BPC6C Cost and Management Accounting. Unit : I to V

|

|

|

- Felicity Simon

- 6 years ago

- Views:

Transcription

1 BPC6C Cost and Management Accounting Unit : I to V

2 UNIT -1 FUNDAMENTALS OF COST ACCOUNTING Nature and scope of Cost Accounting, Distinction between cost and financial accounting, Cost sheet, tenders Characteristics of Management Accounting, Objectives of Management Accounting, Difference between Financial, Cost and Management Accounting, 2

3 FUNDAMENTALS OF COST ACCOUNTING MEANING OF COST ACCOUNTING It is a process of recording, classifying, analyzing, summarizing, allocating and evaluating various alternative courses of action for the control of costs DEFINITION OF COST ACCOUNTING The Institute of Cost and Management Accountant, England (ICMA) has defined Cost Accounting as the process of accounting for the costs from the point at which expenditure incurred, to the establishment of its ultimate relationship with cost centres and cost units For Simple notes click 3

4 COST SHEET FORMAT Particulars Raw materials Consumed direct Labour Direct Expenses Per Unit Total Cost Prime Cost Add: Factory overheads All expenes incurred in manufacturing works cost Add: Office Overheads All expenses incurred in administration Cost of Production Add: Selling & Distribution overheads All expenses incurred in selling distribution Cost of Sales Profit Sales 4

5 COST SHEET FORMAT Particulars Raw materials Consumed direct Labour Direct Expenses Per Unit Total Cost Prime Cost Add: Factory overheads All expenes incurred in manufacturing works cost Add: Office Overheads All expenses incurred in administration Cost of Production Add: Selling & Distribution overheads All expenses incurred in selling distribution Cost of Sales Profit Sales 5

6 FUNDAMENTAL S OF COST ACCOUNTING DIFFERENCE BETWEEN COST ACCOUNTING & FINANCIAL ACCOUNTING Cost Accounting Internal Reporting Point of Difference Purpose Optional Objective Manner Obligation Recording External Reporting mainly to tax authorities & Government Compulsory Subjective Manner Marginal Costing Budgetary Control Standard Costing The cost data helps in evaluation Control No control techniques Evaluation of efficiency Stock is always valued of Valuation of cost price stock Financial Accounting Not sufficient for evaluation Stock is valued at cost or market price 6

7 COST SHEET According to CIMA London Cost Sheet is A statement which provides for the assembly of the detailed cost of a centre or a cost unit. It is also a periodical statement. The expenditure which has been incurred upon product for a period is extracted from the financial books and the store records and set out in a memorandum statement. If this statement is confined to the disclosure of the costs of units produced dividing the period, it is termed as Cost- Sheet, but where the statement records both total cost, profit and sales, it is usually known as Statement of Cost or Production Account. 7

8 COST SHEET FORMAT Particulars Raw materials Consumed direct Labour Direct Expenses Per Unit Total Cost Prime Cost Add: Factory overheads All expenes incurred in manufacturing works cost Add: Office Overheads All expenses incurred in administration Cost of Production Add: Selling & Distribution overheads All expenses incurred in selling distribution Cost of Sales Profit Sales 8

9 COST SHEET Problems need to be worked out under 1. Simple cost sheet 2. Cost Sheet with Stock Adjustment 3. Cost sheet with Tender or Quotation 4. Cost Sheet with Estimated cost for future period 5. Cost Sheet with Hidden Information 6. Reconciliation Statement To check more problems click the following B 9

10 UNIT -II COST SHEET 10

11 Management Accounting Management Accounting is the presentation of accounting information in such a way as to assist management in the creation of policy and in day to day operations of an undertaking - ICMA Providing financial information Cause and effect analysis Use of special techniques and concepts Decision making No fixed conventions Achievement of objectives Improving efficiency Forecasting Providing information and not decisions 11

12 Financial, Cost and Management A/c Cost Accounting Management Accounting Purpose Ascertain and control Provide information to the cost of products or management for efficiently services performing the management functions Emphasis Based on both historical Future projections and present data Principles and Procedures Established procedures No such prescribed practice and practices are are followed followed Data used Quantitative information Scope Cost ascertainment and budgeting, Tax planning control and reporting to management Quantitative and Qualitative 12

13 UNIT II Stores Records, Purchase order, Stores Ledger, Economic Ordering Quantity, Minimum and Maximum Reorder Level Labour, importance of labour cost, Different methods of Wage Payment, Calculation of Wages, Methods of incentive for scheme. 13

14 MATERIALS COST Introduction to Materials Material costs are the costs of acquiring of material resources necessary for business. Raw materials and semi-finished products costs. The cost of acquiring the necessary raw materials and semi-finished products belongs to this group. This group of material costs is often the largest. Fuel and energy costs. Acquisition costs of gasoline, machine oil, gas, solid fuel, electricity, heat belong to this group. Packaging costs. Acquisition costs of various containers (boxes, bales, boxes) belong to these costs. Spare parts costs. Expenses of spare parts used to repair equipment, machinery or vehicles. Building materials costs. The cost of building materials arise when the company is building new facilities or making renovation of existing facilities. Other material cost. All material costs which are not included in the above groups related to other expenses. It may be, for example, waste production or other costs. 14

15 MATERIAL PROCUREMENT SYSTEM 15

16 ECONOMIC ORDERING QUANTITY (EOQ) The Economic Order Quantity (EOQ) is the number of units that a company should add to inventory with each order to minimize the total costs of inventory such as holding costs, order costs, and shortage costs. FORMULA FOR EOQ 16

17 ECONOMIC ORDERING QUANTITY (EOQ) 17

18 MATERIALS COST CONCEPT AND MEANING OF STOCK LEVEL Stock level refers to the different levels of stock which are required for an efficient and effective control of materials and to avoid over and under-stocking of materials. The purpose of materials control is to maintain the sock of raw materials as low as possible and at the same time they may be available as and when required. To avoid over and under-stocking, the storekeeper must fix the inventory level, which is also known as a demand and supply method of stock control. In a scientific system of inventory control the following levels of materials are fixed. 1. Re-order Level 2. Minimum Level Or Safety Level 3. Maximum Level 4. Average stock Level 5.. Danger Level 18

19 MATERIALS COST PURPOSE OF STOCK LEVELS 19

20 MATERIALS COST Maximum Level of Stock = (Reorder Level + Reorder Quantity) (Minimum rate of consumption x Minimum reorder period) Minimum level of stock = Reorder level (Average rate of consumption x Average reorder period) Reorder level or Ordering level = Maximum rate of consumption Maximum reorder period Average Stock level = (Maximum stock level + Minimum stock level) /2 or Minimum Stock level + 14 Reorder Quantity Danger level = Minimum rate of consumption Emergency delivery time 20

21 MATERIALS COST To learn more problems click the following link vel_maximum_stock_level_danger_level_cost_and_management_ accounting&b=42&c=

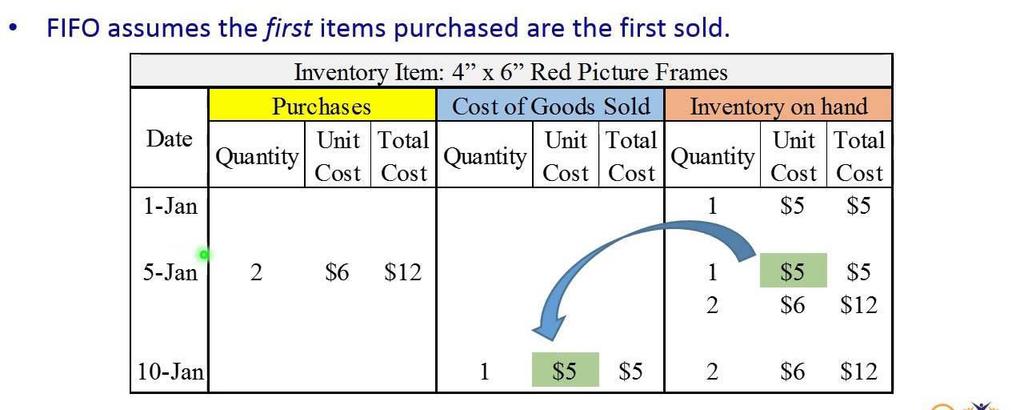

22 MATERIALS COST METHOS OF PRICING OF MATERIAL ISSUES FIFO - FIRST IN FIRST OUT LIFO - LAST IN FIRST OUT HIFO - HIGHEST IN FIRST OUT SAM -SIMPLE AVERAGE METHOD WAM - WEIGHTED AVERAGE METHOD BASE STOCK SPECIFIC PRICE METHOD 22

23 FIFO 23

24 LIFO 24

25 Weighted Average Method 25

26 SPECIFIC PRICE METHOD 26

27 Simple Average Price Method 27

28 BASE STOCK METHOD -FIFO 28

29 Store Ledger Base stock with LIFO 29

30 UNIT III MATERIALS COST WORKOUT PROBLEMS WITH THE HELP OF FOLLOWING LINK

31 LABOUR COST Labour cost - Meaning It is classified as direct and indirect. They form the labour cost which in turn forms a significant percentage of the total cost of production in a manufacturing or service organization. Minimizing costs does not mean reducing cost but means getting optimal and efficient productivity from the employees. Purposes of Labour Cost To calculate the correct gross and net wages for each employee. For financial accounting purposes. For management accounting purposes (i.e. stock valuation) Decision making and control purposes Elements of Labour Cost. Basic Wages. Overtime premium Bonus payment Idle time Labour turnover 31

32 CLASSIFICATION OF LABOUR COST 32

33 REMUNERATION METHODS Time Rate System Wages = No. of hours worked x Rate per hour Piece Rate System Wages = Rate per unit x No. of units produced. Incentive Plans Straight Piece Rate Method Guaranteed Day Work Rowan Premium Bonus Plan Group Incentive Schemes Gantt Task Bonus System Emerson Plan Flat Time Rate Method Taylor Differential Piece Rate Halsey Premium Bonus Plan Merrick Multiple Piece Rate Bedaux Point System Barth Premium System 33

34 LABOUR COST 34

35 LABOUR COST To workout problems refer the following link

36 UNIT III OVERHEADS Overheads overhead Classification, Accounting Manufacturing, Administration, and control of Selling and Distribution (Primary and Secondary Distribution), Allocation Apportionment and Absorption. Machine Hour Rate. 36

37 OVERHEADS Meaning Overhead costs, often referred to as overhead or operating expenses, refer to those expenses associated with running a business that can t be linked to creating or producing a product or service. Types Overhead costs can be broken down into three types: Fixed Variable Semi-variable 37

38 OVERHEAD ANALYSIS OVERHEAD ANALYSIS CAN BE DIVIDED INTO SIX STAGES 1.Overhead Collection - Overhead is said to be collected when it is incurred 2. Overhead Classification - This is the logical grouping of overhead into the major activities undertaken by a business such as production, selling, distribution and administration. 3. Overhead Codification - This refers to the use codes for the identification of overhead costs of different kinds 4. Overhead Allocation - This is charging of whole item of overhead to a single cost centre 5. Overhead Apportionment - This is the charging of proportions of overhead to different cost centres using fair and equitable bases. 6. Overhead Absorption - This is the charging of overhead to cost units using carefully calculated predetermined overhead rates 38

39 OVERHEADS PRIMARY DISTRIBUTION OF OVERHEAD Primary Distribution is the allocation or appointment of different items of overhead to both production and service departments on suitable basis. There is no partiality between production and service department in making primary distribution. IMPORTANT POINTS SHOULD BE KEPT IN MIND The basis for allocation and apportionment should be equitable and practicable. Charges are to be made to different departments in relation to benefits received. The method and basis for allocation and apportionment should not be time consuming and costly 39

40 APPORTIONMENT SECONDARY APPORTIONMENT It reapportions service department overhead to production departments. The objective of this stage is to ensure that only production departments bear all overhead costs, and which will eventually be charged to products. This is because while there is a direct link between the product produced and the production departments, there is no such link between the products and service departments. The absence of a direct link between service cost centres and products will make it difficult to charge service cost centre overheads to products. SERVICE DEPARENTS The departments such as canteen, administration, stores, maintenance, etc that do not take direct part in the production process. They provide support work for the production departments 40

41 UNIT V OVERHEADS Bases of Apportionment 1Cost or value of asset 2Floor space occupied 3Number of employees Overhead Cost Depreciation, insurance, repairs and maintenance, etc. Building depreciation, insurance and repairs, rent and rates, electricity, cleaning cost, Canteen, personnel administration, welfare, supervision, etc. Production or working hours Working hours affect almost all types 5Number of light bulbs 6.Metre reading Electricity Electricity, heating, air conditioning 7.Machine capacity or HP Electrical power 8.Number of requisitions Stores costs 41

42 Statement showing Primary Distribution of Overhead 42

43 Secondary distribution 43

44 UNIT V OVERHEADS 44

45 Over Absorption and Under Absorption of Overhead Over absorption occurs when the overhead absorbed is greater than the actual overhead incurred. Over absorbed overheads represent gains and are therefore credited to the profit and loss account. Under absorption occurs when actual overhead cost incurred is greater than the overhead absorbed. Under-absorbed overhead represents a loss and is therefore debited to the profit and loss account. 45

46 OVERHEADS Overhead Absorption This is the final stage of the overhead analysis process where the overhead of the production departments are charged to the final product. The following is the general formula for calculating overhead absorption rate. Activity level maybe measured using any of the following Cost basis Production hours Output Overhead absorption rates are based on budgeted overhead rather than actual overhead 46

47 UNIT V OVERHEADS Machine Hour Rate: Machine hour rate is a rational method for absorption of factory overhead. The factory overhead costs are allocated to a machine or a group of machines doing the same type of job and the cost per hour of the machine is ascertained dividing the total allocated overhead costs to the machine by number of hours the machine worked during the same period of time for which the costs have been considered. 47

48 MACHINE HOUR RATE 48

49 UNIT V OVERHEADS To workout more problems click the link

50 Unit IV Uses & limitations of funds flow statement Difference between funds flow statement and balance sheet Advantages and limitations of cash flow statement Methods of preparing cash flow statement Objectives of Ratio Analysis Advantages & Limitations of Ratio Analysis Steps in Ratio Analysis Classification of Ratios 50

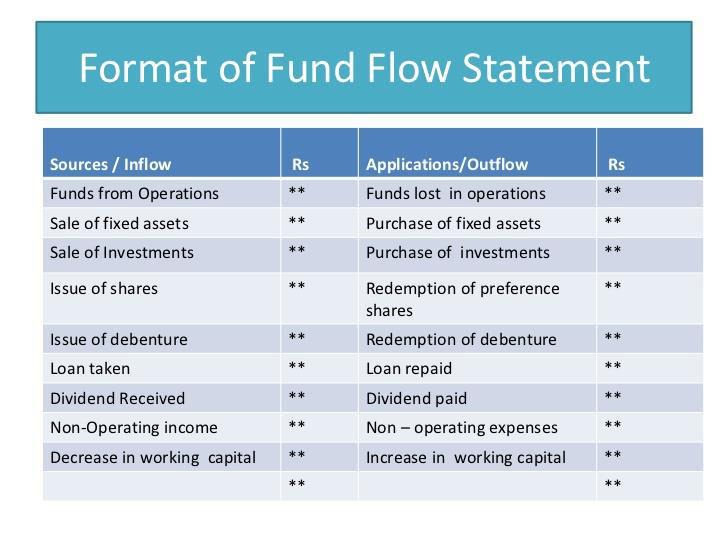

51 Funds Flow Statement It is based on Working Capital concept of funds. It measures inflow and outflow of working capital resulting from different business transactions IMPORTANCE OF FUNDS FLOW STATEMENT Dividend Policy Financial Analysis and Control Useful to Bankers and Money Lenders Knowledge of Business Problems Manageri al Policies Financial Planning Helpful in Comparat ive Study 51

52 TRANSACTIONS THAT WILL AFFECT THE FLOW OF FUNDS The following transactions will bring the change in the working capital: 1. Current Assets and Non-Current Assets 2. Current Assets and Non-Current Liabilities 3. Current Liabilities and Non-Current Liabilities 4. Current Liabilities and Non-Current Assets TRANSACTIONS THAT WILL NOT AFFECT THE FLOW OF FUNDS Current Assets and Current Liabilities Non-Current Assets and Non-Current Liabilities Non-Current Liabilities or Non-Current Assets. 52

53 Funds Flow Statement & Balance Sheet Funds Flow Statement Balance Sheet Shows changes in working capital between 2 balance sheet dates Shows the position of assets and liabilities on a specific date Shows only those items which cause changes in working capital Shows the real and personal accounts of a business Aims at presenting flow of funds over a period Aims at depicting the financial position of a business Tool for financial analysis generally Culmination of the accounting process useful for management of a period meant for usage of stakeholders Based on the data from financial statements Based on trial balance Prepared after financial accounts are completed Prepared after income statement is completed 53

54 Steps in Funds Flow Statement Schedule of Changes in Working Capital is prepared from current assets and current liabilities in order to calculate the increase or decrease in working capital 54

55 Schedule of Changes in Working Capital Particulars Previous Year Rs. Current Year Rs. Changes in Working Capital Increase Decrease Current Assets : Cash Debtors Stocks Bill Receivables Marketable Securities or Shortterm Investment Current Liabilities: Creditors Bills Payable Bank Overdraft Outstanding Expenses Short-term Loan Increase or Decrease in Working Capital 55

56 Adjusted P&L A/c It can be calculated in two forms : Particulars Amount Rs. Amount Rs. Net Profit for Current Year Add : Non fund items Depreciation Goodwill, Patents Preliminary Expenses Written off LESS : Non-fund Items and Nontrading Income,already Credited to P & L A/c. Dividend Received Profit on sale Funds from operations 56

57 Profit and Loss Adjustment A/c Particulars To Depreciation Amount Particulars Amount By opening Balance of P&L Appropriation A/c To Goodwill Written off By Dividend Received To preliminary Expenses written off By Over provisions Written Back To Transfer to sinking fund To Loss on sale of fixed Assets By Funds from operations (Balancing Figure) To Closing Balance of P&L Appropriation A/c 57

58 While preparing funds flow statement, the following rules must be remembered An increase in a fixed assets indicates an application of funds A decrease in a fixed assets indicates a source of funds An increase in a fixed liability indicates a source of funds A decrease in fixed liability indicates an application of funds An increase in share capital indicates a source of funds A decrease in share capital indicates an application of funds Source of Funds -Fixed Assets +Fixed Liabilities +Share Capital Application of Funds +Fixed Assets -Fixed Liabilities -Share Capital 58

59 59

60 Cash Flow Statement Periodic Provides information regarding the liquidity of a firm Explains the reasons for increase or decrease in cash balance from one balance sheet date to the next Classifies the reasons for the change as an operating, investing or financing activity. Reconciles net income with cash flow from operations. 60

61 61

62 Presentation of Cash Flow Statement Indirect Method Increases in Cash Operating (receipts from revenues) Investing (receipts from sales of noncurrent assets) Financing (receipts from issuing equity and debt securities) Decreases in Cash Operating (payments for expenses) Investing (payments for acquiring noncurrent assets) Financing (payments for treasury stock, dividends, and redemption of debt securities) 62 62

63 Cash Flow Statement Cash flows from operating activities Net Income Adjustments to reconcile net income to net cash provided by **** **** **** operating activities **** + Depreciation expense **** + Loss on sale of long-term assets **** - Gain on sale of long-term assets **** - Increases in current assets other than cash **** + Decreases in current assets other than cash **** + Increases in current liabilities **** - Decreases in current liabilities **** Net cash provided by operating activities **** 63

Paying dividends, debt, purchasing")

64 Investing Activities Cash inflows from investing activities arise from Selling fixed assets, investments, intangible assets Cash outflows from investing activities arise from Buying fixed assets, investments, intangible assets Financing Activities Cash inflows from financing activities arise from Issuing debt, equity securities Cash outflows from financing activities arise from (Re)Paying dividends, debt, purchasing treasury stock 64

65 Cash flows from operating activities Direct Method Cash Inflows: 1. Collections from customers including cash received from sales (or services) and collections of A/R. 2. Cash receipts of interests or dividends. 3. Collections of other operating receipts (i.e., unearned revenue, rent revenue). Cash Outflows: 1. Payments to suppliers. 2. Payments to employees. 3. Payments for interest expense. 4. Payments for income taxes. 5. Payments for other expenses(i.e., Prepaid expenses; rent expenses). 65

66 Comparison of Direct & Indirect Method Direct method of presentation calculates cash flow from operations by subtracting cash disbursements to supplies, employees, and others from cash receipts from customers. The indirect method calculates cash flow from operations by adjusting net income for non-cash revenues and expenses. Most firms present their cash flows using the indirect method. Only operating activities section is different between the methods, investing and financing sections are the same. 66

67 Ratio Analysis Ratio is a mathematical relationship between 2 items expressed in quantitative form Ratio analysis is the process of determining and presenting the relationship of items and groups of items in the financial statements Rations may be expressed in: o Proportion o Times o Percentage 67

68 Profitability Ratios 68

69 Profitability Ratios 69

70 Turnover Ratios 70

71 Turnover Ratios 71

72 Short Term Solvency Ratios 72

73 Long Term Solvency Ratios 73

74 Unit V - Syllabus Features of marginal costing Advantages & limitations of marginal costing Marginal & absorption costing Cost Volume Profit analysis Break even charts Difference between forecast and budget Objectives of budgetary control Advantages & limitations of budgetary control Classification of budgets Zero based budgeting 74

75 Marginal Costing Marginal Cost is the amount at any given volume of output by which aggregate costs are changed if volume of output is increased or decreased by one unit.it relates to change in output in particular circumstances under consideration. Marginal costing is the ascertainment of marginal cost and of the effect on profit of changes in volume or type of output by differentiating fixed cost &variable cost.in this technique of costing only variable cost are charged to operation,processes or products leaving all indirect cost to be written off against profits in period in which they arise. 75

76 Sales = Variable Cost + Fixed Cost + Profit S = VC + FC + P Profit = Sales Variable Cost Fixed Cost P = S-VC-FC 76

77 Marginal Cost Equation Tm Contribution = Sales Variable Cost (or) Contribution = Fixed Cost + Profit C = S VC (or) C = FC + P P/V Ratio = Contribution / Sales * 100 P/V Ratio = C/S*100 Break Even Point = Fixed Cost / PV Ratio BEP (Rs.) = FC/PV Ratio BEP (Units) = Fixed Cost / Contribution Per Unit Required Sales = (Fixed Cost + Profit) / PV Ratio *

78 78

79 Margin of Safety = Profit / PV Ratio (or) Margin of Safety = Actual Sales Break Even Sales MOS = P/PV Ratio (or) MOS = S-BES 79

80 Break Even Point 80

81 Budget Budget is defined as a financial or quantitative statement prepared prior to a definite period of time to be pursued during that period for the purpose of attaining a given o je tive ICMA Budgeting refers to the process of preparing budgets Budgetory Control is the process of prparation of budgets for various activities and comparing the budgeted figures for arriving at deviations 81

82 Functional Budgets Purchase Budget Cash Budget Sales Budget Production Budget Materials Budget 82

83 Cash Budget 83

84 Production Budget 84

85 Materials Budget 85

COMMERCE & LAW PROGRAM DIVISION (CLPD) ANSWER KEY TO CS-EXECUTIVE DECEMBER-2014 (ATTEMPT) CODE-C SUBJECT : COST & MANAGEMENT ACCOUNTING

ANSWER KEY TO CS-EXECUTIVE DECEMBER-2014 (ATTEMPT) CODE-C SUBJECT : COST & MANAGEMENT ACCOUNTING") COMMERCE & LAW PROGRAM DIVISION (CLPD) ANSWER KEY TO CS-EXECUTIVE DECEMBER-2014 (ATTEMPT) CODE-C SUBJECT : COST & MANAGEMENT ACCOUNTING 1. If the minimum stock level and average stock level of raw material

COMMERCE & LAW PROGRAM DIVISION (CLPD) ANSWER KEY TO CS-EXECUTIVE DECEMBER-2014 (ATTEMPT) CODE-C SUBJECT : COST & MANAGEMENT ACCOUNTING 1. If the minimum stock level and average stock level of raw material

B.Com II Cost Accounting

B.Com II Cost Accounting Chapter - 1 Cost Accounting: An Overview of Fundamental Aspects 2009 (1) Discuss the objectives of Cost Accounting. 2011 (1) Discuss importance of cost accounting. 2012 (1) What

B.Com II Cost Accounting Chapter - 1 Cost Accounting: An Overview of Fundamental Aspects 2009 (1) Discuss the objectives of Cost Accounting. 2011 (1) Discuss importance of cost accounting. 2012 (1) What

December CS Executive Programme Module - I Paper - 2

December - 2015 CS Executive Programme Module - I Paper - 2 (New Syllabus) Cost and Management Accounting Total number of questions: 100 Maximum marks: 100 Assertion A: 1. In management accounting, firm

December - 2015 CS Executive Programme Module - I Paper - 2 (New Syllabus) Cost and Management Accounting Total number of questions: 100 Maximum marks: 100 Assertion A: 1. In management accounting, firm

COST ACCOUNTING INTERVIEW QUESTIONS

www.globalcma.in Learning Platform for Cost Accountants (CMA) Explain cost sheet? Cost Sheet is a periodical statement of cost designed to show in detail the various elements of cost of goods produced

www.globalcma.in Learning Platform for Cost Accountants (CMA) Explain cost sheet? Cost Sheet is a periodical statement of cost designed to show in detail the various elements of cost of goods produced

Cost and Management Accounting

Paper 2 Cost and Management Accounting Syllabus......................................... 2.2 Line Chart Showing Relative Importance of Chapters...... 2.6 Table Showing Importance of Chapter on the Basis

Paper 2 Cost and Management Accounting Syllabus......................................... 2.2 Line Chart Showing Relative Importance of Chapters...... 2.6 Table Showing Importance of Chapter on the Basis

STUDY MATERIAL BASED CONTENTS

STUDY MATERIAL BASED CONTENTS Paper 3 Cost and Management Accounting Syllabus....................................... 3. Examination Trend Analysis........................ 3.7 Line Chart Showing Relative

STUDY MATERIAL BASED CONTENTS Paper 3 Cost and Management Accounting Syllabus....................................... 3. Examination Trend Analysis........................ 3.7 Line Chart Showing Relative

Answer to PTP_Intermediate_Syllabus 2008_Jun2015_Set 1

Paper 8: Cost & Management Accounting Time Allowed: 3 Hours Full Marks: 100 Question No 1 is Compulsory. Answers any five Questions from the rest. Working Notes should form part of the answer. Question.1

Paper 8: Cost & Management Accounting Time Allowed: 3 Hours Full Marks: 100 Question No 1 is Compulsory. Answers any five Questions from the rest. Working Notes should form part of the answer. Question.1

CS Executive Programme Module - I December Paper - 2 : Cost and Management Accounting

ISBN : 978-93-5034-747-8 Solved Scanner Appendix CS Executive Programme Module - I December - 2013 Paper - 2 : Cost and Management Accounting Chapter - 1 : Introduction to Cost and Management Accounting

ISBN : 978-93-5034-747-8 Solved Scanner Appendix CS Executive Programme Module - I December - 2013 Paper - 2 : Cost and Management Accounting Chapter - 1 : Introduction to Cost and Management Accounting

322 Roll No : 1 : Time allowed : 3 hours Maximum marks : 100

2/2013/CMA (N/S) Roll No : 1 : Time allowed : 3 hours Maximum marks : 100 Total number of questions : 6 Total number of printed pages : 7 NOTE : 1. Answer ALL Questions. 2. All working notes should be

2/2013/CMA (N/S) Roll No : 1 : Time allowed : 3 hours Maximum marks : 100 Total number of questions : 6 Total number of printed pages : 7 NOTE : 1. Answer ALL Questions. 2. All working notes should be

SET - I Paper 2-Fundamentals of Accounting

SET - I Paper 2-Fundamentals of Accounting Full Marks: 100 Time allowed: 3 Hours PART A I. Choose the correct answer from the given four alternatives: [6 1=6] 1. Accounting function does not include (a)

SET - I Paper 2-Fundamentals of Accounting Full Marks: 100 Time allowed: 3 Hours PART A I. Choose the correct answer from the given four alternatives: [6 1=6] 1. Accounting function does not include (a)

I B.Com PA [ ] Semester II Core: Management Accounting - 218A Multiple Choice Questions.

![I B.Com PA [ ] Semester II Core: Management Accounting - 218A Multiple Choice Questions.](/thumbs/80/82536614.jpg "I B.Com PA [ ] Semester II Core: Management Accounting - 218A Multiple Choice Questions.") 1 of 23 1/27/2018, 11:53 AM Dr.G.R.Damodaran College of Science (Autonomous, affiliated to the Bharathiar University, recognized by the UGC)Reaccredited at the 'A' Grade Level by the NAAC and ISO 9001:2008

1 of 23 1/27/2018, 11:53 AM Dr.G.R.Damodaran College of Science (Autonomous, affiliated to the Bharathiar University, recognized by the UGC)Reaccredited at the 'A' Grade Level by the NAAC and ISO 9001:2008

Contents. Chapter 1 Conceptual Foundation

Contents Chapter 1 Conceptual Foundation Meaning of Accounting... 2 Need for Accounting Information... 3 Areas of Accounting... 4 Financial Accounting... 4 Meaning... 4 Objectives... 4 Limitations... 5

Contents Chapter 1 Conceptual Foundation Meaning of Accounting... 2 Need for Accounting Information... 3 Areas of Accounting... 4 Financial Accounting... 4 Meaning... 4 Objectives... 4 Limitations... 5

SYMBIOSIS CENTRE FOR DISTANCE LEARNING (SCDL) Subject: Management Accounting

Subject: Management Accounting") Sample Questions: Section I: Subjective Questions 1. How does Subsidiary Book help in accounting process? Which subsidiary books are used very frequently? 2. Differentiate between the liabilities and assets.

Sample Questions: Section I: Subjective Questions 1. How does Subsidiary Book help in accounting process? Which subsidiary books are used very frequently? 2. Differentiate between the liabilities and assets.

Free of Cost ISBN : CMA (CWA) Inter Gr. II. (Solution upto June & Questions of Dec Included)

Inter Gr. II. (Solution upto June & Questions of Dec Included)") Free of Cost ISBN : 978-93-5034-704-1 Solved Scanner Appendix CMA (CWA) Inter Gr. II (Solution upto June - 2013 & Questions of Dec - 2013 Included) Chapter- 2: Material Accounting 2013 - June [7] (a) Date

Free of Cost ISBN : 978-93-5034-704-1 Solved Scanner Appendix CMA (CWA) Inter Gr. II (Solution upto June - 2013 & Questions of Dec - 2013 Included) Chapter- 2: Material Accounting 2013 - June [7] (a) Date

MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47

Time: 60 min Marks: 47") MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47 Question No: 1 ( Marks: 1 ) - Please choose one Which of the following product cost is Included

MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47 Question No: 1 ( Marks: 1 ) - Please choose one Which of the following product cost is Included

ALL IN ONE MGT 402 MIDTERM PAPERS MORE THAN ( 10 )

") ALL IN ONE MGT 402 MIDTERM PAPERS MORE THAN ( 10 ) MIDTERM EXAMINATION MGT402- Cost & Management Accounting Question No: 1 ( Marks: 1 ) - Please choose one D Corporation uses process costing to calculate

ALL IN ONE MGT 402 MIDTERM PAPERS MORE THAN ( 10 ) MIDTERM EXAMINATION MGT402- Cost & Management Accounting Question No: 1 ( Marks: 1 ) - Please choose one D Corporation uses process costing to calculate

Answer to MTP_Intermediate_Syllabus 2008_Jun2014_Set 1

Paper-8: COST & MANAGEMENT ACCOUNTING SECTION - A Answer Q No. 1 (Compulsory) and any 5 from the rest Question.1 (a) Match the statement in Column 1 with the most appropriate statement in Column 2 : [1

Paper-8: COST & MANAGEMENT ACCOUNTING SECTION - A Answer Q No. 1 (Compulsory) and any 5 from the rest Question.1 (a) Match the statement in Column 1 with the most appropriate statement in Column 2 : [1

Analysing cost and revenues

Osborne Books Tutor Zone Analysing cost and revenues Chapter activities Osborne Books Limited, 2013 2 a n a l y s i n g c o s t s a n d r e v e n u e s t u t o r z o n e 1 An introduction to cost accounting

Osborne Books Tutor Zone Analysing cost and revenues Chapter activities Osborne Books Limited, 2013 2 a n a l y s i n g c o s t s a n d r e v e n u e s t u t o r z o n e 1 An introduction to cost accounting

FOUNDATION EXAMINATION

FOUNDATION EXAMINATION (SYLLABUS 2008) SUGGESTED ANSWERS TO QUESTIONS JUNE 2012 Paper-2 : ACCOUNTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the right side indicate full marks.

FOUNDATION EXAMINATION (SYLLABUS 2008) SUGGESTED ANSWERS TO QUESTIONS JUNE 2012 Paper-2 : ACCOUNTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the right side indicate full marks.

(AA22) COST ACCOUNTING AND REPORTING

COST ACCOUNTING AND REPORTING") All Rights Reserved ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA AA2 EXAMINATION - JULY 2017 (AA22) COST ACCOUNTING AND REPORTING Instructions to candidates (Please Read Carefully): (1) Time Allowed:

All Rights Reserved ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA AA2 EXAMINATION - JULY 2017 (AA22) COST ACCOUNTING AND REPORTING Instructions to candidates (Please Read Carefully): (1) Time Allowed:

Cost and Management Accounting

Paper 2 Cost and Management Accounting Syllabus................................................ 2.2 Line Chart Showing Relative Importance of Chapters............ 2.5 Table Showing Importance of Chapter

Paper 2 Cost and Management Accounting Syllabus................................................ 2.2 Line Chart Showing Relative Importance of Chapters............ 2.5 Table Showing Importance of Chapter

Answer to MTP_Foundation_Syllabus 2012_Dec2016_Set 2 Paper 2- Fundamentals of Accounting

Paper 2- Fundamentals of Accounting Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 2- Fundamentals of Accounting Full Marks :

Paper 2- Fundamentals of Accounting Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 2- Fundamentals of Accounting Full Marks :

BATCH All Batches. DATE: MAXIMUM MARKS: 100 TIMING: 3 Hours. PAPER 3 : Cost Accounting

BATCH All Batches DATE: 25.09.2017 MAXIMUM MARKS: 100 TIMING: 3 Hours PAPER 3 : Cost Accounting Q. No. 1 is compulsory. Wherever necessary suitable assumptions should be made by the candidates. Working

BATCH All Batches DATE: 25.09.2017 MAXIMUM MARKS: 100 TIMING: 3 Hours PAPER 3 : Cost Accounting Q. No. 1 is compulsory. Wherever necessary suitable assumptions should be made by the candidates. Working

Paper 8- Cost Accounting

Paper 8- Cost Accounting Dos, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 8- Cost Accounting Full Marks : 100 Time allowed: 3 hours Section A Question

Paper 8- Cost Accounting Dos, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 8- Cost Accounting Full Marks : 100 Time allowed: 3 hours Section A Question

Suggested Answer_Syl12_Dec2015_Paper 8 INTERMEDIATE EXAMINATION

INTERMEDIATE EXAMINATION GROUP I (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2015 Paper8 : COST ACCOUNTING AND FINANCIAL MANAGEMENT Time Allowed : 3 Hours Full Marks : 100 The figures in the

INTERMEDIATE EXAMINATION GROUP I (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2015 Paper8 : COST ACCOUNTING AND FINANCIAL MANAGEMENT Time Allowed : 3 Hours Full Marks : 100 The figures in the

Cost and Management Accounting

Paper 2B Cost and Management Accounting Syllabus................................................ 2.314 Bird's-Eye View.......................................... 2.315 Line Chart Showing Relative Importance

Paper 2B Cost and Management Accounting Syllabus................................................ 2.314 Bird's-Eye View.......................................... 2.315 Line Chart Showing Relative Importance

(AA22) COST ACCOUNTING AND REPORTING

COST ACCOUNTING AND REPORTING") All Rights Reserved ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA AA2 EXAMINATION - JULY 2016 (AA22) COST ACCOUNTING AND REPORTING Instructions to candidates (Please Read Carefully): (1) Time Allowed:

All Rights Reserved ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA AA2 EXAMINATION - JULY 2016 (AA22) COST ACCOUNTING AND REPORTING Instructions to candidates (Please Read Carefully): (1) Time Allowed:

SYLLABUS. Class B.Com IV Sem. (Hons.)

") SYLLABUS Class B.Com IV Sem. (Hons.) SUBJECT: THEORY & PRACTICE OF COST ACCOUNT Unit I Unit II Unit III Unit IV Unit V Cost Accounting:- Nature, Scope, Methods, Techniques & installation of costing system,

SYLLABUS Class B.Com IV Sem. (Hons.) SUBJECT: THEORY & PRACTICE OF COST ACCOUNT Unit I Unit II Unit III Unit IV Unit V Cost Accounting:- Nature, Scope, Methods, Techniques & installation of costing system,

About the author I-5 Acknowledgement I-7 Preface I-9 Chapter-heads I-11

CONTENTS About the author I-5 Acknowledgement I-7 Preface I-9 Chapter-heads I-11 1 INTRODUCTION u Cost 1 u Costing 2 u Cost accounting 2 u Cost accountancy 2 u Classification of costs 3 u Distinction between

CONTENTS About the author I-5 Acknowledgement I-7 Preface I-9 Chapter-heads I-11 1 INTRODUCTION u Cost 1 u Costing 2 u Cost accounting 2 u Cost accountancy 2 u Classification of costs 3 u Distinction between

Purushottam Sir. Formulas of Costing

Purushottam Sir Formulas of Costing Material Maximum Stock Level= Re-order level + Re-order quantity (Minimum consumption Minimum reorder period) Minimum Stock Level= Re-order level (Average lead time

Purushottam Sir Formulas of Costing Material Maximum Stock Level= Re-order level + Re-order quantity (Minimum consumption Minimum reorder period) Minimum Stock Level= Re-order level (Average lead time

WORK BOOK COST ACCOUNTING

WORK BOOK COST ACCOUNTING INTERMEDIATE GROUP I PAPER 8 The Institute of Cost Accountants of India (Statutory body under an Act of Parliament) www.icmai.in First Edition : March 2018 Completed by : Academics

WORK BOOK COST ACCOUNTING INTERMEDIATE GROUP I PAPER 8 The Institute of Cost Accountants of India (Statutory body under an Act of Parliament) www.icmai.in First Edition : March 2018 Completed by : Academics

MIDTERM EXAMINATION Spring 2009 MGT402- Cost & Management Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one D Corporation uses process costing to calculate the cost of manufacturing

MIDTERM EXAMINATION Spring 2009 MGT402- Cost & Management Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one D Corporation uses process costing to calculate the cost of manufacturing

Unit 1 Theoretical Framework.

Unit 1 Theoretical Framework. A. Answer the Following (1 Mark) 1. What is Accounting equation? 2. Find out the value of assets if: Liabilities=Rs. 5000 and Capital=Rs.1000. 3. Give the classification of

Unit 1 Theoretical Framework. A. Answer the Following (1 Mark) 1. What is Accounting equation? 2. Find out the value of assets if: Liabilities=Rs. 5000 and Capital=Rs.1000. 3. Give the classification of

TEACHING LESSON PLAN- B.Com (Regular) 4 th Semester

4 th Semester") TEACHING LESSON PLAN- B.Com (Regular) 4 th Semester SUBJECT: C 5MC40: COST ACCOUNTING MODULE : BASIC CONCEPTS AND CLASSIFICATION SESSION/ HOURS REQUIRED) 5 Hrs Hours a) Meaning of Cost Accounting, Costing,

TEACHING LESSON PLAN- B.Com (Regular) 4 th Semester SUBJECT: C 5MC40: COST ACCOUNTING MODULE : BASIC CONCEPTS AND CLASSIFICATION SESSION/ HOURS REQUIRED) 5 Hrs Hours a) Meaning of Cost Accounting, Costing,

PRACTICE TEST PAPER - 2 INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT

: GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT") PRACTICE TEST PAPER - 2 INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT Question No. 1 is compulsory. Attempt any five questions from the remaining six questions. Working

PRACTICE TEST PAPER - 2 INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT Question No. 1 is compulsory. Attempt any five questions from the remaining six questions. Working

(AA22) COST ACCOUNTING AND REPORTING

COST ACCOUNTING AND REPORTING") All Rights Reserved ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA AA2 EXAMINATION - JULY 2015 (AA22) COST ACCOUNTING AND REPORTING Instructions to candidates (Please Read Carefully): (1) Time: 03

All Rights Reserved ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA AA2 EXAMINATION - JULY 2015 (AA22) COST ACCOUNTING AND REPORTING Instructions to candidates (Please Read Carefully): (1) Time: 03

COST ACCOUNTING AND FINANCIAL MANAGEMENT

STUDY MATERIAL Intermediate (IPC) Course PAPER : 3 COST ACCOUNTING AND FINANCIAL MANAGEMENT Part 1 : Cost Accounting VOLUME I BOARD OF STUDIES THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA This study

STUDY MATERIAL Intermediate (IPC) Course PAPER : 3 COST ACCOUNTING AND FINANCIAL MANAGEMENT Part 1 : Cost Accounting VOLUME I BOARD OF STUDIES THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA This study

SECTION I 14,000 14,200 19,170 10,000 8,000 10,400 12,400 9,600 8,400 11,200 13,600 18,320

QUESTION ONE SECTION I The following budget and actual results relates to Cypo Ltd. for the last three quarters for the year ended 31 March 200. Budget: Quarter 2 Quarter 3 Quarter to 30/9/2003 to 31/12/2003

QUESTION ONE SECTION I The following budget and actual results relates to Cypo Ltd. for the last three quarters for the year ended 31 March 200. Budget: Quarter 2 Quarter 3 Quarter to 30/9/2003 to 31/12/2003

PTP_Intermediate_Syllabus 2012_Jun2014_Set 1

Paper 8: Cost Accounting & Financial Management Time Allowed: 3 Hours Full Marks: 100 Question.1 Section A-Cost Accounting (Answer Question No. 1 which is compulsory and any three from the rest in this

Paper 8: Cost Accounting & Financial Management Time Allowed: 3 Hours Full Marks: 100 Question.1 Section A-Cost Accounting (Answer Question No. 1 which is compulsory and any three from the rest in this

Analysing cost and revenues

Osborne Books Tutor Zone Analysing cost and revenues Chapter activities answers Osborne Books Limited, 2013 2 a n a l y s i n g c o s t s a n d r e v e n u e s t u t o r z o n e 1 An introduction to cost

Osborne Books Tutor Zone Analysing cost and revenues Chapter activities answers Osborne Books Limited, 2013 2 a n a l y s i n g c o s t s a n d r e v e n u e s t u t o r z o n e 1 An introduction to cost

MGT402 Cost & Management Accounting. Composed By Faheem Saqib MIDTERM EXAMINATION. Spring MGT402- Cost & Management Accounting (Session - 1)

") MGT402 Cost & Management Accounting Composed By Faheem Saqib 14 Midterm Papers 3 of 2010 & 11 of 2009 For more Help Rep At Faheem_saqib2003@yahoo.com Faheem.saqib2003@gmail.com 0334-6034849 MIDTERM EXAMINATION

MGT402 Cost & Management Accounting Composed By Faheem Saqib 14 Midterm Papers 3 of 2010 & 11 of 2009 For more Help Rep At Faheem_saqib2003@yahoo.com Faheem.saqib2003@gmail.com 0334-6034849 MIDTERM EXAMINATION

Examinations for Academic Year Semester I / Academic Year 2015 Semester II. 1. This question paper consists of Section A and Section B.

PROGRAMME COHORT BSc (Hons) Human Resource Management BSc (Hons) Management BHRM/14B/FT BMAN/15A/FT B1, B2 Examinations for Academic Year 2015 2016 Semester I / Academic Year 2015 Semester II MODULE: COST

PROGRAMME COHORT BSc (Hons) Human Resource Management BSc (Hons) Management BHRM/14B/FT BMAN/15A/FT B1, B2 Examinations for Academic Year 2015 2016 Semester I / Academic Year 2015 Semester II MODULE: COST

ST. JOSEPH S COLLEGE OF COMMERCE

ST. JOSEPH S COLLEGE OF COMMERCE (AUTONOMOUS) LESSON PLAN 207-208 EVEN SEMESTER B.Com - Travel and Tourism C2 5 MC 40 Cost Accounting TEACHING LESSON PLAN- B.Com (Travel and Tourism) 4 th Semester SUBJECT:

ST. JOSEPH S COLLEGE OF COMMERCE (AUTONOMOUS) LESSON PLAN 207-208 EVEN SEMESTER B.Com - Travel and Tourism C2 5 MC 40 Cost Accounting TEACHING LESSON PLAN- B.Com (Travel and Tourism) 4 th Semester SUBJECT:

INTERMEDIATE EXAMINATION

INTERMEDIATE EXAMINATION GROUP II (SYLLABUS 2008) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2011 Paper-8 : COST AND MANAGEMENT ACCOUNTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin

INTERMEDIATE EXAMINATION GROUP II (SYLLABUS 2008) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2011 Paper-8 : COST AND MANAGEMENT ACCOUNTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin

Free of Cost ISBN : Scanner Appendix. CS Executive Programme Module - I December Paper - 2 : Cost and Management Accounting

Free of Cost ISBN : 978-93-5034-831-4 Solved Scanner Appendix CS Executive Programme Module - I December - 2013 Paper - 2 : Cost and Management Accounting Chapter - 1: Introduction to Cost and Management

Free of Cost ISBN : 978-93-5034-831-4 Solved Scanner Appendix CS Executive Programme Module - I December - 2013 Paper - 2 : Cost and Management Accounting Chapter - 1: Introduction to Cost and Management

TEACHING LESSON PLAN- B.Com (Regular) 4 th Semester

4 th Semester") TEACHING LESSON PLAN- B.Com (Regular) 4 th Semester SUBJECT: C 5MC40: COST ACCOUNTING MODULE : BASIC CONCEPTS AND CLASSIFICATION 4 Hours a) Meaning of Cost Accounting, Costing, Cost Accountancy, Cost Management

TEACHING LESSON PLAN- B.Com (Regular) 4 th Semester SUBJECT: C 5MC40: COST ACCOUNTING MODULE : BASIC CONCEPTS AND CLASSIFICATION 4 Hours a) Meaning of Cost Accounting, Costing, Cost Accountancy, Cost Management

: 1 : Time allowed : 3 hours Maximum marks : 100. Total number of questions : 8 Total number of printed pages : 8

Roll No : 1 : 262 Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 8 NOTE : All working notes should be shown distinctly. PART A (Answer Question

Roll No : 1 : 262 Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 8 NOTE : All working notes should be shown distinctly. PART A (Answer Question

Roll No : 1 : Time allowed : 3 hours Maximum marks : 100. Total number of questions : 8 Total number of printed pages : 11

Roll No : 1 : Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 11 NOTE : All working notes should be shown distinctly. PART A (Answer Question No.1

Roll No : 1 : Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 11 NOTE : All working notes should be shown distinctly. PART A (Answer Question No.1

Level 2 Cost Accounting

Level 2 Cost Accounting Syllabus Effective for examinations to be held after 1 January 2008 ASPE0483 >f0t@wjy9w2`4s3dpd# Vision Statement Our vision is to contribute to the achievements of learners around

Level 2 Cost Accounting Syllabus Effective for examinations to be held after 1 January 2008 ASPE0483 >f0t@wjy9w2`4s3dpd# Vision Statement Our vision is to contribute to the achievements of learners around

MTP_Intermediate_Syllabus 2012_Jun2017_Set 1 Paper 8- Cost Accounting & Financial Management

Paper 8- Cost Accounting & Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper-8: Cost Accounting & Financial

Paper 8- Cost Accounting & Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper-8: Cost Accounting & Financial

Cost and Management Accounting

Paper 2 Cost and Management Accounting Syllabus... Q&A-2.2 Bird's-Eye View... Q&A-2.5 Line Chart Showing Relative Importance Chapters... Q&A-2.7 Table Showing Importance of Chapter on the Basis of Marks...

Paper 2 Cost and Management Accounting Syllabus... Q&A-2.2 Bird's-Eye View... Q&A-2.5 Line Chart Showing Relative Importance Chapters... Q&A-2.7 Table Showing Importance of Chapter on the Basis of Marks...

Answer to MTP_Intermediate_Syllabus 2012_Jun2017_Set 2 Paper 8- Cost Accounting & Financial Management

Paper 8- Cost Accounting & Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper-8: Cost Accounting & Financial

Paper 8- Cost Accounting & Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper-8: Cost Accounting & Financial

Free of Cost ISBN : Appendix. CMA (CWA) Inter Gr. II (Solution upto Dec & Questions of June 2013 included)

Inter Gr. II (Solution upto Dec & Questions of June 2013 included)") Free of Cost ISBN : 978-93-5034-631-0 Appendix CMA (CWA) Inter Gr. II (Solution upto Dec. 2012 & Questions of June 2013 included) Paper - 8 : Cost and Management Accounting Chapter - 3 : Labour Accounting

Free of Cost ISBN : 978-93-5034-631-0 Appendix CMA (CWA) Inter Gr. II (Solution upto Dec. 2012 & Questions of June 2013 included) Paper - 8 : Cost and Management Accounting Chapter - 3 : Labour Accounting

Question No: 5 ( Marks: 1 ) - Please choose one Which of the following manufacturers is most likely to use a job order cost accounting system?

- Please choose one Which of the following manufacturers is most likely to use a job order cost accounting system?") MGT402 Latest Solved MCQs From Current Papers 2010 By http://vustudents.ning.com Question No: 1 ( Marks: 1 ) - Please choose one If Selling price per unit Rs. 15.00; Direct Materials cost per unit Rs.

MGT402 Latest Solved MCQs From Current Papers 2010 By http://vustudents.ning.com Question No: 1 ( Marks: 1 ) - Please choose one If Selling price per unit Rs. 15.00; Direct Materials cost per unit Rs.

MGT402 - COST & MANAGEMENT ACCOUNTING

MGT402 - COST & MANAGEMENT ACCOUNTING Lesson No. TOPICS Page No. 1 Cost Classification and Cost Behavior 1 2 Important Terminologies 11 3 Financial Statements 15 4 Financial Statements (Continued)....

MGT402 - COST & MANAGEMENT ACCOUNTING Lesson No. TOPICS Page No. 1 Cost Classification and Cost Behavior 1 2 Important Terminologies 11 3 Financial Statements 15 4 Financial Statements (Continued)....

Appendix. IPCC Gr. I (New Course) (Solution upto November & Question of May ) Free of Cost ISBN :

(Solution upto November & Question of May ) Free of Cost ISBN :") Free of Cost ISBN : 978-93-5034-234-3 Appendix IPCC Gr. I (New Course) (Solution upto November - 2011 & Question of May - 2012) Paper - 3A : Cost Accounting Chapter-1 : Basic Concepts 2011 - Nov [5] (i)

Free of Cost ISBN : 978-93-5034-234-3 Appendix IPCC Gr. I (New Course) (Solution upto November - 2011 & Question of May - 2012) Paper - 3A : Cost Accounting Chapter-1 : Basic Concepts 2011 - Nov [5] (i)

PAPER 8- COST ACCOUNTING

PAPER 8- COST ACCOUNTING Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper - 8: COST ACCOUNTING Full Marks: 100 Time Allowed: 3 Hours

PAPER 8- COST ACCOUNTING Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper - 8: COST ACCOUNTING Full Marks: 100 Time Allowed: 3 Hours

UNIT 11: STANDARD COSTING

UNIT 11: STANDARD COSTING Introduction One of the prime functions of management accounting is to facilitate managerial control and the important aspect of managerial control is cost control. The efficiency

UNIT 11: STANDARD COSTING Introduction One of the prime functions of management accounting is to facilitate managerial control and the important aspect of managerial control is cost control. The efficiency

Paper 8- Cost Accounting

Paper 8- Cost Accounting Dos, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 8- Cost Accounting Full Marks : 100 Time allowed: 3 hours Section A Question

Paper 8- Cost Accounting Dos, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 8- Cost Accounting Full Marks : 100 Time allowed: 3 hours Section A Question

PTP_Intermediate_Syllabus 2012_Dec 2015_Set 2 Paper 8: Cost Accounting & Financial Management

Paper 8: Cost Accounting & Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Pg 1 LEVEL B PTP_Intermediate_Syllabus 2012_Dec

Paper 8: Cost Accounting & Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Pg 1 LEVEL B PTP_Intermediate_Syllabus 2012_Dec

SUGGESTED SOLUTION IPCC NOVEMBER 2018 EXAM. Test Code -

SUGGESTED SOLUTION IPCC NOVEMBER 2018 EXAM COSTING Test Code - BRANCH - (MUMBAI-2 (DB) (Date : 01.07.2018) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

SUGGESTED SOLUTION IPCC NOVEMBER 2018 EXAM COSTING Test Code - BRANCH - (MUMBAI-2 (DB) (Date : 01.07.2018) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

Solution Paper 8 COST AND MANAGEMENT ACCOUNTING June Chapter 2 Material

2013 - June [7] (a) Date Receipts Qty (Units) May 2013 1 Opening Balance Solution Paper 8 COST AND MANAGEMENT ACCOUNTING June - 2013 Chapter 2 Material Rate FIFO Method Issue Qty. (Units) Rate Issue LIFO

2013 - June [7] (a) Date Receipts Qty (Units) May 2013 1 Opening Balance Solution Paper 8 COST AND MANAGEMENT ACCOUNTING June - 2013 Chapter 2 Material Rate FIFO Method Issue Qty. (Units) Rate Issue LIFO

NATIONAL 5 Accounting

MADRAS COLLEGE FACULTY OF TECHNOLOGIES DEPARTMENT OF BUSINESS AND ENTERPRISE NATIONAL 5 Accounting Course Information Name: ACCOUNTING NATIONAL 5 COURSE AIMS AND STRUCTURE The course aims to enable learners

MADRAS COLLEGE FACULTY OF TECHNOLOGIES DEPARTMENT OF BUSINESS AND ENTERPRISE NATIONAL 5 Accounting Course Information Name: ACCOUNTING NATIONAL 5 COURSE AIMS AND STRUCTURE The course aims to enable learners

AM Syllabus ( ): Accounting AM SYLLABUS ( ) ACCOUNTING AM 01 SYLLABUS

: Accounting AM SYLLABUS ( ) ACCOUNTING AM 01 SYLLABUS") AM SYLLABUS (2008-2013) ACCOUNTING AM 01 SYLLABUS 1 Accounting AM 01 Syllabus (Available in September) Paper I (3 hrs) + Paper II (3 hrs) Introduction The syllabus builds on the topics set for the SEC

AM SYLLABUS (2008-2013) ACCOUNTING AM 01 SYLLABUS 1 Accounting AM 01 Syllabus (Available in September) Paper I (3 hrs) + Paper II (3 hrs) Introduction The syllabus builds on the topics set for the SEC

CIMA'S Official Learning System PUBLISHING

g$>g CIMA'S Official Learning System PUBLISHING Relevant for 2008/2009 Computer-Based Assessments CIMA terrmcafe in Business Accounting Janet Walker ELSEVIER AMSTERDAM BOSTON HEIDELBERG LONDON NEW YORK

g$>g CIMA'S Official Learning System PUBLISHING Relevant for 2008/2009 Computer-Based Assessments CIMA terrmcafe in Business Accounting Janet Walker ELSEVIER AMSTERDAM BOSTON HEIDELBERG LONDON NEW YORK

F2 FIA FMA. ACCA Qualification ACCA. Accounting. December 2012 Examinations. OpenTuition Course Notes can be downloaded FREE from

ACCA Qualification Course NOTES ACCA F2 FIA FMA Management Accounting December 2012 Examinations OpenTuition Course Notes can be downloaded FREE from www.opentuition.com Copyright belongs to OpenTuition.com

ACCA Qualification Course NOTES ACCA F2 FIA FMA Management Accounting December 2012 Examinations OpenTuition Course Notes can be downloaded FREE from www.opentuition.com Copyright belongs to OpenTuition.com

FOUNDATION EXAMINATION

FOUNDATION EXAMINATION (SYLLABUS 2008) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2011 Paper-2 : ACCOUNTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the right side indicate full

FOUNDATION EXAMINATION (SYLLABUS 2008) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2011 Paper-2 : ACCOUNTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the right side indicate full

7 Solved Mid Term Papers of MGT402 BY.

7 Solved Mid Term Papers of MGT402 BY http://vustudents.ning.com Spring 2009 MGT402- Cost & Management Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one D Corporation uses process

7 Solved Mid Term Papers of MGT402 BY http://vustudents.ning.com Spring 2009 MGT402- Cost & Management Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one D Corporation uses process

PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING QUESTIONS

PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING QUESTIONS 1. (i) ABC Ltd. had an opening inventory value of 1760 (550 units valued at 3.20 each) on 1 st April 2010. The following

PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING QUESTIONS 1. (i) ABC Ltd. had an opening inventory value of 1760 (550 units valued at 3.20 each) on 1 st April 2010. The following

PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING QUESTIONS

PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING QUESTIONS Material 1. The following information has been extracted from the records of a cotton merchant, for the month of March,

PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING QUESTIONS Material 1. The following information has been extracted from the records of a cotton merchant, for the month of March,

FMA. Management Accounting. OpenTuition.com ACCA FIA. March/June 2016 exams. Free resources for accountancy students

OpenTuition.com Free resources for accountancy students March/June 2016 exams ACCA FIA F2 FMA Management Accounting Please spread the word about OpenTuition, so that all ACCA students can benefit. ONLY

OpenTuition.com Free resources for accountancy students March/June 2016 exams ACCA FIA F2 FMA Management Accounting Please spread the word about OpenTuition, so that all ACCA students can benefit. ONLY

CAS-3 : Overheads 1. Introduction

1 CAS-3 : Overheads 1. Introduction 2. Object In Cost Accounting the analysis and collection overheads, their allocation and apportionment to different cost centres and absorption to products or services

1 CAS-3 : Overheads 1. Introduction 2. Object In Cost Accounting the analysis and collection overheads, their allocation and apportionment to different cost centres and absorption to products or services

5_MGT402_Spring_2010_Final_Term_Solved_paper

5_MGT402_Spring_2010_Final_Term_Solved_paper http://vustudents.ning.com Question No: 1 ( Marks: 1 ) - Please choose one BDH produced 30,500 units of Kisty (a product). Each unit of Kisty takes two units

5_MGT402_Spring_2010_Final_Term_Solved_paper http://vustudents.ning.com Question No: 1 ( Marks: 1 ) - Please choose one BDH produced 30,500 units of Kisty (a product). Each unit of Kisty takes two units

Suggested Answer_Syl12_Dec2014_Paper_8 INTERMEDIATE EXAMINATION GROUP I (SYLLABUS 2012)

") INTERMEDIATE EXAMINATION GROUP I (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2014 Paper-8: COST ACCOUNTING AND FINANCIAL MANAGEMENT Time Allowed : 3 Hours Full Marks : 100 The figures in the

INTERMEDIATE EXAMINATION GROUP I (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2014 Paper-8: COST ACCOUNTING AND FINANCIAL MANAGEMENT Time Allowed : 3 Hours Full Marks : 100 The figures in the

MTP_Intermediate_Syllabus 2012_Jun2017_Set 2 Paper 8- Cost Accounting & Financial Management

Paper 8- Cost Accounting & Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper-8: Cost Accounting & Financial

Paper 8- Cost Accounting & Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper-8: Cost Accounting & Financial

LU4: Accounting for Overhead

LU4: Accounting for Overhead Contents Introduction Applied manufacturing overheads Allocation of manufacturing overheads Learning objectives Define overhead costs Distinguish between manufacturing and

LU4: Accounting for Overhead Contents Introduction Applied manufacturing overheads Allocation of manufacturing overheads Learning objectives Define overhead costs Distinguish between manufacturing and

INSTITUTE OF ADVANCED MANAGEMENT AND RESEARCH, GHAZIABAD. Model Question bank. Cost and Management Accounting for Decision Com: 2.

INSTITUTE OF ADVANCED MANAGEMENT AND RESEARCH, GHAZIABAD Model Question bank Cost and Management Accounting for Decision Com: 2.7 Question. 1.What are the elements of cost and what are various types of

INSTITUTE OF ADVANCED MANAGEMENT AND RESEARCH, GHAZIABAD Model Question bank Cost and Management Accounting for Decision Com: 2.7 Question. 1.What are the elements of cost and what are various types of

MTP_Intermediate_Syl2016_June2018_Set 1 Paper 8- Cost Accounting

Paper 8- Cost Accounting DoS, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Cost Accounting Full Marks: 100 Time allowed: 3 hours Section- A Answer the following

Paper 8- Cost Accounting DoS, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Cost Accounting Full Marks: 100 Time allowed: 3 hours Section- A Answer the following

Institute of Certified Bookkeepers

Institute of Certified Bookkeepers Level III Diploma in Costing and Budgeting Introduction: Financial Accounting is the reporting of financial information to users of Financial Statements both internal

Institute of Certified Bookkeepers Level III Diploma in Costing and Budgeting Introduction: Financial Accounting is the reporting of financial information to users of Financial Statements both internal

MOCK TEST PAPER 2 INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT SUGGESTED ANSWERS/ HINTS

: GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT SUGGESTED ANSWERS/ HINTS") 1. (a) Working notes: MOCK TEST PAPER 2 INTERMEDIATE (IPC): GROUP I Test Series: October, 2015 PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT SUGGESTED ANSWERS/ HINTS 1. (i) Number of units sold at

1. (a) Working notes: MOCK TEST PAPER 2 INTERMEDIATE (IPC): GROUP I Test Series: October, 2015 PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT SUGGESTED ANSWERS/ HINTS 1. (i) Number of units sold at

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

II Contents PAPER 4 : COST ACCOUNTING AND FINANCIAL MANAGEMENT Section A : Cost Accounting QUESTIONS 1. (a) Classify each of the followings on the basis of behavioural aspects of cost. (iii) (iv) (v) (vi)

II Contents PAPER 4 : COST ACCOUNTING AND FINANCIAL MANAGEMENT Section A : Cost Accounting QUESTIONS 1. (a) Classify each of the followings on the basis of behavioural aspects of cost. (iii) (iv) (v) (vi)

PRINCIPLES OF COST ACCOUNTING

1. AIMS AND OBJECTIVES PRINCIPLES OF COST ACCOUNTING The aims of this examination are to test candidates ability to a) assemble, analyze and ascertain the cost of producing and procuring goods and services;

1. AIMS AND OBJECTIVES PRINCIPLES OF COST ACCOUNTING The aims of this examination are to test candidates ability to a) assemble, analyze and ascertain the cost of producing and procuring goods and services;

Answer to MTP_Foundation_Syllabus 2012_Jun2017_Set 1 Paper 2- Fundamentals of Accounting

Paper 2- Fundamentals of Accounting Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 2- Fundamentals of Accounting Full Marks :

Paper 2- Fundamentals of Accounting Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 2- Fundamentals of Accounting Full Marks :

NEW HORIZON COLLEGE MARATHALLI, BANGALORE

NEW HORIZON COLLEGE MARATHALLI, BANGALORE (Affiliated to Bangalore University) A Recipient of Prestigious Rajyotsava State Award 2012 conferred by the Government of Karnataka IV SEM BCOM STUDY MATERIAL

NEW HORIZON COLLEGE MARATHALLI, BANGALORE (Affiliated to Bangalore University) A Recipient of Prestigious Rajyotsava State Award 2012 conferred by the Government of Karnataka IV SEM BCOM STUDY MATERIAL

C O V E N A N T U N I V E RS I T Y P R O G R A M M E : A C C O U N T I N G A L P H A S E M E S T E R T U T O R I A L K I T L E V E L

C O V E N A N T U N I V E RS I T Y T U T O R I A L K I T P R O G R A M M E : A C C O U N T I N G A L P H A S E M E S T E R 2 0 0 L E V E L DISCLAIMER The contents of this document are intended for practice

C O V E N A N T U N I V E RS I T Y T U T O R I A L K I T P R O G R A M M E : A C C O U N T I N G A L P H A S E M E S T E R 2 0 0 L E V E L DISCLAIMER The contents of this document are intended for practice

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM SUBJECT- COSTING Test Code - PIN 5043 BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM SUBJECT- COSTING Test Code - PIN 5043 BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

(AA22) COST ACCOUNTING AND REPORTING

COST ACCOUNTING AND REPORTING") All Rights Reserved ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA AA2 EXAMINATION - JANUARY 2019 (AA22) COST ACCOUNTING AND REPORTING Instructions to candidates (Please Read Carefully): (1) Time Allowed:

All Rights Reserved ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA AA2 EXAMINATION - JANUARY 2019 (AA22) COST ACCOUNTING AND REPORTING Instructions to candidates (Please Read Carefully): (1) Time Allowed:

Reconciliation of Cost and Financial A/c

Reconciliation of Cost and Financial A/c Meaning In business concern where Non-integrated Accounting System is followed, cost and financial accounts are maintained separately, the difference between the

Reconciliation of Cost and Financial A/c Meaning In business concern where Non-integrated Accounting System is followed, cost and financial accounts are maintained separately, the difference between the

FOR MORE PAPERS LOGON TO

MGT402 - Cost & Management Accounting Question No: 1 ( Marks: 1 ) - Please choose one Opportunity cost is the best example of: Sunk Cost Standard Cost Relevant Cost Irrelevant Cost Question No: 2 ( Marks:

MGT402 - Cost & Management Accounting Question No: 1 ( Marks: 1 ) - Please choose one Opportunity cost is the best example of: Sunk Cost Standard Cost Relevant Cost Irrelevant Cost Question No: 2 ( Marks:

Budgets and Budgetary Control. By: CA Kapileshwar Bhalla

Budgets and Budgetary Control By: CA Kapileshwar Bhalla Learning Objectives Understand the objectives and importance of budgeting and budgetary control Understand the Advantages and disadvantages of budgetary

Budgets and Budgetary Control By: CA Kapileshwar Bhalla Learning Objectives Understand the objectives and importance of budgeting and budgetary control Understand the Advantages and disadvantages of budgetary

MGT101 All Solved Past Papers of Mid Term Exam in one file By

MGT101 All Solved Past Papers of Mid Term Exam in one file By http://vustudents.ning.com MIDTERM EXAMINATION 7 th Dec 2009 MGT101- Financial Accounting Question No: 1 Income of the business includes: Cash

MGT101 All Solved Past Papers of Mid Term Exam in one file By http://vustudents.ning.com MIDTERM EXAMINATION 7 th Dec 2009 MGT101- Financial Accounting Question No: 1 Income of the business includes: Cash

Please spread the word about OpenTuition, so that all ACCA students can benefit.

ACCA COURSE NOTES June 2014 Examinations ACCA F2 FIA FMA Management Accounting Please spread the word about OpenTuition, so that all ACCA students can benefit. ONLY with your support can the site exist

ACCA COURSE NOTES June 2014 Examinations ACCA F2 FIA FMA Management Accounting Please spread the word about OpenTuition, so that all ACCA students can benefit. ONLY with your support can the site exist

INTER CA MAY Test Code M32 Branch: MULTIPLE Date: (50 Marks) Note: All questions are compulsory.

Note: All questions are compulsory.") (5 Marks) Note: All questions are compulsory. INTER CA MAY 218 COSTING Topic: Contract Costing, Budgetary Control, Labour, Joint & By- Product, Absorption Costing, Overheads, Integral & Non Integral, Marginal

(5 Marks) Note: All questions are compulsory. INTER CA MAY 218 COSTING Topic: Contract Costing, Budgetary Control, Labour, Joint & By- Product, Absorption Costing, Overheads, Integral & Non Integral, Marginal

INTERMEDIATE EXAMINATION

INTERMEDIATE EXAMINATION GROUP II (SYLLABUS 2008) SUGGESTED ANSWERS TO QUESTIONS JUNE 2012 Paper- 8 : COST AND MANAGEMENT ACCOUNTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on

INTERMEDIATE EXAMINATION GROUP II (SYLLABUS 2008) SUGGESTED ANSWERS TO QUESTIONS JUNE 2012 Paper- 8 : COST AND MANAGEMENT ACCOUNTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on

MANAGEMENT ACCOUNTING

MANAGEMENT ACCOUNTING Course Code Chief Course Instructor Course Instructor UM15MB605 Dr. Anitha S Yadav Course Credits 4 No. of Hours Credit pattern ISA 52 Lecture Tutorial Practical/ Seminar Self study

MANAGEMENT ACCOUNTING Course Code Chief Course Instructor Course Instructor UM15MB605 Dr. Anitha S Yadav Course Credits 4 No. of Hours Credit pattern ISA 52 Lecture Tutorial Practical/ Seminar Self study

MIDTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 2)

") MIDTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one Particulars Rs. Opening written down value of machine 1,00,000 Cost of new machine

MIDTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one Particulars Rs. Opening written down value of machine 1,00,000 Cost of new machine

SUGGESTED SOLUTION INTERMEDIATE N 2018 EXAM

SUGGESTED SOLUTION INTERMEDIATE N 2018 EXAM SUBJECT- COSTING Test Code CIN 5013 Date: 02.09.2018 Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 ANSWER-1

SUGGESTED SOLUTION INTERMEDIATE N 2018 EXAM SUBJECT- COSTING Test Code CIN 5013 Date: 02.09.2018 Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 ANSWER-1

Solved Answer COST & F.M. CA IPCC Nov

Solved Answer COST & F.M. CA IPCC Nov. 2009 1 1. Answer any five of the following : [5x2=10 marks] (i) Define the following : (a) Imputed cost (b) Capitalised cost. (ii) Calculate efficiency, and activity

Solved Answer COST & F.M. CA IPCC Nov. 2009 1 1. Answer any five of the following : [5x2=10 marks] (i) Define the following : (a) Imputed cost (b) Capitalised cost. (ii) Calculate efficiency, and activity

MOCK TEST PAPER INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT

: GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT") MOCK TEST PAPER INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT Test Series: March 2018 Answers are to be given only in English except in the case of the candidates who have

MOCK TEST PAPER INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT Test Series: March 2018 Answers are to be given only in English except in the case of the candidates who have

Mark Scheme (Results) Series Pearson LCCI Level 3 COST ACCOUNTING (ASE3017)

Series Pearson LCCI Level 3 COST ACCOUNTING (ASE3017)") Mark Scheme (Results) Series 3 2014 Pearson LCCI Level 3 COST ACCOUNTING (ASE3017) LCCI International Qualifications LCCI International Qualifications are awarded by Pearson, the UK s largest awarding

Mark Scheme (Results) Series 3 2014 Pearson LCCI Level 3 COST ACCOUNTING (ASE3017) LCCI International Qualifications LCCI International Qualifications are awarded by Pearson, the UK s largest awarding