CHAPTER :- 4 CONCEPTUAL FRAMEWORK OF FINANCIAL PERFORMANCE.

|

|

|

- Ruby Smith

- 6 years ago

- Views:

Transcription

1 CHAPTER :- 4 CONCEPTUAL FRAMEWORK OF FINANCIAL PERFORMANCE. 4.1 INTRODUCTION. 4.2 FINANCIAL PERFORMANCE. 4.3 FINANCIAL STATEMENT. 4.4 FINANCIAL STATEMENT ANALYSIS. 4.5 METHODS OF ANALYSIS OF FINANCIAL STATEMENTS COMPARATIVE STATEMENTS COMMON-SIZE STATEMENTS TREND PERCENTAGES STATEMENT OF CHANGES IN WORKING CAPITAL CASH FLOW STATEMENT RATIO ANALYSIS MEANING OF RATIO DEFINITION OF RATIO DEFINATION OF RATIO ANALYSIS IMPORTANCE OF RATIO ANALYSIS OBJECTIVE OF RATIO ANALYSIS USES OF RATIO ANALYSIS LIMITATIONS OF RATIO ANALYSIS CLASSIFICATION OF RATIOS WORKING CAPITAL RATIO. REFERENCES. 172

2 CHAPTER :- 4 CONCEPTUAL FRAMEWORK OF FINANCIAL PERFORMANCE. 4.1 INTRODUCTION:- In this chapter researcher has take to know the financial performance and he has also taken method of analysis of financial statement and with that he has to maser the performance with ratio analysis. 4.2 FINANCIAL PERFORMANCE:- The performance of the firm can be measured by its financial results, i.e., by its size of earnings Riskiness and profitability are two major factors which jointly determine the value of the concern. 1 Financial decisions which increase risks will decrease the value of the firm and on the other hand, financial decisions which increase the profitability will increase value of the firm. Risk and profitability are two essential ingredients of a business concern. There has been a considerable debate about the ultimate objective of firm performance, whether it is profit maximization or wealth maximization. It is observed that while considering the firm performance, the profit and wealth maximization are linked and are effected by oneanother. A company s financial performance therefore is normally judged by a series of ratios or figures, however there are following three ratio 173

3 parameters which can be used to evaluate financial performance, they are: a) Return on Equity b) Earnings per Share and c) Price Earnings Ratio. All three parameters are discussed in detailed along with various other ratios. However, it is to be noted that fundamentally, the balance sheet indicates the financial position of the company as on that point of time. However, profit and loss account is a statement, which is prepared for a particular financial year. In Indian context, where an analyst has to rely upon the audited financial statement for a particular company, the performance is to be judged from the financial statement only. This chapter, however indicates some of the techniques, which can be used for such analysis of financial performance FINANCIAL STATEMENT:- Company is required to present its financial statements every year as required by the provisions of the companies Act. Generally, these financial statements comprise of Balance sheet and Profit and Loss Account is also known as Income Statement. Balance sheet shows the financial position of the company as on the data of balance sheet. The financial position comprises of what company/entity owns and what it owes. In other words, financial position shows what are the assets and liabilities of the enterprise Company records day to day transactions in its books of accounts from this information, financial statements are prepared at the end of the year. 3 These financial statements comprise mainly of the following two 174

4 statements: Balance sheet showing financial position of business : and Profit and loss accounts showing the performance or result of business during the year. Financial statements are prepared in terms of provisions of law. They are prepared in accordance with generally accepted accounting principal and accounting standards. For example, stock is valued at cost or market price whichever is lower. The financial statements are used for various objectives. For example, determining profit for the purpose of managerial remuneration, for making provision for income tax, for determining taxable profit, etc FINANCIAL STATEMENT ANALYSIS:- Financial Analysis is the process of identifying the financial strengths and weaknesses of the company by properly establishing relationships between the items of the balance sheet and the profit and loss account. Financial analysis can be undertaken by management of the firm, or by parties outside the firm, viz. owners, Creditors, investors and others. The nature of analysis will differ depending on the purpose of analyst. Financial ratios are tools for interpreting financial statements to provide a basis for valuing securities and appraising financial and management performance. Information published in financial statements may not be sufficient form the view point of different parties. Different parties or stockholders are interested in arriving at conclusions for their own objectives based on information contained in financial statements. For such conclusions, the information may not be readily available from financial statements. For 175

5 example, position of the company from the viewpoint of 1) liquidity, 2) profitability or 3) solvency may not be known directly from the face of financial statements. For this purpose, information contained in financial statements is not be analyzed based on the figures of financial statements and other related supplementary information. Such conclusions cannot be drawn straight from the number shown in financial statements. For the purpose of analysis different information and figures have to be compared and such information can be obtained in the form of percentage or rate of turnover. Thus, conclusions drawn based on different financial numbers given in the financial statements is known as analysis and the opinions framed based on such conclusion is known as interpretation METHODS OF ANALYSIS OF FINANCIAL STATEMENTS:- One gets information based on financial statements. Analysis of such information by comparison or with the help of percentages or formula and arriving at conclusions based on such analysis is known as financial statement analysis of financial statements: COMPARATIVE STATEMENTS: COMMON-SIZE STATEMENTS: TREND PERCENTAGES: STATEMENT OF CHANGES IN WORKING CAPITAL: CASH FLOW STATEMENT: RATIO ANALYSIS:- 176

6 4.5.1 COMPARATIVE STATEMENTS :- One cannot get an idea about profitability and financial position by analyzing only one year`s financial statements. Under this method of analysis, one needs at least two years` figures. By putting figures of different years together, one can know about the change of trend in business. This method is useful to know about the business trend of various matters. To understand the presentation for analysis of financial statements are prepared in this method: Profit and loss statement. Balance sheet COMMON SIZE STATEMENTS :- These statements are prepared to know percentage of each of assets to total assets and percentage of each element of expense as percentage of total sales. Such statements are also known as hundred percentage statement. Common- size statements are also useful in comparing financial position of two companies. While analyzing balance sheet, each asset as a percentage of total assets and each liability as a percentage of total liabilities is calculated. Similarly, in analyzing profit and loss account, each item expense and income is calculated as percentage of total sales TREND PERCENTAGES :- The Time Series Analysis or Trend Analysis indicates of ratio indicates the direction of changes. The trend analysis is advocated to be studied in light of the following two factors. 177

7 i) The rate of fixed expansion or secular trend in the growth of the business and ii) The general price level. Any increase sales statement may be because of two reasons, one may be the increase in volume of business and another is the variation in prices of the goods / services. For trend analysis, the use of index number is generally advocated. The procedure followed is to assign the number 100 to the items of each base year and to calculate percentage changes in each item of the other years in relation to the base year. This is known as Trend-Percentage Method STATEMENT OF CHANGES IN WORKING CAPITAL :- In financial management, two important decisions are very vital and crucial. They are decision regarding fixed assets/fixed capital and decision regarding working capital/current assets. Both are important and a firm always analyzes their effect to final impact upon profitability and risk. Fixed capital refers to the funds invested in such fixed or permanent assets as land, building, and machinery etc. Whereas working capital refers to the funds locked up in materials, work in progress, finished goods, receivables, and cash etc. Thus, in very simple words, working capital may be defined as capital invested in current assets. Here current assets are those assets, which can be converted into cash within a short period of time and the cash received is gain invested into these assets. 8 Thus, it is constantly 178

8 receiving or circulating. Hence, working capital is also known as circulating capital or floating capital. There are two concepts of working capital. These are: 1. Gross working capital: (Total Current Assets) The gross working capital, simply called as working capital refers to the firm s investment in current assets. Current assets are the assets, which can be converted into cash within an accounting year or operating cycle. Thus, Gross working capital, is the total of all current assets. 2. Net Working Capital: (Total Current Assets Total Current Liabilities) Net working capital refers to the difference between current assets and Current liabilities. 9 Current liabilities are those claims of outsiders, which are expected to mature for payment within an accounting year. 9 Net working capital may be positive or negative. A positive net working capital will arise when current assets exceed current liabilities and a negative net working capital will arise when current liabilities exceed current assets i.e. there is no working capital, but there is a working capital deficit. Working Capital represents the amount of current assets that have not been supplied by current, short term Creditors. 10 Gross working capital refers to the amount of funds invested in current assets that are employed in the business process while, Net Working Capital refers to the difference between current assets and current liabilities

9 Working Capital is the excess of current assets that has been supplied by the long-term Creditors and the stockholders. 12 The two concepts of working capital, gross working capital and net working capital are exclusive. Both are equally important for the efficient management of working capital. The gross working capital focuses attention on two aspects How to optimize investment in current assets? And how should current assets is financed? While, net working capital concept is qualitative. It indicates the liquidity position of the firm and suggests the extent to which working capital needs may be financed by permanent sources of funds CASH FLOW STATEMENT :- Cash flow analysis is primarily used as a tool to evaluate the sources and uses of funds. 13 Cash flow analysis provides insights into how a company is obtaining its financing and deploying its resources. It also is used in cash flow forecasting and as part of liquidity analysis. The cash flow statement was previously known as the flow of Cash statement. The cash flow statement reflects a firm's liquidity. The balance sheet is a snapshot of a firm's financial resources and obligations at a single point in time, and the income statement summarizes a firm's financial transactions over an interval of time. These two financial statements reflect the accrual basis accounting used by firms to match revenues with the expenses associated with generating those revenues. The cash flow statement includes only inflows and outflows of cash and cash equivalents; it excludes transactions that do not directly affect cash receipts and payments. These non-cash transactions include depreciation or write-offs on bad debts or credit losses to name a few. The cash flow 180

10 statement is a cash basis report on three types of financial activities: operating activities, investing activities, and financing activities. Noncash activities are usually reported in footnotes. The cash flow statement is intended to 1. provide information on a firm's liquidity and solvency and its ability to change cash flows in future circumstances 2. provide additional information for evaluating changes in assets, liabilities and equity 3. improve the comparability of different firms' operating performance by eliminating the effects of different accounting methods 4. indicate the amount, timing and probability of future cash flows The cash flow statement has been adopted as a standard financial statement because it eliminates allocations, which might be derived from different accounting methods, such as various timeframes for depreciating fixed assets RATIO ANALYSIS :- Ratio analysis is a powerful tool of financial analysis. A ratio is defined as the indicated quotient of two mathematical expressions" and as the relationship between two or more things. 15 In financial analysis, a ratio is used as a benchmark for evaluating the financial position and performance of a firm. An accounting figure conveys meaning when it is related to some other relevant information. A ratio gets utility by comparison to other data and standards. 181

11 The relationship between two accounting figures, expressed mathematically, is known as a Financial Ratio. Ratios help to summaries large quantities of financial data and to make qualitative judgment about the firm s financial performance. The point to note that a ratio reflecting a quantitative relationship helps to form a qualitative judgment. Financial analysis can be undertaken by management of the firm, or by parties outside the firm, viz. owners, Creditors, investors and others. 16 generally, ratios are divided in four areas of classification that are providing different kind of information liquidity, profitability, activity and leverage ratios. 17 Ratio analysis is a very powerful analytical tool useful for measuring performance of an organization. The ratio analysis helps the assets to current liabilities will work out to be / = 1.5 management to analyze the past performance of the firm and to make further projection. 18 The ratio analysis of working capital can be used by management as a means of checking upon the efficiency with working capital. 19 Ratio analysis is essentially concerned with the calculation of relationships, which after proper identification and interpretation may provide information about the operations and state of affairs of a business enterprise. Ratio analysis is such a significant technique for financial analysis. It indicates relation of two mathematical expressions and the relationship between two or more things. A financial ratio is a relationship between two financial variables. 20 Ratio analysis is a process of comparison of one figure against another, which make a ratio, and the appraisal of the ratios to make 182

12 proper analysis about the strengths and weakness of the firm s operations. The calculation of ratios is a relatively easy and simple task but the proper analysis and interpretation of the ratios can be made only by the skilled analyst. While interpreting the financial information, the analyst has to be careful in limitations imposed by the accounting concepts and methods of valuation. Ratio analysis is extremely helpful in providing valuable insight into a company s financial picture MEANING OF RATIO: DEFINITION OF RATIO: DEFINITION OF RATIO ANALYSIS: IMPORTANCE OF RATIO ANALYSIS: OBJECTIVES FOR RATIO ANALYSIS: USES OF RATIO ANALYSIS: LIMITATION OF RATIO ANALYSIS: CLASSIFICATION OF RATIOS: MEANING OF RATIO :- A ratio is nothing but a simple arithmetical expression of the relationship of one number to another. It may be defined as the indicated quotient of two mathematical expressions. In simple language ratio is one number expressed in terms of anther and can be worked out by dividing one number in to the other. For example, if the current assets of a firm on a given data are Rs and the current liabilities are Rs then the ratio of current 183

13 assets to current liabilities will work out to be / = 1.5 A ratio is the mathematical relationship between two quantities in the form of a fraction or percentage DEFINITION OF RATIO :- The relationship between the two figurer expressed mathematically is called a ratio. - Hingorani, Ramanathans & Crewal DEFINITION OF RATIO ANALYSIS :- A number expressed in terms of another. Ratio is a yardstick used to evaluate the financial condition and performance of a firm relating two pieces of financial data to each other. - James C. Van Harne The relation of one amount, a to another b, expressed as the ratio of a to b. - Kohler Ratio is a fraction whose numerator is the antecedent and denominator the consequent. Ratio is the relationship or proportion that one amount bears to another the first number being the numerator and the later denominator. - H. G. Guthmann Ratio analysis is one of the important tools of financial analysis. They assist the management in its basic function of forecasting, Planning, control and communication. - Dr. S.N.Maheshwari & Sunil Maheshwari 184

14 IMPORTANCE OF RATIO ANALYSIS :- The major benefits arising from ratio analysis are as follows: Ratio analysis is a very powerful analytical tool useful for measuring performance of an organization. 21 Ratio analysis concentrates on the inter-relationship among the figures appearing in the financial statements. Ratio analysis helps the management to analysis the part performance of the firm and to make further projections. Ratio analysis allow interested parties to make evaluations of certain aspects of the firms performance as give below : Shareholders and prospective investors will analysis ratios for taking investment and disinvestment decisions. Bankers who provide working capital will analysis ratio for appraising the credit worthiness of the firm. The financial institutions that provide long-term debt will analysis ratios for project appraisal and debt servicing capacity of the firm. The financial analysis will analyze ratio for making comparison and recommending to the investing public. The credit rating agencies will analyze ratios of a firm to give the credit rating to the firm. The government agencies will analyze ratio of a firm for review of its performance. The company s management will analyze ratios for determining the financial health and its profitability. The ratios will also be used for inter- firm and intra-firm comparison and will also be used in financial planning and decision making. 185

15 OBJECTIVES OF RATIO ANALYSIS :- With the help of ratio analysis financial executives can measure whether the firm is at present financially health or not. The following are some of the important objectives of ratio analysis TO SERVE AS AN AID IN FINANCIAL FORCASTING: TO SERVE AS AN AID IN COMPARISON: TO SERVE AN AID IN COST CONTROL: TO COMMUNICATE: OTHER OBJECTIVES: TO SERVE AS AN AID IN FINANCIAL FORCASTING :- Ratio analysis is very helpful in financial forecasting. Ratio relating to the fast sales, profits and financial position are the vase for the future trends TO SERVE AS AN AID IN COMPARISON :- With the help of ratio analysis ideal ratios can be composed and they can be used for comparison of a particular firms and performance TO SERVE AN AID IN COST CONTROL :- Ratios are very useful for measuring the performance of any organization and it is very useful in cost control. 186

16 TO COMMUNICATE :- Different financial ratios communicate the strengths and financial standing of the firm to both internal and external parties OTHER OBJECTIVES :- Financial ratios are very helpful in the diagnosis of the financial health of a firm. They highlight the liquidity, solvency, profitability and capital gearing etc. of the firm. Thus, ratio analysis serves as a useful tool for analyzing the financial performance of any firm USES OF RATIO ANALYSIS :- The ratio analysis is one of the most powerful tools available in the hands of the management to take sound financial decisions. It is used as a device to analyze and interpret the financial health of an enterprise. The managerial uses of ratio analysis are the following: HELPS IN DECISION MAKING: HELPS IN FINANCIAL FORCASTING AND PLANNING: HELPS IN COMMUNICATING: HELPS IN COORDINATION: HELPS IN CONTROL: FACILITATES INTRA-FIRM COMPARISON: FACILITATES INTER-FIRM COMPARISON:- 187

17 HELPS IN DECISION MAKING:- Ratio analysis helps in making decisions from the information provided in the financial statements HELPS IN FINANCIAL FORCASTING AND PLANNING :- Planning is looking ahead and ratios calculated for a number of years work as a guide for the future. Meaningful conclusions can be drawn for future from these ratios. Thus, ratio analysis helps in forecasting and planning HELPS IN COMMUNICATING :- The financial strength and weakness of a firm are communicated in a more easy and understandable manner by the use of ratios HELPS IN COORDINATION :- Better communication of efficiency and weakness of an enterprise results in better coordination in the enterprise HELPS IN CONTROL :- Ratio analysis even helps in making effective control of the business. Standard ratios can be based upon Performa financial statement 188

18 and variances or deviations, if any, can be found by comparing the actual with the standards so as to take a corrective action at the right time FACILITATES INTRA-FIRM COMPARISON :- Comparison of ratios of the same firm over a period of years can be made. It helps to know the improvements in financial performance over a period of years FACILITATES INTER-FIRM COMPARISON :- Ratios of a firm can be compared with the ratios of similar nature of rims. This comparison will indicate how well the concern is operating relatively to its competitors. follow: LIMITATIONS OF RATIO ANALYSIS :- Ratio analysis has a number of pitfalls. Some of these are as LIMITED USE OF A SINGLE RATIO :- A single ratio dose not conveys much of a sense. To make a better interpretation, a number of ratio have to be calculated which is likely to confuse analyst. 189

19 LAKE OF ADEQUATE STANDARDS :- There are no well-accepted standard or rules of thumb for all ratio which can be accepted as norms, it renders interpretation of the ratios difficult INHERENT LIMITATION OF RATIOS :- Ratios of the past are not necessarily true indicators of the future CHANGE OF ACCOUNTING PROCEDURE :- Change in accounting procedure by a firm often makes ratio analysis misleading WINDOW DRESSING :- Financial statement can easily be window dressed to present a better picture of its financial and profitability position to outsiders. But, it may be very difficult for an outsider to know about the window dressing made by a firm PERSONAL BIAS :- Ratios have to be interpreted and different people may interpret the same ratio in different ways. 190

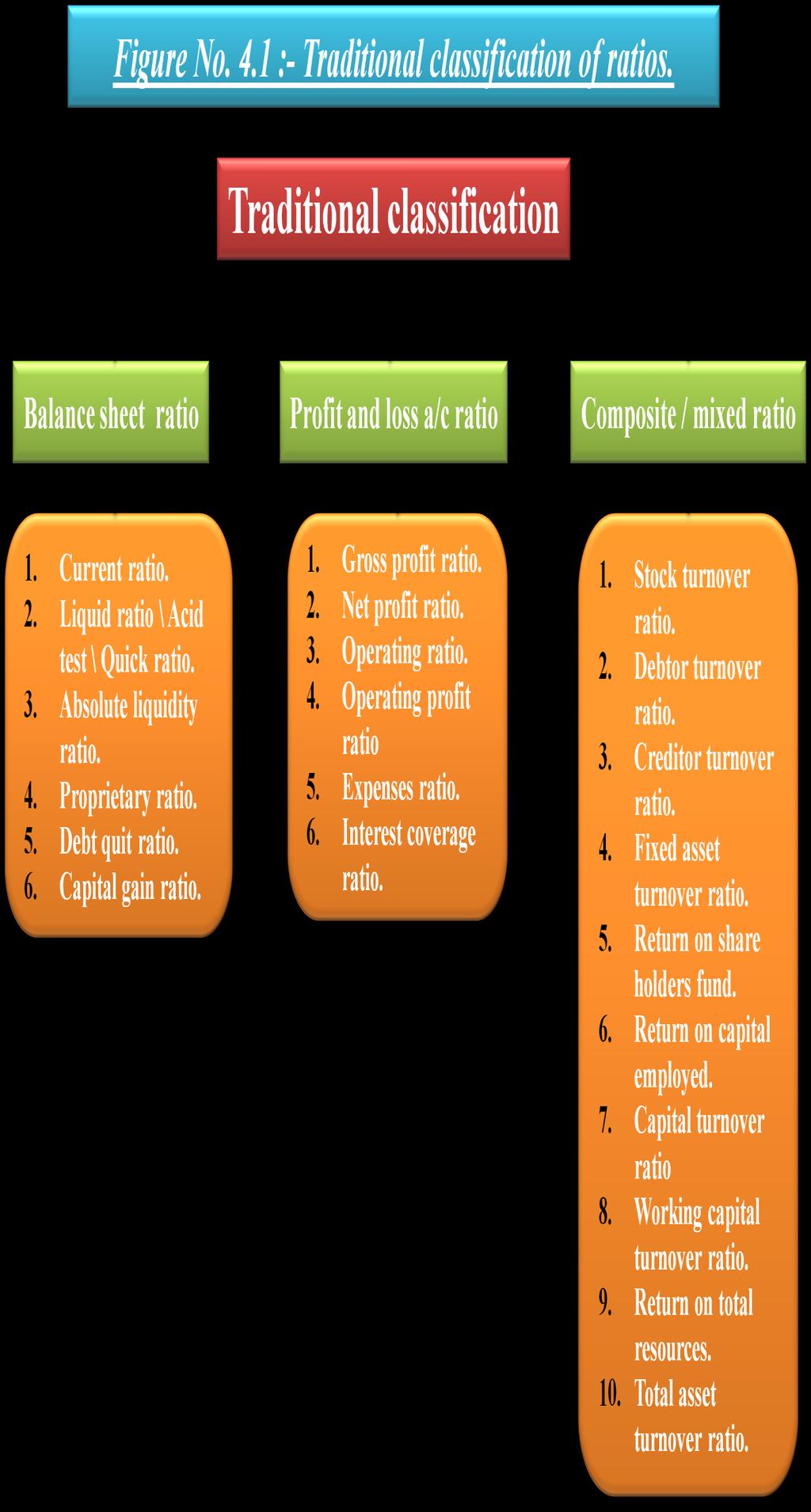

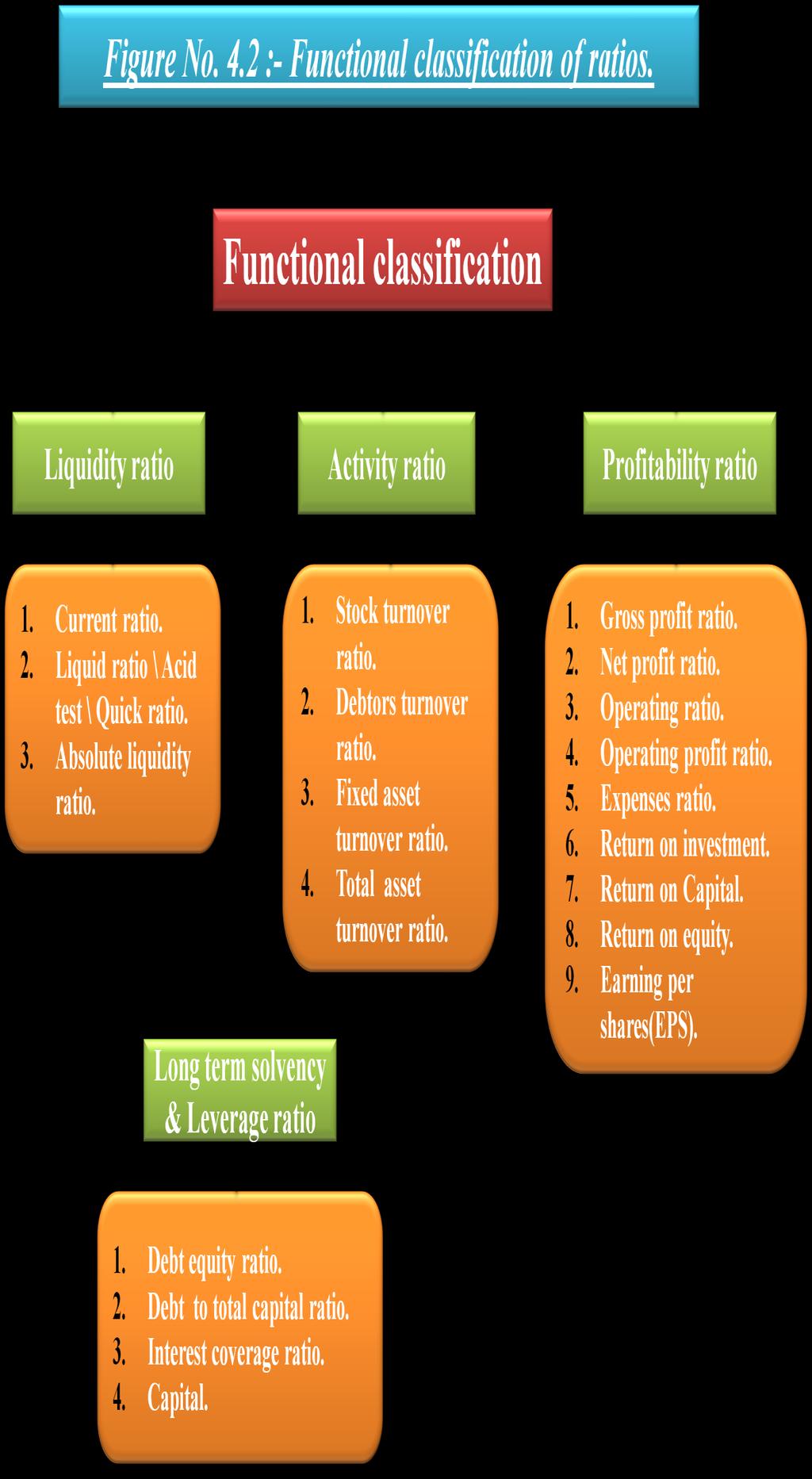

20 INCOMPARABLE :- Not only industries differ in their nature but also the firms of the similar business widely differ in their size and accounting procedures. It makes comparison of ratios difficult and misleading PRICE LEVEL CHANGES :- While making ratio analysis, no consideration is made to the price level and it makes the interpretation of ratio invalid RATIO ON SUBSTITUTES :- Ratios become useless if separated from the statement from which they are computed UNSUITABLE FOR FORECASTING :- Ratios indicate what has happened in the past. Since past is quite different from what is likely to happen in future, it is difficult to use ratio for forecasting purposes CLASSIFICATION OF RATIOS :- Ratio can be classified either on the basis of tradition (statement) or on the basis of their functions. Traditional Classification. Functional Classification. 191

21 192

22 193

23 4.5.7 WORKING CAPITAL RATIO :- Current ratio. Quick ratio. Liquidity ratio. Cash ratio. Interval measure. Net working capital ratio. Inventory turnover. Inventory to working capital ratio. Debtors turnover ratio. Creditors turnover ratio. Current assets turnover. Average collection period. Working capital turnover ratio. Gross profit margin. Net profit margin. Operating expense ratio. 194

24 REFERENCES ME/2004/me5th.pdf 2. Pandey I M (2005) Ninth Edition Financial Management PP Mechatronics.pdf 4. Element of book keeping and accountancy (2009), Gujarat state board of school textbooks Element of book keeping and accountancy (2009), Gujarat state board of school textbooks Element of book keeping and accountancy (2009), Gujarat state board of school textbooks Element of book keeping and accountancy (2009), Gujarat state board of school textbooks James C. Van Horne & John M. Wachowicz, Jr. Fundamentals of Financial Management 11. M. Y. Khan & P K Jain, - Financial Management Text and Problems 12. Prasanna Chandra Financial Management Theory and Practice ch.pdf LEVERAGES.pdf 15. Webster s New Collegiate Dictionary, 8 th Ed., Springfield, 195

25 Mass: G & C, Merriam, 1975, p Foster, G., Financial Statement Analysis, Prentice-Hall, 1986, pp Foster, op. cit Kuchhal S. C. Financial Management ( An analytical and conceptual approach ) Allahabad, chaitanya Publishing House, 1992 p Pandey I. M. Financial Management, Eighth Edition, Vikas Publishing House Pvt. Ltd., New Delhi, 2003, p iew_checklist.pdf 196

6.1 Introduction. 6.2 Meaning of Ratio

6.1 Introduction Ratio analysis has emerged as the principal technique of analysis of financial statements. The system of analysis of financial statements by means of ratio was first made in 1919 be Alexander

6.1 Introduction Ratio analysis has emerged as the principal technique of analysis of financial statements. The system of analysis of financial statements by means of ratio was first made in 1919 be Alexander

Chapter 1. Research Methodology

Chapter 1 Research Methodology 1.1 Introduction: Of all the modern service institutions, stock exchanges are perhaps the most crucial agents and facilitators of entrepreneurial progress. After the independence,

Chapter 1 Research Methodology 1.1 Introduction: Of all the modern service institutions, stock exchanges are perhaps the most crucial agents and facilitators of entrepreneurial progress. After the independence,

A STUDY ON FINANCIAL ANALYSIS WITH REFERENCE TO NDMPMACU LTD., NELLORE, A.P.

A STUDY ON FINANCIAL ANALYSIS WITH REFERENCE TO NDMPMACU LTD., NELLORE, A.P. P. THANUJA ASSISTANT PROFESSOR DEPARTMENT OF MANAGEMENT STUDIES VISVODAYA INSTITUTE OF TECHNOLOGY & SCIENCE S.P.S.R. NELLORE,

A STUDY ON FINANCIAL ANALYSIS WITH REFERENCE TO NDMPMACU LTD., NELLORE, A.P. P. THANUJA ASSISTANT PROFESSOR DEPARTMENT OF MANAGEMENT STUDIES VISVODAYA INSTITUTE OF TECHNOLOGY & SCIENCE S.P.S.R. NELLORE,

Ratio Analysis An Accounting Technique of Analysis and Interpretation of Financial Statements

Ratio Analysis An Accounting Technique of Analysis and Interpretation of Financial Statements IDRISH ALLAD Research Scholar, Rai University, Saroda, Ahmedabad. DR. MAHENDRA H. MAISURIA Research Supervisor,

Ratio Analysis An Accounting Technique of Analysis and Interpretation of Financial Statements IDRISH ALLAD Research Scholar, Rai University, Saroda, Ahmedabad. DR. MAHENDRA H. MAISURIA Research Supervisor,

CHAPTER 2 CONCEPTUAL FRAMEWORK OF DU PONT MODEL AND RATIO ANALYSIS

CHAPTER 2 CONCEPTUAL FRAMEWORK OF DU PONT MODEL AND RATIO ANALYSIS 2.1 Introduction 2.2 Meaning of Financial Performance 2.3 Evolution of Financial Performance 2.4 Meaning of Financial Statements 2.5 Definitions

CHAPTER 2 CONCEPTUAL FRAMEWORK OF DU PONT MODEL AND RATIO ANALYSIS 2.1 Introduction 2.2 Meaning of Financial Performance 2.3 Evolution of Financial Performance 2.4 Meaning of Financial Statements 2.5 Definitions

CHAPTER - VI RATIO ANALYSIS 6.3 UTILITY OF RATIO ANALYSIS 6.4 LIMITATIONS OF RATIO ANALYSIS 6.5 RATIO TABLES, CHARTS, ANALYSIS AND

CHAPTER - VI RATIO ANALYSIS 6.1 INTRODUCTION 6.2 NATURE OF RATIO 6.3 UTILITY OF RATIO ANALYSIS 6.4 LIMITATIONS OF RATIO ANALYSIS 6.5 RATIO TABLES, CHARTS, ANALYSIS AND INTERPRETATION OF DIFFERENT RATIOS

CHAPTER - VI RATIO ANALYSIS 6.1 INTRODUCTION 6.2 NATURE OF RATIO 6.3 UTILITY OF RATIO ANALYSIS 6.4 LIMITATIONS OF RATIO ANALYSIS 6.5 RATIO TABLES, CHARTS, ANALYSIS AND INTERPRETATION OF DIFFERENT RATIOS

FINANCIAL STATEMENTS ANALYSIS - AN INTRODUCTION

Financial Statements Analysis - An Introduction 27 FINANCIAL STATEMENTS ANALYSIS - AN INTRODUCTION You have already learnt about the preparation of financial statements i.e. Balance Sheet and Trading and

Financial Statements Analysis - An Introduction 27 FINANCIAL STATEMENTS ANALYSIS - AN INTRODUCTION You have already learnt about the preparation of financial statements i.e. Balance Sheet and Trading and

A Comparative Financial Analysis of TATA Steel Ltd. and SAIL

IOSR Journal of Economics and Finance (IOSR-JEF) e-issn: 2321-5933, p-issn: 2321-5925.Volume 7, Issue 6 Ver. IV (Nov. - Dec. 2016), PP 01-05 www.iosrjournals.org A Comparative Financial Analysis of TATA

IOSR Journal of Economics and Finance (IOSR-JEF) e-issn: 2321-5933, p-issn: 2321-5925.Volume 7, Issue 6 Ver. IV (Nov. - Dec. 2016), PP 01-05 www.iosrjournals.org A Comparative Financial Analysis of TATA

A Study on Financial Analysis of Steel Trading Company: A Case Study on Kalyani Steel

225 A Study on Financial Analysis of Steel Trading Company: A Case Study on Kalyani Steel Shubham V. Shirsath 1, Pritam B. Bhawar 2 1,2 Student, Department of MBA, MIT School of Management, Pune, India

225 A Study on Financial Analysis of Steel Trading Company: A Case Study on Kalyani Steel Shubham V. Shirsath 1, Pritam B. Bhawar 2 1,2 Student, Department of MBA, MIT School of Management, Pune, India

A study on liquidity and profitability position of national thermal power corporation limited New Delhi

International Journal of Commerce and Management Research ISSN: 2455-627, Impact Factor: RJIF 5.22 www.managejournal.com Volume 3; Issue 2; February 207; Page No. 2-6 A study on liquidity and profitability

International Journal of Commerce and Management Research ISSN: 2455-627, Impact Factor: RJIF 5.22 www.managejournal.com Volume 3; Issue 2; February 207; Page No. 2-6 A study on liquidity and profitability

CHAPTER - 4 ANALYSIS OF PERFORMANCE OF SELECTED FMCG COMPANIES

CHAPTER - 4 ANALYSIS OF PERFORMANCE OF SELECTED FMCG COMPANIES The performance of the FMCG Companies can be evaluated in three ways, they are: (1) Solvency: This is the measure of the firm s ability to

CHAPTER - 4 ANALYSIS OF PERFORMANCE OF SELECTED FMCG COMPANIES The performance of the FMCG Companies can be evaluated in three ways, they are: (1) Solvency: This is the measure of the firm s ability to

AN INTRODUCTION TO ANALYSIS OF FINANCIAL STATEMENT

COURSE 6 Block 1 UNIT-1 AN INTRODUCTION TO ANALYSIS OF FINANCIAL STATEMENT Learning Objectives After reading this chapter, students should be able to: Meaning, definitions and features of financial statement

COURSE 6 Block 1 UNIT-1 AN INTRODUCTION TO ANALYSIS OF FINANCIAL STATEMENT Learning Objectives After reading this chapter, students should be able to: Meaning, definitions and features of financial statement

ANALYSIS OF VALUE ADDED RATIOs

ANALYSIS OF VALUE ADDED RATIOs 4.1 INTRODUCTION. 4.2 MEANING & DEFINITION OF VALUE ADDED RATIO. 4.3 OBJECTIVE & UTILITY OF RATIO ANALYSIS. 4.4 LIMITATION OF RATIO ANALYSIS. 4.5 CLASSIFICATION OF RATIO.

ANALYSIS OF VALUE ADDED RATIOs 4.1 INTRODUCTION. 4.2 MEANING & DEFINITION OF VALUE ADDED RATIO. 4.3 OBJECTIVE & UTILITY OF RATIO ANALYSIS. 4.4 LIMITATION OF RATIO ANALYSIS. 4.5 CLASSIFICATION OF RATIO.

Executive Dashboard. What We ll Cover. Melissa Wood Consultant

Executive Dashboard Melissa Wood Consultant What We ll Cover 1. What kind of information can I find in the Executive Dashboard? 2. Set Up and Save Criteria 3. Using Graphs for More Detail 4. Analyze Financial

Executive Dashboard Melissa Wood Consultant What We ll Cover 1. What kind of information can I find in the Executive Dashboard? 2. Set Up and Save Criteria 3. Using Graphs for More Detail 4. Analyze Financial

Financial statements aim at providing financial

Accounting Ratios 5 LEARNING OBJECTIVES After studying this chapter, you will be able to : Explain the meaning, objectives and limitations of analysis using accounting ratios; Identify the various types

Accounting Ratios 5 LEARNING OBJECTIVES After studying this chapter, you will be able to : Explain the meaning, objectives and limitations of analysis using accounting ratios; Identify the various types

CHAPTER 1 CONCEPT OF FINANCIAL ANALYSIS

CHAPTER 1 CONCEPT OF FINANCIAL ANALYSIS 1 MEANING AND CONCEPT OF FINANCIAL ANALYSIS Financial analysis refers to an assessment of the viability, stability and profitability of a business, sub-business

CHAPTER 1 CONCEPT OF FINANCIAL ANALYSIS 1 MEANING AND CONCEPT OF FINANCIAL ANALYSIS Financial analysis refers to an assessment of the viability, stability and profitability of a business, sub-business

VI SEM BCOM STUDY MATERIAL MANAGEMENT ACCOUNTING. Prepared By SREEJA NAIR PADMA NANDANAN

NEW HORIZON COLLEGE MARATHALLI, BANGALORE (Affiliated to Bangalore University) A Recipient of Prestigious Rajyotsava State Award 2012 conferred by the Government of Karnataka VI SEM BCOM STUDY MATERIAL

NEW HORIZON COLLEGE MARATHALLI, BANGALORE (Affiliated to Bangalore University) A Recipient of Prestigious Rajyotsava State Award 2012 conferred by the Government of Karnataka VI SEM BCOM STUDY MATERIAL

LESSON 6 RATIO ANALYSIS CONTENTS

LESSON 6 RATIO ANALYSIS CONTENTS 6.0 Aims and Objectives 6.1 Introduction 6.2 Definition 6.3 How the Accounting Ratios are Expressed? 6.4 Purpose, Utility & Limitations of Ratio Analysis 6.5 Classification

LESSON 6 RATIO ANALYSIS CONTENTS 6.0 Aims and Objectives 6.1 Introduction 6.2 Definition 6.3 How the Accounting Ratios are Expressed? 6.4 Purpose, Utility & Limitations of Ratio Analysis 6.5 Classification

condition & operating results in a condensed form. Financial statements are used as a

2.1 FINANCIAL ANALYSIS Financial statements are formal records of the financial activities of a business, person or other entity and provide an overview of a business or person s financial condition in

2.1 FINANCIAL ANALYSIS Financial statements are formal records of the financial activities of a business, person or other entity and provide an overview of a business or person s financial condition in

KADI SARVA VISHWAVIDYALAYA B.COM - SEMESTER - 6 B.COM 601 Management Accountancy

KADI SARVA VISHWAVIDYALAYA B.COM - SEMESTER - 6 B.COM 601 Management Accountancy [A] RATIONALE As students have already learnt Financial Accounting, corporate accounting and cost accounting it is necessary

KADI SARVA VISHWAVIDYALAYA B.COM - SEMESTER - 6 B.COM 601 Management Accountancy [A] RATIONALE As students have already learnt Financial Accounting, corporate accounting and cost accounting it is necessary

UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION MODULE - 2

UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION MODULE - 2 UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION Financial Statements: Structure 6.0 Introduction 6.1 Unit Objectives 6.2 Relationship

UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION MODULE - 2 UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION Financial Statements: Structure 6.0 Introduction 6.1 Unit Objectives 6.2 Relationship

CHAPTER 5 FINANCIAL PERFORMANCE APPRAISAL OF EASTERN COALFIELDS LIMITED: A FRAMEWORK OF TOOLS AND TECHNIQUES EMPLOYED FOR DATA ANALYSIS

CHAPTER 5 FINANCIAL PERFORMANCE APPRAISAL OF EASTERN COALFIELDS LIMITED: A FRAMEWORK OF TOOLS AND TECHNIQUES EMPLOYED FOR DATA ANALYSIS Introduction In the previous chapter, we have described the historical

CHAPTER 5 FINANCIAL PERFORMANCE APPRAISAL OF EASTERN COALFIELDS LIMITED: A FRAMEWORK OF TOOLS AND TECHNIQUES EMPLOYED FOR DATA ANALYSIS Introduction In the previous chapter, we have described the historical

CHAPTER-3 OVERVIEW OF FINANCIAL STATEMENT ANALYSIS

CHAPTER-3 OVERVIEW OF FINANCIAL STATEMENT ANALYSIS INDEX SR.NO NAME OF TOPIC 3.1 INTRODUCTION 3.2 MEANING AND CONCEPT OF FINANCIAL ANALYSIS 3.3 DEFINITIONS 3.4 OBJECTIVES AND IMPORTANCE OF FINANCIAL STATEMENT

CHAPTER-3 OVERVIEW OF FINANCIAL STATEMENT ANALYSIS INDEX SR.NO NAME OF TOPIC 3.1 INTRODUCTION 3.2 MEANING AND CONCEPT OF FINANCIAL ANALYSIS 3.3 DEFINITIONS 3.4 OBJECTIVES AND IMPORTANCE OF FINANCIAL STATEMENT

FINANCIAL MANAGEMENT

FINANCIAL MANAGEMENT Financial Statement Analysis The process of determining financial strengths and weaknesses of a firm by establishing strategic relationship between the items of the balance sheet,

FINANCIAL MANAGEMENT Financial Statement Analysis The process of determining financial strengths and weaknesses of a firm by establishing strategic relationship between the items of the balance sheet,

WEEK 10 Analysis of Financial Statements

WEEK 10 Analysis of Financial Statements Learning Objectives 1. Organize a systematic financial statements analysis using common-size financial statements and ratio analysis. 2. Recognize the potential

WEEK 10 Analysis of Financial Statements Learning Objectives 1. Organize a systematic financial statements analysis using common-size financial statements and ratio analysis. 2. Recognize the potential

Class B.Com VI Sem. (Hons.)

") SYLLABUS Class B.Com VI Sem. (Hons.) UNIT I UNIT II UNIT III UNIT IV UNIT V Subject Management Accounting Management Accounting: Meaning, nature, scope and functions of management accounting, Role of management

SYLLABUS Class B.Com VI Sem. (Hons.) UNIT I UNIT II UNIT III UNIT IV UNIT V Subject Management Accounting Management Accounting: Meaning, nature, scope and functions of management accounting, Role of management

US03FBCA01- Financial Accounting and Management. Liquidity ratios Leverage ratios Activity ratios Profitability ratios

Unit 4 Ratio Analysis and Cost-Volume- Profit (CVP) Analysis Types of Ratio Several ratios, calculated from the accounting data, can be grouped into various classes according to financial activity or function

Unit 4 Ratio Analysis and Cost-Volume- Profit (CVP) Analysis Types of Ratio Several ratios, calculated from the accounting data, can be grouped into various classes according to financial activity or function

RATIO ANALYSIS. The preceding chapters concentrated on developing a general but solid understanding

C H A P T E R 4 RATIO ANALYSIS I N T R O D U C T I O N The preceding chapters concentrated on developing a general but solid understanding of accounting principles and concepts and their applications to

C H A P T E R 4 RATIO ANALYSIS I N T R O D U C T I O N The preceding chapters concentrated on developing a general but solid understanding of accounting principles and concepts and their applications to

A Study on Cost of Capital

International Journal of Empirical Finance Vol. 4, No. 1, 2015, 1-11 A Study on Cost of Capital Ravi Thirumalaisamy 1 Abstract Cost of capital which is used as a financial standard plays a crucial role

International Journal of Empirical Finance Vol. 4, No. 1, 2015, 1-11 A Study on Cost of Capital Ravi Thirumalaisamy 1 Abstract Cost of capital which is used as a financial standard plays a crucial role

not to be republished NCERT You have learnt about the financial statements Analysis of Financial Statements 4

Analysis of Financial Statements 4 LEARNING OBJECTIVES After studying this chapter, you will be able to : explain the nature and significance of financial analysis; identify the objectives of financial

Analysis of Financial Statements 4 LEARNING OBJECTIVES After studying this chapter, you will be able to : explain the nature and significance of financial analysis; identify the objectives of financial

E1-E2 Accounting Standards And Ratio analysis

E1-E2 Accounting Standards And Ratio analysis For internal circulation of BSNLonly 1 WELCOME This is a presentation for the E1-E2 (Finance) Module for the Topic: Accounting standards and Ratio analysis

E1-E2 Accounting Standards And Ratio analysis For internal circulation of BSNLonly 1 WELCOME This is a presentation for the E1-E2 (Finance) Module for the Topic: Accounting standards and Ratio analysis

Unit 2: ACCOUNTING CONCEPTS, PRINCIPLES AND CONVENTIONS

Unit 2: ACCOUNTING S, PRINCIPLES AND CONVENTIONS Accounting is a language of the business. Financial statements prepared by the accountant communicate financial information to the various stakeholders

Unit 2: ACCOUNTING S, PRINCIPLES AND CONVENTIONS Accounting is a language of the business. Financial statements prepared by the accountant communicate financial information to the various stakeholders

Financial Performance of RINL Using Financial Ratios and

Financial Performance of RINL Using Financial Ratios and Comparison with TATA, SAIL and JSW Kommu U. K.S. Alekhya, K. Simhachalam Naidu, Tippana Lochana MVGR College of Engineering (A) ABSTRACT: This paper

Financial Performance of RINL Using Financial Ratios and Comparison with TATA, SAIL and JSW Kommu U. K.S. Alekhya, K. Simhachalam Naidu, Tippana Lochana MVGR College of Engineering (A) ABSTRACT: This paper

Engineering Economics and Financial Accounting

Engineering Economics and Financial Accounting Unit 5: Accounting Major Topics are: Balance Sheet - Profit & Loss Statement - Evaluation of Investment decisions Average Rate of Return - Payback Period

Engineering Economics and Financial Accounting Unit 5: Accounting Major Topics are: Balance Sheet - Profit & Loss Statement - Evaluation of Investment decisions Average Rate of Return - Payback Period

MVSR ENGINEERING COLLEGE MBA DEPARTMNET FINANCIAL ACCOUNTING AND ANALYSIS

MVSR ENGINEERING COLLEGE MBA DEPARTMNET FINANCIAL ACCOUNTING AND ANALYSIS Accounting : The systematic and comprehensive recording of financial transactions pertaining to a business. Accounting also refers

MVSR ENGINEERING COLLEGE MBA DEPARTMNET FINANCIAL ACCOUNTING AND ANALYSIS Accounting : The systematic and comprehensive recording of financial transactions pertaining to a business. Accounting also refers

A Comparative Financial Analysis of SAIL and TATA Steel Ltd.

A Comparative Financial Analysis of and TATA Steel Ltd. Ashwini Raghuvanshi Research Scholar, Faculty of Commerce, U.P. Autonomous College, Varanasi, U.P. 221002 Abstract: The present study aims to show

A Comparative Financial Analysis of and TATA Steel Ltd. Ashwini Raghuvanshi Research Scholar, Faculty of Commerce, U.P. Autonomous College, Varanasi, U.P. 221002 Abstract: The present study aims to show

Asian Journal of Multidisciplinary Studies

Asian Journal of Multidisciplinary Studies Volume, Issue, October 4 ISSN: -9 (Online) 4-6 (Print) Impact Factor:.9 Abstract: A Significance of Financial Ratio Analysis in Decisions Making: A Case Study

Asian Journal of Multidisciplinary Studies Volume, Issue, October 4 ISSN: -9 (Online) 4-6 (Print) Impact Factor:.9 Abstract: A Significance of Financial Ratio Analysis in Decisions Making: A Case Study

WORKING CAPITAL ANALYSIS OF SELECT CEMENT COMPANIES IN INDIA

CHAPTER - IV WORKING CAPITAL ANALYSIS OF SELECT CEMENT COMPANIES IN INDIA CHAPTER IV WORKING CAPITAL ANALYSIS OF SELECT CEMENT COMPANIES IN INDIA In this chapter an attempt has been made to analyse the

CHAPTER - IV WORKING CAPITAL ANALYSIS OF SELECT CEMENT COMPANIES IN INDIA CHAPTER IV WORKING CAPITAL ANALYSIS OF SELECT CEMENT COMPANIES IN INDIA In this chapter an attempt has been made to analyse the

CHAPTER 4. ANALYSIS AND INTERPRETATION OF DATA Ratio Analysis - Meaning of Ratio (A) Return on Investment Ratios

Return on Investment Ratios") CHAPTER 4 ANALYSIS AND INTERPRETATION OF DATA Ratio Analysis - Meaning of Ratio (A) Return on Investment Ratios - Concept of Return on Investment - Advantages of ROI - Limitations of ROI - Evaluation of

CHAPTER 4 ANALYSIS AND INTERPRETATION OF DATA Ratio Analysis - Meaning of Ratio (A) Return on Investment Ratios - Concept of Return on Investment - Advantages of ROI - Limitations of ROI - Evaluation of

UNIT IV CAPITAL BUDGETING

UNIT IV CAPITAL BUDGETING Capital Budgeting: Capital budgeting is the process of making investment decision in long-term assets or courses of action. Capital expenditure incurred today is expected to bring

UNIT IV CAPITAL BUDGETING Capital Budgeting: Capital budgeting is the process of making investment decision in long-term assets or courses of action. Capital expenditure incurred today is expected to bring

Basic Financial Statement Analysis Practices: A Study on Infosys

Basic Financial Statement Analysis Practices: A Study on Infosys Medarapu Sudhakar Kakatiya University- Warangal Telangana, INDIA Abstract: The Balance Sheet, also called a statement of financial position,

Basic Financial Statement Analysis Practices: A Study on Infosys Medarapu Sudhakar Kakatiya University- Warangal Telangana, INDIA Abstract: The Balance Sheet, also called a statement of financial position,

Subject- Management Accounting

UNIT-II Financial statements : Meaning, objectives and methods The term Financial Analysis Which is also known as and interpretation of financial statements refer to process of determining financial strength

UNIT-II Financial statements : Meaning, objectives and methods The term Financial Analysis Which is also known as and interpretation of financial statements refer to process of determining financial strength

Week 4 and Week 5 Handout Financial Statement Analysis

Week 4 and Week 5 Handout Financial Statement Analysis Introduction After understanding the basic financial statements, one may be interested in analysing the financial statements to understand the performance

Week 4 and Week 5 Handout Financial Statement Analysis Introduction After understanding the basic financial statements, one may be interested in analysing the financial statements to understand the performance

ANALYSIS OF THE FINANCIAL STATEMENTS

5 ANALYSIS OF THE FINANCIAL STATEMENTS CONTENTS PAGE STUDY OBJECTIVES 166 INTRODUCTION 167 METHODS OF STATEMENT ANALYSIS 167 A. ANALYSIS WITH THE AID OF FINANCIAL RATIOS 168 GROUPS OF FINANCIAL RATIOS

5 ANALYSIS OF THE FINANCIAL STATEMENTS CONTENTS PAGE STUDY OBJECTIVES 166 INTRODUCTION 167 METHODS OF STATEMENT ANALYSIS 167 A. ANALYSIS WITH THE AID OF FINANCIAL RATIOS 168 GROUPS OF FINANCIAL RATIOS

PERFORMANCE APPRAISAL OF HPCL THROUGH FREE CASH FLOW

Indian Journal of Accounting (IJA) 18 ISSN : 0972-1479 (Print) 2395-6127 (Online) Vol. XLVIII (2), December, 2016, pp. 18-24 PERFORMANCE APPRAISAL OF HPCL THROUGH FREE CASH FLOW Dr. S. K. Khatik Dr. Amit

Indian Journal of Accounting (IJA) 18 ISSN : 0972-1479 (Print) 2395-6127 (Online) Vol. XLVIII (2), December, 2016, pp. 18-24 PERFORMANCE APPRAISAL OF HPCL THROUGH FREE CASH FLOW Dr. S. K. Khatik Dr. Amit

A Comparison of Financial Performance Based On Ratio Analysis (With Special Reference to ITC Limited and HUL Limited)

") IOSR Journal Of Humanities And Social Science (IOSR-JHSS) Volume 23, Issue 4, Ver. 3 (April. 2018) PP 59-63 e-issn: 2279-0837, p-issn: 2279-0845. www.iosrjournals.org A Comparison of Financial Performance

IOSR Journal Of Humanities And Social Science (IOSR-JHSS) Volume 23, Issue 4, Ver. 3 (April. 2018) PP 59-63 e-issn: 2279-0837, p-issn: 2279-0845. www.iosrjournals.org A Comparison of Financial Performance

CHAPTER II FINANCIAL MANAGEMENT AND BANKING - AN OVERVIEW

27 CHAPTER II FINANCIAL MANAGEMENT AND BANKING - AN OVERVIEW 28 CONTENTS 2.1 Importance of Finance in Banks 2.2 Meaning of Bank Finance 2.3 Meaning of Financial Management in Banks 2.4 Scope of Financial

27 CHAPTER II FINANCIAL MANAGEMENT AND BANKING - AN OVERVIEW 28 CONTENTS 2.1 Importance of Finance in Banks 2.2 Meaning of Bank Finance 2.3 Meaning of Financial Management in Banks 2.4 Scope of Financial

CHAPTER IV CAPITAL STRUCTURE OF STEEL INDUSTRIES IN TAMILNADU

CHAPTER IV CAPITAL STRUCTURE OF STEEL INDUSTRIES IN TAMILNADU INTRODUCTION In order to run and manage a company, funds are needed. Right from the promotional stage up to end, finances plays an important

CHAPTER IV CAPITAL STRUCTURE OF STEEL INDUSTRIES IN TAMILNADU INTRODUCTION In order to run and manage a company, funds are needed. Right from the promotional stage up to end, finances plays an important

FINANCIAL MANAGEMENT

FINANCIAL MANAGEMENT Question 1: What is financial management? Explain the functions of financial management. (May 13, Nov 11) (Mark 7) Answer: Financial management is that specialized activity which is

FINANCIAL MANAGEMENT Question 1: What is financial management? Explain the functions of financial management. (May 13, Nov 11) (Mark 7) Answer: Financial management is that specialized activity which is

Liquidity and Profitability Analysis Chapter is divided into four parts. comprising of part I dealing with Liquidity Analysis divided into short-term

163 5.1 INTRODUCTION Liquidity and Profitability Analysis Chapter is divided into four parts comprising of part I dealing with Liquidity Analysis divided into short-term and long-term. Part II deals with

163 5.1 INTRODUCTION Liquidity and Profitability Analysis Chapter is divided into four parts comprising of part I dealing with Liquidity Analysis divided into short-term and long-term. Part II deals with

A Case Study on Trend and Growth Analysis of Tata Consultancy Services Limited

A Case Study on Trend and Growth Analysis of Tata Consultancy Services Limited 1 Dr. K. Venkatachalam and 2 J.B. Rajaanjali 1 Assistant Professor, 3 PG Student, 1,2 Department of Commerce, PGP College

A Case Study on Trend and Growth Analysis of Tata Consultancy Services Limited 1 Dr. K. Venkatachalam and 2 J.B. Rajaanjali 1 Assistant Professor, 3 PG Student, 1,2 Department of Commerce, PGP College

DETERMINATION OF WORKING CAPITAL

E- Module 1 DETERMINATION OF WORKING CAPITAL Operating Cycle Approach The operating cycle can be said to be at the heart of the need for working capital 1. Taking the time lag into account for determining

E- Module 1 DETERMINATION OF WORKING CAPITAL Operating Cycle Approach The operating cycle can be said to be at the heart of the need for working capital 1. Taking the time lag into account for determining

CHAPTER-4 ANALYSIS OF LIQUIDITY

CHAPTER-4 ANALYSIS OF LIQUIDITY SR. NO. PARTICULAR P. NO 4.1 INTRODUCTION OF LIQUIDITY 81 4.2 CONCEPT OF LIQUIDITY 81 4.3 SIGNIFICANCE OF THE LIQUIDITY ANALYSIS 82 4.4 LIQUIDITY ANALYSIS OF SELECTEDAUTOMOBILE

CHAPTER-4 ANALYSIS OF LIQUIDITY SR. NO. PARTICULAR P. NO 4.1 INTRODUCTION OF LIQUIDITY 81 4.2 CONCEPT OF LIQUIDITY 81 4.3 SIGNIFICANCE OF THE LIQUIDITY ANALYSIS 82 4.4 LIQUIDITY ANALYSIS OF SELECTEDAUTOMOBILE

CHAPTER-4 ANALYSIS OF FINANCIAL EFFICIENCY. The word efficiency as defined by the Oxford dictionary states that:

CHAPTER-4 ANALYSIS OF FINANCIAL EFFICIENCY 4.1 Concept of Efficiency and Performance The word efficiency as defined by the Oxford dictionary states that: "Efficiency is the accomplishment of or the ability

CHAPTER-4 ANALYSIS OF FINANCIAL EFFICIENCY 4.1 Concept of Efficiency and Performance The word efficiency as defined by the Oxford dictionary states that: "Efficiency is the accomplishment of or the ability

Lesson 5 Ratios, at first glance

Advanced Accounting AY 2017/2018 Lesson 5 Ratios, at first glance Università degli Studi di Trieste D.E.A.M.S. Paolo Altin 160 Financial ratios Provide a quick and (relatively) simple means of evaluating

Advanced Accounting AY 2017/2018 Lesson 5 Ratios, at first glance Università degli Studi di Trieste D.E.A.M.S. Paolo Altin 160 Financial ratios Provide a quick and (relatively) simple means of evaluating

Chapter-4. Data Analysis and Interpretation

Chapter-4 Data Analysis and Interpretation Chapter-4 Data Analysis and Interpretation 4.1 Introduction. 4.2 Meaning of Finance. 4.3 Definition of Financial Efficiency. 4.4 Concept of Financial Efficiency.

Chapter-4 Data Analysis and Interpretation Chapter-4 Data Analysis and Interpretation 4.1 Introduction. 4.2 Meaning of Finance. 4.3 Definition of Financial Efficiency. 4.4 Concept of Financial Efficiency.

UNIT 3 RATIO ANALYSIS

Understanding and Analysis of Financial Statements UNIT 3 RATIO ANALYSIS Structure Page Nos. 3.0 Introduction 52 3.1 Objectives 54 3.2 Categories of Ratios 54 3.2.1 Long-term Solvency Ratios 3.2.2 Liquidity

Understanding and Analysis of Financial Statements UNIT 3 RATIO ANALYSIS Structure Page Nos. 3.0 Introduction 52 3.1 Objectives 54 3.2 Categories of Ratios 54 3.2.1 Long-term Solvency Ratios 3.2.2 Liquidity

Management of cash in Public sector Enterprises - A case study of ECIL, Hyderabad

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668 PP 50-55 www.iosrjournals.org Management of cash in Public sector Enterprises - A case study of ECIL, Hyderabad Dr.N.Jyothi

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668 PP 50-55 www.iosrjournals.org Management of cash in Public sector Enterprises - A case study of ECIL, Hyderabad Dr.N.Jyothi

CHAPTER: - 8. Analysis of Cash flow

CHAPTER: - 8 Analysis of Cash flow Particular Page No. Introduction 231 Meaning of Certain terms 231 Classification of cash flow 231 Information required for cash flow Statement 233 Utility of Cash Flow

CHAPTER: - 8 Analysis of Cash flow Particular Page No. Introduction 231 Meaning of Certain terms 231 Classification of cash flow 231 Information required for cash flow Statement 233 Utility of Cash Flow

FRAMEWORK FOR SUPERVISORY INFORMATION

FRAMEWORK FOR SUPERVISORY INFORMATION ABOUT THE DERIVATIVES ACTIVITIES OF BANKS AND SECURITIES FIRMS (Joint report issued in conjunction with the Technical Committee of IOSCO) (May 1995) I. Introduction

FRAMEWORK FOR SUPERVISORY INFORMATION ABOUT THE DERIVATIVES ACTIVITIES OF BANKS AND SECURITIES FIRMS (Joint report issued in conjunction with the Technical Committee of IOSCO) (May 1995) I. Introduction

ANSWER SHEET EXAMINATION #2

ANSWER SHEET EXAMINATION #2 1) D 2) B 26) D 3) C 27) B 4) A 28) B 5) D 29) C 6) D 30) A 7) D 31) B 8) C 32) D 9) D 33) D 10) B 34) D 11) A 12) A 13) D 14) C 15) A 16) C 17) B 18) B 19) C 20) B 21) B 22)

ANSWER SHEET EXAMINATION #2 1) D 2) B 26) D 3) C 27) B 4) A 28) B 5) D 29) C 6) D 30) A 7) D 31) B 8) C 32) D 9) D 33) D 10) B 34) D 11) A 12) A 13) D 14) C 15) A 16) C 17) B 18) B 19) C 20) B 21) B 22)

CHAPTER 4 COST AND MANAGEMENT ACCOUNTING - THEORITICAL BACKGROUD

CHAPTER 4 COST AND MANAGEMENT ACCOUNTING - THEORITICAL BACKGROUD Sr. No. Contains Page No Introduction 34 4.1 Cost Accounting 35 4.2 Cost and Management Accounting 37 4.3 Financial Statement Analysis 41

CHAPTER 4 COST AND MANAGEMENT ACCOUNTING - THEORITICAL BACKGROUD Sr. No. Contains Page No Introduction 34 4.1 Cost Accounting 35 4.2 Cost and Management Accounting 37 4.3 Financial Statement Analysis 41

Learning Goal 1: Review the contents of the stockholders' report and the procedures for consolidating international financial statements.

Principles of Managerial Finance, 12e (Gitman) Chapter 2 Financial Statements and Analysis Learning Goal 1: Review the contents of the stockholders' report and the procedures for consolidating international

Principles of Managerial Finance, 12e (Gitman) Chapter 2 Financial Statements and Analysis Learning Goal 1: Review the contents of the stockholders' report and the procedures for consolidating international

Chapter 4 Financial Strength Analysis

Chapter 4 Financial Strength Analysis 4.1 Meaning of Financial Strength Finance is an essential requirement for every business enterprise. Various type of finance was needed by the concern for their activity

Chapter 4 Financial Strength Analysis 4.1 Meaning of Financial Strength Finance is an essential requirement for every business enterprise. Various type of finance was needed by the concern for their activity

INDUSTRIAL BUDGETING AND COST ANALYSIS

C h a p t e r INDUSTRIAL BUDGETING AND COST ANALYSIS 10.1 INTRODUCTION Everybody is familiar with the idea of a plan. Not only in business, but in private life also people make plans though there are considerable

C h a p t e r INDUSTRIAL BUDGETING AND COST ANALYSIS 10.1 INTRODUCTION Everybody is familiar with the idea of a plan. Not only in business, but in private life also people make plans though there are considerable

Nature of a Budget. Budgets are an important tool for effective short-term planning and control in organizations.

Budget Preparation Nature of a Budget Budgets are an important tool for effective short-term planning and control in organizations. An operating budget usually covers one year and states the revenues and

Budget Preparation Nature of a Budget Budgets are an important tool for effective short-term planning and control in organizations. An operating budget usually covers one year and states the revenues and

Airo International Research Journal February, 2017 Volume IX, ISSN:

1 SHARING IS WHAT NOT CARING A SHAREHOLDER S WEALTH: A STUDY ON DIVIDEND DECISION TO SHAREHOLDER S WEALTH OF SELECT PHARMACEUTICAL COMPANIES D Rajitha Associate Professor, Trinity college of Engineering

1 SHARING IS WHAT NOT CARING A SHAREHOLDER S WEALTH: A STUDY ON DIVIDEND DECISION TO SHAREHOLDER S WEALTH OF SELECT PHARMACEUTICAL COMPANIES D Rajitha Associate Professor, Trinity college of Engineering

Class B.Com. V Sem. SYLLABUS. Subject Management Accounting

SYLLABUS Class B.Com. V Sem. Subject Management Accounting Unit-I Management accounting: meaning, nature, scope and functions of management accounting, role of management accounting in decision making,

SYLLABUS Class B.Com. V Sem. Subject Management Accounting Unit-I Management accounting: meaning, nature, scope and functions of management accounting, role of management accounting in decision making,

Georgia Banking School Financial Statement Analysis. Dr. Christopher R Pope Terry College of Business University of Georgia

Georgia Banking School Financial Statement Analysis Dr. Christopher R Pope Terry College of Business University of Georgia Introduction Objective My objective is to introduce you to the analysis of financial

Georgia Banking School Financial Statement Analysis Dr. Christopher R Pope Terry College of Business University of Georgia Introduction Objective My objective is to introduce you to the analysis of financial

Financial Performance of BHEL (Visakhapatnam) using Financial Ratios

using Financial Ratios") Financial Performance of BHEL (Visakhapatnam) using Financial Ratios Madhulatha Karri MVGR college of engineering Sheeba.V.Thomas MVGR College Of Engineering Omkar Venkata Chinnam Naidu Murru MVGR College

Financial Performance of BHEL (Visakhapatnam) using Financial Ratios Madhulatha Karri MVGR college of engineering Sheeba.V.Thomas MVGR College Of Engineering Omkar Venkata Chinnam Naidu Murru MVGR College

A STUDY ON CAPACITY UTILIZATION AND THE EFFICIENCY OF FINANCIAL MANAGEMENT OF NATIONAL THERMAL POWER CORPORATION LIMITED NEW DELHI

A STUDY ON CAPACITY UTILIZATION AND THE EFFICIENCY OF FINANCIAL MANAGEMENT OF NATIONAL THERMAL POWER CORPORATION LIMITED NEW DELHI Nasir Rashid* and Dr. B. Manivannan** *PhD Research Scholar, Dept. of

A STUDY ON CAPACITY UTILIZATION AND THE EFFICIENCY OF FINANCIAL MANAGEMENT OF NATIONAL THERMAL POWER CORPORATION LIMITED NEW DELHI Nasir Rashid* and Dr. B. Manivannan** *PhD Research Scholar, Dept. of

INTRODUCTION DEFINITION OF FINANCE

INTRODUCTION Business concern needs finance to meet their requirements in the economic world. Any kind of business activity depends on the finance. Hence, it is called as lifeblood of business organization.

INTRODUCTION Business concern needs finance to meet their requirements in the economic world. Any kind of business activity depends on the finance. Hence, it is called as lifeblood of business organization.

Chapter-6: Analysis of Efficiency of Asset Management of the selected Public Sector Oil and Gas Companies in India

Chapter-6: Analysis of Efficiency of Asset Management of the selected Public Sector Oil and Gas Companies in India 6.1 Introduction Turnover ratios or activity ratios bring out the relationship between

Chapter-6: Analysis of Efficiency of Asset Management of the selected Public Sector Oil and Gas Companies in India 6.1 Introduction Turnover ratios or activity ratios bring out the relationship between

Manpower, Sultanate of Oman.

ISSN: 2249-7196 IJMRR/ December 2014/ Volume 4/Issue 12/Article No-2/1129-1137 Dr. Riyas Kalathinkal et al./ International Journal of Management Research & Review AN ANALYTICAL STUDY ON FINANCIAL PERFORMANCE

ISSN: 2249-7196 IJMRR/ December 2014/ Volume 4/Issue 12/Article No-2/1129-1137 Dr. Riyas Kalathinkal et al./ International Journal of Management Research & Review AN ANALYTICAL STUDY ON FINANCIAL PERFORMANCE

Financial Evaluation of Arasu Rubber Corporation Limited in Kanyakumari District of Tamilnadu-An Empirical study

Financial Evaluation of Arasu Rubber Corpon Limited in Kanyakumari District of Tamilnadu-An Empirical study D.H.Thavamalar & M.Julius prasad Assistant Professor, Department of Commerce, Directorate of

Financial Evaluation of Arasu Rubber Corpon Limited in Kanyakumari District of Tamilnadu-An Empirical study D.H.Thavamalar & M.Julius prasad Assistant Professor, Department of Commerce, Directorate of

INTERNATIONAL JOURNAL OF MULTIDISCIPLINARY RESEARCH CENTRE (IJMRC)

") ISSN: 2454-3659 (P), 2454-3861(E) Volume I, Issue 7 December 2015 International Journal of Multidisciplinary Research Centre Research Article / Survey Paper / Case Study A STUDY ON CAPITAL BUDGETING PROCESS

ISSN: 2454-3659 (P), 2454-3861(E) Volume I, Issue 7 December 2015 International Journal of Multidisciplinary Research Centre Research Article / Survey Paper / Case Study A STUDY ON CAPITAL BUDGETING PROCESS

DO NOT TURN OVER UNTIL TOLD TO BEGIN

THIS PAPER IS NOT TO BE REMOVED FROM THE EXAMINATION HALLS University of London BSc Examination 2012 BA1020 (BBA0020) Business Administration Accounting for Management Day, May 2012: Time DO NOT TURN OVER

THIS PAPER IS NOT TO BE REMOVED FROM THE EXAMINATION HALLS University of London BSc Examination 2012 BA1020 (BBA0020) Business Administration Accounting for Management Day, May 2012: Time DO NOT TURN OVER

Commerce Financial Management Lesson: Leverage Analysis Author: Mr. Vinay Kumar, College/Dept: Aryabhatta College University of Delhi

Commerce Financial Management Lesson: Leverage Analysis Author: Mr. Vinay Kumar, College/Dept: Aryabhatta College University of Delhi Institute of Lifelong Learning, University of Delhi Page 1 Table of

Commerce Financial Management Lesson: Leverage Analysis Author: Mr. Vinay Kumar, College/Dept: Aryabhatta College University of Delhi Institute of Lifelong Learning, University of Delhi Page 1 Table of

Book-III:- Analysis of Financial Statement of a company. Financial Statements of a Company

SUPPORT MATERIAL ACCOUNTANCY CLASS-XII Book-III:- Analysis of Financial Statement of a company Financial Statements of a Company Financial Statements: Financial statements are the end products of accounting

SUPPORT MATERIAL ACCOUNTANCY CLASS-XII Book-III:- Analysis of Financial Statement of a company Financial Statements of a Company Financial Statements: Financial statements are the end products of accounting

FINANCING OF WORKING CAPITAL IN SELECT CEMENT COMPANIES- A POLICY PERSPECTIVE

FINANCING OF WORKING CAPITAL IN SELECT CEMENT COMPANIES- A POLICY PERSPECTIVE Dr. K. Bhagyalakshmi 1, Dr. P. Krishnama Chary 2 1 Lecturer, Dept. of Commerce and Business Management, University College

FINANCING OF WORKING CAPITAL IN SELECT CEMENT COMPANIES- A POLICY PERSPECTIVE Dr. K. Bhagyalakshmi 1, Dr. P. Krishnama Chary 2 1 Lecturer, Dept. of Commerce and Business Management, University College

Analysis of Financial Statement Chapter VI. Answers to the very short answers questions.

Analysis of Financial Statement Chapter VI Answers to the very short answers questions. Ans.1 Ans.2 Analysis of Financial statement is the systematic process of identifying the financial strength and weaknesses

Analysis of Financial Statement Chapter VI Answers to the very short answers questions. Ans.1 Ans.2 Analysis of Financial statement is the systematic process of identifying the financial strength and weaknesses

To Measure the Liquidity Of Selected Private Sector Pharmaceutical Companies in India

To Measure the Liquidity Of Selected Private Sector Pharmaceutical Companies in India Dr.K.Ayappan Assistant Professor, Government Arts College (Autonomous),Kumbakonam Abstract: The Indian pharmaceuticals

To Measure the Liquidity Of Selected Private Sector Pharmaceutical Companies in India Dr.K.Ayappan Assistant Professor, Government Arts College (Autonomous),Kumbakonam Abstract: The Indian pharmaceuticals

CMA Part 2. Financial Decision Making

CMA Part 2 Financial Decision Making SU 8.1 The Capital Budgeting Process Capital budgeting is the process of planning and controlling investment for long-term projects. Will affect the company for many

CMA Part 2 Financial Decision Making SU 8.1 The Capital Budgeting Process Capital budgeting is the process of planning and controlling investment for long-term projects. Will affect the company for many

III YEAR VI SEMESTER COURSE CODE: 4BCO6C2 CORE COURSE XVII MANAGEMENT ACCOUNTING

III YEAR VI SEMESTER COURSE CODE: 4BCO6C2 CORE COURSE XVII MANAGEMENT ACCOUNTING Unit I Management Accounting Meaning Definition Objectives Cost Accounting Vs Financial Accounting Vs Management Accounting

III YEAR VI SEMESTER COURSE CODE: 4BCO6C2 CORE COURSE XVII MANAGEMENT ACCOUNTING Unit I Management Accounting Meaning Definition Objectives Cost Accounting Vs Financial Accounting Vs Management Accounting

ACC 501 Quizzes Lecture 1 to 22

ACC501 Business Finance Composed By Faheem Saqib A mega File of MiD Term Solved MCQ For more Help Rep At Faheem_saqib2003@yahoocom Faheemsaqib2003@gmailcom 0334-6034849 ACC 501 Quizzes Lecture 1 to 22

ACC501 Business Finance Composed By Faheem Saqib A mega File of MiD Term Solved MCQ For more Help Rep At Faheem_saqib2003@yahoocom Faheemsaqib2003@gmailcom 0334-6034849 ACC 501 Quizzes Lecture 1 to 22

FINANCIAL RATIOS. LIQUIDITY RATIOS (and Working Capital) You want current and quick ratios to be > 1. Current Liabilities SAMPLE BALANCE SHEET ASSETS

You want current and quick ratios to be > 1. Current Liabilities SAMPLE BALANCE SHEET ASSETS") FINANCIAL RATIOS ROUND ALL ANSWERS TO TWO DECIMALS UNLESS REQUESTED OTHERWISE IN THE PROBLEM LIQUIDITY RATIOS (and Working Capital) You want current and quick ratios to be > 1 Current Ratio Quick Ratio

FINANCIAL RATIOS ROUND ALL ANSWERS TO TWO DECIMALS UNLESS REQUESTED OTHERWISE IN THE PROBLEM LIQUIDITY RATIOS (and Working Capital) You want current and quick ratios to be > 1 Current Ratio Quick Ratio

CHAPTER 7. Cash Flow AnAlysis. of Sample Real. EstatE CompaniEs

CHAPTER 7 Cash Flow AnAlysis of Sample Real EstatE CompaniEs 226 INTRODUCTION CASH FLOW A cash flow statement is one of the most important financial statements for a project or business. A type of financial

CHAPTER 7 Cash Flow AnAlysis of Sample Real EstatE CompaniEs 226 INTRODUCTION CASH FLOW A cash flow statement is one of the most important financial statements for a project or business. A type of financial

Many decisions in operations management involve large

SUPPLEMENT Financial Analysis J LEARNING GOALS After reading this supplement, you should be able to: 1. Explain the time value of money concept. 2. Demonstrate the use of the net present value, internal

SUPPLEMENT Financial Analysis J LEARNING GOALS After reading this supplement, you should be able to: 1. Explain the time value of money concept. 2. Demonstrate the use of the net present value, internal

Reading Understanding. Financial Statements. A Layman s Guide to Financial Reporting

Reading Understanding & Financial Statements A Layman s Guide to Financial Reporting 1 Introduction Financial statements are an important management tool. When correctly prepared and properly interpreted,

Reading Understanding & Financial Statements A Layman s Guide to Financial Reporting 1 Introduction Financial statements are an important management tool. When correctly prepared and properly interpreted,

Key Business Ratios v 2.0 Course Transcript Presented by: TeachUcomp, Inc.

Key Business Ratios v 2.0 Course Transcript Presented by: TeachUcomp, Inc. Course Introduction Welcome to Key Business Ratios, a presentation of TeachUcomp, Inc. This course examines key ratios used to

Key Business Ratios v 2.0 Course Transcript Presented by: TeachUcomp, Inc. Course Introduction Welcome to Key Business Ratios, a presentation of TeachUcomp, Inc. This course examines key ratios used to

FIXED ASSET MANAGEMENT WITH RESPECT TO WILO MATHER AND PLATT PUMPS PVT LTD

FIXED ASSET MANAGEMENT WITH RESPECT TO WILO MATHER AND PLATT PUMPS PVT LTD Dr. Daniel Penkar Abstract: Fixed assets management is an accounting process that seeks to track fixed assets for the purposes

FIXED ASSET MANAGEMENT WITH RESPECT TO WILO MATHER AND PLATT PUMPS PVT LTD Dr. Daniel Penkar Abstract: Fixed assets management is an accounting process that seeks to track fixed assets for the purposes

Book 3.1 Accounting & Finance in Business

Book 3.1 Accounting & Finance in Business Why are we studying what is accounting?? Accounting is crucial to the running of any business. It is concerned with the flow of economic resources in and out of

Book 3.1 Accounting & Finance in Business Why are we studying what is accounting?? Accounting is crucial to the running of any business. It is concerned with the flow of economic resources in and out of

A Study on Factors Affecting Investment Decision Making in the Context of Portfolio Management

A Study on Factors Affecting Investment Decision Making in the Context of Portfolio Management Anoop Joseph 1 and Josmy Varghese 2 Assistant Professor of Commerce, Pavanatma College, Murickassery 1 Assistant

A Study on Factors Affecting Investment Decision Making in the Context of Portfolio Management Anoop Joseph 1 and Josmy Varghese 2 Assistant Professor of Commerce, Pavanatma College, Murickassery 1 Assistant

Chapter 6. Data Analysis and Interpretation

Chapter 6 Data Analysis and Interpretation 6.1 Introduction. 6.2 Current Ratio. 6.3 Quick Ratio. 6.4 Debt Equity Ratio. 6.5 Interest Coverage Ratio. 6.6 Operating Profit Margin Ratio. 6.7 Net Profit Margin

Chapter 6 Data Analysis and Interpretation 6.1 Introduction. 6.2 Current Ratio. 6.3 Quick Ratio. 6.4 Debt Equity Ratio. 6.5 Interest Coverage Ratio. 6.6 Operating Profit Margin Ratio. 6.7 Net Profit Margin

CHAPTER-3 DATA ANALYSIS PART-1 CAPITAL STRUCTURE

CHAPTER-3 DATA ANALYSIS PART-1 CAPITAL STRUCTURE 87 CHAPTER 3 DATA ANALYSIS PART - 1: CAPITAL STRUCTURE 3.1 CONCEPT OF CAPITAL STRUCTURE:... 90 3.2 CAPITAL STRUCTURE ANALYSIS:... 91 3.2.1 FINANCIAL TOOLS:...

CHAPTER-3 DATA ANALYSIS PART-1 CAPITAL STRUCTURE 87 CHAPTER 3 DATA ANALYSIS PART - 1: CAPITAL STRUCTURE 3.1 CONCEPT OF CAPITAL STRUCTURE:... 90 3.2 CAPITAL STRUCTURE ANALYSIS:... 91 3.2.1 FINANCIAL TOOLS:...

Financial management Notes

Financial management Notes FINANCIAL MANAGEMENT Financial management is an academic discipline which is concerned with decision-making. This decision is concerned with the size and composition of assets

Financial management Notes FINANCIAL MANAGEMENT Financial management is an academic discipline which is concerned with decision-making. This decision is concerned with the size and composition of assets

UNIT 1 FINANCIAL MANAGEMENT: BASICS

UNIT 1 FINANCIAL MANAGEMENT: BASICS UNIT 1 FINANCIAL MANAGEMENT: BASICS Financial Management: Structure 1.0 Introduction 1.1 Unit Objectives 1.2 Importance of Finance 1.3 Meaning of Business Finance 1.4

UNIT 1 FINANCIAL MANAGEMENT: BASICS UNIT 1 FINANCIAL MANAGEMENT: BASICS Financial Management: Structure 1.0 Introduction 1.1 Unit Objectives 1.2 Importance of Finance 1.3 Meaning of Business Finance 1.4

A study on capital structure analysis of Tata motors limited

International Journal of Commerce and Management Research ISSN: 2455-1627, Impact Factor: RJIF 5.22 www.managejournal.com Volume 3; Issue 3; March 2017; Page No. 48-52 A study on capital structure analysis

International Journal of Commerce and Management Research ISSN: 2455-1627, Impact Factor: RJIF 5.22 www.managejournal.com Volume 3; Issue 3; March 2017; Page No. 48-52 A study on capital structure analysis

Reading & Understanding Financial Statements

Reading & Understanding Financial Statements A Guide to Financial Reporting Introduction Financial statements are an important management tool. When correctly prepared and properly interpreted, they contribute

Reading & Understanding Financial Statements A Guide to Financial Reporting Introduction Financial statements are an important management tool. When correctly prepared and properly interpreted, they contribute

Reading & Understanding Financial Statements. A Guide to Financial Reporting

Reading & Understanding Financial Statements A Guide to Financial Reporting Introduction Financial statements are an important management tool. When correctly prepared and properly interpreted, they contribute

Reading & Understanding Financial Statements A Guide to Financial Reporting Introduction Financial statements are an important management tool. When correctly prepared and properly interpreted, they contribute