Georgia Funders Forum June 20, Impact Fees. Georgia s Most Ignored State Law? Bill Ross ROSS+associates

|

|

|

- Meghan Barton

- 5 years ago

- Views:

Transcription

1 Georgia Funders Forum June 20, 2018 Impact Fees Georgia s Most Ignored State Law? Bill Ross ROSS+associates

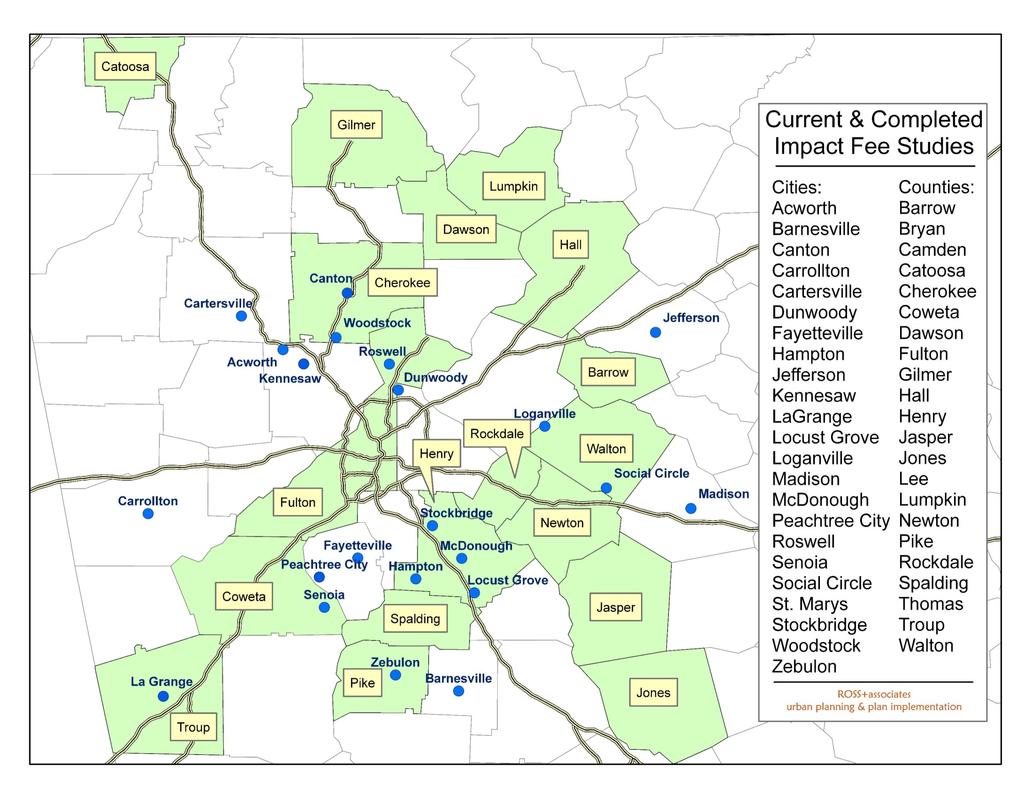

2 Who Is ROSS+associates? Comprehensive Planning Long-Range Comprehensive Plans Land Use and Neighborhood Plans Economic and Business Development Strategies Short Term Work Programs Zoning and Land Development Codes Unified Land Development Codes Zoning and Subdivision Regulations Sign Ordinances Development Permitting and Review Procedures Implementation and Financing Capital Improvement Programs Impact Fees Water and Sewer Connection Fees Community Improvement Districts

3

4

5 What Does the Georgia Impact Fee Act Cover? Certain Public Facility Categories Development Exactions System Improvements Comprehensive Plan Connection

6 What s This?

7 What s This?

8 Development Exactions Any requirement for development approval that compels the payment, dedication, or contribution of goods, services, land, or money as a condition of approval.

9 Public Facilities Covered Water supply, treatment & distribution. Wastewater collection, treatment & disposal. Roads, streets, and bridges. Storm-water and flood control facilities. Parks, open space, and recreation. Police and fire protection, emergency medical, and emergency communications. Libraries.

10 Exactions for System Imps Cities and Counties may impose development exactions for system improvements only by way of development impact fees imposed in accordance with the provisions of the Development Impact Fee Act (DIFA).

11 Project v. System Imps Project Improvements System Improvements Site improvements and facilities that are planned and designed to provide service for a particular development project. Capital improvements that are public facilities and are designed to provide service to the community at large.

12 Exactions Local Subdivision Street Land for School Land for Library Deceleration Lane for a Shopping Center Land for County Courthouse Water Treatment Plant

13 Project v. System Imps Project Improvements System Improvements Site improvements and facilities that are planned and designed to provide service for a particular development project. Capital improvements that are public facilities and are designed to provide service to the community at large.

14 Capital Improvement An improvement with a useful life of ten years or more, by new construction or other action, which increases the service capacity of a public facility. Examples: Land acquisition and building construction A new fire truck A new recreation facilities A water treatment plant, storage and mains A major thoroughfare widening

15 Level of Service A measure of the relationship between service capacity and service demand for public facilities in terms of demand to capacity ratios, the comfort and convenience of use or service of public facilities, or both. Examples: Park acreage per household Number of fire trucks per population Average daily flows (gpd) of water per person Average daily traffic generated by development

16 Comprehensive Plan The Planning Capital Improvements Program Connection Funding Resources Impact Fees

17 The Planning Connection: DIFA Municipalities and counties which have adopted a comprehensive plan containing a capital improvements element are authorized to impose by ordinance development impact fees as a condition of development approval on all development pursuant to and in accordance with the provisions of this chapter.

18 Capital Improvements Element "Capital improvements element" sets out A B C projected needs for system improvements during a planning horizon established in the comprehensive plan, a schedule of capital improvements that will meet the anticipated need for system improvements, and a description of anticipated funding sources for each required improvement.

19 Ga. Dept. of Community Affairs Administers Comprehensive Planning Act. Adopts minimum standards for preparation of Comprehensive Plans and their Capital Improvement Elements. Requires annual updates of Community Work Programs and Financial Reports from impact fee jurisdictions. Publishes guidelines for Adoption of impact fees Preparation of CIEs and annual CIE updates Preparation of Community Work Program updates

20 Impact Fee Study Elements Study Documents

21 EXERCISE Impact Fee for Park Land Community Data Current Population = 50,000 Future (2040) Population = 80,000 Existing Park Acreage = 80 acres LOS Standard = 2 acres per 1,000 population Average household size = 2.5 persons

22 Impact Fee for Park Land FIRST in our example We ll figure out how much DEMAND there is for new park land.

23 Demand Current Population = 50,000 Current Park Need at 2 acres per 1,000 = Current (existing) Park Area = Existing Deficiency = acres 80 acres acres Projected Population in 2040 = New Residential Growth = - 50,000 = Park Land Needed for New Growth at 2 acres per 1,000 = acres TOTAL NEW ACRES NEEDED = acres

24 Demand Current Population = 50,000 Current Park Need at 2 acres per 1,000 = Current (existing) Park Area = Existing Deficiency = acres 80 acres acres Projected Population in 2040 = New Residential Growth = - 50,000 = Park Land Needed for New Growth at 2 acres per 1,000 = acres TOTAL NEW ACRES NEEDED = acres

25 Demand Current Population = 50,000 Current Park Need at 2 acres per 1,000 = Current (existing) Park Area = Existing Deficiency = 100 acres 80 acres acres Projected Population in 2040 = New Residential Growth = - 50,000 = Park Land Needed for New Growth at 2 acres per 1,000 = acres TOTAL NEW ACRES NEEDED = acres

26 Demand Current Population = 50,000 Current Park Need at 2 acres per 1,000 = Current (existing) Park Area = Existing Deficiency = 100 acres 80 acres acres Projected Population in 2040 = New Residential Growth = - 50,000 = Park Land Needed for New Growth at 2 acres per 1,000 = acres TOTAL NEW ACRES NEEDED = acres

27 Demand Current Population = 50,000 Current Park Need at 2 acres per 1,000 = Current (existing) Park Area = Existing Deficiency = 100 acres 80 acres 20 acres Projected Population in 2040 = New Residential Growth = - 50,000 = Park Land Needed for New Growth at 2 acres per 1,000 = acres TOTAL NEW ACRES NEEDED = acres

28 Demand Current Population = 50,000 Current Park Need at 2 acres per 1,000 = Current (existing) Park Area = Existing Deficiency = 100 acres 80 acres 20 acres Projected Population in 2040 = New Residential Growth = - 50,000 = Park Land Needed for New Growth at 2 acres per 1,000 = acres TOTAL NEW ACRES NEEDED = acres

29 Demand Current Population = 50,000 Current Park Need at 2 acres per 1,000 = Current (existing) Park Area = Existing Deficiency = 100 acres 80 acres 20 acres Projected Population in 2040 = 80,000 New Residential Growth = - 50,000 = Park Land Needed for New Growth at 2 acres per 1,000 = acres TOTAL NEW ACRES NEEDED = acres

30 Demand Current Population = 50,000 Current Park Need at 2 acres per 1,000 = Current (existing) Park Area = Existing Deficiency = 100 acres 80 acres 20 acres Projected Population in 2040 = 80,000 New Residential Growth = 80,000-50,000 = Park Land Needed for New Growth at 2 acres per 1,000 = acres TOTAL NEW ACRES NEEDED = acres

31 Demand Current Population = 50,000 Current Park Need at 2 acres per 1,000 = Current (existing) Park Area = Existing Deficiency = 100 acres 80 acres 20 acres Projected Population in 2040 = 80,000 New Residential Growth = 80,000-50,000 = 30,000 Park Land Needed for New Growth at 2 acres per 1,000 = acres TOTAL NEW ACRES NEEDED = acres

32 Demand Current Population = 50,000 Current Park Need at 2 acres per 1,000 = Current (existing) Park Area = Existing Deficiency = 100 acres 80 acres 20 acres Projected Population in 2040 = 80,000 New Residential Growth = 80,000-50,000 = 30,000 Park Land Needed for New Growth at 2 acres per 1,000 = acres TOTAL NEW ACRES NEEDED = acres

33 Demand Current Population = 50,000 Current Park Need at 2 acres per 1,000 = Current (existing) Park Area = Existing Deficiency = 100 acres 80 acres 20 acres Projected Population in 2040 = 80,000 New Residential Growth = 80,000-50,000 = 30,000 Park Land Needed for New Growth at 2 acres per 1,000 = 60 acres TOTAL NEW ACRES NEEDED = acres

34 Demand Current Population = 50,000 Current Park Need at 2 acres per 1,000 = Current (existing) Park Area = Existing Deficiency = 100 acres 80 acres 20 acres Projected Population in 2040 = 80,000 New Residential Growth = 80,000-50,000 = 30,000 Park Land Needed for New Growth at 2 acres per 1,000 = 60 acres TOTAL NEW ACRES NEEDED = acres

35 Demand Current Population = 50,000 Current Park Need at 2 acres per 1,000 = Current (existing) Park Area = Existing Deficiency = 100 acres 80 acres 20 acres Projected Population in 2040 = 80,000 New Residential Growth = 80,000-50,000 = 30,000 Park Land Needed for New Growth at 2 acres per 1,000 = 60 acres TOTAL NEW ACRES NEEDED = 80 acres

36 Impact Fee for Park Land NEXT in our example We ll figure out how much the DEMAND will COST And how much of that cost would be new growth s PROPORTIONAL SHARE

37 Cost Average Land Value = $50,000 per acre Cost of Debt Service, etc., for this example = $0 Total Purchase Price = 80 acres x $50,000 = $ Proportional Share Land Needed for New Growth ( 60 acres) Total Acres ( 80 ) = % New Growth Share = % x Total Purchase Price = $ Cost per New Person = New Growth Share ($ ) New Res Growth (30,000) = $ Future taxes from New Growth for this example = $0 Impact Fee per Household = Cost per New Person ($ ) x Avg. Household Size (2.5) = $

38 Cost Average Land Value = $50,000 per acre Cost of Debt Service, etc., for this example = $0 Total Purchase Price = 80 acres x $50,000 = $ Proportional Share Land Needed for New Growth ( 60 acres) Total Acres ( 80 ) = % New Growth Share = % x Total Purchase Price = $ Cost per New Person = New Growth Share ($ ) New Res Growth (30,000) = $ Future taxes from New Growth for this example = $0 Impact Fee per Household = Cost per New Person ($ ) x Avg. Household Size (2.5) = $

39 Cost Average Land Value = $50,000 per acre Cost of Debt Service, etc., for this example = $0 Total Purchase Price = 80 acres x $50,000 = $ 4,000,000 Proportional Share Land Needed for New Growth ( 60 acres) Total Acres ( 80 ) = % New Growth Share = % x Total Purchase Price = $ Cost per New Person = New Growth Share ($ ) New Res Growth (30,000) = $ Future taxes from New Growth for this example = $0 Impact Fee per Household = Cost per New Person ($ ) x Avg. Household Size (2.5) = $

40 Cost Average Land Value = $50,000 per acre Cost of Debt Service, etc., for this example = $0 Total Purchase Price = 80 acres x $50,000 = $ 4,000,000 Proportional Share Land Needed for New Growth ( 60 acres) Total Acres ( 80 ) = % New Growth Share = % x Total Purchase Price = $ Cost per New Person = New Growth Share ($ ) New Res Growth (30,000) = $ Future taxes from New Growth for this example = $0 Impact Fee per Household = Cost per New Person ($ ) x Avg. Household Size (2.5) = $

41 Cost Average Land Value = $50,000 per acre Cost of Debt Service, etc., for this example = $0 Total Purchase Price = 80 acres x $50,000 = $ 4,000,000 Proportional Share Land Needed for New Growth ( 60 acres) Total Acres ( 80 ) = 75 % New Growth Share = % x Total Purchase Price = $ Cost per New Person = New Growth Share ($ ) New Res Growth (30,000) = $ Future taxes from New Growth for this example = $0 Impact Fee per Household = Cost per New Person ($ ) x Avg. Household Size (2.5) = $

42 Cost Average Land Value = $50,000 per acre Cost of Debt Service, etc., for this example = $0 Total Purchase Price = 80 acres x $50,000 = $ 4,000,000 Proportional Share Land Needed for New Growth ( 60 acres) Total Acres ( 80 ) = 75 % New Growth Share = 75% x Total Purchase Price = $ Cost per New Person = New Growth Share ($ ) New Res Growth (30,000) = $ Future taxes from New Growth for this example = $0 Impact Fee per Household = Cost per New Person ($ ) x Avg. Household Size (2.5) = $

43 Cost Average Land Value = $50,000 per acre Cost of Debt Service, etc., for this example = $0 Total Purchase Price = 80 acres x $50,000 = $ 4,000,000 Proportional Share Land Needed for New Growth ( 60 acres) Total Acres ( 80 ) = 75 % New Growth Share = 75% x Total Purchase Price = $ 3,000,000 Cost per New Person = New Growth Share ($ ) New Res Growth (30,000) = $ Future taxes from New Growth for this example = $0 Impact Fee per Household = Cost per New Person ($ ) x Avg. Household Size (2.5) = $

44 Cost Average Land Value = $50,000 per acre Cost of Debt Service, etc., for this example = $0 Total Purchase Price = 80 acres x $50,000 = $ 4,000,000 Proportional Share Land Needed for New Growth ( 60 acres) Total Acres ( 80 ) = 75 % New Growth Share = 75% x Total Purchase Price = $ 3,000,000 Cost per New Person = New Growth Share ($3,000,000) New Res Growth (30,000) = $ Future taxes from New Growth for this example = $0 Impact Fee per Household = Cost per New Person ($ ) x Avg. Household Size (2.5) = $

Total Acres ( 80 ) = 75 % New Growth Share = 75% x Total")

45 Cost Average Land Value = $50,000 per acre Cost of Debt Service, etc., for this example = $0 Total Purchase Price = 80 acres x $50,000 = $ 400,000 Proportional Share Land Needed for New Growth ( 60 acres) Total Acres ( 80 ) = 75 % New Growth Share = 75% x Total Purchase Price = $ 3,000,000 Cost per New Person = New Growth Share ($3,000,000) New Res Growth (30,000) = $ 100 Future taxes from New Growth for this example = $0 Impact Fee per Household = Cost per New Person ($ ) x Avg. Household Size (2.5) = $

46 Cost Average Land Value = $50,000 per acre Cost of Debt Service, etc., for this example = $0 Total Purchase Price = 80 acres x $50,000 = $ 4,000,000 Proportional Share Land Needed for New Growth ( 60 acres) Total Acres ( 80 ) = 75 % New Growth Share = 75% x Total Purchase Price = $ 3,000,000 Cost per New Person = New Growth Share ($3,000,000) New Res Growth (30,000) = $ 100 Future taxes from New Growth for this example = $0 Impact Fee per Household = Cost per New Person ($ 100) x Avg. Household Size (2.5) = $

47 Cost Average Land Value = $50,000 per acre Cost of Debt Service, etc., for this example = $0 Total Purchase Price = 80 acres x $50,000 = $ 4,000,000 Proportional Share Land Needed for New Growth ( 60 acres) Total Acres ( 80 ) = 75 % New Growth Share = 75% x Total Purchase Price = $ 3,000,000 Cost per New Person = New Growth Share ($3,000,000) New Res Growth (30,000) = $ 100 Future taxes from New Growth for this example = $0 Impact Fee per Household = Cost per New Person ($100) x Avg. Household Size (2.5) = $ 250

48 + Value of existing capacity in the system available to support New Growth Cost of new capital expansion needed to serve New Growth Methodology Overview Water & Sewer Impact Fees = Gross cost of capital improvements to serve New Growth - Future revenue from New Growth to help pay for the improvements = Max amount of cost that can be collected as a capital recovery fee Capacity Added for New Growth (GPD) = Per capacity cost that can be collected as a capital recovery fee Average flow capacity of water meter = Capital Recovery Fee + Cost to set meter or make connection = Total Connection Fee

49 ROSS+associates Bill Ross

Capital Improvements Element

Chapter 6 Capital Improvements Element The Hall County Capital Improvements Element 1, adopted June 25, 2009, is provided as an attachment to Hall County Forward. 1 The 2017-2021 Community Work Program

Chapter 6 Capital Improvements Element The Hall County Capital Improvements Element 1, adopted June 25, 2009, is provided as an attachment to Hall County Forward. 1 The 2017-2021 Community Work Program

Policy CIE The following are the minimum acceptable LOS standards to be utilized in planning for capital improvement needs:

Vision Statement: Provide high quality public facilities that meet and exceed the minimum level of service standards. Goals, Objectives and Policies: Goal CIE-1. The City shall provide for facilities and

Vision Statement: Provide high quality public facilities that meet and exceed the minimum level of service standards. Goals, Objectives and Policies: Goal CIE-1. The City shall provide for facilities and

CAPITAL IMPROVEMENTS ELEMENT

[COMPREHENSIVE PLAN] 2025 INTRODUCTION EXHIBIT F CAPITAL IMPROVEMENTS ELEMENT A primary purpose of the Capital Improvements Element (CIE) is to assess and demonstrate the financial feasibility of the Clay

[COMPREHENSIVE PLAN] 2025 INTRODUCTION EXHIBIT F CAPITAL IMPROVEMENTS ELEMENT A primary purpose of the Capital Improvements Element (CIE) is to assess and demonstrate the financial feasibility of the Clay

CAPITAL IMPROVEMENTS ELEMENT

GOALS, OBJECTIVES AND POLICIES Goal 1.0.0. To annually adopt and utilize a 5-Year Capital Improvements Program and Annual Capital Budget to coordinate the timing and to prioritize the construction and

GOALS, OBJECTIVES AND POLICIES Goal 1.0.0. To annually adopt and utilize a 5-Year Capital Improvements Program and Annual Capital Budget to coordinate the timing and to prioritize the construction and

APPENDIX B. Water/Wastewater Connection Fees. 1. Basis B Authority B Connection Fees B-1thru B Calculating Connection Fees B-2

APPENDIX B Water/Wastewater Connection Fees Article Page 1. Basis B-1 2. Authority B-1 3. Connection Fees B-1thru B-2 4. Calculating Connection Fees B-2 5. Connection Fee Worksheet, Residential Water B-3

APPENDIX B Water/Wastewater Connection Fees Article Page 1. Basis B-1 2. Authority B-1 3. Connection Fees B-1thru B-2 4. Calculating Connection Fees B-2 5. Connection Fee Worksheet, Residential Water B-3

Purpose of LOST SALES AND USE TAXATION. Local Option Sales Tax (LOST) Taxation 101 Larry Hanson City Manager City of Valdosta June 26, /16/2017

Taxation 101 Larry Hanson City Manager City of Valdosta June 26, /16/2017") SALES AND USE TAXATION Taxation 101 Larry Hanson City Manager City of Valdosta June 26, 2017 Local Option Sales Tax (LOST) Purpose of LOST To assist in funding governmental services authorized by the Constitution

SALES AND USE TAXATION Taxation 101 Larry Hanson City Manager City of Valdosta June 26, 2017 Local Option Sales Tax (LOST) Purpose of LOST To assist in funding governmental services authorized by the Constitution

C APITA L IMPRO VEMENTS S CHEDULE (FIGURE CI-14)

") August 20, 2018 Staff Report to the Municipal Planning Board G M P 2 0 1 8-1 0 0 2 0 I TEM 6 S U M M A RY Applicant City of Orlando Requested Actions 1. Amend Figure CI-14 and Policy 2.2.30 of the Capital

August 20, 2018 Staff Report to the Municipal Planning Board G M P 2 0 1 8-1 0 0 2 0 I TEM 6 S U M M A RY Applicant City of Orlando Requested Actions 1. Amend Figure CI-14 and Policy 2.2.30 of the Capital

Presented By: L. Carson Bise II, AICP President

Impact Fee Basics: Methodology and Fee Design Presented By: L. Carson Bise II, AICP President Basic Options for One-Time Infrastructure Charges Funding from broad-based revenues (general taxes) Growth

Impact Fee Basics: Methodology and Fee Design Presented By: L. Carson Bise II, AICP President Basic Options for One-Time Infrastructure Charges Funding from broad-based revenues (general taxes) Growth

C APITA L IMPRO VEMENTS S CHEDULE (FIGURE CI-14)

") August 15, 2017 Staff Report to the Municipal Planning Board G M P 2 0 1 7-0 0 0 1 7 I TEM 3 S U M M A RY Applicant City of Orlando Requested Actions 1. Amend Figure CI-14 and Policy 2.2.30 of the Capital

August 15, 2017 Staff Report to the Municipal Planning Board G M P 2 0 1 7-0 0 0 1 7 I TEM 3 S U M M A RY Applicant City of Orlando Requested Actions 1. Amend Figure CI-14 and Policy 2.2.30 of the Capital

Nassau County 2030 Comprehensive Plan. Capital Improvements Element (CI) Goals, Objectives and Policies. Goal

Goals, Objectives and Policies. Goal") (CI) Goal Based on the premise that existing taxpayers should not have to bear the financial burden of growth-related infrastructure needs, Ensure the orderly and efficient provision of infrastructure

(CI) Goal Based on the premise that existing taxpayers should not have to bear the financial burden of growth-related infrastructure needs, Ensure the orderly and efficient provision of infrastructure

FY Annual Budget: Mobility Solutions, Infrastructure, & Sustainability

FY 2018-19 Annual Budget: Mobility Solutions, Infrastructure, & Sustainability City Council Briefing August 15, 2018 Majed Al-Ghafry, Assistant City Manager Overview FY 2018-19 Budget by Strategic Priority

FY 2018-19 Annual Budget: Mobility Solutions, Infrastructure, & Sustainability City Council Briefing August 15, 2018 Majed Al-Ghafry, Assistant City Manager Overview FY 2018-19 Budget by Strategic Priority

Province of Nova Scotia Service Nova Scotia and Municipal Relations

v214-215.1.1 Province of Nova Scotia Service Nova Scotia and Municipal Relations FINANCIAL INFORMATION RETURN ( as prescribed by the Minister of Service Nova Scotia and Municipal Relations) FOR Municipality

v214-215.1.1 Province of Nova Scotia Service Nova Scotia and Municipal Relations FINANCIAL INFORMATION RETURN ( as prescribed by the Minister of Service Nova Scotia and Municipal Relations) FOR Municipality

Quigley Canyon Ranch Cost/Benefit Study Update

Quigley Canyon Ranch Cost/Benefit Study Update April 26, 2012 RICHARD CAPLAN & ASSOCIATES Mayor Fritz Haemmerle Hailey City Council 115 Main Street Hailey, ID 83333 April 26, 2012 Dear Mayor Haemmerle

Quigley Canyon Ranch Cost/Benefit Study Update April 26, 2012 RICHARD CAPLAN & ASSOCIATES Mayor Fritz Haemmerle Hailey City Council 115 Main Street Hailey, ID 83333 April 26, 2012 Dear Mayor Haemmerle

September 17, 2018 City Council Meeting

September 17, 2018 City Council Meeting Budget Overview Total Proposed 2019 Operating & Capital Budget $83,755,556 Increase of $1,147,156 (1.4%) over 2018 budget $1.2M General Fund $0.6M Mass Transit $380K

September 17, 2018 City Council Meeting Budget Overview Total Proposed 2019 Operating & Capital Budget $83,755,556 Increase of $1,147,156 (1.4%) over 2018 budget $1.2M General Fund $0.6M Mass Transit $380K

UNOFFICIAL COPY OF HOUSE BILL Read and Examined by Proofreaders:

UNOFFICIAL COPY OF HOUSE BILL 1141 L6 (6lr1312) ENROLLED BILL -- Environmental Matters/Education, Health, and Environmental Affairs -- Introduced by Delegates McIntosh, Bobo, Bronrott, Cane, V. Clagett,

UNOFFICIAL COPY OF HOUSE BILL 1141 L6 (6lr1312) ENROLLED BILL -- Environmental Matters/Education, Health, and Environmental Affairs -- Introduced by Delegates McIntosh, Bobo, Bronrott, Cane, V. Clagett,

CAPITAL IMPROVEMENTS. City of St. Augustine Comprehensive Plan EAR-Based Amendments

CAPITAL IMPROVEMENTS City of St. Augustine Comprehensive Plan EAR-Based Amendments CAPITAL IMPROVEMENTS ELEMENT CI Goal 1 The City shall manage its financial resources to adequately provide public facilities

CAPITAL IMPROVEMENTS City of St. Augustine Comprehensive Plan EAR-Based Amendments CAPITAL IMPROVEMENTS ELEMENT CI Goal 1 The City shall manage its financial resources to adequately provide public facilities

The Fiscal Impact of the Proposed City of Sharon Springs on Forsyth County, Georgia

The Fiscal Impact of the Proposed City of Sharon Springs on Forsyth County, Georgia Prepared for: Forsyth County Board of Commissioners December 2015 Table of Contents Executive Summary... 3 Section 1:

The Fiscal Impact of the Proposed City of Sharon Springs on Forsyth County, Georgia Prepared for: Forsyth County Board of Commissioners December 2015 Table of Contents Executive Summary... 3 Section 1:

Capital Improvements

Capital Improvements CAPITAL IMPROVEMENT ELEMENT GOAL 7-1: PROVIDE & MAINTAIN PUBLIC FACILITIES AND SERVICES Provide and maintain public facilities and services which protect and promote the public health,

Capital Improvements CAPITAL IMPROVEMENT ELEMENT GOAL 7-1: PROVIDE & MAINTAIN PUBLIC FACILITIES AND SERVICES Provide and maintain public facilities and services which protect and promote the public health,

City of Redding, California Development Impact Mitigation Fee Nexus Study

, California Development Impact Mitigation Fee Nexus Study December 5, 2017 Prepared by helping communities fund to morrow This page intentionally left blank. TABLE OF CONTENTS Executive Summary...1 Background

, California Development Impact Mitigation Fee Nexus Study December 5, 2017 Prepared by helping communities fund to morrow This page intentionally left blank. TABLE OF CONTENTS Executive Summary...1 Background

LEGEND Bridges Parks Fire Stations Project Locations Libraries Schools A

LEGEND Bridges Parks Fire Stations Project Locations Libraries Schools A Aid to Construction Fund The Aid to Construction Fund (Water) are funds received from customers for requested water service and

LEGEND Bridges Parks Fire Stations Project Locations Libraries Schools A Aid to Construction Fund The Aid to Construction Fund (Water) are funds received from customers for requested water service and

Securing Burbank s Financial Future

Securing Burbank s Financial Future Updated General Fund Status and Revenue Options JUNE 26, 2018 WHAT WILL BE COVERED Strategic Correction Plan: 3 Essential Elements 1. Measure T 2. Council and Labor

Securing Burbank s Financial Future Updated General Fund Status and Revenue Options JUNE 26, 2018 WHAT WILL BE COVERED Strategic Correction Plan: 3 Essential Elements 1. Measure T 2. Council and Labor

Chapter Ten, Capital Improvements Element City of St. Petersburg Comprehensive Plan

CAPITAL IMPROVEMENTS ELEMENT Sections: 10.1 INTRODUCTION 10. 2 GOALS, OBJECTIVES AND POLICIES ISSUE: Construction of needed improvements ISSUE: Adequate provision of public facilities ISSUE: Public expenditure

CAPITAL IMPROVEMENTS ELEMENT Sections: 10.1 INTRODUCTION 10. 2 GOALS, OBJECTIVES AND POLICIES ISSUE: Construction of needed improvements ISSUE: Adequate provision of public facilities ISSUE: Public expenditure

CAPITAL IMPROVEMENT ELEMENT Inventory Analysis

CAPITAL IMPROVEMENT ELEMENT Inventory Analysis 2.191 INTRODUCTION The principal purpose of this element is to identify the capital improvements that are needed to implement the comprehensive plan and ensure

CAPITAL IMPROVEMENT ELEMENT Inventory Analysis 2.191 INTRODUCTION The principal purpose of this element is to identify the capital improvements that are needed to implement the comprehensive plan and ensure

Brunswick Crossing Special Taxing District City of Brunswick, Maryland

Brunswick Crossing Special Taxing District City of Brunswick, Maryland The Brunswick Crossing Special Taxing District consists of approximately 552.7 acres located in Brunswick, Maryland adjacent to the

Brunswick Crossing Special Taxing District City of Brunswick, Maryland The Brunswick Crossing Special Taxing District consists of approximately 552.7 acres located in Brunswick, Maryland adjacent to the

Recommended by City Manager A.C. Gonzalez

Recommended by City Manager A.C. Gonzalez Proposed budget is fiscally responsible, strategically begins restoring services, and positions City to continue growth FY 2014-15 budget is balanced and totals

Recommended by City Manager A.C. Gonzalez Proposed budget is fiscally responsible, strategically begins restoring services, and positions City to continue growth FY 2014-15 budget is balanced and totals

CAPITAL IMPROVEMENT PROGRAM K-1

Fund # begins with a Fund Type Fund Type Description/Restrictions 1 General The City's principal operating fund, which is supported by taxes and fees and which, generally, has no restrictions on its use.

Fund # begins with a Fund Type Fund Type Description/Restrictions 1 General The City's principal operating fund, which is supported by taxes and fees and which, generally, has no restrictions on its use.

Taxes: This 2019 Budget holds property and income taxes for city services at their current rates.

January 30, 2019 Dear Members of City Council: I present to you our 2019 Oakwood City Budget. This is my 17 th budget as your city manager. Many people assisted in the preparation of this document, most

January 30, 2019 Dear Members of City Council: I present to you our 2019 Oakwood City Budget. This is my 17 th budget as your city manager. Many people assisted in the preparation of this document, most

Queen Creek Annual Budget Organizational Structure

Organizational Structure Town Organizational Chart Employees by Department Staffing Level Changes Fund Structure Chart Fund Structure Narrative Where the Money Comes From Where the Money Goes 60 TOWN ORGANIZATIONAL

Organizational Structure Town Organizational Chart Employees by Department Staffing Level Changes Fund Structure Chart Fund Structure Narrative Where the Money Comes From Where the Money Goes 60 TOWN ORGANIZATIONAL

Hometo t w o n w Connection September 2 2, 2 009

Hometown Connection September 22, 2009 Administration And Finance Administration Budget BUDGET DECREASE - FY 2010 FY 2010 Budget $142,266,325 FY 2009 Budget $169,489,120 Budget Decrease $ 27,222,795-16.06%

Hometown Connection September 22, 2009 Administration And Finance Administration Budget BUDGET DECREASE - FY 2010 FY 2010 Budget $142,266,325 FY 2009 Budget $169,489,120 Budget Decrease $ 27,222,795-16.06%

CAPITAL IMPROVEMENT PROGRAM K-1

Fund # begins with a Fund Type Fund Type Description/Restrictions 1 General The City's principal operating fund, which is supported by taxes and fees and which, generally, has no restrictions on its use.

Fund # begins with a Fund Type Fund Type Description/Restrictions 1 General The City's principal operating fund, which is supported by taxes and fees and which, generally, has no restrictions on its use.

CAPITAL IMPROVEMENTS ELEMENT GOALS, OBJECTIVES AND POLICIES. Goal 1: [CI] (EFF. 7/16/90)

![CAPITAL IMPROVEMENTS ELEMENT GOALS, OBJECTIVES AND POLICIES. Goal 1: [CI] (EFF. 7/16/90)](/thumbs/93/114312533.jpg "CAPITAL IMPROVEMENTS ELEMENT GOALS, OBJECTIVES AND POLICIES. Goal 1: [CI] (EFF. 7/16/90)") CAPITAL IMPROVEMENTS ELEMENT GOALS, OBJECTIVES AND POLICIES Goal 1: [CI] (EFF. 7/16/90) To use sound fiscal policies to provide adequate public facilities concurrent with, or prior to development in order

CAPITAL IMPROVEMENTS ELEMENT GOALS, OBJECTIVES AND POLICIES Goal 1: [CI] (EFF. 7/16/90) To use sound fiscal policies to provide adequate public facilities concurrent with, or prior to development in order

HACKBERRY HIDDEN COVE PUBLIC IMPROVEMENT DISTRICT NO. 2 SERVICE AND ASSESSMENT PLAN (UTILITY IMPROVEMENTS)

") HACKBERRY HIDDEN COVE PUBLIC IMPROVEMENT DISTRICT NO. 2 SERVICE AND ASSESSMENT PLAN (UTILITY IMPROVEMENTS) SEPTEMBER 15, 2009 HACKBERRY HIDDEN COVE PUBLIC IMPROVEMENT DISTRICT NO. 2 SERVICE AND ASSESSMENT

HACKBERRY HIDDEN COVE PUBLIC IMPROVEMENT DISTRICT NO. 2 SERVICE AND ASSESSMENT PLAN (UTILITY IMPROVEMENTS) SEPTEMBER 15, 2009 HACKBERRY HIDDEN COVE PUBLIC IMPROVEMENT DISTRICT NO. 2 SERVICE AND ASSESSMENT

9.C.2.a. Attachment: FY 2016 Budget [Revision 1] (1727 : FY2016 Budget) Packet Pg. 75

![9.C.2.a. Attachment: FY 2016 Budget [Revision 1] (1727 : FY2016 Budget) Packet Pg. 75](/thumbs/88/117495514.jpg "9.C.2.a. Attachment: FY 2016 Budget [Revision 1] (1727 : FY2016 Budget) Packet Pg. 75") Packet Pg. 75 Packet Pg. 76 Packet Pg. 77 GENERAL FUND BUDGET SUMMARY REVENUES, OTHER SOURCES, EXPENDITURES, OTHER USES AND FUND BALANCE FY 2016 Initial Budget 2014 2014 2015 Actuals FY 2016 Initial Budget

Packet Pg. 75 Packet Pg. 76 Packet Pg. 77 GENERAL FUND BUDGET SUMMARY REVENUES, OTHER SOURCES, EXPENDITURES, OTHER USES AND FUND BALANCE FY 2016 Initial Budget 2014 2014 2015 Actuals FY 2016 Initial Budget

Item Amend Capital Improvements Element

Item 05-15 Amend Capital Improvements Element CHAPTER 15 CAPITAL IMPROVEMENTS ELEMENT Page 1 of 38 CHAPTER 15 CAPITAL IMPROVEMENTS ELEMENT A. OVERVIEW The Capital Improvements Element is essentially the

Item 05-15 Amend Capital Improvements Element CHAPTER 15 CAPITAL IMPROVEMENTS ELEMENT Page 1 of 38 CHAPTER 15 CAPITAL IMPROVEMENTS ELEMENT A. OVERVIEW The Capital Improvements Element is essentially the

Georgia Studies. Unit 8 Local Governments. Lesson 5 Local Governments. Study Presentation

Georgia Studies Unit 8 Local Governments Lesson 5 Local Governments Study Presentation Lesson 5 - Local Governments ESSENTIAL QUESTION Why do local governments collect and use taxes? Why are there different

Georgia Studies Unit 8 Local Governments Lesson 5 Local Governments Study Presentation Lesson 5 - Local Governments ESSENTIAL QUESTION Why do local governments collect and use taxes? Why are there different

City of Mercer Island CITY S FINANCIAL CHALLENGES: HOUSTON, WE HAVE A PROBLEM

City of Mercer Island CITY S FINANCIAL CHALLENGES: HOUSTON, WE HAVE A PROBLEM Presented by: Julie Underwood, City Manager Chip Corder, Assistant City Manager/Finance Director Presented to: Mercer Island

City of Mercer Island CITY S FINANCIAL CHALLENGES: HOUSTON, WE HAVE A PROBLEM Presented by: Julie Underwood, City Manager Chip Corder, Assistant City Manager/Finance Director Presented to: Mercer Island

SPRINGVILLE CITY CULINARY WATER IMPACT FEE ANALYSIS (IFA) MAY 2014

MAY 2014") SPRINGVILLE CITY CULINARY WATER IMPACT FEE ANALYSIS (IFA) MAY 2014 Adopted May 20, 2014 TABLE OF CONTENTS IMPACT FEE CERTIFICATION... 3 SECTION 1: EXECUTIVE SUMMARY... 4 PROPOSED CULINARY WATER IMPACT

SPRINGVILLE CITY CULINARY WATER IMPACT FEE ANALYSIS (IFA) MAY 2014 Adopted May 20, 2014 TABLE OF CONTENTS IMPACT FEE CERTIFICATION... 3 SECTION 1: EXECUTIVE SUMMARY... 4 PROPOSED CULINARY WATER IMPACT

City of Penticton: Financial Plan Reporting Structure

City of Penticton: Financial Plan Reporting Structure General Utilities General Government Services Recreation and Culture Environmental Health Services Public Health and Safety Protective Services Environmental

City of Penticton: Financial Plan Reporting Structure General Utilities General Government Services Recreation and Culture Environmental Health Services Public Health and Safety Protective Services Environmental

*** Redwood County ***

Page 1 Budget: 2017 BUDGET (ORIG) ORIG 1 - GENERAL Page 2 PROPERTY TAXES 6,688,872 OTHER TAXES 9,3 SPECIAL ASSESSMENTS 35,058 LICENSES & PERMITS 56,750 INTERGOVERNMENTAL S 141,0 PERA RATE REIMBURSEMENT

Page 1 Budget: 2017 BUDGET (ORIG) ORIG 1 - GENERAL Page 2 PROPERTY TAXES 6,688,872 OTHER TAXES 9,3 SPECIAL ASSESSMENTS 35,058 LICENSES & PERMITS 56,750 INTERGOVERNMENTAL S 141,0 PERA RATE REIMBURSEMENT

Nith Peninsula, Brant County Fiscal Impact Study

Fiscal Impact Study October 25, 2017 Fiscal Impact Study Prepared for: Losani Homes Prepared by: 33 Yonge Street Toronto Ontario M5E 1G4 Phone: (416) 641 9500 Fax: (416) 641 9501 economics@altusgroup.com

Fiscal Impact Study October 25, 2017 Fiscal Impact Study Prepared for: Losani Homes Prepared by: 33 Yonge Street Toronto Ontario M5E 1G4 Phone: (416) 641 9500 Fax: (416) 641 9501 economics@altusgroup.com

Description of Fund Types and Funds

Financial activities for local government fall into three broad categories, governmental, proprietary, and fiduciary fund categories. Governmental funds are used to account for activities primarily supported

Financial activities for local government fall into three broad categories, governmental, proprietary, and fiduciary fund categories. Governmental funds are used to account for activities primarily supported

TABLE OF CONTENTS LIST OF TABLES

TABLE OF CONTENTS A. GOALS, OBJECTIVES, AND POLICIES... 3 B. SUMMARY... 17 LIST OF TABLES Table IX 1: City of Winter Springs Five-Year Schedule of Capital Improvements (SCI) FY 2013/14-2017/18... 11 Table

TABLE OF CONTENTS A. GOALS, OBJECTIVES, AND POLICIES... 3 B. SUMMARY... 17 LIST OF TABLES Table IX 1: City of Winter Springs Five-Year Schedule of Capital Improvements (SCI) FY 2013/14-2017/18... 11 Table

Budget in Brief Proposed City Commission Budget FY 2017

City of Treasure Island Budget in Brief Proposed City Commission Budget FY 2017 Where charm meets contemporary All Funds Budget Summary Total Proposed Budget Budget % Fund FY 2016 FY 2017 Change General

City of Treasure Island Budget in Brief Proposed City Commission Budget FY 2017 Where charm meets contemporary All Funds Budget Summary Total Proposed Budget Budget % Fund FY 2016 FY 2017 Change General

Town of Smithfield Rhode Island 2019 Operating Budget

Rhode Island 2019 Operating Budget FINANCIAL TOWN MEETING APPROVED: June 14, 2018 Smithfield Town Hall 64 Farnum Pike Smithfield, RI 02917 Phone: (401) 233-1000 Fax: (401) 233-1080 Hours: 8:30 am 4:30

Rhode Island 2019 Operating Budget FINANCIAL TOWN MEETING APPROVED: June 14, 2018 Smithfield Town Hall 64 Farnum Pike Smithfield, RI 02917 Phone: (401) 233-1000 Fax: (401) 233-1080 Hours: 8:30 am 4:30

TOWN OF LILLINGTON FISCAL YEAR (FY) BUDGET MESSAGE

BUDGET MESSAGE") TOWN OF LILLINGTON June 13, 2017 Mayor Glenn McFadden Mayor Pro Tempore Judy Breeden Commissioner Rupert Langdon Commissioner Dianne Johnson Commissioner Marshall Page Commissioner Paul Phillips FISCAL

TOWN OF LILLINGTON June 13, 2017 Mayor Glenn McFadden Mayor Pro Tempore Judy Breeden Commissioner Rupert Langdon Commissioner Dianne Johnson Commissioner Marshall Page Commissioner Paul Phillips FISCAL

Planning Commission Application Summary

Planning Commission Application Summary Project Name: Galena Park Place Zone Change Address: 538 W. Fox Chase Dr. Current Zoning: CC Hearing Date: April 28, 2016 Background This rezone fixes a zoning discrepancy

Planning Commission Application Summary Project Name: Galena Park Place Zone Change Address: 538 W. Fox Chase Dr. Current Zoning: CC Hearing Date: April 28, 2016 Background This rezone fixes a zoning discrepancy

The Corporation of Haldimand County. Consolidated Financial Statements

Consolidated Financial Statements December 31, 2016 Index to Consolidated Financial Statements December 31, 2016 Page INDEPENDENT AUDITORS' REPORT 2 CONSOLIDATED FINANCIAL STATEMENTS Management's Responsibility

Consolidated Financial Statements December 31, 2016 Index to Consolidated Financial Statements December 31, 2016 Page INDEPENDENT AUDITORS' REPORT 2 CONSOLIDATED FINANCIAL STATEMENTS Management's Responsibility

$180 $160 $140 $120 $100 $80 $60 $40 $20 $ Single Fam -New Apts -New

2012 REVENUE FORECAST Presented by Brian Henshaw September 26, 2011 1 Economic Conditions Housing starts Federal & State deficits Sovereign-debt crisis Bankruptcies Unemployment Stock Market volatility

2012 REVENUE FORECAST Presented by Brian Henshaw September 26, 2011 1 Economic Conditions Housing starts Federal & State deficits Sovereign-debt crisis Bankruptcies Unemployment Stock Market volatility

PLANNING DEPARTMENT ADMINISTRATION

PLANNING DEPARTMENT ADMINISTRATION Long-Range Planning Zoning and Land Development Land Use and Design Community Improvement and Transportation Rezoning and Development Regulations Development Review Transit

PLANNING DEPARTMENT ADMINISTRATION Long-Range Planning Zoning and Land Development Land Use and Design Community Improvement and Transportation Rezoning and Development Regulations Development Review Transit

DEFINITION OF REVENUE SOURCES GENERAL FUND

GENERAL FUND PROPERTY TAX: The valuation of property in the City is determined by the Los Angeles County Tax Assessor, except for Public Utility property, which is assessed by the State Board of Equalization.

GENERAL FUND PROPERTY TAX: The valuation of property in the City is determined by the Los Angeles County Tax Assessor, except for Public Utility property, which is assessed by the State Board of Equalization.

LAFCo 509 W. WEBER AVENUE SUITE 420 STOCKTON, CA 95203

SAN JOAQUIN LOCAL AGENCY FORMATION COMMISSION AGENDA ITEM NO. 2 LAFCo 509 W. WEBER AVENUE SUITE 420 STOCKTON, CA 95203 REVISED EXECUTIVE OFFICER S REPORT March 10, 2016 TO: FROM: SUBJECT: LAFCo Commissioners

SAN JOAQUIN LOCAL AGENCY FORMATION COMMISSION AGENDA ITEM NO. 2 LAFCo 509 W. WEBER AVENUE SUITE 420 STOCKTON, CA 95203 REVISED EXECUTIVE OFFICER S REPORT March 10, 2016 TO: FROM: SUBJECT: LAFCo Commissioners

CITY OF PALM DESERT COMPREHENSIVE GENERAL PLAN

Comprehensive General Plan/Administration and Implementation CITY OF PALM DESERT COMPREHENSIVE GENERAL PLAN CHAPTER II ADMINISTRATION AND IMPLEMENTATION This Chapter of the General Plan addresses the administration

Comprehensive General Plan/Administration and Implementation CITY OF PALM DESERT COMPREHENSIVE GENERAL PLAN CHAPTER II ADMINISTRATION AND IMPLEMENTATION This Chapter of the General Plan addresses the administration

Outcome-Based Budgeting Process

Outcome-Based Budgeting Process Fiscal Year 2011 is the fourth year for the outcome-based budget process in Broward County. The process puts additional focus on results or outcomes in the development of

Outcome-Based Budgeting Process Fiscal Year 2011 is the fourth year for the outcome-based budget process in Broward County. The process puts additional focus on results or outcomes in the development of

2019 Adopted Budget. August 2019

2019 Adopted Budget August 2019 2019 City Budget The Overland Park City Council adopted a budget for fiscal year 2019 in August of 2018. The annual budget is the City s business plan to reflect the community

2019 Adopted Budget August 2019 2019 City Budget The Overland Park City Council adopted a budget for fiscal year 2019 in August of 2018. The annual budget is the City s business plan to reflect the community

City of Phoenix, Arizona. Monthly Financial Report

City of Phoenix, Arizona Monthly Financial Report March 212 Monthly Financial Report March 212 Executive Summary The budget amounts in this report represent the official adopted budget, as approved by

City of Phoenix, Arizona Monthly Financial Report March 212 Monthly Financial Report March 212 Executive Summary The budget amounts in this report represent the official adopted budget, as approved by

CITY OF MAUSTON GENERAL FUND SUMMARY SCHEDULE OF REVENUES AND EXPENDITURES

GENERAL FUND Taxes General Property Taxes $ 1,934,140 $ 1,688,759 $ 1,696,679 $ 1,720,679 $ 1,720,771 $ 21,321 $ 1,742,000 Payment in Lieu of Taxes 125,492 137,264 124,568 147,748 150,707 (1,000) 146,748

GENERAL FUND Taxes General Property Taxes $ 1,934,140 $ 1,688,759 $ 1,696,679 $ 1,720,679 $ 1,720,771 $ 21,321 $ 1,742,000 Payment in Lieu of Taxes 125,492 137,264 124,568 147,748 150,707 (1,000) 146,748

CAPITAL FUNDS 2015 Budget

CAPITAL FUNDS This section provides comparisons of revenues and expenditures/appropriations for all capital funds for 2014 2016, the 2017 budget, and the 2018 2022 plan. Historical fund balances and the

CAPITAL FUNDS This section provides comparisons of revenues and expenditures/appropriations for all capital funds for 2014 2016, the 2017 budget, and the 2018 2022 plan. Historical fund balances and the

JUNEAU COUNTY ALL HAZARDS MITIGATION PLAN UPDATE. OVERSIGHT COMMITTEE KICK-OFF September 21, 2016

JUNEAU COUNTY ALL HAZARDS MITIGATION PLAN UPDATE OVERSIGHT COMMITTEE KICK-OFF September 21, 2016 DARRYL L. LANDEAU, AICP SENIOR PLANNER NORTH CENTRAL WI REGIONAL PLANNING COMMISSION Past Work of NCWRPC

JUNEAU COUNTY ALL HAZARDS MITIGATION PLAN UPDATE OVERSIGHT COMMITTEE KICK-OFF September 21, 2016 DARRYL L. LANDEAU, AICP SENIOR PLANNER NORTH CENTRAL WI REGIONAL PLANNING COMMISSION Past Work of NCWRPC

City Services Appendix

Technical vices 1.0 Introduction... 1 1.1 The Capital Facilities Plan... 1 1.2 Utilities Plan... 2 1.3 Key Principles Guiding Bremerton s Capital Investments... 3 1.4 Capital Facilities and Utilities Addressed

Technical vices 1.0 Introduction... 1 1.1 The Capital Facilities Plan... 1 1.2 Utilities Plan... 2 1.3 Key Principles Guiding Bremerton s Capital Investments... 3 1.4 Capital Facilities and Utilities Addressed

Elected Officials & Citywide Administration Engineering Department Police Department Fire Department...

Page Elected Officials & Citywide Administration. 1 14 Engineering Department.. 15-20 Police Department..... 21-28 Fire Department... 29 33 Public Works Department... 34-46 Planning & Neighborhood Services

Page Elected Officials & Citywide Administration. 1 14 Engineering Department.. 15-20 Police Department..... 21-28 Fire Department... 29 33 Public Works Department... 34-46 Planning & Neighborhood Services

NORTH LEBANON TOWNSHIP PROPOSED BUDGET

NORTH LEBANON TOWNSHIP 2013 PROPOSED BUDGET Prepared by: Cheri Grumbine Presented: 11/19/2012 w/corrections 11/20/2012 North Lebanon Township Description of Various Funds The 2013 Preliminary Budget and

NORTH LEBANON TOWNSHIP 2013 PROPOSED BUDGET Prepared by: Cheri Grumbine Presented: 11/19/2012 w/corrections 11/20/2012 North Lebanon Township Description of Various Funds The 2013 Preliminary Budget and

NOTICE OF SPECIAL MEETING

Publish: 37 NOTICE OF SPECIAL MEETING A special meeting of the Greybull Town Council will be held on Monday, March 18, 2019 at 5:30 pm, Town Hall, 24 South 5 th St., for the purpose of: 1) FY20 Budget

Publish: 37 NOTICE OF SPECIAL MEETING A special meeting of the Greybull Town Council will be held on Monday, March 18, 2019 at 5:30 pm, Town Hall, 24 South 5 th St., for the purpose of: 1) FY20 Budget

SUMMARY OF SERVICES BY STRATEGIC PRIORITY

Public Safety City Attorney's Office Municipal Prosecution $2,287,153 $2,343,199 $2,287,153 $2,343,199 Police Legal Liaison $768,508 $785,703 $768,508 $785,703 Court and Detention Services Adjudication

Public Safety City Attorney's Office Municipal Prosecution $2,287,153 $2,343,199 $2,287,153 $2,343,199 Police Legal Liaison $768,508 $785,703 $768,508 $785,703 Court and Detention Services Adjudication

Fiscal and Economic Impact Analysis of Proposed IKEA in Dublin, California

Final Report Fiscal and Economic Impact Analysis of Proposed IKEA in Dublin, California Prepared for: IKEA Property, Inc. Prepared by: Economic & Planning Systems, Inc. August 22, 2017 EPS #161062 1. INTRODUCTION

Final Report Fiscal and Economic Impact Analysis of Proposed IKEA in Dublin, California Prepared for: IKEA Property, Inc. Prepared by: Economic & Planning Systems, Inc. August 22, 2017 EPS #161062 1. INTRODUCTION

1. identifies the required capacity of capital improvements to serve existing and future development based on level-of-service (LOS) standards;

standards;") DIVISION 4.200 CAPITAL IMPROVEMENTS ELEMENT SECTION 4.201 INTRODUCTION The purpose of the Capital Improvements Element (CIE) is to tie the capital improvement needs identified in the other elements to

DIVISION 4.200 CAPITAL IMPROVEMENTS ELEMENT SECTION 4.201 INTRODUCTION The purpose of the Capital Improvements Element (CIE) is to tie the capital improvement needs identified in the other elements to

HOST OVERVIEW. 05 Oct 2012 (17 pages) Cherokee County where metro meets the mountains

Cherokee County where metro meets the mountains") HOST OVERVIEW On the November 6, 2012 Ballot, Cherokee County voters will be asked to consider a HOST, an additional penny sales tax, which will be used to reduce property taxes 05 Oct 2012 (17 pages)

HOST OVERVIEW On the November 6, 2012 Ballot, Cherokee County voters will be asked to consider a HOST, an additional penny sales tax, which will be used to reduce property taxes 05 Oct 2012 (17 pages)

CITY OF MODESTO COMMUNITY FACILITIES DISTRICT NO (HETCH HETCHY) CFD REPORT

CFD REPORT") CITY OF MODESTO COMMUNITY FACILITIES DISTRICT NO. 2005-1 (HETCH HETCHY) CFD REPORT September 23, 2005 Goodwin Consulting Group, Inc. 555 University Avenue, Suite 280 Sacramento, California 95825 Phone

CITY OF MODESTO COMMUNITY FACILITIES DISTRICT NO. 2005-1 (HETCH HETCHY) CFD REPORT September 23, 2005 Goodwin Consulting Group, Inc. 555 University Avenue, Suite 280 Sacramento, California 95825 Phone

CITY OF BRAMPTON Budget Highlights. As Approved by City Council on February 23, 2011

CITY OF BRAMPTON 2011 Budget Highlights As Approved by City Council on February 23, 2011 EXEXCUTIVE SUMMARY The current economic climate, meeting provincial growth targets and other budget drivers places

CITY OF BRAMPTON 2011 Budget Highlights As Approved by City Council on February 23, 2011 EXEXCUTIVE SUMMARY The current economic climate, meeting provincial growth targets and other budget drivers places

2018 Development Charges Background Study The Cost of Growth. Council Workshop #2

Development Charges Background Study The Cost of Growth Council Workshop #2 June 27, 1 Agenda Review of development charges, legislated requirements and influencing factors City s DC study schedule and

Development Charges Background Study The Cost of Growth Council Workshop #2 June 27, 1 Agenda Review of development charges, legislated requirements and influencing factors City s DC study schedule and

CITY OF WARNER ROBINS, GEORGIA ANNUAL FINANCIAL REPORT YEAR ENDED JUNE 30, 2014

CITY OF WARNER ROBINS, GEORGIA ANNUAL FINANCIAL REPORT YEAR ENDED NICHOLS, CAULEY & ASSOCIATES, LLC Certified Public Accountants Certified Financial Planners Certified Internal Auditors Certified Government

CITY OF WARNER ROBINS, GEORGIA ANNUAL FINANCIAL REPORT YEAR ENDED NICHOLS, CAULEY & ASSOCIATES, LLC Certified Public Accountants Certified Financial Planners Certified Internal Auditors Certified Government

Revenue vs Expense for February 2019

General Fund Sales Tax $7,000,000.00 $1,227,630.12 17.54% County Sales Tax $2,100,000.00 $358,756.42 17.08% Payment of ACT 9 Taxes $50,000.00 $0.00 0.00% Pay in Lieu of Taxes - Util $1,600,000.00 $237,073.45

General Fund Sales Tax $7,000,000.00 $1,227,630.12 17.54% County Sales Tax $2,100,000.00 $358,756.42 17.08% Payment of ACT 9 Taxes $50,000.00 $0.00 0.00% Pay in Lieu of Taxes - Util $1,600,000.00 $237,073.45

General Operating Fund

General Operating Fund Actual Actual Actual Budget 2010 YTD Projected Recommended Projected Projected Revenues 2007 2008 2009 2010 as of 6/30/10 2010 2011 2011 2012 Property Taxes $13,449,730 $13,842,433

General Operating Fund Actual Actual Actual Budget 2010 YTD Projected Recommended Projected Projected Revenues 2007 2008 2009 2010 as of 6/30/10 2010 2011 2011 2012 Property Taxes $13,449,730 $13,842,433

CITY OF NORTH LAS VEGAS, NEVADA DEBT MANAGEMENT POLICY IN ACCORDANCE WITH NRS (C)

") CITY OF NORTH LAS VEGAS, NEVADA DEBT MANAGEMENT POLICY IN ACCORDANCE WITH NRS 350.013 1(C) JUNE 30, 2007 TABLE OF CONTENTS DEBT MANAGEMENT POLICY NRS 350.013 Subsection 1(c)... 1 Summary of Debt... 2 Affordability

CITY OF NORTH LAS VEGAS, NEVADA DEBT MANAGEMENT POLICY IN ACCORDANCE WITH NRS 350.013 1(C) JUNE 30, 2007 TABLE OF CONTENTS DEBT MANAGEMENT POLICY NRS 350.013 Subsection 1(c)... 1 Summary of Debt... 2 Affordability

SUMMARY OF SERVICES BY STRATEGIC PRIORITY

Public Safety Building Services Security Service for City Facilities $4,196,367 $4,262,299 $4,196,367 $4,262,299 City Attorney's Office Municipal Prosecution $2,343,624 $2,397,112 $2,343,624 $2,397,112

Public Safety Building Services Security Service for City Facilities $4,196,367 $4,262,299 $4,196,367 $4,262,299 City Attorney's Office Municipal Prosecution $2,343,624 $2,397,112 $2,343,624 $2,397,112

FINANCIAL REPORT TO THE CITY OF MISSISSAUGA ON THE TRANSITION TO A SINGLE TIER

FINANCIAL REPORT TO THE CITY OF MISSISSAUGA ON THE TRANSITION TO A SINGLE TIER DAY & DAY CHARTERED ACCOUNTANTS NOVEMBER 2003 TABLE OF CONTENTS Page EXECUTIVE SUMMARY...i INTRODUCTION... 1 MUNICIPAL PROFILES...

FINANCIAL REPORT TO THE CITY OF MISSISSAUGA ON THE TRANSITION TO A SINGLE TIER DAY & DAY CHARTERED ACCOUNTANTS NOVEMBER 2003 TABLE OF CONTENTS Page EXECUTIVE SUMMARY...i INTRODUCTION... 1 MUNICIPAL PROFILES...

CITIZEN PERSPECTIVE Citizen Survey. Survey conducted by Prairie Research Associates May 2017

CITIZEN PERSPECTIVE 217 Citizen Survey Survey conducted by Prairie Research Associates May 217 1 What is Market Research? The process of gathering information to learn more about how customers and potential

CITIZEN PERSPECTIVE 217 Citizen Survey Survey conducted by Prairie Research Associates May 217 1 What is Market Research? The process of gathering information to learn more about how customers and potential

TOWN OF SHELBURNE, VERMONT AUDIT REPORT JUNE 30, 2017

AUDIT REPORT AUDIT REPORT TABLE OF CONTENTS Page # Independent Auditor s Report 1-3 Management s Discussion and Analysis 4-12 Basic Financial Statements: Statement of Net Position Exhibit A 13 Statement

AUDIT REPORT AUDIT REPORT TABLE OF CONTENTS Page # Independent Auditor s Report 1-3 Management s Discussion and Analysis 4-12 Basic Financial Statements: Statement of Net Position Exhibit A 13 Statement

2015 Update of Water and Wastewater Impact Fees

2015 Update of Water and Wastewater Impact Fees Prepared for the City of Georgetown Prepared by: Georgetown Utility Services and Chisholm Trail Special Utility District Capital Improvements Advisory Committees

2015 Update of Water and Wastewater Impact Fees Prepared for the City of Georgetown Prepared by: Georgetown Utility Services and Chisholm Trail Special Utility District Capital Improvements Advisory Committees

April 30, 2015 For the first seven months of FY , the General Fund has collected 78% of revenues, primarily due to property taxes. Expenditur

April 30, 2015 For the first seven months of FY 2014-2015, the General Fund has collected 78% of revenues, primarily due to property taxes. Expenditures are 55% of budget. The Fire Department has spent

April 30, 2015 For the first seven months of FY 2014-2015, the General Fund has collected 78% of revenues, primarily due to property taxes. Expenditures are 55% of budget. The Fire Department has spent

VILLAGE OF NEW MARYLAND 2015 GENERAL OPERATING FUND BUDGET. 1. Total Budget - Total Page 17 $4,466,360

1. Total Budget - Total Page 17 $4,466,360 2. Less: Non-Tax Revenue - Total Page 7 $311,392 3. Net Budget $4,154,968 4. Less: Community Funding and Equalization Grant $6,108 5. Warrant to be Raised by

1. Total Budget - Total Page 17 $4,466,360 2. Less: Non-Tax Revenue - Total Page 7 $311,392 3. Net Budget $4,154,968 4. Less: Community Funding and Equalization Grant $6,108 5. Warrant to be Raised by

Public Policy Issues and Sustainability in Southern California. Financing Infrastructure Development

Public Policy Issues and Sustainability in Southern California Financing Infrastructure Development University of California Riverside March 3, 2010 Outline What is Infrastructure?; Infrastructure Need;

Public Policy Issues and Sustainability in Southern California Financing Infrastructure Development University of California Riverside March 3, 2010 Outline What is Infrastructure?; Infrastructure Need;

ORDINANCE NO. 701 (Adopting FY Budget)

") ORDINANCE NO. 701 (Adopting FY 2013-2014 Budget) AN ORDINANCE OF THE CITY OF PARKER, COLLIN COUNTY, TEXAS APPROVING AND ADOPTING A BUDGET FOR THE FISCAL YEAR BEGINNING OCTOBER 1, 2013, AND ENDING SEPTEMBER

ORDINANCE NO. 701 (Adopting FY 2013-2014 Budget) AN ORDINANCE OF THE CITY OF PARKER, COLLIN COUNTY, TEXAS APPROVING AND ADOPTING A BUDGET FOR THE FISCAL YEAR BEGINNING OCTOBER 1, 2013, AND ENDING SEPTEMBER

Rural Based Business License Application

New Applications All forms must be filled out completely, including mailing and business addresses and all available phone/fax/email information. Currently we do not accept applications by mail. $35.00

New Applications All forms must be filled out completely, including mailing and business addresses and all available phone/fax/email information. Currently we do not accept applications by mail. $35.00

OFF-SITE LEVIES UDI ALBERTA & CHBA ALBERTA RECOMMENDATIONS

OFF-SITE LEVIES UDI ALBERTA & CHBA ALBERTA RECOMMENDATIONS 1. OVERVIEW We want to express our appreciation for the work of Municipal Affairs staff throughout the consultation process on the individual

OFF-SITE LEVIES UDI ALBERTA & CHBA ALBERTA RECOMMENDATIONS 1. OVERVIEW We want to express our appreciation for the work of Municipal Affairs staff throughout the consultation process on the individual

INFORMATION ITEMS December 31, 2014 For the first quarter of FY 2014-2015, the General Fund has collected 31% of revenues, primarily due to property taxes (42% collected through December). Expenditures

INFORMATION ITEMS December 31, 2014 For the first quarter of FY 2014-2015, the General Fund has collected 31% of revenues, primarily due to property taxes (42% collected through December). Expenditures

CITY OF LATHROP SPECIAL FINANCING DISTRICTS. Fiscal Year 2011/12

CITY OF LATHROP SPECIAL FINANCING DISTRICTS Fiscal Year 2011/12 East Lathrop North Special Financing Districts East Lathrop North is the area generally bounded by the City limits to the north and east,

CITY OF LATHROP SPECIAL FINANCING DISTRICTS Fiscal Year 2011/12 East Lathrop North Special Financing Districts East Lathrop North is the area generally bounded by the City limits to the north and east,

Revenue vs Expense for December 2017

General Fund Revenue vs Expense for December 2017 Sales Tax $6,900,000.00 $6,869,780.06 99.56% County Sales Tax $2,000,000.00 $2,017,372.46 100.87% Payment of ACT 9 Taxes $22,000.00 $42,085.50 191.30%

General Fund Revenue vs Expense for December 2017 Sales Tax $6,900,000.00 $6,869,780.06 99.56% County Sales Tax $2,000,000.00 $2,017,372.46 100.87% Payment of ACT 9 Taxes $22,000.00 $42,085.50 191.30%

GENERAL FUND REVENUES AND EXPENDITURES FY Through March % of Budget Year

GENERAL FUND REVENUES AND EXPENDITURES Current Actual Projected YTD Budget Final Amended Month Current YTD YTD Projected Actual YTD% Projected % REVENUES Budget Actuals Amount Amount Variance of Budget

GENERAL FUND REVENUES AND EXPENDITURES Current Actual Projected YTD Budget Final Amended Month Current YTD YTD Projected Actual YTD% Projected % REVENUES Budget Actuals Amount Amount Variance of Budget

Development Charges Annual Report

Report No: CS 2018-09 CORPORATE SERVICES Council Date: April 11, 2018 To: From: Warden and Members of County Council Director of Corporate Services Development Charges Annual Report - 2017 RECOMMENDATION

Report No: CS 2018-09 CORPORATE SERVICES Council Date: April 11, 2018 To: From: Warden and Members of County Council Director of Corporate Services Development Charges Annual Report - 2017 RECOMMENDATION

January 31, 2015 For the first four months of FY , the General Fund has collected 55% of revenues, primarily due to property taxes (75% colle

January 31, 2015 For the first four months of FY 2014-2015, the General Fund has collected 55% of revenues, primarily due to property taxes (75% collected through January). Expenditures through Janauary

January 31, 2015 For the first four months of FY 2014-2015, the General Fund has collected 55% of revenues, primarily due to property taxes (75% collected through January). Expenditures through Janauary

City of Keizer Fees and Charges for Services As of July 2017

General Administration Liquor Licenses/Permits Original Application $ 100.00 Change of ownership, location, privilege $ 75.00 Renewal and temporary applications $ 35.00 Special license applications $ 35.00

General Administration Liquor Licenses/Permits Original Application $ 100.00 Change of ownership, location, privilege $ 75.00 Renewal and temporary applications $ 35.00 Special license applications $ 35.00

Introduction to Development Charges (DCs)

") Introduction to Development Charges (DCs) Strategic Priorities and Policy Committee April 13 th, 2015 1 Agenda What are Development Charges & what do they pay for? DC rate setting process Payment of DCs

Introduction to Development Charges (DCs) Strategic Priorities and Policy Committee April 13 th, 2015 1 Agenda What are Development Charges & what do they pay for? DC rate setting process Payment of DCs

Budget Introduction Proposed Budget

Budget Introduction Proposed Budget INTRO - 1 INTRO - 2 Summary of the Budget and Accounting Structure The City of Beverly Hills uses the same basis for budgeting as for accounting. Governmental fund financial

Budget Introduction Proposed Budget INTRO - 1 INTRO - 2 Summary of the Budget and Accounting Structure The City of Beverly Hills uses the same basis for budgeting as for accounting. Governmental fund financial

Monthly Financial Report and Benchmarks. December 2017

Monthly Financial Report and Benchmarks December 2017 This financial overview reflects the City s overall unaudited financial condition through December 2017 or 25% of the fiscal year. The following tables

Monthly Financial Report and Benchmarks December 2017 This financial overview reflects the City s overall unaudited financial condition through December 2017 or 25% of the fiscal year. The following tables

LINDQUIST, VON HUSEN AND JOYCE

F"RED,J. VON HUSEN JOHN F.,JOYCE NORMAN THOMAS ARTHUR F. ROBIN ERIC L HEDEN FRED E _ LUNDBERG RUDOLPH E. LINDQUIST ASSOCIATE LINDQUIST, VON HUSEN AND JOYCE CERTIFIED PUBLIC ACCOUNTANTS 120 MONTGOM ERY

F"RED,J. VON HUSEN JOHN F.,JOYCE NORMAN THOMAS ARTHUR F. ROBIN ERIC L HEDEN FRED E _ LUNDBERG RUDOLPH E. LINDQUIST ASSOCIATE LINDQUIST, VON HUSEN AND JOYCE CERTIFIED PUBLIC ACCOUNTANTS 120 MONTGOM ERY

Chapter VIII. General Plan Implementation A. INTRODUCTION B. SUBMITTAL AND APPROVAL OF SUBSEQUENT PROJECTS C. SPHERE OF INFLUENCE

Chapter VIII General Plan Implementation A. INTRODUCTION This chapter presents a variety of tools available to the (City) to help build the physical city envisioned in Chapter III. While the Modesto provides

Chapter VIII General Plan Implementation A. INTRODUCTION This chapter presents a variety of tools available to the (City) to help build the physical city envisioned in Chapter III. While the Modesto provides

Monthly Financial Report and Benchmarks. November 2017

Monthly Financial Report and Benchmarks November 2017 This financial overview reflects the City s overall unaudited financial condition through November 2017 or 17% of the fiscal year. The following tables

Monthly Financial Report and Benchmarks November 2017 This financial overview reflects the City s overall unaudited financial condition through November 2017 or 17% of the fiscal year. The following tables

8. CAPITAL IMPROVEMENT ELEMENT Goals, Objectives, and Policies

8. Goals, Objectives, and Policies GOAL 8-1: TO USE SOUND FISCAL POLICIES TO PROVIDE PUBLIC FACILITIES AND SERVICES CONCURRENT WITH DEVELOPMENT/REDEVELOPMENT IN ORDER TO ACHIEVE AND MAINTAIN ADOPTED STANDARDS

8. Goals, Objectives, and Policies GOAL 8-1: TO USE SOUND FISCAL POLICIES TO PROVIDE PUBLIC FACILITIES AND SERVICES CONCURRENT WITH DEVELOPMENT/REDEVELOPMENT IN ORDER TO ACHIEVE AND MAINTAIN ADOPTED STANDARDS

2016 CITY MANAGER RECOMMENDED BUDGET. Law Enforcement

2016 CITY MANAGER RECOMMENDED BUDGET Law Enforcement Law Enforcement 2016 Department Overview Motto Community First, Public Safety ALWAYS! Mission The Mission of the Snohomish Police Department is to provide

2016 CITY MANAGER RECOMMENDED BUDGET Law Enforcement Law Enforcement 2016 Department Overview Motto Community First, Public Safety ALWAYS! Mission The Mission of the Snohomish Police Department is to provide

CITIZEN S POPULAR ANNUAL FINANCIAL REPORT

Clearfield City 1 CITIZEN S POPULAR ANNUAL FINANCIAL REPORT A Summary Financial Report of the 2013 Fiscal Year (July 1, 2012 through June 30, 2013) 2 Clearfield City Purpose Statement The intent of the

Clearfield City 1 CITIZEN S POPULAR ANNUAL FINANCIAL REPORT A Summary Financial Report of the 2013 Fiscal Year (July 1, 2012 through June 30, 2013) 2 Clearfield City Purpose Statement The intent of the