M.Sc. in Economic Policy Studies

|

|

|

- Camron Simmons

- 5 years ago

- Views:

Transcription

1 M.Sc. in Economic Policy Studies John FitzGerald, room 3012, 02/10/2015 1

2 Outline of lectures 3: October 16 th Money and the macro-economy Demand for money The demand for money The quantity theory of money Money supply Factors affecting supply Velocity Policy on money demand and supply Targeting money growth The Lucas critique 02/10/2015 2

3 The Demand for Money Transactions demand for money to pay for goods and services If money expensive (opportunity cost, interest rate) use less Affected by technology Example Hold money in bonds and transfer to current account only daily need. This would reduce holdings of money. Precautionary demand a rainy day fund Portfolio demand for money Depends on wealth, expected interest rates on alternative assets, perceived riskiness of alternative assets. (Effects of bank risk). Example: if expect interest rates on bonds to rise then their value will fall in the future. Don t invest and hold cash to avoid a capital loss. Thus the return on a range of assets will affect demand for money 02/10/2015 3

4 Money and the Macro-Economy Money, growth and inflation They are closely related There are no cases of: High money growth and low inflation Low money growth and high inflation When inflation moves from 1% a year to 2% a year does this change behaviour? Buy now before the price increase? Announced increases in VAT and excise However, if inflation moves from 2% a year to 2% a week may change behaviour Use your money before it loses its value wheelbarrows! Inflation and money supply are related: 02/10/2015 4

5 Money and Inflation ECB targets inflation Also concerned with growth in money supply Fed rarely talks about money supply, though it is concerned, inter alia, with inflation. Why the difference? Money different definitions M1 currency M2 currency + current accounts M3 currency + current and deposit accounts Table A3 02/10/2015 5

6 Money Supply - Ireland M1 M2 M3 02/10/2015 6

7 Costs of inflation Changes in rate of inflation costly Contracts are written based on an expected inflation rate e.g. upward only rent reviews Tax distortions capital gains not treated same as income Tax on savings when it rises What is the optimal rate of inflation? Hyperinflation Print money to finance government rather than taxing Using the seignorage More money higher inflation People expect inflation to rise try and game it by raising prices Higher inflation to buy same services need to print even more money To end hyperinflation need to stop printing money and fund services by taxes /10/2015 7

8 Money and consumer prices, Ireland 24 % change, moving average of 4 years M2 Inflation 02/10/2015 8

9 % Money and consumer prices, Iceland 100 Chart Title CPI M3 02/10/2015 9

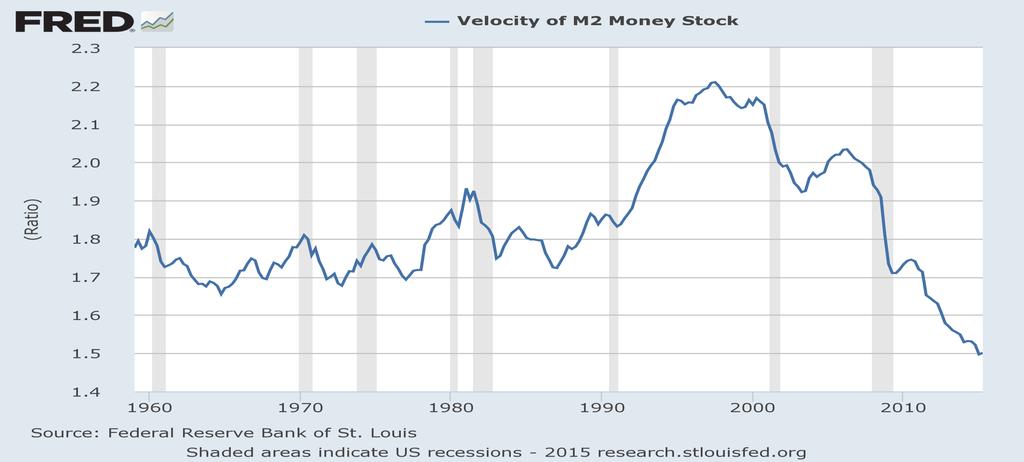

10 The Quantity Theory of Money Money in circulation is controlled by the Central Bank However, money is used in many transactions. Every transaction in the economy (GDP) is paid for with money GDP at current prices (PY) = Quantity of money (M) X Velocity (V) P is the price level and Y is the volume of output PY=MV Money growth + velocity growth = inflation + growth in output Irving Fisher early in 20 th c. assumed: V is constant and money does not change Y Therefore the growth in money supply = inflation 02/10/

11 Measures of velocity in Ireland Velocity-M1 Velocity-M2 Velocity-M3 02/10/

12

13 The Quantity Theory of Money With moderate inflation growth in money exceeds inflation Because output is growing. If velocity is constant then growth in money = growth in value of output However: Central Bank controls M1, currency. Relation to M2 may vary Velocity may change. e.g. will rise if expect inflation to rise. V=PY/M=GDP/M Some stability with M3, not with M1 Why? Implications for post-1992 world? 02/10/

14 Papers modelling Irish demand for money First paper finds M3 best measure however, no good relationship Second paper found a stable relationship for M3, explained by sales, inflation, and an interest rate measure. The justification for including inflation is that when it is high you will hold less cash and have a higher velocity because money is losing its value faster. However, even this model did not prove stable over the coming decades Problem for ECB there is not a stable (predictable) demand for money function for the Euro area. To target inflation need a more sophisticated approach Instead of using the actual supply of money to target its inflation objective use interest rates to indirectly influence the factors driving inflation 02/10/

15 Supply of Money Central Bank prints money cash Issue cash (M1) in return for assets Central bank changes money supply (M1) by open market operations Buy short-term debt raise price of debt reduces interest rates. Results in higher cash in hands of public. Sell short-term debt to increase interest rates and take money out of economy However, cash is small relative to other forms of money - 02/10/

16 Interest rate, i The Liquidity Trap M d M s 1 M s 2 M s 3 Money, M 02/10/

17 ECB s Strategy Based on Bundesbank s Initially targeted money supply and inflation rate Targeting money supply e.g. Assume: Real GDP growth of 2%. Price inflation of 2%. Therefore PY=4% MV=PY with PY growing by 4% then MV needs to grow by 4% Assume V falling by 0.5% - money, M, needs to grow by 4.5% Before crisis a more stable demand for money However, targeting money supply unsatisfactory because V unstable Also the deflator for GDP is not the same as inflation for consumers 02/10/

18 Implications for monetary policy ECB should target inflation in medium term. Short term not possible because noise in data and long lag in effects of policy How can the ECB implement its inflation objective An unstable demand for money Using market interventions (short-term interest rates) Because short interest rates are zero use long interest rates quantitative easing Why does the ECB have problems raising inflation today? What has happened to velocity and why? 02/10/

19 Implications for monetary policy Technological change How have ATMs affected holdings of cash? Money in transit changes in system affects cash in clearing The effects of the crisis on household and firm behaviour Rush to liquidity changing portfolio choice Option value of cash increased Change in opportunity cost of holding cash With zero interest rate just give the money back to the ECB unable to change supply Negative interest rate to force the economy to absorb the cash 02/10/

20 Model of money demand and supply M d = M3 ( including deposit and current accounts) M = money supply CU d = demand for currency by the public D d = demand for deposit accounts i = interest rate Y = real GDP P = price of GDP R = bank reserves H d = demand for central bank money H = supply of central bank money 02/10/

21 Model of money demand and supply Money demand M d = f(yp, i) (1) Money supply = money demand M = f(yp, i) (2) Demand for currency and deposit accounts is a fixed % of money demand, c CU d = cm d (3) D d = (1-c)M d (4) Banks have to hold a share of deposits, θ, as reserves R = θd d (5) R = θ(1-c)m d (6) 02/10/

22 Model of money demand and supply Demand for central bank money by the public and banks: H d = CU d + R (7) Substitute using equations 2, 3, 6 H d = [c+ θ(1-c)] f(yp, i) (8) Supply of central bank money = demand for it H = H d = [c+ θ(1-c)] f(yp, i) (9) Rearrange equation 9 so that the supply of money equals the demand 1 H = f(yp, i) (10) [c+θ 1 c ] 1 >1 this constant is referred to as the money multiplier [c+θ 1 c ] Central bank money has a larger effect when there are banks 02/10/

23 Money demand and supply Example of the money multiplier Central bank buys a bond for 100 increases H by 100 Seller of bond deposits cash in a bank deposits D rise by 100 Bank needs to retain θ, say 10%, of the cash against the deposit The bank buys bonds for 90. The seller deposits it in the bank Bank needs to retain θ, say 10%, of the cash ( 9) against the deposit The bank buys bonds for 81. The seller deposits it in the bank Etc. etc. Eventual change in M= 100( )= (1.9) = /10/

24 Money demand and supply What can change is outside control of Central Bank? f(yp, i) the demand for money (e.g. a rush to liquidity) c share of currency in money demand (e.g. a bank run could change it) Monetary policy is implemented through changes in H, Cash Through open market operations buying and selling assets in return for cash H Effects of monetary policy affected by θ? This may be regulated or could be chosen by banks to maximise expected profits In crisis θ changed as banks wanted to hold more cash and did not trust each other. Central Banks could have imposed a minimum θ but not a maximum Changed effects of Central Bank open market operations 02/10/

25 Demand and Supply of Money i S D 1 D 2 M 02/10/

26 Implications for monetary policy The demand for money and the supply of money determine the short term interest rate the price of money Given the demand for money the ECB can control EITHER the supply of money or the price (interest rate) but not both If there is an unstable demand for money Targeting a particular supply of money may have unpredictable consequences If D1 represents true demand for money changes in supply may have unpredictable consequences, reflected in uncertain interest rates If D2 then more predictable more stable interest rates if choose the supply Interest rate stability (predictability) can insulate real economy from financial shocks 02/10/

27 Implementing Monetary Policy Need research to tell you what drives the demand for money Need to understand is this model stable Shocks to the system may cause a change in behaviour Need to understand what determines supply Not determined directly by the Central Bank Changes in supply behaviour may restrict scope for Central Bank action Need model a demand curve and a supply curve to know how interest rates are determined OR how interest rates may affect demand for money Ultimately need to know how monetary policy affects the real economy, including the rate of inflation The next lecture 02/10/

28 The Lucas Critique Models used for monetary policy making are based on historical data Can we learn from history? Will history repeat itself? Changes in policy may change people s behaviour Also, the public can read the models too. Economic and financial decisions are based on expectations about the future Policy may change expectations and, hence, behaviour. Can make models invalid Models, to be robust, must take account of this learning behaviour Very important in financial sector because behaviour is based on expectations Argues for predictable policy making 02/10/

29 Rational expectations Lucas critique assumes rational expectations The formation of expectations based on rational forecasts Makes for more complex models People s behaviour today depends, not only on a range of variables today, but also on the forecasts of those variables for the future Have to solve models, not just for today, but well into the future in order to predict what people will do today. 02/10/

30 Rational expectations - examples Rational expectations results in sudden jumps with new information Draghi announced quantitative easing in December 2015 Everyone new that in buying bonds over two years many of them would come from foreigners. This would reduce the value of the. The did not change gradually as the bonds were bought. Instead the jumped to a new equilibrium value and has stayed there. Investment and interest rates Investors decide based on expected future profits. Interest rates are crucial in the decision to invest. However, if there is an economy-wide boom in investment the demand for money will rise and there may be inflationary pressures. In turn this may cause interest rates to rise. Could result in a decision not to invest because of expectations of monetary policy consequences of the investment boom. 02/10/

31 Quantitative Easing Liquidity trap Central Bank traditional open market operations: buy short term securities change short-term interest rate Short-term interest fell to zero Banks don t want central bank money lodge it back with ECB Banks cannot make profitable use of Central Bank money. 02/10/

32 Interest rate, i The Liquidity Trap M d M s 1 M s 2 M s 3 Money, M 02/10/

33 Quantitative Easing Liquidity trap Central Bank traditional open market operations: buy short term securities change short-term interest rate Short-term interest fell to zero Banks don t want central bank money lodge it back with ECB Banks cannot make profitable use of Central Bank money. Quantitative easing Buy other assets government bonds Reduces long-term interest rates Hope that sellers of long bonds buy other assets equities or invest. Reduces cost of capital for those who are not over-leveraged 02/10/

34 Quantitative Easing Buying bonds on the market don t care about sellers However, foreign holders of Euro government bonds face a choice The interest rate on Euro area assets has fallen relative to foreign assets sell? ECB buying assets held by foreigners will raise value of foreign currency Fall in value of Euro will make Euro assets less attractive sell? Affects exchange rate Rational expectations: When QE announced foreign holders of Euro bonds knew it would weaken They try to bail out en masse, triggering big change in exchange rate Change in exchange rate makes imports into Euro area more expensive Raises rate of inflation directly 02/10/

35 Policy making under uncertainty Central Banks are not infallible How long does it take for monetary policy to work? The longer it takes the more reliance on theory and models Models are not perfect and people can change behaviour Are the risks higher as a result of an undershoot in the inflation rate or an overshoot in the inflation rate? Plot a stable path or adjust in the face of new information? 02/10/

36 Questions Why does an independent central bank reduce occurrences of extremely high inflation, especially in developing economies? Why was there a fall in velocity during the recent crisis? Look at papers on demand for money in Ireland 02/10/

37 References Cecchetti and Schoenholtz, Money, Banking, and Financial Markets, Chapter 20 Blanchard, Amighini and Giavazzi, Macro-Economics a European Perspective, Chapter 4. Demand for Money QE Somalia and Zimbabwe /10/

Chapter Twenty. In This Chapter 4/29/2018. Chapter 22 Quantity Theory, Inflation and the Demand for Money

Chapter Twenty Chapter 22 Quantity Theory, Inflation and the Demand for Money In This Chapter 1. The quantity theory of money. 2. The velocity of, and demand for, money. 3. Money targeting. Money Growth

Chapter Twenty Chapter 22 Quantity Theory, Inflation and the Demand for Money In This Chapter 1. The quantity theory of money. 2. The velocity of, and demand for, money. 3. Money targeting. Money Growth

Chapter Twenty 11/26/2017. Chapter 20 Money Growth, Money Demand, and Modern Monetary Policy. In This Chapter. 1. The quantity theory of money.

Chapter Twenty Chapter 20 Money Growth, Money Demand, and Modern Monetary Policy In This Chapter 1. The quantity theory of money. 2. The velocity of, and demand for, money. 3. Money targeting. Money Growth

Chapter Twenty Chapter 20 Money Growth, Money Demand, and Modern Monetary Policy In This Chapter 1. The quantity theory of money. 2. The velocity of, and demand for, money. 3. Money targeting. Money Growth

WJEC (Wales) Economics A-level

Economics A-level") WJEC (Wales) Economics A-level Macroeconomics Topic 2: Macroeconomic Objectives 2.3 Inflation and deflation Notes Inflation is the sustained rise in the general price level over time. This means that the

WJEC (Wales) Economics A-level Macroeconomics Topic 2: Macroeconomic Objectives 2.3 Inflation and deflation Notes Inflation is the sustained rise in the general price level over time. This means that the

M.Sc. in Economic Policy Studies

M.Sc. in Economic Policy Studies John FitzGerald, room 3012, jofitzge@tcd.ie 30/10/2015 1 Outline of lectures 5: October 30 th Exchange rates monetary policy and the real economy Exchange rates What drives

M.Sc. in Economic Policy Studies John FitzGerald, room 3012, jofitzge@tcd.ie 30/10/2015 1 Outline of lectures 5: October 30 th Exchange rates monetary policy and the real economy Exchange rates What drives

DEMAND FOR MONEY. Ch. 9 (Ch.19 in the text) ECON248: Money and Banking Ch.9 Dr. Mohammed Alwosabi

ECON248: Money and Banking Ch.9 Dr. Mohammed Alwosabi") Ch. 9 (Ch.19 in the text) DEMAND FOR MONEY Individuals allocate their wealth between different kinds of assets such as a building, income earning securities, a checking account, and cash. Money is what

Ch. 9 (Ch.19 in the text) DEMAND FOR MONEY Individuals allocate their wealth between different kinds of assets such as a building, income earning securities, a checking account, and cash. Money is what

Chapter 19. Quantity Theory, Inflation and the Demand for Money

Chapter 19 Quantity Theory, Inflation and the Demand for Money Quantity Theory of Money Velocity of Money and The Equation of Exchange M = the money supply P = price level Y = aggregate output (income)

Chapter 19 Quantity Theory, Inflation and the Demand for Money Quantity Theory of Money Velocity of Money and The Equation of Exchange M = the money supply P = price level Y = aggregate output (income)

TOPIC 1: IS-LM MODEL...3 TOPIC 2: LABOUR MARKET...23 TOPIC 3: THE AD-AS MODEL...33 TOPIC 4: INFLATION AND UNEMPLOYMENT...41 TOPIC 5: MONETARY POLICY

TOPIC 1: IS-LM MODEL...3 TOPIC 2: LABOUR MARKET...23 TOPIC 3: THE AD-AS MODEL...33 TOPIC 4: INFLATION AND UNEMPLOYMENT...41 TOPIC 5: MONETARY POLICY AND THE RESERVE BANK OF AUSTRALIA...53 TOPIC 6: THE

TOPIC 1: IS-LM MODEL...3 TOPIC 2: LABOUR MARKET...23 TOPIC 3: THE AD-AS MODEL...33 TOPIC 4: INFLATION AND UNEMPLOYMENT...41 TOPIC 5: MONETARY POLICY AND THE RESERVE BANK OF AUSTRALIA...53 TOPIC 6: THE

CIE Economics A-level

CIE Economics A-level Topic 4: The Macroeconomy f) Money supply (theory) Notes Quantity theory of money (MV = PT) The Quantity Theory of Money states that there is inflation if the money supply increases

CIE Economics A-level Topic 4: The Macroeconomy f) Money supply (theory) Notes Quantity theory of money (MV = PT) The Quantity Theory of Money states that there is inflation if the money supply increases

THE FEDERAL RESERVE AND MONETARY POLICY Macroeconomics in Context (Goodwin, et al.)

") Chapter 12 THE FEDERAL RESERVE AND MONETARY POLICY Macroeconomics in Context (Goodwin, et al.) Chapter Overview In this chapter, you will be introduced to a standard treatment of central banking and monetary

Chapter 12 THE FEDERAL RESERVE AND MONETARY POLICY Macroeconomics in Context (Goodwin, et al.) Chapter Overview In this chapter, you will be introduced to a standard treatment of central banking and monetary

International Money and Banking: 6. Problems with Monetarism

International Money and Banking: 6. Problems with Monetarism Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) Money and Inflation Spring 2018 1 / 30 The Basic Elements of Monetarism Last

International Money and Banking: 6. Problems with Monetarism Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) Money and Inflation Spring 2018 1 / 30 The Basic Elements of Monetarism Last

Essex EC248-2-SP Lecture 5. The Demand for Money and Monetary Theory. Alexander Mihailov, 13/02/06

Essex EC248-2-SP Lecture 5 The Demand for Money and Monetary Theory Alexander Mihailov, 13/02/06 Plan of Talk Introduction 1. Theories on the Demand for Money 2. Money in IS-LM and AD-AS Analysis 3. Money

Essex EC248-2-SP Lecture 5 The Demand for Money and Monetary Theory Alexander Mihailov, 13/02/06 Plan of Talk Introduction 1. Theories on the Demand for Money 2. Money in IS-LM and AD-AS Analysis 3. Money

Plan of Talk. Quantity Theory of Money. Aims and Learning Outcomes. P Y Velocity V (definition) M Equation of Exchange M V P Y (identity)

M Equation of Exchange M V P Y (identity)") Essex EC248-2-SP Lecture 5 The Demand for Money and Monetary Theory Alexander Mihailov, 13/02/06 Plan of Talk Introduction 1. Theories on the Demand for Money 2. Money in IS-LM and AD-AS Analysis 3. Money

Essex EC248-2-SP Lecture 5 The Demand for Money and Monetary Theory Alexander Mihailov, 13/02/06 Plan of Talk Introduction 1. Theories on the Demand for Money 2. Money in IS-LM and AD-AS Analysis 3. Money

TOPIC 5. Fed Policy and Money Markets

TOPIC 5 Fed Policy and Money Markets 1 2 Outline What is Money? What does affect the supply of Money? How the banking system works? What is the Fed and how does it work? What is a monetary policy? What

TOPIC 5 Fed Policy and Money Markets 1 2 Outline What is Money? What does affect the supply of Money? How the banking system works? What is the Fed and how does it work? What is a monetary policy? What

Leandro Conte UniSi, Department of Economics and Statistics. Money, Macroeconomic Theory and Historical evidence. SSF_ aa

Leandro Conte UniSi, Department of Economics and Statistics Money, Macroeconomic Theory and Historical evidence SSF_ aa.2017-18 Learning Objectives ASSESS AND INTERPRET THE EMPIRICAL EVIDENCE ON THE VALIDITY

Leandro Conte UniSi, Department of Economics and Statistics Money, Macroeconomic Theory and Historical evidence SSF_ aa.2017-18 Learning Objectives ASSESS AND INTERPRET THE EMPIRICAL EVIDENCE ON THE VALIDITY

Notes VI - Models of Economic Fluctuations

Notes VI - Models of Economic Fluctuations Julio Garín Intermediate Macroeconomics Fall 2017 Intermediate Macroeconomics Notes VI - Models of Economic Fluctuations Fall 2017 1 / 33 Business Cycles We can

Notes VI - Models of Economic Fluctuations Julio Garín Intermediate Macroeconomics Fall 2017 Intermediate Macroeconomics Notes VI - Models of Economic Fluctuations Fall 2017 1 / 33 Business Cycles We can

2. Why is it important for the Fed to know the size and the rate of growth of the money supply?

KOFA HIGH SCHOOL SOCIAL SCIENCES DEPARTMENT AP ECONOMICS EXAM PREP WORKSHOP # 4 > MONEY, MONETARY POLICY, AND ECONOMIC STABILITY NAME : DATE : All About The Ms : 1. What are the three basic functions of

KOFA HIGH SCHOOL SOCIAL SCIENCES DEPARTMENT AP ECONOMICS EXAM PREP WORKSHOP # 4 > MONEY, MONETARY POLICY, AND ECONOMIC STABILITY NAME : DATE : All About The Ms : 1. What are the three basic functions of

Answers to Problem Set #8

Macroeconomic Theory Spring 2013 Chapter 15 Answers to Problem Set #8 1. The five equations that make up the dynamic aggregate demand aggregate supply model can be manipulated to derive long-run values

Macroeconomic Theory Spring 2013 Chapter 15 Answers to Problem Set #8 1. The five equations that make up the dynamic aggregate demand aggregate supply model can be manipulated to derive long-run values

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Econ 330 Spring 2015: EXAM 1 Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) If during the past decade the average rate

Econ 330 Spring 2015: EXAM 1 Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) If during the past decade the average rate

BUSI 101 Capital Markets and Real Estate

BUSI 101 Capital Markets and Real Estate PURPOSE AND SCOPE The Capital Markets and Real Estate course (BUSI 101) is intended to acquaint the student with the basic principles of macroeconomics and to give

BUSI 101 Capital Markets and Real Estate PURPOSE AND SCOPE The Capital Markets and Real Estate course (BUSI 101) is intended to acquaint the student with the basic principles of macroeconomics and to give

Exam Number. Section

Exam Number Section MACROECONOMICS IN THE GLOBAL ECONOMY Core Course Professor Antonio Fatás Final Exam February 24, 2011 9:00-12:00 Instructions: (PLEASE READ) SUGGESTED ANSWERS Space to answer the questions

Exam Number Section MACROECONOMICS IN THE GLOBAL ECONOMY Core Course Professor Antonio Fatás Final Exam February 24, 2011 9:00-12:00 Instructions: (PLEASE READ) SUGGESTED ANSWERS Space to answer the questions

Boğaziçi University, Department of Economics Spring 2016 EC 102 PRINCIPLES of MACROECONOMICS FINAL , Saturday 10:00 TYPE A

NAME: NO: SECTION: Boğaziçi University, Department of Economics Spring 2016 EC 102 PRINCIPLES of MACROECONOMICS FINAL 21.05.2016, Saturday 10:00 TYPE A Turn off your cell phone and put it away. During

NAME: NO: SECTION: Boğaziçi University, Department of Economics Spring 2016 EC 102 PRINCIPLES of MACROECONOMICS FINAL 21.05.2016, Saturday 10:00 TYPE A Turn off your cell phone and put it away. During

MACROECONOMICS. N. Gregory Mankiw. Money and Inflation 8/15/2011. In this chapter, you will learn: The connection between money and prices

% change from 12 mos. earlier % change from 12 mos. earlier 2 0 1 0 U P D A T E S E V E N T H E D I T I O N 8/15/2011 MACROECONOMICS N. Gregory Mankiw PowerPoint Slides by Ron Cronovich C H A P T E R 4

% change from 12 mos. earlier % change from 12 mos. earlier 2 0 1 0 U P D A T E S E V E N T H E D I T I O N 8/15/2011 MACROECONOMICS N. Gregory Mankiw PowerPoint Slides by Ron Cronovich C H A P T E R 4

Principles of Macroeconomics

Principles of Macroeconomics Focus on three key variables (for clarity, other variables implied): 1. Gross Domestic Product (Y) = aggregate real output (GDP). Link to employment: production creates jobs.

Principles of Macroeconomics Focus on three key variables (for clarity, other variables implied): 1. Gross Domestic Product (Y) = aggregate real output (GDP). Link to employment: production creates jobs.

1) List the 3 functions of money: 4) The Federal Reserve is the bank of the USA. It is considered from the Government and has 2 primary goals:

List the 3 functions of money: 4) The Federal Reserve is the bank of the USA. It is considered from the Government and has 2 primary goals:") AP ECONOMICS---Ippolito 2017 Study Guide for Monetary Policy (unit #4) Name: Due Friday December 8 th Multiple Choice Test (25 questions, 100 pts) 1) List the 3 functions of money: 2) What is liquidity?

AP ECONOMICS---Ippolito 2017 Study Guide for Monetary Policy (unit #4) Name: Due Friday December 8 th Multiple Choice Test (25 questions, 100 pts) 1) List the 3 functions of money: 2) What is liquidity?

Elements of Macroeconomics: Homework #6. Due 11/27or 11/28 in assigned Section

Elements of Macroeconomics: Homework #6 Due 11/27or 11/28 in assigned Section Name: Section: Section I Based on the information given below, answer the following questions Brazil s real GDP = 6 trillion

Elements of Macroeconomics: Homework #6 Due 11/27or 11/28 in assigned Section Name: Section: Section I Based on the information given below, answer the following questions Brazil s real GDP = 6 trillion

III. 9. IS LM: the basic framework to understand macro policy continued Text, ch 11

Objectives: To apply IS-LM analysis to understand the causes of short-run fluctuations in real GDP and the short-run impact of monetary and fiscal policies on the economy. To use the IS-LM model to analyse

Objectives: To apply IS-LM analysis to understand the causes of short-run fluctuations in real GDP and the short-run impact of monetary and fiscal policies on the economy. To use the IS-LM model to analyse

Quantitative Easing and the implications for Actuaries & Economics Discussion

Quantitative Easing and the implications for Actuaries & Economics Discussion Colm Fitzgerald Dublin City University / Paragon Research Ltd Society of Actuaries in Ireland May 17 th 2011 Introduction Context

Quantitative Easing and the implications for Actuaries & Economics Discussion Colm Fitzgerald Dublin City University / Paragon Research Ltd Society of Actuaries in Ireland May 17 th 2011 Introduction Context

Lastrapes Fall y t = ỹ + a 1 (p t p t ) y t = d 0 + d 1 (m t p t ).

y t = d 0 + d 1 (m t p t ).") ECON 8040 Final exam Lastrapes Fall 2007 Answer all eight questions on this exam. 1. Write out a static model of the macroeconomy that is capable of predicting that money is non-neutral. Your model should

ECON 8040 Final exam Lastrapes Fall 2007 Answer all eight questions on this exam. 1. Write out a static model of the macroeconomy that is capable of predicting that money is non-neutral. Your model should

2010 Pearson Addison Wesley CHAPTER 1

CHAPTER 1 Money has taken many forms. What is money today? What happens when the bank lends the money we re deposited to someone else? How does the Fed influence the quantity of money? What happens when

CHAPTER 1 Money has taken many forms. What is money today? What happens when the bank lends the money we re deposited to someone else? How does the Fed influence the quantity of money? What happens when

ECON 3560/5040 Week 5

ECON 3560/5040 Week 5 1. What is Money? MONEY AND INFLATION - Definition: the stock of assets that can be readily used to make transaction - The functions of money Store of value: a way to transfer purchasing

ECON 3560/5040 Week 5 1. What is Money? MONEY AND INFLATION - Definition: the stock of assets that can be readily used to make transaction - The functions of money Store of value: a way to transfer purchasing

Money, Banking and the Federal Reserve

Money, Banking and the Federal Reserve What Is Money? Money is any asset that can easily be used to purchase goods and services. Fiat money : Money, such as paper currency, that is authorized by a central

Money, Banking and the Federal Reserve What Is Money? Money is any asset that can easily be used to purchase goods and services. Fiat money : Money, such as paper currency, that is authorized by a central

LECTURE 18. AS/AD in demand-deficient Ireland: Unemployment and Deflation

LECTURE 18 AS/AD in demand-deficient Ireland: Unemployment and Deflation THE AGGREGATE SUPPLY CURVE Aggregate supply curve Each possible price level Quantity of goods & services All nation s businesses

LECTURE 18 AS/AD in demand-deficient Ireland: Unemployment and Deflation THE AGGREGATE SUPPLY CURVE Aggregate supply curve Each possible price level Quantity of goods & services All nation s businesses

13.2 Monetary Policy Rules and Aggregate Demand Introduction 6/24/2014. Stabilization Policy and the AS/AD Framework.

Chapter 13 Stabilization Policy and the / Framework By Charles I. Jones 13.2 Monetary Policy Rules and Aggregate Demand The short-run model consists of three basic equations: Media Slides Created By Dave

Chapter 13 Stabilization Policy and the / Framework By Charles I. Jones 13.2 Monetary Policy Rules and Aggregate Demand The short-run model consists of three basic equations: Media Slides Created By Dave

Principles of Macroeconomics December 15th, 2005 name: Final Exam (100 points)

") EC132.01 Serge Kasyanenko Principles of Macroeconomics December 15th, 2005 name: Final Exam (100 points) This is a closed-book exam - you may not use your notes and textbooks. Calculators are not allowed.

EC132.01 Serge Kasyanenko Principles of Macroeconomics December 15th, 2005 name: Final Exam (100 points) This is a closed-book exam - you may not use your notes and textbooks. Calculators are not allowed.

Problem Set #4 Revised: April 13, 2007

Global Economy Chris Edmond Problem Set #4 Revised: April 13, 2007 Before attempting this problem set, you might like to read over the lecture notes on Business Cycle Indicators, on Money and Inflation,

Global Economy Chris Edmond Problem Set #4 Revised: April 13, 2007 Before attempting this problem set, you might like to read over the lecture notes on Business Cycle Indicators, on Money and Inflation,

Macroeconomic Stabilization

1 Macroeconomic Stabilization A. Inflation and Exchange Rates 1. Inflation Deterioration in the value of the domestic currency. Affects the buying power of domestic goods. 2. Exchange Rate Deterioration/enhancement

1 Macroeconomic Stabilization A. Inflation and Exchange Rates 1. Inflation Deterioration in the value of the domestic currency. Affects the buying power of domestic goods. 2. Exchange Rate Deterioration/enhancement

Lecture 6. Expectations, Output, and Policy. Randall Romero Aguilar, PhD I Semestre 2017 Last updated: April 20, 2017

Lecture 6 Expectations, Output, and Policy Randall Romero Aguilar, PhD I Semestre 2017 Last updated: April 20, 2017 Universidad de Costa Rica EC3201 - Teoría Macroeconómica 2 Table of contents 1. Introduction

Lecture 6 Expectations, Output, and Policy Randall Romero Aguilar, PhD I Semestre 2017 Last updated: April 20, 2017 Universidad de Costa Rica EC3201 - Teoría Macroeconómica 2 Table of contents 1. Introduction

Disputes In Macroeconomics

No G G & T 3-5% Monetary Rule Expectations negate fiscal and monetary Policy. Adam Smith John M. Keynes Milton Friedman Classicals Keynesians Monetarists Robert Lucas Get the G off of our backs. Ronald

No G G & T 3-5% Monetary Rule Expectations negate fiscal and monetary Policy. Adam Smith John M. Keynes Milton Friedman Classicals Keynesians Monetarists Robert Lucas Get the G off of our backs. Ronald

Intermediate Macroeconomic Theory / Macroeconomic Analysis (ECON 3560/5040) Midterm Exam (Answers)

Midterm Exam (Answers)") Intermediate Macroeconomic Theory / Macroeconomic Analysis (ECON 3560/5040) Midterm Exam (Answers) Part A (15 points) State whether you think each of the following questions is true (T), false (F), or

Intermediate Macroeconomic Theory / Macroeconomic Analysis (ECON 3560/5040) Midterm Exam (Answers) Part A (15 points) State whether you think each of the following questions is true (T), false (F), or

Lecture 12: Economic Fluctuations. Rob Godby University of Wyoming

Lecture 12: Economic Fluctuations Rob Godby University of Wyoming Short-Run Economic Fluctuations Economic activity fluctuates from year to year. In some years, the production of goods and services rises.

Lecture 12: Economic Fluctuations Rob Godby University of Wyoming Short-Run Economic Fluctuations Economic activity fluctuates from year to year. In some years, the production of goods and services rises.

The Demand for Money. Lecture Notes for Chapter 7 of Macroeconomics: An Introduction. In this chapter we will discuss -

Lecture Notes for Chapter 7 of Macroeconomics: An Introduction The Demand for Money Copyright 1999-2008 by Charles R. Nelson 2/19/08 In this chapter we will discuss - What does demand for money mean? Why

Lecture Notes for Chapter 7 of Macroeconomics: An Introduction The Demand for Money Copyright 1999-2008 by Charles R. Nelson 2/19/08 In this chapter we will discuss - What does demand for money mean? Why

Midsummer Examinations 2011

Midsummer Examinations 2011 No. of Pages: 7 No. of Questions: 37 Subject ECONOMICS Title of Paper MACROECONOMICS Time Allowed Two Hours (2 Hours) Instructions to candidates This paper is in two sections.

Midsummer Examinations 2011 No. of Pages: 7 No. of Questions: 37 Subject ECONOMICS Title of Paper MACROECONOMICS Time Allowed Two Hours (2 Hours) Instructions to candidates This paper is in two sections.

LIMIT INFLATION Country and Time- Zimbabwe, 2008 Annual Inflation Rate- 79,600,000,000% Time for Prices to Double hours

Inflation 1 Copyright LIMIT INFLATION Country and Time- Zimbabwe, 2008 Annual Inflation Rate- 79,600,000,000% Time for Prices to Double- 24.7 hours What is Inflation? Inflation is rising general level

Inflation 1 Copyright LIMIT INFLATION Country and Time- Zimbabwe, 2008 Annual Inflation Rate- 79,600,000,000% Time for Prices to Double- 24.7 hours What is Inflation? Inflation is rising general level

: Monetary Economics and the European Union. Lecture 8. Instructor: Prof Robert Hill. The Costs and Benefits of Monetary Union II

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

ECON 3010 Intermediate Macroeconomics. Chapter 5 Inflation: Its Causes, Effects, and Social Costs

ECON 3010 Intermediate Macroeconomics Chapter 5 Inflation: Its Causes, Effects, and Social Costs U.S. inflation 1960 2012 12% % change from 12 mos. earlier 10% 8% 6% 4% 2% % change in GDP deflator 0% 1960

ECON 3010 Intermediate Macroeconomics Chapter 5 Inflation: Its Causes, Effects, and Social Costs U.S. inflation 1960 2012 12% % change from 12 mos. earlier 10% 8% 6% 4% 2% % change in GDP deflator 0% 1960

Lecture notes 10. Monetary policy: nominal anchor for the system

Kevin Clinton Winter 2005 Lecture notes 10 Monetary policy: nominal anchor for the system 1. Monetary stability objective Monetary policy was a 20 th century invention Wicksell, Fisher, Keynes advocated

Kevin Clinton Winter 2005 Lecture notes 10 Monetary policy: nominal anchor for the system 1. Monetary stability objective Monetary policy was a 20 th century invention Wicksell, Fisher, Keynes advocated

Case, Fair and Oster Macroeconomics Chapter 12 Problems -- Aggregate Demand in the Goods and Money Markets

Case, Fair and Oster Macroeconomics Chapter 12 Problems -- Aggregate Demand in the Goods and Money Markets Problem 1. ECB cuts interest rates -- why? Faced with a recession, the European Central Bank cut

Case, Fair and Oster Macroeconomics Chapter 12 Problems -- Aggregate Demand in the Goods and Money Markets Problem 1. ECB cuts interest rates -- why? Faced with a recession, the European Central Bank cut

ECON 3560/5040 Week 8-9

ECON 3560/5040 Week 8-9 AGGREGATE DEMAND 1. Keynes s Theory - John Maynard Keynes (1936) criticized classical theory for assuming that AS alone capital, labor, and technology determines national income

ECON 3560/5040 Week 8-9 AGGREGATE DEMAND 1. Keynes s Theory - John Maynard Keynes (1936) criticized classical theory for assuming that AS alone capital, labor, and technology determines national income

Practice Test 1: Multiple Choice

Practice Test 1: Multiple Choice 1. If aggregate planned expenditure exceeds real GDP A. actual inventories decrease below their target. B. firms are not maximizing their profits. C. planned consumption

Practice Test 1: Multiple Choice 1. If aggregate planned expenditure exceeds real GDP A. actual inventories decrease below their target. B. firms are not maximizing their profits. C. planned consumption

Chapter8 3/9/2018. MONEY, THE PRICE LEVEL, AND INFLATION Part 2. The Money Market the Demand for Money

Chapter8 MONEY, THE PRICE LEVEL, AND INFLATION Part 2 the Demand for Money How much money do people and business firms want to hold? Depends on four main factors: The price level (P) Real GDP (Y), The

Chapter8 MONEY, THE PRICE LEVEL, AND INFLATION Part 2 the Demand for Money How much money do people and business firms want to hold? Depends on four main factors: The price level (P) Real GDP (Y), The

Midsummer Examinations 2013

Midsummer Examinations 2013 No. of Pages: 7 No. of Questions: 34 Subject ECONOMICS Title of Paper MACROECONOMICS Time Allowed Two Hours (2 Hours) Instructions to candidates This paper is in two sections.

Midsummer Examinations 2013 No. of Pages: 7 No. of Questions: 34 Subject ECONOMICS Title of Paper MACROECONOMICS Time Allowed Two Hours (2 Hours) Instructions to candidates This paper is in two sections.

ECON MACROECONOMIC THEORY Instructor: Dr. Juergen Jung Towson University

ECON 310 - MACROECONOMIC THEORY Instructor: Dr. Juergen Jung Towson University J.Jung Chapter 12 - Money and Monetary Policy Towson University 1 / 83 Disclaimer These lecture notes are customized for Intermediate

ECON 310 - MACROECONOMIC THEORY Instructor: Dr. Juergen Jung Towson University J.Jung Chapter 12 - Money and Monetary Policy Towson University 1 / 83 Disclaimer These lecture notes are customized for Intermediate

ECON 3010 Intermediate Macroeconomics Final Exam

ECON 3010 Intermediate Macroeconomics Final Exam Multiple Choice Questions. (60 points; 3 pts each) 1. The returns to scale in the production function YY = KK 0.5 LL 0.5 are: A) decreasing. B) constant.

ECON 3010 Intermediate Macroeconomics Final Exam Multiple Choice Questions. (60 points; 3 pts each) 1. The returns to scale in the production function YY = KK 0.5 LL 0.5 are: A) decreasing. B) constant.

Topic 2: Should the inflation target be raised? Lecture to 3 rd year undergrad Current Economic Problems, Bristol, Spring 2015 Tony Yates

Topic 2: Should the inflation target be raised? Lecture to 3 rd year undergrad Current Economic Problems, Bristol, Spring 2015 Tony Yates Overview and motivation Blanchard et al (2010)/Krugman (various):

Topic 2: Should the inflation target be raised? Lecture to 3 rd year undergrad Current Economic Problems, Bristol, Spring 2015 Tony Yates Overview and motivation Blanchard et al (2010)/Krugman (various):

Exam 2 Review. 2. If Y = AK 0.5 L 0.5 and A, K, and L are all 100, the marginal product of capital is: A) 50. B) 100. C) 200. D) 1000.

50. B) 100. C) 200. D) 1000.") Exam 2 Review 1. If output is described by the production function Y = AK 0.2 L 0.8, then the production function has: A) constant returns to scale. B) diminishing returns to scale. C) increasing returns

Exam 2 Review 1. If output is described by the production function Y = AK 0.2 L 0.8, then the production function has: A) constant returns to scale. B) diminishing returns to scale. C) increasing returns

macro macroeconomics Money and Inflation N. Gregory Mankiw CHAPTER FOUR PowerPoint Slides by Ron Cronovich fifth edition

macro CHAPTER FOUR Money and Inflation macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved In this chapter you will learn The classical

macro CHAPTER FOUR Money and Inflation macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved In this chapter you will learn The classical

macro macroeconomics Money and Inflation (chapter 4) N. Gregory Mankiw The classical theory of inflation causes effects social costs

N. Gregory Mankiw The classical theory of inflation causes effects social costs") macro Topic 7: (chapter 4) macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved In this chapter you will learn The classical theory

macro Topic 7: (chapter 4) macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved In this chapter you will learn The classical theory

Business 33001: Microeconomics

Business 33001: Microeconomics Owen Zidar University of Chicago Booth School of Business Week 6 Owen Zidar (Chicago Booth) Microeconomics Week 6: Capital & Investment 1 / 80 Today s Class 1 Preliminaries

Business 33001: Microeconomics Owen Zidar University of Chicago Booth School of Business Week 6 Owen Zidar (Chicago Booth) Microeconomics Week 6: Capital & Investment 1 / 80 Today s Class 1 Preliminaries

ECON 6022B Problem Set 1 Suggested Solutions Fall 2011

ECON 6022B Problem Set Suggested Solutions Fall 20 September 5, 20 Shocking the Solow Model Consider the basic Solow model in Lecture 2. Suppose the economy stays at its steady state in Period 0 and there

ECON 6022B Problem Set Suggested Solutions Fall 20 September 5, 20 Shocking the Solow Model Consider the basic Solow model in Lecture 2. Suppose the economy stays at its steady state in Period 0 and there

Unit 2: Macro Measures REVIEW ACTIVITY Name That Concept Rules: 1. Cannot use the word(s) 2. Focus on the concept not word Ex: Price Maker

2. Focus on the concept not word Ex: Price Maker") 1 Unit 2: Macro Measures 1 REVIEW ACTIVITY Name That Concept Rules: 1. Cannot use the word(s) 2. Focus on the concept not word Ex: Price Maker 2 NAME THAT CONCEPT 1.Macroeconomics 2.Inflation 3.Nominal

1 Unit 2: Macro Measures 1 REVIEW ACTIVITY Name That Concept Rules: 1. Cannot use the word(s) 2. Focus on the concept not word Ex: Price Maker 2 NAME THAT CONCEPT 1.Macroeconomics 2.Inflation 3.Nominal

Econ 102 Final Exam Name ID Section Number

Econ 102 Final Exam Name ID Section Number 1. Assume that the economy is contracting and unemployment is rising. Which of the following would be a logical explanation for a sudden fall in the unemployment

Econ 102 Final Exam Name ID Section Number 1. Assume that the economy is contracting and unemployment is rising. Which of the following would be a logical explanation for a sudden fall in the unemployment

EC202 Macroeconomics

EC202 Macroeconomics Koç University, Summer 2014 by Arhan Ertan Study Questions - 3 1. Suppose a government is able to permanently reduce its budget deficit. Use the Solow growth model of Chapter 9 to

EC202 Macroeconomics Koç University, Summer 2014 by Arhan Ertan Study Questions - 3 1. Suppose a government is able to permanently reduce its budget deficit. Use the Solow growth model of Chapter 9 to

Econ 102 Final Exam Name ID Section Number

Econ 102 Final Exam Name ID Section Number 1. Which of the following is not an accurate statement of core capital goods? A) proxy for business investments B) does not include transportation equipment C)

Econ 102 Final Exam Name ID Section Number 1. Which of the following is not an accurate statement of core capital goods? A) proxy for business investments B) does not include transportation equipment C)

8/23/2018. Where You Are! Course Webpage. Who am I? Dr. John Neri Office: Morrill Hall, Room 1106D, M and W 10:30am to 11:30am

Where You Are! Economics 305 Macroeconomic Theory M, W, F from 12:00pm to 12:50pm The Friday class is primarily graded quizzes and 3 midterm exams see the syllabus. Text: Gregory Mankiw: Macroeconomics,

Where You Are! Economics 305 Macroeconomic Theory M, W, F from 12:00pm to 12:50pm The Friday class is primarily graded quizzes and 3 midterm exams see the syllabus. Text: Gregory Mankiw: Macroeconomics,

MACROECONOMICS. Inflation: Its Causes, Effects, and Social Costs. N. Gregory Mankiw. PowerPoint Slides by Ron Cronovich

5 : Its Causes, Effects, and Social Costs MACROECONOMICS N. Gregory Mankiw Modified for EC 204 by Bob Murphy PowerPoint Slides by Ron Cronovich 2013 Worth Publishers, all rights reserved IN THIS CHAPTER,

5 : Its Causes, Effects, and Social Costs MACROECONOMICS N. Gregory Mankiw Modified for EC 204 by Bob Murphy PowerPoint Slides by Ron Cronovich 2013 Worth Publishers, all rights reserved IN THIS CHAPTER,

Different Schools of Thought in Economics: A Brief Discussion

Different Schools of Thought in Economics: A Brief Discussion Topic 1 Based upon: Macroeconomics, 12 th edition by Roger A. Arnold and A cheat sheet for understanding the different schools of economics

Different Schools of Thought in Economics: A Brief Discussion Topic 1 Based upon: Macroeconomics, 12 th edition by Roger A. Arnold and A cheat sheet for understanding the different schools of economics

Classes and Lectures

Classes and Lectures There are no classes in week 24, apart from the cancelled ones You ve already had 9 classes, as promised, and no doubt you re keen to revise Answers for Question Sheet 5 are on the

Classes and Lectures There are no classes in week 24, apart from the cancelled ones You ve already had 9 classes, as promised, and no doubt you re keen to revise Answers for Question Sheet 5 are on the

Macroeconomics Review Course LECTURE NOTES

Macroeconomics Review Course LECTURE NOTES Lorenzo Ferrari frrlnz01@uniroma2.it August 11, 2018 Disclaimer: These notes are for exclusive use of the students of the Macroeconomics Review Course, M.Sc.

Macroeconomics Review Course LECTURE NOTES Lorenzo Ferrari frrlnz01@uniroma2.it August 11, 2018 Disclaimer: These notes are for exclusive use of the students of the Macroeconomics Review Course, M.Sc.

1. Under what condition will the nominal interest rate be equal to the real interest rate?

Practice Problems III EC 102.03 Questions 1. Under what condition will the nominal interest rate be equal to the real interest rate? Real interest rate, or r, is equal to i π where i is the nominal interest

Practice Problems III EC 102.03 Questions 1. Under what condition will the nominal interest rate be equal to the real interest rate? Real interest rate, or r, is equal to i π where i is the nominal interest

Econ 302 Fall Don t forget to download a copy of the Homework Cover Sheet. Mark the location where you handed in your work.

Econ 302 Fall 2005 Don t forget to download a copy of the Homework Cover Sheet. Mark the location where you handed in your work. Homework #1; Chapter 1. This homework has three parts (A, B, C). Each part

Econ 302 Fall 2005 Don t forget to download a copy of the Homework Cover Sheet. Mark the location where you handed in your work. Homework #1; Chapter 1. This homework has three parts (A, B, C). Each part

II. Determinants of Asset Demand. Figure 1

University of California, Merced EC 121-Money and Banking Chapter 5 Lecture otes Professor Jason Lee I. Introduction Figure 1 shows the interest rates for 3 month treasury bills. As evidenced by the figure,

University of California, Merced EC 121-Money and Banking Chapter 5 Lecture otes Professor Jason Lee I. Introduction Figure 1 shows the interest rates for 3 month treasury bills. As evidenced by the figure,

Model Question Paper Economics - II (MSF1A4)

") Model Question Paper Economics - II (MSF1A4) Answer all 74 questions. Marks are indicated against each question. 1. Which of the following is true if the central bank of a country sells government securities

Model Question Paper Economics - II (MSF1A4) Answer all 74 questions. Marks are indicated against each question. 1. Which of the following is true if the central bank of a country sells government securities

ECF2331 Final Revision

Table of Contents Week 1 Introduction to Macroeconomics... 5 What Macroeconomics is about... 5 Macroeconomics 5 Issues addressed by macroeconomists 5 What Macroeconomists Do... 5 Macro Research 5 Develop

Table of Contents Week 1 Introduction to Macroeconomics... 5 What Macroeconomics is about... 5 Macroeconomics 5 Issues addressed by macroeconomists 5 What Macroeconomists Do... 5 Macro Research 5 Develop

November 25, AP Inflation.notebook. Goal #3 Price Stability. What is inflation? Inflation is a general rise in prices.

AP Inflation.notebook Goal #3 Price Stability Country and Time Zimbabwe, 2008 Annual Inflation Rate 79,600,000,000% Time for Prices to Double 24.7 hours What is inflation? Inflation is a general rise in

AP Inflation.notebook Goal #3 Price Stability Country and Time Zimbabwe, 2008 Annual Inflation Rate 79,600,000,000% Time for Prices to Double 24.7 hours What is inflation? Inflation is a general rise in

Inflation and the Quantity Theory of Money

Chapter 12 MODERN PRINCIPLES OF ECONOMICS Third Edition Inflation and the Quantity Theory of Money Outline Defining and Measuring Inflation The Quantity Theory of Money The Costs of Inflation Why do governments

Chapter 12 MODERN PRINCIPLES OF ECONOMICS Third Edition Inflation and the Quantity Theory of Money Outline Defining and Measuring Inflation The Quantity Theory of Money The Costs of Inflation Why do governments

Global Financial Crisis and China s Countermeasures

Global Financial Crisis and China s Countermeasures Qin Xiao The year 2008 will go down in history as a once-in-a-century financial tsunami. This year, as the crisis spreads globally, the impact has been

Global Financial Crisis and China s Countermeasures Qin Xiao The year 2008 will go down in history as a once-in-a-century financial tsunami. This year, as the crisis spreads globally, the impact has been

Fed Policy and Money Markets

TOPIC 5 Fed Policy and Money Markets 1 Outline What is Money? What affects the supply of money? How does the banking system work? What is the Fed? How does it work? What is monetary policy? What affects

TOPIC 5 Fed Policy and Money Markets 1 Outline What is Money? What affects the supply of money? How does the banking system work? What is the Fed? How does it work? What is monetary policy? What affects

Chapter 4. U.S. inflation & its trend, The connection between money and prices

Chapter 4 The classical theory of inflation causes effects social costs Classical -- assumes prices are flexible & markets clear. Applies to the long run. slide 0 16 U.S. inflation & its trend, 1960-2001

Chapter 4 The classical theory of inflation causes effects social costs Classical -- assumes prices are flexible & markets clear. Applies to the long run. slide 0 16 U.S. inflation & its trend, 1960-2001

Second Edition ROBERT H. FRANK BEN S. BERNANKE LOUIS D. JOHNSTON. Cornell University

Second Edition ROBERT H. FRANK Cornell University BEN S. BERNANKE Princeton University [affiliated] Chairman, Board of Governors of the Federal Reserve System with special contribution by LOUIS D. JOHNSTON

Second Edition ROBERT H. FRANK Cornell University BEN S. BERNANKE Princeton University [affiliated] Chairman, Board of Governors of the Federal Reserve System with special contribution by LOUIS D. JOHNSTON

Econ 110: Introduction to Economic Theory. 35th Class 4/25/11. Keynes vs. Hayek rap:

Econ 0: Introduction to Economic Theory th Class // Keynes vs. Hayek rap: http://www.youtube.com/watch?v=d0nertfo-sk last of three lectures on macroeconomic stabilization policy: macro policy debates It

Econ 0: Introduction to Economic Theory th Class // Keynes vs. Hayek rap: http://www.youtube.com/watch?v=d0nertfo-sk last of three lectures on macroeconomic stabilization policy: macro policy debates It

Objectives for Chapter 24: Monetarism (Continued) Chapter 24: The Basic Theory of Monetarism (Continued) (latest revision October 2004)

Chapter 24: The Basic Theory of Monetarism (Continued) (latest revision October 2004)") 1 Objectives for Chapter 24: Monetarism (Continued) At the end of Chapter 24, you will be able to answer the following: 1. What is the short-run? 2. Use the theory of job searching in a period of unanticipated

1 Objectives for Chapter 24: Monetarism (Continued) At the end of Chapter 24, you will be able to answer the following: 1. What is the short-run? 2. Use the theory of job searching in a period of unanticipated

MONEY, THE PRICE LEVEL, AND INFLATION

24 MONEY, THE PRICE LEVEL, AND INFLATION After studying this chapter, you will be able to: Define money and describe its functions Explain the economic functions of banks Describe the structure and functions

24 MONEY, THE PRICE LEVEL, AND INFLATION After studying this chapter, you will be able to: Define money and describe its functions Explain the economic functions of banks Describe the structure and functions

4. What two variables are always equal for a profit maximizing firm? Ans: Marginal revenue and marginal cost

SET 1 1. What bubble in the late 1990 s to early 2000 s significantly increased productivity growth in the US? Ans: Dot-com bubble, technology bubble 2. What is a market with only a single buyer called?

SET 1 1. What bubble in the late 1990 s to early 2000 s significantly increased productivity growth in the US? Ans: Dot-com bubble, technology bubble 2. What is a market with only a single buyer called?

EC3115 Monetary Economics

EC3115 :: L.8 : Money, inflation and welfare Almaty, KZ :: 30 October 2015 EC3115 Monetary Economics Lecture 8: Money, inflation and welfare Anuar D. Ushbayev International School of Economics Kazakh-British

EC3115 :: L.8 : Money, inflation and welfare Almaty, KZ :: 30 October 2015 EC3115 Monetary Economics Lecture 8: Money, inflation and welfare Anuar D. Ushbayev International School of Economics Kazakh-British

The Model at Work. (Reference Slides I may or may not talk about all of this depending on time and how the conversation in class evolves)

") TOPIC 7 The Model at Work (Reference Slides I may or may not talk about all of this depending on time and how the conversation in class evolves) Note: In terms of the details of the models for changing

TOPIC 7 The Model at Work (Reference Slides I may or may not talk about all of this depending on time and how the conversation in class evolves) Note: In terms of the details of the models for changing

Chapter 5 Inflation: Its Causes, Effects, and Social Costs

Chapter 5 Inflation: Its Causes, Effects, and Social Costs Modified by Yun Wang Eco 3203 Intermediate Macroeconomics Florida International University Summer 2017 2016 Worth Publishers, all rights reserved

Chapter 5 Inflation: Its Causes, Effects, and Social Costs Modified by Yun Wang Eco 3203 Intermediate Macroeconomics Florida International University Summer 2017 2016 Worth Publishers, all rights reserved

International Economics: Theory and Policy

International Economics: Theory and Policy Eleventh Edition Chapter 15 Money, Interest Rates, and Exchange Rates Learning Objectives 15.1 Describe and discuss the national money markets in which interest

International Economics: Theory and Policy Eleventh Edition Chapter 15 Money, Interest Rates, and Exchange Rates Learning Objectives 15.1 Describe and discuss the national money markets in which interest

DP/P = (DP/P) e t+1 + g [Y Y P ] + r. AD Curve (substitute MP Curve into IS Curve)

![DP/P = (DP/P) e t+1 + g [Y Y P ] + r. AD Curve (substitute MP Curve into IS Curve)](/thumbs/71/66085730.jpg "DP/P = (DP/P) e t+1 + g [Y Y P ] + r. AD Curve (substitute MP Curve into IS Curve)") DP/P LRAS SRAS 1 DP/P = (DP/P) e t+1 + g [Y Y P ] + r AD1 Y P Y AD Curve (substitute MP Curve into IS Curve) Y = [C + I + G + NX d f MPC T] * 1 (d + x) * [r + l (DP/P) e t+1 ] 1 - [mpc(1-t)] 1 - [mpc(1-t)]

DP/P LRAS SRAS 1 DP/P = (DP/P) e t+1 + g [Y Y P ] + r AD1 Y P Y AD Curve (substitute MP Curve into IS Curve) Y = [C + I + G + NX d f MPC T] * 1 (d + x) * [r + l (DP/P) e t+1 ] 1 - [mpc(1-t)] 1 - [mpc(1-t)]

Macroeconomics: Principles, Applications, and Tools

Macroeconomics: Principles, Applications, and Tools NINTH EDITION Chapter 16 The Dynamics of Inflation and Unemployment Learning Objectives 16.1 Describe how an economy at full unemployment with inflation

Macroeconomics: Principles, Applications, and Tools NINTH EDITION Chapter 16 The Dynamics of Inflation and Unemployment Learning Objectives 16.1 Describe how an economy at full unemployment with inflation

Econ 330 Final Exam Name ID Section Number

Econ 330 Final Exam Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A group of economists believe that the natural rate

Econ 330 Final Exam Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A group of economists believe that the natural rate

Money Growth and Inflation

Wojciech Gerson (83-90) Seventh Edition Principles of Macroeconomics N. Gregory Mankiw CHAPTER 7 Money Growth and Inflation The Money P the price level (e.g., the CPI or GDP deflator) P is the price of

Wojciech Gerson (83-90) Seventh Edition Principles of Macroeconomics N. Gregory Mankiw CHAPTER 7 Money Growth and Inflation The Money P the price level (e.g., the CPI or GDP deflator) P is the price of

U. S. Productivity Growth:

Macro Lecture 12: Late 1990s, the 2000s, and Mortgages Productivity Growth: 1990-2004 Most economists expected the general decline in productivity growth 8 occurring during the 1950 s, 1960 s, 1970 s,

Macro Lecture 12: Late 1990s, the 2000s, and Mortgages Productivity Growth: 1990-2004 Most economists expected the general decline in productivity growth 8 occurring during the 1950 s, 1960 s, 1970 s,

Disputes Over Macro Theory and Policy

s or Discretion C H A P T E R Disputes Over Macro Theory and Policy 19-1 s or Discretion 19-2 CLASSICAL ECONOMICS AND KEYNES Classical Economics Adam Smith - 1776 Laissez-faire The Classical Vertical Aggregate

s or Discretion C H A P T E R Disputes Over Macro Theory and Policy 19-1 s or Discretion 19-2 CLASSICAL ECONOMICS AND KEYNES Classical Economics Adam Smith - 1776 Laissez-faire The Classical Vertical Aggregate

Sherif Khalifa. Sherif Khalifa () Inflation 1 / 40

Inflation 1 / 40") Sherif Khalifa Sherif Khalifa () Inflation 1 / 40 "The first panacea for a mismanaged nation is inflation of the currency; the second is war. Both bring a temporary prosperity; both bring a permanent ruin.

Sherif Khalifa Sherif Khalifa () Inflation 1 / 40 "The first panacea for a mismanaged nation is inflation of the currency; the second is war. Both bring a temporary prosperity; both bring a permanent ruin.

The Aggregate Demand/Aggregate Supply Model

CHAPTER 27 The Aggregate Demand/Aggregate Supply Model The Theory of Economics... is a method rather than a doctrine, an apparatus of the mind, a technique of thinking which helps its possessor to draw

CHAPTER 27 The Aggregate Demand/Aggregate Supply Model The Theory of Economics... is a method rather than a doctrine, an apparatus of the mind, a technique of thinking which helps its possessor to draw

Name: Days/Times Class Meets: Today s Date:

Name: _ Days/Times Class Meets: Today s Date: Macroeconomics, Fall 2007, Final Exam, several versions, December Read these Instructions carefully! You must follow them exactly! I) On your Scantron card

Name: _ Days/Times Class Meets: Today s Date: Macroeconomics, Fall 2007, Final Exam, several versions, December Read these Instructions carefully! You must follow them exactly! I) On your Scantron card

28 Money, Interest Rates, and Economic Activity

28 Money, Interest Rates, and Economic Activity CHAPTER OUTLINE LEARNING OBJECTIVES (LO) In this chapter you will learn 28.1 UNDERSTANDING BONDS 1 why the price of a bond is inversely related to the market

28 Money, Interest Rates, and Economic Activity CHAPTER OUTLINE LEARNING OBJECTIVES (LO) In this chapter you will learn 28.1 UNDERSTANDING BONDS 1 why the price of a bond is inversely related to the market

Chapter 7: Money and Inflation. Instructor: Dmytro Hryshko

Chapter 7: Money and Inflation Instructor: Dmytro Hryshko Money and Its Functions Money is an asset that can be used to support transactions. Functions of money: 1 A Store of value: use money to support

Chapter 7: Money and Inflation Instructor: Dmytro Hryshko Money and Its Functions Money is an asset that can be used to support transactions. Functions of money: 1 A Store of value: use money to support

Session 12. The New Normal. Deflation and Zero Lower Bound.

Session 12. The New Normal. Deflation and Zero Lower Bound. Deflation and Interest Rates The Zero Lower Bound trap The Great Depression The Great Recession Deflation and the Zero Lower Bound Trap Deflation

Session 12. The New Normal. Deflation and Zero Lower Bound. Deflation and Interest Rates The Zero Lower Bound trap The Great Depression The Great Recession Deflation and the Zero Lower Bound Trap Deflation

Money, Banks and the Federal Reserve

Money, Banks and the Federal Reserve By The Great Gamecock 2009 Prentice Hall Business Publishing Essentials of Economics Hubbard/O Brien, 2e. 1 of 43 2009 Prentice Hall Business Publishing Essentials

Money, Banks and the Federal Reserve By The Great Gamecock 2009 Prentice Hall Business Publishing Essentials of Economics Hubbard/O Brien, 2e. 1 of 43 2009 Prentice Hall Business Publishing Essentials