Managing Economic Exposure And Translation Exposure. J. Gaspar: Adapted from Jeff Madura, International Financial Management

|

|

|

- Lillian Tate

- 6 years ago

- Views:

Transcription

1 Chapter 12 Managing Economic Exposure And Translation Exposure J. Gaspar: Adapted from Jeff Madura, International Financial Management 12. 1

2 Chapter Objectives To explain how an MNC s economic exposure can be managed/hedged; and To explain how an MNC s translation exposure can be managed/hedged

3 Economic Exposure Economic exposure refers to the impact exchange rate fluctuations can have on a firm s Present Value of future cash flows. Recall that corporate cash flows can be affected by exchange rate movements in ways not directly associated with foreign transactions, i.e., a purely domestic firm that faces international competition

4 Economic Exposure The economic impact of currency exchange rates on us is complex because such changes are often linked to variability in real growth, inflation, interest rates, governmental actions, and other factors. These changes, if material, can cause us to adjust our financing and operating strategies. PepsiCo 12. 4

5 Income Statement Analysis to Assess Economic Exposure MNCs can determine the impact of FX exposure by assessing the sensitivity of their cash inflows and outflows to various possible exchange rate scenarios. The MNC can then minimize its FX exposure by restructuring its operations to reduce its net exchange-rate-sensitive cash flows. Use spreadsheets to facilitate analysis

12.")

6 Base Case: Impact of Exchange Rate Movements on Earnings of Madison, Inc. (In Millions) 12. 6

7 Managing Madison Inc. s Economic Exposure Madison Inc. s Net FX Exposure: C$206 m outflow Madison s earnings before taxes is inversely related to the Canadian dollar s strength, since the higher expenses more than offset the higher revenue when the Canadian dollar strengthens. Madison may reduce its exposure by increasing Canadian sales, reducing orders of Canadian materials, and borrowing less in Canadian dollars

8 How to Minimize Economic Exposure Restructuring can reduce economic exposure by shifting the sources of costs or revenue to other locations in order to match cash inflows and outflows in foreign currencies. The new structure is then evaluated by assessing how the revised cash flows are sensitive to various possible exchange rate scenarios

12.")

9 Impact of Possible Exchange Rate Movements on Earnings: Before and After Corporate Restructuring (in Millions) 12. 9

10 Economic Exposure Based on the Original and Proposed Operating Structures

11 Crucial Issues Involved in the Restructuring Decisions Restructuring operations is a long-term solution to reducing economic exposure. It is a much more complex task than hedging any foreign currency transaction. MNCs must be very confident about the long-term potential benefits before they proceed to restructure their operations, because of the high reversal costs

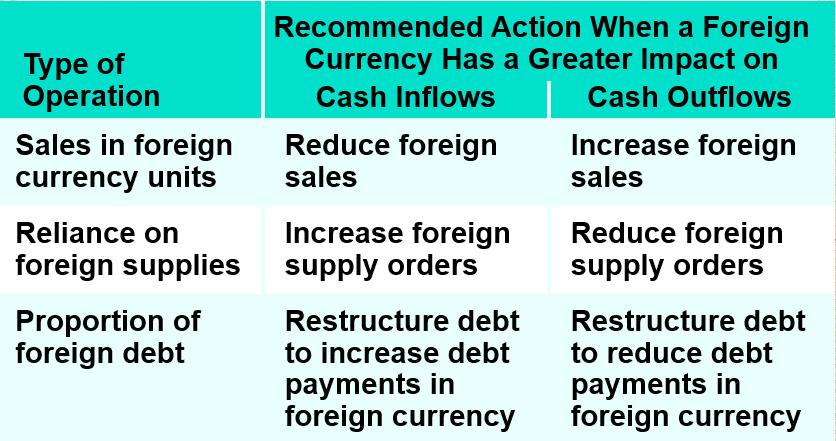

12 Strategies for Restructuring Restructuring may involve: increasing/reducing sales in new or existing foreign markets, increasing/reducing dependency on foreign suppliers, establishing/eliminating production facilities in foreign markets, and/or increasing/reducing the level of debt denominated in foreign currencies

13 12. 13

14 A Case Study in Hedging Economic Exposure Savor Co., a U.S. firm, has three independent units that conduct business in the Eurozone. It is concerned about its exposure to the euro. To determine whether it is exposed and the source of the exposure, Savor applies a series of regression analysis to its cash flows and the euro s movements

15 An Analysis of Savor Co. s Cash Flows and the Euro s Movements

16 A Case Study in Hedging Economic Exposure Assessment of Savor s Exposure: % TotalCashFlow t = a 0 + a 1 % euro t + t The slope coefficient, a 1, is found by regression analysis to be positive and statistically significant. Savor is exposed to the euro s movements

17 A Case Study in Hedging Economic Exposure Assessment of Each Unit s Exposure: % UnitCashFlow t = a 0 + a 1 % euro t + t Unit C is exposed to the euro s movements

18 A Case Study in Hedging Economic Exposure Identifying the Source of Unit C s Exposure: Savor believes that Unit C s cash flows are mainly affected by income statement items. Savor thus applies regression analysis to each income statement item, and finds a significant positive relationship between Unit C s revenue and the euro s value. Savor s economic exposure could be due to foreign competition

19 A Case Study in Hedging Economic Exposure Possible Hedging Strategies: Pricing policy Reduce prices when the euro depreciates. Hedging with forward contracts Sell euros forward to hedge against the adverse effects of a weak euro. Purchasing foreign supplies Costs will be reduced during a weak-euro period

20 A Case Study in Hedging Economic Exposure Possible Hedging Strategies: Financing with foreign funds Costs will be reduced during a weak-euro period. Revising the operations of other units So as to offset the exposure of Unit C

21 Hedging Exposure to Fixed Assets When an MNC has fixed assets (such as buildings or machinery) in a foreign country, the cash flows to be received from the sale of these assets is subject to exchange rate risk. A sale of fixed assets can be hedged by creating a liability that matches the expected value of the assets at the point in the future when they will be sold

22 Translation Exposure Translation exposure results when an MNC translates each subsidiary s financial data from its host country (operating) currency to home country (reporting) currency for consolidated financial reporting. MNCs like Coca Cola, GE, etc. deal with over a hundred operating currencies. Translation exposure does not directly affect cash flows, but some firms are concerned because of its potential impact on reported consolidated earnings

23 Translation Exposure Management A simple example of earnings and balance sheet translation Earnings Translation Management Columbus, Inc., a US-based MNC has a subsidiary in France that is forecast to have an after tax earnings of 20 million during after tax earnings: 20 million Case#1: Repatriate earnings Case of transactions exposure Case#2: Reinvest earnings in France Case of translation exposure Exchange rate Jan 1, 2015 Dec 31, 2015 rate Ave Forward Rate (sell ) quote provided on Jan 1, 2015 $1.30/ spot $1.40/ spot $1.35/ $1.50/ (Dec 31, 2015 delivery) Case#2: Reinvest 20 million earnings in France Strategy #1: No hedging of translation exposure Per FASB-52, Translation of 20 French earning to $ (reporting currency) on Dec 31, 2015 = = $27 million Earnings after translation = $27 million Strategy #2: Hedging translation exposure by selling euros forward at a stronger rate than the actual future spot rate of $1.40/ recorded on December 31, Profit from executing forward contract = Sell euros forward buy euros spot on Dec 31, 2015 = 20 million ( ) = = $2 million Earnings after translation = $27 million + $2*(1-French corporate tax rate) million Strategy #3: Hedging translation exposure by selling euros forward at a weaker rate than the actual future spot rate (say, $1.36/ instead of the recorded $1.40/ spot rate). A loss will be incurred while executing the forward contract, since euros will need to be purchased at say, $1.40/ (future spot rate on December 31, 2015) and the euro sold at a lower forward rate of $1.36/. Loss= 20 million ( ) = 20 x = -$0.8 mn Earnings after translation = $27 million (1.35x20) $0.8 million = $26.2 million Balance Sheet Translation Management Balance Sheet Translation Exposure relates to consolidation of Balance Sheet items in different currencies to reporting currency and can be managed by minimizing Net Exposed Assets Columbus Net exposed assets = Assets Liabilities (i.e., net assets exposed to change in the value of v. $, i.e. from operating currency to reporting currency). J. Gaspar 5/4/

24 Limitations of Hedging Translation Exposure Inaccurate earnings forecasts Inadequate forward contracts for some currencies Accounting distortions Translation gains/losses are based on the average exchange rate (which is unlikely to be the same as the forward rate). Translation losses are also not tax deductible

Financial Management in IB. Foreign Exchange Exposure

Financial Management in IB Foreign Exchange Exposure 1 Exchange Rate Risk Exchange rate risk can be defined as the risk that a company s performance will be negatively affected by exchange rate movements.

Financial Management in IB Foreign Exchange Exposure 1 Exchange Rate Risk Exchange rate risk can be defined as the risk that a company s performance will be negatively affected by exchange rate movements.

Slides by Yee-Tien (Ted) Fu

Fu") Chapter 14 Multinational Capital Budgeting J. Gaspar: Adapted from Jeff Madura, International Financial Management 14. 1 Slides by Yee-Tien (Ted) Fu Capital Budgeting Capital budgeting involves the allocation

Chapter 14 Multinational Capital Budgeting J. Gaspar: Adapted from Jeff Madura, International Financial Management 14. 1 Slides by Yee-Tien (Ted) Fu Capital Budgeting Capital budgeting involves the allocation

Chapter 10. Measuring Exposure to Exchange Rate Fluctuations. Lecture Outline. Relevance of Exchange Rate Risk

Chapter 10 Measuring Exposure to Exchange Rate Fluctuations Lecture Outline Relevance of Exchange Rate Risk Transaction Exposure Estimating Net Cash Flows in Each Currency Exposure of an MNC s Portfolio

Chapter 10 Measuring Exposure to Exchange Rate Fluctuations Lecture Outline Relevance of Exchange Rate Risk Transaction Exposure Estimating Net Cash Flows in Each Currency Exposure of an MNC s Portfolio

BBK3273 International Finance

BBK3273 International Finance Prepared by Dr Khairul Anuar L6: Transaction Exposure www.notes638.wordpress.com Contents 1. Transaction Exposure 2. Policies for Hedging Transaction Exposure 3. Hedging Exposure

BBK3273 International Finance Prepared by Dr Khairul Anuar L6: Transaction Exposure www.notes638.wordpress.com Contents 1. Transaction Exposure 2. Policies for Hedging Transaction Exposure 3. Hedging Exposure

Long-Term Debt Financing

18 Long-Term Debt Financing CHAPTER OBJECTIVES The specific objectives of this chapter are to: explain how an MNC uses debt financing in a manner that minimizes its exposure to exchange rate risk, explain

18 Long-Term Debt Financing CHAPTER OBJECTIVES The specific objectives of this chapter are to: explain how an MNC uses debt financing in a manner that minimizes its exposure to exchange rate risk, explain

Contract and Operating Exposure: Thinking Cash Flows

FIN 700 International Finance Managing Foreign Currency Exposure Professor Robert Hauswald Kogod School of Business, AU Contract and Operating Exposure: Thinking Cash Flows From global markets to corporate

FIN 700 International Finance Managing Foreign Currency Exposure Professor Robert Hauswald Kogod School of Business, AU Contract and Operating Exposure: Thinking Cash Flows From global markets to corporate

BBK3273 International Finance

BBK3273 International Finance Prepared by Dr Khairul Anuar L6: Transaction Exposure www.notes638.wordpress.com Contents 1. Transaction Exposure 2. Policies for Hedging Transaction Exposure 3. Hedging Exposure

BBK3273 International Finance Prepared by Dr Khairul Anuar L6: Transaction Exposure www.notes638.wordpress.com Contents 1. Transaction Exposure 2. Policies for Hedging Transaction Exposure 3. Hedging Exposure

Foreign Exchange Risk. Foreign Exchange Risk. Risks from International Investments. Foreign Exchange Transactions. Topics

Foreign Exchange Risk Topics Foreign Exchange Risk Foreign Exchange Exposure Financial Derivatives Forwards Futures Options Risks from International Investments Additional Risks Political Risk: Uncertainty

Foreign Exchange Risk Topics Foreign Exchange Risk Foreign Exchange Exposure Financial Derivatives Forwards Futures Options Risks from International Investments Additional Risks Political Risk: Uncertainty

Agenda. Learning Objectives. Chapter 19. International Business Finance. Learning Objectives Principles Used in This Chapter

Chapter 19 International Business Finance Agenda Learning Objectives Principles Used in This Chapter 1. Foreign Exchange Markets and Currency Exchange Rates 2. Interest Rate and Purchasing-Power Parity

Chapter 19 International Business Finance Agenda Learning Objectives Principles Used in This Chapter 1. Foreign Exchange Markets and Currency Exchange Rates 2. Interest Rate and Purchasing-Power Parity

Management of Economic Exposure

INTERNATIONAL FINANCIAL MANAGEMENT Seventh Edition EUN / RESNICK 9-0 Copyright 2015 by The McGraw-Hill Companies, Inc. All rights reserved. Management of Economic Exposure 9 Chapter Nine INTERNATIONAL

INTERNATIONAL FINANCIAL MANAGEMENT Seventh Edition EUN / RESNICK 9-0 Copyright 2015 by The McGraw-Hill Companies, Inc. All rights reserved. Management of Economic Exposure 9 Chapter Nine INTERNATIONAL

International Financial Markets Prices and Policies. Second Edition Richard M. Levich. Overview. ❿ Measuring Economic Exposure to FX Risk

International Financial Markets Prices and Policies Second Edition 2001 Richard M. Levich 16C Measuring and Managing the Risk in International Financial Positions Chap 16C, p. 1 Overview ❿ Measuring Economic

International Financial Markets Prices and Policies Second Edition 2001 Richard M. Levich 16C Measuring and Managing the Risk in International Financial Positions Chap 16C, p. 1 Overview ❿ Measuring Economic

Incorporating International Tax Laws Nontraditional Hedging Techniques in Multinational Capital Budgeting

Incorporating International Tax Laws Nontraditional Hedging Techniques in Multinational Capital Budgeting While traditional hedging techniques were covered in the chapter, many other techniques may be

Incorporating International Tax Laws Nontraditional Hedging Techniques in Multinational Capital Budgeting While traditional hedging techniques were covered in the chapter, many other techniques may be

Exchange rates and aviation: examining the links

-50%+ -48% to -50% -44% to -46% -40% to -42% -36% to -38% -32% to -34% -28% to -30% -24% to -26% -20% to -22% -16% to -18% -12% to -14% -8% to -10% -4% to -6% 0% to -2% 0% to 2% 4% to 6% 8% to 10% 12%

-50%+ -48% to -50% -44% to -46% -40% to -42% -36% to -38% -32% to -34% -28% to -30% -24% to -26% -20% to -22% -16% to -18% -12% to -14% -8% to -10% -4% to -6% 0% to -2% 0% to 2% 4% to 6% 8% to 10% 12%

Ch. 10 Translation Exposure. Translation Exposure. Translation Exposure

Ch. 10 Translation Exposure Topics Translation Exposure Functional Currency Translation Methods Current Rate Method Temporal Method Managing Translation Exposure Translation Exposure Translation exposure,

Ch. 10 Translation Exposure Topics Translation Exposure Functional Currency Translation Methods Current Rate Method Temporal Method Managing Translation Exposure Translation Exposure Translation exposure,

International Finance multiple-choice questions

International Finance multiple-choice questions 1. Spears Co. will receive SF1,000,000 in 30 days. Use the following information to determine the total dollar amount received (after accounting for the

International Finance multiple-choice questions 1. Spears Co. will receive SF1,000,000 in 30 days. Use the following information to determine the total dollar amount received (after accounting for the

Currency Option Combinations

APPENDIX5B Currency Option Combinations 160 In addition to the basic call and put options just discussed, a variety of currency option combinations are available to the currency speculator and hedger.

APPENDIX5B Currency Option Combinations 160 In addition to the basic call and put options just discussed, a variety of currency option combinations are available to the currency speculator and hedger.

Siemens financetraining. Area: Accounting Module: Specific Accounting Topics (SAT) Lecture: Foreign Currency Accounting Date:

Lecture: Foreign Currency Accounting Date:") Page 1 of 123 - Version from May 2014 Siemens financetraining Area: Accounting Module: Specific Accounting Topics (SAT) Lecture: Foreign Currency Accounting Date: 2017.09.25 This Lecture covers finance

Page 1 of 123 - Version from May 2014 Siemens financetraining Area: Accounting Module: Specific Accounting Topics (SAT) Lecture: Foreign Currency Accounting Date: 2017.09.25 This Lecture covers finance

Managing and Identifying Risk

Managing and Identifying Risk Fall 2013 Stephen Sapp All of life is the management of risk, not its elimination Risk is the volatility of unexpected outcomes. In the context of financial risk the volatility

Managing and Identifying Risk Fall 2013 Stephen Sapp All of life is the management of risk, not its elimination Risk is the volatility of unexpected outcomes. In the context of financial risk the volatility

Chapter 11. Managing Transaction Exposure. Lecture Outline. Hedging Payables. Hedging Receivables

Chapter 11 Managing Transaction Exposure Lecture Outline Policies for Hedging Transaction Exposure Hedging Most of the Exposure Selective Hedging Hedging Payables Forward or Futures Hedge Money Market

Chapter 11 Managing Transaction Exposure Lecture Outline Policies for Hedging Transaction Exposure Hedging Most of the Exposure Selective Hedging Hedging Payables Forward or Futures Hedge Money Market

If we determine that EE is significant, then a firm should try to manage it.

Rauli Susmel Dept. of Finance Univ. of Houston FINA 4360 International Financial Management 4/21/02 Last Lecture Managing TE - Futures/forwards - Options (with different strike prices). Typical insurance

Rauli Susmel Dept. of Finance Univ. of Houston FINA 4360 International Financial Management 4/21/02 Last Lecture Managing TE - Futures/forwards - Options (with different strike prices). Typical insurance

Note 8: Derivative Instruments

Note 8: Derivative Instruments Derivative instruments are financial contracts that derive their value from underlying changes in interest rates, foreign exchange rates or other financial or commodity prices

Note 8: Derivative Instruments Derivative instruments are financial contracts that derive their value from underlying changes in interest rates, foreign exchange rates or other financial or commodity prices

Financial Accounting Level 4 Module 7

Financial Accounting Level 4 Module 7 IMPORTANT Exchange rates can be stated in two different ways: 1. Canadian dollar equivalent method: This is when we are given how much it will cost in Canadian funds

Financial Accounting Level 4 Module 7 IMPORTANT Exchange rates can be stated in two different ways: 1. Canadian dollar equivalent method: This is when we are given how much it will cost in Canadian funds

IFRS Unaudited Financial Statements and Shareholders Report

IFRS Unaudited Financial Statements and Shareholders Report First Quarter Ended 2014 First Quarter Ended 2014 2014 UNAUDITED INTERIM FINANCIAL STATEMENTS Contents I. Balance Sheets 2 II. Income Statements

IFRS Unaudited Financial Statements and Shareholders Report First Quarter Ended 2014 First Quarter Ended 2014 2014 UNAUDITED INTERIM FINANCIAL STATEMENTS Contents I. Balance Sheets 2 II. Income Statements

CONSOLIDATED FINANCIAL STATEMENTS SIX MONTHS ENDED JUNE 30, Consolidation and Group Reporting Department

CONSOLIDATED FINANCIAL STATEMENTS SIX MONTHS ENDED JUNE 30, 2012 Consolidation and Group Reporting Department CONSOLIDATED BALANCE SHEET Notes June 30, 2012 Dec. 31, 2011 ASSETS Goodwill (3) 11,281 11,041

CONSOLIDATED FINANCIAL STATEMENTS SIX MONTHS ENDED JUNE 30, 2012 Consolidation and Group Reporting Department CONSOLIDATED BALANCE SHEET Notes June 30, 2012 Dec. 31, 2011 ASSETS Goodwill (3) 11,281 11,041

Session 13. Exchange Rate Risk

Session 13 Exchange Rate Risk Programme : Executive Diploma in Accounting, Business & Strategy (EDABS 2017) Course : Corporate Financial Management (EDABS 202) Lecturer : Mr. Asanka Ranasinghe MBA (Colombo),

Session 13 Exchange Rate Risk Programme : Executive Diploma in Accounting, Business & Strategy (EDABS 2017) Course : Corporate Financial Management (EDABS 202) Lecturer : Mr. Asanka Ranasinghe MBA (Colombo),

Chapter 9. Forecasting Exchange Rates. Lecture Outline. Why Firms Forecast Exchange Rates

Chapter 9 Forecasting Exchange Rates Lecture Outline Why Firms Forecast Exchange Rates Forecasting Techniques Technical Forecasting Fundamental Forecasting Market-Based Forecasting Mixed Forecasting Guidelines

Chapter 9 Forecasting Exchange Rates Lecture Outline Why Firms Forecast Exchange Rates Forecasting Techniques Technical Forecasting Fundamental Forecasting Market-Based Forecasting Mixed Forecasting Guidelines

10/7 Chapter 10 Measuring Exposure to FX Changes

Rauli Susmel Dept. of Finance Univ. of Houston FINA 4360 International Financial Management 10/7 Chapter 10 Measuring Exposure to FX Changes Three areas of FX exposure - Transaction exposure: associated

Rauli Susmel Dept. of Finance Univ. of Houston FINA 4360 International Financial Management 10/7 Chapter 10 Measuring Exposure to FX Changes Three areas of FX exposure - Transaction exposure: associated

Capital Budgeting in Global Markets

Capital Budgeting in Global Markets Fall 2013 Stephen Sapp Yes, our chief analyst is recommending further investments in the new year. 1 Introduction Capital budgeting is the process of determining which

Capital Budgeting in Global Markets Fall 2013 Stephen Sapp Yes, our chief analyst is recommending further investments in the new year. 1 Introduction Capital budgeting is the process of determining which

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS Kubota Corporation and Subsidiaries Years Ended March 31, 2000, 1999, and 1998 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES Basis of Financial Statements The

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS Kubota Corporation and Subsidiaries Years Ended March 31, 2000, 1999, and 1998 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES Basis of Financial Statements The

IOLKOS DEVELOPMENT ENTERTAINMENT S.A. 85 MESOGEION AVE., Athens, Greece General Commerce Reg. No SA Reg. No.

85 MESOGEION AVE., 11526 Athens, Greece General Commerce Reg. No. 59231 SA Reg. No. 57343/1/Β/4/47 TRANSLATED ABSTRACT OF ANNUAL FINANCIAL STATEMENTS 1 ST JANUARY TO 31 ST DECEMBER 217 STATEMENT OF FINANCIAL

85 MESOGEION AVE., 11526 Athens, Greece General Commerce Reg. No. 59231 SA Reg. No. 57343/1/Β/4/47 TRANSLATED ABSTRACT OF ANNUAL FINANCIAL STATEMENTS 1 ST JANUARY TO 31 ST DECEMBER 217 STATEMENT OF FINANCIAL

Communicating FX Risk Within the Firm

Communicating FX Risk Within the Firm Carolinas Cash Adventure Presentation May 21, 2018 GPS Capital Markets Wes Seeger Director FX 980-236-0069 wseeger@gpsfx.com David Pierce Director Business Development

Communicating FX Risk Within the Firm Carolinas Cash Adventure Presentation May 21, 2018 GPS Capital Markets Wes Seeger Director FX 980-236-0069 wseeger@gpsfx.com David Pierce Director Business Development

What is a multinational corporation? Why do firms expand into other countries?

What is a multinational corporation? Why do firms expand into other countries? 1. To seek new markets. Coca-Cola and McDonald s have expanded around the world to seek new markets. Likewise, Sony, Toshiba,

What is a multinational corporation? Why do firms expand into other countries? 1. To seek new markets. Coca-Cola and McDonald s have expanded around the world to seek new markets. Likewise, Sony, Toshiba,

Half year financial report

Half year financial report Six-month period ended June 30, 2016 Condensed Consolidated Financial Statements Management Report CEO Attestation Statutory Auditors Review Report Table of contents Condensed

Half year financial report Six-month period ended June 30, 2016 Condensed Consolidated Financial Statements Management Report CEO Attestation Statutory Auditors Review Report Table of contents Condensed

CHAPTER 6. FX OPERATING EXPOSURE

CHAPTER 6. FX OPERATING EXPOSURE Regardless of the scope of a firm s international operations, volatile FX rates can impact profitability and growth. How a firm measures and manages its risk exposure to

CHAPTER 6. FX OPERATING EXPOSURE Regardless of the scope of a firm s international operations, volatile FX rates can impact profitability and growth. How a firm measures and manages its risk exposure to

CONCLUSION AND RECOMMENDATIONS

CHAPTER 5 CONCLUSION AND RECOMMENDATIONS The final chapter presents the conclusion and summary of this research. Next, suggestions for further research are presented. Finally, the chapter ends with valuable

CHAPTER 5 CONCLUSION AND RECOMMENDATIONS The final chapter presents the conclusion and summary of this research. Next, suggestions for further research are presented. Finally, the chapter ends with valuable

FOREIGN EXCHANGE RESERVES

FOREIGN Management of Norges Bank s foreign exchange reserves 4 16 FEBRUARY 17 REPORT FOR FOURTH QUARTER 16 Contents Management of the foreign exchange reserves... 3 The foreign exchange reserves... 4

FOREIGN Management of Norges Bank s foreign exchange reserves 4 16 FEBRUARY 17 REPORT FOR FOURTH QUARTER 16 Contents Management of the foreign exchange reserves... 3 The foreign exchange reserves... 4

2017 Full Year Results. Tuesday 21 November 2017

2017 Full Year Results Tuesday 21 November 2017 Disclaimer Certain information included in the following presentation is forward looking and involves risks, assumptions and uncertainties that could cause

2017 Full Year Results Tuesday 21 November 2017 Disclaimer Certain information included in the following presentation is forward looking and involves risks, assumptions and uncertainties that could cause

Notes to Consolidated Financial Statements Kubota Corporation and Subsidiaries Years Ended March 31, 2002, 2001, and 2000

Notes to Consolidated Financial Statements Kubota Corporation and Subsidiaries Years Ended March 31, 2002, 2001, and 2000 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES Basis of Financial Statements The

Notes to Consolidated Financial Statements Kubota Corporation and Subsidiaries Years Ended March 31, 2002, 2001, and 2000 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES Basis of Financial Statements The

2017 FIRST QUARTER INTERIM REPORT

2017 FIRST QUARTER INTERIM REPORT INTERIM MANAGEMENT S DISCUSSION AND ANALYSIS March 31, 2017 Quarterly highlights 3 Preliminary comments to Management s discussion and analysis 4 Profile and description

2017 FIRST QUARTER INTERIM REPORT INTERIM MANAGEMENT S DISCUSSION AND ANALYSIS March 31, 2017 Quarterly highlights 3 Preliminary comments to Management s discussion and analysis 4 Profile and description

Vanguard research July 2014

The Understanding buck stops the here: hedge return : Vanguard The impact money of currency market hedging funds in foreign bonds Vanguard research July 214 Charles Thomas, CFA; Paul M. Bosse, CFA Hedging

The Understanding buck stops the here: hedge return : Vanguard The impact money of currency market hedging funds in foreign bonds Vanguard research July 214 Charles Thomas, CFA; Paul M. Bosse, CFA Hedging

gement JEFF MADURA "Fldfida'J&lantic University .,. ;. O r> Ll.l K 1 i UNIVERSnAT LIECHTENSTEIN Blbllothett SOUTH-WESTERN CENGAGE Learning- " ^ si-

f f >' ' '^11 ABRIDGED 10TH EDITION gement JEFF MADURA "Fldfida'J&lantic University Ll.l K 1 i.,. ;. O r> UNIVERSnAT LIECHTENSTEIN Blbllothett /, " ^ si- -A- SOUTH-WESTERN CENGAGE Learning- Australia Brazil

f f >' ' '^11 ABRIDGED 10TH EDITION gement JEFF MADURA "Fldfida'J&lantic University Ll.l K 1 i.,. ;. O r> UNIVERSnAT LIECHTENSTEIN Blbllothett /, " ^ si- -A- SOUTH-WESTERN CENGAGE Learning- Australia Brazil

Consolidated financial statements. December 31, 2018

Consolidated financial statements December 31, 2018 Table of contents 1.Consolidated statement of income... 2 2. Consolidated statement of cash flows... 4 3. Consolidated balance sheet... 5 4. Consolidated

Consolidated financial statements December 31, 2018 Table of contents 1.Consolidated statement of income... 2 2. Consolidated statement of cash flows... 4 3. Consolidated balance sheet... 5 4. Consolidated

Half-year report January 1 June

Half-year report January 1 June 30 2012 Result consistent with AP s long-term objectives The Second AP Fund posted a total return of 5.8 percent, excluding costs. Relative to benchmark index, return was

Half-year report January 1 June 30 2012 Result consistent with AP s long-term objectives The Second AP Fund posted a total return of 5.8 percent, excluding costs. Relative to benchmark index, return was

CONSOLIDATED FINANCIAL STATEMENTS DECEMBER 31, Direction de la CONSOLIDATION REPORTING GROUPE

CONSOLIDATED FINANCIAL STATEMENTS DECEMBER 31, 2010 Direction de la CONSOLIDATION REPORTING GROUPE CONSOLIDATED BALANCE SHEET Notes Dec. 31, 2010 Dec. 31, 2009 ASSETS Goodwill (3) 11,030 10,740 Other intangible

CONSOLIDATED FINANCIAL STATEMENTS DECEMBER 31, 2010 Direction de la CONSOLIDATION REPORTING GROUPE CONSOLIDATED BALANCE SHEET Notes Dec. 31, 2010 Dec. 31, 2009 ASSETS Goodwill (3) 11,030 10,740 Other intangible

ACCOUNTING FOR FOREIGN CURRENCY

ACCOUNTING FOR FOREIGN CURRENCY FOREIGN EXCHANGE MARKETS Each country uses its own currency as the unit of value for the purchase and sale of goods and services. The currency used in the United States

ACCOUNTING FOR FOREIGN CURRENCY FOREIGN EXCHANGE MARKETS Each country uses its own currency as the unit of value for the purchase and sale of goods and services. The currency used in the United States

RIBER S.A. GROUP. 31 rue Casimir Perier BEZONS, FRANCE R.C.S. Pontoise

RIBER S.A. GROUP 31 rue Casimir Perier 95 873 BEZONS, FRANCE R.C.S. Pontoise 343 006 151 CONSOLIDATED FINANCIAL STATEMENTS AT DECEMBER 31, 2007 Page 2 of 24 CONTENTS Pages CONSOLIDATED BALANCE SHEET 3-4

RIBER S.A. GROUP 31 rue Casimir Perier 95 873 BEZONS, FRANCE R.C.S. Pontoise 343 006 151 CONSOLIDATED FINANCIAL STATEMENTS AT DECEMBER 31, 2007 Page 2 of 24 CONTENTS Pages CONSOLIDATED BALANCE SHEET 3-4

COPYRIGHTED MATERIAL U.S. ACCOUNTING REQUIREMENTS HIGHLIGHTS FASB 52: REQUIREMENTS OVERVIEW

HIGHLIGHTS 1 U.S. ACCOUNTING REQUIREMENTS FASB 52 Requirements Overview FASB 52 Currency Exchange Rates FASB 52 Currency Translation Organizational Impacts FASB 52: REQUIREMENTS OVERVIEW The Financial

HIGHLIGHTS 1 U.S. ACCOUNTING REQUIREMENTS FASB 52 Requirements Overview FASB 52 Currency Exchange Rates FASB 52 Currency Translation Organizational Impacts FASB 52: REQUIREMENTS OVERVIEW The Financial

Aflac Incorporated Announces Third Quarter Results, Upwardly Revises 2016 Operating EPS Outlook, Increases Fourth Quarter Cash Dividend 4.

News Release FOR IMMEDIATE RELEASE Aflac Incorporated Announces Third Quarter Results, Upwardly Revises 2016 Operating EPS Outlook, Increases Fourth Quarter Cash Dividend 4.9% COLUMBUS, Ga. October 27,

News Release FOR IMMEDIATE RELEASE Aflac Incorporated Announces Third Quarter Results, Upwardly Revises 2016 Operating EPS Outlook, Increases Fourth Quarter Cash Dividend 4.9% COLUMBUS, Ga. October 27,

CONSOLIDATED FINANCIAL STATEMENTS. Year ended 31 December 2016

CONSOLIDATED FINANCIAL STATEMENTS Year ended 31 December 2016 CONTENTS CONSOLIDATED FINANCIAL STATEMENTS 4 PROFIT AND LOSS ACCOUNT FOR THE YEAR ENDED 31 DECEMBER 2016 4 STATEMENT OF NET INCOME AND CHANGES

CONSOLIDATED FINANCIAL STATEMENTS Year ended 31 December 2016 CONTENTS CONSOLIDATED FINANCIAL STATEMENTS 4 PROFIT AND LOSS ACCOUNT FOR THE YEAR ENDED 31 DECEMBER 2016 4 STATEMENT OF NET INCOME AND CHANGES

Investing in a Portfolio of Currencies

APPENDIX 21 Investing in a Portfolio of Currencies Large fi nancial corporations may consider investing in a portfolio of currencies, as illustrated in the following example. Assume that MacFarland Co.,

APPENDIX 21 Investing in a Portfolio of Currencies Large fi nancial corporations may consider investing in a portfolio of currencies, as illustrated in the following example. Assume that MacFarland Co.,

Consolidated Statement of Profit or Loss (in million Euro)

") Consolidated Statement of Profit or Loss (in million Euro) Q3 2015 Q3 2016 % change 9m 2015 9m 2016 % change Revenue 661 625-5.4% 1,974 1,873-5.1% Cost of sales (453) (415) -8.4% (1,340) (1,239) -7.5%

Consolidated Statement of Profit or Loss (in million Euro) Q3 2015 Q3 2016 % change 9m 2015 9m 2016 % change Revenue 661 625-5.4% 1,974 1,873-5.1% Cost of sales (453) (415) -8.4% (1,340) (1,239) -7.5%

Consolidated Statement of Profit or Loss (in million Euro)

") Consolidated Statement of Profit or Loss (in million Euro) Q1 2016 Q1 2017 % change Revenue 603 588-2.5% Cost of sales (408) (396) -2.9% Gross profit 195 192-1.5% Selling expenses (84) (86) 2.4% Research

Consolidated Statement of Profit or Loss (in million Euro) Q1 2016 Q1 2017 % change Revenue 603 588-2.5% Cost of sales (408) (396) -2.9% Gross profit 195 192-1.5% Selling expenses (84) (86) 2.4% Research

Total assets 22,581 21,030 $186,107

Non-Consolidated Balance Sheets As of December 31,2017 and 2016 Thousands of U.S.Dollars Millions of Yen (1US$=\113.00) Assets 2016 2017 2017 Current assets: Cash on hand and in banks 826 1,395 $12,348

Non-Consolidated Balance Sheets As of December 31,2017 and 2016 Thousands of U.S.Dollars Millions of Yen (1US$=\113.00) Assets 2016 2017 2017 Current assets: Cash on hand and in banks 826 1,395 $12,348

Management Consulting Group PLC Half-year report 2016

provides professional services across a wide range of industries and sectors. Strategic report 01 Highlights 02 Chairman s statement 03 Operating and financial review Financials 08 Directors responsibility

provides professional services across a wide range of industries and sectors. Strategic report 01 Highlights 02 Chairman s statement 03 Operating and financial review Financials 08 Directors responsibility

17: Multinational Cost of Capital and Capital Structure

7: Multinational Cost of Capital and Capital Structure An MC finances its operations by using a capital structure (proportion of debt versus equity financing) that can minimize its cost of capital. By

7: Multinational Cost of Capital and Capital Structure An MC finances its operations by using a capital structure (proportion of debt versus equity financing) that can minimize its cost of capital. By

Comprehensive Project

APPENDIX A Comprehensive Project One of the best ways to gain a clear understanding of the key concepts explained in this text is to apply them directly to actual situations. This comprehensive project

APPENDIX A Comprehensive Project One of the best ways to gain a clear understanding of the key concepts explained in this text is to apply them directly to actual situations. This comprehensive project

ETFS Physical US Dollar ETF. ASX code: ZUSD

ETFS Physical US Dollar ETF ASX code: ZUSD The intelligent alternative The Exchange Traded Fund with real currency The intelligent alternative What is ETFS Physical US Dollar ETF? At a glance Benchmark

ETFS Physical US Dollar ETF ASX code: ZUSD The intelligent alternative The Exchange Traded Fund with real currency The intelligent alternative What is ETFS Physical US Dollar ETF? At a glance Benchmark

CIFFA: Managing FX Risks MAY 2016

CIFFA: Managing FX Risks MAY 2016 Today s Objectives 2 Discuss the recent volatility of currency, and what makes the future value of currency so difficult to predict Assess FX risk to freight forwarders

CIFFA: Managing FX Risks MAY 2016 Today s Objectives 2 Discuss the recent volatility of currency, and what makes the future value of currency so difficult to predict Assess FX risk to freight forwarders

Best Practices for Foreign Exchange Risk Management in Volatile and Uncertain Times

erspective P Insights for America s Business Leaders Best Practices for Foreign Exchange Risk Management in Volatile and Uncertain Times Framing the Challenge The appeal of international trade among U.S.

erspective P Insights for America s Business Leaders Best Practices for Foreign Exchange Risk Management in Volatile and Uncertain Times Framing the Challenge The appeal of international trade among U.S.

PRESENTATION CURRENCY AND FUNCTIONAL CURRENCY CHAPTER 15 MULTINATIONAL OPERATIONS CHANGES IN EXCHANGE RATES IMPACT ON SALES: EXAMPLE 1

Presenter s name Presenter s title dd Month yyyy CHAPTER 15 MULTINATIONAL OPERATIONS PRESENTATION CURRENCY AND FUNCTIONAL CURRENCY Presentation currency: In which the company presents its financial statements.

Presenter s name Presenter s title dd Month yyyy CHAPTER 15 MULTINATIONAL OPERATIONS PRESENTATION CURRENCY AND FUNCTIONAL CURRENCY Presentation currency: In which the company presents its financial statements.

(Registration no C) (Registration no C) Financial Results. (unaudited) 11 November 2009

(Registration no C) Financial Results. (unaudited) 11 November 2009") 3 rd Quarter and 9-Month 9 2009 Financial Results (unaudited) 11 November 2009 1 Important note on forward looking statements The presentation herein may contain forward looking statements by the management

3 rd Quarter and 9-Month 9 2009 Financial Results (unaudited) 11 November 2009 1 Important note on forward looking statements The presentation herein may contain forward looking statements by the management

FIN 683 Financial Institutions Management Hedging with Derivatives

FIN 683 Financial Institutions Management Hedging with Derivatives Professor Robert B.H. Hauswald Kogod School of Business, AU Futures and Forwards Third largest group of interest rate derivatives in terms

FIN 683 Financial Institutions Management Hedging with Derivatives Professor Robert B.H. Hauswald Kogod School of Business, AU Futures and Forwards Third largest group of interest rate derivatives in terms

Product Key Facts Franklin Templeton Asia Fund Series Templeton Select Global Equity Fund Last updated: April 2018

Product Key Facts Franklin Templeton Asia Fund Series Templeton Select Global Equity Fund Last updated: April 2018 This statement provides you with key information about this product. This statement is

Product Key Facts Franklin Templeton Asia Fund Series Templeton Select Global Equity Fund Last updated: April 2018 This statement provides you with key information about this product. This statement is

Audited Financial Statements (per IFRS) Year Ended December 31, 2014

Year Ended December 31, 2014") Audited Financial Statements (per IFRS) Contents I. Balance Sheets 3 II. Income Statements 4 III. Statements of Comprehensive Income 5 IV. Cash Flow Statements 6 V. Statements of Changes in Equity 7 VI.

Audited Financial Statements (per IFRS) Contents I. Balance Sheets 3 II. Income Statements 4 III. Statements of Comprehensive Income 5 IV. Cash Flow Statements 6 V. Statements of Changes in Equity 7 VI.

CONSOLIDATED FINANCIAL STATEMENTS SIX MONTHS ENDED JUNE 30, 2006 GROUP CONSOLIDATION AND REPORTING DEPARTMENT

CONSOLIDATED FINANCIAL STATEMENTS SIX MONTHS ENDED JUNE 30, 2006 GROUP CONSOLIDATION AND REPORTING DEPARTMENT This English-language version of this document is a free translation of the original French

CONSOLIDATED FINANCIAL STATEMENTS SIX MONTHS ENDED JUNE 30, 2006 GROUP CONSOLIDATION AND REPORTING DEPARTMENT This English-language version of this document is a free translation of the original French

Ch. 9 Transaction Exposure. FX Exposure. FX Exposure

Ch. 9 Transaction Exposure Topics Foreign Exchange Exposure Transaction Exposure Techniques to Eliminate Transaction Exposure Limitations of Hedging FX Exposure Foreign Exchange Exposure: Measure of the

Ch. 9 Transaction Exposure Topics Foreign Exchange Exposure Transaction Exposure Techniques to Eliminate Transaction Exposure Limitations of Hedging FX Exposure Foreign Exchange Exposure: Measure of the

Use the following to answer questions 19-20: Scenario: Exchange Rates The value of a euro goes from US$1.25 to US$1.50.

Name: Date: 1. Open-economy macroeconomics is the branch of economics that deals with: A) reducing regulations on business. B) the relationships between economies of different nations. C) reducing employment

Name: Date: 1. Open-economy macroeconomics is the branch of economics that deals with: A) reducing regulations on business. B) the relationships between economies of different nations. C) reducing employment

CONSOLIDATED FINANCIAL STATEMENTS SIX MONTHS ENDED JUNE 30, 2008 GROUP CONSOLIDATION AND REPORTING

CONSOLIDATED FINANCIAL STATEMENTS SIX MONTHS ENDED JUNE 30, 2008 GROUP CONSOLIDATION AND REPORTING CONSOLIDATED BALANCE SHEET in millions Notes June 30, 2008 Dec. 31, 2007 ASSETS Goodwill (3) 10,778 9,240

CONSOLIDATED FINANCIAL STATEMENTS SIX MONTHS ENDED JUNE 30, 2008 GROUP CONSOLIDATION AND REPORTING CONSOLIDATED BALANCE SHEET in millions Notes June 30, 2008 Dec. 31, 2007 ASSETS Goodwill (3) 10,778 9,240

2018 THIRD QUARTER INTERIM REPORT

2018 THIRD QUARTER INTERIM REPORT INTERIM MANAGEMENT S DISCUSSION AND ANALYSIS September 30, 2018 Quarterly highlights 3 Preliminary comments to Management s discussion and analysis 4 Profile and description

2018 THIRD QUARTER INTERIM REPORT INTERIM MANAGEMENT S DISCUSSION AND ANALYSIS September 30, 2018 Quarterly highlights 3 Preliminary comments to Management s discussion and analysis 4 Profile and description

CHAPTER 8 MANAGEMENT OF TRANSACTION EXPOSURE ANSWERS & SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS

CHAPTER 8 MANAGEMENT OF TRANSACTION EXPOSURE ANSWERS & SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. How would you define transaction exposure? How is it different from economic exposure?

CHAPTER 8 MANAGEMENT OF TRANSACTION EXPOSURE ANSWERS & SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. How would you define transaction exposure? How is it different from economic exposure?

From CapEx to Cash Capital Markets Day Merkers - November 12th, 2015

K+S Aktiengesellschaft From CapEx to Cash Capital Markets Day Merkers - November 12th, 2015 Dr. Burkhard Lohr, CFO From Capex to Cash Capex Phase Cash Phase 2020 Net debt: 2.2 billion 1) Leverage: 2.1x

K+S Aktiengesellschaft From CapEx to Cash Capital Markets Day Merkers - November 12th, 2015 Dr. Burkhard Lohr, CFO From Capex to Cash Capex Phase Cash Phase 2020 Net debt: 2.2 billion 1) Leverage: 2.1x

Note 10: Derivative Instruments

Note 10: Derivative Instruments Derivative instruments are financial that derive their value from underlying changes in interest rates, foreign exchange rates or other financial or commodity prices or

Note 10: Derivative Instruments Derivative instruments are financial that derive their value from underlying changes in interest rates, foreign exchange rates or other financial or commodity prices or

Foreign Exchange Hedging Strategies at General Motors: Transactional and Translational Exposures

Foreign Exchange Hedging Strategies at General Motors: Transactional and Translational Exposures Prepared By: Danial Wahaj Khan EXECUTIVE SUMMARY: This report is based on a practical scenario solution

Foreign Exchange Hedging Strategies at General Motors: Transactional and Translational Exposures Prepared By: Danial Wahaj Khan EXECUTIVE SUMMARY: This report is based on a practical scenario solution

2016 Financial Performance Review

2016 Financial Performance Review This section provides a review of our enterprise financial performance for 2016 that focuses on the Consolidated Statement of Income included in our consolidated financial

2016 Financial Performance Review This section provides a review of our enterprise financial performance for 2016 that focuses on the Consolidated Statement of Income included in our consolidated financial

2018 FIRST QUARTER INTERIM REPORT

2018 FIRST QUARTER INTERIM REPORT INTERIM MANAGEMENT S DISCUSSION AND ANALYSIS March 31, 2018 Quarterly highlights 3 Preliminary comments to Management s discussion and analysis 4 Profile and description

2018 FIRST QUARTER INTERIM REPORT INTERIM MANAGEMENT S DISCUSSION AND ANALYSIS March 31, 2018 Quarterly highlights 3 Preliminary comments to Management s discussion and analysis 4 Profile and description

J. Gaspar: Adapted from Jeff Madura, International Financial Management. Slides by Yee-Tien (Ted) Fu

Fu") Chapter15 Multinational Restructuring J. Gaspar: Adapted from Jeff Madura, International Financial Management 15. 1 Slides by Yee-Tien (Ted) Fu Corporate Restructuring The business environment in most

Chapter15 Multinational Restructuring J. Gaspar: Adapted from Jeff Madura, International Financial Management 15. 1 Slides by Yee-Tien (Ted) Fu Corporate Restructuring The business environment in most

A Basket Currency for the EAC: Possible Advantages and Issues

A Basket Currency for the EAC: Possible Advantages and Issues By Paul R. Masson, Monetary Union Advisor, Rwanda, funded by TradeMark East Africa September 24, 2012 I. Introduction Creating a monetary union

A Basket Currency for the EAC: Possible Advantages and Issues By Paul R. Masson, Monetary Union Advisor, Rwanda, funded by TradeMark East Africa September 24, 2012 I. Introduction Creating a monetary union

Financial Review. Selected Financial Data 19. Consolidated Balance Sheets 29. Consolidated Statements of Shareholders Equity 30

Financial Review Selected Financial Data 19 Management s Discussion and Analysis 20 Consolidated Statements of Operations 28 Consolidated Balance Sheets 29 Consolidated Statements of Shareholders Equity

Financial Review Selected Financial Data 19 Management s Discussion and Analysis 20 Consolidated Statements of Operations 28 Consolidated Balance Sheets 29 Consolidated Statements of Shareholders Equity

EURO RESSOURCES S.A AUDITED FINANCIAL STATEMENTS. Contents

IFRS Financial Statements and Shareholders Report Fiscal Year Ended 2013 EURO RESSOURCES S.A. 2013 AUDITED FINANCIAL STATEMENTS Contents I. Balance Sheets 1 II. Income Statements 2 III. Statements of Comprehensive

IFRS Financial Statements and Shareholders Report Fiscal Year Ended 2013 EURO RESSOURCES S.A. 2013 AUDITED FINANCIAL STATEMENTS Contents I. Balance Sheets 1 II. Income Statements 2 III. Statements of Comprehensive

AFLAC INCORPORATED ANNOUNCES FIRST QUARTER RESULTS, DECLARES SECOND QUARTER CASH DIVIDEND

News Release FOR IMMEDIATE RELEASE AFLAC INCORPORATED ANNOUNCES FIRST QUARTER RESULTS, DECLARES SECOND QUARTER CASH DIVIDEND COLUMBUS, Georgia April 27, 2010 Aflac Incorporated today reported its first

News Release FOR IMMEDIATE RELEASE AFLAC INCORPORATED ANNOUNCES FIRST QUARTER RESULTS, DECLARES SECOND QUARTER CASH DIVIDEND COLUMBUS, Georgia April 27, 2010 Aflac Incorporated today reported its first

CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED FINANCIAL STATEMENTS 66 Consolidated Statement of Comprehensive Income 67 Consolidated Balance Sheet 68 Consolidated Statement of Changes in Equity 69 Consolidated Statement of Cash Flows

CONSOLIDATED FINANCIAL STATEMENTS 66 Consolidated Statement of Comprehensive Income 67 Consolidated Balance Sheet 68 Consolidated Statement of Changes in Equity 69 Consolidated Statement of Cash Flows

Types of Exposure. Forward Market Hedge. Transaction Exposure. Forward Market Hedge. Forward Market Hedge: an Example INTERNATIONAL FINANCE.

Types of Exposure INTERNATIONAL FINANCE Chapter 8 Transaction exposure sensitivity of realized domestic currency values of the firm s contractual cash flows denominated in foreign currencies to unexpected

Types of Exposure INTERNATIONAL FINANCE Chapter 8 Transaction exposure sensitivity of realized domestic currency values of the firm s contractual cash flows denominated in foreign currencies to unexpected

Report on IFAD s investment portfolio for 2015

Document: EB 2016/117/R.22 Agenda: 17 Date: 9 March 2016 Distribution: Public Original: English E Report on IFAD s investment for 2015 Note to Executive Board representatives Focal points: Technical questions:

Document: EB 2016/117/R.22 Agenda: 17 Date: 9 March 2016 Distribution: Public Original: English E Report on IFAD s investment for 2015 Note to Executive Board representatives Focal points: Technical questions:

Mississippi Prepaid Affordable College Tuition Program

Auditor s Reports and Financial Statements Contents Independent Auditor s Report... 1 Financial Statements Statement of Net Position...3 Statement of Revenues, Expenses and Changes in Net Position...4

Auditor s Reports and Financial Statements Contents Independent Auditor s Report... 1 Financial Statements Statement of Net Position...3 Statement of Revenues, Expenses and Changes in Net Position...4

Global Economic Outlook Brittle Strength

Global Economic Outlook Brittle Strength RISI North American Conference October 2017 Lasse Sinikallas Director Macroeconomics Agenda 1. Global Snapshot Steady 2. North America Performing 3. China In Transition

Global Economic Outlook Brittle Strength RISI North American Conference October 2017 Lasse Sinikallas Director Macroeconomics Agenda 1. Global Snapshot Steady 2. North America Performing 3. China In Transition

E Consolidated Financial Statements

E Consolidated Financial Statements 1. Significant accounting policies 204 2. Accounting estimates and assessments 214 3. Consolidated Group 215 4. Revenue 216 5. Functional costs 217 6. Other operating

E Consolidated Financial Statements 1. Significant accounting policies 204 2. Accounting estimates and assessments 214 3. Consolidated Group 215 4. Revenue 216 5. Functional costs 217 6. Other operating

Chapter 14. Multinational Capital Budgeting. Lecture Outline

Chapter 14 Multinational Capital Budgeting Lecture Outline Subsidiary versus Parent Perspective Tax Differentials Restrictions on Remitted Earnings Exchange Rate Movements Input for Multinational Capital

Chapter 14 Multinational Capital Budgeting Lecture Outline Subsidiary versus Parent Perspective Tax Differentials Restrictions on Remitted Earnings Exchange Rate Movements Input for Multinational Capital

32. Management of financial risks

298 F CONSOLIDATED FINANCIAL STATEMENTS NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 32. Management of financial risks General information on financial risks As a result of its businesses and the global

298 F CONSOLIDATED FINANCIAL STATEMENTS NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 32. Management of financial risks General information on financial risks As a result of its businesses and the global

Belimo Annual Report 2016

Financial Report Consolidated 44 Notes to the Consolidated 48 of BELIMO Holding AG 83 Information for Investors 92 Five-Year Summary 94 43 Consolidated Consolidated Income Statement in CHF 1 000 Note 2016

Financial Report Consolidated 44 Notes to the Consolidated 48 of BELIMO Holding AG 83 Information for Investors 92 Five-Year Summary 94 43 Consolidated Consolidated Income Statement in CHF 1 000 Note 2016

Consolidated Financial Statements. Prince Rupert Port Authority. December 31, 2017

Consolidated Financial Statements Prince Rupert Port Authority December 31, 2017 Contents Page Independent Auditor s Report 1-2 Consolidated Statement of Financial Position 3 Consolidated Statement of

Consolidated Financial Statements Prince Rupert Port Authority December 31, 2017 Contents Page Independent Auditor s Report 1-2 Consolidated Statement of Financial Position 3 Consolidated Statement of

CONSOLIDATED FINANCIAL STATEMENTS. Year ended 31 December 2017

CONSOLIDATED FINANCIAL STATEMENTS Year ended 31 December 2017 CONTENTS CONSOLIDATED FINANCIAL STATEMENTS 4 PROFIT AND LOSS ACCOUNT FOR THE YEAR ENDED 31 DECEMBER 2017 4 STATEMENT OF NET INCOME AND CHANGES

CONSOLIDATED FINANCIAL STATEMENTS Year ended 31 December 2017 CONTENTS CONSOLIDATED FINANCIAL STATEMENTS 4 PROFIT AND LOSS ACCOUNT FOR THE YEAR ENDED 31 DECEMBER 2017 4 STATEMENT OF NET INCOME AND CHANGES

Report on the first half of fiscal 2009

Report on the first half of fiscal 2009 Table of Contents 3 Letter to the Shareholders 4 Management Report 8 Interim Financial Statement 9 Consolidated income statement for the period 01.01.2009 30.06.2009

Report on the first half of fiscal 2009 Table of Contents 3 Letter to the Shareholders 4 Management Report 8 Interim Financial Statement 9 Consolidated income statement for the period 01.01.2009 30.06.2009

Financial Section. Selected Financial Data 26. Consolidated Balance Sheets 28. Consolidated Statements of Income 30

Financial Section Management s Discussion and Analysis of Fiscal Results 22 Selected Financial Data 26 Consolidated Balance Sheets 28 Consolidated Statements of Income 30 Consolidated Statements of Shareholders

Financial Section Management s Discussion and Analysis of Fiscal Results 22 Selected Financial Data 26 Consolidated Balance Sheets 28 Consolidated Statements of Income 30 Consolidated Statements of Shareholders

Investors/Analysts Conference London/New York, February 2010 Ian Bishop

Investors/Analysts Conference London/New York, February 2010 Ian Bishop This presentation contains certain forward-looking statements. These forward-looking statements may be identified by words such as

Investors/Analysts Conference London/New York, February 2010 Ian Bishop This presentation contains certain forward-looking statements. These forward-looking statements may be identified by words such as

Notes to the Group Financial Statements

Notes to the Group Financial Statements 1. Exchange rates The results of operations have been translated into US dollars at the average rates of exchange for the year. In the case of sterling, the translation

Notes to the Group Financial Statements 1. Exchange rates The results of operations have been translated into US dollars at the average rates of exchange for the year. In the case of sterling, the translation

Consolidated Financial Statements. Prince Rupert Port Authority. December 31, 2016

Consolidated Financial Statements Prince Rupert Port Authority December 31, 2016 Contents Page Independent Auditor s Report 1-2 Consolidated Statement of Financial Position 3 Consolidated Statement of

Consolidated Financial Statements Prince Rupert Port Authority December 31, 2016 Contents Page Independent Auditor s Report 1-2 Consolidated Statement of Financial Position 3 Consolidated Statement of

4: Exchange Rate Determination

4: Exchange Rate Determination Financial managers of MNCs that conduct international business must continuously monitor exchange rates because their cash flows are highly dependent on them. They need to

4: Exchange Rate Determination Financial managers of MNCs that conduct international business must continuously monitor exchange rates because their cash flows are highly dependent on them. They need to

E) 39. FINANCIAL INSTRUMENTS AND FINANCIAL RISK MANAGEMENT

39. FINANCIAL INSTRUMENTS AND FINANCIAL RISK MANAGEMENT") E) 39. FINANCIAL INSTRUMENTS AND FINANCIAL RISK MANAGEMENT Financial instruments The following table shows a comparison between the book value of the Group's financial instruments and their fair value.

E) 39. FINANCIAL INSTRUMENTS AND FINANCIAL RISK MANAGEMENT Financial instruments The following table shows a comparison between the book value of the Group's financial instruments and their fair value.

Financial review Refresco Financial review 2017

Financial review 2017 Financial review 2017 Financial review 2017 1 69 Consolidated income statement For the year ended December 31, 2017 (x 1 million euro) Note December 31, 2017 December 31, 2016 Revenue

Financial review 2017 Financial review 2017 Financial review 2017 1 69 Consolidated income statement For the year ended December 31, 2017 (x 1 million euro) Note December 31, 2017 December 31, 2016 Revenue

Management of Transaction Exposure

INTERNATIONAL FINANCIAL MANAGEMENT Seventh Edition EUN / RESNICK Management of Transaction Exposure 8 Chapter Eight INTERNATIONAL Chapter Objective: FINANCIAL MANAGEMENT This chapter discusses various

INTERNATIONAL FINANCIAL MANAGEMENT Seventh Edition EUN / RESNICK Management of Transaction Exposure 8 Chapter Eight INTERNATIONAL Chapter Objective: FINANCIAL MANAGEMENT This chapter discusses various