INTERNATIONAL REGULATION FOR ACCOUNTING

|

|

|

- Josephine Boone

- 5 years ago

- Views:

Transcription

1 1 INTERNATIONAL REGULATION FOR ACCOUNTING STOCKHOLM

2 2 International Regulation for Accounting CONTENT A brief history of global standard settings Older global standards and interpretations still in force Newer global standards and interpretations Global implementation of standards + The work flow Regional implementation of global standards + The EU as example National implementations of regional standards + The EU member states example

3 3 Abbreviations Global + IASC International Accounting Standards Committee + IAS International Accounting Standards + SIC Standing Interpretation Committee + IASB International Accounting Standards Board + IFRS International Financial Reporting Standards + IFRS-enterprises Listed enterprises and other who apply IFRS + IFRIC IFRS Interpretations Committee + GAAP Generally Accepted Accounting Principles + OECD The Organization for Economic Co-operation and Development + BEPS Base Erosion and Profit Shifting Regional + EU European Union + EFRAG European Financial Reporting Advisory Group + ESMA European Securities and Markets Authority + EEA European Economic Area

4 4 Harmonization (or not) in Different Areas 1) Financial Reports + Listed companies: Good uniformity through IFRS + Unlisted companies: Poor uniformity although IFRS for SME + Smaller companies: No uniformity, with IFRS for SME as a too-large framework 2) Income Tax + No overall uniformity, neither globally nor within the EU + Partial uniformity, globally and within the EU + BEPS Project, within the EU as member of the OECD 3) VAT + Good uniformity within the EU 4) VAT versus Income Tax + No overall uniformity, neither globally nor within the EU 5) Accounting versus taxation and VAT + Poor uniformity, globally and regionally

5 5 Chain of Standards for Accounting (1) Global Regional National (main topic of this webinar) 1) Global standards are issued 2) and adopted regionally (by the EU after inspection) 3) and implemented in the member states + As law and/or standard + With national adaption if needed, to legislation for + Accounting + Income taxation + IFRS adopted by the EU also applies to member states in the EEA + Iceland + Liechtenstein + Norway

6 6 Chain of Standards for Accounting (2) Regional National (not covered in this webinar) 1) Regional standards are issued by the EU for companies not applying IFRS + In each regulation there are limits for + What the member states can decide themselves + Wen the regulation should be nationally implemented 2) and implemented in the member states + As law and/or standard + With national adaption if needed and permitted, to legislation for + Accounting + Income taxation + EU standards also applies to member states in the EEA + Iceland + Liechtenstein + Norway

7 7 Chain of Standards for Accounting (3) National (not covered in this webinar) + Each member state within the EU have it s own legislation for accounting topics which are not covered by the EU + Day-by-day accounting + Finalizing the accounts for non-listed companies + And for those who doesn t set up financial reports or consolidated accounts + National limits for categories, and the number of them, within EU legislation + Archiving the accounting + Audit of accounting (regulated by the EU but with wide limits) + IT-related matters

8 8 1. Communication During the Standard Setting Process Representation Comments National EU Representation Comments Committees Drafts IFRS

9 9 2. Adaption of Issued Standards Standard Interpretation Amendment IFRS EU EFRIC Recommendation EU Adaption Adjustments Adaption National

10 10 Global (1) - IASC was the Predecessor Operative Private non-profit organization, based in London Established by auditor organizations in Australia, Canada, France, Germany, Japan, Mexico, Netherlands, Great Britain and Ireland Issued Framework for the Preparation and Presentation of Financial Statements The Framework) + Issued standards (IAS) and interpretations (SIC) Replaced by IASB + Some IAS and SIC have been replaced by IFRS and IFRIC or revoked + But 2018 most IAS and some SIC are still in force, under supervision of IASB + 28 IAS + 8 SIC

11 11 IASC Standards (1) 1) IAS 1 Presentation of Financial Statements 2) IAS 2 Inventories 3) IAS 7 Statement of Cash Flows (Amended 2017) 4) IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors 5) IAS 10 Events after the Reporting Period 6) IAS 11 Construction Contracts 7) IAS 12 Income Taxes (Amended 2017) 8) IAS 16 Property, Plant and Equipment 9) IAS 17 Leases 10) IAS 18 Revenue 11) IAS 19 Employee Benefits Still in Force ) IAS 20 Accounting for Government Grants and Disclosure of Government Assistance 13) IAS 21 The Effects of Changes in Foreign Exchange Rates 14) IAS 23 Borrowing Costs 15) IAS 24 Related Party Disclosures 16) IAS 26 Accounting and Reporting by Retirement Benefit Plans 17) IAS 27 Separate Financial Statements 18) IAS 28 Investments in Associates and Joint Ventures * * Amendment not yet adopted by the EU as per December 12, 2017

12 12 IASC Standards (2) 20) IAS 29 Financial Reporting in Hyperinflationary Economies 21) IAS 32 Financial Instruments: Presentation 22) IAS 33 Earnings per Share 23) IAS 34 Interim Financial Reporting 24) IAS 36 Impairment of Assets 25) IAS 37 Provisions, Contingent Liabilities and Contingent Assets 26) IAS 38 Intangible Assets 27) IAS 39 Financial Instruments: Recognition and Measurement Still in Force ) IAS 40 Investment Property * 21) IAS 41 Agriculture * Amendment not yet adopted by the EU as per December 12, 2017

13 13 IASC Interpretations 1) SIC-7 Introduction of the Euro 2) SIC-10 Government Assistance No Specific Relation to Operating Activities 3) SIC-15 Operating Leases Incentives 4) SIC-25 Income Taxes Changes in the Tax Status of an Entity or its Shareholders 5) SIC-27 Evaluating the Substance of Transactions Involving the Legal Form of a Lease 6) SIC-29 Service Concession Arrangements: Disclosures Still in Force ) SIC-31 Revenue Barter Transactions Involving Advertising Services 8) SIC-32 Intangible Assets Web Site Costs

14 14 Global (2) - IASB is the Successor Operative from Private independent, non-profit organization, based in London + Supported by the G20, the World Bank and other international organizations + Issues standards (IFRS) and interpretations (IFRIC) + Still manages older standards (IAS) and interpretations (SIC) from IASC + The standards are now required in 125 jurisdictions, and permitted in many others Framework and standards Took over the framework from IASC Issued Conceptual Framework for Financial Reporting The IFRS Framework + Not adopted by the EU, therefor no official EU translations : So far issued + The IFRS Framework + 17 IFRS + 20 IFRIC + The IFRS for SMEs Standard + IFRS Taxonomy

15 15 IASB Standards (2) 1) IFRS 1 First-time Adoption of International Financial Reporting Standards 2) IFRS 2 Share-based Payment * 3) IFRS 3 Business Combinations 4) IFRS 4 Insurance Contracts (Amended 2017) 5) IFRS 5 Non-current Assets Held for Sale and Discontinued Operations 6) IFRS 6 Exploration for and Evaluation of Mineral Resources 7) IFRS 7 Financial Instruments: Disclosures 8) IFRS 8 Operating Segments 9) IFRS 9 Financial Instruments ** Issued until ) IFRS 10 Consolidated Financial Statements ** 11) IFRS 11 Joint Arrangements 12) IFRS 12 Disclosure of Interests in Other Entities 13) IFRS 13 Fair Value Measurement 14) IFRS 14 Regulatory Deferral Accounts * 15) IFRS 15 Revenue from Contracts with Customers (Clarified 2017) 16) IFRS 16 Leases (New 2017) 17) IFRS 17 Insurance Contracts * * Not yet adopted by the EU as per December 12, 2017 ** Amendment not yet adopted by the EU as per December 12, 2017

16 16 IASB Interpretations (1) 1) IFRIC 1 Changes in Existing Decommissioning, Restoration and Similar Liabilities 2) IFRIC 2 Members Shares in Co-operative Entities and Similar Instruments 3) IFRIC 4 Determining whether an Arrangement Contains a Lease 4) IFRIC 5 Rights to Interests arising from Decommissioning, Restoration and Environmental Rehabilitation Funds 5) IFRIC 6 Liabilities arising from Participating in a Specific Market Waste Electrical and Electronic Equipment Issued until ) IFRIC 7 Applying the Restatement Approach under IAS 29 Financial Reporting in Hyperinflationary Economies 7) IFRIC 9 Reassessment of Embedded Derivatives 8) IFRIC 10 Interim Financial Reporting and Impairment 9) IFRIC 12 Service Concession Arrangements 10) IFRIC 13 Customer Loyalty Programmes 11) IFRIC 14 IAS 19 The Limit on a Defined Benefit Asset, Minimum Funding Requirements and their Interaction

17 17 IASB Interpretations (2) 12) IFRIC 15 Agreements for the Construction of Real Estate 13) IFRIC 16 Hedges of a Net Investment in a Foreign Operation 14) IFRIC 17 Distributions of Non-cash Assets to Owners 15) IFRIC 18 Transfers of Assets from Customers 16) IFRIC 19 Extinguishing Financial Liabilities with Equity Instruments 17) IFRIC 20 Stripping Costs in the Production Phase of a Surface Mine 18) IFRIC 21 Levies Issued until ) IFRIC 22 Foreign Currency Transactions and Advance Consideration * 20) IFRIC 23 Uncertainty over Income Tax Treatments * Not yet adopted by the EU as per December 12, 2017

18 18 The IFRS Framework (1) Highlights Framework published by the IASC Framework adopted by the IASB Conceptual Framework published by the IASB , Q1 Planned publishing of revised Conceptual Framework Planned update of references to Framework in IFRS Standards Principles and definitions 1) The objective of financial reporting + Providing financial information about the reporting entity that is useful to existing and potential investors, lenders and other creditors in making decisions about providing resources to the entity 2) The qualitative characteristics of useful financial information + Relevance, faithful representation, comparability, verifiability, timeliness and understandability 3) The definition, recognition and measurement of the elements from which financial statements are constructed + Assets and liabilities, Equity, Income and expenses + Helps you solve problems when there is an uncertainty!

19 19 The IFRS Framework (2) Assets F 4.4 (a): An asset is a resource + controlled by the entity + as a result of past events + and from which future economic benefits are expected to flow to the entity F 4.44: An asset is recognized in the balance sheet + when it is probable that the future economic benefits will flow to the entity + and the asset has a cost or value that can be measured reliably. Comment + Q: When should real estates be transferred to a new owner in the accounting? + On the day of contract? + On the day of take-over? + A: The criteria's of an asset and it s recognition are fulfilled on the day of take-over + Possible national timely differences between accounting and income taxation!

20 20 The IFRS Framework (3) Liabilities F 4.4 (b): A liability is a present obligation of the entity + arising from past events, + the settlement of which is expected to result in an outflow from the entity + of resources embodying economic benefits F 4.46: A liability is recognized in the balance sheet + when it is probable that an outflow of resources embodying economic benefits + will result from the settlement of a present obligation + and the amount at which the settlement will take place can be measured reliably

21 21 The IFRS Framework (4) Equity F 4.4 (c): Equity is the residual interest in the assets of the entity, + after deducting all its liabilities

22 22 The IFRS Framework (5) Income F 4.25 (a): Income is increases in economic benefits during the accounting period in the form of + inflows or enhancements of assets or decreases of liabilities that result in increases in equity, + other than those relating to contributions from equity participants F 4.47: Income is recognized in the income statement when an increase in future economic benefits + related to an increase in an asset or a decrease of a liability has arisen that can be measured reliably + recognition of income occurs simultaneously with the recognition of increases in assets or decreases in liabilities + for example, the net increase in assets arising on a sale of goods or services or the decrease in liabilities arising from the waiver of a debt payable

23 23 The IFRS Framework (6) Expenses F 4.25 (b): Expenses are decreases in economic benefits during the accounting period in the form of + outflows or depletions of assets or incurrences of liabilities that result in decreases in equity, + other than those relating to distributions to equity participants F 4.49: Expenses are recognized when a decrease in future economic benefits + related to a decrease in an asset or an increase of a liability has arisen that can be measured reliably + recognition of expenses occurs simultaneously with the recognition of an increase in liabilities or a decrease in assets + for example, the accrual of employee entitlements or the depreciation of equipment

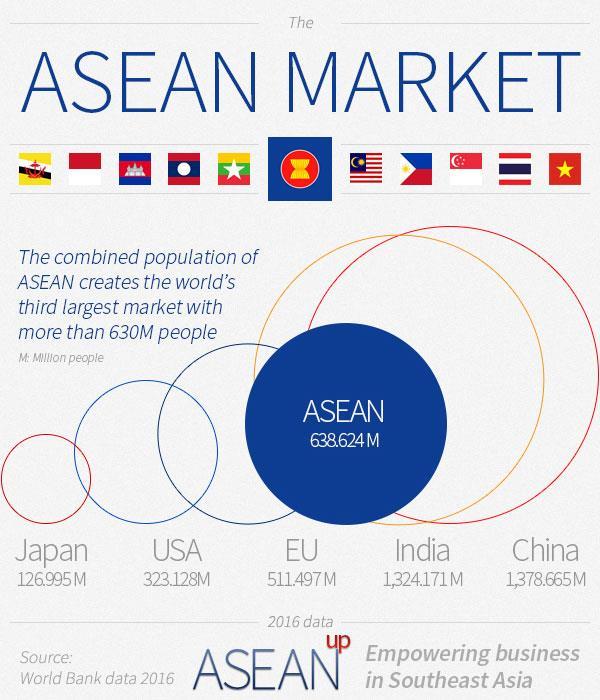

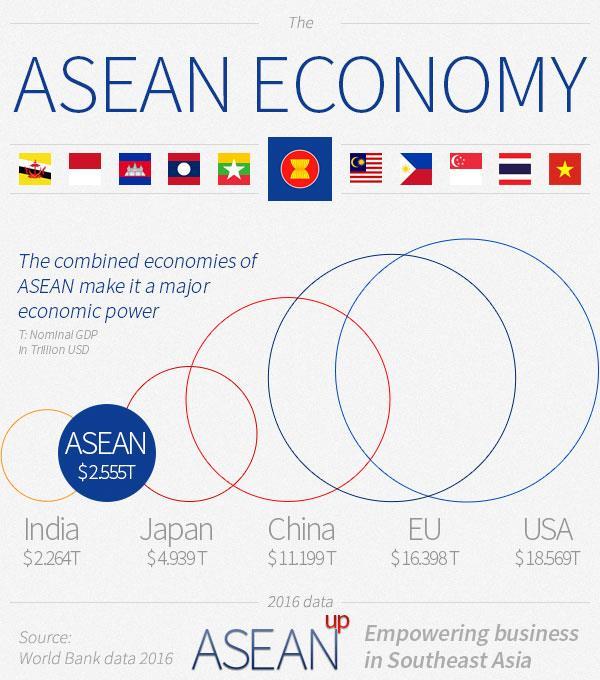

24 24 The Standard Setting Process for IFRS (1) 1) Agenda consultation a) Every 5 years: Priorities and work plan : Better communication in financial statements 2) Research a) Discussion paper, open for public comment 3) Standard-setting a) Review of research and comments on discussion paper b) Exposure draft (proposal of new standard or amendment of existing standard), open for public consultation c) Consultation with stakeholders around the world (parallel with step b) d) Analysis of feedback e) Release of standard or amendment 4) Maintenance a) Consultation on implementation for the new standard or amendment b) Interpretation by IFRIC c) After a few years: Evaluation by a post-implementation review

25 25 The Standard Setting Process for IFRS (3) Phase Research 2. Standardsetting 3. Maintenance

26 26 The Standard Setting Process for IFRS (2) Phase 2 2 a. Exposure Draft 2 b. Public Consultation 2 c. Release

27 27 Regional Implementation The EU (Step 1 of 3) Application of IAS, July 19, 2002 (regulation 1606/2002/EC, 4 pages) + From 2005 companies that are listed within the EU must prepare their consolidated accounts conform to international accounting standards adopted by the EU + Each standard and interpretation from the IASB must be adopted by the EU before they can be applied by the member states + An accounting regulatory committee shall assist the EU Commission (EFRAG)

28 28 Regional Implementation The EU (Step 2 of 3) Adopting certain international accounting standards, November 3, 2008 (regulation 1126/2008, 481 pages) + The Commission followed the advice of EFRAG and adopted all existing standards and interpretations as of October 15, 2008 with one exception + Limited parts of IAS 39 Financial Instruments: Recognition and Measurement were omitted + The regulation itself contains of 2 pages, but it s followed by an annex of 479 pages including every adopted standard and interpretation in full text EUR-Lex the EU database with official translations in all member state languages However the IFRS Framework is missing, since it s not an IFRS standard and not adopted by the EU

29 29 Regional Implementation The EU (Step 3 of 3) Accepting third countries accounting standards, December 12, 2008 (decision 2008/961/EC, 3 pages) + The following standards are considered equivalent to IFRS adopted by the EU, when preparing consolidated financial statements annually and half-yearly + IFRS, in accordance with IAS 1 + GAAP of Japan + GAAP of the USA + Third country company applying GAAP of China, Canada, South Korea and India + The Commission continue to monitor the efforts by third countries towards a changeover to IFRS

30 30 Regional Implementation The EU (EFRAG) Private organization established 2001 with support from the EU + Based in Brussels + Members are European parties and national organizations supporting the development of IFRS + Develops and supports European views in the development of IFRS + Is an active member of, and contributor to, the IASB Accounting Standard Advisory Forum + EFRAG takes part in the public consultations preceding new or amended standards and interpretations + Advices the EU on to which extent new or amended IFRS and IFRIC fulfills the criteria in the IAS-regulation + Comment: The time from an issued IFRS to adoption by the EU can be substantial! + See the page Endorsement Status for link to up-to-date report

31 31 Regional implementation The ASEAN (1) Established Member states + Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, Philippines, Singapore, Thailand, Viet Nam The ASEAN Economic Community (AEC) key characteristics a) a single market and production base b) a highly competitive economic region c) a region of equitable economic development d) a region fully integrated into the global economy World Bank on ASEAN Population/market 639 million, third largest in the world (EU 511 million) + 1) China 2) India + Economy, USD 2,555 trillion, fifths largest in the world (EU 16,398 trillion) + 1) USA 2) EU 3) China, 4) Japan

32 32

33 33

34 34 Regional implementation The ASEAN (2) World Bank Group Report Current Status of the Accounting and Auditing Profession in ASEAN Countries, 88 pages (Sep 2014) + All ASEAN countries have aligned their financial reporting standards to a greater or lesser degree with IFRS (p. 8) + Implementation of IFRS is quite weak in all except the more developed countries (p. 8) + Almost all countries have issued simplified financial reporting standards for SMEs, but with a wide variation across the ASEAN countries (p. 9) + IFRS for SME is too burdensome for most SME in the lesser developed countries, ASEAN should develop a common set of standards for SME

35 35 National Implementation Finland + IFRS applies in Finland as member state of the EU Norway + IFRS applies in Norway as member state of the EEA treaty Sweden + IFRS applies to Sweden as member state of the EU + Every year the private organization RFR issues recommendations on how to apply by the EU adopted standards and interpretations, with adjustments when needed to the Swedish Annual Accounts Act and the Swedish tax laws

36 36 Regional Financial Supervision ESMA is an independent EU authority + Safeguarding the stability of the financial system in the EU + Together with national supervisory authorities ensure that IFRS for listed companies are applied uniformly within the EEA + Established 2009, began operating mission: To enhance investor protection and promote stable and orderly financial market + 3 Objectives: Investor Protection, Orderly Markets, Financial Stability

37 37 Regional Financial Supervision Example ESMA have pointed out prioritized areas for the supervisory authorities in the member states to review in the listed companies financial reports for Disclosures of expected effects of applying new standards first time + IFRS 9 Financial Instruments (amended 2017) + IFRS 15 Revenue from Contracts with Customers (clarified 2017) + IFRS 16 Leases (new 2017) + Specific issues regarding + IFRS 3 Business Combinations + IAS 7 Statement of Cash Flows (amended 2017)

38 38 Källor Litteratur + Peter Berg, IFRS Work Plan consultjourney.com/2017/01/10/iasb-plan-for / Hemsidor + IFRS ifrs.org + IFRS Work Plan ifrs.org/projects/work-plan/ + OECD oecd.org + BEPS Project oecd.org/tax/beps + EU europa.eu + EUR-Lex eur-lex.europa.eu/homepage.html + EFRAG efrag.org + ESMA esma.europa.eu + ASEAN asean.org + World Bank Group worldbank.org + The Consultant s Journey consultjourney.com

39 39 Know the origin and process of the standards and you ll improve significantly - Peter Berg

40 40 KNOWLEDGE HELPS YOU SEE POSSIBILITIES AND AVOID TRAPS

The EU Endorsement Status Report - Position as at 12 October 2017

IASB/IFRIC documents not yet endorsed [Revisions to this schedule are marked in bold] IFRS STANDARDS 1 AND INTERPRETATIONS EFRAG draft advice The EU Endorsement Status Report - Position as at 12 October

IASB/IFRIC documents not yet endorsed [Revisions to this schedule are marked in bold] IFRS STANDARDS 1 AND INTERPRETATIONS EFRAG draft advice The EU Endorsement Status Report - Position as at 12 October

THE EU ENDORSEMENT STATUS REPORT

THE EU ENDORSEMENT STATUS REPORT IASB/IFRIC documents not yet endorsed [Revisions to this schedule are marked in bold] EFRAG draft advice EFRAG advice ARC Vote When might be expected IASB Effective date

THE EU ENDORSEMENT STATUS REPORT IASB/IFRIC documents not yet endorsed [Revisions to this schedule are marked in bold] EFRAG draft advice EFRAG advice ARC Vote When might be expected IASB Effective date

The EU Endorsement Status Report - Position as at 9 November 2017

The EU Endorsement Status Report - Position as at IASB/IFRIC documents not yet endorsed [Revisions to this schedule are marked in bold] EFRAG draft advice EFRAG advice ARC Vote When might be expected IASB

The EU Endorsement Status Report - Position as at IASB/IFRIC documents not yet endorsed [Revisions to this schedule are marked in bold] EFRAG draft advice EFRAG advice ARC Vote When might be expected IASB

The EU Endorsement Status Report - Position as at 27 February 2018

The EU Endorsement Status Report - Position as at 27 February IASB/IFRIC documents not yet endorsed [Revisions to this schedule are marked in bold] IFRS STANDARDS 1 AND INTERPRETATIONS EFRAG draft advice

The EU Endorsement Status Report - Position as at 27 February IASB/IFRIC documents not yet endorsed [Revisions to this schedule are marked in bold] IFRS STANDARDS 1 AND INTERPRETATIONS EFRAG draft advice

Institute of Chartered Accountants of India

Introductory Programme on IFRS for Young Members Organised by Institute of Chartered Accountants of India Presented by Technical Directorate, Institute of Chartered Accountants of India 1 Copyright Recognition

Introductory Programme on IFRS for Young Members Organised by Institute of Chartered Accountants of India Presented by Technical Directorate, Institute of Chartered Accountants of India 1 Copyright Recognition

The EU Endorsement Status Report Position as at 8 December 2016

The EU Endorsement Status Report Position as at 8 December IASB/IFRIC documents not yet endorsed [Revisions to this schedule are marked in bold] EFRAG draft advice EFRAG advice ARC Vote When might be expected

The EU Endorsement Status Report Position as at 8 December IASB/IFRIC documents not yet endorsed [Revisions to this schedule are marked in bold] EFRAG draft advice EFRAG advice ARC Vote When might be expected

The EU endorsement status report Position as at 21 June 2013

The EU endorsement status report Position as at 21 June 2013 IASB/IFRIC documents not yet endorsed [Revisions to this schedule are marked in bold] EFRAG draft endorsement advice EFRAG endorsement advice

The EU endorsement status report Position as at 21 June 2013 IASB/IFRIC documents not yet endorsed [Revisions to this schedule are marked in bold] EFRAG draft endorsement advice EFRAG endorsement advice

The EU Endorsement Status Report Position as at 31 October 2016

IASB/IFRIC documents not yet endorsed [Revisions to this schedule are marked in bold] STANDARDS EFRAG draft advice The EU Endorsement Status Report Position as at 31 October EFRAG advice ARC Vote When

IASB/IFRIC documents not yet endorsed [Revisions to this schedule are marked in bold] STANDARDS EFRAG draft advice The EU Endorsement Status Report Position as at 31 October EFRAG advice ARC Vote When

International Financial Reporting Standards

International Financial Reporting Standards as issued at 1 January 2009 The consolidated text of International Financial Reporting Standards (IFRSs ) including International Accounting Standards (IASs

International Financial Reporting Standards as issued at 1 January 2009 The consolidated text of International Financial Reporting Standards (IFRSs ) including International Accounting Standards (IASs

The EU endorsement status report Position as at 6 July 2016

IASB/IFRIC documents not yet endorsed [Revisions to this schedule are marked in bold] STANDARDS EFRAG draft advice EFRAG advice ARC Vote When might be expected The EU status report Position as at 6 July

IASB/IFRIC documents not yet endorsed [Revisions to this schedule are marked in bold] STANDARDS EFRAG draft advice EFRAG advice ARC Vote When might be expected The EU status report Position as at 6 July

The EU endorsement status report Position as at 20 April 2016

The EU status report Position as at 20 April IASB/IFRIC documents not yet endorsed [Revisions to this schedule are marked in bold] EFRAG draft advice EFRAG advice ARC vote W hen might be expected IASB

The EU status report Position as at 20 April IASB/IFRIC documents not yet endorsed [Revisions to this schedule are marked in bold] EFRAG draft advice EFRAG advice ARC vote W hen might be expected IASB

Revocation of Tier 3 and Tier 4 For-profit Accounting Standards

Revocation of Tier 3 and Tier 4 For-profit Accounting Standards This Revocation was issued on 5 March 2015 by the External Reporting Board pursuant to section 12(f) of the Financial Reporting Act 2013.

Revocation of Tier 3 and Tier 4 For-profit Accounting Standards This Revocation was issued on 5 March 2015 by the External Reporting Board pursuant to section 12(f) of the Financial Reporting Act 2013.

INTERNATIONAL CPD WEBINAR. IFRS Overview. Presented by: Peter Thatcher BSc FCA Aptus Personal Development Consultants

INTERNATIONAL CPD WEBINAR IFRS Overview 18 th January 2018 Presented by: Peter Thatcher BSc FCA Aptus Personal Development Consultants No responsibility for loss occasioned to any person acting or refraining

INTERNATIONAL CPD WEBINAR IFRS Overview 18 th January 2018 Presented by: Peter Thatcher BSc FCA Aptus Personal Development Consultants No responsibility for loss occasioned to any person acting or refraining

Good First-time Adopter (International) Limited

Limited") Good First-time Adopter (International) Limited International GAAP Illustrative financial statements of a first-time adopter for the year ended 31 December 2012 Based on International Financial Reporting

Good First-time Adopter (International) Limited International GAAP Illustrative financial statements of a first-time adopter for the year ended 31 December 2012 Based on International Financial Reporting

International Financial Accounting (IFA)

") International Financial Accounting (IFA) Part I Accounting Regulation; International Accounting DEPARTMENT OF BUSINESS AND LAW ROBERTO DI PIETRA SIENA, NOVEMBER 4, 2013 1 IASB: history, governance and

International Financial Accounting (IFA) Part I Accounting Regulation; International Accounting DEPARTMENT OF BUSINESS AND LAW ROBERTO DI PIETRA SIENA, NOVEMBER 4, 2013 1 IASB: history, governance and

TECHNICAL INFORMATION PAPER - VALUATIONS OF REAL PROPERTY, PLANT & EQUIPMENT FOR USE IN NEW ZEALAND FINANCIAL REPORTS

TECHNICAL INFORMATION PAPER - VALUATIONS OF REAL PROPERTY, PLANT & EQUIPMENT FOR USE IN NEW ZEALAND FINANCIAL REPORTS Reference Effective Review Owner NZVGNTIP# Valuations for Use in New Zealand Financial

TECHNICAL INFORMATION PAPER - VALUATIONS OF REAL PROPERTY, PLANT & EQUIPMENT FOR USE IN NEW ZEALAND FINANCIAL REPORTS Reference Effective Review Owner NZVGNTIP# Valuations for Use in New Zealand Financial

ACCOUNTING STANDARDS BOARD DIRECTIVE 5 DETERMINING THE GRAP REPORTING FRAMEWORK

ACCOUNTING STANDARDS BOARD DIRECTIVE 5 DETERMINING THE GRAP REPORTING FRAMEWORK Issued by the Accounting Standards Board March 2009 Accounting Standards Board P O Box 74219 Lynnwood Ridge 0040 Fax: +27

ACCOUNTING STANDARDS BOARD DIRECTIVE 5 DETERMINING THE GRAP REPORTING FRAMEWORK Issued by the Accounting Standards Board March 2009 Accounting Standards Board P O Box 74219 Lynnwood Ridge 0040 Fax: +27

Ernst & Young IFRS Core Tools. January Good Insurance (International) Limited. statements for the year ended 31 December 2011

Limited. statements for the year ended 31 December 2011") Ernst & Young IFRS Core Tools January 2012 Good Insurance (International) Limited statements for the year ended 31 December 2011 Based on International Financial Reporting Standards in issue at 30 September

Ernst & Young IFRS Core Tools January 2012 Good Insurance (International) Limited statements for the year ended 31 December 2011 Based on International Financial Reporting Standards in issue at 30 September

Good Group (International) Limited

Limited") EY IFRS Core Tools Good Group (International) Limited International GAAP Illustrative financial statements for the year ended 31 December 2013 Based on International Financial Reporting Standards in issue

EY IFRS Core Tools Good Group (International) Limited International GAAP Illustrative financial statements for the year ended 31 December 2013 Based on International Financial Reporting Standards in issue

INITIAL TEST OF COMPETENCE SYLLABUS AND EXAMINABLE PRONOUNCEMENTS JANUARY AND JUNE 2015

Integrity House, P.O. Box CY 1079, Cnr. Bath Road and Second Street Causeway, Harare. Zimbabwe. Tel: 263 4 793674/960/252672/793471 Fax: 263 4 706245 E-mail: administrator@icaz.icon.co.zw INITIAL TEST

Integrity House, P.O. Box CY 1079, Cnr. Bath Road and Second Street Causeway, Harare. Zimbabwe. Tel: 263 4 793674/960/252672/793471 Fax: 263 4 706245 E-mail: administrator@icaz.icon.co.zw INITIAL TEST

IFRS and Indonesia GAAP (IFAS) Similarities and Differences

Similarities and Differences") www.pwc.com/id IFRS and Indonesia GAAP (IFAS) Similarities and Differences August 2016 Introduction This publication provides a summary of the key differences between the Indonesian Financial Accounting

www.pwc.com/id IFRS and Indonesia GAAP (IFAS) Similarities and Differences August 2016 Introduction This publication provides a summary of the key differences between the Indonesian Financial Accounting

ACCOUNTING STANDARDS BOARD DIRECTIVE 5 DETERMINING THE GRAP REPORTING FRAMEWORK

ACCOUNTING STANDARDS BOARD DIRECTIVE 5 DETERMINING THE GRAP REPORTING FRAMEWORK Issued by the Accounting Standards Board March 2009 Copyright 2017 by the Accounting Standards Board All rights reserved.

ACCOUNTING STANDARDS BOARD DIRECTIVE 5 DETERMINING THE GRAP REPORTING FRAMEWORK Issued by the Accounting Standards Board March 2009 Copyright 2017 by the Accounting Standards Board All rights reserved.

IFRS. B V Subramaniam FCMA A CONCEPTUAL ANALYSIS

IFRS 1 A CONCEPTUAL ANALYSIS INTRODUCTION International Financial Reporting Standards (IFRS) are the world-wide accounting standards which consists of 1) Standards (IFRS statements & IAS standards) 2)

IFRS 1 A CONCEPTUAL ANALYSIS INTRODUCTION International Financial Reporting Standards (IFRS) are the world-wide accounting standards which consists of 1) Standards (IFRS statements & IAS standards) 2)

Good Construction Group (International) Limited

Limited") Good Construction Group (International) Limited International GAAP Illustrative financial statements for the year ended 31 December 2012 Based on International Financial Reporting Standards in issue at

Good Construction Group (International) Limited International GAAP Illustrative financial statements for the year ended 31 December 2012 Based on International Financial Reporting Standards in issue at

Good First-time Adopter (International) Limited

Limited") Good First-time Adopter (International) Limited International GAAP Illustrative financial statements of a first-time adopter for the year ended 31 December 2011 Based on International Financial Reporting

Good First-time Adopter (International) Limited International GAAP Illustrative financial statements of a first-time adopter for the year ended 31 December 2011 Based on International Financial Reporting

IFRS and Indonesian GAAP (IFAS) Similarities and Differences

Similarities and Differences") www.pwc.com/id IFRS and Indonesian GAAP (IFAS) Similarities and Differences October 2017 Introduction This publication provides a summary of the key differences between the Indonesian Financial Accounting

www.pwc.com/id IFRS and Indonesian GAAP (IFAS) Similarities and Differences October 2017 Introduction This publication provides a summary of the key differences between the Indonesian Financial Accounting

IMPLEMENTATION PROBLEMS

1 RESEARCHING IFRS IMPLEMENTATION PROBLEMS Overview 1 The IFRS Hierarchy 1 Researching IFRS 4 Researching Accounting Controls 5 Researching Accounting Forms and Reports 6 Researching Accounting Footnotes

1 RESEARCHING IFRS IMPLEMENTATION PROBLEMS Overview 1 The IFRS Hierarchy 1 Researching IFRS 4 Researching Accounting Controls 5 Researching Accounting Forms and Reports 6 Researching Accounting Footnotes

IFRS versus LUX GAAP A comprehensive comparison

IFRS versus LUX GAAP A comprehensive comparison Content Foreword 3 Abbreviations 4 A short history of convergence 5 Current use of IFRS in Luxembourg 8 Comparison of IFRS and LUX GAAP 9 Principles/Policies

IFRS versus LUX GAAP A comprehensive comparison Content Foreword 3 Abbreviations 4 A short history of convergence 5 Current use of IFRS in Luxembourg 8 Comparison of IFRS and LUX GAAP 9 Principles/Policies

Good Investment Fund Limited (Liability)

") EY IFRS Core Tools Good Investment Fund Limited (Liability) International GAAP Illustrative financial statements for the year ended 31 December 2013 Based on International Financial Reporting Standards

EY IFRS Core Tools Good Investment Fund Limited (Liability) International GAAP Illustrative financial statements for the year ended 31 December 2013 Based on International Financial Reporting Standards

Application of Japan s Modified International Standards

Japan s Modified International Standards (JMIS): Accounting Standards Comprising IFRSs and the ASBJ Modifications Application of Japan s Modified International Standards 30 June 2015 Amended 25 July 2016

Japan s Modified International Standards (JMIS): Accounting Standards Comprising IFRSs and the ASBJ Modifications Application of Japan s Modified International Standards 30 June 2015 Amended 25 July 2016

Management s Responsibility for the Financial Statements

REPORT OF THE INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS TO THE MANAGEMENT OF BNP PARIBAS BANGKOK BRANCH We have audited the financial statements of BNP Paribas Bangkok Branch, which comprise the statement

REPORT OF THE INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS TO THE MANAGEMENT OF BNP PARIBAS BANGKOK BRANCH We have audited the financial statements of BNP Paribas Bangkok Branch, which comprise the statement

Introduction & Concepts. ICAI, 3 rd MAY CA Nitish Kirtikar

Introduction & Concepts ICAI, 3 rd MAY 2014 CA Nitish Kirtikar Contents Introduction and concepts 1. Introduction to IFRS 2. Conceptual framework for Financial reporting 3. Convergence process with IFRS

Introduction & Concepts ICAI, 3 rd MAY 2014 CA Nitish Kirtikar Contents Introduction and concepts 1. Introduction to IFRS 2. Conceptual framework for Financial reporting 3. Convergence process with IFRS

IFRS AND IND AS Preface

IFRS AND IND AS CA. Rajkumar S. Adukia http://www.carajkumarradukia.com rajkumarfca@gmail.com +91 98200 61049/09323061049 Preface India, one of the fastest growing global economies is on the verge of converging

IFRS AND IND AS CA. Rajkumar S. Adukia http://www.carajkumarradukia.com rajkumarfca@gmail.com +91 98200 61049/09323061049 Preface India, one of the fastest growing global economies is on the verge of converging

Table 1 IPSAS and Equivalent IFRS Summary 1

Agenda Item 1.6 IPSAS IFRS Alignment Dashboard Table 1 IPSAS and Equivalent IFRS Summary 1 IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements IAS 1 17, Property,

Agenda Item 1.6 IPSAS IFRS Alignment Dashboard Table 1 IPSAS and Equivalent IFRS Summary 1 IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements IAS 1 17, Property,

BNP PARIBAS BANGKOK BRANCH. Financial Statements. Year ended December 31, 2015

BNP PARIBAS BANGKOK BRANCH Financial Statements Year ended December 31, 2015 REPORT OF THE INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS TO THE MANAGEMENT OF BNP PARIBAS BANGKOK BRANCH We have audited the financial

BNP PARIBAS BANGKOK BRANCH Financial Statements Year ended December 31, 2015 REPORT OF THE INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS TO THE MANAGEMENT OF BNP PARIBAS BANGKOK BRANCH We have audited the financial

Table 1 IPSAS and Equivalent IFRS Summary 2

IPSASB Meeting ( 2018) Agenda Item 1.6 IPSAS IFRS Alignment 1 Dashboard Table 1 IPSAS and Equivalent IFRS Summary 2 IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements

IPSASB Meeting ( 2018) Agenda Item 1.6 IPSAS IFRS Alignment 1 Dashboard Table 1 IPSAS and Equivalent IFRS Summary 2 IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements

Management s Responsibility for the Financial Statements

AUDITOR S REPORT To the Board of Directors and Shareholders of Chukai Public Company Limited I have audited the accompanying consolidated of Chukai Public Company Limited and its subsidiaries, which comprise

AUDITOR S REPORT To the Board of Directors and Shareholders of Chukai Public Company Limited I have audited the accompanying consolidated of Chukai Public Company Limited and its subsidiaries, which comprise

Good Bank (International) Limited

Limited") Good Bank (International) Limited International GAAP Illustrative financial statements for the year ended 31 December 2011 Based on International Financial Reporting Standards in issue at 30 September

Good Bank (International) Limited International GAAP Illustrative financial statements for the year ended 31 December 2011 Based on International Financial Reporting Standards in issue at 30 September

THE ZIMBABWE CHARTERED ACCOUNTANTS EXAMINATION BOARD

THE ZIMBABWE CHARTERED ACCOUNTANTS EXAMINATION BOARD Integrity House, P.O. Box CY 1079, Cnr. Bath Road and Second Street Causeway, Harare. Zimbabwe. Tel: 263 4 793674/960/252672 Fax: 263 4 706245 E-mail:

THE ZIMBABWE CHARTERED ACCOUNTANTS EXAMINATION BOARD Integrity House, P.O. Box CY 1079, Cnr. Bath Road and Second Street Causeway, Harare. Zimbabwe. Tel: 263 4 793674/960/252672 Fax: 263 4 706245 E-mail:

IFRS Guidebook Edition. Steven M. Bragg

IFRS Guidebook 2017 Edition Steven M. Bragg Chapter 1 Introduction... 1 Learning Objectives... 1 Introduction... 1 What is IFRS?... 1 The IFRS Conceptual Framework... 2 How This Book is Organized... 4

IFRS Guidebook 2017 Edition Steven M. Bragg Chapter 1 Introduction... 1 Learning Objectives... 1 Introduction... 1 What is IFRS?... 1 The IFRS Conceptual Framework... 2 How This Book is Organized... 4

Table 1 IPSAS and Equivalent IFRS Summary 2

Agenda Item 1.7 IPSAS IFRS Alignment 1 Dashboard Table 1 IPSAS and Equivalent IFRS Summary 2 IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements IAS 1 18, Segment

Agenda Item 1.7 IPSAS IFRS Alignment 1 Dashboard Table 1 IPSAS and Equivalent IFRS Summary 2 IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements IAS 1 18, Segment

Model Financial Statements NZ IFRS and NZ IFRS (RDR) For reporting periods ending 31 December 2015

For reporting periods ending 31 December 2015") Model Financial Statements NZ IFRS and NZ IFRS (RDR) For reporting periods ending 31 December 2015 Denise Hodgkins Partner, Deloitte Auckland Phone +64 9 303 0918 Email: dhodgkins@deloitte.co.nz Peter

Model Financial Statements NZ IFRS and NZ IFRS (RDR) For reporting periods ending 31 December 2015 Denise Hodgkins Partner, Deloitte Auckland Phone +64 9 303 0918 Email: dhodgkins@deloitte.co.nz Peter

IFRS and Indonesian GAAP (IFAS) Similarities and Differences

Similarities and Differences") www.pwc.com/id IFRS and Indonesian GAAP (IFAS) Similarities and Differences May 2018 Introduction This publication provides a summary of the key differences between the Indonesian Financial Accounting

www.pwc.com/id IFRS and Indonesian GAAP (IFAS) Similarities and Differences May 2018 Introduction This publication provides a summary of the key differences between the Indonesian Financial Accounting

April Grant Thornton LLP All rights reserved U.S. member firm of Grant Thornton International Ltd

Comparison between and International Financial Reporting Standards April 2016 Comparison between and International Financial Reporting Standards 2 Contents 1. Introduction... 5 International standards

Comparison between and International Financial Reporting Standards April 2016 Comparison between and International Financial Reporting Standards 2 Contents 1. Introduction... 5 International standards

Amendments to References to the Conceptual Framework in IFRS Standards

March 2018 IFRS Standards Basis for Conclusions Amendments to References to the Conceptual Framework in IFRS Standards Amendments to References to the Conceptual Framework in IFRS Standards Amendments

March 2018 IFRS Standards Basis for Conclusions Amendments to References to the Conceptual Framework in IFRS Standards Amendments to References to the Conceptual Framework in IFRS Standards Amendments

e-modules & educational products

FASTER ICT Financial and Accounting Seminars Targeting European Regions WP3 e-modules & educational products Radoslav Tušan (TUKE) WP3: Tasks Modules - Deliverables Task Module Deliverable 3.1 FASTER Platform

FASTER ICT Financial and Accounting Seminars Targeting European Regions WP3 e-modules & educational products Radoslav Tušan (TUKE) WP3: Tasks Modules - Deliverables Task Module Deliverable 3.1 FASTER Platform

IFRS pocket guide inform.pwc.com

IFRS pocket guide 2016 inform.pwc.com Introduction 1 Introduction This pocket guide provides a summary of the recognition and measurement requirements of International Financial Reporting Standards (IFRS)

IFRS pocket guide 2016 inform.pwc.com Introduction 1 Introduction This pocket guide provides a summary of the recognition and measurement requirements of International Financial Reporting Standards (IFRS)

NZ IFRS (RDR) Model Financial Statements

Model Financial Statements") NZ IFRS (RDR) Model Financial Statements 31 December 2013 This publication is intended as background briefing only. It should only be utilised by someone with a detailed knowledge of New Zealand equivalents

NZ IFRS (RDR) Model Financial Statements 31 December 2013 This publication is intended as background briefing only. It should only be utilised by someone with a detailed knowledge of New Zealand equivalents

(UNOFFICIAL TRANSLATION) AUDITOR S REPORT TO: THE SHAREHOLDERS OF PTT PUBLIC COMPANY LIMITED

AUDITOR S REPORT TO: THE SHAREHOLDERS OF PTT PUBLIC COMPANY LIMITED") AUDITOR S REPORT TO: THE SHAREHOLDERS OF PTT PUBLIC COMPANY LIMITED The Office of the Auditor General of Thailand has audited the accompanying consolidated and separate of PTT Public Company Limited and

AUDITOR S REPORT TO: THE SHAREHOLDERS OF PTT PUBLIC COMPANY LIMITED The Office of the Auditor General of Thailand has audited the accompanying consolidated and separate of PTT Public Company Limited and

CIMB THAI BANK PUBLIC COMPANY LIMITED CONSOLIDATED AND BANK FINANCIAL STATEMENTS 31 DECEMBER 2015

CIMB THAI BANK PUBLIC COMPANY LIMITED CONSOLIDATED AND BANK FINANCIAL STATEMENTS 31 DECEMBER 2015 AUDITOR S REPORT To the Shareholders of CIMB Thai Bank Public Company Limited I have audited the accompanying

CIMB THAI BANK PUBLIC COMPANY LIMITED CONSOLIDATED AND BANK FINANCIAL STATEMENTS 31 DECEMBER 2015 AUDITOR S REPORT To the Shareholders of CIMB Thai Bank Public Company Limited I have audited the accompanying

IFRS News Quarter

IFRS News IFRS News is your quarterly update on all things relating to International Financial Reporting Standards. We ll bring you up to speed on topical issues, provide comment and points of view and

IFRS News IFRS News is your quarterly update on all things relating to International Financial Reporting Standards. We ll bring you up to speed on topical issues, provide comment and points of view and

US GAAP FACT-SHEET. GAAP NO. DESCRIPTION KEY ELEMENTS EQUIVALENT/SIMILAR IFRS Generally Accepted Accounting - GAAP Codification

US GAAP FACT-SHEET GAAP NO. DESCRIPTION KEY ELEMENTS EQUIVALENT/SIMILAR IFRS ASC 105 Generally Accepted Accounting - GAAP Codification - The Conceptual Principles - The Standards Setting Process - CONs

US GAAP FACT-SHEET GAAP NO. DESCRIPTION KEY ELEMENTS EQUIVALENT/SIMILAR IFRS ASC 105 Generally Accepted Accounting - GAAP Codification - The Conceptual Principles - The Standards Setting Process - CONs

Company No H. MIZUHO CORPORATE BANK (MALAYSIA) BERHAD Incorporated in Malaysia

BERHAD Incorporated in Malaysia") Company No. 923693 H MIZUHO CORPORATE BANK (MALAYSIA) BERHAD UNAUDITED INTERIM CONDENSED FINANCIAL STATEMENTS 30 JUNE 2012 MIZUHO CORPORATE BANK (MALAYSIA) BERHAD (923693-H) UNAUDITED INTERIM CONDENSED

Company No. 923693 H MIZUHO CORPORATE BANK (MALAYSIA) BERHAD UNAUDITED INTERIM CONDENSED FINANCIAL STATEMENTS 30 JUNE 2012 MIZUHO CORPORATE BANK (MALAYSIA) BERHAD (923693-H) UNAUDITED INTERIM CONDENSED

Ind AS Overview, Impact and Anaysis

Ind AS Overview, Impact and Anaysis Organised by: Gurugram Branch of NIRC of ICAI Hotel Plazzio, June 9, 2018 IFRS Journey History and Background of IFRS 1. IASG : AICPA, CICA & ICAEW (1966-67) 2. Australia,

Ind AS Overview, Impact and Anaysis Organised by: Gurugram Branch of NIRC of ICAI Hotel Plazzio, June 9, 2018 IFRS Journey History and Background of IFRS 1. IASG : AICPA, CICA & ICAEW (1966-67) 2. Australia,

IFRS: A comparison with Dutch Laws and regulations 2017

IFRS: A comparison with Dutch Laws and regulations 2017 Table of contents Preface to the 2017 edition 3 Instructions for use 4 Application of IFRS 5 Summary of main points 7 Statement of financial position

IFRS: A comparison with Dutch Laws and regulations 2017 Table of contents Preface to the 2017 edition 3 Instructions for use 4 Application of IFRS 5 Summary of main points 7 Statement of financial position

Financial Reporting Matters

Financial Reporting Matters December 2005 Issue 9 A UDIT It is the time of the year again to take stock of financial reporting requirements, both new and anticipated, that have a direct impact on the year-end

Financial Reporting Matters December 2005 Issue 9 A UDIT It is the time of the year again to take stock of financial reporting requirements, both new and anticipated, that have a direct impact on the year-end

IFRS Explained - supplement. Chapter 1 The IASB and the regulatory framework. Chapter 2 Conceptual framework for financial reporting

IFRS Explained - supplement Chapter 1 The IASB and the regulatory framework The organisations mentioned in this chapter were renamed in July 2010 as follows: The IASC Foundation became the IFRS Foundation

IFRS Explained - supplement Chapter 1 The IASB and the regulatory framework The organisations mentioned in this chapter were renamed in July 2010 as follows: The IASC Foundation became the IFRS Foundation

INDEPENDENT AUDITOR S REPORT. To the Shareholders of RICH ASIA CORPORATION PUBLIC COMPANY LIMITED. Opinion

INDEPENDENT AUDITOR S REPORT To the Shareholders of RICH ASIA CORPORATION PUBLIC COMPANY LIMITED Opinion I have audited the accompanying consolidated and separate financial statements of RICH ASIA CORPORATION

INDEPENDENT AUDITOR S REPORT To the Shareholders of RICH ASIA CORPORATION PUBLIC COMPANY LIMITED Opinion I have audited the accompanying consolidated and separate financial statements of RICH ASIA CORPORATION

ACCOUNTING STANDARDS BOARD DIRECTIVE 5 DETERMINING THE GRAP REPORTING FRAMEWORK

ACCOUNTING STANDARDS BOARD DIRECTIVE 5 DETERMINING THE GRAP REPORTING FRAMEWORK Issued by the Accounting Standards Board March 2009 Accounting Standards Board P O Box 74219 Lynnwood Ridge 0040 Fax: +27

ACCOUNTING STANDARDS BOARD DIRECTIVE 5 DETERMINING THE GRAP REPORTING FRAMEWORK Issued by the Accounting Standards Board March 2009 Accounting Standards Board P O Box 74219 Lynnwood Ridge 0040 Fax: +27

Table 1 IPSAS and Equivalent IFRS Summary*

Agenda Item 13.3.2 IPSAS IFRS Alignment Dashboard Table 1 IPSAS and Equivalent IFRS Summary* IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements IAS 1 17, Property,

Agenda Item 13.3.2 IPSAS IFRS Alignment Dashboard Table 1 IPSAS and Equivalent IFRS Summary* IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements IAS 1 17, Property,

Summary Comparison of Canadian GAAP (Part V) and IFRSs (Part I)

and IFRSs (Part I)") Summary Comparison of Canadian GAAP and IFRSs (Part I) as of December 31, 2009 1. This comparison has been prepared by the staff of the Accounting Standards Board (AcSB) and has not been approved by the

Summary Comparison of Canadian GAAP and IFRSs (Part I) as of December 31, 2009 1. This comparison has been prepared by the staff of the Accounting Standards Board (AcSB) and has not been approved by the

IFRS UPDATE. Standards, Amendments and Interpretations. February 2017

IFRS UPDATE Standards, Amendments and Interpretations February 2017 Our summary of the new and revised financial reporting requirements provides an update on IFRS Standards, Amendments and Interpretations

IFRS UPDATE Standards, Amendments and Interpretations February 2017 Our summary of the new and revised financial reporting requirements provides an update on IFRS Standards, Amendments and Interpretations

International Financial Reporting Standards (IFRS)

") International Financial Reporting Standards (IFRS) International Financial Reporting Standards (IFRS) Meaning International Financial Reporting Standards (IFRS) are designed as a common global language

International Financial Reporting Standards (IFRS) International Financial Reporting Standards (IFRS) Meaning International Financial Reporting Standards (IFRS) are designed as a common global language

IFRS: A comparison with Dutch Laws and regulations 2016

IFRS: A comparison with Dutch Laws and regulations 2016 Table of contents Preface 3 Instructions for use 4 Application of IFRS 5 Summary of main points 7 Statement of financial posistion 1 Intangible

IFRS: A comparison with Dutch Laws and regulations 2016 Table of contents Preface 3 Instructions for use 4 Application of IFRS 5 Summary of main points 7 Statement of financial posistion 1 Intangible

AUDITOR S REPORT. To the Board of Directors and Shareholders of Fire Victor Public Company Limited

AUDITOR S REPORT To the Board of Directors and Shareholders of Fire Victor Public Company Limited I have audited the accompanying financial statements of Fire Victor Public Company Limited which comprise

AUDITOR S REPORT To the Board of Directors and Shareholders of Fire Victor Public Company Limited I have audited the accompanying financial statements of Fire Victor Public Company Limited which comprise

Apolus Holding AB is owned by Apolus Holdco S.a.r.l., Luxemburg (B ) and the principal owner is Triton Fund II LP (reg.nr LP701), Jersey.

and the principal owner is Triton Fund II LP (reg.nr LP701), Jersey.") The Board of Directors Apolus Holding AB Org nr 556714-1725 hereby submits the Annual accounts and consolidated accounts for the financial year 1 January - 31 December 2011 Administration report 3 (33)

The Board of Directors Apolus Holding AB Org nr 556714-1725 hereby submits the Annual accounts and consolidated accounts for the financial year 1 January - 31 December 2011 Administration report 3 (33)

DATE ISSUED IASB AcSB

New and Proposed Changes to IFRS Sections for the Two Years Ended NEW AND AMENDED STANDARDS DATE ISSUED IASB AcSB EFFECTIVE DATE Annual Improvements to IFRSs 2012 2014 Cycle (Amendment) September 2014

New and Proposed Changes to IFRS Sections for the Two Years Ended NEW AND AMENDED STANDARDS DATE ISSUED IASB AcSB EFFECTIVE DATE Annual Improvements to IFRSs 2012 2014 Cycle (Amendment) September 2014

SUPPLEMENTARY ACCOUNTING RULES FOR GROUPS

RFR 1.1 This recommendation constitutes a translation of the Swedish recommendation RFR 1.1. In case of uncertainty, the Swedish version takes precedence. December 2007 SUPPLEMENTARY ACCOUNTING RULES FOR

RFR 1.1 This recommendation constitutes a translation of the Swedish recommendation RFR 1.1. In case of uncertainty, the Swedish version takes precedence. December 2007 SUPPLEMENTARY ACCOUNTING RULES FOR

International Financial Reporting Standards

May 2011 International Financial Reporting Standards International Financial Reporting Standards Michael Wells, Director, Education Initiative, IFRS Foundation IFRS Foundation The views expressed in this

May 2011 International Financial Reporting Standards International Financial Reporting Standards Michael Wells, Director, Education Initiative, IFRS Foundation IFRS Foundation The views expressed in this

Overview of Accounting Standards; IASs/IFRS and IPSAS Presentation by: CPA Daniel Kahi Monday, 10 September 2018

Overview of Accounting Standards; IASs/IFRS and IPSAS Presentation by: CPA Daniel Kahi Monday, 10 September 2018 Uphold public interest Presentation agenda Introduction ISAs / IFRSs IPSAS Concluding Remarks

Overview of Accounting Standards; IASs/IFRS and IPSAS Presentation by: CPA Daniel Kahi Monday, 10 September 2018 Uphold public interest Presentation agenda Introduction ISAs / IFRSs IPSAS Concluding Remarks

Agenda Item 13.2: IPSAS IFRS Alignment Dashboard

Agenda Item 13.2: IPSAS IFRS Alignment Dashboard João Fonseca, Principal IPSASB Meeting Toronto, Canada June 19 22, 2018 Page 1 Proprietary and Copyrighted Information Agenda Item 13.2 IPSAS IFRS Alignment

Agenda Item 13.2: IPSAS IFRS Alignment Dashboard João Fonseca, Principal IPSASB Meeting Toronto, Canada June 19 22, 2018 Page 1 Proprietary and Copyrighted Information Agenda Item 13.2 IPSAS IFRS Alignment

M.C.S. STEEL PUBLIC COMPANY LIMITED AND SUBSIDIARIES STATEMENT OF FINANCIAL POSITION AS AT DECEMBER 31, 2017 ASSETS

M.C.S. STEEL PUBLIC COMPANY LIMITED AND SUBSIDIARIES STATEMENT OF FINANCIAL POSITION AS AT ASSETS In Baht Consolidated Separate financial statements financial statements As at December 31, As at December

M.C.S. STEEL PUBLIC COMPANY LIMITED AND SUBSIDIARIES STATEMENT OF FINANCIAL POSITION AS AT ASSETS In Baht Consolidated Separate financial statements financial statements As at December 31, As at December

Agenda Item 1.7: IPSAS-IFRS Alignment Dashboard

Agenda Item 1.7: IPSAS-IFRS Alignment Dashboard João Fonseca, Principal IPSASB Meeting Washington D.C., USA March 12 15, 2019 Page 1 Proprietary and Copyrighted Information Agenda Item 1.7 Outline Change

Agenda Item 1.7: IPSAS-IFRS Alignment Dashboard João Fonseca, Principal IPSASB Meeting Washington D.C., USA March 12 15, 2019 Page 1 Proprietary and Copyrighted Information Agenda Item 1.7 Outline Change

IFRS Newsletter. Deferral Accounts and IFRS 15 Revenue from Contracts with Customers. We

IFRS Newsletter May 2014 Welcome to IFRS Newsletter a newsletter that offers a summary of certain developments in International Financial Reporting Standards (IFRS) along with insights into topical issues.

IFRS Newsletter May 2014 Welcome to IFRS Newsletter a newsletter that offers a summary of certain developments in International Financial Reporting Standards (IFRS) along with insights into topical issues.

IFRS UPDATE. Standards, Amendments and Interpretations. October 2016

IFRS UPDATE Standards, Amendments and Interpretations October 2016 Our summary of the new and revised financial reporting requirements provides an update on IFRS Standards, Amendments and Interpretations

IFRS UPDATE Standards, Amendments and Interpretations October 2016 Our summary of the new and revised financial reporting requirements provides an update on IFRS Standards, Amendments and Interpretations

Good Petroleum (International) Limited

Limited") EY IFRS Core Tools Good Petroleum (International) Limited International GAAP Illustrative financial statements for the year ended 31 December 2013 Based on International Financial Reporting Standards in

EY IFRS Core Tools Good Petroleum (International) Limited International GAAP Illustrative financial statements for the year ended 31 December 2013 Based on International Financial Reporting Standards in

IFRS UPDATE. Standards, Amendments and Interpretations. April 2016

IFRS UPDATE Standards, Amendments and Interpretations April 2016 Our summary of the new and revised financial reporting requirements provides an update on IFRS Standards, Amendments and Interpretations

IFRS UPDATE Standards, Amendments and Interpretations April 2016 Our summary of the new and revised financial reporting requirements provides an update on IFRS Standards, Amendments and Interpretations

HASHEMITE UNIVERSITY. SUMMARY of MAIN ACCOUNTING THEYORY TOPICS Instructor Dr Husam Al-Khadash

HASHEMITE UNIVERSITY SUMMARY of MAIN ACCOUNTING THEYORY TOPICS Instructor Dr Husam Al-Khadash Prepared by Mariam Zaghal, accounting student, 2011 CHAPTER 1 THE DEVELOPMENT OF ACCOUNTING THEORY What is

HASHEMITE UNIVERSITY SUMMARY of MAIN ACCOUNTING THEYORY TOPICS Instructor Dr Husam Al-Khadash Prepared by Mariam Zaghal, accounting student, 2011 CHAPTER 1 THE DEVELOPMENT OF ACCOUNTING THEORY What is

General Announcement::Announcement by Subsidiary, IFS Capital (Thailand) Public... http://infopub.sgx.com/apps?a=cow_corpannouncement_content&b=announcem... Page 1 of 1 2/16/2015 General Announcement::Announcement

General Announcement::Announcement by Subsidiary, IFS Capital (Thailand) Public... http://infopub.sgx.com/apps?a=cow_corpannouncement_content&b=announcem... Page 1 of 1 2/16/2015 General Announcement::Announcement

Use of Full IFRSs Around the World

Use of IFRSs Worldwide, First-time time Adoption of IFRSs, and IFRS Resources Paul Pacter Deloitte IFRS Global Office Deloitte Taiwan IFRS Seminar Taipei 9 December 2008 1 1. Use of International Financial

Use of IFRSs Worldwide, First-time time Adoption of IFRSs, and IFRS Resources Paul Pacter Deloitte IFRS Global Office Deloitte Taiwan IFRS Seminar Taipei 9 December 2008 1 1. Use of International Financial

International Financial Reporting Standards (IFRSs)

") May 2010 International Financial Reporting Standards International Financial Reporting Standards (IFRSs) Gilbert Gélard, IASB member The views expressed in this presentation are those of the presenters,

May 2010 International Financial Reporting Standards International Financial Reporting Standards (IFRSs) Gilbert Gélard, IASB member The views expressed in this presentation are those of the presenters,

PUBLIC BENEFIT ENTITY STANDARDS. IMPACT ASSESSMENT FOR PUBLIC SECTOR PBEs

PUBLIC BENEFIT ENTITY STANDARDS IMPACT ASSESSMENT FOR PUBLIC SECTOR PBEs Prepared June 2012 Issued November 2013 This document contains assessments of the impact for public sector PBEs of transitioning

PUBLIC BENEFIT ENTITY STANDARDS IMPACT ASSESSMENT FOR PUBLIC SECTOR PBEs Prepared June 2012 Issued November 2013 This document contains assessments of the impact for public sector PBEs of transitioning

International Financial Reporting Standard. Small and Medium-sized Entities

A Staff Overview This overview of the IASB s exposure draft of a proposed International Financial Reporting Standard for Small and Medium-sized Entities (IFRS for SMEs) was prepared by Paul Pacter, IASB

A Staff Overview This overview of the IASB s exposure draft of a proposed International Financial Reporting Standard for Small and Medium-sized Entities (IFRS for SMEs) was prepared by Paul Pacter, IASB

IFRS UPDATE. Standards, Amendments and Interpretations. January 2017

IFRS UPDATE Standards, Amendments and Interpretations January 2017 Our summary of the new and revised financial reporting requirements provides an update on IFRS Standards, Amendments and Interpretations

IFRS UPDATE Standards, Amendments and Interpretations January 2017 Our summary of the new and revised financial reporting requirements provides an update on IFRS Standards, Amendments and Interpretations

IFRS AS A TOOL FOR CROSS- BORDER FINANCIAL REPORTING

IFRS AS A TOOL FOR CROSS- BORDER FINANCIAL REPORTING A paper presented by Ismai la M. Zakari FBR, FCA Managing Partner, (Chartered Accountants) Council Member, ICAN Learning Outcomes What is IFRS? What

IFRS AS A TOOL FOR CROSS- BORDER FINANCIAL REPORTING A paper presented by Ismai la M. Zakari FBR, FCA Managing Partner, (Chartered Accountants) Council Member, ICAN Learning Outcomes What is IFRS? What

Comparison between U.S. GAAP and International Financial Reporting Standards

Comparison between and International Financial Reporting Standards April 2014 Comparison between and International Financial Reporting Standards 2 Contents 1. Introduction... 6 International standards

Comparison between and International Financial Reporting Standards April 2014 Comparison between and International Financial Reporting Standards 2 Contents 1. Introduction... 6 International standards

Preface to International Financial Reporting Standards 1

Preface to International Financial Reporting Standards 1 This Preface is issued to set out the objectives and due process of the International Accounting Standards Board and to explain the scope, authority

Preface to International Financial Reporting Standards 1 This Preface is issued to set out the objectives and due process of the International Accounting Standards Board and to explain the scope, authority

Financial Statements for the year ended December 31 st, 2006 in accordance with International Financial Reporting Standards («IFRS»)

") INFO-QUEST S.A. Financial Statements for the year ended December 31 st, 2006 in accordance with International Financial Reporting Standards («IFRS») The attached financial statements have been approved

INFO-QUEST S.A. Financial Statements for the year ended December 31 st, 2006 in accordance with International Financial Reporting Standards («IFRS») The attached financial statements have been approved

International Financial Reporting Standards (IFRSs ) A Briefing for Chief Executives, Audit Committees & Boards of Directors

A Briefing for Chief Executives, Audit Committees & Boards of Directors") 2012 International Financial Reporting Standards (IFRSs ) A Briefing for Chief Executives, Audit Committees & Boards of Directors 2012 International Financial Reporting Standards (IFRSs ) A Briefing for

2012 International Financial Reporting Standards (IFRSs ) A Briefing for Chief Executives, Audit Committees & Boards of Directors 2012 International Financial Reporting Standards (IFRSs ) A Briefing for

IFRS UPDATE. Standards, Amendments and Interpretations. June 2016

IFRS UPDATE Standards, Amendments and Interpretations June 2016 Our summary of the new and revised financial reporting requirements provides an update on IFRS Standards, Amendments and Interpretations

IFRS UPDATE Standards, Amendments and Interpretations June 2016 Our summary of the new and revised financial reporting requirements provides an update on IFRS Standards, Amendments and Interpretations

CIMA F1. Financial Operations Student Notes

CIMA F1 Financial Operations Student Notes Contents CIMA F1...1 Topic 6 The Regulatory Environment...2 International Financial Reporting Standards (IFRSs)...5 Topic 7: The Conceptual Framework...7 Topic

CIMA F1 Financial Operations Student Notes Contents CIMA F1...1 Topic 6 The Regulatory Environment...2 International Financial Reporting Standards (IFRSs)...5 Topic 7: The Conceptual Framework...7 Topic

Our IAS Plus website 2. Use of IFRS 4. Developing IFRS 7 IFRS 13. Summaries of Standards and related Interpretations 19. Current IASB projects 102

IFRS in your pocket 2017 Contents Foreword 1 Our IAS Plus website 2 Use of IFRS 4 Developing IFRS 7 IFRS 13 Summaries of Standards and related Interpretations 19 Current IASB projects 102 Abbreviations

IFRS in your pocket 2017 Contents Foreword 1 Our IAS Plus website 2 Use of IFRS 4 Developing IFRS 7 IFRS 13 Summaries of Standards and related Interpretations 19 Current IASB projects 102 Abbreviations

REPORT: Recognising energy efficiency in value properties: impact on financial accounting and auditing

REPORT: Recognising energy efficiency in value properties: impact on financial accounting and auditing Marco Koot Vanhier The REVALUE project has received funding from the European Union s Horizon 2020

REPORT: Recognising energy efficiency in value properties: impact on financial accounting and auditing Marco Koot Vanhier The REVALUE project has received funding from the European Union s Horizon 2020

TCHAIKAPHARMA HIGH QUALITY MEDICINES INC EXPLANATORY NOTES TO THE INTERIM FINANCIAL REPORT AS OF THE 30 th OF SEPTEMBER 2017

TCHAIKAPHARMA HIGH QUALITY MEDICINES INC THE INTERIM FINANCIAL REPORT AS OF THE 30 th OF SEPTEMBER 2017 TABLE OF CONTENTS APPENDICES TO THE INTERIM FINANCIAL REPORT I. INFORMATION ABOUT THE COMPANY 3 II.

TCHAIKAPHARMA HIGH QUALITY MEDICINES INC THE INTERIM FINANCIAL REPORT AS OF THE 30 th OF SEPTEMBER 2017 TABLE OF CONTENTS APPENDICES TO THE INTERIM FINANCIAL REPORT I. INFORMATION ABOUT THE COMPANY 3 II.

Report. ESMA Report on Enforcement and Regulatory Activities of Accounting Enforcers in March 2016 ESMA/2016/410

Report ESMA Report on Enforcement and Regulatory Activities of Accounting Enforcers in 2015 29 March 2016 ESMA/2016/410 Date: 29 March 2016 ESMA/2016/410 Table of contents 1 EXECUTIVE SUMMARY... 4 2 INTRODUCTION...

Report ESMA Report on Enforcement and Regulatory Activities of Accounting Enforcers in 2015 29 March 2016 ESMA/2016/410 Date: 29 March 2016 ESMA/2016/410 Table of contents 1 EXECUTIVE SUMMARY... 4 2 INTRODUCTION...

BANK OF THE PHILIPPINE ISLANDS Financial Indicators As at December 31, 2016 and Liquidity Ratio 62.44% 66.71% Debt-to-Equity Ratio 37.53% 13.

BANK OF THE PHILIPPINE ISLANDS Financial Indicators As at December 31, 2016 and 2015 2016 2015 Liquidity Ratio 62.44% 66.71% Debt-to-Equity Ratio 37.53% 13.93% Asset-to-Equity Ratio 1,045.03% 1,009.00%

BANK OF THE PHILIPPINE ISLANDS Financial Indicators As at December 31, 2016 and 2015 2016 2015 Liquidity Ratio 62.44% 66.71% Debt-to-Equity Ratio 37.53% 13.93% Asset-to-Equity Ratio 1,045.03% 1,009.00%

IFRS News Quarter

IFRS News Welcome to IFRS News. This is your quarterly update on all things relating to International Financial Reporting Standards. We ll bring you up to speed on topical issues, provide commentary and

IFRS News Welcome to IFRS News. This is your quarterly update on all things relating to International Financial Reporting Standards. We ll bring you up to speed on topical issues, provide commentary and

IFRS: A comparison with Dutch Laws and regulations 2018

IFRS: A comparison with Dutch Laws and 2018 Table of contents Preface to the 2018 edition 3 Instructions for use 4 Application of IFRS 5 Summary of main points 8 Statement of financial position 1 Intangible

IFRS: A comparison with Dutch Laws and 2018 Table of contents Preface to the 2018 edition 3 Instructions for use 4 Application of IFRS 5 Summary of main points 8 Statement of financial position 1 Intangible

Summary of potential inconsistencies between the existing Standards and the Conceptual Framework Exposure Draft

IASB Agenda ref 10D STAFF PAPER REG IASB Meeting Project Paper topic Conceptual Framework October 2014 Summary of potential inconsistencies between the existing Standards and the Conceptual Framework Exposure

IASB Agenda ref 10D STAFF PAPER REG IASB Meeting Project Paper topic Conceptual Framework October 2014 Summary of potential inconsistencies between the existing Standards and the Conceptual Framework Exposure

Presentation to IAASB

International Financial Reporting Standards Presentation to IAASB Prabhakar Kalavacherla PK, IASB Member Michael Stewart, Director of Implementation Activities June 2013 The views expressed in this presentation

International Financial Reporting Standards Presentation to IAASB Prabhakar Kalavacherla PK, IASB Member Michael Stewart, Director of Implementation Activities June 2013 The views expressed in this presentation