GDP growth ticked up for the first time in six quarters

|

|

|

- Britney Doyle

- 5 years ago

- Views:

Transcription

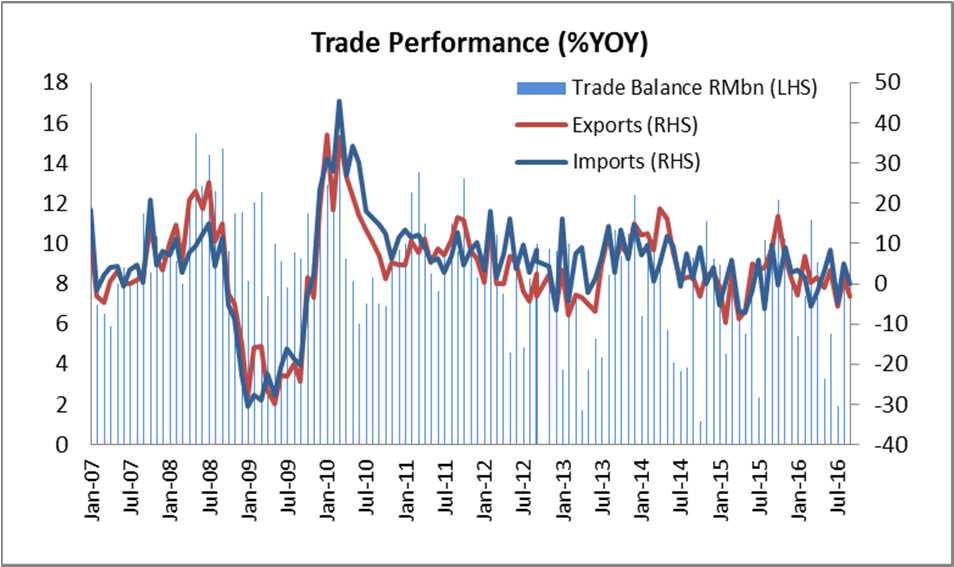

1 Global Markets Research Economics - Malaysia x GDP growth ticked up for the first time in six quarters The Malaysian economy snapped a five straight quarters of growth moderation and increased at its fastest pace in three quarters, by 4.3% YOY in 3Q. A rebound in net exports was the savior, offsetting the softer growth traction in domestic demand dragged by slower public spending and investment. While we see a higher headline GDP print, the rather hefty pullback in domestic demand growth to just 4.7% YOY in 3Q vs 2Q s 6.3% raised concerns if domestic growth momentum is at risks of faltering again. Hence, although the better than expected 3Q GDP print prompted us to revise our full year growth forecast higher to 4.2% (previous 4.0%), it is premature to conclude that the Malaysian economy is on a solid recovery path. In addition, the most recent outcome of the US Presidential election could also reignite global uncertainty and external risks, hence triggering increased market volatility that could have macroeconomic and policy implications. Amid a still uncertain backdrop, we feel it is too early to totally remove an OPR cut from the radar despite acknowledging that recent development has reduced the odds of a cut in the near term. Real GDP grew at its fastest pace in three quarters, by 4.3% YOY in 3Q Malaysia real GDP growth snapped a five straight quarters of moderation to increase 4.3% YOY in 3Q16 (2Q16: +4.0% YOY). This was a pleasant surprise vs our estimate of 3.9% and consensus estimate of 4.0%. Growth bounced back from 2Q s GFC-low and marked its first uptick in six quarters, spurring hopes the Malaysian economy may have seen its trough. The surprisingly upbeat reading was due to a turnaround in net exports to +5.9% YOY (2Q: -7.0%), which offset slower expansion in domestic demand (+4.7% vs +6.3%) dragged by slower growth from both the private and public sectors. While private consumption continued to increase at a faster pace for the 4 th straight quarter, its momentum has abated somewhat (3Q: +6.4%; 2Q: +6.3%; 1Q: +5.3%). Despite this, private consumption remained the main growth driver, amid slower expansions in gross fixed capital formation (+2.0% vs +6.1%) and public expenditure (+3.1% vs +6.5%). On a seasonally adjusted QOQ basis, real GDP growth picked up for the first time in three quarters to 1.5% in 3Q (2Q: +0.7%). Net exports contribution the savior, offsetting slower growth in domestic demand While we see a higher headline GDP print, the rather hefty pullback in domestic demand growth to just 4.7% YOY in 3Q vs 2Q s 6.3% raised concerns if 1

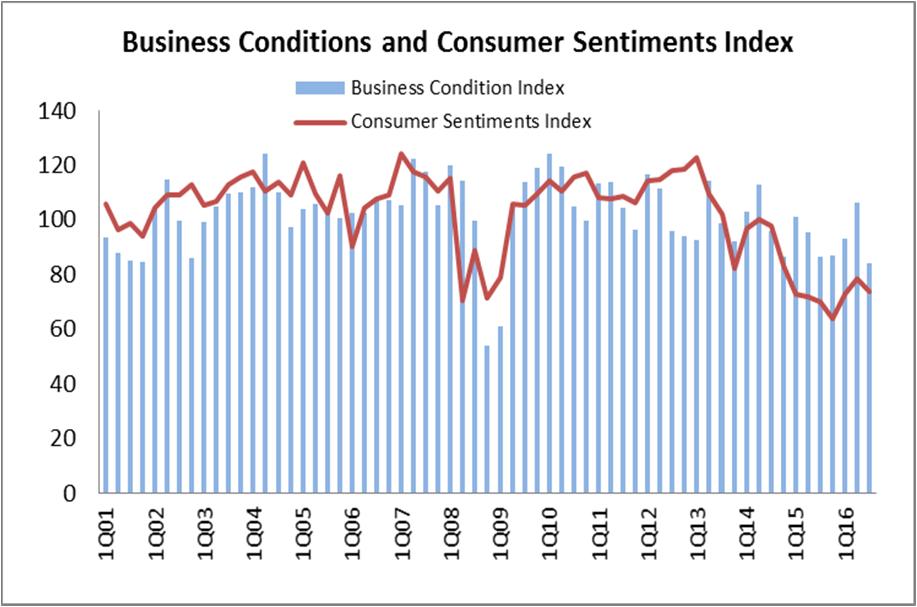

2 domestic growth momentum is at risks of faltering again. This worry is not unfounded since both consumer and business confidence indices by MIER had plunged below the 100-threshold to 73.6 and 83.9 respectively in 3Q, signaling a less optimistic outlook ahead. Private sector activities grew at a slightly slower pace of 6.0% YOY in 3Q (2Q: +6.1%) while growth in public sector activities plummeted to 0.3% YOY in 3Q (2Q: +6.9%), no thanks to a 3.8% YOY contraction in public investment and halved public spending growth of 3.1% YOY. Private sector activities were holding up better as quicker increase in private spending (+6.4% vs +6.3%) cushioned the slower growth in private investment (+4.7% vs +5.6%). Net exports bounced back into positive territory for the first time in three quarters, increasing 5.9% YOY in 3Q (2Q: -7.0%), as exports of goods and services contracted at a smaller pace of 1.3% YOY in 3Q vs a 2.3 YOY decline in imports (2Q: +1.0%; +2.0%). On the contrary, inventories drawdown (-1.6% YOY) remained a drag on overall GDP growth. Services and manufacturing remained in the forefront of growth On the supply side, all sectors registered improvement with the exception of slower growth in the construction sector. Services and manufacturing sectors remained in the forefront in spearheading growth, growing 6.1% and 4.2% YOY respectively in 3Q (2Q: +5.7% and +4.1%). Consumption-related services were the biggest growth driver for services while the manufacturing sector was boosted by export-oriented industries. Higher crude oil production led to quicker growth in mining (+3.6% vs +2.6%) but lagged effect of El Nino on CPO yields resulted in extended, albeit smaller, decline in the agriculture sector (-5.9% vs -7.9%). Meanwhile, growth in the construction sector tapered off to 7.9% YOY in 3Q (2Q: +8.8%), supported by continued expansion in civil engineering subsector. 2

3 Tripling in current account surplus eased concerns on twin deficits In a separate release, Malaysia s current account surplus tripled to RM6.0bn in 3Q16, from RM1.9bn in 2Q16, boosted by an RM6.7bn increase in surplus in the goods account to RM26.5bn (2Q: RM19.8bn). This should further ease concerns of a twin deficits as solid surplus in the goods accounts continued to offset higher deficits in the services and income accounts. Deficit in the services account widened to RM5.1bn while deficit in the income account widened to RM15.4bn in 3Q16 (2Q: -RM4.6bn and -RM13.3bn). The capital account reported a net outflow of RM7m vs a net inflow of RM118m in 2Q16 while the financial account saw net outflows for the first time in three quarters, of RM6.3bn (RM9.5bn in 2Q16) as a result of net outflow of portfolio investment (RM10.6bn) which offset the net inflows of FDI (RM6.5bn). Full year growth revised higher to 4.2%...odds of a OPR cut lower in the near term Despite the better than expected 3Q GDP print which prompted us to revise our full year growth forecast higher to 4.2% (previous 4.0%), it is premature to conclude that the Malaysian economy is on a solid recovery path. While we reckon external risks have dwindled somewhat recently, overall lift in exports could be dampened by signs of softer growth momentum in domestic demand. As mentioned above, both consumer and business sentiments have reversed course and plunged below the 100-threshold separating optimism and pessimism, signaling potential pullback in consumer spending and business activities in the immediate quarters ahead. In addition, the most recent outcome of the US Presidential election could also reignite global uncertainty and external risks, hence triggering increased market volatility that could spill over to the macro front. Amid a still uncertain backdrop, we feel it is too early to totally remove an OPR cut from the radar despite acknowledging that recent development has reduced the odds of a cut in the near term. 3

4 4

5 Hong Leong Bank Berhad Fixed Income & Economic Research, Global Markets Level 6, Wisma Hong Leong 18, Jalan Perak Kuala Lumpur Tel: Fax: DISCLAIMER This report is for information purposes only and does not take into account the investment objectives, financial situation or particular needs of any particular recipient. The information contained herein does not constitute the provision of investment advice and is not intended as an offer or solicitation with respect to the purchase or sale of any of the financial instruments mentioned in this report and will not form the basis or a part of any contract or commitment whatsoever. The information contained in this publication is derived from data obtained from sources believed by Hong Leong Bank Berhad ( HLBB ) to be reliable and in good faith, but no warranties or guarantees, representations are made by HLBB with regard to the accuracy, completeness or suitability of the data. Any opinions expressed reflect the current judgment of the authors of the report and do not necessarily represent the opinion of HLBB or any of the companies within the Hong Leong Bank Group ( HLB Group ). The opinions reflected herein may change without notice and the opinions do not necessarily correspond to the opinions of HLBB. HLBB does not have an obligation to amend, modify or update this report or to otherwise notify a reader or recipient thereof in the event that any matter stated herein, or any opinion, projection, forecast or estimate set forth herein, changes or subsequently becomes inaccurate. HLB Group, their directors, employees and representatives do not have any responsibility or liability to any person or recipient (whether by reason of negligence, negligent misstatement or otherwise) arising from any statement, opinion or information, expressed or implied, arising out of, contained in or derived from or omission from the reports or matter. HLBB may, to the extent permitted by law, buy, sell or hold significantly long or short positions; act as investment and/or commercial bankers; be represented on the board of the issuers; and/or engage in market making of securities mentioned herein. The past performance of financial instruments is not indicative of future results. Whilst every effort is made to ensure that statements of facts made in this report are accurate, all estimates, projections, forecasts, expressions of opinion and other subjective judgments contained in this report are based on assumptions considered to be reasonable as of the date of the document in which they are contained and must not be construed as a representation that the matters referred to therein will occur. Any projections or forecasts mentioned in this report may not be achieved due to multiple risk factors including without limitation market volatility, sector volatility, corporate actions, the unavailability of complete and accurate information. No assurance can be given that any opinion described herein would yield favorable investment results. Recipients who are not market professional or institutional investor customer of HLBB should seek the advice of their independent financial advisor prior to taking any investment decision based on the recommendations in this report. HLBB may provide hyperlinks to websites of entities mentioned in this report, however the inclusion of a link does not imply that HLBB endorses, recommends or approves any material on the linked page or accessible from it. Such linked websites are accessed entirely at your own risk. HLBB does not accept responsibility whatsoever for any such material, nor for consequences of its use. This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. This report is for the use of the addressees only and may not be redistributed, reproduced or passed on to any other person or published, in part or in whole, for any purpose, without the prior, written consent of HLBB. The manner of distributing this report may be restricted by law or regulation in certain countries. Persons into whose possession this report may come are required to inform themselves about and to observe such restrictions. By accepting this report, a recipient hereof agrees to be bound by the foregoing limitations. 5

Surprisingly strong 1Q GDP

Global Markets Research Economics - Malaysia Surprisingly strong 1Q GDP The Malaysian economy grew at a surprisingly strong pace of 5.6% YOY in 1Q17, marking its best growth in two years led by an impressive

Global Markets Research Economics - Malaysia Surprisingly strong 1Q GDP The Malaysian economy grew at a surprisingly strong pace of 5.6% YOY in 1Q17, marking its best growth in two years led by an impressive

BNM Annual Report 2016: Moderate outlook amid higher inflation

Global Markets Research Economics - Malaysia BNM Annual Report 2016: Moderate outlook amid higher inflation The Malaysian economy is expected to expand at a faster pace for the first time in three years,

Global Markets Research Economics - Malaysia BNM Annual Report 2016: Moderate outlook amid higher inflation The Malaysian economy is expected to expand at a faster pace for the first time in three years,

Vietnam grew quicker than expected in 3Q

September 9, 1 Global Markets Research Economics - Vietnam Vietnam grew quicker than expected in 3Q Vietnam s economy grew.93 in the past nine months (1H: +.) as momentum in the manufacturing and services

September 9, 1 Global Markets Research Economics - Vietnam Vietnam grew quicker than expected in 3Q Vietnam s economy grew.93 in the past nine months (1H: +.) as momentum in the manufacturing and services

Auction calendar 2019

Global Markets Research Fixed Income Auction calendar 2019 For 2019, there will be a total of 32 auctions (comprising of 16 MGS and 16 GII issuances) compared to the 33 auctions in 2018 (comprising 15

Global Markets Research Fixed Income Auction calendar 2019 For 2019, there will be a total of 32 auctions (comprising of 16 MGS and 16 GII issuances) compared to the 33 auctions in 2018 (comprising 15

Malaysia- GDP & BOP 1Q17

Real GDP growth surprised on the upside in 1Q17 Real GDP growth rose by 5.6% in 1Q17, exceeding market expectations Malaysia s real GDP growth rose by 5.6% yoy in 1Q17 (4.5% in 4Q16), significantly higher

Real GDP growth surprised on the upside in 1Q17 Real GDP growth rose by 5.6% in 1Q17, exceeding market expectations Malaysia s real GDP growth rose by 5.6% yoy in 1Q17 (4.5% in 4Q16), significantly higher

Global Markets Research Fixed Income

Global Markets Research Fixed Income Fixed Income Daily Market Snapshot Chang Wai Ming Fixed Income Strategist Hong Leong Bank Berhad, Global Markets Fixed Income & Economic Research WMChang@hlbb.hongleong.com.my

Global Markets Research Fixed Income Fixed Income Daily Market Snapshot Chang Wai Ming Fixed Income Strategist Hong Leong Bank Berhad, Global Markets Fixed Income & Economic Research WMChang@hlbb.hongleong.com.my

3Q18 GDP Growth to Ease to 4.2% amid Moderating Agricultural and Industrial Output

ECONOMIC REPORT National Account Preview 13 November 2018 GDP Growth to Ease to 4.2% amid Moderating Agricultural and Industrial Output Moderating business confidences. Looking at leading indicators, Malaysia

ECONOMIC REPORT National Account Preview 13 November 2018 GDP Growth to Ease to 4.2% amid Moderating Agricultural and Industrial Output Moderating business confidences. Looking at leading indicators, Malaysia

Global Markets Research Daily Market Highlights. Key Takeaways. What s Coming Up Next. July 27, Source: Bloomberg. Overnight Economic Data

July 27, 2017 Global Markets Research Daily Market Highlights Key Takeaways Overnight Economic Data US The Fed left Fed Fund Target rate unchanged at 1.00-1.25% as expected. and offered no surprises in

July 27, 2017 Global Markets Research Daily Market Highlights Key Takeaways Overnight Economic Data US The Fed left Fed Fund Target rate unchanged at 1.00-1.25% as expected. and offered no surprises in

Improved Macroeconomic Conditions Boost Consumer Sentiment to Its Highest Level in 3½-Year

ECONOMIC REPORT Business & Consumer Confidence 17 April 2018 Improved Macroeconomic Conditions Boost Consumer Sentiment to Its Highest Level in 3½-Year MIER s CSI rebounded to 3.5-year high. Underpin by

ECONOMIC REPORT Business & Consumer Confidence 17 April 2018 Improved Macroeconomic Conditions Boost Consumer Sentiment to Its Highest Level in 3½-Year MIER s CSI rebounded to 3.5-year high. Underpin by

Global Markets Research Fixed Income

Global Markets Research Fixed Income Fixed Income Daily Market Snapshot US Treasuries UST Tenure Closing (%) Chg (bps) 2-yr UST 2.49 12 5-yr UST 2.50 14 10-yr UST 2.67 12 30-yr UST 2.98 8 MGS GII* Tenure

Global Markets Research Fixed Income Fixed Income Daily Market Snapshot US Treasuries UST Tenure Closing (%) Chg (bps) 2-yr UST 2.49 12 5-yr UST 2.50 14 10-yr UST 2.67 12 30-yr UST 2.98 8 MGS GII* Tenure

Global Markets Research Daily Market Highlights. Key Takeaways. What s Coming Up Next. December 21, Overnight Economic Data

December 21, 2017 Global Markets Research Daily Market Highlights Key Takeaways Overnight Economic Data Overnight financial markets continued to take the hit from the passage of US Tax Bill by the Senate

December 21, 2017 Global Markets Research Daily Market Highlights Key Takeaways Overnight Economic Data Overnight financial markets continued to take the hit from the passage of US Tax Bill by the Senate

Global Markets Research Daily Market Highlights. Key Takeaways. What s Coming Up Next. September 25, 2017

September 25, 2017 Global Markets Research Daily Market Highlights Key Takeaways Fed speaks over last Friday revealed no new details. Kansas City Fed President Esther George stated that muted market reaction

September 25, 2017 Global Markets Research Daily Market Highlights Key Takeaways Fed speaks over last Friday revealed no new details. Kansas City Fed President Esther George stated that muted market reaction

Global Markets Research Fixed Income

Global Markets Research Fixed Income Fixed Income Daily Market Snapshot US Treasuries US Treasuries rallied as the curve shifted lower as investors assessed the impact on the economy and Fed policy from

Global Markets Research Fixed Income Fixed Income Daily Market Snapshot US Treasuries US Treasuries rallied as the curve shifted lower as investors assessed the impact on the economy and Fed policy from

3Q18 Current Account Surplus Lowest Since 3Q16 amid Continued Deficit in Services

n ECONOMIC REPORT Balance of Payment 21 November 218 3Q18 Current Account Surplus Lowest Since 3Q16 amid Continued Deficit in Services Malaysia s current account surplus at 9-quarter low. Current account

n ECONOMIC REPORT Balance of Payment 21 November 218 3Q18 Current Account Surplus Lowest Since 3Q16 amid Continued Deficit in Services Malaysia s current account surplus at 9-quarter low. Current account

Indonesia Outlook. Steady and stable 2018 growth. Thursday, February 07, Highlights

Indonesia Outlook Steady and stable 2018 growth Highlights Thursday, February 07, 2019 Treasury Research Tel: 6530-8384 2018 final quarter GDP growth came out at 5.18% yoy (-1.69% qoq), which was in line

Indonesia Outlook Steady and stable 2018 growth Highlights Thursday, February 07, 2019 Treasury Research Tel: 6530-8384 2018 final quarter GDP growth came out at 5.18% yoy (-1.69% qoq), which was in line

Economics. Market Insight Tuesday, 6 June, Malaysia Economy. Exports and Imports slowed down in April. Chart 1: Malaysia: External Trade

Market Insight Tuesday, 6 June, 2017 RM'bn Jan'10 Jan'11 Jan'12 Jan'13 Jan'14 Jan'15 Jan'16 Jan'17 % y-o-y Imran Nurginias Ibrahim imran@bimbsec.com.my PP16795/03/2013(031743) 03-26131733 www.bisonline.com

Market Insight Tuesday, 6 June, 2017 RM'bn Jan'10 Jan'11 Jan'12 Jan'13 Jan'14 Jan'15 Jan'16 Jan'17 % y-o-y Imran Nurginias Ibrahim imran@bimbsec.com.my PP16795/03/2013(031743) 03-26131733 www.bisonline.com

BNM Maintains OPR at 3.25%, Hawkish About Economic Outlook

7 March 2018 ECONOMIC REVIEW March 2018 BNM MPC BNM Maintains OPR at 3.25%, Hawkish About Economic Outlook Overnight Policy Rate maintained at 3.25%. In line with our expectation, overnight policy rate,

7 March 2018 ECONOMIC REVIEW March 2018 BNM MPC BNM Maintains OPR at 3.25%, Hawkish About Economic Outlook Overnight Policy Rate maintained at 3.25%. In line with our expectation, overnight policy rate,

Global PMI. Global economy set for robust Q2 growth. June 8 th IHS Markit. All Rights Reserved.

Global PMI Global economy set for robust Q2 growth June 8 th 2017 2 PMI indicates robust global growth in Q2 The global economy is on course for a robust second quarter, according to PMI survey data. The

Global PMI Global economy set for robust Q2 growth June 8 th 2017 2 PMI indicates robust global growth in Q2 The global economy is on course for a robust second quarter, according to PMI survey data. The

Youth Unemployment Rate Remains High as Skills Mismatch Stay Prevalent

3 May 2018 ECONOMIC REVIEW 2017 Labour Market Youth Unemployment Rate Remains High as Skills Mismatch Stay Prevalent Youth unemployment rate stays high amid skills mismatch. Based on the latest labour

3 May 2018 ECONOMIC REVIEW 2017 Labour Market Youth Unemployment Rate Remains High as Skills Mismatch Stay Prevalent Youth unemployment rate stays high amid skills mismatch. Based on the latest labour

KINDLY REFER TO THE LAST PAGE OF THIS PUBLICATION FOR IMPORTANT DISCLOSURES

9 May 2017 ECONOMIC REVIEW 2016 Labour Market Youth Unemployment Rate Remain High Youth unemployment rate hits 10.5% with number of unemployed youth reached 273,400 persons in 2016. Youth labour force

9 May 2017 ECONOMIC REVIEW 2016 Labour Market Youth Unemployment Rate Remain High Youth unemployment rate hits 10.5% with number of unemployed youth reached 273,400 persons in 2016. Youth labour force

Stable Labor Market Promotes Wage Growth

2 June 2017 ECONOMIC REVIEW 2016 Salaries & Wages Stable Labor Market Promotes Wage Growth Wage growth registered at 6.4% in 2016. Malaysia s median wage grew by 6.4% to RM1,703 last year. The wage growth

2 June 2017 ECONOMIC REVIEW 2016 Salaries & Wages Stable Labor Market Promotes Wage Growth Wage growth registered at 6.4% in 2016. Malaysia s median wage grew by 6.4% to RM1,703 last year. The wage growth

Monthly Outlook. June Summary

Monthly Outlook June 2015 Summary Yields of US Treasuries (USTs) rallied in May, with the 2-year and 10-year yields up 4 and 9 basis points (bps) respectively as compared to end-april levels. During the

Monthly Outlook June 2015 Summary Yields of US Treasuries (USTs) rallied in May, with the 2-year and 10-year yields up 4 and 9 basis points (bps) respectively as compared to end-april levels. During the

GDP REPORT 10 December 2018

GDP REPORT 10 December 2018 Agriculture caused Q3 s positive surprise; our GDP growth forecast revised to 4.1% Treasury Sales Team +40 372 31 85 88 sales.treasury@otpbank.ro The National Institute of Statistics

GDP REPORT 10 December 2018 Agriculture caused Q3 s positive surprise; our GDP growth forecast revised to 4.1% Treasury Sales Team +40 372 31 85 88 sales.treasury@otpbank.ro The National Institute of Statistics

Sublime. Key Take Away GDP Numbers Detail 1Q16 4Q15 1Q15 Real GDP (y-o-y) Real GDP (q-o-q) Domestic Demand Growth

Real GDP (q-o-q) Domestic Demand Growth") M&A Securities Economic Report: Malaysian 1Q16 GDP PP14767/09/2012(030761) Sublime Friday, May 13, 2016 Key Take Away GDP Numbers Detail 1Q16 4Q15 1Q15 Real GDP (y-o-y) 4.2 4.5 5.7 Real GDP (q-o-q) 1.0

M&A Securities Economic Report: Malaysian 1Q16 GDP PP14767/09/2012(030761) Sublime Friday, May 13, 2016 Key Take Away GDP Numbers Detail 1Q16 4Q15 1Q15 Real GDP (y-o-y) 4.2 4.5 5.7 Real GDP (q-o-q) 1.0

MARKET REVIEW & OUTLOOK February 2018

MARKET REVIEW & OUTLOOK February 2018 1.0 Fixed Income Economics During the month, Malaysia s 4Q2017 GDP was released. Real Gross Domestic Product ( GDP ) grew 5.9% YoY, slightly slower than the 6.2% recorded

MARKET REVIEW & OUTLOOK February 2018 1.0 Fixed Income Economics During the month, Malaysia s 4Q2017 GDP was released. Real Gross Domestic Product ( GDP ) grew 5.9% YoY, slightly slower than the 6.2% recorded

Global Markets Research Daily Market Highlights. Key Takeaways. What s Coming Up Next. November 3, Source: Bloomberg

November 3, 2017 Global Markets Research Daily Market Highlights Key Takeaways Overnight Economic Data US EU UK Singapore Australia Markets turned a little risk averse overnight, somewhat unsettled by

November 3, 2017 Global Markets Research Daily Market Highlights Key Takeaways Overnight Economic Data US EU UK Singapore Australia Markets turned a little risk averse overnight, somewhat unsettled by

Global PMI. Solid Q2 growth masks widening growth differentials. July 7 th IHS Markit. All Rights Reserved.

Global PMI Solid Q2 growth masks widening growth differentials July 7 th 2017 2 Widening developed and emerging world growth trends The global economy enjoyed further steady growth in June, according to

Global PMI Solid Q2 growth masks widening growth differentials July 7 th 2017 2 Widening developed and emerging world growth trends The global economy enjoyed further steady growth in June, according to

Growth to accelerate. A quarterly analysis of trends in the Irish economy

Produced by the Economic Research Unit July 2014 A quarterly analysis of trends in the Irish economy Growth to accelerate Strong start to 2014 Recovery becoming more broad-based GDP growth revised up for

Produced by the Economic Research Unit July 2014 A quarterly analysis of trends in the Irish economy Growth to accelerate Strong start to 2014 Recovery becoming more broad-based GDP growth revised up for

Global Markets Research Daily Market Highlights. Key Takeaways. What s Coming Up Next. March 15, 2018

March 15, 2018 Global Markets Research Daily Market Highlights Key Takeaways Markets turned uneasy again, roiled by ongoing concerns over brewing trade wars and US political development, not forgetting

March 15, 2018 Global Markets Research Daily Market Highlights Key Takeaways Markets turned uneasy again, roiled by ongoing concerns over brewing trade wars and US political development, not forgetting

2,500 2,000 1,500 1, , ,000-1,500-2,000-2,500. May-13. Jun-13. Apr-13. Feb-13. Mar-13

Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 QUARTERLY REVIEW June 213 ECONOMIC REPORT The End of Euphoria Perception vs.

Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 QUARTERLY REVIEW June 213 ECONOMIC REPORT The End of Euphoria Perception vs.

MARKET REPORT AND STRATEGY

MARKET OUTLOOK AND STRATEGY MAY 2009 Market Review The KLCI ended May 53 points or 5.4% higher to close at 1,044 points. Although the announcement of 1Q09 GDP on May 27 was indeed weak at 6.2%, nearly

MARKET OUTLOOK AND STRATEGY MAY 2009 Market Review The KLCI ended May 53 points or 5.4% higher to close at 1,044 points. Although the announcement of 1Q09 GDP on May 27 was indeed weak at 6.2%, nearly

Higher Minimum Wage to Boost Domestic Economy Without Burdening Businesses

7 September 2018 ECONOMIC REVIEW 2019 Minimum Wage Higher Minimum Wage to Boost Domestic Economy Without Burdening Businesses Gradual rise in the national minimum wage will have positive impacts on Malaysia

7 September 2018 ECONOMIC REVIEW 2019 Minimum Wage Higher Minimum Wage to Boost Domestic Economy Without Burdening Businesses Gradual rise in the national minimum wage will have positive impacts on Malaysia

Malaysia- GDP & BOP 3Q16

November 2016 Higher GDP growth in 3Q16, led by net exports Real GDP growth trended higher for the first time since 2Q15 Economic growth rebounded after slowing down for five consecutive quarters since

November 2016 Higher GDP growth in 3Q16, led by net exports Real GDP growth trended higher for the first time since 2Q15 Economic growth rebounded after slowing down for five consecutive quarters since

Global Markets Research Daily Market Highlights. Key Takeaways. What s Coming Up Next. September 21, Source: Bloomberg. Overnight Economic Data

September 21, 2017 Global Markets Research Daily Market Highlights Overnight Economic Data Key Takeaways FOMC kept rates unchanged at 1.00-1.25% and announced that the Fed will begin trimming its balance

September 21, 2017 Global Markets Research Daily Market Highlights Overnight Economic Data Key Takeaways FOMC kept rates unchanged at 1.00-1.25% and announced that the Fed will begin trimming its balance

Growth might show positive surprise

Baltic Outlook Growth might show positive surprise Violeta Klyvienė Senior Baltic Analyst +370 5 2156992, +370 611 24354 April 2011 vkly@danskebank.dk Important disclosures and certifications are contained

Baltic Outlook Growth might show positive surprise Violeta Klyvienė Senior Baltic Analyst +370 5 2156992, +370 611 24354 April 2011 vkly@danskebank.dk Important disclosures and certifications are contained

PPI Contracted for Two Consecutive Months as Prices Fell Further For Agriculture

30 March 2018 ECONOMIC REVIEW February 2018 Producer Price Index Contracted for Two Consecutive Months as Prices Fell Further For Agriculture Producer prices continued to fall for two consecutive months.

30 March 2018 ECONOMIC REVIEW February 2018 Producer Price Index Contracted for Two Consecutive Months as Prices Fell Further For Agriculture Producer prices continued to fall for two consecutive months.

JUL AUG SEP OCT NOV DEC JAN FEB MAR APR MAY JUN

BOT raised GDP growth forecasts for and 2018 BOT kept its policy rate unchanged at 1.5% for eighteen straight month Bank of Thailand (BOT) maintained its policy rate, i.e. one-day repurchase rate, at 1.5%

BOT raised GDP growth forecasts for and 2018 BOT kept its policy rate unchanged at 1.5% for eighteen straight month Bank of Thailand (BOT) maintained its policy rate, i.e. one-day repurchase rate, at 1.5%

Indonesia chart book Consumption trumps weak trade

Economics Indonesia chart book Consumption trumps weak trade Group Research 7 August 2018 Radhika Rao Economist Please direct distribution queries to Violet Lee +65 68785281 violetleeyh@dbs.com 2Q GDP

Economics Indonesia chart book Consumption trumps weak trade Group Research 7 August 2018 Radhika Rao Economist Please direct distribution queries to Violet Lee +65 68785281 violetleeyh@dbs.com 2Q GDP

KINDLY REFER TO THE LAST PAGE OF THIS PUBLICATION FOR IMPORTANT DISCLOSURES

1 June 2017 MONTHLY ECONOMIC REVIEW May 2017 Malaysia Economy Riding High in 1Q17 Leading index recorded the highest in two years. In March 2017, leading index grew by 1.8%yoy, the highest since March

1 June 2017 MONTHLY ECONOMIC REVIEW May 2017 Malaysia Economy Riding High in 1Q17 Leading index recorded the highest in two years. In March 2017, leading index grew by 1.8%yoy, the highest since March

4Q2013 GDP better than expected

Mohd Afzanizam Abdul Rashid Chief Economist 03-2088 8075 afzanizam@bankislam.com.my 4Q2013 GDP better than expected GDP above expectation Malaysia s GDP scorecard for 4Q2013 released on Wednesday saw the

Mohd Afzanizam Abdul Rashid Chief Economist 03-2088 8075 afzanizam@bankislam.com.my 4Q2013 GDP better than expected GDP above expectation Malaysia s GDP scorecard for 4Q2013 released on Wednesday saw the

Malaysia- Fiscal policy

Dec-14 Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 22 July 2016 Higher oil prices may provide some fiscal flexibility

Dec-14 Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 22 July 2016 Higher oil prices may provide some fiscal flexibility

Financial Market Outlook: Stocks Rebounding from July Correction, Further Gains Likely. Bond Yields Range Bound

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Stocks Rebounding from July Correction, Further Gains Likely. Bond

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Stocks Rebounding from July Correction, Further Gains Likely. Bond

Economic Research KDN No.: PP14787/11/2012(030811)

") wider Economic Research KDN No.: PP14787/11/2012(030811) Vol.: ER/014/2015 State of Kuwait: Country Risk Insights Economic Research Led By: Nor Zahidi Alias Chief Economist +603 2082 2277 zahidi@marc.com.my

wider Economic Research KDN No.: PP14787/11/2012(030811) Vol.: ER/014/2015 State of Kuwait: Country Risk Insights Economic Research Led By: Nor Zahidi Alias Chief Economist +603 2082 2277 zahidi@marc.com.my

Economic activity gathers pace

Produced by the Economic Research Unit October 2014 A quarterly analysis of trends in the Irish economy Economic activity gathers pace Positive data flow Recovery broadening out GDP growth revised up to

Produced by the Economic Research Unit October 2014 A quarterly analysis of trends in the Irish economy Economic activity gathers pace Positive data flow Recovery broadening out GDP growth revised up to

Global PMI. Global economy starts 2017 on the front foot, PMI at 22-month high. February 8 th 2016

Global PMI Global economy starts 2017 on the front foot, PMI at 22-month high February 8 th 2016 2016 IHS Markit. All Rights Reserved. 2 Global PMI at 22-month high The global economy started 2017 with

Global PMI Global economy starts 2017 on the front foot, PMI at 22-month high February 8 th 2016 2016 IHS Markit. All Rights Reserved. 2 Global PMI at 22-month high The global economy started 2017 with

Eurozone Economic Watch Higher growth forecasts for January 2018

Eurozone Economic Watch Higher growth forecasts for 2018-19 January 2018 Eurozone Economic Watch January 2018 Eurozone: Higher growth forecasts for 2018-19 Our MICA-BBVA model estimates a broadly stable

Eurozone Economic Watch Higher growth forecasts for 2018-19 January 2018 Eurozone Economic Watch January 2018 Eurozone: Higher growth forecasts for 2018-19 Our MICA-BBVA model estimates a broadly stable

BTMU Focus Latin America Mexico: macroeconomic performance Mexico: (2Q GDP and Current Monthly Indicators)

") BTMU Focus Latin America Mexico: macroeconomic performance Mexico: (Q GDP and Current Monthly Indicators) MUFG UNION BANK Economic Research (New York) Hongrui Zhang Latin America Economist hozhang@us.mufg.jp

BTMU Focus Latin America Mexico: macroeconomic performance Mexico: (Q GDP and Current Monthly Indicators) MUFG UNION BANK Economic Research (New York) Hongrui Zhang Latin America Economist hozhang@us.mufg.jp

Thailand. Respectable Growth in Monday, February 20, 2017

Thailand Respectable Growth in 2016 Treasury Advisory Corporate FX & Structured Products Tel: 6349-1888 / 1881 Interest Rate Derivatives Tel: 6349-1899 Investments & Structured Products Tel: 6349-1886

Thailand Respectable Growth in 2016 Treasury Advisory Corporate FX & Structured Products Tel: 6349-1888 / 1881 Interest Rate Derivatives Tel: 6349-1899 Investments & Structured Products Tel: 6349-1886

Investec Services PMI Ireland

Embargoed until: 06:00 (Dublin) July 4th 18 Investec Services PMI Ireland Sharpest rise in activity since January Investec T: +3-1-421-0496 E: Investec.Economics@investec.ie W: www.investec.ie Investec

Embargoed until: 06:00 (Dublin) July 4th 18 Investec Services PMI Ireland Sharpest rise in activity since January Investec T: +3-1-421-0496 E: Investec.Economics@investec.ie W: www.investec.ie Investec

Global Markets Research Fixed Income

Global Markets Research Fixed Income Fixed Income Daily Market Snapshot UST Tenure Closing (%) Chg (bps) 2-yr UST 2.81 0 5-yr UST 2.87-2 10-yr UST 3.04-2 30-yr UST 3.30-1 MGS GII* Tenure Closing (%) Chg

Global Markets Research Fixed Income Fixed Income Daily Market Snapshot UST Tenure Closing (%) Chg (bps) 2-yr UST 2.81 0 5-yr UST 2.87-2 10-yr UST 3.04-2 30-yr UST 3.30-1 MGS GII* Tenure Closing (%) Chg

Insolvency forecasts. Economic Research August 2017

Insolvency forecasts Economic Research August 2017 Summary We present our new insolvency forecasting model which offers a broader scope of macroeconomic developments to better predict insolvency developments.

Insolvency forecasts Economic Research August 2017 Summary We present our new insolvency forecasting model which offers a broader scope of macroeconomic developments to better predict insolvency developments.

BTMU Focus Latin America Colombia: macroeconomic performance Mexico: (1Q 2015)

") BTMU Focus Latin America Colombia: macroeconomic performance Mexico: (1Q 1) MUFG UNION BANK Economic Research (New York) Hongrui Zhang Latin America Economist hozhang@us.mufg.jp +1(1)7-7 July 7, 1 Contents

BTMU Focus Latin America Colombia: macroeconomic performance Mexico: (1Q 1) MUFG UNION BANK Economic Research (New York) Hongrui Zhang Latin America Economist hozhang@us.mufg.jp +1(1)7-7 July 7, 1 Contents

MARKET OUTLOOK January 2018

MARKET OUTLOOK January 2018 1.0 Fixed Income Fixed Income Outlook & Investment Strategy Given that it was the start of the new trading year, trading volume in the MGS market rebounded sharply in January

MARKET OUTLOOK January 2018 1.0 Fixed Income Fixed Income Outlook & Investment Strategy Given that it was the start of the new trading year, trading volume in the MGS market rebounded sharply in January

Global PMI. Global economic growth kicks higher at start of fourth quarter but outlook darkens. November 14 th 2016

Global PMI Global economic growth kicks higher at start of fourth quarter but outlook darkens November 14 th 2016 2 Global PMI at 11-month high in October Global economic growth kicked higher at the start

Global PMI Global economic growth kicks higher at start of fourth quarter but outlook darkens November 14 th 2016 2 Global PMI at 11-month high in October Global economic growth kicked higher at the start

Leumi. Global Economics Monthly Review. Arie Tal, Research Economist. July 12, Capital Markets Division, Economics Department. leumiusa.

Global Economics Monthly Review July 12, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report

Global Economics Monthly Review July 12, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report

Global Markets Research Daily Market Highlights. Key Takeaways. What s Coming Up Next. April 13, 2018

April 13, 2018 Global Markets Research Daily Market Highlights Key Takeaways Overnight, risk appetite in the markets improved after concerns over US-Russia confrontation over Syrian conflict eased. On

April 13, 2018 Global Markets Research Daily Market Highlights Key Takeaways Overnight, risk appetite in the markets improved after concerns over US-Russia confrontation over Syrian conflict eased. On

Investec Services PMI Ireland

Embargoed until: 06:00 (Dublin) June 6th 18 Investec Services PMI Ireland Investec T: +3-1-421-0496 E: Investec.Economics@investec.ie W: www.investec.ie Investec in Ireland, a member of the Investec Group,

Embargoed until: 06:00 (Dublin) June 6th 18 Investec Services PMI Ireland Investec T: +3-1-421-0496 E: Investec.Economics@investec.ie W: www.investec.ie Investec in Ireland, a member of the Investec Group,

April 13, Economics Research - Globanomics - Q4/16. Globanomics. World s Dashboard of Economic Indicators Q4 2016

April 13, 2017 Economics Research - Globanomics - Q4/16 Globanomics World s Dashboard of Economic Indicators Q4 2016 Globanomics: Global Economic Indicators Q4 16 1 Quarter at a Glance The IMF revised

April 13, 2017 Economics Research - Globanomics - Q4/16 Globanomics World s Dashboard of Economic Indicators Q4 2016 Globanomics: Global Economic Indicators Q4 16 1 Quarter at a Glance The IMF revised

FLASH NOTE EUROPE CHART OF THE WEEK: GERMAN GROWTH A BLIP OR SOMETHING MORE? SUMMARY

Author NADIA GHARBI, CFA ngharbi@pictet.com SUMMARY German GDP figures showed that the German economy contracted in Q3 for the first time since Q1 2015 but markets were prepared. Economic activity was

Author NADIA GHARBI, CFA ngharbi@pictet.com SUMMARY German GDP figures showed that the German economy contracted in Q3 for the first time since Q1 2015 but markets were prepared. Economic activity was

Malaysia Outlook. 100 days later, what should we expect after this? Thursday, August 23, Highlights

Malaysia Outlook 100 days later, what should we expect after this? Highlights Thursday, August 23, 2018 Manifesto promises may probably require a longer time period to be delivered Debt can risk weighing

Malaysia Outlook 100 days later, what should we expect after this? Highlights Thursday, August 23, 2018 Manifesto promises may probably require a longer time period to be delivered Debt can risk weighing

Global PMI. Global economy buoyed by rising US strength. June 12 th IHS Markit. All Rights Reserved.

Global PMI Global economy buoyed by rising US strength June 12 th 2018 2 Global PMI rises but also brings signs of slower future growth At 54.0 in May, the headline JPMorgan Global Composite PMI, compiled

Global PMI Global economy buoyed by rising US strength June 12 th 2018 2 Global PMI rises but also brings signs of slower future growth At 54.0 in May, the headline JPMorgan Global Composite PMI, compiled

Global Markets Research Fixed Income

Global Markets Research Fixed Income Fixed Income Daily Market Snapshot US Treasuries UST Tenure Closing (%) Chg (bps) 2-yr UST 1.47 0 5-yr UST 1.92 0 10-yr UST 2.32 0 30-yr UST 2.87 0 M GS GII* Tenure

Global Markets Research Fixed Income Fixed Income Daily Market Snapshot US Treasuries UST Tenure Closing (%) Chg (bps) 2-yr UST 1.47 0 5-yr UST 1.92 0 10-yr UST 2.32 0 30-yr UST 2.87 0 M GS GII* Tenure

Global Markets Research Daily Market Highlights

September 20, 2018 Global Markets Research Daily Market Highlights Key Takeaways US stocks extended further climb overnight fueled by the gain in financials shares as the yield on US 10Y treasuries rose

September 20, 2018 Global Markets Research Daily Market Highlights Key Takeaways US stocks extended further climb overnight fueled by the gain in financials shares as the yield on US 10Y treasuries rose

ASEAN Insights: Regional trends

ASEAN Insights: Regional trends January 2017 1. Global trends GLOBAL ECONOMY AND EQUITY MARKETS ENTER 2017 ON A STRONG NOTE DESPITE GEOPOLITICAL UNCERTAINTIES The global economy entered 2017 on a strong

ASEAN Insights: Regional trends January 2017 1. Global trends GLOBAL ECONOMY AND EQUITY MARKETS ENTER 2017 ON A STRONG NOTE DESPITE GEOPOLITICAL UNCERTAINTIES The global economy entered 2017 on a strong

FLASH NOTE CHINA: MIXED OCTOBER HARD DATA GOVERNMENT STIMULUS STARTS TO BEAR SOME FRUITS SUMMARY

Author DONG CHEN dochen@pictet.com SUMMARY Hard data out of China for October were mixed. Growth in infrastructure investment picked up, suggesting the government s policy easing may be starting to have

Author DONG CHEN dochen@pictet.com SUMMARY Hard data out of China for October were mixed. Growth in infrastructure investment picked up, suggesting the government s policy easing may be starting to have

Global Markets Research Daily Market Highlights

June 8, 2018 Global Markets Research Daily Market Highlights Key Takeaways Markets turned to a cautious mode overnight ahead of the G7 summit and major central bank meetings, not to forget the Trump-Kim

June 8, 2018 Global Markets Research Daily Market Highlights Key Takeaways Markets turned to a cautious mode overnight ahead of the G7 summit and major central bank meetings, not to forget the Trump-Kim

Economic Research KDN No.: PP14787/11/2012(030811)

") wider Economic Research KDN No.: PP14787/11/2012(030811) Vol.: ER/009/2018 Capital Flows, Renminbi & the Ringgit Trend Economic Research Led By: Nor Zahidi Alias Chief Economist +603 2717 2936 zahidi@marc.com.my

wider Economic Research KDN No.: PP14787/11/2012(030811) Vol.: ER/009/2018 Capital Flows, Renminbi & the Ringgit Trend Economic Research Led By: Nor Zahidi Alias Chief Economist +603 2717 2936 zahidi@marc.com.my

MUFG LATIN AMERICA TOPICS

MUFG LATIN AMERICA TOPICS Colombia s Macroeconomic Performance: Q3 17 GDP and Current Monthly Indicators MUFG UNION BANK, N.A. ECONOMIC RESEARCH (NEW YORK) KAREN MARTINEZ Latin America Economist +1(1)78-78

MUFG LATIN AMERICA TOPICS Colombia s Macroeconomic Performance: Q3 17 GDP and Current Monthly Indicators MUFG UNION BANK, N.A. ECONOMIC RESEARCH (NEW YORK) KAREN MARTINEZ Latin America Economist +1(1)78-78

Australia Real GDP Likely to Increase +3.0% in 2018:4Q and +3.25% in 2019:4Q

Economics Weekly International Highlights Wednesday, March 7, 2018 Dick Rippe 212-446-5636 Dick.Rippe@evercoreisi.com Sean Zhang 212-446-9438 sean.zhang@evercoreisi.com Ed Hyman 212-446-5617 ed.hyman@evercoreisi.com

Economics Weekly International Highlights Wednesday, March 7, 2018 Dick Rippe 212-446-5636 Dick.Rippe@evercoreisi.com Sean Zhang 212-446-9438 sean.zhang@evercoreisi.com Ed Hyman 212-446-5617 ed.hyman@evercoreisi.com

Economic Research KDN No.: PP14787/11/2012(030811)

") wider Economic Research KDN No.: PP14787/11/2012(030811) Vol.: ER/004/2015 Malaysia: Country Risk Insight Economics Team Led By: Nor Zahidi Alias Chief Economist +603 2082 2277 zahidi@marc.com.my www.marc.com.my

wider Economic Research KDN No.: PP14787/11/2012(030811) Vol.: ER/004/2015 Malaysia: Country Risk Insight Economics Team Led By: Nor Zahidi Alias Chief Economist +603 2082 2277 zahidi@marc.com.my www.marc.com.my

Flash Note Switzerland: Q2 GDP growth

FLASH NOTE Flash Note Switzerland: Q2 GDP growth The devil is in the details Pictet Wealth Management - Asset Allocation & Macro Research 7 September 2018 Yes, the Swiss economy is booming. GDP grew by

FLASH NOTE Flash Note Switzerland: Q2 GDP growth The devil is in the details Pictet Wealth Management - Asset Allocation & Macro Research 7 September 2018 Yes, the Swiss economy is booming. GDP grew by

PROPERTY INSIGHTS. Market Overview. Home buyers remain cautious despite stronger GDP growth. Kuala Lumpur Quarter 3, 2017

PROPERTY INSIGHTS Kuala Lumpur Quarter 3, 2017 Home buyers remain cautious despite stronger GDP growth Market Overview The residential market is expected to remain subdued unless the upturn in economy

PROPERTY INSIGHTS Kuala Lumpur Quarter 3, 2017 Home buyers remain cautious despite stronger GDP growth Market Overview The residential market is expected to remain subdued unless the upturn in economy

PPI Inched Up 0.1% in Jun-18 Driven By Rising Commodity Price

31 July 2018 ECONOMIC REVIEW June 2018 Producer Price Index Inched Up 0.1% in Jun-18 Driven By Rising Commodity Price grew for the first time in 2018. Malaysia s producer prices increased by 0.1%yoy in

31 July 2018 ECONOMIC REVIEW June 2018 Producer Price Index Inched Up 0.1% in Jun-18 Driven By Rising Commodity Price grew for the first time in 2018. Malaysia s producer prices increased by 0.1%yoy in

BTMU Focus Latin America Colombia : macroeconomic performance Peru: (2Q GDP and Current Monthly Indicators)

") BTMU Focus Latin America Colombia : macroeconomic performance Peru: (Q GDP and Current Monthly Indicators) MUFG UNION BANK Economic Research (New York) Hongrui Zhang Latin America Economist hozhang@us.mufg.jp

BTMU Focus Latin America Colombia : macroeconomic performance Peru: (Q GDP and Current Monthly Indicators) MUFG UNION BANK Economic Research (New York) Hongrui Zhang Latin America Economist hozhang@us.mufg.jp

China Economic Growth Slows in 1Q

Yao Shaohua, PhD Senior Economist shaohuayao@hangseng.com China Economic Growth Slows in 1Q 15 April 2015 Mainland China s economic growth continued to lose momentum in the first quarter, due largely to

Yao Shaohua, PhD Senior Economist shaohuayao@hangseng.com China Economic Growth Slows in 1Q 15 April 2015 Mainland China s economic growth continued to lose momentum in the first quarter, due largely to

Markit economic overview

Markit Economics Markit economic overview Global economic growth weakest since late-2012 April 13 th 2016 Global economic growth weakest since late-2012 Global economic growth was running at its weakest

Markit Economics Markit economic overview Global economic growth weakest since late-2012 April 13 th 2016 Global economic growth weakest since late-2012 Global economic growth was running at its weakest

Portugal: GDP growth forecasts for 2018 reviewed upwards to 1.7%

13 March 217 ECONOMIC ANALYSIS Portugal: GDP growth forecasts for 218 reviewed upwards to 1.7% Myriam Montañez Growth of the Portuguese economy in 4Q16 reached.6% QoQ 1, once again causing positive surprise

13 March 217 ECONOMIC ANALYSIS Portugal: GDP growth forecasts for 218 reviewed upwards to 1.7% Myriam Montañez Growth of the Portuguese economy in 4Q16 reached.6% QoQ 1, once again causing positive surprise

Latest Macroeconomic Projections - May Vice-Governor Anita Angelovska-Bezhoska

Latest Macroeconomic Projections - May 2018 - Vice-Governor Anita Angelovska-Bezhoska May, 4 2018 Contents Key assumptions on external and domestic environment Macroeconomic scenario 2018-2019 Comparison

Latest Macroeconomic Projections - May 2018 - Vice-Governor Anita Angelovska-Bezhoska May, 4 2018 Contents Key assumptions on external and domestic environment Macroeconomic scenario 2018-2019 Comparison

Monthly Outlook SEPTEMBER 2013

Monthly Outlook SEPTEMBER 2013 In August, the yield curve of US Treasuries continued to steepen as the likelihood of the US Fed tapering to start before year-end became stronger. Asian Local Currency fund

Monthly Outlook SEPTEMBER 2013 In August, the yield curve of US Treasuries continued to steepen as the likelihood of the US Fed tapering to start before year-end became stronger. Asian Local Currency fund

US Q3 GDP acceleration due to inventory build but final domestic demand remains weak

ISSN: 1791 35 35 November 26, 2013 Olga Kosma Economic Analyst okosma@eurobank.gr US Q3 GDP acceleration due to inventory build but final domestic demand remains weak Real GDP accelerated to 2.8% q-o-q

ISSN: 1791 35 35 November 26, 2013 Olga Kosma Economic Analyst okosma@eurobank.gr US Q3 GDP acceleration due to inventory build but final domestic demand remains weak Real GDP accelerated to 2.8% q-o-q

Economic Projections :1

Economic Projections 2017-2020 2018:1 Outlook for the Maltese economy Economic projections 2017-2020 The Central Bank s latest economic projections foresee economic growth over the coming three years to

Economic Projections 2017-2020 2018:1 Outlook for the Maltese economy Economic projections 2017-2020 The Central Bank s latest economic projections foresee economic growth over the coming three years to

Financial Market Outlook: Further Stock Gain on Faster GDP Rebound and Earnings Recovery. Year-end Target Raised

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: FurtherStock Gains Likely, Year-end Target Raised. Bond Under Pressure

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: FurtherStock Gains Likely, Year-end Target Raised. Bond Under Pressure

Malaysia s Exports Performance Steadied in April Despite Sluggish Global Trade

6 June 2016 MONTHLY ECONOMIC REVIEW May 2016 Malaysia s Exports Performance Steadied in April Despite Sluggish Global Trade Exports were up by 1.6%yoy in April, higher than consensus. This was largely

6 June 2016 MONTHLY ECONOMIC REVIEW May 2016 Malaysia s Exports Performance Steadied in April Despite Sluggish Global Trade Exports were up by 1.6%yoy in April, higher than consensus. This was largely

Investec Services PMI Ireland

Embargoed until: 06:00 (Dublin) September 5th 18 Investec Services PMI Ireland Activity rises at sharper pace in August Investec T: +3-1-421-0496 E: Investec.Economics@investec.ie W: www.investec.ie Investec

Embargoed until: 06:00 (Dublin) September 5th 18 Investec Services PMI Ireland Activity rises at sharper pace in August Investec T: +3-1-421-0496 E: Investec.Economics@investec.ie W: www.investec.ie Investec

BANKING SECTOR. Rationale for report: Banking statistics for January 2017

BANKING SECTOR Sector Report 2 March 2017 Kelvin Ong,CFA kelvin-ong@ambankgroup.com 03-20362294 Higher deposit growth with stronger CASA momentum Rationale for report: Banking statistics for January 2017

BANKING SECTOR Sector Report 2 March 2017 Kelvin Ong,CFA kelvin-ong@ambankgroup.com 03-20362294 Higher deposit growth with stronger CASA momentum Rationale for report: Banking statistics for January 2017

Ireland. Eurozone rebalancing. EY Eurozone Forecast June Portugal Slovakia Slovenia Spain. Latvia Lithuania Luxembourg Malta Netherlands

EY Forecast June 2015 rebalancing recovery Outlook for Rising domestic demand improves prospects for 2015 Published in collaboration with Highlights The Irish economy grew by 4.8% last year, which was

EY Forecast June 2015 rebalancing recovery Outlook for Rising domestic demand improves prospects for 2015 Published in collaboration with Highlights The Irish economy grew by 4.8% last year, which was

Markit economic overview

Markit Economics Markit economic overview PMI data highlight growing variations in likely policy paths 9 June 2015 Global growth slows for second month running in May Global economic growth edged lower

Markit Economics Markit economic overview PMI data highlight growing variations in likely policy paths 9 June 2015 Global growth slows for second month running in May Global economic growth edged lower

OCT NOV DEC JAN FEB MAR APR MAY JUN JUL AUG GENERAL

8 September ASEAN manufacturing PMI rose above 50 in August Indonesia inflation rate slowed slightly to 3.82% ASEAN purchasing managers index (PMI) rose above 50 level to 50.4 in August, after falling

8 September ASEAN manufacturing PMI rose above 50 in August Indonesia inflation rate slowed slightly to 3.82% ASEAN purchasing managers index (PMI) rose above 50 level to 50.4 in August, after falling

Ireland Outlook. Economy powering on. February Economic Research Unit

Ireland Outlook February 218 Economy powering on Momentum in the Irish economy remains strong, with activity in the first three quarters of 217 ahead of expectations and high frequency data indicating

Ireland Outlook February 218 Economy powering on Momentum in the Irish economy remains strong, with activity in the first three quarters of 217 ahead of expectations and high frequency data indicating

Flash Note Japan: Second reading of Q2 GDP

FLASH NOTE Flash Note Japan: Second reading of Q2 GDP GDP forecast revised up but external uncertainties persist Pictet Wealth Management - Asset Allocation & Macro Research 11 September 2018 The second

FLASH NOTE Flash Note Japan: Second reading of Q2 GDP GDP forecast revised up but external uncertainties persist Pictet Wealth Management - Asset Allocation & Macro Research 11 September 2018 The second

PROPERTY INSIGHTS. Market Overview. Subdued economic growth dampen investment sentiments. Citigold Private Client

Citigold Private Client PROPERTY INSIGHTS Malaysia Quarter 2, 2016 Subdued economic growth dampen investment sentiments Market Overview Malaysia s economy grew at a slower pace in Q1 2016 due to slower

Citigold Private Client PROPERTY INSIGHTS Malaysia Quarter 2, 2016 Subdued economic growth dampen investment sentiments Market Overview Malaysia s economy grew at a slower pace in Q1 2016 due to slower

The FDI-driven export growth story continues to power ahead despite the US withdrawal from TPP

Vietnam s economy grew 6.2% yoy in 2016, versus 6.7% in 2015, weighed down by a slowdown in the agriculture and mining sectors. There was a further moderation to 5.1% growth in 1Q17. Nonetheless, on the

Vietnam s economy grew 6.2% yoy in 2016, versus 6.7% in 2015, weighed down by a slowdown in the agriculture and mining sectors. There was a further moderation to 5.1% growth in 1Q17. Nonetheless, on the

Growth and Inflation Prospects and Monetary Policy

Growth and Inflation Prospects and Monetary Policy 1. Growth and Inflation Prospects and Monetary Policy The Thai economy expanded by slightly less than the previous projection due to weaker-than-anticipated

Growth and Inflation Prospects and Monetary Policy 1. Growth and Inflation Prospects and Monetary Policy The Thai economy expanded by slightly less than the previous projection due to weaker-than-anticipated

Fund Information. Fund Name. Fund Category. Fund Investment Objective. Fund Performance Benchmark. Fund Distribution Policy

Fund Information Fund Name (PeFAF) Fund Category Mixed Asset Fund Investment Objective To achieve capital growth over the medium to long-term period through a portfolio allocation across equities and fixed

Fund Information Fund Name (PeFAF) Fund Category Mixed Asset Fund Investment Objective To achieve capital growth over the medium to long-term period through a portfolio allocation across equities and fixed

Fund Information. Fund Name. Fund Category. Fund Investment Objective. Fund Performance Benchmark. Fund Distribution Policy

Fund Information Fund Name PB Asia Pacific Dividend Fund () Fund Category Equity Fund Investment Objective To provide income by investing in a portfolio of stocks in domestic and regional markets which

Fund Information Fund Name PB Asia Pacific Dividend Fund () Fund Category Equity Fund Investment Objective To provide income by investing in a portfolio of stocks in domestic and regional markets which

Malaysia Bond Flows Update

Malaysia Bond Flows Update Foreign net selloff lower in August, foreign buying to increase on improving fundamentals Economics Kenanga Investment Bank Berhad T: 603-2172 0880 OVERVIEW Foreign selloff moderated.

Malaysia Bond Flows Update Foreign net selloff lower in August, foreign buying to increase on improving fundamentals Economics Kenanga Investment Bank Berhad T: 603-2172 0880 OVERVIEW Foreign selloff moderated.

MUFG LATIN AMERICA TOPICS

MUFG LATIN AMERICA TOPICS Mexico s Macroeconomic Performance: Q1 2017 and Current Economic Indicators MUFG UNION BANK, N.A. ECONOMIC RESEARCH (NEW YORK) KAREN MARTINEZ Latin America Economist +1(212)782-5708

MUFG LATIN AMERICA TOPICS Mexico s Macroeconomic Performance: Q1 2017 and Current Economic Indicators MUFG UNION BANK, N.A. ECONOMIC RESEARCH (NEW YORK) KAREN MARTINEZ Latin America Economist +1(212)782-5708

GDP Forecast Revised Due to Weak Global Outlook

5 July 2016 MONTHLY ECONOMIC REVIEW Jun 2016 GDP Forecast Revised Due to Weak Global Outlook Exports were down by 0.9%yoy in May, while trade balance moderated to RM3.2 billion. This was largely due to

5 July 2016 MONTHLY ECONOMIC REVIEW Jun 2016 GDP Forecast Revised Due to Weak Global Outlook Exports were down by 0.9%yoy in May, while trade balance moderated to RM3.2 billion. This was largely due to

Balance of Payment Q3 FY (October-December 2012)

") Balance of Payment Q3 FY2012-13 (October-December 2012) Key Highlights: - India s Current Account Deficit (CAD) widened to a record high of 6.7% of GDP in Q3 FY2012-13 on the back of surging oil and gold

Balance of Payment Q3 FY2012-13 (October-December 2012) Key Highlights: - India s Current Account Deficit (CAD) widened to a record high of 6.7% of GDP in Q3 FY2012-13 on the back of surging oil and gold

Global Markets Research Fixed Income

Global Markets Research Fixed Income Fixed Income Daily Market Snapshot UST Tenure Closing (%) Chg (bps) 2-yr UST 2.81-2 5-yr UST 2.94-3 10-yr UST 3.04-3 30-yr UST 3.18-2 MGS GII* Tenure Closing (%) Chg

Global Markets Research Fixed Income Fixed Income Daily Market Snapshot UST Tenure Closing (%) Chg (bps) 2-yr UST 2.81-2 5-yr UST 2.94-3 10-yr UST 3.04-3 30-yr UST 3.18-2 MGS GII* Tenure Closing (%) Chg