Session 34 PD, Healthcare Exchanges: Case Studies in the ACA. Moderator: William James Swacker II, FSA, MAAA

|

|

|

- Norah Jordan

- 5 years ago

- Views:

Transcription

1 Session 34 PD, Healthcare Exchanges: Case Studies in the ACA Moderator: William James Swacker II, FSA, MAAA Presenters: David G. Hayes, FSA, MAAA Michael N. Muldoon, ASA, FCA, MAAA William James Swacker II, FSA, MAAA SOA Antitrust Disclaimer SOA Presentation Disclaimer

2 David G. Hayes, FSA, MAAA Principal and Consulting Actuary Milliman - Atlanta Session 34 Panel Discussion: Healthcare Exchanges: Case Studies in the ACA October 24, 2016

3 Presentation Disclaimer Presentations are intended for educational purposes only and do not replace independent professional judgment. Statements of fact and opinions expressed are those of the participants individually and, unless expressly stated to the contrary, are not the opinion or position of the Society of Actuaries, its cosponsors or its committees. The Society of Actuaries does not endorse or approve, and assumes no responsibility for, the content, accuracy or completeness of the information presented. Attendees should note that the sessions are audio-recorded and may be published in various media, including print, audio and video formats without further notice. 2

4 General Overview Multiple Markets 3

5 Number of Insurers, Grouped by Parent Company, Participating in Marketplaces, State California Colorado Connecticut DC Indiana Maine Maryland Michigan Nevada New Mexico New York Oregon Rhode Island Tennessee Vermont Virginia Washington Average Source: Kaiser Family Foundation 4

6 Monthly Lowest-Cost Silver Premium - 40 YO, Non-Smoker (before tax credits) State Major City (Rating Area #) % Change % Change Average Annual Change California Los Angeles (15) $251 $243 3% 5% 4% Colorado Denver (3) $304 $266 14% 29% 7% Connecticut Hartford (2) $358 $316 13% -1% 4% DC Washington (1) $275 $228 21% -4% 5% Indiana Indianapolis (10) $284 $286-1% -10% -6% Maine Portland (1) $307 $285 8% 4% 3% Maryland Baltimore (1) $267 $243 10% 8% 8% Michigan Detroit (1) $233 $210 11% -4% 7% Nevada Las Vegas (1) $279 $256 9% 8% 6% New Mexico Albuquerque (1) $192 $181 6% 8% 1% New York New York City (4) $425 $366 16% -2% 6% Oregon Portland (1) $302 $240 26% 13% 16% Rhode Island Providence (1) $224 $259-14% 6% -6% Tennessee Nashville (4) $333 $262 27% 19% 23% Vermont Burlington (1) $482 $465 4% 9% 7% Virginia Richmond (7) $296 $264 12% 9% 9% Washington Seattle (1) $232 $224 4% -5% -6% Weighted Average $281 $257 9% 5% 7% Source: Kaiser Family Foundation 5

7 A Step Back in Time Major Considerations for 2014 Rate Development Demographics Basis for rate development Risk adjustment Reinsurance Transitional business (depending on the State) On or off-exchange Competitive position Member subsidies Understanding the rating templates Actuarial value (AV) calculator 6

8 Year 2 Major Considerations for 2015 Rate Development Knowledge gained from 2014 Initial enrollment Initial experience indications Competitive position Pent-up demand Allowable rating parameters (e.g., child load) Area factors and inclusion of risk Benefit design Narrow networks Elimination of platinum and gold plans 7

9 First Year of Experience - Major Considerations for 2016 Rate Development 2014 claims and demographic experience Risk adjustment 2014 results Change in coefficients Changes to the AV calculator Supreme Court ruling (Burwell) Increased regulatory oversite Rate adequacy 8

10 Major Considerations for 2017 Rate Development Risk corridor all but eliminated Risk adjustment Rate adequacy Financial stability Make up of the marketplace Carriers leaving market CO-OP failures Market consolidation Competitive position Economic value of members 9

11 What Keeps Carriers Up at Night? Financial performance and stability Timing of obligations and receivables Elimination of reinsurance Redesign of risk adjustment Shifting risk to providers 10

12 Trey Swacker, FSA, MAAA Actuarial Sr. Director Aetna Session 34 Panel Discussion Healthcare Exchanges: Case Studies in the ACA October 24, 2016

13 Ohio Individual Marketplace 2

14 Ohio Individual Market 2013 $877M earned premium 331K covered lives 82.4% Federal MLR $222 Premium PMPM Aultman 2% Assurant Aetna 3% 4% United 12% Health Span 2% Summa 1% Humana 1% Other 2% Anthem 38% Medical Mutual of Ohio 35% 2013 Supplemental Health Care Exhibit Part 1 Geography: Ohio LOB: Comp Health: Individual 3

15 Ohio Exchange Participants Commercial Government Regional National 4

16 Ohio Individual Market 2014 $1.3B earned premium +48% 378K covered lives +14% 100.5% Federal MLR -18.1% $285 Premium PMPM +28.3% HealthSpan 2% Aultman Assurant 2% 2% Aetna 3% Humana 3% CareSource 6% United 8% Summa 2% Other 3% Medical Mutual of Ohio 40% Anthem 29% 2014 Supplemental Health Care Exhibit Part 1 Geography: Ohio LOB: Comp Health: Individual 5

17 Ohio Individual Market 2015 $1.6B earned premium +19% Aultman 2% 378K covered lives +0% 102.6% Federal MLR -18.1% Assurant 2% Humana 3% HealthSpan 2% Aetna 5% Co-Op 5% Other 5% Anthem 21% $324 Premium PMPM +14% CareSource 9% United 7% Medical Mutual of Ohio 39% 2015 Supplemental Health Care Exhibit Part 1 Geography: Ohio LOB: Comp Health: Individual 6

18 Ohio Exchange Facts Year Participating Carriers Covered Lives Average Approved Rate Increase Average Premium (before subsidies) ,000 N/A $382 PMPM ,000 12% $381 PMPM ,000 13% $405 PMPM TBD 13% TBD 46% market share in % market share in

19 Columbus, Ohio 8

20 Columbus, Ohio Caresource filed five networks per product; slotted providers in based on agreed reimbursment level vs Medicare. Narrow network (6 out of 15 facilities in metro area) HMO product Molina priced based on Medicaid experience; commercial rates with providers ~60% higher. Anthem / MMO had PPO products only Paramount network coverage minimal 9

21 Columbus, Ohio Molina trued up pricing (revisited assumptions applied to baseline data) Caresource used same credibility manual, low pricing trend assumption Assurant trued up rate (aligned with broad network PPO product) Aetna enters market with narrower PPO network (vs other PPOs), centered around Mt. Carmel system United enters market with PPO plans MMO added plans 10

22 Columbus, Ohio United and Anthem introduce HMO products for the first time on-exchange. Molina s experience base (2014 Medicaid) improved vs assumptions; ACA experience not credible Other increases reflective of ACA experience, trend, reduction in reinsurance program Healthspan geographic expansion into Columbus 11

23 Columbus, Ohio Several carriers dropped exchange offerings. Only narrow-network HMOs left. MMO introduces narrow network HMO options (centered around Mercy and Ohio Health systems) Caresource experience driving more of a true-up vs prior years. (risk adjustment insights) 12

24 Columbus, Ohio - Summary Carriers playing in focused geographies Narrow network HMO products Product offering centered around Silver / Bronze tiers Some erosion of unit cost advantages initially built with reimbursement rates relative to Medicare Risk adjustment program continues to drive uncertainty 13

25

26 Colorado Division of Insurance Presented by Chief Actuary - Michael Muldoon, ASA, MAAA, FCA

27

28

29

30

31

32

33 Number of Individual Market On-Exchange Carriers, by County

34 Kaiser Foundation Health Plan of CO Rocky Mountain HMO, Inc. Colorado Health Insurance Cooperative (COOP) Humana Insurance Company Time Insurance Company Anthem - HMO Colorado, Inc. Humana Health Plan, Inc. Colorado Choice Health Plans Cigna Health and Life Insurance Denver Health Medical Plan, Inc. All Savers Insurance Company New Health Ventures, Inc.

35

36 Entering Anthem - Rocky Mountain H&MS BCBS PPO Plans (Off-Exchange only) UnitedHealthcare Life Insurance Company PPO (Off-Exchange only) National Foundation Life Insurance Company PPO (Off-Exchange only) Freedom Life Insurance Company of America PPO (Off-Exchange only) Leaving N/A Anthem entered the Individual ACA market in January 2015 with PPO plans, however they continued to maintain a large block of closed Transitional NGF plan members who were not transitioned into ACA plans until January 2016 when the State of Colorado required all transitional plans to be terminated

37

38 Entering UnitedHealthcare of Colorado HMO (On-Exchange) Golden Rule Insurance Company PPO (Off-Exchange Only) Anthem - Rocky Mountain H&MS BCBS PPO Plans (On-Exchange) Leaving Colorado Health Insurance Cooperative, Inc. (On-Exchange) Assurant - Time Insurance Company PPO (Off-Exchange) New Health Ventures, Inc. (On-Exchange)

39

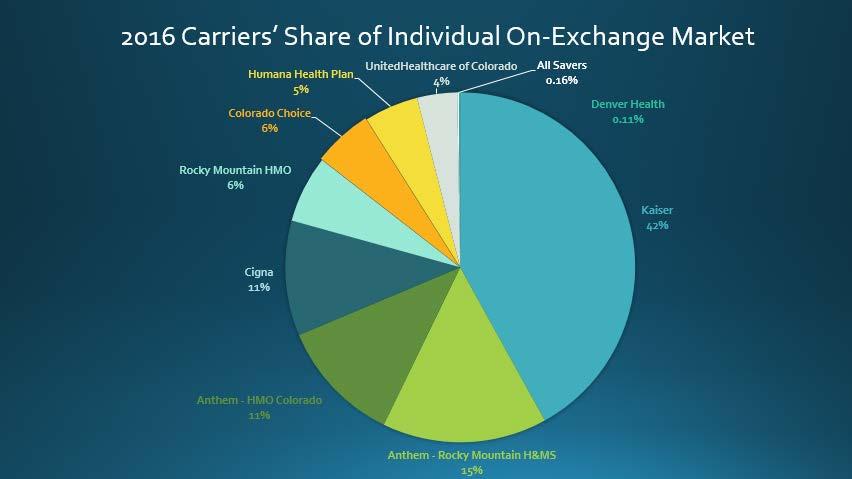

40 Entering Bright Health Plan EPO (On-Exchange) Leaving Percent of On-Exchange Market Anthem Rocky Mountain H&MS PPO (On-Exchange)* 15.23% Rocky Mountain HMO (On-Exchange)** 5.01% Humana Health Plan HMO (On-Exchange) 5.00% UnitedHealthcare of Colorado HMO (On-Exchange) 3.70% All Savers Insurance Company (On-Exchange) 0.16% Humana Insurance Company (Off-Exchange) N/A UnitedHealthcare Life Insurance Company N/A TOTAL 29.10% *Anthem PPO only offering off-exchange catastrophic plan in 2017 **Rocky Mountain HMO pulled out of the market statewide, except for one product (both on/off exchange) in Area 5 (Mesa County)

41

42 HMO Colorado, Inc. (Anthem) Bright Health Plan Cigna Health and Life Insurance Company Denver Health Medical Plan, Inc. Kaiser Foundation Health Plan of Colorado Only carrier that is statewide on-exchange New carrier in 2017, EPO plans in 4 areas along Front Range EPO plans in 6 areas along Front Range HMO plans in limited counties in Denver MSA HMO plans in 7 areas Rocky Mountain H&MS (Anthem) Only offering off-exchange catastrophic plan in 2017 Rocky Mountain HMO Offer one product (both on/off exchange) in Area 5 (Mesa County) Golden Rule Insurance Company National Foundation Life Insurance Company Freedom Life Insurance Company Statewide PPO plans Less than 10 members enrolled Less than 10 members enrolled

43

44

45 2014 Area Factors: 7 MSA + 4 Non-MSA

46

47

48 2015 Area Factors: 7 MSA + 2 Non-MSA

49 On-Exchange HMO Colorado (Anthem) -5.10% COOP -9.63% Kaiser 7.00% Humana Health Plan -3.00% Cigna 6.07% Colorado Choice 2.10% Rocky Mountain HMO 3.10% All Savers 0.00% Denver Health 17.50% New Health Ventures % Off-Exchange Only Humana Insurance Company -8.50% Time Insurance Company 35.00% Weighted Individual Market Average Rate Change: 0.71%

50

7.40% New Health Ventures 26.80% Denver Health 12.")

51 On-Exchange Kaiser 4.00% Rocky Mountain HMO 30.80% Humana Health Plan 20.10% HMO Colorado, Inc. (Anthem) 8.20% COOP 25.20% Colorado Choice 9.40% Cigna** 0.00% Rocky Mountain H&MS (Anthem) 7.40% New Health Ventures 26.80% Denver Health 12.70% All Savers** 0.00% Off-Exchange Only Humana Insurance 14.90% UnitedHealthcare Life -2.30% *based on Issuers with 50+ members enrolled ** Cigna and All Savers had all new network plans for 2016 Weighted Individual Market Average Rate Change: 9.84%

52

53 On-Exchange Kaiser 18.00% HMO Colorado (Anthem) 25.80% Cigna 9.50% Off-Exchange Only Golden Rule 46.20% *based on Issuers with 50+ members enrolled Colorado Choice 42.90% Rocky Mountain H&MS (Anthem) 20.60% Rocky Mountain HMO 34.90% Denver Health -0.46% Weighted Individual Market Average Rate Change: 20.54%

54

55 Rate Changes for Subsidized and Non Subsidized Members With Plans Continuing in the Individual Exchange Market Study by Wakely Consulting Group Data Provided by the Colorado Exchange (C4HCO) and Colorado DOI

56 155,754 With Premium Subsidies 61%* Without Premium Subsidies 39% 132,235 With Premium Subsidies 0% Without Premium Subsidies 100% 287,989 With Premium Subsidies 33% Without Premium Subsidies 67% *Approximately 68% are eligible to receive premium subsidies

57 Metal Tier Enrollees Not Eligible for Subsidies 2016 PMPM Premium 2017 PMPM Premium Auto Renew % Change Over 2016 Gold 3,907 $359 $443 23% Silver 8,308 $329 $403 22% Bronze 20,579 $301 $378 25% Catastrophic 1,222 $170 $207 22% Total 34,016 $310 $385 24%

58 Rating Area Description Enrollees Not Eligible for Subsidies 2016 PMPM Premium 2017 PMPM Premium Auto Renew % Change 1 Boulder 3,839 $300 $367 22% 2 Colorado Springs 3,068 $299 $386 29% 3 Denver 19,373 $296 $355 20% 4 Fort Collins (Larimer) 2,917 $319 $408 28% 5 Grand Junction (Mesa) 325 $414 $592 43% 6 Greeley (Weld) 1,443 $321 $407 27% 7 Pueblo 320 $374 $452 21% 8 East 1,084 $384 $560 46% 9 West 1,647 $414 $551 33%

59 Metal Tier Enrollees Eligible for Subsidies 2016 PMPM Premium 2017 PMPM Premium Auto Renew % Change Over 2016 Gold 3,598 $260 $270 4% Silver 34,048 $143 $136-5% Bronze 33,654 $128 $100-22% Catastrophic* 718 $177 $215 21% Total 72,018 $142 $126-11%

60 Rating Area Description Enrollees Eligible for Subsidies 2016 PMPM Premium After Subsidy 2017 PMPM Premium After Subsidy Auto Renew % Change 1 Boulder 6,233 $143 $125-12% 2 Colorado Springs 5,910 $147 $130-11% 3 Denver 36,557 $142 $129-9% 4 Fort Collins (Larimer) 6,690 $147 $123-17% 5 Grand Junction (Mesa) 2,077 $141 $115-18% 6 Greeley (Weld) 3,418 $152 $123-19% 7 Pueblo 1,228 $138 $99-28% 8 East 4,130 $133 $129-3% 9 West 5,775 $136 $121-11%

61

62

63

Changes in Marketplace Premiums, 2017 to 2018

U.S. Health Reform Monitoring and Impact Changes in Marketplace Premiums, 2017 to 2018 March 2018 By John Holahan, Linda J. Blumberg, and Erik Wengle Support for this research was provided by the Robert

U.S. Health Reform Monitoring and Impact Changes in Marketplace Premiums, 2017 to 2018 March 2018 By John Holahan, Linda J. Blumberg, and Erik Wengle Support for this research was provided by the Robert

2016 Premium Increases in the ACA Marketplaces: Not Nearly as Dramatic as You ve Been Led to Believe

ACA Implementation Monitoring and Tracking 2016 Premium Increases in the ACA Marketplaces: t Nearly as Dramatic as You ve Been Led to Believe vember 2015 John Holahan, Linda J Blumberg, Erik Wengle, and

ACA Implementation Monitoring and Tracking 2016 Premium Increases in the ACA Marketplaces: t Nearly as Dramatic as You ve Been Led to Believe vember 2015 John Holahan, Linda J Blumberg, Erik Wengle, and

Stabilizing Markets with 1332

Stabilizing Markets with 1332 L E S S O N S A N D A N E W T O O L F O R S T A T E S C O N S I D E R I N G R E I N S U R A N C E T u e s d a y, D e c e m b e r 1 1, 2 0 1 8 4-5 p m E T / 1-2 p m P T D i

Stabilizing Markets with 1332 L E S S O N S A N D A N E W T O O L F O R S T A T E S C O N S I D E R I N G R E I N S U R A N C E T u e s d a y, D e c e m b e r 1 1, 2 0 1 8 4-5 p m E T / 1-2 p m P T D i

Health Care Reform Part 1: Strategic Issues

Health Care Reform Part 1: Strategic Issues HealthFlex Summit October 21, 2014 Agenda 1 ACA* Rollout/Implementation Update Outcome in 2014 Outlook for 2015 Marketplace Plans Market Pressure and Strategic

Health Care Reform Part 1: Strategic Issues HealthFlex Summit October 21, 2014 Agenda 1 ACA* Rollout/Implementation Update Outcome in 2014 Outlook for 2015 Marketplace Plans Market Pressure and Strategic

Session 122 PD, Lessons Learned: Two Years of Three Rs. Moderator: Shyam Prasad Kolli, FSA, MAAA

Session 122 PD, Lessons Learned: Two Years of Three Rs Moderator: Shyam Prasad Kolli, FSA, MAAA Presenters: David M. Dillon, FSA, MAAA Andrew Ryan Large, FSA, CERA, MAAA SOA Antitrust Disclaimer SOA Presentation

Session 122 PD, Lessons Learned: Two Years of Three Rs Moderator: Shyam Prasad Kolli, FSA, MAAA Presenters: David M. Dillon, FSA, MAAA Andrew Ryan Large, FSA, CERA, MAAA SOA Antitrust Disclaimer SOA Presentation

ehealth Inventory Report of Major Medical Health Plans Available Off of Government Exchanges

ehealth Inventory Report of Major Medical Health Available Off of Government Exchanges February 2014 Introduction Beginning January 1, 2014, all new major medical health insurance plans were required to

ehealth Inventory Report of Major Medical Health Available Off of Government Exchanges February 2014 Introduction Beginning January 1, 2014, all new major medical health insurance plans were required to

The impact of California s prescription drug cost-sharing cap

The impact of California s prescription drug cost-sharing cap Prepared by Milliman, Inc. Gabriela Dieguez, FSA, MAAA Principal and Consulting Actuary Bruce Pyenson, FSA, MAAA Principal and Consulting Actuary

The impact of California s prescription drug cost-sharing cap Prepared by Milliman, Inc. Gabriela Dieguez, FSA, MAAA Principal and Consulting Actuary Bruce Pyenson, FSA, MAAA Principal and Consulting Actuary

Medicare Advantage Update. Southeastern Actuaries Conference November 15, 2007

Stuart Rachlin, Consulting Actuary Tampa, FL F.S.A., M.A.A.A. Medicare Advantage Update Southeastern Actuaries Conference November 15, 2007 Grand Floridian Resort Orlando, FL Demand for Medicare Medicare

Stuart Rachlin, Consulting Actuary Tampa, FL F.S.A., M.A.A.A. Medicare Advantage Update Southeastern Actuaries Conference November 15, 2007 Grand Floridian Resort Orlando, FL Demand for Medicare Medicare

Insurer Participation on ACA Marketplaces,

November 2018 Issue Brief Insurer Participation on ACA Marketplaces, 2014-2019 Rachel Fehr, Cynthia Cox, Larry Levitt Since the Affordable Care Act health insurance marketplaces opened in 2014, there have

November 2018 Issue Brief Insurer Participation on ACA Marketplaces, 2014-2019 Rachel Fehr, Cynthia Cox, Larry Levitt Since the Affordable Care Act health insurance marketplaces opened in 2014, there have

Market Competition Works: Proposed Silver Premiums in the 2014 Individual and Small Group Markets Are Nearly 20% Lower than Expected

ASPE ISSUE BRIEF Market Competition Works: Proposed Silver Premiums in the 2014 Individual and Small Group Markets Are Nearly 20% Lower than Expected By: Laura Skopec and Richard Kronick, ASPE A goal of

ASPE ISSUE BRIEF Market Competition Works: Proposed Silver Premiums in the 2014 Individual and Small Group Markets Are Nearly 20% Lower than Expected By: Laura Skopec and Richard Kronick, ASPE A goal of

The Launch of the Affordable Care Act in Selected States: Insurer Participation, Competition, and Premiums

ACA Implementation Monitoring and Tracking The Launch of the Affordable Care Act in Selected States: Insurer Participation, Competition, and Premiums March 2014 John Holahan and Rebecca Peters, The Urban

ACA Implementation Monitoring and Tracking The Launch of the Affordable Care Act in Selected States: Insurer Participation, Competition, and Premiums March 2014 John Holahan and Rebecca Peters, The Urban

2014 U.S. Census (2015) Median African-American Household Income Rank, Memphis Included. Household Median Income Ranking, African American Population

Median African-American Household Income Rank, Memphis Included. Household Median Income Ranking, African American Population") 2015 2015 Rankings Report Prepared by Elena Delavega, PhD, MSW Department of Social Work Benjamin L. Hooks Institute for Social Change University of Memphis 2014 U.S. Census (2015) - Rank, Memphis Included

2015 2015 Rankings Report Prepared by Elena Delavega, PhD, MSW Department of Social Work Benjamin L. Hooks Institute for Social Change University of Memphis 2014 U.S. Census (2015) - Rank, Memphis Included

Nevada s Individual Health Insurance Market

Nevada s Individual Health Insurance Market 2013 Individual Market Snapshot 15 carriers actively writing, 13 were Preferred Provider Organizations 96,150 Nevadans were covered under individual policies

Nevada s Individual Health Insurance Market 2013 Individual Market Snapshot 15 carriers actively writing, 13 were Preferred Provider Organizations 96,150 Nevadans were covered under individual policies

Correspondence Summary

SERFF Tracking #: AWLP-130050273 State Tracking #: 201503007 Company Tracking #: State: Connecticut Filing Company: Anthem Health Plans, Inc dba Anthem Blue Cross and Blue Shield of Connecticut TOI/Sub-TOI:

SERFF Tracking #: AWLP-130050273 State Tracking #: 201503007 Company Tracking #: State: Connecticut Filing Company: Anthem Health Plans, Inc dba Anthem Blue Cross and Blue Shield of Connecticut TOI/Sub-TOI:

Factors Affecting Individual Premium Rates in 2014 for California

Factors Affecting Individual Premium Rates in 2014 for California Prepared for: Covered California Prepared by: Robert Cosway, FSA, MAAA Principal and Consulting Actuary 858-587-5302 bob.cosway@milliman.com

Factors Affecting Individual Premium Rates in 2014 for California Prepared for: Covered California Prepared by: Robert Cosway, FSA, MAAA Principal and Consulting Actuary 858-587-5302 bob.cosway@milliman.com

AFFORDABLE CARE ACT ( ACA ) EMPLOYEE COMMUNICATION PART I OVERVIEW OF HEALTHCARE REFORM

EMPLOYEE COMMUNICATION PART I OVERVIEW OF HEALTHCARE REFORM") AFFORDABLE CARE ACT ( ACA ) EMPLOYEE COMMUNICATION PART I OVERVIEW OF HEALTHCARE REFORM Most employees are familiar with the terms healthcare reform, the Affordable Care Act ( ACA ) or Obamacare. The media

AFFORDABLE CARE ACT ( ACA ) EMPLOYEE COMMUNICATION PART I OVERVIEW OF HEALTHCARE REFORM Most employees are familiar with the terms healthcare reform, the Affordable Care Act ( ACA ) or Obamacare. The media

Consulting Actuaries. Carrier Trend Report

Consulting Actuaries Carrier Trend Report January 2014 Analysis Contents 1. Report Overview 1 2. Executive Summary 2 3. Results for January 2014 3 4. Historical Experience 12 5. Participating Providers

Consulting Actuaries Carrier Trend Report January 2014 Analysis Contents 1. Report Overview 1 2. Executive Summary 2 3. Results for January 2014 3 4. Historical Experience 12 5. Participating Providers

Session 113PD, State Flexibility and 1332 Waivers in ACA Marketplaces. Moderator/Presenter: Traci L. Hughes, ASA, MAAA

Session 113PD, State Flexibility and 1332 Waivers in ACA Marketplaces Moderator/Presenter: Traci L. Hughes, ASA, MAAA Presenters: Kristi M. Bohn, FSA, MAAA, EA, MSPA Michael Cohen Ph.D. Danielle W. Hilson,

Session 113PD, State Flexibility and 1332 Waivers in ACA Marketplaces Moderator/Presenter: Traci L. Hughes, ASA, MAAA Presenters: Kristi M. Bohn, FSA, MAAA, EA, MSPA Michael Cohen Ph.D. Danielle W. Hilson,

What Is Next For the Affordable Care Act s Cost-Sharing Reductions?

What Is Next For the Affordable Care Act s Cost-Sharing Reductions? Understanding The Impact on Consumers and Insurance Markets Monday, April 24 th 1:30p.m.-2:15p.m. EDT What Is Next For the Affordable

What Is Next For the Affordable Care Act s Cost-Sharing Reductions? Understanding The Impact on Consumers and Insurance Markets Monday, April 24 th 1:30p.m.-2:15p.m. EDT What Is Next For the Affordable

Aetna Individual Direct Pay Commissions Schedule

Aetna Individual Direct Pay Commissions Schedule Cards Issued Broker Rate Broker Tier Per Year 1st Yr 2nd Yr 3+ Yrs Levels 11-Jan 4.00% 4.00% 3.00% Bronze 24-Dec 6.00% 4.00% 3.00% Silver 25-49 8.00% 4.00%

Aetna Individual Direct Pay Commissions Schedule Cards Issued Broker Rate Broker Tier Per Year 1st Yr 2nd Yr 3+ Yrs Levels 11-Jan 4.00% 4.00% 3.00% Bronze 24-Dec 6.00% 4.00% 3.00% Silver 25-49 8.00% 4.00%

STATE OF CONNECTICUT

STATE OF CONNECTICUT INSURANCE DEPARTMENT Finding of Facts Celtic Insurance Company Individual 2016 Off Exchange Rate Filing 1. This filing is a rate submission for the Celtic ACA-compliant individual

STATE OF CONNECTICUT INSURANCE DEPARTMENT Finding of Facts Celtic Insurance Company Individual 2016 Off Exchange Rate Filing 1. This filing is a rate submission for the Celtic ACA-compliant individual

Session 84 TS, Payment Transfer Formula - The Mystery Revealed. Moderator/Presenter: Julia S. Lambert, FSA, MAAA

Session 84 TS, Payment Transfer Formula - The Mystery Revealed Moderator/Presenter: Julia S. Lambert, FSA, MAAA Presenter: Kelsey Leigh Stevens, FSA, MAAA SOA Health Meeting 2015 Tuesday June 16, 2015

Session 84 TS, Payment Transfer Formula - The Mystery Revealed Moderator/Presenter: Julia S. Lambert, FSA, MAAA Presenter: Kelsey Leigh Stevens, FSA, MAAA SOA Health Meeting 2015 Tuesday June 16, 2015

The Affordable Care Act (ACA) Health Insurance Exchanges

Health Insurance Exchanges") The Affordable Care Act (ACA) Health Insurance Exchanges Dave Chandra Senior Policy Analyst Center on Budget and Policy Priorities March 11, 2013 Linking Americans to Coverage (2014) FPL Unsubsidized 400%

The Affordable Care Act (ACA) Health Insurance Exchanges Dave Chandra Senior Policy Analyst Center on Budget and Policy Priorities March 11, 2013 Linking Americans to Coverage (2014) FPL Unsubsidized 400%

Session 107 PD, Value of ACA Coding Improvement: Market Effects. Moderator: Douglas T. Norris, FSA, MAAA. Presenters: Ksenia Whittal, FSA, MAAA

Session 107 PD, Value of ACA Coding Improvement: Market Effects Moderator: Douglas T. Norris, FSA, MAAA Presenters: Douglas T. Norris, FSA, MAAA Ksenia Whittal, FSA, MAAA SOA Antitrust Disclaimer SOA Presentation

Session 107 PD, Value of ACA Coding Improvement: Market Effects Moderator: Douglas T. Norris, FSA, MAAA Presenters: Douglas T. Norris, FSA, MAAA Ksenia Whittal, FSA, MAAA SOA Antitrust Disclaimer SOA Presentation

Health Care Reform Update

Health Care Reform Update Presented by David Hayes, FSA, MAAA Consulting Actuary Milliman - Atlanta November 16, 2012 Southeastern Actuaries Conference Fall 2012 Agenda This will be an general session

Health Care Reform Update Presented by David Hayes, FSA, MAAA Consulting Actuary Milliman - Atlanta November 16, 2012 Southeastern Actuaries Conference Fall 2012 Agenda This will be an general session

1332 State Innovation Waivers: Getting off the Ground. Manatt Health Solutions July 2015

1 2 1332 State Innovation Waivers: Getting off the Ground Manatt Health Solutions July 2015 3 Agenda Getting Started with 1332 Waivers 1332 Waivers in HealthCare.Gov States Discussion of Future Topics

1 2 1332 State Innovation Waivers: Getting off the Ground Manatt Health Solutions July 2015 3 Agenda Getting Started with 1332 Waivers 1332 Waivers in HealthCare.Gov States Discussion of Future Topics

Changes in Premium and Out-of-Pocket Costs from October 15, 2018 John Pierre Cardenas Director, Policy and Plan Management

Changes in Premium and Out-of-Pocket Costs from 2018-2019 October 15, 2018 John Pierre Cardenas Director, Policy and Plan Management Health Care Costs Changes in Consumer Experience Premiums: The State

Changes in Premium and Out-of-Pocket Costs from 2018-2019 October 15, 2018 John Pierre Cardenas Director, Policy and Plan Management Health Care Costs Changes in Consumer Experience Premiums: The State

Carrier Trend Report. July 2017 Analysis. Consulting Actuaries

Carrier Trend Report July 2017 Analysis Consulting Actuaries Contents 1. REPORT OVERVIEW 1 2. EXECUTIVE SUMMARY 2 3. RESULTS FOR JULY 2017 3 4. HISTORICAL EXPERIENCE 12 5. PARTICIPATING PROVIDERS 18 6.

Carrier Trend Report July 2017 Analysis Consulting Actuaries Contents 1. REPORT OVERVIEW 1 2. EXECUTIVE SUMMARY 2 3. RESULTS FOR JULY 2017 3 4. HISTORICAL EXPERIENCE 12 5. PARTICIPATING PROVIDERS 18 6.

Session 90 L, Learning From the First Two Years of the ACA. Moderator: Syed Muzayan Mehmud, ASA, FCA, MAAA

Session 90 L, Learning From the First Two Years of the ACA Moderator: Syed Muzayan Mehmud, ASA, FCA, MAAA Presenters: Gregory Gierer Syed Muzayan Mehmud, ASA, FCA, MAAA Karan Rustagi, ASA, MAAA SOA Antitrust

Session 90 L, Learning From the First Two Years of the ACA Moderator: Syed Muzayan Mehmud, ASA, FCA, MAAA Presenters: Gregory Gierer Syed Muzayan Mehmud, ASA, FCA, MAAA Karan Rustagi, ASA, MAAA SOA Antitrust

What you need to know about Insurance Exchanges?

What you need to know about Insurance Exchanges? Patrick C. Haynes, Jr. Today s presenter As counsel for Crawford Advisors Employee Benefits and Executive Compensation Group, Mr. Haynes advises employers

What you need to know about Insurance Exchanges? Patrick C. Haynes, Jr. Today s presenter As counsel for Crawford Advisors Employee Benefits and Executive Compensation Group, Mr. Haynes advises employers

Affordable Care Act (ACA) Update / Life & Health Product Review Roundtable

Update / Life & Health Product Review Roundtable") 2014 Industry Conference Navigating the Changing Insurance Environment Affordable Care Act (ACA) Update / Life & Health Product Review Roundtable Richard Robleto, Deputy Commissioner, Life & Health Jack

2014 Industry Conference Navigating the Changing Insurance Environment Affordable Care Act (ACA) Update / Life & Health Product Review Roundtable Richard Robleto, Deputy Commissioner, Life & Health Jack

Health Insurance Price Index for October-December February 2014

Health Insurance Price Index for October-December 2013 February 2014 ehealth 2.2014 Table of Contents Introduction... 3 Executive Summary and Highlights... 4 Nationwide Health Insurance Costs National

Health Insurance Price Index for October-December 2013 February 2014 ehealth 2.2014 Table of Contents Introduction... 3 Executive Summary and Highlights... 4 Nationwide Health Insurance Costs National

Prepared by Marsha Gold and Dawn Phelps i ; and Gretchen Jacobson and Tricia Neuman ii June 2010

MEDICARE ADVANTAGE 2010 DATA SPOTLIGHT Plan Enrollment Patterns and Trends Prepared by Marsha Gold and Dawn Phelps i ; and Gretchen Jacobson and Tricia Neuman ii June 2010 In March 2010, 11.1 million Medicare

MEDICARE ADVANTAGE 2010 DATA SPOTLIGHT Plan Enrollment Patterns and Trends Prepared by Marsha Gold and Dawn Phelps i ; and Gretchen Jacobson and Tricia Neuman ii June 2010 In March 2010, 11.1 million Medicare

ACA impact illustrations Individual and group medical New Jersey

ACA impact illustrations Individual and group medical New Jersey Prepared for and at the request of: Center Forward Prepared by: Margaret A. Chance, FSA, MAAA James T. O Connor, FSA, MAAA 71 S. Wacker

ACA impact illustrations Individual and group medical New Jersey Prepared for and at the request of: Center Forward Prepared by: Margaret A. Chance, FSA, MAAA James T. O Connor, FSA, MAAA 71 S. Wacker

Exchanges year 2: New findings and ongoing trends

Intelligence Brief Exchanges year 2: New findings and ongoing trends The open enrollment period (OEP) for year 2 of the individual exchanges is officially under way, having begun on November 15 th. To

Intelligence Brief Exchanges year 2: New findings and ongoing trends The open enrollment period (OEP) for year 2 of the individual exchanges is officially under way, having begun on November 15 th. To

Consulting Actuaries CARRIER TREND REPORT JANUARY 2016 ANALYSIS

Consulting Actuaries CARRIER TREND REPORT JANUARY 16 ANALYSIS CONTENTS 1. REPORT OVERVIEW 3 2. EXECUTIVE SUMMARY 4 3. RESULTS FOR JANUARY 16 4. HISTORICAL EXPERIENCE 14. PARTICIPATING PROVIDERS 6. EXPOSURES

Consulting Actuaries CARRIER TREND REPORT JANUARY 16 ANALYSIS CONTENTS 1. REPORT OVERVIEW 3 2. EXECUTIVE SUMMARY 4 3. RESULTS FOR JANUARY 16 4. HISTORICAL EXPERIENCE 14. PARTICIPATING PROVIDERS 6. EXPOSURES

MEDICAL PLAN OPTIONS. Presented By Kurt Swardenski, RHU, REBC Advantage Benefits Group

MEDICAL PLAN OPTIONS Presented By Kurt Swardenski, RHU, REBC Advantage Benefits Group Medical Options after CMU 1. Spouse Plan 2. COBRA continuation coverage 3. Marketplace Coverage 4. Individual Coverage

MEDICAL PLAN OPTIONS Presented By Kurt Swardenski, RHU, REBC Advantage Benefits Group Medical Options after CMU 1. Spouse Plan 2. COBRA continuation coverage 3. Marketplace Coverage 4. Individual Coverage

Report on Merging the Individual and Small Group Markets

www.pwc.com Report on Merging the Individual and Small Group Markets Draft October 12, 2018 Prepared by PwC for Covered California (10/12/18) Covered California 1601 Exposition Blvd. Sacramento, CA 95815

www.pwc.com Report on Merging the Individual and Small Group Markets Draft October 12, 2018 Prepared by PwC for Covered California (10/12/18) Covered California 1601 Exposition Blvd. Sacramento, CA 95815

Budget Uncertainty in Medicaid. Federal Funds Information for States

Budget Uncertainty in Medicaid Federal Funds Information for States www.ffis.org NCSL Legislative Summit August 2017 CHIP Funding State Flexibility DSH Cuts Uncertainty Block Grant ACA Expansion Per Capita

Budget Uncertainty in Medicaid Federal Funds Information for States www.ffis.org NCSL Legislative Summit August 2017 CHIP Funding State Flexibility DSH Cuts Uncertainty Block Grant ACA Expansion Per Capita

Center on Budget and Policy Priorities. cbpp.org

1 QHP Certification Process Ac#ve Purchasing Market Organizer Enhanced Cer#fica#on Basic Cer#fica#on QHP Cer#fica#on Model Ac#ve Purchasing Market Organizer Enhanced Cer#fica#on Basic Cer#fica#on Cer#fica#on

1 QHP Certification Process Ac#ve Purchasing Market Organizer Enhanced Cer#fica#on Basic Cer#fica#on QHP Cer#fica#on Model Ac#ve Purchasing Market Organizer Enhanced Cer#fica#on Basic Cer#fica#on Cer#fica#on

Medicare Advantage 2018 Data Spotlight: First Look

Medicare Advantage 2018 Data Spotlight: First Look Gretchen Jacobson, Anthony Damico, Tricia Neuman More than 19 million Medicare beneficiaries (33%) are enrolled in Medicare Advantage in 2017, which are

Medicare Advantage 2018 Data Spotlight: First Look Gretchen Jacobson, Anthony Damico, Tricia Neuman More than 19 million Medicare beneficiaries (33%) are enrolled in Medicare Advantage in 2017, which are

Medicare Part D: A First Look at Plan Offerings in 2014

October 2013 Issue Brief Medicare Part D: A First Look at Plan Offerings in 2014 Jack Hoadley, Juliette Cubanski, Elizabeth Hargrave, and Laura Summer 1 The Centers for Medicare & Medicaid Services (CMS)

October 2013 Issue Brief Medicare Part D: A First Look at Plan Offerings in 2014 Jack Hoadley, Juliette Cubanski, Elizabeth Hargrave, and Laura Summer 1 The Centers for Medicare & Medicaid Services (CMS)

Health Insurance Price Index Report Open Enrollment Period

Health Insurance Price Index Report 2018 Open Enrollment Period SEPTEMBER 2018 2 Health Insurance Price Index Report 2018 Open Enrollment Period 3 Introduction 4 Individual Coverage Costs 7 Family Coverage

Health Insurance Price Index Report 2018 Open Enrollment Period SEPTEMBER 2018 2 Health Insurance Price Index Report 2018 Open Enrollment Period 3 Introduction 4 Individual Coverage Costs 7 Family Coverage

The Academy and Health Reform

The Academy and Health Reform Cori E. Uccello, FSA, MAAA, MPP Senior Health Fellow American Academy of Actuaries CAS Annual Meeting, Session C-25 November 10, 2010 Washington, DC Overview Key provisions

The Academy and Health Reform Cori E. Uccello, FSA, MAAA, MPP Senior Health Fellow American Academy of Actuaries CAS Annual Meeting, Session C-25 November 10, 2010 Washington, DC Overview Key provisions

Moderator: Donna Christine Megregian, FSA, MAAA

Session 46 PD, Newly Proposed ASOPs: Pricing, Modeling and Setting Assumptions Moderator: Donna Christine Megregian, FSA, MAAA Presenters: Donna Christine Megregian, FSA, MAAA James A. Miles, FSA, MAAA

Session 46 PD, Newly Proposed ASOPs: Pricing, Modeling and Setting Assumptions Moderator: Donna Christine Megregian, FSA, MAAA Presenters: Donna Christine Megregian, FSA, MAAA James A. Miles, FSA, MAAA

Nation s Uninsured Rate for Children Drops to Another Historic Low in 2016

Nation s Rate for Children Drops to Another Historic Low in 2016 by Joan Alker and Olivia Pham The number of uninsured children nationwide dropped to another historic low in 2016 with approximately 250,000

Nation s Rate for Children Drops to Another Historic Low in 2016 by Joan Alker and Olivia Pham The number of uninsured children nationwide dropped to another historic low in 2016 with approximately 250,000

Seal of Approval: Product Strategy Evolution and Current State

Seal of Approval: Product Strategy Evolution and Current State ASHLEY HAGUE Deputy Executive Director, Strategy and External Affairs AUDREY GASTEIER Director of Policy and Outreach BRIAN SCHUETZ Director

Seal of Approval: Product Strategy Evolution and Current State ASHLEY HAGUE Deputy Executive Director, Strategy and External Affairs AUDREY GASTEIER Director of Policy and Outreach BRIAN SCHUETZ Director

The Affordable Care Act; 2014 and Beyond

The Affordable Care Act; 2014 and Beyond Presented by: Lacey Robinson, ACA Certified Vice President & Senior Benefits Consultant Gregory & Appel December 10, 2013 Agenda 2014 ACA Mandates ACA Intention

The Affordable Care Act; 2014 and Beyond Presented by: Lacey Robinson, ACA Certified Vice President & Senior Benefits Consultant Gregory & Appel December 10, 2013 Agenda 2014 ACA Mandates ACA Intention

California ARCA / MCA Health Care Reform Presentation

Mark Straus Dee Shaw Disclaimer: The ACA is constantly being revised and updated and the information contained in these slides was based on best information available to date. Atlanta Cleveland Los Angeles

Mark Straus Dee Shaw Disclaimer: The ACA is constantly being revised and updated and the information contained in these slides was based on best information available to date. Atlanta Cleveland Los Angeles

2016 individual market losses are in the high single digits a slight improvement from 2015

June 2017 2016 individual market losses are in the high single digits a slight improvement from 2015 Jim Oatman, Erica Coe A new McKinsey analysis suggests that overall carrier losses in the individual

June 2017 2016 individual market losses are in the high single digits a slight improvement from 2015 Jim Oatman, Erica Coe A new McKinsey analysis suggests that overall carrier losses in the individual

Handout. Table of Contents

Maximizing the Payment of Health-Related VR Services by Private Insurers and Medicaid: The VR Program and the Affordable Care Act Prepared for: Vocational Rehabilitation Research and Training Center By:

Maximizing the Payment of Health-Related VR Services by Private Insurers and Medicaid: The VR Program and the Affordable Care Act Prepared for: Vocational Rehabilitation Research and Training Center By:

State Plan Management Systems and Submission Deadlines for 2015

Plan Management Systems and Submission Deadlines for 2015 Questions related to HIOS may be directed to the HIOS Help Desk at 1-877-343-6507 or insuranceoversight@hhs.gov. Questions related to SERFF may

Plan Management Systems and Submission Deadlines for 2015 Questions related to HIOS may be directed to the HIOS Help Desk at 1-877-343-6507 or insuranceoversight@hhs.gov. Questions related to SERFF may

Consulting Actuaries CARRIER TREND REPORT JULY 2016 ANALYSIS

Consulting Actuaries CARRIER TREND REPORT JULY 16 ANALYSIS CONTENTS 1. REPORT OVERVIEW 1 2. EXECUTIVE SUMMARY 2 3. RESULTS FOR JULY 16 3 4. HISTORICAL EXPERIENCE 12. PARTICIPATING PROVIDERS 18 6. EXPOSURES

Consulting Actuaries CARRIER TREND REPORT JULY 16 ANALYSIS CONTENTS 1. REPORT OVERVIEW 1 2. EXECUTIVE SUMMARY 2 3. RESULTS FOR JULY 16 3 4. HISTORICAL EXPERIENCE 12. PARTICIPATING PROVIDERS 18 6. EXPOSURES

State Minimum Wage Chart (See below for Local/City Minimum Wage Chart)

") State Current Minimum Wage State Minimum Wage Chart (See below for Local/City Minimum Wage Chart) Maximum Tip Credit Allowed for Tipped Employees Federal $7.25 $5.12 $2.13 Minimum Cash Wage for Tipped

State Current Minimum Wage State Minimum Wage Chart (See below for Local/City Minimum Wage Chart) Maximum Tip Credit Allowed for Tipped Employees Federal $7.25 $5.12 $2.13 Minimum Cash Wage for Tipped

2017 Health Insurance Exchange Snapshot

2017 Health Insurance Exchange Snapshot Avalere Health An Inovalon Company January 2017 Figure 1. Exchange Enrollment Continues to Fall Below Expectations EXCHANGE ENROLLMENT AND PROJECTIONS, IN MILLIONS

2017 Health Insurance Exchange Snapshot Avalere Health An Inovalon Company January 2017 Figure 1. Exchange Enrollment Continues to Fall Below Expectations EXCHANGE ENROLLMENT AND PROJECTIONS, IN MILLIONS

Analysis & Background

1 Values shown are June estimates. # # # Analysis & Background Expected Revisions to Colorado Second quarter 2017 Quarterly Census of Employment and Wages (QCEW) results indicate Colorado total nonfarm

1 Values shown are June estimates. # # # Analysis & Background Expected Revisions to Colorado Second quarter 2017 Quarterly Census of Employment and Wages (QCEW) results indicate Colorado total nonfarm

CALL REPORT MEMBER BANK BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM WASHINGTON

MEMBER BANK CALL REPORT BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM WASHINGTON Assets and Liabilities: TABLE OF CONTENTS Of All Member Banks June 0, 98, April iz, 98, and June 0, 97 Of All Member

MEMBER BANK CALL REPORT BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM WASHINGTON Assets and Liabilities: TABLE OF CONTENTS Of All Member Banks June 0, 98, April iz, 98, and June 0, 97 Of All Member

Presented by: Jim Gilbert Registered Health Underwriter & Registered Employee Benefits Consultant

Healthcare Reform Update 18 th Annual Update for Accountants Presented by: Jim Gilbert Registered Health Underwriter & Registered Employee Benefits Consultant Thursday, December 5 th, 2013 What is Health

Healthcare Reform Update 18 th Annual Update for Accountants Presented by: Jim Gilbert Registered Health Underwriter & Registered Employee Benefits Consultant Thursday, December 5 th, 2013 What is Health

Realizing Health Reform s Potential

The COMMONWEALTH FUND Realizing Health Reform s Potential AUGUST 2015 Comparing Individual Health Coverage On and Off the Affordable Care Act s Insurance Exchanges Michael J. McCue and Mark A. Hall The

The COMMONWEALTH FUND Realizing Health Reform s Potential AUGUST 2015 Comparing Individual Health Coverage On and Off the Affordable Care Act s Insurance Exchanges Michael J. McCue and Mark A. Hall The

State of New Jersey Department of Banking and Insurance PO Box 325 Life & Health Actuarial, 11th Floor Trenton, NJ Tel (609) Fax

Fax") State of New Jersey Department of Banking and Insurance PO Box 325 Life & Health Actuarial, 11th Floor Trenton, NJ 08625-0325 Tel (609) 292-7272 Fax (609) 633-0527 1 R. Neil Vance, Managing Actuary NJ

State of New Jersey Department of Banking and Insurance PO Box 325 Life & Health Actuarial, 11th Floor Trenton, NJ 08625-0325 Tel (609) 292-7272 Fax (609) 633-0527 1 R. Neil Vance, Managing Actuary NJ

Minimum Wage per State

per State Future and Notes ALABAMA NONE Federal minimum applies. BIRMINGHAM: July 2016 $ 8.50; July 2017: $10.10 ALASKA $8.75 ARIZONA $8.05 ARKANSAS $7.50 Nov. 4 2014 ballot measure approved to raise minimum

per State Future and Notes ALABAMA NONE Federal minimum applies. BIRMINGHAM: July 2016 $ 8.50; July 2017: $10.10 ALASKA $8.75 ARIZONA $8.05 ARKANSAS $7.50 Nov. 4 2014 ballot measure approved to raise minimum

Washington Health Benefit Exchange 2018 Plan Landscape and Market Stabilization Project

Washington Health Benefit Exchange 2018 Plan Landscape and Market Stabilization Project Exchange Advisory Committee Meeting September 12, 2017 Molly Voris, Policy Director Christine Gibert, Associate Policy

Washington Health Benefit Exchange 2018 Plan Landscape and Market Stabilization Project Exchange Advisory Committee Meeting September 12, 2017 Molly Voris, Policy Director Christine Gibert, Associate Policy

Hospital networks: Perspective from four years of the individual market exchanges

Hospital networks: Perspective from four years of the individual market exchanges McKinsey Center for U.S. Health System Reform May 017 Any use of this material without specific permission of is strictly

Hospital networks: Perspective from four years of the individual market exchanges McKinsey Center for U.S. Health System Reform May 017 Any use of this material without specific permission of is strictly

Moderator: Robert T Eaton FSA,MAAA. Presenters: Bryn T Douds FSA,MAAA Robert T Eaton FSA,MAAA Robert K Yee FSA,MAAA

Session 27PD: The Impact of FASB Targeted Improvements on Health Products Moderator: Robert T Eaton FSA,MAAA Presenters: Bryn T Douds FSA,MAAA Robert T Eaton FSA,MAAA Robert K Yee FSA,MAAA SOA Antitrust

Session 27PD: The Impact of FASB Targeted Improvements on Health Products Moderator: Robert T Eaton FSA,MAAA Presenters: Bryn T Douds FSA,MAAA Robert T Eaton FSA,MAAA Robert K Yee FSA,MAAA SOA Antitrust

MILLIMAN RESEARCH REPORT Medicaid risk-based managed care: Analysis of financial results for June 2017

Medicaid risk-based managed care: Analysis of financial results for 2016 June 2017 Jeremy D. Palmer, FSA, MAAA Christopher T. Pettit, FSA, MAAA Table of Contents INTRODUCTION... 1 SUMMARY OF RESULTS...

Medicaid risk-based managed care: Analysis of financial results for 2016 June 2017 Jeremy D. Palmer, FSA, MAAA Christopher T. Pettit, FSA, MAAA Table of Contents INTRODUCTION... 1 SUMMARY OF RESULTS...

HSA BANK HEALTH & WEALTH INDEX SM. HSA-Based Plans Drive Engagement Among Consumers

HSA BANK HEALTH & WEALTH INDEX SM HSA-Based Plans Drive Engagement Among Consumers 2018 TABLE OF CONTENTS Introduction... 1 Overview... 1 Outcomes... 2 Key Findings... 7 1: Consumers can improve their

HSA BANK HEALTH & WEALTH INDEX SM HSA-Based Plans Drive Engagement Among Consumers 2018 TABLE OF CONTENTS Introduction... 1 Overview... 1 Outcomes... 2 Key Findings... 7 1: Consumers can improve their

Part 3 Actuarial Memorandum

1. GENERAL INFORMATION Insurance Company Name Cigna HealthCare of North Carolina NAIC Company Code 95132 HIOS Issuer ID 73943 State North Carolina Market Type Individual Proposed Effective Date 01/01/2019

1. GENERAL INFORMATION Insurance Company Name Cigna HealthCare of North Carolina NAIC Company Code 95132 HIOS Issuer ID 73943 State North Carolina Market Type Individual Proposed Effective Date 01/01/2019

CCI 2019 LEGISLATIVE ISSUE FORM HHS. 1.) Issue: INDIVIDUAL HEALTH INSURANCE MARKET EQUALITY AND STABILIZATION ACT

Issue: INDIVIDUAL HEALTH INSURANCE MARKET EQUALITY AND STABILIZATION ACT") CCI 2019 LEGISLATIVE ISSUE FORM HHS CCI is soliciting potential legislative issues for the 2019 legislative session. Please answer all of the questions below for each of your county s legislative issues.

CCI 2019 LEGISLATIVE ISSUE FORM HHS CCI is soliciting potential legislative issues for the 2019 legislative session. Please answer all of the questions below for each of your county s legislative issues.

Medicaid & CHIP: December 2014 Monthly Applications, Eligibility Determinations and Enrollment Report February 23, 2015

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services 7500 Security Boulevard, Mail Stop S2-26-12 Baltimore, Maryland 21244-1850 Medicaid & CHIP: December 2014 Monthly Applications,

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services 7500 Security Boulevard, Mail Stop S2-26-12 Baltimore, Maryland 21244-1850 Medicaid & CHIP: December 2014 Monthly Applications,

11/14/2013. Overview. Employer Mandate Exchanges Medicaid Expansion Funding. Medicare Taxes & Fees. Discussion

Michael A. Morrisey, Ph.D. Lister Hill Center for Health Policy University of Alabama at Birmingham Atlanta Federal Reserve Bank November 14, 2013 Individual Mandate Employer Mandate Exchanges Medicaid

Michael A. Morrisey, Ph.D. Lister Hill Center for Health Policy University of Alabama at Birmingham Atlanta Federal Reserve Bank November 14, 2013 Individual Mandate Employer Mandate Exchanges Medicaid

Advancing Sovereignty. Other ACA and IHCIA-related Topics --

Advancing Sovereignty -- Tribal Sponsorship and Other ACA and IHCIA-related Topics -- August 17, 2016 Agenda HHS Essential Community Provider List: Status Update Summary of Benefits and Coverage: HHS release

Advancing Sovereignty -- Tribal Sponsorship and Other ACA and IHCIA-related Topics -- August 17, 2016 Agenda HHS Essential Community Provider List: Status Update Summary of Benefits and Coverage: HHS release

Provider Network Definitions BY METAL TIER

2014 Provider Network Definitions BY METAL TIER This information is subject to change without notice. The information provided herein is provided to you on an as is as available basis without warranty

2014 Provider Network Definitions BY METAL TIER This information is subject to change without notice. The information provided herein is provided to you on an as is as available basis without warranty

HEALTH CARE WAIVERS 101 THURSDAY, JULY 28, :00 PM ET/ 3:00 PM CT/2:00 PM MT/ 1:00 PM PT

HEALTH CARE WAIVERS 101 THURSDAY, JULY 28, 2016 4:00 PM ET/ 3:00 PM CT/2:00 PM MT/ 1:00 PM PT Special Thanks This webinar is supported by the Health Resources and Services Administration (HRSA) of the

HEALTH CARE WAIVERS 101 THURSDAY, JULY 28, 2016 4:00 PM ET/ 3:00 PM CT/2:00 PM MT/ 1:00 PM PT Special Thanks This webinar is supported by the Health Resources and Services Administration (HRSA) of the

Session 024 PD - Life Reinsurance in Bermuda. Moderator: Gokul Sudarsana, FSA, CERA, FCIA

Session 024 PD - Life Reinsurance in Bermuda Moderator: Gokul Sudarsana, FSA, CERA, FCIA Presenters: Manfred Maske Sylvia Martin Oliveira, FSA, MAAA Scott D. Selkirk, FSA, MAAA SOA Antitrust Compliance

Session 024 PD - Life Reinsurance in Bermuda Moderator: Gokul Sudarsana, FSA, CERA, FCIA Presenters: Manfred Maske Sylvia Martin Oliveira, FSA, MAAA Scott D. Selkirk, FSA, MAAA SOA Antitrust Compliance

THE COST OF NOT EXPANDING MEDICAID

REPORT THE COST OF NOT EXPANDING MEDICAID July 2013 PREPARED BY John Holahan, Matthew Buettgens, and Stan Dorn The Urban Institute The Kaiser Commission on Medicaid and the Uninsured provides information

REPORT THE COST OF NOT EXPANDING MEDICAID July 2013 PREPARED BY John Holahan, Matthew Buettgens, and Stan Dorn The Urban Institute The Kaiser Commission on Medicaid and the Uninsured provides information

III.B. Provisions and Parameters for the Permanent Risk Adjustment Program

Dec. 31, 2012 Centers for Medicare & Medicaid Services U.S. Department of Health and Human Services Attention: CMS-9964-P PO Box 8016 Baltimore, MD 21244-8016 Re: Notice of Benefit and Payment Parameters

Dec. 31, 2012 Centers for Medicare & Medicaid Services U.S. Department of Health and Human Services Attention: CMS-9964-P PO Box 8016 Baltimore, MD 21244-8016 Re: Notice of Benefit and Payment Parameters

WHITE PAPER. Impact of CSR De-funding on Market Stability. Executive Summary

WHITE PAPER Impact of CSR De-funding on Market Stability Karan Rustagi, FSA, MAAA 720.282.4965 Karan.Rustagi@wakely.com Michael Cohen, PhD 202.568.0633 Michael.Cohen@wakely.com Al Bingham, Jr., FSA, MAAA

WHITE PAPER Impact of CSR De-funding on Market Stability Karan Rustagi, FSA, MAAA 720.282.4965 Karan.Rustagi@wakely.com Michael Cohen, PhD 202.568.0633 Michael.Cohen@wakely.com Al Bingham, Jr., FSA, MAAA

North Carolina Actuarial Memorandum Requirements for Rate Submissions Effective 1/1/2015 and Later. Small Group Market Non grandfathered Business

North Carolina Actuarial Memorandum Requirements for Rate Submissions Effective 1/1/2015 and Later Small Group Market Non grandfathered Business These actuarial memorandum requirements apply to all products

North Carolina Actuarial Memorandum Requirements for Rate Submissions Effective 1/1/2015 and Later Small Group Market Non grandfathered Business These actuarial memorandum requirements apply to all products

https://youtu.be/emoc1kjptoy ACA IS FAILING Higher premiums and fewer options The percentage of workers at small firms receiving coverage through their employer has declined from nearly half in 2010 to

https://youtu.be/emoc1kjptoy ACA IS FAILING Higher premiums and fewer options The percentage of workers at small firms receiving coverage through their employer has declined from nearly half in 2010 to

Session 47L, Health Reserve Setting. Moderator/Presenter: Marilyn M. McGaffin, ASA, MAAA

Session 47L, Health Reserve Setting Moderator/Presenter: Marilyn M. McGaffin, ASA, MAAA Presenters: David A. Berry, FSA, MAAA Lisa M. Parker, ASA, MAAA Andrew Z. Smith, ASA, MAAA SOA Antitrust Disclaimer

Session 47L, Health Reserve Setting Moderator/Presenter: Marilyn M. McGaffin, ASA, MAAA Presenters: David A. Berry, FSA, MAAA Lisa M. Parker, ASA, MAAA Andrew Z. Smith, ASA, MAAA SOA Antitrust Disclaimer

Deteriorating Health Insurance Coverage from 2000 to 2010: Coverage Takes the Biggest Hit in the South and Midwest

ACA Implementation Monitoring and Tracking Deteriorating Health Insurance Coverage from 2000 to 2010: Coverage Takes the Biggest Hit in the South and Midwest August 2012 Fredric Blavin, John Holahan, Genevieve

ACA Implementation Monitoring and Tracking Deteriorating Health Insurance Coverage from 2000 to 2010: Coverage Takes the Biggest Hit in the South and Midwest August 2012 Fredric Blavin, John Holahan, Genevieve

State-by-State Estimates of the Coverage and Funding Consequences of Full Repeal of the ACA

H E A L T H P O L I C Y C E N T E R State-by-State Estimates of the Coverage and Funding Consequences of Full Repeal of the ACA Linda J. Blumberg, Matthew Buettgens, John Holahan, and Clare Pan March 2019

H E A L T H P O L I C Y C E N T E R State-by-State Estimates of the Coverage and Funding Consequences of Full Repeal of the ACA Linda J. Blumberg, Matthew Buettgens, John Holahan, and Clare Pan March 2019

The Massachusetts Health Connector and Cost Containment After Reform

The Massachusetts Health Connector and Cost Containment After Reform MARISSA WOLTMANN Associate Director of Policy and ACA Implementation Specialist January 12, 2017 Today s Focus Background on the Health

The Massachusetts Health Connector and Cost Containment After Reform MARISSA WOLTMANN Associate Director of Policy and ACA Implementation Specialist January 12, 2017 Today s Focus Background on the Health

Legislative and Regulatory Update. Jeff Williams SVP Actuarial, Economics & Healthcare Regulation SE Actuarial Conference June 20-22, 2018

Legislative and Regulatory Update Jeff Williams SVP Actuarial, Economics & Healthcare Regulation SE Actuarial Conference June 20-22, 2018 Marketplace Update CSR Armageddon Nationwide stats in 2018 vs.

Legislative and Regulatory Update Jeff Williams SVP Actuarial, Economics & Healthcare Regulation SE Actuarial Conference June 20-22, 2018 Marketplace Update CSR Armageddon Nationwide stats in 2018 vs.

Enhancing the Patient-Centeredness of State Health Insurance Markets State Progress Reports

Enhancing the Patient-Centeredness of State Health Insurance Markets State Progress Reports ENHANCING THE PATIENT-CENTEREDNESS OF STATE HEALTH INSURANCE MARKETS 1 Founded in 1920, the NHC is the only organization

Enhancing the Patient-Centeredness of State Health Insurance Markets State Progress Reports ENHANCING THE PATIENT-CENTEREDNESS OF STATE HEALTH INSURANCE MARKETS 1 Founded in 1920, the NHC is the only organization

ACA impact on Puerto Rico small groups (PYMES)

") ACA impact on Puerto Rico small groups (PYMES) Presented by: Luis O. Maldonado, FSA, MAAA Consulting Actuary Agenda Key Elements of Health Care Reform ACA Insurance Market provisions ACA impact for Puerto

ACA impact on Puerto Rico small groups (PYMES) Presented by: Luis O. Maldonado, FSA, MAAA Consulting Actuary Agenda Key Elements of Health Care Reform ACA Insurance Market provisions ACA impact for Puerto

American Dental Association Changing Payment System. Medicare Coverage Addendum

Tax American Dental Association Changing Payment System Medicare Coverage Addendum Contents of Benefit Implementation Strategies 3 Medicare 10 Medicare 15 21 was engaged to perform actuarial services.

Tax American Dental Association Changing Payment System Medicare Coverage Addendum Contents of Benefit Implementation Strategies 3 Medicare 10 Medicare 15 21 was engaged to perform actuarial services.

QUALIFIED HEALTH PLAN SELECTION: CONSIDERATIONS FOR CONSUMERS

QUALIFIED HEALTH PLAN SELECTION: CONSIDERATIONS FOR CONSUMERS January 2014 Support for this resource provided through a grant from the Robert Wood Johnson Foundation s State Health Reform Assistance Network

QUALIFIED HEALTH PLAN SELECTION: CONSIDERATIONS FOR CONSUMERS January 2014 Support for this resource provided through a grant from the Robert Wood Johnson Foundation s State Health Reform Assistance Network

Medicare Advantage: 2015 National Snapshot

Advantage: 2015 National Snapshot July 2015 Prepared by: Avalere LLC Funding for this research was provided by Aetna. Avalere maintained full editorial control. Advantage: 2015 National Snapshot 1 PROGRAM

Advantage: 2015 National Snapshot July 2015 Prepared by: Avalere LLC Funding for this research was provided by Aetna. Avalere maintained full editorial control. Advantage: 2015 National Snapshot 1 PROGRAM

2018 Seal of Approval Preview

2018 Seal of Approval Preview BRIAN SCHUETZ Director of Program and Product Strategy MARIA JOY DAWLEY Product Manager, Health and Dental Plans EMILY BRICE Senior Policy Advisor Board of Directors Meeting,

2018 Seal of Approval Preview BRIAN SCHUETZ Director of Program and Product Strategy MARIA JOY DAWLEY Product Manager, Health and Dental Plans EMILY BRICE Senior Policy Advisor Board of Directors Meeting,

February 11, 2014 By Emily R. Gee

ASPE RESEARCH BRIEF ELIGIBLE UNINSURED LATINOS: 8 IN 10 COULD RECEIVE HEALTH INSURANCE MARKETPLACE TAX CREDITS, MEDICAID OR CHIP February 11, 2014 By Emily R. Gee Under the Affordable Care Act, 10.2 million

ASPE RESEARCH BRIEF ELIGIBLE UNINSURED LATINOS: 8 IN 10 COULD RECEIVE HEALTH INSURANCE MARKETPLACE TAX CREDITS, MEDICAID OR CHIP February 11, 2014 By Emily R. Gee Under the Affordable Care Act, 10.2 million

Session 84 PD, SOA Research Topic: Conversion Mortality Experience. Moderator: James M. Filmore, FSA, MAAA. Presenters: Minyu Cao, FSA, CERA

Session 84 PD, SOA Research Topic: Conversion Mortality Experience Moderator: James M. Filmore, FSA, MAAA Presenters: Minyu Cao, FSA, CERA James M. Filmore, FSA, MAAA Hezhong (Mark) Ma, FSA, MAAA SOA Antitrust

Session 84 PD, SOA Research Topic: Conversion Mortality Experience Moderator: James M. Filmore, FSA, MAAA Presenters: Minyu Cao, FSA, CERA James M. Filmore, FSA, MAAA Hezhong (Mark) Ma, FSA, MAAA SOA Antitrust

Health Reform Coverage Expansions: Impact of Insurance Exchanges & Medicaid Expansion on Michigan Health Plans. July 2014 avalere.

Health Reform Coverage Expansions: Impact of Insurance Exchanges & Medicaid Expansion on Michigan Health Plans July 2014 avalere.com Agenda Health Insurance Exchanges: National and Michigan Trends o Enrollment

Health Reform Coverage Expansions: Impact of Insurance Exchanges & Medicaid Expansion on Michigan Health Plans July 2014 avalere.com Agenda Health Insurance Exchanges: National and Michigan Trends o Enrollment

PRIVATE PAYOR OUTLOOK KELLI BACK, ATTORNEY AND APMA CONSULTANT

PRIVATE PAYOR OUTLOOK KELLI BACK, ATTORNEY AND APMA CONSULTANT Insurance Coverage by Source (2015) Employer Group 49% Non-group (individual and association) 7% Medicaid 20% (includes dual eligibles) Medicare

PRIVATE PAYOR OUTLOOK KELLI BACK, ATTORNEY AND APMA CONSULTANT Insurance Coverage by Source (2015) Employer Group 49% Non-group (individual and association) 7% Medicaid 20% (includes dual eligibles) Medicare

Medicare advantage Enrollment Market Update

Data spotlight Medicare advantage Enrollment Market Update Prepared by Marsha Gold i ; and Gretchen Jacobson, Anthony Damico, and Tricia Neuman ii In millions: EXHIBIT 1 Total Medicare Private Health Plan

Data spotlight Medicare advantage Enrollment Market Update Prepared by Marsha Gold i ; and Gretchen Jacobson, Anthony Damico, and Tricia Neuman ii In millions: EXHIBIT 1 Total Medicare Private Health Plan

EXECUTIVE SUMMARY ENROLLMENT GROWS YET MARGINS DROP FOR OHIO S HEALTH INSURING CORPORATIONS. 970,000 Ohioans remained uninsured in 2014.

OHA exists to collaborate with member hospitals and health systems to ensure a healthy Ohio. February 2016 EXECUTIVE SUMMARY ENROLLMENT GROWS YET MARGINS DROP FOR OHIO S HEALTH INSURING CORPORATIONS In

OHA exists to collaborate with member hospitals and health systems to ensure a healthy Ohio. February 2016 EXECUTIVE SUMMARY ENROLLMENT GROWS YET MARGINS DROP FOR OHIO S HEALTH INSURING CORPORATIONS In

Medicaid & CHIP: March 2015 Monthly Applications, Eligibility Determinations and Enrollment Report June 4, 2015

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services 7500 Security Boulevard, Mail Stop S2-26-12 Baltimore, Maryland 21244-1850 Medicaid & CHIP: March 2015 Monthly Applications,

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services 7500 Security Boulevard, Mail Stop S2-26-12 Baltimore, Maryland 21244-1850 Medicaid & CHIP: March 2015 Monthly Applications,

Medicaid & CHIP: October 2014 Monthly Applications, Eligibility Determinations and Enrollment Report December 18, 2014

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services 7500 Security Boulevard, Mail Stop S2-26-12 Baltimore, Maryland 21244-1850 Medicaid & CHIP: October 2014 Monthly Applications,

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services 7500 Security Boulevard, Mail Stop S2-26-12 Baltimore, Maryland 21244-1850 Medicaid & CHIP: October 2014 Monthly Applications,

Session 112 PD, Medicaid - Hot Topics. Moderator: Clay Farris

Session 112 PD, Medicaid - Hot Topics Moderator: Clay Farris Presenters: Davis Burge, FSA, MAAA Sabrina H. Gibson, FSA, MAAA Christopher John Truffer, FSA, MAAA SOA Antitrust Disclaimer SOA Presentation

Session 112 PD, Medicaid - Hot Topics Moderator: Clay Farris Presenters: Davis Burge, FSA, MAAA Sabrina H. Gibson, FSA, MAAA Christopher John Truffer, FSA, MAAA SOA Antitrust Disclaimer SOA Presentation

2013 Summary of Benefits

2013 Summary of Benefits SilverScript Basic (PDP) SilverScript Choice (PDP) SilverScript Plus (PDP) January 1, 2013 December 31, 2013 S5601 SilverScript Basic (PDP), SilverScript Choice (PDP) and SilverScript

2013 Summary of Benefits SilverScript Basic (PDP) SilverScript Choice (PDP) SilverScript Plus (PDP) January 1, 2013 December 31, 2013 S5601 SilverScript Basic (PDP), SilverScript Choice (PDP) and SilverScript