Ross School of Business at the University of Michigan Independent Study Project Report

|

|

|

- Percival Snow

- 5 years ago

- Views:

Transcription

1 Ross School of Business at the University of Michigan Independent Study Project Report TERM : Spring 1998 COURSE : CS 750 PROFESSOR : Gunter Dufey STUDENT : Nagendra Palle TITLE : Estimating cost of capital for emerging market equity investment

2 By Nagendra Palle A research paper submitted in fulfillment of the requirements for three credits, GRADUATE INDEPENDENT RESEARCH PROJECT Spring Term 1998, Professor Gunter Dufev, Faculty Supervisor

3 Executive Summary In recent years, emerging markets have become very important for investment banks and multinational corporations (MNCs). The attractions to these markets have been to take advantage of diversification opportunities and high growth. Multinationals have an additional benefit from an opportunity to vertically integrate in segments where there are high labour costs. However, emerging markets have also been perceived as risky and uncertain. Investments in these markets are extremely difficult to evaluate. The difficulties arise due to several factors: political, economic and business volatility, among others. Traditionally, Capital Asset Pricing Models (CAPM) have been used to evaluate the cost of capital for investments. CAPM has been seen to work reasonably well for domestic (U.S.) markets but has failed when a world portfolio (including international markets) has been developed. One of the main difficulties with using CAPM is that many of these emerging markets are segmented. Quantifying factors contributing to the segmentation is not easy and several researchers have developed models to estimate the cost of capital for emerging market investments. Most of these models are a modification to traditional CAPM. They typically include adjustments to CAPM to account for the segmentation and other qualitative features of these markets. This report addresses some fundamental issues related to emerging markets - what they and their characteristics are. It presents several models available in literature to evaluate cost of capital for investments in these markets - both from portfolio managers' and MNCs points of view. The goal of this report is to present a conceptual framework to look at these topics and does not emphasize quantitative analysis. The state-of-the-art understanding of this topic still lacks a firm basis for quantitative analysis and it would be premature to carry out extensive quantitative analysis.

4 Estimating Cost of Capital for Equity Investments in Emerging Markets 1. What Are Emerging Markets Definition of an emerging market depends on one's perspective and purpose. Different sectors of industry define emerging markets differently, even though, they often are referring to similar geographic regions or countries. Khanna and Palepu [1] propose to classify markets based on how well they facilitate buyers and sellers coming together. Since, every market needs institutions to facilitate its functions, they argue that markets can be classified based on how developed these institutions are. Examples of these institutions are regulations, judicial systems and reliable information transfer mechanisms. They propose that in advanced economies, these institutions are very well developed and therefore minimize the risk of market failure. On the other hand, stagnant economies usually suffer from near complete market failure. Emerging markets, they say are in between, where, some of these institutions are developed, encouraging good commerce (and therefore the prospect of growth) but they also have some institutional voids that can cause market failures. This perspective is a very broad one, perhaps one from a corporate strategist or economist's standpoint. Mobius [2] describes the term "emerging markets" as first being coined by officers at the World Bank's International Finance Corporation when they were working on the concept of country funds and capital market development in less developed regions of the world. While it is difficult to determine a cut-off between emerging and emerged markets, the World Bank classification of high-, middle- and low-income countries provides a good basis. The low- and middle- income countries are usually considered 1

5 these markets are inherently less developed with significant potential for economic growth however with much uncertainty (risk). 2. Characteristics of Emerging Markets Two characteristics of emerging markets have been mentioned in the previous section: 1) low per capita GNP with higher economic growth rate than developed countries and 2) a higher perceived risk. Both factors are inter-related and a brief discussion on how they are related is presented in this section. 2,1 International Business: Country Risk & Economic Theory Erb et. al. [4] have presented a comprehensive study of country risk in the context of global financial management. They present a framework to understand risk, expected return and their relation to economic growth. A schematic of this framework is shown in Figure 1. 3

6 of the economy. However, inefficiencies do exist and countries are usually not at the optimal level of capital utilization. The important point here is that growth and expected returns (related to return of capital) are positively correlated. 3. Conditional Convergence & Economic Growth: The principle of convergence implies that economies with lower per capita GDP will grow, on average, faster than countries with higher per capita GDP. Conditional convergence implies the same principle but includes the assumption of all other factors being equal. Barro [6], in his neoclassical model of growth theory implies that if all economies were similar in all countries, except for the stage of development (or initial conditions), there would be a convergence to a steady-sate level of GDP. This is an important assumption when considering emerging markets, because all things are not equal in these markets leading to an uncertainty on the rate of growth and therefore leading to convergence only in a conditional sense. Conditional growth also changes the level of risk in various countries. These differences arise from various government poilicies, growth rate of population, savings rate, education levels and fertility rates. We will revisit some of these issues in later sections. Another aspect of Barro's work relates technological change (or R&D) and economic growth. He implies that long term R&D helps to maintain a positive long term economic growth. This aspect of growth theory has an important implication for emerging markets whose long term R&D investment is miniscule compared to the advanced countries. Conditional convergence would still hold in this case because developing countries can "piggyback" on the research of leading countries. While the developed countries can 5

7 differences in these factors between countries lead to differences in risk. We will revisit these factors in greater detail in later sections. 4. Initial Conditions/Conditional Convergence and Financial Returns: This is inferred from-the conditional convergence-economic growth-expected returns relationships outlined in items 1, 2 and 3. It can also be viewed as a conclusion from the principle of diminishing returns of capital, i.e. economies with a lower capital per worker tend to earn higher returns and higher growth. As indicated by the dashed line, this relationship is basically an inferred relationship. 5. Economic Growth & Country Risk: Erb et. al. [4] concluded this relationship by regressing real per capita economic growth on: real GDP per capita, the natural log of the Institutional Investor's Country Credit Rating (a measure of country risk) and the realized change in the rating for 61 countries between 1980 and The regression explained 60% of the cross-sectional variation with a positive correlation between risk and economic growth and a negative coefficient for initial GDP per capita (diminishing growth with a high initial level of per capita GDP). 6. Initial Conditions/Conditional Convergence and Country Risk: Similar to analysis in item 5, Erb et. al. regressed equity market returns in these countries with: the initial conditions represented by real per capital GDP and the Institutional Investor's Country Credit Ratings. The regression produced statistically significant coefficients for both the independent variables (real per capital GDP and credit ratings), thus linking the initial conditions and financial returns. The above discussion provides a general framework to understand how current states of various countries (say, in terms of per capita GDP), their economic growth 7

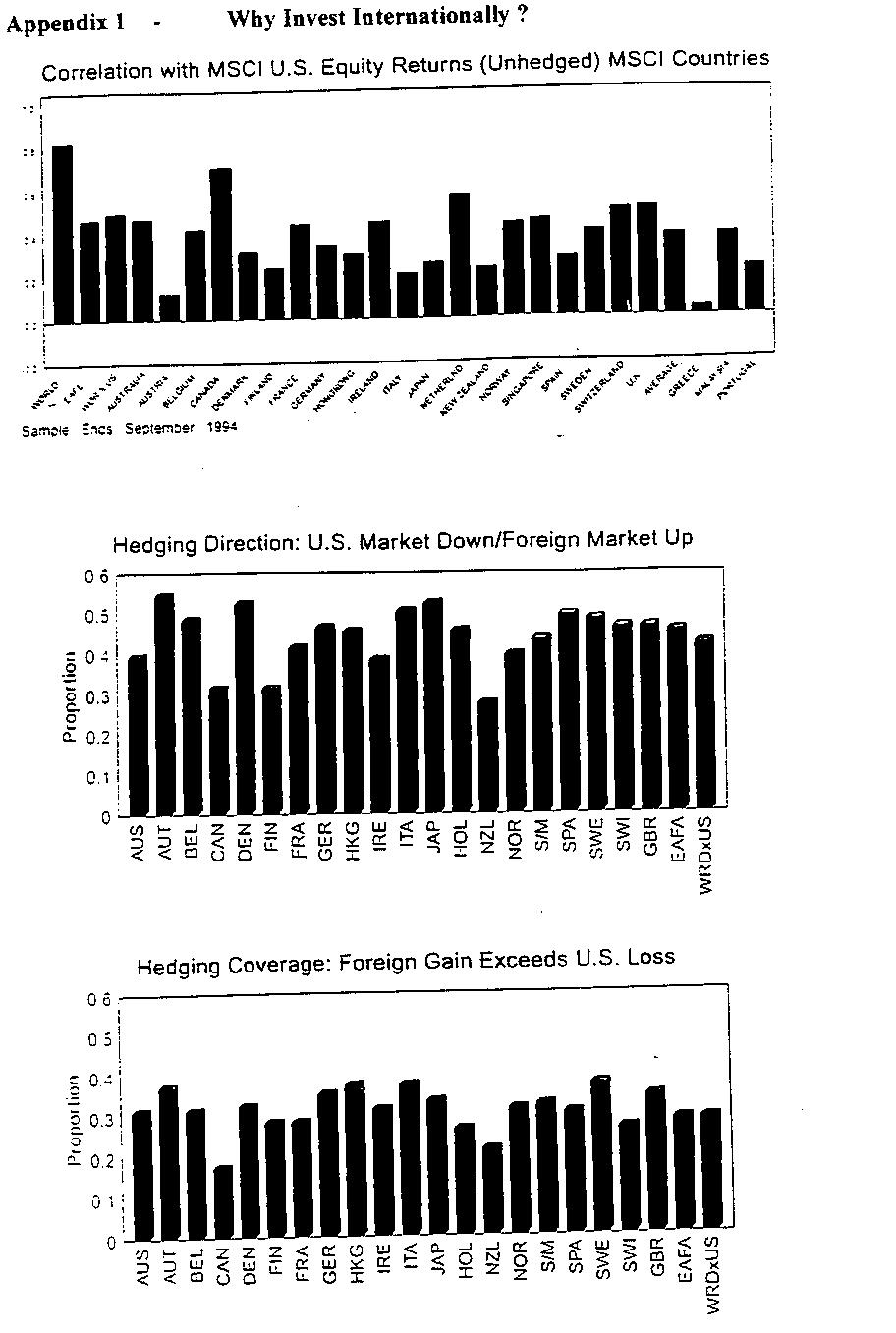

8 2.3 Investing in International Markets Just as there were large capital flows in a period spanning 30 years prior to the first world war, significant integration of international markets is taking place again today. However, there are some major differences [10]: Today, a large number of countries are involved in trade, unlike the 19 th century. Globalization in the latter half of 19 th century was heavily motivated by falling transportation costs whereas, today it is being driven by falling communication costs. Although, the net capital flows are smaller today than in the past, gross capital flows are much bigger. While, there are several indicators of increased integration around the world, markets are still quite segmented. For example, trade between two Canadian provinces is 20 times higher than trade between an American and Canadian province. This is a telling statistic, considering that trading borders between Canada and the United States is one of the least restricted in the world. Segmentation in world markets provides unique opportunities and risks for investors. Many factors that segment markets, also provide basis for country risk. They form the basis for international investing and global financial management Why invest in international markets? Up until the 1970's, the U.S. capitalization of the world market was over 50% [11]. In fact, in the 50's and 60's the U.S. market capitalization was over 75%. For this reason, the U.S. market was considered proxy for the world market. However, today, the U.S. market represents less than 40% of the world market. Therefore, the question is, 9

9

10 2.4 Investing in Emerging Markets Motivation To Invest & Recent Trends in Emerging Markets Some basic information comparing developed and emerging economies is presented in Figure 2. Figure 2 Emerging Markets vs. Developed Markets - Share of the World Figure 2 shows that the emerging markets are a small fraction of the global economy even though them have the majority of the world's population. Starting in the 1980's, however, developing economies began opening up and international capital flows into these markets accelerated. Figure 3, taken from The Economist [13], demonstrates Figure 3 (a) Opening up of emerging economies (b) Capital flows into emerging markets

![Figure 4 Average volatility of developed and emerging financial markets [12] Emerging financial markets can provide higher returns than developed markets (Figure 5) Figure 5 Average annual returns of](/docs-images/94/121310021/images/11-1.jpg "developed and emerging markets [12] Many emerging markets are larger than some smaller developed countries' markets While there is sufficient empirical evidence that suggests and encourages")

11 Figure 4 Average volatility of developed and emerging financial markets [12] Emerging financial markets can provide higher returns than developed markets (Figure 5) Figure 5 Average annual returns of developed and emerging markets [12] Many emerging markets are larger than some smaller developed countries' markets While there is sufficient empirical evidence that suggests and encourages investments in emerging markets, there is very little fundamental understanding of these markets to enable complete and consistent analyses of investments in these countries. The next 15

12 vary across securities and investors. Sometimes, there are restrictions on which investors can buy too, further limiting this model. A detailed discussion of these issues is presented in Stulz [14]. More evidence of the difficulty in understanding international market returns is provided by Cho et al. [15]. Based on an empirical investigation, they reject the hypothesis that the international capital market is integrated and that the arbitrage pricing theory is valid internationally. However, they do not specifically determine if this rejection implies a segmentation of capital markets or the failure of international arbitrage pricing theory. Relationships between inflation and asset returns are well-understood for developed markets, however; they are less clear for emerging markets. Figure 6 shows average inflation data for developed and emerging markets. Furthermore, regressing country credit ratings with inflation, stock market returns, (in local and US currency) or volatility (in local or US currency) does not demonstrate any correlation for emerging markets [12]. In summary, while developed international markets are understood to some extent, parameters influencing emerging market returns are less understood Cost of Capital In Emerging Equity Markets Emerging markets cannot be considered as one market. Each country is different and should be dealt with separately. Investment risks are country specific. The important sources of country risk are: 17

13 proxy to world returns. While they show some changes in the beta values for some periods, their analysis is not conclusive. - Most world market portfolios are heavily weighted by the industrial countries. Based on market capitalization of these countries, it is difficult to determine how close these portfolios are in representing world market behavior. CAPM assumes that investors have access to all stocks and these stocks are traded freely. However, in reality, regulations, costs and logistics of trading in these markets can be costly and complicated, or in other words, the markets are not completely integrated into the world. Harvey [19] has compiled a table (Table 1) listing the regulatory environment for investors in several emerging markets. Obviously, the CAPM model does not take into account these difficulties. The betas estimated by typical single-factor models are assumed to be constants over time. A constant beta implies constant risk over the period considered. Most emerging markets are changing rapidly on all fronts of risk and this assumption is a limitation of most world CAPM models. The above discussion implies that there are several qualitative factors that prevent a conclusive rigorous statistical analysis of these markets. Several researchers have included these factors in a somewhat ad hoc manner as discussed here. 19

14

15 23

16 3.1 Risks for MNC Investments in Emerging Markets There are three primary sources of risks for MNC investments in emerging markets [26]: 1. Political or "sovereign" risk 2. Commercial or "business" risk 3. Currency risk Political or "sovereign" risks can be observed in the yield spreads on the sovereign bonds denominated in US dollars. Business risk can be observed in the volatility of local equity markets. Currency risk can be accounted for by carrying out all financial analyses by converting cash flows from local currency to US dollars. The exchange rate used for this conversion can typically include an upper and lower bound to estimate the bounds on cash flows. 3.2 Discount Rates for Evaluating Investment Opportunities Discount rates are useful for comparing various investment opportunities when performing an NPV analysis. In practice, for corporations, discount rates are computed as a weighted average of relevant debt and equity costs. Estimations of costs of equity are typically done based on the Capital Asset Pricing Model (CAPM). In principle, risks such as sovereign risks would be considered unsystematic risks because investors could diversify away these risks by personally investing in these markets. However, as we have seen from the discussions in earlier sections, emerging markets are not easily accessible to investors. For instance, consider Ford Motor 25

17 27

18

19 31

20 is a great deal of uncertainty associated with cash flows for investments in emerging markets. In fact, I believe, having a handle on cash flows is harder because it requires accurate estimates of economic growth and income distributions in these markets. 6 Acknowledgements The author would like to thank Prof. Gunter Dufey for guiding and supporting this work. Prof. Campbell Harvey of Duke University is gratefully acknowledged for his generosity in sending several working papers and publications. 33

21 12. Harvey, C. R., 1995, "Course Notes: Global Financial Management & Country Risk", Duke University/National Bureau of Economic Research. 13. Schools Brief, October 25-31,1997,"Capital Goes Global", The Economist, Stulz, R. M., 1985, "Pricing Capital Assets in an International Setting: An Introduction", in International Financial Management, ed. D. R. Lessard, 2 nd Ed., John, Wiley & Sons, Inc. 15. Cho, D. C, C. S. Eun and L. M. Senbet, 1996, "International Arbitrage Pricing Theory: An Empirical Investigation", The Journal of Finance, Vol. XLI, No. 2, pp Black, F., 1972, "Capital Market Equilibrium with Restricted Borrowing", Journal of Business, 45, Harvey, C. R., 1995, "The Rsik Exposure of Emerging Equity Markets", The World Bank Economic Review, Vol. 9, No. 1, pp Scholes, M. and J. Williams, 1977, "Estimating Betas from Nonsynchronous Data", Journal of Financial Economics, Vol 5., No. 3, pp Harvey, C. R., 1994, "Emerging Markets: Opportunities and Risks", Wachovia: PFS Training Program, February, Fuqua School of Business, Duke University. 20. Mariscal, J. O. and R. M. Lee, 1993, "The Valuation of Mexican Stocks: An Extension of the CAPM", Goldman Sachs, New York. 21. Annin, M. and D. Falaschetti, 1998, "Equity Risk Premium Still Produced Debate", Risk Pre/, Ibbotson Associates. 22. Erb, C. B., C. R. Harvey and T. E. Viskanta, "Political Risk, Economic Risk and Financial Risk", 1996, Financial Analysts Journal, Nov-Dec, pp

22

23 KRESG BUS. AE UBRAR Faculty Comments Here is the evaluation I put on your paper. We need urgently one more clean copy to be put in the Library. This research paper provides a comprehensive survey of various models used for estimating the cost of capital for investments in emerging markets. The subject is challenging and the author has done an extensive job researching the literature and compiling the major ideas into a readable and generally well-organized report. Small problems in exposition and structure notwithstanding, a grade of EXCELLENT is appropriate in view of the scope of work and the difficulty of the topic.

Risk Analysis and Project Evaluation

International Finance Risk Analysis and Project Evaluation Campbell R. Harvey Duke University, NBER and Investment Strategy Advisor, Man Group, plc February 1, 2017 2 The Setting Prerequisite to any evaluation

International Finance Risk Analysis and Project Evaluation Campbell R. Harvey Duke University, NBER and Investment Strategy Advisor, Man Group, plc February 1, 2017 2 The Setting Prerequisite to any evaluation

Does Portfolio Theory Work During Financial Crises?

Does Portfolio Theory Work During Financial Crises? Harry M. Markowitz, Mark T. Hebner, Mary E. Brunson It is sometimes said that portfolio theory fails during financial crises because: All asset classes

Does Portfolio Theory Work During Financial Crises? Harry M. Markowitz, Mark T. Hebner, Mary E. Brunson It is sometimes said that portfolio theory fails during financial crises because: All asset classes

Conditional Convergence: Evidence from the Solow Growth Model

Conditional Convergence: Evidence from the Solow Growth Model Reginald Wilson The University of Southern Mississippi The Solow growth model indicates that more than half of the variation in gross domestic

Conditional Convergence: Evidence from the Solow Growth Model Reginald Wilson The University of Southern Mississippi The Solow growth model indicates that more than half of the variation in gross domestic

Solow instead assumed a standard neo-classical production function with diminishing marginal product for both labor and capital.

Module 5 Lecture 34 Topics 5.2 Growth Theory II 5.2.1 Solow Model 5.2 Growth Theory II 5.2.1 Solow Model Robert Solow was quick to recognize that the instability inherent in the Harrod- Domar model is

Module 5 Lecture 34 Topics 5.2 Growth Theory II 5.2.1 Solow Model 5.2 Growth Theory II 5.2.1 Solow Model Robert Solow was quick to recognize that the instability inherent in the Harrod- Domar model is

Risk and Return. Nicole Höhling, Introduction. Definitions. Types of risk and beta

Risk and Return Nicole Höhling, 2009-09-07 Introduction Every decision regarding investments is based on the relationship between risk and return. Generally the return on an investment should be as high

Risk and Return Nicole Höhling, 2009-09-07 Introduction Every decision regarding investments is based on the relationship between risk and return. Generally the return on an investment should be as high

ECON FINANCIAL ECONOMICS

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Spring 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Spring 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

Chapter 4 Research Methodology

Chapter 4 Research Methodology 4.1 Introduction An exchange rate (also known as a foreign-exchange rate, forex rate, FX rate or Agio) between two currencies is the rate at which one currency will be exchanged

Chapter 4 Research Methodology 4.1 Introduction An exchange rate (also known as a foreign-exchange rate, forex rate, FX rate or Agio) between two currencies is the rate at which one currency will be exchanged

THE EFFECTS OF THE EU BUDGET ON ECONOMIC CONVERGENCE

THE EFFECTS OF THE EU BUDGET ON ECONOMIC CONVERGENCE Eva Výrostová Abstract The paper estimates the impact of the EU budget on the economic convergence process of EU member states. Although the primary

THE EFFECTS OF THE EU BUDGET ON ECONOMIC CONVERGENCE Eva Výrostová Abstract The paper estimates the impact of the EU budget on the economic convergence process of EU member states. Although the primary

Comment Does the economics of moral hazard need to be revisited? A comment on the paper by John Nyman

Journal of Health Economics 20 (2001) 283 288 Comment Does the economics of moral hazard need to be revisited? A comment on the paper by John Nyman Åke Blomqvist Department of Economics, University of

Journal of Health Economics 20 (2001) 283 288 Comment Does the economics of moral hazard need to be revisited? A comment on the paper by John Nyman Åke Blomqvist Department of Economics, University of

CHAPTER III RISK MANAGEMENT

CHAPTER III RISK MANAGEMENT Concept of Risk Risk is the quantified amount which arises due to the likelihood of the occurrence of a future outcome which one does not expect to happen. If one is participating

CHAPTER III RISK MANAGEMENT Concept of Risk Risk is the quantified amount which arises due to the likelihood of the occurrence of a future outcome which one does not expect to happen. If one is participating

Notes on classical growth theory (optional read)

") Simon Fraser University Econ 855 Prof. Karaivanov Notes on classical growth theory (optional read) These notes provide a rough overview of "classical" growth theory. Historically, due mostly to data availability

Simon Fraser University Econ 855 Prof. Karaivanov Notes on classical growth theory (optional read) These notes provide a rough overview of "classical" growth theory. Historically, due mostly to data availability

Role of Foreign Direct Investment in Knowledge Spillovers: Firm-Level Evidence from Korean Firms Patent and Patent Citations

THE JOURNAL OF THE KOREAN ECONOMY, Vol. 5, No. 1 (Spring 2004), 47-67 Role of Foreign Direct Investment in Knowledge Spillovers: Firm-Level Evidence from Korean Firms Patent and Patent Citations Jaehwa

THE JOURNAL OF THE KOREAN ECONOMY, Vol. 5, No. 1 (Spring 2004), 47-67 Role of Foreign Direct Investment in Knowledge Spillovers: Firm-Level Evidence from Korean Firms Patent and Patent Citations Jaehwa

Topic 3: Endogenous Technology & Cross-Country Evidence

EC4010 Notes, 2005 (Karl Whelan) 1 Topic 3: Endogenous Technology & Cross-Country Evidence In this handout, we examine an alternative model of endogenous growth, due to Paul Romer ( Endogenous Technological

EC4010 Notes, 2005 (Karl Whelan) 1 Topic 3: Endogenous Technology & Cross-Country Evidence In this handout, we examine an alternative model of endogenous growth, due to Paul Romer ( Endogenous Technological

The impact of changing diversification on stability and growth in a regional economy

ABSTRACT The impact of changing diversification on stability and growth in a regional economy Carl C. Brown Florida Southern College Economic diversification has long been considered a potential determinant

ABSTRACT The impact of changing diversification on stability and growth in a regional economy Carl C. Brown Florida Southern College Economic diversification has long been considered a potential determinant

Economic Growth and Financial Liberalization

Economic Growth and Financial Liberalization Draft March 8, 2001 Geert Bekaert and Campbell R. Harvey 1. Introduction From 1980 to 1997, Chile experienced average real GDP growth of 3.8% per year while

Economic Growth and Financial Liberalization Draft March 8, 2001 Geert Bekaert and Campbell R. Harvey 1. Introduction From 1980 to 1997, Chile experienced average real GDP growth of 3.8% per year while

COMPREHENSIVE ANALYSIS OF BANKRUPTCY PREDICTION ON STOCK EXCHANGE OF THAILAND SET 100

COMPREHENSIVE ANALYSIS OF BANKRUPTCY PREDICTION ON STOCK EXCHANGE OF THAILAND SET 100 Sasivimol Meeampol Kasetsart University, Thailand fbussas@ku.ac.th Phanthipa Srinammuang Kasetsart University, Thailand

COMPREHENSIVE ANALYSIS OF BANKRUPTCY PREDICTION ON STOCK EXCHANGE OF THAILAND SET 100 Sasivimol Meeampol Kasetsart University, Thailand fbussas@ku.ac.th Phanthipa Srinammuang Kasetsart University, Thailand

Political and Economic Risk Analysis Case study of Macedonia

Political and Economic Risk Analysis Case study of Macedonia Misko Dzidrov 1, Marjan Dzidrov 2 1 Management School, Wuhan University of Technology, Wuhan, China 2 Faculty of Computer Science and Information

Political and Economic Risk Analysis Case study of Macedonia Misko Dzidrov 1, Marjan Dzidrov 2 1 Management School, Wuhan University of Technology, Wuhan, China 2 Faculty of Computer Science and Information

INVESTING IN LONG-TERM ASSETS: CAPITAL BUDGETING

INVESTING IN LONG-TERM ASSETS: CAPITAL BUDGETING P A R T 4 10 11 12 13 The Cost of Capital The Basics of Capital Budgeting Cash Flow Estimation and Risk Analysis Real Options and Other Topics in Capital

INVESTING IN LONG-TERM ASSETS: CAPITAL BUDGETING P A R T 4 10 11 12 13 The Cost of Capital The Basics of Capital Budgeting Cash Flow Estimation and Risk Analysis Real Options and Other Topics in Capital

ECON FINANCIAL ECONOMICS

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Fall 2017 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Fall 2017 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

The New Growth Theories - Week 6

The New Growth Theories - Week 6 ECON1910 - Poverty and distribution in developing countries Readings: Ray chapter 4 8. February 2011 (Readings: Ray chapter 4) The New Growth Theories - Week 6 8. February

The New Growth Theories - Week 6 ECON1910 - Poverty and distribution in developing countries Readings: Ray chapter 4 8. February 2011 (Readings: Ray chapter 4) The New Growth Theories - Week 6 8. February

A New Strategy for Social Security Investment in Latin America

A New Strategy for Social Security Investment in Latin America Martin Feldstein * Thank you. I m very pleased to be here in Mexico and to have this opportunity to talk to a group that understands so well

A New Strategy for Social Security Investment in Latin America Martin Feldstein * Thank you. I m very pleased to be here in Mexico and to have this opportunity to talk to a group that understands so well

Public Expenditure on Capital Formation and Private Sector Productivity Growth: Evidence

ISSN 2029-4581. ORGANIZATIONS AND MARKETS IN EMERGING ECONOMIES, 2012, VOL. 3, No. 1(5) Public Expenditure on Capital Formation and Private Sector Productivity Growth: Evidence from and the Euro Area Jolanta

ISSN 2029-4581. ORGANIZATIONS AND MARKETS IN EMERGING ECONOMIES, 2012, VOL. 3, No. 1(5) Public Expenditure on Capital Formation and Private Sector Productivity Growth: Evidence from and the Euro Area Jolanta

Real Estate Ownership by Non-Real Estate Firms: The Impact on Firm Returns

Real Estate Ownership by Non-Real Estate Firms: The Impact on Firm Returns Yongheng Deng and Joseph Gyourko 1 Zell/Lurie Real Estate Center at Wharton University of Pennsylvania Prepared for the Corporate

Real Estate Ownership by Non-Real Estate Firms: The Impact on Firm Returns Yongheng Deng and Joseph Gyourko 1 Zell/Lurie Real Estate Center at Wharton University of Pennsylvania Prepared for the Corporate

International journal of advanced production and industrial engineering (A Blind Peer Reviewed Journal)

") IJAPIE-2016-10-406, Vol 1(4), 40-44 International journal of advanced production and industrial engineering (A Blind Peer Reviewed Journal) Consumption and Market Beta: Empirical Evidence from India Nand

IJAPIE-2016-10-406, Vol 1(4), 40-44 International journal of advanced production and industrial engineering (A Blind Peer Reviewed Journal) Consumption and Market Beta: Empirical Evidence from India Nand

INTERNATIONAL FINANCIAL MANAGEMENT

National Research University - Higher School of Economics Faculty of World Economy and International Affairs Course Syllabus and Description INTERNATIONAL FINANCIAL MANAGEMENT Master of International Business

National Research University - Higher School of Economics Faculty of World Economy and International Affairs Course Syllabus and Description INTERNATIONAL FINANCIAL MANAGEMENT Master of International Business

Macroeconomics, Cdn. 4e (Williamson) Chapter 1 Introduction

Chapter 1 Introduction") Macroeconomics, Cdn. 4e (Williamson) Chapter 1 Introduction 1) Which of the following topics is a primary concern of macro economists? A) standards of living of individuals B) choices of individual consumers

Macroeconomics, Cdn. 4e (Williamson) Chapter 1 Introduction 1) Which of the following topics is a primary concern of macro economists? A) standards of living of individuals B) choices of individual consumers

ESTIMATING THE MARKET RISK PREMIUM IN NEW ZEALAND THROUGH THE SIEGEL METHODOLOGY

ESTIMATING THE MARKET RISK PREMIUM IN NEW ZEALAND THROUGH THE SIEGEL METHODOLOGY by Martin Lally School of Economics and Finance Victoria University of Wellington PO Box 600 Wellington New Zealand E-mail:

ESTIMATING THE MARKET RISK PREMIUM IN NEW ZEALAND THROUGH THE SIEGEL METHODOLOGY by Martin Lally School of Economics and Finance Victoria University of Wellington PO Box 600 Wellington New Zealand E-mail:

in-depth Invesco Actively Managed Low Volatility Strategies The Case for

Invesco in-depth The Case for Actively Managed Low Volatility Strategies We believe that active LVPs offer the best opportunity to achieve a higher risk-adjusted return over the long term. Donna C. Wilson

Invesco in-depth The Case for Actively Managed Low Volatility Strategies We believe that active LVPs offer the best opportunity to achieve a higher risk-adjusted return over the long term. Donna C. Wilson

International Financial Markets 1. How Capital Markets Work

International Financial Markets Lecture Notes: E-Mail: Colloquium: www.rainer-maurer.de rainer.maurer@hs-pforzheim.de Friday 15.30-17.00 (room W4.1.03) -1-1.1. Supply and Demand on Capital Markets 1.1.1.

International Financial Markets Lecture Notes: E-Mail: Colloquium: www.rainer-maurer.de rainer.maurer@hs-pforzheim.de Friday 15.30-17.00 (room W4.1.03) -1-1.1. Supply and Demand on Capital Markets 1.1.1.

In Chapter 7, I discussed the teaching methods and educational

Chapter 9 From East to West Downloaded from www.worldscientific.com Innovative and Active Approach to Teaching Finance In Chapter 7, I discussed the teaching methods and educational philosophy and in Chapter

Chapter 9 From East to West Downloaded from www.worldscientific.com Innovative and Active Approach to Teaching Finance In Chapter 7, I discussed the teaching methods and educational philosophy and in Chapter

Optimal Portfolio Inputs: Various Methods

Optimal Portfolio Inputs: Various Methods Prepared by Kevin Pei for The Fund @ Sprott Abstract: In this document, I will model and back test our portfolio with various proposed models. It goes without

Optimal Portfolio Inputs: Various Methods Prepared by Kevin Pei for The Fund @ Sprott Abstract: In this document, I will model and back test our portfolio with various proposed models. It goes without

Country Risk Components, the Cost of Capital, and Returns in Emerging Markets

Country Risk Components, the Cost of Capital, and Returns in Emerging Markets Campbell R. Harvey a,b a Duke University, Durham, NC 778 b National Bureau of Economic Research, Cambridge, MA Abstract This

Country Risk Components, the Cost of Capital, and Returns in Emerging Markets Campbell R. Harvey a,b a Duke University, Durham, NC 778 b National Bureau of Economic Research, Cambridge, MA Abstract This

Donald L Kohn: Asset-pricing puzzles, credit risk, and credit derivatives

Donald L Kohn: Asset-pricing puzzles, credit risk, and credit derivatives Remarks by Mr Donald L Kohn, Vice Chairman of the Board of Governors of the US Federal Reserve System, at the Conference on Credit

Donald L Kohn: Asset-pricing puzzles, credit risk, and credit derivatives Remarks by Mr Donald L Kohn, Vice Chairman of the Board of Governors of the US Federal Reserve System, at the Conference on Credit

Monetary Economics Risk and Return, Part 2. Gerald P. Dwyer Fall 2015

Monetary Economics Risk and Return, Part 2 Gerald P. Dwyer Fall 2015 Reading Malkiel, Part 2, Part 3 Malkiel, Part 3 Outline Returns and risk Overall market risk reduced over longer periods Individual

Monetary Economics Risk and Return, Part 2 Gerald P. Dwyer Fall 2015 Reading Malkiel, Part 2, Part 3 Malkiel, Part 3 Outline Returns and risk Overall market risk reduced over longer periods Individual

Procedia - Social and Behavioral Sciences 109 ( 2014 ) Yigit Bora Senyigit *, Yusuf Ag

Yigit Bora Senyigit *, Yusuf Ag") Available online at www.sciencedirect.com ScienceDirect Procedia - Social and Behavioral Sciences 109 ( 2014 ) 327 332 2 nd World Conference on Business, Economics and Management WCBEM 2013 Explaining

Available online at www.sciencedirect.com ScienceDirect Procedia - Social and Behavioral Sciences 109 ( 2014 ) 327 332 2 nd World Conference on Business, Economics and Management WCBEM 2013 Explaining

Diversification s Impact on Discount Rates in U.S. Cost-Sharing Agreements

Volume 75, Number 9 September 1, 2014 Diversification s Impact on Discount Rates in U.S. Cost-Sharing Agreements by Stuart Webber Reprinted from Tax Notes Int l, September 1, 2014, p. 755 Diversification

Volume 75, Number 9 September 1, 2014 Diversification s Impact on Discount Rates in U.S. Cost-Sharing Agreements by Stuart Webber Reprinted from Tax Notes Int l, September 1, 2014, p. 755 Diversification

Web Extension: Continuous Distributions and Estimating Beta with a Calculator

19878_02W_p001-008.qxd 3/10/06 9:51 AM Page 1 C H A P T E R 2 Web Extension: Continuous Distributions and Estimating Beta with a Calculator This extension explains continuous probability distributions

19878_02W_p001-008.qxd 3/10/06 9:51 AM Page 1 C H A P T E R 2 Web Extension: Continuous Distributions and Estimating Beta with a Calculator This extension explains continuous probability distributions

Copyright 2009 Pearson Education Canada

Operating Cash Flows: Sales $682,500 $771,750 $868,219 $972,405 $957,211 less expenses $477,750 $540,225 $607,753 $680,684 $670,048 Difference $204,750 $231,525 $260,466 $291,722 $287,163 After-tax (1

Operating Cash Flows: Sales $682,500 $771,750 $868,219 $972,405 $957,211 less expenses $477,750 $540,225 $607,753 $680,684 $670,048 Difference $204,750 $231,525 $260,466 $291,722 $287,163 After-tax (1

CHAPTER 2 RISK AND RETURN: Part I

CHAPTER 2 RISK AND RETURN: Part I (Difficulty Levels: Easy, Easy/Medium, Medium, Medium/Hard, and Hard) Please see the preface for information on the AACSB letter indicators (F, M, etc.) on the subject

CHAPTER 2 RISK AND RETURN: Part I (Difficulty Levels: Easy, Easy/Medium, Medium, Medium/Hard, and Hard) Please see the preface for information on the AACSB letter indicators (F, M, etc.) on the subject

Capital Asset Pricing Model - CAPM

Capital Asset Pricing Model - CAPM The capital asset pricing model (CAPM) is a model that describes the relationship between systematic risk and expected return for assets, particularly stocks. CAPM is

Capital Asset Pricing Model - CAPM The capital asset pricing model (CAPM) is a model that describes the relationship between systematic risk and expected return for assets, particularly stocks. CAPM is

Perhaps the most striking aspect of the current

COMPARATIVE ADVANTAGE, CROSS-BORDER MERGERS AND MERGER WAVES:INTER- NATIONAL ECONOMICS MEETS INDUSTRIAL ORGANIZATION STEVEN BRAKMAN* HARRY GARRETSEN** AND CHARLES VAN MARREWIJK*** Perhaps the most striking

COMPARATIVE ADVANTAGE, CROSS-BORDER MERGERS AND MERGER WAVES:INTER- NATIONAL ECONOMICS MEETS INDUSTRIAL ORGANIZATION STEVEN BRAKMAN* HARRY GARRETSEN** AND CHARLES VAN MARREWIJK*** Perhaps the most striking

Testing for Stock Market Overvaluation/ Undervaluation

Chapter 18 Testing for Stock Market Overvaluation/ Undervaluation Ellen R. McGrattan* Federal Reserve Bank of Minneapolis and University of Minnesota and Edward C. Prescott University of Minnesota and

Chapter 18 Testing for Stock Market Overvaluation/ Undervaluation Ellen R. McGrattan* Federal Reserve Bank of Minneapolis and University of Minnesota and Edward C. Prescott University of Minnesota and

Decimalization and Illiquidity Premiums: An Extended Analysis

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 5-2015 Decimalization and Illiquidity Premiums: An Extended Analysis Seth E. Williams Utah State University

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 5-2015 Decimalization and Illiquidity Premiums: An Extended Analysis Seth E. Williams Utah State University

THE EFFECT OF SOCIAL SECURITY ON PRIVATE SAVING: THE TIME SERIES EVIDENCE

NBER WORKING PAPER SERIES THE EFFECT OF SOCIAL SECURITY ON PRIVATE SAVING: THE TIME SERIES EVIDENCE Martin Feldstein Working Paper No. 314 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue

NBER WORKING PAPER SERIES THE EFFECT OF SOCIAL SECURITY ON PRIVATE SAVING: THE TIME SERIES EVIDENCE Martin Feldstein Working Paper No. 314 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue

Pension fund investment: Impact of the liability structure on equity allocation

Pension fund investment: Impact of the liability structure on equity allocation Author: Tim Bücker University of Twente P.O. Box 217, 7500AE Enschede The Netherlands t.bucker@student.utwente.nl In this

Pension fund investment: Impact of the liability structure on equity allocation Author: Tim Bücker University of Twente P.O. Box 217, 7500AE Enschede The Netherlands t.bucker@student.utwente.nl In this

Foreign Direct Investment I

FD Foreign Direct nvestment [My notes are in beta. f you see something that doesn t look right, would greatly appreciate a heads-up.] 1 FD background Foreign direct investment FD) occurs when an enterprise

FD Foreign Direct nvestment [My notes are in beta. f you see something that doesn t look right, would greatly appreciate a heads-up.] 1 FD background Foreign direct investment FD) occurs when an enterprise

LIQUIDITY EXTERNALITIES OF CONVERTIBLE BOND ISSUANCE IN CANADA

LIQUIDITY EXTERNALITIES OF CONVERTIBLE BOND ISSUANCE IN CANADA by Brandon Lam BBA, Simon Fraser University, 2009 and Ming Xin Li BA, University of Prince Edward Island, 2008 THESIS SUBMITTED IN PARTIAL

LIQUIDITY EXTERNALITIES OF CONVERTIBLE BOND ISSUANCE IN CANADA by Brandon Lam BBA, Simon Fraser University, 2009 and Ming Xin Li BA, University of Prince Edward Island, 2008 THESIS SUBMITTED IN PARTIAL

Journal of Central Banking Theory and Practice, 2017, 1, pp Received: 6 August 2016; accepted: 10 October 2016

BOOK REVIEW: Monetary Policy, Inflation, and the Business Cycle: An Introduction to the New Keynesian... 167 UDK: 338.23:336.74 DOI: 10.1515/jcbtp-2017-0009 Journal of Central Banking Theory and Practice,

BOOK REVIEW: Monetary Policy, Inflation, and the Business Cycle: An Introduction to the New Keynesian... 167 UDK: 338.23:336.74 DOI: 10.1515/jcbtp-2017-0009 Journal of Central Banking Theory and Practice,

The Impact of Interest Rate in determining Exchange Rate: Revisiting Interest Rate Parity Theory

The Impact of Interest Rate in determining Exchange Rate: Revisiting Interest Rate Parity Theory P.R.M.R.Perera 1 Lecturer (Temporary) Department of Accountancy, Faculty of Commerce & Management Studies,

The Impact of Interest Rate in determining Exchange Rate: Revisiting Interest Rate Parity Theory P.R.M.R.Perera 1 Lecturer (Temporary) Department of Accountancy, Faculty of Commerce & Management Studies,

Chapter 13 Return, Risk, and Security Market Line

1 Chapter 13 Return, Risk, and Security Market Line Konan Chan Financial Management, Spring 2018 Topics Covered Expected Return and Variance Portfolio Risk and Return Risk & Diversification Systematic

1 Chapter 13 Return, Risk, and Security Market Line Konan Chan Financial Management, Spring 2018 Topics Covered Expected Return and Variance Portfolio Risk and Return Risk & Diversification Systematic

The mathematical model of portfolio optimal size (Tehran exchange market)

") WALIA journal 3(S2): 58-62, 205 Available online at www.waliaj.com ISSN 026-386 205 WALIA The mathematical model of portfolio optimal size (Tehran exchange market) Farhad Savabi * Assistant Professor of

WALIA journal 3(S2): 58-62, 205 Available online at www.waliaj.com ISSN 026-386 205 WALIA The mathematical model of portfolio optimal size (Tehran exchange market) Farhad Savabi * Assistant Professor of

Investment 3.1 INTRODUCTION. Fixed investment

3 Investment 3.1 INTRODUCTION Investment expenditure includes spending on a large variety of assets. The main distinction is between fixed investment, or fixed capital formation (the purchase of durable

3 Investment 3.1 INTRODUCTION Investment expenditure includes spending on a large variety of assets. The main distinction is between fixed investment, or fixed capital formation (the purchase of durable

Financial Markets and Institutions Midterm study guide Jon Faust Spring 2014

180.266 Financial Markets and Institutions Midterm study guide Jon Faust Spring 2014 The exam will have some questions involving definitions and some involving basic real world quantities. These will be

180.266 Financial Markets and Institutions Midterm study guide Jon Faust Spring 2014 The exam will have some questions involving definitions and some involving basic real world quantities. These will be

High Frequency Autocorrelation in the Returns of the SPY and the QQQ. Scott Davis* January 21, Abstract

High Frequency Autocorrelation in the Returns of the SPY and the QQQ Scott Davis* January 21, 2004 Abstract In this paper I test the random walk hypothesis for high frequency stock market returns of two

High Frequency Autocorrelation in the Returns of the SPY and the QQQ Scott Davis* January 21, 2004 Abstract In this paper I test the random walk hypothesis for high frequency stock market returns of two

THE PENNSYLVANIA STATE UNIVERSITY SCHREYER HONORS COLLEGE DEPARTMENT OF FINANCE

THE PENNSYLVANIA STATE UNIVERSITY SCHREYER HONORS COLLEGE DEPARTMENT OF FINANCE EXAMINING THE IMPACT OF THE MARKET RISK PREMIUM BIAS ON THE CAPM AND THE FAMA FRENCH MODEL CHRIS DORIAN SPRING 2014 A thesis

THE PENNSYLVANIA STATE UNIVERSITY SCHREYER HONORS COLLEGE DEPARTMENT OF FINANCE EXAMINING THE IMPACT OF THE MARKET RISK PREMIUM BIAS ON THE CAPM AND THE FAMA FRENCH MODEL CHRIS DORIAN SPRING 2014 A thesis

An Analysis of the Market Price of Cat Bonds

An Analysis of the Price of Cat Bonds Neil Bodoff, FCAS and Yunbo Gan, PhD 2009 CAS Reinsurance Seminar Disclaimer The statements and opinions included in this Presentation are those of the individual

An Analysis of the Price of Cat Bonds Neil Bodoff, FCAS and Yunbo Gan, PhD 2009 CAS Reinsurance Seminar Disclaimer The statements and opinions included in this Presentation are those of the individual

Accounting disclosure, value relevance and firm life cycle: Evidence from Iran

International Journal of Economic Behavior and Organization 2013; 1(6): 69-77 Published online February 20, 2014 (http://www.sciencepublishinggroup.com/j/ijebo) doi: 10.11648/j.ijebo.20130106.13 Accounting

International Journal of Economic Behavior and Organization 2013; 1(6): 69-77 Published online February 20, 2014 (http://www.sciencepublishinggroup.com/j/ijebo) doi: 10.11648/j.ijebo.20130106.13 Accounting

RISK MANAGEMENT IN THE INSURANCE COMPANIES IN KOSOVO (SIGMA COMPANY)

") FACULTY OF ECONOMICS DEPARTMENT: FINANCIAL MARKETS AND BANKS MASTER THESIS RISK MANAGEMENT IN THE INSURANCE COMPANIES IN KOSOVO (SIGMA COMPANY) Mentor: Prof. Dr. Drita Konxheli kandidate: Jeton Nuredini

FACULTY OF ECONOMICS DEPARTMENT: FINANCIAL MARKETS AND BANKS MASTER THESIS RISK MANAGEMENT IN THE INSURANCE COMPANIES IN KOSOVO (SIGMA COMPANY) Mentor: Prof. Dr. Drita Konxheli kandidate: Jeton Nuredini

Correlation vs. Trends in Portfolio Management: A Common Misinterpretation

Correlation vs. rends in Portfolio Management: A Common Misinterpretation Francois-Serge Lhabitant * Abstract: wo common beliefs in finance are that (i) a high positive correlation signals assets moving

Correlation vs. rends in Portfolio Management: A Common Misinterpretation Francois-Serge Lhabitant * Abstract: wo common beliefs in finance are that (i) a high positive correlation signals assets moving

Estimating the Current Value of Time-Varying Beta

Estimating the Current Value of Time-Varying Beta Joseph Cheng Ithaca College Elia Kacapyr Ithaca College This paper proposes a special type of discounted least squares technique and applies it to the

Estimating the Current Value of Time-Varying Beta Joseph Cheng Ithaca College Elia Kacapyr Ithaca College This paper proposes a special type of discounted least squares technique and applies it to the

The Capital Assets Pricing Model & Arbitrage Pricing Theory: Properties and Applications in Jordan

Modern Applied Science; Vol. 12, No. 11; 2018 ISSN 1913-1844E-ISSN 1913-1852 Published by Canadian Center of Science and Education The Capital Assets Pricing Model & Arbitrage Pricing Theory: Properties

Modern Applied Science; Vol. 12, No. 11; 2018 ISSN 1913-1844E-ISSN 1913-1852 Published by Canadian Center of Science and Education The Capital Assets Pricing Model & Arbitrage Pricing Theory: Properties

Equity Research Methodology

Equity Research Methodology Morningstar s Buy and Sell Rating Decision Point Methodology By Philip Guziec Morningstar Derivatives Strategist August 18, 2011 The financial research community understands

Equity Research Methodology Morningstar s Buy and Sell Rating Decision Point Methodology By Philip Guziec Morningstar Derivatives Strategist August 18, 2011 The financial research community understands

Using Microsoft Corporation to Demonstrate the Optimal Capital Structure Trade-off Theory

JOURNAL OF ECONOMICS AND FINANCE EDUCATION Volume 9 Number 2 Winter 2010 29 Using Microsoft Corporation to Demonstrate the Optimal Capital Structure Trade-off Theory John C. Gardner, Carl B. McGowan Jr.,

JOURNAL OF ECONOMICS AND FINANCE EDUCATION Volume 9 Number 2 Winter 2010 29 Using Microsoft Corporation to Demonstrate the Optimal Capital Structure Trade-off Theory John C. Gardner, Carl B. McGowan Jr.,

Economics 689 Texas A&M University

Horizontal FDI Economics 689 Texas A&M University Horizontal FDI Foreign direct investments are investments in which a firm acquires a controlling interest in a foreign firm. called portfolio investments

Horizontal FDI Economics 689 Texas A&M University Horizontal FDI Foreign direct investments are investments in which a firm acquires a controlling interest in a foreign firm. called portfolio investments

Journal Of Financial And Strategic Decisions Volume 7 Number 3 Fall 1994 ASYMMETRIC INFORMATION: THE CASE OF BANK LOAN COMMITMENTS

Journal Of Financial And Strategic Decisions Volume 7 Number 3 Fall 1994 ASYMMETRIC INFORMATION: THE CASE OF BANK LOAN COMMITMENTS James E. McDonald * Abstract This study analyzes common stock return behavior

Journal Of Financial And Strategic Decisions Volume 7 Number 3 Fall 1994 ASYMMETRIC INFORMATION: THE CASE OF BANK LOAN COMMITMENTS James E. McDonald * Abstract This study analyzes common stock return behavior

How Markets React to Different Types of Mergers

How Markets React to Different Types of Mergers By Pranit Chowhan Bachelor of Business Administration, University of Mumbai, 2014 And Vishal Bane Bachelor of Commerce, University of Mumbai, 2006 PROJECT

How Markets React to Different Types of Mergers By Pranit Chowhan Bachelor of Business Administration, University of Mumbai, 2014 And Vishal Bane Bachelor of Commerce, University of Mumbai, 2006 PROJECT

Testing the Solow Growth Theory

Testing the Solow Growth Theory Dilip Mookherjee Ec320 Lecture 4, Boston University Sept 11, 2014 DM (BU) 320 Lect 4 Sept 11, 2014 1 / 25 RECAP OF L3: SIMPLE SOLOW MODEL Solow theory: deviates from HD

Testing the Solow Growth Theory Dilip Mookherjee Ec320 Lecture 4, Boston University Sept 11, 2014 DM (BU) 320 Lect 4 Sept 11, 2014 1 / 25 RECAP OF L3: SIMPLE SOLOW MODEL Solow theory: deviates from HD

Midterm Examination Number 1 February 19, 1996

Economics 200 Macroeconomic Theory Midterm Examination Number 1 February 19, 1996 You have 1 hour to complete this exam. Answer any four questions you wish. 1. Suppose that an increase in consumer confidence

Economics 200 Macroeconomic Theory Midterm Examination Number 1 February 19, 1996 You have 1 hour to complete this exam. Answer any four questions you wish. 1. Suppose that an increase in consumer confidence

THE BEHAVIOUR OF GOVERNMENT OF CANADA REAL RETURN BOND RETURNS: AN EMPIRICAL STUDY

ASAC 2005 Toronto, Ontario David W. Peters Faculty of Social Sciences University of Western Ontario THE BEHAVIOUR OF GOVERNMENT OF CANADA REAL RETURN BOND RETURNS: AN EMPIRICAL STUDY The Government of

ASAC 2005 Toronto, Ontario David W. Peters Faculty of Social Sciences University of Western Ontario THE BEHAVIOUR OF GOVERNMENT OF CANADA REAL RETURN BOND RETURNS: AN EMPIRICAL STUDY The Government of

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice A. Mean-Variance Analysis 1. Thevarianceofaportfolio. Consider the choice between two risky assets with returns R 1 and R 2.

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice A. Mean-Variance Analysis 1. Thevarianceofaportfolio. Consider the choice between two risky assets with returns R 1 and R 2.

ECON828 INTERNATIONAL INVESTMENT & RISK (DEPARTMENT OF ECONOMICS) SECOND SEMESTER 2009 COURSE OUTLINE

SECOND SEMESTER 2009 COURSE OUTLINE") ECON828 INTERNATIONAL INVESTMENT & RISK (DEPARTMENT OF ECONOMICS) SECOND SEMESTER 2009 COURSE OUTLINE Hugh Dougherty Lecturer in Charge ECON828 INTERNATIONAL INVESTMENT & RISK 1. COURSE OBJECTIVES This

ECON828 INTERNATIONAL INVESTMENT & RISK (DEPARTMENT OF ECONOMICS) SECOND SEMESTER 2009 COURSE OUTLINE Hugh Dougherty Lecturer in Charge ECON828 INTERNATIONAL INVESTMENT & RISK 1. COURSE OBJECTIVES This

The Long-Run Equity Risk Premium

The Long-Run Equity Risk Premium John R. Graham, Fuqua School of Business, Duke University, Durham, NC 27708, USA Campbell R. Harvey * Fuqua School of Business, Duke University, Durham, NC 27708, USA National

The Long-Run Equity Risk Premium John R. Graham, Fuqua School of Business, Duke University, Durham, NC 27708, USA Campbell R. Harvey * Fuqua School of Business, Duke University, Durham, NC 27708, USA National

UNIVERSITY Of ILLINOIS LIBRARY AT URBANA-CHAMPA1GN STACKS

UNIVERSITY Of ILLINOIS LIBRARY AT URBANA-CHAMPA1GN STACKS Digitized by the Internet Archive in University of Illinois 2011 with funding from Urbana-Champaign http://www.archive.org/details/analysisofnonsym436kimm

UNIVERSITY Of ILLINOIS LIBRARY AT URBANA-CHAMPA1GN STACKS Digitized by the Internet Archive in University of Illinois 2011 with funding from Urbana-Champaign http://www.archive.org/details/analysisofnonsym436kimm

Concentration and Stock Returns: Australian Evidence

2010 International Conference on Economics, Business and Management IPEDR vol.2 (2011) (2011) IAC S IT Press, Manila, Philippines Concentration and Stock Returns: Australian Evidence Katja Ignatieva Faculty

2010 International Conference on Economics, Business and Management IPEDR vol.2 (2011) (2011) IAC S IT Press, Manila, Philippines Concentration and Stock Returns: Australian Evidence Katja Ignatieva Faculty

Futures and Forward Markets

Futures and Forward Markets (Text reference: Chapters 19, 21.4) background hedging and speculation optimal hedge ratio forward and futures prices futures prices and expected spot prices stock index futures

Futures and Forward Markets (Text reference: Chapters 19, 21.4) background hedging and speculation optimal hedge ratio forward and futures prices futures prices and expected spot prices stock index futures

Introduction and Subject Outline. To provide general subject information and a broad coverage of the subject content of

Introduction and Subject Outline Aims: To provide general subject information and a broad coverage of the subject content of 316-351 Objectives: On completion of this lecture, students should: be aware

Introduction and Subject Outline Aims: To provide general subject information and a broad coverage of the subject content of 316-351 Objectives: On completion of this lecture, students should: be aware

Risky asset valuation and the efficient market hypothesis

Risky asset valuation and the efficient market hypothesis IGIDR, Bombay May 13, 2011 Pricing risky assets Principle of asset pricing: Net Present Value Every asset is a set of cashflow, maturity (C i,

Risky asset valuation and the efficient market hypothesis IGIDR, Bombay May 13, 2011 Pricing risky assets Principle of asset pricing: Net Present Value Every asset is a set of cashflow, maturity (C i,

SENSITIVITY ANALYSIS IN CAPITAL BUDGETING USING CRYSTAL BALL. Petter Gokstad 1

SENSITIVITY ANALYSIS IN CAPITAL BUDGETING USING CRYSTAL BALL Petter Gokstad 1 Graduate Assistant, Department of Finance, University of North Dakota Box 7096 Grand Forks, ND 58202-7096, USA Nancy Beneda

SENSITIVITY ANALYSIS IN CAPITAL BUDGETING USING CRYSTAL BALL Petter Gokstad 1 Graduate Assistant, Department of Finance, University of North Dakota Box 7096 Grand Forks, ND 58202-7096, USA Nancy Beneda

CAN AGENCY COSTS OF DEBT BE REDUCED WITHOUT EXPLICIT PROTECTIVE COVENANTS? THE CASE OF RESTRICTION ON THE SALE AND LEASE-BACK ARRANGEMENT

CAN AGENCY COSTS OF DEBT BE REDUCED WITHOUT EXPLICIT PROTECTIVE COVENANTS? THE CASE OF RESTRICTION ON THE SALE AND LEASE-BACK ARRANGEMENT Jung, Minje University of Central Oklahoma mjung@ucok.edu Ellis,

CAN AGENCY COSTS OF DEBT BE REDUCED WITHOUT EXPLICIT PROTECTIVE COVENANTS? THE CASE OF RESTRICTION ON THE SALE AND LEASE-BACK ARRANGEMENT Jung, Minje University of Central Oklahoma mjung@ucok.edu Ellis,

Assignment 5 The New Keynesian Phillips Curve

Econometrics II Fall 2017 Department of Economics, University of Copenhagen Assignment 5 The New Keynesian Phillips Curve The Case: Inflation tends to be pro-cycical with high inflation during times of

Econometrics II Fall 2017 Department of Economics, University of Copenhagen Assignment 5 The New Keynesian Phillips Curve The Case: Inflation tends to be pro-cycical with high inflation during times of

Foundations of Finance

Foundations of Finance Instructor: Prof. K. Ozgur Demirtas Office: KMC 9-150 Office Hours: Tuesday: 1:00-2:00 pm, Thursday: 1:00-2:00 pm, or by appointment Telephone: 646-312-3484 Email: kdemirta@stern.nyu.edu

Foundations of Finance Instructor: Prof. K. Ozgur Demirtas Office: KMC 9-150 Office Hours: Tuesday: 1:00-2:00 pm, Thursday: 1:00-2:00 pm, or by appointment Telephone: 646-312-3484 Email: kdemirta@stern.nyu.edu

Do Domestic Chinese Firms Benefit from Foreign Direct Investment?

Do Domestic Chinese Firms Benefit from Foreign Direct Investment? Chang-Tai Hsieh, University of California Working Paper Series Vol. 2006-30 December 2006 The views expressed in this publication are those

Do Domestic Chinese Firms Benefit from Foreign Direct Investment? Chang-Tai Hsieh, University of California Working Paper Series Vol. 2006-30 December 2006 The views expressed in this publication are those

Fair and Reasonable Royalty Rate Determination - When is the 25% rule applicable?

Fair and Reasonable Royalty Rate Determination - When is the 25% rule applicable? by Ove Granstrand 1 Article submitted to LES Nouvelles 1 Professor of Industrial Management and Economics, Chalmers University.

Fair and Reasonable Royalty Rate Determination - When is the 25% rule applicable? by Ove Granstrand 1 Article submitted to LES Nouvelles 1 Professor of Industrial Management and Economics, Chalmers University.

Conditional convergence: how long is the long-run? Paul Ormerod. Volterra Consulting. April Abstract

Conditional convergence: how long is the long-run? Paul Ormerod Volterra Consulting April 2003 pormerod@volterra.co.uk Abstract Mainstream theories of economic growth predict that countries across the

Conditional convergence: how long is the long-run? Paul Ormerod Volterra Consulting April 2003 pormerod@volterra.co.uk Abstract Mainstream theories of economic growth predict that countries across the

BUSINESS VALUATION-2 Course Outline

BUSINESS VALUATION-2 Course Outline Faculty: Economics Year: 2014 Course name: Business Valuation Advanced level (Business Valuation-2) Level: Master, 1 year Language of instruction: English Period: Module

BUSINESS VALUATION-2 Course Outline Faculty: Economics Year: 2014 Course name: Business Valuation Advanced level (Business Valuation-2) Level: Master, 1 year Language of instruction: English Period: Module

Chapter URL:

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Taxing Multinational Corporations Volume Author/Editor: Martin Feldstein, James R. Hines

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Taxing Multinational Corporations Volume Author/Editor: Martin Feldstein, James R. Hines

EQUITY RESEARCH AND PORTFOLIO MANAGEMENT

EQUITY RESEARCH AND PORTFOLIO MANAGEMENT By P K AGARWAL IIFT, NEW DELHI 1 MARKOWITZ APPROACH Requires huge number of estimates to fill the covariance matrix (N(N+3))/2 Eg: For a 2 security case: Require

EQUITY RESEARCH AND PORTFOLIO MANAGEMENT By P K AGARWAL IIFT, NEW DELHI 1 MARKOWITZ APPROACH Requires huge number of estimates to fill the covariance matrix (N(N+3))/2 Eg: For a 2 security case: Require

Semester / Term: -- Workload: 300 h Credit Points: 10

Module Title: Corporate Finance and Investment Module No.: DLMBCFIE Semester / Term: -- Duration: Minimum of 1 Semester Module Type(s): Elective Regularly offered in: WS, SS Workload: 300 h Credit Points:

Module Title: Corporate Finance and Investment Module No.: DLMBCFIE Semester / Term: -- Duration: Minimum of 1 Semester Module Type(s): Elective Regularly offered in: WS, SS Workload: 300 h Credit Points:

Examining RADR as a Valuation Method in Capital Budgeting

Examining RADR as a Valuation Method in Capital Budgeting James R. Scott Missouri State University Kee Kim Missouri State University The risk adjusted discount rate (RADR) method is used as a valuation

Examining RADR as a Valuation Method in Capital Budgeting James R. Scott Missouri State University Kee Kim Missouri State University The risk adjusted discount rate (RADR) method is used as a valuation

h Edition Economic Growth in a Cross Section of Countries

In the Name God Sharif University Technology Graduate School Management Economics Economic Growth in a Cross Section Countries Barro (1991) Navid Raeesi Fall 2014 Page 1 A Cursory Look I Are there any

In the Name God Sharif University Technology Graduate School Management Economics Economic Growth in a Cross Section Countries Barro (1991) Navid Raeesi Fall 2014 Page 1 A Cursory Look I Are there any

Convergence of Life Expectancy and Living Standards in the World

Convergence of Life Expectancy and Living Standards in the World Kenichi Ueda* *The University of Tokyo PRI-ADBI Joint Workshop January 13, 2017 The views are those of the author and should not be attributed

Convergence of Life Expectancy and Living Standards in the World Kenichi Ueda* *The University of Tokyo PRI-ADBI Joint Workshop January 13, 2017 The views are those of the author and should not be attributed

COST OF CAPITAL IN INTERNATIONAL MKTS

COST OF CAPITAL IN INTERNATIONAL MKTS Capital Structure and Cost of Capital Cost of Capital - Country Risk affects discount rates - Different countries will have different risk free rates (k f ). - High

COST OF CAPITAL IN INTERNATIONAL MKTS Capital Structure and Cost of Capital Cost of Capital - Country Risk affects discount rates - Different countries will have different risk free rates (k f ). - High

1.1 Please provide the background curricula vitae for all three authors.

C6-6 1.0. TOPIC: Background information REQUEST: 1.1 Please provide the background curricula vitae for all three authors. 1.2 Please indicate whether any of the authors have testified on behalf of a Canadian

C6-6 1.0. TOPIC: Background information REQUEST: 1.1 Please provide the background curricula vitae for all three authors. 1.2 Please indicate whether any of the authors have testified on behalf of a Canadian

Maximum Likelihood Estimation Richard Williams, University of Notre Dame, https://www3.nd.edu/~rwilliam/ Last revised January 13, 2018

Maximum Likelihood Estimation Richard Williams, University of otre Dame, https://www3.nd.edu/~rwilliam/ Last revised January 3, 208 [This handout draws very heavily from Regression Models for Categorical

Maximum Likelihood Estimation Richard Williams, University of otre Dame, https://www3.nd.edu/~rwilliam/ Last revised January 3, 208 [This handout draws very heavily from Regression Models for Categorical

Tax Policy and Foreign Direct Investment in Open Economies

ISSUE BRIEF 05.01.18 Tax Policy and Foreign Direct Investment in Open Economies George R. Zodrow, Ph.D., Baker Institute Rice Faculty Scholar and Allyn R. and Gladys M. Cline Chair of Economics, Rice University

ISSUE BRIEF 05.01.18 Tax Policy and Foreign Direct Investment in Open Economies George R. Zodrow, Ph.D., Baker Institute Rice Faculty Scholar and Allyn R. and Gladys M. Cline Chair of Economics, Rice University

Estimating the Market Risk Premium: The Difficulty with Historical Evidence and an Alternative Approach

Estimating the Market Risk Premium: The Difficulty with Historical Evidence and an Alternative Approach (published in JASSA, issue 3, Spring 2001, pp 10-13) Professor Robert G. Bowman Department of Accounting

Estimating the Market Risk Premium: The Difficulty with Historical Evidence and an Alternative Approach (published in JASSA, issue 3, Spring 2001, pp 10-13) Professor Robert G. Bowman Department of Accounting

Reading map : Structure of the market Measurement problems. It may simply reflect the profitability of the industry

Reading map : The structure-conduct-performance paradigm is discussed in Chapter 8 of the Carlton & Perloff text book. We have followed the chapter somewhat closely in this case, and covered pages 244-259

Reading map : The structure-conduct-performance paradigm is discussed in Chapter 8 of the Carlton & Perloff text book. We have followed the chapter somewhat closely in this case, and covered pages 244-259

The World Economy from a Distance

The World Economy from a Distance It would be difficult for any country today to completely isolate itself. Even tribal populations may find the trials of isolation a challenge. Most features of any economy

The World Economy from a Distance It would be difficult for any country today to completely isolate itself. Even tribal populations may find the trials of isolation a challenge. Most features of any economy

PUT-CALL PARITY AND THE EARLY EXERCISE PREMIUM FOR CURRENCY OPTIONS. Geoffrey Poitras, Chris Veld, and Yuriy Zabolotnyuk * September 30, 2005

1 PUT-CALL PARITY AND THE EARLY EXERCISE PREMIUM FOR CURRENCY OPTIONS By Geoffrey Poitras, Chris Veld, and Yuriy Zabolotnyuk * September 30, 2005 * Geoffrey Poitras is Professor of Finance, and Chris Veld

1 PUT-CALL PARITY AND THE EARLY EXERCISE PREMIUM FOR CURRENCY OPTIONS By Geoffrey Poitras, Chris Veld, and Yuriy Zabolotnyuk * September 30, 2005 * Geoffrey Poitras is Professor of Finance, and Chris Veld

Corporate Leverage and Taxes around the World

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 5-1-2015 Corporate Leverage and Taxes around the World Saralyn Loney Utah State University Follow this and

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 5-1-2015 Corporate Leverage and Taxes around the World Saralyn Loney Utah State University Follow this and