Enterprise Risk Management Economic Capital Modleing and the Financial Crisis

|

|

|

- Barnaby Hall

- 5 years ago

- Views:

Transcription

1 Risk Management and The Crisis Enterprise Risk Management Economic Capital Modleing and the Financial Crisis What worked and what did not

2 Insurance Industry Continues to Respond to Risk Dynamics Risk Sources and Complexity Have Increased Over Time Dynamic Fin l Analysis ERM and Economic Capital Risk Asset-Liability Management Cash Flow Testing Cash Flow Testing Asset-Liability Management Traditional Risk Management Traditional Risk Management Time

3 ERM for all companies? Nature and scope of ERM will vary based on: Complexity of a company Type of products offered Number of products offered Investments Risk Profile of the company Volatility of Earnings/potential significant capital loss (Risk profile) Financial Flexibility Strength of its Traditional Risk management

4 ERM Embedding Risk Management into your Corporate DNA ERM and Economic Capital model must be an integral part of the management process and decision making culture of the institution. Embed your business in ERM and ECM frameworks and then embed your ERM and ECM into your Business Risk awareness is properly embedded in the daily operating procedures employed across the organization

5 Risk Management and BCAR Best s Traditional Approach Weak Risk Management Strong Risk Management BCAR BCAR Guideline LOW HIGH EXPOSURE to EARNINGS and CAPITAL VOLATILITY

6 Impact of ERM - Example of Changing Business Strategy From Volatile to Stabile Lines Volatile Strategy A- Stable Strategy will become A+ sooner BCAR Average Return 160 = Minimum for A+ Today Future Time

7 Impact of ERM on Ratings Ins Co w/inadeq Return for Risk = B+ Ins Co w/adeq Return will become A- sooner Adeq Avg Return BCAR Inadeq Avg Return 130 = Minimum for A- Today Future Time

8 Best s Revised BCAR Approach Will consider allowing insurers to maintain lower BCAR levels relative to the guideline for its rating if they demonstrate: Superior traditional risk management fundamentals Superior capital management and financial flexibility Strong ERM characteristics Strong EC modeling capabilities Weak Risk Management BCAR Strong Risk Management BCAR Guidelines Low High Exposure to Earnings and Capital Volatility

9 Efficiency Frontier ` Strategy B Return Strategy C Strategy A Risk

10 Enhanced Efficiency Frontier Return Strategy X Strategy C Strategy B Strategy A Risk

11 ERM and Reduced Volatility

12 A.M. Best s Rating Evaluation Rating Considerations Secure A++ B+ B Vulnerable D Balance Sheet Strength Outstanding Enterprise Weak Operating Performance Business Profile Very Stable/Strong Strong / Sustainable Advantages Well-Diversified Risk Management Volatile/Poor Questionable Viability Competitive Disadvantages Concentrated Risk

13 ERM Framework and Culture Board & Senior Management Involvement Establishment and Communication of Risk Management Objectives Risk Tolerances Key Risk Metrics Defined Roles/Responsibilities/Oversight Risk Management Objectives and Incentive Compensation

14 ERM is about the E ERM is the process through which insurers identify, quantify, and manage risk on an enterprise-wide, holistic basis ERM takes into consideration the individual risks at hand, as well as any correlations and interdependencies of risk across the entire organization Insurers that create a more structured, integrated risk framework and apply it prudently can Increase the value of the firm and Provide financial security to the organization

15 Role of BCAR BCAR lives on as a baseline for the assessment of risk-adjusted capital for all insurers Many organizations do not have the scale or resources to support an Internal Capital Model Value of BCAR in rating process proven over time through our default statistics Next generation BCAR NOT an economic capital model Tie probability of default to the determination of required capital Incorporate more stochastic elements in the development of risk factors

16 BCAR Requirements Companies Without EC Output (Most of the U.S. Industry) BCAR requirements more closely linked to a company s relative ERM strength and earnings volatility An insurer with strong ERM and low volatility can operate closer to the BCAR guideline for its rating level An insurer with weak ERM and high volatility needs to maintain capital that is several notches above Best s minimum BCAR guidelines Companies With EC Output Best is encouraging leading edge insurers to share their EC output Companies with strong ERM and EC modeling capabilities may have capital requirements that fall below Best s BCAR guidelines, provided the EC output is: Used by management in strategic decision-making Produced by an EC model that Best views as robust

17 Economic Capital Models

18 AMB - ECM Framework Governance and Control Analytical Framework Statistical Quality Tests Calibration Test Valuation Methods Risk Metrics Economic Capital Model Use Test Dependencies and Correlations Time Horizons Validation Documentation

19 How will AMB gain comfort in the integrity of the ECM process and results? Independent assessment of an insurer s ECM process and results Statistical quality test (including appropriateness of methodology and assumptions of model) Calibration test (including extent to which stress and scenario testing is used to determine impact of tail events)

20 How will AMB gain comfort in the integrity of the ECM process and results? Independent assessment of an insurer s ECM process and results Use test and governance (including evaluation of governance and internal controls in place related to ECM) Performance measurement Compensation Pricing Reserving Capital allocation Strategic decision making

21 How will AMB gain comfort in the integrity of the ECM process and results? Objective is to better understand ECM vs. BCAR or other metrics Compare/contrast gross ECM results to BCAR, i.e. pre and post diversification benefit In aggregate, by LOB, by major risk type Compare/contrast net ECM results to BCAR, i.e. postdiversification benefit In aggregate, by LOB, by major risk type Reconcile results for current time period and understand trends

22 Internal Capital Models & Ratings Tier II AMB discussion of key elements of ICM process and results Analytical framework and granularity, flexibility, computability, tractability and auditability of the model Assumptions and scenario testing Timeliness and availability of data Applicability and relevance of data Sample length and relevance Time horizons Risk metrics used (VaR TVaR CTE) Correlations and dependencies Operational, Strategic and Emerging risks ICM and management decision making Disclosure (internal and external) Parameter error / model error and model implementation error considerations Internal and external audit findings Next steps in ICM development

23 100% How will AMB integrate ECM results in the rating analysis? BCAR Relative Weightings ECM 0% 100% A Z Items for Discussion: Can the relative weighting reach 100% ECM? Can credit be given for partial models? What detail should AMB disclose about the analysis and weighting? 0%

24 Model documentation Model development and structure Outline of Technical documentation Change documentation List and Frequency of Parameter calculations, updates, and model calibration Models Sub-Models and Versions if any Documentation understandable and accessible Public disclosure of the documentation

25 Model Validation Internal or external Procedures to check the calibration and appropriateness of the model Validation is iterative Qualitative validation Departments, design teams, management teams, risk ownership at all levels, Model design, Data Quality, Use Test Quantitative Model calibration, back testing, benchmarking, scenario testing Statistical tools and fitness testing, Calibration Model output volatilities across cycles, and across different time periods Cognizant of model risk, parameter risk, simulation errors and parameter errors Transparency

26 Use Test Degree to which risk management considers ECM results ECM is approved by the senior management ECM output is reported to Senior management and to be used in strategy setting ECM is used for Capital allocation, capital attribution, pricing, reserving, objective setting, product development, performance ECM is embedded, instilled and ingrained in enterprise DNA

27 ECM - What have we seen so far? Re-insurers, large primaries Methodologies vary widely Reserves bootstrap, Mack, percent deviations Aggregation Correlation matrix, copulas, Stochastic modeling Time horizon 1yr/ult runoff, 5yr/10runoff, 4yr Risk tolerance VaRs %, 99.5%, 99.95%, 99.97% Risk Metrics VaR, CTE/TVaR Usage Risk Capital, Product Pricing, capital allocation Model/parameter updates qtrly annual Validation Internal validation Documentation Not satisfactory Maintenance and Development of the Model - Nothing No explicit credit given so far..

28

29 Failure of ERM? Failure in ERM?

30 Failure of ERM? Failure in ERM?

31

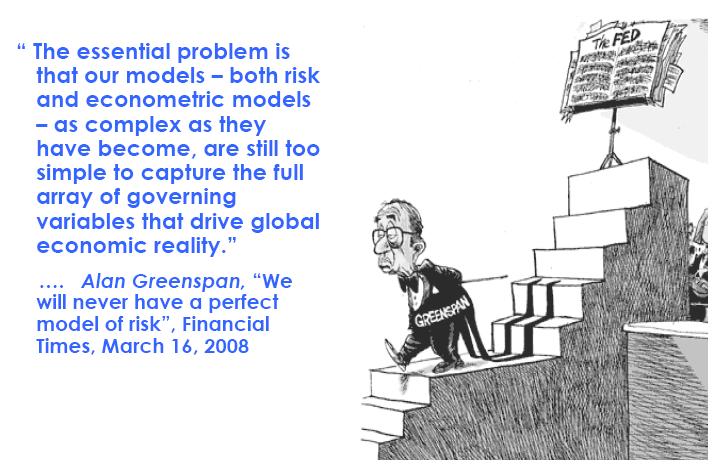

32 Financial Crisis: What worked and what did not? Liquidity Risk Operational Risk Contagion Risk Capital Fungibility Correlations between risk factors Frequent scenario analysis Risk Governance Risk Metrics Risk Communication Risk Compensation Risk and reward/risk performance

33 Risk Metrics

34 Risk Governance and Financial Crisis Risk Management Culture Risk Policy Independence Authority - empowerment Risk Controls Risk Compensation Risk Ownership Alignment of risk management and objectives Risk awareness and underwriting Risk articulation and Communication Risk INFO feed back loops Board and Senior management involvement Integrated comprehensive and holistic

35 Risk Appetite and Financial Crisis Risk Appetite Risk Tolerance Risk Limits Risk targets Risk controls Embedding the risk limits in business Soft and/or hard limits on Risk Limit violations and trigger mechanisms Risk escalation procedures Implementation, effectiveness and changing of risk mitigation strategies

36 Impact of risks on your Business and Risk Rating. Impact Likelihood 1 Insignificant 2 Marginal 3 Significant 4 Critical 5 Catastrophic 5 Catastrophic 4 Critical 3 Significant 2 Marginal 1 Insignificant Tolerance Level

37 Risk Limits: Soft and Hard H i g h Soft Limit Hard Limit L o w Target level of risk

38 Risk Appetite and the Financial Crisis Stakeholder analysis Shareholders Employees Rating agencies Regulators Alignment with Strategic, financial and operational objectives Risk capacity and Risk Propensity Integrated, comprehensive and holistic view of risk Risk Culture

39 Risk Communication and Financial Crisis Key risk indicators Risk dashboards Risk registers risk logs Oversight review of risk events Vision and provision for emerging risk Risk escalation procedures and triggers Frequency and timeliness of communications

40 Risk Categories and Financial Crisis Operational Risks Reputational Risks Contagion Risks Emerging Risks Basis Risks Risk Responses

41 Liquidity Risk and Financial Funding liquidity Asset liquidity Liquidity and Capital Crisis Liquidity risk Management framework Scenario and stress tests Including in ECM Contingency funding and stress testing Conduits and off balance sheet activities Liquidity risk pricing

42 Market Consistent Embedded Value and Financial Crisis Purpose Market Value of Assets Net Worth Value of existing business TVOG CRNHR Frictional Costs Liabilities Present Value of Future Profits MCEV Valuation Performance Disclosure Reporting Pricing Problem with MCEV illiquid Markets Market Volatility No allowance for Credit and Liquidity risk u u Source: CEIOPS `

43 Risk Models and Financial Crisis Correlations between risk factors Capital Fungibility Frequent scenario and stress analysis Liquidity Risk Consideration of non quantifiable risks Model error Model validation Data quality Risk categories covered Flexibility of frameworks and assumptions to deal with contingencies Experience judgment

44 ERM and ECM Not mutually exclusive ECM a subset of ERM ECM not necessary for all companies ECM may be a must for some companies ECM a quantitative tool with in ERM Partial models are possible Risk profile dictates the relationship between ERM and ECM ECM for Pricing of risk

45 Model Error/Validity/applicability

46 Questions and Comments

47 ERM, ECM and the Financial Crisis Raj Guttha Ph.D, PMP Manager, Enterprise Risk Management Economic Capital Modeling A.M. Best Company X

A.M. Best s New Risk Management Standards

A.M. Best s New Risk Management Standards Stephanie Guethlein McElroy, A.M. Best Manager, Rating Criteria and Rating Relations Hubert Mueller, Towers Perrin, Principal March 24, 2008 Introduction A.M.

A.M. Best s New Risk Management Standards Stephanie Guethlein McElroy, A.M. Best Manager, Rating Criteria and Rating Relations Hubert Mueller, Towers Perrin, Principal March 24, 2008 Introduction A.M.

GUIDELINE ON ENTERPRISE RISK MANAGEMENT

GUIDELINE ON ENTERPRISE RISK MANAGEMENT Insurance Authority Table of Contents Page 1. Introduction 1 2. Application 2 3. Overview of Enterprise Risk Management (ERM) Framework and 4 General Requirements

GUIDELINE ON ENTERPRISE RISK MANAGEMENT Insurance Authority Table of Contents Page 1. Introduction 1 2. Application 2 3. Overview of Enterprise Risk Management (ERM) Framework and 4 General Requirements

NAIC OWN RISK AND SOLVENCY ASSESSMENT (ORSA) GUIDANCE MANUAL

GUIDANCE MANUAL") NAIC OWN RISK AND SOLVENCY ASSESSMENT (ORSA) GUIDANCE MANUAL Created by the NAIC Group Solvency Issues Working Group Of the Solvency Modernization Initiatives (EX) Task Force 2011 National Association

NAIC OWN RISK AND SOLVENCY ASSESSMENT (ORSA) GUIDANCE MANUAL Created by the NAIC Group Solvency Issues Working Group Of the Solvency Modernization Initiatives (EX) Task Force 2011 National Association

Statement of Guidance for Licensees seeking approval to use an Internal Capital Model ( ICM ) to calculate the Prescribed Capital Requirement ( PCR )

to calculate the Prescribed Capital Requirement ( PCR )") MAY 2016 Statement of Guidance for Licensees seeking approval to use an Internal Capital Model ( ICM ) to calculate the Prescribed Capital Requirement ( PCR ) 1 Table of Contents 1 STATEMENT OF OBJECTIVES...

MAY 2016 Statement of Guidance for Licensees seeking approval to use an Internal Capital Model ( ICM ) to calculate the Prescribed Capital Requirement ( PCR ) 1 Table of Contents 1 STATEMENT OF OBJECTIVES...

Subject ST9 Enterprise Risk Management Syllabus

Subject ST9 Enterprise Risk Management Syllabus for the 2018 exams 1 June 2017 Aim The aim of the Enterprise Risk Management (ERM) Specialist Technical subject is to instil in successful candidates the

Subject ST9 Enterprise Risk Management Syllabus for the 2018 exams 1 June 2017 Aim The aim of the Enterprise Risk Management (ERM) Specialist Technical subject is to instil in successful candidates the

Economic Capital: Recent Market Trends and Best Practices for Implementation

1 Economic Capital: Recent Market Trends and Best Practices for Implementation 7-11 September 2009 Hubert Mueller 2 Overview Recent Market Trends Implementation Issues Economic Capital (EC) Aggregation

1 Economic Capital: Recent Market Trends and Best Practices for Implementation 7-11 September 2009 Hubert Mueller 2 Overview Recent Market Trends Implementation Issues Economic Capital (EC) Aggregation

Subject SP9 Enterprise Risk Management Specialist Principles Syllabus

Subject SP9 Enterprise Risk Management Specialist Principles Syllabus for the 2019 exams 1 June 2018 Enterprise Risk Management Specialist Principles Aim The aim of the Enterprise Risk Management (ERM)

Subject SP9 Enterprise Risk Management Specialist Principles Syllabus for the 2019 exams 1 June 2018 Enterprise Risk Management Specialist Principles Aim The aim of the Enterprise Risk Management (ERM)

Enhancing Our Risk Appetite Framework. A Case Study

Enhancing Our Risk Appetite Framework A Case Study Desired Outcomes 1. An approach to developing a risk appetite framework and risk appetite statement. 2. Understanding how a risk appetite framework can

Enhancing Our Risk Appetite Framework A Case Study Desired Outcomes 1. An approach to developing a risk appetite framework and risk appetite statement. 2. Understanding how a risk appetite framework can

Capturing Risk Appetite Through ERM - Implementation Challenges

Capturing Risk Appetite Through ERM - Implementation Challenges ERM Symposium, Chicago March 14-16, 2011 Varun Agarwal, SVP, Risk Strategy, HSBC Venkat Veeramani, Manager, Risk Strategy, HSBC Table of

Capturing Risk Appetite Through ERM - Implementation Challenges ERM Symposium, Chicago March 14-16, 2011 Varun Agarwal, SVP, Risk Strategy, HSBC Venkat Veeramani, Manager, Risk Strategy, HSBC Table of

INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS

Guidance Paper No. 2.2.x INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS GUIDANCE PAPER ON ENTERPRISE RISK MANAGEMENT FOR CAPITAL ADEQUACY AND SOLVENCY PURPOSES DRAFT, MARCH 2008 This document was prepared

Guidance Paper No. 2.2.x INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS GUIDANCE PAPER ON ENTERPRISE RISK MANAGEMENT FOR CAPITAL ADEQUACY AND SOLVENCY PURPOSES DRAFT, MARCH 2008 This document was prepared

2014 Own Risk and Solvency Assessment (ORSA) Feedback Pilot Project Observations of the Group Solvency Issues (E) Working Group

Feedback Pilot Project Observations of the Group Solvency Issues (E) Working Group") 2014 Own Risk and Solvency Assessment (ORSA) Feedback Pilot Project Observations of the Group Solvency Issues (E) Working Group During October 2014 through June 2015, a third ORSA Feedback Pilot Project

2014 Own Risk and Solvency Assessment (ORSA) Feedback Pilot Project Observations of the Group Solvency Issues (E) Working Group During October 2014 through June 2015, a third ORSA Feedback Pilot Project

Guidance paper on the use of internal models for risk and capital management purposes by insurers

Guidance paper on the use of internal models for risk and capital management purposes by insurers October 1, 2008 Stuart Wason Chair, IAA Solvency Sub-Committee Agenda Introduction Global need for guidance

Guidance paper on the use of internal models for risk and capital management purposes by insurers October 1, 2008 Stuart Wason Chair, IAA Solvency Sub-Committee Agenda Introduction Global need for guidance

Rating Methodology Stephen Irwin, Vice President, A.M. Best Doniella Pliss, Managing Senior Financial Analyst, A.M. Best

Rating Methodology 2017 Stephen Irwin, Vice President, A.M. Best Doniella Pliss, Managing Senior Financial Analyst, A.M. Best Impetus for Change Timeline Building Block Approach Rating Implications Questions

Rating Methodology 2017 Stephen Irwin, Vice President, A.M. Best Doniella Pliss, Managing Senior Financial Analyst, A.M. Best Impetus for Change Timeline Building Block Approach Rating Implications Questions

ECONOMIC CAPITAL MODELING CARe Seminar JUNE 2016

ECONOMIC CAPITAL MODELING CARe Seminar JUNE 2016 Boston Catherine Eska The Hanover Insurance Group Paul Silberbush Guy Carpenter & Co. Ronald Wilkins - PartnerRe Economic Capital Modeling Safe Harbor Notice

ECONOMIC CAPITAL MODELING CARe Seminar JUNE 2016 Boston Catherine Eska The Hanover Insurance Group Paul Silberbush Guy Carpenter & Co. Ronald Wilkins - PartnerRe Economic Capital Modeling Safe Harbor Notice

Preparing for an Own Risk & Solvency Assessment

www.pwc.com Preparing for an Own Risk & Solvency Assessment March 2013 Brian Paton Director, Insurance Risk and Capital Practice brian.paton@us.pwc.com Contents 1. ORSA challenges 2. ORSA readiness and

www.pwc.com Preparing for an Own Risk & Solvency Assessment March 2013 Brian Paton Director, Insurance Risk and Capital Practice brian.paton@us.pwc.com Contents 1. ORSA challenges 2. ORSA readiness and

Methodology Review Seminar

etc.venues St.Paul s, London Methodology Review Seminar 16 November 2016 Methodology Review Seminar Welcome and Introduction Overview of the Structural Changes to Best's Credit Rating Methodology Greg

etc.venues St.Paul s, London Methodology Review Seminar 16 November 2016 Methodology Review Seminar Welcome and Introduction Overview of the Structural Changes to Best's Credit Rating Methodology Greg

INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS

Guidance Paper No. 2.2.6 INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS GUIDANCE PAPER ON ENTERPRISE RISK MANAGEMENT FOR CAPITAL ADEQUACY AND SOLVENCY PURPOSES OCTOBER 2007 This document was prepared

Guidance Paper No. 2.2.6 INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS GUIDANCE PAPER ON ENTERPRISE RISK MANAGEMENT FOR CAPITAL ADEQUACY AND SOLVENCY PURPOSES OCTOBER 2007 This document was prepared

ORSA reports: gaps and opportunities

ORSA reports: gaps and opportunities Market benchmarking of ORSA reports for Singapore general insurers Industry-wide Own Risk and Solvency Assessment (ORSA) 1 2 Contents 1 Executive summary 2 Our assessment

ORSA reports: gaps and opportunities Market benchmarking of ORSA reports for Singapore general insurers Industry-wide Own Risk and Solvency Assessment (ORSA) 1 2 Contents 1 Executive summary 2 Our assessment

Own Risk and Solvency Assessment (ORSA)

") Own Risk and Solvency Assessment (ORSA) Presentations to OCCA (Nov. 19, 2014) and AAIARD (Nov. 21, 2014) Jacqueline Friedland, FCIA, FCAS, FSA, MAAA Chief Actuary, RSA Canada Presentation Outline What

Own Risk and Solvency Assessment (ORSA) Presentations to OCCA (Nov. 19, 2014) and AAIARD (Nov. 21, 2014) Jacqueline Friedland, FCIA, FCAS, FSA, MAAA Chief Actuary, RSA Canada Presentation Outline What

Sections of the ORSA Report

Lessons Learned From Orsa Reviews Impact on Risk Focused Examination NAIC Insurance Summit INS Companies Joe Fritsch, Director INS Companies Don Carbone, Exam Manager INS Companies Sections of the ORSA

Lessons Learned From Orsa Reviews Impact on Risk Focused Examination NAIC Insurance Summit INS Companies Joe Fritsch, Director INS Companies Don Carbone, Exam Manager INS Companies Sections of the ORSA

ERM and ORSA Assuring a Necessary Level of Risk Control

ERM and ORSA Assuring a Necessary Level of Risk Control Dave Ingram, MAAA, FSA, CERA, FRM, PRM Chair of IAA Enterprise & Financial Risk Committee Executive Vice President, Willis Re September, 2012 1 DISCLAIMER

ERM and ORSA Assuring a Necessary Level of Risk Control Dave Ingram, MAAA, FSA, CERA, FRM, PRM Chair of IAA Enterprise & Financial Risk Committee Executive Vice President, Willis Re September, 2012 1 DISCLAIMER

Prudential Standard GOI 3 Risk Management and Internal Controls for Insurers

Prudential Standard GOI 3 Risk Management and Internal Controls for Insurers Objectives and Key Requirements of this Prudential Standard Effective risk management is fundamental to the prudent management

Prudential Standard GOI 3 Risk Management and Internal Controls for Insurers Objectives and Key Requirements of this Prudential Standard Effective risk management is fundamental to the prudent management

ENTERPRISE RISK MANAGEMENT, INTERNAL MODELS AND OPERATIONAL RISK FOR LIFE INSURERS DISCUSSION PAPER DP14-09

ENTERPRISE RISK MANAGEMENT, INTERNAL MODELS AND FOR LIFE INSURERS DISCUSSION PAPER DP14-09 This paper is issued by the Insurance and Pensions Authority ( the IPA ), the regulatory authority responsible

ENTERPRISE RISK MANAGEMENT, INTERNAL MODELS AND FOR LIFE INSURERS DISCUSSION PAPER DP14-09 This paper is issued by the Insurance and Pensions Authority ( the IPA ), the regulatory authority responsible

A.M. Best s Updated Credit Rating Methodology and Capital Model. Robert Raber Senior Financial Analyst A.M. Best Company

A.M. Best s Updated Credit Rating Methodology and Capital Model Robert Raber Senior Financial Analyst A.M. Best Company 1 Contents A.M. Best Company Overview Updated Best s Credit Rating Methodology (BCRM)

A.M. Best s Updated Credit Rating Methodology and Capital Model Robert Raber Senior Financial Analyst A.M. Best Company 1 Contents A.M. Best Company Overview Updated Best s Credit Rating Methodology (BCRM)

Stress Tests From stressful times to business as usual an updated point of view

Stress Tests From stressful times to business as usual an updated point of view Informational presentation for our clients May 2009 1 Point of view From stressful times to business as usual Stress test

Stress Tests From stressful times to business as usual an updated point of view Informational presentation for our clients May 2009 1 Point of view From stressful times to business as usual Stress test

A.M. Best s 2010 Supplemental Rating Questionnaire (SRQ)

") A.M. Best s 2010 Supplemental Rating Questionnaire (SRQ) A briefing on Best s new SRQ questions January 2011 2011 Towers Watson. All rights reserved. BACKGROUND By February 1, A.M. Best will be releasing

A.M. Best s 2010 Supplemental Rating Questionnaire (SRQ) A briefing on Best s new SRQ questions January 2011 2011 Towers Watson. All rights reserved. BACKGROUND By February 1, A.M. Best will be releasing

New Actuarial Standards of Practice No. 46 Risk Evaluation in ERM No. 47 Risk Treatment in ERM

New Actuarial Standards of Practice No. 46 Risk Evaluation in ERM No. 47 Risk Treatment in ERM August 1, 2013 1 Professional Disclaimer Any opinions expressed within this presentation are the presenter

New Actuarial Standards of Practice No. 46 Risk Evaluation in ERM No. 47 Risk Treatment in ERM August 1, 2013 1 Professional Disclaimer Any opinions expressed within this presentation are the presenter

INSURANCE CORE PRINCIPLES, STANDARDS, GUIDANCE AND ASSESSMENT METHODOLOGY

INSURANCE CORE PRINCIPLES, STANDARDS, GUIDANCE AND ASSESSMENT METHODOLOGY Revised ICP 8 and the additional ComFrame material in ICP 8 for public consultation (redline version) This public consultation

INSURANCE CORE PRINCIPLES, STANDARDS, GUIDANCE AND ASSESSMENT METHODOLOGY Revised ICP 8 and the additional ComFrame material in ICP 8 for public consultation (redline version) This public consultation

Certified Enterprise Risk Professional (CERP) Test Content Outline

Test Content Outline") Certified Enterprise Risk Professional (CERP) Test Content Outline SECTION 1: RISK GOVERNANCE Domain 1: Board and Senior Management Oversight (8%) Task 1: Provide relevant, timely, and accurate information

Certified Enterprise Risk Professional (CERP) Test Content Outline SECTION 1: RISK GOVERNANCE Domain 1: Board and Senior Management Oversight (8%) Task 1: Provide relevant, timely, and accurate information

Best s Credit Rating Methodology (BCRM) & MPL Insurer Ratings

& MPL Insurer Ratings") Special Presentation at the PIAA CEO/COO Meeting Best s Credit Rating Methodology (BCRM) & MPL Insurer Ratings Stefan Holzberger Chief Rating Officer Scottsdale, Arizona 16 March 2017 Disclaimer (1) AM

Special Presentation at the PIAA CEO/COO Meeting Best s Credit Rating Methodology (BCRM) & MPL Insurer Ratings Stefan Holzberger Chief Rating Officer Scottsdale, Arizona 16 March 2017 Disclaimer (1) AM

The Rating Agency View of Capital Modelling. Simon Harris Team Managing Director European Insurance

The Rating Agency View of Capital Modelling Simon Harris Team Managing Director European Insurance September 2007 Agenda The importance of risk and capitalisation in the rating process Moody s approach

The Rating Agency View of Capital Modelling Simon Harris Team Managing Director European Insurance September 2007 Agenda The importance of risk and capitalisation in the rating process Moody s approach

The use of an Economic Capital Model within an Enterprise Risk Management framework

The use of an Economic Capital Model within an Enterprise Risk Management framework David Ingram, Senior Director Standard & Poor s Ratings Services December, 2007 Copyright (c) 2006 Standard & Poor s,

The use of an Economic Capital Model within an Enterprise Risk Management framework David Ingram, Senior Director Standard & Poor s Ratings Services December, 2007 Copyright (c) 2006 Standard & Poor s,

ERM, the New Regulatory Requirements and Quantitative Analyses

ERM, the New Regulatory Requirements and Quantitative Analyses Presenters Lisa Cosentino, Managing Director, SMART DEVINE Kim Piersol, Consulting Actuary, Huggins Actuarial Services, Inc. 2 Objectives

ERM, the New Regulatory Requirements and Quantitative Analyses Presenters Lisa Cosentino, Managing Director, SMART DEVINE Kim Piersol, Consulting Actuary, Huggins Actuarial Services, Inc. 2 Objectives

The Real World: Dealing With Parameter Risk. Alice Underwood Senior Vice President, Willis Re March 29, 2007

The Real World: Dealing With Parameter Risk Alice Underwood Senior Vice President, Willis Re March 29, 2007 Agenda 1. What is Parameter Risk? 2. Practical Observations 3. Quantifying Parameter Risk 4.

The Real World: Dealing With Parameter Risk Alice Underwood Senior Vice President, Willis Re March 29, 2007 Agenda 1. What is Parameter Risk? 2. Practical Observations 3. Quantifying Parameter Risk 4.

American Academy of Actuaries Webinar: The Practice of ERM in the Insurance Industry. Enterprise Risk Management Committee November 19, 2013

American Academy of Actuaries Webinar: The Practice of ERM in the Insurance Industry Enterprise Risk Management Committee November 19, 2013 All Rights Reserved. 1 Presenters Bruce Jones, MAAA, FCAS, CERA

American Academy of Actuaries Webinar: The Practice of ERM in the Insurance Industry Enterprise Risk Management Committee November 19, 2013 All Rights Reserved. 1 Presenters Bruce Jones, MAAA, FCAS, CERA

Criteria Insurance General: Refined Methodology For Assessing An Insurer's Risk Appetite. Table Of Contents

March 30, 2010 Criteria Insurance General: Refined Methodology For Assessing An Insurer's Risk Appetite Primary Credit Analyst: Marcus Bowser, London +44(207) 176 7052; marcus_bowser@standardandpoors.com

March 30, 2010 Criteria Insurance General: Refined Methodology For Assessing An Insurer's Risk Appetite Primary Credit Analyst: Marcus Bowser, London +44(207) 176 7052; marcus_bowser@standardandpoors.com

INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS GUIDELINE. Nepal Rastra Bank Bank Supervision Department. August 2012 (updated July 2013)

") INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS GUIDELINE Nepal Rastra Bank Bank Supervision Department August 2012 (updated July 2013) Table of Contents Page No. 1. Introduction 1 2. Internal Capital Adequacy

INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS GUIDELINE Nepal Rastra Bank Bank Supervision Department August 2012 (updated July 2013) Table of Contents Page No. 1. Introduction 1 2. Internal Capital Adequacy

BERGRIVIER MUNICIPALITY. Risk Management Risk Appetite Framework

BERGRIVIER MUNICIPALITY Risk Management Risk Appetite Framework APRIL 2018 1 Document review and approval Revision history Version Author Date reviewed 1 2 3 4 5 This document has been reviewed by Version

BERGRIVIER MUNICIPALITY Risk Management Risk Appetite Framework APRIL 2018 1 Document review and approval Revision history Version Author Date reviewed 1 2 3 4 5 This document has been reviewed by Version

ERM in the Rating Process: A Practical Perspective

ERM in the Rating Process: A Practical Perspective Jeffrey Mango, Group Vice President, A.M. Best Michelle Baurkot, Assistant Vice President, A.M. Best Tom Zitelli, Managing Senior Financial Analyst, A.M.

ERM in the Rating Process: A Practical Perspective Jeffrey Mango, Group Vice President, A.M. Best Michelle Baurkot, Assistant Vice President, A.M. Best Tom Zitelli, Managing Senior Financial Analyst, A.M.

INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS MODULE

INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS Table of Contents IC-A IC-1 Date Last Changed Introduction IC-A.1 Purpose 07/2018 IC-A.2 Module History 07/2018 General Requirements IC-1.1 Overview 07/2018

INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS Table of Contents IC-A IC-1 Date Last Changed Introduction IC-A.1 Purpose 07/2018 IC-A.2 Module History 07/2018 General Requirements IC-1.1 Overview 07/2018

Risk Appetite. What is risk appetite?

Risk Appetite Presented by Mike Claffey 30 March 2011 What is risk appetite? Risk appetite is the degree of risk that an organisation is willing to accept in order to achieve its objectives, both in terms

Risk Appetite Presented by Mike Claffey 30 March 2011 What is risk appetite? Risk appetite is the degree of risk that an organisation is willing to accept in order to achieve its objectives, both in terms

Risk Appetite for Life Offices IFoA working party

Risk Appetite for Life Offices IFoA working party Gautam Kakar, Chairman 30 October 2015 Members of Working Party: Gautam Kakar Lana Nguyen Shayanthan Pathmanathan Rod Bryn-Hussey Fabio Schiaffini Crystal

Risk Appetite for Life Offices IFoA working party Gautam Kakar, Chairman 30 October 2015 Members of Working Party: Gautam Kakar Lana Nguyen Shayanthan Pathmanathan Rod Bryn-Hussey Fabio Schiaffini Crystal

Best s Credit Rating Methodology (BCRM) & Market Segment Outlooks

& Market Segment Outlooks") Special Presentation at the Gen Re Winter Forum Best s Credit Rating Methodology (BCRM) & Market Segment Outlooks Stefan Holzberger Chief Rating Officer St. Petersburg, Florida 19 January 2017 Disclaimer

Special Presentation at the Gen Re Winter Forum Best s Credit Rating Methodology (BCRM) & Market Segment Outlooks Stefan Holzberger Chief Rating Officer St. Petersburg, Florida 19 January 2017 Disclaimer

NAIC OWN RISK AND SOLVENCY ASSESSMENT (ORSA) GUIDANCE MANUAL

GUIDANCE MANUAL") NAIC OWN RISK AND SOLVENCY ASSESSMENT (ORSA) GUIDANCE MANUAL As of December 2017 The NAIC is the authoritative source for insurance industry information. Our expert solutions support the efforts of regulators,

NAIC OWN RISK AND SOLVENCY ASSESSMENT (ORSA) GUIDANCE MANUAL As of December 2017 The NAIC is the authoritative source for insurance industry information. Our expert solutions support the efforts of regulators,

OWN RISK AND SOLVENCY ASSESSMENT. ERM Seminar Compliance All Dealing from the same deck now

OWN RISK AND SOLVENCY ASSESSMENT ERM Seminar - 2014 Compliance All Dealing from the same deck now Own and Solvency Assessment! Originated in the UK about 10 years ago Now a global insurance regulatory

OWN RISK AND SOLVENCY ASSESSMENT ERM Seminar - 2014 Compliance All Dealing from the same deck now Own and Solvency Assessment! Originated in the UK about 10 years ago Now a global insurance regulatory

A.M. Best Ratings Impact from the New Rating Methodology and Stochastic-based BCAR

A.M. Best Ratings Impact from the New Rating Methodology and Stochastic-based BCAR September 2017 Prepared by Aon Benfield Executive Summary A.M. Best is expected to finalize new rating criteria by mid-october

A.M. Best Ratings Impact from the New Rating Methodology and Stochastic-based BCAR September 2017 Prepared by Aon Benfield Executive Summary A.M. Best is expected to finalize new rating criteria by mid-october

IAIS: Enterprise Risk Management for Capital Adequacy & Solvency Purposes. George Brady. IAIS Deputy Secretary General

IAIS: Enterprise Risk Management for Capital Adequacy & Solvency Purposes George Brady IAIS Deputy Secretary General Table of Contents 1. Introduction 2. Governance and an Enterprise Risk Management (ERM)

IAIS: Enterprise Risk Management for Capital Adequacy & Solvency Purposes George Brady IAIS Deputy Secretary General Table of Contents 1. Introduction 2. Governance and an Enterprise Risk Management (ERM)

Enterprise Risk Management (ERM)

") Southeastern Actuaries Conference Enterprise Risk Management (ERM) November 16, 2007 ING. Your future. Made easier. Agenda ERM Are you doing it? Definition of ERM What is it? Industry Overview What is

Southeastern Actuaries Conference Enterprise Risk Management (ERM) November 16, 2007 ING. Your future. Made easier. Agenda ERM Are you doing it? Definition of ERM What is it? Industry Overview What is

Lloyd s Minimum Standards MS13 Modelling, Design and Implementation

Lloyd s Minimum Standards MS13 Modelling, Design and Implementation January 2019 2 Contents MS13 Modelling, Design and Implementation 3 Minimum Standards and Requirements 3 Guidance 3 Definitions 3 Section

Lloyd s Minimum Standards MS13 Modelling, Design and Implementation January 2019 2 Contents MS13 Modelling, Design and Implementation 3 Minimum Standards and Requirements 3 Guidance 3 Definitions 3 Section

Enterprise Risk Management

Enterprise Risk Management Its implications, benefits and process by Janice Englesbe, CFA, and Abbe Bensimon, FCAS, MAAA, Gen Re Capital Consultants A Berkshire Hathaway Company The 2005 hurricane season

Enterprise Risk Management Its implications, benefits and process by Janice Englesbe, CFA, and Abbe Bensimon, FCAS, MAAA, Gen Re Capital Consultants A Berkshire Hathaway Company The 2005 hurricane season

29th India Fellowship Seminar

29th India Fellowship Seminar Is Risk Based Capital way forward? Adaptability to Indian Context & Comparison of various market consistent measures Guide: Sunil Sharma Presented by: Rakesh Kumar Niraj Kumar

29th India Fellowship Seminar Is Risk Based Capital way forward? Adaptability to Indian Context & Comparison of various market consistent measures Guide: Sunil Sharma Presented by: Rakesh Kumar Niraj Kumar

Defining the Internal Model for Risk & Capital Management under the Solvency II Directive

14 Defining the Internal Model for Risk & Capital Management under the Solvency II Directive Mark Dougherty is an international Senior Corporate Governance and Risk Management professional and Chartered

14 Defining the Internal Model for Risk & Capital Management under the Solvency II Directive Mark Dougherty is an international Senior Corporate Governance and Risk Management professional and Chartered

STRESS TESTING GUIDELINE

c DRAFT STRESS TESTING GUIDELINE November 2011 TABLE OF CONTENTS Preamble... 2 Introduction... 3 Coming into effect and updating... 6 1. Stress testing... 7 A. Concept... 7 B. Approaches underlying stress

c DRAFT STRESS TESTING GUIDELINE November 2011 TABLE OF CONTENTS Preamble... 2 Introduction... 3 Coming into effect and updating... 6 1. Stress testing... 7 A. Concept... 7 B. Approaches underlying stress

Economic Capital Follow-up from November 12 ERRC

Practical Implications of Developing and Implementing a Return on Economic Capital Framework Economic Capital Follow-up from November 12 ERRC ERM Symposium June 11, 2015 Adam Walter, Allstate Tim Borst,

Practical Implications of Developing and Implementing a Return on Economic Capital Framework Economic Capital Follow-up from November 12 ERRC ERM Symposium June 11, 2015 Adam Walter, Allstate Tim Borst,

FINANCIAL INSTITUTIONS

FINANCIAL INSTITUTIONS Quality Of Trading Risk Management Practices Varies In Financial Institutions Primary Credit Analysts: Prodyot Samanta New York (1) 212-438-2009 prodyot_samanta@ standardandpoors.com

FINANCIAL INSTITUTIONS Quality Of Trading Risk Management Practices Varies In Financial Institutions Primary Credit Analysts: Prodyot Samanta New York (1) 212-438-2009 prodyot_samanta@ standardandpoors.com

Use of Internal Models for Determining Required Capital for Segregated Fund Risks (LICAT)

") Canada Bureau du surintendant des institutions financières Canada 255 Albert Street 255, rue Albert Ottawa, Canada Ottawa, Canada K1A 0H2 K1A 0H2 Instruction Guide Subject: Capital for Segregated Fund

Canada Bureau du surintendant des institutions financières Canada 255 Albert Street 255, rue Albert Ottawa, Canada Ottawa, Canada K1A 0H2 K1A 0H2 Instruction Guide Subject: Capital for Segregated Fund

Harmonizing Risk Appetites within a Stress Testing Framework. April 2013

Harmonizing Risk Appetites within a Stress Testing Framework April 2013 Contents The Regulatory Evolution and Risk Appetites 3 Deloitte s Approach 9 Definition of Risk Appetite 10 Risk Appetite Framework

Harmonizing Risk Appetites within a Stress Testing Framework April 2013 Contents The Regulatory Evolution and Risk Appetites 3 Deloitte s Approach 9 Definition of Risk Appetite 10 Risk Appetite Framework

Exploring the New Era of ORSA Enterprise Risk Management (ERM)/ Own Risk and Solvency Assessment (ORSA) Committee

/ Own Risk and Solvency Assessment (ORSA) Committee") Exploring the New Era of ORSA Enterprise Risk Management (ERM)/ Own Risk and Solvency Assessment (ORSA) Committee Copyright 2015 by the American Academy of Actuaries. All Rights Reserved. Presenters Tricia

Exploring the New Era of ORSA Enterprise Risk Management (ERM)/ Own Risk and Solvency Assessment (ORSA) Committee Copyright 2015 by the American Academy of Actuaries. All Rights Reserved. Presenters Tricia

Enterprise Risk Management

ASSOCIATION ACTUARIELLE INTERNATIONALE INTERNATIONAL ACTUARIAL ASSOCIATION Enterprise Risk Management All of life is the management of risk, not its elimination Walter Wriston, former chairman of Citicorp

ASSOCIATION ACTUARIELLE INTERNATIONALE INTERNATIONAL ACTUARIAL ASSOCIATION Enterprise Risk Management All of life is the management of risk, not its elimination Walter Wriston, former chairman of Citicorp

Supervisory Views on Bank Economic Capital Systems: What are Regulators Looking For?

Supervisory Views on Bank Economic Capital Systems: What are Regulators Looking For? Prepared By: David M Wright Group, Vice President Federal Reserve Bank of San Francisco July, 2007 Any views expressed

Supervisory Views on Bank Economic Capital Systems: What are Regulators Looking For? Prepared By: David M Wright Group, Vice President Federal Reserve Bank of San Francisco July, 2007 Any views expressed

Navigating Financial. Maintaining the Momentum in Shifting Tides

Navigating Financial Strength Ratings Maintaining the Momentum in Shifting Tides Aon Benfield s Rating Agency Advisory group has substantial experience helping clients navigate various criteria changes

Navigating Financial Strength Ratings Maintaining the Momentum in Shifting Tides Aon Benfield s Rating Agency Advisory group has substantial experience helping clients navigate various criteria changes

Solvency II Update. Latest developments and industry challenges (Session 10) Réjean Besner

Réjean Besner") Solvency II Update Latest developments and industry challenges (Session 10) Canadian Institute of Actuaries - Annual Meeting, 29 June 2011 Réjean Besner Content Solvency II framework Solvency II equivalence

Solvency II Update Latest developments and industry challenges (Session 10) Canadian Institute of Actuaries - Annual Meeting, 29 June 2011 Réjean Besner Content Solvency II framework Solvency II equivalence

Solvency Assessment and Management: Pillar 2 - Sub Committee ORSA and Use Test Task Group Discussion Document 35 (v 3) Use Test

Use Test") Solvency Assessment and Management: Pillar 2 - Sub Committee ORSA and Use Test Task Group Discussion Document 35 (v 3) Use Test EXECUTIVE SUMMARY 1. INTRODUCTION AND PURPOSE The purpose of this document

Solvency Assessment and Management: Pillar 2 - Sub Committee ORSA and Use Test Task Group Discussion Document 35 (v 3) Use Test EXECUTIVE SUMMARY 1. INTRODUCTION AND PURPOSE The purpose of this document

A.M. Best s Rating Criteria Seminar

A.M. Best Europe Rating Services Ltd 19 October 2012 A.M. Best s Rating Criteria Seminar Stefan Holzberger, Managing Director, Analytics Mahesh Mistry, Associate Director, Analytics Carlos Wong-Fupuy,

A.M. Best Europe Rating Services Ltd 19 October 2012 A.M. Best s Rating Criteria Seminar Stefan Holzberger, Managing Director, Analytics Mahesh Mistry, Associate Director, Analytics Carlos Wong-Fupuy,

Guidance Note: Stress Testing Credit Unions with Assets Greater than $500 million. May Ce document est également disponible en français.

Guidance Note: Stress Testing Credit Unions with Assets Greater than $500 million May 2017 Ce document est également disponible en français. Applicability This Guidance Note is for use by all credit unions

Guidance Note: Stress Testing Credit Unions with Assets Greater than $500 million May 2017 Ce document est également disponible en français. Applicability This Guidance Note is for use by all credit unions

Guidance Note. Securitization. March Ce document est aussi disponible en français. Revised in October 2018

Guidance Note Securitization March 2018 Revised in October 2018 Ce document est aussi disponible en français. Applicability The Guidance Note: Securitization (Guidance Note) is for use by all credit unions

Guidance Note Securitization March 2018 Revised in October 2018 Ce document est aussi disponible en français. Applicability The Guidance Note: Securitization (Guidance Note) is for use by all credit unions

Opinion of the EBA on Good Practices for ETF Risk Management

EBA-Op-2013-01 7 March 2013 Opinion of the EBA on Good Practices for ETF Risk Management Table of contents Table of contents 2 Introduction 4 I. Good Practices for ETF business 6 II. Considerations for

EBA-Op-2013-01 7 March 2013 Opinion of the EBA on Good Practices for ETF Risk Management Table of contents Table of contents 2 Introduction 4 I. Good Practices for ETF business 6 II. Considerations for

Solvency II Insights for North American Insurers. CAS Centennial Meeting Damon Paisley Bill VonSeggern November 10, 2014

Solvency II Insights for North American Insurers CAS Centennial Meeting Damon Paisley Bill VonSeggern November 10, 2014 Agenda 1 Introduction to Solvency II 2 Pillar I 3 Pillar II and Governance 4 North

Solvency II Insights for North American Insurers CAS Centennial Meeting Damon Paisley Bill VonSeggern November 10, 2014 Agenda 1 Introduction to Solvency II 2 Pillar I 3 Pillar II and Governance 4 North

GUIDELINES FOR THE INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS FOR LICENSEES

SUPERVISORY AND REGULATORY GUIDELINES: 2016 Issued: 2 August 2016 GUIDELINES FOR THE INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS FOR LICENSEES 1. INTRODUCTION 1.1 The Central Bank of The Bahamas ( the

SUPERVISORY AND REGULATORY GUIDELINES: 2016 Issued: 2 August 2016 GUIDELINES FOR THE INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS FOR LICENSEES 1. INTRODUCTION 1.1 The Central Bank of The Bahamas ( the

Understanding Best s Capital Adequacy Ratio (BCAR) for U.S. Property/Casualty Insurers

for U.S. Property/Casualty Insurers") Understanding Best s Capital Adequacy Ratio (BCAR) for U.S. Property/Casualty Insurers Analytical Contact March 1, 216 Thomas Mount, Oldwick +1 (98) 439-22 Ext. 5155 Thomas.Mount@ambest.com Understanding

Understanding Best s Capital Adequacy Ratio (BCAR) for U.S. Property/Casualty Insurers Analytical Contact March 1, 216 Thomas Mount, Oldwick +1 (98) 439-22 Ext. 5155 Thomas.Mount@ambest.com Understanding

Economic Capital in a Canadian Context

Economic Capital in a Canadian Context ERM Seminar May 2005 Topics 1. Rationale for Economic Capital 2. Canadian Regulatory Context 3. Economic Capital Principles 4. Economic Capital Issues 5. Economic

Economic Capital in a Canadian Context ERM Seminar May 2005 Topics 1. Rationale for Economic Capital 2. Canadian Regulatory Context 3. Economic Capital Principles 4. Economic Capital Issues 5. Economic

Enterprise Risk Management

Enterprise Risk Management Southeastern Actuaries Conference Rebecca Scotchie June 2011 ERM is 2 1 Agenda What is ERM? Why is risk management important? ERM maturity model/evolution of ERM ERM Framework

Enterprise Risk Management Southeastern Actuaries Conference Rebecca Scotchie June 2011 ERM is 2 1 Agenda What is ERM? Why is risk management important? ERM maturity model/evolution of ERM ERM Framework

LEGAL & GENERAL GROUP PLC risk management supplement

LEGAL & GENERAL GROUP PLC 2017 risk management supplement Supplement contents Within this supplement we set out descriptions of the risks we face, how our risk management framework operates, as well as

LEGAL & GENERAL GROUP PLC 2017 risk management supplement Supplement contents Within this supplement we set out descriptions of the risks we face, how our risk management framework operates, as well as

TABLE OF CONTENTS. Lombardi, Chapter 1, Overview of Valuation Requirements. A- 22 to A- 26

iii TABLE OF CONTENTS FINANCIAL REPORTING PriceWaterhouseCoopers, Chapter 3, Liability for Income Tax. A- 1 to A- 2 PriceWaterhouseCoopers, Chapter 4, Income for Tax Purposes. A- 3 to A- 6 PriceWaterhouseCoopers,

iii TABLE OF CONTENTS FINANCIAL REPORTING PriceWaterhouseCoopers, Chapter 3, Liability for Income Tax. A- 1 to A- 2 PriceWaterhouseCoopers, Chapter 4, Income for Tax Purposes. A- 3 to A- 6 PriceWaterhouseCoopers,

Risk management. Ari Kaperi Group CRO

Risk management Ari Kaperi Group CRO 1 The least volatile Nordic bank Factors driving risk down Nordea vs. peers 26-Q1 215, % Large and diversified client base Quarterly net profit volatility 15 Geographical

Risk management Ari Kaperi Group CRO 1 The least volatile Nordic bank Factors driving risk down Nordea vs. peers 26-Q1 215, % Large and diversified client base Quarterly net profit volatility 15 Geographical

Presented by Kristina Narvaez President & CEO ERM Strategies, LLC

Presented by Kristina Narvaez President & CEO ERM Strategies, LLC www.erm-strategies.com Regulations to Support Value Creation Sarbanes Oxley 2002 NYSE 2004 SEC 33-9089 Dodd Frank Section 165 Part C S

Presented by Kristina Narvaez President & CEO ERM Strategies, LLC www.erm-strategies.com Regulations to Support Value Creation Sarbanes Oxley 2002 NYSE 2004 SEC 33-9089 Dodd Frank Section 165 Part C S

Academy Presentation to NAIC ORSA Implementation (E) Subgroup

Subgroup") Academy Presentation to NAIC ORSA Implementation (E) Subgroup Tricia Matson, MAAA, FSA Chairperson, Enterprise Risk Management (ERM) and Own Risk and Solvency Assessment (ORSA) Committee August 10, 2016

Academy Presentation to NAIC ORSA Implementation (E) Subgroup Tricia Matson, MAAA, FSA Chairperson, Enterprise Risk Management (ERM) and Own Risk and Solvency Assessment (ORSA) Committee August 10, 2016

The Counterparty Risk Management Policy Group III Report Includes Detailed Suggestions for Financial Intermediaries

News Bulletin August 11, 2008 The Counterparty Risk Management Policy Group III Report Includes Detailed Suggestions for Financial Intermediaries Overview On August 6, 2008, the Counterparty Risk Management

News Bulletin August 11, 2008 The Counterparty Risk Management Policy Group III Report Includes Detailed Suggestions for Financial Intermediaries Overview On August 6, 2008, the Counterparty Risk Management

Guideline. Own Risk and Solvency Assessment. Category: Sound Business and Financial Practices. No: E-19 Date: November 2015

Guideline Subject: Category: Sound Business and Financial Practices No: E-19 Date: November 2015 This guideline sets out OSFI s expectations with respect to the Own Risk and Solvency Assessment (ORSA)

Guideline Subject: Category: Sound Business and Financial Practices No: E-19 Date: November 2015 This guideline sets out OSFI s expectations with respect to the Own Risk and Solvency Assessment (ORSA)

ORSA An International Development

ORSA An International Development 25.02.14 Agenda What is an ORSA? Global reach Comparison of requirements Common challenges Potential solutions Origin of ORSA FSA ICAS Solvency II IAIS ICP16 What is an

ORSA An International Development 25.02.14 Agenda What is an ORSA? Global reach Comparison of requirements Common challenges Potential solutions Origin of ORSA FSA ICAS Solvency II IAIS ICP16 What is an

RESERVE BANK OF MALAWI

RESERVE BANK OF MALAWI GUIDELINES ON INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS (ICAAP) Bank Supervision Department March 2013 Table of Contents 1.0 INTRODUCTION... 2 2.0 MANDATE... 2 3.0 RATIONALE...

RESERVE BANK OF MALAWI GUIDELINES ON INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS (ICAAP) Bank Supervision Department March 2013 Table of Contents 1.0 INTRODUCTION... 2 2.0 MANDATE... 2 3.0 RATIONALE...

Risk Appetite Survey Current state of the Insurance Industry

Risk Appetite Survey Current state of the Insurance Industry Deloitte Belgium and The Netherlands Financial Services Industry The survey was conducted during July 2013 till December 2013 Introduction The

Risk Appetite Survey Current state of the Insurance Industry Deloitte Belgium and The Netherlands Financial Services Industry The survey was conducted during July 2013 till December 2013 Introduction The

RISK APPETITE FRAMEWORK

RISK APPETITE FRAMEWORK TRANSLATING A BANK B/S INTO A REGULATORY B/S Accounting Balance Sheet Capital Typology Sources of Capital Basis of Capital Requirement Market Risk Credit Risk Operational Risk Other

RISK APPETITE FRAMEWORK TRANSLATING A BANK B/S INTO A REGULATORY B/S Accounting Balance Sheet Capital Typology Sources of Capital Basis of Capital Requirement Market Risk Credit Risk Operational Risk Other

Managing Health Care Reserves: Aligning Operating Assets with Broader Organizational Goals

Managing Health Care Reserves: Aligning Operating Assets with Broader Organizational Goals Enterprise Risk Management for Health Care Organizations June 2017 Investment advice and consulting services provided

Managing Health Care Reserves: Aligning Operating Assets with Broader Organizational Goals Enterprise Risk Management for Health Care Organizations June 2017 Investment advice and consulting services provided

CAPITAL MANAGEMENT GUIDELINE

CAPITAL MANAGEMENT GUIDELINE May 2015 Capital Management Guideline 1 Preambule TABLE OF CONTENTS Preamble... 3 Scope... 4 Coming into effect and updating... 5 Introduction... 6 1. Capital management...

CAPITAL MANAGEMENT GUIDELINE May 2015 Capital Management Guideline 1 Preambule TABLE OF CONTENTS Preamble... 3 Scope... 4 Coming into effect and updating... 5 Introduction... 6 1. Capital management...

ORSA An international requirement

Prepared by: Padraic O'Malley, Principal, Dublin Eamonn Phelan, Principal, Dublin December 2013 ORSA An international requirement Title Author a [Footer - regular] Month YYYY Title Author b [Footer - regular]

Prepared by: Padraic O'Malley, Principal, Dublin Eamonn Phelan, Principal, Dublin December 2013 ORSA An international requirement Title Author a [Footer - regular] Month YYYY Title Author b [Footer - regular]

ERM Concepts and Framework. Paul Duffy

Society of Actuaries in Ireland ERM Concepts and Framework Paul Duffy 13 th May 2010 *connectedthinking Lecture Plan Introduction to ERM Describe the concept of ERM Discuss the framework for risk management

Society of Actuaries in Ireland ERM Concepts and Framework Paul Duffy 13 th May 2010 *connectedthinking Lecture Plan Introduction to ERM Describe the concept of ERM Discuss the framework for risk management

BERMUDA INSURANCE (GROUP SUPERVISION) RULES 2011 BR 76 / 2011

RULES 2011 BR 76 / 2011") QUO FA T A F U E R N T BERMUDA INSURANCE (GROUP SUPERVISION) RULES 2011 BR 76 / 2011 TABLE OF CONTENTS 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 Citation and commencement PART 1 GROUP RESPONSIBILITIES

QUO FA T A F U E R N T BERMUDA INSURANCE (GROUP SUPERVISION) RULES 2011 BR 76 / 2011 TABLE OF CONTENTS 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 Citation and commencement PART 1 GROUP RESPONSIBILITIES

Unlocking Value with Enterprise Risk Management. presented by Jim Toole, FSA, CERA, MAAA Bob Daino, FCAS, MAAA

Unlocking Value with Enterprise Risk Management presented by Jim Toole, FSA, CERA, MAAA Bob Daino, FCAS, MAAA August, 2009 Our Talk Today Why Enterprise Risk Management? The ERM Process A Risk Vocabulary

Unlocking Value with Enterprise Risk Management presented by Jim Toole, FSA, CERA, MAAA Bob Daino, FCAS, MAAA August, 2009 Our Talk Today Why Enterprise Risk Management? The ERM Process A Risk Vocabulary

PRINCIPLES FOR RISK MANAGEMENT IN NORGES BANK INVESTMENT MANAGEMENT LAID DOWN BY THE EXECUTIVE BOARD 10 JUNE 2009, LAST AMENDED 21 NOVEMBER 2018

PRINCIPLES FOR RISK MANAGEMENT IN NORGES BANK INVESTMENT MANAGEMENT LAID DOWN BY THE EXECUTIVE BOARD 10 JUNE 2009, LAST AMENDED 21 NOVEMBER 2018 1. Purpose and objective These principles represent our

PRINCIPLES FOR RISK MANAGEMENT IN NORGES BANK INVESTMENT MANAGEMENT LAID DOWN BY THE EXECUTIVE BOARD 10 JUNE 2009, LAST AMENDED 21 NOVEMBER 2018 1. Purpose and objective These principles represent our

Harmonizing Risk Appetites within a Stress Testing Framework

Harmonizing Risk Appetites within a Stress Testing Framework H. Walter Young Audit & Enterprise Risk Services April 2013 Contents The Regulatory Evolution and Risk Appetites 3 Deloitte s Approach 9 Definition

Harmonizing Risk Appetites within a Stress Testing Framework H. Walter Young Audit & Enterprise Risk Services April 2013 Contents The Regulatory Evolution and Risk Appetites 3 Deloitte s Approach 9 Definition

Enterprise Risk Management How much risk do you want to take? Mark Lim Risk Consulting and Software Towers Watson

Enterprise Risk Management How much risk do you want to take? Mark Lim Risk Consulting and Software Towers Watson 1 Agenda 1 Introduction 2 Developing an ERM framework 3 Defining and integrating Risk Appetite

Enterprise Risk Management How much risk do you want to take? Mark Lim Risk Consulting and Software Towers Watson 1 Agenda 1 Introduction 2 Developing an ERM framework 3 Defining and integrating Risk Appetite

ECB Guide to the internal liquidity adequacy assessment process (ILAAP)

") ECB Guide to the internal liquidity adequacy assessment process (ILAAP) March 2018 Contents 1 Introduction 2 1.1 Purpose 3 1.2 Scope and proportionality 3 2 Principles 5 Principle 1 The management body

ECB Guide to the internal liquidity adequacy assessment process (ILAAP) March 2018 Contents 1 Introduction 2 1.1 Purpose 3 1.2 Scope and proportionality 3 2 Principles 5 Principle 1 The management body

DEVELOPING A GROUP CAPITAL CALCULATION

Bill Schwegler, Senior Actuary, AEGON DEVELOPING A GROUP CAPITAL CALCULATION Presentation to NAIC s Group Solvency Issues Working Group March 25, 2011 Economic capital models: critical decisions 1. Definition

Bill Schwegler, Senior Actuary, AEGON DEVELOPING A GROUP CAPITAL CALCULATION Presentation to NAIC s Group Solvency Issues Working Group March 25, 2011 Economic capital models: critical decisions 1. Definition

D7 Risk Management Policy

D7 Risk Management Policy Purpose and scope The aim of Kelda s policy is to establish and embed effective risk management in normal business process and culture. This will improve Kelda s ability to predict

D7 Risk Management Policy Purpose and scope The aim of Kelda s policy is to establish and embed effective risk management in normal business process and culture. This will improve Kelda s ability to predict

Risk Architecture: Agenda. Leon Bloom, Partner, Deloitte & Touche LLP

Risk Architecture: Alignment of Investor Objectives and Strategic and Business Objectives and Risk Appetite and Limits Leon Bloom, Partner, Deloitte & Touche LLP lebloom@deloitte.ca Agenda Alignment of

Risk Architecture: Alignment of Investor Objectives and Strategic and Business Objectives and Risk Appetite and Limits Leon Bloom, Partner, Deloitte & Touche LLP lebloom@deloitte.ca Agenda Alignment of

REGULATORY GUIDELINE Liquidity Risk Management Principles TABLE OF CONTENTS. I. Introduction II. Purpose and Scope III. Principles...

REGULATORY GUIDELINE Liquidity Risk Management Principles SYSTEM COMMUNICATION NUMBER Guideline 2015-02 ISSUE DATE June 2015 TABLE OF CONTENTS I. Introduction... 1 II. Purpose and Scope... 1 III. Principles...

REGULATORY GUIDELINE Liquidity Risk Management Principles SYSTEM COMMUNICATION NUMBER Guideline 2015-02 ISSUE DATE June 2015 TABLE OF CONTENTS I. Introduction... 1 II. Purpose and Scope... 1 III. Principles...

Insurance companies make money by managing various types of risk the risk of

A.M. BEST METHODOLOGY April 2, 2013 Risk and the Rating Process for Insurance Companies Insurance companies make money by managing various types of risk the risk of dying too young, experiencing a loss

A.M. BEST METHODOLOGY April 2, 2013 Risk and the Rating Process for Insurance Companies Insurance companies make money by managing various types of risk the risk of dying too young, experiencing a loss

BERMUDA MONETARY AUTHORITY DISCUSSION PAPER ON THE OWN RISK AND SOLVENCY ASSESSMENT PROCESS

DISCUSSION PAPER ON THE OWN RISK AND SOLVENCY ASSESSMENT PROCESS Table of Contents FOREWORD... 2 0. PURPOSE AND EXECUTIVE SUMMARY... 3 1. INTRODUCTION... 5 Bermuda Regulatory Developments... 5 Relationship

DISCUSSION PAPER ON THE OWN RISK AND SOLVENCY ASSESSMENT PROCESS Table of Contents FOREWORD... 2 0. PURPOSE AND EXECUTIVE SUMMARY... 3 1. INTRODUCTION... 5 Bermuda Regulatory Developments... 5 Relationship

ORSA: A relevant part of the governance system within Solvency II

ORSA: A relevant part of the governance system within Solvency II Prof. Dr. Martin Balleer, Georg-August-Universität Göttingen Germany Faculty of Economics Belgrade University 18th May 2016, Belgrade Solvency

ORSA: A relevant part of the governance system within Solvency II Prof. Dr. Martin Balleer, Georg-August-Universität Göttingen Germany Faculty of Economics Belgrade University 18th May 2016, Belgrade Solvency