Information System Audit Engr. Abdul-Rahman Mahmood MS, PMP, MCP, QMR(ISO9001:2000)

|

|

|

- Melissa Lambert

- 5 years ago

- Views:

Transcription

armahmood786@yahoo.")

1 Information System Audit Engr. Abdul-Rahman Mahmood MS, PMP, MCP, QMR(ISO9001:2000) alphapeeler.sf.net/pubkeys/pkey.htm pk.linkedin.com/in/armahmood abdulmahmood-sss alphasecure mahmood_cubix VC++, VB, ASP

2

3 Objectives Discuss why adequate audit planning is essential. Make client acceptance decisions and perform initial audit planning. Gain an understanding of the client s business and industry. Assess client business risk. Perform preliminary analytical procedures. State the purposes of analytical procedures and the timing of each purpose. Select the most appropriate analytical procedure from among the five major types. Compute common financial ratios.

4 Learning Objective 1 Discuss why adequate audit planning is essential.

5 Three Main Reasons for Planning 1. To obtain sufficient appropriate evidence for the circumstances 2. To help keep audit costs reasonable 3. To avoid misunderstanding with the client

6 8 parts for Audit Planning

7 Risk Terms Acceptable audit risk measure of how willing the auditor is to accept that the financial statements may be materially misstated after the audit is completed. Inherent risk measure of likelihood that there are material misstatements in an account balance before considering the effectiveness of internal control.

8 Learning Objective 2 Make client acceptance decisions and perform initial audit planning.

9 Initial Audit Planning Initial audit planning involves four things: 1. Client acceptance or continuance. experienced auditor. 2. Identify client s reasons for audit. 3. Obtain an understanding with the client. (terms of the engagement) 4. Develop overall audit strategy. (including engagement staffing and any required audit specialists.)

10 Client Acceptance and Continuance New client investigations If previously audited by CPA firm, new auditor is required to communicate with the predecessor auditor Client permission required (Code of Professional Conduct) Continuing clients Annual evaluations whether to continue based on issues, fees, and client integrity

11 Identify Reasons for the Audit Two major factors affecting acceptable risk Likely statement users Intended uses of the statements Likely to accumulate more evidence for companies that are Publicly held Have extreme indebtedness Likely to be sold

12 Obtaining an Understanding with the Client Engagement terms should be understood between CPA and client. Standards require an engagement letter describing: objectives responsibilities of auditor and management schedules and fees Informs client that auditor cannot guarantee all acts of fraud will be discovered See figure (Engagement Letter)

13 Engagement Letter

14 Develop Overall Audit Strategy Preliminary audit strategy should consider client s business and industry material misstatement risk areas number of client locations past effectiveness of controls Preliminary strategy helps auditor determine resource requirements and staffing staff continuity need for specialists

15 Learning Objective 3 Gain an understanding of the client s business and industry.

16 Understanding of the Client s Business and Industry Client business risk is the risk that the client will fail to meet its objectives. Economic conditions around the world Information technology Clients expanded operations globally Human capital & intangible assets has increased accounting complexity

17 Understanding of the Client s Business and Industry

18 Industry and External Environment Reasons for obtaining an understanding of the client s industry and external environment: 1. Risks associated with specific industries 2. Inherent risks common to all clients in certain industries 3. Unique accounting requirements

19 Business Operations and Processes Factors the auditor should understand: Major sources of revenue Key customers and suppliers Sources of financing Information about related parties

20 Tour the Plant and Offices Touring the physical facilities enables the auditor to assess asset safeguards and interpret accounting data related to assets.

21 Identify Related Parties Affiliated companies Principal owners of the client Any other party with which the client deals A party who can influence management or client policies

22 Management and Governance Governance includes: Organizational structure Board activities Audit committee activities. Governance insights: Corporate charter and bylaws Code of ethics Meeting minutes Management establishes the strategies and processes followed by the client s business.

23 Code of Ethics In response to the Sarbanes-Oxley Act, the SEC now requires each public company to disclose whether is has adopted a code of ethics that applies to senior management. The SEC also requires companies to disclose amendments and waivers to the code of ethics.

24 Client Objectives and Strategies Strategies are approaches to achieve organizational objectives. Auditors should understand client objectives. Financial reporting reliability Effectiveness and efficiency of operations Compliance with laws and regulations

25 Measurement and Performance The client s performance measurement system includes key performance indicators. Examples: market share sales per employee unit sales growth Web site visitors same-store sales sales/square foot Performance measurement includes ratio analysis and benchmarking against key competitors.

26 Learning Objective 4 Assess client business risk.

27 Assess Client Business Risk Client business risk is the risk that the client will fail to achieve its objectives. What is the auditor s primary concern? Material misstatements in the financial statements due to client business risk

28 Client s Business, Risk, and Risk of Material Misstatement

29 Sarbanes-Oxley Act Management must certify it has designed disclosure controls and procedures to ensure that material information about business risks is made known to them. Management must certify it has informed the auditor and audit committee of any significant control deficiencies.

30 Learning Objective 5 Perform preliminary analytical procedures.

31 Preliminary Analytical Procedures Comparison of client ratios to industry or competitor benchmarks provides an indication of the company s performance. Preliminary tests can reveal unusual changes in ratios.

32 Examples of Planning Analytical Procedures

33 Summary of the Parts of Auditing Planning A major purpose is to gain an understanding of the client s business and industry.

34 Planning an Audit and Designing an Audit Approach Set materiality and assess acceptable audit risk and inherent risk. Understand internal control and assess control risk Gather information to assess fraud risks Develop overall audit plan and audit program

35 Learning Objective 6 State the purposes of analytical procedures and the timing of each procedure.

36 Analytical Procedures AU 329 emphasizes the expectations developed by the auditor. 1. Required in the planning phase 2. Often done during the testing phase 3. Required during the completion phase

37 Timing and Purposes of Analytical Procedures

38 Learning Objective 7 Select the most appropriate analytical procedure from among the five major types.

39 Five Types of Analytical Procedures Compare client data with: 1. Industry data 2. Similar prior-period data 3. Client-determined expected results 4. Auditor-determined expected results 5. Expected results using nonfinancial data.

40 Compare Client and Industry Data Client Industry Inventory turnover Gross margin 26.3% 26.4% 27.3% 26.2%

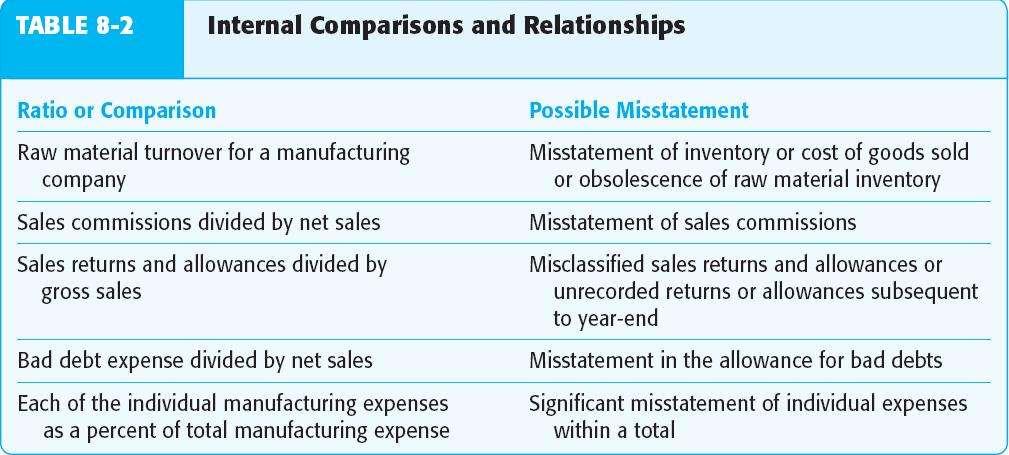

41 Internal Comparisons

42 Compare Client Data with Similar Prior Period Data (000) Prelim % of Net sales (000) Prelim % of Net sales Net sales $143, $131, Cost of goods sold 103, , Gross profit $ 39, $ 36, Selling expense 14, , Administrative expense 17, , Other 1, , Earnings before taxes $ 5, $ 4, Income taxes 1, , Net income $ 3, $ 3,

43 Learning Objective 8 Compute common financial ratios.

44 Common Financial Ratios Short-term debt-paying ability Liquidity activity ratios Ability to meet long-term debt obligations Profitability ratios

45 Short-term Debt-paying Ability Cash ratio Quick ratio Current ratio = = = (Cash + Marketable securities) Current liabilities (Cash + Marketable securities + Net accounts receivable) Current liabilities Current assets Current liabilities

46 Liquidity Activity Ratios Accounts receivable turnover Days to collect receivable Inventory turnover Days to sell inventory = = = = Net sales Average gross receivables 365 days Accounts receivable turnover Cost of goods sold Average inventory 365 days Inventory turnover

47 Ability to Meet Long-term Debt Obligation Debt to equity = Total liabilities Total equity Times interest earned = Operating income Interest expense

48 Profitability Ratios Earnings per share = Net income Average common shares outstanding Gross profit percent Profit margin = = (Net sales Cost of goods sold) Net sales Operating income Net sales

49 Profitability Ratios Return on assets Return on common equity = = Income before taxes Average total assets (Income before taxes Preferred dividends) Average stockholders equity

50 Explained

51 Common financial ratios. Auditors analytical procedures includes the use of general financial ratios during planning and final review of the audited financial statements. These are useful for understanding recent events and the financial status of the business and for viewing the statements from the perspective of a user. The general financial analysis may be effective for identifying possible problem areas. The most important comparisons are to those of previous years for the company and to industry averages or similar companies for the same year.

52 Accounting terms Liquidity: Cash is the most liquid asset, while real estate, fine art and collectibles are all relatively illiquid. Market liquidity: In business, economics or investment, market liquidity is a market's ability to facilitate the purchase or sale of an asset without causing drastic change in the asset's price. Leverage ratio: A leverage ratio is any one of several financial measurements that look at how much capital comes in the form of debt (loans), or assesses the ability of a company to meet financial obligations. Equity: the value of the shares issued by a company. "he owns 62% of the group's equity."

53 Accounting terms Cash ratio: ratio of a company's total cash + cash equivalents to its current liabilities. It is most commonly used as a measure of company liquidity. cash ratio = (cash + cash equivalents)/ (total current liabilities) Example: Ally's Palace is a restaurant that is looking to remodel its dining room. Ally is asking her bank for a loan of $100,000. Ally's balance sheet lists these items: Cash: $10,000, Cash Equivalents: $2,000 Accounts Payable: $5,000, Current Taxes Payable: $1,000 Current Long-term Liabilities: $10,000 Ally's cash ratio is calculated like this: CR = (10,000+2,000)/ (5,000+1,000+10,000) = 0.75 This means that Ally only has enough cash and equivalents to pay off 75 % of her current liabilities.

54 Accounting terms Quick ratio: compares the total amount of cash + marketable securities + accounts receivable to the amount of current liabilities. The quick ratio is also known as the acid test ratio. The quick ratio is an indicator of a company s short-term liquidity. The quick ratio measures a company s ability to meet its short-term obligations with its most liquid assets. For this reason, the ratio excludes inventories from current assets, and is calculated as follows: Quick ratio = (current assets inventories) / current liabilities, or = (cash and equivalents + marketable securities + accounts receivable) / current liabilities

55 Accounting terms Current ratio: The current ratio is a liquidity ratio that measures a company's ability to pay short-term and long-term obligations. To gauge this ability, the current ratio considers the total assets of a company (both liquid and illiquid) relative to that company s total liabilities. Current Ratio = Current Assets / Current Liabilities The current ratio is called current because, unlike some other liquidity ratios, it incorporates all current assets and liabilities.

56 Accounting terms Accounts receivable (AR): refers to money owed by customers (individuals or corporations) to another entity in exchange for goods or services that have been delivered or used, but not yet paid for. Accounts payable (AP): is an accounting entry that represents an entity's obligation to pay off a short-term debt to its creditors. Accounts payable entry is found on balance sheet under the heading current liabilities. Debt - Equity Ratio: indicates how much debt a company is using to finance its assets relative to the amount of value represented in shareholders equity. D-E Ratio = Total Liabilities / Shareholders' Equity

57 Accounting terms Times interest earned: (TIE) a metric used to measure company's ability to meet its debt obligations. TIE = (earnings before interest and taxes (EBIT))/ (total interest payable on bonds & contractual debt). It indicates how many times a company can cover its interest charges on a pretax basis. Failing to meet these obligations could force a company into bankruptcy. Gross profit: Gross profit is a company's total revenue (equivalent to total sales) minus the cost of goods sold. Gross profit is the profit a company makes after deducting the costs associated with making and selling its products, or the costs associated with providing its services. formula: Gross profit = revenue (total sales) - cost of goods sold

58 Accounting terms Net profit: No. of sales dollars remaining after all operating expenses, interest, taxes and preferred stock dividends have been deducted from total revenue. (Example): Net profit is also referred to as the bottom line, net income, or net earnings. The formula for net profit is as follows: Total Revenue -Total Expenses = Net Profit Net profit is found on the last line of the income statement, which is why it's often referred to as the bottom line. Let's look at a hypothetical income statement for Company XYZ: Income Statement of XYZ, Inc. - December 31, 2008: Total Revenue $100,000 Cost of Goods Sold ($ 20,000) Gross Profit $ 80,000 Operating Expenses Salaries $10,000 Rent $10,000 Utilities $ 5,000 Depreciation $ 5,000 Total Operating Expenses ($ 30,000) Interest Expense ($ 10,000) Taxes ($ 10,000) Net Profit = $100,000 - $20,000 - $30,000, - $10,000 - $10,000 = $30,000

59 Accounting terms Profit Margin = Net Income / Net Sales (revenue) Return on equity (ROE): is the amount of net income returned as a percentage of shareholders equity. Return on equity measures a corporation's profitability by revealing how much profit a company generates with the money shareholders have invested. Return on Equity = Net Income/Shareholder's Equity Return on common equity (ROCE): can be defined as the amount of profit or net income a company earns per investment dollar. Return on common equity, explained is a measure of how well a company uses its investment dollars to generate profits. ROCE = Net Income (NI)/ Average Common Shareholder s Equity The average common equity is found by combining the beginning common stock for the year on the balance sheet, and the ending common stock value. These values are then divided by two for the average amount in the year.

60 Hillsburg Hardware Overall Test of Interest Expense December 31, 2011

61 Short-term Debt-Paying Ability Liquidity Activity Ratios

62 Summary of Analytical Procedures Compare ratios of recorded amounts to auditor expectations. Used in planning to understand client s business and industry. Used throughout the audit to identify possible misstatements reduce detailed tests assess going-concern issues.

Information System Audit Engr. Abdul-Rahman Mahmood MS, PMP, MCP, QMR(ISO9001:2000)

") Information System Audit Engr. Abdul-Rahman Mahmood MS, PMP, MCP, QMR(ISO9001:2000) armahmood786@yahoo.com alphasecure@gmail.com alphapeeler.sf.net/pubkeys/pkey.htm http://alphapeeler.sourceforge.net pk.linkedin.com/in/armahmood

Information System Audit Engr. Abdul-Rahman Mahmood MS, PMP, MCP, QMR(ISO9001:2000) armahmood786@yahoo.com alphasecure@gmail.com alphapeeler.sf.net/pubkeys/pkey.htm http://alphapeeler.sourceforge.net pk.linkedin.com/in/armahmood

1LINK & MNET Engr. Abdul-Rahman Mahmood MS, PMP, MCP, QMR(ISO9001:2000)

") 1LINK & MNET Engr. Abdul-Rahman Mahmood MS, PMP, MCP, QMR(ISO9001:2000) armahmood786@yahoo.com alphasecure@gmail.com alphapeeler.sf.net/pubkeys/pkey.htm http://alphapeeler.sourceforge.net pk.linkedin.com/in/armahmood

1LINK & MNET Engr. Abdul-Rahman Mahmood MS, PMP, MCP, QMR(ISO9001:2000) armahmood786@yahoo.com alphasecure@gmail.com alphapeeler.sf.net/pubkeys/pkey.htm http://alphapeeler.sourceforge.net pk.linkedin.com/in/armahmood

Chapter 15 Accounting & Financial Analysis

Chapter 15 Accounting & Financial Analysis Professor Muriel Anderson, CPA MGG 150: Introduction to Business November 12, 2013 Chapter Outline How Firms Use Accounting Responsible Financial Reporting Interpreting

Chapter 15 Accounting & Financial Analysis Professor Muriel Anderson, CPA MGG 150: Introduction to Business November 12, 2013 Chapter Outline How Firms Use Accounting Responsible Financial Reporting Interpreting

Financial Statements, Forecasts, and Planning Chapter 6

C H A P T E R 6 Financial Statements, Forecasts, and Planning Chapter 6 Chapter Objectives Identify the elements of the balance sheet. Identify the elements of the income statement. Discuss the cash flow

C H A P T E R 6 Financial Statements, Forecasts, and Planning Chapter 6 Chapter Objectives Identify the elements of the balance sheet. Identify the elements of the income statement. Discuss the cash flow

Accounting Functions. The various financial statements are- Income Statement Balance Sheet

Accounting Functions The accounting system provides a structure of maintaining details of business transactions that represent the finances of the organization. The various financial statements are- Income

Accounting Functions The accounting system provides a structure of maintaining details of business transactions that represent the finances of the organization. The various financial statements are- Income

Corporate Finance, 3Ce (Berk, DeMarzo, Strangeland) Chapter 2 Introduction to Financial Statement Analysis

Chapter 2 Introduction to Financial Statement Analysis") Corporate Finance, 3Ce (Berk, DeMarzo, Strangeland) Chapter 2 Introduction to Financial Statement Analysis 2.1 The Disclosure of Financial Information 1) Canadian public companies are required to file

Corporate Finance, 3Ce (Berk, DeMarzo, Strangeland) Chapter 2 Introduction to Financial Statement Analysis 2.1 The Disclosure of Financial Information 1) Canadian public companies are required to file

Professional Designation Ratios: Formulas & Definitions Used in Credit Risk Assessment

Professional Designation Ratios: Formulas & Definitions Used in Credit Risk Assessment Profitability Ratios Measure management's ability to control expenses and to earn a return on the resources committed

Professional Designation Ratios: Formulas & Definitions Used in Credit Risk Assessment Profitability Ratios Measure management's ability to control expenses and to earn a return on the resources committed

Chapter Seventeen. Learning Objectives

Chapter Seventeen Using Accounting Information Learning Objectives 1. Explain why accounting information and audited financial statements are important. 2. Identify the people who use accounting information

Chapter Seventeen Using Accounting Information Learning Objectives 1. Explain why accounting information and audited financial statements are important. 2. Identify the people who use accounting information

Learning Goal 1: Review the contents of the stockholders' report and the procedures for consolidating international financial statements.

Principles of Managerial Finance, 12e (Gitman) Chapter 2 Financial Statements and Analysis Learning Goal 1: Review the contents of the stockholders' report and the procedures for consolidating international

Principles of Managerial Finance, 12e (Gitman) Chapter 2 Financial Statements and Analysis Learning Goal 1: Review the contents of the stockholders' report and the procedures for consolidating international

Corporate Finance. Week 3 Financial Statement Analysis II

Corporate Finance 1-1 Week 3 Financial Statement Analysis II 1-1 Asset Efficiency or Turnover Measures 1-2 A first broad measure of efficiency is asset turnover: Sales Asset Turnover = Total Assets Fixed

Corporate Finance 1-1 Week 3 Financial Statement Analysis II 1-1 Asset Efficiency or Turnover Measures 1-2 A first broad measure of efficiency is asset turnover: Sales Asset Turnover = Total Assets Fixed

FINANCIAL RATIOS. LIQUIDITY RATIOS (and Working Capital) You want current and quick ratios to be > 1. Current Liabilities SAMPLE BALANCE SHEET ASSETS

You want current and quick ratios to be > 1. Current Liabilities SAMPLE BALANCE SHEET ASSETS") FINANCIAL RATIOS ROUND ALL ANSWERS TO TWO DECIMALS UNLESS REQUESTED OTHERWISE IN THE PROBLEM LIQUIDITY RATIOS (and Working Capital) You want current and quick ratios to be > 1 Current Ratio Quick Ratio

FINANCIAL RATIOS ROUND ALL ANSWERS TO TWO DECIMALS UNLESS REQUESTED OTHERWISE IN THE PROBLEM LIQUIDITY RATIOS (and Working Capital) You want current and quick ratios to be > 1 Current Ratio Quick Ratio

The Role of Accountants and Accounting Information

Slide 1 BA-101 Introduction to Business The Role of Accountants and Accounting Information Chapter Fourteen 1-1 Slide 2 What Is Accounting, and Who Uses Accounting Information? Accounting comprehensive

Slide 1 BA-101 Introduction to Business The Role of Accountants and Accounting Information Chapter Fourteen 1-1 Slide 2 What Is Accounting, and Who Uses Accounting Information? Accounting comprehensive

Chapter 2. Introduction to Financial Statement Analysis

Chapter 2 Introduction to Financial Statement Analysis 2-1. In a firm s annual report, five financial statements can be found: the balance sheet, the income statement, the statement of cash flows, the

Chapter 2 Introduction to Financial Statement Analysis 2-1. In a firm s annual report, five financial statements can be found: the balance sheet, the income statement, the statement of cash flows, the

Financial Statement Analysis

Financial Statement Analysis Lakehead University September 2003 Overview of the Lecture 2.1 Financial Statements 2.2 Ratio Analysis 2.4 Common-Size Analysis 2.3 Changing Prices 2.5 International Considerations

Financial Statement Analysis Lakehead University September 2003 Overview of the Lecture 2.1 Financial Statements 2.2 Ratio Analysis 2.4 Common-Size Analysis 2.3 Changing Prices 2.5 International Considerations

ECON132 Exam #1 Summer 2005 Session B

ECON132 Exam #1 Summer 2005 Session B Name: Perm #: Please answer questions 1-35 on your green scantron. If the question is a true false question, answer A for true and B for false. The short answer/ essay

ECON132 Exam #1 Summer 2005 Session B Name: Perm #: Please answer questions 1-35 on your green scantron. If the question is a true false question, answer A for true and B for false. The short answer/ essay

CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B. Com.

MANAGEMENT OF FINANCIAL RESOURCES AND PERFORMANCE SESSIONS 5 & 6 FINANCIAL DATA, PERFORMANCE ANALYSIS & MANAGEMENT AND DECISION MAKING June 10 to 24, 2013 CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B. Com.

MANAGEMENT OF FINANCIAL RESOURCES AND PERFORMANCE SESSIONS 5 & 6 FINANCIAL DATA, PERFORMANCE ANALYSIS & MANAGEMENT AND DECISION MAKING June 10 to 24, 2013 CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B. Com.

Financial Statement Analysis

Without financial statement analysis, finance statements would be comprised of primarily historical data. The analysis converts the data into information that is useful to understanding the company and

Without financial statement analysis, finance statements would be comprised of primarily historical data. The analysis converts the data into information that is useful to understanding the company and

Basic Financial Analysis and Valuation

30 Sep 2017 Basic Financial Analysis and Valuation By Puah Soon Lim, CFA 2 Disclaimer The information in this workshop is for general information purposes only and is provided on an as is basis without

30 Sep 2017 Basic Financial Analysis and Valuation By Puah Soon Lim, CFA 2 Disclaimer The information in this workshop is for general information purposes only and is provided on an as is basis without

Georgia Banking School Financial Statement Analysis. Dr. Christopher R Pope Terry College of Business University of Georgia

Georgia Banking School Financial Statement Analysis Dr. Christopher R Pope Terry College of Business University of Georgia Introduction Objective My objective is to introduce you to the analysis of financial

Georgia Banking School Financial Statement Analysis Dr. Christopher R Pope Terry College of Business University of Georgia Introduction Objective My objective is to introduce you to the analysis of financial

Working with Financial Statements

Working with Financial Statements Lakehead University September 2004 Overview of the Lecture 3.1 Cash Flow and Financial Statements 3.2 Standardizes Financial Statements 3.3 Ratio Analysis 3.4 Dupont Identity

Working with Financial Statements Lakehead University September 2004 Overview of the Lecture 3.1 Cash Flow and Financial Statements 3.2 Standardizes Financial Statements 3.3 Ratio Analysis 3.4 Dupont Identity

Working with Financial Statements

Working with Financial Statements Lakehead University September 2004 Overview of the Lecture 3.1 Cash Flow and Financial Statements 3.2 Standardizes Financial Statements 3.3 Ratio Analysis 3.4 Dupont Identity

Working with Financial Statements Lakehead University September 2004 Overview of the Lecture 3.1 Cash Flow and Financial Statements 3.2 Standardizes Financial Statements 3.3 Ratio Analysis 3.4 Dupont Identity

Key Business Ratios v 2.0 Course Transcript Presented by: TeachUcomp, Inc.

Key Business Ratios v 2.0 Course Transcript Presented by: TeachUcomp, Inc. Course Introduction Welcome to Key Business Ratios, a presentation of TeachUcomp, Inc. This course examines key ratios used to

Key Business Ratios v 2.0 Course Transcript Presented by: TeachUcomp, Inc. Course Introduction Welcome to Key Business Ratios, a presentation of TeachUcomp, Inc. This course examines key ratios used to

Corporate Finance, 3e (Berk/DeMarzo) Chapter 2 Introduction to Financial Statement Analysis. 2.1 Firms' Disclosure of Financial Information

Chapter 2 Introduction to Financial Statement Analysis. 2.1 Firms' Disclosure of Financial Information") Corporate Finance, 3e (Berk/DeMarzo) Chapter 2 Introduction to Financial Statement Analysis 2.1 Firms' Disclosure of Financial Information 1) U.S. public companies are required to file their annual financial

Corporate Finance, 3e (Berk/DeMarzo) Chapter 2 Introduction to Financial Statement Analysis 2.1 Firms' Disclosure of Financial Information 1) U.S. public companies are required to file their annual financial

CMA 2010 Support Package

CMA 2010 Support Package Ratio Definitions CMA EXAM RATIO DEFINITIONS Abbreviations EBIT = Earnings before interest and taxes EBITDA = Earnings before interest, taxes, depreciation and amortization EBT

CMA 2010 Support Package Ratio Definitions CMA EXAM RATIO DEFINITIONS Abbreviations EBIT = Earnings before interest and taxes EBITDA = Earnings before interest, taxes, depreciation and amortization EBT

Excellence in. Management

Excellence in Financial Management Course 1: Evaluating Financial Performance Prepared by: Matt H. Evans, CPA, CMA, CFM Chapter 1: Return on Equity Why use ratios? It has been said that you must measure

Excellence in Financial Management Course 1: Evaluating Financial Performance Prepared by: Matt H. Evans, CPA, CMA, CFM Chapter 1: Return on Equity Why use ratios? It has been said that you must measure

Fundamentals of Corporate Finance, 2e (Berk) Chapter 2 Introduction to Financial Statement Analysis. 2.1 Firms' Disclosure of Financial Information

Chapter 2 Introduction to Financial Statement Analysis. 2.1 Firms' Disclosure of Financial Information") Fundamentals of Corporate Finance, 2e (Berk) Chapter 2 Introduction to Financial Statement Analysis 2.1 Firms' Disclosure of Financial Information 1) In the United States, publicly traded companies can

Fundamentals of Corporate Finance, 2e (Berk) Chapter 2 Introduction to Financial Statement Analysis 2.1 Firms' Disclosure of Financial Information 1) In the United States, publicly traded companies can

Working with Financial Statements, Part II

Working with Financial Statements, Part II Faculty of Business Administration Lakehead University Spring 2003 May 7, 2003 Outline of Chapter 3, Part II 3.3 Ratio Analysis 3.4 The DuPont Identity 3.5 Using

Working with Financial Statements, Part II Faculty of Business Administration Lakehead University Spring 2003 May 7, 2003 Outline of Chapter 3, Part II 3.3 Ratio Analysis 3.4 The DuPont Identity 3.5 Using

Fundamentals of Corporate Finance, 3e (Berk/DeMarzo/Harford) Chapter 2 Introduction to Financial Statement Analysis

Chapter 2 Introduction to Financial Statement Analysis") Fundamentals of Corporate Finance, 3e (Berk/DeMarzo/Harford) Chapter 2 Introduction to Financial Statement Analysis 2.1 Firms' Disclosure of Financial Information 1) In the United States, publicly traded

Fundamentals of Corporate Finance, 3e (Berk/DeMarzo/Harford) Chapter 2 Introduction to Financial Statement Analysis 2.1 Firms' Disclosure of Financial Information 1) In the United States, publicly traded

Chapter 17. Page 1. Company Analysis. Learning Objectives. INVESTMENTS: Analysis and Management Second Canadian Edition

INVESTMENTS: Analysis and Management Second Canadian Edition W. Sean Cleary Charles P. Jones Chapter 17 Company Analysis Learning Objectives Define fundamental analysis at the company level. Explain the

INVESTMENTS: Analysis and Management Second Canadian Edition W. Sean Cleary Charles P. Jones Chapter 17 Company Analysis Learning Objectives Define fundamental analysis at the company level. Explain the

REVIEW OF BASIC UNDERSTANDING AND ANALYSIS OF FINANCIAL STATEMENTS

REVIEW OF BASIC UNDERSTANDING AND ANALYSIS OF FINANCIAL STATEMENTS Payear Sangiumvibool, Ph.D., CPA (US) ดร. พเย ย เสง ยมว บ ล Webster University Thailand Faculty, Accounting and Management สภาว ชาช พบ

REVIEW OF BASIC UNDERSTANDING AND ANALYSIS OF FINANCIAL STATEMENTS Payear Sangiumvibool, Ph.D., CPA (US) ดร. พเย ย เสง ยมว บ ล Webster University Thailand Faculty, Accounting and Management สภาว ชาช พบ

STAFF GUIDANCE CHANGES TO THE AUDITOR'S REPORT EFFECTIVE FOR AUDITS OF FISCAL YEARS ENDING ON OR AFTER DECEMBER 15, 2017

1666 K Street NW Washington, DC 20006 Office: (202) 207-9100 Fax: (202) 862-8430 www.pcaobus.org STAFF GUIDANCE CHANGES TO THE AUDITOR'S REPORT EFFECTIVE FOR AUDITS OF FISCAL YEARS ENDING ON OR AFTER DECEMBER

1666 K Street NW Washington, DC 20006 Office: (202) 207-9100 Fax: (202) 862-8430 www.pcaobus.org STAFF GUIDANCE CHANGES TO THE AUDITOR'S REPORT EFFECTIVE FOR AUDITS OF FISCAL YEARS ENDING ON OR AFTER DECEMBER

How Well Am I Doing? Financial Statement Analysis

How Well Am I Doing? Financial Statement Analysis Chapter 16 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Limitations of Financial Statement Analysis Differences

How Well Am I Doing? Financial Statement Analysis Chapter 16 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Limitations of Financial Statement Analysis Differences

Finance & accounting for non-financial energy professionals. September 11, 2014

Finance & accounting for non-financial energy professionals September 11, 2014 Objectives On completion of this training each participant should be able to: Understand basic financial statement analysis

Finance & accounting for non-financial energy professionals September 11, 2014 Objectives On completion of this training each participant should be able to: Understand basic financial statement analysis

Financial & Managerial Accounting Practice with Ratios and Analysis

Financial & Managerial Accounting Practice with Ratios and Analysis A company had the following income statement for the year and the balance sheet accounts at the end of the year. Use the information

Financial & Managerial Accounting Practice with Ratios and Analysis A company had the following income statement for the year and the balance sheet accounts at the end of the year. Use the information

Measuring Vendor Financial Strength

Measuring Vendor Financial Strength Presented by Michael Greene, City of Tempe Presentation Overview Why is it important to consider a firm s financial strength Review the three typical financial statements:

Measuring Vendor Financial Strength Presented by Michael Greene, City of Tempe Presentation Overview Why is it important to consider a firm s financial strength Review the three typical financial statements:

Ratio Analysis. Assets = Liabilities + Shareholder s Equity

Ratio Analysis The purpose of a financial statement is to disclose information about the financial position of an entity to interested parties. By reporting the finances, shareholders are able to make

Ratio Analysis The purpose of a financial statement is to disclose information about the financial position of an entity to interested parties. By reporting the finances, shareholders are able to make

Accounting: Decision Making by the Numbers BUSN

Accounting: Decision Making by the Numbers What is accounting? How is accounting information used? What are career opportunities in accounting? What are the goals of generally accepted accounting principles?

Accounting: Decision Making by the Numbers What is accounting? How is accounting information used? What are career opportunities in accounting? What are the goals of generally accepted accounting principles?

Understanding Accounting and Financial Information

Chapter Seventeen Understanding Accounting and Financial Information McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. SEAN PERICH Bakery Barn A lifelong weightlifter

Chapter Seventeen Understanding Accounting and Financial Information McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. SEAN PERICH Bakery Barn A lifelong weightlifter

Chapter 05. Audit Evidence and Documentation. McGraw-Hill/Irwin. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 05 Audit Evidence and Documentation McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Audit Risk The possibility that the auditors may unknowingly fail to

Chapter 05 Audit Evidence and Documentation McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Audit Risk The possibility that the auditors may unknowingly fail to

Gleim CPA Review Updates to Auditing 2011 Edition, 1st Printing June 3, 2011

Page 1 of 7 Gleim CPA Review Updates to Auditing 2011 Edition, 1st Printing June 3, 2011 NOTE: Text that should be deleted from the outline is displayed with a line through the text. New text is shown

Page 1 of 7 Gleim CPA Review Updates to Auditing 2011 Edition, 1st Printing June 3, 2011 NOTE: Text that should be deleted from the outline is displayed with a line through the text. New text is shown

Chapter 9. #17 is a bad question if it is changed as follows the answer is d

Chapter 9 Multiple choice 1. a 2. d 3. b 4. d 5. b 6. b 7. d 8. c 9. b 10. b 11. b 12. c 13. d 14. b 15. b 16. c #17 is a bad question if it is changed as follows the answer is d 17. The audit of accounts

Chapter 9 Multiple choice 1. a 2. d 3. b 4. d 5. b 6. b 7. d 8. c 9. b 10. b 11. b 12. c 13. d 14. b 15. b 16. c #17 is a bad question if it is changed as follows the answer is d 17. The audit of accounts

Advanced Valuation Methods. Analyzing Historical Performance. Financial Analysis

1 Advanced Valuation Methods Analyzing Historical Performance Financial Analysis Goal Assess performance of a firm in the context of shareholder value versus competitive advantage Productivity of employed

1 Advanced Valuation Methods Analyzing Historical Performance Financial Analysis Goal Assess performance of a firm in the context of shareholder value versus competitive advantage Productivity of employed

A/P Turnover (Activity)

") A/P Turnover (Activity) 1a COGS Avg A/P 1b A/R Turnover (Activity) 2a Net Credit Sales Avg Net Receivables [A/R quality & success in collecting outstanding A/R] 2b A/R Turnover in Days (Activity) 3a Avg

A/P Turnover (Activity) 1a COGS Avg A/P 1b A/R Turnover (Activity) 2a Net Credit Sales Avg Net Receivables [A/R quality & success in collecting outstanding A/R] 2b A/R Turnover in Days (Activity) 3a Avg

4 Chapter 2 Chapter 2: Financial Statement and Cash Flow Analysis

4 Chapter 2 Chapter 2: Financial Statement and Cash Flow Analysis Answers to End of Chapter Questions 2-1. Financial statement analysis provides information about the company s financial health, and its

4 Chapter 2 Chapter 2: Financial Statement and Cash Flow Analysis Answers to End of Chapter Questions 2-1. Financial statement analysis provides information about the company s financial health, and its

Who of the following make a broader use of accounting information?

Who of the following make a broader use of accounting information? Accountants Financial Analysts Auditors Marketers Which of the following is NOT an internal use of financial statements information? Planning

Who of the following make a broader use of accounting information? Accountants Financial Analysts Auditors Marketers Which of the following is NOT an internal use of financial statements information? Planning

FINANCIAL PERFORMANCE ANALYSIS OF BEXIMCO PHARMACEUTICALS LTD. AND SQUARE PHARMACEUTICALS LTD. Submitted to. M. Nurul Amin.

FINANCIAL PERFORMANCE ANALYSIS OF BEXIMCO PHARMACEUTICALS LTD. AND SQUARE PHARMACEUTICALS LTD. Submitted to M. Nurul Amin Submitted by Date-31 st July, 2010 North South University Financial Performance

FINANCIAL PERFORMANCE ANALYSIS OF BEXIMCO PHARMACEUTICALS LTD. AND SQUARE PHARMACEUTICALS LTD. Submitted to M. Nurul Amin Submitted by Date-31 st July, 2010 North South University Financial Performance

Analysis and Interpretation of Financial Statements

Chapter 23 Analysis and Interpretation of Financial Statements o Prepare comparative financial statements using horizontal analysis o Prepare comparative financial statements using vertical analysis o

Chapter 23 Analysis and Interpretation of Financial Statements o Prepare comparative financial statements using horizontal analysis o Prepare comparative financial statements using vertical analysis o

Chapter 3 Working with Financial Statements

Chapter 3 Working with Financial Statements This chapter is a continuation of Chapter 2. We use accounting numbers because of the unavailability of market numbers. We prefer to use market numbers. Common-Size

Chapter 3 Working with Financial Statements This chapter is a continuation of Chapter 2. We use accounting numbers because of the unavailability of market numbers. We prefer to use market numbers. Common-Size

Business Ratios. Current Ratio

Current Ratio Business Ratios Measures whether or not the firm has enough resources to pay its debt over the next 12 months formula: Current Ratio = Current Assets Current Liabilities Acceptable ratios

Current Ratio Business Ratios Measures whether or not the firm has enough resources to pay its debt over the next 12 months formula: Current Ratio = Current Assets Current Liabilities Acceptable ratios

> > > > > > > > Chapter 16. Understanding Accounting and Financial Statements

> > > > > > > > Chapter 16 Understanding Accounting and Financial Statements 1 2 3 Explain the functions and importance of accounting, and identify the three basic activities involving accounting. Describe

> > > > > > > > Chapter 16 Understanding Accounting and Financial Statements 1 2 3 Explain the functions and importance of accounting, and identify the three basic activities involving accounting. Describe

AU-C Section 930, Interim Financial Information Proposed SSARS Review of Financial Statements Explanation for Differences

Comparison of AU-C section 930, Interim Financial Information, with Proposed Statement on Standards for Accounting and Review Services Review of Financial Statements This document demonstrates how the

Comparison of AU-C section 930, Interim Financial Information, with Proposed Statement on Standards for Accounting and Review Services Review of Financial Statements This document demonstrates how the

STAFF GUIDANCE CHANGES TO THE AUDITOR'S REPORT EFFECTIVE FOR AUDITS OF FISCAL YEARS ENDING ON OR AFTER DECEMBER 15, 2017

1666 K Street NW Washington, DC 20006 Office: (202) 207-9100 Fax: (202) 862-8430 www.pcaobus.org STAFF GUIDANCE CHANGES TO THE AUDITOR'S REPORT EFFECTIVE FOR AUDITS OF FISCAL YEARS ENDING ON OR AFTER DECEMBER

1666 K Street NW Washington, DC 20006 Office: (202) 207-9100 Fax: (202) 862-8430 www.pcaobus.org STAFF GUIDANCE CHANGES TO THE AUDITOR'S REPORT EFFECTIVE FOR AUDITS OF FISCAL YEARS ENDING ON OR AFTER DECEMBER

A CLEAR UNDERSTANDING OF THE INDUSTRY

A CLEAR UNDERSTANDING OF THE INDUSTRY IS CFA INSTITUTE INVESTMENT FOUNDATIONS RIGHT FOR YOU? Investment Foundations is a certificate program designed to give you a clear understanding of the investment

A CLEAR UNDERSTANDING OF THE INDUSTRY IS CFA INSTITUTE INVESTMENT FOUNDATIONS RIGHT FOR YOU? Investment Foundations is a certificate program designed to give you a clear understanding of the investment

Identifying Risk: Understanding the Entity and its Environment

CASE STUDY: PIZZA SHOP, INC. Identifying Risk: Understanding the Entity and its Environment Pizza Shop, Inc. (PSI or the Entity) owns and operates dine-in restaurants offering Italian cuisine. PSI was

CASE STUDY: PIZZA SHOP, INC. Identifying Risk: Understanding the Entity and its Environment Pizza Shop, Inc. (PSI or the Entity) owns and operates dine-in restaurants offering Italian cuisine. PSI was

Agenda Item 2A PROPOSED STATEMENT ON STANDARDS FOR ACCOUNTING AND REVIEW SERVICES REVIEW OF FINANCIAL STATEMENTS CONTENTS

ARSC Meeting August 21-23, 2012 Agenda Item 2A PROPOSED STATEMENT ON STANDARDS FOR ACCOUNTING AND REVIEW SERVICES REVIEW OF FINANCIAL STATEMENTS Introduction CONTENTS Prepared by: Mike Glynn (August 2012)

ARSC Meeting August 21-23, 2012 Agenda Item 2A PROPOSED STATEMENT ON STANDARDS FOR ACCOUNTING AND REVIEW SERVICES REVIEW OF FINANCIAL STATEMENTS Introduction CONTENTS Prepared by: Mike Glynn (August 2012)

Using Financial Statements in the Credit Review Process. Wendi Rosenblatt, Hearst Television

Using Financial Statements in the Credit Review Process Wendi Rosenblatt, Hearst Television Agenda What is Available Financial Statement Overview DineEquity, Inc. Annual Report/Form 10K Review Availability

Using Financial Statements in the Credit Review Process Wendi Rosenblatt, Hearst Television Agenda What is Available Financial Statement Overview DineEquity, Inc. Annual Report/Form 10K Review Availability

Chapter 3. The Balance Sheet and Financial Disclosures

Chapter 3 The Balance Sheet and Financial Disclosures AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments,

Chapter 3 The Balance Sheet and Financial Disclosures AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments,

Chapter 12. Final work: general principles, analytical review of financial. trade receivables

Chapter 12 Final work: general principles, analytical review of financial statements, noncurrent assets and trade receivables Learning objectives To explain the importance of planning the year-end examination

Chapter 12 Final work: general principles, analytical review of financial statements, noncurrent assets and trade receivables Learning objectives To explain the importance of planning the year-end examination

Financial statements present the results of operations and the financial position of the company.

Accounting Fundamentals Lesson 1 1. The Financial Statements Financial statements present the results of operations and the financial position of the company. Publicly traded companies commonly prepare

Accounting Fundamentals Lesson 1 1. The Financial Statements Financial statements present the results of operations and the financial position of the company. Publicly traded companies commonly prepare

Report on Inspection of Mark Shelley CPA (Headquartered in Mesa, Arizona) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2014 (Headquartered in Mesa, Arizona) Issued by the Public Company Accounting Oversight

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2014 (Headquartered in Mesa, Arizona) Issued by the Public Company Accounting Oversight

LIQUIDITY MANAGEMENT Presentation by: CPA Richard Kamami Secretary, PSB,Murang a PSB 23rd November 2017

LIQUIDITY MANAGEMENT Presentation by: CPA Richard Kamami Secretary, PSB,Murang a PSB 23rd November 2017 Uphold public interest Outline Definitions Assessment of Liquidity Criticism Liquidity Management

LIQUIDITY MANAGEMENT Presentation by: CPA Richard Kamami Secretary, PSB,Murang a PSB 23rd November 2017 Uphold public interest Outline Definitions Assessment of Liquidity Criticism Liquidity Management

WEEK 10 Analysis of Financial Statements

WEEK 10 Analysis of Financial Statements Learning Objectives 1. Organize a systematic financial statements analysis using common-size financial statements and ratio analysis. 2. Recognize the potential

WEEK 10 Analysis of Financial Statements Learning Objectives 1. Organize a systematic financial statements analysis using common-size financial statements and ratio analysis. 2. Recognize the potential

PCAOB Update. Maryland Association of CPAs 2014 Accounting Education Conference

PCAOB Update Maryland Association of CPAs 2014 Accounting Education Conference Jeanette M. Franzel, Board Member Public Company Accounting Oversight Board January 10, 2014 Columbia, MD The views I express

PCAOB Update Maryland Association of CPAs 2014 Accounting Education Conference Jeanette M. Franzel, Board Member Public Company Accounting Oversight Board January 10, 2014 Columbia, MD The views I express

PCAOB Update. Maryland Association of CPAs 2014 Accounting Education Conference

PCAOB Update Maryland Association of CPAs 2014 Accounting Education Conference Jeanette M. Franzel, Board Member Public Company Accounting Oversight Board January 10, 2014 Columbia, MD 2 The views I express

PCAOB Update Maryland Association of CPAs 2014 Accounting Education Conference Jeanette M. Franzel, Board Member Public Company Accounting Oversight Board January 10, 2014 Columbia, MD 2 The views I express

Report on Inspection of PricewaterhouseCoopers Kyoto (Headquartered in Kyoto, Japan) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2013 Inspection of PricewaterhouseCoopers Kyoto (Headquartered in Kyoto, Japan) Issued

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2013 Inspection of PricewaterhouseCoopers Kyoto (Headquartered in Kyoto, Japan) Issued

Disciplined thinking focuses inspiration rather than constricts it. ~ Anonymous

Ratio Analysis Disciplined thinking focuses inspiration rather than constricts it. ~ Anonymous Ratio Analysis compares significant numbers from your financial statements. Rather than focusing on specific

Ratio Analysis Disciplined thinking focuses inspiration rather than constricts it. ~ Anonymous Ratio Analysis compares significant numbers from your financial statements. Rather than focusing on specific

During this session, we ll cover: Benefits of using ratios Information gathering Types of ratios and when to use them How to calculate them More

During this session, we ll cover: Benefits of using ratios Information gathering Types of ratios and when to use them How to calculate them More importantly, how to interpret them Pinpoint potential problem

During this session, we ll cover: Benefits of using ratios Information gathering Types of ratios and when to use them How to calculate them More importantly, how to interpret them Pinpoint potential problem

CHAPTER 8: Accounting

CHAPTER 8: Accounting DECISION MAKING BY THE NUMBERS 1 LOOKING AHEAD What is accounting? How is accounting information used? What are career opportunities in accounting? What are the goals of generally

CHAPTER 8: Accounting DECISION MAKING BY THE NUMBERS 1 LOOKING AHEAD What is accounting? How is accounting information used? What are career opportunities in accounting? What are the goals of generally

ASSIGNMENT. Financial Management. TOPIC Ratio Analysis on Shinepukur Ceramics Limited ( ) Submitted to. S. M. Arifuzzaman Course Instructor

Submitted to. S. M. Arifuzzaman Course Instructor") ASSIGNMENT Financial Management TOPIC Ratio Analysis on Shinepukur Ceramics Limited (2008-2010) Submitted to S. M. Arifuzzaman Course Instructor Financial Management Department of Accounting & Finance

ASSIGNMENT Financial Management TOPIC Ratio Analysis on Shinepukur Ceramics Limited (2008-2010) Submitted to S. M. Arifuzzaman Course Instructor Financial Management Department of Accounting & Finance

a $33.17 $33.33 $33.50 $28.57

What is the book value per share for a company that has total stockholders' equity of $10,000,000, preferred stock of $50,000, and 300,000 common shares outstanding? a $33.17 $33.33 $33.50 $28.57 "'Your

What is the book value per share for a company that has total stockholders' equity of $10,000,000, preferred stock of $50,000, and 300,000 common shares outstanding? a $33.17 $33.33 $33.50 $28.57 "'Your

1 See Staff Inspection Brief, Preview of Observations from 2015 Inspections of Auditors of Issuers, Vol. 2016/1, issued in April of

Vol. 2016/3 July 2016 Staff Inspection Brief The staff of the ( PCAOB or Board ) prepares Inspection Briefs to assist auditors, audit committees, investors, and preparers in understanding the PCAOB inspection

Vol. 2016/3 July 2016 Staff Inspection Brief The staff of the ( PCAOB or Board ) prepares Inspection Briefs to assist auditors, audit committees, investors, and preparers in understanding the PCAOB inspection

Session 2, Sunday, April 2nd (1:30-5:00) v Association for Financial Professionals. All rights reserved. Session 3-1

v Association for Financial Professionals. All rights reserved. Session 3-1") Session 2, Sunday, April 2nd (1:30-5:00) v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Financial Accounting and Reporting: Part I, Domain B Chapter

Session 2, Sunday, April 2nd (1:30-5:00) v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Financial Accounting and Reporting: Part I, Domain B Chapter

Report on Inspection of B F Borgers CPA PC (Headquartered in Lakewood, Colorado) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Lakewood, Colorado) Issued by the Public Company Accounting

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Lakewood, Colorado) Issued by the Public Company Accounting

CASH FLOW FORECASTING

CASH FLOW FORECASTING 1 2 3 4 5 6 Goal of Accurate Projections Key Elements Methodology Sales Forecast Key Sales Questions Staffing Forecast 7 8 9 10 11 12 Key Staffing Questions Operating Expenses Balance

CASH FLOW FORECASTING 1 2 3 4 5 6 Goal of Accurate Projections Key Elements Methodology Sales Forecast Key Sales Questions Staffing Forecast 7 8 9 10 11 12 Key Staffing Questions Operating Expenses Balance

Chapter 23 Audit of Cash and Financial Instruments. Copyright 2014 Pearson Education

Chapter 23 Audit of Cash and Financial Instruments Identify the major types of cash and financial instruments accounts maintained by business entities. Show the relationship of cash in the bank to the

Chapter 23 Audit of Cash and Financial Instruments Identify the major types of cash and financial instruments accounts maintained by business entities. Show the relationship of cash in the bank to the

Breaking Down ROE Using the DuPont Formula. R eturn on equity. By Z. Joe Lan, CFA

Breaking Down ROE Using the DuPont Formula By Z. Joe Lan, CFA Article Highlights ROE calculates the return a company earns from shareholder s equity. The DuPont formula reveals the source of those returns:

Breaking Down ROE Using the DuPont Formula By Z. Joe Lan, CFA Article Highlights ROE calculates the return a company earns from shareholder s equity. The DuPont formula reveals the source of those returns:

Report on Inspection of MaloneBailey, LLP (Headquartered in Houston, Texas) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Houston, Texas) Issued by the Public Company Accounting Oversight

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Houston, Texas) Issued by the Public Company Accounting Oversight

The principal purposes of the Audit Committee (Committee) of the Board of Directors (Board) of Vistra Energy Corp.

of the Board of Directors (Board) of Vistra Energy Corp.") VISTRA ENERGY CORP. AUDIT COMMITTEE CHARTER I. PURPOSES OF THE COMMITTEE The principal purposes of the Audit Committee (Committee) of the Board of Directors (Board) of Vistra Energy Corp. (Company) are

VISTRA ENERGY CORP. AUDIT COMMITTEE CHARTER I. PURPOSES OF THE COMMITTEE The principal purposes of the Audit Committee (Committee) of the Board of Directors (Board) of Vistra Energy Corp. (Company) are

RATIO ANALYSIS. The preceding chapters concentrated on developing a general but solid understanding

C H A P T E R 4 RATIO ANALYSIS I N T R O D U C T I O N The preceding chapters concentrated on developing a general but solid understanding of accounting principles and concepts and their applications to

C H A P T E R 4 RATIO ANALYSIS I N T R O D U C T I O N The preceding chapters concentrated on developing a general but solid understanding of accounting principles and concepts and their applications to

HANDOUT ANALYSIS FINANCIAL RATIO S. COURSE : FINANCIAL STATEMENT ANALYSIS LECTURER : PATRIANI W. DEWANTI, M.Acc.

HANDOUT ANALYSIS FINANCIAL RATIO S COURSE : FINANCIAL STATEMENT ANALYSIS LECTURER : PATRIANI W. DEWANTI, M.Acc. ACCOUNTING DEPARTMENT FACULTY OF ECONOMICS YOGYAKARTA STATE UNIVERSITY 1 FINANCIAL STATEMENT

HANDOUT ANALYSIS FINANCIAL RATIO S COURSE : FINANCIAL STATEMENT ANALYSIS LECTURER : PATRIANI W. DEWANTI, M.Acc. ACCOUNTING DEPARTMENT FACULTY OF ECONOMICS YOGYAKARTA STATE UNIVERSITY 1 FINANCIAL STATEMENT

STUDY UNIT TWO FINANCIAL PERFORMANCE METRICS FINANCIAL RATIOS

STUDY UNIT TWO FINANCIAL PERFORMANCE METRICS FINANCIAL RATIOS 1 2.1 Liquidity Ratios.......................................................... 2 2.2 Leverage and Solvency Ratios..............................................

STUDY UNIT TWO FINANCIAL PERFORMANCE METRICS FINANCIAL RATIOS 1 2.1 Liquidity Ratios.......................................................... 2 2.2 Leverage and Solvency Ratios..............................................

Audit and Assurance. Certificate in Accounting and Business II Examination September 2012 THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA

SUGGESTED SOLUTIONS 06204 - Audit and Assurance Certificate in Accounting and Business II Examination September 2012 THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA All Rights Reserved (1) Answer No.

SUGGESTED SOLUTIONS 06204 - Audit and Assurance Certificate in Accounting and Business II Examination September 2012 THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA All Rights Reserved (1) Answer No.

Accounting For Managers

Accounting For Managers Professor ZHOU Ning SCHOOL OF ECONOMICS AND MANAGEMENT BEIHANG UNIVERSITY zning80@buaa.edu.cn Chapter 13 Financial Statement Analysis The objectives of Chapter 13 Business objectives

Accounting For Managers Professor ZHOU Ning SCHOOL OF ECONOMICS AND MANAGEMENT BEIHANG UNIVERSITY zning80@buaa.edu.cn Chapter 13 Financial Statement Analysis The objectives of Chapter 13 Business objectives

Chapter 6 Statement of Cash Flows

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

Chapter 3 Analysis of Financial Statements. Ratio Analysis Please refer to the attached financial statements, and industry average ratios

Chapter 3 Analysis of Financial Statements Ratio Analysis Please refer to the attached financial statements, and industry average ratios In this chapter, we will cover Liquidity ratios Asset management

Chapter 3 Analysis of Financial Statements Ratio Analysis Please refer to the attached financial statements, and industry average ratios In this chapter, we will cover Liquidity ratios Asset management

Gaiam, Inc. Gaiam, Inc. Financial Snapshot. Operating Performance. Fast Facts. SWOT Analysis. [Figure] Gaiam, Inc. - SWOT Profile Page 1

![Gaiam, Inc. Gaiam, Inc. Financial Snapshot. Operating Performance. Fast Facts. SWOT Analysis. [Figure] Gaiam, Inc. - SWOT Profile Page 1](/thumbs/86/94009915.jpg "Gaiam, Inc. Gaiam, Inc. Financial Snapshot. Operating Performance. Fast Facts. SWOT Analysis. [Figure] Gaiam, Inc. - SWOT Profile Page 1") Gaiam, Inc. Fast Facts Headquarters Address Telephone Fax Website Ticker Symbol, Stock Exchange Financial Snapshot Operating Performance The company reported revenue of US$XX million during the fiscal

Gaiam, Inc. Fast Facts Headquarters Address Telephone Fax Website Ticker Symbol, Stock Exchange Financial Snapshot Operating Performance The company reported revenue of US$XX million during the fiscal

Current Accounting Issues Red Flags of Credit Analysis

Current Accounting Issues Red Flags of Credit Analysis Presented by: Dennis M. Schleper, Principal dschleper@larsonallen.com 267-419-1144 Objectives Understand the current accounting issues and pronouncements

Current Accounting Issues Red Flags of Credit Analysis Presented by: Dennis M. Schleper, Principal dschleper@larsonallen.com 267-419-1144 Objectives Understand the current accounting issues and pronouncements

This is How Do Managers Use Financial and Nonfinancial Performance Measures?, chapter 13 from the book Accounting for Managers (index.html) (v. 1.0).

(v. 1.0).") This is How Do Managers Use Financial and Nonfinancial Performance Measures?, chapter 13 from the book Accounting for Managers (index.html) (v. 1.0). This book is licensed under a Creative Commons by-nc-sa

This is How Do Managers Use Financial and Nonfinancial Performance Measures?, chapter 13 from the book Accounting for Managers (index.html) (v. 1.0). This book is licensed under a Creative Commons by-nc-sa

Kavous Ardalan. Marist College, New York, USA

Journal of Modern Accounting and Auditing, July 2017, Vol. 13, No. 7, 294-298 doi: 10.17265/1548-6583/2017.07.002 D DAVID PUBLISHING Advancing the Interpretation of the Du Pont Equation Kavous Ardalan

Journal of Modern Accounting and Auditing, July 2017, Vol. 13, No. 7, 294-298 doi: 10.17265/1548-6583/2017.07.002 D DAVID PUBLISHING Advancing the Interpretation of the Du Pont Equation Kavous Ardalan

Curriculum designed for use with the Iowa Electronic Markets Cynthia J. Brown Marilyn M. Dutton Thomas A. Rietz

Financial Statement Analysis Curriculum designed for use with the Iowa Electronic Markets by Cynthia J. Brown Marilyn M. Dutton Thomas A. Rietz ١ Financial Statement Analysis: Lecture Outline Review of

Financial Statement Analysis Curriculum designed for use with the Iowa Electronic Markets by Cynthia J. Brown Marilyn M. Dutton Thomas A. Rietz ١ Financial Statement Analysis: Lecture Outline Review of

Classification: 1. Profitability. 2. Efficiency. 3. Liquidity

BUSS1030 Semester 2 2012 1 - Simple means of examining the health of a business - Help highlight the financial strengths and weaknesses of a business o Cannot, however, explain why certain strengths/weaknesses

BUSS1030 Semester 2 2012 1 - Simple means of examining the health of a business - Help highlight the financial strengths and weaknesses of a business o Cannot, however, explain why certain strengths/weaknesses

Clarified Auditing Standards and PCAOB Standards

Clarified ing Standards and PCAOB Standards 177 Appendix B Clarified ing Standards and PCAOB Standards The auditing content in this guide focuses primarily on generally accepted auditing standards issued

Clarified ing Standards and PCAOB Standards 177 Appendix B Clarified ing Standards and PCAOB Standards The auditing content in this guide focuses primarily on generally accepted auditing standards issued

Financial Statements. For the Year Ended March 31, 2016

Financial Statements For the Year Ended March 31, 2016 Table of Contents Statement of Management Responsibility...3 Independent Auditors Report...4 Statement of Financial Position...6 Statement of Operations

Financial Statements For the Year Ended March 31, 2016 Table of Contents Statement of Management Responsibility...3 Independent Auditors Report...4 Statement of Financial Position...6 Statement of Operations

n Financial Statement Analysis n Dollar and Percentage Changes n Common Sized Statements n Ratio Analysis McGraw-Hill /Irwin McGraw-Hill /Irwin

14-1 Today s Agenda Management Accounting Lecture 3 (Chapter 14) Financial Statement Analysis Bangor University Transfer Abroad Programme n Financial Statement Analysis n Dollar and Percentage Changes

14-1 Today s Agenda Management Accounting Lecture 3 (Chapter 14) Financial Statement Analysis Bangor University Transfer Abroad Programme n Financial Statement Analysis n Dollar and Percentage Changes

CHAPTER 2. Capital Structure and Debt Capacity. Balancing Operating / Business Risk and Financial Risk

CHAPTER 2 Capital Structure and Debt Capacity Balancing Operating / Business Risk and Financial Risk A company s capital structure is comprised of a combination of debt and equity that is used to fund

CHAPTER 2 Capital Structure and Debt Capacity Balancing Operating / Business Risk and Financial Risk A company s capital structure is comprised of a combination of debt and equity that is used to fund

Chapter 1: Business Decisions and Financial Accounting

Test Bank Fundamentals Of Financial Accounting 5th Edition by Fred Phillips, Robert Libby, Patricia Libby, completed download: https://testbankarea.com/download/fundamentals-financialaccounting-5th-edition-test-bank-fred-phillips-robert-libby-patricialibby/

Test Bank Fundamentals Of Financial Accounting 5th Edition by Fred Phillips, Robert Libby, Patricia Libby, completed download: https://testbankarea.com/download/fundamentals-financialaccounting-5th-edition-test-bank-fred-phillips-robert-libby-patricialibby/

2 BASIC FINANCIAL STATEMENTS

Chapter 02 Basic Financial Statements 2 BASIC FINANCIAL STATEMENTS Chapter Summary Financial statements are the primary means of communicating financial information to users. Chapter 2 covers the income

Chapter 02 Basic Financial Statements 2 BASIC FINANCIAL STATEMENTS Chapter Summary Financial statements are the primary means of communicating financial information to users. Chapter 2 covers the income

CANADA: FINANCIAL STATEMENTS AND ACCOUNTING STANDARDS

: FINANCIAL STATEMENTS AND ACCOUNTING STANDARDS Chartered Professional Accountants of Canada (CPA Canada) is the national organization established to support a unified Canadian accounting profession. CPA

: FINANCIAL STATEMENTS AND ACCOUNTING STANDARDS Chartered Professional Accountants of Canada (CPA Canada) is the national organization established to support a unified Canadian accounting profession. CPA

Supply chain management and return on total net assets Understanding the impact of SCM decisions on financial performance

Supply chain management and return on total net assets Understanding the impact of SCM decisions on financial performance CASE STUDY SUPPLY CHAIN MANAGEMENT Simon Templar AUTHOR BIOGRAPHY DR SIMON TEMPLAR

Supply chain management and return on total net assets Understanding the impact of SCM decisions on financial performance CASE STUDY SUPPLY CHAIN MANAGEMENT Simon Templar AUTHOR BIOGRAPHY DR SIMON TEMPLAR

Report on Inspection of Arnett Carbis Toothman LLP (Headquartered in Charleston, West Virginia) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Charleston, West Virginia) Issued by the Public Company Accounting

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Charleston, West Virginia) Issued by the Public Company Accounting