Topic 8: Financial Frictions and Shocks Part1: Asset holding developments

|

|

|

- Ethel Reynolds

- 5 years ago

- Views:

Transcription

1 Topic 8: Financial Frictions and Shocks Part1: Asset holding developments - The relaxation of capital account restrictions in many countries over the last two decades has produced dramatic increases in international asset flows, - with a temporary slowdown during financial crisis. - The accumulation of large foreign asset positions have implications for theories studied earlier in this course. - Integrated financial markets provides channel of international transmission of financial shocks, as in Global Financial Crisis of

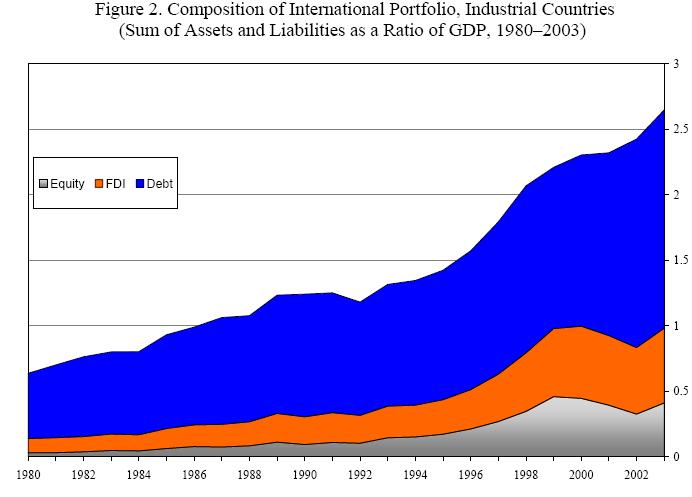

2 a) Observations (Lane and Milesi Ferretti papers) - The sum of assets plus liabilities has grown much, especially in the late 1990s. - Financial integration has grown faster than goods trade integration. - Gross holdings (assets plus liabilities) has grown much more than net holdings (assets minus liabilities). - Returns on US assets abroad have tended to be higher than US liabilities. This explains why US net interest income was positive until recently, even though it has been a net debtor since

3 Chinn-Ito index of caitgal account openness ranges -2.5 to 2.5 3

4 4

5 5

6 6

7 source: Benertrix, Lane, Shambaugh (2015) 7

8 8

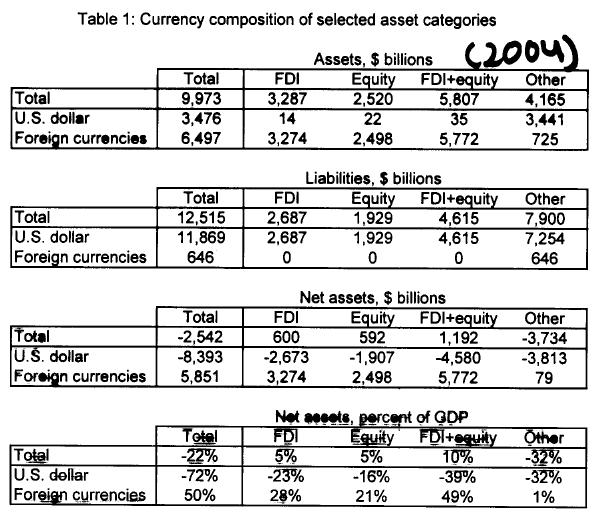

9 b) the US portfolio is special: - While US gross assets are primarily in foreign currency, its liabilities are largely in US dollars. - While the US is a net creditor in foreign currency assets (50% of US GDP in 2004) it is net debtor in dollar assets (72% of GDP). Overall, net debt position of 22% of GDP. - This implies that a change in the nominal exchange rate affects the value of the net asset position: a 10% depreciation of dollar transfers 5% of US GDP. - Implications of this fact will be developed in a theoretical model in the third section of this lecture. 9

10 10

11 11

12 12

13 Part2: Financial Adjustment: Gourinchas and Rey - This paper studies how capital gains on gross external assets provide an alternative channel for international BOP adjustment to the familiar channel via trade flows. - We have seen in our intertemporal models that a country running a current account deficit to smooth over a shock needs to finance this by trade surpluses in future periods. - An alternative way of satisfying the budget constraint would be for the valuation of foreign holdings of home assets to drop. - A likely way that this would occur would be through exchange rate depreciation. 13

14 a) Theory - The theory is analogous to that used for the Present Value tests of Campbell, used to test the intertemporal approach to the current account used in this course. - The authors refer to their approach as an intertemporal approach to the Financial account. - Begin with a rewriting of the BOP (budget) constraint: NAt 1 Rt 1 NAt NX t Where - NA is defined as the difference between gross foreign assets (A) and gross foreign liabilities (L). - NX is net exports, exports (X) minus imports (M). - R is total return on net foreign asset portfolio. 14

15 - As in the earlier present value tests, linearize this budget constraint: 1 nat 1 rt 1 1 nxt nat Where 1 is the steady state ratio of net exports to net assets (NX /NA). - The total rate of return on the net foreign asset portfolio can be approximated as a weighted combination of the rates of return on the countries external assets and that on the country s external liabilities (which can differ) r r r a l t 1 a t 1 l t 1 15

16 - For reference later, define a linear combination of net exports and net assets: nxa nx na x m a l t t t x t m t a t l l t Which can be interpreted as the deviation from trend of the ratio of net exports to net foreign assets (NX /NA). - The intertemporal budget constraint implies a condition analogous to the test condition from the present value CA literature: t j j 1 t t j t j nxa E r nx (key PV condition) 16

17 - This shows that movements in the trade balance and the net foreign asset position must forecast either future portfolio returns, or future net exports growth, or both. - So there are two channels of adjustment to a net export imbalance: the usual trade channel, and an asset valuation channel. - Note that the latter, represented in r, can take place by changes in the nominal exchange rate, if the gross asset positions for assets and liabilities tend to be denominated in different currencies. 17

18 b) Empirical Implementation and Results Data: The authors must work quite hard to collect the data needed to compute the series for total returns, r, as this requires estimates on weights for different categories of assets and their returns. Present value test: - The authors follow Campbell methodology in testing the PV condition above. - They use a VAR to generate forecasts for the expected discounted sums of r and NX above. 18

19 - They then can use the equation above to compute a model-consistent forecast of nxa, which then can compare to the data using a Wald test. - They find a chi-squared statistic of 0.325, and with three restrictions, the p-value is So they cannot reject the restriction of the Present value condition above. 19

20 Decomposition: The authors decompose nxa into the two channels implied by the PV condition: j - the trade channel ( Et nxt j ) j 1 t j j 1 t t j t j nxa E r nx j -and the valuation channel ( Et rt j ). j 1 - The valuation channel plays an important role, accounting for 31% of overall external adjustment. - They conclude that the valuation channel does not replace the need for the US to generate net exports in the future, but it does significantly reduce the magnitude of adjustment needed along the trade channel. 20

21 21

22 22

23 Part 3: Implications for monetary policy models: Tille a) Model: - Two country model sticky price model like OR (1995), but with new asset market features. - Can hold home and foreign bonds and equities. Nominal bonds in H and F currency (one period and perpetuity bonds that pay a fixed nominal interest rate for all future periods). - Equities share in firm in H and F, which are mutual fund claim to other countries nominal profits. 23

24 - assume steady state with zero net foreign asset position, so can get closed form solution. - Nonetheless, there are nonzero gross holdings in each currency. - Calibration: representative of US case. Foreign currency - assets represent 50% of home GDP (either bonds, equities, or combination of the two). Four cases for asset market in each table: 1) no international asset positions 2) bonds only economy 3) equities only 4) mixture of bonds and equities matching US case. 24

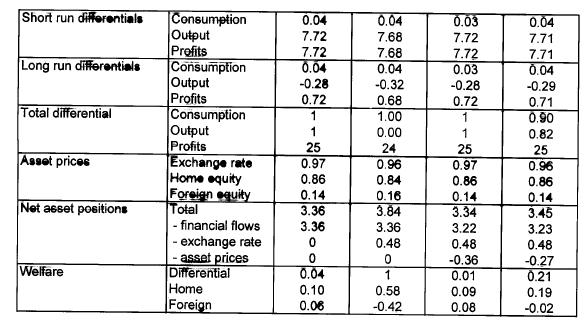

25 b) Findings (sticky price version of model) With no financial integration (column 1), get something close to the basic Obstfeld-Rogoff (1995) story: Increase money supply raises production and consumption. Bonds only economy: (Column 2) - We see evidence of a wealth transfer. - May appear that the asset valuation effect has little impact on consumption - But note the fall in home long-run output. - It is also very clear in the effect on home welfare, which rises 5.8 times larger than in the no asset case. 25

26 26

27 Part 4: International transmission of financial shocks and Global Financial Crisis International comovement was particularly strong during recent financial crisis. But was temporary, associated with particular financial shock. Countries with greater financial linkages to US tended to experience US Great Recession more strongly. 27

28 28

29 29

GDP during past recessions: 30")

30 a) International Recession (Perri and Quadrini, 2016) (slides from Angsoka Y. Paundralingga) GDP during past recessions: 30

31 31

32 32

33 33

34 34

35 35

36 36

37 37

38 38

39 39

40 40

41 41

42 42

43 43

44 44

45 45

46 46

47 47

48 48

49 49

50 50

51 Result 1: Asymmetry: Credit contractions have larger macroeconomic and asset price effects than expansions 51

52 Result 2: Recessions Led by Credit Booms: The severity of crises increases with the duration of the credit expansion 52

53 Result 3: Employment and Asset Price Volatility: Credit shocks generate large fluctuations in employment and asset prices 53

54 Result 4: Heterogeneous Responses of Labor:Heterogeneous response of employment but similar responses of financial variables and other real variables 54

55 55

56 Conclusions: 56

57 57

58 58

59 b) Devereux and Yetman: Leverage Constraints and the International Transmission of Shocks Slides courtesy of Luca Macedoni 59

60 60

61 61

62 62

63 63

64 64

65 65

66 66

67 67

68 68

69 69

70 70

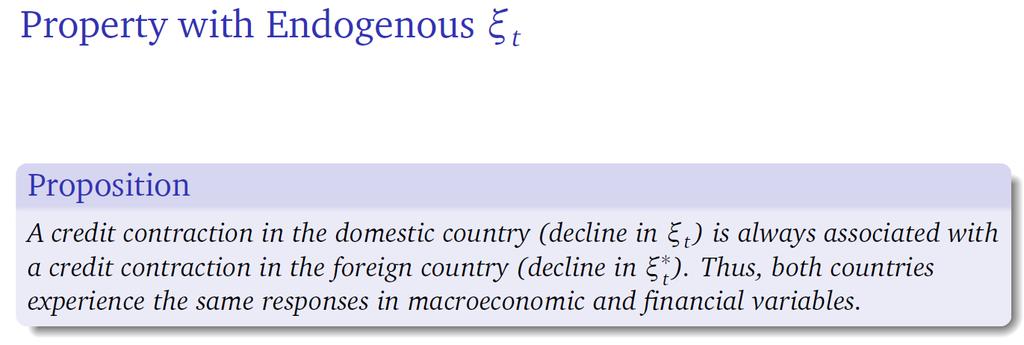

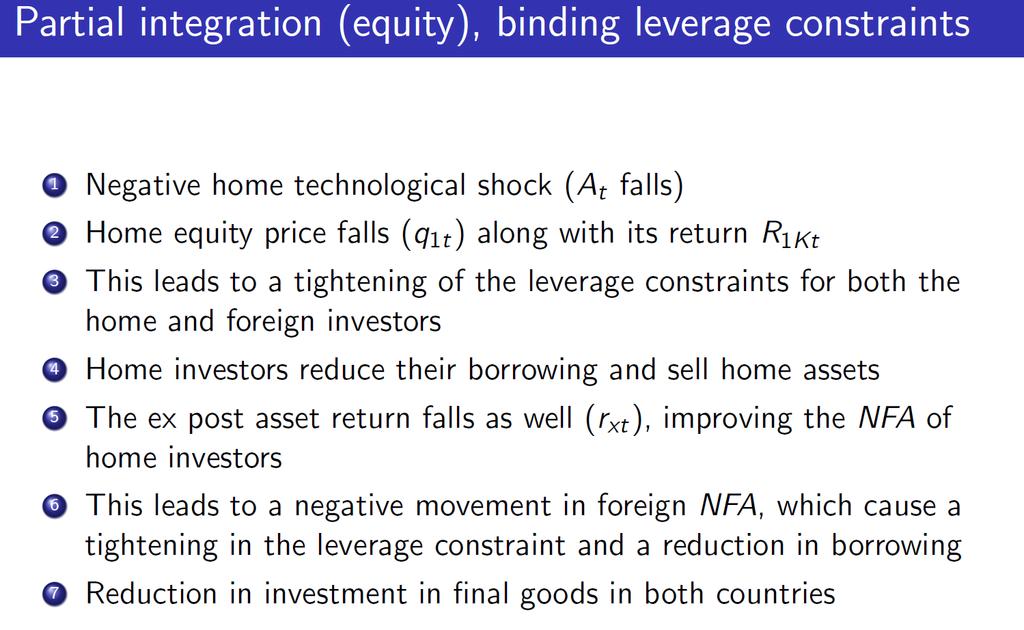

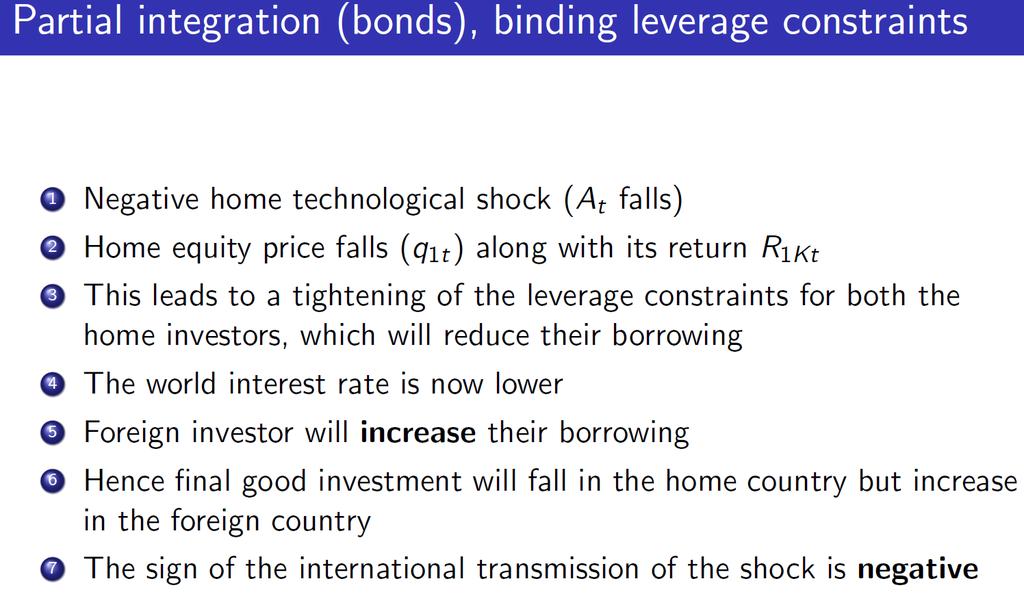

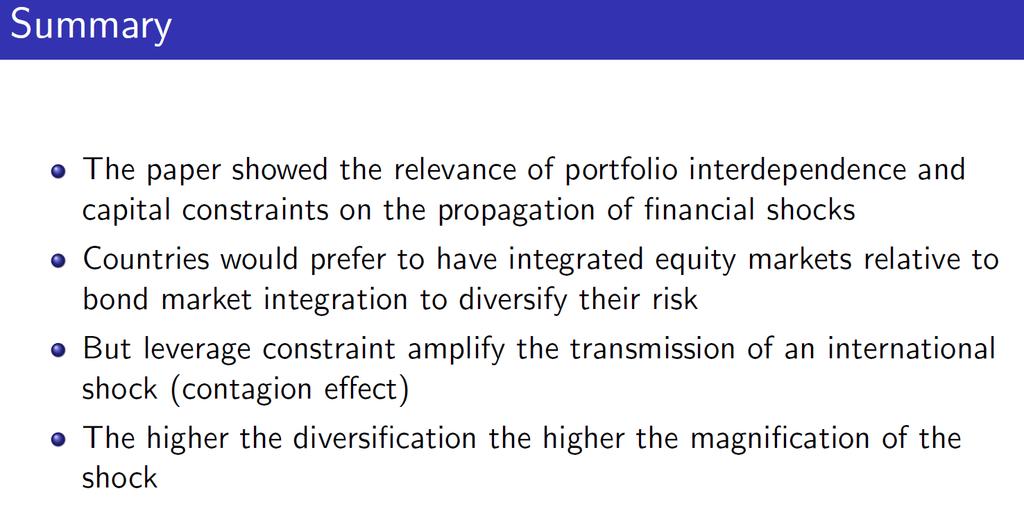

71 71

72 72

73 73

74 74

75 75

76 76

77 77

78 78

79 There is a clear positive comovement across countries. Qualitatively, the transmission is similar to Figs 5 and 6, except now there is a single world debt market. Shock leads to a fall in the price of the home asset and, from arbitrage condition (8), the foreign asset price also falls. Given the hedged portfolio position of the home country, the fall in the return on the home asset leads to an increase in home NFA due to valuation effects. For the foreign country these valuation effects are negative, leading to tightening of foreign leverage constraint. 79

80 80

Topic 10: Asset Valuation Effects

Topic 10: Asset Valuation Effects Part1: Document Asset holding developments - The relaxation of capital account restrictions in many countries over the last two decades has produced dramatic increases

Topic 10: Asset Valuation Effects Part1: Document Asset holding developments - The relaxation of capital account restrictions in many countries over the last two decades has produced dramatic increases

19.2 Exchange Rates in the Long Run Introduction 1/24/2013. Exchange Rates and International Finance. The Nominal Exchange Rate

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

Draft: The Trilemma and Long Run Financial Adjustment

Draft: The Trilemma and Long Run Financial Adjustment William Swanson September 13, 2016 Abstract Rich and poor countries have aggregate portfolios that are starkly different. First, Net Foreign Assets

Draft: The Trilemma and Long Run Financial Adjustment William Swanson September 13, 2016 Abstract Rich and poor countries have aggregate portfolios that are starkly different. First, Net Foreign Assets

International Finance and Macroeconomics (Econ 422)

") Professor Eric van Wincoop Econ 422 Department of Economics Spring 2015 231 Monroe Hall TR 9:30-10:45 Office Hours: Monday 2-3, Tuesday 11-12 Monroe 116 E-mail: vanwincoop@virginia.edu Phone: 924-3997

Professor Eric van Wincoop Econ 422 Department of Economics Spring 2015 231 Monroe Hall TR 9:30-10:45 Office Hours: Monday 2-3, Tuesday 11-12 Monroe 116 E-mail: vanwincoop@virginia.edu Phone: 924-3997

GLOBAL IMBALANCES FROM A STOCK PERSPECTIVE

GLOBAL IMBALANCES FROM A STOCK PERSPECTIVE Ángel Estrada and Francesca Viani (*) 14 th EMERGING MARKET WORKSHOP Madrid (*) The views expressed here do not necessarily coincide with those of Banco de España

GLOBAL IMBALANCES FROM A STOCK PERSPECTIVE Ángel Estrada and Francesca Viani (*) 14 th EMERGING MARKET WORKSHOP Madrid (*) The views expressed here do not necessarily coincide with those of Banco de España

GRA 6639 Topics in Macroeconomics

Lecture 9 Spring 2012 An Intertemporal Approach to the Current Account Drago Bergholt (Drago.Bergholt@bi.no) Department of Economics INTRODUCTION Our goals for these two lectures (9 & 11): - Establish

Lecture 9 Spring 2012 An Intertemporal Approach to the Current Account Drago Bergholt (Drago.Bergholt@bi.no) Department of Economics INTRODUCTION Our goals for these two lectures (9 & 11): - Establish

Financial integration: Patterns, effects and challenges.

Financial integration: Patterns, effects and challenges. Viktoria Hnatkovska UBC and Wharton School BREAD-IGC-ISI Summer School, Delhi July 23 2012 Introduction New Delhi, March 2012: Mr Kaushik Basu,

Financial integration: Patterns, effects and challenges. Viktoria Hnatkovska UBC and Wharton School BREAD-IGC-ISI Summer School, Delhi July 23 2012 Introduction New Delhi, March 2012: Mr Kaushik Basu,

Exorbitant Privilege and Exorbitant Duty P.O. Gourinchas, H. Rey, N. Govillot Comments

Exorbitant Privilege and Exorbitant Duty P.O. Gourinchas, H. Rey, N. Govillot Comments Banco de España - Banco Mundial - CREI Financial Globalization: Shifting Balances Banco de España, Madrid July 1-2,

Exorbitant Privilege and Exorbitant Duty P.O. Gourinchas, H. Rey, N. Govillot Comments Banco de España - Banco Mundial - CREI Financial Globalization: Shifting Balances Banco de España, Madrid July 1-2,

Topic 3: International Risk Sharing and Portfolio Diversification

Topic 3: International Risk Sharing and Portfolio Diversification Part 1) Working through a complete markets case - In the previous lecture, I claimed that assuming complete asset markets produced a perfect-pooling

Topic 3: International Risk Sharing and Portfolio Diversification Part 1) Working through a complete markets case - In the previous lecture, I claimed that assuming complete asset markets produced a perfect-pooling

Creditor countries and debtor countries: some asymmetries in the dynamics of external wealth accumulation

ECONOMIC BULLETIN 3/218 ANALYTICAL ARTICLES Creditor countries and debtor countries: some asymmetries in the dynamics of external wealth accumulation Ángel Estrada and Francesca Viani 6 September 218 Following

ECONOMIC BULLETIN 3/218 ANALYTICAL ARTICLES Creditor countries and debtor countries: some asymmetries in the dynamics of external wealth accumulation Ángel Estrada and Francesca Viani 6 September 218 Following

Capital markets liberalization and global imbalances

Capital markets liberalization and global imbalances Vincenzo Quadrini University of Southern California, CEPR and NBER February 11, 2006 VERY PRELIMINARY AND INCOMPLETE Abstract This paper studies the

Capital markets liberalization and global imbalances Vincenzo Quadrini University of Southern California, CEPR and NBER February 11, 2006 VERY PRELIMINARY AND INCOMPLETE Abstract This paper studies the

Autarky vs Openness in a Neoclassical Growth Model. George Alogoskoufis Athens University of Economics and Business

Autarky vs Openness in a Neoclassical Growth Model! George Alogoskoufis Athens University of Economics and Business Financial Autarky vs Openness During the 1950s and the 1960s the domestic financial systems

Autarky vs Openness in a Neoclassical Growth Model! George Alogoskoufis Athens University of Economics and Business Financial Autarky vs Openness During the 1950s and the 1960s the domestic financial systems

Global Real Rates: A Secular Approach

Global Real Rates: A Secular Approach Pierre-Olivier Gourinchas 1 Hélène Rey 2 1 UC Berkeley & NBER & CEPR 2 London Business School & NBER & CEPR FRBSF Fed, April 2017 Prepared for the conference Do Changes

Global Real Rates: A Secular Approach Pierre-Olivier Gourinchas 1 Hélène Rey 2 1 UC Berkeley & NBER & CEPR 2 London Business School & NBER & CEPR FRBSF Fed, April 2017 Prepared for the conference Do Changes

GLOBAL IMBALANCES FROM A STOCK PERSPECTIVE

GLOBAL IMBALANCES FROM A STOCK PERSPECTIVE Enrique Alberola (BIS), Ángel Estrada and Francesca Viani (BdE) (*) (*) The views expressed here do not necessarily coincide with those of Banco de España, the

GLOBAL IMBALANCES FROM A STOCK PERSPECTIVE Enrique Alberola (BIS), Ángel Estrada and Francesca Viani (BdE) (*) (*) The views expressed here do not necessarily coincide with those of Banco de España, the

Week 5. Remainder of chapter 9: the complete real model Chapter 10: money Copyright 2008 Pearson Addison-Wesley. All rights reserved.

Week 5 Remainder of chapter 9: the complete real model Chapter 10: money 10-1 A Decrease in the Current Capital Stock This could arise due to a war or natural disaster. Output may rise or fall, depending

Week 5 Remainder of chapter 9: the complete real model Chapter 10: money 10-1 A Decrease in the Current Capital Stock This could arise due to a war or natural disaster. Output may rise or fall, depending

Global Financial Cycle

Global Financial Cycle Hélène Rey London Business School & NBER & CEPR IMF 2017 Prepared for Jacques Polak ARC 18th 1 / 31 Global Financial Cycle Fluctuations in financial activity (risk taking, credit

Global Financial Cycle Hélène Rey London Business School & NBER & CEPR IMF 2017 Prepared for Jacques Polak ARC 18th 1 / 31 Global Financial Cycle Fluctuations in financial activity (risk taking, credit

Empirical Modeling of Dollar Exchange Rates

Empirical Modeling of Dollar Exchange Rates Forecasting and Policy Implications Menzie D. Chinn UW-Madison & NBER Presentation at Congressional Budget Office June 29, 2005 Motivation (I) Uncovered interest

Empirical Modeling of Dollar Exchange Rates Forecasting and Policy Implications Menzie D. Chinn UW-Madison & NBER Presentation at Congressional Budget Office June 29, 2005 Motivation (I) Uncovered interest

CONFERENCE PROCEEDINGS. Current Account Sustainability in Major Advanced Economies

CONFERENCE PROCEEDINGS Current Account Sustainability in Major Advanced Economies This conference, held at the University of Wisconsin on 28 and 29 of April 2006, presented research on theoretical and

CONFERENCE PROCEEDINGS Current Account Sustainability in Major Advanced Economies This conference, held at the University of Wisconsin on 28 and 29 of April 2006, presented research on theoretical and

The US Current Account Deficit and Its Exchange Rate Consequences. By Ali Al-Eyd Ray Barrell and Olga Pomerantz

The US Current Account Deficit and Its Exchange Rate Consequences By Ali Al-Eyd Ray Barrell and Olga Pomerantz The emerging deficit The US current account (as a % of GDP) has been progressively deteriorating

The US Current Account Deficit and Its Exchange Rate Consequences By Ali Al-Eyd Ray Barrell and Olga Pomerantz The emerging deficit The US current account (as a % of GDP) has been progressively deteriorating

Exchange Rates and External Imbalances

Exchange Rates and External Imbalances Christian Grisse and Thomas Nitschka Swiss National Bank First draft: September 21, 212 This draft: February 15, 213 Preliminary. Comments welcome, please do not

Exchange Rates and External Imbalances Christian Grisse and Thomas Nitschka Swiss National Bank First draft: September 21, 212 This draft: February 15, 213 Preliminary. Comments welcome, please do not

Recent developments in the euro area suggest. What caused current account imbalances in euro area periphery countries?

No. 31 October 16 What caused current account imbalances in euro area periphery countries? Daniele Siena Directorate General Economics and International Relations The views expressed here are those of

No. 31 October 16 What caused current account imbalances in euro area periphery countries? Daniele Siena Directorate General Economics and International Relations The views expressed here are those of

An Introduction to Macroeconomics

An Introduction to Macroeconomics Economics 4353 - Intermediate Macroeconomics Aaron Hedlund University of Missouri Fall 2015 Econ 4353 (University of Missouri) Introduction Fall 2015 1 / 19 What is Macroeconomics?

An Introduction to Macroeconomics Economics 4353 - Intermediate Macroeconomics Aaron Hedlund University of Missouri Fall 2015 Econ 4353 (University of Missouri) Introduction Fall 2015 1 / 19 What is Macroeconomics?

Topic 2: International Comovement Part1: International Business cycle Facts: Quantities

Topic 2: International Comovement Part1: International Business cycle Facts: Quantities Issue: We now expand our study beyond consumption and the current account, to study a wider range of macroeconomic

Topic 2: International Comovement Part1: International Business cycle Facts: Quantities Issue: We now expand our study beyond consumption and the current account, to study a wider range of macroeconomic

Session 2. Saving and Investment. The Real Interest Rate. National Accounting

Session 2. Saving and. The Real Interest Rate. v National Accounting Identity v Consumption and Saving v v Equilibrium and the real interest rate v Applications: Farewell to cheap capital? National Accounting

Session 2. Saving and. The Real Interest Rate. v National Accounting Identity v Consumption and Saving v v Equilibrium and the real interest rate v Applications: Farewell to cheap capital? National Accounting

International Macroeconomics

Slides for Chapter 6: External Adjustment in Small and Large Economies International Macroeconomics Schmitt-Grohé Uribe Woodford Columbia University May 1, 2016 1 A Graphical Approach to Studying External

Slides for Chapter 6: External Adjustment in Small and Large Economies International Macroeconomics Schmitt-Grohé Uribe Woodford Columbia University May 1, 2016 1 A Graphical Approach to Studying External

Oil Shocks and the Zero Bound on Nominal Interest Rates

Oil Shocks and the Zero Bound on Nominal Interest Rates Martin Bodenstein, Luca Guerrieri, Christopher Gust Federal Reserve Board "Advances in International Macroeconomics - Lessons from the Crisis," Brussels,

Oil Shocks and the Zero Bound on Nominal Interest Rates Martin Bodenstein, Luca Guerrieri, Christopher Gust Federal Reserve Board "Advances in International Macroeconomics - Lessons from the Crisis," Brussels,

Helpful Hint Fiscal Policy and the AS-AD Model

Helpful Hint Fiscal Policy and the AS-AD Model In this Helpful Hint, we analyze the effects of a change in fiscal policy using the AS-AD model. In doing so, it is useful to consider a specific example.

Helpful Hint Fiscal Policy and the AS-AD Model In this Helpful Hint, we analyze the effects of a change in fiscal policy using the AS-AD model. In doing so, it is useful to consider a specific example.

Eco202 Review, April 2011, Prof. Bill Even. I. Introduction. A. The causes of the great recession B. Government responses to great recession

Eco202 Review, April 2011, Prof. Bill Even I. Introduction. A. The causes of the great recession B. Government responses to great recession II. III. Chapter 4: Measuring GDP and Economic Growth A. Definition

Eco202 Review, April 2011, Prof. Bill Even I. Introduction. A. The causes of the great recession B. Government responses to great recession II. III. Chapter 4: Measuring GDP and Economic Growth A. Definition

Lecture 1. Global Imbalances

Lecture 1 Global Imbalances Saverio Simonelli University of Naples Federico II Fall 2017 International Macroeconomics Practical information Meeting: Monday, Tuesday and Wednesday, 10:15-12:00 Room: Dipartimento,

Lecture 1 Global Imbalances Saverio Simonelli University of Naples Federico II Fall 2017 International Macroeconomics Practical information Meeting: Monday, Tuesday and Wednesday, 10:15-12:00 Room: Dipartimento,

Global Imbalances in Current Account Balances

Journal of Applied Finance & Banking, vol. 2, no. 6, 2012, 83-93 ISSN: 1792-6580 (print version), 1792-6599 (online) Scienpress Ltd, 2012 Global Imbalances in Current Account Balances Melike Bildirici

Journal of Applied Finance & Banking, vol. 2, no. 6, 2012, 83-93 ISSN: 1792-6580 (print version), 1792-6599 (online) Scienpress Ltd, 2012 Global Imbalances in Current Account Balances Melike Bildirici

Introduction Copyright 2011 Pearson Addison-Wesley. All rights reserved.

Lecture 1 Introduction Copyright 2011 Pearson Addison-Wesley. All rights reserved. Course Overview Welcome to Advanced Macroeconomics What you will NOT learn in this class How to make money by predicting

Lecture 1 Introduction Copyright 2011 Pearson Addison-Wesley. All rights reserved. Course Overview Welcome to Advanced Macroeconomics What you will NOT learn in this class How to make money by predicting

Prof. Dr. Paul JJ Welfens University of Wuppertal December 2016

Prof. Dr. Paul JJ Welfens www.eiiw.eu University of Wuppertal December 2016 Additional Aspects on Regulations; Role of International (Gross) Inflows and Current Account Deficit See (slides): AL-SAFFAR,

Prof. Dr. Paul JJ Welfens www.eiiw.eu University of Wuppertal December 2016 Additional Aspects on Regulations; Role of International (Gross) Inflows and Current Account Deficit See (slides): AL-SAFFAR,

Exorbitant Duty. Hélène Rey London Business School CEPR & NBER Nicolas Govillot Mines de Paris

Exorbitant Privilege and Exorbitant Duty PO P.O. Gourinchas UC Berkeley, CEPR & NBER Hélène Rey London Business School CEPR & NBER Nicolas Govillot Mines de Paris Research Agenda on balance sheet of countries

Exorbitant Privilege and Exorbitant Duty PO P.O. Gourinchas UC Berkeley, CEPR & NBER Hélène Rey London Business School CEPR & NBER Nicolas Govillot Mines de Paris Research Agenda on balance sheet of countries

MONETARY POLICY EXPECTATIONS AND BOOM-BUST CYCLES IN THE HOUSING MARKET*

Articles Winter 9 MONETARY POLICY EXPECTATIONS AND BOOM-BUST CYCLES IN THE HOUSING MARKET* Caterina Mendicino**. INTRODUCTION Boom-bust cycles in asset prices and economic activity have been a central

Articles Winter 9 MONETARY POLICY EXPECTATIONS AND BOOM-BUST CYCLES IN THE HOUSING MARKET* Caterina Mendicino**. INTRODUCTION Boom-bust cycles in asset prices and economic activity have been a central

Intermediate Macroeconomics, EC2201. L4: National income in the open economy

Intermediate Macroeconomics, EC2201 L4: National income in the open economy Anna Seim Department of Economics, Stockholm University Spring 2017 1 / 50 Contents and literature The balance of payments. National

Intermediate Macroeconomics, EC2201 L4: National income in the open economy Anna Seim Department of Economics, Stockholm University Spring 2017 1 / 50 Contents and literature The balance of payments. National

Financial Integration, Financial Deepness and Global Imbalances

Financial Integration, Financial Deepness and Global Imbalances Enrique G. Mendoza University of Maryland, IMF & NBER Vincenzo Quadrini University of Southern California, CEPR & NBER José-Víctor Ríos-Rull

Financial Integration, Financial Deepness and Global Imbalances Enrique G. Mendoza University of Maryland, IMF & NBER Vincenzo Quadrini University of Southern California, CEPR & NBER José-Víctor Ríos-Rull

6 The Open Economy. This chapter:

6 The Open Economy This chapter: Balance of Payments Accounting Savings and Investment in the Open Economy Determination of the Trade Balance and the Exchange Rate Mundell Fleming model Exchange Rate Regimes

6 The Open Economy This chapter: Balance of Payments Accounting Savings and Investment in the Open Economy Determination of the Trade Balance and the Exchange Rate Mundell Fleming model Exchange Rate Regimes

Intermediate Macroeconomics

Intermediate Macroeconomics L1: National Income in Closed and Open Economies Anna Seim Department of Economics, Stockholm University Spring 2015 Topics The relationship between Saving and investment in

Intermediate Macroeconomics L1: National Income in Closed and Open Economies Anna Seim Department of Economics, Stockholm University Spring 2015 Topics The relationship between Saving and investment in

Valuation Effects in China:Scale, Structure and Its Function in the External Adjustment

Valuation Effects in China:Scale, Structure and Its Function in the External Adjustment Fangxiu Song, Tianjiao Feng School of Economics, Peking University Working Paper No. E-2014-003 October-21-2014 Copyright

Valuation Effects in China:Scale, Structure and Its Function in the External Adjustment Fangxiu Song, Tianjiao Feng School of Economics, Peking University Working Paper No. E-2014-003 October-21-2014 Copyright

Comment on: Capital Controls and Monetary Policy Autonomy in a Small Open Economy by J. Scott Davis and Ignacio Presno

Comment on: Capital Controls and Monetary Policy Autonomy in a Small Open Economy by J. Scott Davis and Ignacio Presno Fabrizio Perri Federal Reserve Bank of Minneapolis and CEPR fperri@umn.edu December

Comment on: Capital Controls and Monetary Policy Autonomy in a Small Open Economy by J. Scott Davis and Ignacio Presno Fabrizio Perri Federal Reserve Bank of Minneapolis and CEPR fperri@umn.edu December

ECO 403 L0301 Developmental Macroeconomics. Lecture 8 Balance-of-Payment Crises

ECO 403 L0301 Developmental Macroeconomics Lecture 8 Balance-of-Payment Crises Gustavo Indart Slide 1 The Capitalist Economic System Capitalism is basically an unstable economic system Disequilibrium is

ECO 403 L0301 Developmental Macroeconomics Lecture 8 Balance-of-Payment Crises Gustavo Indart Slide 1 The Capitalist Economic System Capitalism is basically an unstable economic system Disequilibrium is

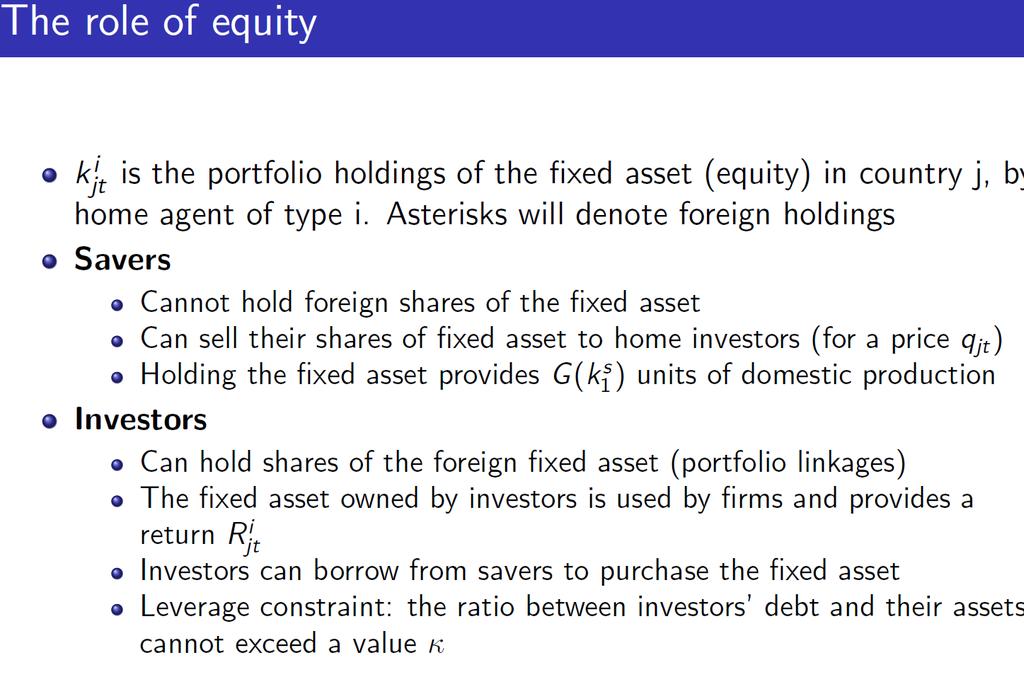

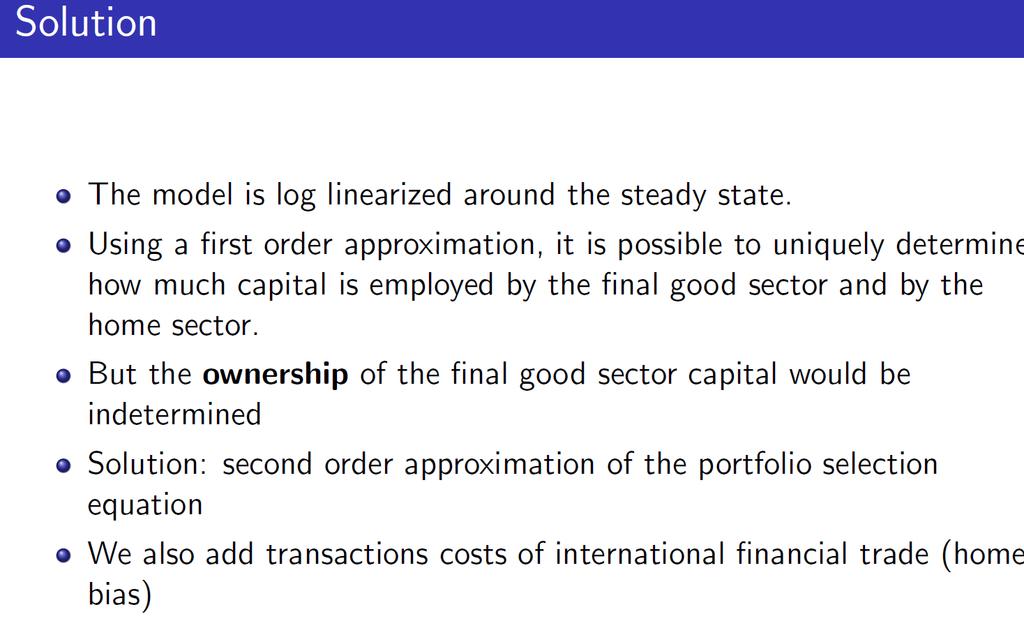

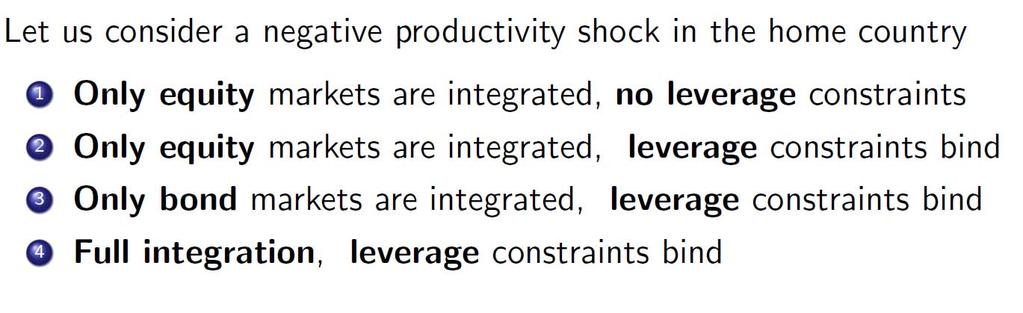

International Transmission, and international financial. Michael B. Devereux UBC James Yetman BIS

Leverage Constraints International Transmission, and international financial integration Michael B. Devereux UBC James Yetman BIS (Alan Sutherland) Financial markets and international business cycles Typical

Leverage Constraints International Transmission, and international financial integration Michael B. Devereux UBC James Yetman BIS (Alan Sutherland) Financial markets and international business cycles Typical

Corporate leverage and investment in the aftermath of the financial crisis

ECB-UNRESTRICTED FINAL Corporate leverage and investment in the aftermath of the financial crisis Philip Vermeulen European Central Bank Directorate General Research Copyright rests with the author. All

ECB-UNRESTRICTED FINAL Corporate leverage and investment in the aftermath of the financial crisis Philip Vermeulen European Central Bank Directorate General Research Copyright rests with the author. All

A Real Intertemporal Model with Investment Copyright 2014 Pearson Education, Inc.

Chapter 11 A Real Intertemporal Model with Investment Copyright Chapter 11 Topics Construct a real intertemporal model that will serve as a basis for studying money and business cycles in Chapters 12-14.

Chapter 11 A Real Intertemporal Model with Investment Copyright Chapter 11 Topics Construct a real intertemporal model that will serve as a basis for studying money and business cycles in Chapters 12-14.

Flows between sectors. Over a given period of time, income flows and spending flows run within each sector and between sectors.

Basic macroeconomic accounting The threesector division An economy can be divided into three sectors: (i) the domestic private sector (households, firms, and banks); (ii) the domestic government sector

Basic macroeconomic accounting The threesector division An economy can be divided into three sectors: (i) the domestic private sector (households, firms, and banks); (ii) the domestic government sector

macro macroeconomics Government Debt (chapter 15) N. Gregory Mankiw

N. Gregory Mankiw") macro Topic 14: (chapter 15) macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved In this chapter you will learn about the size of

macro Topic 14: (chapter 15) macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved In this chapter you will learn about the size of

The External Balance Sheets of China and Returns Differentials

The External Balance Sheets of China and Returns Differentials Yi Huang The Graduate Institute of International and Development Studies, Geneva International Conference on Capital Flows and Safe Assets

The External Balance Sheets of China and Returns Differentials Yi Huang The Graduate Institute of International and Development Studies, Geneva International Conference on Capital Flows and Safe Assets

Exam Number. Section

Exam Number Section MACROECONOMICS IN THE GLOBAL ECONOMY Core Course ANSWER KEY Final Exam March 1, 2010 Note: These are only suggested answers. You may have received partial or full credit for your answers

Exam Number Section MACROECONOMICS IN THE GLOBAL ECONOMY Core Course ANSWER KEY Final Exam March 1, 2010 Note: These are only suggested answers. You may have received partial or full credit for your answers

BIS Working Papers. Global imbalances from a stock perspective. The asymmetry between creditors and debtors. No 707. Monetary and Economic Department

BIS Working Papers No 707 Global imbalances from a stock perspective. The asymmetry between creditors and debtors by Enrique Alberola, Ángel Estrada and Francesca Viani Monetary and Economic Department

BIS Working Papers No 707 Global imbalances from a stock perspective. The asymmetry between creditors and debtors by Enrique Alberola, Ángel Estrada and Francesca Viani Monetary and Economic Department

Class Notes. Chapter 5 Saving and Investment in the Open Economy Learning Objectives

1 Chapter 5 Saving and Investment in the Open Economy Learning Objectives A. Explain how the balance of payments is calculated (Sec. 5.1) B. Discuss goods market equilibrium in an open economy (Sec. 5.2)

1 Chapter 5 Saving and Investment in the Open Economy Learning Objectives A. Explain how the balance of payments is calculated (Sec. 5.1) B. Discuss goods market equilibrium in an open economy (Sec. 5.2)

International Macroeconomics

Slides for Chapter 3: Theory of Current Account Determination International Macroeconomics Schmitt-Grohé Uribe Woodford Columbia University May 1, 2016 1 Motivation Build a model of an open economy to

Slides for Chapter 3: Theory of Current Account Determination International Macroeconomics Schmitt-Grohé Uribe Woodford Columbia University May 1, 2016 1 Motivation Build a model of an open economy to

The Long and Short of it: Determinants of Foreign Currency Exposure in External Balance Sheets

CONFERENCE ON INTERNATIONAL MACRO-FINANCE APRIL 24-25, 2008 The Long and Short of it: Determinants of Foreign Currency Exposure in External Balance Sheets Philip R. Lane and Jay C. Shambaugh Presented

CONFERENCE ON INTERNATIONAL MACRO-FINANCE APRIL 24-25, 2008 The Long and Short of it: Determinants of Foreign Currency Exposure in External Balance Sheets Philip R. Lane and Jay C. Shambaugh Presented

Argentina s Crisis and Recovery: A Demand Side Story Alberto Martin November 2013

Argentina s Crisis and Recovery: A Demand Side Story 1998 2006 by Ariel Burstein and Ivan Werning Alberto Martin November 2013 Overview Revisit argentine experience 1998 2002: Prolonged recession: 5.4%

Argentina s Crisis and Recovery: A Demand Side Story 1998 2006 by Ariel Burstein and Ivan Werning Alberto Martin November 2013 Overview Revisit argentine experience 1998 2002: Prolonged recession: 5.4%

The trade balance and fiscal policy in the OECD

European Economic Review 42 (1998) 887 895 The trade balance and fiscal policy in the OECD Philip R. Lane *, Roberto Perotti Economics Department, Trinity College Dublin, Dublin 2, Ireland Columbia University,

European Economic Review 42 (1998) 887 895 The trade balance and fiscal policy in the OECD Philip R. Lane *, Roberto Perotti Economics Department, Trinity College Dublin, Dublin 2, Ireland Columbia University,

Econ520. Spring Prof. Lutz Hendricks. March 28, 2017

Practice Problems: Trade Deficits Econ520. Spring 2017. Prof. Lutz Hendricks. March 28, 2017 Jones, Charles I. (2008). Macroeconomics (1st ed.). W. W. Norton, ch. 14, questions 1, 3-8. 1 Basics 1. Explain

Practice Problems: Trade Deficits Econ520. Spring 2017. Prof. Lutz Hendricks. March 28, 2017 Jones, Charles I. (2008). Macroeconomics (1st ed.). W. W. Norton, ch. 14, questions 1, 3-8. 1 Basics 1. Explain

Lecture 22. Aggregate demand and aggregate supply

Lecture 22 Aggregate demand and aggregate supply By the end of this lecture, you should understand: three key facts about short-run economic fluctuations how the economy in the short run differs from the

Lecture 22 Aggregate demand and aggregate supply By the end of this lecture, you should understand: three key facts about short-run economic fluctuations how the economy in the short run differs from the

Monetary Theory and Policy. Fourth Edition. Carl E. Walsh. The MIT Press Cambridge, Massachusetts London, England

Monetary Theory and Policy Fourth Edition Carl E. Walsh The MIT Press Cambridge, Massachusetts London, England Contents Preface Introduction xiii xvii 1 Evidence on Money, Prices, and Output 1 1.1 Introduction

Monetary Theory and Policy Fourth Edition Carl E. Walsh The MIT Press Cambridge, Massachusetts London, England Contents Preface Introduction xiii xvii 1 Evidence on Money, Prices, and Output 1 1.1 Introduction

The Role of Stock-Flow Adjustment during the Global Financial Crisis

The Role of Stock-Flow Adjustment during the Global Financial Crisis Katharina Bergant December 31, 2017 Abstract While the recent contraction of current account imbalances that followed the Global Financial

The Role of Stock-Flow Adjustment during the Global Financial Crisis Katharina Bergant December 31, 2017 Abstract While the recent contraction of current account imbalances that followed the Global Financial

Lecture 12: Economic Fluctuations. Rob Godby University of Wyoming

Lecture 12: Economic Fluctuations Rob Godby University of Wyoming Short-Run Economic Fluctuations Economic activity fluctuates from year to year. In some years, the production of goods and services rises.

Lecture 12: Economic Fluctuations Rob Godby University of Wyoming Short-Run Economic Fluctuations Economic activity fluctuates from year to year. In some years, the production of goods and services rises.

Chapter 5. Measuring a Nation s Production and Income. Macroeconomics: Principles, Applications, and Tools NINTH EDITION

Macroeconomics: Principles, Applications, and Tools NINTH EDITION Chapter 5 Measuring a Nation s Production and Income During the recent deep economic downturn, economists, business writers, and politicians

Macroeconomics: Principles, Applications, and Tools NINTH EDITION Chapter 5 Measuring a Nation s Production and Income During the recent deep economic downturn, economists, business writers, and politicians

Chapter 5. Saving and Investment in the Open Economy. Copyright 2009 Pearson Education Canada

Chapter 5 Saving and Investment in the Open Economy Copyright 2009 Pearson Education Canada Balance of Payments Accounting The balance of payments accounts are the record of country s international transactions.

Chapter 5 Saving and Investment in the Open Economy Copyright 2009 Pearson Education Canada Balance of Payments Accounting The balance of payments accounts are the record of country s international transactions.

Inflation Stabilization and Default Risk in a Currency Union. OKANO, Eiji Nagoya City University at Otaru University of Commerce on Aug.

Inflation Stabilization and Default Risk in a Currency Union OKANO, Eiji Nagoya City University at Otaru University of Commerce on Aug. 10, 2014 1 Introduction How do we conduct monetary policy in a currency

Inflation Stabilization and Default Risk in a Currency Union OKANO, Eiji Nagoya City University at Otaru University of Commerce on Aug. 10, 2014 1 Introduction How do we conduct monetary policy in a currency

International Macroeconomics

Slides for Chapter 2: Current Account Sustainability International Macroeconomics Schmitt-Grohé Uribe Woodford Columbia University May 1, 2016 1 Motivation A natural question that arises from our description

Slides for Chapter 2: Current Account Sustainability International Macroeconomics Schmitt-Grohé Uribe Woodford Columbia University May 1, 2016 1 Motivation A natural question that arises from our description

Lecture 7. Unemployment and Fiscal Policy

Lecture 7 Unemployment and Fiscal Policy The Multiplier Model As we ve seen spending on investment projects tends to cluster. What are the two reasons for this? 1. Firms may adopt a new technology at

Lecture 7 Unemployment and Fiscal Policy The Multiplier Model As we ve seen spending on investment projects tends to cluster. What are the two reasons for this? 1. Firms may adopt a new technology at

Where Did All The Borrowing Go? A Forensic Analysis of the U.S. External Position

Discussion of paper by Philip Lane & Gian Maria Milesi-Ferretti on Where Did All The Borrowing Go? A Forensic Analysis of the U.S. External Position Marcel Fratzscher European Central Bank SNB-IMF Conference

Discussion of paper by Philip Lane & Gian Maria Milesi-Ferretti on Where Did All The Borrowing Go? A Forensic Analysis of the U.S. External Position Marcel Fratzscher European Central Bank SNB-IMF Conference

International Monetary Theory and Policy Economics 5602

Department of Economics Raul Razo-Garcia Carleton University Fall 2009 International Monetary Theory and Policy Economics 5602 CONTACT INFORMATION Professor: Raul Razo-Garcia Office: A-804 Loeb Building

Department of Economics Raul Razo-Garcia Carleton University Fall 2009 International Monetary Theory and Policy Economics 5602 CONTACT INFORMATION Professor: Raul Razo-Garcia Office: A-804 Loeb Building

Sustainability of Current Account Deficits in Turkey: Markov Switching Approach

Sustainability of Current Account Deficits in Turkey: Markov Switching Approach Melike Elif Bildirici Department of Economics, Yıldız Technical University Barbaros Bulvarı 34349, İstanbul Turkey Tel: 90-212-383-2527

Sustainability of Current Account Deficits in Turkey: Markov Switching Approach Melike Elif Bildirici Department of Economics, Yıldız Technical University Barbaros Bulvarı 34349, İstanbul Turkey Tel: 90-212-383-2527

International Monetary Theory and Policy ECON 5602 S

Department of Economics Carleton University International Monetary Theory and Policy ECON 5602 S Raul Razo-Garcia 2011 Early Summer CONTACT INFORMATION Professor: Raul Razo-Garcia Office: A-804 Loeb Building

Department of Economics Carleton University International Monetary Theory and Policy ECON 5602 S Raul Razo-Garcia 2011 Early Summer CONTACT INFORMATION Professor: Raul Razo-Garcia Office: A-804 Loeb Building

Macroeconomics: Policy, 31E23000

Macroeconomics: Policy, 31E23000 Lecture 1 Pertti Aalto University School of Business 22.02.2016 About this course 1 Current crisis: Role of policies in creating it? Role of policies in helping to get

Macroeconomics: Policy, 31E23000 Lecture 1 Pertti Aalto University School of Business 22.02.2016 About this course 1 Current crisis: Role of policies in creating it? Role of policies in helping to get

Europe and Global Imbalances

WP/07/144 Europe and Global Imbalances Philip R. Lane and Gian Maria Milesi-Ferretti 2007 International Monetary Fund WP/07/144 IMF Working Paper Research Department Europe and Global Imbalances Prepared

WP/07/144 Europe and Global Imbalances Philip R. Lane and Gian Maria Milesi-Ferretti 2007 International Monetary Fund WP/07/144 IMF Working Paper Research Department Europe and Global Imbalances Prepared

THE SHRINKING CURRENT ACCOUNT DEFICIT: Remarks by Thomas C. Melzer St. Louis Society of Financial Analysts St. Louis, Missouri May 28, 1992

THE SHRINKING CURRENT ACCOUNT DEFICIT: Remarks by Thomas C. Melzer St. Louis Society of Financial Analysts St. Louis, Missouri May 28, 1992 A CLOSER LOOK During the 1980s, the U.S. current account balance

THE SHRINKING CURRENT ACCOUNT DEFICIT: Remarks by Thomas C. Melzer St. Louis Society of Financial Analysts St. Louis, Missouri May 28, 1992 A CLOSER LOOK During the 1980s, the U.S. current account balance

Intermediate Macroeconomics, 7.5 ECTS

STOCKHOLMS UNIVERSITET Intermediate Macroeconomics, 7.5 ECTS SEMINAR EXERCISES STOCKHOLMS UNIVERSITET page 1 SEMINAR 1. Mankiw-Taylor: chapters 3, 5 and 7. (Lectures 1-2). Question 1. Assume that the production

STOCKHOLMS UNIVERSITET Intermediate Macroeconomics, 7.5 ECTS SEMINAR EXERCISES STOCKHOLMS UNIVERSITET page 1 SEMINAR 1. Mankiw-Taylor: chapters 3, 5 and 7. (Lectures 1-2). Question 1. Assume that the production

Nominal Exchange Rates and Net Foreign Assets Dynamics: the Stabilization Role of Valuation Effects

Nominal Exchange Rates and Net Foreign Assets Dynamics: the Stabilization Role of Valuation Effects Sara Eugeni Durham University Business School First draft: May 2013 April 6, 2016 Abstract Recent empirical

Nominal Exchange Rates and Net Foreign Assets Dynamics: the Stabilization Role of Valuation Effects Sara Eugeni Durham University Business School First draft: May 2013 April 6, 2016 Abstract Recent empirical

VII. Short-Run Economic Fluctuations

Macroeconomic Theory Lecture Notes VII. Short-Run Economic Fluctuations University of Miami December 1, 2017 1 Outline Business Cycle Facts IS-LM Model AD-AS Model 2 Outline Business Cycle Facts IS-LM

Macroeconomic Theory Lecture Notes VII. Short-Run Economic Fluctuations University of Miami December 1, 2017 1 Outline Business Cycle Facts IS-LM Model AD-AS Model 2 Outline Business Cycle Facts IS-LM

ECON2010 test 2 study guide

ECON2010 test 2 study guide 1) In a closed economy public saving plus private saving is equal to a The budget deficit b The budget surplus c Taxes minus transfers d Investment 2) Which of the following

ECON2010 test 2 study guide 1) In a closed economy public saving plus private saving is equal to a The budget deficit b The budget surplus c Taxes minus transfers d Investment 2) Which of the following

ECO403 Macroeconomics Solved Online Quiz For Midterm Exam Preparation Spring 2013

ECO403 Macroeconomics Solved Online Quiz For Midterm Exam Preparation Spring 2013 Question # 1 of 15 ( Start time: 03:22:55 PM ) Total Marks: 1 If the U.S. real exchange rate increases, then U.S. ----------------

ECO403 Macroeconomics Solved Online Quiz For Midterm Exam Preparation Spring 2013 Question # 1 of 15 ( Start time: 03:22:55 PM ) Total Marks: 1 If the U.S. real exchange rate increases, then U.S. ----------------

Macroeconomics. 1.1 What Is Macroeconomics? Part 1: Preliminaries. Third Edition. Introduction to. Macroeconomics. In this chapter, we learn:

1.1 What Is? Third Edition by In this chapter, we learn: What macroeconomics is and consider some questions. How macroeconomics uses models, and why. The book s basic three-part structure: the long run,

1.1 What Is? Third Edition by In this chapter, we learn: What macroeconomics is and consider some questions. How macroeconomics uses models, and why. The book s basic three-part structure: the long run,

Business cycle fluctuations Part II

Understanding the World Economy Master in Economics and Business Business cycle fluctuations Part II Lecture 7 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 7: Business cycle fluctuations

Understanding the World Economy Master in Economics and Business Business cycle fluctuations Part II Lecture 7 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 7: Business cycle fluctuations

Monetary Systems and Macro Policy Slides for KOMIF Ch08 (KOMIE Ch19)

") Slides for KOMIF Ch08 (KOMIE Ch19) American University 2017-11-30 Preview Macroeconomic Policy Goals of macroeconomic policies Persistent current account deficits Monetary standards Gold standard International

Slides for KOMIF Ch08 (KOMIE Ch19) American University 2017-11-30 Preview Macroeconomic Policy Goals of macroeconomic policies Persistent current account deficits Monetary standards Gold standard International

Financial Globalization. Bilò Valentina. Maran Elena

Financial Globalization Bilò Valentina Maran Elena Three types of international transactions Goods and services Goods and services Assets Assets The Ricardian model of comparative advantage A country has

Financial Globalization Bilò Valentina Maran Elena Three types of international transactions Goods and services Goods and services Assets Assets The Ricardian model of comparative advantage A country has

ECON 1120: Macroeconomics

ECON 1120: Macroeconomics General Information: Term: 2018 Summer Session Instructor: Staff Language of Instruction: English Classroom: TBA Office hours: TBA Class Sessions Per Week: 5 Total Weeks: 5 Total

ECON 1120: Macroeconomics General Information: Term: 2018 Summer Session Instructor: Staff Language of Instruction: English Classroom: TBA Office hours: TBA Class Sessions Per Week: 5 Total Weeks: 5 Total

Macroeconomics, Cdn. 4e (Williamson) Chapter 1 Introduction

Chapter 1 Introduction") Macroeconomics, Cdn. 4e (Williamson) Chapter 1 Introduction 1) Which of the following topics is a primary concern of macro economists? A) standards of living of individuals B) choices of individual consumers

Macroeconomics, Cdn. 4e (Williamson) Chapter 1 Introduction 1) Which of the following topics is a primary concern of macro economists? A) standards of living of individuals B) choices of individual consumers

Notes on Obstfeld-Rogoff Ch.1

Notes on Obstfeld-Rogoff Ch.1 Open Economy = domestic economy trading with ROW Macro level: focus on intertemporal issues (not: multiple good, added later) OR 1.1-1.2: Small economy = Easiest setting to

Notes on Obstfeld-Rogoff Ch.1 Open Economy = domestic economy trading with ROW Macro level: focus on intertemporal issues (not: multiple good, added later) OR 1.1-1.2: Small economy = Easiest setting to

The Current Account, the Spot Exchange Rate and the Demand for Money

The Current Account, the Spot Exchange Rate and the Demand for Money Anthony Joseph Department of Computer Science Seidenberg School of Computer Science and Information Systems, Pace University 163 William

The Current Account, the Spot Exchange Rate and the Demand for Money Anthony Joseph Department of Computer Science Seidenberg School of Computer Science and Information Systems, Pace University 163 William

The Public Debt Crisis of the United States

The Public Debt Crisis of the United States Enrique G. Mendoza University of Pennsylvania, NBER & PIER Seminario sobre Sostenibilidad de la Deuda Pública: AIReF September 5, 2017 Madrid, Spain What debt

The Public Debt Crisis of the United States Enrique G. Mendoza University of Pennsylvania, NBER & PIER Seminario sobre Sostenibilidad de la Deuda Pública: AIReF September 5, 2017 Madrid, Spain What debt

Foreign Ownership of US Safe Assets. Good or Bad?

: Good or Bad? Jack Favilukis, Sydney C. Ludvigson, and Stijn Van Nieuwerburgh London School of Economics, New York University, and NYU Stern Global Imbalances Introduction Last 20 years: sharp rise in

: Good or Bad? Jack Favilukis, Sydney C. Ludvigson, and Stijn Van Nieuwerburgh London School of Economics, New York University, and NYU Stern Global Imbalances Introduction Last 20 years: sharp rise in

No 03. Chapter 2. Chapter Outline. Gross Domestic Product. Measuring Macroeconomic Variables

No 03. Chapter 2 Measuring Macroeconomic Variables Chapter Outline National Income Accounting: The Measurement of Production, Income, and Expenditure (Gross Domestic Product) Saving and Wealth Real GDP,

No 03. Chapter 2 Measuring Macroeconomic Variables Chapter Outline National Income Accounting: The Measurement of Production, Income, and Expenditure (Gross Domestic Product) Saving and Wealth Real GDP,

MACROECONOMICS FOR ECONOMIC POLICY

COURSE SYLLABUS MACROECONOMICS FOR ECONOMIC POLICY Instructors: Adam Reiff (lecturer), Rita Peto (TA) Department: Department of Economics, Central European University Semester and year: Fall, 2014/2015

COURSE SYLLABUS MACROECONOMICS FOR ECONOMIC POLICY Instructors: Adam Reiff (lecturer), Rita Peto (TA) Department: Department of Economics, Central European University Semester and year: Fall, 2014/2015

International Macroeconomics

Slides for Chapter 1: Global Imbalances International Macroeconomics Schmitt-Grohé Uribe Woodford Columbia University January 22, 2018 1 Motivation Countries trade a lot with one another, and the United

Slides for Chapter 1: Global Imbalances International Macroeconomics Schmitt-Grohé Uribe Woodford Columbia University January 22, 2018 1 Motivation Countries trade a lot with one another, and the United

ECON 012: Macroeconomics

General Information ECON 012: Macroeconomics Term: 2018 Summer Session Class Sessions Per Week: 5 Instructor: Staff Total Weeks: 6 Language of Instruction: English Total Class Sessions: 30 Classroom: TBA

General Information ECON 012: Macroeconomics Term: 2018 Summer Session Class Sessions Per Week: 5 Instructor: Staff Total Weeks: 6 Language of Instruction: English Total Class Sessions: 30 Classroom: TBA

Global Real Rates: A Secular Approach

Global Real Rates: A Secular Approach Pierre-Olivier Gourinchas 1 Hélène Rey 2 1 UC Berkeley & NBER & CEPR 2 London Business School & NBER & CEPR Bank for International Settlements, Zurich, June 2018 17th

Global Real Rates: A Secular Approach Pierre-Olivier Gourinchas 1 Hélène Rey 2 1 UC Berkeley & NBER & CEPR 2 London Business School & NBER & CEPR Bank for International Settlements, Zurich, June 2018 17th

II.2. Member State vulnerability to changes in the euro exchange rate ( 35 )

") II.2. Member State vulnerability to changes in the euro exchange rate ( 35 ) There have been significant fluctuations in the euro exchange rate since the start of the monetary union. This section assesses

II.2. Member State vulnerability to changes in the euro exchange rate ( 35 ) There have been significant fluctuations in the euro exchange rate since the start of the monetary union. This section assesses

GLOBAL EDITION. Macroeconomics EIGHTH EDITION. Abel Bernanke Croushore

GLOBAL EDITION Macroeconomics EIGHTH EDITION Abel Bernanke Croushore Symbols Used in This Book A productivity B government debt BASE monetary base C consumption CA current account balance CU currency held

GLOBAL EDITION Macroeconomics EIGHTH EDITION Abel Bernanke Croushore Symbols Used in This Book A productivity B government debt BASE monetary base C consumption CA current account balance CU currency held

Economic Fluctuations

Sherif Khalifa Sherif Khalifa () Economic Fluctuations 1 / 43 Definition The business cycle is the fluctuations in the production output of goods and services in an economy. Definition The business cycle

Sherif Khalifa Sherif Khalifa () Economic Fluctuations 1 / 43 Definition The business cycle is the fluctuations in the production output of goods and services in an economy. Definition The business cycle

PART XII: SHORT-RUN ECONOMIC FLUCTUATIONS AGGREGATE DEMAND AND AGGREGATE SUPPLY. Chapter 33

1 PART XII: SHORT-RUN ECONOMIC FLUCTUATIONS AGGREGATE DEMAND AND AGGREGATE SUPPLY Chapter 33 What did we learn so far? Macroeconomics studies the economy as a whole It aims to explain economic events that

1 PART XII: SHORT-RUN ECONOMIC FLUCTUATIONS AGGREGATE DEMAND AND AGGREGATE SUPPLY Chapter 33 What did we learn so far? Macroeconomics studies the economy as a whole It aims to explain economic events that

Principles of Macroeconomics December 17th, 2005 name: Final Exam (100 points)

") EC132.02 Serge Kasyanenko Principles of Macroeconomics December 17th, 2005 name: Final Exam (100 points) This is a closed-book exam - you may not use your notes and textbooks. Calculators are not allowed.

EC132.02 Serge Kasyanenko Principles of Macroeconomics December 17th, 2005 name: Final Exam (100 points) This is a closed-book exam - you may not use your notes and textbooks. Calculators are not allowed.

ECON 012: Macroeconomics

ECON 012: Macroeconomics General Information: Term: 2019 Summer Session Instructor: Staff Language of Instruction: English Classroom: TBA Office Hours: TBA Class Sessions Per Week: 5 Total Weeks: 5 Total

ECON 012: Macroeconomics General Information: Term: 2019 Summer Session Instructor: Staff Language of Instruction: English Classroom: TBA Office Hours: TBA Class Sessions Per Week: 5 Total Weeks: 5 Total

ECON 012: Macroeconomics

ECON 012: Macroeconomics General Information: Term: 2018 Summer Session Instructor: Staff Language of Instruction: English Classroom: TBA Office Hours: TBA Class Sessions Per Week: 5 Total Weeks: 6 Total

ECON 012: Macroeconomics General Information: Term: 2018 Summer Session Instructor: Staff Language of Instruction: English Classroom: TBA Office Hours: TBA Class Sessions Per Week: 5 Total Weeks: 6 Total

Macroeconomic Analysis Econ 6022 Level I

1 / 37 Macroeconomic Analysis Econ 6022 Level I Lecture 2 Fall, 2011 2 / 37 Overview Let s start our tour in macroeconomics by introducing a few building blocks, which will be used repeatedly later on.

1 / 37 Macroeconomic Analysis Econ 6022 Level I Lecture 2 Fall, 2011 2 / 37 Overview Let s start our tour in macroeconomics by introducing a few building blocks, which will be used repeatedly later on.

Aggregate Demand and Aggregate Supply

Aggregate Demand and Aggregate Supply Chapter 19 Copyright 2001 by Harcourt, Inc. All rights reserved. Requests for permission to make copies of any part of the work should be mailed to: Permissions Department,

Aggregate Demand and Aggregate Supply Chapter 19 Copyright 2001 by Harcourt, Inc. All rights reserved. Requests for permission to make copies of any part of the work should be mailed to: Permissions Department,