Basel III Leverage Ratio

|

|

|

- Judith Nash

- 6 years ago

- Views:

Transcription

1 Basel III Leverage Ratio Prepared for Asia Risk Jakarta May 2018 by Mike Duncan

2 Agenda Overview of Basel III What is the Leverage Ratio? Basic principles and calculations Exposure Measure On-balance sheet exposures Off balance sheet exposures (OBS) Derivatives exposures Securities Financing Transactions (SFT) Exposures Leverage Ratio standard disclosure How does Leverage Ratio interplay with LCR and NSFR? Conclusion Q&A

Why?")

3 Overview of Basel III What is Basel III? An extension of existing Basel II framework Builds on existing 3 Pillars concept Introduces new capital and liquidity standards (requirements) Why? A result of the Financial crisis of 2008 Governments requiring banks to be more robust, through additional levels of capital, regulation and supervision

4

5 Overview of Basel III To get a better understanding of Basel III, need to know more about Basel II Accord Basel II result of substantial bank losses in the early 1990 s attributed to poor risk management Basel II made it mandatory for FI s to use Standardised measurements for credit, market risk and operational risk FI able to pursue advanced risk management approaches to free up capital Uses a 3 Pillars concept Pillar 1 Minimal capital requirements (addressing risk) Credit Risk calculated 3 ways, Standardised Approach (SA), Foundation Internal Rating based Approach (IRB) & advanced IRB Operational Risk Basic Indicator Approach (BIA), Standardised Approach (STA) & Internal Measurement Approach (AMA) Market Risk allows for Standardised and Internal approaches. Preferred is Value at Risk (VaR)

6 Overview of Basel III Uses a 3 Pillars concept Pillar 2 Supervisory review Regulatory response to the 1 st pillar, provides regulators better tools than previously Also provided framework for dealing with Pension Risk, Systemic Risk, Concentration Risk, Strategic Risk, Reputational Risk, Liquidity Risk and Legal Risk combined under the accord as Residual Risk Market Risk allows for Standardised and Internal approaches. Preferred is Value at Risk (VaR) Pillar 3 Market Discipline Designed to encourage market discipline by developing a set of disclosure requirements which allow market participants to assess key pieces of information on the scope of allocation, capital, risk exposure, risk assessment processes i.e. the capital adequacy of the FI MD supplements Pillar 2 as sharing of information facilitates assessments (i.e. comparisons) of the banks by others (investors, analysts, customers, clients, competitors and rating agencies) provides a common framework

7 Overview of Basel III Hence Basel III builds on the foundation of Basel II Focus on Pillar 1 Minimal Capital requirements (increased) Response to inadequate capital maintained by banks up to 2008 Banks required to hold more capital & higher quality capital under Basel II rules Explicit definitions of what Capital is - Tier 1 and Tier 2 Leverage Ratio (LR) introduced to supplement risk-based minimum capital requirements Liquidity Ratios to ensure adequate funding is maintained in the case of the next banking crisis But wait there is more

8 Overview of Basel III Created by the Basel Committee on Bank Supervision (BCBS) BCBS is a group of international banking authorities who work to strengthen the regulation, supervision and practices of banks and improve financial stability worldwide Members include; Argentina, Australia, Belgium, Brazil, Canada, China, France, Germany, Hong Kong SAR, India, Indonesia, Italy, Japan, Korea, Luxembourg, Mexico, the Netherlands, Russia, Saudi Arabia, Singapore, South Africa, Spain, Sweden, Switzerland, Turkey, the United Kingdom and the United States Basel III regulations/policies have no legal authority. They have to be passed into law by the applicable authorities in each respective jurisdiction Hence applicable rules or applications will differ in various jurisdictions

9

10 Leverage Ratio Basic principals and calculations What is it? Also known as the Supplementary Leverage Ratio (SLR) Non-risk-based backstop to the risk-based capital rules does not distinguish between safer or riskier assets Designed to be credible supplementary measure to risk-based capital requirements Limits excessive build-up in leverage Tier 1 capital of the bank must be at least 3% of the banks on & off balance sheet exposures (other jurisdictions it is higher e.g. US) LR applicable to all internationally active banks Public disclosure requirements allow for calibration and comparison across banks Basel III 2017 reforms at an additional buffer for Global Systematically Important Banks (G- SIBs)

11 LR Basic principals and calculations Calculation Leverage Ratio = Capital Measure Exposure Measure 3% Where Capital Measure = Tier 1 Capital (mostly Common Equity & some additional Tier 1 Capital Exposure Measure = Sum of on-balance sheet exposures, derivatives exposures, securities finance transactions (SFT) exposures & off-balance sheet exposures (OBS) For G-SIB LR buffer will be set at 50% of it s risk-based capital buffer. i.e. a G-SIB with a 2% risk-based buffer will have a 1% LR buffer so will have to maintain a total LR of 4%

12 LR basic principles & calculations Why is there a LR? An underlying cause of the GFC was the build up of excessive on- and off-balance sheet leverage in the banking system (e.g. Lehman Bros, RBS). In many case leveraged significantly while maintaining seemingly strong risk-based capital ratios. The deleveraging process at the height of the crisis created a vicious circle of losses and reduced the availability of credit in the real economy. Fears about bank solvency lead to wholesale funding markets freezing. BCBS introduced the LR in Basel III to reduce the risk of such period of deleveraging in the future. LR also intended to reinforce the risk-based capital requirements with a simple, non-risk based backstop

13 LR Exposure measurement The exposure measure should generally follow the account value subject to the following; 1. On-balance sheet, non-derivative exposures are included in the exposure measure net of specific provisions or accounting valuation adjustments (e.g. accounting credit valuation adjustments 2. Netting of loans and deposits is not allowed 3. Unless specified in the exposure types banks must not take account of physical or financial collateral, guarantees or other credit risk mitigation techniques to reduce the exposure measure Total exposure measure = On-balance sheet exposures + Derivative exposures +Securities financing transactions (SFT) + Off-balance sheet exposures (OBS)

14 LR Exposure measurement On-balance Sheet Exposures Banks must include all balance sheet assets in their exposure measure including on-balance sheet derivatives collateral Collateral for SFTs Exception is on-balance sheet derivative and SFT assets (covered in their specific sections) For consistency balance sheet assets deducted from Tier 1 Capital may be deducted from the exposure measure e.g. when an subsidiary entity is not included in the regulatory scope of consolidation Liability items (e.g. gains/losses on fair valued liabilities) must not be deducted from the exposure measure Balance sheet products cash, loans, securities, deposits, borrowing, equity

15 LR Exposure measurement Off-balance Sheet Exposures Incorporation OBS items as defined in Basel II framework into LR exposure measure OBS items defined as; Commitments (liquidity facilities) Direct credit substitutes - purchasing a subordinated cert of another bank's securitisation, guaranteeing mezzanine cert of another bank's securitization, providing a letter of credit to ABCP program Acceptances Standby letters of credit Trade letters of credit OBS items converted under the standardised approach (SA-CCR) into credit equivalents via use credit conversion factors (CCF) which are applied to the notional amount

16 LR Exposure measurement Derivative Exposures Banks required to calculate derivative exposures as a replacement cost (RC) for the current exposure (i.e. MTM) plus an add-on for potential future exposure (PFE) or the credit risk Includes when banks writes credit protection (sells CDS), which are subject to additional treatment In cases of bilateral netting contracts alternative treatments may be applied For single derivative exposure not covered by a bilateral netting agreement the amount of the exposure measure is as follows; Exposure measure = replacement cost (RC) + add-on where RC = replacement cost of contract (MTM), where the contract has a positive value Add-on = amount of PFE over remaining life of contract calculated by applying an add-on factor to notional principal of the derivative

17 LR Exposure measurement Derivative Exposures

18 LR Exposure measurement Derivative Exposures

19 LR Exposure measurement Derivative Exposures Bilateral Netting When a bilateral netting contract is used the RC for the set of derivatives covered by the contract will be the net replacement cost and the add-on will be Anet This is the sum of the net MTM replacement cost, if positive, plus an add-on based on the notional underlying principal. The add-on for the netted transactions (Anet) equals the weighted average of the gross add-on (AGross) and the gross add-on adjusted by the ratio of net current replacement cost to gross current replacement cost (NGR). Anet = 0.4 x Agross * NGR x Agross Where NGR = level of net replacement cost/level of gross replacement cost for transactions subject to legally enforceable netting agreements Agross = sum individual add-on amounts (multiplying notional amount by appropriate add-on factors) of all transactions subject to the netting agreement with one counterparty

20 LR Exposure measurement Derivative Exposures Collateral BCBS notes that collateral has two effects on leverage 1. Reduces counterparty exposure 2. Can increase economic resources available to the bank as bank can use the collateral for leverage (if no restriction on rehypothecation) Collateral received - may not be netted against underlying derivative exposures whether or not netting is permitted accounting or risk-based framework so banks cannot reduce the exposure amount by any collateral received from the counterparty Collateral provided banks must gross up their exposure measure by the amount of derivatives collateral provided where the provision of that capital has reduce the value of their balance sheet assets under their accounting framework Cash Variation margin cash portion of variation margin BCBS treating as form of presettlement payment

21 LR Exposure measurement Derivative Exposures Cash Variation margin (CVM) cash portion of variation margin BCBS treating as form of presettlement payment if following met: For trades not cleared through a QCCP cash received by recipient counterparty is not segregated CVM calculated and exchanged on a daily basis based on MTM valuation of derivative positions CVM is received in the same currency as the currency of settlement of the derivative contract CVM exchanged is the full amount that would be necessary to fully extinguish the MTM exposure of the derivative subject to the threshold and minimum transfer amounts applicable to the counterparty Derivatives transactions and variation margins are covered by a single master netting agreement (MNA) between the counterparties in the derivatives transaction If conditions above met; 1. cash portion of variation margin received can be used to reduce the RC portion of the LR exposure measure 2. receivables assets from CVM provided can be deducted from LR exposure measure as follows CVM received receiving bank can reduce RC (not the add-on portion)of the exposure amount by the amount of cash received if the positive MTM value has not already been reduced by the same amount CVM received under the banks accounting framework CVM provided to a counterparty, posting bank can deduct resulting receivable from its LR exposure measure where CVM has been recognized as an asset under the banks accounting framework CVM can not be used to reduce PFE amount,including calculation of NGR

22 LR Exposure measurement Derivative Exposures Treatment of clearing services bank acting as clearing member (CM) Where bank offers clearing services to clients, the CM trade exposures to the CCP that arise when the clearing member is obligated to cover the client for any losses suffered due to changes in value of transaction is CCP defaults must be captured as per usual treatment as other derivatives If CM based on contracts with client is not obligated to cover client for any losses suffered from default of CCP, CM need not recognize resulting trade exposures to CCP in LR exposure measure. Likewise when CM guarantees performance of a clients derivative trade exposures to a CCP must be included in LR exposure measure

23 LR Exposure measurement Derivative Exposures Additional treatment for written credit derivatives In addition to the CCR exposure arising from MTM value of the contracts, written credit derivatives (sold protection) create a notional credit exposure arising from the credit worthiness of the reference entity. Hence required to treat sold protection consistently with cash instruments (e.g. loans, bonds) for purposes of LR exposure measure. Effective notional amount of a written credit derivative can be reduced by any negative change in MTM value incorporated into calculation of Tier 1 capital with respect to the written credit derivative. The amount may be further reduced by the effective notional amount of a purchased credit derivative on the same reference name if 1. Credit protection purchased on the reference obligor which ranks pari passu with or is junior to the underlying reference obligor of the written credit derivative in case of singe name 2. Remaining maturity of credit protection purchased is equal to or greater than the remaining maturity of the written credit derivatives

24 LR Exposure measurement Securities Financing Transactions (SFT) Exposures Treatment designed to ensure consistent international implementation by providing a common measure for dealing main differences in operative accounting frameworks SFTs include following where transaction values depend on market valuations and transactions often subject to margin agreements; Repurchase agreements (repos) Reverse repurchase agreements (reverse repos) Security lending and borrowing(i.e. stock, borrowing & lending) Margin lending transactions

25 LR Exposure measurement Securities Financing Transactions (SFT) Exposures General Treatment (Bank Acting as principle) Gross SFT assets recognized for accounting purposes (i.e. no recognition of accounting netting) adjusted as follows Excluding from the exposure measure value of any securities received under an SFT, where the bank has recognized the securities as an asset on its balance sheet Cash payables and receivables in SFTs with same counterparty may be measured net: Transactions have same explicit final settlement date Right to set off amount owed to counterparty with the amount owed to the counterparty is legally enforceable currently in the normal course of business and in event of (i) default, (iii) insolvency and (iii) bankruptcy Counterparties intend to settle net and settle simultaneously (or transactions in system that has same effect)

26 LR Exposure measurement Securities Financing Transactions (SFT) Exposures General Treatment (Bank Acting as principle) A measure of CCR calculated as current exposure without an add-on for PFE, calculated as follows; With a qualifying master netting agreement (MNA), current exposure (E*) is greater of zero and total value of securities and cash lent to a counterparty included in the MNA ( Ei) less total value of cash and securities received from the counterparty for those transactions ( Cj) E = max 0, Ej Cj Where no MNA, current exposure for transactions with a counterparty must be calculated on a transaction basis (individual) i.e. each transaction treated as its own netting set E = max 0, Ei Cj

27 LR Exposure measurement Securities Financing Transactions (SFT) Exposures Bank Acting as agent prime broker, stock borrowing and lending Bank usually provides an indemnity or guarantee to only one of the parties involved, and only for the difference between the value of the security or cash its customer has lent and the value of the collateral the borrower as provided. Bank is only exposed to the counterparty of its customer for the difference in values, rather than the full exposure of the underlying security of the transaction When bank does not own/control the underlying cash or security resource that resource can t be leveraged by the bank i.e. no rehypothecation If bank provides an indemnity to a customer or counterparty as described above then bank has to use General Treatment without an MNA i.e. transactional basis, NO NETTING, NO OFFSET = OUCH!!! As doubling banks exposure to a relatively risk-free business

28 Disclosure Requirements Banks required to publicly disclose their LR on a consolidated basis from1 Jan 2015 Frequency concurrent with publication of the jurisdictions financial statements (i.e. halfyearly or quarterly), however Under basel II Pillar 3 (market discipline), large banks are subject to a minimum disclosure requirement to defined key capital ratios & elements on a quarterly basis regardless of frequency of publication of financial statements Disclosures must be either included in banks published financial statements or at a minimum provide a direct link to the completed disclosures on banks websites Banks must make available on their websites (or through publicly available regulatory reports) an ongoing archive of reconciliation & disclosure templates To enable participants to reconcile LR disclosures from period to period, to compare Capital Adequacy of banks across jurisdictions / accountancy frameworks necessitated a common consistency in formats of disclosures.

29 Disclosure Requirements Public disclosure requirements require internationally active banks to publish LR accounting to a common set of templates Summary comparison table provides comparison banks total accounting assets amounts & LR exposures Common disclosure template provide breakdown of main LR regulatory elements Reconciliation requirement details sources of material differences between banks total balance sheet assets in Financial Statements & on-balance sheet exposures in common disclosure template Other disclosures frequency of disclosure, location of disclosures, archives of disclosures

30 Disclosure Requirements Summary comparison table provides comparison banks total accounting assets amounts & LR exposures

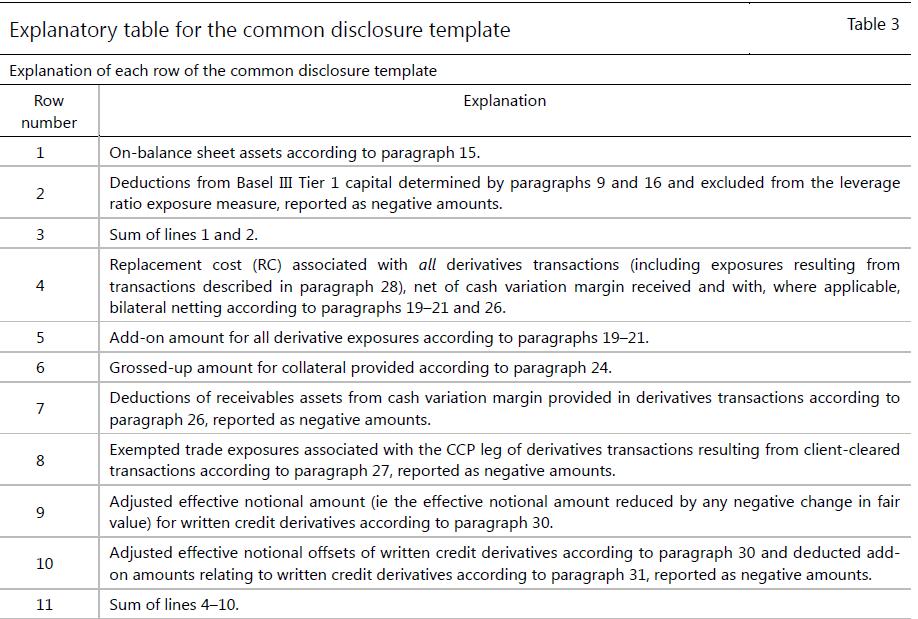

31 Disclosure Requirements Common disclosure template provide breakdown of main LR regulatory elements

32 Disclosure Requirements Common disclosure template provide breakdown of main LR regulatory elements

33 Disclosure Requirements

34 Disclosure Requirements example JPM JP Morgan Chase & Co

35 Disclosure Requirements example JPM

36 How does LR interplay with CR, LCR & NSFR Capital Ratio Risk-based, increases in RWA require in Regulatory Capital Risk models used to calculate RWA can either incorrectly model the risk or misstate completely e.g. CDO Risk based Capital Ratio = Regulatory Capital Risk Weighted Assets LCR Liquidity coverage ratio minimum liquidity inventory level Requires banks to pass 30-day liquidity stress test to support expected liability run-offs over a 30 day period i.e. banks have to have sufficient cash or govt securities to survive stress conditions for 30 days LCR = High Quality Liquid Assets (HQLA) Net cash outflows (30 days) 100%

37 How does LR interplay with CR, LCR & NSFR NSFR Net stable funding ratio 1 year time horizon Assesses tenors of assets (loans etc) to liabilities (funding) Extends the maturity of the funding mix for banks Punitive to banks that are overly reliant to wholesale funding Concept of borrow short, lend long is restricted further NSFR = Available Stable Funding Required Stable Funding 100%

38 How does LR interplay with CR, LCR & NSFR Ultimately the regulators seek to prevent the chaos of GFC occurring in future via the banks Key aspects to the GFC were excessive leverage insufficient stable funding poor quality assets as collateral, poor assets in general insufficient capital reliance on short term funding Weaknesses in risk models and a result RWA, understated risk for numerous products (CDO, RBMS,CMBS, Leveraged Loans) e.g. CDO for risk purposes considered virtually riskless minimal RWA Poor underwriting standards e.g. NINJA loans, loan types with teasers, non-recourse loans CR - risk-based capital constraint risk-based leverage capital constraint weakness potentially with models, gaming the system etc LR - leverage constraint, used as a backstop to the capital constraint non-risk based simple ratio Avoids model risk and measurement error with CR

39 How does LR interplay with CR, LCR & NSFR LCR - minimum funding balance over stressed 30-day horizon NSFR mandates banks to have longer dated funding, relative to assets tenors Risk-weighted, lower quality assets discounted in formula Either > levels HQLA or extend tenors of funding The ratios work together to prevent excessive leverage in the banking sector outright leverage constraints International banks (DB, Deutsche, Citi bank etc) CR - key leverage constraint local and less sophisticated banks LR key leverage constraint on activity Liquidity constraints are LCR and NSFR working such that bank leverage levels are actively underpinned by solid liquidity (ability to fund assets) and quality assets/collateral. i.e. the ability support excessive is now curtailed significantly Lehman Bros scenario, LR and CR would have prevented them from having 40 times leverage Either CR or LR would have been exceeded requiring more regulatory capital, or a sell down in assets NSFR would have prevented the use of primarily ABCP to fund their growth (30 days of less maturity) LCR would have required switch to better quality assets and longer term funding (bond issuance)

40 Conclusion LR is a non risk-based measure designed to curtail excessive leverage Not as simple as it is implied devil is in the small print No model risk but exposure calculation is required for various product types there is model risk Has achieved objective of reducing leverage in banking system Also resulted in the withdrawal of players from business lines Clearing, Prime Services, bond market making etc Those that remain, margins eroded and costs increased Creation of bigger too big to fail institutions - US top 10 banks clear over 80% swaps - CCP s now systematically important (and consolidating) concentration of cleared derivatives in less hands This has let to less liquidity, more volatility, reduced ability to execute some trades. In a crises situation this will be exacerbated Initial versions extremely draconian toned down considerably, still improvements to be made Creates confusion where previously these was none clearing derivatives, collateral Makes trading more complicated in some cases Future focus of Basel on FRTB

41 Q&A Questions

Basel Committee on Banking Supervision

Basel Committee on Banking Supervision Basel III leverage ratio framework and disclosure requirements January 2014 This publication is available on the BIS website (www.bis.org). Bank for International

Basel Committee on Banking Supervision Basel III leverage ratio framework and disclosure requirements January 2014 This publication is available on the BIS website (www.bis.org). Bank for International

MODULE 11. Guidance to completing the Leverage Ratio module of BSL/2

MODULE 11 Guidance to completing the Leverage Ratio module of BSL/2 Glossary The following abbreviations are used within the document: CCF CCP CM MNA OBS PFE QCCP RC SFT Credit Conversion Factors Central

MODULE 11 Guidance to completing the Leverage Ratio module of BSL/2 Glossary The following abbreviations are used within the document: CCF CCP CM MNA OBS PFE QCCP RC SFT Credit Conversion Factors Central

RBI/ /396 DBR.No.BP.BC.58/ / January 8, 2015

RBI/2014-15/396 DBR.No.BP.BC.58/21.06.201/2014-15 January 8, 2015 The Chairman and Managing Director/ Chief Executive Officer All Scheduled Commercial Banks (Excluding Regional Rural Banks and Local Area

RBI/2014-15/396 DBR.No.BP.BC.58/21.06.201/2014-15 January 8, 2015 The Chairman and Managing Director/ Chief Executive Officer All Scheduled Commercial Banks (Excluding Regional Rural Banks and Local Area

Revised Basel III Leverage Ratio Visual Memorandum

Revised Basel III Leverage Ratio Visual Memorandum January 21, 2014 2014 Davis Polk & Wardwell LLP 450 Lexington Avenue New York, NY 10017 Davis Polk & Wardwell LLP Notice: This publication, which we believe

Revised Basel III Leverage Ratio Visual Memorandum January 21, 2014 2014 Davis Polk & Wardwell LLP 450 Lexington Avenue New York, NY 10017 Davis Polk & Wardwell LLP Notice: This publication, which we believe

Leverage Ratio Rules and Guidelines

BASEL III FRAMEWORK Leverage Ratio Rules and Guidelines Month YYYY CAYMAN ISLANDS MONETARY AUTHORITY Table of Contents 1. INTRODUCTION... 3 2. SCOPE OF APPLICATION... 3 3. DEFINITION AND MINIMUM REQUIREMENT...

BASEL III FRAMEWORK Leverage Ratio Rules and Guidelines Month YYYY CAYMAN ISLANDS MONETARY AUTHORITY Table of Contents 1. INTRODUCTION... 3 2. SCOPE OF APPLICATION... 3 3. DEFINITION AND MINIMUM REQUIREMENT...

Basel Committee on Banking Supervision

Basel Committee on Banking Supervision Implementation of Basel standards A report to G20 Leaders on implementation of the Basel III regulatory reforms August 2016 This publication is available on the BIS

Basel Committee on Banking Supervision Implementation of Basel standards A report to G20 Leaders on implementation of the Basel III regulatory reforms August 2016 This publication is available on the BIS

Leverage Ratio Rules and Guidelines

BASEL III FRAMEWORK Leverage Ratio Rules and Guidelines 1 December 2019 CAYMAN ISLANDS MONETARY AUTHORITY Table of Contents 1. INTRODUCTION... 4 2. SCOPE OF APPLICATION... 4 3. DEFINITION AND MINIMUM REQUIREMENT...

BASEL III FRAMEWORK Leverage Ratio Rules and Guidelines 1 December 2019 CAYMAN ISLANDS MONETARY AUTHORITY Table of Contents 1. INTRODUCTION... 4 2. SCOPE OF APPLICATION... 4 3. DEFINITION AND MINIMUM REQUIREMENT...

Basel III Pillar 3 Quantitative Disclosures

Basel III Pillar 3 Quantitative Disclosures 30 June 2018 Bank Albilad Basel III Pillar 3 Disclosures June 2018 Page 1 of 15 Basel III Pillar 3 Quantitative Disclosures Tables and templates Template ref.#

Basel III Pillar 3 Quantitative Disclosures 30 June 2018 Bank Albilad Basel III Pillar 3 Disclosures June 2018 Page 1 of 15 Basel III Pillar 3 Quantitative Disclosures Tables and templates Template ref.#

This article is on Capital Adequacy Ratio and Basel Accord. It contains concepts like -

This article is on Capital Adequacy Ratio and Basel Accord It contains concepts like - Capital Adequacy Capital Adequacy Ratio (CAR) Benefits of CAR Basel Accord Origin Basel Accords I, II, III Expected

This article is on Capital Adequacy Ratio and Basel Accord It contains concepts like - Capital Adequacy Capital Adequacy Ratio (CAR) Benefits of CAR Basel Accord Origin Basel Accords I, II, III Expected

Basel Committee on Banking Supervision. Fourteenth progress report on adoption of the Basel regulatory framework

Basel Committee on Banking Supervision Fourteenth progress report on adoption of the Basel regulatory framework April 2018 This publication is available on the BIS website (www.bis.org). Bank for International

Basel Committee on Banking Supervision Fourteenth progress report on adoption of the Basel regulatory framework April 2018 This publication is available on the BIS website (www.bis.org). Bank for International

BASEL III Basel Committee on Banking Supervision (BCBS)

") BASEL III 1.0. Basel Committee on Banking Supervision (BCBS) Following the failure of German Herstatt Bank in the early 1970 s, the Basel Committee on Banking Supervision (BCBS) was created as a Committee

BASEL III 1.0. Basel Committee on Banking Supervision (BCBS) Following the failure of German Herstatt Bank in the early 1970 s, the Basel Committee on Banking Supervision (BCBS) was created as a Committee

Basel Committee on Banking Supervision

Basel Committee on Banking Supervision Implementation of Basel standards A report to G20 Leaders on implementation of the Basel III regulatory reforms November 2018 This publication is available on the

Basel Committee on Banking Supervision Implementation of Basel standards A report to G20 Leaders on implementation of the Basel III regulatory reforms November 2018 This publication is available on the

Basel Committee on Banking Supervision. Ninth progress report on adoption of the Basel regulatory framework

Basel Committee on Banking Supervision Ninth progress report on adoption of the Basel regulatory framework October 2015 This publication is available on the BIS website (www.bis.org). Bank for International

Basel Committee on Banking Supervision Ninth progress report on adoption of the Basel regulatory framework October 2015 This publication is available on the BIS website (www.bis.org). Bank for International

Samba Financial Group Basel III - Pillar 3 Disclosure Report. June 2018 PUBLIC

Basel III - Pillar 3 Disclosure Report June 2018 Basel III - Pillar 3 Disclosure Report as at June 30, 2018 Page 1 of 19 Table of Contents Capital Structure Page Statement of financial position - Step

Basel III - Pillar 3 Disclosure Report June 2018 Basel III - Pillar 3 Disclosure Report as at June 30, 2018 Page 1 of 19 Table of Contents Capital Structure Page Statement of financial position - Step

Public Disclosure Requirements related to Basel III Leverage Ratio

Guideline Subject: Category: Accounting and Disclosures No: D-12 Date: Revised: September 2014 Effective Date: November 201 / January 2018 1 On January 12, 2014, the Basel Committee on Banking Supervision

Guideline Subject: Category: Accounting and Disclosures No: D-12 Date: Revised: September 2014 Effective Date: November 201 / January 2018 1 On January 12, 2014, the Basel Committee on Banking Supervision

Press release Press enquiries:

Press release Press enquiries: +41 61 280 8188 press@bis.org www.bis.org Ref no: 35/2010 12 September 2010 Group of Governors and Heads of Supervision announces higher global minimum capital standards

Press release Press enquiries: +41 61 280 8188 press@bis.org www.bis.org Ref no: 35/2010 12 September 2010 Group of Governors and Heads of Supervision announces higher global minimum capital standards

The Bank of East Asia, Limited 東亞銀行有限公司. Banking Disclosure Statement

Banking Disclosure Statement For the period ended 30 September 2018 Table of contents Introduction... 1 Template KM1: Key prudential ratios... 2 Template OV1: Overview of RWA... 3 Template LR2: Leverage

Banking Disclosure Statement For the period ended 30 September 2018 Table of contents Introduction... 1 Template KM1: Key prudential ratios... 2 Template OV1: Overview of RWA... 3 Template LR2: Leverage

Regulatory Disclosures 30 September 2018

Regulatory Disclosures 30 September CONTENTS PAGE 1. Basis of reporting 1 2. Key prudential ratios and overview of RWA 2 KM1: Key prudential ratios 2 OV1: Overview of RWA 3 3. Leverage ratio 4 LR2: Leverage

Regulatory Disclosures 30 September CONTENTS PAGE 1. Basis of reporting 1 2. Key prudential ratios and overview of RWA 2 KM1: Key prudential ratios 2 OV1: Overview of RWA 3 3. Leverage ratio 4 LR2: Leverage

Deutsche Bank AG Johannesburg Pillar 3 disclosure

Deutsche Bank AG Johannesburg For the half year ended 30 Deutsche Bank Risk & Capital Management Deutsche Bank Contents Page Overview 1 Financial performance 2 Financial position 3 Capital structure 4

Deutsche Bank AG Johannesburg For the half year ended 30 Deutsche Bank Risk & Capital Management Deutsche Bank Contents Page Overview 1 Financial performance 2 Financial position 3 Capital structure 4

Blackline: Basel Committee s Basel III Leverage Ratio Framework and Disclosure Requirements. January 2014 Final Version vs. June 2013 Proposed Version

Blackline: Basel Committee s Basel III Leverage Ratio Framework and Disclosure Requirements January 2014 Final Version vs. June 2013 Proposed Version Introduction 1. An underlying featurecause of the global

Blackline: Basel Committee s Basel III Leverage Ratio Framework and Disclosure Requirements January 2014 Final Version vs. June 2013 Proposed Version Introduction 1. An underlying featurecause of the global

Samba Financial Group Basel III - Pillar 3 Disclosure Report. September 2018 PUBLIC

Basel III - Pillar 3 Disclosure Report September 2018 Basel III - Pillar 3 Disclosure Report as at September 30, 2018 Page 1 of 6 Table of Contents Liquidity Page LIQ1 - Liquidity coverage ratio ( LCR

Basel III - Pillar 3 Disclosure Report September 2018 Basel III - Pillar 3 Disclosure Report as at September 30, 2018 Page 1 of 6 Table of Contents Liquidity Page LIQ1 - Liquidity coverage ratio ( LCR

Pillar 3 and regulatory disclosures Credit Suisse Group AG 2Q17

Pillar 3 and regulatory disclosures Credit Suisse Group AG 2Q17 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse, the Group, we, us and our mean Credit Suisse

Pillar 3 and regulatory disclosures Credit Suisse Group AG 2Q17 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse, the Group, we, us and our mean Credit Suisse

African Bank Holdings Limited and African Bank Limited

African Bank Holdings Limited and African Bank Limited Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 CONTENTS 1. Executive summary... 3 2. Basis of compilation... 7 3. Supplementary

African Bank Holdings Limited and African Bank Limited Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 CONTENTS 1. Executive summary... 3 2. Basis of compilation... 7 3. Supplementary

2016 Seminar for Senior Bank Supervisors from Emerging Economies. Implementation of Basel III Liquidity Requirements in Emerging Markets

2016 Seminar for Senior Bank Supervisors from Emerging Economies Implementation of Basel III Liquidity Requirements in Emerging Markets Christopher Wilson Monetary and Capital Markets Department International

2016 Seminar for Senior Bank Supervisors from Emerging Economies Implementation of Basel III Liquidity Requirements in Emerging Markets Christopher Wilson Monetary and Capital Markets Department International

African Bank Holdings Limited and African Bank Limited

African Bank Holdings Limited and African Bank Limited Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 CONTENTS 1. Executive summary... 3 2. Basis of compilation... 5 3. Supplementary

African Bank Holdings Limited and African Bank Limited Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 CONTENTS 1. Executive summary... 3 2. Basis of compilation... 5 3. Supplementary

Basel III Pillar 3 Disclosures. 30 June 2018

Basel III Pillar 3 Disclosures 30 June 2018 Table of Contents PART 2 OVERVIEW OF RISK MANAGEMENT AND RWA... 3 KM1 Key metrics (at consolidated group level)... 3 OV1 Overview of RWA... 4 PART 5 MICROPRUDENTIAL

Basel III Pillar 3 Disclosures 30 June 2018 Table of Contents PART 2 OVERVIEW OF RISK MANAGEMENT AND RWA... 3 KM1 Key metrics (at consolidated group level)... 3 OV1 Overview of RWA... 4 PART 5 MICROPRUDENTIAL

Samba Financial Group Basel III - Pillar 3 Disclosure Report. September 2017 PUBLIC

Basel III - Pillar 3 Disclosure Report September 2017 Basel III - Pillar 3 Disclosure Report as at September 30, 2017 Page 1 of 12 Table of contents Capital Structure Page Statement of financial position

Basel III - Pillar 3 Disclosure Report September 2017 Basel III - Pillar 3 Disclosure Report as at September 30, 2017 Page 1 of 12 Table of contents Capital Structure Page Statement of financial position

African Bank Holdings Limited and African Bank Limited. Annual Public Pillar III Disclosures

African Bank Holdings Limited and African Bank Limited Annual Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 as at 30 September 2016 1 African Bank Holdings Limited and African

African Bank Holdings Limited and African Bank Limited Annual Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 as at 30 September 2016 1 African Bank Holdings Limited and African

SUPPLEMENTARY REGULATORY CAPITAL AND PILLAR 3 DISCLOSURE

SUPPLEMENTARY REGULATORY CAPITAL AND PILLAR 3 DISCLOSURE FIRST QUARTER 209 (unaudited) For more information: Ghislain Parent, Chief Financial Officer and Executive Vice-President Finance, Tel: 54 394-6807

SUPPLEMENTARY REGULATORY CAPITAL AND PILLAR 3 DISCLOSURE FIRST QUARTER 209 (unaudited) For more information: Ghislain Parent, Chief Financial Officer and Executive Vice-President Finance, Tel: 54 394-6807

FORM SR-2A (extract): CAPITAL DEFINITION (CET1, ADDITIONAL TIER 1, TIER 2, TOTAL CAPITAL, MEMORANDUM ITEMS) COMPLETION GUIDANCE

: CAPITAL DEFINITION (CET1, ADDITIONAL TIER 1, TIER 2, TOTAL CAPITAL, MEMORANDUM ITEMS) COMPLETION GUIDANCE") FORM SR-2A (extract): CAPITAL DEFINITION (CET1, ADDITIONAL TIER 1, TIER 2, TOTAL CAPITAL, MEMORANDUM ITEMS) COMPLETION GUIDANCE Item Description Guidance A Common Equity Tier 1 Capital: instruments and

FORM SR-2A (extract): CAPITAL DEFINITION (CET1, ADDITIONAL TIER 1, TIER 2, TOTAL CAPITAL, MEMORANDUM ITEMS) COMPLETION GUIDANCE Item Description Guidance A Common Equity Tier 1 Capital: instruments and

African Bank Holdings Limited and African Bank Limited

African Bank Holdings Limited and African Bank Limited Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 CONTENTS 1. Executive summary... 3 2. Basis of compilation... 7 3. Supplementary

African Bank Holdings Limited and African Bank Limited Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 CONTENTS 1. Executive summary... 3 2. Basis of compilation... 7 3. Supplementary

African Bank Holdings Limited and African Bank Limited

African Bank Holdings Limited and African Bank Limited Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 CONTENTS 1. Executive summary... 3 2. Basis of compilation... 9 3. Supplementary

African Bank Holdings Limited and African Bank Limited Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 CONTENTS 1. Executive summary... 3 2. Basis of compilation... 9 3. Supplementary

The Leverage Ratio. The Author. Background. Abstract. Basel III Framework. December Scott Warner

The Author Background Abstract Scott Warner Leverage means the relative size of an institution's assets, offbalance sheet obligations and contingent obligations to pay or to deliver or to provide collateral,

The Author Background Abstract Scott Warner Leverage means the relative size of an institution's assets, offbalance sheet obligations and contingent obligations to pay or to deliver or to provide collateral,

Prudential supervisors and external auditors. Marc Pickeur, CBFA Brussels, 27 October

Prudential supervisors and external auditors Marc Pickeur, CBFA Brussels, 27 October 2010 1 Disclaimer The views expressed by the speaker are entirely his own, and are not to be taken to represent those

Prudential supervisors and external auditors Marc Pickeur, CBFA Brussels, 27 October 2010 1 Disclaimer The views expressed by the speaker are entirely his own, and are not to be taken to represent those

Basel Committee on Banking Supervision. Twelfth progress report on adoption of the Basel regulatory framework

Basel Committee on Banking Supervision Twelfth progress report on adoption of the Basel regulatory framework April 2017 This publication is available on the BIS website (www.bis.org). Bank for International

Basel Committee on Banking Supervision Twelfth progress report on adoption of the Basel regulatory framework April 2017 This publication is available on the BIS website (www.bis.org). Bank for International

BANK OF SHANGHAI (HONG KONG) LIMITED

LIMITED") For the First six months ended 3 June 217 CONTENTS Pages Introduction 1 Capital Adequacy 1 Composition of Capital 3 Leverage Ratio 13 Overview of Risk-weighted Amount 16 Credit Risk 17 Counterparty Credit

For the First six months ended 3 June 217 CONTENTS Pages Introduction 1 Capital Adequacy 1 Composition of Capital 3 Leverage Ratio 13 Overview of Risk-weighted Amount 16 Credit Risk 17 Counterparty Credit

China Construction Bank Corporation, Johannesburg Branch

China Construction Bank Corporation, Johannesburg Branch Pillar 3 Disclosure (Half Year ended 30 June 2018) Builds a better future CONTENTS 1. OVERVIEW... 3 2. COMPOSITION OF CAPITAL... 4 3. LIQUIDITY...12

China Construction Bank Corporation, Johannesburg Branch Pillar 3 Disclosure (Half Year ended 30 June 2018) Builds a better future CONTENTS 1. OVERVIEW... 3 2. COMPOSITION OF CAPITAL... 4 3. LIQUIDITY...12

ALLIED BANKING CORPORATION (HONG KONG) LIMITED

LIMITED") ALLIED BANKING CORPORATION (HONG KONG) LIMITED Pillar 3 Regulatory Disclosures For the year ended 3 June 218 (Unaudited) Table of contents Template KM1: Key prudential ratios 1 Template OV1: Overview of

ALLIED BANKING CORPORATION (HONG KONG) LIMITED Pillar 3 Regulatory Disclosures For the year ended 3 June 218 (Unaudited) Table of contents Template KM1: Key prudential ratios 1 Template OV1: Overview of

Regulatory Disclosures 30 September 2018

Regulatory Disclosures 30 September CONTENTS PAGE 1. Key prudential ratios and overview of RWA KM1: Key prudential ratios 1 OV1: Overview of RWA 2 2. Leverage ratio LR2: Leverage ratio 3 3. Liquidity LIQ1:

Regulatory Disclosures 30 September CONTENTS PAGE 1. Key prudential ratios and overview of RWA KM1: Key prudential ratios 1 OV1: Overview of RWA 2 2. Leverage ratio LR2: Leverage ratio 3 3. Liquidity LIQ1:

Disclosure Report. Investec Limited Basel Pillar III semi-annual disclosure report

Disclosure Report 2017 Investec Basel Pillar III semi-annual disclosure report Cross reference tools 1 2 Page references Refers readers to information elsewhere in this report Website Indicates that additional

Disclosure Report 2017 Investec Basel Pillar III semi-annual disclosure report Cross reference tools 1 2 Page references Refers readers to information elsewhere in this report Website Indicates that additional

COPYRIGHTED MATERIAL. Bank executives are in a difficult position. On the one hand their shareholders require an attractive

chapter 1 Bank executives are in a difficult position. On the one hand their shareholders require an attractive return on their investment. On the other hand, banking supervisors require these entities

chapter 1 Bank executives are in a difficult position. On the one hand their shareholders require an attractive return on their investment. On the other hand, banking supervisors require these entities

Samba Financial Group Basel III - Pillar 3 Disclosure Report. March 2018 PUBLIC

Basel III - Pillar 3 Disclosure Report March 2018 Basel III - Pillar 3 Disclosure Report as at March 31, 2018 Page 1 of 11 Table of contents Capital structure Statement of financial position - Step 1 (

Basel III - Pillar 3 Disclosure Report March 2018 Basel III - Pillar 3 Disclosure Report as at March 31, 2018 Page 1 of 11 Table of contents Capital structure Statement of financial position - Step 1 (

Basel Committee on Banking Supervision

Basel Committee on Banking Supervision Seventh progress report on adoption of the Basel regulatory framework October 2014 This publication is available on the BIS website (www.bis.org). Bank for International

Basel Committee on Banking Supervision Seventh progress report on adoption of the Basel regulatory framework October 2014 This publication is available on the BIS website (www.bis.org). Bank for International

Supplementary Leverage Ratio (SLR) Visual Memorandum

Visual Memorandum") Supplementary Leverage Ratio (SLR) Visual Memorandum September 12, 2014 2014 Davis Polk & Wardwell LLP 450 Lexington Avenue New York, NY 10017 Davis Polk & Wardwell LLP Notice: This publication, which

Supplementary Leverage Ratio (SLR) Visual Memorandum September 12, 2014 2014 Davis Polk & Wardwell LLP 450 Lexington Avenue New York, NY 10017 Davis Polk & Wardwell LLP Notice: This publication, which

TABLE 2: CAPITAL STRUCTURE - September 30, 2018

TABLE 2: CAPITAL STRUCTURE - September 30, 2018 Balance sheet - Step 1 (Table 2(b)) All figures are in SAR '000 Assets Balance sheet in Published financial statements Adjustment of banking associates /

TABLE 2: CAPITAL STRUCTURE - September 30, 2018 Balance sheet - Step 1 (Table 2(b)) All figures are in SAR '000 Assets Balance sheet in Published financial statements Adjustment of banking associates /

Intraday Liquidity Monitoring Solution

Treasury and Trade Solutions Global Clearing & FI Payments Citi Academy for Financial Institutions July 2015 Intraday Liquidity Monitoring Solution Carolina Caballero Intraday Liquidity Product Manager

Treasury and Trade Solutions Global Clearing & FI Payments Citi Academy for Financial Institutions July 2015 Intraday Liquidity Monitoring Solution Carolina Caballero Intraday Liquidity Product Manager

Fubon Bank (Hong Kong) Limited. Quarterly financial disclosures As at 30 September 2018

Limited. Quarterly financial disclosures As at 30 September 2018") Fubon Bank (Hong Kong) Limited Quarterly financial disclosures As at 30 September 2018 Table of Contents Template KM1: Key prudential ratios Page 2 Template OV1: Overview of RWA.. Page 3 Template LR2:

Fubon Bank (Hong Kong) Limited Quarterly financial disclosures As at 30 September 2018 Table of Contents Template KM1: Key prudential ratios Page 2 Template OV1: Overview of RWA.. Page 3 Template LR2:

Valiant Holding AG. 3 General part / Reconciliation of accounting values to regulatory values. 9 Information on credit risk

disclosures of capital adequacy and liquidity valiant holding ag 31 / 12 / 2017 Valiant Holding AG Disclosures of capital adequacy and liquidity 3 General part / Reconciliation of accounting values to

disclosures of capital adequacy and liquidity valiant holding ag 31 / 12 / 2017 Valiant Holding AG Disclosures of capital adequacy and liquidity 3 General part / Reconciliation of accounting values to

African Bank Holdings Limited and African Bank Limited. Quarterly Public Pillar III Disclosures

African Bank Holdings Limited and African Bank Limited Quarterly Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 as at 31 December 2016 1 African Bank Holdings Limited and African

African Bank Holdings Limited and African Bank Limited Quarterly Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 as at 31 December 2016 1 African Bank Holdings Limited and African

Public Finance Limited

Semi-annual Disclosures For the period ended 30 June 2018 (Solo Basis and Unaudited) Table of contents Template KM1: Key prudential ratios.... 1 Template OV1: Overview of RWA... 3 Template CC1: Composition

Semi-annual Disclosures For the period ended 30 June 2018 (Solo Basis and Unaudited) Table of contents Template KM1: Key prudential ratios.... 1 Template OV1: Overview of RWA... 3 Template CC1: Composition

Leverage Ratio Disclosure Template A. Summary Comparison (Table 1)

") A. Summary Comparison (Table 1) Summary comparison of accounting assets versus leverage ratio exposure measure Row Item In SR 000 s # 1 Total consolidated assets as per published financial statements 115,005,067

A. Summary Comparison (Table 1) Summary comparison of accounting assets versus leverage ratio exposure measure Row Item In SR 000 s # 1 Total consolidated assets as per published financial statements 115,005,067

Nippon Wealth Limited

Nippon Wealth Limited (the Company ) is a restricted license bank incorporated in Hong Kong, its principal activities are the provision of wealth management services, insurance agency, securities dealing

Nippon Wealth Limited (the Company ) is a restricted license bank incorporated in Hong Kong, its principal activities are the provision of wealth management services, insurance agency, securities dealing

Basel Committee on Banking Supervision. Progress report on Basel III implementation

Basel Committee on Banking Supervision Progress report on Basel III implementation April 2012 Copies of publications are available from: Bank for International Settlements Communications CH-4002 Basel,

Basel Committee on Banking Supervision Progress report on Basel III implementation April 2012 Copies of publications are available from: Bank for International Settlements Communications CH-4002 Basel,

Public Finance Limited

Quarterly Disclosures For the period ended 30 September (Solo Basis and Unaudited) Table of contents Template KM1: Key prudential ratios.... 1 Template OV1: Overview of RWA... 3 Template LR2: Leverage

Quarterly Disclosures For the period ended 30 September (Solo Basis and Unaudited) Table of contents Template KM1: Key prudential ratios.... 1 Template OV1: Overview of RWA... 3 Template LR2: Leverage

Lombard Odier Group Pillar 3 Disclosures at 30 June 2018

Lombard Odier Group Pillar 3 Disclosures at 30 June 2018 Contents Introduction 5 Consolidation scope 5 Composition of capital 7 Risk-weighted assets and minimum capital requirements 9 Market Risks 10

Lombard Odier Group Pillar 3 Disclosures at 30 June 2018 Contents Introduction 5 Consolidation scope 5 Composition of capital 7 Risk-weighted assets and minimum capital requirements 9 Market Risks 10

Valiant Holding AG. 3 General part/reconciliation of accounting values to regulatory values. 6 Information on credit risk

disclosures of capital adequacy and liquidity valiant holding ag 30/06/2018 Valiant Holding AG Capital adequacy and liquidity disclosures 3 General part/reconciliation of accounting values to regulatory

disclosures of capital adequacy and liquidity valiant holding ag 30/06/2018 Valiant Holding AG Capital adequacy and liquidity disclosures 3 General part/reconciliation of accounting values to regulatory

Public Bank (Hong Kong) Limited

Limited") Quarterly Disclosures For the period ended (Consolidated and Unaudited) Table of contents Template KM1: Key prudential ratios...1 Template OV1: Overview of RWA...3 Template LR2: Leverage ratio.....5 Glossary....7

Quarterly Disclosures For the period ended (Consolidated and Unaudited) Table of contents Template KM1: Key prudential ratios...1 Template OV1: Overview of RWA...3 Template LR2: Leverage ratio.....5 Glossary....7

CHINA CONSTRUCTION BANK (ASIA) CORPORATION LIMITED. Regulatory Disclosures For the six months ended 30 June 2017 (Unaudited)

CORPORATION LIMITED. Regulatory Disclosures For the six months ended 30 June 2017 (Unaudited)") CHINA CONSTRUCTION BANK (ASIA) CORPORATION LIMITED For the six months ended 30 June 2017 (Unaudited) Table of contents Page Key capital ratios 1 Template OV1: Overview of 2 Template CR1: Credit quality

CHINA CONSTRUCTION BANK (ASIA) CORPORATION LIMITED For the six months ended 30 June 2017 (Unaudited) Table of contents Page Key capital ratios 1 Template OV1: Overview of 2 Template CR1: Credit quality

Official Journal of the European Union

17.1.2015 L 11/37 COMMISSION DELEGATED REGULATION (EU) 2015/62 of 10 October 2014 amending Regulation (EU) No 575/2013 of the European Parliament and of the Council with regard to the leverage ratio (Text

17.1.2015 L 11/37 COMMISSION DELEGATED REGULATION (EU) 2015/62 of 10 October 2014 amending Regulation (EU) No 575/2013 of the European Parliament and of the Council with regard to the leverage ratio (Text

TABLE 2: CAPITAL STRUCTURE - December 31, 2015

Frequency : Quarterly Location : Quarterly Financial Statement TABLE 2: CAPITAL STRUCTURE - December 31, 2015 Balance sheet - Step 1 (Table 2(b)) All figures are in SAR '000 Assets Balance sheet in Published

Frequency : Quarterly Location : Quarterly Financial Statement TABLE 2: CAPITAL STRUCTURE - December 31, 2015 Balance sheet - Step 1 (Table 2(b)) All figures are in SAR '000 Assets Balance sheet in Published

Information on Capital Structure, Liquidity Coverage and Leverage Ratios as per Basel-III Framework as at June 30, 2016

Information on Capital Structure, Liquidity Coverage and Leverage Ratios as per Basel-III Framework as at June 30, 2016 Table of Contents Capital Structure Statement of Financial Position - Step 1 ( Table

Information on Capital Structure, Liquidity Coverage and Leverage Ratios as per Basel-III Framework as at June 30, 2016 Table of Contents Capital Structure Statement of Financial Position - Step 1 ( Table

Basel III Pillar 3 Disclosures 30 June 2018 J. Safra Sarasin Holding Ltd.

Basel III Pillar 3 Disclosures 30 June 2018 J. Safra Sarasin Holding Ltd. Table of contents Basel III Pillar 3 Disclosures (FINMA circ. 2016/1) Table 39 (MR1): Market risk: Capital requirements under the

Basel III Pillar 3 Disclosures 30 June 2018 J. Safra Sarasin Holding Ltd. Table of contents Basel III Pillar 3 Disclosures (FINMA circ. 2016/1) Table 39 (MR1): Market risk: Capital requirements under the

Progress of Financial Regulatory Reforms

THE CHAIRMAN 12 February 2013 To G20 Ministers and Central Bank Governors Progress of Financial Regulatory Reforms Financial market conditions have improved over recent months. Nonetheless, medium-term

THE CHAIRMAN 12 February 2013 To G20 Ministers and Central Bank Governors Progress of Financial Regulatory Reforms Financial market conditions have improved over recent months. Nonetheless, medium-term

EBF response to the BCBS consultation on the revision to the Basel III leverage ratio framework. 1- General comments. Ref: EBF_ OT

Ref: EBF_021367 - OT 06.07.16 EBF response to the BCBS consultation on the revision to the Basel III leverage ratio framework 1- General comments The European Banking Federation welcomes the opportunity

Ref: EBF_021367 - OT 06.07.16 EBF response to the BCBS consultation on the revision to the Basel III leverage ratio framework 1- General comments The European Banking Federation welcomes the opportunity

BASEL III - Leverage Ratio 31 December 2017

BASEL III - Leverage Ratio 31 December 2017 Table 1 A. Summary comparison of accounting assets vs leverage ratio exposure measure Summary comparison of accounting assets versus leverage ratio exposure

BASEL III - Leverage Ratio 31 December 2017 Table 1 A. Summary comparison of accounting assets vs leverage ratio exposure measure Summary comparison of accounting assets versus leverage ratio exposure

Basel III Pillar 3 Disclosures 31 December 2017 J. Safra Sarasin Holding Ltd.

Basel III Pillar 3 Disclosures 31 December 2017 J. Safra Sarasin Holding Ltd. Table of contents Basel III Pillar 3 Disclosures (FINMA circ. 2016/1) Introduction 3 Consolidation perimeter 3 Table 1: Composition

Basel III Pillar 3 Disclosures 31 December 2017 J. Safra Sarasin Holding Ltd. Table of contents Basel III Pillar 3 Disclosures (FINMA circ. 2016/1) Introduction 3 Consolidation perimeter 3 Table 1: Composition

Bridgewater Bank Regulatory Disclosures December 31, 2017

Bridgewater Bank Regulatory Disclosures December 31, 2017 This document was prepared to fulfill regulatory requirements of the Office of the Superintendent of Financial Institutions Canada. Public disclosure

Bridgewater Bank Regulatory Disclosures December 31, 2017 This document was prepared to fulfill regulatory requirements of the Office of the Superintendent of Financial Institutions Canada. Public disclosure

SAUDI BRITISH BANK BASEL III - LEVERAGE RATIO DISCLOSURE AS AT

SAUDI BRITISH BANK BASEL III LEVERAGE RATIO DISCLOSURE AS AT 31st March 2015 PUBLIC Page 1 of 7 Table of Contents Page Leverage Ratio Exposures (Table 1)...... 3 Leverage Ratio Regulatory Elements (Table

SAUDI BRITISH BANK BASEL III LEVERAGE RATIO DISCLOSURE AS AT 31st March 2015 PUBLIC Page 1 of 7 Table of Contents Page Leverage Ratio Exposures (Table 1)...... 3 Leverage Ratio Regulatory Elements (Table

Bridgewater Bank Regulatory Disclosures March 31, 2017

Bridgewater Bank Regulatory Disclosures March 31, 2017 This document was prepared to fulfill regulatory requirements of the Office of the Superintendent of Financial Institutions Canada. Public disclosure

Bridgewater Bank Regulatory Disclosures March 31, 2017 This document was prepared to fulfill regulatory requirements of the Office of the Superintendent of Financial Institutions Canada. Public disclosure

DBS BANK (HONG KONG) LIMITED

LIMITED") 星展銀行 ( 香港 ) 有限公司 DBS BANK (HONG KONG) LIMITED (Incorporated in Hong Kong with limited liability) REGULATORY DISCLOSURE STATEMENTS For the quarter ended CONTENTS Pages 1 INTRODUCTION... 1 2 KEY PRUDENTIAL

星展銀行 ( 香港 ) 有限公司 DBS BANK (HONG KONG) LIMITED (Incorporated in Hong Kong with limited liability) REGULATORY DISCLOSURE STATEMENTS For the quarter ended CONTENTS Pages 1 INTRODUCTION... 1 2 KEY PRUDENTIAL

Basel III Pillar 3 Disclosures Report. For the Quarterly Period Ended June 30, 2016

BASEL III PILLAR 3 DISCLOSURES REPORT For the quarterly period ended June 30, 2016 Table of Contents Page 1 Morgan Stanley... 1 2 Capital Framework... 1 3 Capital Structure... 2 4 Capital Adequacy... 2

BASEL III PILLAR 3 DISCLOSURES REPORT For the quarterly period ended June 30, 2016 Table of Contents Page 1 Morgan Stanley... 1 2 Capital Framework... 1 3 Capital Structure... 2 4 Capital Adequacy... 2

RISK REPORT PILLAR

A French corporation with share capital of EUR 1,009,897,137.75 Registered office: 29 boulevard Haussmann - 75009 PARIS 552 120 222 R.C.S. PARIS RISK REPORT PILLAR 3 30.09.2018 CONTENTS 1 CAPITAL MANAGEMENT

A French corporation with share capital of EUR 1,009,897,137.75 Registered office: 29 boulevard Haussmann - 75009 PARIS 552 120 222 R.C.S. PARIS RISK REPORT PILLAR 3 30.09.2018 CONTENTS 1 CAPITAL MANAGEMENT

Standard Chartered Bank (Hong Kong) Limited. Supplementary Notes to Condensed Consolidated Interim Financial Statements (unaudited)

Limited. Supplementary Notes to Condensed Consolidated Interim Financial Statements (unaudited)") Standard Chartered Bank (Hong Kong) Limited Supplementary Notes to Condensed Consolidated Interim Financial Statements (unaudited) For period ended 30 June 2017 Standard Chartered Bank (Hong Kong) Limited

Standard Chartered Bank (Hong Kong) Limited Supplementary Notes to Condensed Consolidated Interim Financial Statements (unaudited) For period ended 30 June 2017 Standard Chartered Bank (Hong Kong) Limited

Basel III Capital & Liquidity Rules

Basel III Capital & Liquidity Rules Prepared for Asia Risk Jakarta May 2018 by Mike Duncan mike.duncan@outlook.com www.linkedin.com/in/mike-duncan/ Agenda Overview of Basel III Objectives of the introduction

Basel III Capital & Liquidity Rules Prepared for Asia Risk Jakarta May 2018 by Mike Duncan mike.duncan@outlook.com www.linkedin.com/in/mike-duncan/ Agenda Overview of Basel III Objectives of the introduction

TABLE 2: CAPITAL STRUCTURE - June 30, 2018

TABLE 2: CAPITAL STRUCTURE - June 30, 2018 Balance sheet - Step 1 (Table 2(b)) All figures are in SAR '000 Assets Balance sheet in Published financial statements Adjustment of banking associates / other

TABLE 2: CAPITAL STRUCTURE - June 30, 2018 Balance sheet - Step 1 (Table 2(b)) All figures are in SAR '000 Assets Balance sheet in Published financial statements Adjustment of banking associates / other

Bridgewater Bank Regulatory Disclosures March 31, 2016

Bridgewater Bank Regulatory Disclosures March 31, 2016 This document was prepared to fulfill regulatory requirements of the Office of the Superintendent of Financial Institutions Canada. Public disclosure

Bridgewater Bank Regulatory Disclosures March 31, 2016 This document was prepared to fulfill regulatory requirements of the Office of the Superintendent of Financial Institutions Canada. Public disclosure

Standard Chartered Bank (Singapore) Limited Registration Number: C. Pillar 3 Disclosures as at 31 December 2017

Limited Registration Number: C. Pillar 3 Disclosures as at 31 December 2017") Standard Chartered Bank (Singapore) Limited Registration Number: 201224747C Pillar 3 Disclosures as at 31 December 2017 1 Contents 1. Capital Adequacy and Leverage Ratio... 2 2. Overview of RWA... 3 3.

Standard Chartered Bank (Singapore) Limited Registration Number: 201224747C Pillar 3 Disclosures as at 31 December 2017 1 Contents 1. Capital Adequacy and Leverage Ratio... 2 2. Overview of RWA... 3 3.

TABLE 2: CAPITAL STRUCTURE - March 31, 2016

c Frequency : Quarterly Location : Quarterly Financial Statement Balance sheet - Step 1 (Table 2(b)) All figures are in SAR '000 Assets Balance sheet in Published financial statements Adjustment of banking

c Frequency : Quarterly Location : Quarterly Financial Statement Balance sheet - Step 1 (Table 2(b)) All figures are in SAR '000 Assets Balance sheet in Published financial statements Adjustment of banking

Basel III Pillar 3 Disclosures Report. For the Quarterly Period Ended December 31, 2015

BASEL III PILLAR 3 DISCLOSURES REPORT For the quarterly period ended December 31, 2015 Table of Contents Page 1 Morgan Stanley... 1 2 Capital Framework... 1 3 Capital Structure... 2 4 Capital Adequacy...

BASEL III PILLAR 3 DISCLOSURES REPORT For the quarterly period ended December 31, 2015 Table of Contents Page 1 Morgan Stanley... 1 2 Capital Framework... 1 3 Capital Structure... 2 4 Capital Adequacy...

UBS Group AG and significant regulated subsidiaries and sub-groups

UBS Group AG and significant regulated subsidiaries and sub-groups Third quarter 2017 Pillar 3 report Table of contents UBS Group AG consolidated 2 Section 1 Introduction 3 Section 2 Risk-weighted assets

UBS Group AG and significant regulated subsidiaries and sub-groups Third quarter 2017 Pillar 3 report Table of contents UBS Group AG consolidated 2 Section 1 Introduction 3 Section 2 Risk-weighted assets

2016 RISK AND PILLAR III REPORT SECOND UPDATE AS OF JUNE 30, 2017

2016 RISK AND PILLAR III REPORT SECOND UPDATE AS OF JUNE 30, 2017 NATIXIS - 2016 Risk & Pillar III Report second update as of June 30, 2017 2 TABLE OF CONTENTS Update by chapter of the Risk and Pillar

2016 RISK AND PILLAR III REPORT SECOND UPDATE AS OF JUNE 30, 2017 NATIXIS - 2016 Risk & Pillar III Report second update as of June 30, 2017 2 TABLE OF CONTENTS Update by chapter of the Risk and Pillar

Q4 18. Supplementary Regulatory Capital Information. For the Quarter Ended October 31, For further information, contact:

Supplementary Regulatory Capital Information For the Quarter Ended October 31, 2018 For further information, contact: JILL HOMENUK CHRISTINE VIAU Head, Investor Relations Director, Investor Relations 416.867.4770

Supplementary Regulatory Capital Information For the Quarter Ended October 31, 2018 For further information, contact: JILL HOMENUK CHRISTINE VIAU Head, Investor Relations Director, Investor Relations 416.867.4770

Regulatory Disclosures 30 June 2018

Regulatory Disclosures 30 June 2018 CONTENTS PAGES KM1: Key prudential ratios 1 OV1: Overview of RWA 2 CC1: Composition of regulatory capital 3 CC2: Reconciliation of regulatory capital to balance sheet

Regulatory Disclosures 30 June 2018 CONTENTS PAGES KM1: Key prudential ratios 1 OV1: Overview of RWA 2 CC1: Composition of regulatory capital 3 CC2: Reconciliation of regulatory capital to balance sheet

Regulatory Capital Pillar 3 Disclosures

Regulatory Capital Pillar 3 Disclosures December 31, 2016 Table of Contents Background 1 Overview 1 Corporate Governance 1 Internal Capital Adequacy Assessment Process 2 Capital Demand 3 Capital Supply

Regulatory Capital Pillar 3 Disclosures December 31, 2016 Table of Contents Background 1 Overview 1 Corporate Governance 1 Internal Capital Adequacy Assessment Process 2 Capital Demand 3 Capital Supply

Basel Committee on Banking Supervision. Proportionality in bank regulation and supervision a survey on current practices

Basel Committee on Banking Supervision Proportionality in bank regulation and supervision a survey on current practices March 2019 This publication is available on the BIS website (www.bis.org). Bank for

Basel Committee on Banking Supervision Proportionality in bank regulation and supervision a survey on current practices March 2019 This publication is available on the BIS website (www.bis.org). Bank for

DISCLOSURE OBLIGATIONS REGARDING CAPITAL ADEQUACY AND LIQUIDITY DECEMBER 2016

DISCLOSURE OBLIGATIONS REGARDING CAPITAL ADEQUACY AND LIQUIDITY DECEMBER 2016 JULIUS BAER GROUP LTD. ACCORDING TO FINMA-CIRCULAR 2016/1 DISCLOSURE BANKS CONTENTS DISCLOSURE OBLIGATIONS REGARDING CAPITAL

DISCLOSURE OBLIGATIONS REGARDING CAPITAL ADEQUACY AND LIQUIDITY DECEMBER 2016 JULIUS BAER GROUP LTD. ACCORDING TO FINMA-CIRCULAR 2016/1 DISCLOSURE BANKS CONTENTS DISCLOSURE OBLIGATIONS REGARDING CAPITAL

Basel III - Pillar 3. Semiannual Disclosures

138943.4 Basel III - Pillar 3 Semiannual Disclosures As at 30th June 2017 Table of Contents Item Part 2 Overview of risk management and RWA Tables and templates* Template ref. # Page No. OV1 Overview of

138943.4 Basel III - Pillar 3 Semiannual Disclosures As at 30th June 2017 Table of Contents Item Part 2 Overview of risk management and RWA Tables and templates* Template ref. # Page No. OV1 Overview of

The bank safety net: institutions and rules for preserving the stability of the banking system

The bank safety net: institutions and rules for preserving the stability of the banking system Professor Dr. Christos V. Gortsos Professor of Public Economic Law, Law School, National and Kapodistrian

The bank safety net: institutions and rules for preserving the stability of the banking system Professor Dr. Christos V. Gortsos Professor of Public Economic Law, Law School, National and Kapodistrian

Regulatory Disclosures March 31, 2018

Regulatory Disclosures March 31, 2018 SCOPE of DISCLOSURE... 3 CORPORATE PROFILE... 3 CAPITAL... 3 Capital structure... 4 Common shares... 4 Subordinated debt... 4 RISK MANAGEMENT... 4 Risk management

Regulatory Disclosures March 31, 2018 SCOPE of DISCLOSURE... 3 CORPORATE PROFILE... 3 CAPITAL... 3 Capital structure... 4 Common shares... 4 Subordinated debt... 4 RISK MANAGEMENT... 4 Risk management

Royal Bank of Canada. Pillar 3 Report

Royal Bank of Canada Pillar 3 Report As at January 3, 09 TABLE OF CONTENTS CAUTION REGARDING FORWARD-LOOKING STATEMENTS... ABOUT ROYAL BANK OF CANADA... CAPITAL FRAMEWORK... TLAC FRAMEWORK... DISCLOSURE

Royal Bank of Canada Pillar 3 Report As at January 3, 09 TABLE OF CONTENTS CAUTION REGARDING FORWARD-LOOKING STATEMENTS... ABOUT ROYAL BANK OF CANADA... CAPITAL FRAMEWORK... TLAC FRAMEWORK... DISCLOSURE

Habib Bank AG Zurich. Annual disclosures according to Basel III (Year 2015)

") Annual disclosures according to Basel III (Year 2015) 1 Annual disclosures according to Basel III (Year 2015) 1. Scope of consolidation Scope of consolidation for capital adequacy purposes The scope of

Annual disclosures according to Basel III (Year 2015) 1 Annual disclosures according to Basel III (Year 2015) 1. Scope of consolidation Scope of consolidation for capital adequacy purposes The scope of

Basel III Pillar 3 Disclosures Report. For the Quarterly Period Ended September 30, 2016

Basel III Pillar 3 Disclosures Report For the Quarterly Period Ended September 30, 2016 BASEL III PILLAR 3 DISCLOSURES REPORT For the quarterly period ended September 30, 2016 Table of Contents Page 1

Basel III Pillar 3 Disclosures Report For the Quarterly Period Ended September 30, 2016 BASEL III PILLAR 3 DISCLOSURES REPORT For the quarterly period ended September 30, 2016 Table of Contents Page 1

Samba Financial Group Basel III - Pillar 3 Disclosure Report. December 2017 PUBLIC

Basel III - Pillar 3 Disclosure Report December 2017 Basel III - Pillar 3 Disclosure Report as at December 31, 2017 Page 1 of 39 Capital Structure Table of Contents Page Statement of financial position

Basel III - Pillar 3 Disclosure Report December 2017 Basel III - Pillar 3 Disclosure Report as at December 31, 2017 Page 1 of 39 Capital Structure Table of Contents Page Statement of financial position

MORGAN STANLEY ASIA INTERNATIONAL LIMITED. Interim Financial Disclosure Statements

Interim Financial Disclosure Statements INTERIM FINANCIAL DISCLOSURE STATEMENTS CONTENTS PAGE Corporate Information 1 Unaudited income statement 2 Unaudited statement of comprehensive income 3 Unaudited

Interim Financial Disclosure Statements INTERIM FINANCIAL DISCLOSURE STATEMENTS CONTENTS PAGE Corporate Information 1 Unaudited income statement 2 Unaudited statement of comprehensive income 3 Unaudited

Disclosure in terms of Regulation 43 relating to banks, issued under section 90 of the Banks Act, No. 94 of 1990, as amended.

Mercantile Bank Holdings Limited and its subsidiaries ( the Group ) unaudited bi-annual disclosure as at (incorporating quarterly disclosure) Disclosure in terms of Regulation 43 relating to banks, issued

Mercantile Bank Holdings Limited and its subsidiaries ( the Group ) unaudited bi-annual disclosure as at (incorporating quarterly disclosure) Disclosure in terms of Regulation 43 relating to banks, issued

Citibank (Hong Kong) Limited. Regulatory Disclosures

Limited. Regulatory Disclosures") Citibank (Hong Kong) Limited Regulatory Disclosures For the Period ended September 30, Table of contents Template KM1: Key prudential ratios Template OV1: Overview of Risk-Weighted Assets Template LR2:

Citibank (Hong Kong) Limited Regulatory Disclosures For the Period ended September 30, Table of contents Template KM1: Key prudential ratios Template OV1: Overview of Risk-Weighted Assets Template LR2:

Project Editor, Yale Program on Financial Stability (YPFS), Yale School of Management

, Yale School of Management") yale program on financial stability case study 2014-1b-v1 november 1, 2014 Basel III B: 1 Basel III Overview Christian M. McNamara 2 Michael Wedow 3 Andrew Metrick 4 Abstract In the wake of the financial

yale program on financial stability case study 2014-1b-v1 november 1, 2014 Basel III B: 1 Basel III Overview Christian M. McNamara 2 Michael Wedow 3 Andrew Metrick 4 Abstract In the wake of the financial

The Net Stable Funding Ratio. Tomihiro Teranishi May 21-22, 2014 Asia Pacific CRO Forum

The Net Stable Funding Ratio Tomihiro Teranishi May 21-22, 2014 Asia Pacific CRO Forum Basel III - Liquidity Final: Liquidity Coverage Ratio (LCR) finalized Jan 2013 LCR disclosure standard - finalized

The Net Stable Funding Ratio Tomihiro Teranishi May 21-22, 2014 Asia Pacific CRO Forum Basel III - Liquidity Final: Liquidity Coverage Ratio (LCR) finalized Jan 2013 LCR disclosure standard - finalized

Traded Risk & Regulation

DRAFT Traded Risk & Regulation University of Essex Expert Lecture 14 March 2014 Dr Paula Haynes Managing Partner Traded Risk Associates 2014 www.tradedrisk.com Traded Risk Associates Ltd Contents Introduction

DRAFT Traded Risk & Regulation University of Essex Expert Lecture 14 March 2014 Dr Paula Haynes Managing Partner Traded Risk Associates 2014 www.tradedrisk.com Traded Risk Associates Ltd Contents Introduction

Pillar 3, Liquidity Coverage Ratio ("LCR") and Net Stable Funding Ratio ("NSFR") Disclosures

and Net Stable Funding Ratio (NSFR) Disclosures") Pillar 3, Liquidity Coverage Ratio ("LCR") and Net Stable Funding Ratio ("NSFR") Disclosures Second Quarter 2018 DBS Group Holdings Ltd Incorporated in the Republic of Singapore Company Registration Number:

Pillar 3, Liquidity Coverage Ratio ("LCR") and Net Stable Funding Ratio ("NSFR") Disclosures Second Quarter 2018 DBS Group Holdings Ltd Incorporated in the Republic of Singapore Company Registration Number: