Mixed Bag in 2Q, Array Growth Accelerates

|

|

|

- Everett Hodge

- 5 years ago

- Views:

Transcription

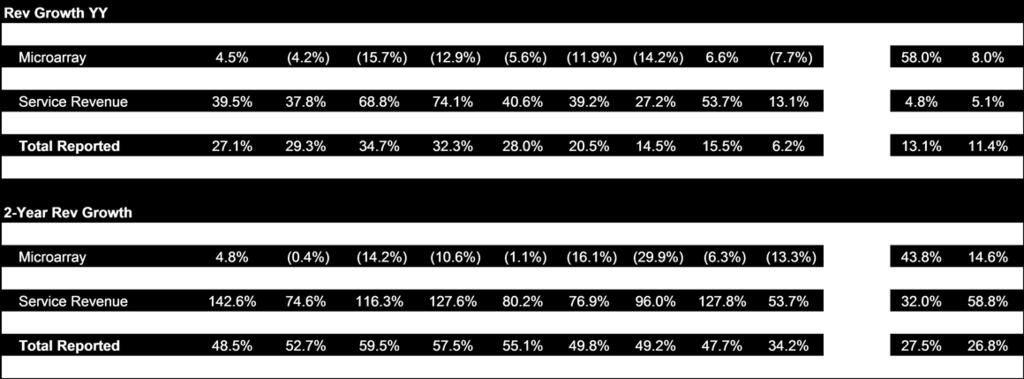

1 July MONTH 27, 2016 DD, YYYY 07:00 HH:MM AM GMT AM/PM GMT Illumina Inc. Mixed Bag in 2Q, Array Growth Accelerates Stock Rating Underweight Industry View In-Line Price Target $ Sequencing growth was again <10% in 2Q, and commentary on Arrays suggests consensus sequencing expectations were likely optimistic. PT to $115 from $110 on stronger Array growth. Clarity on the drivers of the guidance suggests sequencing growth slower than some expected. Our cautious view on ILMN ( Underweight on End Market Pressures (05 Jul) ) was rooted in concerns about the timelines for clinical reacceleration and growth for the HiSeq franchise, and the 2Q16 result was a mixed bag in terms of updates. Oncology growth +45% was positive, driven by a subset of large customers, that was at odds with our diligence. Sequencing sales growth was however below our forecast (8% vs. our 10%) in spite of the Oncology result. ILMN s new disclosure that the Array growth embedded in the (unchanged) 12% total revenue growth guidance is >10% subsequently suggests that sequencing growth for the full year is expected to be in the low double digits, in line with our thinking but likely below investor thinking, as Array growth was historically slower. Net-net, a perception of slower sequencing growth and another quarter of sequencing instrument declines over 20% likely offset the impact of better Oncology growth and keep ILMN sentiment more balanced than the beat in the quarter might have implied. Instrument trends leave the debate unresolved. HiSeq franchise shipments were stable qr/qr and instrument revenues in total for sequencing were down over 20%. Guidance for 2H16 calls for a reacceleration of sequential growth, which would be at odds with our diligence. Considering the book to bill was ~1 in the quarter and 2Q16 results did not demonstrate a reacceleration in the instrument segment, we believe there remains uncertainty in the outlook. Sequential growth in the instrument franchise is a management focus, called out by new CEO DeSouza, as the guidance implies sequential growth in 2H16 accelerates substantially vs 1H16 and instrument revenues are a key driver. Decomposing the P&L beat. The 16% EPS beat to MSe in 2Q16 primarily reflects lower SBC expenses and new cost control initiatives driving EBIT margins >200bps ahead of our expectations at 32.6% (MSe forecasts at 30.3% see Exhibit 7 ). The 2Q16 performance translates to a 4% increase in EPS to guidance ($3.53) and the company assumes no changes with regards to GRAIL/Helix impact. Incorporating both the 2Q16 outperformance and our updated revenues outlook of +11% in '16E to account for >10% Array growth in '16E drives our updated EPS estimate of $3.50, +7% from previous estimates. For more details on estimate changes, see Exhibit 6. MORGAN STANLEY & CO. LLC Steve Beuchaw EQUITY ANALYST Steve.Beuchaw@morganstanley.com Liza C Garcia RESEARCH ASSOCIATE Liza.Garcia@morganstanley.com Illumina Inc. ( ILMN.O, ILMN US ) Life Science Tools & Diagnostics / United States of America Stock Rating Underweight Industry View In-Line Price target $ Shr price, close (Jul 26, 2016) $ Mkt cap, curr (mm) $22, Week Range $ Fiscal Year Ending 12/15 12/16e 12/17e 12/18e ModelWare EPS ($) Prior ModelWare EPS ($) P/E Consensus EPS ($) Div yld (%) Unless otherwise noted, all metrics are based on Morgan Stanley ModelWare framework = Consensus data is provided by Thomson Reuters Estimates e = Morgan Stanley Research estimates QUARTERLY MODELWARE EPS ($) 2016e 2016e 2017e 2017e Quarter 2015 Prior Current Prior Current Q a Q a Q Q e = Morgan Stanley Research estimates, a = Actual Company reported data Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision. For analyst certification and other important disclosures, refer to the Disclosure Section, located at the end of this report. 1

2 Notable updates from the call. European traction is recovering more slowly, offsetting positive Asia trends. The China PMI is driving a majority of HiSeq X orders, but the US is expected to be a stronger driver over the balance of the year; total X customers are now 34, up by 3 qr/qr. ILMN has not budgeted for Brexit impacts in the guidance, any pressures thus far are limited and anecdotal. Throughput on NextSeq was strong and drove an increase to (pullthrough) guidance, with support from NIPT volumes. Japan is slowly improving off a low base. We continue to believe the stock is expensive estimate revisions drive our updated PT$115. Revenue growth in the low double digits, instrument revenue declines, and the steady deceleration of sequencing consumables remain at odds with the NTM P/E >40x. We continue to believe the markets are simply not growing fast enough to support the multiple or consensus expectations for 17 growth acceleration. Our updated PT$115 reflects our ~150bps upward revision to '16E revenue estimates accounting for Array >10% growth expectations ( Exhibit 15 ). 2

3 Risk Reward Growth unlikely to satisfy the multiple $ $ $ (+27%) $ (-23%) $50.00 (-67%) 0 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Price Target (Jul-17) Historical Stock Performance WARNINGDONOTEDIT_RRS4RL~ILMN.O~ Current Stock Price Source: Thomson Reuters, Morgan Stanley Research. Bull $190 6x CY20E bull case revenue, Discounted at 9% NGS for cancer and prenatal becomes the standard of care in the next 36 months. Market penetration follows an adoption curve more like a new drug than a new diagnostic test, as regulatory approvals and guideline inclusion drive clinicians to adopt new approaches to cancer and prenatal care. Guidelines are revised in to support cancer and prenatal testing uptake. Reimbursement for clinical applications improves as tests are standardized, guideline revisions are supportive, and Medicare coding is refined. Research market growth improves, and ILMN successfully penetrates smaller labs. Base $115 25x CY20E base case EPS, Discounted at 9% Uptake supports growth at >10% topline, but the inflection in oncology remains a event. Uptake of NGS for clinical applications remaining concentrated in academic and not community hospitals through 2017, as refinements for ease of use with new software and sample preparation systems are ongoing. Regulatory approvals and guideline inclusion are anticipated but do not emerge in Reimbursement improves but administration remains challenging for new providers of clinical testing through Research market growth remains limited and competition emerges through the medium term. Bear $50 14x CY20E bear case EPS, Discounted at 9% Growth moderates ahead of broader clinical adoption. Placements of HiSeq X systems slow in as demand proves to be limited outside of major genome centers. Uptake of NGS for clinical applications remains concentrated in academic and not community centers through 2019, as refinements for ease of use with new software and sample preparation systems are ongoing. Reimbursement for clinical applications remains limited in the private pay group despite progress on Medicare codes and rates. Regulatory approvals and guideline inclusion for cancer and prenatal applications are uncertain, as calls for longer-term outcomes data become more pronounced. Research markets remain roughly flat, as government budgets are pressured. Interest in competitive platforms grows over the medium term threatening ILMN dominance in the space. Investment Thesis Illumina is the dominant player in nextgeneration sequencing (NGS) with an applicable TAM opportunity >$20bn We expect broader application of NGS as a diagnostic aid for cancer and prenatal applications over the longer term, but traction to be measured ahead of updates to clinical guidelines and widespread reimbursement emerging in '17-'19 Core markets likely remain solid, but are more mature with moderate growth profiles Key Value Drivers Physician group support for clinical guideline evolution and broader adoption of NGS in clinical settings, look for publications from expert consortia and clinical trials FDA and insurer support, including regulatory approvals of standardized tests and positive reimbursement policies Expanding interest in research to tailor genomically guided therapies Rapid innovation on sample preparation and software to support adoption by users in smaller clinics and hospitals Potential Catalysts Clinical trial readouts in do not support broader human sequencing for oncology applications Private insurer reimbursement decisions limit NGS diagnostics for oncology Increasing trend of out sourcing sequencing by labs limits instrument demand Risks to Achieving Price Target Clinical trials ahead of our timelines support broad human sequencing driving updated clinical guidelines in support of NGS Insurer reimbursement decisions support broad use of NGS for oncology applications Reacceleration of research channel Meaningful competition does not emerge over the medium term 3

4 Supplementary Exhibits Exhibit 1: Quarterly revenue analysis Source: Company Data, Morgan Stanley Research Exhibit 2: Organic growth trends Source: Company Data, Morgan Stanley Research 4

5 Exhibit 3: Instrument Unit Shipments Source: Company Data, Morgan Stanley Research Exhibit 4: EBIT margin trends Source: Company Data, Morgan Stanley Research 5

6 Exhibit 5: Guidance tracker Exhibit 6: Changes to forecasts Source: Company Data, Morgan Stanley Research estimates Source: Company Data, Morgan Stanley Research estimates 6

7 Exhibit 7: Results variance Source: Company Data, Morgan Stanley Research estimates 7

8 Exhibit 8: Illumina consumable growth Exhibit 9: Illumina instrument growth Source: Company Data and Morgan Stanley Research Source: Company Data and Morgan Stanley Research 8

9 Valuation and Risks Exhibit 10: Valuation on EV/Sales elevated at 90th %ile relative to our fast growth peer group Exhibit 11: Valuation on P/E is just below the 75th %ile relative to our fast growth peer group Source: Thomson Reuters and Morgan Stanley Research Exhibit 12: Relative NTM P/E vs LST Index Source: Thomson Reuters and Morgan Stanley Research Exhibit 13: Relative NTM P/E vs S&P 500 Source: Thomson Reuters and Morgan Stanley Research Source: Thomson Reuters and Morgan Stanley Research Exhibit 14: 3 yrs Indexed Price Performance Source: Thomson Reuters and Morgan Stanley Research 9

10 Exhibit 15: Sum-of-the-parts valuation Revenue Based Valuation Summary $mn ex per- 2016e Hypothetical '16E-'20E Sales 2020E '17E Value Value share items Sales 2020 Sales CAGR Mult. WACC per Share Base Business 1,669 2, % 4.0x $ 8,914 $ 6,921 $ Population Seq % 4.0x $ 2,096 $ 1,590 $ Clinical Oncology % 7.0x $ 5,032 $ 3,817 $ NIPT % 7.0x $ 3,953 $ 2,999 $ Total 2,453 4, % 5.0x $ 19,994 $ 15,326 $ Share Price Including Net Cash ($) $ 21,503 $ 16,311 $ Source: Company data, Morgan Stanley Research Valuation methodology/risk section ILMN.O Our $115 price target is based on our '20E revenue build, yielding a composite 5x EV/ '20E revenue multiple from the company's various business units and respective growth outlook for each piece of the business, then discounting back to '17E to reach our PT using a 9% discount rate. Our view is based on uptake of NGS for clinical applications remaining concentrated in academic and not community hospitals through 2017, as refinements for ease of use with new software and sample preparation systems are ongoing. Regulatory approvals and guideline inclusion are anticipated but do not emerge in Reimbursement improves but administration remains challenging for new providers of clinical testing through Research market growth remains limited and competition emerges through the medium term. Key value drivers include 1) Physician group support for clinical guideline evolution and broader adoption of NGS systems, including publications from expert consortia and clinical trial groups; 2) FDA and insurer support, including regulatory approvals of standardized tests and positive reimbursement policies; 3) Expanding interest in research to support and tailor genomically guided therapies; and 4) Rapid innovation on sample preparation and software to support adoption by users in smaller clinics and hospitals. Risks include clinical trial and guideline timelines, hospital and government budget constraints, and new competition. 10

11 Exhibit 16: ILMN Income Statement Source: Company data, Morgan Stanley Research estimates 11

12 Exhibit 17: ILMN Revenue Build Source: Company data, Morgan Stanley Research estimates 12

13 Disclosure Section The information and opinions in Morgan Stanley Research were prepared by Morgan Stanley & Co. LLC, and/or Morgan Stanley C.T.V.M. S.A., and/or Morgan Stanley Mexico, Casa de Bolsa, S.A. de C.V., and/or Morgan Stanley Canada Limited. As used in this disclosure section, "Morgan Stanley" includes Morgan Stanley & Co. LLC, Morgan Stanley C.T.V.M. S.A., Morgan Stanley Mexico, Casa de Bolsa, S.A. de C.V., Morgan Stanley Canada Limited and their affiliates as necessary. For important disclosures, stock price charts and equity rating histories regarding companies that are the subject of this report, please see the Morgan Stanley Research Disclosure Website at or contact your investment representative or Morgan Stanley Research at 1585 Broadway, (Attention: Research Management), New York, NY, USA. For valuation methodology and risks associated with any recommendation, rating or price target referenced in this research report, please contact the Client Support Team as follows: US/Canada ; Hong Kong ; Latin America (U.S.); London +44 (0) ; Singapore ; Sydney +61 (0) ; Tokyo +81 (0) Alternatively you may contact your investment representative or Morgan Stanley Research at 1585 Broadway, (Attention: Research Management), New York, NY USA. Analyst Certification The following analysts hereby certify that their views about the companies and their securities discussed in this report are accurately expressed and that they have not received and will not receive direct or indirect compensation in exchange for expressing specific recommendations or views in this report: Steve Beuchaw. Unless otherwise stated, the individuals listed on the cover page of this report are research analysts. Global Research Conflict Management Policy Morgan Stanley Research has been published in accordance with our conflict management policy, which is available at Important US Regulatory Disclosures on Subject Companies As of June 30, 2016, Morgan Stanley beneficially owned 1% or more of a class of common equity securities of the following companies covered in Morgan Stanley Research: Bruker Corp, Illumina Inc., Myriad Genetics Inc., NanoString Technologies Inc, Qiagen NV, Thermo Fisher Scientific Inc.. Within the last 12 months, Morgan Stanley managed or co-managed a public offering (or 144A offering) of securities of Thermo Fisher Scientific Inc.. Within the last 12 months, Morgan Stanley has received compensation for investment banking services from Bruker Corp, Natera Inc, Thermo Fisher Scientific Inc.. In the next 3 months, Morgan Stanley expects to receive or intends to seek compensation for investment banking services from Agilent Technologies, Inc., Bruker Corp, Cepheid, Illumina Inc., Mettler-Toledo International Inc., Myriad Genetics Inc., NanoString Technologies Inc, Natera Inc, PerkinElmer Inc., T2 Biosystems Inc, Thermo Fisher Scientific Inc., Waters Corp.. Within the last 12 months, Morgan Stanley has received compensation for products and services other than investment banking services from Agilent Technologies, Inc., Illumina Inc., Qiagen NV, Thermo Fisher Scientific Inc.. Within the last 12 months, Morgan Stanley has provided or is providing investment banking services to, or has an investment banking client relationship with, the following company: Agilent Technologies, Inc., Bruker Corp, Cepheid, Illumina Inc., Mettler-Toledo International Inc., Myriad Genetics Inc., NanoString Technologies Inc, Natera Inc, PerkinElmer Inc., T2 Biosystems Inc, Thermo Fisher Scientific Inc., Waters Corp.. Within the last 12 months, Morgan Stanley has either provided or is providing non-investment banking, securities-related services to and/or in the past has entered into an agreement to provide services or has a client relationship with the following company: Agilent Technologies, Inc., Cepheid, Illumina Inc., Myriad Genetics Inc., Qiagen NV, Thermo Fisher Scientific Inc.. Morgan Stanley & Co. LLC makes a market in the securities of Agilent Technologies, Inc., Bruker Corp, Cepheid, Illumina Inc., Mettler-Toledo International Inc., Myriad Genetics Inc., NanoString Technologies Inc, Natera Inc, PerkinElmer Inc., Qiagen NV, T2 Biosystems Inc, Thermo Fisher Scientific Inc., Waters Corp.. The equity research analysts or strategists principally responsible for the preparation of Morgan Stanley Research have received compensation based upon various factors, including quality of research, investor client feedback, stock picking, competitive factors, firm revenues and overall investment banking revenues. Equity Research analysts' or strategists' compensation is not linked to investment banking or capital markets transactions performed by Morgan Stanley or the profitability or revenues of particular trading desks. Morgan Stanley and its affiliates do business that relates to companies/instruments covered in Morgan Stanley Research, including market making, providing liquidity, fund management, commercial banking, extension of credit, investment services and investment banking. Morgan Stanley sells to and buys from customers the securities/instruments of companies covered in Morgan Stanley Research on a principal basis. Morgan Stanley may have a position in the debt of the Company or instruments discussed in this report. Morgan Stanley trades or may trade as principal in the debt securities (or in related derivatives) that are the subject of the debt research report. Certain disclosures listed above are also for compliance with applicable regulations in non-us jurisdictions. STOCK RATINGS Morgan Stanley uses a relative rating system using terms such as Overweight, Equal-weight, Not-Rated or Underweight (see definitions below). Morgan Stanley does not assign ratings of Buy, Hold or Sell to the stocks we cover. Overweight, Equal-weight, Not-Rated and Underweight are not the equivalent of buy, hold and sell. Investors should carefully read the definitions of all ratings used in Morgan Stanley Research. In addition, since Morgan Stanley Research contains more complete information concerning the analyst's views, investors should carefully read Morgan Stanley Research, in its entirety, and not infer the contents from the rating alone. In any case, ratings (or research) should not be used or relied upon as investment advice. An investor's decision to buy or sell a stock should depend on individual circumstances (such as the investor's existing holdings) and other considerations. Global Stock Ratings Distribution (as of June 30, 2016) The Stock Ratings described below apply to Morgan Stanley's Fundamental Equity Research and do not apply to Debt Research produced by the Firm. For disclosure purposes only (in accordance with NASD and NYSE requirements), we include the category headings of Buy, Hold, and Sell alongside our ratings of Overweight, Equal-weight, Not-Rated and Underweight. Morgan Stanley does not assign ratings of Buy, Hold or Sell to the stocks we cover. Overweight, Equal-weight, Not-Rated and Underweight are not the equivalent of buy, hold, and sell but represent recommended relative weightings (see definitions below). To satisfy regulatory requirements, we correspond Overweight, our most positive stock rating, with a buy recommendation; we correspond Equal-weight and Not-Rated to hold and Underweight to sell recommendations, respectively. 13

14 STOCK RATING CATEGORY COVERAGE UNIVERSE INVESTMENT BANKING CLIENTS (IBC) OTHER MATERIAL INVESTMENT SERVICES CLIENTS (MISC) COUNT % OF TOTAL COUNT % OF TOTAL IBC % OF RATING CATEGORY COUNT % OF TOTAL OTHER MISC Overweight/Buy % % 24% % Equal-weight/Hold % % 24% % Not-Rated/Hold 78 2% 8 1% 10% 11 1% Underweight/Sell % 94 13% 15% % TOTAL 3, Data include common stock and ADRs currently assigned ratings. Investment Banking Clients are companies from whom Morgan Stanley received investment banking compensation in the last 12 months. Analyst Stock Ratings Overweight (O). The stock's total return is expected to exceed the average total return of the analyst's industry (or industry team's) coverage universe, on a risk-adjusted basis, over the next months. Equal-weight (E). The stock's total return is expected to be in line with the average total return of the analyst's industry (or industry team's) coverage universe, on a risk-adjusted basis, over the next months. Not-Rated (NR). Currently the analyst does not have adequate conviction about the stock's total return relative to the average total return of the analyst's industry (or industry team's) coverage universe, on a risk-adjusted basis, over the next months. Underweight (U). The stock's total return is expected to be below the average total return of the analyst's industry (or industry team's) coverage universe, on a risk-adjusted basis, over the next months. Unless otherwise specified, the time frame for price targets included in Morgan Stanley Research is 12 to 18 months. Analyst Industry Views Attractive (A): The analyst expects the performance of his or her industry coverage universe over the next months to be attractive vs. the relevant broad market benchmark, as indicated below. In-Line (I): The analyst expects the performance of his or her industry coverage universe over the next months to be in line with the relevant broad market benchmark, as indicated below. Cautious (C): The analyst views the performance of his or her industry coverage universe over the next months with caution vs. the relevant broad market benchmark, as indicated below. Benchmarks for each region are as follows: North America - S&P 500; Latin America - relevant MSCI country index or MSCI Latin America Index; Europe - MSCI Europe; Japan - TOPIX; Asia - relevant MSCI country index or MSCI sub-regional index or MSCI AC Asia Pacific ex Japan Index. Stock Price, Price Target and Rating History (See Rating Definitions) 14

15 Important Disclosures for Morgan Stanley Smith Barney LLC Customers Important disclosures regarding the relationship between the companies that are the subject of Morgan Stanley Research and Morgan Stanley Smith Barney LLC or Morgan Stanley or any of their affiliates, are available on the Morgan Stanley Wealth Management disclosure website at For Morgan Stanley specific disclosures, you may refer to Each Morgan Stanley Equity Research report is reviewed and approved on behalf of Morgan Stanley Smith Barney LLC. This review and approval is conducted by the same person who reviews the Equity Research report on behalf of Morgan Stanley. This could create a conflict of interest. Other Important Disclosures Morgan Stanley & Co. International PLC and its affiliates have a significant financial interest in the debt securities of Agilent Technologies, Inc., Thermo Fisher Scientific Inc.. Morgan Stanley Research policy is to update research reports as and when the Research Analyst and Research Management deem appropriate, based on developments with the issuer, the sector, or the market that may have a material impact on the research views or opinions stated therein. In addition, certain Research publications are intended to be updated on a regular periodic basis (weekly/monthly/quarterly/annual) and will ordinarily be updated with that frequency, unless the Research Analyst and Research Management determine that a different publication schedule is appropriate based on current conditions. Morgan Stanley is not acting as a municipal advisor and the opinions or views contained herein are not intended to be, and do not constitute, advice within the meaning of Section 975 of the Dodd-Frank Wall Street Reform and Consumer Protection Act. Morgan Stanley produces an equity research product called a "Tactical Idea." Views contained in a "Tactical Idea" on a particular stock may be contrary to the recommendations or views expressed in research on the same stock. This may be the result of differing time horizons, methodologies, market events, or other factors. For all research available on a particular stock, please contact your sales representative or go to Matrix at Morgan Stanley Research is provided to our clients through our proprietary research portal on Matrix and also distributed electronically by Morgan Stanley to clients. Certain, but not all, Morgan Stanley Research products are also made available to clients through third-party vendors or redistributed to clients through alternate electronic means as a convenience. For access to all available Morgan Stanley Research, please contact your sales representative or go to Matrix at Any access and/or use of Morgan Stanley Research is subject to Morgan Stanley's Terms of Use ( By accessing and/or using Morgan Stanley Research, you are indicating that you have read and agree to be bound by our Terms of Use ( In addition you consent to Morgan Stanley processing your personal data and using cookies in accordance with our Privacy Policy and our Global Cookies Policy ( including for the purposes of setting your preferences and to collect readership data so that we can deliver better and more personalized service and products to you. To find out more information about how Morgan Stanley processes personal data, how we use cookies and how to reject cookies see our Privacy Policy and our Global Cookies Policy ( If you do not agree to our Terms of Use and/or if you do not wish to provide your consent to Morgan Stanley processing your personal data or using cookies please do not access our research. Morgan Stanley Research does not provide individually tailored investment advice. Morgan Stanley Research has been prepared without regard to the circumstances and objectives of those who receive it. Morgan Stanley recommends that investors independently evaluate particular investments and strategies, and encourages investors to seek the advice of a financial adviser. The appropriateness of an investment or strategy will depend on an investor's 15

16 circumstances and objectives. The securities, instruments, or strategies discussed in Morgan Stanley Research may not be suitable for all investors, and certain investors may not be eligible to purchase or participate in some or all of them. Morgan Stanley Research is not an offer to buy or sell or the solicitation of an offer to buy or sell any security/instrument or to participate in any particular trading strategy. The value of and income from your investments may vary because of changes in interest rates, foreign exchange rates, default rates, prepayment rates, securities/instruments prices, market indexes, operational or financial conditions of companies or other factors. There may be time limitations on the exercise of options or other rights in securities/instruments transactions. Past performance is not necessarily a guide to future performance. Estimates of future performance are based on assumptions that may not be realized. If provided, and unless otherwise stated, the closing price on the cover page is that of the primary exchange for the subject company's securities/instruments. The fixed income research analysts, strategists or economists principally responsible for the preparation of Morgan Stanley Research have received compensation based upon various factors, including quality, accuracy and value of research, firm profitability or revenues (which include fixed income trading and capital markets profitability or revenues), client feedback and competitive factors. Fixed Income Research analysts', strategists' or economists' compensation is not linked to investment banking or capital markets transactions performed by Morgan Stanley or the profitability or revenues of particular trading desks. The "Important US Regulatory Disclosures on Subject Companies" section in Morgan Stanley Research lists all companies mentioned where Morgan Stanley owns 1% or more of a class of common equity securities of the companies. For all other companies mentioned in Morgan Stanley Research, Morgan Stanley may have an investment of less than 1% in securities/instruments or derivatives of securities/instruments of companies and may trade them in ways different from those discussed in Morgan Stanley Research. Employees of Morgan Stanley not involved in the preparation of Morgan Stanley Research may have investments in securities/instruments or derivatives of securities/instruments of companies mentioned and may trade them in ways different from those discussed in Morgan Stanley Research. Derivatives may be issued by Morgan Stanley or associated persons. With the exception of information regarding Morgan Stanley, Morgan Stanley Research is based on public information. Morgan Stanley makes every effort to use reliable, comprehensive information, but we make no representation that it is accurate or complete. We have no obligation to tell you when opinions or information in Morgan Stanley Research change apart from when we intend to discontinue equity research coverage of a subject company. Facts and views presented in Morgan Stanley Research have not been reviewed by, and may not reflect information known to, professionals in other Morgan Stanley business areas, including investment banking personnel. Morgan Stanley Research personnel may participate in company events such as site visits and are generally prohibited from accepting payment by the company of associated expenses unless pre-approved by authorized members of Research management. Morgan Stanley may make investment decisions that are inconsistent with the recommendations or views in this report. To our readers in Taiwan: Information on securities/instruments that trade in Taiwan is distributed by Morgan Stanley Taiwan Limited ("MSTL"). Such information is for your reference only. The reader should independently evaluate the investment risks and is solely responsible for their investment decisions. Morgan Stanley Research may not be distributed to the public media or quoted or used by the public media without the express written consent of Morgan Stanley. Information on securities/instruments that do not trade in Taiwan is for informational purposes only and is not to be construed as a recommendation or a solicitation to trade in such securities/instruments. MSTL may not execute transactions for clients in these securities/instruments. To our readers in Hong Kong: Information is distributed in Hong Kong by and on behalf of, and is attributable to, Morgan Stanley Asia Limited as part of its regulated activities in Hong Kong. If you have any queries concerning Morgan Stanley Research, please contact our Hong Kong sales representatives. Morgan Stanley is not incorporated under PRC law and the research in relation to this report is conducted outside the PRC. Morgan Stanley Research does not constitute an offer to sell or the solicitation of an offer to buy any securities in the PRC. PRC investors shall have the relevant qualifications to invest in such securities and shall be responsible for obtaining all relevant approvals, licenses, verifications and/or registrations from the relevant governmental authorities themselves. Neither this report nor any part of it is intended as, or shall constitute, provision of any consultancy or advisory service of securities investment as defined under PRC law. Such information is provided for your reference only. Morgan Stanley Research is disseminated in Brazil by Morgan Stanley C.T.V.M. S.A.; in Mexico by Morgan Stanley México, Casa de Bolsa, S.A. de C.V which is regulated by Comision Nacional Bancaria y de Valores. Paseo de los Tamarindos 90, Torre 1, Col. Bosques de las Lomas Floor 29, Mexico City; in Japan by Morgan Stanley MUFG Securities Co., Ltd. and, for Commodities related research reports only, Morgan Stanley Capital Group Japan Co., Ltd; in Hong Kong by Morgan Stanley Asia Limited (which accepts responsibility for its contents) and by Morgan Stanley Asia International Limited, Hong Kong Branch; in Singapore by Morgan Stanley Asia (Singapore) Pte. (Registration number Z) and/or Morgan Stanley Asia (Singapore) Securities Pte Ltd (Registration number H), regulated by the Monetary Authority of Singapore (which accepts legal responsibility for its contents and should be contacted with respect to any matters arising from, or in connection with, Morgan Stanley Research) and by Morgan Stanley Asia International Limited, Singapore Branch (Registration number T11FC0207F); in Australia to "wholesale clients" within the meaning of the Australian Corporations Act by Morgan Stanley Australia Limited A.B.N , holder of Australian financial services license No , which accepts responsibility for its contents; in Australia to "wholesale clients" and "retail clients" within the meaning of the Australian Corporations Act by Morgan Stanley Wealth Management Australia Pty Ltd (A.B.N , holder of Australian financial services license No , which accepts responsibility for its contents; in Korea by Morgan Stanley & Co International plc, Seoul Branch; in India by Morgan Stanley India Company Private Limited; in Indonesia by PT Morgan Stanley Asia Indonesia; in Canada by Morgan Stanley Canada Limited, which has approved of and takes responsibility for its contents in Canada; in Germany by Morgan Stanley Bank AG, Frankfurt am Main and Morgan Stanley Private Wealth Management Limited, Niederlassung Deutschland, regulated by Bundesanstalt fuer Finanzdienstleistungsaufsicht (BaFin); in Spain by Morgan Stanley, S.V., S.A., a Morgan Stanley group company, which is supervised by the Spanish Securities Markets Commission (CNMV) and states that Morgan Stanley Research has been written and distributed in accordance with the rules of conduct applicable to financial research as established under Spanish regulations; in the US by Morgan Stanley & Co. LLC, which accepts responsibility for its contents. Morgan Stanley & Co. International plc, authorized by the Prudential Regulatory Authority and regulated by the Financial Conduct Authority and the Prudential Regulatory Authority, disseminates in the UK research that it has prepared, and approves solely for the purposes of section 21 of the Financial Services and Markets Act 2000, research which has been prepared by any of its affiliates. RMB Morgan Stanley (Proprietary) Limited is a member of the JSE Limited and regulated by the Financial Services Board in South Africa. RMB Morgan Stanley (Proprietary) Limited is a joint venture owned equally by Morgan Stanley International Holdings Inc. and RMB Investment Advisory (Proprietary) Limited, which is wholly owned by FirstRand Limited. The information in Morgan Stanley Research is being disseminated by Morgan Stanley Saudi Arabia, regulated by the Capital Market Authority in the Kingdom of Saudi Arabia, and is directed at Sophisticated investors only. The information in Morgan Stanley Research is being communicated by Morgan Stanley & Co. International plc (DIFC Branch), regulated by the Dubai Financial Services Authority (the DFSA), and is directed at Professional Clients only, as defined by the DFSA. The financial products or financial services to which this research relates will only be made available to a customer who we are satisfied meets the regulatory criteria to be a Professional Client. The information in Morgan Stanley Research is being communicated by Morgan Stanley & Co. International plc (QFC Branch), regulated by the Qatar Financial Centre Regulatory Authority (the QFCRA), and is directed at business customers and market counterparties only and is not intended for Retail Customers as defined by the QFCRA. As required by the Capital Markets Board of Turkey, investment information, comments and recommendations stated here, are not within the scope of investment advisory activity. Investment advisory service is provided exclusively to persons based on their risk and income preferences by the authorized firms. Comments and recommendations stated here are general in nature. These opinions may not fit to your financial status, risk and return preferences. For this reason, to make an investment decision by relying solely to this information stated here may not bring about outcomes that fit your expectations. The trademarks and service marks contained in Morgan Stanley Research are the property of their respective owners. Third-party data providers make no warranties or representations relating to the accuracy, completeness, or timeliness of the data they provide and shall not have liability for any damages relating 16

17 to such data. The Global Industry Classification Standard (GICS) was developed by and is the exclusive property of MSCI and S&P. Morgan Stanley Research, or any portion thereof may not be reprinted, sold or redistributed without the written consent of Morgan Stanley. INDUSTRY COVERAGE: Life Science Tools & Diagnostics COMPANY (TICKER) RATING (AS OF) PRICE* (07/26/2016) Steve Beuchaw Agilent Technologies, Inc. (A.N) E (09/08/2014) $46.95 Bruker Corp (BRKR.O) E (09/15/2015) $24.38 Cepheid (CPHD.O) E (06/15/2016) $32.79 Illumina Inc. (ILMN.O) U (07/05/2016) $ Mettler-Toledo International Inc. (MTD.N) E (04/02/2015) $ Myriad Genetics Inc. (MYGN.O) U (11/10/2014) $32.37 NanoString Technologies Inc (NSTG.O) O (11/10/2014) $13.29 Natera Inc (NTRA.O) O (08/14/2015) $12.84 PerkinElmer Inc. (PKI.N) O (09/08/2014) $55.44 Qiagen NV (QGEN.O) O (09/15/2015) $23.13 T2 Biosystems Inc (TTOO.O) E (09/02/2014) $5.26 Thermo Fisher Scientific Inc. (TMO.N) O (09/08/2014) $ Waters Corp. (WAT.N) U (09/08/2014) $ Stock Ratings are subject to change. Please see latest research for each company. * Historical prices are not split adjusted Morgan Stanley 17

Video March 1, StratTV at the TMT Conference. Watch the video: Related Research

March 1, 2016 Video StratTV at the TMT Conference MORGAN STANLEY & CO. LLC Adam S. Parker, Ph.D. Adam.Parker@morganstanley.com Video March 1, 2016 +1 212 761-1755 Watch the video: Related Research US Equity

March 1, 2016 Video StratTV at the TMT Conference MORGAN STANLEY & CO. LLC Adam S. Parker, Ph.D. Adam.Parker@morganstanley.com Video March 1, 2016 +1 212 761-1755 Watch the video: Related Research US Equity

Interview with CFO Stephen Nolan

March 31, 2016 Video Vista Outdoor Inc. Interview with CFO Stephen Nolan MORGAN STANLEY & CO. LLC Jay Sole Jay.Sole@morganstanley.com +1 212 761-5866 Watch the video: Stephen M. Nolan is Chief Financial

March 31, 2016 Video Vista Outdoor Inc. Interview with CFO Stephen Nolan MORGAN STANLEY & CO. LLC Jay Sole Jay.Sole@morganstanley.com +1 212 761-5866 Watch the video: Stephen M. Nolan is Chief Financial

Can P-VOD Save Hollywood?

July 10, 2017 09:00 AM GMT Video Media Can P-VOD Save Hollywood? MORGAN STANLEY & CO. LLC Benjamin Swinburne, CFA EQUITY ANALYST Benjamin.Swinburne@morganstanley.com +1 212 761-7527 Watch the video: Related

July 10, 2017 09:00 AM GMT Video Media Can P-VOD Save Hollywood? MORGAN STANLEY & CO. LLC Benjamin Swinburne, CFA EQUITY ANALYST Benjamin.Swinburne@morganstanley.com +1 212 761-7527 Watch the video: Related

January TIC Data Update: Overseas Investors Decreased Agency MBS by $3.6bn

March 15, 2016 Agency MBS Brief January TIC Data Update: Overseas Investors Decreased Agency MBS by $3.6bn MORGAN STANLEY & CO. LLC Michael H Ortiz Michael.Ortiz@morganstanley.com Devan K Knoetze Devan.Knoetze@morganstanley.com

March 15, 2016 Agency MBS Brief January TIC Data Update: Overseas Investors Decreased Agency MBS by $3.6bn MORGAN STANLEY & CO. LLC Michael H Ortiz Michael.Ortiz@morganstanley.com Devan K Knoetze Devan.Knoetze@morganstanley.com

No Substitute for Execution; Remain OW

July 23, 2015 Thermo Fisher Scientific Inc. No Substitute for Execution; Remain OW MORGAN STANLEY & CO. LLC Steve Beuchaw Steve.Beuchaw@morganstanley.com Michael Clerico Michael.Clerico@morganstanley.com

July 23, 2015 Thermo Fisher Scientific Inc. No Substitute for Execution; Remain OW MORGAN STANLEY & CO. LLC Steve Beuchaw Steve.Beuchaw@morganstanley.com Michael Clerico Michael.Clerico@morganstanley.com

Who s Using XBRL Data & Why: Case Studies

M O R G A N S T A N L E Y R E S E A R C H North America Accounting & Valuation Todd Castagno, CFA, CPA Equity Strategist Todd.Castagno@morganstanley.com +1 212 761 6893 Morgan Stanley does and seeks to

M O R G A N S T A N L E Y R E S E A R C H North America Accounting & Valuation Todd Castagno, CFA, CPA Equity Strategist Todd.Castagno@morganstanley.com +1 212 761 6893 Morgan Stanley does and seeks to

Tobacco Pricing Power Far From Extinguished

January 14, 2016 Video Global Insight Tobacco Pricing Power Far From Extinguished Our affordability deep dive suggests sustained visibility to 5%+ global pricing, with surprisingly high affordability in

January 14, 2016 Video Global Insight Tobacco Pricing Power Far From Extinguished Our affordability deep dive suggests sustained visibility to 5%+ global pricing, with surprisingly high affordability in

Steel March 15, Mid-Quarter Guidance Preview: Looking

March 15, 2016 Steel Mid-Quarter Guidance Preview: Looking for a Beat from STLD We have updated our estimates ahead of mid-quarter guidance likely out later this week and next. Our STLD estimates are comfortably

March 15, 2016 Steel Mid-Quarter Guidance Preview: Looking for a Beat from STLD We have updated our estimates ahead of mid-quarter guidance likely out later this week and next. Our STLD estimates are comfortably

Deep Discount Cigarette Share Gains Elevate Pricing Concerns

August 1, 2018 04:01 AM GMT Tobacco Deep Discount Cigarette Share Gains Elevate Pricing Concerns Deep discount share increased 70 bps in 2Q18. Widening Marlboro price gaps and MO share losses (-70 bps

August 1, 2018 04:01 AM GMT Tobacco Deep Discount Cigarette Share Gains Elevate Pricing Concerns Deep discount share increased 70 bps in 2Q18. Widening Marlboro price gaps and MO share losses (-70 bps

Research Tactical Idea

March 1, 2017 10:14 PM GMT Santos Research Tactical Idea Stock Rating Overweight Industry View In-Line Price Target A$5.08 We believe the share price will rise in absolute terms over the next 60 days.

March 1, 2017 10:14 PM GMT Santos Research Tactical Idea Stock Rating Overweight Industry View In-Line Price Target A$5.08 We believe the share price will rise in absolute terms over the next 60 days.

Should We Be Concerned About Industrial Exposure?

January 25, 2016 Mettler-Toledo International Inc. Should We Be Concerned About Industrial Exposure? MORGAN STANLEY & CO. LLC Steve Beuchaw Steve.Beuchaw@morganstanley.com Michael Clerico Michael.Clerico@morganstanley.com

January 25, 2016 Mettler-Toledo International Inc. Should We Be Concerned About Industrial Exposure? MORGAN STANLEY & CO. LLC Steve Beuchaw Steve.Beuchaw@morganstanley.com Michael Clerico Michael.Clerico@morganstanley.com

2018 Hong Kong Summit Feedback

March 7, 2018 06:33 AM GMT NagaCorp 2018 Hong Kong Summit Feedback MORGAN STANLEY ASIA LIMITED+ Praveen K Choudhary EQUITY ANALYST Praveen.Choudhary@morganstanley.com Jeremy An RESEARCH ASSOCIATE Jeremy.An@morganstanley.com

March 7, 2018 06:33 AM GMT NagaCorp 2018 Hong Kong Summit Feedback MORGAN STANLEY ASIA LIMITED+ Praveen K Choudhary EQUITY ANALYST Praveen.Choudhary@morganstanley.com Jeremy An RESEARCH ASSOCIATE Jeremy.An@morganstanley.com

1st Take: FDA wants to educate US physicians about the basics of biosimilars

October 24, 2017 11:11 PM GMT Celltrion Inc. 1st Take: FDA wants to educate US physicians about the basics of biosimilars Stock Rating Underweight Industry View In-Line Price Target W80,000 The FDA has

October 24, 2017 11:11 PM GMT Celltrion Inc. 1st Take: FDA wants to educate US physicians about the basics of biosimilars Stock Rating Underweight Industry View In-Line Price Target W80,000 The FDA has

ASEAN4 Most Productive Companies

July 29, 2015 Video ASEAN Equity Strategy ASEAN4 Most Productive Companies ASEAN equity strategist Hozefa Topiwalla discusses ASEAN4's Most Productive Companies framework, which could potentially help

July 29, 2015 Video ASEAN Equity Strategy ASEAN4 Most Productive Companies ASEAN equity strategist Hozefa Topiwalla discusses ASEAN4's Most Productive Companies framework, which could potentially help

Our Thoughts On the Preannouncement

October 14, 2015 Manitowoc Co Inc Our Thoughts On the Preannouncement Industry View In-Line Stock Rating Overweight This evening, MTW provided preliminary 3Q15 results, and expects to report net sales

October 14, 2015 Manitowoc Co Inc Our Thoughts On the Preannouncement Industry View In-Line Stock Rating Overweight This evening, MTW provided preliminary 3Q15 results, and expects to report net sales

First Take: Building on the core

March 27, 2017 10:20 PM GMT FAR Ltd First Take: Building on the core Stock Rating Overweight Industry View In-Line Price Target A$0.13 FAR has announced a farm-in deal with Erin Energy. The deal expands

March 27, 2017 10:20 PM GMT FAR Ltd First Take: Building on the core Stock Rating Overweight Industry View In-Line Price Target A$0.13 FAR has announced a farm-in deal with Erin Energy. The deal expands

SHARED AUTONOMY. Adam Jonas, CFA Apple is covered by Katy Huberty; Google is covered by Brian Nowak

SHARED AUTONOMY Adam Jonas, CFA Adam.Jonas@morganstanley.com +1 212 761-1726 Apple is covered by Katy Huberty; Google is covered by Brian Nowak Morgan Stanley does and seeks to do business with companies

SHARED AUTONOMY Adam Jonas, CFA Adam.Jonas@morganstanley.com +1 212 761-1726 Apple is covered by Katy Huberty; Google is covered by Brian Nowak Morgan Stanley does and seeks to do business with companies

1Q16 EPS Above Lowered Expectations

May 4, 2016 Allstate Corporation 1Q16 EPS Above Lowered Expectations MORGAN STANLEY & CO. LLC Kai Pan Kai.Pan@MorganStanley.com Chai Gohil Chaitanya.Gohil@morganstanley.com Allstate Corporation May 4,

May 4, 2016 Allstate Corporation 1Q16 EPS Above Lowered Expectations MORGAN STANLEY & CO. LLC Kai Pan Kai.Pan@MorganStanley.com Chai Gohil Chaitanya.Gohil@morganstanley.com Allstate Corporation May 4,

Making the Right Moves in Sports Betting

August 1, 2018 02:05 AM GMT MGM Resorts International Making the Right Moves in Sports Betting Stock Rating Overweight Industry View In-Line Price Target $38.00 Over the course of two days, MGM has announced

August 1, 2018 02:05 AM GMT MGM Resorts International Making the Right Moves in Sports Betting Stock Rating Overweight Industry View In-Line Price Target $38.00 Over the course of two days, MGM has announced

Proposed China Tariff on US Pork Negative for HRL/TSN

March 23, 2018 01:32 01:46 PM GMT Protein Proposed China Tariff on US Pork Negative for HRL/TSN China's potential 25% tariff on US pork represents a meaningful headwind to HRL's profitability. Despite

March 23, 2018 01:32 01:46 PM GMT Protein Proposed China Tariff on US Pork Negative for HRL/TSN China's potential 25% tariff on US pork represents a meaningful headwind to HRL's profitability. Despite

XL Group PLC February 3, 2016

February 3, 2016 XL Group PLC 4Q15: Underlying EPS Miss; Integration On Track MORGAN STANLEY & CO. LLC Kai Pan Kai.Pan@MorganStanley.com Chai Gohil Chaitanya.Gohil@morganstanley.com XL Group PLC February

February 3, 2016 XL Group PLC 4Q15: Underlying EPS Miss; Integration On Track MORGAN STANLEY & CO. LLC Kai Pan Kai.Pan@MorganStanley.com Chai Gohil Chaitanya.Gohil@morganstanley.com XL Group PLC February

USD Sensitivity. Source: Getty Images

September 19, 2014 US Economics USD Sensitivity The nominal trade-weighted major currencies USD index has jumped by more than 3% since early June. We find that a sustained increase of 10% hampers US GDP

September 19, 2014 US Economics USD Sensitivity The nominal trade-weighted major currencies USD index has jumped by more than 3% since early June. We find that a sustained increase of 10% hampers US GDP

Sinisi's Shop Food Retail Pricing Study (Vol. 45, August '18)

") August 1, 2018 04:01 AM GMT Food Retailers Sinisi's Shop Food Retail Pricing Study (Vol. 45, August '18) Whole Foods pricing was +0.3% m/m and -2.0% y/y for Sinisi's Shop basket in our eleventh check post-amazon

August 1, 2018 04:01 AM GMT Food Retailers Sinisi's Shop Food Retail Pricing Study (Vol. 45, August '18) Whole Foods pricing was +0.3% m/m and -2.0% y/y for Sinisi's Shop basket in our eleventh check post-amazon

Paradise. 4Q13: In line with consensus

ASIA/PACIFIC Morgan Stanley & Co. International plc, Seoul Branch+ HyunTaek Lee HyunTaek.Lee@morganstanley.com +82 2 399 9854 Morgan Stanley Asia Limited+ Praveen K Choudhary Praveen.Choudhary@morganstanley.com

ASIA/PACIFIC Morgan Stanley & Co. International plc, Seoul Branch+ HyunTaek Lee HyunTaek.Lee@morganstanley.com +82 2 399 9854 Morgan Stanley Asia Limited+ Praveen K Choudhary Praveen.Choudhary@morganstanley.com

Canadian Pacific Railway Ltd. (CP.N) Closed Research Tactical Idea

Closed Research Tactical Idea") NORTH AMERICA Morgan Stanley & Co. LLC William J. Greene, CFA William.Greene@morganstanley.com +1 212 761 8017 (CP.N) Closed Research Tactical Idea Effective immediately, the Tactical Idea published on

NORTH AMERICA Morgan Stanley & Co. LLC William J. Greene, CFA William.Greene@morganstanley.com +1 212 761 8017 (CP.N) Closed Research Tactical Idea Effective immediately, the Tactical Idea published on

Lowering Outlook Following 3Q, Merger Filing Forecast

November 24, 2015 Cablevision Systems Lowering Outlook Following 3Q, Merger Filing Forecast MORGAN STANLEY & CO. LLC Benjamin Swinburne, CFA Benjamin.Swinburne@morganstanley.com Ryan Fiftal Ryan.Fiftal@MorganStanley.com

November 24, 2015 Cablevision Systems Lowering Outlook Following 3Q, Merger Filing Forecast MORGAN STANLEY & CO. LLC Benjamin Swinburne, CFA Benjamin.Swinburne@morganstanley.com Ryan Fiftal Ryan.Fiftal@MorganStanley.com

Visa Inc. February 29, 2016

February 29, 2016 Visa Inc. Visa at MS TMT Conference: Cautious on macro near-term, but unchanged growth drivers long-term Industry View In-Line Stock Rating Overweight Price Target $90.00 Staying cautious

February 29, 2016 Visa Inc. Visa at MS TMT Conference: Cautious on macro near-term, but unchanged growth drivers long-term Industry View In-Line Stock Rating Overweight Price Target $90.00 Staying cautious

1st Take: November Sales On Track Despite YoY Decline

December 12, 2016 12:16 PM GMT Toung Loong Textile 1st Take: November Sales On Track Despite YoY Decline Stock Rating Overweight Industry View In-Line Price Target NT$110.00 Toung Loong Textile (TLT) reported

December 12, 2016 12:16 PM GMT Toung Loong Textile 1st Take: November Sales On Track Despite YoY Decline Stock Rating Overweight Industry View In-Line Price Target NT$110.00 Toung Loong Textile (TLT) reported

Portfolio Strategy. The Endowment Model: Theory and More Experience

NORTH AMERICA Morgan Stanley & Co. Incorporated Martin Leibowitz Martin.Leibowitz@morganstanley.com +1 (1)212 761 7597 Anthony Bova Anthony.Bova@morganstanley.com +1 (1)212 761 3781 The Endowment Model:

NORTH AMERICA Morgan Stanley & Co. Incorporated Martin Leibowitz Martin.Leibowitz@morganstanley.com +1 (1)212 761 7597 Anthony Bova Anthony.Bova@morganstanley.com +1 (1)212 761 3781 The Endowment Model:

4Q16 Diagnostics Tracker: US Market Catches the Flu?

March 21, 21, 2017 2017 05:00 05:03 AM AM GMT GMT Life Science Tools & Diagnostics 4Q16 Diagnostics Tracker: US Market Catches the Flu? Global diagnostics/dx market growth slowed in 4Q16, with 160bps deceleration

March 21, 21, 2017 2017 05:00 05:03 AM AM GMT GMT Life Science Tools & Diagnostics 4Q16 Diagnostics Tracker: US Market Catches the Flu? Global diagnostics/dx market growth slowed in 4Q16, with 160bps deceleration

In the Penalty Box But Valuation Remains Compelling

March 16, 2016 Connecture Inc In the Penalty Box But Valuation Remains Compelling Industry View In-Line Stock Rating Overweight Price Target $7.00 CNXR shares are in the penalty box after missing 4Q revenue

March 16, 2016 Connecture Inc In the Penalty Box But Valuation Remains Compelling Industry View In-Line Stock Rating Overweight Price Target $7.00 CNXR shares are in the penalty box after missing 4Q revenue

Kohl's May 14, Not So Great 1Q; Bull Thesis Fading

May 14, 2015 Kohl's Not So Great 1Q; Bull Thesis Fading MORGAN STANLEY & CO. LLC Kimberly C Greenberger Kimberly.Greenberger@morganstanley.com Lauren Cassel Lauren.Cassel@morganstanley.com +1 212 761-6284

May 14, 2015 Kohl's Not So Great 1Q; Bull Thesis Fading MORGAN STANLEY & CO. LLC Kimberly C Greenberger Kimberly.Greenberger@morganstanley.com Lauren Cassel Lauren.Cassel@morganstanley.com +1 212 761-6284

Price/Earnings Ratios, Risk Premiums and the g* Adjustment

April 23, 2018 02:18 PM GMT Portfolio Strategy Price/Earnings Ratios, Risk Premiums and the g* Adjustment MORGAN STANLEY & CO. LLC Martin Leibowitz PORTFOLIO ANALYST Martin.Leibowitz@morganstanley.com

April 23, 2018 02:18 PM GMT Portfolio Strategy Price/Earnings Ratios, Risk Premiums and the g* Adjustment MORGAN STANLEY & CO. LLC Martin Leibowitz PORTFOLIO ANALYST Martin.Leibowitz@morganstanley.com

Strong Underlying Metrics Point To Upside Potential

May 4, 2016 Healthcare Realty Trust Inc. Strong Underlying Metrics Point To Upside Potential MORGAN STANLEY & CO. LLC Vikram Malhotra Vikram.Malhotra@morganstanley.com Landon Park Landon.Park@morganstanley.com

May 4, 2016 Healthcare Realty Trust Inc. Strong Underlying Metrics Point To Upside Potential MORGAN STANLEY & CO. LLC Vikram Malhotra Vikram.Malhotra@morganstanley.com Landon Park Landon.Park@morganstanley.com

Acquisition of Lafarge/Holcim assets

February 2, 2015 CRH Acquisition of Lafarge/Holcim assets Industry View In-Line Stock Rating ++ CRH is the buyer of the Lafarge/Holcim assets. CRH has announced the acquisition of all of the assets as

February 2, 2015 CRH Acquisition of Lafarge/Holcim assets Industry View In-Line Stock Rating ++ CRH is the buyer of the Lafarge/Holcim assets. CRH has announced the acquisition of all of the assets as

Slower near-term momentum but we expect long-term targets to be reached in OW

November 16, 2015 International Flavors & Fragrances Slower near-term momentum but we expect long-term targets to be reached in 2016 - OW Industry View In-Line Stock Rating Overweight Price Target US$130.00

November 16, 2015 International Flavors & Fragrances Slower near-term momentum but we expect long-term targets to be reached in 2016 - OW Industry View In-Line Stock Rating Overweight Price Target US$130.00

2018 Guidance Reduction Sets an Achievable Bar

July 19, 2018 11:28 PM GMT Philip Morris International Inc 2018 Guidance Reduction Sets an Achievable Bar Stock Rating Overweight Industry View In-Line Price Target $102.00 Q2 results reflected improved

July 19, 2018 11:28 PM GMT Philip Morris International Inc 2018 Guidance Reduction Sets an Achievable Bar Stock Rating Overweight Industry View In-Line Price Target $102.00 Q2 results reflected improved

Earnings Observations: EPS Beats Driving Outsized Moves, Where to Go from Here

August 3, 2015 Business & Education Services Earnings Observations: EPS Beats Driving Outsized Moves, Where to Go from Here Sticking with our top calls: VRSK Overweight, IHS Underweight. What's new: Last

August 3, 2015 Business & Education Services Earnings Observations: EPS Beats Driving Outsized Moves, Where to Go from Here Sticking with our top calls: VRSK Overweight, IHS Underweight. What's new: Last

New Pipeline Investment Supportive, But We Still See Downside to Consensus

February 4, 2016 Laclede Group Inc New Pipeline Investment Supportive, But We Still See Downside to Consensus Industry View In-Line Stock Rating Underweight Price Target $62.00 Yesterday Laclede Group

February 4, 2016 Laclede Group Inc New Pipeline Investment Supportive, But We Still See Downside to Consensus Industry View In-Line Stock Rating Underweight Price Target $62.00 Yesterday Laclede Group

2017 Results Largely In Line

March 26, 2018 07:03 PM GMT Sinotrans Limited 2017 Results Largely In Line Stock Rating Overweight Industry View In-Line Price Target HK$6.60 Sinotrans 2017 net profit of Rmb2,304mn missed MSe by 2%, but

March 26, 2018 07:03 PM GMT Sinotrans Limited 2017 Results Largely In Line Stock Rating Overweight Industry View In-Line Price Target HK$6.60 Sinotrans 2017 net profit of Rmb2,304mn missed MSe by 2%, but

More Visibility on FY After Q1 Upside, But Valuation Now Appropriate

February 3, 2016 Edgewell Personal Care More Visibility on FY After Q1 Upside, But Valuation Now Appropriate Industry View In-Line Stock Rating Equal-weight Price Target $87.00 We remain Equal-weight on

February 3, 2016 Edgewell Personal Care More Visibility on FY After Q1 Upside, But Valuation Now Appropriate Industry View In-Line Stock Rating Equal-weight Price Target $87.00 We remain Equal-weight on

Healthcare Premium Priced In

August 2, 2015 IMS Health Holdings Inc Healthcare Premium Priced In Industry View In-Line Stock Rating Equal-weight Price Target $31.00 MORGAN STANLEY & CO. LLC Toni Kaplan Toni.Kaplan@morganstanley.com

August 2, 2015 IMS Health Holdings Inc Healthcare Premium Priced In Industry View In-Line Stock Rating Equal-weight Price Target $31.00 MORGAN STANLEY & CO. LLC Toni Kaplan Toni.Kaplan@morganstanley.com

CTSH: Is The Bar Low Enough?

October 27, 2016 04:02 AM GMT Cognizant Technology Solutions Corp CTSH: Is The Bar Low Enough? Stock Rating Overweight Industry View Cautious Price Target $61.00 MORGAN STANLEY & CO. LLC Brian Essex, CFA

October 27, 2016 04:02 AM GMT Cognizant Technology Solutions Corp CTSH: Is The Bar Low Enough? Stock Rating Overweight Industry View Cautious Price Target $61.00 MORGAN STANLEY & CO. LLC Brian Essex, CFA

Field Trip Takeaways: Sustained Focus on Network Efficiency

January 7, 2018 05:27 PM GMT ZTO Express Field Trip Takeaways: Sustained Focus on Network Efficiency Stock Rating Overweight Industry View In-Line Price Target US$21.20 MORGAN STANLEY ASIA LIMITED+ Edward

January 7, 2018 05:27 PM GMT ZTO Express Field Trip Takeaways: Sustained Focus on Network Efficiency Stock Rating Overweight Industry View In-Line Price Target US$21.20 MORGAN STANLEY ASIA LIMITED+ Edward

1st Take: Stronger than Expected December Shipments Thanks to Upturn

January 11, 2015 TCL Communication 1st Take: Stronger than Expected December Shipments Thanks to Upturn in China Industry View In-Line Stock Rating Overweight TCLC reported December smartphone shipments

January 11, 2015 TCL Communication 1st Take: Stronger than Expected December Shipments Thanks to Upturn in China Industry View In-Line Stock Rating Overweight TCLC reported December smartphone shipments

Emergency Liquidity Assistance in the Euro Area

Emergency Liquidity Assistance in the Euro Area November 2010 Laurence Mutkin Head of European Interest Rate Strategy Laurence.Mutkin@morganstanley.com Morgan Stanley & Co. International plc+ Rachael Featherstone

Emergency Liquidity Assistance in the Euro Area November 2010 Laurence Mutkin Head of European Interest Rate Strategy Laurence.Mutkin@morganstanley.com Morgan Stanley & Co. International plc+ Rachael Featherstone

Nike Inc. October 15, 2015

October 15, 2015 Nike Inc. Very Bullish Analyst Day; Nike Remains Our Top Pick MORGAN STANLEY & CO. LLC Jay Sole Jay.Sole@morganstanley.com Joseph Wyatt, CFA Joseph.Wyatt@morganstanley.com Nike Inc. October

October 15, 2015 Nike Inc. Very Bullish Analyst Day; Nike Remains Our Top Pick MORGAN STANLEY & CO. LLC Jay Sole Jay.Sole@morganstanley.com Joseph Wyatt, CFA Joseph.Wyatt@morganstanley.com Nike Inc. October

Weaker NPAT, driven by higher. formation; LDR over 100%

October 18, 2016 02:28 PM GMT The Siam Commercial Bank Public Company Weaker NPAT, driven by higher loan loss, rise in new NPL formation; LDR over 100% Stock Rating Equal-weight Industry View In-Line Price

October 18, 2016 02:28 PM GMT The Siam Commercial Bank Public Company Weaker NPAT, driven by higher loan loss, rise in new NPL formation; LDR over 100% Stock Rating Equal-weight Industry View In-Line Price

1st Take: OJK suspends new account opening

March 22, 2017 04:34 AM GMT Bank Tabungan Negara 1st Take: OJK suspends new account opening Stock Rating Overweight Industry View In-Line Price Target Rp2,102 OJK suspension: Kontan newspaper today reported

March 22, 2017 04:34 AM GMT Bank Tabungan Negara 1st Take: OJK suspends new account opening Stock Rating Overweight Industry View In-Line Price Target Rp2,102 OJK suspension: Kontan newspaper today reported

Research Tactical Idea

May 26, 2017 10:58 AM GMT Jinko Solar Research Tactical Idea Stock Rating Underweight Industry View Attractive Price Target US$16.40 We believe the share price will fall in absolute terms over the next

May 26, 2017 10:58 AM GMT Jinko Solar Research Tactical Idea Stock Rating Underweight Industry View Attractive Price Target US$16.40 We believe the share price will fall in absolute terms over the next

Model Updates. March 15, Healthcare Services & Distribution MORGAN STANLEY RESEARCH. Ashley E Ponce

March 15, 2016 LH + DGX Model Updates We are updating our models and extending estimates to 2018 - when we think PAMA will likely affect pricing vs. previous estimate of 2017. Trim LH PT to $133, remain

March 15, 2016 LH + DGX Model Updates We are updating our models and extending estimates to 2018 - when we think PAMA will likely affect pricing vs. previous estimate of 2017. Trim LH PT to $133, remain

4Q15 Miss: Yet Refiners Hit Seasonal Inflection

February 24, 2016 HollyFrontier Corporation 4Q15 Miss: Yet Refiners Hit Seasonal Inflection MORGAN STANLEY & CO. LLC Evan Calio Evan.Calio@morganstanley.com Benny Wong Benny.Wong@morganstanley.com +1 212

February 24, 2016 HollyFrontier Corporation 4Q15 Miss: Yet Refiners Hit Seasonal Inflection MORGAN STANLEY & CO. LLC Evan Calio Evan.Calio@morganstanley.com Benny Wong Benny.Wong@morganstanley.com +1 212

Indra May 12, Problem contracts & elections drive significant 1Q15 shortfall. Problem contracts and elections falling away drove a topline miss

May 12, 2015 Indra Problem contracts & elections drive significant 1Q15 shortfall MORGAN STANLEY & CO. INTERNATIONAL PLC+ Adam Wood Adam.Wood@morganstanley.com Sid Mehra Sid.Mehra@morganstanley.com William

May 12, 2015 Indra Problem contracts & elections drive significant 1Q15 shortfall MORGAN STANLEY & CO. INTERNATIONAL PLC+ Adam Wood Adam.Wood@morganstanley.com Sid Mehra Sid.Mehra@morganstanley.com William

Q Conference October 18 th, 2006 Santa Barbara, CA

Martin Leibowitz martin.leibowitz@morganstanley.com +1 (212) 761-7597 Anthony Bova anthony.bova@morganstanley.com +1 (212) 761-3781 Q Conference October 18 th, 2006 Santa Barbara, CA Morgan Stanley does

Martin Leibowitz martin.leibowitz@morganstanley.com +1 (212) 761-7597 Anthony Bova anthony.bova@morganstanley.com +1 (212) 761-3781 Q Conference October 18 th, 2006 Santa Barbara, CA Morgan Stanley does

7 Key Takes from Meetings with SFM Management

March 16, 2016 Sprouts Farmers Market Inc 7 Key Takes from Meetings with SFM Management MORGAN STANLEY & CO. LLC Vincent J Sinisi Vincent.Sinisi@morganstanley.com Andrew R Ruben Andrew.Ruben@morganstanley.com

March 16, 2016 Sprouts Farmers Market Inc 7 Key Takes from Meetings with SFM Management MORGAN STANLEY & CO. LLC Vincent J Sinisi Vincent.Sinisi@morganstanley.com Andrew R Ruben Andrew.Ruben@morganstanley.com

Coffee Talk: A Look at February US Scanner Data

March 8, 2016 Food and Restaurants Coffee Talk: A Look at February US Scanner Data Total coffee sales contracted 0.2% L4W, a deceleration from +1.7% L12W as both R&G (-3.5%) and K-Cup (+6.0%) trends softened.

March 8, 2016 Food and Restaurants Coffee Talk: A Look at February US Scanner Data Total coffee sales contracted 0.2% L4W, a deceleration from +1.7% L12W as both R&G (-3.5%) and K-Cup (+6.0%) trends softened.

The Worst Behind Them; Raising PT, Upgrade to EW

November 24, 2015 Schnitzer Steel Industries The Worst Behind Them; Raising PT, Upgrade to EW MORGAN STANLEY & CO. LLC Evan L Kurtz, CFA Evan.Kurtz@morganstanley.com Piyush Sood Piyush.Sood@morganstanley.com

November 24, 2015 Schnitzer Steel Industries The Worst Behind Them; Raising PT, Upgrade to EW MORGAN STANLEY & CO. LLC Evan L Kurtz, CFA Evan.Kurtz@morganstanley.com Piyush Sood Piyush.Sood@morganstanley.com

The Robotic Dilemma. Do surgical robots equate to an existential dilemma for SN's orthopedics business? Overweight. Attractive.

March 21, 2017 05:00 AM GMT Smith & Nephew The Robotic Dilemma Stock Rating Overweight Industry View Attractive Price Target 1,301p Do surgical robots equate to an existential dilemma for SN's orthopedics

March 21, 2017 05:00 AM GMT Smith & Nephew The Robotic Dilemma Stock Rating Overweight Industry View Attractive Price Target 1,301p Do surgical robots equate to an existential dilemma for SN's orthopedics

Industry Analysis. BRICs and Motors

Equity Research Europe BRICs and Motors Adam M. Jonas, CFA European Auto Analyst adam.jonas@morganstanley.com +44 207 425 2177 Industry Analysis EMs account for 80 to >100% of unit growth EMs already account

Equity Research Europe BRICs and Motors Adam M. Jonas, CFA European Auto Analyst adam.jonas@morganstanley.com +44 207 425 2177 Industry Analysis EMs account for 80 to >100% of unit growth EMs already account

ACCC, A4ANZ, BARA & BARNZ vs Airports, MQA in the ASX100

March 10, 2017 12:19 AM GMT Australia Infrastructure ACCC, A4ANZ, BARA & BARNZ vs Airports, MQA in the ASX100 The ACCC has flagged it will seek additional price regulation powers at the next review of

March 10, 2017 12:19 AM GMT Australia Infrastructure ACCC, A4ANZ, BARA & BARNZ vs Airports, MQA in the ASX100 The ACCC has flagged it will seek additional price regulation powers at the next review of

2Q16: External Pressures Return

July MONTH 28, 2016 DD, YYYY 01:35 HH:MM AM GMTAM/PM GMT Marriott International Inc. 2Q16: External Pressures Return Stock Rating Equal-weight Industry View In-Line Price Target $73.00 MAR reported 2Q

July MONTH 28, 2016 DD, YYYY 01:35 HH:MM AM GMTAM/PM GMT Marriott International Inc. 2Q16: External Pressures Return Stock Rating Equal-weight Industry View In-Line Price Target $73.00 MAR reported 2Q

BorsodChem MDI Suspension Likely to Further Boost Market Sentiment; Positive for Wanhua

August 15, 2017 04:40 PM GMT Wanhua Chemical BorsodChem MDI Suspension Likely to Further Boost Market Sentiment; Positive for Wanhua Stock Rating Overweight Industry View Attractive Price Target Rmb41.46

August 15, 2017 04:40 PM GMT Wanhua Chemical BorsodChem MDI Suspension Likely to Further Boost Market Sentiment; Positive for Wanhua Stock Rating Overweight Industry View Attractive Price Target Rmb41.46

March 22, Is An Ultra-Bear Scenario in Play?

March 22, 2016 ESRX Is An Ultra-Bear Scenario in Play? Industry View In-Line Stock Rating Equal-weight Price Target $67.00 With ANTM/ESRX dispute escalating to litigation, probability of contract renewal

March 22, 2016 ESRX Is An Ultra-Bear Scenario in Play? Industry View In-Line Stock Rating Equal-weight Price Target $67.00 With ANTM/ESRX dispute escalating to litigation, probability of contract renewal

Corporate Travel Survey 2018 Stronger Trends: Intra-EU & Asia Are Key Drivers

November 15, 2017 05:00 AM GMT Airlines Corporate Travel Survey 2018 Stronger Trends: Intra-EU & Asia Are Key Drivers In this report we summarise the key observations from our 2018 AlphaWise Corporate

November 15, 2017 05:00 AM GMT Airlines Corporate Travel Survey 2018 Stronger Trends: Intra-EU & Asia Are Key Drivers In this report we summarise the key observations from our 2018 AlphaWise Corporate

Green Dot Corp February 25, 2016

February 25, 2016 Green Dot Corp 4Q15: The Six Step Program MORGAN STANLEY & CO. LLC Vasundhara Govil Vasundhara.Govil@morganstanley.com Danyal Hussain, CFA Danyal.Hussain@morganstanley.com +1 212 761-3609

February 25, 2016 Green Dot Corp 4Q15: The Six Step Program MORGAN STANLEY & CO. LLC Vasundhara Govil Vasundhara.Govil@morganstanley.com Danyal Hussain, CFA Danyal.Hussain@morganstanley.com +1 212 761-3609

4Q15 Earnings Preview

January 26, 2016 Cummins Inc. 4Q15 Earnings Preview Industry View In-Line Stock Rating Underweight Price Target $71.00 We forecast a $0.04 miss vs. consensus and expect CMI to provide a 2016e framework

January 26, 2016 Cummins Inc. 4Q15 Earnings Preview Industry View In-Line Stock Rating Underweight Price Target $71.00 We forecast a $0.04 miss vs. consensus and expect CMI to provide a 2016e framework

Letter from New York. In-Line. Equal-weight $ What's new: we hosted a day of investor meetings in NY with Dunkin Brand CFO Paul Carbone.

October 27, 2016 04:02 AM GMT Dunkin Brands Group Inc Letter from New York Stock Rating Equal-weight Industry View In-Line Price Target $48.00 Coffee focus, product innovation and reduced food complexity

October 27, 2016 04:02 AM GMT Dunkin Brands Group Inc Letter from New York Stock Rating Equal-weight Industry View In-Line Price Target $48.00 Coffee focus, product innovation and reduced food complexity

PASPA Overturned: US Sports Betting To Open Up

May 14, 2018 02:33 PM GMT US Sports Betting PASPA Overturned: US Sports Betting To Open Up The US Supreme Court has ruled that PASPA, the law which prohibits states from legalising sports betting, is unconstitutional.

May 14, 2018 02:33 PM GMT US Sports Betting PASPA Overturned: US Sports Betting To Open Up The US Supreme Court has ruled that PASPA, the law which prohibits states from legalising sports betting, is unconstitutional.

Upbeat Tone in Barcelona - Questions

November 16, 2015 Telecom Services Upbeat Tone in Barcelona - Questions for US Carriers This week's European TMT conference in Barcelona featured a record attendance amidst a generally upbeat overall tone.

November 16, 2015 Telecom Services Upbeat Tone in Barcelona - Questions for US Carriers This week's European TMT conference in Barcelona featured a record attendance amidst a generally upbeat overall tone.

Prudent Bet On Low Oil Prices

March 16, 2016 Tsakos Energy Navigation LTD Prudent Bet On Low Oil Prices MORGAN STANLEY & CO. LLC Fotis Giannakoulis Fotis.Giannakoulis@morganstanley.com Sherif Elmaghrabi Sherif.Elmaghrabi@morganstanley.com

March 16, 2016 Tsakos Energy Navigation LTD Prudent Bet On Low Oil Prices MORGAN STANLEY & CO. LLC Fotis Giannakoulis Fotis.Giannakoulis@morganstanley.com Sherif Elmaghrabi Sherif.Elmaghrabi@morganstanley.com

Tower Tour Reinforces Our Positive View on the Towers

May 15, 2015 Telecom Services Tower Tour Reinforces Our Positive View on the Towers MORGAN STANLEY & CO. LLC Simon Flannery Simon.Flannery@morganstanley.com Armintas Sinkevicius, CFA, CPA Armintas.Sinkevicius@morganstanley.com

May 15, 2015 Telecom Services Tower Tour Reinforces Our Positive View on the Towers MORGAN STANLEY & CO. LLC Simon Flannery Simon.Flannery@morganstanley.com Armintas Sinkevicius, CFA, CPA Armintas.Sinkevicius@morganstanley.com

Structural Headwinds Likely Continue Beyond 2017

March 1, 2016 Halyard Health Structural Headwinds Likely Continue Beyond 2017 MORGAN STANLEY & CO. LLC David R. Lewis David.R.Lewis@morganstanley.com Jonathan L Demchick Jonathan.Demchick@morganstanley.com

March 1, 2016 Halyard Health Structural Headwinds Likely Continue Beyond 2017 MORGAN STANLEY & CO. LLC David R. Lewis David.R.Lewis@morganstanley.com Jonathan L Demchick Jonathan.Demchick@morganstanley.com

Global Strategy Forum: Renaissance Meets Reality

Morgan Stanley & Co. LLC : Renaissance Meets Reality Introduction: In today s Strategy Forum we look at the conclusions of the latest Morgan Stanley Blue Paper, US Manufacturing Renaissance: Is It a Masterpiece

Morgan Stanley & Co. LLC : Renaissance Meets Reality Introduction: In today s Strategy Forum we look at the conclusions of the latest Morgan Stanley Blue Paper, US Manufacturing Renaissance: Is It a Masterpiece

Raiffeisen International

EUROPE Morgan Stanley & Co. International Limited+ Maciej J Szczesny Maciej.Szczesny@morganstanley.com +44 (0)20 7425 8828 Stock Rating Underweight Industry View No Rating 2Q 06 Results Preview Quick Comment:

EUROPE Morgan Stanley & Co. International Limited+ Maciej J Szczesny Maciej.Szczesny@morganstanley.com +44 (0)20 7425 8828 Stock Rating Underweight Industry View No Rating 2Q 06 Results Preview Quick Comment:

Some Puts and Takes in Q2; Thesis Unchanged, Stay EW

August 30, 2018 02:15 AM GMT Dick's Sporting Goods Some Puts and Takes in Q2; Thesis Unchanged, Stay EW Stock Rating Equal-weight Industry View In-Line Price Target $35.00 Q2 EPS beat on better margins

August 30, 2018 02:15 AM GMT Dick's Sporting Goods Some Puts and Takes in Q2; Thesis Unchanged, Stay EW Stock Rating Equal-weight Industry View In-Line Price Target $35.00 Q2 EPS beat on better margins

GoPro Inc January 13, 2016

January 13, 2016 GoPro Inc Picture Not Likely to Clear Up for a While Industry View Cautious Stock Rating Underweight Price Target $12.00 The to-do list is long (better usability, new cameras, etc.), inventories

January 13, 2016 GoPro Inc Picture Not Likely to Clear Up for a While Industry View Cautious Stock Rating Underweight Price Target $12.00 The to-do list is long (better usability, new cameras, etc.), inventories

Baby Steps. Equal-weight. Attractive

July MONTH 28, 2016 DD, YYYY 04:01 HH:MM AM GMT AM/PM GMT Care.com Baby Steps Stock Rating Equal-weight Industry View Attractive Price Target $9.50 CRCM has improved profitability, making us more optimistic

July MONTH 28, 2016 DD, YYYY 04:01 HH:MM AM GMT AM/PM GMT Care.com Baby Steps Stock Rating Equal-weight Industry View Attractive Price Target $9.50 CRCM has improved profitability, making us more optimistic

1Q Report Doesn't Answer Main Question; Stay EW

August 3, 2015 Deckers Outdoor Corp 1Q Report Doesn't Answer Main Question; Stay EW MORGAN STANLEY & CO. LLC Jay Sole Jay.Sole@morganstanley.com Joseph Wyatt, CFA Joseph.Wyatt@morganstanley.com +1 212

August 3, 2015 Deckers Outdoor Corp 1Q Report Doesn't Answer Main Question; Stay EW MORGAN STANLEY & CO. LLC Jay Sole Jay.Sole@morganstanley.com Joseph Wyatt, CFA Joseph.Wyatt@morganstanley.com +1 212

Our Thoughts on Biosimilar hype

October 18, 2017 03:35 PM GMT Celltrion Inc. Our Thoughts on Biosimilar hype Stock Rating Underweight Industry View In-Line Price Target W80,000 Celltrion Group stocks' rallies have drawn interest from

October 18, 2017 03:35 PM GMT Celltrion Inc. Our Thoughts on Biosimilar hype Stock Rating Underweight Industry View In-Line Price Target W80,000 Celltrion Group stocks' rallies have drawn interest from

5 Telco Questions Ahead of MS SF TMT Conference

February 25, 2016 Telecom Services 5 Telco Questions Ahead of MS SF TMT Conference MORGAN STANLEY & CO. LLC Simon Flannery Simon.Flannery@morganstanley.com Lisa Lam, CFA Lisa.Lam@morganstanley.com Spencer

February 25, 2016 Telecom Services 5 Telco Questions Ahead of MS SF TMT Conference MORGAN STANLEY & CO. LLC Simon Flannery Simon.Flannery@morganstanley.com Lisa Lam, CFA Lisa.Lam@morganstanley.com Spencer

IT Hardware February 29, 2016

February 29, 2016 IT Hardware TMT Conference: Takeaways from Day 1 We hosted Fitbit, Western Digital, Seagate, and Electronics for Imaging on Day 1 of the MS TMT conference. Key takeaways from company

February 29, 2016 IT Hardware TMT Conference: Takeaways from Day 1 We hosted Fitbit, Western Digital, Seagate, and Electronics for Imaging on Day 1 of the MS TMT conference. Key takeaways from company

Balanced Portfolio and Gross Margin Upside Drive 1Q Results

May 4, 2016 CDW Corporation Balanced Portfolio and Gross Margin Upside Drive 1Q Results MORGAN STANLEY & CO. LLC Katy L. Huberty, CFA Kathryn.Huberty@morganstanley.com Jerry Liu Jerry.Y.Liu@morganstanley.com

May 4, 2016 CDW Corporation Balanced Portfolio and Gross Margin Upside Drive 1Q Results MORGAN STANLEY & CO. LLC Katy L. Huberty, CFA Kathryn.Huberty@morganstanley.com Jerry Liu Jerry.Y.Liu@morganstanley.com

GPhA thoughts and highlights: further consolidation appears inevitable

February 25, 2016 Specialty Pharmaceuticals GPhA thoughts and highlights: further consolidation appears inevitable We attended the annual GPhA (Generic Pharmaceutical Association) meeting in Florida Feb

February 25, 2016 Specialty Pharmaceuticals GPhA thoughts and highlights: further consolidation appears inevitable We attended the annual GPhA (Generic Pharmaceutical Association) meeting in Florida Feb

Closed-End Equity Funds

RESEARCH WEALTH MANAGEMENT INVESTMENT RESOURCES MAY 25, 2016 Closed-End Equity Funds NORTH AMERICA CHRISTOPHER K. BAXTER Morgan Stanley Wealth Management Christopher.Baxter@morganstanley.com +1 212 296-2562

RESEARCH WEALTH MANAGEMENT INVESTMENT RESOURCES MAY 25, 2016 Closed-End Equity Funds NORTH AMERICA CHRISTOPHER K. BAXTER Morgan Stanley Wealth Management Christopher.Baxter@morganstanley.com +1 212 296-2562

Strong 4Q15 Results. Stock Rating Equal-weight. Price target $7.50. Industry View In-Line

February 29, 2016 Scorpio Tankers Inc. Strong 4Q15 Results MORGAN STANLEY & CO. LLC Fotis Giannakoulis Fotis.Giannakoulis@morganstanley.com Sherif Elmaghrabi Sherif.Elmaghrabi@morganstanley.com +1 212

February 29, 2016 Scorpio Tankers Inc. Strong 4Q15 Results MORGAN STANLEY & CO. LLC Fotis Giannakoulis Fotis.Giannakoulis@morganstanley.com Sherif Elmaghrabi Sherif.Elmaghrabi@morganstanley.com +1 212

Tax Reform Still at the Drawing Board

November 3, 2017 12:22 AM GMT US Public Policy Brief Tax Reform Still at the Drawing Board Takeaways: Outcomes skew toward modest stimulus with execution risk; a controversial international system; limited