The Affordable Care Act: A Summary on Healthcare Reform. The Wyoming Department of Insurance

|

|

|

- Bernice Day

- 6 years ago

- Views:

Transcription

1 The Affordable Care Act: A Summary on Healthcare Reform The Wyoming Department of Insurance

2 Additional Resources Wyoming Insurance Department: or toll free at 1-(800) Information on the Federal Healthcare Reform: Internal Revenue Service Information on the Penalty: For Employers: and-answers-on-employer-shared-responsibility-provisions- Under-the-Affordable-Care-Act For Individuals: Answers-on-the-Individual-Shared-Responsibility-Provision The Henry J. Kaiser Family Foundation General Information on Health Insurance and Health Care Reform:

3 This information is solely for informational purposes. It is not intended to provide legal advice, accounting advice or any opinions. This presentation is to provide only general, nonspecific information and is only a general guide. It does not include all the details found in the Act and is not intended to express any opinions of the State of Wyoming as to the interpretation of the Act nor is it bound by its content. For the application of the Act to a particular situation, the reader is advised to consult the specific provisions of the Act and obtain advice from the appropriate source.

4 Health Reform Quiz Will the health reform law require nearly all Americans to have health insurance starting in 2014 or else pay a penalty? Yes. Starting in 2014, most U.S. citizens and legal residents will be required to obtain health coverage, or pay a penalty. 64% answered this question correctly.

5 Will the health reform law provide financial help to low and moderate income Americans who don t get insurance through their jobs to help them purchase coverage? Yes. Individuals who purchase coverage through the new insurance marketplaces and have incomes between % of the federal poverty level will be eligible for premium tax credits based on their income. 72% answered this question correctly.

6 Will the health reform law prohibit insurance companies from denying coverage because of a person s medical history or health condition? Yes. Starting in 2014, all health insurers will be required to sell coverage to everyone who applies, regardless of their medical history or health status. 67% answered this question correctly.

7 Will the health reform law require all businesses, even the smallest ones, to provide health insurance for their employees? No. The law does not require employers to provide health benefits. However, it does impose penalties, in some cases, on larger employers (those with 50 or more workers) that do not provide insurance to their workers or that provide coverage that is considered unaffordable. 25% answered this question correctly.

8 Will the health reform law create a new government run insurance plan to be offered along with private plans? No. The law does not create a new government-run health insurance plan. 27% answered this question correctly.

9 Will the health reform law allow undocumented immigrants to receive financial help from the government to buy health insurance? No. Undocumented immigrants are not eligible to receive financial help from the government to buy health insurance, nor are they eligible for Medicaid or to purchase insurance with their own money in the new marketplaces. 42% answered this question correctly.

10 Healthcare Reform So Far September 23, 2010 Immediate reforms: No lifetime limits and restricted annual limits Internal and external review standards Elimination of denial for pre-existing conditions for children under age 19 Adult Dependent Child coverage up to age 26 Coverage of preventive benefits Temporary High-Risk Pools (enrollment suspended Feb 2013) Rate Review Standards (rate increases 10%+ reviewed) Medical Loss Ratios with Rebates Summary of Benefits and Coverage (September 2013)

11 2014 Market Reforms For Small Group and Individual Coverage Sold or Renewed on or after January 1, 2014: Guaranteed Issue (cannot be denied or rated because of any health condition) No Pre-Existing Condition Exclusions Insurance Rating Guidelines Essential Health Benefits & Cost-Sharing Must Meet Established Value Levels These apply inside and outside of a marketplace

12 Insurance Rating Guidelines For the Small Group and Individual Markets: No rating based on health status Maximum age variation of 3:1 (ages 21-64) Maximum variation based on tobacco use of 1.5:1 Rates based on geographic areas Family rates built up based on age and tobacco use of each member A family premium is the sum of the individual premium for each adult and each child up to 3 under age 21.

13 Benefit Design Individual and small group plans must include Essential Health Benefits (EHBs). Large group and self-insured plans may not have annual or lifetime limits on EHBs. EHBs based on benchmark plan in each state Benefit levels: Platinum = 90% value Gold = 80% value Silver = 70% value Bronze = 60% value Catastrophic Plan (limited to young and those without affordable option in the market)

14 Do I have to do anything?

15 Individual Mandate Individuals required to have minimum qualified coverage beginning January 1, 2014 Penalties $95 per adult up to $285 or 1% of household income, whichever is higher $325 per adult up to $975 or 2% of household income, whichever is higher $695 per adult up to $2,085 or 2.5% of household income, whichever is higher Penalty for a child is ½ that of an adult Penalties indexed to the growth of CPI after 2016

16 Individual Mandate What is Minimum Essential Coverage Medicare Medicaid CHIP Tri-Care Employer Sponsored Coverage Individual Market Coverage Grandfathered Coverage Exemptions: Cost of coverage is more than 8% of household income Religious objection Financial hardship Tribal members

17 What will I do?

18 What will I do? Keep what I have Purchase inside the marketplace Purchase outside the marketplace Do nothing

19 Grandfathered Plans Coverage in which individuals were enrolled prior to March 23, 2010 are exempt from most provisions of the bill. Provisions that DO Apply: Lifetime limits Restrictions on rescissions Extension of dependent coverage Medical loss ratios Annual limits (group only) Preexisting condition exclusions (group only) Grandfather Status Can Be Lost Grandfathered plans will satisfy individual mandate Check with insurance agent or company to see if your current plan qualifies for grandfather status.

20 What is a marketplace? Virtual marketplace Qualifies individuals for Medicaid, CHIP or premium subsidies Offers only qualified health plans and dental plans Two marketplaces 1 Individuals 1 Small Groups Three types of marketplaces State based Partnership Federally facilitated marketplace (Wyoming) On October 1, 2013 you can enroll for health insurance at:

21 Marketplace

22 Product Portfolio Individual and small group plans must include Essential Health Benefits (EHBs). Large group and self-insured plans may not have annual or lifetime limits on EHBs. EHBs based on benchmark plan in each state Benefit levels: Platinum = 90% value (Insurance should pay 90% of covered health care costs) Gold = 80% value Silver = 70% value Bronze = 60% value Catastrophic Plan (limited to young and those without affordable option in the market)

23 Plan Design A child-only plan must be offered at the same metal tier as any health plan that the issuer offers. Limited to individuals who are under age 21 as of the beginning of the plan year. A catastrophic plan is available to individuals who are under age 30 or who are exempt from the individual mandate due to a hardship or where cost of coverage, exceed 8% of income. Each issuer selling in the marketplace must offer at least one silver level, one gold level, and a child-only.

Multi-State Plans (not available in")

24 Plans Available in the Marketplace Qualified Health Plans Stand-Alone Dental Plans CO-OP Plans (not available in Wyoming) Multi-State Plans (not available in Wyoming)

25 2013 Federal Poverty Level Table Updated annually usually in late January

26 Premium Cap as % of Income Subsidies: Premium Tax Credit Available from 100% - 400% FPL. Covers the difference between premium for the second-lowest-cost Silver plan and a percentage of income. Advanced to insurer. Must purchase coverage in the individual marketplace Calculated based upon estimated income recipients may have to repay excess credits if actual income is higher. Premium Tax Credits 10% 9% 8% 7% 6% 5% 4% 3% 2% 1% 0% 100% 133% 150% 200% 250% 300% 400% Household Income as % of FPL

27 Premium Tax Credit Calculation Example: Family of Four with Income of $50,000, Purchases Benchmark Plan The Premium Tax credit is generally based on the benchmark plan. The family s expected contribution is a percentage of the family s household income. Income as a Percentage of FPL: 224% Expected Family Contribution: $3,570 Premium for Benchmark Plan: $9,000 Premium Tax Credit: $5,430 ($9,000 - $3,570) Premium for Plan Family Chooses: $9,000 Actual Family Contribution: $3,570

28 Cost-Sharing Reductions Lowers the out-of-pocket costs at the point of service and has the effect of increasing the actuarial value of a plan. Only available to individuals enrolled in a silver-level qualified health plan. The amount varies with income: There will be no cost-sharing for a Tribal member with household income below 300% FPL. There will be no cost-sharing for any Tribal member who receives care from Indian Health Services or related provider. Due to mid-year income fluctuations, reconciliation will occur annually.

29 Individual Coverage and Enrollment Initial open enrollment period will be October 1, 2013 March 31, Annual enrollment will occur between October 15 December 7. Special enrollment period of 60 days from the triggering event. In the marketplace special enrollment period will be 60 days from the triggering event.

30 Marketplace Responsibility The Marketplace is responsible for determining the date the special enrollment period begins. Special enrollment triggers include: An individual or dependent losing minimum essential coverage; An individual gaining or becoming a dependent through marriage, birth, adoption, or placement of adoption; An individual experiencing an error in enrollment; When a plan or issuer substantially violates a material provision of the contract in which the individual is enrolled; An individual becomes newly eligible or newly ineligible for subsidies or a change in cost-sharing reductions; or When new coverage becomes available as a result of a permanent move.

31 How Do I Enroll? Toll free number to be established Navigators Potential Consumer s Assistors across the State Potentially Agents/Brokers

32 Outside the Marketplace An issuer can offer only in the Marketplace, only outside the Marketplace, or a combination of both. No subsidy or cost sharing reduction outside the marketplace Outside the marketplace companies may have products that will not qualify as minimum essential health coverage (Tax penalty) Limited benefit plans Specific illness plans (cancer policy) Need to check with agent/company to see if plan satisfies the Federal mandate Contact agents/brokers/companies to purchase Insurers may restrict sales of new policies in the individual market to open enrollment periods that align with those for marketplaces.

33 What Size of a Group Do I Have?

34 How to determine Full Time Equivalent (FTE)? ACA refers to FTE rather than actual number of employees. To calculate total FTEs, add the following: All employees who work at least 30 hours per week (full time); PLUS Total number of hours worked in a month by part-time employees (<30 hours per week) divided by 120.

35 FTE Calculation Example Employer has 35 employees regularly working at least 30 hours per week and 16 employees regularly working 24 hours per week (total of 96 hours per month). Full time = 35 Part time = [16 employees X 96 hours] = 12.8 Total FTE = Federal government guidelines specify to round down to the nearest whole number

36 Seasonal Employee: Definition: Performs labor or services exclusively during certain seasons or periods of the year which, from its nature, is not continuous or carried on throughout the year. Includes retail workers employed exclusively during holiday seasons. If employer s workforce exceeds 50 FTE for no more than 120 days during the calendar year and the employees in excess of 50 were seasonal workers, then the employer is not considered to have more than 50 employees.

37 New Employees: If the new employee is reasonably expected to consistently work at least 30 hours per week, then consider the employee as full time.

38 Small Employers 1-49 full-time or full-time equivalent employees during the preceding calendar year. The fulltime equivalent employee count includes seasonal employees (if they work more than 120 days per year). There is NO penalty for small employers who do not offer health insurance to their employees.

39 Subsidies: Small Business Tax Credit Businesses with 25 or fewer employees. Average wages less than $50,000. Contribute at least 50% of premium. Phases out as size and wages of business increase : Up to 35% of total employer contribution and later: Up to 50% of contribution.

40 The Marketplaces) Small Group (SHOP) Marketplace: For small employers 1-49 ( 1 defined as employer and one employee) 70% participation rate allowed in federal SHOP. Employer may choose coverage level and allow employees to choose from insurers offering at that level beginning in Marketplace collects and combines premiums and sends to insurers beginning in 2015.

41 Small Group Coverage and Enrollment Initial open enrollment period will be October 1, 2013 March 31, Enrollment may occur at any time if that small employer has a 70% minimum participation rate (the level of participation of the employees). Annual enrollment period will occur between November 15 December 15. Special enrollment period of 30 days (60 days for those losing Medicaid or CHIP coverage) from triggering event. Enrollment periods will be the same inside and outside the Marketplace.

42 Large Employers 50+ full-time or full-time equivalent employees during the preceding calendar year. The full-time equivalent employee count includes seasonal employees (if they work more than 120 days per year) Large employers MUST provide minimum essential and affordable health insurance or pay a penalty. Minimum essential coverage means that insurance pays for at least 60% of covered healthcare expenses. Affordable means it cannot cost the employee more than 9.5% of that employee s income.

43 Employer Responsibilities Employers of over 200 employees must auto-enroll with opt-out (final rules and regulations have not been released) The penalty for large groups (50+ FTE) not providing health insurance, if at least one employee receives a subsidy from the Marketplace, will be $2,000 per each full-time employee above the first 30 workers. Example: A business employs 55 full-time employees; 2 receive a subsidy. The employer would pay a penalty of $50,000. ($2,000 x (55-30) = penalty). The penalty for not providing affordable coverage will be $3,000 annually for each full-time employee who receives a subsidy from the Marketplace, with a maximum of $2,000 times the number of full-time employees above the first 30 workers. Example: A business with 55 full-time employees; 2 receive a subsidy. The employer would pay a penalty of $6,000. ($3,000 x 2) = penalty. The maximum penalty for this business would be $50,000. ($2,000 x (55-30) = penalty).

44 Self-Insured Groups Self-insured groups are not required to: Cover essential health benefits Limit deductibles Justify large rate increases Extend health insurance to anyone who applies (but they cannot discriminate based on a pre-existing condition) Guarantee to renew coverage Standardize cost-sharing tiers based on actuarial value Prohibit higher premiums based on health status

45 Penalties for Employers not offering affordable coverage START HERE Does the employer have at least 50 full-time equivalent employees? No Penalties do not apply to small employers If the employer has 25 fewer employees and average wage up to $50,000.00, it may be eligible for a health insurance tax credit. Yes Does the employer offer coverage to its workers? No Did at least one employee receive a premium tax credit or cost sharing subsidy in an Exchange? Yes The employer must pay a penalty for not offering coverage The penalty is $2,000 annually times the number of full-time employees minus 30. The penalty is increased each year by the growth in insurance premiums.. Yes There is no penalty payment required of the employer since it offers affordable coverage. No Does the insurance pay for at least 60% of covered health care expenses for a typical population? Yes Do any employees have to pay more than 9.5% of family income for the employer coverage? No Yes Employees can choose to buy coverage in an Exchange and receive a premium tax credit. Those employees can choose to buy coverage in an Exchange and receive a premium tax credit. The employer must pay a penalty for not offering affordable coverage The penalty is $3,000 annually for each full-time employee receiving a tax credit, up to a maximum of $2,000 times the number of full-time employees minus 30. The penalty is increased each year by the growth in insurance premiums.

The Affordable Care Act: A Summary on Healthcare Reform. The Wyoming Department of Insurance

The Affordable Care Act: A Summary on Healthcare Reform The Wyoming Department of Insurance The ACA is a federal law that impacts Wyoming and its citizens. The State of Wyoming has filed a lawsuit against

The Affordable Care Act: A Summary on Healthcare Reform The Wyoming Department of Insurance The ACA is a federal law that impacts Wyoming and its citizens. The State of Wyoming has filed a lawsuit against

The Affordable Care Act: Information for Wyoming Consumers

The Affordable Care Act: Information for Wyoming Consumers The Wyoming Department of Insurance The Affordable Care Act is a federally-mandated health care and health insurance law. Wyoming citizens and

The Affordable Care Act: Information for Wyoming Consumers The Wyoming Department of Insurance The Affordable Care Act is a federally-mandated health care and health insurance law. Wyoming citizens and

8/7/2013 INSURANCE MADE SIMPLE. 1

Presented by: Mark E. Baker Vice President Employee Benefits INSURANCE MADE SIMPLE. 1 Health Care Reform provisions in effect 2010-2012 Large Employer Defined Pay or Play Mandate and Penalties Small Employer

Presented by: Mark E. Baker Vice President Employee Benefits INSURANCE MADE SIMPLE. 1 Health Care Reform provisions in effect 2010-2012 Large Employer Defined Pay or Play Mandate and Penalties Small Employer

Health Care Reform Update. April 2013

Health Care Reform Update April 2013 2013 Compliance Issues Summary of Benefits and Coverage Simple explanation of benefits and costs 4 double sided pages, 12 point or larger font Can provide in paper

Health Care Reform Update April 2013 2013 Compliance Issues Summary of Benefits and Coverage Simple explanation of benefits and costs 4 double sided pages, 12 point or larger font Can provide in paper

Frequently Asked Questions about Health Care Reform and the Affordable Care Act

Frequently Asked Questions about Health Care Reform and the Affordable Care Act HEALTH CARE REFORM OVERVIEW Q 1: What ACA changes are already in place? There are no lifetime dollar limits on essential

Frequently Asked Questions about Health Care Reform and the Affordable Care Act HEALTH CARE REFORM OVERVIEW Q 1: What ACA changes are already in place? There are no lifetime dollar limits on essential

Health Care Reform: General Q&A for Employees

From Health Care Reform: General Q&A for Employees Common questions answered I ve heard a lot about the health care reform law. When do the reforms become effective? The health care reform bill was signed

From Health Care Reform: General Q&A for Employees Common questions answered I ve heard a lot about the health care reform law. When do the reforms become effective? The health care reform bill was signed

Health Care Reform. Navigating The Maze Of. What s Inside

Navigating The Maze Of Health Care Reform What s Inside Questions and Answers on Health Care Reform Health Care Reform Timeline Health Care Reform Glossary Questions and Answers on Health Care Reform I

Navigating The Maze Of Health Care Reform What s Inside Questions and Answers on Health Care Reform Health Care Reform Timeline Health Care Reform Glossary Questions and Answers on Health Care Reform I

Rhode Island League of Cities and Towns. Health Care Reform and the State Exchanges: What Cities and Towns Should Be Doing Now

Rhode Island League of Cities and Towns Health Care Reform and the State Exchanges: What Cities and Towns Should Be Doing Now Rick Johnson Senior Vice President, National Public Sector Health Practice

Rhode Island League of Cities and Towns Health Care Reform and the State Exchanges: What Cities and Towns Should Be Doing Now Rick Johnson Senior Vice President, National Public Sector Health Practice

Tennessee Public Health Association. Overview of the Affordable Care Act

Tennessee Public Health Association Overview of the Affordable Care Act Susie Baird Director of Policy Health Care Finance and Administration September 12, 2013 1 Origins of ACA Signed into law on March

Tennessee Public Health Association Overview of the Affordable Care Act Susie Baird Director of Policy Health Care Finance and Administration September 12, 2013 1 Origins of ACA Signed into law on March

THE AFFORDABLE CARE ACT...2

Table of Contents THE AFFORDABLE CARE ACT...2 Health Insurance Marketplace (Exchange)...3 Metallic Levels...4 Catastrophic Plans...4 Individual Mandate...5 Subsidies...5 Open Enrollment Period...6 Special

Table of Contents THE AFFORDABLE CARE ACT...2 Health Insurance Marketplace (Exchange)...3 Metallic Levels...4 Catastrophic Plans...4 Individual Mandate...5 Subsidies...5 Open Enrollment Period...6 Special

UNIVERSAL HEALTHCARE COUNCIL 2013 OVERVIEW OF THE AFFORDABLE CARE ACT

UNIVERSAL HEALTHCARE COUNCIL 2013 OVERVIEW OF THE AFFORDABLE CARE ACT Introduction The Patient Protection and Affordable Care Act (ACA) was signed into federal law on March 23, 2010. While many reforms

UNIVERSAL HEALTHCARE COUNCIL 2013 OVERVIEW OF THE AFFORDABLE CARE ACT Introduction The Patient Protection and Affordable Care Act (ACA) was signed into federal law on March 23, 2010. While many reforms

Complying with Health Care Reform

Complying with Health Care Reform April 17, 2013 1 1 What Happened? In March 2010, Congress passed and the President signed health reform in: The Patient Protection and Affordable Care Act The Health Care

Complying with Health Care Reform April 17, 2013 1 1 What Happened? In March 2010, Congress passed and the President signed health reform in: The Patient Protection and Affordable Care Act The Health Care

The Affordable Care Act Update

The Affordable Care Act Update Presented by: The Union Labor Life Insurance Company SOLUTIONS FOR THE UNION WORKPLACE SPECIALTY INSURANCE INVESTMENTS Overview I. Key Provisions II. Major Challenges III.

The Affordable Care Act Update Presented by: The Union Labor Life Insurance Company SOLUTIONS FOR THE UNION WORKPLACE SPECIALTY INSURANCE INVESTMENTS Overview I. Key Provisions II. Major Challenges III.

Key Medicaid, CHIP, and Low-Income Provisions in the Senate Bill Patient Protection and Affordable Care Act (Released November 18, 2009)

") Key Medicaid, CHIP, and Low-Income Provisions in the Senate Bill Patient Protection and Affordable Care Act (Released November 18, 2009) On November 18, 2009, the Senate released its health care reform

Key Medicaid, CHIP, and Low-Income Provisions in the Senate Bill Patient Protection and Affordable Care Act (Released November 18, 2009) On November 18, 2009, the Senate released its health care reform

Health Policy Essentials: Private Health Insurance. Bernadette Fernandez, Annie Mach, Janemarie Mulvey March 1, 2013

Health Policy Essentials: Private Health Insurance Bernadette Fernandez, Annie Mach, Janemarie Mulvey March 1, 2013 Private Health Insurance Insurance provides protection from economic loss Risk likelihood

Health Policy Essentials: Private Health Insurance Bernadette Fernandez, Annie Mach, Janemarie Mulvey March 1, 2013 Private Health Insurance Insurance provides protection from economic loss Risk likelihood

2014 AFFORDABLE CARE ACT (OBAMA CARE)

") 2014 AFFORDABLE CARE ACT (OBAMA CARE) Planning for 2014 Tax Return Filings O Beginning 2014, the ACA requires all persons be covered by health insurance O Individuals not covered by Medicare, their employers,

2014 AFFORDABLE CARE ACT (OBAMA CARE) Planning for 2014 Tax Return Filings O Beginning 2014, the ACA requires all persons be covered by health insurance O Individuals not covered by Medicare, their employers,

Navigating the New Health Care Law

Navigating the New Health Care Law For Sole Proprietors and Small Businesses (50 employees or less) This presentation is intended for educational purposes only and not intended as a legal, tax, or insurance

Navigating the New Health Care Law For Sole Proprietors and Small Businesses (50 employees or less) This presentation is intended for educational purposes only and not intended as a legal, tax, or insurance

Pay or Play Employer Shared Responsibility Penalties

Brought to you by Olson Insurance Pay or Play Employer Shared Responsibility Penalties The Affordable Care Act (ACA) requires applicable large employers (ALEs) to offer affordable, minimum value health

Brought to you by Olson Insurance Pay or Play Employer Shared Responsibility Penalties The Affordable Care Act (ACA) requires applicable large employers (ALEs) to offer affordable, minimum value health

Patient Protection and Affordable Care Act of 2009: Health Insurance Market Reforms

Patient Protection and Affordable Care Act of 2009: Health Insurance Market Reforms Provision Notes Standards SUBTITLE C Quality Health Insurance Coverage for All Americans PART I HEALTH INSURANCE MARKET

Patient Protection and Affordable Care Act of 2009: Health Insurance Market Reforms Provision Notes Standards SUBTITLE C Quality Health Insurance Coverage for All Americans PART I HEALTH INSURANCE MARKET

Pay or Play Employer Shared Responsibility Penalties

Brought to you by Biggs Insurance Services Pay or Play Employer Shared Responsibility Penalties The Affordable Care Act (ACA) requires certain large employers to offer affordable, minimum value health

Brought to you by Biggs Insurance Services Pay or Play Employer Shared Responsibility Penalties The Affordable Care Act (ACA) requires certain large employers to offer affordable, minimum value health

Health Insurance Webinar Series: The Affordable Care Act Updates for 2017

Health Insurance Webinar Series: The Affordable Care Act Updates for 2017 What is the Affordable Care Act (ACA)? The Patient Protection and Affordable Care Act (PPACA) of 2010 or Affordable Care Act (ACA),

Health Insurance Webinar Series: The Affordable Care Act Updates for 2017 What is the Affordable Care Act (ACA)? The Patient Protection and Affordable Care Act (PPACA) of 2010 or Affordable Care Act (ACA),

OVERVIEW OF THE AFFORDABLE CARE ACT. September 23, 2013

OVERVIEW OF THE AFFORDABLE CARE ACT September 23, 2013 Outline The New Continuum of Coverage Medicaid and CHIP Are Changing The New Marketplaces Insurance Affordability Programs Shared Responsibility Requirement

OVERVIEW OF THE AFFORDABLE CARE ACT September 23, 2013 Outline The New Continuum of Coverage Medicaid and CHIP Are Changing The New Marketplaces Insurance Affordability Programs Shared Responsibility Requirement

Health care reform update

Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned and managed member of Baker Tilly International. Health care reform update Agenda > Recent updates for 2014 and beyond > Individual

Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned and managed member of Baker Tilly International. Health care reform update Agenda > Recent updates for 2014 and beyond > Individual

Questions from Agents/Producers

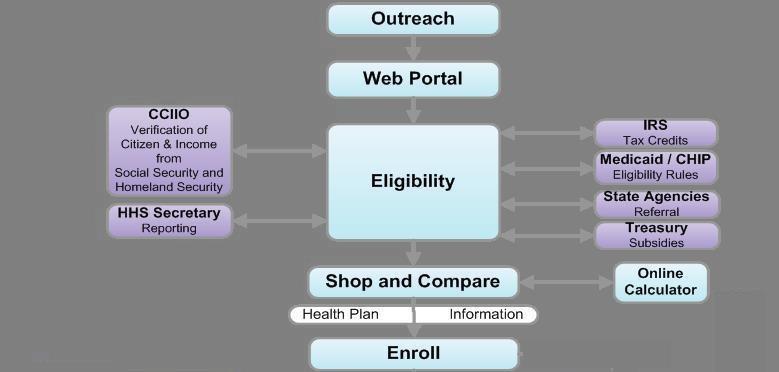

Questions from Agents/Producers Q. How will income be determined? Will we take the word of the consumer about their income without verifying? A. Incomes will be verified by the data hub on the Federal

Questions from Agents/Producers Q. How will income be determined? Will we take the word of the consumer about their income without verifying? A. Incomes will be verified by the data hub on the Federal

The Affordable Care Act (ACA) Health Insurance Exchanges

Health Insurance Exchanges") The Affordable Care Act (ACA) Health Insurance Exchanges Dave Chandra Senior Policy Analyst Center on Budget and Policy Priorities March 11, 2013 Linking Americans to Coverage (2014) FPL Unsubsidized 400%

The Affordable Care Act (ACA) Health Insurance Exchanges Dave Chandra Senior Policy Analyst Center on Budget and Policy Priorities March 11, 2013 Linking Americans to Coverage (2014) FPL Unsubsidized 400%

Key Facts You Need to Know About: Premium Tax Credits

Updated September 2014 Key Facts You Need to Know About: Premium Tax Credits In 2014, millions of Americans became eligible for a new premium tax credit that helps them pay for health coverage. This collection

Updated September 2014 Key Facts You Need to Know About: Premium Tax Credits In 2014, millions of Americans became eligible for a new premium tax credit that helps them pay for health coverage. This collection

Navajo County Schools EBT

Navajo County Schools EBT Affordable Care Act (ACA) Update Aaron Polkoski Segal Consulting January 31st, 2014 Copyright 2013 by The Segal Group, Inc., parent of The Segal Company. All rights reserved.

Navajo County Schools EBT Affordable Care Act (ACA) Update Aaron Polkoski Segal Consulting January 31st, 2014 Copyright 2013 by The Segal Group, Inc., parent of The Segal Company. All rights reserved.

Health Care Reform Update 6/12/2014

Health Care Reform Update 6/12/2014 Disclaimer The information contained herein is for general information only. It is not intended as and does not constitute legal or tax advice. The information should

Health Care Reform Update 6/12/2014 Disclaimer The information contained herein is for general information only. It is not intended as and does not constitute legal or tax advice. The information should

The Affordable Care Act Update

The Affordable Care Act Update Presented by: The Union Labor Life Insurance Company SOLUTIONS FOR THE UNION WORKPLACE SPECIALTY INSURANCE INVESTMENTS Overview of Presentation 1. 2010 2014 Provisions overview

The Affordable Care Act Update Presented by: The Union Labor Life Insurance Company SOLUTIONS FOR THE UNION WORKPLACE SPECIALTY INSURANCE INVESTMENTS Overview of Presentation 1. 2010 2014 Provisions overview

2014 and Beyond. This timeline explains how and when the Affordable Care Act (ACA) provisions will be implemented over the next few years.

provisions will be implemented over the next few years.") December This timeline explains how and when the Affordable Care Act (ACA) provisions will be implemented over the next few years. Get Covered Illinois, the Official Health Marketplace of Illinois While

December This timeline explains how and when the Affordable Care Act (ACA) provisions will be implemented over the next few years. Get Covered Illinois, the Official Health Marketplace of Illinois While

Pennsylvania Association of Health Underwriters Advisors and Advocates for Employers, Employees and Health Care Consumers

Pennsylvania Association of Health Underwriters Advisors and Advocates for Employers, Employees and Health Care Consumers Timeline for Health Care Reform March 26, 2010 The Patient Protection and Affordable

Pennsylvania Association of Health Underwriters Advisors and Advocates for Employers, Employees and Health Care Consumers Timeline for Health Care Reform March 26, 2010 The Patient Protection and Affordable

GENERAL INFORMATION BULLETIN

AFL-CIO California School Employees Association GENERAL INFORMATION BULLETIN March 15, 2013 General Information Bulletin No. 17 13 AFFORDABLE CARE ACT (ACA) QUESTION & ANSWER RESOURCE DOCUMENT Action for

AFL-CIO California School Employees Association GENERAL INFORMATION BULLETIN March 15, 2013 General Information Bulletin No. 17 13 AFFORDABLE CARE ACT (ACA) QUESTION & ANSWER RESOURCE DOCUMENT Action for

The Patient Protection and Affordable Care Act. An In-Depth Analysis of Provisions Directly or Indirectly Affecting Group Health Plans

The Patient Protection and Affordable Care Act An In-Depth Analysis of Provisions Directly or Indirectly Affecting Group Health Plans Table of Contents Section 1 Insurance Plan Provisions Prohibition on

The Patient Protection and Affordable Care Act An In-Depth Analysis of Provisions Directly or Indirectly Affecting Group Health Plans Table of Contents Section 1 Insurance Plan Provisions Prohibition on

ACA in Brief 2/18/2014. It Takes Three Branches... Overview of the Affordable Care Act. Health Insurance Coverage, USA, % 16% 55% 15% 10%

Health Insurance Coverage, USA, 2011 16% Uninsured Overview of the Affordable Care Act 55% 16% Medicaid Medicare Private Non-Group Philip R. Lee Institute for Health Policy Studies Janet Coffman, MPP,

Health Insurance Coverage, USA, 2011 16% Uninsured Overview of the Affordable Care Act 55% 16% Medicaid Medicare Private Non-Group Philip R. Lee Institute for Health Policy Studies Janet Coffman, MPP,

Health Care Reform at-a-glance

Health Care Reform at-a-glance August 2015 Table of Contents Employer mandate...3 Individual mandate...3 Health plan provisions applying to both grandfathered and non-grandfathered employer plans...4 Health

Health Care Reform at-a-glance August 2015 Table of Contents Employer mandate...3 Individual mandate...3 Health plan provisions applying to both grandfathered and non-grandfathered employer plans...4 Health

AFFORDABLE CARE ACT (ACA)

") AFFORDABLE CARE ACT (ACA) Presented By ANDREW H. HOOK, CELA, CFP, AEP 295 Bendix Road, Suite 170, Virginia Beach, VA 23452 5806 Harbour View Blvd., Suite 203, Suffolk, VA 23435 Tel: 757-399-7506 Fax: 757-397-1267

AFFORDABLE CARE ACT (ACA) Presented By ANDREW H. HOOK, CELA, CFP, AEP 295 Bendix Road, Suite 170, Virginia Beach, VA 23452 5806 Harbour View Blvd., Suite 203, Suffolk, VA 23435 Tel: 757-399-7506 Fax: 757-397-1267

Health Care Reform: General Q&A for Employees

Health Care Reform: General Q&A for Employees I ve heard a lot about the health care reform law. When do the reforms become effective? The health care reform bill was signed into law in March 2010. The

Health Care Reform: General Q&A for Employees I ve heard a lot about the health care reform law. When do the reforms become effective? The health care reform bill was signed into law in March 2010. The

HEALTH CARE REFORM Focus on Group Coverage Blue Cross and Blue Shield of Minnesota. All rights reserved.

HEALTH CARE REFORM Focus on Group Coverage 2011 Blue Cross and Blue Shield of Minnesota. All rights reserved. Current Insurance Coverage Environment Minnesota United States Uninsured 9% Ot her Public 1%

HEALTH CARE REFORM Focus on Group Coverage 2011 Blue Cross and Blue Shield of Minnesota. All rights reserved. Current Insurance Coverage Environment Minnesota United States Uninsured 9% Ot her Public 1%

AFFORDABLE CARE ACT FAQ

AFFORDABLE CARE ACT FAQ What is the Healthcare Insurance Marketplace? The Marketplace is a new way to find quality health coverage. It can help if you don t have coverage now or if you have it but want

AFFORDABLE CARE ACT FAQ What is the Healthcare Insurance Marketplace? The Marketplace is a new way to find quality health coverage. It can help if you don t have coverage now or if you have it but want

The Patient Protection and Affordable Care Act in Colorado

The Patient Protection and Affordable Care Act in Colorado Colorado Center on Law and Policy 789 Sherman St., Suite 300, Denver, CO 80203 303-573-5669 September 20, 2013 The Problem 50 million uninsured

The Patient Protection and Affordable Care Act in Colorado Colorado Center on Law and Policy 789 Sherman St., Suite 300, Denver, CO 80203 303-573-5669 September 20, 2013 The Problem 50 million uninsured

Open Enrollment is here!

Navigating the Federal Marketplace AFFORDABLE CARE Open Enrollment is here! Reminders On November 20 at 9:30 AM ET, IPHCA is hosting a call with Matt Cesnik from FSSA again. CMS has released guidance on

Navigating the Federal Marketplace AFFORDABLE CARE Open Enrollment is here! Reminders On November 20 at 9:30 AM ET, IPHCA is hosting a call with Matt Cesnik from FSSA again. CMS has released guidance on

Health Care Reform Update. Michelle VanDellen, CPA Tax Senior Manager

Health Care Reform Update Michelle VanDellen, CPA Tax Senior Manager 1 The material appearing in this presentation is for informational purposes only and is not legal or accounting advice. Communication

Health Care Reform Update Michelle VanDellen, CPA Tax Senior Manager 1 The material appearing in this presentation is for informational purposes only and is not legal or accounting advice. Communication

Overview of the Affordable Care Act.

Overview of the Affordable Care Act www.insurance.illinois.gov Regulates Insurance Companies and Agents who sell Life, Health, Home and Auto Policies The Affordable Care Act (ACA) offers important benefits

Overview of the Affordable Care Act www.insurance.illinois.gov Regulates Insurance Companies and Agents who sell Life, Health, Home and Auto Policies The Affordable Care Act (ACA) offers important benefits

Health Care Reform Frequently Asked Questions

Health Care Reform Frequently Asked Questions What are health exchanges, or marketplaces, and when are they going to be available? Health insurance exchanges, now called health insurance marketplaces,

Health Care Reform Frequently Asked Questions What are health exchanges, or marketplaces, and when are they going to be available? Health insurance exchanges, now called health insurance marketplaces,

The Patient Protection and Affordable Care Act

The Patient Protection and Affordable Care Act 2015 marks the beginning of the fifth full year of the Patient Protection and Affordable Care Act (ACA). We want to take the opportunity to look ahead and

The Patient Protection and Affordable Care Act 2015 marks the beginning of the fifth full year of the Patient Protection and Affordable Care Act (ACA). We want to take the opportunity to look ahead and

Overview of the ACA and Wisconsin Medicaid Reforms. Covering Kids & Families Wisconsin Wisconsin Primary Health Care Association

Overview of the ACA and Wisconsin Medicaid Reforms Covering Kids & Families Wisconsin Wisconsin Primary Health Care Association Updated September 9, 2013 Topics to be Covered What is the ACA? Wisconsin

Overview of the ACA and Wisconsin Medicaid Reforms Covering Kids & Families Wisconsin Wisconsin Primary Health Care Association Updated September 9, 2013 Topics to be Covered What is the ACA? Wisconsin

Understanding Obamacare

Understanding Obamacare What is The Affordable Care Act? The stated purpose of The Patient Protection and Affordable Care Act or Affordable Care Act, or ACA, or Obamacare is to "increase the number of

Understanding Obamacare What is The Affordable Care Act? The stated purpose of The Patient Protection and Affordable Care Act or Affordable Care Act, or ACA, or Obamacare is to "increase the number of

Washington Health Benefit Exchange

Washington Health Benefit Exchange HEALTHCARE REFORM SEMINAR November 25th, 2013 ACA INFORMATIONAL SESSION FOR SMALL BUSINESS OWNERS The Affordable Care Act Exchange Basics Today s Agenda Exchange Functions

Washington Health Benefit Exchange HEALTHCARE REFORM SEMINAR November 25th, 2013 ACA INFORMATIONAL SESSION FOR SMALL BUSINESS OWNERS The Affordable Care Act Exchange Basics Today s Agenda Exchange Functions

President Obama speaks about the Affordable Care Act at the White House on May 10.

POLITICAL LANDSCAPE Washington s political dynamic is fractured House actions are tempered by conservative pressure and tight Democratic majority in the Senate and President Obama GOP is struggling with

POLITICAL LANDSCAPE Washington s political dynamic is fractured House actions are tempered by conservative pressure and tight Democratic majority in the Senate and President Obama GOP is struggling with

Key Facts: Premium Tax Credit

Updated September 13, 2018 Key Facts: Premium Tax Credit As a result of the Affordable Care Act (ACA), millions of Americans are eligible for a premium tax credit that helps them pay for health coverage.

Updated September 13, 2018 Key Facts: Premium Tax Credit As a result of the Affordable Care Act (ACA), millions of Americans are eligible for a premium tax credit that helps them pay for health coverage.

THE AFFORDABLE CARE ACT: 2014 AND BEYOND

THE AFFORDABLE CARE ACT: 2014 AND BEYOND October 28, 2013 Howard Van Mersbergen, Vice President of Employee Benefits, Christian Schools International Julie Sessions, Principal, Mercer Patient Protection

THE AFFORDABLE CARE ACT: 2014 AND BEYOND October 28, 2013 Howard Van Mersbergen, Vice President of Employee Benefits, Christian Schools International Julie Sessions, Principal, Mercer Patient Protection

Health Care Reform under the Patient Protection and Affordable Care Act ( PPACA ) provisions effective January 1, 2014

provisions effective January 1, 2014") The New Health Care Landscape Today s Agenda Health Care Reform under the Patient Protection and Affordable Care Act ( PPACA ) provisions effective January 1, 2014 Exchanges and Qualified Health Plans

The New Health Care Landscape Today s Agenda Health Care Reform under the Patient Protection and Affordable Care Act ( PPACA ) provisions effective January 1, 2014 Exchanges and Qualified Health Plans

HEALTH CARE REFORM: EMPLOYER SHARED RESPONSIBILITY RULES

HEALTH CARE REFORM: EMPLOYER SHARED RESPONSIBILITY RULES The Affordable Care Act (ACA) requires applicable large employers (ALEs) to offer affordable, minimum value health coverage to their full-time employees

HEALTH CARE REFORM: EMPLOYER SHARED RESPONSIBILITY RULES The Affordable Care Act (ACA) requires applicable large employers (ALEs) to offer affordable, minimum value health coverage to their full-time employees

Health Reform Employer Perspective

Health Reform Employer Perspective Copyright 2008 McGraw Wentworth, Inc. All rights reserved. 1 Government Requirements Expanding Federal requirements effecting employers expanded significantly in 2009

Health Reform Employer Perspective Copyright 2008 McGraw Wentworth, Inc. All rights reserved. 1 Government Requirements Expanding Federal requirements effecting employers expanded significantly in 2009

Understanding the Impacts of Health Care Reform on Employers : 2014 and beyond

2013 CliftonLarsonAllen LLP Understanding the Impacts of Health Care Reform on Employers : 2014 and beyond cliftonlarsonallen.com Peoria County Bar Association January 25, 2014 Deb Freeland Objectives

2013 CliftonLarsonAllen LLP Understanding the Impacts of Health Care Reform on Employers : 2014 and beyond cliftonlarsonallen.com Peoria County Bar Association January 25, 2014 Deb Freeland Objectives

American Health Care Act (House-Passed Bill)

") This chart compares the to provisions of both the House-passed and the Senate Discussion Draft, called the. This chart is current as of June 26, 2017. Individual shared responsibility penalty for not having

This chart compares the to provisions of both the House-passed and the Senate Discussion Draft, called the. This chart is current as of June 26, 2017. Individual shared responsibility penalty for not having

Health Care Reform Overview

Publication date: March 2014 Health Care Reform Overview for Large Group (51+) Plans The following chart provides a breakdown of key Affordable Care Act (ACA) provisions by year for large group plans,

Publication date: March 2014 Health Care Reform Overview for Large Group (51+) Plans The following chart provides a breakdown of key Affordable Care Act (ACA) provisions by year for large group plans,

Affordable Care Act and You

Affordable Care Act and You The Affordable Care Act (also called ACA, federal health care reform or sometimes Obamacare ) expands health coverage to millions of previously uninsured Americans and makes

Affordable Care Act and You The Affordable Care Act (also called ACA, federal health care reform or sometimes Obamacare ) expands health coverage to millions of previously uninsured Americans and makes

Health Reform: An Overview. Hinda Chaikind February 25, 2011

Health Reform: An Overview Hinda Chaikind February 25, 2011 Introduction Expanded coverage and reform Insurance and subsidies through Exchanges Medicaid expansion CHIP funding (Children s Health Insurance

Health Reform: An Overview Hinda Chaikind February 25, 2011 Introduction Expanded coverage and reform Insurance and subsidies through Exchanges Medicaid expansion CHIP funding (Children s Health Insurance

Affordable Care Act (ACA) An Overview of Key Provisions

An Overview of Key Provisions") Affordable Care Act (ACA) An Overview of Key Provisions Locey & Cahill, LLC Presentation to the: New York State Association of Management Advocates for School Labor Affairs, Inc. 36 th Annual Summer Conference

Affordable Care Act (ACA) An Overview of Key Provisions Locey & Cahill, LLC Presentation to the: New York State Association of Management Advocates for School Labor Affairs, Inc. 36 th Annual Summer Conference

In this training, the law is referred to as The Affordable Care Act.

1 This training discusses the goals of the new health care law, The Patient Protection and Affordable Care Act of 2010 (as amended by the Health Care and Education Reconciliation Act of 2010) and its major

1 This training discusses the goals of the new health care law, The Patient Protection and Affordable Care Act of 2010 (as amended by the Health Care and Education Reconciliation Act of 2010) and its major

Employer Obligations and Coverage Options under the Affordable Care Act in 2014/2015

Employer Obligations and Coverage Options under the Affordable Care Act in 2014/2015 C H I C A G O S O U T H L A N D C H A M B E R O F C O M M E R C E J U L Y 1 5, 2 0 1 3 L A U R A M I N Z E R E X E C

Employer Obligations and Coverage Options under the Affordable Care Act in 2014/2015 C H I C A G O S O U T H L A N D C H A M B E R O F C O M M E R C E J U L Y 1 5, 2 0 1 3 L A U R A M I N Z E R E X E C

Health Care Reform: The Financial Impact on the Employer

Health Care Reform: The Financial Impact on the Employer WP&BC August 15, 2012 1 1 Supreme Court Examines Constitutionality U.S. Supreme Court Ruling: June 28, 2012 Individual Mandate - Constitutional

Health Care Reform: The Financial Impact on the Employer WP&BC August 15, 2012 1 1 Supreme Court Examines Constitutionality U.S. Supreme Court Ruling: June 28, 2012 Individual Mandate - Constitutional

Effects of the Affordable Health Care Act

Effects of the Affordable Health Care Act A Focus on Financial, Administrative and Plan Impacts February 27, 2013 Presented By J.W. Terrill Consulting Services Agenda Introduction: Patient Protection &

Effects of the Affordable Health Care Act A Focus on Financial, Administrative and Plan Impacts February 27, 2013 Presented By J.W. Terrill Consulting Services Agenda Introduction: Patient Protection &

U.S. HEALTH-CARE REFORM: THE PATIENT PROTECTION AND AFFORDABLE CARE ACT

C The Journal of Risk and Insurance, 2010, Vol. 77, No. 3, 703-708 DOI: 10.1111/j.1539-6975.2010.01371.x U.S. HEALTH-CARE REFORM: THE PATIENT PROTECTION AND AFFORDABLE CARE ACT Scott E. Harrington ABSTRACT

C The Journal of Risk and Insurance, 2010, Vol. 77, No. 3, 703-708 DOI: 10.1111/j.1539-6975.2010.01371.x U.S. HEALTH-CARE REFORM: THE PATIENT PROTECTION AND AFFORDABLE CARE ACT Scott E. Harrington ABSTRACT

Health Care Reform: Be Prepared for 2014

Health Care Reform: Be Prepared for 2014 Your Health Care Reform Team: Moderator Eboni Britt POMCO Group Marketing Manager Co-presenter Jessica Marabella POMCO Group Account Manager Co-presenter Amy Zell

Health Care Reform: Be Prepared for 2014 Your Health Care Reform Team: Moderator Eboni Britt POMCO Group Marketing Manager Co-presenter Jessica Marabella POMCO Group Account Manager Co-presenter Amy Zell

Presentation by: Champaign County Health Care Consumers (CCHCC) October 26, Welcome!

October 26, Welcome!") The Affordable Care Act (ACA): The Health Insurance Marketplace and Medicaid Presentation by: Champaign County Health Care Consumers (CCHCC) October 26, 2017 Welcome! Goals of the Affordable Care Act (ACA)

The Affordable Care Act (ACA): The Health Insurance Marketplace and Medicaid Presentation by: Champaign County Health Care Consumers (CCHCC) October 26, 2017 Welcome! Goals of the Affordable Care Act (ACA)

06/29/2015_830 AM. Healthcare Reform How Will Your Business be Affected in 2015 and Beyond? Introduction

Healthcare Reform How Will Your Business be Affected in 2015 and Beyond? Introduction Overview of ACA Healthcare Reform in 2015 What s on the Horizon Potential Legislative Actions Patient Protection and

Healthcare Reform How Will Your Business be Affected in 2015 and Beyond? Introduction Overview of ACA Healthcare Reform in 2015 What s on the Horizon Potential Legislative Actions Patient Protection and

The Affordable Care Act: Update for Employers. Agenda

The Affordable Care Act: Update for Employers Attorney Gesina (Ena)Seiler gseiler@axley.com Agenda General Overview Health Insurance Marketplaces Employer Shared Responsibility ( Play or Pay ) Employer

The Affordable Care Act: Update for Employers Attorney Gesina (Ena)Seiler gseiler@axley.com Agenda General Overview Health Insurance Marketplaces Employer Shared Responsibility ( Play or Pay ) Employer

Implementing Health Care Reform in the Workplace. Nancy E. Taylor Greenberg Traurig

Implementing Health Care Reform in the Workplace Nancy E. Taylor Greenberg Traurig 1 Health Care Reform THESE PROVISIONS CAN CHANGE A LOT IS UNCERTAIN AND WILL BE SUBJECT TO REGULATIONS/GUIDANCE. WILL

Implementing Health Care Reform in the Workplace Nancy E. Taylor Greenberg Traurig 1 Health Care Reform THESE PROVISIONS CAN CHANGE A LOT IS UNCERTAIN AND WILL BE SUBJECT TO REGULATIONS/GUIDANCE. WILL

Health Insurance Premium Tax Credits and Cost-Sharing Subsidies: In Brief

Health Insurance Premium Tax Credits and Cost-Sharing Subsidies: In Brief Bernadette Fernandez Specialist in Health Care Financing February 10, 2017 Congressional Research Service 7-5700 www.crs.gov R44425

Health Insurance Premium Tax Credits and Cost-Sharing Subsidies: In Brief Bernadette Fernandez Specialist in Health Care Financing February 10, 2017 Congressional Research Service 7-5700 www.crs.gov R44425

Looking for a Life Vest?

Looking for a Life Vest? November 20 th, 2014 @thomasharte Agenda: Looking for a Life Vest? Health Care Reform: What s new with ACA?? Provisions Already in Effect Preparing for Health Care Reform Primary

Looking for a Life Vest? November 20 th, 2014 @thomasharte Agenda: Looking for a Life Vest? Health Care Reform: What s new with ACA?? Provisions Already in Effect Preparing for Health Care Reform Primary

PPACA Implementation and the Marketplaces aka Exchanges. Presented by: Cathy Cooper November 15, 2013

PPACA Implementation and the Marketplaces aka Exchanges Presented by: Cathy Cooper November 15, 2013 Today s Agenda 2014 Provisions Groups over 50 in 2014 Groups under 50 in 2014 Marketplaces aka Exchanges

PPACA Implementation and the Marketplaces aka Exchanges Presented by: Cathy Cooper November 15, 2013 Today s Agenda 2014 Provisions Groups over 50 in 2014 Groups under 50 in 2014 Marketplaces aka Exchanges

The Affordable Care Act: Time to Prepare for 2014 and Beyond

The Affordable Care Act: Time to Prepare for 2014 and Beyond Howard Van Mersbergen Vice President of Employee Benefits, Christian Schools International Brian C. Meekhof Benefits Administrator, Christian

The Affordable Care Act: Time to Prepare for 2014 and Beyond Howard Van Mersbergen Vice President of Employee Benefits, Christian Schools International Brian C. Meekhof Benefits Administrator, Christian

Important Consumer Considerations in Design of Pediatric Dental Benefits

Important Consumer Considerations in Design of Pediatric Dental Benefits Pediatric dental benefits are essential health benefits (EHBs) under federal and state law. 1 Both inside and outside of the Exchange,

Important Consumer Considerations in Design of Pediatric Dental Benefits Pediatric dental benefits are essential health benefits (EHBs) under federal and state law. 1 Both inside and outside of the Exchange,

ACA and The Marketplace. Also known as the (Federal) Exchange

Exchange") ACA and The Marketplace Also known as the (Federal) Exchange 1 Qualified Health Plan and Minimum Essential Coverage (Indiv., Small Group & Large Group Coverage) Needs to Meet the Following (At a Minimum):

ACA and The Marketplace Also known as the (Federal) Exchange 1 Qualified Health Plan and Minimum Essential Coverage (Indiv., Small Group & Large Group Coverage) Needs to Meet the Following (At a Minimum):

Needs for publicly funded behavioral health services under the Patient Protection and Affordable Care Act (ACA): What gaps will remain?

: What gaps will remain?") Needs for publicly funded behavioral health services under the Patient Protection and Affordable Care Act (ACA): What gaps will remain? February 4, 2014 Stan Dorn (sdorn@urban.org) Senior Fellow, Health

Needs for publicly funded behavioral health services under the Patient Protection and Affordable Care Act (ACA): What gaps will remain? February 4, 2014 Stan Dorn (sdorn@urban.org) Senior Fellow, Health

Affordable Care Act and Employers

Affordable Care Act and Employers Important Details about Health Care Reform The Affordable Care Act (ACA, i.e., federal health care reform) makes significant changes to health insurance practices nationwide.

Affordable Care Act and Employers Important Details about Health Care Reform The Affordable Care Act (ACA, i.e., federal health care reform) makes significant changes to health insurance practices nationwide.

The Affordable Care Act (ACA)

") Life Guide The Affordable Care Act (ACA) The Affordable Care Act, or ACA, is the nation's health insurance reform law, initially enacted in March 2010 and being gradually phased in over a period of years.

Life Guide The Affordable Care Act (ACA) The Affordable Care Act, or ACA, is the nation's health insurance reform law, initially enacted in March 2010 and being gradually phased in over a period of years.

T R U S T E D A D V I S O R S. Providing Outstanding Client Service Boston /Cambridge/Newport / Providence / Waltham

T R U S T E D A D V I S O R S Providing Outstanding Client Service Boston /Cambridge/Newport / Providence / Waltham www.kahnlitwin.com Health Care Reform Overview Applicable Large Employer Determination

T R U S T E D A D V I S O R S Providing Outstanding Client Service Boston /Cambridge/Newport / Providence / Waltham www.kahnlitwin.com Health Care Reform Overview Applicable Large Employer Determination

Washington Health Benefit Exchange

Washington Health Benefit Exchange AFFORDABLE CARE ACT 101 APRIL 26, 2013 Christine Brown Navigator/In-person Assister Program Today s Agenda History of the Affordable Care Act (ACA) Highlights of the

Washington Health Benefit Exchange AFFORDABLE CARE ACT 101 APRIL 26, 2013 Christine Brown Navigator/In-person Assister Program Today s Agenda History of the Affordable Care Act (ACA) Highlights of the

Health Care Reform Toolkit Large Employers

Health Care Reform Toolkit Large Employers Table of Contents Introduction... 3 Plan Design and Coverage Issues: 2014 and Beyond... 4 Employer Obligations... 11 Notice and Disclosure Requirements... 19

Health Care Reform Toolkit Large Employers Table of Contents Introduction... 3 Plan Design and Coverage Issues: 2014 and Beyond... 4 Employer Obligations... 11 Notice and Disclosure Requirements... 19

Understanding Health Care Reform

Understanding Health Care Reform Dear adidas Group Employee: Included in this mailing is an important legally required notice that helps you understand the implications of Health Care Reform for 2014.

Understanding Health Care Reform Dear adidas Group Employee: Included in this mailing is an important legally required notice that helps you understand the implications of Health Care Reform for 2014.

Some Basics on the Individual Mandate, Subsidies, and Medicaid Expansion Lisa Klinger, J.D.

Some Basics on the Individual Mandate, Subsidies, and Medicaid Expansion Lisa Klinger, J.D. www.leavitt.com/healthcarereform.com 10-23- 2013 As of January 1, 2014, the Patient Protection and Affordable

Some Basics on the Individual Mandate, Subsidies, and Medicaid Expansion Lisa Klinger, J.D. www.leavitt.com/healthcarereform.com 10-23- 2013 As of January 1, 2014, the Patient Protection and Affordable

Health Insurance Premium Tax Credits and Cost-Sharing Subsidies

Health Insurance Premium Tax Credits and Cost-Sharing Subsidies Bernadette Fernandez Specialist in Health Care Financing April 24, 2018 Congressional Research Service 7-5700 www.crs.gov R44425 Summary

Health Insurance Premium Tax Credits and Cost-Sharing Subsidies Bernadette Fernandez Specialist in Health Care Financing April 24, 2018 Congressional Research Service 7-5700 www.crs.gov R44425 Summary

Healthcare Reform: The Affordable Care Act Implications for Employers and Individuals

Healthcare Reform: The Affordable Care Act Implications for Employers and Individuals Chet Lilly Business Manager June 2013 P C A R e t i r e m e n t & B e n e f i t s, I n c. H e a l t h c a r e R e f

Healthcare Reform: The Affordable Care Act Implications for Employers and Individuals Chet Lilly Business Manager June 2013 P C A R e t i r e m e n t & B e n e f i t s, I n c. H e a l t h c a r e R e f

It s a new world! Health Care Changes and the ACA

It s a new world! Health Care Changes and the ACA Today s Agenda 2 MHC Who we are Understanding the Problem Understanding the Affordable Care Act Understanding Insurance Exchanges Moving Forward Montana

It s a new world! Health Care Changes and the ACA Today s Agenda 2 MHC Who we are Understanding the Problem Understanding the Affordable Care Act Understanding Insurance Exchanges Moving Forward Montana

What s Inside STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT (ACA)

") What s Inside Step 1: What Understand what you re buying 4 Step 2: How How can you buy health insurance? 18 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT (ACA) Want to know more about the health reform

What s Inside Step 1: What Understand what you re buying 4 Step 2: How How can you buy health insurance? 18 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT (ACA) Want to know more about the health reform

H E A L T H C A R E R E F O R M T I M E L I N E

H E A L T H C A R E R E F O R M T I M E L I N E On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act (ACA), into law. The ACA makes sweeping changes to the U.S.

H E A L T H C A R E R E F O R M T I M E L I N E On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act (ACA), into law. The ACA makes sweeping changes to the U.S.

What s Inside STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT (ACA)

") What s Inside Step 1: What Understand what you re buying 4 Step 2: How How can you buy health insurance? 20 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT (ACA) Want to know more about the health reform

What s Inside Step 1: What Understand what you re buying 4 Step 2: How How can you buy health insurance? 20 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT (ACA) Want to know more about the health reform

Nonappropriated Fund (NAF)

") Nonappropriated Fund (NAF) AFFORDABLE CARE ACT FOR NAF EMPLOYEES AND RETIREES Questions and Answers 2014 The below questions and answers only apply to those NAF employees eligible for the DoD NAF Health

Nonappropriated Fund (NAF) AFFORDABLE CARE ACT FOR NAF EMPLOYEES AND RETIREES Questions and Answers 2014 The below questions and answers only apply to those NAF employees eligible for the DoD NAF Health

The Affordable Care Act; 2014 and Beyond

The Affordable Care Act; 2014 and Beyond Presented by: Lacey Robinson, ACA Certified Vice President & Senior Benefits Consultant Gregory & Appel December 10, 2013 Agenda 2014 ACA Mandates ACA Intention

The Affordable Care Act; 2014 and Beyond Presented by: Lacey Robinson, ACA Certified Vice President & Senior Benefits Consultant Gregory & Appel December 10, 2013 Agenda 2014 ACA Mandates ACA Intention

TO UNDERSTANDING THE AFFORDABLE CARE ACT

3 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT What s Inside Step 1: What Understand what you re buying 4 Step 2: How How can you buy health insurance? 20 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT

3 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT What s Inside Step 1: What Understand what you re buying 4 Step 2: How How can you buy health insurance? 20 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT

Health Reform Update. April 1, Presented by: Chip Kerby Liberté Group LLC (202)

") Health Reform Update April 1, 2010 Presented by: Chip Kerby Liberté Group LLC chip@libertegroup.com (202) 756-2459 Agenda Background Key elements Impact on stakeholders 1 Background Sources of Coverage

Health Reform Update April 1, 2010 Presented by: Chip Kerby Liberté Group LLC chip@libertegroup.com (202) 756-2459 Agenda Background Key elements Impact on stakeholders 1 Background Sources of Coverage

MYTHS & REALITIES OF HEALTH CARE REFORM

MYTHS & REALITIES OF HEALTH CARE REFORM The Florida Bar Solo & Small Firm Annual Conference January 25, 2014 Presented By: Kirsten Vignec Shareholder Introduction On March 23, 2010, the Patient Protection

MYTHS & REALITIES OF HEALTH CARE REFORM The Florida Bar Solo & Small Firm Annual Conference January 25, 2014 Presented By: Kirsten Vignec Shareholder Introduction On March 23, 2010, the Patient Protection

Monitoring the ACA s. Vital Signs. The Affordable Care Act A Progress Report

Monitoring the ACA s Vital Signs The Affordable Care Act A Progress Report Today s Discussion Affordable Care Act Some Foundational Knowledge Affordable Care Act Compliance Requirements Plan Design Reporting

Monitoring the ACA s Vital Signs The Affordable Care Act A Progress Report Today s Discussion Affordable Care Act Some Foundational Knowledge Affordable Care Act Compliance Requirements Plan Design Reporting

THE PATIENT PROTECTION AND AFFORDABLE CARE ACT UPDATE

THE PATIENT PROTECTION AND AFFORDABLE CARE ACT UPDATE February 21, 2013 Jonathan Alexander, Esq. Compliance Counsel Pinnacle Claims Management, Inc. Copyright 2013 Pinnacle Claims Management, Inc. Reproduction

THE PATIENT PROTECTION AND AFFORDABLE CARE ACT UPDATE February 21, 2013 Jonathan Alexander, Esq. Compliance Counsel Pinnacle Claims Management, Inc. Copyright 2013 Pinnacle Claims Management, Inc. Reproduction

By Larry Grudzien Attorney at Law

By Larry Grudzien Attorney at Law 1 What is a small employer? Fees and Taxes 90 day Waiting Period Pre-existing condition Out-of Pocket Limits Wellness Programs Approved Clinical Trials Cafeteria Plans

By Larry Grudzien Attorney at Law 1 What is a small employer? Fees and Taxes 90 day Waiting Period Pre-existing condition Out-of Pocket Limits Wellness Programs Approved Clinical Trials Cafeteria Plans

Dennis G. Shea, Ph.D. Associate Dean for Undergraduate Programs and Outreach Professor of Health Policy and Administration College of Health and

Dennis G. Shea, Ph.D. Associate Dean for Undergraduate Programs and Outreach Professor of Health Policy and Administration College of Health and Human Development Summary of before 2010 Overview What is

Dennis G. Shea, Ph.D. Associate Dean for Undergraduate Programs and Outreach Professor of Health Policy and Administration College of Health and Human Development Summary of before 2010 Overview What is

The New Healthcare Law and Its Impact on Small Business

U. S. Small Business Administration Washington Metropolitan Area District Office The New Healthcare Law and Its Impact on Small Business Julie C. Verratti Advisor U.S. Small Business Administration Julie.Verratti@sba.gov

U. S. Small Business Administration Washington Metropolitan Area District Office The New Healthcare Law and Its Impact on Small Business Julie C. Verratti Advisor U.S. Small Business Administration Julie.Verratti@sba.gov