The Role of Derivatives in corporate risk management. Introduction: Basics of Derivatives:

|

|

|

- Barnaby Stafford

- 5 years ago

- Views:

Transcription

1 The Role of Derivatives in corporate risk management Introduction: Basics of Derivatives: Derivatives are financial instruments that are mainly used to protect against and manage risks, very often also serve arbitrage or investment purpose, provide various advantages compared to securities. Derivatives are various types and can differentiated by how they are traded, the underlying they refer to, and product type etc. We will discuss two FTSE100 and one NYS companies who use derivatives for risk management tool. Aviva plc is the UK s largest life and general insurer with strong business in selected international markets. Aviva plc a FTSE 100 company. The Group uses derivatives to mitigate risk. The Aviva uses a variety of derivatives financial instruments, including both exchange traded and over the counter in line with their overall risk management strategy. The objectives are exposure management for price, foreign current and / or interest rate risk on existing assets or liabilities, as well as planned or anticipated investment purchases. In the narration and tables / figures are given for both notional amounts and fair values of these instruments. 1 P age

2 If we go through the annual accounts 1 it shows that Group entered into number of interest rate swats in order to hedge fluctuations in the fair value part of its portfolio of mortgage loans and debt securities in the US. The notional value of these interest rate swap is indicated in the table and these hedges were fully effective during the year. To reduce its exposure to foreign currency risk, the Group has entered into net investment hedges: The Group has designed a portion of its euro and US dollars denominated debt as a hedge of the net investment in its European and American subsidiaries. 1 Aviva plc annual report P age

3 Group also indicates in its report the derivatives not qualifying for hedge accounting, because certain derivatives either do not qualify for hedge accounting under IAS39 2 or the portion to hedge account has not been taken. Diageo: Diageo Plc is a British company which is on FTSE100, Diageo distils, brews, packages, and distributor of spirits, beer, wine, and ready to drink beverages. It offers many market leader brands. The company is founded in 1886 and based in UK. The Group uses derivatives financial instruments to hedge its exposures to fluctuations in interest and exchange rates risks. The annual accounts 3 shows that derivatives instruments used by Diageo mainly of currency forward, foreign currency swaps, interest rate swaps and cross currency interest rate swaps. Diageo uses derivatives to manage the foreign exchange risk and use hedging ongoing basis, the group hedges a substantial portion of its exposure to fluctuation in the sterling value of its foreign operations by designating net borrowings held in foreign currencies and by using foreign spots, forwards, swaps and other financial derivatives. The board recently revised risk management strategy to manage hedging of foreign exchange risk arising from net investment in foreign operations. 4 - HILTON HOTELS HEDGE USING AN INTEREST RATE SWAP Hilton Hotels (hereafter referred to as Hilton), together with its subsidiaries, is involved with the ownership, management and development of hotels, resorts and timeshare properties and the franchising of lodging properties. During the period of the interest rate swap, Hilton owned and operated 60 hotels, leased and operated 203 hotels, owned an interest in and operated 53 hotels, managed 343 hotels owned by others and franchised 2,242 hotels owned and operated by third parties. Hilton was founded in International Accounting Standards IAS 3 Annual accounts Please accept this example as an exceptional case because they have explained derivatives in details, as I was asked to include all FTS100 companies, as it is not on FTSE P age

4 4 P age

5 5 P age

6 Given our assumption about the initial spot value date of 12/15/2002, the first reset is on 6/15/2002 and subsequent reset dates fall on the December 15 and June 15. To calculate the 6 P age

7 futures hedge rates for all exposures, we use the futures prices of the two futures contracts that immediately follow the hedge value dates. Table 3 shows the hedge value dates, futures contracts chosen, futures prices as of 12/15/2002, the corresponding futures rates, computed futures hedge rates and par yields. Earnings impact Hilton reported in its 10-K report that the interest rate swap qualifies as a fair-value hedge. In a fair-value hedge, as summarized in Section III, a company uses a derivative to hedge the exposure to changes in the fair value of a recognized asset or liability. In this case, the hedged liability is the issued senior notes that pay a fixed rate of 7.95%. Hilton discloses in its 10-K report: We have an interest rate swap on certain fixed rate senior notes which qualifies as a fair value hedge. This derivative impacts earnings to the extent of increasing or decreasing actual interest expense on the hedged notes to simulate a floating interest rate. Changes in the fair value of the derivative are offset by an adjustment to the value of the hedged notes." Based on this statement, we can conclude that only the interest expense item on the income statement will be affected by the swap. The entry for another item, net other (loss) gain, will have a value of zero, reflecting the difference between the fair value of the bond and the fair value of the swap. The net income and as a result, the earnings per share (EPS) will change with our replication using exchange-traded derivatives, as we start changing the position that Hilton has taken from paying a floating side of a swap to being long a strip of Eurodollar futures. We make the assumption that only the interest expense will change, and we are going to include the mark-to-market of all futures contracts in the interest expense as well. 7 P age

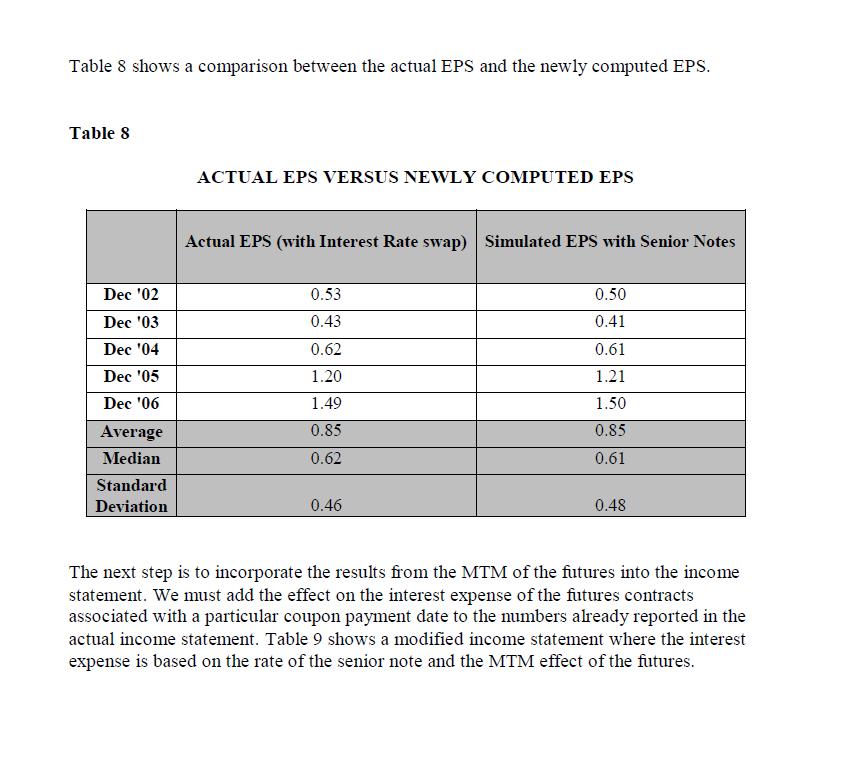

8 Table 7 shows the income statement, where the interest expense is substituted with the one computed above, and the net income and EPS are as a result changed. HILTON HOTELS INCOME STATEMENT CHANGES FROM 2002 THROUGH P age

9 9 P age

or from 0.47 to 0.46 (a 2.")

10 Table 10 shows a comparison between the actual EPS and the newly computed EPS. Note that the interest rate swap is the best option in terms of EPS volatility. Next is the futures hedge, and the worst case is no hedge at all. The OTC interest rate swap helps reduce volatility in EPS from 0.48 to 0.46 (a 4.2% reduction) or from 0.47 to 0.46 (a 2.1 % reduction) versus exchange-traded contracts. These are important results showing the benefits of OTC derivatives as compared to exchange-traded contracts, especially when you consider this is only one $375 million debt financing transaction for a firm with total long-term debt of $4,554 million and total assets of $8,348 million in Larger hedges in OTC markets can further reduce earnings volatility. 10 P age

11 Due to being on the favourable side of the hedge, Hilton s cash flow benefited from the MTM of the ED futures contracts. This is why we see that the average EPS went up; however, the volatility increased as well. 11 P age

12 Derivatives as corporate risk management tools: In the wake of the financial crises, regulatory proposals were made that would enforce margin requirements on non-cleared derivatives for market participants. Such regulations would limit the ability of non-financial firms to effectively manage risk. However, an exemption for non-financial companies was included within the US Dodd Frank Act and European Market Infrastructure Regulation (EMIR) which excuse those firms that use derivatives to hedge commercial risk from mandatory central clearing rules. Non systemically important non financial institutions will also be exempt from posting margin on non-cleared transactions, according to rules finalized by the Basel Committee on Banking Supervision and International Organization of Securities Commissions in September 2013, nonetheless, it is important to note there may be indirect costs for corporate end-users 7 the derivative statistics on the BIS website, including the total notional principal amount outstanding (np) as December 2012, are as follows: 8 1. Interest rate contracts: forward rate agreements, interest rate swaps ($489,703 billion np globally; non-financial firms are $34,731 billion np (7.1%) 2. Foreign exchange contracts: forwards and forex swaps, currency swaps ($67,358 billion np globally; non-financial firms are $9,693 billion np (14.4%) 5 Dodd Fran Wall Street Reform and Consumer Protection Act The Regulation (EU) No 648/2012 of the European Parliament and of the Council of 4 th July 2012 on OTC derivatives, central counterparties (CCPs) and trade repositories (TRs (EMIR) entered into force on 16 th August As of September 2013, the margin requirements for uncleared trades only apply to financial institutions and systemically important non-financial entities. Non-financial firms are exempt from clearing if the hedges are used for hedging commercial risk. There may be indirect impact. Under Basel III, dealers are required to hold higher capital for unclear trades, and they also need to apply a credit valuation adjustment (CVA) capital charge. This charge may be high for uncleared, non-collateralized trades. The dealer may also hedge its exposure with another dealer which would be subject to margin requirements (cleared or uncleared). The dealer may pass part or all of the funding cost, plus the capital charges, back to the non-financial. Under European rules, European banks do not need to apply a CVA charge when trading with a non-financial, but this exemption was not adopted in the US 8 A report by Keybridge Research (2010) provides analysis of the impact on non-financial firms if mandatory margin requirements were required. This research was done before the new rules were finalized and nonfinancials were exempted. While these results do not apply now, the findings are insightful, especially if the rules were changed in the future. The key findings are as follows: (1) About 72% of survey participants report that proposed regulations would have a significant impact on their hedging activities. (2) A 3% margin requirement, assuming no exemptions, would require total collateral of $33.1 billion for non-financial, publicly traded BRT firms. (3) Non-financial publicly traded BRT firms would likely respond to the imposition of margin requirements on OTC derivatives by reducing capital spending 0.9% to 1.1% (approximately $2 billion to $2.5 billion) and (4) Extending their estimates to S&P 500 companies indicates a reduction in capital spending of $5 billion to $6 billion per year and an estimated loss of 100,000 to 120,000 jobs. See Bank for International Settlements 2013 in the references and 12 P age

13 3. Credit default swaps: single-name instruments, multi-name instruments ($25,069 billion np globally; non-financial firms are $200 billion np (0.8%) 4. Equity-linked contracts: forwards and swaps, options ($6,251 billion np globally; nonfinancial firms are $755 billion np (12.1%) 5. Commodity contracts: forwards and swaps, options ($2,587 billion np; non-financial firms not available). Motivations for Hedging - Researcher has shown that there are important motivations for firms to hedge using derivatives and that hedging can increase firm value. Smithson and Simkins (2005) provide a comprehensive review of the literature in this area. Reasons to firms to hedge include to: Reduce expected taxes (Nance, Smith, and Smithson, 1993 and Graham and Rogers, 2002) Reduce expected costs of financial distress (Stulz, 1996) Reduce agency costs (Smith and Stulz, 1985). Reduce costs associated with under-investment opportunities (Froot, Scharfstein, and Stein, 1993, Gay and Nam 1998, among others. Studies including Nance, Smith, and Smithson (1993), Dolde (1995) and Geczy, Minton, and Schrand (1997), and Allayannis and Ofed (1998) have shown that hedging using foreign derivatives is consistent with shareholder wealth maximization. Other studies have demonstrated the value of interest rate derivatives. For example, Simkins and Rogers (2000) find that firms using interest rate swaps to create synthetic fixed rate financing are more likely to undergo credit quality upgrades. This evidence is consistent with the use of corporate risk management to reduce the probability of financial distress. Financial distress and corporate risk management is explained in Amiyatosh Purnanandam (2008) 9 A number of studies have directly examined if hedging can increase firm value. Most studies have shown positive relation between corporate risk management and value of the firm. For example, Allayannis and Weston (2001) examine the use of foreign currency (FX) derivatives 9 Purnanandam A Financial distress and corporate risk management: Theory and evidence, Journal of Financial Economics 87 (2008) P age

14 by large non financial firms between 1990 and 1995, and find that FX hedging is associated with 4.8% premium for companies with FX exposure (as measured by foreign sales). Regarding hedging using commodity derivatives, Carter, Rogers, and Simkins (2005) show that fuel price hedging by airlines is associated with significantly higher firm values. A study of oil and gas firms by Jin and Jorion (2005) find that while hedging reduced the firm s stock price sensitive to oil and gas prices, it did not appear to increase value. Academic article and research paper wrote by David J, Richard D. Philips, Stephen D. Smith (1998) 10 in this research paper they have formulated and tested number of hypotheses regarding insurance participation and volume decisions in derivatives markets. The results provide a considerable amount of support for the hypothesis that insurances hedge to maximize value, insurers are motivated to use financial derivatives to reduce the expected costs of financial distress the decision to use derivatives is inversely related to the capital to-asset ratio for both life and property liability insurers. It has also evident that insurers use derivatives to hedge asset volatility, liquidity, and exchange rate risks. Life insurers appear to use derivatives to manage interest rate risk and risk from embedded options present in their individual life insurance and GIC liabilities Conclusion: An alternative vision for policy makers in the after math of Lehman Brother s bankruptcy would have involved greater consideration of how liquidity can become constrained so quickly, as in the commercial paper and repo markets, and an effort to mandate the type and amount of collateral provided in these asset classes. More regulations required to regulated derivatives and self established risk management system should be in place. As Georg Santayana so famously remarked, Those who do not understand history are doomed to repeat. 10 J.David Cummins, Richard D. Philips, Stephen D. Smith Derivatives and Corporate Risk Management: Participation and Volume Decisions in the Insurance Industry, The Wharton Financial Institutions Centre 14 P age

15 References: Bank for International Settlements (BIS), 2013, Statistical Release: OTC Derivatives Statistics at End-December 2012, May. Dolde, W., 1995, Hedging, Leverage, and Primitive Risk, Journal of Financial Engineering 4, Jin and Jorion, 2006, Firm Value and Hedging: Evidence from U.S. Oil and Gas Producers, Journal of Finance, 61, Gay, G.D., and J. Nam, 1998, The Underinvestment Problem and Corporate Derivatives Use, Financial Management 27 (4), Froot, Kenneth, David Scharfstein, and Jeremy Stein, 1993, Risk Management: Coordinating Investment and Financing Policies, The Journal of Finance 48, Jin and Jorion, 2006, Firm Value and Hedging: Evidence from U.S. Oil and Gas Producers, Journal of Finance, 61, Géczy, C., B.A. Minton, and C. Schrand, 1997, Why Firms Use Currency Derivatives, Journal of Finance 52, Graham, J.R., and D.A. Rogers, 2002, Do Firms Hedge in Response to Tax Incentives? Journal of Finance 57, Grinblatt, M., and N. Jegadeesh, 1996, Relative Pricing of Eurodollar Futures and Forward Contracts, Journal of Finance 51, Gupta, A., and M.G. Subrahmanyam, 2000, An Empirical Examination of the Convexity Bias in the Pricing of Interest Rate Swaps, Journal of Financial Economics 55, Hovakimian, A. and G. Hovakimian, 2009, Cash Flow Sensitivity of Investment, European Financial Management, 15 (1), Kavussanos M., and I. Visvikis, 2004, Market Interactions in Returns and Volatilities between Spot and Forward Shipping Freight Markets, Journal of Banking & Finance 28, Kawaller, Ira, 1994, Comparing Eurodollar strips to interest rate swaps, The Journal of Derivatives 2 (1), pp Kawaller, Ira, 1997, Tailing Futures Hedges/Tailing Spreads, The Journal of Derivatives, 5 (2), FMC Corporation, 2012, The Impact of Dodd-Frank on Customers, Credit, and Job Creators, Hearing before the Subcommittee on Capital Markets and Government Sponsored Enterprises Committee on Financial Services U.S. House of Representatives, Testimony of Thomas C. Deas, Jr., July P age

16 Gregory W. Brown, 2000, Managing foreign exchange risk with derivatives, Journal of Financial Economics 60 (2001) Graham, J, Smith C, Tax incentives to hedge. Journal of Finance 54, Dolde, W, Hedging, leverage, and primitive risk. The Journal of Financial Engineeering4, Gerald D. Gay, Chen Miano Lin, Stephan D Smith, 2011 Corporate Derivatives use and the cost of equity, Journal of Banking and Finance 35 (2011) P age

If the market is perfect, hedging would have no value. Actually, in real world,

2. Literature Review If the market is perfect, hedging would have no value. Actually, in real world, the financial market is imperfect and hedging can directly affect the cash flow of the firm. So far,

2. Literature Review If the market is perfect, hedging would have no value. Actually, in real world, the financial market is imperfect and hedging can directly affect the cash flow of the firm. So far,

Why Do Non-Financial Firms Select One Type of Derivatives Over Others?

Why Do Non-Financial Firms Select One Type of Derivatives Over Others? Hong V. Nguyen University of Scranton The increase in derivatives use over the past three decades has stimulated both theoretical

Why Do Non-Financial Firms Select One Type of Derivatives Over Others? Hong V. Nguyen University of Scranton The increase in derivatives use over the past three decades has stimulated both theoretical

A Review of the Literature on Commodity Risk Management for Nonfinancial Firms

A Review of the Literature on Commodity Risk Management for Nonfinancial Firms Presentation by: Betty J. Simkins, Ph.D. Williams Companies Chair & Professor of Finance Department Head of Finance Oklahoma

A Review of the Literature on Commodity Risk Management for Nonfinancial Firms Presentation by: Betty J. Simkins, Ph.D. Williams Companies Chair & Professor of Finance Department Head of Finance Oklahoma

The Use of Foreign Currency Derivatives and Firm Value In U.S.

The Use of Foreign Currency Derivatives and Firm Value In U.S. Master thesis Rui Zhang ANR: 484834 23 Aug 2012 International Management Faculty of Economics and Business Administration Supervisor: Dr.

The Use of Foreign Currency Derivatives and Firm Value In U.S. Master thesis Rui Zhang ANR: 484834 23 Aug 2012 International Management Faculty of Economics and Business Administration Supervisor: Dr.

Determinants of exchange rate hedging an empirical analysis of U.S. small-cap industrial firms

University of Central Florida HIM 1990-2015 Open Access Determinants of exchange rate hedging an empirical analysis of U.S. small-cap industrial firms 2011 Zachary M. Lehner University of Central Florida

University of Central Florida HIM 1990-2015 Open Access Determinants of exchange rate hedging an empirical analysis of U.S. small-cap industrial firms 2011 Zachary M. Lehner University of Central Florida

How Much do Firms Hedge with Derivatives?

How Much do Firms Hedge with Derivatives? Wayne Guay The Wharton School University of Pennsylvania 2400 Steinberg-Dietrich Hall Philadelphia, PA 19104-6365 (215) 898-7775 guay@wharton.upenn.edu and S.P.

How Much do Firms Hedge with Derivatives? Wayne Guay The Wharton School University of Pennsylvania 2400 Steinberg-Dietrich Hall Philadelphia, PA 19104-6365 (215) 898-7775 guay@wharton.upenn.edu and S.P.

The Value of Investing in ERM

The Value of Investing in ERM By Richard D. Phillips C.V. Starr Professor of Risk Management and Insurance Georgia State University Martin F. Grace Georgia State University mgrace@gsu.edu Richard D. Phillips

The Value of Investing in ERM By Richard D. Phillips C.V. Starr Professor of Risk Management and Insurance Georgia State University Martin F. Grace Georgia State University mgrace@gsu.edu Richard D. Phillips

Regulatory Landscape and Challenges

TITLE: Regulatory Landscape and Challenges AUTHOR: Adrian Orr Chief Executive EVENT PRESENTATION: September 2012 PG 2 Overview Significant regulatory and legislative reform globally: banking, insurance,

TITLE: Regulatory Landscape and Challenges AUTHOR: Adrian Orr Chief Executive EVENT PRESENTATION: September 2012 PG 2 Overview Significant regulatory and legislative reform globally: banking, insurance,

Corporate Risk Management: Costs and Benefits

DePaul University From the SelectedWorks of Ali M Fatemi 2002 Corporate Risk Management: Costs and Benefits Ali M Fatemi, DePaul University Carl Luft, DePaul University Available at: https://works.bepress.com/alifatemi/5/

DePaul University From the SelectedWorks of Ali M Fatemi 2002 Corporate Risk Management: Costs and Benefits Ali M Fatemi, DePaul University Carl Luft, DePaul University Available at: https://works.bepress.com/alifatemi/5/

Interest Rate Swaps and Nonfinancial Real Estate Firm Market Value in the US

Interest Rate Swaps and Nonfinancial Real Estate Firm Market Value in the US Yufeng Hu Senior Thesis in Economics Professor Gary Smith Spring 2018 1. Abstract In this paper I examined the impact of interest

Interest Rate Swaps and Nonfinancial Real Estate Firm Market Value in the US Yufeng Hu Senior Thesis in Economics Professor Gary Smith Spring 2018 1. Abstract In this paper I examined the impact of interest

The Strategic Motives for Corporate Risk Management

April 2004 The Strategic Motives for Corporate Risk Management Amrita Nain* Abstract This paper investigates how the benefits of hedging currency risk and the incentives of a firm to hedge are affected

April 2004 The Strategic Motives for Corporate Risk Management Amrita Nain* Abstract This paper investigates how the benefits of hedging currency risk and the incentives of a firm to hedge are affected

Master Thesis Finance Foreign Currency Exposure, Financial Hedging Instruments and Firm Value

Master Thesis Finance 2012 Foreign Currency Exposure, Financial Hedging Instruments and Firm Value Author : P.N.G Tobing Student number : U1246193 ANR : 187708 Department : Finance Supervisor : Dr.M.F.Penas

Master Thesis Finance 2012 Foreign Currency Exposure, Financial Hedging Instruments and Firm Value Author : P.N.G Tobing Student number : U1246193 ANR : 187708 Department : Finance Supervisor : Dr.M.F.Penas

Interest Rate Hedging under Financial Distress: The Effects of Leverage and Growth Opportunities

University of Massachusetts - Amherst ScholarWorks@UMass Amherst International CHRIE Conference-Refereed Track 2009 ICHRIE Conference Jul 29th, 3:15 PM - 4:15 PM Interest Rate Hedging under Financial Distress:

University of Massachusetts - Amherst ScholarWorks@UMass Amherst International CHRIE Conference-Refereed Track 2009 ICHRIE Conference Jul 29th, 3:15 PM - 4:15 PM Interest Rate Hedging under Financial Distress:

Kristine Watson Hankins * ABSTRACT

ARE ACQUISITIONS AN OPERATIONAL HEDGE? THE INTERACTION OF FINANCIAL AND OPERATIONAL HEDGING Kristine Watson Hankins * kristine.hankins@uky.edu ABSTRACT This paper investigates the substitution of financial

ARE ACQUISITIONS AN OPERATIONAL HEDGE? THE INTERACTION OF FINANCIAL AND OPERATIONAL HEDGING Kristine Watson Hankins * kristine.hankins@uky.edu ABSTRACT This paper investigates the substitution of financial

Regulatory Reform and Collateral Management: The Impact on Major Participants in the OTC Derivatives Markets

Regulatory Reform and Collateral Management: The Impact on Major Participants in the OTC Derivatives Markets 4 J.P. Morgan thought / Winter 2012 The new regulations that will take effect in the wake of

Regulatory Reform and Collateral Management: The Impact on Major Participants in the OTC Derivatives Markets 4 J.P. Morgan thought / Winter 2012 The new regulations that will take effect in the wake of

Firm Value and Hedging: Evidence from U.S. Oil and Gas Producers

THE JOURNAL OF FINANCE VOL. LXI, NO. 2 APRIL 2006 Firm Value and Hedging: Evidence from U.S. Oil and Gas Producers YANBO JIN and PHILIPPE JORION ABSTRACT This paper studies the hedging activities of 119

THE JOURNAL OF FINANCE VOL. LXI, NO. 2 APRIL 2006 Firm Value and Hedging: Evidence from U.S. Oil and Gas Producers YANBO JIN and PHILIPPE JORION ABSTRACT This paper studies the hedging activities of 119

Firm Value and Hedging: Evidence from U.S. Oil and Gas Producers

Firm Value and Hedging: Evidence from U.S. Oil and Gas Producers YANBO JIN and PHILIPPE JORION* ABSTRACT This paper studies the hedging activities of 119 U.S. oil and gas producers from 1998 to 2001 and

Firm Value and Hedging: Evidence from U.S. Oil and Gas Producers YANBO JIN and PHILIPPE JORION* ABSTRACT This paper studies the hedging activities of 119 U.S. oil and gas producers from 1998 to 2001 and

Course Structure and Standard Syllabus. Course Area: Financial Sector Policies. Course Title: Financial Markets and Instruments (FMI)

") Course Structure and Standard Syllabus Course Area: Financial Sector Policies Course Title: Financial Markets and Instruments (FMI) Objectives: This two-week course aims at providing participant with the

Course Structure and Standard Syllabus Course Area: Financial Sector Policies Course Title: Financial Markets and Instruments (FMI) Objectives: This two-week course aims at providing participant with the

The Determinants of Corporate Hedging and Firm Value: An Empirical Research of European Firms

The Determinants of Corporate Hedging and Firm Value: An Empirical Research of European Firms Ying Liu S882686, Master of Finance, Supervisor: Dr. J.C. Rodriguez Department of Finance, School of Economics

The Determinants of Corporate Hedging and Firm Value: An Empirical Research of European Firms Ying Liu S882686, Master of Finance, Supervisor: Dr. J.C. Rodriguez Department of Finance, School of Economics

Journal of Energy and Management

J o u r n a l o f e n e r g y a n d m a n a g e m e n t ( 2 0 1 6 ) V o l. 1 P a g e 44 Journal of Energy and Management Journal homepage: https://www.pdpu.ac.in/jem.html COMMODITY HEDGING THROUGH ZERO-COST

J o u r n a l o f e n e r g y a n d m a n a g e m e n t ( 2 0 1 6 ) V o l. 1 P a g e 44 Journal of Energy and Management Journal homepage: https://www.pdpu.ac.in/jem.html COMMODITY HEDGING THROUGH ZERO-COST

The Determinants of Corporate Hedging Policies

International Journal of Business and Social Science Vol. 2 No. 6; April 2011 The Determinants of Corporate Hedging Policies Xuequn Wang Faculty of Business Administration, Lakehead University 955 Oliver

International Journal of Business and Social Science Vol. 2 No. 6; April 2011 The Determinants of Corporate Hedging Policies Xuequn Wang Faculty of Business Administration, Lakehead University 955 Oliver

Operational and Financial Hedging: Friend or Foe? Evidence from the U.S. Airline Industry

Operational and Financial Hedging: Friend or Foe? Evidence from the U.S. Airline Industry Stephen D. Treanor California State University David A. Carter Oklahoma State University Daniel A. Rogers Portland

Operational and Financial Hedging: Friend or Foe? Evidence from the U.S. Airline Industry Stephen D. Treanor California State University David A. Carter Oklahoma State University Daniel A. Rogers Portland

Interest Rate Risk Management Refresher. April 29, Presented to: Howard Sakin Section I. Basics of Interest Rate Hedging?

Interest Rate Risk Management Refresher April 29, 2011 Presented to: Howard Sakin 410-237-5315 Section I Basics of Interest Rate Hedging? 1 What Is An Interest Rate Hedge? Interest rate hedges are contracts

Interest Rate Risk Management Refresher April 29, 2011 Presented to: Howard Sakin 410-237-5315 Section I Basics of Interest Rate Hedging? 1 What Is An Interest Rate Hedge? Interest rate hedges are contracts

Interest Rate Risk Management Refresher. April 27, Presented to: Section I. Basics of Interest Rate Hedging?

Interest Rate Risk Management Refresher April 27, 2012 Presented to: Section I Basics of Interest Rate Hedging? What Is An Interest Rate Hedge? Interest rate hedges are contracts between parties designed

Interest Rate Risk Management Refresher April 27, 2012 Presented to: Section I Basics of Interest Rate Hedging? What Is An Interest Rate Hedge? Interest rate hedges are contracts between parties designed

Measuring Efficiency of Using Currency Derivatives to Hedge Foreign Exchange Risk: A Study on Advanced Chemical Industries (ACI) in Bangladesh

in Bangladesh") International Journal of Economics, Finance and Management Sciences 2016; 4(2): 57-66 Published online March 7, 2016 (http://www.sciencepublishinggroup.com/j/ijefm) doi: 10.11648/j.ijefm.20160402.14 ISSN:

International Journal of Economics, Finance and Management Sciences 2016; 4(2): 57-66 Published online March 7, 2016 (http://www.sciencepublishinggroup.com/j/ijefm) doi: 10.11648/j.ijefm.20160402.14 ISSN:

How Does the Selection of Hedging Instruments Affect Company Financial Measures? Evidence from UK Listed Firms

How Does the Selection of Hedging Instruments Affect Company Financial Measures? Evidence from UK Listed Firms George Emmanuel Iatridis (Corresponding author) University of Thessaly, Department of Economics,

How Does the Selection of Hedging Instruments Affect Company Financial Measures? Evidence from UK Listed Firms George Emmanuel Iatridis (Corresponding author) University of Thessaly, Department of Economics,

ING response to the draft Technical Standards for the Regulation on OTC Derivatives, CCPs and Trade Repositories

ING response to the draft Technical Standards for the Regulation on OTC Derivatives, CCPs and Trade Repositories 3 August 2012 About ING Contact: Jeroen Groothuis Group Public & Government Affairs T +31

ING response to the draft Technical Standards for the Regulation on OTC Derivatives, CCPs and Trade Repositories 3 August 2012 About ING Contact: Jeroen Groothuis Group Public & Government Affairs T +31

Cash Holdings from a Risk Management Perspective

Department of Business Administration FEKN90, Business Administration Degree Project Master of Science in Business and Economics Spring 2015 Cash Holdings from a Risk Management Perspective - A study on

Department of Business Administration FEKN90, Business Administration Degree Project Master of Science in Business and Economics Spring 2015 Cash Holdings from a Risk Management Perspective - A study on

THE TIME VARYING PROPERTY OF FINANCIAL DERIVATIVES IN

THE TIME VARYING PROPERTY OF FINANCIAL DERIVATIVES IN ENHANCING FIRM VALUE Bach Dinh and Hoa Nguyen* School of Accounting, Economics and Finance Faculty of Business and Law Deakin University 221 Burwood

THE TIME VARYING PROPERTY OF FINANCIAL DERIVATIVES IN ENHANCING FIRM VALUE Bach Dinh and Hoa Nguyen* School of Accounting, Economics and Finance Faculty of Business and Law Deakin University 221 Burwood

THE 31ST ANNUAL CONFERENCE OF THE BANKING & FINANCIAL SERVICES LAW ASSOCIATION

THE 31ST ANNUAL CONFERENCE OF THE BANKING & FINANCIAL SERVICES LAW ASSOCIATION G2 REFORMS - HOW FAR HAVE WE COME, HOW FAR YET TO GO? MR DANIEL MCAULIFFE, MANAGER, BANKING AND CAPITAL MARKETS REGULATION

THE 31ST ANNUAL CONFERENCE OF THE BANKING & FINANCIAL SERVICES LAW ASSOCIATION G2 REFORMS - HOW FAR HAVE WE COME, HOW FAR YET TO GO? MR DANIEL MCAULIFFE, MANAGER, BANKING AND CAPITAL MARKETS REGULATION

Dynamic Corporate Risk Management: Motivations and Real Implications

Forthcoming in Journal of Banking and Finance Dynamic Corporate Risk Management: Motivations and Real Implications Georges Dionne, corresponding author Canada Research Chair in Risk Management HEC Montreal

Forthcoming in Journal of Banking and Finance Dynamic Corporate Risk Management: Motivations and Real Implications Georges Dionne, corresponding author Canada Research Chair in Risk Management HEC Montreal

Interest rate swap usage for hedging and speculation by. Dutch listed non-financial firms

Interest rate swap usage for hedging and speculation by Dutch listed non-financial firms Master Thesis: Business Administration Track: Financial Management University of Twente Faculty of Behavioral, Management

Interest rate swap usage for hedging and speculation by Dutch listed non-financial firms Master Thesis: Business Administration Track: Financial Management University of Twente Faculty of Behavioral, Management

Eurex Clearing. Response. Joint CFTC SEC request for comment on international swap and clearinghouse regulation

Eurex Clearing Response to Joint CFTC SEC request for comment on international swap and clearinghouse regulation CFTC Release No. Frankfurt am Main, 26 September 2011 Eurex Clearing AG wishes to thank

Eurex Clearing Response to Joint CFTC SEC request for comment on international swap and clearinghouse regulation CFTC Release No. Frankfurt am Main, 26 September 2011 Eurex Clearing AG wishes to thank

Advanced Risk Management

Winter 2015/2016 Advanced Risk Management Part I: Decision Theory and Risk Management Motives Lecture 4: Risk Management Motives Perfect financial markets Assumptions: no taxes no transaction costs no

Winter 2015/2016 Advanced Risk Management Part I: Decision Theory and Risk Management Motives Lecture 4: Risk Management Motives Perfect financial markets Assumptions: no taxes no transaction costs no

1.2 Product nature of credit derivatives

1.2 Product nature of credit derivatives Payoff depends on the occurrence of a credit event: default: any non-compliance with the exact specification of a contract price or yield change of a bond credit

1.2 Product nature of credit derivatives Payoff depends on the occurrence of a credit event: default: any non-compliance with the exact specification of a contract price or yield change of a bond credit

The Determinants of Foreign Currency Hedging by UK Non- Financial Firms

The Determinants of Foreign Currency Hedging by UK Non- Financial Firms Amrit Judge Economics Group, Middlesex University The Burroughs, Hendon London NW4 4BT Tel: 020 8411 6344 Fax: 020 8411 4739 A.judge@mdx.ac.uk

The Determinants of Foreign Currency Hedging by UK Non- Financial Firms Amrit Judge Economics Group, Middlesex University The Burroughs, Hendon London NW4 4BT Tel: 020 8411 6344 Fax: 020 8411 4739 A.judge@mdx.ac.uk

29 January Dear Commissioner, Re: Call for evidence on EU regulatory framework for financial services

29 January 2016 Jonathan Hill, Lord Hill of Oareford Commissioner Financial Stability, Financial Services and Capital Markets Union European Commission Rue de la Loi / Wetstraat 200 1049 Brussels Belgium

29 January 2016 Jonathan Hill, Lord Hill of Oareford Commissioner Financial Stability, Financial Services and Capital Markets Union European Commission Rue de la Loi / Wetstraat 200 1049 Brussels Belgium

Chapter 8. Swaps. Copyright 2009 Pearson Prentice Hall. All rights reserved.

Chapter 8 Swaps Introduction to Swaps A swap is a contract calling for an exchange of payments, on one or more dates, determined by the difference in two prices A swap provides a means to hedge a stream

Chapter 8 Swaps Introduction to Swaps A swap is a contract calling for an exchange of payments, on one or more dates, determined by the difference in two prices A swap provides a means to hedge a stream

Hedging and Firm Value in the European Airline Industry

Hedging and Firm Value in the European Airline Industry - Does jet fuel price hedging increase firm value? Master Thesis, Copenhagen Business School MSC in Economics and Business Administration Finance

Hedging and Firm Value in the European Airline Industry - Does jet fuel price hedging increase firm value? Master Thesis, Copenhagen Business School MSC in Economics and Business Administration Finance

CURRENT CONTEXT OF USING DERIVATIVES AS RISK MANAGEMENT TECHNIQUE OF SRI LANKAN LISTED COMPANIES

International Journal of Business and General Management (IJBGM) ISSN(P): 2319-2267; ISSN(E): 2319-2275 Vol. 2, Issue 5, Nov 2013, 1-10 IASET CURRENT CONTEXT OF USING DERIVATIVES AS RISK MANAGEMENT TECHNIQUE

International Journal of Business and General Management (IJBGM) ISSN(P): 2319-2267; ISSN(E): 2319-2275 Vol. 2, Issue 5, Nov 2013, 1-10 IASET CURRENT CONTEXT OF USING DERIVATIVES AS RISK MANAGEMENT TECHNIQUE

How much do firms hedge with derivatives? $

Journal of Financial Economics 70 (2003) 423 461 How much do firms hedge with derivatives? $ Wayne Guay a, S.P Kothari b, * a The Wharton School, University of Pennsylvania, Philadelphia, PA 19104-6355,

Journal of Financial Economics 70 (2003) 423 461 How much do firms hedge with derivatives? $ Wayne Guay a, S.P Kothari b, * a The Wharton School, University of Pennsylvania, Philadelphia, PA 19104-6355,

Risk Management Determinants Affecting Firms' Values in the Gold Mining Industry: New Empirical Results

Risk Management Determinants Affecting Firms' Values in the Gold Mining Industry: New Empirical Results by Georges Dionne* and Martin Garand Risk Management Chair, HEC Montreal * Corresponding author:

Risk Management Determinants Affecting Firms' Values in the Gold Mining Industry: New Empirical Results by Georges Dionne* and Martin Garand Risk Management Chair, HEC Montreal * Corresponding author:

BLACKROCK FUNDS II BlackRock Low Duration Bond Portfolio (the Fund ) Class K Shares

Class K Shares") BLACKROCK FUNDS II BlackRock Low Duration Bond Portfolio (the Fund ) Class K Shares Supplement dated March 28, 2018 to the Summary Prospectus and Prospectus, each dated January 26, 2018, as supplemented

BLACKROCK FUNDS II BlackRock Low Duration Bond Portfolio (the Fund ) Class K Shares Supplement dated March 28, 2018 to the Summary Prospectus and Prospectus, each dated January 26, 2018, as supplemented

Finance: Risk Management

Winter 2010/2011 Module III: Risk Management Motives steinorth@bwl.lmu.de Perfect financial markets Assumptions: no taxes no transaction costs no costs of writing and enforcing contracts no restrictions

Winter 2010/2011 Module III: Risk Management Motives steinorth@bwl.lmu.de Perfect financial markets Assumptions: no taxes no transaction costs no costs of writing and enforcing contracts no restrictions

STRENGTHENING FINANCIAL STABILITY EUROPEAN MARKET INFRASTRUCTURE REGULATION (EMIR) OVERVIEW AND INDUSTRY PRIORITIES

OVERVIEW AND INDUSTRY PRIORITIES") STRENGTHENING FINANCIAL STABILITY EUROPEAN MARKET INFRASTRUCTURE REGULATION (EMIR) OVERVIEW AND INDUSTRY PRIORITIES BACKGROUND AND CONTEXT In the wake of the 2008 Financial Crisis, world leaders met in

STRENGTHENING FINANCIAL STABILITY EUROPEAN MARKET INFRASTRUCTURE REGULATION (EMIR) OVERVIEW AND INDUSTRY PRIORITIES BACKGROUND AND CONTEXT In the wake of the 2008 Financial Crisis, world leaders met in

The Information Conveyed in Hiring Announcements of Senior Executives Overseeing Enterprise-Wide Risk Management Processes

The Information Conveyed in Hiring Announcements of Senior Executives Overseeing Enterprise-Wide Risk Management Processes Mark Beasley Professor of Accounting and ERM Initiative Director Don Pagach Professor

The Information Conveyed in Hiring Announcements of Senior Executives Overseeing Enterprise-Wide Risk Management Processes Mark Beasley Professor of Accounting and ERM Initiative Director Don Pagach Professor

Essays on foreign currency risk management

Louisiana State University LSU Digital Commons LSU Doctoral Dissertations Graduate School 2011 Essays on foreign currency risk management Sungjae Francis Kim Louisiana State University and Agricultural

Louisiana State University LSU Digital Commons LSU Doctoral Dissertations Graduate School 2011 Essays on foreign currency risk management Sungjae Francis Kim Louisiana State University and Agricultural

Modeling Fixed-Income Securities and Interest Rate Options

jarr_fm.qxd 5/16/02 4:49 PM Page iii Modeling Fixed-Income Securities and Interest Rate Options SECOND EDITION Robert A. Jarrow Stanford Economics and Finance An Imprint of Stanford University Press Stanford,

jarr_fm.qxd 5/16/02 4:49 PM Page iii Modeling Fixed-Income Securities and Interest Rate Options SECOND EDITION Robert A. Jarrow Stanford Economics and Finance An Imprint of Stanford University Press Stanford,

P2.T6. Credit Risk Measurement & Management. Jon Gregory, The xva Challenge: Counterparty Credit Risk, Funding, Collateral, and Capital

P2.T6. Credit Risk Measurement & Management Jon Gregory, The xva Challenge: Counterparty Credit Risk, Funding, Collateral, and Capital Bionic Turtle FRM Study Notes Sample By David Harper, CFA FRM CIPM

P2.T6. Credit Risk Measurement & Management Jon Gregory, The xva Challenge: Counterparty Credit Risk, Funding, Collateral, and Capital Bionic Turtle FRM Study Notes Sample By David Harper, CFA FRM CIPM

MiFID II: Information on Financial instruments

MiFID II: Information on Financial instruments A. Introduction This information is provided to you being categorized as a Professional client to inform you on financial instruments offered by Rabobank

MiFID II: Information on Financial instruments A. Introduction This information is provided to you being categorized as a Professional client to inform you on financial instruments offered by Rabobank

Credit Risk Management: A Survey of Practices

DePaul University From the SelectedWorks of Ali M Fatemi 2006 Credit Risk Management: A Survey of Practices Ali M Fatemi, DePaul University Iraj Fooladi, Dalhousie University Available at: https://works.bepress.com/alifatemi/3/

DePaul University From the SelectedWorks of Ali M Fatemi 2006 Credit Risk Management: A Survey of Practices Ali M Fatemi, DePaul University Iraj Fooladi, Dalhousie University Available at: https://works.bepress.com/alifatemi/3/

EMIR and DODD-FRANK FAQs. January 2017

This FAQs document relates to: EMIR and DODD-FRANK FAQs January 2017 the European Market Infrastructure Regulation or EMIR, Regulation (EU) No 648/2012 of the European Parliament and of the Council of

This FAQs document relates to: EMIR and DODD-FRANK FAQs January 2017 the European Market Infrastructure Regulation or EMIR, Regulation (EU) No 648/2012 of the European Parliament and of the Council of

Two essays on corporate hedging: the choice of instruments and methods

Louisiana State University LSU Digital Commons LSU Doctoral Dissertations Graduate School 2003 Two essays on corporate hedging: the choice of instruments and methods Pinghsun Huang Louisiana State University

Louisiana State University LSU Digital Commons LSU Doctoral Dissertations Graduate School 2003 Two essays on corporate hedging: the choice of instruments and methods Pinghsun Huang Louisiana State University

E.ON General Statement to Margin requirements for non-centrally-cleared derivatives

E.ON AG Avenue de Cortenbergh, 60 B-1000 Bruxelles www.eon.com Contact: Political Affairs and Corporate Communications E.ON General Statement to Margin requirements for non-centrally-cleared derivatives

E.ON AG Avenue de Cortenbergh, 60 B-1000 Bruxelles www.eon.com Contact: Political Affairs and Corporate Communications E.ON General Statement to Margin requirements for non-centrally-cleared derivatives

THE IMPACT OF EMIR IS YOUR ORGANISATION READY?

THE IMPACT OF EMIR IS YOUR ORGANISATION READY? November 2013 Introduction to EMIR EMIR is part of the G20 commitments to prevent future financial crises Both the European Union and the United States have

THE IMPACT OF EMIR IS YOUR ORGANISATION READY? November 2013 Introduction to EMIR EMIR is part of the G20 commitments to prevent future financial crises Both the European Union and the United States have

Derivatives and Corporate Risk Management: Participation and Volume Decisions in the Insurance Industry

Derivatives and Corporate Risk Management: Participation and Volume Decisions in the Insurance Industry J. David Cummins, Richard D. Phillips, and Stephen D. Smith Federal Reserve Bank of Atlanta Working

Derivatives and Corporate Risk Management: Participation and Volume Decisions in the Insurance Industry J. David Cummins, Richard D. Phillips, and Stephen D. Smith Federal Reserve Bank of Atlanta Working

A strategic approach to global derivative trade reporting

A strategic approach to global derivative trade reporting Perspective for the buy side kpmg.com Aim: Key considerations for buy-side firms to evaluate a global derivative trade reporting approach that

A strategic approach to global derivative trade reporting Perspective for the buy side kpmg.com Aim: Key considerations for buy-side firms to evaluate a global derivative trade reporting approach that

SUMMARY PROSPECTUS. BlackRock Allocation Target Shares BATS: Series E Portfolio Series E Portfolio BATEX. July 28, 2017

July 28, 2017 SUMMARY PROSPECTUS BlackRock Allocation Target Shares BATS: Series E Portfolio Series E Portfolio BATEX Before you invest, you may want to review the Fund s prospectus, which contains more

July 28, 2017 SUMMARY PROSPECTUS BlackRock Allocation Target Shares BATS: Series E Portfolio Series E Portfolio BATEX Before you invest, you may want to review the Fund s prospectus, which contains more

The road to reform. Helping commercial end users of OTC derivatives comply with Dodd-Frank s Title VII

The road to reform Helping commercial end users of OTC derivatives comply with Dodd-Frank s Title VII Wide-ranging impact A survey conducted by the International Swaps & Derivatives Association (ISDA)

The road to reform Helping commercial end users of OTC derivatives comply with Dodd-Frank s Title VII Wide-ranging impact A survey conducted by the International Swaps & Derivatives Association (ISDA)

** Department of Accounting and Finance Faculty of Business and Economics PO Box 11E Monash University Victoria 3800 Australia

CORPORATE USAGE OF FINANCIAL DERIVATIVES AND INFORMATION ASYMMETRY Hoa Nguyen*, Robert Faff** and Alan Hodgson*** * School of Accounting, Economics and Finance Faculty of Business and Law Deakin University

CORPORATE USAGE OF FINANCIAL DERIVATIVES AND INFORMATION ASYMMETRY Hoa Nguyen*, Robert Faff** and Alan Hodgson*** * School of Accounting, Economics and Finance Faculty of Business and Law Deakin University

HOW DOES HEDGING AFFECT FIRM VALUE EVIDENCE FROM THE U.S. AIRLINE INDUSTRY. Mengdong He. A Thesis

HOW DOES HEDGING AFFECT FIRM VALUE EVIDENCE FROM THE U.S. AIRLINE INDUSTRY Mengdong He A Thesis In The John Molson School of Business Presented in Partial Fulfillment of the Requirements for the Degree

HOW DOES HEDGING AFFECT FIRM VALUE EVIDENCE FROM THE U.S. AIRLINE INDUSTRY Mengdong He A Thesis In The John Molson School of Business Presented in Partial Fulfillment of the Requirements for the Degree

Fixed-Income Analysis. Assignment 5

FIN 684 Professor Robert B.H. Hauswald Fixed-Income Analysis Kogod School of Business, AU Assignment 5 Please be reminded that you are expected to use contemporary computer software to solve the following

FIN 684 Professor Robert B.H. Hauswald Fixed-Income Analysis Kogod School of Business, AU Assignment 5 Please be reminded that you are expected to use contemporary computer software to solve the following

Glossary of Swap Terminology

Glossary of Swap Terminology Arbitrage: The opportunity to exploit price differentials on tv~otherwise identical sets of cash flows. In arbitrage-free financial markets, any two transactions with the same

Glossary of Swap Terminology Arbitrage: The opportunity to exploit price differentials on tv~otherwise identical sets of cash flows. In arbitrage-free financial markets, any two transactions with the same

OTC Derivatives The new cost of trading

OTC Derivatives The new cost of trading Contents Executive summary 1 Data sources and methodology 3 Costs for OTC derivative transactions that will need to be centrally cleared 5 Costs for OTC derivative

OTC Derivatives The new cost of trading Contents Executive summary 1 Data sources and methodology 3 Costs for OTC derivative transactions that will need to be centrally cleared 5 Costs for OTC derivative

Trade Repositories and their role in the financial marketplace

Trade Repositories and their role in the financial marketplace Manish Kumar Singh Susan Thomas Indira Gandhi Institute of Development Research March 2011 Contents 1 Background 1 2 What is a trade repository?

Trade Repositories and their role in the financial marketplace Manish Kumar Singh Susan Thomas Indira Gandhi Institute of Development Research March 2011 Contents 1 Background 1 2 What is a trade repository?

Financing Risk & Reinsurance

JOHN A. MAJOR, GARY G. VENTER 1 Guy Carpenter & Co., Inc. Two World Trade Center New York, NY 10048 (212) 323-1605 john.major@guycarp.com Financing Risk & Reinsurance WHY TRANSFER RISK? Ever since Modigliani

JOHN A. MAJOR, GARY G. VENTER 1 Guy Carpenter & Co., Inc. Two World Trade Center New York, NY 10048 (212) 323-1605 john.major@guycarp.com Financing Risk & Reinsurance WHY TRANSFER RISK? Ever since Modigliani

2017 DFAST Mid-Cycle Stress Test Disclosure Citi Severely Adverse Scenario

Citi 2017 2017 DFAST Mid-Cycle Stress Test Disclosure Citi Severely Adverse Scenario October 27, 2017 2017 Mid-Cycle Stress Test Overview Under the stress testing requirements of the Dodd-Frank Wall Street

Citi 2017 2017 DFAST Mid-Cycle Stress Test Disclosure Citi Severely Adverse Scenario October 27, 2017 2017 Mid-Cycle Stress Test Overview Under the stress testing requirements of the Dodd-Frank Wall Street

An insight into the derivatives trading of firms in the euro area

Nicola Benatti Francesco Napolitano DG-Statistics, European Central Bank An insight into the derivatives trading of firms in the euro area 9 th IFC Conference on Are post-crisis statistical initiatives

Nicola Benatti Francesco Napolitano DG-Statistics, European Central Bank An insight into the derivatives trading of firms in the euro area 9 th IFC Conference on Are post-crisis statistical initiatives

Potential Impact to Foreign Exchange Risk Management - Dodd-Frank Bill!

Potential Impact to Foreign Exchange Risk Management - Dodd-Frank Bill! April 7, 2011 Presented by: Mary Ann Dowling, Principal 2011 Treasury Strategies, Inc. All rights reserved. Dodd-Frank Act Passed

Potential Impact to Foreign Exchange Risk Management - Dodd-Frank Bill! April 7, 2011 Presented by: Mary Ann Dowling, Principal 2011 Treasury Strategies, Inc. All rights reserved. Dodd-Frank Act Passed

Derivative Instruments and Their Use For Hedging by U.S. Non-Financial Firms: A Review of Theories and Empirical Evidence

Journal of Applied Business and Economics Derivative Instruments and Their Use For Hedging by U.S. Non-Financial Firms: A Review of Theories and Empirical Evidence Hong V. Nguyen University of Scranton

Journal of Applied Business and Economics Derivative Instruments and Their Use For Hedging by U.S. Non-Financial Firms: A Review of Theories and Empirical Evidence Hong V. Nguyen University of Scranton

ON THE DETERMINANTS OF FOREIGN EXCHANGE DERIVATIVE USAGE BY LARGE INDIAN FIRMS

IJEBR : Vol. 6, No. 1, June 2016 ON THE DETERMINANTS OF FOREIGN EXCHANGE DERIVATIVE USAGE BY LARGE INDIAN FIRMS B. Charumathi Department of Management Studies, School of Management, Pondicherry University,

IJEBR : Vol. 6, No. 1, June 2016 ON THE DETERMINANTS OF FOREIGN EXCHANGE DERIVATIVE USAGE BY LARGE INDIAN FIRMS B. Charumathi Department of Management Studies, School of Management, Pondicherry University,

11 th July Summary views

Record Currency Management Limited response to European Supervisory Authorities Consultation Paper Draft regulatory technical standards on risk-mitigation techniques for OTC-derivative contracts not cleared

Record Currency Management Limited response to European Supervisory Authorities Consultation Paper Draft regulatory technical standards on risk-mitigation techniques for OTC-derivative contracts not cleared

Collateralized Banking

Collateralized Banking A Post-Crisis Reality Dr. Matthias Degen Senior Manager, KPMG AG ETH Risk Day 2014 Zurich, 12 September 2014 Definition Collateralized Banking Totality of aspects and processes relating

Collateralized Banking A Post-Crisis Reality Dr. Matthias Degen Senior Manager, KPMG AG ETH Risk Day 2014 Zurich, 12 September 2014 Definition Collateralized Banking Totality of aspects and processes relating

REGIS-TR the European Trade Repository for Derivatives. 10./11. May 2012 Clearstream CEE Conference

the European Trade Repository for Derivatives 10./11. Clearstream CEE Conference Agenda 1. Trade Repository Offering 2. Regulation in the making Status Europe 3. Regulation driving structural changes in

the European Trade Repository for Derivatives 10./11. Clearstream CEE Conference Agenda 1. Trade Repository Offering 2. Regulation in the making Status Europe 3. Regulation driving structural changes in

Counterparty Credit Risk

Counterparty Credit Risk The New Challenge for Global Financial Markets Jon Gregory ) WILEY A John Wiley and Sons, Ltd, Publication Acknowledgements List of Spreadsheets List of Abbreviations Introduction

Counterparty Credit Risk The New Challenge for Global Financial Markets Jon Gregory ) WILEY A John Wiley and Sons, Ltd, Publication Acknowledgements List of Spreadsheets List of Abbreviations Introduction

Increasing value by derivative hedging

Increasing value by derivative hedging Research on relationship between firm value and derivative hedging in UK Master thesis for the department of Finance and Accounting Faculty of Management and Governance

Increasing value by derivative hedging Research on relationship between firm value and derivative hedging in UK Master thesis for the department of Finance and Accounting Faculty of Management and Governance

Note 8: Derivative Instruments

Note 8: Derivative Instruments Derivative instruments are financial contracts that derive their value from underlying changes in interest rates, foreign exchange rates or other financial or commodity prices

Note 8: Derivative Instruments Derivative instruments are financial contracts that derive their value from underlying changes in interest rates, foreign exchange rates or other financial or commodity prices

The Theory and Practice of Corporate Risk Management: Evidence from the Field

The Theory and Practice of Corporate Risk Management: Evidence from the Field Erasmo Giambona, John R. Graham, Campbell R. Harvey, and Gordon M. Bodnar We survey more than 1,100 risk managers from around

The Theory and Practice of Corporate Risk Management: Evidence from the Field Erasmo Giambona, John R. Graham, Campbell R. Harvey, and Gordon M. Bodnar We survey more than 1,100 risk managers from around

Shorts and Derivatives in Portfolio Statistics

Shorts and Derivatives in Portfolio Statistics Morningstar Methodology Paper April 17, 2007 2007 Morningstar, Inc. All rights reserved. The information in this document is the property of Morningstar,

Shorts and Derivatives in Portfolio Statistics Morningstar Methodology Paper April 17, 2007 2007 Morningstar, Inc. All rights reserved. The information in this document is the property of Morningstar,

Introduction to Derivative Instruments Part 2

Link n Learn Introduction to Derivative Instruments Part 2 Leading Business Advisors Contacts Elaine Canty - Manager Financial Advisory Ireland Email: ecanty@deloitte.ie Tel: 00 353 417 2991 Fabian De

Link n Learn Introduction to Derivative Instruments Part 2 Leading Business Advisors Contacts Elaine Canty - Manager Financial Advisory Ireland Email: ecanty@deloitte.ie Tel: 00 353 417 2991 Fabian De

Information Conveyed in Hiring Announcements of Senior Executives Overseeing Enterprise-Wide Risk Management Processes

Information Conveyed in Hiring Announcements of Senior Executives Overseeing Enterprise-Wide Risk Management Processes Mark Beasley Professor of Accounting and ERM Initiative Director Don Pagach Professor

Information Conveyed in Hiring Announcements of Senior Executives Overseeing Enterprise-Wide Risk Management Processes Mark Beasley Professor of Accounting and ERM Initiative Director Don Pagach Professor

Dreyfus/Standish Global Fixed Income Fund

Dreyfus/Standish Global Fixed Income Fund Summary Prospectus May 1, 2018 Class A C I Y Ticker DHGAX DHGCX SDGIX DSDYX Before you invest, you may want to review the fund's prospectus, which contains more

Dreyfus/Standish Global Fixed Income Fund Summary Prospectus May 1, 2018 Class A C I Y Ticker DHGAX DHGCX SDGIX DSDYX Before you invest, you may want to review the fund's prospectus, which contains more

Dynamic Corporate Risk Management: Motivations and Real Implications

Dynamic Corporate Risk Management: Motivations and Real Implications Georges Dionne Jean-Pierre Gueyie Mohamed Mnasri July 2016 Georges Dionne 1,2,*, Jean-Pierre Gueyie 3, Mohamed Mnasri 2 1 Interuniversity

Dynamic Corporate Risk Management: Motivations and Real Implications Georges Dionne Jean-Pierre Gueyie Mohamed Mnasri July 2016 Georges Dionne 1,2,*, Jean-Pierre Gueyie 3, Mohamed Mnasri 2 1 Interuniversity

Traded Risk & Regulation

DRAFT Traded Risk & Regulation University of Essex Expert Lecture 14 March 2014 Dr Paula Haynes Managing Partner Traded Risk Associates 2014 www.tradedrisk.com Traded Risk Associates Ltd Contents Introduction

DRAFT Traded Risk & Regulation University of Essex Expert Lecture 14 March 2014 Dr Paula Haynes Managing Partner Traded Risk Associates 2014 www.tradedrisk.com Traded Risk Associates Ltd Contents Introduction

THE VALUE OF HEDGING THROUGH CORPORATE GOVERNANCE: A LITERATURE REVIEW AND DIRECTIONS FOR FUTURE RESEARCH

School of Economics and Management TECNICAl. UNIVERSITY OF LISBON THE VALUE OF HEDGING THROUGH CORPORATE GOVERNANCE: A LITERATURE REVIEW AND DIRECTIONS FOR FUTURE RESEARCH Maria Jofio Jorge School of Technology

School of Economics and Management TECNICAl. UNIVERSITY OF LISBON THE VALUE OF HEDGING THROUGH CORPORATE GOVERNANCE: A LITERATURE REVIEW AND DIRECTIONS FOR FUTURE RESEARCH Maria Jofio Jorge School of Technology

Liability aware investing

August 2017 Liability aware investing The benefits of integrating your liability hedging and growth portfolios This document is for investment professionals only and should not be distributed to or relied

August 2017 Liability aware investing The benefits of integrating your liability hedging and growth portfolios This document is for investment professionals only and should not be distributed to or relied

Journal of Financial and Strategic Decisions Volume 13 Number 2 Summer 2000 MANAGERIAL COMPENSATION AND OPTIMAL CORPORATE HEDGING

Journal of Financial and Strategic Decisions Volume 13 Number 2 Summer 2000 MANAGERIAL COMPENSATION AND OPTIMAL CORPORATE HEDGING Steven B. Perfect *, Kenneth W. Wiles and Shawn D. Howton ** Abstract This

Journal of Financial and Strategic Decisions Volume 13 Number 2 Summer 2000 MANAGERIAL COMPENSATION AND OPTIMAL CORPORATE HEDGING Steven B. Perfect *, Kenneth W. Wiles and Shawn D. Howton ** Abstract This

EMIR - What should Hedge Funds be doing?

www.pwc.co.uk EMIR - What should Hedge Funds be doing? Sept 2009 2008 credit crisis 2008: OTC market collapse Weaknesses revealed in crisis Collapse of Bear Stearns and Lehmans Heightened levels of counterparty

www.pwc.co.uk EMIR - What should Hedge Funds be doing? Sept 2009 2008 credit crisis 2008: OTC market collapse Weaknesses revealed in crisis Collapse of Bear Stearns and Lehmans Heightened levels of counterparty

Financial Derivatives

Derivatives in ALM Financial Derivatives Swaps Hedge Contracts Forward Rate Agreements Futures Options Caps, Floors and Collars Swaps Agreement between two counterparties to exchange the cash flows. Cash

Derivatives in ALM Financial Derivatives Swaps Hedge Contracts Forward Rate Agreements Futures Options Caps, Floors and Collars Swaps Agreement between two counterparties to exchange the cash flows. Cash

Frank J. Fabozzi, CFA

SEVENTH EDITION Frank J. Fabozzi, CFA Professor in the Practice of Finance Yale School of Management Boston San Francisco New York London Toronto Sydney Tokyo Singapore Madrid Mexico City Munich Paris

SEVENTH EDITION Frank J. Fabozzi, CFA Professor in the Practice of Finance Yale School of Management Boston San Francisco New York London Toronto Sydney Tokyo Singapore Madrid Mexico City Munich Paris

Federated Institutional High Yield Bond Fund

Prospectus December 31, 2017 Share Class Ticker Institutional FIHBX R6 FIHLX Federated Institutional High Yield Bond Fund A Portfolio of Federated Institutional Trust A mutual fund seeking high current

Prospectus December 31, 2017 Share Class Ticker Institutional FIHBX R6 FIHLX Federated Institutional High Yield Bond Fund A Portfolio of Federated Institutional Trust A mutual fund seeking high current

A Firm-Specific Analysis of Taiwan Foreign Exchange Rate Exposure: A Panel Data Approach

A Firm-Specific Analysis of Taiwan Foreign Exchange Rate Exposure: A Panel Data Approach R. F. Franck Varga 1 Department of Global Political Economy Tamkang University, Lanyang Campus, 180 Linwei Road,Jiaoshi,

A Firm-Specific Analysis of Taiwan Foreign Exchange Rate Exposure: A Panel Data Approach R. F. Franck Varga 1 Department of Global Political Economy Tamkang University, Lanyang Campus, 180 Linwei Road,Jiaoshi,

Revised trade reporting requirements under EMIR June 2017

Revised trade reporting requirements under EMIR June 2017 Background Article 9 of the European Market Infrastructure Regulation (EMIR) requires counterparties to report details of any derivative contract

Revised trade reporting requirements under EMIR June 2017 Background Article 9 of the European Market Infrastructure Regulation (EMIR) requires counterparties to report details of any derivative contract

The Changing Landscape for Derivatives. John Hull Joseph L. Rotman School of Management University of Toronto.

The Changing Landscape for Derivatives John Hull Joseph L. Rotman School of Management University of Toronto hull@rotman.utoronto.ca April 2014 ABSTRACT This paper describes the changes taking place in

The Changing Landscape for Derivatives John Hull Joseph L. Rotman School of Management University of Toronto hull@rotman.utoronto.ca April 2014 ABSTRACT This paper describes the changes taking place in

The Use of Options in Corporate Risk Management

MPRA Munich Personal RePEc Archive The Use of Options in Corporate Risk Management Söhnke M. Bartram Lancaster University 7. January 2004 Online at http://mpra.ub.uni-muenchen.de/6663/ MPRA Paper No. 6663,

MPRA Munich Personal RePEc Archive The Use of Options in Corporate Risk Management Söhnke M. Bartram Lancaster University 7. January 2004 Online at http://mpra.ub.uni-muenchen.de/6663/ MPRA Paper No. 6663,

Changes in US OTC markets since the crisis

Changes in US OTC markets since the crisis Nina Boyarchenko Federal Reserve Bank of New York The views expressed herein are the author s and are not representative of the views of the Federal Reserve Bank

Changes in US OTC markets since the crisis Nina Boyarchenko Federal Reserve Bank of New York The views expressed herein are the author s and are not representative of the views of the Federal Reserve Bank

Demystifying Dodd Frank s Impact on Corporate Hedging

Demystifying Dodd Frank s Impact on Corporate Hedging Overview Section 1: Dodd Frank on Swaps and the End User Section 2: How Companies Can prepare Section 3: What Tools are Available? 2 Section 1: End

Demystifying Dodd Frank s Impact on Corporate Hedging Overview Section 1: Dodd Frank on Swaps and the End User Section 2: How Companies Can prepare Section 3: What Tools are Available? 2 Section 1: End

THE DODD-FRANK ACT & DERIVATIVES MARKET

THE DODD-FRANK ACT & DERIVATIVES MARKET By Khader Shaik Author of Managing Derivatives Contracts This presentation can be used as a supplement to Chapter 9 - The Dodd-Frank Act Agenda Introduction Major

THE DODD-FRANK ACT & DERIVATIVES MARKET By Khader Shaik Author of Managing Derivatives Contracts This presentation can be used as a supplement to Chapter 9 - The Dodd-Frank Act Agenda Introduction Major

Basel Committee on Banking Supervision & Board of the International Organisation of Securities Commissions

1 Basel Committee on Banking Supervision & Board of the International Organisation of Securities Commissions Margin requirements for non-centrally cleared derivatives Response provided by: Standard Life

1 Basel Committee on Banking Supervision & Board of the International Organisation of Securities Commissions Margin requirements for non-centrally cleared derivatives Response provided by: Standard Life

Point De Vue: Operational challenges faced by asset managers to price OTC derivatives Laurent Thuilier, SGSS. Avec le soutien de

Point De Vue: Operational challenges faced by asset managers to price OTC derivatives 2012 01 Laurent Thuilier, SGSS Avec le soutien de JJ Mois Année Operational challenges faced by asset managers to price

Point De Vue: Operational challenges faced by asset managers to price OTC derivatives 2012 01 Laurent Thuilier, SGSS Avec le soutien de JJ Mois Année Operational challenges faced by asset managers to price