Michigan Association of County Treasurers

|

|

|

- Dylan Hart

- 5 years ago

- Views:

Transcription

1 Michigan Association of County Treasurers Summer Conference - Boyne August 8, 2011 Michigan Dept. of Treasury Roxanne Nicholas, Senior Auditor 1 From the Michigan Department of Treasury What will we cover? Accounting for Jail Inmates Accounting for Jail Commissary Funds Accounting for Drug Forfeiture Funds County Treasurer s Responsibility for Trust Accounts Updates on Escheating 2

2 Accounting for Jail Inmates A draft numbered letter is in the process of being approved. 3 Accounting for Jail Inmates The Inmate Trust Fund may be found in counties that have a jail facility. The accounting for funds belonging to inmates lodged at the county jail is the responsibility of the county sheriff. Such moneys must be deposited with the county treasurer. The sheriff office has the responsibility for the individual inmate accounts and for authorizing payments of these moneys by the county treasurer or from an imprest inmate trust bank account with subsequent replenishment of the imprest accounts. 4

3 Accounting for Jail Inmates 5 As inmates are admitted to the jail, their personal funds are place in this trust fund. Friends and relatives may also make deposits for the benefit of an individual inmate. Money may be withdrawn only for the benefit of the particular inmate. Each withdrawal must be properly authorized. Written procedures must be established for the handling of these funds to safeguard the inmate s money held in trust. This fund must have its own depository bank account that is reconciled monthly. Individual inmate accounts must be maintained and reconciled to the total of the depository bank account. Accounting for Jail Inmates Accounting procedures are similar whether the money is in the custody of the sheriff or the county treasurer. All inmate funds should be placed in a bank account and all disbursements made by check. 6

4 Accounting for Jail Inmates Receipting: Official pre-numbered receipts (or computerized equivalent) should be obtained. The heading on the receipts should include the name of the department (sheriff), name of the county, and the type of account, such as Inmate Funds or Inmate Trust Account. A receipt is prepared in duplicate for all moneys taken from the inmate at the time of incarceration and other moneys received on behalf of the inmate. The original is for the inmate or the person depositing the money on behalf of the inmate. The duplicate is retained at the receipt book. An inmate must be informed of moneys deposited in his behalf by another party. 7 Accounting for Jail Inmates 8 Bank Deposits: Money should be deposited intact and daily if at all possible. This means the deposit should equal exactly the amount collected and receipted for. Bank accounts should be reconciled monthly. Bank reconciliations are done by sheriff department. Make sure that your auditor is aware of those accounts and that they are being reviewed as part of the audit.

5 Accounting for Jail Inmates 9 Checks: Pre-numbered checks are essential. All moneys collected are deposited in a bank account. All payments are made by check. This includes any purchases made on behalf of an inmate and amounts returned to the inmate upon release from jail. Where moneys are deposited on behalf of an inmate by another party, it should be ascertained whether any remaining moneys are to be paid to the depositor or to the inmate upon release from jail. This should be stipulated in writing at the time of the deposit. Accounting for Jail Inmates 10 Purchases and/or Account Withdrawals: It is not necessary that a separate check be issued for each account withdrawal, except payment of the account balance upon release from jail. A voucher, shopping list, order form, etc., may be used where the amounts to be charged to individual inmate accounts are compiled in a single document. Such document or listing must include the signature of the individual inmate to insure that account withdrawals are properly authorized. A single check may be written for the total amount to be paid and the individual inmate accounts may be charged from the listing. When an inmate is released from jail, a voucher or check authorization form must be prepared to authorize payment of the individual account balance. The check number should be placed on each listing or voucher and all of the documents filed and retained for audit purposes.

6 Accounting for Jail Inmates 11 Individual Accounts: The sheriff must insure that an account is maintained for each individual inmate. This record should include the date, receipt or check number, amount received, amount paid out, and the balance. Each receipt written is posted to the applicable account. Withdrawals, or charges, are entered from check copies, vouchers, or other listings. Balances on the accounts are computed after each posting. The total of the individual accounts should at all times equal the amount on cash on hand and in the bank. Accounts should be reconciled monthly with the bank balance plus cash on hand, if any, and also reconciled by the detail of the open inmates accounts. Accounting for Jail Inmates 12 Imprest Cash: Where numerous small purchases are necessary, the sheriff may authorize an imprest cash fund from the inmate funds. Under this procedure, a check is written from the account for the amount to be used as imprest (petty) cash. It is necessary that each payment from this cash fund be supported by a signed voucher. On the basis of such vouchers, the imprest (petty) cash is replenished from time to time. The amount in this fund should at all times equal the cash on hand plus paid vouchers on hand. Where this system is used, individual accounts should be charged from the signed petty cash vouchers.

7 Accounting for Jail Inmates Budget Requirements: An approved budget is not required for this fund. 13 Controls Where possible, deputies or other personnel working at the jail (or sheriff department) should be assigned accounting duties in a manner to insure that all moneys are properly accounted for. For instance, the individual who writes receipts and makes bank deposits should not prepare the bank reconcilements; those who post individual accounts should not handle the cash or write checks; those who prepare disbursement vouchers should not write the checks. Checks will be signed by the sheriff or any other individual(s) designated by the sheriff. Accounting for Jail Inmates 14 The use of a checking account (as previously explained) for the money of inmates held for a period of less than 24 hours may be cumbersome for the added internal control obtained from the use of the bank account. The following procedure could be used in lieu of the bank account. Other procedures or deviations from this suggestion could be developed that provide control for the safekeeping of inmates valuables as well as administrative efficiency. The inmate s property and valuables could be stored in an envelope with the details written on the outside. You could also use a cover sheet with a duplicate in which on copy could be kept in the inmate file and the second sheet given to the inmate or to a transfer agency. Receipts in at lease duplicate should be prepared and signed by the inmate for partial withdrawals of valuables or money. A copy should be retained in sheriff files and the other put in the inmate s envelope (file).

8 Accounting for Jail Inmates It is very important to make sure that everyone that might be handling inmates valuables or personal property is bonded. 15 The inmate does have the right to retain currency and coins that have a collectors or keepsake value. Examples are silver certificate currency, gold coins, etc. These valuables should be retained for and returned to the inmate. They should not be deposited in a financial institution. List the description of the item including date, value, serial number, etc. as applicable to specifically describe the item(s). Accounting for Jail Commissary Funds A draft numbered letter is in the process of being approved. 16

9 Accounting for Jail Commissary Funds 17 The accounting for funds for the operation of the commissary at the county jail is the responsibility of the county treasurer and county sheriff. Such moneys must be deposited with the county treasurer. The sheriff is responsible for inventory control and accounting records, properly charging the inmate accounts for commissary purchases and proper accounting for the receipts of the commissary. Accounting for Jail Commissary Funds All commissary funds should be placed in the Jail Commissary Fund (595) by the county treasurer. 18

10 Accounting for Jail Commissary Funds 19 Establishment--The Jail Commissary Fund is established by resolution of the county board of commissioners. The establishing resolution should provide guidelines for the operation of the commissary, types of inventory to be maintained, markup, sales tax license, and authorized use of the profits of the commissary. The county sheriff may be authorized to purchase inventory and other items for resale to the inmates. Purchase of items for resale to the employees of the county must be prohibited. The county board of commissioners must review and approve any expense of the commissary and any use of the profits. Accounting for Jail Commissary Funds Receipting--Official pre-numbered receipts should be obtained. The heading on the receipts should include the name of the department (sheriff), name of the county, and the name of the fund, Jail Commissary Fund. A receipt must be prepared in duplicate for all moneys transferred from the Inmate Trust Fund for purchases from the commissary and for any other sales, refunds or other commissary revenue. The duplicate is retained in the receipt book. 20

11 Accounting for Jail Commissary Funds Deposits--Money should be deposited intact with the county treasurer on a timely, routine basis. Intact means the deposit should equal exactly the amount collected and receipted for. 21 Accounting for Jail Commissary Funds 22 Imprest Checking Account--An imprest checking account may be established for the purchase of small inventory replenishment purposes. Most payments from the Fund must be made through the county purchasing system and with the appropriate approvals. Prenumbered checks are essential. It is necessary that each payment from this imprest checking fund be supported by a signed voucher and/or original vendor receipt. On the basis of such vouchers and/or original vendor receipts, the imprest checking account is replenished from time to time. The balance in the bank account plus paid vouchers on hand must at all times equal the imprest amount established for this fund. The bank account must be reconciled monthly and should be done by the county treasurer's office. The sheriff department must provide a listing of checks issued each month for reconciliation purposes.

12 Accounting for Jail Commissary Funds 23 Controls--Deputies or other personnel working at the jail (or sheriff department) should be assigned accounting duties in a manner to insure that all moneys are properly accounted for. For instance, the individual who writes receipts and makes bank deposits should not prepare the bank reconcilements; those who post individual accounts should not handle the cash or write checks; those who prepare disbursement vouchers should not write the checks. Checks will be signed by the sheriff or any other individual(s) designated by the sheriff. Accounting for Jail Commissary Funds What happens when the fund builds up? Counties should not purchase large items directly from this fund. If there is an excess of amount from this fund, the Board of Commissioners may appropriate the funds to the General Fund for purchases that directly support the jail. Examples are: Surveillance camera system for the jail Fuel for transporting inmates Palm scanning equipment Inmate transportation vehicle It should be noted that if there is a purchase made through the general fund (using funds appropriated from the Jail Commissary) and there is an amount not covered, it is the General Fund s responsibility to cover. 24

13 Accounting for Drug Forfeiture Funds Refer to Treasury Numbered Letter The Drug Forfeiture Account and Fund are under the control of the county treasurer. The fund number is 265. This fund is mandatory if the unit has received forfeited assets. This fund must be established by resolution of the governing body of the unit. This is a special revenue fund. 25 Accounting for Drug Forfeiture Funds 26 The money and proceeds from the sale of seized property in substance abuse criminal complaints (as specified in MCL a) and optional county appropriations are deposited into fund number 265. The expenditures and a budget for this fund should be approved by the board of county commissioners. There is limited usage (for drug law enforcement) of its assets.

14 Accounting for Drug Forfeiture Funds 27 Funds should not be credited to an expenditure account when they come in (this circumvents the budget process). This fund may be found in any county or local unit having budgetary authority over an agency which may seize property involved in the violation of controlled substance statutes. Money for the operation of this fund is normally supplied by forfeited money, negotiable instruments, securities, and the proceeds of the sale of the other property and articles of value. Accounting for Drug Forfeiture Funds Expenditures include payments for expenses of seizure, forfeiture and sale. The available balance is to be used to enhance law enforcement efforts pertaining to controlled substances. 28

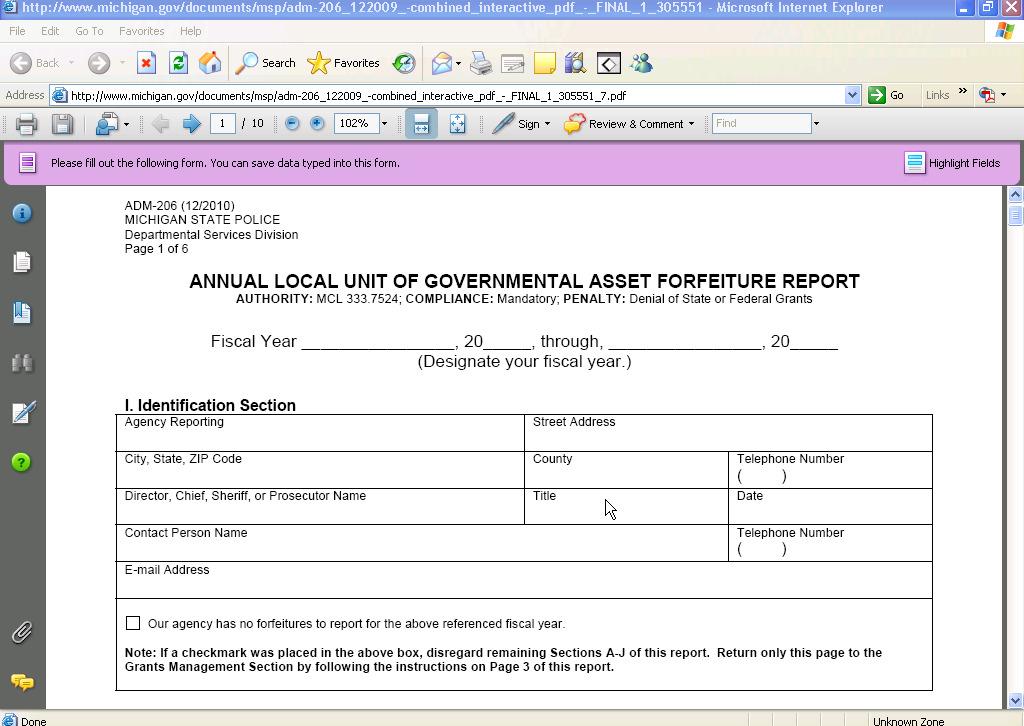

15 Accounting for Drug Forfeiture Funds 29 Each year, local units of government are required to report certain asset forfeiture information by February 1 to the Grants Management Section of the Michigan State Police. Even if a local unit does not effectuate any forfeiture proceedings during the fiscal year, local units are asked to fill out the identification section of the form, indicate that there were no forfeiture proceedings and return it. The form is available at (Byrne JAG Grant Funding/Forms). This is usually completed by the sheriff office. 30

16 31 32

meet and establish written procedures for the use and operations of the money in this fund.")

17 33 Accounting for Drug Forfeiture Funds 34 We recommend that the board of county commissioners or committee of the board, prosecuting attorney, sheriff, and county treasurer (or clerk who will give input into the record keeping procedures) meet and establish written procedures for the use and operations of the money in this fund. The procedures may allow the sheriff to have sufficient imprest cash for use on an emergency basis to make drug purchases.

18 Accounting for Drug Forfeiture Funds 35 Care must be taken to protect the law enforcement effort and names of individuals. This can be accomplished by the assignment of a number or code name for specific expenditures. They can be approved jointly by the sheriff and prosecuting attorney or other procedures deemed in the best interest of law enforcement and with sufficient internal accounting control over the assets of this fund. Note that state statute states shall be distributed by the court having jurisdiction over the forfeiture proceedings to the entity having budgetary authority over the seizing agency. County Treasurer s Responsibility for Trust Accounts Refer to Dick Baldermann s handout to this conference from

19 County Treasurer s Responsibility for Trust Accounts 37 MCL states, It shall be the duty of the county treasurer to receive all moneys belonging to the county, from whatever source they may be derived, and all moneys received by him for the use of the county, shall be paid by him only on the order of the board of supervisors, signed by their clerk, and counter signed by their chairman, except when special provisions for payment thereof is or shall be otherwise made by law. District Courts: The most common two bank accounts established for each District Court are the Bond (or trust) Account and a District Court Control Unit Depository Account in accordance with the Michigan State Court Administrative Reference Guide Michigan Department of Treasury Uniform Chart of Accounts Fund 760 District Court Fund-may be established by resolution of the legislative body of the local unit at the request of the court. Bank account may be established only when the account is necessary. County Treasurer s Responsibility for Trust Accounts (continued) It is important that these bank accounts be reconciled at least monthly. The Bond Account should be reconcile to the open individual bonds which make up the reconciled bank balance at the end of the month. Friend of the Court The UCA does not define a specific fund number for the Friend of the Court Trust Fund, however a open trust and agency fund number may be used. The State Court Administrative Reference Guide authorizes one bank account for the friend of the court offices Friend of the Court Trust Account. Financial Reporting of All Court Trust Funds Michigan Committee on Governmental Accounting and Auditing Statement 4 Definition of the County Financial Reporting Entity 38 These accounts usually maintained by county court personnel in their official capacity as county court employees should be reflected in the financial statements of the county.

20 County Treasurer s Responsibility for Trust Accounts The County Treasurer is responsible for the bank reconciliations for all bank accounts except Jail Inmate, District Court Bond and District Court Depository. 39 County Treasurer s Responsibility for Trust Accounts 40 Pursuant to the previous discussion, following is a list of bank accounts which are currently being used by the courts which should be in the county treasurer s name and be reconciled by the county treasurer or by court personnel and a copy provided to the county treasurer. Circuit Court Court Ordered Account(s) District Court Depository Account Bond Account Court Ordered Account(s) Friend of the Court Support Payment and Trust Account Court Ordered Account(s) Probate Court Court Ordered Account(s)

21 Updates on Escheating 41 A recent change in the Uniform Unclaimed Property Act, PA 29 of 1995, has moved the reporting dates and shortened the dormancy periods of most properties, beginning in Regardless of property types, all government entities must report all properties after one year of dormancy. Although there has been a change in reporting, the accounting is the same as in the past. Updates on Escheating The program is administered by the Michigan Department of Treasury and it serves as the State of Michigan s central depository for abandoned and unclaimed property. 42

.")

22 Updates on Escheating The Michigan Department of Treasury, Unclaimed Property Division (UPD) released an updated Manual for Reporting Unclaimed Property in May The following The link to the new manual is: For more specific questions, call (new phone number for holders). The telephone number for claiming property is

23 Updates on Escheating Interest will be charged for holder reports filed after the July 1 due date and for individual properties contained in the holder report which, in accordance with the applicable dormancy period, should have been reported and remitted in prior years. 45 Updates on Escheating What s new? Beginning in 2011, the due date for the annual unclaimed property report (holder report) will change from November 1 to July 1 for property reaching its dormancy period s of March

24 Updates on Escheating The dormancy period for most property has been shortened to three years. Unclaimed property reaching the new dormancy periods as of March 31 must be reported and remitted to the State on or before July 1. Entities having no unclaimed property reportable under the Uniform Unclaimed Property Act must complete Form 4305 and file it with the Michigan Department of Treasury by July 1. Form 4305 is available on the web. 47 Updates on Escheating CD-ROM is the preferred reporting media for submitting Holder Reports. Paper reporting is allowed only if reporting fewer than ten properties for the entity each year. Filing on diskette will continue to be accepted for 2011 reporting, but we encourage holders to take steps to upgrade their technology to allow for CD-ROM reporting in future years. Holders should not report and remit worthless securities as unclaimed property. 48

25 Updates on Escheating 49 Highlights of the reporting process: The main objective of the UPD is to reunite owners or heirs with their lost or forgotten funds. UPD s goal is to process claims in less than 90 days. Michigan law requires holders to send written notice to owners at their last known address informing them that they hold property subject to being turned over to the State. This requirement applies if all of the following conditions exist: The address for the owner does not appear to be inaccurate. The property has a value of $50 or more. The statue of limitation does not bar the claim of the owner. Updates on Escheating 50 For property where the owner is not known, enter unknown in the Last Name field. List any descriptive or identifying information in the Property Description field. Copies of reports and supporting records must be kept for ten years. A person who fails to pay or deliver property within the time prescribed by the act shall pay interest at the current monthly rate of one percentage point above the adjusted prime rate, per year, per month, on the property or value of the property, from the date the property should have been delivered.

26 Updates on Escheating 51 Who should report? The Uniform Unclaimed Property Act is silent as to what official has the responsibility to complete the report and escheat unclaimed property to the State of Michigan. MCL states, the person holding property presumed abandoned and subject to the State s custody as unclaimed property under this act shall report to the administrator (State Treasurer) concerning the property as provided in this section. However, in other statutory provisions, the local governmental unit treasurer has the statutory responsibility as the custodian of all funds in the local unit of government. Updates on Escheating 52 For example, outstanding checks, drafts or similar instruments not cashed for 90 days or older that are payable in the General Fund should be transferred to the Trust and Agency Fund. The Uniform Chart of Accounts requires that the amount of the outstanding checks that are abandoned and to be escheated to the State be maintained in account number 268 Escheatable Money within the Trust and Agency Fund. A detailed list would be maintained of the transferred outstanding checks and then reconciled on a monthly basis as part of the bank reconciliation process.

27 Updates on Escheating In a county, the county treasurer would have the responsibility to complete the report under MCL as the person holding the property presumed abandoned and subject to the State s custody as unclaimed property under this act. In the case of the county, a letter should be sent to the various departments directing them to send all unclaimed outstanding checks over 90 days old to the county treasurer for deposit into the Trust and Agency Fund as Escheatable Money. 53 What we covered Accounting for Jail Inmates Accounting for Jail Commissary Funds Accounting for Drug Forfeiture Funds County Treasurer s Responsibility for Trust Accounts Updates on Escheating 54

28 Any Questions? You may contact me directly: Roxanne Nicholas Soon to be: 55

MICHIGAN ASSOCIATION OF COUNTY TREASURERS Summer Conference Amway Grand Hotel Grand Rapids, Michigan. August 10, 1998

MICHIGAN ASSOCIATION OF COUNTY TREASURERS Summer Conference Amway Grand Hotel Grand Rapids, Michigan August 10, 1998 County Treasurer's Responsibility for Trust Accounts Prepared by Richard L. Baldermann,

MICHIGAN ASSOCIATION OF COUNTY TREASURERS Summer Conference Amway Grand Hotel Grand Rapids, Michigan August 10, 1998 County Treasurer's Responsibility for Trust Accounts Prepared by Richard L. Baldermann,

TABLE OF CONTENTS. Introduction. Required Basic Accounting Records. Internal Control Requirement. Chapter 1--Uniform Chart of Accounts

www.michigan.gov (To Print: use your browser's print function) Release Date: December 18, 2001 Last Update: May 14, 2002 Uniform Accounting Procedures Manual TABLE OF CONTENTS Introduction Required Basic

www.michigan.gov (To Print: use your browser's print function) Release Date: December 18, 2001 Last Update: May 14, 2002 Uniform Accounting Procedures Manual TABLE OF CONTENTS Introduction Required Basic

SALT LAKE COUNTY COUNTYWIDE POLICY ON PETTY CASH AND OTHER IMPREST FUNDS

1203 SALT LAKE COUNTY COUNTYWIDE POLICY ON PETTY CASH AND OTHER IMPREST FUNDS Purpose - Scope - This policy provides procedures for establishing, operating, reconciling, handling discrepancies in, reviewing,

1203 SALT LAKE COUNTY COUNTYWIDE POLICY ON PETTY CASH AND OTHER IMPREST FUNDS Purpose - Scope - This policy provides procedures for establishing, operating, reconciling, handling discrepancies in, reviewing,

DESCHUTES COUNTY ADULT JAIL L. Shane Nelson, Sheriff Jail Operations Approved by: February 8, 2016 INMATE ACCOUNT

DESCHUTES COUNTY ADULT JAIL CD-1-3 L. Shane Nelson, Sheriff Jail Operations Approved by: February 8, 2016 INMATE ACCOUNT POLICY. Cash in an inmate s possession at the time of dress-in will be deposited

DESCHUTES COUNTY ADULT JAIL CD-1-3 L. Shane Nelson, Sheriff Jail Operations Approved by: February 8, 2016 INMATE ACCOUNT POLICY. Cash in an inmate s possession at the time of dress-in will be deposited

CONTRA COSTA COUNTY Office of the County Administrator ADMINISTRATIVE BULLETIN SUBJECT: CASH RECEIVING, SAFEGUARDING AND DEPOSITING

Number: 205.1 Date: February 20, 2008 Section: Budget & Fiscal CONTRA COSTA COUNTY Office of the County Administrator ADMINISTRATIVE BULLETIN SUBJECT: CASH RECEIVING, SAFEGUARDING AND DEPOSITING This bulletin

Number: 205.1 Date: February 20, 2008 Section: Budget & Fiscal CONTRA COSTA COUNTY Office of the County Administrator ADMINISTRATIVE BULLETIN SUBJECT: CASH RECEIVING, SAFEGUARDING AND DEPOSITING This bulletin

Report on the. Office of Sheriff. Marshall County, Alabama January 1, 2012 through February 28, Filed: August 14, 2015

Report on the Marshall County, Alabama January 1, 2012 through February 28, 2014 Filed: August 14, 2015 Department of Examiners of Public Accounts 50 North Ripley Street, Room 3201 P.O. Box 302251 Montgomery,

Report on the Marshall County, Alabama January 1, 2012 through February 28, 2014 Filed: August 14, 2015 Department of Examiners of Public Accounts 50 North Ripley Street, Room 3201 P.O. Box 302251 Montgomery,

CHAPTER IX SECTION IX-ASB ASSOCIATED STUDENT BODY FUND (ASB)

") CHAPTER IX SECTION IX-ASB ASSOCIATED STUDENT BODY FUND (ASB) Special Revenue Funds -- to account for the proceeds of specific revenue sources (other than expendable trust or for major capital projects)

CHAPTER IX SECTION IX-ASB ASSOCIATED STUDENT BODY FUND (ASB) Special Revenue Funds -- to account for the proceeds of specific revenue sources (other than expendable trust or for major capital projects)

Policy on Petty Cash Fund

Policy on Petty Cash Fund Department responsible: Finance and Administrative Services Effective date: December 8, 2005 Amended on: March 1, 2014 and February 17, 2016 Approved by: Resolution #EC 2016-050

Policy on Petty Cash Fund Department responsible: Finance and Administrative Services Effective date: December 8, 2005 Amended on: March 1, 2014 and February 17, 2016 Approved by: Resolution #EC 2016-050

ASSOCIATED STUDENT BODY FUND (ASB)

") The modified accrual basis of accounting is to be used in measuring financial position and operating results unless the district had less than 1,000 full-time equivalent students the previous fiscal year

The modified accrual basis of accounting is to be used in measuring financial position and operating results unless the district had less than 1,000 full-time equivalent students the previous fiscal year

CHAPTER III SECTION III-G-4 GUIDELINE NO. 4 - EXPENDITURES AND DISBURSEMENTS. * Dates and/or time travel charges were incurred.

CHAPTER III SECTION III-G-4 GUIDELINE NO. 4 - EXPENDITURES AND DISBURSEMENTS This section contains guidance on the treatment of expenditure and disbursement documents. Employee Travel Travel reimbursements

CHAPTER III SECTION III-G-4 GUIDELINE NO. 4 - EXPENDITURES AND DISBURSEMENTS This section contains guidance on the treatment of expenditure and disbursement documents. Employee Travel Travel reimbursements

Procedure REVISION DATE CHAPTER TITLE CHAPTER NO. ADMINISTRATIVE MANUAL Financial & Management 7 MILWAUKEE COUNTY

7.17 IMPREST FUND (Petty Cash) PROCEDURES (1) PURPOSE. To provide a uniform method for replenishing a Petty Cash Imprest Fund for direct disbursements. (2) POLICY. It is the policy of Milwaukee County

7.17 IMPREST FUND (Petty Cash) PROCEDURES (1) PURPOSE. To provide a uniform method for replenishing a Petty Cash Imprest Fund for direct disbursements. (2) POLICY. It is the policy of Milwaukee County

Date: 5/22/2017. Scope: 1/1/12 3/31/17 **Our original audit scope was 1/1/15 12/31/16 but was extended after initial review**

Date: 5/22/2017 This audit was requested by Acting District Attorney Bokelman via an email on March 12 th, 2017. The Acting DA Bokelman specifically asked for an audit of the District Attorney s Special

Date: 5/22/2017 This audit was requested by Acting District Attorney Bokelman via an email on March 12 th, 2017. The Acting DA Bokelman specifically asked for an audit of the District Attorney s Special

Cash Operations Training Mary H. Loomis, CPA, Comptroller

Cash Operations Training - 2012 Mary H. Loomis, CPA, Comptroller Purpose of the Cash Operations Manual The purpose of the cash operations manual is to consolidate the cash handling/cash operations policies

Cash Operations Training - 2012 Mary H. Loomis, CPA, Comptroller Purpose of the Cash Operations Manual The purpose of the cash operations manual is to consolidate the cash handling/cash operations policies

MICHIGAN CONSERVATION DISTRICT UNIFORM ACCOUNTING PROCEDURES MANUAL REVISED TABLE OF CONTENTS TABLE OF CONTENTS...1 INTRODUCTION...

TABLE OF CONTENTS TABLE OF CONTENTS...1 INTRODUCTION...3 REQUIRED BASIC ACCOUNTING RECORDS...4 PART ONE...5 UNIFORM CHART OF ACCOUNTS...5 ACCOUNT STRUCTURE...6 ACTIVITIES...6 BALANCE SHEET ACCOUNTS...8

TABLE OF CONTENTS TABLE OF CONTENTS...1 INTRODUCTION...3 REQUIRED BASIC ACCOUNTING RECORDS...4 PART ONE...5 UNIFORM CHART OF ACCOUNTS...5 ACCOUNT STRUCTURE...6 ACTIVITIES...6 BALANCE SHEET ACCOUNTS...8

PROCEDURE - ASSOCIATED STUDENT BODY BUDGETS

PROCEDURE - ASSOCIATED STUDENT BODY BUDGETS 7415P The combined budgets for all the student activity groups will complete the Associated Student Body (ASB) program budget for the school. After the proposed

PROCEDURE - ASSOCIATED STUDENT BODY BUDGETS 7415P The combined budgets for all the student activity groups will complete the Associated Student Body (ASB) program budget for the school. After the proposed

BASIC POLICY STATEMENT

SAMPLE A Well Known FINANCIAL Philosophy POLICIES For & High PROCEDURES Standards HANDBOOK BASIC POLICY STATEMENT The BEST NONPROFIT, INCORPORATED (BIN) is committed to responsible financial management.

SAMPLE A Well Known FINANCIAL Philosophy POLICIES For & High PROCEDURES Standards HANDBOOK BASIC POLICY STATEMENT The BEST NONPROFIT, INCORPORATED (BIN) is committed to responsible financial management.

CHAPTER 9 Information Unique to Each Fund

CHAPTER 9 Information Unique to Each Fund Table of Contents Page INTRODUCTION... 1 GENERAL FUND... 1 ASSOCIATED STUDENT BODY FUND (ASB)... 2 Introduction... 2 Associated Student Body Moneys... 2 Trust

CHAPTER 9 Information Unique to Each Fund Table of Contents Page INTRODUCTION... 1 GENERAL FUND... 1 ASSOCIATED STUDENT BODY FUND (ASB)... 2 Introduction... 2 Associated Student Body Moneys... 2 Trust

FINANCE COMMITTEE PROCEDURES. Committee Responsibilities. Audit Process

1 FINANCE COMMITTEE PROCEDURES Committee Responsibilities The committee is responsible for overseeing financial operations. This includes: 1. Hiring a bookkeeper 2. Preparing a budget 3. Conducting an

1 FINANCE COMMITTEE PROCEDURES Committee Responsibilities The committee is responsible for overseeing financial operations. This includes: 1. Hiring a bookkeeper 2. Preparing a budget 3. Conducting an

CASH ACCOUNTING MANUAL

Auditor-Controller & Treasurer-Tax Collector March 2011 1. INTRODUCTION... 4 1.1. Purpose of manual... 4 1.2. Applicability of manual... 4 1.3. Using the manual... 4 2. AUTHORITY AND RESPONSIBILITY...

Auditor-Controller & Treasurer-Tax Collector March 2011 1. INTRODUCTION... 4 1.1. Purpose of manual... 4 1.2. Applicability of manual... 4 1.3. Using the manual... 4 2. AUTHORITY AND RESPONSIBILITY...

TITLE II ADMINISTRATIVE REGULATIONS

TITLE II ADMINISTRATIVE REGULATIONS CHAPTER 18 CASH HANDLING POLICY 18.01 Purpose The Cash Handling Policy was established for the purpose of ensuring adequate internal controls to account for the handling

TITLE II ADMINISTRATIVE REGULATIONS CHAPTER 18 CASH HANDLING POLICY 18.01 Purpose The Cash Handling Policy was established for the purpose of ensuring adequate internal controls to account for the handling

CONSTITUTIONAL OFFICERS THE COMPENSATION BOARD. Robyn de Socio, Executive Secretary Compensation Board March 24, 2018 AND

CONSTITUTIONAL OFFICERS AND THE COMPENSATION BOARD Robyn de Socio, Executive Secretary Compensation Board March 24, 2018 CONSTITUTIONAL OFFICERS Constitution of Virginia, 1901 revisions, sets out 5 locallyelected

CONSTITUTIONAL OFFICERS AND THE COMPENSATION BOARD Robyn de Socio, Executive Secretary Compensation Board March 24, 2018 CONSTITUTIONAL OFFICERS Constitution of Virginia, 1901 revisions, sets out 5 locallyelected

IMPREST ACCOUNTS. Policy i

Table of Contents IMPREST ACCOUNTS Policy 511.1 PURPOSE... 1.4 ESTABLISHMENT... 1.5 PETTY CASH... 1 5.1 USE AND DOCUMENTATION OF PETTY CASH... 1 5.1 PROHIBITED USES... 2 5.2 PETTY CASH REPLENISHMENT...

Table of Contents IMPREST ACCOUNTS Policy 511.1 PURPOSE... 1.4 ESTABLISHMENT... 1.5 PETTY CASH... 1 5.1 USE AND DOCUMENTATION OF PETTY CASH... 1 5.1 PROHIBITED USES... 2 5.2 PETTY CASH REPLENISHMENT...

OVERVIEW: Establish Petty Cash or Imprest Funds. Turnover Rate and Increasing or Decreasing Funds

OVERVIEW: A petty cash fund may be established so that cash payments can be made for small, incidental expenses or refunds. An imprest fund is a petty cash fund that has been converted into a checking

OVERVIEW: A petty cash fund may be established so that cash payments can be made for small, incidental expenses or refunds. An imprest fund is a petty cash fund that has been converted into a checking

Sonoma County. Internal Audit Report. Auditor Controller Treasurer Tax Collector

For the Period: July 1, 2015 June 30, 2017 Sonoma County Auditor Controller Treasurer Tax Collector Internal Audit Report Engagement No: 3485 Report Date: December 27, 2017 Erick Roeser Auditor Controller

For the Period: July 1, 2015 June 30, 2017 Sonoma County Auditor Controller Treasurer Tax Collector Internal Audit Report Engagement No: 3485 Report Date: December 27, 2017 Erick Roeser Auditor Controller

Guidelines for Parish Financial Procedures and Controls

ADMINISTRATION Parish-6 6/30/2011 Guidelines for Parish Financial Procedures and Controls Diocese of San Diego PREFACE The purpose of this guideline is to provide parishes with the basic controls and procedures

ADMINISTRATION Parish-6 6/30/2011 Guidelines for Parish Financial Procedures and Controls Diocese of San Diego PREFACE The purpose of this guideline is to provide parishes with the basic controls and procedures

Index as: STATE ASSET FORFEITURE MANAGEMENT I. PURPOSE AND GENERAL DESCRIPTION OF STATE ASSET FORFEITURE LAWS

Ref: CALEA Standard 74.4.1 DEPARTMENTAL GENERAL ORDER F-6 Index as: Rev. State Asset Forfeiture Management STATE ASSET FORFEITURE MANAGEMENT The purpose of this order is to set forth policy and procedures

Ref: CALEA Standard 74.4.1 DEPARTMENTAL GENERAL ORDER F-6 Index as: Rev. State Asset Forfeiture Management STATE ASSET FORFEITURE MANAGEMENT The purpose of this order is to set forth policy and procedures

County of Chester Office of the Sheriff

County of Chester Office of the Sheriff Management Letter Margaret Reif, Controller To: Carolyn B. Welsh, Sheriff Introduction On June 4, 2018, Internal Audit completed an audit of the Office of the Sheriff

County of Chester Office of the Sheriff Management Letter Margaret Reif, Controller To: Carolyn B. Welsh, Sheriff Introduction On June 4, 2018, Internal Audit completed an audit of the Office of the Sheriff

Petty Cash Policies and Procedures

Petty Cash Policies and Procedures January 2018 Table of Contents 1. POLICY... 2 2. SCOPE... 2 3. DEFINITIONS... 2 4. GUIDELINES... 3 4.1. Establishing a Petty Cash Fund... 3 4.2. Designating a Petty Cash

Petty Cash Policies and Procedures January 2018 Table of Contents 1. POLICY... 2 2. SCOPE... 2 3. DEFINITIONS... 2 4. GUIDELINES... 3 4.1. Establishing a Petty Cash Fund... 3 4.2. Designating a Petty Cash

SPECIFIC PRACTICES Cash Management Page 1

SPEIFI PRATIES 4510 ash Management Page 1 SUBJET: Petty ash and hange Fund Accounts PURPOSE: To describe a procedure for the creation and management of a petty cash or change fund account. DISUSSION: This

SPEIFI PRATIES 4510 ash Management Page 1 SUBJET: Petty ash and hange Fund Accounts PURPOSE: To describe a procedure for the creation and management of a petty cash or change fund account. DISUSSION: This

CITY OF MONT BELVIEU CITY COUNCIL POLICY

Page 1 of 14 4.01 Purpose The Cash Handling Policy was established for the purpose of ensuring adequate internal controls to accounts for the handling of Mont Belvieu s municipal cash and to maintain public

Page 1 of 14 4.01 Purpose The Cash Handling Policy was established for the purpose of ensuring adequate internal controls to accounts for the handling of Mont Belvieu s municipal cash and to maintain public

GLASA. Greater Los Angeles Softball Association. Accounting Policies & Procedures Manual

GLASA Greater Los Angeles Softball Association Accounting Policies & Procedures Manual 7/2015 TABLE OF CONTENTS I. General Practices... 1 II. Cash Receipts... 2 III. Cash Disbursements... 3 IV. Other Financial

GLASA Greater Los Angeles Softball Association Accounting Policies & Procedures Manual 7/2015 TABLE OF CONTENTS I. General Practices... 1 II. Cash Receipts... 2 III. Cash Disbursements... 3 IV. Other Financial

A Bill Regular Session, 2009 HOUSE BILL 1430

Stricken language would be deleted from and underlined language would be added to the law as it existed prior to this session of the General Assembly. 0 State of Arkansas th General Assembly A Bill Regular

Stricken language would be deleted from and underlined language would be added to the law as it existed prior to this session of the General Assembly. 0 State of Arkansas th General Assembly A Bill Regular

Comparison of Newly Adopted Delaware Rules of Professional Conduct with ABA Model Rules DELAWARE

Comparison of Newly Adopted Delaware Rules of Professional Conduct with ABA Model Rules DELAWARE Final rules approved by the Delaware Supreme Court to be effective July 1, 2003. Amendments to Rule 5.5

Comparison of Newly Adopted Delaware Rules of Professional Conduct with ABA Model Rules DELAWARE Final rules approved by the Delaware Supreme Court to be effective July 1, 2003. Amendments to Rule 5.5

Sonoma County. Internal Audit Report. Auditor Controller Treasurer Tax Collector

Inmate Welfare and Jail Store Trust Funds For the Period July 1, 2013 through June 30, 2015 Sonoma County Auditor Controller Treasurer Tax Collector Internal Audit Report Engagement No: 3485 Report Date:

Inmate Welfare and Jail Store Trust Funds For the Period July 1, 2013 through June 30, 2015 Sonoma County Auditor Controller Treasurer Tax Collector Internal Audit Report Engagement No: 3485 Report Date:

Corridor District of the North Carolina Conference The United Methodist Church

Audit Information Corridor District of the North Carolina Conference Section 258.4(d) of the 2012 Book of Discipline makes it MANDATORY that every church finance committee shall make provision for an annual

Audit Information Corridor District of the North Carolina Conference Section 258.4(d) of the 2012 Book of Discipline makes it MANDATORY that every church finance committee shall make provision for an annual

Washington State Auditor s Office. Accountability Audit Report. Grant County. Audit Period January 1, 2002 through December 31, Report No.

Washington State Auditor s Office Accountability Audit Report Audit Period Report No. 65534 Issue Date October 10, 2003 Audit Summary ABOUT THE AUDIT This report contains the results of our independent

Washington State Auditor s Office Accountability Audit Report Audit Period Report No. 65534 Issue Date October 10, 2003 Audit Summary ABOUT THE AUDIT This report contains the results of our independent

Registry of the Court

Registry of the Court 2014 On the Road Training Amarillo Paul S. Lyon, CPA January 17, 2014 Contact Information Paul Lyon, CPA First Assistant Travis County Auditor s Office Email paul.lyon@co.travis.tx.us

Registry of the Court 2014 On the Road Training Amarillo Paul S. Lyon, CPA January 17, 2014 Contact Information Paul Lyon, CPA First Assistant Travis County Auditor s Office Email paul.lyon@co.travis.tx.us

UNIFORM UNCLAIMED PROPERTY ACT Act 29 of The People of the State of Michigan enact:

UNIFORM UNCLAIMED PROPERTY ACT Act 29 of 1995 AN ACT concerning unclaimed property; to provide for the reporting and disposition of unclaimed property; to make uniform the law concerning unclaimed property;

UNIFORM UNCLAIMED PROPERTY ACT Act 29 of 1995 AN ACT concerning unclaimed property; to provide for the reporting and disposition of unclaimed property; to make uniform the law concerning unclaimed property;

Internal Accounting Control Procedures

Internal Accounting Control Procedures The City of Clearwater wants to ensure public confidence and retain a financially healthy Community. Therefore it is the intent of the Internal Accounting Control

Internal Accounting Control Procedures The City of Clearwater wants to ensure public confidence and retain a financially healthy Community. Therefore it is the intent of the Internal Accounting Control

CUYAHOGA COUNTY DEPARTMENT OF INTERNAL AUDITING

CUYAHOGA COUNTY DEPARTMENT OF INTERNAL AUDITING TO: Clifford Pinkney, Cuyahoga County Sheriff FROM: Cory Swaisgood, Director, Department of Internal Auditing DATE: November 27, 2018 RE: Sheriff s Office

CUYAHOGA COUNTY DEPARTMENT OF INTERNAL AUDITING TO: Clifford Pinkney, Cuyahoga County Sheriff FROM: Cory Swaisgood, Director, Department of Internal Auditing DATE: November 27, 2018 RE: Sheriff s Office

Chapter II: Internal Controls II-10

Chapter II: Internal Controls II-10 Section C. Internal Control Questionnaire The following Internal Control Questionnaire is intended to provide guidance for setting up an accounting system and a checklist

Chapter II: Internal Controls II-10 Section C. Internal Control Questionnaire The following Internal Control Questionnaire is intended to provide guidance for setting up an accounting system and a checklist

COUNCIL AUDITOR S OFFICE P R O C E D U R E S S U R R O U N D I N G C I T Y I M P R E S T A C C O U N T S

COUNCIL AUDITOR S OFFICE P R O C E D U R E S S U R R O U N D I N G C I T Y I M P R E S T A C C O U N T S Executive Summary Report #706 Background We performed a series of audits of imprest checking accounts

COUNCIL AUDITOR S OFFICE P R O C E D U R E S S U R R O U N D I N G C I T Y I M P R E S T A C C O U N T S Executive Summary Report #706 Background We performed a series of audits of imprest checking accounts

Peralta Community College District AP 6300

ADMINISTRATIVE PROCEDURE 6300 GENERAL ACCOUNTING A. Functions The Accounting Office, under the direction of the Vice Chancellor for Finance and Administration and the Associate Vice Chancellor for Finance

ADMINISTRATIVE PROCEDURE 6300 GENERAL ACCOUNTING A. Functions The Accounting Office, under the direction of the Vice Chancellor for Finance and Administration and the Associate Vice Chancellor for Finance

CITY OF RICHARDSON INTERDEPARTMENTAL POLICY AND PROCEDURES

Revised May 1, 2018 CITY OF RICHARDSON INTERDEPARTMENTAL POLICY AND PROCEDURES PETTY CASH/CHANGE FUNDS POLICY Petty cash funds are established to reimburse City employees for small cash expenditures. Petty

Revised May 1, 2018 CITY OF RICHARDSON INTERDEPARTMENTAL POLICY AND PROCEDURES PETTY CASH/CHANGE FUNDS POLICY Petty cash funds are established to reimburse City employees for small cash expenditures. Petty

Managing Client Trusts Accounts

Managing Client Trusts Accounts Rules, Regulations and Common Sense This booklet has been prepared by the Washington State Bar Association as a guide for both new and experienced lawyers in dealing with

Managing Client Trusts Accounts Rules, Regulations and Common Sense This booklet has been prepared by the Washington State Bar Association as a guide for both new and experienced lawyers in dealing with

Fundamental Accounting Principles, Volume 1, Fifteenth Canadian Edition

Chapter 7 Internal Control and Cash 1) A properly designed internal control system is a key part of systems design, analysis, and performance. Answer: TRUE Diff: 1 Type: TF Topic: 07-02 Purpose of Internal

Chapter 7 Internal Control and Cash 1) A properly designed internal control system is a key part of systems design, analysis, and performance. Answer: TRUE Diff: 1 Type: TF Topic: 07-02 Purpose of Internal

Manatee County, Florida Sheriff s Office

AUDITED FINANCIAL STATEMENTS September 30, 2018 Sheriff's Office Table of Contents September 30, 2018 TAB: REPORT Independent Auditors Report 1 TAB: FINANCIAL STATEMENTS Balance Sheet Governmental Funds

AUDITED FINANCIAL STATEMENTS September 30, 2018 Sheriff's Office Table of Contents September 30, 2018 TAB: REPORT Independent Auditors Report 1 TAB: FINANCIAL STATEMENTS Balance Sheet Governmental Funds

February 17, Dear Mr. Wallace, Sheriff Farber and Members of the County Legislature:

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 February 17, 2015 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 February 17, 2015 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT

Union County Policy and Procedures For Credit Cards

Union County Policy and Procedures For Credit Cards Background The program is designed to provide a new, easier and faster method to make blanket purchases. Authority Ohio Revised Code 301.27 permits counties

Union County Policy and Procedures For Credit Cards Background The program is designed to provide a new, easier and faster method to make blanket purchases. Authority Ohio Revised Code 301.27 permits counties

KENTUCKY COMMUNITY AND TECHNICAL COLLEGE SYSTEM BUSINESS PROCEDURES MANUAL

Procedure 4.24 Page 1 of 8 Effective: July 01, 2013 Supersedes: dated July 01, 2008 Applies to: Colleges Procedure Responsibility: Treasury, Business Services, Purchasing, Accounts Payable Imprest Cash

Procedure 4.24 Page 1 of 8 Effective: July 01, 2013 Supersedes: dated July 01, 2008 Applies to: Colleges Procedure Responsibility: Treasury, Business Services, Purchasing, Accounts Payable Imprest Cash

Departmental Petty Cash Fund Procedures. Table of Contents. Page

Accounts Payable; MSN 3C1; Tel: 3-2580; Fax: 3-2589 Departmental Petty Cash Fund Procedures Table of Contents Petty Cash Fund Policy Statement... 2 Definitions... 2 P-Card... 3 Establishing a Petty Cash

Accounts Payable; MSN 3C1; Tel: 3-2580; Fax: 3-2589 Departmental Petty Cash Fund Procedures Table of Contents Petty Cash Fund Policy Statement... 2 Definitions... 2 P-Card... 3 Establishing a Petty Cash

Audit of the Shenandoah County Sheriff s Office s Equitable Sharing Program Activities Woodstock, Virginia

Office of the Inspector General U.S. Department of Justice Audit of the Shenandoah County Sheriff s Office s Equitable Sharing Program Activities Woodstock, Virginia Audit Division GR-30-15-004 June 2015

Office of the Inspector General U.S. Department of Justice Audit of the Shenandoah County Sheriff s Office s Equitable Sharing Program Activities Woodstock, Virginia Audit Division GR-30-15-004 June 2015

CUYAHOGA COUNTY DEPARTMENT OF INTERNAL AUDITING

CUYAHOGA COUNTY DEPARTMENT OF INTERNAL AUDITING TO: FROM: Cuyahoga County Crime Stoppers Board Cory Swaisgood, Director, Department of Internal Auditing DATE: October 5, 2017 RE: Crime Stoppers Follow-Up

CUYAHOGA COUNTY DEPARTMENT OF INTERNAL AUDITING TO: FROM: Cuyahoga County Crime Stoppers Board Cory Swaisgood, Director, Department of Internal Auditing DATE: October 5, 2017 RE: Crime Stoppers Follow-Up

(385) ; TTY / fax. Scope and Methodology. May 22, 2018

; TTY / fax. Scope and Methodology. May 22, 2018") Salt Lake County Library Services 8030 South 1825 West West Jordan, UT 84088 SCOTT TINGLEY CIA, CGAP Salt Lake County Auditor STingley@slco.org CHERYLANN JOHNSON MBA, CIA, CFE Chief Deputy Auditor CAJohnson@slco.org

Salt Lake County Library Services 8030 South 1825 West West Jordan, UT 84088 SCOTT TINGLEY CIA, CGAP Salt Lake County Auditor STingley@slco.org CHERYLANN JOHNSON MBA, CIA, CFE Chief Deputy Auditor CAJohnson@slco.org

INTERNAL CONTROLS MICHAEL N. WATKINS, ASSOCIATE REGIONAL DIRECTOR/FINANCE BOY SCOUTS OF AMERICA, SOUTHERN REGION, P.O. BOX , KENNESAW, GA 30160

INTERNAL CONTROLS MICHAEL N. WATKINS, ASSOCIATE REGIONAL DIRECTOR/FINANCE BOY SCOUTS OF AMERICA, SOUTHERN REGION, P.O. BOX 440728, KENNESAW, GA 30160 INTERNAL CONTROLS Executive Summary The following suggestions

INTERNAL CONTROLS MICHAEL N. WATKINS, ASSOCIATE REGIONAL DIRECTOR/FINANCE BOY SCOUTS OF AMERICA, SOUTHERN REGION, P.O. BOX 440728, KENNESAW, GA 30160 INTERNAL CONTROLS Executive Summary The following suggestions

HARDEE COUNTY PURCHASING CARD PROGRAM POLICIES AND PROCEDURES AMENDED 10/01/2015

HARDEE COUNTY PURCHASING CARD PROGRAM POLICIES AND PROCEDURES AMENDED 10/01/2015 1 INTRODUCTION ---------------------------------------------------------------------------------------- 3 What is the Purchasing

HARDEE COUNTY PURCHASING CARD PROGRAM POLICIES AND PROCEDURES AMENDED 10/01/2015 1 INTRODUCTION ---------------------------------------------------------------------------------------- 3 What is the Purchasing

COOPERATIVE ORGANIZATIONS THE SCHOOL DISTRICT OF LEE COUNTY

COOPERATIVE ORGANIZATIONS THE SCHOOL DISTRICT OF LEE COUNTY TABLE OF CONTENTS Section Page Number Guidelines 1-3 Annual Checklist 4 Forms and Instructions 5-9 Technical Assistance 10-12 (Non Authoritative/Best

COOPERATIVE ORGANIZATIONS THE SCHOOL DISTRICT OF LEE COUNTY TABLE OF CONTENTS Section Page Number Guidelines 1-3 Annual Checklist 4 Forms and Instructions 5-9 Technical Assistance 10-12 (Non Authoritative/Best

Section II Chapter 1 Depositories/Investment of Funds

Page 1-1 Chapter 1 Depositories/Investment of Funds I. GENERAL DESCRIPTION The Internal Fund activities are managed at the school site level. In order for a school to account for its financial transactions,

Page 1-1 Chapter 1 Depositories/Investment of Funds I. GENERAL DESCRIPTION The Internal Fund activities are managed at the school site level. In order for a school to account for its financial transactions,

State Capitol Building Des Moines, Iowa

OFFICE OF AUDITOR OF STATE STATE OF IOWA State Capitol Building Des Moines, Iowa 50319-0006 Mary Mosiman, CPA Auditor of State Telephone (515) 281-5834 Facsimile (515) 242-6134 NEWS RELEASE Contact: Mary

OFFICE OF AUDITOR OF STATE STATE OF IOWA State Capitol Building Des Moines, Iowa 50319-0006 Mary Mosiman, CPA Auditor of State Telephone (515) 281-5834 Facsimile (515) 242-6134 NEWS RELEASE Contact: Mary

FUNDS HANDLING (Cash Receipts) GUIDELINES AND PROCEDURES

GUIDELINES AND PROCEDURES") FUNDS HANDLING (Cash Receipts) GUIDELINES AND PROCEDURES Reference: Policy No.3600 Revision: August 20, 2014 Funds Handling and Deposit of State and Local Funds 2014.1 1.0 Guidelines 2.0 Definitions 3.0

FUNDS HANDLING (Cash Receipts) GUIDELINES AND PROCEDURES Reference: Policy No.3600 Revision: August 20, 2014 Funds Handling and Deposit of State and Local Funds 2014.1 1.0 Guidelines 2.0 Definitions 3.0

Fiscal Policies and Procedures for County Councils. Responsibilities

Fiscal Policies and Procedures for County Councils Fiscal management policies established for county outreach and extension councils are based on the Missouri Revised Statutes, University of Missouri policies

Fiscal Policies and Procedures for County Councils Fiscal management policies established for county outreach and extension councils are based on the Missouri Revised Statutes, University of Missouri policies

INSTRUCTIONS FOR OPERATION OF STUDENT ACTIVITY ACCOUNTS. September 2006 Maine School Administrative District No RHR Smith & Company

INSTRUCTIONS FOR OPERATION OF STUDENT ACTIVITY ACCOUNTS September 2006 Maine School Administrative District No. 1000 RHR Smith & Company INSTRUCTIONS FOR OPERATION OF STUDENT ACTIVITY ACCOUNTS TABLE OF

INSTRUCTIONS FOR OPERATION OF STUDENT ACTIVITY ACCOUNTS September 2006 Maine School Administrative District No. 1000 RHR Smith & Company INSTRUCTIONS FOR OPERATION OF STUDENT ACTIVITY ACCOUNTS TABLE OF

FINANCIAL POLICIES & PROCEDURES HANDBOOK

MAINE ASSOCIATION OF PLANNERS FINANCIAL POLICIES & PROCEDURES HANDBOOK 0 P a g e Contents I. BASIC POLICY STATEMENT... 2 II. LINE OF AUTHORITY... 2 III. INDEMNITY POLICY... 3 IV. INVESTMENT POLICY... 3

MAINE ASSOCIATION OF PLANNERS FINANCIAL POLICIES & PROCEDURES HANDBOOK 0 P a g e Contents I. BASIC POLICY STATEMENT... 2 II. LINE OF AUTHORITY... 2 III. INDEMNITY POLICY... 3 IV. INVESTMENT POLICY... 3

Livingston County Probation Department

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Livingston County Probation Department Financial Operations Report of Examination

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Livingston County Probation Department Financial Operations Report of Examination

- REVISED CODE OF WAHKIAKUM COUNTY. Title 10 FUNDS

Title 10 Chapters: FUNDS Chapter 10.02 - INVESTMENT OF FUNDS Chapter 10.06 - POLICY FOR SUPPLEMENTAL APPROPRIATIONS AS THE RESULT OF UNANTICIPATED FUNDS FROM LOCAL REVENUE SOURCES Chapter 10.30 - SALARY

Title 10 Chapters: FUNDS Chapter 10.02 - INVESTMENT OF FUNDS Chapter 10.06 - POLICY FOR SUPPLEMENTAL APPROPRIATIONS AS THE RESULT OF UNANTICIPATED FUNDS FROM LOCAL REVENUE SOURCES Chapter 10.30 - SALARY

SECTION 5 FINANCE AND ACCOUNTING

SECTION 5 FINANCE AND ACCOUNTING 5.01 ACCOUNTING POLICIES It shall be the policy of Collegiate Hall Charter School ( Collegiate Hall ) to create and maintain accounting, billing, and cash control policies,

SECTION 5 FINANCE AND ACCOUNTING 5.01 ACCOUNTING POLICIES It shall be the policy of Collegiate Hall Charter School ( Collegiate Hall ) to create and maintain accounting, billing, and cash control policies,

Unclaimed Property Process Report

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp Unclaimed Property

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp Unclaimed Property

OZAUKEE COUNTY POLICY AND PROCEDURE MANUAL

CHAPTER 5 Table of Contents 5.01 COUNTY FINANCE... 2 (1) Deposits of Fees and Moneys:... 2 (2) County Investment Policy:... 2 (3) Authorization for Independent Bank Accounts:... 6 (4) Fund Transfers/Supplemental

CHAPTER 5 Table of Contents 5.01 COUNTY FINANCE... 2 (1) Deposits of Fees and Moneys:... 2 (2) County Investment Policy:... 2 (3) Authorization for Independent Bank Accounts:... 6 (4) Fund Transfers/Supplemental

Section 3 FINANCE Policies and Procedures

Section 3 FINANCE Policies and Procedures 3.1 Introduction... 2 311 Purpose... 2 312 Definitions... 2 3.2 Budgeting Policies & Procedures... 2 321 Budget Principles... 2 322 Budget Preparation and Adoption...

Section 3 FINANCE Policies and Procedures 3.1 Introduction... 2 311 Purpose... 2 312 Definitions... 2 3.2 Budgeting Policies & Procedures... 2 321 Budget Principles... 2 322 Budget Preparation and Adoption...

CLERK OF COURTS HIGHLANDS COUNTY, FLORIDA FINANCIAL STATEMENTS YEAR ENDED SEPTEMBER 30, 2018

FINANCIAL STATEMENTS YEAR ENDED TABLE OF CONTENTS YEAR ENDED INDEPENDENT AUDITORS REPORT 1 FINANCIAL STATEMENTS BALANCE SHEET GOVERNMENTAL FUNDS 4 STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND

FINANCIAL STATEMENTS YEAR ENDED TABLE OF CONTENTS YEAR ENDED INDEPENDENT AUDITORS REPORT 1 FINANCIAL STATEMENTS BALANCE SHEET GOVERNMENTAL FUNDS 4 STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND

Lac qui Parle County Job Description

Lac qui Parle County Job Description Job Title: Deputy ATC Office Support Specialist Department: County Auditor-Treasurer-Coordinator Reports to: Supervises: Job Type: Auditor-Treasurer-Coordinator, Property

Lac qui Parle County Job Description Job Title: Deputy ATC Office Support Specialist Department: County Auditor-Treasurer-Coordinator Reports to: Supervises: Job Type: Auditor-Treasurer-Coordinator, Property

Office of Budget and Finance. Cash Accountability Policy

Office of Budget and Finance Cash Accountability Policy Effective Date: January 1, 2018 Agenda Cash Accountability Policy Cash Certification / Acknowledgment Forms Exceptions and Alternative Procedures

Office of Budget and Finance Cash Accountability Policy Effective Date: January 1, 2018 Agenda Cash Accountability Policy Cash Certification / Acknowledgment Forms Exceptions and Alternative Procedures

Peter M. Guilfoyle Assistant State Auditor July 30, 1997

The Honorable Deborah T. Poritz Chief Justice of the Supreme Court The Honorable Christine Todd Whitman Governor of New Jersey The Honorable Donald T. DiFrancesco President of the Senate The Honorable

The Honorable Deborah T. Poritz Chief Justice of the Supreme Court The Honorable Christine Todd Whitman Governor of New Jersey The Honorable Donald T. DiFrancesco President of the Senate The Honorable

Policies of the University of North Texas. Chapter 10. Fiscal Management General Payment Information

Policies of the University of North Texas 10.016 General Payment Information Chapter 10 Fiscal Management Policy Statement. It is the policy of the University to review each payment document prior to final

Policies of the University of North Texas 10.016 General Payment Information Chapter 10 Fiscal Management Policy Statement. It is the policy of the University to review each payment document prior to final

HILLSBOROUGH COUNTY, FLORIDA SHERIFF

FINANCIAL STATEMENTS As of and for the Year Ended September 30, 2017 And Reports of Independent Auditor TABLE OF CONTENTS REPORT OF INDEPENDENT AUDITOR... 1-3 FINANCIAL STATEMENTS Balance Sheet Governmental

FINANCIAL STATEMENTS As of and for the Year Ended September 30, 2017 And Reports of Independent Auditor TABLE OF CONTENTS REPORT OF INDEPENDENT AUDITOR... 1-3 FINANCIAL STATEMENTS Balance Sheet Governmental

Approved: Effective: June 15, 2016 Review: May 15,2016 Office: Comptroller, General Accounting Office Topic No.: k REVOLVING FUNDS

Approved: Effective: June 15, 2016 Review: May 15,2016 Office: Comptroller, General Accounting Office Topic No.: 350-080-303-k Department of Transportation PURPOSE: REVOLVING FUNDS To provide direction

Approved: Effective: June 15, 2016 Review: May 15,2016 Office: Comptroller, General Accounting Office Topic No.: 350-080-303-k Department of Transportation PURPOSE: REVOLVING FUNDS To provide direction

OZAUKEE COUNTY POLICY AND PROCEDURE MANUAL

CHAPTER Table of Contents.0 COUNTY FINANCE... () Deposits of Fees and Moneys:... () County Investment Policy:... () Authorization for Independent Bank Accounts:... () Fund Transfers/Supplemental Appropriations:...

CHAPTER Table of Contents.0 COUNTY FINANCE... () Deposits of Fees and Moneys:... () County Investment Policy:... () Authorization for Independent Bank Accounts:... () Fund Transfers/Supplemental Appropriations:...

Guidelines for Church Financial Review

Guidelines for Church Financial Review Catawba Presbytery - October 2016 The following are suggested procedures to be used by churches when they have their financial review to meet Presbytery/ Synod s

Guidelines for Church Financial Review Catawba Presbytery - October 2016 The following are suggested procedures to be used by churches when they have their financial review to meet Presbytery/ Synod s

26. PURCHASING CARD POLICY

26. PURCHASING CARD POLICY POLICY It is the policy of Scott County to have a Purchasing Card Program. This program is intended to replace blanket purchase orders, purchase orders used to purchase items

26. PURCHASING CARD POLICY POLICY It is the policy of Scott County to have a Purchasing Card Program. This program is intended to replace blanket purchase orders, purchase orders used to purchase items

Florida State Courts System Office of Inspector General. Annual Report Fiscal Year

Florida State Courts System Office of Inspector General Annual Report Fiscal Year 2014-15 July 28, 2015 CONTENTS Inspector General s Message 2 Introduction 2 Audits 3 Consulting Activities 5 Investigations

Florida State Courts System Office of Inspector General Annual Report Fiscal Year 2014-15 July 28, 2015 CONTENTS Inspector General s Message 2 Introduction 2 Audits 3 Consulting Activities 5 Investigations

OPN Jan 27, The Honorable Ruth D. Lee Clay County Tax Collector P.O. Box 218 Green Cove Springs, Florida

OPN 94-0003 Jan 27, 1994 The Honorable Ruth D. Lee Clay County Tax Collector P.O. Box 218 Green Cove Springs, Florida 32043-0218 RE: Taxes; Refunds; Surplus Funds; Distribution of Interest and Principal

OPN 94-0003 Jan 27, 1994 The Honorable Ruth D. Lee Clay County Tax Collector P.O. Box 218 Green Cove Springs, Florida 32043-0218 RE: Taxes; Refunds; Surplus Funds; Distribution of Interest and Principal

THE CORPORATION OF THE CITY OF WINDSOR POLICY

THE CORPORATION OF THE CITY OF WINDSOR POLICY Primary Owner: Finance Policy No.: CS.A7.07 Secondary Owner: n/a Approval Date: January 21, 2013 1. POLICY Approved By: M20-2013 Subject: Corporate-Wide Cash

THE CORPORATION OF THE CITY OF WINDSOR POLICY Primary Owner: Finance Policy No.: CS.A7.07 Secondary Owner: n/a Approval Date: January 21, 2013 1. POLICY Approved By: M20-2013 Subject: Corporate-Wide Cash

CHAPTER III - ADMINISTRATION OF CITY GOVERNMENT... 2

CHAPTER III - ADMINISTRATION OF CITY GOVERNMENT... 2 Section 300 Officers and departments... 2 300.01. City administrator.... 2 300.03. City clerk.... 2 300.05. Finance officer/treasurer.... 3 300.07.

CHAPTER III - ADMINISTRATION OF CITY GOVERNMENT... 2 Section 300 Officers and departments... 2 300.01. City administrator.... 2 300.03. City clerk.... 2 300.05. Finance officer/treasurer.... 3 300.07.

RULE 1.15: SAFEKEEPING PROPERTY

American Bar Association CPR Policy Implementation Committee Variations of the ABA Model Rules of Professional Conduct RULE 1.15: SAFEKEEPING PROPERTY (a) A lawyer shall hold property of clients or third

American Bar Association CPR Policy Implementation Committee Variations of the ABA Model Rules of Professional Conduct RULE 1.15: SAFEKEEPING PROPERTY (a) A lawyer shall hold property of clients or third

VIRGINIA MILITARY INSTITUTE REVIEW OF CONTROLS OVER CASHIERING FUNCTION MARCH 2006

VIRGINIA MILITARY INSTITUTE REVIEW OF CONTROLS OVER CASHIERING FUNCTION MARCH 2006 March 23, 2006 The Honorable Timothy M. Kaine Governor of Virginia The Honorable Lacey E. Putney Chairman, Joint Legislative

VIRGINIA MILITARY INSTITUTE REVIEW OF CONTROLS OVER CASHIERING FUNCTION MARCH 2006 March 23, 2006 The Honorable Timothy M. Kaine Governor of Virginia The Honorable Lacey E. Putney Chairman, Joint Legislative

Arenac County Road Commission. Financial Statements

(A Component Unit of Arenac County, Michigan) Standish, Michigan Financial Statements For the Year Ended December 31, 2016 SMITH & KLACZKIEWICZ, PC Certified Public Accountants (A Component Unit of Arenac

(A Component Unit of Arenac County, Michigan) Standish, Michigan Financial Statements For the Year Ended December 31, 2016 SMITH & KLACZKIEWICZ, PC Certified Public Accountants (A Component Unit of Arenac

DEPARTMENT OF NATURAL RESOURCES LAW ENFORCEMENT DIVISION GENERAL RULES

DEPARTMENT OF NATURAL RESOURCES LAW ENFORCEMENT DIVISION GENERAL RULES (By authority conferred on the department of natural resources by sections 80121 and 80164 of 1994 PA 451, MCL 324.80121 and MCL 324.80164)

DEPARTMENT OF NATURAL RESOURCES LAW ENFORCEMENT DIVISION GENERAL RULES (By authority conferred on the department of natural resources by sections 80121 and 80164 of 1994 PA 451, MCL 324.80121 and MCL 324.80164)

CASH HANDLING POLICIES

CASH HANDLING POLICIES Administered by the Skagit County Treasurer Revised May 8, 2017 Policy TABLE OF CONTENTS I. Mandatory training for Cash Handlers 3 II. Temporary Employees as Cash Handlers 4 III.

CASH HANDLING POLICIES Administered by the Skagit County Treasurer Revised May 8, 2017 Policy TABLE OF CONTENTS I. Mandatory training for Cash Handlers 3 II. Temporary Employees as Cash Handlers 4 III.

Audit: Controls and Accountability For Police Asset Forfeiture Deposit Accounts Need Improvement

Office of the City Auditor CONSENT CALENDAR September 11, 2007 To: From: Subject: Honorable Mayor and Members of the City Council Ann-Marie Hogan, City Auditor Audit: Controls and Accountability For Police

Office of the City Auditor CONSENT CALENDAR September 11, 2007 To: From: Subject: Honorable Mayor and Members of the City Council Ann-Marie Hogan, City Auditor Audit: Controls and Accountability For Police

Updated 07/07/2018 ID 19, Page 1 of 6

Requirement: Frequency: Due Date: Purpose Financial Management Requirements 2 C.F.R., part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards; The U.S.

Requirement: Frequency: Due Date: Purpose Financial Management Requirements 2 C.F.R., part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards; The U.S.

CLERK OF THE COURTS HIGHLANDS COUNTY, FLORIDA FINANCIAL STATEMENTS AND SUPPLEMENTAL REPORTS YEAR ENDED SEPTEMBER 30, 2013

FINANCIAL STATEMENTS AND SUPPLEMENTAL REPORTS YEAR ENDED SEPTEMBER 30, 2013 TABLE OF CONTENTS YEAR ENDED SEPTEMBER 30, 2013 INDEPENDENT AUDITORS' REPORT 1 SPECIAL-PURPOSE FINANCIAL STATEMENTS SPECIAL-PURPOSE

FINANCIAL STATEMENTS AND SUPPLEMENTAL REPORTS YEAR ENDED SEPTEMBER 30, 2013 TABLE OF CONTENTS YEAR ENDED SEPTEMBER 30, 2013 INDEPENDENT AUDITORS' REPORT 1 SPECIAL-PURPOSE FINANCIAL STATEMENTS SPECIAL-PURPOSE

TOWN OF EMERALD ISLE INTERNAL CONTROL POLICY

TOWN OF EMERALD ISLE INTERNAL CONTROL POLICY Goals The Town of Emerald Isle has set forth the following internal control procedures to ensure compliance with all applicable laws and regulations. Internal

TOWN OF EMERALD ISLE INTERNAL CONTROL POLICY Goals The Town of Emerald Isle has set forth the following internal control procedures to ensure compliance with all applicable laws and regulations. Internal

Schedule of Federal Audit Findings and Questioned Costs

Schedule of Federal Audit Findings and Questioned Costs Riverside Fire Authority Lewis County January 1, 2009 through December 31, 2009 1. The Authority s internal controls are inadequate to ensure compliance

Schedule of Federal Audit Findings and Questioned Costs Riverside Fire Authority Lewis County January 1, 2009 through December 31, 2009 1. The Authority s internal controls are inadequate to ensure compliance

Sparta Area School District Purchasing Card Program and Employee Use Agreement

All employees responsible for the use or custodial responsibilities of the PCard must read, understand, and sign this agreement before a card may be checked out to them. Introduction and Purpose A Purchasing

All employees responsible for the use or custodial responsibilities of the PCard must read, understand, and sign this agreement before a card may be checked out to them. Introduction and Purpose A Purchasing

OVERVIEW OF THE STATE OF TENNESSEE COLLATERAL POOL

OVERVIEW OF THE STATE OF TENNESSEE COLLATERAL POOL PURPOSE In March of 1990, the Tennessee General Assembly enacted legislation which permitted the creation of a statewide Collateral Pool. This legislation,

OVERVIEW OF THE STATE OF TENNESSEE COLLATERAL POOL PURPOSE In March of 1990, the Tennessee General Assembly enacted legislation which permitted the creation of a statewide Collateral Pool. This legislation,

THE UNIVERSITY OF ALABAMA IN HUNTSVILLE CASH HANDLING POLICY

Number THE UNIVERSITY OF ALABAMA IN HUNTSVILLE CASH HANDLING POLICY Division Accounting & Financial Reporting Date April 18, 2012 Purpose To reduce the risk of theft, loss or misplacement of cash and checks

Number THE UNIVERSITY OF ALABAMA IN HUNTSVILLE CASH HANDLING POLICY Division Accounting & Financial Reporting Date April 18, 2012 Purpose To reduce the risk of theft, loss or misplacement of cash and checks

Salt Lake County Library Imprest Fund

A Review of the A Report to the Citizens of Salt Lake County, the Mayor, and the County Council Salt Lake County Library Imprest Fund December 2010 Jeff Hatch Salt Lake County Auditor A Review of the

A Review of the A Report to the Citizens of Salt Lake County, the Mayor, and the County Council Salt Lake County Library Imprest Fund December 2010 Jeff Hatch Salt Lake County Auditor A Review of the

The title "School Finance Officer" shall be used herein to designate the position responsible for handling the School Activity Funds.

The Regulations of the State Board of Education define school activity funds as all funds received from extracurricular school activities, such as entertainment, athletic contests, club dues, school fund-raising,

The Regulations of the State Board of Education define school activity funds as all funds received from extracurricular school activities, such as entertainment, athletic contests, club dues, school fund-raising,

MANAGEMENT LETTER. Noncompliance Findings

MANAGEMENT LETTER City of Richmond Heights 26789 Highland Road Richmond Heights, Ohio 44143 To the City Council: We have audited the financial statements of the City of Richmond Heights,, Ohio (the City)

MANAGEMENT LETTER City of Richmond Heights 26789 Highland Road Richmond Heights, Ohio 44143 To the City Council: We have audited the financial statements of the City of Richmond Heights,, Ohio (the City)

Chapter 06 - Cash and Internal Controls. Chapter Outline

I. Internal Control A. Purpose of Internal Control A properly designed internal control system is a key part of system design, analysis, and performance. Internal controls do not provide guarantees, but

I. Internal Control A. Purpose of Internal Control A properly designed internal control system is a key part of system design, analysis, and performance. Internal controls do not provide guarantees, but