NAB Quarterly SME Survey

|

|

|

- Isabel Parker

- 5 years ago

- Views:

Transcription

1 NAB Quarterly SME Survey by NAB Group Economics Key Points: The NAB Quarterly SME Survey is the leading business survey on small businesses in Australia. It offers a rich repertoire of insights into factors affecting these firms conditions by state, industry and size, as well as an assessment on their outlook for investment and output. SME business conditions fell marginally to +3 index points in Q4 from +4 index points in Q3. Within the components of business conditions, trading conditions were strongest, while profitability remained positive as well. However, employment conditions still lacked momentum. Conditions also continued to vary across business size with low-tier firms facing the most challenging conditions. Meanwhile, SME business confidence regained some of its loss in Q3 to be at +3 index points, a level which is slightly above the long-run average of +2 index points. That said, SME confidence has been on a general slowing trend since late It is also worth noting that the survey was conducted prior to the recent rout in global financial and commodity markets, which may act to erode confidence. The majority of SME industries experienced lower business conditions in the quarter, but in level terms business conditions in most industries remained positive. Finance firms continued to outperform other industries, while retail, wholesale and transportation SMEs were the weakest. Business conditions have trended higher in manufacturing in recent quarters ( see Industry Focus, P5, for further detail). SME business conditions were mostly weaker across states as well. However, NSW and VIC conditions were still resilient overall, while the mining/partly-mining states of QLD, WA and SA continued to be mired in negative territory. Most states confidence improved in the quarter, except for WA s which sank further into negative territory to reach the lowest level since the GFC. Capacity utilisation fell marginally in Q4. Similarly, capex by firms has also lost further momentum in the quarter. However, the still-positive readings of the capex and forward orders indices indicate that SME firms continue to operate in an expansionary mode on balance. Table 1: Business conditions & confidence Dec qtr Table 2: Conditions and confidence by industry (net balance, s.a.) Dec qtr Embargoed until: 11:30am Thursday 11 February 2016 Dec quarter Q4 Q3 Q4 Business Conditions Low-tier firms Mid-tier irms High-tier firms Business Confidence Low-tier firms Mid-tier irms High-tier firms Trading Conditions Low-tier firms Mid-tier irms 7 11 High-tier firms Profitability Low-tier firms Mid-tier irms High-tier firms Employment Low-tier firms Mid-tier irms High-tier firms Note*: Low-tier : turnover $2-3m p.a. Mid-tier: turnover $3-5m p.a. High-tier: turnover $5-m p.a. Table 3: Q3 Conditions and confidence by state (net balance, s.a.) Dec qtr Contacts: Alan Oster, Chief Economist: (03) or , Riki Polygenis, Head of Australian Economics: (03) , Alt. Vyanne Lai, Economist: (03)

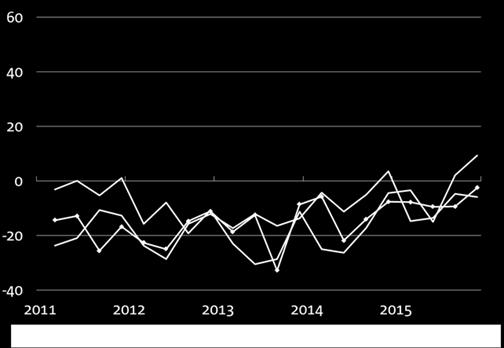

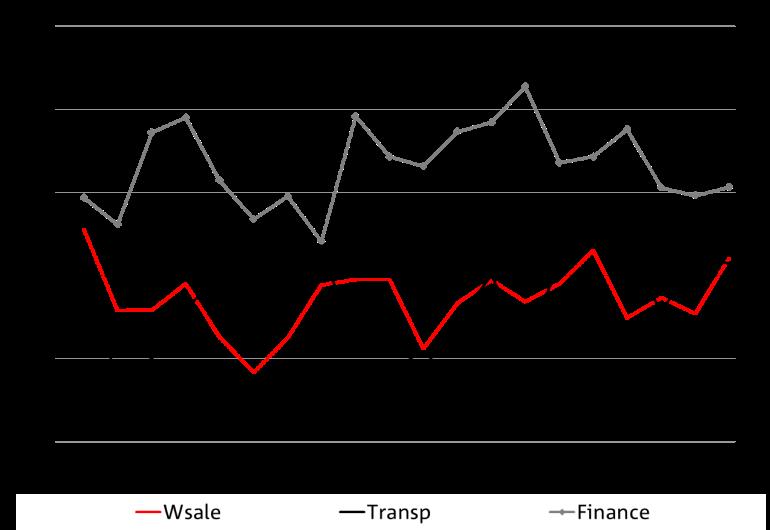

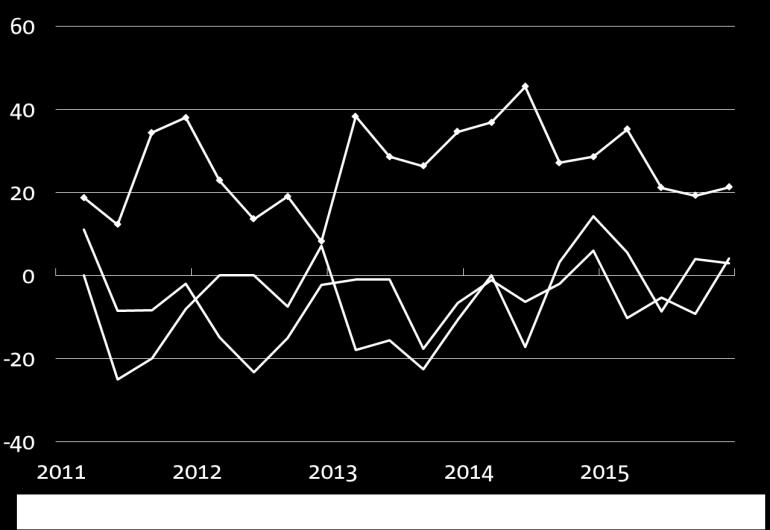

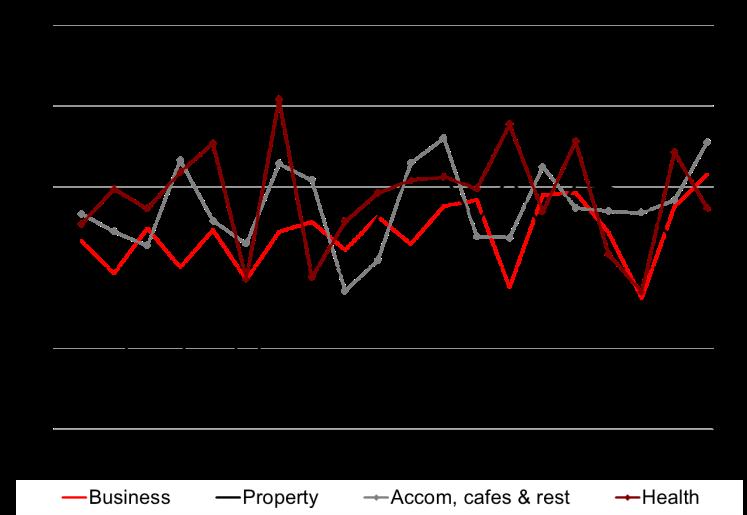

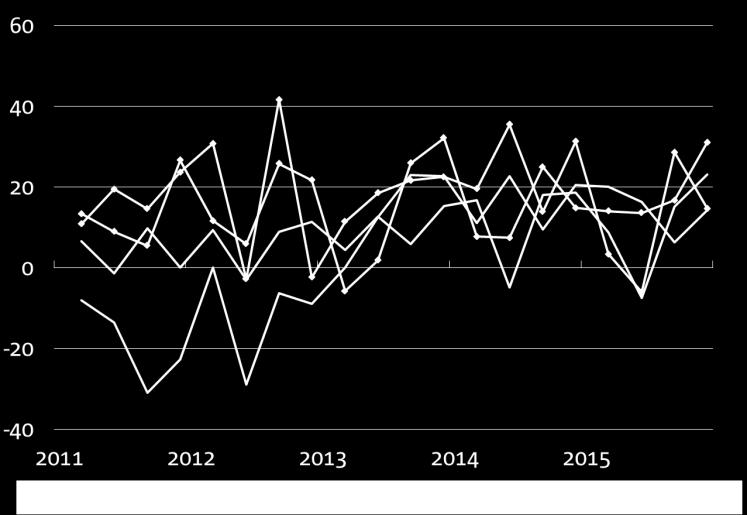

2 The disparity in SME conditions between high and low-tier firms widens Business conditions for SMEs fell slightly to +3 index points in the December quarter from +4 index points in the September quarter. Business confidence, however, reversed its loss last quarter to be back in positive territory at +2 index points. SME conditions diverged further from those of general businesses indicated by NAB Quarterly Business Survey (QBS) in the quarter, driven by the much weaker conditions of low-tier SMEs. This is particularly the case for SMEs in retail and wholesale, suggesting that they may not as well-positioned as the larger businesses to maximise the benefits/tackle the challenges arising from changes in the currency. SMEs in manufacturing, however, are experiencing more positive business conditions (see Industry Focus on P5). Despite recording a 4-point fall in the quarter to +9 index points, SME trading conditions have generally held up quite well since early 2014 to average around + index points. The profitability index was positive in most quarters over the period as well, albeit at a lower level a possible reflection of weak margins. That said, employment conditions remained subdued, to be slightly at odds with official ABS data which showed strong employment growth. Overall, the survey results point to a broadening non-mining sector recovery into late Business conditions remain strongest in services industries, with the finance sector (at +14 index points) continuing to outperform other industries. Accommodations/cafes/restaurants tied with property services in second spot at +12 index points. Meanwhile, retail, wholesale and transportation sectors were the only ones with negative readings in the quarter. For retail and wholesale, higher import costs associated with a lower AUD could be contributing. By state, the two largest states of NSW and VIC continued to outperform at +11 and +5 index points respectively. SA business conditions weakened further this quarter to -12, while mining states of WA and Qld remained mired in negative territory at -8 and -5 index points respectively. The widening disparity between the bestperforming and worst-performing states suggests that the rebalancing of growth away from mining states to non-mining states is gaining traction. Business confidence in most states improved in the quarter, except for WA s which sank further into negative territory to reach the lowest level since the GFC. By industry, business confidence mostly improved in the quarter, with the majority reporting positive results. Accommodations/cafes/restaurants and wholesale were the most confident at +7 index points, while health confidence fell points to be the weakest at -8 index points. Compared to the larger businesses in the QBS, SME business conditions were lower in all industries except for manufacturing. Analysis by the size of firms shows that low-tier SME firms with $2 to 3 million annual revenue continued to report significantly weaker conditions compared to their larger counterparts. Incidentally they also reported the weakest confidence in the quarter Business Conditions (net bal, sa.), SME & QBS SME Business Conditions Components (net bal, sa.) Business Conditions (latest quarter, sa.) Larger firms (QBS) conditions SME firms conditions SME Conditions QBS Conditions Trading Profit Employment ** Data are seasonally adjusted by NAB, except SME cashflow (insufficient time series available). All data are net balance indices. Fieldwork for this Survey conducted from 23 November to 11 December 2015 covering around 707 SME (non-farm) firms. 2

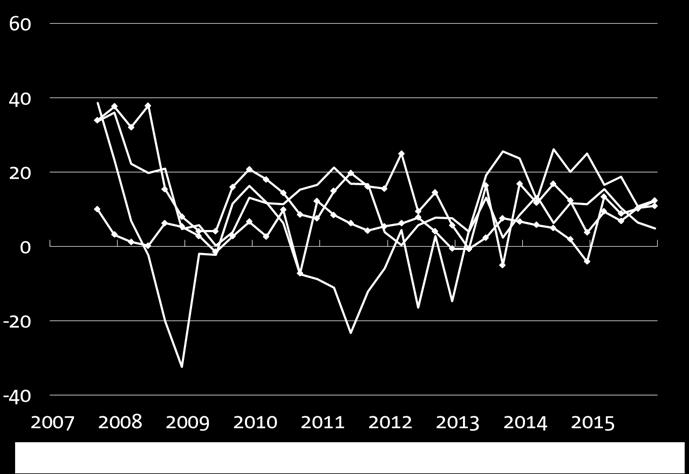

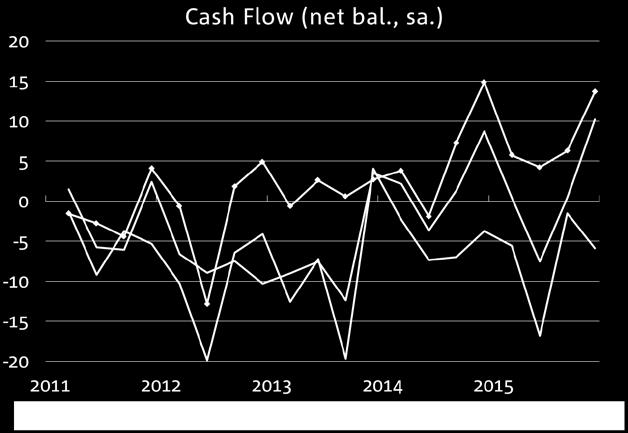

3 Forward and financial indicators moderated in Q4 In the December quarter, SME forward orders fell marginally by 1 point to +3 index points, to be still higher than the long-run average of -2 index points. This was broadly consistent with the result for general businesses as reported in the QBS. The SME forward index has largely tracked sideways since early 2014, with little evidence of a significantly lower AUD providing much impetus. The generally positive readings for forward orders since early last year are consistent with a moderate recovery in real economic activity. Property services, which reported the strongest orders across industries in Q3, experienced a sharp decline of 11 points in its forward orders index to +1 index point in Q4. Seeing through the quarterly volatility, the data suggests that the overall trend in property services forward orders is a slowing one, consistent with cooling housing market activity nationally. As a sign of improving conditions in the manufacturing sector, forward orders for the sector maintained at around the 6-year high level at +9 index points in the quarter. Meanwhile, a continuous slowdown in engineering and dwelling construction activity was reflected in the lacklustre reading for the construction sector (+2), a long way below its recent peak of +14 in mid Retail (at -6), health (at -1) and transportation (at 0) reported the weakest forward orders in the quarter. The SME stock index remained largely unchanged in the quarter at +2 index points, a level consistent with a moderate pick-up in underlying demand and slightly below that in the QBS. By industry, manufacturing (+7) and wholesale (+6) continued to report the highest levels of stocks. Meanwhile stocks were the lowest in accommodations, cafes and restaurants (-9) while the construction stock index relapsed into negative territory after barely nudging into positive territory last quarter. Overall, at their current levels, the forward and financial indicators point to a moderate but tentative pick-up in activity in coming months. Cash flow rebounded back into positive territory SME Business Conditions & Cash Flow (net bal) SME forward orders lost some momentum in Q4 Forward Orders (Net bal, sa.), SME & QBS Trading conditions continued to be the key driver for overall conditions, but profitability stayed positive as well SME Business Conditions Components (net bal, sa.) Trading Profit Employment SME stock index slipped below that of QBS Stocks (Net bal., sa.), SME & QBS Conditions (s.a.) Cash Flow (n.s.a) SME Orders QBS Orders SME Stocks QBS Stocks 3

by SMEs lost further momentum in the December quarter to stay below the capex reading for larger businesses as indicated by the QBS.")

4 SME capacity utilisation fell marginally in the quarter SME capacity utilisation deteriorated in the December quarter by 1ppt to 78%, consistent with a decline in business conditions and remained below those of general businesses indicated by the QBS. Services industries continued to report higher capacity utilisation rates in general, with health ranked top at 84.2%, but this level was significantly below its recent peak of 88.2% achieved in Q This was followed by business services and property services at 83.5% and 81.4% respectively. Meanwhile manufacturing continued to report the weakest capacity utilisation out of all industries at 73.4%. Despite improving business conditions, manufacturing capacity utilisation has failed to gain substantial momentum over the past two years. Analysis by the size of firms suggests that SMEs of all sizes experienced a fall in capacity utilisation in the quarter, driven largely by mid-tier and low-tier firms, which recorded declines of 1.8ppts and 0.6ppt to 78.1% and 77.1% respectively. Meanwhile the capacity utilisation rate of high-tier SME firms was more resilient to be at 78.5%, down from 78.8% in Q3. Capital expenditure (capex) by SMEs lost further momentum in the December quarter to stay below the capex reading for larger businesses as indicated by the QBS. Since peaking in Q3 2014, SME capex has been trending downwards. However, positive readings for both the SMEs and QBS capital expenditure indices indicate that firms continue to operate in an expansionary mode on balance. The capex series of individual industries show a high level of volatility from quarter to quarter. This is demonstrated by a 24-point increase in the capex index of transportation to +24 index points to be the strongest performing sector in the quarter. Meanwhile health, which was the best performer last quarter, experienced a 23-point decline to +4 index points over the same time. At -2 index points, construction had the lowest capex reading out of all industries. Aggregate longer-term capex intentions improved, with 12- month capex expectations picking up to +15 in the quarter from +14 the same quarter last year. SME capacity utilisation reversed the gains in Q3 Capex points to moderate expansion in near-term activity 4

.")

5 Industry Focus : Manufacturing A strong appreciation in the AUD between 20 and 2013 placed a disproportionate amount of pressure on manufacturing firms in Australia through the erosion of international competitiveness, despite lowering their import costs at the same time. Along with the steady devaluations in the currency since 2013, business conditions experienced by manufacturing firms started to recover gradually, with manufacturing SMEs breaching into positive territory in early While smaller firms tend to experience certain sizespecific challenges relative to their larger industry counterparts, this does not seem to be the case for manufacturing SMEs. In 2015, business conditions for manufacturing SMEs have outperformed general manufacturing businesses indicated by the QBS. This may be because smaller manufacturers often operate in niche markets where they may not be competing as heavily on price or because their business model is more nimble in terms of responding to specific customer needs. While a lower AUD has improved the external competitiveness of manufacturing SMEs, it has also driven purchase cost growth higher in the past two years (see chart at top right hand corner). However, purchase cost inflation has moderated significantly since its peak in 2014, while other sources of cost growth remain relatively well-contained. A moderating trend in overheads growth suggests that manufacturing firms have been undertaking steady cost-cutting to counter higher purchase costs. As such, the cost environment facing manufacturing SMEs has become more benign of late, which appears to have bolstered their trading and cash flow conditions. That said, profitability is more subdued, possibly reflecting weak margins given subdued final product price growth. Forward-looking indicators for manufacturing SMEs such as forward orders and stocks have also been improving. Somewhat surprisingly, however, this has not translated into higher capacity utilisation, which has been tracking sideways at a low level over the past two years. This suggests that manufacturing SMEs continue to face a challenging demand environment. Manufacturing SMEs are outperforming their larger industry counterparts Trading conditions have improved markedly, but employment and profitability remain subdued Input costs for manufacturing SMEs are decelerating, but final product inflation is subdued A recovery in forward orders and stocks conditions has not translated into higher capacity utilisation 5

Pattern in SMEs business strategies is largely stable In the December quarter, we")

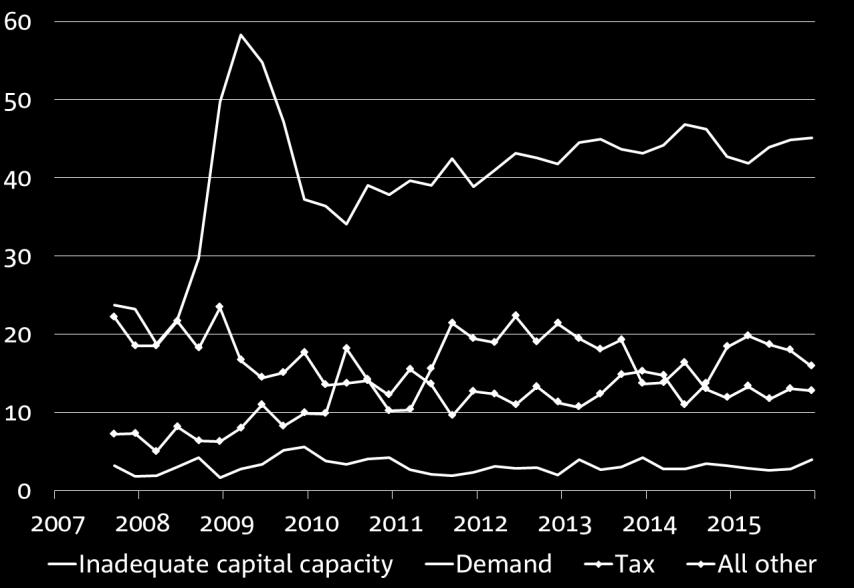

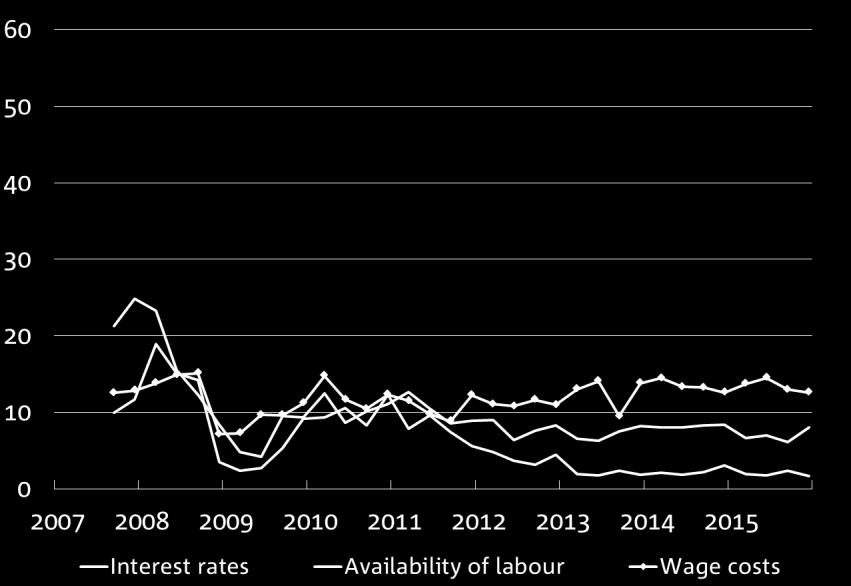

6 Significant constraints affecting SMEs long-term decisions lifted in the quarter Easing global volatility and risk aversion in Q4 from the their height in Q3 was demonstrated by the amelioration in most of the constraining factors affecting SME s long-term decisions in the quarter. It is worth noting that the survey was polled prior to the recent rout in global financial and commodity markets, which may act to erode business and investor confidence. Given the above, SMEs reported an improvement in most of the significant constraints affecting their long-term decisions, except for credit and staffing availability. Even so, supply-side factors, including credit, staffing availability, as well as interest rates, continued to be relatively benign overall. Despite a fall in the quarter, demand conditions were still regarded as the most constraining factor at +43 index points. Most significant constraining factors for SMEs (per cent, multiple responses) Pattern in SMEs business strategies is largely stable In the December quarter, we again asked firms whether they had employed any new strategies over the past 12 months to improve their competitiveness in the market. There were no significant changes in their strategies in the quarter compared to the same quarter in the previous year, but the results perhaps showed a lesser use of more resource-intensive (and costly) strategies such as R&D and offline marketing, with a preference for strategies such as online marketing. Part of this could reflect the relatively weak investment appetite of SME firms still, despite generally benign business conditions. 6

7 Constraints facing SMEs output and profitability Constraint on output (% of firms) Constraint on profitability (% of firms) 7

8 Detail by industry Business conditions by industry (net balance) Business confidence by industry (net balance) 8

9 Detail by state Business conditions by state (net balance) Business confidence by state (net balance) 9

10 Detail by SME firm size

11")

11 Detail by firm size (cont.) 11

12 Group Economics Alan Oster Group Chief Economist International Economics Tom Taylor Head of Economics, International Global Markets Research Peter Jolly Global Head of Research New Zealand Stephen Toplis Head of Research, NZ Jacqui Brand Personal Assistant Australian Economics and Commodities Riki Polygenis Head of Australian Economics +(61 3) James Glenn Senior Economist Australia +(61 3) Vyanne Lai Economist Australia +(61 3) Amy Li Economist Australia +(61 3) Phin Ziebell Economist Agribusiness +(61 4) Industry Analysis Dean Pearson Head of Industry Analysis +(61 3) Robert De Iure Senior Economist Industry Analysis +(61 3) Brien McDonald Senior Economist Industry Analysis +(61 3) Tony Kelly Senior Economist International +(61 3) Gerard Burg Senior Economist Asia +(61 3) John Sharma Economist Sovereign Risk +(61 3) Australia Economics Ivan Colhoun Chief Economist, Markets David de Garis Senior Economist Tapas Strickland Economist FX Strategy Ray Attrill Global Co-Head of FX Strategy Rodrigo Catril Currency Strategist Interest Rate Strategy Skye Masters Head of Interest Rate Strategy Credit Research Michael Bush Head of Credit Research Simon Fletcher Senior Credit Analyst FI Andrew Jones Credit Analyst Distribution Barbara Leong Research Production Manager Craig Ebert Senior Economist Doug Steel Markets Economist Kymberly Martin Senior Market Strategist Jason Wong Currency Strategist Yvonne Liew Publications & Web Administrator Asia Christy Tan Head of Markets Strategy/Research, Asia, Julian Wee Senior Markets Strategist, Asia UK/Europe Nick Parsons Head of Research, UK/Europe, and Global Co-Head of FX Strategy Gavin Friend Senior Markets Strategist Derek Allassani Research Production Manager Important Notice This document has been prepared by National Australia Bank Limited ABN AFSL ("NAB"). Any advice contained in this document has been prepared without taking into account your objectives, financial situation or needs. Before acting on any advice in this document, NAB recommends that you consider whether the advice is appropriate for your circumstances. NAB recommends that you obtain and consider the relevant Product Disclosure Statement or other disclosure document, before making any decision about a product including whether to acquire or to continue to hold it. Please click here to view our disclaimer and terms of use.

NAB Quarterly SME Survey

NAB Quarterly SME Survey by NAB Group Economics Embargoed until: 11:3am Thursday 28 July 216 Jun qtr 216 Key Points: The NAB SME Survey revealed very strong results across a wide range of indicators in

NAB Quarterly SME Survey by NAB Group Economics Embargoed until: 11:3am Thursday 28 July 216 Jun qtr 216 Key Points: The NAB SME Survey revealed very strong results across a wide range of indicators in

CONTACTS Alan Oster, Chief Economist, Riki Polygenis, Head of Australian Economics, Amy Li, Economist,

EMBARGOED UNTIL: 11.3AM THURSDAY 26 OCTOBER 217 NAB QUARTERLY SME SURVEY SEPTEMBER 217 Key points: The NAB Small and Medium Enterprises (SME) Business Survey showed an improvement in both business conditions

EMBARGOED UNTIL: 11.3AM THURSDAY 26 OCTOBER 217 NAB QUARTERLY SME SURVEY SEPTEMBER 217 Key points: The NAB Small and Medium Enterprises (SME) Business Survey showed an improvement in both business conditions

NAB Consumer Anxiety Index: Q by NAB Group Economics Embargoed until: 11.30am Wednesday 9 September 2015

NAB Consumer Anxiety Index: Q3 215 by NAB Group Economics Embargoed until: 11.3am Wednesday 9 September 215 Australian consumers are feeling less anxious. Cost of living concerns have fallen but are still

NAB Consumer Anxiety Index: Q3 215 by NAB Group Economics Embargoed until: 11.3am Wednesday 9 September 215 Australian consumers are feeling less anxious. Cost of living concerns have fallen but are still

NAB Monthly Business Survey

NAB Monthly Business Survey by NAB Group Economics Embargoed until: :3am Tuesday 9 December November Key Points: Last months spike in business conditions was again short-lived, pulling back towards long

NAB Monthly Business Survey by NAB Group Economics Embargoed until: :3am Tuesday 9 December November Key Points: Last months spike in business conditions was again short-lived, pulling back towards long

NAB Commercial Property Survey - Market Overview Q3 2014

Embargoed until: 11.3 am Wednesday 29 October 14 NAB Commercial Property Survey - Market Overview Q3 14 Summary NAB Commercial Property Index records its first positive read since Q1 11 (rising to +2 points

Embargoed until: 11.3 am Wednesday 29 October 14 NAB Commercial Property Survey - Market Overview Q3 14 Summary NAB Commercial Property Index records its first positive read since Q1 11 (rising to +2 points

NAB Consumer Anxiety Index: Q by NAB Group Economics

NAB Consumer Anxiety Index: Q2 2015 by NAB Group Economics Embargoed until: 11.30am Thursday 25 June 2015 Overall consumer anxiety rose despite falling concern over government policy post the federal budget.

NAB Consumer Anxiety Index: Q2 2015 by NAB Group Economics Embargoed until: 11.30am Thursday 25 June 2015 Overall consumer anxiety rose despite falling concern over government policy post the federal budget.

China s economy at a glance by NAB Group Economics

China s economy at a glance by NAB Group Economics Construction activity continued ramp up in April, but we are concerned about the sustainability of growth A rebound in real estate investment in early

China s economy at a glance by NAB Group Economics Construction activity continued ramp up in April, but we are concerned about the sustainability of growth A rebound in real estate investment in early

NAB Wellbeing Index: Q by NAB Group Economics

NAB Wellbeing Index: Q4 by NAB Group Economics Embargoed until: 11.30am Thursday 29 January 2015 Economic Overall wellbeing deteriorated slightly in Q4 with anxiety levels reaching a new high. Wellbeing

NAB Wellbeing Index: Q4 by NAB Group Economics Embargoed until: 11.30am Thursday 29 January 2015 Economic Overall wellbeing deteriorated slightly in Q4 with anxiety levels reaching a new high. Wellbeing

China s economy at a glance by NAB Group Economics 13 December 2015

more give, less take China s economy at a glance by NAB Group Economics 13 December 2 The modest recovery in industry unlikely to continue, China is moving away from the old economy Indicators of China

more give, less take China s economy at a glance by NAB Group Economics 13 December 2 The modest recovery in industry unlikely to continue, China is moving away from the old economy Indicators of China

NAB Monthly Business Survey

NAB Monthly Business Survey by NAB Group Economics Embargoed until: :3am Tuesday 9 September August Key Points: Business confidence remains resilient despite easing a little in August, supported by positive

NAB Monthly Business Survey by NAB Group Economics Embargoed until: :3am Tuesday 9 September August Key Points: Business confidence remains resilient despite easing a little in August, supported by positive

NAB Consumer Anxiety Index: Q by NAB Group Economics

NAB Consumer Anxiety Index: Q3 by NAB Group Economics Embargoed until: 11.30am Wednesday 17 September Consumer anxiety moderates after the post budget jump, but concerns over government policy and health

NAB Consumer Anxiety Index: Q3 by NAB Group Economics Embargoed until: 11.30am Wednesday 17 September Consumer anxiety moderates after the post budget jump, but concerns over government policy and health

Asian Emerging Economies Update

International > Economics 26 February 2014 Asian Emerging Economies Update Moderate economic growth continues across the emerging market economies of East Asia (ASEAN, HK, South Korea and Taiwan) with

International > Economics 26 February 2014 Asian Emerging Economies Update Moderate economic growth continues across the emerging market economies of East Asia (ASEAN, HK, South Korea and Taiwan) with

MARCH 2017 CONTENTS. Key points CONTACTS EMBARGOED UNTIL: 11.30AM TUESDAY 11 APRIL Table 1: Key monthly business statistics

EMBARGOED UNTIL:.AM TUESDAY APRIL NAB MONTHLY BUSINESS SURVEY MARCH NEXT RELEASE: APRIL MARCH QUARTERLY 9 MAY APRIL MONTHLY Key points: Results from the March NAB Monthly Business Survey indicate an overall

EMBARGOED UNTIL:.AM TUESDAY APRIL NAB MONTHLY BUSINESS SURVEY MARCH NEXT RELEASE: APRIL MARCH QUARTERLY 9 MAY APRIL MONTHLY Key points: Results from the March NAB Monthly Business Survey indicate an overall

NAB Wellbeing Index: Q by NAB Group Economics

NAB Wellbeing Index: Q3 2015 by NAB Group Economics s wellbeing has risen to its highest level since mid-2013, with happiness, life satisfaction, life worth and anxiety all improving. Anxiety (especially

NAB Wellbeing Index: Q3 2015 by NAB Group Economics s wellbeing has risen to its highest level since mid-2013, with happiness, life satisfaction, life worth and anxiety all improving. Anxiety (especially

CHINA S ECONOMY AT A GLANCE

CHINA S ECONOMY AT A GLANCE AUGUST 217 CONTENTS Key points 2 Industrial Production 3 Investment 4 International trade - trade balance and imports International trade - exports 6 Retail sales and inflation

CHINA S ECONOMY AT A GLANCE AUGUST 217 CONTENTS Key points 2 Industrial Production 3 Investment 4 International trade - trade balance and imports International trade - exports 6 Retail sales and inflation

CHINA S ECONOMY AT A GLANCE

CHINA S ECONOMY AT A GLANCE MARCH 217 CONTENTS Key points 2 National People's Congress 3 Industrial Production 4 Investment 5 International trade - trade balance and imports International trade - exports

CHINA S ECONOMY AT A GLANCE MARCH 217 CONTENTS Key points 2 National People's Congress 3 Industrial Production 4 Investment 5 International trade - trade balance and imports International trade - exports

U.S. Economic Update by NAB Group Economics 15 January 2016

U.S. Economic Update by NAB Group Economics 15 January 216 Economic We expect another year of moderate growth in 216, with further labour market improvement and inflation starting to move back towards

U.S. Economic Update by NAB Group Economics 15 January 216 Economic We expect another year of moderate growth in 216, with further labour market improvement and inflation starting to move back towards

China s economy at a glance by NAB Group Economics

more give, less take China s economy at a glance by NAB Group Economics China s economic growth was stable in Q2, but can services maintain momentum post equity correction? An influx of new investors and

more give, less take China s economy at a glance by NAB Group Economics China s economic growth was stable in Q2, but can services maintain momentum post equity correction? An influx of new investors and

INDIA MONETARY POLICY OCTOBER 2017 NAB Group Economics

INDIA MONETARY POLICY OCTOBER 217 NAB Group The RBI held the benchmark policy Repo rate at 6%. This was expected, in light of recent higher readings for headline and core inflation. NAB is forecasting

INDIA MONETARY POLICY OCTOBER 217 NAB Group The RBI held the benchmark policy Repo rate at 6%. This was expected, in light of recent higher readings for headline and core inflation. NAB is forecasting

NAB Quarterly Business Survey

NAB Quarterly Business Survey by NAB Group Economics Embargoed until: 11:3am Wednesday 4 February 215 December Quarter 214 For more information contact: Alan Oster, Chief Economist: (3) 8634 2927 or 414

NAB Quarterly Business Survey by NAB Group Economics Embargoed until: 11:3am Wednesday 4 February 215 December Quarter 214 For more information contact: Alan Oster, Chief Economist: (3) 8634 2927 or 414

INDIA MONETARY POLICY OCTOBER 2016

INDIA MONETARY POLICY OCTOBER 1 NAB Group The RBI cut the policy rate by bp to.% at the October meeting. This decision was chaired by the -member Monetary Policy Committee under the newlyappointed Governor,

INDIA MONETARY POLICY OCTOBER 1 NAB Group The RBI cut the policy rate by bp to.% at the October meeting. This decision was chaired by the -member Monetary Policy Committee under the newlyappointed Governor,

MLC Quarterly Australian Wealth Sentiment Survey

Q4 14 More than 1 in 2 Australians believe they will not have money, almost 3% expect with less than $,, and 1 in will have to sell the family home. Post retirement, Australians also expect to have to

Q4 14 More than 1 in 2 Australians believe they will not have money, almost 3% expect with less than $,, and 1 in will have to sell the family home. Post retirement, Australians also expect to have to

Quarterly SME Survey December quarter 2012

Quarterly SME Survey December quarter 212 SME confidence & conditions weaken a touch in Q4 and poor relative to history; sentiment and activity of SMEs a touch weaker than their larger counterparts. Forward

Quarterly SME Survey December quarter 212 SME confidence & conditions weaken a touch in Q4 and poor relative to history; sentiment and activity of SMEs a touch weaker than their larger counterparts. Forward

Quarterly ASX 300 Business Survey March 2014

Embargoed until: 11:3am 28 April 214 Quarterly ASX 3 Business Survey March 214 Business conditions for ASX 3 maintained momentum in the first quarter of 214 the broader economy weakened as it dipped back

Embargoed until: 11:3am 28 April 214 Quarterly ASX 3 Business Survey March 214 Business conditions for ASX 3 maintained momentum in the first quarter of 214 the broader economy weakened as it dipped back

China Economic Briefing by NAB Group Economics July 2014

China Economic Briefing by NAB Group Economics July 21 Economic Government financial reforms could ease local government debt fears In late June, China s politburo agreed to fiscal and taxation reforms

China Economic Briefing by NAB Group Economics July 21 Economic Government financial reforms could ease local government debt fears In late June, China s politburo agreed to fiscal and taxation reforms

State Update: Northern Territory January 2016

State Update: Northern Territory January 1 more give, less take NAB Group Economics Contents Key points In Focus: LNG in context 3 Business and consumer sectors Residential property 5 Labour market Demographics

State Update: Northern Territory January 1 more give, less take NAB Group Economics Contents Key points In Focus: LNG in context 3 Business and consumer sectors Residential property 5 Labour market Demographics

Quarterly ASX 300 Business Survey March 2013

Quarterly ASX 3 Business Survey March 13 ASX 3 show greater resilience than the broader economy in Q1, with conditions stable. Finance, Business & Property considerably stronger. Confidence rebounded but

Quarterly ASX 3 Business Survey March 13 ASX 3 show greater resilience than the broader economy in Q1, with conditions stable. Finance, Business & Property considerably stronger. Confidence rebounded but

East Asian emerging market economies November 2014

East Asian emerging market economies November 2014 Key Points: Figure 1: Moderate economic growth set to continue Moderate sub-trend growth continues across the emerging market economies of East Asia (S

East Asian emerging market economies November 2014 Key Points: Figure 1: Moderate economic growth set to continue Moderate sub-trend growth continues across the emerging market economies of East Asia (S

NAB COMMERCIAL PROPERTY SURVEY Q1 2017

EMBARGOED UNTIL 11.30 AM 26 APRIL 17 NAB COMMERCIAL PROPERTY SURVEY Q1 17 Date April 17 NAB Behavioural & Industry Economics KEY FINDINGS Commercial property market sentiment climbed to a new high in Q1

EMBARGOED UNTIL 11.30 AM 26 APRIL 17 NAB COMMERCIAL PROPERTY SURVEY Q1 17 Date April 17 NAB Behavioural & Industry Economics KEY FINDINGS Commercial property market sentiment climbed to a new high in Q1

OCTOBER 2017 CONTENTS. Key points:

EMBARGOED UNTIL: 11.3AM TUESDAY 14 NOVEMBER 217 NAB MONTHLY BUSINESS SURVEY OCTOBER 217 Key points: Table 1: Key monthly business statistics * All data seasonally adjusted and subject to revision. Cost

EMBARGOED UNTIL: 11.3AM TUESDAY 14 NOVEMBER 217 NAB MONTHLY BUSINESS SURVEY OCTOBER 217 Key points: Table 1: Key monthly business statistics * All data seasonally adjusted and subject to revision. Cost

Canada Economic Update

Canada Economic Update NAB Group Economics July 24 Summary & Overview The Canadian economy recorded a moderate.3% increase during the March quarter,24, impacted by weather related disruptions. Group Economics

Canada Economic Update NAB Group Economics July 24 Summary & Overview The Canadian economy recorded a moderate.3% increase during the March quarter,24, impacted by weather related disruptions. Group Economics

Gold Market Update June 2015

Gold Market Update June 215 NAB Group Economics Key Points: A low-volatility global environment for equity and commodity markets in April and May to date have helped to keep gold prices largely range bound

Gold Market Update June 215 NAB Group Economics Key Points: A low-volatility global environment for equity and commodity markets in April and May to date have helped to keep gold prices largely range bound

China Briefing. International > Economics 17 April 2014

International > Economics 17 April 21 China Briefing There were few surprises in the latest Chinese data release, with the weakening trends evident since the latter part of last year continuing into the

International > Economics 17 April 21 China Briefing There were few surprises in the latest Chinese data release, with the weakening trends evident since the latter part of last year continuing into the

INDIA MONETARY POLICY AUGUST 2016

INDIA MONETARY POLICY AUGUST 16 NAB Group The RBI held the policy (Repo) rate at 6.%, as expected. NAB is forecasting a bp cut in rates to 6.% in the December quarter, on expectation of softer food prices.

INDIA MONETARY POLICY AUGUST 16 NAB Group The RBI held the policy (Repo) rate at 6.%, as expected. NAB is forecasting a bp cut in rates to 6.% in the December quarter, on expectation of softer food prices.

United States Economic Update by NAB Group Economics 10 April 2015

United States Economic Update by NAB Group Economics 1 April 15 Economic Economy has got off to a slow start in 15. While we expect it to be a temporary slowdown, we have revised our 15 forecast to 2.7%

United States Economic Update by NAB Group Economics 1 April 15 Economic Economy has got off to a slow start in 15. While we expect it to be a temporary slowdown, we have revised our 15 forecast to 2.7%

US ECONOMIC UPDATE FEBRUARY 2017

US Economic Update 1 February 17 US ECONOMIC UPDATE FEBRUARY 17 NAB Group Economics Moderate growth in the US is expected to continue, but with some strengthening later in the year if, as expected, the

US Economic Update 1 February 17 US ECONOMIC UPDATE FEBRUARY 17 NAB Group Economics Moderate growth in the US is expected to continue, but with some strengthening later in the year if, as expected, the

United States Economic Update by NAB Group Economics 9 September 2014

United States Economic Update by NAB Group Economics 9 September 214 Economic Indicators remain generally positive, consistent with our forecast of solid, above trend, growth of 3.% qoq (annualised) in

United States Economic Update by NAB Group Economics 9 September 214 Economic Indicators remain generally positive, consistent with our forecast of solid, above trend, growth of 3.% qoq (annualised) in

US ECONOMIC UPDATE NOV. 2016

US ECONOMIC UPDATE NOV. 016 Economy is solid although election result increases uncertainty NAB Group The election result increases uncertainty around the economic outlook as we wait to see what parts

US ECONOMIC UPDATE NOV. 016 Economy is solid although election result increases uncertainty NAB Group The election result increases uncertainty around the economic outlook as we wait to see what parts

CHINA S ECONOMY AT A GLANCE

CHINA S ECONOMY AT A GLANCE OCTOBER 217 CONTENTS Key points 2 Gross domestic product 3 Industrial Production 4 Investment 5 International trade - trade balance and imports International trade - exports

CHINA S ECONOMY AT A GLANCE OCTOBER 217 CONTENTS Key points 2 Gross domestic product 3 Industrial Production 4 Investment 5 International trade - trade balance and imports International trade - exports

AUSTRALIAN ECONOMIC UPDATE

AUSTRALIAN ECONOMIC UPDATE Business and government led growth NAB Group Economics December 17 Bottom line: Moderate growth momentum in Q3, mainly led by business and government investment. Households are

AUSTRALIAN ECONOMIC UPDATE Business and government led growth NAB Group Economics December 17 Bottom line: Moderate growth momentum in Q3, mainly led by business and government investment. Households are

India Monetary Policy by Group Economics August 2015

India Monetary Policy by Group Economics August 15 Summary & Overview The RBI maintained the Repo rate 7.5%, as expected. The Government and the RBI are broadly in agreement regarding the future composition

India Monetary Policy by Group Economics August 15 Summary & Overview The RBI maintained the Repo rate 7.5%, as expected. The Government and the RBI are broadly in agreement regarding the future composition

INDIA GDP & MONETARY POLICY JUNE 2017 NAB Group Economics

INDIA GDP & MONETARY POLICY JUNE 17 NAB Group The Indian economy experienced a demonetisation-induced slowdown in growth to.1% in the March quarter, with investment spending contracting. The RBI held the

INDIA GDP & MONETARY POLICY JUNE 17 NAB Group The Indian economy experienced a demonetisation-induced slowdown in growth to.1% in the March quarter, with investment spending contracting. The RBI held the

East Asian emerging market economies June 2014

East Asian emerging market economies June 2014 Key Points: Figure 1: Moderate economic growth set to continue Moderate sub-trend growth continues across the emerging market economies of East Asia (S Korea,

East Asian emerging market economies June 2014 Key Points: Figure 1: Moderate economic growth set to continue Moderate sub-trend growth continues across the emerging market economies of East Asia (S Korea,

AUGUST 2017 CONTENTS. Key points:

EMBARGOED UNTIL: 11.3AM TUESDAY 12 SEPTEMBER 217 NAB MONTHLY BUSINESS SURVEY AUGUST 217 Key points: Table 1: Key monthly business statistics * All data seasonally adjusted and subject to revision. Cost

EMBARGOED UNTIL: 11.3AM TUESDAY 12 SEPTEMBER 217 NAB MONTHLY BUSINESS SURVEY AUGUST 217 Key points: Table 1: Key monthly business statistics * All data seasonally adjusted and subject to revision. Cost

Chart 4: Other key indicators (Australia) Chart 5: Other key indicators (NSW FO firms v Other state FO firms)

Chart 5: Other key indicators (NSW FO firms v Other state FO firms)") NAB MULTINATIONAL BUSINESS SURVEY December Quarter 216 (Embargoed until 11.3am Tuesday 14 th March) By Group Economics FOREIGN OWNED MULTINATIONALS ENJOY STRONG CONDITIONS IN THEIR AUSTRALIAN OPERATIONS.

NAB MULTINATIONAL BUSINESS SURVEY December Quarter 216 (Embargoed until 11.3am Tuesday 14 th March) By Group Economics FOREIGN OWNED MULTINATIONALS ENJOY STRONG CONDITIONS IN THEIR AUSTRALIAN OPERATIONS.

NAB QUARTERLY SME SURVEY 2018 Q1 SME BUSINESS CONDITIONS STEADY AT THE START OF 2018

EMBARGOED UNTIL: 11:3AM AEST, 26 APRIL 218 NAB QUARTERLY SME SURVEY 218 Q1 SME BUSINESS CONDITIONS STEADY AT THE START OF 218 NAB Australian Economics SME business conditions were unchanged in 218 Q1,

EMBARGOED UNTIL: 11:3AM AEST, 26 APRIL 218 NAB QUARTERLY SME SURVEY 218 Q1 SME BUSINESS CONDITIONS STEADY AT THE START OF 218 NAB Australian Economics SME business conditions were unchanged in 218 Q1,

Quarterly Business Survey December quarter 2012

Embargoed until: 11.3am Thursday 7 February 13 Quarterly Business Survey December quarter 1 Business conditions weaken to lowest level since June quarter 9; weakness very apparent in construction, manufacturing

Embargoed until: 11.3am Thursday 7 February 13 Quarterly Business Survey December quarter 1 Business conditions weaken to lowest level since June quarter 9; weakness very apparent in construction, manufacturing

NAB Consumer Behaviour Survey: Q Summary Report by NAB Behavioural & Industry Economics Embargoed until: 11.

NAB Consumer Behaviour Survey: Q1 216 Summary Report by NAB Behavioural & Industry Embargoed until: 11.3am 7 April 216 Consumer anxiety falls again despite growing concern over government policy ahead

NAB Consumer Behaviour Survey: Q1 216 Summary Report by NAB Behavioural & Industry Embargoed until: 11.3am 7 April 216 Consumer anxiety falls again despite growing concern over government policy ahead

NAB Consumer Behaviour Survey: Q Summary Report by NAB Behavioural & Industry Economics Embargoed until: 11.30am 7 July 2016

NAB Consumer Behaviour Survey: Q2 216 Summary Report by NAB Behavioural & Industry Embargoed until: 11.3am 7 July 216 Consumer anxiety fell for the fourth straight quarter as lower anxiety associated with

NAB Consumer Behaviour Survey: Q2 216 Summary Report by NAB Behavioural & Industry Embargoed until: 11.3am 7 July 216 Consumer anxiety fell for the fourth straight quarter as lower anxiety associated with

INDIA GROWTH PUZZLE - OCTOBER 2017

India Economic Update 24 October 217 INDIA GROWTH PUZZLE - OCTOBER 217 NAB Group Economics The Indian economy has slowed considerably since the first half of 216. The demonetisation program and the recently-implemented

India Economic Update 24 October 217 INDIA GROWTH PUZZLE - OCTOBER 217 NAB Group Economics The Indian economy has slowed considerably since the first half of 216. The demonetisation program and the recently-implemented

Budget : Agriculture. May 2016

Budget 2016-17: Agriculture May 2016 We welcome the measures announced to support and promote Australian Agriculture. At NAB, we re confident in the future of Australian agriculture and we re proud to

Budget 2016-17: Agriculture May 2016 We welcome the measures announced to support and promote Australian Agriculture. At NAB, we re confident in the future of Australian agriculture and we re proud to

Quarterly Australian Commercial Property Survey: Q4 2013

Embargoed until: 11.3am Wednesday 6 February 14 Quarterly n Commercial Property Survey: Q4 13 Sentiment rises further in Q4, with NAB s Commercial Property reaching a -year high (but still negative overall).

Embargoed until: 11.3am Wednesday 6 February 14 Quarterly n Commercial Property Survey: Q4 13 Sentiment rises further in Q4, with NAB s Commercial Property reaching a -year high (but still negative overall).

International > Economics 31 January 2014 US Economic Update US GDP, 2013 Q4. QoQ % ch ppts

International > Economics 31 January 2014 US Economic Update US GDP, 2013 Q4 US GDP rose by a reasonably strong 3.2% (annualized rate) in the December quarter, completing a strong second half to the year.

International > Economics 31 January 2014 US Economic Update US GDP, 2013 Q4 US GDP rose by a reasonably strong 3.2% (annualized rate) in the December quarter, completing a strong second half to the year.

AUSTRALIAN ECONOMIC UPDATE

AUSTRALIAN ECONOMIC UPDATE GDP Q 1 Another decent outcome NAB Group Economics 5 September 1 Bottom line: GDP recorded another solid outcome in Q (+.9% q/q and +3.% y/y). Growth was again supported by domestic

AUSTRALIAN ECONOMIC UPDATE GDP Q 1 Another decent outcome NAB Group Economics 5 September 1 Bottom line: GDP recorded another solid outcome in Q (+.9% q/q and +3.% y/y). Growth was again supported by domestic

State Update: Victoria January 2015

State Update: Victoria January 15 more give, less take NAB Group Economics Content: Key points In Focus: A strengthening labour market in Victoria 3 Consumer and household sector Business sector 5 Commercial

State Update: Victoria January 15 more give, less take NAB Group Economics Content: Key points In Focus: A strengthening labour market in Victoria 3 Consumer and household sector Business sector 5 Commercial

CONSUMER ANXIETY FALLS TO ITS LOWEST LEVEL SINCE MID-2013 NAB CONSUMER ANXIETY INDEX NAB CONSUMER ANXIETY TRENDS

CONSUMER BEHAVIOUR SURVEY Q3 16 CONSUMER ANXIETY EASES AS CONCERNS OVER JOBS, THE COST OF LIVING AND GOVERNMENT POLICY CONTINUE TO MODERATE. NAB Behavioural & Industry Economics Consumer anxiety fell again

CONSUMER BEHAVIOUR SURVEY Q3 16 CONSUMER ANXIETY EASES AS CONCERNS OVER JOBS, THE COST OF LIVING AND GOVERNMENT POLICY CONTINUE TO MODERATE. NAB Behavioural & Industry Economics Consumer anxiety fell again

Asian Emerging Economies Update

International > Economics 3 October 213 Asian Emerging Economies Update Behind the volatility in the monthly data, the trend pace of growth in the emerging market economies of East Asia (which stretch

International > Economics 3 October 213 Asian Emerging Economies Update Behind the volatility in the monthly data, the trend pace of growth in the emerging market economies of East Asia (which stretch

NAB MONTHLY BUSINESS SURVEY JANUARY 2018 FURTHER CONFIRMATION OF BUSINESS STRENGTH

EMBARGOED UNTIL: :3AM AEDT, 3 FEBRUARY 28 NAB MONTHLY BUSINESS SURVEY JANUARY 28 FURTHER CONFIRMATION OF BUSINESS STRENGTH NAB Australian Economics Strong trend business conditions provide further confirmation

EMBARGOED UNTIL: :3AM AEDT, 3 FEBRUARY 28 NAB MONTHLY BUSINESS SURVEY JANUARY 28 FURTHER CONFIRMATION OF BUSINESS STRENGTH NAB Australian Economics Strong trend business conditions provide further confirmation

NAB MONTHLY BUSINESS SURVEY APRIL 2018 BUSINESS CONDITIONS AT RECORD LEVELS

EMBARGOED UNTIL: 11:3AM AEST, 7 MAY 218 NAB MONTHLY BUSINESS SURVEY APRIL 218 BUSINESS CONDITIONS AT RECORD LEVELS NAB Australian Economics There was a significant improvement in business conditions in

EMBARGOED UNTIL: 11:3AM AEST, 7 MAY 218 NAB MONTHLY BUSINESS SURVEY APRIL 218 BUSINESS CONDITIONS AT RECORD LEVELS NAB Australian Economics There was a significant improvement in business conditions in

NAB QUARTERLY BUSINESS SURVEY 2018 Q2 FAVOURABLE BUSINESS CONDITIONS PERSIST

EMBARGOED UNTIL: 11:3AM AEST, 19 JULY 218 NAB QUARTERLY BUSINESS SURVEY 218 Q2 FAVOURABLE BUSINESS CONDITIONS PERSIST NAB Australian Economics After strengthening to historically high levels in Q1, business

EMBARGOED UNTIL: 11:3AM AEST, 19 JULY 218 NAB QUARTERLY BUSINESS SURVEY 218 Q2 FAVOURABLE BUSINESS CONDITIONS PERSIST NAB Australian Economics After strengthening to historically high levels in Q1, business

EMBARGOED UNTIL: 11:30AM AEDT, 30 JANUARY 2018 NAB MONTHLY BUSINESS SURVEY

EMBARGOED UNTIL: 11:3AM AEDT, 3 JANUARY 18 NAB MONTHLY BUSINESS SURVEY THE STATE OF PLAY ACCORDING TO BUSINESS - DECEMBER 17 NAB Australian Economics The NAB Monthly Business Survey indicate a strong business

EMBARGOED UNTIL: 11:3AM AEDT, 3 JANUARY 18 NAB MONTHLY BUSINESS SURVEY THE STATE OF PLAY ACCORDING TO BUSINESS - DECEMBER 17 NAB Australian Economics The NAB Monthly Business Survey indicate a strong business

GDP growth rebounds in March quarter

International > Economics 29 April 2013 US Economic Update US GDP, 2013 Q1 US GDP rose by 2.5% (annualized rate) in the March quarter. Underlying trend is modest growth. Growth in the quarter was largely

International > Economics 29 April 2013 US Economic Update US GDP, 2013 Q1 US GDP rose by 2.5% (annualized rate) in the March quarter. Underlying trend is modest growth. Growth in the quarter was largely

Global & Australian Forecasts by NAB Group Economics

Global & Australian Forecasts by NAB Group Economics June 25 Key Points: There was no evidence of an acceleration in the pace of global growth in early 25. Weak GDP results in the US, UK and Canada outweighed

Global & Australian Forecasts by NAB Group Economics June 25 Key Points: There was no evidence of an acceleration in the pace of global growth in early 25. Weak GDP results in the US, UK and Canada outweighed

Foreign Trade: A closer look

India GDP & Monetary Policy by Group Economics December 15 Summary & Overview India s economy accelerated in the September quarter 15, with Real GDP growing by 7.4% yoy, up from 7% in the June quarter.

India GDP & Monetary Policy by Group Economics December 15 Summary & Overview India s economy accelerated in the September quarter 15, with Real GDP growing by 7.4% yoy, up from 7% in the June quarter.

NAB MONTHLY BUSINESS SURVEY JUNE 2018

EMBARGOED UNTIL: 11:3AM AEST, 1 JULY 218 NAB MONTHLY BUSINESS SURVEY JUNE 218 CONFIDENCE AND CONDITIONS HOLD STEADY NAB Australian Economics There was little change in headline business conditions and

EMBARGOED UNTIL: 11:3AM AEST, 1 JULY 218 NAB MONTHLY BUSINESS SURVEY JUNE 218 CONFIDENCE AND CONDITIONS HOLD STEADY NAB Australian Economics There was little change in headline business conditions and

NAB Manufacturing Activity Index Q1 2013

NAB Activity Index Q1 2013 The Activity Index improved in Q1, up to neutral levels driven largely by less negative levels for business confidence. The index implies no growth in quarterly manufacturing

NAB Activity Index Q1 2013 The Activity Index improved in Q1, up to neutral levels driven largely by less negative levels for business confidence. The index implies no growth in quarterly manufacturing

MLC Quarterly Australian Wealth Sentiment Survey Q1 2014

Q1 14 Consumer balance sheets are becoming more conservative, with a heavy emphasis on deposits and paying off debt, and a decline in intentions to invest in direct and superannuation. Less than % of Australians

Q1 14 Consumer balance sheets are becoming more conservative, with a heavy emphasis on deposits and paying off debt, and a decline in intentions to invest in direct and superannuation. Less than % of Australians

NAB MONTHLY BUSINESS SURVEY FEBRUARY 2018 BUSINESS CONDITIONS SURGE

EMBARGOED UNTIL: 11:3AM AEDT, 13 MARCH 18 NAB MONTHLY BUSINESS SURVEY FEBRUARY 18 BUSINESS CONDITIONS SURGE NAB Australian Economics Business conditions were at a record high in February, with the broad-based

EMBARGOED UNTIL: 11:3AM AEDT, 13 MARCH 18 NAB MONTHLY BUSINESS SURVEY FEBRUARY 18 BUSINESS CONDITIONS SURGE NAB Australian Economics Business conditions were at a record high in February, with the broad-based

NAB Quarterly Australian Consumer Anxiety Index: Q4 2013

Embargoed until: 11:30am Tuesday 14 January 2014 NAB Quarterly Australian Consumer Index: Q4 2013 Consumer anxiety rises amid ongoing weakness in the domestic economy. Consumer anxiety rose to 61.5 points

Embargoed until: 11:30am Tuesday 14 January 2014 NAB Quarterly Australian Consumer Index: Q4 2013 Consumer anxiety rises amid ongoing weakness in the domestic economy. Consumer anxiety rose to 61.5 points

India Monetary Policy Review

International > Economics April 1 India Monetary Policy Review At its first bi-monthly Monetary policy statement for 1-1, the RBI maintained the policy Repo rate at %, as expected. India s headline inflation

International > Economics April 1 India Monetary Policy Review At its first bi-monthly Monetary policy statement for 1-1, the RBI maintained the policy Repo rate at %, as expected. India s headline inflation

TRUMP, TRADE AND AUSTRALIA JULY 2016

TRUMP, TRADE AND AUSTRALIA JULY 2016 Republican candidate continues hard line on trade NAB Group Mr Trump s economic platform is radical in many respects, calling for big tax cuts, alongside continued

TRUMP, TRADE AND AUSTRALIA JULY 2016 Republican candidate continues hard line on trade NAB Group Mr Trump s economic platform is radical in many respects, calling for big tax cuts, alongside continued

CHINA S ECONOMY AT A GLANCE

CHINA S ECONOMY AT A GLANCE APRIL 218 CONTENTS Key points 2 Gross Domestic Product 3 Industrial Production 4 Investment 5 International trade - trade balance and imports International trade - exports 6

CHINA S ECONOMY AT A GLANCE APRIL 218 CONTENTS Key points 2 Gross Domestic Product 3 Industrial Production 4 Investment 5 International trade - trade balance and imports International trade - exports 6

NAB MONTHLY BUSINESS SURVEY NOVEMBER 2018

EMBARGOED UNTIL: 11:3AM AEDT, 11 DECEMBER 218 NAB MONTHLY BUSINESS SURVEY NOVEMBER 218 DOWNWARD TREND CONTINUES NAB Australian Economics Key Messages from the Survey: Both business conditions and confidence

EMBARGOED UNTIL: 11:3AM AEDT, 11 DECEMBER 218 NAB MONTHLY BUSINESS SURVEY NOVEMBER 218 DOWNWARD TREND CONTINUES NAB Australian Economics Key Messages from the Survey: Both business conditions and confidence

Embargoed until 11.30am Thursday 8 November % of Responses

Embargoed until 11.3am Thursday 8 November 212 Of respondents looking to undertake new works, 57 are looking to do so with land-banked stock held for future development (59 in Q1 12). NSW (33), Victoria

Embargoed until 11.3am Thursday 8 November 212 Of respondents looking to undertake new works, 57 are looking to do so with land-banked stock held for future development (59 in Q1 12). NSW (33), Victoria

Quarterly Australian Commercial Property Survey: Q2 2013

Summary Report Embargoed until: 11.3am Wednesday 7 August 13 Quarterly n Commercial Property Survey: Q2 13 Sentiment in the commercial property market weakened notably in Q2 13. The recent softening in

Summary Report Embargoed until: 11.3am Wednesday 7 August 13 Quarterly n Commercial Property Survey: Q2 13 Sentiment in the commercial property market weakened notably in Q2 13. The recent softening in

Global & Australian Forecasts by NAB Group Economics

Global & Australian Forecasts by NAB Group Economics Embargoed until: :3am Tuesday 4 July 25 July 25 Key Points: The Chinese share market correction and concerns that Greece could exit from the Euro-zone

Global & Australian Forecasts by NAB Group Economics Embargoed until: :3am Tuesday 4 July 25 July 25 Key Points: The Chinese share market correction and concerns that Greece could exit from the Euro-zone

NAB Quarterly Australian Wellbeing Index: Q4 2013

NAB Quarterly Australian Index: Q4 2013 National wellbeing deteriorates for the second straight quarter. The NAB Australian Index fell to 63.5 points in Q4 (64.4 points in Q3), with all four survey questions

NAB Quarterly Australian Index: Q4 2013 National wellbeing deteriorates for the second straight quarter. The NAB Australian Index fell to 63.5 points in Q4 (64.4 points in Q3), with all four survey questions

India GDP& Monetary Policy by Group Economics June 2015

India GDP& Monetary Policy by Group Economics June 21 Summary & Overview The Indian economy expanded by 7.% over the year to March 21. Services (9.2%) was the best performing, particularly Hospitality

India GDP& Monetary Policy by Group Economics June 21 Summary & Overview The Indian economy expanded by 7.% over the year to March 21. Services (9.2%) was the best performing, particularly Hospitality

Emerging Asia. NAB Group Economics September 2015

Emerging Asia NAB Group Economics September 215 1 Summary & Overview Contents Concerns about the extent of slowing in China, the anticipated rise in the US Fed Funds rate, and sharp declines in commodity

Emerging Asia NAB Group Economics September 215 1 Summary & Overview Contents Concerns about the extent of slowing in China, the anticipated rise in the US Fed Funds rate, and sharp declines in commodity

China Economic Comment

International > Economics 9 September 13 China Economic Comment China s policy puzzle There has been a large divergence in views over the future path of China s monetary policy/stimulus over the medium

International > Economics 9 September 13 China Economic Comment China s policy puzzle There has been a large divergence in views over the future path of China s monetary policy/stimulus over the medium

Gold Market Update. Gold Demand. Recent Price Developments. Australia > Commodities 3 May 2013

Australia > Commodities 3 May 213 Gold Market Update The gold price fell by 6.6% over April. Recent gold demand appears to have fallen sharply on news of soft US inflation, slowing Chinese growth as well

Australia > Commodities 3 May 213 Gold Market Update The gold price fell by 6.6% over April. Recent gold demand appears to have fallen sharply on news of soft US inflation, slowing Chinese growth as well

VIEW FROM NAB ECONOMICS VIEW FROM PROPERTY EXPERTS. NAB Behavioural & Industry Economics NAB HEDONIC HOUSE PRICE FORECASTS (%)*

*") NAB RESIDENTIAL PROPERTY SURVEY Q4-18 CURRENT MARKET SENTIMENT AND CONFIDENCE AMONG PROPERTY PROFESSIONALS SINK TO NEW SURVEY LOWS (PULLED DOWN BY NSW & VIC) SUGGESTING HOUSING MARKET DOWNTURN HAS FURTHER

NAB RESIDENTIAL PROPERTY SURVEY Q4-18 CURRENT MARKET SENTIMENT AND CONFIDENCE AMONG PROPERTY PROFESSIONALS SINK TO NEW SURVEY LOWS (PULLED DOWN BY NSW & VIC) SUGGESTING HOUSING MARKET DOWNTURN HAS FURTHER

CONTENTS CONTACT. AUTHORS Gerard Burg Tom Taylor EMBARGOED UNTIL: 11.30AM THURSDAY 15 MARCH 2018 THE FORWARD VIEW GLOBAL. NAB Group Economics

EMBARGOED UNTIL: 11.AM THURSDAY 1 MARCH 1 THE FORWARD VIEW GLOBAL MARCH 1 Summary sabre rattling ahead of a potential trade war? The global economic environment remains the most encouraging it has been

EMBARGOED UNTIL: 11.AM THURSDAY 1 MARCH 1 THE FORWARD VIEW GLOBAL MARCH 1 Summary sabre rattling ahead of a potential trade war? The global economic environment remains the most encouraging it has been

India GDP &Monetary Policy by Group Economics December 2014

India GDP &Monetary Policy by Group Economics December 1 Summary & Overview The Indian economy expanded by.3% over the year to the September quarter. Whilst lower than the June quarter s (.7%) result,

India GDP &Monetary Policy by Group Economics December 1 Summary & Overview The Indian economy expanded by.3% over the year to the September quarter. Whilst lower than the June quarter s (.7%) result,

THE FORWARD VIEW: AUSTRALIA JULY 2018

EMBARGOED UNTIL 11.3 AM WEDNESDAY 11 JULY 218 THE FORWARD VIEW: AUSTRALIA JULY 218 Forecasts broadly unchanged but new risks to watch OVERVIEW Fundamentally we have not changed our core views on the outlook

EMBARGOED UNTIL 11.3 AM WEDNESDAY 11 JULY 218 THE FORWARD VIEW: AUSTRALIA JULY 218 Forecasts broadly unchanged but new risks to watch OVERVIEW Fundamentally we have not changed our core views on the outlook

NAB COMMERCIAL PROPERTY SURVEY Q3 2017

EMBARGOED UNTIL 11.30 AM WEDNESDAY 18 OCTOBER 2017 NAB COMMERCIAL PROPERTY SURVEY Q3 2017 Date October 2017 NAB Behavioural & Industry Economics KEY FINDINGS Overall sentiment in commercial property markets

EMBARGOED UNTIL 11.30 AM WEDNESDAY 18 OCTOBER 2017 NAB COMMERCIAL PROPERTY SURVEY Q3 2017 Date October 2017 NAB Behavioural & Industry Economics KEY FINDINGS Overall sentiment in commercial property markets

Australian Markets Weekly A weekly outlook for Australia, key global economies and markets

Australia > Economics Australian Markets Weekly A weekly outlook for Australia, key global economies and markets 13 April 2015 Record employment and the NAB survey Chart 1: Employment growth close to stabilising

Australia > Economics Australian Markets Weekly A weekly outlook for Australia, key global economies and markets 13 April 2015 Record employment and the NAB survey Chart 1: Employment growth close to stabilising

NAB COMMERCIAL PROPERTY SURVEY Q2 2018

EMBARGOED UNTIL 11.30 AM WEDNESDAY 25 JULY 2018 NAB COMMERCIAL PROPERTY SURVEY Q2 2018 Date July 2018 NAB Behavioural & Industry Economics KEY FINDINGS The NAB Commercial Property Index fell 4 points to

EMBARGOED UNTIL 11.30 AM WEDNESDAY 25 JULY 2018 NAB COMMERCIAL PROPERTY SURVEY Q2 2018 Date July 2018 NAB Behavioural & Industry Economics KEY FINDINGS The NAB Commercial Property Index fell 4 points to

India GDP Update (Sept Qtr 2013)

") International > Economics December 13 India GDP Update (Sept Qtr 13) Indian growth accelerated to.%, in year ended terms, in the September Quarter, up from.% in the June quarter. An improvement in the

International > Economics December 13 India GDP Update (Sept Qtr 13) Indian growth accelerated to.%, in year ended terms, in the September Quarter, up from.% in the June quarter. An improvement in the

China Economic Update

International > Economics 2 February 21 China Economic Update Growing local government debt a degree of concern, but it can be carefully managed In late December, China s National Audit Office (NAO) released

International > Economics 2 February 21 China Economic Update Growing local government debt a degree of concern, but it can be carefully managed In late December, China s National Audit Office (NAO) released

Brief China Economic Update

International > Economics 1 uary 13 Brief China Economic Update Today s economic data releases for China came in broadly in line with expectations, providing evidence that the economic slowdown may have

International > Economics 1 uary 13 Brief China Economic Update Today s economic data releases for China came in broadly in line with expectations, providing evidence that the economic slowdown may have

NOVEMBER 2017 Summary

EMBARGOED UNTIL: 11.3AM THURSDAY 1 NOVEMBER 17 THE FORWARD VIEW GLOBAL NOVEMBER 17 Summary Global upturn continues, with growth next year set to just beat its long-term trend. Inflation remains subdued

EMBARGOED UNTIL: 11.3AM THURSDAY 1 NOVEMBER 17 THE FORWARD VIEW GLOBAL NOVEMBER 17 Summary Global upturn continues, with growth next year set to just beat its long-term trend. Inflation remains subdued

JULY 2018 Summary trade risks to the fore

EMBARGOED UNTIL: 11.3AM THURSDAY 1 JULY 18 THE FORWARD VIEW GLOBAL JULY 18 Summary trade risks to the fore The imposition on July of a % tariff by the on around $3b of imports from China, immediately followed

EMBARGOED UNTIL: 11.3AM THURSDAY 1 JULY 18 THE FORWARD VIEW GLOBAL JULY 18 Summary trade risks to the fore The imposition on July of a % tariff by the on around $3b of imports from China, immediately followed

NOVEMBER 2018 Summary global growth is above average but slowing

EMBARGOED UNTIL: 11.AM THURSDAY 1 NOVEMBER 1 THE FORWARD VIEW GLOBAL NOVEMBER 1 Summary global growth is above average but slowing While global growth remains above average, available GDP data for Q point

EMBARGOED UNTIL: 11.AM THURSDAY 1 NOVEMBER 1 THE FORWARD VIEW GLOBAL NOVEMBER 1 Summary global growth is above average but slowing While global growth remains above average, available GDP data for Q point

Gold Market Update. Recent Price Developments. Gold Demand. Australia > Commodities 23 August 2013

Australia > Commodities 23 August 213 Gold Market Update The price of gold fell by a notable 4.3% in July, but has stabilised more recently, recovering by a modest 2.8% over August to date. Spot gold is

Australia > Commodities 23 August 213 Gold Market Update The price of gold fell by a notable 4.3% in July, but has stabilised more recently, recovering by a modest 2.8% over August to date. Spot gold is

India Update - GDP. GDP Production and Partials. International Economics > India 13 June 2013

International Economics > India 13 June 13 India Update - GDP The Indian economy (Production, at factor cost) expanded by.% in the March 13 quarter. Annual growth over the 1-13 fiscal was %, the lowest

International Economics > India 13 June 13 India Update - GDP The Indian economy (Production, at factor cost) expanded by.% in the March 13 quarter. Annual growth over the 1-13 fiscal was %, the lowest

US-CHINA TARIFFS AN UPDATE SEPT. 2018

US-CHINA TARIFFS AN UPDATE SEPT. 2018 Impacts contained for now, but still risk of further escalation with ending unclear NAB Group Economics 21 September 2018 Recent tariff announcements are a modest

US-CHINA TARIFFS AN UPDATE SEPT. 2018 Impacts contained for now, but still risk of further escalation with ending unclear NAB Group Economics 21 September 2018 Recent tariff announcements are a modest

India Budget:

India Budget: 2014-15 NAB Group Economics July 2014 Summary & Overview India s new Finance Minister, Arun Jaitley, delivered his maiden Budget on the 10 th of July. It was a good document, albeit not a

India Budget: 2014-15 NAB Group Economics July 2014 Summary & Overview India s new Finance Minister, Arun Jaitley, delivered his maiden Budget on the 10 th of July. It was a good document, albeit not a

EMBARGOED UNTIL: 11.30AM WEDNESDAY 13 SEPTEMBER 2017 THE FORWARD VIEW - AUSTRALIA. RBA to remove some emergency accommodation in 2018

EMBARGOED UNTIL:.AM WEDNESDAY SEPTEMBER 7 THE FORWARD VIEW - AUSTRALIA SEPTEMBER 7 RBA to remove some emergency accommodation in Stronger employment, GDP and investment data have seen us revise our forecasts

EMBARGOED UNTIL:.AM WEDNESDAY SEPTEMBER 7 THE FORWARD VIEW - AUSTRALIA SEPTEMBER 7 RBA to remove some emergency accommodation in Stronger employment, GDP and investment data have seen us revise our forecasts

Gold Market Update. Recent Price Developments. Australia > Commodities 31 October 2013

Australia > Commodities 31 October 213 Gold Market Update The average price of gold eased by around 2½% in October, though the daily spot price generally strengthened over the second half of the month

Australia > Commodities 31 October 213 Gold Market Update The average price of gold eased by around 2½% in October, though the daily spot price generally strengthened over the second half of the month