World Steel Industry Development and Market Prospects 13 th International Market and Trade Conference

|

|

|

- Griselda Willis

- 6 years ago

- Views:

Transcription

1 World Steel Industry Development and Market Prospects 13 th International Market and Trade Conference

2 Global Steel Industry in the post-crisis Period

3 Global economic recovery continues to disappoint The global economy grows on a single engine With strong fundamentals, the US remains the bright spot The Eurozone recovery is firming, but still lacking strength China decelerating, other emerging economies struggling Geopolitical tensions continue to undermine growth in some regions Sources: IMF, Haver Analytics 3

4 Uneven recovery in steel demand Post-crisis recovery led by the emerging economies Steel Demand Recovery Apparent Steel Use, finished steel (SRO April 2015) 2007= World Developed Economies Emerging & Developing Economies excl. China China 2014 as % of 2007 World United States 98.7 European Union (28) 73.2 Germany 91.7 Japan 83.2 China India Brazil ASEAN (5) MENA

5 Steel demand shifts to low gear with China deceleration Steel Demand Evolution (Apparent Steel Use, finished steel) China, Mt Developed, Mt Developing ex China, Mt World, y-o-y % growth China Developing ex China Developed y-o-y % growth

6 How are other industries doing? Sources: different, OICA, worldsteel, IAI, USGS 6

7 Overcapacity to stay During 00~ 14, global crude steel capacity increased by1300 Mt to reach 2351 Mt vs. crude steel production up by 815 MT to 1665 Mt Chinese capacity increased by 990 Mt to 1140 Mt, production up by 694 Mt to 823 Mt Global Capacity vs Demand (2000=100) = Apparent steel use, crude steel equivalent Capacity Utilization Ratio

8 Steel industry stuck in low performance Steel companies profitability converges at a low level due to overcapacity and high raw material prices Sources: different, companies reports, Thomson Reuters 8

9 Steel Market Prospects

10 Factors shaping future steel market development Deleveraging in the developed economies Deceleration of investment-led growth in China Structural reforms in the developing and emerging economies Geopolitical stability and transformation of MENA countries Lower oil prices (at least in the medium term) GDP Growth Forecasts, % Fixed investments growth, % Source: IHS Global Insight 10

11 Impact of low oil prices Negative Investment in the energy sector will slow Infrastructure projects in oil revenue dependent countries to be scaled down Positive Lower energy cost to boost manufacturing and consumer spending Lower inflationary pressure provides more space for supportive monetary policy in high inflation countries and energy price reform Saudi Arabia United Arab Emirates Venezuela Nigeria Russia Ghana Vietnam Mexico Canada Malaysia Egypt Argentina Brazil United Kingdom Indonesia Turkey France United States Germany Italy China Japan Spain Poland South Korea Thailand Oil net exports as % of GDP in 2013 Fiscal breakeven oil price (USD/bbl) Iran 131 Nigeria 123 Venezuela 118 Russia 105 Saudi Arabia 104 United Arab Emirates % Source: - worldsteel calculations based on GI nominal GDP (USD) and UN Comtrade trade (USD, HS 2709), 2013 (2011 for UAE, 2010 for Turkey), selected countries - fiscal breakeven oil price, USD per barrel, Deutsche Bank and IMF 11

12 Deleveraging in the developed economies Deleveraging in the developed economies is progressing only at a slow speed, differentiated Public sector debt has increased as a result of anti-crisis measures and slow growth Deflationary pressure to aggravate debt burden Source: Haver Analytics 12

13 Diverging growth prospects of the developing economies Structural reform will define growth potential Brazil and Russia trapped in structural problems Mexico has brighter prospects thanks to the strong reform agenda ASEAN countries with reform agenda will outperform others MENA outlook clouded by low oil prices and geopolitical instability India getting ready for a take off with renewed reform initiatives 13

14 Unleashing potential of emerging markets Structural reform agenda is a prerequisite for unleashing potentials in the developing countries Low oil prices to facilitate reform environment GDP/capita, USD Urbanization, % Population,(mln) Steel use per capita, kg India Indonesia Vietnam Thailand Egypt Sources: UN, Global Insight 14

15 Conclusion Steel industry will face new normal of low growth and low profit With China deceleration, lacking a strong growth engine Unleashing other emerging economies potential requires time Capacity build ups in newly emerging economies cause concern Steel industry s sustainability under great stress Current profitability inadequate to meet huge R&D bill to meet the challenges of climate change Inter-material competition and more efficient use of steel reduces steel market expansion potential Focus on value creation rather than expansion 15

16 worldsteel.org

PMITM. The world s leading economic indicator

PMITM The world s leading economic indicator The Purchasing Managers IndexTM (PMITM) is based on monthly surveys of carefully selected companies representing major and developing economies worldwide. KEY

PMITM The world s leading economic indicator The Purchasing Managers IndexTM (PMITM) is based on monthly surveys of carefully selected companies representing major and developing economies worldwide. KEY

Moderate but continued growth expected for global steel demand

PRESS RELEASE Moderate but continued growth expected for global steel demand worldsteel Short Range Outlook October 2017 Brussels, 16 October 2017 - The World Steel Association (worldsteel) today released

PRESS RELEASE Moderate but continued growth expected for global steel demand worldsteel Short Range Outlook October 2017 Brussels, 16 October 2017 - The World Steel Association (worldsteel) today released

Global Steel Market Outlook. OECD Steel Committee Meeting, Sep 28, 2017, Paris

Global Steel Market Outlook OECD Steel Committee Meeting, Sep 28, 2017, Paris Disclaimer text This document is protected by copyright. Distribution to third parties or reproduction in any format is not

Global Steel Market Outlook OECD Steel Committee Meeting, Sep 28, 2017, Paris Disclaimer text This document is protected by copyright. Distribution to third parties or reproduction in any format is not

A short history of debt

A short history of debt In the words of the late Charles Kindleberger, debt/financial crises are a hardy perennial we have been here many times before. Over the past decade and a half the ratio of global

A short history of debt In the words of the late Charles Kindleberger, debt/financial crises are a hardy perennial we have been here many times before. Over the past decade and a half the ratio of global

Progress Towards Strong, Sustainable, and Balanced Growth. Figure 1: Recovery From Financial Crisis (100 = First Quarter of Real GDP contraction)

") Progress Towards Strong, Sustainable, and Balanced Growth Figure 1: Recovery From Financial Crisis ( = First Quarter of Real GDP contraction) 13 125 196-26 AE Recessions' Range*** 196-26 AE Recessions**

Progress Towards Strong, Sustainable, and Balanced Growth Figure 1: Recovery From Financial Crisis ( = First Quarter of Real GDP contraction) 13 125 196-26 AE Recessions' Range*** 196-26 AE Recessions**

Progress towards Strong, Sustainable and Balanced Growth. Figure 1: Recovery from Financial Crisis (100 = First Quarter of Real GDP Contraction)

") Progress towards Strong, Sustainable and Balanced Growth Figure 1: Recovery from Financial Crisis (100 = First Quarter of Real GDP Contraction) Source: OECD May 2014 Forecast, Haver Analytics, Rogoff and

Progress towards Strong, Sustainable and Balanced Growth Figure 1: Recovery from Financial Crisis (100 = First Quarter of Real GDP Contraction) Source: OECD May 2014 Forecast, Haver Analytics, Rogoff and

New in 2013: Greater emphasis on capital flows Refinements to EBA methodology Individual country assessments

As in 212: Stock-take: multilaterally consistent assessment of external sector policies of the largest economies Feeds into Article IVs Draws on External Balance Assessment (EBA) methodology/other Identifies

As in 212: Stock-take: multilaterally consistent assessment of external sector policies of the largest economies Feeds into Article IVs Draws on External Balance Assessment (EBA) methodology/other Identifies

Chart Collection for Morning Briefing

Chart Collection for Morning Briefing November 17, 2 Dr. Edward Yardeni 16-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box 13 13 Figure

Chart Collection for Morning Briefing November 17, 2 Dr. Edward Yardeni 16-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box 13 13 Figure

Market Correlations: S&P 500

Market Correlations: S&P 500 September 25, 2017 Dr. Edward Yardeni 516-972-7683 eyardeni@ Debbie Johnson 480-664-1333 djohnson@ Mali Quintana 480-664-1333 aquintana@ Please visit our sites at www. blog.

Market Correlations: S&P 500 September 25, 2017 Dr. Edward Yardeni 516-972-7683 eyardeni@ Debbie Johnson 480-664-1333 djohnson@ Mali Quintana 480-664-1333 aquintana@ Please visit our sites at www. blog.

US Economic Indicators: Import Prices, PPI, & CPI

US Economic Indicators: Import Prices, PPI, & CPI December 1, 17 Dr. Edward Yardeni 51-97-73 eyardeni@ Debbie Johnson --1333 djohnson@ Please visit our sites at blog. thinking outside the box Table Of

US Economic Indicators: Import Prices, PPI, & CPI December 1, 17 Dr. Edward Yardeni 51-97-73 eyardeni@ Debbie Johnson --1333 djohnson@ Please visit our sites at blog. thinking outside the box Table Of

Stock Market Briefing: S&P 500 Revenues & the Economy

Stock Market Briefing: S&P Revenues & the Economy December 21, 217 Dr. Edward Yardeni 16-972-7683 eyardeni@ Joe Abbott 732-497-36 jabbott@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at

Stock Market Briefing: S&P Revenues & the Economy December 21, 217 Dr. Edward Yardeni 16-972-7683 eyardeni@ Joe Abbott 732-497-36 jabbott@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at

Actuarial Supply & Demand. By i.e. muhanna. i.e. muhanna Page 1 of

By i.e. muhanna i.e. muhanna Page 1 of 8 040506 Additional Perspectives Measuring actuarial supply and demand in terms of GDP is indeed a valid basis for setting the actuarial density of a country and

By i.e. muhanna i.e. muhanna Page 1 of 8 040506 Additional Perspectives Measuring actuarial supply and demand in terms of GDP is indeed a valid basis for setting the actuarial density of a country and

Economic Outlook. Macro Research Itaú Unibanco

Economic Outlook Macro Research Itaú Unibanco June, 2013 Agenda Economia Global Heterogeneous growth: U.S. growing faster, Europe in recession. Deceleration in the emerging economies. The Fed signals a

Economic Outlook Macro Research Itaú Unibanco June, 2013 Agenda Economia Global Heterogeneous growth: U.S. growing faster, Europe in recession. Deceleration in the emerging economies. The Fed signals a

Gold demand statistics

Gold demand statistics Table 2: Gold demand (tonnes) 2014 2015 Q2 14 Q3 14 Q4 14 Q2 15 Q3 15 Q4 15 Jewellery 2,482.0 2,397.5 589.5 591.5 686.0 596.9 513.7 623.7 663.2 481.9-19 Technology 348.5 333.8 86.6

Gold demand statistics Table 2: Gold demand (tonnes) 2014 2015 Q2 14 Q3 14 Q4 14 Q2 15 Q3 15 Q4 15 Jewellery 2,482.0 2,397.5 589.5 591.5 686.0 596.9 513.7 623.7 663.2 481.9-19 Technology 348.5 333.8 86.6

Global Construction 2030 Expo EDIFICA 2017 Santiago Chile. 4-6 October 2017

Global Construction 2030 Expo EDIFICA 2017 Santiago Chile 4-6 October 2017 Graham Robinson Global Construction Perspectives Global Construction 2030 is the fourth in a series of global studies of the construction

Global Construction 2030 Expo EDIFICA 2017 Santiago Chile 4-6 October 2017 Graham Robinson Global Construction Perspectives Global Construction 2030 is the fourth in a series of global studies of the construction

Economic Stimulus Packages and Steel: A Summary

Economic Stimulus Packages and Steel: A Summary Steel Committee Meeting 8-9 June 2009 Sources of information on stimulus packages Questionnaire to Steel Committee members, full participants and observers

Economic Stimulus Packages and Steel: A Summary Steel Committee Meeting 8-9 June 2009 Sources of information on stimulus packages Questionnaire to Steel Committee members, full participants and observers

Global Macroeconomic Outlook March 2016

Prepared by Meketa Investment Group Global Economic Outlook Projections for global growth continue to be lowered, as the economic recovery in many countries remains weak. The IMF reduced their 206 global

Prepared by Meketa Investment Group Global Economic Outlook Projections for global growth continue to be lowered, as the economic recovery in many countries remains weak. The IMF reduced their 206 global

MENA Benchmarking Report Arab-EU Business Facilitation Network

MENA Benchmarking Report Arab-EU Business Facilitation Network www.ae-network.org September 2014 Agenda Objective of the Report Macroeconomic Analysis Business Environment Index MENA Rankings 2 Objective

MENA Benchmarking Report Arab-EU Business Facilitation Network www.ae-network.org September 2014 Agenda Objective of the Report Macroeconomic Analysis Business Environment Index MENA Rankings 2 Objective

Global economic overview and the new oil price environment

IHS AUTOMOTIVE Presentation Global economic overview and the new oil price environment IHS Automotive Conference Tokyo 5 March 215 ihs.com Sara Johnson, Senior Research Director, Global Economics +1 781

IHS AUTOMOTIVE Presentation Global economic overview and the new oil price environment IHS Automotive Conference Tokyo 5 March 215 ihs.com Sara Johnson, Senior Research Director, Global Economics +1 781

Financial wealth of private households worldwide

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

Market Correlations: Trade-Weighted Dollar

Market Correlations: Trade-Weighted Dollar March 11, 218 Dr. Edward Yardeni 516-972-7683 eyardeni@ Joe Abbott 732-497-536 jabbott@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog.

Market Correlations: Trade-Weighted Dollar March 11, 218 Dr. Edward Yardeni 516-972-7683 eyardeni@ Joe Abbott 732-497-536 jabbott@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog.

Market Correlations: Expected Inflation in TIPS

Market Correlations: in TIPS April, 8 Dr. Edward Yardeni 56-97-768 eyardeni@ Joe Abbott 7-497-56 jabbott@ Mali Quintana 48-664- aquintana@ Please visit our sites at www. blog. thinking outside the box

Market Correlations: in TIPS April, 8 Dr. Edward Yardeni 56-97-768 eyardeni@ Joe Abbott 7-497-56 jabbott@ Mali Quintana 48-664- aquintana@ Please visit our sites at www. blog. thinking outside the box

SMSF Investment Seminar Sydney. 18 Oct 2010

SMSF Investment Seminar Sydney 18 Oct 2010 Important Notice This document has been prepared by Asian Masters Fund Limited (Asian Masters Fund). The material that follows is a presentation of general background

SMSF Investment Seminar Sydney 18 Oct 2010 Important Notice This document has been prepared by Asian Masters Fund Limited (Asian Masters Fund). The material that follows is a presentation of general background

Chart Collection for Morning Briefing

Chart Collection for Morning Briefing February 7, 1 Dr. Edward Yardeni 1-97-73 eyardeni@ Mali Quintana --1333 aquintana@ Please visit our sites at www. blog. thinking outside the box 3 3 Figure 1. S&P

Chart Collection for Morning Briefing February 7, 1 Dr. Edward Yardeni 1-97-73 eyardeni@ Mali Quintana --1333 aquintana@ Please visit our sites at www. blog. thinking outside the box 3 3 Figure 1. S&P

Market Briefing: S&P 500 Forward Earnings & the Economy

Market Briefing: S&P Forward Earnings & the Economy January, 18 Dr. Edward Yardeni 516-972-7683 eyardeni@ Joe Abbott 732-497-56 jabbott@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www.

Market Briefing: S&P Forward Earnings & the Economy January, 18 Dr. Edward Yardeni 516-972-7683 eyardeni@ Joe Abbott 732-497-56 jabbott@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www.

Jörg Decressin Deputy Director

World Economic Outlook October 13 Jörg Decressin Deputy Director Research Department, IMF 1 Outline Prospects for Advanced Economies Recent Developments and Implications for Emerging Economies Medium-term

World Economic Outlook October 13 Jörg Decressin Deputy Director Research Department, IMF 1 Outline Prospects for Advanced Economies Recent Developments and Implications for Emerging Economies Medium-term

Planning Global Compensation Budgets for 2018 November 2017 Update

Planning Global Compensation Budgets for 2018 November 2017 Update Planning Global Compensation Budgets for 2018 The year is rapidly coming to a close, and we are now in the midst of 2018 global compensation

Planning Global Compensation Budgets for 2018 November 2017 Update Planning Global Compensation Budgets for 2018 The year is rapidly coming to a close, and we are now in the midst of 2018 global compensation

EQUITY REPORTING & WITHHOLDING. Updated May 2016

EQUITY REPORTING & WITHHOLDING Updated May 2016 When you exercise stock options or have RSUs lapse, there may be tax implications in any country in which you worked for P&G during the period from the

EQUITY REPORTING & WITHHOLDING Updated May 2016 When you exercise stock options or have RSUs lapse, there may be tax implications in any country in which you worked for P&G during the period from the

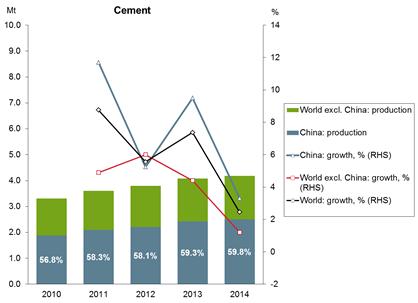

Global cement markets Current and future trends

Global cement markets Current and future trends Presented at CemTech conference Dubai, February 2015 M O R G A N S T A N L E Y R E S E A R C H Europe Morgan Stanley & Co. International plc+ Yuri Serov

Global cement markets Current and future trends Presented at CemTech conference Dubai, February 2015 M O R G A N S T A N L E Y R E S E A R C H Europe Morgan Stanley & Co. International plc+ Yuri Serov

Chart Collection for Morning Briefing

Chart Collection for Morning Briefing November 14, 217 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box 16 Figure

Chart Collection for Morning Briefing November 14, 217 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box 16 Figure

Air Passenger Forecasts

www.iata.org/pax-forecast Example report: numbers are for illustration purposes only Global report Page Table of Contents 1 Top Markets 2 Top Domestic Markets 3 Top International Country Pairs 4 Largest

www.iata.org/pax-forecast Example report: numbers are for illustration purposes only Global report Page Table of Contents 1 Top Markets 2 Top Domestic Markets 3 Top International Country Pairs 4 Largest

Market Correlations: Brent Crude Oil

Market Correlations: Brent Crude Oil March 6, 2018 Dr. Edward Yardeni 516-972-7683 eyardeni@ Debbie Johnson 480-664-1333 djohnson@ Mali Quintana 480-664-1333 aquintana@ Please visit our sites at blog.

Market Correlations: Brent Crude Oil March 6, 2018 Dr. Edward Yardeni 516-972-7683 eyardeni@ Debbie Johnson 480-664-1333 djohnson@ Mali Quintana 480-664-1333 aquintana@ Please visit our sites at blog.

Global growth weakening as some risks materialise

OECD INTERIM ECONOMIC OUTLOOK Global growth weakening as some risks materialise 6 March 2019 Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE blog: oecdecoscope.wordpress.com

OECD INTERIM ECONOMIC OUTLOOK Global growth weakening as some risks materialise 6 March 2019 Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE blog: oecdecoscope.wordpress.com

Market Briefing: Correlated Markets

Market Briefing: Correlated Markets September 25, 217 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box Table

Market Briefing: Correlated Markets September 25, 217 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box Table

EXPORT PERFORMANCE MONITOR

Export Performance Monitor Statistics department, EEPC Head Office Exports growing steadily According to the provisional data available from DGCI&S up to September 2007, Exports during September, 2007

Export Performance Monitor Statistics department, EEPC Head Office Exports growing steadily According to the provisional data available from DGCI&S up to September 2007, Exports during September, 2007

San Francisco Retiree Health Care Trust Fund Education Materials on Public Equity

M E K E T A I N V E S T M E N T G R O U P 5796 ARMADA DRIVE SUITE 110 CARLSBAD CA 92008 760 795 3450 fax 760 795 3445 www.meketagroup.com The Global Equity Opportunity Set MSCI All Country World 1 Index

M E K E T A I N V E S T M E N T G R O U P 5796 ARMADA DRIVE SUITE 110 CARLSBAD CA 92008 760 795 3450 fax 760 795 3445 www.meketagroup.com The Global Equity Opportunity Set MSCI All Country World 1 Index

COMCEC Trade OUTLOOK 2015

COMCEC Trade OUTLOOK 2015 Trade Working Group 6 th Meeting September 17, 2015 Ankara, Turkey OUTLINE Recent Trends in Trade Between the OIC Member States and the World Recent Trends in Intra-OIC Trade

COMCEC Trade OUTLOOK 2015 Trade Working Group 6 th Meeting September 17, 2015 Ankara, Turkey OUTLINE Recent Trends in Trade Between the OIC Member States and the World Recent Trends in Intra-OIC Trade

The Long View How will the global economic order change by 2050?

www.pwc.com The World in 2050 Summary report The Long View How will the global economic order change by 2050? February 2017 Emerging markets will dominate the world s top 10 economies in 2050 (GDP at PPPs)

www.pwc.com The World in 2050 Summary report The Long View How will the global economic order change by 2050? February 2017 Emerging markets will dominate the world s top 10 economies in 2050 (GDP at PPPs)

Fiscal Policy and the Global Crisis

Fiscal Policy and the Global Crisis Presentation at Koҫ University, Istanbul Carlo Cottarelli Director IMF Fiscal Affairs Department June 9, 2009 1 Two fiscal questions What is the appropriate fiscal policy

Fiscal Policy and the Global Crisis Presentation at Koҫ University, Istanbul Carlo Cottarelli Director IMF Fiscal Affairs Department June 9, 2009 1 Two fiscal questions What is the appropriate fiscal policy

Economic Outlook. Ottawa Chamber of Commerce/ Ottawa Business Journal: Mayor s Breakfast Series Ottawa, Ontario 27 April 2012.

Economic Outlook Ottawa Chamber of Commerce/ Ottawa Business Journal: Mayor s Breakfast Series Ottawa, Ontario 27 April 2012 Mark Carney Mark Carney Governor Agenda Three global forces The consequences

Economic Outlook Ottawa Chamber of Commerce/ Ottawa Business Journal: Mayor s Breakfast Series Ottawa, Ontario 27 April 2012 Mark Carney Mark Carney Governor Agenda Three global forces The consequences

STATISTICS Last update: 03/07/2017

STATISTICS 2012-2016 Last update: 03/07/2017 BU NEWS BUSINESS [USD, BILLIONS] New business by year, vs. total world exports 3,000 2,500 2,000 1,500 1,000 500 12,131 1,138 40 127 971 14,023 1,323 53 143

STATISTICS 2012-2016 Last update: 03/07/2017 BU NEWS BUSINESS [USD, BILLIONS] New business by year, vs. total world exports 3,000 2,500 2,000 1,500 1,000 500 12,131 1,138 40 127 971 14,023 1,323 53 143

Capital Flows to Emerging Markets - The Perspective from the IIF

Capital Flows to Emerging Markets - The Perspective from the IIF Felix Huefner Global Macroeconomic Analysis Department Institute of International Finance 1 st Meeting of the COMCEC Financial Cooperation

Capital Flows to Emerging Markets - The Perspective from the IIF Felix Huefner Global Macroeconomic Analysis Department Institute of International Finance 1 st Meeting of the COMCEC Financial Cooperation

Global Economic Outlook John Hawksworth Chief Economist, PwC September 2012

www.pwc.co.uk/economics Global Economic Outlook John Hawksworth Chief Economist, September 2012 Agenda Global overview Short term prospects for Europe, US and BRICs Long term trends: demographics, growth

www.pwc.co.uk/economics Global Economic Outlook John Hawksworth Chief Economist, September 2012 Agenda Global overview Short term prospects for Europe, US and BRICs Long term trends: demographics, growth

Market Correlation: Emerging Markets MSCI

Market Correlation: MSCI March 2, 218 Dr. Edward Yardeni 516-972-7683 eyardeni@ Joe Abbott 732-497-536 jabbott@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside

Market Correlation: MSCI March 2, 218 Dr. Edward Yardeni 516-972-7683 eyardeni@ Joe Abbott 732-497-536 jabbott@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside

CEOs Less Optimistic about Global Economy for 2015

Press Release Date 22 January 2014 Contact Vu Thi Thu Nguyet Tel: (04) 3946 2246, Ext. 4690; Mobile: 0947 093 998 E-mail: vu.thi.thu.nguyet@vn.pwc.com Pages 6 CEOs Less Optimistic about Global Economy

Press Release Date 22 January 2014 Contact Vu Thi Thu Nguyet Tel: (04) 3946 2246, Ext. 4690; Mobile: 0947 093 998 E-mail: vu.thi.thu.nguyet@vn.pwc.com Pages 6 CEOs Less Optimistic about Global Economy

Key Economic Challenges in Japan and Asia. Changyong Rhee IMF Asia and Pacific Department February

Key Economic Challenges in Japan and Asia Changyong Rhee IMF Asia and Pacific Department February 2017 1 Global and Asia Outlook 2 Global activity strengthening, with rising dispersion and uncertainty

Key Economic Challenges in Japan and Asia Changyong Rhee IMF Asia and Pacific Department February 2017 1 Global and Asia Outlook 2 Global activity strengthening, with rising dispersion and uncertainty

Emerging markets and mining growth

Emerging markets and mining growth Aditya Mittal CFO and member of Group Management Board Plant Tour Brazil - 24-26 March 21 Disclaimer Forward-Looking Statements This document may contain forward-looking

Emerging markets and mining growth Aditya Mittal CFO and member of Group Management Board Plant Tour Brazil - 24-26 March 21 Disclaimer Forward-Looking Statements This document may contain forward-looking

Short-term momentum: Will it be sustained?

OECD INTERIM ECONOMIC OUTLOOK Projections published:20 Sept Short-term momentum: Will it be sustained? David TURNER Project LINK Meeting, UNCTAD in Geneva Oct 3-5, 2017 www.oecd.org/economy/economicoutlook.htm

OECD INTERIM ECONOMIC OUTLOOK Projections published:20 Sept Short-term momentum: Will it be sustained? David TURNER Project LINK Meeting, UNCTAD in Geneva Oct 3-5, 2017 www.oecd.org/economy/economicoutlook.htm

EU-28 STEEL SCRAP STATISTICS. by Rolf Willeke Statistics Advisor of the BIR Ferrous Division For EFR a branch of EuRIC (30 October 2017)

") EU-28 STEEL SCRAP STATISTICS (JANUARY JUNE 2017) by Rolf Willeke Statistics Advisor of the BIR Ferrous Division For EFR a branch of EuRIC (30 October 2017) C O N T E N T S EU-28 and World Crude Steel Production

EU-28 STEEL SCRAP STATISTICS (JANUARY JUNE 2017) by Rolf Willeke Statistics Advisor of the BIR Ferrous Division For EFR a branch of EuRIC (30 October 2017) C O N T E N T S EU-28 and World Crude Steel Production

Global growth fragile: The global economy is projected to grow at 3.5% in 2019 and 3.6% in 2020, 0.2% and 0.1% below October 2018 projections.

Monday January 21st 19 1:05pm International Prepared by: Ravi Kurjah, Senior Economic Analyst (Research & Analytics) ravi.kurjah@firstcitizenstt.com World Economic Outlook: A Weakening Global Expansion

Monday January 21st 19 1:05pm International Prepared by: Ravi Kurjah, Senior Economic Analyst (Research & Analytics) ravi.kurjah@firstcitizenstt.com World Economic Outlook: A Weakening Global Expansion

HSBC Trade Connections: Trade Forecast Quarterly Update October 2011

HSBC Trade Connections: Trade Forecast Quarterly Update October 2011 New quarterly forecast exploring the future of world trade and the opportunities for international businesses World trade will grow

HSBC Trade Connections: Trade Forecast Quarterly Update October 2011 New quarterly forecast exploring the future of world trade and the opportunities for international businesses World trade will grow

Rebalancing Economic Themes and Emerging Risks for the Balance of 2016

Rebalancing Economic Themes and Emerging Risks for the Balance of 2016 Page 1 Themes Oil s Not Well A world of cheap petroleum Eastern Anxiety China attempts a difficult transition Growing Prospects Central

Rebalancing Economic Themes and Emerging Risks for the Balance of 2016 Page 1 Themes Oil s Not Well A world of cheap petroleum Eastern Anxiety China attempts a difficult transition Growing Prospects Central

Market Briefing: Gold

Market Briefing: Gold January 3, 218 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box Table Of Contents Table

Market Briefing: Gold January 3, 218 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box Table Of Contents Table

Methodology Calculating the insurance gap

Methodology Calculating the insurance gap Insurance penetration Methodology 3 Insurance Insurance Penetration Rank Rank Rank penetration penetration difference 2018 2012 change 2018 report 2012 report

Methodology Calculating the insurance gap Insurance penetration Methodology 3 Insurance Insurance Penetration Rank Rank Rank penetration penetration difference 2018 2012 change 2018 report 2012 report

Latin America: the shadow of China

Latin America: the shadow of China Juan Ruiz BBVA Research Chief Economist for South America Latin America Outlook Second Quarter Madrid, 13 May Latin America Outlook / May Key messages 1 2 3 4 5 The global

Latin America: the shadow of China Juan Ruiz BBVA Research Chief Economist for South America Latin America Outlook Second Quarter Madrid, 13 May Latin America Outlook / May Key messages 1 2 3 4 5 The global

December Nigeria's operating landscape

Nigeria's operating landscape Caveat This document has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information

Nigeria's operating landscape Caveat This document has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information

Economic Indicators. Roland Berger Institute

Economic Indicators Roland Berger Institute October 2017 Overview Key points Economic Indicators A publication, compiled by the Roland Berger Institute, that provides you with the most important macroeconomic

Economic Indicators Roland Berger Institute October 2017 Overview Key points Economic Indicators A publication, compiled by the Roland Berger Institute, that provides you with the most important macroeconomic

Global Economic Indictors: CRB Raw Industrials & Global Economy

Global Economic Indictors: & Global Economy December 14, 2017 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 480-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box

Global Economic Indictors: & Global Economy December 14, 2017 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 480-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box

Economic Outlook. EAGLEs

Economic Outlook EAGLEs Annual Report 212 Economic Analysis The group of emerging countries which compose the EAGLEs and the Nest (our watch list of countries which could eventually become an EAGLE) is

Economic Outlook EAGLEs Annual Report 212 Economic Analysis The group of emerging countries which compose the EAGLEs and the Nest (our watch list of countries which could eventually become an EAGLE) is

Market Briefing: Daily Markets Overview

Market Briefing: Daily Markets Overview September 25, 217 Dr. Edward Yardeni 516-972-7683 eyardeni@ Joe Abbott 732-497-536 jabbott@ Please visit our sites at blog. thinking outside the box Table Of Contents

Market Briefing: Daily Markets Overview September 25, 217 Dr. Edward Yardeni 516-972-7683 eyardeni@ Joe Abbott 732-497-536 jabbott@ Please visit our sites at blog. thinking outside the box Table Of Contents

These figures are to be attached to Polterovich and Popov's paper.

These figures are to be attached to Polterovich and Popov's paper. Fig. 3.1. Foreign Exchange Reserves as a % of GDP, Average Ratios for 19-99 Congo, Rep. US Mexico Russia (1993-99) India Brazil UK Pakistan

These figures are to be attached to Polterovich and Popov's paper. Fig. 3.1. Foreign Exchange Reserves as a % of GDP, Average Ratios for 19-99 Congo, Rep. US Mexico Russia (1993-99) India Brazil UK Pakistan

Note: G20 includes only the 19 member countries (excludes European Union).

.") Note: G20 includes only the 19 member countries (excludes European Union). (Per cent) Variable 2007 2008 2009 2010 2011 2012 2013 2014 2015* GDP 5.7 3.1 0.0 5.4 4.2 3.4 3.3 3.4 3.1 Trade 7.9 2.9-10.3 12.5

Note: G20 includes only the 19 member countries (excludes European Union). (Per cent) Variable 2007 2008 2009 2010 2011 2012 2013 2014 2015* GDP 5.7 3.1 0.0 5.4 4.2 3.4 3.3 3.4 3.1 Trade 7.9 2.9-10.3 12.5

Retail Banking and Wealth Management

Retail Banking and Wealth Management Results and Strategy John Flint, Chief Executive, RBWM John Greene, Chief Financial Officer, RBWM March 2013 Forward-looking statements This presentation and subsequent

Retail Banking and Wealth Management Results and Strategy John Flint, Chief Executive, RBWM John Greene, Chief Financial Officer, RBWM March 2013 Forward-looking statements This presentation and subsequent

Global investment event Winners and losers from the recent oil price rally

For client use only Global investment event Winners and losers from the recent oil price rally Since mid-2017, oil prices have been on an upward trend. Strong oil demand growth, OPECled production cuts,

For client use only Global investment event Winners and losers from the recent oil price rally Since mid-2017, oil prices have been on an upward trend. Strong oil demand growth, OPECled production cuts,

Chart Collection for Morning Briefing

Chart Collection for Morning Briefing February 12, 219 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at blog. thinking outside the box 25 Figure

Chart Collection for Morning Briefing February 12, 219 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at blog. thinking outside the box 25 Figure

2010 Results. Paris - March 2, 2011

2010 Results Paris - March 2, 2011 > Highlights of 2010 > Financial results > Strategy and outlook 2010 Results 2 2010: A Year of Acceleration Highlights of 2010 Revenue of 3,892m, up 19.1% Operating profit

2010 Results Paris - March 2, 2011 > Highlights of 2010 > Financial results > Strategy and outlook 2010 Results 2 2010: A Year of Acceleration Highlights of 2010 Revenue of 3,892m, up 19.1% Operating profit

Growth has peaked amidst escalating risks

OECD ECONOMIC OUTLOOK Growth has peaked amidst escalating risks 1 November 18 Ángel Gurría OECD Secretary-General Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE

OECD ECONOMIC OUTLOOK Growth has peaked amidst escalating risks 1 November 18 Ángel Gurría OECD Secretary-General Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE

2013 Global Survey of Accounting Assumptions. for Defined Benefit Plans. Executive Summary

2013 Global Survey of Accounting Assumptions for Defined Benefit Plans Executive Summary Executive Summary In broad terms, accounting standards aim to enable employers to approximate the cost of an employee

2013 Global Survey of Accounting Assumptions for Defined Benefit Plans Executive Summary Executive Summary In broad terms, accounting standards aim to enable employers to approximate the cost of an employee

Market Briefing: Daily Markets Overview

Market Briefing: Daily Markets Overview April 3, 18 Dr. Edward Yardeni 516-972-7683 eyardeni@ Joe Abbott 732-497-536 jabbott@ Please visit our sites at www. blog. thinking outside the box Table Of Contents

Market Briefing: Daily Markets Overview April 3, 18 Dr. Edward Yardeni 516-972-7683 eyardeni@ Joe Abbott 732-497-536 jabbott@ Please visit our sites at www. blog. thinking outside the box Table Of Contents

EDHECinfra Broad Market Index Families

EDHECinfra Broad Market Index Families Unlisted Infrastructure Equity Index Families Global Unlisted Infrastructure Equity Global Project Finance Equity Advanced Markets Unlisted Infrastructure Equity

EDHECinfra Broad Market Index Families Unlisted Infrastructure Equity Index Families Global Unlisted Infrastructure Equity Global Project Finance Equity Advanced Markets Unlisted Infrastructure Equity

Strategist s Handbook: Chart Updates

Strategist s Handbook: Chart Updates February 1, 1 Dr. Edward Yardeni 1-2- eyardeni@ Please visit our sites at www. blog. thinking outside the box Table Of Contents Table Of Contents Stock Prices 1 S&P

Strategist s Handbook: Chart Updates February 1, 1 Dr. Edward Yardeni 1-2- eyardeni@ Please visit our sites at www. blog. thinking outside the box Table Of Contents Table Of Contents Stock Prices 1 S&P

Marine. Global Programmes. cunninghamlindsey.com. A Cunningham Lindsey service

Marine Global Programmes A Cunningham Lindsey service Marine global presence Marine Global Programmes Cunningham Lindsey approach Managing your needs With 160 marine surveyors and claims managers in 36

Marine Global Programmes A Cunningham Lindsey service Marine global presence Marine Global Programmes Cunningham Lindsey approach Managing your needs With 160 marine surveyors and claims managers in 36

Vietnam. HSBC Global Connections Report. October 2013

HSBC Global Connections Report October 2013 Vietnam The pick-up in GDP growth will be modest this year, with weak domestic demand and exports still dampening industrial confidence. A stronger recovery

HSBC Global Connections Report October 2013 Vietnam The pick-up in GDP growth will be modest this year, with weak domestic demand and exports still dampening industrial confidence. A stronger recovery

Market Correlations: CRB Raw Industrials Spot Price Index

Market Correlations: Spot Price Index December 15, 2017 Dr. Edward Yardeni 516-972-7683 eyardeni@ Debbie Johnson 480-664-1333 djohnson@ Mali Quintana 480-664-1333 aquintana@ Please visit our sites at www.

Market Correlations: Spot Price Index December 15, 2017 Dr. Edward Yardeni 516-972-7683 eyardeni@ Debbie Johnson 480-664-1333 djohnson@ Mali Quintana 480-664-1333 aquintana@ Please visit our sites at www.

Market Briefing: Daily Markets Overview

Market Briefing: Daily Markets Overview ruary, 218 Dr. Edward Yardeni 16-972-7683 eyardeni@ Joe Abbott 732-497-36 jabbott@ Please visit our sites at www. blog. thinking outside the box Table Of Contents

Market Briefing: Daily Markets Overview ruary, 218 Dr. Edward Yardeni 16-972-7683 eyardeni@ Joe Abbott 732-497-36 jabbott@ Please visit our sites at www. blog. thinking outside the box Table Of Contents

2013Q3 Scissors and Similar Articles Produced by IAR Team Focus Technology Co., Ltd.

2013Q3 Scissors and Similar Articles 2013.10 Produced by IAR Team Focus Technology Co., Ltd. Contents 1. China Scissors and Similar Articles Main Original Places of Exported Goods from Jan. to June in

2013Q3 Scissors and Similar Articles 2013.10 Produced by IAR Team Focus Technology Co., Ltd. Contents 1. China Scissors and Similar Articles Main Original Places of Exported Goods from Jan. to June in

Quarterly Economic Outlook: Quarter on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War

Foregin Direct Investment (Billion USD) China U.S. Asia World Quarterly Economic Outlook: Quarter 3 2018 on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War Thai Economy: Thai

Foregin Direct Investment (Billion USD) China U.S. Asia World Quarterly Economic Outlook: Quarter 3 2018 on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War Thai Economy: Thai

The effects of the financial crisis on developing countries mapping out the issues. By Julian Jessop

The effects of the financial crisis on developing countries mapping out the issues By Julian Jessop 1. Plan of My Talk The outlook for advanced economies. Impact on developing countries. Some losers and

The effects of the financial crisis on developing countries mapping out the issues By Julian Jessop 1. Plan of My Talk The outlook for advanced economies. Impact on developing countries. Some losers and

Global Economic Outlook

Global Economic Outlook Will growth continue and at what pace? International Containerboard Conference Chicago November 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary

Global Economic Outlook Will growth continue and at what pace? International Containerboard Conference Chicago November 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary

Chart Collection for Morning Briefing

Chart Collection for Morning Briefing December 19, 216 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box 38 36

Chart Collection for Morning Briefing December 19, 216 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box 38 36

Global Consumer Confidence

Global Consumer Confidence The Conference Board Global Consumer Confidence Survey is conducted in collaboration with Nielsen 4TH QUARTER 2017 RESULTS CONTENTS Global Highlights Asia-Pacific Africa and

Global Consumer Confidence The Conference Board Global Consumer Confidence Survey is conducted in collaboration with Nielsen 4TH QUARTER 2017 RESULTS CONTENTS Global Highlights Asia-Pacific Africa and

Global Exhibition Barometer 13 th edition (July 2014)

") Global Exhibition Barometer 13 th edition A UFI report based on the results of a survey conducted in June among UFI*, SISO**, AFIDA*** & EXSA**** Members (*) Global (**) USA (***) Central & South America

Global Exhibition Barometer 13 th edition A UFI report based on the results of a survey conducted in June among UFI*, SISO**, AFIDA*** & EXSA**** Members (*) Global (**) USA (***) Central & South America

A Country Picker's Market

A Country Picker's Market February 12, 2018 by Christopher Dhanraj of ishares It s a country picker s market. The most synchronized global economy in a decade comes with an unusual counterpart: the most

A Country Picker's Market February 12, 2018 by Christopher Dhanraj of ishares It s a country picker s market. The most synchronized global economy in a decade comes with an unusual counterpart: the most

Stronger growth, but risks loom large

OECD ECONOMIC OUTLOOK Stronger growth, but risks loom large Ángel Gurría OECD Secretary-General Álvaro S. Pereira OECD Chief Economist ad interim Paris, 3 May Global growth will be around 4% Investment

OECD ECONOMIC OUTLOOK Stronger growth, but risks loom large Ángel Gurría OECD Secretary-General Álvaro S. Pereira OECD Chief Economist ad interim Paris, 3 May Global growth will be around 4% Investment

The Global Economic Crisis: Asia and the role of China Elliott School of International Affairs, George Washington University March 31, 2009

The Global Economic Crisis: Asia and the role of China Elliott School of International Affairs, George Washington University March 31, 29 Anoop Singh Asia and Pacific Department IMF 1 Five key questions

The Global Economic Crisis: Asia and the role of China Elliott School of International Affairs, George Washington University March 31, 29 Anoop Singh Asia and Pacific Department IMF 1 Five key questions

Global Economic Outlook

Global Economic Outlook Will the growth continue and at what pace? Latin American Conference São Paulo August 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary Information

Global Economic Outlook Will the growth continue and at what pace? Latin American Conference São Paulo August 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary Information

2010 Annual Results. February 10, 2011

2010 Annual Results February 10, 2011 Disclaimer This presentation contains forward-looking statements. The use of the words "aim(s)," "expect(s)," "feel(s)," "will," "may," "believe(s)," "anticipate(s)"

2010 Annual Results February 10, 2011 Disclaimer This presentation contains forward-looking statements. The use of the words "aim(s)," "expect(s)," "feel(s)," "will," "may," "believe(s)," "anticipate(s)"

Public Pension Spending Trends and Outlook in Emerging Europe. Benedict Clements Fiscal Affairs Department International Monetary Fund March 2013

Public Pension Spending Trends and Outlook in Emerging Europe Benedict Clements Fiscal Affairs Department International Monetary Fund March 13 Plan of Presentation I. Trends and drivers of public pension

Public Pension Spending Trends and Outlook in Emerging Europe Benedict Clements Fiscal Affairs Department International Monetary Fund March 13 Plan of Presentation I. Trends and drivers of public pension

Economic Indicators. Roland Berger Institute

Economic Indicators Roland Berger Institute November 2018 Overview Key points Economic Indicators A publication, compiled by the Roland Berger Institute, that provides you with the most important macroeconomic

Economic Indicators Roland Berger Institute November 2018 Overview Key points Economic Indicators A publication, compiled by the Roland Berger Institute, that provides you with the most important macroeconomic

2018 Edelman Trust Barometer

2018 Edelman Trust Barometer Snapshot Australia #TrustBarometer Trust Index A World of Distrust Average trust in institutions, general population, 2017 vs. 2018 Global Trust Index remains at distruster

2018 Edelman Trust Barometer Snapshot Australia #TrustBarometer Trust Index A World of Distrust Average trust in institutions, general population, 2017 vs. 2018 Global Trust Index remains at distruster

Boost competitiveness, attract foreign capital. Italy's Plan for new Investment

Boost competitiveness, attract foreign capital Italy's Plan for new Investment intro Economic recovery presents new opportunities to contribute to the country's growth. But investment needs fertile terrain

Boost competitiveness, attract foreign capital Italy's Plan for new Investment intro Economic recovery presents new opportunities to contribute to the country's growth. But investment needs fertile terrain

Monetary Policy under Fed Normalization and Other Challenges

Javier Guzmán Calafell, Deputy Governor, Banco de México* Santander Latin America Day London, June 28 th, 2018 */ The opinions and views expressed in this document are the sole responsibility of the author

Javier Guzmán Calafell, Deputy Governor, Banco de México* Santander Latin America Day London, June 28 th, 2018 */ The opinions and views expressed in this document are the sole responsibility of the author

OECD ECONOMIC OUTLOOK

OECD ECONOMIC OUTLOOK (A EUROPEAN AND GLOBAL PERSPECTIVE) GIC Conference, London, 3 June, 2016 Christian Kastrop Director, Economics Department Key messages 1 The global economy is stuck in a low growth

OECD ECONOMIC OUTLOOK (A EUROPEAN AND GLOBAL PERSPECTIVE) GIC Conference, London, 3 June, 2016 Christian Kastrop Director, Economics Department Key messages 1 The global economy is stuck in a low growth

Chart Collection for Morning Briefing

Chart Collection for Morning Briefing January, 17 Dr. Edward Yardeni 16-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box 16 Figure 1.

Chart Collection for Morning Briefing January, 17 Dr. Edward Yardeni 16-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box 16 Figure 1.

WORLD ECONOMIC OUTLOOK January 2018 Research Department, International Monetary Fund

WORLD ECONOMIC OUTLOOK January 2018 Research Department, International Monetary Fund Global activity has gained further momentum Global growth picked up further in 2017H2; outlook is for higher annual

WORLD ECONOMIC OUTLOOK January 2018 Research Department, International Monetary Fund Global activity has gained further momentum Global growth picked up further in 2017H2; outlook is for higher annual

Total Imports by Volume (Gallons per Country)

") 3/7/2018 Imports by Volume (Gallons per Country) YTD YTD Country 01/2017 01/2018 % Change 2017 2018 % Change MEXICO 54,235,419 58,937,856 8.7 % 54,235,419 58,937,856 8.7 % NETHERLANDS 12,265,935 10,356,183

3/7/2018 Imports by Volume (Gallons per Country) YTD YTD Country 01/2017 01/2018 % Change 2017 2018 % Change MEXICO 54,235,419 58,937,856 8.7 % 54,235,419 58,937,856 8.7 % NETHERLANDS 12,265,935 10,356,183

IMF forecasts India s GDP growth to improve from 6.7% in FY2018 to 7.4% in FY2019 : World Economic Outlook

All Members, IMF forecasts India s GDP growth to improve from 6.7% in FY2018 to 7.4% in FY2019 : World Economic Outlook International monetary fund (IMF) in its latest update on World Economic Outlook

All Members, IMF forecasts India s GDP growth to improve from 6.7% in FY2018 to 7.4% in FY2019 : World Economic Outlook International monetary fund (IMF) in its latest update on World Economic Outlook

2017 PhRMA Annual Membership Survey

2017 PhRMA Annual Membership Survey DEFINITION OF TERMS as well as developmental activities carried on Research and Development (R&D) Expenditure Definitions or supported in the pharmaceutical, biological,

2017 PhRMA Annual Membership Survey DEFINITION OF TERMS as well as developmental activities carried on Research and Development (R&D) Expenditure Definitions or supported in the pharmaceutical, biological,

26 MAY Boustead Singapore Limited / Boustead Projects Limited Joint FY2015 Financial Results Presentation

26 MAY 2015 Boustead Singapore Limited / Boustead Projects Limited Joint FY2015 Financial Results Presentation Disclaimer This presentation contains certain statements that are not statements of historical

26 MAY 2015 Boustead Singapore Limited / Boustead Projects Limited Joint FY2015 Financial Results Presentation Disclaimer This presentation contains certain statements that are not statements of historical

PhRMA Annual Membership Survey

PhRMA Annual Membership Survey DEFINITION OF TERMS Research and Development Expenditure Definitions R&D Expenditures: Expenditures within PhRMA member companies US and/or foreign research laboratories

PhRMA Annual Membership Survey DEFINITION OF TERMS Research and Development Expenditure Definitions R&D Expenditures: Expenditures within PhRMA member companies US and/or foreign research laboratories