PhD course in Empirical Finance. Dr. Cesario Mateus

|

|

|

- Clarissa McLaughlin

- 5 years ago

- Views:

Transcription

1 PhD course in Empirical Finance Dr. Cesario Mateus Session 3: December, 12 th,

2 Announcement Price The announcement was unexpected and there is a positive market reaction The announcement was expected or there are no market reaction The announcement was unexpected and there is a negative market reaction Announcement Time 2

3 α and β are estimated using OLS, for period (example) -255 to -21 days before the announcement Event Window 3

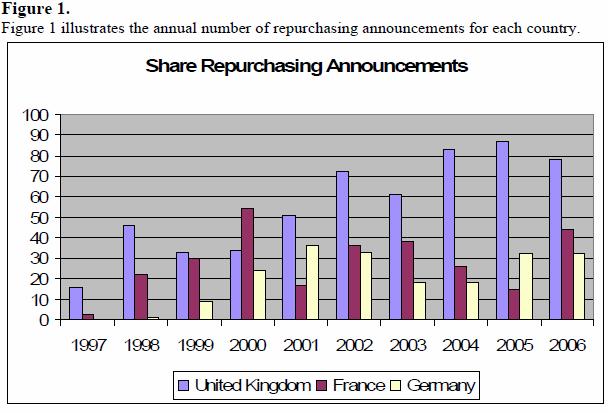

4 Share Repurchases in Europe. Underlying signals and regulatory frameworks: a Cross-country Analysis, Dimitrios Andriosopoulos and M. Ameziane Lasfer Market Reaction to Share Repurchases announcement in the UK, France and Germany from 1997 to 2006 (10 years) In the UK and Germany the market reaction is positive. In France, the market reaction is negative 4

5 5

6 6

7 7

8 8

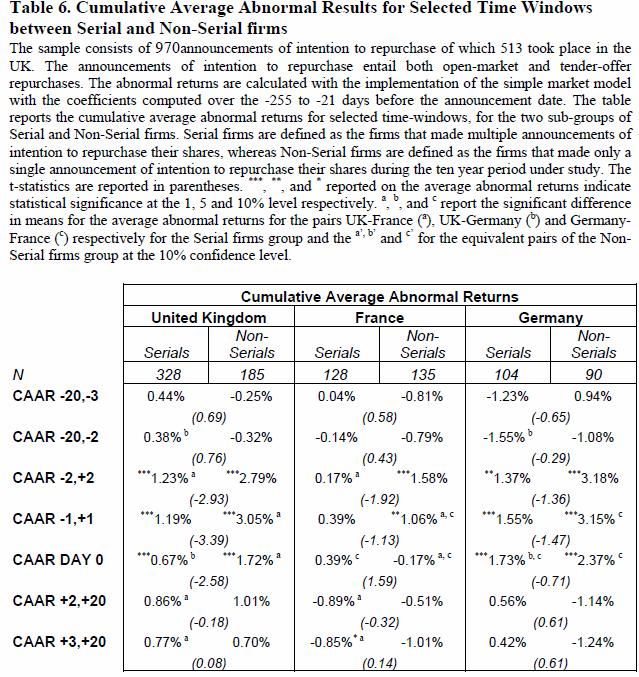

9 Table 5 considers only the initial announcement (from the firms in the sample that had multiple announcements) as well the ones that announced the intention of just a single share repurchase (by firma and country). Summary UK larger reaction in the pre-event period (0.13% and 0.29%) France and Germany, poorer reaction for initial announcements than for to total announcements. Significant difference in CAARs for each event window. 9

10 10

11 11

12 12

13 13

14 14

15 15

16 16

17 Terrorist Attacks and Financial Markets New York London Madrid 17

18 An Empirical Analysis of the Impact of Terrorism on Global Financial Markets Tandoh and Mateus Terrorism Definition United Nations: Act of terrorism in peacetime is equivelent of war Crime Central Intelligence Agency: Terrorism means premeditated, politically motivated violence perpreted agians non-combatent targets by subnational groups or clandestine agents, usually intendfed to influence na audience Aljazeere: terrorists are actors who don t belong to any recognized armed forces and who don t adhere to their rules and who are therefore regarded as rogue actors. Terrorism comes from tem French word terrorisme, which is based on Latin language verb terrere (to frighten) and deterrere (to frighten from) 18

19 Most studies WTC (9/11) Comparative study among NY, London and Madrid Establish impact differences among industries Analyses 10 markets and 13 industries Markets react negatively to terrorist attacks (statistical significance for 1 and 5 percent levels) Markets recover after the initial impact to previous levels (22 days in the case of World Index after NY attack) NY attack is the one with the largest impact in the stock market 1) Occurs with a previous stock market decline 2) Was an attack to the financial sector 19

20 Event Study Structure Event Definition Selection Criteria Normal and Abnormal Returns Estimates Tests Interpretation 20

21 Indexes Methodology Average adjusted returns Abnormal Returns on Stock Markets (t = 0) S&P 500 Russell 3000 NYSE Composit NIKKEI 225 NASDAQ Composite New York September 11th Attack Madrid March 11th Attack London July 7th Attack FTSE100 CAC40 World Index Returns 21

22 As a benchmark index, the Dow Jones Wilshire Global Total Market Index consists of 58 county-level Indexes and it has more than 98% of global market capitalization Source: Official site of Dow Jones Wilshire 22

23 Abnormal Returns 6.00% 6 Days Cummulative Abnormal Returns 4.00% 2.00% 0.00% -2.00% -4.00% -6.00% September 11th 2001 Event Madrid March 11th 2004 Event London July 7th Event -8.00% % % World Index CAC40 FTSE100 NASDAQ Composite NIKKEI 225 NYSE Composit Russell 3000 S&P 500 Stock Markets 23

24 Abnormal Returns 8.00% 11 Days Cummulative Abnormal Returns 6.00% 4.00% 2.00% 0.00% -2.00% -4.00% -6.00% -8.00% September 11th 2001 Event Madrid March 11th 2004 Event London July 7th Event % % World Index CAC40 FTSE100 NASDAQ Composite NIKKEI 225 NYSE Composit Russell 3000 S&P 500 Stock Markets 24

25 Returns 5.00% Cummulative Abnormal Return - World Index 0.00% % % London July 7th Attack Madrid March 11th Attack New York September 11th Attack % % % T=-10 to T=+10 25

26 Returns Cummulative Abnormal Returns - S&P500 Index 5.00% 0.00% -5.00% London July 7th Attack Madrid March 11th Attack New York September 11th Attack % % % T = -10 to T =

27 Returns Cummulative Abnormal Returns - NYSE Composite Index 5.00% 0.00% -5.00% London July 7th Attack Madrid March 11th Attack New York September 11th Attack % % % T = -10 to T =

28 Returns Cummulative Abnormal Returns - NASDAQ Composite Index 5.00% 0.00% -5.00% London July 7th Attack % % Madrid March 11th Attack New York September 11th Attack % % % T = -10 to T =

29 Returns 5.00% Cummulative Abnormal Returns - CAC40 Index 0.00% -5.00% London July 7th Attack % Madrid March 11th Attack % New York September 11th Attack % % % T = -10 to T =

30 Returns Cummulative Abnormal Returns - FTSE100 Index 5.00% 0.00% -5.00% London July 7th Attack Madrid March 11th Attack % New York September 11th Attack % % % T = -10 to T =

31 Returns Cummulative Abnormal Returns - Nikkei 225 Index 15.00% 10.00% 5.00% London July 7th Attack 0.00% -5.00% Madrid March 11th Attack New York September 11th Attack % % % T = -10 to T =

32 Industry Abnormal Returns for Industry Sector (t = 0) Non-Cyclical Cyclical Basic Industries General Industries Automobile Banks Financials Media Phamaceutical Telecoms Utilities Technology Energy London July 7th Event Madrid March 11th 2004 Event September 11th 2001 Event Returns 32

33 Abnormal Returns 6 Day Cummulative Abnormal Returns for the Industry Sector Indices 5.00% 0.00% -5.00% % % September 11th 2001 Event Madrid March 11th 2004 Event London July 7th Event % % Energy Technology Utilities Telecoms Phamaceutical Media Financials Banks Sector Automobile General Industries Basic Industries Cyclical Non-Cyclical 33

34 Abnormal Returns 11 days Cummulative Abnormal Returns for the Industry Sector Indices 10.00% 5.00% 0.00% -5.00% % September 11th 2001 Event Madrid March 11th 2004 Event London July 7th Event % % % Energy Technology Utilities Telecoms Phamaceutical Media Financials Banks Sector Automobile General Industries Basic Industries Cyclical Non-Cyclical 34

35 Price Discounts in Rights Issues: Why Do Managers Insist On What Investors Hate? Significant mean price discounts (25% for financial and 29% for nonfinancial firms) in rights issues in the UK using a sample of 264 observations for the period of 1994 to sample is comprised by 264 rights issues deals that occurred during the period of , with 229 and 35 deals for non-financial and financial firms Pre and post-announcement 35

36 Variables Description Expected Sign Pre-announcement Price Discount Price Discount = 1 (issue price divided by last price) Dependent Variable Leverage Leverage = Total debt divided by total assets (+) Bid_Ask Stock s bid ask spread in the 260 days prior to the (+) right issue announcement Loss Binary variable equal to one if return on assets is (+) negative and zero otherwise M_Sentiment Binary variable equal to one if last year market return (previous to announcement) is positive and zero otherwise (-) 36

37 Variables Description Expected Sign Post-announcement CAR_Rights Cumulative abnormal returns around announcement of rights issues terms Price Discount Price Discount = 1 (issue price divided by last price) Dependent Variable Size Natural logarithm of firm s market value (+) ROA Return on Assets = Net Income divided by (+) lagged total assets Tobin s Q Market value of Equity plus Book value of Debt divided by book value of debt and Equity C_Held_Shares Closely held shares = percentage shares held by majority shareholders F_Sentiment Binary variable equal to one if firm s cumulative return in prior 90 days to announcement is positive and zero otherwise (-) (+) (-)/(+) (+) 37

38 Price Discount i,t = α + +β 1 Leverage i,t + +β 2 Bid_Ask i,t + β 3 Loss i,t + β 4 M_Sentiment i,t + ε i,t AAR i, t = 2 t= 2 R i, t ER i, t CAR RIGHTS i,t = α + +β 1 Price Discount i,t + +β 2 Size i,t + β 3 ROA i,t + β 4 TOBIN Q i,t +β 5 C_Held_Shares i,t + β 6 F_Sentiment i,t + ε i,t 38

39 Pre-announcement Non-Financials Model (1) Model (2) Model (3) Model (4) Leverage 0.327*** (2.851) 0.308*** (2.915) 0.305*** (2.911) 0.308*** (2.931) Bid-Ask 1.632*** (3.792) 1.277*** (2.814) 1.276*** (2.813) Loss 0.110*** (2.426) 0.109* (2.419) M_Sentiment (1.059) Constant 0.204*** 0.123*** 0.099*** 0.076*** (6.437) (3.858) (3.431) (2.077) R-squared

40 Financials Model (1) Model (2) Model (3) Model (4) Leverage (0.434) * (-1.704) (-0.985) (-1.075) Bid-Ask 6.127*** (3.605) 3.151** (2.085) 3.074** (2.138) Loss 0.322*** (3.223) 0.347*** (4.011) M_Sentiment (0.749) Constant 0.221*** 0.105* (3.468) (1.755) (1.245) (0.154) R-squared

41 Post-announcement (Non Financials) Variables Model (1) Model (2) Model (3) Model (4) Model (5) Model (6) Price Discount * * * * ** (-1.922) (-1.626) (-1.721) (-1.917) (-1.968) (-1.991) Size 0.008** (2.354) 0.007** (2.083) 0.008** (2.153) 0.010** (2.442) 0.009** (2.091) Tobin s Q 0.004** (2.390) 0.004** (2.302) 0.004** (2.176) 0.003* (1.711) ROA (-0.608) (-0.630) (-0.898) C_Held_Shares (1.164) (1.091) F_Sentiment 0.037*** (2.765) Constant (-1.343) ** (-2.561) *** (-2.945) *** (-2.991) *** (-2.997) *** (-3.400) Adj. R-squared

42 Post-announcement (Financials) Variables Model (1) Model (2) Model (3) Model (4) Model (5) Model (6) Price Discount * * * (-2.027) (-1.939) (-1.661) (-1.345) (-1.193) (-1.027) Size (0.248) (0.443) (0.245) (0.101) (-0.356) Tobin s Q (0.658) (0.840) (0.846) (1.128) ROA 0.132*** (3.500) C_Held_Shares 0.135*** (3.646) (-0.444) 0.117*** (3.516) (-0.771) F_Sentiment 0.068* (1.878) Constant (0.531) (-0.090) (-0.484) (-0.455) (-0.115) (-0.554) Adj. R-squared

43 References Event Studies: Short-run abnormal returns MacKinlay, A. Craig, 1997, Event studies in economics and finance, Journal of Economics Literature 35, Campbell, Lo and MacKinlay, 1997, The Econometrics of Financial Markets. Princeton: Princeton University Press, 1997 (p ) Brown, Stephen and Jerold Warner, 1980, Measuring security price performance, Journal of Financial Economics 8, Brown, Stephen and JeroldWarner, 1985, Using daily stock returns: The case of event studies, Journal of Financial Economics 14, Ball, C., and W. Torous, 1988, Investigating security price performance in the presence of event date uncertainty, Journal of Financial Economics 22, Boehmer, E., J. Musumeci, and A. Poulsen, 1991, Event study methodology under conditions of event-induced variance, Journal of Financial Economics 30, Cooper, M. J., Dimitrov, O., Rau, R. (2001). A rose.com by Any Other Name. The Journal of Finance, 56, 6,

44 Eckbo, B. Espen, Vojislav Maksimovic, and Joseph Williams, 1990, Consistent estimation of cross-sectional models in event studies, Review of Financial Studies 3, Prabhala, N. R., 1997, Conditional methods in event studies and an equilibrium justification for standard event study procedures, Review of Financial Studies 10, 1-38 Long-Run Abnormal Performance Fama, Eugene, 1998, Market efficiency, long-term returns, and behavioral finance, Journal of Financial Economics 49, Kothari, S.P. and Jerold Warner, 1997, Measuring long-run security price performance, Journal of Financial Economics 43, Barder, Brad and John Lyon, 1997, Detecting long-run abnormal stock returns: The empirical power and specification of test statistics, Journal of Financial Economics 43, Lyon, John, Brad Barder and Chih Tsai, 1999, Improved methods for tests of long-run abnormal stock returns, Journal of Finance 54, Loughran, Tim, and Jay R. Ritter, 2000, Uniformly least powerful tests of market efficiency, Journal of Financial Economics 55,

45 Mitchell, Mark L., and Erik Stafford, 2000, Managerial decisions and long-term stock price performance, Journal of Business 73, Ritter, Jay R., 2003, Investment banking and securities issuance, Chapter 5 in Handbook of the Economics and Finance. Others Fama, E.F. and MacBeth, J.D. (1973) Risk, Return and Equilibrium : Empirical Tests, Journal of Political Economy, pp Roll, R. (1977) A Critique of Asset Pricing Theory s Tests, Journal of Financial Economics, Vol. 4, pp Fama, E.F. and French, K. (1993) Common Risk Factors in the Returns on Stocks and Bonds, Journal of Financial Economics, Vol. 33, pp

Does Calendar Time Portfolio Approach Really Lack Power?

International Journal of Business and Management; Vol. 9, No. 9; 2014 ISSN 1833-3850 E-ISSN 1833-8119 Published by Canadian Center of Science and Education Does Calendar Time Portfolio Approach Really

International Journal of Business and Management; Vol. 9, No. 9; 2014 ISSN 1833-3850 E-ISSN 1833-8119 Published by Canadian Center of Science and Education Does Calendar Time Portfolio Approach Really

Event Study. Dr. Qiwei Chen

Event Study Dr. Qiwei Chen Event Study Analysis Definition: An event study attempts to measure the valuation effects of an economic event, such as a merger or earnings announcement, by examining the response

Event Study Dr. Qiwei Chen Event Study Analysis Definition: An event study attempts to measure the valuation effects of an economic event, such as a merger or earnings announcement, by examining the response

Analysis of Stock Price Behaviour around Bonus Issue:

BHAVAN S INTERNATIONAL JOURNAL of BUSINESS Vol:3, 1 (2009) 18-31 ISSN 0974-0082 Analysis of Stock Price Behaviour around Bonus Issue: A Test of Semi-Strong Efficiency of Indian Capital Market Charles Lasrado

BHAVAN S INTERNATIONAL JOURNAL of BUSINESS Vol:3, 1 (2009) 18-31 ISSN 0974-0082 Analysis of Stock Price Behaviour around Bonus Issue: A Test of Semi-Strong Efficiency of Indian Capital Market Charles Lasrado

Dr. Khalid El Ouafa Cadi Ayyad University, PO box 4162, FPD Sidi Bouzid, Safi, Morroco

Information Content of Annual Earnings Announcements: Evidence from Moroccan Stock Market Dr. Khalid El Ouafa Cadi Ayyad University, PO box 4162, FPD Sidi Bouzid, Safi, Morroco Abstract The objective of

Information Content of Annual Earnings Announcements: Evidence from Moroccan Stock Market Dr. Khalid El Ouafa Cadi Ayyad University, PO box 4162, FPD Sidi Bouzid, Safi, Morroco Abstract The objective of

UNIVERSITY OF ROCHESTER

UNIVERSITY OF ROCHESTER William E. Simon Graduate School of Business Administration FIN 532 Professor G. William Schwert Advanced Topics in Capital Markets CS 3-110L, 275-2470 Fax: 461-5475 Email: schwert@schwert.ssb.rochester.edu

UNIVERSITY OF ROCHESTER William E. Simon Graduate School of Business Administration FIN 532 Professor G. William Schwert Advanced Topics in Capital Markets CS 3-110L, 275-2470 Fax: 461-5475 Email: schwert@schwert.ssb.rochester.edu

2. The Efficient Markets Hypothesis - Generalized Method of Moments

Useful textbooks for the course are SYLLABUS UNSW PhD Seminar Empirical Financial Economics June 19-21, 2006 J. Cochrane, (JC) 2001, Asset Pricing (Princeton University Press, Princeton NJ J. Campbell,

Useful textbooks for the course are SYLLABUS UNSW PhD Seminar Empirical Financial Economics June 19-21, 2006 J. Cochrane, (JC) 2001, Asset Pricing (Princeton University Press, Princeton NJ J. Campbell,

A Note on Intraday Event Studies

A Note on Intraday Event Studies Ben R. Marshall* Massey University b.marshall@massey.ac.nz Nhut H. Nguyen Massey University n.h.nguyen@massey.ac.nz Nuttawat Visaltanachoti Massey University n.visaltanachoti@massey.ac.nz

A Note on Intraday Event Studies Ben R. Marshall* Massey University b.marshall@massey.ac.nz Nhut H. Nguyen Massey University n.h.nguyen@massey.ac.nz Nuttawat Visaltanachoti Massey University n.visaltanachoti@massey.ac.nz

Testing the Robustness of. Long-Term Under-Performance of. UK Initial Public Offerings

Testing the Robustness of Long-Term Under-Performance of UK Initial Public Offerings by Susanne Espenlaub* Alan Gregory** and Ian Tonks*** 22 July, 1998 * Manchester School of Accounting and Finance, University

Testing the Robustness of Long-Term Under-Performance of UK Initial Public Offerings by Susanne Espenlaub* Alan Gregory** and Ian Tonks*** 22 July, 1998 * Manchester School of Accounting and Finance, University

Completely predictable and fully anticipated? Step ups in warrant exercise prices

Applied Economics Letters, 2005, 12, 561 565 Completely predictable and fully anticipated? Step ups in warrant exercise prices Luis Garcia-Feijo o a, *, John S. Howe b and Tie Su c a Department of Finance,

Applied Economics Letters, 2005, 12, 561 565 Completely predictable and fully anticipated? Step ups in warrant exercise prices Luis Garcia-Feijo o a, *, John S. Howe b and Tie Su c a Department of Finance,

Share Price Behaviour of Indian Pharmaceutical Companies. Ms. S. Padmavathy 1, Dr. J. Ashok

Share Price Behaviour of Indian Pharmaceutical Companies Ms. S. Padmavathy 1, Dr. J. Ashok 2 1 Asst. Professor, Department of Management Studies, Kongu Engineering College, Erode, Tamilnadu, India - 638052.

Share Price Behaviour of Indian Pharmaceutical Companies Ms. S. Padmavathy 1, Dr. J. Ashok 2 1 Asst. Professor, Department of Management Studies, Kongu Engineering College, Erode, Tamilnadu, India - 638052.

Shariah-compliant Investment and Shareholders Value: An Empirical Investigation

Global Economy and Finance Journal Vol. 4. No. 1. March 2011 Pp. 44-61 Shariah-compliant Investment and Shareholders Value: An Empirical Investigation Mehdi Sadeghi * This paper investigates the impacts

Global Economy and Finance Journal Vol. 4. No. 1. March 2011 Pp. 44-61 Shariah-compliant Investment and Shareholders Value: An Empirical Investigation Mehdi Sadeghi * This paper investigates the impacts

CORPORATE ANNOUNCEMENTS OF EARNINGS AND STOCK PRICE BEHAVIOR: EMPIRICAL EVIDENCE

CORPORATE ANNOUNCEMENTS OF EARNINGS AND STOCK PRICE BEHAVIOR: EMPIRICAL EVIDENCE By Ms Swati Goyal & Dr. Harpreet kaur ABSTRACT: This paper empirically examines whether earnings reports possess informational

CORPORATE ANNOUNCEMENTS OF EARNINGS AND STOCK PRICE BEHAVIOR: EMPIRICAL EVIDENCE By Ms Swati Goyal & Dr. Harpreet kaur ABSTRACT: This paper empirically examines whether earnings reports possess informational

THE UNIVERSITY OF NEW SOUTH WALES SCHOOL OF BANKING AND FINANCE

THE UNIVERSITY OF NEW SOUTH WALES SCHOOL OF BANKING AND FINANCE SESSION 1, 2005 FINS 4774 FINANCIAL DECISION MAKING UNDER UNCERTAINTY Instructor Dr. Pascal Nguyen Office: Quad #3071 Phone: (2) 9385 5773

THE UNIVERSITY OF NEW SOUTH WALES SCHOOL OF BANKING AND FINANCE SESSION 1, 2005 FINS 4774 FINANCIAL DECISION MAKING UNDER UNCERTAINTY Instructor Dr. Pascal Nguyen Office: Quad #3071 Phone: (2) 9385 5773

THE EFFECTS AND COMPETITIVE EFFECTS OF SEASONED EQUITY OFFERINGS. Mikel Hoppenbrouwers Master Thesis Finance Program

Firms conducting SEOs outperform nonissuing firms in the same industry. THE EFFECTS AND COMPETITIVE EFFECTS OF SEASONED EQUITY OFFERINGS The Impact on Stock Price Performance Mikel Hoppenbrouwers Master

Firms conducting SEOs outperform nonissuing firms in the same industry. THE EFFECTS AND COMPETITIVE EFFECTS OF SEASONED EQUITY OFFERINGS The Impact on Stock Price Performance Mikel Hoppenbrouwers Master

Journal Of Financial And Strategic Decisions Volume 7 Number 3 Fall 1994 ASYMMETRIC INFORMATION: THE CASE OF BANK LOAN COMMITMENTS

Journal Of Financial And Strategic Decisions Volume 7 Number 3 Fall 1994 ASYMMETRIC INFORMATION: THE CASE OF BANK LOAN COMMITMENTS James E. McDonald * Abstract This study analyzes common stock return behavior

Journal Of Financial And Strategic Decisions Volume 7 Number 3 Fall 1994 ASYMMETRIC INFORMATION: THE CASE OF BANK LOAN COMMITMENTS James E. McDonald * Abstract This study analyzes common stock return behavior

Indian Institute of Management Calcutta. Working Paper Series. WPS No. 798 April 2017

Indian Institute of Management Calcutta Working Paper Series WPS No. 798 April 2017 Impact of Stock Splits on Returns: Evidence from Indian Stock Market Binay Bhushan Chakrabarti Retd. Professor, Indian

Indian Institute of Management Calcutta Working Paper Series WPS No. 798 April 2017 Impact of Stock Splits on Returns: Evidence from Indian Stock Market Binay Bhushan Chakrabarti Retd. Professor, Indian

IMPACT OF DEMONETIZATION ON STOCK MARKET: EVENT STUDY METHODOLOGY

Indian Journal of Accounting (IJA) 127 ISSN : 0972-1479 (Print) 2395-6127 (Online) Vol. XLIX (1), June, 2017, pp. 127-132 IMPACT OF DEMONETIZATION ON STOCK MARKET: EVENT STUDY METHODOLOGY Swati Chauhan

Indian Journal of Accounting (IJA) 127 ISSN : 0972-1479 (Print) 2395-6127 (Online) Vol. XLIX (1), June, 2017, pp. 127-132 IMPACT OF DEMONETIZATION ON STOCK MARKET: EVENT STUDY METHODOLOGY Swati Chauhan

Open Market Repurchase Programs - Evidence from Finland

International Journal of Economics and Finance; Vol. 9, No. 12; 2017 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education Open Market Repurchase Programs - Evidence from

International Journal of Economics and Finance; Vol. 9, No. 12; 2017 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education Open Market Repurchase Programs - Evidence from

Analysis of Market Reaction Around the Bonus Issues in Indian Market

Analysis of Market Reaction Around the Bonus Issues in Indian Market Dhanya Alex Ph.D Associate Professor, FISAT Business School, Mookkannoor, Angamaly, Kochi, PO Box 683577, India Abstract When the companies

Analysis of Market Reaction Around the Bonus Issues in Indian Market Dhanya Alex Ph.D Associate Professor, FISAT Business School, Mookkannoor, Angamaly, Kochi, PO Box 683577, India Abstract When the companies

Stock split and reverse split- Evidence from India

Stock split and reverse split- Evidence from India Ruzbeh J Bodhanwala Flame University Abstract: This study expands on why managers decide to split and reverse split their companies share and what are

Stock split and reverse split- Evidence from India Ruzbeh J Bodhanwala Flame University Abstract: This study expands on why managers decide to split and reverse split their companies share and what are

Journal Of Financial And Strategic Decisions Volume 10 Number 3 Fall 1997

Journal Of Financial And Strategic Decisions Volume 0 Number 3 Fall 997 EVENT RISK BOND COVENANTS AND SHAREHOLDER WEALTH: EVIDENCE FROM CONVERTIBLE BONDS Terrill R. Keasler *, Delbert C. Goff * and Steven

Journal Of Financial And Strategic Decisions Volume 0 Number 3 Fall 997 EVENT RISK BOND COVENANTS AND SHAREHOLDER WEALTH: EVIDENCE FROM CONVERTIBLE BONDS Terrill R. Keasler *, Delbert C. Goff * and Steven

An Empirical Analysis on the Management Strategy of the Growth in Dividend Payout Signal Transmission Based on Event Study Methodology

International Business and Management Vol. 7, No. 2, 2013, pp. 6-10 DOI:10.3968/j.ibm.1923842820130702.1100 ISSN 1923-841X [Print] ISSN 1923-8428 [Online] www.cscanada.net www.cscanada.org An Empirical

International Business and Management Vol. 7, No. 2, 2013, pp. 6-10 DOI:10.3968/j.ibm.1923842820130702.1100 ISSN 1923-841X [Print] ISSN 1923-8428 [Online] www.cscanada.net www.cscanada.org An Empirical

Impact of Dividends on Share Price Performance of Companies in Indian Context

Impact of Dividends on Share Price Performance of Companies in Indian Context Kavita Chavali and Nusratunnisa School of Business - Alliance University, Bangalore Abstract The study aims at finding the

Impact of Dividends on Share Price Performance of Companies in Indian Context Kavita Chavali and Nusratunnisa School of Business - Alliance University, Bangalore Abstract The study aims at finding the

Biases in the IPO Pricing Process

University of Rochester William E. Simon Graduate School of Business Administration The Bradley Policy Research Center Financial Research and Policy Working Paper No. FR 01-02 February, 2001 Biases in

University of Rochester William E. Simon Graduate School of Business Administration The Bradley Policy Research Center Financial Research and Policy Working Paper No. FR 01-02 February, 2001 Biases in

NBER WORKING PAPER SERIES A REHABILITATION OF STOCHASTIC DISCOUNT FACTOR METHODOLOGY. John H. Cochrane

NBER WORKING PAPER SERIES A REHABILIAION OF SOCHASIC DISCOUN FACOR MEHODOLOGY John H. Cochrane Working Paper 8533 http://www.nber.org/papers/w8533 NAIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts

NBER WORKING PAPER SERIES A REHABILIAION OF SOCHASIC DISCOUN FACOR MEHODOLOGY John H. Cochrane Working Paper 8533 http://www.nber.org/papers/w8533 NAIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts

Appendix. In this Appendix, we present the construction of variables, data source, and some empirical procedures.

Appendix In this Appendix, we present the construction of variables, data source, and some empirical procedures. A.1. Variable Definition and Data Source Variable B/M CAPX/A Cash/A Cash flow volatility

Appendix In this Appendix, we present the construction of variables, data source, and some empirical procedures. A.1. Variable Definition and Data Source Variable B/M CAPX/A Cash/A Cash flow volatility

The Journal of Applied Business Research January/February 2013 Volume 29, Number 1

Stock Price Reactions To Debt Initial Public Offering Announcements Kelly Cai, University of Michigan Dearborn, USA Heiwai Lee, University of Michigan Dearborn, USA ABSTRACT We examine the valuation effect

Stock Price Reactions To Debt Initial Public Offering Announcements Kelly Cai, University of Michigan Dearborn, USA Heiwai Lee, University of Michigan Dearborn, USA ABSTRACT We examine the valuation effect

Share repurchase announcements

Share repurchase announcements The influence of firm performances on the share price impact Master Thesis Finance Student name: Administration number: Study Program: Michiel (M.M.T.) van Lent S166433 Finance

Share repurchase announcements The influence of firm performances on the share price impact Master Thesis Finance Student name: Administration number: Study Program: Michiel (M.M.T.) van Lent S166433 Finance

Impact of US election results on Indian stock market: An event study approach

2017; 3(5): 09-13 ISSN Print: 2394-7500 ISSN Online: 2394-5869 Impact Factor: 5.2 IJAR 2017; 3(5): 09-13 www.allresearchjournal.com Received: 05-03-2017 Accepted: 06-04-2017 Madhu Iyengar Prof. CMA (US),

2017; 3(5): 09-13 ISSN Print: 2394-7500 ISSN Online: 2394-5869 Impact Factor: 5.2 IJAR 2017; 3(5): 09-13 www.allresearchjournal.com Received: 05-03-2017 Accepted: 06-04-2017 Madhu Iyengar Prof. CMA (US),

THE EFFECT OF SHARE REPURCHASES ON STOCK PRICE PERFORMANCE

TILBURG UNIVERSITY THE EFFECT OF SHARE REPURCHASES ON STOCK PRICE PERFORMANCE Empirical evidences from The Netherlands and Belgium Master thesis Student name : Thanh Huyen Vu Student number : 1259219 Administration

TILBURG UNIVERSITY THE EFFECT OF SHARE REPURCHASES ON STOCK PRICE PERFORMANCE Empirical evidences from The Netherlands and Belgium Master thesis Student name : Thanh Huyen Vu Student number : 1259219 Administration

EVENT STUDY ON STOCK SPLITS

BAJRA Ujkan & HASANI Burim - Event study on stock splits EVENT STUDY ON STOCK SPLITS Ujkan BAJRA, PhD. C *Univeristy of Prishtrina, Faculty of Applied Sciences of Business in Peja Burim HASANI, Msc. Univeirsty

BAJRA Ujkan & HASANI Burim - Event study on stock splits EVENT STUDY ON STOCK SPLITS Ujkan BAJRA, PhD. C *Univeristy of Prishtrina, Faculty of Applied Sciences of Business in Peja Burim HASANI, Msc. Univeirsty

Columbia, V2N 4Z9, Canada Version of record first published: 30 Mar 2009.

This article was downloaded by: [UNBC Univ of Northern British Columbia] On: 30 March 2013, At: 17:30 Publisher: Routledge Informa Ltd Registered in England and Wales Registered Number: 1072954 Registered

This article was downloaded by: [UNBC Univ of Northern British Columbia] On: 30 March 2013, At: 17:30 Publisher: Routledge Informa Ltd Registered in England and Wales Registered Number: 1072954 Registered

Returns to shareholders in Acquisitions into the U.S. Pharmaceutical Companies. Samra Chaudary Lahore School of Economics, Pakistan

International Journal of Health and Economic Development, 1(2), 14-27, July 2015 14 Returns to shareholders in Acquisitions into the U.S. Pharmaceutical Companies Samra Chaudary Lahore School of Economics,

International Journal of Health and Economic Development, 1(2), 14-27, July 2015 14 Returns to shareholders in Acquisitions into the U.S. Pharmaceutical Companies Samra Chaudary Lahore School of Economics,

LONG-RUN ABNORMAL STOCK PERFORMANCE: SOME ADDITIONAL EVIDENCE

LONG-RUN ABNORMAL STOCK PERFORMANCE: SOME ADDITIONAL EVIDENCE J.F. BACMANN a AND M. DUBOIS a First Draft: February 2002 a Université de Neuchâtel, Pierre-à-Mazel 7, 2000 Neuchâtel, Switzerland Tel: +41

LONG-RUN ABNORMAL STOCK PERFORMANCE: SOME ADDITIONAL EVIDENCE J.F. BACMANN a AND M. DUBOIS a First Draft: February 2002 a Université de Neuchâtel, Pierre-à-Mazel 7, 2000 Neuchâtel, Switzerland Tel: +41

Testing for efficient markets

IGIDR, Bombay May 17, 2011 What is market efficiency? A market is efficient if prices contain all information about the value of a stock. An attempt at a more precise definition: an efficient market is

IGIDR, Bombay May 17, 2011 What is market efficiency? A market is efficient if prices contain all information about the value of a stock. An attempt at a more precise definition: an efficient market is

The Characteristics of Bidding Firms and the Likelihood of Cross-border Acquisitions

The Characteristics of Bidding Firms and the Likelihood of Cross-border Acquisitions Han Donker, Ph.D., University of orthern British Columbia, Canada Saif Zahir, Ph.D., University of orthern British Columbia,

The Characteristics of Bidding Firms and the Likelihood of Cross-border Acquisitions Han Donker, Ph.D., University of orthern British Columbia, Canada Saif Zahir, Ph.D., University of orthern British Columbia,

Available on Gale & affiliated international databases. AsiaNet PAKISTAN. JHSS XX, No. 2, 2012

Available on Gale & affiliated international databases AsiaNet PAKISTAN Journal of Humanities & Social Sciences University of Peshawar JHSS XX, No. 2, 2012 Impact of Interest Rate and Inflation on Stock

Available on Gale & affiliated international databases AsiaNet PAKISTAN Journal of Humanities & Social Sciences University of Peshawar JHSS XX, No. 2, 2012 Impact of Interest Rate and Inflation on Stock

Investor Behavior and the Timing of Secondary Equity Offerings

Investor Behavior and the Timing of Secondary Equity Offerings Dalia Marciukaityte College of Administration and Business Louisiana Tech University P.O. Box 10318 Ruston, LA 71272 E-mail: DMarciuk@cab.latech.edu

Investor Behavior and the Timing of Secondary Equity Offerings Dalia Marciukaityte College of Administration and Business Louisiana Tech University P.O. Box 10318 Ruston, LA 71272 E-mail: DMarciuk@cab.latech.edu

The Performance of Acquisitions in the Real Estate Investment Trust Industry

The Performance of Acquisitions in the Real Estate Investment Trust Industry Author Olgun F. Sahin Abstract This study examines the performance of acquisitions in the Real Estate Investment Trust (REIT)

The Performance of Acquisitions in the Real Estate Investment Trust Industry Author Olgun F. Sahin Abstract This study examines the performance of acquisitions in the Real Estate Investment Trust (REIT)

Outline. The Impact of Share Repurchases on Closed-End Funds. Repurchases: Stylised Facts. Repurchases Now Equal Dividends in Magnitude

The Impact of Share Repurchases on Closed-End Funds Outline Jingfeng An * Gordon Gemmill # Dylan C. Thomas* November 5.Background and previous work on repurchases. How repurchases may affect closed-end

The Impact of Share Repurchases on Closed-End Funds Outline Jingfeng An * Gordon Gemmill # Dylan C. Thomas* November 5.Background and previous work on repurchases. How repurchases may affect closed-end

The Impact of Optimistic and Pessimistic Managers on Firm Performance and Corporate Decisions

Working Paper The Impact of Optimistic and Pessimistic Managers on Firm Performance and Corporate Decisions Jens Martin 1 Swiss Finance Institute, University of Lugano May 2008 This paper investigates

Working Paper The Impact of Optimistic and Pessimistic Managers on Firm Performance and Corporate Decisions Jens Martin 1 Swiss Finance Institute, University of Lugano May 2008 This paper investigates

Journal of Internet Banking and Commerce

ZHAO R Journal of Internet Banking and Commerce An open access Internet journal (http://www.icommercecentral.com) Journal of Internet Banking and Commerce, April 2016, vol. 21, no. 1 Index effects: Evidence

ZHAO R Journal of Internet Banking and Commerce An open access Internet journal (http://www.icommercecentral.com) Journal of Internet Banking and Commerce, April 2016, vol. 21, no. 1 Index effects: Evidence

Corporate Ethical Behaviours and Equity Value

Corporate Ethical Behaviours and Equity Value Evidence from the GPFG s ethical exclusions Vaska Atta-Darkua Judge Business School, University of Cambridge January 9, 2019 Motivation In the United States,

Corporate Ethical Behaviours and Equity Value Evidence from the GPFG s ethical exclusions Vaska Atta-Darkua Judge Business School, University of Cambridge January 9, 2019 Motivation In the United States,

Class Action, Halliburton II, & Event Studies. Sanjai Bhagat University of Colorado

Class Action, Halliburton II, & Event Studies Sanjai Bhagat University of Colorado Executive Summary In Halliburton Co. v. Erica P. John Fund, Inc., 134 S. Ct. 2398 (2014) (Halliburton II), the U.S. Supreme

Class Action, Halliburton II, & Event Studies Sanjai Bhagat University of Colorado Executive Summary In Halliburton Co. v. Erica P. John Fund, Inc., 134 S. Ct. 2398 (2014) (Halliburton II), the U.S. Supreme

Seasonal Analysis of Abnormal Returns after Quarterly Earnings Announcements

Seasonal Analysis of Abnormal Returns after Quarterly Earnings Announcements Dr. Iqbal Associate Professor and Dean, College of Business Administration The Kingdom University P.O. Box 40434, Manama, Bahrain

Seasonal Analysis of Abnormal Returns after Quarterly Earnings Announcements Dr. Iqbal Associate Professor and Dean, College of Business Administration The Kingdom University P.O. Box 40434, Manama, Bahrain

Impact of EXPO 2020 on Dubai Financial Market An Event Study on Banks, Investment and Insurance Sectors

Impact of EXPO 2020 on Dubai Financial Market An Event Study on Banks, Investment and Insurance Sectors Ganga Bhavani 1 & Sai Geetha Kukunuru 1 1 Skyline University College, Sharjah, UAE Correspondence:

Impact of EXPO 2020 on Dubai Financial Market An Event Study on Banks, Investment and Insurance Sectors Ganga Bhavani 1 & Sai Geetha Kukunuru 1 1 Skyline University College, Sharjah, UAE Correspondence:

Long-term Equity and Operating Performances following Straight and Convertible Debt Issuance in the U.S. *

Asia-Pacific Journal of Financial Studies (2009) v38 n3 pp337-374 Long-term Equity and Operating Performances following Straight and Convertible Debt Issuance in the U.S. * Mookwon Jung Kookmin University,

Asia-Pacific Journal of Financial Studies (2009) v38 n3 pp337-374 Long-term Equity and Operating Performances following Straight and Convertible Debt Issuance in the U.S. * Mookwon Jung Kookmin University,

The stock market reaction towards acquisition announcements in different business cycles

Master Degree Project in Finance The stock market reaction towards acquisition announcements in different business cycles Mathias Karlsson and Jacob Sundquist Supervisor: Martin Holmén Master Degree Project

Master Degree Project in Finance The stock market reaction towards acquisition announcements in different business cycles Mathias Karlsson and Jacob Sundquist Supervisor: Martin Holmén Master Degree Project

DIVIDEND POLICY OF BANK INITIAL PUBLIC OFFERINGS

DIVIDEND POLICY OF BANK INITIAL PUBLIC OFFERINGS Wolfgang Bessler Professor of Finance Center for Finance and Banking Justus-Liebig-University Giessen, Germany James P. Murtagh Clinical Assistant Professor

DIVIDEND POLICY OF BANK INITIAL PUBLIC OFFERINGS Wolfgang Bessler Professor of Finance Center for Finance and Banking Justus-Liebig-University Giessen, Germany James P. Murtagh Clinical Assistant Professor

What Is Fundamental Indexation?

What Is Fundamental Indexation? Passive investing is the market portfolio in market proportions. Strictly speaking, all else is active investing. Active investing incurs administrative costs and transaction

What Is Fundamental Indexation? Passive investing is the market portfolio in market proportions. Strictly speaking, all else is active investing. Active investing incurs administrative costs and transaction

Systematic liquidity risk and stock price reaction to shocks: Evidence from London Stock Exchange

Systematic liquidity risk and stock price reaction to shocks: Evidence from London Stock Exchange Khelifa Mazouz a,*, Dima W.H. Alrabadi a, and Shuxing Yin b a Bradford University School of Management,

Systematic liquidity risk and stock price reaction to shocks: Evidence from London Stock Exchange Khelifa Mazouz a,*, Dima W.H. Alrabadi a, and Shuxing Yin b a Bradford University School of Management,

Earnings Information and Stock Market Efficiency

American Scientific Research Journal for Engineering, Technology, and Sciences (ASRJETS) ISSN (Print) 23134410, ISSN (Online) 23134402 Global Society of Scientific Research and Researchers http://asrjetsjournal.org/

American Scientific Research Journal for Engineering, Technology, and Sciences (ASRJETS) ISSN (Print) 23134410, ISSN (Online) 23134402 Global Society of Scientific Research and Researchers http://asrjetsjournal.org/

Share Repurchases in Europe:

Master Thesis Finance Share Repurchases in Europe: A View over Managerial Hubris, EU Regulations and Country Legal Origins. Author: João Diogo Correia de Matos (ANR: 202419) Supervisor: Fabio Castiglionesi

Master Thesis Finance Share Repurchases in Europe: A View over Managerial Hubris, EU Regulations and Country Legal Origins. Author: João Diogo Correia de Matos (ANR: 202419) Supervisor: Fabio Castiglionesi

Information Content of PE Ratio, Price-to-book Ratio and Firm Size in Predicting Equity Returns

01 International Conference on Innovation and Information Management (ICIIM 01) IPCSIT vol. 36 (01) (01) IACSIT Press, Singapore Information Content of PE Ratio, Price-to-book Ratio and Firm Size in Predicting

01 International Conference on Innovation and Information Management (ICIIM 01) IPCSIT vol. 36 (01) (01) IACSIT Press, Singapore Information Content of PE Ratio, Price-to-book Ratio and Firm Size in Predicting

Institutional Finance Financial Crises, Risk Management and Liquidity

Institutional Finance Financial Crises, Risk Management and Liquidity Markus K. Brunnermeier Preceptor: Delwin Olivan Princeton University 1 Overview Efficiency concepts EMH implies Martingale Property

Institutional Finance Financial Crises, Risk Management and Liquidity Markus K. Brunnermeier Preceptor: Delwin Olivan Princeton University 1 Overview Efficiency concepts EMH implies Martingale Property

EFFECT OF EX-DIVIDEND DATE ON STOCK RETURNS OF NIFTY STOCKS IN INDIA

Lakshmi Rawat & Mary Jessica Special Issue Volume 2 Issue 1, pp. 236-248 DOI-http://dx.doi.org/10.20319/ pijss.2016.s21.236248 EFFECT OF EX-DIVIDEND DATE ON STOCK RETURNS OF NIFTY STOCKS IN INDIA Lakshmi

Lakshmi Rawat & Mary Jessica Special Issue Volume 2 Issue 1, pp. 236-248 DOI-http://dx.doi.org/10.20319/ pijss.2016.s21.236248 EFFECT OF EX-DIVIDEND DATE ON STOCK RETURNS OF NIFTY STOCKS IN INDIA Lakshmi

The Free Cash Flow Effects of Capital Expenditure Announcements. Catherine Shenoy and Nikos Vafeas* Abstract

The Free Cash Flow Effects of Capital Expenditure Announcements Catherine Shenoy and Nikos Vafeas* Abstract In this paper we study the market reaction to capital expenditure announcements in the backdrop

The Free Cash Flow Effects of Capital Expenditure Announcements Catherine Shenoy and Nikos Vafeas* Abstract In this paper we study the market reaction to capital expenditure announcements in the backdrop

TRADING VOLUME REACTIONS AND THE ADOPTION OF INTERNATIONAL ACCOUNTING STANDARD (IAS 1): PRESENTATION OF FINANCIAL STATEMENTS IN INDONESIA

: PRESENTATION OF FINANCIAL STATEMENTS IN INDONESIA") TRADING VOLUME REACTIONS AND THE ADOPTION OF INTERNATIONAL ACCOUNTING STANDARD (IAS 1): PRESENTATION OF FINANCIAL STATEMENTS IN INDONESIA Beatrise Sihite, University of Indonesia Aria Farah Mita, University

TRADING VOLUME REACTIONS AND THE ADOPTION OF INTERNATIONAL ACCOUNTING STANDARD (IAS 1): PRESENTATION OF FINANCIAL STATEMENTS IN INDONESIA Beatrise Sihite, University of Indonesia Aria Farah Mita, University

Stock Market Reaction to Dividend Announcements from a Special Institutional Environment of Vietnamese Stock Market

International Journal of Economics and Finance; Vol. 7, No. 9; 2015 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education Stock Market Reaction to Dividend Announcements

International Journal of Economics and Finance; Vol. 7, No. 9; 2015 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education Stock Market Reaction to Dividend Announcements

Post-Earnings-Announcement Drift: The Role of Revenue Surprises and Earnings Persistence

Post-Earnings-Announcement Drift: The Role of Revenue Surprises and Earnings Persistence Joshua Livnat Department of Accounting Stern School of Business Administration New York University 311 Tisch Hall

Post-Earnings-Announcement Drift: The Role of Revenue Surprises and Earnings Persistence Joshua Livnat Department of Accounting Stern School of Business Administration New York University 311 Tisch Hall

Would You Follow MM or a Profitable Trading Strategy? Brian Baturevich. Gulnur Muradoglu*

Would You Follow MM or a Profitable Trading Strategy? Brian Baturevich Gulnur Muradoglu* Abstract We investigate the ability of company capital structures to be used as a predictor for abnormal returns.

Would You Follow MM or a Profitable Trading Strategy? Brian Baturevich Gulnur Muradoglu* Abstract We investigate the ability of company capital structures to be used as a predictor for abnormal returns.

Aggregate Earnings Surprises, & Behavioral Finance

Stock Returns, Aggregate Earnings Surprises, & Behavioral Finance Kothari, Lewellen & Warner, JFE, 2006 FIN532 : Discussion Plan 1. Introduction 2. Sample Selection & Data Description 3. Part 1: Relation

Stock Returns, Aggregate Earnings Surprises, & Behavioral Finance Kothari, Lewellen & Warner, JFE, 2006 FIN532 : Discussion Plan 1. Introduction 2. Sample Selection & Data Description 3. Part 1: Relation

Investment Management Course Syllabus

ICEF, Higher School of Economics, Moscow Bachelor Programme, Academic Year 2015-201 Investment Management Course Syllabus Lecturer: Luca Gelsomini (e-mail: lgelsomini@hse.ru) Class Teacher: Dmitry Kachalov

ICEF, Higher School of Economics, Moscow Bachelor Programme, Academic Year 2015-201 Investment Management Course Syllabus Lecturer: Luca Gelsomini (e-mail: lgelsomini@hse.ru) Class Teacher: Dmitry Kachalov

Prediction of open market share repurchases and portfolio returns: evidence from France, Germany and the UK

Prediction of open market share repurchases and portfolio returns: evidence from France, Germany and the UK Dimitris Andriosopoulos 1*, Chrysovalantis Gaganis 2, Fotios Pasiouras 3,4 1 Department of Accounting

Prediction of open market share repurchases and portfolio returns: evidence from France, Germany and the UK Dimitris Andriosopoulos 1*, Chrysovalantis Gaganis 2, Fotios Pasiouras 3,4 1 Department of Accounting

UNIVERSITY OF ROCHESTER. Home work Assignment #4 Due: May 24, 2012

UNIVERSITY OF ROCHESTER William E. Simon Graduate School of Business Administration FIN 532 Advanced Topics in Capital Markets Home work Assignment #4 Due: May 24, 2012 The point of this assignment is

UNIVERSITY OF ROCHESTER William E. Simon Graduate School of Business Administration FIN 532 Advanced Topics in Capital Markets Home work Assignment #4 Due: May 24, 2012 The point of this assignment is

TABLE OF CONTENTS WHAT ARE INDICES? 3 HOW INDICES ARE PRICED 4 WHY TRADE INDICES? 5 HOW INDEX FUTURES ARE TRADED 6 TYPES OF INDICES 7

TABLE OF CONTENTS WHAT ARE INDICES? 3 HOW INDICES ARE PRICED 4 WHY TRADE INDICES? 5 HOW INDEX FUTURES ARE TRADED 6 TYPES OF INDICES 7 AN EXAMPLE OF AN INDICES CFD TRADE 8 UNDERSTANDING INDICES WHAT ARE

TABLE OF CONTENTS WHAT ARE INDICES? 3 HOW INDICES ARE PRICED 4 WHY TRADE INDICES? 5 HOW INDEX FUTURES ARE TRADED 6 TYPES OF INDICES 7 AN EXAMPLE OF AN INDICES CFD TRADE 8 UNDERSTANDING INDICES WHAT ARE

MARKET REACTION TO & ANTICIPATION OF ACCOUNTING NUMBERS

MARKET REACTION TO & ANTICIPATION OF ACCOUNTING NUMBERS One way in which accounting numbers can be assessed is to see how they relate to stock returns. Accounting numbers which update the market s beliefs

MARKET REACTION TO & ANTICIPATION OF ACCOUNTING NUMBERS One way in which accounting numbers can be assessed is to see how they relate to stock returns. Accounting numbers which update the market s beliefs

Decimalization and Illiquidity Premiums: An Extended Analysis

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 5-2015 Decimalization and Illiquidity Premiums: An Extended Analysis Seth E. Williams Utah State University

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 5-2015 Decimalization and Illiquidity Premiums: An Extended Analysis Seth E. Williams Utah State University

Abstract. Master thesis. Keywords: mergers and acquisitions, long-term performance, event study, buy-and-hold abnormal returns.

Master thesis Hit or miss? - Do acquisitions create value for the acquiring company s shareholders? A long-term event study on acquisitions performed by Swedish IT companies. Abstract In this paper, we

Master thesis Hit or miss? - Do acquisitions create value for the acquiring company s shareholders? A long-term event study on acquisitions performed by Swedish IT companies. Abstract In this paper, we

High-Frequency Data Analysis and Market Microstructure [Tsay (2005), chapter 5]

![High-Frequency Data Analysis and Market Microstructure [Tsay (2005), chapter 5]](/thumbs/79/79153367.jpg "High-Frequency Data Analysis and Market Microstructure [Tsay (2005), chapter 5]") 1 High-Frequency Data Analysis and Market Microstructure [Tsay (2005), chapter 5] High-frequency data have some unique characteristics that do not appear in lower frequencies. At this class we have: Nonsynchronous

1 High-Frequency Data Analysis and Market Microstructure [Tsay (2005), chapter 5] High-frequency data have some unique characteristics that do not appear in lower frequencies. At this class we have: Nonsynchronous

CLASS ACTION LAWSUITS AND VENUE: DOES THE MARKET CARE

CLASS ACTION LAWSUITS AND VENUE: DOES THE MARKET CARE PHILIP L. TEW, JD / Ph.D ASSISTANT PROFESSOR OF FINANCE ARKANSAS STATE UNIVERSITY PO BOX 239 STATE UNIVERSITY, AR 72467 PTEW@ASTATE.EDU 870-972-3742

CLASS ACTION LAWSUITS AND VENUE: DOES THE MARKET CARE PHILIP L. TEW, JD / Ph.D ASSISTANT PROFESSOR OF FINANCE ARKANSAS STATE UNIVERSITY PO BOX 239 STATE UNIVERSITY, AR 72467 PTEW@ASTATE.EDU 870-972-3742

Does Debt Help Managers? Using Cash Holdings to Explain Acquisition Returns

University of Colorado, Boulder CU Scholar Undergraduate Honors Theses Honors Program Spring 2017 Does Debt Help Managers? Using Cash Holdings to Explain Acquisition Returns Michael Evans Michael.Evans-1@Colorado.EDU

University of Colorado, Boulder CU Scholar Undergraduate Honors Theses Honors Program Spring 2017 Does Debt Help Managers? Using Cash Holdings to Explain Acquisition Returns Michael Evans Michael.Evans-1@Colorado.EDU

A Perspective on Industry Classification and Market Reaction to Corporate News: Evidence from India

Scientific Annals of Economics and Business 65 (1), 2018, 31-50 DOI: 10.2478/saeb-2018-0001 A Perspective on Industry Classification and Market Reaction to Corporate News: Evidence from India Nayanjyoti

Scientific Annals of Economics and Business 65 (1), 2018, 31-50 DOI: 10.2478/saeb-2018-0001 A Perspective on Industry Classification and Market Reaction to Corporate News: Evidence from India Nayanjyoti

Do Stock Markets Underreact to Spinoff Announcements? The European Evidence

Do Stock Markets Underreact to Spinoff Announcements? The European Evidence Binsheng Qian Cranfield School of Management Cranfield University Cranfield, MK43 0AL United Kingdom binsheng.qian@gmail.com

Do Stock Markets Underreact to Spinoff Announcements? The European Evidence Binsheng Qian Cranfield School of Management Cranfield University Cranfield, MK43 0AL United Kingdom binsheng.qian@gmail.com

Are Bank Loans Special? Evidence on the Post-Announcement Performance of Bank Borrowers

Are Bank Loans Special? Evidence on the Post-Announcement Performance of Bank Borrowers by Matthew T. Billett a Henry B. Tippie College of Business, University of Iowa Mark J. Flannery b Warrington College

Are Bank Loans Special? Evidence on the Post-Announcement Performance of Bank Borrowers by Matthew T. Billett a Henry B. Tippie College of Business, University of Iowa Mark J. Flannery b Warrington College

High Frequency Autocorrelation in the Returns of the SPY and the QQQ. Scott Davis* January 21, Abstract

High Frequency Autocorrelation in the Returns of the SPY and the QQQ Scott Davis* January 21, 2004 Abstract In this paper I test the random walk hypothesis for high frequency stock market returns of two

High Frequency Autocorrelation in the Returns of the SPY and the QQQ Scott Davis* January 21, 2004 Abstract In this paper I test the random walk hypothesis for high frequency stock market returns of two

The relationship between share repurchase announcement and share price behaviour

The relationship between share repurchase announcement and share price behaviour Name: P.G.J. van Erp Submission date: 18/12/2014 Supervisor: B. Melenberg Second reader: F. Castiglionesi Master Thesis

The relationship between share repurchase announcement and share price behaviour Name: P.G.J. van Erp Submission date: 18/12/2014 Supervisor: B. Melenberg Second reader: F. Castiglionesi Master Thesis

IPO IMPACT ON INDUSTRY INCUMBENTS. Nuno Filipe Matamouros Resende Frade Campos, nr. 1016

A Work Project, presented as part of the requirements for the Award of a Masters Degree in Economics / Finance / Management from the Faculdade de Economia da Universidade Nova de Lisboa. IPO IMPACT ON

A Work Project, presented as part of the requirements for the Award of a Masters Degree in Economics / Finance / Management from the Faculdade de Economia da Universidade Nova de Lisboa. IPO IMPACT ON

UNEXPECTED QUARTERLY EARNINGS ANNOUNCEMENTS, FIRM SIZE, AND STOCK PRICE REACTION

Unexpected Quarterly Earnings... UNEXPECTED QUARTERLY EARNINGS ANNOUNCEMENTS, FIRM SIZE, AND STOCK PRICE REACTION Sana Tauseef 1 Abstract This study examines the stock price reaction to the unexpected

Unexpected Quarterly Earnings... UNEXPECTED QUARTERLY EARNINGS ANNOUNCEMENTS, FIRM SIZE, AND STOCK PRICE REACTION Sana Tauseef 1 Abstract This study examines the stock price reaction to the unexpected

Access to Retirement Savings and its Effects on Labor Supply Decisions

Access to Retirement Savings and its Effects on Labor Supply Decisions Yan Lau Reed College May 2015 IZA / RIETI Workshop Motivation My Question: How are labor supply decisions affected by access of Retirement

Access to Retirement Savings and its Effects on Labor Supply Decisions Yan Lau Reed College May 2015 IZA / RIETI Workshop Motivation My Question: How are labor supply decisions affected by access of Retirement

Long Run Stock Returns after Corporate Events Revisited. Hendrik Bessembinder. W.P. Carey School of Business. Arizona State University.

Long Run Stock Returns after Corporate Events Revisited Hendrik Bessembinder W.P. Carey School of Business Arizona State University Feng Zhang David Eccles School of Business University of Utah May 2017

Long Run Stock Returns after Corporate Events Revisited Hendrik Bessembinder W.P. Carey School of Business Arizona State University Feng Zhang David Eccles School of Business University of Utah May 2017

State Ownership at the Oslo Stock Exchange. Bernt Arne Ødegaard

State Ownership at the Oslo Stock Exchange Bernt Arne Ødegaard Introduction We ask whether there is a state rebate on companies listed on the Oslo Stock Exchange, i.e. whether companies where the state

State Ownership at the Oslo Stock Exchange Bernt Arne Ødegaard Introduction We ask whether there is a state rebate on companies listed on the Oslo Stock Exchange, i.e. whether companies where the state

Applied Macro Finance

Master in Money and Finance Goethe University Frankfurt Week 2: Factor models and the cross-section of stock returns Fall 2012/2013 Please note the disclaimer on the last page Announcements Next week (30

Master in Money and Finance Goethe University Frankfurt Week 2: Factor models and the cross-section of stock returns Fall 2012/2013 Please note the disclaimer on the last page Announcements Next week (30

Is There a Friday Effect in Financial Markets?

Economics and Finance Working Paper Series Department of Economics and Finance Working Paper No. 17-04 Guglielmo Maria Caporale and Alex Plastun Is There a Effect in Financial Markets? January 2017 http://www.brunel.ac.uk/economics

Economics and Finance Working Paper Series Department of Economics and Finance Working Paper No. 17-04 Guglielmo Maria Caporale and Alex Plastun Is There a Effect in Financial Markets? January 2017 http://www.brunel.ac.uk/economics

A Note on Event Studies in Finance and Management Research. Ivana Naumovska INSEAD,

Working Paper Series 2015/84/EFE A Note on Event Studies in Finance and Management Research Ivana Naumovska INSEAD, ivana.naumovska@insead.edu Abe de Jong Erasmus University, ajong@rsm.nl This article

Working Paper Series 2015/84/EFE A Note on Event Studies in Finance and Management Research Ivana Naumovska INSEAD, ivana.naumovska@insead.edu Abe de Jong Erasmus University, ajong@rsm.nl This article

The Impact of Leverage on the Delisting Decision of AIM Companies

The Impact of Leverage on the Delisting Decision of AIM Companies Eilnaz Kashefi Pour 1 and Meziane Lasfer Cass Business School, City University, 106 Bunhill Row, London EC1Y 8TZ Abstract We analyse the

The Impact of Leverage on the Delisting Decision of AIM Companies Eilnaz Kashefi Pour 1 and Meziane Lasfer Cass Business School, City University, 106 Bunhill Row, London EC1Y 8TZ Abstract We analyse the

D. Agus Harjito Faculty of Economics, Universitas Islam Indonesia

ISSN : 1410-9018 SINERGI KA JIAN BISNIS DAN MANAJEMEN Vol. 8 No. 1, Januari 2006 Hal. 1-12 THE EFFECT OF MERGER AND ACQUISITION ANNOUNCEMENTS ON STOCK PRICE BEHAVIOUR AND FINANCIAL PERFORMANCE CHANGES:

ISSN : 1410-9018 SINERGI KA JIAN BISNIS DAN MANAJEMEN Vol. 8 No. 1, Januari 2006 Hal. 1-12 THE EFFECT OF MERGER AND ACQUISITION ANNOUNCEMENTS ON STOCK PRICE BEHAVIOUR AND FINANCIAL PERFORMANCE CHANGES:

Bessembinder / Zhang (2013): Firm characteristics and long-run stock returns after corporate events. Discussion by Henrik Moser April 24, 2015

: Firm characteristics and long-run stock returns after corporate events. Discussion by Henrik Moser April 24, 2015") Bessembinder / Zhang (2013): Firm characteristics and long-run stock returns after corporate events Discussion by Henrik Moser April 24, 2015 Motivation of the paper 3 Authors review the connection of

Bessembinder / Zhang (2013): Firm characteristics and long-run stock returns after corporate events Discussion by Henrik Moser April 24, 2015 Motivation of the paper 3 Authors review the connection of

IPO Underpricing and Information Disclosure. Laura Bottazzi (Bologna and IGIER) Marco Da Rin (Tilburg, ECGI, and IGIER)

Marco Da Rin (Tilburg, ECGI, and IGIER)") IPO Underpricing and Information Disclosure Laura Bottazzi (Bologna and IGIER) Marco Da Rin (Tilburg, ECGI, and IGIER) !! Work in Progress!! Motivation IPO underpricing (UP) is a pervasive feature of

IPO Underpricing and Information Disclosure Laura Bottazzi (Bologna and IGIER) Marco Da Rin (Tilburg, ECGI, and IGIER) !! Work in Progress!! Motivation IPO underpricing (UP) is a pervasive feature of

Merger and Acquisitions of IPO firms in Taiwan

Journal of Applied Finance & Banking, vol. 5, no. 3, 2015, 145-157 ISSN: 1792-6580 (print version), 1792-6599 (online) Scienpress Ltd, 2015 Merger and Acquisitions of IPO firms in Taiwan Jean Yu 1 and

Journal of Applied Finance & Banking, vol. 5, no. 3, 2015, 145-157 ISSN: 1792-6580 (print version), 1792-6599 (online) Scienpress Ltd, 2015 Merger and Acquisitions of IPO firms in Taiwan Jean Yu 1 and

CHAPTER 6: CONCLUSION AND RECOMMENDATIONS. market react efficiently to both announcements? Following the objectives, three

CHAPTER 6: CONCLUSION AND RECOMMENDATIONS 6.1 Summary and conclusion The purpose of this research is to find out whether there is any impact of political and national budget announcements on the stock

CHAPTER 6: CONCLUSION AND RECOMMENDATIONS 6.1 Summary and conclusion The purpose of this research is to find out whether there is any impact of political and national budget announcements on the stock

The Effect of Earnings Management and Earnings Persistence on Earnings Response Coefficient: Evidence from Indonesia

The Effect of Earnings Management and Earnings Persistence on Earnings Response Coefficient: Evidence from Indonesia Suwarno Universitas Muhammadiyah Gresik, Indonesia E-mail: suwarno@umg.ac.id Received:

The Effect of Earnings Management and Earnings Persistence on Earnings Response Coefficient: Evidence from Indonesia Suwarno Universitas Muhammadiyah Gresik, Indonesia E-mail: suwarno@umg.ac.id Received:

Keywords: Equity firms, capital structure, debt free firms, debt and stocks.

Working Paper 2009-WP-04 May 2009 Performance of Debt Free Firms Tarek Zaher Abstract: This paper compares the performance of portfolios of debt free firms to comparable portfolios of leveraged firms.

Working Paper 2009-WP-04 May 2009 Performance of Debt Free Firms Tarek Zaher Abstract: This paper compares the performance of portfolios of debt free firms to comparable portfolios of leveraged firms.

Institutional Finance Financial Crises, Risk Management and Liquidity

Institutional Finance Financial Crises, Risk Management and Liquidity Markus K. Brunnermeier Preceptor: Dong Beom Choi Princeton University 1 Overview Efficiency concepts EMH implies Martingale Property

Institutional Finance Financial Crises, Risk Management and Liquidity Markus K. Brunnermeier Preceptor: Dong Beom Choi Princeton University 1 Overview Efficiency concepts EMH implies Martingale Property

An Online Appendix of Technical Trading: A Trend Factor

An Online Appendix of Technical Trading: A Trend Factor In this online appendix, we provide a comparative static analysis of the theoretical model as well as further robustness checks on the trend factor.

An Online Appendix of Technical Trading: A Trend Factor In this online appendix, we provide a comparative static analysis of the theoretical model as well as further robustness checks on the trend factor.

Day of the Week Effect of Stock Returns: Empirical Evidence from Bombay Stock Exchange

International Journal of Research in Social Sciences Vol. 8 Issue 4, April 2018, ISSN: 2249-2496 Impact Factor: 7.081 Journal Homepage: Double-Blind Peer Reviewed Refereed Open Access International Journal

International Journal of Research in Social Sciences Vol. 8 Issue 4, April 2018, ISSN: 2249-2496 Impact Factor: 7.081 Journal Homepage: Double-Blind Peer Reviewed Refereed Open Access International Journal

A Study on the Short-Term Market Effect of China A-share Private Placement and Medium and Small Investors Decision-Making Shuangjun Li

A Study on the Short-Term Market Effect of China A-share Private Placement and Medium and Small Investors Decision-Making Shuangjun Li Department of Finance, Beijing Jiaotong University No.3 Shangyuancun

A Study on the Short-Term Market Effect of China A-share Private Placement and Medium and Small Investors Decision-Making Shuangjun Li Department of Finance, Beijing Jiaotong University No.3 Shangyuancun

Early evidence on the efficient market hypothesis was quite favorable to it. In recent

Appendix to chapter 7 Evidence on the Efficient Market Hypothesis Early evidence on the efficient market hypothesis was quite favorable to it. In recent years, however, deeper analysis of the evidence

Appendix to chapter 7 Evidence on the Efficient Market Hypothesis Early evidence on the efficient market hypothesis was quite favorable to it. In recent years, however, deeper analysis of the evidence

Errors in Estimating Unexpected Accruals in the Presence of Large Net External Financing THINK.CHANGE.DO

Errors in Estimating Unexpected Accruals in the Presence of Large Net External Financing THINK.CHANGE.DO Yaowen Shan Stephen Taylor Terry Walter University of Technology, Sydney UEXAC = β PART + ε Motivations

Errors in Estimating Unexpected Accruals in the Presence of Large Net External Financing THINK.CHANGE.DO Yaowen Shan Stephen Taylor Terry Walter University of Technology, Sydney UEXAC = β PART + ε Motivations

Discussion Paper No. DP 07/02

SCHOOL OF ACCOUNTING, FINANCE AND MANAGEMENT Essex Finance Centre Can the Cross-Section Variation in Expected Stock Returns Explain Momentum George Bulkley University of Exeter Vivekanand Nawosah University

SCHOOL OF ACCOUNTING, FINANCE AND MANAGEMENT Essex Finance Centre Can the Cross-Section Variation in Expected Stock Returns Explain Momentum George Bulkley University of Exeter Vivekanand Nawosah University