Critical Reflection of Two State-of-the-Art Risk Management Frameworks (SRM004)

|

|

|

- Mervin Casey

- 5 years ago

- Views:

Transcription

1

2 Critical Reflection of Two State-of-the-Art Risk Management Frameworks (SRM004) Speakers: Dr. Kathrin Anne Meier, Chief Risk Officer, Allianz Global Corporate & Specialty John Adams, VP Global ERM, PepsiCo

3 Content 1. Allianz Risk Management Framework 2. PepsiCo Risk Management Framework 3. Discussion of selected Risk Management Elements 4. Summary and Q&A

4 Learning Objectives At the end of this session, you will: Understand critical elements of a comprehensive Risk Management framework Better understand how two different companies approach governance, risk tolerance and risk identification approaches

5 Allianz Over 85 million Allianz customers 122.3bn in Revenue: among the top 30 of the world s largest corporations based on revenues 10.4bn Operating Profit Net income attributable to shareholders of 6.2bn Number 1 in P&C business globally: P&C segment delivered more than half of Allianz Group s operating profit, with 5.4bn; Gross Written Premium rose to 48.3bn Among the top 5 in Life/Health business worldwide: statutory premiums grew by 18.6% to 67.3bn from 56.8bn in 2013 Number 1 in Credit insurance globally One of the largest Asset Managers globally Worldwide leader in travel insurance, assistance services and personal services All figures as per 12/31/2014

6 Allianz Global Corporate & Specialty Allianz s center of excellence for corporate clients and mid-sized businesses with complex and specialized insurance and risk control needs. Diversified product portfolio Wide range of complementary services, including specialist non-traditional risk transfer solutions provided by our subsidiary Allianz Risk Transfer Financial strength: 5.4 billion Gross Written Premium (2014)* Consistently strong ratings: AA ( Very Strong ) from Standard & Poor s, A+ ( Superior ) from A.M. Best** Global reach: integrated in the Allianz network of more than 160 countries worldwide Extensive international experience: manages some 2,300 International Insurance Programs More than 3,600 dedicated employees * All Allianz Global Corporate & Specialty companies ** Allianz Global Corporate & Specialty, correct as at 02/2015

7 Allianz Risk Framework Set-up driven by various internal and external requirements Taking on and managing risks is Allianz' core competency and we continuously improve and adapt our risk framework to the needs of Allianz, its clients and other external stakeholders (Regulators: in particular Solvency II (SII) in Europe and other new Solvency regimes, Rating Agencies) Set-up influenced by introduction of SII SII initiated because of capital market crisis at the beginning of this century Economic risk-based solvency capital regime (as from 1 Jan 2016) Linkage between risk and capital Crucial role to be played by risk management Well developed risk culture with the right tone from the top

8 Role of Risk Management under SII SII Directive establishes ground rules for good governance Key functions: Risk Management, Actuarial, Compliance, Internal Audit Three lines of defense, key functions are independent Documented policies and evidence of implementation and effectiveness Fit & proper requirements for persons running the business The Risk Management system under SII Must comprise strategies, processes, continuous reporting on risks at individual and aggregated level as well as their interdependencies Must be effective and well integrated into organizational structure and in decision-making process Companies are required to conduct ORSA Regular and ad-hoc Own Risk and Solvency Assessments (ORSA) to determine the Solvency Capital Requirement risk measure and calibration

9 Added Value by Risk Management

10 Governance Structure Allianz Group Allianz Global Coporate & Specialty Risk Committee (board committee) Chief Risk Officer Function / Project Branch Subsidiary Allianz Group Risk Committee Allianz Group Risk Sound Governance Structure where decisions are delegated to Committees Risk Committee tasks: To decide on structure and scope of risk and control frameworks To review ORSA, Internal Control System, procedures for identification, assessment and reporting of risks To propose risk mitigation actions To overview risk landscape To decide and monitor risk tolerance Quarterly Risk Committee meetings

11 Policy Framework Our Governance framework consists of ten policies and various underlying standards and functional rules:

12 Risk Policy Framework How business is steered and controlled within the company is documented in a set of corporate rules, establishing binding regulation and guidelines within the company

13 Risk Management Process Our Top Risk Assessment process is managed in four steps: Risk Management Process Identification Analysis & Evaluation Steering Monitoring Objective Be aware of the most material risks Allianz is exposed to Be in a position to judge the main impacts on Allianz Take measures necessary to limit risks and focus risk mitigating measures Monitor risk developments and changes in the risk environment Risk Scenarios Heat Map Risk Report and Quarterly Risk Updates Tools

14 Risk Categories Market Risk: changes in market prices (e.g. driven by equity prices, interest rates, real estate prices, exchange rates, credit spreads and implied volatilities). Credit Risk: deterioration in the credit quality of counterparties. Liquidity Risk: failure to meet payment obligations, and/or refinancing is only possible at higher interest rates or by liquidating assets at a discount. Underwriting Risk: inadequacy of reserves or unpredictability of mortality or longevity. Business Risk: decrease in actual results compared to business assumptions. This includes lapse risk. Operational Risk: inadequate or failed internal processes and systems, from human misbehavior/errors or from external events. Reputational Risk: drop in the value of Allianz caused by a decline in the reputation. Strategic Risk: negative changes in Allianz s value arising from the adverse effect of management decisions regarding business strategies and their implementation

15 Risk Strategy The Risk Tolerance System is governed in the Risk Strategy: Capital Adequacy Limits Risk Strategy Target Ratings for Top Risks Internal Risk Capital Risk Standards Retention Management Principles Financial Limits

16 Capital Model Internal Model is used for capital management Solvency capital calculation Stress testing Assets Liabilities Free Assets Internal Model is used in business decisions Incorporation in pricing tools Used for outwards reinsurance structuring Internal Model is used to steer business RoRC (Return on Risk Capital) as forward-looking profitability measure RoRC = Economic Profit : Risk Capital Comparison of relative economic attractiveness of lines of business Market value of assets SCR MCR Technical Provisions SCR: Solvency Capital Ratio MCR: Minimum Capital Ratio

17 Risk Reporting Internal / Regulatory Reporting on Risk Quarterly Risk report on risk landscape, risk tolerances and mitigation actions to Senior Management and Regulator Annual & ad-hoc ORSA reports on assessment of overall risk position and solvency needs, ensuring business underwritten is supported by right amount of capital Regular Supervisory Report Quantitative Reporting Templates to Regulator Public Disclosure on Risk Annual Solvency and Financial Condition Report to public

18 PepsiCo Leading global food and beverage company with a portfolio of iconic brands 2014 full year results; Market Capitalization as of 4/1/15 Ø $66 Billion in revenue 51% US, 49% Int l Foods: 53%; Beverages: 47% Ø 22 Billion dollar brands Ø Available in more than 200 countries and territories Ø ~20% of revenue in nutrition Ø Market capitalization - $142bn Ø Largest Food & Bev. contributor to US retail sales growth Ø 10 of the top 50 new Food and Beverage launches in North America in 14

19 PepsiCo Risk Framework

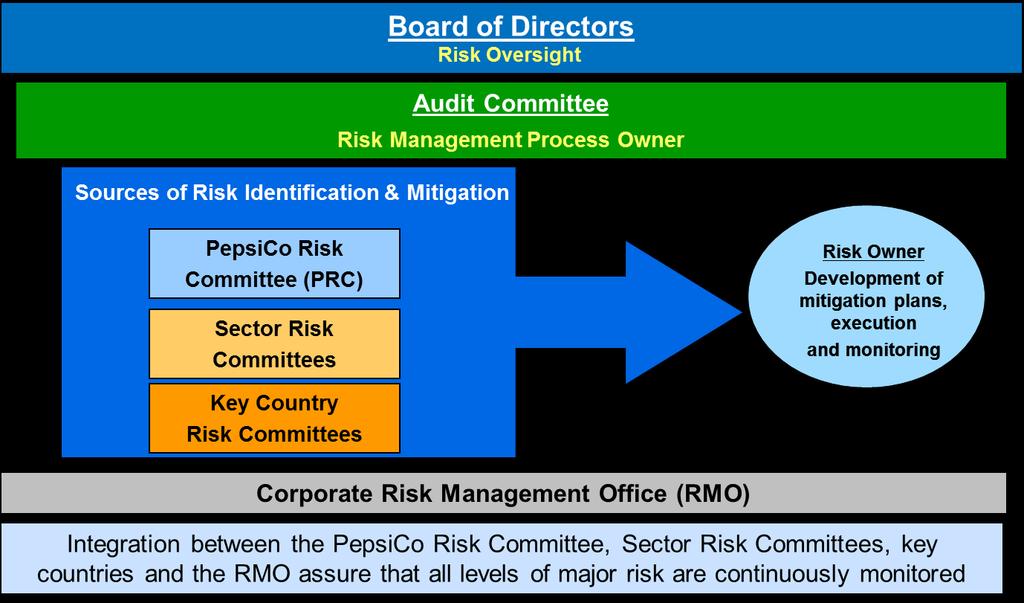

20 Governance Model

21 Executive Risk Committees

22 Corporate Risk Management Office (RMO) RMO role: Ø Ø Ø Ø Ø Ø Set the PepsiCo ERM agenda Define the framework, establish the processes, develop tools Engage with Corporate/Sectors to identify and assess risks and ensure risk owners are identified and mitigation plans put in place Ensure on-going risk monitoring and reporting to the PRC and the Board Educate the organization on ERM and drive best practice sharing Build further risk capability and drive program improvements To be effec(ve, the RMO needs to work collabora(vely with the sectors and other corporate func(ons

23 Risk Categories Risk Category Strategic Definition Risks that can have a material impact on our strategic objectives arising from internal or external factors Opera(ng Regulatory Financial Issues which may affect or compromise execution of business functions Governmental/NGO actions that can have a material impact on the achievement of our business objectives or an adverse impact on our reputation or sustainability Risks which can cause unexpected variability or volatility in our topline, margins, EPS or returns

24 End-to-End Process

25 Risk Identification

26 Prioritization and Assessment

27 Risk Mitigation Ø Risk owner identified and accountability established Ø Simply stated definition of the risk describing how it may impact the achievement of our business objectives and the impact of the risk occurring Ø Discussion of risk mitigation plans already in place, progress made to date, and additional mitigation actions that we will take to further mitigate the risk Ø Identification of additional capital and/or resources required or new capabilities Ø The targeted end-state, what does success look like Ø Key milestones and metrics that we will use to monitor our progress Ø Risk tolerance

28 Monitoring Progress Simple, concise risk Dashboards and Scorecards are used to monitor and report our risk mitigation progress Risk Dashboard Risk Scorecard

Ø Risk Assessment template required for all capexes above a certain threshold to address various non-financial")

29 Embedded in Core Processes Strategic Planning Ø Identification of the top risks to achieving each strategic objective Ø Template to facilitate discussions at strategic plan meetings Ø Discussion of the top risks during strategic plan presentations Capital Investment Decisions (Capex) Ø Risk Assessment template required for all capexes above a certain threshold to address various non-financial business risks Ø Key project risks are identified and communicated to ensure the appropriate risk tradeoff decisions Ø RMO represented on the capex committee for review/approval of investment decisions M&A Due Diligence Ø Due Diligence checklist revised to ensure all appropriate non-financial risks are identified and mitigation costs considered in our assessment and negotiations.

30 Cadence For Review

31 Discussion Governance Allianz Effective system of governance ensured by a transparent organizational structure with a clear allocation and appropriate segregation of responsibilities Risk Committee is Executive Committee, chaired by the CFO Risk Management is the process owner Risk Management reports into CFO Documentation (polices, standards, etc.) clarifies roles and responsibilities PepsiCo Board has oversight of the top PepsiCo risks Executive risk committee chaired by the CEO Risk committees at the Sector and key Country level Audit Committee is the process owner; Risk Management office is the corporate process owner Risk Management reports into Strategy Group and CFO Three lines of defense principle applied Documented process to ensure consistency across the organization

32 Discussion Risk Tolerance Allianz Limits applied not only to market, credit and insurance risk, but also to operational risk, e.g. key risk indicators on data quality risk, IT risk, key personnel risk Risk appetite to be decided by Executive Management based on Risk Management s risk tolerance proposal. This is captured in the Risk Strategy. The Risk Strategy is to be aligned with the business strategy PepsiCo Limits managed by the business divisions and functions, e.g. Finance, etc. Applies to specific risks Integration of risk into business strategy and capital investment decisions Driven by business strategies Targeted end state developed for each risk

33 Discussion Risk Identification Allianz Internal and external input to risk landscape Many risk assessments and workshops (operational risk, compliance risk) Emerging risk identification Scenario building helps greatly to discuss about risks Risk Ownership on top management level is key PepsiCo Top down and bottom up process Includes both internal and external perspectives Includes existing and emerging risks Formal annual process; ongoing identification and escalation as warranted Tools to assist the process country level risk survey Scenario analysis used selectively

34 Summary A sound risk management framework addresses: Risk governance, incl. documented processes, procedures and policies All risk types at individual, aggregated and interdependent levels Decision-making processes, e.g. limit systems Important elements: The tone from the top is indispensable for a good risk culture Risk management should be embedded at all levels of the organization Operational independence of Risk Management department is needed Quantitative assessments should always be complemented by qualitative assessments In general: Risk management should not prevent deals but should help the company to execute its risk strategy in a controlled way Risk management should aid the businesses in the achievement of their short and long term goals and inform and improve senior management s allocation of resources and decision making

35 Q & A

36 Back Up

37 Solvency II Basic Architecture Solvency II Pillar 1 Pillar 2 Pillar 3 Quantitative requirements Market-consistent valuation of assets and liabilities Own Funds Risk-based Solvency Capital Requirement Qualitative requirements and supervisory review System of Governance Own Risk and Solvency Assessment Internal Model Governance Use Test Supervisory review process Supervisory reporting and public disclosure Regular Supervisory Reporting Solvency and Financial Condition Report Support of risk-based supervision through market mechanisms

38 Three Lines of Defense 1 st Line of Defense Business Underwriting, Pricing, Claims, Finance, Human Resources, Distribution Management, Customer Service, Agents, etc 2 nd Line of Defense Control Functions Risk Management, Compliance, Actuarial, Legal 3 rd Line of Defense Internal Audit Internal Audit Management, Board Members, CEOs, Business Unit Managers, etc. Senior management is ultimately responsible for both the profitability and risk in their business Design control environment Develop frameworks Support business for managing risks Independent risk oversight Monitor and control risk exposure Challenge risk management controls, processes and systems Independent verification that policies are being adhered to and control environment is effective

Solvency II Insights for North American Insurers. CAS Centennial Meeting Damon Paisley Bill VonSeggern November 10, 2014

Solvency II Insights for North American Insurers CAS Centennial Meeting Damon Paisley Bill VonSeggern November 10, 2014 Agenda 1 Introduction to Solvency II 2 Pillar I 3 Pillar II and Governance 4 North

Solvency II Insights for North American Insurers CAS Centennial Meeting Damon Paisley Bill VonSeggern November 10, 2014 Agenda 1 Introduction to Solvency II 2 Pillar I 3 Pillar II and Governance 4 North

ERM/ORSA Training Thai General Insurance Association (TGIA)

") ERM/ORSA Training Thai General Insurance Association (TGIA) 10 October 2017 Agenda Time Topics 8.30-9.00 Registration ORSA for Non-life Insurance Top 10 global business risk in 2017 Weakness and past failures

ERM/ORSA Training Thai General Insurance Association (TGIA) 10 October 2017 Agenda Time Topics 8.30-9.00 Registration ORSA for Non-life Insurance Top 10 global business risk in 2017 Weakness and past failures

Title of the presentational;;l

Title of the presentational;;l Allianz Global Corporate & Specialty SE Singapore Branch 2017 Allianz Global Corporate & Specialty SE Singapore Branch Supplementary Information 2017 This Disclosure is a

Title of the presentational;;l Allianz Global Corporate & Specialty SE Singapore Branch 2017 Allianz Global Corporate & Specialty SE Singapore Branch Supplementary Information 2017 This Disclosure is a

American Academy of Actuaries Webinar: The Practice of ERM in the Insurance Industry. Enterprise Risk Management Committee November 19, 2013

American Academy of Actuaries Webinar: The Practice of ERM in the Insurance Industry Enterprise Risk Management Committee November 19, 2013 All Rights Reserved. 1 Presenters Bruce Jones, MAAA, FCAS, CERA

American Academy of Actuaries Webinar: The Practice of ERM in the Insurance Industry Enterprise Risk Management Committee November 19, 2013 All Rights Reserved. 1 Presenters Bruce Jones, MAAA, FCAS, CERA

Risk Appetite Survey Current state of the Insurance Industry

Risk Appetite Survey Current state of the Insurance Industry Deloitte Belgium and The Netherlands Financial Services Industry The survey was conducted during July 2013 till December 2013 Introduction The

Risk Appetite Survey Current state of the Insurance Industry Deloitte Belgium and The Netherlands Financial Services Industry The survey was conducted during July 2013 till December 2013 Introduction The

INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS

Guidance Paper No. 2.2.x INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS GUIDANCE PAPER ON ENTERPRISE RISK MANAGEMENT FOR CAPITAL ADEQUACY AND SOLVENCY PURPOSES DRAFT, MARCH 2008 This document was prepared

Guidance Paper No. 2.2.x INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS GUIDANCE PAPER ON ENTERPRISE RISK MANAGEMENT FOR CAPITAL ADEQUACY AND SOLVENCY PURPOSES DRAFT, MARCH 2008 This document was prepared

Title of the presentational;;l

Title of the presentational;;l Allianz Global Corporate & Specialty SE Singapore Branch 2016 Allianz Global Corporate & Specialty SE Singapore Branch Supplementary Information 2016 This Disclosure is a

Title of the presentational;;l Allianz Global Corporate & Specialty SE Singapore Branch 2016 Allianz Global Corporate & Specialty SE Singapore Branch Supplementary Information 2016 This Disclosure is a

Solvency II Implementation

Solvency II Implementation Allianz Life Korea October 21, 2015 Solvency II in history 2001-02 Financial Crisis Solvency I not risk based, especially on asset side Basel II seen as a success in banking

Solvency II Implementation Allianz Life Korea October 21, 2015 Solvency II in history 2001-02 Financial Crisis Solvency I not risk based, especially on asset side Basel II seen as a success in banking

Own Risk Solvency Assessment (ORSA) Linking Risk Management, Capital Management and Strategic Planning

Linking Risk Management, Capital Management and Strategic Planning") Own Risk Solvency Assessment (ORSA) Linking Risk Management, Capital Management and Strategic Planning Moderator: David Holland, Risk Director, Ally Insurance SPEAKERS Mary-ellen Coggins, Managing Director,

Own Risk Solvency Assessment (ORSA) Linking Risk Management, Capital Management and Strategic Planning Moderator: David Holland, Risk Director, Ally Insurance SPEAKERS Mary-ellen Coggins, Managing Director,

The Changing face of ERM: The Insurance Company s Perspective

The Changing face of ERM: The Insurance Company s Perspective Karen Tan, Chief Risk Officer, Reinsurance Asia, Swiss Re FNLIA Discussion Series, December 1, 2015 History of Risk Management as a professional

The Changing face of ERM: The Insurance Company s Perspective Karen Tan, Chief Risk Officer, Reinsurance Asia, Swiss Re FNLIA Discussion Series, December 1, 2015 History of Risk Management as a professional

A (personal) view. Philip Whittingham, European Chief Enterprise Risk Officer. 22 March 2010

view. Philip Whittingham, European Chief Enterprise Risk Officer. 22 March 2010") The role of the risk profession in a Solvency II world A (personal) view Philip Whittingham, European Chief Enterprise Risk Officer XL Group plc 22 March 2010 Session Aims Successful Solvency II implementation

The role of the risk profession in a Solvency II world A (personal) view Philip Whittingham, European Chief Enterprise Risk Officer XL Group plc 22 March 2010 Session Aims Successful Solvency II implementation

The Challenges of Solvency II

Solvency II The Challenges of Solvency II Gain-Line & Solvency II Solvency II is the biggest ever exercise in bringing together insurers and re-insurers under one regulatory regime. Solvency II is a set

Solvency II The Challenges of Solvency II Gain-Line & Solvency II Solvency II is the biggest ever exercise in bringing together insurers and re-insurers under one regulatory regime. Solvency II is a set

SOLVENCY AND FINANCIAL CONDITION REPORT EUROLIFE LTD

SOLVENCY AND FINANCIAL CONDITION REPORT EUROLIFE LTD FOR THE YEAR ENDING 31 DECEMBER 2016 1 Table of Contents 1.Executive Summary... 5 1.1 Overview... 5 1.2 Business and performance... 5 1.3 System of

SOLVENCY AND FINANCIAL CONDITION REPORT EUROLIFE LTD FOR THE YEAR ENDING 31 DECEMBER 2016 1 Table of Contents 1.Executive Summary... 5 1.1 Overview... 5 1.2 Business and performance... 5 1.3 System of

INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS

Guidance Paper No. 2.2.6 INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS GUIDANCE PAPER ON ENTERPRISE RISK MANAGEMENT FOR CAPITAL ADEQUACY AND SOLVENCY PURPOSES OCTOBER 2007 This document was prepared

Guidance Paper No. 2.2.6 INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS GUIDANCE PAPER ON ENTERPRISE RISK MANAGEMENT FOR CAPITAL ADEQUACY AND SOLVENCY PURPOSES OCTOBER 2007 This document was prepared

SOLVENCY AND FINANCIAL CONDITION REPORT EUROLIFE LTD

SOLVENCY AND FINANCIAL CONDITION REPORT EUROLIFE LTD FOR THE YEAR ENDING 31 DECEMBER 2017 1 Table of Contents 1. Executive Summary... 5 1.1 Overview... 5 1.2 Business and performance... 5 1.3 System of

SOLVENCY AND FINANCIAL CONDITION REPORT EUROLIFE LTD FOR THE YEAR ENDING 31 DECEMBER 2017 1 Table of Contents 1. Executive Summary... 5 1.1 Overview... 5 1.2 Business and performance... 5 1.3 System of

IAIS: Enterprise Risk Management for Capital Adequacy & Solvency Purposes. George Brady. IAIS Deputy Secretary General

IAIS: Enterprise Risk Management for Capital Adequacy & Solvency Purposes George Brady IAIS Deputy Secretary General Table of Contents 1. Introduction 2. Governance and an Enterprise Risk Management (ERM)

IAIS: Enterprise Risk Management for Capital Adequacy & Solvency Purposes George Brady IAIS Deputy Secretary General Table of Contents 1. Introduction 2. Governance and an Enterprise Risk Management (ERM)

WHITE PAPER. Solvency II Compliance and beyond: Title The essential steps for insurance firms

WHITE PAPER Solvency II Compliance and beyond: Title The essential steps for insurance firms ii Contents Introduction... 1 Step 1 Data Management... 1 Step 2 Risk Calculations... 3 Solvency Capital Requirement

WHITE PAPER Solvency II Compliance and beyond: Title The essential steps for insurance firms ii Contents Introduction... 1 Step 1 Data Management... 1 Step 2 Risk Calculations... 3 Solvency Capital Requirement

Guidance Note: Internal Capital Adequacy Assessment Process (ICAAP) Credit Unions with Total Assets Greater than $1 Billion.

Credit Unions with Total Assets Greater than $1 Billion.") Guidance Note: Internal Capital Adequacy Assessment Process (ICAAP) Credit Unions with Total Assets Greater than $1 Billion January 2018 Ce document est aussi disponible en français. Applicability This

Guidance Note: Internal Capital Adequacy Assessment Process (ICAAP) Credit Unions with Total Assets Greater than $1 Billion January 2018 Ce document est aussi disponible en français. Applicability This

ERM Implementation and the Own Risk and Solvency Assessment (ORSA)

") ERM Implementation and the Own Risk and Solvency Assessment (ORSA) Kevin Olberding June 2013 1 Agenda ERM IMPLEMENTATION AND THE OWN RISK AND SOLVENCY ASSESSMENT (ORSA) Evolution of Enterprise Risk Management

ERM Implementation and the Own Risk and Solvency Assessment (ORSA) Kevin Olberding June 2013 1 Agenda ERM IMPLEMENTATION AND THE OWN RISK AND SOLVENCY ASSESSMENT (ORSA) Evolution of Enterprise Risk Management

The ORSA opportunity:

The ORSA opportunity: Compliance and business value 12 March 2014 Today s agenda Background and regulatory update ORSA overview Industry perspectives Achieving long-term business value Page 2 Today s agenda

The ORSA opportunity: Compliance and business value 12 March 2014 Today s agenda Background and regulatory update ORSA overview Industry perspectives Achieving long-term business value Page 2 Today s agenda

Life under Solvency II Be prepared!

Life under Solvency II Be prepared! Moderator: Hugh Rosenbaum, Towers Watson Speakers: Tomas Wittbjer, Global Head of Insurance, IKANO SA Lorraine Stack, Marsh Management Services Dublin Session Overview

Life under Solvency II Be prepared! Moderator: Hugh Rosenbaum, Towers Watson Speakers: Tomas Wittbjer, Global Head of Insurance, IKANO SA Lorraine Stack, Marsh Management Services Dublin Session Overview

Link between Pillar 1 and Pillar 2

Link between Pillar 1 and Pillar 2 XXIV International Seminar on Insurance and Surety, November 2014, Mexico City Olaf Ermert, BaFin Link between Pillar 1 and Pillar 2 Content Introduction Own Risk and

Link between Pillar 1 and Pillar 2 XXIV International Seminar on Insurance and Surety, November 2014, Mexico City Olaf Ermert, BaFin Link between Pillar 1 and Pillar 2 Content Introduction Own Risk and

Solvency II: Implementation Challenges & Experiences Learned

Solvency II: Implementation Challenges & Experiences Learned Appointed Actuary Symposium Actuarial Society of Hong Kong (ASHK) Jonathan Zhao - Actuarial Services Practice Leader, Asia Pacific 3 November

Solvency II: Implementation Challenges & Experiences Learned Appointed Actuary Symposium Actuarial Society of Hong Kong (ASHK) Jonathan Zhao - Actuarial Services Practice Leader, Asia Pacific 3 November

NAIC OWN RISK AND SOLVENCY ASSESSMENT (ORSA) GUIDANCE MANUAL

GUIDANCE MANUAL") NAIC OWN RISK AND SOLVENCY ASSESSMENT (ORSA) GUIDANCE MANUAL Created by the NAIC Group Solvency Issues Working Group Of the Solvency Modernization Initiatives (EX) Task Force 2011 National Association

NAIC OWN RISK AND SOLVENCY ASSESSMENT (ORSA) GUIDANCE MANUAL Created by the NAIC Group Solvency Issues Working Group Of the Solvency Modernization Initiatives (EX) Task Force 2011 National Association

SOLVENCY II INSIGHTS FOR NORTH AMERICAN INSURERS. CAS Centennial Meeting Melissa Salton November 10, 2014

SOLVENCY II INSIGHTS FOR NORTH AMERICAN INSURERS CAS Centennial Meeting Melissa Salton 609-243-4424 November 10, 2014 Risk Management Components at MRG provides a framework for all US entities Disclosure

SOLVENCY II INSIGHTS FOR NORTH AMERICAN INSURERS CAS Centennial Meeting Melissa Salton 609-243-4424 November 10, 2014 Risk Management Components at MRG provides a framework for all US entities Disclosure

Sections of the ORSA Report

Lessons Learned From Orsa Reviews Impact on Risk Focused Examination NAIC Insurance Summit INS Companies Joe Fritsch, Director INS Companies Don Carbone, Exam Manager INS Companies Sections of the ORSA

Lessons Learned From Orsa Reviews Impact on Risk Focused Examination NAIC Insurance Summit INS Companies Joe Fritsch, Director INS Companies Don Carbone, Exam Manager INS Companies Sections of the ORSA

Mediolanum International Life dac

Contents Executive Summary... 3 A. Business and Performance... 6 A.1 Business and External Environment... 6 A.2 Performance from Underwriting Activities... 7 A.3 Performance from Investment Activities...

Contents Executive Summary... 3 A. Business and Performance... 6 A.1 Business and External Environment... 6 A.2 Performance from Underwriting Activities... 7 A.3 Performance from Investment Activities...

Forsikringsselskabet Privatsikring A/S. Solvency and Financial Condition Report

Forsikringsselskabet Privatsikring A/S Solvency and Financial Condition Report 2017 Introduction... 3 Summary... 4 A. Business and Performance... 6 A.1 Business... 6 A.2 Underwriting Performance... 9 A.3

Forsikringsselskabet Privatsikring A/S Solvency and Financial Condition Report 2017 Introduction... 3 Summary... 4 A. Business and Performance... 6 A.1 Business... 6 A.2 Underwriting Performance... 9 A.3

Presentation by: Nasumba Kizito Kwatukha CPA,CIA, CISA,CFE,CISSP,CRMA,CISM,IIK 6 th JULY 2017

ENTERPRISE RISK MANAGEMENT SEMINAR Enterprise Risk Management in case of Financial Institutions Presentation by: Nasumba Kizito Kwatukha CPA,CIA, CISA,CFE,CISSP,CRMA,CISM,IIK 6 th JULY 2017 Uphold public

ENTERPRISE RISK MANAGEMENT SEMINAR Enterprise Risk Management in case of Financial Institutions Presentation by: Nasumba Kizito Kwatukha CPA,CIA, CISA,CFE,CISSP,CRMA,CISM,IIK 6 th JULY 2017 Uphold public

ERM and ORSA Assuring a Necessary Level of Risk Control

ERM and ORSA Assuring a Necessary Level of Risk Control Dave Ingram, MAAA, FSA, CERA, FRM, PRM Chair of IAA Enterprise & Financial Risk Committee Executive Vice President, Willis Re September, 2012 1 DISCLAIMER

ERM and ORSA Assuring a Necessary Level of Risk Control Dave Ingram, MAAA, FSA, CERA, FRM, PRM Chair of IAA Enterprise & Financial Risk Committee Executive Vice President, Willis Re September, 2012 1 DISCLAIMER

TD BANK INTERNATIONAL S.A.

TD BANK INTERNATIONAL S.A. Pillar 3 Disclosures Year Ended October 31, 2013 1 Contents 1. Overview... 3 1.1 Purpose...3 1.2 Frequency and Location...3 2. Governance and Risk Management Framework... 4 2.1

TD BANK INTERNATIONAL S.A. Pillar 3 Disclosures Year Ended October 31, 2013 1 Contents 1. Overview... 3 1.1 Purpose...3 1.2 Frequency and Location...3 2. Governance and Risk Management Framework... 4 2.1

Increased Corporate Governance Requirements for Insurers

Increased Corporate Governance Requirements for Insurers 0 INCREASED CORPORATE GOVERNANCE REQUIREMENTS FOR INSURERS Introduction On 17 December 2009, the definitive text of the Solvency II Directive (2009/138/EC)

Increased Corporate Governance Requirements for Insurers 0 INCREASED CORPORATE GOVERNANCE REQUIREMENTS FOR INSURERS Introduction On 17 December 2009, the definitive text of the Solvency II Directive (2009/138/EC)

Solvency and Financial Condition Report

Solvency and Financial Condition Report December 2016 1 P a g e Solvency and Financial Condition Report Contents Summary... 3 A. Business and performance... 3 A.1 Business... 3 A.2 Underwriting Performance...

Solvency and Financial Condition Report December 2016 1 P a g e Solvency and Financial Condition Report Contents Summary... 3 A. Business and performance... 3 A.1 Business... 3 A.2 Underwriting Performance...

CATTOLICA LIFE DAC SOLVENCY AND FINANCIAL CONDITION REPORT 31 ST DECEMBER 2017

CATTOLICA LIFE DAC SOLVENCY AND FINANCIAL CONDITION REPORT 31 ST DECEMBER 2017 May 3, 2018 TABLE OF CONTENTS EXECUTIVE SUMMARY 3 A. BUSINESS AND PEFORMANCE 5 A.1 Business A.2 Underwriting Performance 5

CATTOLICA LIFE DAC SOLVENCY AND FINANCIAL CONDITION REPORT 31 ST DECEMBER 2017 May 3, 2018 TABLE OF CONTENTS EXECUTIVE SUMMARY 3 A. BUSINESS AND PEFORMANCE 5 A.1 Business A.2 Underwriting Performance 5

A.M. Best s New Risk Management Standards

A.M. Best s New Risk Management Standards Stephanie Guethlein McElroy, A.M. Best Manager, Rating Criteria and Rating Relations Hubert Mueller, Towers Perrin, Principal March 24, 2008 Introduction A.M.

A.M. Best s New Risk Management Standards Stephanie Guethlein McElroy, A.M. Best Manager, Rating Criteria and Rating Relations Hubert Mueller, Towers Perrin, Principal March 24, 2008 Introduction A.M.

GUIDELINE ON ENTERPRISE RISK MANAGEMENT

GUIDELINE ON ENTERPRISE RISK MANAGEMENT Insurance Authority Table of Contents Page 1. Introduction 1 2. Application 2 3. Overview of Enterprise Risk Management (ERM) Framework and 4 General Requirements

GUIDELINE ON ENTERPRISE RISK MANAGEMENT Insurance Authority Table of Contents Page 1. Introduction 1 2. Application 2 3. Overview of Enterprise Risk Management (ERM) Framework and 4 General Requirements

Prudential Standard GOI 3 Risk Management and Internal Controls for Insurers

Prudential Standard GOI 3 Risk Management and Internal Controls for Insurers Objectives and Key Requirements of this Prudential Standard Effective risk management is fundamental to the prudent management

Prudential Standard GOI 3 Risk Management and Internal Controls for Insurers Objectives and Key Requirements of this Prudential Standard Effective risk management is fundamental to the prudent management

Gregg Clifton. CFO Aurigen Reinsurance

Gregg Clifton CFO Aurigen Reinsurance Regulatory Capital When it comes to regulatory capital, is there a discernable clicking sound of a ratchet? More onerous Canadian capital requirements and the inherent

Gregg Clifton CFO Aurigen Reinsurance Regulatory Capital When it comes to regulatory capital, is there a discernable clicking sound of a ratchet? More onerous Canadian capital requirements and the inherent

TYRE REINSURANCE (IRELAND) DAC. Solvency and Financial Condition Report. For Financial Year Ending 31 st December 2016 (the reporting period )

DAC. Solvency and Financial Condition Report. For Financial Year Ending 31 st December 2016 (the reporting period )") TYRE REINSURANCE (IRELAND) DAC Solvency and Financial Condition Report For Financial Year Ending 31 st December 2016 (the reporting period ) 1 P a g e Executive Summary Tyre Reinsurance (Ireland) DAC (

TYRE REINSURANCE (IRELAND) DAC Solvency and Financial Condition Report For Financial Year Ending 31 st December 2016 (the reporting period ) 1 P a g e Executive Summary Tyre Reinsurance (Ireland) DAC (

Risk Appetite. What is risk appetite?

Risk Appetite Presented by Mike Claffey 30 March 2011 What is risk appetite? Risk appetite is the degree of risk that an organisation is willing to accept in order to achieve its objectives, both in terms

Risk Appetite Presented by Mike Claffey 30 March 2011 What is risk appetite? Risk appetite is the degree of risk that an organisation is willing to accept in order to achieve its objectives, both in terms

Society of Actuaries in Ireland Solvency II for Beginners. Mike Frazer. 19 May 2011

Society of Actuaries in Ireland Solvency II for Beginners Mike Frazer 19 May 2011 1 Agenda Why has Solvency II been created? Structure of Solvency II The Solvency II Balance Sheet Pillar II & III Aspects

Society of Actuaries in Ireland Solvency II for Beginners Mike Frazer 19 May 2011 1 Agenda Why has Solvency II been created? Structure of Solvency II The Solvency II Balance Sheet Pillar II & III Aspects

Preparing for SII and IDD what is the best approach for local stakeholders to consider?

Preparing for SII and IDD what is the best approach for local stakeholders to consider? Experience with Solvency II implementation in Croatia Croatian Financial Services Supervisory Agency Gordana Letica,

Preparing for SII and IDD what is the best approach for local stakeholders to consider? Experience with Solvency II implementation in Croatia Croatian Financial Services Supervisory Agency Gordana Letica,

Does the ORSA add value? Challenges and initial achievements. Lukas Ziewer Risk Management Perspectives, 18/11/2014

Does the ORSA add value? Challenges and initial achievements Lukas Ziewer Risk Management Perspectives, 18/11/2014 My three wishes for a prudential regime 1. Capital as a single currency for risk as a

Does the ORSA add value? Challenges and initial achievements Lukas Ziewer Risk Management Perspectives, 18/11/2014 My three wishes for a prudential regime 1. Capital as a single currency for risk as a

Solvency II overview

Solvency II overview David Payne, FIA Casualty Loss Reserve Seminar 21 September 2010 INTNL-2: Solvency II - Update and Current Events Antitrust Notice The Casualty Actuarial Society is committed to adhering

Solvency II overview David Payne, FIA Casualty Loss Reserve Seminar 21 September 2010 INTNL-2: Solvency II - Update and Current Events Antitrust Notice The Casualty Actuarial Society is committed to adhering

Pillar 3 As at 31st March 2011

Pillar 3 As at 31 st March 2011 Purpose of Disclosure This document sets out the Pillar 3 market disclosures for Threadneedle Asset Management Holdings an authorised and regulated limited license firm

Pillar 3 As at 31 st March 2011 Purpose of Disclosure This document sets out the Pillar 3 market disclosures for Threadneedle Asset Management Holdings an authorised and regulated limited license firm

The Role of Finance and Accounting as Critical Players in ERM and ORSA

The Role of Finance and Accounting as Critical Players in ERM and ORSA Session Number 404 Jim Stangroom Baker Tilly John Romano Baker Tilly John Holdorf NYCM Insurance Amy Purdy Godleski Columbian Financial

The Role of Finance and Accounting as Critical Players in ERM and ORSA Session Number 404 Jim Stangroom Baker Tilly John Romano Baker Tilly John Holdorf NYCM Insurance Amy Purdy Godleski Columbian Financial

CAPITAL MANAGEMENT GUIDELINE

CAPITAL MANAGEMENT GUIDELINE May 2015 Capital Management Guideline 1 Preambule TABLE OF CONTENTS Preamble... 3 Scope... 4 Coming into effect and updating... 5 Introduction... 6 1. Capital management...

CAPITAL MANAGEMENT GUIDELINE May 2015 Capital Management Guideline 1 Preambule TABLE OF CONTENTS Preamble... 3 Scope... 4 Coming into effect and updating... 5 Introduction... 6 1. Capital management...

Pillar III Disclosure Report 2017

Pillar III Disclosure Report 2017 Content Section 1. Introduction and basis for preparation 3 Section 2. Risk management objectives and policies 5 Section 3. Information on the scope of application of

Pillar III Disclosure Report 2017 Content Section 1. Introduction and basis for preparation 3 Section 2. Risk management objectives and policies 5 Section 3. Information on the scope of application of

2014 Own Risk and Solvency Assessment (ORSA) Feedback Pilot Project Observations of the Group Solvency Issues (E) Working Group

Feedback Pilot Project Observations of the Group Solvency Issues (E) Working Group") 2014 Own Risk and Solvency Assessment (ORSA) Feedback Pilot Project Observations of the Group Solvency Issues (E) Working Group During October 2014 through June 2015, a third ORSA Feedback Pilot Project

2014 Own Risk and Solvency Assessment (ORSA) Feedback Pilot Project Observations of the Group Solvency Issues (E) Working Group During October 2014 through June 2015, a third ORSA Feedback Pilot Project

Solvency II Update. Latest developments and industry challenges (Session 10) Réjean Besner

Réjean Besner") Solvency II Update Latest developments and industry challenges (Session 10) Canadian Institute of Actuaries - Annual Meeting, 29 June 2011 Réjean Besner Content Solvency II framework Solvency II equivalence

Solvency II Update Latest developments and industry challenges (Session 10) Canadian Institute of Actuaries - Annual Meeting, 29 June 2011 Réjean Besner Content Solvency II framework Solvency II equivalence

ORSA An International Development

ORSA An International Development 25.02.14 Agenda What is an ORSA? Global reach Comparison of requirements Common challenges Potential solutions Origin of ORSA FSA ICAS Solvency II IAIS ICP16 What is an

ORSA An International Development 25.02.14 Agenda What is an ORSA? Global reach Comparison of requirements Common challenges Potential solutions Origin of ORSA FSA ICAS Solvency II IAIS ICP16 What is an

ORSA reports: gaps and opportunities

ORSA reports: gaps and opportunities Market benchmarking of ORSA reports for Singapore general insurers Industry-wide Own Risk and Solvency Assessment (ORSA) 1 2 Contents 1 Executive summary 2 Our assessment

ORSA reports: gaps and opportunities Market benchmarking of ORSA reports for Singapore general insurers Industry-wide Own Risk and Solvency Assessment (ORSA) 1 2 Contents 1 Executive summary 2 Our assessment

Swiss Re Portfolio Partners S.A. Solvency and Financial Condition Report

Swiss Re Portfolio Partners S.A. (formerly iptiq Insurance S.A.) Solvency and Financial Condition Report For the period ended 31 December 2016 Swiss Re Portfolio Partners S.A. 2A, rue Albert Borschette

Swiss Re Portfolio Partners S.A. (formerly iptiq Insurance S.A.) Solvency and Financial Condition Report For the period ended 31 December 2016 Swiss Re Portfolio Partners S.A. 2A, rue Albert Borschette

Exploring the New Era of ORSA Enterprise Risk Management (ERM)/ Own Risk and Solvency Assessment (ORSA) Committee

/ Own Risk and Solvency Assessment (ORSA) Committee") Exploring the New Era of ORSA Enterprise Risk Management (ERM)/ Own Risk and Solvency Assessment (ORSA) Committee Copyright 2015 by the American Academy of Actuaries. All Rights Reserved. Presenters Tricia

Exploring the New Era of ORSA Enterprise Risk Management (ERM)/ Own Risk and Solvency Assessment (ORSA) Committee Copyright 2015 by the American Academy of Actuaries. All Rights Reserved. Presenters Tricia

Insurance Summit Mr Raymond Tam Executive Director (Policy and Development) Insurance Authority 21 September 2017

Insurance Authority 21 September 2017") Insurance Summit 2017 Mr Raymond Tam Executive Director (Policy and Development) Insurance Authority 21 September 2017 Priority of Policy Initiatives Development of risk-based capital regime Facilitation

Insurance Summit 2017 Mr Raymond Tam Executive Director (Policy and Development) Insurance Authority 21 September 2017 Priority of Policy Initiatives Development of risk-based capital regime Facilitation

Preparing for an Own Risk & Solvency Assessment

www.pwc.com Preparing for an Own Risk & Solvency Assessment March 2013 Brian Paton Director, Insurance Risk and Capital Practice brian.paton@us.pwc.com Contents 1. ORSA challenges 2. ORSA readiness and

www.pwc.com Preparing for an Own Risk & Solvency Assessment March 2013 Brian Paton Director, Insurance Risk and Capital Practice brian.paton@us.pwc.com Contents 1. ORSA challenges 2. ORSA readiness and

Actuaries and the Regulatory Environment. Role of the Actuary in the Solvency II framework

Actuaries and the Regulatory Environment Role of the Actuary in the Solvency II framework IAA Fund Southeast Europe Actuarial Seminar, Zagreb, 3 October 2011 1 Solvency II primary objectives fundamental

Actuaries and the Regulatory Environment Role of the Actuary in the Solvency II framework IAA Fund Southeast Europe Actuarial Seminar, Zagreb, 3 October 2011 1 Solvency II primary objectives fundamental

Guidance Note System of Governance - Insurance Transition to Governance Requirements established under the Solvency II Directive

Guidance Note Transition to Governance Requirements established under the Solvency II Directive Issued : 31 December 2013 Table of Contents 1.Introduction... 4 2. Detailed Guidelines... 4 General governance

Guidance Note Transition to Governance Requirements established under the Solvency II Directive Issued : 31 December 2013 Table of Contents 1.Introduction... 4 2. Detailed Guidelines... 4 General governance

Sampo Group Risk Management Principles. 9 May 2018

Sampo Group Risk Management Principles 9 May 2018 Table of contents 1. The Objectives, Tasks and Motivation of the Risk Management Process 4 2. General Group Level Risk Statements 7 2.1 Risk Appetite 7

Sampo Group Risk Management Principles 9 May 2018 Table of contents 1. The Objectives, Tasks and Motivation of the Risk Management Process 4 2. General Group Level Risk Statements 7 2.1 Risk Appetite 7

Solvency & Financial Condition Report. Surestone Insurance dac March

Solvency & Financial Condition Report Surestone Insurance dac March 31 2018 Contents SUMMARY... 1 A BUSINESS AND PERFORMANCE... 3 B SYSTEM OF GOVERNANCE... 7 C. RISK PROFILE... 23 D. VALUATION FOR SOLVENCY

Solvency & Financial Condition Report Surestone Insurance dac March 31 2018 Contents SUMMARY... 1 A BUSINESS AND PERFORMANCE... 3 B SYSTEM OF GOVERNANCE... 7 C. RISK PROFILE... 23 D. VALUATION FOR SOLVENCY

2013 Conference Risk, Recovery & Real Growth" 23rd Annual CAA Conference Secrets Wild Orchid Montego Bay, Jamaica. 4 th to 6 th December 2013

2013 Conference Risk, Recovery & Real Growth" 23rd Annual CAA Conference Secrets Wild Orchid Montego Bay, Jamaica. 4 th to 6 th December 2013 Regulatory developments in life assurance Nick Dumbreck Milliman

2013 Conference Risk, Recovery & Real Growth" 23rd Annual CAA Conference Secrets Wild Orchid Montego Bay, Jamaica. 4 th to 6 th December 2013 Regulatory developments in life assurance Nick Dumbreck Milliman

Risk Report. 42 Introduction 43 Risk and Capital Overview 43 Key Risk Metrics 44 Overall Risk Assessment 44 Risk Profile

Risk Report 42 Introduction 43 Risk and Capital Overview 43 Key Risk Metrics 44 Overall Risk Assessment 44 Risk Profile 46 Risk and Capital Framework 46 Risk Management Principles 47 Risk Governance 50

Risk Report 42 Introduction 43 Risk and Capital Overview 43 Key Risk Metrics 44 Overall Risk Assessment 44 Risk Profile 46 Risk and Capital Framework 46 Risk Management Principles 47 Risk Governance 50

Enterprise Risk Management Policy Adopted by the AMP Limited Board on 2 February 2017

Enterprise Management Policy Adopted by the AMP Limited Board on 2 February 2017 AMP s promise is to help people own tomorrow. To achieve this promise, risks must be managed effectively within the Board

Enterprise Management Policy Adopted by the AMP Limited Board on 2 February 2017 AMP s promise is to help people own tomorrow. To achieve this promise, risks must be managed effectively within the Board

Solvency and Financial Condition Report. Friends First Managed Pension Funds SOLVENCY AND FINANCIAL CONDITION REPORT

Friends First Managed Pension Funds Solvency and Financial Condition Report RSR Friends First Managed Pension Fund 2016 1 2016 TABLE OF CONTENTS 1. Introduction 4 A. Business and performance 6 A.1. Business

Friends First Managed Pension Funds Solvency and Financial Condition Report RSR Friends First Managed Pension Fund 2016 1 2016 TABLE OF CONTENTS 1. Introduction 4 A. Business and performance 6 A.1. Business

Advent Insurance dac. Solvency and Financial Condition Report ( SFCR ) for the financial year ended 31 December P a g e 1

for the financial year ended 31 December P a g e 1") Advent Insurance dac Solvency and Financial Condition Report ( SFCR ) for the financial year ended 31 December 2016 P a g e 1 Contents EXECUTIVE SUMMARY... 4 A BUSINESS AND PERFORMANCE... 6 A.1 BUSINESS...

Advent Insurance dac Solvency and Financial Condition Report ( SFCR ) for the financial year ended 31 December 2016 P a g e 1 Contents EXECUTIVE SUMMARY... 4 A BUSINESS AND PERFORMANCE... 6 A.1 BUSINESS...

SOLVENCY & FINANCIAL CONDITION REPORT. SureStone Insurance dac

SOLVENCY & FINANCIAL CONDITION REPORT SureStone Insurance dac March 31 2017 TABLE OF CONTENTS SUMMARY 1 A BUSINESS AND PERFORMANCE 2 B SYSTEM OF GOVERNANCE 5 C RISK PROFILE 19 D VALUATION FOR SOLVENCY

SOLVENCY & FINANCIAL CONDITION REPORT SureStone Insurance dac March 31 2017 TABLE OF CONTENTS SUMMARY 1 A BUSINESS AND PERFORMANCE 2 B SYSTEM OF GOVERNANCE 5 C RISK PROFILE 19 D VALUATION FOR SOLVENCY

INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS GUIDELINE. Nepal Rastra Bank Bank Supervision Department. August 2012 (updated July 2013)

") INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS GUIDELINE Nepal Rastra Bank Bank Supervision Department August 2012 (updated July 2013) Table of Contents Page No. 1. Introduction 1 2. Internal Capital Adequacy

INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS GUIDELINE Nepal Rastra Bank Bank Supervision Department August 2012 (updated July 2013) Table of Contents Page No. 1. Introduction 1 2. Internal Capital Adequacy

SOLVENCY ASSESSMENT AND MANAGEMENT (SAM) FRAMEWORK

FRAMEWORK") SOLVENCY ASSESSMENT AND MANAGEMENT (SAM) FRAMEWORK Hantie van Heerden Head: Actuarial Insurance Department 5 October 2010 High-level summary of Solvency II Background to SAM Agenda Current Structures Progress

SOLVENCY ASSESSMENT AND MANAGEMENT (SAM) FRAMEWORK Hantie van Heerden Head: Actuarial Insurance Department 5 October 2010 High-level summary of Solvency II Background to SAM Agenda Current Structures Progress

Risk Appetite for Life Offices IFoA working party

Risk Appetite for Life Offices IFoA working party Gautam Kakar, Chairman 30 October 2015 Members of Working Party: Gautam Kakar Lana Nguyen Shayanthan Pathmanathan Rod Bryn-Hussey Fabio Schiaffini Crystal

Risk Appetite for Life Offices IFoA working party Gautam Kakar, Chairman 30 October 2015 Members of Working Party: Gautam Kakar Lana Nguyen Shayanthan Pathmanathan Rod Bryn-Hussey Fabio Schiaffini Crystal

SOLVENCY AND FINANCIAL CONDITION REPORT AS AT 31ST DECEMBER 2017

SOLVENCY AND FINANCIAL CONDITION REPORT AS AT 31ST DECEMBER 2017 May 2018 Executive Summary Business performance The principal activities of Hellenic Alico Life Insurance Company Limited are the underwriting

SOLVENCY AND FINANCIAL CONDITION REPORT AS AT 31ST DECEMBER 2017 May 2018 Executive Summary Business performance The principal activities of Hellenic Alico Life Insurance Company Limited are the underwriting

Solvency and Financial Condition Report Aegon Ireland

Solvency and Financial Condition Report Aegon Ireland 2017 Page 1 of 58 Contents Scope of the report... 4 Summary... 5 Business and Performance... 5 System of Governance... 5 Risk Profile... 6 Valuation

Solvency and Financial Condition Report Aegon Ireland 2017 Page 1 of 58 Contents Scope of the report... 4 Summary... 5 Business and Performance... 5 System of Governance... 5 Risk Profile... 6 Valuation

ERM Concepts and Framework. Paul Duffy

Society of Actuaries in Ireland ERM Concepts and Framework Paul Duffy 13 th May 2010 *connectedthinking Lecture Plan Introduction to ERM Describe the concept of ERM Discuss the framework for risk management

Society of Actuaries in Ireland ERM Concepts and Framework Paul Duffy 13 th May 2010 *connectedthinking Lecture Plan Introduction to ERM Describe the concept of ERM Discuss the framework for risk management

REPORT. Solvency and Financial Conditions Report (SFCR) FOR. Gefion Insurance A/S AND. Gefion Forsikringsholding Aktieselskab

FOR. Gefion Insurance A/S AND. Gefion Forsikringsholding Aktieselskab") REPORT ON Solvency and Financial Conditions Report (SFCR) FOR Gefion Insurance A/S AND Gefion Forsikringsholding Aktieselskab DFSA registration number: 53117 (Gefion Insurance A/S) and 96017 (Gefion Forsikringsholding

REPORT ON Solvency and Financial Conditions Report (SFCR) FOR Gefion Insurance A/S AND Gefion Forsikringsholding Aktieselskab DFSA registration number: 53117 (Gefion Insurance A/S) and 96017 (Gefion Forsikringsholding

ERM Benchmark Survey Report

ERM Benchmark Survey Report A report on PACICC s fifth ERM benchmarking survey October 2017 2011 2013 2015 2016 2017 Member Survey on ERM Practices A report on PACICC s fifth ERM benchmarking survey October

ERM Benchmark Survey Report A report on PACICC s fifth ERM benchmarking survey October 2017 2011 2013 2015 2016 2017 Member Survey on ERM Practices A report on PACICC s fifth ERM benchmarking survey October

SOLVENCY AND FINANCIAL CONDITION REPORT

SOLVENCY AND FINANCIAL CONDITION REPORT Reporting year 2017 Table of Contents Page Table of Contents 2 Executive Summary 4 A Business and Performance 7 A.1 Business 7 A.2 Underwriting Performance 8 A.3

SOLVENCY AND FINANCIAL CONDITION REPORT Reporting year 2017 Table of Contents Page Table of Contents 2 Executive Summary 4 A Business and Performance 7 A.1 Business 7 A.2 Underwriting Performance 8 A.3

Risk Disclosure. Deutsche Bank AG, Colombo Branch. as at 31 December Deutsche Bank

Deutsche Bank AG, Colombo Branch Risk Disclosure as at 31 December 2015 Note: The sequence of this document follows the Central Bank of Sri Lanka, Bank Supervision Department direction no. 02/17/900/001/04

Deutsche Bank AG, Colombo Branch Risk Disclosure as at 31 December 2015 Note: The sequence of this document follows the Central Bank of Sri Lanka, Bank Supervision Department direction no. 02/17/900/001/04

The Solvency II project and the work of CEIOPS

Thomas Steffen CEIOPS Chairman Budapest, 16 May 07 The Solvency II project and the work of CEIOPS Outline Reasons for a change in the insurance EU regulatory framework The Solvency II project Drivers Process

Thomas Steffen CEIOPS Chairman Budapest, 16 May 07 The Solvency II project and the work of CEIOPS Outline Reasons for a change in the insurance EU regulatory framework The Solvency II project Drivers Process

Solvency II update. Shirley Beglinger Shires Partnership Ltd Global Association of Risk Professionals. December 2014

Solvency II update Shirley Beglinger Shires Partnership Ltd Global Association of Risk Professionals December 2014 The views expressed in the following material are the author s and do not necessarily

Solvency II update Shirley Beglinger Shires Partnership Ltd Global Association of Risk Professionals December 2014 The views expressed in the following material are the author s and do not necessarily

SAM QRT Workshop Asset Templates April 2013

SAM QRT Workshop Asset Templates April 2013 1 Agenda Welcome and introduction Background and guiding principles to the development of QRT s SAM Balance Sheet Asset QRT s General Questions and closure Renewed

SAM QRT Workshop Asset Templates April 2013 1 Agenda Welcome and introduction Background and guiding principles to the development of QRT s SAM Balance Sheet Asset QRT s General Questions and closure Renewed

Managed Pension Funds Limited

. Managed Pension Funds Limited Solvency and Financial Condition Report as at 31 December 2017 Managed Pension Funds Limited General Contents Summary... 4 Section A: Business and Performance... 7 A.1 Business...

. Managed Pension Funds Limited Solvency and Financial Condition Report as at 31 December 2017 Managed Pension Funds Limited General Contents Summary... 4 Section A: Business and Performance... 7 A.1 Business...

AIA Group Limited. Terms of Reference for the Board Risk Committee

AIA Group Limited AIA Restricted and Proprietary Information Issued by : Board of AIA Group Limited Date : 26 February 2018 Version : 7.0 Definitions 1. For the purposes of these terms of reference (these

AIA Group Limited AIA Restricted and Proprietary Information Issued by : Board of AIA Group Limited Date : 26 February 2018 Version : 7.0 Definitions 1. For the purposes of these terms of reference (these

Basel II Pillar 3- Qualitative Disclosure

Basel II Pillar 3- Qualitative Disclosure 1. Scope This qualitative disclosure applies to Alinma bank, Saudi Arabia. Alinma bank is a Saudi joint stock company formed in accordance with Royal Decree No.

Basel II Pillar 3- Qualitative Disclosure 1. Scope This qualitative disclosure applies to Alinma bank, Saudi Arabia. Alinma bank is a Saudi joint stock company formed in accordance with Royal Decree No.

Western Captive Insurance Company DAC. Solvency and Financial Condition Report. For Financial Year Ending 31 st December 2016 (the reporting period )

") Western Captive Insurance Company DAC Solvency and Financial Condition Report For Financial Year Ending 31 st December 2016 (the reporting period ) 1 Executive Summary Western Captive Insurance Company

Western Captive Insurance Company DAC Solvency and Financial Condition Report For Financial Year Ending 31 st December 2016 (the reporting period ) 1 Executive Summary Western Captive Insurance Company

ORSA: A relevant part of the governance system within Solvency II

ORSA: A relevant part of the governance system within Solvency II Prof. Dr. Martin Balleer, Georg-August-Universität Göttingen Germany Faculty of Economics Belgrade University 18th May 2016, Belgrade Solvency

ORSA: A relevant part of the governance system within Solvency II Prof. Dr. Martin Balleer, Georg-August-Universität Göttingen Germany Faculty of Economics Belgrade University 18th May 2016, Belgrade Solvency

Economic Capital Modeling

Economic Capital Modeling Proxy Model Implementation Experience Clint Thompson Chief Risk Officer, Hannover Life Reassurance Co. of America ERM Symposium June 2015 Agenda 1. Risk appetite and linkage to

Economic Capital Modeling Proxy Model Implementation Experience Clint Thompson Chief Risk Officer, Hannover Life Reassurance Co. of America ERM Symposium June 2015 Agenda 1. Risk appetite and linkage to

SUMMARY... 3 A BUSINESS AND PERFORMANCE... 8 B SYSTEM OF GOVERNANCE C RISK PROFILE D VALUATION FOR SOLVENCY PURPOSES...

Solvency and Financial Condition Report (SFCR) Valuation date: 31st of December 2017 Table of Contents SUMMARY... 3 A BUSINESS AND PERFORMANCE... 8 BUSINESS... 8 UNDERWRITING PERFORMANCE... 10 INVESTMENT

Solvency and Financial Condition Report (SFCR) Valuation date: 31st of December 2017 Table of Contents SUMMARY... 3 A BUSINESS AND PERFORMANCE... 8 BUSINESS... 8 UNDERWRITING PERFORMANCE... 10 INVESTMENT

INSURANCE CORE PRINCIPLES, STANDARDS, GUIDANCE AND ASSESSMENT METHODOLOGY

INSURANCE CORE PRINCIPLES, STANDARDS, GUIDANCE AND ASSESSMENT METHODOLOGY Revised ICP 8 and the additional ComFrame material in ICP 8 for public consultation (redline version) This public consultation

INSURANCE CORE PRINCIPLES, STANDARDS, GUIDANCE AND ASSESSMENT METHODOLOGY Revised ICP 8 and the additional ComFrame material in ICP 8 for public consultation (redline version) This public consultation

DRAFT 3/18/14 Financial Analysis Handbook 2014 Annual/2015 Quarterly

ORSA Summary Report The NAIC Risk Management and Own Risk and Solvency Assessment Model Act (Model #505) requires all insurers with direct written premium and unaffiliated assumed premium of $500 million

ORSA Summary Report The NAIC Risk Management and Own Risk and Solvency Assessment Model Act (Model #505) requires all insurers with direct written premium and unaffiliated assumed premium of $500 million

The road to Solvency II: The Regulatory View

The road to Solvency II: The Regulatory View Rob Curtis Director, KPMG 1 June 2011 Background to developments The Global Financial Crisis (GFC) highlighted: Regulatory focus at individual firm level and

The road to Solvency II: The Regulatory View Rob Curtis Director, KPMG 1 June 2011 Background to developments The Global Financial Crisis (GFC) highlighted: Regulatory focus at individual firm level and

BAILLIE GIFFORD. Baillie Gifford Life Limited Solvency and Financial Condition Report (SFCR) As at 31 March 2018

As at 31 March 2018") BAILLIE GIFFORD Baillie Gifford Life Limited Solvency and Financial Condition Report (SFCR) As at 31 March 2018 Contents Page Summary 3 A Business and Performance 5 B System of Governance 8 C Risk Profile

BAILLIE GIFFORD Baillie Gifford Life Limited Solvency and Financial Condition Report (SFCR) As at 31 March 2018 Contents Page Summary 3 A Business and Performance 5 B System of Governance 8 C Risk Profile

OIC & ORSA. Thanita Anusonadisai Director of Capital and Solvency Standard Department Office of Insurance Commission, Thailand

OIC & ORSA Thanita Anusonadisai Director of Capital and Solvency Standard Department Office of Insurance Commission, Thailand Agenda http://www.oic.or.th Changes in insurance regulatory approach Update

OIC & ORSA Thanita Anusonadisai Director of Capital and Solvency Standard Department Office of Insurance Commission, Thailand Agenda http://www.oic.or.th Changes in insurance regulatory approach Update

Actuaries Club of the Southwest

www.pwc.com Actuaries Club of the Southwest 3-2-1-ORSA Drivers of Enterprise Risk Management ( ERM ) Fed 1. Rating Agencies AM Best SRQ ERM Questions & S&P ERM Level III Reviews FASB/IASB 2. IAIS ICP 16

www.pwc.com Actuaries Club of the Southwest 3-2-1-ORSA Drivers of Enterprise Risk Management ( ERM ) Fed 1. Rating Agencies AM Best SRQ ERM Questions & S&P ERM Level III Reviews FASB/IASB 2. IAIS ICP 16

Solvency and Financial Condition Report 20I6

Solvency and Financial Condition Report 20I6 Contents Contents... 2 Director s Statement... 4 Report of the External Independent Auditor... 5 Summary... 9 Company Information... 9 Purpose of the Solvency

Solvency and Financial Condition Report 20I6 Contents Contents... 2 Director s Statement... 4 Report of the External Independent Auditor... 5 Summary... 9 Company Information... 9 Purpose of the Solvency

The Components of a Sound Emerging Risk Management Framework

North American CRO Council The Components of a Sound Emerging Risk Management Framework December 6, 2012 2012 North American CRO Council Incorporated chairperson@crocouncil.org North American CRO Council

North American CRO Council The Components of a Sound Emerging Risk Management Framework December 6, 2012 2012 North American CRO Council Incorporated chairperson@crocouncil.org North American CRO Council

CAPTIVE BEST PRACTICE GUIDELINES

CAPTIVE BEST PRACTICE GUIDELINES Version 01:01/11 1 Table of Contents 1. Introduction... 3 2. General Governance Requirements... 4 3. Risk Management System... 5 4. Actuarial Function... 7 5. Outsourcing...

CAPTIVE BEST PRACTICE GUIDELINES Version 01:01/11 1 Table of Contents 1. Introduction... 3 2. General Governance Requirements... 4 3. Risk Management System... 5 4. Actuarial Function... 7 5. Outsourcing...

Tara Insurance DAC. Solvency & Financial Condition Report (SFCR) 31 August, 2016

31 August, 2016") Tara Insurance DAC Solvency & Financial Condition Report (SFCR) 31 August, 2016 Contents 1. Introduction 3 2. Business & Performance 3 3. System of Governance 5 4. Risk Profile 16 5. Valuation for Solvency

Tara Insurance DAC Solvency & Financial Condition Report (SFCR) 31 August, 2016 Contents 1. Introduction 3 2. Business & Performance 3 3. System of Governance 5 4. Risk Profile 16 5. Valuation for Solvency

SOLVENCY AND FINANCIAL CONDITION REPORT If P&C Insurance Ltd (publ)

") SOLVENCY AND FINANCIAL CONDITION REPORT 2017 If P&C Insurance Ltd (publ) CONTENT Summary... 1 1 Business and Performance...3 1.1 Business... 3 1.2 Underwriting performance... 4 1.3 Investment Performance...5

SOLVENCY AND FINANCIAL CONDITION REPORT 2017 If P&C Insurance Ltd (publ) CONTENT Summary... 1 1 Business and Performance...3 1.1 Business... 3 1.2 Underwriting performance... 4 1.3 Investment Performance...5

COLUMBIA THREADNEEDLE Threadneedle Pensions Limited Solvency and Financial Condition Report

COLUMBIA THREADNEEDLE Threadneedle Pensions Limited Solvency and Financial Condition Report 31 December 2016 Report date: 19 May 2017 Contents 1. Summary... 3 1.1 Business and performance... 3 1.2 System

COLUMBIA THREADNEEDLE Threadneedle Pensions Limited Solvency and Financial Condition Report 31 December 2016 Report date: 19 May 2017 Contents 1. Summary... 3 1.1 Business and performance... 3 1.2 System

Risk appetite. Getting in shape building and sustaining your risk appetite. 27 February 2014

Getting in shape building and sustaining your risk appetite 27 February 2014 Getting in shape building and sustaining your risk appetite James Maher Insurance and Actuarial Services Leader FSO Ireland

Getting in shape building and sustaining your risk appetite 27 February 2014 Getting in shape building and sustaining your risk appetite James Maher Insurance and Actuarial Services Leader FSO Ireland

29th India Fellowship Seminar

29th India Fellowship Seminar Is Risk Based Capital way forward? Adaptability to Indian Context & Comparison of various market consistent measures Guide: Sunil Sharma Presented by: Rakesh Kumar Niraj Kumar

29th India Fellowship Seminar Is Risk Based Capital way forward? Adaptability to Indian Context & Comparison of various market consistent measures Guide: Sunil Sharma Presented by: Rakesh Kumar Niraj Kumar