Ex-ante Impacts of Agricultural Insurance: Evidence from a Field Experiment in Mali

|

|

|

- Lora Newton

- 5 years ago

- Views:

Transcription

1 Ex-ante Impacts of Agricultural Insurance: Evidence from a Field Experiment in Mali Ghada Elabed* & Michael R Carter** *Mathematica Policy Research **University of California, Davis & NBER BASIS Assets & Market Access Research Program & I 4 Index Insurance Innovation Initiative Annual Global Development Conference, Casablanca 13 June 2015

2 Uninsured Risk Is Costly Risk is costly: Makes Households Poor when it leads them to adopt less risky, but lower returning activities Keeps Households Poor not only when it de-capitalizes them in the wake of a shock, but also when it leads them to accumulate unproductive 'buer' assets in anticipation of shocks Can insurance have real development impacts? Not just ex post smoothing eects (see previous work) But allowing farmers to ex ante prudentially invest more and increase their average incomes This presentation looks at the investment and income impacts of index insurance for cotton farmers in Mali

3 Logic of Index Insurance Conventional insurance (based on individual loss adjustment) has a dismal record Costly to verify losses for smallholders Moral hazard if do not/cannot reliably verify losses Adverse selection Index insurance does not pay based on (veried) individual losses, but instead based on a cheap to measure 'index' that is correlated with individual losses (e.g., average yields in a zone, or rainfall) Cuts costs Eliminates moral hazard & adverse selection

4 Cotton Production in Mali Most farmers are smallholders and grow a mix of subsistence crops and cotton Cotton is their main (and often only) source of cash Cotton is a protable, but risky crop Production organized in cooperatives Cotton is controlled by the Compagnie malienne pour le développement du textile (CMDT), a parastatal CMDT provides input loans and buys the harvest at a price announced before planting

5 Risk and Capital Constraints in Mali Farmers access credit via group loans: Amount of loan is on average 95, 000CFA/ha, and the net revenue from cotton is 105, 000CFA/ha If the cooperative yield falls below 750 kg/ha, loan repayment is tenuous P(yield < 750) = 10% Consequences of default are substantial (informal collateral) The collateral risk of default appears to discourage farmers from growing as much cotton as they otherwise mightclassic example of risk rationing Output can be taxed away to pay for others in the group

6 Dual Scale Area-yield Index Contract To address these issues, developed an area-yield insurance contract Can do this easily because monopsony buyer (CMDT) already measures area and output Insured unit is the cooperative (as it holds the joint liability debt for all farmers in the village) Payouts based on the average yield of the cooperative and of the ZPA grouping (an agglomeration of village cooperatives) This dual scale area-yield contract has a low level of basis risk: Conditional on a loss, the probability of getting a payment is 80%, and the probability that net proceeds are less than the value of 750 kg of cotton per-hectare drops to 2%

7 The Mali Pilot Project In cooperation with PlaNet Guarantee implemented a randomized control trial for the 2011/12 year 87 cooperatives: 59 were randomly selected for treatment (oered insurance), 28 served as control An encouragement design: reduced the price of contract to 50%, 75%, or 100% of the actuarially fair premium Decisions to buy the insurance made in May 2011 (planting season) 30% of the treated cooperatives purchased the insurance contract

8 The Mali Pilot Project Note that the insurance purchase decision was a joint decision by co-op Creates the possibility that an individual farmer may not know s/he is insured (e.g., if missed meeting) Ex ante eects can of course only occur if farmers know they are insured In the analysis to follow, we will both look at the impacts of being insured (co-op purchased insurance) and also impact if farmer reports that s/he is insured.

9 Research design Unfortunately, we discovered aws in roll-out (not all treated co-ops were actually oered insurance) Fortunately, we had audit questions that allowed us to gure out what really happened But only 22.5% of the treated households believed they were insured (and 10% of non-treated households!) Results shown here use the audit-based reclassication of treatment and control areas Paper includes all resultssimilar estimated impacts but less precise Audit-adjusted treatment & control groups are balanced in terms of observable covariates Let's focus now on key outcome variables

10 Econometric Method The decision to buy insurance (and to know insured) are of course economically & econometrically endogenous To obtain unbiased estimates of the impacts of insurance purchase and farming knowing insured, we exploit our randomized controlled trial and use instrumental variable methods to recover standard local average treatment eects.

11 Impacts if Co-op Purchased Insurance

12 Impacts if Farmer Knows Insured

13 Conclusion Impact of insurance are substantial at the extensive margin: Area in cotton rose by 1.3 to 1.4 hectares (a 60% increase) Matching increases in loans and inputs No impacts on input intensity, nor any impact on reduction in other ag activity Output (and income) increases are estimated to be about 40%, but this gure is not signicant (noisy outcome measure) We thus see that insurance can have substantial development impact New pilot in Burkina Fasostay tuned!

14 Extra Material

15 Cumulative cotton area in 2011 Cumulatives: Coton area in 2011, below 3 ha Cumulatives: Coton area in 2011, above 3 ha Area (ha) Area (ha) cdf_insurance cdf_control cdf_insurance cdf_control

.")

16 Prior Evidence on Risk TransferImpact of Index Insurance Maize producers in Ghana invest more when insured Randomly oered some farmers insurance at variable prices Other farmers oered a capital grant for purchasing inputs Found that farmers oered insurance: Expand area cultivated by 15% Increase input use by 40% Capital grants by themselves have little impact Source: Karlan et al. (2014). Agricultural Decisions after Relaxing Risk & Credit Constraints, Quarterly J of Econ.

17 Logic of Index Insurance Comparison of Index versus Conventional Insurance in Ecuador

18 Dual Scale Area-yield Index Contract Equivalently priced single & dual-scale contracts (Mali) Source: Elabed, Carter, Guirking & Bellemare (2014). Managing Basis Risk with Multi-scale Index Insurance Contracts, Agricultural Economics

19 Risk Rationing and Cotton Production Loans come with a binding joint liability clause Consequences of default are substantial (informal collateral) Survey in 2006: 32% of the farmers growing cotton had diculty with their loan repayment 38% had to sell their assets 4% sent one of their children to work for another farmer Some saw their credit line reduced and faced exclusion from the credit group The collateral risk of default appears to discourage farmers from growing as much cotton as they otherwise mightclassic example of risk rationing

20 Research question and Research Strategy There is modest but growing evidence that risk transfer (via insurance) & risk reduction (via stress tolerant varieties) has economically notable impacts Protecting current and future assets: Janzen and Carter (2014) Relaxing risk and capital constraints: Karlan et al (2014) Incentivizing technology adoption: Mobarak and Rosenzweig (2012) Use the remainder of our time to look at the investment and income impacts of insurance for cotton farmers in Mali We designed an insurance contract for cotton cooperatives in Mali We randomly oered insurance to 87 cotton cooperatives

21 Behavior of the Insured versus Uninsured These are NOT impact results

22 Risk Rationing and Cotton Production Loans come with a binding joint liability clause Consequences of default are substantial (informal collateral) Survey in 2006: 32% of the farmers growing cotton had diculty with their loan repayment 38% had to sell their assets 4% sent one of their children to work for another farmer Some saw their credit line reduced and faced exclusion from the credit group The collateral risk of default appears to discourage farmers from growing as much cotton as they otherwise mightclassic example of risk rationing

23 Dual Scale Area-yield Index Contract To address these issues, developed an area-yield insurance contract Can do this easily because monopsony buyer (CMDT) already measures area and output Insured unit is the cooperative (as it holds the joint liability debt for all farmers in the village) But at what scale set the trigger or strikepoint that determines payment? If take average across a larger area, basis risk increases If take average across too small an area, collusion and moral hazard possible

24 Dual Scale Area-yield Index Contract Rather than face the tradeo between a village level yield trigger (moral hazard) versus a yield trigger based on a larger ZPA grouping (an agglomeration of village cooperatives), designed a dual scale contract Payouts based on the average yield of the cooperative AND of the ZPA Can think of the ZPA trigger as an audit ruleonly believe village yields are low due to nature if neighboring villages are also showing some signs of stress Conditional on a loss, the probability of getting a payment is 80%, and the probability that net proceeds are less than the value of 750 kg of cotton per-hectare drops to 2%

25 Logic of Index Insurance Conventional insurance (based on individual loss adjustment) has a dismal record Costly to verify losses for smallholders Moral hazard if do not/cannot reliably verify losses Adverse selection Index insurance does not pay based on (veried) individual losses, but instead based on a cheap to measure 'index' that is correlated with individual losses (e.g., average yields in a zone, or rainfall) Cuts costs Eliminates moral hazard & adverse selection

26 Baseline Balance on Key Variables

27 Econometric Method The decision to buy insurance (and to know insured) are of course economically & econometrically endogenous To obtain unbiased estimates of the impacts of insurance purchase and farming knowing insured, we exploit our randomized controlled trial and use instrumental variable methods to recover standard local average treatment eects: Y jc = α + βîjc + γx jc + ε jc where Y jc is the outcome variable of interest (e.g., yields) for farmer j in co-op c, X jc are a set of control variables (baseline wealth, experience, etc.), and Î jc is the rst stage estimate of whether or not individual jc is, or feels, insured.

28 Econometric Method We derive these rst stage estimates of insurance status by estimating two equations of this form: I jc = α + δ 1 T jc + δ 2 P jc + ε jc where I jc = 1 if individual jc is (or believes) that is insured, T jc is the randomly determined treatment variable (equals 1 if co-op was oered insurance) and P ic is a measure of the strike point penalty randomly imposed by the reinsurance company

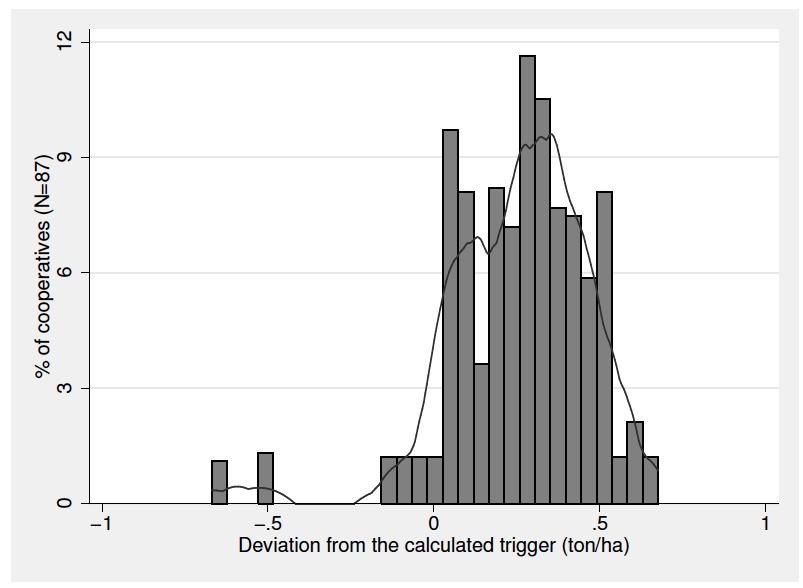

29 Strikepoint Penalty Research team designed & then priced the contract under the assumption that yields for dierent co-ops in the same area are driven by a common parametric probability structure Structure was allowed to parametrically shift with each co-op's average long-term yields Resulted in a set of spatially stable prices

30 Strikepoint Penalty Reinsurance partner rejected this approach and priced each co-op separately using burn rates based on the short time series available on each co-op Resulted in often radical downward shift in strike points, with neighboring co-ops sometimes oered radically dierent contracts Also resulted in no contracts being oered to more than half the co-ops in pilot area Because these strike point dierences were driven by randomness (did one co-op happen to have an especially bad year in its time series, whereas its neighbor did not), a measure of this strike point penalty should serve as a statistically valid and strong instrument to explain insurance purchase

31 Strikepoint Penalty

Sharing the Risk and the Uncertainty: Public- Private Reinsurance Partnerships for Viable Agricultural Insurance Markets

I4 Brief no. 2013-1 July 2013 Sharing the Risk and the Uncertainty: Public- Private Reinsurance Partnerships for Viable Agricultural Insurance Markets by Michael R. Carter The Promise of Agricultural Insurance

I4 Brief no. 2013-1 July 2013 Sharing the Risk and the Uncertainty: Public- Private Reinsurance Partnerships for Viable Agricultural Insurance Markets by Michael R. Carter The Promise of Agricultural Insurance

The Effects of Rainfall Insurance on the Agricultural Labor Market. A. Mushfiq Mobarak, Yale University Mark Rosenzweig, Yale University

The Effects of Rainfall Insurance on the Agricultural Labor Market A. Mushfiq Mobarak, Yale University Mark Rosenzweig, Yale University Background on the project and the grant In the IGC-funded precursors

The Effects of Rainfall Insurance on the Agricultural Labor Market A. Mushfiq Mobarak, Yale University Mark Rosenzweig, Yale University Background on the project and the grant In the IGC-funded precursors

Ex-ante Impacts of Agricultural Insurance:

Ex-ante Impacts of Agricultural Insurance: Evidence from a Field Experiment in Mali Ghada Elabed and Michael Carter PRELIMINARY DRAFT: April 24 2014 Abstract Anticipating a negative income shock, uninsured

Ex-ante Impacts of Agricultural Insurance: Evidence from a Field Experiment in Mali Ghada Elabed and Michael Carter PRELIMINARY DRAFT: April 24 2014 Abstract Anticipating a negative income shock, uninsured

CLIENT VALUE & INDEX INSURANCE

CLIENT VALUE & INDEX INSURANCE TARA STEINMETZ, ASSISTANT DIRECTOR FEED THE FUTURE INNOVATION LAB FOR ASSETS & MARKET ACCESS Fairview Hotel, Nairobi, Kenya 4 JULY 2017 basis.ucdavis.edu Photo Credit Goes

CLIENT VALUE & INDEX INSURANCE TARA STEINMETZ, ASSISTANT DIRECTOR FEED THE FUTURE INNOVATION LAB FOR ASSETS & MARKET ACCESS Fairview Hotel, Nairobi, Kenya 4 JULY 2017 basis.ucdavis.edu Photo Credit Goes

Pisco Sour? Insights from an Area Yield Pilot program in Pisco, Peru

Pisco Sour? Insights from an Area Yield Pilot program in Pisco, Peru Steve Boucher University of California, Davis I-4/FAO Conference: Economics of Index Insurance Rome, January 15-16, 2010 Pilot Insurance

Pisco Sour? Insights from an Area Yield Pilot program in Pisco, Peru Steve Boucher University of California, Davis I-4/FAO Conference: Economics of Index Insurance Rome, January 15-16, 2010 Pilot Insurance

International Economic Development Spring 2017 Midterm Examination

Please complete the following questions in the space provided. Each question has equal value. Please be concise, but do write in complete sentences. Question 1 In thinking about economic growth among poor

Please complete the following questions in the space provided. Each question has equal value. Please be concise, but do write in complete sentences. Question 1 In thinking about economic growth among poor

Behavioral Economics & the Design of Agricultural Index Insurance in Developing Countries

Behavioral Economics & the Design of Agricultural Index Insurance in Developing Countries Michael R Carter Department of Agricultural & Resource Economics BASIS Assets & Market Access Research Program

Behavioral Economics & the Design of Agricultural Index Insurance in Developing Countries Michael R Carter Department of Agricultural & Resource Economics BASIS Assets & Market Access Research Program

Making Index Insurance Work for the Poor

Making Index Insurance Work for the Poor Xavier Giné, DECFP April 7, 2015 It is odd that there appear to have been no practical proposals for establishing a set of markets to hedge the biggest risks to

Making Index Insurance Work for the Poor Xavier Giné, DECFP April 7, 2015 It is odd that there appear to have been no practical proposals for establishing a set of markets to hedge the biggest risks to

Testing for Poverty Traps: Asset Smoothing versus Consumption Smoothing in Burkina Faso (with some thoughts on what to do about it)

") Testing for Poverty Traps: Asset Smoothing versus Consumption Smoothing in Burkina Faso (with some thoughts on what to do about it) Travis Lybbert Michael Carter University of California, Davis Risk &

Testing for Poverty Traps: Asset Smoothing versus Consumption Smoothing in Burkina Faso (with some thoughts on what to do about it) Travis Lybbert Michael Carter University of California, Davis Risk &

Development Economics Part II Lecture 7

Development Economics Part II Lecture 7 Risk and Insurance Theory: How do households cope with large income shocks? What are testable implications of different models? Empirics: Can households insure themselves

Development Economics Part II Lecture 7 Risk and Insurance Theory: How do households cope with large income shocks? What are testable implications of different models? Empirics: Can households insure themselves

Indirect protection: the impact of cotton insurance on farmers income portfolio in Burkina Faso

Indirect protection: the impact of cotton insurance on farmers income portfolio in Burkina Faso Quentin Stoeffler, Wouter Gelade, Catherine Guirkinger, and Michael Carter May 2016 Abstract While risk is

Indirect protection: the impact of cotton insurance on farmers income portfolio in Burkina Faso Quentin Stoeffler, Wouter Gelade, Catherine Guirkinger, and Michael Carter May 2016 Abstract While risk is

Risk, Insurance and Wages in General Equilibrium. A. Mushfiq Mobarak, Yale University Mark Rosenzweig, Yale University

Risk, Insurance and Wages in General Equilibrium A. Mushfiq Mobarak, Yale University Mark Rosenzweig, Yale University 750 All India: Real Monthly Harvest Agricultural Wage in September, by Year 730 710

Risk, Insurance and Wages in General Equilibrium A. Mushfiq Mobarak, Yale University Mark Rosenzweig, Yale University 750 All India: Real Monthly Harvest Agricultural Wage in September, by Year 730 710

Index Insurance: Financial Innovations for Agricultural Risk Management and Development

Index Insurance: Financial Innovations for Agricultural Risk Management and Development Sommarat Chantarat Arndt-Corden Department of Economics Australian National University PSEKP Seminar Series, Gadjah

Index Insurance: Financial Innovations for Agricultural Risk Management and Development Sommarat Chantarat Arndt-Corden Department of Economics Australian National University PSEKP Seminar Series, Gadjah

Disaster Management The

Disaster Management The UKRAINIAN Agricultural AGRICULTURAL Dimension WEATHER Global Facility for RISK Disaster MANAGEMENT Recovery and Reduction Seminar Series February 20, 2007 WORLD BANK COMMODITY RISK

Disaster Management The UKRAINIAN Agricultural AGRICULTURAL Dimension WEATHER Global Facility for RISK Disaster MANAGEMENT Recovery and Reduction Seminar Series February 20, 2007 WORLD BANK COMMODITY RISK

Financial Literacy, Social Networks, & Index Insurance

Financial Literacy, Social Networks, and Index-Based Weather Insurance Xavier Giné, Dean Karlan and Mũthoni Ngatia Building Financial Capability January 2013 Introduction Introduction Agriculture in developing

Financial Literacy, Social Networks, and Index-Based Weather Insurance Xavier Giné, Dean Karlan and Mũthoni Ngatia Building Financial Capability January 2013 Introduction Introduction Agriculture in developing

The Educa*on of Co/on Farmers in Mali

The Educa*on of Co/on Farmers in Mali Marc F. Bellemare Duke University Catherine Guirkinger University of Namur Michael R. Carter University of California, Davis Ghada Elabed University of California,

The Educa*on of Co/on Farmers in Mali Marc F. Bellemare Duke University Catherine Guirkinger University of Namur Michael R. Carter University of California, Davis Ghada Elabed University of California,

Agricultural Commodity Risk Management: Policy Options and Practical Instruments with Emphasis on the Tea Economy

Agricultural Commodity Risk Management: Policy Options and Practical Instruments with Emphasis on the Tea Economy Alexander Sarris Director, Trade and Markets Division, FAO Presentation at the Intergovernmental

Agricultural Commodity Risk Management: Policy Options and Practical Instruments with Emphasis on the Tea Economy Alexander Sarris Director, Trade and Markets Division, FAO Presentation at the Intergovernmental

A Microfinance Model of Insurable Covariate Risk and Endogenous Effort. John P. Dougherty. Ohio State University.

A Microfinance Model of Insurable Covariate Risk and Endogenous Effort John P. Dougherty Ohio State University dougherty.148@osu.edu Mario J. Miranda Ohio State University Selected Paper prepared for presentation

A Microfinance Model of Insurable Covariate Risk and Endogenous Effort John P. Dougherty Ohio State University dougherty.148@osu.edu Mario J. Miranda Ohio State University Selected Paper prepared for presentation

Innovations for Agriculture

DIME Impact Evaluation Workshop Innovations for Agriculture 16-20 June 2014, Kigali, Rwanda Facilitating Savings for Agriculture: Field Experimental Evidence from Rural Malawi Lasse Brune University of

DIME Impact Evaluation Workshop Innovations for Agriculture 16-20 June 2014, Kigali, Rwanda Facilitating Savings for Agriculture: Field Experimental Evidence from Rural Malawi Lasse Brune University of

Poverty Traps and Social Protection

Christopher B. Barrett Michael R. Carter Munenobu Ikegami Cornell University and University of Wisconsin-Madison May 12, 2008 presentation Introduction 1 Multiple equilibrium (ME) poverty traps command

Christopher B. Barrett Michael R. Carter Munenobu Ikegami Cornell University and University of Wisconsin-Madison May 12, 2008 presentation Introduction 1 Multiple equilibrium (ME) poverty traps command

Informal Risk Sharing, Index Insurance and Risk-Taking in Developing Countries

Working paper Informal Risk Sharing, Index Insurance and Risk-Taking in Developing Countries Ahmed Mushfiq Mobarak Mark Rosenzweig December 2012 When citing this paper, please use the title and the following

Working paper Informal Risk Sharing, Index Insurance and Risk-Taking in Developing Countries Ahmed Mushfiq Mobarak Mark Rosenzweig December 2012 When citing this paper, please use the title and the following

NBER WORKING PAPER SERIES RISK, INSURANCE AND WAGES IN GENERAL EQUILIBRIUM. Ahmed Mushfiq Mobarak Mark Rosenzweig

NBER WORKING PAPER SERIES RISK, INSURANCE AND WAGES IN GENERAL EQUILIBRIUM Ahmed Mushfiq Mobarak Mark Rosenzweig Working Paper 19811 http://www.nber.org/papers/w19811 NATIONAL BUREAU OF ECONOMIC RESEARCH

NBER WORKING PAPER SERIES RISK, INSURANCE AND WAGES IN GENERAL EQUILIBRIUM Ahmed Mushfiq Mobarak Mark Rosenzweig Working Paper 19811 http://www.nber.org/papers/w19811 NATIONAL BUREAU OF ECONOMIC RESEARCH

Add Presenter Name Here. Index Insurance for Agricultural Risk Management

Add Presenter Name Here Index Insurance for Agricultural Risk Management IMAGINE FOR A MOMENT: You re a smallholder farmer. You re just near the poverty line, either above or below just making ends meet

Add Presenter Name Here Index Insurance for Agricultural Risk Management IMAGINE FOR A MOMENT: You re a smallholder farmer. You re just near the poverty line, either above or below just making ends meet

A Quasi-experimental Study of a Discontinued Insurance Product in Haiti

A Quasi-experimental Study of a Discontinued Insurance Product in Haiti Emily Breza, Dan Osgood, Aaron Baum (Columbia University) Carine Roenen (Fonkoze) Benedique Paul (State University of Haiti) BASIS

A Quasi-experimental Study of a Discontinued Insurance Product in Haiti Emily Breza, Dan Osgood, Aaron Baum (Columbia University) Carine Roenen (Fonkoze) Benedique Paul (State University of Haiti) BASIS

Module 6 Book A: Principles of Contract Design. Agriculture Risk Management Team Agricultural and Rural Development The World Bank

+ Module 6 Book A: Principles of Contract Design Agriculture Risk Management Team Agricultural and Rural Development The World Bank + Module 6 in the Process of Developing Index Insurance Initial Idea

+ Module 6 Book A: Principles of Contract Design Agriculture Risk Management Team Agricultural and Rural Development The World Bank + Module 6 in the Process of Developing Index Insurance Initial Idea

3 RD MARCH 2009, KAMPALA, UGANDA

INNOVATIVE NEW PRODUCTS WEATHER INDEX INSURANCE IN MALAWI SHADRECK MAPFUMO VICE PRESIDENT, AGRICULTURE INSURANCE 3 RD MARCH 2009, KAMPALA, UGANDA Acknowledgements The Commodity Risk Management Group at

INNOVATIVE NEW PRODUCTS WEATHER INDEX INSURANCE IN MALAWI SHADRECK MAPFUMO VICE PRESIDENT, AGRICULTURE INSURANCE 3 RD MARCH 2009, KAMPALA, UGANDA Acknowledgements The Commodity Risk Management Group at

Rural Financial Intermediaries

Rural Financial Intermediaries 1. Limited Liability, Collateral and Its Substitutes 1 A striking empirical fact about the operation of rural financial markets is how markedly the conditions of access can

Rural Financial Intermediaries 1. Limited Liability, Collateral and Its Substitutes 1 A striking empirical fact about the operation of rural financial markets is how markedly the conditions of access can

Public-Private Partnerships for Agricultural Risk Management through Risk Layering

I4 Brief no. 2011-01 April 2011 Public-Private Partnerships for Agricultural Risk Management through Risk Layering by Michael Carter, Elizabeth Long and Stephen Boucher Public and Private Risk Management

I4 Brief no. 2011-01 April 2011 Public-Private Partnerships for Agricultural Risk Management through Risk Layering by Michael Carter, Elizabeth Long and Stephen Boucher Public and Private Risk Management

Business Statistics 41000: Homework # 2

Business Statistics 41000: Homework # 2 Drew Creal Due date: At the beginning of lecture # 5 Remarks: These questions cover Lectures #3 and #4. Question # 1. Discrete Random Variables and Their Distributions

Business Statistics 41000: Homework # 2 Drew Creal Due date: At the beginning of lecture # 5 Remarks: These questions cover Lectures #3 and #4. Question # 1. Discrete Random Variables and Their Distributions

Credit Markets in Africa

Credit Markets in Africa Craig McIntosh, UCSD African Credit Markets Are highly segmented Often feature vibrant competitive microfinance markets for urban small-trading. However, MF loans often structured

Credit Markets in Africa Craig McIntosh, UCSD African Credit Markets Are highly segmented Often feature vibrant competitive microfinance markets for urban small-trading. However, MF loans often structured

Crop Price Indemnified Loans for Farmers: A Pilot Experiment in Rural Ghana. Dean Karlan, Ed Kutsoati, Margaret McMillan, and Chris Udry

Crop Price Indemnified Loans for Farmers: A Pilot Experiment in Rural Ghana Dean Karlan, Ed Kutsoati, Margaret McMillan, and Chris Udry January 15, 2010 Contributions to this research made by a member

Crop Price Indemnified Loans for Farmers: A Pilot Experiment in Rural Ghana Dean Karlan, Ed Kutsoati, Margaret McMillan, and Chris Udry January 15, 2010 Contributions to this research made by a member

Workshop / Atelier. Disaster Risk Financing and Insurance (DRFI) Financement et Assurance des Risques de Désastres Naturels

Financement et Assurance des Risques de Désastres Naturels") Workshop / Atelier Disaster Risk Financing and Insurance (DRFI) Financement et Assurance des Risques de Désastres Naturels Thursday-Friday, June 4-5, 2015 Jeudi-Vendredi 4-5 Juin 2015 Managing Risk with

Workshop / Atelier Disaster Risk Financing and Insurance (DRFI) Financement et Assurance des Risques de Désastres Naturels Thursday-Friday, June 4-5, 2015 Jeudi-Vendredi 4-5 Juin 2015 Managing Risk with

Public Disclosure Authorized. Project Name Mali - Third Structural Adjustment Credit (SAC III) Public Disclosure Authorized

Public Disclosure Authorized") Public Disclosure Authorized Report No. PID10817 Project Name Mali - Third Structural Adjustment Credit (SAC III) Region Sector Project ID Africa Multi-sectoral MLPE72785 Borrower Republic of Mali Public

Public Disclosure Authorized Report No. PID10817 Project Name Mali - Third Structural Adjustment Credit (SAC III) Region Sector Project ID Africa Multi-sectoral MLPE72785 Borrower Republic of Mali Public

Measurement of Price Risk in Revenue Insurance: 1 Introduction Implications of Distributional Assumptions A variety of crop revenue insurance programs

Measurement of Price Risk in Revenue Insurance: Implications of Distributional Assumptions Matthew C. Roberts, Barry K. Goodwin, and Keith Coble May 14, 1998 Abstract A variety of crop revenue insurance

Measurement of Price Risk in Revenue Insurance: Implications of Distributional Assumptions Matthew C. Roberts, Barry K. Goodwin, and Keith Coble May 14, 1998 Abstract A variety of crop revenue insurance

Problems in Rural Credit Markets

Problems in Rural Credit Markets Econ 435/835 Fall 2012 Econ 435/835 () Credit Problems Fall 2012 1 / 22 Basic Problems Low quantity of domestic savings major constraint on investment, especially in manufacturing

Problems in Rural Credit Markets Econ 435/835 Fall 2012 Econ 435/835 () Credit Problems Fall 2012 1 / 22 Basic Problems Low quantity of domestic savings major constraint on investment, especially in manufacturing

EU i (x i ) = p(s)u i (x i (s)),

= p(s)u i (x i (s)),") Abstract. Agents increase their expected utility by using statecontingent transfers to share risk; many institutions seem to play an important role in permitting such transfers. If agents are suitably

Abstract. Agents increase their expected utility by using statecontingent transfers to share risk; many institutions seem to play an important role in permitting such transfers. If agents are suitably

Inequalities and Investment. Abhijit V. Banerjee

Inequalities and Investment Abhijit V. Banerjee The ideal If all asset markets operate perfectly, investment decisions should have very little to do with the wealth or social status of the decision maker.

Inequalities and Investment Abhijit V. Banerjee The ideal If all asset markets operate perfectly, investment decisions should have very little to do with the wealth or social status of the decision maker.

Ex ante moral hazard on borrowers actions

Lecture 9 Capital markets INTRODUCTION Evidence that majority of population is excluded from credit markets Demand for Credit arises for three reasons: (a) To finance fixed capital acquisitions (e.g. new

Lecture 9 Capital markets INTRODUCTION Evidence that majority of population is excluded from credit markets Demand for Credit arises for three reasons: (a) To finance fixed capital acquisitions (e.g. new

Weathering the Risks: Scalable Weather Index Insurance in East Africa

Weathering the Risks: Scalable Weather Index Insurance in East Africa Having enough food in East Africa depends largely on the productivity of smallholder farms, which in turn depends on farmers ability

Weathering the Risks: Scalable Weather Index Insurance in East Africa Having enough food in East Africa depends largely on the productivity of smallholder farms, which in turn depends on farmers ability

Financial Economics Field Exam August 2008

Financial Economics Field Exam August 2008 There are two questions on the exam, representing Macroeconomic Finance (234A) and Corporate Finance (234C). Please answer both questions to the best of your

Financial Economics Field Exam August 2008 There are two questions on the exam, representing Macroeconomic Finance (234A) and Corporate Finance (234C). Please answer both questions to the best of your

Oil Price Movements and the Global Economy: A Model-Based Assessment. Paolo Pesenti, Federal Reserve Bank of New York, NBER and CEPR

Oil Price Movements and the Global Economy: A Model-Based Assessment Selim Elekdag, International Monetary Fund Douglas Laxton, International Monetary Fund Rene Lalonde, Bank of Canada Dirk Muir, Bank

Oil Price Movements and the Global Economy: A Model-Based Assessment Selim Elekdag, International Monetary Fund Douglas Laxton, International Monetary Fund Rene Lalonde, Bank of Canada Dirk Muir, Bank

CROP PRICE INDEMNIFIED LOANS FOR FARMERS: A PILOT EXPERIMENT IN RURAL GHANA

C The Journal of Risk and Insurance, 2011, Vol. 78, No. 1, 37-55 DOI: 10.1111/j.1539-6975.2010.01406.x CROP PRICE INDEMNIFIED LOANS FOR FARMERS: A PILOT EXPERIMENT IN RURAL GHANA Dean Karlan Ed Kutsoati

C The Journal of Risk and Insurance, 2011, Vol. 78, No. 1, 37-55 DOI: 10.1111/j.1539-6975.2010.01406.x CROP PRICE INDEMNIFIED LOANS FOR FARMERS: A PILOT EXPERIMENT IN RURAL GHANA Dean Karlan Ed Kutsoati

Credit Market Problems in Developing Countries

Credit Market Problems in Developing Countries September 2007 () Credit Market Problems September 2007 1 / 17 Should Governments Intervene in Credit Markets Moneylenders historically viewed as exploitive:

Credit Market Problems in Developing Countries September 2007 () Credit Market Problems September 2007 1 / 17 Should Governments Intervene in Credit Markets Moneylenders historically viewed as exploitive:

Development Economics 455 Prof. Karaivanov

Development Economics 455 Prof. Karaivanov Notes on Credit Markets in Developing Countries Introduction ------------------ credit markets intermediation between savers and borrowers: o many economic activities

Development Economics 455 Prof. Karaivanov Notes on Credit Markets in Developing Countries Introduction ------------------ credit markets intermediation between savers and borrowers: o many economic activities

Risk & Resilience Ample evidence that risk Makes people poor by reducing incomes & destroying assets, sometimes pushing households into a situation fr

Scaling Tools for Resilient Drylands Professor, University of California, Davis, Giannini Foundation & NBER Director, Feed the Future Assets & Market Access Innovation Lab October 11, 2016 Risk & Resilience

Scaling Tools for Resilient Drylands Professor, University of California, Davis, Giannini Foundation & NBER Director, Feed the Future Assets & Market Access Innovation Lab October 11, 2016 Risk & Resilience

Drought and Informal Insurance Groups: A Randomised Intervention of Index based Rainfall Insurance in Rural Ethiopia

Drought and Informal Insurance Groups: A Randomised Intervention of Index based Rainfall Insurance in Rural Ethiopia Guush Berhane, Daniel Clarke, Stefan Dercon, Ruth Vargas Hill and Alemayehu Seyoum Taffesse

Drought and Informal Insurance Groups: A Randomised Intervention of Index based Rainfall Insurance in Rural Ethiopia Guush Berhane, Daniel Clarke, Stefan Dercon, Ruth Vargas Hill and Alemayehu Seyoum Taffesse

THE INSTITUTE OF CHARTERED ACCOUNTANTS (GHANA) MICRO-ECONOMICS QUESTION PAPER NOVEMBER 2014 SECTION A: (MICRO-ECONOMICS)

MICRO-ECONOMICS QUESTION PAPER NOVEMBER 2014 SECTION A: (MICRO-ECONOMICS)") SECTION A: (MICRO-ECONOMICS) NB: answer only three (3) questions in this section QUESTION 1 The table below shows the various combinations of yam and maize that a hypothetical country can produce per farming

SECTION A: (MICRO-ECONOMICS) NB: answer only three (3) questions in this section QUESTION 1 The table below shows the various combinations of yam and maize that a hypothetical country can produce per farming

Subsidy Policies and Insurance Demand 1

Subsidy Policies and Insurance Demand 1 Jing Cai 2 University of Michigan Alain de Janvry Elisabeth Sadoulet University of California, Berkeley 11/30/2013 Preliminary and Incomplete Do not Circulate, Do

Subsidy Policies and Insurance Demand 1 Jing Cai 2 University of Michigan Alain de Janvry Elisabeth Sadoulet University of California, Berkeley 11/30/2013 Preliminary and Incomplete Do not Circulate, Do

Index-based weather insurance for developing countries: A review of evidence and a set of propositions for up-scaling Outline Abstract

Index-based weather insurance for developing countries: A review of evidence and a set of propositions for up-scaling by Michael Carter +, Alain de Janvry ++, Elisabeth Sadoulet ++, and Alexander Sarris

Index-based weather insurance for developing countries: A review of evidence and a set of propositions for up-scaling by Michael Carter +, Alain de Janvry ++, Elisabeth Sadoulet ++, and Alexander Sarris

Interlinking Product and Insurance Markets: Experimental Evidence from Contract Farming in Kenya

Interlinking Product and Insurance Markets: Experimental Evidence from Contract Farming in Kenya Lorenzo Casaburi Stanford University Jack Willis Harvard University March 2015 Preliminary and Incomplete

Interlinking Product and Insurance Markets: Experimental Evidence from Contract Farming in Kenya Lorenzo Casaburi Stanford University Jack Willis Harvard University March 2015 Preliminary and Incomplete

Credit Market Problems in Developing Countries

Credit Market Problems in Developing Countries November 2007 () Credit Market Problems November 2007 1 / 25 Basic Problems (circa 1950): Low quantity of domestic savings major constraint on investment,

Credit Market Problems in Developing Countries November 2007 () Credit Market Problems November 2007 1 / 25 Basic Problems (circa 1950): Low quantity of domestic savings major constraint on investment,

Formal and informal insurance: experimental evidence from Ethiopia

Formal and informal insurance: experimental evidence from Ethiopia Guush Berhane International Food Policy Research Institute Stefan Dercon University of Oxford Ruth Vargas Hill* World Bank Alemayehu Seyoum

Formal and informal insurance: experimental evidence from Ethiopia Guush Berhane International Food Policy Research Institute Stefan Dercon University of Oxford Ruth Vargas Hill* World Bank Alemayehu Seyoum

The role of asymmetric information

LECTURE NOTES ON CREDIT MARKETS The role of asymmetric information Eliana La Ferrara - 2007 Credit markets are typically a ected by asymmetric information problems i.e. one party is more informed than

LECTURE NOTES ON CREDIT MARKETS The role of asymmetric information Eliana La Ferrara - 2007 Credit markets are typically a ected by asymmetric information problems i.e. one party is more informed than

Moral Hazard. Economics Microeconomic Theory II: Strategic Behavior. Instructor: Songzi Du

Moral Hazard Economics 302 - Microeconomic Theory II: Strategic Behavior Instructor: Songzi Du compiled by Shih En Lu (Chapter 25 in Watson (2013)) Simon Fraser University July 9, 2018 ECON 302 (SFU) Lecture

Moral Hazard Economics 302 - Microeconomic Theory II: Strategic Behavior Instructor: Songzi Du compiled by Shih En Lu (Chapter 25 in Watson (2013)) Simon Fraser University July 9, 2018 ECON 302 (SFU) Lecture

Time vs. State in Insurance: Experimental Evidence from Contract Farming in Kenya

Time vs. State in Insurance: Experimental Evidence from Contract Farming in Kenya Lorenzo Casaburi Stanford University Jack Willis Harvard University October 29, 2015 Abstract The gains from insurance

Time vs. State in Insurance: Experimental Evidence from Contract Farming in Kenya Lorenzo Casaburi Stanford University Jack Willis Harvard University October 29, 2015 Abstract The gains from insurance

Insured v. The management company brings a claim against the association for breach of management

Insured v. Insured Exclusion What is it all About in the Community Association s Directors and Officers Policy by Joel W. Meskin, Esq., CIRMS Featured in Community Interests, May 2009 The directors & officers

Insured v. Insured Exclusion What is it all About in the Community Association s Directors and Officers Policy by Joel W. Meskin, Esq., CIRMS Featured in Community Interests, May 2009 The directors & officers

Master in Industrial Organization and Markets. Spring 2012 Microeconomics III Assignment 1: Uncertainty

Master in Industrial Organization and Markets. Spring Microeconomics III Assignment : Uncertainty Problem Determine which of the following assertions hold or not. Justify your answers with either an example

Master in Industrial Organization and Markets. Spring Microeconomics III Assignment : Uncertainty Problem Determine which of the following assertions hold or not. Justify your answers with either an example

Borrowing Culture and Debt Relief: Evidence from a Policy Experiment

Borrowing Culture and Debt Relief: Evidence from a Policy Experiment Sankar De (Shiv Nadar University, India) Prasanna Tantri (Centre for Analytical Finance, Indian School of Business) IGIDR Emerging Market

Borrowing Culture and Debt Relief: Evidence from a Policy Experiment Sankar De (Shiv Nadar University, India) Prasanna Tantri (Centre for Analytical Finance, Indian School of Business) IGIDR Emerging Market

Risk, Financial Markets, and Human Capital in a Developing Country, by Jacoby and Skouas

Risk, Financial Markets, and Human Capital in a Developing Country, by Jacoby and Skouas Mark Klee 12/11/06 Risk, Financial Markets, and Human Capital in a Developing Country, by Jacoby and Skouas 2 1

Risk, Financial Markets, and Human Capital in a Developing Country, by Jacoby and Skouas Mark Klee 12/11/06 Risk, Financial Markets, and Human Capital in a Developing Country, by Jacoby and Skouas 2 1

Final Exam. Part I. (60 minutes) Answer each of the following questions in the time allowed.

Answer each of the following questions in the time allowed.") Final Exam Econ. 116 December 17, 2016 180 MINUTES (one point per minute) REMEMBER: ONE PART PER BLUE BOOK Part I. (60 minutes) Answer each of the following questions in the time allowed. 1. (6 minutes)

Final Exam Econ. 116 December 17, 2016 180 MINUTES (one point per minute) REMEMBER: ONE PART PER BLUE BOOK Part I. (60 minutes) Answer each of the following questions in the time allowed. 1. (6 minutes)

Small Farmers Perspectives on Agricultural Insurance in Africa

Africa - Asia Conclave on Loss and Damage Due to Climate Change - - - Small Farmers Perspectives on Agricultural Insurance in Africa - - - August 25-26 2016, Nairobi intro. Climate changes and Insurance

Africa - Asia Conclave on Loss and Damage Due to Climate Change - - - Small Farmers Perspectives on Agricultural Insurance in Africa - - - August 25-26 2016, Nairobi intro. Climate changes and Insurance

AGRICULTURAL DECISIONS AFTER RELAXING CREDIT AND RISK CONSTRAINTS* Dean Karlan Robert Osei Isaac Osei-Akoto Christopher Udry

AGRICULTURAL DECISIONS AFTER RELAXING CREDIT AND RISK CONSTRAINTS* Dean Karlan Robert Osei Isaac Osei-Akoto Christopher Udry The investment decisions of small-scale farmers in developing countries are

AGRICULTURAL DECISIONS AFTER RELAXING CREDIT AND RISK CONSTRAINTS* Dean Karlan Robert Osei Isaac Osei-Akoto Christopher Udry The investment decisions of small-scale farmers in developing countries are

Adverse Selection on Maturity: Evidence from On-Line Consumer Credit

Adverse Selection on Maturity: Evidence from On-Line Consumer Credit Andrew Hertzberg (Columbia) with Andrés Liberman (NYU) and Daniel Paravisini (LSE) Credit and Payments Markets Oct 2 2015 The role of

Adverse Selection on Maturity: Evidence from On-Line Consumer Credit Andrew Hertzberg (Columbia) with Andrés Liberman (NYU) and Daniel Paravisini (LSE) Credit and Payments Markets Oct 2 2015 The role of

UNDERWRITING AREA-BASED YIELD INSURANCE TO CROWD-IN CREDIT SUPPLY AND DEMAND*

UNDERWRITING AREA-BASED YIELD INSURANCE TO CROWD-IN CREDIT SUPPLY AND DEMAND* MICHAEL R. CARTER University of Wisconsin, Madison - mrcarter@wisc.edu FRANCISCO GALARZA University of Wisconsin, Madison -

UNDERWRITING AREA-BASED YIELD INSURANCE TO CROWD-IN CREDIT SUPPLY AND DEMAND* MICHAEL R. CARTER University of Wisconsin, Madison - mrcarter@wisc.edu FRANCISCO GALARZA University of Wisconsin, Madison -

Agricultural Markets. Spring Lecture 24

Agricultural Markets Spring 2014 Two Finance Concepts My claim: the two critical ideas of finance (what you learn in MBA program). 1. Time Value of Money. 2. Risk Aversion and Pooling. Time Value of Money

Agricultural Markets Spring 2014 Two Finance Concepts My claim: the two critical ideas of finance (what you learn in MBA program). 1. Time Value of Money. 2. Risk Aversion and Pooling. Time Value of Money

Where and How Index Insurance Can Boost the Adoption of Improved Agricultural Technologies

Where and How Index Insurance Can Boost the Adoption of Improved Agricultural Technologies Michael R. Carter University of California, Davis Lan Cheng Unviversity of California, Davis Alexandros Sarris

Where and How Index Insurance Can Boost the Adoption of Improved Agricultural Technologies Michael R. Carter University of California, Davis Lan Cheng Unviversity of California, Davis Alexandros Sarris

Lecture Notes - Insurance

1 Introduction need for insurance arises from Lecture Notes - Insurance uncertain income (e.g. agricultural output) risk aversion - people dislike variations in consumption - would give up some output

1 Introduction need for insurance arises from Lecture Notes - Insurance uncertain income (e.g. agricultural output) risk aversion - people dislike variations in consumption - would give up some output

Credit Lecture 23. November 20, 2012

Credit Lecture 23 November 20, 2012 Operation of the Credit Market Credit may not function smoothly 1. Costly/impossible to monitor exactly what s done with loan. Consumption? Production? Risky investment?

Credit Lecture 23 November 20, 2012 Operation of the Credit Market Credit may not function smoothly 1. Costly/impossible to monitor exactly what s done with loan. Consumption? Production? Risky investment?

Endogenous Insurance and Informal Relationships

Endogenous Insurance and Informal Relationships Xiao Yu Wang Duke May 2014 Wang (Duke) Endogenous Informal Insurance 05/14 1 / 20 Introduction The Idea "Informal institution": multi-purpose relationships

Endogenous Insurance and Informal Relationships Xiao Yu Wang Duke May 2014 Wang (Duke) Endogenous Informal Insurance 05/14 1 / 20 Introduction The Idea "Informal institution": multi-purpose relationships

Growing emphasis on insurance systems

Growing emphasis on insurance systems Roger C Stone, University of Southern Queensland, Australia. World Meteorological Organisation, Commission for Agricultural Meteorology. IDMP Geneva September 14-16,

Growing emphasis on insurance systems Roger C Stone, University of Southern Queensland, Australia. World Meteorological Organisation, Commission for Agricultural Meteorology. IDMP Geneva September 14-16,

Econ 277A: Economic Development I. Final Exam (06 May 2012)

") Econ 277A: Economic Development I Semester II, 2011-12 Tridip Ray ISI, Delhi Final Exam (06 May 2012) There are 2 questions; you have to answer both of them. You have 3 hours to write this exam. 1. [30

Econ 277A: Economic Development I Semester II, 2011-12 Tridip Ray ISI, Delhi Final Exam (06 May 2012) There are 2 questions; you have to answer both of them. You have 3 hours to write this exam. 1. [30

Definition of Incomplete Contracts

Definition of Incomplete Contracts Susheng Wang 1 2 nd edition 2 July 2016 This note defines incomplete contracts and explains simple contracts. Although widely used in practice, incomplete contracts have

Definition of Incomplete Contracts Susheng Wang 1 2 nd edition 2 July 2016 This note defines incomplete contracts and explains simple contracts. Although widely used in practice, incomplete contracts have

Causes and Implications of Credit Rationing in Rural Ethiopia

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Policy Research Working Paper 6096 Causes and Implications of Credit Rationing in Rural

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Policy Research Working Paper 6096 Causes and Implications of Credit Rationing in Rural

CALIFORNIA INSTITUTE OF TECHNOLOGY

DIVISION OF THE HUMANITIES AND SOCIAL SCIENCES CALIFORNIA INSTITUTE OF TECHNOLOGY PASADENA, CALIFORNIA 91125 MORAL HAZARD, FINANCIAL CONSTRAINTS AND SHARECROPPING IN EL OULJA Jean-Jacques Laffont California

DIVISION OF THE HUMANITIES AND SOCIAL SCIENCES CALIFORNIA INSTITUTE OF TECHNOLOGY PASADENA, CALIFORNIA 91125 MORAL HAZARD, FINANCIAL CONSTRAINTS AND SHARECROPPING IN EL OULJA Jean-Jacques Laffont California

1 Each factor of production earns an income. What correctly identifies the income for labour and capital?

Economics 0455, Solved MCQ Paper Oct / Nov 2016 /12, (Total MCQ: 30; Max Time Mnts (30+5); Total Marks: 30) 1 Each factor of production earns an income. What correctly identifies the income for labour

Economics 0455, Solved MCQ Paper Oct / Nov 2016 /12, (Total MCQ: 30; Max Time Mnts (30+5); Total Marks: 30) 1 Each factor of production earns an income. What correctly identifies the income for labour

Outline. Commodity Risk Management Group. Microeconomic Problems of Commodity Price Volatility. Macroeconomic Problems of Commodity Price Volatility

Commodity Risk Management Group Panos Varangis / Julie Dana CRM, The World Bank Outline Price Risk Management Problems Background of Project Activities Lessons Learned Presentation to ICAC Research Associates

Commodity Risk Management Group Panos Varangis / Julie Dana CRM, The World Bank Outline Price Risk Management Problems Background of Project Activities Lessons Learned Presentation to ICAC Research Associates

STEP 7. Before starting Step 7, you will have

STEP 7 Gap analysis Handing out mosquito nets in Bubulo village, Uganda Photo credit: Geoff Sayer/Oxfam Step 7 completes the gap-analysis strand. It should produce a final estimate of the total shortfall

STEP 7 Gap analysis Handing out mosquito nets in Bubulo village, Uganda Photo credit: Geoff Sayer/Oxfam Step 7 completes the gap-analysis strand. It should produce a final estimate of the total shortfall

GLOSSARY. 1 Crop Cutting Experiments

GLOSSARY 1 Crop Cutting Experiments Crop Cutting experiments are carried out on all important crops for the purpose of General Crop Estimation Surveys. The same yield data is used for purpose of calculation

GLOSSARY 1 Crop Cutting Experiments Crop Cutting experiments are carried out on all important crops for the purpose of General Crop Estimation Surveys. The same yield data is used for purpose of calculation

Development Economics 855 Lecture Notes 7

Development Economics 855 Lecture Notes 7 Financial Markets in Developing Countries Introduction ------------------ financial (credit) markets important to be able to save and borrow: o many economic activities

Development Economics 855 Lecture Notes 7 Financial Markets in Developing Countries Introduction ------------------ financial (credit) markets important to be able to save and borrow: o many economic activities

CASE STUDY AGLEND LOAN APPLICATION. Solutions & Explanations

CASE STUDY AGLEND LOAN APPLICATION Solutions & Explanations Questions: 1. Come up with basic criteria that AGLEND can review within 5 10 minutes to decide whether a client qualifies for a loan. You also

CASE STUDY AGLEND LOAN APPLICATION Solutions & Explanations Questions: 1. Come up with basic criteria that AGLEND can review within 5 10 minutes to decide whether a client qualifies for a loan. You also

INTERNATIONAL COTTON ADVISORY COMMITTEE

INTERNATIONAL COTTON ADVISORY COMMITTEE Standing Committee Attachment III to SC-N-493 Washington, DC May 12, 2008 Government Support to the Cotton Industry Direct government subsidies currently provided

INTERNATIONAL COTTON ADVISORY COMMITTEE Standing Committee Attachment III to SC-N-493 Washington, DC May 12, 2008 Government Support to the Cotton Industry Direct government subsidies currently provided

Portfolio Investment

Portfolio Investment Robert A. Miller Tepper School of Business CMU 45-871 Lecture 5 Miller (Tepper School of Business CMU) Portfolio Investment 45-871 Lecture 5 1 / 22 Simplifying the framework for analysis

Portfolio Investment Robert A. Miller Tepper School of Business CMU 45-871 Lecture 5 Miller (Tepper School of Business CMU) Portfolio Investment 45-871 Lecture 5 1 / 22 Simplifying the framework for analysis

Group Lending or Individual Lending?

Group Lending or Individual Lending? Evidence from a Randomized Field Experiment in Mongolia O. Attanasio 1 B. Augsburg 2 R. De Haas 3 E. Fitzsimons 2 H. Harmgart 3 1 University College London and Institute

Group Lending or Individual Lending? Evidence from a Randomized Field Experiment in Mongolia O. Attanasio 1 B. Augsburg 2 R. De Haas 3 E. Fitzsimons 2 H. Harmgart 3 1 University College London and Institute

Experimental Identification of Asymmetric Information: Evidence on Crop Insurance in the Philippines

Experimental Identification of Asymmetric Information: Evidence on Crop Insurance in the Philippines Snaebjorn Gunnsteinsson * January 31, 2017 Abstract Asymmetric information imposes costs on a wide range

Experimental Identification of Asymmetric Information: Evidence on Crop Insurance in the Philippines Snaebjorn Gunnsteinsson * January 31, 2017 Abstract Asymmetric information imposes costs on a wide range

After the Drought: The Impact of Microinsurance on Consumption Smoothing and Asset Protection

After the Drought: The Impact of Microinsurance on Consumption Smoothing and Asset Protection December 29, 2017 Michael R. Carter Sarah A. Janzen Montana State University Ph: (406) 994-3714 sarah.janzen@montana.edu

After the Drought: The Impact of Microinsurance on Consumption Smoothing and Asset Protection December 29, 2017 Michael R. Carter Sarah A. Janzen Montana State University Ph: (406) 994-3714 sarah.janzen@montana.edu

Information Asymmetries in Crop Insurance:

Information Asymmetries in Crop Insurance: Theory and Experimental Evidence from the Philippines Snaebjorn Gunnsteinsson * September 7, 2016 Abstract Asymmetric information can be costly in insurance markets

Information Asymmetries in Crop Insurance: Theory and Experimental Evidence from the Philippines Snaebjorn Gunnsteinsson * September 7, 2016 Abstract Asymmetric information can be costly in insurance markets

Designing index-based safety nets for village Africa

Designing index-based safety nets for village Africa Bart van den Boom Vasco Molini Centre for World Food Studies, VU University Amsterdam Weather Deivatives and Risk January 28, 2010 Humboldt Universität

Designing index-based safety nets for village Africa Bart van den Boom Vasco Molini Centre for World Food Studies, VU University Amsterdam Weather Deivatives and Risk January 28, 2010 Humboldt Universität

Catastrophe Risk Financing Instruments. Abhas K. Jha Regional Coordinator, Disaster Risk Management East Asia and the Pacific

Catastrophe Risk Financing Instruments Abhas K. Jha Regional Coordinator, Disaster Risk Management East Asia and the Pacific Structure of Presentation Impact of Disasters in developing Countries The Need

Catastrophe Risk Financing Instruments Abhas K. Jha Regional Coordinator, Disaster Risk Management East Asia and the Pacific Structure of Presentation Impact of Disasters in developing Countries The Need

Crop Insurance Contracting: Moral Hazard Costs through Simulation

Crop Insurance Contracting: Moral Hazard Costs through Simulation R.D. Weaver and Taeho Kim Selected Paper Presented at AAEA Annual Meetings 2001 May 2001 Draft Taeho Kim, Research Assistant Department

Crop Insurance Contracting: Moral Hazard Costs through Simulation R.D. Weaver and Taeho Kim Selected Paper Presented at AAEA Annual Meetings 2001 May 2001 Draft Taeho Kim, Research Assistant Department

Practice Problems 1: Moral Hazard

Practice Problems 1: Moral Hazard December 5, 2012 Question 1 (Comparative Performance Evaluation) Consider the same normal linear model as in Question 1 of Homework 1. This time the principal employs

Practice Problems 1: Moral Hazard December 5, 2012 Question 1 (Comparative Performance Evaluation) Consider the same normal linear model as in Question 1 of Homework 1. This time the principal employs

11 06 Class 12 Forwards and Futures

11 06 Class 12 Forwards and Futures From banks to futures markets Financial i l markets as insurance markets Instruments and exchanges; The counterparty risk problem 1 From last time Banks face bank runs

11 06 Class 12 Forwards and Futures From banks to futures markets Financial i l markets as insurance markets Instruments and exchanges; The counterparty risk problem 1 From last time Banks face bank runs

Basis Risk and Compound-Risk Aversion: Evidence from a WTP Experiment in Mali

Basis Risk and Compound-Risk Aversion: Evidence from a WTP Experiment in Mali Ghada Elabed Ph.D. Candidate Department of Ag & Res Economics University of California, Davis elabed@primal.ucdavis.edu Michael

Basis Risk and Compound-Risk Aversion: Evidence from a WTP Experiment in Mali Ghada Elabed Ph.D. Candidate Department of Ag & Res Economics University of California, Davis elabed@primal.ucdavis.edu Michael

Insights from Behavioral Economics on Index Insurance

Insights from Behavioral Economics on Index Insurance Michael Carter Professor, Agricultural & Resource Economics University of California, Davis Director, BASIS Collaborative Research Support Program

Insights from Behavioral Economics on Index Insurance Michael Carter Professor, Agricultural & Resource Economics University of California, Davis Director, BASIS Collaborative Research Support Program

Index Based Crop Insurance Initiative Kenya April 2012

Index Based Crop Insurance Initiative Kenya April 2012 Presentation Outline 1. What is Index Insurance? 2. Why do farmers need insurance? 3. What is Kilimo Salama? 4. How does Kilimo Salama work? 5. Key

Index Based Crop Insurance Initiative Kenya April 2012 Presentation Outline 1. What is Index Insurance? 2. Why do farmers need insurance? 3. What is Kilimo Salama? 4. How does Kilimo Salama work? 5. Key

Price Discrimination As Portfolio Diversification. Abstract

Price Discrimination As Portfolio Diversification Parikshit Ghosh Indian Statistical Institute Abstract A seller seeking to sell an indivisible object can post (possibly different) prices to each of n

Price Discrimination As Portfolio Diversification Parikshit Ghosh Indian Statistical Institute Abstract A seller seeking to sell an indivisible object can post (possibly different) prices to each of n

DETERMINANTS OF DEBT CAPACITY. 1st set of transparencies. Tunis, May Jean TIROLE

DETERMINANTS OF DEBT CAPACITY 1st set of transparencies Tunis, May 2005 Jean TIROLE I. INTRODUCTION Adam Smith (1776) - Berle-Means (1932) Agency problem Principal outsiders/investors/lenders Agent insiders/managers/entrepreneur

DETERMINANTS OF DEBT CAPACITY 1st set of transparencies Tunis, May 2005 Jean TIROLE I. INTRODUCTION Adam Smith (1776) - Berle-Means (1932) Agency problem Principal outsiders/investors/lenders Agent insiders/managers/entrepreneur

Economics 101A (Lecture 25) Stefano DellaVigna

Stefano DellaVigna") Economics 101A (Lecture 25) Stefano DellaVigna April 29, 2014 Outline 1. Hidden Action (Moral Hazard) II 2. The Takeover Game 3. Hidden Type (Adverse Selection) 4. Evidence of Hidden Type and Hidden Action

Economics 101A (Lecture 25) Stefano DellaVigna April 29, 2014 Outline 1. Hidden Action (Moral Hazard) II 2. The Takeover Game 3. Hidden Type (Adverse Selection) 4. Evidence of Hidden Type and Hidden Action

University of Groningen

University of Groningen Does the group leader matter? The impact of monitoring activities and social ties of group leaders on the repayment performance of groupbased lending Eritrea Hermes, Cornelis; Lensink,

University of Groningen Does the group leader matter? The impact of monitoring activities and social ties of group leaders on the repayment performance of groupbased lending Eritrea Hermes, Cornelis; Lensink,

Population Economics Field Exam Spring This is a closed book examination. No written materials are allowed. You can use a calculator.

Population Economics Field Exam Spring 2011 Instructions You have 4 hours to complete this exam. This is a closed book examination. No written materials are allowed. You can use a calculator. YOU MUST

Population Economics Field Exam Spring 2011 Instructions You have 4 hours to complete this exam. This is a closed book examination. No written materials are allowed. You can use a calculator. YOU MUST

Credit II Lecture 25

Credit II Lecture 25 November 27, 2012 Operation of the Credit Market Last Tuesday I began the discussion of the credit market (Chapter 14 in Development Economics. I presented material through Section

Credit II Lecture 25 November 27, 2012 Operation of the Credit Market Last Tuesday I began the discussion of the credit market (Chapter 14 in Development Economics. I presented material through Section