Flood Compliance by the Case

|

|

|

- Deirdre Kelley

- 6 years ago

- Views:

Transcription

1 Flood Compliance by the Case A CASE STUDY APPROACH FOR LENDERS Presented by: 1 Topic 1: Private Flood Insurance Topic 2: Force Placement Topic 3: Condo Conundrum Here s our agenda for today Topic 4: Escrows Topic 5: Detached Structures Exemption Topic 6: Insurable Value Topic 7: Resources 3 1

2 Topic 1 PRIVATE FLOOD INSURANCE 4 Private Flood Questions Ask The Expert Private Flood Insurance Q. How does a bank ensure adequacy to regulations when presented with a private flood policy? Q. What are the safety & soundness risks faced when NFIP limits on commercial insurance are $500K but a building has insurable value of $2M? Should banks be requiring more flood insurance? 5 2/20/2018 2

3 Private Flood Insurance Talking Points History of Private Flood Insurance: Private Flood Insurance Suggested guidelines appeared in Mandatory Purchase booklet for years March 2012: FEMA clarified its position (advisory, not regulatory) July 2012: BW-12 enacted (Sec defined components) October 2013: Joint Notice of Proposed Rulemaking (Safe harbors) March 2014: HFIAA enacted No private flood insurance amendment June 25, 2015: H.R & S introduced in Congress November 7, 2016: Joint Notice of Proposed Rulemaking Loans in Areas Have Special Flood Hazards - Private Flood Insurance Federal Register publication date 7 Private Flood Insurance Talking Points Private Flood Insurance NFIP set to expire 9/30/17 requires reauthorization (Extended to 3/23/18) Flood Insurance Market Parity and Modernization Act (Private Flood Insurance Market Development Act of 2017) H.R passed the House 4/28/16 (H.R /8/17) S received in Senate 5/9/16 (S /8/17) Proposes that Federal Flood Insurance and Private Flood Insurance are equal remedies for mandatory purchase of flood insurance Establishes that any period of continuous coverage by private flood insurance meets the standard and is considered a period of continuous coverage for any statutory, regulatory or administrative continuous coverage requirement 8 3

4 Private Flood Insurance Talking Points Private Flood Insurance Proposes requirements regarding financial strength of private flood insurance companies That do not affect or conflict with any state law, regulation or procedure concerning the regulation of the business of insurance Environment favorable to private flood insurance market Admitted insurance carriers vs. Non-admitted carriers Resolving the Confusion About Admitted and Non-Admitted Carriers 9 Non-NFIP Flood Coverage Examples of other types of flood policies/coverage Standalone Flood Policy Admitted carrier Non-admitted carrier Difference in Condition Policy (DIC) Commercial Property Policy w/flood endorsement Mobile-Home policies All-Risk Builder s Risk Policy Manuscript Policy Self-insurance Coverage Excess Flood Policy Got You Confused? 10 4

5 Private Flood Insurance Talking Points Private Flood Insurance Loans in Areas Having Special Flood Hazards Private Flood Insurance (Joint Notice of Proposed Rulemaking) A. Definitions Mutual Aid Society Private Flood Insurance At least as broad as (1/2 dozen items to research specific, not simple) B. Requirement to purchase flood insurance Meets statutory definition of private flood insurance Meets the mandatory purchase requirement C. Compliance aid for mandatory purchase Meets definition of private flood insurance if: Policy has written summary describing how it meets definition Lender verification in writing that policy meets definition Endorsement/provision within policy that states definition met 11 Private Flood Insurance Talking Points Private Flood Insurance Loans in Areas Having Special Flood Hazards Private Flood Insurance (Joint Notice of Proposed Rulemaking) D. Discretionary Acceptance Authorized insurer Covers lender and borrower as loss payees Cancellation for same reasons as SFIP Coverage as broad as or similar to SFIP Exception for mutual aid societies Discretionary acceptance for non-residential property 12 5

6 Private Flood Questions Ask The Expert Non-NFIP Flood Insurance Q: In the absence of regulations, how does a lender determine whether a private flood insurance policy is acceptable? 14 2/20/ Private Flood Insurance Talking Points Private Flood Insurance Original private flood insurance criteria: Licensure Licensed, admitted or approved by State insurance regulator Surplus lines recognition (non-residential commercial) Carrier should be recognized, or not disapproved, as a surplus lines carrier Requirement of 45-day cancellation/non-renewal notice Policy should be as restrictive as SFIP s cancellation provisions Breadth of policy coverage Similar mortgage clause Legal recourse 15 6

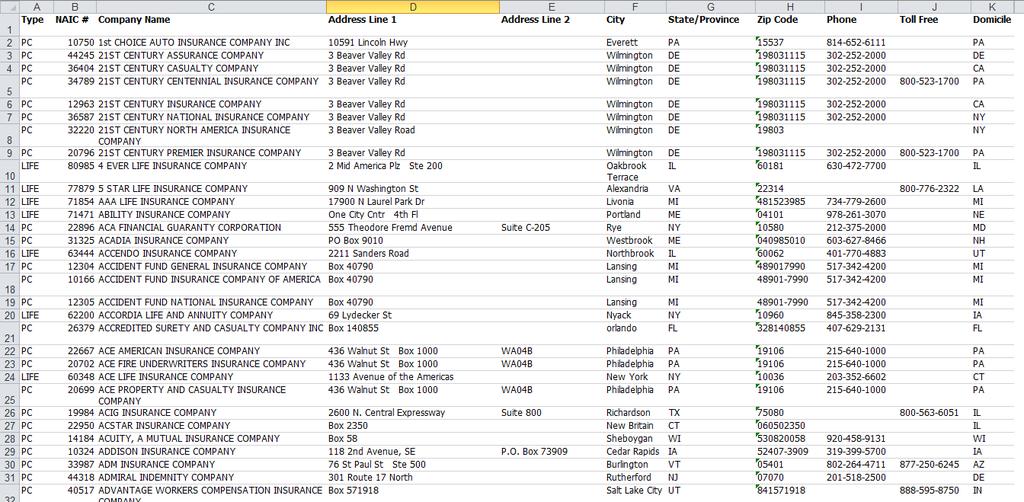

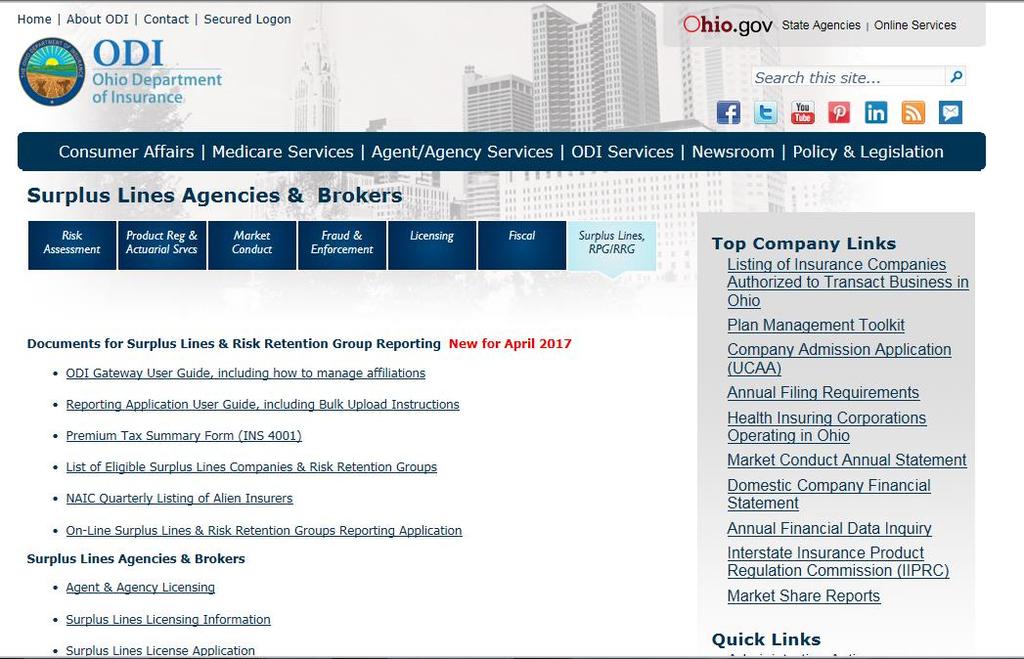

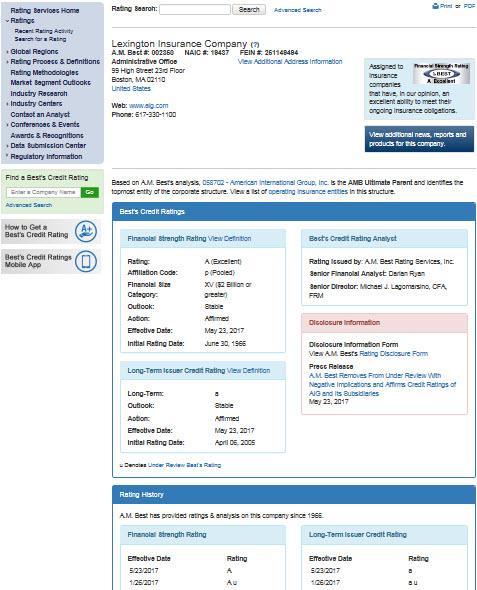

7 Private Flood Insurance Talking Points Private Flood Insurance Resources for vetting private market flood insurance carriers Department of insurance websites Demo 1: Ohio Department of Insurance Demo 2: Florida Office of Insurance Regulation Demo 3: A.M. Best Rating Service by Company Demo 4: Best s Financial Strength Rating Guide 16 7

8 8

9 9

10 10

11 Private Flood Insurance Talking Points Private Flood Insurance Resources for vetting private market flood insurance carriers Department of insurance websites Demo 1: Ohio Department of Insurance Demo 2: Florida Office of Insurance Regulation Demo 3: A.M. Best Rating Service by Company Demo 4: Best s Financial Strength Rating Guide 25 11

12 12

13 Private Flood Insurance Talking Points Private Flood Insurance Resources for vetting private market flood insurance carriers Department of insurance websites Demo 1: Ohio Department of Insurance Demo 2: Florida Office of Insurance Regulation Demo 3: A.M. Best Rating Service by Company Demo 4: Best s Financial Strength Rating Guide 28 A.M. Best Rating Guide 13

14 A.M. Best Rating Guide 14

15 Private Flood Insurance Talking Points Private Flood Insurance Resources for vetting private market flood insurance carriers Department of insurance websites Demo 1: Ohio Department of Insurance Demo 2: Florida Office of Insurance Regulation Demo 3: A.M. Best Rating Service by Company Demo 4: Best s Financial Strength Rating Guide 32 15

16 Private Flood Questions Ask The Expert Non-NFIP Flood Insurance Q: What are some considerations for a borrower when switching to private flood insurance? 34 2/20/ Private Flood Insurance Talking Points Private Flood Insurance Pros: In competitive market, coverage may be less expensive Coverage may be broader Available coverage limits may be higher Greater flexibility with deductibles. Cons: Private market may not always be price competitive Possible loss of rating subsidy if borrower (insured) returns to NFIP for coverage Private market capacity and availability may vary with market conditions 35 16

17 Topic 1 CASE FILE Reform legislation encourages expansion of private flood insurance 2. FEMA guidance advisory, not regulatory 3. Legislators and regulators are reevaluating their approaches to private flood insurance CASE FILE NOTES 37 17

18 Topic 2 FORCE PLACEMENT 38 Force Placement Question Ask The Expert Force Placement Question I am confused about when I can force place flood insurance and when I have to send the notice. Seems like every time I think I have it down, something else comes along that seems to change what I think I know. When I determine that my borrower s flood coverage has lapsed and I send out the 45-day notice, can I force place the coverage right away so there s not any interruption in the coverage? 39 2/20/

19 Force Placement Overview Lender determines at any time during the life of the loan that property securing the loan is located in SFHA; Flood insurance is available; Flood insurance is inadequate or does not exist; and After required notice, borrower fails to purchase appropriate amount of coverage. Send 45 day letter Allow time for borrower to purchase flood insurance Force Place? 40 Impact of Biggert-Waters Reform Act Sec Force Placement Final Rule Required 45-day notice must be sent: Upon receipt of a notice of cancellation or expiration from an insurance provider or internal flood monitoring system When lender learns a property is now a designated loan due to a map change FINAL RULE Clarifies that the required notice must be sent following the date of lapse or insufficient coverage notification. Only courtesy notice prior

20 Impact of Biggert-Waters Reform Act Sec Force Placement Premium and fees a lender or servicer may charge include: Premium or fees incurred for coverage Beginning on the date flood insurance coverage lapsed or, Did not provide sufficient coverage amount FINAL RULE Lapsed date = policy expiration date or effective date the policy is cancelled 42 Impact of Biggert-Waters Reform Act Sec Force Placement Final Rule clarifies a lender or servicer may force place coverage: Any time during 45-day notice period Do not have to wait 45 days after providing notice to force place Force placing prior to expiration of 45-day notice period may create additional work effort NOTE There can be a distinction made between when a policy is put in place and when it is effective. Consider force placing effective the day after expiration

21 Impact of Biggert-Waters Reform Act Sec Force Placement Requires lender or servicer within 30 days of: Receiving confirmation of borrower s coverage Notify insurer to terminate force-place insurance Refund all force-placed premium and fees paid by borrower During any overlap in coverage FINAL RULE Lender required to notify insurer to cancel. 44 Impact of Biggert-Waters Reform Act Sec Force Placement Requires lender or servicer to: Accept borrower s existing policy declarations page as confirmation Declarations page must include: Identity/Contact information for insurance company or agent Existing policy number Lender may accept alternative evidence FINAL RULE Lender responsible for determining adequacy of coverage. If inadequate, notify borrower

22 Topic 2 CASE FILE Can charge force place premium and fees from date of lapse 2. Date of lapse equals the policy s expiration date or the effective date the policy is cancelled 3. Notify insurer to terminate force placed policy within 30 days of confirmation of borrower s existing flood insurance coverage CASE FILE NOTES 47 22

23 Force Placement Question Ask The Expert Force Placement Question When I force place flood coverage for one of my borrowers, is that considered a MIRE event? I have heard conflicting opinions on this topic. 48 2/20/2018 Three Categories Force Place as MIRE Event Category 1 Premium/fees added to UPB Insurance amount must include FP premium and fees Triggering event depends on loan contract Category 2 Premium/fees added to an unsecured account If FP is in separate, unsecured account: Not an increase Not a triggering event Category 3 Premium/fees billed to borrower Not an increase/triggering event If borrower fails to pay, see Categories 1 &

X 1.00 = $2,000 UPB increases to $202,000 Amount of FP = $200,000 $2,0(00) X 1.00 = $20 UPB increases to $202,020 Amount of FP = $202,000 $100 X 1.")

24 Single family dwelling: $350,000 insurable value $200,000 loan amount Fails to renew flood policy Need to force place Adding premium/fees to UPB Cost of FP flood policy: $2,000 Equals $1 per $100 coverage limit $200,0(00) X 1.00 = $2,000 UPB increases to $202,000 Amount of FP = $200,000 $2,0(00) X 1.00 = $20 UPB increases to $202,020 Amount of FP = $202,000 $100 X 1.00 = $1 UPB increases to $202,021 Amount of FP = $202, Force Placement Question Ask The Expert Force Placement Question Q. Can we renew a loan using an existing lender force placed flood insurance policy? A. Assuming the force placed policy is in effect and otherwise satisfies the regulatory coverage standards, then that policy may satisfy the mandatory purchase requirement. The term flood insurance is sufficiently broad in scope to include force placed policies. 51 2/20/2018 (Interagency Flood Insurance Regulation Update 10/22/15, Q. 8) 24

25 Topic 3 CONDO CONUNDRUM 52 Condo Conundrum Question Ask The Expert Condo Conundrum Part 1 I found your training very informative. My only complaint it was not long enough. I do have a question on Condo insurance. We have a Condo policy RCBAP that has $500,000 in coverage and has four units. We were dividing the $500,000 by 4 = $125,000 per unit. The customer s loan has a balance of $131,000. We are requiring the customer to obtain his own policy for $6,000 to cover the balance. Is that correct? 53 2/20/

26 Condo Condundrum Question Ask The Expert Condo Conundrum Part 2 I have spoken to you before at the Minnesota Bankers Association Advanced Compliance Workshops. I hope you can help answer a question for me. We have a loan secured by a condo in Florida. The RCV on the building is $35,249,400, but the RCBAP policy is written at a limit of $28,199,500, which is 80% of RCV. Policy says 100% Replacement Cost. It appears this is ok per the FEMA guidelines. However, there are 126 units, so this is flood coverage of $223, per unit. We have a loan for greater than $250,000 and the unit value is more than $250,000. My Question: Are we required to have $250,000 of flood insurance coverage? If so, this means the borrower will have to purchase a policy for the difference of $26, /20/ Condo Coverage Talking Points Condo Conundrum RCBAP co-insurance clause/penalty Avoid if insured to max limit, or 80% of RCV at time of loss At 80%, building is 20% uninsured Coverage limit division Assumes all units are identical Discuss 4-unit condo building Discuss 126-unit condo building 55 26

27 Condo Coverage Talking Points Condo Conundrum 4-unit residential condominium building 3 units identical in size and value 4 th unit is two floors - double size and value of other 3 units 126-unit residential condominium building Building has 1, 2 and 3 bedroom units All different sizes all 2 bedrooms not the same size Cookie cutter approach all units equal Approach used in Q Interagency Q&As May look to percentage of ownership see assessments 56 4-Unit Residential Condo Building Unit 4 Unit 3 Unit 2 Unit 1 $500,000 Coverage Limit Unit 4 $500K X.40 = $200,000 vs. $500K X.25 = $125,000 Unit 1 = 20% Ownership Unit 2 = 20% Ownership Unit 3 = 20% Ownership Unit 4 = 40% Ownership 57 27

28 Topic 4 ESCROWS 59 Revised Escrow Requirements Reform Legislation Escrows Revised escrow provisions effective 1/1/16 Applies to residential improved real estate with a triggering event only Escrow notification part of notice to borrower Notice of Special Flood Hazards updated Small lender and loan exceptions to escrow requirement Mandatory escrows in place since National Flood Insurance Reform Act of

29 Escrow Question Ask The Expert Escrows Q: If a small lender requires the escrow of taxes or insurance premiums only under certain conditions or for only a portion of the loan term, is it considered to have a policy of consistently and uniformly requiring escrows? 62 2/20/ Small Lender Exception Less than $1 billion in assets if on or before July 6, 2012: Not required under Federal or State law to: Deposit taxes, insurance premiums, fees, or any other charges in an escrow account for the entire term of the loan secured by residential improved real estate or a mobile home and: Did not have a policy of consistently and uniformly requiring: The deposit of taxes, insurance premiums, fees, or any other charges in an escrow account for any loans secured by residential improved real estate or a mobile home. Less than $1 billion in assets: Either of prior two calendar years as of 12/31: Less than $1 billion on 12/31/16 More than $1 billion on 12/31/17 Small lender exception applies on 1/1/18 If still more than $1billion on 12/31/18: Lose small lender exception (2 prior years > $1B) Change in Status: More than $1 billion in assets (2 prior years): Effective July 1 First calendar year of changed status Must escrow flood insurance premium and fees Designated loans: Made, Increase, Renewed or Extended On or after July

30 Escrow Question Ask The Expert Escrows Q: If a small lender requires the escrow of taxes or insurance premiums only under certain conditions or for only a portion of the loan term, is it considered to have a policy of consistently and uniformly requiring escrows? 64 2/20/ Escrow Talking Points Escrows Does institution pass all three tests for small exception? Does institution have total assets < $1 billion in one or both of two prior calendar years? (Key Date: 12/31) Was not required as of BW-12 date of enactment (7/6/12) under federal or state law to deposit taxes, insurance premiums, fees, etc. into an escrow account for the entire term of any loan secured by residential improved real estate/mobile home. (HPML?) Did not have a policy of consistently and uniformly requiring deposit of taxes, premiums, fees, etc. into an escrow account for any loans secured (PMI/taxes above LTV threshold?) 65 30

31 EXCEPTIONS Reform Legislation Escrows Escrows: Final Joint Regulatory Guidance Six exceptions to escrow requirement: 1. Loan primarily for business, commercial or agricultural purpose 2. Subordinate liens when flood insurance is provided at time of loan origination 3. Condominiums, cooperatives, homeowner associations, etc. 4. Home equity lines of credit 5. Non-performing loans (90 or more days past due) 6. Short-term loans 66 EXCEPTION 1 Reform Legislation Escrows Escrow Exceptions: Final Joint Regulatory Guidance Loan primarily for business, commercial or agricultural purpose: Residential improved real estate or mobile home Portion of collateral Escrow requirement does not apply 67 31

32 EXCEPTION 2 Reform Legislation Escrows Escrow Exceptions: Final Joint Regulatory Guidance Subordinate liens when flood insurance is provided at time of loan origination: No requirement to monitor lien position prospectively If lender determines the exception no longer applies Receives notice senior lien paid off Determines at subsequent triggering event Must begin escrowing premium and fees 68 EXCEPTION 3 Reform Legislation Escrows Escrow Exceptions: Final Joint Regulatory Guidance Condominiums, cooperatives, homeowner associations, etc.: Flood insurance meets mandatory purchase requirements Is provided and premium paid for by: Condominium Association Cooperative Homeowner Association or other applicable group Escrows required if: Borrower purchases own coverage 69 32

33 EXCEPTION 4 Reform Legislation Escrows Escrow Exceptions: Final Joint Regulatory Guidance Home equity lines of credit: Statute does not include any exclusion to the HELOC exception Fully drawn HELOCs included Escrows are not required 70 EXCEPTION 5 Reform Legislation Escrows Escrow Exceptions: Final Joint Regulatory Guidance Non-performing loans (90 or more days past due): Remains non-performing unless: Permanently modified Entire past due amount collected or discharged Principal Accrued interest Penalty interest 71 33

34 EXCEPTION 6 Reform Legislation Escrows Escrow Exceptions: Final Joint Regulatory Guidance Short-term loans: Must be no longer than 12 months to qualify Extensions of 12 month or less Exception applies Triggering event 72 Escrow Talking Points Reform Legislation Escrows Escrows: Final Joint Regulatory Guidance Escrow Notice Mail or deliver notice to borrower that escrow of premiums and fees may be required Provide the escrow notice as part of Notice of Special Flood Hazards and Availability of Federal Disaster Relief Sample notice provided by regulators in Appendix A of bulletin 73 34

35 Escrow Talking Points Reform Legislation Escrows Escrows: Final Joint Regulatory Guidance Escrow Notice Clarification Notice required for excepted loans May lose exception during term of loan Will be informed escrows may be required Federal law may require a lender or its servicer to escrow all premiums and fees for flood insurance that covers any residential building or mobile home securing a loan that is located in an area with special flood hazards. If your lender notifies you that an escrow account is required for your loan, then you must pay your flood insurance premiums and fees to the lender or its servicer with the same frequency as you make loan payments for the duration of your loan. 74 Option to Escrow (01/16) Required lenders to offer and make available to borrower the option to escrow Option does not apply to: Loans or lenders excepted as of 01/01/16 Loans already escrowing for flood insurance Deliver notice to borrowers by June 30, 2016 Change of status lenders: September 30 th First calendar year of status change Can be separate notice or added to another disclosure, eg. Periodic statements When requested, begin escrow as soon as reasonably practicable 75 35

36 Escrow Question Ask The Expert Escrows Q: Do map changes trigger the mandatory escrow rules? Don t confuse mandatory purchase with mandatory escrow Need tripwire for escrow 76 2/20/ Escrow Question Ask The Expert Escrows Q: If you have previously waived escrow for taxes and hazard insurance, do you still have to escrow for flood insurance? Can flood escrow be waived? If you are required to escrow for flood under the revised escrow rule, then you must escrow for flood regardless of your decision on other escrows. 77 2/20/

37 Escrow Question Ask The Expert Escrows Q: Do lenders need to escrow for flood when a property is not in an SFHA but the borrower buys flood insurance? Required when: Secured by residential improved real estate Located in a Special Flood Hazard Area Experienced a triggering event on or after 1/1/ /20/ Topic 4 CASE FILE 79 37

38 1. Escrows affect residential improved real estate or mobile homes with triggering event 2. A small lender exception applies to regulated lending institutions with total assets < $1 billion 3. Six loan exceptions to the escrow requirement exist CASE FILE NOTES 80 Topic 5 DETACHED STRUCTURES 81 38

39 Detached Structures Question Ask The Expert Detached Structures I am hoping you can answer a question for me. We attended a webinar and were given information concerning exclusion from the mandatory purchase requirement. It stated The act authorizes the exclusion of detached structures that are not used for residential purposes from the mandatory purchase of flood insurance requirement. We currently have a loan that has the dwelling in zone X but the barn is in zone AE. Do we have to have flood insurance for the barn? 82 2/20/2018 Detached Structures Talking Points Detached Structures Exemption - HFIAA Profile of Issue: HFIAA allows mandatory purchase exemption for certain detached structures (3) DETACHED STRUCTURES. Notwithstanding any other provision of this section, flood insurance shall not be required, in the case of any residential property, for any structure that is a part of such property but is detached from the primary residential structure of such property and does not serve as a residence. Three Components Required: Applies to Residential Property Detached from primary residential structure Does not serve as a residence 83 39

40 Detached Structures Talking Points Final Joint Regulatory Guidance: Although you may not be required to maintain flood insurance on all structures, you may still wish to do so, and your mortgage lender may still require you to do so to protect the collateral securing the mortgage. If you choose not to maintain flood insurance on a structure and it floods, you are responsible for all flood losses relating to the structure. Detached Structures Exemption - HFIAA Regulators agree exemption became effective upon enactment. Exemption addresses concerns on low-value structures Provides discretionary authority to require coverage Notice of Special Flood Hazards amended 84 3 Components Detached Structures Exemption 1 Applies to a residential property Purpose of loan is immaterial when residence secures a loan Broadly defined to include any residential building A structure that is part of a residential property: Refers to a property used primarily for personal, family or household purposes Not commercial, agricultural or other business use 2 Applies to a detached structure Detached from the primary residential structure Detached is defined as a building that stands alone Not joined by any structural connection to the residential structure 3 Does not serve as a residence No single bright line test; Focus on structure s intended use Rely on good faith determination of lender Could serve as residence if it generally includes sleeping, bathroom or kitchen facilities 85 40

41 Detached Structures Talking Points Detached Structures Exemption - HFIAA Final Joint Regulatory Guidance: Further Clarification on serves as a residence : Detached structures can vary greatly Sleeping, bathroom and kitchen all three not necessary to serve as a residence No duty to monitor status of detached structure Must re-examine on future triggering event Send borrower notice if lender determines building becomes subject to mandatory purchase 86 Detached Structures Question Ask The Expert Detached Structures Exemption Q: If a commercial loan is secured by a personal guaranty provided by the principal owner of a commercial entity, with a mortgage on his or her residence, may a detached structure on the residential property be eligible for the exemption? 88 2/20/

42 Detached Structures Talking Points Detached Structures Exemption Exemption applies regardless of the purpose of the loan* Just so long as a residential property is secured Affordability issues are the same Exemption only a remedy for residential properties and not commercial, business or agricultural Homeowner Flood Insurance Affordability Act not Business or Farm owner *NOTE: Escrow requirement only consumer loans 89 Detached Structures Question Ask The Expert Detached Structures Exemption Q: If one of our borrowers currently has a flood policy on a detached structure that meets the exemption s requirements, can we cancel our requirement for flood insurance? Can our borrower cancel their policy and get a refund? 90 2/20/

43 Detached Structures Talking Points Detached Structures Exemption Borrower is no longer required by statute to have flood insurance on a building(s) meeting the exemption s requirements Lender may rescind its flood insurance mandate For safety and soundness, lender may want to continue coverage mandate on higher valued detached structures NFIP policies can be cancelled mid-term with cancellation effective the date the cancellation request and supporting documentation are received by insurance carrier Documentation: Signed statement from policyholder that policy no longer required by lender for a detached structure 91 Topic 5 CASE FILE 92 43

44 1. Applies to property used primarily for personal, family or household purposes. 2. Lenders can exercise discretion in their use of the exemption. 3. To be exempted the detached structure may not serve as a residence. CASE FILE NOTES 93 Topic 6 INSURABLE VALUE 94 44

45 Calculating Insurable Value 96 Calculating Insurable Value

46 RCV vs. ACV Replacement Cost Value Cost to repair or replace a building Material of similar kind and quality No deduction for depreciation RCV does not include land values RCV is not market value Calculating Insurable Value 101 RCV vs. ACV Actual Cash Value Cost to replace an insured item of property at time of loss Less the value of its physical depreciation Based on age, wear and tear Replacement cost less depreciation Calculating Insurable value

47 Types of Policies Which to use? What s the purpose of the structure? 103 Applies to: Residential building for 1 to 4 families Also applies to: Individual condo units Manufactured homes Renters (for contents) Dwelling Form

48 Replacement Cost Loss Settlement Building Coverage Only Single Family Dwellings Principal Residence Properly Insured to Value 80% of RCV Max Limit Available Dwelling Form 105 Actual Cash Value Loss Settlement 2 4 Family Dwellings Mobile Homes <16 ft wide and 600 sq. ft. Single Family Not insured to value Not principal residence Contents Detached Garage 10% extension Dwelling Form

49 Actual Cash Value Loss Settlement Residential (More than 4 families) Non-residential buildings Commercial Schools, churches Farm buildings Industrial buildings Warehouses Hotels < 6 months Mixed-use buildings less than 75% residential General Property Form 107 Replacement Cost Loss Settlement** Replacement Cost Loss Settlement** Buildings owned by condo associations 75% of floor area residential High rise buildings Low rise buildings Townhouse/Rowhouse Detached single family condos Residential Condominium Building Association Policy 108 ** Subject to co-insurance penalty if not properly insured to value. 49

50 Replacement Cost Value (RCV) RCV Single Family Dwelling Principal Residence Insured to Value Residential Condo Buildings RCBAP Coverage Form Insured to Value Replacement Cost Loss Settlement Summary 109 Actual Cash Value (ACV) Everything Else Actual Cash Value Loss Settlement Summary

51 Insurable Value Final Answer Appraisal based on cost-value approach Reconstruction cost Reconstruction less depreciation Insurance value approaches/methods 111 Insurable Value Final Answer Appraisal based on cost-value approach Construction-cost calculation Residential cost estimators Commercial cost estimators Google on Internet Industry leader obvious Replacement cost calculations Depreciated values Insurance value approaches/methods

52 Insurable Value Final Answer Appraisal based on cost-value approach Construction-cost calculation Insurable value used in hazard policy Insurance value approaches/methods 113 Insurable Value Final Answer Appraisal based on cost-value approach Construction-cost calculation Insurable value used in hazard policy Any other reasonable approach that can be supported Insurance value approaches/methods

53 Topic 6 CASE FILE No one single solution to calculating insurable value. 2. NFIP losses are typically settled on either an Actual Cash Value or Replacement Cost Value basis. 3. Regulators have defined a series of approaches to defining insurable value. CASE FILE NOTES

54 Topic 7 RESOURCES 126 National Flood Insurance Program Home Page

http://www.occ.")

55 NFIP Flood Insurance Manual Access the NFIP Flood Insurance Manual: Online at the Flood Insurance Library: Links to Final Rule Loans in Areas Having Special Flood Hazards (June 2015) a.pdf

")

56 Links to Interagency Q&As Interagency Q & As Regarding Flood Insurance (July 2009) Interagency Q & As Regarding Flood Insurance (October 2011) Proposed Rule: Private Flood Insurance Federal Register Publication: Click Here

57 Reform Act Legislation and more Online at: Visit the Map Service Center

58 Evaluations - Online All attendees will be receiving an with a link to a survey and feedback form. Please take time to complete and help us improve our training effort! Presented by: 134 Training Information Like us on Facebook at: Rich Slevin rich@h2opartnersusa.com Mike Moye mmoye@h2opartnersusa.com Melanie Graham melanie@h2opartnersusa.com Rich Waalkes rwaalkes@h2opartnersusa.com Aaron Montanez producer@h2opartnersusa.com

, The National Flood Insurance Program (NFIP), any Federal Entity for Lending Regulation or Government")

59 Any views or opinions presented in this webinar are solely those of the speakers. They do not represent the Federal Emergency Management Agency (FEMA), The National Flood Insurance Program (NFIP), any Federal Entity for Lending Regulation or Government Sponsored Enterprise (GSE). Always consult your regulatory entity for definitive guidance

Flood Compliance: Final Rules in 60!

Flood Compliance: Final Rules in 60! A RULE-BY-RULE APPROACH FOR LENDERS Presented by: 1 Flood Compliance: Final Rules in 60! A RULE-BY-RULE APPROACH FOR LENDERS Rich Slevin Flood Compliance & Education

Flood Compliance: Final Rules in 60! A RULE-BY-RULE APPROACH FOR LENDERS Presented by: 1 Flood Compliance: Final Rules in 60! A RULE-BY-RULE APPROACH FOR LENDERS Rich Slevin Flood Compliance & Education

Key Fundamentals of Flood Compliance!

a Welcome to Key Fundamentals of Flood Compliance! An entry-level approach for lenders [Photo credit: Oliver Gruener] We will get started in a few minutes. Presented Meanwhile, by: let s perform a warm

a Welcome to Key Fundamentals of Flood Compliance! An entry-level approach for lenders [Photo credit: Oliver Gruener] We will get started in a few minutes. Presented Meanwhile, by: let s perform a warm

Welcome to Demystifying the Interagency Q&A! 10/28/2013. National Flood Insurance Program. Demystifying the Lender Q&As

Demystifying the Lender Q&As National Flood Insurance Program 1 Welcome to Demystifying the Interagency Q&A! We will get started in a few minutes. Meanwhile, let s perform a warm up exercise. 2 1 Seminar

Demystifying the Lender Q&As National Flood Insurance Program 1 Welcome to Demystifying the Interagency Q&A! We will get started in a few minutes. Meanwhile, let s perform a warm up exercise. 2 1 Seminar

Flood Insurance Requirements

Flood Insurance Requirements Patti Joyner Blenden, CRCM Financial Solutions April 2018 1 Flood Disaster Protection Act (FDPA) Requires homeowners in flood hazard areas to purchase insurance to close a

Flood Insurance Requirements Patti Joyner Blenden, CRCM Financial Solutions April 2018 1 Flood Disaster Protection Act (FDPA) Requires homeowners in flood hazard areas to purchase insurance to close a

TOP 10 Flood Insurance Changes

TOP 10 Flood Insurance Changes What Every Floodplain Official Should Know Rich Slevin, H 2 O Partners Dorothy Martinez, H 2 O Partners 1 TOP 10 Flood Insurance Changes What Every Floodplain Official Should

TOP 10 Flood Insurance Changes What Every Floodplain Official Should Know Rich Slevin, H 2 O Partners Dorothy Martinez, H 2 O Partners 1 TOP 10 Flood Insurance Changes What Every Floodplain Official Should

Introduction to Lender Compliance. National Flood Insurance Program

Introduction to Lender Compliance National Flood Insurance Program 1 Welcome to Introduction to Lender Compliance! We will get started in a few minutes. Meanwhile, let s perform a warm up exercise. 2 1

Introduction to Lender Compliance National Flood Insurance Program 1 Welcome to Introduction to Lender Compliance! We will get started in a few minutes. Meanwhile, let s perform a warm up exercise. 2 1

Flood Disaster Protection Act Flood Disaster Protection Act

Flood Disaster Protection Act 10/2017 American Bankers Association Page 1 Menu Course Introduction Overview Monitoring, Notice, and Force Placement Course Conclusion 10/2017 American Bankers Association

Flood Disaster Protection Act 10/2017 American Bankers Association Page 1 Menu Course Introduction Overview Monitoring, Notice, and Force Placement Course Conclusion 10/2017 American Bankers Association

Servicers' Guide to Flood Insurance Requirements

Welcome to Servicers' Guide to Flood Insurance Requirements February 18, 2016 Moderated by: Sara Singhas, Policy Advisor, Residential Policy, Mortgage Bankers Association Presented by: Kathleen Dufraine,

Welcome to Servicers' Guide to Flood Insurance Requirements February 18, 2016 Moderated by: Sara Singhas, Policy Advisor, Residential Policy, Mortgage Bankers Association Presented by: Kathleen Dufraine,

CALL ME! FLOOD INSURANCE QUESTIONS? ANNE LOLLEY. and Total Training Solutions CALL OR E MAIL ANNE x4

FLOOD INSURANCE SPECIAL CREDIT UNION EDITION ANNE LOLLEY and Total Training Solutions CALL ME! QUESTIONS? CALL OR E MAIL ANNE 877 778 5192 x4 alolley@cox.net 1 THE NEW STUFF Detached structure exemption...

FLOOD INSURANCE SPECIAL CREDIT UNION EDITION ANNE LOLLEY and Total Training Solutions CALL ME! QUESTIONS? CALL OR E MAIL ANNE 877 778 5192 x4 alolley@cox.net 1 THE NEW STUFF Detached structure exemption...

Key Fundamentals of Flood Insurance

a Welcome to Key Fundamentals of Flood Insurance An entry-level approach for real estate professionals [Photo credit: Oliver Gruener] We will get started in a few minutes. Presented Meanwhile, by: let

a Welcome to Key Fundamentals of Flood Insurance An entry-level approach for real estate professionals [Photo credit: Oliver Gruener] We will get started in a few minutes. Presented Meanwhile, by: let

11/18/2011. FEMA All rights reserved. FEMA All rights reserved. Session Overview

3 Session Overview 4 1 Welcome to Session 2 of the FEMA NFIP Agent Training Program! Dorothy Martinez Rich Slevin Recall your learning from the previous session and share at least one important takeaway.

3 Session Overview 4 1 Welcome to Session 2 of the FEMA NFIP Agent Training Program! Dorothy Martinez Rich Slevin Recall your learning from the previous session and share at least one important takeaway.

Loans in Areas Having Special Flood Hazards; Interagency Questions and Answers Regarding Flood Insurance

Loans in Areas Having Special Flood Hazards; Interagency Questions and Answers Regarding Flood Insurance Note: This document is extracted from the Federal Register publication at 74 FR 35914 (July 21,

Loans in Areas Having Special Flood Hazards; Interagency Questions and Answers Regarding Flood Insurance Note: This document is extracted from the Federal Register publication at 74 FR 35914 (July 21,

2018 Northwest Compliance Conference October 4, 2018

Flood Changes 2018 Northwest Compliance Conference October 4, 2018 Kathleen O. Blanchard, CRCM Key Compliance Services, LLC History of Flood Insurance History of Flood Insurance National Flood Insurance

Flood Changes 2018 Northwest Compliance Conference October 4, 2018 Kathleen O. Blanchard, CRCM Key Compliance Services, LLC History of Flood Insurance History of Flood Insurance National Flood Insurance

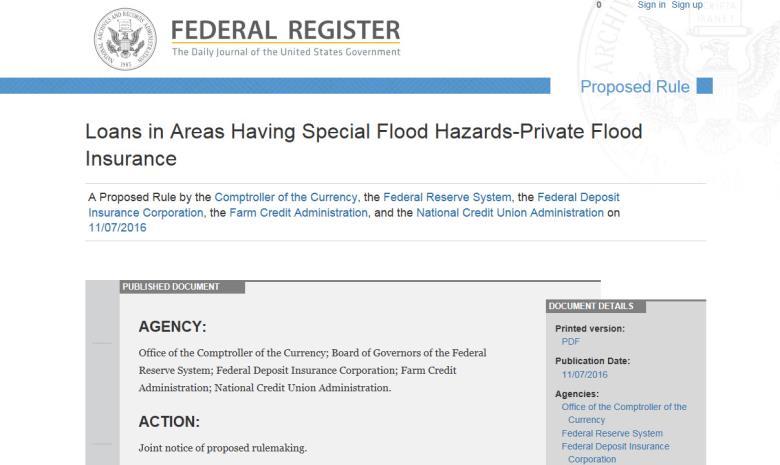

Re: Joint Notice of Proposed Rulemaking on Loans in Areas Having Special Flood Hazards -- Private Flood Insurance

Office of the Comptroller of the Currency Legislative and Regulatory Activities Division 400 7 th Street SW., Suite 3E-218, Mail Stop 9W-11 Washington, DC 20219 Docket ID OCC 2016 0005; RIN 1557 AD67 Board

Office of the Comptroller of the Currency Legislative and Regulatory Activities Division 400 7 th Street SW., Suite 3E-218, Mail Stop 9W-11 Washington, DC 20219 Docket ID OCC 2016 0005; RIN 1557 AD67 Board

BIGGERT-WATERS 2012 TALKING POINTS

BIGGERT-WATERS 2012 TALKING POINTS No Extension of Subsidy on the Pre-FIRM Properties in SFHA s & Zone D Effective October 1, 2013, the NFIP will no longer provide any extension of premium rate subsidy

BIGGERT-WATERS 2012 TALKING POINTS No Extension of Subsidy on the Pre-FIRM Properties in SFHA s & Zone D Effective October 1, 2013, the NFIP will no longer provide any extension of premium rate subsidy

October 1, Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP) Servicing Agent

Principal Coordinators and the National Flood Insurance Program (NFIP) Servicing Agent") U.S. Department of Homeland Security Washington, D.C. 20472 October 1, 2015 MEMORANDUM FOR: Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP) Servicing Agent FROM:

U.S. Department of Homeland Security Washington, D.C. 20472 October 1, 2015 MEMORANDUM FOR: Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP) Servicing Agent FROM:

OCC Mission and Vision

FLOOD DISASTER PROTECTION ACT 12 C.F.R. 22 Michelle Mitchell, NBE Comptroller of the Currency Little Rock, Arkansas 1 OCC Mission and Vision Mission To ensure that national banks and federal savings associations

FLOOD DISASTER PROTECTION ACT 12 C.F.R. 22 Michelle Mitchell, NBE Comptroller of the Currency Little Rock, Arkansas 1 OCC Mission and Vision Mission To ensure that national banks and federal savings associations

Frequently Asked Questions and Answers Concerning Flood Insurance

Frequently Asked Questions and Answers Concerning Flood Insurance Sources Used: (1) www.floodsmart.gov (2) National Flood Insurance Program, Answers to Questions about the NFIP, FEMA F-084/ March 2011.

Frequently Asked Questions and Answers Concerning Flood Insurance Sources Used: (1) www.floodsmart.gov (2) National Flood Insurance Program, Answers to Questions about the NFIP, FEMA F-084/ March 2011.

Flood Insurance Update. Proposed Private Flood Insurance Regulations

Flood Insurance Update Proposed Private Flood Insurance Regulations On November 7, 2016, the FDIC, OCC, Board of Governors of the Federal Reserve System, National Credit Union Administration and Farm Credit

Flood Insurance Update Proposed Private Flood Insurance Regulations On November 7, 2016, the FDIC, OCC, Board of Governors of the Federal Reserve System, National Credit Union Administration and Farm Credit

F E M A Mapping Changes. FEMA Mapping Changes. National Flood Insurance Program

FEMA Mapping Changes National Flood Insurance Program 1 Welcome to FEMA Mapping Changes! We will get started in a few minutes. Meanwhile, let s perform a warm up exercise. 2 1 Training Agenda Section 1-

FEMA Mapping Changes National Flood Insurance Program 1 Welcome to FEMA Mapping Changes! We will get started in a few minutes. Meanwhile, let s perform a warm up exercise. 2 1 Training Agenda Section 1-

Impacts of Map Changes -Flood Insurance-

Impacts of Map Changes -Flood Insurance- 1 Effective Dates Waiting Periods 30-day 1-day 0 day 2 Flood Zones Moderate- and Low-Risk B, C, X, Shaded X Over 35% of Arizona flood claims occur here High-Risk

Impacts of Map Changes -Flood Insurance- 1 Effective Dates Waiting Periods 30-day 1-day 0 day 2 Flood Zones Moderate- and Low-Risk B, C, X, Shaded X Over 35% of Arizona flood claims occur here High-Risk

Flood Insurance Regulations: Wading through the Tide of Change

Flood Insurance Regulations: Wading through the Tide of Change Presented by Ken Agle AdvisX President About Our Presenter As president of AdvisX, Mr. Agle brings over 28 years of regulatory and FI experience

Flood Insurance Regulations: Wading through the Tide of Change Presented by Ken Agle AdvisX President About Our Presenter As president of AdvisX, Mr. Agle brings over 28 years of regulatory and FI experience

Biggert-Waters Flood Insurance Reform and Modernization Act of 2012

Biggert-Waters Flood Insurance Reform and Modernization Act of 2012 On July 6, 2012, President Obama signed into law the Biggert-Waters Flood Insurance Reform Act of 2012, which reauthorizes and reforms

Biggert-Waters Flood Insurance Reform and Modernization Act of 2012 On July 6, 2012, President Obama signed into law the Biggert-Waters Flood Insurance Reform Act of 2012, which reauthorizes and reforms

Changes to the National Flood Insurance Program What to Expect

Changes to the National Flood Insurance Program What to Expect Impact of changes to the NFIP under Homeowner Flood Insurance Affordability Act of 2014 BW-12: What Changed Subsidies to be phased out Non-primary

Changes to the National Flood Insurance Program What to Expect Impact of changes to the NFIP under Homeowner Flood Insurance Affordability Act of 2014 BW-12: What Changed Subsidies to be phased out Non-primary

Mortgage Servicing: Flood Insurance Administration after Biggert-Waters

NAIC Examination Oversight (E) Task Force Climate Change and Global Warming (E) Working Group Testimony of J. Kevin A. McKechnie, Senior Vice President & Director ABA Office of Insurance Advocacy, to be

NAIC Examination Oversight (E) Task Force Climate Change and Global Warming (E) Working Group Testimony of J. Kevin A. McKechnie, Senior Vice President & Director ABA Office of Insurance Advocacy, to be

December 21, Dear Chairman McWilliams, Comptroller Otting, Vice Chairman Quarles, Chairman McWatters, and Chairman Tonsager:

December 21, 2018 The Honorable Jelena McWilliams The Honorable J. Mark McWatters Chairman Chairman Federal Deposit Insurance Corporation National Credit Union Administration 550 17 th Street, NW 1775

December 21, 2018 The Honorable Jelena McWilliams The Honorable J. Mark McWatters Chairman Chairman Federal Deposit Insurance Corporation National Credit Union Administration 550 17 th Street, NW 1775

May 5, Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP) Servicing Agent

Principal Coordinators and the National Flood Insurance Program (NFIP) Servicing Agent") U.S. Department of Homeland Security 500 C Street, SW Washington, DC 20472 W-13026 May 5, 2013 MEMORANDUM FOR: Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP)

U.S. Department of Homeland Security 500 C Street, SW Washington, DC 20472 W-13026 May 5, 2013 MEMORANDUM FOR: Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP)

Re: Loans in Areas Having Special Flood Hazards; RIN 1557-AD84; RIN 71-AE22; RIN AE27; RIN 3052-AC93; RIN 3133-AE40

December 18, 2014 By electronic delivery to: Legislative and Regulatory Activities Division Office of the Comptroller of the Currency 400 7 th Street, S.W., Suite 3E-218 MAIL Stop 9W-11 Washington, D.C.

December 18, 2014 By electronic delivery to: Legislative and Regulatory Activities Division Office of the Comptroller of the Currency 400 7 th Street, S.W., Suite 3E-218 MAIL Stop 9W-11 Washington, D.C.

Changes Coming to the National Flood Insurance Program What to Expect. Impact of changes to the NFIP under Section 205 of the Biggert-Waters Act

Changes Coming to the National Flood Insurance Program What to Expect Impact of changes to the NFIP under Section 205 of the Biggert-Waters Act Flood Risk Flood risks and the costs of flooding Weather

Changes Coming to the National Flood Insurance Program What to Expect Impact of changes to the NFIP under Section 205 of the Biggert-Waters Act Flood Risk Flood risks and the costs of flooding Weather

Changes to the National Flood Insurance Program What to Expect

Changes to the National Flood Insurance Program What to Expect Impact of changes to the NFIP under Homeowner Flood Insurance Affordability Act of 2014 More Changes are Coming to the NFIP On March 21, 2014,

Changes to the National Flood Insurance Program What to Expect Impact of changes to the NFIP under Homeowner Flood Insurance Affordability Act of 2014 More Changes are Coming to the NFIP On March 21, 2014,

SECTION 5 FLOOD DISASTER PROTECTION ACT

2018 CUNA MORTGAGE LENDING REGULATIONS 5-1 Section 5 Flood Disaster Protection Act Background The Flood Disaster Protection Act (FDPA) of 1973 and the National Flood Insurance Reform Act (NFIRA) of 1994

2018 CUNA MORTGAGE LENDING REGULATIONS 5-1 Section 5 Flood Disaster Protection Act Background The Flood Disaster Protection Act (FDPA) of 1973 and the National Flood Insurance Reform Act (NFIRA) of 1994

National Flood Insurance Program, Biggert-Waters 2012, and Homeowners Flood Insurance Affordability Act 2014

National Flood Insurance Program, Biggert-Waters 2012, and Homeowners Flood Insurance Affordability Act 2014 Janice Mitchell, Insurance Specialist Floodplain Management and Insurance Branch FEMA Region

National Flood Insurance Program, Biggert-Waters 2012, and Homeowners Flood Insurance Affordability Act 2014 Janice Mitchell, Insurance Specialist Floodplain Management and Insurance Branch FEMA Region

National Flood Insurance Program 3. FEMA All rights reserved

National Flood Insurance Program 3 Poll Question 1 A very upset property owner comes to you with a letter from the Bank. The letter states he has now been moved into a high risk zone and Flood Insurance

National Flood Insurance Program 3 Poll Question 1 A very upset property owner comes to you with a letter from the Bank. The letter states he has now been moved into a high risk zone and Flood Insurance

On March 21, 2014, President Obama signed the Homeowner Flood Insurance Affordability Act of 2014 into law.

On March 21, 2014, President Obama signed the Homeowner Flood Insurance Affordability Act of 2014 into law. This law repeals and modifies certain provisions of the Biggert-Waters Flood Insurance Reform

On March 21, 2014, President Obama signed the Homeowner Flood Insurance Affordability Act of 2014 into law. This law repeals and modifies certain provisions of the Biggert-Waters Flood Insurance Reform

Presented by: Brian T. Ford, CPCU, MBA of Insurance Resources and Ashley Tharp of Wright Flood

Presented by: Brian T. Ford, CPCU, MBA of Insurance Resources and Ashley Tharp of Wright Flood National Flood Insurance Program 1/28/69 Goals Prevent future loss of life & property Reduce public monies

Presented by: Brian T. Ford, CPCU, MBA of Insurance Resources and Ashley Tharp of Wright Flood National Flood Insurance Program 1/28/69 Goals Prevent future loss of life & property Reduce public monies

2012 Conference Report on National Flood Insurance Reform Legislation (Passed by House & Senate)

") 2012 Conference Report on National Flood Insurance Reform Legislation (Passed by House & Senate) Provision Biggert-Waters Flood Insurance Reform Act of 2012 (112th Congress) Title Biggert-Waters Flood

2012 Conference Report on National Flood Insurance Reform Legislation (Passed by House & Senate) Provision Biggert-Waters Flood Insurance Reform Act of 2012 (112th Congress) Title Biggert-Waters Flood

APRIL 2013 BIGGERT-WATERS SPECIAL EDITION

News from Region X Inside this Issue April 2013 Volume 3, Issue 5 SPECIAL EDITION Biggert-Waters Reform Biggert-Waters Reform The National Flood Insurance Program (NFIP), administered by the Department

News from Region X Inside this Issue April 2013 Volume 3, Issue 5 SPECIAL EDITION Biggert-Waters Reform Biggert-Waters Reform The National Flood Insurance Program (NFIP), administered by the Department

May 16th, FEMA Region I. MA Agents Association Live-Stream on May 16, 2017 AGENDA

May 16th, 2017 FEMA Region I MA Agents Association Live-Stream on May 16, 2017 AGENDA 1. April 1, 2017 Changes 2. October 2017 Changes 3. Section 28 Clear Communications 4. Private Flood Insurance 5. Misc.

May 16th, 2017 FEMA Region I MA Agents Association Live-Stream on May 16, 2017 AGENDA 1. April 1, 2017 Changes 2. October 2017 Changes 3. Section 28 Clear Communications 4. Private Flood Insurance 5. Misc.

National Flood Insurance Program Making Sense of. April 2018 Changes. April

National Flood Insurance Program Making Sense of April 2018 Changes April 2018 Introduction Table of Contents As you may know, the National Flood Insurance Program (NFIP) implements program changes biannually.

National Flood Insurance Program Making Sense of April 2018 Changes April 2018 Introduction Table of Contents As you may know, the National Flood Insurance Program (NFIP) implements program changes biannually.

National Flood Insurance Program BW-12

National Flood Insurance Program BW-12 Janice Mitchell, Insurance Specialist, Floodplain Management and Insurance Branch FEMA, Region 4 Janice.mitchell@fema.dhs.gov Biggert-Waters 2012 - What Everyone

National Flood Insurance Program BW-12 Janice Mitchell, Insurance Specialist, Floodplain Management and Insurance Branch FEMA, Region 4 Janice.mitchell@fema.dhs.gov Biggert-Waters 2012 - What Everyone

CONDOMINIUMS I. METHODS OF INSURING CONDOMINIUMS. Important Notice to Agents/Producers:

Previous Section Main Menu Table of Contents Next Section Important Notice to Agents/Producers: CONDOMINIUMS Boards of directors of condominium associations typically are responsible under their by-laws

Previous Section Main Menu Table of Contents Next Section Important Notice to Agents/Producers: CONDOMINIUMS Boards of directors of condominium associations typically are responsible under their by-laws

NFIP: October 2016 Updates and Community Decision Impacts on Individual Rates

NFIP: October 2016 Updates and Community Decision Impacts on Individual Rates Carl Watts, Regional Liaison NFIP-iService, Region VI cwatts@nfip-iservice.com P: 405-257-9000 1 1 NFIP: Review and October

NFIP: October 2016 Updates and Community Decision Impacts on Individual Rates Carl Watts, Regional Liaison NFIP-iService, Region VI cwatts@nfip-iservice.com P: 405-257-9000 1 1 NFIP: Review and October

REQUIREMENT TO PURCHASE FLOOD INSURANCE

REQUIREMENT TO PURCHASE FLOOD INSURANCE SEC. 102. (a) After the expiration of sixty days following the date of enactment of this Act, no Federal officer or agency shall approve any financial assistance

REQUIREMENT TO PURCHASE FLOOD INSURANCE SEC. 102. (a) After the expiration of sixty days following the date of enactment of this Act, no Federal officer or agency shall approve any financial assistance

Managing Flood And Other Risks

A WNC Presentation WNC Insurance Services, Inc. 899 El Centro Street, South Pasadena, CA 91030 800-423-2497 / www.wncinsuranceservices.com WNC Fast Facts Celebrating 50 Years Of Service In 2012 With More

A WNC Presentation WNC Insurance Services, Inc. 899 El Centro Street, South Pasadena, CA 91030 800-423-2497 / www.wncinsuranceservices.com WNC Fast Facts Celebrating 50 Years Of Service In 2012 With More

OCC BULLETIN OCC Date: June 9, 2010

OCC 2010-20 OCC BULLETIN Page 1 of 5 Date: June 9, 2010 TO: Chief Executive Officers and Compliance Officers of All National Banks, Department and Division Heads, All Examining Personnel, and Other Interested

OCC 2010-20 OCC BULLETIN Page 1 of 5 Date: June 9, 2010 TO: Chief Executive Officers and Compliance Officers of All National Banks, Department and Division Heads, All Examining Personnel, and Other Interested

June 26, Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP) Direct Servicing Agent (DSA)

Principal Coordinators and the National Flood Insurance Program (NFIP) Direct Servicing Agent (DSA)") June 26, 2014 MEMORANDUM FOR: FROM: SUBJECT: Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP) Direct Servicing Agent (DSA) David L. Miller Associate Administrator

June 26, 2014 MEMORANDUM FOR: FROM: SUBJECT: Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP) Direct Servicing Agent (DSA) David L. Miller Associate Administrator

ATTACHMENT A UNDERWRITING GUIDELINES OCTOBER 1, 2014 REFUND PROCEDURES

ATTACHMENT A UNDERWRITING GUIDELINES OCTOBER 1, 2014 REFUND PROCEDURES Underwriting Guidelines for HFIAA Section 3 and Section 5 Refund Procedures Background Section 3 of HFIAA requires FEMA to restore

ATTACHMENT A UNDERWRITING GUIDELINES OCTOBER 1, 2014 REFUND PROCEDURES Underwriting Guidelines for HFIAA Section 3 and Section 5 Refund Procedures Background Section 3 of HFIAA requires FEMA to restore

Many of the changes to the NFIP were recently revised on March 21, 2014 by the Homeowner Flood Insurance Affordability Act of 2014.

F l oodawa r e ne swe e k Ma r c h19-ma r c h25 2017 Below is a summary of the topics we will discuss today. On July 6, 2012, the Biggert-Waters Flood Insurance Reform Act of 2012 was passed by Congress

F l oodawa r e ne swe e k Ma r c h19-ma r c h25 2017 Below is a summary of the topics we will discuss today. On July 6, 2012, the Biggert-Waters Flood Insurance Reform Act of 2012 was passed by Congress

LOCAL OFFICIALS MEETING Lake Wausau Physical Map Revision MARATHON COUNTY, WISCONSIN FEBRUARY 9, 2017

LOCAL OFFICIALS MEETING Lake Wausau Physical Map Revision MARATHON COUNTY, WISCONSIN FEBRUARY 9, 2017 Welcome & Introduction Michelle Staff Floodplain Management Policy Coordinator, WDNR Michelle.Staff@Wisconsin.gov

LOCAL OFFICIALS MEETING Lake Wausau Physical Map Revision MARATHON COUNTY, WISCONSIN FEBRUARY 9, 2017 Welcome & Introduction Michelle Staff Floodplain Management Policy Coordinator, WDNR Michelle.Staff@Wisconsin.gov

UHM Insurance Requirements (Hazard, Condominium, H0-6 and Flood)

") This Insurance Guide is provided by Union Home Mortgage Corp. ( UHM ), having its principal place of business at 8241 Dow Circle West, Strongsville, OH 44136. UHM publishes this via its secured website

This Insurance Guide is provided by Union Home Mortgage Corp. ( UHM ), having its principal place of business at 8241 Dow Circle West, Strongsville, OH 44136. UHM publishes this via its secured website

National Flood Insurance Program Making Sense of April 2019 Changes

National Flood Insurance Program Making Sense of April 2019 Changes Foreword The National Flood Insurance Program (NFIP) provides an important means for property owners to protect themselves financially

National Flood Insurance Program Making Sense of April 2019 Changes Foreword The National Flood Insurance Program (NFIP) provides an important means for property owners to protect themselves financially

May 1, Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP) Servicing Agent

Principal Coordinators and the National Flood Insurance Program (NFIP) Servicing Agent") U.S. Department of Homeland Security 500 C St. SW Washington, D.C. 20472 W-15016 May 1, 2015 MEMORANDUM FOR: Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP)

U.S. Department of Homeland Security 500 C St. SW Washington, D.C. 20472 W-15016 May 1, 2015 MEMORANDUM FOR: Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP)

National Flood Insurance Program (NFIP) Biggert-Waters Act 2012 (BW12)

Biggert-Waters Act 2012 (BW12)") National Flood Insurance Program (NFIP) Biggert-Waters Act 2012 (BW12) NFIP Re-Authorization & Reform Todd Bass Natural Hazards Program Specialist Floodplain Management and Insurance Branch Mitigation

National Flood Insurance Program (NFIP) Biggert-Waters Act 2012 (BW12) NFIP Re-Authorization & Reform Todd Bass Natural Hazards Program Specialist Floodplain Management and Insurance Branch Mitigation

Flood Insurance Reform Act of 2012

Flood Insurance Reform Act of 2012 Impact of changes to the NFIP Note: This Fact Sheet deals specifically with Sections 205 and 207 of the Act. In 2012, the U.S. Congress passed the Flood Insurance Reform

Flood Insurance Reform Act of 2012 Impact of changes to the NFIP Note: This Fact Sheet deals specifically with Sections 205 and 207 of the Act. In 2012, the U.S. Congress passed the Flood Insurance Reform

ATTACHMENT A SUMMARY OF THE NFIP PROGRAM CHANGES EFFECTIVE APRIL 1, 2018 AND JANUARY 1, 2019

ATTACHMENT A SUMMARY OF THE NFIP PROGRAM CHANGES EFFECTIVE APRIL 1, 2018 AND JANUARY 1, 2019 National Flood Insurance Program April 1, 2018 and January 1, 2019 Program Changes: A Summary The changes outlined

ATTACHMENT A SUMMARY OF THE NFIP PROGRAM CHANGES EFFECTIVE APRIL 1, 2018 AND JANUARY 1, 2019 National Flood Insurance Program April 1, 2018 and January 1, 2019 Program Changes: A Summary The changes outlined

Making the NFIP Work for Taxpayers and Policy Holders: Increasing Consumer Participation

Making the NFIP Work for Taxpayers and Policy Holders: Increasing Consumer Participation November 3, 2016 This paper was developed in conjunction with C. Scott Canady, owner and Principal at Tambala Strategy,

Making the NFIP Work for Taxpayers and Policy Holders: Increasing Consumer Participation November 3, 2016 This paper was developed in conjunction with C. Scott Canady, owner and Principal at Tambala Strategy,

Connecticut Avenue Securities TM Investor Call Mortgage Insurance Primer

Connecticut Avenue Securities TM Investor Call Mortgage Insurance Primer Co-hosted by October 2017 2017 Fannie Mae. Trademarks of Fannie Mae. 1 Disclaimer This presentation contains a number of estimates,

Connecticut Avenue Securities TM Investor Call Mortgage Insurance Primer Co-hosted by October 2017 2017 Fannie Mae. Trademarks of Fannie Mae. 1 Disclaimer This presentation contains a number of estimates,

W October 1, Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP) Servicing Agent

Principal Coordinators and the National Flood Insurance Program (NFIP) Servicing Agent") U.S. Department of Homeland Security 500 C St. SW Washington, D.C. 20472 W-14053 October 1, 2014 MEMORANDUM FOR: Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP)

U.S. Department of Homeland Security 500 C St. SW Washington, D.C. 20472 W-14053 October 1, 2014 MEMORANDUM FOR: Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP)

YAVAPAI COUNTY FLOOD CONTROL DISTRICT STAKEHOLDER WORKSHOP. March 30 th & 31 st, 2015

YAVAPAI COUNTY FLOOD CONTROL DISTRICT STAKEHOLDER WORKSHOP March 30 th & 31 st, 2015 1 Floods Happen In Yavapai County September 1983 Northwest Prescott Area: - Willow Creek - Bottleneck Wash - Granite

YAVAPAI COUNTY FLOOD CONTROL DISTRICT STAKEHOLDER WORKSHOP March 30 th & 31 st, 2015 1 Floods Happen In Yavapai County September 1983 Northwest Prescott Area: - Willow Creek - Bottleneck Wash - Granite

National Flood Insurance Program

National Flood Insurance Program A Discussion in Three Parts: The Nature of Flood Risk An Overview of the NFIP Impact of Recent Legislation (BW-12 & HFIAA-14) Nature of Flood Risk FLOODS ARE AN ACT OF

National Flood Insurance Program A Discussion in Three Parts: The Nature of Flood Risk An Overview of the NFIP Impact of Recent Legislation (BW-12 & HFIAA-14) Nature of Flood Risk FLOODS ARE AN ACT OF

National Flood Insurance Program and Biggert-Waters 2012

National Flood Insurance Program and Biggert-Waters 2012 National Flood Insurance Program NFIP was created by Congress in 1968 Coverage underwritten by the Federal Government, administered by FEMA NFIP

National Flood Insurance Program and Biggert-Waters 2012 National Flood Insurance Program NFIP was created by Congress in 1968 Coverage underwritten by the Federal Government, administered by FEMA NFIP

Flood Insurance for Local Officials and Floodplain Managers. What Every Community Official Needs to Know About Flood Insurance

Flood Insurance for Local Officials and Floodplain Managers What Every Community Official Needs to Know About Flood Insurance Illinois Association for Floodplain and Stormwater Management 2011 Annual Conference

Flood Insurance for Local Officials and Floodplain Managers What Every Community Official Needs to Know About Flood Insurance Illinois Association for Floodplain and Stormwater Management 2011 Annual Conference

Welcome to The NFIP s Basic Agent Tutorial: Key Fundamentals of Flood Insurance

a Welcome to The NFIP s Basic Agent Tutorial: Key Fundamentals of Flood Insurance Focused on flood insurance basics for insurance professionals (Part 2) 1 Here s our AGENDA Section 1 Introduction and General

a Welcome to The NFIP s Basic Agent Tutorial: Key Fundamentals of Flood Insurance Focused on flood insurance basics for insurance professionals (Part 2) 1 Here s our AGENDA Section 1 Introduction and General

Kevin Wagner Maryland Department of the Environment

Kevin Wagner Maryland Department of the Environment Topics Overview of the National Flood Insurance Program (NFIP) Mapping Regulations Insurance Mitigation Community Rating System (CRS) Questions Know

Kevin Wagner Maryland Department of the Environment Topics Overview of the National Flood Insurance Program (NFIP) Mapping Regulations Insurance Mitigation Community Rating System (CRS) Questions Know

Flood Insurance THE TOPIC OCTOBER 2012

Flood Insurance THE TOPIC OCTOBER 2012 Because of frequent flooding of the Mississippi River during the 1960s and the rising cost of taxpayer funded disaster relief for flood victims, in 1968 Congress

Flood Insurance THE TOPIC OCTOBER 2012 Because of frequent flooding of the Mississippi River during the 1960s and the rising cost of taxpayer funded disaster relief for flood victims, in 1968 Congress

FAQs About RESPA for Industry

FAQs About RESPA for Industry Scope of RESPA 1. What kinds of transactions are covered under RESPA? Transactions involving a federally related mortgage loan, which includes most loans secured by a lien

FAQs About RESPA for Industry Scope of RESPA 1. What kinds of transactions are covered under RESPA? Transactions involving a federally related mortgage loan, which includes most loans secured by a lien

Changes to the National Flood Insurance Program: From Biggert-Waters. to Grimm-Waters. Click to edit Master title style

Changes to the National Flood Insurance Program: From Biggert-Waters Click to edit Master title style to Grimm-Waters Click to edit Master subtitle style Thomas Ruppert Coastal Planning Specialist Florida

Changes to the National Flood Insurance Program: From Biggert-Waters Click to edit Master title style to Grimm-Waters Click to edit Master subtitle style Thomas Ruppert Coastal Planning Specialist Florida

CALHFA SCHOOL PROGRAM Product Codes: ECTP

PROGRAM SUMMARY The School Teacher and Employee Assistance Program (School Program) is a deferred payment, simple interest rate subordinate loan that is combined with a CalHFA first mortgage. Your low

PROGRAM SUMMARY The School Teacher and Employee Assistance Program (School Program) is a deferred payment, simple interest rate subordinate loan that is combined with a CalHFA first mortgage. Your low

CANCELLATION/NULLIFICATION

Previous Section Main Menu Table of Contents Next Section Fld insurance coverage may be terminated by either canceling or nullifying the policy, only in accordance with a valid reason for the transaction,

Previous Section Main Menu Table of Contents Next Section Fld insurance coverage may be terminated by either canceling or nullifying the policy, only in accordance with a valid reason for the transaction,

Pennsylvania. Senate Banking & Insurance and Senate Environmental Resources & Energy Committees. Joint Public Hearing on Flood Insurance

Pennsylvania Senate Banking & Insurance and Senate Environmental Resources & Energy Committees Joint Public Hearing on Flood Insurance January 28, 2014 Respectfully submitted by: Donald L. Griffin, CPCU,

Pennsylvania Senate Banking & Insurance and Senate Environmental Resources & Energy Committees Joint Public Hearing on Flood Insurance January 28, 2014 Respectfully submitted by: Donald L. Griffin, CPCU,

ATTACHMENT A SUMMARY OF THE NFIP OCTOBER 2013 PREMIUM RATE AND RULE CHANGES

ATTACHMENT A SUMMARY OF THE NFIP OCTOBER 2013 PREMIUM RATE AND RULE CHANGES National Flood Insurance Program October 1, 2013, Premium Rate and Rule Changes: A Summary 1. Premium Increases Premiums will

ATTACHMENT A SUMMARY OF THE NFIP OCTOBER 2013 PREMIUM RATE AND RULE CHANGES National Flood Insurance Program October 1, 2013, Premium Rate and Rule Changes: A Summary 1. Premium Increases Premiums will

If you have any questions or concerns please give us a call at , or Walter Jenkins at (ext 300).

.") FLORIDA FLOODZONE SERVICES Flood Insurance and Zone Consulting 461 SE 3 rd Terrace Pompano Beach, FL 33060 Phone 954-290-7420 bspencer@florida-floodzone.com March 15, 2010 Dear Portofino Lakes Homeowner:

FLORIDA FLOODZONE SERVICES Flood Insurance and Zone Consulting 461 SE 3 rd Terrace Pompano Beach, FL 33060 Phone 954-290-7420 bspencer@florida-floodzone.com March 15, 2010 Dear Portofino Lakes Homeowner:

Diane P. Horn Analyst in Flood Insurance and Emergency Management. April 6, Congressional Research Service

Federal Disaster Assistance: The National Flood Insurance Program and Other Federal Disaster Assistance Programs Available to Individuals and Households After a Flood Diane P. Horn Analyst in Flood Insurance

Federal Disaster Assistance: The National Flood Insurance Program and Other Federal Disaster Assistance Programs Available to Individuals and Households After a Flood Diane P. Horn Analyst in Flood Insurance

VFMA Workshop October 16, David M. Gunn, P.E., CFM Henrico County DPW

VFMA Workshop October 16, 2014 David M. Gunn, P.E., CFM Henrico County DPW Agenda NFIP Virginia Statistics BW-12 GW-14 Community Actions Flood Damages are not the result of a Natural Disaster, They are

VFMA Workshop October 16, 2014 David M. Gunn, P.E., CFM Henrico County DPW Agenda NFIP Virginia Statistics BW-12 GW-14 Community Actions Flood Damages are not the result of a Natural Disaster, They are

Commonwealth Schools of Insurance, Inc.

Commonwealth Schools of Insurance P.O. Box 22414, Louisville, KY 40252-0414 502.425.5987 FAX 502.429.0755 E-mail: info@commonwealthschools.com INSTRUCTIONS TO COMPLETE THE CONTINUING EDUCATION COURSE Thank

Commonwealth Schools of Insurance P.O. Box 22414, Louisville, KY 40252-0414 502.425.5987 FAX 502.429.0755 E-mail: info@commonwealthschools.com INSTRUCTIONS TO COMPLETE THE CONTINUING EDUCATION COURSE Thank

FGMC Correspondent Announcement: First Guaranty Mortgage Corporation Correspondent Lending Seller Guide Updates

01-30-2017 FGMC Correspondent Announcement: First Guaranty Mortgage Corporation Correspondent Lending Seller Guide Updates The Seller Guide has been updated to include changes to the following: Loan delivery

01-30-2017 FGMC Correspondent Announcement: First Guaranty Mortgage Corporation Correspondent Lending Seller Guide Updates The Seller Guide has been updated to include changes to the following: Loan delivery

ASFPM Update and NFIP Reform. KAMM 10 th Anniversary Conference September 9, 2014

ASFPM Update and NFIP Reform KAMM 10 th Anniversary Conference September 9, 2014 AND HE SAID Floods are 'acts of God,' but flood losses are largely acts of man. 1945 PhD Dissertation Human Adjustments

ASFPM Update and NFIP Reform KAMM 10 th Anniversary Conference September 9, 2014 AND HE SAID Floods are 'acts of God,' but flood losses are largely acts of man. 1945 PhD Dissertation Human Adjustments

ComplianceAction. Flood Tide Rising. by Patti Blenden

ComplianceAction VOLUME 20 YOUR SOURCE FOR REGULATORY COMPLIANCE NUMBER 9 EDITOR LUCY GRIFFIN BOARD OF ADVISORS JOHN J. BYRNE ROBERT P. CHAMNESS CLIFF E. COOK DAVID DICKINSON PHILLIPS G. GAY, JR. MICHAEL

ComplianceAction VOLUME 20 YOUR SOURCE FOR REGULATORY COMPLIANCE NUMBER 9 EDITOR LUCY GRIFFIN BOARD OF ADVISORS JOHN J. BYRNE ROBERT P. CHAMNESS CLIFF E. COOK DAVID DICKINSON PHILLIPS G. GAY, JR. MICHAEL

Residential Real Estate Lending. Key Highlights of Residential Compliance Regulations and Common Problem Areas

Residential Real Estate Lending Key Highlights of Residential Compliance Regulations and Common Problem Areas 2 Agenda Key Considerations in Assessing Risk for Residential Real Estate (RRE) Lending Overview

Residential Real Estate Lending Key Highlights of Residential Compliance Regulations and Common Problem Areas 2 Agenda Key Considerations in Assessing Risk for Residential Real Estate (RRE) Lending Overview

Federal Flood Insurance Changes (National Flood Insurance Program NFIP)

") Federal Flood Insurance Changes (National Flood Insurance Program NFIP) Biggert-Waters (BW-12) Flood Insurance Reform Act 2012 HR 4348 Signed by the President on July 6, 2012 Public Works, Engineering

Federal Flood Insurance Changes (National Flood Insurance Program NFIP) Biggert-Waters (BW-12) Flood Insurance Reform Act 2012 HR 4348 Signed by the President on July 6, 2012 Public Works, Engineering

Key Fundamentals of Flood Insurance in the NFIP!

a Welcome to Key Fundamentals of Flood Insurance in the NFIP! A Before and After approach for Housing Counselors Presented by: 1 Before the Flood Presenter Melanie Graham After the Flood Presenter Erin

a Welcome to Key Fundamentals of Flood Insurance in the NFIP! A Before and After approach for Housing Counselors Presented by: 1 Before the Flood Presenter Melanie Graham After the Flood Presenter Erin

How Does Flood Insurance Work?

How Does Flood Insurance Work? The National Flood Insurance Program (NFIP) Makes Available: flood insurance disaster assistance grants and loans In Exchange For: Local adoption of a floodplain ordinance

How Does Flood Insurance Work? The National Flood Insurance Program (NFIP) Makes Available: flood insurance disaster assistance grants and loans In Exchange For: Local adoption of a floodplain ordinance

42 USC 4012a. NB: This unofficial compilation of the U.S. Code is current as of Jan. 4, 2012 (see

TITLE 42 - THE PUBLIC HEALTH AND WELFARE CHAPTER 50 - NATIONAL FLOOD INSURANCE SUBCHAPTER I - THE NATIONAL FLOOD INSURANCE PROGRAM 4012a. Flood insurance purchase and compliance requirements and escrow

TITLE 42 - THE PUBLIC HEALTH AND WELFARE CHAPTER 50 - NATIONAL FLOOD INSURANCE SUBCHAPTER I - THE NATIONAL FLOOD INSURANCE PROGRAM 4012a. Flood insurance purchase and compliance requirements and escrow

SECTION 6 LOAN PREPARATION

SECTION 6 LOAN PREPARATION 6.1 Terms and Conditions of Loans 6.2 Title Insurance 6.3 Hazard/Flood Insurance 6.4 Property Description 6.5 Appraisal Requirements Rev. 2-2018 Page 1 Section 6 Loan Preparation

SECTION 6 LOAN PREPARATION 6.1 Terms and Conditions of Loans 6.2 Title Insurance 6.3 Hazard/Flood Insurance 6.4 Property Description 6.5 Appraisal Requirements Rev. 2-2018 Page 1 Section 6 Loan Preparation

11 th Annual Eastern Secondary Market Conference. February 5-7, 2014 The Hyatt Regency Orlando

11 th Annual Eastern Secondary Market Conference February 5-7, 2014 The Hyatt Regency Orlando Scott D. Samlin Partner Scott Samlin is a New York partner in the firm s Financial Services & Products Group.

11 th Annual Eastern Secondary Market Conference February 5-7, 2014 The Hyatt Regency Orlando Scott D. Samlin Partner Scott Samlin is a New York partner in the firm s Financial Services & Products Group.

CALENDAR YEAR The Annual Report of the Flood Insurance Advocate OFFICE OF THE FLOOD INSURANCE ADVOCATE

CALENDAR YEAR 2017 The Annual Report of the Flood Insurance Advocate The Annual Report of the Flood Insurance Advocate Table of Contents MESSAGE FROM THE ADVOCATE 1 Update on the OFIA..................................1

CALENDAR YEAR 2017 The Annual Report of the Flood Insurance Advocate The Annual Report of the Flood Insurance Advocate Table of Contents MESSAGE FROM THE ADVOCATE 1 Update on the OFIA..................................1

TILA-RESPA Integrated Disclosure rule

May 2018 TILA-RESPA Integrated Disclosure rule Small entity compliance guide Guide for creating on-brand reports Version Log The Bureau updates this Guide on a periodic basis to reflect finalized clarifications

May 2018 TILA-RESPA Integrated Disclosure rule Small entity compliance guide Guide for creating on-brand reports Version Log The Bureau updates this Guide on a periodic basis to reflect finalized clarifications

COMMUNITY RATING SYSTEM FLORIDA RESPONSE TO BW-12. Bryan W. Koon Director Division of Emergency Management

COMMUNITY RATING SYSTEM FLORIDA RESPONSE TO BW-12 Bryan W. Koon Director Division of Emergency Management 2014 Biggert-Waters Reform Act 2012 Signed into law on July 6, 2012, reauthorizing the program

COMMUNITY RATING SYSTEM FLORIDA RESPONSE TO BW-12 Bryan W. Koon Director Division of Emergency Management 2014 Biggert-Waters Reform Act 2012 Signed into law on July 6, 2012, reauthorizing the program

Floodplain Management. City Council Work Session April 16, 2013

Floodplain Management City Council Work Session April 16, 2013 1 Discussion Agenda Flood Insurance Rate Changes Community Rating System Recommendation Floodplain Ordinance Enhancements Modifications Public

Floodplain Management City Council Work Session April 16, 2013 1 Discussion Agenda Flood Insurance Rate Changes Community Rating System Recommendation Floodplain Ordinance Enhancements Modifications Public

March 29, Write Your Own (WYO) Company Principal Coordinators and the National Flood Insurance Program (NFIP) Servicing Agent

Company Principal Coordinators and the National Flood Insurance Program (NFIP) Servicing Agent") U.S. Department of Homeland Security 500 C Street, SW Washington, DC 20472 W-10029 March 29, 2010 MEMORANDUM FOR: Write Your Own (WYO) Company Principal Coordinators and the National Flood Insurance Program

U.S. Department of Homeland Security 500 C Street, SW Washington, DC 20472 W-10029 March 29, 2010 MEMORANDUM FOR: Write Your Own (WYO) Company Principal Coordinators and the National Flood Insurance Program

Diane P. Horn Analyst in Flood Insurance and Emergency Management. November 28, Congressional Research Service

Federal Disaster Assistance: The National Flood Insurance Program and Other Federal Disaster Assistance Programs Available to Individuals and Households After a Flood Diane P. Horn Analyst in Flood Insurance

Federal Disaster Assistance: The National Flood Insurance Program and Other Federal Disaster Assistance Programs Available to Individuals and Households After a Flood Diane P. Horn Analyst in Flood Insurance

National Flood Insurance Program Changes Effective April 1, 2016

National Flood Insurance Program Changes Effective April 1, 2016 Beginning April 1, 2016, the National Flood Insurance Program (NFIP) will begin implementing additional flood insurance program changes

National Flood Insurance Program Changes Effective April 1, 2016 Beginning April 1, 2016, the National Flood Insurance Program (NFIP) will begin implementing additional flood insurance program changes

INTRODUCTION AND GENERAL RULES. Welcome to The NFIP s Basic Agent Tutorial: Key Fundamentals of Flood Insurance. Section 1

a Welcome to The NFIP s Basic Agent Tutorial: Key Fundamentals of Flood Insurance Focused on flood insurance basics for insurance professionals 1 Section 1 INTRODUCTION AND GENERAL RULES 2 1 Here s our

a Welcome to The NFIP s Basic Agent Tutorial: Key Fundamentals of Flood Insurance Focused on flood insurance basics for insurance professionals 1 Section 1 INTRODUCTION AND GENERAL RULES 2 1 Here s our

NCUA Update: Looking Ahead to 2014

NCUA Update: Looking Ahead to 2014 NAFCU s Regulatory Affairs Team December 10, 2013: 2:00pm-3:30pm NAFCU NCUA Update Webcast Presented by: Michael J. Coleman, Esq., NCCO Director of Regulatory Affairs

NCUA Update: Looking Ahead to 2014 NAFCU s Regulatory Affairs Team December 10, 2013: 2:00pm-3:30pm NAFCU NCUA Update Webcast Presented by: Michael J. Coleman, Esq., NCCO Director of Regulatory Affairs

Changes to the National Flood Insurance Program: From Biggert to Grimm Waters. Click to edit Master title style. Click to edit Master subtitle style