ANNUITY FUNDED LIFE INSURANCE

|

|

|

- Natalie McDonald

- 5 years ago

- Views:

Transcription

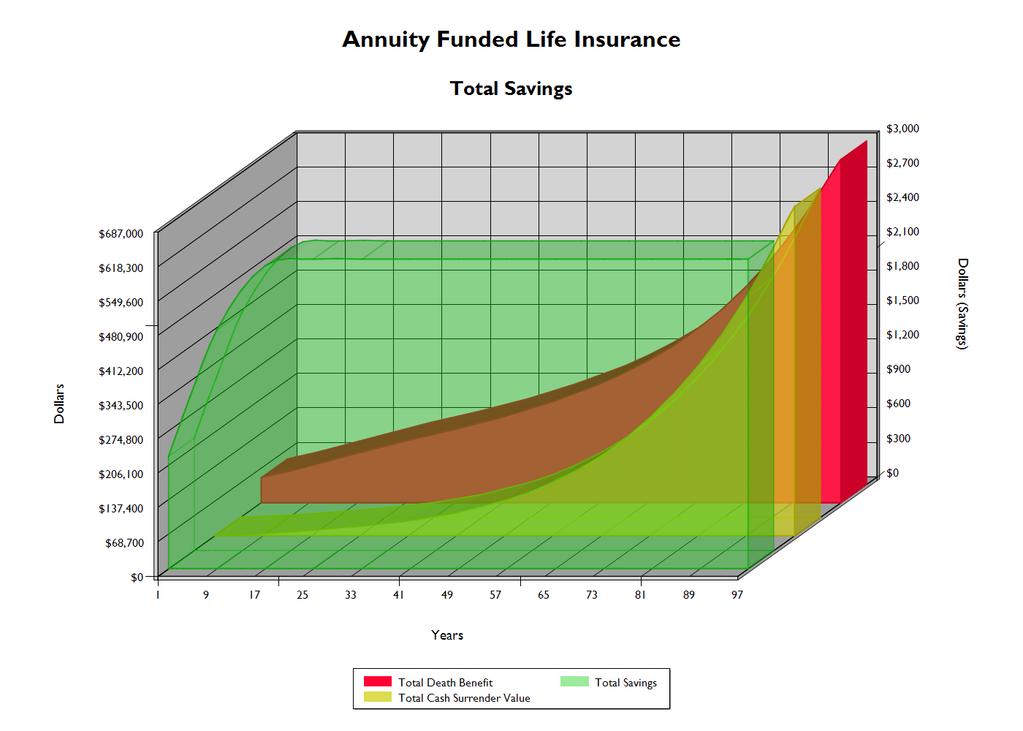

1 ANNUITY FUNDED LIFE INSURANCE June Proposal For Funded Life Insurance Prepared By: Retail Insurance Marketing Victoria Park Ave Toronto, ON M2J5A (fax)

2 Funded Life Insurance Strategy Introducing a strategy for clients looking to pre-fund life insurance premiums with one payment. By using an Empire Life term certain annuity to pre-pay life insurance premiums, clients can save money and time, and enjoy peace-of-mind in the process. How this works Pay Once and Pay Less For clients applying for a life insurance policy from Empire Life who want to pre-fund future premiums using an Empire Life term certain annuity, follow these easy steps: 1) Purchase an Empire Life insurance policy. Apply for a life insurance policy and indicate that payments will be made via a term certain annuity (no bank account information is necessary). 2) Purchase an Empire Life term certain annuity. Once the life insurance policy is issued, apply for a term certain annuity after confirming the deposit amount required to pay the insurance premiums for the desired length of time. 3) Confirm payment details. The client needs to indicate Empire Life as the payee of the annuity income and reference the insurance policy number(s) on their annuity application Pay Once and Pay Less! Simple and easy way to pre-fund future life insurance premiums for a set period of time. Perfect for clients who are starting their estate plan, want to provide a gift for loved ones, or fund future payments on their existing life insurance. June E.&O.E. Page 2 of 10

3 June E.&O.E. Page 3 of 10

4 When this strategy works well While other scenarios are possible, using a term certain annuity to pre-fund the premiums for a life insurance policy should work well if: The life insured is also the annuitant. This helps ensure the annuity income is available to pay the life insurance premiums until the life insured/annuitant dies. Both plans have the same pay period. Choose a limited pay life insurance policy (eg. 20 years) where the period to pay premiums on the life insurance policy matches the guaranteed payment period on the term certain annuity. income matches the life insurance premium exactly. This can help avoid the need to use additional funds to pay life insurance premiums. Contingent Owner of the life insurance policy and the Beneficiary of the annuity is the same person. Recommended if the Life Insured is someone other than the Annuitant. This can help ensure future funding for life insurance premiums if the annuitant dies during the annuity guaranteed period. Both plans are set up on an annual pay basis. This makes determining the amount of the annuity deposit easier and results in savings on the insurance premiums. There is only one annuity per life insurance policy. This provides better control where funds are directed from the annuity to the life insurance contract should the annuitant die. Funding multiple life insurance policies may be permitted under certain circumstances. Other important information Submitting applications: Apply for the Term Certain annuity only after the life insurance policy is issued. contract can t be changed or cancelled: Once the Term Certain is purchased, it cannot be changed or cancelled. If annuity income is no longer required to pay the life insurance premiums (eg. client elects early coverage termination or reduced paid-up coverage), the owner decides who receives future annuity income. Annuitant age and deposit limits: The annuitant can be any age between 18 and 70. The current annuity deposit limits are between $7,500 and $1,000,000. First payment: Make sure the first annuity payment occurs within 30 days from date of issue of the life insurance policy to ensure life insurance premiums are paid on time. If there are multiple life policies involved, all must be issued within 30 days of each other as only one payment per annuity will be made. Taxes on income: A portion of the income from the term certain annuity is taxable. Using a prescribed annuity can lessen how much income is taxable up front. Empire Life will provide a tax slip to the policy owner each year. Continuation of funding: If the life insured is someone other than the annuitant, it is important to remember that if the annuitant dies before all life insurance premiums are paid, alternative funding arrangements are needed to pay the remaining insurance premiums. Children s policies: If pre-funding multiple children s life insurance policies, a separate annuity should be set up for each child when possible and a contingent owner should be named for the insurance policy. However, one annuity used to fund multiple life insurance policies is possible as long as the annuitant/owner understands the risks should they die before all insurance premiums are paid. Changes to life insurance policy: If changes occur within the life insurance policy that result in an increase to the overall policy premiums, the policy owner will have to pay the difference in premium amount if the annuity income is not sufficient. Other payment options: While this concept works best when used to pay all premiums on a limited pay product, the client could elect alternative payment options. June E.&O.E. Page 4 of 10

5 Net Present Value (NPV): In order to give a reasonable approximation of the savings prior to the end of the premium payment period, the savings are calculated as the total premiums paid plus the net present value (NPV) of the remaining annuity payouts less the amount invested in the annuity. While the annual premiums would cease in the event of the death of the insured, the annuity payouts would continue on schedule. The NPV is used to factor in inflation erosion of the future payouts of the annuity in order to give a more realistic picture of the value of those payouts in the year of the death of the insured. June E.&O.E. Page 5 of 10

6 CONCEPT ASSUMPTIONS Insureds Insured... Funded Life Insurance, Male, Age 0, Smoker Product Name... $50,000 Optimax Wealth, Single Life Planned Deposits (20 years) Investment... $10,659 Marginal Tax Rate % NPV Discount Rate % Savings... $2,701 Special Notes Withdrawals from the policy may be subject to income tax, depending on the adjusted cost basis (ACB) of the policy, at the time of withdrawal. However, the proceeds of a life insurance policy upon death of the insured are received taxfree in the hands of the beneficiaries. Important Information This illustration is not a contract and the values are not guaranteed. The tax treatment of this illustration is based on the current Canadian Federal Tax laws and regulations. Any changes will affect the amounts shown on the illustration. It is advisable to contact a competent professional advisor in determining whether this Strategy is suitable to your situation. If this strategy shows a corporately owned scenario with an Alternate Investment, this illustration shows the net estate value assuming that the alternative investment and the insurance are paid out as a dividend at death. It does not reflect any capital gain on the deemed disposition of the shares at death. This strategy uses an Empire Life insurance policy. The amounts shown in the illustration may or may not be achieved depending on assumptions used. Corporate Owned Life Insurance only: The General anti-avoidance Rule (GAAR) in the Tax Act may deny a tax benefit that is the result of an avoidance transaction, unless it is undertaken primarily for purposes other than to obtain the tax benefit. Since the main purpose of this strategy is to provide a business with a higher tax-free value of the business for the estate or surviving shareholders, the GAAR rule is unlikely to apply. This document consists of two parts: the presentation and the Empire Life illustration. The presentation and the illustration are designed to read together, to fully understand how some of the values shown in the illustrations may vary. If either part is missing, this document is non-compliant and incomplete. This document is for illustrative purposes only and is not a contract or offer of insurance. Illustrated values are not guaranteed. Empire Life and its employees, distribution partners, and independent advisors do not provide specific legal, accounting, or tax advice. The provision of information provided on this presentation and corresponding illustration and any oral or written communication regarding the same should not be construed as such. This illustration is incomplete without all pages. Registered trademark of The Empire Life Insurance Company. Policies are issued by The Empire Life Insurance Company. June E.&O.E. Page 6 of 10

7 Policy year Taxable Portion Tax Payable Net Total Annual Premium Life Insurance Total Cash Surrender Value Total Death Benefit 1 $ ,000 2 $ ,798 3 $ ,901 4 $ ,447 57,954 5 $ ,964 60,974 6 $ ,472 63,987 7 $ ,016 67,011 8 $ ,599 70,044 9 $ ,223 73, $ ,891 76, $ ,605 79, $ ,368 82, $ ,180 85, $ ,046 88, $ ,966 92, $ ,943 95,392 17* $ ,979 98, $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , ,257 ** Values shown beginning/ end of policy year. Tax payable is not withheld from the policy and may be higher or lower and is not guaranteed.* Break even point CSV = purchase amount June E.&O.E. Page 7 of 10

8 Policy year Taxable Portion Tax Payable Net Total Annual Premium Life Insurance Total Cash Surrender Value Total Death Benefit 46 $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , ,682 ** Values shown beginning/ end of policy year. Tax payable is not withheld from the policy and may be higher or lower and is not guaranteed.* Break even point CSV = purchase amount June E.&O.E. Page 8 of 10

9 Policy year Taxable Portion Tax Payable Net Total Annual Premium Life Insurance Total Cash Surrender Value Total Death Benefit 91 $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , , $ , ,194 ** Values shown beginning/ end of policy year. Tax payable is not withheld from the policy and may be higher or lower and is not guaranteed.* Break even point CSV = purchase amount June E.&O.E. Page 9 of 10

10 June E.&O.E. Page 10 of 10

CORPORATE LEGACY BUILDER

CORPORATE LEGACY BUILDER June-06-17 Proposal For Corporate Legacy Builder Prepared By: Retail Insurance Marketing 500-2550 Victoria Park Ave Toronto, ON M2J5A9 4164942972 18775481881 4164942972 (fax) john.quirt@empire.ca

CORPORATE LEGACY BUILDER June-06-17 Proposal For Corporate Legacy Builder Prepared By: Retail Insurance Marketing 500-2550 Victoria Park Ave Toronto, ON M2J5A9 4164942972 18775481881 4164942972 (fax) john.quirt@empire.ca

The Corporate Asset Transfer Plan

BMO Insurance Advisor Guide The Corporate Asset Transfer Plan Someone is going to profit from your client s hard work. Shouldn t it be their family? Introduction 3 Overview of the Corporate Asset Transfer

BMO Insurance Advisor Guide The Corporate Asset Transfer Plan Someone is going to profit from your client s hard work. Shouldn t it be their family? Introduction 3 Overview of the Corporate Asset Transfer

ANNUITY-FUNDED LIFE INSURANCE STRATEGY

ANNUITY-FUNDED LIFE INSURANCE STRATEGY Case Study Jesse Jesse is a 35 year old non-smoking healthy male. Insurance Needs Working with his advisor, Jesse s life insurance needs will include an EstateMax

ANNUITY-FUNDED LIFE INSURANCE STRATEGY Case Study Jesse Jesse is a 35 year old non-smoking healthy male. Insurance Needs Working with his advisor, Jesse s life insurance needs will include an EstateMax

Your Payout Annuity policy

64075536 Your Payout Annuity policy In this document, "you" and "your" means the owner of this policy, or the policyholder. "We", "our", "us" and the "Company" means Sun Life Assurance Company of Canada.

64075536 Your Payout Annuity policy In this document, "you" and "your" means the owner of this policy, or the policyholder. "We", "our", "us" and the "Company" means Sun Life Assurance Company of Canada.

Lifetime Income Benefit Rider

for a secure Retirement Lifetime Income Benefit Rider (LIBR-2010)* Included automatically on most Fixed Indexed Annuities** for use with Fixed Indexed Annuities *May vary by state. Not available in all

for a secure Retirement Lifetime Income Benefit Rider (LIBR-2010)* Included automatically on most Fixed Indexed Annuities** for use with Fixed Indexed Annuities *May vary by state. Not available in all

The Intergenerational Wealth Transfer of Life Insurance Policies (Cascading Policies)

") The Intergenerational Wealth Transfer of Life Insurance Policies (Cascading Policies) This document will review the tax issues associated with Cascading Policies. This is the terminology used to describe

The Intergenerational Wealth Transfer of Life Insurance Policies (Cascading Policies) This document will review the tax issues associated with Cascading Policies. This is the terminology used to describe

Tax implications of a life insurance policy transfer

Tax implications of a life insurance policy transfer Jean Turcotte, Attorney, B.B.A., LL.B., D.Fisc, Fin.Pl., TEP Director, Tax, Wealth and Insurance Planning Group Sun Life Financial March 2017 1 Tax

Tax implications of a life insurance policy transfer Jean Turcotte, Attorney, B.B.A., LL.B., D.Fisc, Fin.Pl., TEP Director, Tax, Wealth and Insurance Planning Group Sun Life Financial March 2017 1 Tax

SPIA. Consider securing a steady, lifetime income. A SPIA can help provide a dependable, guaranteed stream of income for a lifetime.

SINGLE PREMIUM IMMEDIATE ANNUITY (SPIA) SPIA A SPIA can help provide a dependable, guaranteed stream of income for a lifetime. Consider securing a steady, lifetime income A SPIA, a single premium immediate

SINGLE PREMIUM IMMEDIATE ANNUITY (SPIA) SPIA A SPIA can help provide a dependable, guaranteed stream of income for a lifetime. Consider securing a steady, lifetime income A SPIA, a single premium immediate

SHARING INTERESTS IN A LIFE INSURANCE POLICY

SHARING INTERESTS IN A LIFE INSURANCE POLICY A GUIDE FOR LAWYERS AND ACCOUNTANTS Shared ownership and shared benefit life insurance arrangements Life s brighter under the sun This guide is designed to

SHARING INTERESTS IN A LIFE INSURANCE POLICY A GUIDE FOR LAWYERS AND ACCOUNTANTS Shared ownership and shared benefit life insurance arrangements Life s brighter under the sun This guide is designed to

December 3, Prepared on SAMPLE. Your SunFlex Retirement Income policy

60003599 Your SunFlex Retirement Income policy In this document, "you" and "your" means the owner of this policy, who is the annuitant and policyholder. "We", "our", "us" and the "Company" means Sun Life

60003599 Your SunFlex Retirement Income policy In this document, "you" and "your" means the owner of this policy, who is the annuitant and policyholder. "We", "our", "us" and the "Company" means Sun Life

A Retirement Income Strategy: A Split Annuity Review

A Retirement Income Strategy: A Split Annuity Review The biggest financial risk that anyone faces during retirement is the risk that savings will be depleted... the risk that income will be outlived! Table

A Retirement Income Strategy: A Split Annuity Review The biggest financial risk that anyone faces during retirement is the risk that savings will be depleted... the risk that income will be outlived! Table

New York Life Insurance and Annuity Corporation NYL Guaranteed Lifetime Income Annuity II - Joint Life

Annuitant & Policy Information New York Life Insurance and Annuity Corporation Summary Primary Name: John Example Type of Funds: Non-Qualified Date of Birth: 02/01/1940 Payment Frequency: Annual Sex: Male

Annuitant & Policy Information New York Life Insurance and Annuity Corporation Summary Primary Name: John Example Type of Funds: Non-Qualified Date of Birth: 02/01/1940 Payment Frequency: Annual Sex: Male

RRSPs and RRIFs on death Frequently Asked Questions

RRSPs and RRIFs on death Frequently Asked Questions W E A L T H T R A N S F E R S T R A T E G Y 8 Most Canadians are familiar with the tax advantages of using registered savings plans to save for their

RRSPs and RRIFs on death Frequently Asked Questions W E A L T H T R A N S F E R S T R A T E G Y 8 Most Canadians are familiar with the tax advantages of using registered savings plans to save for their

MY Guaranteed Solution II IM (4/14) Fixed annuity offered by Horace Mann Life Insurance Co.

Fixed annuity offered by Horace Mann Life Insurance Co.") MY Guaranteed Solution II IM-007014 (4/14) Fixed annuity offered by Horace Mann Life Insurance Co. Dedicated to the educational community At Horace Mann, we believe educators are taking care of our children

MY Guaranteed Solution II IM-007014 (4/14) Fixed annuity offered by Horace Mann Life Insurance Co. Dedicated to the educational community At Horace Mann, we believe educators are taking care of our children

RRSPs and RRIFs on death frequently asked questions

TAX, RETIREMENT & ESTATE PLANNING SERVICES WEALTH TRANSFER STRATEGY 8 RRSPs and RRIFs on death frequently asked questions Most Canadians are familiar with the tax advantages of using registered savings

TAX, RETIREMENT & ESTATE PLANNING SERVICES WEALTH TRANSFER STRATEGY 8 RRSPs and RRIFs on death frequently asked questions Most Canadians are familiar with the tax advantages of using registered savings

Annuities in Retirement Income Planning

For much of the recent past, individuals entering retirement could look to a number of potential sources for the steady income needed to maintain a decent standard of living: Defined benefit (DB) employer

For much of the recent past, individuals entering retirement could look to a number of potential sources for the steady income needed to maintain a decent standard of living: Defined benefit (DB) employer

FOR REPRESENTATIVES ONLY GUARANTEED INVESTMENT FUNDS. Taxation. Desjardins Insurance refers to Desjardins Financial Security Life Assurance Company.

GUARANTEED INVESTMENT FUNDS FOR REPRESENTATIVES ONLY Taxation Desjardins Insurance refers to Desjardins Financial Security Life Assurance Company. SECTION 1 Income Allocation Table of Contents SECTION

GUARANTEED INVESTMENT FUNDS FOR REPRESENTATIVES ONLY Taxation Desjardins Insurance refers to Desjardins Financial Security Life Assurance Company. SECTION 1 Income Allocation Table of Contents SECTION

RRSPs and RRIFs on death frequently asked questions

Tax, Retirement & Estate Planning Services WEALTH TRANSFER STRATEGY 8 RRSPs and RRIFs on death frequently asked questions Most Canadians are familiar with the tax advantages of using registered savings

Tax, Retirement & Estate Planning Services WEALTH TRANSFER STRATEGY 8 RRSPs and RRIFs on death frequently asked questions Most Canadians are familiar with the tax advantages of using registered savings

Palladium. Immediate Annuity Series. Palladium Single Premium Immediate Annuity Palladium Single Premium Immediate Annuity - NY

Palladium Immediate Annuity Series Palladium Single Premium Immediate Annuity Palladium Single Premium Immediate Annuity - NY 1 Securing Income for Your Needs One of the major fears we face today is outliving

Palladium Immediate Annuity Series Palladium Single Premium Immediate Annuity Palladium Single Premium Immediate Annuity - NY 1 Securing Income for Your Needs One of the major fears we face today is outliving

GET IT AND FORGET IT Using a Term Certain Annuity to prearrange funding for Equimax participating whole life

Page 1 of 17 Equimax FOR ADVISOR USE ONLY Sales Track: Products The need The solution Client profile Advisor profile Client attention grabber Positioning the concept GET IT AND FORGET IT Using a Term Certain

Page 1 of 17 Equimax FOR ADVISOR USE ONLY Sales Track: Products The need The solution Client profile Advisor profile Client attention grabber Positioning the concept GET IT AND FORGET IT Using a Term Certain

HOUSE OF FINANCE PENSIONS INVESTMENTS PROTECTION. A Guide to Annuities

HOUSE OF FINANCE PENSIONS INVESTMENTS PROTECTION Contents I m approaching retirement, what are my financial options? What is a Financial Broker? Why would I need to use a Financial Broker? What is an annuity?

HOUSE OF FINANCE PENSIONS INVESTMENTS PROTECTION Contents I m approaching retirement, what are my financial options? What is a Financial Broker? Why would I need to use a Financial Broker? What is an annuity?

ATLANTIC COAST LIFE INSURANCE COMPANY

SAFE ANCHOR MARKET GUARANTEE 5 YEAR FIXED RATE WITH INDEXING OPTION STANDARD BROCHURE (All States Except Florida) ATLANTIC COAST LIFE INSURANCE COMPANY ACLANBRANCHOR-OT 082817 As the length of retirement

SAFE ANCHOR MARKET GUARANTEE 5 YEAR FIXED RATE WITH INDEXING OPTION STANDARD BROCHURE (All States Except Florida) ATLANTIC COAST LIFE INSURANCE COMPANY ACLANBRANCHOR-OT 082817 As the length of retirement

December 3, Prepared on SAMPLE. Your SunFlex Retirement Income policy

60003581 Your SunFlex Retirement Income policy In this document, "you" and "your" means the owner of this policy, who is the annuitant and policyholder. "We", "our", "us" and the "Company" means Sun Life

60003581 Your SunFlex Retirement Income policy In this document, "you" and "your" means the owner of this policy, who is the annuitant and policyholder. "We", "our", "us" and the "Company" means Sun Life

ADVISOR USE ONLY PAYOUT ANNUITY OVERCOMING OBJECTIONS. Life s brighter under the sun

ADVISOR USE ONLY PAYOUT ANNUITY OVERCOMING OBJECTIONS Life s brighter under the sun Overcoming objections Overview > > Payout annuities are a powerful retirement tool and have been an important product

ADVISOR USE ONLY PAYOUT ANNUITY OVERCOMING OBJECTIONS Life s brighter under the sun Overcoming objections Overview > > Payout annuities are a powerful retirement tool and have been an important product

Insurance and Annuities

Presented for Valued Client Presented by John M. Webster HMS Insurance Associates, Inc. johnwebster@financialguide.com 443-632-3436 Page 1 of 8 The Annuity Concept An annuity contract specifies that the

Presented for Valued Client Presented by John M. Webster HMS Insurance Associates, Inc. johnwebster@financialguide.com 443-632-3436 Page 1 of 8 The Annuity Concept An annuity contract specifies that the

The BMO. Insurance Corporate Insured Retirement Plan. A life insurance solution that provides security and flexibility to access cash.

BMO Insurance Advisor Guide The BMO Insurance Corporate Insured Retirement Plan A life insurance solution that provides security and flexibility to access cash. Introduction 3 Table of Contents The Opportunity

BMO Insurance Advisor Guide The BMO Insurance Corporate Insured Retirement Plan A life insurance solution that provides security and flexibility to access cash. Introduction 3 Table of Contents The Opportunity

LEVERAGING A LIFE INSURANCE POLICY A GUIDE FOR LAWYERS, ACCOUNTANTS AND INSURANCE ADVISORS

ADVISOR USE ONLY LEVERAGING A LIFE INSURANCE POLICY A GUIDE FOR LAWYERS, ACCOUNTANTS AND INSURANCE ADVISORS Using life insurance as collateral for personal and business planning Life s brighter under the

ADVISOR USE ONLY LEVERAGING A LIFE INSURANCE POLICY A GUIDE FOR LAWYERS, ACCOUNTANTS AND INSURANCE ADVISORS Using life insurance as collateral for personal and business planning Life s brighter under the

SEATTLE PACIFIC UNIVERSITY. Defined Contribution Retirement Plan

SEATTLE PACIFIC UNIVERSITY Defined Contribution Retirement Plan SUMMARY PLAN DESCRIPTION July 1, 2013 8.1 When will my retirement benefits be paid?... 11 8.2 In what form will my benefit be paid?... 11

SEATTLE PACIFIC UNIVERSITY Defined Contribution Retirement Plan SUMMARY PLAN DESCRIPTION July 1, 2013 8.1 When will my retirement benefits be paid?... 11 8.2 In what form will my benefit be paid?... 11

Designating a Beneficiary for Your IRA

Retirement Planning Designating a Beneficiary for Your IRA You have likely named beneficiaries many times over the years for things like your life insurance policies, annuity contracts, IRAs, company pension

Retirement Planning Designating a Beneficiary for Your IRA You have likely named beneficiaries many times over the years for things like your life insurance policies, annuity contracts, IRAs, company pension

Table of Contents I. Annuities 2 A. Who... 2 B. What... 2 C. Where... 2 D. When... 3 Annuity Phases... 3 a) Immediate Annuity...

Immediate Annuity...") Table of Contents I. Annuities 2 A. Who... 2 B. What... 2 C. Where... 2 D. When... 3 Annuity Phases... 3 a) Immediate Annuity... 3 b) Deferred Annuity... 3 E. Why... 4 F. How do I put my money in?... 4

Table of Contents I. Annuities 2 A. Who... 2 B. What... 2 C. Where... 2 D. When... 3 Annuity Phases... 3 a) Immediate Annuity... 3 b) Deferred Annuity... 3 E. Why... 4 F. How do I put my money in?... 4

The Capital Dividend Account. January 2017 Jean Turcotte, B.B.A., LL.B., D.Fisc, Fin.Pl., TEP Director, Tax, Wealth and Insurance Planning Group

The Capital Dividend Account January 2017 Jean Turcotte, B.B.A., LL.B., D.Fisc, Fin.Pl., TEP Director, Tax, Wealth and Insurance Planning Group Capital Dividend Account Why the Capital Dividend Account

The Capital Dividend Account January 2017 Jean Turcotte, B.B.A., LL.B., D.Fisc, Fin.Pl., TEP Director, Tax, Wealth and Insurance Planning Group Capital Dividend Account Why the Capital Dividend Account

SecureOption Select A fixed deferred annuity. safety and certainty on your terms. hij abc

SecureOption Select A fixed deferred annuity safety and certainty on your terms hij abc SecureOption Select safety, certainty and control What is an annuity? Annuities are offered by insurance companies

SecureOption Select A fixed deferred annuity safety and certainty on your terms hij abc SecureOption Select safety, certainty and control What is an annuity? Annuities are offered by insurance companies

The ScotiaMcLeod Wealth Planning Series. Early Retirement Options Handbook

The ScotiaMcLeod Wealth Planning Series Early Retirement Options Handbook ScotiaMcLeod s Wealth Planning Services Early Retirement Options Handbook Most of us will accumulate assets during our working

The ScotiaMcLeod Wealth Planning Series Early Retirement Options Handbook ScotiaMcLeod s Wealth Planning Services Early Retirement Options Handbook Most of us will accumulate assets during our working

North Carolina Agents Checklist For Submitting Fixed Annuity New Business. General Information

North Carolina Agents Checklist For Submitting Fixed Annuity New Business General Information... 1 Non-Qualified Single Premium Tax Deferred Annuity... 2 Traditional IRA (Qualified Annuity)... 3 Roth IRA

North Carolina Agents Checklist For Submitting Fixed Annuity New Business General Information... 1 Non-Qualified Single Premium Tax Deferred Annuity... 2 Traditional IRA (Qualified Annuity)... 3 Roth IRA

NV Energy Retirement Plan MPAT Employees January, [Type text] Page 1

![NV Energy Retirement Plan MPAT Employees January, [Type text] Page 1](/thumbs/89/98385230.jpg "NV Energy Retirement Plan MPAT Employees January, [Type text] Page 1") NV Energy Retirement Plan MPAT Employees January, 2014 [Type text] Page 1 Who Do I Call and Where Do I Look? Contact Telephone Website Vanguard 1-800-523-1188 5:30 a.m. 6:00 p.m. PT Monday - Friday www.vanguard.com

NV Energy Retirement Plan MPAT Employees January, 2014 [Type text] Page 1 Who Do I Call and Where Do I Look? Contact Telephone Website Vanguard 1-800-523-1188 5:30 a.m. 6:00 p.m. PT Monday - Friday www.vanguard.com

Guaranteeing an Income for Life: An Immediate Fixed Income Annuity Review

Guaranteeing an Income for Life: An Immediate Fixed Income Annuity Review The biggest financial risk that anyone faces during retirement is the risk that savings will be depleted...the risk that income

Guaranteeing an Income for Life: An Immediate Fixed Income Annuity Review The biggest financial risk that anyone faces during retirement is the risk that savings will be depleted...the risk that income

Annuities. Preparing for a secure financial future. FIN1763-2

Annuities Preparing for a secure financial future. FIN1763-2 We all dream of living comfortably in the future Your dreams of a comfortable, financially secure future for you and your family are as individual

Annuities Preparing for a secure financial future. FIN1763-2 We all dream of living comfortably in the future Your dreams of a comfortable, financially secure future for you and your family are as individual

CLIENT GUIDE. a solution that s just for you. Life s brighter under the sun

S U N P A R A C C U M U L A T O R I I CLIENT GUIDE a solution that s just for you Life s brighter under the sun Sun Par Accumulator II a solution that s just for you 4 Benefits for you 5 How your plan

S U N P A R A C C U M U L A T O R I I CLIENT GUIDE a solution that s just for you Life s brighter under the sun Sun Par Accumulator II a solution that s just for you 4 Benefits for you 5 How your plan

FIXED INCOME ANNUITY QUESTIONS & ANSWERS

Metropolitan Life Insurance Company FIXED INCOME ANNUITY QUESTIONS & ANSWERS Important Information about Fixed Income Annuities for FRS Investment Plan Participants This information will help you decide

Metropolitan Life Insurance Company FIXED INCOME ANNUITY QUESTIONS & ANSWERS Important Information about Fixed Income Annuities for FRS Investment Plan Participants This information will help you decide

STATEMENT OF BENEFIT INFORMATION

STATEMENT OF BENEFIT INFORMATION CONTRACT SUMMARY Pacific Life Insurance Company P.O. Box 2378 Omaha, NE 68103-2378 (800) 722-4448 Contract Owners (800) 722-2333 - Registered Representatives/Producers

STATEMENT OF BENEFIT INFORMATION CONTRACT SUMMARY Pacific Life Insurance Company P.O. Box 2378 Omaha, NE 68103-2378 (800) 722-4448 Contract Owners (800) 722-2333 - Registered Representatives/Producers

It s All About the Business

It s All About the Business Planning Strategies Integrated with Life Insurance to Help a Business Owner Accomplish Goals for Retirement, Business Perpetuation, Successful Business Transition, and Estate

It s All About the Business Planning Strategies Integrated with Life Insurance to Help a Business Owner Accomplish Goals for Retirement, Business Perpetuation, Successful Business Transition, and Estate

Summary Plan Description 2016

Summary Plan Description 2016 Active and Former Team Members, Beneficiaries and Alternate Payees Retirement Plan TSI062716 3.4M DP DATE: July 2016 TO: FROM: RE: Benefit Plan Participants Human Resources,

Summary Plan Description 2016 Active and Former Team Members, Beneficiaries and Alternate Payees Retirement Plan TSI062716 3.4M DP DATE: July 2016 TO: FROM: RE: Benefit Plan Participants Human Resources,

STANDARD LIFE TRUST COMPANY TAX-FREE SAVINGS ACCOUNT FOR ELIGIBLE PARTICIPANTS OF THE STANDARD LIFE ADVANTAGE PROGRAM

STANDARD LIFE TRUST COMPANY TAX-FREE SAVINGS ACCOUNT FOR ELIGIBLE PARTICIPANTS OF THE STANDARD LIFE ADVANTAGE PROGRAM Arranged in conjunction with THE STANDARD LIFE ASSURANCE COMPANY OF CANADA and STANDARD

STANDARD LIFE TRUST COMPANY TAX-FREE SAVINGS ACCOUNT FOR ELIGIBLE PARTICIPANTS OF THE STANDARD LIFE ADVANTAGE PROGRAM Arranged in conjunction with THE STANDARD LIFE ASSURANCE COMPANY OF CANADA and STANDARD

Annuities. Understanding. ABC Company 123 Main Street Anywhere, USA

Understanding Annuities Your promotional imprint here and/or back cover. ABC Company 123 Main Street Anywhere, USA 12345 www.sampleabccompany.com 800.123.4567 It may bring you peace of mind to have a regular

Understanding Annuities Your promotional imprint here and/or back cover. ABC Company 123 Main Street Anywhere, USA 12345 www.sampleabccompany.com 800.123.4567 It may bring you peace of mind to have a regular

Segregated Funds SEGREGATED FUNDS. Savings and Retirement PIVOTAL SELECT. Contract and Information Folder

Segregated Funds SEGREGATED FUNDS Savings and Retirement PIVOTAL SELECT TM Contract and Information Folder Any amount that is allocated to a segregated fund is invested at the risk of the contractholder(s)

Segregated Funds SEGREGATED FUNDS Savings and Retirement PIVOTAL SELECT TM Contract and Information Folder Any amount that is allocated to a segregated fund is invested at the risk of the contractholder(s)

Insurance Solutions for Individual Needs

Insurance Solutions for Individual Needs This brochure looks at some of the different needs individuals can experience and it shows how insurance can help meet those needs. Leaving a Legacy at Death Life

Insurance Solutions for Individual Needs This brochure looks at some of the different needs individuals can experience and it shows how insurance can help meet those needs. Leaving a Legacy at Death Life

orporate Investment Shelter

C (a orporate Investment Shelter strategy utilizing exempt life insurance) Sun Life Financial Sales Desk Sun Life Financial 225 King Street West - 9th Floor Toronto, Ontario M5V 3C5 1-800-800-4786 Option

C (a orporate Investment Shelter strategy utilizing exempt life insurance) Sun Life Financial Sales Desk Sun Life Financial 225 King Street West - 9th Floor Toronto, Ontario M5V 3C5 1-800-800-4786 Option

OPTION PLUS GROUP RSP APPLICATION FOR MEMBERSHIP

VERSION DATE: DECEMBER 2015 OPTION PLUS GROUP RSP APPLICATION FOR MEMBERSHIP When you receive your Certificate, record your Certificate number here for future reference. Certificate number: ANY AMOUNT

VERSION DATE: DECEMBER 2015 OPTION PLUS GROUP RSP APPLICATION FOR MEMBERSHIP When you receive your Certificate, record your Certificate number here for future reference. Certificate number: ANY AMOUNT

MYGA Annuity Product Training

MYGA Annuity Product Training Definitions Multi-Year Guarantee Deferred Annuity (MYGA) MYGA Contract Overview MYGA Contract Plan Schedules Preferred Choice (3, 5, 6 and 7 years) Premium Preferred (5 and

MYGA Annuity Product Training Definitions Multi-Year Guarantee Deferred Annuity (MYGA) MYGA Contract Overview MYGA Contract Plan Schedules Preferred Choice (3, 5, 6 and 7 years) Premium Preferred (5 and

Immediate Annuity Quotation

Immediate Annuity Quotation Personalized for: Primary Annuitant Prepared by: Ivon T Hughes Tel: 514-842-9001 Email: info@trustco.ca Fax: 514-842-1085 Reference #: 213331.1 Date Prepared: June 27, 2013

Immediate Annuity Quotation Personalized for: Primary Annuitant Prepared by: Ivon T Hughes Tel: 514-842-9001 Email: info@trustco.ca Fax: 514-842-1085 Reference #: 213331.1 Date Prepared: June 27, 2013

Retirement Income Options for Group Retirement Plan Members

Retirement Income Options for Group Retirement Plan Members Everything you should know about your retirement income options Make the choice that s right for you You ve been enjoying the benefit of saving

Retirement Income Options for Group Retirement Plan Members Everything you should know about your retirement income options Make the choice that s right for you You ve been enjoying the benefit of saving

STEPUP. Registered Assets & Disabled Beneficiaries. Vol. 13, No. 09. Sales Tax Estate Planning Underwriting & Product Newsletter

STEPUP Sales Tax Estate Planning Underwriting & Product Newsletter Registered Assets & Disabled Beneficiaries Parents and families of people with disabilities value peace of mind when considering and making

STEPUP Sales Tax Estate Planning Underwriting & Product Newsletter Registered Assets & Disabled Beneficiaries Parents and families of people with disabilities value peace of mind when considering and making

12/ A. Titling Options for Your Nonqualified Deferred Annuity Contract

12/15 23236-15A Titling Options for Your Nonqualified Deferred Annuity Contract Planning for Retirement Whether you re approaching retirement or already retired, this is the time when your financial focus

12/15 23236-15A Titling Options for Your Nonqualified Deferred Annuity Contract Planning for Retirement Whether you re approaching retirement or already retired, this is the time when your financial focus

MassMutual Odyssey Select SM Product Disclosure

Annuity Issuer MassMutual Odyssey Select SM (Policy form # MUFA10.1, MUFA10.1-Rev, ICC12-MUFA10.1) is a fixed deferred annuity contract issued by Massachusetts Mutual Life Insurance Company (MassMutual),

Annuity Issuer MassMutual Odyssey Select SM (Policy form # MUFA10.1, MUFA10.1-Rev, ICC12-MUFA10.1) is a fixed deferred annuity contract issued by Massachusetts Mutual Life Insurance Company (MassMutual),

PPL Retirement Plan Summary Plan Description for Management Employees

PPL Retirement Plan Summary Plan Description for Management Employees TABLE OF CONTENTS Page # The Retirement Plan... 1 About Your Participation... 2 Eligibility... 2 When Participation Begins... 3 Some

PPL Retirement Plan Summary Plan Description for Management Employees TABLE OF CONTENTS Page # The Retirement Plan... 1 About Your Participation... 2 Eligibility... 2 When Participation Begins... 3 Some

Lincoln Benefit Life Company A Stock Company

Lincoln Benefit Life Company A Stock Company 2940 South 84 th Street, Lincoln, Nebraska 68506 Flexible Premium Deferred Annuity Contract This Contract is issued to the Owner in consideration of the initial

Lincoln Benefit Life Company A Stock Company 2940 South 84 th Street, Lincoln, Nebraska 68506 Flexible Premium Deferred Annuity Contract This Contract is issued to the Owner in consideration of the initial

Understanding Life Insurance: A Lesson in Life Insurance

Understanding Life Insurance: A Lesson in Life Insurance If something happens to you, how will your family replace your earning power? Table of Contents Page Your Earning Power 2 Life Insurance Questions

Understanding Life Insurance: A Lesson in Life Insurance If something happens to you, how will your family replace your earning power? Table of Contents Page Your Earning Power 2 Life Insurance Questions

VALIC Financial Advisors, Inc. An array of financial planning and investment services SAVING : INVESTING : PLANNING

VALIC Financial Advisors, Inc. An array of financial planning and investment services SAVING : INVESTING : PLANNING Your financial advisor will work with you to help make sure your financial plan fits

VALIC Financial Advisors, Inc. An array of financial planning and investment services SAVING : INVESTING : PLANNING Your financial advisor will work with you to help make sure your financial plan fits

Early Distribution Options Ellen Dawson

Early Distribution Options Ellen Dawson Presented by: Joseph Davis, CLU, ChFC 215 Broad Street Charlotte, North Carolina 26292 Phone: 704-927-5555 Mobile Phone: 704-549-5555 Fax: 704-549-6666 Email: joseph.davis@aol.com

Early Distribution Options Ellen Dawson Presented by: Joseph Davis, CLU, ChFC 215 Broad Street Charlotte, North Carolina 26292 Phone: 704-927-5555 Mobile Phone: 704-549-5555 Fax: 704-549-6666 Email: joseph.davis@aol.com

THE ALTERNATIVE USING LIFE INSURANCE. Ruth and Al Sample

THE ALTERNATIVE USING LIFE INSURANCE 00307140 CV Prepared for: Ruth and Al Sample This proposal by Pension Concepts has been designed to illustrate how you may increase your retirement income over your

THE ALTERNATIVE USING LIFE INSURANCE 00307140 CV Prepared for: Ruth and Al Sample This proposal by Pension Concepts has been designed to illustrate how you may increase your retirement income over your

Nicholson Financial Services, Inc. March 15, 2018

Nicholson Financial Services, Inc. David S. Nicholson Financial Advisor 89 Access Road Ste. C Norwood, MA 02062 781-255-1101 866-668-1101 david@nicholsonfs.com www.nicholsonfs.com Variable Annuities Variable

Nicholson Financial Services, Inc. David S. Nicholson Financial Advisor 89 Access Road Ste. C Norwood, MA 02062 781-255-1101 866-668-1101 david@nicholsonfs.com www.nicholsonfs.com Variable Annuities Variable

The value of your Foresters membership. Whole Life Insurance. Helping your family prepare for final expenses. Foresters PlanRight

Whole Life Insurance Compliments of: The value of your Foresters membership None of us like to think about our own mortality. But, on a purely practical front, we need to think about the costs associated

Whole Life Insurance Compliments of: The value of your Foresters membership None of us like to think about our own mortality. But, on a purely practical front, we need to think about the costs associated

SURVIVOR SUPPLEMENTAL RETIREMENT INCOME FUNDED WITH LIFE INSURANCE. Presented for Valued Client

Presented for Valued Client Presented by John M. Webster HMS Insurance Associates, Inc. johnwebster@financialguide.com 443-632-3436 Page 1 of 8 The Purpose Survivor supplemental retirement income funded

Presented for Valued Client Presented by John M. Webster HMS Insurance Associates, Inc. johnwebster@financialguide.com 443-632-3436 Page 1 of 8 The Purpose Survivor supplemental retirement income funded

Immediate Annuity Quotation

Immediate Annuity Quotation Personalized for: Primary Annuitant Prepared by: Ivon T Hughes Tel: 514-842-9001 Email: info@trustco.ca Fax: 514-842-1085 Reference #: 239360.1 Date Prepared: April 9, 2014

Immediate Annuity Quotation Personalized for: Primary Annuitant Prepared by: Ivon T Hughes Tel: 514-842-9001 Email: info@trustco.ca Fax: 514-842-1085 Reference #: 239360.1 Date Prepared: April 9, 2014

Maximizing Your Pension Income

Maximizing Your Pension Income These materials are not intended to be used to avoid tax penalties and were prepared to support the promotion or marketing of the matter addressed in this document. Neither

Maximizing Your Pension Income These materials are not intended to be used to avoid tax penalties and were prepared to support the promotion or marketing of the matter addressed in this document. Neither

Focused Growth Annuity 5, 7 and 10

Focused Growth Annuity 5, 7 and 10 A Rewarding Combination of Safety, Tax Deferral and Choice Standard Insurance Company A Deferred Annuity Is An Insurance Contract A deferred annuity contract is chiefly

Focused Growth Annuity 5, 7 and 10 A Rewarding Combination of Safety, Tax Deferral and Choice Standard Insurance Company A Deferred Annuity Is An Insurance Contract A deferred annuity contract is chiefly

An Insider s Guide to Annuities. The Safe Money Guide. retirement security investment growth

The Safe Money Guide retirement security investment growth An Insider s Guide to Annuities 1 Presented by Joe Brown Brown Advisory Group, LLC http://joebrown.retirevillage.com An Insider s Guide to Annuities

The Safe Money Guide retirement security investment growth An Insider s Guide to Annuities 1 Presented by Joe Brown Brown Advisory Group, LLC http://joebrown.retirevillage.com An Insider s Guide to Annuities

Income protection to cover life s essentials

RiverSource Income Protection Life term insurance Income protection to cover life s essentials 291358 F (11/13) Helping you protect an important financial asset your paycheck. If you re like most people,

RiverSource Income Protection Life term insurance Income protection to cover life s essentials 291358 F (11/13) Helping you protect an important financial asset your paycheck. If you re like most people,

Planning ahead. Understanding your 403(b) plan. Plan Participant Guide RETIREMENT PLAN SERVICES

plan. Plan Participant Guide RETIREMENT PLAN SERVICES") Planning ahead Understanding your 403(b) plan The Lincoln National Life Insurance Company Lincoln Life & Annuity Company of New York Plan Participant Guide RETIREMENT PLAN SERVICES 2073285 It all starts

Planning ahead Understanding your 403(b) plan The Lincoln National Life Insurance Company Lincoln Life & Annuity Company of New York Plan Participant Guide RETIREMENT PLAN SERVICES 2073285 It all starts

Purchase Payments. Annuity Options

CONTRACT SUMMARY Pacific Life Insurance Company P.O. Box 2378 Omaha, NE 68103-2378 (800) 722-4448 Contract Owners (800) 722-2333 Registered Representatives www.pacificlife.com Pacific Secure Income Annuity

CONTRACT SUMMARY Pacific Life Insurance Company P.O. Box 2378 Omaha, NE 68103-2378 (800) 722-4448 Contract Owners (800) 722-2333 Registered Representatives www.pacificlife.com Pacific Secure Income Annuity

SunSpectrum Joint Term

SunSpectrum Joint Term Policy number: LI-1234,567-8 Owner: John Doe Mary Doe The following policy wording is provided solely for your convenience and reference. It is incomplete and reflects only some

SunSpectrum Joint Term Policy number: LI-1234,567-8 Owner: John Doe Mary Doe The following policy wording is provided solely for your convenience and reference. It is incomplete and reflects only some

Table of Contents. Introduction Jurisdiction Transferring Your Money to a Prescribed Registered Retirement Income Fund...

RETIREMENT OPTIONS Table of Contents Page Introduction... 1 Jurisdiction... 2 Transferring Your Money to a Prescribed Registered Retirement Income Fund... 4 Locked-in Retirement Account... 7 Protecting

RETIREMENT OPTIONS Table of Contents Page Introduction... 1 Jurisdiction... 2 Transferring Your Money to a Prescribed Registered Retirement Income Fund... 4 Locked-in Retirement Account... 7 Protecting

Understanding Life Insurance: A Lesson in Life Insurance

Understanding Life : A Lesson in Life If something happens to you, how will your family replace your earning power? Table of Contents Page Your Earning Power 2 Life Questions 3 Types of Term 4 Term Variations

Understanding Life : A Lesson in Life If something happens to you, how will your family replace your earning power? Table of Contents Page Your Earning Power 2 Life Questions 3 Types of Term 4 Term Variations

Human Resources Benefits Office. For Your Benefit. PVA Benefits Program 2013 Summary Plan Description

Human Resources Benefits Office For Your Benefit PVA Benefits Program 2013 Summary Plan Description TABLE OF CONTENTS Page HOW THE PLAN WORKS... 5 Overview... 5 What is a Voluntary Tax Deferred Annuity

Human Resources Benefits Office For Your Benefit PVA Benefits Program 2013 Summary Plan Description TABLE OF CONTENTS Page HOW THE PLAN WORKS... 5 Overview... 5 What is a Voluntary Tax Deferred Annuity

Provider Single Premium Immediate Annuity

Provider Single Premium Immediate Annuity Type Issue Ages Free Look Minimum/Maximum Contributions Income Options Single Premium Immediate Annuity (Product features may vary by state.) 0-95 Qualified and

Provider Single Premium Immediate Annuity Type Issue Ages Free Look Minimum/Maximum Contributions Income Options Single Premium Immediate Annuity (Product features may vary by state.) 0-95 Qualified and

Getting to Know NATIONWIDE SURVIVORSHIP LEGACY PROVIDER UNIVERSAL LIFE. Nationwide Survivorship Legacy Provider Universal Life SM

Getting to Know NATIONWIDE SURVIVORSHIP LEGACY PROVIDER UNIVERSAL LIFE Nationwide Survivorship Legacy Provider Universal Life SM After a lifetime of planning and saving, you ve created a comfortable living

Getting to Know NATIONWIDE SURVIVORSHIP LEGACY PROVIDER UNIVERSAL LIFE Nationwide Survivorship Legacy Provider Universal Life SM After a lifetime of planning and saving, you ve created a comfortable living

CHAPTER 10 ANNUITIES

CHAPTER 10 ANNUITIES Annuities are contracts sold by life insurance companies that pay monthly, quarterly, semiannual, or annual income benefits for the life of a person (the annuitant), for the lives

CHAPTER 10 ANNUITIES Annuities are contracts sold by life insurance companies that pay monthly, quarterly, semiannual, or annual income benefits for the life of a person (the annuitant), for the lives

INDEX. pro-rating, 11

INDEX A grandfathered policies, 11, 12, 13 21-year deemed disposition rule, keyperson insurance strategy and, 301 302 205, 207, 208 Crummey trust and, 325 pro-rating, 11 Accounting for life insurance,

INDEX A grandfathered policies, 11, 12, 13 21-year deemed disposition rule, keyperson insurance strategy and, 301 302 205, 207, 208 Crummey trust and, 325 pro-rating, 11 Accounting for life insurance,

Options available on retrenchment (Applicable to members leaving post March 2009) The contents of this document

The contents of this document") Options available on retrenchment (Applicable to members leaving post March 2009) The contents of this document This document explains the different options you have available to you when you leave your

Options available on retrenchment (Applicable to members leaving post March 2009) The contents of this document This document explains the different options you have available to you when you leave your

Give your beneficiaries an Edge

Enhanced Death Benefit Rider Give your beneficiaries an Edge Not a bank or credit union deposit, obligation or guarantee May lose value Not FDIC or NCUA/NCUSIF insured Not insured by any federal government

Enhanced Death Benefit Rider Give your beneficiaries an Edge Not a bank or credit union deposit, obligation or guarantee May lose value Not FDIC or NCUA/NCUSIF insured Not insured by any federal government

Personal Financial Plan

Personal Financial Plan Pete and Carrie Mitchell 918 Richmond Street Toronto, Ontario M5N 1V5 Disclaimer This document has been prepared to assist in the analysis of your current financial position, thereby

Personal Financial Plan Pete and Carrie Mitchell 918 Richmond Street Toronto, Ontario M5N 1V5 Disclaimer This document has been prepared to assist in the analysis of your current financial position, thereby

Your Company Name RRIF Estate Maximizer (current date) page 1 of 7

page 1 of 7") (current date) page 1 of 7 "Pay tax on your RRIF income only once!" Are you now receiving more RRIF income than what you need to live on? Are you accumulating additional assets that you would like to pass

(current date) page 1 of 7 "Pay tax on your RRIF income only once!" Are you now receiving more RRIF income than what you need to live on? Are you accumulating additional assets that you would like to pass

Trusts An introduction

Trusts An introduction Trusts can be highly effective wealth management vehicles, especially for income splitting, tax and estate planning purposes and wealth protection. A trust is an arrangement whereby

Trusts An introduction Trusts can be highly effective wealth management vehicles, especially for income splitting, tax and estate planning purposes and wealth protection. A trust is an arrangement whereby

RETIREMENT PLAN OF THE CITY OF BRISTOL. Summary Plan Description

RETIREMENT PLAN OF THE CITY OF BRISTOL Summary Plan Description July 2007 TABLE OF CONTENTS GENERAL INFORMATION... 1 TYPE OF PLAN... 1 ELIGIBILITY AND PARTICIPATION... 1 CONTRIBUTIONS TO THE PLAN... 1

RETIREMENT PLAN OF THE CITY OF BRISTOL Summary Plan Description July 2007 TABLE OF CONTENTS GENERAL INFORMATION... 1 TYPE OF PLAN... 1 ELIGIBILITY AND PARTICIPATION... 1 CONTRIBUTIONS TO THE PLAN... 1

Your Company Name Corporate Redemption of Shares November 16, 1999 page 1 of 6

November 16, 1999 page 1 of 6 "Pay the cost of your Corporate Share Redemption Insurance from your company bank account and minimize the impact of capital gains taxation at death!" Many shareholders of

November 16, 1999 page 1 of 6 "Pay the cost of your Corporate Share Redemption Insurance from your company bank account and minimize the impact of capital gains taxation at death!" Many shareholders of

A discussion of corporate-owned life insurance

A discussion of corporate-owned life insurance Persons who seek their livelihood in business are often motivated by a need to place their fate in their own hands. Of course, the desire to make money for

A discussion of corporate-owned life insurance Persons who seek their livelihood in business are often motivated by a need to place their fate in their own hands. Of course, the desire to make money for

PERSONAL CHOICE PLUS+

You now have more options when it comes to your future Sentinel Plan PERSONAL CHOICE PLUS+ Client Brochure California SSLPCPBR-CA 010118 Retirement options you can depend on As the length of retirement

You now have more options when it comes to your future Sentinel Plan PERSONAL CHOICE PLUS+ Client Brochure California SSLPCPBR-CA 010118 Retirement options you can depend on As the length of retirement

Immediate Annuity Quotation

Immediate Annuity Quotation Personalized for: Prime Annuitant Prepared by: Quote No: AZGNT2 Date Prepared: March 1, 2017 Page1of6 Manulife Investments Annuities can assist with your income needs through

Immediate Annuity Quotation Personalized for: Prime Annuitant Prepared by: Quote No: AZGNT2 Date Prepared: March 1, 2017 Page1of6 Manulife Investments Annuities can assist with your income needs through

MassMutual Odyssey Select SM

MassMutual Odyssey Select SM A Flexible Premium Deferred Fixed Annuity Save for retirement your way MassMutual Odyssey Select (Odyssey Select) is a flexible premium deferred fixed annuity issued by Massachusetts

MassMutual Odyssey Select SM A Flexible Premium Deferred Fixed Annuity Save for retirement your way MassMutual Odyssey Select (Odyssey Select) is a flexible premium deferred fixed annuity issued by Massachusetts

Sharing Interests in a Life Insurance Policy

Sharing Interests in a Life Insurance Policy Shared Ownership and Shared Benefit Life Insurance Arrangements A GUIDE FOR LAWYERS AND ACCOUNTANTS Financial planning goals Our sales concept materials support

Sharing Interests in a Life Insurance Policy Shared Ownership and Shared Benefit Life Insurance Arrangements A GUIDE FOR LAWYERS AND ACCOUNTANTS Financial planning goals Our sales concept materials support

The Taxation of Non-Registered Segregated Funds

The Taxation of Non-Registered Segregated Funds Segregated funds (also referred to as individual variable insurance contracts, or IVICs) are an appropriate part of many Canadians portfolios. In very simple

The Taxation of Non-Registered Segregated Funds Segregated funds (also referred to as individual variable insurance contracts, or IVICs) are an appropriate part of many Canadians portfolios. In very simple

Lifetime Income Benefit Rider

Lifetime Income Benefit Rider Choice Series Version American Equity Simple Choices for a Secure Retirement The one who works for you! You ve Done the Work. Now Enjoy the Ride. You worked hard. From saving

Lifetime Income Benefit Rider Choice Series Version American Equity Simple Choices for a Secure Retirement The one who works for you! You ve Done the Work. Now Enjoy the Ride. You worked hard. From saving

individual life product solutions

individual life product solutions 1 make the most of every hard-earned dollar. You work hard for your money. Now make it work just as hard for you. At Sanlam we can help you transform your money into something

individual life product solutions 1 make the most of every hard-earned dollar. You work hard for your money. Now make it work just as hard for you. At Sanlam we can help you transform your money into something

Planned Giving CHARITABLE WILL BEQUESTS. The Benefits to You

Planned Giving Thank you for your interest in supporting the Unitarian Church of Edmonton and our many programs. For more information on our planned giving program, please call us at (780) 454-8073. CHARITABLE

Planned Giving Thank you for your interest in supporting the Unitarian Church of Edmonton and our many programs. For more information on our planned giving program, please call us at (780) 454-8073. CHARITABLE

INDEX. Segregated funds, Structured pre-1990 contracts, settlements deferred annuities, accrual taxation rules,

INDEX 21-year deemed disposition rule, 328 329 Crummey trust and, 353 A Accounting for life insurance, 224 226 Accounting standards, 71 72 Accrual reporting annuities, 431 433 keyperson insurance strategy

INDEX 21-year deemed disposition rule, 328 329 Crummey trust and, 353 A Accounting for life insurance, 224 226 Accounting standards, 71 72 Accrual reporting annuities, 431 433 keyperson insurance strategy

Guaranteeing an Income for Life: An Immediate Income Annuity Review

Guaranteeing an Income for Life: An Immediate Income Annuity Review The biggest financial risk that anyone faces during retirement is the risk that savings will be depleted...the risk that income will

Guaranteeing an Income for Life: An Immediate Income Annuity Review The biggest financial risk that anyone faces during retirement is the risk that savings will be depleted...the risk that income will

SUMMIT BONUS INDEX FIELD GUIDE SINGLE PREMIUM, DEFFERED ANNUITY

SUMMIT BONUS INDEX SINGLE PREMIUM, DEFFERED ANNUITY FIELD GUIDE SENTINEL SECURITY LIFE INSURANCE COMPANY PO BOX 27248 SALT LAKE CITY, UTAH 84127-0248 STATE OF DOMICILE: UTAH SSLIANFLDGD REV.062015 SUMMIT

SUMMIT BONUS INDEX SINGLE PREMIUM, DEFFERED ANNUITY FIELD GUIDE SENTINEL SECURITY LIFE INSURANCE COMPANY PO BOX 27248 SALT LAKE CITY, UTAH 84127-0248 STATE OF DOMICILE: UTAH SSLIANFLDGD REV.062015 SUMMIT

Accumulating Funds in an Annuity: A Deferred Fixed Interest and Indexed Annuity Review

Accumulating Funds in an Annuity: A Deferred Fixed Interest and Indexed Annuity Review Did you know that an annuity can be used to systematically accumulate money for retirement purposes, as well as to

Accumulating Funds in an Annuity: A Deferred Fixed Interest and Indexed Annuity Review Did you know that an annuity can be used to systematically accumulate money for retirement purposes, as well as to

Segregated funds policy Information folder

SEGREGATED FUNDS ESTATE PROTECTION Segregated funds policy Information folder The Canada Life Assurance Company is the sole issuer of the individual variable annuity policy described in this information

SEGREGATED FUNDS ESTATE PROTECTION Segregated funds policy Information folder The Canada Life Assurance Company is the sole issuer of the individual variable annuity policy described in this information

Annuity Answer Booklet

Annuity Answer Booklet Explanations of Annuity Concepts and Language Standard Insurance Company Annuity Answer Booklet Explanations of Annuity Concepts and Language Annuity Definition... 3 Interest Rates...

Annuity Answer Booklet Explanations of Annuity Concepts and Language Standard Insurance Company Annuity Answer Booklet Explanations of Annuity Concepts and Language Annuity Definition... 3 Interest Rates...