Global economic outlook: Are we headed for another global recession? Sarah Hunter Head of Americas macro consulting

|

|

|

- June Quinn

- 5 years ago

- Views:

Transcription

1 Global economic outlook: Are we headed for another global recession? Sarah Hunter Head of Americas macro consulting 10 th March 2016

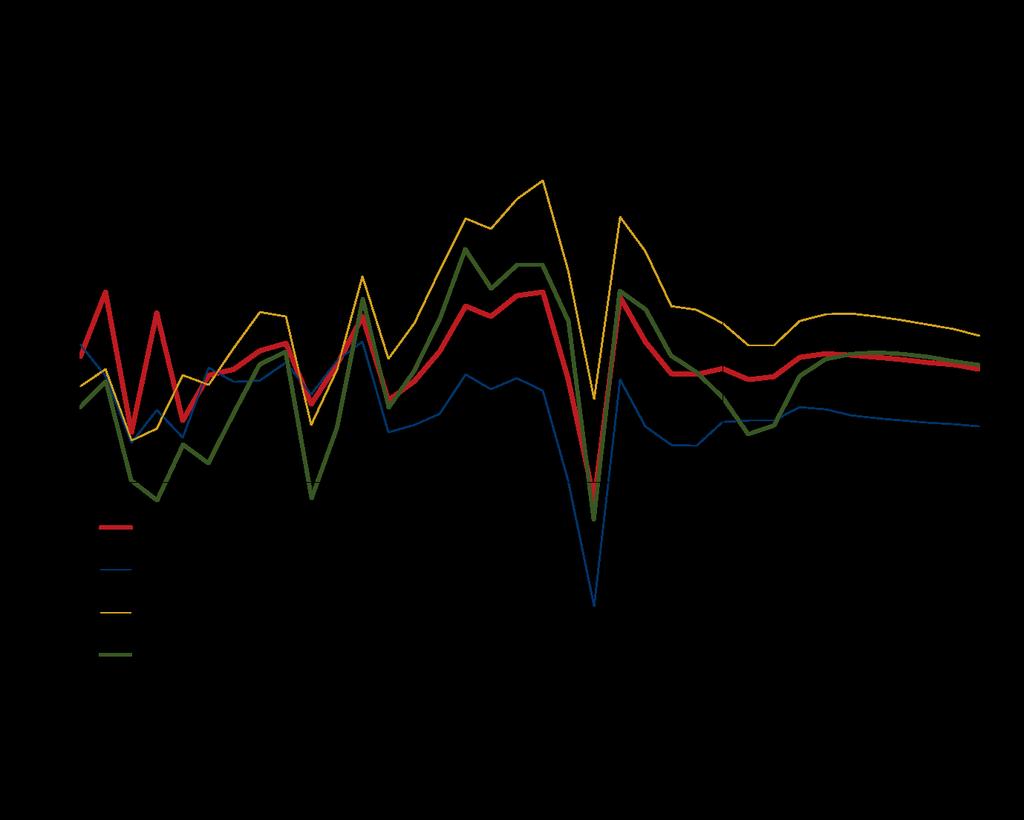

2 Oxford Economics forecast highlights Baseline world GDP forecast for 2016 now seen at 2.3% slowest pace of global growth since Sell-off in global financial markets since start of 2016 a factor; overall financial conditions have tightened significantly since mid Also some signs of weakness in real economy broadening from industry/commodity sector to services. Currently expect US economy to grow around 2% this year, down from a 2.6% forecast in December. Other major economies have also been downgraded; Japan (to 0.8% from 1.2%), Eurozone (to 1.6% from 1.8%), Brazil (to -3.6% from -2.6%) and Russia (to -2.4% from -0.9%). Our concern is that the financial market slump could create negative credit and confidence shocks and negative wealth effects, which will slow growth further. 2

3 Stress signals are becoming louder... US: High yield bond spread % spread, high yield-aaa corporate bond yields 18 World 16 recessions Average spread in recessions High yield bond spread Source : Oxford Economics/Haver Analytics US: Credit standards and equity prices % quarter Wilshire 5000 index (LHS) % Q Q Q Net % of banks tightening C&I loan standards (RHS, inverted) Source : Oxford Economics/Haver Analytics 60 80

4 and are starting to spill over to real activity World: PMI surveys Diffusion index, 50=neutral US composite PMI World: Economic surprise indices % G Global manufacturing PMI China Caixin manufacturing PMI Emerging markets Source : Oxford Economics/Haver Analytics Source : Oxford Economics/Citigroup 4

5 with global growth forecast weakest since 2009 World: Industrial output and recessions % quarter World: GDP % year 5 4 Long-term average Forecast World recessions G7 industrial output Source : Oxford Economics/Haver Analytics Source : Oxford Economics/Haver Analytics 2016 growth set to be the lowest since the recession year of Considerable downgrade since mid-2015 reflecting weaker incoming data and big financial market sell-off. Weakness in the world economy is still mostly centred in industry; manufacturing in the G7 is likely to be in a technical recession at the moment. And there have been tentative signs of softening activity in services too in January surveys e.g. in the US and Eurozone. Positive factors for services and consumption are low oil prices and still-solid property markets in most advanced economies but property markets have tended to move with stocks in recent years and there is weakness in some emerging and Asian property markets. 5

6 Overall picture amber alert We conclude that the situation is one of amber alert, not red alert High frequency economic data do not suggest recession but some financial market indicators are consistent with past recession periods All these indicators are fallible; the financial indicators tend to flag recessions around 50% of the time Current conditions are quite similar to , a period of weakening world growth rather than recession World growth could edge down to 2% or even below this year, a very slow pace The last time this happened, we got QE3 from the Fed. Where is the circuit-breaker this time? 6 Current risk indicators and historical context Indicator Current Average 3 months Worst point in level before recessions recessions (av.) G7 Industrial output, qoq World stocks, 6m chge Real non-oil commodity prices, 6m chge US high yield spread, % US corporate credit standards, % Source: Oxford Economics

7 What could the alternative look like? Financial fragility Chinese hard landing (15%) Housing sales slump sharply, triggering renewed house price falls and a sharp fall in housing construction. Domestic and external confidence is hit hard, resulting in lower FDI inflows, private investment and consumption The shock to growth spills over to emerging economies and sparks major currency realignment Geopolitical tensions (2%) A dramatic worsening in Saudi-Iranian relations triggers a violent reversal of recent oil price declines Crude oil prices rise back above $80 per barrel While the disruption is relatively short-lived, the global impact is material and varies hugely across countries Financial market contagion (10%) Amid signs of weakening growth, the current market gloom persists and weighs on global growth Equity price falls generate negative wealth effects, consumer and business confidence fade, and credit conditions tighten The Fed responds and reverses course; but some EMs are forced into rate hikes to defend their currencies Commodity demand weakness (10%) Oil prices fall further as global demand weakness weighs on commodity markets At current low oil prices, that drags modestly on global growth The boost to energy importers is outweighed by strains placed on exporter sovereigns and the US shale industry Emerging market commodity producers and the US are among those hit hardest Domestic demand fragility

8 US locomotive: A muffled whistle as we enter

9 Service sector still holding up, but mfg contracting 9

10 Domestic fundamentals remain quite strong Jan , , ,000 10

11 Maturing labor market will mean smaller job gains 11

12 but wage growth should pick up the income baton 12

13 Housing continues gradual recovery Drivers: Income growth Low interest rates Modest home price inflation Pent-up demand 13

14 Headwinds from strong $ and weak global growth 14

15 IP technically in a recession, but not truly Only 26% of manufacturing sector contracting in December

16 Fed to tighten at most 50bps this year 16

17 Eurozone: H2 weakness to extend into 2016 Eurozone Composite PMI & GDP Index GDP (RHS) Composite PMI (LHS) % change q/q Eurozone: Industrial production and manu. PMI Index % 3-month on 3-month Manufacturing PMI (LHS) 6 Industrial production excluding construction (RHS) Source : Oxford Economics/Haver Analytics/Markit Source : Oxford Economics/Haver Analytics 17

18 Deposit rate to move deeper into negative territory The ECB look set to implement further monetary easing this month, as inflation expectations and forecasts drop back towards zero. We think that major changes to the QE programme are unlikely and that the main policy initiative will be a 20bp reduction in the deposit rate. Given concerns about the associated tax on banks, such a change may be augmented by a tiering of the deposit rate. Eurozone: CPI Inflation (Bottom-up f'cast model) % y/y / contr ibution Core Energy Food alcohol and tobacco Headline Source : Oxford Economics/Haver Analytics Forecast 18

19 Japan: GDP growth close to 1% pa in 16 and 17 19

20 Long-term rates turn negative 20

21 as stronger exchange rate hurts profits and exports 21

22 China: Real growth slowed more than data show Real GDP growth % y/y GDP, Oxford Econmics estimate GDP, NBS Source: Oxford Economics, CEIC Data 22

23 Truly a two-track economy Real growth per sector % yoy Primary Secondary Tertiary Source: Oxford Economics, CEIC Data Nominal growth per sector % yoy Primary Secondary Tertiary Source: Oxford Economics, CEIC Data 23

24 ...with excess capacity in industry still on the rise Production and capacity in industry 2007=100 Value added in industry 250 Production capacity in industry* 200 Excess capacity (RHS) % Source: Oxford Economics, CEIC Data * From growth accounting 24

25 Financial leverage is rising Bank lending and total social financing % GDP 200 Total social financing 150 Bank loans Source: Oxford Economics, CEIC Data 25

26 and capital outflows have accelerated China: Financial capital flows US$bn Composition net financial outflows (Q3 2015) Chinese outflows other than foreign lending 16% Repayment foreign loans 23% Errors and omissions BOP -150 Foreign assets -200 Foreign liabilities Net financial flows Source : Oxford Economics, CEIC Data Foreign lending 31% Source: Oxford Economics, CEIC Data Repatriation foreign inflows 30% 26

27 Growth is expected to slow as economy rebalances 27

28 Commodity-dependent EMs continue to struggle 28

29 with Russia and Brazil in outright recessions BRICs: Manufacturing Purchasing Managers' Index Index, breakeven level= China Russia India Brazil Source : PMI/Markit/China NBS/Haver Analytics 29

30 Oil supply/demand balance not restored until 2017? Global Demand chg mb/d Global Supply chg mb/d o/w OPEC o/w US Stock Build Brent Oil Price Source: Oxford Economics/ IEA 30

31 Global forecast summary 31 World GDP growth % change on previous year Real GDP North America United States Canada Europe Eurozone Germany France Italy UK EU Asia Japan Emerging Asia, excl Japan China India World World 2005 PPPs World trade

32 What could the alternative look like? Financial fragility Chinese hard landing (15%) Housing sales slump sharply, triggering renewed house price falls and a sharp fall in housing construction. Domestic and external confidence is hit hard, resulting in lower FDI inflows, private investment and consumption The shock to growth spills over to emerging economies and sparks major currency realignment Geopolitical tensions (2%) A dramatic worsening in Saudi-Iranian relations triggers a violent reversal of recent oil price declines Crude oil prices rise back above $80 per barrel While the disruption is relatively short-lived, the global impact is material and varies hugely across countries Financial market contagion (10%) Amid signs of weakening growth, the current market gloom persists and weighs on global growth Equity price falls generate negative wealth effects, consumer and business confidence fade, and credit conditions tighten The Fed responds and reverses course; but some EMs are forced into rate hikes to defend their currencies Commodity demand weakness (10%) Oil prices fall further as global demand weakness weighs on commodity markets At current low oil prices, that drags modestly on global growth The boost to energy importers is outweighed by strains placed on exporter sovereigns and the US shale industry Emerging market commodity producers and the US are among those hit hardest Domestic demand fragility

33 Alternative 1: China hard landing Domestic financial stress buildings in China, with banks non-performing loans rising, house prices dropping sharply and the equity market undergoing further falls. Investment collapses as credit dries up and demand for housing falls, and consumers cut back on their spending as a result of falling real incomes and weaker confidence. Outflows spike, as investors pull out of China. The authorities intervene to stabilise the currency, and allow it to depreciate by 10% relative to the USD. Other emerging market currencies also depreciate, while the JPY and EUR gain on a trade-weighted basis. 33

34 China hard landing: Impact on GDP 34

35 Alternative 2: Financial market contagion With real economic indicators showing signs of weakness, this scenario assumes that conditions worsen further in financial markets. Equity prices fall, particularly in the US where stocks remain overvalued, consumer and business confidence drops and credit conditions tighten globally. The US is hit hard, as the epicentre of the scenario. But contagion means that all countries experience a deterioration in financial conditions, particularly vulnerable EMs who experience a flight away from their assets. 35

36 Financial market contagion: Impact on GDP 36

37 Alternative 3: Commodity demand weakens further In this scenario demand for commodities weakens further, increasing the pressure in commodity-dependent economies. Emerging Markets such as Russia and Saudi Arabia are badly affected, and the impact is also felt in Australia, Canada and even the US, where the extraction sector sees sharp falls in equity prices and rises in corporate spreads. The impact on the rest of the world is limited. Growth is slowed by the downturn in the US and other commodity producers, but this is broadly offset by the positive boost provided by lower commodity prices. 37

38 Commodity demand weakens further: Impact on GDP 38

39 Thank you! Any questions? Sarah Hunter:

Fed monetary policy amid a global backdrop of negative interest rates

Fed monetary policy amid a global backdrop of negative interest rates Kathy Bostjancic Head of US Macro Investor Services kathybostjancic@oxfordeconomics.com April 2016 Oxford Economics forecast highlights

Fed monetary policy amid a global backdrop of negative interest rates Kathy Bostjancic Head of US Macro Investor Services kathybostjancic@oxfordeconomics.com April 2016 Oxford Economics forecast highlights

Global Risk Outlook May 2016

Global Risk Outlook May 2016 Scott Livermore Managing Director and COO slivermore@oxfordeconomics.com About Oxford Economics Oxford Economics is a world leader in global forecasting and quantitative analysis.

Global Risk Outlook May 2016 Scott Livermore Managing Director and COO slivermore@oxfordeconomics.com About Oxford Economics Oxford Economics is a world leader in global forecasting and quantitative analysis.

Global MT outlook: Will the crisis in emerging markets derail the recovery?

Global MT outlook: Will the crisis in emerging markets derail the recovery? John Walker Chairman and Chief Economist jwalker@oxfordeconomics.com March 2014 Oxford Economics Oxford Economics is one of the

Global MT outlook: Will the crisis in emerging markets derail the recovery? John Walker Chairman and Chief Economist jwalker@oxfordeconomics.com March 2014 Oxford Economics Oxford Economics is one of the

Emerging Markets Weekly Economic Briefing

Emerging Markets Weekly Economic Briefing The risks of renewed capital flight from emerging markets Recent episodes of capital flight from emerging markets have highlighted the vulnerability of a number

Emerging Markets Weekly Economic Briefing The risks of renewed capital flight from emerging markets Recent episodes of capital flight from emerging markets have highlighted the vulnerability of a number

World Economic outlook

Frontier s Strategy Note: 01/23/2014 World Economic outlook IMF has just released the World Economic Update on the 21st January 2015 and we are displaying the main points here. Even with the sharp oil

Frontier s Strategy Note: 01/23/2014 World Economic outlook IMF has just released the World Economic Update on the 21st January 2015 and we are displaying the main points here. Even with the sharp oil

Eurozone Economic Watch Higher growth forecasts for January 2018

Eurozone Economic Watch Higher growth forecasts for 2018-19 January 2018 Eurozone Economic Watch January 2018 Eurozone: Higher growth forecasts for 2018-19 Our MICA-BBVA model estimates a broadly stable

Eurozone Economic Watch Higher growth forecasts for 2018-19 January 2018 Eurozone Economic Watch January 2018 Eurozone: Higher growth forecasts for 2018-19 Our MICA-BBVA model estimates a broadly stable

Global Economic Outlook

Global Economic Outlook Will the growth continue and at what pace? Latin American Conference São Paulo August 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary Information

Global Economic Outlook Will the growth continue and at what pace? Latin American Conference São Paulo August 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary Information

Summary. Economic Update 1 / 7 January 2019

Economic Update Economic Update 1 / 7 Summary 2 Global Global economic growth is expected to have peaked in 2018 at 3.0% and to ease to 2.8% in 2019. Tightening global monetary conditions, fading US fiscal

Economic Update Economic Update 1 / 7 Summary 2 Global Global economic growth is expected to have peaked in 2018 at 3.0% and to ease to 2.8% in 2019. Tightening global monetary conditions, fading US fiscal

Teetering on the brink: is the world heading for another financial crisis?

Teetering on the brink: is the world heading for another financial crisis? Adrian Cooper CEO & Chief Economist acooper@oxfordeconomics.com Peter Suomi Director petersuomi@oxfordeconomics.com October 2011

Teetering on the brink: is the world heading for another financial crisis? Adrian Cooper CEO & Chief Economist acooper@oxfordeconomics.com Peter Suomi Director petersuomi@oxfordeconomics.com October 2011

Eurozone Economic Watch. July 2018

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

Global Economy & the Machine Tool Outlook. Jan 2010 Rhys Herbert

Global Economy & the Machine Tool Outlook Jan 21 Rhys Herbert rherbert@oxfordeconomics.com Which scenario do you favour? Short-term outlook (a) W -shaped cycle Growth initially boosted by inventory rebuild

Global Economy & the Machine Tool Outlook Jan 21 Rhys Herbert rherbert@oxfordeconomics.com Which scenario do you favour? Short-term outlook (a) W -shaped cycle Growth initially boosted by inventory rebuild

Leumi. Global Economics Monthly Review. Arie Tal, Research Economist. May 8, The Finance Division, Economics Department. leumiusa.

Global Economics Monthly Review May 8, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report Key

Global Economics Monthly Review May 8, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report Key

Global investment event Winners and losers from the recent oil price rally

For client use only Global investment event Winners and losers from the recent oil price rally Since mid-2017, oil prices have been on an upward trend. Strong oil demand growth, OPECled production cuts,

For client use only Global investment event Winners and losers from the recent oil price rally Since mid-2017, oil prices have been on an upward trend. Strong oil demand growth, OPECled production cuts,

Global PMI. Global growth lifted by emerging market upturn. August 8 th 2016

Global PMI Global growth lifted by emerging market upturn August 8 th 2016 2 Global PMI buoyed by emerging market upturn Global economic growth edged higher at the start of the third quarter, but failed

Global PMI Global growth lifted by emerging market upturn August 8 th 2016 2 Global PMI buoyed by emerging market upturn Global economic growth edged higher at the start of the third quarter, but failed

Global Economic Outlook Brittle Strength

Global Economic Outlook Brittle Strength RISI North American Conference October 2017 Lasse Sinikallas Director Macroeconomics Agenda 1. Global Snapshot Steady 2. North America Performing 3. China In Transition

Global Economic Outlook Brittle Strength RISI North American Conference October 2017 Lasse Sinikallas Director Macroeconomics Agenda 1. Global Snapshot Steady 2. North America Performing 3. China In Transition

The Global Economy Modest Improvement

Title line 1 Title line 2 The Global Economy Modest Improvement Name David Katsnelson, Director Title, date RISI Macroeconomic Service 3 June, 2015 1 Agenda 1. Global Snapshot 2. China 3. External Environment

Title line 1 Title line 2 The Global Economy Modest Improvement Name David Katsnelson, Director Title, date RISI Macroeconomic Service 3 June, 2015 1 Agenda 1. Global Snapshot 2. China 3. External Environment

Financial Market Outlook: Further Stock Gain on Faster GDP Rebound and Earnings Recovery. Year-end Target Raised

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: FurtherStock Gains Likely, Year-end Target Raised. Bond Under Pressure

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: FurtherStock Gains Likely, Year-end Target Raised. Bond Under Pressure

Global Economic Outlook

Global Economic Outlook Will growth continue and at what pace? International Containerboard Conference Chicago November 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary

Global Economic Outlook Will growth continue and at what pace? International Containerboard Conference Chicago November 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary

Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy February 2017 Global Stock Market Rally likely to Continue with Solid Q4 Earnings & Stronger 2017 Earnings, ECB

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy February 2017 Global Stock Market Rally likely to Continue with Solid Q4 Earnings & Stronger 2017 Earnings, ECB

SEPTEMBER Overview

Overview SEPTEMBER 214 Global growth. Global growth has been weaker than expected so far this year, as economic activity disappointed in a number of major countries in the first six months (Figure 1).

Overview SEPTEMBER 214 Global growth. Global growth has been weaker than expected so far this year, as economic activity disappointed in a number of major countries in the first six months (Figure 1).

Global Economic Outlook

Global Economic Outlook Will growth continue and at what pace? North American Conference San Francisco October 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary Information

Global Economic Outlook Will growth continue and at what pace? North American Conference San Francisco October 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary Information

Eurozone Economic Watch

BBVA Research - Global Economic Watch December 2018 / 1 Eurozone Economic Watch December 2018 Eurozone GDP growth still slows gradually, but high uncertainty could take its toll GDP growth could grow by

BBVA Research - Global Economic Watch December 2018 / 1 Eurozone Economic Watch December 2018 Eurozone GDP growth still slows gradually, but high uncertainty could take its toll GDP growth could grow by

Summary of macroeconomic forecasts GDP Growth Inflation Curr. Account / GDP Fiscal balances / GDP

ECONOMIC RESEARCH DEPARTMENT Summary of macroeconomic forecasts GDP Growth Inflation Curr. Account / GDP Fiscal balances / GDP % 216 e 217 e 218 e 216 e 217 e 218 e 216 e 217 e 218 e 216 e 217 e 218 e

ECONOMIC RESEARCH DEPARTMENT Summary of macroeconomic forecasts GDP Growth Inflation Curr. Account / GDP Fiscal balances / GDP % 216 e 217 e 218 e 216 e 217 e 218 e 216 e 217 e 218 e 216 e 217 e 218 e

Global economy in charts

Global economy in charts Ian Stewart, Debapratim De, Tom Simmons & Peter Ireson Economics & Markets Research, Deloitte, London Summary 1. Global activity easing 2. Slowdown most apparent in euro area 3.

Global economy in charts Ian Stewart, Debapratim De, Tom Simmons & Peter Ireson Economics & Markets Research, Deloitte, London Summary 1. Global activity easing 2. Slowdown most apparent in euro area 3.

Prudential International Investments Advisers, LLC. Global Investment Strategy June 2009

Prudential International Investments Advisers, LLC. Global Investment Strategy June 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Prudential International Investments Advisers, LLC. Global Investment Strategy June 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Global growth fragile: The global economy is projected to grow at 3.5% in 2019 and 3.6% in 2020, 0.2% and 0.1% below October 2018 projections.

Monday January 21st 19 1:05pm International Prepared by: Ravi Kurjah, Senior Economic Analyst (Research & Analytics) ravi.kurjah@firstcitizenstt.com World Economic Outlook: A Weakening Global Expansion

Monday January 21st 19 1:05pm International Prepared by: Ravi Kurjah, Senior Economic Analyst (Research & Analytics) ravi.kurjah@firstcitizenstt.com World Economic Outlook: A Weakening Global Expansion

Prudential International Investments Advisers, LLC. Global Investment Strategy March 2010

Prudential International Investments Advisers, LLC. Global Investment Strategy March 2010 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Prudential International Investments Advisers, LLC. Global Investment Strategy March 2010 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Financial Market Outlook: Stock Rally Continues with Faster & Stronger GDP Rebound, Earnings Recovery & Liquidity

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Further Stock Gains with Macro Sweet Spot & Earnings Recovery.

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Further Stock Gains with Macro Sweet Spot & Earnings Recovery.

Commercial Cards & Payments Leo Abruzzese October 2015 New York

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

Eurozone. Economic Watch FEBRUARY 2017

Eurozone Economic Watch FEBRUARY 2017 EUROZONE WATCH FEBRUARY 2017 Eurozone: A slight upward revision to our GDP growth projections The recovery proceeded at a steady and solid pace in, resulting in an

Eurozone Economic Watch FEBRUARY 2017 EUROZONE WATCH FEBRUARY 2017 Eurozone: A slight upward revision to our GDP growth projections The recovery proceeded at a steady and solid pace in, resulting in an

Explore the themes and thinking behind our decisions.

ASSET ALLOCATION COMMITTEE VIEWPOINTS First Quarter 2017 These views are informed by a subjective assessment of the relative attractiveness of asset classes and subclasses over a 6- to 18-month horizon.

ASSET ALLOCATION COMMITTEE VIEWPOINTS First Quarter 2017 These views are informed by a subjective assessment of the relative attractiveness of asset classes and subclasses over a 6- to 18-month horizon.

OECD Interim Economic Projections Real GDP 1 Percentage change September 2015 Interim Projections. Outlook

ass Interim Economic Outlook 16 September 2015 Puzzles and uncertainties Global growth prospects have weakened slightly and become less clear in recent months. World trade growth has stagnated and financial

ass Interim Economic Outlook 16 September 2015 Puzzles and uncertainties Global growth prospects have weakened slightly and become less clear in recent months. World trade growth has stagnated and financial

Europe Outlook. Third Quarter 2015

Europe Outlook Third Quarter 2015 Main messages 1 2 3 4 5 Moderation of global growth and slowdown in emerging economies, with downside risks The recovery continues in the eurozone, but still marked by

Europe Outlook Third Quarter 2015 Main messages 1 2 3 4 5 Moderation of global growth and slowdown in emerging economies, with downside risks The recovery continues in the eurozone, but still marked by

Economic and market snapshot for January 2016

From left to right: Herman van Papendorp (Head of Macro Research and Asset Allocation), Sanisha Packirisamy (Economist) Economic and market snapshot for January 2016 Global economic developments United

From left to right: Herman van Papendorp (Head of Macro Research and Asset Allocation), Sanisha Packirisamy (Economist) Economic and market snapshot for January 2016 Global economic developments United

Nigeria's economic recovery Defining the path for economic growth

www.pwc.com/ng Nigeria's economic recovery Defining the path for economic growth Nigeria's economy has turned a corner The oil price shock, which started in mid-2014, severely affected the Nigerian economy.

www.pwc.com/ng Nigeria's economic recovery Defining the path for economic growth Nigeria's economy has turned a corner The oil price shock, which started in mid-2014, severely affected the Nigerian economy.

The Outlook for the World Economy

AIECE General Meeting Brussels, 14/15 November 218 The Outlook for the World Economy Downward risks are rising Klaus-Jürgen Gern Kiel Institute for the World Economy Forecasting Center Global growth has

AIECE General Meeting Brussels, 14/15 November 218 The Outlook for the World Economy Downward risks are rising Klaus-Jürgen Gern Kiel Institute for the World Economy Forecasting Center Global growth has

November PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy November 2015 John Praveen, PhD Chief Investment Strategist FOR MORE INFORMATION CONTACT: Theresa Miller Phone:

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy November 2015 John Praveen, PhD Chief Investment Strategist FOR MORE INFORMATION CONTACT: Theresa Miller Phone:

Prudential International Investments Advisers, LLC. Global Investment Strategy May 2008

Prudential International Investments Advisers, LLC. Global Investment Strategy May 2008 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Prudential International Investments Advisers, LLC. Global Investment Strategy May 2008 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Eurozone Economic Watch

BBVA Research Eurozone Economic Watch November 2018 / 1 Eurozone Economic Watch November 2018 Eurozone: Growth to recover in 4Q18, but concerns about the slowdown next year are growing Eurozone GDP growth

BBVA Research Eurozone Economic Watch November 2018 / 1 Eurozone Economic Watch November 2018 Eurozone: Growth to recover in 4Q18, but concerns about the slowdown next year are growing Eurozone GDP growth

Leumi. Global Economics Monthly Review. Arie Tal, Research Economist. July 12, Capital Markets Division, Economics Department. leumiusa.

Global Economics Monthly Review July 12, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report

Global Economics Monthly Review July 12, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report

Prudential International Investments Advisers, LLC. Global Investment Strategy & Outlook For 2009

Prudential International Investments Advisers, LLC. Global Investment Strategy & Outlook For 2009 December 17, 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact:

Prudential International Investments Advisers, LLC. Global Investment Strategy & Outlook For 2009 December 17, 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact:

Financial Market Outlook: Stocks Rebounding from July Correction, Further Gains Likely. Bond Yields Range Bound

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Stocks Rebounding from July Correction, Further Gains Likely. Bond

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Stocks Rebounding from July Correction, Further Gains Likely. Bond

Summary. Economic Update 1 / 7 December 2017

Economic Update Economic Update 1 / 7 Summary 2 Global Strengthening of the pickup in global growth, with GDP expected to increase 2.9% in 2017 and 3.1% in 2018. 3 Eurozone The eurozone recovery is upholding

Economic Update Economic Update 1 / 7 Summary 2 Global Strengthening of the pickup in global growth, with GDP expected to increase 2.9% in 2017 and 3.1% in 2018. 3 Eurozone The eurozone recovery is upholding

What could debt restructuring imply for the Eurozone? Adrian Cooper

What could debt restructuring imply for the Eurozone? Adrian Cooper acooper@oxfordeconomics.com June 2011 What could debt restructuring imply for the Eurozone? New stage in Eurozone debt crisis: first

What could debt restructuring imply for the Eurozone? Adrian Cooper acooper@oxfordeconomics.com June 2011 What could debt restructuring imply for the Eurozone? New stage in Eurozone debt crisis: first

PMI and economic outlook

PMI and economic outlook Chris Williamson Chief Business Economist, IHS Markit 1 st November 2017 2 PMI coverage Current coverage Expansion pipeline 40+ Countries covered 27,000+ Companies surveyed every

PMI and economic outlook Chris Williamson Chief Business Economist, IHS Markit 1 st November 2017 2 PMI coverage Current coverage Expansion pipeline 40+ Countries covered 27,000+ Companies surveyed every

Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy John Praveen, PhD Chief Investment Strategist FOR MORE INFORMATION CONTACT: Mayura Hooper Phone: 973-367-7930 Email:

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy John Praveen, PhD Chief Investment Strategist FOR MORE INFORMATION CONTACT: Mayura Hooper Phone: 973-367-7930 Email:

Global Investment Strategy. Scenario Analysis Winter 2012/13

Global Investment Strategy Scenario Analysis Winter 2012/13 Introduction Our central scenario is for a reacceleration in global growth in 2013 and 2014, which should be help risk assets outperform during

Global Investment Strategy Scenario Analysis Winter 2012/13 Introduction Our central scenario is for a reacceleration in global growth in 2013 and 2014, which should be help risk assets outperform during

Asia Watch. The US giveth, the US taketh away. Group Economics Emerging Markets Research. Group Economics: Enabling smart decisions.

Asia Watch Group Economics Emerging Markets Research 1 June 18 Arjen van Dijkhuizen Senior Economist Tel: +31 68 85 arjen.van.dijkhuizen@nl.abnamro.com The US giveth, the US taketh away Growth momentum

Asia Watch Group Economics Emerging Markets Research 1 June 18 Arjen van Dijkhuizen Senior Economist Tel: +31 68 85 arjen.van.dijkhuizen@nl.abnamro.com The US giveth, the US taketh away Growth momentum

OVERVIEW. The EU recovery is firming. Table 1: Overview - the winter 2014 forecast Real GDP. Unemployment rate. Inflation. Winter 2014 Winter 2014

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

South African Reserve Bank STATEMENT OF THE MONETARY POLICY COMMITTEE. Issued by Lesetja Kganyago, Governor of the South African Reserve Bank

South African Reserve Bank PRESS STATEMENT 24 January 2017 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the previous meeting of

South African Reserve Bank PRESS STATEMENT 24 January 2017 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the previous meeting of

Global growth weakening as some risks materialise

OECD INTERIM ECONOMIC OUTLOOK Global growth weakening as some risks materialise 6 March 2019 Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE blog: oecdecoscope.wordpress.com

OECD INTERIM ECONOMIC OUTLOOK Global growth weakening as some risks materialise 6 March 2019 Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE blog: oecdecoscope.wordpress.com

Financial Market Outlook & Strategy: Stocks Bottoming On Track to Recovery. Near-term Risks

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Stocks Bottoming On Track to Recovery. Near-term Risks John Praveen

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Stocks Bottoming On Track to Recovery. Near-term Risks John Praveen

Global PMI. Global economy set for robust Q2 growth. June 8 th IHS Markit. All Rights Reserved.

Global PMI Global economy set for robust Q2 growth June 8 th 2017 2 PMI indicates robust global growth in Q2 The global economy is on course for a robust second quarter, according to PMI survey data. The

Global PMI Global economy set for robust Q2 growth June 8 th 2017 2 PMI indicates robust global growth in Q2 The global economy is on course for a robust second quarter, according to PMI survey data. The

HIGHLIGHTS from CHAPTER 1: GLOBAL OUTLOOK DARKENING SKIES

Key Points HIGHLIGHTS from CHAPTER 1: GLOBAL OUTLOOK DARKENING SKIES Global growth has moderated, and it is expected to slow from 3 percent in 18 to.9 percent in. International trade and manufacturing

Key Points HIGHLIGHTS from CHAPTER 1: GLOBAL OUTLOOK DARKENING SKIES Global growth has moderated, and it is expected to slow from 3 percent in 18 to.9 percent in. International trade and manufacturing

Global PMI. Solid Q2 growth masks widening growth differentials. July 7 th IHS Markit. All Rights Reserved.

Global PMI Solid Q2 growth masks widening growth differentials July 7 th 2017 2 Widening developed and emerging world growth trends The global economy enjoyed further steady growth in June, according to

Global PMI Solid Q2 growth masks widening growth differentials July 7 th 2017 2 Widening developed and emerging world growth trends The global economy enjoyed further steady growth in June, according to

Saudi Economy: still shining

Saudi Economy: still shining - - - For comments and queries please contact the author: Fahad Alturki Senior Economist falturki@jadwa.com Real GDP growth 199 1 F Saudi Arabia World Advanced economies Head

Saudi Economy: still shining - - - For comments and queries please contact the author: Fahad Alturki Senior Economist falturki@jadwa.com Real GDP growth 199 1 F Saudi Arabia World Advanced economies Head

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

NOVEMBER 2018 Summary global growth is above average but slowing

EMBARGOED UNTIL: 11.AM THURSDAY 1 NOVEMBER 1 THE FORWARD VIEW GLOBAL NOVEMBER 1 Summary global growth is above average but slowing While global growth remains above average, available GDP data for Q point

EMBARGOED UNTIL: 11.AM THURSDAY 1 NOVEMBER 1 THE FORWARD VIEW GLOBAL NOVEMBER 1 Summary global growth is above average but slowing While global growth remains above average, available GDP data for Q point

GLOBAL OUTLOOK ECONOMIC WATCH. July 2017

GLOBAL OUTLOOK ECONOMIC WATCH July 2017 Positive global outlook, with projections revised across areas The global outlook remains positive. Our BBVA-GAIN model estimates global GDP growth at 1% QoQ in,

GLOBAL OUTLOOK ECONOMIC WATCH July 2017 Positive global outlook, with projections revised across areas The global outlook remains positive. Our BBVA-GAIN model estimates global GDP growth at 1% QoQ in,

All the BRICs dampening world trade in 2015

Aug Weekly Economic Briefing Emerging Markets All the BRICs dampening world trade in World trade in has been hit by an unexpectedly sharp drag from the very largest emerging economies. The weakness in

Aug Weekly Economic Briefing Emerging Markets All the BRICs dampening world trade in World trade in has been hit by an unexpectedly sharp drag from the very largest emerging economies. The weakness in

Global PMI. Global economic growth kicks higher at start of fourth quarter but outlook darkens. November 14 th 2016

Global PMI Global economic growth kicks higher at start of fourth quarter but outlook darkens November 14 th 2016 2 Global PMI at 11-month high in October Global economic growth kicked higher at the start

Global PMI Global economic growth kicks higher at start of fourth quarter but outlook darkens November 14 th 2016 2 Global PMI at 11-month high in October Global economic growth kicked higher at the start

SOUTH ASIA. Chapter 2. Recent developments

SOUTH ASIA GLOBAL ECONOMIC PROSPECTS January 2014 Chapter 2 s GDP growth rose to an estimated 4.6 percent in 2013 from 4.2 percent in 2012, but was well below its average in the past decade, reflecting

SOUTH ASIA GLOBAL ECONOMIC PROSPECTS January 2014 Chapter 2 s GDP growth rose to an estimated 4.6 percent in 2013 from 4.2 percent in 2012, but was well below its average in the past decade, reflecting

Global scenario service. December 2011

December Contents Executive Summary... Overview... scenario... Disorderly Eurozone default... China hard landing... 7 Corporate reawakening... Conclusion... December Executive Summary The global economic

December Contents Executive Summary... Overview... scenario... Disorderly Eurozone default... China hard landing... 7 Corporate reawakening... Conclusion... December Executive Summary The global economic

US Economy Update May 2014

US Economy Update May 2014 MACRO REPORT Key Insights Monica Defend Head of Global Asset Allocation Research Annalisa Usardi Economist, US & LATAM Global Asset Allocation Research Also contributing Riccardo

US Economy Update May 2014 MACRO REPORT Key Insights Monica Defend Head of Global Asset Allocation Research Annalisa Usardi Economist, US & LATAM Global Asset Allocation Research Also contributing Riccardo

Markit economic overview

Markit Economics Markit economic overview Global economic growth weakest since late-2012 April 13 th 2016 Global economic growth weakest since late-2012 Global economic growth was running at its weakest

Markit Economics Markit economic overview Global economic growth weakest since late-2012 April 13 th 2016 Global economic growth weakest since late-2012 Global economic growth was running at its weakest

An interim assessment

What is the economic outlook for OECD countries? An interim assessment Paris, 8 September 2011 11h00 Paris time Pier Carlo Padoan OECD Chief Economist and Deputy Secretary-General Activity has come close

What is the economic outlook for OECD countries? An interim assessment Paris, 8 September 2011 11h00 Paris time Pier Carlo Padoan OECD Chief Economist and Deputy Secretary-General Activity has come close

Global Economic Prospects

Global Economic Prospects Assuring growth over the medium term Andrew Burns DEC Prospects Group January 213 1 Despite better financial conditions, stronger growth remains elusive More than 4 years after

Global Economic Prospects Assuring growth over the medium term Andrew Burns DEC Prospects Group January 213 1 Despite better financial conditions, stronger growth remains elusive More than 4 years after

Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy March 2017 Global Stock Markets Rally likely to Continue, Driven by Strong Earnings & Strengthening GDP Growth.

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy March 2017 Global Stock Markets Rally likely to Continue, Driven by Strong Earnings & Strengthening GDP Growth.

Global Investment Strategy. Scenario Analysis Autumn 2012

Global Investment Strategy Scenario Analysis Autumn 212 Introduction 2 The combination of bullish investors, low market volatility and low financial stress suggests that risk assets are vulnerable to a

Global Investment Strategy Scenario Analysis Autumn 212 Introduction 2 The combination of bullish investors, low market volatility and low financial stress suggests that risk assets are vulnerable to a

In the US The Euro area, e 2019 e e 2019 e Advanced 2,3 2,4 1,7 1,8 2,1 1,9 Euro Area 2,6 2,2 1,7 1,5 1,8 1,8

In the US, activity wasn t as dynamic as expected at the start of the year, however this could be due to temporary factors Economy should continue to expand at a 3 percent path or so in 218, thanks to

In the US, activity wasn t as dynamic as expected at the start of the year, however this could be due to temporary factors Economy should continue to expand at a 3 percent path or so in 218, thanks to

March PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy March 2016 Stocks likely to Recover Further with Improving Growth & Recession Fears Easing, Fresh Stimulus from

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy March 2016 Stocks likely to Recover Further with Improving Growth & Recession Fears Easing, Fresh Stimulus from

Prudential International Investments Advisers, LLC. Global Investment Strategy February 2010

Prudential International Investments Advisers, LLC. Global Investment Strategy February 2010 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Prudential International Investments Advisers, LLC. Global Investment Strategy February 2010 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Our goal is to provide a clear perspective on the global financial markets, as well as a logical framework to discuss them, thereby enabling

Our goal is to provide a clear perspective on the global financial markets, as well as a logical framework to discuss them, thereby enabling investors to recognize both the opportunities and risks that

Our goal is to provide a clear perspective on the global financial markets, as well as a logical framework to discuss them, thereby enabling investors to recognize both the opportunities and risks that

Prudential International Investments Advisers, LLC. Global Investment Strategy October 2009

Prudential International Investments Advisers, LLC. Global Investment Strategy October 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Prudential International Investments Advisers, LLC. Global Investment Strategy October 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

The Global Economy Heightened Risks

The Global Economy Heightened Risks RISI North American Conference 5 October, 2016 David Katsnelson Director, Macroeconomics Agenda 1. Global Snapshot 2. USA Steady Growth 3. Europe Growing Slowly 4. China

The Global Economy Heightened Risks RISI North American Conference 5 October, 2016 David Katsnelson Director, Macroeconomics Agenda 1. Global Snapshot 2. USA Steady Growth 3. Europe Growing Slowly 4. China

Spain Economic Outlook Q FIRST QUARTER. Economic Outlook. Spain. Economic Outlook. Spain

Economic Outlook FIRST QUARTER 2016 Spain Economic Outlook Spain The world economy will continue to grow, but at a slower pace than in the past and with more risks Spain's economy has started 2016 with

Economic Outlook FIRST QUARTER 2016 Spain Economic Outlook Spain The world economy will continue to grow, but at a slower pace than in the past and with more risks Spain's economy has started 2016 with

Global Sovereign Conference Singapore 6 September

Global Sovereign Conference Singapore September 1 --- --- Politics, Populism and the Global Economy Brian Coulton Chief Economist --- --- Key Messages World economy muddling along but global macro risks

Global Sovereign Conference Singapore September 1 --- --- Politics, Populism and the Global Economy Brian Coulton Chief Economist --- --- Key Messages World economy muddling along but global macro risks

GLOBAL ECONOMICS CHART BOOK

th January 9 GLOBAL ECONOMICS CHART BOOK The cycle is turning Many of the indicators that tend to turn first around peaks in the business cycle are now flashing red in several major economies. Admittedly,

th January 9 GLOBAL ECONOMICS CHART BOOK The cycle is turning Many of the indicators that tend to turn first around peaks in the business cycle are now flashing red in several major economies. Admittedly,

Global Macroeconomic Monthly Review

Global Macroeconomic Monthly Review October 16 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Please see disclaimer on the last page of this report 1 Key Issues Global

Global Macroeconomic Monthly Review October 16 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Please see disclaimer on the last page of this report 1 Key Issues Global

AUGUST 2018 Summary growth remains above trend, but risks a concern

EMBARGOED UNTIL: 11.3AM THURSDAY 1 AUGT 1 THE FORWARD VIEW GLOBAL AUGT 1 Summary growth remains above trend, but risks a concern As expected, after hitting a soft patch in Q1, major advanced economy growth

EMBARGOED UNTIL: 11.3AM THURSDAY 1 AUGT 1 THE FORWARD VIEW GLOBAL AUGT 1 Summary growth remains above trend, but risks a concern As expected, after hitting a soft patch in Q1, major advanced economy growth

Growth has peaked amidst escalating risks

OECD ECONOMIC OUTLOOK Growth has peaked amidst escalating risks 1 November 18 Ángel Gurría OECD Secretary-General Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE

OECD ECONOMIC OUTLOOK Growth has peaked amidst escalating risks 1 November 18 Ángel Gurría OECD Secretary-General Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE

Market Insight Economy and Asset Classes December Oil Prices Downtrending: The Real Global Economic Stimulus

Market Insight Economy and Asset Classes December 2014 Oil Prices Downtrending: The Real Global Economic Stimulus 2 Equities Markets Feature In Citi analysts view, the expansion phase the US are enjoying

Market Insight Economy and Asset Classes December 2014 Oil Prices Downtrending: The Real Global Economic Stimulus 2 Equities Markets Feature In Citi analysts view, the expansion phase the US are enjoying

Taiwan chart book Policy remains neutral

Economics Taiwan chart book Policy remains neutral Group Research October 18 Ma Tieying Economist Please direct distribution queries to Violet Lee +6 687881 violetleeyh@dbs.com Charts of the month Export

Economics Taiwan chart book Policy remains neutral Group Research October 18 Ma Tieying Economist Please direct distribution queries to Violet Lee +6 687881 violetleeyh@dbs.com Charts of the month Export

Global Economic and Market Outlook for Gavyn Davies, Chairman, Fulcrum Asset Management

Global Economic and Market Outlook for 2018 Gavyn Davies, Chairman, Fulcrum Asset Management After many years of persistent downgrades to consensus GDP forecasts, 2017 has seen the first upgrades since

Global Economic and Market Outlook for 2018 Gavyn Davies, Chairman, Fulcrum Asset Management After many years of persistent downgrades to consensus GDP forecasts, 2017 has seen the first upgrades since

By John Praveen, Chief Investment Strategist of Prudential International Investments Advisers, LLC.*

By John Praveen, Chief Investment Strategist of Prudential International Investments Advisers, LLC.* For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

By John Praveen, Chief Investment Strategist of Prudential International Investments Advisers, LLC.* For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Global PMI. Global economy starts 2017 on the front foot, PMI at 22-month high. February 8 th 2016

Global PMI Global economy starts 2017 on the front foot, PMI at 22-month high February 8 th 2016 2016 IHS Markit. All Rights Reserved. 2 Global PMI at 22-month high The global economy started 2017 with

Global PMI Global economy starts 2017 on the front foot, PMI at 22-month high February 8 th 2016 2016 IHS Markit. All Rights Reserved. 2 Global PMI at 22-month high The global economy started 2017 with

Emerging Markets Weekly Economic Briefing

1 Emerging Markets Emerging Markets Weekly Economic Briefing Forecasts eased down again as trade remains sluggish We have cut our forecast for China again following weak growth in Q1. We now expect the

1 Emerging Markets Emerging Markets Weekly Economic Briefing Forecasts eased down again as trade remains sluggish We have cut our forecast for China again following weak growth in Q1. We now expect the

Global Economic Prospects. South Asia. June 2014 Andrew Burns

Global Economic Prospects South Asia June 214 Andrew Burns Main Messages 214 Global forecast has been downgraded, mainly reflecting one-off factors Financing conditions have eased temporarily, but are

Global Economic Prospects South Asia June 214 Andrew Burns Main Messages 214 Global forecast has been downgraded, mainly reflecting one-off factors Financing conditions have eased temporarily, but are

Global Macroeconomic Monthly Review

Global Macroeconomic Monthly Review August 14 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department 1 Please see disclaimer on the last page of this report Key Issues Global

Global Macroeconomic Monthly Review August 14 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department 1 Please see disclaimer on the last page of this report Key Issues Global

Russia: Macro Outlook for 2019

October 2018 Russia: Macro Outlook for 2019 Natalia Orlova Head of Alfa Bank Macro Insights +7 495 795 36 77 norlova@alfabank.ru Egypt Saudi Arabia Brazil S. Africa UAE Iraq China Japan US Mexico UK Russia

October 2018 Russia: Macro Outlook for 2019 Natalia Orlova Head of Alfa Bank Macro Insights +7 495 795 36 77 norlova@alfabank.ru Egypt Saudi Arabia Brazil S. Africa UAE Iraq China Japan US Mexico UK Russia

Markit economic overview

Markit Economics Markit economic overview PMI data highlight growing variations in likely policy paths 9 June 2015 Global growth slows for second month running in May Global economic growth edged lower

Markit Economics Markit economic overview PMI data highlight growing variations in likely policy paths 9 June 2015 Global growth slows for second month running in May Global economic growth edged lower

Inflation projection of Narodowy Bank Polski based on the NECMOD model

Economic Institute Inflation projection of Narodowy Bank Polski based on the NECMOD model Warsaw / 9 March Inflation projection of the NBP based on the NECMOD model Outline: Introduction Changes between

Economic Institute Inflation projection of Narodowy Bank Polski based on the NECMOD model Warsaw / 9 March Inflation projection of the NBP based on the NECMOD model Outline: Introduction Changes between

FIXED INCOME STRATEGY

12 QUARTERLY INVESTMENT STRATEGY FIXED INCOME STRATEGY GLOBAL FIXED INCOME FIXED INCOME DEVELOPED DM Government DM Credit EMERGING EM Government -- - N + ++ Our overall fixed income strategy is to stay

12 QUARTERLY INVESTMENT STRATEGY FIXED INCOME STRATEGY GLOBAL FIXED INCOME FIXED INCOME DEVELOPED DM Government DM Credit EMERGING EM Government -- - N + ++ Our overall fixed income strategy is to stay

In the US The Euro area, GDP Growth Inflation e 2020 e e 2020 e Advanced

In the US, activity has been buoyant so far, largely thanks to tax cuts. For the foreseeable period, a slowdown is more than a possibility Interest rates hikes and tariffs increases on worth $3bn of imports

In the US, activity has been buoyant so far, largely thanks to tax cuts. For the foreseeable period, a slowdown is more than a possibility Interest rates hikes and tariffs increases on worth $3bn of imports

Global Economic Prospects: Spillovers amid Weak Growth. Select Publications from DECPG

// Global Economic Prospects: Spillovers amid Weak Growth February M. Ayhan Kose Disclaimer! The views presented here are those of the authors and do NOT necessarily reflect the views and policies of the

// Global Economic Prospects: Spillovers amid Weak Growth February M. Ayhan Kose Disclaimer! The views presented here are those of the authors and do NOT necessarily reflect the views and policies of the

Three Big Global Questions

Three Big Global Questions Nick Kounis Head Macro & Financial Markets Research Marine Money Athens 14 October 2015 Will developed economies continue to recover? 2 US consumer making a comeback Job gains,

Three Big Global Questions Nick Kounis Head Macro & Financial Markets Research Marine Money Athens 14 October 2015 Will developed economies continue to recover? 2 US consumer making a comeback Job gains,

Global Update. 6 th October, Global Prospects. Contacts: Madan Sabnavis Chief Economist

Global Update Global Prospects 6 th October, 2010 Contacts: Madan Sabnavis Chief Economist 91-022-6754 3489 Samruddha Paradkar Associate Economist 91-022-6754 3407 Krithika Subramanian Associate Economist

Global Update Global Prospects 6 th October, 2010 Contacts: Madan Sabnavis Chief Economist 91-022-6754 3489 Samruddha Paradkar Associate Economist 91-022-6754 3407 Krithika Subramanian Associate Economist

Global Economic Prospects: A Fragile Recovery. June M. Ayhan Kose Four Questions

//7 Global Economic Prospects: A Fragile Recovery June 7 M. Ayhan Kose akose@worldbank.org Four Questions How is the health of the global economy? Recovery underway, broadly as expected How important is

//7 Global Economic Prospects: A Fragile Recovery June 7 M. Ayhan Kose akose@worldbank.org Four Questions How is the health of the global economy? Recovery underway, broadly as expected How important is

GDP Growth Inflation e 2018 e e 2018 e Advanced 1,6 2,1 1,9 0,8 1,6 1,7 Euro Area 1,7 2,1 1,6 0,2 1,5 1,1

GDP Growth % 216 217 e 218 e 216 217 e 218 e Advanced 1,6 2,1 1,9,8 1,6 1,7 United-States 1,6 2,3 2,6 1,3 1,9 2,3 Japan 1, 1,7 1, -,1,4,6 United-Kingdom 1,8 1,5 1,,6 2,8 2,8 Euro Area 1,7 2,1 1,6,2 1,5

GDP Growth % 216 217 e 218 e 216 217 e 218 e Advanced 1,6 2,1 1,9,8 1,6 1,7 United-States 1,6 2,3 2,6 1,3 1,9 2,3 Japan 1, 1,7 1, -,1,4,6 United-Kingdom 1,8 1,5 1,,6 2,8 2,8 Euro Area 1,7 2,1 1,6,2 1,5

South African Reserve Bank STATEMENT OF THE MONETARY POLICY COMMITTEE. Issued by Lesetja Kganyago, Governor of the South African Reserve Bank

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 20 November 2014 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 20 November 2014 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the