Econ 234C Corporate Finance Lecture 2: Internal Investment (I)

|

|

|

- Sabina Hoover

- 5 years ago

- Views:

Transcription

1 Econ 234C Corporate Finance Lecture 2: Internal Investment (I) Ulrike Malmendier UC Berkeley January 30, 2008

2 1 Corporate Investment 1.1 A few basics from last class Baseline model of investment and financing Three-periods, firm has existing assets A and s shares outstanding. Ass. 1: financing with internal cash or equity issuance; no debt Ass. 2: zero interest rate Timeline t = 0: return function R(I) becomes known to CEO + investors; R defined on [0, ), R 0 > 0, R 00 < 0, R 0 (I) > 1 for some I. t = 1: cashflow C is realized (firm s new net worth A + C); CEO chooses I. t = 2: R(I) realized.

3 CEO s optimization problem CEO maximizes shareholder value subject to the financing constraint: s max I s + s0(a + R(I)) s.t. s 0 (A + R(I)) = I C s + s0 if I>C = First-order condition: R 0 (I) =1.

4 Digression: We are assuming that a CEO (in a world without incentive problems, without asymmetric information) maximizes s/(s + s 0 ) (A + R(I)). What does this mean? What alternative assumption would make sense (i.e., is consistent with shareholder-vaue maximization )? How does the maximization problem look like now? Would it make a difference? If so for what?

5 1.2 Empirical Evidence on Investment Theory: In a frictionless world, investment cash flow. (Firm can borrow at market interest rate.) Baseline empirical test: I k,t = α + βc k,t + X 0 k,t Γ + μ k + ν t + ε k,t where C is cash-flow of company k in year t, X k,t includes a proxy for investment opportunities (Q k,t ) Much of the empirical evidence is about testing whether coefficient β significantly different from 0.

6 Remark: What bigger question are we trying to address here (indirectly)? Why don t we ask it directly? Can you think of ways of asking directly? Can you think of OTHER ways of asking this question indirectly?

7 Identification of Investment-Cash Flow Sensitivity Model: I k,t = α + βc k,t + X 0 k,t Γ + μ k + ν t + ε k,t Identification: Need exogenous shock to C k,t 1. Unexpected gains from law-suits (Blanchard, Lopez-de-Silanes, Shleifer, JFE 1994): windfall gains used for acquisitions. 2. Oil price shocks (Lamont, JF 1997): impact on investment in non-oil segments of oil companies. 3. Hurricanes (Froot-O Connell, 1997): reinsurers supply less earthquake coverage after post-hurricane payments. 4. Non-linearities in pension fund requirements (Rauh, JF 2006).

8 Identification using Oil Price Shocks (Lamont, JF 1997) Idea: Step1: exogenous shock to cash flow available to a firm = oil price exogenously determined + affects CF of oil firms Step2: exogenous shock needs to be orthogonal to investment opportunities (quality of investment projects) = non-oil subsidiaries of oil companies

9 Caveat: joint hypothesis test with financial frictions + internal capital markets ( corporate socialism ) Data: Focus on 1986 oil price decrease. Argument 1: size of price change: 50% (from $26.60/barrel in 12/1985 to $12.67/barrel in 4/1986). Argument 2: unanticipated (What is otherwise the problem?) Def. oil company: primary or secondary SIC as oil/gas extraction AND 25% of C k,1985 from oil/gas extraction. Def. non-oil-segment: ρ(profit, oil price) 0.

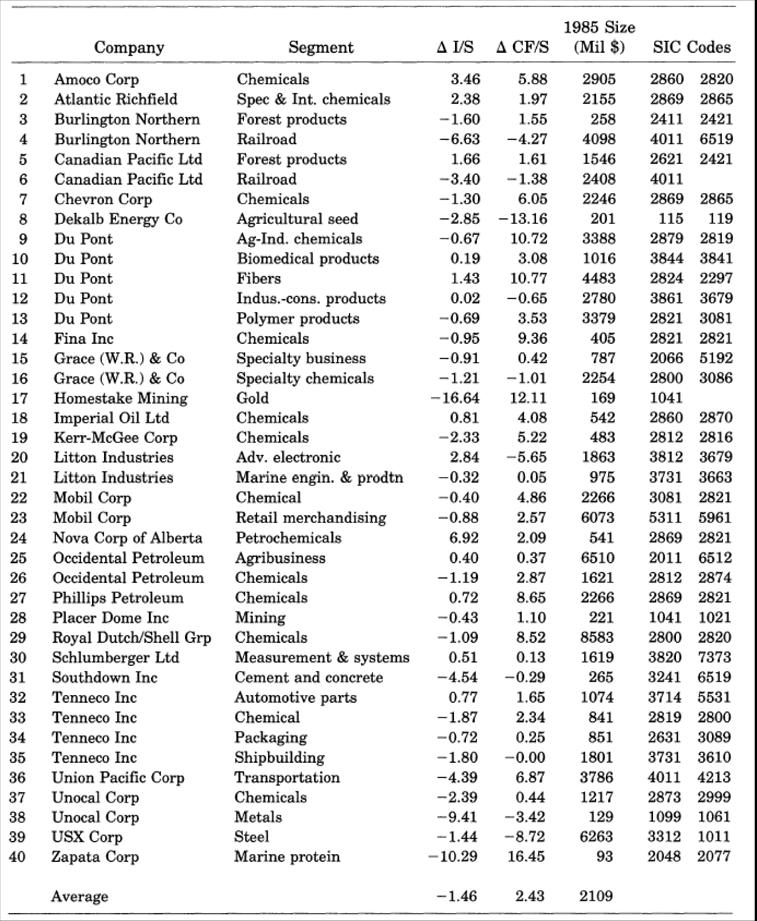

10 Final sample: 26 firms, 40 segments Note: Exclusion of financial or services industry as it is standard (because of complex accounting variables) Concrete examples; quotes from newspapers, annoual reports! Appendix with full listing, including the excluded firms. Results: Table III ( = ) : eye-ball test increase in CF in nonoil segments decrease in investment in nonoil segments

11

12

13 Limits: Mere time-series identification. = What is the problem? See Table I, Panel A: Increase in non-energy profit rate in 1986 supports identifcation. Explosion in 1987 casts doubt on identification. (Why?)

14 Other Evidence Windfall gains from law-suits (Blanchard, Lopez-de-Silanes, Shleifer, JFE 1994) Problem: N =11 Non-linearities in pension fund requirements (Rauh, JF 2006) Firms that sponsor defined benefit (DB) pension plans must make financial contributions to their pension funds. If underfunded, mandatory contributions. If overfunded, contributions only up to a limit. Contributions affect internal financial resources. If a firm is financially constrained, contributions thus affect ability to invest.

15 Mandatory Contributions (%) Mandatory Contribution as % of Underfunding 60% 50% 40% 30% 20% 10% Minimum Funding Contribution 1974-present Deficit Reduction Contribution Deficit Reduction Contribution 1995-present 0% Funding Status (%) Minimum funding contribution drawn for a firm with sample mean characteristics: liabilities of $37.3m, a normal cost of $1.3m, and prior credits of $0.5m.

16 Issues (many of which explored by Rauh himself in follow-up papers!) Claim: Required contributions exogenous relative to investment opportunities. But: investment & hiring / age structure / turnover etc? Manipulation similar to earnings manipulation? As with Lamont: investment further before and further after. Does not exploit (much) the discontinuity between funded and underfunded. (Only within underfunded)

17 Broad conclusions from above papers: I/CF sensitivity exists It remains hard to put a $$ amount on it. It remains hard to understand generalizability.

18 1.3 Why is Investment Sensitive to Cash Flow? Prime hypothesis: financial constraints. Cost of external equity finance > cost of external debt finance > cost of internal finance. (Pecking order) Illustration from Fazzari, Hubbard and Petersen (1988) D 1 /D 2 /D 3 = low/medium/high level of investment demand (depending on Q)

19

20 I k,t = α + βc k,t + X 0 k,t Γ + μ k + ν t + ε k,t Fazzari, Hubbard and Petersen (1988) sort on a priori measures of constraint (dividends) and interpret β. Kaplan and Zingales (1997) show that β is not higher for firms that truly appear constrained. Sample: 49 low-dividend paying firms from FHP (1988) Data source: letters to shareholders, management discussions of operations and liquidity, financial statements with notes (from annual report / 10-K filings); COMPUSTAT instead of VALUELINE data

21 Establish comparability of sample

22 Next step:split firms in quintiles of severity of being financial constrained and show that I/CF sensitivity is not increasing in financial constraints.

23 Main insights: 1. Dividends is not a good proxy for financial constraints. The median firm in the highest quintile coud have paid large dividends (58% of investment) without seeking additional funding / permission from current lenders. 2. Financial constraints do not explain I/CF sensitivity. Nver-constrained firms have the hightes I/CF sensitivity. Side product: KZ index as a measure of financial constraint. KZ it = CF it K it Q it Lev it Dividend it C it K it 1 ==> Typical use: quintiled. ==> Often double-lagged (endogeneity). K it 1 (Other ex-ante measures of financial constraints: age, debt-rating)

24 Theories relating to I/CF sensitivity Asymmetric information Implies underinvestment (external financing more costly than internal financing) Myers and Majluf (1984) Manager-shareholder agency problems Tendency to over-invest; (internal resources easier to divert) Jensen and Meckling (1976), Stulz (1990), Hart and Moore (1995) Overoptimism/overconfidence Tendency to over-invest; but perceived undervaluation may lead to underinvestment in the case of equity-financing Heaton (2002); Malmendier and Tate (2005)

25 1.4 Required reading for next class: Myers, Stewart and N. Majluf (1984), Corporate Financing and Investment Decisions when Firms Have Information that Investors Do Not Have, Journal of Financial Economics 13, pp Jensen, Michael and William Meckling (1976), Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure, Journal of Financial Economics 3, pp Jensen, Michael (1986), Agency Costs of Free Cash Flow, Corporate Finance, and Takeovers, American Economic Review 76, pp

26 1.5 Take away & Research Ideas If your main field is not finance: Clean estimates of the phenomenon (in education economics, development economcis). Exploring explanations other than financial constraints in areas where financial constraints is the typical explanation (e.g. firm-level growth data in development). Use investment-cf sensitivity where you are really interested in investment quality (as a measure of the degree of suboptimality ). If your field is finance: My guess (my personal taste?): little room for yet another identification / criticism (despite lack of the perfect paper).

27 Direct measures of investment quality? Look at frictions other than sensitivity to cash flow, e.g. over-/underadjustment to demographic trends.

Econ 234C Corporate Finance Lecture 1: Topics and Tools

Econ 234C Corporate Finance Lecture 1: Topics and Tools Ulrike Malmendier UC Berkeley January 16, 2006 Outline 1. Syllabus and Organization 2. Topics in Corporate Finance 3. Tools and Methods in Corporate

Econ 234C Corporate Finance Lecture 1: Topics and Tools Ulrike Malmendier UC Berkeley January 16, 2006 Outline 1. Syllabus and Organization 2. Topics in Corporate Finance 3. Tools and Methods in Corporate

How Costly is External Financing? Evidence from a Structural Estimation. Christopher Hennessy and Toni Whited March 2006

How Costly is External Financing? Evidence from a Structural Estimation Christopher Hennessy and Toni Whited March 2006 The Effects of Costly External Finance on Investment Still, after all of these years,

How Costly is External Financing? Evidence from a Structural Estimation Christopher Hennessy and Toni Whited March 2006 The Effects of Costly External Finance on Investment Still, after all of these years,

Causes and consequences of Cash Flow Sensitivity: Empirical Tests of the US Lodging Industry

Journal of Hospitality Financial Management The Professional Refereed Journal of the International Association of Hospitality Financial Management Educators Volume 15 Issue 1 Article 11 2007 Causes and

Journal of Hospitality Financial Management The Professional Refereed Journal of the International Association of Hospitality Financial Management Educators Volume 15 Issue 1 Article 11 2007 Causes and

Investment Cash Flow Sensitivity and Effect of Managers Ownership: Difference between Central Owned and Private Owned Companies in China

International Journal of Economics and Financial Issues Vol. 4, No. 3, 2014, pp.449-456 ISSN: 2146-4138 www.econjournals.com Investment Cash Flow Sensitivity and Effect of Managers Ownership: Difference

International Journal of Economics and Financial Issues Vol. 4, No. 3, 2014, pp.449-456 ISSN: 2146-4138 www.econjournals.com Investment Cash Flow Sensitivity and Effect of Managers Ownership: Difference

Dr. Syed Tahir Hijazi 1[1]

![Dr. Syed Tahir Hijazi 1[1]](/thumbs/79/79837134.jpg "Dr. Syed Tahir Hijazi 1[1]") The Determinants of Capital Structure in Stock Exchange Listed Non Financial Firms in Pakistan By Dr. Syed Tahir Hijazi 1[1] and Attaullah Shah 2[2] 1[1] Professor & Dean Faculty of Business Administration

The Determinants of Capital Structure in Stock Exchange Listed Non Financial Firms in Pakistan By Dr. Syed Tahir Hijazi 1[1] and Attaullah Shah 2[2] 1[1] Professor & Dean Faculty of Business Administration

Econ 234C Corporate Finance Lecture 8: External Investment (finishing up) Capital Structure

Capital Structure") Econ 234C Corporate Finance Lecture 8: External Investment (finishing up) Capital Structure Ulrike Malmendier UC Berkeley March 13, 2007 Outline 1. Organization: Exams 2. External Investment (IV): Managerial

Econ 234C Corporate Finance Lecture 8: External Investment (finishing up) Capital Structure Ulrike Malmendier UC Berkeley March 13, 2007 Outline 1. Organization: Exams 2. External Investment (IV): Managerial

Investment and Financing Constraints

Investment and Financing Constraints Nathalie Moyen University of Colorado at Boulder Stefan Platikanov Suffolk University We investigate whether the sensitivity of corporate investment to internal cash

Investment and Financing Constraints Nathalie Moyen University of Colorado at Boulder Stefan Platikanov Suffolk University We investigate whether the sensitivity of corporate investment to internal cash

Financial Constraints and the Risk-Return Relation. Abstract

Financial Constraints and the Risk-Return Relation Tao Wang Queens College and the Graduate Center of the City University of New York Abstract Stock return volatilities are related to firms' financial

Financial Constraints and the Risk-Return Relation Tao Wang Queens College and the Graduate Center of the City University of New York Abstract Stock return volatilities are related to firms' financial

Financing Constraints and Corporate Investment

Financing Constraints and Corporate Investment Basic Question Is the impact of finance on real corporate investment fully summarized by a price? cost of finance (user) cost of capital required rate of

Financing Constraints and Corporate Investment Basic Question Is the impact of finance on real corporate investment fully summarized by a price? cost of finance (user) cost of capital required rate of

Paul Gompers EMCF 2009 March 5, 2009

Paul Gompers EMCF 2009 March 5, 2009 Examine two papers that use interesting cross sectional variation to identify their tests. Find a discontinuity in the data. In how much you have to fund your pension

Paul Gompers EMCF 2009 March 5, 2009 Examine two papers that use interesting cross sectional variation to identify their tests. Find a discontinuity in the data. In how much you have to fund your pension

DETERMINANTS OF DEBT CAPACITY. 1st set of transparencies. Tunis, May Jean TIROLE

DETERMINANTS OF DEBT CAPACITY 1st set of transparencies Tunis, May 2005 Jean TIROLE I. INTRODUCTION Adam Smith (1776) - Berle-Means (1932) Agency problem Principal outsiders/investors/lenders Agent insiders/managers/entrepreneur

DETERMINANTS OF DEBT CAPACITY 1st set of transparencies Tunis, May 2005 Jean TIROLE I. INTRODUCTION Adam Smith (1776) - Berle-Means (1932) Agency problem Principal outsiders/investors/lenders Agent insiders/managers/entrepreneur

CORPORATE CASH HOLDING AND FIRM VALUE

CORPORATE CASH HOLDING AND FIRM VALUE Cristina Martínez-Sola Dep. Business Administration, Accounting and Sociology University of Jaén Jaén (SPAIN) E-mail: mmsola@ujaen.es Pedro J. García-Teruel Dep. Management

CORPORATE CASH HOLDING AND FIRM VALUE Cristina Martínez-Sola Dep. Business Administration, Accounting and Sociology University of Jaén Jaén (SPAIN) E-mail: mmsola@ujaen.es Pedro J. García-Teruel Dep. Management

Investment-Cash Flow Sensitivity for Swedish Firms

Stockholm School of Economics Bachelor Thesis Accounting & Financial Management Spring 2016 Investment-Cash Flow Sensitivity for Swedish Firms Is overinvestment and underinvestment related to positive

Stockholm School of Economics Bachelor Thesis Accounting & Financial Management Spring 2016 Investment-Cash Flow Sensitivity for Swedish Firms Is overinvestment and underinvestment related to positive

Discussion of Overinvestment of free cash flow

Rev Acc Stud (2006) 11:191 202 DOI 10.1007/s11142-006-9002-3 Discussion of Overinvestment of free cash flow Daniel Bergstresser Published online: 20 May 2006 Ó Springer Science+Business Media, LLC 2006

Rev Acc Stud (2006) 11:191 202 DOI 10.1007/s11142-006-9002-3 Discussion of Overinvestment of free cash flow Daniel Bergstresser Published online: 20 May 2006 Ó Springer Science+Business Media, LLC 2006

ENTREPRENEURIAL OPTIMISM, CREDIT AVAILABILITY, AND COST OF FINANCING: EVIDENCE FROM U.S. SMALL BUSINESSES

ENTREPRENEURIAL OPTIMISM, CREDIT AVAILABILITY, AND COST OF FINANCING: EVIDENCE FROM U.S. SMALL BUSINESSES DISCLAIMER The Securities and Exchange Commission, as a matter of policy, disclaims responsibility

ENTREPRENEURIAL OPTIMISM, CREDIT AVAILABILITY, AND COST OF FINANCING: EVIDENCE FROM U.S. SMALL BUSINESSES DISCLAIMER The Securities and Exchange Commission, as a matter of policy, disclaims responsibility

Managerial Optimism, Investment Efficiency, and Firm Valuation

1 Managerial Optimism, Investment Efficiency, and Firm Valuation I-Ju Chen* Yuan Ze University, Taiwan Shin-Hung Lin Yuan Ze University, Taiwan This study investigates the relationship between managerial

1 Managerial Optimism, Investment Efficiency, and Firm Valuation I-Ju Chen* Yuan Ze University, Taiwan Shin-Hung Lin Yuan Ze University, Taiwan This study investigates the relationship between managerial

A Model with Costly Enforcement

A Model with Costly Enforcement Jesús Fernández-Villaverde University of Pennsylvania December 25, 2012 Jesús Fernández-Villaverde (PENN) Costly-Enforcement December 25, 2012 1 / 43 A Model with Costly

A Model with Costly Enforcement Jesús Fernández-Villaverde University of Pennsylvania December 25, 2012 Jesús Fernández-Villaverde (PENN) Costly-Enforcement December 25, 2012 1 / 43 A Model with Costly

Cash Flow Sensitivity of Investment: Firm-Level Analysis

Cash Flow Sensitivity of Investment: Firm-Level Analysis Armen Hovakimian Baruch College and Gayane Hovakimian * Fordham University May 12, 2005 ABSTRACT Using firm level estimates of investment-cash flow

Cash Flow Sensitivity of Investment: Firm-Level Analysis Armen Hovakimian Baruch College and Gayane Hovakimian * Fordham University May 12, 2005 ABSTRACT Using firm level estimates of investment-cash flow

The Determinants of Capital Structure of Stock Exchange-listed Non-financial Firms in Pakistan

The Pakistan Development Review 43 : 4 Part II (Winter 2004) pp. 605 618 The Determinants of Capital Structure of Stock Exchange-listed Non-financial Firms in Pakistan ATTAULLAH SHAH and TAHIR HIJAZI *

The Pakistan Development Review 43 : 4 Part II (Winter 2004) pp. 605 618 The Determinants of Capital Structure of Stock Exchange-listed Non-financial Firms in Pakistan ATTAULLAH SHAH and TAHIR HIJAZI *

THE WILLIAM DAVIDSON INSTITUTE AT THE UNIVERSITY OF MICHIGAN BUSINESS SCHOOL

THE WILLIAM DAVIDSON INSTITUTE AT THE UNIVERSITY OF MICHIGAN BUSINESS SCHOOL Financial Dependence, Stock Market Liberalizations, and Growth By: Nandini Gupta and Kathy Yuan William Davidson Working Paper

THE WILLIAM DAVIDSON INSTITUTE AT THE UNIVERSITY OF MICHIGAN BUSINESS SCHOOL Financial Dependence, Stock Market Liberalizations, and Growth By: Nandini Gupta and Kathy Yuan William Davidson Working Paper

Cash holdings determinants in the Portuguese economy 1

17 Cash holdings determinants in the Portuguese economy 1 Luísa Farinha Pedro Prego 2 Abstract The analysis of liquidity management decisions by firms has recently been used as a tool to investigate the

17 Cash holdings determinants in the Portuguese economy 1 Luísa Farinha Pedro Prego 2 Abstract The analysis of liquidity management decisions by firms has recently been used as a tool to investigate the

Do Peer Firms Affect Corporate Financial Policy?

1 / 23 Do Peer Firms Affect Corporate Financial Policy? Journal of Finance, 2014 Mark T. Leary 1 and Michael R. Roberts 2 1 Olin Business School Washington University 2 The Wharton School University of

1 / 23 Do Peer Firms Affect Corporate Financial Policy? Journal of Finance, 2014 Mark T. Leary 1 and Michael R. Roberts 2 1 Olin Business School Washington University 2 The Wharton School University of

Managerial Overconfidence, Moral Hazard Problems, and

Managerial Overconfidence, Moral Hazard Problems, and Excessive Life-cycle Debt Sensitivity. Richard Fairchild, School of Management, University of Bath, UK March 27 th, 2009 Abstract We analyse the effects

Managerial Overconfidence, Moral Hazard Problems, and Excessive Life-cycle Debt Sensitivity. Richard Fairchild, School of Management, University of Bath, UK March 27 th, 2009 Abstract We analyse the effects

Ownership Structure and Capital Structure Decision

Modern Applied Science; Vol. 9, No. 4; 2015 ISSN 1913-1844 E-ISSN 1913-1852 Published by Canadian Center of Science and Education Ownership Structure and Capital Structure Decision Seok Weon Lee 1 1 Division

Modern Applied Science; Vol. 9, No. 4; 2015 ISSN 1913-1844 E-ISSN 1913-1852 Published by Canadian Center of Science and Education Ownership Structure and Capital Structure Decision Seok Weon Lee 1 1 Division

Corporate Liquidity Management and Financial Constraints

Corporate Liquidity Management and Financial Constraints Zhonghua Wu Yongqiang Chu This Draft: June 2007 Abstract This paper examines the effect of financial constraints on corporate liquidity management

Corporate Liquidity Management and Financial Constraints Zhonghua Wu Yongqiang Chu This Draft: June 2007 Abstract This paper examines the effect of financial constraints on corporate liquidity management

Market Value of the Firm, Market Value of Equity, Return Rate on Capital and the Optimal Capital Structure

Market Value of the Firm, Market Value of Equity, Return Rate on Capital and the Optimal Capital Structure Chao Chiung Ting Michigan State University, USA E-mail: tingtch7ti@aol.com Received: September

Market Value of the Firm, Market Value of Equity, Return Rate on Capital and the Optimal Capital Structure Chao Chiung Ting Michigan State University, USA E-mail: tingtch7ti@aol.com Received: September

I. Introduction In an influential paper, Jensen (1986) argues that cash inflows (equivalently, cash holdings) enable managers to extract private benef

argues that cash inflows (equivalently, cash holdings) enable managers to extract private benef") Note: Preliminary, please ask authors before citing Do Corporate Cash Holdings Cause Agency Problems? Deniz Okat Hong Kong University of Science and Technology Mikael Paaso Aalto University of School of

Note: Preliminary, please ask authors before citing Do Corporate Cash Holdings Cause Agency Problems? Deniz Okat Hong Kong University of Science and Technology Mikael Paaso Aalto University of School of

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Investment and Financing Policies of Nepalese Enterprises

Investment and Financing Policies of Nepalese Enterprises Kapil Deb Subedi 1 Abstract Firm financing and investment policies are central to the study of corporate finance. In imperfect capital market,

Investment and Financing Policies of Nepalese Enterprises Kapil Deb Subedi 1 Abstract Firm financing and investment policies are central to the study of corporate finance. In imperfect capital market,

Do Financial Frictions Amplify Fiscal Policy?

Do Financial Frictions Amplify Fiscal Policy? Evidence from Business Investment Stimulus Eric Zwick and James Mahon* NTA Annual Conference on Taxation, November 13th, 2014 *The views expressed here are

Do Financial Frictions Amplify Fiscal Policy? Evidence from Business Investment Stimulus Eric Zwick and James Mahon* NTA Annual Conference on Taxation, November 13th, 2014 *The views expressed here are

Dynamic Capital Structure Choice

Dynamic Capital Structure Choice Xin Chang * Department of Finance Faculty of Economics and Commerce University of Melbourne Sudipto Dasgupta Department of Finance Hong Kong University of Science and Technology

Dynamic Capital Structure Choice Xin Chang * Department of Finance Faculty of Economics and Commerce University of Melbourne Sudipto Dasgupta Department of Finance Hong Kong University of Science and Technology

Corporate Liquidity. Amy Dittmar Indiana University. Jan Mahrt-Smith London Business School. Henri Servaes London Business School and CEPR

Corporate Liquidity Amy Dittmar Indiana University Jan Mahrt-Smith London Business School Henri Servaes London Business School and CEPR This Draft: May 2002 We are grateful to João Cocco, David Goldreich,

Corporate Liquidity Amy Dittmar Indiana University Jan Mahrt-Smith London Business School Henri Servaes London Business School and CEPR This Draft: May 2002 We are grateful to João Cocco, David Goldreich,

Role of financial leverage in determining corporate investment in Pakistan

Role of financial leverage in determining corporate investment in Pakistan Abdul Haque Department of Management Science COMSATS Institute of Information Technology, Lahore, Pakistan Keywords Financial

Role of financial leverage in determining corporate investment in Pakistan Abdul Haque Department of Management Science COMSATS Institute of Information Technology, Lahore, Pakistan Keywords Financial

THE CAPITAL STRUCTURE S DETERMINANT IN FIRM LOCATED IN INDONESIA

THE CAPITAL STRUCTURE S DETERMINANT IN FIRM LOCATED IN INDONESIA Linna Ismawati Sulaeman Rahman Nidar Nury Effendi Aldrin Herwany ABSTRACT This research aims to identify the capital structure s determinant

THE CAPITAL STRUCTURE S DETERMINANT IN FIRM LOCATED IN INDONESIA Linna Ismawati Sulaeman Rahman Nidar Nury Effendi Aldrin Herwany ABSTRACT This research aims to identify the capital structure s determinant

The Impact of Uncertainty on Investment: Empirical Evidence from Manufacturing Firms in Korea

The Impact of Uncertainty on Investment: Empirical Evidence from Manufacturing Firms in Korea Hangyong Lee Korea development Institute December 2005 Abstract This paper investigates the empirical relationship

The Impact of Uncertainty on Investment: Empirical Evidence from Manufacturing Firms in Korea Hangyong Lee Korea development Institute December 2005 Abstract This paper investigates the empirical relationship

Debt/Equity Ratio and Asset Pricing Analysis

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies Summer 8-1-2017 Debt/Equity Ratio and Asset Pricing Analysis Nicholas Lyle Follow this and additional works

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies Summer 8-1-2017 Debt/Equity Ratio and Asset Pricing Analysis Nicholas Lyle Follow this and additional works

Tax Policy and Heterogeneous Investment Behavior

Tax Policy and Heterogeneous Investment Behavior Eric Zwick and James Mahon* *The views expressed here are the authors and do not necessarily reflect those of the Internal Revenue Service or the Office

Tax Policy and Heterogeneous Investment Behavior Eric Zwick and James Mahon* *The views expressed here are the authors and do not necessarily reflect those of the Internal Revenue Service or the Office

Discussion Paper No. 593

Discussion Paper No. 593 MANAGEMENT OWNERSHIP AND FIRM S VALUE: AN EMPIRICAL ANALYSIS USING PANEL DATA Sang-Mook Lee and Keunkwan Ryu September 2003 The Institute of Social and Economic Research Osaka

Discussion Paper No. 593 MANAGEMENT OWNERSHIP AND FIRM S VALUE: AN EMPIRICAL ANALYSIS USING PANEL DATA Sang-Mook Lee and Keunkwan Ryu September 2003 The Institute of Social and Economic Research Osaka

M&A Activity in Europe

M&A Activity in Europe Cash Reserves, Acquisitions and Shareholder Wealth in Europe Master Thesis in Business Administration at the Department of Banking and Finance Faculty Advisor: PROF. DR. PER ÖSTBERG

M&A Activity in Europe Cash Reserves, Acquisitions and Shareholder Wealth in Europe Master Thesis in Business Administration at the Department of Banking and Finance Faculty Advisor: PROF. DR. PER ÖSTBERG

Financial Economics Field Exam August 2011

Financial Economics Field Exam August 2011 There are two questions on the exam, representing Macroeconomic Finance (234A) and Corporate Finance (234C). Please answer both questions to the best of your

Financial Economics Field Exam August 2011 There are two questions on the exam, representing Macroeconomic Finance (234A) and Corporate Finance (234C). Please answer both questions to the best of your

Credit Constraints and Investment-Cash Flow Sensitivities

Credit Constraints and Investment-Cash Flow Sensitivities Heitor Almeida September 30th, 2000 Abstract This paper analyzes the investment behavior of rms under a quantity constraint on the amount of external

Credit Constraints and Investment-Cash Flow Sensitivities Heitor Almeida September 30th, 2000 Abstract This paper analyzes the investment behavior of rms under a quantity constraint on the amount of external

Abnormal accruals and external financing

Abnormal accruals and external financing Theodore H. Goodman Eller College of Management University of Arizona McClelland Hall Tucson, AZ 85721-0108 tgoodman@email.arizona.edu August 2007 ABSTRACT In this

Abnormal accruals and external financing Theodore H. Goodman Eller College of Management University of Arizona McClelland Hall Tucson, AZ 85721-0108 tgoodman@email.arizona.edu August 2007 ABSTRACT In this

Capital Market Conditions and the Financial and Real Implications of Cash Holdings *

Capital Market Conditions and the Financial and Real Implications of Cash Holdings * Aziz Alimov University of Arizona Wayne Mikkelson University of Oregon This draft: October 18, 2009 Abstract We investigate

Capital Market Conditions and the Financial and Real Implications of Cash Holdings * Aziz Alimov University of Arizona Wayne Mikkelson University of Oregon This draft: October 18, 2009 Abstract We investigate

Corporate Financial Management. Lecture 3: Other explanations of capital structure

Corporate Financial Management Lecture 3: Other explanations of capital structure As we discussed in previous lectures, two extreme results, namely the irrelevance of capital structure and 100 percent

Corporate Financial Management Lecture 3: Other explanations of capital structure As we discussed in previous lectures, two extreme results, namely the irrelevance of capital structure and 100 percent

The Determinants of Capital Structure: Analysis of Non Financial Firms Listed in Karachi Stock Exchange in Pakistan

Analysis of Non Financial Firms Listed in Karachi Stock Exchange in Pakistan Introduction The capital structure of a company is a particular combination of debt, equity and other sources of finance that

Analysis of Non Financial Firms Listed in Karachi Stock Exchange in Pakistan Introduction The capital structure of a company is a particular combination of debt, equity and other sources of finance that

Internal Capital Markets in Business Groups

Internal Capital Markets in Business Groups Krislert Samphantharak November, 2002 Abstract Business groups are important in many countries. Several studies have looked at the performance and behavior of

Internal Capital Markets in Business Groups Krislert Samphantharak November, 2002 Abstract Business groups are important in many countries. Several studies have looked at the performance and behavior of

Internet Appendix to: Common Ownership, Competition, and Top Management Incentives

Internet Appendix to: Common Ownership, Competition, and Top Management Incentives Miguel Antón, Florian Ederer, Mireia Giné, and Martin Schmalz August 13, 2016 Abstract This internet appendix provides

Internet Appendix to: Common Ownership, Competition, and Top Management Incentives Miguel Antón, Florian Ederer, Mireia Giné, and Martin Schmalz August 13, 2016 Abstract This internet appendix provides

Johannes Beyenbach, Marc Steffen Rapp, and Daniel Powell

Family control and the sensitivity of investment to cash flow: Evidence from a Multi-Equation Approach Johannes Beyenbach, Marc Steffen Rapp, and Daniel Powell 19th Workshop on Corporate Governance and

Family control and the sensitivity of investment to cash flow: Evidence from a Multi-Equation Approach Johannes Beyenbach, Marc Steffen Rapp, and Daniel Powell 19th Workshop on Corporate Governance and

Controlling Shareholders Expropriation and the Sensitivity of Investment to Cash Flow

Controlling Shareholders Expropriation and the Sensitivity of Investment to Cash Flow Zheng (Nadal) Wang University of California, Santa Barbara October 12, 2017 Abstract This paper argues that investment-cash

Controlling Shareholders Expropriation and the Sensitivity of Investment to Cash Flow Zheng (Nadal) Wang University of California, Santa Barbara October 12, 2017 Abstract This paper argues that investment-cash

Journal of Financial and Strategic Decisions Volume 13 Number 2 Summer 2000 MANAGERIAL COMPENSATION AND OPTIMAL CORPORATE HEDGING

Journal of Financial and Strategic Decisions Volume 13 Number 2 Summer 2000 MANAGERIAL COMPENSATION AND OPTIMAL CORPORATE HEDGING Steven B. Perfect *, Kenneth W. Wiles and Shawn D. Howton ** Abstract This

Journal of Financial and Strategic Decisions Volume 13 Number 2 Summer 2000 MANAGERIAL COMPENSATION AND OPTIMAL CORPORATE HEDGING Steven B. Perfect *, Kenneth W. Wiles and Shawn D. Howton ** Abstract This

Does financial liberalisation reduce credit constraints: A study of firms in the Indian private corporate sector

Proceedings of FIKUSZ 09 Symposium for Young Researchers, 2009, 147-160 The Author(s). Conference Proceedings compilation Budapest Tech Keleti Károly Faculty of Economics 2009. Published by Budapest Tech

Proceedings of FIKUSZ 09 Symposium for Young Researchers, 2009, 147-160 The Author(s). Conference Proceedings compilation Budapest Tech Keleti Károly Faculty of Economics 2009. Published by Budapest Tech

Depression Babies: Do Macroeconomic Experiences Affect Risk-Taking?

Depression Babies: Do Macroeconomic Experiences Affect Risk-Taking? October 19, 2009 Ulrike Malmendier, UC Berkeley (joint work with Stefan Nagel, Stanford) 1 The Tale of Depression Babies I don t know

Depression Babies: Do Macroeconomic Experiences Affect Risk-Taking? October 19, 2009 Ulrike Malmendier, UC Berkeley (joint work with Stefan Nagel, Stanford) 1 The Tale of Depression Babies I don t know

Bakke & Whited [JF 2012] Threshold Events and Identification: A Study of Cash Shortfalls Discussion by Fabian Brunner & Nicolas Boob

![Bakke & Whited [JF 2012] Threshold Events and Identification: A Study of Cash Shortfalls Discussion by Fabian Brunner & Nicolas Boob](/thumbs/85/92264989.jpg "Bakke & Whited [JF 2012] Threshold Events and Identification: A Study of Cash Shortfalls Discussion by Fabian Brunner & Nicolas Boob") Bakke & Whited [JF 2012] Threshold Events and Identification: A Study of Cash Shortfalls Discussion by Background and Motivation Rauh (2006): Financial constraints and real investment Endogeneity: Investment

Bakke & Whited [JF 2012] Threshold Events and Identification: A Study of Cash Shortfalls Discussion by Background and Motivation Rauh (2006): Financial constraints and real investment Endogeneity: Investment

Debt Covenants and the Macroeconomy: The Interest Coverage Channel

Debt Covenants and the Macroeconomy: The Interest Coverage Channel Daniel L. Greenwald MIT Sloan EFA Lunch, April 19 Daniel L. Greenwald Debt Covenants and the Macroeconomy EFA Lunch, April 19 1 / 6 Introduction

Debt Covenants and the Macroeconomy: The Interest Coverage Channel Daniel L. Greenwald MIT Sloan EFA Lunch, April 19 Daniel L. Greenwald Debt Covenants and the Macroeconomy EFA Lunch, April 19 1 / 6 Introduction

CORPORATE TAX INCENTIVES AND CAPITAL STRUCTURE: EVIDENCE FROM UK TAX RETURN DATA

CORPORATE TAX INCENTIVES AND CAPITAL STRUCTURE: EVIDENCE FROM UK TAX RETURN DATA Jing Xing, Giorgia Maffini, and Michael Devereux Centre for Business Taxation Saïd Business School University of Oxford

CORPORATE TAX INCENTIVES AND CAPITAL STRUCTURE: EVIDENCE FROM UK TAX RETURN DATA Jing Xing, Giorgia Maffini, and Michael Devereux Centre for Business Taxation Saïd Business School University of Oxford

Innovative Capability and Financing Constraints for Innovation: More Money, More Innovation?

Innovative Capability and Financing Constraints for Innovation: More Money, More Innovation? Hanna Hottenrott and Bettina Peters Presented by 陈亚会 2017.12.4 Introduction Discussion Paper from European Economic

Innovative Capability and Financing Constraints for Innovation: More Money, More Innovation? Hanna Hottenrott and Bettina Peters Presented by 陈亚会 2017.12.4 Introduction Discussion Paper from European Economic

CASH HOLDING POLICY AND ABILITY TO INVEST: HOW DO FIRMS DETERMINE

CASH HOLDING POLICY AND ABILITY TO INVEST: HOW DO FIRMS DETERMINE THEIR CAPITAL EXPENDITURES? NEW EVIDENCE FROM THE UK MARKET Maria-Teresa Marchica Manchester Accounting and Finance Group Manchester Business

CASH HOLDING POLICY AND ABILITY TO INVEST: HOW DO FIRMS DETERMINE THEIR CAPITAL EXPENDITURES? NEW EVIDENCE FROM THE UK MARKET Maria-Teresa Marchica Manchester Accounting and Finance Group Manchester Business

The U-Shaped Investment Curve

MSc in Finance and International Business Aarhus School of Business University of Aarhus Master thesis The U-Shaped Investment Curve Empirical evidence from a panel of US manufacturing and mining firms

MSc in Finance and International Business Aarhus School of Business University of Aarhus Master thesis The U-Shaped Investment Curve Empirical evidence from a panel of US manufacturing and mining firms

Long Term Performance of Divesting Firms and the Effect of Managerial Ownership. Robert C. Hanson

Long Term Performance of Divesting Firms and the Effect of Managerial Ownership Robert C. Hanson Department of Finance and CIS College of Business Eastern Michigan University Ypsilanti, MI 48197 Moon H.

Long Term Performance of Divesting Firms and the Effect of Managerial Ownership Robert C. Hanson Department of Finance and CIS College of Business Eastern Michigan University Ypsilanti, MI 48197 Moon H.

Financial Innovation and Borrowers: Evidence from Peer-to-Peer Lending

Financial Innovation and Borrowers: Evidence from Peer-to-Peer Lending Tetyana Balyuk BdF-TSE Conference November 12, 2018 Research Question Motivation Motivation Imperfections in consumer credit market

Financial Innovation and Borrowers: Evidence from Peer-to-Peer Lending Tetyana Balyuk BdF-TSE Conference November 12, 2018 Research Question Motivation Motivation Imperfections in consumer credit market

R&D sensitivity to asset sale proceeds: New evidence on financing constraints and intangible investment

Finance Publication Finance 1-2013 R&D sensitivity to asset sale proceeds: New evidence on financing constraints and intangible investment Ginka Borisova Iowa State University, ginka@iastate.edu James

Finance Publication Finance 1-2013 R&D sensitivity to asset sale proceeds: New evidence on financing constraints and intangible investment Ginka Borisova Iowa State University, ginka@iastate.edu James

Executive Compensation, Financial Constraint and Product Market Strategies

Executive Compensation, Financial Constraint and Product Market Strategies Jaideep Chowdhury January 17, 01 Abstract In this paper, we provide an additional factor that can explain a firm s product market

Executive Compensation, Financial Constraint and Product Market Strategies Jaideep Chowdhury January 17, 01 Abstract In this paper, we provide an additional factor that can explain a firm s product market

Managerial Incentives and Corporate Cash Holdings

Managerial Incentives and Corporate Cash Holdings Tracy Xu University of Denver Bo Han University of Washington We examine the impact of managerial incentive on firms cash holdings policy. We find that

Managerial Incentives and Corporate Cash Holdings Tracy Xu University of Denver Bo Han University of Washington We examine the impact of managerial incentive on firms cash holdings policy. We find that

Controlling Shareholders Expropriation and the Sensitivity of Investment to Cash Flow

Controlling Shareholders Expropriation and the Sensitivity of Investment to Cash Flow Zheng (Nadal) Wang University of California, Santa Barbara October 7, 2017 Abstract This paper argues that investment-cash

Controlling Shareholders Expropriation and the Sensitivity of Investment to Cash Flow Zheng (Nadal) Wang University of California, Santa Barbara October 7, 2017 Abstract This paper argues that investment-cash

Credit Constraints and Search Frictions in Consumer Credit Markets

in Consumer Credit Markets Bronson Argyle Taylor Nadauld Christopher Palmer BYU BYU Berkeley-Haas CFPB 2016 1 / 20 What we ask in this paper: Introduction 1. Do credit constraints exist in the auto loan

in Consumer Credit Markets Bronson Argyle Taylor Nadauld Christopher Palmer BYU BYU Berkeley-Haas CFPB 2016 1 / 20 What we ask in this paper: Introduction 1. Do credit constraints exist in the auto loan

Investment, Alternative Measures of Fundamentals, and Revenue Indicators

Investment, Alternative Measures of Fundamentals, and Revenue Indicators Nihal Bayraktar, February 03, 2008 Abstract The paper investigates the empirical significance of revenue management in determining

Investment, Alternative Measures of Fundamentals, and Revenue Indicators Nihal Bayraktar, February 03, 2008 Abstract The paper investigates the empirical significance of revenue management in determining

Motivated Institutional Investors and Firm Investment

Motivated Institutional Investors and Firm Investment Efficiency Charles Ward 1, Chao Yin 1, and Yeqin Zeng 1 1 University of Reading January 13, 2017 Abstract This paper investigates whether firms with

Motivated Institutional Investors and Firm Investment Efficiency Charles Ward 1, Chao Yin 1, and Yeqin Zeng 1 1 University of Reading January 13, 2017 Abstract This paper investigates whether firms with

How Does Earnings Management Affect Innovation Strategies of Firms?

How Does Earnings Management Affect Innovation Strategies of Firms? Abstract This paper examines how earnings quality affects innovation strategies and their economic consequences. Previous literatures

How Does Earnings Management Affect Innovation Strategies of Firms? Abstract This paper examines how earnings quality affects innovation strategies and their economic consequences. Previous literatures

Determinants of Target Capital Structure: The Case of Dual Debt and Equity Issues

Determinants of Target Capital Structure: The Case of Dual Debt and Equity Issues Armen Hovakimian Baruch College Gayane Hovakimian Fordham University Hassan Tehranian Boston College We thank Jim Booth,

Determinants of Target Capital Structure: The Case of Dual Debt and Equity Issues Armen Hovakimian Baruch College Gayane Hovakimian Fordham University Hassan Tehranian Boston College We thank Jim Booth,

Sources of Financing in Different Forms of Corporate Liquidity and the Performance of M&As

Sources of Financing in Different Forms of Corporate Liquidity and the Performance of M&As Zhenxu Tong * University of Exeter Jian Liu ** University of Exeter This draft: August 2016 Abstract We examine

Sources of Financing in Different Forms of Corporate Liquidity and the Performance of M&As Zhenxu Tong * University of Exeter Jian Liu ** University of Exeter This draft: August 2016 Abstract We examine

Pension fund investment: Impact of the liability structure on equity allocation

Pension fund investment: Impact of the liability structure on equity allocation Author: Tim Bücker University of Twente P.O. Box 217, 7500AE Enschede The Netherlands t.bucker@student.utwente.nl In this

Pension fund investment: Impact of the liability structure on equity allocation Author: Tim Bücker University of Twente P.O. Box 217, 7500AE Enschede The Netherlands t.bucker@student.utwente.nl In this

Financial Constraints for Norwegian Non-Listed Firms

Elise Botten Marthe Kristine Hafsahl Karset BI Norwegian School of Management-Thesis GRA 19003 MSc Thesis Financial Constraints for Norwegian Non-Listed Firms Date of submission: 01.09.2010 Campus: BI

Elise Botten Marthe Kristine Hafsahl Karset BI Norwegian School of Management-Thesis GRA 19003 MSc Thesis Financial Constraints for Norwegian Non-Listed Firms Date of submission: 01.09.2010 Campus: BI

American Finance Association

American Finance Association CEO Overconfidence and Corporate Investment Author(s): Ulrike Malmendier and Geoffrey Tate Source: The Journal of Finance, Vol. 60, No. 6 (Dec., 2005), pp. 2661-2700 Published

American Finance Association CEO Overconfidence and Corporate Investment Author(s): Ulrike Malmendier and Geoffrey Tate Source: The Journal of Finance, Vol. 60, No. 6 (Dec., 2005), pp. 2661-2700 Published

A Model of Financial Intermediation

A Model of Financial Intermediation Jesús Fernández-Villaverde University of Pennsylvania December 25, 2012 Jesús Fernández-Villaverde (PENN) A Model of Financial Intermediation December 25, 2012 1 / 43

A Model of Financial Intermediation Jesús Fernández-Villaverde University of Pennsylvania December 25, 2012 Jesús Fernández-Villaverde (PENN) A Model of Financial Intermediation December 25, 2012 1 / 43

The Impact of Ownership Structure and Capital Structure on Financial Performance of Vietnamese Firms

International Business Research; Vol. 7, No. 2; 2014 ISSN 1913-9004 E-ISSN 1913-9012 Published by Canadian Center of Science and Education The Impact of Ownership Structure and Capital Structure on Financial

International Business Research; Vol. 7, No. 2; 2014 ISSN 1913-9004 E-ISSN 1913-9012 Published by Canadian Center of Science and Education The Impact of Ownership Structure and Capital Structure on Financial

This content downloaded from on Wed, 10 Feb :52:16 UTC All use subject to JSTOR Terms and Conditions

Capital Market Imperfections and the Sensitivity of Investment to Stock Prices Author(s): Alexei V. Ovtchinnikov and John J. McConnell Source: The Journal of Financial and Quantitative Analysis, Vol. 44,

Capital Market Imperfections and the Sensitivity of Investment to Stock Prices Author(s): Alexei V. Ovtchinnikov and John J. McConnell Source: The Journal of Financial and Quantitative Analysis, Vol. 44,

Financial Constraints, Asset Tangibility, and Corporate Investment*

Financial Constraints, Asset Tangibility, and Corporate Investment* Heitor Almeida New York University halmeida@stern.nyu.edu Murillo Campello University of Illinois campello@uiuc.edu This Draft: May 21,

Financial Constraints, Asset Tangibility, and Corporate Investment* Heitor Almeida New York University halmeida@stern.nyu.edu Murillo Campello University of Illinois campello@uiuc.edu This Draft: May 21,

Firm Diversification and the Value of Corporate Cash Holdings

Firm Diversification and the Value of Corporate Cash Holdings Zhenxu Tong University of Exeter* Paper Number: 08/03 First Draft: June 2007 This Draft: February 2008 Abstract This paper studies how firm

Firm Diversification and the Value of Corporate Cash Holdings Zhenxu Tong University of Exeter* Paper Number: 08/03 First Draft: June 2007 This Draft: February 2008 Abstract This paper studies how firm

Controlling Shareholders Expropriation and the Sensitivity of Investment to Cash Flow

Controlling Shareholders Expropriation and the Sensitivity of Investment to Cash Flow Zheng (Nadal) Wang University of California, Santa Barbara November 1, 2017 Abstract This paper argues that investment-cash

Controlling Shareholders Expropriation and the Sensitivity of Investment to Cash Flow Zheng (Nadal) Wang University of California, Santa Barbara November 1, 2017 Abstract This paper argues that investment-cash

Related Party Transactions, Investments and External Financing. Avishek Bhandari University of Wisconsin - Whitewater

Related Party Transactions, Investments and External Financing Avishek Bhandari University of Wisconsin - Whitewater Mark Kohlbeck * Florida Atlantic University Brian Mayhew University of Wisconsin - Madison

Related Party Transactions, Investments and External Financing Avishek Bhandari University of Wisconsin - Whitewater Mark Kohlbeck * Florida Atlantic University Brian Mayhew University of Wisconsin - Madison

Dividends, Investment, and Financial Flexibility *

Dividends, Investment, and Financial Flexibility * Naveen D. Daniel LeBow College of Business Drexel University nav@drexel.edu David J. Denis Krannert School of Management Purdue University djdenis@purdue.edu

Dividends, Investment, and Financial Flexibility * Naveen D. Daniel LeBow College of Business Drexel University nav@drexel.edu David J. Denis Krannert School of Management Purdue University djdenis@purdue.edu

International Journal of Asian Social Science OVERINVESTMENT, UNDERINVESTMENT, EFFICIENT INVESTMENT DECREASE, AND EFFICIENT INVESTMENT INCREASE

International Journal of Asian Social Science ISSN(e): 2224-4441/ISSN(p): 2226-5139 journal homepage: http://www.aessweb.com/journals/5007 OVERINVESTMENT, UNDERINVESTMENT, EFFICIENT INVESTMENT DECREASE,

International Journal of Asian Social Science ISSN(e): 2224-4441/ISSN(p): 2226-5139 journal homepage: http://www.aessweb.com/journals/5007 OVERINVESTMENT, UNDERINVESTMENT, EFFICIENT INVESTMENT DECREASE,

financial constraints and hedging needs

Corporate investment, debt and liquidity choices in the light of financial constraints and hedging needs Christina E. Bannier and Carolin Schürg August 11, 2015 Abstract We examine firms simultaneous choice

Corporate investment, debt and liquidity choices in the light of financial constraints and hedging needs Christina E. Bannier and Carolin Schürg August 11, 2015 Abstract We examine firms simultaneous choice

The Applicability of Pecking Order Theory in Kenyan Listed Firms

The Applicability of Pecking Order Theory in Kenyan Listed Firms Dr. Fredrick M. Kalui Department of Accounting and Finance, Egerton University, P.O.Box.536 Egerton, Kenya Abstract The focus of this study

The Applicability of Pecking Order Theory in Kenyan Listed Firms Dr. Fredrick M. Kalui Department of Accounting and Finance, Egerton University, P.O.Box.536 Egerton, Kenya Abstract The focus of this study

CORPORATE CASH HOLDINGS AND FIRM VALUE EVIDENCE FROM CHINESE INDUSTRIAL MARKET

CORPORATE CASH HOLDINGS AND FIRM VALUE EVIDENCE FROM CHINESE INDUSTRIAL MARKET by Lixian Cao Bachelor of Business Administration in International Accounting Nankai University, 2013 and Chen Chen Bachelor

CORPORATE CASH HOLDINGS AND FIRM VALUE EVIDENCE FROM CHINESE INDUSTRIAL MARKET by Lixian Cao Bachelor of Business Administration in International Accounting Nankai University, 2013 and Chen Chen Bachelor

1 No capital mobility

University of British Columbia Department of Economics, International Finance (Econ 556) Prof. Amartya Lahiri Handout #7 1 1 No capital mobility In the previous lecture we studied the frictionless environment

University of British Columbia Department of Economics, International Finance (Econ 556) Prof. Amartya Lahiri Handout #7 1 1 No capital mobility In the previous lecture we studied the frictionless environment

The Effect of Financial Constraints, Investment Policy and Product Market Competition on the Value of Cash Holdings

The Effect of Financial Constraints, Investment Policy and Product Market Competition on the Value of Cash Holdings Abstract This paper empirically investigates the value shareholders place on excess cash

The Effect of Financial Constraints, Investment Policy and Product Market Competition on the Value of Cash Holdings Abstract This paper empirically investigates the value shareholders place on excess cash

Corporate Financial Policy and the Value of Cash

THE JOURNAL OF FINANCE VOL. LXI, NO. 4 AUGUST 2006 Corporate Financial Policy and the Value of Cash MICHAEL FAULKENDER and RONG WANG ABSTRACT We examine the cross-sectional variation in the marginal value

THE JOURNAL OF FINANCE VOL. LXI, NO. 4 AUGUST 2006 Corporate Financial Policy and the Value of Cash MICHAEL FAULKENDER and RONG WANG ABSTRACT We examine the cross-sectional variation in the marginal value

Corporate Governance, Internal Financing and Investment Policy: Evidence from Anti-takeover Legislation

Corporate Governance, Internal Financing and Investment Policy: Evidence from Anti-takeover Legislation Bill Francis, Iftekhar Hasan, Liang Song * Lally School of Management and Technology of Rensselaer

Corporate Governance, Internal Financing and Investment Policy: Evidence from Anti-takeover Legislation Bill Francis, Iftekhar Hasan, Liang Song * Lally School of Management and Technology of Rensselaer

GRA Master Thesis. BI Norwegian Business School - campus Oslo

BI Norwegian Business School - campus Oslo GRA 19502 Master Thesis Component of continuous assessment: Thesis Master of Science Final master thesis Counts 80% of total grade The Effect of Corporate Tax

BI Norwegian Business School - campus Oslo GRA 19502 Master Thesis Component of continuous assessment: Thesis Master of Science Final master thesis Counts 80% of total grade The Effect of Corporate Tax

Corporate Valuation and Financing

Corporate Valuation and Financing Empirical Capital Structure Prof H. Pirotte Questions 2 What level of debt? What financing next time? Determinants in practice? Weight of determinants? Impact on securities

Corporate Valuation and Financing Empirical Capital Structure Prof H. Pirotte Questions 2 What level of debt? What financing next time? Determinants in practice? Weight of determinants? Impact on securities

Corporate Demand for Liquidity*

Corporate Demand for Liquidity* Heitor Almeida New York University halmeida@stern.nyu.edu Murillo Campello University of Illinois m-campe@uiuc.edu Michael S. Weisbach University of Illinois and NBER weisbach@uiuc.edu

Corporate Demand for Liquidity* Heitor Almeida New York University halmeida@stern.nyu.edu Murillo Campello University of Illinois m-campe@uiuc.edu Michael S. Weisbach University of Illinois and NBER weisbach@uiuc.edu

Is There a Relationship between EBITDA and Investment Intensity? An Empirical Study of European Companies

2012 International Conference on Economics, Business Innovation IPEDR vol.38 (2012) (2012) IACSIT Press, Singapore Is There a Relationship between EBITDA and Investment Intensity? An Empirical Study of

2012 International Conference on Economics, Business Innovation IPEDR vol.38 (2012) (2012) IACSIT Press, Singapore Is There a Relationship between EBITDA and Investment Intensity? An Empirical Study of

Young Innovative Firms, Investment-Cash Flow Sensitivities and Technological Misallocation

Young Innovative Firms, Investment-Cash Flow Sensitivities and Technological Misallocation Oscar Mauricio Valencia-Arana Jose Eduardo Gomez-Gonzalez Andrés Garcia-Suaza SERIE DOCUMENTOS DE TRABAJO No.

Young Innovative Firms, Investment-Cash Flow Sensitivities and Technological Misallocation Oscar Mauricio Valencia-Arana Jose Eduardo Gomez-Gonzalez Andrés Garcia-Suaza SERIE DOCUMENTOS DE TRABAJO No.

Why Does the Law Matter? Investor Protection and Its Effects on Investment, Finance, and Growth

THE JOURNAL OF FINANCE VOL. LXVII, NO. 1 FEBRUARY 2012 Why Does the Law Matter? Investor Protection and Its Effects on Investment, Finance, and Growth R. DAVID MCLEAN, TIANYU ZHANG, and MENGXIN ZHAO ABSTRACT

THE JOURNAL OF FINANCE VOL. LXVII, NO. 1 FEBRUARY 2012 Why Does the Law Matter? Investor Protection and Its Effects on Investment, Finance, and Growth R. DAVID MCLEAN, TIANYU ZHANG, and MENGXIN ZHAO ABSTRACT

GRA Master Thesis. BI Norwegian Business School - campus Oslo

BI Norwegian Business School - campus Oslo GRA 19502 Master Thesis Component of continuous assessment: Thesis Master of Science Final master thesis Counts 80% of total grade Three Perspectives on the Cash

BI Norwegian Business School - campus Oslo GRA 19502 Master Thesis Component of continuous assessment: Thesis Master of Science Final master thesis Counts 80% of total grade Three Perspectives on the Cash

Real Options: Theory Meets Practice REAL OPTION, FINANCIAL FRICTIONS AND COLLATERALIZED DEBT: THEORY AND EVIDENCE FROM REAL ESTATE COMPANIES

Real Options: Theory Meets Practice 16 th Annual Conference, June 27th 30th 2012, London, England REAL OPTION, FINANCIAL FRICTIONS AND COLLATERALIZED DEBT: THEORY AND EVIDENCE FROM REAL ESTATE COMPANIES

Real Options: Theory Meets Practice 16 th Annual Conference, June 27th 30th 2012, London, England REAL OPTION, FINANCIAL FRICTIONS AND COLLATERALIZED DEBT: THEORY AND EVIDENCE FROM REAL ESTATE COMPANIES

FINANCIAL ECONOMICS II ECO SPRING 2019

FINANCIAL ECONOMICS II ECO 2504 - SPRING 2019 Instructor: Prof. V. Aivazian Office: 150 St. George St. Room 272 Telephone: (416)978-2375 E-mail: varouj.aivazian@utoronto.ca The focus of this course is

FINANCIAL ECONOMICS II ECO 2504 - SPRING 2019 Instructor: Prof. V. Aivazian Office: 150 St. George St. Room 272 Telephone: (416)978-2375 E-mail: varouj.aivazian@utoronto.ca The focus of this course is

The Real Effects of Analyst Coverage

The Real Effects of Analyst Coverage FRANÇOIS DERRIEN and AMBRUS KECSKÉS * Abstract We study the causal effects of analyst coverage on corporate investment, financing, and payout policies. We hypothesize

The Real Effects of Analyst Coverage FRANÇOIS DERRIEN and AMBRUS KECSKÉS * Abstract We study the causal effects of analyst coverage on corporate investment, financing, and payout policies. We hypothesize

How much is too much? Debt Capacity and Financial Flexibility

How much is too much? Debt Capacity and Financial Flexibility Dieter Hess and Philipp Immenkötter January 2012 Abstract We analyze corporate financing decisions with focus on the firm s debt capacity and

How much is too much? Debt Capacity and Financial Flexibility Dieter Hess and Philipp Immenkötter January 2012 Abstract We analyze corporate financing decisions with focus on the firm s debt capacity and