Beyond The realm Of possibilities

|

|

|

- Clementine Holland

- 5 years ago

- Views:

Transcription

1 Beyond The realm Of possibilities nd Quarter Report

2 Table of Contents - Outlook of U.S. Real Estate Products Performance Review Performance: DFSP Series Market Outlook 25-28

3 Outlook of U.S. Real Estate

4 U.S. economic growth is improving The US recovery continues to be on track from its trough. The US economy is expected to expand at a rate of 2.1% in Q According to the economic forecast provided by Federal Reserve, the Real GDP growth for 2013 and 2014 are expected to be approximately 2.0% and 2.8%, respectively. United States Economic Data (Actual/Forecasts) Source: Bloomberg

5 U.S. consumer confidence index increases Figures show that the US economic recovery did not stall, but rather continue its growth at a steady pace. US Consumer Confidence index has increased to 81.4 in June from The increase in confidence is due to: US Conference Board Consumer Confidence Index Higher expectation of more jobs Better stock market performance Rising home prices Source: Bloomberg

6 Better stock market performance U.S. unemployment rate has multiple consecutive months of decline from 2010 highs, while Fed s monetary stimulus has also pushed up the US stock prices to record highs as well as real estate prices remain strong trend. US Unemployment Rate Dow Jones Industrial Average Source: Bloomberg Source: Bloomberg

7 Housing data remains robust Sales of new homes rose to the highest level in nearly five years in May, indicating substantial strength in the housing sector ahead of recent worries about rising mortgage rates. US New home sales rose 2.1% in May 2013 to an annual rate (seasonally adjusted) of 476,000 new homes. This was the highest level since July Single-Family Home Sales Source: National Association of Realtors ( NAR ), Census Bureau

8 Rapid increase in price According to National Association of Realtors, sales of previously owned homes climbed 4.2% to 5.2 million in May, their highest level since 2009, while median prices jumped 15% on the year. The data suggested the real-estate developers to call for a rapid increase in home building to temper the rapid increase in prices. Median Price of Home Sales Source: National Association of Realtors ( NAR ), Census Bureau

9 Housing price increase in Metro Areas House prices continue to rise. According to the S&P Case-Shiller home price index, which tracks 20 metropolitan regions across the US, showed prices increased 12% year-over-year in April (from in April 2012 to in April 2013), the largest increase since March 2006 and ahead of the previous month s 9.3% annual rise. 20 Metro Areas Housing Data Source:, Zillow, S&P Case-Shiller

10 Housing price increase in Metro Areas Similar to the Case-Shiller release, the CoreLogic house price indices also showed 12% year-over-year appreciation. The Zillow home value index posted a relatively modest year-over-year increase of 5.4% in May. Some of the variation between different house price indices can be explained by difference in data sources and index methodology. U.S. Zillow Home Value Index Source: Zillow

11 Individual cities housing figures For individual cities, on a year-over-year basis, all 20 cities that Case-Shiller tracks have recorded home-price growth for at least four straight months. In April, 19 cities showed improvement on M-o-M basis, with only Detroit remained flat. On the West coast, Phoenix and Las Vegas both saw growth of price gains of roughly 22% Y-o-Y in April. From the above housing figures, the U.S. housing market remains strong upside potential. And in some individual cities, the prices are still well below average. With the situation that U.S. economy continues to improve, the housing price appreciation was expected.

12 Our view We are positive on the housing recovery. The double-digit annual home price appreciation observed in recent months states the strength in the housing market. We expect home price can still rise at a steady pace of 4-5% over the next few years, taking in the consideration of rising rates prompt questions about the impact on house prices. And we expect this will be only a minimal negative effect because housing is still very affordable currently. Price-to-Rent Ratio and Housing Affordability Index Source: CoreLogic, BLS, NAR, GS Global ECS Research

13 Our view Another part of the reasons is recent data indicate the banks are easing credit restrictions. To cope with rising mortgage rates, borrowers may switch between fixed rate and adjustable rate loans. We think banks credit quality and restrictions are always more important than level of mortgage rates. Market and Effective Mortgage Rate Source: Freddie Mac, BEA.

14 Our view Extremely low levels of new housing starts over the past few years means a large number of new housing units will likely need to be built but in the meantime, prices should rise due to demand / supply imbalance. Housing Starts Source: National Association of Home Builders ( NAHB ), Census Bureau

15 Our view Lastly, Fed has clearly indicated a schedule to taper the asset purchase, we believe: Policymakers seeing diminished downside risks to economic outlook Labor market has shown further improvement Thus, we expect various housing activity indicators will stay on their upward trend due to the improving US economy and higher affordability.

16 Conclusion Low Real Estate prices provide an attractive yield for institutional and other investors. Under the international inflation economic situation, real estate investment offers investors a stable and sustainable growth investment opportunities. From the above housing figures, the U.S. housing market possesses a strong upside potential. Demand for existing homes has surged, while limited supply over the past 4-5 years does not meet current demand which provides support to home prices. In addition, these affordable investments accelerate investors to make trading decisions and increase market liquidity thereby.

17 Products Performances 17

18 POWERFUND

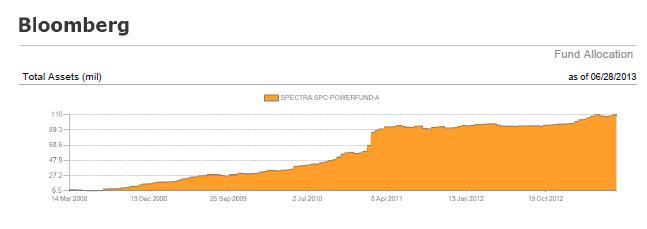

19 POWERFUND Stable and Persistent Positive Return The Q2 performance of POWERFUND was in line with the expectation of the fund manger. The fund s NAV was up 1.53% in the second quarter, i.e. bringing the YTD return to 3.24%. The monthly returns were about 0.56%, in line with our target, i.e. diversification through correlations with traditional assets. 19

20 20

21 21

22 Performance Review: DFSP Series 22

23 Diversified FX Trading Segregated Portfolio (USD & EUR) DFSP USD Fund rose 1.85% in Q2 of Regardless of the market conditions, DFSP Serial Fund is able to deliver a stable return. DFPS EUR Fund of rose 2.47% in Q2 of The return mainly derived from the performance in arbitrary operation. Comparing to traditional equity fund, the Fund demonstrates its capability to disperse risk and attain higher return-to-risk ratio. 23

24 24

25 25

26 Market Outlook

27 Market Outlook Markets were caught by surprise as Ben Bernanke announced the tapering of the stimulus package. On grounds of an improving stability in the US economy based on general economic data in the 1st quarter of 2013, most importantly GDP growth. This has led to a sharp reversal of the Dollar of almost 5%, with increased volatility in the recent months. US Dollar Index Future Daily Price Chart We view the US treasury and Mortgaged- Backed Securities bond funds sell off in the past few months as Dollar positive. This continual sell off of bonds will in effect drive yields higher along with the currency. Our general outlook is bullish on the Dollar for next quarter, as more tapering for reducing stimulus is announced.

28 Market Outlook The Euro is slightly higher versus the Dollar as the currency found support near the 1.28 level set by positions made in the beginning of the 2nd Quarter; off the selloff of the currency in the beginning of February. EURUSD Daily Price Chart Growth and inflation are on a slow recovery, fiscal related problems such as the sovereign debt crisis and rising unemployment implies that economic growth is yet to be anytime soon. We believe the ECB rates will not change any time soon in order to maintain liquidity with banks. We believe there is somewhat of an internal struggle in the bloc which is one of the main constraining factors for the ECB to take decisive action. Short-term we remain neutral on this currency, though look for increased volatility around the end of next quarter.

29 Market Outlook GBP/USD Daily Price Chart GBPUSD saw a significant reversal in losses during the end of the first quarter, since then markets have been fluctuating in and out of gains and losses as the currency pairing was little changed this quarter. The general economy in UK has somewhat improved in this quarter as better than expected data over June indicated moderate GDP growth. Strong retail figures, employment and wages and housing incomes and spending were all positive. Despite all this, the GBP has not been able to make significant ground versus the Dollar. In our opinion the UK s fiscal austerity has constrained economic growth and further easing speculations will continue weigh on the currency. USD/JPY Daily Price Chart USDJPY has reached a high of during this quarter, not seen since the 4th Quarter of Prime Minister Shinzo Abe s objective of 2% target inflation, low interest rates and quantitative easing has weakened the currency by close to 25% since the first quarter of We believe this milestone will cause speculators to increase risk appetite and volatility. Despite this, we believe the BOJ is unlikely to announce new easing measures, as domestic growth remains slow but sure. In the short term there may be a reversal in the Yen, however, in the longer term it is fairly obvious to stick with the Dollar because the US currency is the best performing currency thus far, and the Yen is one of the worst.

30 For further information, please contact Web : Important Notice : This documentation is for discussion purpose only and may not be appropriate for any investor. Without limitation, this document does not constitute an offer. Information, views or opinions expressed in this presentation originates from many different sources and contributors throughout the general community. Please note that the contents do not necessarily represent or reflect the views and opinions of WEALTH MANAGEMENT or their affiliates.

Beyond The realm Of possibilities

Beyond The realm Of possibilities 2014 2nd Quarter Report 目錄 Table of Contents Market Outlook US Dollar Index. 4 EURUSD... 5 GBPUSD. 6 USDJPY.... 7 Products Performance Review POWERFUND. 9 12 Ayers Alliance

Beyond The realm Of possibilities 2014 2nd Quarter Report 目錄 Table of Contents Market Outlook US Dollar Index. 4 EURUSD... 5 GBPUSD. 6 USDJPY.... 7 Products Performance Review POWERFUND. 9 12 Ayers Alliance

Beyond The realm Of possibilities

Beyond The realm Of possibilities 2013 3rd Quarter Report 目錄 Table of Contents Market Outlook 3 7 US Dollar Index. 4 EURUSD... 5 GBPUSD. 6 USDJPY.... 7 Products Performance Review 8 16 POWERFUND.. 9-12

Beyond The realm Of possibilities 2013 3rd Quarter Report 目錄 Table of Contents Market Outlook 3 7 US Dollar Index. 4 EURUSD... 5 GBPUSD. 6 USDJPY.... 7 Products Performance Review 8 16 POWERFUND.. 9-12

Explore the themes and thinking behind our decisions.

ASSET ALLOCATION COMMITTEE VIEWPOINTS Fourth Quarter 2016 These views are informed by a subjective assessment of the relative attractiveness of asset classes and subclasses over a 6- to 18-month horizon.

ASSET ALLOCATION COMMITTEE VIEWPOINTS Fourth Quarter 2016 These views are informed by a subjective assessment of the relative attractiveness of asset classes and subclasses over a 6- to 18-month horizon.

Explore the themes and thinking behind our decisions.

ASSET ALLOCATION COMMITTEE VIEWPOINTS First Quarter 2017 These views are informed by a subjective assessment of the relative attractiveness of asset classes and subclasses over a 6- to 18-month horizon.

ASSET ALLOCATION COMMITTEE VIEWPOINTS First Quarter 2017 These views are informed by a subjective assessment of the relative attractiveness of asset classes and subclasses over a 6- to 18-month horizon.

Lawrence Yun, Ph.D. Chief Economist NATIONAL ASSOCIATION OF REALTORS. Presentation at NAR Leadership Summit Chicago, IL

Lawrence Yun, Ph.D. Chief Economist NATIONAL ASSOCIATION OF REALTORS Presentation at NAR Leadership Summit Chicago, IL August 21, 2008 60 50 Home Sales Starting to Recover from Improving Affordability

Lawrence Yun, Ph.D. Chief Economist NATIONAL ASSOCIATION OF REALTORS Presentation at NAR Leadership Summit Chicago, IL August 21, 2008 60 50 Home Sales Starting to Recover from Improving Affordability

THE STATE OF THE ECONOMY

THE STATE OF THE ECONOMY ANGELA GUO Portland State University Moderate growth continued in the United States economy through the second quarter of 2013, though forecasters had anticipated an acceleration

THE STATE OF THE ECONOMY ANGELA GUO Portland State University Moderate growth continued in the United States economy through the second quarter of 2013, though forecasters had anticipated an acceleration

Weekly FX Insight. Weekly FX Insight. Dec 30, 2013 with data as of Dec 27. Citibank Wealth Management. FX & Eco. Figures Forecast

Citibank Wealth Management Weekly FX Insight Weekly FX Insight Dec 30, 2013 with data as of Dec 27 Market Review & Focus FX Analysis Weekly FX Recap 01 GBP/USD 03 USD/JPY 04 Weekly FX Focus 02 NZD/USD

Citibank Wealth Management Weekly FX Insight Weekly FX Insight Dec 30, 2013 with data as of Dec 27 Market Review & Focus FX Analysis Weekly FX Recap 01 GBP/USD 03 USD/JPY 04 Weekly FX Focus 02 NZD/USD

INDEX. Forex market outlook Donald Trump s rise and impact on the US dollar. Fed s policy and their hawkish stance

FOREX MARKET OUTLOOK 2018 1 INDEX Forex market outlook 2018 Donald Trump s rise and impact on the US dollar Fed s policy and their hawkish stance EUR/USD s recovery and Euro zone s political challenges

FOREX MARKET OUTLOOK 2018 1 INDEX Forex market outlook 2018 Donald Trump s rise and impact on the US dollar Fed s policy and their hawkish stance EUR/USD s recovery and Euro zone s political challenges

The Office of Economic Policy HOUSING DASHBOARD. March 16, 2016

The Office of Economic Policy HOUSING DASHBOARD March 16, 216 Recent housing market indicators suggest that housing activity continues to strengthen. Solid residential investment in 215Q4 contributed.3

The Office of Economic Policy HOUSING DASHBOARD March 16, 216 Recent housing market indicators suggest that housing activity continues to strengthen. Solid residential investment in 215Q4 contributed.3

Market Insight Economy and Asset Classes December Oil Prices Downtrending: The Real Global Economic Stimulus

Market Insight Economy and Asset Classes December 2014 Oil Prices Downtrending: The Real Global Economic Stimulus 2 Equities Markets Feature In Citi analysts view, the expansion phase the US are enjoying

Market Insight Economy and Asset Classes December 2014 Oil Prices Downtrending: The Real Global Economic Stimulus 2 Equities Markets Feature In Citi analysts view, the expansion phase the US are enjoying

Provided to you by Lee McLain

Provided to you by Lee McLain Lee McLain First Federal Bank of Kansas City 816.728.7700 lee.mclain@ffbkc.com NMLS:680316 Contents Weekly Review: week of September 24, 2018 Economic Calendar week of October

Provided to you by Lee McLain Lee McLain First Federal Bank of Kansas City 816.728.7700 lee.mclain@ffbkc.com NMLS:680316 Contents Weekly Review: week of September 24, 2018 Economic Calendar week of October

Interest Rates Headed Higher. What that Means for Housing.

NOVEMBER 2016 Interest Rates Headed Higher. What that Means for Housing. Interest rates surged higher over the past two weeks following the U.S. presidential election. The 10-year Treasury closed at 2.35

NOVEMBER 2016 Interest Rates Headed Higher. What that Means for Housing. Interest rates surged higher over the past two weeks following the U.S. presidential election. The 10-year Treasury closed at 2.35

Financial Concepts Unlimited, Inc.

Financial Concepts Unlimited, Inc. 30B West Street Annapolis, MD 21401 Phone: (301) 315-6344 Fax: (301) 315-6343 Toll Free:(866)-444-5122 http://www.fcuinc.com John R. Taylor Jr. President & CEO October

Financial Concepts Unlimited, Inc. 30B West Street Annapolis, MD 21401 Phone: (301) 315-6344 Fax: (301) 315-6343 Toll Free:(866)-444-5122 http://www.fcuinc.com John R. Taylor Jr. President & CEO October

After housing s best year in a decade, what s next?

DECEMBER 2016 After housing s best year in a decade, what s next? The year is drawing to a close and it is time to take stock of where housing and mortgage markets have been and where they likely are headed.

DECEMBER 2016 After housing s best year in a decade, what s next? The year is drawing to a close and it is time to take stock of where housing and mortgage markets have been and where they likely are headed.

Rising Risks for the Housing Outlook

Rising Risks for the Housing Outlook Master Builders Association of Pierce County October 17, 2018 Robert Dietz, Ph.D. NAHB Chief Economist Population Growth Pierce County population growing faster than

Rising Risks for the Housing Outlook Master Builders Association of Pierce County October 17, 2018 Robert Dietz, Ph.D. NAHB Chief Economist Population Growth Pierce County population growing faster than

PRESS RELEASE. Home Prices Continue Climbing in June 2013 According to the S&P/Case-Shiller Home Price Indices

Home Prices Continue Climbing in June 2013 According to the S&P/Case-Shiller Home Price Indices New York, August 27, 2013 Data through June 2013, released today by for its S&P/Case-Shiller 1 Home Price

Home Prices Continue Climbing in June 2013 According to the S&P/Case-Shiller Home Price Indices New York, August 27, 2013 Data through June 2013, released today by for its S&P/Case-Shiller 1 Home Price

DECEMBER 7, 2018 Market Commentary by Scott J. Brown, Ph.D., Chief Economist

DECEMBER 7, 2018 Market Commentary by Scott J. Brown, Ph.D., Chief Economist Two key issues rattled stock market investors: trade policy and the yield curve. The weekend meeting between President Trump

DECEMBER 7, 2018 Market Commentary by Scott J. Brown, Ph.D., Chief Economist Two key issues rattled stock market investors: trade policy and the yield curve. The weekend meeting between President Trump

QUARTERLY MARKET REVIEW: JANUARY - MARCH Dear Clients,

Financial Concepts Unlimited, Inc. 30B West Street Annapolis, MD 21401 Phone: (301) 315-6344 Fax: (301) 315-6343 Toll Free:(866)-444-5122 http://www.fcuinc.com John R. Taylor Jr. President & CEO April

Financial Concepts Unlimited, Inc. 30B West Street Annapolis, MD 21401 Phone: (301) 315-6344 Fax: (301) 315-6343 Toll Free:(866)-444-5122 http://www.fcuinc.com John R. Taylor Jr. President & CEO April

within the longer term downward trend that began almost a year ago. In our opinion, it s the latter that continues to look the most likely scenario.

WHAT ARE THE CHANCES Risk Insight Volume 6, Issue 12-30 March 2015..that EURUSD will touch 1.15 within the next month? 11.0% The Big Picture Is the euro primed for another leg lower? fter reaching a 12

WHAT ARE THE CHANCES Risk Insight Volume 6, Issue 12-30 March 2015..that EURUSD will touch 1.15 within the next month? 11.0% The Big Picture Is the euro primed for another leg lower? fter reaching a 12

Medium Risk Portfolio QUANTUM FUNDS PORTFOLIO REVIEW NOVEMBER DECEMBER 2014 OBJECTIVE AND STRATEGY COMPOSITION OF PORTFOLIO QUANTUM FUNDS

QUANTUM FUNDS ($500 INVESTMENT) Medium Risk Portfolio QUANTUM FUNDS PORTFOLIO REVIEW NOVEMBER OBJECTIVE AND STRATEGY The fund pursues the objective of long-term total returns combined with capital preservation.

QUANTUM FUNDS ($500 INVESTMENT) Medium Risk Portfolio QUANTUM FUNDS PORTFOLIO REVIEW NOVEMBER OBJECTIVE AND STRATEGY The fund pursues the objective of long-term total returns combined with capital preservation.

Provided to you by Lee McLain

Provided to you by Lee McLain Lee McLain First Federal Bank of Kansas City 816.728.7700 lee.mclain@ffbkc.com NMLS:680316 Contents Weekly Review: week of October 22, 2018 Economic Calendar - week of October

Provided to you by Lee McLain Lee McLain First Federal Bank of Kansas City 816.728.7700 lee.mclain@ffbkc.com NMLS:680316 Contents Weekly Review: week of October 22, 2018 Economic Calendar - week of October

U.S. Economic Outlook: recent developments

U.S. Economic Outlook Recent developments Washington, D.C., 6 February 2018 This document was prepared by Helvia Velloso, Economic Affairs Officer, under the supervision of Inés Bustillo, Director, ECLAC

U.S. Economic Outlook Recent developments Washington, D.C., 6 February 2018 This document was prepared by Helvia Velloso, Economic Affairs Officer, under the supervision of Inés Bustillo, Director, ECLAC

ANALYSIS OF THE CENTRAL VIRGINIA AREA HOUSING MARKET

ANALYSIS OF THE CENTRAL VIRGINIA AREA HOUSING MARKET 2018 First Quarter Report by John McClain, Senior Policy Fellow Ryan Price, Senior Associate George Mason University Center for Regional Analysis National

ANALYSIS OF THE CENTRAL VIRGINIA AREA HOUSING MARKET 2018 First Quarter Report by John McClain, Senior Policy Fellow Ryan Price, Senior Associate George Mason University Center for Regional Analysis National

Editor: Thomas Nilsson. The Week Ahead Key Events Jul, 2017

Editor: Thomas Nilsson The Week Ahead Key Events 10 16 Jul, 2017 European Sovereign Rating Reviews Recent rating reviews Upcoming rating reviews Source: Bloomberg Monday 10, 08.00 NOR: CPI (Jun) SEB Cons.

Editor: Thomas Nilsson The Week Ahead Key Events 10 16 Jul, 2017 European Sovereign Rating Reviews Recent rating reviews Upcoming rating reviews Source: Bloomberg Monday 10, 08.00 NOR: CPI (Jun) SEB Cons.

[ ] WEEKLY CHANGES AGAINST THE USD

![[ ] WEEKLY CHANGES AGAINST THE USD](/thumbs/78/77362224.jpg "[ ] WEEKLY CHANGES AGAINST THE USD") January 15, 2018 [ ] MACRO & MARKETS COMMENTARY» The European central bank (ECB) has indicated it should revisit its communication stance in early 2018, according to the ECB s minutes of December meeting

January 15, 2018 [ ] MACRO & MARKETS COMMENTARY» The European central bank (ECB) has indicated it should revisit its communication stance in early 2018, according to the ECB s minutes of December meeting

June 24th, Rate Reversal. Author: Benjamin Struck President

June 24th, 2013 Rate Reversal Author: Benjamin Struck President 1 Economic Summary 3 Strategic Allocation 5 Tactical Allocation 6 2 Last week s selloff was broad based and applied to nearly all asset classes.

June 24th, 2013 Rate Reversal Author: Benjamin Struck President 1 Economic Summary 3 Strategic Allocation 5 Tactical Allocation 6 2 Last week s selloff was broad based and applied to nearly all asset classes.

APRIL 18, 2019 Market Commentary by Scott J. Brown, Ph.D., Chief Economist

APRIL 18, 2019 Market Commentary by Scott J. Brown, Ph.D., Chief Economist The economic data reports were mixed, but generally consistent with moderate growth in the near term. Retail sales rose 1.6% in

APRIL 18, 2019 Market Commentary by Scott J. Brown, Ph.D., Chief Economist The economic data reports were mixed, but generally consistent with moderate growth in the near term. Retail sales rose 1.6% in

Growth May Slow to End 2016 But Sentiment Brightens

Economic Developments December 2016 Growth May Slow to End 2016 But Sentiment Brightens We expect economic growth to moderate to less than two percent this quarter, with full-year 2016 growth at 1.8 percent.

Economic Developments December 2016 Growth May Slow to End 2016 But Sentiment Brightens We expect economic growth to moderate to less than two percent this quarter, with full-year 2016 growth at 1.8 percent.

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook September 2013 Financial Market Outlook: Stocks likely to Remain in Modest Uptrend with Low Rates & Plentiful Liquidity, Improving

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook September 2013 Financial Market Outlook: Stocks likely to Remain in Modest Uptrend with Low Rates & Plentiful Liquidity, Improving

Financial Market Outlook: Stocks Rebounding from July Correction, Further Gains Likely. Bond Yields Range Bound

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Stocks Rebounding from July Correction, Further Gains Likely. Bond

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Stocks Rebounding from July Correction, Further Gains Likely. Bond

Provided to you by Lee McLain

Provided to you by Lee McLain Lee McLain First Federal Bank of Kansas City 816.728.7700 lee.mclain@ffbkc.com NMLS:680316 Contents Weekly Review: week of November 26, 2018 Economic Calendar - week of December

Provided to you by Lee McLain Lee McLain First Federal Bank of Kansas City 816.728.7700 lee.mclain@ffbkc.com NMLS:680316 Contents Weekly Review: week of November 26, 2018 Economic Calendar - week of December

October 2016 Market Update

Market Update (10/2016) Allianz Investment Management LLC October 2016 Market Update Key Points The lack of further easing measures from both the Bank of Japan and the European Central Bank are causing

Market Update (10/2016) Allianz Investment Management LLC October 2016 Market Update Key Points The lack of further easing measures from both the Bank of Japan and the European Central Bank are causing

Financial Market Outlook: Further Stock Gain on Faster GDP Rebound and Earnings Recovery. Year-end Target Raised

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: FurtherStock Gains Likely, Year-end Target Raised. Bond Under Pressure

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: FurtherStock Gains Likely, Year-end Target Raised. Bond Under Pressure

Q EARNINGS PREVIEW:

LPL RESEARCH WEEKLY MARKET COMMENTARY July 5 216 216 EARNINGS PREVIEW: BETTER TIMES AHEAD? Burt White Chief Investment Officer, LPL Financial Jeffrey Buchbinder, CFA Market Strategist, LPL Financial KEY

LPL RESEARCH WEEKLY MARKET COMMENTARY July 5 216 216 EARNINGS PREVIEW: BETTER TIMES AHEAD? Burt White Chief Investment Officer, LPL Financial Jeffrey Buchbinder, CFA Market Strategist, LPL Financial KEY

Global Equities PUTTING RECENT MARKET VOLATILITY IN PERSPECTIVE

PRICE POINT February 2018 Timely intelligence and analysis for our clients. Global Equities PUTTING RECENT MARKET VOLATILITY IN PERSPECTIVE KEY POINTS The upswing in equity market volatility can be attributed

PRICE POINT February 2018 Timely intelligence and analysis for our clients. Global Equities PUTTING RECENT MARKET VOLATILITY IN PERSPECTIVE KEY POINTS The upswing in equity market volatility can be attributed

COMPTROLLER LEMBO REPORTS EARLY INDICATIONS THAT STATE COULD END FISCAL YEAR 2019 IN SURPLUS

COMPTROLLER LEMBO REPORTS EARLY INDICATIONS THAT STATE COULD END FISCAL YEAR 2019 IN SURPLUS Comptroller Kevin Lembo today said that there are reasons for cautious optimism that the state could end Fiscal

COMPTROLLER LEMBO REPORTS EARLY INDICATIONS THAT STATE COULD END FISCAL YEAR 2019 IN SURPLUS Comptroller Kevin Lembo today said that there are reasons for cautious optimism that the state could end Fiscal

Outlook for the Hawai'i Economy

Outlook for the Hawai'i Economy May 3, 2001 Dr. Carl Bonham University of Hawai'i Economic Research Organization Summary The Hawaii economy entered 2001 in its best shape in more than a decade. While the

Outlook for the Hawai'i Economy May 3, 2001 Dr. Carl Bonham University of Hawai'i Economic Research Organization Summary The Hawaii economy entered 2001 in its best shape in more than a decade. While the

Currencies Daily Report

Currencies Daily Report www.karvycurrency.com Friday 02 Jun 2017 Market Overview Asian shares were mostly higher today with attention on U.S. jobs data later in the day. Overnight, U.S. stocks made a winning

Currencies Daily Report www.karvycurrency.com Friday 02 Jun 2017 Market Overview Asian shares were mostly higher today with attention on U.S. jobs data later in the day. Overnight, U.S. stocks made a winning

Q WestEnd Advisors. Macroeconomic Highlights. (888)

") Q1 2017 WestEnd Advisors Macroeconomic Highlights www.westendadvisors.com info@westendadvisors.com (888) 500-9025 1 U.S. Economic Picture Prior to the November Election 3-Month Moving Average 1.0 0.5 0.0-0.5-1.0-1.5-2.0

Q1 2017 WestEnd Advisors Macroeconomic Highlights www.westendadvisors.com info@westendadvisors.com (888) 500-9025 1 U.S. Economic Picture Prior to the November Election 3-Month Moving Average 1.0 0.5 0.0-0.5-1.0-1.5-2.0

New England Economic Partnership May 2013: Massachusetts

Executive Summary and Highlights MASSACHUSETTS ECONOMIC OUTLOOK The Massachusetts economy is in the fourth year of the expansion that began in the summer of 2009. During this expansion, real gross state

Executive Summary and Highlights MASSACHUSETTS ECONOMIC OUTLOOK The Massachusetts economy is in the fourth year of the expansion that began in the summer of 2009. During this expansion, real gross state

US Economic Outlook Improving

Government Bonds Have Never Looked Less Attractive OUTLOOK Executive Summary Kenneth J. Taubes Chief Investment Officer, US Economic Outlook US GDP growth may lead growth among developed nations, at approximately

Government Bonds Have Never Looked Less Attractive OUTLOOK Executive Summary Kenneth J. Taubes Chief Investment Officer, US Economic Outlook US GDP growth may lead growth among developed nations, at approximately

Strong Economic Growth Despite Weaker Housing Market Activity

AUGUST 2018 Strong Economic Growth Despite Weaker Housing Market Activity The U.S. economy accelerated in the second quarter of 2018, with real GDP growth at 4.1 percent, which was the strongest quarterly

AUGUST 2018 Strong Economic Growth Despite Weaker Housing Market Activity The U.S. economy accelerated in the second quarter of 2018, with real GDP growth at 4.1 percent, which was the strongest quarterly

How Affordability Affects Housing s Spring Season

MARCH 2017 How Affordability Affects Housing s Spring Season Recent indications of stronger growth convinced the Federal Reserve to raise the Federal funds rate this month and to signal further increases

MARCH 2017 How Affordability Affects Housing s Spring Season Recent indications of stronger growth convinced the Federal Reserve to raise the Federal funds rate this month and to signal further increases

Raymond James WEEKLY MARKET SNAPSHOT

Page 1 of 5 June 21, 2013 MARKET COMMENTARY BY SCOTT J. BROWN, PH.D., CHIEF ECONOMIST The Federal Open Market Committee left short-term interest rates unchanged, did not alter its forward guidance on the

Page 1 of 5 June 21, 2013 MARKET COMMENTARY BY SCOTT J. BROWN, PH.D., CHIEF ECONOMIST The Federal Open Market Committee left short-term interest rates unchanged, did not alter its forward guidance on the

SEPTEMBER S&P CORELOGIC CASE-SHILLER NATIONAL HOME PRICE NSA INDEX UP 6.2% IN LAST 12 MONTHS

SEPTEMBER S&P CORELOGIC CASE-SHILLER NATIONAL HOME PRICE NSA INDEX UP 6.2% IN LAST 12 MONTHS NEW YORK, NOVEMBER 28, 2017 S&P Dow Jones Indices today released the latest results for the S&P CoreLogic Case-Shiller

SEPTEMBER S&P CORELOGIC CASE-SHILLER NATIONAL HOME PRICE NSA INDEX UP 6.2% IN LAST 12 MONTHS NEW YORK, NOVEMBER 28, 2017 S&P Dow Jones Indices today released the latest results for the S&P CoreLogic Case-Shiller

Economic and Portfolio Outlook 4th Quarter 2014 (Released October 2014)

") Economic and Portfolio Outlook 4th Quarter 2014 (Released October 2014) Our economic outlook for the fourth quarter of 2014 for the U.S. is continued slow growth. We stated in our 3 rd quarter Economic

Economic and Portfolio Outlook 4th Quarter 2014 (Released October 2014) Our economic outlook for the fourth quarter of 2014 for the U.S. is continued slow growth. We stated in our 3 rd quarter Economic

Smith Leonard PLLC Kenneth D. Smith, CPA Mark S. Laferriere, CPA

FURNITURE INSIGHTS Smith Leonard PLLC s Industry Newsletter May 2018 HIGHLIGHTS - EXECUTIVE SUMMARY A fter hearing about how sluggish business was in the first quarter, our survey of residential furniture

FURNITURE INSIGHTS Smith Leonard PLLC s Industry Newsletter May 2018 HIGHLIGHTS - EXECUTIVE SUMMARY A fter hearing about how sluggish business was in the first quarter, our survey of residential furniture

Economic and Financial Markets Monthly Review & Outlook Detailed Report. June 2014

Economic and Financial Markets Monthly Review & Outlook Detailed Report June 1 Overview of the Economy In the U.S., the Federal Reserve s Beige Book report on the economy through late May indicated that

Economic and Financial Markets Monthly Review & Outlook Detailed Report June 1 Overview of the Economy In the U.S., the Federal Reserve s Beige Book report on the economy through late May indicated that

LAS VEGAS LEADS PRICE GAINS IN JUNE ACCORDING TO S&P CORELOGIC CASE-SHILLER INDEX

LAS VEGAS LEADS PRICE GAINS IN JUNE ACCORDING TO S&P CORELOGIC CASE-SHILLER INDEX NEW YORK, AUGUST 28, 2018 S&P Dow Jones Indices today released the latest results for the S&P CoreLogic Case-Shiller Indices,

LAS VEGAS LEADS PRICE GAINS IN JUNE ACCORDING TO S&P CORELOGIC CASE-SHILLER INDEX NEW YORK, AUGUST 28, 2018 S&P Dow Jones Indices today released the latest results for the S&P CoreLogic Case-Shiller Indices,

Financial Market Outlook & Strategy: Stocks Bottoming On Track to Recovery. Near-term Risks

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Stocks Bottoming On Track to Recovery. Near-term Risks John Praveen

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Stocks Bottoming On Track to Recovery. Near-term Risks John Praveen

Prudential International Investments Advisers, LLC. Global Investment Strategy October 2009

Prudential International Investments Advisers, LLC. Global Investment Strategy October 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Prudential International Investments Advisers, LLC. Global Investment Strategy October 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Key takeaways. What it may mean for investors FIRST A NALYSIS NEWS OR EVENTS T HAT MAY AFFECT Y OUR INVESTMENTS. Global Investment Strategy Team

FIRST A NALYSIS NEWS OR EVENTS T HAT MAY AFFECT Y OUR INVESTMENTS Global Investment Strategy Team February 5, 2018 Market Sell-off What Investors Need to Know Now Key takeaways» A swift climb in the 10-year

FIRST A NALYSIS NEWS OR EVENTS T HAT MAY AFFECT Y OUR INVESTMENTS Global Investment Strategy Team February 5, 2018 Market Sell-off What Investors Need to Know Now Key takeaways» A swift climb in the 10-year

Recap of 2017 Markets and Economy

Welcome to 2018! As always, our primary goal this year is to continue our tradition of helping clients achieve their personal financial goals. To make that process more efficient, please review the 2018

Welcome to 2018! As always, our primary goal this year is to continue our tradition of helping clients achieve their personal financial goals. To make that process more efficient, please review the 2018

Haruhiko Kuroda: Japan s economy and monetary policy

Haruhiko Kuroda: Japan s economy and monetary policy Speech by Mr Haruhiko Kuroda, Governor of the Bank of Japan, at a meeting with business leaders, Osaka, 28 September 2015. Introduction * * * It is

Haruhiko Kuroda: Japan s economy and monetary policy Speech by Mr Haruhiko Kuroda, Governor of the Bank of Japan, at a meeting with business leaders, Osaka, 28 September 2015. Introduction * * * It is

Editor: Felix Ewert. The Week Ahead Key Events Mar 2018

Editor: Felix Ewert The Week Ahead Key Events 12 18 Mar 2018 Monday 12, 08.00 SWE: Unemployment, registered (Feb) SEB Cons. Prev. Open 3.9 --- 4.0 Open, seas. adj. 3.8 --- 3.8 Total seas. adj. 7.1 ---

Editor: Felix Ewert The Week Ahead Key Events 12 18 Mar 2018 Monday 12, 08.00 SWE: Unemployment, registered (Feb) SEB Cons. Prev. Open 3.9 --- 4.0 Open, seas. adj. 3.8 --- 3.8 Total seas. adj. 7.1 ---

Global FX 2 Apr 2012

Global FX 2 Apr 2012 Uncertainty reigned in the currency market over the past two weeks, with the dollar fluctuating in rather tight ranges against most other major currencies. The greenback initially

Global FX 2 Apr 2012 Uncertainty reigned in the currency market over the past two weeks, with the dollar fluctuating in rather tight ranges against most other major currencies. The greenback initially

By John Praveen, Chief Investment Strategist of Prudential International Investments Advisers, LLC.*

By John Praveen, Chief Investment Strategist of Prudential International Investments Advisers, LLC.* For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

By John Praveen, Chief Investment Strategist of Prudential International Investments Advisers, LLC.* For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

June & July 2012 CURRENCY FORECAST

June & July 2012 CURRENCY FORECAST Foreign Exchange & Global Payments CURRENCY FORECAST CHART GBP/USD EXCHANGE RATES MAY Avg. JUNE & JULY f 2012 Q4 f USD/CAD 1.0107 1.0100-1.0600 0.9900 EUR/USD 1.2800

June & July 2012 CURRENCY FORECAST Foreign Exchange & Global Payments CURRENCY FORECAST CHART GBP/USD EXCHANGE RATES MAY Avg. JUNE & JULY f 2012 Q4 f USD/CAD 1.0107 1.0100-1.0600 0.9900 EUR/USD 1.2800

Annual Market Review 2016

Annual Market Review 2016 Overview The year 2016 likely will be remembered for the election of Donald Trump as the 45th president of the United States and the Brexit vote. This year also saw the Fed raise

Annual Market Review 2016 Overview The year 2016 likely will be remembered for the election of Donald Trump as the 45th president of the United States and the Brexit vote. This year also saw the Fed raise

Housing Demand Holding Steady Amidst Rising Mortgage and Home Prices

MAY 2018 Housing Demand Holding Steady Amidst Rising Mortgage and Home Prices Real Gross Domestic Product (GDP) grew at an annualized rate of 2.3 percent in the first quarter of 2018, down from 2.9 percent

MAY 2018 Housing Demand Holding Steady Amidst Rising Mortgage and Home Prices Real Gross Domestic Product (GDP) grew at an annualized rate of 2.3 percent in the first quarter of 2018, down from 2.9 percent

PRESS RELEASE. Home Price Gains Continue to Moderate According to the S&P/Case-Shiller Home Price Indices

Home Price Gains Continue to Moderate According to the S&P/Case-Shiller Home Price Indices New York, July 29, 2014 Data through May 2014, released today by for its S&P/Case-Shiller 1 Home Price Indices,

Home Price Gains Continue to Moderate According to the S&P/Case-Shiller Home Price Indices New York, July 29, 2014 Data through May 2014, released today by for its S&P/Case-Shiller 1 Home Price Indices,

Currency Research Desk

Currency Research Desk Currency weekly October 29, 2012 Global economic review Economic performance All the Financial markets remained at tenterhook expect some of the Asian bourses. However, the two largest

Currency Research Desk Currency weekly October 29, 2012 Global economic review Economic performance All the Financial markets remained at tenterhook expect some of the Asian bourses. However, the two largest

Economy Check-In: Post 2008 Crisis Market Update Special Report

Insight. Education. Analysis. Economy Check-In: Post 2008 Crisis Market Update Special Report By Kevin Chambers The 2008 crisis was one of the worst downturns in American economic history. News reports

Insight. Education. Analysis. Economy Check-In: Post 2008 Crisis Market Update Special Report By Kevin Chambers The 2008 crisis was one of the worst downturns in American economic history. News reports

COMMENTARY NUMBER 378 June Retail Sales, PPI, May Trade Deficit. July 14, 2011

COMMENTARY NUMBER 378 June Retail Sales, PPI, May Trade Deficit July 14, 2011 At Best, Inflation-Adjusted Retail Sales Showed No Growth in Second-Quarter 2011 Trade Data Should Offer a Positive Contribution

COMMENTARY NUMBER 378 June Retail Sales, PPI, May Trade Deficit July 14, 2011 At Best, Inflation-Adjusted Retail Sales Showed No Growth in Second-Quarter 2011 Trade Data Should Offer a Positive Contribution

2014 Annual Review & Outlook

2014 Annual Review & Outlook As we enter 2014, the current economic expansion is 4.5 years in duration, roughly the average life of U.S. economic expansions. There is every reason to believe it will continue,

2014 Annual Review & Outlook As we enter 2014, the current economic expansion is 4.5 years in duration, roughly the average life of U.S. economic expansions. There is every reason to believe it will continue,

FX Insights. Chart Of The Day USD/JPY: Next significant support at Friday, 29 April 2016

Quek Ser Leang Quek.SerLeang@uobgroup.com Lee Sue Ann Lee.SueAnn@uobgroup.com Global Economics & Markets Research Email: GlobalEcoMktResearch@uobgroup.com URL: www.uob.com.sg/research Chart Of The Day

Quek Ser Leang Quek.SerLeang@uobgroup.com Lee Sue Ann Lee.SueAnn@uobgroup.com Global Economics & Markets Research Email: GlobalEcoMktResearch@uobgroup.com URL: www.uob.com.sg/research Chart Of The Day

US Dollar Struggles as Euro Gains Top Spot - A review of the Major Global Currencies

US Dollar Struggles as Euro Gains Top Spot - A review of the Major Global Currencies 26 th November 2017 My colleagues have been urging me to write a weekly commentary on Bitcoin/Cryptocurrencies. However,

US Dollar Struggles as Euro Gains Top Spot - A review of the Major Global Currencies 26 th November 2017 My colleagues have been urging me to write a weekly commentary on Bitcoin/Cryptocurrencies. However,

FX Insights. Chart Of The Day USD/CNH: Expect deep pull-back towards with lower odds for extension to Friday, 22 July 2016

Quek Ser Leang Quek.SerLeang@uobgroup.com Lee Sue Ann Lee.SueAnn@uobgroup.com Global Economics & Markets Research Email: GlobalEcoMktResearch@uobgroup.com URL: www.uob.com.sg/research Chart Of The Day

Quek Ser Leang Quek.SerLeang@uobgroup.com Lee Sue Ann Lee.SueAnn@uobgroup.com Global Economics & Markets Research Email: GlobalEcoMktResearch@uobgroup.com URL: www.uob.com.sg/research Chart Of The Day

2014: Started with a Deep Hole, Ending with a Whimper Growth Received an Upgrade But Some Payback is in the Cards

2014: Started with a Deep Hole, Ending with a Whimper The year 2014 will be remembered for its roller-coaster pattern of economic growth. The unusually cold winter weather helped put growth in deep negative

2014: Started with a Deep Hole, Ending with a Whimper The year 2014 will be remembered for its roller-coaster pattern of economic growth. The unusually cold winter weather helped put growth in deep negative

Daily Market Reflection

Daily Market Reflection Commodity Market Outlook Gold edged higher on Wednesday as the dollar weakened after the previous session's rally, though gains were seen as limited by a recovery in equity markets

Daily Market Reflection Commodity Market Outlook Gold edged higher on Wednesday as the dollar weakened after the previous session's rally, though gains were seen as limited by a recovery in equity markets

Economic Slowdown Ahead

Economic Slowdown Ahead NAHB Meeting of the Members February 20, 2019 Robert Dietz, Ph.D. NAHB Chief Economist GDP Growth Economic slowdown approaching 10% 8% 6% Q/Q Percent Change, SAAR Annual Growth

Economic Slowdown Ahead NAHB Meeting of the Members February 20, 2019 Robert Dietz, Ph.D. NAHB Chief Economist GDP Growth Economic slowdown approaching 10% 8% 6% Q/Q Percent Change, SAAR Annual Growth

Financial Market Outlook: Stock Rally Continues with Faster & Stronger GDP Rebound, Earnings Recovery & Liquidity

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Further Stock Gains with Macro Sweet Spot & Earnings Recovery.

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Further Stock Gains with Macro Sweet Spot & Earnings Recovery.

Danske Bank March 1 ST 2016 Economic Update,

Monthly update: Tuesday 1 March 2016 Danske Bank Chief Economist, Twitter: angela_mcgowan Local job and investment announcements during January 2016: The NI economy suffered a significant blow during the

Monthly update: Tuesday 1 March 2016 Danske Bank Chief Economist, Twitter: angela_mcgowan Local job and investment announcements during January 2016: The NI economy suffered a significant blow during the

Smith Leonard PLLC Kenneth D. Smith, CPA Mark S. Laferriere, CPA

Smith Leonard PLLC s Industry Newsletter January 2018 HIGHLIGHTS - EXECUTIVE SUMMARY A ccording to our latest survey of residential furniture manufacturers and distributors, new orders in November 2017

Smith Leonard PLLC s Industry Newsletter January 2018 HIGHLIGHTS - EXECUTIVE SUMMARY A ccording to our latest survey of residential furniture manufacturers and distributors, new orders in November 2017

Flash Note Japan: Macro and market outlook

FLASH NOTE Flash Note Japan: Macro and market outlook Strong growth and Abenomics mean Japanese equities continue to provide opportunities Pictet Wealth Management - Asset Allocation & Macro Research 26

FLASH NOTE Flash Note Japan: Macro and market outlook Strong growth and Abenomics mean Japanese equities continue to provide opportunities Pictet Wealth Management - Asset Allocation & Macro Research 26

Commentary March 2013

Market Price of Bond Market Price of Bond Commentary March 2013 Interest Rates: Creeping Higher Interest rates and bond yields are at multi-generational lows and are expected to trend higher over the next

Market Price of Bond Market Price of Bond Commentary March 2013 Interest Rates: Creeping Higher Interest rates and bond yields are at multi-generational lows and are expected to trend higher over the next

G10 FX Week Ahead: Waiting for the ECB

Economic and Financial Analysis 23 October 2017 FX 23 October 2017 Article G10 FX Week Ahead: Waiting for the ECB The key focus for FX markets is the ECB meeting on Thursday. Here's our view of major currency

Economic and Financial Analysis 23 October 2017 FX 23 October 2017 Article G10 FX Week Ahead: Waiting for the ECB The key focus for FX markets is the ECB meeting on Thursday. Here's our view of major currency

Quarterly Currency Outlook

Mature Economies Quarterly Currency Outlook MarketQuant Research Writing completed on July 12, 2017 Content 1. Key elements of background for mature market currencies... 4 2. Detailed Currency Outlook...

Mature Economies Quarterly Currency Outlook MarketQuant Research Writing completed on July 12, 2017 Content 1. Key elements of background for mature market currencies... 4 2. Detailed Currency Outlook...

SIP Aggressive Portfolio

SIP LIFESTYLE PORTFOLIOS FACT SHEET (NOV 2015) SIP Aggressive Portfolio SIP Aggressive Portfolio is a unitized fund, which is designed to provide long term capital growth. It is designed for those who

SIP LIFESTYLE PORTFOLIOS FACT SHEET (NOV 2015) SIP Aggressive Portfolio SIP Aggressive Portfolio is a unitized fund, which is designed to provide long term capital growth. It is designed for those who

2018 ECONOMIC OUTLOOK

LPL RESEARCH WEEKLY ECONOMIC COMMENTARY December 4 207 208 ECONOMIC OUTLOOK EXPECT BETTER GROWTH WORLDWIDE John Lynch Chief Investment Strategist, LPL Financial Barry Gilbert, PhD, CFA Asset Allocation

LPL RESEARCH WEEKLY ECONOMIC COMMENTARY December 4 207 208 ECONOMIC OUTLOOK EXPECT BETTER GROWTH WORLDWIDE John Lynch Chief Investment Strategist, LPL Financial Barry Gilbert, PhD, CFA Asset Allocation

PRESS RELEASE. Widespread Slowdown in Home Price Gains According to the S&P/Case-Shiller Home Price Indices

Widespread Slowdown in Home Price Gains According to the S&P/Case-Shiller Home Price Indices New York, August 26, 2014 Data through June 2014, released today by for its S&P/Case-Shiller 1 Home Price Indices,

Widespread Slowdown in Home Price Gains According to the S&P/Case-Shiller Home Price Indices New York, August 26, 2014 Data through June 2014, released today by for its S&P/Case-Shiller 1 Home Price Indices,

S&P CORELOGIC CASE-SHILLER NATIONAL HOME PRICE NSA INDEX CONTINUES STEADY GAINS IN OCTOBER

S&P CORELOGIC CASE-SHILLER NATIONAL HOME PRICE NSA INDEX CONTINUES STEADY GAINS IN OCTOBER NEW YORK, DECEMBER 26, 2017 S&P Dow Jones Indices today released the latest results for the S&P CoreLogic Case-Shiller

S&P CORELOGIC CASE-SHILLER NATIONAL HOME PRICE NSA INDEX CONTINUES STEADY GAINS IN OCTOBER NEW YORK, DECEMBER 26, 2017 S&P Dow Jones Indices today released the latest results for the S&P CoreLogic Case-Shiller

BCA 4Q 2018 Review and 2019 Outlook Russ Allen, CIO. Summary Outlook

BCA 4Q 2018 Review and 2019 Outlook Russ Allen, CIO Summary Outlook January 15, 2019 Markets in 2019 will be choppy with volatility more like this past year than the placid trading of 2017. The Fed is

BCA 4Q 2018 Review and 2019 Outlook Russ Allen, CIO Summary Outlook January 15, 2019 Markets in 2019 will be choppy with volatility more like this past year than the placid trading of 2017. The Fed is

MID-TERM REVIEW OF THE 2014 MONETARY POLICY STATEMENT

MID-TERM REVIEW OF THE 2014 MONETARY POLICY STATEMENT 1. INTRODUCTION 1.1 The Mid-Term Review (MTR) of the 2014 Monetary Policy Statement (MPS) examines recent price developments and reviews key financial

MID-TERM REVIEW OF THE 2014 MONETARY POLICY STATEMENT 1. INTRODUCTION 1.1 The Mid-Term Review (MTR) of the 2014 Monetary Policy Statement (MPS) examines recent price developments and reviews key financial

MTFX ANALYTICS OCTOBER 2012 CURRENCY FORECAST

MTFX ANALYTICS OCTOBER 2012 CURRENCY FORECAST Foreign Exchange & Global Payments MONTHLY CURRENCY FORECAST CHART GBP/USD EXCHANGE RATES SEP Avg OCT f 2012 Q4 f USD/CAD 0.9790 0.9600 1.0200 0.9800 EUR/USD

MTFX ANALYTICS OCTOBER 2012 CURRENCY FORECAST Foreign Exchange & Global Payments MONTHLY CURRENCY FORECAST CHART GBP/USD EXCHANGE RATES SEP Avg OCT f 2012 Q4 f USD/CAD 0.9790 0.9600 1.0200 0.9800 EUR/USD

Economic Outlook Spring 2014

Economic Outlook Spring 2014 Accelerating Economic Growth Ahead FROM ANTHONY CHAN, PHD, CHIEF ECONOMIST FOR CHASE Summary After a strong 2013 finish with U.S. and European stock markets posting double-digit

Economic Outlook Spring 2014 Accelerating Economic Growth Ahead FROM ANTHONY CHAN, PHD, CHIEF ECONOMIST FOR CHASE Summary After a strong 2013 finish with U.S. and European stock markets posting double-digit

Global Economic Outlook 2014 Year Ahead Outlook January 2014

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Economic Outlook 2014 Year Ahead Outlook January 2014 2014 Year Ahead - Global Economic Outlook Global Growth Strengthens as U.S. & U.K. GDP Growth

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Economic Outlook 2014 Year Ahead Outlook January 2014 2014 Year Ahead - Global Economic Outlook Global Growth Strengthens as U.S. & U.K. GDP Growth

THE STATE OF THE ECONOMY

THE STATE OF THE ECONOMY CARLY HARRISON Portland State University The economy continues to grow at a steady rate, with slight increases in global and national GDP, a lower national unemployment rate, and

THE STATE OF THE ECONOMY CARLY HARRISON Portland State University The economy continues to grow at a steady rate, with slight increases in global and national GDP, a lower national unemployment rate, and

Housing & Mortgage Market Outlook

Housing & Mortgage Market Outlook 2005 Economic Outlook Symposium Federal Reserve Bank of Chicago December 2005 David W. Berson Vice President & Chief Economist What You Want to Know: We expect economic

Housing & Mortgage Market Outlook 2005 Economic Outlook Symposium Federal Reserve Bank of Chicago December 2005 David W. Berson Vice President & Chief Economist What You Want to Know: We expect economic

Risk Insight. The Central Bank Tightening Party: Who Will Be Next To Join? What are the chances... Volume 8, Issue th July 2017.

Inside this issue Big Picture... 1-2 GBPUSD... 3 GBPEUR... 4 Risk Insight Volume 8, Issue 31 24 th July 2017 EURUSD... 5 USDCAD... 6 Economic Data and Market Indicators... 7 Appendix... 8 The Central Bank

Inside this issue Big Picture... 1-2 GBPUSD... 3 GBPEUR... 4 Risk Insight Volume 8, Issue 31 24 th July 2017 EURUSD... 5 USDCAD... 6 Economic Data and Market Indicators... 7 Appendix... 8 The Central Bank

Banks at a Glance: Economic and Banking Highlights by State 2Q 2018

Economic and Banking Highlights by State 2Q 2018 These semi-annual reports highlight key indicators of economic and banking conditions within each of the nine states comprising the 12th Federal Reserve

Economic and Banking Highlights by State 2Q 2018 These semi-annual reports highlight key indicators of economic and banking conditions within each of the nine states comprising the 12th Federal Reserve

National Housing Market Summary

1st 2017 June 2017 HUD PD&R National Housing Market Summary The Housing Market Recovery Showed Progress in the First The housing market improved in the first quarter of 2017. Construction starts rose for

1st 2017 June 2017 HUD PD&R National Housing Market Summary The Housing Market Recovery Showed Progress in the First The housing market improved in the first quarter of 2017. Construction starts rose for

Banks at a Glance: Alaska

Banks at a Glance: Financial Institution Supervision and Credit sf.fisc.publications@sf.frb.org Economic and Banking Highlights Data as of 12/31/216 's economy continued to struggle, driven by weaknesses

Banks at a Glance: Financial Institution Supervision and Credit sf.fisc.publications@sf.frb.org Economic and Banking Highlights Data as of 12/31/216 's economy continued to struggle, driven by weaknesses

Currencies Daily Report

Currencies Daily Report Powered by Karvy Forex & Currencies Pvt. Ltd. www.karvyforex.com Thursday 08 Jun 2017 Market Overview Political winds from elections in the U.K. and testimony to Congress by the

Currencies Daily Report Powered by Karvy Forex & Currencies Pvt. Ltd. www.karvyforex.com Thursday 08 Jun 2017 Market Overview Political winds from elections in the U.K. and testimony to Congress by the

Empire State Manufacturing Survey.

February 218 Empire State Manufacturing Survey Business activity continued to expand in New York State, according to firms responding to the February 218 Empire State Manufacturing Survey. The headline

February 218 Empire State Manufacturing Survey Business activity continued to expand in New York State, according to firms responding to the February 218 Empire State Manufacturing Survey. The headline

The state of the nation s Housing 2013

The state of the nation s Housing 2013 Fact Sheet PURPOSE The State of the Nation s Housing report has been released annually by Harvard University s Joint Center for Housing Studies since 1988. Now in

The state of the nation s Housing 2013 Fact Sheet PURPOSE The State of the Nation s Housing report has been released annually by Harvard University s Joint Center for Housing Studies since 1988. Now in

A Divided Real Estate Nation

Real Estate Reality Check Explanation of "What Happened" from the 26 Leadership Conference Boom ended August 2 Mortgage rates rose almost one point Affordability conditions deteriorated Speculative investors

Real Estate Reality Check Explanation of "What Happened" from the 26 Leadership Conference Boom ended August 2 Mortgage rates rose almost one point Affordability conditions deteriorated Speculative investors

MORGANTOWN METROPOLITAN STATISTICAL AREA OUTLOOK COLLEGE OF BUSINESS AND ECONOMICS. Bureau of Business and Economic Research

2013 MORGANTOWN METROPOLITAN STATISTICAL AREA OUTLOOK COLLEGE OF BUSINESS AND ECONOMICS Bureau of Business and Economic Research 1 MORGANTOWN METROPOLITAN STATISTICAL AREA OUtlook 2013 EXECUTIVE SUMMARY

2013 MORGANTOWN METROPOLITAN STATISTICAL AREA OUTLOOK COLLEGE OF BUSINESS AND ECONOMICS Bureau of Business and Economic Research 1 MORGANTOWN METROPOLITAN STATISTICAL AREA OUtlook 2013 EXECUTIVE SUMMARY

Smith Leonard PLLC Kenneth D. Smith, CPA Mark S. Laferriere, CPA

FURNITURE INSIGHTS Smith Leonard PLLC s Industry Newsletter August 2018 N HIGHLIGHTS - EXECUTIVE SUMMARY ew orders in June 2018 were up 5% over June 2017, according to our recent survey of residential

FURNITURE INSIGHTS Smith Leonard PLLC s Industry Newsletter August 2018 N HIGHLIGHTS - EXECUTIVE SUMMARY ew orders in June 2018 were up 5% over June 2017, according to our recent survey of residential

Putnam Stable Value Fund

Product profile Q1 2016 Putnam Stable Value Fund Inception date February 28, 1991 Total portfolio assets $5.7B Putnam Stable as of March 31, 2016 Value Weighted average maturity 2.66 Effective duration

Product profile Q1 2016 Putnam Stable Value Fund Inception date February 28, 1991 Total portfolio assets $5.7B Putnam Stable as of March 31, 2016 Value Weighted average maturity 2.66 Effective duration