Rationale for report : Sector Update

|

|

|

- Collin Wells

- 5 years ago

- Views:

Transcription

1 Investment Highlights MALT LIQUOR SECTOR Slump in price of malting barley a boon for June 2012 NEUTRAL Low Soo Fang low-soo-fang@ambankgroup.com Rationale for report : Sector Update (Maintained) Higher MLM growth forecast of 6%-7% We have raised our MLM growth forecast to 6%-7% for , up from 5%-6% previously. Our channel checks at selected F&B outlets within the Klang Valley suggest a relatively resilient demand, with the recent 3% price hike wellabsorbed by end-consumers. To recap, the higher pricing structure was implemented by both brewers Carlsberg Brewery Malaysia Bhd (CAB) and Guinness Anchor Bhd (GAB) back in May Robust beer volume growth seen Notwithstanding the effect from the Euro 2012 special event, the industry s longer-term upward growth trajectory remains intact. We see healthy demand growth well underpinned by: -1) the status quo in alcohol excise duty at RM7.40/litre; 2) positive consumer spending sentiment and; 3) on-going major A&P campaigns to boost sales. Slump in price of malting barley to drive margin expansion in Robust beer volume growth aside and more importantly, we believe brewers are poised for an earnings upgrade from margin expansion on the back of cheaper input costs going forward. We see a sustained easing in prices of malting barley due to:- 1) additional global supply on increased plantings and favourable weather conditions, and 2) Flattish demand from Europe alongside the bearish macroeconomic outlook in the region. As it is, the current price of malting barley at EUR219/MT is down a further 12% from 2 months ago, extending its downward trend from the YTD high of EUR288/MT (Feb 2012). This brings the present price level on par to that last seen in 2009, prior to the heat wave-induced price surge in Much as we witnessed a notable margin expansion back then, we expect a similar re-run going into CY13F. EPS forecast raised by 7% to 9% - We anticipate a margin improvement of 2ppts to 3ppts for next year as new and cheaper inventories of malting barley filter through. Both brewers have locked in their respective raw material requirements for CY12. Next to excise duties, raw materials & packaging costs account for approximately 15%-17% of total operating costs. Consequently, our earnings forecasts for CAB and GAB have been nudged upwards by 7% to 9% for FY13F-14F. Our revised earnings models now suggest a 3-year earnings CAGR of 8% for GAB and a higher 10% for CAB. Dividend yield of 5% p.a. is still decent As we have seen, the recent share price rally comes in largely in line with the re-rating of the broader consumer sector, mainly due to rising interests by investors seeking a defensive portfolio strategy. Nonetheless, net dividend yields of 5% per annum (p.a.) are still decent especially in view of renewed uncertainties in the global capital markets. Re-affirm BUY on CAB, FV: RM14.00/share - We re-affirm our BUY recommendation on CAB with a higher DCF-based fair value of RM14.00/share post a revised long-term growth rate assumption of 4% vs. 3% previously. CAB remains our preferred pick for exposure to the brewery sector for its solid earnings prospects on the back of an expanding market share and a deepening market penetration. A strong portfolio of premium beers and in-house brewing of imported labels (Asahi, Kronenbourg 1664 and Kronenbourg Blanc) will further bolster long-term growth. Maintain HOLD on GAB, FV: RM14.50/share We maintain our HOLD recommendation on GAB with a higher DCF-based fair value of RM14.50/share, as we upped our long-term growth rate assumption from 2% to 3%.GAB s dividend yield of 5% per annum (p.a.) as premised on a generous dividend payout of 90% is well supported by the group s strong brand equity and dominant MLM market share at 60%-62%. Additionally, the stock is a potential beneficiary of capital management initiatives which could result in the establishment of a higher dividend payout policy as part of management s effort to optimise its cost of capital. TABLE 1 : SECTOR VALUATION MATRIX Div Target Share Price EPS (sen) PE (x) P/BV ROE Potential Yield Price Rating (RM) CY12F CY13F CY12F CY13F (x) (%) (%) (RM) Upside (%) Carlsberg Buy Guinness Hold Source: Company, AmResearch estimates Share prices as at 26 June 2012 PP 12246/05/2013 (032379)

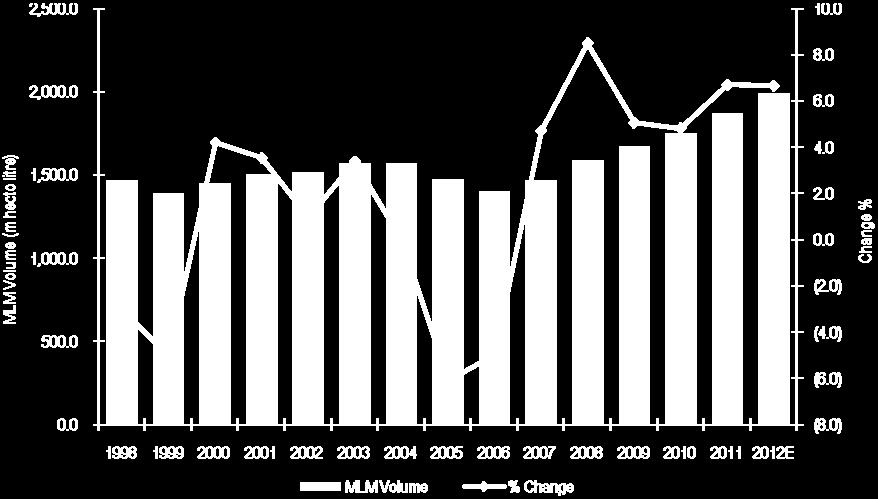

2 SLUMP IN PRICE OF MALTING BARLEY A BOON FOR 2013 Higher MLM growth forecast of 6%-7% We have raised our MLM growth forecast to 6%-7% for , up from 5%-6% previously. Our channel checks at selected food & beverage outlets within the Klang Valley suggest a relatively resilient demand, with the recent 3% price hike well absorbed by endconsumers. To recap, the higher pricing structure was implemented by both brewers Carlsberg Brewery Malaysia Bhd (CAB) and Guinness Anchor Berhad (GAB) back in May Industry s upward growth trajectory remains intact Notwithstanding the effect from the Euro 2012 special event, the industry s longer-term upward growth trajectory remains intact (See Chart 10). We see healthy demand growth well underpinned by: -1) the status quo in alcohol excise duty at RM7.40/litre; 2) positive consumer spending sentiment and; 3) on-going major A&P campaigns to boost sales. This brings the present prices on par to that last seen in 2009, prior to the heat wave-induced price surge in Russia which prompted the government s ban on exports to meet local demand (See Charts 1 and 2). Russia is the single largest exporter of barley behind the European Union, accounting for circa 12% of global exports. Much as we witnessed a notable margin expansion back then, we expect a similar re-run going into CY13F. Raising earnings forecast by 7% to 9% for FY13F- 14F We anticipate a margin improvement of 2ppts to 3ppts for next year as new and cheaper inventories of malting barley filter through. Both brewers have locked in their respective raw material requirements for CY12. Consequently, our earnings forecasts for CAB and GAB have been nudged upwards by 7% to 9% for FY13F-14F. Our revised earnings models now suggest 3-year earnings CAGR of 8% for GAB and a higher 10% for CAB. Slump in price of malting barley to drive margin expansion for brewers Robust beer volume growth aside and more importantly, we believe brewers are poised for an earnings upgrade from margin expansions going forward. This will come on the back of cheaper input costs, notably malting barley and packaging costs such as aluminium cans. Next to excise duties, raw materials & packaging costs account for approximately 15%-17% of total operating costs. Excise duties are the largest determinant at roughly 63%-65% of total operating costs. Sustained easing in malting barley prices due to demand & supply fundamentals We see a sustained easing in malting barley prices due to:- 1) additional global supply on increased plantings and favourable weather conditions and; 2) Flattish demand from Europe alongside the bearish macroeconomic outlook in the region. As it is, the current price of malting barley at EUR219/MT is down a further 12% from 2 months ago, extending its downward trend from year-to-date high of EUR288/MT (February 2012). Dividend yield of 5% per annum is still decent As we have seen, the recent share price rally comes in largely in line with the re-rating of the broader consumer sector, mainly due to rising interests by investors seeking a defensive portfolio strategy. Nonetheless, net dividend yields of 5% per annum (p.a.) are still decent especially in view of renewed uncertainties in the global capital markets. Re-affirm BUY on CAB, fair value of RM14.00/share We re-affirm our BUY recommendation on CAB with a higher DCF-based fair value of RM14.00/share, post a revised long-term growth rate assumption of 4% versus 3% previously (WACC: 9%). CAB remains our preferred pick for exposure to the brewery sector for its solid earnings prospects on the back of an expanding market share and a deepening market penetration. A strong portfolio of premium beers and in-house brewing of imported labels (Asahi, Kronenbourg 1664 and Kronenbourg Blanc) will further bolster long-term growth. AmResearch Sdn Bhd 2

3 Maintain HOLD on GAB, fair value of RM14.50/share We maintain our HOLD recommendation on GAB with a higher DCF-based fair value of RM14.50/share, as we upped our long-term growth rate assumption from 2% to 3% (WACC: 9%). GAB s dividend yield of 5% per annum (p.a.) as premised on a generous dividend payout of 90% is well supported by the group s strong brand equity and dominant MLM market share at 60%-62%. Additionally, the stock is a potential beneficiary of capital management initiatives which could result in the establishment of a higher dividend payout policy as part of management s effort to optimise its cost of capital. AmResearch Sdn Bhd 3

AmResearch Sdn Bhd 4")

4 CHART 1 : PRICE TREND OF MALTING BARLEY ( JAN 2012) CHART 2 : PRICE TREND OF MALTING BARLEY (AS AT JUN 2012) AmResearch Sdn Bhd 4

5 CHART 3 : EASING ALUMINIUM FUTURES TO LIFT MARGIN PRESSURE ON PACKAGING COSTS CHART 4 : SECTOR ENJOYS VALUATION PREMIUM FOR ITS DEFENSIVE ATTRIBUTES AmResearch Sdn Bhd 5

")

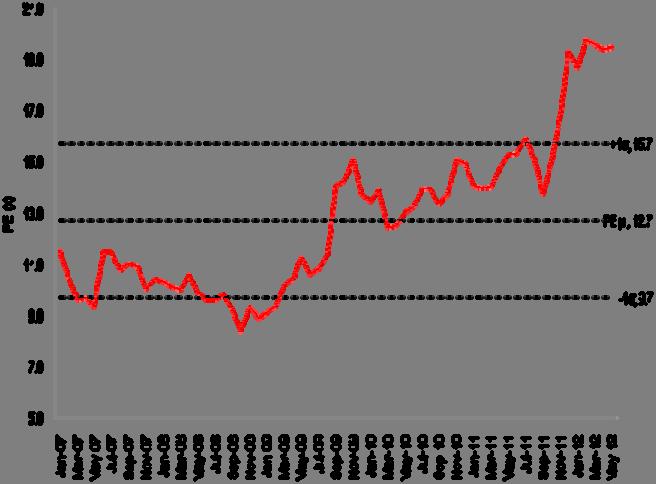

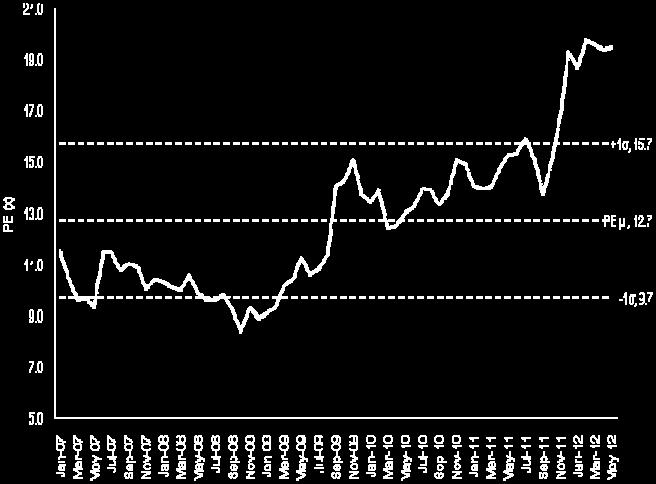

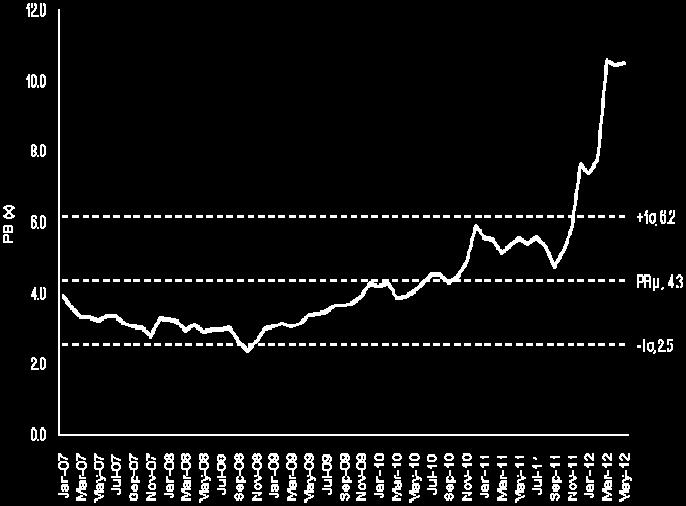

6 CHART 5 : PE(X) TREND OF CAB CHART 6 : PE(X) TREND OF GAB CHART 7 : P/B TREND OF CAB CHART 8 : P/B TREND OF GAB AmResearch Sdn Bhd 6

7 CHART 9 : COMPARISON OF PRODUCT PORTFOLIO Source: CAB, GAB, AmResearch CHART 10 : UPTREND IN TIV REMAINS INTACT Source: CAB, GAB, AmResearch estimates AmResearch Sdn Bhd 7

8 CHART 11 : ALCOHOL EXCISE DUTY AT STATUS QUO Source: CAB, GAB, AmResearch estimates CHART 12 : MLM VOLUME DOMINATED BY BLONDE BEER Source: CAB, GAB, AmResearch AmResearch Sdn Bhd 8

9 TABLE 2 : CAB FINANCIAL DATA Income Statement (RMmil, YE 31 Dec) F 2013F 2014F Revenue 1, , , , ,784.9 EBITDA Depreciation (17.7) (20.1) (21.3) (20.2) (21.2) Operating income (EBIT) Other income & associates Net interest (1.3) (1.2) (0.3) (0.3) (0.3) Exceptional items Pretax profit Taxation (42.4) (53.0) (57.5) (66.2) (70.3) Minorities/pref dividends (0.9) (1.2) (1.2) (1.3) (1.3) Net profit Core net profit Balance Sheet (RMmil, YE 31 Dec) F 2013F 2014F Fixed assets Intangible assets Other long-term assets Total non-current assets Cash & equivalent Stock Trade debtors Other current assets Total current assets Trade creditors Short-term borrowings Other current liabilities Total current liabilities Long-term borrowings Other long-term liabilities Total long-term liabilities Shareholders funds Minority interests BV/share (RM) Cash Flow (RMmil, YE 31 Dec) F 2013F 2014F Pretax profit Depreciation Net change in working capital 67.6 (55.4) 12.6 (6.1) (4.3) Others (39.3) (30.5) (63.0) (71.7) (75.8) Cash flow from operations Capital expenditure (25.1) (28.5) (30.0) (30.0) (30.0) Net investments & sale of fixed assets Others (193.8) Cash flow from investing (218.9) (21.6) (30.0) (30.0) (30.0) Debt raised/(repaid) 44.4 (30.7) (5.0) (5.0) (5.0) Equity raised/(repaid) Dividends paid (58.5) (127.3) (174.7) (127.3) (145.3) Others (5.1) (4.8) (0.4) (0.4) (0.4) Cash flow from financing (19.2) (162.7) (180.0) (132.6) (150.7) Net cash flow (15.6) (29.8) Net cash/(debt) b/f (59.9) Net cash/(debt) c/f Key Ratios (YE 31 Dec) F 2013F 2014F Revenue growth (%) EBITDA growth (%) Pretax margins (%) Net profit margins (%) Interest cover (x) Effective tax rate (%) Net dividend payout (%) Debtors turnover (days) Stock turnover (days) Creditors turnover (days) Source: Company, AmResearch estimates AmResearch Sdn Bhd 9

10 TABLE 3 : GAB FINANCIAL DATA Income Statement (RMmil, YE 31 Dec) F 2013F 2014F Revenue 1, , , , ,784.9 EBITDA Depreciation (17.7) (20.1) (21.3) (20.2) (21.2) Operating income (EBIT) Other income & associates Net interest (1.3) (1.2) (0.3) (0.3) (0.3) Exceptional items Pretax profit Taxation (42.4) (53.0) (57.5) (66.2) (70.3) Minorities/pref dividends (0.9) (1.2) (1.2) (1.3) (1.3) Net profit Core net profit Balance Sheet (RMmil, YE 31 Dec) F 2013F 2014F Fixed assets Intangible assets Other long-term assets Total non-current assets Cash & equivalent Stock Trade debtors Other current assets Total current assets Trade creditors Short-term borrowings Other current liabilities Total current liabilities Long-term borrowings Other long-term liabilities Total long-term liabilities Shareholders funds Minority interests BV/share (RM) Cash Flow (RMmil, YE 31 Dec) F 2013F 2014F Pretax profit Depreciation Net change in working capital 67.6 (55.4) 12.6 (6.1) (4.3) Others (39.3) (30.5) (63.0) (71.7) (75.8) Cash flow from operations Capital expenditure (25.1) (28.5) (30.0) (30.0) (30.0) Net investments & sale of fixed assets Others (193.8) Cash flow from investing (218.9) (21.6) (30.0) (30.0) (30.0) Debt raised/(repaid) 44.4 (30.7) (5.0) (5.0) (5.0) Equity raised/(repaid) Dividends paid (58.5) (127.3) (174.7) (127.3) (145.3) Others (5.1) (4.8) (0.4) (0.4) (0.4) Cash flow from financing (19.2) (162.7) (180.0) (132.6) (150.7) Net cash flow (15.6) (29.8) Net cash/(debt) b/f (59.9) Net cash/(debt) c/f Key Ratios (YE 31 Dec) F 2013F 2014F Revenue growth (%) EBITDA growth (%) Pretax margins (%) Net profit margins (%) Interest cover (x) Effective tax rate (%) Net dividend payout (%) Debtors turnover (days) Stock turnover (days) Creditors turnover (days) Source: Company, AmResearch estimates AmResearch Sdn Bhd 10

11 Published by AmResearch Sdn Bhd ( P) (A member of the AmInvestment Bank Group) 15th Floor Bangunan AmBank Group 55 Jalan Raja Chulan Kuala Lumpur Tel: (03) (research) Fax: (03) Printed by AmResearch Sdn Bhd ( P) (A member of the AmInvestment Bank Group) 15th Floor Bangunan AmBank Group 55 Jalan Raja Chulan Kuala Lumpur Tel: (03) (research) Fax: (03) The information and opinions in this report were prepared by AmResearch Sdn Bhd. The investments discussed or recommended in this report may not be suitable for all investors. This report has been prepared for information purposes only and is not an offer to sell or a solicitation to buy any securities. The directors and employees of AmResearch Sdn Bhd may from time to time have a position in or with the securities mentioned herein. Members of the AmInvestment Group and their affiliates may provide services to any company and affiliates of such companies whose securities are mentioned herein. The information herein was obtained or derived from sources that we believe are reliable, but while all reasonable care has been taken to ensure that stated facts are accurate and opinions fair and reasonable, we do not represent that it is accurate or complete and it should not be relied upon as such. No liability can be accepted for any loss that may arise from the use of this report. All opinions and estimates included in this report constitute our judgement as of this date and are subject to change without notice. For AmResearch Sdn Bhd Benny Chew Managing Director AmResearch Sdn Bhd 11

COCOALAND HOLDINGS BUY. 9MFY15: On track for a record year. Company report. (Maintained) CONSUMER

CONSUMER") CONSUMER COCOALAND HOLDINGS (COLA MK EQUITY, CCLD.KL) 26 Nov 2015 Company report Cheryl Tan, CFA cheryl-tan@ambankgroup.com 03-2036 2333 9MFY15: On track for a record year Rationale for report: Company

CONSUMER COCOALAND HOLDINGS (COLA MK EQUITY, CCLD.KL) 26 Nov 2015 Company report Cheryl Tan, CFA cheryl-tan@ambankgroup.com 03-2036 2333 9MFY15: On track for a record year Rationale for report: Company

SUNWAY BUY. FY15 operating earnings within expectations. Company report. (Maintained) CONGLOMERATE

CONGLOMERATE") SUNWAY CONGLOMERATE (SWB MK EQUITY, SWAY.KL) 29 Feb 2016 FY15 operating earnings within expectations Company report Thomas Soon soon-guan-chuan@ambankgroup.com 03-2036 2300 Rationale for report: Company

SUNWAY CONGLOMERATE (SWB MK EQUITY, SWAY.KL) 29 Feb 2016 FY15 operating earnings within expectations Company report Thomas Soon soon-guan-chuan@ambankgroup.com 03-2036 2300 Rationale for report: Company

PUNCAK NIAGA HOLD. Water deal completion imminent. Company report. (Maintained) UTILITIES. Max Koh

UTILITIES. Max Koh") PUNCAK NIAGA UTILITIES (PNH MK EQUITY, PNHB.KL) 06 Feb 2015 Company report Max Koh max-koh@ambankgroup.com 03-2036 2299 Water deal completion imminent Rationale for report: Company update HOLD (Maintained)

PUNCAK NIAGA UTILITIES (PNH MK EQUITY, PNHB.KL) 06 Feb 2015 Company report Max Koh max-koh@ambankgroup.com 03-2036 2299 Water deal completion imminent Rationale for report: Company update HOLD (Maintained)

IJM PLANTATIONS BUY. Earnings recovery in FY14F. Company report. (Maintained) Rationale for report: Company Update PLANTATION

Rationale for report: Company Update PLANTATION") PLANTATION IJM PLANTATIONS (IJMP MK, IJMP.KL) 4 July 2012 Company report Gan Huey Ling, CFA gan-huey-ling@ambankgroup.com 03 2036 2305 Earnings recovery in FY14F Rationale for report: Company Update BUY

PLANTATION IJM PLANTATIONS (IJMP MK, IJMP.KL) 4 July 2012 Company report Gan Huey Ling, CFA gan-huey-ling@ambankgroup.com 03 2036 2305 Earnings recovery in FY14F Rationale for report: Company Update BUY

BURSA MALAYSIA BUY. Riding on sustained trading interest. Company report. (Maintained) Rationale for report: Company Result STOCK EXCHANGE

Rationale for report: Company Result STOCK EXCHANGE") STOCK EXCHANGE BURSA MALAYSIA (BURSA MK, BMYS.KL) 22 October 22 Company report Cheryl Tan cheryltan@ambankgroup.com +63 236 2293 Riding on sustained trading interest Rationale for report: Company Result

STOCK EXCHANGE BURSA MALAYSIA (BURSA MK, BMYS.KL) 22 October 22 Company report Cheryl Tan cheryltan@ambankgroup.com +63 236 2293 Riding on sustained trading interest Rationale for report: Company Result

GENT PLANTATIONS BUY. Positioned for growth from Indonesia. Company report. (Maintained) Rationale for report: Company Update PLANTATION

Rationale for report: Company Update PLANTATION") PLANTATION GENT PLANTATIONS (GENP MK, GENS.SI) 27 June 22 Company report Gan Huey Ling, CFA gan-huey-ling@ambankgroup.com 3 236 235 Positioned for growth from Indonesia Rationale for report: Company Update

PLANTATION GENT PLANTATIONS (GENP MK, GENS.SI) 27 June 22 Company report Gan Huey Ling, CFA gan-huey-ling@ambankgroup.com 3 236 235 Positioned for growth from Indonesia Rationale for report: Company Update

HOCK SENG LEE BUY. Results below expectations; more job newsflow expected in 2H. Company report. (Maintained) Rationale for report: Company result

Rationale for report: Company result") Company report AmResearch Sdn Bhd www.amesecurities.com.my 603 2036 2300 CONSTRUCTION HOCK SENG LEE (HSL MK, HSLB.KL) 23 May 2012 Results below expectations; more job newsflow expected in 2H Rationale

Company report AmResearch Sdn Bhd www.amesecurities.com.my 603 2036 2300 CONSTRUCTION HOCK SENG LEE (HSL MK, HSLB.KL) 23 May 2012 Results below expectations; more job newsflow expected in 2H Rationale

TELEKOM MALAYSIA HOLD. Results missed, searching for a bottom. Company report. (Maintained) TELECOMMUNICATION

TELECOMMUNICATION") TELECOMMUNICATION TELEKOM MALAYSIA (T MK EQUITY, TLMM.KL) 27 Nov 2014 Company report Hafriz Hezry hafriz-hezry@ambankgroup.com 03-2036 2280 Results missed, searching for a bottom Rationale for report:

TELECOMMUNICATION TELEKOM MALAYSIA (T MK EQUITY, TLMM.KL) 27 Nov 2014 Company report Hafriz Hezry hafriz-hezry@ambankgroup.com 03-2036 2280 Results missed, searching for a bottom Rationale for report:

SUNWAY BUY. 9MFY15 within expectations. Company report. (Maintained) CONGLOMERATE. Thomas Soon

CONGLOMERATE. Thomas Soon") SUNWAY CONGLOMERATE (SWB MK EQUITY, SWAY.KL) 27 Nov 2015 9MFY15 within expectations Company report Thomas Soon soon-guan-chuan@ambankgroup.com 03-2036 2300 Rationale for report: Company result BUY (Maintained)

SUNWAY CONGLOMERATE (SWB MK EQUITY, SWAY.KL) 27 Nov 2015 9MFY15 within expectations Company report Thomas Soon soon-guan-chuan@ambankgroup.com 03-2036 2300 Rationale for report: Company result BUY (Maintained)

SUNWAY BUY. Acquires prime land in Kelana Jaya at RM386/sq ft. Company report. (Maintained) CONGLOMERATE

CONGLOMERATE") Aug-11 Nov-11 May-12 Nov-12 May-13 Nov-13 May-14 Nov-14 Company report SUNWAY CONGLOMERATE (SWB MK EQUITY, SWAY.KL) 12 May 2015 Acquires prime land in Kelana Jaya at RM386/sq ft Thomas Soon soon-guan-chuan@ambankgroup.com

Aug-11 Nov-11 May-12 Nov-12 May-13 Nov-13 May-14 Nov-14 Company report SUNWAY CONGLOMERATE (SWB MK EQUITY, SWAY.KL) 12 May 2015 Acquires prime land in Kelana Jaya at RM386/sq ft Thomas Soon soon-guan-chuan@ambankgroup.com

PRESTARIANG. (PRES MK EQUITY, PSTG.KL) 23 May UniMy closer to breakeven. Rationale for report: Company result Investment Highlights

23 May UniMy closer to breakeven. Rationale for report: Company result Investment Highlights") Price Fair Value 52-week High/Low Key Changes Fair value EPS Company report Lavis Chong RM2.35 RM2.60 RM2.53/RM1.69 PRESTARIANG TECHNOLOGY (PRES MK EQUITY, PSTG.KL) 23 May 2017 UniMy closer to breakeven

Price Fair Value 52-week High/Low Key Changes Fair value EPS Company report Lavis Chong RM2.35 RM2.60 RM2.53/RM1.69 PRESTARIANG TECHNOLOGY (PRES MK EQUITY, PSTG.KL) 23 May 2017 UniMy closer to breakeven

KL KEPONG BUY. Young trees to underpin long-term growth. Company report. (Maintained) Rationale for report: Company Update PLANTATION

Rationale for report: Company Update PLANTATION") PLANTATION KL KEPONG (KLK MK, KLKK.KL) 20 March 2013 Company report Gan Huey Ling, CFA gan-huey-ling@ambankgroup.com 03 2036 2305 Young trees to underpin long-term growth Rationale for report: Company

PLANTATION KL KEPONG (KLK MK, KLKK.KL) 20 March 2013 Company report Gan Huey Ling, CFA gan-huey-ling@ambankgroup.com 03 2036 2305 Young trees to underpin long-term growth Rationale for report: Company

3 November 2014 NEUTRAL

Sector Report Proposed changes in credit card fees 3 November 2014 NEUTRAL Rachel Huang huang-teng-siang@ambankgroup.com +603 2036 2293 Investment Highlights BANKING SECTOR Rationale for report : Sector

Sector Report Proposed changes in credit card fees 3 November 2014 NEUTRAL Rachel Huang huang-teng-siang@ambankgroup.com +603 2036 2293 Investment Highlights BANKING SECTOR Rationale for report : Sector

WCT HOLDINGS. (WCTHG MK EQUITY, WCTE.KL) 03 May WCT wins in AEON Bukit Tinggi dispute. Rationale for report: Company update

03 May WCT wins in AEON Bukit Tinggi dispute. Rationale for report: Company update") WCT HOLDINGS CONSTRUCTION (WCTHG MK EQUITY, WCTE.KL) 03 May 2018 Company report Joshua Ng ng-chin-yuing@ambankgroup.com 03-2036 2293 WCT wins in AEON Bukit Tinggi dispute Rationale for report: Company

WCT HOLDINGS CONSTRUCTION (WCTHG MK EQUITY, WCTE.KL) 03 May 2018 Company report Joshua Ng ng-chin-yuing@ambankgroup.com 03-2036 2293 WCT wins in AEON Bukit Tinggi dispute Rationale for report: Company

PRESTARIANG BUY. 4Q core profit surges over 4x YoY. Company report. (Maintained) TECHNOLOGY. Lavis Chong

TECHNOLOGY. Lavis Chong") PRESTARIANG TECHNOLOGY (PRES MK EQUITY, PSTG.KL) 28 Feb 2018 Company report Lavis Chong chong-guang-wei@ambankgroup.com 03-2036 2291 4Q core profit surges over 4x YoY Rationale for report: Company results

PRESTARIANG TECHNOLOGY (PRES MK EQUITY, PSTG.KL) 28 Feb 2018 Company report Lavis Chong chong-guang-wei@ambankgroup.com 03-2036 2291 4Q core profit surges over 4x YoY Rationale for report: Company results

UMW OIL & GAS CORPORATION

Company report Alex Goh alexgoh@ambankgroup.com 03-2036 2280 OIL & GAS UMW OIL & GAS CORPORATION (UMWOG MK EQUITY, UMWOG.KL) 14 June 2017 Pricing ahead of massive rights Rationale for report: Company update

Company report Alex Goh alexgoh@ambankgroup.com 03-2036 2280 OIL & GAS UMW OIL & GAS CORPORATION (UMWOG MK EQUITY, UMWOG.KL) 14 June 2017 Pricing ahead of massive rights Rationale for report: Company update

HONG LEONG BANK BHD (HLBK MK, HLBB.KL) 28 February 2012

28 February 2012") - BANKING HONG LEONG BANK BHD (HLBK MK, HLBB.KL) 28 February 2012 Strong realisation of merger synergies Company report Rachel Huang huang-teng-siang@ambankgroup.com +603 2036 2293 Rationale for report:

- BANKING HONG LEONG BANK BHD (HLBK MK, HLBB.KL) 28 February 2012 Strong realisation of merger synergies Company report Rachel Huang huang-teng-siang@ambankgroup.com +603 2036 2293 Rationale for report:

SUNWAY CONSTRUCTION. (SCGB MK EQUITY, SCOG.KL) 15 Sep Poised to surpass FY17 target for job wins. Rationale for report: Company update

15 Sep Poised to surpass FY17 target for job wins. Rationale for report: Company update") Price Fair Value 52-week High/Low Key Changes Fair value EPS Company report AmInvestment Bank www.amesecurities.com.my 03-2036 2250 RM2.30 RM2.60 RM2.41/RM1.56 YE to Dec FY16 FY17F FY18F FY19F Revenue

Price Fair Value 52-week High/Low Key Changes Fair value EPS Company report AmInvestment Bank www.amesecurities.com.my 03-2036 2250 RM2.30 RM2.60 RM2.41/RM1.56 YE to Dec FY16 FY17F FY18F FY19F Revenue

CONSTRUCTION (SARAWAK)

") Thomas Soon Sector report 12 Dec 2014 soon-guan-chuan@ambankgroup.com 03-2036 2300 Investment Highlights CONSTRUCTION (SARAWAK) No stopping SCORE now Rationale for report: Sector update OVERWEIGHT (Maintained)

Thomas Soon Sector report 12 Dec 2014 soon-guan-chuan@ambankgroup.com 03-2036 2300 Investment Highlights CONSTRUCTION (SARAWAK) No stopping SCORE now Rationale for report: Sector update OVERWEIGHT (Maintained)

WCT HOLDINGS HOLD. Growing order book, paring gearing. Company report. (Maintained) CONSTRUCTION. Joshua Ng

CONSTRUCTION. Joshua Ng") WCT HOLDINGS CONSTRUCTION (WCTHG MK EQUITY, WCTE.KL) 25 Aug 2017 Company report Joshua Ng ng-chin-yuing@ambankgroup.com 03-2036 2293 Growing order book, paring gearing Rationale for report: Company update

WCT HOLDINGS CONSTRUCTION (WCTHG MK EQUITY, WCTE.KL) 25 Aug 2017 Company report Joshua Ng ng-chin-yuing@ambankgroup.com 03-2036 2293 Growing order book, paring gearing Rationale for report: Company update

SUPERMAX HOLD. Diversifying its downstream activities. Company report. Initiation. Rationale for report: Initiation Coverage

SUPERMAX (SUCB MK, SUPM.KL) 22 November 2012 Company report Cheryl Tan cheryl-tan@ambankgroup.com +603 2036 2333 Diversifying its downstream activities Rationale for report: Initiation Coverage HOLD (Initiation)

SUPERMAX (SUCB MK, SUPM.KL) 22 November 2012 Company report Cheryl Tan cheryl-tan@ambankgroup.com +603 2036 2333 Diversifying its downstream activities Rationale for report: Initiation Coverage HOLD (Initiation)

EONMETALL GROUP BUY. Strong earnings growth remains visible. Company report. (Maintained) MANUFACTURING

MANUFACTURING") MANUFACTURING EONMETALL GROUP (EONM MK EQUITY, EONM.KL) 18 July 2017 Company report AmInvestment Bank ww.amesecurities.com.my 03-2036 2250 Strong earnings growth remains visible Rationale for report: Company

MANUFACTURING EONMETALL GROUP (EONM MK EQUITY, EONM.KL) 18 July 2017 Company report AmInvestment Bank ww.amesecurities.com.my 03-2036 2250 Strong earnings growth remains visible Rationale for report: Company

TELEKOM MALAYSIA BUY. Focused on convergence & digitisation. Company report. (Maintained) TELECOMMUNICATION

TELECOMMUNICATION") TELECOMMUNICATION TELEKOM MALAYSIA (T MK EQUITY, TLMM.KL) 24 May 2017 Company report Alex Goh alexgoh@ambankgroup.com 03-2036 2280 Focused on convergence & digitisation Rationale for report: Company update

TELECOMMUNICATION TELEKOM MALAYSIA (T MK EQUITY, TLMM.KL) 24 May 2017 Company report Alex Goh alexgoh@ambankgroup.com 03-2036 2280 Focused on convergence & digitisation Rationale for report: Company update

MALAYAN BANKING HOLD. Dividend boost in final quarter Company report. (Maintained) Rationale for report: Company Result BANKING

Rationale for report: Company Result BANKING") BANKING MALAYAN BANKING (MAY MK, MBBM.KL) 22 February 2013 Dividend boost in final quarter Company report Rachel Huang huang-teng-siang@ambankgroup.com +603 2036 2293 Rationale for report: Company Result

BANKING MALAYAN BANKING (MAY MK, MBBM.KL) 22 February 2013 Dividend boost in final quarter Company report Rachel Huang huang-teng-siang@ambankgroup.com +603 2036 2293 Rationale for report: Company Result

IOI CORPORATION HOLD. Dividends are sustainable for now. Company report. (Maintained) PLANTATION

PLANTATION") PLANTATION IOI CORPORATION (IOI MK,IOIC.KL) 26 July 2018 Company report Gan Huey Ling, CFA gan-huey-ling@ambankgroup.com 03 2036 2305 Dividends are sustainable for now Rationale for report: Company Update

PLANTATION IOI CORPORATION (IOI MK,IOIC.KL) 26 July 2018 Company report Gan Huey Ling, CFA gan-huey-ling@ambankgroup.com 03 2036 2305 Dividends are sustainable for now Rationale for report: Company Update

GENTING MALAYSIA BUY. What is GenM s return on its investments? Company report. (Maintained) Rationale for report: Company Update CASINO

Rationale for report: Company Update CASINO") CASINO GENTING MALAYSIA (GENM MK) 29 January 2013 Company report Gan Huey Ling, CFA gan-huey-ling@ambankgroup.com 03 2036 2305 What is GenM s return on its investments? Rationale for report: Company Update

CASINO GENTING MALAYSIA (GENM MK) 29 January 2013 Company report Gan Huey Ling, CFA gan-huey-ling@ambankgroup.com 03 2036 2305 What is GenM s return on its investments? Rationale for report: Company Update

WCT HOLDINGS. (WCTHG MK EQUITY, WCTE.KL) 28 February First, put the house in order. Rationale for report: Company update. Investment Highlights

28 February First, put the house in order. Rationale for report: Company update. Investment Highlights") WCT HOLDINGS CONSTRUCTION (WCTHG MK EQUITY, WCTE.KL) 28 February 2018 Company report Joshua Ng ng-chin-yuing@ambankgroup.com 03-2036 2293 First, put the house in order Rationale for report: Company update

WCT HOLDINGS CONSTRUCTION (WCTHG MK EQUITY, WCTE.KL) 28 February 2018 Company report Joshua Ng ng-chin-yuing@ambankgroup.com 03-2036 2293 First, put the house in order Rationale for report: Company update

BANKING SECTOR. Final guidelines issued for BASEL III capital framework 2 January 2013 OVERWEIGHT. Rationale for report : Sector update

BANKING SECTOR Final guidelines issued for BASEL III capital framework 2 January 2013 OVERWEIGHT Rachel Huang huang-teng-siang@ambankgroup.com +603 2036 2293 Rationale for report : Sector update (Maintained)

BANKING SECTOR Final guidelines issued for BASEL III capital framework 2 January 2013 OVERWEIGHT Rachel Huang huang-teng-siang@ambankgroup.com +603 2036 2293 Rationale for report : Sector update (Maintained)

WCT HOLDINGS HOLD. De-gearing still the key focus. Company report. (Maintained) CONSTRUCTION. Joshua Ng

CONSTRUCTION. Joshua Ng") WCT HOLDINGS CONSTRUCTION (WCTHG MK EQUITY, WCTE.KL) 23 Nov 2017 Company report Joshua Ng ng-chin-yuing@ambankgroup.com 03-2036 2293 De-gearing still the key focus Rationale for report: Company update

WCT HOLDINGS CONSTRUCTION (WCTHG MK EQUITY, WCTE.KL) 23 Nov 2017 Company report Joshua Ng ng-chin-yuing@ambankgroup.com 03-2036 2293 De-gearing still the key focus Rationale for report: Company update

Results Review. 3QFY13: Downsizing its workforce. Technology Bloomberg Ticker: UNI MK Bursa Code: November 2013

Results Review (Member of Alliance Bank group) PP7766/03/2013 (032116) 8 November 2013 Analyst Toh Woo Kim wookim@alliancefg.com +603 2604 3917 12-month upside potential Previous target price 0.89 Revised

Results Review (Member of Alliance Bank group) PP7766/03/2013 (032116) 8 November 2013 Analyst Toh Woo Kim wookim@alliancefg.com +603 2604 3917 12-month upside potential Previous target price 0.89 Revised

WCT HOLDINGS. (WCTHG MK EQUITY, WCTE.KL) 23 Jan Straight From The New Team. Rationale for report: Company update. Investment Highlights

23 Jan Straight From The New Team. Rationale for report: Company update. Investment Highlights") WCT HOLDINGS CONSTRUCTION (WCTHG MK EQUITY, WCTE.KL) 23 Jan 2017 Company report Joshua Ng ng-chin-yuing@ambankgroup.com 03-2036 2293 Straight From The New Team Rationale for report: Company update HOLD

WCT HOLDINGS CONSTRUCTION (WCTHG MK EQUITY, WCTE.KL) 23 Jan 2017 Company report Joshua Ng ng-chin-yuing@ambankgroup.com 03-2036 2293 Straight From The New Team Rationale for report: Company update HOLD

Uchi Tech UCHI MK Sector: Technology

Still all about its yields Uchi s stock price has righfully re-rated over the past 2 years on its attractive valuations and above-average dividend yields. While the latter remains attractive at just under

Still all about its yields Uchi s stock price has righfully re-rated over the past 2 years on its attractive valuations and above-average dividend yields. While the latter remains attractive at just under

SAPURAKENCANA PETROLEUM (SAKP MK) 16 May 2012

16 May 2012") Company report OIL & GAS SAPURAKENCANA PETROLEUM (SAKP MK) 16 May 2012 Dominant offshore service provider Alex Goh alexgoh@ambankgroup.com +603 2036 2291 Rationale for report: Initiation Price RM2.24 (Reference

Company report OIL & GAS SAPURAKENCANA PETROLEUM (SAKP MK) 16 May 2012 Dominant offshore service provider Alex Goh alexgoh@ambankgroup.com +603 2036 2291 Rationale for report: Initiation Price RM2.24 (Reference

MARKET STRATEGY. MGS foreign outflows: a blip or the start of a trend? 4 December 2014

MARKET STRATEGY 4 December 14 MGS foreign outflows: a blip or the start of a trend? Benny Chew, CFA benny-chew@ambankgroup.com +3 31 26 Rationale for report : Market Strategy Investment Highlights Our

MARKET STRATEGY 4 December 14 MGS foreign outflows: a blip or the start of a trend? Benny Chew, CFA benny-chew@ambankgroup.com +3 31 26 Rationale for report : Market Strategy Investment Highlights Our

Market Access. M&A Securities. Results Review (1Q15) TSH Resources Berhad HOLD (TP: RM2.38) A Tough Quarter - More Room to Grow.

TSH Resources Berhad HOLD (TP: RM2.38) A Tough Quarter - More Room to Grow.") M&A Securities Results Review (1Q15) PP14767/09/2012(030761) TSH Resources Berhad Thursday, May 21, 2015 HOLD (TP: RM2.38) A Tough Quarter - More Room to Grow Results Review Actual vs. expectations. TSH

M&A Securities Results Review (1Q15) PP14767/09/2012(030761) TSH Resources Berhad Thursday, May 21, 2015 HOLD (TP: RM2.38) A Tough Quarter - More Room to Grow Results Review Actual vs. expectations. TSH

Market Access. Results Review (3Q15) M&A Securities. Dutch Lady Milk Industries Berhad. Double Whammy. Wednesday, November 18, 2015 HOLD (TP: RM47.

M&A Securities. Dutch Lady Milk Industries Berhad. Double Whammy. Wednesday, November 18, 2015 HOLD (TP: RM47.") Market Access M&A Securities Results Review (3Q15) PP14767/4/212(296 Dutch Lady Milk Industries Berhad Double Whammy Results Review Actual vs. expectations. Dutch Lady Milk Industries Berhad (Dutch Lady)

Market Access M&A Securities Results Review (3Q15) PP14767/4/212(296 Dutch Lady Milk Industries Berhad Double Whammy Results Review Actual vs. expectations. Dutch Lady Milk Industries Berhad (Dutch Lady)

Market Access. Company Note. M&A Securities. Nestle Malaysia Berhad. Steering Away From Turbulence. Tuesday, June 21, 2016 HOLD (TP: RM79.

M&A Securities Company Note PP14767/09/2012(030761) Nestle Malaysia Berhad Steering Away From Turbulence 1Q16 results review. To recap, Nestle Malaysia Berhad (Nestle) registered its 1Q16 revenue at RM1.3

M&A Securities Company Note PP14767/09/2012(030761) Nestle Malaysia Berhad Steering Away From Turbulence 1Q16 results review. To recap, Nestle Malaysia Berhad (Nestle) registered its 1Q16 revenue at RM1.3

Market Access. M&A Securities. Results Review 1Q15. Malayan Banking Bhd BUY (TP: RM10.70) Stabilizing Period. Results Review

Stabilizing Period. Results Review") M&A Securities Results Review 1Q15 PP14767/09/2012(030761) Malayan Banking Bhd BUY (TP: RM10.70) Friday, May 29, 2015 Stabilizing Period Results Review Actual vs. expectation. Malayan Banking Berhad (Maybank)

M&A Securities Results Review 1Q15 PP14767/09/2012(030761) Malayan Banking Bhd BUY (TP: RM10.70) Friday, May 29, 2015 Stabilizing Period Results Review Actual vs. expectation. Malayan Banking Berhad (Maybank)

Market Access. Results Review 4Q15. M&A Securities. Digi.Com Berhad. Survives the Headwinds BUY (TP:RM5.90) Results Review

Results Review") M&A Securities Results Review 4Q15 PP14767/09/2012(030761) Digi.Com Berhad BUY (TP:RM5.90) Wednesday, February 10, 2016 Results Review Survives the Headwinds Current Price (RM) New Fair Value (RM) Previous

M&A Securities Results Review 4Q15 PP14767/09/2012(030761) Digi.Com Berhad BUY (TP:RM5.90) Wednesday, February 10, 2016 Results Review Survives the Headwinds Current Price (RM) New Fair Value (RM) Previous

TRC Synergy. Hold. Equity Malaysia Construction. Bags RM499m building job in Putrajaya. 05 Dec Price RM0.58 Target Price RM0.62 (from RM0.

Equity Malaysia Construction 05 Dec 2018 Hold Price RM0.58 Target Price RM0.62 (from RM0.59) Market Data Bloomberg Code TRC MK No. of shares (m) 480.5 Market cap (RMm) 276.3 52-week high/low (RM) 0.79

Equity Malaysia Construction 05 Dec 2018 Hold Price RM0.58 Target Price RM0.62 (from RM0.59) Market Data Bloomberg Code TRC MK No. of shares (m) 480.5 Market cap (RMm) 276.3 52-week high/low (RM) 0.79

Malaysia. RCE Capital Results within; proposes bonus & rights. Hold (unchanged) Results Review 15 February 2012

Results Review 15 February 2012") PP16832/01/2013 (031128) Malaysia Results Review 15 February 2012 Hold (unchanged) Share price: Target price: RM0.515 Wong Chew Hann, CA wchewh@maybank-ib.com (603) 2297 8686 Stock Information RM0.45 (unchanged)

PP16832/01/2013 (031128) Malaysia Results Review 15 February 2012 Hold (unchanged) Share price: Target price: RM0.515 Wong Chew Hann, CA wchewh@maybank-ib.com (603) 2297 8686 Stock Information RM0.45 (unchanged)

MRCB. Equity Malaysia Property

Equity Malaysia Property 30 August 2017 Buy Price RM1.19 Target price RM1.40 (from RM1.48) Market data Bloomberg code MRC MK No. of shares (m) 2,192.6 Market cap (RMm) 2,609.2 52-week high/low (RM) 1.74

Equity Malaysia Property 30 August 2017 Buy Price RM1.19 Target price RM1.40 (from RM1.48) Market data Bloomberg code MRC MK No. of shares (m) 2,192.6 Market cap (RMm) 2,609.2 52-week high/low (RM) 1.74

Impact of new export tax rate system 15 October 2012 OVERWEIGHT. Rationale for report : Sector update

Investment Highlights PLANTATION SECTOR Impact of new export tax rate system 15 October 2012 OVERWEIGHT Gan Huey Ling gan-huey-ling@ambankgroup.com +603 2036 2305 Rationale for report : Sector update (Maintained)

Investment Highlights PLANTATION SECTOR Impact of new export tax rate system 15 October 2012 OVERWEIGHT Gan Huey Ling gan-huey-ling@ambankgroup.com +603 2036 2305 Rationale for report : Sector update (Maintained)

Market Access. Results Review 4Q FY16. M&A Securities. Hartalega HoldingsBerhad. Double-Digit Growth amid Challenging Times BUY (TP:RM4.

M&A Securities Results Review 4Q FY16 PP14767/09/2012(030761) Hartalega HoldingsBerhad BUY (TP:RM4.78) Wednesday, May 04, 2016 Double-Digit Growth amid Challenging Times Results Review Current Price (RM)

M&A Securities Results Review 4Q FY16 PP14767/09/2012(030761) Hartalega HoldingsBerhad BUY (TP:RM4.78) Wednesday, May 04, 2016 Double-Digit Growth amid Challenging Times Results Review Current Price (RM)

Market Access. Results Review (1Q16) M&A Securities. Tan Chong Motor Holdings Bhd. Lacking the X-Factor SELL (TP: RM1.

M&A Securities. Tan Chong Motor Holdings Bhd. Lacking the X-Factor SELL (TP: RM1.") M&A Securities Results Review (1Q16) PP14767/09/2012(030761) Tan Chong Motor Holdings Bhd Wednesday, May 11, 2016 SELL (TP: RM1.87) Lacking the X-Factor Results Review Actual vs. expectations. Tan Chong

M&A Securities Results Review (1Q16) PP14767/09/2012(030761) Tan Chong Motor Holdings Bhd Wednesday, May 11, 2016 SELL (TP: RM1.87) Lacking the X-Factor Results Review Actual vs. expectations. Tan Chong

RHB CAPITAL BUY. Making sense of a possible MBSB merger Company report. (Maintained) Rationale for report: Company Update BANKING

Rationale for report: Company Update BANKING") BANKING RHB CAPITAL (RHBC MK, RHBC.KL) 5 July 212 Making sense of a possible MBSB merger Company report Rachel Huang huang-teng-siang@ambankgroup.com +63 236 2293 Rationale for report: Company Update BUY

BANKING RHB CAPITAL (RHBC MK, RHBC.KL) 5 July 212 Making sense of a possible MBSB merger Company report Rachel Huang huang-teng-siang@ambankgroup.com +63 236 2293 Rationale for report: Company Update BUY

Market Access. Results Review 1Q16. M&A Securities. Digi.Com Berhad. Equipped for Competition BUY (TP:RM5.75) Results Review

Results Review") M&A Securities Results Review 1Q16 PP14767/09/2012(030761) Digi.Com Berhad BUY (TP:RM5.75) Monday, April 25, 2016 Equipped for Competition Results Review Actual vs. expectations. Digi.Com (Digi) started

M&A Securities Results Review 1Q16 PP14767/09/2012(030761) Digi.Com Berhad BUY (TP:RM5.75) Monday, April 25, 2016 Equipped for Competition Results Review Actual vs. expectations. Digi.Com (Digi) started

Market Access. Results Review 1Q FY17. M&A Securities. Hartalega Holdings Berhad. Record Sales with Lower Margins BUY (TP:RM4.

M&A Securities Results Review 1Q FY17 PP14767/09/2012(030761) Hartalega Holdings Berhad BUY (TP:RM4.78) Wednesday, August 03, 2016 Record Sales with Lower Margins Results Review Current Price (RM) New

M&A Securities Results Review 1Q FY17 PP14767/09/2012(030761) Hartalega Holdings Berhad BUY (TP:RM4.78) Wednesday, August 03, 2016 Record Sales with Lower Margins Results Review Current Price (RM) New

Market Access. M&A Securities. Results Review 1Q16. Malayan Banking Berhad. Hampered by Loan Loss. Monday, May 30, 2016 HOLD (TP: RM9.

M&A Securities Results Review 1Q16 PP14767/09/2012(030761) Malayan Banking Berhad Monday, May 30, 2016 HOLD (TP: RM9.10) Hampered by Loan Loss Results Review Actual vs. expectations. Malayan Banking Bhd

M&A Securities Results Review 1Q16 PP14767/09/2012(030761) Malayan Banking Berhad Monday, May 30, 2016 HOLD (TP: RM9.10) Hampered by Loan Loss Results Review Actual vs. expectations. Malayan Banking Bhd

BUY QUALITY ASSETS AT GOOD PRICE ISSUES TO CONSIDER ACTIONABLE IDEAS KEY CATALYSTS KEY RISKS MALAYSIAN RESEARCH

16 October 2009 YTL Power International BUY RM2.17 QUALITY ASSETS AT GOOD PRICE YTL Power is extracting much more value from its PowerSeraya acquisition than we initially thought. The company continues

16 October 2009 YTL Power International BUY RM2.17 QUALITY ASSETS AT GOOD PRICE YTL Power is extracting much more value from its PowerSeraya acquisition than we initially thought. The company continues

Market Access. Results Review (1Q15) M&A Securities. Nestle Malaysia Berhad. Pre-GST Buying. Thursday, April 23, 2015 SELL (TP: RM59.

M&A Securities. Nestle Malaysia Berhad. Pre-GST Buying. Thursday, April 23, 2015 SELL (TP: RM59.") M&A Securities Results Review (1Q15) PP14767/9/212(3761) Nestle Malaysia Berhad Pre-GST Buying Results Review Actual vs. expectations. Nestle Malaysia Berhad (Nestle) recorded a revenue of RM1.27 billion

M&A Securities Results Review (1Q15) PP14767/9/212(3761) Nestle Malaysia Berhad Pre-GST Buying Results Review Actual vs. expectations. Nestle Malaysia Berhad (Nestle) recorded a revenue of RM1.27 billion

Market Access. Results Review 2Q16. M&A Securities. RHB Capital Berhad. Recovery in Decent Traction. Thursday, August 25, 2016 BUY (TP: RM5.

M&A Securities Results Review 2Q16 PP14767/09/2012(030761) RHB Capital Berhad BUY (TP: RM5.80) Thursday, August 25, 2016 Recovery in Decent Traction Results Review Actual vs. expectations. RHB Bank Berhad

M&A Securities Results Review 2Q16 PP14767/09/2012(030761) RHB Capital Berhad BUY (TP: RM5.80) Thursday, August 25, 2016 Recovery in Decent Traction Results Review Actual vs. expectations. RHB Bank Berhad

Market Access. Briefing Notes. M&A Securities. Digi.Com Berhad. 4G is the Way Forward BUY (TP:RM6.10)

") M&A Securities Briefing Notes PP14767/09/2012(030761) Digi.Com Berhad BUY (TP:RM6.10) Tuesday, September 08, 2015 4G is the Way Forward Digi hosted its Analyst s Day yesterday where the senior management

M&A Securities Briefing Notes PP14767/09/2012(030761) Digi.Com Berhad BUY (TP:RM6.10) Tuesday, September 08, 2015 4G is the Way Forward Digi hosted its Analyst s Day yesterday where the senior management

Sunway Berhad. OUTPERFORM Price: RM2.65 Target Price: RM3.08 KENANGA RESEARCH. Within expectations. Results Note KENANGA RESEARCH.

Results Note 02 December 2013 Sunway Berhad Within expectations Period 3Q13 / 9M13 Actual vs. Expectations Dividends None as expected. Key Results Highlights At 73% of our full-year FY13 estimates, the

Results Note 02 December 2013 Sunway Berhad Within expectations Period 3Q13 / 9M13 Actual vs. Expectations Dividends None as expected. Key Results Highlights At 73% of our full-year FY13 estimates, the

Market Access. Briefing Notes. M&A Securities. BIMB Holdings Bhd BUY (TP:RM4.60) Shifting into High Gears

Shifting into High Gears") M&A Securities Briefing Notes PP14767/09/2012(030761) BIMB Holdings Bhd BUY (TP:RM4.60) Monday, October 12, 2015 Shifting into High Gears We attended post-1h15 results briefing organized by BIMB Holdings

M&A Securities Briefing Notes PP14767/09/2012(030761) BIMB Holdings Bhd BUY (TP:RM4.60) Monday, October 12, 2015 Shifting into High Gears We attended post-1h15 results briefing organized by BIMB Holdings

Bermaz Auto Implications of Mazda s supply chain transplant

21 November 2016 Corporate Update Bermaz Auto Implications of Mazda s supply chain transplant INVESTMENT THESIS APM-Delta JV reflects Mazda s move to transplant its supply chain and transform its Malaysian

21 November 2016 Corporate Update Bermaz Auto Implications of Mazda s supply chain transplant INVESTMENT THESIS APM-Delta JV reflects Mazda s move to transplant its supply chain and transform its Malaysian

Market Access. Results Review (2Q15) M&A Securities. Genting Plantations Berhad. Hit by Plantation-Malaysia Segment. Wednesday, August 26, 2015

M&A Securities. Genting Plantations Berhad. Hit by Plantation-Malaysia Segment. Wednesday, August 26, 2015") M&A Securities Results Review (2Q15) PP14767/09/2012(030761) Genting Plantations Berhad Wednesday, August 26, 2015 HOLD (TP: RM9.66) Hit by Plantation-Malaysia Segment Results Review Actual vs. expectations.

M&A Securities Results Review (2Q15) PP14767/09/2012(030761) Genting Plantations Berhad Wednesday, August 26, 2015 HOLD (TP: RM9.66) Hit by Plantation-Malaysia Segment Results Review Actual vs. expectations.

Market Access. M&A Securities. Results Review 2Q15. Axiata Group Berhad. Satisfactory, Need to Push in 2H15. Friday, August 21, 2015 HOLD (TP:RM7.

M&A Securities Results Review 2Q15 PP14767/09/2012(030761) Axiata Group Berhad Friday, August 21, 2015 HOLD (TP:RM7.10) Satisfactory, Need to Push in 2H15 Results Review Actual vs. expectations. Axiata

M&A Securities Results Review 2Q15 PP14767/09/2012(030761) Axiata Group Berhad Friday, August 21, 2015 HOLD (TP:RM7.10) Satisfactory, Need to Push in 2H15 Results Review Actual vs. expectations. Axiata

MMC MMC MK Sector: Utilities

Weakness continues into 2Q MMC reported a lacklustre set of earnings for 1H17, as PATAMI of RM118m (-3 yoy) was below expectations. 1H17 results constituted 22% of our and consensus full year forecast.

Weakness continues into 2Q MMC reported a lacklustre set of earnings for 1H17, as PATAMI of RM118m (-3 yoy) was below expectations. 1H17 results constituted 22% of our and consensus full year forecast.

Pharmaniaga MARKET PERFORM. 1Q15 Inline but Rich Valuations. Results Note. Price: RM6.91 Target Price: RM6.95. PP7004/02/2013(031762) Page 1 of 5

Page 1 of 5") Pharmaniaga 1Q15 Inline but Rich Valuations By the Kenanga Research Team l research@kenanga.com.my Period 1Q15 Actual vs. Expectations 1Q15 PATAMI of RM31.8m (+21% YoY) came in at 32% and 31% of our and

Pharmaniaga 1Q15 Inline but Rich Valuations By the Kenanga Research Team l research@kenanga.com.my Period 1Q15 Actual vs. Expectations 1Q15 PATAMI of RM31.8m (+21% YoY) came in at 32% and 31% of our and

EconWatch. Qualms of forex volatility; strong USD prior to policy tightening in the US. 21 August 2015

EconWatch 21 August 2015 Patricia Oh Swee Ling patricia-oh@ambankgroup.com 603-2036 2240 Qualms of forex volatility; strong USD prior to policy tightening in the US Investment Highlights Qualms of currency

EconWatch 21 August 2015 Patricia Oh Swee Ling patricia-oh@ambankgroup.com 603-2036 2240 Qualms of forex volatility; strong USD prior to policy tightening in the US Investment Highlights Qualms of currency

Market Access. M&A Securities. Results Review (3Q15) Padini Holdings Berhad. A good Quarter BUY (TP: RM1.80) Wednesday, May 20, 2015.

Padini Holdings Berhad. A good Quarter BUY (TP: RM1.80) Wednesday, May 20, 2015.") Market Access M&A Securities PP14767/04/2012(029607) [ Padini Holdings Berhad Results Review (3Q15) BUY (TP: RM1.80) Wednesday, May 20, 2015 A good Quarr Results Review Actual vs. expectations. Padini

Market Access M&A Securities PP14767/04/2012(029607) [ Padini Holdings Berhad Results Review (3Q15) BUY (TP: RM1.80) Wednesday, May 20, 2015 A good Quarr Results Review Actual vs. expectations. Padini

APM AUTOMOTIVE. (APM MK EQUITY, APMA.KL) 17 Mar Hopes pinned on M&A. Rationale for report: Initiation. Investment Highlights

17 Mar Hopes pinned on M&A. Rationale for report: Initiation. Investment Highlights") APM AUTOMOTIVE AUTOMOBILE (APM MK EQUITY, APMA.KL) 17 Mar 2017 Company report Al Zaquan al-zaquan@ambankgroup.com 03-2036 2304 Hopes pinned on M&A Rationale for report: Initiation HOLD (Initiation) Price

APM AUTOMOTIVE AUTOMOBILE (APM MK EQUITY, APMA.KL) 17 Mar 2017 Company report Al Zaquan al-zaquan@ambankgroup.com 03-2036 2304 Hopes pinned on M&A Rationale for report: Initiation HOLD (Initiation) Price

Market Access. M&A Securities. Results Review 1Q15. Axiata Group Berhad. Slow in Recovery. Wednesday, May 20, 2015 HOLD (TP:RM7.

M&A Securities Results Review 1Q15 PP14767/09/2012(030761) Axiata Group Berhad Wednesday, May 20, 2015 HOLD (TP:RM7.40) Slow in Recovery Results Review Actual vs. expectations. Axiata Group Bhd (Axiata)

M&A Securities Results Review 1Q15 PP14767/09/2012(030761) Axiata Group Berhad Wednesday, May 20, 2015 HOLD (TP:RM7.40) Slow in Recovery Results Review Actual vs. expectations. Axiata Group Bhd (Axiata)

Company Note Company Update. Sime Darby Berhad. Meet The Enlarged Sime Darby. Target Price Raised to RM12.40.

Company Note Company Update Monday, 13 August 2007 For Internal Circulation Only KLCI : 1,287.70 Sector : PLANTATIONS 13 Aug 2007 Bloomberg : SDY MK Analyst : James Ratnam E- : james@ta.com.my : 20721277

Company Note Company Update Monday, 13 August 2007 For Internal Circulation Only KLCI : 1,287.70 Sector : PLANTATIONS 13 Aug 2007 Bloomberg : SDY MK Analyst : James Ratnam E- : james@ta.com.my : 20721277

Tenaga Nasional Berhad TP: RM17.38 (+16.5%)

") COMPANY UPDATE Wednesday, December 20, 2017 FBMKLCI: 1,736.95 Sector: Power & Utilities THIS REPORT IS STRICTLY FOR INTERNAL CIRCULATION ONLY* Tenaga Nasional Berhad TP: RM17.38 (+16.5%) RP2 Uncertainty

COMPANY UPDATE Wednesday, December 20, 2017 FBMKLCI: 1,736.95 Sector: Power & Utilities THIS REPORT IS STRICTLY FOR INTERNAL CIRCULATION ONLY* Tenaga Nasional Berhad TP: RM17.38 (+16.5%) RP2 Uncertainty

Star Media STAR MK Sector: Media

Print remains under pressure We expect prospects for the print media industry to remain weak in 2016 given the challenging market environment, poor consumer sentiment as well as the structurally declining

Print remains under pressure We expect prospects for the print media industry to remain weak in 2016 given the challenging market environment, poor consumer sentiment as well as the structurally declining

Market Access. Company Update. M&A Securities. Public Bank Berhad. Wednesday, April 27, BUY (Target Price: RM21.38) Proves to be Bellwether

Proves to be Bellwether") M&A Securities Company Update PP14767/09/2012(030761) Public Bank Berhad Wednesday, April 27, 2016 BUY (Target Price: RM21.38) Proves to be Bellwether We recommend investors to accumulate Public Bank Bhd

M&A Securities Company Update PP14767/09/2012(030761) Public Bank Berhad Wednesday, April 27, 2016 BUY (Target Price: RM21.38) Proves to be Bellwether We recommend investors to accumulate Public Bank Bhd

Market Access. M&A Securities. Results Review 3Q15. Telekom Malaysia Berhad. Hampered by Forex Translation Loss. Friday, November 27, 2015

M&A Securities Results Review 3Q15 PP14767/09/2012(030761) Telekom Malaysia Berhad Friday, November 27, 2015 HOLD (TP:RM6.87) Hampered by Forex Translation Loss Results Review Actual vs. expectation. Telekom

M&A Securities Results Review 3Q15 PP14767/09/2012(030761) Telekom Malaysia Berhad Friday, November 27, 2015 HOLD (TP:RM6.87) Hampered by Forex Translation Loss Results Review Actual vs. expectation. Telekom

Buy (Maintained) Above Expectations. Technology - Software & Services Target Price: SGD1.00 Market Cap: USD1,540m Price: SGD0.86

Above Expectations. Technology - Software & Services Target Price: SGD1.00 Market Cap: USD1,540m Price: SGD0.86") May-13 Jul-13 Sep-13 Nov-13 Jan-14 Mar-14 Vol m Results Review, Buy (Maintained) Technology - Software & Services Target Price: SGD1.00 Market Cap: USD1,540m Price: SGD0.86 Above Expectations Macro Risks

May-13 Jul-13 Sep-13 Nov-13 Jan-14 Mar-14 Vol m Results Review, Buy (Maintained) Technology - Software & Services Target Price: SGD1.00 Market Cap: USD1,540m Price: SGD0.86 Above Expectations Macro Risks

Market Access. M&A Securities. Company Update. Tenaga Nasional Berhad. A Look into Debt. Tuesday, July 14, 2015 BUY (TP: RM15.20) Latest Development

Latest Development") M&A Securities Company Update PP14767/09/2012(030761) Tenaga Nasional Berhad BUY (TP: RM15.20) Tuesday, July 14, 2015 A Look into Debt Latest Development Debt position. Tenaga Nasional Bhd (TNB) core business

M&A Securities Company Update PP14767/09/2012(030761) Tenaga Nasional Berhad BUY (TP: RM15.20) Tuesday, July 14, 2015 A Look into Debt Latest Development Debt position. Tenaga Nasional Bhd (TNB) core business

Rough Start. Results Note. Price: RM5.40 Target Price: RM4.95. By Desmond Chong l

UMW Holdings Rough Start By Desmond Chong l cwchong@kenanga.com.my 1Q16 core PATAMI of RM16.9m (>100% QoQ; -90% YoY) came in way below estimates, making up only 5% of both our and consensus estimates.

UMW Holdings Rough Start By Desmond Chong l cwchong@kenanga.com.my 1Q16 core PATAMI of RM16.9m (>100% QoQ; -90% YoY) came in way below estimates, making up only 5% of both our and consensus estimates.

Company Update. Deleum Berhad. On the lookout for earnings surprises. Oil & Gas Bloomberg Ticker: DLUM MK Bursa Code: 5132.

Company Update (Member of Alliance Bank group) PP7766/03/2013 (032116) 3 May 2013 Analyst Arhnue Tan arhnue@alliancefg.com +603 2604 3909 12-month upside potential Target price 2.70 Current price (as at

Company Update (Member of Alliance Bank group) PP7766/03/2013 (032116) 3 May 2013 Analyst Arhnue Tan arhnue@alliancefg.com +603 2604 3909 12-month upside potential Target price 2.70 Current price (as at

IPO Report KIM TECK CHEONG BERHAD MERCURY SECURITIES SDN BHD SUBSCRIBE ACE MARKET. Initial Public Offering ACE Market TRAD/SERV

MERCURY SECURITIES SDN BHD (A Participating Organisation of Bursa Malaysia Securities Berhad) KIM TECK CHEONG BERHAD Initial Public Offering ACE Market IPO Report Monday, 2 November, 2015 ACE MARKET TRAD/SERV

MERCURY SECURITIES SDN BHD (A Participating Organisation of Bursa Malaysia Securities Berhad) KIM TECK CHEONG BERHAD Initial Public Offering ACE Market IPO Report Monday, 2 November, 2015 ACE MARKET TRAD/SERV

PUBLIC INVESTMENT BANK

PUBLIC INVESTMENT BANK PublicInvest Research Non-Rated Note Tuesday, April 19, 2016 KDN PP17686/03/2013(032117) MAGNI-TECH INDUSTRIES Fair Value: RM5.08 DESCRIPTION Is involved in manufacturing and sales

PUBLIC INVESTMENT BANK PublicInvest Research Non-Rated Note Tuesday, April 19, 2016 KDN PP17686/03/2013(032117) MAGNI-TECH INDUSTRIES Fair Value: RM5.08 DESCRIPTION Is involved in manufacturing and sales

BANKING SECTOR. Rationale for report: Banking statistics for January 2017

BANKING SECTOR Sector Report 2 March 2017 Kelvin Ong,CFA kelvin-ong@ambankgroup.com 03-20362294 Higher deposit growth with stronger CASA momentum Rationale for report: Banking statistics for January 2017

BANKING SECTOR Sector Report 2 March 2017 Kelvin Ong,CFA kelvin-ong@ambankgroup.com 03-20362294 Higher deposit growth with stronger CASA momentum Rationale for report: Banking statistics for January 2017

Market Access. Company Update. M&A Securities. UMW Oil and Gas Corporation Bhd. Awards for NAGA 7 SELL (TP: RM0.90)

") M&A Securities Company Update PP14767/9/212(3761) Friday, October 3, 215 UMW Oil and Gas Corporation Bhd Awards for NAGA 7 SELL (TP: RM.9) Current Price (RM) New Target Price (RM) Previous Target Price

M&A Securities Company Update PP14767/9/212(3761) Friday, October 3, 215 UMW Oil and Gas Corporation Bhd Awards for NAGA 7 SELL (TP: RM.9) Current Price (RM) New Target Price (RM) Previous Target Price

THAI BEVERAGE PLC CORPORATES. No. 183/ November 2018 RATIONALE

THAI BEVERAGE PLC No. 183/ 16 November CORPORATES Company Rating: Issue Ratings: Senior unsecured Outlook: Last Review Date : Date Rating Outlook/Alert 15/02/18 Stable Company Rating History: Date Rating

THAI BEVERAGE PLC No. 183/ 16 November CORPORATES Company Rating: Issue Ratings: Senior unsecured Outlook: Last Review Date : Date Rating Outlook/Alert 15/02/18 Stable Company Rating History: Date Rating

Evergreen Fibreboard

PP10551/09/2011(028936) 09 November 2010 The Research Team +60 (3) 9207 7663 Research2 @my.oskgroup.com Company Update Evergreen Fibreboard MALAYSIA EQUITY Investment Research Daily Softer Second Half

PP10551/09/2011(028936) 09 November 2010 The Research Team +60 (3) 9207 7663 Research2 @my.oskgroup.com Company Update Evergreen Fibreboard MALAYSIA EQUITY Investment Research Daily Softer Second Half

Market Access. Results Review (4Q14) M&A Securities. Genting Plantations Berhad. Hit by Plantation-Malaysia Segment. Thursday, May 28, 2015

M&A Securities. Genting Plantations Berhad. Hit by Plantation-Malaysia Segment. Thursday, May 28, 2015") M&A Securities Results Review (4Q14) PP14767/09/2012(030761) Genting Plantations Berhad Thursday, May 28, 2015 HOLD (TP: RM10.77) Hit by Plantation-Malaysia Segment Results Review Actual vs. expectations.

M&A Securities Results Review (4Q14) PP14767/09/2012(030761) Genting Plantations Berhad Thursday, May 28, 2015 HOLD (TP: RM10.77) Hit by Plantation-Malaysia Segment Results Review Actual vs. expectations.

Market Access. Results Review (4Q16) M&A Securities. Scientex Berhad. Unstoppable Growth Amid Challenging Times. Tuesday, September 27, 2016

M&A Securities. Scientex Berhad. Unstoppable Growth Amid Challenging Times. Tuesday, September 27, 2016") Market Access M&A Securities Results Review (4Q16) PP14767/04/2012(029 Tuesday, September 27, 2016 Scientex Berhad Unstoppable Growth Amid Challenging Times BUY (TP: RM8.33) Current Price (RM) New Target

Market Access M&A Securities Results Review (4Q16) PP14767/04/2012(029 Tuesday, September 27, 2016 Scientex Berhad Unstoppable Growth Amid Challenging Times BUY (TP: RM8.33) Current Price (RM) New Target

Market Access. M&A Securities. Results Review 1Q15. BIMB Holdings Bhd BUY (TP:RM4.84) Brilliant Beginning. Results Review

Brilliant Beginning. Results Review") M&A Securities Results Review 1Q15 PP14767/09/2012(030761) BIMB Holdings Bhd BUY (TP:RM4.84) Wednesday, May 27, 2015 Brilliant Beginning Results Review Actual vs. expectation. BIMB Holdings Berhad (BIMB)

M&A Securities Results Review 1Q15 PP14767/09/2012(030761) BIMB Holdings Bhd BUY (TP:RM4.84) Wednesday, May 27, 2015 Brilliant Beginning Results Review Actual vs. expectation. BIMB Holdings Berhad (BIMB)

UMW Oil & Gas Corporation Bhd Expensive Acquisition Aborted

A Member of the TA Group MENARA TA ONE, 22 JALAN P. RAMLEE, 50250 KUALA LUMPUR, MALAYSIA TEL: +603-20721277 / FAX: +603-20325048 UMW Oil & Gas Corporation Bhd Expensive Acquisition Aborted THIS REPORT

A Member of the TA Group MENARA TA ONE, 22 JALAN P. RAMLEE, 50250 KUALA LUMPUR, MALAYSIA TEL: +603-20721277 / FAX: +603-20325048 UMW Oil & Gas Corporation Bhd Expensive Acquisition Aborted THIS REPORT

Malaysia. Padini Holdings Strong earnings momentum. Buy (unchanged) Results Review 30 November 2011

Results Review 30 November 2011") PP16832/01/2012 (029059) Malaysia Results Review 30 November 2011 Buy (unchanged) Share price: Target price: RM1.05 Kang Chun Ee chunee@maybank-ib.com (603) 2297 8675 Stock Information RM1.16 (unchanged)

PP16832/01/2012 (029059) Malaysia Results Review 30 November 2011 Buy (unchanged) Share price: Target price: RM1.05 Kang Chun Ee chunee@maybank-ib.com (603) 2297 8675 Stock Information RM1.16 (unchanged)

Market Access. M&A Securities. Results Review (2Q16) SapuraKencana Petroleum Berhad. Solid Orderbook as a Shield BUY (TP: RM2.

SapuraKencana Petroleum Berhad. Solid Orderbook as a Shield BUY (TP: RM2.") M&A Securities Results Review (2Q16) PP14767/09/2012(030761) SapuraKencana Petroleum Berhad Thursday, September 17, 2015 BUY (TP: RM2.55) Solid Orderbook as a Shield Results Review Actual vs. expectations.

M&A Securities Results Review (2Q16) PP14767/09/2012(030761) SapuraKencana Petroleum Berhad Thursday, September 17, 2015 BUY (TP: RM2.55) Solid Orderbook as a Shield Results Review Actual vs. expectations.

Market Access. M&A Securities. Result Review (3Q16) Cahya Mata Sarawak Berhad. Loss-Making Business Turns Into Black BUY (TP: RM4.

Cahya Mata Sarawak Berhad. Loss-Making Business Turns Into Black BUY (TP: RM4.") M&A Securities Result Review (3Q16) PP14767/09/2012(030761) Cahya Mata Sarawak Berhad Thursday, Dec 1, 2016 BUY (TP: RM4.66) Loss-Making Business Turns Into Black Result Review Actual vs. expectation.

M&A Securities Result Review (3Q16) PP14767/09/2012(030761) Cahya Mata Sarawak Berhad Thursday, Dec 1, 2016 BUY (TP: RM4.66) Loss-Making Business Turns Into Black Result Review Actual vs. expectation.

Market Access. Results Review (1Q16) M&A Securities. Dayang Enterprise Holdings Bhd. A Quiet Quarter. Thursday, May 26, 2016 HOLD (TP: RM1.

M&A Securities. Dayang Enterprise Holdings Bhd. A Quiet Quarter. Thursday, May 26, 2016 HOLD (TP: RM1.") M&A Securities Results Review (1Q16) PP14767/9/212(3761) Dayang Enterprise Holdings Bhd Thursday, May 26, 216 HOLD (TP: RM1.16) Results Review A Quiet Quarter Current Price (RM) New Target Price (RM) Previous

M&A Securities Results Review (1Q16) PP14767/9/212(3761) Dayang Enterprise Holdings Bhd Thursday, May 26, 216 HOLD (TP: RM1.16) Results Review A Quiet Quarter Current Price (RM) New Target Price (RM) Previous

Signature International Berhad Cooking up better growth ahead

09 May 2017 Small Cap Highlight Signature International Berhad Cooking up better growth ahead INVESTMENT HIGHLIGHTS Orderbook of RM220m Facility expansion to cater for more value-added products Tapping

09 May 2017 Small Cap Highlight Signature International Berhad Cooking up better growth ahead INVESTMENT HIGHLIGHTS Orderbook of RM220m Facility expansion to cater for more value-added products Tapping

KPJ Healthcare. Company Update. A Fresh Start BUY. MALAYSIA EQUITY Investment Research Daily News

PP10551/10/2010(025682) 07 January 2010 Norfauzi Nasron +60 (3) 9207 7644 analyst.name@osk.com.my Company Update KPJ Healthcare MALAYSIA EQUITY Investment Research Daily News BUY Target Previous Price

PP10551/10/2010(025682) 07 January 2010 Norfauzi Nasron +60 (3) 9207 7644 analyst.name@osk.com.my Company Update KPJ Healthcare MALAYSIA EQUITY Investment Research Daily News BUY Target Previous Price

SCGM Berhad (Not Rated)

") SCGM Berhad (Not Rated) Great package deals Highlights Catalysts Risks Forecasts - A one stop leading thermo-vacuum formed plastic packaging manufacturer SCGM manufactures and sells its thermos-vacuum

SCGM Berhad (Not Rated) Great package deals Highlights Catalysts Risks Forecasts - A one stop leading thermo-vacuum formed plastic packaging manufacturer SCGM manufactures and sells its thermos-vacuum

Tenaga Nasional Bonus earnings not sustainable

29 January 2018 1QFY18 Results Review Tenaga Nasional Bonus earnings not sustainable 1QFY18 within estimates RP1 earnings inflated by favourable customer mix Bonus regulated earnings not sustainable in

29 January 2018 1QFY18 Results Review Tenaga Nasional Bonus earnings not sustainable 1QFY18 within estimates RP1 earnings inflated by favourable customer mix Bonus regulated earnings not sustainable in

Economics. Market Insight Tuesday, 6 June, Malaysia Economy. Exports and Imports slowed down in April. Chart 1: Malaysia: External Trade

Market Insight Tuesday, 6 June, 2017 RM'bn Jan'10 Jan'11 Jan'12 Jan'13 Jan'14 Jan'15 Jan'16 Jan'17 % y-o-y Imran Nurginias Ibrahim imran@bimbsec.com.my PP16795/03/2013(031743) 03-26131733 www.bisonline.com

Market Insight Tuesday, 6 June, 2017 RM'bn Jan'10 Jan'11 Jan'12 Jan'13 Jan'14 Jan'15 Jan'16 Jan'17 % y-o-y Imran Nurginias Ibrahim imran@bimbsec.com.my PP16795/03/2013(031743) 03-26131733 www.bisonline.com

PUBLIC INVESTMENT BANK

PUBLIC INVESTMENT BANK PublicInvest Research Results Review Wednesday, February 28, 2018 KDN PP17686/03/2013(032117) PRESTARIANG Outperform DESCRIPTION An ICT service provider focusing on ICT training

PUBLIC INVESTMENT BANK PublicInvest Research Results Review Wednesday, February 28, 2018 KDN PP17686/03/2013(032117) PRESTARIANG Outperform DESCRIPTION An ICT service provider focusing on ICT training

Muhibbah Engineering (M) Bhd BUY. 3Q FY2017 results update. 30 Nov 2017

Bhd BUY. 3Q FY2017 results update. 30 Nov 2017") 3Q FY2017 results update 30 Nov 2017 Muhibbah Engineering (M) Bhd 3Q2017 results within expectations Large RM1.9b order-book to underpin earnings Rising oil prices auger well for more capex and jobs Attractive

3Q FY2017 results update 30 Nov 2017 Muhibbah Engineering (M) Bhd 3Q2017 results within expectations Large RM1.9b order-book to underpin earnings Rising oil prices auger well for more capex and jobs Attractive

Bermaz Auto Darkest before dawn

14 June 2017 4QFY17 Results Review Bermaz Auto Darkest before dawn Maintain BUY Unchanged Target Price (TP):RM2.50 INVESTMENT THESIS 4QFY17 within our expectation, below consensus Impacted by weak RM but

14 June 2017 4QFY17 Results Review Bermaz Auto Darkest before dawn Maintain BUY Unchanged Target Price (TP):RM2.50 INVESTMENT THESIS 4QFY17 within our expectation, below consensus Impacted by weak RM but

KINDLY REFER TO THE LAST PAGE OF THIS PUBLICATION FOR IMPORTANT DISCLOSURES

21 January 2016 Sector Update Automotive Maintain NEUTRAL Time to scrap? INVESTMENT HIGHLIGHTS Domestic autos looks set to enter its third straight year of earnings contraction. A relook at a vehicle scrapping

21 January 2016 Sector Update Automotive Maintain NEUTRAL Time to scrap? INVESTMENT HIGHLIGHTS Domestic autos looks set to enter its third straight year of earnings contraction. A relook at a vehicle scrapping

Market Access. M&A Securities. Company Update. MMHE Holdings Berhad. Multiple Awards worth RM527 million. Monday, December 28, 2015 HOLD (TP: RM1.

M&A Securities Company Update PP14767/9/212(3761) MMHE Holdings Berhad Monday, December 28, 215 HOLD (TP: RM1.4) Multiple Awards worth RM527 million Malaysia Marine and Heavy Engineering Berhad (MMHE)

M&A Securities Company Update PP14767/9/212(3761) MMHE Holdings Berhad Monday, December 28, 215 HOLD (TP: RM1.4) Multiple Awards worth RM527 million Malaysia Marine and Heavy Engineering Berhad (MMHE)

EARNINGS UPDATE Nigerian Breweries Plc. February 2018

Thousands RATING: HOLD Target Price: NGN128 Income Statement Summary FY2017 FY2016 NGN'bn NGN'bn Revenue 344.56 313.74 9.82% Cost of sales 201.01 178.22 12.79% Finance cost 10.66 13.65-21.85% PBT 46.63

Thousands RATING: HOLD Target Price: NGN128 Income Statement Summary FY2017 FY2016 NGN'bn NGN'bn Revenue 344.56 313.74 9.82% Cost of sales 201.01 178.22 12.79% Finance cost 10.66 13.65-21.85% PBT 46.63

Petra Energy PENB MK Sector: Oil & Gas

Small hiccup, turnaround remains in motion Petra Energy (PENB) remains a strong contender to win the upcoming modification, construction and maintenance (MCM) contract from Petronas, which is to be split

Small hiccup, turnaround remains in motion Petra Energy (PENB) remains a strong contender to win the upcoming modification, construction and maintenance (MCM) contract from Petronas, which is to be split

Fundamental Analysis for GUINNESS ANCHOR BHD

Fundamental Analysis for GUINNESS ANCHOR BHD Date of Analysis: 3-Jun-11 Company Name: GUINNESS ANCHOR BHD Board: Main Stock Code (Bursa): GAB FBMKLCI: N Stock Code (Bloomberg): GUIN:MK Sector: CONSUMER

Fundamental Analysis for GUINNESS ANCHOR BHD Date of Analysis: 3-Jun-11 Company Name: GUINNESS ANCHOR BHD Board: Main Stock Code (Bursa): GAB FBMKLCI: N Stock Code (Bloomberg): GUIN:MK Sector: CONSUMER