine if the participant should have fees waived or reduced. We will not require proof of income or hardship. The faculty/staff member shall strive to make provisions in their budget to obtain funds from sponsors and others to underwrite fees for these participants and offer scholarships whenever necessary. Sources of funds to cover costs may include grants, contracts, gifts, sponsors, donations, program underwriting, and participant fees. The opportunity or need to recover costs shall not be the major determining factor in setting program priorities and/or evaluating program results. 2 P age

4 Revenue generated from cost recovery shall remain with the county or counties from which it was generated and be deposited into the local extension checking account in the appropriate program sub-account. Accountability of these funds is critical. All funds collected will be managed according to the UGA Cooperative Extension County Funds policy. Each faculty/staff member will be accountable for the funds collected for their programs. Oversight will be provided by the County Extension Coordinator. Accountability of these funds is critical. All funds collected will be managed according to the UGA Cooperative Extension County Funds policy. Each faculty/staff member will be accountable for the funds collected for their programs. Oversight will be provided by the County Extension Coordinator. Funds may be utilized to pay the direct cost of the program or service including travel, meeting room rental, cost of publications and supplies, meals and breaks, printing, postage and personnel expenses to hire contractual employees that support the program effort. You may also include indirect costs such as professional development, and overhead costs to pay for things like computer equipment, software, etc. Funds cannot be used to offset the salaries and benefits of employees who are paid from federal, state and local extension funds. A cost recovery worksheet shall be developed by the responsible faculty/staff member for each major program and reviewed by the appropriate County Extension Coordinator (CEC) or in the case of a program conducted by the CEC, the worksheet shall be reviewed by the appropriate Program Development Coordinator/Specialist or by the District Extension Director (DED). Cost recovery through sponsorship is also allowed for underwriting of county Extension newsletters. However, this opportunity needs to be widely available to organizations and there must be understanding among all parties that underwriting does not imply endorsement of particular products, services or organizations. On such newsletters use the following statement: Sponsorship of this newsletter does not imply endorsement of the sponsor by the University of Georgia Cooperative Extension. Obviously there are some businesses, and/or products that we would not want associated with our programs even with the disclaimer stated above. For example, it is probably generally accepted that we would not want the local liquor store sponsoring our 4-H newsletter. We reserve the right to refuse sponsorship funds from any business or organization that we would deem inappropriate to be associated with extension programs and services. Membership and Participation Fees for 4-H There is no membership fee for a student to join the Georgia 4-H Club. 4-H club members may be charged a fee to cover costs associated with participation in certain 4-H club activities. Charges associated with these activities may include direct costs as well as a limited amount for indirect costs. No 4-H club member shall be denied the opportunity to participate in educational programs based on their inability to pay the participation fee. 3 P age

5 COST RECOVERY OPTIONS AND TYPES OF PROGRAMS The type of audience a program is designed to reach is one of the guiding factors in determining what level of cost recovery is appropriate. Cost recovery for Extension programs should be viewed as a continuum on a scale ranging from no cost recovery to full cost recovery. This continuum can be viewed as follows: No Cost Recovery Partial Cost Recovery Full Cost Recovery No Cost Recovery. These are programs that are primary and fundamental to the mission of UGA Cooperative Extension. These programs have no charge or minimal charge. Generally they would be open to the general public, would contribute to the public good and would be part of the agent s base program or included in their issue based plan of work. Examples: Any program targeted at low income audiences (eg. EFNEP), farm visits to commercial farmers, general 4-H club programs and training for Extension volunteers who do not receive any personal benefit from the training (Master Gardener training would not fall into this category since the participants gain knowledge that is of personal value). Partial Cost Recovery. These programs are highly targeted and content specific and are also primary and fundamental to the mission of UGA Cooperative Extension. They are based on existing programs, and are modified or customized for a specific individual, business, or narrowly defined group that is the primary beneficiary. They may be classified as programs for the public good, but may not be offered without additional financial resources. Partial cost recovery should include direct costs and may include recovery of indirect costs if administratively approved. Examples: Crop production meetings, home gardening classes, soil and plant testing, private pesticide applicator training, 4-H summer day camps, 4-H Project Achievement, 4-H horse clubs, food preservation classes. Full Cost Recovery. Customized programs developed for a specific group, individual, or business that realizes primary economic benefits; i.e. where there is an identifiable private good to the individuals, group and/or business. In addition to programming, this could include ongoing one-on-one advising for a specific individual, group, or business on a topic that may be beyond the scope of our day to day responsibilities. Examples: Food safety certification program for restaurant workers, commercial pesticide applicator training for a company s employees, forest tax training for CPA s, child care provider training for licensing and/or renewal, a strategic planning retreat conducted for a local non-profit agency. 4 P age

6 Additional Overview of UGA Cooperative Extension Cost Recovery Options and Programs The types of programs offered by Extension differ widely. Some programs are targeted toward individuals, families, community and government groups, and businesses. These programs generally fall in the category of no cost or partial cost recovery. Then too, there are programs requested that provide customized educational offerings for exclusive or private audiences. These programs fall into the category of full cost recovery. A general overview of the programs and how they may be viewed in making a determination about the level of cost recovery is reiterated below: Characteristics of programs involving no cost or partial cost recovery: - Anyone may attend the program. - Materials are available broadly and may be shared with others. - Subject matter expertise is readily available. - Time needed to develop the program is a part of the overall plan of work. - Time needed to deliver the program is reasonable within the professional s work assignment. - The program is part of ongoing efforts and may be broadly applied and utilized. - No formal certification or credits are offered. Characteristics of programs where there would be full cost recovery: - Attendance is only for an exclusive group where there is an identifiable private good related to the programming effort. - Programs and services require customizing the curriculum for an exclusive group. - Subject matter is appropriate for Extension, but current faculty may not have the expertise to develop and conduct the program. Consequently, such efforts would require specialized training, development, etc. to fulfill the programming request. - Continuing education units or certificates may be provided for completing the course/program. ADMINISTRATION OF COST RECOVERY GUIDELINES Fees may include both direct and indirect costs and shall be determined using the Program Cost Recovery Worksheet (Appendix C). Funds collected shall be deposited into the local extension checking account. Fees must be collected, deposited, and expended following the UGA Extension County Funds Policy. It is the responsibility of the faculty/staff member coordinating the program to ensure that appropriate university and extension policies are followed when fees are charged. A cost recovery worksheet must be prepared by the faculty/staff member for all major programs and reviewed by the appropriate CEC or in the case of programs offered by the CEC, the worksheet shall be reviewed by the appropriate PDC/S or DED. For any program for which partial or full cost recovery is utilized, the Program Cost Recovery Worksheet shall be kept as part of the official program files. When a standard program is offered in multiple locations around the state it may be determined that a standard registration fee is beneficial. In this case, a request shall be made to the appropriate state program leader and that individual (with input from the Extension Leadership Team) will determine whether a standard fee should be applied and will help to determine the amount of the registration fee to be charged. In some cases, for programs that 5 P age

7 may also be offered by entities other than Extension, there may be a need to charge the prevailing fee in order to avoid undercutting the competition. In these cases the standard fee could be higher than the amount determined using the Program Cost Recovery Worksheet The Program Cost Recovery Worksheet and these guidelines shall be located on the County Operations website on the Extension Intranet. The worksheet will be available as a pdf file that can be printed and filled out by hand and as an Excel spreadsheet that can be filled out and saved as an electronic file. SPONSORSHIP AND DONATIONS Program sponsors may be secured to pay some or all of the costs that would otherwise be recovered through user fees. Program sponsors should be recognized appropriately in program publicity and materials. A disclaimer statement must be used on the printed materials to ensure that sponsorship does not imply an endorsement; e.g. Sponsorship of this program does not imply endorsement of the sponsor by the University of Georgia Cooperative Extension. 6 P age

8 Appendix A Federal Cost Recovery Regulations The United States Department of Agriculture Administrative Handbook for Cooperative Extension Work details user fee regulations in chapter 3. These guidelines clearly preclude charging user fees to offset the salaries of Cooperative Extension faculty and staff that are funded at least in part with county, state, or federal general-purpose funds. In compliance with this federal policy, state and county cost recovery efforts may not extend to the salaries of these personnel. Fees cannot be substituted for state or county appropriated funds. The Handbook further states that clients be informed what the fees include. Per USDA guidelines, educational activities and services for which fees may be charged to partly or wholly recover costs include the following: 1. Services that enhance the basic educational program, like mediated instruction transmission and associated costs (e.g. video conference production and transmission expenses), publications and other materials, computer analysis, computer software, and the overhead costs associated with providing these types of enhanced services. 2. Conference-related activities that contribute to agent and specialist teaching, such as expenses for outside instructors, materials, specialized electronic equipment, audiovisual equipment, and rental costs for meeting rooms. 3. Supplemental educational programs funded entirely through county or private sources. 4. Non-educational costs, such as meals and refreshments, which are always subject to full-cost recovery. 5. Services such as water testing, forage testing, plant analysis, farm record analysis, and pest identification, etc. 6. Programs not supported with government appropriations such as those designed for or restricted to a specific individual, group or business are not subject to USDA cost recovery regulations and shall be handled on a grant, contract, or participation fee basis. These programs shall be entirely self-supported with corresponding fees charged or grant or contract funding received. 7 P age

9 Appendix B Extension Publications Publications and other educational materials developed and/or paid for with federal or offset funds (e.g., state and county tax funds) are subject to federal regulations administered by USDA. Although each state is encouraged, to the extent feasible, to provide publications and materials without charge, it is permissible to recover costs related to reproduction, mailing, and handling. New publications that are part of grant-funded programs should include a budget that reflects the true cost of publications development, e.g. design, editing, printing, and distribution, when appropriate. The college has both "free" and "for-sale" (cost recovery) publication programs. State and federal funds are allocated to support our "free" Extension publications program. UGA Cooperative Extension will support providing a single copy of any non-cost recovery publication requested by an individual, group, or business within Georgia. For individuals or groups requesting multiple copies of publications for non-extension programs a fee may be charged to cover the cost of printing. Publications required for emergency response, in general will be made available without charge. The cost for publications used in educational programs may be covered through registration fees whenever appropriate. 8 P age

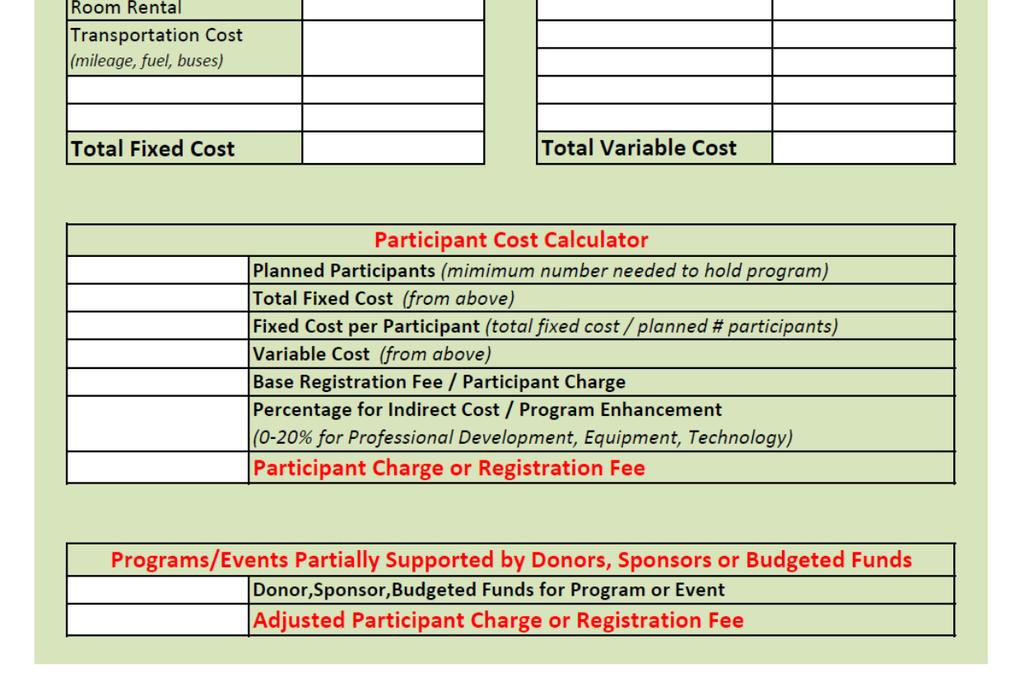

10 APPENDIX C 9 PAGE

Tu Tran, Associate Vice President. Contact: Jing Yu. Title:

Page 1 of 5 Responsible Officer: Responsible Office: Tu Tran, Associate Vice President Office of the Controller and Business Services (OCBS) Issuance Date: 07/25/2017 Effective Date: 07/25/2017 Last Review

Page 1 of 5 Responsible Officer: Responsible Office: Tu Tran, Associate Vice President Office of the Controller and Business Services (OCBS) Issuance Date: 07/25/2017 Effective Date: 07/25/2017 Last Review

Association for Communication Excellence (ACE) In Agriculture, Natural Resources, and Life and Human Sciences RFP FOR ASSOCIATION MANAGEMENT SERVICES

In Agriculture, Natural Resources, and Life and Human Sciences RFP FOR ASSOCIATION MANAGEMENT SERVICES") Association for Communication Excellence (ACE) In Agriculture, Natural Resources, and Life and Human Sciences RFP FOR ASSOCIATION MANAGEMENT SERVICES HISTORY OF ACE Since 1913, ACE has been providing professional

Association for Communication Excellence (ACE) In Agriculture, Natural Resources, and Life and Human Sciences RFP FOR ASSOCIATION MANAGEMENT SERVICES HISTORY OF ACE Since 1913, ACE has been providing professional

Current Operating Funds

Current Operating Funds Business Officer s Certification Program October 20, 2004 Objective Gain a better understanding of current funds in accounting systems Apply the above understanding to Clemson University

Current Operating Funds Business Officer s Certification Program October 20, 2004 Objective Gain a better understanding of current funds in accounting systems Apply the above understanding to Clemson University

30-DAY ACTION PLAN DISTRICT DIRECTOR 1. COORDINATE THE HANDOFF. Your name: District: Term start date:

DISTRICT DIRECTOR 30-DAY ACTION PLAN Your name: District: Term start date: 1. COORDINATE THE HANDOFF As district director, you are responsible to oversee the entire district transition. Schedule a meeting

DISTRICT DIRECTOR 30-DAY ACTION PLAN Your name: District: Term start date: 1. COORDINATE THE HANDOFF As district director, you are responsible to oversee the entire district transition. Schedule a meeting

W.O. SMITH NASHVILLE COMMUNITY MUSIC SCHOOL, INC. NASHVILLE, TENNESSEE FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT JUNE 30, 2017 AND 2016

NASHVILLE, TENNESSEE FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT NASHVILLE, TENNESSEE FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT CONTENTS INDEPENDENT AUDITOR S REPORT... 1 PAGE FINANCIAL

NASHVILLE, TENNESSEE FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT NASHVILLE, TENNESSEE FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT CONTENTS INDEPENDENT AUDITOR S REPORT... 1 PAGE FINANCIAL

Functions at West Virginia University

Functions at West Virginia University Function is used to classify the University's expenditures in multiple ways. The classifications are necessary to report the activity to the Federal government, sponsors

Functions at West Virginia University Function is used to classify the University's expenditures in multiple ways. The classifications are necessary to report the activity to the Federal government, sponsors

The Institute of Internal Auditors. Austin Chapter. Policies and Procedures

1. Polling Board Members by e-mail: The Institute of Internal Auditors Austin Chapter Policies and Procedures The Chapter President, or his/her designee, may poll the Board members by e-mail when a decision

1. Polling Board Members by e-mail: The Institute of Internal Auditors Austin Chapter Policies and Procedures The Chapter President, or his/her designee, may poll the Board members by e-mail when a decision

TABLE OF CONTENTS ASB INTRODUCTION... 2 ARTICLE I PURPOSE... 2 ARTICLE 2 DEFINITIONS... 2 ARTICLE 3 FUND MANAGEMENT...

FINANCIAL CODE TABLE OF CONTENTS ASB INTRODUCTION... 2 ARTICLE I PURPOSE... 2 ARTICLE 2 DEFINITIONS... 2 ARTICLE 3 FUND MANAGEMENT... 3 OBJECTIVE...3 USE OF FUNDS*...3 SECTION 3. LIMITATIONS*...4 SECTION

FINANCIAL CODE TABLE OF CONTENTS ASB INTRODUCTION... 2 ARTICLE I PURPOSE... 2 ARTICLE 2 DEFINITIONS... 2 ARTICLE 3 FUND MANAGEMENT... 3 OBJECTIVE...3 USE OF FUNDS*...3 SECTION 3. LIMITATIONS*...4 SECTION

CHECKLIST C505. Factors Indicating the Presence of Unrelated Business Income (UBI) (See Chapter 12)

(See Chapter 12)") C 82 990 1/15 CHECKLIST C505 Factors Indicating the Presence of Unrelated Business Income (UBI) (See Chapter 12) Client: Preparer s Initials and Date: Year: Reviewer s Initials and Date: Part I Initial

C 82 990 1/15 CHECKLIST C505 Factors Indicating the Presence of Unrelated Business Income (UBI) (See Chapter 12) Client: Preparer s Initials and Date: Year: Reviewer s Initials and Date: Part I Initial

THE APPALACHIAN TRAIL CONSERVANCY. Harpers Ferry, West Virginia FINANCIAL STATEMENTS DECEMBER 31, 2017

THE APPALACHIAN TRAIL CONSERVANCY Harpers Ferry, West Virginia FINANCIAL STATEMENTS DECEMBER 31, 2017 C O N T E N T S INDEPENDENT AUDITOR'S REPORT 1 and 2 Page FINANCIAL STATEMENTS Statement of financial

THE APPALACHIAN TRAIL CONSERVANCY Harpers Ferry, West Virginia FINANCIAL STATEMENTS DECEMBER 31, 2017 C O N T E N T S INDEPENDENT AUDITOR'S REPORT 1 and 2 Page FINANCIAL STATEMENTS Statement of financial

Creating A Program Budget

Creating A Program Budget Defining a Program Budget ORGANIZATIONAL BUDGET: Applies to an entire organization's activity, including everything that the organization does. Therefore all the programs and

Creating A Program Budget Defining a Program Budget ORGANIZATIONAL BUDGET: Applies to an entire organization's activity, including everything that the organization does. Therefore all the programs and

CAMP KUDZU, INC. FINANCIAL STATEMENTS SEPTEMBER 30, 2016 AND 2015

FINANCIAL STATEMENTS TABLE OF CONTENTS INDEPENDENT AUDITORS REPORT 1 FINANCIAL STATEMENTS Statements of Financial Position 2 Statements of Activities 3 Statement of Functional Expenses 2016 4 Statement

FINANCIAL STATEMENTS TABLE OF CONTENTS INDEPENDENT AUDITORS REPORT 1 FINANCIAL STATEMENTS Statements of Financial Position 2 Statements of Activities 3 Statement of Functional Expenses 2016 4 Statement

CAMPS & CLINICS Table of Contents

CAMPS & CLINICS Table of Contents DISTRICT GUIDELINES.. 2 Guidelines for School Sponsored Events.4 Extracurricular Addenda Agreement W-9 Financial Summary for Camps and Clinics Payroll Expenses 1099 Expenses

CAMPS & CLINICS Table of Contents DISTRICT GUIDELINES.. 2 Guidelines for School Sponsored Events.4 Extracurricular Addenda Agreement W-9 Financial Summary for Camps and Clinics Payroll Expenses 1099 Expenses

SAF Finances and Treasurer Role

SAF Finances and Treasurer Role Big Picture Understand the interrelationship of finances between the chapter, state, Northwest Office and National What are the funding sources and opportunities Impact

SAF Finances and Treasurer Role Big Picture Understand the interrelationship of finances between the chapter, state, Northwest Office and National What are the funding sources and opportunities Impact

Booster Clubs Questions and Answers (in italics)

") Booster Clubs Questions and Answers (in italics) Board Policy (Employees) DBD Regulations: Employees and Financial Capacity 1. If an employee is in charge of a concession stand, does that fall in the same

Booster Clubs Questions and Answers (in italics) Board Policy (Employees) DBD Regulations: Employees and Financial Capacity 1. If an employee is in charge of a concession stand, does that fall in the same

SASFAA Guide to Financial Management TABLE OF CONTENTS

1 SASFAA UPDATED 03/16/2016 SASFAA Guide to Financial Management Section 1: Purpose and Scope TABLE OF CONTENTS Section 2: Budget Planning and Preparation 2.1 Budget Preparation 2.2 Initial Operating Budget

1 SASFAA UPDATED 03/16/2016 SASFAA Guide to Financial Management Section 1: Purpose and Scope TABLE OF CONTENTS Section 2: Budget Planning and Preparation 2.1 Budget Preparation 2.2 Initial Operating Budget

UNITED WAY OF GREATER MILWAUKEE, INC. Milwaukee, Wisconsin. FINANCIAL STATEMENTS June 30, 2013 and 2012

Milwaukee, Wisconsin FINANCIAL STATEMENTS TABLE OF CONTENTS PAGE INDEPENDENT AUDITORS REPORT... 1 FINANCIAL STATEMENTS Statements of Financial Position... 3 Statements of Activities... 4 Statements of

Milwaukee, Wisconsin FINANCIAL STATEMENTS TABLE OF CONTENTS PAGE INDEPENDENT AUDITORS REPORT... 1 FINANCIAL STATEMENTS Statements of Financial Position... 3 Statements of Activities... 4 Statements of

Part 10: SSAI SCSEP Program Finance Procedures

SSAI SCSEP Policy and Procedure Manual Part 10: SSAI SCSEP Program Finance Procedures 1000 Sponsor Agreement, Budget Instructions and Administrative Requirements A. SSAI SCSEP Sponsor Agreement B. SSAI

SSAI SCSEP Policy and Procedure Manual Part 10: SSAI SCSEP Program Finance Procedures 1000 Sponsor Agreement, Budget Instructions and Administrative Requirements A. SSAI SCSEP Sponsor Agreement B. SSAI

Evaluation of Annual Action Plan (ongoing) and Institutional Effectiveness Plans Responsibility: Component Leadership

and Institutional Effectiveness Plans Responsibility: Component Leadership") August, 2018 Evaluation of 17-18 Annual Action Plan (ongoing) and Institutional Plans Annual 17-18 committee reports posted on website for College Committee review Responsibility: Committee Chairs and

August, 2018 Evaluation of 17-18 Annual Action Plan (ongoing) and Institutional Plans Annual 17-18 committee reports posted on website for College Committee review Responsibility: Committee Chairs and

Title: Business Expense Policy and Guidelines Prepared by: Controller s Office Administrator: University Controller Created: July 1, 2012

Title: Business Expense Policy and Guidelines Prepared by: Controller s Office Administrator: University Controller Created: July 1, 2012 Policy Statement The basic principle governing business expenses

Title: Business Expense Policy and Guidelines Prepared by: Controller s Office Administrator: University Controller Created: July 1, 2012 Policy Statement The basic principle governing business expenses

POLICY. Number: Sponsored Research Cost Sharing Responsible Office: Research & Innovation

POLICY USF System USF USFSP USFSM Number: 0-313 Title: Sponsored Research Cost Sharing Responsible Office: Research & Innovation Date of Origin: 11-2-09 Date Last Amended: Date Last Reviewed: I. INTRODUCTION

POLICY USF System USF USFSP USFSM Number: 0-313 Title: Sponsored Research Cost Sharing Responsible Office: Research & Innovation Date of Origin: 11-2-09 Date Last Amended: Date Last Reviewed: I. INTRODUCTION

Pediatric Brain Tumor Foundation of the United States, Inc.

Pediatric Brain Tumor Foundation of the United States, Inc. Financial Statements Years Ended December 31, 2017 and 2016 Pediatric Brain Tumor Foundation 0f The United States, Inc. Table of Contents Independent

Pediatric Brain Tumor Foundation of the United States, Inc. Financial Statements Years Ended December 31, 2017 and 2016 Pediatric Brain Tumor Foundation 0f The United States, Inc. Table of Contents Independent

THE APPALACHIAN TRAIL CONSERVANCY. Harpers Ferry, West Virginia FINANCIAL STATEMENTS DECEMBER 31, 2016

THE APPALACHIAN TRAIL CONSERVANCY Harpers Ferry, West Virginia FINANCIAL STATEMENTS DECEMBER 31, 2016 C O N T E N T S INDEPENDENT AUDITOR'S REPORT 1 and 2 Page FINANCIAL STATEMENTS Statement of financial

THE APPALACHIAN TRAIL CONSERVANCY Harpers Ferry, West Virginia FINANCIAL STATEMENTS DECEMBER 31, 2016 C O N T E N T S INDEPENDENT AUDITOR'S REPORT 1 and 2 Page FINANCIAL STATEMENTS Statement of financial

FINANCIAL STATEMENTS DECEMBER 31, 2017 AND 2016

FINANCIAL STATEMENTS TABLE OF CONTENTS Page Report of Independent Auditors... 1 Financial Statements: Statements of Financial Position... 3 Statements of Activities and Changes in Net Assets... 4 Statements

FINANCIAL STATEMENTS TABLE OF CONTENTS Page Report of Independent Auditors... 1 Financial Statements: Statements of Financial Position... 3 Statements of Activities and Changes in Net Assets... 4 Statements

Delaware 4-H Club Financial Guidelines For Chartered 4-H Clubs and Other Groups Authorized to Use the 4-H Name and Emblem in Delaware

Delaware 4-H Club Financial Guidelines For Chartered 4-H Clubs and Other Groups Authorized to Use the 4-H Name and Emblem in Delaware The Delaware 4-H Youth Development program is part of the Delaware

Delaware 4-H Club Financial Guidelines For Chartered 4-H Clubs and Other Groups Authorized to Use the 4-H Name and Emblem in Delaware The Delaware 4-H Youth Development program is part of the Delaware

NORTH CAROLINA AGRICULTURAL AND TECHNICAL STATE UNIVERSITY

Intellectual Property page 1. NORTH CAROLINA AGRICULTURAL AND TECHNICAL STATE UNIVERSITY SECTION V INTELLECUAL PROPERTY 1.0 I. PREAMBLE INTELLECTUAL PROPERTY UNIVERSITY POLICY Since its establishment in

Intellectual Property page 1. NORTH CAROLINA AGRICULTURAL AND TECHNICAL STATE UNIVERSITY SECTION V INTELLECUAL PROPERTY 1.0 I. PREAMBLE INTELLECTUAL PROPERTY UNIVERSITY POLICY Since its establishment in

Are You Willing to Work For It?

Are You Willing to Work For It? NTCC Work Scholarship Program ~ A Groundbreaking Opportunity available in the summer of 2014 at NTCC s Eagle Ranch NTCC Wants You? NTCC is looking for a select group of

Are You Willing to Work For It? NTCC Work Scholarship Program ~ A Groundbreaking Opportunity available in the summer of 2014 at NTCC s Eagle Ranch NTCC Wants You? NTCC is looking for a select group of

Fiscal Policies and Procedures for County Councils. Responsibilities

Fiscal Policies and Procedures for County Councils Fiscal management policies established for county outreach and extension councils are based on the Missouri Revised Statutes, University of Missouri policies

Fiscal Policies and Procedures for County Councils Fiscal management policies established for county outreach and extension councils are based on the Missouri Revised Statutes, University of Missouri policies

UNITED WAY OF GREATER MILWAUKEE & WAUKESHA COUNTY, INC. Milwaukee, Wisconsin. FINANCIAL STATEMENTS June 30, 2016 and 2015

UNITED WAY OF GREATER MILWAUKEE & WAUKESHA COUNTY, INC. Milwaukee, Wisconsin FINANCIAL STATEMENTS TABLE OF CONTENTS PAGE INDEPENDENT AUDITORS REPORT... 1 FINANCIAL STATEMENTS Statements of Financial Position...

UNITED WAY OF GREATER MILWAUKEE & WAUKESHA COUNTY, INC. Milwaukee, Wisconsin FINANCIAL STATEMENTS TABLE OF CONTENTS PAGE INDEPENDENT AUDITORS REPORT... 1 FINANCIAL STATEMENTS Statements of Financial Position...

AMERICAN YOUTH FOUNDATION

FINANCIAL STATEMENTS and SUPPLEMENTARY INFORMATION FOR THE YEARS ENDED DECEMBER 31, 2013 AND 2012 Vredeveld Haefner LLC TABLE OF CONTENTS Page Independent Auditors Report 1-2 Financial Statements Statements

FINANCIAL STATEMENTS and SUPPLEMENTARY INFORMATION FOR THE YEARS ENDED DECEMBER 31, 2013 AND 2012 Vredeveld Haefner LLC TABLE OF CONTENTS Page Independent Auditors Report 1-2 Financial Statements Statements

Name of Reporting Institution: Kenyon College Information for the Reporting Year: II (with football)

") file:///y /Surveys/22-3/NCAA%2Financial%2Report/np.jsp.htm Name of Reporting Institution: Kenyon College Information for the Reporting Year: 22 Check to release your information to your conference This

file:///y /Surveys/22-3/NCAA%2Financial%2Report/np.jsp.htm Name of Reporting Institution: Kenyon College Information for the Reporting Year: 22 Check to release your information to your conference This

Ivy Tech Community College

Ivy Tech Community College POLICY TITLE International Travel for Faculty/Staff POLICY NUMBER ASOM 7.15 PRIMARY RESPONSIBILITY Academic Affairs CREATION/REVISION/EFFECTIVE DATES Created July 2013/Effective

Ivy Tech Community College POLICY TITLE International Travel for Faculty/Staff POLICY NUMBER ASOM 7.15 PRIMARY RESPONSIBILITY Academic Affairs CREATION/REVISION/EFFECTIVE DATES Created July 2013/Effective

Leadership, Education and Athletics in Partnership, Inc. Financial Statements and Independent Auditor's Report. August 31, 2013 and 2012

Leadership, Education and Athletics in Partnership, Inc. Financial Statements and Independent Auditor's Report August 31, 2013 and 2012 Index Page Independent Auditor's Report 2-3 Statements of Financial

Leadership, Education and Athletics in Partnership, Inc. Financial Statements and Independent Auditor's Report August 31, 2013 and 2012 Index Page Independent Auditor's Report 2-3 Statements of Financial

Communication and Public Information

School Fund Raising Guidelines Introduction Student Activity accounts are those funds which are owned, operated, and managed by organizations, clubs, or groups within the student body under the guidance

School Fund Raising Guidelines Introduction Student Activity accounts are those funds which are owned, operated, and managed by organizations, clubs, or groups within the student body under the guidance

Leadership, Education and Athletics in Partnership, Inc. Financial Statements and Independent Auditors' Report. August 31, 2012 and 2011

Leadership, Education and Athletics in Partnership, Inc. Financial Statements and Independent Auditors' Report August 31, 2012 and 2011 Index Page Independent Auditors' Report 2 Statements of Financial

Leadership, Education and Athletics in Partnership, Inc. Financial Statements and Independent Auditors' Report August 31, 2012 and 2011 Index Page Independent Auditors' Report 2 Statements of Financial

Evaluation of Annual Action Plan (ongoing) and Institutional Effectiveness Plans Responsibility: Component Leadership

and Institutional Effectiveness Plans Responsibility: Component Leadership") August, 2016 Evaluation of 15-16 Annual Action Plan (ongoing) and Institutional Plans Annual 15-16 committee reports posted on website for College review Responsibility: Committee Chairs and Director of

August, 2016 Evaluation of 15-16 Annual Action Plan (ongoing) and Institutional Plans Annual 15-16 committee reports posted on website for College review Responsibility: Committee Chairs and Director of

Vernon College Annual Planning Calendar Academic Year

August, 2016 Evaluation of 16-17 Annual Action Plan (ongoing) and Institutional Plans Annual 16-17committee reports posted on website for College Committee review Responsibility: Committee Chairs and Director

August, 2016 Evaluation of 16-17 Annual Action Plan (ongoing) and Institutional Plans Annual 16-17committee reports posted on website for College Committee review Responsibility: Committee Chairs and Director

AR 3600 Auxiliary Organizations

AR 3600 Auxiliary Organizations References: Education Code Sections 72670 et seq.; Government Code Sections 12580 et seq.; Title 5 Sections 59250 et seq. Definitions Board of Directors: The term board

AR 3600 Auxiliary Organizations References: Education Code Sections 72670 et seq.; Government Code Sections 12580 et seq.; Title 5 Sections 59250 et seq. Definitions Board of Directors: The term board

Reporting Institution: Kenyon College Reporting Year (FY): 2015

: 2015") School Info Reporting Institution: Kenyon College Reporting Year (FY): 2015 PLEASE NOTE: Some of the data collected on this page will require input from the Financial Aid Office and/or the University Business

School Info Reporting Institution: Kenyon College Reporting Year (FY): 2015 PLEASE NOTE: Some of the data collected on this page will require input from the Financial Aid Office and/or the University Business

CALIFORNIA STATE UNIVERSITY CHANNEL ISLANDS EVENTS AND FACILITIES USE PROCEDURAL GUIDELINES

CALIFORNIA STATE UNIVERSITY CHANNEL ISLANDS EVENTS AND FACILITIES USE PROCEDURAL GUIDELINES Draft Revisions: August 2012 EVENTS AND FACILITIES USE PROCEDURAL GUIDELINES TABLE OF CONTENTS INTRODUCTION 1

CALIFORNIA STATE UNIVERSITY CHANNEL ISLANDS EVENTS AND FACILITIES USE PROCEDURAL GUIDELINES Draft Revisions: August 2012 EVENTS AND FACILITIES USE PROCEDURAL GUIDELINES TABLE OF CONTENTS INTRODUCTION 1

University of Maine System ADMINISTRATIVE PRACTICE LETTER

Page 1 of 6 Unrelated Business Income (UBI) is the income from a trade or business that is regularly carried on by an exempt organization and that is not substantially related to the performance by the

Page 1 of 6 Unrelated Business Income (UBI) is the income from a trade or business that is regularly carried on by an exempt organization and that is not substantially related to the performance by the

Fundraising Guidelines for Faculty, Staff and Campus Organizations

Fundraising Guidelines for Faculty, Staff and Campus Organizations August 2006 A. Purposes 1. To distinguish between (a) fundraising efforts in which St. Norbert College (hereafter the College ) is an

Fundraising Guidelines for Faculty, Staff and Campus Organizations August 2006 A. Purposes 1. To distinguish between (a) fundraising efforts in which St. Norbert College (hereafter the College ) is an

THE MIAMI FOUNDATION, INC.

CONSOLIDATED FINANCIAL STATEMENTS TABLE OF CONTENTS INDEPENDENT AUDITOR S REPORT 1 CONSOLIDATED FINANCIAL STATEMENTS Consolidated Statements of Financial Position 2 Consolidated Statements of Activities

CONSOLIDATED FINANCIAL STATEMENTS TABLE OF CONTENTS INDEPENDENT AUDITOR S REPORT 1 CONSOLIDATED FINANCIAL STATEMENTS Consolidated Statements of Financial Position 2 Consolidated Statements of Activities

Name of Reporting Institution: Kenyon College Information for the Reporting Year: III (with football)

") file:///o /Institutional%Research/Surveys/-/NCAA%Financial%Report/np.jsp-final.htm Name of Reporting Institution: Kenyon College Information for the Reporting Year: Check to release your information to

file:///o /Institutional%Research/Surveys/-/NCAA%Financial%Report/np.jsp-final.htm Name of Reporting Institution: Kenyon College Information for the Reporting Year: Check to release your information to

Page 1 of 58 School Info Reporting Institution: University of Texas at El Paso Reporting Year (FY): 2016 PLEASE NOTE: Some of the data collected on this page will require input from the Financial Aid Office

Page 1 of 58 School Info Reporting Institution: University of Texas at El Paso Reporting Year (FY): 2016 PLEASE NOTE: Some of the data collected on this page will require input from the Financial Aid Office

Terms and Conditions

Terms and Conditions Acceptance of Terms The STEM Shoppe, LLC (collectively, The STEM Shoppe, we, or us ) is a Utah limited liability company with its principal place of business at 822 W Sheppard Lane,

Terms and Conditions Acceptance of Terms The STEM Shoppe, LLC (collectively, The STEM Shoppe, we, or us ) is a Utah limited liability company with its principal place of business at 822 W Sheppard Lane,

Pediatric Brain Tumor Foundation of the United States, Inc.

Pediatric Brain Tumor Foundation of the United States, Inc. Financial Statements Years Ended December 31, 2016 and 2015 Pediatric Brain Tumor Foundation 0f The United States, Inc. Table of Contents Independent

Pediatric Brain Tumor Foundation of the United States, Inc. Financial Statements Years Ended December 31, 2016 and 2015 Pediatric Brain Tumor Foundation 0f The United States, Inc. Table of Contents Independent

VIRGINIA CENTER FOR INCLUSIVE COMMUNITIES

VIRGINIA CENTER FOR INCLUSIVE COMMUNITIES Financial Statements For the year ended (with comparative financial information for the year ended June 30, 2016) VIRGINIA CENTER FOR INCLUSIVE COMMUNITIES Contents

VIRGINIA CENTER FOR INCLUSIVE COMMUNITIES Financial Statements For the year ended (with comparative financial information for the year ended June 30, 2016) VIRGINIA CENTER FOR INCLUSIVE COMMUNITIES Contents

Reporting Institution: Merrimack College Reporting Year (FY): 2015

: 2015") School Info Reporting Institution: Merrimack College Reporting Year (FY): 2015 PLEASE NOTE: Some of the data collected on this page will require input from the Financial Aid Office and/or the University

School Info Reporting Institution: Merrimack College Reporting Year (FY): 2015 PLEASE NOTE: Some of the data collected on this page will require input from the Financial Aid Office and/or the University

Money, Money, Money!

Money, Money, Money! Why Are We Making Changes? 1. Federal mandate for oversight of 4-H programs 2. State regulations & increased public scrutiny 3. Need for consistency in management and accounting across

Money, Money, Money! Why Are We Making Changes? 1. Federal mandate for oversight of 4-H programs 2. State regulations & increased public scrutiny 3. Need for consistency in management and accounting across

Report on application of certain agreed-upon procedures to assist the University in complying with NCAA Bylaw

Report on application of certain agreed-upon procedures to assist the University in complying with NCAA Bylaw 3.2.4.15 Oklahoma State University June 30, 2016 Contents REPORT OF INDEPENDENT CERTIFIED PUBLIC

Report on application of certain agreed-upon procedures to assist the University in complying with NCAA Bylaw 3.2.4.15 Oklahoma State University June 30, 2016 Contents REPORT OF INDEPENDENT CERTIFIED PUBLIC

Institutional Code of Conduct for Education loans Iowa Western Community College June 2016

Institutional Code of Conduct for Education loans Iowa Western Community College June 2016 Introduction Iowa Code Section 261F.2, Sections 487(a)(25)(A) and 487(e) of Title IV of the Higher Education Act

Institutional Code of Conduct for Education loans Iowa Western Community College June 2016 Introduction Iowa Code Section 261F.2, Sections 487(a)(25)(A) and 487(e) of Title IV of the Higher Education Act

SAMPLE DOCUMENT. Date: 2011 USE STATEMENT & COPYRIGHT NOTICE

SAMPLE DOCUMENT Type of Document: Financial Policies & Procedures Museum Name: Alutiiq Museum and Archaeological Repository Date: 2011 Type: Natural History Budget Size: $5 million to $9.9 million Budget

SAMPLE DOCUMENT Type of Document: Financial Policies & Procedures Museum Name: Alutiiq Museum and Archaeological Repository Date: 2011 Type: Natural History Budget Size: $5 million to $9.9 million Budget

Tiffany Lynch direct line: Finance Manager fax:

Tiffany Lynch direct line: 206-727-8247 Finance Manager fax: 206-727-8310 Washington State Bar Association e-mail: tiffanyl@wsba.org May 21, 2012 Dear Section Chairs, Chairs-Elect, and Treasurers: The

Tiffany Lynch direct line: 206-727-8247 Finance Manager fax: 206-727-8310 Washington State Bar Association e-mail: tiffanyl@wsba.org May 21, 2012 Dear Section Chairs, Chairs-Elect, and Treasurers: The

Reporting Institution: Western Michigan University Reporting Year (FY): 2015

: 2015") School Info Reporting Institution: Western Michigan University Reporting Year (FY): 2015 PLEASE NOTE: Some of the data collected on this page will require input from the Financial Aid Office and/or the

School Info Reporting Institution: Western Michigan University Reporting Year (FY): 2015 PLEASE NOTE: Some of the data collected on this page will require input from the Financial Aid Office and/or the

Budget Committee Standard Operating Procedure

Budget Committee Standard Operating Procedure February 20, 2007 (revised 11/4/15) The Budget Committee (BC) has three main responsibilities pursuant to the TCKS Fiscal Management Policy (FMP) to prepare

Budget Committee Standard Operating Procedure February 20, 2007 (revised 11/4/15) The Budget Committee (BC) has three main responsibilities pursuant to the TCKS Fiscal Management Policy (FMP) to prepare

INTERVARSITY CHRISTIAN FELLOWSHIP/USA

INTERVARSITY CHRISTIAN FELLOWSHIP/USA Consolidated Financial Statements With Independent Auditors Report Table of Contents Page Independent Auditors' Report 1 Financial Statements Consolidated Statements

INTERVARSITY CHRISTIAN FELLOWSHIP/USA Consolidated Financial Statements With Independent Auditors Report Table of Contents Page Independent Auditors' Report 1 Financial Statements Consolidated Statements

Service Center Procedure Appendix to Service Center Policy

Service Center Procedure Appendix to Service Center Policy I. Introduction These procedures provide a framework for the fiscal operations of the University of Nebraska at Omaha (UNO) service centers that

Service Center Procedure Appendix to Service Center Policy I. Introduction These procedures provide a framework for the fiscal operations of the University of Nebraska at Omaha (UNO) service centers that

Credit Union Statement of Commitment to Members

Credit Union Statement of Commitment to Members As a member-owned, not-for-profit financial cooperative, Forest Area Federal Credit Union is committed to our members. We will uphold our fundamental responsibility

Credit Union Statement of Commitment to Members As a member-owned, not-for-profit financial cooperative, Forest Area Federal Credit Union is committed to our members. We will uphold our fundamental responsibility

Code Name Definition 0100 PHYSICAL PLANT ADMINISTRATION

0100 PHYSICAL PLANT ADMINISTRATION 0200 UTILITIES 0300 BUILDING MAINTENANCE 0500 CUSTODIAL SERVICES 1100 GENERAL ACADEMIC INSTRUCTION 1105 GRAD I - MASTERS LEVEL STUDNTS 1160 IFAS INSTRUCTION 2100 INSTITUTES

0100 PHYSICAL PLANT ADMINISTRATION 0200 UTILITIES 0300 BUILDING MAINTENANCE 0500 CUSTODIAL SERVICES 1100 GENERAL ACADEMIC INSTRUCTION 1105 GRAD I - MASTERS LEVEL STUDNTS 1160 IFAS INSTRUCTION 2100 INSTITUTES

BUDGET PACKET Student Organization President or Advisor

BUDGET PACKET 2011-2012 TO: FROM: Student Organization President or Advisor CGA Budget Committee RE: 2011-2012 Budget Information Enclosed with this memo you should find several items: 1. 2011-2012 Budget

BUDGET PACKET 2011-2012 TO: FROM: Student Organization President or Advisor CGA Budget Committee RE: 2011-2012 Budget Information Enclosed with this memo you should find several items: 1. 2011-2012 Budget

CALIFORNIA STATE UNIVERSITY, STANISLAUS AUXILIARY AND BUSINESS SERVICES OPERATING BUDGET FISCAL YEAR

CALIFORNIA STATE UNIVERSITY, STANISLAUS AUXILIARY AND BUSINESS SERVICES OPERATING BUDGET FISCAL YEAR 2013-14 CALIFORNIA STATE UNIVERSITY, STANISLAUS AUXILIARY AND BUSINESS SERVICES OPERATING BUDGET FISCAL

CALIFORNIA STATE UNIVERSITY, STANISLAUS AUXILIARY AND BUSINESS SERVICES OPERATING BUDGET FISCAL YEAR 2013-14 CALIFORNIA STATE UNIVERSITY, STANISLAUS AUXILIARY AND BUSINESS SERVICES OPERATING BUDGET FISCAL

HF 2690 Model Education Loan Code of Conduct for Covered Postsecondary Institutions

HF 2690 Model Education Loan Code of Conduct for Covered Postsecondary Institutions An institution may, but is not required to, use this model code of conduct to fulfill the requirements of Iowa Code,

HF 2690 Model Education Loan Code of Conduct for Covered Postsecondary Institutions An institution may, but is not required to, use this model code of conduct to fulfill the requirements of Iowa Code,

Reporting Institution: Louisiana State University Reporting Year (FY): 2015

: 2015") School Info Reporting Institution: Louisiana State University Reporting Year (FY): 2015 PLEASE NOTE: Some of the data collected on this page will require input from the Financial Aid Office and/or the

School Info Reporting Institution: Louisiana State University Reporting Year (FY): 2015 PLEASE NOTE: Some of the data collected on this page will require input from the Financial Aid Office and/or the

Frequently Asked Questions (FAQs) about NKU s New Budget Model

about NKU s New Budget Model") Frequently Asked Questions (FAQs) about NKU s New Budget Model Philosophy and guiding principles Why did NKU need a new budget model? Internal and external factors pointed to the need for a more flexible,

Frequently Asked Questions (FAQs) about NKU s New Budget Model Philosophy and guiding principles Why did NKU need a new budget model? Internal and external factors pointed to the need for a more flexible,

THE MIAMI FOUNDATION, INC.

CONSOLIDATED FINANCIAL STATEMENTS TABLE OF CONTENTS INDEPENDENT AUDITOR S REPORT 1 CONSOLIDATED FINANCIAL STATEMENTS Consolidated Statements of Financial Position 2 Consolidated Statements of Activities

CONSOLIDATED FINANCIAL STATEMENTS TABLE OF CONTENTS INDEPENDENT AUDITOR S REPORT 1 CONSOLIDATED FINANCIAL STATEMENTS Consolidated Statements of Financial Position 2 Consolidated Statements of Activities

POSITIVE COACHING ALLIANCE

FINANCIAL STATEMENTS C O N T E N T S Page(s) Independent Auditors Report 1 Financial Statements: Statements of Financial Position 2 Statements of Activities 3 Statement of Functional Expenses for the Year

FINANCIAL STATEMENTS C O N T E N T S Page(s) Independent Auditors Report 1 Financial Statements: Statements of Financial Position 2 Statements of Activities 3 Statement of Functional Expenses for the Year

POLK MUSEUM OF ART, INC. FINANCIAL STATEMENTS YEARS ENDED JUNE 30, 2016 AND 2015

FINANCIAL STATEMENTS YEARS ENDED TABLE OF CONTENTS YEARS ENDED INDEPENDENT AUDITORS' REPORT 1 FINANCIAL STATEMENTS STATEMENTS OF FINANCIAL POSITION 3 STATEMENTS OF ACTIVITIES 4 STATEMENTS OF FUNCTIONAL

FINANCIAL STATEMENTS YEARS ENDED TABLE OF CONTENTS YEARS ENDED INDEPENDENT AUDITORS' REPORT 1 FINANCIAL STATEMENTS STATEMENTS OF FINANCIAL POSITION 3 STATEMENTS OF ACTIVITIES 4 STATEMENTS OF FUNCTIONAL

FARM AID, INC. Financial Statements. December 31, 2017 and 2016

Financial Statements December 31, 2017 and 2016 December 31, 2017 and 2016 CONTENTS Independent Auditor s Report... 1 Statements of Financial Position... 2 Statements of Activities and Changes in Net Assets...

Financial Statements December 31, 2017 and 2016 December 31, 2017 and 2016 CONTENTS Independent Auditor s Report... 1 Statements of Financial Position... 2 Statements of Activities and Changes in Net Assets...

CONSOLIDATED FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS REPORT

CONSOLIDATED FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS REPORT June 30, 2015 and 2014 IVY TECH FOUNDATION, INC. CONTENTS Page CONSOLIDATED FINANCIAL STATEMENTS Independent Auditors Report 1-2 Consolidated

CONSOLIDATED FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS REPORT June 30, 2015 and 2014 IVY TECH FOUNDATION, INC. CONTENTS Page CONSOLIDATED FINANCIAL STATEMENTS Independent Auditors Report 1-2 Consolidated

ALUCA. Click to edit Master title style STRATEGIC PLAN Educate, develop, connect. Edit Master text styles

Click to edit Master title style ALUCA Second level STRATEGIC PLAN 2020 Educate, develop, connect ALUCA Strategic Plan 2017-2020 The 2020 Journey Click to edit Master title style To future proof life insurance

Click to edit Master title style ALUCA Second level STRATEGIC PLAN 2020 Educate, develop, connect ALUCA Strategic Plan 2017-2020 The 2020 Journey Click to edit Master title style To future proof life insurance

NCAA Membership Financial Reporting System

School Info Reporting Institution: Eastern Michigan University Reporting Year (FY): 2015 Institutional Contacts: PLEASE NOTE: Some of the data collected on this page will require input from the Financial

School Info Reporting Institution: Eastern Michigan University Reporting Year (FY): 2015 Institutional Contacts: PLEASE NOTE: Some of the data collected on this page will require input from the Financial

INTERVARSITY CHRISTIAN FELLOWSHIP/USA. Combined Financial Statements With Independent Auditors Report. June 30, 2016 and 2015

INTERVARSITY CHRISTIAN FELLOWSHIP/USA Combined Financial Statements With Independent Auditors Report Table of Contents Page Independent Auditors' Report 1 Financial Statements Combined Statements of Financial

INTERVARSITY CHRISTIAN FELLOWSHIP/USA Combined Financial Statements With Independent Auditors Report Table of Contents Page Independent Auditors' Report 1 Financial Statements Combined Statements of Financial

PALM HEALTHCARE FOUNDATION, INC. AND SUBSIDIARY REPORT ON AUDIT OF CONSOLIDATED FINANCIAL STATEMENTS

REPORT ON AUDIT OF CONSOLIDATED (with comparable totals for 2016) TABLE OF CONTENTS PAGE INDEPENDENT AUDITOR'S REPORT 1-2 CONSOLIDATED Consolidated Statement of Financial Position 3 Consolidated Statement

REPORT ON AUDIT OF CONSOLIDATED (with comparable totals for 2016) TABLE OF CONTENTS PAGE INDEPENDENT AUDITOR'S REPORT 1-2 CONSOLIDATED Consolidated Statement of Financial Position 3 Consolidated Statement

Young Men s Christian Association of Dane County, Inc. Financial Report

Young Men s Christian Association of Dane County, Inc. Financial Report 12.31.2011 Contents Independent Auditor s Report 1 Financial Statements Statements of Financial Position Statements of Activities

Young Men s Christian Association of Dane County, Inc. Financial Report 12.31.2011 Contents Independent Auditor s Report 1 Financial Statements Statements of Financial Position Statements of Activities

Unrelated Business Income Basic Concepts and UGA Applicability. October 13,

Unrelated Business Income Basic Concepts and UGA Applicability University it of Georgia October 13, 2009 Janice Ratica, CPA, JD jratica@cbh.com Objectives After this presentation, we hope you will: Understand

Unrelated Business Income Basic Concepts and UGA Applicability University it of Georgia October 13, 2009 Janice Ratica, CPA, JD jratica@cbh.com Objectives After this presentation, we hope you will: Understand

BLUE RIDGE AREA FOOD BANK, INC. FINANCIAL REPORT

BLUE RIDGE AREA FOOD BANK, INC. FINANCIAL REPORT YEAR ENDED JUNE 30, 2017 BLUE RIDGE AREA FOOD BANK, INC. FINANCIAL REPORT YEAR ENDED JUNE 30, 2017 TABLE OF CONTENTS PAGE Independent Auditors Report...

BLUE RIDGE AREA FOOD BANK, INC. FINANCIAL REPORT YEAR ENDED JUNE 30, 2017 BLUE RIDGE AREA FOOD BANK, INC. FINANCIAL REPORT YEAR ENDED JUNE 30, 2017 TABLE OF CONTENTS PAGE Independent Auditors Report...

Financial Statements September 30, 2014 and 2013 Native Seeds/Southwestern Endangered Aridland Resource Clearing House, Inc.

Financial Statements Native Seeds/Southwestern Endangered Aridland Resource Clearing House, Inc. www.eidebailly.com Table of Contents Independent Auditor s Report... 1 Financial Statements... 3 Statements

Financial Statements Native Seeds/Southwestern Endangered Aridland Resource Clearing House, Inc. www.eidebailly.com Table of Contents Independent Auditor s Report... 1 Financial Statements... 3 Statements

W.O. SMITH NASHVILLE COMMUNITY MUSIC SCHOOL, INC. NASHVILLE, TENNESSEE FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT JUNE 30, 2016 AND 2015

NASHVILLE, TENNESSEE FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT NASHVILLE, TENNESSEE FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT CONTENTS INDEPENDENT AUDITOR S REPORT... 1 PAGE FINANCIAL

NASHVILLE, TENNESSEE FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT NASHVILLE, TENNESSEE FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT CONTENTS INDEPENDENT AUDITOR S REPORT... 1 PAGE FINANCIAL

COLLAGE DANCE COLLECTIVE, INC.

Financial Statements For the Years Ended June 30, 2016 and 2015 COLLAGE DANCE COLLECTIVE. INC. Table of Contents For years ended June 30, 2016 and 2015 Page Independent Auditors Report... 2-3 Financial

Financial Statements For the Years Ended June 30, 2016 and 2015 COLLAGE DANCE COLLECTIVE. INC. Table of Contents For years ended June 30, 2016 and 2015 Page Independent Auditors Report... 2-3 Financial

UNITED WAY OF GREATER MILWAUKEE & WAUKESHA COUNTY, INC. Milwaukee, Wisconsin. FINANCIAL STATEMENTS June 30, 2017 and 2016

UNITED WAY OF GREATER MILWAUKEE & WAUKESHA COUNTY, INC. Milwaukee, Wisconsin FINANCIAL STATEMENTS TABLE OF CONTENTS PAGE INDEPENDENT AUDITORS REPORT... 1 FINANCIAL STATEMENTS Statements of Financial Position...

UNITED WAY OF GREATER MILWAUKEE & WAUKESHA COUNTY, INC. Milwaukee, Wisconsin FINANCIAL STATEMENTS TABLE OF CONTENTS PAGE INDEPENDENT AUDITORS REPORT... 1 FINANCIAL STATEMENTS Statements of Financial Position...

University of Nebraska at Omaha Service Center Procedure Appendix to Service Center Policy

University of Nebraska at Omaha Service Center Procedure Appendix to Service Center Policy I. Introduction These procedures provide a framework for the fiscal operations of the University of Nebraska at

University of Nebraska at Omaha Service Center Procedure Appendix to Service Center Policy I. Introduction These procedures provide a framework for the fiscal operations of the University of Nebraska at

Benewah County Policy and Procedures for Handling Finances for 4 H Clubs/Groups

Background/Statement of Need Benewah County Policy and Procedures for Handling Finances for 4 H Clubs/Groups County volunteer leaders, including the 4 H Council and 4 H club/activity, are an integral part

Background/Statement of Need Benewah County Policy and Procedures for Handling Finances for 4 H Clubs/Groups County volunteer leaders, including the 4 H Council and 4 H club/activity, are an integral part

THE NEA FOUNDATION FOR THE IMPROVEMENT OF EDUCATION

THE NEA FOUNDATION FOR THE IMPROVEMENT OF EDUCATION Financial Statements and Report Thereon TABLE OF CONTENTS Page Independent Auditor s Report... 1-2 Financial Statements Statements of Financial Position...

THE NEA FOUNDATION FOR THE IMPROVEMENT OF EDUCATION Financial Statements and Report Thereon TABLE OF CONTENTS Page Independent Auditor s Report... 1-2 Financial Statements Statements of Financial Position...

OBJECT CODE GUIDELINES. Revised: 12/3/2013

OBJECT CODE GUIDELINES Revised: 12/3/2013 Purpose: The purpose of this document is to provide general guidance to users on appropriate object code use for the procurement of goods or services. These guidelines

OBJECT CODE GUIDELINES Revised: 12/3/2013 Purpose: The purpose of this document is to provide general guidance to users on appropriate object code use for the procurement of goods or services. These guidelines

Student Clubs and Agency Funds Policy

Student Clubs and Agency Funds Policy POLICY CONTENTS Policy Statement Effective Date: June, 21 2016 Reason for Policy Last Updated: August 25, 2016 Who Should Read this Policy Policy Text Responsible

Student Clubs and Agency Funds Policy POLICY CONTENTS Policy Statement Effective Date: June, 21 2016 Reason for Policy Last Updated: August 25, 2016 Who Should Read this Policy Policy Text Responsible

Financial Statements For The Years Ended June 30, 2010 and 2009

Financial Statements For The Years Ended June 30, 2010 and 2009 Johnson Certified Public Accountant, PLLC & Consulting 2501 Franklin Turnpike Danville, Virginia 24540 www.cpa-johnson.com Phone: (434) 836-4498

Financial Statements For The Years Ended June 30, 2010 and 2009 Johnson Certified Public Accountant, PLLC & Consulting 2501 Franklin Turnpike Danville, Virginia 24540 www.cpa-johnson.com Phone: (434) 836-4498

Chesapeake College Foundation. Investment Management Services

Chesapeake College Foundation Investment Management Services Request for Proposals September 11, 2016 1 Table of Contents RFP Timetable 3 Introduction and Background 4 Scope of Work 5 RFP Terms and Conditions

Chesapeake College Foundation Investment Management Services Request for Proposals September 11, 2016 1 Table of Contents RFP Timetable 3 Introduction and Background 4 Scope of Work 5 RFP Terms and Conditions

Situation Permissible Non Permissible 1. Awards A. Clean Tree Contest 1. Cash Award

ND State Soil Conservation Committee North Dakota State University NDSU Extension Service Supervisor's Handbook Section District Operation: Policy Guidelines This sub section contains the following topics:

ND State Soil Conservation Committee North Dakota State University NDSU Extension Service Supervisor's Handbook Section District Operation: Policy Guidelines This sub section contains the following topics:

National Charity League, Inc Fundraising Policy

National Charity League, Inc Fundraising Policy Introduction As 501 (c) (3) organizations, NCL Chapters are legally permitted to accept donations from their members as well as from sources outside of the

National Charity League, Inc Fundraising Policy Introduction As 501 (c) (3) organizations, NCL Chapters are legally permitted to accept donations from their members as well as from sources outside of the

UNITED STATES FIELD HOCKEY ASSOCIATION, INC.

UNITED STATES FIELD HOCKEY ASSOCIATION, INC. Financial Statements and Supplemental Schedules For the Years Ended December 31, 2013 and 2012 And Independent Auditors' Report UNITED STATES FIELD HOCKEY ASSOCIATION,

UNITED STATES FIELD HOCKEY ASSOCIATION, INC. Financial Statements and Supplemental Schedules For the Years Ended December 31, 2013 and 2012 And Independent Auditors' Report UNITED STATES FIELD HOCKEY ASSOCIATION,

Community Foundation of Greater New Britain

Community Foundation of Greater New Britain Financial Statements December 31, 2017 and 2016 ASSURANCE ADVISORY TAX TECHNOLOGY COMMUNITY FOUNDATION OF GREATER NEW BRITAIN Table of Contents December 31,

Community Foundation of Greater New Britain Financial Statements December 31, 2017 and 2016 ASSURANCE ADVISORY TAX TECHNOLOGY COMMUNITY FOUNDATION OF GREATER NEW BRITAIN Table of Contents December 31,

Leadership, Education and Athletics in Partnership, Inc. Report on Financial Statements. Years Ended August 31, 2011 and 2010

Leadership, Education and Athletics in Partnership, Inc. Report on Financial Statements Years Ended August 31, 2011 and 2010 Index Report of Independent Public Accountants 2 Statements of Financial Position

Leadership, Education and Athletics in Partnership, Inc. Report on Financial Statements Years Ended August 31, 2011 and 2010 Index Report of Independent Public Accountants 2 Statements of Financial Position

ADMINISTRATIVE PRACTICE LETTER

Page 1 of 6 Unrelated Business Income (UBI) is the income from a trade or business that is regularly carried on by an exempt organization and that is not substantially related to the performance by the

Page 1 of 6 Unrelated Business Income (UBI) is the income from a trade or business that is regularly carried on by an exempt organization and that is not substantially related to the performance by the

Oklahoma State University

Report on application of certain agreed-upon procedures to assist the University in complying with NCAA Constitution 3.2.4.16.1 Oklahoma State University June 30, 2015 Contents REPORT OF INDEPENDENT CERTIFIED

Report on application of certain agreed-upon procedures to assist the University in complying with NCAA Constitution 3.2.4.16.1 Oklahoma State University June 30, 2015 Contents REPORT OF INDEPENDENT CERTIFIED

National Kidney Foundation, Inc.

Consolidated Financial Statements Year Ended June 30, 2014 The report accompanying these financial statements was issued by BDO USA, LLP, a Delaware limited liability partnership and the U.S. member of

Consolidated Financial Statements Year Ended June 30, 2014 The report accompanying these financial statements was issued by BDO USA, LLP, a Delaware limited liability partnership and the U.S. member of

1/74

School Info Reporting Institution: University of Minnesota, Twin Cities Reporting Year (FY): 2016 PLEASE NOTE: Some of the data collected on this page will require input from the Financial Aid Office and/or

School Info Reporting Institution: University of Minnesota, Twin Cities Reporting Year (FY): 2016 PLEASE NOTE: Some of the data collected on this page will require input from the Financial Aid Office and/or

WINNING FUTURES FINANCIAL STATEMENTS DECEMBER 31, 2016

FINANCIAL STATEMENTS DECEMBER 31, 2016 Independent Auditors Report To the Board of Directors of Winning Futures We have audited the accompanying financial statements of Winning Futures (a Nonprofit Organization),

FINANCIAL STATEMENTS DECEMBER 31, 2016 Independent Auditors Report To the Board of Directors of Winning Futures We have audited the accompanying financial statements of Winning Futures (a Nonprofit Organization),

University Program Resource

University Program Resource A GUIDE FOR UNIVERSITY ACTUARIAL PROGRAMS Access the digital version of this guide at UniversityProgramResourceGuide.SOA.org. Contents 3 Welcome! 4 Who Can Benefit from This

University Program Resource A GUIDE FOR UNIVERSITY ACTUARIAL PROGRAMS Access the digital version of this guide at UniversityProgramResourceGuide.SOA.org. Contents 3 Welcome! 4 Who Can Benefit from This

COALITION FOR CHRISTIAN OUTREACH

COALITION FOR CHRISTIAN OUTREACH Financial Statements as of and for the Years Ended August 31, 2015 and 2014 and Independent Auditors' Report COALITION FOR CHRISTIAN OUTREACH TABLE OF CONTENTS Independent

COALITION FOR CHRISTIAN OUTREACH Financial Statements as of and for the Years Ended August 31, 2015 and 2014 and Independent Auditors' Report COALITION FOR CHRISTIAN OUTREACH TABLE OF CONTENTS Independent