Financial Factors in Business Cycles

|

|

|

- Luke Briggs

- 5 years ago

- Views:

Transcription

1 Financial Factors in Business Cycles Lawrence J. Christiano, Roberto Motto, Massimo Rostagno 30 November 2007 The views expressed are those of the authors only

2 What We Do? Integrate financial factors into a rather standard macro model Fit the model to EA and US data Evaluate credibility of model: What are the shocks that drove booms and recessions? How good is the model at out-of-sample forecasting? How important are financial factors? Are they an important new source of shocks? Are they important sources of propagation? Our Finding: YES - Lending contract are denominated in nominal terms

3 Model Dynamic General Equilibrium Model: Core model:» Christiano, Eichenbaum and Evans (2005) Banking system:» Chari, Christiano and Eichenbaum (1995) Financial frictions:» Bernanke, Gertler and Gilchrist (1999), as modified in CMR (2003) We add many shocks as in Smets and Wouters (2003)

4 Model Overview Households - Consumption - Labour supply / wage - Portfolio (currency, demand deposits, saving deposits, time deposits) Firms - Monopolistic competition - Sticky prices - Trend growth in efficiency of labour - Working capital channel Entrepreneurs - Ownership of capital stock - Own equity + Borrowing - Rent out capital services Monetary and Fiscal Authorities Capital producers -Transform consumption goods into investment goods - Produce installed capital Banks - Assets and Liabilities - Financial imperfections (agency costs) - Nominal frictions (contracts in nominal terms)

5 Households Household s Problem: Consume with habit formation Monopolistic supplier of specialized labor input and sticky wages Enjoy differentiated liquidity services Invest also in one-period assets (backed by loan contract) and n-period bonds

6 Goods Production and Pricing Standard Dixit-Stiglitz aggregator for final-goods production Intermediate-goods production function Hybrid Phillips curve with cost channel. In linearised form:

7 Capital Producers Technology to transform final goods into investment goods: which implies: Technology to transform investment goods into installed capital: so that

8 Entrepreneurs Purchase new capital from capital producers using internal finance and loans: CSV contract observe idiosyncratic productivity shock: decide capital utilization rate: bear a cost to intensity of capital utilization: rent out capital services earning a rent sell capital and pay off debt if cannot repay debt, monitored and must turn over everything nominal amount owed to households is not contingent on shocks realised in period t+1

9 Entrepreneurs Evolution of net worth: Standard models: With financial frictions, in linearised form:

10 Banks Banks are in two businesses: Intermediation of loans to Entrepreneurs Extension of working-capital loans to firms and provision of liquidity services (to households/firms)

11 Banks Fractional-reserve system: A spectrum of interest rates:

12 Estimation State-observer set-up with measurement error: 14 observed variables (including Monetary aggregates, premium, spread, stock market) Use Kalman Filter to construct Likelihood Steady state parameters: A subset set exogenously, e.g. capital depreciation A subset found to match steady state great ratios, velocities and interest rates with corresponding data means, e.g.: Elasticities, shock parameters and std. of measurement errors: Bayesian approach: Maximum Likelihood combined with prior distributions

13 Steady State

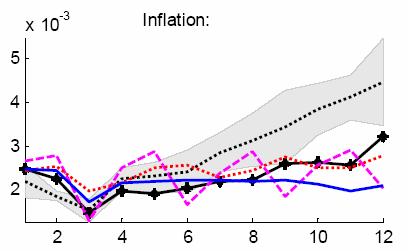

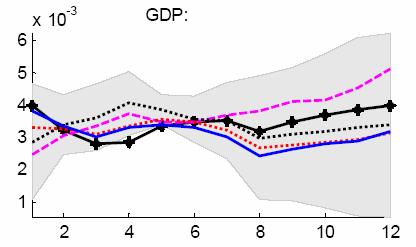

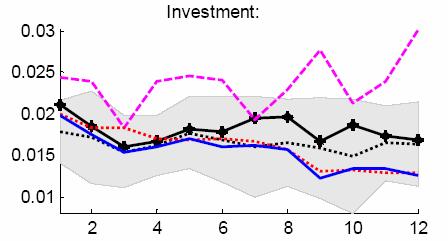

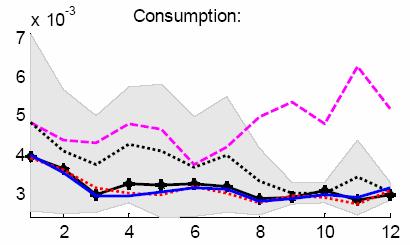

14 EA: Out-of-Sample Performance

15 Shock Decomposition: EA GDP growth Q1 1989Q3 1991Q1 1992Q3 1994Q1 1995Q3 1997Q1 1998Q3 2000Q1 2001Q3 2003Q1 2004Q3 2006Q1 Mark-up Demand Money demand and Banking Capital producers and Entrepreneurs Monetary policy Goods supply GDP Grow th (in deviation from sample mean)

16 Shock Decomposition: US GDP growth

17 Stock Market and Shock Identification Stock market can help to identify shocks driving business cycle If capital increases at the same time that its price increases, this should come from demand and not to supply forces. This demand shock comes from our financial factors When we leave out financial factors and do not use stock market data, we find main driving force is favourable supply shocks in technology for constructing capital

18 Capital Formation

19 Stock Market and Shock Identification Stock market can help to identify shocks driving business cycle If capital increases at the same time that its price increases, this should come from demand and not to supply forces. This demand shock comes from our financial factors When we leave out financial factors and do not use stock market data, we find main driving force is favourable supply shocks in technology for constructing capital

20 Stock Market and Shock Identification

21 Stock Market and Shock Identification

22 Financial Sector We have argued that financial sector is an important source of shocks How important for propagation of non-financial shocks? Nominal frictions in debt contract generate large and persistent effects. Amplification of shocks that move output and inflation in same direction. Mitigate other shocks Banks amplify shocks

23 Propagation of Shocks Impulse response to monetary policy shock Impulse response to neutral technology shock

24 Policy Implications: Taylor Frontier

25 Conclusions Constructed a model that provides useful interpretation of economic fluctuations Financial Frictions are important Source of Shocks Source of Propagation

Fluctuations. Roberto Motto

Financial Factors in Economic Fluctuations Lawrence Christiano Roberto Motto Massimo Rostagno What we do Integrate t financial i frictions into a standard d equilibrium i model and estimate the model using

Financial Factors in Economic Fluctuations Lawrence Christiano Roberto Motto Massimo Rostagno What we do Integrate t financial i frictions into a standard d equilibrium i model and estimate the model using

Incorporate Financial Frictions into a

Incorporate Financial Frictions into a Business Cycle Model General idea: Standard model assumes borrowers and lenders are the same people..no conflict of interest Financial friction models suppose borrowers

Incorporate Financial Frictions into a Business Cycle Model General idea: Standard model assumes borrowers and lenders are the same people..no conflict of interest Financial friction models suppose borrowers

Notes for a Model With Banks and Net Worth Constraints

Notes for a Model With Banks and Net Worth Constraints 1 (Revised) Joint work with Roberto Motto and Massimo Rostagno Combines Previous Model with Banking Model of Chari, Christiano, Eichenbaum (JMCB,

Notes for a Model With Banks and Net Worth Constraints 1 (Revised) Joint work with Roberto Motto and Massimo Rostagno Combines Previous Model with Banking Model of Chari, Christiano, Eichenbaum (JMCB,

Using VARs to Estimate a DSGE Model. Lawrence Christiano

Using VARs to Estimate a DSGE Model Lawrence Christiano Objectives Describe and motivate key features of standard monetary DSGE models. Estimate a DSGE model using VAR impulse responses reported in Eichenbaum

Using VARs to Estimate a DSGE Model Lawrence Christiano Objectives Describe and motivate key features of standard monetary DSGE models. Estimate a DSGE model using VAR impulse responses reported in Eichenbaum

Output Gap, Monetary Policy Trade-Offs and Financial Frictions

Output Gap, Monetary Policy Trade-Offs and Financial Frictions Francesco Furlanetto Norges Bank Paolo Gelain Norges Bank Marzie Taheri Sanjani International Monetary Fund Seminar at Narodowy Bank Polski

Output Gap, Monetary Policy Trade-Offs and Financial Frictions Francesco Furlanetto Norges Bank Paolo Gelain Norges Bank Marzie Taheri Sanjani International Monetary Fund Seminar at Narodowy Bank Polski

Financial Frictions Under Asymmetric Information and Costly State Verification

Financial Frictions Under Asymmetric Information and Costly State Verification General Idea Standard dsge model assumes borrowers and lenders are the same people..no conflict of interest. Financial friction

Financial Frictions Under Asymmetric Information and Costly State Verification General Idea Standard dsge model assumes borrowers and lenders are the same people..no conflict of interest. Financial friction

Policy options at the zero lower bound

Policy options at the zero lower bound Session 5: How to implement stabilization policies with high public debt? Timo Wollmershäuser & Atanas Hristov Ifo Institute Introduction very weak recovery from

Policy options at the zero lower bound Session 5: How to implement stabilization policies with high public debt? Timo Wollmershäuser & Atanas Hristov Ifo Institute Introduction very weak recovery from

Risk Shocks. Lawrence Christiano (Northwestern University), Roberto Motto (ECB) and Massimo Rostagno (ECB)

, Roberto Motto (ECB) and Massimo Rostagno (ECB)") Risk Shocks Lawrence Christiano (Northwestern University), Roberto Motto (ECB) and Massimo Rostagno (ECB) Finding Countercyclical fluctuations in the cross sectional variance of a technology shock, when

Risk Shocks Lawrence Christiano (Northwestern University), Roberto Motto (ECB) and Massimo Rostagno (ECB) Finding Countercyclical fluctuations in the cross sectional variance of a technology shock, when

Financial intermediaries in an estimated DSGE model for the UK

Financial intermediaries in an estimated DSGE model for the UK Stefania Villa a Jing Yang b a Birkbeck College b Bank of England Cambridge Conference - New Instruments of Monetary Policy: The Challenges

Financial intermediaries in an estimated DSGE model for the UK Stefania Villa a Jing Yang b a Birkbeck College b Bank of England Cambridge Conference - New Instruments of Monetary Policy: The Challenges

Risk Shocks and Economic Fluctuations. Summary of work by Christiano, Motto and Rostagno

Risk Shocks and Economic Fluctuations Summary of work by Christiano, Motto and Rostagno Outline Simple summary of standard New Keynesian DSGE model (CEE, JPE 2005 model). Modifications to introduce CSV

Risk Shocks and Economic Fluctuations Summary of work by Christiano, Motto and Rostagno Outline Simple summary of standard New Keynesian DSGE model (CEE, JPE 2005 model). Modifications to introduce CSV

Financial Frictions in Macroeconomics. Lawrence J. Christiano Northwestern University

Financial Frictions in Macroeconomics Lawrence J. Christiano Northwestern University Balance Sheet, Financial System Assets Liabilities Bank loans Securities, etc. Bank Debt Bank Equity Frictions between

Financial Frictions in Macroeconomics Lawrence J. Christiano Northwestern University Balance Sheet, Financial System Assets Liabilities Bank loans Securities, etc. Bank Debt Bank Equity Frictions between

Leverage Restrictions in a Business Cycle Model

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda SAIF, December 2014. Background Increasing interest in the following sorts of questions: What restrictions should be

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda SAIF, December 2014. Background Increasing interest in the following sorts of questions: What restrictions should be

On the new Keynesian model

Department of Economics University of Bern April 7, 26 The new Keynesian model is [... ] the closest thing there is to a standard specification... (McCallum). But it has many important limitations. It

Department of Economics University of Bern April 7, 26 The new Keynesian model is [... ] the closest thing there is to a standard specification... (McCallum). But it has many important limitations. It

Discussion of: Financial Factors in Economic Fluctuations by Christiano, Motto, and Rostagno

Discussion of: Financial Factors in Economic Fluctuations by Christiano, Motto, and Rostagno Guido Lorenzoni Bank of Canada-Minneapolis FED Conference, October 2008 This paper Rich DSGE model with: financial

Discussion of: Financial Factors in Economic Fluctuations by Christiano, Motto, and Rostagno Guido Lorenzoni Bank of Canada-Minneapolis FED Conference, October 2008 This paper Rich DSGE model with: financial

Euro Area and U.S. External Adjustment: The Role of Commodity Prices and Emerging Market Shocks

Euro Area and U.S. External Adjustment: The Role of Commodity Prices and Emerging Market Shocks Massimo Giovannini (European Commission, Joint Research Centre) Robert Kollmann (ECARES, Université Libre

Euro Area and U.S. External Adjustment: The Role of Commodity Prices and Emerging Market Shocks Massimo Giovannini (European Commission, Joint Research Centre) Robert Kollmann (ECARES, Université Libre

... The Great Depression and the Friedman-Schwartz Hypothesis Lawrence J. Christiano, Roberto Motto and Massimo Rostagno

The Great Depression and the Friedman-Schwartz Hypothesis Lawrence J. Christiano, Roberto Motto and Massimo Rostagno Background Want to Construct a Dynamic Economic Model Useful for the Analysis of Monetary

The Great Depression and the Friedman-Schwartz Hypothesis Lawrence J. Christiano, Roberto Motto and Massimo Rostagno Background Want to Construct a Dynamic Economic Model Useful for the Analysis of Monetary

... The Great Depression and the Friedman-Schwartz Hypothesis Lawrence J. Christiano, Roberto Motto and Massimo Rostagno

The Great Depression and the Friedman-Schwartz Hypothesis Lawrence J. Christiano, Roberto Motto and Massimo Rostagno 1 Background Want to Construct a Dynamic Economic Model Useful for the Analysis of Monetary

The Great Depression and the Friedman-Schwartz Hypothesis Lawrence J. Christiano, Roberto Motto and Massimo Rostagno 1 Background Want to Construct a Dynamic Economic Model Useful for the Analysis of Monetary

Analysis of DSGE Models. Lawrence Christiano

Specification, Estimation and Analysis of DSGE Models Lawrence Christiano Overview A consensus model has emerged as a device for forecasting, analysis, and as a platform for additional analysis of financial

Specification, Estimation and Analysis of DSGE Models Lawrence Christiano Overview A consensus model has emerged as a device for forecasting, analysis, and as a platform for additional analysis of financial

Notes on Financial Frictions Under Asymmetric Information and Costly State Verification. Lawrence Christiano

Notes on Financial Frictions Under Asymmetric Information and Costly State Verification by Lawrence Christiano Incorporating Financial Frictions into a Business Cycle Model General idea: Standard model

Notes on Financial Frictions Under Asymmetric Information and Costly State Verification by Lawrence Christiano Incorporating Financial Frictions into a Business Cycle Model General idea: Standard model

Asymmetric Information and Costly State Verification. Lawrence Christiano

Asymmetric Information and Costly State Verification Lawrence Christiano General Idea Standard dsge model assumes borrowers and lenders are the same people..no conflict of interest. Financial friction

Asymmetric Information and Costly State Verification Lawrence Christiano General Idea Standard dsge model assumes borrowers and lenders are the same people..no conflict of interest. Financial friction

Comment. The New Keynesian Model and Excess Inflation Volatility

Comment Martín Uribe, Columbia University and NBER This paper represents the latest installment in a highly influential series of papers in which Paul Beaudry and Franck Portier shed light on the empirics

Comment Martín Uribe, Columbia University and NBER This paper represents the latest installment in a highly influential series of papers in which Paul Beaudry and Franck Portier shed light on the empirics

Discussion of. Optimal Fiscal and Monetary Policy in a Medium-Scale Macroeconomic Model By Stephanie Schmitt-Grohe and Martin Uribe

Discussion of Optimal Fiscal and Monetary Policy in a Medium-Scale Macroeconomic Model By Stephanie Schmitt-Grohe and Martin Uribe Marc Giannoni Columbia University, CEPR and NBER International Research

Discussion of Optimal Fiscal and Monetary Policy in a Medium-Scale Macroeconomic Model By Stephanie Schmitt-Grohe and Martin Uribe Marc Giannoni Columbia University, CEPR and NBER International Research

Leverage Restrictions in a Business Cycle Model

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Disclaimer: The views expressed are those of the authors and do not necessarily reflect those of the Bank of Japan.

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Disclaimer: The views expressed are those of the authors and do not necessarily reflect those of the Bank of Japan.

Monetary Policy and a Stock Market Boom-Bust Cycle

Monetary Policy and a Stock Market Boom-Bust Cycle Lawrence Christiano, Cosmin Ilut, Roberto Motto, and Massimo Rostagno Asset markets have been volatile Should monetary policy react to the volatility?

Monetary Policy and a Stock Market Boom-Bust Cycle Lawrence Christiano, Cosmin Ilut, Roberto Motto, and Massimo Rostagno Asset markets have been volatile Should monetary policy react to the volatility?

Comment on Risk Shocks by Christiano, Motto, and Rostagno (2014)

") September 15, 2016 Comment on Risk Shocks by Christiano, Motto, and Rostagno (2014) Abstract In a recent paper, Christiano, Motto and Rostagno (2014, henceforth CMR) report that risk shocks are the most

September 15, 2016 Comment on Risk Shocks by Christiano, Motto, and Rostagno (2014) Abstract In a recent paper, Christiano, Motto and Rostagno (2014, henceforth CMR) report that risk shocks are the most

Leverage Restrictions in a Business Cycle Model. March 13-14, 2015, Macro Financial Modeling, NYU Stern.

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Northwestern University Bank of Japan March 13-14, 2015, Macro Financial Modeling, NYU Stern. Background Wish to address

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Northwestern University Bank of Japan March 13-14, 2015, Macro Financial Modeling, NYU Stern. Background Wish to address

Macroeconomic Effects of Financial Shocks: Comment

Macroeconomic Effects of Financial Shocks: Comment Johannes Pfeifer (University of Cologne) 1st Research Conference of the CEPR Network on Macroeconomic Modelling and Model Comparison (MMCN) June 2, 217

Macroeconomic Effects of Financial Shocks: Comment Johannes Pfeifer (University of Cologne) 1st Research Conference of the CEPR Network on Macroeconomic Modelling and Model Comparison (MMCN) June 2, 217

Leverage Restrictions in a Business Cycle Model. Lawrence J. Christiano Daisuke Ikeda

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Background Increasing interest in the following sorts of questions: What restrictions should be placed on bank leverage?

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Background Increasing interest in the following sorts of questions: What restrictions should be placed on bank leverage?

Involuntary (Unlucky) Unemployment and the Business Cycle. Lawrence Christiano Mathias Trabandt Karl Walentin

Unemployment and the Business Cycle. Lawrence Christiano Mathias Trabandt Karl Walentin") Involuntary (Unlucky) Unemployment and the Business Cycle Lawrence Christiano Mathias Trabandt Karl Walentin Background New Keynesian (NK) models receive lots of attention ti in central lbanks. People

Involuntary (Unlucky) Unemployment and the Business Cycle Lawrence Christiano Mathias Trabandt Karl Walentin Background New Keynesian (NK) models receive lots of attention ti in central lbanks. People

How Important are Financial Frictions in the U.S. and the Euro Area

Sveriges riksbank 223 working paper series How Important are Financial Frictions in the U.S. and the Euro Area Virginia Queijo von Heideken May 28 Working papers are obtainable from Sveriges Riksbank Information

Sveriges riksbank 223 working paper series How Important are Financial Frictions in the U.S. and the Euro Area Virginia Queijo von Heideken May 28 Working papers are obtainable from Sveriges Riksbank Information

Econ590 Topics in Macroeconomics. Lecture 1 : Business Cycle Models : The Current Consensus (Part C)

") 2015-2016 Econ590 Topics in Macroeconomics Lecture 1 : Business Cycle Models : The Current Consensus (Part C) Paul Beaudry & Franck Portier franck.portier@tse-fr.eu Vancouver School of Economics Version

2015-2016 Econ590 Topics in Macroeconomics Lecture 1 : Business Cycle Models : The Current Consensus (Part C) Paul Beaudry & Franck Portier franck.portier@tse-fr.eu Vancouver School of Economics Version

MONETARY POLICY EXPECTATIONS AND BOOM-BUST CYCLES IN THE HOUSING MARKET*

Articles Winter 9 MONETARY POLICY EXPECTATIONS AND BOOM-BUST CYCLES IN THE HOUSING MARKET* Caterina Mendicino**. INTRODUCTION Boom-bust cycles in asset prices and economic activity have been a central

Articles Winter 9 MONETARY POLICY EXPECTATIONS AND BOOM-BUST CYCLES IN THE HOUSING MARKET* Caterina Mendicino**. INTRODUCTION Boom-bust cycles in asset prices and economic activity have been a central

Boom-bust Cycles and Monetary Policy. Lawrence Christiano

MACRO-LINKAGES, OIL PRICES AND DEFLATION WORKSHOP JANUARY 6 9, 2009 Boom-bust Cycles and Monetary Policy Lawrence Christiano Boom-bust Cycles and Monetary Policy It has often been argued that there is

MACRO-LINKAGES, OIL PRICES AND DEFLATION WORKSHOP JANUARY 6 9, 2009 Boom-bust Cycles and Monetary Policy Lawrence Christiano Boom-bust Cycles and Monetary Policy It has often been argued that there is

Financial Frictions in Macroeconomics. Lawrence J. Christiano Northwestern University

Financial Frictions in Macroeconomics Lawrence J. Christiano Northwestern University Balance Sheet, Financial System Assets Liabilities Bank loans Bank Debt Securities, etc. Bank Equity Balance Sheet,

Financial Frictions in Macroeconomics Lawrence J. Christiano Northwestern University Balance Sheet, Financial System Assets Liabilities Bank loans Bank Debt Securities, etc. Bank Equity Balance Sheet,

The Macroeconomic Implications of Changes in Bank Capital and Liquidity Requirements in Canada: Insights from BoC-GEM-Fin

The Macroeconomic Implications of Changes in Bank Capital and Liquidity Requirements in Canada: Insights from BoC-GEM-Fin Carlos de Resende Ali Dib Nikita Perevalov August 17, 2010 Abstract The authors

The Macroeconomic Implications of Changes in Bank Capital and Liquidity Requirements in Canada: Insights from BoC-GEM-Fin Carlos de Resende Ali Dib Nikita Perevalov August 17, 2010 Abstract The authors

1 Business-Cycle Facts Around the World 1

Contents Preface xvii 1 Business-Cycle Facts Around the World 1 1.1 Measuring Business Cycles 1 1.2 Business-Cycle Facts Around the World 4 1.3 Business Cycles in Poor, Emerging, and Rich Countries 7 1.4

Contents Preface xvii 1 Business-Cycle Facts Around the World 1 1.1 Measuring Business Cycles 1 1.2 Business-Cycle Facts Around the World 4 1.3 Business Cycles in Poor, Emerging, and Rich Countries 7 1.4

Discussion of Monetary Policy, the Financial Cycle, and Ultra-Low Interest Rates

Discussion of Monetary Policy, the Financial Cycle, and Ultra-Low Interest Rates Marc P. Giannoni Federal Reserve Bank of New York 1. Introduction Several recent papers have documented a trend decline

Discussion of Monetary Policy, the Financial Cycle, and Ultra-Low Interest Rates Marc P. Giannoni Federal Reserve Bank of New York 1. Introduction Several recent papers have documented a trend decline

Credit Shocks and the U.S. Business Cycle. Is This Time Different? Raju Huidrom University of Virginia. Midwest Macro Conference

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

Shocks, frictions and monetary policy Frank Smets

Shocks, frictions and monetary policy Frank Smets OECD Workshop Paris, 14 June 2007 Outline Two results from the Inflation Persistence Network (IPN) and their monetary policy implications Based on Altissimo,

Shocks, frictions and monetary policy Frank Smets OECD Workshop Paris, 14 June 2007 Outline Two results from the Inflation Persistence Network (IPN) and their monetary policy implications Based on Altissimo,

Credit Risk and the Macroeconomy

and the Macroeconomy Evidence From an Estimated Simon Gilchrist 1 Alberto Ortiz 2 Egon Zakrajšek 3 1 Boston University and NBER 2 Oberlin College 3 Federal Reserve Board XXVII Encuentro de Economistas

and the Macroeconomy Evidence From an Estimated Simon Gilchrist 1 Alberto Ortiz 2 Egon Zakrajšek 3 1 Boston University and NBER 2 Oberlin College 3 Federal Reserve Board XXVII Encuentro de Economistas

Macro Modelling: From the Financial Crisis to the Long Slump in the EA

Macro Modelling: From the Financial Crisis to the Long Slump in the EA Werner Roeger (European Commission, DG ECFIN) April 216 The views expressed in this presentation are those of the author and should

Macro Modelling: From the Financial Crisis to the Long Slump in the EA Werner Roeger (European Commission, DG ECFIN) April 216 The views expressed in this presentation are those of the author and should

Discussion of. An Estimated Two-Country DSGE Model for the Euro Area and the US Economy. by Gregory de Walque, Frank Smets and Raf Wouters

Discussion of An Estimated Two-Country DSGE Model for the Euro Area and the US Economy by Gregory de Walque, Frank Smets and Raf Wouters Martin Ellison University of Warwick and CEPR Summary of the contribution

Discussion of An Estimated Two-Country DSGE Model for the Euro Area and the US Economy by Gregory de Walque, Frank Smets and Raf Wouters Martin Ellison University of Warwick and CEPR Summary of the contribution

crisis: an estimated DSGE model

School of Economics and Management TECHNICAL UNIVERSITY OF LISBON Department of Economics Carlos Pestana Barros & Nicolas Peypoch Rossana Merola The A Comparative role of financial Analysis of frictions

School of Economics and Management TECHNICAL UNIVERSITY OF LISBON Department of Economics Carlos Pestana Barros & Nicolas Peypoch Rossana Merola The A Comparative role of financial Analysis of frictions

External Financing and the Role of Financial Frictions over the Business Cycle: Measurement and Theory. November 7, 2014

External Financing and the Role of Financial Frictions over the Business Cycle: Measurement and Theory Ali Shourideh Wharton Ariel Zetlin-Jones CMU - Tepper November 7, 2014 Introduction Question: How

External Financing and the Role of Financial Frictions over the Business Cycle: Measurement and Theory Ali Shourideh Wharton Ariel Zetlin-Jones CMU - Tepper November 7, 2014 Introduction Question: How

Inflation in the Great Recession and New Keynesian Models

Inflation in the Great Recession and New Keynesian Models Marco Del Negro, Marc Giannoni Federal Reserve Bank of New York Frank Schorfheide University of Pennsylvania BU / FRB of Boston Conference on Macro-Finance

Inflation in the Great Recession and New Keynesian Models Marco Del Negro, Marc Giannoni Federal Reserve Bank of New York Frank Schorfheide University of Pennsylvania BU / FRB of Boston Conference on Macro-Finance

Unemployment in an Estimated New Keynesian Model

Unemployment in an Estimated New Keynesian Model Jordi Galí Frank Smets Rafael Wouters March 24, 21 Abstract Following Gali (29), we introduce unemployment as an observable variable in the estimation of

Unemployment in an Estimated New Keynesian Model Jordi Galí Frank Smets Rafael Wouters March 24, 21 Abstract Following Gali (29), we introduce unemployment as an observable variable in the estimation of

Lecture 4. Extensions to the Open Economy. and. Emerging Market Crises

Lecture 4 Extensions to the Open Economy and Emerging Market Crises Mark Gertler NYU June 2009 0 Objectives Develop micro-founded open-economy quantitative macro model with real/financial interactions

Lecture 4 Extensions to the Open Economy and Emerging Market Crises Mark Gertler NYU June 2009 0 Objectives Develop micro-founded open-economy quantitative macro model with real/financial interactions

Introduction The Story of Macroeconomics. September 2011

Introduction The Story of Macroeconomics September 2011 Keynes General Theory (1936) regards volatile expectations as the main source of economic fluctuations. animal spirits (shifts in expectations) econ

Introduction The Story of Macroeconomics September 2011 Keynes General Theory (1936) regards volatile expectations as the main source of economic fluctuations. animal spirits (shifts in expectations) econ

An Estimated Two-Country DSGE Model for the Euro Area and the US Economy

An Estimated Two-Country DSGE Model for the Euro Area and the US Economy Discussion Monday June 5, 2006. Practical Issues in DSGE Modelling at Central Banks Stephen Murchison Presentation Outline 1. Paper

An Estimated Two-Country DSGE Model for the Euro Area and the US Economy Discussion Monday June 5, 2006. Practical Issues in DSGE Modelling at Central Banks Stephen Murchison Presentation Outline 1. Paper

Estimating Contract Indexation in a Financial Accelerator Model

Estimating Contract Indexation in a Financial Accelerator Model Charles T. Carlstrom a, Timothy S. Fuerst b, Alberto Ortiz c, Matthias Paustian d a Senior Economic Advisor, Federal Reserve Bank of Cleveland,

Estimating Contract Indexation in a Financial Accelerator Model Charles T. Carlstrom a, Timothy S. Fuerst b, Alberto Ortiz c, Matthias Paustian d a Senior Economic Advisor, Federal Reserve Bank of Cleveland,

The bank lending channel in monetary transmission in the euro area:

The bank lending channel in monetary transmission in the euro area: evidence from Bayesian VAR analysis Matteo Bondesan Graduate student University of Turin (M.Sc. in Economics) Collegio Carlo Alberto

The bank lending channel in monetary transmission in the euro area: evidence from Bayesian VAR analysis Matteo Bondesan Graduate student University of Turin (M.Sc. in Economics) Collegio Carlo Alberto

Dual Wage Rigidities: Theory and Some Evidence

MPRA Munich Personal RePEc Archive Dual Wage Rigidities: Theory and Some Evidence Insu Kim University of California, Riverside October 29 Online at http://mpra.ub.uni-muenchen.de/18345/ MPRA Paper No.

MPRA Munich Personal RePEc Archive Dual Wage Rigidities: Theory and Some Evidence Insu Kim University of California, Riverside October 29 Online at http://mpra.ub.uni-muenchen.de/18345/ MPRA Paper No.

Oil Shocks and the Zero Bound on Nominal Interest Rates

Oil Shocks and the Zero Bound on Nominal Interest Rates Martin Bodenstein, Luca Guerrieri, Christopher Gust Federal Reserve Board "Advances in International Macroeconomics - Lessons from the Crisis," Brussels,

Oil Shocks and the Zero Bound on Nominal Interest Rates Martin Bodenstein, Luca Guerrieri, Christopher Gust Federal Reserve Board "Advances in International Macroeconomics - Lessons from the Crisis," Brussels,

A Model with Costly-State Verification

A Model with Costly-State Verification Jesús Fernández-Villaverde University of Pennsylvania December 19, 2012 Jesús Fernández-Villaverde (PENN) Costly-State December 19, 2012 1 / 47 A Model with Costly-State

A Model with Costly-State Verification Jesús Fernández-Villaverde University of Pennsylvania December 19, 2012 Jesús Fernández-Villaverde (PENN) Costly-State December 19, 2012 1 / 47 A Model with Costly-State

Utility Maximizing Entrepreneurs and the Financial Accelerator

Utility Maximizing Entrepreneurs and the Financial Accelerator Mikhail Dmitriev and Jonathan Hoddenbagh August, 213 Job Market Paper In the financial accelerator literature developed by Bernanke, Gertler

Utility Maximizing Entrepreneurs and the Financial Accelerator Mikhail Dmitriev and Jonathan Hoddenbagh August, 213 Job Market Paper In the financial accelerator literature developed by Bernanke, Gertler

Macroprudential Policies in a Low Interest-Rate Environment

Macroprudential Policies in a Low Interest-Rate Environment Margarita Rubio 1 Fang Yao 2 1 University of Nottingham 2 Reserve Bank of New Zealand. The views expressed in this paper do not necessarily reflect

Macroprudential Policies in a Low Interest-Rate Environment Margarita Rubio 1 Fang Yao 2 1 University of Nottingham 2 Reserve Bank of New Zealand. The views expressed in this paper do not necessarily reflect

Endogenous Money or Sticky Wages: A Bayesian Approach

Endogenous Money or Sticky Wages: A Bayesian Approach Guangling Dave Liu 1 Working Paper Number 17 1 Contact Details: Department of Economics, University of Stellenbosch, Stellenbosch, 762, South Africa.

Endogenous Money or Sticky Wages: A Bayesian Approach Guangling Dave Liu 1 Working Paper Number 17 1 Contact Details: Department of Economics, University of Stellenbosch, Stellenbosch, 762, South Africa.

A bayesian estimation of a DSGE model with nancial frictions

Rossana Merola University of Rome "Tor Vergata" and Université Catholique de Louvain la neuve (Belgium) A bayesian estimation of a DSGE model with nancial frictions Abstract Episodes of crises that have

Rossana Merola University of Rome "Tor Vergata" and Université Catholique de Louvain la neuve (Belgium) A bayesian estimation of a DSGE model with nancial frictions Abstract Episodes of crises that have

Discussion of Gerali, Neri, Sessa, Signoretti. Credit and Banking in a DSGE Model

Discussion of Gerali, Neri, Sessa and Signoretti Credit and Banking in a DSGE Model Jesper Lindé Federal Reserve Board ty ECB, Frankfurt December 15, 2008 Summary of paper This interesting paper... Extends

Discussion of Gerali, Neri, Sessa and Signoretti Credit and Banking in a DSGE Model Jesper Lindé Federal Reserve Board ty ECB, Frankfurt December 15, 2008 Summary of paper This interesting paper... Extends

Three Essays on a Financial Crisis: A New Keynesian DSGE Approach with Financial Frictions

Three Essays on a Financial Crisis: A New Keynesian DSGE Approach with Financial Frictions Kanghoon Keah Doctor of Philosophy University of York Economics 2014 Abstract This thesis aims at enhancing our

Three Essays on a Financial Crisis: A New Keynesian DSGE Approach with Financial Frictions Kanghoon Keah Doctor of Philosophy University of York Economics 2014 Abstract This thesis aims at enhancing our

The Role of Investment Wedges in the Carlstrom-Fuerst Economy and Business Cycle Accounting

MPRA Munich Personal RePEc Archive The Role of Investment Wedges in the Carlstrom-Fuerst Economy and Business Cycle Accounting Masaru Inaba and Kengo Nutahara Research Institute of Economy, Trade, and

MPRA Munich Personal RePEc Archive The Role of Investment Wedges in the Carlstrom-Fuerst Economy and Business Cycle Accounting Masaru Inaba and Kengo Nutahara Research Institute of Economy, Trade, and

Working Paper. Risk Shocks and Divergence between the Euro area and the US. Highlights. Thomas Brand & Fabien Tripier

No 2014-11 July Working Paper Risk Shocks and Divergence between the Euro area and the US Thomas Brand & Fabien Tripier Highlights Highly synchronized during the Great recession of 2008-2009, the Euro

No 2014-11 July Working Paper Risk Shocks and Divergence between the Euro area and the US Thomas Brand & Fabien Tripier Highlights Highly synchronized during the Great recession of 2008-2009, the Euro

Booms and Banking Crises

Booms and Banking Crises F. Boissay, F. Collard and F. Smets Macro Financial Modeling Conference Boston, 12 October 2013 MFM October 2013 Conference 1 / Disclaimer The views expressed in this presentation

Booms and Banking Crises F. Boissay, F. Collard and F. Smets Macro Financial Modeling Conference Boston, 12 October 2013 MFM October 2013 Conference 1 / Disclaimer The views expressed in this presentation

Real-Time DSGE Model Density Forecasts During the Great Recession - A Post Mortem

The views expressed in this talk are those of the authors and do not necessarily reflect the views of the Federal Reserve Bank of New York or the Federal Reserve System. Real-Time DSGE Model Density Forecasts

The views expressed in this talk are those of the authors and do not necessarily reflect the views of the Federal Reserve Bank of New York or the Federal Reserve System. Real-Time DSGE Model Density Forecasts

Business cycle fluctuations Part II

Understanding the World Economy Master in Economics and Business Business cycle fluctuations Part II Lecture 7 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 7: Business cycle fluctuations

Understanding the World Economy Master in Economics and Business Business cycle fluctuations Part II Lecture 7 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 7: Business cycle fluctuations

The financial crisis dramatically demonstrated

The BoC-GEM-Fin: Banking in the Global Economy Carlos de Resende and René Lalonde, International Economic Analysis Department The 2007 09 financial crisis demonstrated the significant interdependence between

The BoC-GEM-Fin: Banking in the Global Economy Carlos de Resende and René Lalonde, International Economic Analysis Department The 2007 09 financial crisis demonstrated the significant interdependence between

Output Gap, Monetary Policy Trade-offs and Financial. Frictions

Output Gap, Monetary Policy Trade-offs and Financial Frictions Francesco Furlanetto Norges Bank Paolo Gelain Norges Bank April 217 Marzie Taheri Sanjani International Monetary Fund Abstract This paper

Output Gap, Monetary Policy Trade-offs and Financial Frictions Francesco Furlanetto Norges Bank Paolo Gelain Norges Bank April 217 Marzie Taheri Sanjani International Monetary Fund Abstract This paper

Financial Frictions and Exchange Rate Regimes in the Prospective Monetary Union of the ECOWAS Countries

Financial Frictions and Exchange Rate Regimes in the Prospective Monetary Union of the ECOWAS Countries Presented by: Lacina BALMA Prepared for the African Economic Conference Johannesburg, October 28th-3th,

Financial Frictions and Exchange Rate Regimes in the Prospective Monetary Union of the ECOWAS Countries Presented by: Lacina BALMA Prepared for the African Economic Conference Johannesburg, October 28th-3th,

Gali Chapter 6 Sticky wages and prices

Gali Chapter 6 Sticky wages and prices Up till now: o Wages taken as given by households and firms o Wages flexible so as to clear labor market o Marginal product of labor = disutility of labor (i.e. employment

Gali Chapter 6 Sticky wages and prices Up till now: o Wages taken as given by households and firms o Wages flexible so as to clear labor market o Marginal product of labor = disutility of labor (i.e. employment

... Monetary Policy and a Stock Market Boom-Bust Cycle. Lawrence Christiano, Roberto Motto, Massimo Rostagno

... Monetary Policy and a Stock Market Boom-Bust Cycle Lawrence Christiano, Roberto Motto, Massimo Rostagno ... Stock Market Boom-Bust Cycle: Episode in Which: Stock Prices, Consumption, Investment, Employment,

... Monetary Policy and a Stock Market Boom-Bust Cycle Lawrence Christiano, Roberto Motto, Massimo Rostagno ... Stock Market Boom-Bust Cycle: Episode in Which: Stock Prices, Consumption, Investment, Employment,

Risky Mortgages in a DSGE Model

1 / 29 Risky Mortgages in a DSGE Model Chiara Forlati 1 Luisa Lambertini 1 1 École Polytechnique Fédérale de Lausanne CMSG November 6, 21 2 / 29 Motivation The global financial crisis started with an increase

1 / 29 Risky Mortgages in a DSGE Model Chiara Forlati 1 Luisa Lambertini 1 1 École Polytechnique Fédérale de Lausanne CMSG November 6, 21 2 / 29 Motivation The global financial crisis started with an increase

Macroeconomics 2. Lecture 6 - New Keynesian Business Cycles March. Sciences Po

Macroeconomics 2 Lecture 6 - New Keynesian Business Cycles 2. Zsófia L. Bárány Sciences Po 2014 March Main idea: introduce nominal rigidities Why? in classical monetary models the price level ensures money

Macroeconomics 2 Lecture 6 - New Keynesian Business Cycles 2. Zsófia L. Bárány Sciences Po 2014 March Main idea: introduce nominal rigidities Why? in classical monetary models the price level ensures money

Understanding the Great Recession

Understanding the Great Recession Lawrence Christiano Martin Eichenbaum Mathias Trabandt Ortigia 13-14 June 214. Background Background GDP appears to have suffered a permanent (1%?) fall since 28. Background

Understanding the Great Recession Lawrence Christiano Martin Eichenbaum Mathias Trabandt Ortigia 13-14 June 214. Background Background GDP appears to have suffered a permanent (1%?) fall since 28. Background

Macroeconomic Modelling at the Central Bank of Brazil. Angelo M. Fasolo Research Department

Macroeconomic Modelling at the Central Bank of Brazil Angelo M. Fasolo Research Department Introduction Economic analysis at the BCB based on three type of models: Small-scale semi-structural models, focused

Macroeconomic Modelling at the Central Bank of Brazil Angelo M. Fasolo Research Department Introduction Economic analysis at the BCB based on three type of models: Small-scale semi-structural models, focused

Samba: Stochastic Analytical Model with a Bayesian Approach. DSGE Model Project for Brazil s economy

Samba: Stochastic Analytical Model with a Bayesian Approach DSGE Model Project for Brazil s economy Working in Progress - Preliminary results Solange Gouvea, André Minella, Rafael Santos, Nelson Souza-Sobrinho

Samba: Stochastic Analytical Model with a Bayesian Approach DSGE Model Project for Brazil s economy Working in Progress - Preliminary results Solange Gouvea, André Minella, Rafael Santos, Nelson Souza-Sobrinho

Chasing the Gap: Speed Limits and Optimal Monetary Policy

Chasing the Gap: Speed Limits and Optimal Monetary Policy Matteo De Tina University of Bath Chris Martin University of Bath January 2014 Abstract Speed limit monetary policy rules incorporate a response

Chasing the Gap: Speed Limits and Optimal Monetary Policy Matteo De Tina University of Bath Chris Martin University of Bath January 2014 Abstract Speed limit monetary policy rules incorporate a response

UNIVERSITY OF TOKYO 1 st Finance Junior Workshop Program. Monetary Policy and Welfare Issues in the Economy with Shifting Trend Inflation

UNIVERSITY OF TOKYO 1 st Finance Junior Workshop Program Monetary Policy and Welfare Issues in the Economy with Shifting Trend Inflation Le Thanh Ha (GRIPS) (30 th March 2017) 1. Introduction Exercises

UNIVERSITY OF TOKYO 1 st Finance Junior Workshop Program Monetary Policy and Welfare Issues in the Economy with Shifting Trend Inflation Le Thanh Ha (GRIPS) (30 th March 2017) 1. Introduction Exercises

Business Cycle Effects of Credit and Technology Shocks in a DSGE Model with Firm Defaults

Business Cycle Effects of Credit and Technology Shocks in a DSGE Model with Firm Defaults M. Hashem Pesaran and TengTeng Xu 5 October 2 CWPE 59 Business Cycle Effects of Credit and Technology Shocks in

Business Cycle Effects of Credit and Technology Shocks in a DSGE Model with Firm Defaults M. Hashem Pesaran and TengTeng Xu 5 October 2 CWPE 59 Business Cycle Effects of Credit and Technology Shocks in

The Liquidity Effect in Bank-Based and Market-Based Financial Systems. Johann Scharler *) Working Paper No October 2007

Working Paper No October 2007") DEPARTMENT OF ECONOMICS JOHANNES KEPLER UNIVERSITY OF LINZ The Liquidity Effect in Bank-Based and Market-Based Financial Systems by Johann Scharler *) Working Paper No. 0718 October 2007 Johannes Kepler

DEPARTMENT OF ECONOMICS JOHANNES KEPLER UNIVERSITY OF LINZ The Liquidity Effect in Bank-Based and Market-Based Financial Systems by Johann Scharler *) Working Paper No. 0718 October 2007 Johannes Kepler

Real wages and monetary policy: A DSGE approach

MPRA Munich Personal RePEc Archive Real wages and monetary policy: A DSGE approach Bryan Perry and Kerk L. Phillips and David E. Spencer Brigham Young University 29. February 2012 Online at https://mpra.ub.uni-muenchen.de/36995/

MPRA Munich Personal RePEc Archive Real wages and monetary policy: A DSGE approach Bryan Perry and Kerk L. Phillips and David E. Spencer Brigham Young University 29. February 2012 Online at https://mpra.ub.uni-muenchen.de/36995/

Loan Securitization and the Monetary Transmission Mechanism

Loan Securitization and the Monetary Transmission Mechanism Bart Hobijn Federal Reserve Bank of San Francisco Federico Ravenna University of California - Santa Cruz First draft: August 1, 29 This draft:

Loan Securitization and the Monetary Transmission Mechanism Bart Hobijn Federal Reserve Bank of San Francisco Federico Ravenna University of California - Santa Cruz First draft: August 1, 29 This draft:

1 Figure 1 (A) shows what the IS LM model looks like for the case in which the Fed holds the

shows what the IS LM model looks like for the case in which the Fed holds the") 1 Figure 1 (A) shows what the IS LM model looks like for the case in which the Fed holds the money supply constant. Figure 1 (B) shows what the model looks like if the Fed adjusts the money supply to hold

1 Figure 1 (A) shows what the IS LM model looks like for the case in which the Fed holds the money supply constant. Figure 1 (B) shows what the model looks like if the Fed adjusts the money supply to hold

The Uncertainty Multiplier and Business Cycles

The Uncertainty Multiplier and Business Cycles Hikaru Saijo University of California, Santa Cruz May 6, 2013 Abstract I study a business cycle model where agents learn about the state of the economy by

The Uncertainty Multiplier and Business Cycles Hikaru Saijo University of California, Santa Cruz May 6, 2013 Abstract I study a business cycle model where agents learn about the state of the economy by

Financial Conditions and Labor Productivity over the Business Cycle

Financial Conditions and Labor Productivity over the Business Cycle Carlos A. Yépez September 5, 26 Abstract The cyclical behavior of productivity has noticeably changed since the mid- 8s. Importantly,

Financial Conditions and Labor Productivity over the Business Cycle Carlos A. Yépez September 5, 26 Abstract The cyclical behavior of productivity has noticeably changed since the mid- 8s. Importantly,

Habit Formation in State-Dependent Pricing Models: Implications for the Dynamics of Output and Prices

Habit Formation in State-Dependent Pricing Models: Implications for the Dynamics of Output and Prices Phuong V. Ngo,a a Department of Economics, Cleveland State University, 22 Euclid Avenue, Cleveland,

Habit Formation in State-Dependent Pricing Models: Implications for the Dynamics of Output and Prices Phuong V. Ngo,a a Department of Economics, Cleveland State University, 22 Euclid Avenue, Cleveland,

Notes on Financial Frictions Under Asymmetric Information and Costly State Verification. Lawrence Christiano

Notes on Financial Frictions Under Asymmetric Information and Costly State Verification by Lawrence Christiano Incorporating Financial Frictions into a Business Cycle Model General idea: Standard model

Notes on Financial Frictions Under Asymmetric Information and Costly State Verification by Lawrence Christiano Incorporating Financial Frictions into a Business Cycle Model General idea: Standard model

Multistep prediction error decomposition in DSGE models: estimation and forecast performance

Multistep prediction error decomposition in DSGE models: estimation and forecast performance George Kapetanios Simon Price Kings College, University of London Essex Business School Konstantinos Theodoridis

Multistep prediction error decomposition in DSGE models: estimation and forecast performance George Kapetanios Simon Price Kings College, University of London Essex Business School Konstantinos Theodoridis

The Real Business Cycle Model

The Real Business Cycle Model Economics 3307 - Intermediate Macroeconomics Aaron Hedlund Baylor University Fall 2013 Econ 3307 (Baylor University) The Real Business Cycle Model Fall 2013 1 / 23 Business

The Real Business Cycle Model Economics 3307 - Intermediate Macroeconomics Aaron Hedlund Baylor University Fall 2013 Econ 3307 (Baylor University) The Real Business Cycle Model Fall 2013 1 / 23 Business

The Role of Investment Wedges in the Carlstrom-Fuerst Economy and Business Cycle Accounting

RIETI Discussion Paper Series 9-E-3 The Role of Investment Wedges in the Carlstrom-Fuerst Economy and Business Cycle Accounting INABA Masaru The Canon Institute for Global Studies NUTAHARA Kengo Senshu

RIETI Discussion Paper Series 9-E-3 The Role of Investment Wedges in the Carlstrom-Fuerst Economy and Business Cycle Accounting INABA Masaru The Canon Institute for Global Studies NUTAHARA Kengo Senshu

Monetary Economics July 2014

ECON40013 ECON90011 Monetary Economics July 2014 Chris Edmond Office hours: by appointment Office: Business & Economics 423 Phone: 8344 9733 Email: cedmond@unimelb.edu.au Course description This year I

ECON40013 ECON90011 Monetary Economics July 2014 Chris Edmond Office hours: by appointment Office: Business & Economics 423 Phone: 8344 9733 Email: cedmond@unimelb.edu.au Course description This year I

Financial Factors and Labor Market Fluctuations

Financial Factors and Labor Market Fluctuations Yahong Zhang January 25, 215 Abstract What are the effects of financial market imperfections on fluctuations in unemployment and vacancies for the US economy?

Financial Factors and Labor Market Fluctuations Yahong Zhang January 25, 215 Abstract What are the effects of financial market imperfections on fluctuations in unemployment and vacancies for the US economy?

Shocks, Structures or Monetary Policies? The Euro Area and US After 2001

Shocks, Structures or Monetary Policies? The Euro Area and US After 2001 Lawrence Christiano, Roberto Motto, and Massimo Rostagno April 23, 2007 Abstract We describe a model we have estimated using US

Shocks, Structures or Monetary Policies? The Euro Area and US After 2001 Lawrence Christiano, Roberto Motto, and Massimo Rostagno April 23, 2007 Abstract We describe a model we have estimated using US

Discussion of The Great Escape? A Quantitative Evaluation of the Fed s Non- Standard Policies by Del Negro, Eggertsson, Ferrero, and Kiyotaki

Discussion of The Great Escape? A Quantitative Evaluation of the Fed s Non- Standard Policies by Del Negro, Eggertsson, Ferrero, and Kiyotaki Zheng Liu, FRB San Francisco March 5, 2010 The opinions expressed

Discussion of The Great Escape? A Quantitative Evaluation of the Fed s Non- Standard Policies by Del Negro, Eggertsson, Ferrero, and Kiyotaki Zheng Liu, FRB San Francisco March 5, 2010 The opinions expressed

Capital Flows, Financial Intermediation and Macroprudential Policies

Capital Flows, Financial Intermediation and Macroprudential Policies Matteo F. Ghilardi International Monetary Fund 14 th November 2014 14 th November Capital Flows, 2014 Financial 1 / 24 Inte Introduction

Capital Flows, Financial Intermediation and Macroprudential Policies Matteo F. Ghilardi International Monetary Fund 14 th November 2014 14 th November Capital Flows, 2014 Financial 1 / 24 Inte Introduction

Sebastian Sienknecht. Inflation persistence amplification in the Rotemberg model

Sebastian Sienknecht Friedrich-Schiller-University Jena, Germany Inflation persistence amplification in the Rotemberg model Abstract: This paper estimates a Dynamic Stochastic General Equilibrium (DSGE)

Sebastian Sienknecht Friedrich-Schiller-University Jena, Germany Inflation persistence amplification in the Rotemberg model Abstract: This paper estimates a Dynamic Stochastic General Equilibrium (DSGE)

Chapter 2. Literature Review

Chapter 2 Literature Review There is a wide agreement that monetary policy is a tool in promoting economic growth and stabilizing inflation. However, there is less agreement about how monetary policy exactly

Chapter 2 Literature Review There is a wide agreement that monetary policy is a tool in promoting economic growth and stabilizing inflation. However, there is less agreement about how monetary policy exactly

Should the Monetary Policy Rule Be Different in a Financial Crisis? By Monika Piazzesi i

Should the Monetary Policy Rule Be Different in a Financial Crisis? By Monika Piazzesi i It s a pleasure to read and discuss this very nice and well-written paper by Nikolsko- Rzhevskyy, Papell and Prodan.

Should the Monetary Policy Rule Be Different in a Financial Crisis? By Monika Piazzesi i It s a pleasure to read and discuss this very nice and well-written paper by Nikolsko- Rzhevskyy, Papell and Prodan.

Bank Capital, Agency Costs, and Monetary Policy. Césaire Meh Kevin Moran Department of Monetary and Financial Analysis Bank of Canada

Bank Capital, Agency Costs, and Monetary Policy Césaire Meh Kevin Moran Department of Monetary and Financial Analysis Bank of Canada Motivation A large literature quantitatively studies the role of financial

Bank Capital, Agency Costs, and Monetary Policy Césaire Meh Kevin Moran Department of Monetary and Financial Analysis Bank of Canada Motivation A large literature quantitatively studies the role of financial

Monetary Policy and Resource Mobility

Monetary Policy and Resource Mobility 2th Anniversary of the Bank of Finland Carl E. Walsh University of California, Santa Cruz May 5-6, 211 C. E. Walsh (UCSC) Bank of Finland 2th Anniversary May 5-6,

Monetary Policy and Resource Mobility 2th Anniversary of the Bank of Finland Carl E. Walsh University of California, Santa Cruz May 5-6, 211 C. E. Walsh (UCSC) Bank of Finland 2th Anniversary May 5-6,

Quantitative Significance of Collateral Constraints as an Amplification Mechanism

RIETI Discussion Paper Series 09-E-05 Quantitative Significance of Collateral Constraints as an Amplification Mechanism INABA Masaru The Canon Institute for Global Studies KOBAYASHI Keiichiro RIETI The

RIETI Discussion Paper Series 09-E-05 Quantitative Significance of Collateral Constraints as an Amplification Mechanism INABA Masaru The Canon Institute for Global Studies KOBAYASHI Keiichiro RIETI The