A Little Bit of History Repeating?

|

|

|

- Sharleen Douglas

- 5 years ago

- Views:

Transcription

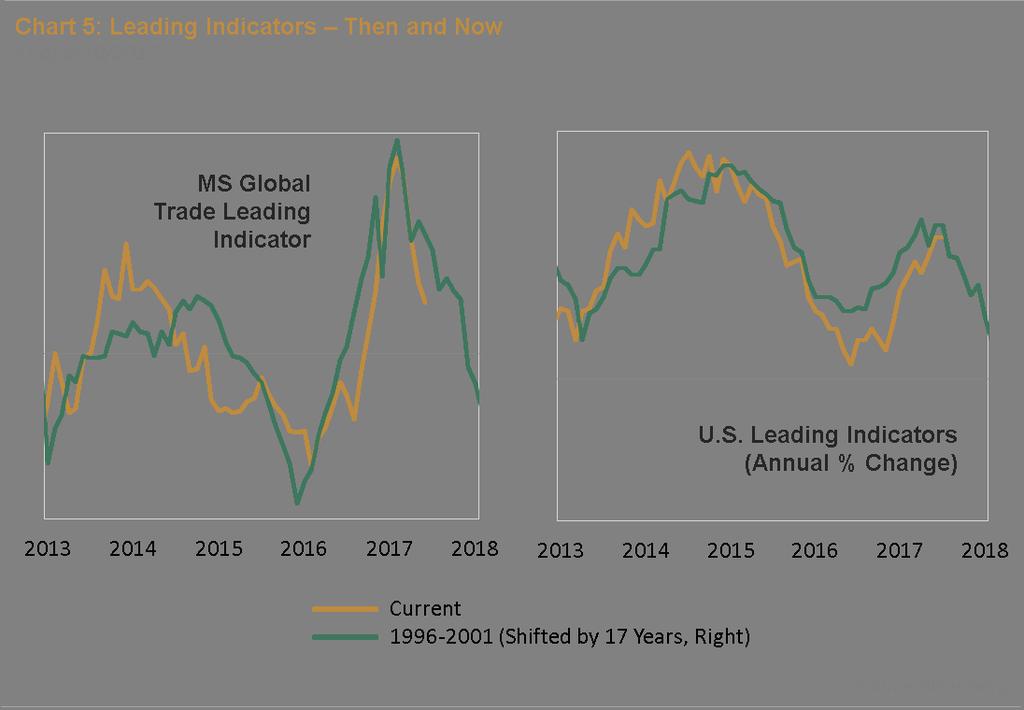

1 JUL A Little Bit of History Repeating? Dorothee Rainis» Historical patterns are among many indicators that can be helpful in the analysis of financial markets, since they can reveal valuable information of drivers or patterns pertinent to assets or events. It should be self-evident however that history only rhymes, so any historical analog has to be treated carefully in order to not jump to conclusions, which can be a costly mistake in financial markets. One thing that caught our eye last year were the pronounced movements in oil prices, which dropped by over 50% year-over-year in 2014, only to retrace nearly all their losses starting in the first half of It was indeed an interesting movement, given that a 50% drop followed by an almost complete retracement of the losses has happened only once outside a recession over the last 35 years, namely between 1997 and Without going into too many details of what drove oil prices in the late 1990s remember, history only rhymes, so we have to stick to the big picture we looked at other indicators to better understand the consequences of such a move, including the grease in the financial system: liquidity. The undisputed central banker of the world in the 1990s was the United States, whereas now the marginal provider of liquidity might very well be China, as my colleague Anujeet Sareen pointed out. So how do liquidity conditions of those two periods compare? Taking the fed funds rate as an admittedly coarse proxy for the U.S., and the credit impulse consistent of changes in total social financing and local government debt for China, we can see that those two liquidity measures overlap fairly well they rhyme.

2 Armed with the assumption that oil prices themselves are strongly related to liquidity since oil producers are paid mainly in U.S. dollars, we can deduce how those liquidity impulses worked their way through the financial system in an ebb and flow of deflation and reflation. With a contraction in liquidity, demand for commodities tends to decline, and we see that the contraction in both time periods was meaningful enough to cause a pronounced drop in a whole range of commodities. Note that we are looking for similar patterns, not similar price levels; after all, the global economy has changed dramatically since the 1990s, but general economic relationships should still bear strong resemblance.

3 Receding liquidity shouldn t only have an impact on commodity prices, but naturally on imports and export orders around the world. As a matter of fact, producer prices responded to the moves in orders and commodities just how we d expect them to: a distinct correction, followed by a strong reflationary rebound once the liquidity impulse turned firmly positive.

4 Now, considering that a marked contraction in orders, production, and prices was followed by a clear-cut expansionary period, businesses reacted exactly like we believe they should once work starts pouring in after a dry spell, with skyrocketing optimism, plans to increase capital expenditures, and stronger hiring intentions. Here s a Chart of the Moment we issued on U.S. business confidence earlier this year.

5

6 Not surprisingly, asset markets also behaved in a similar way. It becomes clear that emerging markets were bound to profit vastly from the inflationary impulse that was waiting to happen in the second half of 2016 and while we concede the timing of markets to rally to the Trump election we d have to point out that higher demand was already in the pipeline, ready to burst higher. Calling the recent rally a Trump trade might hence only be marginally correct.

7 Curiously, the ebb and flow of the reflationary impulse happened at a very similar point in the business cycle of the United States, with unemployment, wages and profit growth seeing comparable developments. Cause and effect of this observation are harder to assess.

8 Further, it would be a poor research practice to avoid pointing out differences in this analogy. Apart from markets that have changed in composition or size and are hence less prone to the same reactions, the biggest difference can be seen in financial stress indicators. Generally, interest rates are where demand for and supply of credit clears. However, if we can observe that the household sector is still reluctant to borrow despite unprecedented low interest rates, it might be an indication that consumers got burned so badly in the Great Financial Crisis that they are simply unwilling to borrow, no matter how low interest rates are. As a consequence, interest rates can at least partially lose their signaling function we re so used to, which in turn, would cause spreads and financial stress indicators which are in large part determined by interest rates and spreads to behave differently this time around, and is exactly what can be observed.

9 This analogy begets the question: Do we believe the global economy is awaiting the same fate we saw play out in the early 2000s? As stated in the beginning, we d advise anyone to not jump to any conclusions. We re pointing out in our latest macro outlook that there is plenty of evidence of a much more favorable backdrop for the global economy. Correlations never persist. It is really the task of an investment manager to determine when and how those correlations might change, and also the prime reason why the study of financial markets is both challenging and extremely engaging at the same time! Groupthink is bad, especially at investment management firms. Brandywine Global therefore takes special care to ensure our corporate culture and investment processes support the articulation of diverse viewpoints. This blog is no different. The opinions expressed by our bloggers may sometimes challenge active positioning within one or more of our strategies. Each blogger represents one market view amongst many expressed at Brandywine Global. Although individual opinions will differ, our investment process and macro outlook will remain driven by a team approach.

10 2019 Brandywine Global Investment Management, LLC. All Rights Reserved. Social Media Guidelines Brandywine Global Investment Management, LLC ("Brandywine Global") is an investment adviser registered with the U.S. Securities and Exchange Commission ("SEC"). Brandywine Global may use Social Media sites to convey relevant information regarding portfolio manager insights, corporate information and other content. Any content published or views expressed by Brandywine Global on any Social Media platform are for informational purposes only and subject to change based on market and economic conditions as well as other factors. They are not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy. This information should not be considered a solicitation or an offer to provide any Brandywine Global service in any jurisdiction where it would be unlawful to do so under the laws of that jurisdiction. Additionally, any views expressed by Brandywine Global or its employees should not be construed as investment advice or a recommendation for any specific security or sector. Brandywine Global will monitor its Social Media pages and any third-party content or comments posted on its Social Media pages. Brandywine Global reserves the right to delete any comment or post that it, in its sole discretion, deems inappropriate or prevent from posting any person who posts inappropriate or offensive content. Any opinions expressed by persons submitting comments don't necessarily represent the views of Brandywine Global. Brandywine Global is not affiliated with any of the Social Media sites it uses and is, therefore, not responsible for the content, terms of use or privacy or security policies of such sites. You are advised to review such terms and policies.

Has the Phillips Curve Flatlined?

AUG 21 2017 Has the Phillips Curve Flatlined? Richard Lawrence» One of the most puzzling aspects of this long, sluggish global recovery has been the pace of increases in average hourly earnings despite

AUG 21 2017 Has the Phillips Curve Flatlined? Richard Lawrence» One of the most puzzling aspects of this long, sluggish global recovery has been the pace of increases in average hourly earnings despite

Can Emerging Markets Hold Steady?

SEP 25 2017 Can Emerging Markets Hold Steady? Carol Lye» China stepped on the stimulus gas pedal last year, marking the turn for emerging market (EM) assets. The weakening trend in the U.S. dollar and

SEP 25 2017 Can Emerging Markets Hold Steady? Carol Lye» China stepped on the stimulus gas pedal last year, marking the turn for emerging market (EM) assets. The weakening trend in the U.S. dollar and

What Are Markets Saying?

JAN 05 2016 What Are Markets Saying? Chen Zhao» Everyone agrees that global growth is weak, but there is no agreement on whether the world economy will strengthen or weaken in 2016. Optimists predict that

JAN 05 2016 What Are Markets Saying? Chen Zhao» Everyone agrees that global growth is weak, but there is no agreement on whether the world economy will strengthen or weaken in 2016. Optimists predict that

It Ain't Over til the Fat Lady Sings or Financial Conditions Get Too Tight

APR 23 2018 It Ain't Over til the Fat Lady Sings or Financial Conditions Get Too Tight Richard Lawrence» In our work as a global macro-focused team, we have to pay attention to a myriad of variables, some

APR 23 2018 It Ain't Over til the Fat Lady Sings or Financial Conditions Get Too Tight Richard Lawrence» In our work as a global macro-focused team, we have to pay attention to a myriad of variables, some

Ground Zero for Brexit: The Fate of Pound Sterling

NOV 14 2016 Ground Zero for Brexit: The Fate of Pound Sterling J. Patrick Bradley» Introduction Much has been written about the impact Brexit may have on the U.K. and its trading partners across Europe

NOV 14 2016 Ground Zero for Brexit: The Fate of Pound Sterling J. Patrick Bradley» Introduction Much has been written about the impact Brexit may have on the U.K. and its trading partners across Europe

All Aboard the Peso-Coaster

JAN 08 2018 All Aboard the Peso-Coaster Richard Lawrence» Few currencies have garnered more press over the past 18 months than the Mexican peso. The peso has experienced a rollercoaster ride courtesy of

JAN 08 2018 All Aboard the Peso-Coaster Richard Lawrence» Few currencies have garnered more press over the past 18 months than the Mexican peso. The peso has experienced a rollercoaster ride courtesy of

Will the Mortgage Whale Torpedo the Market Rally?

MAY 01 2017 Will the Mortgage Whale Torpedo the Market Rally? Tracy Chen, CFA, CAIA» The Federal Reserve (Fed) has telegraphed its intention to start tapering its balance sheet, causing investors to evaluate

MAY 01 2017 Will the Mortgage Whale Torpedo the Market Rally? Tracy Chen, CFA, CAIA» The Federal Reserve (Fed) has telegraphed its intention to start tapering its balance sheet, causing investors to evaluate

External Shocks, Stagflation and Policy Response

JUL 14 2015 External Shocks, Stagflation and Policy Response Chen Zhao» The collapse in commodity prices since 2011 has spurred serious economic difficulties for most commodity-producing countries. Indeed,

JUL 14 2015 External Shocks, Stagflation and Policy Response Chen Zhao» The collapse in commodity prices since 2011 has spurred serious economic difficulties for most commodity-producing countries. Indeed,

4th Quarter Global Macro Webcast. Presented by. Francis A. Scotland Director of Global Macro Research

4th Quarter 2016 Global Macro Webcast Presented by Francis A. Scotland Director of Global Macro Research 2017 Brandywine Global Investment Management, LLC. All rights reserved. The views expressed herein

4th Quarter 2016 Global Macro Webcast Presented by Francis A. Scotland Director of Global Macro Research 2017 Brandywine Global Investment Management, LLC. All rights reserved. The views expressed herein

Venture Capital 4% Strategy. Mega/Large Buyout 29% Highlights from the 2016 GP Dashboard include:

GP Dashboard We are pleased to present Hamilton Lane s GP Dashboard, which captures the opinions and expectations of general partners from around the world and offers insight into where the GP community

GP Dashboard We are pleased to present Hamilton Lane s GP Dashboard, which captures the opinions and expectations of general partners from around the world and offers insight into where the GP community

Key takeaways. What it may mean for investors FIRST A NALYSIS NEWS OR EVENTS T HAT MAY AFFECT Y OUR INVESTMENTS. Global Investment Strategy Team

FIRST A NALYSIS NEWS OR EVENTS T HAT MAY AFFECT Y OUR INVESTMENTS Global Investment Strategy Team February 5, 2018 Market Sell-off What Investors Need to Know Now Key takeaways» A swift climb in the 10-year

FIRST A NALYSIS NEWS OR EVENTS T HAT MAY AFFECT Y OUR INVESTMENTS Global Investment Strategy Team February 5, 2018 Market Sell-off What Investors Need to Know Now Key takeaways» A swift climb in the 10-year

A Different Take on Money Management

A Different Take on Money Management www.simple4xsystem.net Anyone who read one of my books or spent time in one of my trade rooms knows I put a lot of emphasis on using sound Money Management principles

A Different Take on Money Management www.simple4xsystem.net Anyone who read one of my books or spent time in one of my trade rooms knows I put a lot of emphasis on using sound Money Management principles

Income Fund Update: Building Resiliency in Volatile Markets

Income Fund Update: Building Resiliency in Volatile Markets January 28, 2019 by Dan Ivascyn, Alfred Murata of PIMCO SUMMARY During the fourth quarter of 2018, high quality assets were the key drivers of

Income Fund Update: Building Resiliency in Volatile Markets January 28, 2019 by Dan Ivascyn, Alfred Murata of PIMCO SUMMARY During the fourth quarter of 2018, high quality assets were the key drivers of

Charles I Plosser: Strengthening our monetary policy framework through commitment, credibility, and communication

Charles I Plosser: Strengthening our monetary policy framework through commitment, credibility, and communication Speech by Mr Charles I Plosser, President and Chief Executive Officer of the Federal Reserve

Charles I Plosser: Strengthening our monetary policy framework through commitment, credibility, and communication Speech by Mr Charles I Plosser, President and Chief Executive Officer of the Federal Reserve

Economic Perspectives 3 rd Quarter Executive Summary. TRICIA NEWCOMB CIMA Associate, Senior Strategy Analyst

Economic Perspectives 3 rd Quarter 2017 Executive Summary The final estimate of Q2 GDP indicated that the economy grew at a 3.1% rate, the highest quarterly growth rate since Q1 of 2015. Consumer spending

Economic Perspectives 3 rd Quarter 2017 Executive Summary The final estimate of Q2 GDP indicated that the economy grew at a 3.1% rate, the highest quarterly growth rate since Q1 of 2015. Consumer spending

Technical Analysis Basics. Identifying Tops

Technical Analysis Basics. Identifying Tops June 2011 1 Sign Up Now to Upshots forex trade signals disclaimer The information provided in this report is for educational purposes only. It is not a recommendation

Technical Analysis Basics. Identifying Tops June 2011 1 Sign Up Now to Upshots forex trade signals disclaimer The information provided in this report is for educational purposes only. It is not a recommendation

Erlanger Squeeze Play - Squeezeometer. Erlanger Squeeze Play

Page 1 of 5 Indicator Focus: Squeezeometer by Phil Erlanger Erlanger Squeeze Play A core function of our research centers on the concept of advance phases and decline phases. Whether we're in a bull or

Page 1 of 5 Indicator Focus: Squeezeometer by Phil Erlanger Erlanger Squeeze Play A core function of our research centers on the concept of advance phases and decline phases. Whether we're in a bull or

2019 Outlook: Don t Fight the PBOC

2019 Outlook: Don t Fight the PBOC December 18, 2018 by Team of VanEck Jan van Eck, CEO, shares his investment outlook. Watch Now Don t fight the Fed is an old investing mantra, suggesting that investments

2019 Outlook: Don t Fight the PBOC December 18, 2018 by Team of VanEck Jan van Eck, CEO, shares his investment outlook. Watch Now Don t fight the Fed is an old investing mantra, suggesting that investments

Australian Equity IMPROVING OUTLOOK FOR A TRANSITIONING ECONOMY

FOR INVESTMENT PROFESSIONALS ONLY. NOT FOR FURTHER DISTRIBUTION. PRICE POINT December 2015 Timely intelligence and analysis for our clients. Australian Equity IMPROVING OUTLOOK FOR A TRANSITIONING ECONOMY

FOR INVESTMENT PROFESSIONALS ONLY. NOT FOR FURTHER DISTRIBUTION. PRICE POINT December 2015 Timely intelligence and analysis for our clients. Australian Equity IMPROVING OUTLOOK FOR A TRANSITIONING ECONOMY

Myths & misconceptions

ALTERNATIVE INVESTMENTS Myths & misconceptions Many investors mistakenly think of alternative investments as being only for ultra-high-net-worth individuals and institutions. However, due to a number of

ALTERNATIVE INVESTMENTS Myths & misconceptions Many investors mistakenly think of alternative investments as being only for ultra-high-net-worth individuals and institutions. However, due to a number of

2018: Goldilock or Frankenstein

2018: Goldilock or Frankenstein Steen Jakobsen Chief Investment Officer March 2018 Disclaimer NON-INDEPENDENT INVESTMENT RESEARCH None of the information contained herein constitutes an offer (or solicitation

2018: Goldilock or Frankenstein Steen Jakobsen Chief Investment Officer March 2018 Disclaimer NON-INDEPENDENT INVESTMENT RESEARCH None of the information contained herein constitutes an offer (or solicitation

Tips for Traders 5/26/ :35:00 AM Calling All Traders: Get Ready to Make Money Shorting the Market

Tips for Traders 5/26/2009 10:35:00 AM Calling All Traders: Get Ready to Make Money Shorting the Market I am not trying to paint a grim picture of the US stock market and the US economy. I sat quietly

Tips for Traders 5/26/2009 10:35:00 AM Calling All Traders: Get Ready to Make Money Shorting the Market I am not trying to paint a grim picture of the US stock market and the US economy. I sat quietly

What to Consider for Reserve Governance IDENTIFY KEY QUESTIONS AND CONSTRAINTS BUILD INVESTMENT FRAMEWORK

Association Specialty Practice Managing Reserves When Cash Flows are Uneven EXECUTIVE SUMMARY Many associations struggle with issues surrounding asset allocation in light of their complex liquidity and

Association Specialty Practice Managing Reserves When Cash Flows are Uneven EXECUTIVE SUMMARY Many associations struggle with issues surrounding asset allocation in light of their complex liquidity and

ING Fixed Income Perspectives - November 2013

ING Fixed Income Perspectives - November 2013 November 29, 2013 by Christine Hurtsellers and Matt Toms of ING Investement Management ING U.S. Investment Management Fixed Income Perspectives November 27,

ING Fixed Income Perspectives - November 2013 November 29, 2013 by Christine Hurtsellers and Matt Toms of ING Investement Management ING U.S. Investment Management Fixed Income Perspectives November 27,

Multi-Asset Outlook 2017: More Growth, More Inflation, More Politics

Multi-Asset Outlook 2017: More Growth, More Inflation, More Politics January 11, 2017 by Paul O Connor of Henderson Global Investors Paul O Connor, Head of Multi-Asset, reviews 2016 s lessons, and details

Multi-Asset Outlook 2017: More Growth, More Inflation, More Politics January 11, 2017 by Paul O Connor of Henderson Global Investors Paul O Connor, Head of Multi-Asset, reviews 2016 s lessons, and details

Notes 6: Examples in Action - The 1990 Recession, the 1974 Recession and the Expansion of the Late 1990s

Notes 6: Examples in Action - The 1990 Recession, the 1974 Recession and the Expansion of the Late 1990s Example 1: The 1990 Recession As we saw in class consumer confidence is a good predictor of household

Notes 6: Examples in Action - The 1990 Recession, the 1974 Recession and the Expansion of the Late 1990s Example 1: The 1990 Recession As we saw in class consumer confidence is a good predictor of household

Strengthening Our Monetary Policy Framework Through Commitment, Credibility, and Communication

Strengthening Our Monetary Policy Framework Through Commitment, Credibility, and Communication Global Interdependence Center's 2011 Global Citizen Award Luncheon November 8, 2011 Union League Club, Philadelphia,

Strengthening Our Monetary Policy Framework Through Commitment, Credibility, and Communication Global Interdependence Center's 2011 Global Citizen Award Luncheon November 8, 2011 Union League Club, Philadelphia,

10º Congresso Value Investing Brasil

www.cvib.com.br 10º Congresso Value Investing Brasil 23 de maio de 2017 Macro global coerente insights variantes Jonathan Tepper Variant Perception Our Company Who We Are: Variant Perception is an independent

www.cvib.com.br 10º Congresso Value Investing Brasil 23 de maio de 2017 Macro global coerente insights variantes Jonathan Tepper Variant Perception Our Company Who We Are: Variant Perception is an independent

Lecture 8: Inflation and Monetary Policy

Lecture 8: Inflation and Monetary Policy INFLATION IS INFLATION BAD OR GOOD? Think of pensioners or others whose income is fixed in nominal terms. Why would inflation be bad for them? People with nominal

Lecture 8: Inflation and Monetary Policy INFLATION IS INFLATION BAD OR GOOD? Think of pensioners or others whose income is fixed in nominal terms. Why would inflation be bad for them? People with nominal

Appropriate monetary policy and the strong economy Before the Committee on Banking and Financial Services, U.S. House of Representatives July 23, 1997

Appropriate monetary policy and the strong economy Before the Committee on Banking and Financial Services, U.S. House of Representatives July 23, 1997 I would like to begin by expressing my appreciation

Appropriate monetary policy and the strong economy Before the Committee on Banking and Financial Services, U.S. House of Representatives July 23, 1997 I would like to begin by expressing my appreciation

Quantitative & Strategy

Cam Hui, CFA January 30, 2018 cam@pennock@ideahub.com THE PAIN TRADE SIGNALS FROM THE BOND MARKET Highlights As the 10-year Treasury yield staged an upside breakout at 2.6%, and luminary investors such

Cam Hui, CFA January 30, 2018 cam@pennock@ideahub.com THE PAIN TRADE SIGNALS FROM THE BOND MARKET Highlights As the 10-year Treasury yield staged an upside breakout at 2.6%, and luminary investors such

Q Quarterly Market Update Video

Q2 2015 Quarterly Market Update Video Hello, I m Dirk Hofschire of Fidelity Investments. On behalf of my colleagues in the asset allocation research team, I d like to share with you some of our perspectives

Q2 2015 Quarterly Market Update Video Hello, I m Dirk Hofschire of Fidelity Investments. On behalf of my colleagues in the asset allocation research team, I d like to share with you some of our perspectives

Prudential International Investments Advisers, LLC. Global Investment Strategy & Outlook For 2009

Prudential International Investments Advisers, LLC. Global Investment Strategy & Outlook For 2009 December 17, 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact:

Prudential International Investments Advisers, LLC. Global Investment Strategy & Outlook For 2009 December 17, 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact:

State and National Job Figures Show Signs of Firming, but Jobless Rates Remain Unacceptably High

December 2011 State and National Job Figures Show Signs of Firming, but Jobless Rates Remain Unacceptably High New Jersey Recent job gains in the state have erased the storm-induced losses of last summer.

December 2011 State and National Job Figures Show Signs of Firming, but Jobless Rates Remain Unacceptably High New Jersey Recent job gains in the state have erased the storm-induced losses of last summer.

Investment Outlook. Investment Outlook Mid-year review and outlook. December June 2017

Investment Outlook Mid-year review and outlook June 2017 Investment Outlook 2018 December 2017 This commentary provides a high level overview of the recent economic environment and our outlook, and is

Investment Outlook Mid-year review and outlook June 2017 Investment Outlook 2018 December 2017 This commentary provides a high level overview of the recent economic environment and our outlook, and is

Reconciling FOMC Forecasts and Forward Guidance. Mickey D. Levy Blenheim Capital Management

Reconciling FOMC Forecasts and Forward Guidance Mickey D. Levy Blenheim Capital Management Prepared for Shadow Open Market Committee September 20, 2013 Reconciling FOMC Forecasts and Forward Guidance Mickey

Reconciling FOMC Forecasts and Forward Guidance Mickey D. Levy Blenheim Capital Management Prepared for Shadow Open Market Committee September 20, 2013 Reconciling FOMC Forecasts and Forward Guidance Mickey

FOREWORD I have a great job. I travel the world, give speeches, advise corporations, nurture companies, write about investing, and talk about investin

I have a great job. I travel the world, give speeches, advise corporations, nurture companies, write about investing, and talk about investing on television. It s the kind of job that has its share of

I have a great job. I travel the world, give speeches, advise corporations, nurture companies, write about investing, and talk about investing on television. It s the kind of job that has its share of

The Waiting: Wage Growth and Inflation Finally Getting in Gear?

The Waiting: Wage Growth and Inflation Finally Getting in Gear? October 10, 2017 by Liz Ann Sonders of Charles Schwab Key Points Hurricanes impacted job growth; but not unemployment or wages, which both

The Waiting: Wage Growth and Inflation Finally Getting in Gear? October 10, 2017 by Liz Ann Sonders of Charles Schwab Key Points Hurricanes impacted job growth; but not unemployment or wages, which both

Portfolio Management Commentary

Portfolio Management Commentary Quarter Ending March 31, 2017 Patrick A. Choquette, CFP, CIM, FCSI Portfolio Manager We begin with a thorough review of the past quarter. The concern over market valuations

Portfolio Management Commentary Quarter Ending March 31, 2017 Patrick A. Choquette, CFP, CIM, FCSI Portfolio Manager We begin with a thorough review of the past quarter. The concern over market valuations

Summary. The RMB continues to depreciate against the dollar. While there are a number of factors

Summary Editor: Tristan Zhuo Senior Economist Phone: +852 2826 6193 Email: tristanzhuo@bochk.com The protectionist rhetoric of U.S. President-elect Trump during his campaign has prompted fears of escalation

Summary Editor: Tristan Zhuo Senior Economist Phone: +852 2826 6193 Email: tristanzhuo@bochk.com The protectionist rhetoric of U.S. President-elect Trump during his campaign has prompted fears of escalation

Explore the themes and thinking behind our decisions.

ASSET ALLOCATION COMMITTEE VIEWPOINTS First Quarter 2017 These views are informed by a subjective assessment of the relative attractiveness of asset classes and subclasses over a 6- to 18-month horizon.

ASSET ALLOCATION COMMITTEE VIEWPOINTS First Quarter 2017 These views are informed by a subjective assessment of the relative attractiveness of asset classes and subclasses over a 6- to 18-month horizon.

Thomas Jordan: Challenges facing the Swiss National Bank

Thomas Jordan: Challenges facing the Swiss National Bank Speech by Mr Thomas Jordan, Chairman of the Governing Board of the Swiss National Bank, to the General Meeting of Shareholders of the Swiss National

Thomas Jordan: Challenges facing the Swiss National Bank Speech by Mr Thomas Jordan, Chairman of the Governing Board of the Swiss National Bank, to the General Meeting of Shareholders of the Swiss National

Struggling to Find Value

Struggling to Find Value The S&P 500 has returned 21% per year (appreciation and dividends) over the past four years (4/1/09-3/31/13). Investors who hesitated to invest in recent years are pouring money

Struggling to Find Value The S&P 500 has returned 21% per year (appreciation and dividends) over the past four years (4/1/09-3/31/13). Investors who hesitated to invest in recent years are pouring money

Macroeconomic Outlook November 2015

Macroeconomic Outlook November 2015 Philippe WAECHTER Head of Economic Research My twitter account @phil_waechter or http://twitter.com/phil_waechter My blog http://philippewaechter.en.nam.natixis.com

Macroeconomic Outlook November 2015 Philippe WAECHTER Head of Economic Research My twitter account @phil_waechter or http://twitter.com/phil_waechter My blog http://philippewaechter.en.nam.natixis.com

Taking Stock of the Market s Mood

LEADERSHIP SERIES JUNE 2017 A feature article from our U.S. partners Taking Stock of the Market s Mood International stocks continue to outperform, while U.S. equity returns may be choppy and more subdued

LEADERSHIP SERIES JUNE 2017 A feature article from our U.S. partners Taking Stock of the Market s Mood International stocks continue to outperform, while U.S. equity returns may be choppy and more subdued

Wicked Skew: When Extreme Losses are Standard Outcomes

Wicked Skew: When Extreme Losses are Standard Outcomes January 25, 2016 by John Hussman of Hussman Funds Following the market decline of recent weeks, historically reliable valuation measures remain roughly

Wicked Skew: When Extreme Losses are Standard Outcomes January 25, 2016 by John Hussman of Hussman Funds Following the market decline of recent weeks, historically reliable valuation measures remain roughly

Economic Cycle model, Recession Probability model & Leading Indicators A Holistic Perspective

Economic Cycle model, Recession Probability model & Leading Indicators A Holistic Perspective White Paper RecessionProtect.com Whilst history doesn't repeat itself, it often rhymes, so the saying goes.

Economic Cycle model, Recession Probability model & Leading Indicators A Holistic Perspective White Paper RecessionProtect.com Whilst history doesn't repeat itself, it often rhymes, so the saying goes.

Economic recovery dashboard

CURRENT AS OF OCTOBER 31, 2009 Economic recovery dashboard Summary of current state Market indicators Most indicators changed little over the previous month. VIX increased, closing the month at 30.69,

CURRENT AS OF OCTOBER 31, 2009 Economic recovery dashboard Summary of current state Market indicators Most indicators changed little over the previous month. VIX increased, closing the month at 30.69,

Lessons from a Trading Great: Bruce Kovner

Lessons from a Trading Great: Bruce Kovner Bruce Kovner retired in 2011 from Caxton Associates, the hedge fund he founded and ran for 28 years. Over that time the fund returned an average of 21 percent

Lessons from a Trading Great: Bruce Kovner Bruce Kovner retired in 2011 from Caxton Associates, the hedge fund he founded and ran for 28 years. Over that time the fund returned an average of 21 percent

Are we on the road to recovery?

Are we on the road to recovery? Transcript Catherine Gordon: Hi, I m Catherine Gordon. We re here with Joe Davis, Vanguard s chief economist, to talk about economic trends and the outlook for the rest

Are we on the road to recovery? Transcript Catherine Gordon: Hi, I m Catherine Gordon. We re here with Joe Davis, Vanguard s chief economist, to talk about economic trends and the outlook for the rest

- Mark Twain s notice to readers of Huckleberry Finn

February 14, 2018 PERSONS attempting to find a motive in this narrative will be prosecuted; persons attempting to find a moral in it will be banished; persons attempting to find a plot in it will be shot.

February 14, 2018 PERSONS attempting to find a motive in this narrative will be prosecuted; persons attempting to find a moral in it will be banished; persons attempting to find a plot in it will be shot.

MONETARY POLICY COMING OUT OF RECESSION. Anna J. Schwartz National Bureau of Economic Research

MONETARY POLICY COMING OUT OF RECESSION Anna J. Schwartz National Bureau of Economic Research Since 1959 the U. S. has experienced six recessions, not counting the recession that began, according to the

MONETARY POLICY COMING OUT OF RECESSION Anna J. Schwartz National Bureau of Economic Research Since 1959 the U. S. has experienced six recessions, not counting the recession that began, according to the

WELCOME TO THE FOURTH QUARTER

LPL RESEARCH WEEKLY MARKET COMMENTARY IBG FINANCIAL ADVISORS October 3 2016 WELCOME TO THE FOURTH QUARTER Burt White Chief Investment Officer, LPL Financial Ryan Detrick, CMT Senior Market Strategist,

LPL RESEARCH WEEKLY MARKET COMMENTARY IBG FINANCIAL ADVISORS October 3 2016 WELCOME TO THE FOURTH QUARTER Burt White Chief Investment Officer, LPL Financial Ryan Detrick, CMT Senior Market Strategist,

The yellow highlighted areas are bear markets with NO recession.

Part 3, Final Report: Major Market Reversal Model This is the third and final report on my major market reversal model. This portion of the model focuses on the domestic and international economy. I ve

Part 3, Final Report: Major Market Reversal Model This is the third and final report on my major market reversal model. This portion of the model focuses on the domestic and international economy. I ve

Commercial Real Estate Outlook June Must Own Property Names to Buy During Interest Rate Fears

Jonathan Litt Founder & CEO Must Own Property Names to Buy During Interest Rate Fears REITs have sold off 9.5% since their peak in mid-may on fears of rising interest rates. Historically, sell-offs related

Jonathan Litt Founder & CEO Must Own Property Names to Buy During Interest Rate Fears REITs have sold off 9.5% since their peak in mid-may on fears of rising interest rates. Historically, sell-offs related

Marcuard Heritage: Quarterly Asset Allocation Outlook

Marcuard Heritage: Quarterly Asset Allocation Outlook 4 th Quarter 2010 The current Status Concerns of sluggish global economic growth and ongoing stress in the EMU Sovereign countries have gripped the

Marcuard Heritage: Quarterly Asset Allocation Outlook 4 th Quarter 2010 The current Status Concerns of sluggish global economic growth and ongoing stress in the EMU Sovereign countries have gripped the

US: Dangerous deficits?

Article 5 March 2018 US: Dangerous deficits? Economic and Financial Analysis Global Economics Given the pace of economic growth and record levels of employment, it's remarkable that there is a possibility

Article 5 March 2018 US: Dangerous deficits? Economic and Financial Analysis Global Economics Given the pace of economic growth and record levels of employment, it's remarkable that there is a possibility

October Stock Indexes September 2009 Market Indexes September S&P 500 Index +3.6% +17.0% HFRX Global Hedge Fund Index +2.2% +11.

October 2009 Dear Investor, In September, stocks continued modestly higher, both in the US and globally. There have been a few notable exceptions to the gains, as stock indexes in China and Japan (among

October 2009 Dear Investor, In September, stocks continued modestly higher, both in the US and globally. There have been a few notable exceptions to the gains, as stock indexes in China and Japan (among

"Phenomenal" Expectations

"Phenomenal" Expectations March 4, 2017 by Liz Ann Sonders, Brad Sorensen and Jeffrey Kleintop of Charles Schwab Key Points U.S. stock indexes broke to the upside, on better economic data but also heightened

"Phenomenal" Expectations March 4, 2017 by Liz Ann Sonders, Brad Sorensen and Jeffrey Kleintop of Charles Schwab Key Points U.S. stock indexes broke to the upside, on better economic data but also heightened

Technical Analysis. Weekly Comment. Global. SPX Overbought Relief Rally in Europe!! Equities Sales Trading Commentary

h Technical Analysis Equities Sales Trading Commentary Weekly Comment Global Michael Riesner Marc Müller 03/07/2012 michael.riesner@ubs.com marc.mueller@ubs.com +41-44-239 1676 +41-44-239 1789 SPX Overbought

h Technical Analysis Equities Sales Trading Commentary Weekly Comment Global Michael Riesner Marc Müller 03/07/2012 michael.riesner@ubs.com marc.mueller@ubs.com +41-44-239 1676 +41-44-239 1789 SPX Overbought

One Policymaker s Wait for Better Economic Data

EMBARGOED UNTIL June 1, 2015 at 9:00 A.M. Eastern Time OR UPON DELIVERY One Policymaker s Wait for Better Economic Data Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston

EMBARGOED UNTIL June 1, 2015 at 9:00 A.M. Eastern Time OR UPON DELIVERY One Policymaker s Wait for Better Economic Data Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston

The Value of Referrals. Guide to Growth: Leveraging Research and Industry Experience to Achieve Best Practices

Guide to Growth: Leveraging Research and Industry Experience to Achieve Best Practices The Value of Referrals Cetera Financial Institutions is a marketing name of Cetera Investment Services LLC, member

Guide to Growth: Leveraging Research and Industry Experience to Achieve Best Practices The Value of Referrals Cetera Financial Institutions is a marketing name of Cetera Investment Services LLC, member

Implications of Low Inflation Rates for Monetary Policy

Implications of Low Inflation Rates for Monetary Policy Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston Washington and Lee University s H. Parker Willis Lecture in

Implications of Low Inflation Rates for Monetary Policy Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston Washington and Lee University s H. Parker Willis Lecture in

How costly is for Spain to be in the EURO?

How costly is for to be in the EURO? Are members of a monetary Union fatally handicapped to recover from recessions and solve financial crisis? By Domingo Cavallo 1 Countries with a long history of low

How costly is for to be in the EURO? Are members of a monetary Union fatally handicapped to recover from recessions and solve financial crisis? By Domingo Cavallo 1 Countries with a long history of low

Know Your Risks. Investment Update

August 2013 Investment Update Know Your Risks Risk is the chance that you won't be able to meet your financial goals or that you'll have to recalibrate your goals because your investment comes up short.

August 2013 Investment Update Know Your Risks Risk is the chance that you won't be able to meet your financial goals or that you'll have to recalibrate your goals because your investment comes up short.

Letter from Linda. December 31, Valuations Have Declined Below Historical Averages

December 31, The last four months of were the most eventful for the U.S. stock market in years. After peaking on 9/20, the S&P 500 Index declined just shy of 20% by 12/24. This was the largest drop since

December 31, The last four months of were the most eventful for the U.S. stock market in years. After peaking on 9/20, the S&P 500 Index declined just shy of 20% by 12/24. This was the largest drop since

MACRO MUSINGS February 23, 2018

INFLATION FIXATION MACRO MUSINGS February 23, 2018 Rush Zarrabian, CFA Portfolio Manager Corbett Road Investment Mgmt SUMMARY The most recent MACROCAST TM score surged six points to a score of +13. This

INFLATION FIXATION MACRO MUSINGS February 23, 2018 Rush Zarrabian, CFA Portfolio Manager Corbett Road Investment Mgmt SUMMARY The most recent MACROCAST TM score surged six points to a score of +13. This

Personal Finance REBALANCING CAN HELP MITIGATE MARKET RISK

PRICE PERSPECTIVE February 17 In-depth analysis and insights to inform your decision-making. Personal Finance REBALANCING CAN HELP MITIGATE MARKET RISK EXECUTIVE SUMMARY The global equity markets have

PRICE PERSPECTIVE February 17 In-depth analysis and insights to inform your decision-making. Personal Finance REBALANCING CAN HELP MITIGATE MARKET RISK EXECUTIVE SUMMARY The global equity markets have

Article from: Health Watch. October 2012 Issue 70

Article from: Health Watch October 2012 Issue 70 Enterprise Risk Management: One Size Does Not Fit All By Mark Whitford Mark Whitford, FSA, CERA, MAAA, is Director, Business Development and Insurance Strategy,

Article from: Health Watch October 2012 Issue 70 Enterprise Risk Management: One Size Does Not Fit All By Mark Whitford Mark Whitford, FSA, CERA, MAAA, is Director, Business Development and Insurance Strategy,

Analysing the IS-MP-PC Model

University College Dublin, Advanced Macroeconomics Notes, 2015 (Karl Whelan) Page 1 Analysing the IS-MP-PC Model In the previous set of notes, we introduced the IS-MP-PC model. We will move on now to examining

University College Dublin, Advanced Macroeconomics Notes, 2015 (Karl Whelan) Page 1 Analysing the IS-MP-PC Model In the previous set of notes, we introduced the IS-MP-PC model. We will move on now to examining

ANOTHER TOUGH WEEK COMMENTARY REASSURANCE KEY TAKEAWAYS LPL RESEARCH WEEKLY MARKET. October

LPL RESEARCH WEEKLY MARKET COMMENTARY October 29 2018 ANOTHER TOUGH WEEK John Lynch Chief Investment Strategist, LPL Financial Jeffrey Buchbinder, CFA Equity Strategist, LPL Financial Ryan Detrick, CMT

LPL RESEARCH WEEKLY MARKET COMMENTARY October 29 2018 ANOTHER TOUGH WEEK John Lynch Chief Investment Strategist, LPL Financial Jeffrey Buchbinder, CFA Equity Strategist, LPL Financial Ryan Detrick, CMT

Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy February 2017 Global Stock Market Rally likely to Continue with Solid Q4 Earnings & Stronger 2017 Earnings, ECB

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy February 2017 Global Stock Market Rally likely to Continue with Solid Q4 Earnings & Stronger 2017 Earnings, ECB

2014 Annual Review & Outlook

2014 Annual Review & Outlook As we enter 2014, the current economic expansion is 4.5 years in duration, roughly the average life of U.S. economic expansions. There is every reason to believe it will continue,

2014 Annual Review & Outlook As we enter 2014, the current economic expansion is 4.5 years in duration, roughly the average life of U.S. economic expansions. There is every reason to believe it will continue,

Research Global inflation scare: Overview

Investment Research February Research Global inflation scare: Overview With the global recovery strengthening and commodity prices rising sharply, inflation has returned as a market theme. In a series

Investment Research February Research Global inflation scare: Overview With the global recovery strengthening and commodity prices rising sharply, inflation has returned as a market theme. In a series

27PercentWeekly. By Ryan Jones. Part II in the Series Start Small and Retire Early Trading Weekly Options

By Ryan Jones Part II in the Series Start Small and Retire Early Trading Weekly Options Important My 27% Option Strategy is one of the best option trading opportunities you will come across. When you see

By Ryan Jones Part II in the Series Start Small and Retire Early Trading Weekly Options Important My 27% Option Strategy is one of the best option trading opportunities you will come across. When you see

Three Techniques for Spotting Market Twists and Turns. Riding the Roller

Three Techniques for Spotting Market Twists and Turns Riding the Roller Coaster Learn to Spot the Twists and Turns Whether you re new to forex or you ve been trading a while, you know how the unexpected

Three Techniques for Spotting Market Twists and Turns Riding the Roller Coaster Learn to Spot the Twists and Turns Whether you re new to forex or you ve been trading a while, you know how the unexpected

March 16, Dear Investors:

March 16, 2019 Crescat Capital LLC 1560 Broadway Denver, CO 80202 (303) 271-9997 info@crescat.net www.crescat.net Dear Investors: At Crescat we remain positioned to capitalize on a downturn in the economic

March 16, 2019 Crescat Capital LLC 1560 Broadway Denver, CO 80202 (303) 271-9997 info@crescat.net www.crescat.net Dear Investors: At Crescat we remain positioned to capitalize on a downturn in the economic

May Market Update Podcast

May Market Update Podcast Schuster: In the most recent month, risk assets, many of which have experienced doubledigit gains year-to-date, remain generally positive, despite perceptions of slowing global

May Market Update Podcast Schuster: In the most recent month, risk assets, many of which have experienced doubledigit gains year-to-date, remain generally positive, despite perceptions of slowing global

Positioning Equity Portfolios for When Rates Rise

October 2017 Positioning Equity Portfolios for When Rates Rise The current equity bull market is now more than eight years old and has survived several calls for its demise. So far, it has weathered economic

October 2017 Positioning Equity Portfolios for When Rates Rise The current equity bull market is now more than eight years old and has survived several calls for its demise. So far, it has weathered economic

Navigating the New Environment

Navigating the New Environment May 12, 2018 by Liz Ann Sonders, Jeffrey Kleintop & Brad Sorensen of Charles Schwab Key Points U.S. stock indexes have rebounded from their correction lows, although remain

Navigating the New Environment May 12, 2018 by Liz Ann Sonders, Jeffrey Kleintop & Brad Sorensen of Charles Schwab Key Points U.S. stock indexes have rebounded from their correction lows, although remain

July Economic Outlook

July Economic Outlook Going forward, I will not write a monthly economic outlook. Major trends in the economy such as GDP, interest rates, CPI, retail sales, don t change that much, especially month to

July Economic Outlook Going forward, I will not write a monthly economic outlook. Major trends in the economy such as GDP, interest rates, CPI, retail sales, don t change that much, especially month to

Inflation Talk Dividend Strategy under the Rising Rate Environment

Inflation Talk Dividend Strategy under the Rising Rate Environment Summary The traditional dividend discount model is based on simplified assumptions and does not accurately represent all dividend paying

Inflation Talk Dividend Strategy under the Rising Rate Environment Summary The traditional dividend discount model is based on simplified assumptions and does not accurately represent all dividend paying

Chapter 4.3. Speculating with CFDs

1 Chapter 4.3 Speculating with CFDs 0 Contents SPECULATING WITH CFDS Traders often have moments when they feel the stars are aligned to favour a particular trade. And, though they may not be able to explain

1 Chapter 4.3 Speculating with CFDs 0 Contents SPECULATING WITH CFDS Traders often have moments when they feel the stars are aligned to favour a particular trade. And, though they may not be able to explain

The Long-Term Investing Myth

The Long-Term Investing Myth January 3, 2017 by Lance Roberts of Real Investment Advice During my morning routine of caffeine supported information injections, I ran across several articles that just contained

The Long-Term Investing Myth January 3, 2017 by Lance Roberts of Real Investment Advice During my morning routine of caffeine supported information injections, I ran across several articles that just contained

Friday, February 21, Dear Valued Clients and Friends,

Friday, February 21, 2014 Dear Valued Clients and Friends, Another week behind us, and with it, the vast majority of earnings season is complete (though some results will continue to trickle in). I spend

Friday, February 21, 2014 Dear Valued Clients and Friends, Another week behind us, and with it, the vast majority of earnings season is complete (though some results will continue to trickle in). I spend

skyrocketing, production and exploration efforts tend to ramp up to capture the potential

December 15, 2014 Vice President, Research Analyst Franklin Equity Group Portfolio Manager, Franklin Natural Resources Fund When oil prices are skyrocketing, production and exploration efforts tend to

December 15, 2014 Vice President, Research Analyst Franklin Equity Group Portfolio Manager, Franklin Natural Resources Fund When oil prices are skyrocketing, production and exploration efforts tend to

Jekyll and Hyde Quarter

Jekyll and Hyde Quarter May 9, 2018 by Team of Perritt Capital Management The first quarter of 2018 was remarkable in several ways. We saw record highs in equity markets, but also a fierce resurgence in

Jekyll and Hyde Quarter May 9, 2018 by Team of Perritt Capital Management The first quarter of 2018 was remarkable in several ways. We saw record highs in equity markets, but also a fierce resurgence in

Financial Market Outlook: Stock Rally Continues with Faster & Stronger GDP Rebound, Earnings Recovery & Liquidity

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Further Stock Gains with Macro Sweet Spot & Earnings Recovery.

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Further Stock Gains with Macro Sweet Spot & Earnings Recovery.

Q MARKETS REVIEW

Stock markets around the world continued their ascent during the quarter as investors took solace in continuing corporate earnings growth, fueled by strong global economic growth, and U.S. tax cuts. Overview

Stock markets around the world continued their ascent during the quarter as investors took solace in continuing corporate earnings growth, fueled by strong global economic growth, and U.S. tax cuts. Overview

The Labor Force Participation Puzzle

The Labor Force Participation Puzzle May 23, 2013 by David Kelly of J.P. Morgan Funds Slow growth and mediocre job creation have been common themes used to describe the U.S. economy in recent years, as

The Labor Force Participation Puzzle May 23, 2013 by David Kelly of J.P. Morgan Funds Slow growth and mediocre job creation have been common themes used to describe the U.S. economy in recent years, as

Nordic Companies in China less optimistic - But they continue to expand their presence

Nordic Companies in China less optimistic - But they continue to expand their presence THE SEB CHINA FINANCIAL INDEX AT 63.4, down from 70 in March. All indicators are falling in the September survey.

Nordic Companies in China less optimistic - But they continue to expand their presence THE SEB CHINA FINANCIAL INDEX AT 63.4, down from 70 in March. All indicators are falling in the September survey.

Market & Portfolio Update April 2017

Reaching Higher Market & Portfolio Update April 2017 2500 Chamber Center Dr. Suite 202 Ft. Mitchell, KY 41017 Office: 859-815-8566 Toll Free: 800-350-0493 Fax: 859-815-8567 Market Update The global economic

Reaching Higher Market & Portfolio Update April 2017 2500 Chamber Center Dr. Suite 202 Ft. Mitchell, KY 41017 Office: 859-815-8566 Toll Free: 800-350-0493 Fax: 859-815-8567 Market Update The global economic

The Stock Market Is Worried About Inflation. Should It Be?

Instruction for term paper, Eco202H, Spring, 2018 This term paper is worth 20 effective points. The paper should be less than five pages, double-spaced with standard margins and fonts of 11. The complete

Instruction for term paper, Eco202H, Spring, 2018 This term paper is worth 20 effective points. The paper should be less than five pages, double-spaced with standard margins and fonts of 11. The complete

2019 Fixed Income Survey: Is a Change in Market Dynamics Afoot?

2019 Fixed Income Survey: Is a Change in Market Dynamics Afoot? February 21, 2019 by Adam Smears of Russell Investments Throughout the year we ask leading bond and currency managers to consider valuations,

2019 Fixed Income Survey: Is a Change in Market Dynamics Afoot? February 21, 2019 by Adam Smears of Russell Investments Throughout the year we ask leading bond and currency managers to consider valuations,

3 Things: Fed Levitation, Employment, Savings Rate

3 Things: Fed Levitation, Employment, Savings Rate March 31, 2016 by Lance Roberts of Real Investment Advice Fed Levitation What is going on at the Federal Reserve? On Tuesday, Janet Yellen comes out and

3 Things: Fed Levitation, Employment, Savings Rate March 31, 2016 by Lance Roberts of Real Investment Advice Fed Levitation What is going on at the Federal Reserve? On Tuesday, Janet Yellen comes out and

THIS IS JUST THE BEGINNING

THIS IS JUST THE BEGINNING The following is an extract from the December 07 Issue of The Global Speculator sent to subscribers on the 4 th of January 2008. As many of you are already aware the Gold price

THIS IS JUST THE BEGINNING The following is an extract from the December 07 Issue of The Global Speculator sent to subscribers on the 4 th of January 2008. As many of you are already aware the Gold price

Volatility/Vix Trading. Your Step-by- Step Guide to Stock Trading

Volatility/Vix Trading Your Step-by- Step Guide to Stock Trading and Options Trading with Volatility Table Of Contents Introduction Chapter 1 What Is Volatility? Chapter 2 The Volatility Index Chapter

Volatility/Vix Trading Your Step-by- Step Guide to Stock Trading and Options Trading with Volatility Table Of Contents Introduction Chapter 1 What Is Volatility? Chapter 2 The Volatility Index Chapter

Observation. January 18, credit availability, credit

January 18, 11 HIGHLIGHTS Underlying the improvement in economic indicators over the last several months has been growing signs that the economy is also seeing a recovery in credit conditions. The mortgage

January 18, 11 HIGHLIGHTS Underlying the improvement in economic indicators over the last several months has been growing signs that the economy is also seeing a recovery in credit conditions. The mortgage

BULL MARKETS DON T DIE OF OLD AGE

BULL MARKETS DON T DIE OF OLD AGE Issue #11 September/October 2017 Multi asset views from RLAM Royal London Asset Management manages 106.2 billion in life insurance, pensions and third party funds*. The

BULL MARKETS DON T DIE OF OLD AGE Issue #11 September/October 2017 Multi asset views from RLAM Royal London Asset Management manages 106.2 billion in life insurance, pensions and third party funds*. The